Embed Size (px)

Citation preview

AnnuAl RepoRt 2013

TUR

KIS

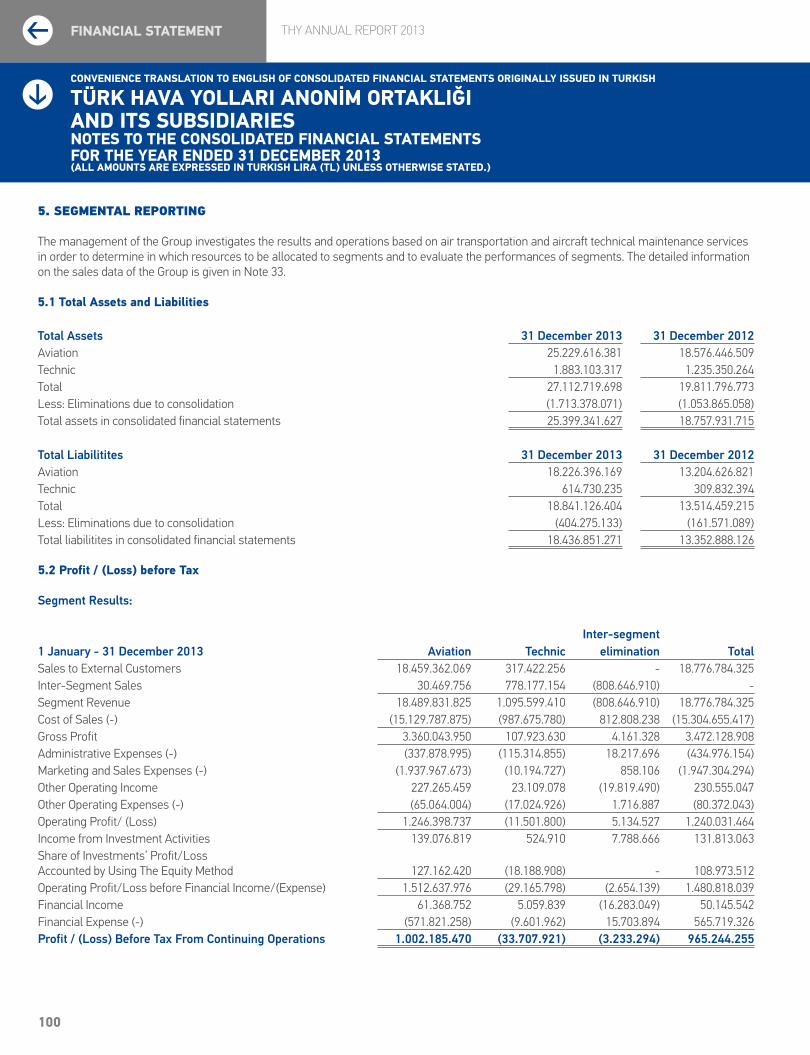

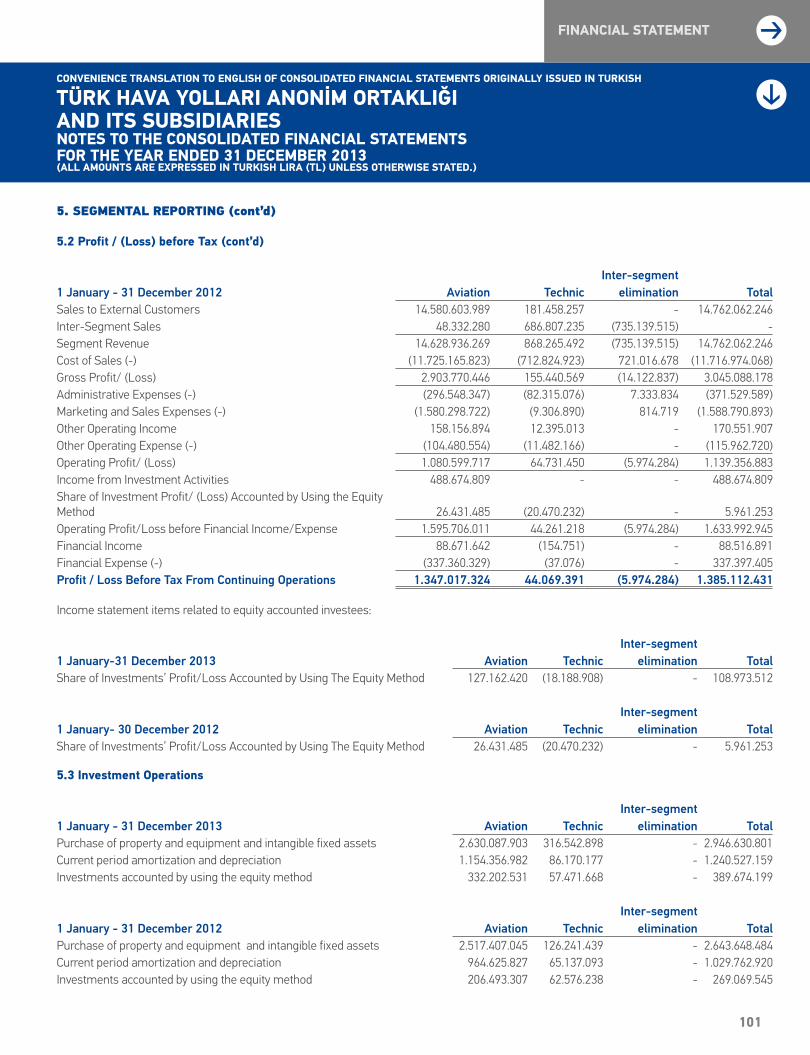

H A

IRLIN

ES An

nu

Al RepoRt 2013

TURKISH AIRLINES HEADQUARTERSAtatürk Hava Limanı Yeşilköy 34149 Istanbul/Turkey

Tel: +90212 463 6363 Fax: +90212 465 2121Reservation: 444 0849

[email protected] (Investor Relations)

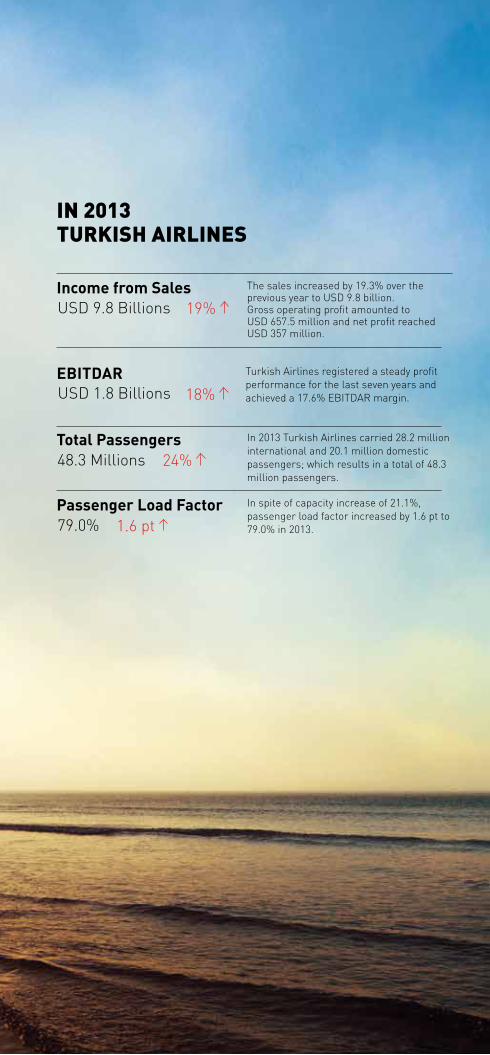

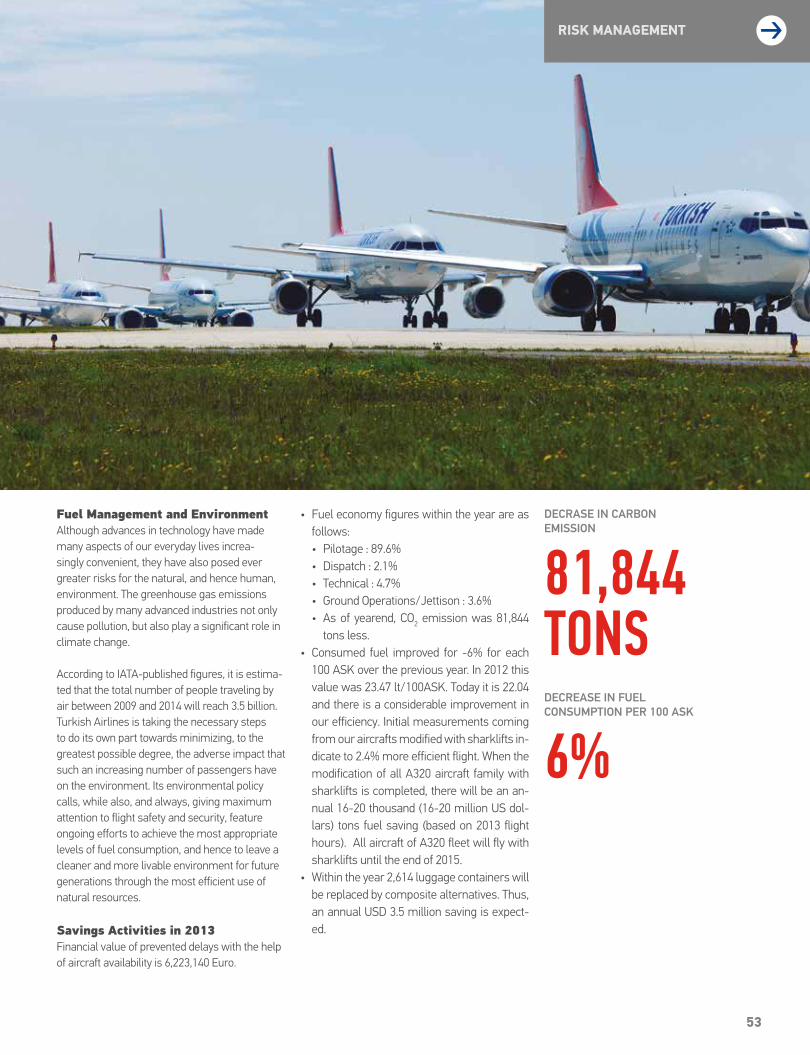

In 2013 TurkIsh AIrlInes

Income from Sales

EBITDAR

Total Passengers

Passenger Load Factor

USD 9.8 Billions

USD 1.8 Billions

48.3 Millions

79.0%

19%

18%

24%

1.6 pt

The sales increased by 19.3% over the previous year to USD 9.8 billion. Gross operating profit amounted to USD 657.5 million and net profit reached USD 357 million.

Turkish Airlines registered a steady profit performance for the last seven years and achieved a 17.6% EBITDAR margin.

In 2013 Turkish Airlines carried 28.2 million international and 20.1 million domestic passengers; which results in a total of 48.3 million passengers.

In spite of capacity increase of 21.1%, passenger load factor increased by 1.6 pt to 79.0% in 2013.

Turkish Airlines has been named as the ‘Airline of the Year’ at this year’s CAPA (Center for Asia Pasific Aviation) Aviation Awards for Excellence. The title is given to the carrier that has had the greatest impact on the development of the airline industry, established itself as a leader and is a benchmark for others to follow. Turkish Airlines has established itself as a formidable competitor in a geographic region that boasts many of the world’s leading airlines. With the world’s largest flight network, Turkish Airlines flies to 200 international destinations from its Istanbul hub.

Turkish Airlines has been named as the ‘Airline of the Year’ at this year’s CAPA Aviation Awards for Excellence. The title is given to the carrier that has had the greatest impact on the development of the airline industry, established itself as a leader and is a benchmark for others to follow.

AIR

LIN

E O

F TH

E YE

AR

Turkish Airlines has received the Skytrax “Best Airline in Europe” award for the third year running. As an internationally recognized brand, executing industrial surveys independent of commercial concerns, Skytrax annually presents awards to airline companies, based on their performance. During the 10 month survey period, airline customers from over 160 different nationalities participated in this customer satisfaction survey. By adding ‘Flying Chef’ service for Business Class passengers on its long flights, Turkish Airlines has been also named as the winner in the category, “Best Business Class Catering”.

While expanding our flight network, we also put emphasis on increasing quality. Crowned with Skytrax “Best Airline in Europe” award for the third time successively, we share our accomplishments with all our customers.

BES

T A

IRLI

NE

IN E

UR

OPE

By the end of 2013, Turkish Airlines has flown to 245 destinations, while increasing passenger numbers by 23.6% to 48.3 million. Within the next decade 100 new destinations are planned. Turkish Airlines aims at increasing the number of aircrafts to over 400 by 2020. By the end of 2013, Turkish Airlines introduced 26 new destinations and upgraded the number of flight points to 245 in 105 countries. The Company’s international destinations coverage is greater than any other airline in the world.

LE

AD

ER F

LIG

HT

NET

WO

RK

New Destinations opened in 2013LIBREVILLECOLOMBOHOUSTONAQABAKUALA LUMPURFRIEDRICHSHAFENSANTIAGO DE COMPOSTELAMALTASALZBURGEL KASIMMARSEILLECONSTANZATALINNVILNIUSLUXEMBURGKATHMANDUMAZAR-I-SHARIF LAHORKANONDJAMENAÇORLUISPARTA KASTAMONUBİNGÖLŞIRNAKKOCAELİ

NEW

BR

AN

D S

TRA

TEG

YTurkish Airlines, with its superior service quality, offers a pleasant travel experience to everyone especially those who are brave challengers and passionate explorers. The Company’s new stance is also reflected in its brand communication. The “Widen Your World” motto is an open invitation to explore new horizons. The renewed brand strategy indicates how the Company surpasses being a global brand. Turkish Airlines ensures maximum passenger satisfaction with the Inflight Entertainment System, containing about 400 movies, 1,000 music CD’s, radio and news channels. Furthermore, the “Invest On Board” digital platform, features entrepreneurs from all over the world matched with prominent business leaders. Live TV broadcasting via satellite are all part of the services offered in the skies.

If you look at diversities as a symbol of richness, if you are a determined pursuer of challenges and if you want to learn by experience; then the world is an amazing playground. Believe in yourself and enjoy.

