Embed Size (px)

Citation preview

1

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

CONSOLIDATED ANNUAL REPORT 2016

List of contents

CONSOLIDATED MANAGEMENT REPORT 3

AUDIT REPORT 6

CONSOLIDATED BALANCE SHEET 9

CONSOLIDATED OFF BALANCE SHEET 11

CONSOLIDATED PROFIT AND LOSS ACCOUNT 13

NOTES TO THE CONSOLIDATED ANNUAL ACCOUNTS 16

3

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

CONSOLIDATED MANAGEMENT REPORT

The quantitative easing program put in

place by the European Central Bank (ECB)

had further increased pressure on interest

rates due to the scarcity of high quality

paper. From January to September, core

European sovereign 10-year benchmark

rates reached levels close to 0%. This

trend has been reversed since October

due to the return of inflation expectations,

political risk in Europe and uncertainties

linked to the potential outcomes from the

US elections.

In March 2016, the deposit facility interest

rate at ECB was reduced from -0.30% to

-0.40%. This second cut in the space of four

months increased the challenge of negative

interest rates for the whole banking sector

and underlines the work to be done in Asset

and Liability Management as this trend is

expected to be maintained in the short term.

The Group took profit from this disruptive

economic environment and increased its

result on financial operations from EUR

2.3m in 2015 to EUR 12.0m in 2016.

The Group continued to focus on developing

its core business during 2016. The

disinvestment from KLP S.A, which began

mid-2015 with the transfer of the insurance

portfolio to another professional insurance

company, has been closed in December

following the sale of the entity.

In terms of development, 2016 was

characterized by two additional acquisitions

completed during the year: Banco Popolare

Luxembourg (renamed Banque Havilland

Institutional Services S.A.), mainly focused on

services to institutional clients, in February

and Banque Pasche Switzerland (renamed

Banque Havilland (Suisse) S.A.) in April.

The combination of acquisitions and global

business development raised the balance

sheet from EUR 1.39bn in 2015 up to

EUR 1.95bn in 2016.

Investments into fixed income have seen an

increase in the size of the portfolio from EUR

654.6m to EUR 777.4m. Asset diversification

pushed by the low interest environment

resulted in the growth of the Group’s loan

portfolio to customers from EUR 389.0m to

CONSOLIDATED MANAGEMENT REPORT

4

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

EUR 669.6m. Such lending activity is always

linked to private banking and is focused on

primary residence mortgages and Lombard

loans, both at conservative loan-to-value

levels. This prudent approach results in a

strong solvency ratio of 33.0%. The extension

of the lending activity is made in the framework

of maintaining strong regulatory ratios.

The Group has successfully been able to

stimulate the organic growth of the private

banking business, which can be seen in the

increase of amounts owed to clients from

EUR 1.06bn to EUR 1.63bn.

The total consolidated operating income

of the Group increased from EUR 37.4m to

EUR 73.5m, driven by strong net interest

income of EUR 33.4m (2015: EUR 21.8m),

which is a result of the continued focus

on development of loans to customers as

indicated above. Commissions grew from

EUR 11.6m to EUR 19.1m in 2016, including

the contribution of acquired entities.

As a continuation of the previous year, in

2016 the Group has further invested in

resources as well as in systems to support

its growth and its role as a hub within a fairly

centralised operating model. The latest

investments in staff and infrastructure have

favourably positioned the Bank to further

consolidate the Group and to maintain

expansion capabilities.

Investments made in people as well as the

Group expansion brought staff cost up from

EUR 17.4m in 2015 to EUR 27.5m in 2016.

Administrative expenses went up by EUR

5m to EUR 18.3m.

We are proud to announce a 2016 net result

after value adjustments and taxes of EUR

14.2m, demonstrating strong progression

from 2015 (EUR 2.5m).

CAPITAL AND RISK MANAGEMENT

The Group’s business is exposed to several

risks, such as credit, market, liquidity,

operational and other business risks.

The Bank continues to maintain a robust

approach to risk management with an

independent department reporting directly

to the Executive Management and the

Board of Directors. The Risk Management

Department ensures that each key risk

of the business is identified and properly

managed by applying a holistic view. Key risk

areas are managed through a framework of

policies, procedures and limits with regular

reviews of such framework. During 2016, the

Group has enhanced its control framework

both in terms of staff and technology to face

the increase in business. The Group has no

direct or indirect exposure towards sub-

prime credit or structured credit obligations

(such as CDOs, SIVs and CLOs) in its loan or

bond portfolios. Additional information on

risk management is available on request in

accordance with part 8 of the EU Regulation

No 575/2013 (CRR: “Capital Requirements

Regulation”). For further information on the

Group’s exposure to risks, please refer to

notes 7.3 and 7.4 of these annual accounts.

This period saw the strong development of

the Group’s CFD (Contracts For Differences )

activity. The business consists of the issuing

5

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Peter Lang

Deputy CEO

Harley Rowland

Member of the Board of Directors

Luxembourg, 12 June 2017

of CFD contracts to clients served by the

Group. The CFDs issued are fully hedged by

the acquisition of the underlying asset or by

backing the operation with another CFD on

the market.

ACTIVITIES OF THE GROUP IN THE FIELD

OF RESEARCH AND DEVELOPMENT

The Group did not undertake any activities

in terms of Research and Development.

Acquisition of own shares

No entity within the Group acquired own

shares in 2016 and does not hold own shares.

Representation offices

The Group has opened one representative

office in Dubai in 2016 and continues to

maintain its subsidiary in Moscow (BH LLC)

as a representative office.

Post-closing events

Banque Havilland Institutional Services

(formerly Banco Popolare Luxembourg S.A.)

will be merged by absorption with Banque

Havilland S.A. during the course of 2017 and

will become a dedicated business line of the

Bank. All services to institutional investors

will be maintained and further developed by

the institutional business line. This operation

is submitted to the approval of the CSSF.

OUR PRIORITIES FOR 2017

In 2017, the Group will further integrate

recently acquired subsidiaries into its

centralized operating model. Banque

Havilland Switzerland’s core banking

system will be aligned with the Group’s

standards and the entity will be able to

capitalize on developments made available

to the rest of the Group.

6

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Audit reportTo the Board of directors of Banque Havilland S.A.

REPORT ON THE CONSOLIDATED

ANNUAL ACCOUNTS

We have audited the accompanying

consolidated annual accounts of Banque

Havilland S.A., which comprise the

consolidated balance sheet as at 31

December 2016, the consolidated profit and

loss account for the year then ended and a

summary of significant accounting policies

and other explanatory information.

Board of Directors' responsibility for

the consolidated annual accounts

The Board of Directors is responsible for

the preparation and fair presentation of

these consolidated annual accounts in

accordance with Luxembourg legal and

regulatory requirements relating to the

preparation of the consolidated annual

accounts, and for such internal control as the

Board of Directors determines is necessary

to enable the preparation of consolidated

annual accounts that are free from material

misstatement, whether due to fraud or error.

Responsibility of the "Réviseur

d'entreprises agréé"

Our responsibility is to express an opinion

on these consolidated annual accounts

based on our audit. We conducted our audit

in accordance with International Standards

on Auditing as adopted for Luxembourg

by the "Commission de Surveillance du

Secteur Financier". Those standards

require that we comply with ethical

requirements and plan and perform the

audit to obtain reasonable assurance about

whether the consolidated annual accounts

are free from material misstatement.

An audit involves performing procedures

to obtain audit evidence about the amounts

and disclosures in the consolidated

annual accounts. The procedures

selected depend on the judgment of the

"Reviseur d'entreprises agréé", including

the assessment of the risks of material

misstatement of the consolidated annual

accounts, whether due to fraud or error.

In making those risk assessments, the

"Réviseur d'entreprises agréé" considers

internal control relevant to the entity's

preparation and fair presentation of the

consolidated annual accounts in order

to design audit procedures that are

appropriate in the circumstances , but not

for the purpose of expressing an opinion

on the effectiveness of the entity's internal

control. An audit also includes evaluating

7

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

the appropriateness of accounting policies

used and the reasonableness of accounting

estimates made by the Board of Directors, as

well as evaluating the overall presentation

of the consolidated annual accounts.

We believe that the audit evidence we have

obtained is sufficient and appropriate to

provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated annual

accounts give a true and fair view of the

consolidated financial position of Banque

Havilland S.A. as of 31 December 2016, and

of the consolidated results of its operations

for the year then ended in accordance

with Luxembourg legal and regulatory

requirements relating to the preparation of

the consolidated annual accounts.

Other information

The Board of Directors is responsible for the

other information. The other information

comprises the information included in

the consolidated management report but

does not include the consolidated annual

accounts and our audit report thereon.

