Embed Size (px)

Citation preview

Brewin Dolphin Holdings PLC, 12 Smithfield Street, London EC1A 9BD

T 020 7246 1000 F 020 3201 3001 W brewin.co.uk E [email protected]

Annual R

eport and Accounts 2013

Annual Report and Accounts 2013

Brewin Dolphin provides a range of investment management, financial advice and execution only services in the UK and Eire.

“Our priorities are clear. They are to reinforce our high standard of service to clients and ensure an improved return to shareholders. Discretionary Investment Management is currently the core of our business model and our mission is to provide a compelling and consistent offering, relevant to all our clients. Over the past decade we have evolved from a stockbroker into a private client investment manager. Our evolution must continue as we strive to become the leading provider of personal Discretionary Wealth Management in the UK.” David Nicol, Chief Executive

Investment proposition• Strongclientrelationshipswithalong-termtrackrecordofpersonalisedservice

• Growthmarketwithgoodlong-termprospects

• Newmanagementteamwithcleargoalsandastrategytoachievethem

• Ourstrategywillgeneratevalueforallstakeholders

We are already creating value in 2013• Totalincomegrewby9%to£283.7m

• Adjustedprofitbeforetaxgrewby22%to£52.3m

• Adjustedprofitmarginincreasedfrom16.5%to18.5%

• Discretionaryfundsundermanagement(FUM)grewby17%to£21.3bn

• Adjustedearningspershare(EPS)grewby19.2%to14.9p(2012:12.5p)

• Fullyeardividendincreasedby20%to8.6p

• TotalShareholderReturnwas63%

01

Busin

ess re

view

Section 1FinancialHighlights 02BusinessHighlights 03Chairman’s Statement 04Overview of the Business and Strategy 06StrategicReport 08

A. Business Description 09B. Market Environment 10C. ObjectivesandStrategy 11D. ProgressReport 12E. ResultsfortheYear 18F. PrincipalRisksandUncertainties 27G. FutureDevelopments 31H. CorporateResponsibility 31

Section 2Directors and their Biographies 32Directors’ Report 34Corporate Responsibility 36CorporateGovernance 39Risk Committee Report 44Audit Committee Report 46Directors’ Remuneration Report 49Directors’ Responsibilities 66

Section 3Independent Auditor’s Report 67Consolidated Income Statement 70Consolidated Statement of Comprehensive Income 71Consolidated Balance Sheet 72Consolidated Statement of Changes in Equity 73Company Balance Sheet 74CompanyStatementofChangesinEquity 75ConsolidatedCashFlowStatement 76CompanyCashFlowStatement 77NotestotheFinancialStatements 78

Section 4FiveYearRecord 120Shareholdersat11November2013 121Appendix–CalculationofKPIs 122Directors, Secretary and Officers 123Branch Address List 124

Busin

ess re

view

Dire

cto

rs’ Report &

G

ove

rnance

Fin

ancial S

tatem

ents

Oth

er

Info

rmatio

n

Contents

02 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Financial Highlights

At 29 September 2013 At 30 September 20121TheSeptember2012incomefigurehasbeenadjustedtoexcludesharedrevenuewhichpriortotheRetailDistributionReview(“RDR”)wasrecordedasincomeforBrewinDolphinwithacorrespondingoperatingexpenseapportioningtheincometoexternalparties.

2Thesefigureshavebeenadjustedtoexcluderedundancycosts,additionalFSCSlevy,onerouscontractsprovision,amortisationofclientrelationshipsanddisposalofavailable–for–saleinvestments.

The Board is implementing a new dividend policy from 2014 based on a target dividend payout ratio of between 60-80%ofadjustedearningspershare.

Profit before tax £28.6m2013

2012 £29.9m

Earnings per share

Basic earnings per share

2013

2012 9.1p

Final dividend

5.05p 40% increaseFull year dividend

8.6p 20% increase

Diluted earnings per share

2013

2012 8.6p

Adjusted2 earnings per share

Basic earnings per share

2013

2012

19.7% increase13.2p

Diluted earnings per share

2013

2012

19.2% increase12.5p

Adjusted2 profit before tax £52.3m2013

2012

22.0% increase£42.9m

Total adjusted income £283.7m2013

20121

9.0% increase£260.4m

Total income £283.7m2013

2012

5.3% increase£269.5m

4.4% decrease

8.0p8.5p

14.9p15.8p

03

Busin

ess re

view

At 29 September 2013 At 30 September 2012

Business Highlights

Strategy We are now two and a half years into the transformation and growth strategy announced in 2011. This strategy has twomainpriorities:continuedstronggrowthandincreasedefficiency. These priorities are underpinned by a series of initiatives to transform the business, ensuring it is best placed to enhance client service, meet regulatory demands and generate shareholder returns.

To improve shareholder returns and value, we have added twofurtherstrategicpriorities:

1) ensuringwemaintainsufficientcapitaltodeliverourstrategy; and

2) aligningdividendgrowthwithunderlyingearnings.

This year we announced a new operating margin target of 25%,whichweaimtoachievebytheendofthe financial year 2016.

Capital Wesuccessfullyraised£38.6mthroughanequityplacing in May 2013 to improve our capital strength and investment capacity. This will allow us to accelerate the strategy, capitalise on our competitive position and drive future growth in earnings and shareholder returns.

Management Team The Board of the Company has been restructured with the appointmentofthreenewExecutiveDirectors,DavidNicol–ChiefExecutive,AndrewWestenberger–FinanceDirectorandStephenFord–HeadofInvestmentManagementwhohavejoinedfellowExecutiveDirector,MichaelWilliams.Thenew management team has been in place since March. They areintentonexpandingthebusinesstotakeadvantageofthe opportunities they perceive in the much changed market environment today. The management team has thoroughly reviewedandrefocusedthe2011StrategicPlan.

Adjusted profit margin2 18.5%2013

2012 16.5%

Total managed funds £28.2bn2013

2012 £25.9bn

Discretionary funds £21.3bn2013

2012 £18.2bn

04 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Chairman’s Statement

Dear Shareholder,

2013 has been a year of significant change for Brewin Dolphin. This has encompassed a comprehensive review ofeveryaspectofthewayinwhichtheGroupoperatesand has resulted in a series of actions which have materially strengthened its position as one of the UK’s leading independentwealthmanagerswithinexcessof100,000clientsand£28billionundermanagement.

Board changesJamie Matheson, my predecessor, retired at the end of March and I would once more like to pay tribute to his long andsuccessfultenure.HenryAlgeo,BenSpeke,BarryHowardandSarahSoarstooddownatthesametime.David McCorkell retired in October 2012 and Robin Bayford in December 2012. In October 2013 Angela Wright retired as Company Secretary and continues to work for Brewin DolphinasGroupChiefAccountant.Ishouldliketorecordthe Board’s appreciation of their substantial contribution to theGroupovermanyyears.

FollowingthesechangestheBoardhasbeenreshapedandthis process continues. In accordance with the UK Corporate GovernanceCode,therolesofChairmanandCEOhavebeensplit.IwasappointedNon-ExecutiveChairman,DavidNicolbecameChiefExecutive,StephenFordwasappointedHeadofInvestmentManagementandtogetherwithAndrewWestenberger,thenewFinanceDirector,andMichaelWilliams,theyarethefourkeyexecutivesinthe firm. These appointments have been accompanied by other management changes designed to create greater accountability and clearer lines of responsibility.1 BiographyofIanDewarwillbeincludedinthenoticeofAGM.

TheUKCorporateGovernanceCodealsorequiresthattheboards of listed businesses should have at least an equal numberofindependentNon-ExecutiveDirectorsexcludingthe Chairman.

