Embed Size (px)

Citation preview

National Financial Inclusion Strategy Annual Report 2019 1

ANNUAL REPORT 2019

National Financial Inclusion Strategy Annual Report 2019 3

Annual Report2019

National Financial Inclusion Strategy Annual Report 2019 4

Abbreviations and Acronyms 5

Foreword 7

Message from the Governor 11

Executive Summary 12

NFIS Achievements for 2019 Report from the Financial Inclusion Technical Secretariat 15Monitoring and Evaluation Framework 22 Impact Indicators 22

Intermediate Indicators 26

Communication 34FISC Working Groups 51Pictorial Highlights of the National Financial Inclusion Activities 53Pictorial Highlights of PSOJ Access to Finance Panel 62Highlights of FSC Town Halls 63Appendix 1 – Summary of NFIS Goals 71Appendix 2 - Details of activities under the NFIS Pillars 83

Financial Access and Usage 83

Financial Resilience 85

Financial Growth 85

MSME Finance 86

Housing Finance 87

Responsible Finance 88

Supporting Infrastructure 88

Contents

National Financial Inclusion Strategy Annual Report 2019 5

Abbreviations andAcronyms

AGD Accountant General’s Department

AML/CFT Anti-moneylaundering/Counter-financingofterrorism

BOJ BankofJamaica

CAC ConsumerAffairsCommission

CDD Customer Due Diligence

DBJ DevelopmentBankofJamaica

DTI Deposit Taking Institutions

ERPS Electronic Retail Payment Services

FISC Financial Inclusion Steering Committee

FSC Financial Services Commission

FTC Fair Trading Commission

JMB Jamaica Mortgage Bank

IDB Inter-American Development Bank

KYC Know Your Customer

MEGJC MinistryofEconomicGrowthandJobCreation

MOFPS MinistryofFinanceandthePublicService

MICAF MinistryofIndustry,Commerce,AgricultureandFisheries

NFIS National Financial Inclusion Strategy

NHT National Housing Trust

OTA OfficeofTechnicalAssistance,UnitedStatesDepartmentofTreasury

PIOJ PlanningInstituteofJamaica

STATIN StatisticalInstituteofJamaica

Photography by Derron Wright of Wright Focus Photography

Animation done by George Hay

National Financial Inclusion Strategy Annual Report 2019 6

Foreword

The Hon. Nigel A. Clarke, D.Phil., MP.Minister of Finance and the Public Service Chairman of the National Financial Inclusion Council

National Financial Inclusion Strategy Annual Report 2019 7

TheGovernmentofJamaicacontinuesitsworkontheimplementationoftheNationalFinancialInclusion Strategy to empower Jamaican citizens, and to catalyse the Government’sobjectiveof‘EconomicOpportunityforAll.’

This Government recognizes that increasingaccess to financial services and productsgreatlyenhances theabilityof Jamaicans topursuetheirownfinancialpath,andpersonalfinancialindependence.

As Jamaican firms increasingly participatein global value chains, the availability andutilisationofdigitalpaymentsiscritical.Digitalpayments require easier account opening processes,whilemaintainingsoundanti-moneylaundering and counter-terrorism financingmechanisms. To ensure the appropriatebalance between robust anti-moneylaundering and counter-terrorism requirements and financial inclusion, the Governmentenacted amendments to the Proceeds ofCrime Act and other relevant legislation. Acritical amendment was to the Proceedsof Crime (Money Laundering Prevention)Regulations, which introduced simplifiedcustomer due diligence requirements. Theseamendmentsarepartofabroaderrisk-basedapproachwhich provide financial institutionsthe flexibility to update their customeridentification and verification processes toaccommodate low-risk consumers seeking to open bank accounts, thereby increasingfinancialaccessforconsumers.

‘Economic Opportunity for All’ also meanscreating a financial system that especiallyincentivises more MSMEs to formalise theirbusinesses; produce financial products andservicesthatrespondtotheneedsofMSMEs;and,stimulategreatergrowthandexpansionoftheseenterprises.Toincreasetheopportunityformicro, smallandmediumsizedbusinessesto raise capital through equity financing,the Government has focused on creatingthe enabling environment for increasedaccess to the financial markets. In August2019, the Government of Jamaica enactedamendmentstothePensions(SuperannuationFunds and Retirement Schemes) InvestmentRegulations. These amendments increasedthethresholdsfor investmentinprivateequityandventurecapitalfunds.

Additionally,theGovernmentcontinueditsworkonimprovingMSMEfinancethroughareviewoftheSecurityInterestsinPersonalPropertyActin conjunctionwith the International FinanceCorporation. Led by the Ministry of Industry,Commerce, Agriculture and Fisheries withthesupportofkeystakeholders intheprivateandpublicsector,theGovernmentengagedthe banking industry and legal fraternity onadvancingMSMEFinancethroughmoveableassetsandthesecuredtransactionsregime.Allstakeholders,includingtheDevelopmentBankof Jamaica and deposit taking institutionsrecognisethatgreaterutilisationofmoveablecollateralprovidestheopportunitytoincreaselending to the private sector, particularlyMSMEs.

I am particularly excited about the workon the Access to Finance project beingspearheaded by the Development Bank ofJamaica to implement its electronic reverse factoring platform, which will improve thetimeforpaymentforapprovedinvoicesissuedby MSMEs to their clients, by leveraging thecreditworthinessoflargeenterprisesasanchorfirms.

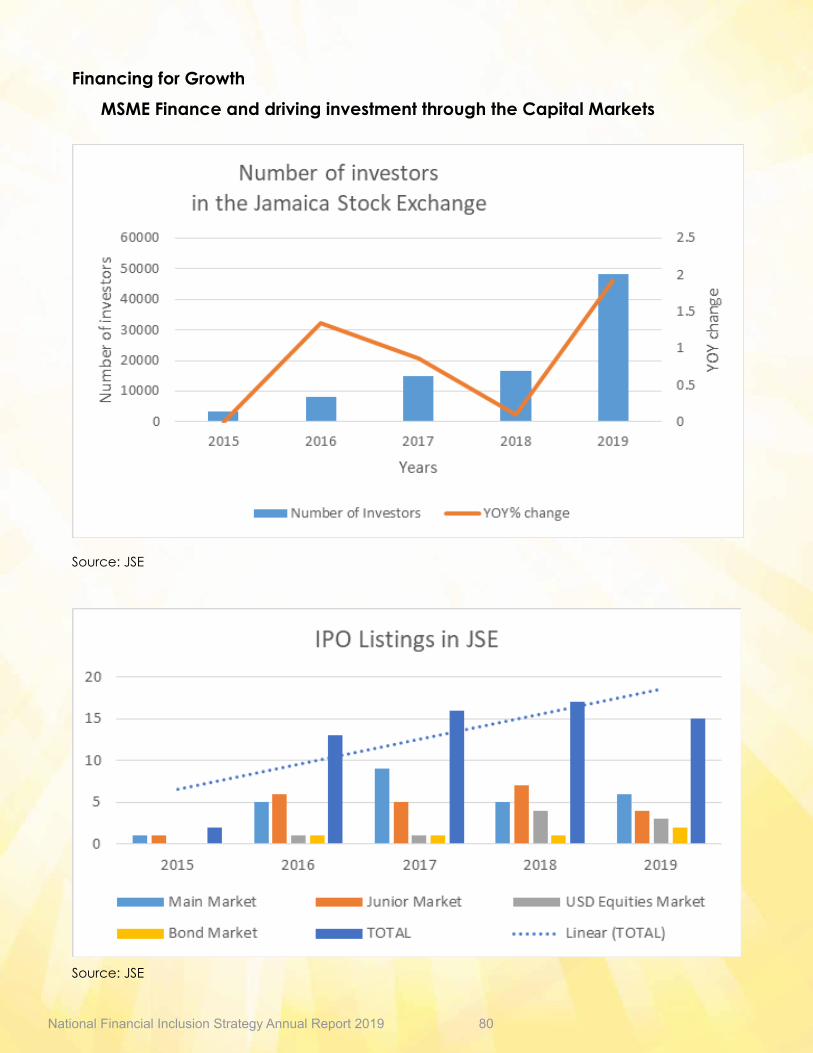

Broadening the ownership base of theJamaican economy is an important strategy inachieving‘EconomicOpportunityforAll.’Assuch,in2019,therewasaconcertedefforttoincrease the number of ordinary Jamaicansparticipating in the stock market throughthe earmarking of investment opportunitiesin initialpublicofferings, includingoneof thelargest in the history of the Jamaican StockExchange, Wigton Windfarm. The JamaicaStock Exchange reported that over 32,000JamaicansrespondedtotheIPOwithbidsthatexceeded$14billion.

Even as the Government continues its work,wemusteducateourpopulationsothattheycanbecome financially capableandbetterprotect their interests when selecting theproducts,theyneed.

Toachievethis,BankofJamaicaimplementedits national financial inclusion outreachprogramme, which sensitized the public keyfinancial literacy concepts and consumerprotectionconcepts.

Weareexcitedaboutwhatwehaveachievedin financial inclusion and financial literacy to

The Hon. Nigel A. Clarke, D.Phil., MP.Minister of Finance and the Public Service Chairman of the National Financial Inclusion Council

National Financial Inclusion Strategy Annual Report 2019 8

date,evenaswerecognizemuchmoremustbedonetopromotefinancialliteracyofourpopulation,especiallyouryouth,toachievesustainableeconomicgrowth. IencourageyoutosupporttheGovernmentofJamaicaonthisjourney.

Hon. Nigel A. Clarke, D.Phil., MP. c. Chairman, National Financial Inclusion Council

National Financial Inclusion Strategy Annual Report 2019 9

National Financial Inclusion Strategy Annual Report 2019 10

Richard Byles Governor, Bank of Jamaica

National Financial Inclusion Strategy Annual Report 2019 11

BankofJamaica’sroleinpromotingfinancialinclusion is captured in our pledge to “Build an inclusiveeconomy.”

Too often, Jamaican citizens and businesseshavebeenperplexedandintimidatedbythecomplexity of the formal financial system, itsrules and laws. Bank of Jamaica appearedtobe justanotherpartofa slowbureacracywhichwas unresponsive to the needs of themarket.

With the continued implementation of theNational Financial Inclusion Strategy, I ampleasedtonotethatBankofJamaicaistrulybeingseenasthe Bank of Jamaica, belongingto the people of Jamaica, committed andaccessible, relevant and accountable. Bankof Jamaica is more than a citadel on thebeautiful KingstonHarbour. Bankof Jamaicaexists to protect, shape and manage theeconomyofJamaica.

In2019,BankofJamaicabeganitsgrass-rootspublic sensitization on the National FinancialInclusion Strategy. Going across the Island,BankofJamaicasoughttohaveaconversationwith our fellow Jamaicans to explain keyeconomicconcepts and the role of BankofJamaica,asregulatorandimplementoroftheNational Financial Inclusion Strategy. BankofJamaica and its financial inclusion partnersfrom across the public and private sectors,visited 6 parishes, educating persons on theBankingServices(ConsumerRelatedMatters)CodeofConduct, theCredit ReportingAct,the Payment Clearing and Settlements ActandtheProceedsofCrimeActandsimpliedcustomerduediligencerequirements.In2019,BankofJamaicaalsoupdatedourguidanceon provisioning for expected credit losses,making reference to the Security Interestsin Personal Property Act. Bank of Jamaicaencouraged the greater use of securedtransactions, supported the developmentof new asset based lending products, suchas reverse factoring; and championed theenhancementoffinancialliteracyanddigitalpayments.

InkeepingwiththecompletionoftheBankingCompetition Study, Bank of Jamaica madethestrategicdecision tocreatetheenablingenvironment for digital finance, throughdevelopingpoliciesto improveaccesstotheretail payments infrastructureanddeliveryof

welfarebenefitselectronically.

Oneofthecrowningachievementsforfinancialinclusion, was the enactment in October2019 of the amendments to the Proceedsof Crime Act and the Proceeds of Crime(Money Laundering Prevention) Regulations,whichallowedfortheapplicationofsimplifiedcustomer due diligence requirements. Withthis legislative change, financial institutionswerenowable to implementeasieraccountopeningproceduresforclientswhichposedalowriskofmoneylaunderingandfinancingofterrorism.Akey legalbarriertoaccessingtheformalfinancialsystemhadbeenmodifiedtoallowforanimprovedrisk-basedapproachtoanti-moneylaunderingandcounter-financingofterrorismregulation.

In2019,asinpreviousyears,BankofJamaicabenefittedgreatlyfromtheworkofitsfinancialinclusion partners. In July 2019, the PrivateSector Organisation of Jamaica (PSOJ)launched its PSOJ Access to Finance Panel,which identified the critical success factorsforfinancial inclusion fromtheperspectiveofmicro, small and medium-sized enterprises.Through the creative use of workshops andconferenceswhichwereaccessibleonsocialmedia, more businesses began to equipthemselveswiththetoolsneededtoscaleuptheiroperationsandgodigital inthedeliveryoftheirservices.

In 2020, Jamaica, like the rest of the World,had to face newchallenges to its economybecauseoftheglobalpandemicofCovid-19.ThesignificantgainsmadeinimrpovingaccesstofinanceforMSMEsandachieveinggreaterfinancialgrowthwerethreatenedbyCovid-19andthereductionofeconomicactivity.

Inthemidstofthischallengehowever,BankofJamaicaidentifiedopportunitiestoacceleratework on financial inclusion through theexpansionofdigitalpaymentsand improvedconsumer protection. Our work to achievefinancial inclusion has accelerated, as webuildanewdigital–and inclusiveeconomy.Ourjourneycontinues,withBankofJamaicaatthevanguardofthetransformation.Welcometoournewinclusiveeconomy.

Richard Byles, GovernorBank of Jamaica Richard Byles

Governor, Bank of Jamaica

National Financial Inclusion Strategy Annual Report 2019 12

The goal of the National Financial InclusionStrategy is to

“createaninclusivefinancialsysteminwhicheveryadultandenterprisehasaccessto,andisabletomakefulluseofarangeofadequate,qualityandaffordableservices”

Through the commitment of the public andprivate sector partners, 2019 was the yearwithinwhich severalof thefinancial inclusioninitiativesbegantobearfruit.TheenactmentoftheamendmentstotheProceedsofCrime(Money Laundering Prevention) Regulationscreated the enabling legislation for theapplicationof simplified know your customerrequirements for individuals and businesses,thereby facilitating easier account openingpractices by financial institutions for low-riskclients.

To advance capital market development,amendments were made to the Pensions(Superannuation Funds and RetirementSchemes) (Investment) Regulations, whichresulted in therevised limits for investments inprivate equity by approved private pensionplans.

TheMinistryofIndustry,Commerce,Agricultureand Fisheries (MICAF) continued its work toempowerMSMEs,throughitsworkonimprovingthe operational processes for online businessname registration by the Companies Office.Further, research on the possibility of utilizingunclaimed fundsasa sourceoffinancing forMSMEswascompletedinAugust2019.MICAFin partnership with the International FinanceCorporation spearheaded the developmentof educational materials on assets basedlending products, such as reverse factoring,whichcouldbeusedbyfinancialinstitutionstoadvancecredittoMSMEs.

Bank of Jamaica supported these efforts,by the issuance of its updated supervisoryguidanceontheStandardofSoundPracticefor provisioning and managing expectedcredit losses, whichmade specific referencetotheStandardofSoundPracticeforProblemAssetManagement,ProvisioningRequirementsand Accounting for Expected Credit Lossesand Asset Based Lending Product. This workcomplementedthecompletionoftheBanking

Competition Study, which highlighted theimportanceofdigitalpaymentsandfintechasadriveroffinancialinclusion.

Bank of Jamaica accelerated its financialinclusion outreach, with a strong presenceon traditional and social media on relevant topics, such as access to finance, digitalpayments,consumerprotectionandfinancialliteracy. With outdoor radio broadcasts andtownhalls insix(6)parishes,BankofJamaicahad the conversation on financial inclusionwithJamaicancitizensandfirms.Thediasporawasalsoengaged,aswastheprivatesector.

July 2019 was the moment in which theprivate sector, through the PSOJ Access toFinanceFacilitationPanel,advancedworkonfinancialinclusion.Inapartnershipoffinancialinstitutions, regulators, industry associations,lawyers and MSMEs, the PSOJ Access toFinance Facilitation Panel demonstrated that all financial institutions wanted to dobusiness with MSMEs. The MSMEs outlinedtheirchallengeswithobtainingfinancingandbusiness support services, and the financialinstitutionscommittedthemselvestoresolutionoftheseissues.

Thetimingofthiscollaborationwasfortuitous,as six impact indicators improved;and threeintermediate indicators improved. Detailsof these achievements and ongoing work-streamsare in theAppendices to the report.The work of building an inclusive economycontinues.

Executive Summary

National Financial Inclusion Strategy Annual Report 2019 13

National Financial Inclusion Strategy Annual Report 2019 14

Melanie Williams Financial Inclusion Technical Secretariat, Bank of Jamaica

Message

National Financial Inclusion Strategy Annual Report 2019 15

Report from the Financial Inclusion Technical Secretariat, Bank of Jamaica

Throughout 2019, the Financial InclusionTechnical Secretariat continued to driveBank of Jamaica’s financial inclusionprojects, incollaborationwith its financialinclusionpartners.BelowarethehighlightsoftheachievementsofBankofJamaica.

A. Technical Assistance, Conferences and WorkshopsBankofJamaica,throughtheFinancialInclusion Technical Secretariat, inassociationwiththeOfficeofTechnicalAssistance staged a workshop on“Leveraging data to drive financialinclusion” on 31 January 2019.ParticipantsincludedBankofJamaica,theStatistical Instituteof Jamaica, theDevelopment Bank of Jamaica andthe Ministry of Industry, Commerce,AgricultureandFisheries.