Our opinion on the consolidated annual

accounts does not cover the other

information and we do not express any

form of assurance conclusion thereon.

In connection with our audit of the consolidated

annual accounts, our responsibility is to

read the other information and, in doing so,

consider whether the other information is

materially inconsistent with the consolidated

annual accounts or our knowledge obtained

in the audit or otherwise appears to be

materially misstated. If, based on the work

we have performed, we conclude that there

is a material misstatement of this other

information, we are required to report this

fact. We have nothing to report in this regard.

Report on other legal and regulatory

requirements

The consolidated management report is

consistent with the consolidated annual

accounts and has been prepared in

accordance with the applicable legal

requirements.

PricewaterhouseCoopers,

Société coopérative

Luxembourg, 12 June 2017

Cyril Lamorlette

PricewaterhouseCoopers Société coopérative2, Rue Gerhard MercatorB.P. 1443L-1014 LuxembourgTelephone +352 494848-1Facsimile +352 494848-2900www.pwc.lu

Cabinet de révision agréé. Expert-comptable(autorisation gouvernementale n°10028256)R.C.S. Luxembourg B 65 477TVA LU25482518

9

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

BANQUE HAVILLAND S.A.CONSOLIDATED BALANCE SHEET AS AT 31st DECEMBER 2016 (EXPRESSED IN EURO)

ASSETS NOTES 31/12/2016 31/12/2015

Cash in hand, balances with central banks and post

office banks 4.1,7.1 213 217 341 127 021 096

Loans and advances to credit institutions

- repayable on demand

- other loans and advances

4.2, 7.1, 7.3130 044 919

6 872 715119 819 597

4 750 000

136 917 634 124 569 597

Loans and advances to customers 2.5.3, 4.3, 7.1, 7.3 669 615 250 388 977 645

Bonds and other fixed-income transferable securities

- Issued by public bodies

- Issued by other borrowers

2.5.1, 4.4, 7.1, 7.3163 350 379614 026 353

51 703 154 602 859 018

777 376 732 654 562 172

Shares and other variable-yield transferable securities 2.5.2, 4.5,7.1, 7.3 90 055 401 47 172 108

Shares in affiliated undertakings - - 80 290

Intangible assets 2.4.1, 4.6 3 004 521 3 062 494

Goodwill of first consolidation 2.3, 4.6 7 554 810 10 576 734

Tangible assets 2.4.2, 4.6 26 074 925 12 506 132

Other assets 4.7 20 865 849 14 767 231

Prepayments and accrued income - 7 933 798 5 067 746

TOTAL ASSETS 4.8 1 952 616 261 1 388 363 245

The accompanying notes form an integral part of these consolidated annual accounts.

10

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

LIABILITIES NOTES 31/12/2016 31/12/2015

Amounts owed to credit institutions

- repayable on demand

- with agreed maturity dates or periods of notice

5.1, 7.1759 790

6 144 76584 329 72129 365 152

6 904 555 113 694 873

Amounts owed to customers other debts

- repayable on demand

- with agreed maturity dates or periods of notice

5.2, 7.11 490 726 435

134 584 154945 078 359 116 915 092

1 625 310 589 1 061 993 451

Other liabilities 5.3 61 247 142 26 016 274

Accruals and deferred income 2 437 886 947 312

Provisions

- provisions for taxation

- other provisions 5.82 876 390

26 365 7534 703 8854 712 568

29 242 143 9 416 453

Fund for general banking risks 2.6 13 248 793 16 768 791

Subscribed capital 5.4, 5.6 170 000 000 130 000 000

Share premium account 5.6 1 260 709 1 260 709

Reserves and profit or loss brought forward 5.5, 5.6 12 431 072 9 700 736

Profit for the financial year attributable to the Group 5.6 14 180 754 2 489 346

Minority interests 5.6 16 352 618 16 075 300

TOTAL LIABILITIES 5.7 1 952 616 261 1 388 363 245

The accompanying notes form an integral part of these consolidated annual accounts.

BANQUE HAVILLAND S.A.CONSOLIDATED BALANCE SHEET AS AT 31st DECEMBER 2016 (EXPRESSED IN EURO)

11

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

BANQUE HAVILLAND S.A.CONSOLIDATED OFF BALANCE SHEET FOR THE YEAR ENDED 31st DECEMBER 2016

(EXPRESSED IN EURO)

OFF BALANCE SHEET NOTES 31/12/2016 31/12/2015

Contingent liabilities

of which:

- Guarantees and assets pledged as collateral security

- Acceptances and endorsements

6.1, 7.1,7.3 8 188 367

11 002 839501 492

14 746 303

14 746 303-

Fiduciary transactions 844 230 867 -

Commitments 399 168 -

The accompanying notes form an integral part of these consolidated annual accounts.

13

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

NOTES 2016 2015

Interest receivable and similar income

of which: arising from fixed-income transferable

securities

Interest payable and similar charges

8.1 39 818 568

8 869 521(6 440 024)

24 122 487

10 431 527(2 302 624)

Net interest income 33 378 544 21 819 863

Income from transferable securities

Income from shares and other variable-yield securities 5 113 2 346

Commission receivable

Commission payable

8.1 27 721 378(8 650 788)

19 803 115(8 204 712)

Net commission income 19 070 590 11 598 403

Net profit or net loss on financial operations 8.1 11 988 973 2 291 849

Other operating income 8.2 9 039 248 1 686 358

Total operating income 73 482 468 37 398 819

General administrative expenses

Staff costs

of which:

- wages and salaries

- social security costs

of which: pension costs

Other administrative expenses

9.3, 9.4

9.5

(27 543 523)

(22 000 515)(3 449 167)(1 370 968)

(18 332 543)

(17 411 990)

(14 248 220)(2 048 289)

(821 673)(13 328 532)

(45 876 066) (30 740 522)

Value adjustments in respect of tangible,

intangible and goodwill of first consolidation (5 469 841) (4 715 508)

Other operating charges 8.3 (2 943 636) (2 738 894)

Value adjustments in respect of loans and advances and

provisions for contingent liabilities and for commitments8.4

(4 780 269) (825 840)

The accompanying notes form an integral part of these consolidated annual accounts.

BANQUE HAVILLAND S.A.CONSOLIDATED PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31ST DECEMBER 2016

(EXPRESSED IN EURO)

14

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

NOTES 2016 2015

Value re-adjustments in respect of loans and

advances and provisions for contingent liabilities

and for commitments 8.4 157 900 1 892 800

Value re-adjustment in respect of securities held

as financial fixed assets, participating interests

and shares in affiliated undertakings - (209 970)

Income from the reversal of amounts included in

the fund for general banking risks 458 777 (299 493)

Profit before tax 15 029 333 (238 608)

Tax on profit or loss on ordinary activities 8.5 (21 287) (26 750)

Profit or loss on ordinary activities after tax 15 008 046 (265 358)

Extraordinary income 210 195 1 480 403

Extraordinary charges (159 845) -

Other taxes not shown in the preceding items (831 663) (524 555)

Profit or loss for the financial year 14 226 733 690 490

Thereof minority interests 45 979 (1 798 856)

Profit for the financial year attributable to the Group 14 180 754 2 489 346

The accompanying notes form an integral part of these consolidated annual accounts.

BANQUE HAVILLAND S.A.CONSOLIDATED PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31ST DECEMBER 2016

(EXPRESSED IN EURO)

16

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

1 GENERAL

Banque Havilland S.A. (the “Bank”) was incorporated in the Grand-Duchy of

Luxembourg on July 10, 2009 as a limited liability company (“Société Anonyme”). The

Ministry of Finance granted the company a banking licence on June 25, 2009.

The Bank was created through a non cash contribution of assets and liabilities from

a former bank. This non cash contribution was calculated as the lower of net book

value or fair value as at the date of the contribution. As a consequence, the Bank

is now carrying all former assets and liabilities and reflects the historical cost and

accumulated depreciation.

The Bank is registered at the Luxembourg “Registre du Commerce et des Sociétés”

under the number B0147029. The head office is located 35a, Avenue J.F. Kennedy,

L-1855 Luxembourg.

The share capital of the Bank is expressed in Euro (EUR) and the accounting records

are prepared and maintained in this currency. The Bank’s accounting year is defined

as the calendar year.

The Bank is permitted to carry out all banking activities. Its principal activity is

private banking.

As of December 31, 2016, the Bank has one branch established in the UK (5 Savile

Row, London, United Kingdom) with private banking activity.

