Embed Size (px)

Citation preview

ASX RELEASE 30 November 2011

Perth: Level 2 Aquila Centre, 1 Preston Street, Como WA 6151 Telephone (61) 8 9423 0111Facsimile (61) 8 9423 0133 Brisbane: Level 11, 10 Market Street, Brisbane QLD 4000 Telephone (61) 7 3229 5630 Facsimile (61) 7 3229 5631 Thabazimbi: C/O Platina and Lood Avenue, Thabazimbi 0380, South Africa Telephone (27) 14 772 3337 Facsimile (27) 14 772 3337 Northern Cape: Stand 585 Opwag, Groblershoop, Northern Cape, South Africa Telephone (27) 798 816 459 Facsimile (27) 866 838 065 Indonesia: Level 2 Zone B Wisma Raharja, JI. TB Simatupang Kav 1, Jakarta 12560 Telephone (62) 21 7884 7214 Facsimile (62) 21 7884 7215

Annual General Meeting Presentation

Aquila Resources Limited is pleased to attach a copy of the powerpoint presentation that will be delivered today by Mr Tony Poli, CEO, at the Company’s Annual General Meeting to be held at the Novotel Perth Langley Hotel. Tony Poli Executive Chairman For further information regarding this announcement, please contact Tony Poli. Telephone: (08) 9423 0111 Facsimile: (08) 9423 0133 Email address: [email protected] Visit us at: www.aquilaresources.com.au

For

per

sona

l use

onl

y

PowerPoint Presentation TemplateAnnual General Meeting November 2011

For

per

sona

l use

onl

y

No representation or liability: No representation or warranty is made as to the fairness, currency, accuracy, completeness, reliability or reasonableness of this presentation, or any opinions, conclusions and forward-looking statements it contains or any other information which Aquila provides to you (whether in this presentation or otherwise). Except to the extent required by law, Aquila Resources Limited (“Aquila”) does not undertake to advise any person of any information coming to its attention (including, without limitation, correcting or updating information) relating to the financial condition, status or affairs of Aquila or its related bodies corporate.

To the maximum extent permitted by law, Aquila and its related bodies corporate and officers, employees and advisers are not liable for any loss or damage (including, without limitation, any direct, indirect or consequential loss or damage) suffered by any person directly or indirectly as a result of relying on this presentation or otherwise in connection with it.

Forward-looking statements: This presentation is heavily dependent on forecasts, projections or forward-looking statements (together the “Forward-looking Statements”). No representation or warranty is given as to the accuracy, completeness, reliability, financial feasibility, likelihood of achievement or reasonableness of any Forward-looking Statements contained in the presentation. Forward-looking Statements are by their nature subject to significant uncertainties and contingencies and no representation is made that any Forward-looking Statements will come to pass.

Seek your own independent advice: Do not rely on this presentation to make an investment decision. This presentation has been prepared without consideration of your objectives and needs (including, without limitation, the need if any for the information to be accurate, reasonable, complete or reliable) and financial situation. You should make your own independent assessment of the information in the presentation and seek your own independent professional financial, taxation and legal advice in relation to the information and before taking any action in relation to any matter contained in the presentation.

Not an offer: This presentation is not intended to be an offer for subscription, invitation, solicitation or recommendation with respect to securities in Aquila in any jurisdiction. Without limiting the foregoing, this presentation is not intended as an offer, invitation, solicitation or recommendation with respect to the purchase or sale of any security in the United States, United Kingdom or Australia or to any person to whom it is unlawful to make such an offer, invitation, solicitation or recommendation. No shares or other securities in Aquila have been nor will be registered under the US Securities Act.

This presentation does not constitute an advertisement for an offer or proposed offer of securities. It is not intended to induce any person to engage in, or refrain from engaging in, any transaction.

2

DISCLAIMER

For

per

sona

l use

onl

y

3

Tony PoliExecutive Chairman

For

per

sona

l use

onl

y

ASX 200 public company with

market capitalisation of ~A$2.3bn1

~A$171m cash and liquids2

Focus on significant projects in the key steel making raw materials of metallurgical coal and iron ore

Production and sales from Isaac Plains Coal Mine

Significant near term growth from development of West Pilbara Iron Ore Project and Eagle Downs Hard Coking Coal Project

Experienced management team with a focus on maximising shareholder value

Isaac Plains(Met/Thermal Coal)Eagle Downs (Metallurgical Coal)Washpool (Metallurgical Coal)Talwood (Metallurgical Coal)

West Pilbara(Iron Ore)

Thabazimbi (Iron ore)Avontuur (Manganese)

10Mtpa*

>30Mtpa*

1-2Mtpa* up to 4Mtpa*1. As at 29 Nov 20112. As at 30 Sep 2011* Target production on 100% basis