LOU

NG

E IS

TAN

BU

L

Turkish Airlines, operating the world’s most comprehensive network of 105 countries; meets the expectations of its passengers by constantly introducing novelties. Its expanded and refurbished private passenger lounge, Turkish Airlines Lounge Istanbul, functions as the gate to the world; presenting a new level in pleasure and comfort. The newly added second floor of the lounge brings greater service choices to the customer. “Lounge Istanbul” was nominated to the international top 10 premium airport lounge list. This newly expanded lounge, which combines both modern and traditional design, aims to be the best.

“Turkish Airlines Lounge Istanbul”, among international top 10 private passenger lounges list, functions as the gate to the world; presenting a new level in pleasure and comfort.

AnnuAl RepoRt 2013

2

TURKISH AIRLINES ANNUAL REvIEw

CONTENTS

01 Turkish Airlines Annual Review

02 To Our Shareholders 02 Financial Analysis 06 Industry Developments and the Forecast for 2014 08 Chairman’s Message 10 Board of Directors 13 Our Mission and Vision 14 Our Strategy

18 Turkish Airlines Group 18 Our Subsidiaries 22 2013 Traffic Results 24 Fleet 26 Flight Networks 28 Our Activities 28 Cargo 30 MRO 32 Catering 34 Ground Handling 36 Training 40 Other Services 47 Human Resources 51 Quality and Corporate Social Responsibility 54 Risk Management 58 Organizational Chart 60 Corporate Governance Principles Compliance Report

67 Consolidated Financial Statements 67 Consolidated Financial Statements and Notes as of December 31, 2013

1

TURKISH AIRLINES ANNUAL REvIEw

Established in 1933, Turkish Airlines’ main fields of activity are all types of domestic and international passenger and cargo air transportation.

As for the shareholding structure of the Company; 50.88% are held publicly and 49.12% by the Prime Ministry, Privatization Directorate. The registered share capital of the Incorporation is TL 2 billion . The Company has 12 subsidiaries; 3 are directly owned and 9 are joint ventures.

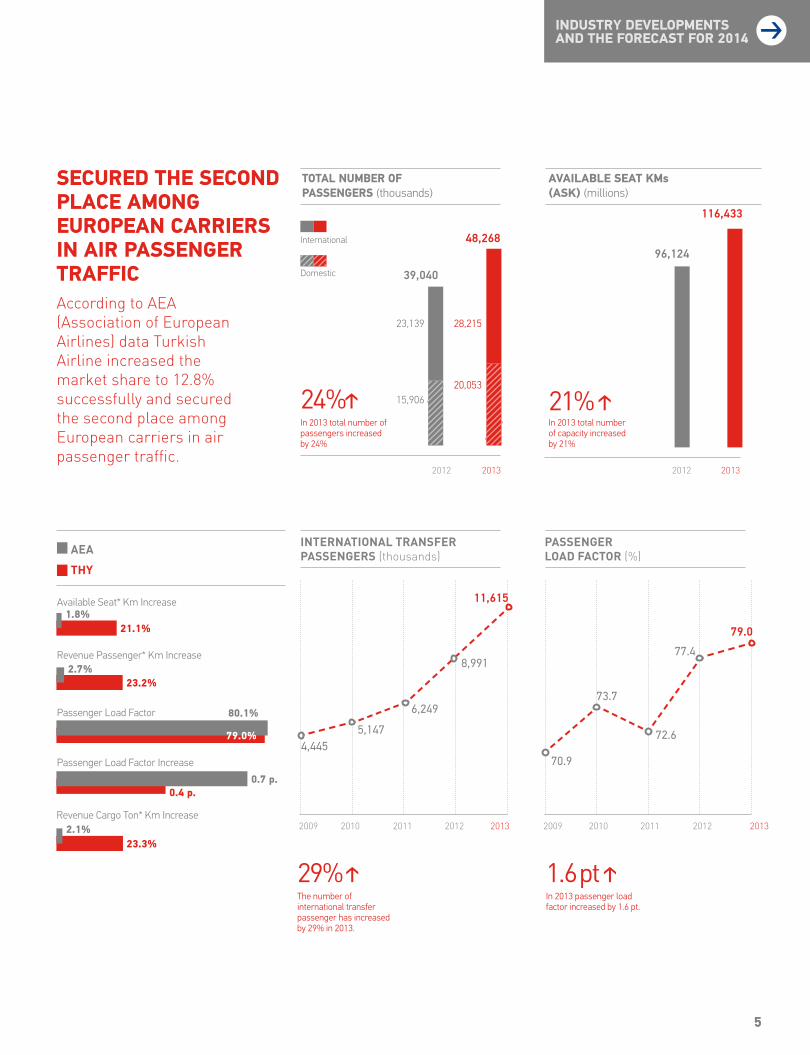

Turkish Airlines flies to 43 domestic and 202 international destination, which brings the total number to 245 destinations. Over the previous year the Company has increased 39 million passenger numbers by 23.6% and carried 48.3 million passengers in 2013. The number of passengers increases by 26.1% on the domestic routes and by 21.9% of international routes. According to AEA (Association of European Airlines) data Turkish Airline increased its market share to 12.8% successfully and has taken second place among European carriers as regards to air passenger traffic. Corresponding to a capacity increase of 21.2%, the passenger load factor increased by 1.6 pt to 79.0% in 2013, which contributed to turnout. Cargo and mail transportation rose in parallel to the passenger increase and grew by 20.1% to 565,391 tons.

Turkish Airlines flies to 43 domestic and 202 international airports, which brings the total number to 245 destinations. Over the previous year the Company has increased its 39 million passenger number by 23.6% and carried 48.3 million passengers in 2013.

FINANCIAL ANALYSIS

50.88%

49.12%

Other (Public)

Republic of Turkey, Prime Ministry, Privatization Administration

AnnuAl RepoRt 2013

2

TURKISH AIRLINES ANNUAL REvIEw

FINANCIAL ANALYSIS

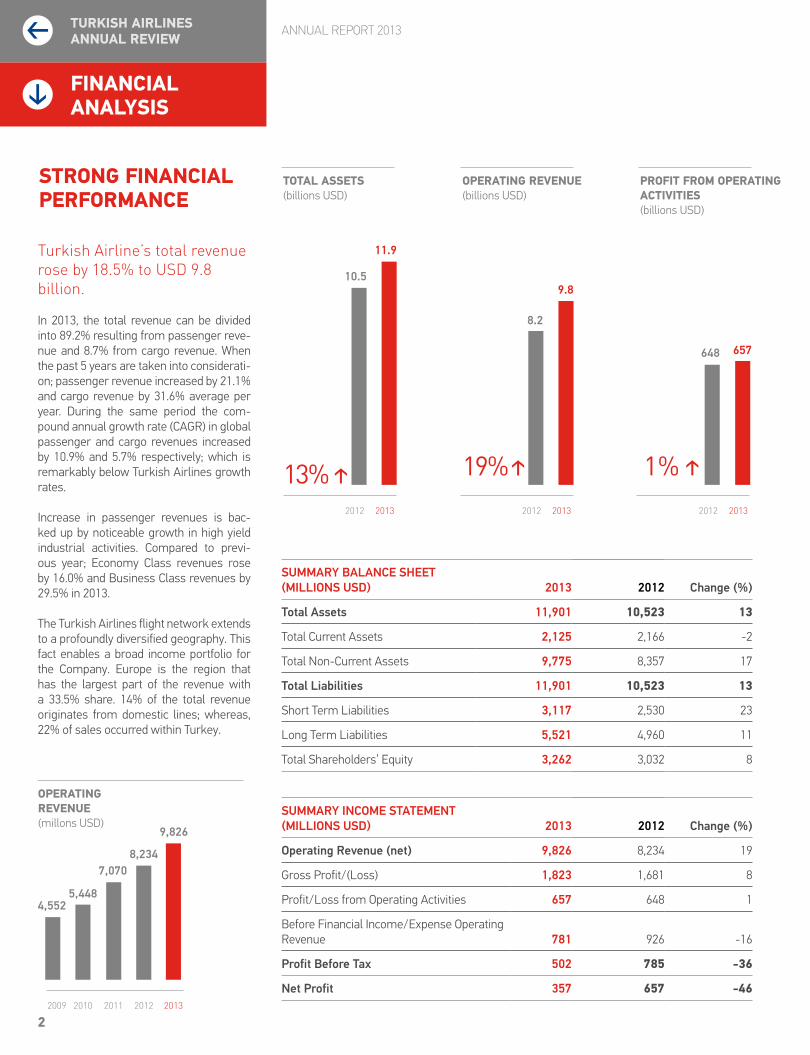

summary Balance sheet (millions UsD) 2013 2012 change (%)

total assets 11,901 10,523 13

Total Current Assets 2,125 2,166 -2

Total Non-Current Assets 9,775 8,357 17

total liabilities 11,901 10,523 13

Short Term Liabilities 3,117 2,530 23

Long Term Liabilities 5,521 4,960 11

Total Shareholders’ Equity 3,262 3,032 8

sUmmary income statement (millions UsD) 2013 2012 change (%)

operating revenue (net) 9,826 8,234 19

Gross Profit/(Loss) 1,823 1,681 8

Profit/Loss from Operating Activities 657 648 1

Before Financial Income/Expense Operating Revenue 781 926 -16

Profit Before tax 502 785 -36

net Profit 357 657 -46

Turkish Airline’s total revenue rose by 18.5% to USD 9.8 billion.

In 2013, the total revenue can be divided into 89.2% resulting from passenger reve-nue and 8.7% from cargo revenue. When the past 5 years are taken into considerati-on; passenger revenue increased by 21.1% and cargo revenue by 31.6% average per year. During the same period the com-pound annual growth rate (CAGR) in global passenger and cargo revenues increased by 10.9% and 5.7% respectively; which is remarkably below Turkish Airlines growth rates.

Increase in passenger revenues is bac-ked up by noticeable growth in high yield industrial activities. Compared to previ-ous year; Economy Class revenues rose by 16.0% and Business Class revenues by 29.5% in 2013. The Turkish Airlines flight network extends to a profoundly diversified geography. This fact enables a broad income portfolio for the Company. Europe is the region that has the largest part of the revenue with a 33.5% share. 14% of the total revenue originates from domestic lines; whereas, 22% of sales occurred within Turkey.

STRONG FINANCIAL PERFORMANCE

1%

PROFIT FROM OPERATING ACTIvITIES (billions USD)

657648

19%

OPERATING REvENUE(billions USD)

9.8

8.2

13%

11.9

10.5

4,5525,448

7,0708,234

9,826

TOTAL ASSETS(billions USD)

2013

2012 2013

2013 20132012

2009 2010 2011

2012 2012

OPERATING REvENUE(millons USD)

3

FINANCIAL ANALYSIS

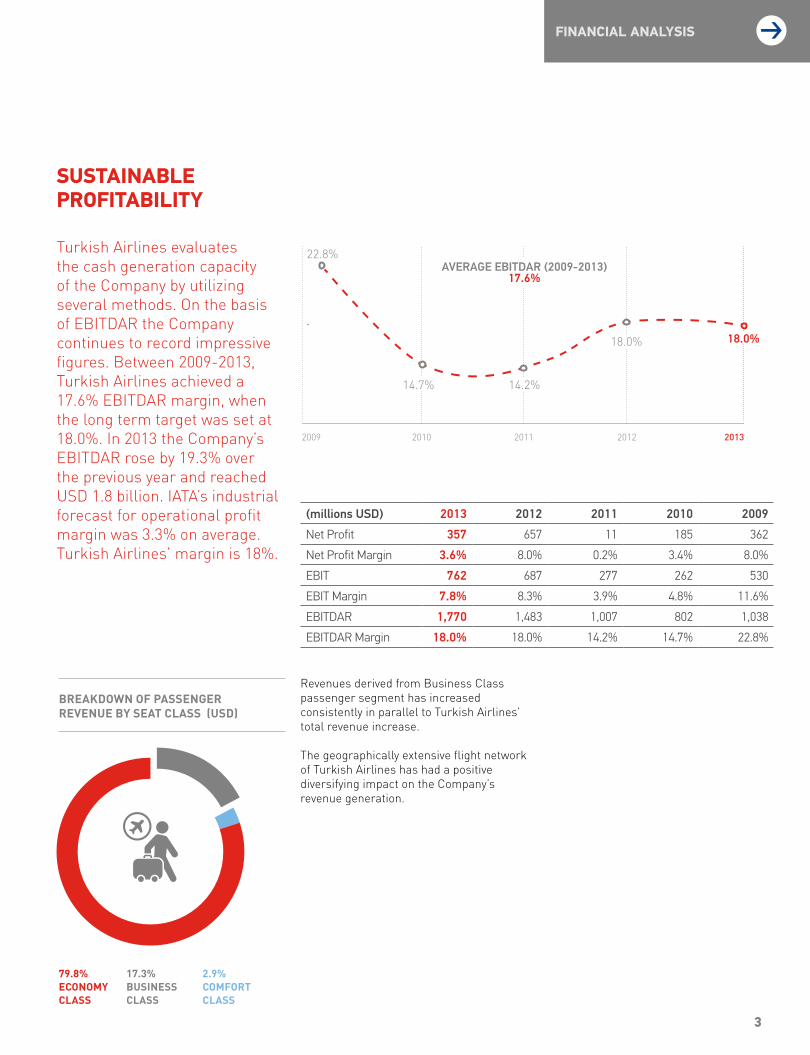

(millions UsD) 2013 2012 2011 2010 2009

Net Profit 357 657 11 185 362

Net Profit Margin 3.6% 8.0% 0.2% 3.4% 8.0%

EBIT 762 687 277 262 530

EBIT Margin 7.8% 8.3% 3.9% 4.8% 11.6%

EBITDAR 1,770 1,483 1,007 802 1,038

EBITDAR Margin 18.0% 18.0% 14.2% 14.7% 22.8%

Turkish Airlines evaluates the cash generation capacity of the Company by utilizing several methods. On the basis of EBITDAR the Company continues to record impressive figures. Between 2009-2013, Turkish Airlines achieved a 17.6% EBITDAR margin, when the long term target was set at 18.0%. In 2013 the Company’s EBITDAR rose by 19.3% over the previous year and reached USD 1.8 billion. IATA’s industrial forecast for operational profit margin was 3.3% on average. Turkish Airlines’ margin is 18%.

