Embed Size (px)

Citation preview

Celebratin

g

Success

Annual Report 2016

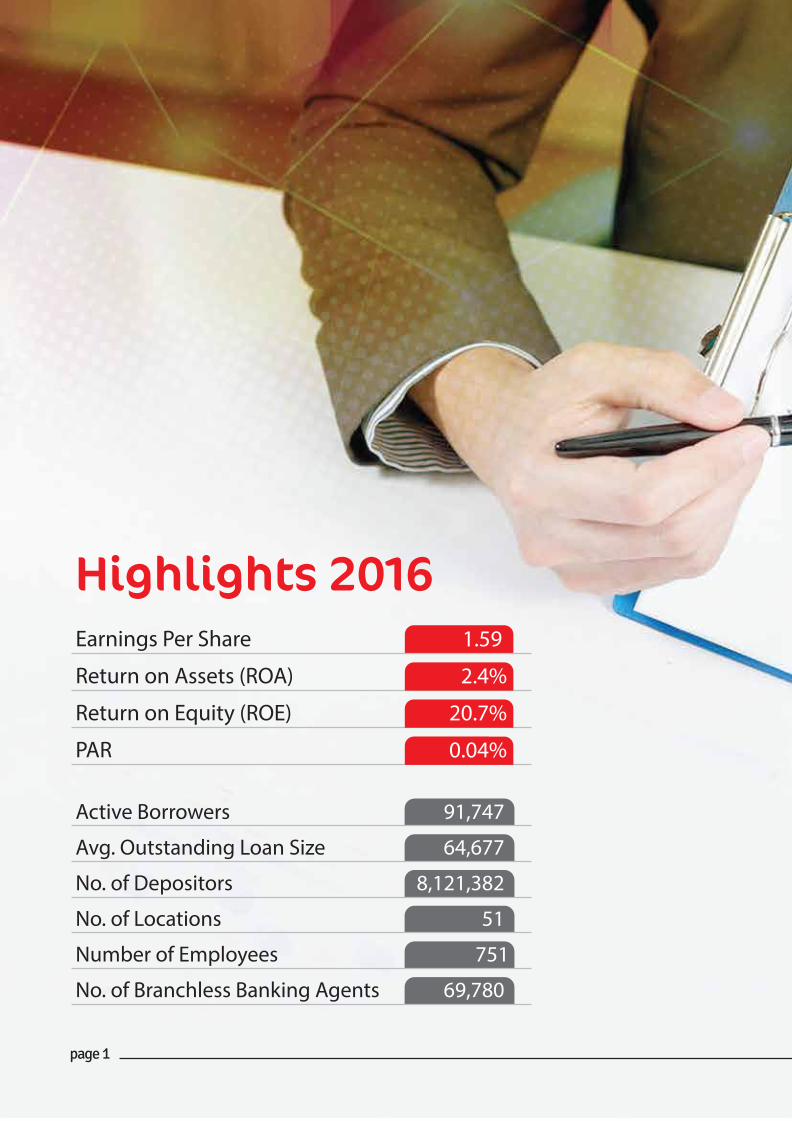

Highlights 2016

Innovative Financial Solutions

About Mobilink Bank

Board of Directors

Management Team

Vision, Mission & Values

Our Products

Branch Network

Five Year Journey

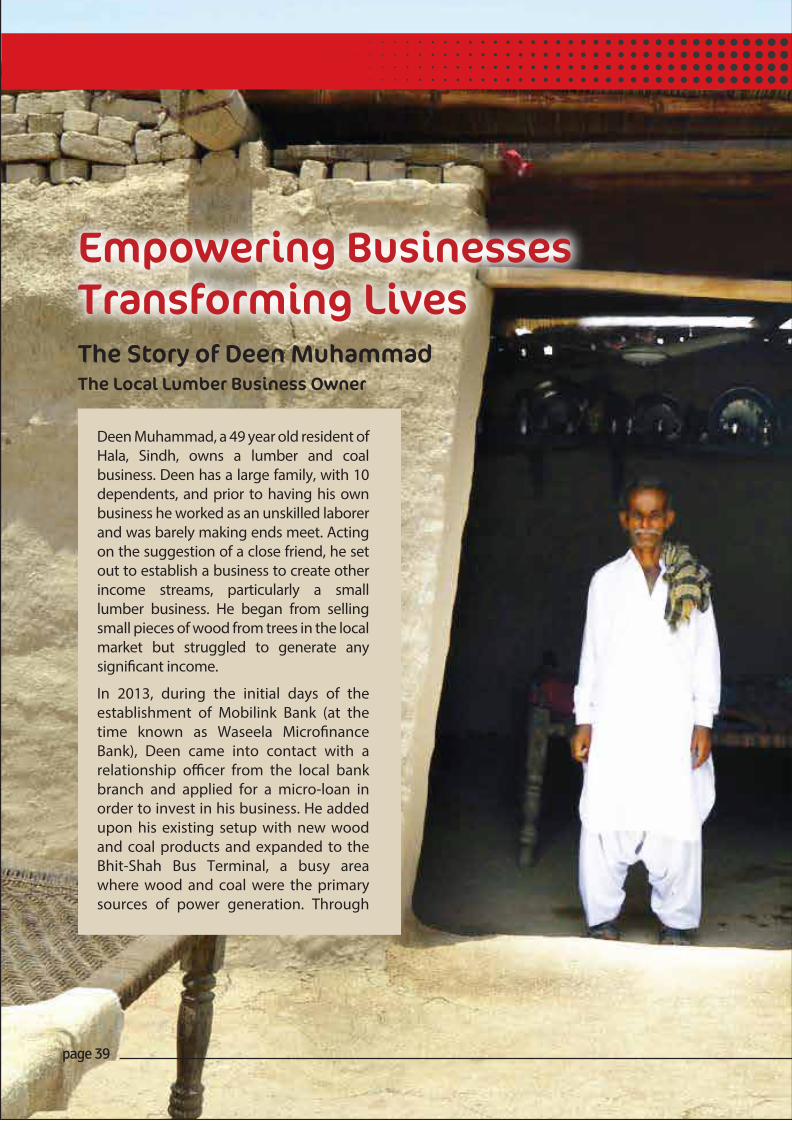

Empowering Businesses: The Story of Deen Muhammad

Director’s Report

CEO’s Message

Chief Digital & Financial Services Officer’s Message

Auditor’s Report

Financial Statements

Notes to Financial Statements

01

06

17

21

23

27

29

31

33

39

42

45

47

49

51

56

Contents

Active Borrowers

Avg. Outstanding Loan Size

No. of Depositors

No. of Locations

Number of Employees

No. of Branchless Banking Agents

Earnings Per Share

Return on Assets (ROA)

Return on Equity (ROE)

PAR

1.59

2.4%

20.7%

0.04%

Highlights 2016

91,747

64,677

8,121,382

51

751

69,780

page 1

The Power of Progress

Mobilink

Microfinance Bank“A/A1”Credit RatingBy PACRA

page 2

MobileAccount*786#

page 3

PAY BILLS

SAVINGS &

INSURANCE

100

MOBILE LOAD

100

PAYMENTS

ATM CARD

SEND MONEY

Rs.

page 4

page 5

Innovative Financial Solutions Drivers of Growth & Success Our innovative financial solutions include a diversified range of products and services such as Domestic Remittance, International Remittance, G2P Disbursements, Utility Bills Payment, Inter-Bank Fund Transfer (IBFT), Pre & Post-Paid Top-Ups, Real time Fee/Loan/Donation/Insurance/Passport/ Tickets Payments, Digital Account opening through bio-metric verification, Loans Disbursements, CASA/TDR accounts, Bankers Cheques and Running Finance. These services are accessible through both Branch and Branchless Banking Platforms, and can be accessed real time through Branchless Banking, Over-the-Counter, Internet Banking, Mobile Application, CCDMs/ATMs/POS/Other-ADC Channels. Our financial solutions have transformed the microfinance industry in Pakistan. In the last five years we have introduced a diversified portfolio of financial products and spearheaded the launch of a cutting-edge branchless banking service under the brand JazzCash making us a leading player in technology driven microfinance solutions in Pakistan.

page 6

page 7

Pakistan’s Largest DigitalBank

page 8

First

Microfinance Bank

to Introduce

page 9

page 10

CCDMCash & Cheque

Deposit Machine

page 11

page 12

Internet Banking

&

Mobile Banking App

page 13

page 14

Visa Classic

QURAT-UL-AEIN

Visa Debit Card

page 15

Visa Classic

QURAT-UL-AEIN

page 16

* Coming Soon

page 17

With over 11 million mobile wallets, Mobilink Bank has become Pakistan’s largest digital bank in a short span of 4 years. Mobilink Microfinance Bank, formerly Waseela MF Bank, a Global Telecom - VEON Group company, started operations in April 2012 and launched branchless banking operations under the brand name ‘Jazzcash’ in partnership with Pakistan's largest telecom operator ‘Jazz’ in November 2012.

Being a hybrid model, that combines traditional microfinance with mobile / digital banking and agent based banking, the bank now operates with 51 branches, a nationwide network of 70,000 branchless banking agents and a USSD (GSM) based digital channel offering savings, micro-enterprise loans, small housing loans, remittances, collections (of utility bills and loan instalments), mobile wallets, insurance, G2P, B2B & B2P payments, the bank currently plays a leading role in the promotion of financial inclusion. Despite being a young bank, Mobilink Bank has emerged as a front

About Mobilink BankAbout Mobilink Bank

page 18

runner in the sector, having achieved financial break-even within four years of commencement of operations, one of the fastest in the industry.

Mobilink Bank & Jazz, under the brand of Jazzcash, envision to become market leaders in digital financial services. Due to rapid increase in the smartphone user base in the country, distinction between traditional and mobile financial services is rapidly diminishing. Therefore, the Bank continues to invest in technology and systems to maintain it’s lead in digitalization of financial services. Mobilink Bank’s strategy is to take banking from the confines of a limited number of brick and mortar structures to customers’ cell phones thereby removing a major barrier in expanding coverage and outreach, significantly increasing access to financial services such as savings, loans, insurance and transactional services.

• 0pened 26 new branches, reaching a total of 30• Ended the year with deposits of Rs. 644 million (573.9% increase from

2012) and 66,279 depositors• GLP closed at Rs. 178 Million• Jazz Cash agents reached a count of 26,578, 2.51 million remittance

transactions and 5.5 million Utility Bill Payments.

2013

• Opened 8 new Booths• Launched Interbank Fund Transfer (IBFT) service in November 2014.• Launched ATM card on May 02, 2014 and installed its first ATM

machine on July 07, 2014.• Closed deposits at Rs. 1.3 Billion with 311,748 depositors • GLP was closed at Rs. 500 Million • Jazz Cash agents reached to 49,586 with 15.8 million remittance

transactions 9.314 million utility bill payments.

2014

• Opened first branch on May 2, 2012• Pilot launch of branchless banking on May 31, 2012• Commercial launch of branchless banking on November 5, 2012 with

brand name Mobicash.• Opened four branches and six service centers • Ended year with Rs. 112 Million deposit with 8,655 depositors• Ended year at GLP of Rs. 6.5 Million• Branchless banking agents reached to 5,030, had 5,885 home

remittance transactions and 62,375 Utility Bill Payments.

2012

page 19

• MMBL launched Banca assurance for its customers• Closed its deposit at Rs. 3.2 Billion with 3.2 Million depositors• GLP was closed at Rs. 1.4 Billion• Jazz Cash agents reached to 58,818 with 28.4 Million remittance

transactions and 2.2 Million Utility Bill Payments.• Launched international remittance services on August 18, 2015. • Launched savings account products for mobile wallet accounts in

August 2015.

2015

• Opened 05 new branches & 8 new booths in 2016 with total number of branches reaching 35 with 16 booths.

• Launched NFC payments for mobile wallets in March 2016• Re-branded from Waseela Microfinance Bank Limited to Mobilink

Microfinance Bank Limited in May 2016.• Launched Internet Banking services In November, 2016, being the first

MFB to offer these services.• Started disbursement of loans straight to mobile wallets in November

2016.• Closed its deposit at Rs. 10.3 Billion with 8.12 Million depositors • GLP was closed at Rs. 5.9 Billion • Jazz Cash agents reached to 69,767 with 36 Million remittance

transactions and 4.5 Million Utility Bill Payments

2016

page 20

Aamir Hafeez IbrahimDirector / Chairman

A highly motivated leader with the proven ability to develop organizations and drive revenues. Mr. Ibrahim possesses vast cross-functional experience that encompasses strategic marketing & sales, stakeholder management and corporate strategy. His track record includes successful leadership roles in Pakistan as well as Thailand, UK, UAE, Switzerland and USA across the telecom and automotive industry.

Niaz BrohiDirector

Presently the Chief Legal Officer at Jazz and having previously worked with the Pakistan Telecom Authority, Mr. Brohi, has over 15 years of experience in the telecom sector specialising in regulatory and corporate affairs, litigation and management, due diligence, mergers and acquisitions, risk assessment and advising the board of directors.

Salim Nooruddin JiwaniDirector

With over 15 years of experience in policy planning, financial management, institutional assessment and transformation of microfinance institutions, Mr. Jiwani believes in poverty reduction and economic empowerment. He has previously served on the Board of Directors of the First Microfinance Bank, Kashf Microfinance Bank and Pakistan Microfinance Network.

Muhammad Usman BajwaDirector

A corporate finance professional with over 10 years of experience in treasury and financial management. Mr. Bajwa is a qualified Chartered Financial Analyst (CFA) with a proven record of managing extensive operations, large teams and various types of financing, debt and capital transactions.

page 21

Board of Directors:

Ghazanfar AzzamDirector

Ghazanfar Azzam is the President and CEO of Mobilink Microfinance Bank Limited. He has vast experience and exceptional achievements to his credit in retail, commercial, consumer, SME and micro-banking segments.In a career spanning over 30 years, Ghazanfar has worked for some of the best banks in Pakistan including HBL, Union Bank, Prime Bank & Bank Alfalah in retail, commercial, consumer, SME Banking and Training & Development.In recognition of his contributions to HR Development in banking industry, he was awarded the prestigious Hubert Humphrey Fellowship by the United States Government for the year 2000-01 under Fulbright Program. He has attended advanced seminars and management development programs at LUMS, World Bank Institute in Washington DC and Harvard Business School.

page 22

Azfar ManzoorDirector

Mr. Azfar is a seasoned professional having 22 years’ experience in the Telecommunication industry. He had done his Electrical engineering from USA & MBA from Lahore University of Management Sciences. He presently is board member of Universal Service Fund and Regional Chair of Massachusetts Institute of Technology. Currently serving as Vice President/ Head of B2B Business Unit & CEO Link.Net Telecom Ltd.

David Leslie Christopher Dobbie Director

A young professional having 14 years’ experience in Legal and corporate affairs. He is an expert in International Transactions with specialties in international cross border transactions and mergers & acquisitions. Mr. Dobbie is a graduate from University of Auckland with in Law & Accounting. He is currently working as Deputy General Counsel in Vimpel Com.

Management Team:

Ghazanfar AzzamPresident / CEO

Ghazanfar Azzam is the President and CEO of Mobilink Microfinance Bank Limited. He has vast experience and exceptional achievements to his credit in retail, commercial, consumer, SME and micro-banking segments.In a career spanning over 30 years, Ghazanfar has worked for some of the best banks in Pakistan including HBL, Union Bank, Prime Bank & Bank Alfalah in retail, commercial, consumer, SME Banking and Training & Development.In recognition of his contributions to HR Development in banking industry, he was awarded the prestigious Hubert Humphrey Fellowship by the United States Government for the year 2000-01 under Fulbright Program. He has attended advanced seminars and management development programs at LUMS, World Bank Institute in Washington DC and Harvard Business School.

Muhammad Asim AnwarChief Operating Officer (COO)

A Seasoned Microfinance Professional with more than 16 years of diversified experience across key business segments including Business Banking, Bank Operations, Branchless Banking, Administration & Procurement. While managing larger workforce across various locations in the country, Asim has been deeply involved in mobilizing the field operations and achieving bank revenue targets through quality portfolios, diversified business products and effective client management.

page 23

Ghazanfar SiddiqueGroup Head IT & Operations

Business and Technology Integration Specialist with 20 years of diversified experience in Banking, Digital Transformation and IT industries having domain exposure of Retail, Branchless Banking, Payment and Card Solutions. Worked as senior management positions in Pakistan, Malaysia and North Africa in Standard Chartered, Jaiz Bank PLC.