On12June2019,theFinancialInclusionTechnicalSecretariatpresentedattheNational Bank of Ukraine’s FinancialInclusion Forum, which focusedon developing a cashless societyand Jamaica’s experiences withthe implementation of the NFIS. For

additional information, please see thehyperlinkbelow:https://www.youtube.com/watch?v=DqIzwBgt0T8

The Financial Inclusion TechnicalSecretariat continues to partner withthe Private Sector Organisation ofJamaica (PSOJ) on the PSOJ Accessto Finance Panel and the series ofworkshopstobuildthefinancialliteracyof MSMEs and address the barriersto accessing credit for MSMEs. TheSecretariat participated in a panel on 3July2019whichdiscussedchallengeswith accessing loans from deposittakinginstitutions,theneedfortrainingof front-line staff engaged in creditadjudication processes and simplifiedcustomerduediligencerequirements.

On 1 – 2 October 2019, the FinancialInclusion Technical Secretariat inpartnershipwiththeMinistryofIndustry,Commerce, Agriculture and Fisheries,the International FinanceCorporation,the Inter-AmericanDevelopmentBankandtheWorldBankstagedaworkshopon MSME Growth and Developmentthroughmoveableassetbasedfinance,on1–2October2019.TopicscoveredincludedpresentationsontheNationalFinancial Inclusion Strategy, theStandardofSoundPracticeonProblemAsset Management, ProvisioningMelanie Williams

Financial Inclusion Technical Secretariat, Bank of Jamaica

NFIS Achievements for 2019

National Financial Inclusion Strategy Annual Report 2019 16

Requirements and Accounting forExpected Credit Losses; and AssetBasedLendingProducts.

B. Participation in the Regional Diaspora Conference 17 – 19 June 2019BOJ’s Research and EconomicProgramming Division in collaborationwith the Financial Inclusion TechnicalSecretariat prepared and administered asurveytoconferenceparticipantsonremittances and access to financialproducts and services to identifynew investment opportunities for thediaspora.

C. External Outreach and CommunicationOn 22 January 2019, through theMinistry of Finance’s communicationteam,theFinancialInclusionTechnicalSecretariatparticipatedintheMinistry’sradio programme “Let’s talk Finance”whichwasairedonNationwideFMon6February2019.Futureradiobroadcastswere recorded on 13 February and20 February, which featured the NFISBrandAmbassadors.

The Financial Inclusion public serviceannouncementwaspublishedbyBOJonitsTwitterpageon24January2019.AsecondPSA,featuringthejingleandanimation for the National FinancialInclusionStrategywaspublishedon28January 2019. The responses to bothtweetswasquitepositive.

On 30 January 2019, in partnership

with theMinistry of Finance, copies ofthe NFIS brochure, which summarizesthe strategy were distributed by theHon. Fayval Williams, M.P. during apublicoutreachprogrammeheldinSt.Andrew.

On 24 February 2019, the FinancialInclusion Technical Secretariat hadits Financial Inclusion Church Serviceat Swallowfield Chapel. Participantsincluded representatives from theJamaica Deposit Insurance Corporation (JDIC)andBankofJamaica.

The Financial Inclusion TechnicalSecretariatcollaboratedwiththePublicRelationsteamonthedevelopmentofaradioprogramme“CentrallySpeaking”to educate the public on BOJ’s rolein implementing monetary policy,creating an inclusive economy and supervisionofdeposittakinginstitutions.

In2019,theFinancialInclusionTechnicalSecretariat and its financial inclusionpartners staged 6outdoorbroadcastswithIrieFMaspartofpublicsensitizationprogramme.

Starting in October 2019, staffengagement videos on financialinclusion were posted to BOJ’s intranet to communicate the key thematicareasoftheNationalFinancialInclusionStrategy.

Partners that haveparticipated in the

National Financial Inclusion Strategy Annual Report 2019 17

outreachincludetheMinistryofIndustry,Commerce, Agriculture and Fisheries,the Companies Office of Jamaica,the Consumer Affairs Commission,the Development Bank of Jamaica,the Financial Services Commission,the Jamaica Business DevelopmentCorporation, the Jamaica DepositInsurance Corporation, the PrivateSector Organisation and the PSOJAccesstoFinancePanel.

AFinancialInclusionTownHallwasheldat Bankof Jamaicaon 19 September2019bytheFinancialInclusionTechnicalSecretariat in conjunction with theInternationalMonetaryFund.

On7October2019,apresentationonfinancialinclusionandfinancialliteracywasmadeattheUniversityoftheWestIndies,MonaSchoolofBusiness.

The Secretariat partnered with theNational Consumers League on 4December2019topresentonfinancialinclusionandconsumerprotection.

Under the Law – Public Sensitization about important legal mattersStarting November 2019, Bank ofJamaicasponsoredfour(4)episodesin“UndertheLaw”programme.

For a full listing of communicationinitiatives,pleaseseesection5.0.

D. Graded Customer Due Diligence Requirements under the Proceeds of Crime ActOn 11 September 2019, the Ministryof National Security circulated the Billcontaining proposed amendments totheProceedsofCrimeActandthePOCA (Money LaunderingPrevention)Regulations. The Financial InclusionTechnical Secretariat provided itscomments on 12 September 2019 inrelationtothesimplifiedcustomerduediligencerequirements.Theenactmentoftheselegislativeamendments,wereacriticalpartoftheenablingframeworkfor risk-based supervision of moneylaundering and financing of terrorismrisks.

Updated bills were received on 30September and 4 October from theMinistry of National Security andfeedbackwasprovidedbytheFinancialInclusionTechnicalSecretariat.

On28October2019,Parliamentpassedthe amendments to the Proceeds ofCrimeActandtheTerrorismPreventionAct.

The proposed amendments to thePOCA (Money LaunderingPrevention)RegulationswerepassedbyParliamentin October 2019. These amendmentsincludedchangestopermitarisk-basedapproach tobe takenwhenopeningaccounts and to allow financialinstitutions to administer simplified

National Financial Inclusion Strategy Annual Report 2019 18

customerduediligencerequirements.

The Financial Inclusion TechnicalSecretariatcontinuedtoworkwiththeFinancialMarketsInfrastructureDivisionto strengthen the legal framework forthe regulation of payment servicesproviders.

E. Digitization of Government Payments

The Financial Inclusion TechnicalSecretariat completed its researchpaper on improving financial accessthrough digitization of governmentpayments and presented the findingstotheChairoftheRetailPaymentsandFinancial InfrastructureWorkingGroupon6November2019.

F. Research Paper on improving access and interoperability

In August 2019, the Financial InclusionTechnical Secretariat submittedits research paper on improvinginteroperability and access to thefinancial infrastructure to the RetailPayments and Financial InfrastructureWorking Group. Comments werereceived from key stakeholders,including the Planning Institute ofJamaicaandMultiLink.

The Financial Inclusion TechnicalSecretariat presented its paper to the National Payments Council on 23October 2019. Comments were alsosolicitedontheimplementationplanforimproving financialaccessanddigitalpayments.

G. Presentation to the Economic Growth Council – 17 October 2019The Ministry of Finance and Bank ofJamaicametwiththeEconomicGrowthCouncil to discuss matters related to the NFIS MSME Finance agenda andthe Financial Deepening Agenda.Work continues with the pursuing theobjectives of the Access to FinanceProject led by theDevelopment BankofJamaica.

H. Development of demand side surveysThe Financial Inclusion TechnicalSecretariat developed survey instrumentstomeasureanumberofkeymetricsforfinancialinclusion,namely:

(a) Easeofaccesstofinancialservices;(b) Usage of financial services (payment

services);(c) Accesstocredit;and(d) AccesstoInsuranceandPensions.

Oncefinalized,thesewillbesharedwiththeConsumerProtectionandFinancialCapability Working Group and theRetailPaymentsFinancialInfrastructureWorkingGroupfortheircomments.

Workwasdoneondevelopmentofthetermsofreferenceforabaselinesurveyfor financial literacy. On completion,that document will be shared withthe Ministry of Education, Youth andInformation and the members of theConsumer Protection and Financial CapabilityWorkingGroup.

National Financial Inclusion Strategy Annual Report 2019 19

National Financial Inclusion Strategy Annual Report 2019 20

I. Banking Competition StudyBOJhadtwovirtualmeetingswith theConsultants (Menns SRPL) on 22 May2019andon18June2019todiscuss:

• Comments on the Final Draft InterimReport;

• Proposedfocusgroupstobeheldwiththebankedandunbankedcustomersas identified by the Consumer AffairsCommission and the Fair TradingCommission;and

• Further discussions with the deposittaking institutions, and micro-financeinstitutions to identify factors thatmayinfluencethecompetitivebehaviourofthemarketparticipants inthebankingservicesindustry.

The Fair Trading Commission (FTC)and BOJ provided their commentson theFinal InterimReporton17June2019 and subsequently on 24 June2019. Comments were received fromthe Financial Inclusion TechnicalSecretariat, the Financial Stability, theFinancialMarketInfrastructureandtheFinancial Institutions Supervisory Division teamsofBOJ.

The Consultants presented theirfindings to theMinistryof Financeandthe Public Service, Bank of Jamaicaand the Fair Trading Commission andotherstakeholderson10–11October2019. The Financial Inclusion TechnicalSecretariat confirmed on 31 October2019, that ithadno furthercommentsonthedraftfinalstudy.

J. Utilisation of Unclaimed Funds

BOJ provided comments on thedraft interim report on the proposedutilization of unclaimed funds to driveMSMEgrowth.ThisreportwaspreparedbyConsultantstotheMinistryofIndustry,Commerce, Agriculture and Fisheries(MICAF). The report was finalized inAugust2019.

K. Legislative review of the Credit Reporting ActBank of Jamaica (BOJ) received thesecondinterimreportinJune2019.TheFinancialInclusionTechnicalSecretariatandtheFinancialInstitutionsSupervisoryDivisionprovidedcomments.

L. The Financial Inclusion Steering CommitteeThe Financial Inclusion SteeringCommitteemeton28May2019.

National Financial Inclusion Strategy Annual Report 2019 21

National Financial Inclusion Strategy Annual Report 2019 22

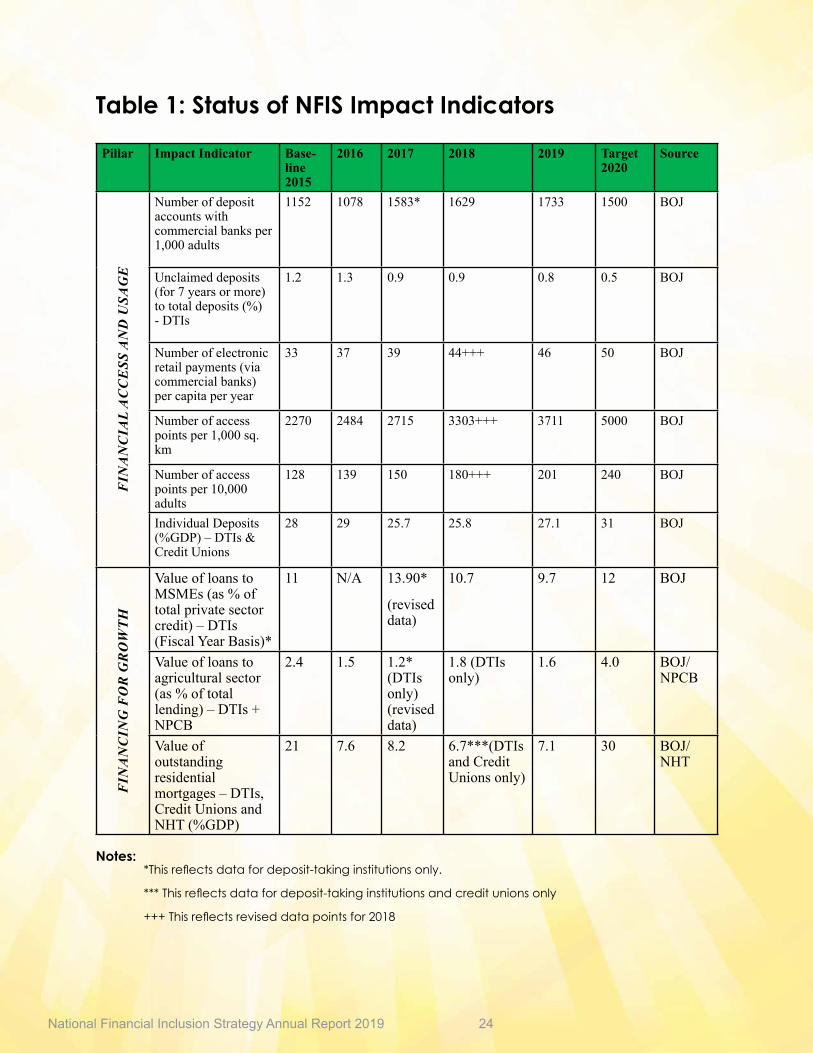

3.1. For the period under review, theFinancial Inclusion TechnicalSecretariat reviewed data on theintermediateandimpactindicators.These aremeasured annually as amethodoftrackingprogressontheNFISobjectives.

Impact Indicators3.2 Six (6) impact indicatorsadvanced

positively towards the 2020 targets.These indicators are all in thedimensions of access to financialservices and usage of financialservices.

3.3 Access impact indicators whichadvanced towards 2020 targets werethe:

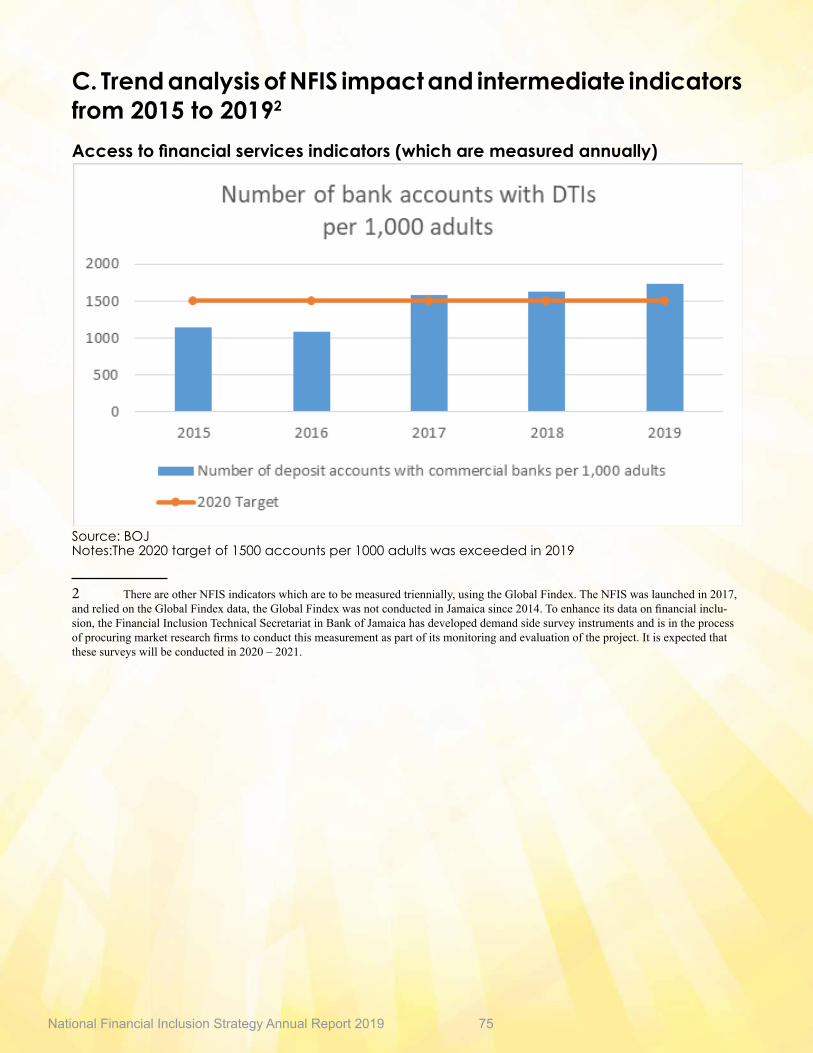

a. Number of deposit accounts withcommercialbanksper1,000adults,

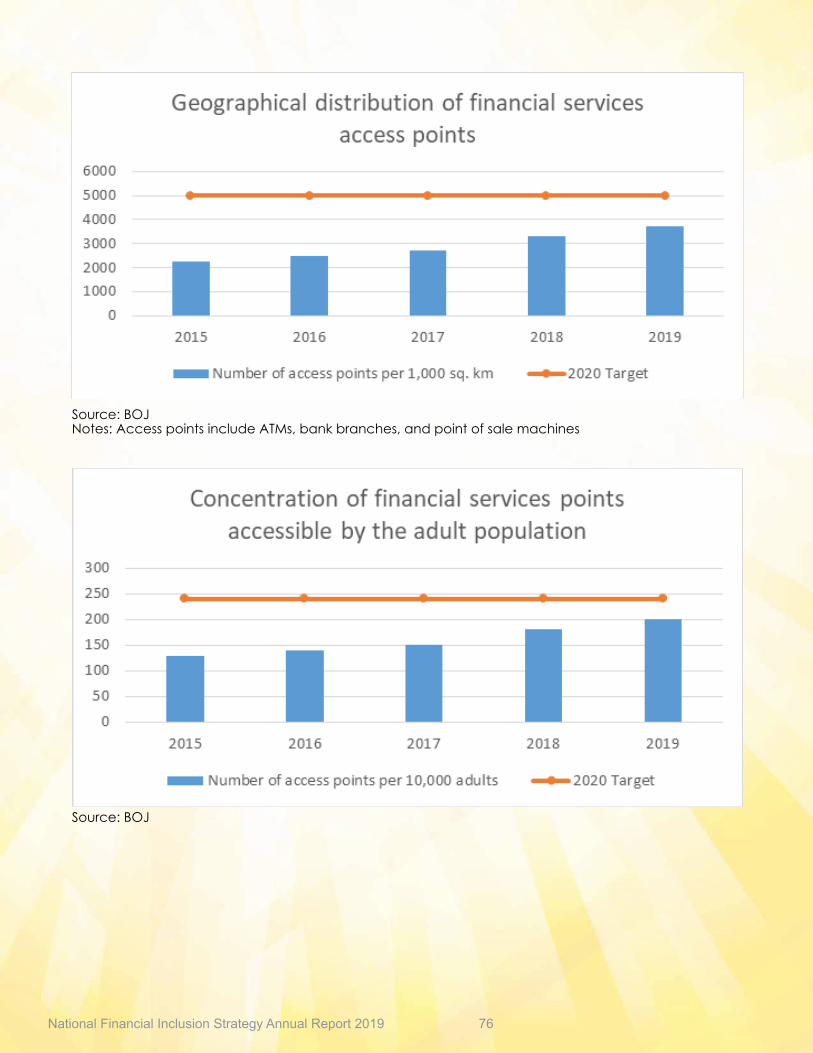

b. Number of access points per 1,000squarekilometres;and

c. Numberofaccesspointsper10,000adults.

