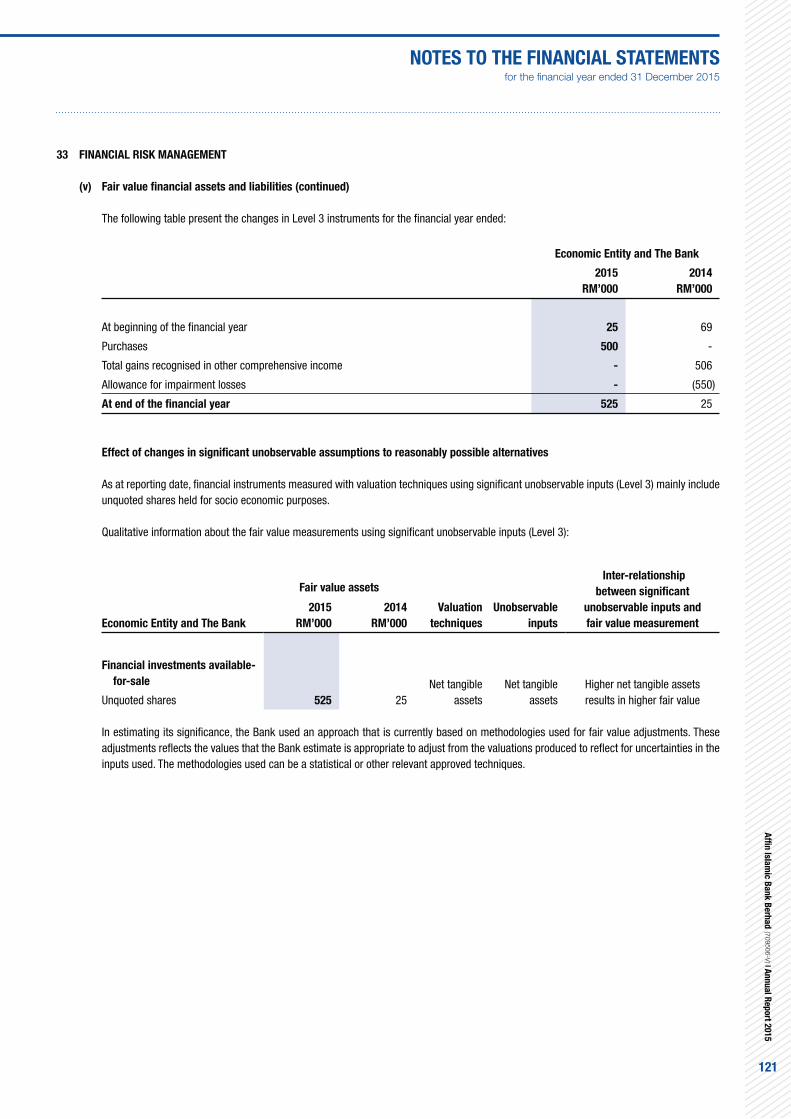

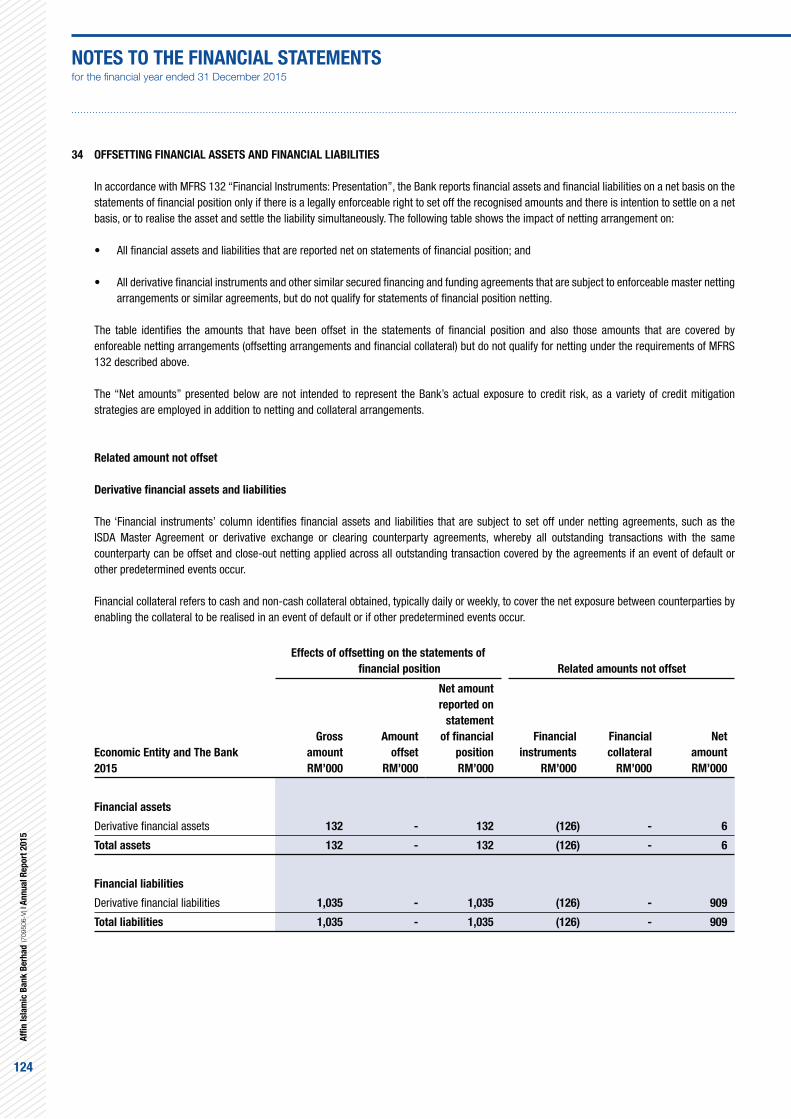

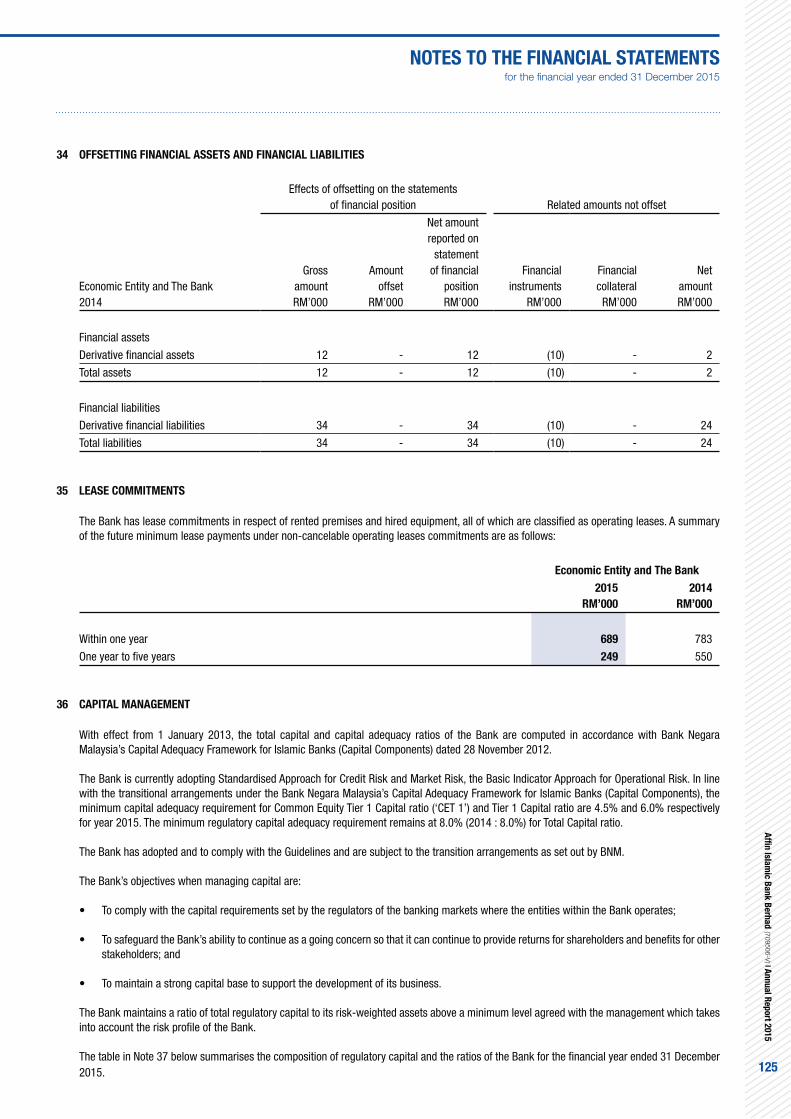

Embed Size (px)

Citation preview

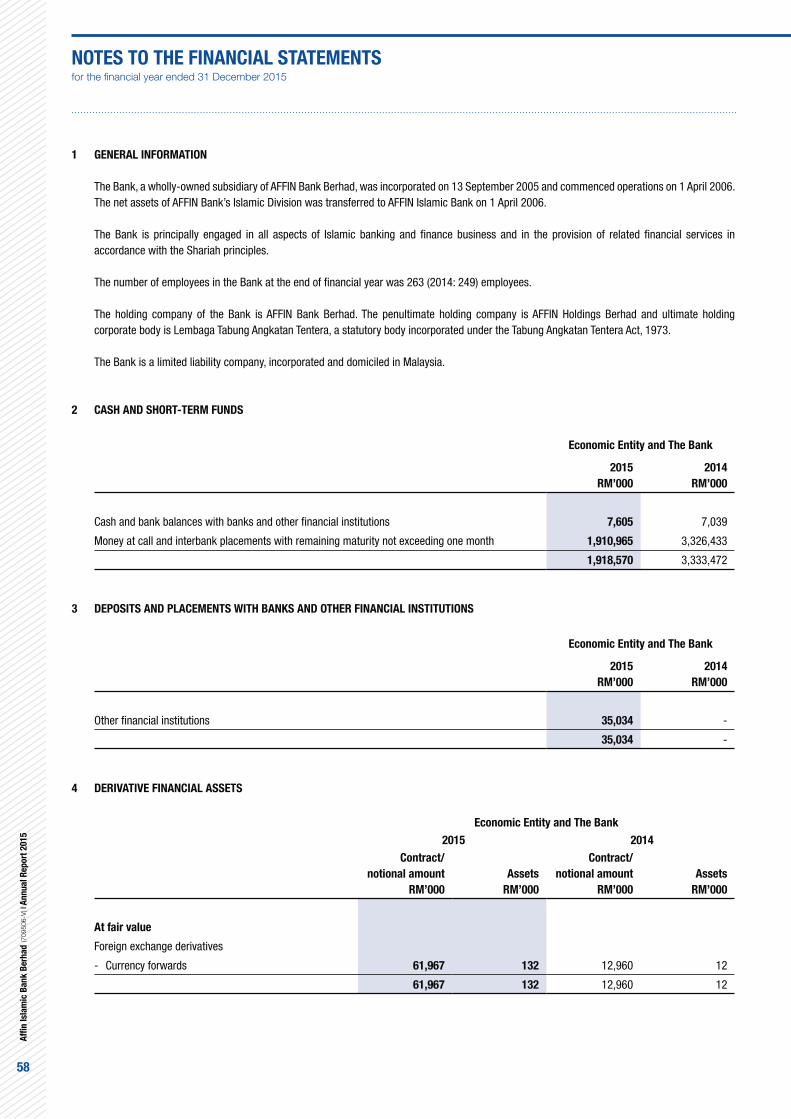

Annual Report 2015

COVER RATIONALE

Identifying and converting potential can be challenging, especially in volatile markets.

It requires conviction, discipline and a focus on the long term.

At AFFIN ISLAMIC, we understand the value of potential.

With expertise across a wide array of disciplines, backed by our focus on results,

we constantly think ahead and strive to anticipate change before it happens.

This forward thinking approach helps our customers look to the future with confidence.

TABLE OF CONTENTS

FINANCIAL STATEMENTS

25 Financial Statements

ORGANISATION

02 Corporate Information

03 Corporate Structure

04 Board of Directors

05 Profile of Board of Directors

09 Management Team

10 Shariah Committee Members

11 Profile of Shariah Committee Members

EXECUTIVE SUMMARY

14 Chairman’s Statement

17 CEO’s Performance Review

20 Corporate Diary

22 Financial Highlights

OTHER INFORMATION

23 Network of Branches

24 Notice of Annual General Meeting

OUR VISION

AFFIN ISLAMIC to play a significant role in the

ever expanding Islamic banking world by providing

innovative Shariah Compliant financial solutions and

services, which will establish itself as a “PREMIER

LOCAL AND INTERNATIONAL ISLAMIC FINANCIAL

INSTITUTION”.