TherearefourNon-ExecutiveDirectorsontheBoard,excludingme.JockWorsleyretiresfromtheBoardattheAGMinFebruary2014after10yearsofservice.Hehas been Chairman of the Audit Committee and was appointed Senior Independent Director at the end of March 2013. Hiswisecounselwillbegreatlymissed.IanDewar,who wasappointedtotheBoardonthe15November2013, will succeed Jock as Chairman of the Audit Committee. Angela Knight will become Senior Independent Director. WewillseektorecruitonemoreNon-ExecutiveDirectorduring the current year. Brewin Dolphin will then be fully compliantwiththeUKCorporateGovernanceCode.

Biographies of each director are contained on pages 32 and 33.1

Running the businessTheBoardsofBrewinDolphinHoldingsPLCandBrewinDolphin Limited, the principal operating company, are now identical, although their respective roles are slightly different. The smaller board format serves the business effectively and allows for more focused discussion.

The business is run on a day to day basis by the Chief ExecutivesupportedbyanExecutiveCommittee.Thereare four Board committees, Audit, Risk, Remuneration and Nomination.EachoftheseischairedbyanIndependentNon-ExecutiveDirector.

05

Busin

ess re

view

FocusOur focus remains unchanged. It is to promote continued strong growth and increased efficiency, thereby ensuring improved returns to shareholders. These are the pillars upon which decisions will be made.

The UK wealth management sector has been the focus of much attention over the past year. The impact of the RetailDistributionReview(‘RDR’)whichcameintoeffectinJanuary2013hascausedthesectortore-examinethewaybusiness has been carried out historically and the result will undoubtedlybeinthelong-terminterestsofbothclientsandmanagers.Thechangeinregulator,fromtheFinancialServices Authority into two successor organisations, will likewise result in changes in how the sector operates. These are designed to make the industry more transparent and accountable to its clients and Brewin Dolphin aims to take a leading role in continuing the development of industry best practice.

EnhancingtheprofitabilityoftheGroupremainsakeyobjectiveoftheBoard.Anexerciseexaminingcostsandefficiencies was undertaken in the second half of the year and savings were identified and made.

RemunerationThe Remuneration Committee has recently undertaken a review of the current remuneration packages of the Company’sExecutiveDirectors.Followingthisreview,theCommittee proposes to rebalance the packages of the ChiefExecutive,theFinanceDirectorandtheHeadofInvestment Management towards more emphasis on longer termdeliveryoftheCompany’sstrategicfinancialobjectives.

The plan has been structured to take into account best practice guidelines from institutional shareholders and shareholder representative bodies.

DividendTheBoardisproposingafinaldividendof5.05ppershare, tobepaidon28March2014toshareholdersontheregisteron28February2014.Thiswillbringthetotaldividendfor theperiodto8.6ppershare(2012:7.15p).

ShareholdersBrewin Dolphin has some 1,000 shareholders, representing a widerangeofinstitutionsandindividuals.Approximately18%of the equity is held by present employees of the business.

Shareholders’ support enabled the company to raise £38.6minMaybywayofaplacingatasmalldiscounttothe market price. Your Board welcomes interaction with shareholders and is committed to maintaining an open and regular dialogue.

Thisyear’sAGMwillbeheldat11.30amon17February2014attheLincolnCentre,18Lincoln’sInnFields,LondonWC2A 3ED. I very much hope you will be able to attend.

Simon Miller 3 December 2013

Our focus remains unchanged. It is to promote continued strong growth and increased efficiency, thereby ensuring improved returns to shareholders. These are the pillars upon which decisions will be made.

06 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Our businessBrewin Dolphin provides a range of investment management, financialadviceandexecutiononlyservicesprimarilytoindividuals and families throughout the UK and Eire. Our aim is to help clients make the most from their money.

• Weearnthetrustofclientsandtherebycreateloyalandlong term client relationships.

• Weofferapersonalapproachtoclientservice,combinedwiththeexpertiseofourprofessionallyqualifiedstaff.

• Wechargeclientsforservicesbasedonthevalueofassets we manage and/or the investment business we transact, on their behalf.

• Wehavealonghistoryandhavegrownrapidlythroughacquisitions.

• Wehave35officesintheUKandEire.

• Wehavemorethan100,000clientsand1,877employees.

• Wemanagemorethan£28billionofinvestmentsonbehalf of clients.

Our marketWeoperateinagrowthmarketwithgoodlong-termprospects from increasing demand for our service.

• Ourindustryfacesbigchallenges:

–Increasingregulatoryfocus

–Changingclientbehaviours

–Harnessingnewtechnology

–Industryconsolidation

• Competitionisintensifying.

Our industry offers many opportunitiesThe market environment has changed considerably in recent years, presenting challenges and opportunities. Increased transparency combined with growth has encouraged both new entrants and new business models to challenge the status quo in the industry.

Our Strategy – Overview

Overview of the Business and Strategy

To be the leading

provider of personal discretionary wealth

management in the UK

Vision

PrimaryGoal

Corporate Objectives

Strategic Priorities

Generateshareholdervalueby growing revenue and delivering a high quality service to our clients efficiently

Build a business to be proud of based on values of client service, teamwork and integrity

Beanexcellent employer

Manage responsibly forlong-term

Growourdividendinline with earnings

Improve our efficiency

Maintain sufficient capitaltomaximiseopportunities and

cover risks

Growthenumberofclients we serve and therefore the revenue

we generate

Initiatives Improve market competitiveness and drive organic growth Achieveoperationalexcellencetoimprovequalityandlowercosts

Enhance the service model for our clients

Invest in technology to improve quality of service

Invest in our people

Develop plans to attract new clients

Focusourbusinessaroundourprimaryservices

Sustainable and transparent pricing

Increased cost discipline

Simplify and streamline our operating model

Harnessourtechnologytolowercosts

07

Busin

ess re

view

Strategy and business model

–Correlationofearningstofinancialmarkets

–Culturalinertia,poorprojectmanagementpreventing change

–Overrelianceonkeyemployeesandclientrelationships

–Possibleweakduediligence/executionofpastacquisitions

Operational

–Unsuitableadviceorinvestmentservice

–Breachofregulatoryrules/reportingrequirements

–Failureofprocesses,technologyorexternalservices

–Compensationclaims/industrylevies

ProgressWe have already made good progress.

1ControlledFunction30(CF30)isanFCAapprovedcustomerfunctionofdealingin,advisingonormanaginginvestmentsonbehalfofclients.

Strategic Priority KPI Progress this year Target

Revenue Growth DiscretionaryFUMinflows 6% 5%

Discretionary service yield 91 96 bps 95bps

Managed Advisory service yield 46 56bps 75bps

Revenue growth 9% n/a

Improved Efficiency AdjustedPBTmargin 16.5 18.5% 25%+

DiscretionaryincomeperCF301 £283k £370k £490k

%ofmanagedFUMinDiscretionaryservice 70 76% 80%

DiscretionaryFUMperCF30 £33m £41m £50m

SupportstafftoCF30ratio 2.5to1 2.0 to 1

Average client portfolio £420k £500k

Capital Sufficiency Solvency ratio 226% Min150%

Dividend Growth Dividend pay out 57 58% 60-80%

AdjustedEPSgrowth 19.2% n/a

Dividend growth 20% n/a

Key Risks• Somekeyrisksanduncertaintiescouldhoweverthreatenfurtherprogress.

• Weareseekingtomanagerisksbyrefocusingstrategicprioritiestoreducecertainkeyrisks.

• Thebusinessisnowwellcapitalisedtobothdeliverstrategyandcoverrisks.

