Embed Size (px)

Citation preview

ANNUAL REPORT

2010

DIRECTORS’ REPORTANNUAL REPORT 2010

Table of Contents

ANNUAL GENERAL MEETING

2010 Annual General Meeting of ThinkSmart Limited will be

held at Level 36, 250 St George’s Tce, Perth, Western Australia

on Monday 16th May at 3.30 pm.

A FOCUSED, GLOBAL BUSINESS 2

AN INNOVATIVE GROWTH COMPANY 4

GROWTH OPPORTUNITIES FOR THE FUTURE 6

EXECUTIVE CHAIRMAN & CEO REPORT 10

TRADING RESULTS UPDATE 12

CORPORATE & SOCIAL RESPONSIBILITY 15

DELIVERING VALUE THROUGH..... 16

FINANCIAL REPORT 17

1

ANNUAL REPORT 2011ANNUAL REPORT 2011

ThinkSmart Limited is a leading international financial services company in the provision of finance to small businesses and consumers shopping in electrical retailing stores.

ThinkSmart’s products fill the gap between a credit card and a bank loan, enabling its customers to get on-the-spot approval for the technology they need via a tax and cash flow friendly operating lease.

It’s a niche in which ThinkSmart has a leading international footprint.

2

DIRECTORS’ REPORT

ThinkSmart has long term distribution agreements with some of the world’s leading electrical retailers and banking institutions across Europe and Australasia.

ThinkSmart’s funding agreements are contracted to dates between 2011 and 2014

A Focused, Global BusinessDirectors’ Meetings

The following table sets out the number of directors’

meetings held during the financial year. During the financial

year 7 Board meetings were held.

Audit Nomination andandRisk Remuneration

Board Committee CommitteeDirector Meetings Meetings Meeting

A B A B A B

Peter Mansell 7 7 2 2 1 1

David Griffiths 6 7 2 2 1 1

Ned Montarello 7 7 2* - 1 1

Steven Penglis 7 7 1* - 1 1

A – Number of meetings attended

B – Number of meetings held during the time the director heldoffice during the year

* – Attendance by invitation from the Committee

Corporate Governance Statement

This statement outlines the main corporate governance

practices in place throughout the financial year, which comply

with the ASX Corporate Governance Council

recommendations, unless otherwise stated.

BOARD OF DIRECTORS

Role of the Board

The Board’s primary role is the protection and enhancement

of long-term shareholder value.

Matters which are specifically reserved for the Board or its

Committees under the Board Charter include:

� appointment of a chair;

� appointment and removal of the CEO;

� appointment of directors to fill a vacancy or as additional

directors;

� establishment of Board Committees, their membership

and delegated authorities;

� approval of dividends;

� development and review of corporate governance

principles and policies;

� approval of operational budgets, major capital

expenditure, acquisitions and divestitures in excess of

authority levels delegated to management;

� calling of meetings of shareholders; and

� any other specific matters nominated by the Board from

time to time.

It is also responsible for approving and monitoring financial

and other reporting. Detail of the Board’s charter is located in

the Company’s website (www.thinksmartworld.com).

The Board, together with the Nomination and Remuneration

Committee, determines the size and composition of the

Board, subject to the terms of the constitution.

The Board has delegated responsibility for operations and

administration of the Company to the Chief Executive Officer

and executive management. Responsibilities are delineated

by formal authority delegations.

ANNUAL REPORT 2010

3

ANNUAL REPORT 2011

Product and technology innovation delivers growth, profit and new opportunities.

PRODUCTFUNDINGCAPACITY

DELIVERYSYSTEMS

Product innovationdelivers services based

rental product

New funding platformssignificantly increasegrowth opportunities

Australian Patented QuickSmart

technology platformfacilitates fast and

efficient instore andonline approval process

• Volume growth• Access to new markets

• Efficiency• Customer satisfaction

• Shareholder Value

ANNUAL REPORT 2011

4

DIRECTORS’ REPORT

An Innovative Growth Company

In FY 2010, ThinkSmart increased net profit after tax by 31% to a record result of $6.8m} }Recent Achievements• Completed a $16m equity raising, providing capital to support $160m of new funding lines in

UK and Australia.

• Executed funding agreement with Secure Trust Bank in UK to provide GBP40m revolving

facility for Business and Consumer customers. In Australia, $200m Multi Funder

Securitisation platform on track for completion in first half of 2011.

• Implemented “Infinity” services based rental product for Consumers in UK market.

• Enhanced the online application and approval web portal leading to the grant of an Australian

Innovation Patent on the online rental process and creating a technological competitive

advantage in ThinkSmart’s chosen markets.

• Extended key retail agreements in UK and Australia.

• Delivered sustainable operating efficiencies through systems capabilities resulting in the

cost of doing business reducing by 17%.

• Integrated ThinkSmart’s application and approval system into Dixons retail point of sale

system across all UK retail franchises.

2010 Financial Highlights

• Grew NPAT 31% to $6.8m to deliver a record profit at the top end of market EBITDA

guidance.

• Delivered EBITDA CAGR of 17% from 2007 to 2010.

• Achieved 34% growth in EBITDA from our Australian business with a 45% uplift in new

business volumes.

• Grew EBITDA Margins by 5% delivered by reducing the cost of doing business by 17%.

• Grew Earnings Per Share by 23%.

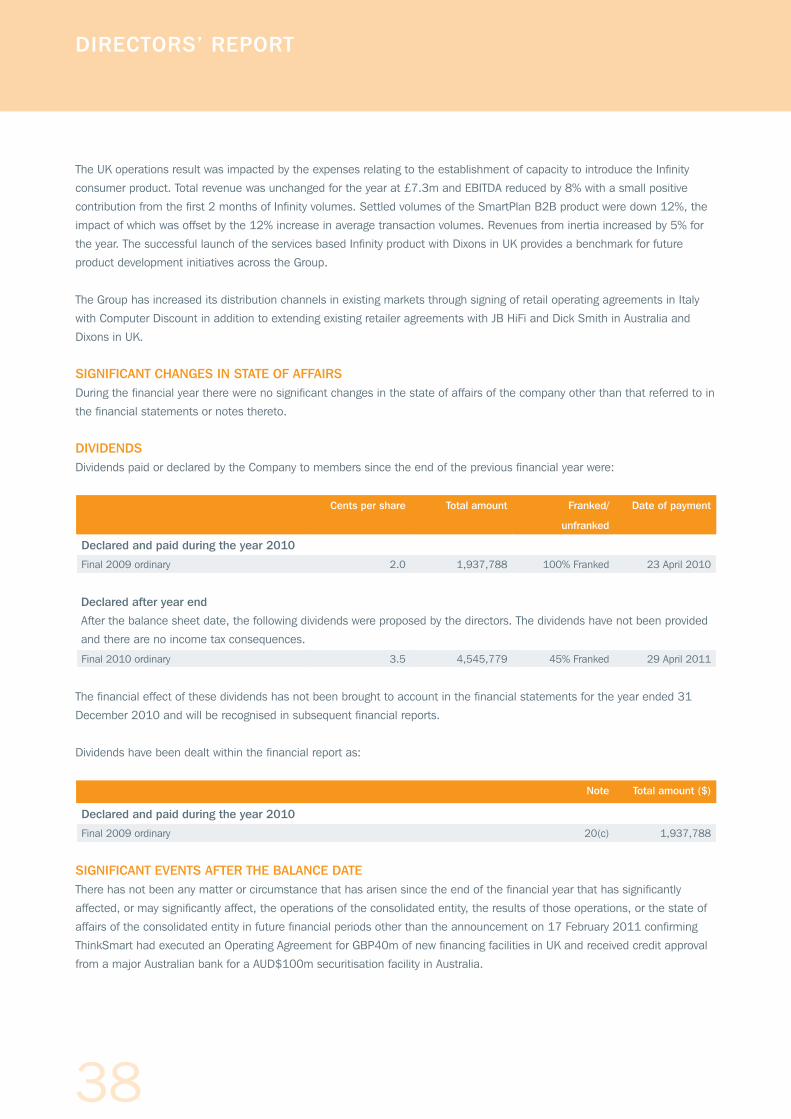

• Paid shareholders 3.5 cents total dividend for the 2010 year.

ANNUAL REPORT 2010

5

ANNUAL REPORT 2011

$40,000

40.0%

8000

$30,000

30.0%

6000

$20,000

20.0%

4000

$10,000

10.0%

2000

$0

0.0%

$0

$45,000

45.0%

9000

$35,000

35.0%

7000

$25,000

25.0%

5000

$15,000

15.0%

3000

$5,000

5.0%

1000

2007

2007

2007

NPAT

Revenue

2008

2008

20082009

2009

20092010

2010

2010

Revenue +14%

$42.1m

Cost of Doing Business -17%

The Cost of Doing Business is the difference between the gross margin and EBITDA margin.

CAGR

(2007 - 2010)

NPAT +31%

$6.8m

-40.0% -20.0% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0% 120.0%

Cost of Doing Business

FY2010 FY2009 % change

NPAT $6.8m $5.2m +31%

Total Revenue $42.1m $36.8m +14%

Earnings Per Share 6.5¢ 5.3¢ +23%

EBITDA $13.3m $11.9m +12%

EBITDA Margin (pre Corp Dev costs) 42% 40% +5%

Cost of Doing Business 22% 27% -17%

Final Dividend - partly franked 3.5cps 3.5cps no change

ANNUAL REPORT 2011

6

DIRECTORS’ REPORT

Growth Opportunities For The Future

ThinkSmart has successfully positioned its business through the challenging global economic environment by

staying true to three guiding principles for growth:

ThinkSmart adopted a strategic plan in 2009 with the aim of cementing its position as the leading international

provider of point-of-sale finance in its chosen markets. The plan involved innovative product design to provide

a compelling value proposition to customers, enhancing web based application and approval systems to

deliver a simple, fast and efficient platform for retail staff and customers, and finally to create funding

capacity to support future growth arising from these leading edge developments. Elements of the plan have

been implemented and have contributed to the Group’s 37% growth in new business volumes in 2010.

Execution of complimentary strategic projects in 2011 for product, funding and delivery systems creates further significant growth opportunities.

