Embed Size (px)

Citation preview

Our people, our value

ANNUAL INTEGRATED REPORT

contents

About this report 1 Introduction

Group overview 2 Group profile

3 Group structure

Performance summary 4 Highlights

6 Ten-year review

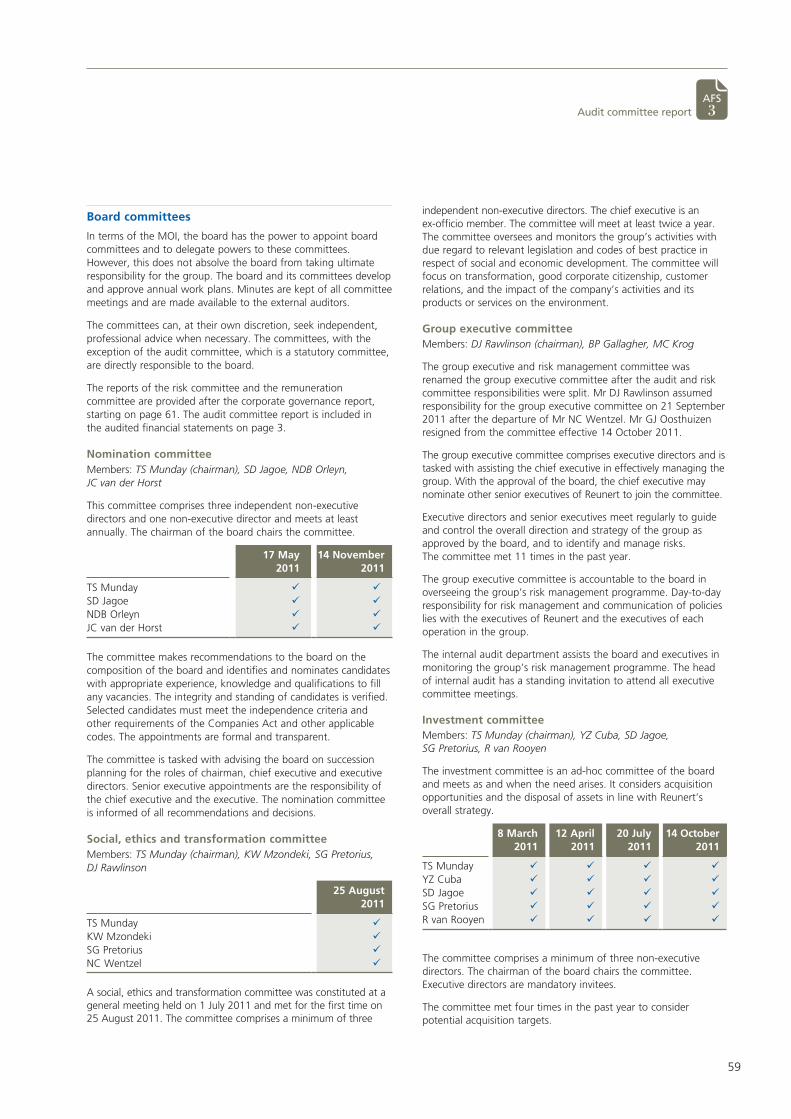

Leadership10 Non-executive directors

12 Chairman’s statement

14 Executive directors

15 Chief executive’s report

19 Financial director’s report

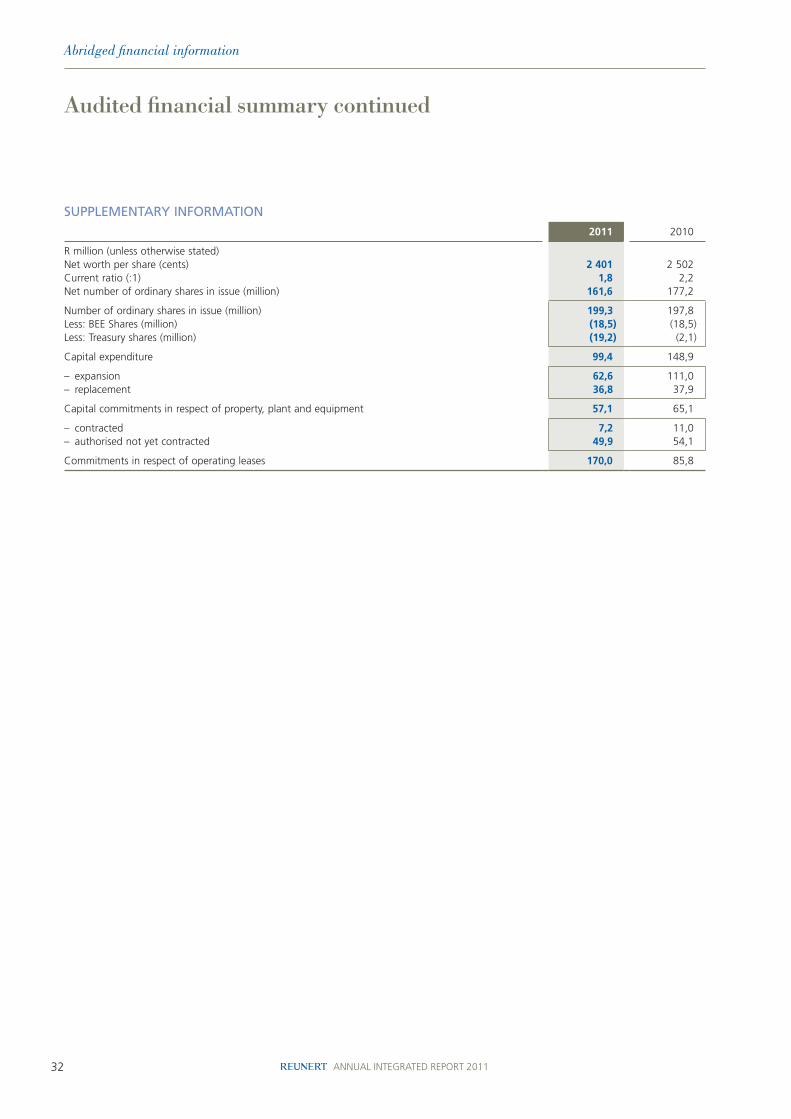

Abridged financial information22 Value-added statement

24 Audited financial summary

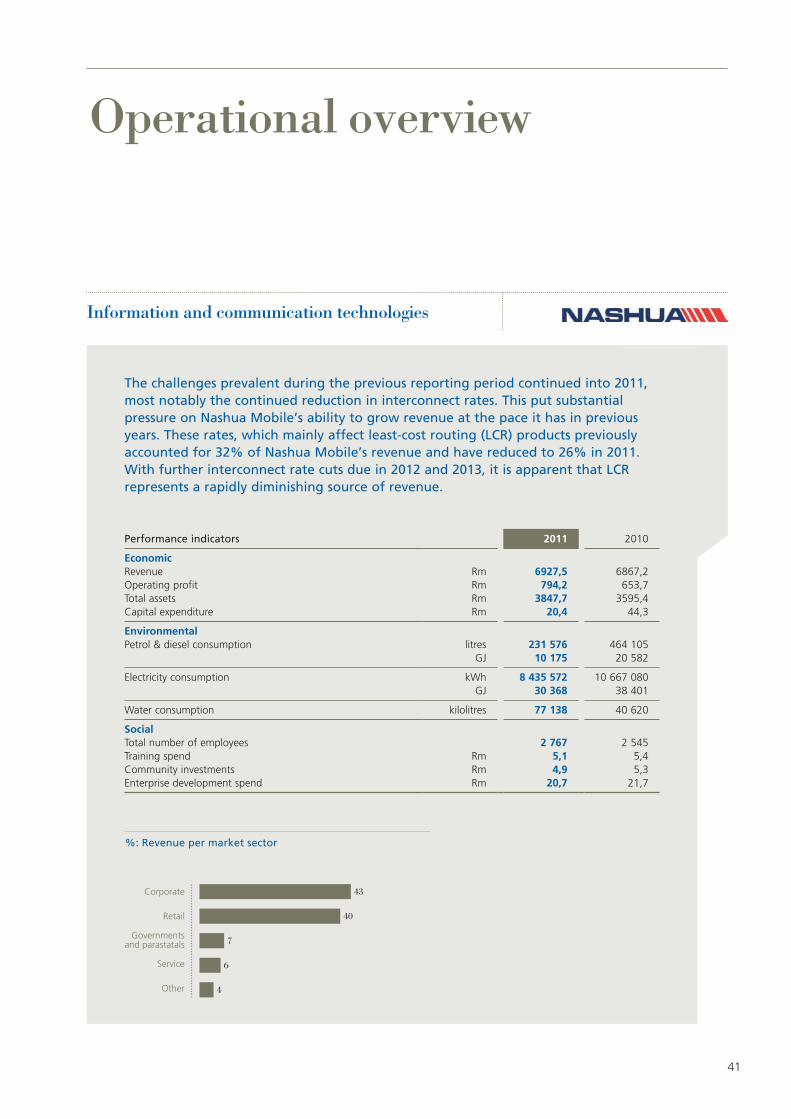

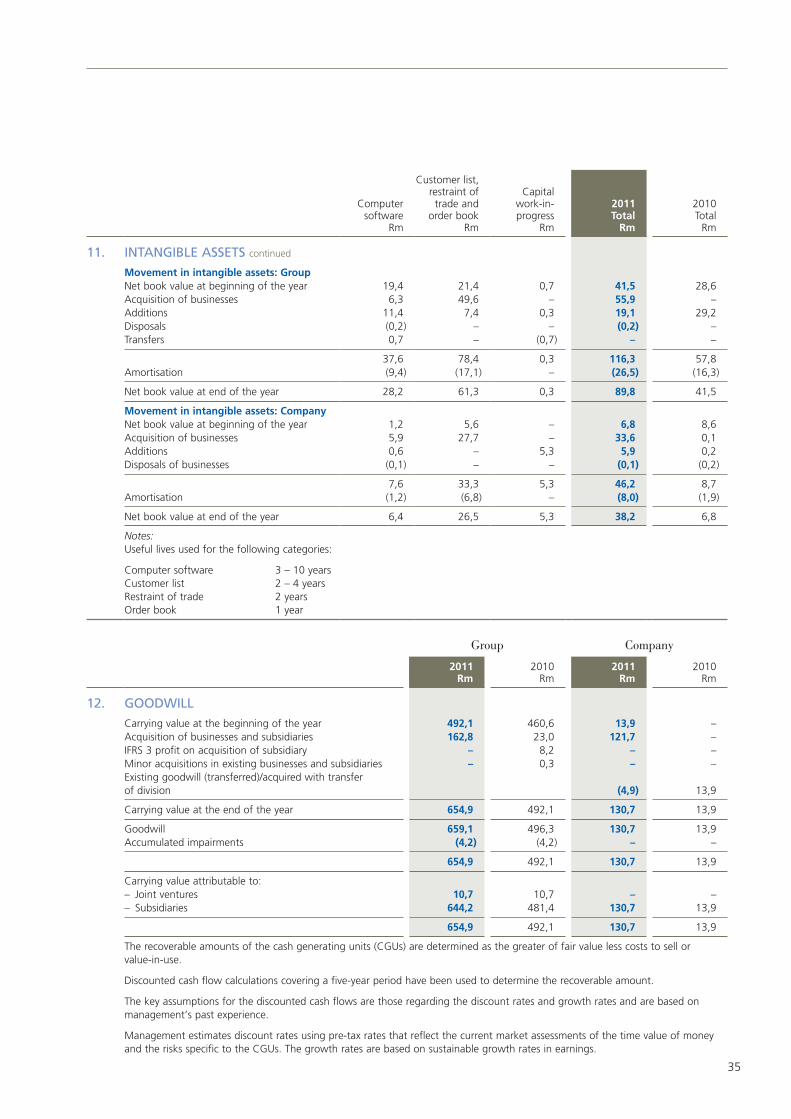

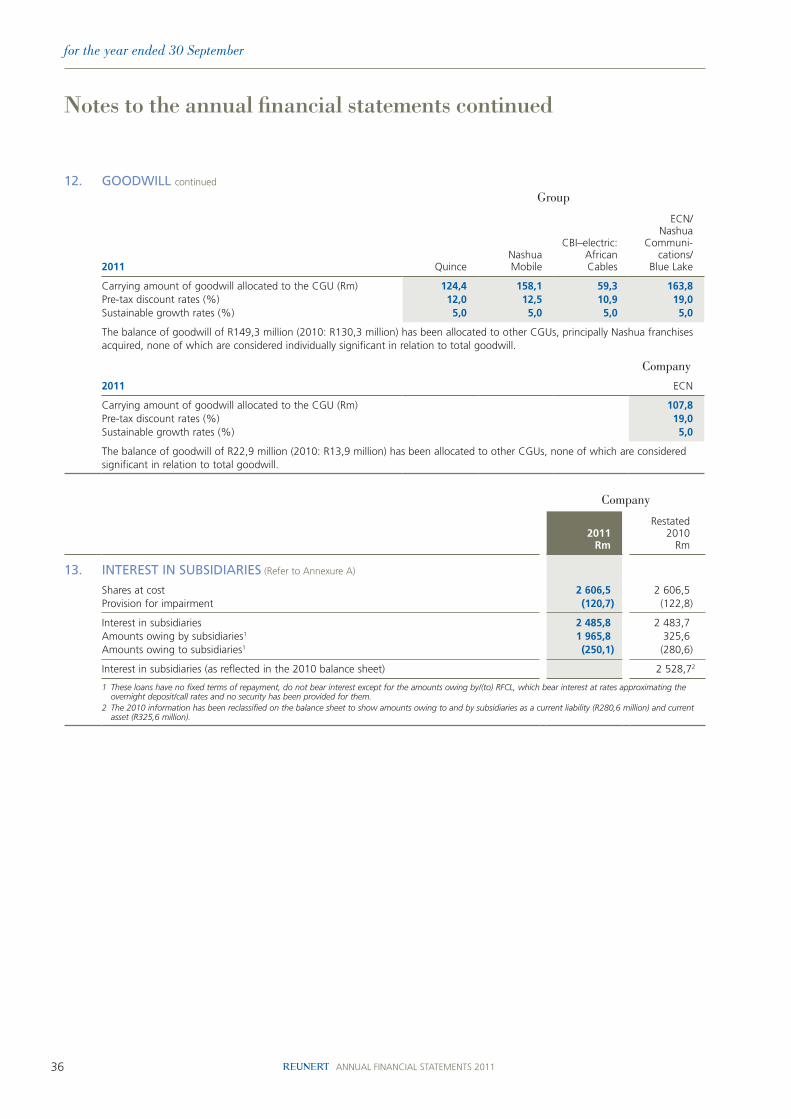

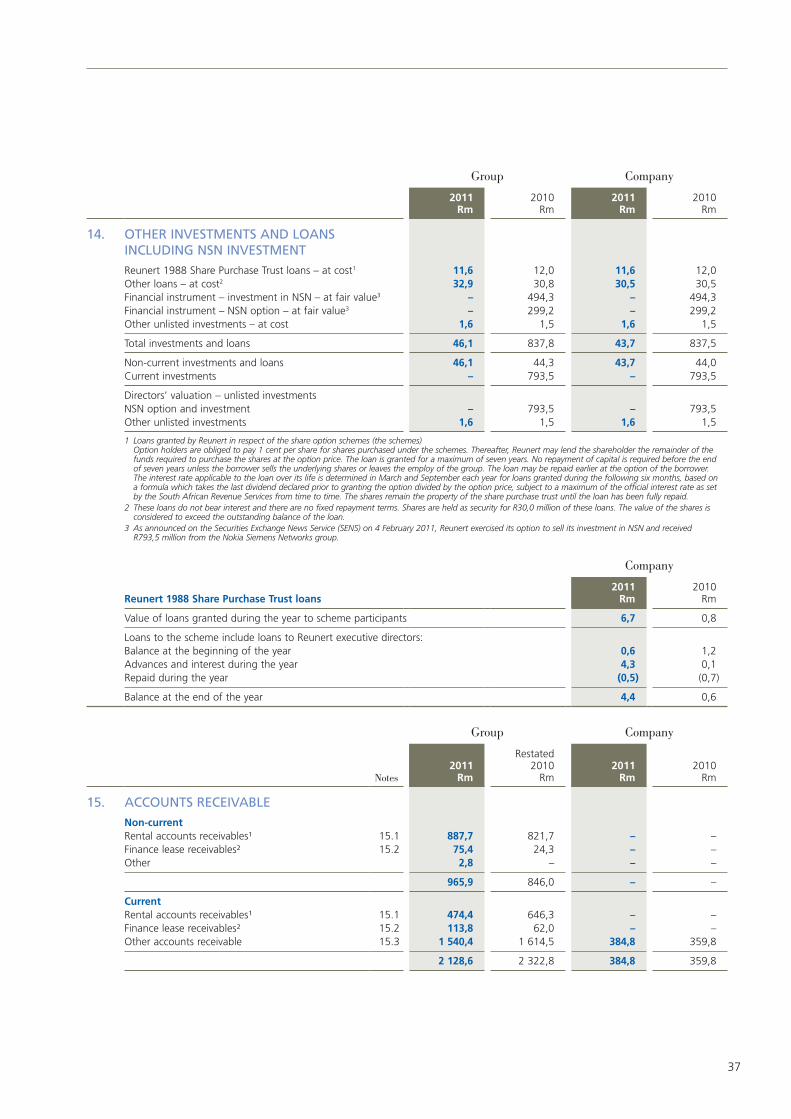

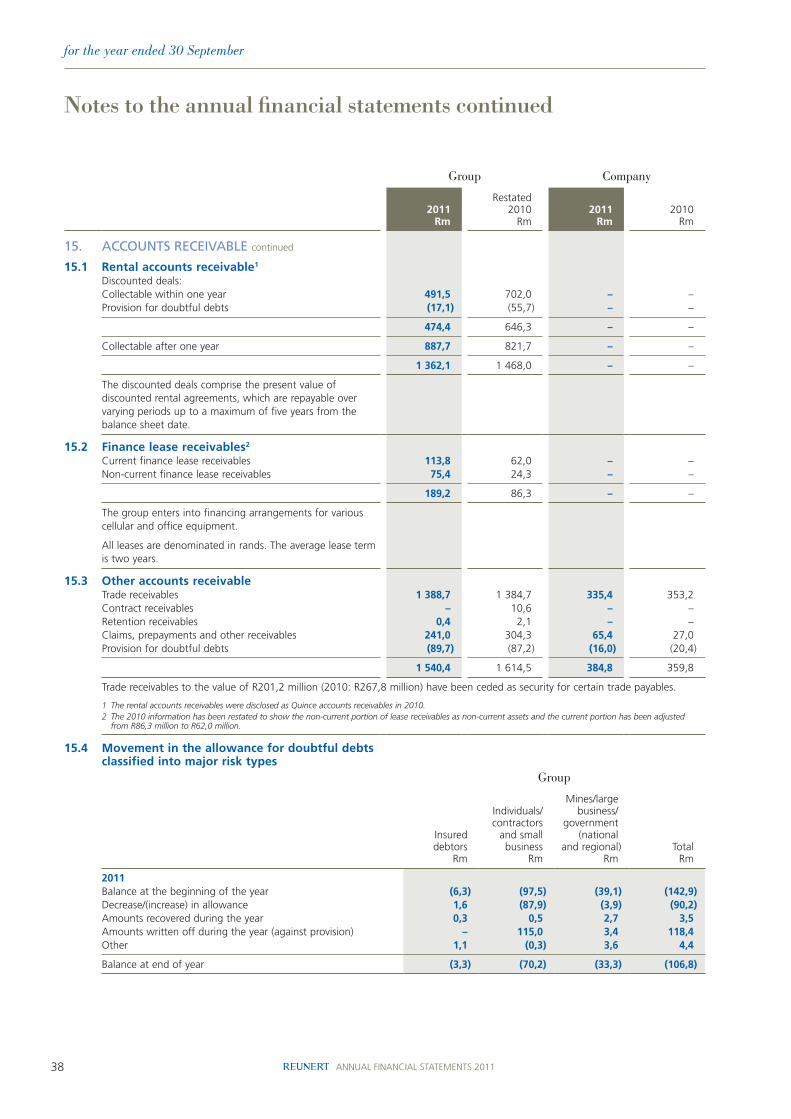

Operational overview34 CBI-electric

40 Nashua

48 Reutech

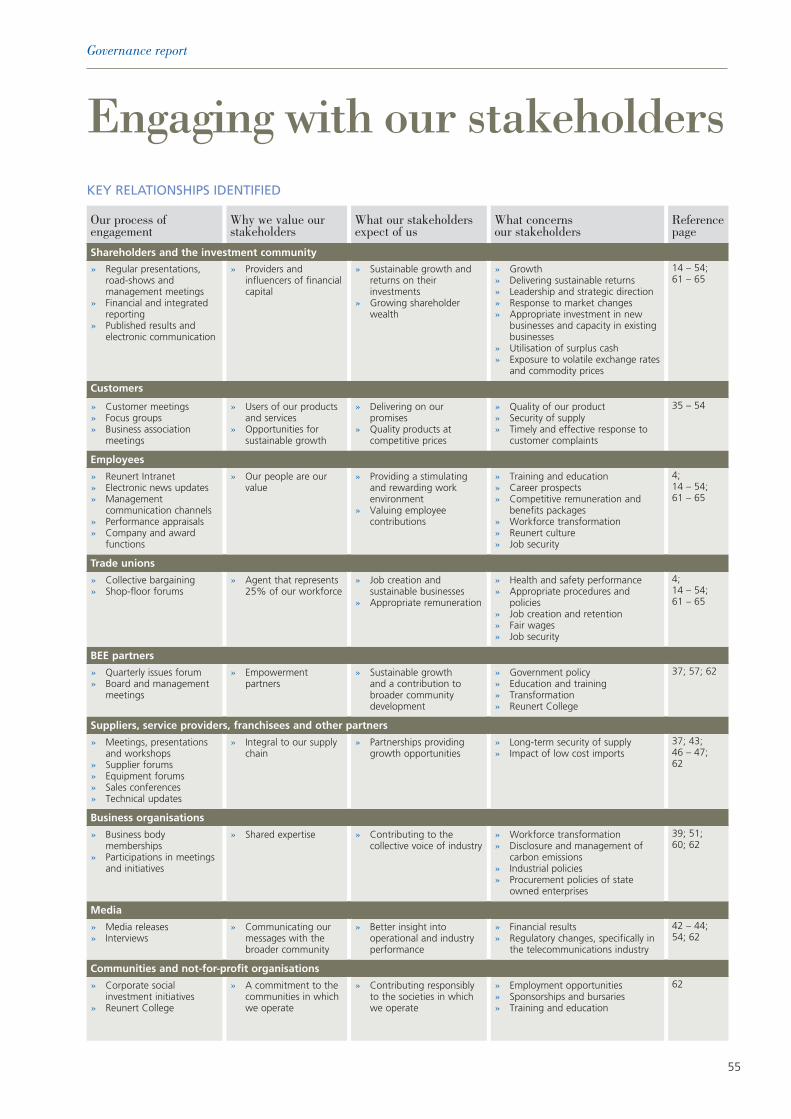

Governance report55 Engaging with our stakeholders

56 Corporate governance

61 Risk committee report

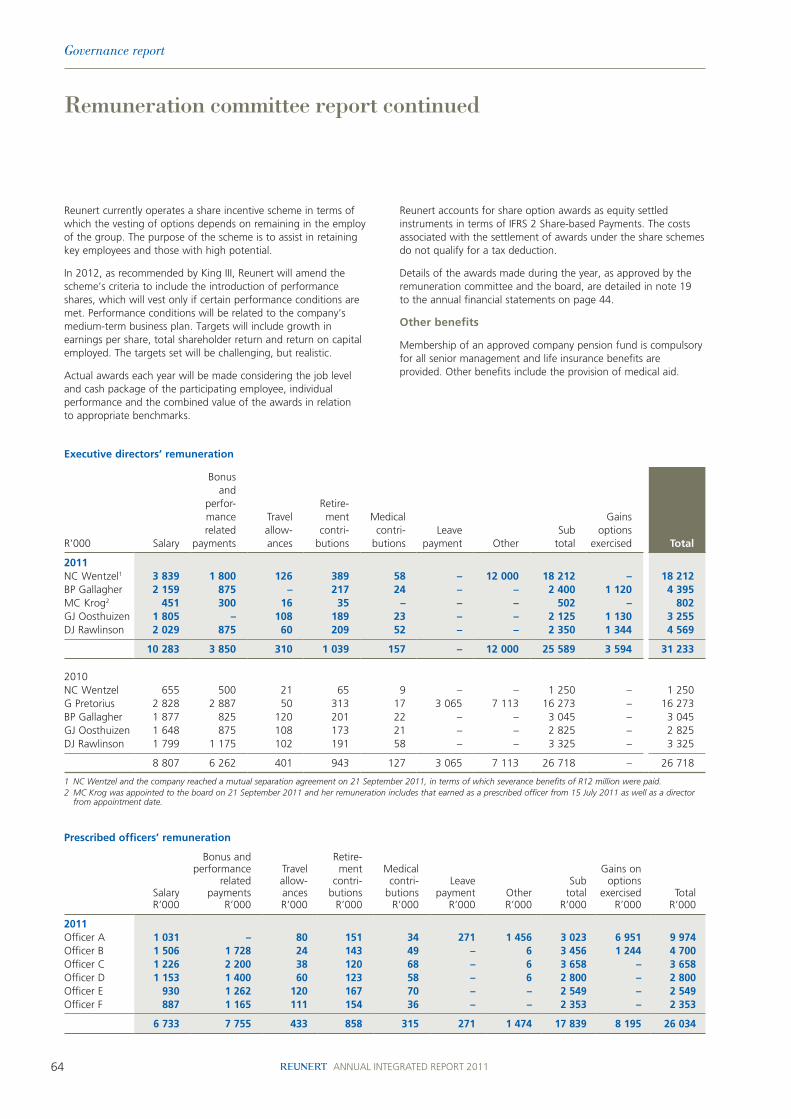

63 Remuneration committee report

Scope and boundary of the report

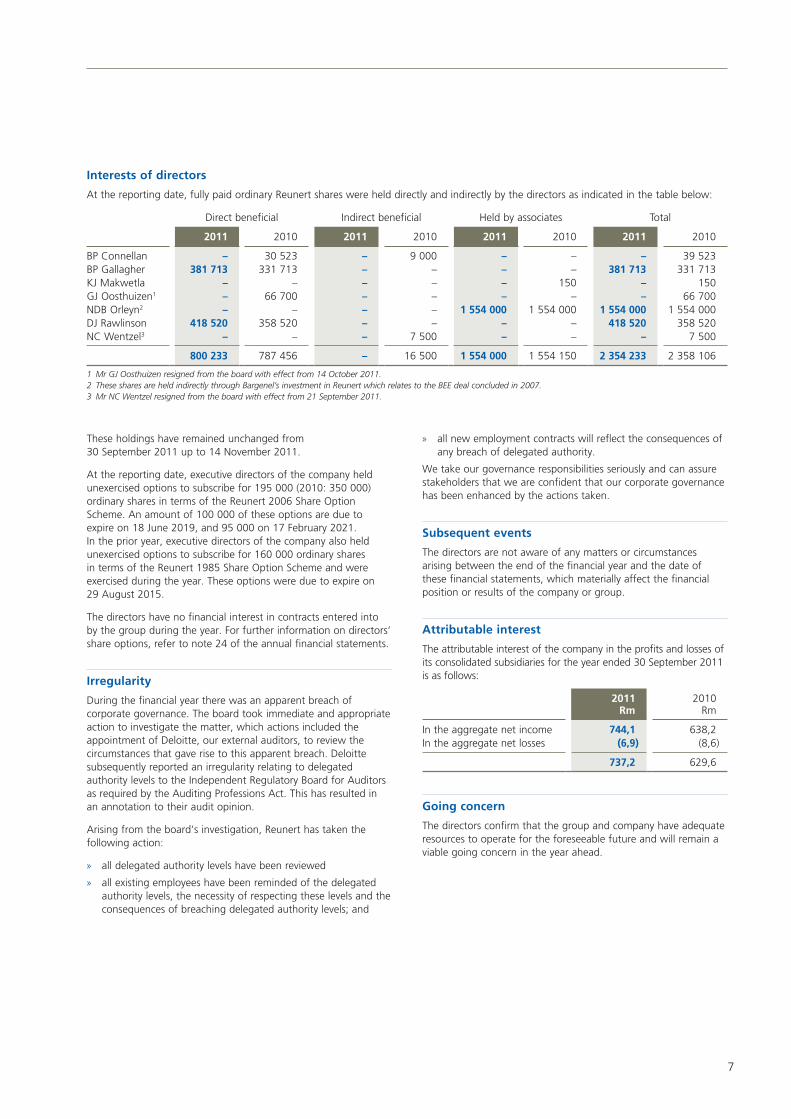

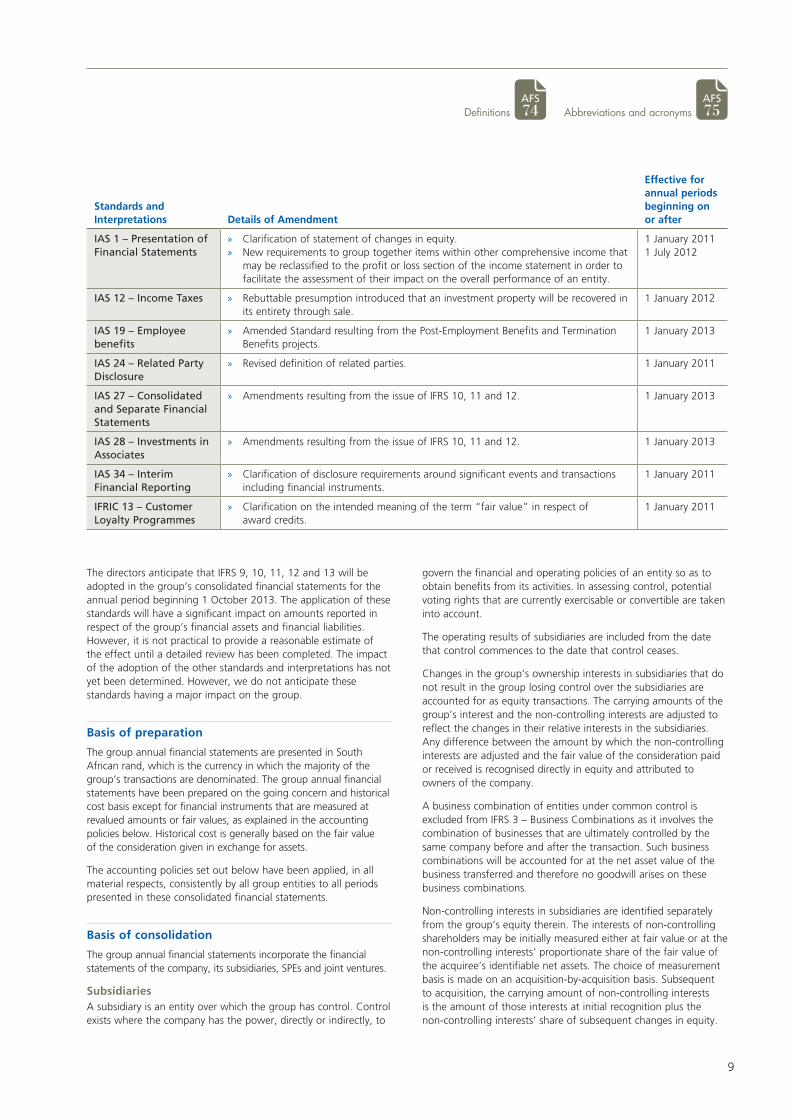

This is our primary report and it covers strategy, financial and non-financial performance, and prospects of Reunert Limited and its subsidiaries (the Reunert group) for the financial year 1 October 2010 to 30 September 2011. The group operates mainly in South Africa.

In preparing the report, management has considered the draft guidelines on integrated reporting provided by the Integrated Reporting Committee (IRC) of South Africa. The audited financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). Sustainability related information, which is integrated into the commentary and newly introduced operating reviews, has been compiled using the G3.1 guidelines of the Global Reporting Initiative (GRI). A consolidated GRI response table can be found on our website.

For this report, we have defined materiality as issues or occurrences that have a significant financial impact on the short-term performance or prospects of Reunert. In the year to come we will work together with our stakeholders on qualifying materiality more specifically according to their interests, particularly in the environmental and social spheres.

Certain statistical information is provided for comparative purposes for up to ten years. Information covers subsidiary, joint venture and investment companies. For sustainability elements, information relating to managed operations is disclosed on a 100% basis, and for our joint venture in CBI-electric: Aberdare ATC telecom cables on a 50% basis.

In the current year we have condensed the presentation relating to our finance company, Quince Capital, in respect of the income statement and balance sheet. Comparatives have been restated accordingly. Details can be found on page 31.

Key dates (dates are subject to change)

Financial calendar

Annual general meeting: 15 February 2012

Interim results announcement: 28 May 2012

Final results announcements: 20 November 2012

Cash dividend to ordinary shareholders

Payment date for the 2011 year: 23 January 2012

Date trading commences ex dividend: 16 January 2012

www.reunert.co.zawww.reunert.com

Visit our website for additional information on the company including results announcements and management presentations

IR pg

AFS pg

Integrated report

Annual financial statements

1

Heading

Section

Introduction

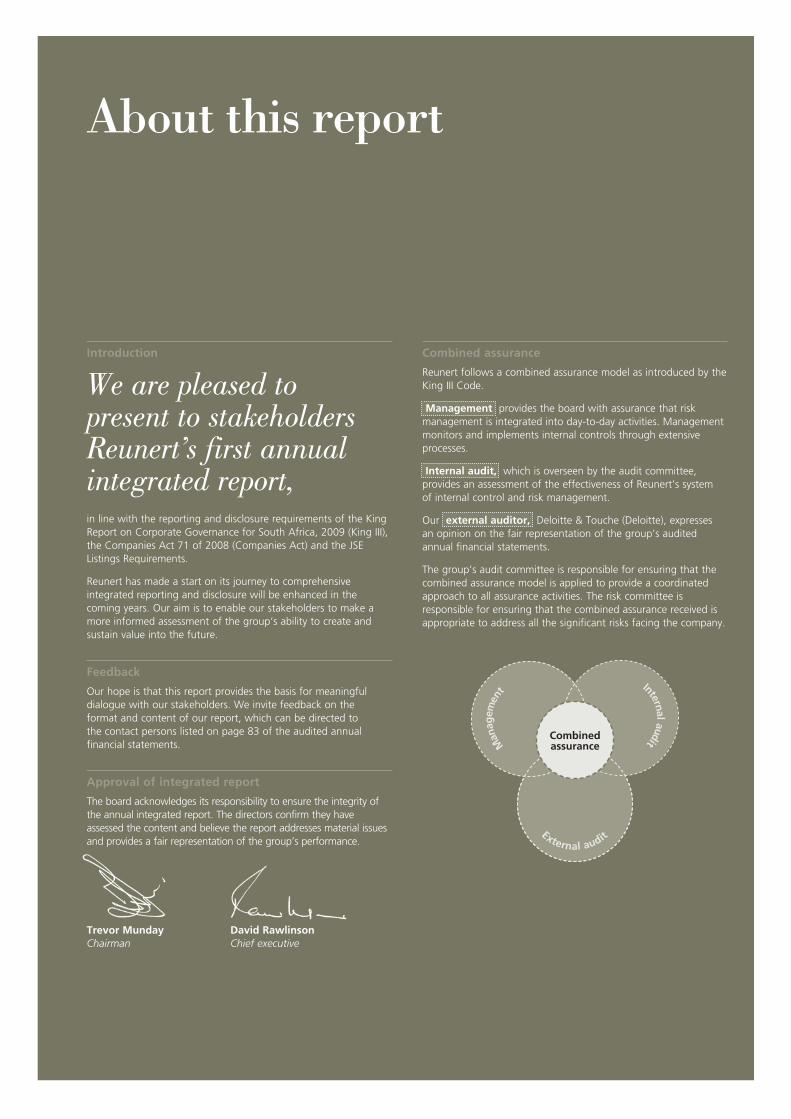

We are pleased to present to stakeholders Reunert’s first annual integrated report, in line with the reporting and disclosure requirements of the King Report on Corporate Governance for South Africa, 2009 (King III), the Companies Act 71 of 2008 (Companies Act) and the JSE Listings Requirements.

