Embed Size (px)

Citation preview

A N N U A L R E P O R T 2 0 0 7

Branch locations

C O N T E N T S

Board of Directors 4

Executive Management 5

Chairman’s Statement 6-7

Managing Director Message 8

Financial Highlights 9

Business Review

- Corporate Banking 10

- Private Banking 11

- Retail Banking 12

- Human Resources 13

Auditor’s Report 14

Balance Sheet 15

Income Statement 16

Statement of Cash Flows 17

Statement of Changes in Equity 18

Notes to the Financial Statements 19-57

International Bank of Qatar (Q.S.C.)

Branch locations

Suhaim Bin Hamad StreetP.O. Box 2001Doha, State of Qatar

Telephone : +974 4473700Facsimile : +974 4473710E-mail: [email protected]

Markhiya BranchBin Towar Centre, Near TV RoundaboutTel: +974 4473871

C Ring RoadNear Cinema SignalTel: +974 4473860

Salwa Road BranchSalwa Road (near Qatar Decoration Roundabout) Doha, QatarTel: +974 4473745

West Bay BranchAl Fardan Tower (next to the Ministry of Commerce),Doha, QatarTel: +974 4473050

Virgin Megastore BranchVillagio MallTel.: +974 4473952

In the Name

of Allah,

Most Gracious,

Most Merciful

His Highness

Sheikh Tamim Bin Hamad Al-Thani

Heir Apparent

His Highness

Sheikh Hamad Bin Khalifa Al-Thani

Emir of the State of Qatar

4

Board of Directors

H. E. Sheikh Hamad Bin Jassim Bin Jabor Al-Thani

Chairman

Ibrahim Dabdoub

Vice Chairman

Sheikh Jabor Bin Hamad Bin Jassim Al-Thani

Board Member

Sheikh Sultan Bin Jassim Bin Mohammed Al-Thani

Board Member

Sheikh Abdulla Bin Hamad Bin Khalifa Al-Thani

Board Member

Mohammed Ali Al-Kubaisi

Board Member

Mohammad Al-Okar

Board Member

Sheikha Al Bahar

Board Member

George Nasra

Board Member

5

Executive Management

George Nasra

Managing Director

Muhannad Kamal

Deputy General Manager

Peter Wilkes

Deputy General Manager

Bhupendra Jain

Head of Corporate Banking

Chaouki Daher

Head of Private Banking

Philip King

Head of Retail

Brian Stubbs

Head of IT

Chandramohan Pillai

Head of Administration and Facilities

Ashok Thirwani

Chief Financial Officer

6

Chairman’s Statement

of this strong performance the Board of Directors is

proposing a cash dividend for 2007 of QAR 180 million

representing 56% of issued capital.

We also witnessed strong growth in the balance

sheet which saw loans increasing by 74% to QAR

6,517 million and total assets by 61% to QAR 10,771

million. Deposits also grew to support this increase in

business activity and at the year-end stood at QAR

6,952 million, an increase of 42%.

The capital of the Bank was again increased during

the year and Shareholders’ funds at 31st December

stood at QAR 1,928 million. This strong capital base

has helped the Bank’s continued expansion of its

business with existing and new clients and increasingly

Qatar’s international profile has been increasing rapidly

over recent years across a number of fronts and there is

much excitement at the prospect of the forthcoming bid

for the 2016 Olympics following the widely recognised

success of the Asian Games and other major sporting

events.

We also remain optimistic at the future potential in the

Bank after another record year in 2007. The excellent

results demonstrate the significant progress that has been

made since 2004 when we began our partnership with the

National Bank of Kuwait as shareholders and managers

of the Bank. Net profit in 2007 of QAR 234.3 million

was 56% over 2006’s figure of QAR 150.5 million and

was seven times the level reported in 2004 representing a

compounded annual growth rate of 93%. On the back

On behalf of the Board of Directors of IBQ I am pleased to present the Annual Report for the Bank

together with the Financial Statements and the Auditors’ Report.

This was another year of real progress for the State of Qatar with GDP continuing to grow robustly. Oil

and gas continue to represent a major part of GDP by way of exports but the investment being made

in the development of down-stream processing and related projects is beginning to make an increased

contribution to growth. Other initiatives to broaden the economic base are progressing well with Qatar

now on course to becoming a knowledge-based economy.

Sheikh Hamad Bin Jassim Bin Jabor Al-Thani

7

appreciation and gratitude are also extended to His

Highness the Heir Apparent, Sheikh Tamim Bin Hamad

Al-Thani for his contribution to the well-being of the

country.

Our appreciation and thanks are also extended to His

Excellency the Governor of the Qatar Central Bank,

Sheikh Abdullah Bin Soud Al-Thani and his colleagues

for their support and guidance to the Bank.

Our staff numbers grew significantly through the year

and we expect further growth during 2008. We also

wish to extend our thanks and appreciation to the staff

for their commitment and contribution in making 2007

such a successful year for the Bank.

A key factor to our success is the continued support of

our customers. We thank them for their trust in IBQ and

we will endeavour to serve them well at all times.

Sheikh Hamad Bin Jassim Bin Jabor Al-Thani

with international companies who are looking to

develop their own business connections in Qatar. Also

important has been the fact that NBK offers IBQ and

its customers an international dimension through its

overseas network. NBK’s confidence in IBQ has been

demonstrated by its increased shareholding which now

stands at 30%.

As well as the excellent financial performance, the

Bank’s infrastructure has continued to grow with one

further branch opened during the year and one ready

to open early in 2008. This brings IBQ up to 6 branches

with further additions planned during 2008 and 2009

supported by significant increases in the number of IBQ

ATM’s. These will enhance the Bank’s increased emphasis

on retail banking which has also been seen with major

product launches such as our Mortgage scheme and our

co-branded credit card with Virgin Megastore. We expect

to see more such initiatives in 2008.

We would like to express our sincere gratitude and

appreciation to His Highness the Emir, Sheikh Hamad

Bin Khalifa Al-Thani for his wise leadership of the State of

Qatar and his support of the banking sector in Qatar. OurChairmanMarch 2008

8

to a QAR 0.7 million recovery in 2006. Taking into account total provisions, risk reserve and interest in suspense, non-performing loans are 780% covered. Non-performing loans account for 0.21% of the loan book compared with 0.60% in 2006.

Balance Sheet

The overall balance sheet grew to QAR 10,771 million largely from the increase in the loan book but also through increased inter-bank activity.

The increase in capital during the year resulted in a capital adequacy ratio of 16.9% which compares withthe Qatar Central Bank minimum of 10%.

Shareholder Value

IBQ’s return on average equity for 2007 was 14.83%. Basic earnings per share increased to QAR 7.86 compared to QAR 6.11 in 2006.

This past year IBQ was recognized by The Banker Middle East magazine as the bank offering the “Best Customer Service Middle East 2007”. We are extremely grateful for this prestigious award as it is evidence of our unwavering focus on giving our customers the personalized banking service they deserve.

George NasraManaging Director

Managing Director Message

Profitability

At IBQ we are committed to providing our customers with the very best banking experience possible. This devotion to excellence is reflected in the growth we achieved in 2007.

IBQ’s operating income at QAR 327.3 million was 40 % above 2006. The post provisions profit of QAR 234.3 million was a record for the Bank and represented a 56% increase on 2006.

Net interest income was QAR 255.9 million, an 29% increase over 2006. The increase was a result of higher risk assets including a 74% increase in year-end loans and advances. Net interest margins also improved during the year.

Fees, commissions, foreign exchange and other income also showed an upward trend with a rise to QAR 71.5 million compared with QAR 35.7 million in 2006. We saw an increase in our trade finance activity with letters of credit, guarantees and acceptances increasing by 63% from QAR 2,571 million to QAR 1,573 million. This benefited both fee income and exchange business. General and administrative expenses and depreciation rose to QAR 96.5 million. This was in line with expectations and reflects investment in the Bank’s infrastructure and human resources to support growth in the business. The Statement of Income reflects investment impairment losses of QAR 1.8 million resulting from the significant drop in the Qatar stock market which mirrored markets throughout the region affecting investors across the board. However the Bank also saw a net recovery of impairment losses on loans and advances of QAR 5.3 million compared

9

Financial Highlights

10

Business Review

Corporate Banking

At IBQ our relationships

are our best investments

and success means

anticipating our clients’

needs. In 2007 the

Corporate Banking

team took these existing

relationships and gave

our clients expanded

options, services, and products. Through our long-

standing relationship with the National Bank of Kuwait,

and its 18 international branches and representative

offices, we are the only local bank to offer our clients

this level of expanded service on a truly global scale.

Corporate Banking achieved many successes in 2007

as our treasury income increased in concordance with

our treasury and trade capacity. We also doubled our

loan portfolio, created a syndication department,

and diversified income generated from mainly asset-

based and fee income. Our Corporate Banking

team also focused on building their new client base

by establishing relationships with all major private

corporations in Qatar.

Attracting new corporate business to the bank was

a priority to IBQ in 2007 and will continue to be so

in the future. As we build new relationships we will

also continue to set new standards of excellence in

Qatar’s banking industry. Our goal is to more than

match our clients’ expectations. We want to exceed

them. As our clients’ needs expand, we will be

ready and prepared to assist them. The vision for

our Corporate Banking remains unchanged. IBQ will

offer the highest possible standard of service, staff,

and integrity.

Strong relationships and outstanding customer service were the foundation of IBQ’s Corporate Banking

success in 2007.

Our range of Corporate Banking services includes asset finance along with trade, project, and working

capital finance. Our Treasury Department provides clients with money market services and competitive

pricing for both interest rate and foreign exchange. Each of these sectors demonstrated significant

growth in 2007 and has continued to position IBQ as a trusted source of sound financial stability amongst

its corporate client base.

11

Business Review

Private Banking

IBQ has deep roots in Qatar’s private banking industry and we take special pride in the relationships we

have built over the last fifty years. These longstanding relationships have developed into second and

third generation clients and are an integral part of our banking success.

We offer our customers

full onshore and off-

shore banking, invest-

ment, financial products,

and real estate services.

In 2007 we added

several private banking

specialists whose roles

are solely dedicated to assisting our clients in all areas

of their financial matters. This team is supported by

regular visits from international investment experts

who personally present elite investment opportunities

to our clients.

In 2007 we continued our tradition of offering our

Private Banking clients exceptional services tailored

to their needs and delivered with the highest

standards of personal attention and confidentiality.