02

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

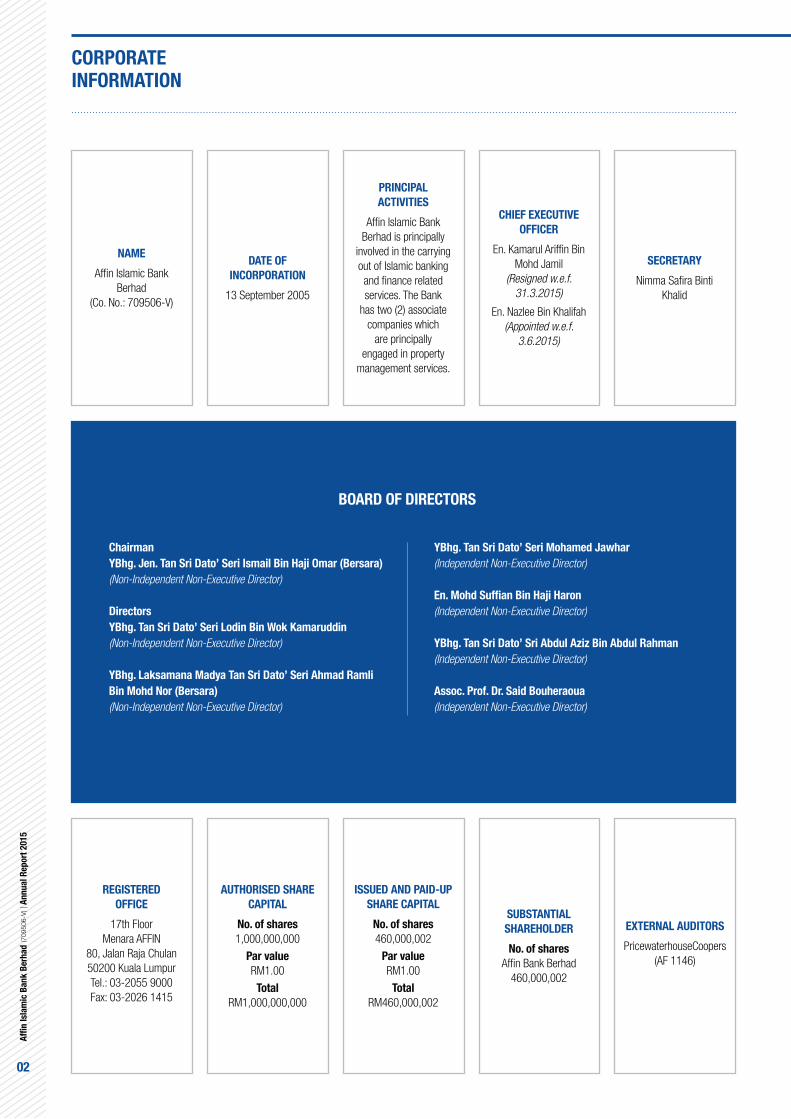

CORPORATE

INFORMATION

Chairman

YBhg. Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara)

(Non-Independent Non-Executive Director)

Directors

YBhg. Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin

(Non-Independent Non-Executive Director)

YBhg. Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli

Bin Mohd Nor (Bersara)

(Non-Independent Non-Executive Director)

YBhg. Tan Sri Dato’ Seri Mohamed Jawhar

(Independent Non-Executive Director)

En. Mohd Suffian Bin Haji Haron

(Independent Non-Executive Director)

YBhg. Tan Sri Dato’ Sri Abdul Aziz Bin Abdul Rahman

(Independent Non-Executive Director)

Assoc. Prof. Dr. Said Bouheraoua

(Independent Non-Executive Director)

BOARD OF DIRECTORS

NAME

Affin Islamic Bank

Berhad

(Co. No.: 709506-V)

REGISTERED

OFFICE

17th Floor

Menara AFFIN

80, Jalan Raja Chulan

50200 Kuala Lumpur

Tel.: 03-2055 9000

Fax: 03-2026 1415

DATE OF

INCORPORATION

13 September 2005

AUTHORISED SHARE

CAPITAL

No. of shares

1,000,000,000

Par value

RM1.00

Total

RM1,000,000,000

PRINCIPAL

ACTIVITIES

Affin Islamic Bank

Berhad is principally

involved in the carrying

out of Islamic banking

and finance related

services. The Bank

has two (2) associate

companies which

are principally

engaged in property

management services.

ISSUED AND PAID-UP

SHARE CAPITAL

No. of shares

460,000,002

Par value

RM1.00

Total

RM460,000,002

CHIEF EXECUTIVE

OFFICER

En. Kamarul Ariffin Bin

Mohd Jamil

(Resigned w.e.f.

31.3.2015)

En. Nazlee Bin Khalifah

(Appointed w.e.f.

3.6.2015)

SUBSTANTIAL

SHAREHOLDER

No. of shares

Affin Bank Berhad

460,000,002

SECRETARY

Nimma Safira Binti

Khalid

EXTERNAL AUDITORS

PricewaterhouseCoopers

(AF 1146)

03

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CORPORATE STRUCTURE

as at 31 December 2015

1 Dormant companies – inactive but company currently holding asset.2 Associate companies.3 Companies where application to strike-off has been filed by the Bank.

OTHERS

AFFIN HOLDINGS BERHAD

AFFIN Bank BerhadAFFIN Islamic Bank Berhad

Lembaga Tabung Angkatan Tentera

AXA AFFIN Life Insurance Berhad

AXA AFFIN General Insurance Berhad

AFFIN MoneyBrokers Sdn Bhd

AFFIN-ACF Holdings Sdn Bhd

AFFIN Hwang Investment Bank Berhad

AFFIN Investment Berhad

(formerly known as AFFIN Investment Bank Berhad)

AFFIN-i Nadayu Sdn Bhd 2

(jointly owned by AFFIN Islamic Bank Berhad and Jurus Positif Sdn Bhd with a 50:50 ownership)

Boustead Holdings Berhad Bank of East Asia Limited

AFFIN Hwang Nominees

(Tempatan) Sdn Bhd

AFFIN Hwang Futures

Sdn Bhd

AFFIN Hwang Nominees

(Asing) Sdn Bhd

AFFIN Nominees

(Tempatan) Sdn Bhd

AFFIN Hwang Asset Management

Berhad

AFFIN Nominees

(Asing) Sdn Bhd

Asian Islamic Investment

Management Sdn Bhd

AFFIN Capital Services Berhad

(formerly known as AFFIN Fund Management Berhad)

PAB Properties Sdn Bhd

ABB Trustee Berhad 2

(80% held by Directors of AFFIN Bank Berhad in trust for AFFIN Bank Berhad)

AFFIN Futures Sdn Bhd 1

ABB IT & Services Sdn Bhd 1

BSNCB Nominees (Tempatan) Sdn Bhd 1

AFFIN Recoveries Berhad 1

ABB Nominee (Tempatan) Sdn Bhd AFFIN-ACF Nominees (Tempatan) Sdn Bhd 3

AFFIN Factors Sdn Bhd 1

ABB Nominee (Asing) Sdn Bhd 1

PAB Property Development Sdn Bhd 3

BSNC Nominees (Tempatan) Sdn Bhd 3

59.98%

20.69%

100%

100%

100%

51%

34.5%

100%

100%

100% 100%

100% 100%

70% 100%

100%

100%

100%

100% 100%

100%

100% 100%

100%

100%

100%

100%

100%

100%

100%

50%

23.52% 20.51%

35.28%

KL South Development Sdn Bhd 2

(jointly owned by AFFIN Islamic Bank Berhad and Albatha Bukit Kiara Holdings Sdn Bhd with a 30:70 ownership)

30%

04

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

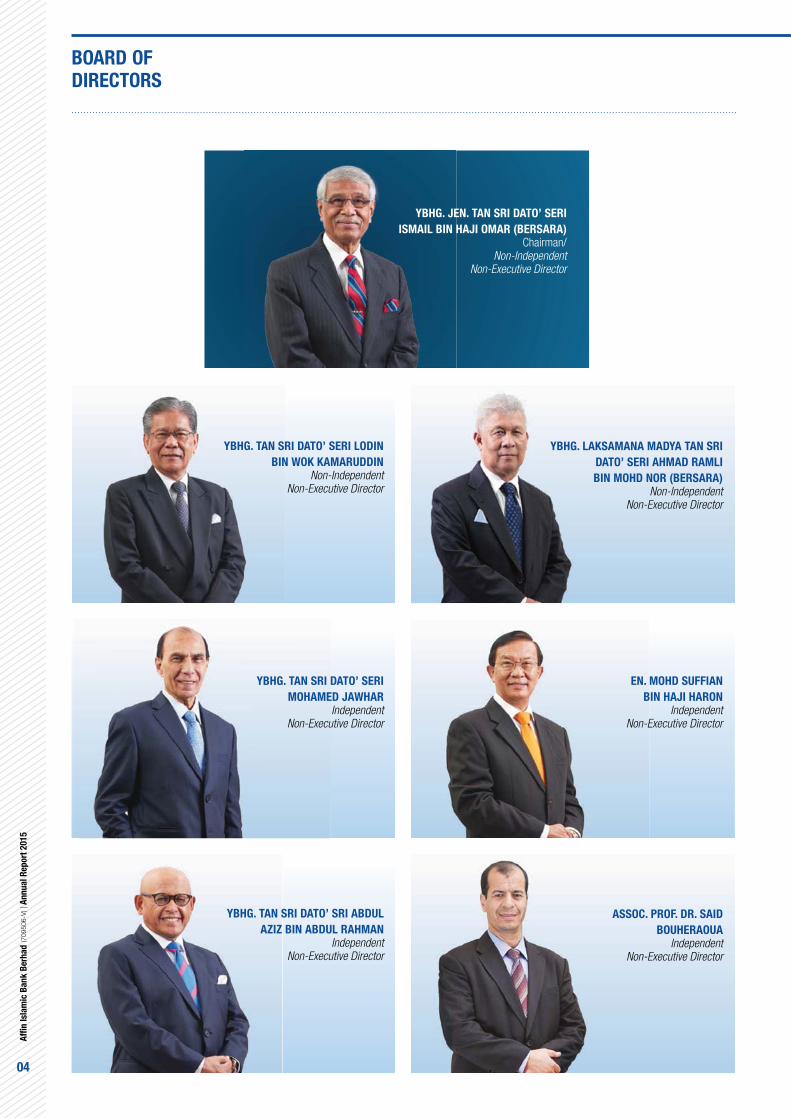

BOARD OF

DIRECTORS

YBHG. LAKSAMANA MADYA TAN SRI

DATO’ SERI AHMAD RAMLI

BIN MOHD NOR (BERSARA)

Non-Independent Non-Executive Director

YBHG. TAN SRI DATO’ SRI ABDUL

AZIZ BIN ABDUL RAHMAN

Independent Non-Executive Director

ASSOC. PROF. DR. SAID

BOUHERAOUA

Independent Non-Executive Director

YBHG. JEN. TAN SRI DATO’ SERI

ISMAIL BIN HAJI OMAR (BERSARA)

Chairman/Non-Independent

Non-Executive Director

EN. MOHD SUFFIAN

BIN HAJI HARON

Independent Non-Executive Director

YBHG. TAN SRI DATO’ SERI LODIN

BIN WOK KAMARUDDIN

Non-Independent Non-Executive Director

YBHG. TAN SRI DATO’ SERI

MOHAMED JAWHAR

Independent Non-Executive Director

05

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

PROFILE OF

DIRECTORS

YBHG. JEN. TAN SRI DATO’ SERI ISMAIL BIN HAJI OMAR (BERSARA)

Chairman / Non-Independent Non-Executive Director

YBHG. TAN SRI DATO’ SERI LODIN BIN WOK KAMARUDDIN

Non-Independent Non-Executive Director

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara), aged 74, was appointed as Director and Chairman

of AFFIN ISLAMIC on 1 April 2006.

