Embed Size (px)

Citation preview

AnnuAl RepoRt 2012

2

title | 2011

CONTENTS

letter to our Shareholders 5

Mission & Strategy 7

Financial Review 8

Stock Review 10

products 13

legacy products 18

partnerships 20

technology 23

Corporate Governance 27

Consolidated Financial Statements 43

Statutory Financial Statements of evolva Holding SA 81

this annual report contains certain forward-looking statements. these forward-looking statements may be identified by words such as “believes”, “expects”, “anticipates”, “projects”, “should”, “seeks”, “estimates”, “future” or similar expres-sions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially from those reflected in the forward-looking statements contained in this annual report. this annual report is available in english only. A German summary is available on request.

5

Letter to Our Shareholders

letter to our Shareholders

Dear Evolva shareholder,

In 2012, and even more so in early 2013, the strategic shift that we embarked upon some three years ago delivered tangible results.

particularly notable were:

� new deals with IFF and Roquette

� Milestones for BASF and Roquette

� A major collaboration with Cargill on our stevia product

� A collaboration with Ajinomoto – applying our technology to new applications in personal care

� the entry of our vanillin product into pre-production in collaboration with IFF

� A lower cash outflow than in previous years

In late 2012 we also acquired our first marketed product – resveratrol – which perfectly complements the rest of our product port-

folio in terms of both production method (fermentation in yeast) and market focus (ingredients for health, wellness and nutrition).

Another key event completed in March 2013 was the raising of CHF 31.3 million in funds from existing and new shareholders. We

thank our existing shareholders for their confidence in the company as evidenced by their high level of participation and are pleased to

welcome several high quality new investors including Cargill and some well-respected Swiss and uS institutions.

the capital increase was significantly oversubscribed and the funds provide a solid basis to carry our company towards profitability

over the next few years. the proceeds will primarily be invested in the development and commercialisation of our products, as well as our

technology platform.

of course not everything went quite so well during 2012. Although we obtained good efficacy results from our phase IIa study on

eV-077, we were disappointed to also observe transient liver enzyme elevations in some individuals. We do see this sort of result, which

is of course very common in drug development, as validating our shift in strategy towards innovative, high value ingredients for health,

wellness and nutrition.

the last 12 months has seen a number of management team changes. Alexandra Santana Sorensen, one of the founders of the

company, left in March 2012, after eight years helping build the company. norbert Bender will leave as Chief Medical officer at the end

of May 2013, and recently Jutta Heim, our Chief Scientific officer, decided to step down. We would like to thank all of them for their

contribution to evolva’s development. We are very pleased that Jutta will remain as an advisor, as well as being willing to join the Board

of Directors. Jutta will be replaced as CSo by Jørgen Hansen, who has run evolva’s Danish research team for the last eight years, during

which time he has been in particular responsible for our vanillin and stevia projects.

In early 2013 the approval of the “Minder initiative” paved the way to changes in Swiss corporate governance over the next few years.

overall evolva is ready to implement the key elements of the initiative that we believe will strengthen the links between companies and

their shareholders. Accordingly at our AGM this May we will start to pro-actively implement some of the envisaged changes.

We are proud of the progress that our company has achieved during the first eight years of its existence but recognise that we are

now entering a crucial period. over the next three years, we will be working hard to launch and drive the sales of several products – some

with a partner, some, like resveratrol, ourselves. As our products enter commercialisation we will face many new challenges, but ones that

we are privileged to have.

once again, we thank our employees for their immense contribution and you, our shareholders, for your support for evolva and hope

you will continue to accompany us on our journey.

With best regards,

Sir Tom McKillop Neil GoldsmithChairman of the Board of Directors Ceo and Managing Director

Reinach, Switzerland, 9 April 2013

7

Mission & Strategy

Mission & Strategy

evolva follows a business-to-business

model, providing ingredients (and technolo-

gies for making ingredients) to other compa-

nies, in particular in the food and beverage,

consumer health and pharmaceutical sec-

tors. We aim to be excellent at the discovery

and implementation of new ingredient pro-

duction routes, as well as the discovery of

novel functional ingredients

our internal focus is on high-value in-

gredients with relatively low production vol-

umes – tonnes or hundreds of tonnes per

year, rather than hundreds of thousands of

tonnes. We see this focus as best fitting our

competitive strengths as a small, highly in-

novative company. In line with this we do

not ourselves pursue low-margin, low-price

sectors such as biofuels or bulk chemicals –

though we are happy to help companies who

do have such a focus, in return for a share of

the value we bring.

our strategy has been developed with

reference to three key factors, namely:

1. Evolva’s competitive strengths

our key competitive strengths lie in our

innovative technologies, as well as an entre-

preneurial mindset. At the same time our

background in highly regulated, science-

driven, sectors means we are comfortable

with the regulation of products that are

consumed by people – whether as foods,

personal care products or pharmaceuticals.

2. Favourable global macrotrends

the number of “medium-affluent” con-

sumers across the world is increasing sharp-

ly. Such individuals typically desire better

health and better quality food at an afford-

able price. this coincides with generally in-

creased consumer awareness of health and

nutrition, and the fact that we are all (not

only as individuals, but as populations) get-

ting older – again increasing our focus on

health. Similar trends are, to a lesser extent,

driving demand for products that are envir-

onmentally sustainable. Yet at the same time

consumers want such benefits without com-

promising on the intrinsic appeal (taste,

smell, look) of a product, or its cost, or indeed

its ease of use. Finally pressures in the de-

veloped world for governments to reduce

expenditure are creating demand (from both

governments and consumers) for products

that can provide health benefits without the

high costs of novel pharmaceuticals.

3. Risk-adjusted returns

the discovery and provision of ingredi-

ents for nutrition and consumer products

have much lower development costs and

risks, and much shorter timelines to market

than is the case for novel chemical entity

pharmaceuticals. At the same time margins

can still be very attractive. Further there are

often major synergies in the discovery and

development of apparently different ingredi-

ents. thus the work we have put into vanillin

also can be used to create capsaicinoids (the

active ingredients of chilli peppers) with ap-

plications ranging from analgesia to weight

loss. Combined, these factors mean a focus

on ingredients that has, we believe, the po-

tential for a better risk-adjusted return than

the conventional biotech emphasis on novel

pharmaceuticals.

Evolva discovers and provides innovative, high-value, sustainable ingredients – in particular for

health, wellness and nutrition.

8

Financial Review

Financial Review | 2012

Overview

Despite a drop in total revenues (as fore-

cast in August 2012), evolva posted a signifi-

cantly lower net loss in 2012 than in the

previous year as it managed to significantly

reduce total costs. As a consequence, the

Company had a relatively solid cash position

at the end of 2012 as it was actively prepar-

ing for the financing round.

total revenues in 2012 reached CHF 7.0

million compared with CHF 11.1 million in

2011. the decrease is primarily due to the ex-

piry (as per contract) in 2011 and early 2012 of

two biodefence projects performed for the uS

Department of Defense. In contrast, revenues

from corporate partnerships increased from

CHF 4.1 million to CHF 6.4 million.

operating expenses decreased by 27% to

CHF 27.1 million. the net loss decreased from

CHF 22.9 million to CHF 16.7 million, below

the estimated loss in november 2012.

At the end of 2012, the total cash

position amounted to CHF 9.1 million

(2011: CHF 22.7 million).

Income statement

During 2012, the Company completed

the shift of its revenue base from projects for

the uS Department of Defense (2% of total

revenues in 2012 versus 51% in 2011 and

80% in 2010) to revenues from corporate cli-

ents such as IFF, Roquette and Roche which

accounted for 90% of total revenues in 2012.