Our customers are part of our family and treated

accordingly. This year we dedicated an exclusive floor

in our corporate headquarters to accommodate our

valuable private banking customers. Now when they

visit our office, they are welcomed by a face and a

name they know. And as always, when they call us

by phone, they are talking to trusted advisors

While our customers are local, their banking needs

are global. IBQ’s partnership with the National Bank

of Kuwait (NBK) allows our clients the privilege of a

wide regional and international network. Our NBK

partners in each of these locations work directly

with us to ensure our customers have access to the

same wide range of exclusive banking services they

have come to expect from us in Qatar.

IBQ’s Private Banking department is a trusted

source of confidential, professional expertise in

Qatar. We believe in building relationships that are

handed down from generation to generation. This

is a privilege and responsibility we take seriously and

relationships we are committed to enhance.

12

Business Review

Retail Banking

IBQ’s Retail Banking division experienced unprecedented growth in 2007. Significant progress was made

against our five-year strategic plan in all areas of this division. Our ongoing goal is to become the lead-

ing retail bank in Qatar by offering distinctive retail products and services to our customers that reflect

their individual banking needs. We made outstanding progress on that goal in 2007 by offering a diver-

sified range of innovative products and services.

Customers are at the core of our business and in 2007

we continued to find innovative ways to serve our rapidly

growing family of loyal customers.

During 2007 IBQ launched the innovative "Win a Home"

campaign which reinforced our position as putting the

customer at the core of our business. The campaign was

the first of its kind in Qatar, offering customers who start

a relationship with the bank by transferring their salary

the opportunity to win an apartment valued at one million

Qatari Riyals in the prestigious West Bay area. This campaign

immediately garnered enormous attention and popularity

and concluded with an exciting draw in January, 2008

when one lucky customer’s name was picked.

In April 2007, the bank introduced mortgage loans offering

competitive terms and conditions. To deliver on its promise

to make customers experience first class service, IBQ

forged partnerships with key developers in Qatar's real

estate industry to give our customers an even wider range

of choice and flexibility. This is a major distinguishing factor

in the IBQ mortgage offering.

Taking this experience to new heights IBQ introduced

a specially branded mortgage vehicle, the IBQ

Hummer, which brings the mortgage team to the

customer, ensuring that more people have access to

the advice they need when and where they most

need it. To enforce the element of transparency

and customer care, we also offer customers a

special mortgage calculator to assist customers in

calculating and budgeting for their mortgage payments.

The VIP IBQ card was another milestone for IBQ during

2007. In November, in collaboration with Virgin Megastore,

the bank launched Qatar’s first co-branded entertainment

credit card, the Virgin Important Person (VIP) - IBQ

MasterCard. This launch represents an exclusive three-

year agreement between IBQ and Virgin Megastore to

give Qatar a VIP customer loyalty programme unlike any

other. The VIP IBQ card provides customers with discounts

not only at Virgin Megastore but a host of other partners

from the lifestyle, leisure and entertainment industries.

IBQ also opened its first ever Kiosk Branch inside the Virgin

Store at Villagio Shopping Mall with an instant issuance

facility of the VIP IBQ card so customers can benefit from

the discounts instantly.

In 2007 IBQ continued to expand and enhance its outreach

to customers by increasing our ATM network to service 13

strategic locations with cash deposit functionality. We also

continued to improve our alternate delivery channels by

upgrading the Call Center to accommodate the increase

in volume of incoming calls.

SMS banking was also introduced in 2007 for our customers

who prefer the ultimate in on-the-go banking services.

2008 promises to be another significant year for IBQ, as we

continue to roll out our plans for expansion in Qatar, and

continually strive to give our customers a truly rewarding

experience for starting a banking relationship with us.

13

Human Resources

The foundation of IBQ’s success lies in the professionalism and dedication of its employees. The value

of our employees is reflected in the service and products we offer our customers. As the bank continues

to grow, we continue to heavily invest in the development of our employees and their skills, as we un-

derstand how crucial this is in achieving our business objectives.

Our main focus during 2007 was to attract high

caliber enthusiastic talent in all areas of business to

help the Bank realize its aggressive plans for growth.

The number of our employees almost doubled to

reach 285 at the end of December 2007.

During 2007, the Bank set out a rigorous training and

development plan with the objective of upgrading the

skills of its employees to create a knowledgeable and

well experienced workforce that is capable of taking

IBQ forward. Training opportunities included courses

in banking at the College of North Atlantic, training

in leadership skills, workshops on customer services

and negotiation skills, in addition to attendance at

conferences and seminars both locally and abroad. IBQ

also offered staff fully paid tuition at courses of their

choice to improve their language or communication

skills or any courses for their own personal interest.

Qatari Development Program

As a rapidly growing bank, we are committed to support

the nationalization drive of the country and develop the

potential Qatari talent who will one day become

Qatar’s future financiers and decision makers. As such

we embarked on an aggressive Qatarization plan with

the aim of attracting and recruiting local talent. We

developed a unique Qatari Development Program which

offers Qatari secondary school and university graduates

a customized career development path that is tailored to

suit each applicant’s skills and interests individually. Our

Qatari Development Program succeeded in attracting a

pool of talented young Qataris who have joined us in

different capacities and are pursuing a career in banking.

IBQ recognizes the value of employee development will

continue during 2008 to reinforce its values of integrity,

collaboration and enthusiasm to create a workplace

environment that fosters learning, training and

empowerment for all employees.

Business Review

14

Auditor’s Report

INDEPENDENT AUDITORS’ REPORT TO THE SHAREHOLDERS OF

INTERNATIONAL BANK OF QATAR (Q.S.C.)

Report on the financial statements

We have audited the accompanying financial statements of

International Bank of Qatar (Q.S.C.) (the “Bank”) which comprises

the balance sheet as at 31 December 2007, and the statements of

income, cash flows and changes in equity for the year then ended,

and a summary of significant accounting policies and other

explanatory notes.

Directors’ responsibility for the financial statements

The Directors are responsible for the preparation of these financial

statements in accordance with International Financial Reporting

Standards and Qatar Central Bank regulations. This responsibility

includes: designing, implementing and maintaining internal control

relevant to the preparation and fair presentation of financial

statements that are free from material misstatement, whether due

to fraud or error; selecting and applying appropriate accounting

policies; and making accounting estimates that are reasonable in

the circumstances.

Auditors’ responsibility

Our responsibility is to express an opinion on these financial

statements based on our audit. We conducted our audit in

accordance with International Standards on Auditing. Those

standards require that we comply with ethical requirements and

plan and perform the audit to obtain reasonable assurance whether

the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence

about the amounts and disclosures in the financial statements. The

procedures selected depend on the auditor’s judgment, including

the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk

assessments, the auditor considers internal control relevant to the

entity’s preparation and fair presentation of the financial statements

in order to design audit procedures that are appropriate for the

circumstances but not for the purpose of expressing an opinion on

the effectiveness of the entity’s internal control. An audit also

includes evaluating the appropriateness of accounting policies used

and the reasonableness of accounting estimates made by the

management, as well as evaluating the overall presentation of the

financial statements.

We believe that the audit evidence we have obtained is sufficient

and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material

respects, the financial position of the Bank as of 31 December

2007 and of its financial performance and its cash flows for the

year then ended in accordance with International Financial Reporting

Standards and Qatar Central Bank regulations.

Report on other legal and regulatory requirements

We have obtained all the information and explanations which

we considered necessary for the purpose of our audit. We

further confirm that the financial information included in the

Annual Report of the Board of Directors is in agreement with

the books and records of the Bank and that we are not aware

of any contravention by the Bank of its Articles of Association,

Qatar Commercial Companies Law No. 5 of 2002, Qatar Central

Bank law No. 33 of 2006 and the related amendments and

directives of Qatar Central Bank during the financial year that

would materially affect its activities or its financial position.