The Bank and the subsidiaries described in note 3 are referred to as the “Group”.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016

17

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND VALUATION RULES

2.1 BASIS OF PRESENTATION

The Group prepares its consolidated annual accounts using the historical cost

principle, in accordance with the laws and regulations in force in the Grand Duchy

of Luxembourg and on the basis of accounting principles generally accepted by the

banking sector in the Grand Duchy of Luxembourg. The accounting policies and the

valuation principles are determined and applied by the Board of Directors, apart

from those which are defined by law and by the Commission de Surveillance du

Secteur Financier.

The preparation of consolidated annual accounts requires the use of a certain

critical accounting estimates. It also requires the Board of Directors to exercise its

judgment in the process of applying accounting policies. Changes in assumptions

may have a significant impact on the consolidated annual accounts in the period in

which the assumptions changed. The Board of Directors believes that the underlying

assumptions are appropriate and that the consolidated annual accounts therefore

present the financial position and results fairly.

The Board of Directors makes estimates and assumptions that affect the reported

amounts of assets and liabilities in the next financial year. Estimates and judgments

are continually evaluated and are based on historical experience and other factors,

including expectations of future events that are believed to be reasonable under

the circumstances.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

18

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2.2 CONSOLIDATION METHOD

The Group has adopted the full consolidation method for its subsidiaries (direct or

indirect holding of more than 50%).

2.3 DIFFERENCES OF FIRST CONSOLIDATION

Differences of first consolidation represent the difference between the cost of the

parent company’s investment in the consolidated subsidiaries and its share of the

net assets of these companies as at the date of acquisition of its investment.

Positive differences of first consolidation are disclosed on the asset side of the

balance sheet (as goodwill of first consolidation) and amortized over 5 years on a

linear basis.

Negative differences of first consolidation are either disclosed on the liability side

of the balance sheet in the consolidated reserves. When it corresponds to future

expected losses, they are disclosed under “Provisions”.

The reversal of negative differences of first consolidation disclosed in provision into

the profit and loss account is made to offset a loss in the results of the acquired

business.

2.4 FIXED ASSETS

2.4.1 Intangible assets

Intangible assets are included at purchase price less accumulated depreciation.

Intangible assets consist of:

• Software amortised over 4 years on a linear basis;

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

19

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

• Goodwill acquired for valuable consideration and amortised over 4 years on a

linear basis;

• Formation expenses and costs in relation to capital increases are directly

expensed when incurred.

In case of durable reduction in value, intangible assets are subject to value

adjustments regardless of whether their utilisation is limited. The valuation of the

inferior value is not maintained if the reason for which the value adjustment were

made no longer exist.

2.4.2 Tangible assets

Tangible assets are included at purchase price less accumulated depreciation.

Tangible assets are depreciated over their expected useful life.

The rates and methods of depreciation are as follows:

RATES METHOD

Office equipment, fixtures & fittings 25.0% linear

Company cars 25.0% linear

Building 1.5% - 4.0% linear

Fixtures and fittings costing less than EUR 867 or whose expected useful life does not

exceed one year are charged directly to profit and loss account for the year.

In case of durable reduction in value, tangible assets are subject to value adjustments

regardless of whether their utilisation is limited. The valuation of the inferior value is not

maintained if the reasons for which the value adjustment were made no longer exist.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

20

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2.5 CURRENT ASSETS

2.5.1 Debt securities and other fixed-income securities

The Group has divided its portfolio of fixed-income transferable securities into three

categories whose principal characteristics are the following:

- an investment portfolio of financial fixed assets which are intended to be used

on a continuing basis in the Bank’s activities;

- a trading portfolio of securities purchased with the intention of resale in the

short term;

- a structural portfolio of securities which do not fall into either of the two other

categories.

Fixed income securities are recorded at their acquisition price and valued as follows

at the balance sheet date:

Investment portfolio of financial fixed assets

Fixed-income transferable securities included in the investment portfolio of financial

fixed assets are valued at acquisition price. In case of long-term depreciations, the

securities concerned are subject to value adjustments in order to give them the

lower value which is to be assigned to them on the balance sheet date.

When the purchase price of fixed-income transferable securities included in

the Bank’s investment portfolio exceed their redemption price or is below their

redemption price, the difference is recorded in profit or loss in instalments over the

period remaining to maturity.

As at December 31, 2016 and December 31, 2015, the Group does not hold

fixed-income securities of this category.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

21

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Trading portfolio

Fixed-income transferable securities included in the trading portfolio are valued at

the lower of cost or market value.

As at December 31, 2016 and December 31, 2015, the Group does not hold

fixed-income securities of this category.

Structural portfolio

Fixed-income transferable securities included in the structural portfolio are valued

at the lower of cost or market value.

Value adjustments are made for securities in the structural portfolio for which the

valuation is lower than the purchase price. The valuation is the market value on

the balance sheet date, the estimated realisable value or the quotation, which best

represents the inherent value of the securities held.

2.5.2 Shares and other variable-yield securities

Shares and other variable-yield securities are classified in the structural portfolio of

the Bank and recorded at purchase price. At the balance sheet date, they are valued

at the lower of purchase price or market value. A value adjustment is recorded when

the market value is lower than the purchase price.

2.5.3 Loans and advances

Loans and advances are disclosed at their nominal value. Accrued interests are

recorded under the heading “Prepayments and accrued income” on the asset side

of the balance sheet.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

22

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2.5.4 Value adjustments in respect of current assets

The policy of the Group is to establish specific provisions to cover the risk of loss and

of the non-recovery of debtors.

Value adjustments are deducted from the relevant current assets.

2.5.5 Provision for assets at risk

A tax free lump-sum provision is accounted for based on the Group’s assets at

risk. These assets are determined in accordance with the regulatory provisions

governing the computation of the capital adequacy ratio. The lump-sum provision

is split between the relevant assets at risk in accordance with the provisions of the

Luxembourg Monetary Institute circular letter dated December 16, 1997. The portion

related to the assets at risk is deducted from these assets.

2.6 FUND FOR GENERAL BANKING RISKS

The Group has established a fund for general banking risks to cover the particular

risks associated with banking. Transfers to this fund are booked from income

after tax, but before determination of net income. This fund is not subject to any

quantitative limit.

In 2016, an amount of EUR 4 060 789 has been used in relation with a payment

related to a claim.

2.7 PURCHASE PRICE OF FUNGIBLE ASSETS

The Group values fungible assets by the weighted average price method.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

23

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2.8 VALUATION OF FOREIGN CURRENCY BALANCES AND TRANSACTIONS

2.8.1 Foreign currency

The share capital of the Group is expressed in Euro (“EUR”) and the accounting

records are maintained in that currency.

Shares in affiliated undertakings included in fixed assets are converted at the spot

rate prevailing at the balance sheet date.

Intangible and tangible assets are converted at the historic rate. All other assets and

liabilities denominated in a currency other than EUR are converted into EUR at the

rate of exchange ruling at the balance sheet date.

Income and charges in foreign currencies are converted into EUR at the rate of

exchange ruling on the date of the transaction.

Foreign currency differences arising from these valuation principles are taken to the

profit and loss account.

The annual accounts of subsidiaries whose operating currency is not the EUR are

converted using the closing rate method. Under this method, all assets, liabilities

and result brought forward, both monetary and non-monetary, are converted using

the spot exchange rate at the balance sheet date. Income and expense items are

converted at the average rate for the year.

2.8.2 Valuation of transactions not subject to currency risk

Swap transactions not linked to balance sheet items

The spot result realised in cash terms is offset by the result arising from the

revaluation of the forward leg. The premium/discount is spread prorata temporis.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

24

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Over-the-counter closed forward transactions

Future profits that are certain to arise are deducted from future losses that are

certain to arise in the same currency.

A provision is created for any excess losses; any excess profits are deferred.

2.8.3 Valuation of transactions subject to currency risk

Over-the-counter speculative forward transactions

Provision is made for unrealised losses on forward transactions, which do not

represent the hedging of a spot position. Unrealised gains are not accounted for.

The Group only enters into financial instruments for hedging purposes.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

25

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

3 SCOPE OF CONSOLIDATION

NAME OF THE COMPANY REGISTERED OFFICE

PROPORTION OF THE CAPITAL HELD BY THE PARENT COMPANY

31/12/2016

Parent company

Banque Havilland S.A. Luxembourg -

Full consolidation

Banque Havilland (Monaco) S.A.M. Monaco 100.0%

Banque Havilland (Liechtenstein) AG Liechtenstein 52.5%

Banque Havilland (Bahamas) Ltd. Bahamas 100.0%

BH International Limited Liability Company (2) Russia 100.0%

Banque Havilland (Suisse) S.A. (3) Switzerland 100.0%

Banque Havilland Institutional Services S.A. (4) Luxembourg 100.0%

31/12/2015

Parent company

Banque Havilland S.A. Luxembourg -

Full consolidation

Banque Havilland (Monaco) S.A.M. Monaco 100.0%

Kaupthing Life and Pension S.A. (“KLP”) (1) Luxembourg 100.0%

Banque Havilland (Liechtenstein) AG Liechtenstein 52.5%

Banque Havilland (Bahamas) Ltd. Bahamas 100.0%

Out of consolidation scope

BH International Limited Liability Company (2) Russia 100.0%

(1) sold in December 2016

(2) 99.5% held by Banque Havilland S.A. and 0.5% by Banque Havilland (Liechtenstein) AG. BH International Limited Liability Company

is included in the scope of consolidation as from the year 2016.