Shahzad Nazir KhanHead Risk Management

A Risk Management professional with diverse banking experience with International and Local Financial Institutions. Having extensive exposure to Business Banking as well as Risk Management in segments ranging from Corporate, SMEs to Microfinance, Shahzad has an effective ability to understand, assess and respond to the ever changing business dynamics. Always promoting a team based and constant learning culture at all levels enables Shahzad to keenly drive the evolution of Microfinance to Digital Banking while effectively safeguarding the interest of all stakeholders. Being a Change Management leader, Shahzad believes that effective communication and repeated transmission of MMBL’s core values not only strengthens our organization but also our people at an individual level.

page 24

Management Team:

page 25

Tayseer AliChief Financial Officer (CFO)

Tayseer is a Chartered Accountant from ICAEW and a Fellow Chartered Certified Accountant. He joined the Bank in January 2017 and was previously working for Pak China Investment Co. as CFO. Tayseer has been associated with the financial sector since 2011.

Syed Sajjad QayyumGroup Head Compliance Affairs

and Service Quality

S. Sajjad Q. Ashraf is an experienced banker having worked in different Instutitions in various capacities, including Leadership roles. Sajjad’ s experience covers key banking functions such as Credit, Operations, Business Banking, Compliance, risk management, Strategic Planning/Business Initiatives, and teams building. He is MBA, LLB(Pb.), D.A.I.B.P.

Naj-Mus-Sahar SabzwariHead Internal Audit

Sabzwari has about 20 years of extensive experience in the field of audit encompassing both commercial and microfinance banking environment. He is a Fellow member of Institute of Chartered Accountants of Pakistan (ICAP) with added qualifications of CISA, CISM and CIA. He is reporting to the Board Audit Committee.

Samiha Ali ZahidHead HR and Trainings

Samiha Ali Zahid brings with her 15 years of cross functional experience in OD, Staffing & HRM resulting in creating cohesive and high performing teams that contribute towards business goals. She holds a Masters’ Degree in Public Administration and is a Certified Trainer. She has been recently Certified by Korn Ferry for their product suite "Korn Ferry Leadership Architect".

Samiha has proven experience of collaborating with other Business functions to initiate programs aimed at developing and sustaining a positive employer image crucial to attract and retain talent. Her expertise include development of policy guidelines aiming to bring internal and external equity for employees. For the last 6 years she has addressed and implemented strategic plans for managing people experience, compensation structure, retention and succession plans.

page 26

Mobilink Microfinance Bank aims to provide financial solutions to the economically underprivileged for their economic freedom by using innovative ADC’s and promoting micro businesses through an ethical and passionate team, which strives to deliver beyond expectations.

Missi n

Visi nMobilink Microfinance Bank aims to alleviate poverty and promote financial inclusion by providing innovative solutions.

page 27

CorporateValues

Collaborative Truthful

Entrepreneurial

Customer Obsessed Innovative

page 28

Solution forFinancial Empowerment

Salary Loan LSO loans Ready Cash

Micro Enterprise Loan Karobar Loan Khushhal Kisan Loan Fori Cash Loan

Livestock Loan Agri Passbook Loan Mobi House Tractor Loan

page 29

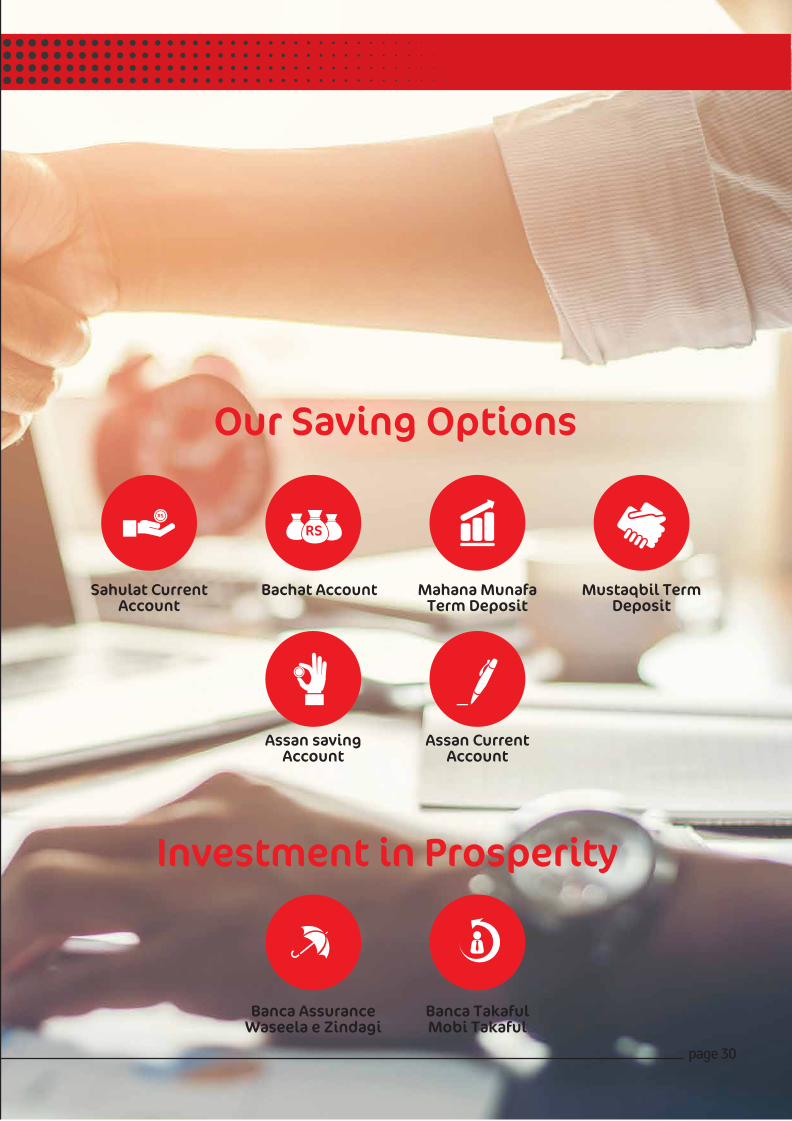

Our Saving Options

Sahulat CurrentAccount

Bachat Account Mahana MunafaTerm Deposit

Mustaqbil TermDeposit

Assan savingAccount

Assan CurrentAccount

Investment in Prosperity

Banca AssuranceWaseela e Zindagi

Banca TakafulMobi Takaful

page 30

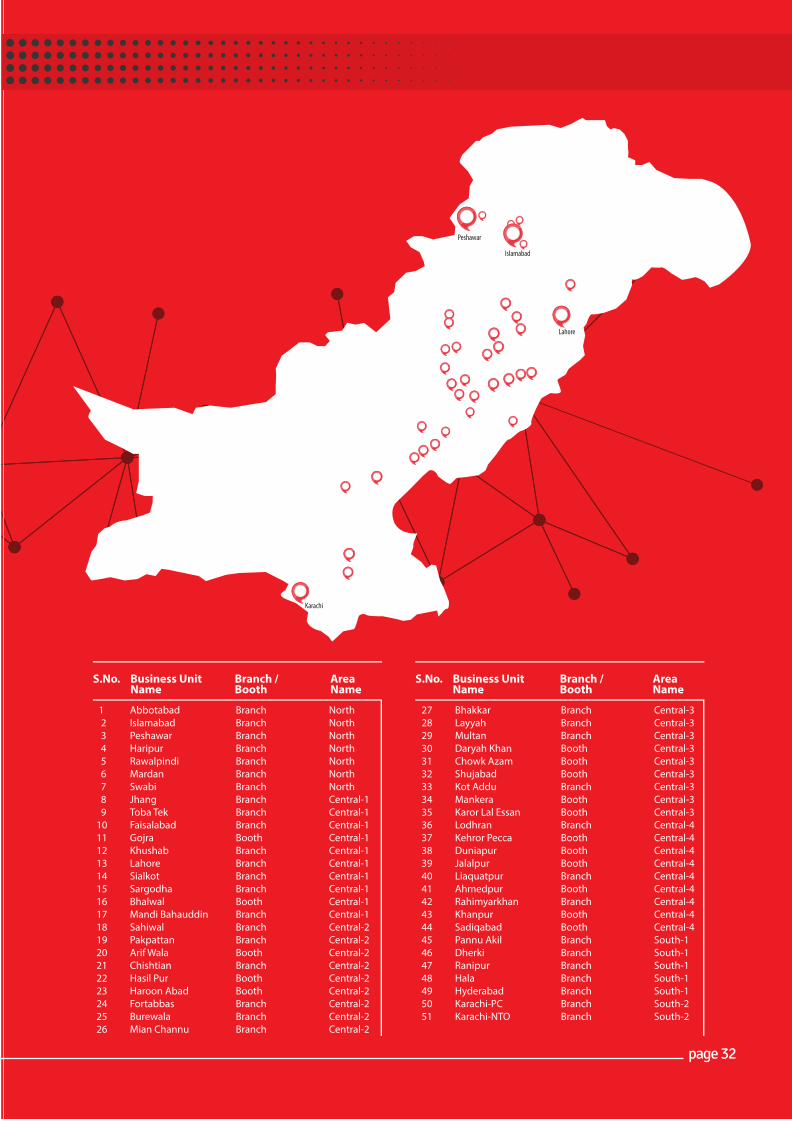

Branches51

BusinessAreas

06

10Central 1

09Central 2

09Central 3

07North

07South

09Central 4

Multan & LayyahFaisalabad & Sargooda

Pannu AqilPeshawar

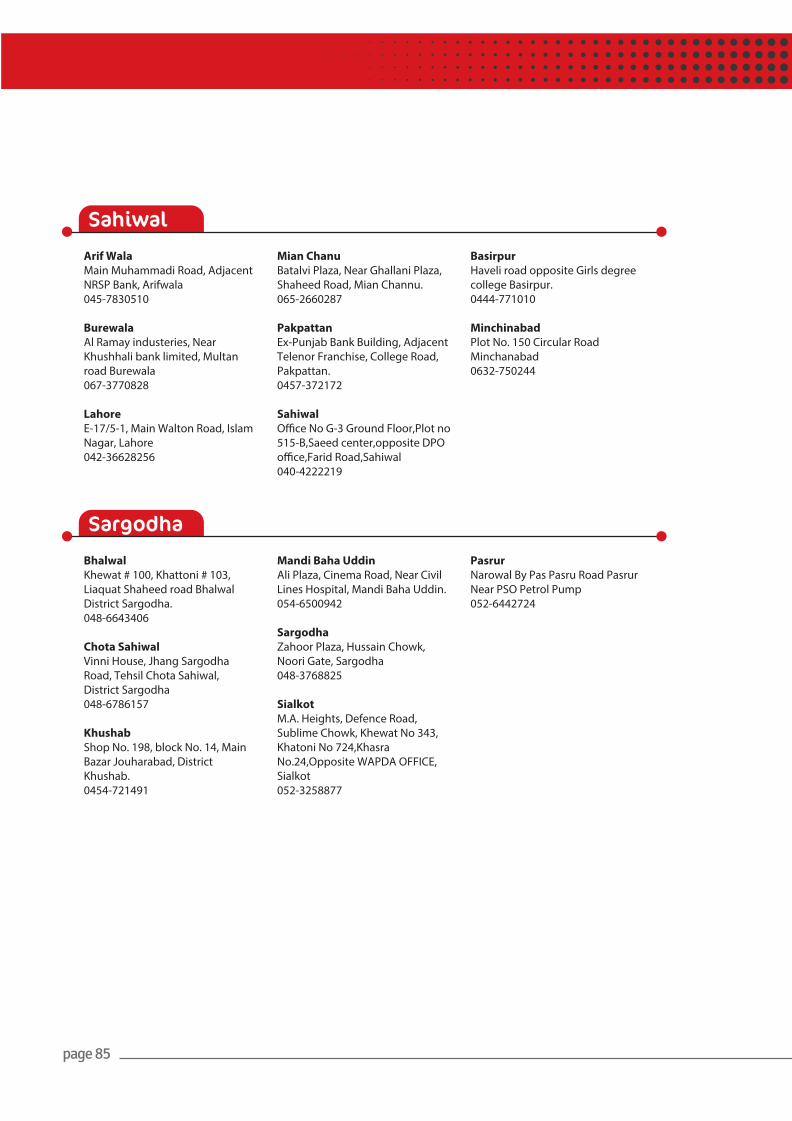

Rahim Yar KhanSahiwal

Business Areas

Branches Network

page 31

Peshawar

Islamabad

Lahore

Karachi

1 Abbotabad Branch North 2 Islamabad Branch North 3 Peshawar Branch North 4 Haripur Branch North 5 Rawalpindi Branch North 6 Mardan Branch North 7 Swabi Branch North 8 Jhang Branch Central-1 9 Toba Tek Branch Central-1 10 Faisalabad Branch Central-1 11 Gojra Booth Central-1 12 Khushab Branch Central-1 13 Lahore Branch Central-1 14 Sialkot Branch Central-1 15 Sargodha Branch Central-1 16 Bhalwal Booth Central-1 17 Mandi Bahauddin Branch Central-1 18 Sahiwal Branch Central-2 19 Pakpattan Branch Central-2 20 Arif Wala Booth Central-2 21 Chishtian Branch Central-2 22 Hasil Pur Booth Central-2 23 Haroon Abad Booth Central-2 24 Fortabbas Branch Central-2 25 Burewala Branch Central-2 26 Mian Channu Branch Central-2

27 Bhakkar Branch Central-3 28 Layyah Branch Central-3 29 Multan Branch Central-3 30 Daryah Khan Booth Central-3 31 Chowk Azam Booth Central-3 32 Shujabad Booth Central-3 33 Kot Addu Branch Central-3 34 Mankera Booth Central-3 35 Karor Lal Essan Booth Central-3 36 Lodhran Branch Central-4 37 Kehror Pecca Booth Central-4 38 Duniapur Booth Central-4 39 Jalalpur Booth Central-4 40 Liaquatpur Branch Central-4 41 Ahmedpur Booth Central-4 42 Rahimyarkhan Branch Central-4 43 Khanpur Booth Central-4 44 Sadiqabad Booth Central-4 45 Pannu Akil Branch South-1 46 Dherki Branch South-1 47 Ranipur Branch South-1 48 Hala Branch South-1 49 Hyderabad Branch South-1 50 Karachi-PC Branch South-2 51 Karachi-NTO Branch South-2