He was formerly Chief Defence Forces (CDF) Malaysia from 1995 until his retirement in 1998,

after 38 years of military service. He graduated from the Royal Military Academy, Sandhurst, United

Kingdom in 1961 and subsequently attended professional and management development courses at

several institutions including the Land Forces Command and Staff College, Canada; the United Nations

International Peace Academy, Vienna; the National Defence College, India and the National Institute of

Public Administration (INTAN), Malaysia.

His military service saw Key Command and Staff appointments at all levels of the Armed Forces. As CDF,

his responsibilities included key roles in Malaysia’s Regional and International Defence Relations.

He was the Chairman of Affin Holdings Berhad and Affin-ACF Finance Berhad from 1999, prior to joining

AFFINBANK. He currently holds directorships in AFFINBANK, ABB Trustee Berhad, EP Engineering Sdn

Bhd and Global Medical Alliance Sdn Bhd.

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara) attended all 11 scheduled monthly Board Meetings

and all 3 Special Board Meetings held during the financial year ended 31 December 2015.

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin, aged 66, was reappointed to the Board of Directors of

AFFIN ISLAMIC on 4 October 2010. He was appointed as the Managing Director of Affin Holdings Berhad

in February 1991 and redesignated as Deputy Chairman on 1 July 2008.

He has extensive experience in managing a provident fund and in the establishment, restructuring and

management of various business interests ranging from plantation, trading, financial services, property

development to oil and gas, pharmaceuticals and shipbuilding.

Tan Sri Dato’ Seri Lodin is the Chief Executive of LTAT and the Deputy Chairman/Group Managing

Director of Boustead Holdings Berhad. Prior to joining LTAT, he was the General Manager of Perbadanan

Kemajuan Bukit Fraser for 9 years.

He is also the Chairman of Boustead Heavy Industries Corporation Berhad, Boustead Naval Shipyard Sdn

Bhd, Pharmaniaga Berhad and Boustead Petroleum Marketing Sdn Bhd. He sits on the Board of The

University of Nottingham in Malaysia, Minority Shareholder Watchdog Group, FIDE Forum, AFFINBANK,

Affin Hwang Investment Bank Berhad, AXA Affin Life Insurance Berhad and Boustead Plantations Berhad.

Tan Sri Dato’ Seri Lodin graduated from the University of Toledo, Ohio, USA with a Bachelor of Business

Administration and a Master of Business Administration. Among the many awards he received todate

include the Chevalier De La Legion D’Honneur from the French Government, the Malaysian Outstanding

Entrepreneurship Award, the Degree of Doctor of Laws (honoris causa) (LLD) from the University of

Nottingham, United Kingdom, the UiTM Alumnus of the Year 2010 Award and The BrandLaureate Most

Eminent Brand ICON Leadership Award 2012 by Asia Pacific Brands Foundation. He is also a Chartered

Banker, AICB.

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin attended all 11 scheduled monthly Board Meetings and all

3 Special Board Meetings held during the financial year ended 31 December 2015.

06

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

YBHG. LAKSAMANA MADYA TAN SRI DATO’ SERI AHMAD RAMLI BIN MOHD NOR (BERSARA)

Non-Independent Non-Executive Director

YBHG. TAN SRI DATO’ SERI MOHAMED JAWHAR

Independent Non-Executive Director

Tan Sri Dato’ Seri Ahmad Ramli Bin Mohd Nor, aged 71, was appointed to the Board of Directors of AFFIN

ISLAMIC on 1 July 2006.

He graduated from the Brittania Royal Naval College Dartmouth, United Kingdom in 1965, the Indonesia

Naval Staff College in 1976, the United States Naval War College and Naval Post-Graduate School

Monterey in 1981. He also holds a Masters Degree in Public Administration from the Harvard University,

United States of America. He was in the Malaysian Navy and retired as Chief of Royal Malaysian Navy

in 1999.

Presently he is the Executive Deputy Chairman / Managing Director of Boustead Heavy Industries

Corporation Berhad. He is also the Board member of Favelle Favco Berhad.

Tan Sri Dato’ Seri Ahmad Ramli Bin Mohd Nor attended 10 out of 11 scheduled monthly Board Meetings

and all 3 Special Board Meetings held during the financial year ended 31 December 2015.

Tan Sri Dato’ Seri Mohamed Jawhar, aged 71, was appointed to the Board of Directors of AFFIN ISLAMIC

on 1 July 2006.

His other positions include: Independent Non-Executive Director, AFFINBANK; Non-Executive Chairman, New

Straits Times Press (Malaysia) Berhad; Member of Securities Commission Malaysia; Member, Operations

Review Panel, Malaysian Anti-Corruption Commission; Distinguished Fellow, Institute of Diplomacy and

Foreign Relations (IDFR); Distinguished Fellow, Malaysian Institute of Defence and Security (MiDAS);

Fellow, Institute of Public Security of Malaysia (IPSOM), Ministry of Home Affairs; Board Member, Institute

of Advanced Islamic Studies (IAIS); and Member, Laureate Advisory Board, INTI International University and

Colleges. He is also the Expert and Eminent Person from Malaysia for the ASEAN Regional Forum (ARF).

He was also Co-Chair, Network of East Asia Think-tanks (NEAT) 2005-2006; Chairman, Malaysian

National Committee, Pacific Economic Cooperation Council (PECC) 2006-2010; and Co-Chair, Council

for Security Cooperation in the Asia Pacific (CSCAP) 2007-2009.

He served with the government for over 20 years before he joined Institute of Strategic

& International Studies (ISIS) Malaysia as Deputy Director-General in 1990. He was

appointed Director-General in March 1997 and later as Chairman and CEO in 2006. He

was appointed Chairman ISIS Malaysia on 9 January 2010 relinquished the position on

8 January 2015.

During his government service, his positions include Director-General, Department of National Unity;

Under-Secretary, Ministry of Home Affairs; Director (Analysis) Research Division, Prime Minister’s

Department; and Principal Assistant Secretary, National Security Council. He also served as Counselor in

the Malaysian Embassies in Indonesia and Thailand.

Tan Sri Dato’ Seri Mohamed Jawhar attended all 11 scheduled monthly Board Meetings and all 3 Special

Board Meetings held during the financial year ended 31 December 2015.

PROFILE OF

DIRECTORS

07

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

EN. MOHD SUFFIAN BIN HAJI HARON

Independent Non-Executive Director

YBHG. TAN SRI DATO’ SRI ABDUL AZIZ BIN ABDUL RAHMAN

Independent Non-Executive Director

En. Mohd Suffian Bin Haji Haron, aged 70, was appointed to the Board of Directors of AFFIN ISLAMIC on

1 July 2006

He graduated from the University of Malaya (1970) with a Bachelor of Economics and holds a Master of

Business Administration from University of Oregon (USA) in 1976.

He started his career as a Diplomatic and Administrative Officer, attached to the Prime Minister’s

Department and the Ministry of Public Enterprises. Whilst at the Prime Minister’s Department, he was

also assigned as the Assistant to the Special Economic Adviser to the Government. He served the Board of

Directors of Fraser’s Hill Development Corporation, the State Development Corporations of Perak, Pahang

and Terengganu as well as the Board of Directors of Bank Pembangunan Malaysia Berhad, Kompleks

Kewangan Malaysia Berhad, HICOM and the Council of Majlis Amanah Rakyat (MARA). After thirteen

years of service, he left the Government Service to serve a GLC involved in international business, after

which he ventured on his own to be the Managing Director of Insurance Broking Company. Amongst his

other involvements after that were in the securities industry and asset management activities. He has

also served as a Director of Hitachi Sales (Malaysia) Sdn Bhd, Meiden Electric Engineering Sdn Bhd, Far

East Computers (India) and Affin Discount Berhad. He also brings with him vast experience in general

trading, power generation and transmission, aircraft maintenance as well as the oil and gas services

sectors.

Presently he is a Board member of AFFINBANK, ABB Trustee Berhad, L.K & Associates Sdn Bhd and

Pharmaniaga Berhad.

En. Mohd Suffian Bin Haji Haron attended all 11 scheduled monthly Board Meetings and all 3 Special

Board Meetings held during the financial year ended 31 December 2015.

Tan Sri Dato’ Sri Abdul Aziz Bin Abdul Rahman, aged 69, was appointed to the Board of Directors of AFFIN

ISLAMIC on 1 November 2011.

He graduated with a Bachelor of Commerce from University of New South Wales, Sydney, Australia. He is

a member of the Malaysian Institute of Certified Public Accountants (MICPA) and the Malaysian Institute

of Accountants (MIA).

He has served as Chairman and Board member of several government institutions, agencies and public

listed companies, both in Australia and Malaysia.

At the corporate level, he was with PricewaterhouseCoopers Sydney, Malaysia Airlines Berhad and

Managing Director of Bank Kerjasama Rakyat Malaysia Berhad before venturing into politics and public

service as the Pahang State Assemblyman, State Executive Councillor and Deputy Chief Minister of

Pahang. He was a Senator of Malaysian Parliament for a maximum period of two (2) terms.

Presently he is a Board member of the International Islamic University Malaysia.

Tan Sri Dato’ Sri Abdul Aziz Bin Abdul Rahman attended 10 out of 11 scheduled monthly Board Meetings

and 2 out of 3 Special Board Meetings held during the financial year ended 31 December 2015.

PROFILE OF

DIRECTORS

08

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

ASSOC. PROF. DR. SAID BOUHERAOUA

Independent Non-Executive Director

Assoc. Prof. Dr. Said Bouheraoua, aged 48, was appointed to the Board of Directors of AFFIN ISLAMIC

on 19 June 2014.

Dr. Said, an Algerian, obtained his Ph.D in Fiqh/Usul Fiqh (Shariah) from International Islamic University

Malaysia (IIUM) in 2002. He was also an Associate Professor at Department of Islamic Law, Ahmad

Ibrahim Kulliyyah of Laws, IIUM. He is currently a Senior Researcher at the International Shariah Research

Academy for Islamic Finance (ISRA) and the editor-in-chief of ISRA International Journal of Islamic

Finance.

Dr. Said has throughout his career as Lecturer/Researcher published several books and articles in

international referred journals. He has also presented papers in international conferences and conducted

training sessions in Islamic finance in Malaysia and abroad.

Assoc. Prof. Dr. Said Bouheraoua attended 8 out of 11 scheduled monthly Board Meetings and all 3

Special Board Meetings held during the financial year ended 31 December 2015

PROFILE OF

DIRECTORS

09

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

MANAGEMENT

TEAM

EN. MOHD RUSLEE BIN OMAR

Head, Strategic Business Alliances

EN. MOHD FAIZ BIN RAHIM

Head, Shariah Supervisory

EN. MOHD FIZAR BIN MOHIDIN

Head, Islamic TreasuryPN. JOZAIMAH BINTI JOHAN ALI

Head, Strategic Management

EN. FERDAUS TOH BIN ABDULLAHDeputy Chief Executive Officer

PN. RADZIAH BINTI AHMAD

Head, Islamic Consumer & Bancatakaful

EN. KAMARUL ARIFFIN BIN MOHD JAMIL

Chief Executive Officer(Resigned w.e.f 31.3.2015)

EN. NAZLEE BIN KHALIFAH

Chief Executive Officer(Appointed w.e.f. 3.6.2015)

PN. ZURINA AYU BINTI SAMSUDIN

Head, Product Development

EN. HAZLAN BIN HASANHead, Investment & Structured Finance

CIK NORAZLINDA BINTI MOHD FADZIL

Head, Promotion & Marketing Communications

10

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

SHARIAH

COMMITTEE MEMBERS

ASSOCIATE PROFESSOR

DR. SAID BOUHERAOUA

ASSOCIATE PROFESSOR

DR. ZULKIFLI HASAN

USTAZ AHMAD

ALFISYAHRIN JAMILIN

ASSOCIATE PROFESSOR

DR. AHMAD AZAM OTHMAN

USTAZ MOHAMMAD

MAHBUBI ALI

11

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

PROFILE OF SHARIAH

COMMITTEE MEMBERS

ASSOCIATE PROFESSOR DR. SAID BOUHERAOUA

ASSOCIATE PROFESSOR DR. AHMAD AZAM OTHMAN

Associate Professor Dr. Said Bouheraoua was appointed as a Director of AFFIN ISLAMIC on 19 June

2014. Dr. Said, an Algerian, obtained a Bachelor in Fiqh and Usul Fiqh from the University of Algiers

in 1991, Master of Quran and Sunnah in 1998 and Ph.D in Fiqh/Usul Fiqh (Shariah) from International

Islamic University Malaysia (IIUM) in 2002. He was also an Associate Professor at Department of Islamic

Law, Ahmad Ibrahim Kulliyyah of Laws, IIUM. He is currently a Senior Researcher at the International

Shariah Research Academy for Islamic Finance (ISRA), and is the editor-in-chief of ISRA International

Journal of Islamic Finance. Dr. Said has throughout his career as Lecturer/ Researcher published four

books, five chapters in books and several articles in international referred journals. He has also presented

several papers in international conferences and conducted several training sessions in Islamic finance

in Malaysia and abroad.