About 10% of the revenues in 2012 origin-

ated from research grants from national and

eu institutions.

total operating expenses declined from

CHF 37.0 million to CHF 27.1 million, a drop

of CHF 9.9 million of which CHF 1.8 million

represented lower charges for the Compa-

ny‘s option programme.

technology and discovery costs (excl.

option charges) declined from CHF 17.7 mil-

lion to CHF 15.0 million primarily due to the

expiry (as per contract) of a biodefence pro-

ject in early 2012, which led to the closure of

the Company’s subsidiary in palo Alto,

California, in March 2012.

Costs for development (excl. option

charges) dropped from CHF 8.2 million in

2011 to CHF 3.5 million. this reflected partly

the expiry in 2011 of a major biodefence pro-

ject, partly that costs for the clinical develop-

ment of eV-077 were not recurring, and fi-

nally a reduction in development staff costs

in 2012.

the Company incurred non-cash ex-

penses of CHF 3.3 million in 2012 for its in-

centive option plans, compared with CHF 5.0

million in 2011.

Both financial income and financial ex-

penses declined during 2012 mainly because

of significantly lower currency fluctuations

during the reporting period compared to

2011.

Key financials1

CHF million 2008 2009 2010 2011 2012

Revenues 11.9 18.9 18.6 11.1 7.0

R&D costs -16.2 -21.2 -30.9 -27.5 -19.5

G&A costs -3.8 -6.6 -10.8 -9.5 -7.5

Net result -8.7 -9.6 -23.3 -22.9 -16.7

equity financing 4.0 45.6 3.6 0.9 1.9

Cash (year-end) 6.2 52.9 37.7 22.7 9.12

Net cash flow -1.1 +46.7 -15.2 -15.0 -12.62

Net equity (year-end) 3.3 67.9 53.0 73.2 61.2

earnings per share (CHF) -0.39 -0.15 -0.17 -0.14 -0.09

1 the financials for 2008 - 2009 (prior to the combination with Arpida) only include evolva SA and its subsidiaries.2 Cash at year-end 2012 and net cash-flow of 2012 do not include CHF 1 million in restricted cash.

9

Financial Review | 2012

the Company posted a gain of CHF 2.6

million in 2012 because of the expiry of the

earn-out commitment to the former Abunda

shareholders.

total general & administrative costs

(excl. option charges) declined from CHF 7.1

million to CHF 5.7 million. this drop reflects

partly the transaction costs in 2011 in con-

nection with the Abunda acquisition and the

SeDA agreement, partly a general reduction

in facility and administration costs across

the evolva Group.

Balance sheet and cash flow

evolva’s cash balance decreased from

CHF 22.7 million at the end of 2011 to CHF

9.1 million at the end of 2012. Including the

CHF 1 million in restricted cash at year-end

2012, the total net cash burn in 2012

amounted to CHF 12.6 million, which was

CHF 2.4 million or 16% lower than in 2011.

the cash outflow from operating activ-

ities was reduced from CHF 17.4 million to

CHF 13.4 million, reflecting lower expenditure

in all major expense categories. Cash inflow

from financing declined from CHF 3.5 million

in 2011 (when proceeds from the Abunda

acquisition represented the major part) to

CHF 1.5 million (before allocation to restricted

cash). proceeds from SeDA financing amount-

ed to CHF 1.9 million compared to CHF 0.8

million in 2011.

total assets declined from CHF 106.5

million to CHF 90.4 million largely reflecting

the decline in the cash position and depreci-

ation of intangible assets.

non-current liabilities declined because

one of the mortgage loans has been trans-

ferred to current liabilities. Deferred income

increased due to the signing of contracts

with Roquette and IFF and deferred income

related to these contracts.

equity decreased from CHF 73.2 million

to CHF 61.3 million at the end of 2012 main-

ly as a result of the net loss in 2012.

Outlook 2013

the Company expects revenues in 2013

to increase to CHF 10-13 million (2012:

CHF 7 million) as a result of new R&D part-

nerships, incl. the agreement with Ajinomoto

(signed in January 2013). existing R&D part-

nerships are expected to continue through-

out the year.

operating costs are expected to increase

as a consequence of new R&D partnerships,

additional investment in internal projects

(incl. the stevia project partnered with Cargill)

as well as financing costs. the net cash out-

flow from operating and investing activities is

expected to be approx. CHF 12-15 million.

the Company conducted an equity

financing in March 2013 which provided

net proceeds of approx. CHF 28.3 million.

taking into account the cash available

before the financing and the projected

operating cash flow, the Company expects

the cash position at the end of 2013 to be at

least CHF 25 million.

10

Stock Review | 2012

10

Key data (as at 31 December 2012)

Stock exchange SIX Swiss exchange

total number of shares 173,343,279

nominal value per share CHF 0.20

ISIn CH0021218067

Symbol eVe

number of registered shareholders 4,939

Stock Review

the evolva stock price ended the year

2012 at CHF 0.36, compared with CHF 0.54 at

the end of 2011. this performance was in line

with the negative trend among other biosyn-

thetic companies. on average, some 202,000

evolva shares were traded per day in 2012

(2011: 98,000).

0

0.10

0.20

0.30

0.40

0.50

0.60

Jan Feb Mar April May June July Aug Sept Oct Nov Dec0

100,000

200,000

300,000

400,000

500,000

600,000

CHF

Num

ber o

f sha

res

Share price (end of month, LH scale) Average daily volume (RH scale)

Development of the Evolva stock in 2012

Source: SIX

11

Stock Review | 2012

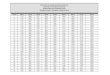

The table below gives an overview of the shareholdings before and after the rights issue.

Million shares Year-end 2012

Changes Q1 2013

Share issue March 2013

End-March 2013

End-March 2013 as %

Investors >3%

Abunda 25.3 - 1.8 27.1 11.3%

Sunstone 16.8 3.0 2.5 22.3 9.3%

Wellington 11.0 - - 11.0 4.6%

Aravis 9.4 -3.0 1.6 8.0 3.3%

entrepreneurs Fund 7.4 - 2.2 9.6 4.0%

Cargill - - 7.5 7.5 3.1%

Total >3% 69.9 0.0 15.5 85.4 35.6%

treasury shares 0.2 0.0 14.0 14.2 5.9%

Smaller and unregistered investors 103.2 0.0 36.7 139.9 58.4%

Total 173.3 0.0 66.2 239.6 100.0%

During 2012, the total number of shares

outstanding rose from 172.9 million to 173.3

million. A detailed overview of the changes

during 2012 is available on page 29 of this

report. As per year-end 2012, the stock mar-

ket capitalisation was CHF 62.4 million on an

undiluted basis.

evolva Holding has only registered com-

mon shares outstanding. A total of 4,939

shareholders, including nominees, were

entered in the share register as per year-end

2012, representing 73% of the total out-

standing capital.

Capital increase March 2013

In March 2013, evolva successfully

raised additional funds through a rights is-

sue to existing investors. Due to the high

level of demand from international institu-

tional investors, evolva increased the size of

the financing from the level indicated in Au-

gust 2012 (CHF 10-20 million) to CHF 31.3

million. As part of the collaboration on ste-

viol glycosides with evolva, Cargill, Inc. in-

vested CHF 4.5 million in the financing.