AreaName

S.No. Business UnitName

Branch /Booth

AreaName

S.No. Business UnitName

Branch /Booth

page 32

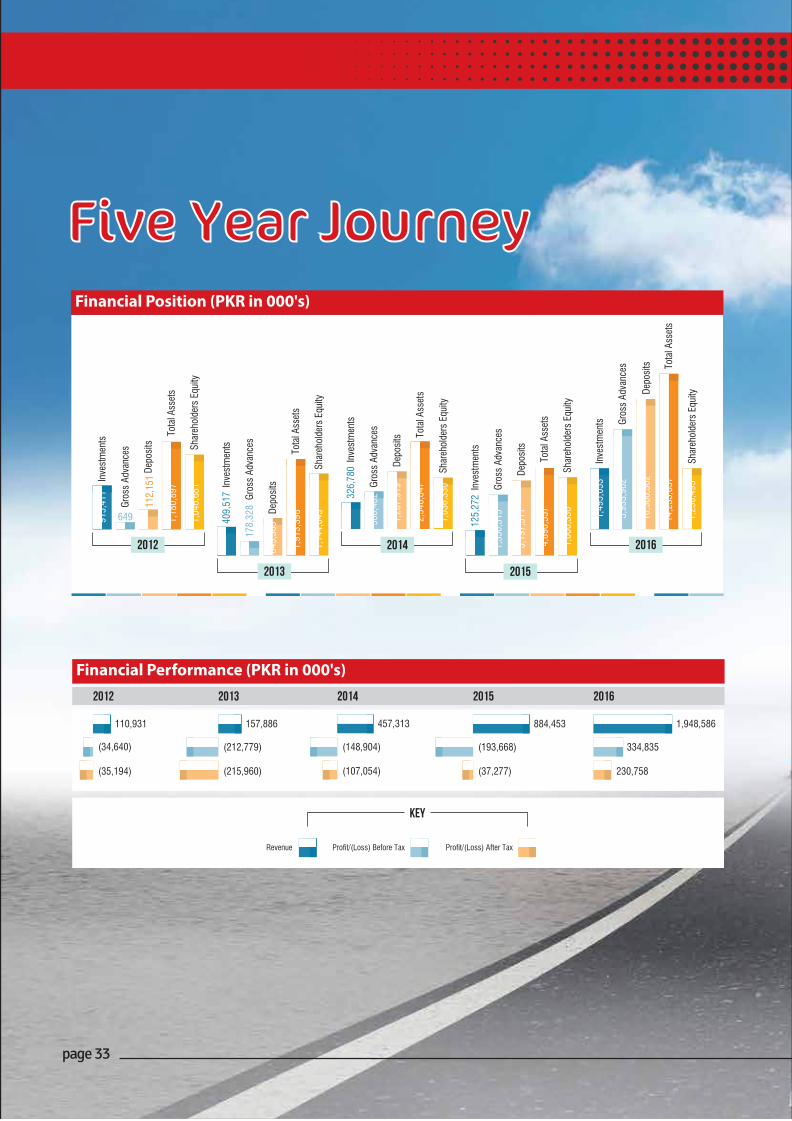

Five Year Journey

649

Investm

ents

Gro

ss A

dvances

Deposits

Tota

l A

ssets

Share

hold

ers

Equity

112,1

51

1,1

80,8

97

915,4

11

1,0

46,6

81

2012

409,5

17

178,3

28

Investm

ents

Gro

ss A

dvances

Deposits

Tota

l A

ssets

Share

hold

ers

Equity

645,3

69

1,9

13,3

98

1,1

44,0

45

2013

125,2

72

Investm

ents

Gro

ss A

dvances

Deposits

Share

hold

ers

Equity

1,3

50,3

15

3,1

97,3

11

4,8

90,5

57

1,0

00,3

36

2015

Investm

ents G

ross A

dvances

Deposits Tota

l A

ssets

Share

hold

ers

Equity

2016

1,4

95,0

53

5,9

33,9

62

10,3

06,3

62

14,2

33,8

57

1,2

30,4

93

Financial Position (PKR in 000's)

(34,640)

Revenue Profit/(Loss) Before Tax

Key

Profit/(Loss) After Tax

2012 2013

(35,194)

110,931

(212,779)

(215,960)

157,886

2014

(148,904)

(107,054)

457,313

2015

(193,668)

(37,277)

884,453

2016

334,835

230,758

1,948,586

Financial Performance (PKR in 000's)

326,7

80

Investm

ents

Gro

ss A

dvances

Deposits T

ota

l A

ssets

Tota

l A

ssets

Share

hold

ers

Equity

2,5

40,8

47

1,2

87,9

19

500,4

02

1,0

36,3

30

2014

page 33

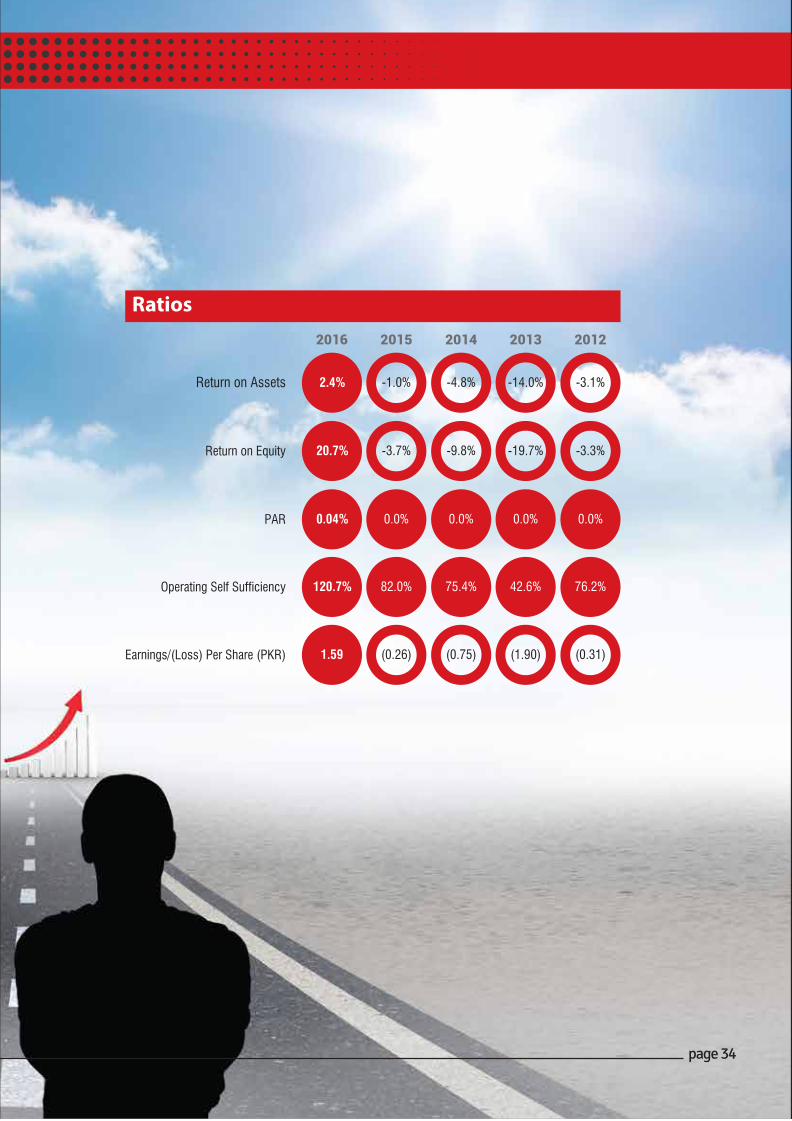

Return on Assets 2.4% -1.0% -4.8% -14.0% -3.1%

Ratios2016 2015 2014 2013 2012

Return on Equity 20.7% -3.7% -9.8% -19.7% -3.3%

Earnings/(Loss) Per Share (PKR) 1.59 (0.26) (0.75) (1.90) (0.31)

PAR 0.04% 0.0% 0.0% 0.0% 0.0%

Operating Self Sufficiency 120.7% 82.0% 75.4% 42.6% 76.2%

page 34

page 35

page 36

page 37

Business Units

Key Stats

Branches/Booths

2012

20132014

2015

2016

BranchLeSs banking agents

2012

20132014

2015

2016

Employees

2012

20132014

2015

201610

3641

41

51 -

26,550

49,573

58,568

69,780

346

130

475

620

751

Active Borrowers

2012

20132014

2015

201629

11,402

4,407 27,225

91,747

Depositors

2012

20132014

2015

20166,850

66,693

311,920

3,185,600

8,121,382

page 38

The Story of Deen Muhammad

Deen Muhammad, a 49 year old resident of Hala, Sindh, owns a lumber and coal business. Deen has a large family, with 10 dependents, and prior to having his own business he worked as an unskilled laborer and was barely making ends meet. Acting on the suggestion of a close friend, he set out to establish a business to create other income streams, particularly a small lumber business. He began from selling small pieces of wood from trees in the local market but struggled to generate any significant income.

In 2013, during the initial days of the establishment of Mobilink Bank (at the time known as Waseela Microfinance Bank), Deen came into contact with a relationship officer from the local bank branch and applied for a micro-loan in order to invest in his business. He added upon his existing setup with new wood and coal products and expanded to the Bhit-Shah Bus Terminal, a busy area where wood and coal were the primary sources of power generation. Through

The Local Lumber Business Owner

Empowering BusinessesTransforming Lives

page 39

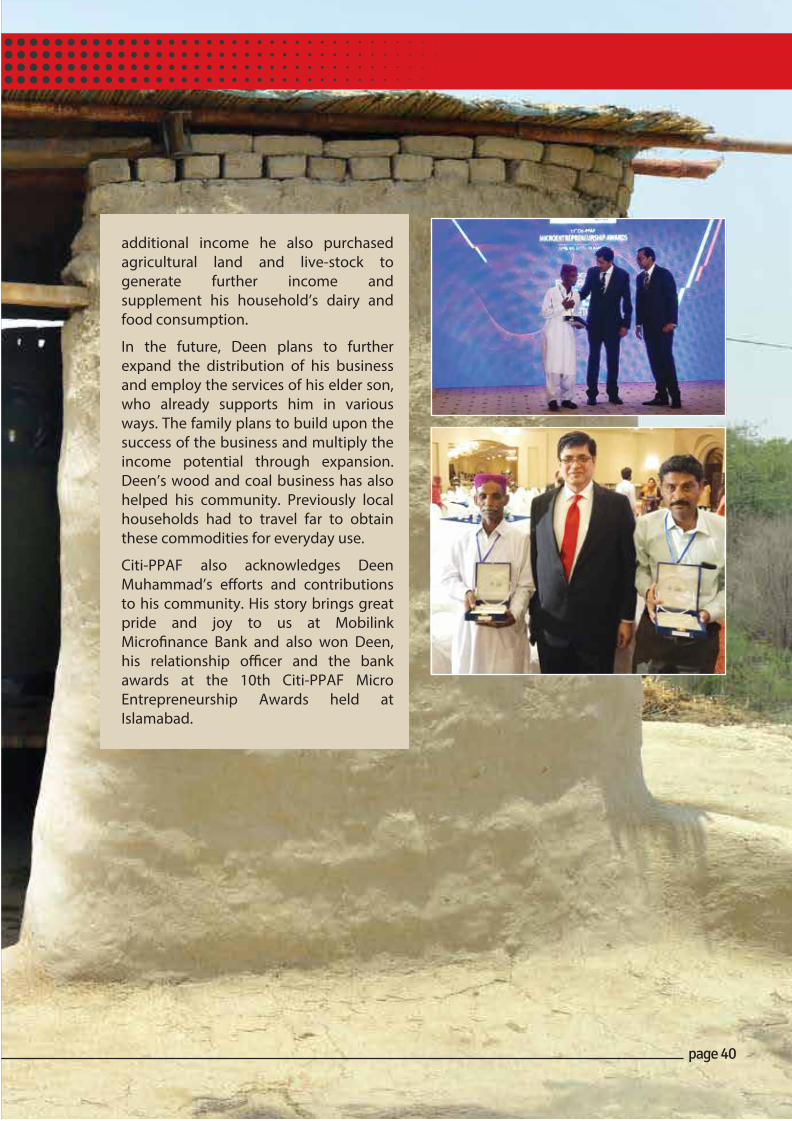

additional income he also purchased agricultural land and live-stock to generate further income and supplement his household’s dairy and food consumption.

In the future, Deen plans to further expand the distribution of his business and employ the services of his elder son, who already supports him in various ways. The family plans to build upon the success of the business and multiply the income potential through expansion. Deen’s wood and coal business has also helped his community. Previously local households had to travel far to obtain these commodities for everyday use.

Citi-PPAF also acknowledges Deen Muhammad’s efforts and contributions to his community. His story brings great pride and joy to us at Mobilink Microfinance Bank and also won Deen, his relationship officer and the bank awards at the 10th Citi-PPAF Micro Entrepreneurship Awards held at Islamabad.

page 40

ChairmanAamir Hafeez Ibrahim

page 41

For the year ended December 31, 2016

Financial Highlights:

Operational achievements/milestones:

Controls Framework:

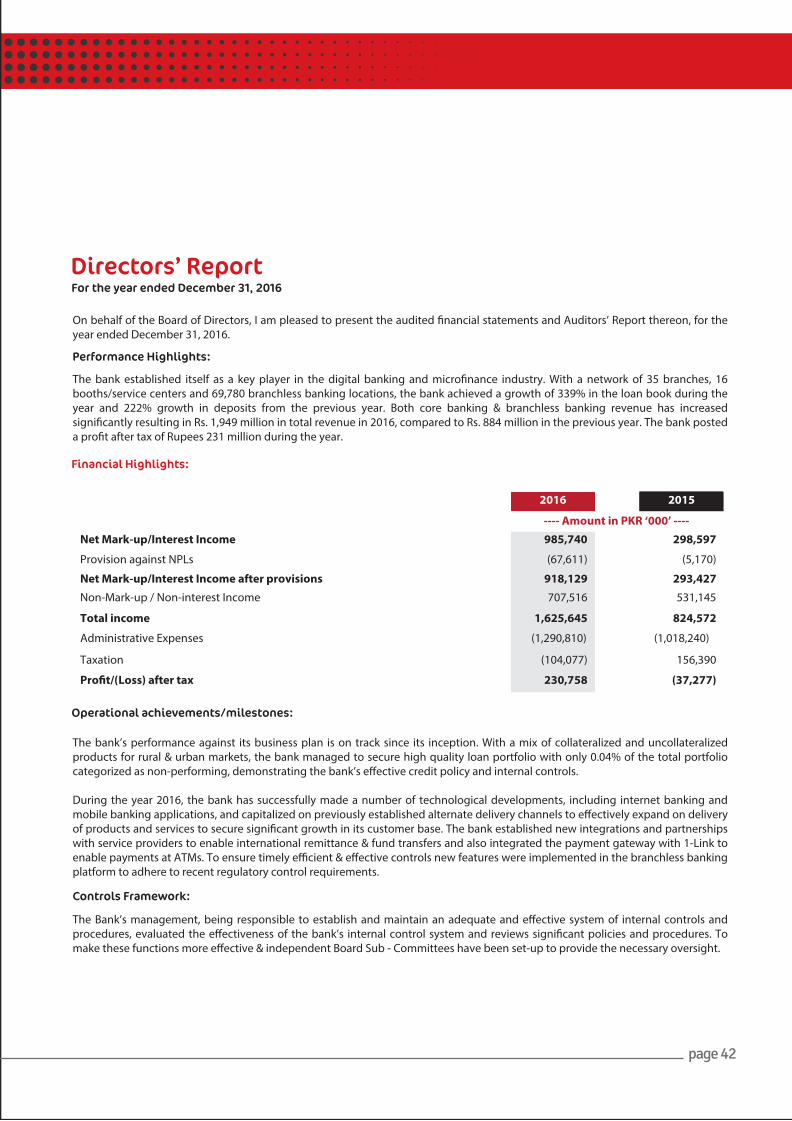

Directors’ Report

On behalf of the Board of Directors, I am pleased to present the audited financial statements and Auditors’ Report thereon, for the year ended December 31, 2016.

Performance Highlights:

The bank established itself as a key player in the digital banking and microfinance industry. With a network of 35 branches, 16 booths/service centers and 69,780 branchless banking locations, the bank achieved a growth of 339% in the loan book during the year and 222% growth in deposits from the previous year. Both core banking & branchless banking revenue has increased significantly resulting in Rs. 1,949 million in total revenue in 2016, compared to Rs. 884 million in the previous year. The bank posted a profit after tax of Rupees 231 million during the year.

The bank’s performance against its business plan is on track since its inception. With a mix of collateralized and uncollateralized products for rural & urban markets, the bank managed to secure high quality loan portfolio with only 0.04% of the total portfolio categorized as non-performing, demonstrating the bank’s effective credit policy and internal controls.

During the year 2016, the bank has successfully made a number of technological developments, including internet banking and mobile banking applications, and capitalized on previously established alternate delivery channels to effectively expand on delivery of products and services to secure significant growth in its customer base. The bank established new integrations and partnerships with service providers to enable international remittance & fund transfers and also integrated the payment gateway with 1-Link to enable payments at ATMs. To ensure timely efficient & effective controls new features were implemented in the branchless banking platform to adhere to recent regulatory control requirements.

The Bank’s management, being responsible to establish and maintain an adequate and effective system of internal controls and procedures, evaluated the effectiveness of the bank’s internal control system and reviews significant policies and procedures. To make these functions more effective & independent Board Sub - Committees have been set-up to provide the necessary oversight.