Reunert has made a start on its journey to comprehensive integrated reporting and disclosure will be enhanced in the coming years. Our aim is to enable our stakeholders to make a more informed assessment of the group’s ability to create and sustain value into the future.

Feedback

Our hope is that this report provides the basis for meaningful dialogue with our stakeholders. We invite feedback on the format and content of our report, which can be directed to the contact persons listed on page 83 of the audited annual financial statements.

Approval of integrated report

The board acknowledges its responsibility to ensure the integrity of the annual integrated report. The directors confirm they have assessed the content and believe the report addresses material issues and provides a fair representation of the group’s performance.

Trevor Munday David RawlinsonChairman Chief executive

About this report

Combined assurance

Reunert follows a combined assurance model as introduced by the King III Code.

Management provides the board with assurance that risk management is integrated into day-to-day activities. Management monitors and implements internal controls through extensive processes.

Internal audit, which is overseen by the audit committee, provides an assessment of the effectiveness of Reunert’s system of internal control and risk management.

Our external auditor, Deloitte & Touche (Deloitte), expresses an opinion on the fair representation of the group’s audited annual financial statements.

The group’s audit committee is responsible for ensuring that the combined assurance model is applied to provide a coordinated approach to all assurance activities. The risk committee is responsible for ensuring that the combined assurance received is appropriate to address all the significant risks facing the company.

CombinedassuranceM

anag

emen

t Internal audit

External audit

2 ANNUAL INTEGRATED REPORT 2011

Group overview

Group profile & structure

Group profile

Established in 1888 and first listed on the JSE in 1948, Reunert Limited is a leading South African company. The group is listed in the industrial goods and services (electronic and electrical equipment) sector of the JSE (ticker symbol: RLO). The group operates mainly in South Africa with minor operations situated in Australia, Lesotho, USA and Zimbabwe.

The Reunert group manages businesses in the services, electronics and electrical engineering sectors, supplying value-added products, services, solutions and systems to local and international markets. Each of these businesses will remain capable of meeting the group’s objectives for sustainable growth and earnings. We will seek meaningful growth opportunities that are either compatible with our leading competencies or which are sensible, strategically-aligned extensions of our existing businesses.

Reunert currently manages three main operating segments: CBI-electric, Nashua and Reutech. Our businesses strive to achieve first or second positions in their key markets. The group promotes a decentralised management style. While our goal is to retain all the positive aspects of this decentralised structure, we will strengthen it going forward by centrally synchronising group-wide values, governance standards and policies and procedures relating particularly to upholding our leading brands and effectiveness in our risk management, human resources and financial and accounting functions.

“The Reunert group manages businesses in the services, electronics and electrical engineering sectors, supplying value-added products, services, solutions and systems to local and international markets.”