Based on the 3-for-10 subscription

ratio, the maximum number of shares to be

issued was 52.2 million. At a subscription

price of CHF 0.60 per share, the maximum

proceeds were CHF 31.3 million.

the subscription period ran from 12

March until 19 March. the rights were not

tradable.

existing shareholders took up 24.2 million

shares, or 46.3% of the total of 52.2 million

shares, available in the rights offering. After

allowing for the subscription of existing

shareholders, 28.0 million new shares were

placed with Cargill, Inc. and institutional

investors. As reported on 6 March 2013,

Cargill, institutional investors as well as evolva

Board and management had pre-committed

to purchase up to 47.4 million shares

(CHF 28.5 million), so that not all pre-commit-

ments by new investors could be satisfied.

the capital increase also included the

issuance of 14 million treasury shares to

evolva. these will be used to satisfy part of

evolva’s obligations towards ApIDC/Ventur-

east (conversion agreement as explained in

the 2012 annual report, page 27) and the

SeDA arrangement with YA Global (see press

release 11 August 2011).

Source: evolva share register and SIX reporting of significant shareholders

13

Products

Products

Evolva has a proprietary, fermentation-based platform that allows radically different approaches

to the production of ingredients for the food, beverage and consumer health sectors.

Although evolva historically has derived

its revenues from its R&D partnerships and

expects these R&D partnerships to contribute

the majority of its revenues for at least the

next two to three years, it is a key part of evol-

va’s strategy to gradually build an additional

and, ultimately, primary revenue base through

the commercialisation of its own products,

either with or without partners. evolva’s prod-

ucts at the most advanced stages of develop-

ment and/or commercialisation include fer-

mentation-derived resveratrol, vanillin, stevia

and saffron, which it considers to be its “core

products”.

Resveratrol

Resveratrol is a compound produced in

grapes and other plants. It occurs in red wine,

albeit at low concentrations. Scientific re-

search indicates that resveratrol may have

protective benefits against age-related health

conditions. In particular, several animal stud-

ies have shown positive effects of resveratrol

on diabetes, inflammation and cardiovascular

conditions. Currently, several clinical studies

are being conducted in order to demonstrate

the potential effects of resveratrol on

humans. A recent study by professor David

Sinclair, Harvard Medical School professor of

genetics, demonstrates where and how

resveratrol works. these findings are

published in the 8 March 2013 issue of the

journal Science.

Most resveratrol products on the market

today are sourced from grapes or from the

Japanese knotweed plant, but there is also a

synthetic version. evolva’s resveratrol is pro-

duced by yeast fermentation.

Market opportunity

A 2012 report by market research firm

Frost & Sullivan, estimated total resveratrol

sales at approximately uSD 50 million in 2011,

with north America representing approxi-

mately 88% of global revenues. In the same

report, Frost & Sullivan estimated that sales in

Asia-pacific and europe will grow by more

than 20% p.a. in the 2013-2018 period. Res-

veratrol is currently consumed primarily as a

nutritional supplement, however, evolva be-

lieves that resveratrol can also be commercial-

ised as an ingredient in beverages and other

consumer goods. Based on the research by

Frost & Sullivan as well as its own estimates

regarding potential market expansion, evolva

estimates that the total addressable market

for its resveratrol product (i.e. the size of the

total market in which evolva’s resveratrol

product will compete) will amount to approxi-

mately uSD 400 million in the year 2020.

As compared to agriculturally derived res-

veratrol, evolva’s fermentation-derived res-

veratrol production has the benefits of a

traceable supply chain and potentially lower

production costs and is expected to result in a

high-quality product. In contrast to synthetic

resveratrol, evolva believes that fermentation-

derived resveratrol addresses an increasing

consumer demand for products that are con-

sidered ‘‘natural’’.

Status and plans

evolva acquired its resveratrol product

from Fluxome Sciences A/S (Denmark) (‘‘Flux-

ome’’) in november 2012. the Fluxome prod-

uct has been on the uS market since 2010, but

primarily due to Fluxome’s high production

costs has not generated significant sales. It

has Self-Affirmed GRAS (“Generally Recog-

nised As Safe”) status in the united States and

obtained novel Foods authorisation from the

european Commission in January 2012

through the notification procedure.

evolva expects to leverage the technology

platform to reduce production costs, and

thereby further strengthen the competitive

position of its resveratrol product. the product

will be toll-manufactured by specialised third-

party manufacturers. evolva expects to be

able to bring down the cost of goods of its

resveratrol product to an economically viable

level, so that it may generate a positive cash

flow by 2014. evolva does not intend to build

a significant sales and marketing organisation

for resveratrol but will instead work with dis-

tributors and major consumer goods compa-

nies to drive sales of the product once the cost

of goods reaches an economically viable level.

Resveratrol

14

Products

Stevia (steviol glycosides)

Stevia (Stevia rebaudiana) is a leafy green

plant that is widely grown around the world

and used in a variety of forms as a natural,

zero-calorie, high-intensity sweetener, espe-

cially in beverages. Stevia leaves contain a

number of individual molecules (steviol glyco-

sides) that give the leaves of the plant their

sweet taste. purified stevia extract can contain

one steviol glycoside, such as Rebaudioside A

(“Reb A”), or a combination of several. Reb A is

a popular steviol glycoside due to its sweet-

ness and abundance in the stevia leaf. Accord-

ing to the International Stevia Council, the

sweetness intensity of Reb A is approximately

200 times that of sugar.

Steviol glycosides are used as a sweetener

either alone or in combination with other in-

gredients such as sugar. Steviol glycosides are

used in a wide variety of food and beverages,

as well as tabletop sweeteners. Stevia has gar-

nered attention because of the strong rise in

consumer demand for natural, low-calorie al-

ternatives to sugar. Hundreds of products

sweetened with steviol glycosides have been

launched in recent years. Steviol glycosides do

not raise blood glucose, which makes it par-

ticularly suitable for diabetic or obese indi-

viduals who have to strictly adhere to a carbo-

hydrate-reduced diet.

A growing number of health and nutrition

authorities, including the American Academy

of nutrition and Dietetics, International Food

Information Council, european Food Informa-

tion Council, and the Calorie Control Council,

support the use of stevia-based and other non-

nutritive sweeteners as tools for calorie reduc-

tion for weight loss management. Steviol gly-

cosides have been approved as sweetening

ingredients for use in foods and beverages by

major governing bodies, including the europe-

an Commission and the uS DA.

the only commercially available steviol

glycosides available today are derived from ste-

via plants grown and harvested in an agricul-

tural setting. evolva believes it is the first com-

pany to successfully adapt fermentation

technology to produce a range of commercially

relevant steviol glycosides, using sustainable,

low-cost, carbohydrate feedstocks, which can

be sourced virtually anywhere on the planet.

Market opportunity

evolva aims to develop and commercial-

ise a range of high-purity steviol glycosides

produced through yeast fermentation.

evolva has already succeeded in making

some of the key steviol glycosides using low-

cost, natural carbohydrate feedstocks.

Fermentation-derived steviol glycosides

will benefit food and beverage manufacturers

in a number of ways: � First, it will allow better tasting steviol-

glycoside-based products (the best-tast-

ing stevia leaf molecules, known as mi-

nor steviol glycosides, are not currently

commercially available due to their very

low concentrations in the plant).

� Second, it will allow steviol glycosides to

become a more economic product for

companies and consumers alike.

� Finally, it will allow steviol glycosides to

be produced using a simplified and scal-

able supply chain.

Fermentation allows the large-scale pro-

duction of minor steviol glycosides, opening

up the possibility of new formulations for

the food and beverage industry that were

previously not possible due to limitations as-

sociated with taste and cost. Based on these

advantages, evolva believes that fermenta-

tion-derived steviol glycosides have the po-

tential to accelerate the adoption of steviol

glycosides and significantly expand the mar-

ket for such sweeteners.