4

COMPANY OVERVIEW

For

per

sona

l use

onl

y

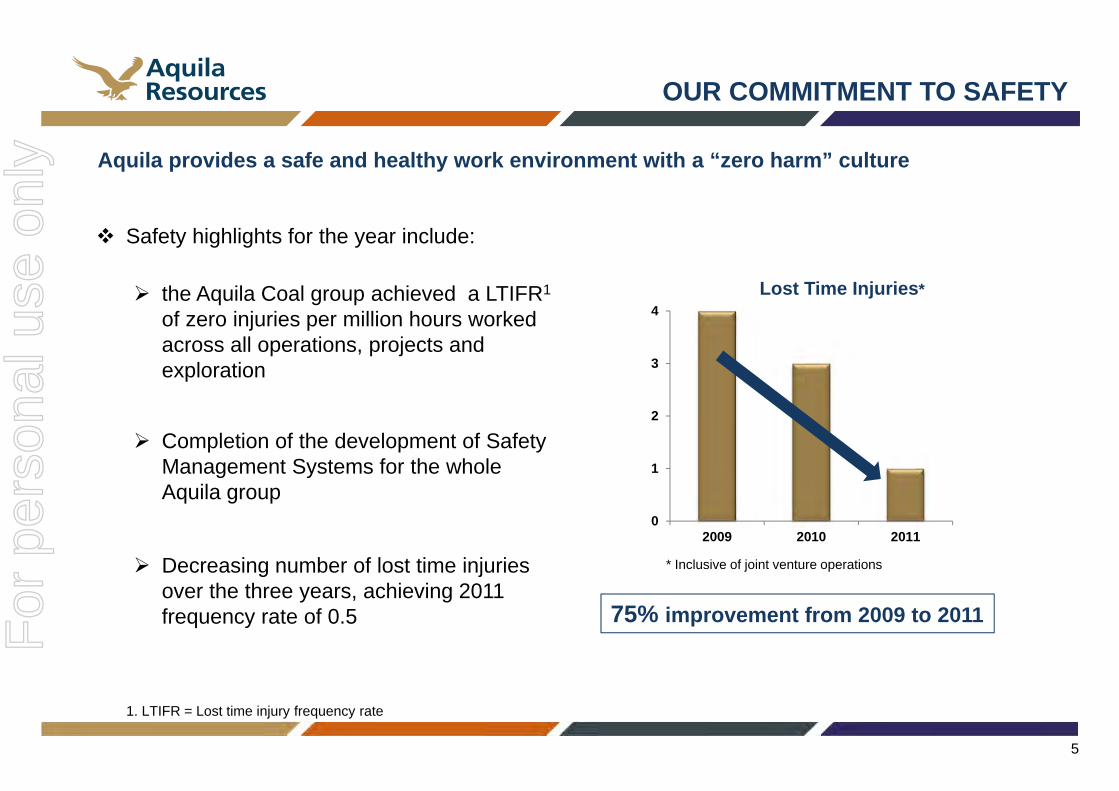

Safety highlights for the year include:

the Aquila Coal group achieved a LTIFR1

of zero injuries per million hours worked across all operations, projects and exploration

Completion of the development of Safety Management Systems for the whole Aquila group

Decreasing number of lost time injuries over the three years, achieving 2011 frequency rate of 0.5

OUR COMMITMENT TO SAFETY

Aquila provides a safe and healthy work environment with a “zero harm” culture

0

1

2

3

4

2009 2010 2011

Lost Time Injuries*

75% improvement from 2009 to 2011

* Inclusive of joint venture operations

1. LTIFR = Lost time injury frequency rate

5

For

per

sona

l use

onl

y

Community highlights for the year include:

Native Title Agreement negotiations are progressing well for mine and rail development activities for the West Pilbara Iron Ore Project

A Social Impact Assessment was conducted for the Washpool Hard Coking Coal Project with the local community of Blackwater and extended Central QLD regional community

The proposed Social & Labour Plan projects for the Gravenhage Manganese Project were ratified by the Joe MorolongLocal Municipality during May 2011

OUR CONTRIBUTION TO COMMUNITY

Aquila is committed to building strong, lasting relationships with communities and key stakeholder groups as it is integral to the success of Aquila’s projects

Donations & sponsorships totalling $350,000 for the year

Aquila’s latest initiative is to donate computers to Groblershoop High School in South Africa

6

For

per

sona

l use

onl

y

In the last 10 years, China has accounted for the entire growth in seaborne trade in iron ore

China will continue to be the dominant market for seaborne iron ore, with urbanisation and large scale infrastructure development continuing to drive steel consumption

IRON ORE DEMAND

7

For

per

sona

l use

onl

y

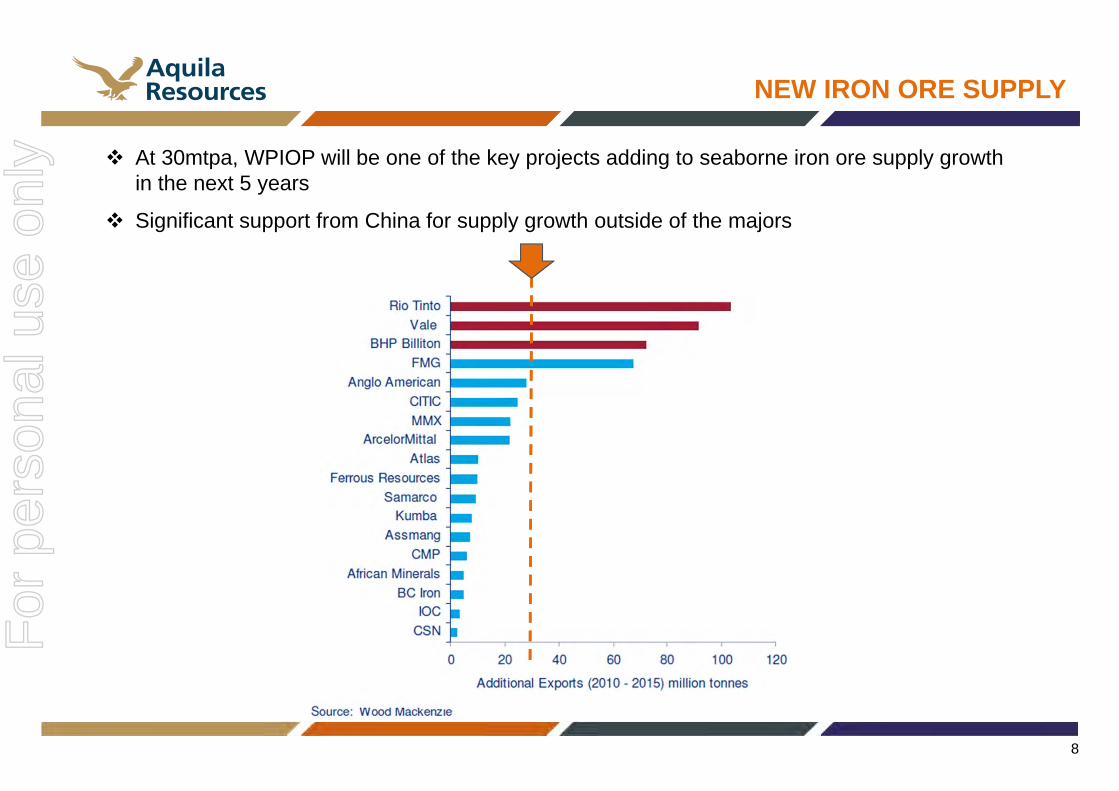

At 30mtpa, WPIOP will be one of the key projects adding to seaborne iron ore supply growth in the next 5 years