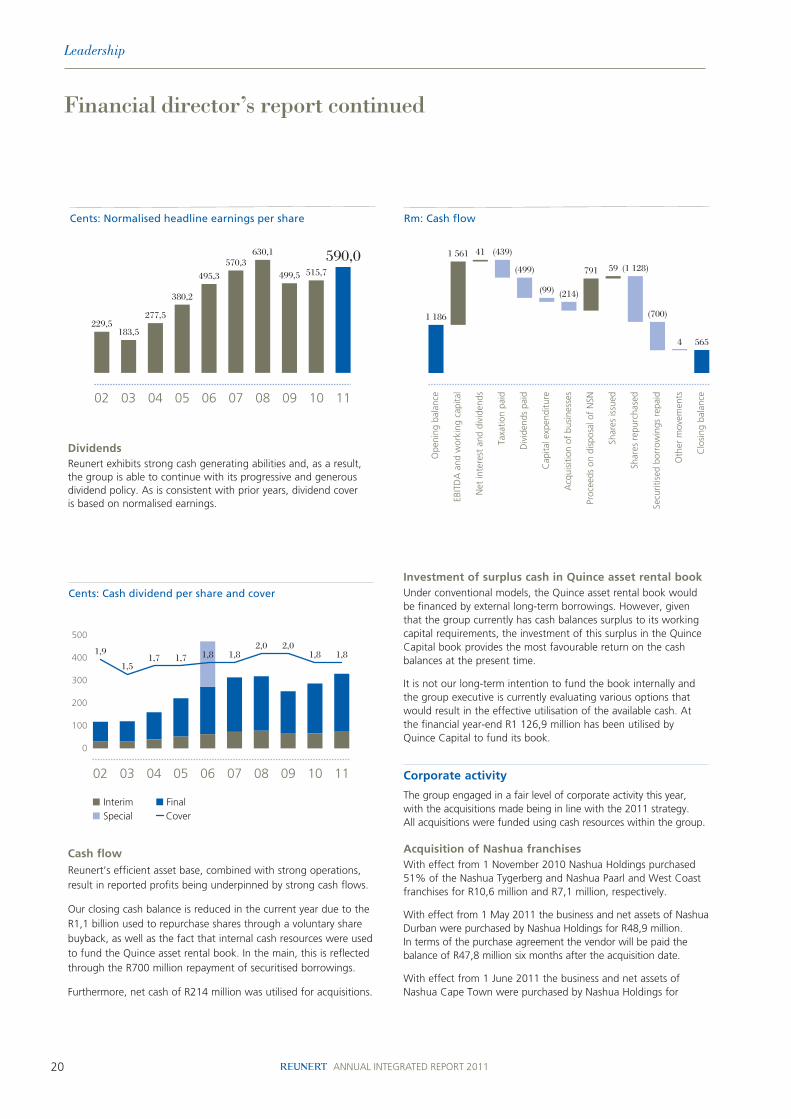

229,5

590,0

02 03 04 05 06 07 08 09 10 11

Cents: Normalised headline earnings per share

183,5

277,5

380,2

495,3

570,3630,1

499,5 515,7

3

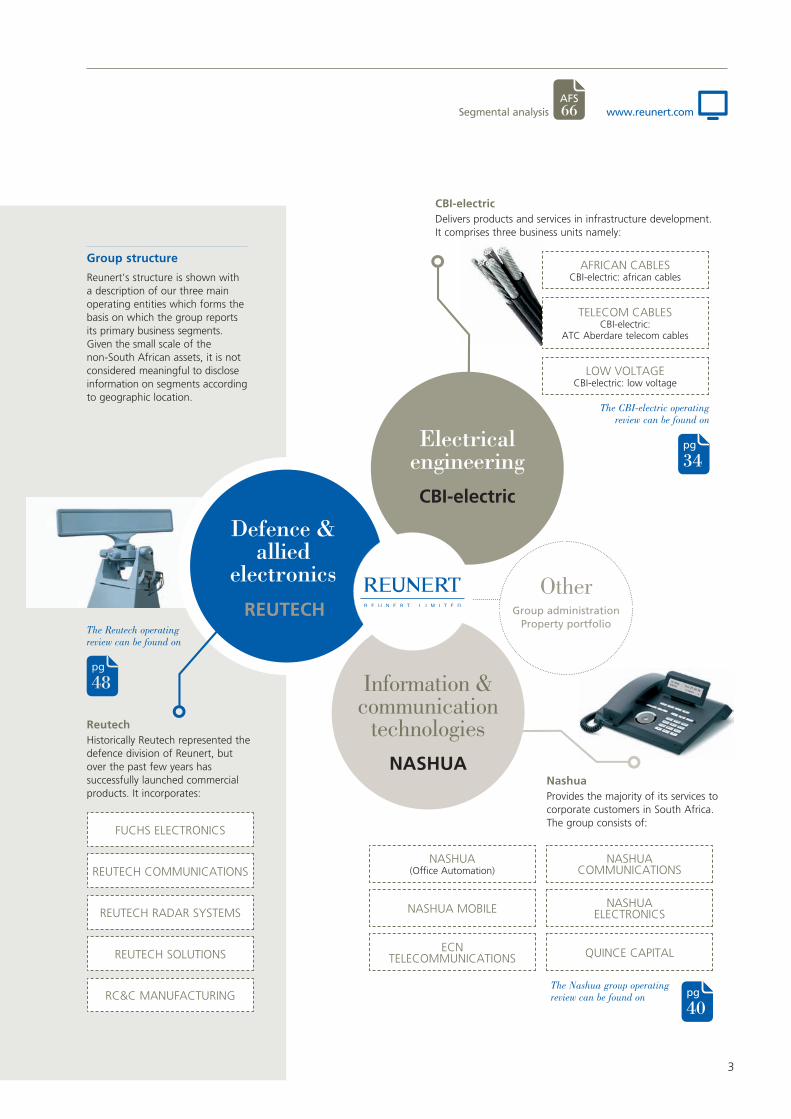

Group structure

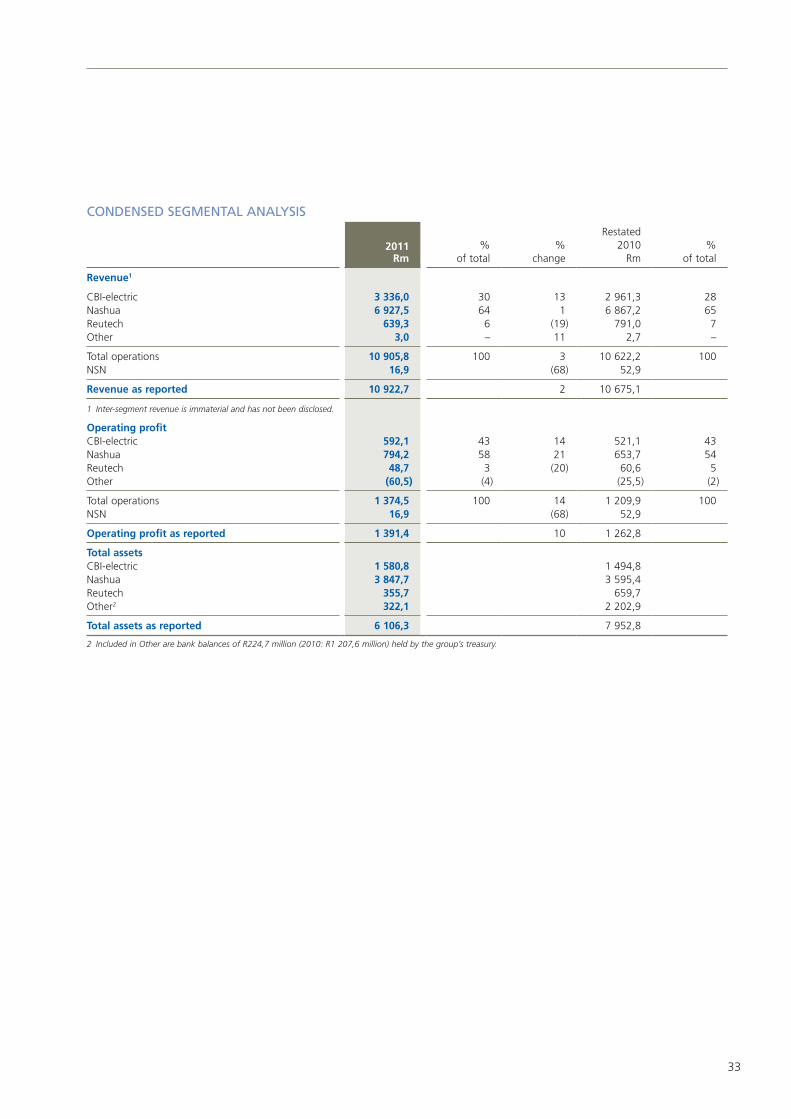

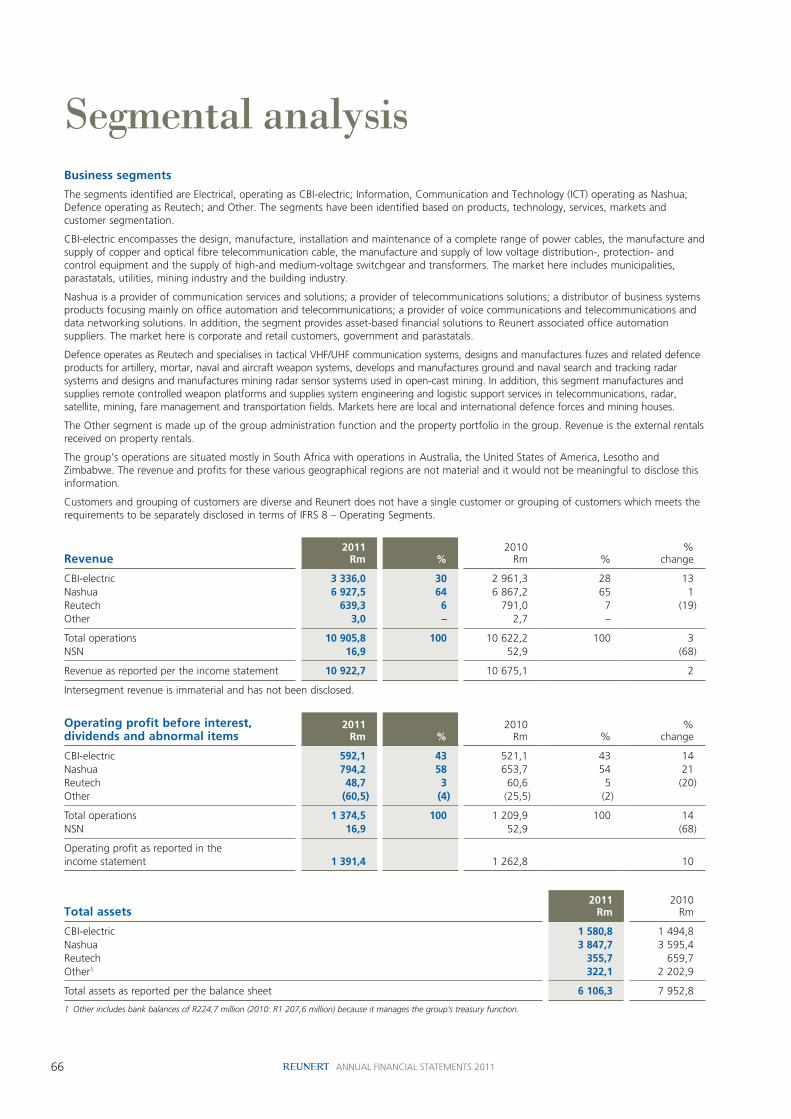

Reunert’s structure is shown with a description of our three main operating entities which forms the basis on which the group reports its primary business segments. Given the small scale of the non-South African assets, it is not considered meaningful to disclose information on segments according to geographic location.

NASHUA(Office Automation)

NASHUA MOBILE

ECN TELECOMMUNICATIONS

NASHUA COMMUNICATIONS

NASHUA ELECTRONICS

QUINCE CAPITAL

AFRICAN CABLESCBI-electric: african cables

TELECOM CABLESCBI-electric:

ATC Aberdare telecom cables

LOW VOLTAGECBI-electric: low voltage

FUCHS ELECTRONICS

REUTECH COMMUNICATIONS

REUTECH RADAR SYSTEMS

REUTECH SOLUTIONS

RC&C MANUFACTURING

The Reutech operating review can be found on

The Nashua group operating review can be found on

The CBI-electric operating review can be found on

pg

40

pg

34

pg

48

CBI-electric Delivers products and services in infrastructure development. It comprises three business units namely:

NashuaProvides the majority of its services to corporate customers in South Africa. The group consists of:

Reutech Historically Reutech represented the defence division of Reunert, but over the past few years has successfully launched commercial products. It incorporates:

OtherGroup administration

Property portfolio

Electrical engineeringCBI-electric

Defence & allied

electronicsREUTECH

Information & communication

technologies

NASHUA

AFS 66Segmental analysis www.reunert.com

4 ANNUAL INTEGRATED REPORT 2011

Performance summary

Highlights

OPERATIONS

CBI-electric Revenue up 13%

2011: R3 336,0m2010: R2 961,3m

» Growth in Power Installations’ contribution

» Sustainable return to profitability of Australian operation

Nashua » Strategic acquisition of ECN

to bring converged solutions

» Greater ownership of office automation supply chain

» Nashua Mobile increased subscriber base by 27 436 customers

ReutechMines worldwide using Reutech surveillance radar

2011: 462010: 29

» Building strong order books

Employee profile

Occupational Levels

Total number of employees

in Reunert

African, Indian & Coloured

Total Male Female

Top management 80 10% 9% 1%

Senior management 130 19% 11% 8%

Professionally qualified, experienced specialists and mid management 503 21% 16% 5%

Junior management, skilled technical and academically qualified workers, supervisors, foremen and superintendents 2 471 49% 34% 15%

Semi-skilled and discretionary decision making 1 393 78% 51% 27%

Unskilled and defined decision making 1 117 99% 23% 76%

Total permanent 5 694 62% 33% 29%

Contract workers 223 66% 28% 38%

Temporary 333 77% 52% 25%

Trainees 16 94% 63% 31%

Total non-permanent 572 74% 43% 31%

Total South Africa and Lesotho 6 266 63% 34% 29%

Australia and USA 58

Total 6 324

253cper share final dividend

330cper share total dividendfor the year

Cash dividend

Wealth created per employee

R636 148

5

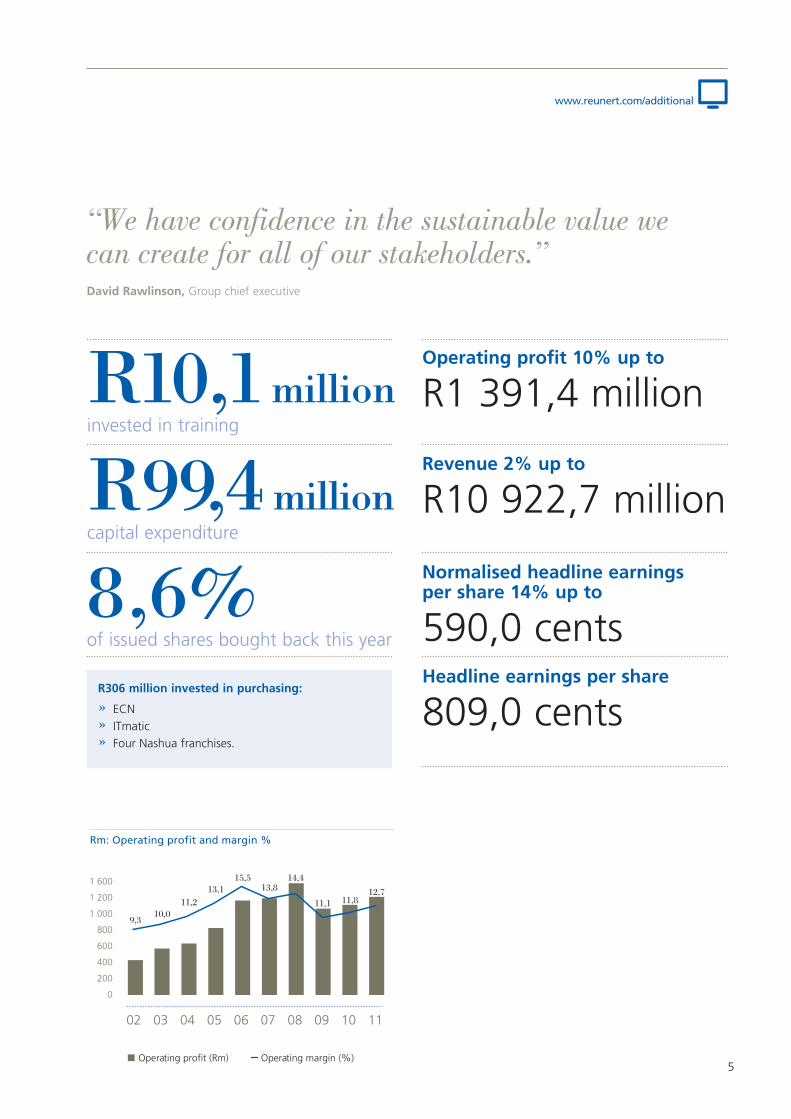

R10,1 millioninvested in training

R99,4 millioncapital expenditure

8,6%of issued shares bought back this year

“We have confidence in the sustainable value we can create for all of our stakeholders.”David Rawlinson, Group chief executive

1 600

1 200

1 000

800

600

400

200

0

02 03 04 05 06 07 08 09 10 11

Rm: Operating profit and margin %

9,310,0

11,213,1

15,513,8

14,4

Operating profit (Rm) Operating margin (%)

12,711,1 11,8

Operating profit 10% up to

R1 391,4 million

Revenue 2% up to

R10 922,7 million

R306 million invested in purchasing:

» ECN» ITmatic» Four Nashua franchises.