08 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

A. Business Description 09B. Market Environment 10C.ObjectivesandStrategy 11D.ProgressReport 12E.ResultsfortheYear 18F. PrincipalRisksandUncertainties 27G.FutureDevelopments 31H.CorporateResponsibility 31

Strategic Report

09

Busin

ess re

view

A. Business Description

Brewin Dolphin is one of the largest providers of personalised investment management services in the UK and Eire. We offer a range of services from managing portfolios on anadvisoryordiscretionarybasis(ourprimaryservices)todealing,withoutadvice(executiononly)andwithadvice(advisorydealing).Ourclientsaremainlyindividuals,but also include Charities, Trusts and Institutions.

In recent years, as part of our primary offering, we have developed our financial planning service which we offer to clients, increasingly on an integrated basis with our investment management service, in order to offer a comprehensive solution to the demands of today’s investors.

TheGrouptodayisprincipallyaninvestmentmanagementbusiness,thoughourrootsdateback250yearsandare in stockbroking. We have grown rapidly since becoming listedontheLondonStockExchangein1994byacquiringsmaller regional private client stockbroking firms and hiring teams of investment managers. Over the past decade, the business has changed from predominantly offering executiononlyandadvisorydealingservicestoonewhich is focused on discretionary investment management. This is evidenced by the significant growth in discretionary assetswhichnowmakeup76%ofourmanagedassets,comparedtoc.40%in2004.

Our business model is based on providing a personalised service,combinedwiththeinvestmentexpertiseofeachindividual investment manager supported by our award winning research. Over recent years we have developed risk rated model portfolios for our smaller accounts.

The advice we offer is comprehensive. A complete wealth management service for private client portfolios, incorporating IndividualSavingsAccounts,Self-InvestedPersonalPensionsandEstatePlanningthroughtohighlyspecialisedinvestmentmandatesonbehalfofCharities,PensionFundsandInstitutions.

Localpresenceandproximitytoourclientshavealwaysbeena key component of Brewin Dolphin and helps us maintain a high level of personalised service. We are committed to this approach.Weprovideourservicevia35officesthroughouttheUKandEirewiththesupportof1,877employees.

We are committed to building the firm into the best in our industry for wealth management

10 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Strategic Report(continued)

B. Market Environment

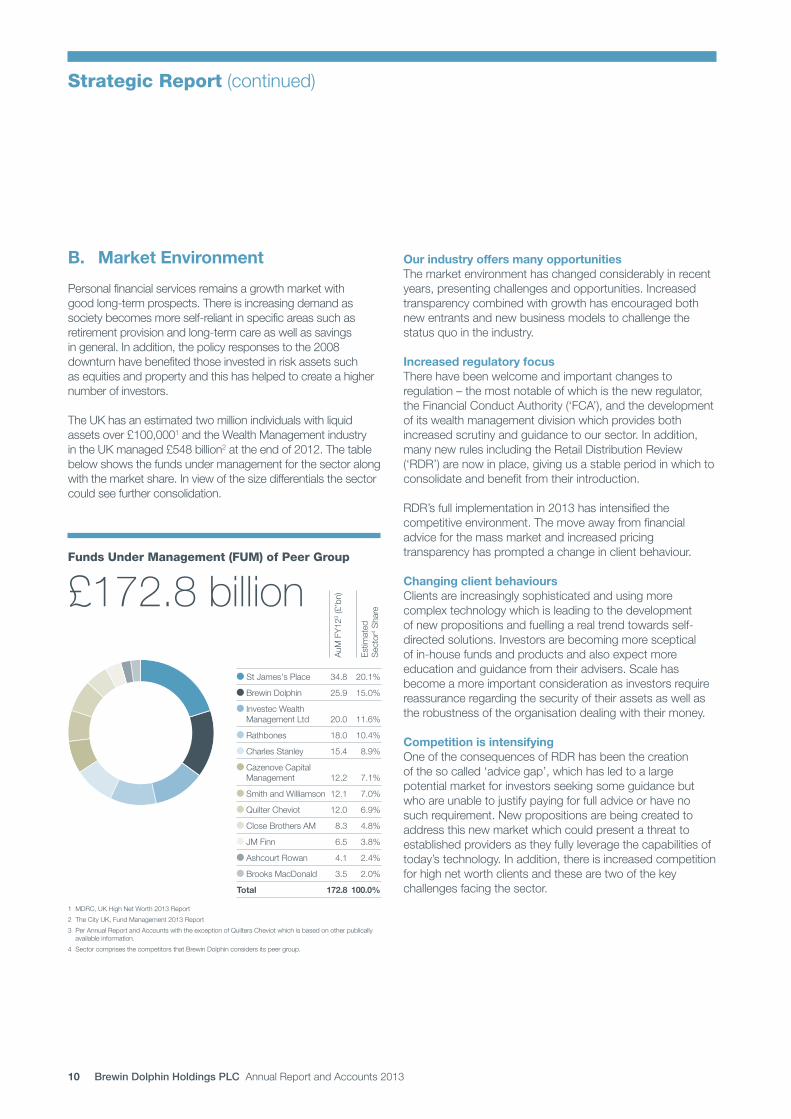

Personalfinancialservicesremainsagrowthmarketwith goodlong-termprospects.Thereisincreasingdemandassocietybecomesmoreself-reliantinspecificareassuchasretirementprovisionandlong-termcareaswellassavings ingeneral.Inaddition,thepolicyresponsestothe2008downturn have benefited those invested in risk assets such as equities and property and this has helped to create a higher number of investors.

The UK has an estimated two million individuals with liquid assetsover£100,0001 and the Wealth Management industry intheUKmanaged£548billion2 at the end of 2012. The table below shows the funds under management for the sector along with the market share. In view of the size differentials the sector could see further consolidation.

Our industry offers many opportunitiesThe market environment has changed considerably in recent years, presenting challenges and opportunities. Increased transparency combined with growth has encouraged both new entrants and new business models to challenge the status quo in the industry.

Increased regulatory focusThere have been welcome and important changes to regulation–themostnotableofwhichisthenewregulator,theFinancialConductAuthority(‘FCA’),andthedevelopmentof its wealth management division which provides both increased scrutiny and guidance to our sector. In addition, many new rules including the Retail Distribution Review (‘RDR’)arenowinplace,givingusastableperiodinwhichtoconsolidate and benefit from their introduction.

RDR’s full implementation in 2013 has intensified the competitive environment. The move away from financial advice for the mass market and increased pricing transparency has prompted a change in client behaviour.

Changing client behavioursClients are increasingly sophisticated and using more complextechnologywhichisleadingtothedevelopmentofnewpropositionsandfuellingarealtrendtowardsself-directed solutions. Investors are becoming more sceptical ofin-housefundsandproductsandalsoexpectmoreeducation and guidance from their advisers. Scale has become a more important consideration as investors require reassurance regarding the security of their assets as well as the robustness of the organisation dealing with their money.

Competition is intensifyingOne of the consequences of RDR has been the creation ofthesocalled‘advicegap’,whichhasledtoalargepotential market for investors seeking some guidance but whoareunabletojustifypayingforfulladviceorhavenosuchrequirement.Newpropositionsarebeingcreatedtoaddress this new market which could present a threat to established providers as they fully leverage the capabilities of today’s technology. In addition, there is increased competition for high net worth clients and these are two of the key challenges facing the sector.

StJames'sPlace 34.8 20.1%

BrewinDolphin 25.9 15.0%

Investec Wealth ManagementLtd 20.0 11.6%

Rathbones 18.0 10.4%

CharlesStanley 15.4 8.9%

Cazenove Capital Management 12.2 7.1%

SmithandWilliamson 12.1 7.0%

QuilterCheviot 12.0 6.9%

CloseBrothersAM 8.3 4.8%

JMFinn 6.5 3.8%

AshcourtRowan 4.1 2.4%

BrooksMacDonald 3.5 2.0%

Total 172.8 100.0%

Funds Under Management (FUM) of Peer Group

£172.8 billion

1 MDRC,UKHighNetWorth2013Report

2 TheCityUK,FundManagement2013Report

3PerAnnualReportandAccountswiththeexceptionofQuiltersCheviotwhichisbasedonotherpublicallyavailable information.