Firas Qoussous of Ernst & YoungAuditor’s Registration No. 236

Date: 26 February 2008

Doha

15

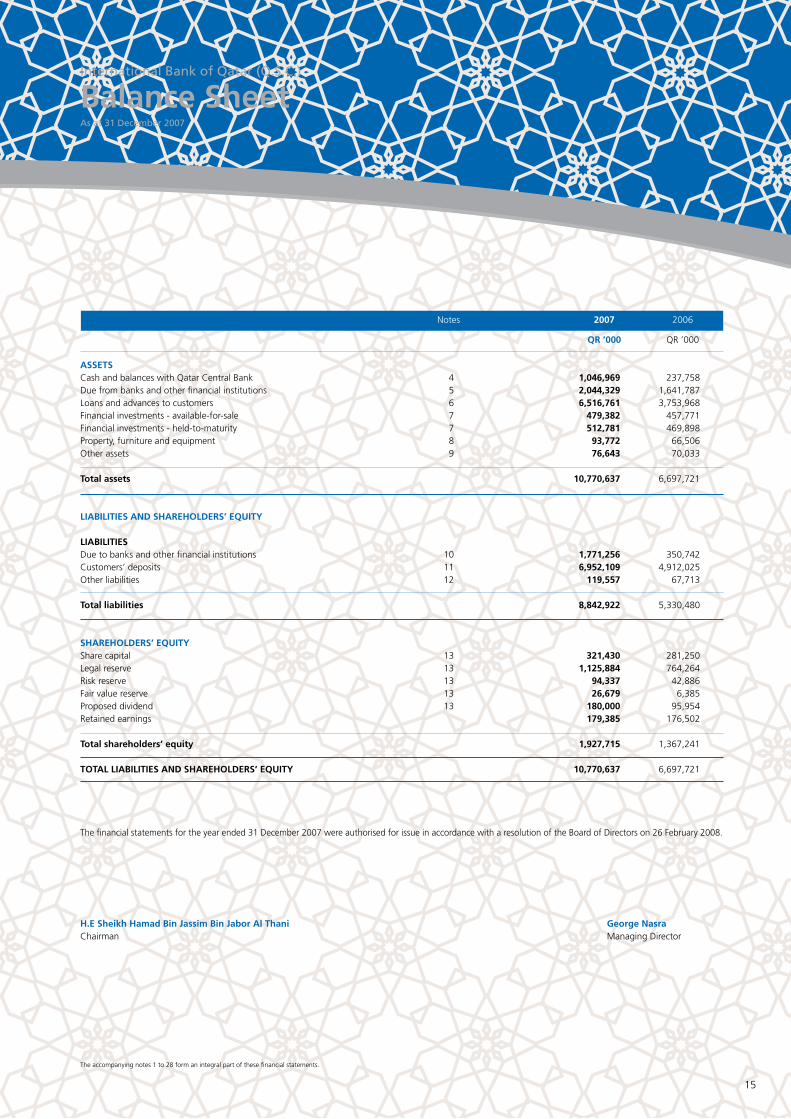

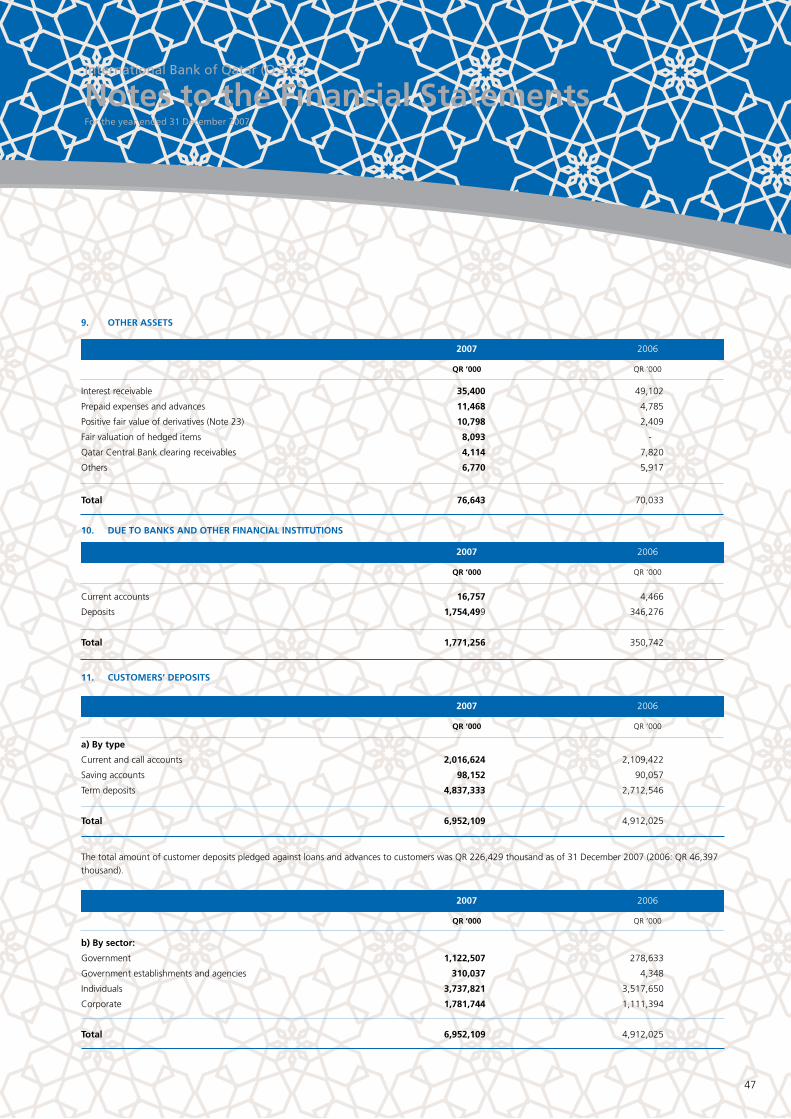

Notes 2007 2006

QR ’000 QR ’000

ASSETSCash and balances with Qatar Central Bank 4 1,046,969 237,758 Due from banks and other financial institutions 5 2,044,329 1,641,787 Loans and advances to customers 6 6,516,761 3,753,968 Financial investments - available-for-sale 7 479,382 457,771 Financial investments - held-to-maturity 7 512,781 469,898 Property, furniture and equipment 8 93,772 66,506 Other assets 9 76,643 70,033

Total assets 10,770,637 6,697,721

LIABILITIES AND SHAREHOLDERS’ EQUITY

LIABILITIES Due to banks and other financial institutions 10 1,771,256 350,742 Customers’ deposits 11 6,952,109 4,912,025 Other liabilities 12 119,557 67,713

Total liabilities 8,842,922 5,330,480

SHAREHOLDERS’ EQUITY Share capital 13 321,430 281,250 Legal reserve 13 1,125,884 764,264 Risk reserve 13 94,337 42,886 Fair value reserve 13 26,679 6,385 Proposed dividend 13 180,000 95,954 Retained earnings 179,385 176,502

Total shareholders’ equity 1,927,715 1,367,241

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 10,770,637 6,697,721

The financial statements for the year ended 31 December 2007 were authorised for issue in accordance with a resolution of the Board of Directors on 26 February 2008.

H.E Sheikh Hamad Bin Jassim Bin Jabor Al Thani George NasraChairman Managing Director

International Bank of Qatar (Q.S.C.)

Balance SheetAs at 31 December 2007

The accompanying notes 1 to 28 form an integral part of these financial statements.

16

Interest income 14 485,246 338,538 Interest expense 15 (229,393) (140,515)

Net interest income 255,853 198,023

Fee and commission income 40,317 22,134 Fee and commission expense (2,698) (945)

Net fee and commission income 16 37,619 21,189

Dividend income from available-for-sale investments 2,444 1,246 Net gain from foreign exchange 17 25,321 13,245 Net gain on trading activities 18 6,096 44

NET OPERATING INCOME 327,333 233,747

General and administrative expenses 19 (90,541) (48,664)Depreciation 8 (5,935) (4,771)Net recoveries of provision for credit losses on loans and advances to customers 5,254 679 Impairment loss on financial investments - available-for-sale (1,777) (30,471)

PROFIT FOR THE YEAR 234,334 150,520

Earnings per shareBasic and diluted - (QR) 20 7.86 6.07

The accompanying notes 1 to 28 form an integral part of these financial statements.

Notes 2007 2006

QR ’000 QR ’000

International Bank of Qatar (Q.S.C.)

Income StatementFor the year ended 31 December 2007

17The accompanying notes 1 to 28 form an integral part of these financial statements.

Notes 2007 2006 QR ’000 QR ’000

International Bank of Qatar (Q.S.C.)

Statement of Cash FlowsFor the year ended 31 December 2007

CASH FLOWS FROM OPERATING ACTIVITIES

Profit for the year 234,334 150,520Adjustments for:

Provision for credit losses on loans and advances to customers 3,227 1,425Recoveries of provision for credit losses on loans and advances to customers (8,481) (2,104)Depreciation 8 5,935 4,771 Amortisation of premium on investments in bonds 4,486 4,280 Provision for employees’ end of service benefits 12a 3,035 2,567 Net gain on sale of financial investments – available-for-sale (6,153) -Impairment loss on financial investments – available-for-sale 1,777 30,471

Cash flows from operating profits before changes in operating assets and liabilities 238,160 191,930

Net decrease (increase) in assetsCash reserve with Qatar Central Bank (68,088) (54,378)Due from banks and other financial institutions 559 (546)Loans and advances to customers (net) (2,757,539) (1,507,091)Other assets (6,610) (31,469)

Net increase (decrease) in liabilitiesDue to banks and other financial institutions 1,420,514 239,371 Customers’ deposits 2,040,084 1,326,318 Other liabilities 50,135 3,941

Cash generated from operations 917,215 168,076 Employees’ end of service benefits paid 12a (1,326) (480)

Net cash from operating activities 915,889 167,596

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of financial investments (69,122) (21,266)Proceeds from sale/redemption of financial investments 24,812 5,830 Purchase of property, furniture and equipment 8 (33,201) (17,042)

Net cash used in investing activities (77,511) (32,478)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from issue of new shares 13a & 13b 401,800 375,000 Dividends paid during the year 13f (95,954) -

Net cash from financing activities 305,846 375,000

NET INCREASE IN CASH AND CASH EQUIVALENTS 1,144,224 510,118 Cash and cash equivalents at 1 January 25 1,688,266 1,178,148

CASH AND CASH EQUIVALENTS AT 31 DECEMBER 25 2,832,490 1,688,266

Operational cash flow from interest and dividendInterest paid 212,067 123,562 Interest received 498,948 316,875 Dividend received 2,444 1,246

18

International Bank of Qatar (Q.S.C.)

Statement of Changes in EquityFor the year ended 31 December 2007

Balance at 1 January 2007 281,250 764,264 42,886 6,385 95,954 176,502 1,367,241

Transfer to risk reserve during the year 13d - - 51,451 - - (51,451) -

Net movements in fair value during the year 13e - - - 20,294 - - 20,294

Total changes recognized directly in equity - - 51,451 20,294 - (51,451) 20,294

Profit for the year - - - - - 234,334 234,334

Total recognized income and expense for the year - - 51,451 20,294 - 182,883 254,628

Shares issued and fully paid 13a 40,180 - - - - - 40,180

Premium on shares issued and fully paid 13b - 361,620 - - - - 361,620

Dividends paid during the year 13f - - - - (95,954) - (95,954)

Proposed dividends 13f - - - - 180,000 (180,000) -

Balance at 31 December 2007 321,430 1,125,884 94,337 26,679 180,000 179,385 1,927,715

Share Legal Risk Fair Value Proposed Retained Notes Capital Reserve Reserve Reserve Divedends Earnings Total QR‘000 QR‘000 QR‘000 QR‘000 QR‘000 QR‘000 QR‘000

Share Legal Risk Fair Value Proposed Retained Notes Capital Reserve Reserve Reserve Divedends Earnings Total QR‘000 QR‘000 QR‘000 QR‘000 QR‘000 QR‘000 QR‘000

Balance at 1 January 2006 187,500 483,014 20,304 66,070 - 144,518 901,406

Transfer to risk reserve during the year 13d - - 22,582 - - (22,582) -

Net movements in fair value during the year 13e - - - (59,685) - - (59,685)

Total changes recognized directly in equity - - 22,582 (59,685) - (22,582) (59,685)

Profit for the year - - - - - 150,520 150,520

Total recognized income and expense for the year - - 22,582 (59,685) - 127,938 90,835

Shares issued and fully paid 13a 93,750 - - - - - 93,750

Premium on shares issued and fully paid 13b - 281,250 - - - - 281,250

Proposed dividends 13f - - - - 95,954 (95,954) -

Balance at 31 December 2006 281,250 764,264 42,886 6,385 95,954 176,502 1,367,241

The accompanying notes 1 to 28 form an integral part of these financial statements.

19

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

1. CORPORATE INFORMATION

The International Bank of Qatar Q.S.C. (the “Bank”) was incorporated in the State of Qatar on 31 July 2000 as Grindlays Qatar Bank under Emiri Decree Number 4 of 2000.The principal shareholders were four Qatari incorporated companies with limited liability (W.L.L.) holding 60% of the Bank’s share capital and Standard Chartered Grindlays Bank Ltd. holding 40%.

Standard Chartered Grindlays Bank Ltd. sold its shareholding to Qatari shareholders on 31 May 2003.

On 30 August 2004, National Bank of Kuwait S.A.K (“NBK”) acquired 20% of the shareholding in the Bank and the name of the Bank was changed to International Bankof Qatar (Q.S.C.) effective 1 September 2004. The Bank entered into a Management Service Agreement with NBK for a period of five years, for an agreed annual managementfee of 1% of the net profit. Subsequently, the shareholding of NBK was increased to 30% effective 1 August 2007.