Governing Principles

1. Growth Through Cash Flow Not Debt

Expand Accessible Market through Consumer Rental

• Significantly expands total available market in UK

• Potential to introduce to other existing territories

Grow Distribution in New and Existing Territories

• Targeting new Retail partnerships

• Grow the internet acquisition channel in all markets

Grow Revenue Lines and Continue to Diversify Income

• Follow Australian mature territory model

• Repeat customer strategy

Improve Delivery and Customer Experience

• QuickSmart & Eclipse systems automate process at stores and significantly reduce costs of doing business

2. Pace of Expansion Governed by Performance

3. Alignment with Market Leading Retailers

Strategic Focus

ANNUAL REPORT 2010

7

ANNUAL REPORT 2011

Expand Accessible Market through Consumer Rental

ThinkSmart launched consumer rental in to the UK market in November 2010 with the Infinity product. This

services based product is a compelling value proposition for customers. A similar move into Consumer in

Australia over 5 years ago has seen consumer volumes increase at a compound annual growth rate of around

50% and this segment of the market now accounts for 70%+ of new business volumes in Australia.

Consumer rentals in the UK represent a material growth opportunity for 2011 and beyond, evidenced by the

relative size of the currently available Business segment across Dixons and the Consumer segment which is

4 times larger.

Outside of the UK, ThinkSmart is exploring the appetite from existing and potential retail partners to expand

ThinkSmart’s operations to include Consumer.

Grow Distribution in New and Existing Territories

ThinkSmart currently originates 32% of new business volumes in Australia online where the customer applies

through ThinkSmart’s website and once approval is notified the customer can execute the rental agreement

and collect the rental equipment instore. In addition to expanding distribution through traditional channels,

ThinkSmart is looking to increase its customer acquisition through Internet sales.

Recent technology developments in the UK market have seen ThinkSmart’s systems integrated with its retail

partner Dixons point of sale systems. When a customer is approved for rental finance at home they can print

out an approval confirmation that carries a unique barcode. This document can be scanned by any Dixons

point of sale terminal to authenticate the approved application and allow the customer to select equipment

up to the pre-approved limit. Equipment details are automatically captured by Dixons point of sale process

and added to the rental contract prior to execution by the customer.

The next phase of this evolution will deliver electronic signature technology to the application and approval

process creating the opportunity for ThinkSmart to offer rental finance to customers choosing to purchase

technology products through the Internet without visiting a traditional retail store. This innovative and leading

edge development will allow ThinkSmart to expand the distribution reach with existing retail partners in

addition to creating new relationship opportunities with participants in the online retail space. ThinkSmart’s

opportunity to expand distribution into new territories using online capability will reduce the establishment

costs and operating risks of expanding the Group’s international footprint.

ANNUAL REPORT 2011

8

DIRECTORS’ REPORT

Grow Revenue Lines and Continue to Diversify Income

ThinkSmart’s existing territories create opportunities to diversify the revenue base and grow total income. The

RentSmart business in Australia was established in 1996 and generates income from brokerage (Commercial

and Consumer rental finance), insurance, inertia and warranty services. In contrast, Italy operations were

established in 2007 and generate income from Commercial rental finance only. As each territory matures

the opportunity to grow revenue lines increases as demonstrated by the UK business which has recently

introduced the Consumer product.

Growth Opportunities For The Future (continued)

Improve Delivery and Customer Experience

ThinkSmart has transitioned from a telephone based applications and approval process to a web portal that

allows the customer to apply for rental finance from instore or from the comfort of their home or office. This

innovative approach has seen the time to complete the end to end process reduced to a few minutes thereby

delivering a significantly improved experience for customers and retailers alike. In addition, ThinkSmart has

achieved operating efficiencies that has led to a 17% reduction in the cost of doing business in 2010.

The QuickSmart system has been developed inhouse and has recently been awarded an Australian Innovation

Patent. Further developments including e-signature technology will further improve efficiency and the overall

experience for customers and retailers. The process establishes ThinkSmart as a global leader in this niche

and strengthens its competitive advantage in the markets it chooses to operate in.

13%

41%35%

5%19%

49% 51% 100%37%

20%

11%

19%

Commercial Consumer Insurance Warranty Inertia

Maturity Of Business Model

Australia(est 1996)

United Kingdom(est 2003)

Spain(est 2005)

Italy(est 2007)

ANNUAL REPORT 2010

9

ANNUAL REPORT 2011

To effectively capture the growth opportunities it has created, ThinkSmart has negotiated material increases

in funding capacity. Delivering increased funding facilities at a lower overall cost was achieved by ThinkSmart

developing in conjunction with banks an alternate funding model that can co-exist with the traditional funding

structures. In Australia, ThinkSmart is well advanced in the implementation of a Master Trust Multi Funder

Securitisation Program that doubles existing capacity. Key elements of the transformation plan are:

• Leases are written “on balance sheet” rather than initiated under a brokerage model on behalf of funding

banks.

• Master Trust structure is non-recourse to ThinkSmart.

• Platform supports additional funders on as needs basis and provides access to securitization markets

to further increase future capacity.

• Improved margins delivered through a transition to an annuity revenue stream and lower funding costs.

• No refinancing risk – all facilities pay down in line with repayments from customers.

• $160m in additional funding capacity initially created across UK and Australia.

• New and existing funding sufficient to settle 3x 2010 business volumes in all territories going forward.

70

50

40

20

-

80

60

40

30

10

2009 2010

UK Funding Capacity (GBPm)

CashUndrawnDrawn

200

150

100

50

-

225

175

125

75

25

2009 2010

Australian Funding Capacity ($Am)

CashUndrawnDrawn

ANNUAL REPORT 2011

10

DIRECTORS’ REPORT

Executive Chairman & CEO Report

Dear Shareholders

I am pleased to be able to report that, for the Financial Year ended 31st December 2010, ThinkSmart delivered

a record full-year Net Profit after Tax of $6.8 million, up 31% on the previous year and delivering to the top end

of the full year EBITDA target. This result was achieved through increased revenue of 14% and a 17% reduction

in the cost of doing business.

Not only have we continued to prove our model’s resilience through the challenges of the global economic

downturn evidenced by 4 consecutive years of record profit growth since listing on the ASX in 2007, but we

have also reinforced with investors that ThinkSmart continues to be a growth company with a 37% uplift in new

business volumes in the year.

A Growth Company

To support the growth momentum ThinkSmart has successfully accessed increased global funding capacity to

support significant levels of future growth. In recent months ThinkSmart has captured $160 million in additional

funding capacity across Australia and UK which together with pre-existing capacity is sufficient to settle 3 times

2010 business volumes. The new funding arrangements provide flexibility and the structure supports additional

funders when growth in demand requires increased capacity, and overall lower funding costs will grow margins

over time.

Access to global funding lines requires a level of capital support and given the magnitude of additional funding

this lead to ThinkSmart raising $16m of additional equity in October 2010. It is expected that any future capital

requirements to support organic growth will be satisfied by internally generated capital.

Systems

The Australian deployment of our new “QuickSmart” online application portal in 2009 has been followed by

deployment to the UK in October 2010. The recently patented QuickSmart system makes the application

experience easier and faster for store sales people; delivering notable efficiency gains for our call centre teams;

and reduced our overall cost of doing business by 17%. The instore experience for the sales person and the

customer is vastly improved leading to increased penetration rates on computer sales. QuickSmart also creates

the opportunity to expand our distribution channels significantly through the growth of our Internet business.

Through a set of improvements to our online process and marketing, we have grown the Internet channel in

Australia to account for up to 32% of all volume in a month, up from 27% a year earlier.

Product

The introduction of services to the rental product in Australia has contributed to increases in volumes of 45% in

2010, far in excess of the computer sales growth of our retail partners. Following the success of the Australian

product initiatives, a more comprehensive services based consumer rental product was introduced to the

UK market in November 2010 though our long term retail partner Dixons. Together with the integration of

ANNUAL REPORT 2010

11

ANNUAL REPORT 2011

ThinkSmart’s systems into Dixons point of sale system, the Company is optimistic that the new Infinity consumer

product will drive growth and increased profitability in our UK operations in 2011 and beyond.

Markets

Retailing in Europe continues to be challenging however there are opportunities to grow the UK operations

leveraging the Infinity consumer product delivered through more efficient online systems and stable funding

capacity at an appropriate pricing structure. In Australia, the retailing outlook is stable however ThinkSmart sees

opportunities to leverage online capability together with lower delivery costs and increased funding capacity to

further grow future new business volumes.

ThinkSmart will continue to work towards leveraging and adapting its existing business model to capitalise on

opportunities in new territories. Further development of expansion opportunities will occur in 2011 with a view to

target new markets in 2012.

Growth Opportunities

ThinkSmart has successfully delivered the key elements of a successful growth strategy being:

• distribution through leading international retailers across global markets;

• capital to support growth expectations;

• product innovation recognised by retail partners as contributing value to their businesses;

• funding capacity to adequately support growth expectations;

• delivery systems that are leading edge and provide competitive advantage.

These elements have global application and support ThinkSmart’s growth ambitions in selected markets. In

2011 and beyond we seek to successfully leverage these strategic elements and profitably grow the international

businesses thereby delivering enhanced shareholder value.

Final Dividend

Finally, on 29 April 2011 we paid a final dividend of 3.5 cents per share partly franked, representing the full

dividend entitlement for the year. We thank all our staff for their continued hard work and enthusiasm and look

forward to continuing to grow together in 2011 and beyond.