2016 2015

---- Amount in PKR ‘000’ ---- Net Mark-up/Interest Income 985,740 298,597

Provision against NPLs (67,611) (5,170)

Net Mark-up/Interest Income after provisions 918,129 293,427 Non-Mark-up / Non-interest Income 707,516 531,145

Total income 1,625,645 824,572

Administrative Expenses (1,290,810) (1,018,240)

Taxation (104,077) 156,390

Profit/(Loss) after tax 230,758 (37,277)

page 42

page 43

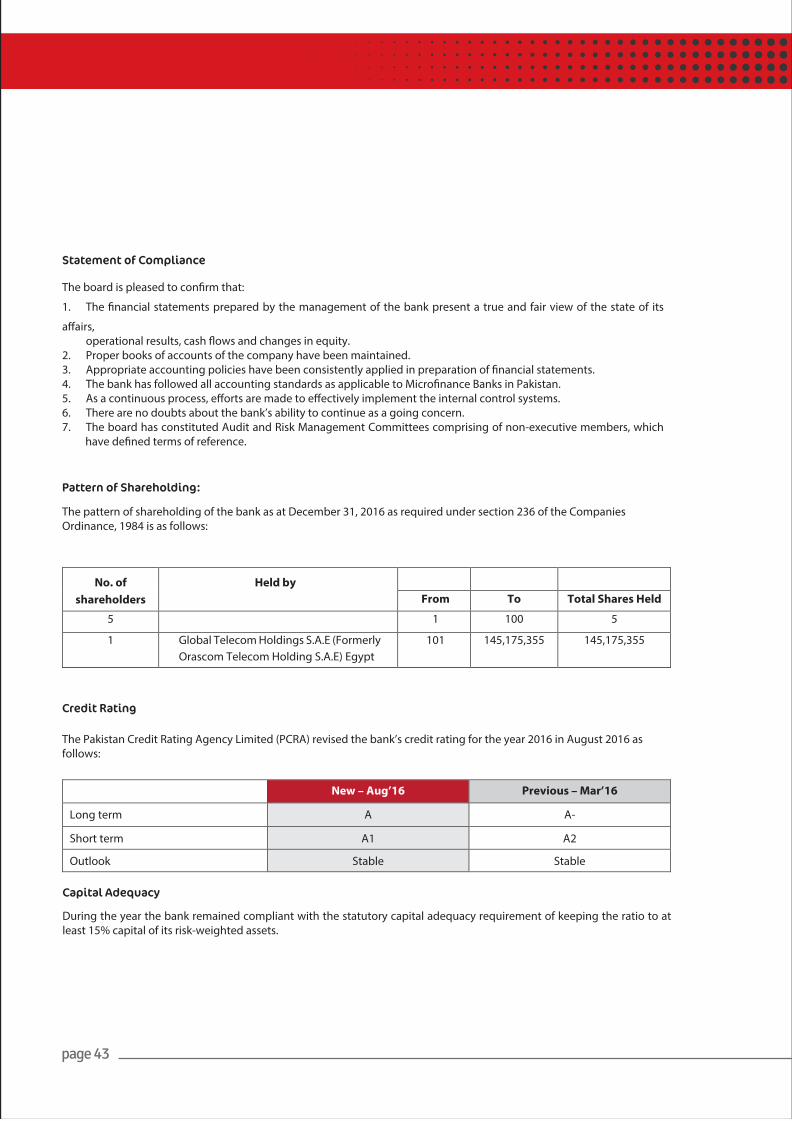

Statement of Compliance

Pattern of Shareholding:

The pattern of shareholding of the bank as at December 31, 2016 as required under section 236 of the Companies Ordinance, 1984 is as follows:

Credit Rating

The Pakistan Credit Rating Agency Limited (PCRA) revised the bank’s credit rating for the year 2016 in August 2016 as follows:

The board is pleased to confirm that:

1. The financial statements prepared by the management of the bank present a true and fair view of the state of its

affairs, operational results, cash flows and changes in equity.2. Proper books of accounts of the company have been maintained.3. Appropriate accounting policies have been consistently applied in preparation of financial statements.4. The bank has followed all accounting standards as applicable to Microfinance Banks in Pakistan. 5. As a continuous process, efforts are made to effectively implement the internal control systems. 6. There are no doubts about the bank’s ability to continue as a going concern.7. The board has constituted Audit and Risk Management Committees comprising of non-executive members, which

have defined terms of reference.

No. of shareholders

Held by

From To Total Shares Held

5 1 100 5

1 Global Telecom Holdings S.A.E (Formerly Orascom Telecom Holding S.A.E) Egypt

101 145,175,355 145,175,355

Capital Adequacy

During the year the bank remained compliant with the statutory capital adequacy requirement of keeping the ratio to at least 15% capital of its risk-weighted assets.

New – Aug’16 Previous – Mar’16

Long term A A-

Short term A1 A2

Outlook Stable Stable

page 44

Acknowledgements:

Aamir Hafeez IbrahimChairman

On behalf of the Board of Directors, I would like to appreciate the hard work put in by the employees of the bank in taking various initiatives during the year. I, on behalf of the Board, express gratitude to the State Bank of Pakistan for its continued support and guidance. Taking this opportunity, I would also thank, on behalf of the Board & the management, the customers for entrusting confidence in us and assure them that we remain committed to maintaining high service standards and a strong corporate governance and compliance in all our endeavors.

For and on behalf of the Board

became accessible to all mobile subscribers in Pakistan.

Resultantly the Bank achieved aggressive growth in all key indicators. The total asset base stood at PKR 14.2 billion, a growth of 191% from the previous year’s base of PKR 4.89 billion. The bank’s loan and deposit portfolios grew exponentially, closing the year at PKR 5.9 billion ( 339%) and PKR 10.3 billion ( 222%) respectively, with a pre-tax profit of PKR 334.8 million, a swing of 273% from last year’s loss of 193.6 million. The bank’s share of the country’s microfinance banking portfolio grew to 6.6%, from 2.4%, and our credit rating was improved to A/A-1 by PACRA.

Our strategy for the year, deemed ‘Quantum Leap 2016’, built upon our strength of being a digital and versatile institution, yielded outstanding results and I am proud of all we have managed to achieve. We now serve over 91,000 active loan customers, 137,000+ branch banking customers and close to 8 million mobile wallet accounts. During the year Jazzcash gained majority market share in active mobile wallets making it the leading mobile financial service in the country.

We progress into the new year seeking to face greater challenges, aiming higher and geared up to accomplish more. Leveraging on our strengths we will optimize our systems and operating structure towards enhanced efficiency and control to continue to grow effectively while maintaining standards of service delivery. The market we serve offers immense opportunity for growth and our edge of being digital and innovative will be pivotal to expanding on the services and value we offer to the country’s microfinance and digital financial ecosystem.

On behalf of the Board of Directors and the management, I would like to congratulate the team at Mobilink Microfinance Bank Limited (MMBL) on the close of the bank’s most impressive and successful year. In 2016 we took on the challenge to grow and expand on our business, products and services and in doing so we achieved tremendous goals and greatly enhanced our level of service delivery.

As the microfinance industry continues to grow on the premise of financial inclusion, it remains in need of disruptive intervention. The market stands at PKR 137 billion in outstanding micro-loans, 65% catered to by microfinance banks, with a total banked population of less than 18%. The opportunity remains quite vast with demand continuing to increase. Mobile financial services remain at the forefront of inclusion efforts as local and international influence guides efforts to further strengthen delivery channels and penetration of digital services.

In an evolving market, we felt it necessary to reposition ourselves in the arena of digital financial services. This included rebranding ourselves, to Mobilink Microfinance Bank, to better capitalize on the brand strength of our sister company. With our new image we set new goals for the organization and it is my pleasure to acknowledge that the team collectively strived and worked tirelessly to successfully achieve them.

We launched our state of the art internet banking services and mobile applications, expanded on our loan and deposit products, added 13 addition locations to our branch network and our branchless banking service, rebranded to Jazzcash, launched innovative insurance and remittance products, an online payment gateway and the Jazzcash account

CEO’s MESSAGEGhazanfar Azzam

page 45

page 46

In line with State Bank’s National Financial Inclusion Strategy, our focus is to take banking services to the masses. Our short term goal is to bring people in the financial net and offer them basic services like domestic transfers, bill payments, top ups and disbursements, and in the long run upgrade these customers to more sophisticated products like micro loans, online payments and debit cards. I would also like to thank State bank for all their guidance and support.

The world is changing at a very fast pace, but this is what makes our jobs and lives more exciting. We saw opportunity in the change; we re-thought and re-shaped our business to become more agile and innovative. Our ambition is to become a digital organization and we want to reshape the digital landscape in Pakistan. We need to continuously work on adapting ways to make things easier for our stakeholders both internally and externally. I would like to wish the best of luck to the Bank’s team for the years to come.

First of all, I would like to congratulate Mobilink Microfinance Bank on the completion of 5 successful years. It has been a phenomenal journey so far. We have secured a leading position in the Mobile Financial services category with more than 2 Million monthly active mobile accounts. On the traditional banking front we made great progress in the last five years. 2016 was a special year. The bank saw over 300% growth in its Gross Loan Portfolio and over 200% in Deposits. We closed the year with Rs.5.93 billion in receivables and Rs.10.3 billion in deposits. This was made possible by the hardwork, dedication and support extended by the bank, not to mention effectively managing the relationship with the State Bank. I deeply value, appreciate and acknowledge the commitment of Mobilink Bank’s employees. It is your passion to do things differently, and your promise and determination to act with integrity and transparency in everything you do, that has made it possible for us to live upto our values, and deliver on the promise made to our stakeholders.

Chief Digital & Financial Services OfficerAniqa Afzal Sandhu

page 47

page 48

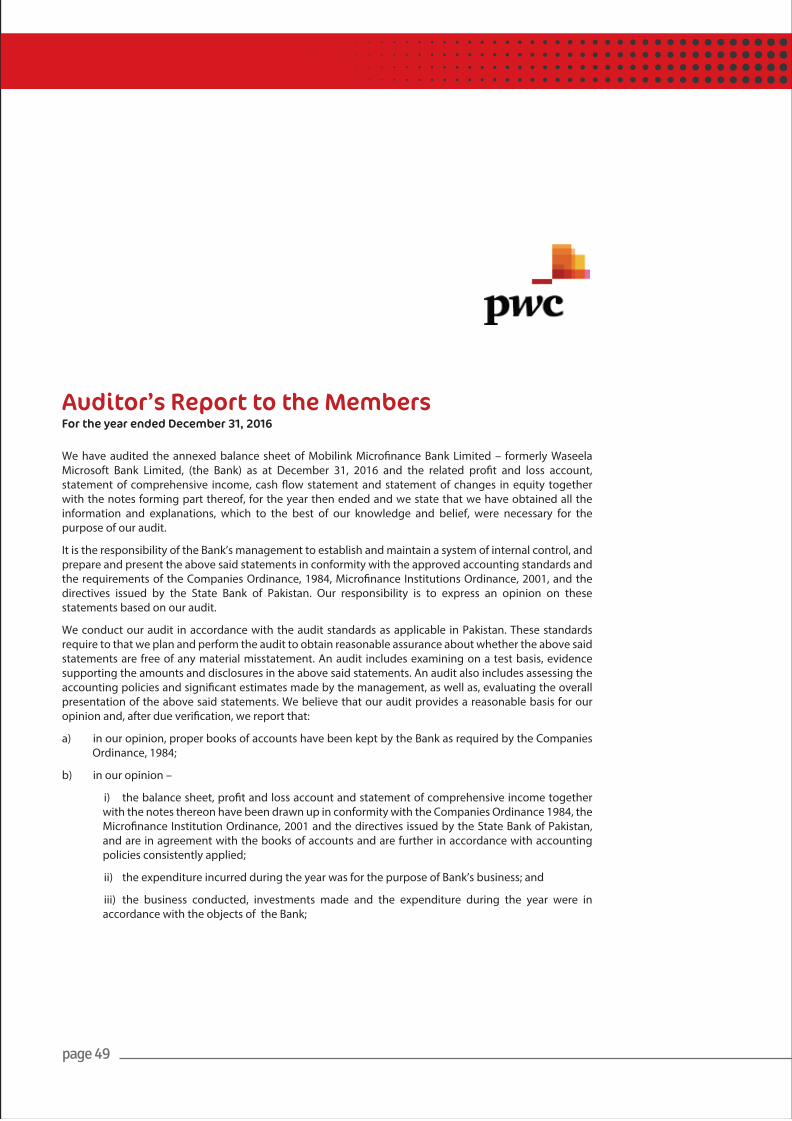

For the year ended December 31, 2016Auditor’s Report to the Members

We have audited the annexed balance sheet of Mobilink Microfinance Bank Limited – formerly Waseela Microsoft Bank Limited, (the Bank) as at December 31, 2016 and the related profit and loss account, statement of comprehensive income, cash flow statement and statement of changes in equity together with the notes forming part thereof, for the year then ended and we state that we have obtained all the information and explanations, which to the best of our knowledge and belief, were necessary for the purpose of our audit.

It is the responsibility of the Bank’s management to establish and maintain a system of internal control, and prepare and present the above said statements in conformity with the approved accounting standards and the requirements of the Companies Ordinance, 1984, Microfinance Institutions Ordinance, 2001, and the directives issued by the State Bank of Pakistan. Our responsibility is to express an opinion on these statements based on our audit.

We conduct our audit in accordance with the audit standards as applicable in Pakistan. These standards require to that we plan and perform the audit to obtain reasonable assurance about whether the above said statements are free of any material misstatement. An audit includes examining on a test basis, evidence supporting the amounts and disclosures in the above said statements. An audit also includes assessing the accounting policies and significant estimates made by the management, as well as, evaluating the overall presentation of the above said statements. We believe that our audit provides a reasonable basis for our opinion and, after due verification, we report that:

a) in our opinion, proper books of accounts have been kept by the Bank as required by the Companies Ordinance, 1984;

b) in our opinion –

i) the balance sheet, profit and loss account and statement of comprehensive income together with the notes thereon have been drawn up in conformity with the Companies Ordinance 1984, the Microfinance Institution Ordinance, 2001 and the directives issued by the State Bank of Pakistan, and are in agreement with the books of accounts and are further in accordance with accounting policies consistently applied;

ii) the expenditure incurred during the year was for the purpose of Bank’s business; and

iii) the business conducted, investments made and the expenditure during the year were in accordance with the objects of the Bank;

page 49

page 50

Chartered Accountants

Islamabad: March 24, 2017

Engagement Partner: JehanZeb Amin

c) in our opinion and to the best of our information and according to the explanations given to us, the balance sheet profit and loss account, statement of comprehensive income, cash flow statement and statement of changes in equity together with the notes forming part thereof conform with approved accounting standards as applicable in Pakistan, and give the information required by the Companies Ordinance, 1984, the Microfinance Institutions Ordinance, 2001 and the directives issued by the State Bank of Pakistan, in the manner so required and respectively give a true and fair view of the state of Bank’s affairs as at December 31, 2016 and of the profit, its cash flows and changes in equity for the year then ended; and

d) in our opinion, Zakat deductible at source under the Zakat and Usher Ordinance, 1980 (xviii 0f 1980), was deducted by the Bank and deposited in the Central Zakat Fund established under section 7 of that Ordinance.