The Bank is engaged in commercial banking activities and operates through its Head Office located at Suhaim Bin Hamad Street in Doha (postal address P.O. Box 2001,Doha, Qatar) and five branches established in the State of Qatar.

2. ACCOUNTING POLICIES

2.1 BASIS OF PREPARATION

The financial statements have been prepared under the historical cost convention, except for measurement at fair value of derivatives and financial investments – availablefor-sale. The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and Qatar Central Bank regulations.

The financial statements are presented in Qatari Riyals (QR) and all values are rounded to the nearest QR thousand except when otherwise indicated.

2.2 CHANGES IN ACCOUNTING POLICIES AND DISCLOSURES

The accounting policies adopted are consistent with those of the previous year except as follows:

During the year, the Bank has adopted the following new and amended IFRS and IFRIC Interpretation, which are mandatory for the financial year beginning on or after 1January 2007:

IFRS 7 Financial Instruments: Disclosures This standard requires disclosures that enable users of the financial statements to evaluate the significance of the Bank’s financial instruments and the nature and extent of risks arising from those financial instruments. The new disclosures are included throughout the financial statements. While there has been no effect on the financial position or results, comparative information has been revised where needed. IAS 1 Presentation of Financial Statements (Amendment) – Capital Disclosures

This amendment requires the Bank to make new disclosures to enable users of the financial statements to evaluate the Bank’s objectives, policies, and processes for managing capital.

2.3 IASB STANDARDS AND INTERPRETATIONS ISSUED BUT NOT ADOPTED

The following IASB Standards and Interpretation have been issued but are not yet mandatory, and have not yet been adopted by the Bank:

IFRS 8 Operating Segments IFRIC 11 - IFRS 2 Group and Treasury Share Transactions

20

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

2. ACCOUNTING POLICIES (continued)

2.3 IASB STANDARDS AND INTERPRETATIONS ISSUED BUT NOT ADOPTED (continued)

The Bank has evaluated the effect of the above standard and interpretation and does not expect these to have a significant impact on the financial statements of the Bankwhen implemented.

IAS 1 Presentation of Financial Statements (Revised)

The application of this standard will result in amendments to the presentation of the financial statements when implemented in 2009.

2.4 SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies applied in the preparation of these financial statements are set below:

(a) Foreign currency transactions

The financial statements are presented in Qatari Riyals which is the currency of the Bank.

Transactions in foreign currencies are translated into the functional currency at the exchange rates ruling at the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies are retranslated into functional currency at the rates ruling at the balance sheet date. Exchange gains and losses resulting therefrom appear in the income statement under ‘Net gain from foreign exchange’.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates as at the dates of the initial transactions.Non-monetary items measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined and the differencesare included in equity as part of the fair value adjustment of the respective assets, unless part of an effective hedging strategy.

(b) Financial instruments – initial recognition and subsequent measurement

(i) Date of recognition of financial transactions

All financial assets are recognised using the settlement date. Any changes in the fair value of the asset between the trade date and the settlement date is not recognised for assets carried at cost or amortised cost and is recognised in equity for assets classified as available for sale.

(ii) Derivatives recorded at fair value through profit or loss

Derivatives include interest rate swaps and forward foreign exchange contracts. Derivatives are recorded at fair value and are included in other assets when their fair valueis positive and other liabilities when their fair values are negative. Changes in the fair value of derivatives held for trading are included in the income statement under‘Net (loss) gain on trading activities’.

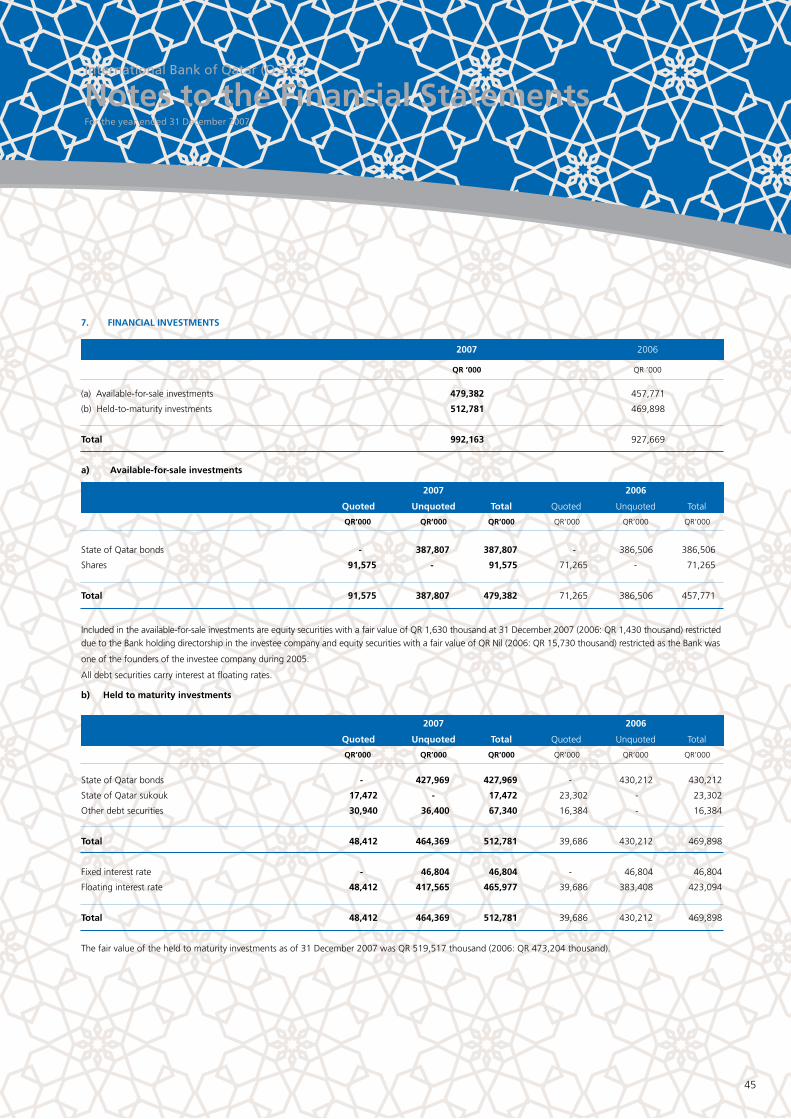

(iii) Financial investments – held-to-maturity

After initial measurement, financial investments – held-to-maturity investments are measured at amortized cost using the effective interest rate method, less provision forimpairment. Amortized cost is calculated by taking into account any discount or premium on the issue and costs that are integral part of the effective interest rate. Theamortization is included in ‘Interest income’ in the income statement.

(iv) Financial investments – available-for-sale

Financial investments – available-for-sale are those which are designated as such or do not qualify to be classified as held-to-maturity or loans and advances. These includeequity and debt instruments.

21

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

2. ACCOUNTING POLICIES (continued)

2.4 SIGNIFICANT ACCOUNTING POLICIES (continued)

After initial measurement, Financial investments - available-for-sale are subsequently measured at fair value. Unrealized gains or losses arising from a change in the fairvalue are recognised directly in the fair value reserve under shareholders’ equity until the investment is sold, at which time the cumulative gain or loss previously recognisedin shareholders’ equity is included in the income statement. Interest earned whilst holding financial investments – available-for-sale is reported as interest income using theeffective interest rates. Dividends earned whilst holding Financial investments - available-for-sale are recognised in the income statement under ‘dividend income’ whenthe right of payment has been established. The impairment losses arising from such investments are recognised in the income statement in ‘Impairment loss on financialinvestments – available-for-sale’.

(v) Due from banks and loans and advances to customers

After initial measurement, amounts due from banks and loans and advances to customers are stated at amortized cost using the effective interest rate method, less anyprovision for their credit losses and interest in suspense. The amortisation is included in ‘Interest income’ in the income statement. The losses arising from impairment arerecognised in the income statement in ‘Net recoveries of provision for credit losses of loans and advances’.

(c) Derecognition of financial assets and liabilities

Financial assets are derecognised when the rights to receive cash flows from the assets have expired or when the Bank has transferred its contractual rights to receive cashflows from the assets.

Financial liabilities are derecognised when they are extinguished, which is when the obligation is discharged or cancelled or expire.

(d) Fair values

The fair value of financial assets traded in organised financial markets is determined by reference to quoted market bid prices on regulated exchange at the close of businesson the balance sheet date.

For all other financial assets not listed in an active market, a reasonable estimate of fair value is determined by reference to the current market value of another instrumentwhich is similar or based on expected cash flows discounted at current rates applicable for items with similar terms and risk characteristics. The fair value of liabilities witha demand feature is the amount payable on demand.

(e) Impairment of financial assets

The Bank assesses at each balance sheet date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or agroup of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after theinitial recognition of the asset (an incurred loss event) and that loss events has an impact on the estimated future cash flows of the financial asset or the group of financialassets that can be reliably estimated.

(i) Financial investments – held-to-maturity

For financial investments – held-to-maturity, the Bank assesses individually whether there is objective evidence of impairment. If there is objective evidence that an impairment loss has been incurred, the amount of loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows. The carrying amount of the asset is reduced by using a provision account and the impairment loss is recognised in the income statement. If, in a subsequent year, the amount of the estimated impairment loss decreases because of an event occurring after the impairment loss was recognised, any amounts previously charged to income statement are credited to ‘Impairment loss on financial investments’.

(ii) Financial investments – available-for-sale

For financial investments – available-for-sale, the Bank assesses individually whether there is objective evidence of impairment.

In case of equity investments classified as available-for-sale, objective evidence would include a significant or prolonged decline in the fair value of the investment belowits cost.

22

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

2. ACCOUNTING POLICIES (continued)

2.4 SIGNIFICANT ACCOUNTING POLICIES (continued)

Where there is evidence of impairment, the cumulative loss – measured as the difference between the acquisition cost and the current fair value, less any impairment losson that investment previously recognised in the income statement – is removed from equity and recognised in the income statement. Impairment losses on debt instrumentsare charged to the income statement through a provision account, while impairment losses on equity instruments are treated as direct write-offs. Impairment losses onequity investments are not reversed through the income statement and are treated as increase in fair value through the statement of changes in equity. Impairment losseson debt instruments are reversed through the income statement.

(iii) Due from banks and loans and advances to customers

If there is objective evidence that an impairment loss has been incurred, the estimated recoverable amount of that asset is determined and any impairment loss is recognisedin the income statement.