Based on sales volume data published in

2011 by the industry research group lMC Inter-

national and data published by other sources,

evolva estimates that total sales of all sweet-

eners amount to approximately uSD 60 billion

p.a., with sugar representing an estimated

85% of total sales. Stevia-based sweeteners

are believed to be the fastest-growing seg-

ment because of increasing consumer de-

mand for products that are low-carbohydrate

and low-sugar. Steviol glycosides can already

be found in hundreds of food and beverage

products, including carbonated soft drinks,

teas, juices, flavoured milks, yogurts, baked

goods, cereals, salad dressings, confectionery,

and as a tabletop sweetener.

STEvIa

15

Products

According to one analyst report (Mira-

baud Securities llp, october 2012), the value

of retail sales in the uS of stevia-sweetened

food and beverage products increased by 45%

from the second quarter of 2011 to the second

quarter of 2012. the same report estimates

that more than 56 million uS households pur-

chased products made with stevia-based

sweeteners in the twelve months to August

2012.

A landmark development in September

2012 was the launch of a stevia- and sugar-

sweetened, 30%-reduced-calorie version of

pepsi next in Australia. According to Beverage

Daily, the launch is significant because it

marks the first time that stevia components

have been used in a front-line cola brand. Also

noteworthy were the launches in the uK and

France of Sprite reformulated with steviol gly-

cosides.

Based on data published in 2012 by Mira-

baud Securities llp and in 2011 by industry

research group lMC International, as well as

other third-party sources and its own market

forecasts, evolva estimates that the total ad-

dressable market for its steviol glycoside

product (i.e. the size of the total market in

which its steviol glycoside product will com-

pete) will amount to approximately uSD 4 bil-

lion in the year 2020.

Status and plans

In 2009, evolva entered a R&D partner-

ship with Abunda nutrition, Inc. (“Abunda”)

for the discovery and development of certain

food ingredients, with a particular focus on

producing the key steviol glycosides by fer-

mentation. In July 2011, evolva acquired

Abunda and gained full ownership of Abun-

da’s steviol glycoside programme, which at

that time was in an early research phase.

evolva’s steviol glycoside R&D is primarily

conducted at its Copenhagen site, with com-

mercial business development activities in the

united States.

on 5 March 2013, evolva entered into a

product partnership with Cargill to jointly de-

velop and commercialise fermentation-de-

rived steviol glycosides. Cargill will be respon-

sible for commercialisation and has agreed to

make a CHF 4.5 million (approximately uSD

4.8 million) equity investment in evolva. Add-

itionally, evolva stands to receive up to uSD

7.5 million in milestone payments and has the

right to a 45% participation in the final busi-

ness. If evolva decides not to exercise this op-

tion it will receive royalty payments from

global sales of the co-developed steviol glyco-

side products; these royalties will scale from

mid-single digit to low double-digit percent-

ages as a function of sales volume and other

parameters. pursuant to the terms of the

partnership, Cargill has the exclusive right to

commercialise any fermentation-derived

steviol glycosides developed as a result of the

partnership.

the steviol glycoside product is expected

to progress into pilot scale in 2014. Based on

current plans and expectations, the first fer-

mentation-derived steviol glycoside product

is expected to be available for commercial

launch in 2015/2016.

vanillin

Vanilla is a complex blend of flavour and

fragrance compounds extracted from the

seed pods of the vanilla orchid. Commercially,

the most widely used compound in the blend

is vanillin, and because of the cost and supply

chain variability of natural vanilla, most prod-

ucts that contain “vanilla” in fact just contain

synthetic vanillin made from petrochemical or

other feedstocks.

Both natural vanilla extract and synthetic

vanillin are used as flavouring agents, primar-

ily in foods and beverages, including, for ex-

ample, in confectionery and dairy products.

Vanillin is also used in the fragrance industry

(for example in perfumes and cleaning prod-

ucts) and to mask unpleasant tastes in medi-

cines or livestock fodder as well as an inter-

mediate in the manufacture of certain

pharmaceuticals. evolva’s vanillin product is

fermentation-derived.

Market opportunity

Vanilla and vanillin are among the most

widely used flavouring products in the world,

with current total annual sales and produc-

tion volumes estimated by evolva to be ap-

proximately uSD 650 million and 16,000 met-

ric tons, respectively. natural vanilla represents

less than 1% of total sales by volume. Sales

prices range from about uSD 1,500 per kg for

natural vanilla extract to uSD 10-20 per kg for

synthetic vanillin.

evolva sees a market opportunity in pro-

viding a competitively priced product with

taste and fragrance superior to, and an inher-

ently greater naturalness than, synthetic

16

Products

vanillin. evolva believes such properties will al-

low fermentation-derived vanillin to be used in

a wide variety of food and other products and

evolva’s product to penetrate a meaningful

part of the total vanillin market. evolva does

not believe that its product will significantly

replace vanilla obtained from the orchid.

Based on the above estimated sales vol-

umes, evolva expects that the total addressa-

ble market for its vanillin product (i.e. the size

of the total market in which its vanillin prod-

uct will compete) will amount to approxi-

mately uSD 600 million in the year 2020.

Status and plans

In January 2011, evolva entered into a

product partnership with IFF with the purpose

of collaborating on the implementation of a

commercial viable biosynthetic route for the

production of vanillin. pursuant to the terms

of the partnership, IFF has the exclusive right

to commercialise any fermentation-derived

vanillin product developed as a result of the

partnership in certain market segments.

evolva has successfully constructed the

production route to vanillin and has filed a

number of patent applications (some already

granted) for this production approach. As of

February 2013, evolva has achieved the pro-

duction yield, titre (i.e. concentration) and

productivity that will allow the commercial

launch of its vanillin product. evolva is con-

tinuing to research ways to further improve

the production process with the aim of

lowering the cost of goods over time.

on 5 February 2013, evolva and IFF an-

nounced that they have entered into the pre-

production phase to develop and scale up,

via a third-party, fermentation-derived van-

illin for commercial application through a

cost-effective, natural and sustainable route.

the two companies are working to confirm

scalability and yield targets through a yeast-

based fermentation route during the pre-

manufacturing phase.

Based on current plans and expectations,

evolva expects its fermentation-derived van-

illin product to be available for commercial

launch in 2014.

vanillin pathway products

Based on the production route for vanil-

lin, evolva believes that it will be able to de-

velop and commercialise other products that

are derived from the same pathway as vanil-

lin. the aim is to launch the first such prod-

ucts by 2016.

Saffron

Saffron is one of the world’s most ex-

pensive spices by weight, as well as one of

the oldest. It comes from the stigma of the

saffron crocus and is used for colouring

and flavouring (e.g. in soups, bread and rice

dishes) as well as for its aroma properties

(such as in soaps and candles).

the characteristic flavour, colour and

odour of saffron come from several com-

ponents, of which the most important are

picrocrocin, crocin and safranal. evolva aims

to develop and commercialise saffron pro-

duced by yeast fermentation.

Market opportunity

Saffron is grown by mostly small farm-

ers in a few regions of the world, with an

estimated 90% or more of the world’s pro-

duction (estimated at about 300 tonnes a

year in 2012) in Iran. the Company estimates

current total annual saffron sales to be ap-

proximately uSD 450 million. Cultivation is

highly labour-intensive (approximately

150,000 crocuses need to be picked, and

their stigma removed, to produce 1 kilo of

saffron), which is the main reason for the

high cost of saffron.

the saffron market is poorly document-

ed, as much of the trade in saffron occurs in

informal markets (most notably in the Mid-

dle east) and there can be significant alter-

ation of the product as it flows through the

supply chain. Both the amount of saffron

and the price of saffron can vary significant-

ly from year to year. evolva believes that

prices for agriculturally derived saffron cur-

rently average around uSD 1,500 per kg with

significant variation depending on the grade.

evolva believes that by providing saffron

at significantly lower prices and with a ro-

bust and stable supply chain that is free of

both geopolitical and adulteration issues, use

of saffron in the world can be significantly

expanded. In particular:

� evolva believes that a significant latent

demand for saffron exists, mainly in

Asia. providing a more affordable, fer-

mentation-derived form of saffron to

mid-market consumers in, for example,

India and other Asian countries can po-

tentially lead to increased use.