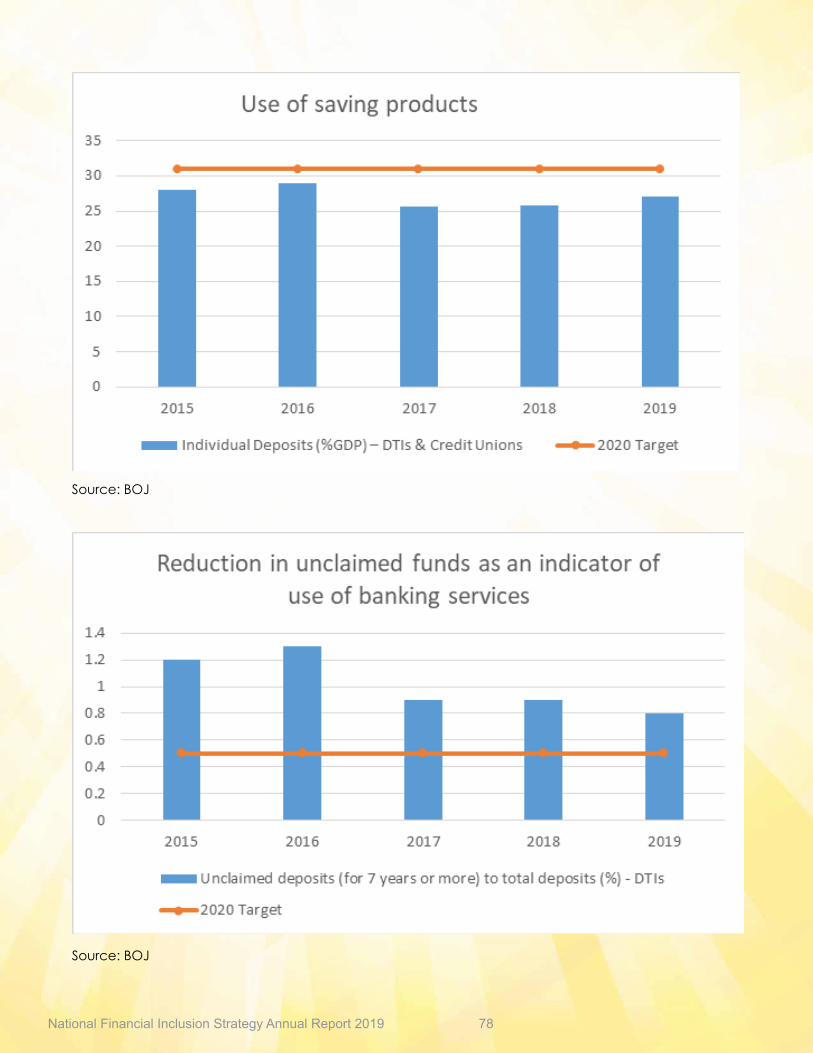

3.4 Usageimpactindicatorswhich advanced towards 2020 targets

a. Unclaimeddepositsasapercentageoftotaldeposits,

b. Electronic retail payments (viacommercialbanks)percapita;and

c. Individual deposits as a percentage ofgrossdomesticproduct.

3.5Withregardtotheimpactindicatorsforfinancialgrowth,theimpact indicator measuring improvement in MSMEFinancedeclinedbelowits2018measurements.

3.6 There is incomplete data for themeasurement of the impactindicatoronthevalueofoutstandingresidential mortgages, and thevalue of loans to the agriculturalsector. Such data as is availablewas limited tocredit advancedbydeposittakinginstitutionsonly.

3.0 Monitoring and Evaluation Framework

National Financial Inclusion Strategy Annual Report 2019 23

National Financial Inclusion Strategy Annual Report 2019 24

Table 1: Status of NFIS Impact Indicators

Pillar Impact Indicator Base-line 2015

2016 2017 2018 2019 Target 2020

Source

FIN

AN

CIA

L A

CC

ESS

AN

D U

SAG

E

Number of deposit accounts with commercial banks per 1,000 adults

1152 1078 1583* 1629 1733 1500 BOJ

Unclaimed deposits (for 7 years or more) to total deposits (%) - DTIs

1.2 1.3 0.9 0.9 0.8 0.5 BOJ

Number of electronic retail payments (via commercial banks) per capita per year

33 37 39 44+++ 46 50 BOJ

Number of access points per 1,000 sq. km

2270 2484 2715 3303+++ 3711 5000 BOJ

Number of access points per 10,000 adults

128 139 150 180+++ 201 240 BOJ

Individual Deposits (%GDP) – DTIs & Credit Unions

28 29 25.7 25.8 27.1 31 BOJ

FIN

AN

CIN

G F

OR

GR

OW

TH

Value of loans to MSMEs (as % of total private sector credit) – DTIs (Fiscal Year Basis)*

11 N/A 13.90*

(revised data)

10.7 9.7 12 BOJ

Value of loans to agricultural sector (as % of total lending) – DTIs + NPCB

2.4 1.5 1.2* (DTIs only) (revised data)

1.8 (DTIs only)

1.6 4.0 BOJ/ NPCB

Value of outstanding residential mortgages – DTIs, Credit Unions and NHT (%GDP)

21 7.6 8.2 6.7***(DTIs and Credit Unions only)

7.1 30 BOJ/NHT

Notes:*Thisreflectsdatafordeposit-takinginstitutionsonly.

***Thisreflectsdatafordeposit-takinginstitutionsandcreditunionsonly

+++Thisreflectsreviseddatapointsfor2018

National Financial Inclusion Strategy Annual Report 2019 25

National Financial Inclusion Strategy Annual Report 2019 26

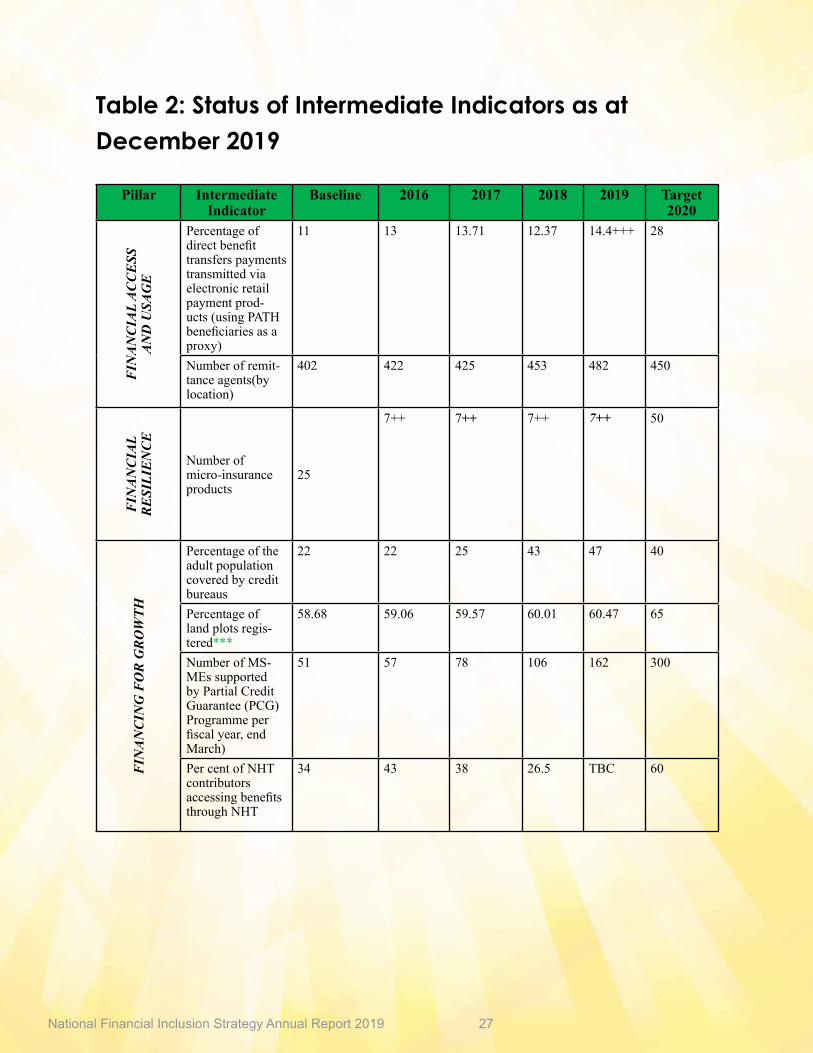

1.1 Aspartofthemonitoringandevaluationframework,therearetenintermediateindicators, which measure Jamaica’sprogress towards financial inclusionthroughouttheproject’stime-line.SeeTable 2.

1.2 Ofthese,fortheperiodunderreview,four intermediate indicators aremoving in a positive direction towards the2020targets.

1.3 Theseare:a) ThenumberofPATHbeneficiarieswho

received theirbenefits throughdigitalpayments;

b) The number of remittance agents(determinedbylocation);

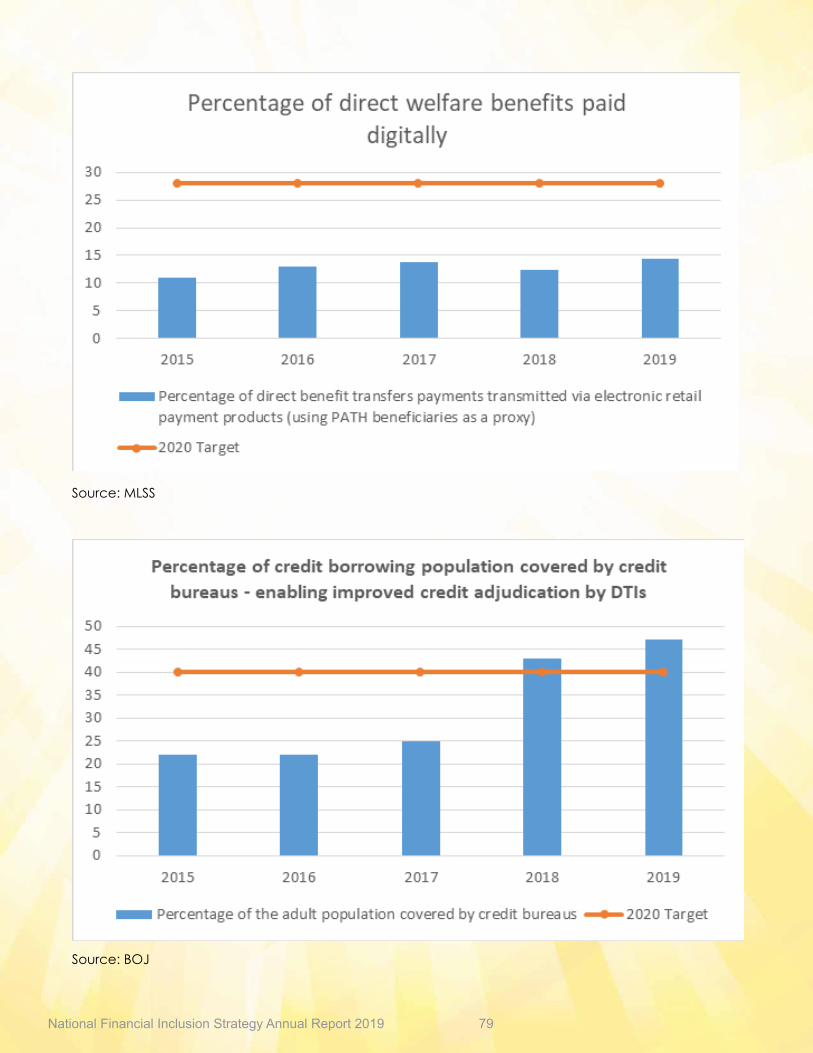

c) Thepercentageoftheadultpopulationcoveredbythecreditbureaus;and

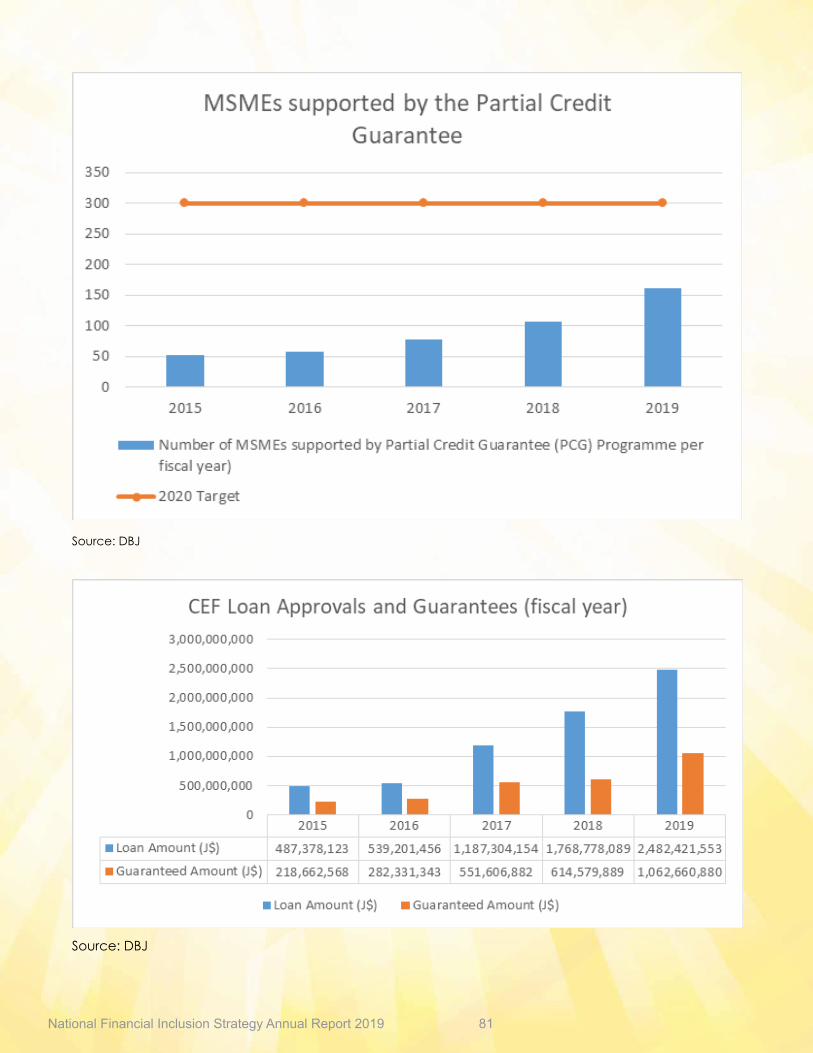

d) The number of micro, small andmedium-sized enterprises supported bythePartialCreditGuarantee(PCG).

1.4 Ofthese,twoindicatorshavemettheir2020targets,whichare:

a) Financial access – number ofremittanceagentlocations;and

b) Financing for growth – percentageof thecreditutilizingadultpopulationwhichiscoveredbyacreditbureau.

1.5 The number of micro-insuranceproductsinthemarketplaceremainedunchanged for the past three years,as the legislativeamendments to theInsuranceAct for themicro-insuranceindustrywerenotenacted.