Specific provisions for credit losses of loans and advances to customers are calculated based on the difference between the book value of the loans and advances and theirrecoverable amount, being the net present value of the expected future cash flows, discounted at the original interest rates. If a loan has a variable interest rate, the discountrate for measuring any impairment loss is the current effective interest rate. The calculation of the present value of the estimated future cash flows of a collateralized financialasset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable.

Loans and advances are written off and charged against specific provision only in circumstances where all reasonable restructuring and collection activities have been exhausted.

(f) Hedge accounting

The Bank makes use of derivatives to manage exposures to interest rate and foreign currency risks including exposures arising from forecast highly probable transactions.

In order to manage particular risks, the Bank applies hedge accounting for transactions which meets the specified criteria. For the purpose of hedge accounting, hedgesare classified as either fair value or cash flow hedges. Fair value hedges hedge the exposure to change in the fair value of a recognised asset or liability. Cash flow hedgeshedge exposure to the variability in cash flows that is either attributable to a particular risk associated with a recognised asset or liability or a forecasted highly probabletransactions.

For hedges which do not qualify for hedge accounting, any gains or losses arising from changes in the fair value of the hedging instrument are taken directly to the incomestatement for the period.

Discontinuation of hedge accountingHedge accounting is discontinued when the hedging instrument expires, is terminated or exercised, or no longer qualifies for hedge accounting. For effective fair valuehedges of financial instruments with fixed maturities any adjustment arising from hedge accounting is amortised over the remaining term to maturity. For effective cashflow hedges, any cumulative gain or loss on the hedging instrument recognised in shareholders’ equity is held therein until the forecasted transaction occurs.

If a hedge transaction is no longer expected to occur, the net cumulative gain or loss recognised in shareholders’ equity is transferred to the income statement.

(i) Fair value hedges

For designated and qualifying fair value hedges, any gain or loss from remeasuring the hedging instrument to fair value is recognised immediately in the income statementunder ‘Net trading income’ . The related aspect of the hedged item is adjusted against the carrying amount of the hedged item and is also recognised in the income statement under ‘Net trading income’.

For fair value hedges of financial instruments with fixed maturities any adjustment arising from hedge accounting is amortised over the remaining term to maturity.

(ii) Cash flow hedges

For designated and qualifying cash flow hedges, the effective portion of the gain or loss on the hedging instrument is initially recognised in equity. The ineffective portionof the gain or loss on the hedging instrument is recognised immediately in the income statement under ‘Net trading income’.

23

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

2. ACCOUNTING POLICIES (continued)

2.4 SIGNIFICANT ACCOUNTING POLICIES (continued)

The gains or losses on cash flow hedges initially recognised in shareholders’ equity are transferred to the income statement in the period in which the hedged transactionimpacts the income statement. Any cumulative gain or loss on the hedging instrument recognised in shareholders’ equity is held therein until the forecasted transactionoccurs. If a hedge transaction is no longer expected to occur, the net cumulative gain or loss recognised in shareholders’ equity is transferred to the income statement.Where the hedged transaction results in the recognition of an asset or a liability, the associated gains or losses that had initially been recognised in the shareholders’ equityare included in the initial measurement of the cost of the related asset or liability.

g) Revenue recognition

Revenue is recognised to the extent that it is possible that the economic benefits will flow to the Bank and can be reliably measured. Revenues are recognised on an accrualbasis. The following specific recognition criteria must also be met before revenue is recognised:

(i) Interest and similar income

For all financial instruments measured at amortised cost and debt instruments classified as available-for-sale financial investments, interest income is recorded at the effectiveinterest rate, which is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or a shorter period,where appropriate, to the net carrying amount of the financial asset or financial liability. The calculation takes into account all contractual terms of the financial instrument(for example, payment options) including any fees or incremental costs that are directly attributable to the instrument and are an integral part of the effective interest rate,but not future credit losses. The carrying amount of the financial asset or financial liability is adjusted if the Bank revises its estimates of payments or receipts. The adjustedcarrying amount is calculated based on original effective interest rate. The change in carrying amount is recorded as interest income. Interest income on non performingloans is suspended if doubt exists with regard to the collectability of the interest or the original loan. Notional interest is recognized on impaired loans and advances tocustomers and other financial assets based on the rate used to discount future cash flows to their net present values.

(ii) Fee and commission income

The Bank earns fee and commission income from a diverse range of services it provides to its customers. Fee income can be divided into the following two categories:

Fee income earned from services that are provided over a certain period of time

Fees earned for the provision of services over a period of time are accrued over that period. These fees include commission income and other management and advisoryfees. Loan commitment fees for loans that are likely to be drawn down and other credit related fees are deferred (together with any incremental costs) and recognised asan adjustment to the effective interest rate of the loan.

Fee income from providing transaction services

Fees arising from negotiation or participating in the negotiation of a transaction for a third party – such as the arrangement of acquisition of shares or other securities orthe purchase or sale of businesses – are recognised on completion of the underlying transaction. Fees or components of fees that are linked to a certain performance arerecognised after fulfilling the corresponding criteria. These fees include underwriting fees, corporate finance fees, and brokerage fees. Loan syndication fees are recognisedin the income statement when the syndication has been completed and the Bank retains no part of the loans for itself or retains part of the loan at the same effective rateas for the other participants.

(iii) Dividend income

Revenue is recognised when the Bank’s right to receive the payment is established.

h) Properties acquired against settlement of debts

Properties acquired against settlement of debts appear under other assets at their net acquired values. Unrealized losses due to diminution in the value of these assets appearin the income statement. Future unrealized gains on these properties are recognised in the income statement to the extent of unrealized losses previously recognised. In accordance with Qatar Central Bank regulations, all properties acquired against settlement of debts must be sold within three years. Any extension or transfer to propertyand equipment must be with Qatar Central Bank approval.

24

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

2. ACCOUNTING POLICIES (continued)

2.4 SIGNIFICANT ACCOUNTING POLICIES (continued)

i) Property, furniture and equipment

Property, furniture and equipment are stated at cost less accumulated depreciation and accumulated impairment in value. Freehold land is not depreciated. All other property,furniture and equipment are depreciated on a straight-line basis over their estimated useful lives as follows:

Leasehold improvements 5-7 yearsComputer equipment 3 yearsFurniture and equipment 5-7 yearsVehicles 5 years

j) Employees’ termination benefits and pension funds

The Bank provides end of service benefits to its expatriate employees. The entitlement to these benefits is based upon the employees’ final salary and length of service,subject to the completion of a minimum service period. The expected cost of these benefits is accrued over the period of employment. The provision for employees’ endof service benefits is disclosed under ‘Other liabilities’.

With respect to Qatari employees, the Bank makes contributions to the Qatari Pension Fund calculated as a percentage of the employees’ salaries. The Bank’s obligationsare limited to these contributions. The cost is considered as part of general and administrative expenses.

k) Other provisions

The Bank makes a provision for any expected obligations (legal or constructive) or financial liabilities as a charge to the income statement based on the likelihood andexpected amount of such liabilities at the balance sheet date.

l) Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the balance sheet if, and only if, there is a currently enforceable legal right to offset therecognised amounts and there is an intention to settle on a net basis, or to realise the asset and settle the liability simultaneously. This is not generally the case with masternetting agreements, and the related assets and liabilities are presented gross in the balance sheet.

m) Cash and cash equivalents

For the purpose of the cash flow statement, cash and cash equivalents include cash and balances with Qatar Central Bank other than mandatory cash reserve and balances with banks and other financial institutions with an original maturity of three months or less as disclosed in note 25.

n) Fiduciary assets

Assets held in a fiduciary capacity are not treated as assets of the Bank in the balance sheet.

o) Contingent liabilities other commitments

As at balance sheet date contingent liabilities and other commitments do not represent actual assets or liabilities of the Bank.

p) Financial guarantees

In the ordinary course of business, the Bank gives financial guarantees, consisting of letters of credit, guarantees and acceptances. Financial guarantees are initially recognisedin the financial statements at fair value, being the premium received. Subsequent to initial recognition, the Bank’s liability under each guarantee is measured at the higherof the amortised premium and the best estimate of expenditure required to settle any financial obligation arising as a result of the guarantee.

Any increase in the liability relating to financial guarantees is taken to the income statement and is included in ‘Provision for credit losses of loans and advances’. Thepremium received is recognised in the income statement in ‘Fee and commission income’ on a straight line basis over the life of the guarantee.

25

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS

3.1 FINANCIAL INSTRUMENTS

a) Definition and classification

Financial instruments cover all financial assets and financial liabilities of the Bank

Financial assets include cash and balances with Qatar Central Bank, Due from banks and other financial institutions, loans and advances to customers and financial investments.Financial liabilities include customer deposits and due to banks and other financial institutions. Financial instruments also include certain contingent liabilities and commitmentsincluded in off-balance sheet items.

The significant accounting policies adopted by the Bank in respect of recognition and measurement of the key financial instruments and their related income and expensesare disclosed in note (2) “significant accounting policies”.

b) Fair value of financial instruments

Set out below is a comparison by class, of the carrying amounts and fair values of the Bank’s financial instruments that are carried in the financial statements. The tabledoes not include the fair values of non-financial assets and non-financial liabilities.

Carrying Fair Unrecognized Carrying Fair Unrecognized value value gain/(loss) value value gain/(loss) 2007 2007 2007 2006 2006 2006

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000

Financial assets

Cash and balances with Qatar Central Bank 1,046,969 1,046,969 - 237,758 237,758 -

Due from banks and other financial institutions 2,044,329 2,044,329 - 1,641,787 1,641,787 -

Loans and advances to customers 6,516,761 6,522,146 5,385 3,753,968 3,764,703 10,735

Financial investments – available-for-sale 479,382 479,382 - 457,771 457,771 -

Financial investments – held-to-maturity 512,781 519,517 6,736 469,898 473,204 3,306

Derivative financial instruments 10,798 10,798 - 2,409 2,409 -

10,611,020 10,623,141 12,121 6,563,591 6,577,632 14,041

Financial liabilities

Due to banks and other financial institutions 1,771,256 1,771,256 - 350,742 350,742 -

Customers’ deposits 6,952,109 6,952,109 - 4,912,025 4,912,025 -

Derivative financial instruments 11,388 11,388 - 983 983 -

8,734,753 8,734,753 - 5,263,750 5,263,750 -

Totalunrecognizedchangeinunrealizedfairvalue 12,121 14,041

26

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS (continued)

3.1 FINANCIAL INSTRUMENTS (continued)

b) Fair value of financial instruments (continued)

The following describes the methodologies and assumptions used to determine fair values for those financial instruments which are not already recorded at fair value inthe financial statements.