Sincerely

NED MONTARELLO

Executive Chairman & CEO

ANNUAL REPORT 2011

12

DIRECTORS’ REPORT

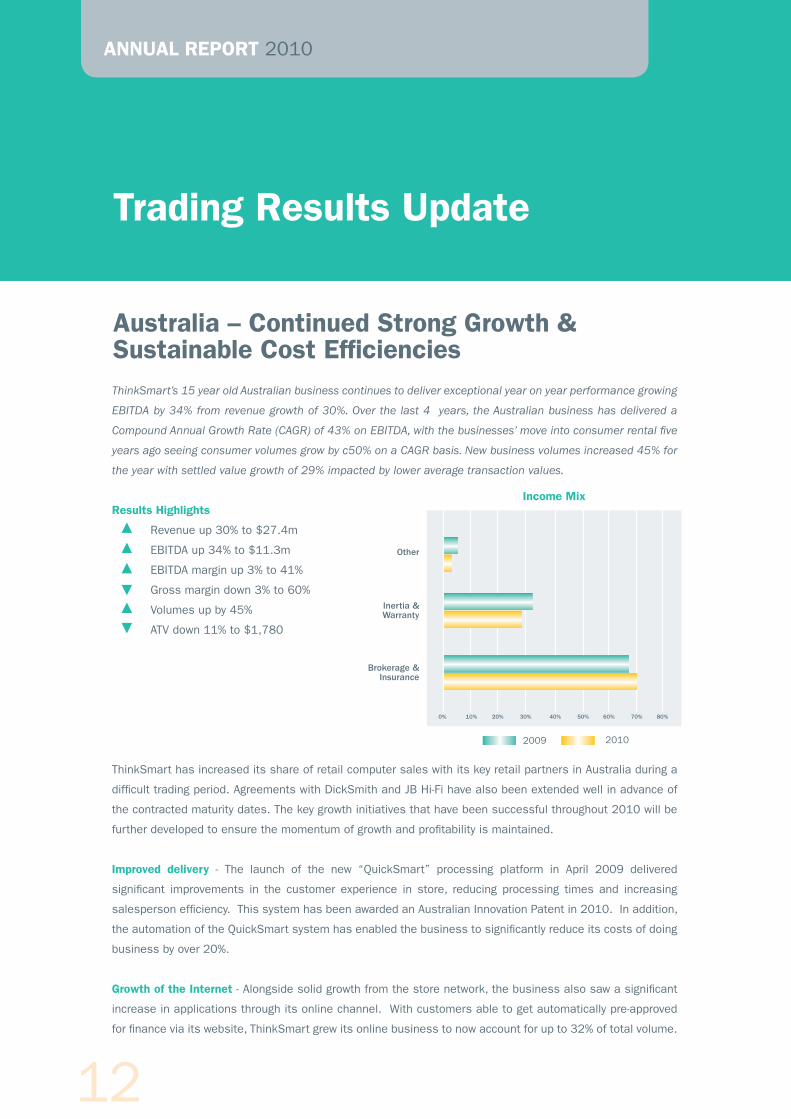

ThinkSmart’s 15 year old Australian business continues to deliver exceptional year on year performance growing

EBITDA by 34% from revenue growth of 30%. Over the last 4 years, the Australian business has delivered a

Compound Annual Growth Rate (CAGR) of 43% on EBITDA, with the businesses’ move into consumer rental five

years ago seeing consumer volumes grow by c50% on a CAGR basis. New business volumes increased 45% for

the year with settled value growth of 29% impacted by lower average transaction values.

Results Highlights

Revenue up 30% to $27.4m

EBITDA up 34% to $11.3m

EBITDA margin up 3% to 41%

Gross margin down 3% to 60%

Volumes up by 45%

ATV down 11% to $1,780

ThinkSmart has increased its share of retail computer sales with its key retail partners in Australia during a

difficult trading period. Agreements with DickSmith and JB Hi-Fi have also been extended well in advance of

the contracted maturity dates. The key growth initiatives that have been successful throughout 2010 will be

further developed to ensure the momentum of growth and profitability is maintained.

Improved delivery - The launch of the new “QuickSmart” processing platform in April 2009 delivered

significant improvements in the customer experience in store, reducing processing times and increasing

salesperson efficiency. This system has been awarded an Australian Innovation Patent in 2010. In addition,

the automation of the QuickSmart system has enabled the business to significantly reduce its costs of doing

business by over 20%.

Growth of the Internet - Alongside solid growth from the store network, the business also saw a significant

increase in applications through its online channel. With customers able to get automatically pre-approved

for finance via its website, ThinkSmart grew its online business to now account for up to 32% of total volume.

Australia – Continued Strong Growth & Sustainable Cost Efficiencies

Trading Results Update

Income Mix

0% 10% 20% 30% 40% 50% 60% 70% 80%

Other

Inertia & Warranty

Brokerage & Insurance

20102009

ANNUAL REPORT 2010

13

ANNUAL REPORT 2011

The growth of the online channel has helped reduce customer acquisition costs, and attracts a higher average

spend. However, this is partially offset by a 20 percentage point lower conversion rate. This experience in

online initiated business is transportable to other existing and future territories.

Product improvements – With the goal of improving customer acquisition and retention, in January 2010,

ThinkSmart rolled out a major new enhancement to its core rental product in Australia to include a suite of

added value service offerings that the customer benefits from over the life of their contract. This provides

more than $500 worth of added value on an average $2,000 deal. Based on the successful launch of the

UK Infinity consumer product, ThinkSmart is looking to further refine the Australian product offering to provide

broader appeal to customers and grow market share further.

The business is strongly positioned for 2011 and beyond with strong and committed retail relationships,

significant growth in funding capacity to support growth ambitions, and consistent and increasing revenue

from inertia and warranty.

United Kingdom - Stable EBITDA with Consumer creating growth opportunities

The focus of 2010 was to maintain the existing B2B product and at the same time develop an exciting and

compelling proposition for the Consumer customer. The Infinity product for Consumers was introduced in early

November and has been positively accepted by Dixons, our retail partner in the UK. The product is expected to

make a positive EBITDA contribution in 2011.

Results Highlights

Revenue unchanged at £7.3m

EBITDA down 5% to £3.5m

EBITDA margin down 9% to 47%

Gross margin down 4% to 79%

Volumes (B2B) down by 12%

ATV up 12% to £881

Income Mix

0% 10% 20% 30% 40% 50% 60% 70% 80%

Other

Inertia

Brokerage & Insurance

20102009

ANNUAL REPORT 2011

14

DIRECTORS’ REPORT

Against a backdrop of a challenging retail trading environment the business has maintained its position and

at the same time created opportunities in the Consumer segment that is expected to deliver significant future

value.

ThinkSmart has secured a strong funding proposition in the UK through the execution of a new GBP40m

revolving facility with Secure Trust Bank which initially runs to 2014. Negotiations with other potential funders

in this market continue as ThinkSmart seeks to move towards a multi funder platform in its key territories.

The Infinity product is available in all Curry’s outlets providing greater market share opportunity. ThinkSmart’s

QuickSmart application and approval system is integrated into Curry’s retail point of sales system thereby

delivering the most advanced and efficient in store process offered by ThinkSmart. This market leading

process provides a competitive advantage and achieves a high level of scaleability as volumes begin to grow

as retail markets improve.

In 2011, ThinkSmart plans to adopt e-signature technology to further enhance the experience for customers

and retail staff whilst further reducing ThinkSmart’s cost of delivery and broadening the appeal of the product

to online purchasers of technology. Encouragingly, the UK businesses second half 2010 application volumes

and EBITDA (over the first half) returned to growth providing a level of expectation for growth in 2011.

Mainland Europe – Stable performance during difficult trading

Spain - ThinkSmart’s Spanish business maintained positive EBITDA in FY 2010, growing its contribution off

a low base. New business volumes grew by over 60% for the year. Inertia revenues from business written in

2006 and 2007 continue to underpin profit performance

ThinkSmart continues to pursue opportunities to develop Spain into a multi-channel territory.

Italy - In Italy, ThinkSmart currently is reviewing its market strategy to incorporate an online approach.

France - France currently remains a challenging market for ThinkSmart, and its success is dependent upon

aligning with the right retail partners in the territory and our ability to secure a supportive funding partner.

There are no immediate plans to commence trading in this territory.

Trading Results Update (continued)

ANNUAL REPORT 2010

15

ANNUAL REPORT 2011

People

ThinkSmart recognises the value of its staff in delivering on its corporate goals. Accordingly, ThinkSmart is

committed to providing the right training, tools, leadership and professional support, required to enable its

employees to develop into highly productive, knowledgeable, and loyal individuals. ThinkSmart also seeks to

create a values based culture, providing the guiding principles within which our employees can develop and

excel.

These goals are primarily fostered through our “PeopleSmart” programme in Australia and the “Investor in

People” accreditation of our UK business. The PeopleSmart programme aims to build a great place to work

and cultivate the values of “people, performance, and culture”. PeopleSmart is made up of a committee of

employees from various departments to organize activities that align employees to the ThinkSmart values.

PeopleSmart also acts as a forum for the discussion of workplace issues, in order to improve the work

environment for ThinkSmart’s employees.

Community

At a corporate level, and through its PeopleSmart initiative, ThinkSmart looks to give back to the community

both financially and by donating time. At a corporate level ThinkSmart is a contributor to the St John of God

Cancer Centre for the treatment of cancer patients, as well as the provision of hospitality to their families.

ThinkSmart has donated a number of computers and other equipment to a Queensland primary school which

had lost all its technology equipment in the 2010 floods.

At a team level, ThinkSmart supports employee driven charitable initiatives both by making the time available

and in most cases, matching employee donations. Employees in the business have given generously and

participated actively in a range of community based initiatives including: the Premiers Disaster Relief Appeal

for the recent Queensland floods; blood and financial donations to the Red Cross; Make a Wish Foundation;

and Movember (Prostate Cancer Foundation and Beyond Blue).

Responsible Lending

ThinkSmart has been a practitioner of responsible lending practices for a number of years. Primarily these

practices are reflected within its lending criteria; however ThinkSmart is also a member of an approved

external dispute resolution scheme and regularly reviews the competence of its lending staff and its end to

end processes as it strives to achieve best practice. ThinkSmart regularly undertakes research and elicits

customer feedback to ensure that its product offering is aligned to community needs and that its customer

service is the best it can be.

Corporate & Social Responsibility

ANNUAL REPORT 2011

16

DIRECTORS’ REPORT

Delivering Value Through...

1. Proven track record of growth - ThinkSmart has delivered a 17% CAGR in underlying EBITDA over the last

four years (2007-2010) since listing on ASX, delivering a very strong EBITDA and Margin performance during

a tough global trading period.

2. Leading International Footprint - ThinkSmart has exclusive and entrenched partnerships with market

leading retailers and funders in Australia and Europe, providing it with a diverse platform for growth.

3. Strong Customer Value Proposition - ThinkSmart’s products provide a compelling and highly profitable

value proposition for retail partners, customers and funders.

4. Capacity for Continued Profitable Strong Growth - ThinkSmart has secured the funding capacity, the

distribution relationships and the compelling product offerings to deliver future growth in its chosen markets.

5. Predictable recurring income lines - The timing of ThinkSmart’s income model provides predictable,

recurring income lines across the life of each customer contract, thereby managing ThinkSmart’s exposure to

demand fluctuations in any one year.

6. Shrinking cost of doing business - The delivery of ThinkSmart’s products through in store portals is

significantly reducing its cost of doing business and thereby improving EBITDA margins. Online capability

provides broader market access and potentially lowers the cost of establishing a new territory.