4 Sector comprises the competitors that Brewin Dolphin considers its peer group.

AuM

FY12

3 (£’bn)

Estim

ated

S

ecto

r4 S

hare

11

Busin

ess re

view

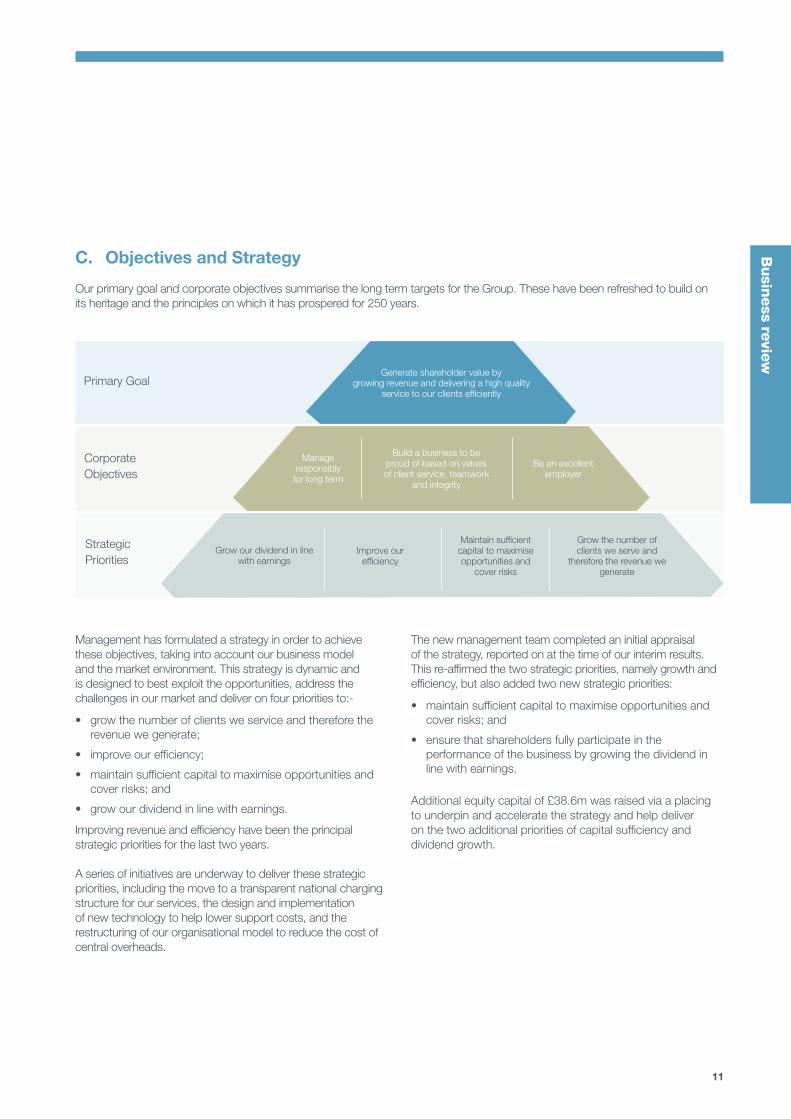

Management has formulated a strategy in order to achieve theseobjectives,takingintoaccountourbusinessmodeland the market environment. This strategy is dynamic and isdesignedtobestexploittheopportunities,addressthechallengesinourmarketanddeliveronfourprioritiesto:-

• growthenumberofclientsweserviceandthereforetherevenue we generate;

• improveourefficiency;

• maintainsufficientcapitaltomaximiseopportunitiesandcover risks; and

• growourdividendinlinewithearnings.

Improving revenue and efficiency have been the principal strategic priorities for the last two years.

A series of initiatives are underway to deliver these strategic priorities, including the move to a transparent national charging structure for our services, the design and implementation of new technology to help lower support costs, and the restructuring of our organisational model to reduce the cost of central overheads.

C. Objectives and Strategy

OurprimarygoalandcorporateobjectivessummarisethelongtermtargetsfortheGroup.Thesehavebeenrefreshedtobuildonitsheritageandtheprinciplesonwhichithasprosperedfor250years.

The new management team completed an initial appraisal of the strategy, reported on at the time of our interim results. Thisre-affirmedthetwostrategicpriorities,namelygrowthandefficiency,butalsoaddedtwonewstrategicpriorities:

• maintainsufficientcapitaltomaximiseopportunitiesandcover risks; and

• ensurethatshareholdersfullyparticipateintheperformance of the business by growing the dividend in line with earnings.

Additionalequitycapitalof£38.6mwasraisedviaaplacingto underpin and accelerate the strategy and help deliver on the two additional priorities of capital sufficiency and dividend growth.

PrimaryGoal

Corporate Objectives

Strategic Priorities

Generateshareholdervalueby growing revenue and delivering a high quality

service to our clients efficiently

Build a business to be proud of based on values of client service, teamwork

and integrity

Beanexcellent employer

Manage responsibly

for long term

Growourdividendinlinewith earnings

Improve our efficiency

Maintain sufficient capitaltomaximiseopportunities and

cover risks

Growthenumberofclients we serve and

therefore the revenue we generate

12 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Thenewfocusreflectsourviewthattomeetourobjectivessuccessfully in this environment our business model needs to evolve,inparticular:

• weneedtosimplifywhatwedoandconcentrateonourprimary services. This will not only help us maintain our competitive position by improving the quality of what we can do best for clients, it will also help improve operational efficiency and create additional capacity to invest in the business; and

• weneedtoinvestinourprimaryservices,successfullyintegrate technology and continue to improve the client experience.

The business will grow and prosper if it simplifies and focuses the business model. A strategy of growth purely reliant on team acquisitions is, in our view, unsustainable in the current market environment. We believe that by building a simplified scalable business, focused on delivering our primary services we can achieve a leadership position in the industry.

Ourstrategydoesallowforexpansionthroughwholebusinessacquisition and hiring of individuals but only when we can successfully integrate them into our culture and business model. In the past our acquisitions strategy has involved insufficient integration which has led to inefficiencies and lack of standardisation in key business processes. This has resulted in higher operational costs, which have impaired the ability of the business to reinvest in new technology to continue improving client service. It has also had a negative impact on shareholder returns and the management of risk.

The strategy has sought to address these issues over the last two years and we have been successful at standardising elements of the business such as pricing, client valuations and client communication. There is significant scope to further improve the business processes without changing the

personalised nature of the service we offer. This challenge will be addressed by many of our current strategic initiatives in ordertode-riskandimprovetheefficiencyofthebusiness.

A series of actions, some of which are underway and others completed are helping to deliver our strategic priorities. These are being pursued by management to grow the number of clients we service and therefore the revenue we generate andtoimproveourefficiencysothatweachieveour25%margin target.

D. Progress report

Manyprojectshavebeenundertakenoverthepastyeartosupport our strategic priorities.

GrowthWe have completed moving our Discretionary and a large portionoftheManagedAdvisoryandExecutionOnlyservicesontostandardnationalpricing.Wenowhavecirca£20bn onnationalpricingbutthereisstillapproximately40%of our Managed Advisory business to complete during 2014. This has allowed us to continue to remove Unit Trust trail from the business and standardise the yield we receive for theservicesweofferatamoresustainablelevel:

Service 2013 Yield bps

2012 Yield bps

Discretionary 96 91

Advisory Managed 56 46

Advisory Dealing 29 42

ExecutionOnly 30 26

Over the last year many clients have moved away from our dealing based services into our primary managed services and this is evident in our client fund flows.