Financial instruments for which fair values approximates carrying valuesFor financial assets and financial liabilities that are liquid or having short term maturities (less than three months), the carrying amounts approximate to their fair values.

This assumption is also applied to demand deposits, savings accounts without a specific maturity and variable rate financial instruments.

Fixed rate financial instrumentsThe fair value of fixed rate financial assets and liabilities carried at amortised cost are estimated by comparing market interest rates when they were first recognised with

current market rates offered for similar financial instruments. The estimated fair value of fixed interest bearing deposits is based on discounted cash flows using prevailing

money-market interest rates for debts with similar credit risk and maturity. For quoted debt issued the fair values are calculated based on quoted market prices. For those

notes issued where quoted market prices are not available, a discounted cash flow model is used based on a current interest rate yield curve appropriate for the remaining

term to maturity.

3.2 RISK MANAGEMENT

3.2.1 Risk management framework

Risk is inherent in the Bank’s activities but it is managed through a process of ongoing identification, measurement and monitoring, subject to risk limits and other controls.

This process of risk management is critical to the Bank’s continuing profitability and each individual within the Bank is accountable for the risk exposures relating to his or

her responsibilities. The Bank is exposed to credit risk, liquidity risk, operating risk and market risk, which include trading and non-trading risks.

The independent risk control process does not include business risks such as changes in the environment, technology and industry. They are monitored through the Bank’s

strategic planning process.

Risk management structureThe Board of Directors is ultimately responsible for identifying and controlling risks; however, there are separate independent bodies responsible for managing and monitoring

risks.

Risk CommitteeThe Risk Committee has the overall responsibility for the development of the risk strategy and implementing principles, frameworks, policies and limits. The committee is

responsible for reviewing all risk issues of the Bank and report to the Audit Committee of the Board of Directors.

Other committeesThe Board of Directors evaluates the specific risks faced by the Bank through the following committees:

• CreditCommitteeoftheBoardreviewsallaspectsrelatedtocreditrisk.

• AuditandRiskCommitteeoftheBoardreviewsthescopeandcoverageofexternalandinternalauditandriskactivities.

• TheAssetandLiabilityCommittee(ALCO)isamanagementcommitteeprimarilyresponsiblefortheAssetandLiabilityManagement(ALM)process,establishing

overall risk parameters relating to liquidity risk and market risk, developing the relevant policies and managing all market risks, including the interest rate and currency

risks inherent in the balance sheet.

27

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS (continued)

3.2 RISK MANAGEMENT (continued)

3.2.1 Risk management framework (continued)

Internal auditRisk management processes throughout the Bank are audited annually by the internal audit function, which examines both the adequacy of the procedures and the Bank’scompliance with the procedures. Internal Audit discusses the results of all assessments with management, and reports its findings and recommendations to the AuditCommittee.

Risk measurement and reporting systems Monitoring and controlling risks is primarily performed based on limits established by the Board. These limits reflect the business strategy of the Board and the marketenvironment as well as the level of risk that the Board is willing to accept, with additional emphasis on selected industries.

Information compiled from all the businesses is examined and processed in order to analyze, control and identify early risks. This information is presented and explained tothe Board of Directors, the Risk Committee, and the head of each business division.

Risk mitigationAs part of its overall risk management, the Bank uses derivatives and other instruments to manage exposures resulting from changes in interest rates, foreign currencies,equity risks, credit risks, and exposures arising from forecast transactions. The risk profile is assessed before entering into hedge transactions, which are authorised by theappropriate level of authority within the Bank. The effectiveness of all hedge relationships are monitored by the Risk management monthly. In situations of ineffectiveness,the Bank will enter into a new hedge relationship to mitigate risk on a continuous basis.

3.2.2 Credit risk

Credit risk is the risk that a customer or counterparty of the Bank will be unable or unwilling to meet a commitment entered into with the Bank. It arises from lending,trade finance, treasury and other activities undertaken by the Bank. The Bank has in place standards, policies and procedures for the control and monitoring of all suchrisks.

The Bank seeks to manage its credit risks exposure through diversification of its lending, investing and financing activities to avoid undue concentrations of risks withindividuals or groups of customers in specific businesses. It also obtains security when appropriate. The types of collateral obtained include cash, mortgages over real estateproperties and pledge over equity instruments.

The Bank uses the same credit risk procedures when entering into derivative transactions that it does for traditional lending products.

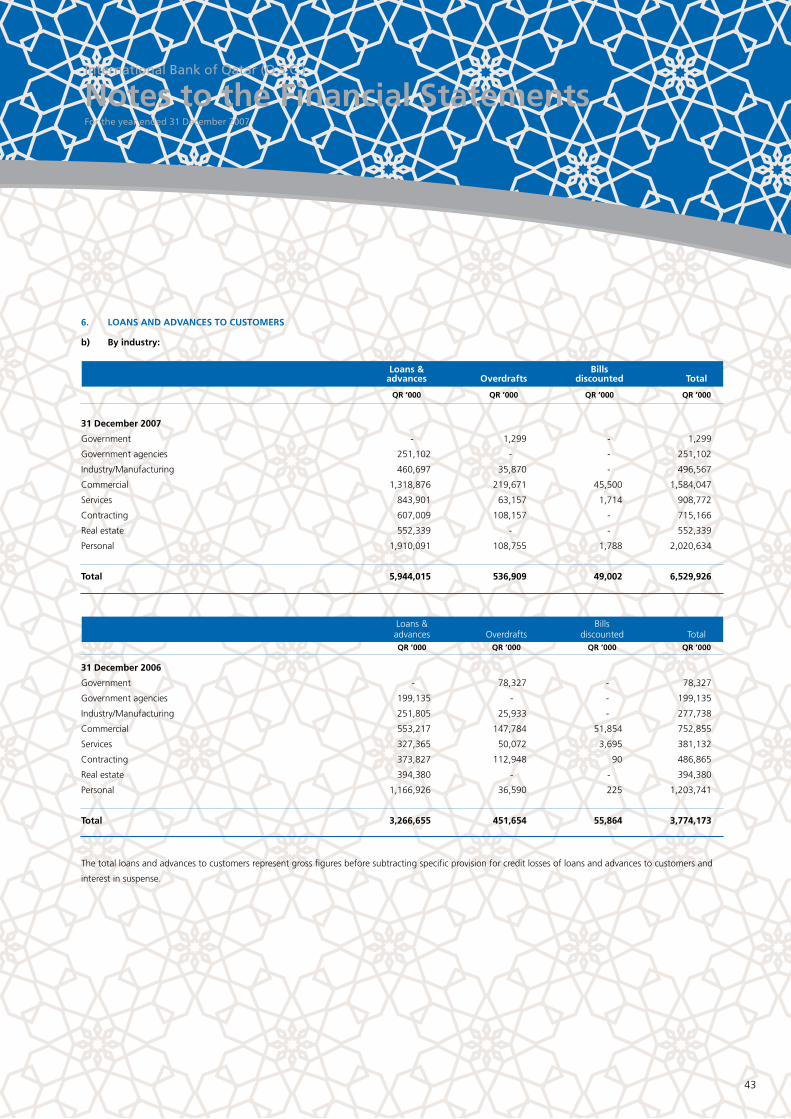

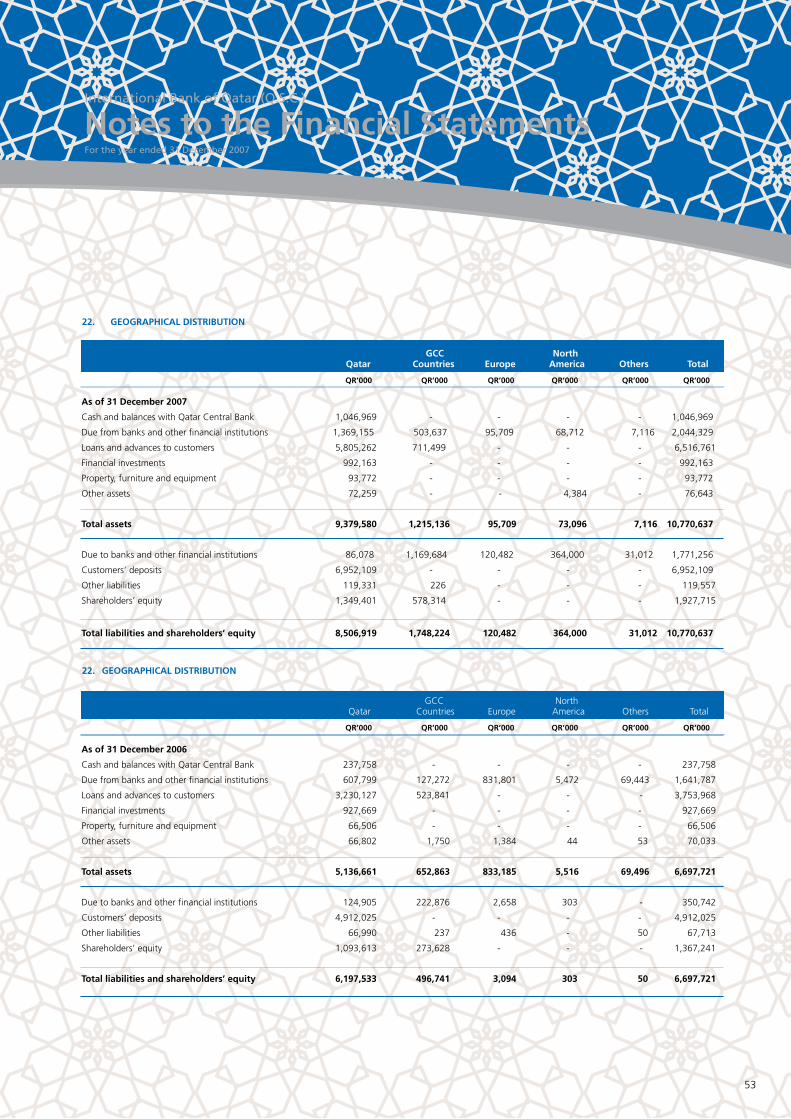

Note 6(b) discloses the distribution of loans and advances to customers by industrial sector. Note 22 discloses the geographical distribution of the Bank’s assets and liabilitiesat the balance sheet date.

28

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS (continued)

3.1 FINANCIAL INSTRUMENTS (continued)

3.2.2 Credit risk (continued)

i) Maximum credit exposure

The table below shows the maximum exposure to credit risk for the components of balance sheet, including off balance sheet items. The maximum exposure is showngross, before the effect of mitigation through the use of master netting and collateral agreements.