SUSTAINABLE PROFITABILITY

22.8%

20132012201120102009

14.7% 14.2%

18.0% 18.0%

aVeraGe eBitDar (2009-2013)17.6%

2.9%ComFoRT CLASS

BREAKDoWN oF PASSENgER REvENuE BY SEAT CLASS (uSD)

79.8%ECoNomY CLASS

17.3%BuSINESS CLASS

Revenues derived from Business Class passenger segment has increased consistently in parallel to Turkish Airlines’ total revenue increase.

The geographically extensive flight network of Turkish Airlines has had a positive diversifying impact on the Company’s revenue generation.

AnnuAl RepoRt 2013

4

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

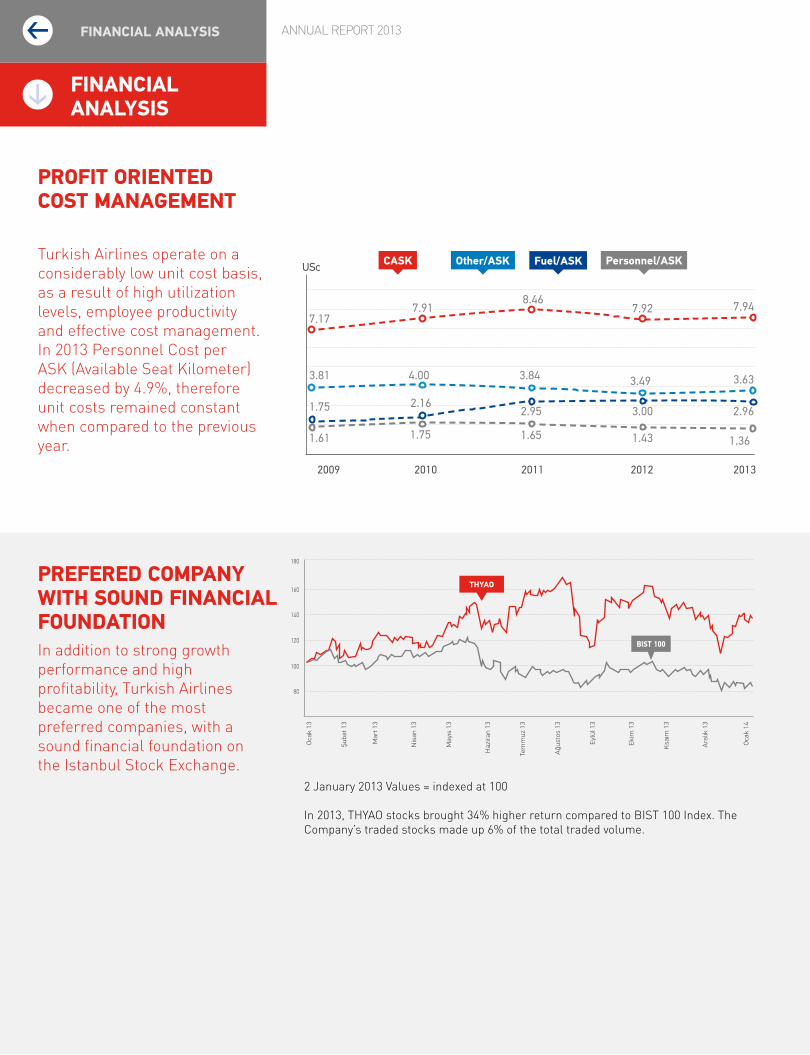

Turkish Airlines operate on a considerably low unit cost basis, as a result of high utilization levels, employee productivity and effective cost management. In 2013 Personnel Cost per ASK (Available Seat Kilometer) decreased by 4.9%, therefore unit costs remained constant when compared to the previous year.

2 January 2013 Values = indexed at 100

In 2013, THYAO stocks brought 34% higher return compared to BIST 100 Index. The Company’s traded stocks made up 6% of the total traded volume.

PROFIT ORIENTED COST MANAGEMENT

PREFERED COMPANY wITH SOUND FINANCIAL FOUNDATION

180

160

140

120

100

80

In addition to strong growth performance and high profitability, Turkish Airlines became one of the most preferred companies, with a sound financial foundation on the Istanbul Stock Exchange.

Oca

k 13

Şub

at 1

3

Mar

t 13

Nis

an 1

3

May

ıs 1

3

Haz

iran

13

Tem

muz

13

Ağu

stos

13

Eyl

ül 1

3

Eki

m 1

3

Ksa

ım 1

3

Ara

lık 1

3

Oca

k 14

2009

USc

2010 2011 2012 2013

CASK Personnel/ASKOther/ASK Fuel/ASK

3.81

7.17

1.75

1.61 1.75 1.431.65 1.36

2.162.95 3.00 2.96

4.00 3.84 3.49 3.63

7.918.46

7.92 7.94

THYAO

BIST 100

5

79.0

77.48,991

11,615

72.6

6,24973.7

5,147

70.94,445

SECURED THE SECOND PLACE AMONG EUROPEAN CARRIERS IN AIR PASSENGER TRAFFIC

INDUSTRY DEvELOPMENTS AND THE FORECAST FOR 2014

INTERNATIoNAL TRANSFER PASSENgERS (thousands)

PASSENgER LoAD FACToR (%)

21%

AvAILABLE SEAT KMs (ASK) (millions)

116,433

96,124

24%

48,268

39,040

23,139 28,215

15,90620,053

TOTAL NUMBER OF PASSENGERS (thousands)

2013 20132012 2012

According to AEA (Association of European Airlines) data Turkish Airline increased the market share to 12.8% successfully and secured the second place among European carriers in air passenger traffic.

International

Domestic

In 2013 total number of passengers increased by 24%

In 2013 total number of capacity increased by 21%

20132013 20122012 20112011 20102010 20092009

AEA

THY

Available Seat* Km Increase1.8%

21.1%

Revenue Passenger* Km Increase2.7%

23.2%

Passenger Load Factor 80.1%

79.0%

Passenger Load Factor Increase

0.7 p.0.4 p.

Revenue Cargo Ton* Km Increase2.1%

23.3%

29% 1.6pt The number of international transfer passenger has increased by 29% in 2013.

In 2013 passenger load factor increased by 1.6 pt.

AnnuAl RepoRt 2013

6

INDUSTRY DEvELOPMENTS AND THE FORECAST FOR 2014

In 2013 there were increasing indications that the US economy was coming out of the cri-sis. As the main actor, the FED was leading expansionary policies since 2007 with USD 85 billion in monthly bond purchases in emer-ging markets. This year was marked by FED’s implications in the direction of slowing down and then closing the monetary expansion. Initially invented as a solution for decreasing unemployment and rejuvenating economy; this monetary expansion policy was soon turned into an instrument used for obtaining cheap money in more reliable markets that yielded higher interest rates. Following the FED decision to discontinue monetary expan-sion, easy obtainable credit tended to move out from emerging markets and return to its country of origin. In 2013, emerging markets were affected by by turbulence month after month. During the year attempts were made against the alarming decrease in foreign exc-hange reserves by utilizing instruments such as high interest and high exchange rates.

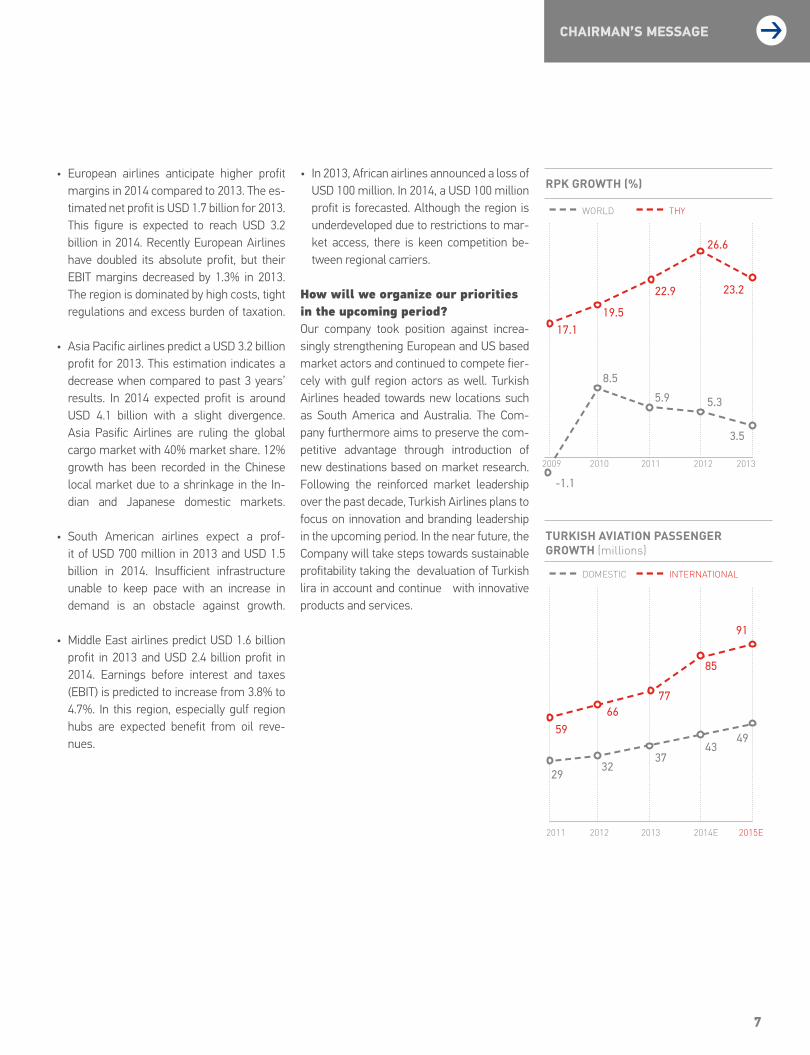

The Turkish economy, on the other hand ex-perienced a low interest rate at 4.6% in 2013; but subsequently economic and political tensions started to build up. In 2013, Turkish Airlines solidified its reputation as a network carrier. The Company’s profitability and doub-le digit growth performance, which continued for the past 11 years successively, also mar-ked 2013. The12 months’ figures reflect that the Company has achieved higher growth ra-tes than set in its target budget. Both growth in domestic and international lines and an inc-rease in load factor are indicative of a succes-sful year for Turkish Airlines in terms of load factor. Among AEA members Turkish Airline secured the second place in air passenger traffic.

In 2013 Turkish Airlines solidified its reputation as a network carrier. The Company’s profitability and double digit growth performance, which continued for the past 11 years successively, marked 2013 as well.

Our Company’s growth performance over the past 11 years strongly resembles that of air-line companies headquartered in South Ame-rica, Middle East and Far East Asia. On the ot-her hand, the growth matrix (curve) of airline companies, operating in advanced markets that are struggling with stagnation and crisis, is fairly static. The growth trouble of Europe-an and American airlines are closely related to structural problems rather than difficulties faced in the last couple of years. Aging fleets, high labor costs, increased tax rates are the primary issues in cost management for Euro-pean and American airlines. All actors in the European Union (EU) market went through hard times beyond comparison. Consolidation or state aids proved to be a life saver for the industry, where many actors stepped out of the market.

Turkish Airlines gained global market visibility by continuing to grow steadily and opening up to new markets over the past decade. Geo-e-conomic advantage, growth success and ma-nagement decisions to enter new markets resulted in revenue increase and well mana-ged costs. These on return contributed to the network and led to lower unit costs.

Actual results in 2013 and expected results for 2014 along IATA regional forecasts is as follows;

North American airlines target a revenue of USD 5.8 billion in 2013 and targets a USD 8.3 billion revenue in 2014. In order to reach absolute maximum profit and a strong EBIT margin, North American Airlines are expected to perform better than the rest of the industry.

FINANCIAL ANALYSIS

gDP DEvELoPmENT FoRECAST (2012-2032)

ANNuAL RPK DEvELoPmENT FoRECAST (2012-2032)

ASIA PACIFIC

AFRICA

LATIN AMERICA

MIDDLE EAST

CIS COUNTRIES

WORLD

NORTH AMERICA

EUROPE

Source: Boeing Current Market Outlook (2012-2032)

4.5%6.3%

5.7%

6.9%

6.3%

4.5%

5.0%

2.7%

4.2%

4.4%

4.0%

3.8%

3.4%

3.2%

2.5%

1.8%

7

• European airlines anticipate higher profit margins in 2014 compared to 2013. The es-timated net profit is USD 1.7 billion for 2013. This figure is expected to reach USD 3.2 billion in 2014. Recently European Airlines have doubled its absolute profit, but their EBIT margins decreased by 1.3% in 2013. The region is dominated by high costs, tight regulations and excess burden of taxation.

• Asia Pacific airlines predict a USD 3.2 billion profit for 2013. This estimation indicates a decrease when compared to past 3 years’ results. In 2014 expected profit is around USD 4.1 billion with a slight divergence. Asia Pasific Airlines are ruling the global cargo market with 40% market share. 12% growth has been recorded in the Chinese local market due to a shrinkage in the In-dian and Japanese domestic markets.

• South American airlines expect a prof-it of USD 700 million in 2013 and USD 1.5 billion in 2014. Insufficient infrastructure unable to keep pace with an increase in demand is an obstacle against growth.

• Middle East airlines predict USD 1.6 billion profit in 2013 and USD 2.4 billion profit in 2014. Earnings before interest and taxes (EBIT) is predicted to increase from 3.8% to 4.7%. In this region, especially gulf region hubs are expected benefit from oil reve-nues.

• In 2013, African airlines announced a loss of USD 100 million. In 2014, a USD 100 million profit is forecasted. Although the region is underdeveloped due to restrictions to mar-ket access, there is keen competition be-tween regional carriers.

How will we organize our priorities in the upcoming period?Our company took position against increa-singly strengthening European and US based market actors and continued to compete fier-cely with gulf region actors as well. Turkish Airlines headed towards new locations such as South America and Australia. The Com-pany furthermore aims to preserve the com-petitive advantage through introduction of new destinations based on market research. Following the reinforced market leadership over the past decade, Turkish Airlines plans to focus on innovation and branding leadership in the upcoming period. In the near future, the Company will take steps towards sustainable profitability taking the devaluation of Turkish lira in account and continue with innovative products and services.