Normalised headline earnings per share 14% up to

590,0 centsHeadline earnings per share

809,0 cents

www.reunert.com/additional

6 ANNUAL INTEGRATED REPORT 2011

Ten-year review

Performance summary

IFRS2011

Rm

IFRS2010

Rm

IFRS2009

Rm

IFRS2008

Rm

IFRS2007

Rm

IFRS2006

Rm

IFRS2005

Rm

SA GAAP2004

Rm

SA GAAP2003

Rm

SA GAAP2002

Rm

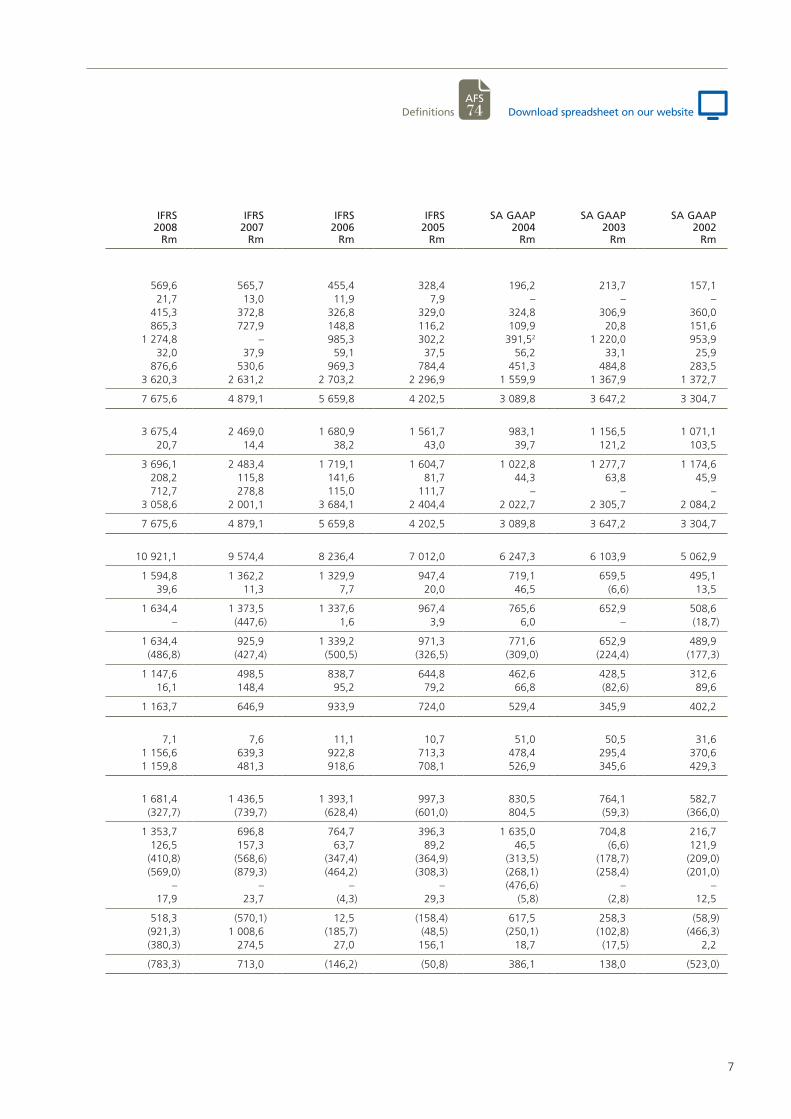

Condensed balance sheetsASSETSProperty, plant and equipment and investment property 612,2 593,8 559,3 569,6 565,7 455,4 328,4 196,2 213,7 157,1 Intangible assets 89,8 41,5 28,6 21,7 13,0 11,9 7,9 – – – Goodwill 654,9 492,1 460,6 415,3 372,8 326,8 329,0 324,8 306,9 360,0 Investments and loans 46,1 837,8 853,9 865,3 727,9 148,8 116,2 109,9 20,8 151,6 Non-current accounts receivable1 965,9 846,0 993,6 1 274,8 – 985,3 302,2 391,52 1 220,0 953,9 Deferred taxation assets 32,2 40,4 29,1 32,0 37,9 59,1 37,5 56,2 33,1 25,9 Cash and cash equivalents1 643,0 1 878,1 1 700,7 876,6 530,6 969,3 784,4 451,3 484,8 283,5 Other current assets1, 3 3 062,2 3 223,1 3 071,6 3 620,3 2 631,2 2 703,2 2 296,9 1 559,9 1 367,9 1 372,7

Total assets 6 106,3 7 952,8 7 697,4 7 675,6 4 879,1 5 659,8 4 202,5 3 089,8 3 647,2 3 304,7

EQUITY AND LIABILITIESOrdinary and preference equity holders of Reunert 3 880,4 4 433,1 4 034,4 3 675,4 2 469,0 1 680,9 1 561,7 983,1 1 156,5 1 071,1 Non-controlling interests 55,2 37,9 26,7 20,7 14,4 38,2 43,0 39,7 121,2 103,5

Total equity 3 935,6 4 471,0 4 061,1 3 696,1 2 483,4 1 719,1 1 604,7 1 022,8 1 277,7 1 174,6 Deferred taxation liabilities 99,6 122,0 140,3 208,2 115,8 141,6 81,7 44,3 63,8 45,9 Long-term borrowings 0,7 710,9 710,9 712,7 278,8 115,0 111,7 – – – Current liabilities3 2 070,4 2 648,9 2 785,1 3 058,6 2 001,1 3 684,1 2 404,4 2 022,7 2 305,7 2 084,2

Total equity and liabilities 6 106,3 7 952,8 7 697,4 7 675,6 4 879,1 5 659,8 4 202,5 3 089,8 3 647,2 3 304,7

Condensed income statementsRevenue1 10 922,7 10 675,1 10 270,8 10 921,1 9 574,4 8 236,4 7 012,0 6 247,3 6 103,9 5 062,9

Operating profit1 1 391,4 1 262,8 1 210,2 1 594,8 1 362,2 1 329,9 947,4 719,1 659,5 495,1 Net interest and dividends received/(paid)1 40,9 59,2 38,4 39,6 11,3 7,7 20,0 46,5 (6,6) 13,5

Profit before abnormal items 1 432,3 1 322,0 1 248,6 1 634,4 1 373,5 1 337,6 967,4 765,6 652,9 508,6 Abnormal items 346,4 (34,0) 299,2 – (447,6) 1,6 3,9 6,0 – (18,7)

Profit before taxation 1 778,7 1 288,0 1 547,8 1 634,4 925,9 1 339,2 971,3 771,6 652,9 489,9 Taxation (425,9) (376,6) (374,3) (486,8) (427,4) (500,5) (326,5) (309,0) (224,4) (177,3)

Profit after taxation 1 352,8 911,4 1 173,5 1 147,6 498,5 838,7 644,8 462,6 428,5 312,6 Share of associate companies’ profits/(losses) – – – 16,1 148,4 95,2 79,2 66,8 (82,6) 89,6

Profit for the year 1 352,8 911,4 1 173,5 1 163,7 646,9 933,9 724,0 529,4 345,9 402,2

Profit for the year attributable to:Non-controlling interests 15,7 12,0 9,0 7,1 7,6 11,1 10,7 51,0 50,5 31,6 Equity holders of Reunert 1 337,1 899,4 1 164,5 1 156,6 639,3 922,8 713,3 478,4 295,4 370,6 Headline earnings attributable to equity holders of Reunert 988,9 903,4 1 163,1 1 159,8 481,3 918,6 708,1 526,9 345,6 429,3

Condensed cash flow statementsEBITDA 1 513,2 1 375,5 1 306,6 1 681,4 1 436,5 1 393,1 997,3 830,5 764,1 582,7 Changes in working capital 47,7 318,3 757,4 (327,7) (739,7) (628,4) (601,0) 804,5 (59,3) (366,0)

Cash generated from operations 1 560,9 1 693,8 2 064,0 1 353,7 696,8 764,7 396,3 1 635,0 704,8 216,7 Net interest and dividends received 40,9 59,2 38,4 126,5 157,3 63,7 89,2 46,5 (6,6) 121,9 Taxation paid (438,8) (407,9) (477,5) (410,8) (568,6) (347,4) (364,9) (313,5) (178,7) (209,0)Dividends paid (498,5) (456,8) (550,3) (569,0) (879,3) (464,2) (308,3) (268,1) (258,4) (201,0)Share buy back (1 127,9) (125,7) – – – – – (476,6) – – Other (net) (1,6) 26,3 42,6 17,9 23,7 (4,3) 29,3 (5,8) (2,8) 12,5

Net cash flows from operating activities (465,0) 788,9 1 117,2 518,3 (570,1) 12,5 (158,4) 617,5 258,3 (58,9)Net cash flows from investing activities 484,7 (313,3) (130,8) (921,3) 1 008,6 (185,7) (48,5) (250,1) (102,8) (466,3)Net cash flows from financing activities (641,0) 21,9 2,5 (380,3) 274,5 27,0 156,1 18,7 (17,5) 2,2

Net cash (utilised)/generated (621,3) 497,5 988,9 (783,3) 713,0 (146,2) (50,8) 386,1 138,0 (523,0)

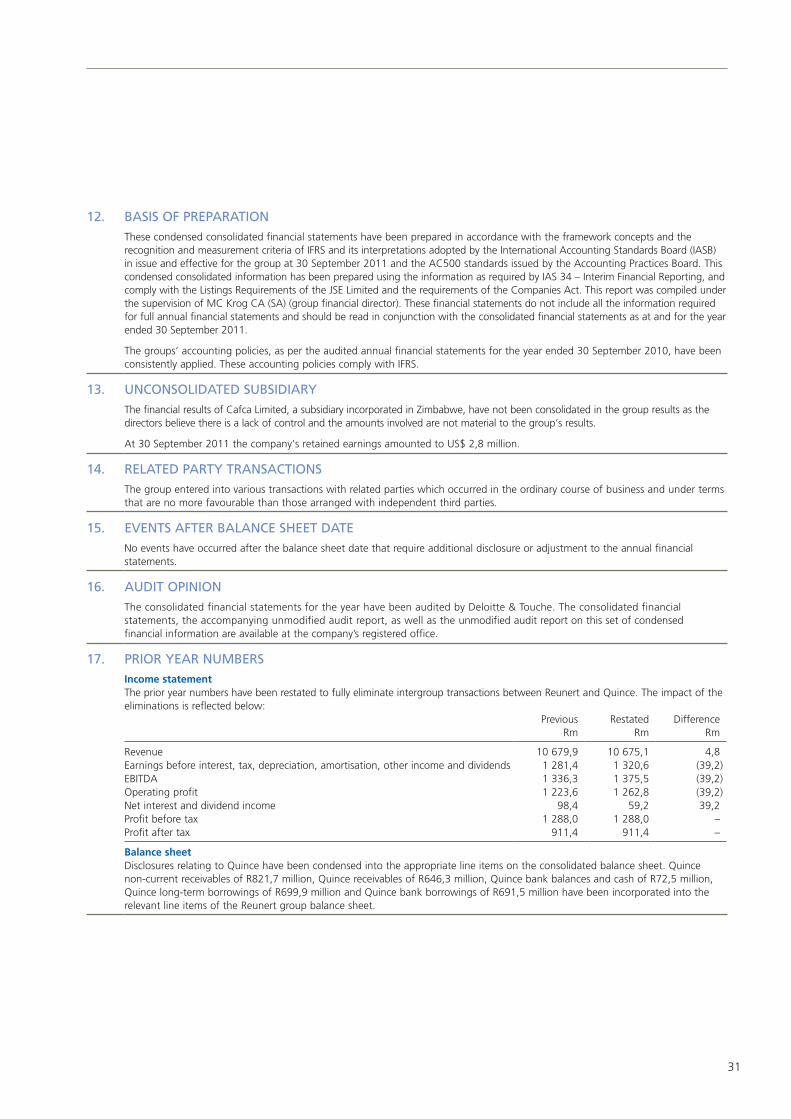

1 All intergroup transactions between Reunert and Quince are now fully eliminated and disclosures related to Quince have been condensed into the appropriate lines on the balance sheet. Comparative information in all financial years has been restated accordingly.

2 In December 2003, R1 255,5 million was received on the sale of the Quince debtors book.3 In years prior to 2008 inventory items were shown net of advance payments received from customers.

These advance payments are now disclosed in current liabilities.

7

IFRS2011

Rm

IFRS2010

Rm

IFRS2009

Rm

IFRS2008

Rm

IFRS2007

Rm

IFRS2006

Rm

IFRS2005

Rm

SA GAAP2004

Rm

SA GAAP2003

Rm

SA GAAP2002

Rm

Condensed balance sheetsASSETSProperty, plant and equipment and investment property 612,2 593,8 559,3 569,6 565,7 455,4 328,4 196,2 213,7 157,1 Intangible assets 89,8 41,5 28,6 21,7 13,0 11,9 7,9 – – – Goodwill 654,9 492,1 460,6 415,3 372,8 326,8 329,0 324,8 306,9 360,0 Investments and loans 46,1 837,8 853,9 865,3 727,9 148,8 116,2 109,9 20,8 151,6 Non-current accounts receivable1 965,9 846,0 993,6 1 274,8 – 985,3 302,2 391,52 1 220,0 953,9 Deferred taxation assets 32,2 40,4 29,1 32,0 37,9 59,1 37,5 56,2 33,1 25,9 Cash and cash equivalents1 643,0 1 878,1 1 700,7 876,6 530,6 969,3 784,4 451,3 484,8 283,5 Other current assets1, 3 3 062,2 3 223,1 3 071,6 3 620,3 2 631,2 2 703,2 2 296,9 1 559,9 1 367,9 1 372,7

Total assets 6 106,3 7 952,8 7 697,4 7 675,6 4 879,1 5 659,8 4 202,5 3 089,8 3 647,2 3 304,7

EQUITY AND LIABILITIESOrdinary and preference equity holders of Reunert 3 880,4 4 433,1 4 034,4 3 675,4 2 469,0 1 680,9 1 561,7 983,1 1 156,5 1 071,1 Non-controlling interests 55,2 37,9 26,7 20,7 14,4 38,2 43,0 39,7 121,2 103,5

Total equity 3 935,6 4 471,0 4 061,1 3 696,1 2 483,4 1 719,1 1 604,7 1 022,8 1 277,7 1 174,6 Deferred taxation liabilities 99,6 122,0 140,3 208,2 115,8 141,6 81,7 44,3 63,8 45,9 Long-term borrowings 0,7 710,9 710,9 712,7 278,8 115,0 111,7 – – – Current liabilities3 2 070,4 2 648,9 2 785,1 3 058,6 2 001,1 3 684,1 2 404,4 2 022,7 2 305,7 2 084,2

Total equity and liabilities 6 106,3 7 952,8 7 697,4 7 675,6 4 879,1 5 659,8 4 202,5 3 089,8 3 647,2 3 304,7

Condensed income statementsRevenue1 10 922,7 10 675,1 10 270,8 10 921,1 9 574,4 8 236,4 7 012,0 6 247,3 6 103,9 5 062,9

Operating profit1 1 391,4 1 262,8 1 210,2 1 594,8 1 362,2 1 329,9 947,4 719,1 659,5 495,1 Net interest and dividends received/(paid)1 40,9 59,2 38,4 39,6 11,3 7,7 20,0 46,5 (6,6) 13,5

Profit before abnormal items 1 432,3 1 322,0 1 248,6 1 634,4 1 373,5 1 337,6 967,4 765,6 652,9 508,6 Abnormal items 346,4 (34,0) 299,2 – (447,6) 1,6 3,9 6,0 – (18,7)

Profit before taxation 1 778,7 1 288,0 1 547,8 1 634,4 925,9 1 339,2 971,3 771,6 652,9 489,9 Taxation (425,9) (376,6) (374,3) (486,8) (427,4) (500,5) (326,5) (309,0) (224,4) (177,3)

Profit after taxation 1 352,8 911,4 1 173,5 1 147,6 498,5 838,7 644,8 462,6 428,5 312,6 Share of associate companies’ profits/(losses) – – – 16,1 148,4 95,2 79,2 66,8 (82,6) 89,6

Profit for the year 1 352,8 911,4 1 173,5 1 163,7 646,9 933,9 724,0 529,4 345,9 402,2

Profit for the year attributable to:Non-controlling interests 15,7 12,0 9,0 7,1 7,6 11,1 10,7 51,0 50,5 31,6 Equity holders of Reunert 1 337,1 899,4 1 164,5 1 156,6 639,3 922,8 713,3 478,4 295,4 370,6 Headline earnings attributable to equity holders of Reunert 988,9 903,4 1 163,1 1 159,8 481,3 918,6 708,1 526,9 345,6 429,3

Condensed cash flow statementsEBITDA 1 513,2 1 375,5 1 306,6 1 681,4 1 436,5 1 393,1 997,3 830,5 764,1 582,7 Changes in working capital 47,7 318,3 757,4 (327,7) (739,7) (628,4) (601,0) 804,5 (59,3) (366,0)

Cash generated from operations 1 560,9 1 693,8 2 064,0 1 353,7 696,8 764,7 396,3 1 635,0 704,8 216,7 Net interest and dividends received 40,9 59,2 38,4 126,5 157,3 63,7 89,2 46,5 (6,6) 121,9 Taxation paid (438,8) (407,9) (477,5) (410,8) (568,6) (347,4) (364,9) (313,5) (178,7) (209,0)Dividends paid (498,5) (456,8) (550,3) (569,0) (879,3) (464,2) (308,3) (268,1) (258,4) (201,0)Share buy back (1 127,9) (125,7) – – – – – (476,6) – – Other (net) (1,6) 26,3 42,6 17,9 23,7 (4,3) 29,3 (5,8) (2,8) 12,5

Net cash flows from operating activities (465,0) 788,9 1 117,2 518,3 (570,1) 12,5 (158,4) 617,5 258,3 (58,9)Net cash flows from investing activities 484,7 (313,3) (130,8) (921,3) 1 008,6 (185,7) (48,5) (250,1) (102,8) (466,3)Net cash flows from financing activities (641,0) 21,9 2,5 (380,3) 274,5 27,0 156,1 18,7 (17,5) 2,2

Net cash (utilised)/generated (621,3) 497,5 988,9 (783,3) 713,0 (146,2) (50,8) 386,1 138,0 (523,0)

1 All intergroup transactions between Reunert and Quince are now fully eliminated and disclosures related to Quince have been condensed into the appropriate lines on the balance sheet. Comparative information in all financial years has been restated accordingly.

2 In December 2003, R1 255,5 million was received on the sale of the Quince debtors book.3 In years prior to 2008 inventory items were shown net of advance payments received from customers.

These advance payments are now disclosed in current liabilities.