Dr. Ahmad Azam Othman is currently an Associate Professor at Islamic Law Department, Ahmad

Ibrahim Kulliyyah of Laws (AIKOL), International Islamic University Malaysia (IIUM). He was the Director

of Harun M. Hashim Law Centre, AIKOL, IIUM and the Head of Islamic Law Department, AIKOL, IIUM. His

specialised areas are Islamic Law of Property, Obligations, Transactions, Personal Bankruptcy, Banking

and Takaful as well as comparative laws. He has vast experience in teaching for postgraduate as well

as undergraduate courses. He is also an internal examiner and supervisor to a number of PhD Theses

and Master Dissertation in various areas including Islamic Banking, Islamic Microfinance, Islamic Capital

Market, Takaful and Waqf. Dr. Ahmad Azam Othman holds a PhD from University of Wales, UK. In addition,

he holds a Master of Comparative Laws from IIUM where he also obtained his LLB (Bachelor of Laws) and

LLB.S (Bachelor of Shariah) as his first degree.

12

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

PROFILE OF SHARIAH

COMMITTEE MEMBERS

USTAZ MOHAMMAD MAHBUBI ALI

Mohammad Mahbubi Ali was a researcher at the International Shari’ah Research Academy for Islamic

Finance (ISRA). During his stint in ISRA, he had contributed to numerous ISRA’s research publications,

mainly involving in Central Bank of Malaysia’s Shari’ah Standards. Currently, he serves as a Shariah

consultant for ZICO Shariah Advisory, Shariah/research consultant for ISRA and ISRA Consultancy Sdn

Bhd, associate consultant for IIFIN Consulting Sdn Bhd, and associate trainer for Amanie Academy Centre

of Excellence. He was also a lecturer at University of Kuala Lumpur and Unitar International University. In

his young age, he has managed to contribute extensively in Islamic Finance through his regular writings

featured in the Islamic Finance News (IFN), Business Islamica, The General Council for Islamic Banks

and Financial Institutions (CIBAFI), Epicentre and many others. He has published numerous articles in

international and local referred academic journals, written several book chapters and presented a number

of papers in various international conferences. His paper entitled: “A Framework of Income Purification

for Islamic Financial Institutions,” co-authored with Dato’ Dr. Asyraf Wajdi Dusuki and Lokmanulhakim

Hussain, was conferred best paper presentation in Sharia Economics Conference, University of Hannover,

Germany, 2013. He received a bachelor degree in Shari’ah Business and Finance from Islamic Business

School, Tazkia Indonesia and Chartered Islamic Finance Professional (CIFP) from INCEIF, The Global

University in Islamic Finance, Malaysia. He is a PhD candidate in Islamic Banking and Finance from the

Institute of Islamic Banking and Finance, International Islamic University Malaysia (IIUM).

ASSOCIATE PROFESSOR DR. ZULKIFLI HASAN

Dr. Zulkifli Hasan is an Associate Professor at the Faculty of Syariah and Law, Universiti Sains Islam Malaysia

(USIM). He has vast experiences in applied banking and finance including takaful and these include as

an advocate and solicitor, in-house counsel for Bank Muamalat Malaysia Berhad, member of Rules and

Regulations Working Committee for Association of Islamic Banking Institutions Malaysia and member

of corporate governance working committee for Awqaf South Africa. He also underwent internship at

Hawkamah, the Institute for Corporate Governance, Dubai International Financial Centre whereby he was

involved in developing corporate governance guidelines for Islamic Financial Institutions in the Middle

East and North Africa (MENA) as well as in the Task Force on Environmental, Social and Governance (ESG)

which led towards development of the S&P/ Hawkamah Pan Arab ESG Index. His articles and books have

been published in reputable academic journals and publishers and he has presented numerous papers

in various conferences both local and abroad. His book entitled ‘Shari’ah Governance in Islamic Bank’

published by the Edinburgh University Press won the MAPIM Best Publication in the category of social

science. In 2013, he represented Malaysia in the prestigious Young Muslim Intellectuals in Southeast

Asia Programme in Japan organized by Japan Foundation. He has been selected as a recipient of a 2014

grant to conduct scholarly research at Fordham University, New York, United States of America by the J.

William Fulbright Foreign Scholarship Board through the Fulbright US-ASEAN Visiting Scholars Initiative.

Dr. Zulkifli Hasan holds a PhD in Islamic Finance from Durham University, UK. Besides this, he holds a

Master of Comparative Laws from International Islamic University of Malaysia where he also obtained his

LLB (Bachelor of Laws) and LLB.S (Bachelor of Shariah) as his first degree. His research interest include

corporate and Shari’ah governance and regulation in Islamic finance.

13

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

PROFILE OF SHARIAH

COMMITTEE MEMBERS

USTAZ AHMAD ALFISYAHRIN JAMILIN

(Appointed w. e. f.1 September 2015)

Ahmad Alfisyahrin Jamilin is currently the Head of Shariah at First Gulf Bank, United Arab Emirates.

He was previously the Chief Shariah Officer at Al Rajhi Bank Malaysia and Shariah Counsel at HSBC

(Amanah) Middle East based in Dubai, United Arab Emirates. Alfisyahrin came with a colorful experience

in his career where he was a Vice President in Global Markets and Structured Investment for Al Rajhi

Bank Malaysia and a Shariah specialist for Sukuk and syndication for Global HSBC Amanah while he

holds a Bachelor in Shariah (honours) from the Islamic University of Madinah, Saudi Arabia.

Alfisyahrin practiced Islamic banking and finance in multiple areas such as front-liner, product structurer

and developer, Shariah specialist and documentation expert. He used to be the originator, transactor and

developer for Sukuk and Treasury products and transactions, and had experience in the conversion of

conventional bank to Islamic. Apart from that, he undertake corporate financial advisory for specialized

or non-vanilla requirements in the areas which include general corporate finance, structured finance,

capital management, contract finance and project finance, managing global Shariah affairs in the global

Islamic banking presence including but not limited to United Arab Emirates, Bahrain, Qatar, Saudi Arabia,

United States of America, United Kingdom, Mauritius, Bangladesh, Malaysia, Indonesia, Brunei and

Singapore. He also has experience in establishing and managing Shariah division and fund custodial and

administrative services by providing Shariah advisory, equity screening, audit and purification process.

14

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CHAIRMAN’S

STATEMENT

DEAR SHAREHOLDERS,

It gives me pleasure to present the financial and operational highlights of

AFFIN ISLAMIC, given the Bank’s very encouraging performance within

a challenging economic environment that faces the financial industry in

Malaysia.

The Board of Directors is committed to ensure the Bank continues to grow

from strength to strength, building on its fundamentals in order to ensure its

long-term sustainability and steady returns to stakeholders. Since the Bank

was established in 2006, we have kept a keen eye on its progress and been

pleased not only by its financial scorecard but also with increasing market

awareness of the brand and its reputation as an Islamic bank that keeps

innovating to introduce Shariah compliant products that appeal to the various

segments of the market.

We are also committed to play our role in advancing Islamic banking

more generally within the local financial landscape. In 2015, we made a

quantum leap in this direction when AFFIN ISLAMIC joined forces with five

other Islamic banking institutions to form a consortium offering an Islamic

Account Platform (IAP). Through the IAP, we will be presenting investment

opportunities in local businesses and entrepreneurs that have been risk-

assessed by the participating banks. We also see the IAP as presenting a new

medium to facilitate greater public-private partnerships in financing strategic

ventures within specific industries. It is also envisaged for IAP to be eventually

positioned to facilitate fund intermediation across borders.

Along with enhanced governance in the Islamic banking sector, we believe

that Islamic financial institutions in general are better positioned to meet the

requirements of the market. AFFIN ISLAMIC in particular has been focusing

intently on fulfilling both the investment and financing needs of our growing

customer base.

As a result, I am pleased to share that the Bank has grown our assets by

5.2%, increased our profit before zakat and taxation (PBZT) by 28.1% to

RM117.4 million, and our earnings per share to 23.5 sen compared to 18.5

sen in 2014.

In addition to increasing our shareholder value in financial terms, the Bank has

also been working assiduously to grow our market reputation and integrate

ourselves more fully into local communities via a series of community outreach

programmes and zakat (business tithes) contributions. These initiatives are

undertaken not out of a sense of obligation but because we truly believe that,

by giving back to the communities that surround us, we are building our brand

thus increasing the intrinsic and long-term value of the Bank.

In 2015, AFFIN ISLAMIC contributed a total of RM5.5 million in zakat to

different causes and sectors of the under-served population. We contributed

a total of RM1.5 million to the six state zakat centres, while also channelling

RM4.0 million in direct contributions to deserving individuals and charitable

organisations. Of this sum, RM2.6 million went towards helping the poor

and needy to provide for themselves. A total of RM478,842 was channelled

towards knowledge cause (Fisabilillah), inclusive of Muallaf activities. Among

our Muallaf contributions were RM60,000 to Multiracial Reverted Muslim

(MRM) and RM25,000 to Interactive Da’wah Training to assist newly converted

Muslims. On our educational aid, AFFIN ISLAMIC contributed RM250,000 to

support deserving students pursuing tertiary education at local institutions

of higher learning such as Universiti Teknologi MARA (UiTM), Universiti

JEN. TAN SRI DATO’ SERI ISMAIL

BIN HAJI. OMAR (BERSARA)

Chairman

RM117.4million

PROFIT BEFORE

ZAKAT AND TAXATION

(PBZT) RM13.4billion

TOTAL ASSETS

“Our total assets grew 5.2% to RM13.4 billion

and profit before zakat and taxation (PBZT)

increased by 28.1% to RM117.4 million.”

15

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CHAIRMAN’S

STATEMENT

Contribution to Tabung Zakat Angkatan Tentera Malaysia.

Contibution from AFFIN Barakah Charity Account-i to PDK Kasih Autisma.

name a few. To help eligible recipients to settle their debts, the Bank disbursed

RM45,212.43 under Gharimin. Meanwhile, we also contributed RM75,000

towards Riqab (rehabilitation of Aqidah), which included RM50,000 to Pusat

Jagaan Remaja Puteri Raudhatus Sakinah.

In addition, we contributed RM700,000 to Tabung Zakat Angkatan Tentera

Malaysia, which manages funds to be allocated to deserving members of the

armed forces.

Besides our zakat contribution, through the AFFIN Barakah Charity Account-i,

AFFIN ISLAMIC donated RM18,360 to Yayasan Kanser Malaysia (YKM) for

the purchase of basic medical needs and equipment for poor patients; and

RM20,000 to Pemulihan Dalam Komuniti (PDK) Kasih Templer Autisma to

assist children with autism and other special needs.

We launched the AFFIN Barakah Charity Account-i as a Mudharabah savings

account in 2013 to facilitate charitable donations by depositors. Via the

account, customers pledge to donate a certain percentage of their monthly

earned investment profit to a worthy cause.

We also support corporate responsibility initiatives together with our parent

company, AFFINBANK. Every year, we join forces to hold a ‘Majlis Berbuka

Puasa Bersama Anak-anak Yatim’, at AFFINBANK’s Head Office to bring

cheer to orphans. This year, about 160 children from three orphanages in

the Klang Valley were invited to a ‘buka puasa’ (breaking of fast) dinner which

was attended by Senior Management from both banks during the month of

Ramadhan. We also presented the children with a token of ‘duit raya’ to add

to the occasion.

In addition, we jointly sponsored Utusan Melayu’s Tutor Pull-out Programme

under which specially prepared Tutor Pull-out were distributed to primary and

secondary school students, to supplement their normal curriculum learning

materials.

16

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

CHAIRMAN’S

STATEMENT

Zakat presentation to Management & Science University (MSU).

Presentation of Zakat to Pusat Jagaan Remaja Puteri Raudhatus Sakinah.