CHAIRMAN’S MESSAGE

5.9

37

5.3

43

3.5

49

8.5

3229

17.1

59

19.5

66

22.9

77

26.6

85

23.2

91

-1.1

RPK gRoWTH (%)

TuRKISH AvIATIoN PASSENgER gRoWTH (millions)

2013

2015E

2012

2014E

2011

2013

2010

20122011

wORlD

DOMESTIC

THY

INTERNATIONAl

2009

AnnuAl RepoRt 2013

8

Esteemed stakeholders, valued business partners and employees,In 2013 Turkish Airlines continued its tradi-tional growth as it has in the past 11 years. The year was marked by increased passenger traffic and was crowned with positive financial results. The company managed to satisfy its customers with friendly service and its sta-keholders with successful financial results.

The global aviation industry continues to grow despite several economic crises it has faced. Industry research reveals that international commercial relations, cultural affairs and touristic travels are the major driving forces behind this growth. However, an increase in traffic numbers does not always signify pro-fitability. When operating in an industry whe-re profit margins are very low, companies should pursue a tight monetary policy in or-der to end the financial year with profitability.

Turkish Airlines carried out all growth plans according to its 2023 vision and has consequ-ently achieved a higher growth rate compared to industrial average. The Company is cons-tantly expanding its flight network, increasing market share in all destinations thanks to an appropriate strategy and carefully calculated

rates. Turkish Airlines is distinguishing itself as a company with incre-

asing brand value with the help of strong com-

munications strategies and targets at high profitability.

We have to note that Istanbul owns 66% of the international passenger traffic as a hub. Within 3 hours of flying distance to Tur-key and Istanbul, 41 countries and

78 cities are within reach. Within 4 hours of fl-ying distance, 53 countries and 118 cities; wit-hin 5 hours of flying distance 66 countries and 143 cities are accessible. In order to get our rightful share of passenger traffic we imposed our strategies successfully. Today our global market share is 2%.

In 2012 Turkish Airlines had a total of 219 flight destinations (182 international and 37 domestic lines), whereas in 2013 we had flights to 245 points (202 international, 43 domestic lines) utilizing a fleet of 233 aircrafts. Turkish Airlines, operating the most comprehensive network of 105 contries worldwide, is strongly determined to countries its leadership.

Our fleet size increased from 202 to 233 airc-raft by the end of 2013. 265 new aircraft, which was ordered earlier, will be delivered in time. By the end of 2020 Turkish Airlines fleet will be including 427 aircraft inclusive cargo airp-lanes. With the added aircraft, the average fle-et age, which is currently 6.7 will come down to 5. Here I would like to share with you some fi-gures from the previous year, which you can examine in more detail in the financial report.

Our passenger number in 2012 of 39 million, increased by 23.6% to 48.3 million. The incre-ase in domestic lines is 26.1% and 21.9% in international lines. Thus, Turkish Airlines suc-cessfully increased its market share to 12.8% and secured the second place among Europe-an carriers in air passenger traffic according to AEA (Association of European Airlines) data. In spite of capacity increase by 21.2% , passenger load factor increased by 1.6 pt to 79.0% in 2013, which contributed to succes-sful turnout. Cargo and mail transportation rose in parallel to passenger increase and increased by 20.1% to 565,391 tons. When we take a closer look at the financial indicators, our sales increased by 27% over the previous year and rose to TL 18.8 billion. Our gross pro-fit is TL 1,240 million and net profit is TL 682 million.

CHAIRMAN’S MESSAGE

According to (AEA) Association of European Airlines data Turkish Airlines successfully increased its market share to 12.8% and secured the second place among European carriers in air passenger traffic.

INDUSTRY DEvELOPMENTS AND THE FORECAST FOR 2014

9

Esteemed shareholders,In short, Turkish Airlines subsidiaries will sig-nificantly contribute to our future growth. Our subsidiaries take us beyond being just an air-line company, carrying passengers and cargo.

In 2013, the HABOM project was inaugura-ted where a major investment with Turkish Technic was made. A 384 thousand square meters hangar at Sabiha Gökçen Airport has been completed for the most part and work has started on the Narrow Body Hangar. In the near future, a Wide Body Hangar will also be put into service.

TGS, Turkish DO&CO contributes significant-ly to the comfort level of passengers who choose Turkish Airlines for their flights. Our catering company operates our CIP lounges as well. In 2013 Turkish DO&CO received gre-at recognition with its new concept as in the past years. TGS, extending its service network to Bodrum and Dalaman, operates in eight airports. We want TGS to become a global actor by entering international markets in the future.

Turkish-Opet maintained market leadership as in the previous year. The company reac-hed the eight position in the Turkish energy industry and achieved sales of USD 2.5 billion. Turkish-Opet operates at all airports in Tur-key.

Our seat manufacturing company Turkish Seat Industries (TSI) took an important step and built the first local economy seat. Owing to their lightweight properties and comfort, our fuel cost decreased and service quality increased. Our first airplane, refurbished with these seats has been put into service on do-mestic flights.

The Turkish Engine Center (TEC) which was established as the largest motor maintenance center in the region; today continues to serve customers both from Turkey and other count-ries in the region.

TCI, manufacturing kitchen and restroom units along international standards, entered the Boeing Company’s approved suppliers list. TCI Cabin Interiors is on the way to becoming an influential player in international markets.

In 2013 the landing field and taxiway of Aydın Çıldır Airport was completed and the flying academy commenced to operation. This pro-ject will enable us to meet the demand for well trained and high class pilots. Turkbine, another subsidiary of Turkish Airlines comp-leted the certification process in 2013 and started sales and marketing activities in its business segment. Esteemed shareholders,Turkish Airlines moves confidently into the future. Our goals are constructed on solid foundation. Every year we reevaluate our vi-sion and goals along Turkey’s vision for 2023; which is the 100th Anniversary of our Republic. During 2014 we plan continued growth for our company.

This year we aim to carry 26.2 million domes-tic and 32.3 international passengers inclu-ding pilgrimage flights and now our target is total of 59.5 million passengers. We plan to reach 141 billion ASK with a total increase of 21%, broken down as follows: 33% domestic lines, 29% South America; 25% Africa, 22% Far East, North America 20%, 16% Europe and 13% Middle East. Passenger load factor is expected to reach 78.8%. In cargo transpor-tation we predict 653 thousand tons which translates to a 23% increase.

BOARD OF DIRECTORS

The total number of aircraft will increase to 265 (201 narrow body, 57 wide body and 7 cargo aircraft) and flight destinations to 259 (16 new routes will be entered into service).

I am strongly of the opinion that the Turkish Airlines family, with more than 36 thousand personnel (including our subsidiaries) will go beyond its financial targets.

While continuing our financial growth; our service quality continued to grow at the same pace. In 2013 we received new Skytrax awards in “Best Airline in Europe”, “Best Airline in South Europe” and “Best Business Class Onboard Catering” categories and preserved our title as the Best of Europe.

I would like to express my sincere thanks to our passengers for their courtesy in preferring Turkish Airlines, our investors for showing trust, our executive staff, our employees and business partners. Their contribution is in-dispensable to our success. I greet your with great respect and hope sincerely that 2014 proves to be another successful year for our Company.

HAmDI TOPçUChairman of the Board and Chairman of the Executive Committee

AnnuAl RepoRt 2013

10

Mr. Topçu was born in Çayeli, Rize in 1964. In 1986, he graduated from the Marmara University, receiving a degree in Economics and Administrative Sciences. He is a certified financial advisor. Mr. Topçu retains his positions on the Turkish Football Federation Auditing Committee and as Chairman of the Board of Directors of the Company’s subsidiaries; THY Turkish Technic, THY DO&CO Catering Services, TGS Ground Services, THY Opet Aviation Fuels and HABOM Aviation Maintenance Repair and Modification Center. Hamdi Topçu is married and has four children.

Mr. Şanlı was born in Manisa in 1950. In 1977 he graduated from the Faculty of Law of Istanbul University, and in the same year began to work as an Assistant at the Istanbul University Law School. In 1985 he received his Doctorate of Law for his thesis “International Commercial Arbitration”. He completed his PhD dissertation on International Arbitration at the Institute of Advanced Legal Studies affiliated to London University. In 1987, he became Assistant Associate Professor, in 1990 Associate Professor, and in 1996 full Professor. He is currently the head of the International Private Law Department of the Faculty of Law at Istanbul University. Prof. Şanlı is a Board Member in the Company’s subsidiaries, THY Turkish Technical and HABOM Aviation Maintenance Repair and Modification Center. He has published many books, articles and monographs in the field of international private law, and especially international arbitration. Cemal Şanlı is married and has four children.

CHAIRMAN’S MESSAGE

BOARD OF DIRECTORS

Mr. Kotil was born in Rize in 1959. In 1983 he graduated from the Aeronautical Engineering Department at Istanbul Technical University (ITU). In 1986, he received his first Master’s degree in the United States from the Aircraft Engineering Department of Michigan University Ann Arbor, followed in 1987 by his second Master’s degree in Mechanical Engineering, and his Doctorate in Mechanical Engineering in 1991 at the same university. From 1991-93 Kotil established and managed the Aviation and Advanced Composite Laboratories of ITU’s Faculty of Aeronautics and Astronautics, where he also served as Assistant Professor and Associate Professor. From 1993-94 he served as Department Faculty Vice President and as Faculty Assistant Dean. Mr. Kotil also served as Head of the Research, Planning and Coordination Department of the Istanbul Metropolitan Municipality. He then served as a guest professor at Illinois University, and then as Department Head at the Research and Engineering Department of AIT Inc. New York. In 2003 he began his career with Turkish Airlines as Vice President of the Technical Department. In 2005 Mr. Kotil was appointed General Manager. And in 2006, he was elected as a member of the IATA Boards of Directors. In 2010, he was appointed as a Board Member of the Association of European Airlines and as Vice President between 2012-2013 and as Chairman in 2014. Mr. Kotil, married with four children, has authored many articles and publications.

Prof. Dr. Cemal Şanlı Vice Chairman of the Board of Directors and Executive Committee

Doç. Dr. Temel KoTİlMember of the Board of Directors and Executive Committee, CEO

HamDİ ToPçuChairman of the Board and Chairman of the Executive Committee

11

Born in Gaziantep in 1961, Mr. Büyükekşi graduated from the Faculty of Architecture at Yıldız Technical University in 1984. He attended Business Administration courses at the Marmara University and Business Administration and English courses in the UK. In addition to being a Board Member of Turkish Airlines, Mr. Büyükekşi is the President of the Turkish Exporters’ Assembly (TİM), a member of the Board of Directors of Türk Eximbank, of the Istanbul Chamber of Industry (ISO), the Istanbul Development Agency, the Istanbul Leather and Leather Products Exporters’ Association (İDMİB), and the Energy Efficiency Association (ENVERDER), and is the General Coordinator of Ziylan Group. Mr. Büyükekşi has been a board member at the Turkish Leather Foundation (TÜRDEV), Organized Industrial Zones and Technology Development Regions (TOBBİS), International Commerce Center Inc. (TOBTIM), and Turkish DO&CO. He was the president of the Turkish Association of Footwear Manufacturers, Chairman of the Istanbul Leather and Leather Products Exporters’ Association (İDMİB), as well as the Founding Chairman of the Turkish Footwear Industry Research Development and Education Foundation (TASEV) from 1997-2008. He is married and has three children.

Born in 1962, Mr. Akpınar graduated from Saint-Michel French High School and the Bosphorus University Department of Management Science. His professional career commenced in 1986 when he became the founder shareholder of Penta Textile. In 1993 he was appointed CEO of KVK Mobil Telefon Hizmetleri A.Ş.. Subsequently, Mr. Akpınar served as the CEO of MV Holding A.Ş. and played an active role in the creation of Fintur Holding BV. Between the years of 2002 and 2006 Mr. Akpınar served as the CEO of Turkcell. He is an independent Board Member of Turkish Airlines and serves as Chairman of the Board at Dost Energy, as Vice Chairman of MV Holding, Chairman of the Board at Portmobil and as a Member of the Board of Kimya Teknik. He remains an entrepreneur and investor in the fields of renewable energy, technology, chemicals and construction. Mr. Akpınar is married and has two children.

Born in Çan, Çanakkale in 1963, Mr. Gerçek graduated from the Public Administration Department of the Ankara University Faculty of Political Sciences in 1985. He received his MA in the USA in 1994. His career began in the position of assistant inspector at the Ministry of Finance Review Committee in the same year. Until 1998 he worked as a finance inspector and finance inspector general. And from 1995-1997 Mr. Gerçek was deputy assistant District Treasurer in Istanbul and has pursued his career as a chartered accountant since 1998. He is an independent Board Member at Turkish Airlines and Member of the Audit Committee at Joint Funds Bank Inc., a Member of the Board of Trustees at Fatih Sultan Mehmet Foundation University, and Auditor at the Participation Banks Association of Turkey.

OUR MISSION AND OUR vISION

meHmeT BüyüKeKŞİ Member of the Board and Corporate Management Committee

mUzAFFER AKPINAR Member of the Board and Financial Audit Committee

İsmaİl GerçeK Member of the Board, Financial Audit and Corporate Management Committee

AnnuAl RepoRt 2013

12

Mehmet Nuri Yazıcı, born in Rize in 1949, gra-duated from the Istanbul University, Academy of Economics and Commercial Sciences in 1975. From 1990 to 1991 he was the Consu-late General of the Republic of Turkey, at the Ministry of Foreign Affairs in Brussels. He also served as Councilor and Advisor to the Chairman at Istanbul Metropolitan Municipa-lity from 1994-2008. Mr. Yazıcı is married and has one child.

Prof. Dr. Mecit Eş, born in 1953 in Samsun; received his degree from the Istanbul University School of Economics in 1974. Having held several offices, he commenced his academic projects and received his Doctorate in 1985. He became Associate Professor in 1990 and Professor in 1986. And having then worked at Dumlupınar University from 1992 and 2012, Mr. Eş continues his academic studies as a Professor of the Academy of Commercial Sciences at Istanbul Commerce University He has published many books and articles, and is married with three children.