AFS 74Definitions Download spreadsheet on our website

8 ANNUAL INTEGRATED REPORT 2011

Performance summary

IFRS2011

IFRS2010

IFRS2009

IFRS2008

IFRS2007

IFRS2006

IFRS2005

SA GAAP2004

SA GAAP2003

SA GAAP2002

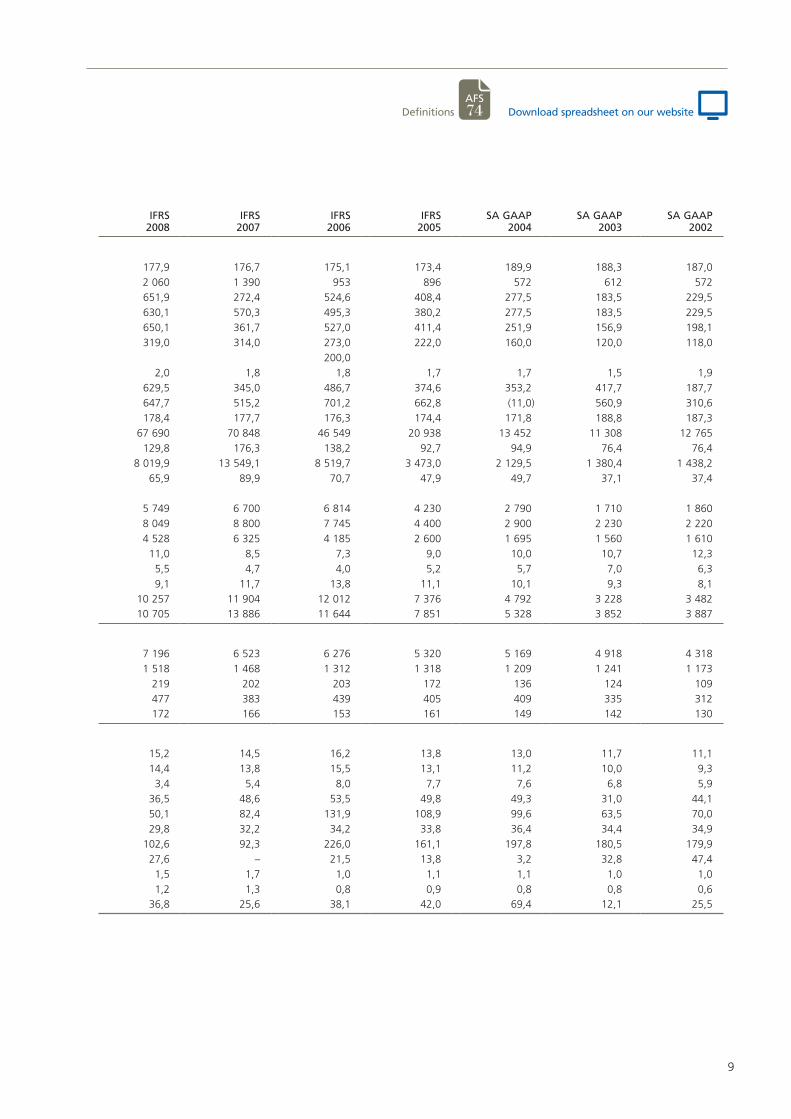

SharesNumber of ordinary shares on which earnings per share is calculated millions 165,3 178,7 178,5 177,9 176,7 175,1 173,4 189,9 188,3 187,0

Net worth per share cents 2 401 2 502 2 258 2 060 1 390 953 896 572 612 572

Headline earnings per share cents 598,3 505,5 651,6 651,9 272,4 524,6 408,4 277,5 183,5 229,5

Normalised headline earnings per share cents 590,0 515,7 499,5 630,1 570,3 495,3 380,2 277,5 183,5 229,5

Basic earnings per share cents 809,0 503,3 652,4 650,1 361,7 527,0 411,4 251,9 156,9 198,1

Dividends per share – normal cents 330,0 287,0 253,0 319,0 314,0 273,0 222,0 160,0 120,0 118,0

– special cents 200,0

Dividend cover times 1,8 1,8 2,0 2,0 1,8 1,8 1,7 1,7 1,5 1,9

Cashflow per share cents 702,8 767,4 797,8 629,5 345,0 486,7 374,6 353,2 417,7 187,7

Cashflow per share (excluding rental book) cents 638,7 635,6 797,6 647,7 515,2 701,2 662,8 (11,0) 560,9 310,6

Ordinary shares in issue (net of treasury shares) millions 161,6 177,2 178,7 178,4 177,7 176,3 174,4 171,8 188,8 187,3

Number of transactions – JSE 99 875 85 444 71 666 67 690 70 848 46 549 20 938 13 452 11 308 12 765

Number of shares traded millions 106,5 134,4 107,7 129,8 176,3 138,2 92,7 94,9 76,4 76,4

Value of shares traded Rm 6 579,4 7 644,8 4 780,6 8 019,9 13 549,1 8 519,7 3 473,0 2 129,5 1 380,4 1 438,2

Number of shares traded as a percentage of gross issued shares 53,4 67,9 54,6 65,9 89,9 70,7 47,9 49,7 37,1 37,4

Market price per share

– year end cents 5 885,0 6 201,0 5 600 5 749 6 700 6 814 4 230 2 790 1 710 1 860

– highest cents 6 970,0 6 247,0 5 900 8 049 8 800 7 745 4 400 2 900 2 230 2 220

– lowest cents 5 101,0 4 950,0 3 201 4 528 6 325 4 185 2 600 1 695 1 560 1 610

Earnings yield % 10,0 8,3 8,9 11,0 8,5 7,3 9,0 10,0 10,7 12,3

Dividend yield % 5,6 4,6 4,5 5,5 4,7 4,0 5,2 5,7 7,0 6,3

Price: Earnings ratio times 10,0 12,0 11,2 9,1 11,7 13,8 11,1 10,1 9,3 8,1

Market capitalisation (net of treasury shares) Rm 9 512 10 988 10 006 10 257 11 904 12 012 7 376 4 792 3 228 3 482JSE actuaries’ electronics sector index at 30 September 9 780 10 462 9 866 10 705 13 886 11 644 7 851 5 328 3 852 3 887

OtherNumber of employees 6 324 6 422 6 321 7 196 6 523 6 276 5 320 5 169 4 918 4 318

Revenue per employee R’000 1 727 1 662 1 625 1 518 1 468 1 312 1 318 1 209 1 241 1 173

Operating profit per employee R’000 220 197 180 219 202 203 172 136 124 109

Wealth created per employee R’000 636 527 530 477 383 439 405 409 335 312Employment cost per employee R’000 248 229 194 172 166 153 161 149 142 130

Profitability, asset management, liquidity and leverageEBITDA as a percentage of revenue1, 2 % 13,9 12,9 12,0 15,2 14,5 16,2 13,8 13,0 11,7 11,1

Operating margin (%)2 % 12,7 11,8 11,1 14,4 13,8 15,5 13,1 11,2 10,0 9,3

Net asset turn2 times 5,4 2,9 2,9 3,4 5,4 8,0 7,7 7,6 6,8 5,9

Normalised return on ordinary shareholders’ funds % 23,5 21,8 23,1 36,5 48,6 53,5 49,8 49,3 31,0 44,1

Return on net operating assets2 % 68,9 34,1 32,0 50,1 82,4 131,9 108,9 99,6 63,5 70,0

Taxation as a percentage of profit before taxation3 % 29,7 28,5 27,0 29,8 32,2 34,2 33,8 36,4 34,4 34,9

Total liabilities to total shareholders’ funds2, 4 % 52,6 75,1 86,7 102,6 92,3 226,0 161,1 197,8 180,5 179,9

Net borrowings to total shareholders’ funds5 % – – 0,6 27,6 – 21,5 13,8 3,2 32,8 47,4

Current ratio 1,8 2,2 1,7 1,5 1,7 1,0 1,1 1,1 1,0 1,0

Quick ratio 1,4 1,9 1,5 1,2 1,3 0,8 0,9 0,8 0,8 0,6 Interest cover (times)2 times 210,8 175,4 54,0 36,8 25,6 38,1 42,0 69,4 12,1 25,5

1 The 2008 percentages have been increased by 1,3% each as a result of the NSN commission now disclosed in operating income, whereas income from NSN was previously disclosed as income from associates.

2 All intergroup transactions between Reunert and Quince are now fully eliminated and disclosures related to Quince have been condensed into the appropriate lines on the balance sheet. The ratios for 2010 only have been restated accordingly.

3 Abnormal items, the STC on a special dividend in 2006 and the share buyback in 2004 have been excluded from this calculation.4 These ratios have been restated in 2003 to 2007 to take account of the reallocation of the advance payments from inventory and contracts in progress to trade and

other payables. 5 There were no net borrowings in 2007 mainly due to Quince being equity accounted.

Ten-year review continued

9

IFRS2011

IFRS2010

IFRS2009

IFRS2008

IFRS2007

IFRS2006

IFRS2005

SA GAAP2004

SA GAAP2003

SA GAAP2002

SharesNumber of ordinary shares on which earnings per share is calculated millions 165,3 178,7 178,5 177,9 176,7 175,1 173,4 189,9 188,3 187,0

Net worth per share cents 2 401 2 502 2 258 2 060 1 390 953 896 572 612 572

Headline earnings per share cents 598,3 505,5 651,6 651,9 272,4 524,6 408,4 277,5 183,5 229,5

Normalised headline earnings per share cents 590,0 515,7 499,5 630,1 570,3 495,3 380,2 277,5 183,5 229,5

Basic earnings per share cents 809,0 503,3 652,4 650,1 361,7 527,0 411,4 251,9 156,9 198,1

Dividends per share – normal cents 330,0 287,0 253,0 319,0 314,0 273,0 222,0 160,0 120,0 118,0

– special cents 200,0

Dividend cover times 1,8 1,8 2,0 2,0 1,8 1,8 1,7 1,7 1,5 1,9

Cashflow per share cents 702,8 767,4 797,8 629,5 345,0 486,7 374,6 353,2 417,7 187,7

Cashflow per share (excluding rental book) cents 638,7 635,6 797,6 647,7 515,2 701,2 662,8 (11,0) 560,9 310,6

Ordinary shares in issue (net of treasury shares) millions 161,6 177,2 178,7 178,4 177,7 176,3 174,4 171,8 188,8 187,3

Number of transactions – JSE 99 875 85 444 71 666 67 690 70 848 46 549 20 938 13 452 11 308 12 765

Number of shares traded millions 106,5 134,4 107,7 129,8 176,3 138,2 92,7 94,9 76,4 76,4

Value of shares traded Rm 6 579,4 7 644,8 4 780,6 8 019,9 13 549,1 8 519,7 3 473,0 2 129,5 1 380,4 1 438,2

Number of shares traded as a percentage of gross issued shares 53,4 67,9 54,6 65,9 89,9 70,7 47,9 49,7 37,1 37,4

Market price per share

– year end cents 5 885,0 6 201,0 5 600 5 749 6 700 6 814 4 230 2 790 1 710 1 860

– highest cents 6 970,0 6 247,0 5 900 8 049 8 800 7 745 4 400 2 900 2 230 2 220

– lowest cents 5 101,0 4 950,0 3 201 4 528 6 325 4 185 2 600 1 695 1 560 1 610

Earnings yield % 10,0 8,3 8,9 11,0 8,5 7,3 9,0 10,0 10,7 12,3

Dividend yield % 5,6 4,6 4,5 5,5 4,7 4,0 5,2 5,7 7,0 6,3

Price: Earnings ratio times 10,0 12,0 11,2 9,1 11,7 13,8 11,1 10,1 9,3 8,1

Market capitalisation (net of treasury shares) Rm 9 512 10 988 10 006 10 257 11 904 12 012 7 376 4 792 3 228 3 482JSE actuaries’ electronics sector index at 30 September 9 780 10 462 9 866 10 705 13 886 11 644 7 851 5 328 3 852 3 887

OtherNumber of employees 6 324 6 422 6 321 7 196 6 523 6 276 5 320 5 169 4 918 4 318

Revenue per employee R’000 1 727 1 662 1 625 1 518 1 468 1 312 1 318 1 209 1 241 1 173

Operating profit per employee R’000 220 197 180 219 202 203 172 136 124 109

Wealth created per employee R’000 636 527 530 477 383 439 405 409 335 312Employment cost per employee R’000 248 229 194 172 166 153 161 149 142 130

Profitability, asset management, liquidity and leverageEBITDA as a percentage of revenue1, 2 % 13,9 12,9 12,0 15,2 14,5 16,2 13,8 13,0 11,7 11,1

Operating margin (%)2 % 12,7 11,8 11,1 14,4 13,8 15,5 13,1 11,2 10,0 9,3

Net asset turn2 times 5,4 2,9 2,9 3,4 5,4 8,0 7,7 7,6 6,8 5,9

Normalised return on ordinary shareholders’ funds % 23,5 21,8 23,1 36,5 48,6 53,5 49,8 49,3 31,0 44,1

Return on net operating assets2 % 68,9 34,1 32,0 50,1 82,4 131,9 108,9 99,6 63,5 70,0

Taxation as a percentage of profit before taxation3 % 29,7 28,5 27,0 29,8 32,2 34,2 33,8 36,4 34,4 34,9

Total liabilities to total shareholders’ funds2, 4 % 52,6 75,1 86,7 102,6 92,3 226,0 161,1 197,8 180,5 179,9

Net borrowings to total shareholders’ funds5 % – – 0,6 27,6 – 21,5 13,8 3,2 32,8 47,4

Current ratio 1,8 2,2 1,7 1,5 1,7 1,0 1,1 1,1 1,0 1,0

Quick ratio 1,4 1,9 1,5 1,2 1,3 0,8 0,9 0,8 0,8 0,6 Interest cover (times)2 times 210,8 175,4 54,0 36,8 25,6 38,1 42,0 69,4 12,1 25,5

1 The 2008 percentages have been increased by 1,3% each as a result of the NSN commission now disclosed in operating income, whereas income from NSN was previously disclosed as income from associates.

2 All intergroup transactions between Reunert and Quince are now fully eliminated and disclosures related to Quince have been condensed into the appropriate lines on the balance sheet. The ratios for 2010 only have been restated accordingly.

3 Abnormal items, the STC on a special dividend in 2006 and the share buyback in 2004 have been excluded from this calculation.4 These ratios have been restated in 2003 to 2007 to take account of the reallocation of the advance payments from inventory and contracts in progress to trade and

other payables. 5 There were no net borrowings in 2007 mainly due to Quince being equity accounted.

AFS 74Definitions Download spreadsheet on our website

10 ANNUAL INTEGRATED REPORT 2011

Non-executive directors

Leadership

(from left to right)

Trevor Munday (62)Appointed 1 June 2008 and as chairman from 1 June 2009» Strategic vision» Corporate leadership» Financial acumen

Sean Jagoe (60)Appointed in 2000 » Corporate finance

expertise» Corporate governance

best practise» Experience in

remuneration policy

Thandi Orleyn (55)Appointed in 2007» Government relationships’

experience» Corporate leadership» Legal and administrative

expertise

Johannes van der Horst (67)Appointed in 1993 » Investment insight» Corporate leadership» Understanding of complex

change processes

Yolanda Cuba (34)Appointed 1 January 2011» Financial and investment

expertise» Empowerment and

transformation know-how» Corporate leadership

11

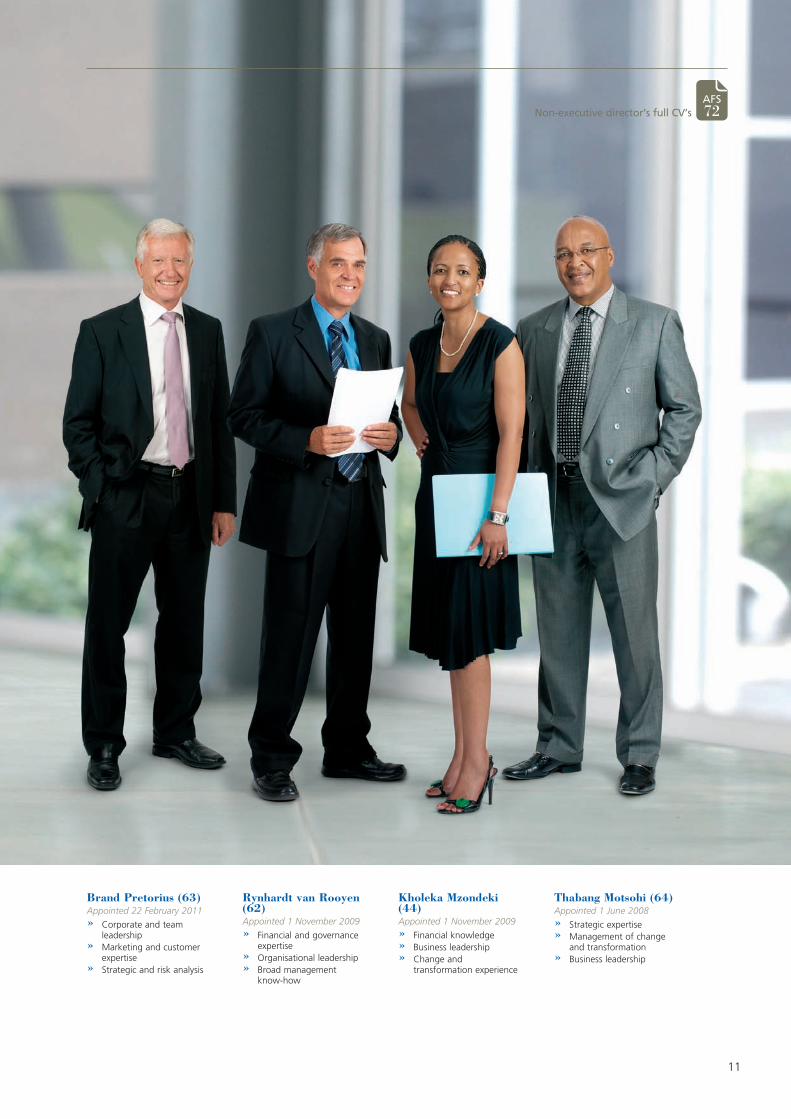

Rynhardt van Rooyen (62)Appointed 1 November 2009» Financial and governance

expertise» Organisational leadership» Broad management

know-how

Kholeka Mzondeki (44)Appointed 1 November 2009 » Financial knowledge» Business leadership» Change and

transformation experience

Brand Pretorius (63)Appointed 22 February 2011» Corporate and team

leadership» Marketing and customer

expertise» Strategic and risk analysis

Thabang Motsohi (64)Appointed 1 June 2008» Strategic expertise» Management of change

and transformation » Business leadership

AFS 72Non-executive director’s full CV’s

12 ANNUAL INTEGRATED REPORT 2011

Chairman’s statement

Overview

The Reunert group recorded a satisfactory performance under challenging conditions this year. In various market sectors, depressed economic conditions adversely affected demand for our products and services and most of our operations faced increased competition, which put additional pressure on margins.

Change programmes which were introduced to streamline various operations and improve productivity yielded pleasing short-term benefits although on-going and close management oversight of them will be required to ensure that the improvements achieved remain sustainable in the long term. Operations actively sought opportunities to diversify revenue sources and worked hard to bring on stream products, services and systems that will add value to their offerings.

Reunert remained a strong cash generator in 2011 and we continued to seek meaningful growth opportunities that are either compatible with our leading competencies or which are sensible, strategically-aligned extensions of our existing businesses. During the year under review, ECN was acquired at a cost of some R172 million. This is a pleasing, value-enhancing addition to Nashua’s product and service offering.

Reunert’s balance sheet and key financial indicators remained robust throughout the year.

Segmental comment

All CBI-electric operations performed well this year. African Cables benefited from the South African government’s commitment to continue investing in basic infrastructure and services. Low Voltage achieved considerable success in tough export markets despite rand strength. These operations, as well as Telecoms Cables, have invested in value-added services and products that should in future further differentiate them from their competitors.

Nashua was negatively affected by the general economic slowdown and, in particular, by government-mandated reductions in mobile interconnect rates. In a mobile market which is now almost fully mature, various cost-reduction initiatives were initiated.

Lower interconnect rates impacted directly on the business’ least-cost routing offering. The board believes that the acquisition of ECN was an important, timely acquisition that will enable Nashua to retain its market leadership by substituting least-cost routing with a voice-over-internet-protocol offering.

Reutech’s diverse operations ended 2011 well positioned to take advantage of new opportunities both locally and internationally. In 2012, sales of mining radar systems are expected to continue building on the successes achieved in 2011. Renewable energy is an emerging sector in which the group is planning to play a leading role.

Corporate governance and sustainability

The board is fully cognisant of its responsibility to the company. In discharging our obligations, both legal and moral, we recognise the roles and rights of all major stakeholders including shareholders, customers, employees, suppliers, government and their various representative bodies. We seek to achieve equity and fairness as we continue to pursue an inclusive strategy for sustainable performance across the group.

The directors and management of the group aspire to sound governance principles and practices in all of our activities. We foster respect for ethical business practices and expect common sense and transparency to underpin our quest to be a responsible corporate citizen.

We are committed to the King Code of Governance Principles 2009 (King III). We present the board’s review of our progress against these standards in the corporate governance report starting on page 56. We provide explanations in those instances where we presently do not comply.

Reunert has complied with the requirements of the new Companies Act, 2008 since it was introduced on 1 May 2011. Senior executives and management throughout the group are required to attest annually in writing that they comply with relevant laws and regulations, most notably the Competition Act.

In terms of our business structure and organisational philosophy, we are in the process of enhancing Reunert’s federal model which has historically provided a high level of decentralised authority and operating autonomy to our various businesses. While our goal is to retain all of the positive aspects of this decentralised structure, we will strengthen it going forward by centrally synchronising group-wide values, governance standards and policies and procedures relating particularly to upholding our leading brands and the effectiveness of our risk management, human resources and financial and accounting functions. As a consequence, while

Trevor MundayChairman14 November 2011Sandton

Leadership

13

our operating subsidiary boards will retain essential aspects of authority, the role and scope of the group executive committee will be substantially elevated and strengthened.

During the year under review, the terms of reference and composition of the board and its various committees were reviewed and amended. The risk committee was established as a separate entity and a social, ethics and transformation committee was constituted in accordance with the requirements of the new Companies Act. This committee is in the formative stages of its activities.