7. Highly scalable model - ThinkSmart operates a simple, highly scalable model with processing centres in

Europe and Australasia which can be leveraged to enable it to enter new markets at a very low cost.

8. Significant Growth Opportunities - ThinkSmart’s entry into Consumer Rental in the UK has the opportunity

to significantly grow the UK market with immediate profit contribution.

ANNUAL REPORT 2010

17

ANNUAL REPORT 2011

FINANCIAL REPORT FINANCIAL YEAR ENDED 31 DECEMBER 2010

Corporate Information 18

Directors’ Report 19

Auditor’s Independence Declaration 42

Directors’ Declaration 43

Statement of Comprehensive Income 44

Statement of Financial Position 45

Statements of Changes in Equity 46

Statement of Cash Flow 47

Notes to the Financial Statements 48

Independent Audit Report 95

Shareholder Information 97

18

CORPORATE INFORMATION

ABN 24 092 319 698

DIRECTORSN R Montarello (Chairman and Chief Executive Officer)

D Griffiths (Deputy Chairman)

S Penglis

F de Vicente

COMPANY SECRETARYN Barker

REGISTERED OFFICELevel 1, The West Centre

1260 Hay Street

West Perth, WA 6005

Australia

PRINCIPAL PLACE OF BUSINESSLevel 1, The West Centre

1260 Hay Street

West Perth, WA 6005

Australia

Phone: +61 8 9463 7500

SHARE REGISTER Computershare Investor Services Pty Limited

Level 2, 45 St Georges Terrace

Perth, WA 6000

Australia

Phone: 1300 850 505

ThinkSmart Limited shares are listed on the Australian

Securities Exchange (ASX code: TSM)

SOLICITORSFreehills

250 St Georges Terrace

Perth, WA 6000

Australia

BANKERSANZ

West Perth

Australia

AUDITORSKPMG

Australia

19

ANNUAL REPORT 2011

DIRECTORS’ REPORT

The Directors of ThinkSmart Limited (the “Company”) submit

herewith the annual financial report of the Company and the

Group for the financial year ended 31 December 2010 and

the auditor’s report thereon. In order to comply with the

provisions of the Corporations Act 2001, the directors report

as follows:

DIRECTORSThe names and details of the Company’s directors in office

during the financial year and until the date of this report

are as follows. Directors were in office for this entire period

unless otherwise stated.

Names, qualifications, experience and special

responsibilities

NED MONTARELLO (AGE 49)

Executive Chairman and Chief Executive Officer

Ned Montarello has over 20 years experience in the finance

industry and joined the Board on 7 April 2000 and was

appointed Chairman on 22 May 2010. Mr Montarello

founded ThinkSmart over 14 years ago and through this

vehicle has been credited with elevating the nano-ticket

rental market sector in Australia, receiving the Telstra and

Australian Government’s Entrepreneur of the Year Award in

1998. He steered the expansion of the business into Europe

in 2002/2003, establishing agreements with the UK’s largest

electrical retailer, DSG International and the Halifax Bank

of Scotland. Following the establishment of a beachhead

European operations centre in Manchester, England, Mr

Montarello has driven its growth across Europe where it now

also operates in Spain and Italy.

DAVID GRIFFITHS (AGE 60)

B. Ec (Hons), M. Ec, D. Ec (Hon), FAICD

Non-Executive Director, Deputy Chairman

David Griffiths joined the Board on 28 November 2000

and was appointed Deputy Chairman on 22 May 2010. Mr

Griffiths has served in a wide range of senior finance roles,

most recently as Division Director of Macquarie Bank Limited

and previously as Executive Chairman of Porter Western

Limited.

Mr Griffiths holds an Honours Degree in Economics from

The University of Western Australia, a Masters Degree in

Economics from Australian National University and is a Fellow

of the Australian Institute of Company Directors. David also

sits on the Board of the Perth International Arts Festival.

Mr Griffiths is currently a chairman of Automotive Holdings

Group Limited and Northern Iron Limited. In the past three

years Mr Griffiths has been a director of the following listed

companies: ARC Energy Limited, Great Southern Limited and

Antaria Limited.

PETER MANSELL (AGE 64)

B.Com, LLB, H. Dip Tax, FAICD

Non-Executive Director

Peter Mansell joined the Board on 12 April 2007 and was

appointed Chairman on the 7 May 2007. Mr Mansell has

subsequently resigned from the Board on 22 May 2010. Mr

Mansell practiced as a business lawyer for over 40 years and

has a wide range of experience in corporate matters. He was

at various times the Freehills National Chairman (1995-

2000), Managing Partner of the Perth office (1992-2002)

and a member of the firm’s National Board (1989-2002).

Mr Mansell is a Fellow of the Australian Institute of Company

Directors, having been President of the Western Australian

division and having sat on its National Board from 2002 to

2003. He is currently a director of the following Australian

listed companies: Ampella Mining Ltd (Chairman) and

Bunnings Property Management Limited (responsible entity

for the Bunnings Warehouse Property Trust). In the past

three years Mr Mansell has been a director of the following

listed companies: Great Southern Limited, West Australian

Newspaper Holdings Ltd, Oz Minerals Limited, Zinifex Ltd and

Western Power Corporation.

STEVEN PENGLIS (AGE 50)

B. Juris and B. Law

Non-Executive Director

Steven Penglis joined the Board on 1 July 2000 and stepped

down as Chairman on the 6 May 2007. Mr Penglis is a

Partner at Freehills since 1987 and former Chairman of

the Legal Practice Board of Western Australia. Mr Penglis

specialises in the area of Corporate and Corporations

Law Litigation, advising many public companies, including

ThinkSmart, before his appointment to the Board. He

is a part-time Senior Member of the Commonwealth

Administrative Appeals Tribunal; an elected member of

the Legal Practice Board of Western Australia and former

chairman; and an elected member of the Council of the Law

Society of Western Australia.

20

DIRECTORS’ REPORT

FERNANDO DE VICENTE (AGE 43)

B. Econ, MBA Bus

Non-Executive Director

Fernando de Vicente is a citizen of Spain whom has

joined the Board on 7 April 2010. Mr de Vicente has a

Degree in Economics (International Development) from the

University Complutense in Madrid, and an Executive MBA

from IESE Business School in Madrid. Mr de Vicente spent

nine years at DSG International, one of Europe’s largest

electrical retailers, where he most recently held the role of

International Managing Director, with responsibility for DSG’s

Central & Southern European operations, a A$3 billion

business with 350 stores across six countries.

Mr de Vicente started his career with DSG as Finance

Director for PC City Spain, and became the MD for Spain

in 2003. In 2006 he was promoted to Regional Managing

Director for South-East Europe based in Greece, before

assuming the role of International Managing Director in

2008. In March 2010, Mr de Vicente left DSG to become

the Executive Chairman of BodyBell Group, one of Spain’s

largest speciality retailers.

COMPANY SECRETARYNEIL BARKER

B.Bus, FCPA

Neil Barker is a Certified Practicing Accountant (Fellow)

with over 27 years experience in banking and finance. Prior

to joining ThinkSmart, Mr Barker was the Group Financial

Controller of Alinta Limited, an Australian public listed

company. Prior to joining Alinta, he was employed with the

NAB Group in senior finance roles based in the UK and

Australia.

DIRECTORS’ MEETINGSThe following table sets out the number of directors’

meetings held during the financial year. During the financial

year 10 Board meetings were held.

Audit Nomination and

and Risk Remuneration

Board Committee Committee

Director Meetings Meetings Meetings

A B A B A B

N Montarello** 9 9^ 2* - 1 1

D Griffiths 10 10 2 2 1 1

S Penglis 9 10 1 1 1 1

P Mansell*** 3 3 1 1 1 1

F de Vicente 6 7 - - - -

A Number of meetings attended.

B Number of meetings held during the time the director held office during

the year.

* Attendance by invitation from the Committee.

** Mr Montarello resigned from the Nomination and Remuneration

Committee on 21 May 2010.

*** Mr Mansell resigned from the Board on 22 May 2010.

^ Mr Montarello was not eligible to attend a board meeting as the meeting

was in relation to a matter in which Mr Montarello held an interest.

21

ANNUAL REPORT 2011

CORPORATE GOVERNANCE STATEMENTThis statement outlines the main corporate governance

practices in place throughout the financial year, which comply

with the ASX Corporate Governance Council recommendations,

unless otherwise stated.

BOARD OF DIRECTORS

Role of the Board

The Board’s primary role is the protection and enhancement

of long-term shareholder value.

To fulfil this role, the Board has adopted a charter

which establishes the relationship between the Board

and management and describes their functions and

responsibilities. The Board’s responsibilities, as set out in the

Board Charter, include:

n working with management to establish ThinkSmart’s

strategic direction;

n monitoring management and financial performance;

n monitoring compliance and risk management;

n reviewing procedures in place for appointment of senior

management and monitoring of its performance and for

succession planning; and

n ensuring effective disclosure policies and procedures.

Matters which are specifically reserved for the Board or its

Committees under the Board Charter include:

n appointment of a chair;

n appointment and removal of the CEO;

n appointment of directors to fill a vacancy or as

additional directors;

n establishment of Board Committees, their membership

and delegated authorities;

n approval of dividends;

n development and review of corporate governance

principles and policies;

n approval of operational budgets, major capital

expenditure, acquisitions and divestitures in excess of

authority levels delegated to management;

n calling of meetings of shareholders; and

n any other specific matters nominated by the Board from

time to time.

It is also responsible for approving and monitoring financial

and other reporting. Detail of the Board’s charter is located

in the Company’s website (www.thinksmartworld.com).

The Board, together with the Nomination and Remuneration

Committee, determines the size and composition of the

Board, subject to the terms of the constitution.

The Board has delegated responsibility for operations and

administration of the Company to the Chief Executive Officer

and executive management. Responsibilities are delineated

by formal authority delegations.

Board process

To assist in the execution of its responsibilities, the Board

has established a Nomination and Remuneration Committee,

as well as an Audit and Risk Committee. These Committees

have written mandates and operating procedures, which are

reviewed on a regular basis. The Board has also established

framework for management of the Group including a system

of internal control, a business risk management process and

the establishment of appropriate ethical standards.

Independent professional advice and access to company

information

Following consultation with the chairperson, directors may

seek independent professional advice at the Company’s

expense. Generally, this advice will be available to all

directors.