Significant support from China for supply growth outside of the majors

NEW IRON ORE SUPPLY

8

For

per

sona

l use

onl

y

IRON ORE PRICING OUTLOOK

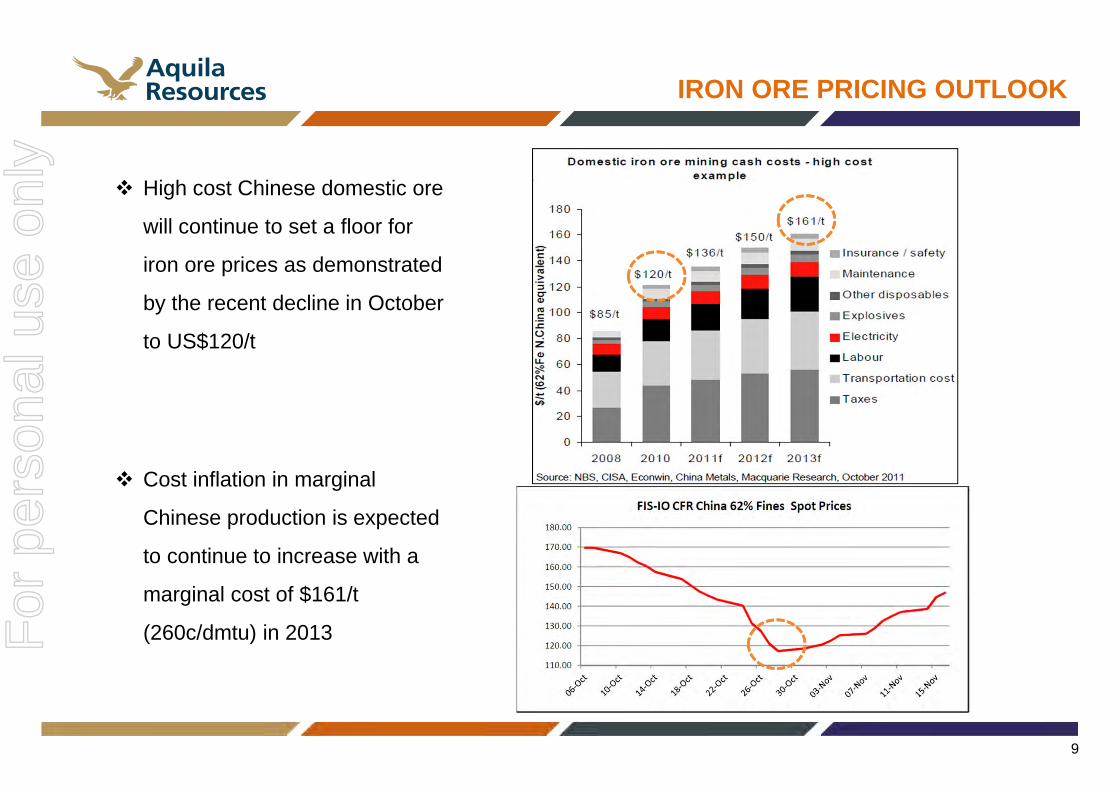

High cost Chinese domestic ore

will continue to set a floor for

iron ore prices as demonstrated

by the recent decline in October

to US$120/t

Cost inflation in marginal

Chinese production is expected

to continue to increase with a

marginal cost of $161/t

(260c/dmtu) in 2013

9

For

per

sona

l use

onl

y

Seaborne supply will continue to remain heavily reliant on Queensland (Bowen Basin)

New coking coal reserves are increasingly hard to find – emerging regions of Mozambique and

Mongolia have significant infrastructure challenges

COKING COAL SUPPLY CONSTRAINTS

Metallurgical coal trade flows

10

For

per

sona

l use

onl

y

COAL PRICE OUTLOOK

Corporate interest in the Australian coal sector has remained very strong, as evidenced by the

large number of M&A transactions, despite volatile markets

Rising capital costs mean that the marginal price (for zero return) for many projects is now in

excess of US$150/t real

11

For

per

sona

l use

onl

y

Issue the Definitive Feasibility Study for the Gravenhage Manganese Project

Issue the Definitive Feasibility Study for the West Pilbara Iron Ore Project

Secure rail and port infrastructure solution for Eagle Downs

Secure West Pilbara project financing and complete non-core asset divestments

Start construction on the Eagle Downs Hard Coking Coal Project; and

Start construction on the West Pilbara Iron Ore Project

OUR 2011/12 OBJECTIVES

12

Focus on Completing Phase One

Focus on Commencing Phase Two

For

per

sona

l use

onl

y

Stephen PilcherGeneral Manager - Coal

13

For

per

sona

l use

onl

y

ISAAC PLAINS COAL MINE (50%)

RESOURCES: 127.9 MILLION TONNESRESERVES: 49.7 MILLION TONNES

EAGLE DOWNS HARD COKING COAL PROJECT (50%)