Strategic Report(continued)

Therefocusedstrategyisunderpinnedbyseveralinitiatives:

Initiatives Improve market competitiveness and drive organic growth Achieveoperationalexcellencetoimprovequalityandlowercosts

Enhance the service model for our clients

Invest in technology to improve quality of service

Invest in our people

Develop plans to attract new clients

Focusourbusinessaroundourprimaryservices

Sustainable and transparent pricing

Increased cost discipline

Simplify and streamline our operating model

Harnessourtechnologytolowercosts

13

Busin

ess re

view

Totalmanagedandadvisedfundswere£28.2bn,upby8.9%from a year ago. The strategy of focusing on our Discretionary service and our move to fair and consistent national pricing across all client services has resulted in a continued move away from Advisory to Discretionary services.

Discretionaryfundsgrewby£3.1bnintheyear,a17%increase(2012:16.7%increase)asaresultofcontinuinggoodnetinflowsof£1.1bn(2012:£1.0bn)andhigher marketlevels£2.0bn(2012:£1.6bn).

Advisoryfundsfellby£0.8bnintheyear,a10.4%decline(2012:8.3%decrease),asaresultofnetoutflowsof £1.5bn(2012:£1.1bn)partiallyoffsetbyhighermarketlevels£0.7bn(2012:£0.4bn).Thefiguresalsoshowthelackofdemand from new clients for our Advisory Managed and Advisory Dealing services which continue to see outflows. The reduction in demand for these services combined withtheabsenceofanyyieldpremium(tocovertherisk ofprovidinginvestmentadvice)andtheflowtoExecutionOnly has shaped Management’s view that we should withdraw our Advisory Dealing service.

ClientfundsheldonanExecutionOnlybasisgrewby £1.3bn,a24%increaseofwhich£0.9bnrepresentednewinflowsand£0.7bnwastransferredfromAdvisorytoExecutionOnlyasaresultofourservicereviewandmovetostandardpricing.Duringtheyear,theFTSE100indexincreasedby13.4%andtheFTSEAPCIMSBalancedIndexincreasedby10.0%.

Discretionaryfundsnowmakeup76%(2012:70%)oftotalmanaged and advised funds, continuing the long term trend andrepresentinggoodprogresstowardsourtargetof80%by 2016.

During 2014 we will introduce an enhanced investment process.Weaimtoimprovetheclientexperiencearounda consistent structure which will be supported by new technology to underpin the change. This will mean we can consolidate our operating model within a national framework andensureweofferamoreconsistentclientexperience.

£bn (roundedtoonedecimalplace)

30 September

2012 Inflows Outflows

Transfers within

Managed/ Advised

Other Transfers NetFlows

Market Movement

29 September

2013

Discretionary Managed

18.2 2.1 (1.0) 0.3 (0.3) 1.1 2.0 21.3

Advisory Managed 4.9 0.1 (0.5) (0.0) (0.1) (0.6) 0.5 4.8Advisory Dealing 2.8 0.1 (0.4) (0.2) (0.3) (0.9) 0.2 2.1

Total Advisory 7.7 0.2 (1.0) (0.3) (0.4) (1.5) 0.6 6.9

Total Managed/Advised 25.9 2.3 (2.0) (0.0) (0.7) (0.4) 2.7 28.2

ExecutionOnly 5.4 0.9 (0.7) n/a 0.7 0.9 0.4 6.7

Total Funds 31.3 3.2 (2.7) (0.0) 0.0 0.5 3.1 34.9

Indices 29 September 2013

30 September 2012 Change

FTSEAPCIMSPrivateInvestorSeriesBalancedPortfolio 3,315 3,014 10.0%

FTSE100 6,513 5,742 13.4%

Funds under management (“FUM”)

14 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

To benefit from our enhanced investment process and more focused service offering, we intend to develop five growth channelstoachieveourtargetof5%pagrowthfromnetinflows in Discretionary business.

a) Direct –AnewwebsitedueinSpring2014willfocuson our primary services combined with a number of marketing initiatives.

b)Agent –FinancialAdvisersarebigsupportersofourbusiness and we believe our enhanced investment process will facilitate new, national partnerships.

c) Customer Advocacy–Ourexistingclientsareourbestadvocatesandweintendtobuilduponourhigh“NetPromoterScore”.

d)Professional Services–Ourpropositiontoaccountantsand solicitors will be updated during 2014.

e) Direct to Client Proposition –Thereisasignificantdemand for a simplified, lower cost service. We have an award winning model portfolio service and we are working on delivering this service directly to consumers.

We believe that the best way to grow is organically and our energies are devoted to building the brand value and meeting the needs of the market.

Improving EfficiencyWe have made progress in simplifying the business model in parallel to the development of our new IT systems. We successfully implemented the first stage of our new core operatingsystemintoStocktrade,ourExecutionOnlyservice, in September 2013 and we are already seeing the benefits. We will now roll the system out across the rest oftheGroupduring2014andimplementnewsoftwaretosupportourInvestmentManagementandFinancialPlanningservices. Technology and process improvement is critical to our success and we will continue to invest in these areas over the foreseeable future.

Inconjunctionwiththedevelopmentofournewoperatingsystem we are also simplifying our service offerings. We have reviewed the risk, profitability and demand for our ancillary services many of which are either in the process of being closed or are no longer available to new business. This will lead to a greater concentration of resource around our primary discretionary wealth service.

The rationalisation of our services, combined with our enhanced investment process and supported by new technology, should facilitate a more efficient balance of AdviserstoFundsunderManagement.

We have reviewed the number of offices which resulted in sixofficesbeingmergedorclosed(Inverness,Teesside,Bradford,Hereford,StokeandSwansea).AtthesametimewehaveexperiencedthedepartureofasmallnumberofteamsincludingthemajorityofourLeicesteroffice.Despitethese reorganisations and departures, some of which were to competitor firms, early indications of clients remaining are positive. This has been achieved without having to hire any new staff.

We also reviewed the Appointed Representatives of the Groupinthecontextofourrefocusedstrategyandconcludedthattherisksofself-employedagentsprovidingadvice under our brand, in return for half the commission they generated was an out of date approach and not in the best interests of our clients. Over the year several Appointed Representatives have transferred their business elsewhere and one has become an employee.

Maintaining Capital SufficiencyAshighlightedinourobjectivesandstrategysection,wehaveadded a new strategic priority to ensure that sufficient capital solvencyismaintainedinorderto:

1 Financethenecessaryinvestmentinthebusiness,todeliverthe strategic priorities and stated operating margin target; and

2 Providesufficientcapacitytosupportthekeyrisksanduncertainties.

TheGroupsuccessfullyraised£38.6mequitycapitalviaaplacing, in order to increase capital levels. Together with profits retained during the year, this helped our capital solvencylevelsincreasefrom123%inSeptember2012to226%inSeptember2013.

Weintendtooperateataminimumsolvencylevelof150% in future.

Growing the Dividend to ShareholdersThe Board is implementing a dividend policy from 2014 basedonatargetdividendpayoutratioofbetween60%to80%ofannualreportedadjusteddilutedearningspershareto deliver the new strategic priority of ensuring that dividends growinlinewithunderlyingadjustedearnings.Theobjectiveof this priority is to ensure that shareholders fully benefit in a timely way from any improvement to earnings.

Historically,theBoardhasadoptedapolicyofpayingbroadlyequal interim and final dividends on the ordinary shares. In the future, the Board intends to establish an interim dividend and grow it in real terms. The variable final dividend will be baseduponthefullyeartargetdividendpayoutratioof60%to80%ofadjustedearningspershare.

Strategic Report(continued)

15

Busin

ess re

view

Discretionary income per CF301

£283k £370k £490k Target

2012 2013

Target

% of managed FUM in discretionary service

70% 76% 80% Target

2012 2013

Discretionary FUM per CF301

£33m £41m £50m Target

2012 2013

Target

Average client portfolio

1 ControlledFunction30(CF30)isanFCAapprovedcustomerfunctionofdealingin,advisingonormanaging investments on behalf of clients.