Composition of the Board

The names of the directors of the Company in the office at

the date of this report are set out in the Directors’ report on

page 19 and 20 of this report. The composition of the Board

is determined using the following principles:

n The Board does not believe that it should establish a

limit on tenure. While tenure limits can help to ensure

that there are fresh ideas and viewpoints available to

the Board, they hold the disadvantage of losing the

contribution of directors who have been able to develop,

over a period of time, increasing insight in the Company

and its operation and, therefore, an increasing

contribution to the Board as a whole.

n It is intended that the Board should comprise a majority

of independent Non-Executive Directors and comprise

directors with a broad range of skills, expertise and

experience from a diverse range of backgrounds.

n The Board regularly reviews the independence of each

director in light of the interests disclosed to the Board.

22

DIRECTORS’ REPORT

On 22 May 2010, Mr Mansell retired from his role

as Chairman of the Board after leading the Company

through a successful transition to being a publicly listed

company, and Mr Montarello was subsequently appointed

Executive Chairman. The Board acknowledges the ASX

Recommendation that the Chairman be an Independent

Director, however, the Board views the appointment of Mr

Montarello as an advantage given his history of leadership

in the Company and finance industry, and his clear incentive

to maximize the interests of the Company. Mr Montarello

founded the Company over 14 years ago, and has been

involved in expanding the business through Australia and

overseas. His experience and insights continue to be

invaluable to the Group.

The Board is conscious of the ASX Corporate Governance

Recommendation stipulates that the roles of Chair and

Chief Executive Officer should not be exercised by the same

individual. Given the breadth of the Group’s operations and

the Executive Chairman’s extensive business experience, the

Board considers it appropriate that the Executive Chairman

be considered the most senior executive overseeing and

supervising the Group as well as managing the Group’s small

executive team in regard to this.

NOMINATION AND REMUNERATION COMMITTEE

The objective of the Nomination and Remuneration

Committee is to help the Board ensure that ThinkSmart has a

Board of an effective composition, size and the commitment

to adequately discharge its responsibilities and duties, and

to determine and review the compensation arrangements for

the Directors and senior management team.

The Nomination and Remuneration Committee reviews and

makes recommendations to the Board on remuneration

packages and policies applicable to the executives and

directors of the Company as well as the Group. On an annual

basis:

n Directors will provide written feedback in relation to

the Board and its Committees against an agreed set of

criteria and each Committee will do the same regarding

its own performance;

n Feedback will be collected by the chair of the Board,

or an external facilitator, and discussed by the Board,

with consideration being given as to whether any steps

should be taken to improve performance of the Board

or its Committees;

n The CEO will also provide feedback from senior

management in connection with any issues that may

be relevant in the context of the Board performance

review; and

n Where appropriate to facilitate the review process,

assistance may be obtained from third party advisers.

The current members of the Committee are S Penglis (Chair),

D Griffiths, and F De Vicente.

The Committee will meet as often as the Committee

members deem necessary in order to fulfil their role.

However, it is intended that the Committee will normally

meet at least annually.

The Committee consists of a minimum of 3 members,

majority being Non-Executive Directors, and an independent

director as chair. The Nomination and Remuneration

Committee has a documented charter, approved by

the Board, which is available on the website (www.

thinksmartworld.com).

REMUNERATION REPORT - AUDITED

The remuneration report for 2010, as presented below,

has been prepared for consideration by shareholders. The

remuneration report is set out under the following main

headings:

A: Principles of compensation

B: Directors’ and executive officers’ remuneration

C: Service agreements

D: Share-based compensation (options)

E: Share-based compensation (shares)

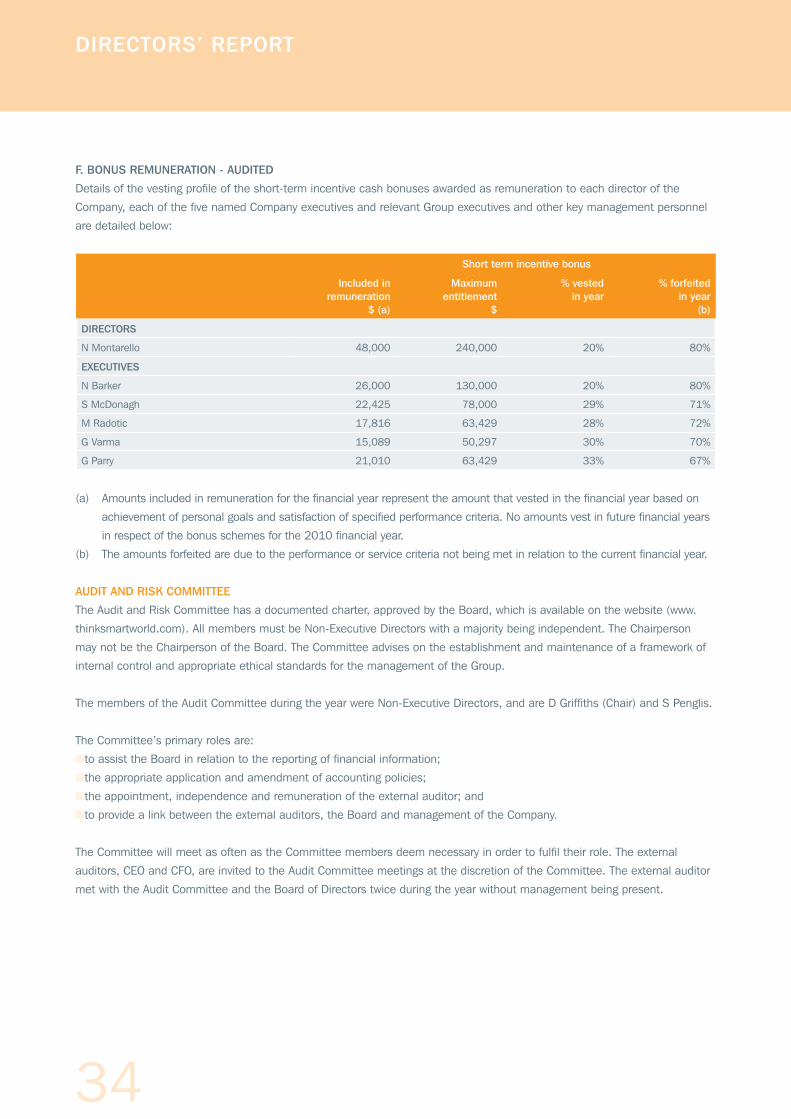

F: Bonus remuneration

A. PRINCIPLES OF COMPENSATION - AUDITED

Remuneration is referred to as compensation throughout

this report. Key management personnel have authority and

responsibility for planning, directing and controlling the

activities of the Company and the Group, including directors

of the Company and other executives. Key management

personnel comprise the directors of the Company and

executives for the Company and the Group including the five

most highly remunerated executives.

23

ANNUAL REPORT 2011

Compensation levels for key management personnel and

secretaries of the Company, and key management personnel

of the Group are competitively set with a view to:

n Maintain alignment with shareholders’ interests; and

n Ensure remuneration remains competitive to retain

and attract talented people who are key to delivering

sustained profitable growth of the Company.

The Nomination and Remuneration Committee obtains

independent advice on the appropriateness of compensation

packages of both the Company and the Group given trends

in comparative companies both locally and internationally

and the objectives of the Company’s compensation strategy.

The compensation structures explained below are

designed to attract suitably qualified candidates, reward

the achievement of strategic objectives, and achieve the

broader outcome of creation of value for shareholders. The

compensation structures take into account:

n the capability and experience of the key management

personnel;

n the key management personnel’s ability to control the

relevant segment/s’ performance; and

n the Group’s performance.

Compensation packages include a mix of fixed and variable

compensation and short-term and long-term performance-

based incentives.

Linking Executive Remuneration to Group Performance

The Directors of ThinkSmart Limited understand that linking

executive remuneration to Group performance is a driver of

performance. Since the Company raised equity and listed in

2007, it has delivered consistent growth in EBITDA (before

listing costs) and basic EPS.

The graph below demonstrates the Group’s consistent growth

in cash net profit after taxation measured on a like for like

basis since the Company listed on the ASX in 2007. The

Cash NPAT calculations for each year exclude from NPAT, on

a net of tax basis, amortisation costs, depreciation costs,

and unrealised foreign exchange costs. In addition, non

recurring items net of any applicable taxation are excluded

being redundancy costs in 2009, US operating costs in

2008 and IPO costs in 2007.

In considering the Group’s performance and benefits for

shareholder wealth, the Executive Chairman and Nomination

and Remuneration Committee have regard to the following

indices of the current financial year and the previous four

financial years.

2010 2009 2008 2007

Profit attributable toowners of the company $6,773,013 $5,171,776 $3,210,752 $738,066

Basic EPS 6.52 cents 5.35 cents 3.34 cents 0.80 cents

Dividends paid $1,937,788 $2,900,682 $1,933,788 -

Dividend paid per share 2 cents 3 cents 2 cents -

Share price at year end $0.73 $0.90 $0.17 $1.92

Change in share price ($0.17) $0.71 ($1.73) ($0.23)^

Return on capital employed 36% 34% 22% 6%

^Initial listing price of $2.15 is used as opening share price.

Profit is considered as one of the financial performance

target setting of the short term incentive. Profit amounts

for 2007 to 2010 have been calculated in accordance with

Australia Accounting Standards (AASBs).

The overall level of key management personnel

compensation takes into account the performance of the

Group over a number of years. Over the past four years, the

group’s profit from ordinary activities after income tax has

grown at an average rate per annum of over 109%. During

the same period, average key management personnel

compensation has grown by approximately 5.7% per annum.

10000

9000

8000

7000

6000

5000

4000

3000

2000

1000

2007 2008 2009 2010

Cash NPAT $’000s

Cash NPAT Non recurring items

24

DIRECTORS’ REPORT

The Directors of ThinkSmart Limited consider that a variety

of factors, including the broad economic environment,

market sentiment and financial performance, contribute to

the Company’s share price. In addition, there are no closely

comparable companies that would provide a meaningful

relative share price measure. As a result, the Executive

remuneration is linked to the Group’s financial performance.

Non-Executive Directors

Fees and payments to non-executive directors reflect the

demands which are made on and the responsibilities of the

Non-Executive Directors. Non-executive directors’ fees and

payments are reviewed annually by the Board. Non-Executive

Directors do not receive Share Options.