RESOURCES: 959 MILLION TONNES*RESERVES: 254.1 MILLION TONNES

COAL

AUSTRALIA

* 69Mt of the Eagle Downs resource is deemed PCI quality

14

For

per

sona

l use

onl

y

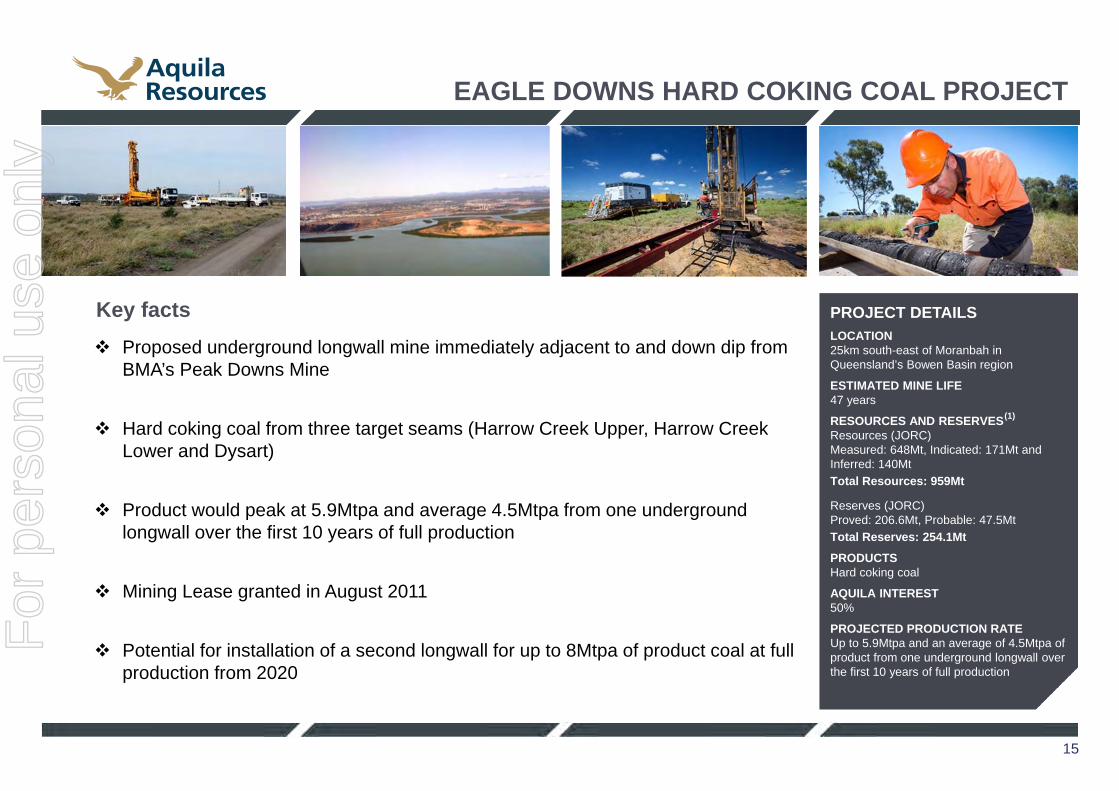

PROJECT DETAILSLOCATION25km south-east of Moranbah in Queensland’s Bowen Basin region

ESTIMATED MINE LIFE47 years

RESOURCES AND RESERVES Resources (JORC) Measured: 648Mt, Indicated: 171Mt and Inferred: 140Mt

Total Resources: 959Mt

Reserves (JORC)Proved: 206.6Mt, Probable: 47.5Mt

Total Reserves: 254.1Mt

PRODUCTSHard coking coal

AQUILA INTEREST50%

PROJECTED PRODUCTION RATEUp to 5.9Mtpa and an average of 4.5Mtpa of product from one underground longwall over the first 10 years of full production

EAGLE DOWNS HARD COKING COAL PROJECT

Proposed underground longwall mine immediately adjacent to and down dip from BMA’s Peak Downs Mine

Hard coking coal from three target seams (Harrow Creek Upper, Harrow Creek Lower and Dysart)

Product would peak at 5.9Mtpa and average 4.5Mtpa from one underground longwall over the first 10 years of full production

Mining Lease granted in August 2011

Potential for installation of a second longwall for up to 8Mtpa of product coal at full production from 2020

Key facts

15

(1)

For

per

sona

l use

onl

y

EAGLE DOWNS HARD COKING COAL PROJECT

16

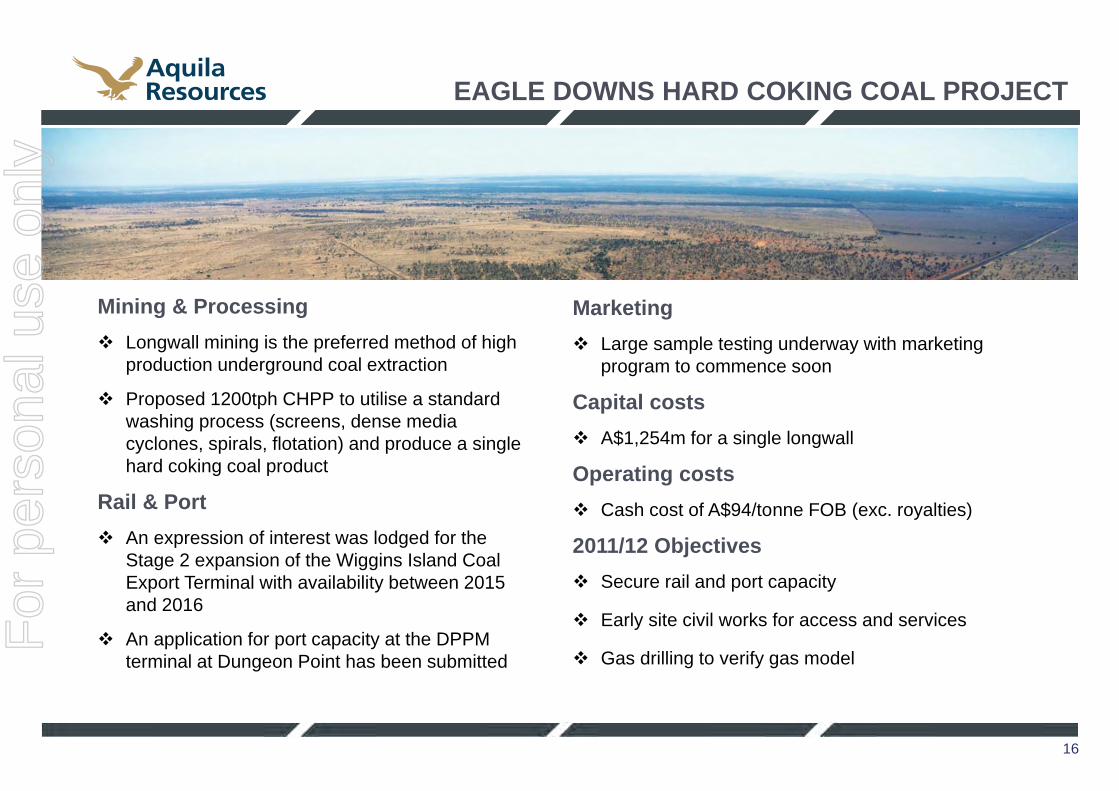

Marketing

Large sample testing underway with marketing program to commence soon

Capital costs

A$1,254m for a single longwall

Operating costs

Cash cost of A$94/tonne FOB (exc. royalties)