Intermediate Indicators

National Financial Inclusion Strategy Annual Report 2019 27

Table 2: Status of Intermediate Indicators as at December 2019

Pillar Intermediate Indicator

Baseline 2016 2017 2018 2019 Target 2020

FIN

AN

CIA

L A

CC

ESS

A

ND

USA

GE

Percentage of direct benefit transfers payments transmitted via electronic retail payment prod-ucts (using PATH beneficiaries as a proxy)

11 13 13.71 12.37 14.4+++ 28

Number of remit-tance agents(by location)

402 422 425 453 482 450

FIN

AN

CIA

L R

ESI

LIE

NC

E

Number of micro-insurance products

25

7++ 7++ 7++ 7++ 50

FIN

AN

CIN

G F

OR

GR

OW

TH

Percentage of the adult population covered by credit bureaus

22 22 25 43 47 40

Percentage of land plots regis-tered***

58.68 59.06 59.57 60.01 60.47 65

Number of MS-MEs supported by Partial Credit Guarantee (PCG) Programme per fiscal year, end March)

51 57 78 106 162 300

Per cent of NHT contributors accessing benefits through NHT

34 43 38 26.5 TBC 60

National Financial Inclusion Strategy Annual Report 2019 28

Pillar Intermediate Indicator Baseline 2016 2017 2018 2019 Target 2020

RE

SPO

NSI

BLE

F

INA

NC

E

A: Per cent of finan-cial consumer com-plaint cases resolved (of those received)

76 53* 56 58 98 N/A

B: Number of com-plaints received (via BOJ, FSC, CAC)

214 195 223 211 170 N/A

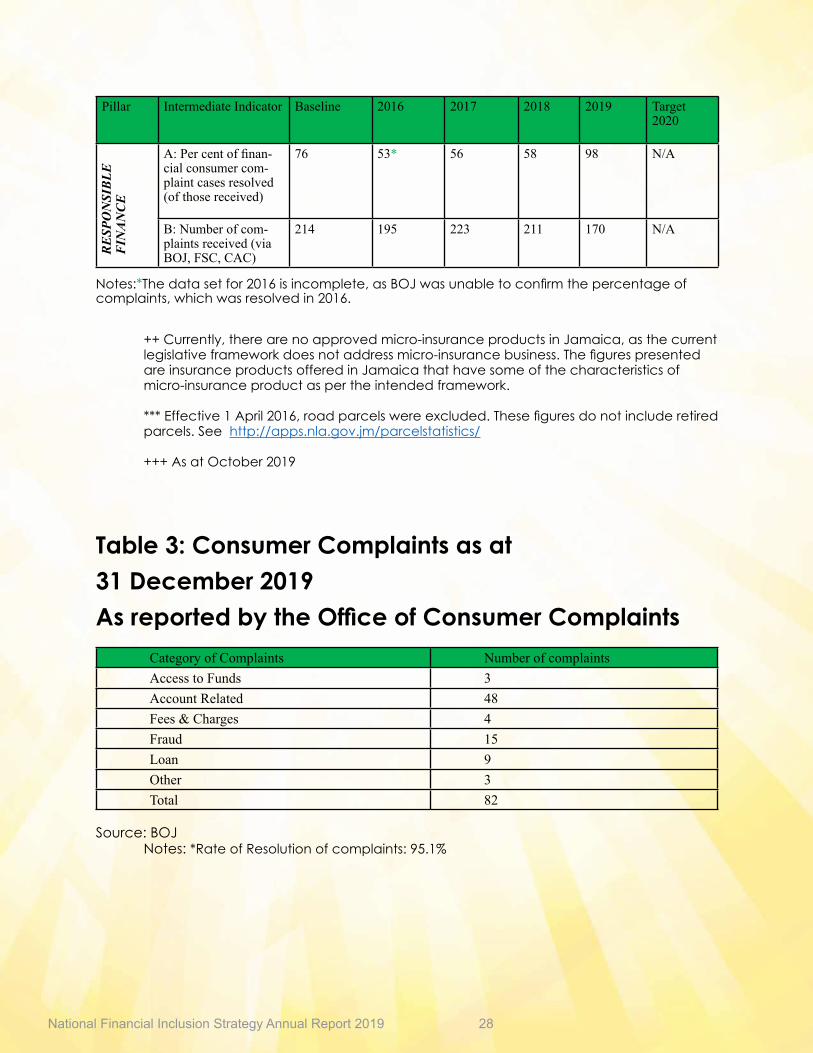

Notes:*Thedatasetfor2016isincomplete,asBOJwasunabletoconfirmthepercentageofcomplaints,whichwasresolvedin2016.

++ Currently,therearenoapprovedmicro-insuranceproductsinJamaica,asthecurrentlegislativeframeworkdoesnotaddressmicro-insurancebusiness.ThefigurespresentedareinsuranceproductsofferedinJamaicathathavesomeofthecharacteristicsofmicro-insuranceproductaspertheintendedframework.

***Effective1April2016,roadparcelswereexcluded.Thesefiguresdonotincluderetiredparcels.Seehttp://apps.nla.gov.jm/parcelstatistics/

+++AsatOctober2019

Table 3: Consumer Complaints as at31 December 2019As reported by the Office of Consumer Complaints

Category of Complaints Number of complaintsAccess to Funds 3Account Related 48Fees & Charges 4Fraud 15Loan 9Other 3Total 82

Source:BOJNotes:*RateofResolutionofcomplaints:95.1%

National Financial Inclusion Strategy Annual Report 2019 29

National Financial Inclusion Strategy Annual Report 2019 30

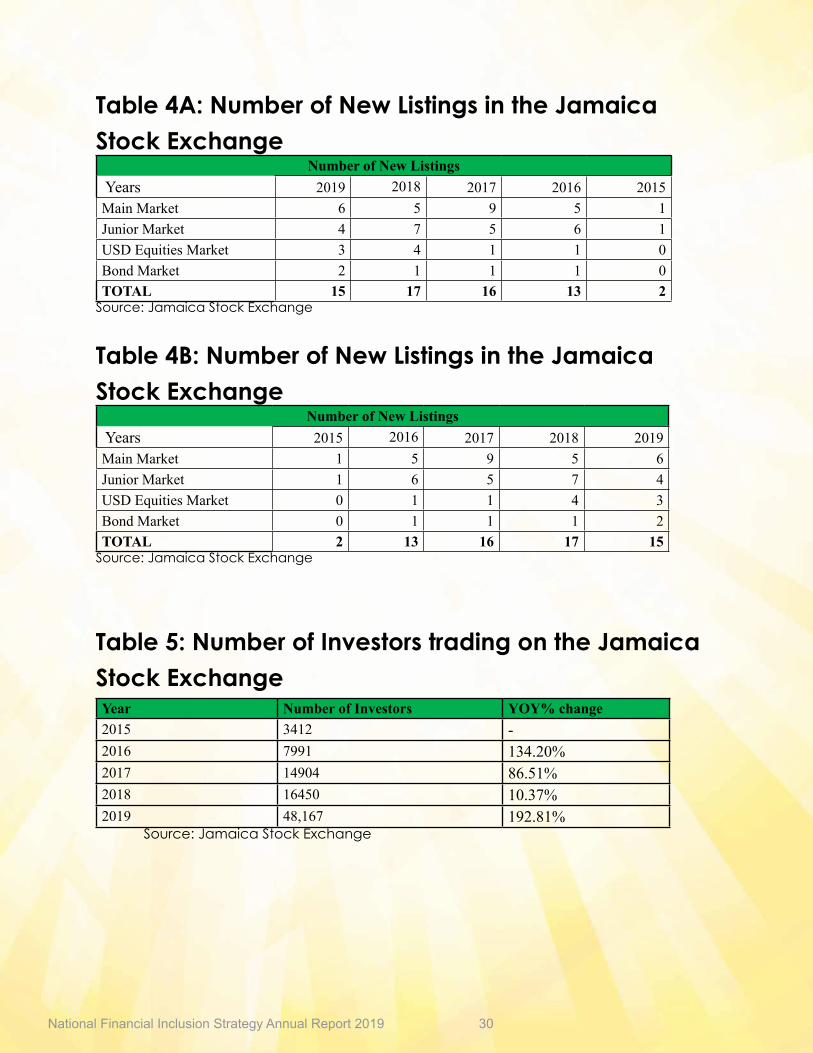

Table 4A: Number of New Listings in the Jamaica Stock Exchange

Number of New Listings Years 2019 2018 2017 2016 2015Main Market 6 5 9 5 1Junior Market 4 7 5 6 1USD Equities Market 3 4 1 1 0Bond Market 2 1 1 1 0TOTAL 15 17 16 13 2Source:JamaicaStockExchange

Table 4B: Number of New Listings in the Jamaica Stock Exchange

Number of New Listings Years 2015 2016 2017 2018 2019Main Market 1 5 9 5 6Junior Market 1 6 5 7 4USD Equities Market 0 1 1 4 3Bond Market 0 1 1 1 2TOTAL 2 13 16 17 15Source:JamaicaStockExchange

Table 5: Number of Investors trading on the Jamaica Stock ExchangeYear Number of Investors YOY% change2015 3412 -2016 7991 134.20%2017 14904 86.51%2018 16450 10.37%2019 48,167 192.81% Source:JamaicaStockExchange

National Financial Inclusion Strategy Annual Report 2019 31

Table 6: Annual Market Capitalization in Junior JSE Market and Main JSE Market

Years 2019 2018 2017 2016 2015Main Market (J$) $1,929,947,681,342.09 $1,383,834,940,068.79 $1,048,739,993,889.94 $697,446,825,637.37 $615,559,573,602.85Junior Market (J$) $151,356,360,107.15 $139,776,812,503.52 $114,795,266,054.62 $103,417,577,608.87 $67,946,699,870.58Combined Market (J$) $2,081,304,041,449.24 $1,523,611,752,572.31 $1,163,535,259,944.56 $800,864,403,246.24 $683,506,273,473.43

Market Capitalization

Source:JamaicaStockExchange

Table 7: Volume and Value of Electronic Retail Payment Transactions for the years 2017 - 2019

Source:BOJ

Notes:Accountsarerecordedasastockfigure

National Financial Inclusion Strategy Annual Report 2019 32

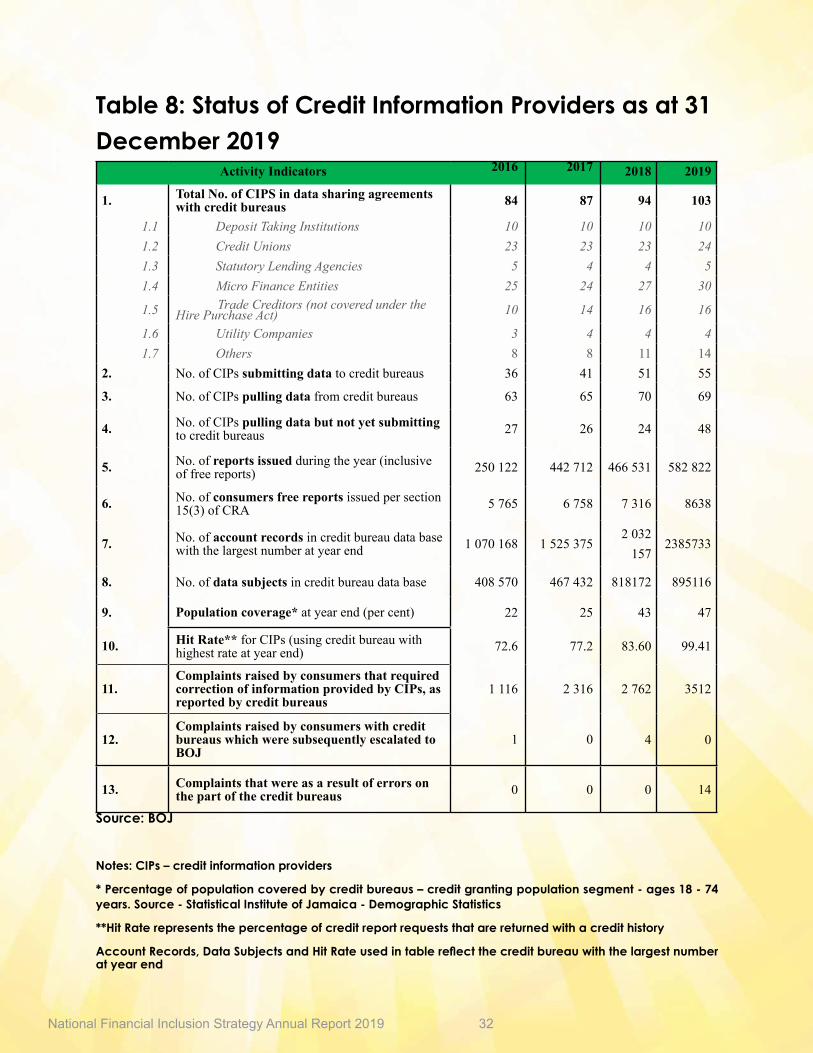

Table 8: Status of Credit Information Providers as at 31 December 2019

Activity Indicators 2016 2017 2018 2019

1. Total No. of CIPS in data sharing agreements with credit bureaus 84 87 94 103

1.1 Deposit Taking Institutions 10 10 10 101.2 Credit Unions 23 23 23 241.3 Statutory Lending Agencies 5 4 4 51.4 Micro Finance Entities 25 24 27 30

1.5 Trade Creditors (not covered under the Hire Purchase Act) 10 14 16 16

1.6 Utility Companies 3 4 4 41.7 Others 8 8 11 14

2. No. of CIPs submitting data to credit bureaus 36 41 51 55

3. No. of CIPs pulling data from credit bureaus 63 65 70 69

4. No. of CIPs pulling data but not yet submitting to credit bureaus 27 26 24 48

5. No. of reports issued during the year (inclusive of free reports) 250 122 442 712 466 531 582 822

6. No. of consumers free reports issued per section 15(3) of CRA 5 765 6 758 7 316 8638

7. No. of account records in credit bureau data base with the largest number at year end 1 070 168 1 525 375

2 032 157

2385733

8. No. of data subjects in credit bureau data base 408 570 467 432 818172 895116

9. Population coverage* at year end (per cent) 22 25 43 47

10. Hit Rate** for CIPs (using credit bureau with highest rate at year end) 72.6 77.2 83.60 99.41

11.Complaints raised by consumers that required correction of information provided by CIPs, as reported by credit bureaus

1 116 2 316 2 762 3512

12.Complaints raised by consumers with credit bureaus which were subsequently escalated to BOJ

1 0 4 0

13. Complaints that were as a result of errors on the part of the credit bureaus 0 0 0 14

Source: BOJ

Notes: CIPs – credit information providers

* Percentage of population covered by credit bureaus – credit granting population segment - ages 18 - 74 years. Source - Statistical Institute of Jamaica - Demographic Statistics

**Hit Rate represents the percentage of credit report requests that are returned with a credit history

Account Records, Data Subjects and Hit Rate used in table reflect the credit bureau with the largest number at year end

National Financial Inclusion Strategy Annual Report 2019 33

National Financial Inclusion Strategy Annual Report 2019 34

5.1 Bank of Jamaica recognized thatit is crucial that we communicateeffectively to our stakeholders toensurethatourmessagesonfinancialinclusionareheard,understoodandfeedback received fromour fellowJamaican citizens and businesses,especiallyourMSMEs.Toooften,theuseofcomplexjargoncanobscurethe message, which causes ourpeopletoloseinterestinthemessageandeitherchangethechannel–orinoursocialmediaworld–scrollon.

5.2 In July 2018, the Financial InclusionTechnical Secretariat of Bank ofJamaicaembarkedonacampaigntoconnectandsharewithJamaicainformationthatourpeoplewantedtounderstand.Ourfinancialinclusionmessages were crafted for ourpeople,and the Financial InclusionTechnicalSecretariathitthestreets,the airwaves and the television.Wediscussedmatterspertaining tomonetary and financial stability, aseducating the public about Bankof Jamaica’s responsibilities assupervisor of financial institutions,overseer of payment systemsand regulator of deposit takinginstitutions, cambios, remittanceservice companies and electronic retail payment service providers.Jamaican citizens and businesseswere eager to learn about theirrightsundertheBankingServicesAct(CustomerRelatedMatters)Codeof

Conduct, theCreditReportingAct,theOperatingDirectionsforcambiosand the Operating Directions forremittanceserviceproviders.

5.3 In2019,wetookthemessagesoftheBank into several communities across Jamaica, through our communityengagement programmes. Here,wesoughttoensureunderstandingof our messages to broaden anddeepenpublicunderstandingwhileweempowerconsumers,especiallythose at the lower end of thefinancialspectrum.BankofJamaicaheldtownhallsonfinancialinclusionat the Bank as well as outdoorbroadcastsinpartnershipwithIrieFMinsix(6)parishes.Inpartnershipwiththe radio series “Under the Law”,we shared relevant information onremittances, credit reporting andtheCodeofConduct toempowerour fellow Jamaican citizens andMSMEs.

5.4 Bank of Jamaica also leveragedour NFIS network and our alliances withkeyfinancialinclusionpartners,including the Ministry of Financeand thePublic Service, theMinistryof Industry, Commerce, AgricultureandFisheries,theDevelopmentBankofJamaica,EXIMBank,theFinancialServices Commission, JamaicaBusiness Development Corporation andtheJamaicaDepositInsuranceCorporation. Through workshops,townhalls, seminars and radio wewereabletosharevaluablecontent

5.0 Communication – the art of engaging, listening, learning and adapting

National Financial Inclusion Strategy Annual Report 2019 35

on how to register a companyonline,thebenefitsoftheSecurityInterests in Personal Property Act and its electronic registry, anddigitalpayments.

5.5 In 2019, Bank of Jamaicacollaborated with multilaterals,such as, the Inter-AmericanDevelopment Bank, theInternationalMonetary Fund, theInternational Finance Corporation andtheWorldBankoninnovativeproducts to driveMSME finance,such as asset based lending,factoring and receivablefinancing. The target audiencefor thesemessages including thebanking industry, representativesfrommicrofinanceinstitutionsandthelegalfraternity.

5.6 Bank of Jamaica not onlyspoke –butwe listened. Theartof effective communicationis based on respect andunderstanding. The concerns ofour citizens informed the designof our Financial inclusion andfinancialliteracycampaigns.

5.7 Bank of Jamaica is pleasedto recognise the leadershiprole played by the PrivateOrganisation of Jamaica (PSOJ)in forming its PSOJ Access toFinance Panel, which held itsinaugural conference on 3 July2019. Since the formationof thispublic-private partnership, therewere three (3) workshops heldwhichidentifiedkeyimpedimentsto growth of small andmedium-sized enterprises, whilearticulating potential solutions to theseproblems.BankofJamaica

is pleased to partner with thePSOJ Access to Finance Panel in itsworktoachievedeepeningofthecapitalmarketsandgreaterfinancialinclusion.

5.8 To ensure reach and messageconnection, Bank of Jamaicabegan to expand the channelsof communication to includeFacebookandYouTube,buildingon the Bank’s use of its Twitterchannel, which had started in2018.Theseeffortsweresupportedby the use of traditionalmedia,giving consumers access to information,pertinenttotheBankon any device, any platform,anywhereandanytime.