Non-Executive Director’s fees

The Non-Executive Directors shall be paid by way of fees for

services the maximum aggregate sum as may be approved

from time to time by ThinkSmart in general meeting. The

fees include Director’s fee as well as Board Committee

membership fee. The current maximum aggregate annual

sum approved by shareholders at a previous general

meeting is $600,000 (2009: $600,000). Any change to

that aggregate annual sum needs to be approved by the

shareholders. The constitution also makes provision for

ThinkSmart to pay all reasonable expenses of directors in

attending meetings and carrying out their duties.

Executive pay

The Company’s remuneration is market competitive and

aims to attract, retain and motivate high calibre employees

who contribute to the sustained growth of the ThinkSmart

business with a mix of the following four components:

n base pay and benefits;

n short-term performance incentives (STIs);

n long-term incentives through participation in the

ThinkSmart Long Term Incentive Plan; and

n other remuneration such as superannuation.

The purpose of STIs is to make a significant contribution to

the total reward package subject to meeting various targets

linked to the Company’s business objectives. An incentivised

reward structure is necessary to ensure a competitive

package in Australian and global marketplace for executives.

Incentives are designed to focus and motivate employees

to achieve outcomes beyond the expectation of normal

professional competence.

Remuneration is reviewed annually. In reviewing each

Executives’ salary, consideration is given to external

competitiveness, position responsibilities and individual

skills and experience. The STI component of Executive

remuneration is based on annual performance targets

and delivered in the form of cash. In 2010, the Company

has also introduced a new Long Term Incentive Plan

which recognises performance and behaviour that delivers

sustainable long term shareholder value and seeks to align

the interests of management with those of the shareholders.

Base pay

Executives are offered a competitive salary that comprises

the components of base pay and benefits that reflects the

applied professional competence of each Executive according

to his/her knowledge, experience and accountabilities. Base

pay for Executives is reviewed annually by Executive Director

to ensure the executive’s pay is competitive with the market.

An executive’s pay is also reviewed on promotion. Base pay

for Executive Chairman in reviewed annually by Nomination

and Remuneration Committee.

Short-term performance incentive

Short-term performance incentives (STIs) vary according to

individual contracts, however, for Executives they are broadly

based as follows:

n a component of the STI is linked to the individual

performance of the executive (this is based on a

number of factors, including performance against

budgets, achievement of key performance indicators

(KPIs) and other personal objectives).

n a component of the STI is linked to the financial

performance of the business or measured against

budgets determined at the beginning of each financial

year.

Using various profit performance targets and personal

performance objectives assessed against KPIs which are

aligned with achievement of the Board’s strategic objectives,

the Company ensures variable reward is only paid when

value has been created for shareholders. For middle and

lower level management, total STIs are linked to individual

performance measures and also to the financial performance

of the business. The STI bonus is delivered in the form of

cash.

25

ANNUAL REPORT 2011

For the 2010 financial year, STI performance targets for Executives were based on the respective territories’ targets of

Earnings before Interest, Tax, Depreciation and Amortisation (“EBITDA”), penetration rate, application volumes, settlement

volumes, Average Transaction Value and territory expansion targets. These targets were selected on the basis that the Group

has, and is likely to have for sometime, a small number of experienced executives and ensuring that employment practices

support and encourage continuity of team engagement with sustained and profitable growth of the Company.

The short-term bonus payments may be adjusted up or down in line with under or over achievement against the target

performance levels. This is at the discretion of the Senior Executives. The STI target annual payment is reviewed annually.

Information on the STI is detailed on section F of the Remuneration Report.

Long term incentive

Long-term incentives to the Chief Executive Officer and certain senior employees were historically provided via the ThinkSmart

Limited Executive Share Option Plan (“ESOP”) as a retention based reward. The Company has a pre-existing ESOP, as an

equity-based long-term incentive, which was initiated before the Company was listed. Given the retention focus of these

grants, vesting of the options is subject to service conditions and not linked to satisfaction of performance targets. There have

been no retention based options granted since the Company’s listing in June 2007.

The table below sets out the details of the currently existing retention options issued to Key Management Personnel that were

issued in 2006 and 2007 before the Company’s listing:

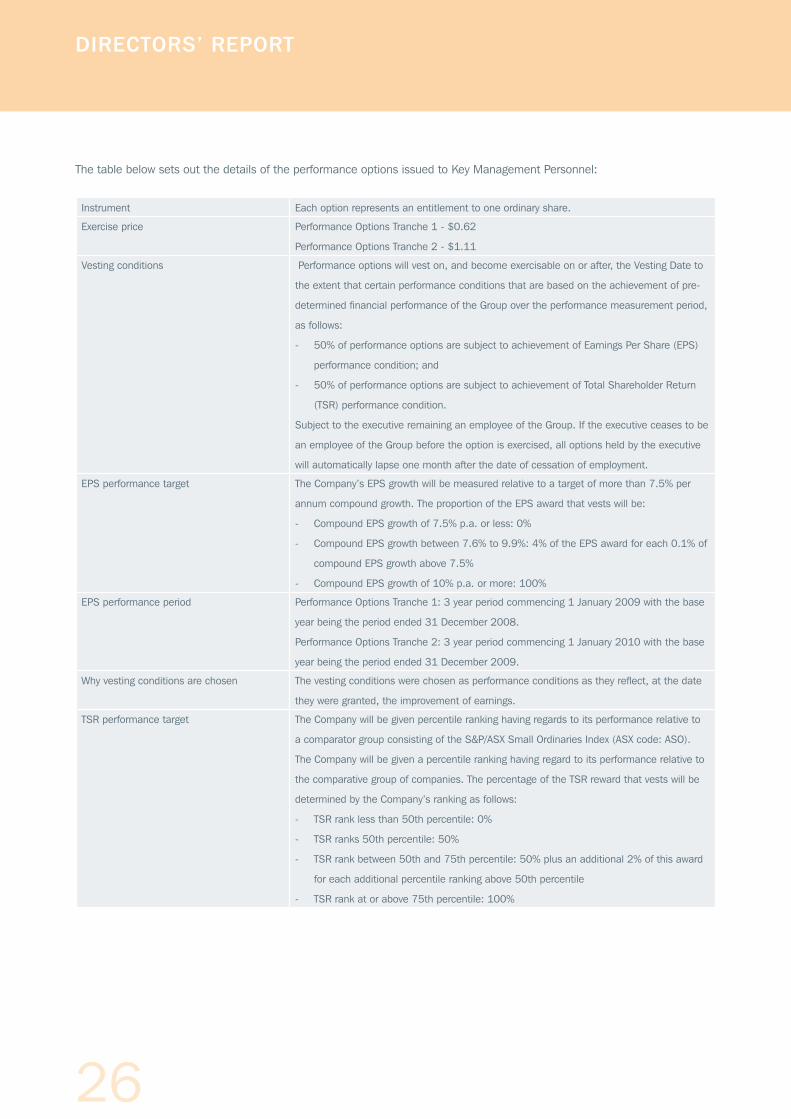

Instrument Each option represents an entitlement to one ordinary share.

Exercise price Retention Options Tranche 5: $1.375

Retention Options Tranche 6: $3.00

Vesting conditions Subject to the executive remaining an employee of the Group. If the executive ceases to be

an employee of the Group before the option is exercised, all options held by the executive

will automatically lapse one month after the date of cessation of employment. There are no

performance hurdles applicable to the retention options.

Why vesting conditions are chosen The vesting conditions are designed to ensure retention of key executives.

Vesting date Retention Options Tranche 5 & 6: 1 January 2009

Exercise period Retention Options Tranche 5 & 6: From vesting date to expiry date

Expiry date Retention Options Tranche 5 & 6: 31 December 2011

Disposal restriction No disposal restriction imposed at the time of this grant.

During 2010, the Company completed a comprehensive review of current remuneration arrangements for senior executives

to determine an appropriate structure to support the Company’s short term and long term business strategies and be aligned

to corporate governance principles. The review included input from external consultants on comparative remuneration levels,

trends and practices. As part of the review, the Board has agreed to reactivate the ESOP which recognises performance and

behaviour that delivers sustainable long term shareholder value and seeks to align the interests of management with those of

the shareholders. Consequently, options are issued to executives, and the ability to exercise the options is conditional on the

Group achieving the pre-determined performance criteria.

26

DIRECTORS’ REPORT

The table below sets out the details of the performance options issued to Key Management Personnel:

Instrument Each option represents an entitlement to one ordinary share.

Exercise price Performance Options Tranche 1 - $0.62

Performance Options Tranche 2 - $1.11

Vesting conditions Performance options will vest on, and become exercisable on or after, the Vesting Date to

the extent that certain performance conditions that are based on the achievement of pre-

determined financial performance of the Group over the performance measurement period,

as follows:

- 50% of performance options are subject to achievement of Earnings Per Share (EPS)

performance condition; and

- 50% of performance options are subject to achievement of Total Shareholder Return

(TSR) performance condition.

Subject to the executive remaining an employee of the Group. If the executive ceases to be

an employee of the Group before the option is exercised, all options held by the executive

will automatically lapse one month after the date of cessation of employment.

EPS performance target The Company’s EPS growth will be measured relative to a target of more than 7.5% per

annum compound growth. The proportion of the EPS award that vests will be:

- Compound EPS growth of 7.5% p.a. or less: 0%

- Compound EPS growth between 7.6% to 9.9%: 4% of the EPS award for each 0.1% of

compound EPS growth above 7.5%

- Compound EPS growth of 10% p.a. or more: 100%

EPS performance period Performance Options Tranche 1: 3 year period commencing 1 January 2009 with the base

year being the period ended 31 December 2008.

Performance Options Tranche 2: 3 year period commencing 1 January 2010 with the base

year being the period ended 31 December 2009.

Why vesting conditions are chosen The vesting conditions were chosen as performance conditions as they reflect, at the date

they were granted, the improvement of earnings.

TSR performance target The Company will be given percentile ranking having regards to its performance relative to

a comparator group consisting of the S&P/ASX Small Ordinaries Index (ASX code: ASO).