2011/12 Objectives

Secure rail and port capacity

Early site civil works for access and services

Gas drilling to verify gas model

Mining & Processing

Longwall mining is the preferred method of high production underground coal extraction

Proposed 1200tph CHPP to utilise a standard washing process (screens, dense media cyclones, spirals, flotation) and produce a single hard coking coal product

Rail & Port

An expression of interest was lodged for the Stage 2 expansion of the Wiggins Island Coal Export Terminal with availability between 2015 and 2016

An application for port capacity at the DPPM terminal at Dungeon Point has been submitted

For

per

sona

l use

onl

y

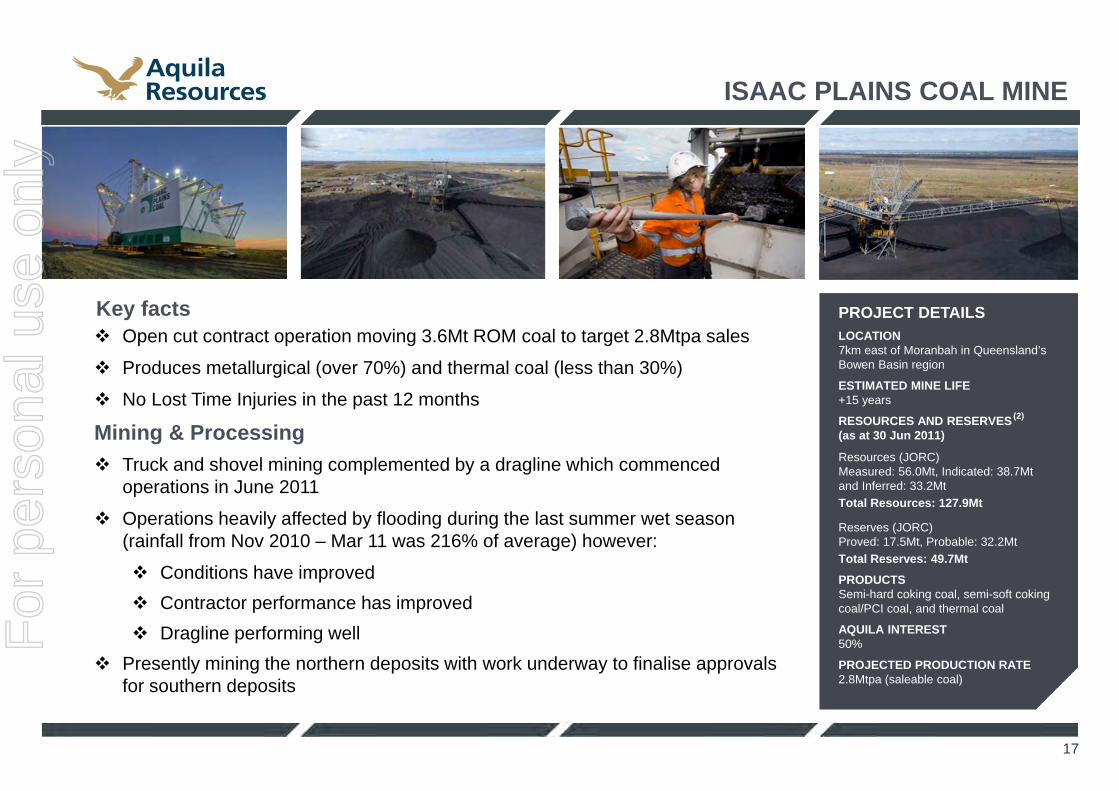

PROJECT DETAILSLOCATION7km east of Moranbah in Queensland’s Bowen Basin region

ESTIMATED MINE LIFE+15 years

RESOURCES AND RESERVES (as at 30 Jun 2011)

Resources (JORC) Measured: 56.0Mt, Indicated: 38.7Mtand Inferred: 33.2Mt

Total Resources: 127.9Mt

Reserves (JORC)Proved: 17.5Mt, Probable: 32.2Mt

Total Reserves: 49.7Mt

PRODUCTSSemi-hard coking coal, semi-soft coking coal/PCI coal, and thermal coal

AQUILA INTEREST50%

PROJECTED PRODUCTION RATE2.8Mtpa (saleable coal)

ISAAC PLAINS COAL MINE

Open cut contract operation moving 3.6Mt ROM coal to target 2.8Mtpa sales

Produces metallurgical (over 70%) and thermal coal (less than 30%)

No Lost Time Injuries in the past 12 months

Mining & Processing

Truck and shovel mining complemented by a dragline which commenced operations in June 2011

Operations heavily affected by flooding during the last summer wet season (rainfall from Nov 2010 – Mar 11 was 216% of average) however:

Conditions have improved

Contractor performance has improved

Dragline performing well

Presently mining the northern deposits with work underway to finalise approvals for southern deposits

Key facts

17

(2)

For

per

sona

l use

onl

y

ISAAC PLAINS COAL MINE

18

Rail & Port

Logistics contracts in place with Queensland Rail, Pacific National and Dalrymple Bay Coal Terminal for full 2.8Mtpa

Marketing

Aquila has now assumed marketing responsibility for its 50% share of product from the Isaac Plains Coal Mine

Operating costs

Average cash cost of ~A$95/tonne FOB (exc. royalties)