5.9 Bank of Jamaica’s digitalfootprint made it possible forthe private sector and thepublic to notice our efforts asour unique and innovative communication strategy exemplified how to connectwith Jamaican enterprises andindividuals on economic policies andregulation,topicswhichhasprovenchallenginginthepast.

5.10 The Bank also produced itsinaugural flagship televisionproduction Centrally Speaking,which was aired on TelevisionJamaica(TVJ). Theprogrammeisalsoavailableonseveraldigitalchannels to include, Twitter,Facebook and YouTube. Ourradio series of the same namewas aired on Irie FM as well as on RJR.

National Financial Inclusion Strategy Annual Report 2019 36

5.11 BankofJamaica’spodcastseriescommenced in mid-year 2019 on four platforms including BuzzSprout, Soundcloud, StitcherandApplepodcast.In2020,theBank will pursue its 360-degreecommunication strategy as we seek to retain and reach newstakeholdersandimprovepublicconfidence.

National Financial Inclusion Strategy Annual Report 2019 37

MembersoftheaudienceinOchoRioslistenattentivelytotheperformanceoftheFinancialInclusionPlaybytheKennySalmonactingtroupe

Brand AmbassadorsTishaunaMullings and TheodoreHenry at BOJ’s financialinclusion outdoor broadcastinSt.Thomas

Highlights from BOJ’s Financial Inclusion outdoor broadcasts

National Financial Inclusion Strategy Annual Report 2019 38

BOJ Financial Inclusion Team At Their Outdoor Broadcasts

National Financial Inclusion Strategy Annual Report 2019 39

National Financial Inclusion Strategy Annual Report 2019 40

National Financial Inclusion Strategy Annual Report 2019 41

National Financial Inclusion Strategy Annual Report 2019 42

National Financial Inclusion Strategy Annual Report 2019 43

MICAF’sCliffordSpencer,speakingatBOJ’sFinancial Inclusion Outdoor Broadcast in Port

Maria

National Financial Inclusion Strategy Annual Report 2019 44

Mr.PaulChinfromDBJ,speakingat BOJ’s Financial Inclusion outdoor

broadcastinPortMaria

National Financial Inclusion Strategy Annual Report 2019 45

CourtneyLodge,sonofPortMariapresentingonfinancialliteracyandMSME Finance at BOJ's outdoor broadcast.

National Financial Inclusion Strategy Annual Report 2019 46

National Financial Inclusion Strategy Annual Report 2019 47

KennySalmon’sActingTroupedramatizetheincreasedopportunitiesforaccesstofinancefromcommercialbanksandDBJ’spartialcreditguaranteescheme

National Financial Inclusion Strategy Annual Report 2019 48

Table 9: Financial Inclusion Outreach Activities for 2019

Date Location ActivityFriday, 3 January 2019 Ministry of Finance and the Public

Service, KingstonAppearance on the radio

programme “Let’s Talk Finance” with Nationwide FM

Tuesday, 29 January 2019 Bank of Jamaica “Leveraging Data to drive Financial Inclusion” workshop with the US Treasury, Office of

Technical AssistanceThursday, 6 February 2019 Ministry of Finance and the Public

Service, KingstonAppearance on the radio

programme “Let’s Talk Finance” with Nationwide FM

Thursday, 13 February 2019 Ministry of Finance and the Public Service, Kingston

Appearance on the radio programme “Let’s Talk Finance”

with Nationwide FMThursday, 20 February 2019 Ministry of Finance and the Public

Service, KingstonAppearance on the radio

programme “Let’s Talk Finance” with Nationwide FM

Friday, 28 February 2019 Ministry of Finance and the Public Service, Kingston

Appearance on the radio programme “Let’s Talk Finance”

with Nationwide FMSunday, 23 February 2019 Swallowfield Church

St. Andrew

Church Service and official launch of the Financial Inclusion

Communication Strategy

Thursday, 5 March 2019 Ministry of Finance and the Public Service, Kingston

Appearance on the radio programme “Let’s Talk Finance”

with Nationwide FMSaturday, 30 March 2019 Sam Sharpe Square, Montego Bay JDIC Town Hall on Financial

InclusionThursday, 4 April 2019 Morant Bay Plaza, St. Thomas Outdoor Radio Broadcast and

Education Booth with IRIE FMTuesday, 28 May 2019 Television Jamaica Limited,

St. Andrew

Appearance on the television programme “Smile Jamaica” on

TV JThursday, 30 May 2019 Port Maria, St. Mary Outdoor Radio Broadcast and

Education Booth with IRIE FM with Ministry of Industry, Commerce, Agriculture and

Fisheries, Development Bank of Jamaica

Wednesday, 3 July 2019 Terra Nova Hotel,

St. Andrew

PSOJ Access to Finance Panel Workshop

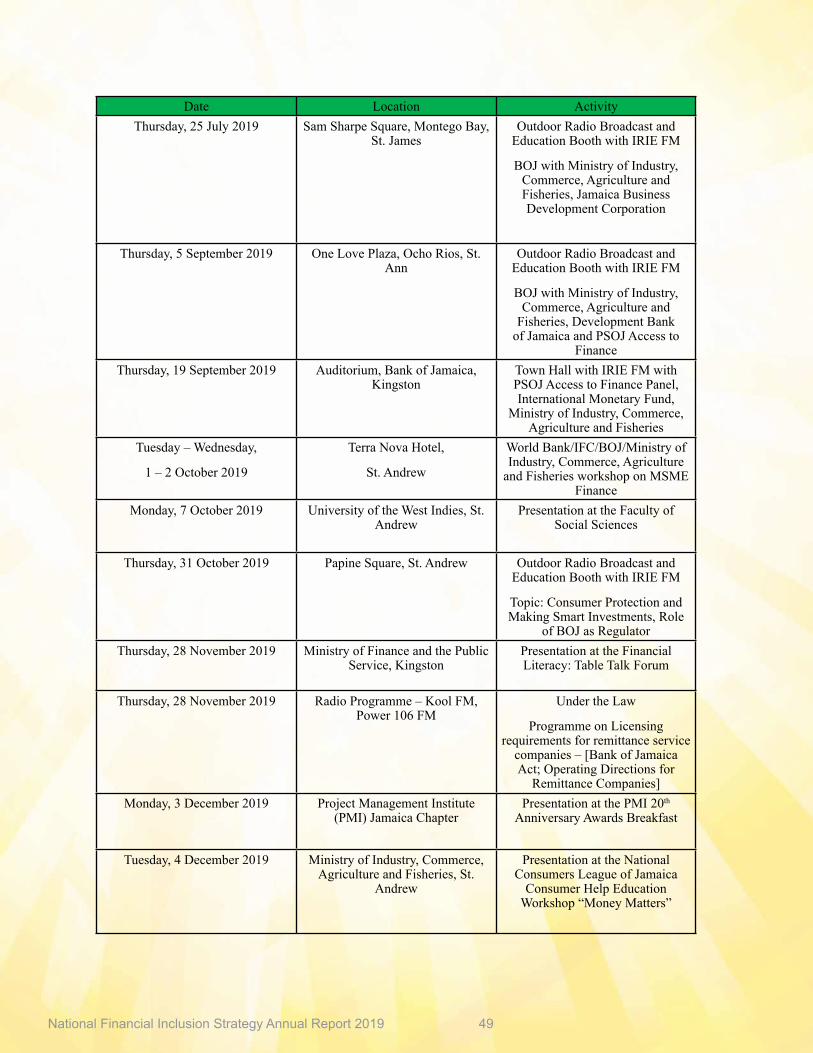

National Financial Inclusion Strategy Annual Report 2019 49

Date Location ActivityThursday, 25 July 2019 Sam Sharpe Square, Montego Bay,

St. JamesOutdoor Radio Broadcast and

Education Booth with IRIE FM

BOJ with Ministry of Industry, Commerce, Agriculture and Fisheries, Jamaica Business Development Corporation

Thursday, 5 September 2019 One Love Plaza, Ocho Rios, St. Ann

Outdoor Radio Broadcast and Education Booth with IRIE FM

BOJ with Ministry of Industry, Commerce, Agriculture and

Fisheries, Development Bank of Jamaica and PSOJ Access to

FinanceThursday, 19 September 2019 Auditorium, Bank of Jamaica,

KingstonTown Hall with IRIE FM with PSOJ Access to Finance Panel, International Monetary Fund,

Ministry of Industry, Commerce, Agriculture and Fisheries

Tuesday – Wednesday,

1 – 2 October 2019

Terra Nova Hotel,

St. Andrew

World Bank/IFC/BOJ/Ministry of Industry, Commerce, Agriculture

and Fisheries workshop on MSME Finance

Monday, 7 October 2019 University of the West Indies, St. Andrew

Presentation at the Faculty of Social Sciences

Thursday, 31 October 2019 Papine Square, St. Andrew Outdoor Radio Broadcast and Education Booth with IRIE FM

Topic: Consumer Protection and Making Smart Investments, Role

of BOJ as RegulatorThursday, 28 November 2019 Ministry of Finance and the Public

Service, KingstonPresentation at the Financial Literacy: Table Talk Forum

Thursday, 28 November 2019 Radio Programme – Kool FM, Power 106 FM

Under the Law

Programme on Licensing requirements for remittance service

companies – [Bank of Jamaica Act; Operating Directions for

Remittance Companies]Monday, 3 December 2019 Project Management Institute

(PMI) Jamaica ChapterPresentation at the PMI 20th

Anniversary Awards Breakfast

Tuesday, 4 December 2019 Ministry of Industry, Commerce, Agriculture and Fisheries, St.

Andrew

Presentation at the National Consumers League of Jamaica

Consumer Help Education Workshop “Money Matters”

National Financial Inclusion Strategy Annual Report 2019 50

Date Location ActivityThursday, 5 December 2019 Radio Programme – Kool FM,

Power 106 FMUnder the Law

Programme on Resolution of Consumer Complaints – [Banking Services Act (Consumer Related

Matters) Code of Conduct)]Monday, 9 December 2019 Half Way Tree Transport Centre,

St. AndrewOutdoor Radio Broadcast and

Education Booth with IRIE FM, in partnership with Consumer Affairs Commission, Financial Services

Commission and Jamaica Deposit Insurance Corporation. Topics;

“Consumer Protection”Thursday, 12 December 2019 Radio Programme – Kool FM,

Power 106 FMUnder the Law

Programme on Bank Charges – [Banking Services Act (Consumer

Related Matters) Code of Conduct)]

Thursday, 19 December 2019 Radio Programme – Kool FM, Power 106 FM

Under the Law

Programme on obtaining a Free Credit Report – [Credit Reporting

Act]

National Financial Inclusion Strategy Annual Report 2019 51

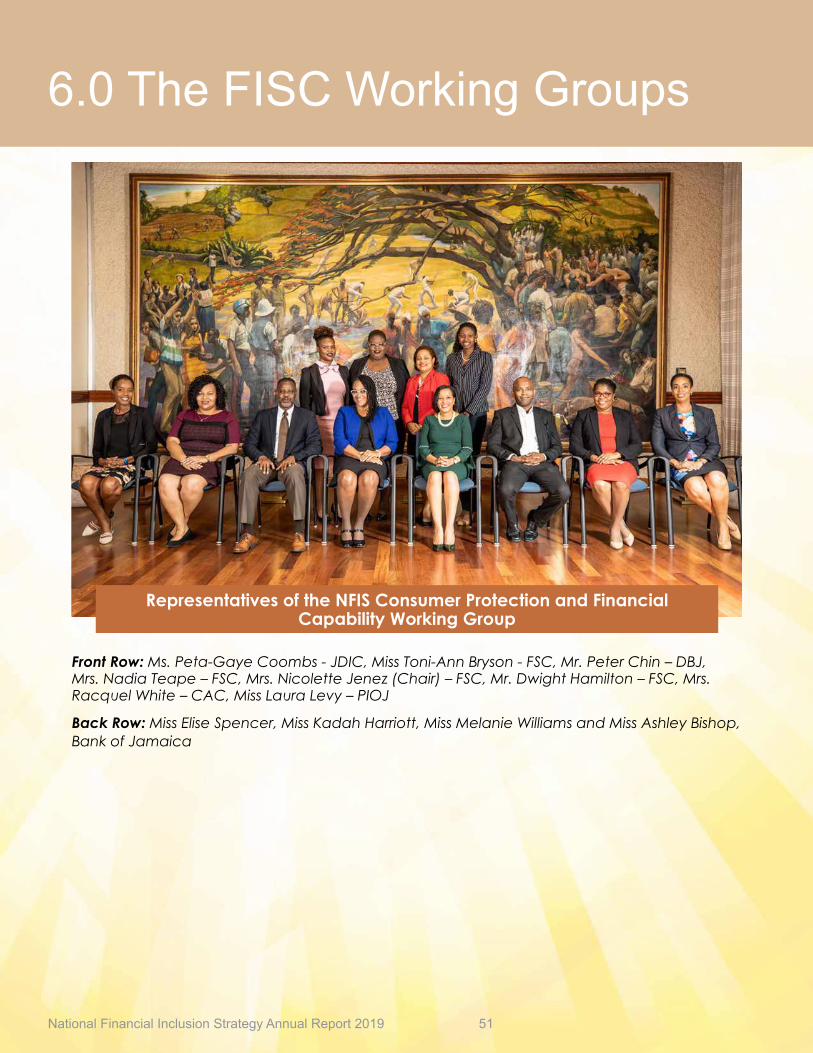

Front Row: Ms. Peta-Gaye Coombs - JDIC, Miss Toni-Ann Bryson - FSC, Mr. Peter Chin – DBJ, Mrs. Nadia Teape – FSC, Mrs. Nicolette Jenez (Chair) – FSC, Mr. Dwight Hamilton – FSC, Mrs. Racquel White – CAC, Miss Laura Levy – PIOJ

Back Row: Miss Elise Spencer, Miss Kadah Harriott, Miss Melanie Williams and Miss Ashley Bishop, Bank of Jamaica

6.0 The FISC Working Groups

Representatives of the NFIS Consumer Protection and Financial Capability Working Group

National Financial Inclusion Strategy Annual Report 2019 52

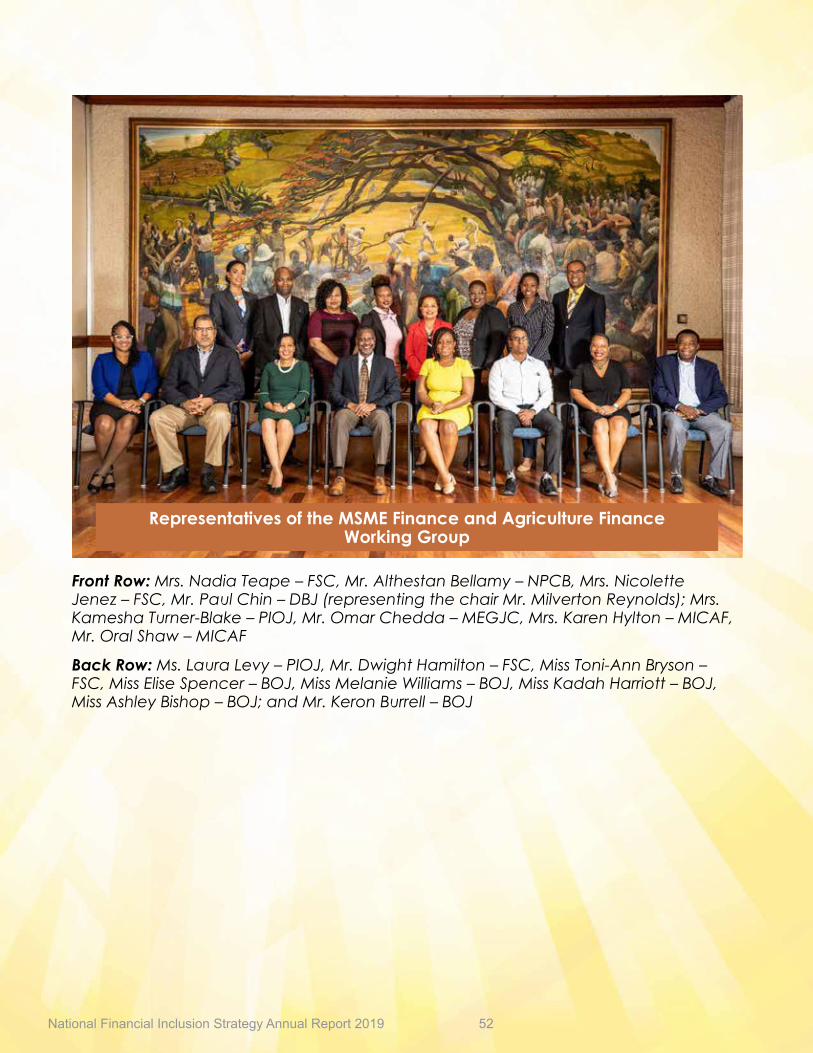

Front Row: Mrs. Nadia Teape – FSC, Mr. Althestan Bellamy – NPCB, Mrs. Nicolette Jenez – FSC, Mr. Paul Chin – DBJ (representing the chair Mr. Milverton Reynolds); Mrs. Kamesha Turner-Blake – PIOJ, Mr. Omar Chedda – MEGJC, Mrs. Karen Hylton – MICAF, Mr. Oral Shaw – MICAF

Back Row: Ms. Laura Levy – PIOJ, Mr. Dwight Hamilton – FSC, Miss Toni-Ann Bryson – FSC, Miss Elise Spencer – BOJ, Miss Melanie Williams – BOJ, Miss Kadah Harriott – BOJ, Miss Ashley Bishop – BOJ; and Mr. Keron Burrell – BOJ