The Company will be given a percentile ranking having regard to its performance relative to

the comparative group of companies. The percentage of the TSR reward that vests will be

determined by the Company’s ranking as follows:

- TSR rank less than 50th percentile: 0%

- TSR ranks 50th percentile: 50%

- TSR rank between 50th and 75th percentile: 50% plus an additional 2% of this award

for each additional percentile ranking above 50th percentile

- TSR rank at or above 75th percentile: 100%

27

ANNUAL REPORT 2011

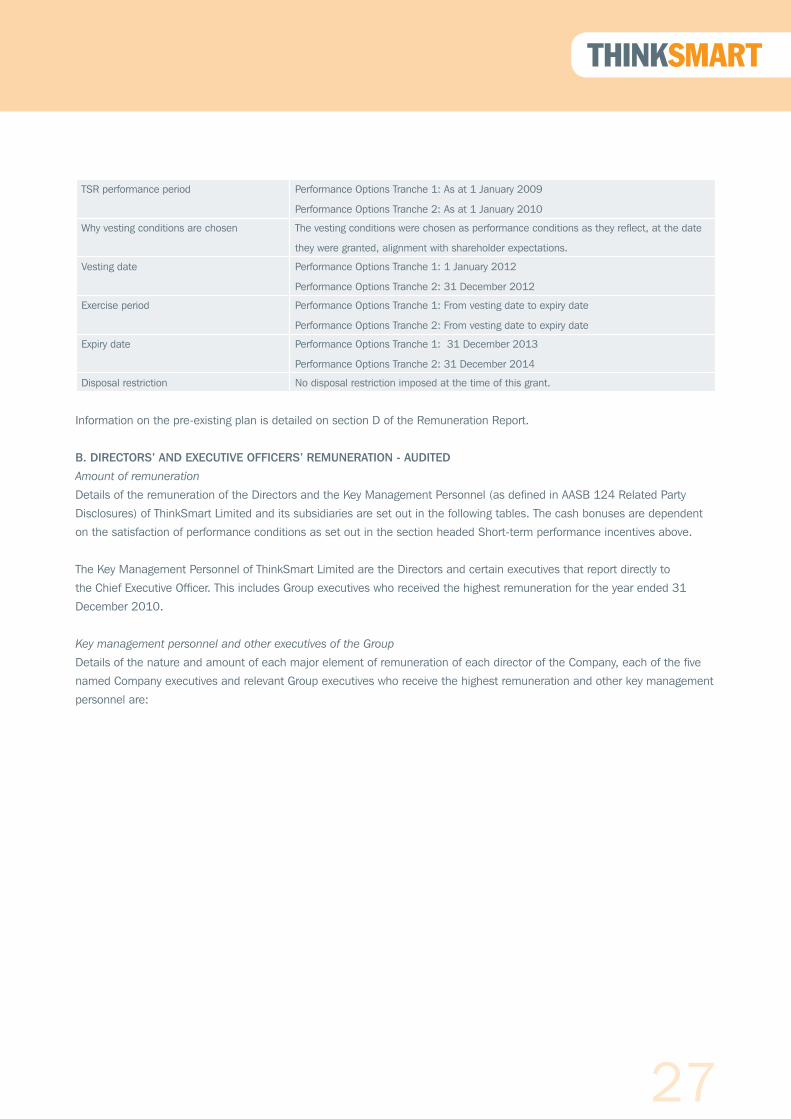

TSR performance period Performance Options Tranche 1: As at 1 January 2009

Performance Options Tranche 2: As at 1 January 2010

Why vesting conditions are chosen The vesting conditions were chosen as performance conditions as they reflect, at the date

they were granted, alignment with shareholder expectations.

Vesting date Performance Options Tranche 1: 1 January 2012

Performance Options Tranche 2: 31 December 2012

Exercise period Performance Options Tranche 1: From vesting date to expiry date

Performance Options Tranche 2: From vesting date to expiry date

Expiry date Performance Options Tranche 1: 31 December 2013

Performance Options Tranche 2: 31 December 2014

Disposal restriction No disposal restriction imposed at the time of this grant.

Information on the pre-existing plan is detailed on section D of the Remuneration Report.

B. DIRECTORS’ AND EXECUTIVE OFFICERS’ REMUNERATION - AUDITED

Amount of remuneration

Details of the remuneration of the Directors and the Key Management Personnel (as defined in AASB 124 Related Party

Disclosures) of ThinkSmart Limited and its subsidiaries are set out in the following tables. The cash bonuses are dependent

on the satisfaction of performance conditions as set out in the section headed Short-term performance incentives above.

The Key Management Personnel of ThinkSmart Limited are the Directors and certain executives that report directly to

the Chief Executive Officer. This includes Group executives who received the highest remuneration for the year ended 31

December 2010.

Key management personnel and other executives of the Group

Details of the nature and amount of each major element of remuneration of each director of the Company, each of the five

named Company executives and relevant Group executives who receive the highest remuneration and other key management

personnel are:

28

Short TermPost

employmentShare-based

payments Proportion of remu-neration perfor-mance related

Value of options as pro-

portion of remu-

nerationSalary

and fee

STI cash

bonus

Non-monetary benefits Total

Superan-nuation benefits

Termi-nation ben-efits

Options and

rights Shares Total

$ $ $ $ $ $ $ $ % %

DIRECTORS

Non-Executive Directors

P Mansell* 2010 24,751 - - 24,751 2,228 - - - 26,979 - -

2009 64,599 - - 64,599 5,814 - - - 70,413 - -

S Penglis 2010 62,145 - - 62,145 5,593 - - - 67,738 - -

2009 55,000 - - 55,000 4,950 - - - 59,950 - -

D Griffiths 2010 67,500 - - 67,500 6,075 - - - 73,575 - -

2009 58,750 - - 58,750 5,288 - - - 64,038 - -

F de Vicente* 2010 49,050 - - 49,050 - - - - 49,050 - -

2009 - - - - - - - - - - -

Executive Director

N Montarello 2010 649,527 48,000 - 697,527 31,651 - 87,531 - 816,709 17% 11%

2009 594,444 - - 594,444 40,318 - 14,174 - 648,936 2% 2%

EXECUTIVES

A Baum* 2010 141,666 - - 141,666 10,000 - 10,903 24,889 187,458 6% 6%

2009 - - - - - - - - - - -

N Barker 2010 322,996 26,000 - 348,996 31,410 - 35,671 - 416,077 15% 9%

2009 321,330 10,000 - 331,330 29,820 - 8,847 - 369,996 5% 2%

M Radotic** 2010 103,859 17,816 15,317 136,992 9,076 - 5,949 - 152,017 16% 4%

2009 233,922 34,692 20,653 289,267 21,410 - 2,591 - 313,267 12% 1%

S McDonagh* 2010 165,046 22,425 - 187,471 16,872 - - - 204,343 11% -

2009 259,231 6,500 - 265,731 23,916 - 2,591 - 292,237 3% 1%

G Varma 2010 268,623 15,089 - 283,712 25,534 - 13,872 - 323,118 4% 4%

2009 251,487 50,000 - 301,487 27,134 - 5,825 - 334,445 2% 2%

G Parry 2010 228,807 21,010 9,946 259,763 11,440 - 18,685 - 289,889 14% 6%

2009 248,790 19,824 11,686 280,300 12,439 - 2,591 - 295,330 8% 1%

Total 2010 2,083,970 150,340 25,263 2,259,573 149,879 - 172,612 24,889 2,606,953 12% 7%

Total 2009 2,087,552 121,016 32,339 2,240,907 171,088 - 36,617 - 2,448,612 6% 1%

* During the year, the Key Management Personnel has either resigned or been appointed. Please refer to the following page for details.

** Remuneration up to 30 June 2010, as Mr Radotic was reposted to a new role, where he is no longer classified as a KMP.

DIRECTORS’ REPORT

29

ANNUAL REPORT 2011

The following are Key Management Personnel of the Group:

Executive Director

n N Montarello (Chairman, Managing Director and Chief Executive Officer, ThinkSmart Limited)

Non-Executive Director

n P Mansell (Chairman, ThinkSmart Limited) – resigned 22 May 2010

n D Griffiths (Deputy Chairman, ThinkSmart Limited) – appointed Deputy Chairman 22 May 2010

n S Penglis (Non-Executive Director, ThinkSmart Limited)

n F de Vicente (Non-Executive Director, ThinkSmart Limited) – appointed to Board on the 7 April 2010

Executives

n A Baum (Group Chief Operating Officer, ThinkSmart Limited) – appointed 1 September 2010

n N Barker (Group Chief Financial Officer, ThinkSmart Limited)

n S McDonagh (Executive General Manager, RentSmart Unit Trust) – resigned 23 July 2010

n M Radotic (General Manager Sales & Marketing Continental Europe, RentSmart Limited) – ceased being a KMP after

reposting as General Manager Customer Care, RentSmart Unit Trust, on the 1 July 2010

n G Varma (Group Chief Information Officer, ThinkSmart Limited)

n G Parry (Managing Director - UK, RentSmart Limited)

C. SERVICE AGREEMENTS - AUDITED

Service agreements can provide for the provision of short-term performance incentives, eligibility for the ThinkSmart ESOP,

other benefits including the use of a Company motor vehicle, tax advisory fees, payment of benefits forgone at a previous

employer, relocation, living, tax equalisation, travel and accommodation expenses whilst an executive is required to live away

from their normal place of residence.

Only remuneration and other terms of employment for the Managing Director are formalised in a service agreement. The

Managing Director’s employment agreement has been extended to a fixed term of 3 years to 28 August 2012. All other

employment agreements are unlimited in term but capable of termination with one to three months’ notice by either the

Company or the executive. The Company can make a payment in lieu of notice.

In the event of retrenchment, the executives listed in the table on page 28 are entitled to the payment provided for in the

service agreement, where applicable. The employment of the executives may be terminated by the Company without notice by

payment in lieu of notice.

The service agreements also contain confidentiality and restraint of trade clauses.

D. SHARE BASED COMPENSATION (OPTIONS) - AUDITED

All options refer to options over ordinary shares of ThinkSmart Limited, which are exercisable on a one-for-one basis under

the Employee Share Options Plan (“ESOP”).

Options and rights over equity instruments granted as compensation – audited

Details on options over ordinary shares in the Company that were granted as compensation to each key management person

during the reporting period and details on options that vested during the reporting period are as follows:

30

DIRECTORS’ REPORT

No of options granted during

2010

Grant date Fair value per option at grant

date ($)

Exercise price per option

($)

Expiry date No of options vested during

2010

DIRECTORS

N Montarello 1,000,000 05/05/2010 0.2746 1.11 31/12/2014 -

EXECUTIVES

A Baum 333,333 01/09/2010 0.2287 1.11 31/12/2014 -

N Barker 333,333 05/05/2010 0.2746 1.11 31/12/2014 -

M Radotic 100,000 05/05/2010 0.2746 1.11 31/12/2014 -

G Varma 100,000 05/05/2010 0.2746 1.11 31/12/2014 -

G Parry 200,000 05/05/2010 0.2746 1.11 31/12/2014 -

No options are granted since the end of the financial year. The options are provided at no cost to the recipients.