� evolva believes that many potential uses

of saffron in mass market consumer

goods (such as skin creams, teas, air

fresheners, baked and savoury goods) are

SaFFRON

vaNIllIN

17

inhibited by a combination of the price,

supply chain and physical form (which

comes in threads) of saffron today. pro-

viding a form of saffron that removes

these constraints should allow such use.

� producing the key components of saf-

fron on an individual basis will allow

the production of customised varieties

of saffron that are particularly rich in

aroma, taste and/or colour and that can

be adapted to specific food formulations

and regional preferences.

the saffron market is poorly document-

ed, however, based on 2012 statements

made by a representative of the national

Saffron Council, information published in

The Hindu Business Line and other third-

party sources, as well as its own estimates

regarding potential market expansion, evol-

va estimates that the total addressable mar-

ket for its saffron product (i.e. the size of the

total market in which its saffron product will

compete) will amount to approximately uSD

800 million in the year 2020.

Status and plans

Research on saffron is primarily con-

ducted at evolva’s Chennai site. After identi-

fying pathways and filing multiple patent

applications, evolva has introduced the

pathway into yeast and produced individu-

ally the key saffron components responsible

for the three prime attributes of saffron,

namely flavour, fragrance and colour. evolva

is currently optimising the production pro-

cess in order to enable commercial produc-

tion of these components.

evolva expects fermentation-derived

saffron to be available for commercial

launch in 2016. evolva’s current aim is to

bring its saffron product as far as possible

towards manufacturing and commercialisa-

tion before it considers entering into a prod-

uct partnership with respect to the product.

Pomecin™

pomecinstM are evolva’s proprietary

compounds, originating from plants, for

the prevention of mould and yeast growth,

with potential uses in crop protection, per-

sonal care, food preservation and consumer

health care.

evolva has conducted pre- and post-

harvest field studies with two pomecintM

compounds that indicate a potential to pre-

vent fungal attacks in various crops. evolva

has also developed an innovative formula-

tion of pomecintM for topical treatment of

onychomycosis (nail fungus). one family of

patents is granted and in force and other

related subject matter is covered in currently

pending patent applications.

evolva has decided to exploit the

pomecintM family of antifungals in collabor-

ation with partners, with only limited further

investment by evolva beyond their current

stage. A number of early-stage partnering

discussions are in progress, but evolva has no

certainty that any of these discussions will

result in a signed agreement.

POMECIN™

18

Legacy Products

Legacy Products

Although it believes these legacy prod-

ucts are potentially highly attractive and

have significant value, any continuing devel-

opment of these products would be done ei-

ther via out-licensing or a spin-off and evol-

va does not plan to make any further

material investment with respect to such

products, with the exception of certain small

investments to maintain their value.

eV-077 and eV-035, the two pharma-

ceutical product families constituting these

legacy products are described below.

Ev-077 for treatment of complications of diabetes

eV-077 is a novel, reversible antagonist

of isoprostanes and prostanoids. It is an oral,

small-molecule compound, belonging to a

new chemical class. the compound is in clin-

ical phase IIa for treatment of vascular in-

flammation and complications of diabetes.

In August 2012, evolva announced top-

line results for 32 patients enrolled in a

phase IIa study for eV-077. the study showed

promising efficacy data, indicating that

300 mg eV-077 given orally twice daily to

patients with type 2 diabetes provided anti-

platelet (anti-thrombotic) activity, reduced

exercise-induced proteinuria (excess protein

in the urine) and increased blood flow in the

forearm.

the analysis also indicated that eV-077

was generally well tolerated, though some

adverse events were observed with respect to

increases in liver enzymes, which were tran-

sient or resolved after discontinuation.

In December 2012, evolva discussed the

future clinical development programme of

eV-077 with BfArM (the German drug au-

thority), in particular with respect to the ob-

served adverse events. the proposed clinical

development programme was perceived as a

reasonable approach by BfArM and the next

clinical trial is intended to be a dose range-

finding study in diabetic patients, investigat-

ing lower doses of eV-077 than the one ad-

ministered in the initial phase IIa study with

the intention to find a dose level for eV-077

that retains the efficacious effects observed

to date, whilst avoiding the increases in liver

enzymes. Consistent with evolva’s strategy, it

is intended to partner eV-077 via out-licens-

ing or spin-off, prior to conducting this

study.

evolva owns all rights to eV-077.

Multiple patent applications have been filed

regarding the compositions and uses of

eV-077, some of which have already been

granted.

Until 2010, the activities of Evolva were primarily focused on the discovery and clinical devel-

opment of novel pharmaceutical products. However, Evolva gradually refocused its strategy to

discovering, developing and producing innovative ingredients that have application in the health,

nutrition and wellness sectors. Evolva has a small number of clinical-stage or preclinical pharma-

ceutical product candidates, which, due to this strategy shift, it considers to be “legacy products”.

Ev-077

19

Legacy Products

Ev-035 for the treatment of bacterial infections

Marketed antibiotics are increasingly los-

ing their efficacy primarily because of bacter-

ial resistance and new antibacterial agents are

urgently needed to close this widening gap in

medical practice. particularly problematic is

the rise of multidrug-resistance among po-

tentially life-threatening pathogens.

eV-035 is a novel bacterial type II topoi-

somerase inhibitor, belonging to the chem-

ical class of 2-pyridones, showing excellent

broad-spectrum activity against pathogens

such as Staphylococcus, Streptococcus, en-

terococcus, escherichia, pseudomonas, Aci-

netobacter and Haemophilus, as well as sev-

eral potential biothreat agents. Most

importantly, eV-035 shows activity not only

on drug-sensitive strains, but also on those

resistant to marketed antibiotics (including

quinolones), and has a very low propensity of

developing new resistance. eV-035 has a

very favourable in vitro safety profile and its

pharmacokinetic properties allow for intra-

venous as well as oral dosing.

In early in vivo infection models, eV-

035 has shown an efficacy comparable or

better than gold standard drugs against

both Gram-positive and Gram-negative

strains, including e. coli and MRSA, as well

as other multidrug-resistant pathogens. In

2012, further biochemical and microbio-

logical profiling of the selected lead com-

pound confirmed its broad range of activ-

ity on multidrug-resistant pathogens, in

combination with excellent tolerability. In

September 2012, evolva presented exten-

sive preclinical data on eV-035 at ICAAC, the

world’s premier international conference on

antimicrobial agents and infectious diseases.