page 51

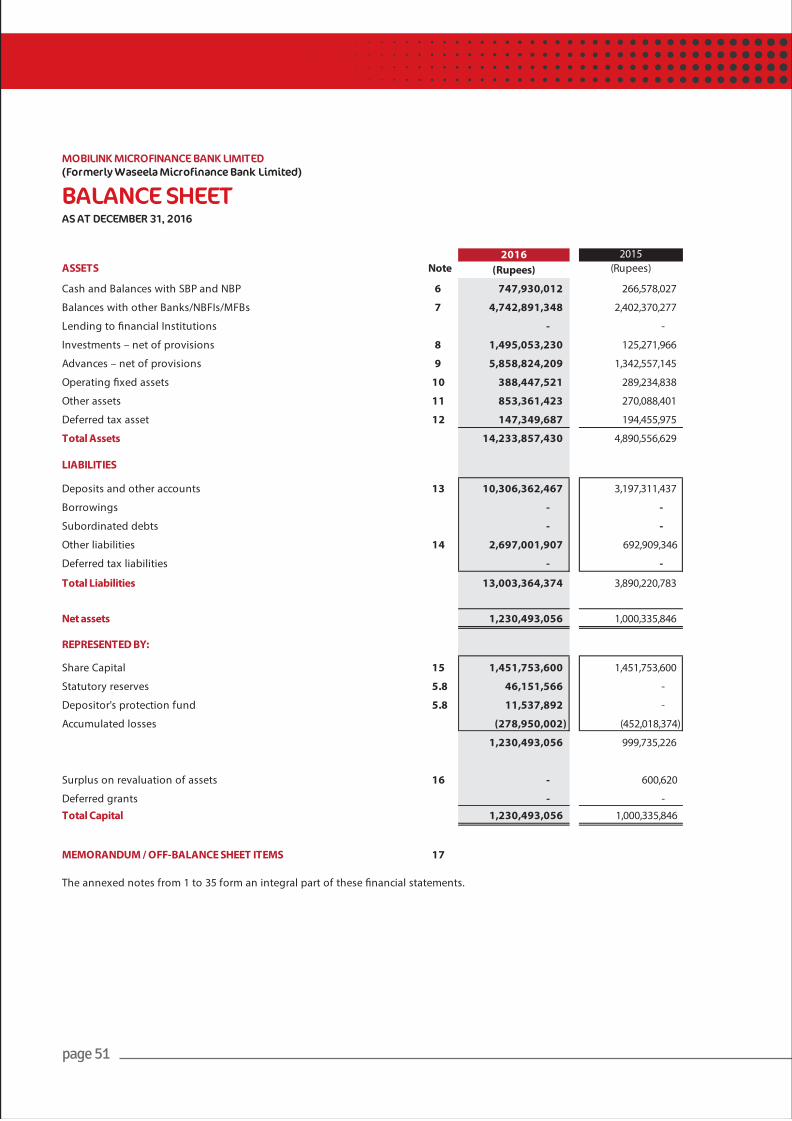

MOBILINK MICROFINANCE BANK LIMITED(Formerly Waseela Microfinance Bank Limited)

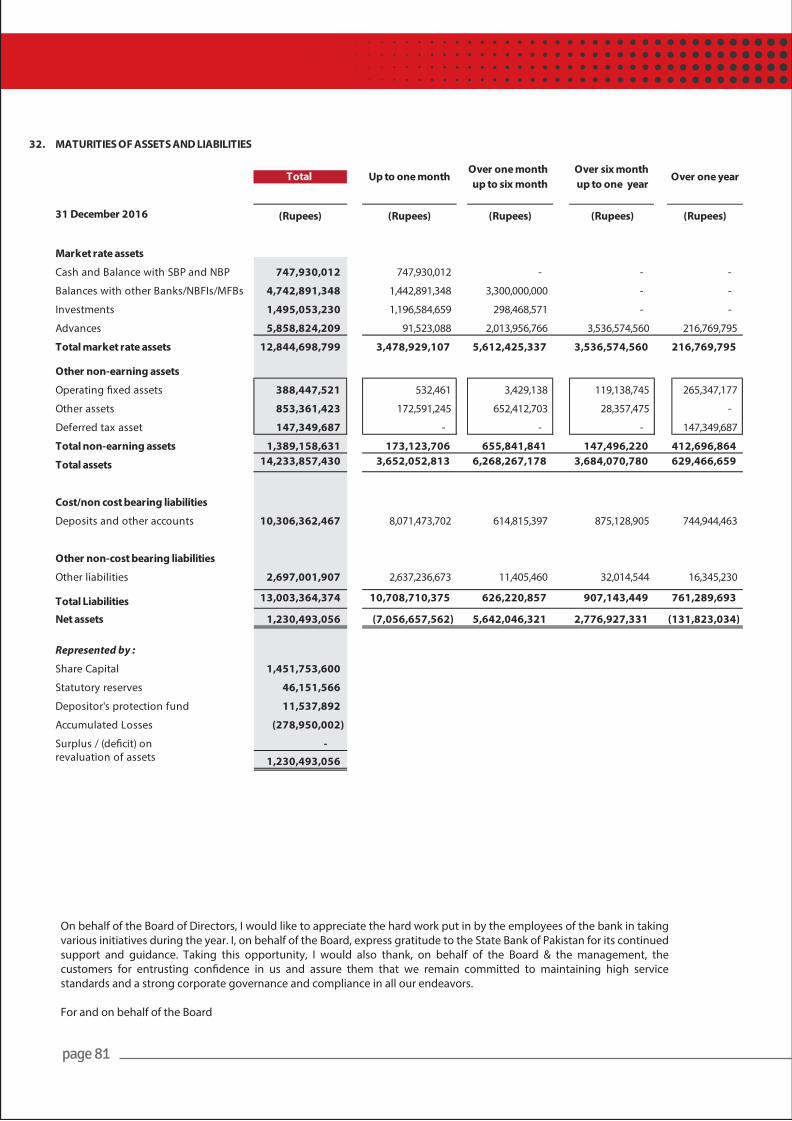

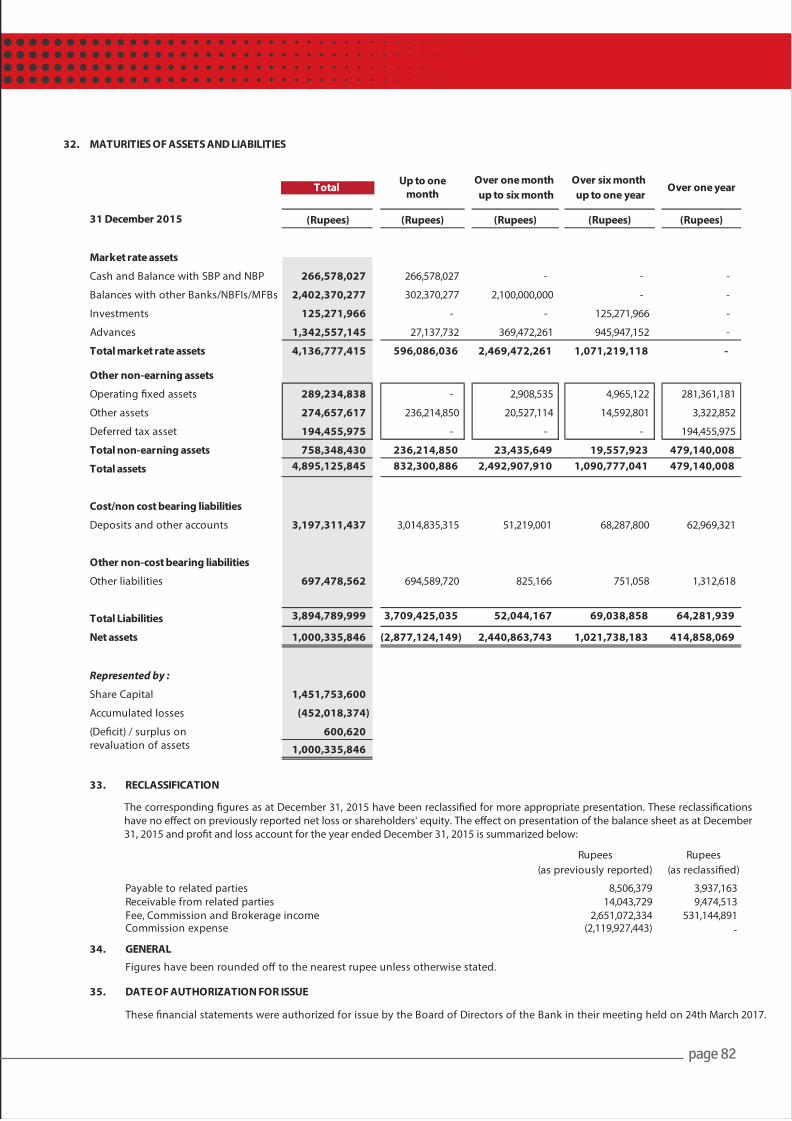

BALANCE SHEET AS AT DECEMBER 31, 2016

2016 2015ASSETS Note (Rupees) (Rupees)

Cash and Balances with SBP and NBP 6 747,930,012 266,578,027

Balances with other Banks/NBFIs/MFBs 7 4,742,891,348 2,402,370,277

Lending to financial Institutions - -

Investments – net of provisions 8 1,495,053,230 125,271,966

Advances – net of provisions 9 5,858,824,209 1,342,557,145

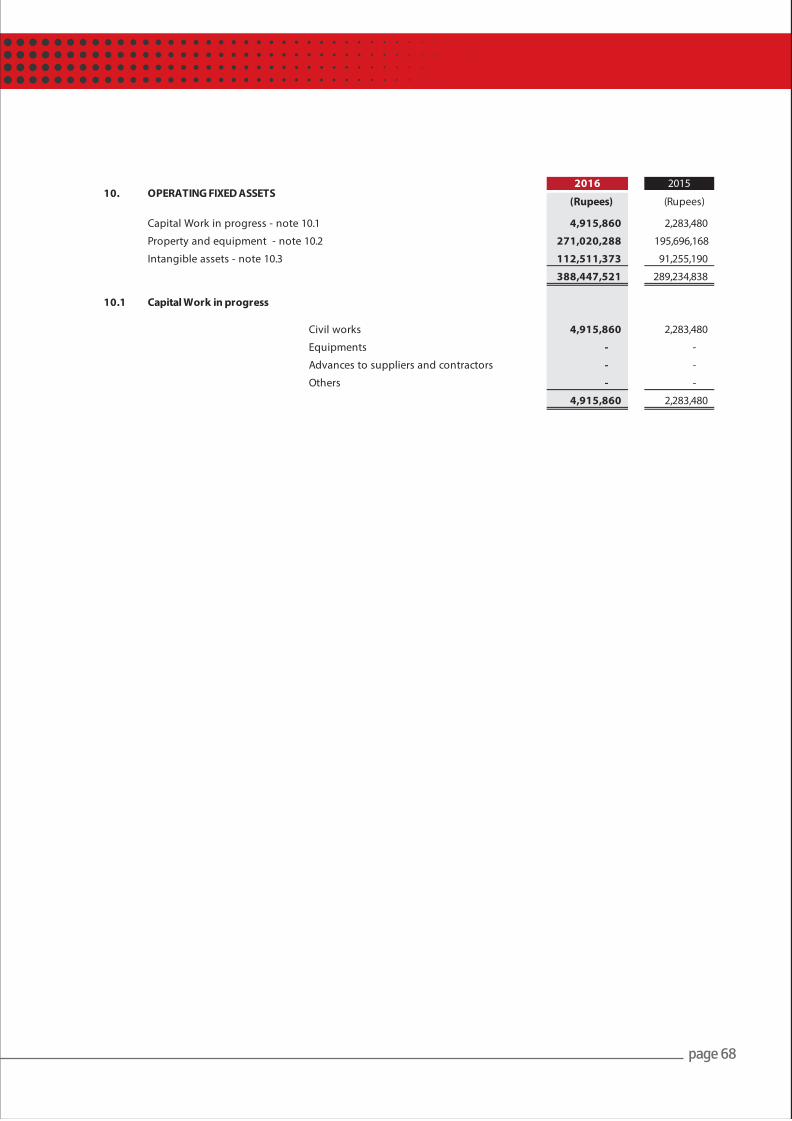

Operating fixed assets 10 388,447,521 289,234,838

Other assets 11 853,361,423 270,088,401

Deferred tax asset 12 147,349,687 194,455,975

Total Assets 14,233,857,430 4,890,556,629

LIABILITIES

Deposits and other accounts 13 10,306,362,467 3,197,311,437

Borrowings - -

Subordinated debts - -

Other liabilities 14 2,697,001,907 692,909,346

Deferred tax liabilities - -

Total Liabilities 13,003,364,374 3,890,220,783

Net assets 1,230,493,056 1,000,335,846

REPRESENTED BY:

Share Capital 15 1,451,753,600 1,451,753,600

Statutory reserves 5.8 46,151,566 -

Depositor's protection fund 5.8 11,537,892 -

Accumulated losses (278,950,002) (452,018,374)

1,230,493,056 999,735,226

Surplus on revaluation of assets 16 - 600,620

Deferred grants - - Total Capital 1,230,493,056 1,000,335,846

MEMORANDUM / OFF-BALANCE SHEET ITEMS 17

The annexed notes from 1 to 35 form an integral part of these financial statements.

page 52

MOBILINK MICROFINANCE BANK LIMITED(Formerly Waseela Microfinance Bank Limited)

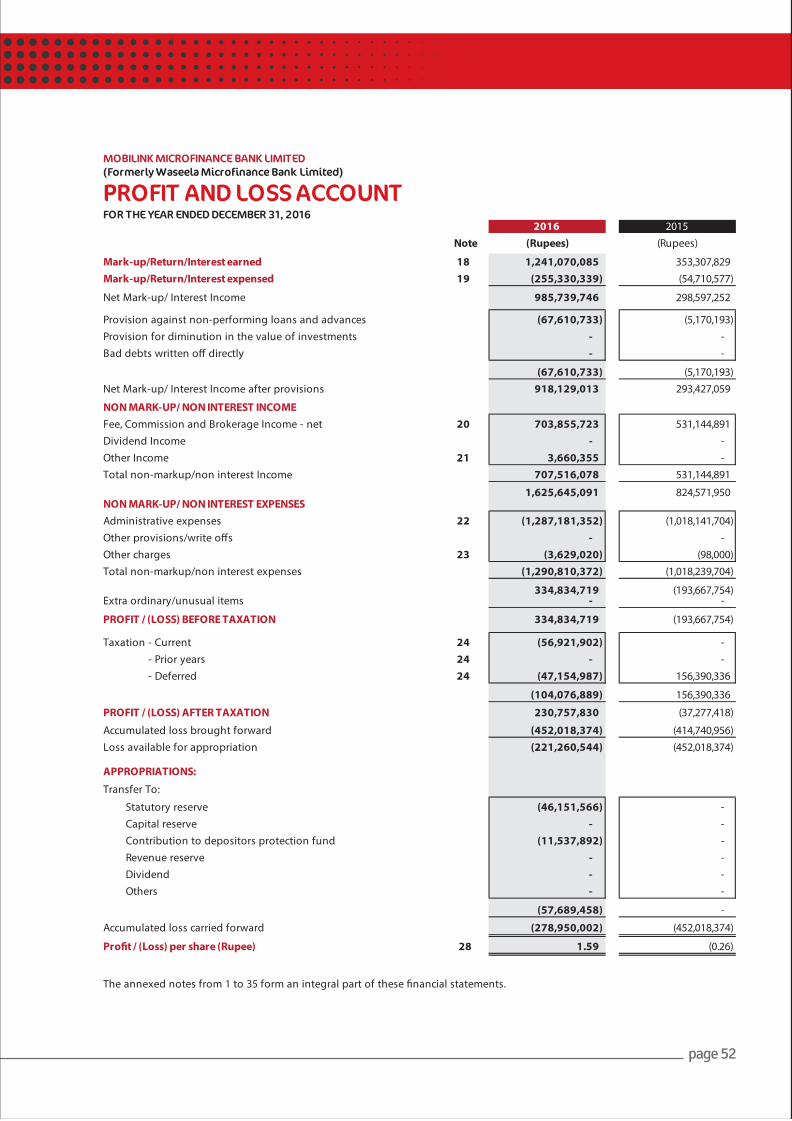

PROFIT AND LOSS ACCOUNTFOR THE YEAR ENDED DECEMBER 31, 2016

2016 2015Note (Rupees) (Rupees)

Mark-up/Return/Interest earned 18 1,241,070,085 353,307,829 Mark-up/Return/Interest expensed 19 (255,330,339) (54,710,577)

Net Mark-up/ Interest Income 985,739,746 298,597,252

Provision against non-performing loans and advances (67,610,733) (5,170,193) Provision for diminution in the value of investments - - Bad debts written off directly - -

(67,610,733) (5,170,193) Net Mark-up/ Interest Income after provisions 918,129,013 293,427,059

NON MARK-UP/ NON INTEREST INCOMEFee, Commission and Brokerage Income - net 20 703,855,723 531,144,891 Dividend Income - - Other Income 21 3,660,355 - Total non-markup/non interest Income 707,516,078 531,144,891

1,625,645,091 824,571,950 NON MARK-UP/ NON INTEREST EXPENSESAdministrative expenses 22 (1,287,181,352) (1,018,141,704) Other provisions/write offs - - Other charges 23 (3,629,020) (98,000) Total non-markup/non interest expenses (1,290,810,372) (1,018,239,704)

334,834,719 (193,667,754) Extra ordinary/unusual items - -

PROFIT / (LOSS) BEFORE TAXATION 334,834,719 (193,667,754)

Taxation - Current 24 (56,921,902) - Taxation - Prior years 24 - - Taxation - Deferred 24 (47,154,987) 156,390,336

(104,076,889) 156,390,336

PROFIT / (LOSS) AFTER TAXATION 230,757,830 (37,277,418)

Accumulated loss brought forward (452,018,374) (414,740,956) Loss available for appropriation (221,260,544) (452,018,374)

APPROPRIATIONS:Transfer To:

Statutory reserve (46,151,566) - Capital reserve - - Contribution to depositors protection fund (11,537,892) - Revenue reserve - - Dividend - - Others - -

(57,689,458) -

Accumulated loss carried forward (278,950,002) (452,018,374)

Profit / (Loss) per share (Rupee) 28 1.59 (0.26)

The annexed notes from 1 to 35 form an integral part of these financial statements.