(3) The Bank acquired in May 2016 99.99% of the shares of Banque Pasche S.A. renamed Banque Havilland (Suisse) S.A..

(4) The Bank acquired in February 2016 100% of the shares of Banco Popolare Luxembourg S.A. renamed Banque Havilland

Institutional Services S.A.. Please also refer to note 9.6.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

26

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

4 DETAILED DISCLOSURES RELATING TO ASSET HEADINGS

4.1 CASH IN HAND, BALANCES WITH CENTRAL BANKS AND POST OFFICE BANKS

In accordance with the requirements of the European Central Bank, the Central

Bank of Luxembourg implemented effective January 1, 1999, a system of mandatory

minimum reserves which applies to all Luxembourg credit institutions. The

reserve balance as at December 31, 2016 held by the Group with the Central Bank

of Luxembourg amounted to EUR 138 084 878 (2015: EUR 82 015 465). The Group

has no overnight deposit at the Central Bank of Luxembourg as at December 31,

2016 (2015: EUR 0). The reserve balance as at December 31, 2016 held by the Group

with the Banque de France amounted to EUR 19 539 113 (2015: EUR 9 372 651).

The reserve balance as at December 31, 2016 held by the Group with the Swiss

National Bank amounted to EUR 52 864 664 (2015: EUR 33 746 405). The reserve

balance as at December 31, 2016 held by the Group with the Central Bank of the

Bahamas amounted to EUR 459 590 (2014: EUR 416 186).

4.2 LOANS AND ADVANCES TO CREDIT INSTITUTIONS

As at December 31, 2016, the Group has no loan granted to affiliated credit institutions

(2015: EUR 0).

4.3 LOANS AND ADVANCES TO CUSTOMERS

As at December 31, 2016, loans and advances to related parties amount to

EUR 133 234 084. (2015: EUR 147 326 491).

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

27

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

4.4 TRANSFERABLE SECURITIES

This heading includes debt securities, whether quoted on a recognised market or

not, issued by public bodies, credit institutions or other issuers and which are not

included under another balance sheet heading.

Quoted and non-quoted securities are analysed as follows:

2016 EUR

2015EUR

Securities quoted on a recognised market 761 967 980 638 559 896

Securities not quoted on a recognised market 15 408 752 16 002 276

TOTAL 777 376 732 654 562 172

Debt securities and other fixed-income securities held are included in the structural

portfolio. The Group uses the European Central Bank Monetary Policy Operations to

finance a part of its eligible securities portfolio.

As at December 31, 2015, the Group was committed in sale and repurchase

agreements with a firm repurchase obligation for an amount of EUR 120 059 549

(2016: EUR 0).

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

28

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

4.5 SHARES AND OTHER VARIABLE-YIELD TRANSFERABLE SECURITIES

This heading includes shares, holdings in investment funds and other variable-yield

securities whether quoted on a recognised market or not which are not included in

fixed asset investments.

Quoted and non-quoted shares and other variable-yield securities are analysed as follows:

2016 EUR

2015EUR

Securities quoted on a recognised market 90 020 354 47 167 503

Securities not quoted on a recognised market 35 047 4 605

TOTAL 90 055 401 47 172 108

All shares and other variable-yield securities held are included in the structural portfolio.

As at December 31, 2016, the Group holds shares and other variable-yield

transferable securities amounting to EUR 77 923 642 for hedging purposes in the

frame of contracts for differences (“CFD”) with clients (2015: EUR 29 744 589).

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

29

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

4.6 MOVEMENTS IN FIXED ASSETS

FIXED ASSETS (IN EUR)

GROSS VALUE AT THE

BEGINNING OF THE

FINANCIAL YEAR

ADDITIONS DISPOSALS / ADJUST-

MENTS

GROSS VALUE AT

THE END OF THE

FINANCIAL YEAR

CUMULATIVE VALUE

ADJUSTMENTS AT THE BEGINNING

OF THE FINANCIAL YEAR

CUMULATIVE VALUE

ADJUSTMENT(*)

NET BOOK VALUE AS AT

31/12/2016

NET BOOK VALUE AS AT

31/12/2015

1. Goodwill of first

consolidation 15 109 620 - - 15 109 620 (4 532 886) (7 554 810) 7 554 810 10 576 734

2. Intangible assets

of which:

- Goodwill acquired for

valuable consideration

- Software

- Other intangible assets

12 030 125

2 875 3588 460 647

694 120

9 631 417

-2 646 6706 984 747

-

---

21 661 542

2 875 35811 107 317

7 678 867

(8 967 631)

(1 161 519)(7 806 112)

-

(18 657 021)

(2 008 017)(9 776 698)(6 872 306)

3 004 521

867 3411 330 619

806 561

3 062 494

1 713 839654 535694 120

3. Tangible assets

of which:

- Office equipment,

fixtures and fittings

- Company cars

- Building

30 522 754

13 913 170211 731

16 397 853

36 971 422

9 895 607241 739

26 834 076

(130 942)

(130 942)--

67 363 234

23 677 835453 470

43 231 929

(18 016 622)

(13 308 968)(104 132)

(4 603 522)

(41 288 309)

(22 860 162)(203 517)

(18 224 630)

26 074 925

817 673249 953

25 007 299

12 506 132

604 202107 599

11 794 331

(*) Including lump sum provision.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

30

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

4.7 OTHER ASSETS

This heading consists of the following:

2016 EUR (*)

2015 EUR (*)

Tax advances 3 899 161 3 431 152

Guarantee called 343 777 300 558

Management and performance fees receivable 318 427 714 883

Margin calls on contracts for differences with clients 9 576 998 9 917 442

Invoices issued 134 089 145 226

Receivable on sales of securities 370 008 -

Cheques in transitory 4 934 587 -

Other receivables 1 288 802 257 970

TOTAL 20 865 849 14 767 231

(*) Including lump-sum provision

4.8 ASSETS DENOMINATED IN FOREIGN CURRENCIES

Assets denominated in currencies other than EUR have a total value of EUR 1 260 383 689

(2015: EUR 851 251 351) as at December 31, 2016. The majority of the gap between non

EUR denominated assets and non EUR denominated liabilities is covered by exchange

rates derivatives instruments.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

31

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

5 DETAILED DISCLOSURES RELATING TO LIABILITY HEADINGS

5.1 AMOUNTS OWED TO CREDIT INSTITUTIONS

As at December 31, 2016, the Group has no amount owed to affiliated credit

institutions (2015: EUR 0).

5.2 AMOUNTS OWED TO CUSTOMERS

As at December 31, 2016, amounts owed to related parties amount to EUR 60 523 154

(2015: EUR 66 294 111).

5.3 OTHER LIABILITIES

2016 EUR

2015 EUR

Invoice payable 1 207 744 2 018 558

Guarantee payable 119 050 119 050

Payable on sales of securities 22 377 089 17 755 221

Business introducers commissions payables 1 314 949 1 006 586

Cheques in transitory 5 316 953 170 550

Other payable 3 848 858 3 830 549

Transitory margin accounts on contracts for differences 14 871 679 -

Payable on sales of structured products 11 494 930 -

Preferential creditors 695 890 1 115 760

TOTAL 61 247 142 26 016 274

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

32

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

5.4 SUBSCRIBED CAPITAL

As at December 31, 2016, the subscribed and fully paid share capital of the Group is

EUR 170 000 000 made up of 170 000 shares with a nominal value of EUR 1 000 each.

During the year 2016, the Bank carried out a EUR 40 000 000 capital increase,

corresponding to the issue of 40 000 new shares with a nominal value of EUR 1 000

each; this capital increase was approved by the Extraordinary General Meeting dated

May 20, 2016.

5.5 LEGAL RESERVE

In accordance with article 72 of the Luxembourg company law, an amount of 5% of

net profits should be allocated to a non distributable legal reserve, until this reserve

reaches 10% of the subscribed capital. As a result, the annual general meeting of

Banque Havilland S.A. held on April 14, 2016 has allocated an amount of EUR 192 785

to the legal reserve, in respect of the 2015 financial year.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

33

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

5.6 CHANGES IN SHAREHOLDERS’ EQUITY

The movements of shareholders’ equity of Banque Havilland S.A. may be summarised

as follows:

5.7 LIABILITIES DENOMINATED IN FOREIGN CURRENCIES

Liabilities denominated in currencies other than EUR have a total value of

EUR 1 121 688 197 (2015: EUR 837 434 957) as at December 31, 2016. The majority of

the gap between non EUR denominated assets and non EUR denominated liabilities

is covered by exchange rates derivative instruments.