The non-executive members of the board, individually and collectively, offer wide-ranging experience and knowledge both to the board and the various committees on which they serve. From a transformation perspective, four of our nine non-executive members are black, three of them women. I am grateful to all members of the board for their diligent and committed approach to their duties in what has been a challenging year.

To ensure the group’s sustainability and its moral licence to operate in South Africa, it is imperative that we improve our transformation credentials, especially by appointing more senior management from designated groups. We have an inspiring pipeline of talented black professionals at our middle-management level and we must ensure that they are nurtured, retained and developed to their full potential. We can, and must, do better in this respect and, as a result, the performance criteria for incentive schemes throughout the group are being altered to ensure heightened management focus and success in this critical area.

We are appreciative of the continuing sound relationship with our lead empowerment partner, the Peotona group, and are particularly grateful for their active contributions to various aspects of our transformation ambitions.

The Reunert College remains an important part of our investment in education and in developing our youth. An independent survey commissioned during the year highlighted various aspects of the college’s activities where improvements are both desirable and necessary. These will be attended to and implemented in the year ahead.

We are well aware of our responsibilities towards the environment and communities that may be affected by our operations. We strive, in all respects, to minimise or eradicate any negative impacts our operations may have. The group has a low to medium environmental impact but, as we position ourselves to become a player in providing renewable energy, it is incumbent on all Reunert operations to implement clean energy solutions wherever feasible.

Prospects

The South African economy and those of most of our export markets remain fragile and 2012 is expected to be yet another challenging year. We will continue to promote innovation, a commitment to meeting our customers’ requirements, sound governance principles and a people-oriented culture.

The board has the utmost confidence in the group’s new executive leadership team with its balance of deep understanding of the group and fresh perspectives, and is satisfied that chief executive David Rawlinson, and his senior team possess the skills,

knowledge and vision needed to develop and grow our various businesses.

Subject to prevailing economic conditions not worsening, we anticipate achieving growth in earnings in the year ahead.*

Directorate

At the annual general meeting held on 8 February 2011, Mr Brian Connellan and Mr Bobby Makwetla retired from the board. Brian served as a member for twelve years and Bobby just a year less. Brian’s and Bobby’s contributions to the board during their tenure are deeply admired and appreciated.

Brian set extremely high standards as a non-executive director and his business acumen, probing questions and staunch defence of ethical conduct, sound governance and fairness will be remembered. We thank him and wish him and Merle a healthy and happy retirement. Bobby always stood out as a gentleman and we valued his well-considered counsel and experience. Our very best wishes accompany him and Angie in their retirement.

Ms Yolanda Cuba and Mr Brand Pretorius joined the board as independent non-executive directors early in the year. We welcome them.

Prior to their appointments, an exercise was undertaken to analyse the skills, knowledge and experience profile of the board and its members. Certain requirements in terms of strategic competencies and marketing and financial management capabilities were identified. Yolanda and Brand both bring varied and valuable attributes to the board and their respective appointments admirably address these requirements.

As announced on the Stock Exchange News Service at the

time, chief executive Nick Wentzel left Reunert under a mutual separation agreement on 21 September 2011. We wish him well in his future endeavours. On that date, financial director David Rawlinson was appointed as chief executive and Manuela Krog was appointed as financial director. We are delighted that Manuela has joined the board. We welcome both David and Manuela to their new roles and wish them much success.

On 14 October 2011, executive director Gerrit Oosthuizen left Reunert under a mutual separation agreement. We also wish Gerrit well in his future endeavours.

Dividend

The board remains committed to returning value to shareholders. Given the group’s strong cash reserves, we are pleased to declare a final cash dividend for the year of 253 cents per share. With the interim cash dividend, announced in May 2011 of 77 cents per share, this translates into a total payout for 2011 of 330 cents per share (2010: 287 cents per share).

Appreciation

I thank the members of the board and our executives and employees for their hard work and contribution to Reunert during the past year. Their commitment and energy in a demanding year is highly appreciated. We in turn thank our customers and various business partners for their support and assure them of our continuing quest for mutually beneficial relationships and the shared pursuit of lasting value.

* The financial information on which the above forecast is based has not been reviewed or reported on by the company’s external auditors.

IR 56Corporate governance sectionReunert College

14 ANNUAL INTEGRATED REPORT 2011

Executive directors

Leadership

David Rawlinson (62)Chief executiveAppointed to the board in 1992 and on 21 September 2011 as chief executive» Strategic vision» In-depth understanding of

the Reunert group» Organisational leadership

experience

Manuela Krog (42)Financial directorAppointed to the board 21 September 2011» Wide-ranging business and

industry knowledge» Financial expertise» High-level strategic planning

Pat Gallagher (61)Executive directorAppointed to the board in 1993» Practical operational leadership» In-depth understanding of the

Reunert group» Top-level strategic thinking

AFS 73Executive director’s full CV’s

15

Chief executive’s report

Transformation

The group is underperforming in certain of its transformation objectives. We will ensure progress on our transformation targets for management control, employment equity and skills development by sharpening our focus on these goals and by incentivising executives to reach these targets. These are areas that, given our reliance on human capital and indeed government business, have been prioritised for significant improvement.

Key performance indicators

Our reporting against key performance indicators has traditionally been dominated by financial values, although we have actively managed our environmental and social performance in each of our operations. In 2012 the group will begin to formulate broader non-financial key performance indicators to focus our reporting in these critical areas.

The environment

There were no material environmental incidents during 2011. Despite the fact that 36% of our business is in the manufacturing field, the group managed to lower its electricity consumption by approximately 5%. Since 2009 the unit cost of electricity has increased 50% and more focus will be placed on energy management in the year ahead.

Our people, our value

The past year has been a challenging one for the Reunert group.

We have undergone changes at operational leadership level while facing challenges at all of our operations and in all of our markets. These challenges have thoroughly tested our mettle. I am pleased to be able to report that in 2011 Reunert overcame these challenges and enters the new financial year in robust good health with reinvigorated leadership at the head of all its operations.

The Reunert that enters 2012 is one that has profound confidence in its board, its management and its people. The recent executive changes have confirmed the depth of management talent within the group. Our management teams have eagerly embraced the opportunities and responsibilities assigned to them. As group management, we are well aware that our ability to continue creating value into the future is in the hands of our talented and dedicated people.

We also emerge from the year confident of our products, our pricing, our solutions and our systems. As a result, we have confidence in the sustainable value we believe we can create for all of our stakeholders, notwithstanding the tough economic environment and specific risks we face in our individual markets.

The philosophy that underpins the group and that is part of the fibre of each of our operations is the “glue” that binds together the diversified businesses of the group. These Reunert values include respect for each other, our customers and partners and a deep-rooted desire to innovate and work harder to be the best, lowest-cost provider of world- class products and solutions.

Given the important unifying effect of values-driven leadership and behaviour, in the year ahead we will develop our “common truths” through consultation and by entrenching our values across the group. In tandem with this values process, we will also strive to communicate respectfully and openly with our stakeholders, broadening this engagement beyond our shareholders and the investment community. To this end we will initiate a more structured, frank and mutually beneficial engagement with employees, suppliers and partners as well as communities, customers and civil society.

Electricity consumption

2011 2010 2009kWh GJ kWh GJ kWh GJ

CBI-electric 42 065 890 151 437 42 738 432 153 858 47 421 624 170 718Nashua 8 435 572 30 368 10 667 080 38 401 8 152 779 29 350Reutech 5 093 818 18 338 5 277 569 18 999 5 074 523 18 268Other 970 203 3 493 1 065 217 3 835 930 115 3 348

Total 56 565 483 203 636 59 748 298 215 094 61 579 041 221 685

“The Reunert that enters 2012 is one that has

profound confidence in its board, its management

and its people.”

ANNUAL INTEGRATED REPORT 201116

Leadership

Overview of group financial performance

Revenue for the year has remained relatively static, with an increase of 2% from R10,7 billion to R10,9 billion. Operating profit, on the other hand, increased by 10% to R1,4 billion, while normalised headline earnings per share rose 14% to 590,0 cents.

The abnormal item of R346,4 million relates to the gain on the sale of the NSN investment, which led to earnings per share increasing by 60% to 809,0 cents. Normalised headline earnings per share increased 14%, compared to a 10% rise in operating profit. This was due to the impact of the share buy-back programme concluded in February 2011.

The solid top-line earnings growth achieved by our electrical businesses demonstrated the counter-cyclical ability of these operations to contribute significantly to revenue and profit.

The Nashua operations were not able to achieve revenue growth mainly due to the reduction in the interconnect rates and Pansolutions exiting the Panasonic consumer business. Voice-over-internet-protocol (VoIP) specialist ECN was bought during the year and successfully integrated into the group.

CBI-electric

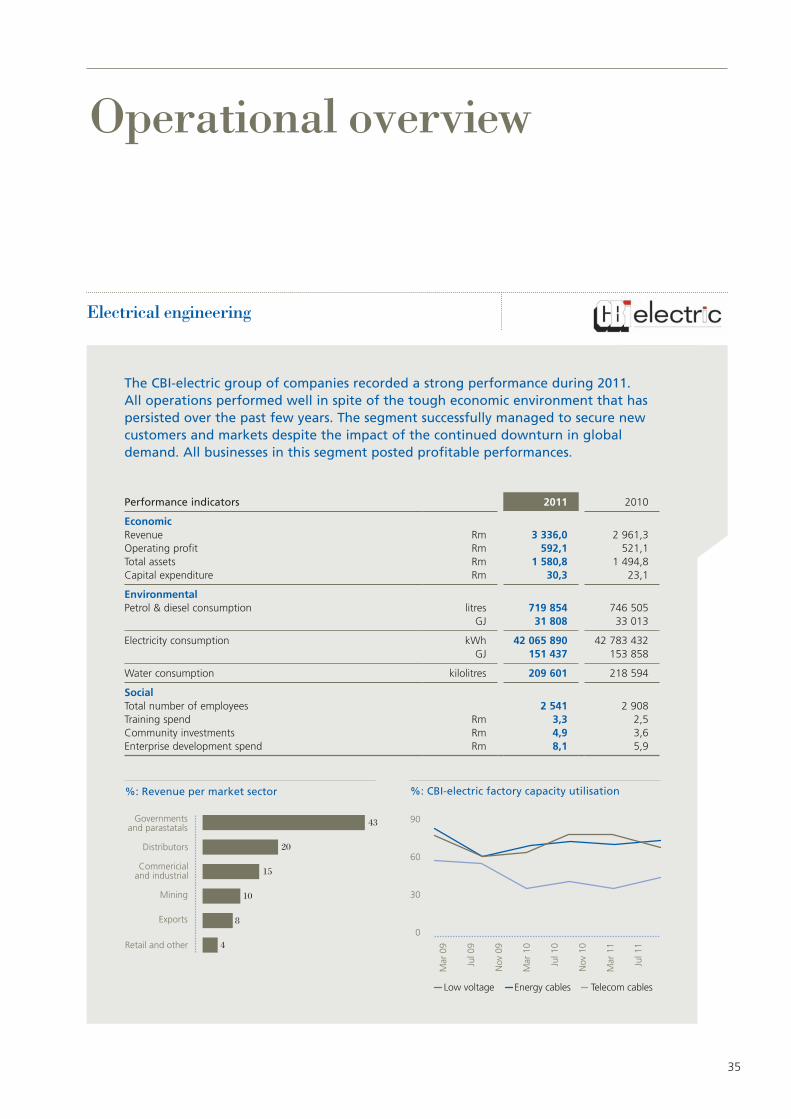

The CBI-electric group of companies recorded a strong performance during 2011. All operations performed well in light of the tough environment that has persisted over the past few years. Revenue increased by 13% to R3,3 billion and operating profit improved by 14% to R592,1 million. This is a pleasing performance with both the Cables and Low Voltage operations retaining or increasing market share. The stringent and ongoing focus on efficiencies and cost containment allowed the division to improve margins.

The demand for energy cables has continued at reasonably buoyant levels. The price of copper has remained at a high, but relatively stable level during the year. The higher revenue achieved at these copper prices has had a small impact on margins as we have continued to keep copper stocks at levels as low as possible. This strategy minimises stock losses should the price of copper reduce. In 2011 the power installation operation showed strong growth and is expected to contribute some 25% to revenue by 2014.

Low Voltage had a pleasing year, increasing turnover by 9% and operating profit by 18%. The export performance was good, given the state of markets that were – without exception – suffering the ongoing effects of the global financial crisis. While difficulties were encountered in Germany, where the sales office was closed and operations relocated to Sweden, the operation in Australia achieved record sales. Domestically the new housing, commercial, industrial and residential refurbishment markets all showed little growth.

In 2011 Low Voltage acquired ITmatic, a system design and system integrator with in-depth technical expertise and a presence throughout Africa. In the new year it is anticipated that ITmatic will make a healthy contribution to revenue and profits.

As expected, the slowdown in infrastructural spend in South Africa negatively impacted our joint venture operation, CBI-electric: Aberdare ATC Telecom Cables, in the past year. Revenues

declined sharply in the first six months of the year but improved markedly in the second half. The overall result was a small decline in turnover and profits. The business is, however, well entrenched with major local telecoms operators including Telkom, Neotel and the mobile networks. Market share in the industrial, IT, mining and power sectors has been maintained and should expand in the short term with new projects, including the National Long Haul Project, coming on line.

Nashua

Nashua performed to expectation in a quiet market. A number of acquisitions were made in the division which added to revenue, enabling marginal growth of 1% to be achieved. These acquisitions, which included four franchises and ECN, together with substantial increases in the contributions from Quince Capital and Nashua Electronics, resulted in operating profit growth of 21% to R794,2 million.

One of the highlights of the year was the acquisition of ECN on 1 June 2011. The energy and expertise of the ECN team has been beneficial to the group. They have achieved good market penetration and are currently billing over 50 million minutes a month. The conversion of the least-cost routing (LCR) business to ECN’s VoIP network is meeting our customers’ expectations. While this migration will take another 24 months, we are confident that we will retain the majority of our LCR customers during this process.

Quince Capital’s profitability returned to normal levels with the reduction in bad debts. The business is now focussed on financing our office automation and telecommunications equipment customers. We are confident that bad debts will be negligible in the year ahead.

Nashua Electronics’ sales reduced due to the operation exiting the consumer market. The addition of Kyocera Mita to its product offering has been positive and the profitability achieved was very pleasing.

Nashua Mobile had a satisfactory year despite the reduction in interconnect rates. The conversion of its LCR business to ECN’s VoIP platform is ongoing. The focus on mobile data and voice resulted in more than 27 000 net connections during the year.

The Office Automation operations experienced increased unit sales but a competitive market resulted in margins remaining under pressure. Increased offerings in the print service, data management and storage areas increased the operation’s share of the tender business. Nashua acquired the Durban and Cape Town franchises during the year, two of our most important outlets. Customer service in these important markets will be emphasised and the strategy of purchasing our larger franchises will continue in order to get closer to our customers.

Reutech

Revenue for the year decreased by 19% to R639,3 million, while operating profit was reduced by 20% to R48,7 million. The contribution from Fuchs was substantially lower due to the late receipt of an export order. The Radar company, through its mining surveillance radars, has had a successful year while the other businesses performed as expected.

Chief executive’s report continued

17

NSN

Reunert exercised its option to sell its shares in NSN in January 2011. The sale of the investment realised R793,5 million, which resulted in an abnormal profit of R346,4 million.

Capital investment and cash management

Capital expenditure investment of R99,4 million will ensure that we have both the capability and capacity to meet future demand.

Reunert has invested R306 million in acquiring four Nashua franchises, ITmatic and ECN in the past year. The acquisition of the four franchises is in line with the group’s strategy to acquire the larger franchises.

ECN has enhanced Reunert’s capability to successfully migrate LCR customers to a VoIP solution. ECN’s network enables us to provide customers with voice and data solutions while the ITmatic acquisition at CBI-electric: low voltage gives us the capability of being a systems integrator with extensive technical capabilities as well as a footprint in Africa.

Cash resources of R1 127,9 million were used to repurchase 17,1 million shares at an average price of R66,14. Returning cash to shareholders through the mechanism of share buybacks has proven beneficial to the group. We will continue to review our share buyback policy. Changes to the Secondary Tax on Companies, due to come into effect in April 2012, make this strategy more compelling.

Group cash currently used to finance the Quince asset rental book is accessible in the event that this cash is required for investment. There are various alternative mechanisms for funding the Quince book. However, using Reunert’s surplus cash to fund the book is the most earnings-enhancing method while the group has surplus funds.

The balance sheet has remained robust with cash and cash equivalents amounting to R564,6 million.

Strategic direction

The diverse nature and operations of the group have served us well during a period that has been trying for many active in the fields of electrical equipment, manufacturing, telecommunications and office automation.

The group’s executive leadership believes that its primary function is to manage and guide the extremely capable leaders at the helm of our various operations. The executive team and board will investigate ways to improve the allocation of capital and the streamlining of shared services while strengthening the federal organisational model as described in the chairman’s statement, and empowering strong operational leaders to keep improving and growing their businesses.

As I stated at the outset, Reunert’s greatest asset is its human capital and to this end we envisage investing more time and resources in creating a culture of excellence at all of our operations. To achieve this it is imperative that employees at all levels feel that their contributions to our success are valued and respected.

The year ahead

Prospects for the group are generally favourable although the economic outlook, both in South Africa and in our major export markets, remains uncertain at the time of writing. The strength of the rand favoured those operations (principally Nashua) which import and distribute products but counted against those with significant export markets, while fuelling imports of often inferior competing products.

Reutech is particularly well placed to grow revenues in 2012, having developed and improved a number of exciting new products and systems. This optimism was borne out by the signing of a number of sizeable new contracts towards the end of the year. The outlook for sales of our proprietary mining surveillance radar and radio frequency tracking technologies is especially positive.

The electrical generating capacity currently being built for Eskom has to be transmitted and distributed and this fact, together with the upgrading of the electrical networks required by municipalities, will ensure a steady demand for our electrical products into the future.

Nashua’s brand remains very strong among consumers and business customers, a fact that is recognised by those service providers with whom we will soon be entering into licence renegotiations. Convergence will continue to drive the industry and in this area, Nashua Mobile is, through the ECN acquisition, able to convert its customers to VoIP while enhancing the level and range of services. The Nashua group will continue to invest cautiously in its telecommunications convergence capability, mainly utilising ECN’s networks and development expertise.

Appreciation

My thanks are due to Trevor Munday and the board for their advice and support, as well as to the Reunert executives, operational management and employees who have energetically assisted me. I am proud to head a dynamic leadership team, one that faces the future with confidence in our ability to continue offering our shareholders, and other stakeholders, a compelling value proposition.

David RawlinsonChief executive14 November 2011Sandton

IR 34Operational reviews

IR 28Audited financial summaryAdditional sustainability information

18 ANNUAL INTEGRATED REPORT 2011

Increase value added services In a market that is becoming increasingly commoditised it is imperative that we strengthen the CBI-electric product and services offering. This will be achieved through introducing and reinforcing our investments in:

» Systems design» Systems integration» Growing maintenance outsourcing contracts for municipalities; and» Adding to our existing Power Installations and ITmatic offerings.

Explore business opportunities in Africa and Australia

In order to grow our market we need to expand our electrical offerings into Africa and to grow our operation in Australia. We will expand our sales effort into Africa and pursue synergistic acquisitions to complement our existing business in Australia.

Continued improvement of operational efficiencies

To succeed in the competitive electrical market it is imperative to be a low-cost producer. We will continue to focus on operational efficiencies through:

» Continued improvement of processes and procedures» Maintenance; and » Scrap reduction, quality and optimising material usage.