£420k £500k Target

2012 2013

Managed advisory service yield

46bps 56bps 75bps Target

2012 2013

Discretionary service yield

91bps 96bps

2012 2013

Minimum 150%

20132012

Solvency ratio

123%

226%

2013 20162012

Adjusted PBT margin

5

10

15

20

25

16.5%

18.5%

Target 25%

Discretionary FUM inflows

2012 2013 2014

6.5% 6% Target +5%

Final Dividend

2012 2013

3.6p5.05p

Full Year Dividend

2012 2013

7.15p8.6p

95bps Target

Key performance illustrations

16 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

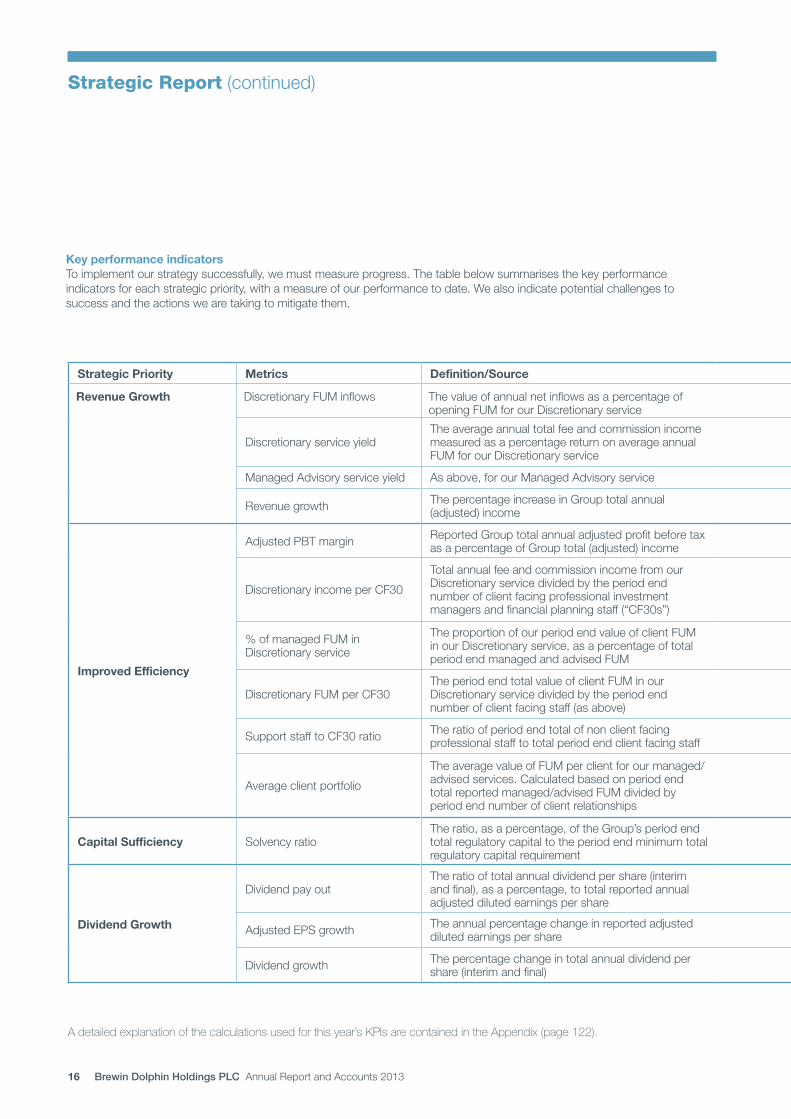

Strategic Priority Metrics Definition/Source Progress Targets Potential challenges/(response)

Revenue Growth DiscretionaryFUMinflows The value of annual net inflows as a percentage of openingFUMforourDiscretionaryservice

6% 5% Failuretoinnovateservice–Strategy focused on increasing competitiveness with investment in service

FailuretocompletetransitiontonationalratecardforAdvisorymanagedservice–Centrally led project has been key strategic initiative

Adverse financial market conditions, loss of clients, key staff,failuretostaycompetitive–Key focus of strategy, staff incentive schemes

Discretionary service yieldThe average annual total fee and commission income measured as a percentage return on average annual FUMforourDiscretionaryservice

91 96bps 95bps

Managed Advisory service yield As above, for our Managed Advisory service 46 56bps 75bps

Revenue growth ThepercentageincreaseinGrouptotalannual(adjusted)income 9% n/a

Improved Efficiency

AdjustedPBTmargin ReportedGrouptotalannualadjustedprofitbeforetaxasapercentageofGrouptotal(adjusted)income 16.5 18.5% 25%+

Failuretoachieveoperationalefficienciestoenablereducedsupportheadcount–Key focus of strategy

Failuretodelivernewtechnologytoimprovecapacitytomanagemoreclientsperhead–Key focus of strategy

Inability to attract new clients or accounts of sufficient value–Key focus of strategy

DiscretionaryincomeperCF30

Total annual fee and commission income from our Discretionary service divided by the period end number of client facing professional investment managersandfinancialplanningstaff(“CF30s”)

£283k £370k £490k

%ofmanagedFUMinDiscretionary service

TheproportionofourperiodendvalueofclientFUMin our Discretionary service, as a percentage of total periodendmanagedandadvisedFUM

70 76% 80%

DiscretionaryFUMperCF30TheperiodendtotalvalueofclientFUMinourDiscretionary service divided by the period end numberofclientfacingstaff(asabove)

£33m £41m £50m

SupportstafftoCF30ratio The ratio of period end total of non client facing professional staff to total period end client facing staff 2.5to1 2.0 to 1

Average client portfolio

TheaveragevalueofFUMperclientforourmanaged/advised services. Calculated based on period end totalreportedmanaged/advisedFUMdividedbyperiod end number of client relationships

£420k £500k

Capital Sufficiency Solvency ratioTheratio,asapercentage,oftheGroup’speriodendtotal regulatory capital to the period end minimum total regulatory capital requirement

226% Min150%

Dividend Growth

Dividend pay outTheratiooftotalannualdividendpershare(interimandfinal),asapercentage,tototalreportedannualadjusteddilutedearningspershare

57 58% 60-80%Loss of profitability

Availability of distributable reserves as impacted by non-adjustedlossese.g.furtherexceptionals, write-offs

AdjustedEPSgrowth Theannualpercentagechangeinreportedadjusteddiluted earnings per share 19.2% n/a

Dividend growth The percentage change in total annual dividend per share(interimandfinal) 20% n/a

Strategic Report(continued)

Key performance indicatorsTo implement our strategy successfully, we must measure progress. The table below summarises the key performance indicators for each strategic priority, with a measure of our performance to date. We also indicate potential challenges to success and the actions we are taking to mitigate them.

A detailed explanation of the calculations used for this year’s KPIs are contained in the Appendix (page 122).