SUBSCRIBED CAPITAL

EUR

SHARE PREMIUM

EUR

LEGAL RESERVE

EUR

CONSOLIDATED RESERVES

AND PROFIT BROUGHT

FORWARD EUR

MINORITY INTERESTS

EUR

PROFIT OF THE YEAR

(GROUP) EUR

TOTAL OWN

FUNDS EUR

Balance at

December 31, 2015 130 000 000 1 260 709 1 866 810 7 833 926 16 075 300 2 489 346 159 526 091

Capital increase 40 000 000 - - - - - 40 000 000

Transfer to legal

reserve - - 192 785 - - (192 785) -

Translation impact on:

- group reserves

- minority interests

--

--

--

240 990-

-231 339

--

24 990231 339

Profit brought forward - - - 2 296 561 - (2 296 561) -

Current year profit - - - - 45 979 14 180 754 14 226 733

BALANCE AT DECEMBER 31, 2016

170 000 000

1 260 709

2 059 595

10 371 477

16 352 618

14 180 754

214 225 153

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

34

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

5.8 OTHER PROVISIONS

This heading consists of the following:

2016 EUR

2015 EUR

Claims 4 171 775 1 497 951

Bonus 1 810 854 854 094

LRF and LGDS provision (ex-AGDL provision) 1 003 312 261 541

Differences of first consolidation (note 2.3) 15 681 350 -

Others 3 698 462 2 098 982

TOTAL 26 365 753 4 712 568

Differences of first consolidation arises from the acquisition by the Bank of

Banque Havilland (Suisse) S.A. and Banque Havilland Institutional Services S.A..

Please refer to note 3.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

35

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

6 CONTINGENT LIABILITIES AND COMMITMENTS

6.1 CONTINGENT LIABILITIES

Contingent liabilities consist of guarantees and other direct substitutes for loans.

6.2 LUXEMBOURG RESOLUTION FUND ("LRF") AND LUXEMBOURG DEPOSIT

GUARANTEE SCHEME ("LGDS")

The law related to the resolution, reorganisation and winding-up measures of credit

institutions and certain investment firms and on deposit guarantee and investor

compensation schemes (“the Law”), transposing into Luxembourgish law the directive

2014/59/EU establishing a framework for the recovery and resolution of credit

institutions and investment firms and the directive 2014/49/EU related to deposit

guarantee and investor compensation schemes, was passed on 18 December 2015.

The deposit guarantee and investor compensation scheme previously in place through

the “Association pour la Garantie des Dépôts Luxembourg” (AGDL) has been replaced

by a new contribution based system of deposit guarantee and investor compensation

scheme. This new system covers eligible deposits of each depositor up to an amount

of EUR 100,000 (Luxembourg Deposit Guarantee Scheme) and investments up to an

amount of EUR 20,000 (Luxembourg Investors Compensation Scheme).

The Law also provides that deposits resulting from specific transactions or fulfilling

a specific social or other purpose are covered for an amount above EUR 100,000 for

a period of 12 months.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

36

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Provisions which were booked in the annual accounts of the credit institutions

throughout the years in order to respect the obligations of the AGDL are reversed in

proportion to the contribution paid on the new “Luxembourg Resolution Fund” (LRF)

and “Luxembourg Deposit Guarantee Scheme” (LDGS).

The funded amount of the LRF shall reach by the end of 2024 at least 1% of covered

deposits, as defined in article 1 number 36 of the Law, of all authorized credit

institutions all participating Member States. This amount will be collected from the

credit institutions through annual contributions during the years 2015 to 2024 using

the previously constituted AGDL provision.

The target level of funding of the LDGS is set at 0.8% of covered deposits, as

defined in article 163 number 8 of the Law, of the relevant credit institutions

arid is to be reached by the end of 2018 through annual contributions using the

previously constituted AGDL provision. When the level of 0.8% will be reached, the

Luxembourgish credit institutions are to continue to contribute for 8 additional

years in order to constitute an additional safety buffer of 0.8% of covered deposits

as defined in article 163 number 8 of the Law.

As of 31 December 2016, the Group has made total advance payments in relation to

a call for guarantee arising from the suspension of payment of three Luxembourg

credit institutions, in the amount of EUR 473,574. As of 31 December 2016, the Group

has received back the amount of EUR 318,871.

According to the Law, the Group decided to use the AGDL provision constituted up to

31 December 2015 to cover LRF and LDGS charges occurring during the year.

During 2016, the AGDL provision was used to cover LRF and LDGS charges for

respectively EUR 289 171 and EUR 66 727.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

37

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

6.3 OPEN FORWARD AGREEMENTS AT THE BALANCE SHEET DATE

The Group is engaged in forward foreign exchange transactions (swaps, outrights) in

the normal course of its banking business. A significant portion of these transactions

has been contracted to hedge the effects of fluctuations in exchange rates (see notes

7.2. and 7.3. for additional information).

6.4 MANAGEMENT AND FIDUCIARY SERVICES

The Group’s services to third parties consist of:

• Portfolio management and investment advice;

• Custody and administration of transferable securities;

• Credit activities;

• Fund administration.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

38

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

7 INFORMATION RELATING TO FINANCIAL INSTRUMENTS

7.1 DISCLOSURES RELATING TO PRIMARY FINANCIAL INSTRUMENTS IN

RELATION TO NON-TRADING ACTIVITIES

The following tables provide an analysis of the carrying amount of primary financial

assets and financial liabilities of the Group into relevant maturity groupings based

on the remaining periods to repayment.

As at December 31, 2016, primary financial assets and liabilities are analysed as

follows (in EUR):