Defining our telecommunications offering for the future

In the short term our separate telecommunication businesses, being Nashua Mobile, Nashua Communications and ECN, have immediate, focused individual strategies that include the migration of LCR customers, improving service levels, customer retention and renewing network agreements.

As we move towards becoming a comprehensive telecommunications services operator, the combined customer base of close to one million customers will be the focus for integrating our communications offering.

Exploring and leveraging our customer base

Continue to evaluate and pursue cross-selling opportunities within our customer base.

Getting closer to our customers Continue to acquire the larger Nashua franchises as they become available.

Stabilise and drive value from our distribution and franchise channel

Continue to maximise the opportunities available within our distribution channels.

Pursue commercial opportunities In order to secure more predictable and sustainable revenue streams it is important for Reutech to continue its drive to pursue commercial opportunities arising from their developments. The following products will continue to be driven commercially:

» Mining surveillance radars» Set-top box manufacturing» Mine winch development; and» Security surveillance.

Strengthen partnerships with government

Continue partnerships between the government and our defence operations to provide radar and communications equipment, border surveillance and intruder detection radar.

Providing latest generation communications for South Africa’s ground forces.

Executive team focus for 2012

Group-wide focus areasRenewed focus on values-driven behaviour

We will revisit the Reunert code of conduct and continue to establish appropriate group wide values. We aim to instill pride in our employees so as to deliver sustainable profits to our stakeholders.

Diversity and transformation Transformation is a key focus area for 2012 and the years ahead. Individual targets have been set for all business operations to further transform and grow our businesses.

Engaging with our stakeholders We will continue engagement with our key stakeholders to get a better understanding of their expectations such that we can continue to build a sustainable business.

19

Leadership

Financial director’s report

Introduction

This report is intended to provide additional insight on matters of a financial nature that are not dealt with comprehensively elsewhere in the integrated report.

Normalised headline earningsNormalised headline earnings are used by the group as an indicator of its sustainable earnings. The basis for computation thereof is consistent from year to year.

The adjustment made to headline earnings to arrive at normalised headline earnings was R13,8 million. This adjustment relates to the imputed minority share of profits earned by our BEE minority shareholders, where, in terms of IFRS the risks and rewards of ownership related to these shares has not been transferred, resulting in a full consolidation of profits by the Reunert group.

Financial performance

The prolonged tough economic environment has proved to be challenging, with revenue increasing modestly to R10,9 billion from R10,7 billion. However, a focus on efficiencies and certain cost reductions have allowed for a respectable increase in operating profit from R1,3 billion to R1,4 billion.

Effective tax rate reduced by 5,2 percentage points to

24%

Highlights

Normalised headline earnings per share increased by 14% from 516cps to

590cps

Operating profit increased by 10% from R1 264 million to

R1 391 m Operating cash flows of

R662,9 m generated

20 ANNUAL INTEGRATED REPORT 2011

229,5

590,0

02 03 04 05 06 07 08 09 10 11

Cents: Normalised headline earnings per share

183,5

277,5

380,2

495,3

570,3630,1

499,5 515,7

DividendsReunert exhibits strong cash generating abilities and, as a result, the group is able to continue with its progressive and generous dividend policy. As is consistent with prior years, dividend cover is based on normalised earnings.

Investment of surplus cash in Quince asset rental bookUnder conventional models, the Quince asset rental book would be financed by external long-term borrowings. However, given that the group currently has cash balances surplus to its working capital requirements, the investment of this surplus in the Quince Capital book provides the most favourable return on the cash balances at the present time.

It is not our long-term intention to fund the book internally and the group executive is currently evaluating various options that would result in the effective utilisation of the available cash. At the financial year-end R1 126,9 million has been utilised by Quince Capital to fund its book.

Corporate activity

The group engaged in a fair level of corporate activity this year, with the acquisitions made being in line with the 2011 strategy. All acquisitions were funded using cash resources within the group.

Acquisition of Nashua franchisesWith effect from 1 November 2010 Nashua Holdings purchased 51% of the Nashua Tygerberg and Nashua Paarl and West Coast franchises for R10,6 million and R7,1 million, respectively.

With effect from 1 May 2011 the business and net assets of Nashua Durban were purchased by Nashua Holdings for R48,9 million. In terms of the purchase agreement the vendor will be paid the balance of R47,8 million six months after the acquisition date.

With effect from 1 June 2011 the business and net assets of Nashua Cape Town were purchased by Nashua Holdings for

Cash flow

Reunert’s efficient asset base, combined with strong operations, result in reported profits being underpinned by strong cash flows.

Our closing cash balance is reduced in the current year due to the R1,1 billion used to repurchase shares through a voluntary share buyback, as well as the fact that internal cash resources were used to fund the Quince asset rental book. In the main, this is reflected through the R700 million repayment of securitised borrowings.

Furthermore, net cash of R214 million was utilised for acquisitions.

Financial director’s report continued

Leadership

21

Our largest exposure to commodity price risk exists within African Cables, where copper is a significant input cost. Supply contracts with customers in the formal sector, such as Eskom and the municipalities provide for the cost of copper to be passed onto the customer. However, in respect of other customers, the group is exposed to movements in the commodity price. In certain instances, where the supply contract stipulates a fixed price, commodity futures are purchased to match the terms of the contract.

R67,0 million. In terms of the purchase agreement with the vendor, the balance of R41,1 million is payable six months after the acquisition date.

Acquisition of ECNWith effect from 1 June 2011 Reunert purchased the business and net assets of ECN for R171,9 million.

Key financial risks

Global economyWe expect that the economic conditions will continue to be challenging in the short to medium term. As such, our businesses are expected to remain under pressure in terms of their levels of activity and profitability.

Exchange rates and commodity price movementsCommodity price volatility and currency risks are two of the most significant financial risks that are faced by the group. In the current year we have seen continued buoyancy in commodity prices and then a significant weakening in the rand against all major currencies towards the end of the financial year.

To this end, the group actively monitors its exchange risk and commodity price risk on an on-going basis. Forward cover is taken on foreign exchange exposures by factoring in the impact of natural hedges that exist within the operations. Overall, the management of the exposure is based on price sensitivity, competitor practices, rand parity estimates, volatility and timing.

Potential exposures arising from exports are actively managed on a day-to-day basis. Advance payments are utilised to purchase materials for export orders and the balance is held in CFC accounts. Cover is taken in the form of forward exchange contracts, zero cost collars, or currency options, where such cover is deemed appropriate.

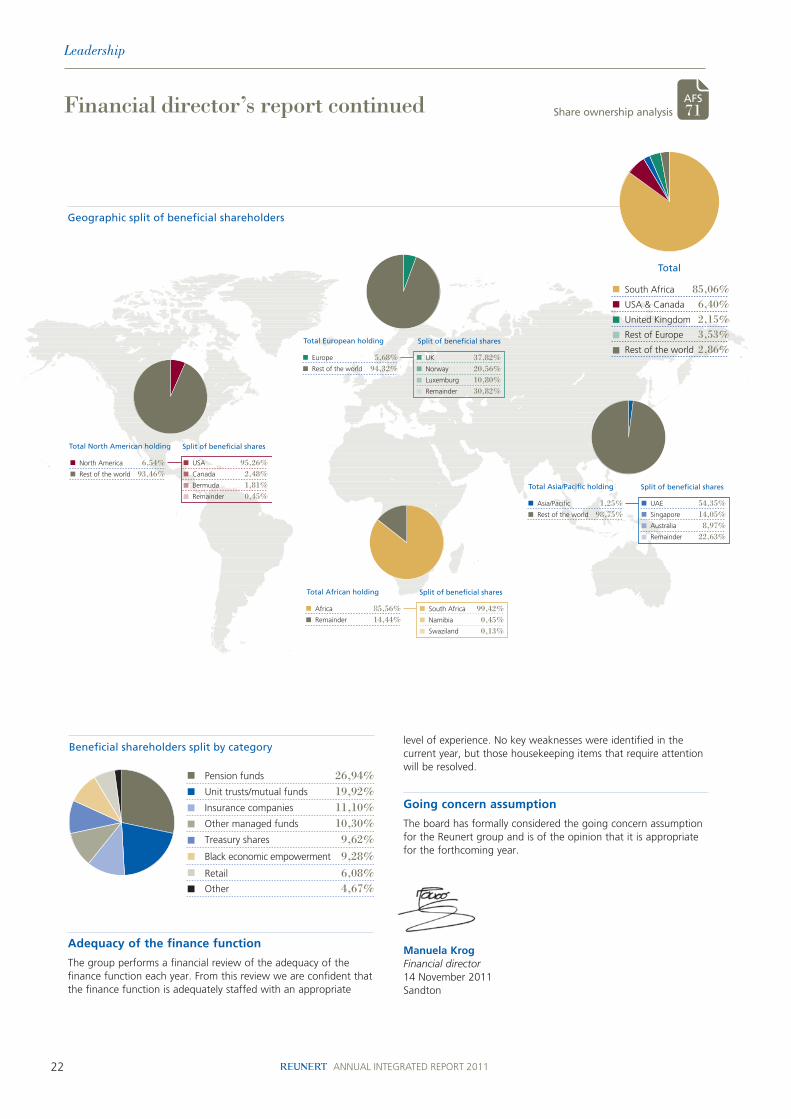

Shareholders’ statistics

Reunert shares continued to trade actively on the JSE in the past year. The total value of shares traded was R6,6 billion, resulting in 53,4% of the market capitalisation of the company being traded during the year. Some 106,5 million shares were traded in over 99 000 transactions.

Fund managers and investors have an active interest in the group, mainly due to its exposure to infrastructure spending through its electrical operations.

22 ANNUAL INTEGRATED REPORT 2011

level of experience. No key weaknesses were identified in the current year, but those housekeeping items that require attention will be resolved.

Going concern assumption

The board has formally considered the going concern assumption for the Reunert group and is of the opinion that it is appropriate for the forthcoming year.

Manuela KrogFinancial director14 November 2011Sandton

Adequacy of the finance function

The group performs a financial review of the adequacy of the finance function each year. From this review we are confident that the finance function is adequately staffed with an appropriate

Financial director’s report continued

Leadership

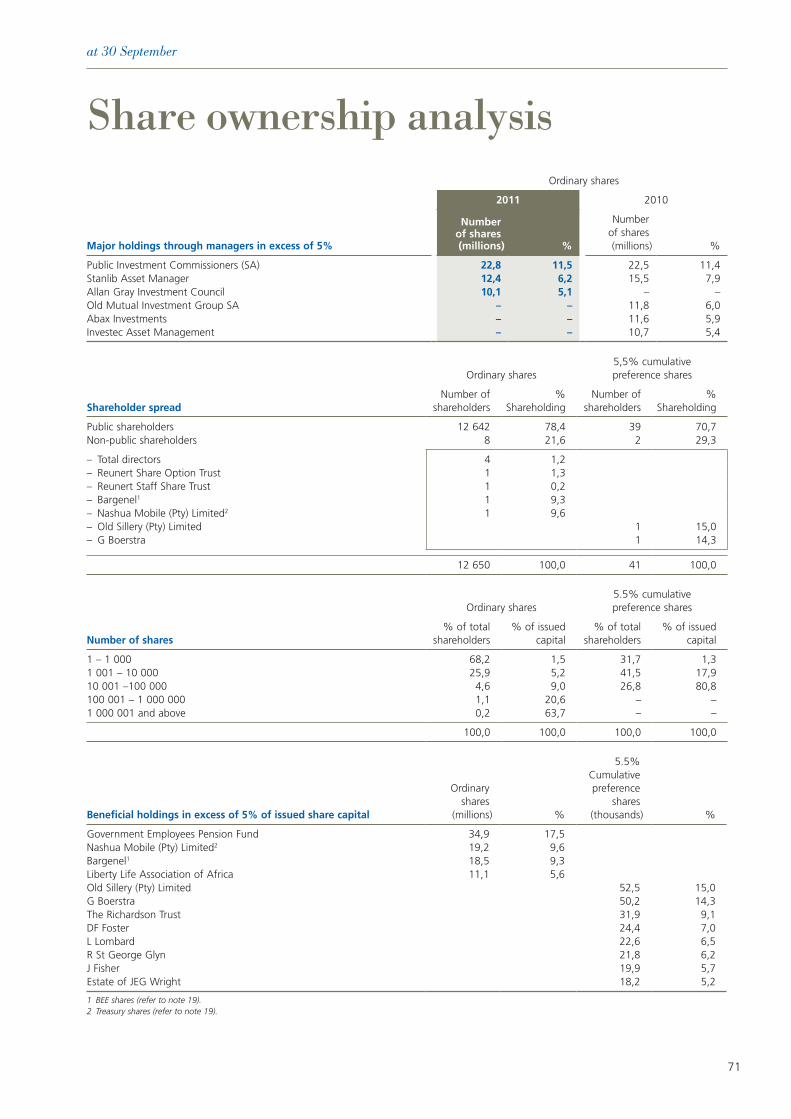

AFS 71Share ownership analysis

23

Value-added statement

Abridged financial information

2011 Rm %

2010 Rm %

% change2011

over 2010

Revenue 10 922,7 10 675,1 2 Paid to suppliers for materials and services 6 946,8 7 356,2 (6)

Value added 3 975,9 99 3 318,9 98 20 Income from investments 47,5 1 66,4 2 (28)

Total wealth created 4 023,4 100 3 385,3 100 –

Distributed as follows:EmployeesRemuneration and service benefits 1 321,3 1 252,6 Add PAYE collected on behalf of government 247,2 219,1

Gross remuneration and service benefits 1 568,5 39 1 471,7 43 7

Providers of capitalDividends to Reunert shareholders 494,3 13 456,0 14 8

Dividends to outside shareholders in subsidiaries 4,2 – 0,8 – 425 Interest paid on borrowings 6,6 – 7,2 – (8)

505,1 13 464,0 14 9

Payments to governmentTaxation on profits and dividends 425,9 407,9 VAT, customs duties and other taxes 507,1 460,4

933,0 23 868,3 26 7

Social investmentVoluntary contributions and investment of funds in the broader community, including enterprise development 40,7 1 39,7 1

Retained in the group to develop future growthAmortisation, depreciation and impairments 121,8 3 118,3 3 3 Accumulated profit 854,3 21 423,3 13 102

976,1 24 541,6 16 80

Total wealth distributed 4 023,4 100 3 385,3 100 –

24 ANNUAL INTEGRATED REPORT 2011

Abridged financial information

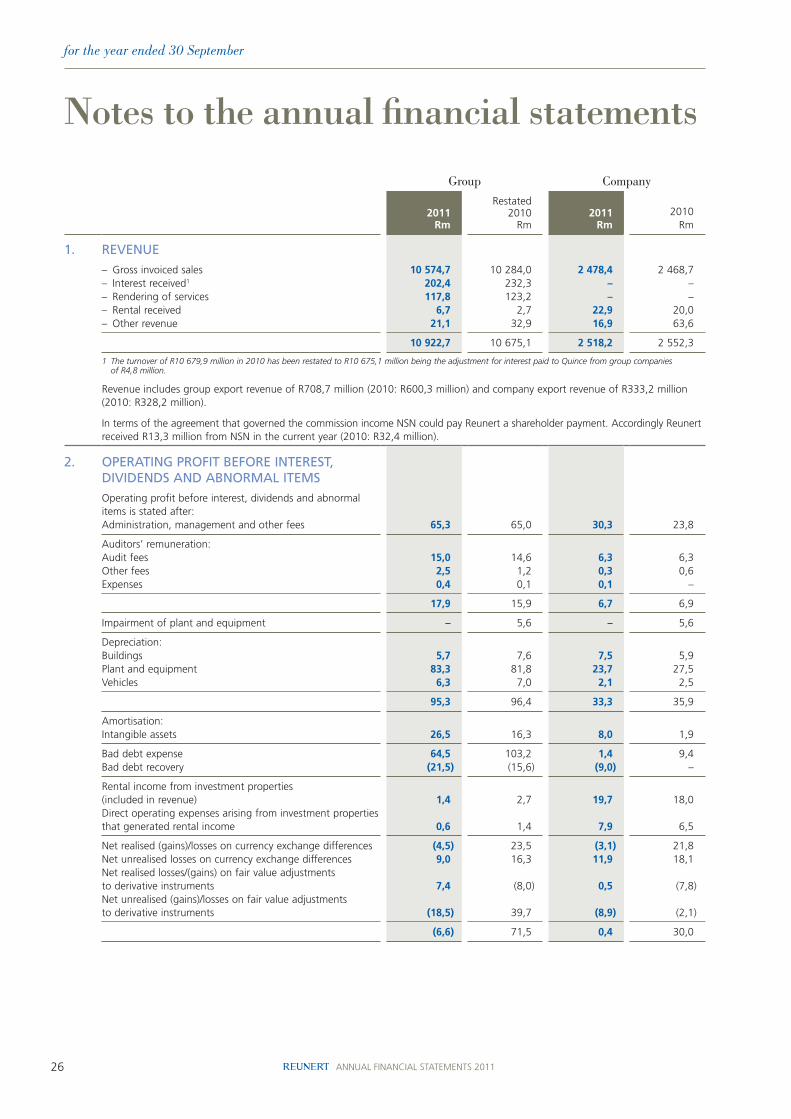

CONDENSED GROuP INCOmE STATEmENTFOR ThE yEAR ENDED 30 SEPTEmbER

Notes2011

Rm%

change

Restated2010

Rm

Revenue 10 922,7 2 10 675,1Earnings before interest, taxation, depreciation, amortisation, other income and dividends 1 472,7 12 1 320,6Other income 40,5 54,9

Earnings before interest, taxation, depreciation and amortisation (EBITDA) 1 1 513,2 10 1 375,5Depreciation and amortisation 121,8 8 112,7

Operating profit 1 391,4 10 1 262,8Net interest and dividend income 2 40,9 (31) 59,2Abnormal items 3 346,4 (34,0)

Profit before taxation 1 778,7 38 1 288,0Taxation 425,9 13 376,6

Profit after taxation 1 352,8 48 911,4

Profit attributable to:Non-controlling interests 15,7 31 12,0Equity holders of Reunert 1 337,1 49 899,4

Basic earnings per share (cents) 5 & 6 809,0 61 503,3Diluted earnings per share (cents) 5 & 6 803,3 61 498,8

Headline earnings per share (cents) 5 & 6 598,3 18 505,5Diluted headline earnings per share (cents) 5 & 6 594,1 19 501,1

Normalised headline earnings per share (cents) 5 & 6 590,0 14 515,7Normalised diluted headline earnings per share (cents) 5 & 6 585,9 15 511,1Cash dividend per ordinary share declared (cents) 330,0 15 287,0Taxation rate including abnormal item 23,9 18 29,2Taxation rate excluding abnormal item 29,7 4 28,5EBITDA as a % of revenue 13,9 8 12,9

CONDENSED GROuP STATEmENT OF COmPREhENSIVE INCOmEFOR ThE yEAR ENDED 30 SEPTEmbER

2011Rm

2010Rm

Profit after taxation 1 352,8 911,4Other comprehensive income, net of taxation:Losses arising from translating the financial results of foreign subsidiaries – (1,9)Gain on disposal of investment (348,6) –Effective portion of gains on hedging instruments 4,2 6,0Income tax relating to components of other comprehensive income (1,2) 1,2

Total comprehensive income 1 007,2 916,7

Total comprehensive income attributable to:Non-controlling interests 15,7 12,0Equity holders of Reunert 991,5 904,7