Ev-035

20

Partnerships

Partnerships

Evolva has, and intends to maintain, a number of partnerships around its technology and research

capabilities – deploying its technology to provide a competitive edge to partner companies and

sharing in the returns they make. 2012 saw additional partnerships in food and nutrition, as well

as good progress on existing projects. The first quarter of 2013 brought several breakthroughs in

our partnering portfolio.

evolva’s revenues to date have been de-

rived from research and development pro-

jects with partners in the uS, europe and

Asia. these R&D partnerships involve the

use of the technology platform to develop

new products and production methods for

new and existing products that are of inter-

est to our partners. We expect these R&D

partnerships to continue to contribute the

majority of revenues for at least the next

two to three years. However, it is a key part

of our strategy to gradually build an add-

itional and, ultimately, primary revenue

base through the commercialisation of our

products, either with or without partners.

evolva has been working with Inter-

national Flavors & Fragrances (IFF) since

January 2011 on the implementation of a

commercially viable biosynthetic route for

the production of vanillin. IFF has the exclu-

sive right to commercialise any fermenta-

tion-derived vanillin product developed as a

result of the partnership in certain market

segments. evolva achieved a key milestone

on this project, prompting a payment by IFF

in the first half of 2012. on 5 February 2013,

evolva and IFF announced entering into the

pre-production phase to develop and scale

up, via a third-party, fermentation-derived

vanillin for commercial application through

a cost-effective, natural and sustainable

route. the two companies are working to

confirm scalability and yield targets through

a yeast-based fermentation route during

the pre-manufacturing phase.

In May 2012, we added a second project

with IFF. Just as in the first IFF project, the

objective is to implement a commercially vi-

able biosynthetic route for the sustainable

production of a flavouring ingredient.

In the early days of 2012, we announced

a partnership with Roquette. this project

aims to find novel and optimised biosyn-

thetic production routes for an ingredient

with important applications in food prod-

ucts. the Roquette collaboration involves

some 7% of evolva’s R&D headcount. evol-

va achieved the first milestone in the pro-

ject in September 2012.

the collaboration with BaSF, which got

underway in March 2011, is now focusing

on the more promising of the initial two

projects. evolva has produced a yeast strain

that achieves a fermentation yield that sig-

nificantly exceeds the requirement for this

project. Based on this achievement, BASF

has made a low six-digit Swiss franc mile-

stone payment to evolva.

the active part of the research collabor-

ation with Roche came to an end during the

first half of 2012, with Roche taking certain

compounds forward internally. More

recently Roche has decided to reprioritise

its focus indications, and rights to these

compounds have been returned to evolva.

evolva is evaluating how to progress the

compounds, whether internally or with

third parties.

the partnerships with the US Depart-

ment of Defense came to a successful con-

clusion, leading to a new series of antibac-

terials which was presented at several

scientific conferences.

We made good progress on the smaller

projects, such as Divinocell and Diabat and

evolva landed an additional project within

the IMI framework. the Innovative Medi-

cines Initiative (IMI) is europe’s largest

public-private initiative aiming to speed up

the development of better and safer medi-

cines for patients.

In the first quarter of 2013 alone, evolva

announced the following partnerships:

In March 2013, evolva entered into a

product partnership with Cargill, Inc., a

global producer and marketer of food, agri-

cultural, financial and industrial products,

for the development of fermentation-

derived stevia components (steviol glyco-

sides) and their subsequent commerciali-

sation. In connection with this partnership,

Cargill also invested CHF 4.5 million in

evolva’s capital increase that was complet-

21

Partnerships

ed on 27 March 2013. Additionally, evolva

stands to receive up to uSD 7.5 million in

milestone payments and has the right to a

45% participation in the final business. If

evolva decides not to exercise this option, it

will receive royalty payments from global

sales of the co-developed steviol glycoside

products; these royalties will scale from mid-

single digit to low double-digit percentages

as a function of sales volume and other

parameters.

Cargill brings to the collaboration

its vast manufacturing and commercial ex-

pertise in bulk sweeteners, food ingredients,

and of course stevia sweeteners. Cargill is a

global market leader in the stevia-based

sweetener category with consumer prod-

ucts and as an ingredient, which can be

found in a variety of branded food products

and beverages sold in the uS, europe,

Mexico, and South America.

In January 2013, evolva entered into an

R&D partnership with ajinomoto Co., Inc.

(Japan), a global manufacturer of season-

ings, processed foods, beverages, amino

acids, pharmaceuticals and speciality chem-

icals, pursuant to which Ajinomoto will

fund evolva’s R&D activities focused on

developing new production routes for a

natural ingredient for use by Ajinomoto in

products for personal care.

the partnership is designed to run for

three and half years and involves evolva’s

application of the technology platform ini-

tially to build a new pathway for the ingredi-

ent and subsequently to improve production

yield through scale-up and manufacturing

phases. evolva expects that on average seven

of its full-time scientists will be working on

this partnership at any given time.

Ajinomoto paid evolva an upfront ex-

clusivity and technology access fee and will

pay evolva quarterly research fees during

the partnership. evolva will receive add-

itional payments from Ajinomoto upon

achieving certain milestones in terms of

yield, productivity and production costs.

the aggregate exclusivity and technology

access and research fees as well as mile-

stone payments made to evolva during the

partnership are expected to amount to

more than CHF 10 million. If Ajinomoto

commercialises a product using the rele-

vant ingredient, it will pay evolva royalties

as a percentage of the product sales.

22

Technology

23

Technology

Technology

Evolva’s technologies are based on yeast. Every day, all over the world, yeast is used to make

food and drink. Breads, beers, wines and many other products are made using yeast. Many soci-

eties have been using yeast for such purposes for thousands of years. Yeast forms a normal part

of our daily diet.

Yeast’s importance has led to it being

well studied scientifically, and in recent years

this has led it to being used in the production

of not only food and food ingredients, but

also pharmaceuticals and vaccines.

evolva’s approach bridges the modern

and the traditional uses of yeast. on the

modern side, we create yeasts with the abil-

ity to make existing and new ingredients. on

the traditional side, our production methods

would be recognisable to any brewer.

Despite the fact that our technology is

rather complex, we use it for just two things:

We create new ways to make “tried and

tested” natural ingredients – for example

the ingredients that make saffron look, taste

and smell like saffron. the existing produc-

tion methods for many such ingredients

have significant problems (too expensive, too

variable, not pure enough, too limited in

scale, not ecologically sustainable, etc.) and

by solving these problems we can widen the

number of people who can enjoy, and benefit

from these ingredients.

We create novel functional compounds.

using our technologies yeast can be used to

make diverse, novel, functional compounds

with potential utility as novel pharmaceut-

icals, crop protection products, etc. Manu-

facture of these compounds can then take

place either by fermentations, or by chemical

synthesis.

Benefits

Improving existing ingredients

Making natural ingredients by fermenta-

tion confers a series of important benefits.

Improved product quality

Many natural ingredients contain un-

desirable elements – for example elements

that make the product bitter, that discolour it,

or that make it difficult to formulate. By mak-

ing pure ingredients by fermentation, evolva

can avoid such contaminants, improving

product quality. For example with stevia, the

bitter tasting components that occur in agri-

culturally produced stevia can be avoided

when using fermentation. the increased

standardisation of products from fermenta-

tion can also be an important quality benefit.

Improved supply chain integrity

Many natural ingredients involve long

and complex supply chains, including mul-

tiple groups in multiple countries. this not

only raises costs, but makes ensuring the in-

tegrity of the supply chain challenging. With

fermentation the supply chain can be greatly

shortened and simplified (being located close

to key customers, if desired). this makes it

less costly, intrinsically more robust, and far

easier to safeguard.

In addition many natural ingredients

vary sharply in their annual production, with

drought, floods, pests or similar “events” fur-

ther complicating supply chains and prices.

For many specialty crops a shortfall in one

year’s harvest cannot be made up until the

next year. By contrast fermentation is far

more stable, and a shortfall in one batch can

be made up the next week.

Reduced cost

nature has not evolved to maximise the

efficiency of production. the saffron crocus

produces very little saffron per crocus; musk

cannot be obtained from the musk deer

without killing it, and so on. this inefficiency

imposes cost, and this cost in turn often lim-

its the potential uses of many ingredients.