FINANCIAL ASSETS

LESS THAN THREE

MONTHS

BETWEEN THREE

MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND FIVE

YEARS

MORE THAN FIVE YEARS

NO MATURITY

TOTAL

Cash, balances with central

banks and post office banks 213 217 341 - - - - 213 217 341

Loans and advances to

credit institutions 132 167 634 4 750 000 - - - 136 917 634

Loans and advances to

customers 394 842 361 136 671 926 130 899 279 7 201 684 - 669 615 250

Debt securities

and other fixed-income

securities

138 893 362 75 737 808 446 794 401 107 647 240 8 303 921 777 376 732

Shares and other variable-

yield securities - - - - 90 055 401 90 055 401

TOTAL 879 120 698 217 159 734 577 693 680 114 848 924 98 359 322 1 187 182 358

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

39

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

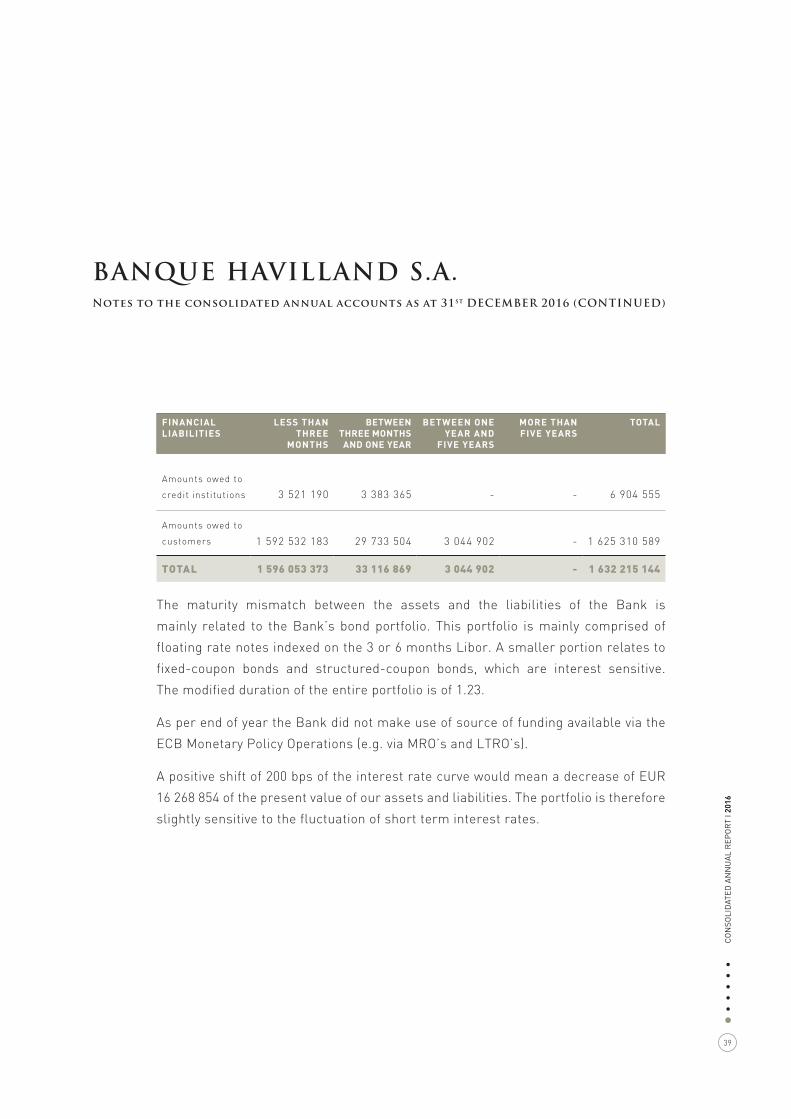

FINANCIALLIABILITIES

LESS THAN THREE

MONTHS

BETWEEN THREE MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND

FIVE YEARS

MORE THAN FIVE YEARS

TOTAL

Amounts owed to

credit institutions 3 521 190 3 383 365 - - 6 904 555

Amounts owed to

customers 1 592 532 183 29 733 504 3 044 902 - 1 625 310 589

TOTAL 1 596 053 373 33 116 869 3 044 902 - 1 632 215 144

The maturity mismatch between the assets and the liabilities of the Bank is

mainly related to the Bank’s bond portfolio. This portfolio is mainly comprised of

floating rate notes indexed on the 3 or 6 months Libor. A smaller portion relates to

fixed-coupon bonds and structured-coupon bonds, which are interest sensitive.

The modified duration of the entire portfolio is of 1.23.

As per end of year the Bank did not make use of source of funding available via the

ECB Monetary Policy Operations (e.g. via MRO’s and LTRO’s).

A positive shift of 200 bps of the interest rate curve would mean a decrease of EUR

16 268 854 of the present value of our assets and liabilities. The portfolio is therefore

slightly sensitive to the fluctuation of short term interest rates.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

40

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

FINANCIAL ASSETS

LESS THAN THREE

MONTHS

BETWEEN THREE

MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND FIVE

YEARS

MORE THAN FIVE

YEARS

NO MATURITY

TOTAL

Cash, balances with

central banks and

post office banks 127 021 096 - - - - 127 021 096

Loans and advances

to credit institutions 119 819 597 - 4 750 000 - - 124 569 597

Loans and advances

to customers 196 582 766 64 252 210 123 604 739 4 537 930 - 388 977 645

Debt securities

and other fixed-

income securities 25 661 676 62 814 936 466 644 488 91 101 643 8 339 429 654 562 172

Shares and other

variable-yield

securities - - - - 47 172 108 47 172 108

TOTAL 469 085 135 127 067 146 594 999 227 95 639 573 55 511 537 1 342 302 618

FINANCIALLIABILITIES

LESS THAN THREE

MONTHS

BETWEEN THREE MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND

FIVE YEARS

MORE THAN FIVE YEARS

TOTAL

Amounts owed to

central banks 80 000 000 - - - 80 000 000

Amounts owed to

credit institutions 33 694 873 - - - 33 694 873

Amounts owed to

customers 1 054 867 830 7 125 621 - - 1 061 993 451

TOTAL 1 168 562 703 7 125 621 - - 1 175 688 324

As at December 31, 2015, primary financial assets and liabilities are analysed as

follows (in EUR):

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

41

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

7.2 DISCLOSURES RELATING TO DERIVATIVE FINANCIAL INSTRUMENTS

The following tables provide an analysis of the derivative financial assets and liabilities

of the Bank into relevant maturity groupings based on the remaining periods to

repayment. As at December 31, 2016, over-the-counter derivative financial assets

and liabilities are analysed as follows (in EUR):

LESS THAN THREE MONTHS

BETWEEN THREE MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND FIVE YEARS

TOTAL ASSETS & LIABILITIES

CONTRACT / NOTIONAL

AMOUNT (EUR)

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

Foreign Exchange OTC

Forward currency

contracts

Currency swap

contracts

Options

91 290 546

108 047 538340 240

1 580 708

181 7027 293

1 771 531

396 1957 293

306

--

4 269

113 091-

944

--

944

--

1 581 958

181 7027 293

1 776 744

509 2867 293

Interest rates

Exchange-traded

- Futures 13 800 133 114 602 - - - - - 114 602 -

Equities

OTC

- Contracts for

difference

Exchange-traded

- Options

223 304 379

1 209 977

9 441 270

53 805

25 949 505

33 915

-

7 097

-

3 175

-

-

-

-

9 441 270

60 902

25 949 505

37 090

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

42

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

As at December 31, 2015, over-the-counter derivative financial assets and liabilities

are analysed as follows (in EUR):

7.3 DISCLOSURES RELATING TO CREDIT RISK

The Group is exposed to credit risk mainly through its lending, investing and

hedging activities and in cases where the Group acts as an intermediary on behalf of

customers and issues guarantees.

The Group’s primary exposure to credit risk arises from its loans and advances and

debt securities. The credit exposure in this regard is represented by the carrying

amounts of the assets in the balance sheet.

The Group is also exposed to off-balance sheet credit risk through guarantees

issued and instruments linked to exchange, interest and other market rates

(forward transactions, swaps and option contracts). The credit exposure in respect

of instruments linked to exchange, interest and other market rates are equal to the

equivalent at risk according to the initial risk approach.

LESS THAN THREE MONTHS

BETWEEN THREE MONTHS AND ONE YEAR

BETWEEN ONE YEAR AND FIVE YEARS

TOTAL ASSETS & LIABILITIES

CONTRACT / NOTIONAL

AMOUNT (EUR)

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

FINANCIAL ASSETS

FINANCIAL LIABILITIES

Foreign Exchange OTC

- Forward currency contracts

- Currency swap contracts

10 650 168225 386 676

80 627458 474

635656 158

-16 296

-8 304

--

--

80 627474 770

635664 462

Equities

OTC

- Contracts for difference

Exchange-traded

- Options

92 535 025

11 000

13 413 590

3 500

5 317 564

3 500

-

-

-

-

-

-

-

-

13 413 590

3 500

5 317 564

3 500

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

43

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

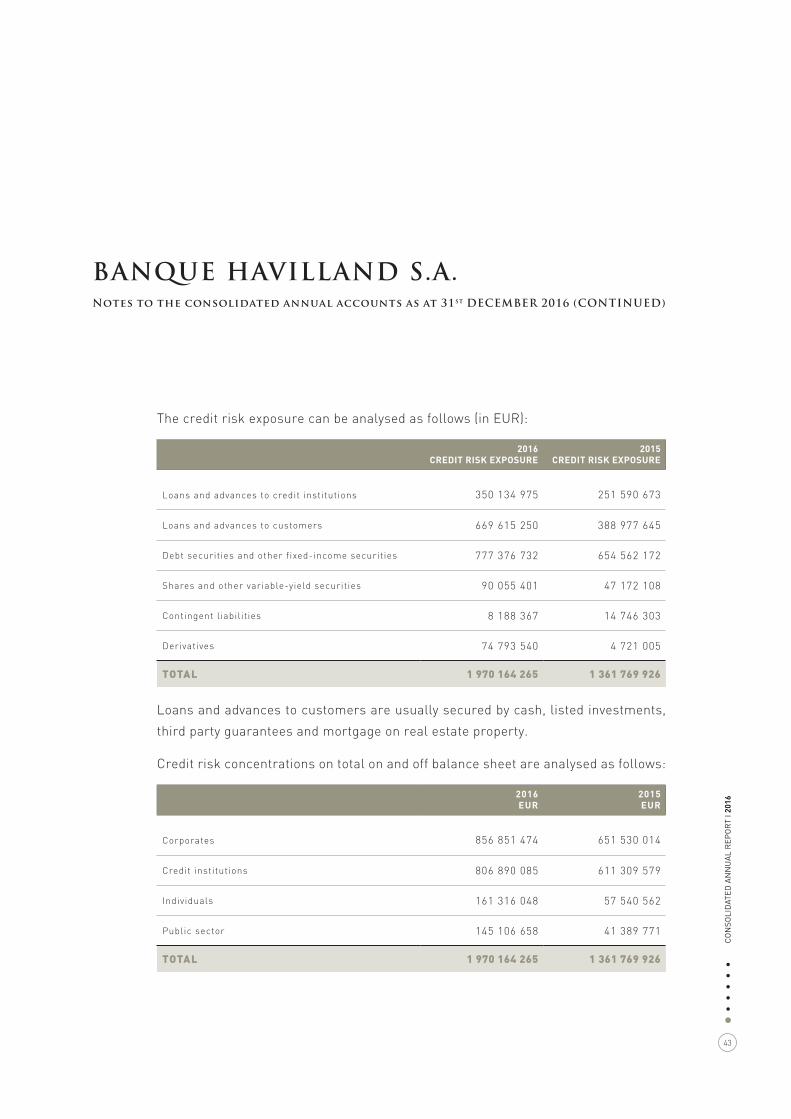

The credit risk exposure can be analysed as follows (in EUR):

2016 CREDIT RISK EXPOSURE

2015 CREDIT RISK EXPOSURE

Loans and advances to credit institutions 350 134 975 251 590 673

Loans and advances to customers 669 615 250 388 977 645

Debt securities and other fixed-income securities 777 376 732 654 562 172

Shares and other variable-yield securities 90 055 401 47 172 108

Contingent liabilities 8 188 367 14 746 303

Derivatives 74 793 540 4 721 005

TOTAL 1 970 164 265 1 361 769 926

Loans and advances to customers are usually secured by cash, listed investments,

third party guarantees and mortgage on real estate property.