Ultimately, we function to serve the needs of the nation. This is reflected

not only in our corporate responsibility initiatives but also in the emphasis

we place on providing our customers with products that truly meet their

needs. I’m pleased to share that in January 2016, as part of a Group

Strategic Transformation Programme, we are conducting a thorough review

of our position within the Islamic finance industry, assessing segments of

the population that we are ideally suited to serve, and plan strategically to

deliver products that will add value to these target markets. In addition, we are

building on our customer service to further enhance our customer experience.

The idea is ensure we keep relevant to a rapidly changing marketplace and

become a ‘dream bank’ not only for our customers but also our employees.

Our employees, after all, are our most valued assets. I would like to take this

opportunity to thank them, on behalf of the Board of Directors, for their hard

work and commitment to the Bank. I would also like to acknowledge our

Management for their able leadership which has seen the Bank grow over

the years. Finally, I would like to express my sincerest appreciation to all other

stakeholders from the regulators to our business partners, shareholders and

customers for their continued support. We value all your contributions, which

have helped us achieve all our successes to date, and are committed to keep

growing so we can attain even greater heights in the Islamic banking space

in the years to come.

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara)

Chairman

17

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CEO’S

PERFORMANCE REVIEW

EN. NAZLEE BIN KHALIFAH

Chief Executive Officer

GROWTH IN

NET

FINANCING

28.5%GROWTH IN PROFIT

BEFORE ZAKAT AND

TAXATION

28.1%

The year 2015 was challenging for the banking

sector in Malaysia - both Islamic and conventional

- due to a bearish capital market and decline of

our currency which, combined with an increase

in US interest rates, led to capital outflow. This

necessitated conscious efforts to increase

our capital adequacy, hence competition and

increased cost for deposits.

Despite the narrowing net profit margin (NPM) and challenging environment,

however, AFFIN ISLAMIC continued to grow our overall financing and assets

as compared to the previous year while increasing our profit before zakat and

taxation (PBZT) by 28.1% to RM117.4 million year-on-year, exceeding the

2015 target by 16.7%.

This has been the result of conscientious efforts to strengthen the Bank at

our core – building its fundamentals while strengthening our relationships

with retail and commercial customers. We have continued to identify and

segmentalise our key markets, and invest in products that are relevant and

provide extra value to them.

FINANCIAL RESULTS

In defiance of the challenging environment, the Bank’s performance for the

year ended 31 December 2015 was extremely encouraging, with positive

results in all key financial parameters. AFFIN ISLAMIC achieved a total

financing growth of 28.5% and experienced an increase in net financing,

advances & other financing to RM9.2 billion with our net impaired financing

ratio stable at 1.1%.

The bank’s deposit portfolio continued to grow, surpassing the RM10.0 billion

mark, as a result of various collaborations with our parent, AFFINBANK. These

included promotions such as the AFFIN Best Deposit Campaign, Merdeka

Combo Campaign and Year End Bonanza 2015. Together, these enabled AFFIN

ISLAMIC to end the year with total assets of RM13.4 billion, an expansion by

5.2% from the previous financial year.

In an increasingly competitive environment, it is more important than ever to

operate at a high level of efficiency, and I am pleased to say that constant

efforts towards this end have had a positive effect on our balance sheet. By

managing our operating costs effectively, AFFIN ISLAMIC managed to improve

our cost to income ratio from 55.48% in 2014 to 47.61%. This played a part

in the increase in PBZT as reported above, and a 27.3% increase in profit

after zakat and taxation from RM66.6 million to RM84.8 million.

BUSINESS INITIATIVES

We continued to explore different market segments in order to better

understand consumers’ characteristics, needs and how we can better serve

them.

Our marketing efforts were concentrated on channels that appeal to an

increasingly more tech-savvy and ‘connected’ population via various online

and social media interaction. During the year, we organised competitions on

social media such as ‘Create Your Own Version of Raya Song’ and ‘Guess

for an iPad’. Supplementing on our online efforts, we extended our reach to

consumers belonging to Gen Y via more direct approach, such as presenting

a talk geared specifically towards first-time home buyers during Prospek

Hartanah.

These targeted efforts were supplemented by mass advertising in order to

increase brand visibility among the public. We ran a nationwide advertisement

campaign using digital displays at Giant hypermarkets, while also promoting

Ar-Rahnu and AFFIN ISLAMIC Impian Haji, a Term Deposit-i campaign, on

digital screens at selected locations.

18

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

CEO’S

PERFORMANCE REVIEW

Ground breaking ceremony of Kompleks At-Tijarah AFFIN-UiTM.

Additionally, we created more awareness of our Term Deposit-i by advertising

it on a highly visible billboard in Petaling Jaya. Other products were advertised

in the New Straits Times daily and i-Property, Prospek Hartanah and Solusi

magazines. The Bank collaborated with strategic business partners such as

MARA, Management & Science University (MSU) and Universiti Teknologi

MARA to organise events and create awareness on Islamic banking.

2015 also saw AFFIN ISLAMIC work with other Islamic banking institutions

to raise the bar of Islamic financial services in the country, enabling Islamic

banks to become financial intermediaries. In October, the Bank, along with

five others chosen by Bank Negara Malaysia, set up a consortium - Raeed

Holdings Sdn Bhd - to offer a Shariah compliant Investment Account Platform

(IAP) providing investors the opportunity to fund businesses, corporates, new

growth industries as well as entrepreneurs with viable projects.

The IAP is an exciting development as it marks the first cooperation among

Islamic banks to create a new Shariah compliant investment avenue with

attractive returns. The initiative is particularly beneficial to investors who

do not have dedicated risk assessment resources, as this function will be

overseen by the sponsoring banks. IAP will also be positioned to facilitate

more public-private partnerships in financing strategic ventures within

specific industries. Through the IAP, government agencies can identify viable

ventures to invest in and create opportunities for the private sector to partially

fund them. It is also envisaged for IAP to be eventually positioned to facilitated

fund intermediation across borders.

The fact that AFFIN ISLAMIC was chosen by BNM to be part of this IAP

speaks volumes of our credibility and integrity, which are qualities that we will

continue to uphold as we serve our valued customers.

During the year, we also strengthened our position in the community via

various contributions. Key among these were a RM4.5 million contributed

to help build Kompleks At-Tijarah UiTM; and RM18,360 to Yayasan Kanser

Malaysia (YKM). The amount channelled to YKM was partly derived from our

AFFIN Barakah Charity Account-i, through which customers pledge a certain

percentage of their monthly profits to charity. This year, RM20,000 from this

savings account was also channelled towards Pemulihan Dalam Komuniti

(PDK) Kasih Templer Autisma, which cares for children with autism and other

special needs.

OUTLOOK & PROSPECTS

The year 2016 is going to be challenging for the banking industry, given the

expected slowdown in both global and local economies. We expect intense

competition for market share and more stringent regulatory requirement,

therefore; it is essential for banks to manage the envolving of customer

behaviours and expectations.

In response, AFFIN ISLAMIC together with our parent, AFFINBANK, are

embarking on a comprehensive Strategic Transformation Programme that will

analyze our position in the industry to capture greater growth, profitability and

sustainability.

In 2016, we continue to invest in new product capabilities and infrastructure

to seize opportunities offered by new affluent segments. Together, we will

step up efforts to enhance our efficiency and productivity to establish a high-

performance culture by integrating strategic functions of AFFIN ISLAMIC with

AFFINBANK for greater operational effectiveness and optimal utilization of

resources.

19

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CEO’S

PERFORMANCE REVIEW

Distributing ‘duit raya’ to orphans from selected orphanages.

The bank will continue to safeguard strong asset quality, pursuing disciplined

risk management framework, while maintaining best practices in corporate

governance and adhering to the regulators’ capital and liquidity requirements.

The launch of IAP with our partner banks will elevate our role in the expanding

Islamic banking world. We will continue to launch innovative Shariah-based

financial solutions and services to strengthen AFFIN ISLAMIC’s position as a

premier local and international Islamic financial institution.

ACKNOWLEDGEMENTS

The Bank is at an exciting juncture in our onward journey. We have achieved

much over the years, and in 2015, for which I would like to thank our various

stakeholders - from our customers to our partners and investors as well as to

our Board of Directors, Management Team and Shariah Committee members.

To everyone who has contributed to AFFIN ISLAMIC, thank you for your

support. Let us continue to work together for even better performance and

results in the future.

EN. NAZLEE BIN KHALIFAH

Chief Executive Officer

Launching of Kompleks At-Tijarah AFFIN-UiTM.

20

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

CORPORATE

DIARY

FEBPusat Zakat Perak

Contribution of RM364,800 to Pusat Zakat Perak

was presented by Encik Kamarul Ariffin, Chief

Executive Officer of AFFIN ISLAMIC during Corporate

Zakat Presentation Ceremony which was graced

by Duli Yang Maha Mulia Paduka Seri Sultan

Nazrin Muizzuddin Shah, the Sultan of Perak. The

ceremony was witnessed by Menteri Besar Perak,

Dato’ Seri Dr. Zambry Abdul Kadir.

JAN Zakat contribution to Pusat Zakat Melaka

AFFIN ISLAMIC contributed RM364,800 of its Zakat

funds to eligible Asnaf of Pusat Zakat Melaka. The

mock cheque was presented by Ustaz Mohd Faiz

Rahim, Head of Shariah Supervisory to Yang Dipertua

Negeri Melaka, Tun Mohd Khalil Yaakob during

Sambutan Maulidur Rasul held at Bukit Falah, Melaka.

JANWakaf Desa Fahmi

A total of RM350,000 was contributed to Wakaf

Desa Fahmi, a centre that offers accommodation to

hardcore poor, homeless, neglected Muslims and

tahfiz students. The mock cheque was presented

by Deputy CEO AFFIN ISLAMIC, En. Ferdaus Toh

Abdullah to Dr. Kamarolzaman Hajar, founder of

Wakaf Desa Fahmi.

MARYayasan Kanser Malaysia

Yayasan Kanser Malaysia, a non-profit organisation

received donation of RM18,360.49. The amount

was raised from customers’ dividends through

AFFIN Barakah Charity Account-i, which provides

customers the option to donate a certain percentage

of their monthly earned Hibah (profit/dividend)

to a worthy cause.

APRIslamic Relief Malaysia

A mock cheque of RM15,000 zakat contribution

was presented by Ustaz Helmi Afizal Zainal from

Zakat Management to En. Zairulshahfuddin Zainal

Abidin, Country Director of Islamic Relief Malaysia

in a ceremony held at Bangi, Selangor. Islamic Relief

Malaysia is a Non-Government Organisation (NGO)

that provides humanitarian aid in Asia Pacific region.

JULZakat contribution to Management and

Science University (MSU)

Management and Science University (MSU) received

a total of RM100,000 to assist Asnaf students

and RM30,000 for MSU Mobile Clinic.The zakat

contribution was presented by Deputy Chief Executive

Officer of AFFIN ISLAMIC, En. Ferdaus Toh Abdullah

to President of MSU, Prof. Tan Sri Dato’ Wira Dr. Mohd

Shukri Ab. Yajid.

OCTPusat Jagaan Bakti Cahaya Hati

AFFIN ISLAMIC spreads cheer and happiness to

45 children of Pusat Jagaan Bakti Cahaya Hati

(PJBCH). The centre is a welfare home for orphans

and underprivileged children. The mock cheque was

presented by Head of Shariah Supervisory AFFIN

ISLAMIC, Ustaz Mohd Faiz Rahim, to Puan Hajah

Wahyuning, founder of PJBCH in Rawang, Selangor.

NOVMSU Islamic Finance Conference 2015

AFFIN ISLAMIC presented a seminar entitled Islamic

Finance: Maturing Towards Sustainable Talent at MSU

Islamic Finance Conference 2015. The event was

attended by 800 students from universities around

Selangor and KL.

NOVMajlis Pelancaran Tabung Pendidikan

Kanak-kanak PDK Kasih Autisma

Ninety autistic and disabled children of PDK Kasih

Templer Autisma, a community rehabilitation

centre for autistic and disabled children received a

contribution amounting to RM20,000 from AFFIN

Barakah Charity Account-i. The mock cheque was

presented by Chief Executive Officer of AFFIN ISLAMIC,

En. Nazlee Khalifah and Deputy Chief Executive

Officer, En. Ferdaus Toh Abdullah to Dato’ Saiful

Bahri Abdul Hadi, Chairman of PDK Kasih Autisma at

Putrajaya Lake Club.