Dalrymple Bay Coal Terminal For

per

sona

l use

onl

y

19

Russell TipperGeneral Manager – Iron Ore

For

per

sona

l use

onl

y

AUSTRALIA

RESOURCES: 1, 223 MILLION TONNES @ 57.1% FeRESERVES: 445 MILLION TONNES @ 57.1% Fe

WEST PILBARA IRON ORE PROJECT

20

For

per

sona

l use

onl

y

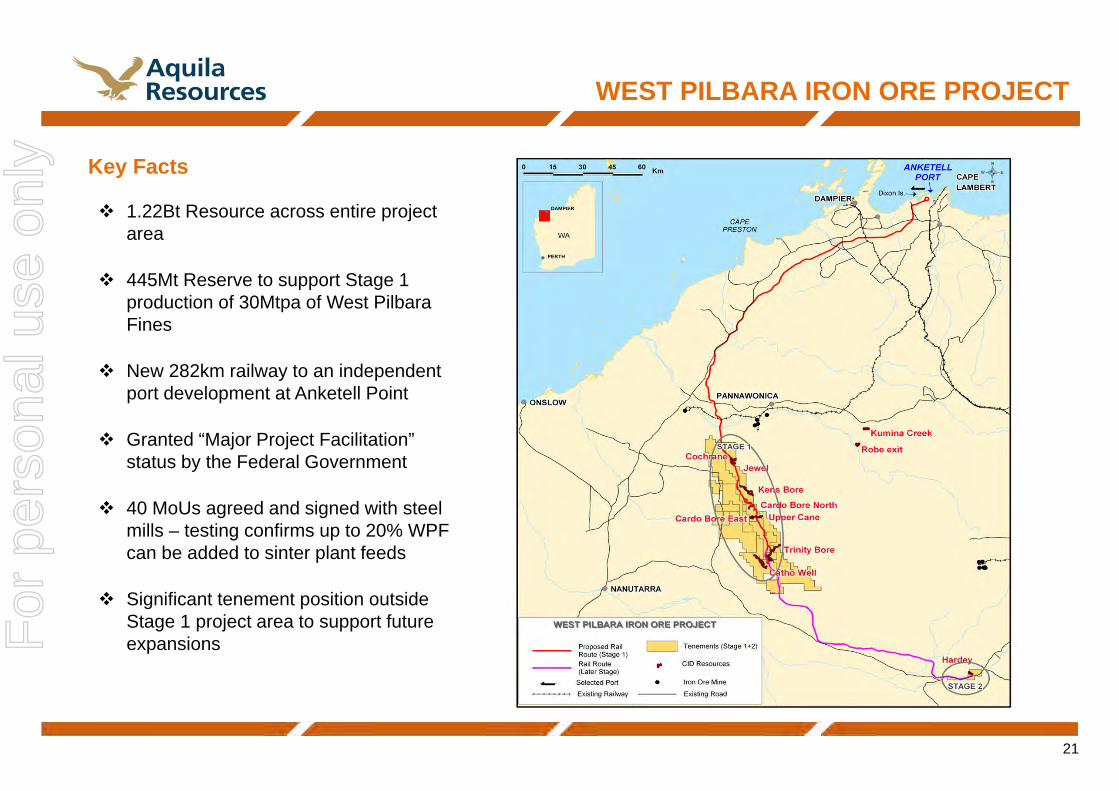

1.22Bt Resource across entire project area

445Mt Reserve to support Stage 1 production of 30Mtpa of West Pilbara Fines

New 282km railway to an independent port development at Anketell Point

Granted “Major Project Facilitation” status by the Federal Government

40 MoUs agreed and signed with steel mills – testing confirms up to 20% WPF can be added to sinter plant feeds

Significant tenement position outside Stage 1 project area to support future expansions

WEST PILBARA IRON ORE PROJECT

21

Key Facts

For

per

sona

l use

onl

y

PROJECT DETAILSLOCATIONStage 1: 70km south of Pannawonicain the Pilbara region of Western Australia

ESTIMATED MINE LIFEAt least 15 years from Stage 1

RESOURCES AND RESERVES Resources (JORC) Measured: 209Mt @ 57.8% Fe,

Indicated: 392Mt @ 56.2% Fe and Inferred: 86Mt @ 55.4% Fe

Total Resources: 687Mt @ 56.6% Fe

Reserves (JORC)Proved: 165.7Mt @ 58.0% Fe,

Probable: 279.4Mt @ 56.5% Fe

Total Reserves: 445.1Mt @ 57.05% Fe

PRODUCTSDirect ship channel iron and bedded iron fines

AQUILA INTEREST50%

PROJECTED PRODUCTION RATEAt least 30Mtpa from Stage 1

Stage 1 production capacity of 30Mtpa

Definitive Feasibility Study due for completion Q4 CY2011

Mining Lease applications submitted

Environmental approval of the mine and rail development recommended by the EPA

Preferred Project Managing Contractor (PMC) identified

Mining & Processing

3 mining hubs: north, central and south

Drill & blast, load and haul operation

Overburden to Ore ratio of 1.13:1

Rail

Negotiations under way for a State Agreement for the Project railway

Key Facts

22

(3)