Audited financial summary

25

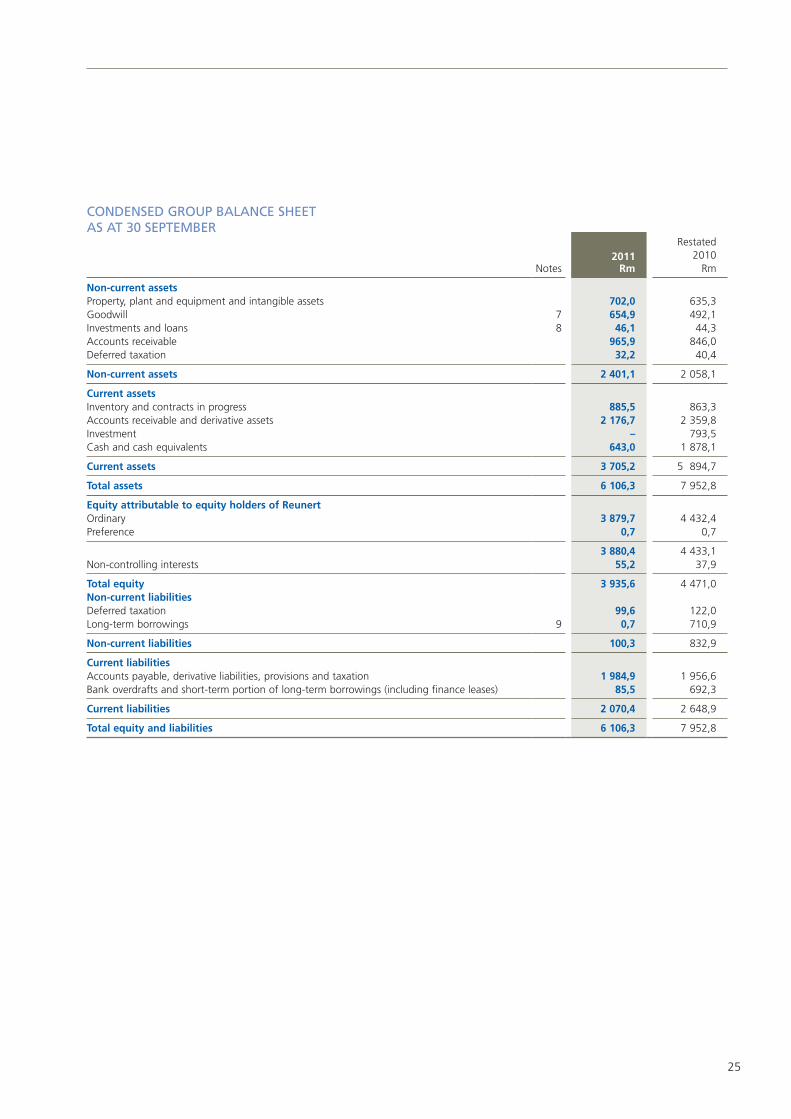

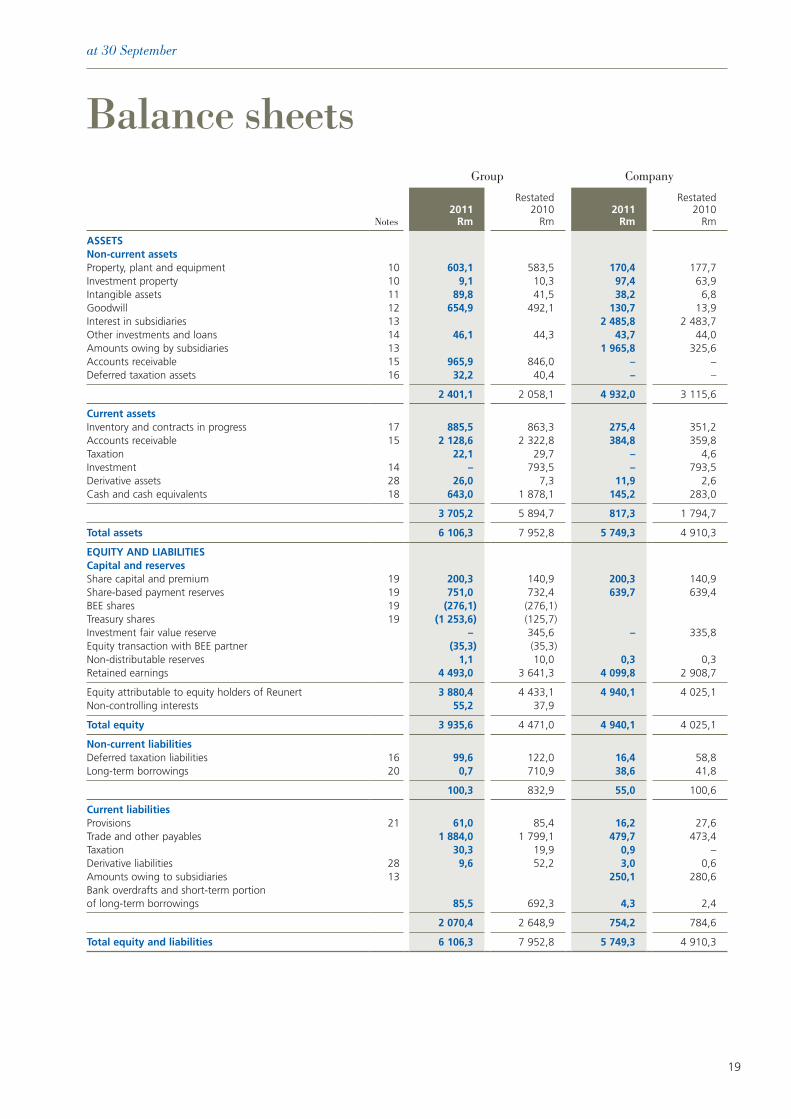

CONDENSED GROuP bALANCE ShEETAS AT 30 SEPTEmbER

Notes2011

Rm

Restated2010

Rm

Non-current assetsProperty, plant and equipment and intangible assets 702,0 635,3Goodwill 7 654,9 492,1Investments and loans 8 46,1 44,3Accounts receivable 965,9 846,0Deferred taxation 32,2 40,4

Non-current assets 2 401,1 2 058,1

Current assetsInventory and contracts in progress 885,5 863,3Accounts receivable and derivative assets 2 176,7 2 359,8Investment – 793,5Cash and cash equivalents 643,0 1 878,1

Current assets 3 705,2 5 894,7

Total assets 6 106,3 7 952,8

Equity attributable to equity holders of ReunertOrdinary 3 879,7 4 432,4Preference 0,7 0,7

3 880,4 4 433,1Non-controlling interests 55,2 37,9

Total equity 3 935,6 4 471,0Non-current liabilitiesDeferred taxation 99,6 122,0Long-term borrowings 9 0,7 710,9

Non-current liabilities 100,3 832,9

Current liabilitiesAccounts payable, derivative liabilities, provisions and taxation 1 984,9 1 956,6Bank overdrafts and short-term portion of long-term borrowings (including finance leases) 85,5 692,3

Current liabilities 2 070,4 2 648,9

Total equity and liabilities 6 106,3 7 952,8

26 ANNUAL INTEGRATED REPORT 2011

Audited financial summary continued

Abridged financial information

CONDENSED GROuP STATEmENT OF ChANGES IN EquITyFOR ThE yEAR ENDED 30 SEPTEmbER

2011Rm

2010Rm

Share capital and premium

Balance at the beginning of the year 140,9 116,0 Issue of shares 59,4 24,9

Balance at the end of the year 200,3 140,9Share-based payment reserve

Balance at the beginning of the year 732,4 679,6 Share-based payment expense and deferred taxation thereon 18,6 52,8

Balance at the end of the year 751,0 732,4Fair value adjustment reserve1

Balance at the beginning of the year 345,6 338,4 Other comprehensive income (345,6) 7,2

Balance at the end of the year – 345,6Equity transaction with BEE partner (35,3) (35,3)BEE shares2 (276,1) (276,1)Treasury shares3

Balance at the beginning of the year (125,7) – Purchases made during the year (1 127,9) (125,7)

Balance at the end of the year (1 253,6) (125,7)Non-distributable reserves

Balance at the beginning of the year 10,0 11,9 Other comprehensive income – (1,9) Transfer to retained earnings (8,9) –

Balance at the end of the year 1,1 10,0Retained earnings Balance at the beginning of the year 3 641,3 3 199,9

Profit after taxation attributable to equity holders of Reunert 1 337,1 899,4 Transfer from non-distributable reserves 8,9 – Taxation charge on transaction with BEE partner – (2,0) Cash dividends declared and paid (494,3) (456,0)

Balance at the end of the year 4 493,0 3 641,3

Equity attributable to equity holders of Reunert 3 880,4 4 433,1Non-controlling interests

Balance at the beginning of the year 37,9 26,7 Share of total comprehensive income 15,7 12,0 Dividends declared and paid (4,2) (0,8) Non-controlling interest introduced 2,0 – Other 3,8 –

Balance at the end of the year 55,2 37,9

Total equity at end of the year 3 935,6 4 471,0

1 This reserve related to fair value adjustments on financial assets classified as “available-for-sale” financial assets.2 These are shares held by Bargenel Investment Limited (Bargenel), a company sold by Reunert to an accredited BEE partner in 2007. Until the amount owing by the BEE

partner is repaid to Reunert, Bargenel is to be consolidated by the group as the significant risks and rewards of ownership of the equity have not passed to the BEE partner.

3 Commencing in August 2010, a group subsidiary purchased Reunert shares on the open market. Up to 30 September 2010, 2,1 million shares had been bought at an average price of R59,18 per share. No further purchases were made after 4 February 2011 at which time a total of 19,2 million shares had been bought at an average price of R65,37 per share.

27

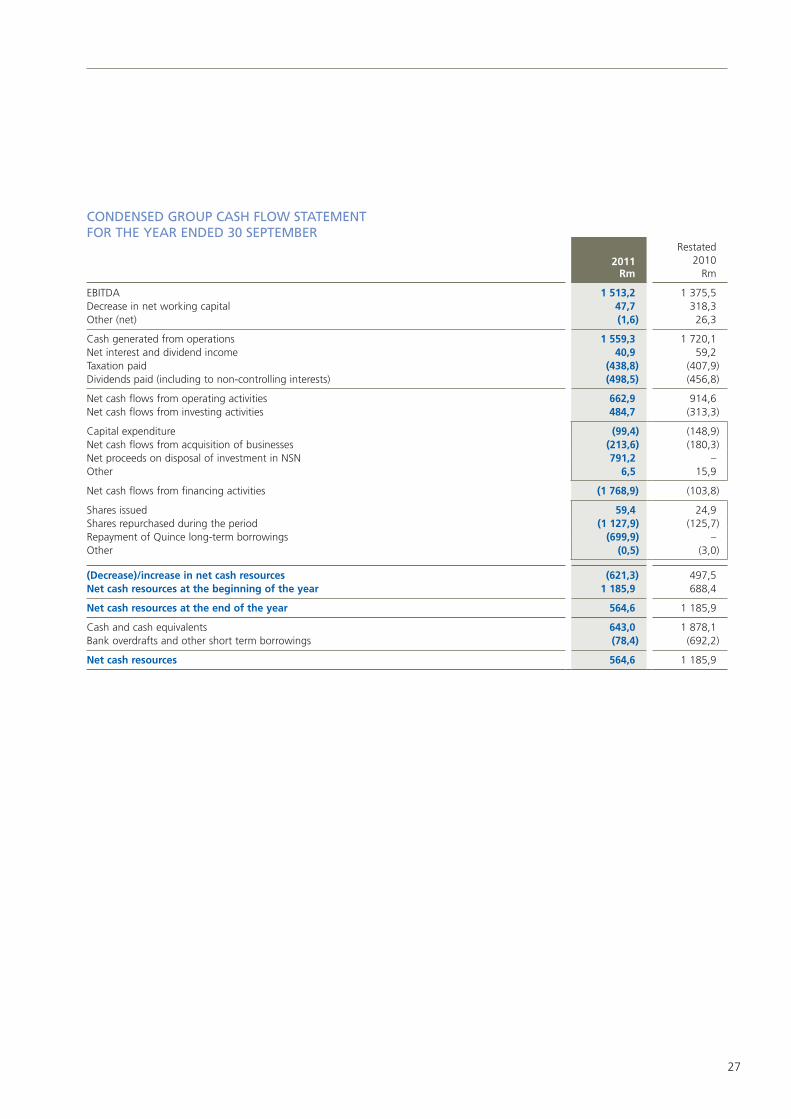

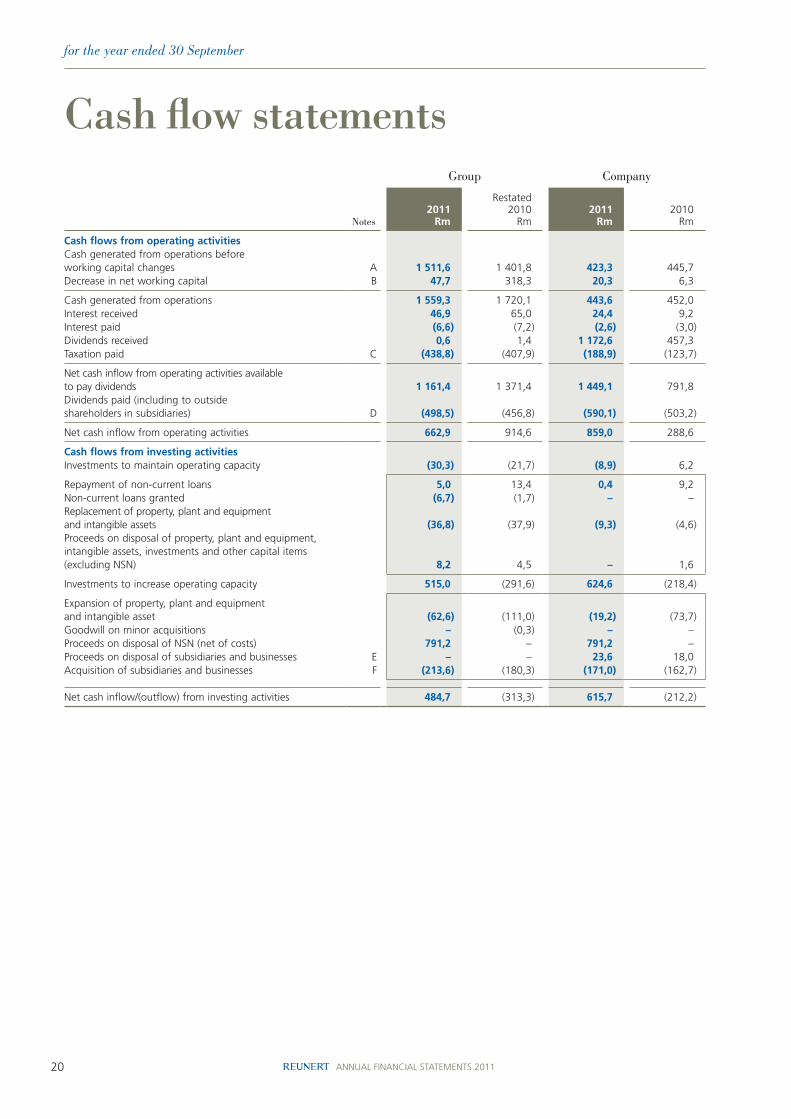

CONDENSED GROuP CASh FLOW STATEmENTFOR ThE yEAR ENDED 30 SEPTEmbER

2011Rm

Restated2010

Rm

EBITDA 1 513,2 1 375,5Decrease in net working capital 47,7 318,3Other (net) (1,6) 26,3

Cash generated from operations 1 559,3 1 720,1Net interest and dividend income 40,9 59,2Taxation paid (438,8) (407,9)Dividends paid (including to non-controlling interests) (498,5) (456,8)

Net cash flows from operating activities 662,9 914,6Net cash flows from investing activities 484,7 (313,3)

Capital expenditure (99,4) (148,9)Net cash flows from acquisition of businesses (213,6) (180,3)Net proceeds on disposal of investment in NSN 791,2 –Other 6,5 15,9

Net cash flows from financing activities (1 768,9) (103,8)

Shares issued 59,4 24,9Shares repurchased during the period (1 127,9) (125,7)Repayment of Quince long-term borrowings (699,9) – Other (0,5) (3,0)

(Decrease)/increase in net cash resources (621,3) 497,5Net cash resources at the beginning of the year 1 185,9 688,4

Net cash resources at the end of the year 564,6 1 185,9

Cash and cash equivalents 643,0 1 878,1Bank overdrafts and other short term borrowings (78,4) (692,2)

Net cash resources 564,6 1 185,9

28 ANNUAL INTEGRATED REPORT 2011

Audited financial summary continued

Abridged financial information

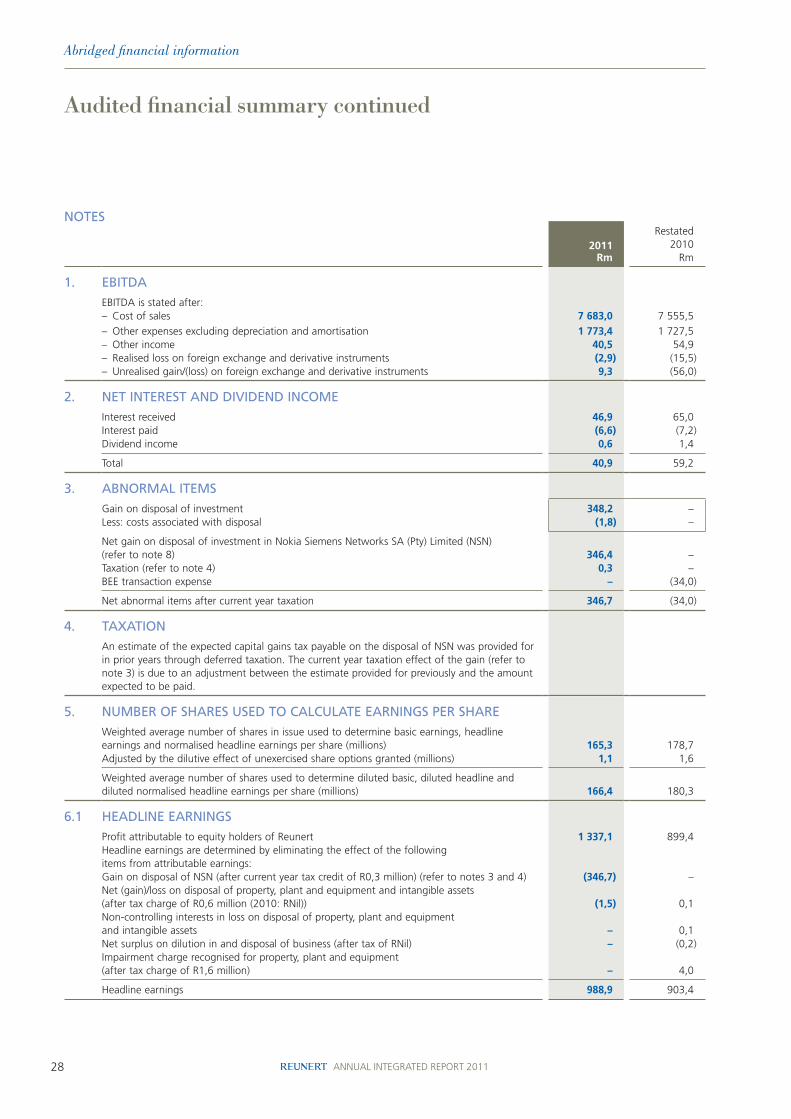

NOTES

2011Rm

Restated2010

Rm

1. EbITDA

EBITDA is stated after:– Cost of sales 7 683,0 7 555,5