BOARD OF DIRECTORS

BOARD OF DIRECTORS

Mr. Ağbal was born in Bayburt in 1968. He graduated from the Public Administration Department of the Istanbul University Faculty of Political Sciences in 1989. In 1998 he re-ceived his MBA from Exeter University in the UK. In 1989 he became Assistant Inspector at the Ministry of Finance, in 1993 Inspector at the Ministry of Finance, and in 1999, became Inspector General. Having served as Vice President of the Financial Review Commit-tee, he was appointed Head of Department at the Inland Revenue in 2003, and served as a Ministerial Advisor in 2004. In 2006 Mr. Ağbal was appointed acting General Mana-ger of Budget and Financial Control at the Ministry of Finance, and Vice President of the Inland Revenue in the same year. In 2009 he became the Undersecretary of Finance. He is also a member of the Council of Higher Education and of the Board of Trustees at Yesevi University. Mr. Ağbal is married with two children.

naCİ ağBal Member of the Board

meHmeT nurİ yazıCı Member of the Board

Prof. Dr. meCİT eŞMember of the Board

13

OUR MISSION AND OUR vISION

• to develop the company’s standing as a global airline by expanding the coverage of its long-range flight network.

• to develop the company’s standing by developing its technical maintenance unit into a major regional resource.

• to develop the company’s standing as a service provider in all strategically important aspects of civil aviation, including ground handling services and flight training.

• to defend the company’s standing as the leader of the domestic airline industry.

• to provide an uninterrupted and superior flight service by entering into a collaborative agreement with a global airline alliance that complements its own network so as to advance its international image and marketing abilities.

• to safeguard and improve upon istanbul’s reputation as a regional aviation hub in its capacity as the flag carrier of the republic of turkey in the civil aviation industry, to be a leading european airline and an active global player by virtue of its flight safety and security record, and its product diversity, service quality, and competitive edge.

• to accomplish istanbul a significant (hub) destination.

OUR MISSION OUR vISION

• sustained growth of above the industry average

• a zero accident and crash record

• the most envied service levels worldwide

• Unit costs equal to those of low-cost carriers

• sales and distribution costs of below industry averages

• loyal customers who manage their own reservation, ticketing, and boarding formalities themselves

• Personnel who constantly develop their qualifications with an awareness of the close relationship between benefits for the company and the added value that they contribute

• a sense of entrepreneurship that creates business opportunities for fellow members in the star alliance and takes advantage of the business potential provided by them

• a management team, whose members identify with modern governance principles, and who distinguish themselves by being mindful of the best interests of shareholders and all stakeholders alike

OUR STRATEGY

AnnuAl RepoRt 2013

14

OUR STRATEGY

Turkish Airline keeps track of flight demand for various destinations worldwide. In order to cater to passengers’ needs, the Company manages its flight network accordingly. In 2013 Turkish Airline offered flights to 106 count-ries (including Turkey) and became an airline with the largest flight network as per country number. The Company positioned itself as the largest carrier worldwide by international desti-nation number (202 destinations) in 2013.

Our Company is aware of the fact that the center of aviation industry is shifting towards East. Therefore effort is made to strengthen the flight network in Middle East, Africa and Far East regions. In Africa and Middle East region Turkish Airlines offers the highest number of pairs of arrival and departure. In Far East flights Turkish Airlines flight network is on the third place as per destination number. In order to strengthen flight network, 16 new routes and frequency increase in present routes are planned for 2014. We aim to rise number of direct and transfer passenger to maximum and to keep our operational efficiency at the highest possible level. Our Company managed to sur-pass other airlines in many flight points where high competition prevails and became number one choice for passengers.

while heading towards top we are well aware of our competitive advantages. we are determined to preserve our power and use our strengths effectively.

The main factors behind Turkish Airlines stable growth are satisfaction and trust offered to customers. The Company moves on well aware of this fact. Customer satisfaction is a critical issue at each phase of the service offered. Turkish Airlines provides a variety of choices before and during flight with the help of friendly staff. Specially designed CIP lounges offer homelike comfort before flight. Personalized menu prepared by professional cooks during flight and tea service in traditional Turkish style ‘samovar’ are much appreciated by customers. On-time departure rate is over 85%. Turkish Airline has the highest on time departure performance among top 10 European Airlines. Rate of missing bags, which is an important part of customer satisfaction is decreased and kept at a low level in 2013. Successfully reaching this goal Turkish Airline is the carrier with the lowest rate of lost luggage among top 10 European Airlines. Turkish Airline won CAPA “Airline of the Year Award” thanks to superior customer satisfaction policy. The Company won Skytrax “Best Airline Europe Award” for the third time and a new award in “Best Business Class Catering”category too. Turkish Airline is determined to continue increasing service quality in the future and to enhance products through innovation and maximize customer satisfaction during their travelling experience.

Leader with strong fLight

network

Customer satisfaCtion

oriented management

ComPETITIvE ADvANTAgES

OUR MISSION AND OUR vISION

60 miLLions

1.9%

PassenGer tarGet in 2014

GloBal marKet sHare tarGet

15

Turkish Airlines gained high brand awareness thanks to good quality service and extensive flight network. Today the Company strives to heighten the existing level through various pro-jects. Turkish Airlines now invites passengers to widen their world with the newly adopted brand slogan “Widen Your World”. New slogan points to İstanbul’s linking character between two con-tinents. It invites potential customers to fly with Turkish Airlines and introduces the Companys extending flight network to existing passengers who love discoveries and new experiences. In order to increase brand awareness and brand value, Turkish Airlines conducted social media campaigns for flights, granted several sponsor-ships and used celebrity advertising effectively. In consequence of these activities Turkish Air-lines gained strength against traditional airline brands with widespread reputation. Now the Company is a preferred airline globally.

With each passing day Turkish Airline is coming to the forefront among airline carriers. In 2013 global average ASK ratio increased by 4.7%, whereas Turkish Airlines had 21% increase. 0.2 pt increase has been achieved with this ratio in globally offered capacity (ASK) and passenger market share. 2014 goal for capacity increase is 21%. With this goal realized, market share will increase by 0.3 pt and reach 1.9%. Capacity increase is planned along flight network strate-gies. Transfer and local passenger potential is also taken into consideration. Capacity increase targets are; 33% for Turkey, 29% for South America, 25% for Africa, 22% for Far East, 20% for North America, 16% for Europe and 13% for Middle East. 23% increase in passenger number is planned while balancing capacity increase with passenger load factor increase. Thus total number of 60 million passengers is set as tar-get for 2014. In 2013 global passenger market share was 1.5%. It will rise by 0.3 and reach 1.8% in 2014. Top airline carriers plan with 1% capacity increase in 2014. Turkish Airlines plans to grow faster than its competitors in 2014. The Company will continue to advance in top airline carriers list in 2014 like in previous year. In regard to international passengers Turkish Airlines got to 10th place in 2013. The Company owns this success to its strategy designed especially for transfer passengers and will sustain it. Turkish Airlines goal is to increase international transfer passengers in the same pace with total passengers and to attain this objective İstanbul’s adventegous geographical location will be utilized.

Turkish Airlines has a noteworthy cost advanta-ge over its competitors and in order to preserve this strength the Company works on new strategies. To sustain competitive advantage in total unit cost; saving strategies, cost cutting strategies and financial risk management stra-tegies are implemented. Maintaining a young fleet and pursuing an efficient fuel consumption policy are other saving strategies in progress. In order to reduce sales costs various projects are designed to increase sales via direct sales channels. Regional and point target strategies, through which Turkish Airlines takes preceden-ce of its competitors, will also be enhanced. The Company will continue to invest in technology to decrease costs, to increase efficiency and to enhance product experience as in 2013. With respect to personnel efficiency Turkish Airlines aims to preserve its existing strength by making careful plans to support increase and avoid inef-ficiency. The Company plans to increase aircraft efficiency by 2% and thus preserve high aircraft efficiency, which is one of the most important cost advantages presently. Aircraft fuel costs stemming from fluctuations in the oil prices are controlled by using financial instruments. This is an important financial risk management strategy, implemented as part of commodity risk management. Management by process and tracking system projects are indispensible components of general management and help Turkish Airlines to gear along strategic goals in a standardized way.

high Brand awareness

BaLanCed, PLanned and raPid growth

Low unit Cost advantage

OUR STRATEGY

AnnuAl RepoRt 2013

16

OUR STRATEGY

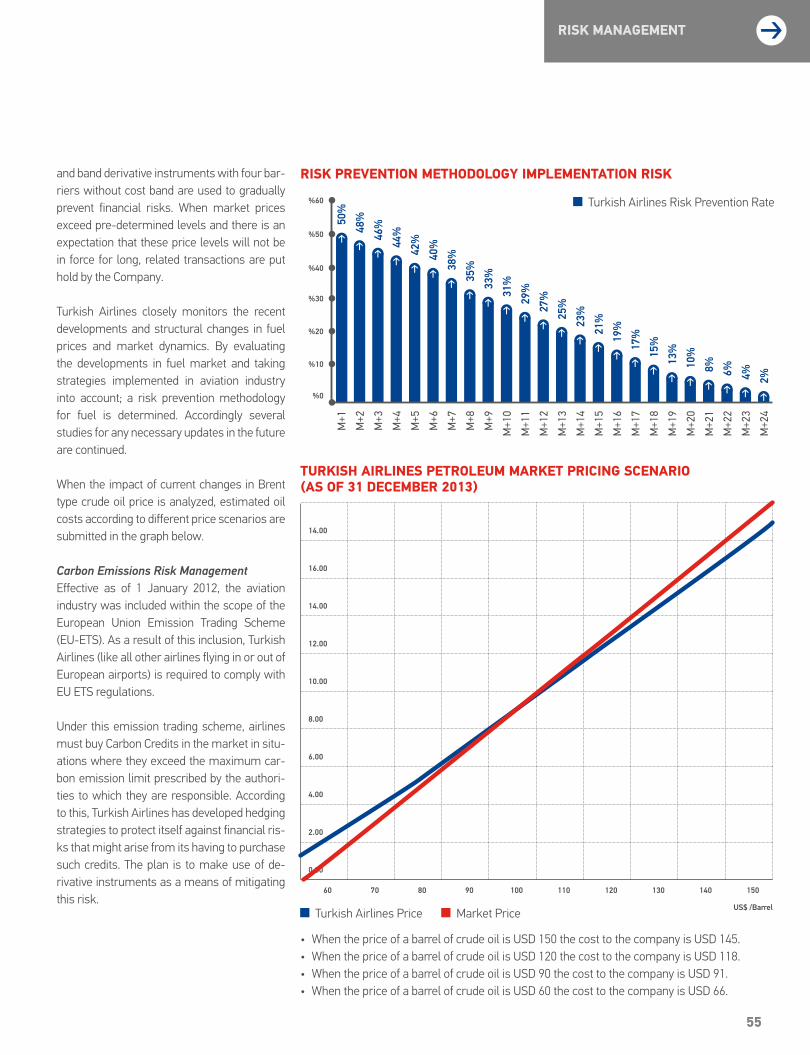

INDuSTRIAL RISKS

OUR STRATEGY

Our Company keeps an eye on the fluctua-tions in neighbouring regions and is always on alert for crisis management. Potential risks are incorporated in plans and income, expenses and capacity distribution is alloca-ted accordingly to prevent damages. Turkish Airlines completed its risk plans for 2014 as in previous years and established a structu-re where the Company can react to potential instabilities with the help of dynamic capacity, income management and financial risk ma-nagement when necesserary.

Recently capacity limits in Atatürk Airport and its negative impact on Turkish Airlines’ growth became an issue. With effective flight plan-ning our Company will use the present capa-city in the most efficient way and will include new route to its flight network and continue growth in Atatürk Airport. Turkish Airlines will perform its duty consciously in order to use Atatürk Airport’s available capacity for maxi-mum efficiency. Sabiha Gökçen and Esenbo-ğa based operations will be increased as well. With the new airline the Company intends to use Istanbul’s, which is one of the leading international hubs, geographical advantage more efficiently.

Industrial changes increase market share of low cost carriers and competition with each passing day. Other notable industry changes to consider are; consolidations in Europe and America and strategic alliances formed in Asia and Middle East regions. Turkish Air-lines’ will sustain its strengths and will use its competitive advantages against low cost carriers and airlines growing through conso-lidation. Our Company intends to increase its market share in the industry with low costs, operational efficiency, financial strength, well balanced growth strategy, product quality and brand recognition.

CaPaCity Limits in istanBuL atatürk

airPort

inCreasing ComPetitive

Conditions PriCe oriented

eConomiC and PoLitiCaL

instaBiLities in the neighBouring

regions

Turkish Airlines will sustain its strengths and will use its competitive advantages against low cost carriers and airlines growing through consolidation.