MOBILINK MICROFINANCE BANK LIMITED(Formerly Waseela Microfinance Bank Limited)

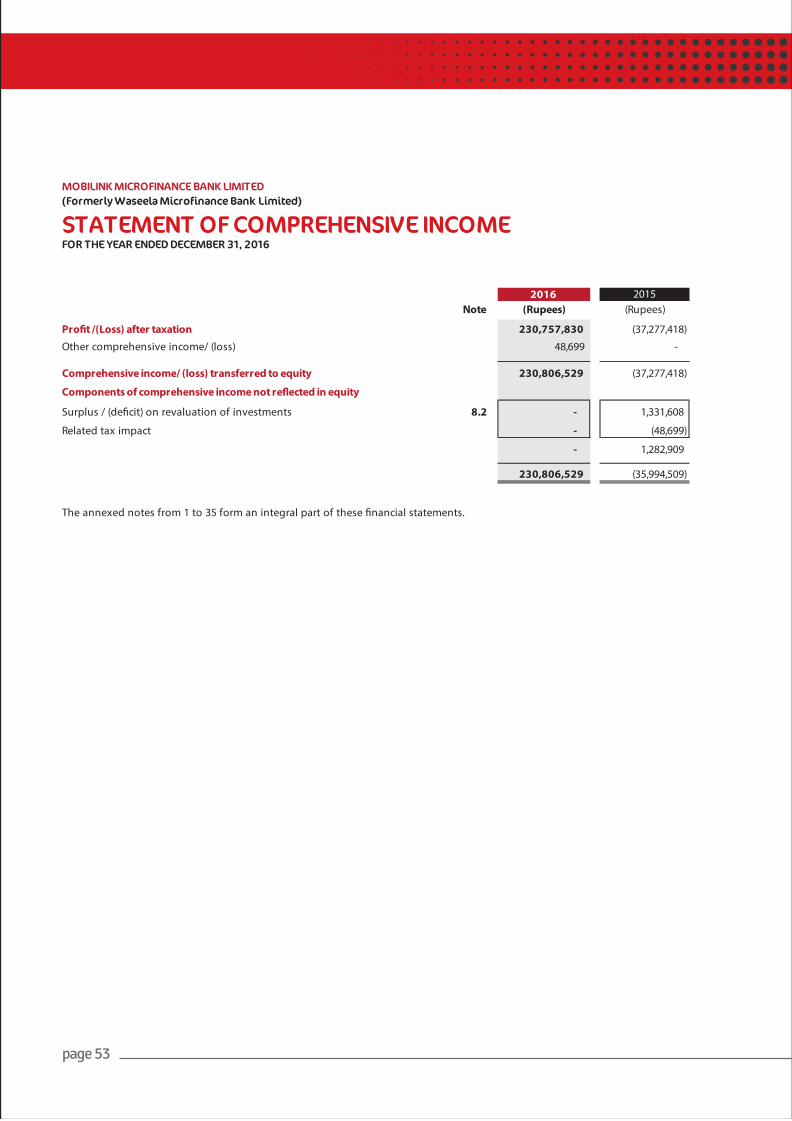

STATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED DECEMBER 31, 2016

2016 2015Note (Rupees) (Rupees)

Profit /(Loss) after taxation 230,757,830 (37,277,418) Other comprehensive income/ (loss) 48,699 -

Comprehensive income/ (loss) transferred to equity 230,806,529 (37,277,418)

Components of comprehensive income not reflected in equity

Surplus / (deficit) on revaluation of investments 8.2 - 1,331,608

Related tax impact - (48,699)

- 1,282,909

230,806,529 (35,994,509)

The annexed notes from 1 to 35 form an integral part of these financial statements.

page 53

MOBILINK MICROFINANCE BANK LIMITED(Formerly Waseela Microfinance Bank Limited)

CASH FLOW STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2016

CASH FLOWS FROM OPERATING ACTIVITIESProfit / (Loss) before taxationLess: Dividend income

Adjustments for non-cash charges

DepreciationAmortizationProvision for gratuityProvision against non-performing advancesProvision for diminution in the value of investments/ other assets(Gain) /loss on sale of fixed assets- netAssets transferred to related party

(Increase)/ decrease in operating assets Lending to financial institutionsAdvancesOther assets (excluding advance taxation)

Increase/ (decrease) in operating liabilities Bills payableBorrowings from financial institutionsDepositsOther liabilities (excluding current taxation)

Gratuity paidPayments against provisions held against off-balance sheet obligationsIncome tax paid

Net cash inflow from operating activitiesCASH FLOWS FROM INVESTING ACTIVITIES

Net investment in available-for-sale securitiesNet investment in held-to-maturity securitiesDividend incomeInvestments in operating fixed assetsSale proceeds of property and equipment disposed–off

Net cash (outflow) / inflow from investing activitiesCASH FLOWS FROM FINANCING ACTIVITIES

Receipts/ payments of Sub-ordinated loanReceipts/ payments of lease obligationsIssue of share capital

Dividend paidNet cash flow from financing activitiesIncrease / (decrease) in cash and cash equivalents

Cash and cash equivalents at beginning of the yearCash and cash equivalents at end of the year

The annexed notes from 1 to 35 form an integral part of these financial statements.

2016 2015Note (Rupees) (Rupees)

334,834,719 (193,667,754) - -

334,834,719 (193,667,754)

88,332,296 65,418,020 32,897,932 17,311,184

5,024,139 4,730,073 67,610,733 5,170,193

- - (2,462,889) 87,247

- 12,777

191,402,211 92,729,494

526,236,930 (100,938,260)

- - (4,583,877,797) (849,914,872)

(594,577,185) (77,949,066)

(5,178,454,982) (927,863,938)

28,551,824 33,755,730 - -

7,109,051,030 1,909,392,697 1,972,053,060 444,545,173

9,109,655,914 2,387,693,600

4,457,437,862 1,358,891,402 (1,536,462) (2,150,381)

- - (45,617,739) (15,812,984)

4,410,283,661 1,340,928,037

(1,370,430,583) 202,839,400 - - - -

(221,888,203) (152,646,719) 3,908,181 1,544,000

(1,588,410,605) 51,736,681

- - - - - -

- - - -

2,821,873,056 1,392,664,718

2,668,948,304 1,276,283,586

30 5,490,821,360 2,668,948,304

page 54

- - - - - - - -

MO

BILI

NK

MIC

ROFI

NA

NCE

BA

NK

LIM

ITED

(Fo

rmer

ly W

asee

la M

icro

fina

nce

Bank

Lim

ited

)

STA

TEM

ENT

OF

CHA

NG

ES IN

EQ

UIT

Y FO

R TH

E YE

AR

END

ED D

ECEM

BER

31,

20

16

Sha

re C

apita

l C

apita

l Re

serv

e S

tatu

tory

Res

erve

R

even

ue

Rese

rve

Dep

osito

rs

Prot

ectio

n Fu

nd

Adv

ance

aga

inst

is

sue

of sh

ares

A

ccum

ulat

ed lo

sses

T

otal

(Rup

ees)

(Rup

ees)

(Rup

ees)

(Rup

ees)

(Rup

ees)

(Rup

ees)

(Rup

ees)

(Rup

ees)

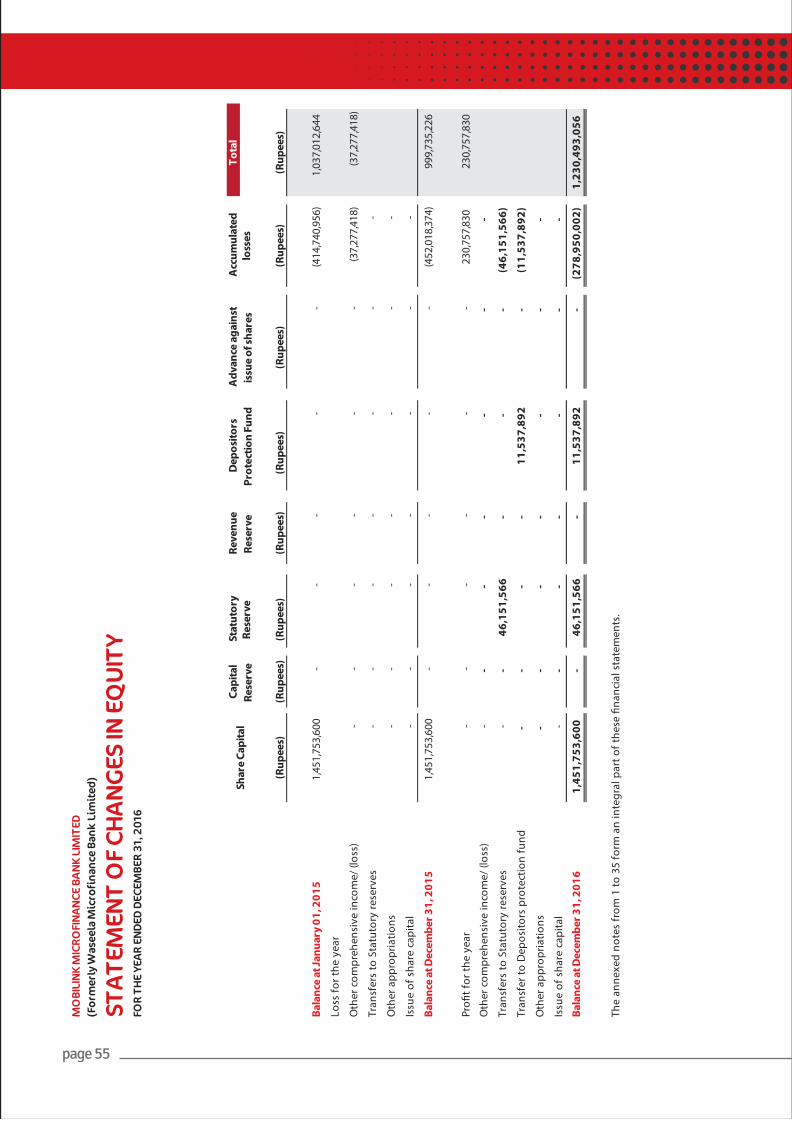

Bala

nce

at Ja

nuar

y 01

, 201

51,

451,

753,

600

-

-

-

-

-

(414

,740

,956

)

1,03

7,01

2,64

4

Loss

for t

he y

ear

Oth

er c

ompr

ehen

sive

inco

me/

(los

s)-

-

-

-

-

-

(37,

277,

418)

(37,

277,

418)

Tran

sfer

s to

Sta

tuto

ry re

serv

es-

-

-

-

-

-

-

Oth

er a

ppro

pria

tions

-

-

-

-

-

-

-

Issu

e of

sha

re c

apita

l-

-

-

-

-

-

-

Bala

nce

at D

ecem

ber 3

1, 2

015

1,45

1,75

3,60

0

-

-

-

-

-

(4

52,0

18,3

74)

99

9,73

5,22

6

Profi

t for

the

year

-

-

-

-

-

-

23

0,75

7,83

0

230,

757,

830

Oth

er c

ompr

ehen

sive

inco

me/

(los

s)-

-

-

-

-

-

-

Tran

sfer

s to

Sta

tuto

ry re

serv

es-

-

46

,151

,566

-

-

-

(46,

151,

566)

Tran

sfer

to D

epos

itors

pro

tect

ion

fund

-

-

-

-

11,5

37,8

92

-

(11,

537,

892)

Oth

er a

ppro

pria

tions

-

-

-

-

-

-

-

Issu

e of

sha

re c

apita

l-

-

-

-

-

-

-

Ba

lanc

e at

Dec

embe

r 31,

201

61,

451,

753,

600

-

46

,151

,566

-

11

,537

,892

-

(2

78,9

50,0

02)

1,

230,

493,

056

The

anne

xed

note

s fr

om 1

to 3

5 fo

rm a

n in

tegr

al p

art o

f the

se fi

nanc

ial s

tate

men

ts.

page 55

MOBILINK MICROFINANCE BANK LIMITED(Formerly Waseela Microfinance Bank Limited)

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2016

1 STATUS AND NATURE OF BUSINESS

2 BASIS OF PRESENTATION

3 STATEMENT OF COMPLIANCE

These financial statements have been presented in accordance with the Banking Supervision Department (BSD) Circular No.11 dated December 30, 2003 issued by the State Bank of Pakistan.

These financial statements have been prepared in accordance with the approved accounting standards as applicable inPakistan. Approved accounting standards comprise of International Financial Reporting Standards (IFRSs) issued by theInternational Accounting Standards Board (IASB) as are notified under the Companies Ordinance, 1984, the requirements ofthe Companies Ordinance, 1984, the Microfinance Institutions Ordinance, 2001, and the regulations/ directives issued by theSECP and the SBP. Wherever the requirements of the Companies Ordinance, 1984, the Microfinance Institutions Ordinance,2001, or regulations/ directives issued by the SECP and SBP differ with the requirements of IFRSs, the requirements of theCompanies Ordinance, 1984, the Microfinance Institutions Ordinance, 2001, or the requirements of the said regulations/directives shall prevail.

The SBP vide BSD Circular No. 10, dated August 26, 2002 has deferred the applicability of International Accounting Standard(IAS) 39, "Financial Instruments: Recognition and Measurement" and IAS 40, "Investment Property" till further instructions.Accordingly, the requirements of these standards have not been considered in the preparation of these financialstatements. However, investments have been measured in accordance with the Prudential Regulations (the Regulations) ofthe SBP and presented in accordance with the requirements of SBP BSD Circular No. 11 dated December 30, 2003. Further,the SECP vide its S.R.O No. 411 (I)/ 2008 dated April 28, 2008 has deferred the applicability of International FinancialReporting Standard (IFRS) 7 "Financial Instruments: Disclosures", which is applicable for annual periods beginning on orafter July 01, 2009, till further orders.

Mobilink Microfinance Bank Limited formerly known as Waseela Microfinance Bank Limited (the Bank) was incorporated inPakistan on November 29, 2010 as a public limited company under the Companies Ordinance, 1984. The Bank obtainedlicense for Microfinance from the State Bank of Pakistan (SBP) on September 12, 2011 to operate on a nationwide basis andreceived the certificate of commencement of business from Securities and Exchange Commission of Pakistan (SECP) onFebruary 13, 2012 whereas certificate of commencement of business from SBP was received on April 20, 2012. The Bank has51 business locations / touch points comprising of 35 branches and 16 booths / service centres (2015: 41 business locations/ touch points comprising of 30 branches and 11 booths/ service centres) in operation. The Bank is a subsidiary of GlobalTelecom Holding S.A.E. (the holding company) which owns 99.99% shareholding in the Bank. The Bank's registered andprincipal office is situated at Plot No. 3-A/2, F-8 Markaz, Islamabad, Pakistan. The Bank's principal business is to providemicrofinance banking and related services to the poor and under served segment of the society under the MicrofinanceInstitution Ordinance, 2001. The Bank is also offering Branchless Banking Services through agency agreement with PakistanMobile Communications Limited (PMCL), a related party, under the Branchless Banking license from the SBP.