Fermentation allows for far more efficient

production of such ingredients, reducing the

cost (often substantially) and making them

affordable to many more individuals all over

the world.

Improved sustainability

Many agricultural production systems

are perfectly sustainable. But not all. the in-

efficiency of nature (see above) can mean

that growing the plant, or raising the animal,

takes more land, more water or more energy

24

Technology

than it really should. extracting the ingredi-

ent from its original source may require solv-

ents or other processes which generate

significant waste. In such cases making the

ingredient by fermentation can improve a

product’s sustainability, freeing land or other

resources for other uses.

Improved product “customisation”

Many natural ingredients (for example

saffron or stevia) are mixtures of different

components. these components each con-

tribute their own taste, smell, colour, func-

tionality, etc. to the mixture. But not all of

these properties may be desirable in all prod-

ucts, or desired by all consumer demograph-

ics – a blue colour may be desirable in a

sweet, but not in a meat coating, etc. Fer-

mentation allows ingredients to be broken

down to their individual components, and

hence allows companies to customise their

offer more precisely to the needs and desires

of particular customers.

Improved solubility and bio-availability

evolva’s glycosylation technologies allow

many ingredients to be improved in terms of

their solubility and bio-availability. this can

improve their efficacy, make them easier to

formulate and reduce their cost of production.

Making “impossible” ingredients possible

In some cases the ingredients we make

occur in nature, but only in settings that have

made their commercialisation to date “impos-

sible”. evolva’s approach can liberate the avail-

ability of such ingredients. two examples: � natural product drugs, scents and crop

protection products. Many interesting

compounds are made by plants, marine

organisms and other species. However,

often they are made in such small

amounts, or the species is so rare, or dif-

ficult to harvest (corals for example) that

the compounds remain out of reach.

Many of these compounds can be fer-

mented using evolva technologies, mak-

ing them accessible to the world.

� endogenous human metabolites. Many

fascinating and important molecules oc-

cur naturally in humans. Yet harvesting

these molecules from humans (or our

relatives) is often ethically unacceptable

and/or economically impractical. pro-

duction of many of these metabolites by

chemical synthesis is often impossible.

Such molecules can be made by fermen-

tation in our yeasts.

Creating new active ingredients

Whilst much of our work focuses on find-

ing new ways to make existing ingredients, we

also create new compounds, based on the

creation of biosynthetic pathways that do not

occur in nature, or that use non-natural

building blocks as their starting point. Very

often, though not always, this approach is

combined with functional selection for ingre-

dients that have particularly desirable proper-

ties (break a protein:protein interaction, stop a

virus replicating through a cell, etc.).

Such novel active ingredients have their

primary utility in the pharmaceutical indus-

try, but are also relevant to crop protection,

specialty chemicals and some other sectors.

Importantly the compounds that we ob-

tain in this manner have highly attractive

structural characteristics, in particular: � A high level of novelty (c. 80% novelty,

including c. 20% core scaffold novelty);

� A low molecular weight, averaging

around 300 daltons;

� Relatively high three-dimensional com-

plexity despite the small size;

� Good observance of all drug-likeness

rules (lipophilicity, number of rotatable

bonds, etc).

Technical implementation

evolva has four significant technology

capabilities, all associated with getting yeast

to make valuable products.

Combinatorial genetics

Evolva can create billions of different

yeast cells expressing multiple new gene

combinations.

We have an array of technologies that

allow us to rapidly insert and express tens to

hundreds of genes in billions of individual

yeast cells in a highly combinatorial fashion.

this allows us to explore large numbers of

gene combinations and hence find those

gene combinations that are necessary to

make (biosynthesise) a given ingredient. It

also allows us to find those gene combina-

tions that give the highest production rate

(and hence the lowest production cost). the

same approach can create novel pathways

that generate diverse small molecules for

drug discovery and similar activities. the

genes that we use are either sourced (in

compliance with the CBD) from various spe-

cies or constructed de novo based on online

databases or other sequence data.

25

Technology

Screening and analytical technologies

Evolva has an array of advanced screen-

ing tools that can select those yeast cells that

produce desirable ingredients from a back-

ground of a large number of cells.

We have both function-led and struc-

ture-led screening tools that allow us to rap-

idly identify which yeasts are making desired

ingredients and/or which have acquired de-

sired functions (as a result of making certain

ingredients).

� Function-led screens are typically based on

fluorescence- or survival-based read-outs

and have throughputs of up to 1 billion

screening events per day. We have used

such screens to discover novel molecules

with potential utility against cancer and

infectious disease, amongst others. the

approach can also be used to find new

functionalities for food ingredients.

� Structure-led screens use state-of-the-

art capabilities that combine ultra-high

performance liquid chromatography

with time-of-flight mass spectroscopy,

nMR and a large internal database for

the identification. they are primarily used

to elaborate production pathways for

known ingredients.

Pathway optimisation technologies

Evolva has a number of tools that can

improve the efficiency with which yeast pro-

duces the desired product, which results in a

lower cost as well as other benefits.

once a biosynthetic route has been

established, it is important to improve it with

respect to purity of product, yield, speed of

conversion and final titre. the more these

elements are optimised, the lower the cost of

production of the ingredient. In addition to

our combinatorial genetics approach, one

important tool is the ability to simultan-

eously insert (and test) multiple (>10) genes

into the yeast genome. We also optimise

pathways using a combination of molecular

engineering, enzyme co-factor balancing,

metabolic engineering and pathway flux

analysis.

Decoration technologies

Evolva has proprietary technologies that

allow it to enhance the properties of ingredi-

ents, as well as their economics.

We have multiple collections of enzymes

that allow us to “decorate” ingredients and

hence enhance their properties. one particu-

lar focus is glycosylation (the process of

attaching glucose or other sugars to mol-

ecules). Glycosylation allows us to: � Make ingredients (such as stevia and

saffron) whose natural properties de-

pend on their glycosylation patterns.

� Improve the bio-availability of certain

molecules, hence improving their

effectiveness in nutritional or pharma-

ceutical use (or allowing a reduced

amount of the relevant molecule to have

the same effect as the larger amount).

� Improve manufacturing efficiencies by

orders of magnitude, resulting in reduc-

tions in the relevant ingredient’s manu-

facturing cost.

other decoration technologies allow us

to functionalise molecules for further

chemical derivatisation, alter lipophilicity or

stability, etc.

26

27

Corporate Governance

Evolva Holding SA is a Swiss stock corporation established under the laws of Switzerland with

registered office in Reinach (Canton Basel-Landschaft). Its business purpose is to to engage

in the research, development and marketing of products and processes with applications in

food, nutritional, pharmaceutical and other areas. The Company is listed on the SIX Swiss Stock

Exchange and is therefore subject to the rules of SIX, including the Directive on Information

Relating to Corporate Governance.

Group structure year-end 2012

Name Domicile Issued share capital Shareholder % of equity capital held

evolva SA Switzerland CHF 6,369,540 evolva Holding SA 100%

evolva Biotech A/S Denmark DKK 4,311,583 evolva SA 100%

evolva Biotech private limited India InR 169,930 evolva SA 60% 1

evolva nutrition, Inc. uSA uSD 0.01 evolva SA 100%

evolva, Inc. uSA uSD 0.01 evolva SA 100%

Arpida uK ltd. united Kingdom GBp 1,000 evolva Holding SA 100%

Corporate Governance

Group structure and shareholders

Group structure

As of 31 December 2012, the evolva

group (“evolva”) consisted of evolva Holding

SA (“the Company”) as holding company and

the following non-listed direct or indirect

subsidiaries:

Shareholder structure

the section “Stock review” on page 10-11

of this annual report contains extensive infor-

mation on evolva’s shareholder structure.