17

OUR SUBSIDIARIES

AnnuAl RepoRt 2013

18

OUR SUBSIDIARIES

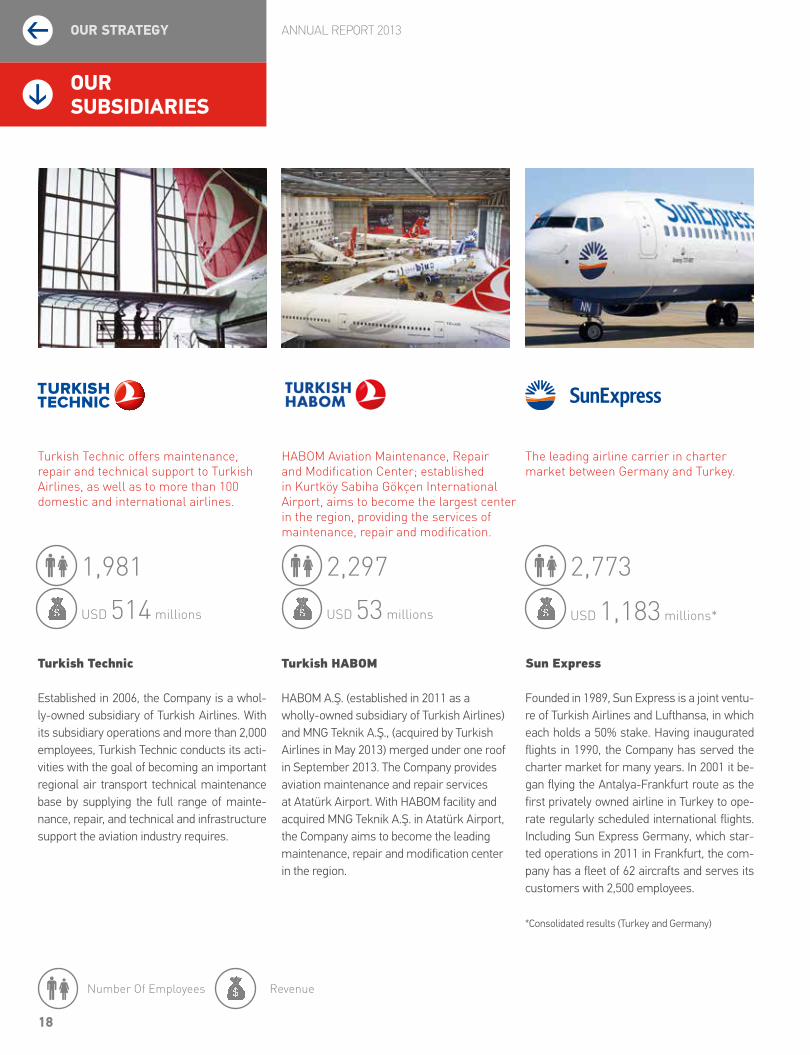

Turkish Technic offers maintenance, repair and technical support to Turkish Airlines, as well as to more than 100 domestic and international airlines.

HABOM Aviation Maintenance, Repair and Modification Center; established in Kurtköy Sabiha Gökçen International Airport, aims to become the largest center in the region, providing the services of maintenance, repair and modification.

The leading airline carrier in charter market between Germany and Turkey.

OUR STRATEGY

Turkish HABOm

HABOM A.Ş. (established in 2011 as a wholly-owned subsidiary of Turkish Airlines) and MNG Teknik A.Ş., (acquired by Turkish Airlines in May 2013) merged under one roof in September 2013. The Company provides aviation maintenance and repair services at Atatürk Airport. With HABOM facility and acquired MNG Teknik A.Ş. in Atatürk Airport, the Company aims to become the leading maintenance, repair and modification center in the region.

Turkish Technic

Established in 2006, the Company is a whol-ly-owned subsidiary of Turkish Airlines. With its subsidiary operations and more than 2,000 employees, Turkish Technic conducts its acti-vities with the goal of becoming an important regional air transport technical maintenance base by supplying the full range of mainte-nance, repair, and technical and infrastructure support the aviation industry requires.

Sun Express

Founded in 1989, Sun Express is a joint ventu-re of Turkish Airlines and Lufthansa, in which each holds a 50% stake. Having inaugurated flights in 1990, the Company has served the charter market for many years. In 2001 it be-gan flying the Antalya-Frankfurt route as the first privately owned airline in Turkey to ope-rate regularly scheduled international flights. Including Sun Express Germany, which star-ted operations in 2011 in Frankfurt, the com-pany has a fleet of 62 aircrafts and serves its customers with 2,500 employees.

*Consolidated results (Turkey and Germany)

1,981 2,297 2,773

USD 514 millions USD 53 millions USD 1,183 millions*

Number Of Employees Revenue

19

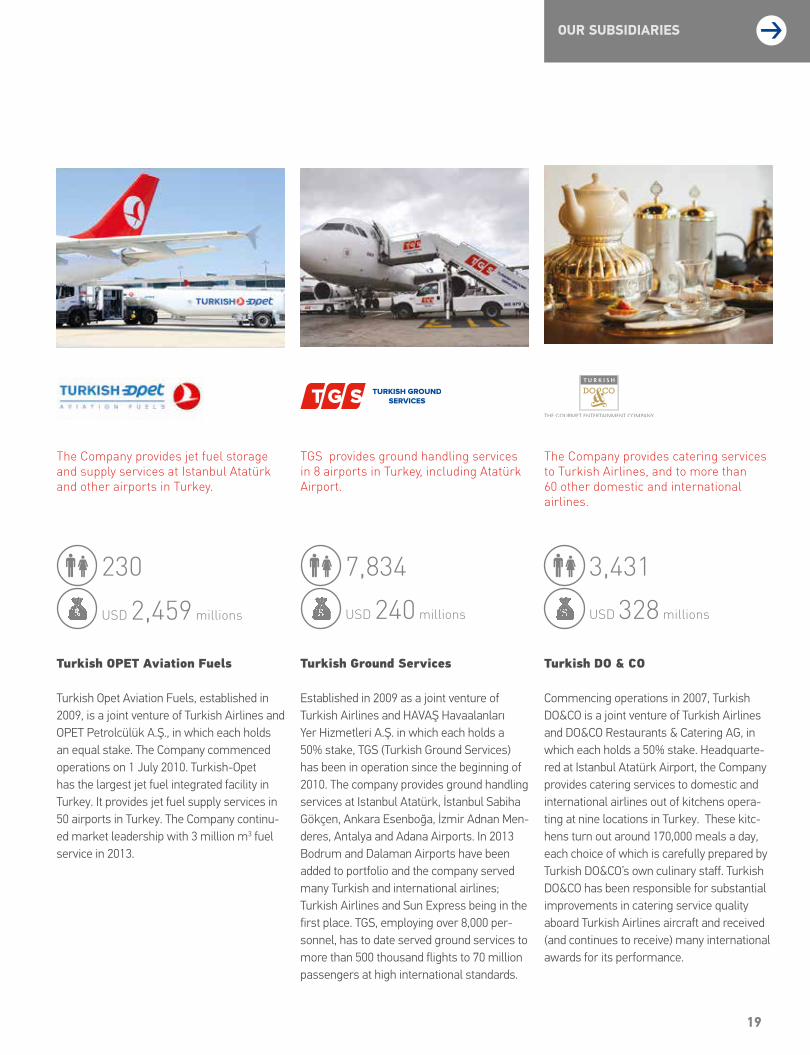

The Company provides jet fuel storage and supply services at Istanbul Atatürk and other airports in Turkey.

Turkish OPET Aviation Fuels

Turkish Opet Aviation Fuels, established in 2009, is a joint venture of Turkish Airlines and OPET Petrolcülük A.Ş., in which each holds an equal stake. The Company commenced operations on 1 July 2010. Turkish-Opet has the largest jet fuel integrated facility in Turkey. It provides jet fuel supply services in 50 airports in Turkey. The Company continu-ed market leadership with 3 million m3 fuel service in 2013.

TGS provides ground handling services in 8 airports in Turkey, including Atatürk Airport.

Turkish Ground Services

Established in 2009 as a joint venture of Turkish Airlines and HAVAŞ Havaalanları Yer Hizmetleri A.Ş. in which each holds a 50% stake, TGS (Turkish Ground Services) has been in operation since the beginning of 2010. The company provides ground handling services at Istanbul Atatürk, İstanbul Sabiha Gökçen, Ankara Esenboğa, İzmir Adnan Men-deres, Antalya and Adana Airports. In 2013 Bodrum and Dalaman Airports have been added to portfolio and the company served many Turkish and international airlines; Turkish Airlines and Sun Express being in the first place. TGS, employing over 8,000 per-sonnel, has to date served ground services to more than 500 thousand flights to 70 million passengers at high international standards.

OUR SUBSIDIARIES

The Company provides catering services to Turkish Airlines, and to more than 60 other domestic and international airlines.

Turkish DO & CO

Commencing operations in 2007, Turkish DO&CO is a joint venture of Turkish Airlines and DO&CO Restaurants & Catering AG, in which each holds a 50% stake. Headquarte-red at Istanbul Atatürk Airport, the Company provides catering services to domestic and international airlines out of kitchens opera-ting at nine locations in Turkey. These kitc-hens turn out around 170,000 meals a day, each choice of which is carefully prepared by Turkish DO&CO’s own culinary staff. Turkish DO&CO has been responsible for substantial improvements in catering service quality aboard Turkish Airlines aircraft and received (and continues to receive) many international awards for its performance.

230

USD 2,459 millions

7,834

USD 240 millions

3,431

USD 328 millions

AnnuAl RepoRt 2013

20

The Company provides aircraft engine maintenance, repair, and overhaul services to customers in Turkey and its hinterland.

Turkish Engine Center (TEC)

This Company, established in 2008, is a joint venture of Turkish Airlines and United Technologies, a subsidiary of Pratt&Whitney (49%) and Turkish Airlines (51%). Operating out of a high-tech, environmentally-friend-ly maintenance center with an area of around 25,000 m² at Istanbul Sabiha Gökçen International Airport, TEC has the capacity to perform maintenance on more than 200 aircraft engines a year.

At the Gebze facilities, high quality services for maintenance and repair of nacelles and thrust reversers is provided.

Goodrich Turkish Airlines Technic Service Center

Established in 2010, the Goodrich Turkish Airlines Technical Service Center is a joint venture of Turkish Technic (40%) and TSA-Ri-na Holdings (60%), the latter a subsidiary of Goodrich Corporation. The Goodrich Turkish Airlines Technical Service Center aims to be an important player in the industry by providing maintenance and repair services meeting international standards to Turkish Airlines and other international airline com-panies.

TCI’s present objective is meet Turkish Airlines demand for cabin interior systems and to win a share of international markets in the future.

Turkish Cabin Interior Systems

The Company is formed in 2011, stakes of 30%, 21%, and 49% are held respectively by Turkish Airlines, Turkish Technic and Türk Havacılık ve Uzay Sanayi A.Ş. (TUSAŞ -TAI). TCI’s objective is to undertake the design, manufacture, logistical support, modificati-on, and marketing of aircraft cabin interior systems and components, and to win a share of international markets with the goods and services that it produces. TCI took an impor-tant step by becoming an approved Boeing vendor and delivered the initial products for assembling to Turkish Airlines.

OUR SUBSIDIARIES

OUR SUBSIDIARIES

204 22 72

USD 130 millions USD 8 millions USD 1,333 thousands

Number Of Employees Revenue

21

The Company designs and manufactures airline seats, and makes, modifies, markets, and sell spare parts. Production has started at the end of 2013.

TSI Aviation Seats

The Company was formed as a joint venture with the Assan Hanil Group, which was the leading company in car seats manufacturing in 2011. Stakes are held 50%, 45%, and 5% by Assan Hanil Group, Turkish Airlines, and Tur-kish Tecnic respectively. In 2014, the first set of passenger seats have been assembled for Turkish Airline aircrafts. The Company aims to design and manufacture airline seats, and to make, modify, market, and sell spare parts to Turkish Airlines and other international airline companies in the future.

2013 TRAFFIC RESULTS

The Company is a collaboration that derives its strength from international experience, technically competent personnel and strong brand underpinning.

TURKBINE Gas Turbines

Established in 2011, the Company is a joint venture of Turkish Technic and Zorlu O&M Enerji Tesisleri İşletme ve Bakım Hizmetleri A.Ş., in which each holds an equal stake. The signed agreement envisions the provision of maintenance, repair, and overhaul services for a variety of aircraft engines that are be-yond the activity scope of existing subsidia-ries, and also for industrial gas turbines used at power plants.

The Company was established in 2012 as a wholly-owned subsidiary of Turkish Airlines.

aydın çıldır airport services

The Company was established to operate Aydin Çıldır Airport, provide aviation training, organize sports-training flights and conduct all activities related to the transportation of passengers with aircraft types appropriate to the prevailing runway length. Following the completion of landing field and taxiway of Aydın Çıldır Airport flying academy commenced operation. The company will contribute to education of well-trained pilots for the aviation industry.

25 16

USD 896 thousands USD 1,033 thousands

AnnuAl RepoRt 2013

22

OUR SUBSIDIARIES

2013 TRAFFIC RESULTS

total traffic results 2013 2012 2011 2010 2009Revenue Passenger (000) 48,268 39,045 32,648 29,119 25,102Available Seats-Km (millions) 116,433 96,124 81,193 65,100 56,574Revenue Passenger-Km (millions) 91,997 74,410 58,933 47,950 40,130Passenger Load Factor (%) 79.0 77.4 72.6 73.7 70.9Number of Destinations 245 219 196 174 158Number of Landings 377,400 308,384 270,618 245,226 213,953Km’s flown (000) 690,572 542,339 419,113 358,370 311,869Cargo (tons) 546,822 454,293 375,042 302,983 230,709Mail (tons) 18,569 16,570 12,796 10,973 7,351Excess Baggage (tons) 6,231 3,683 4,170 3,629 3,734Available Ton-Km (millions) 17,519 14,288 11,926 9,036 7,795Revenue Ton-Km (millions) 11,571 9,425 7,467 5,894 4,784Overall Load Factor (%) 66.0 66.0 62.6 65.2 61.4

international traffic results 2013 2012 2011 2010 2009Revenue Passenger (000) 28,215 23,139 18,160 15,474 13,410Available Seats-Km (millions) 101.000 84.112 70.029 54.663 47.536Revenue Passenger-Km (millions) 79,696 64,945 50,349 39,943 33,311Passenger Load Factor (%) 78.9 77.2 71.9 73.1 70.1Number of Destinations 202 182 152 132 120Number of Landings 220,037 179,843 149,941 132,384 116,256Km’s flown (000) 592,911 464,772 348,356 292,794 255,556Cargo (tons) 503,021 417,141 340,627 267,630 197,672Mail (tons) 14,827 13,622 9,771 7,002 3,802Excess Baggage (tons) 4,040 2,162 2,291 1,929 2,284Available Ton-Km (millions) 15,757 12,916 10,653 7,845 6,748Revenue Ton-Km (millions) 10,438 8,538 6,654 5,137 4,132Overall Load Factor (%) 66.2 66.1 62.5 65.5 61.2