Cash and balances with Qatar Central Bank 1,018,247 181,193

Due from banks and other financial institutions 2,044,329 1,641,787

Loans and advances to customers 6,516,761 3,753,968

Financial investments – held-to-maturity 512,781 469,898

Financial investments – available-for-sale 387,807 386,506

Other assets 65,175 65,248

Total on balance sheet 10,545,100 6,498,600

Contingent liabilities 2,570,754 1,573,067

Other commitments 1,237,097 1,160,013

Total off balance sheet 3,807,851 2,733,080

Total exposure 14,352,951 9,231,680

Gross maximum exposure Total Total 2007 2006 QR ’000 QR ’000

29

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS (continued)

3.1 FINANCIAL INSTRUMENTS (continued)

3.2.2 Credit risk (continued)

ii) Risk concentration for maximum exposure to credit risk by industry sector

Government 1,857,443 1,857,443 1,170,600 1,170,600

Government agencies 307,203 307,203 273,727 273,727

Industry/Manufacturing 753,698 623,698 442,756 334,556

Commercial 2,673,846 2,643,933 1,457,035 1,432,138

Services 4,011,515 3,878,103 2,585,377 2,474,337

Contracting 1,548,755 1,544,534 1,200,342 1,196,829

Real estate 726,451 358,655 532,767 226,650

Personal 2,409,089 1,771,289 1,563,160 1,032,317

Others 64,951 64,951 5,916 5,916

Total 14,352,951 13,049,809 9,231,680 8,147,070

iii) Credit risk exposure for each internal risk rating

It is the Bank’s policy to maintain accurate and consistent risk ratings across the credit portfolio. This facilitates focused management of the applicable risks and the comparison

of credit exposures across all lines of business, geographic regions and products. The rating system is supported by a variety of financial analytics, combined with processed

market information to provide the main inputs for the measurement of counterparty risk. All internal risk ratings are tailored to the various categories and are derived in

accordance with the Bank’s rating policy. Also, the ratings used by the Bank are in line with the ratings and definitions published by international rating agencies. The

attributable risk ratings are assessed and updated regularly.

Unsecured Total Unsecured Total share 2007 share 2006 of exposure QR ‘000 of exposure QR ‘000

Equivalent Grades % %

AAA to AA- 100.00 2,034,535 100.00 1,944,549

A+ to A- 93.95 4,130,777 94.80 1,731,186

BBB+ to BBB- 93.88 3,854,202 95.48 2,418,893

BB+ to B- 80.27 4,143,341 70.68 3,018,780

Below B- 100.00 727 100.00 3,104

Unrated 100.00 189,369 100.00 115,168

Total (gross maximum exposure) 14,352,951 9,231,680

Gross Net Gross Net maximum maximum maximum maximum exposure exposure exposure exposure 2007 2007 2006 2006 QR ’000 QR ’000 QR ’000 QR ’000

30

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. RISK MANAGEMENT OF FINANCIAL INSTRUMENTS (continued)

3.1 FINANCIAL INSTRUMENTS (continued)

3.2.2 Credit risk (continued)

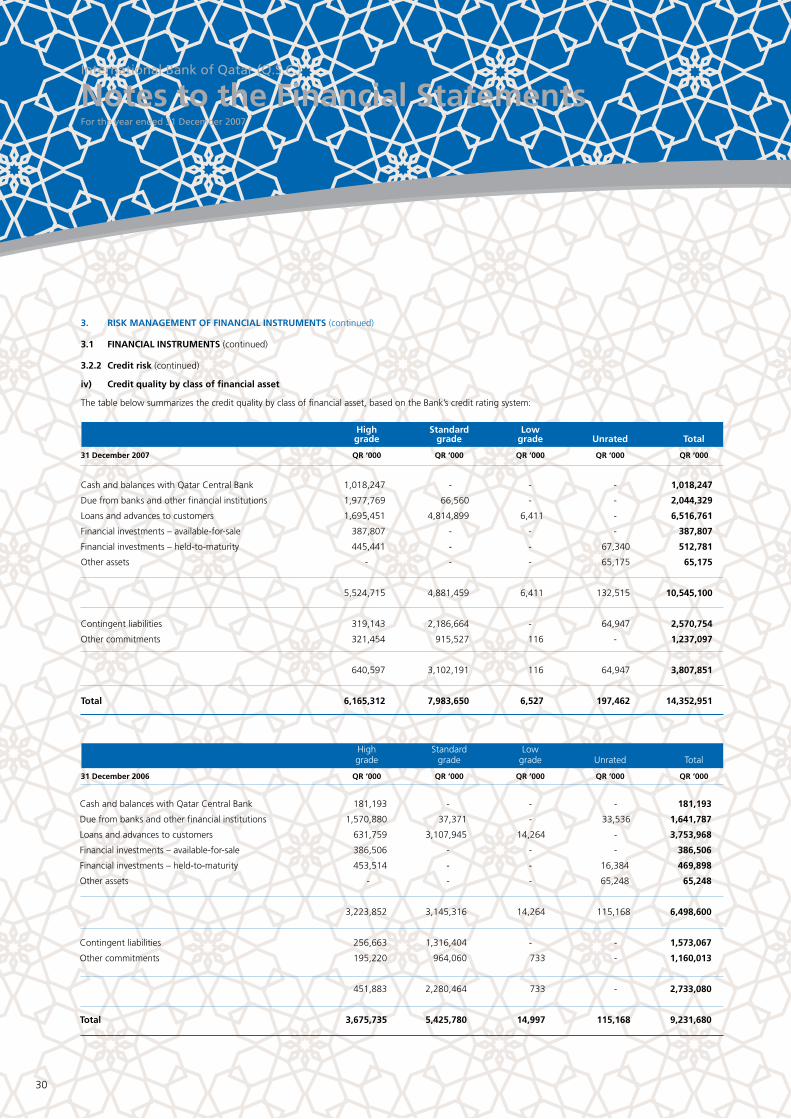

iv) Credit quality by class of financial asset

The table below summarizes the credit quality by class of financial asset, based on the Bank’s credit rating system:

High Standard Low grade grade grade Unrated Total

31 December 2007 QR ‘000 QR ‘000 QR ‘000 QR ‘000 QR ‘000

Cash and balances with Qatar Central Bank 1,018,247 - - - 1,018,247

Due from banks and other financial institutions 1,977,769 66,560 - - 2,044,329

Loans and advances to customers 1,695,451 4,814,899 6,411 - 6,516,761

Financial investments – available-for-sale 387,807 - - - 387,807

Financial investments – held-to-maturity 445,441 - - 67,340 512,781

Other assets - - - 65,175 65,175

5,524,715 4,881,459 6,411 132,515 10,545,100

Contingent liabilities 319,143 2,186,664 - 64,947 2,570,754

Other commitments 321,454 915,527 116 - 1,237,097

640,597 3,102,191 116 64,947 3,807,851

Total 6,165,312 7,983,650 6,527 197,462 14,352,951

High Standard Low grade grade grade Unrated Total

31December2006 QR‘000 QR‘000 QR‘000 QR‘000 QR‘000

Cash and balances with Qatar Central Bank 181,193 - - - 181,193

Due from banks and other financial institutions 1,570,880 37,371 - 33,536 1,641,787

Loans and advances to customers 631,759 3,107,945 14,264 - 3,753,968

Financial investments – available-for-sale 386,506 - - - 386,506

Financial investments – held-to-maturity 453,514 - - 16,384 469,898

Other assets - - - 65,248 65,248

3,223,852 3,145,316 14,264 115,168 6,498,600

Contingent liabilities 256,663 1,316,404 - - 1,573,067

Other commitments 195,220 964,060 733 - 1,160,013

451,883 2,280,464 733 - 2,733,080

Total 3,675,735 5,425,780 14,997 115,168 9,231,680

31

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.2 Credit risk (continued)

v) Aging analysis of past due but not impaired loans and advances

Less than 31 to 60 61 to 90 30 days days days Total

31 December 2007 QR ’000 QR ’000 QR ’000 QR ’000

Less than 31 to 60 61 to 90 30 days days days Total

31 December 2006 QR’000 QR’000 QR’000 QR’000

Loans and advances to customers

Retail - 5,400 400 5,800

Loans and advances to customers

Retail - 10,212 1,681 11,893

There were no other past due but not impaired financial assets at 31 December 2007 (2006: Nil).

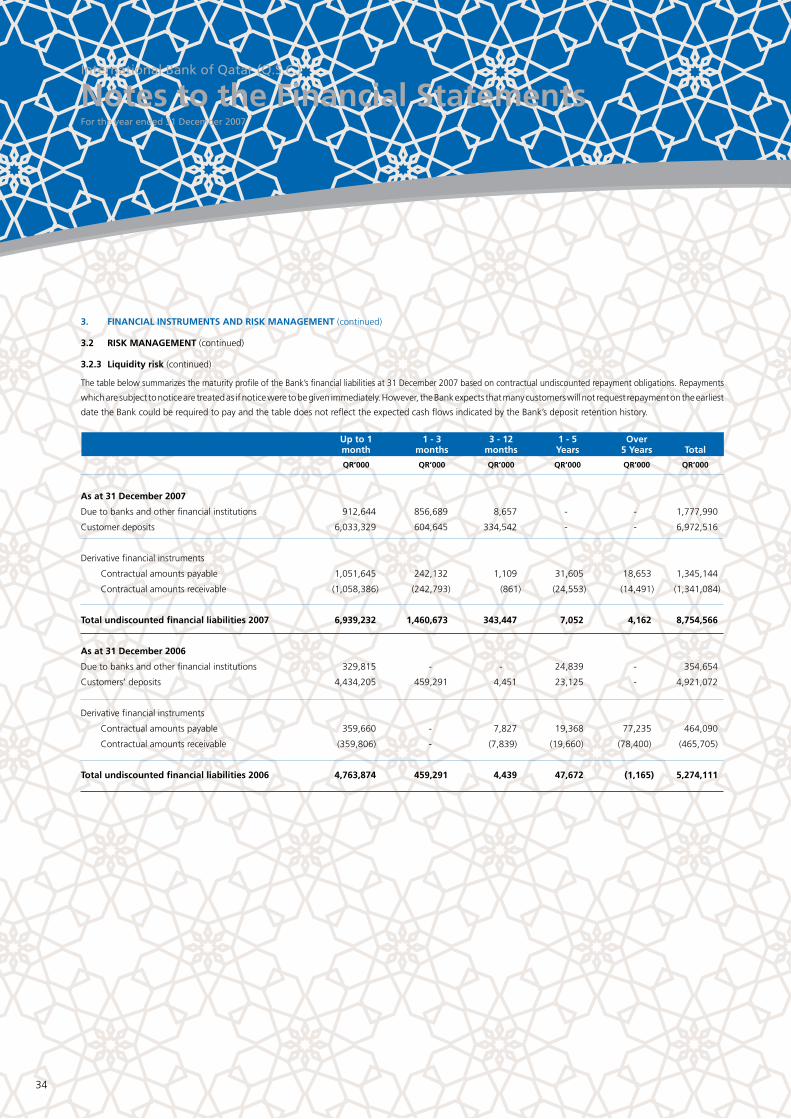

3.2.3 LIQUIDITY RISK

Liquidity risk is the risk that the Bank will be unable to meet its funding requirements. Liquidity risk arises from fluctuations in cash flows due to market disruptions orcredit down grades, which may cause certain sources of funding to cease immediately. The Bank maintains a portfolio of highly marketable and diverse assets that can beeasily liquidated in the event of an unforeseen interruption of cash flow. In addition, the Bank maintains a statutory deposit with the Qatar Central Bank. The liquidityposition is assessed and managed under a variety of scenarios, giving due consideration to stress factors relating to both the market in general and specifically to the Bank.