WPIOP - STAGE 1

For

per

sona

l use

onl

y

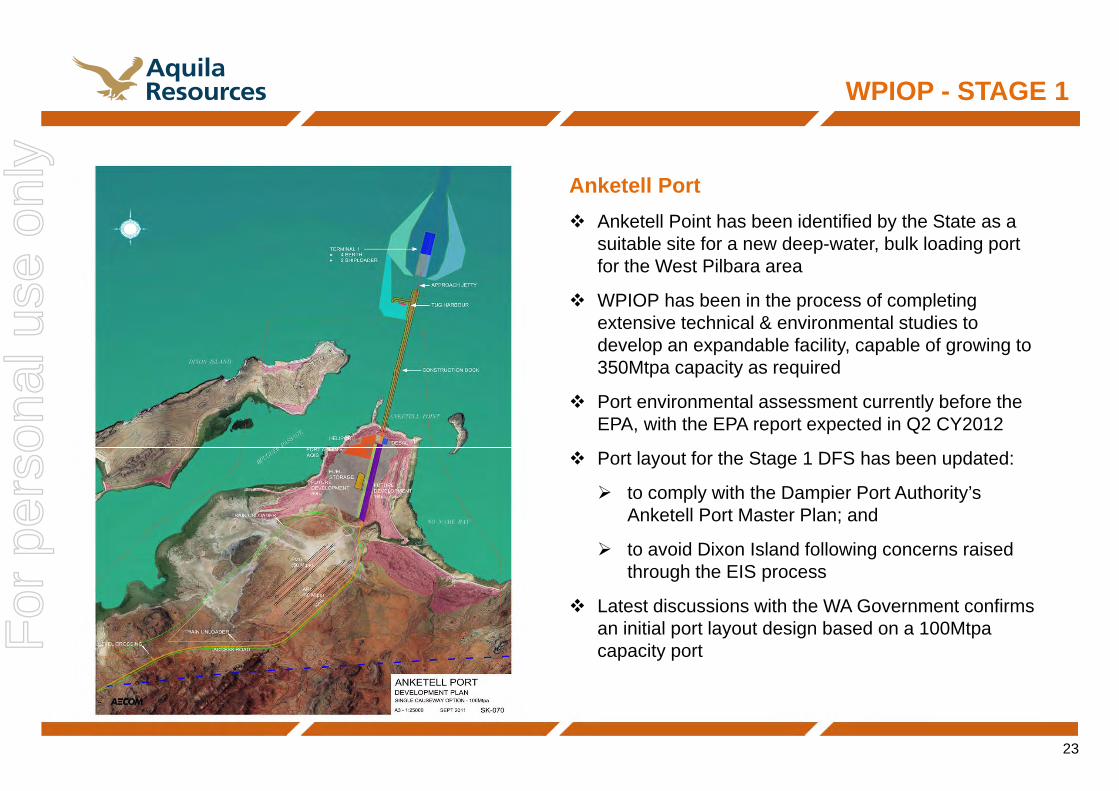

Anketell Port

Anketell Point has been identified by the State as a suitable site for a new deep-water, bulk loading port for the West Pilbara area

WPIOP has been in the process of completing extensive technical & environmental studies to develop an expandable facility, capable of growing to 350Mtpa capacity as required

Port environmental assessment currently before the EPA, with the EPA report expected in Q2 CY2012

Port layout for the Stage 1 DFS has been updated:

to comply with the Dampier Port Authority’s Anketell Port Master Plan; and

to avoid Dixon Island following concerns raised through the EIS process

Latest discussions with the WA Government confirms an initial port layout design based on a 100Mtpa capacity port

23

WPIOP - STAGE 1

For

per

sona

l use

onl

y

24

Key facts

Pre-feasibility Study for Hardey Iron Ore Deposit completed

Targeted Hardey production rate of 10Mtpa

Rail & Port

Potential for an additional 150km of new rail to be constructed to connect with the proposed rail for Stage 1

Minimal incremental port capex with additional berth to be added to the Stage 1 jetty

Marketing

Hardey Deposit comprises both Brockman and Marra Mamba ores which will be blended to form a single fines product for export

Project Timeline

Construction planned to be integrated with Stage 1 development activities (subject to approvals)

First shipment of Hardey BID product expected in 2016/2017

WPIOP – STAGE 2

For

per

sona

l use

onl

y

25

Martin AlciaturiGeneral Manager –Finance & Corporate

For

per

sona

l use

onl

y

Debt funding negotiations with CDB nearing conclusion

Washpool Hard Coking Coal Project

Expression’s of interest

Provision of Information Memorandum

Indicative bids and shortlisting of parties

Detailed due diligence, management presentation & site visits

A concluded sale agreement is expected before end 2011

China Development Bank

FINANCING

26

Avontuur Manganese Project

Expression’s of Interest

Provision of Information Memorandum

Indicative bids and shortlisting of parties

Announcement of DFS coincides with commencement of detailed due diligence for shortlisted parties

Management presentations and site visits commencing in December 2011

Final bids expected in Q1 2012

For

per

sona

l use

onl

y

Gravenhage Manganese Project

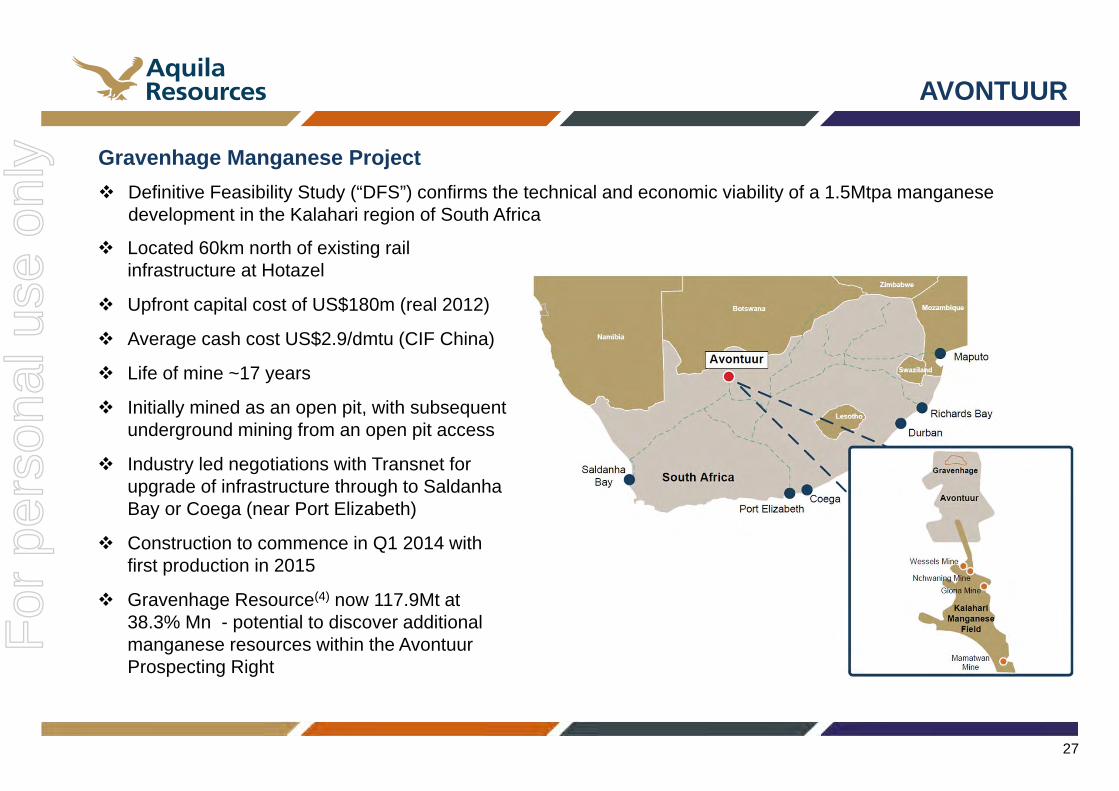

Definitive Feasibility Study (“DFS”) confirms the technical and economic viability of a 1.5Mtpa manganese development in the Kalahari region of South Africa