Modification of terms of equity-settled share-based payment transactions - audited

No terms of equity-settled share-based payment transactions (including options and rights granted as compensation to a key

management person) have been altered or modified by the issuing entity during the reporting period or the prior period.

Exercise of options granted as compensation - audited

During the reporting period, the following shares were issued as a result of the exercise of options in the 2010 financial year.

No of shares Amount paid $/share

EXECUTIVES

N Barker 280,000 0.625

31

ANNUAL REPORT 2011

Analysis of options and rights over equity instruments granted as compensation - audited

Details of vesting profiles of the options granted as remuneration to each director of the Company and each of the five

named Company executives and relevant Group executives and other key management personnel are detailed below.

Options granted

Number of shares Grant Date % vested in year % forfeited in year (a)

Financial year in which grant vest

DIRECTORS

N Montarello 1,400,000 28/08/2006 -% -% 2009

1,000,000 30/06/2009 -% -% 2012

1,000,000 05/05/2010 -% -% 2012

EXECUTIVES

A Baum 333,333 01/09/2010 -% -% 2013

N Barker *280,000 05/01/2006 33% -% 2010

160,000 17/04/2007 -% -% 2009

120,000 17/04/2007 -% -% 2009

500,000 30/06/2009 -% -% 2012

333,333 05/05/2010 -% -% 2013

S McDonagh 300,000 30/06/2009 -% 100% 2012

M Radotic 160,000 17/04/2007 -% -% 2009

120,000 17/04/2007 -% -% 2009

300,000 30/06/2009 -% -% 2012

100,000 05/05/2010 -% -% 2013

G Varma *280,000 05/01/2006 33% -% 2010

150,000 30/06/2009 -% -% 2012

100,000 05/05/2010 -% -% 2013

G Parry 160,000 17/04/2007 -% -% 2009

120,000 17/04/2007 -% -% 2009

300,000 30/06/2009 -% -% 2012

200,000 05/05/2010 -% -% 2013

(a) The % forfeited in the year represents the reduction from the maximum number of options available to vest due to the

highest level performance criteria not being achieved.

* Option series vest equally over 3 years on 1 January 2008, 2009 and 2010.

32

DIRECTORS’ REPORT

Analysis of movement of options - audited

The movement during the reporting period, by value of options over ordinary shares in the Company held by each Company

director and each of the five named Company executives and relevant Group executives and other key management

personnel is detailed below.

Granted in year $ (a) Exercised in year $ (b) Lapsed in year $ (c)

DIRECTORS

N Montarello 274,600 - -

EXECUTIVES

A Baum 76,233 - -

N Barker 91,533 56,200 -

S McDonagh - - 87,000

M Radotic 27,460 - -

G Varma 27,460 - 19,600

G Parry 54,920 - -

Total 552,206 56,200 106,600

(a) The value of options granted in the year is the fair value of the options calculated at grant date using a binominal

option-pricing model. The total value of the options granted is included in the table above. This amount is allocated to

remuneration over the vesting period.

(b) The value of options exercised during the year is calculated as the market price of shares of the Company on the

Australian Securities Exchange as at close of trading on the date the options were exercised after deducting the price

paid to exercise the option.

(c) The value of the options that lapsed during the year represents the benefit forgone and is calculated at the date the

option lapsed using a binominal option-pricing model with no adjustments for whether the performance criteria had been

achieved.

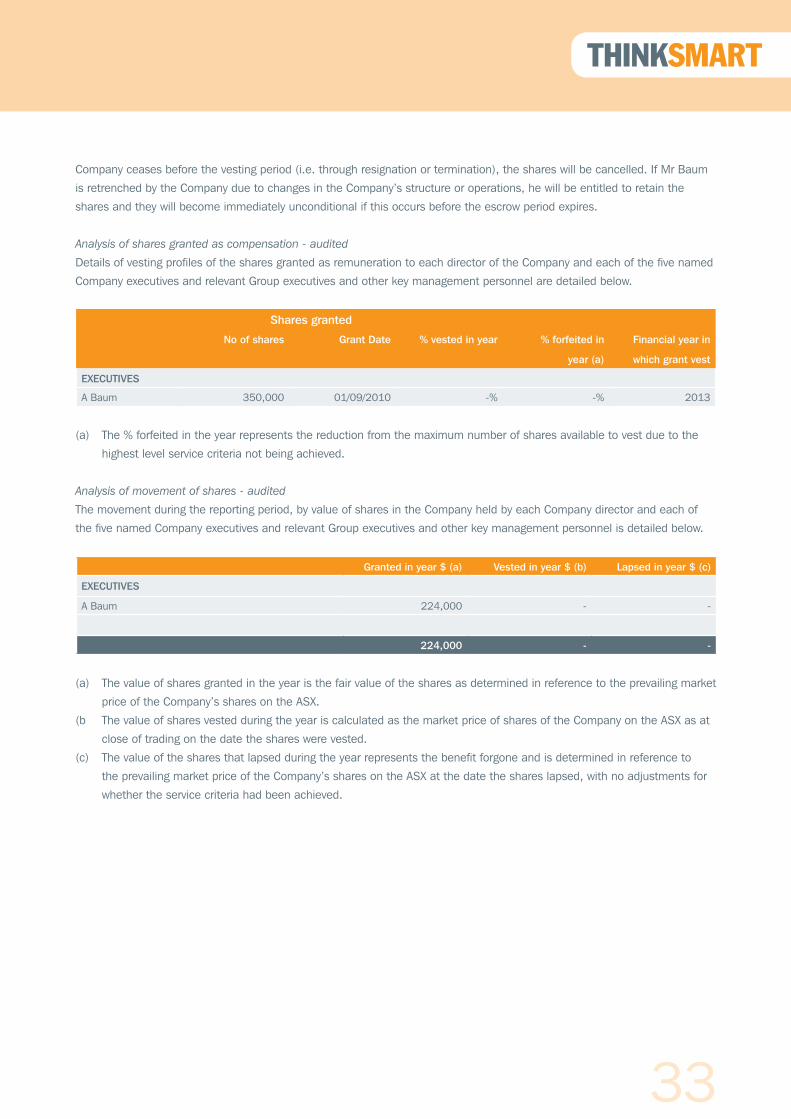

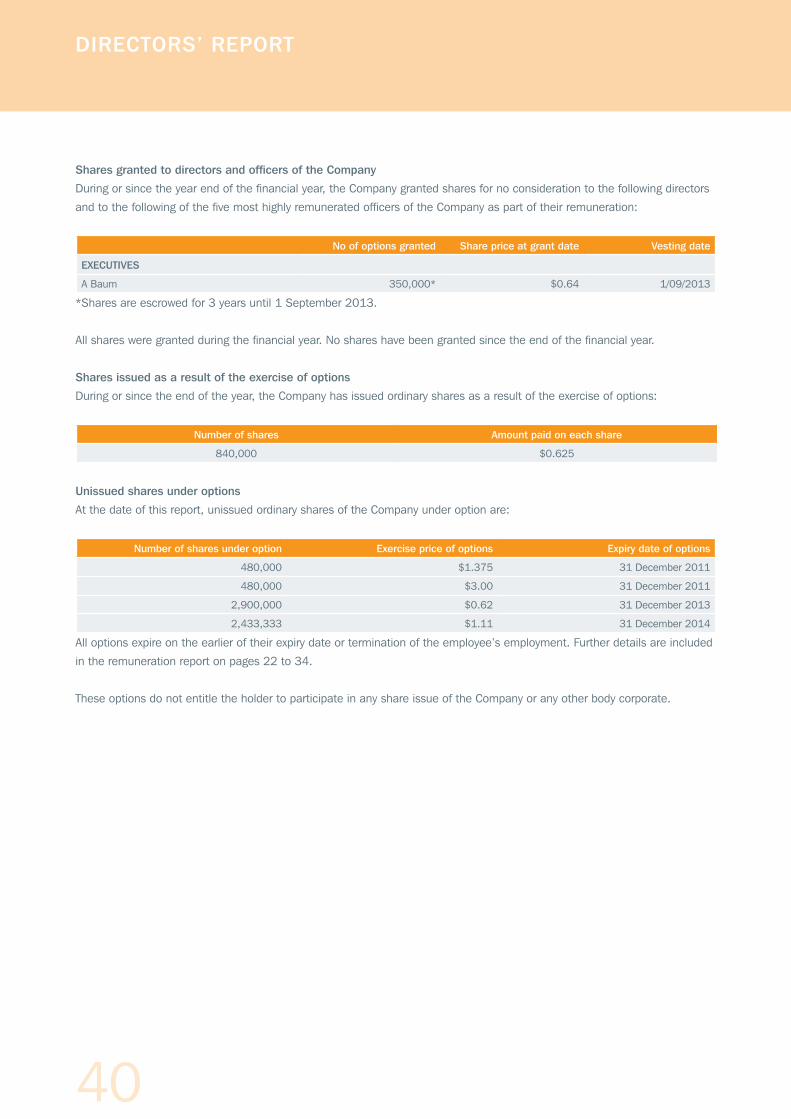

E. SHARE BASED COMPENSATION (SHARES) - AUDITED

All shares refer to shares over ordinary shares of ThinkSmart Limited.

Shares granted as compensation – audited

Details on shares of the Company that were granted as compensation to each key management person during the reporting

period and details on shares vested during the reporting period are as follows:

No of shares

granted during

2010

Grant Date Fair value at grant

date ($)

Vesting period No of shares vested

during 2010

EXECUTIVES

A Baum 350,000 01/09/2010 0.64 3 years -

No shares are granted since the end of the financial year. The shares are provided at no cost to the recipient.

These shares were issued to A Baum upon him joining ThinkSmart Ltd and are held in escrow. The shares are ordinary shares

in the Company and will vest upon completion of a 3-year service period. During this period, Mr Baum is entitled to any

dividends declared by the Company and normal voting rights are attached. In the event that Mr Baum’s employment with the

33

ANNUAL REPORT 2011

Company ceases before the vesting period (i.e. through resignation or termination), the shares will be cancelled. If Mr Baum