32

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.3 Liquidity risk (continued)

The table below set out the maturity profile of the Bank’s assets and liabilities. The contractual maturities of assets and liabilities have been determined on the basis ofthe remaining period at the balance sheet date to the contractual maturity date and do not take account of the effective maturities as indicated by the Bank’s depositretention history. Management monitors the maturity profile to ensure that adequate liquidity is maintained.

As at 31 December 2007

Up to 1 1 - 3 3 - 12 1 - 5 Over month months months Years 5 Years Total

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000

Cash and balances with Qatar Central Bank 1,046,969 - - - - 1,046,969

Due from banks and other financial institutions 1,974,049 17,500 36,400 16,380 - 2,044,329

Loans and advances to customers 922,202 478,711 1,069,010 3,568,616 478,222 6,516,761

Financial investments - - - 961,223 30,940 992,163

Property, furniture and equipment - - - - 93,772 93,772

Other assets 4,114 - 64,436 743 7,350 76,643

Total assets 3,947,334 496,211 1,169,846 4,546,962 610,284 10,770,637

Due to banks and other financial institutions 910,948 851,844 8,464 - - 1,771,256

Customers’ deposits 6,023,760 601,233 327,116 - - 6,952,109

Other liabilities - - 119,557 - - 119,557

Shareholders’ equity - - - - 1,927,715 1,927,715

Total liabilities and equity 6,934,708 1,453,077 455,137 - 1,927,715 10,770,637

Net liquidity gap (2,987,374) (956,866) 714,709 4,546,962 (1,317,431) -

Cumulative liquidity gap (2,987,374) (3,944,240) (3,229,531) 1,317,431 - -

33

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.3 Liquidity risk (continued)

As at 31 December 2006

Up to 1 1 - 3 3 - 12 1 - 5 Over month months months Years 5 Years Total

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000

Cash and balances with Qatar Central Bank 237,758 - - - - 237,758

Due from banks and other financial institutions 1,517,031 71,417 546 52,793 - 1,641,787

Loans and advances to customers 823,470 23,306 765,322 1,506,374 635,496 3,753,968

Financial investments - - - 927,669 - 927,669

Property, furniture and equipment - - - - 66,506 66,506

Other assets 7,820 - 62,213 - - 70,033

Total assets 2,586,079 94,723 828,081 2,486,836 702,002 6,697,721

Due to banks and other financial institutions 329,035 - - 21,707 - 350,742

Customers’ deposits 4,429,128 457,273 4,374 21,250 - 4,912,025

Other liabilities - - 67,713 - - 67,713

Shareholders’ equity - - - - 1,367,241 1,367,241

Total liabilities and equity 4,758,163 457,273 72,087 42,957 1,367,241 6,697,721

Net liquidity gap (2,172,084) (362,550) 755,994 2,443,879 (665,239) -

Cumulative liquidity gap (2,172,084) (2,534,634) (1,778,640) 665,239 - -

34

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.3 Liquidity risk (continued)

The table below summarizes the maturity profile of the Bank’s financial liabilities at 31 December 2007 based on contractual undiscounted repayment obligations. Repayments

which are subject to notice are treated as if notice were to be given immediately. However, the Bank expects that many customers will not request repayment on the earliest

date the Bank could be required to pay and the table does not reflect the expected cash flows indicated by the Bank’s deposit retention history.

Up to 1 1 - 3 3 - 12 1 - 5 Over month months months Years 5 Years Total

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000

As at 31 December 2007

Due to banks and other financial institutions 912,644 856,689 8,657 - - 1,777,990

Customer deposits 6,033,329 604,645 334,542 - - 6,972,516

Derivative financial instruments

Contractual amounts payable 1,051,645 242,132 1,109 31,605 18,653 1,345,144

Contractual amounts receivable (1,058,386) (242,793) (861) (24,553) (14,491) (1,341,084)

Total undiscounted financial liabilities 2007 6,939,232 1,460,673 343,447 7,052 4,162 8,754,566

As at 31 December 2006

Due to banks and other financial institutions 329,815 - - 24,839 - 354,654

Customers’ deposits 4,434,205 459,291 4,451 23,125 - 4,921,072

Derivative financial instruments

Contractual amounts payable 359,660 - 7,827 19,368 77,235 464,090

Contractual amounts receivable (359,806) - (7,839) (19,660) (78,400) (465,705)

Total undiscounted financial liabilities 2006 4,763,874 459,291 4,439 47,672 (1,165) 5,274,111

35

At 31 December 2007

Contingent liabilities 240,244 1,118,420 1,194,088 18,002 - 2,570,754

Unused credit facilities 461,898 239,769 535,429 - - 1,237,096

Total 702,142 1,358,189 1,729,517 18,002 - 3,807,850

At 31 December 2006

Contingent liabilities 343,136 339,338 879,549 11,044 - 1,573,067

Unused credit facilities 592,542 16,770 550,701 - - 1,160,013

Total 935,678 356,108 1,430,250 11,044 - 2,733,080

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.3 Liquidity risk (continued)

The table below shows the contractual expiry by maturity of the Bank’s contingent liabilities and commitments:

Up to 1 1 - 3 3 - 12 1 - 5 Over month months months Years 5 Years Total

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000

3.2.4 Market risk

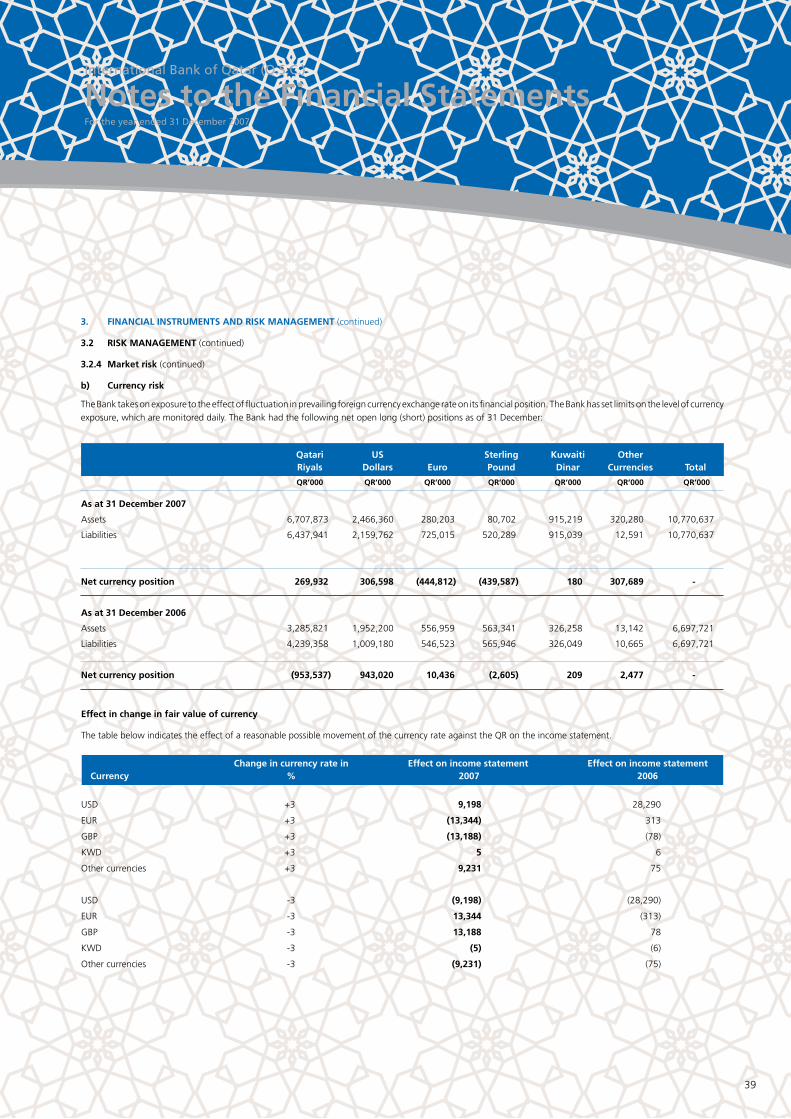

Market risk is the risk that the fair value or future cash flows of financial instruments will fluctuate due to changes in market variables such as interest rates, foreign exchange

rates, and equity prices.

a) Interest rate risk

Interest rate risk arises from the possibility that changes in interest rates might affect the future cash flow or the fair value of financial instruments. Exposure to interest

rate risk is managed by the Bank using, where appropriate, various off-balance sheet instruments, primarily interest rate swaps. Maturities of assets and liabilities have

been determined on the basis of contractual repricing or maturity dates, whichever date is earlier.

The following table summarizes the repricing profile of the Bank assets, liabilities and off balance sheet exposures:

36

International Bank of Qatar (Q.S.C.)

Notes to the Financial StatementsFor the year ended 31 December 2007

3. FINANCIAL INSTRUMENTS AND RISK MANAGEMENT (continued)

3.2 RISK MANAGEMENT (continued)

3.2.3 Liquidity risk (continued)

a) Interest rate risk (continued)

As at 31 December 2007

Effective Up to 1 1 - 3 3 - 12 1 - 5 Non-interest Interest month months months Years sensitive Total Rate

QR’000 QR’000 QR’000 QR’000 QR’000 QR’000 (%)

Cash and balances with Qatar Central Bank 163,000 - - - 883,969 1,046,969 4.02

Due from banks and other financial institutions 1,855,491 53,900 - - 134,938 2,044,329 3.39

Loans and advances to customers 3,871,432 1,871,806 766,576 6,947 - 6,516,761 7.11

Financial investments - - 853,784 46,804 91,575 992,163 5.94