Representatives of the MSME Finance and Agriculture Finance Working Group

National Financial Inclusion Strategy Annual Report 2019 53

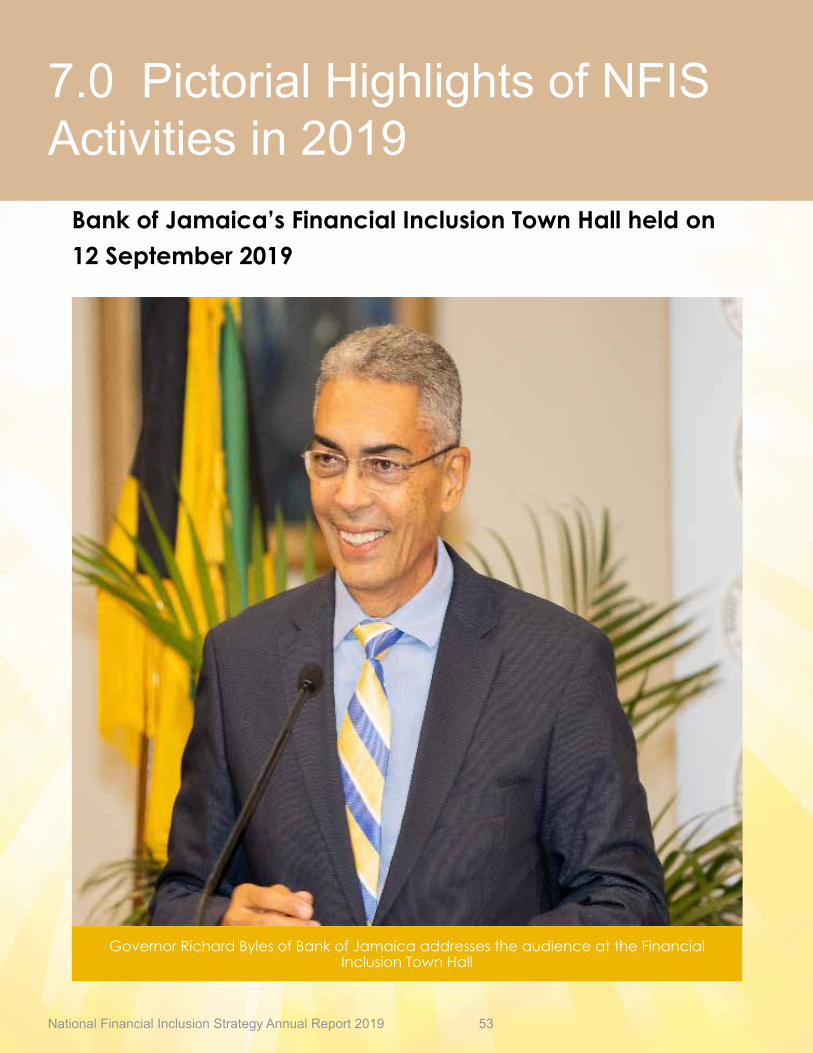

Bank of Jamaica’s Financial Inclusion Town Hall held on 12 September 2019

7.0 Pictorial Highlights of NFIS Activities in 2019

GovernorRichardBylesofBankofJamaicaaddressestheaudienceattheFinancialInclusion Town Hall

National Financial Inclusion Strategy Annual Report 2019 54

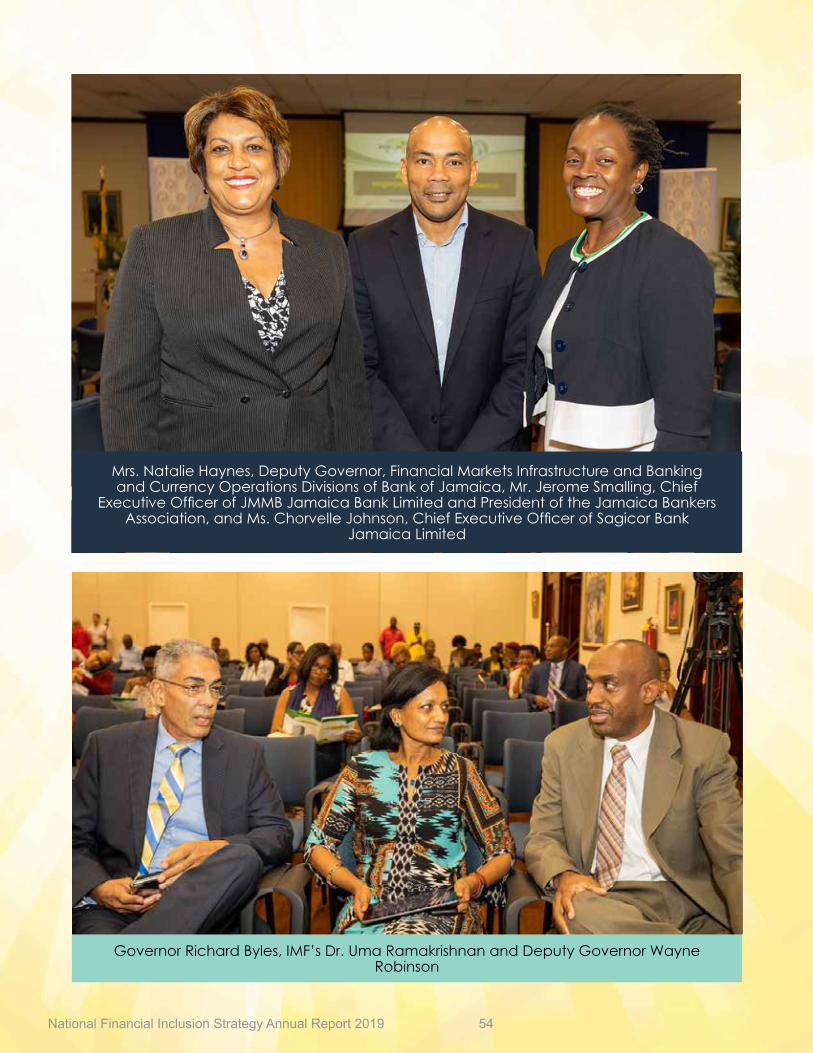

GovernorRichardByles,IMF’sDr.UmaRamakrishnanandDeputyGovernorWayneRobinson

Mrs.NatalieHaynes,DeputyGovernor,FinancialMarketsInfrastructureandBankingandCurrencyOperationsDivisionsofBankofJamaica,Mr.JeromeSmalling,Chief

ExecutiveOfficerofJMMBJamaicaBankLimitedandPresidentoftheJamaicaBankersAssociation,andMs.ChorvelleJohnson,ChiefExecutiveOfficerofSagicorBank

Jamaica Limited

National Financial Inclusion Strategy Annual Report 2019 55

Mr.KarimYoussef,IMFResidentRepresentativeforJamaicaandMr.JeromeSmalling,PresidentoftheJamaicaBankersAssociationinananimateddiscussionatBankof

Jamaica’sFinancialInclusionTownHall,September2019

TheInternationalMonetaryFund’sDr.UmaRamakrishnan

National Financial Inclusion Strategy Annual Report 2019 56

Mr.KeithDuncan,PresidentofthePrivateSectorOrganisationofJamaica

Mr.MilvertonReynolds,ManagingDirectorofDevelopmentBankofJamaica

National Financial Inclusion Strategy Annual Report 2019 57

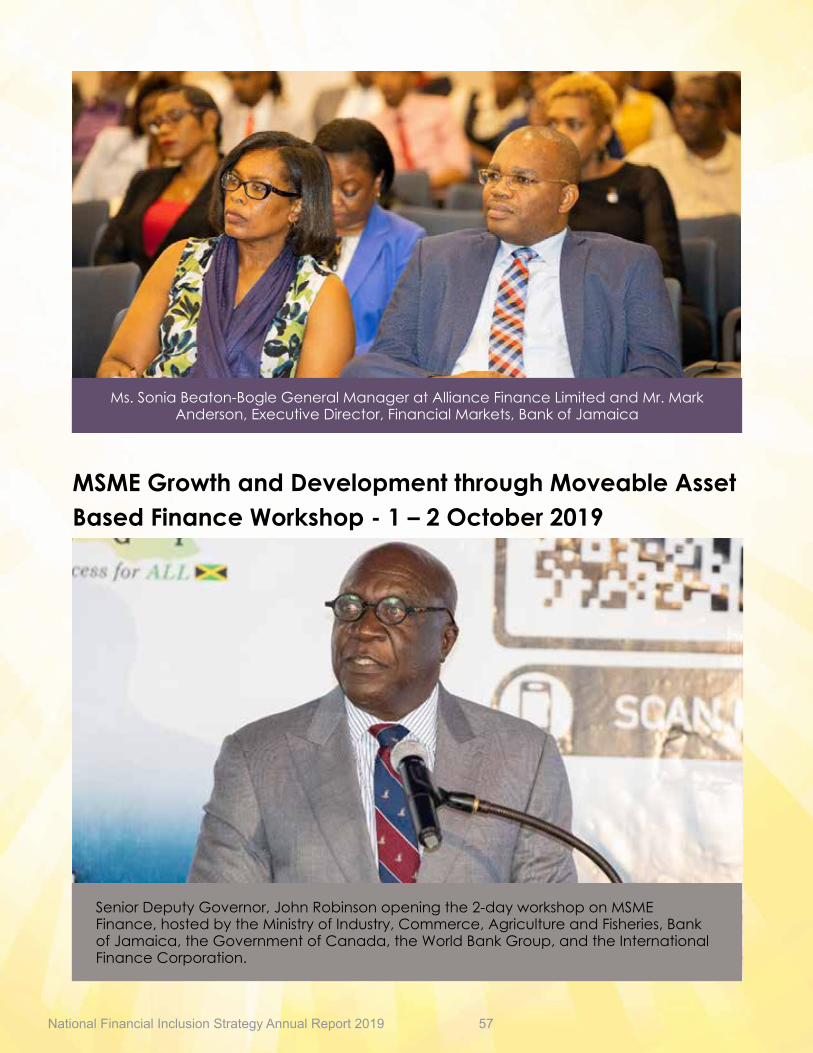

MSME Growth and Development through Moveable Asset Based Finance Workshop - 1 – 2 October 2019

Ms.SoniaBeaton-BogleGeneralManageratAllianceFinanceLimitedandMr.MarkAnderson,ExecutiveDirector,FinancialMarkets,BankofJamaica

SeniorDeputyGovernor,JohnRobinsonopeningthe2-dayworkshoponMSMEFinance,hostedbytheMinistryofIndustry,Commerce,AgricultureandFisheries,BankofJamaica,theGovernmentofCanada,theWorldBankGroup,andtheInternationalFinanceCorporation.

National Financial Inclusion Strategy Annual Report 2019 58

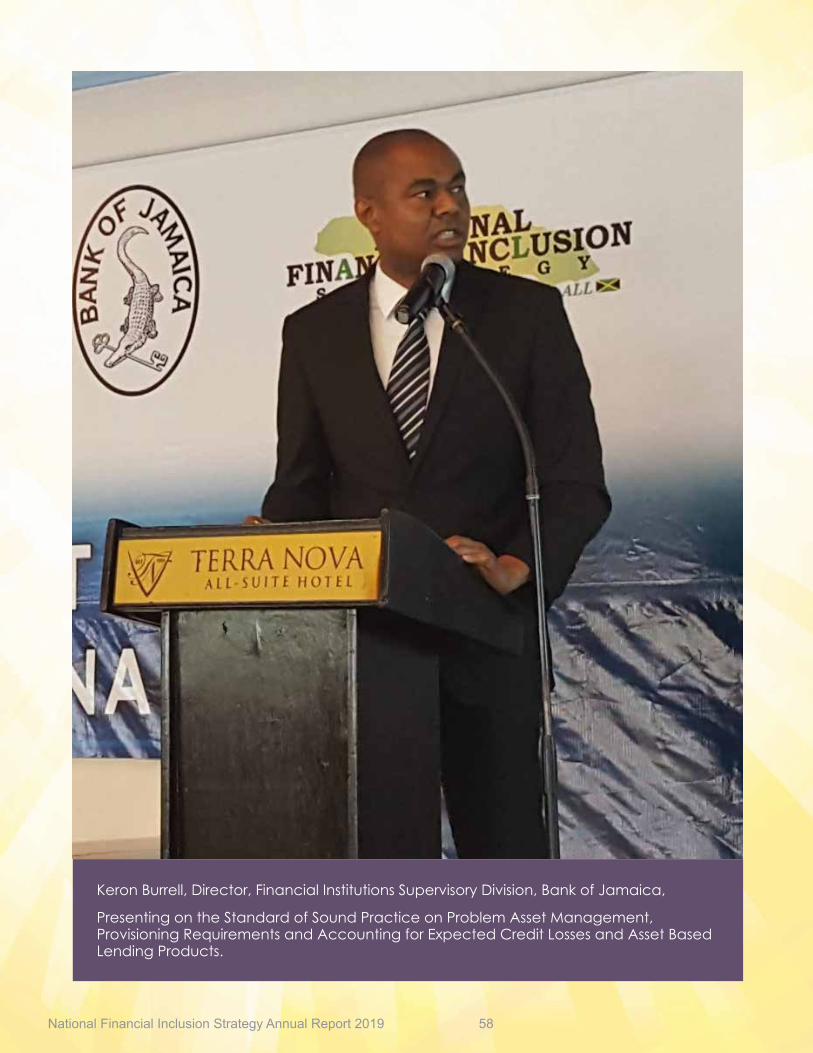

KeronBurrell,Director,FinancialInstitutionsSupervisoryDivision,BankofJamaica,

PresentingontheStandardofSoundPracticeonProblemAssetManagement,ProvisioningRequirementsandAccountingforExpectedCreditLossesandAssetBasedLendingProducts.

National Financial Inclusion Strategy Annual Report 2019 59

MelanieWilliams,NationalFinancialInclusionCoordinatorPresenting on the National Financial Inclusion Strategy

Mr.OralShaw,PrincipalDirector,MSMEOffice,MinistryofIndustry,Commerce,AgricultureandFisheries

National Financial Inclusion Strategy Annual Report 2019 60

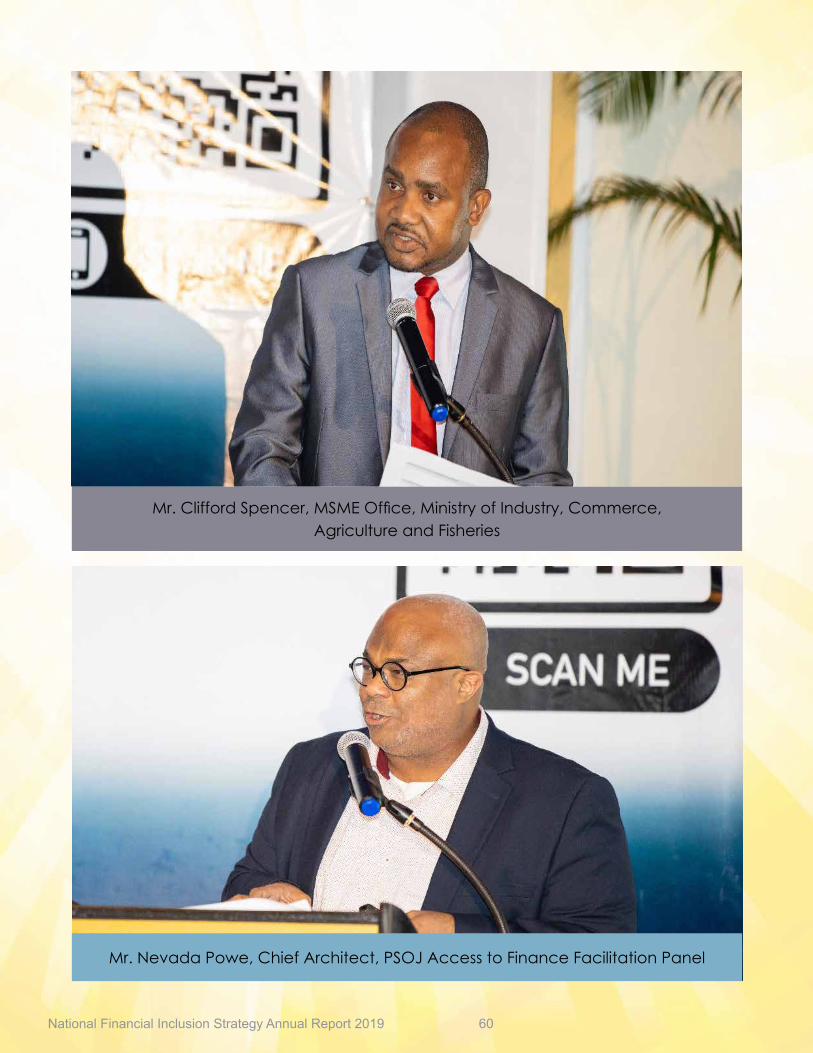

Mr.CliffordSpencer,MSMEOffice,MinistryofIndustry,Commerce,AgricultureandFisheries

Mr.NevadaPowe,ChiefArchitect,PSOJAccesstoFinanceFacilitationPanel

National Financial Inclusion Strategy Annual Report 2019 61

Panelistsrespondtoaquestionfromtheaudience

Mrs.GailDixon,PresidentofJAMFIN

Mr.ImtiazAhmad,ConsultanttotheDevelopmentBankofJamaica

Presenting on the DBJ’s Electronic Factoring Platform

National Financial Inclusion Strategy Annual Report 2019 62

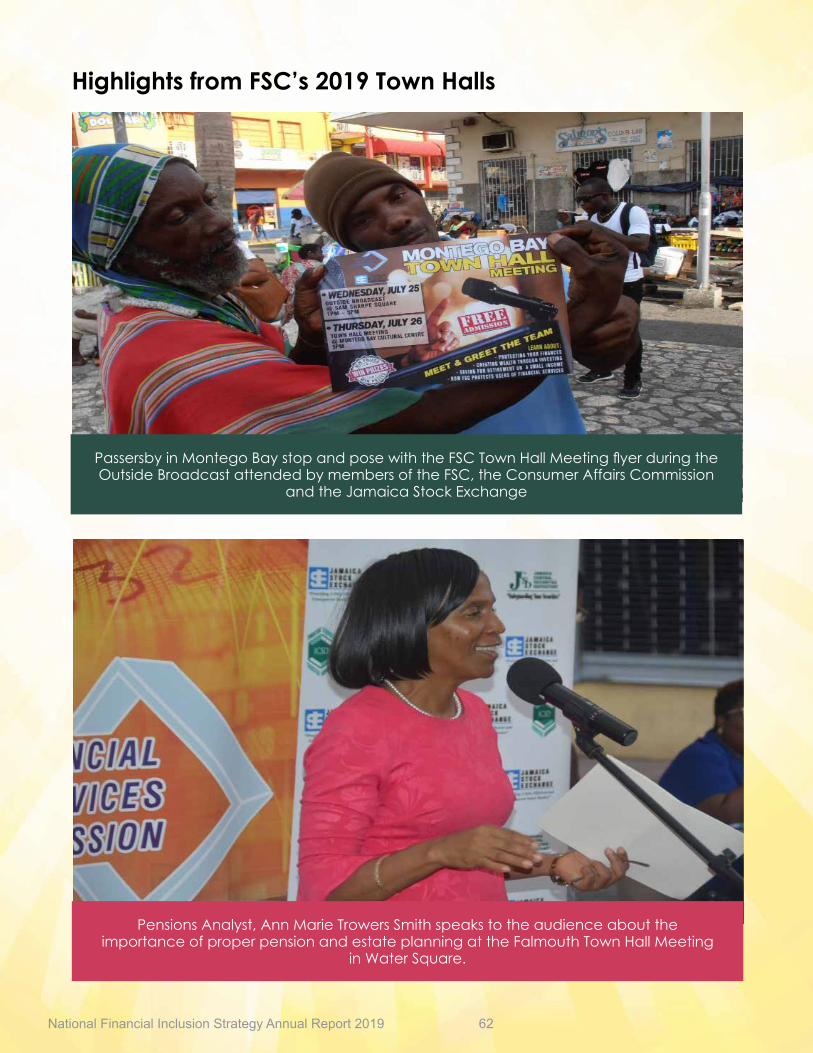

Highlights from FSC’s 2019 Town Halls

PensionsAnalyst,AnnMarieTrowersSmithspeakstotheaudienceabouttheimportanceofproperpensionandestateplanningattheFalmouthTownHallMeeting

inWaterSquare.