During 2012, shareholders submitted a

limited number of disclosures regarding their

crossing of reportable thresholds under the

Swiss disclosure rules (Art. 20 Stock exchange

Act, SeStA). the detailed notifications are

available on the evolva website

www.evolva.com and on the SIX website

www.six-swiss-exchange.com.

Cross-shareholdings

As of 31 December 2012, no cross-share-

holdings existed.

Capital structure

Issued share capital

As of 31 December 2012, 173,343,279

registered common shares were issued and

outstanding with a nominal value of CHF

0.20 each, representing a nominal share

capital of CHF 34,668,655.80. All shares are

1 Ventureast trustee Company (p) limited (“Ventureast”) and ApIDC Venture Capital (p) limited (“ApIDC”) hold, collectively, 40% of the shares (i.e. 6,683 shares) in evolva Biotech private limited. pursuant to a conversion agreement entered into by the Company, evolva SA, evolva India, ApIDC and Ventureast in December 2009 (and amended in September 2011), (i) ApIDC and Ventureast shall contribute their shares in evolva Biotech private limited to evolva SA in exchange for 27,813 newly issued shares of evolva SA, with a nominal value of CHF 20 each, and (ii) thereafter, ApIDC and Ventureast shall contribute such shares in evolva SA to the Company in exchange for 10,697,260 shares, in each case subject to the terms and conditions of such agreement, including approval of the relevant Indian governmental authorities. once approved and completed, evolva Biotech private limited will become a wholly owned direct subsidiary of evolva SA.

28

Corporate Governance

fully paid up. An overview of changes in is-

sued capital during 2012 is included in the

notes to the Consolidated Financial State-

ments on page 68 of this report.

Treasury shares

As of 31 December 2011, evolva held

7,508,346 shares in treasury. In 2012, 4.67

million of these treasury shares were de-

livered to YA Global and 1.08 million served

as consideration for the purchase of the

resveratrol-related assets from Fluxome

Science A/S. A description of the SeDA

arrangement with YA Global is available in

the notes to the Consolidated Financial

Statements on page 70 of this report.

Overview treasury shares 2012

Number of shares

Start of year 7,508,346

Consideration for purchase of resveratrol assets -1,077,006

SeDA advances -4,667,480

end of year 1,763,860

Conditional capital for incentive option

plans

As of 31 December 2011, conditional

capital of CHF 5,622,977.60 was available for

the issuance of 28,114,888 shares under the

incentive option plan to employees of the

Company or its subsidiaries, Board members

and other key persons. During 2012, 98,648

shares were issued under the 2009 evolva

plan. on balance, conditional capital of CHF

5,603,248.00 was available for the issuance

of 28,016,240 shares under the incentive op-

tion plans as of 31 December 2012. For de-

tails regarding the terms and conditions of

such options, please refer to the notes to the

Consolidated Financial Statements on pages

71-72.

authorised capital for internal Group

reorganisation purposes

Article 3b of the Articles of Association

was related to the intended conversion of a

direct participation of Ventureast trustee

Company (p) limited (“Ventureast”) and

ApIDC Venture Capital (p) limited (“ApIDC”) in

evolva Biotech private limited (“evolva India”)

into a participation in evolva SA, immediately

followed by a conversion of this new partici-

pation in evolva SA into a participation in

evolva Holding SA. this authorisation expired

on 9 June 2012 and was not extended.

Capital for financing purposes

A small part of the conditional capital

for financing purposes has been used in

2012 for an earn-out payment related to the

acquisition of Abunda nutrition, Inc.

29

Corporate Governance

Development of share capital for financing purposes, available in the Articles

(in million shares) Combined capital authorised capital Conditional capital Total

Articles of Association old 3a new 3a new 3abis

Year-end 2009 14.0 - - 14.0

AGM 2010 +8.5 - - +8.5

Year-end 2010 22.5 - - 22.5

AGM 2011 -22.5 +60.0 +32.0 +69.5

Abunda acquisition - -25.0 - -25.0

Issue treasury shares - -8.0 - -8.0

Year-end 2011 0.0 27.0 32.0 59.0

Abunda earn-out - - -0.3 -0.3

AGM 2012 - +50.0 +23.0 +73.0

Year-end 2012 0.0 77.0 54.7 131.7

For detailed information regarding the

capital structure, reference is made to the

Articles of Association, which are available

on the evolva website.

Changes in capital

For changes in capital that took place in

2009 or earlier, reference is made to the 2009

annual report.

Development issued share capital

Number of shares Nominal value (CHF)

Year-end 2009 139,178,594 27,835,718.80

option exercise 381,531 76,306.20

Year-end 2010 139,560,125 27,912,025.00

Abunda acquisition 25,000,000 5,000,000.00

Issue treasury shares from authorised capital 8,000,000 1,600,000.00

option exercise 344,885 68,977.00

Year-end 2011 172,905,010 34,581,002.00

Issue from conditional capital, related to Abunda earn-out 339,621 67,924.20

option exercise 98,648 19,729.60

Year-end 2012 173,343,279 34,668,655.80

30

Corporate Governance

Description of the shares

As of 31 December 2012, the Company

had only common shares outstanding. no

bearer shares or participation certificates

have been issued. All shares have a nominal

value of CHF 0.20. each share carries one

vote at the shareholders’ meetings of the

Company – subject to limitations as de-

scribed below. the shareholders’ meeting

may at any time convert registered shares

into bearer shares and bearer shares into

registered shares through an amendment of

the Articles of Association.

limitations on transferability and nom-

inee registration

A transfer of shares is effected by a cor-

responding entry in the books of a bank or

depository institution following an assign-

ment in writing by the selling shareholder

and notification of such assignment to the

Company by the bank or the depository insti-

tution. A transfer of shares further requires

that a shareholder file a share registration

form in order to be registered in the share

register of the Company with voting rights.

Failing such registration, a shareholder may

not vote at or participate in a shareholders’

meeting.

A purchaser of shares will be recorded in

the Company’s share register as a sharehold-

er with voting rights if the purchaser dis-

closes its name, citizenship or registered of-

fice and address and gives a declaration that

it has acquired the shares in its own name

and for its own account.

the Articles of Association (Art. 5) pro-

vide that a person or entity not explicitly

stating in its registration request that it will

hold the shares for its own account (“nom-

inee”) may be entered as a shareholder in the

share register with voting rights for shares

up to a maximum of 5% of the outstanding

nominal share capital. Shares held by a nom-

inee that exceed this limit are only registered

in the share register with voting rights if

such nominee declares in writing to disclose

name, address and shareholding of any per-

son or legal entity for whose account it is

holding 1% or more of the outstanding

nominal share capital. the limit of 5% shall

apply correspondingly to nominees who are

related to one another through capital own-

ership or voting rights or have a common

management or are otherwise interrelated.

the Company has nominee agreements with

two nominees. this should facilitate share-

holder identification and the voting proced-

ure for shareholders’ meetings.

A share being indivisible, the Company

will only recognise one representative for

each share. Furthermore, shares may only be

pledged to the bank that administers the

bank entries of such shares for the account

of the pledging shareholders; in such case,

the Company must be notified.

Convertible bonds and options

As of 31 December 2012, the Company

did not have any convertible bonds or war-

rants outstanding.

evolva Holding SA has established sev-

eral incentive option plans in order to at-

tract, motivate and retain key staff and thus

enhance the value of the Company by giving

key people an opportunity to become share-

holders of the Company. the terms of the

incentive option plans are determined by the