17

Busin

ess re

view

Strategic Priority Metrics Definition/Source Progress Targets Potential challenges/(response)

Revenue Growth DiscretionaryFUMinflows The value of annual net inflows as a percentage of openingFUMforourDiscretionaryservice

6% 5% Failuretoinnovateservice–Strategy focused on increasing competitiveness with investment in service

FailuretocompletetransitiontonationalratecardforAdvisorymanagedservice–Centrally led project has been key strategic initiative

Adverse financial market conditions, loss of clients, key staff,failuretostaycompetitive–Key focus of strategy, staff incentive schemes

Discretionary service yieldThe average annual total fee and commission income measured as a percentage return on average annual FUMforourDiscretionaryservice

91 96bps 95bps

Managed Advisory service yield As above, for our Managed Advisory service 46 56bps 75bps

Revenue growth ThepercentageincreaseinGrouptotalannual(adjusted)income 9% n/a

Improved Efficiency

AdjustedPBTmargin ReportedGrouptotalannualadjustedprofitbeforetaxasapercentageofGrouptotal(adjusted)income 16.5 18.5% 25%+

Failuretoachieveoperationalefficienciestoenablereducedsupportheadcount–Key focus of strategy

Failuretodelivernewtechnologytoimprovecapacitytomanagemoreclientsperhead–Key focus of strategy

Inability to attract new clients or accounts of sufficient value–Key focus of strategy

DiscretionaryincomeperCF30

Total annual fee and commission income from our Discretionary service divided by the period end number of client facing professional investment managersandfinancialplanningstaff(“CF30s”)

£283k £370k £490k

%ofmanagedFUMinDiscretionary service

TheproportionofourperiodendvalueofclientFUMin our Discretionary service, as a percentage of total periodendmanagedandadvisedFUM

70 76% 80%

DiscretionaryFUMperCF30TheperiodendtotalvalueofclientFUMinourDiscretionary service divided by the period end numberofclientfacingstaff(asabove)

£33m £41m £50m

SupportstafftoCF30ratio The ratio of period end total of non client facing professional staff to total period end client facing staff 2.5to1 2.0 to 1

Average client portfolio

TheaveragevalueofFUMperclientforourmanaged/advised services. Calculated based on period end totalreportedmanaged/advisedFUMdividedbyperiod end number of client relationships

£420k £500k

Capital Sufficiency Solvency ratioTheratio,asapercentage,oftheGroup’speriodendtotal regulatory capital to the period end minimum total regulatory capital requirement

226% Min150%

Dividend Growth

Dividend pay outTheratiooftotalannualdividendpershare(interimandfinal),asapercentage,tototalreportedannualadjusteddilutedearningspershare

57 58% 60-80%Loss of profitability

Availability of distributable reserves as impacted by non-adjustedlossese.g.furtherexceptionals, write-offs

AdjustedEPSgrowth Theannualpercentagechangeinreportedadjusteddiluted earnings per share 19.2% n/a

Dividend growth The percentage change in total annual dividend per share(interimandfinal) 20% n/a

18 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Strategic Report(continued)

E. Results for the Year

Financial HighlightsThe strong underlying results for the year ended 29 September 2013 reflect the combination of improving market conditions andprogresswehavemadeondeliveringourstrategicobjectives.Adjustedprofitbeforetaxgrewby22%to£52.3mfrom£42.9mlastyearandadjusteddilutedEPSgrewby19%to14.9ppersharefrom12.5plastyear.

Theunderlyingadjustedprofitgrowthwasdrivenbyincreasedincome,9%higherthanprioryear,togetherwithimprovingefficiencyasreflectedbyfixedoperatingcostgrowthbeinglimitedto3%andtheincreaseinadjustedprofitbeforetaxmarginto18.5%from16.5%intheprioryear.

Profitbeforetaxfortheyearwas£28.6m(2012:£29.9m),a4%declineontheprioryear.Thiswasaresultofsignificantrestructuringcostsincurredintheyearandmaterialprovisionsforonerouscontractswhichareexplainedbelow.

2013 £m

2012 £m

Change

Total income 283.7 260.4 9%

Salaries (105.3) (98.6) 7%

Other operating costs (83.4) (85.1) -2%

Total fixed operating costs (188.7) (183.7) 3%

Adjustedprofitbeforevariablestaffcosts1 95.0 76.7 24%

Variable staff costs (43.7) (34.6) 26%

Adjustedoperatingprofit1 51.3 42.1

Netfinanceincomeandothergainsandlosses 1.0 0.8

Adjusted profit before tax1 52.3 42.9 22%

Exceptionalcosts/gains (11.2) (1.1)

Amortisation of client relationships (12.5) (11.9)

Profit before tax 28.6 29.9 -4%

Taxation (7.3) (8.4)

Profitaftertax 21.3 21.5

Earnings per share

Basic earnings per share 8.5p 9.1p

Diluted earnings per share 8.0p 8.6p

Earnings per share1

Basic earnings per share 15.8p 13.2p

Diluted earnings per share 14.9p 12.5p

1 Excluding redundancy costs, additional FSCS levy, onerous contracts provision, amortisation of client relationships and disposal of available-for-sale investment.

19

Busin

ess re

view

Reconciliation of adjusted income and operating expenses to financial statements

2013 £m

2012 £m

Income–perfinancialstatements 283.7 269.5

Reclassificationofitemspreviouslyreportedasoperatingexpenses – (9.1)

Adjusted income used for purposes of financial highlights and strategic report 283.7 260.4

Otheroperatingcosts–perfinancialstatements 83.4 94.2

Reclassification of items previously reported as income – (9.1)

Adjusted other operating expenses used for purposes of financial highlights and strategic report 83.4 85.1

PriortotheintroductionofRDR(1January2013),BrewinDolphincollectedincomefromclientportfoliosonbehalfofintermediarieswhichitrecordedasincomewithanoffsettingexpense.PostRDR,intermediariesarerequiredtocollectandrecord their income directly from clients and consequently this income is no longer recorded in Brewin Dolphin’s results.

Thishasnoimpactonreportedprofit,howeverwehavechosentoadjustthecomparativefiguresfor2012tobeonapostRDRbasis as we believe this offers a more fair and appropriate analysis of underlying income and cost trends.

IncomeTotalincomegrewby9%to£283.7m(2012:£260.4m)intheyearandisanalysedasfollows:

2013 £m

2012 £m

Change

Commissions 93.5 84.1

Fees 152.0 121.4

Core income1 245.5 205.5 19%

FinancialPlanning 11.7 9.3

Trail 14.8 29.2

Interest 11.7 16.4

Other income 38.2 54.9 -30%

Total income 283.7 260.4 9%

1 Core income is defined as income derived from fees and commissions charged on management and/or advice and execution activities relating to client portfolios.

20 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

CoreincomefromourDiscretionary,AdvisoryandExecutionOnlyservices,grewstronglyby19%to£245.5m(2012:£205.5m).This was driven by a combination of increased average client fund balances due to higher market levels and continued inflows, and improved returns as a result of the move to new pricing structures.

Income and yield by service type

2013 £m

2012 £m

Change

Income

Discretionary 192.7 156.3 23%

Advisory Managed 27.5 23.3 18%

Advisory Dealing 7.2 12.8 -44%

Total Managed/Advised 227.4 192.4 18%

ExecutionOnly 18.1 13.1 38%

Total 245.5 205.5 19%

Yield Bps Bps

Discretionary 96 91

Advisory Managed 56 46

Advisory Dealing 29 42

ExecutionOnly 30 26

Strategic Report(continued)

21

Busin

ess re

view

ThestronggrowthinFUMandimprovedyieldresultedina23%increaseinincometo£192.7m(2012:£156.3m)fromourDiscretionaryservice.DespitelowerlevelsofAdvisoryManagedFUM,overallincomefromManaged/Advisedservicesincreasedby18%duetotheimprovedyieldfromre-pricing.Thedeclineinincomefromadvisorydealingresultedfromthesteepdeclineinfundsunderthiscategoryasaresultoftheservicereviewandre-pricinginitiative.

Overallfeesandcommissionsgrew,withfeesgrowingparticularlystrongly,up25%to£152.0m(2012:£121.4m)asaresultofthegrowthinDiscretionaryservicesandtheon-goingintroductionoffeestoallAdvisoryManagedaccountsinlinewithnewpricing structures.

Aggregateotherincomedeclinedby30%to£38.2mfrom£54.9min2012,primarilyduetotheplannedsignificantreduction intrailincomewhichdecreasedto£14.8m(2012:£29.2m)asaresultofourinitiativetoswitchtotrailfree‘cleanunits’.Sincethebeginningofthisyearallnewfundshavebeenpurchasedona‘clean’basisposttheimplementationofRDR.