PassersbyinMontegoBaystopandposewiththeFSCTownHallMeetingflyerduringtheOutsideBroadcastattendedbymembersoftheFSC,theConsumerAffairsCommission

andtheJamaicaStockExchange

National Financial Inclusion Strategy Annual Report 2019 63

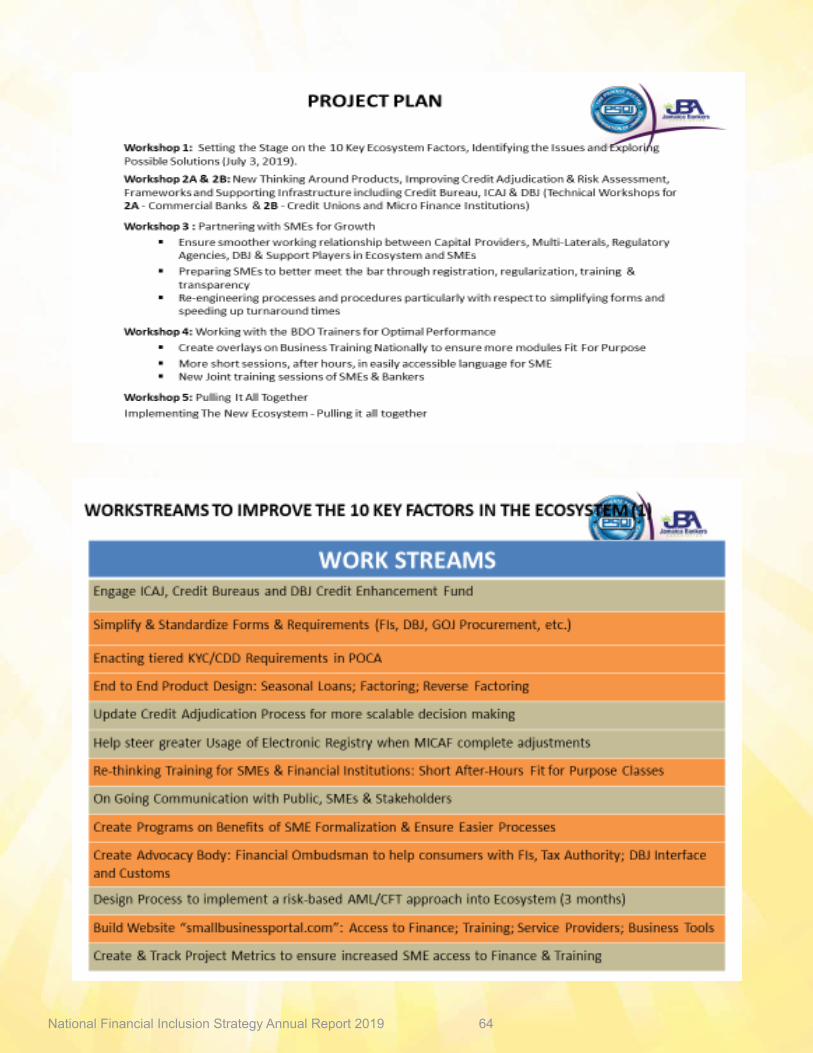

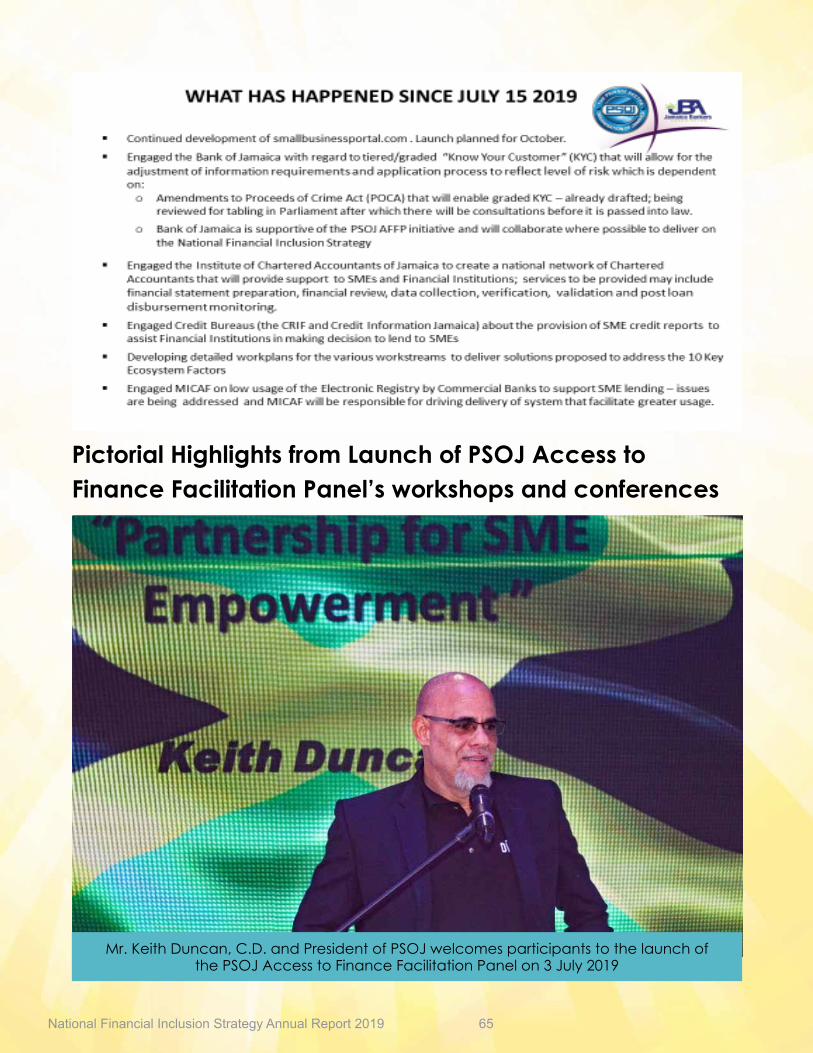

8.1 In July 2019, the Private SectorOrganisation of Jamaica launched itsAccess to Finance Facilitation Panel. Aninitiative that brought together fifteen(15) public and private sector entitiesbroughtarenewedprivatesectorfocustoadvancing financial inclusion,particularlyincreasing MSME Finance for small andmedium-sizedenterprises.

8.2 TheworkofthePSOJAFFPfosteredthepublic-private partnership needed toadvance the work of financial inclusionthroughdevelopmentof “fit forpurpose”solutions for small and medium-sizedenterprises.

8.3 Presented beloware key highlightsfrom the PSOJ Access to Finance workstreamsin2019.

8.0 Highlights from the PSOJ Access to Finance Facilitation Panel (PSOJ AFFP)

National Financial Inclusion Strategy Annual Report 2019 64

National Financial Inclusion Strategy Annual Report 2019 65

Pictorial Highlights from Launch of PSOJ Access to Finance Facilitation Panel’s workshops and conferences

Mr.KeithDuncan,C.D.andPresidentofPSOJwelcomesparticipantstothelaunchofthePSOJAccesstoFinanceFacilitationPanelon3July2019

National Financial Inclusion Strategy Annual Report 2019 66

MembersofthePrivateSectorgathertodisplayproudlythesigningoftheMOU(memorandumofunderstanding)byfinancialinstitutions

DavidNoel,PresidentandCEO,ScotiabankJamaica

National Financial Inclusion Strategy Annual Report 2019 67

Mr.NevadaPoweLeadArchitect,PSOJAFFP,and

MichelleCoulton,ManagingDirector,SoHoBoutique

TheHon.MinisterFloydGreenM.P.,MinisterofAgriculture

andFisheries

National Financial Inclusion Strategy Annual Report 2019 68

TheHon.AudleyShaw,CD,MP,MinisterofIndustry,InvestmentandCommercebeingwelcomedbyKeithDuncan,CD,President,ThePrivateSector

OrganisationofJamaica(PSOJ)

Smallbusinessownersgatheredaroundatableinconversation

National Financial Inclusion Strategy Annual Report 2019 69

Ms.RochelleCameron,ChiefProjectExecutive,PSOJAccesstoFinanceFacilitationPanel(AFFP)beamsasshehoststhePSOJAccesstoFinancePanelworkshop

MembersofthePSOJAccesstoFinancePanelandfinancialinstitutionsatWorkshop2heldinNovember2019,whichwasgearedtothebankingindustryandMSMEs.

National Financial Inclusion Strategy Annual Report 2019 70

National Financial Inclusion Strategy Annual Report 2019 71

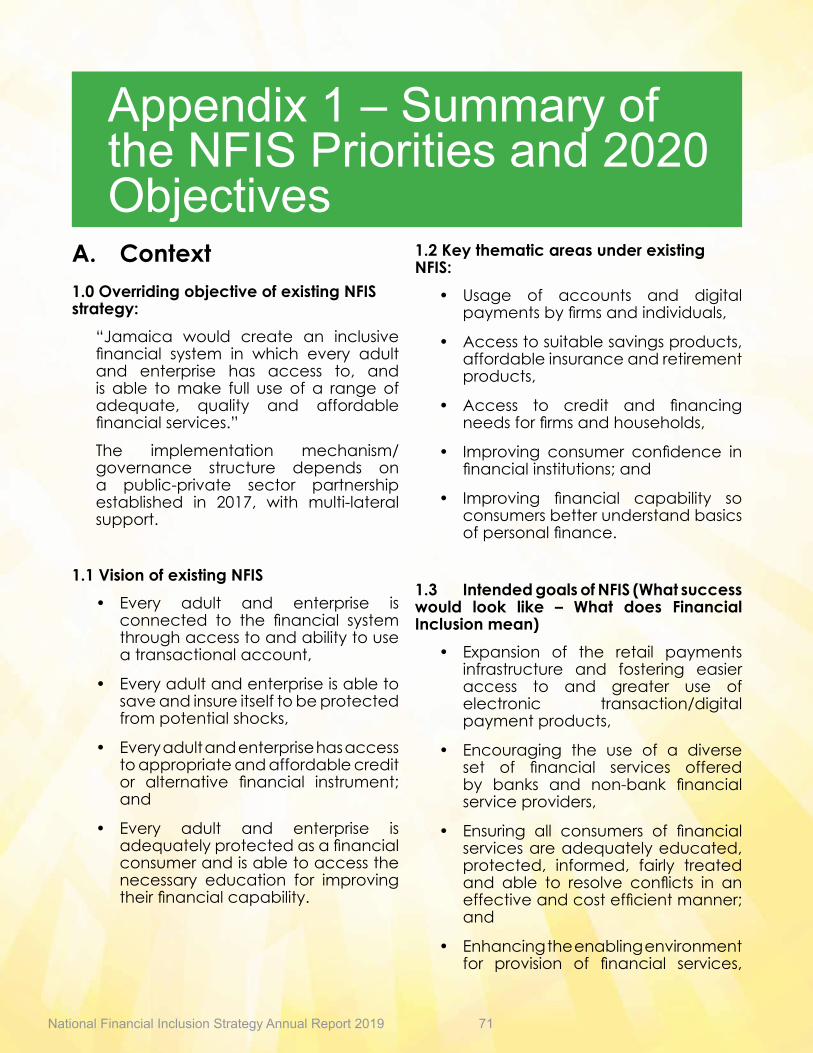

A. Context1.0 Overriding objective of existing NFIS strategy:

“Jamaica would create an inclusive financial system in which every adultand enterprise has access to, andis able tomake full use of a rangeofadequate, quality and affordablefinancialservices.”

The implementation mechanism/governance structure depends on a public-private sector partnershipestablished in 2017, with multi-lateralsupport.

1.1 Vision of existing NFIS• Every adult and enterprise is

connected to the financial systemthroughaccesstoandabilitytouseatransactionalaccount,

• Everyadultandenterpriseisabletosaveandinsureitselftobeprotectedfrompotentialshocks,

• Everyadultandenterprisehasaccesstoappropriateandaffordablecreditor alternative financial instrument;and

• Every adult and enterprise is adequatelyprotectedasafinancialconsumerandisabletoaccessthenecessary education for improvingtheirfinancialcapability.

1.2 Key thematic areas under existing NFIS:

• Usage of accounts and digitalpaymentsbyfirmsandindividuals,

• Accesstosuitablesavingsproducts,affordableinsuranceandretirementproducts,

• Access to credit and financingneedsforfirmsandhouseholds,

• Improving consumer confidence infinancialinstitutions;and

• Improving financial capability soconsumersbetterunderstandbasicsofpersonalfinance.

1.3 Intended goals of NFIS (What success would look like – What does Financial Inclusion mean)

• Expansion of the retail paymentsinfrastructure and fostering easieraccess to and greater use ofelectronic transaction/digital paymentproducts,

• Encouraging the use of a diverseset of financial services offeredby banks and non-bank financialserviceproviders,

• Ensuring all consumers of financialservicesareadequatelyeducated,protected, informed, fairly treatedand able to resolve conflicts in aneffectiveandcostefficientmanner;and

• Enhancingtheenablingenvironmentfor provision of financial services,

Appendix 1 – Summary of the NFIS Priorities and 2020 Objectives

National Financial Inclusion Strategy Annual Report 2019 72

including the improvement in thefinancial infrastructure and thelegal, regulatory and supervisoryframework.

B. Summary of key action items to achieve financial inclusion outcomes1

2.0 To achieve greater access Bank of Jamaica and its financial inclusion partners completed the following project activities:

• Legislativereformtopromoteeasieraccount opening processes as part of a risk-based approach to anti-money laundering and counter-financingofterrorism;

• Strengthening the supervisory andlegalframeworkforpaymentserviceproviders (non-DTIs) to offer digitalpaymentande-commerceservices;

• Enablinggreateraccesstofinancialmarket infrastructure (paymentsystems) for non-DTIs (i.e. paymentserviceproviders),throughupdatingthe, Retail Payments Strategy andpreparing its research paper oninteroperability and the NationalPaymentswitch;

• Encouraging digital payment ofgovernmentwelfarebenefitsthroughbank accounts or transactionalaccounts;

• Conducting the bankingcompetitionstudy;

1 These actions were further revised based on the recommendations of the Banking Competition Study, completed in 2019; and the recommendations of the Credit Reporting Act legislative review, both of which Bank of Jamaica’s Financial Inclusion Technical Secretariat and FISD coordinated in collab-oration with other financial inclusion partners, MOFPS, MICAF, the Fair Trading Commission and the Consumer.Affairs Commission.

• Legislating the use of nationalidentification mechanisms (e.g.NIDS) to ease account openingprocesses (data protection law toprovideprivacyprotections);

• Promoting greater competition in the prices for financial servicesthrough innovation (e.g. fintech),removingbarrierstoentryforserviceproviders and wide circulation ofinformationonfeesandchargesforfinancialservices;

• Worktowardsstandardisationofthedescription of banking services toallow foreasiercomparisonof feesandcharges;

• Financial literacy and financialinclusion outreach via traditionalandsocialmedia;

• Enhancing the use of securedtransactions through revisionof thesupervisoryframeworkformanagingexpectedcreditlossesandassessingcreditrisk;and

• Expanding MSME finance throughthe use of asset based lendingproducts, venture capital andimprovingaccesstocapital.