AVONTUUR

27

Located 60km north of existing rail infrastructure at Hotazel

Upfront capital cost of US$180m (real 2012)

Average cash cost US$2.9/dmtu (CIF China)

Life of mine ~17 years

Initially mined as an open pit, with subsequent underground mining from an open pit access

Industry led negotiations with Transnet for upgrade of infrastructure through to SaldanhaBay or Coega (near Port Elizabeth)

Construction to commence in Q1 2014 with first production in 2015

Gravenhage Resource(4) now 117.9Mt at 38.3% Mn - potential to discover additional manganese resources within the Avontuur Prospecting Right

For

per

sona

l use

onl

y

(1) The information in this presentation that relates to the Eagle Downs Resource Statement has been based on information compiled by Mr MalBlaik who is a member of the Australasian Institute of Mining and Metallurgy. Mr Blaik has over 30 years experience in geology and over 20years experience in coal resource evaluation. Mr Blaik is a Principal Consultant of JB Mining Services Pty Ltd. Mr Blaik is a qualified geologist(BSc App Geol (Hons) University of QLD, 1979) and is a member of the Australasian Institute of Mining and Metallurgy and as such qualifiesas a Competent Person under the JORC Code. Mr Blaik consents to the inclusion in the presentation of the matters based on their informationin the form and context in which it appears.

The information in this presentation that relates to Eagle Downs Coal Reserves, is based on information reviewed by Mr J Steenekamp, who isa Fellow of the Australasian Institute of Mining and Metallurgy. Mr Steenekamp has sufficient experience which is relevant to the style ofmineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as definedin the 2004 edition of the JORC Code. Mr Steenekamp is a full time employee of Mining Consultancy Services (Australia) Pty Ltd and holdsthe position of Managing Director. Mr Steenekamp has consented to the inclusion in the presentation of the matters relating to Coal Reservesbased on the information he has reviewed, in the form and context in which it appears.

(2) The information in this presentation that relates to the Isaac Plains Resource Statement has been compiled by Mr Mal Blaik. Mr Blaik is aPrincipal Consultant of JB Mining Services Pty Ltd. Mr Blaik is a qualified geologist (BSc App Geol (Hons) University of Queensland, 1979)with over 20 years experience in coal geology and over 15 years experience in resource evaluation. Mr Blaik is a Member of the AustralasianInstitute of Mining and Metallurgy and as such qualifies as a Competent Person under the JORC code. The Resource Statement has beenprepared under the guidelines of the December 2004 edition of the Australian Code for Reporting of Mineral Resources and Ore Reserves(the JORC Code). Neither Mr Blaik nor JB Mining Services Pty Ltd (JBMS) have any material interest or entitlement, direct or indirect, in thesecurities of Bowen Central Coal or any companies associated with Bowen Central Coal. Fees for the preparation of this report are on a timeand materials basis.

The information in this presentation that relates to the Isaac Plains Reserves Estimate has been prepared by Mr Mark Bowater. The estimatesof Coal Reserves for Isaac Plains North (ML 70342) and Isaac Plains South (MLa 70361) have been carried out in accordance with the 2004edition of the Australian Code for Reporting of Mineral Resources and Ore Reserves (The JORC Code). Mr Bowater is the Director of EchelonMining Services. Mr Bowater has a Bachelor in Civil Engineering from Queensland University of Technology and a Bachelor in Business fromUniversity of South Queensland. Mr Bowater has over 20 years experience in the open cut mining industry, including 18 years in Queenslandcoal. Mr Bowater has substantial experience in mining operations financial evaluations, including previously conducted reserves statements.Mr Bowater is a Member of the Australasian Institute of Mining and Metallurgy and as such qualifies as a Competent Person under the JORCCode. Neither Mr Bowater nor Echelon Mining Services have any material interest or entitlement, direct or indirect, in the securities of BowenCentral Coal or any associated companies. Fees for the preparation of this report are on a time and materials basis.

COMPETENCY STATEMENTS

28

For

per

sona

l use

onl

y

(3) The information in this presentation that relates to Mineral Resource Estimates was prepared under the supervision of Mr Stuart Tuckey. MrTuckey is a member of the Australasian Institute of Mining and Metallurgy and full-time employee of the API Management Pty Ltd. Mr Tuckeyhas sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he isundertaking to qualify as a Competent Persons as defined in the 2004 Edition of the ‘Australasian Code of Reporting of Exploration Results,Mineral Resources and Ore Reserves’. Mr Tuckey consents to the inclusion in the presentation of the matters based on his information in theform and context in which it appears.

The information in this presentation that relates to Ore Reserves is based on information compiled by Mr Steve Craig, Managing Director ofORElogy (Mining Consultants). Mr Craig is a Member of the Australasian Institute of Mining and Metallurgy and has sufficient experiencewhich is relevant to the style of mineralisation and type of deposit under consideration, and to the activity he is undertaking, to qualify as aCompetent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and OreReserves”. Mr Craig consents to the inclusion of the matters based on his information in the form and context in which it appears in thispresentation.

(4) The information in this presentation that relates to the Gravenhage Manganese Resource was prepared under the supervision of Brent EGreen who is a member of the Australian Institute of Geoscientists, and who has more than five years’ experience in the field of activity beingreported on. Mr Green is a full-time employee of Aquila Resources Limited. Mr Green has sufficient experience which is relevant to the styleof mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person asdefined in the 2004 Edition of the ‘Australasian Code of Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Greenconsents to the inclusion in the presentation of the matters based on the information in the form and context in which it appears.

COMPETENCY STATEMENTS

29

For

per

sona

l use

onl

y