Credit risk concentrations on total on and off balance sheet are analysed as follows:

2016 EUR

2015 EUR

Corporates 856 851 474 651 530 014

Credit institutions 806 890 085 611 309 579

Individuals 161 316 048 57 540 562

Public sector 145 106 658 41 389 771

TOTAL 1 970 164 265 1 361 769 926

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

44

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

Credit institutions, corporates, individuals and public sector are essentially issued

from OECD countries, main ones being Luxembourg, United States, Switzerland,

France and the United Kingdom.

Geographical Concentration of credit risk (in EUR):

2016EUR

Luxembourg 419 826 433

United States 256 589 901

Switzerland 241 179 638

British Virgin Islands 161 982 510

France 126 005 643

United Kingdom 125 071 329

Germany 78 215 582

Canada 39 661 149

Monaco 36 113 483

Turkey 35 072 701

Italy 33 691 418

Cyprus 26 217 496

Mauritius 25 571 078

Cayman Islands 22 304 897

Sweden 19 592 140

Netherlands 18 519 198

Belgium 17 802 708

Russia 17 789 718

Spain 17 606 604

Hong Kong 17 483 195

Jersey 16 659 457

Australia 16 303 148

Austria 15 943 279

Panama 14 743 495

Czech Republic 13 951 003

Azerbaijan 13 887 827

Malta 12 085 388

Denmark 11 687 498

Liechtenstein 10 446 415

Ireland 9 751 287

United Arab Emirates 9 458 577

China 8 924 784

South Korea 7 620 119

Japan 7 278 515

Guernsey 6 686 322

Singapore 5 631 003

Other 52 809 327

TOTAL 1 970 164 265

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

45

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

7.4 INFORMATION ON THE MANAGEMENT OF OTHER RISKS

Liquidity Risk

A cash management system enables the Group to achieve a daily automatic

“vostro-nostro” reconciliation of its main correspondent accounts.

The Group is able to identify possible cash flow errors, to determine adjusted

opening balances and generate an accurate liquidity gap to better channel short-

term liquidity needs.

The Asset and Liability Committee (“ALCO”) receives a daily report on the overall

liquidity situation of the Group, the upcoming liquidity risks and the cash buffer.

Interest Rate Risk

The Group monitors its interest rate risk by analysing the different maturity gaps in

the balance sheet.

The Group is not exposed to interest rate risks due to the nature of its business. Less

than 10% of the assets are fixed rate denominated.

Stress tests are performed quarterly by analysing parallel curve shifts.

Exchange Rate Risk

The Group’s main exposure to foreign exchange risk (“FX”) arises from USD, CHF,

DKK, GBP, SEK, NOK and ISK.

A foreign exchange position system provides an overall view of the currency risk and

related profit or loss impact by business line, turnover and margins.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

46

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

The implementation of a Value at Risk (“VaR”) model gives a view of the potential loss

of the overnight position.

The ALCO members monitor and control the exchange rate risk through the daily

report received from the Treasury department.

Market Risk

The Group’s Market Risk is managed in both a qualitative and a quantitative manner.

The profit and loss of the Group’s investment and FX book is reported daily by the

Treasury to the ALCO members. An in-depth analysis of the Group’s investment

portfolio is performed twice a month in terms of geographic segmentation, sector

segmentation, type of products, last important news on the issuer, yield analysis,

rating agency’s views, liquidity, issuer’s healthiness, etc. The FX overnight’s risk is

computed daily through a 99% Expected Shortfall. These documents are sent to the

ALCO. All the investment’s decisions are subject to the ALCO approval and need to

be compliant with the Investment Guidelines as agreed by the Board of Directors.

The monitoring and control of CFD positions is operationalized, among others,

through the production of two daily reports: a CFD control report and a CFD

statement report. The details for each position, corresponding margin call, profit

and loss, computed VaR are indicated in these documents.

In case of any breach the Relationship Manager of the client and the credit department

are immediately informed. The Credit Department with the support of the Relation

Manager has to solve the breach wether by margin calling the client, either by closing

the CFD’s contract.

The Treasury of the Group can hedge the client’s CFDs either by backing the CFD on

the market with a CFD provider, either by taking positions on the underlying. In any

case, the Group’s book has to be delta neutral.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

47

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

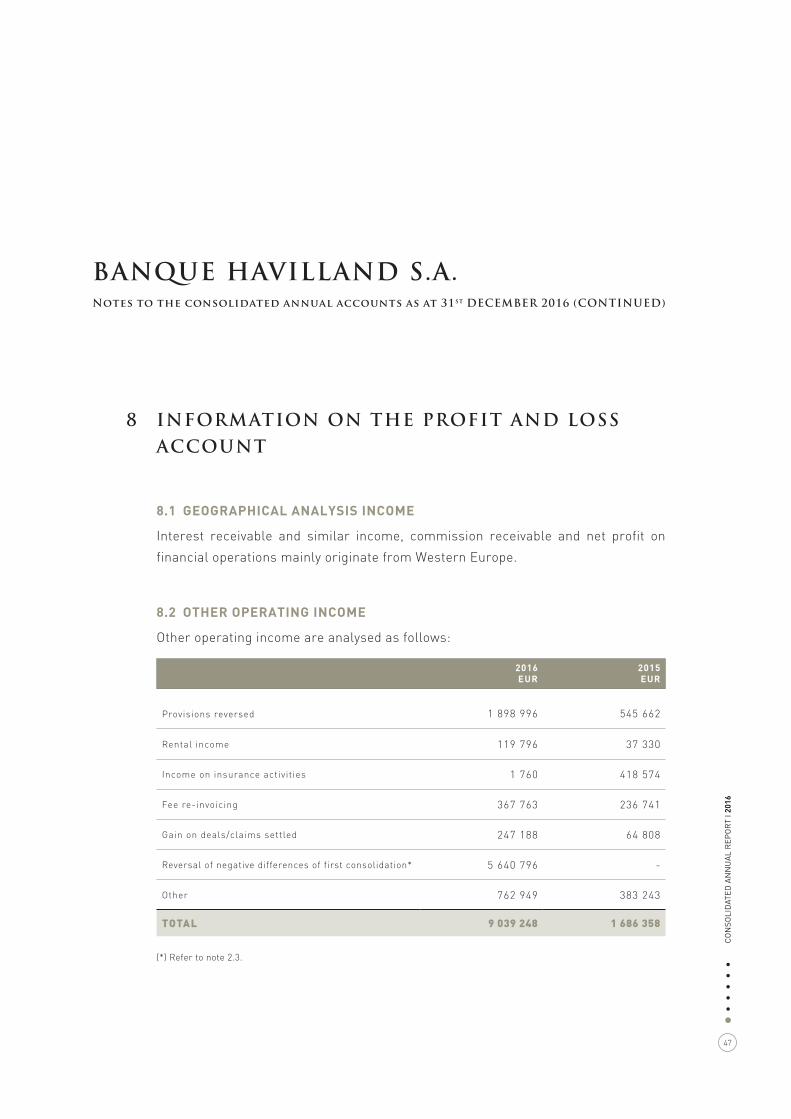

8 INFORMATION ON THE PROFIT AND LOSS ACCOUNT

8.1 GEOGRAPHICAL ANALYSIS INCOME

Interest receivable and similar income, commission receivable and net profit on

financial operations mainly originate from Western Europe.