Further, pursuant to the special resolution passed in the Extraordinary General Meeting of the shareholders held on 2016and approval of SBP and the SECP, the name of the Bank was changed from "Waseela Microfinance Bank Limited" to"Mobilink Microfinance Bank Limited" with effect from April 29, 2016.

page 56

page 57

4 BASIS OF MEASURMENT

4.1 Functional and presentation currency

4.2 Significant accounting estimates

a) Impairment of investments

b) Advances

c) Taxation

The Bank takes into account the current income tax law and decisions taken by the taxation authorities. Those amounts areshown as contingent liabilities wherein, the Bank's views differ from the views taken by the taxation authorities at theassessment stage and where the Bank considers that its view on items of material nature is in accordance with law.

These financial statements have been prepared under the historical cost basis except "available for sale" investments whichare measured at fair value.

These financial statements are presented in Pakistan Rupee (PKR), which is the Bank’s functional currency. All financialinformation presented in PKR has been rounded to the nearest of PKR, unless otherwise stated.

The preparation of financial statements in conformity with approved accounting standards, as applicable in Pakistan,requires management to make judgments/ estimates and associated assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. These judgments/ estimates and associated assumptionsare based on historical experience and various other factors that are believed to be reasonable under the circumstances,the result of which form the basis of making the estimates about carrying value of assets and liabilities that are not readilyapparent from other sources. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates arerecognized in the period in which the estimates are revised if the revision affects only that period, or in the period of therevision and future periods if the revision affects both current and future periods. Information about significant areas ofestimation, uncertainty and critical judgments in applying accounting policies that have significant effect on the amountsrecognized in the financial statements relates to valuation and impairment of investments, advances, determination ofuseful lives of depreciable assets and intangible assets, provision for income taxes and other provisions which arediscussed in following paragraphs:

Impairment in the value of investments is made after considering objective evidence of impairment. Provision fordiminution in the value of investments is made as per the Regulations issued by SBP.

The Bank reviews its micro credit loan portfolio to assess amount of non-performing advances and provision requiredthere against on regular basis. While assessing this requirement, the Regulations of SBP are taken into consideration.

page 58

d) Operating fixed assets/ intangible assets

e) Provisions and contingencies

f) Impairment of financial assets

g) Other provisions

5 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

5.1 Cash and cash equivalents

5.2 Investment

a) Held for trading

Estimates of residual values and useful lives of operating fixed assets and intangible assets are reassessed annually andany change in estimate is taken into account in the determination of depreciation/ amortization charge and impairmentloss. Changes in estimates are accounted for over the estimated remaining useful life of the assets.

The Bank reviews the status of all the legal cases on a regular basis. Based on the expected outcome and consideration ofopinion of its legal advisor, appropriate provision/ disclosure is made.

A financial asset is considered to be impaired if objective evidence indicates that one or more events would have anegative effect on the estimated future cash flows of that asset.

An impairment loss in respect of a financial asset measured at amortized cost is calculated as the difference between itscarrying amount, and the present value of the estimated future cash flows discounted at the original interest rate.

Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets areassessed collectively in groups that share similar credit risk characteristics. All impairment losses are recognized in profitand loss account.

Estimates of the amount of provisions recognized are based on current legal and constructive requirements. As actualoutflows can differ from estimates due to changes in laws, regulations, public expectations, prices and conditions, and cantake many years in the future, the carrying amounts of provisions are regularly reviewed and adjusted to take account ofsuch changes.

Cash and cash equivalents comprise cash in hand, balance with SBP/ National Bank of Pakistan (NBP) and other banks/ Non-Banking Financial Institutions (NBFIs)/ Microfinance Banks (MFBs).

All purchases and sale of investments are recognized using settlement date accounting. Settlement date is the date onwhich investments are delivered to or by the Bank. All investments are derecognized when the right to receive economicbenefits from the investments has expired or has been transferred or the Bank has transferred substantially all the risksand rewards of ownership.

Investments of the Bank are classified into the following categories:

These represent securities acquired with the intention to trade by taking advantage of short-term market / interest ratemovements. These securities are disposed off within 90 days from the date of their acquisition. These are marked to marketand surplus / deficit arising on revaluation of ‘held for trading’ investments is taken to profit and loss account inaccordance with the requirements prescribed by SBP.

b) Held to maturity

c) Available-for-sale

5.3 Advances

a) Other assets especially mentioned

b) Substandard

c) Doubtful

d) Loss

Investments which may be sold in response to needs for liquidity or changes in interest rates, exchange rates or equityprices are classified as available for sale. Available-for-sale investments are initially recognized at cost and subsequentlymeasured at fair value. Profit on available-for-sale investments is recognized on a time proportion basis taking into account the effective yield on the investments.

The surplus / (deficit) arising on revaluation of available for sale investments is kept in "surplus/(deficit) on revaluation ofassets" through statement of comprehensive income. The surplus/(deficit) arising on these investments is taken to profitand loss account, when actually realized upon disposal of the investment.

Advances are stated net of provision for non-performing advances. The outstanding principal and mark-up of the loansand advances, payments against which are overdue for 30 days or more are classified as non-performing loans (NPLs). Theunrealized interest / profit / mark-up / service charges on NPLs is suspended and credited to interest suspense account.Further the NPLs are divided into following categories:

These are advances in arrears (payments/instalments overdue) for 30 days or more but less than 60 days.

These are advances in arrears (payments/instalments overdue) for 60 days or more but less than 90 days.

These are advances in arrears (payments/instalments overdue) for 90 days or more but less than 180 days.

These are advances in arrears (payments/instalments overdue) for 180 days or more.

In addition the Bank maintains a Watch List of all accounts overdue for 5-29 days. However, such accounts are not treatedas non-performing for the purpose of classification/ provisioning.

Premium or discount on acquisition of held to maturity investments is amortized through profit and loss account over theremaining period till maturity.

Investments with fixed maturity, where management has both the intention and the ability to hold to maturity, areclassified as held to maturity. Subsequent to initial recognition at cost, these investments are measured at amortized cost,less provision for impairment in value, if any. Amortized cost is calculated taking into account effective interest ratemethod. Profit on held to maturity investments is recognized on a time proportion basis taking into account the effectiveyield on the investments.

Other assets especially mentioned Nil

Substandard 25% of outstanding principal net of cash collaterals

Doubtful 50% of outstanding principal net of cash collaterals

Loss 100% of outstanding principal net of cash collaterals

In accordance with the Regulations, the Bank maintains specific provision of outstanding principal net of cash collateralsand Gold (ornaments and bullion) realizable without recourse to a Court of Law at the following rates:

page 59

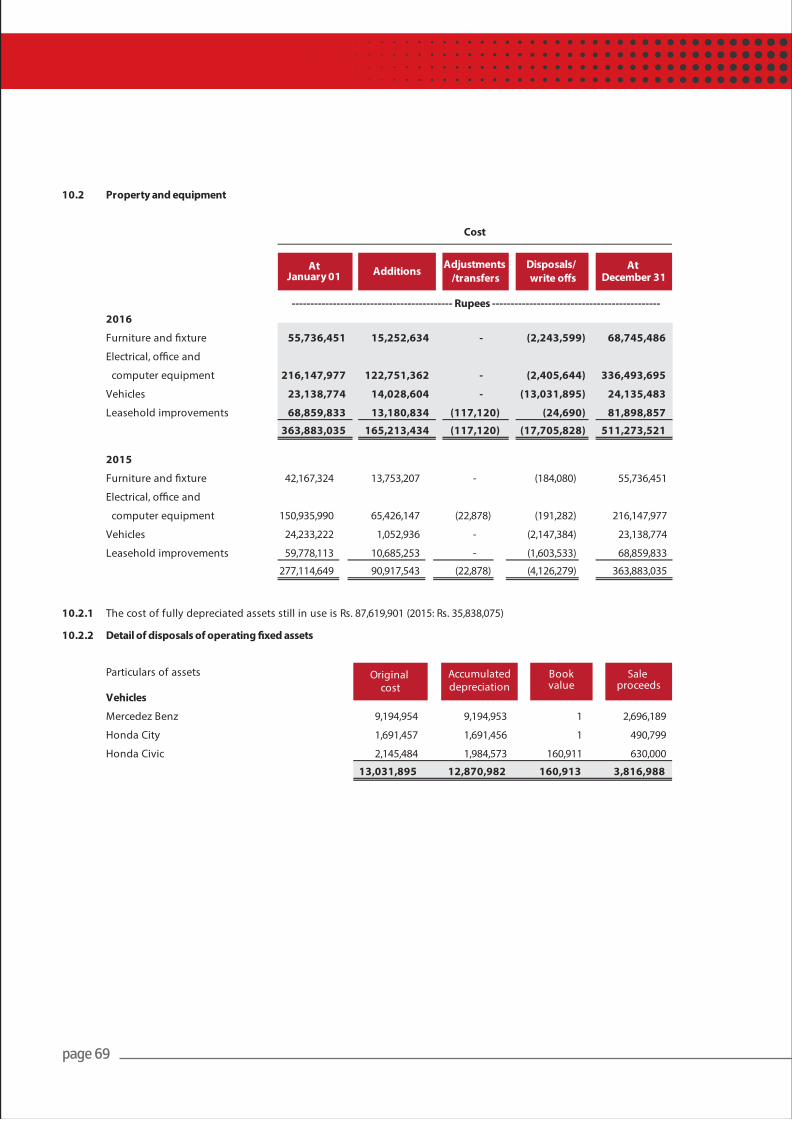

5.4 Operating fixed assets

a) Property and equipment

b) Capital work-in-progress

Non-performing advances are written off one month after the loan is classified as “Loss”. However, the Bank continues itsefforts for recovery of the written off balances.

Property and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Costincludes expenditure that is directly attributable to the acquisition of the asset and the costs of dismantling and removingthe items and restoring on which they are located, if any.

Depreciation is charged on the straight line method at rates specified note 10.2 to the financial statements, so as to writeoff the cost of assets over their estimated useful lives.

Full month's depreciation is charged in the month of addition while no depreciation is charged in the month of deletion.

Subsequent costs are included in the assets carrying amount when it is probable that future economic benefits associatedwith the item will flow to the Bank and the cost of the item can be measured reliably. Carrying amount of the replaced partis derecognized. All other repair and maintenance are charged to income during the year.

Gains or losses on disposal of an item of property and equipment are determined by comparing the proceeds fromdisposal with the carrying amounts. Gains are recognized within "other income" while losses are recognized inadministrative expenses in the profit and loss account.

Capital work-in-progress is stated at cost less impairment losses, if any.

General and specific provisions are charged to the profit and loss account in the period in which they occur.

In addition to above, a general provision is made equivalent to 1.5% (2015: 1%) of the net outstanding balance (advancesnet of specific provisions) in accordance with the requirement of the Regulations.

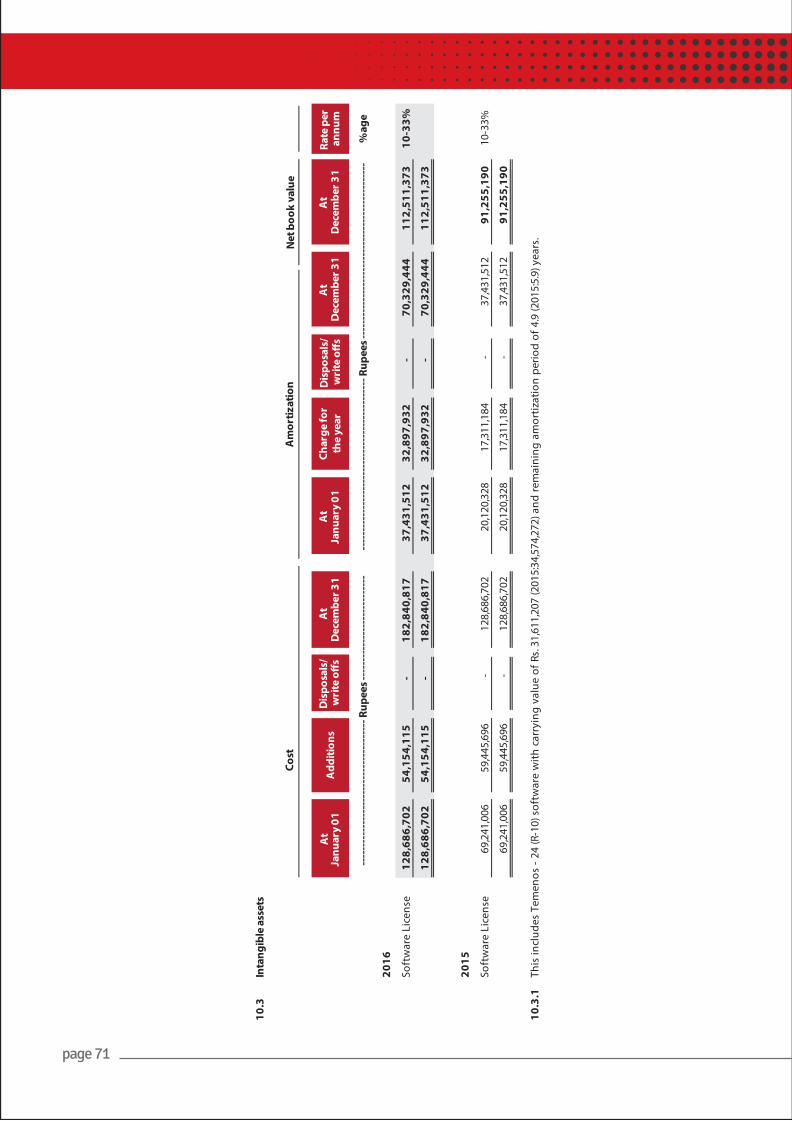

c) Intangible assets

5.5 Deposits

An intangible asset is recognized if it is probable that the future economic benefits that are attributable to the asset willflow to the Bank and that the cost of such asset can also be measured reliably. These are stated at cost less accumulatedamortization and impairment losses, if any.

Intangible assets comprise of computer software and related applications. Intangible assets are amortized over theirestimated useful lives at rate specified in note 10.3 to the financial statements. Subsequent expenditure is capitalized onlywhen it increases the future economic benefit embodied in the specific asset to which it relates. All other expenditure isrecognized in profit and loss account as incurred.

Deposits are initially recorded at the amount of proceeds received. Mark-up accrued on deposits, if any, is recognizedseparately as part of other liabilities and is charged to the profit and loss account over the period.

page 60

page 61

anthe

5.6 Taxation

a) Current

b) Deferred

The Bank takes into account the current income tax law and decisions taken by the taxation authorities. Those amounts areshown as contingent liabilities wherein, the Bank's views differ from the views taken by the taxation authorities at theassessment stage and where the Bank considers that its view on items of material nature is in accordance with law.

Current tax is the tax due on the taxable income for the year, using tax rates enacted or substantively enacted at thereporting date, taking into account tax credits, rebates and tax losses, if any, and any adjustment to tax payable in respectof previous years.

Deferred tax is accounted for on all major taxable temporary differences between the carrying amounts of assets and theirtaxation base. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will beavailable against which the asset can be utilized. Deferred tax assets are reduced to the extent that it is no longer probablethat the related tax benefit will be realized. At each balance sheet date, the Bank reassesses the carrying and theunrecognized amount of deferred tax assets.

Deferred tax assets and liabilities are calculated at the rate that are expected to apply to the period when the asset isrealized or the liability is settled, based on the tax rates (and tax laws) that have been enacted or substantively enacted bythe balance sheet date.

Income tax on the profit or loss for the year comprises current and deferred tax. Income tax is recognized in the profit andloss account, except to the extent that it relates to items recognized directly in other comprehensive income or belowequity, its related tax is recognized in other comprehensive income or below equity.

5.7 Staff retirement benefits

a) Provident fund

b) Gratuity

5.8 Reserves

a) Statutory reserve

The Bank participates in a defined contribution provident fund for its eligible employees. Monthly contributions are madeby the Bank and its employees at rate of 10% of basic salary.

The Bank maintains provision of gratuity for all its contractual employees, according to the agreement signed with HRSGOutsourcing (Pvt) Limited, an outsourcing company. Gratuity equivalent to one month's last drawn basic salary for eachcompleted year of service is paid to outgoing employees with at least 1 year of past service rendered.