JUNGround breaking ceremony of Kompleks

At-Tijarah AFFIN-UiTM

The ground breaking ceremony of Kompleks

At-Tijarah AFFIN UiTM which was funded by

AFFINBANK & AFFIN ISLAMIC was held at UiTM

Puncak Alam campus on 11 June. The ceremonious

event was graced by Chairman of AFFINBANK

& AFFIN ISLAMIC, YBhg. Jen. Tan Sri Dato’ Seri

Ismail Hj. Omar (Bersara), Managing Director/

CEO of AFFINBANK, En. Kamarul Ariffin Mohd

Jamil, Chief Executive Officer of AFFIN ISLAMIC,

En. Nazlee Khalifah, Deputy Chief Executive Officer of

AFFIN ISLAMIC, En. Ferdaus Toh Abdullah, and Vice

Chancellor of Universiti Teknologi Mara, YBhg. Tan

Sri Dato’ Sri Prof. Ir. Dr. Sahol Hamid Abu Bakar. The

first in UiTM, the complex of Islamic Centre consists

of four components which are ‘Rukhsah’, Food &

Beverages, Da’wah and Medical & Health.

JULInternational Islamic University Malaysia

(IIUM) Hijrah Grand Iftar

In the month of Ramadhan, AFFIN ISLAMIC presented

zakat contribution amounting RM100,000 to

deserving students of International Islamic University

Malaysia (IIUM). The mock cheque was presented by

En. Nazlee Khalifah, Chief Executive Officer of Affin

Islamic Bank Berhad to, The Honourable Tan Sri Dato’

Seri Utama Dr. Rais Yatim, Advisor to the Government

of Malaysia and President of IIUM in a Hijrah Grand

Iftar held at IIUM Gombak.

JUL Majlis Penyampaian Sumbangan Angkatan

Tentera Malaysia (ATM)

AFFIN ISLAMIC contributed zakat funds amounting

to RM700,000 to ‘Tabung Zakat Angkatan Tentera

Malaysia’. The zakat contribution was presented by

AFFIN ISLAMIC Independent Non-Executive Director,

YBhg. Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman,

to Minister of Defence, YB Datuk Seri Hishammuddin

Tun Hussein during Majlis Penyampaian Sumbangan

Hari Raya Aidilfitri held at Ministry of Defence,

Kuala Lumpur.

21

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CORPORATE

DIARY

22

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

FINANCIAL HIGHLIGHTS

Earnings Per Share (EPS)Sen

Profit Before Zakat And TaxationRM’million

Total AssetsRM’billion

Net Financing, Advances & Other FinancingRM’billion

Deposits From CustomersRM’billion

Shareholders’ EquityRM’million

AFFIN ISLAMIC’s EPS for the financial year ended 31 December

2015 stood at 23.5 sen compared to 18.5 sen the year before

with an increase of 27.0%.

‘15 23.5

‘14 18.5

‘13 16.4

‘12 25.8

AFFIN ISLAMIC achieved profit before zakat and taxation of

RM117.4 million for the year ended 31 December 2015 with

an increase of 28.1% compared with RM91.7 million in 2014.

‘15 117.4

‘14 91.7

‘13 87.3

‘12 106.4

AFFIN ISLAMIC’s financial position as at 31 December 2015

continued to remain strong with total assets of RM13.4 billion,

an increase of 5.2% compared with RM12.7 billion as at

31 December 2014.

‘15 13.4

‘14 12.7

‘13 12.3

‘12 11.7

AFFIN ISLAMIC’s net financing, advances and financing grew by

28.5% to RM9.2 billion compared to RM7.2 billion in 2014.

‘15 9.2

‘14 7.2

‘13 6.0

‘12 5.1

Total deposits increased by 1.3% year-on-year to RM10.0 billion

as at 31 December 2015 compared to RM9.9 billion in the year

before.

‘15 10.0

‘14 9.9

‘13 9.3

‘12 9.0

Total shareholders’ equity of AFFIN ISLAMIC is RM954.8 million

as at 31 December 2015 with an increase of 23.7% compared

to RM772.1 million in 2014.

‘15 954.8

‘14 772.1

‘13 704.4

‘12 655.0

23

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

NETWORKOF BRANCHES

WILAYAH PERSEKUTUAN

1. Fraser

20-G & 20-1,Jalan Metro Pudu,Fraser Business Park,55100 Kuala Lumpur.Tel : 03-9222 8877Fax : 03-9222 9877

SELANGOR

1. Bangi

No.175 & 177 Ground Floor,Jalan 8/1, Seksyen 8,43650 Bandar Baru Bangi, Selangor.Tel : 03-8925 7333Fax : 03-8927 4815

2. MSU Shah Alam

Management & Science University,2nd Floor, University Drive,Persiaran Olahraga, Section 13,40100 Shah Alam, Selangor.Tel : 03-5510 0425Fax : 03-5510 0563

3. SS2

161-163,Jalan SS2/24,47300 Petaling Jaya, Selangor.Tel : 03-7874 3513Fax : 03-7874 3480

NEGERI SEMBILAN

1. Senawang

No. 312-G & 312-1,Jalan Bandar Senawang 17,Pusat Bandar Senawang,70450 Seremban, Negeri Sembilan.Tel : 06-675 7066Fax : 06-675 7188

JOHOR

1. Taman Molek

No. 23, 23-01, 23-02,Jalan Molek 1/29,Taman Molek,81100 Johor Bahru, Johor.Tel : 07-351 9522Fax : 07-357 9522

PULAU PINANG

1. Juru Auto-City

No. 1813A,Jalan Perusahaan, Auto-City,North-South Highway,Juru Interchange,13600 Prai, Pulau Pinang.Tel : 04-507 7422Fax : 04-507 6522 / 0522

KEDAH

1. Jitra

No. 17, Jalan Tengku Maheran 2,Taman Tengku Maheran, Fasa 4,06000 Jitra, Kedah.Tel : 04-919 0888Fax : 04-919 0380

TERENGGANU

1. Kuala Terengganu

63 & 63-A,Jalan Sultan Ismail,20200 Kuala Terengganu, Terengganu.Tel : 09-622 3725Fax : 09-623 6496

24

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

NOTICE OF

ANNUAL GENERAL MEETING

AGENDA

1. To receive the Statutory Statements of Accounts for the year ended 31 December 2015 together with the

Directors’ and Auditors’ Reports thereon.

2. To re-elect Assoc. Prof. Dr. Said Bouheraoua who retire pursuant to Article 68 of the Company’s Articles of

Association and who, being eligible, offer himselves for re-election.

3. To consider and if thought fit, to pass the following resolutions in accordance with Section 129(6) of the

Companies Act, 1965:

(a) That YBhg. Jen. Tan Sri Dato’ Seri Ismail bin Haji Omar (Bersara), retiring in accordance with Section 129(6)

of the Companies Act, 1965, be and is hereby re-appointed as a Director of the Company to hold office until

the conclusion of the next Annual General Meeting.

(b) That YBhg. Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli bin Mohd Nor (Bersara), retiring in

accordance with Section 129(6) of the Companies Act, 1965, be and is hereby re-appointed as a Director

of the Company to hold office until the conclusion of the next Annual General Meeting.

(c) That En. Mohd Suffian bin Haji Haron, retiring in accordance with Section 129(6) of the Companies Act,

1965, be and is hereby re-appointed as a Director of the Company to hold office until the conclusion of the

next Annual General Meeting

(d) That YBhg. Tan Sri Dato’ Seri Mohamed Jawhar, retiring in accordance with Section 129(6) of the Companies

Act, 1965, be and is hereby re-appointed as a Director of the Company to hold office until the conclusion

of the next Annual General Meeting.

(e) That YBhg. Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman, retiring in accordance with Section 129(6) of

the Companies Act, 1965, be and is hereby re-appointed as a Director of the Company to hold office until

the conclusion of the next Annual General Meeting.

4. To approve the payment of Directors’ fees and Committees’ fees for financial year ended 31 December 2015.

5. To re-appoint Messrs PricewaterhouseCoopers as Auditors for the financial year ending 31 December 2016 and

to authorise the Directors to fix their remuneration.

6. To transact any other ordinary business of the Company.

BY ORDER OF THE BOARD

NIMMA SAFIRA BINTI KHALID

Secretary

NOTE:

1. A member entitled to attend and vote at the Meeting is entitled to appoint a proxy to attend and vote instead of him and the proxy need not be a

member of the Company.

The instrument appointing a proxy shall be in writing under the hand of the appointor or his attorney duly authorised in writing or, if the appointor is a

corporation, either under the seal or in some other manner approved by Directors.

The instrument appointing a proxy and the power of attorney or other authority, if any, under which it is signed or a notarially certified copy of such

power or authority shall be deposited at the Company’s registered office at the 17th Floor, Menara Affin, 80, Jalan Raja Chulan, 50200 Kuala Lumpur,

at least forty-eight (48) hours before the time appointed for holding the Meeting or adjourned Meeting as the case may be otherwise the person so

named shall not be entitled to vote in respect thereof.

2. Reference is made to Recommendation 3.2 and 3.3 of the Malaysian Code on Corporate Governance 2012 which states that the tenure of an

Independent Director should not exceed a cumulative term of nine (9) years.

Tan Sri Dato’ Seri Mohamed Jawhar and En. Mohd Suffian bin Haji Haron have served on the Board as Independent Non-Executive Directors for a

cumulative term exceeding nine (9) years, however, they remain independent as they are free from any business or other relationship, which could

interfere with the exercise of independent judgement or the ability to act in the best interest of the Company. The Nominating Committee and the

Board have determined at the annual assessment carried out that Tan Sri Dato’ Seri Mohamed Jawhar and En. Mohd Suffian bin Haji Haron remain

independent in mind and character. They participate actively in the Board as well as Board Committees’ deliberations and decision making.