Domestic traffic results 2013 2012 2011 2010 2009Revenue Passengers (000) 20,053 15,906 14,488 13,645 11,692Available Seats-Km (millions) 15,433 12,012 11,164 10,437 9,038Revenue Passenger-Km (millions) 12,301 9,465 8,584 8,007 6,819Passenger Load Factor (%) 79.7 78.8 76.9 76.7 75.4Number of Destinations 43 37 44 42 38Number of Landings 157,363 128,541 120,677 112,842 97,697Km’s flown (000) 97,660 77,567 70,757 65,576 56,313Cargo (tons) 43,802 37,152 34,415 35,353 33,037Mail (tons) 3,742 2,948 3,025 3,971 3,549Excess Baggage (tons) 2,191 1,521 1,879 1,700 1,450Available Ton-Km (millions) 1,763 1,372 1,273 1,191 1,047Revenue Ton-Km (millions) 1,133 887 813 757 652Overall Load Factor (%) 64.3 64.7 63.9 63.6 62.3

Traffic Results

InternatIonalrevenue

Passengers(000)

28,215InternatIonal

Passenger load Factor

78.9%

Passenger load Factor

79.0% total number oF Passengers (000)

48,268

DOMESTIC REVENUE PASSENGERS

(000)

20,053domestIc

Passenger load Factor

79.7%

23

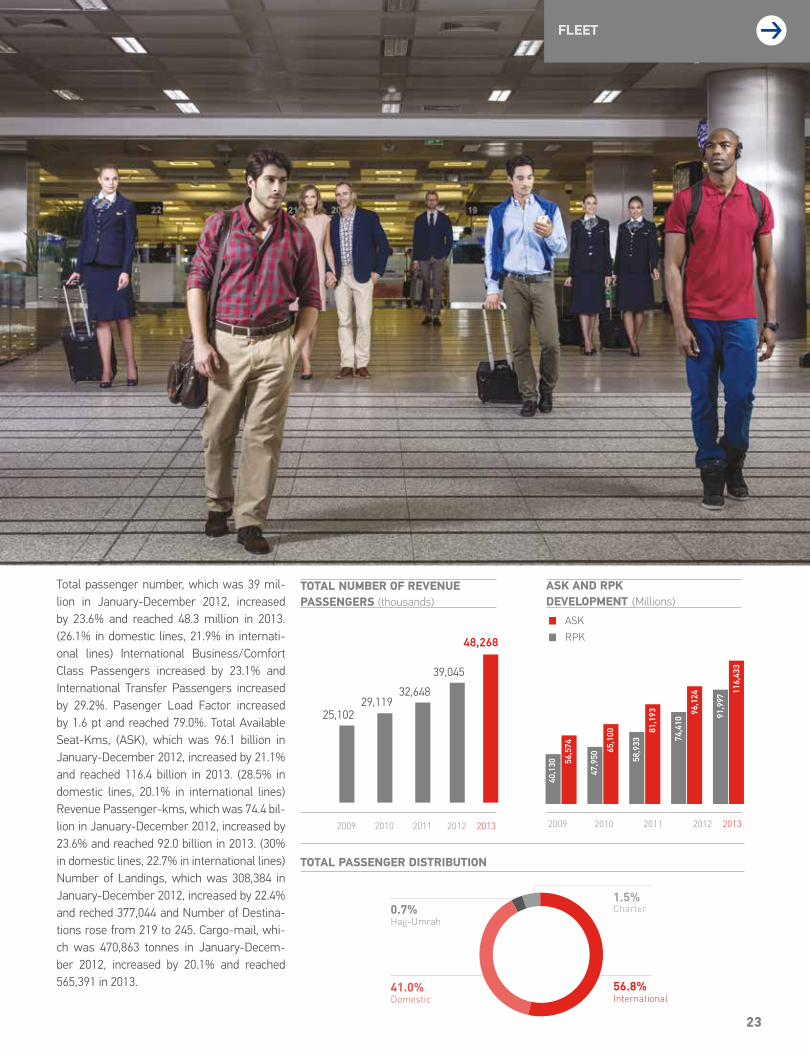

Total passenger number, which was 39 mil-lion in January-December 2012, increased by 23.6% and reached 48.3 million in 2013. (26.1% in domestic lines, 21.9% in internati-onal lines) International Business/Comfort Class Passengers increased by 23.1% and International Transfer Passengers increased by 29.2%. Pasenger Load Factor increased by 1.6 pt and reached 79.0%. Total Available Seat-Kms, (ASK), which was 96.1 billion in January-December 2012, increased by 21.1% and reached 116.4 billion in 2013. (28.5% in domestic lines, 20.1% in international lines) Revenue Passenger-kms, which was 74.4 bil-lion in January-December 2012, increased by 23.6% and reached 92.0 billion in 2013. (30% in domestic lines, 22.7% in international lines) Number of Landings, which was 308,384 in January-December 2012, increased by 22.4% and reched 377,044 and Number of Destina-tions rose from 219 to 245. Cargo-mail, whi-ch was 470,863 tonnes in January-Decem-ber 2012, increased by 20.1% and reached 565,391 in 2013.

TOTAL NUMBER OF REvENUE PASSENGERS (thousands)

TOTAL PASSENGER DISTRIBUTION

48,268

39,045

32,64829,119

25,102

20132012201120102009

ASK AND RPK DEvELOPMENT (Millions)

20132012201120102009

40,1

30 56,5

74

47,9

50

65,1

00

58,9

33

81,1

93

74,4

10

96,1

24

91,9

97

116,

433

ASKRPK

FLEET

1.5%

56.8%

0.7%

41.0%

Charter

International

Hajj-Umrah

Domestic

AnnuAl RepoRt 2013

24

FLEET

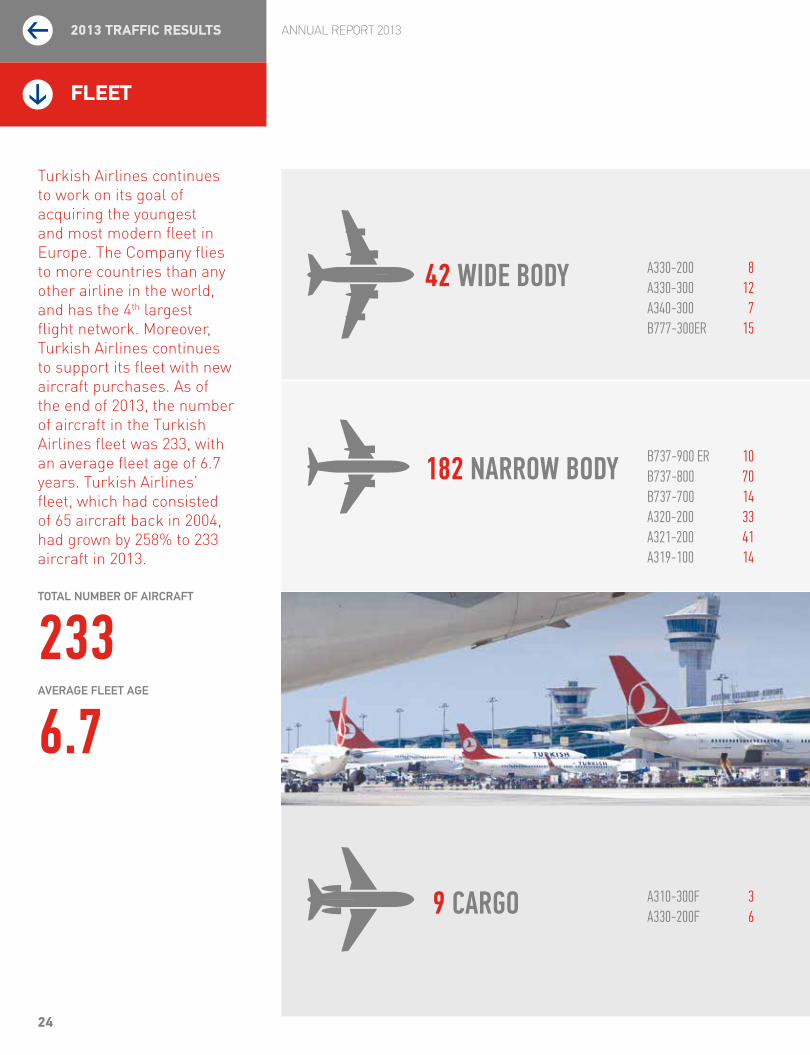

6.7233total nUmBer oF aircraFt

aVeraGe Fleet aGe

Turkish Airlines continues to work on its goal of acquiring the youngest and most modern fleet in Europe. The Company flies to more countries than any other airline in the world, and has the 4th largest flight network. Moreover, Turkish Airlines continues to support its fleet with new aircraft purchases. As of the end of 2013, the number of aircraft in the Turkish Airlines fleet was 233, with an average fleet age of 6.7 years. Turkish Airlines’ fleet, which had consisted of 65 aircraft back in 2004, had grown by 258% to 233 aircraft in 2013.

A330-200 8 A330-300 12 A340-300 7 B777-300ER 15

B737-900 ER 10 B737-800 70 B737-700 14 A320-200 33 A321-200 41 A319-100 14

42 wide Body

182 narrow Body

A310-300F 3 A330-200F 6 9 Cargo

2013 TRAFFIC RESULTS

25

Turkish Airlines continues to work on its goal of acquiring the youngest and most modern fleet in Europe. The Company flies to more countries than any other airline in the world, and has the 4th largest flight network. More-over, Turkish Airlines continues to support its fleet with new aircraft purchases. As of the end of 2013, the number of aircraft in the Turkish Airlines fleet was 233, with an average fleet age of 6.7 years. Turkish Airline’s fleet, which had consisted of 65 aircraft back in 2004, had grown by 258% to 233 aircraft in 2013.

While purchasing aircraft Turkish Airlines ta-kes into consideration the following points; changes in passenger traffic, varying custo-mer needs, passenger comfort and safety, high technology equipment, fuel economy and environmental friendliness. Thus the Company takes important steps towards strengthening its brand. As a consequence of long term fleet projection, 20 B777-300ER and 20 A330-300 aircraft have been ordered, whi-ch will meet the demand for long haul aircraft in the coming period. A330-300 aircraft orde-red will be delivered by the end of 2016 and B777-300ER aircraft ordered will be delivered between 2014 and 2017.

In 2013 a purchase order for 117 aircraft has been sent to Airbus Company, which is the largest one-time order ever placed in Turkish Civil Aviation history. The Company ordered 25 A321 CEO, 4 A320 NEO and 88 A321 NEO

to meet narrow-body aircraft demand. Accor-ding to plan ordered aircraft are will be taken into operation between 2015 and 2020.

In addition to 117 aircraft order, a purchase or-der of 95 aircraft has been sent to Boing Com-pany. The order includes 20 B737-800 NG, 65 B737-8 MAX and 10 B737-9 MAX aircraft. According to plan ordered aircraft are will be delivered between 2016 and 2021.

In 2013 major airlines are went through con-solidation or formed strategic alliances un-der cost pressure. Placing a purchase order for 212 aircraft reflects Turkish Airlines’ self confidence and provides assurance to its sta-keholders.

When compared to the existing fleet, 15% fuel economy is expected after delivery of the or-dered narrow and wide body aircraft. In additi-on long haul aircraft will contribute positively to network extension and passenger increase.

The Company updates fleet plans at the end of each year, within the scope of the following strategies: Exploiting opportunities, risk ma-nagement, sustainability, dynamic capacity planning, a broadening of the flight network and increased frequency. During the year, aircraft numbers are revised according to deli-veries and demand and fleet rejuvenation ne-eds. Interim solutions are also implemented, such as using leased aircraft in light of market conditions, which does not increase fleet age or damage the integrity of aircraft.

In 2013 a purchase order for 117 aircraft has been sent to Airbus company, which is the largest one-time order ever placed in Turkish Civil Aviation history.

TOTAL SEAT CAPACITY

DAILY UTILIZATION RATE

42,236

12:40

36,504

12:12

33,007

11:38

28,030

12:02

23,549

11:39

2013

2013

2012

2012

2011

2011

2010

2010

2009

2009

FLIGHT NETwORK

AnnuAl RepoRt 2013

26

FLIGHT NETwORK

In 2013, Turkish Airlines flights to 3 destinations in Africa, two in the Middle East, nine in Europe, five in the Far East and one in the USA commenced. In addition to 20 international routes, Turkish Airlines opened 6 domestic routes and added 26 new destinations to its flight map. North America

South America

Turkish Airlines added 20 new destinations in 9 countries during 2013 to widen the world of their passengers. The Company invites them to discover Aqaba and Al Qassim in Middle East, Friedrichshafen, Salzburg, Tallinn, Vilnius, Santiago de Compostela, Luxemburg, Marsilia and Malta in Europe, Colombo, Lahor, Kathmandu, Kuala Lumpur and Mazar-i Sharif in Asia, Houston in USA, N’djamena, Kano and Libreville in Africa and Constanta in the Balkans. With the new destinations offered, passengers can fly to 245 flight destinations in 105 countries. Our Company connects cities where no inter-national connection was present before, to Turkey and many other international flight points; so that passengers can get anywhere in the world they want to.