In compliance with the related regulatory requirements, the Bank is required to maintain statutory reserve to whichappropriation equivalent to 20% of the profit after tax is required to be made till such time the reserve fund equalspaid up capital of the Bank. However, thereafter, the contribution is to be reduced to 5% of the profit after tax.

page 62

b) Depositor's protection fund

c) Cash reserve

d) Statutory liquidity requirement

5.9 Provisions

5.10 Foreign currency transactions

A provision is recognized when, and only when, the Bank has a present obligation (legal or constructive) as a result of apast event, it is probable that an outflow of resources embodying economic benefits will be required to settle theobligation, and a reliable estimate can be made of the amount of the obligation.

The financial statements are presented in Pakistani Rupee, which is the Bank's functional currency. Transactions in foreigncurrencies are translated into Pak Rupee at exchange rate on the date of transaction. All monetary assets and liabilities inforeign currencies are translated into Pak Rupee at the rate of exchange approximating those ruling at the balance sheetdate. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at theyear end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized in profit andloss account.

In compliance with the related regulatory requirements, the Bank is required to maintain liquidity equivalent to at least10% of its total demand liabilities and time liabilities with tenor of less than one year in form of liquid assets i.e. cash, gold,unencumbered treasury bills, Pakistan Investment Bonds and Government of Pakistan sukuk bonds. Treasury bills andPakistan Investment Bonds held under depositor protection fund are excluded for the purpose of determining liquidity.

The Bank is required under the Microfinance Institutions Ordinance, 2001, to contribute 5% of annual after tax profit andprofit earned on investments of the fund to be credited to depositors protection fund for the purpose of providingsecurity or guarantee to persons depositing money in the Bank.

In compliance with the related regulatory requirements, the Bank is required to maintain a cash reserve equivalent to notless than 5% of its deposits (including demand deposits and time deposits with tenor of less than 1 year) in a currentaccount opened with the State Bank or its agent.

5.11 Revenue recognition

a) Markup / income on advances

b) Income from investments

Markup / income / return / service charges on advances is recognized on accrual / time proportion basis using effectiveinterest rate method at the Bank's prevailing interest rates for the loan products. Markup/ income on advances is collectedwith loan instalments. Due but unpaid service charges / income are accrued on overdue advances for period up to 30 days.After 30 days, overdue advances are classified as non-performing and recognition of unpaid service charges / incomeceases. Further, accrued markup on non-performing advances are reversed and credited to suspense account.Subsequently, markup recoverable on non-performing advances is recognized on a receipt basis in accordance with therequirements of the Regulations.

Markup / income on investments is recognized on accrual / time proportion basis using the effective interest method.Where debt securities are purchased at premium or discount, those premiums / discounts are amortized through profit andloss account over the remaining period of maturity.

c) Fee, commission and brokerage income

d) Income from inter bank deposits

e) Gain/ loss on sale of operating fixed assets

f) Gain/ loss on sale of investments

5.12 Financial instruments

a) Financial assets

Financial assets are cash and balances with SBP and NBP, balances with other banks/NBFls/MFBs, lending to financialinstitutions, investments, advances and other receivables. Advances are stated at their nominal value as reduced byappropriate provisions against non-performing advances, while other financial assets excluding investments are stated atcost. Investments classified as held for trading and available for sale are valued at year end prices and investmentsclassified as held to maturity are stated at amortized cost.

All financial assets and liabilities are initially measured at cost which is the fair value of the consideration given andreceived respectively. These financial assets and liabilities are subsequently measured at fair value, amortized cost orhistorical cost, as the case may be.

Fee, commission and brokerage income is recognized when the related services are rendered.

Income from inter bank deposits in saving accounts is recognized in the profit and loss account as it accrues using theeffective interest method .

Gain on sale of operating fixed assets are recognized under other income in the profit and loss account.

Loss on sale of operating fixed assets are recognized under administrative expenses in the profit and loss account.

Gains and losses on sale of investments are recognised in the profit and loss account.

Financial assets and liabilities are recognized when the Bank becomes a party to the contractual provisions of theinstrument. These are derecognized when the Bank ceases to be the party to the contractual provisions of the instrument.

b) Financial liabilities

5.13 Off-setting

Financial liabilities are classified according to the substance of the contractual arrangement entered into. Financial liabilities include deposit and other accounts and other liabilities which are stated at their nominal value. Financial charges areaccounted for on accrual basis.

Any gain or loss on the recognition and derecognition of the financial assets and liabilities is included in the net profit andloss for the year in which it arises.

Financial assets and financial liabilities and tax assets and tax liabilities are only off-set and the net amount is reported inthe financial statements when there is a legally enforceable right to set off the recognized amount and the Bank intendseither to settle on net basis or to realize the assets and to settle the liabilities simultaneously. Income and expense items ofsuch assets and liabilities are also off-set and the net amount is reported in the financial statements.

page 63

5.14 Borrowing costs

5.15 Mark-up bearing borrowings

5.16 Grants

5.17 Earnings per share

Mark-up bearing borrowings are recognized initially at cost being the fair value of consideration received, less attributabletransaction costs. Subsequent to initial recognition mark-up bearing borrowings are stated at original cost less subsequentrepayments.

The grant related to an asset is recognized in the balance sheet initially as deferred income when grant is received or thereis reasonable assurance that it will be received and that the Bank will comply with the conditions attached to it. Grants thatcompensate the Bank for expenses incurred are recognized as revenue in the profit and loss account on a systematic basisin the same periods in which the expenses are incurred. Grants that compensate the Bank for the cost of an asset arerecognized in the profit and loss account as other operating income on a systematic basis over the useful life of the asset.

The Bank presents basic and diluted earnings per share (EPS) for its shareholders. Basic EPS is calculated by dividing theprofit or loss attributable to ordinary shareholders of the Bank by the weighted average number of ordinary sharesoutstanding during the year. Diluted EPS, if any is determined by adjusting the profit or loss attributable to ordinaryshareholders and the weighted average number of ordinary shares outstanding for the effects of all dilutive potentialordinary shares. There were no dilutive potential ordinary shares in issue at December 31, 2016.

Borrowing costs are recognized as an expense in the period in which they are incurred except where such costs relate tothe acquisition, construction or production of a qualifying asset in which case such costs are capitalized as part of the costof that asset. Borrowing cost includes exchange differences arising from foreign currency borrowings to the extent theseare regarded as an adjustment to borrowing costs.

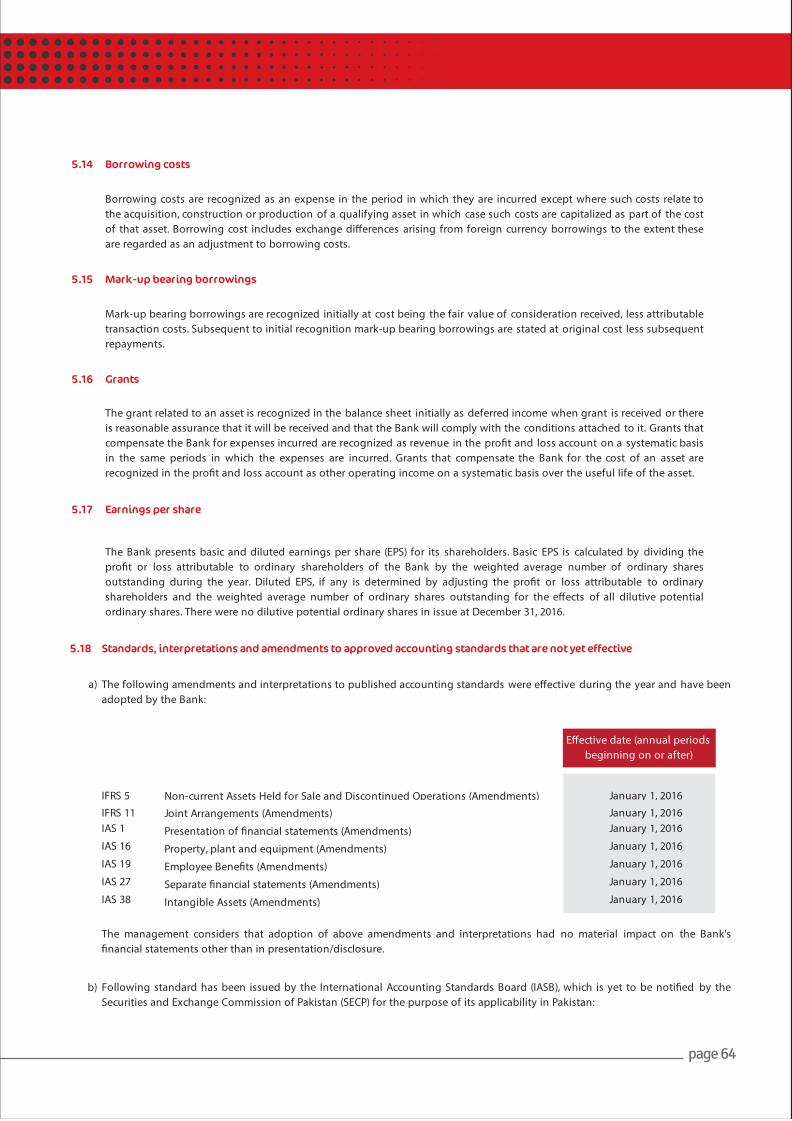

5.18

a)

IFRS 5IFRS 11IAS 1

IAS 16

IAS 19

IAS 27

IAS 38

b)

The management considers that adoption of above amendments and interpretations had no material impact on the Bank'sfinancial statements other than in presentation/disclosure.

Following standard has been issued by the International Accounting Standards Board (IASB), which is yet to be notified by theSecurities and Exchange Commission of Pakistan (SECP) for the purpose of its applicability in Pakistan:

Employee Benefits (Amendments) January 1, 2016

Separate financial statements (Amendments) January 1, 2016

Intangible Assets (Amendments) January 1, 2016

Joint Arrangements (Amendments) January 1, 2016

Presentation of financial statements (Amendments) January 1, 2016

Property, plant and equipment (Amendments) January 1, 2016

Non-current Assets Held for Sale and Discontinued Operations (Amendments) January 1, 2016

Standards, interpretations and amendments to approved accounting standards that are not yet effective

The following amendments and interpretations to published accounting standards were effective during the year and have beenadopted by the Bank:

Effective date (annual periods beginning on or after)

page 64

IFRS 1

IFRS 14 Regulatory Deferral Accounts

c)

IFRS 1

IFRS 2

IFRS 4

IFRS 7

IFRS 12

IFRS 15

IFRS 16

IAS 12

IAS 39

IAS 40 Investment property (Amendments) July 1, 2018

The management anticipates that adoption of above standards and amendments in future periods will have no material impacton the Bank's financial statements other than in presentation/disclosure.

Leases January 1, 2019

Income taxes (Amendments) January 1, 2017

Financial Instruments: Recognition and Measurement (Amendments) January 1, 2018

Financial Instruments (Amendments) January 1, 2018

Disclosure of Interests in Other Entities (Amendments) January 1, 2017

Revenue from Contracts with Customers January 1, 2018

First-time Adoption of International Financial Reporting Standards (Amendments)

January 1, 2018

Share-based payment (Amendments) January 1, 2018

Insurance Contracts January 1, 2018

January 1, 2016

Following standards and amendments to published accounting standards will be effective in future periods and have not beenearly adopted by the Bank.

Effective date (annual periods beginning on or after)

Effective date (annual periods beginning on or after)

First-Time Adoption of International Financial Reporting Standards (Amendments)

July 1, 2009

page 65

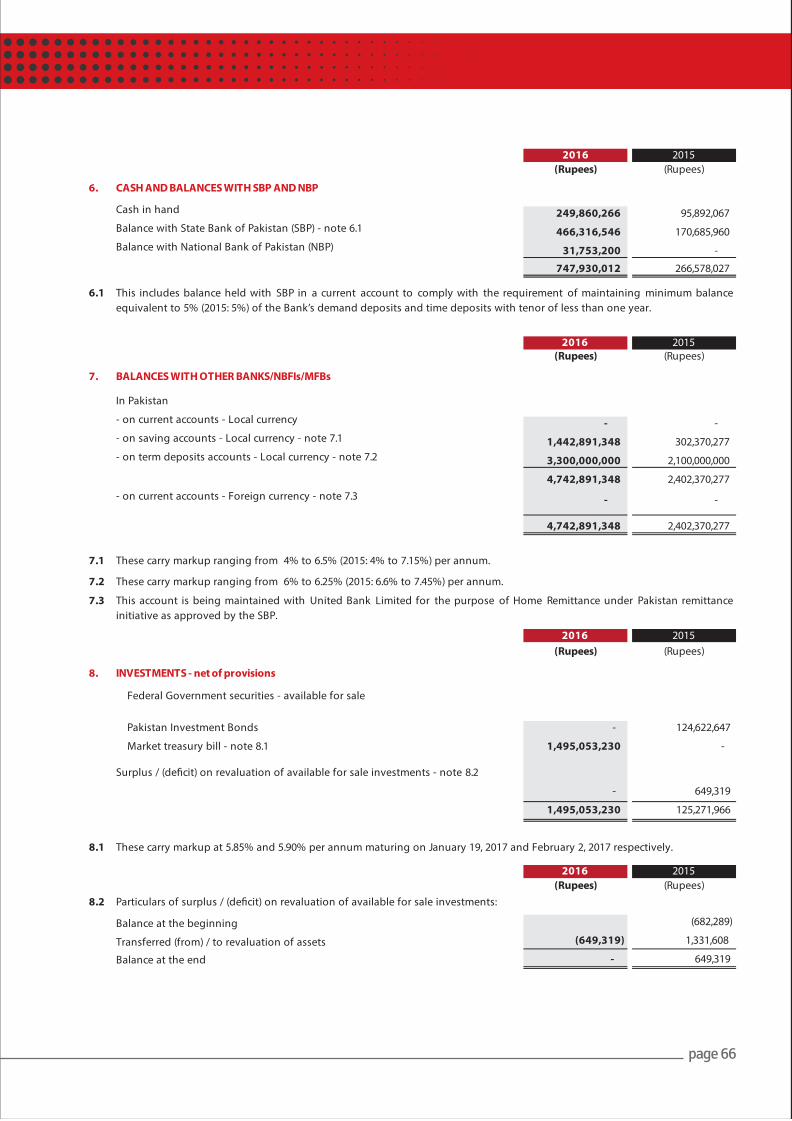

2016 2015(Rupees) (Rupees)

6. CASH AND BALANCES WITH SBP AND NBP

Cash in hand 249,860,266 95,892,067 Balance with State Bank of Pakistan (SBP) - note 6.1 466,316,546 170,685,960 Balance with National Bank of Pakistan (NBP) 31,753,200 -

747,930,012 266,578,027

6.1

2016 2015

7. BALANCES WITH OTHER BANKS/NBFIs/MFBs

(Rupees) (Rupees)

In Pakistan

- on current accounts - Local currency - - - on saving accounts - Local currency - note 7.1 1,442,891,348 302,370,277 - on term deposits accounts - Local currency - note 7.2 3,300,000,000 2,100,000,000

4,742,891,348 2,402,370,277 - on current accounts - Foreign currency - note 7.3 - -

4,742,891,348 2,402,370,277

7.1

7.2

7.3

2016 2015

8. INVESTMENTS - net of provisions

(Rupees) (Rupees)

Federal Government securities - available for sale

Pakistan Investment Bonds - 124,622,647

Market treasury bill - note 8.1 1,495,053,230 -

- 649,319

1,495,053,230 125,271,966

8.1

2016 2015(Rupees) (Rupees)

8.2 Particulars of surplus / (deficit) on revaluation of available for sale investments:

Balance at the beginning 649,319 (682,289)

Transferred (from) / to revaluation of assets (649,319) 1,331,608

Balance at the end - 649,319

Surplus / (deficit) on revaluation of available for sale investments - note 8.2

These carry markup at 5.85% and 5.90% per annum maturing on January 19, 2017 and February 2, 2017 respectively.

This includes balance held with SBP in a current account to comply with the requirement of maintaining minimum balanceequivalent to 5% (2015: 5%) of the Bank’s demand deposits and time deposits with tenor of less than one year.