National Financial Inclusion Strategy Annual Report 2019 73

2.1 To achieve greater usage of financial products, in 2019, the NFIS public sector entities pursued the following project activities:

• StrengtheningFSC’smarketconductregulation of its entities (securitiesdealers,insurancecompanies);

• Legislative and supervisory reformto promote the use of securedtransactions (asset based lendingsuch as reverse factoring, leasing,use of moveable collateral andcredit reporting utilization) toincreaseaccesstofinance;

• Proposing legislative amendments to the Insurance Act to promotemicro-insuranceproducts;

• Developing policy proposals forlegislativereformtopromotegreateraccess to debt financing for firmsthrough capital markets (venturecapital, easier exempt distributionprocesses, easier registration ofbusinessnames);

• Commencing improved financialliteracy/financial capabilityprogrammes (focused on BOJ’sresponsibilities as regulator ofspecified entities, legal obligationsofentitiesandconsumers);

• Restructuring the CreditEnhancement Fund, so thatguarantees could be issued on aportfolio basis rather than a policybasis.

• TablinginParliamenttheMicro-creditBill to bring micro-credit financialinstitutions under a regulated regime;and

• Promotinggreater financial literacyand awareness of existing legalprotections for consumers offinancialservicesthroughoutreach,townhallsandseminars.

2.2 To achieve greater financial growth in 2020, the NFIS partners will continue their work on the following initiatives:

• Implementing reforms to reduceinformality by incentivizing businessnameregistrationoffirms,

• Promoting MSME Finance throughasset based lending products,such as reverse factoring, revisionof SIPPA, revision of Income TaxAct to promote venture capital and encouraging banks to createfinancial inclusion plans (e.g.partnership with PSOJ Access toFinanceFacilitationPanel),

• Encouraging the development ofsecondary markets for moveablecollateral to allow for objectivevaluation/pricingand realization ofsecurity,

• Creating theenablingenvironmentfor expansion of credit informationproviders (CIPs) through legislativerevisions of the Credit ReportingAct to expand categories of CIPsand implementing principles ofmandatory reporting and reciprocity toaccesscreditprofiles,

• Promoting fintech andinteroperabilityofpaymentservicesthrough thedevelopmentofpolicyproposals for the enhancement ofthelegalandsupervisoryframeworkforpaymentserviceproviders,

• Developing housing micro-financesolutionsforlowincomecontributorstoNHT,

• CapacitybuildingforMSMEs,

• Encouraging greater formalizationofMSMEsinpartnershipwithMICAF,

• Utilisation of unclaimed funds as asourceoffundingforMSMEs,

• Enhancing the businessenabling environment throughimplementation of simplifiedcustomer due diligence requirements

National Financial Inclusion Strategy Annual Report 2019 74

forMSMEsandindividuals,

• Encouraging financial institutions todevelop internal financial inclusionplans,whichwould facilitateeasieraccount-opening processes and the design of suitable products forMSMEsandindividuals;

• Developing demand side surveys to measure financial literacycompetencies,consumers’financialknowledge, behaviour andattitudes, factors impacting use ofdigital payments, credit facilities,insurance and pension products;and

• Launching financial literacycampaigns on matters related to savings, cambios, credit reporting,consumerprotection,andsimplifiedCDDrequirements.

National Financial Inclusion Strategy Annual Report 2019 75

C. Trend analysis of NFIS impact and intermediate indicators from 2015 to 20192

Access to financial services indicators (which are measured annually)

Source:BOJNotes:The2020targetof1500accountsper1000adultswasexceededin2019

2 There are other NFIS indicators which are to be measured triennially, using the Global Findex. The NFIS was launched in 2017, and relied on the Global Findex data, the Global Findex was not conducted in Jamaica since 2014. To enhance its data on financial inclu-sion, the Financial Inclusion Technical Secretariat in Bank of Jamaica has developed demand side survey instruments and is in the process of procuring market research firms to conduct this measurement as part of its monitoring and evaluation of the project. It is expected that these surveys will be conducted in 2020 – 2021.

National Financial Inclusion Strategy Annual Report 2019 76

Source:BOJNotes:AccesspointsincludeATMs,bankbranches,andpointofsalemachines

Source:BOJ

National Financial Inclusion Strategy Annual Report 2019 77

Source:BOJNotes:The2020targetof450locationswasexceededin2019

Usage indicators (measured annually)

Source:BOJNotes:ElectronicretailpaymentsincludespaymentsviaACH,Jamclear®-RTGS

National Financial Inclusion Strategy Annual Report 2019 78

Source:BOJ

Source:BOJ

National Financial Inclusion Strategy Annual Report 2019 79

Source:MLSS

Source:BOJ

National Financial Inclusion Strategy Annual Report 2019 80

Financing for Growth MSME Finance and driving investment through the Capital Markets

Source:JSE

Source:JSE

National Financial Inclusion Strategy Annual Report 2019 81

Source:DBJ

Source:DBJ

National Financial Inclusion Strategy Annual Report 2019 82

Source:BOJNotes:SourceofthisdataisBOJbasedonthestatutoryfilingsfromDTIs.Datafor2016wasnotavailable.

National Financial Inclusion Strategy Annual Report 2019 83

1.0 Financial Access and Usage Pillar

1.1. Under the Financial Access andUsage Pillar, the following were theachievements for the period underreview:

Enhance the regulatory framework for appointment of DTI agents to facilitate greater penetration

a. February 2019 – The FinancialInclusion Technical Secretariatpreparedabriefonagentbanking.Adetailed researchpaper isbeingdone on the existing regulation ofDTIagentstodeterminehowbesttofosterfinancialinclusion.

Promote competitive practices in payment services to increase access, market penetrations and competitive prices for consumers

b. August 2019 – Completion of thepolicy proposal paper on proposals tofacilitatetopromotewideraccesstopaymentsystemsandservices.

Bank of Jamaica’s policy papernotedthatacriticalfactorimpedingthe expansion of digital paymentsolutionswere:

(a) barriers faced by non-deposittaking institutions in accessing the existing paymentsinfrastructure;and

(b) the lack of interoperabilityof existing electronic retail

paymentservices.

In seeking to address these challengesand promote greater financial inclusionthroughdigitalpayments,BankofJamaicaconsidered international standards and principlesonthedevelopmentoffinancialmarketinfrastructure.

The paper proposed solutions that couldwidenaccessandpromoteinteroperability.Fouroptionswereidentified,namely:

(i) Proposal 1: connecting throughmessaging standards such asISO20022. Canada and UK arecountries that used this methodtoprovideinteroperability.

(ii) Proposal 2: leveraging existinginfrastructure using the hubandspokes model, as was done inBelizeandMexico.

(iii) Proposal 3: developing andimplementing a national payment switch, such as in thecaseofMauritius.

(iv) Takingamultifacetedapproachthat incorporates proposals one(1) through three (3) in stages,which would allow for greaterpenetration.

In September 2019, the policyproposal paper was circulated to themembersoftheRetailPaymentsandFinancialInfrastructureWorkingGroupfortheircomments.

Appendix 2 Details of activities under the NFIS Pillars

National Financial Inclusion Strategy Annual Report 2019 84

As a subsequent development,exploratory work began on thefeasibility of a national paymentswitchinJanuary2020.

f. October2019–CompletionoftheBankingCompetitionStudy,whichoutlinedrecommendationsforpromotingdigitalfinancethroughfintechanddigitalpaymentsolutions.

g. October 2019 – Enactment of theAmendments to the Proceedsof Crime Act and Regulationsto facilitate application ofsimplified customer due diligencerequirements. As part of thelegislativeamendmentstoenhancetheintegrityofthefinancialsystem,the Government of Jamaicatook steps to encourage financialinclusionbyenactingprovisionsthatallowedforarisk-basedapproachin the application of customerdue diligence requirements.Critically, amendments weremade to the Proceeds of Crime(Money Laundering Prevention)(Amendment) Regulations 2019,whichpermittedregulatedentities,including financial institutions toapply simplified customer duediligence requirements based ontheirassessmentoftheriskofmoneylaundering posed by a potentialcustomer.Inaddition,thelegislationpermittedfirmstoacceptoneformofGovernmentissuedidentificationasameansofcustomerverification.For further information, pleasesee the link below to access thelegislation:

http://www.boj.org.jm/financial_sys/supervised_legislation.php

h. November 2019 – Completion ofresearch paper on digitizationof Government Payments and

presentationtotheRetailPaymentsandFinancialInfrastructureWorkingGroup.

Evaluate, design and implement a policy framework for opening transaction accounts with graded KYC requirements

i. December2019-BankofJamaicadeterminedthattheenhancementofthelegalandregulatoryframeworkfor the regulation of electronicretail payment service providers wasacritical factor indevelopingthe enabling environment fordigital payments. A determinationwasmadetocommenceresearchon comparative legal jurisdictionsto inform the policy proposals forthe relevant statute under whichnon-DTIs offering electronic retailpayment service providers could beregulated

Review and revise the regulatory framework to facilitate the development of financial products linked to remittances, including remittance-based cards

j. November 2019 – The review ofthe regulatory framework wascompletedinAugust2016,withanamendment being made to theOperatingDirectionsforRemittanceServices to permit remittances to be paid via cards which werelinked to bank accounts. As partof its financial inclusion publicsensitization, Bank of Jamaicausedthe“UndertheLaw”seriestohighlightthelicensingrequirementsforremittancebusinesses.Ongoingeducationontheoversightpowersof Bank of Jamaica continued in2019.

National Financial Inclusion Strategy Annual Report 2019 85

2.0 Financial Resilience Pillar

2.1The Financial Resilience pillarsupportsreformsthatwillcontributetoincreasedsavings,insurance,andretirement accounts for the low-income and informal segments ofthepopulation.

2.2 Thefollowingweretheachievementsfortheperiodunderreview:

Develop a legal and regulatory framework for micro-insurance

a. March 2019 – FSC published itsconsultation paper on policy proposals for micro-insuranceregulations. Thepolicyproposalsincluded definitions for keyterms such as “Micro-insurancebusiness”, “Micro-insuranceinstitution” and “Bundledmicro-insurance product”.This consultation paper furtherrefined policy proposals whichwere developed by the FSC inMarch2017,initsmicro-insuranceframework policy paper“Creatingaregulatoryframeworkforinclusiveinsurance.”

For further information on theMicro-Insurance Consultation Paper, please see: http://www.f sc jamaica.o rg/ regu lated-industries/content-1229.html

b. May 2019 – FSC completedits review of the Bill to amendthe Insurance Act to facilitatemicro-insurance and provided its comments to the MOFPSon 16 May 2019. The FSC alsosubmitted its conceptpaper onthe proposed micro-insurance

regulations to the Ministry ofFinance and the Public Serviceon16May2019,havingreceivedcomments from the industry onthepaper.

c. September 2019 - Following theinitial drafting of amendmentsto the Insurance Act andRegulations,theMinistrypreparedadraftCabinetsubmissionontheamendments to the InsuranceAct and Regulations. This wassent to the Attorney-General’sDepartment for its review andcomment.

d. November 2019 – In November2019,theFSCreceivedquestionsfrom MOFPS for clarificationson micro-insurance. The FSCprovided a response on 28November2019.

Promote a retirement product for low-income and the informally employed

e. December 2019 - Theprocurement of a suitableconsultant was completed and the contract for micro pensionconsultancywasawarded.

3.0 Financing for Growth

3.1 Thispillarhas22action itemswhichcover the thematicareasofMSMEFinance, Agriculture Finance andHousingFinance.Ofthese,progresswas made on MSME Finance and HousingFinance.

National Financial Inclusion Strategy Annual Report 2019 86

MSME Finance

3.2Under MSME Finance, there arenine action items including matters relatedtofactoring,leasing,venturecapital and capacity building ofMSMEs.

3.3Thefollowingaretheupdatesunderthis thematicarea for this reportingperiod:

World Bank Access to Finance Project

Component 1: Enhancement to the CEF

a. In January 2019, DBJ reportedthat for the fiscal year of2018/2019, work began on thedevelopment of the businessplan, the financial model,policies and procedures forthe operations of the CreditEnhancement Fund (CEF). Aspartoftheprogramme,softwarewould be procured to assistDBNJ’sriskunitwithassessingthequalifications of the approvedfinancial institutions (AFIs)underthe programme and provideDBJwithtechnicalassistanceintheareaofriskassessment.

b. April 2019 - The business planand financial model for theCEF were completed, as wellas the policies and proceduresfor theenhancedCEF. TheCEFwouldmove froman individualscheme to a portfolio-basedscheme. Initial sensitizationabout the changes werecommunicated to the publicvia the Financial InclusionTechnical Secretariat’s townhalls and outdoor broadcasts,pending the implementation

ofDBJ’smarketingplan for theenhancedCEF.

c. June 2019 – Capitalisation ofthe Partial Credit Guaranteescheme was achieved, withthefirsttrancheofUS$1.5millionbeingreceivedinJune2019.Thiswas used as additional capital fortheCEFtosupportadditionalguarantees.

Component 2: Supporting the establishment of a SME Fund

d. The consultancy for thedevelopment of new productsand a marketing plan was completedin2019.

IDB Credit Enhancement Programme for MSMEs

e. September 2019 – Theidentification of key monitoringandevaluation indicatorswhichwere developed to measure the impact of the programme.These included the numberof guarantees approved, thepercent of women ownedbusinesses receiving guaranteesand the percentage ofguarantees supporting loans forenergyprojects.

f. September2019–FortheperiodJanuary2018toSeptember2019,165 guarantees were approvedwith a value of close to $1billion (J$ 979,000,000), whichsupported loans of 2.4 billion(J$2,400,000,000). Fifty percent(50%) of businesses benefittingfromtheguaranteeswereownedbywomen;withfivepercent(5%)

National Financial Inclusion Strategy Annual Report 2019 87

of the guarantees supportingenergy loans. Forty-two (42) ofthe one hundred and sixty-five(165) guarantees were issued insupport of loansmade tomicroentrepreneurs, with fifty-three(53) benefitting medium-sizedenterprises.

Venture Capital

g. August 2019 – Amendmentswere made to the Pensions(Superannuation Fundsand Retirement Schemes)(Investment) Regulations topermit investments in private equityandventurecapitalfunds.

3.0 Housing Finance

3.1 InMarch2019,NHTannouncedthat it would reduce interestrates for all its mortgagors byone percent (1%). In addition,NHTwideneditsincomebands,by increasingtheceilingofthelowest interest rate band from$12,000to$15,000.Thischangewould enable more personsto access the Home Grantfacility. Further, the loan limitswere increased by 18% from$5.5 million to $6.5 million toallowlowerincomecontributorsto offset the higher costs ofconstruction.

3.2 NHTannouncedtheissuanceof“Intergenerational mortgages”whichwouldprovideflexibilityinrelatives servicing a mortgage obligation in the event of thedeath or retirement of themortgagor.

3.3 NHT continued its partnershipwith select financial institutionsunder the Joint Financingmortgage programme. Underthe terms of the agreement,the NHT invested funds withparticipating institutions for thesolepurposeoftheseinstitutionslending funds to qualifiedcontributors to the NHT. As atMarch 2019, the participatinginstitutionswerenine(9)deposittakinginstitutions.

3.4 March 2019 - Under the NHTcontinued its Housing Micro FinanceLoanProgramme,underwhich theNHTentered intoanagreement with participatingcreditunionstoprovidefundstolowincomecontributorstoassistwith their housing needs.AsatMarch2019,themaximumloanamountwaseighthundredandfiftythousanddollars(J$850,000)which could be used forrepairs, home improvementor to construct homes. Theloans were offered at 9% perannum unsecured and 4.5%per annum secured for a loantermofsix(6)monthstofive(5)years. As at December 2019,thefourparticipatinginstitutionswere Educom Cooperative Credit Union, Community &Workers of Jamaica (C&WJ)Cooperative Credit Union,Jamaica Police Cooperative CreditUnionandLascellesandPartnerCreditUnion.300microloansweredisbursedvaluedat$194,683,058.67.

National Financial Inclusion Strategy Annual Report 2019 88

4.0 Responsible Finance

4.1 Therearetenactionitemsunderthispillar, which fall into the thematicareasofconsumerprotectionandfinancialcapability.

4.2 The following action itemsadvanced under this pillar duringthereportingperiod.Theseare:

a. January 2019 – FSC issuedits updated Guidelines on Market Conduct for InsuranceCompaniesandIntermediaries.The Guidelines establishedspecificminimumstandards foracceptable business practicesfor protection of policyholders.For more information, pleasesee:http://www.fscjamaica.org/regulated-industries/content-1229.html

b. August2019–TheFSCpublisheditsdraftrevisedmarketconductguidelines for the securitiesindustry on the FSC’s website.The draft Guidelines were alsocirculated to the industry for itscomments.

c. October 2019 – The Bankingcompetition study was completed, which maderecommendations on revisiting theexistingregulatorytreatmentoffintechandinnovativedigitalpayment solutions as a key driver for financial inclusion.Recommendations were also madeontheAML/CFTregulationoffinancialservices,tofacilitatea risk-basedapproach toAML/CFToversightoflow-riskclients.

d. December 2019 – Workcontinuedon the reviewof theCredit Reporting Act, with theconsultant preparing his finalreport for the considerationof Bank of Jamaica and theMinistry of Finance and thePublicService.

5.0 Supporting Infrastructure

5.1 Useofunclaimedfunds

Consultants completed theirresearchonthefeasibilityofusingof unclaimed funds in deposittaking institutions. The potentialuses of the funds included theformation of a MSME fund, afund for financial literacy forMSMEs and ensuring appropriate safeguards were included tomeet any claims made regarding theentitlementtosuchfunds.

5.2 TheMicro-CreditBillandCreditUnions(SpecialProvisions)Bill

a. TheMicro-CreditBillwastabledinParliamentinFebruary2019.

b. Stakeholder consultationcontinued on the draft CreditUnions(SpecialProvisions)Bill.

National Financial Inclusion Strategy Annual Report 2019 89

National Financial Inclusion Strategy Annual Report 2019 90