NOTICE IS HEREBY

GIVEN THAT THE 10TH

ANNUAL GENERAL

MEETING OF

AFFIN ISLAMIC

BANK BERHAD

WILL BE HELD AT THE

BOARD ROOM,

19TH FLOOR,

MENARA AFFIN,

80, JALAN RAJA

CHULAN, 50200

KUALA LUMPUR ON

TUESDAY,

22 MARCH 2016

AT 8.30 A.M. FOR

THE TRANSACTION

OF THE FOLLOWING

BUSINESSES:-

FINANCIAL STATEMENTS26 Directors’ Report

38 Statements of Financial Position

39 Income Statements

40 Statements of Comprehensive Income

41 Statements of Changes in Equity

43 Statements of Cash Flows

45 Summary of Significant Accounting Policies

58 Notes to the Financial Statements

128 Statement by Directors

128 Statutory Declaration

129 Independent Auditors’ Report

130 Shariah Committee’s Report

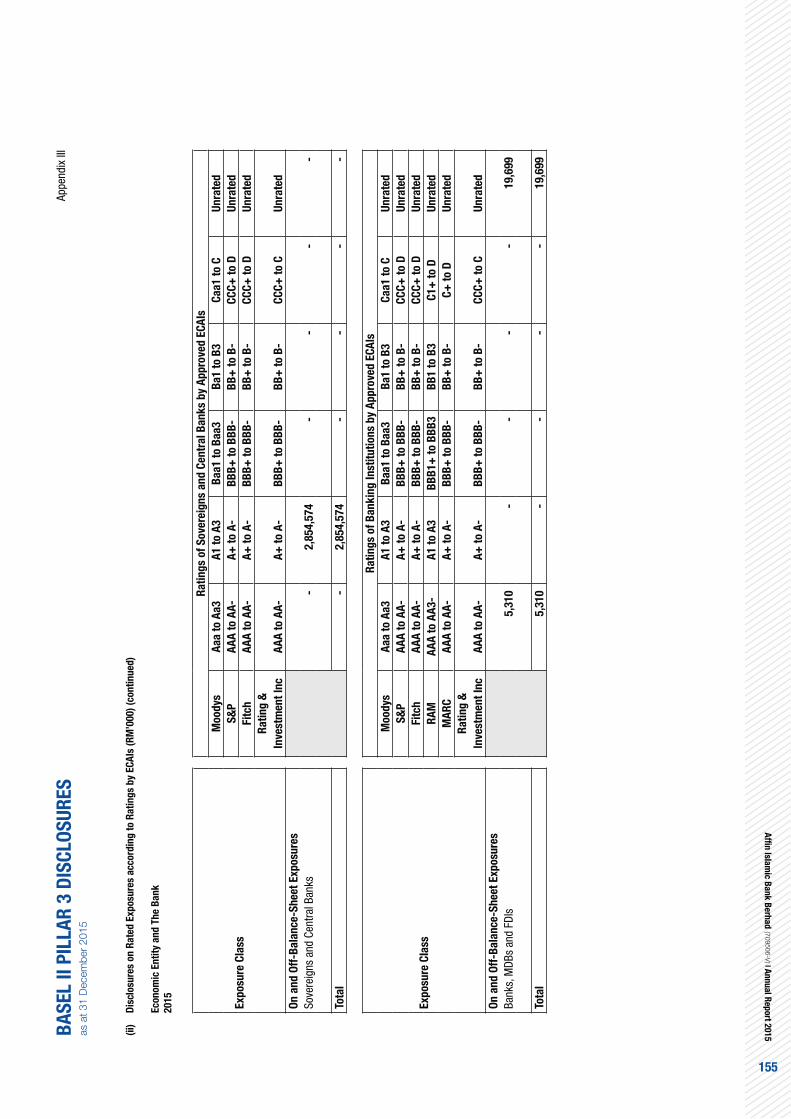

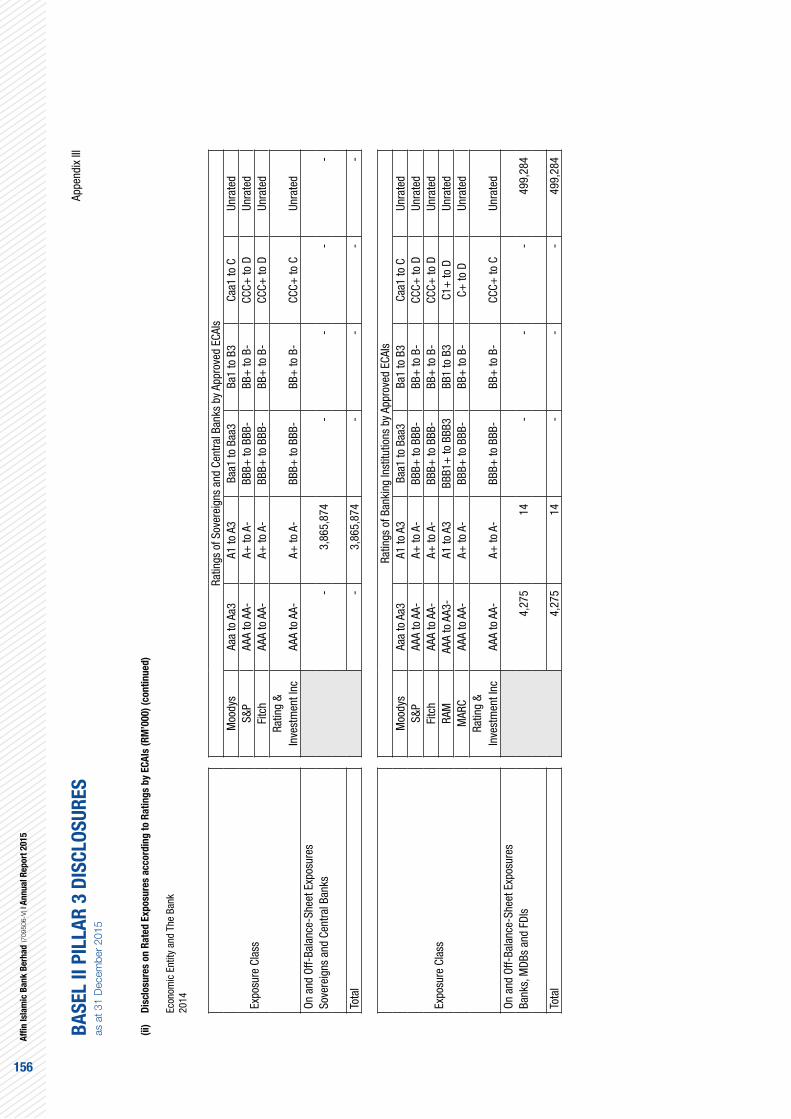

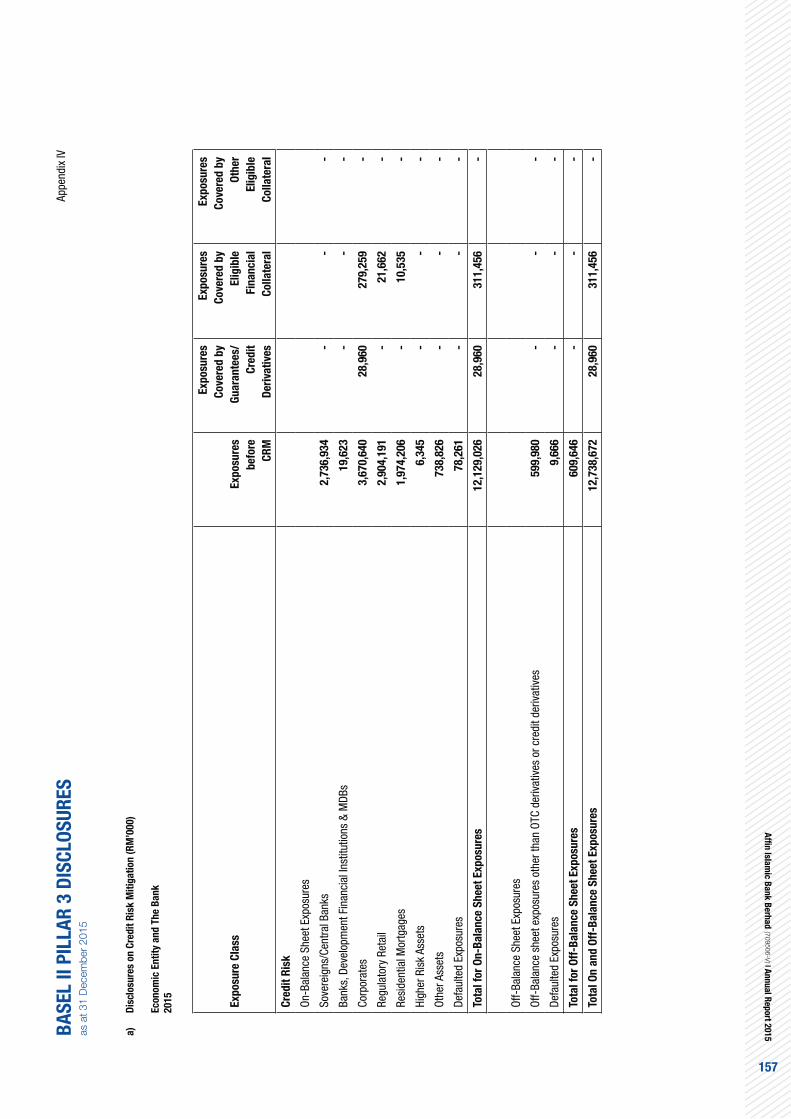

132 Basel II Pillar 3 Disclosures

26

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

The Directors hereby submit their report together with the audited financial statements of the Bank for the financial year ended 31 December 2015.

PRINCIPAL ACTIVITIES

The principal activities of the Bank are Islamic banking business and the provision of related financial services. There were no significant changes in these activities during the financial year.

FINANCIAL RESULTS

Economic Entity

and The Bank

RM’000

Profit before zakat and taxation 117,375

Zakat (3,779)

Profit before taxation 113,596

Taxation (28,811)

Net profit for the financial year 84,785

DIVIDENDS

No dividends have been paid by the Bank in respect of the financial year ended 31 December 2014 and 2015.

The Directors do not recommend the payment of any dividend in respect of the current financial year.

RESERVES AND PROVISIONS

All material transfers to or from reserves or provisions during the financial year are shown in the financial statements and notes to the financial statements.

BAD AND DOUBTFUL FINANCING

Before the financial statements of the Bank were made out, the Directors took reasonable steps to ascertain that actions had been taken in relation to the writing off of bad financing and the making of allowances for doubtful financing, and have satisfied themselves that all known bad financing had been written off and adequate allowances had been made for bad and doubtful financing.

At the date of this report, the Directors are not aware of any circumstances which would render the amount written off for bad financing, or the amount of the allowance for doubtful financing in the financial statements of the Bank, inadequate to any substantial extent.

CURRENT ASSETS

Before the financial statements of the Bank were made out, the Directors took reasonable steps to ascertain that any current assets, other than financing, which were unlikely to be realised in the ordinary course of business, their values as shown in the accounting records of the Bank have been written down to an amount which they might expected so to realise.

At the date of this report, the Directors are not aware of any circumstances which would render the values attributed to the current assets in the financial statements of the Bank misleading.

VALUATION METHODS

At the date of this report, the Directors are not aware of any circumstances which have arisen which render adherence to the existing methods of valuation of assets or liabilities in the Bank’s financial statements misleading or inappropriate.

27

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CONTINGENT AND OTHER LIABILITIES

At the date of this report there does not exist:

(a) any charge on the assets of the Bank which has arisen since the end of the financial year which secures the liabilities of any other person; or

(b) any contingent liability in respect of the Bank that has arisen since the end of the financial year other than those in the ordinary course of banking business or activities of the Bank.

No contingent or other liability of the Bank has become enforceable, or is likely to become enforceable within the period of twelve months after the end of the financial year which, in the opinion of the Directors, will or may substantially affect the ability of the Bank to meet its obligations as and when they fall due.

CHANGE OF CIRCUMSTANCES

At the date of this report, the Directors are not aware of any circumstances, not otherwise dealt with in this report or the financial statements of the Bank, that would render any amount stated in the financial statements misleading.

ITEMS OF AN UNUSUAL NATURE

The results of the operations of the Bank during the financial year were not, in the opinion of the Directors, substantially affected by any item, transaction or event of a material and unusual nature.

There has not arisen in the interval between the end of the financial year and the date of this report any item, transaction or event of a material and unusual nature likely, in the opinion of the Directors, to affect substantially the results of the operations of the Bank for the current financial year in which this report is made.

SIGNIFICANT EVENT DURING THE FINANCIAL YEAR

There is no significant event during the financial year.

SUBSEQUENT EVENTS

There were no material events subsequent to the reporting date that require disclosure or adjustments to the financial statements.

DIRECTORS

The Directors of the Bank who have held office since the date of the last report and at the date of this report are:

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara)Chairman/ Non-Independent Non-Executive Director

Tan Sri Dato’ Seri Lodin Bin Wok KamaruddinNon-Independent Non-Executive Director

Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli Bin Mohd Nor (Bersara)Non-Independent Non-Executive Director

Tan Sri Dato’ Seri Mohamed JawharIndependent Non-Executive Director

En. Mohd Suffian Bin Haji HaronIndependent Non-Executive Director

Tan Sri Dato’ Sri Abdul Aziz Bin Abdul RahmanIndependent Non-Executive Director

Associate Professor Dr. Said BouheraouaNon-Independent Non-Executive Director

28

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

RESPONSIBILITY STATEMENT BY BOARD OF DIRECTORS

In the course of preparing the annual financial statements of the Bank, the Directors are collectively responsible in ensuring that these financial statements are drawn up in accordance with Malaysian Financial Reporting Standards, International Financial Reporting Standards and the requirements of the Companies Act, 1965 in Malaysia.

It is the responsibility of the Directors to ensure that the financial reporting of the Bank present a true and fair view of the state of affairs of the Bank as at 31 December 2015 and of the financial results and cash flows of the Bank for the financial year then ended.

The financial statements are prepared on the going concern basis and the Directors have ensured that proper accounting records are kept, applied the appropriate accounting policies on a consistent basis and made accounting estimates that are reasonable and fair so as to enable the preparation of the financial statements of the Bank with reasonable accuracy.

The Directors have also taken the necessary steps to ensure that appropriate systems are in place for the assets of the Bank to be properly safeguarded for the prevention and detection of fraud and other irregularities. The systems, by their nature, can only provide reasonable and not absolute assurance against material misstatements, whether due to fraud or error.

The Statement by Directors pursuant to Section 169 of the Companies Act, 1965 is set out on page 128 of the financial statements.