8.2 OTHER OPERATING INCOME

Other operating income are analysed as follows:

2016EUR

2015EUR

Provisions reversed 1 898 996 545 662

Rental income 119 796 37 330

Income on insurance activities 1 760 418 574

Fee re-invoicing 367 763 236 741

Gain on deals/claims settled 247 188 64 808

Reversal of negative differences of first consolidation* 5 640 796 -

Other 762 949 383 243

TOTAL 9 039 248 1 686 358

(*) Refer to note 2.3.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

48

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

8.3 OTHER OPERATING CHARGES

Other operating charges are analysed as follows:

2016 EUR

2015EUR

Write-off of receivables 703 156 1 514 373

Administrative fees reinvoiced 377 532 218 489

Provision for claims 1 000 000 -

Expenses on insurance activities 189 321 29 766

AGDL contributions - 170 484

Tax adjustments related to previous years 380 757 -

Other 292 870 805 782

TOTAL 2 943 636 2 738 894

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

49

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

8.4 NET VALUE ADJUSTMENTS IN RESPECT OF LOANS AND ADVANCES AND

PROVISION FOR CONTINGENT LIABILITIES AND FOR COMMITMENTS

This heading is analysed as follows:

2016EUR

2015EUR

Specific value adjustments on loans to customers

- Additions

- Reversals

3 187 924(36 030)

425 840(104 390)

Loan to customers fully impaired

Reversal of value adjustment on loan to customers fully impaired

Lump sum provision additions

12 209(154 006)1 612 272

400 000(1 788 410)

-

TOTAL (4 622 369) (1 066 960)

As at December 31, 2016, the lump sum provision amounts to EUR 7 075 938

(2015: EUR 2 491 893).

8.5 TAX INFORMATION

The parent company is liable to taxes on income and net assets in line with the

Luxembourg legislation.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

50

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

9 OTHER INFORMATION

9.1 COUNTRY BY COUNTRY INFORMATION

According to Article 38-3 of the law of April 5, 1993 as amended by the law of

July 23, 2015, the credit institutions, financial holding companies and investment

companies must publish information on their locations and activities, included in

their scope of consolidation in each state or territory.

As at December 31, 2016, country by country information are analysed as follows (in EUR):

EU MEMBER COUNTRIES

STATUTORY OPERATING

INCOME

STATUTORY PROFIT OR LOSS

BEFORE TAX

STATUTORY TAX ON PROFIT OR

LOSS

NUMBER OF EMPLOYEES

Luxembourg* 49 052 996 12 412 205 (546 921) 125

United Kingdom* 3 303 677 561 191 - 15

NON-EU MEMBER COUNTRIES

STATUTORY OPERATING

INCOME

STATUTORY PROFIT OR LOSS

BEFORE TAX

STATUTORY TAX ON PROFIT OR

LOSS

NUMBER OF EMPLOYEES

Bahamas 3 154 162 (2 092 254) - 11

Liechtenstein 7 199 473 118 086 21 287 20

Monaco 3 630 689 164 076 - 15

Switzerland 3 526 215 (3 642 783) - 40

Russia - (485 699) (77 093) 3

(*) Audited

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

51

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

No public subsidies have been received by the Group during the year that ended

December 31, 2016.

As at December 31, 2015, country by country information are analysed as follows (in EUR):

EU MEMBER COUNTRIES

STATUTORY OPERATING

INCOME

STATUTORY PROFIT OR LOSS

BEFORE TAX

STATUTORY TAX ON PROFIT OR

LOSS

NUMBER OF EMPLOYEES

(FTE)

Luxembourg* 29 813 339 5 026 160 (531 710) 77

United Kingdom* 1 423 290 (992 083) - 13

NON-EU MEMBER COUNTRIES

STATUTORY OPERATING

INCOME

STATUTORY PROFIT OR LOSS

BEFORE TAX

STATUTORY TAX ON PROFIT OR

LOSS

NUMBER OF EMPLOYEES

(FTE)

Bahamas 2 795 869 (1 287 515) (18 472) 11

Liechtenstein 3 890 023 (3 785 943) (1 123) 36

Monaco 3 333 072 141 530 - 14

No public subsidies have been received by the Group during the year that ended

December 31, 2015.

9.2 RETURN ON ASSETS

The return on assets of the Group for the year ended December 31, 2016 stands to 0.73%

(0.18% for the previous year). The return on assets is calculated as being the net profit

divided by the total balance sheet.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

52

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

9.3 PERSONNEL EMPLOYED

The average number of persons employed during the financial year was as follows:

2016 2015

Management 30 16

Employees 191 130

TOTAL 221 146

9.4 MEMBERS OF THE ADMINISTRATION, MANAGERIAL AND SUPERVISORY

BODIES

Remuneration paid to the various bodies of the Group during the financial year was

as follows:

2016EUR

2015EUR

Management 4 553 528 3 130 432

Supervisory body 721 867 209 040

TOTAL 5 275 395 3 339 472

Loans and advances granted to members of the Management and the Board of

Directors as at December 31, 2016 amount to 3 586 494 (2015: EUR 0).

As at December 31, 2016, no guarantee has been issued in favour of member of the

Management and the Board of Directors.

It was decided at the Annual General Meeting held on April 14, 2016 that three

Board members of the Bank in Luxembourg received emoluments in respect of their

duties for a total gross amount of EUR 195 000 related to the fiscal year ended

December 31, 2016 (2015: EUR 195 000).

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

53

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

9.5 INDEPENDENT AUDITOR’S FEES

Fees billed (excluding VAT) to the Group by PricewaterhouseCoopers, Société

coopérative, Luxembourg and other member firms of the PricewaterhouseCoopers

network during the year are as follows:

2016EUR

2015EUR

Audit fees 1 131 684 672 811

Audit-related fees 14 689 -

Tax-related fees 25 219 22 496

Other fees 172 522 562 743

TOTAL 1 344 114 1 258 050

Such fees are presented under other administrative expenses in the consolidated

profit and loss account.

9.6 SUBSEQUENT EVENT

Banque Havilland Institutional Services (formerly Banco Popolare Luxembourg S.A.)

will be merged by absorption with the Bank during 2017 and will become a dedicated

business line of the Bank. All services to institutional investors will be maintained

and further developed by the Institutional business line. The merger application has

been submitted to the CSSF for approval.

BANQUE HAVILLAND S.A.Notes to the consolidated annual accounts as at 31st DECEMBER 2016 (CONTINUED)

“A PASSING WAVE IN HOOKENA” by Jean–Marie Ghislain

“SYMPHONY IN HOOKENA” by Jean–Marie Ghislain

“SPRING IN HOOKENA” by Jean–Marie Ghislain

©Jean–Marie Ghislain - www.ghislainjm.com

“A PASSING WAVE IN HOOKENA” par Jean–Marie Ghislain

“SYMPHONY IN HOOKENA” par Jean–Marie Ghislain

“SPRING IN HOOKENA” par Jean–Marie Ghislain

56

CO

NSO

LID

ATE

D A

NN

UA

L R

EP

OR

T I 2016

••••••

2017_1w. banquehavilland.com

BANQUE HAVILLAND S.A.

35a, avenue J.F. Kennedy • L-1855 Luxembourg • t. +352 463 131 • f. +352 463 132 • R.C.S. Luxembourg B 147029 T.V.A. LU23366742

BANQUE HAVILLAND INSTITUTIONAL SERVICES S.A.

35a, avenue J.F. Kennedy • L-1855 Luxembourg • t. +352 463 131 • f. +352 463 132 • R.C.S. Luxembourg B 47796 T.V.A. LU16027373

BANQUE HAVILLAND S.A. (UK BRANCH)

5 Savile Row • London • W1S 3PB • United Kingdom • t. +44 20 7087 7999 • f. +44 20 7087 7995 • Company Registration N° BR014651 • V.A.T. N° GB167 1621 10Supervised by the Financial Conduct Authority and Prudential Regulation Authority in UK and regulated by the Commission de Surveillance du Secteur Financier in Luxembourg

BANQUE HAVILLAND (MONACO) S.A.M. Société Anonyme Monégasque au capital de 20.000.000 euros

Le Monte Carlo Palace • 3-7, Boulevard des Moulins • MC-98000 Monaco • t. +377 999 995 00 • f. +377 999 995 01 R.C.I. 08s04856 • T.V.A. FR 00 00008050 6

BANQUE HAVILLAND (LIECHTENSTEIN) AG

Austrasse 61 • LI - 9490 Vaduz • Liechtenstein • t. +423 239 33 33 • f. +423 239 33 00 • Handelsregister Nr. FL-1.542.492-8 • MWST. Nr. 53652

BANQUE HAVILLAND (BAHAMAS) LTD.

Unit 1 Western New Providence • Mt. Pleasant Village, Western Road • P.O. Box AP-59241 • Nassau • Bahamas t. +242 702 2900 • f. +242 362 6186 • Company Registration N° 39 268

BH INTERNATIONAL LLC