6

2

43202245

10526

Domestic Destinations

international Destinations

total nUmBer oF Destinations

total nUmBer oF coUntries

Destinations laUncHeD in 2013

FLEET

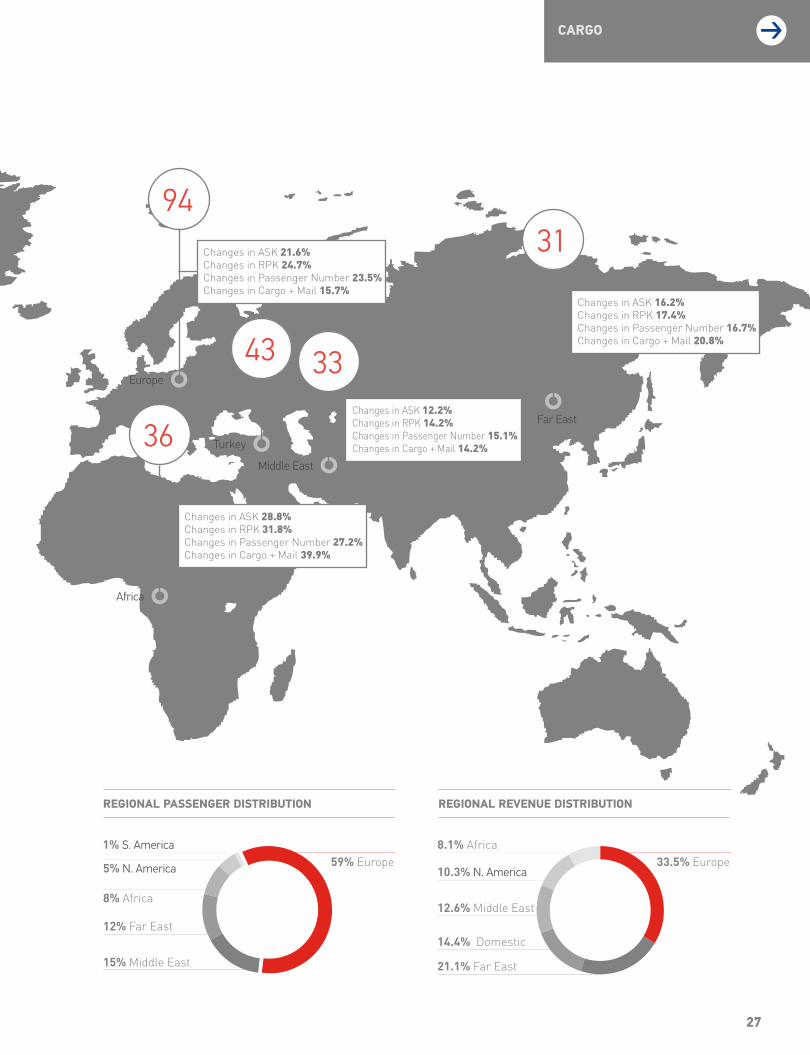

Changes in ASK 22.8% Changes in RPK 25.3%Changes in Passenger Number 23.9%Changes in Cargo + Mail 23.3%

Changes in ASK 40.8% Changes in RPK 75.8%Changes in Passenger Number 135.0%Changes in Cargo + Mail 54.5%

27

Africa

Middle East

Turkey

Far East

36

43 33

31

Europe

94

CARGO

1% S. America

5% N. America

8% Africa

12% Far East

15% Middle East

59% Europe

Changes in ASK 28.8%Changes in RPK 31.8%Changes in Passenger Number 27.2%Changes in Cargo + Mail 39.9%

Changes in ASK 12.2%Changes in RPK 14.2%Changes in Passenger Number 15.1%Changes in Cargo + Mail 14.2%

Changes in ASK 16.2%Changes in RPK 17.4%Changes in Passenger Number 16.7%Changes in Cargo + Mail 20.8%

Changes in ASK 21.6%Changes in RPK 24.7%Changes in Passenger Number 23.5%Changes in Cargo + Mail 15.7%

REGIONAL PASSENGER DISTRIBUTION REGIONAL REvENUE DISTRIBUTION

8.1% Africa

10.3% N. America

12.6% Middle East

14.4% Domestic

21.1% Far East

33.5% Europe

AnnuAl RepoRt 2013

28

CARGO

Turkish Cargo, a sub-brand of Turkish Airlines, has achieved consistent growth since 2000, des-pite the global recession, which started in 2008 and has left its traces until today. By increasing the volume from 470,863 (2012) tons to 565,391 tons in 2013; Turkish Cargo has continuously increased its services during that recession time while other airline and cargo carriers cut back on their capacity and traffic. Turkish Cargo recording a growth 21.8% became the rising star in the in-dustry with this achievement. We have shown our recognition and confidence in our brand by developing and modernizing our fleet. We have incorporated 6 new-generation wide-body and long haul Airbus A330-200F and 3 A310-200F cargo aircraft. With A330-200F cargo aircraft Turkish Cargo acquired the necessary long-haul capability for direct cargo transfer and introdu-ced Shanghai and Hong Kong routes. Cargo ca-pacity in present destinations; Frankfurt, Maast-richt, Milan, Madrid, Helsinki, Stockholm, Kiev, Budapest increased. At the same time high qu-ality cargo service started for new destinations; Kuwait, Riyadh, Tehran, Karachi, Ashkhabad, Guangzhou, Astana, Dacca, Bombay, Singapore, Seoul, Bangkok, Islamabad, Akra, Entebbe, La-gos, Khartoum, Johannesburg, Nairobi.

Turkish Airlines strengthened its fleet by inclu-ding new generation, wide body and long-haul Boeing 777 and Airbus A330 passenger aircraft. Using belly cargo capacity of these wide body aircraft, Asia and America being in the first place,

business partners in many other new commer-cial centers were contacted and greater cargo capacity was provided to further flight points in the market.

Turkish Cargo continues its investments without deceleration. The new storage area which was built on 10,500 m² area at Ataturk International Airport is inaugurated in September 2013. Cargo terminal construction with 43,000 m² enclosed area is continuing. The estimated date for inau-guration is September 2014.

Turkish Cargo, has started to use a new softwa-re solution, instead of TACTIC system which has been used for process management of cargo operations since 1990. According to plans ICar-go, which is a new generation integrated solu-tion, that meets passenger & cargo carriers, ground handling agents and airport operators needs in a single suit, containing cargo sales & reservation, terminal operations, mail handling & accounting, cargo revenue accounting and ULD management modules; will go live in 2015.

Turkish Cargo will have 150,000 m² enclosed area in the 3rd airport in Istanbul.

The Company will continue developing cargo services to offer high quality cargo services. Turkish Cargo is strongly committed to increase service quality day by day and to promote İstan-bul to become a logistics center.

By increasing the volume from 470,863 (2012) tons to 565,391 tons in 2013 and recording a growth 21.8% Turkish Cargo became the rising star in the industry with this achievement

9nUmBer oF carGo aircraFt

CARGO+MAIL DEvELOPMENT (TONS)

565,391

470,863

387,838

313,956

238,060

20132012201120102009

FLIGHT NETwORK

29

Sales Based Income Percentage by Cargo Regions (%)

Sales Based Tonnage Percentage by Cargo Regions (%)

EUROPE1

AFRICA

TURKEY

MIDDLE EAST

EUROPE2 FAR EAST

AMERICA

19.6

2.2

22.9

3.4

7.1 37.8

7.0

19.0

2.6

32.9

4.9

7.6 25.8

7.1

MRO

AnnuAl RepoRt 2013

30

MRO

The services that Turkish Technic provides its customers primarily consist of line, station, and component maintenance. In addition to Turkish Airlines aircraft, the company also makes com-ponent pool services available to the fleets of other carriers. The number of Component Pool service customers reached 400 in 2013.

Turkish Technic’s four hangars in Istanbul and Ankara have a total combined enclosed space of 73,500 m², at which it provides maintenance and repair services for airlines and VIP jet operators. Turkish Technic provides maintenance and repa-ir services, through various specialized compo-nent shops, from station maintenance, engines, APU (auxiliary power units) to landing gear. And while it’s most important customer is Turkish Airlines, Turkish Technic also serves more than 600 other companies located on four continents.

Turkish Technic provides line and station main-tenance services for the following aircraft: Boe-ing 737 Classic and Next Generation (NG), Boe-ing 777, Airbus A320 series, Airbus A300, Airbus A310, Airbus A330, Airbus A340, Gulfstream G-IV, Gulfstream 550, Cessna 172, and Diamond

DA42. In addition, it has the ability to conduct a full range of maintenance-repair services on an aircraft including landing gear, avionics compo-nents, hydraulic/pneumatic components, brake systems, tires and rims, and mechanical com-ponents. In brief, Turkish Technic offers all ne-cessary maintenance and repair activities at its own facilities for the aforementioned aircraft.

First local plane seat is manufactured The Company has started to renew seats made by Koito Industries installed on Boeing 737-800 passenger aircraft, which were included during the years 1998 to 2000 to the fleet and were used for the past 14 years. These seats are today be-low Turkish Airlines current standarts in regard to comfort and esthetics. Following the planning, seats manufactured by Turkish Airlines’ subsi-diary TSI have been chosen. Refurbishment has been made in TC-JFI aircraft economy class, bu-siness class and moving curtains. The plane is put into service thereafter.

Turkish Technic’s four hangars in Istanbul and Ankara have a total combined enclosed space of 73,500 m², at which it provides maintenance and repair services for airlines and VIP jet operators. Turkish Technic provides maintenance and repair services, through various specialized component shops, from station maintenance, engines, APU (auxiliary power units) to landing gear. while it’s most important customer is Turkish Airlines, Turkish Technic also serves more than 600 other customers located on four continents.

CARGO

73,500 m²

more than 600 Customers LoCated on 4 Continents

total encloseD sPace

cUstomer nUmBer

First local in-cabin kitchen set (Galley Equipments)Turkish Airline subsidiary TCI (Turkish Cabin Interior) produced in-cabin kitchen sets are ap-proved by Boeing Company. The equipments are assembled in B737-800/900 aircraft, which will be delivered throughout 2014 and 2015. The assembly process was completed in Boeing fa-cilities.

Sharklet modification of A320FAm aircraft Turkish Technic provided sharklet modification for Turkish Airlines A320FAM aircraft for fuel economy. An average decrease by 2.5% fuel

31

consumption is expected varying subject to flight duration. The modification has been made in two A321 aircraft.

Boeing 777 GCS (Internet and TV) modificationModification in B777-300ER aircraft with Panaso-nic GCS-Global Communication Suite, which will enable provision of wireless internet and live TV service for passengers, is completed. Thus Wide-band Internet and Live TV service is provided for passengers in all Boeing 777 aircraft.

Contribution to International Aviation Projects Turkish Airline provides support for SESAR (Sing-le European Sky ATM Research) collaborative project coordinated by EUROCONTROL and where many airlines, aircraft component manufacturers and ANSP’s (Air Navigation Service Provider) take part.

EFB (Electronic Flight Bag) IntegrationIntegration process for EFB (Electronic Flight Bag) system in our aircraft, which is used to transfer cabin crew documents into digital media, has been started. EFB system enables fast access to

any document, means less paper work, simplifies taxi management, provides noteworthy novelties in flight safety and flight economy.

AmO AuthorizationWith the approval of AMO Authorization, our Company completed the transition from Main-tenance Management System to AMO. On 13th of December 2013, AMO approval certificate for our Company has been published. Turkish Air-lines has been authorized to provide continued airworthiness for A310, A319/320/321, A330, A340, B737-400/700/800/900 and B777 types. Thus audits performeby General Directorate for Civil Aviation each year will be transferred to our Company with this approval. Turkish Airlines will publish sertificates after assessment of compa-tibility.

Turkish Technic provided sharklet modification for Turkish Airlines A320FAM aircraft for fuel economy. An average decrease by 2.5% fuel consumption is expected varying subject to flight duration.

CATERING

2.5%FUel consUmPtion

AnnuAl RepoRt 2013

32

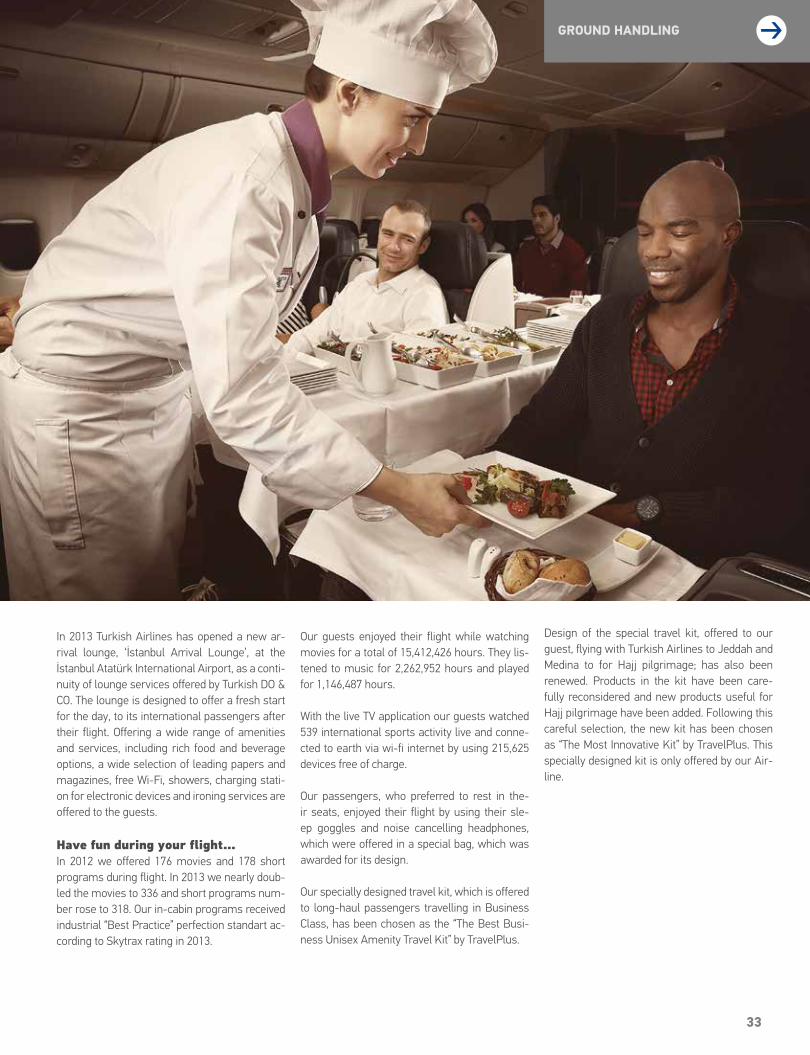

MRO

CATERING

Commencing operations in 2007, Turkish DO&-CO is a joint venture of Turkish Airlines and DO&CO Restaurants & Catering AG. It provides catering services to more than 60 domestic and international airlines at nine locations (Istanbul Atatürk, Sabiha Gökcen, Ankara, Antalya, Izmir, Bodrum, Trabzon, Dalaman and Adana) in Tur-key. The company now controls around a 70% share of the in-flight catering market in Turkey.

Our Company has been awarded with “Europe’s Best Airline Company” in 2013 as in the past two years. This year Turkish Airline received “Best Business Class Onboard Catering Award” in long haul flights, thanks to Business Class catering offered to passengers. According to APEX/IFSA rating Turkish Airlines took the first place in “Best Food & Beverage” category.