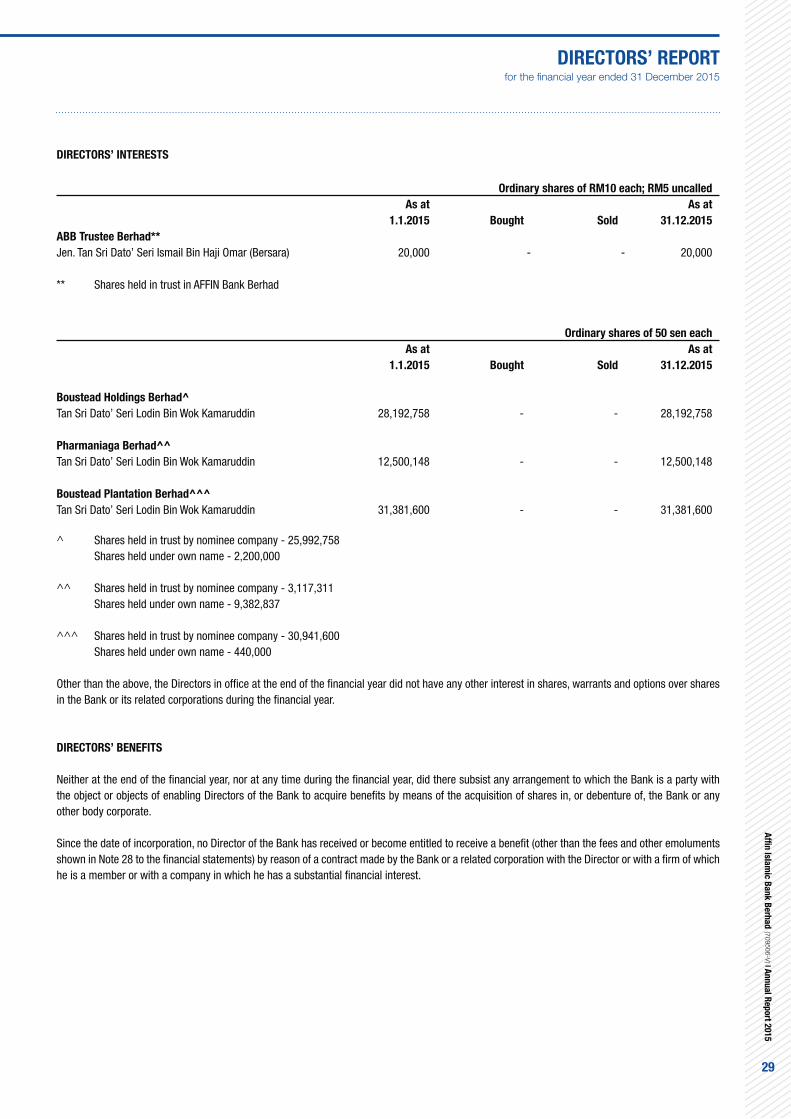

DIRECTORS’ INTERESTS

According to the register of Directors’ shareholdings, the interest of Directors in office at the end of the financial year in shares, warrants and options of related companies is as follows:

Ordinary shares of RM1 each

As at As at

1.1.2015 Bought Sold 31.12.2015

AFFIN Holdings Berhad

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin *1,051,328 - - *1,051,328

Boustead Heavy Industries Corporation Berhad

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin *2,000,000 - - *2,000,000

Boustead Petroleum Sdn Bhd

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 5,916,465 - - 5,916,465

* Shares held in trust by nominee company

29

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

DIRECTORS’ INTERESTS

Ordinary shares of RM10 each; RM5 uncalled

As at As at

1.1.2015 Bought Sold 31.12.2015

ABB Trustee Berhad**

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara) 20,000 - - 20,000

** Shares held in trust in AFFIN Bank Berhad

Ordinary shares of 50 sen each

As at As at

1.1.2015 Bought Sold 31.12.2015

Boustead Holdings Berhad^

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 28,192,758 - - 28,192,758

Pharmaniaga Berhad^^

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 12,500,148 - - 12,500,148

Boustead Plantation Berhad^^^

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 31,381,600 - - 31,381,600

^ Shares held in trust by nominee company - 25,992,758 Shares held under own name - 2,200,000

^^ Shares held in trust by nominee company - 3,117,311 Shares held under own name - 9,382,837

^^^ Shares held in trust by nominee company - 30,941,600 Shares held under own name - 440,000

Other than the above, the Directors in office at the end of the financial year did not have any other interest in shares, warrants and options over shares in the Bank or its related corporations during the financial year.

DIRECTORS’ BENEFITS

Neither at the end of the financial year, nor at any time during the financial year, did there subsist any arrangement to which the Bank is a party with the object or objects of enabling Directors of the Bank to acquire benefits by means of the acquisition of shares in, or debenture of, the Bank or any other body corporate.

Since the date of incorporation, no Director of the Bank has received or become entitled to receive a benefit (other than the fees and other emoluments shown in Note 28 to the financial statements) by reason of a contract made by the Bank or a related corporation with the Director or with a firm of which he is a member or with a company in which he has a substantial financial interest.

30

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

CORPORATE GOVERNANCE

The Board of Directors is committed to ensure the highest standards of corporate governance throughout the organisation with the objectives of safeguarding the interests of all stakeholders and enhancing the shareholders’ value and financial performance of the Bank. The Board considers that it has applied the Best Practices as set out in the Malaysian Code of Corporate Governance throughout the financial year. The Bank is also required to comply with BNM’s Guidelines on Corporate Governance for Licensed Islamic Banks.

(i) Board of Directors Responsibility and Oversight

The Board of Directors

The direction and control of the Bank rest firmly with the Board as it effectively assumes the overall responsibility for corporate governance, strategic direction, formulation of policies and overseeing the investments and operations of the Bank. The Board exercises independent oversight on the management and bears the overall accountability for the performance of the Bank and compliance with the principle of good governance.

There is a clear division of responsibility between the Chairman and the Chief Executive Officer (‘CEO’) to ensure that there is a balance of power and authority. The Board is responsible for reviewing and approving the longer term strategic plans of the Bank as well as the business strategies. It is also responsible for identifying the principal risks and implementation of appropriate systems to manage those risks as well as reviewing the adequacy and integrity of the Bank’s internal control systems, management information systems, including systems for compliance with applicable laws, regulations and guidelines.

Whilst the Management Committee, headed by the CEO, is responsible for the implementation of the strategies and internal control as well as monitoring performance, the Committee is also a forum to deliberate issues pertaining to the Bank’s business, strategic initiatives, risk management, manpower development, supporting technology platform and business processes.

The Board Meetings

Throughout the financial year, 14 Board meetings were held. All Directors have complied with the minimum number of attendances for Board meetings as stipulated by Bank Negara Malaysia. All Directors review Board papers or reports providing updates on operational, financial and corporate developments prior to the Board meetings. These papers and reports are circulated prior to the meeting to enable the Directors to obtain further explanations and having sufficient time to deliberate on the issues and make decisions during the meeting.

31

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n Is

lam

ic B

an

k B

erh

ad (709506-V

) | An

nu

al R

ep

ort 2

015

CORPORATE GOVERNANCE

(i) Board of Directors Responsibility and Oversight (continued)

Board Balance

Currently the Board has seven members, comprising three Non-Independent Non-Executive Directors (including the Chairman) and four Independent Non-Executive Directors. The Board of Directors meetings are presided by Non-Independent Non-Executive Chairman whose role is clearly separated from the role of CEO. The composition of the Board and the number of meetings attended by each Director are as follows:

Directors Total Meetings Attended

Jen. Tan Sri Dato’ Seri Ismail Bin Haji Omar (Bersara) 14 / 14

Chairman/ Non-Independent Non-Executive Director

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 14 / 14

Member/ Non-Independent Non-Executive Director

Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli Bin Mohd Nor (Bersara) 13 / 14

Member/ Non-Independent Non-Executive Director

Tan Sri Dato’ Seri Mohamed Jawhar 14 / 14

Member/ Independent Non-Executive Director

En. Mohd Suffian Bin Haji Haron 14 / 14

Member/ Independent Non-Executive Director

Tan Sri Dato’ Sri Abdul Aziz Bin Abdul Rahman 12 / 14

Member/ Independent Non-Executive Director

Associate Professor Dr. Said Bouheraoua 11 / 14

Member/ Independent Non-Executive Director

32

DIRECTORS’ REPORTfor the financial year ended 31 December 2015

Affi

n I

sla

mic

Ba

nk

Berh

ad (7

0950

6-V

) | A

nn

ua

l R

ep

ort

2015

CORPORATE GOVERNANCE

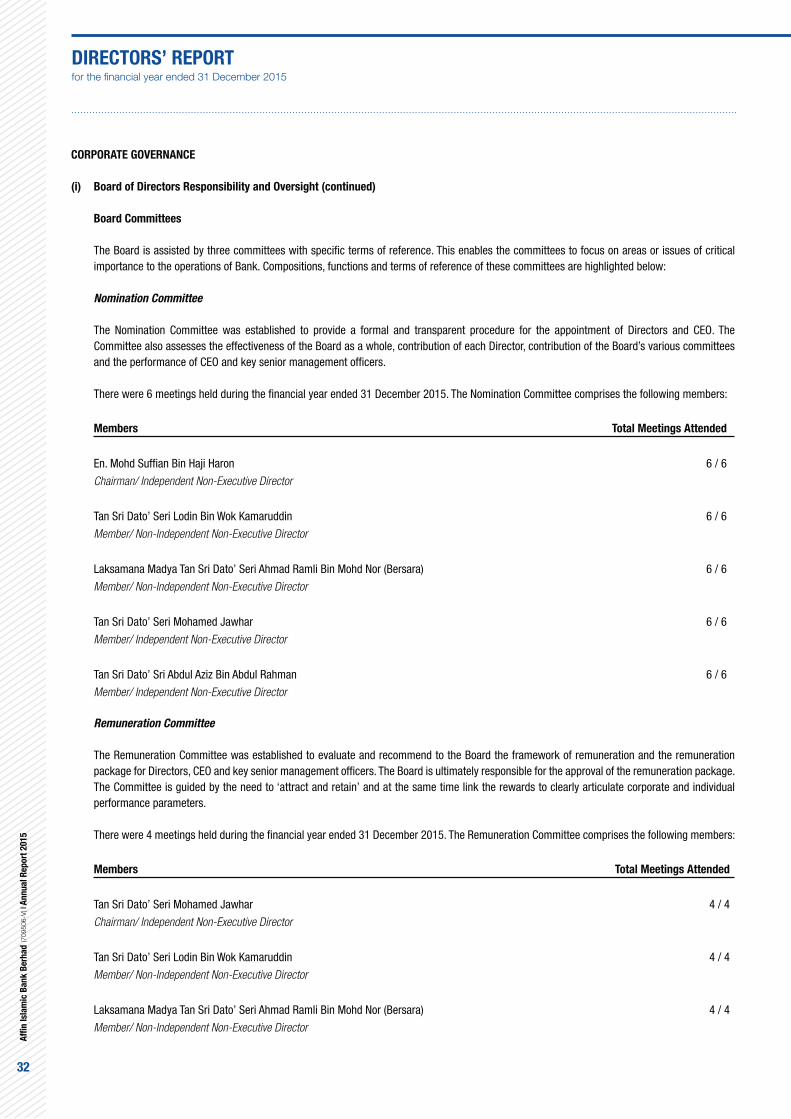

(i) Board of Directors Responsibility and Oversight (continued)

Board Committees

The Board is assisted by three committees with specific terms of reference. This enables the committees to focus on areas or issues of critical importance to the operations of Bank. Compositions, functions and terms of reference of these committees are highlighted below:

Nomination Committee

The Nomination Committee was established to provide a formal and transparent procedure for the appointment of Directors and CEO. The Committee also assesses the effectiveness of the Board as a whole, contribution of each Director, contribution of the Board’s various committees and the performance of CEO and key senior management officers.

There were 6 meetings held during the financial year ended 31 December 2015. The Nomination Committee comprises the following members:

Members Total Meetings Attended

En. Mohd Suffian Bin Haji Haron 6 / 6

Chairman/ Independent Non-Executive Director

Tan Sri Dato’ Seri Lodin Bin Wok Kamaruddin 6 / 6

Member/ Non-Independent Non-Executive Director

Laksamana Madya Tan Sri Dato’ Seri Ahmad Ramli Bin Mohd Nor (Bersara) 6 / 6

Member/ Non-Independent Non-Executive Director