Incomefromfinancialplanningactivitiesgrewby26%duringtheyearto£11.7m(2012:£9.3m)asaresultofourstrategytooffer an integrated wealth management service.

Netinterestearnedfromthemanagementofclientcashdepositsreducedby29%intheyearto£11.7m(2012:£16.4m)asaresultof reduced interest rates on deposits available from our banks, whilst maintaining interest rates payable on client cash balances.

Costs

Reconciliation of adjusted operating expenses to financial statements

2013 £m

2012 £m

Change

Fixedstaffcost 105.3 98.7 7%

Underlyingnon-staffcosts 84.2 89.7 -6%

Insurance recovery (0.8) (4.7)

Non-staffcosts 83.4 85.0 -2%

Totaladjustedfixedoperatingcosts 188.7 183.7 3%

Variable staff costs 43.7 34.6 26%

Redundancy costs 4.8 0.6

Additional FSCS levy 1.1 0.5

Onerous contracts 6.2 –

Totalexceptionalcosts 12.1 1.1

Amortisation of client relationships 12.5 11.9

Total adjusted operating expenses 257.0 231.3

Reclassification1 – 9.1

As reported in Income Statement 257.0 240.4

1 Reconciliation of adjusted income and operating expenses to financial statements (page 19)

22 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Strategic Report(continued)

Significant progress has been made in bringing costs under control during the year.

Fixed staff costsFixedstaffcostgrowthwaslimitedto7%yearonyear,belowtherateofincomegrowth,areversalofpreviousyears’trendsand contributing to the improved operating margin. This was achieved through a combination of hiring discipline together with reducedrunratecentralfunctioncostsfollowingtherestructuringexerciseundertakenduringtheyear.Theexceptionalcostsassociated with this are described below.

Variable staff costsVariablestaffcostsincreasedby26%to£43.7m(2012:£34.6m).Theincreasewasdrivenprimarilybytheriseinadjustedprofitbeforevariablestaffcosts(+24%)towhichthemajorityofvariablestaffcostislinked,andmanagement’sdecisiontoincreasethe overall level of variable staff compensation to assist in staff retention.

Theoverallratiooftotal(fixedandvariable)staffcoststoadjustedincomeincreasedaccordinglyduringtheyearto53%from51%in2012.

Non-staff costsAsignificantreductioninunderlyingnon-staffcostsof6%yearonyearwasachieved,fallingto£84.2mfrom£89.7min2012.

Thiswasduetotightercontrolsarounddiscretionaryexpenditure,inparticularinareassuchasmarketing,advertisingandlegal/consulting fees, and the reduction contributed significantly to the improvement in operating margin during the year.

Insurance recoveryDuringtheyeartheGroupreachedfinalsettlementwithitsinsurerswithrespecttocertainmaterialpastclaimsrelatingtoinsuredlossesincurredinprioryears.Thisresultedinanadditional£0.8m(2012:£4.7m)recoverybeingrecognisedintheyear.

Exceptional costs

Redundancy costsRedundancycostsof£4.8m(2012:£0.6m)incurredintheyearprimarilyresultedfromtwoorganisationalrestructurings:

1) InMarchvariousheadofficefunctionswererestructuredinordertobetterservicebusinessneedsandreducecosts. Thisresultedinapproximately£3.0minredundancypaymentsandreducedcentralfunctionsheadcountbyapproximately100.Thisresultedinanongoingstaffcostssavingof£6.0mperannum.

2) Duringthesecondhalf,arationalisationofthebranchnetworkwasundertaken,resultingintheclosureofouroffices inInverness,Teesside,HerefordandSwansea.Themanagementofclientstogetherwithsomeofthestaffmovedto locallargerofficeswhereweconsiderwearebetterabletoserveourclients’needsinthelongerterm.Afurther£1.4m of redundancy payments were incurred as a consequence, with run rate savings to branch staff costs to be felt from 2014 onwards.

Onerous contracts provisionsProvisionsinrespectofonerouscontractstotalling£6.2m,£5.7mrelatingtosurpluspropertyspacewhichmaynotbeabletobecontinuallysub-let,weremadeintheyear.

Ofthis,approximately£0.5mrelatestotheremainingleasecommitmentsofuptofouryearsonrecentlyclosedoffices,£4.3mrelatestoleasecommitmentsofupto20yearsonexcessspaceresultingfromtheconsolidationofoperationsintooneofficeinEdinburgh,and£0.9mfromexcessspaceresultingfromtheconsolidationintooneofficeinLondon.The£0.4mnon-propertyrelated provision relates to software applications no longer being used as a result of the central functions restructuring. The maximumtotalfutureundiscountedexposureresultingfromtheaggregateoftheonerouspropertyleasesisapproximately£23.0m.

Exceptional gainDuringtheyeartheGroupsolditsremainingstakeinNPLUS1SingerLtdrealisinganexceptionalgainondisposalof£0.9m.

23

Busin

ess re

view

Cash flow and capital expenditureOur strategy aims to deliver not only growing earnings, but also rising free cash flow, being the cash generated from operations less what we invest in the business. This will ensure that dividend growth can be aligned with earnings growth without material short term reductions to tangible equity.

Thetablebelowshowshowunderlyingprofitabilitytranslatedintocashgeneration:

2013 £m

2012 £m

Adjusted profit before tax 52.3 42.9

Less–Exceptionalcosts/gains (11.2) (1.1)Amortisation of client relationships (12.5) (11.9)

Statutory PBT 28.6 30.0Add–noncashexpensesincluded 27.1 26.9 Less–discontinuedoperations – (3.5)Less–pensioncontributionsnotincludedabove (3.0) (3.0)

Operating cash flows before working capital 52.7 50.4Less–taxpaid (6.3) (5.9)

Underlying cash from operations 46.4 44.5Net investment–Purchaseofclientrelationships (3.4) (6.9)–Purchaseoffixedassets (4.5) (7.4)–Purchaseofsoftware (15.1) (16.4)–Netgainsanddividendsonavailable-for-saleinvestment 1.2 0.3

(21.8) (30.4)

Underlying free cash flow 24.6 14.1

Net financing –Dividendspaid (18.1) (16.9)–Sharespurchased (0.2) (1.9)–Sharesissuedforcash 41.9 0.7

23.6 (18.1)

Underlying increase/(decrease) in cash 48.2 (4.0)

Decrease/(increase)inworkingcapital 17.6 (12.1)

Movement in firm's cash 65.8 (16.0)

Movement in client balances (3.5) 2.6

Movement in total cash 62.3 (13.4)

Reconciliation to reported cash from operationsUnderlying cash from operations per above 46.4 44.5Movement in client balances per above (3.5) 2.6Movement in working capital per above 17.6 (12.1)

Cash from operations per note 34 60.5 35.0

24 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

TheGroup’scashbalancesincreasedmateriallyby£65.8mto£113.5mat29September2013,from£47.8mat 30 September 2012.

Inadditiontounderlyingcashgeneratedfromoperationsof£46.4m(2012:£44.5m),thelargeincreasewastheresult primarilyoftheequitycapitalraisinginMay2013,generatingnetproceedsof£38.6m,inadditiontopositiveworking capitalmovementof£17.6mintheyear.

Underlyingfreecashflowincreasedto£24.6mfrom£14.1min2012,duetolowertotalcapitalinvestmentintheyear (£21.8m,versus2012:£30.4m).

Upfrontcashspentonacquiringteamsofinvestmentmanagersandtheirclientrelationshipsdeclinedto£3.4mfrom £6.9min2012duetothesignificantabsenceoffurtherteamhiresintheyearbeyondwhatwasalreadyinprogressat 30 September 2012.

Investmentinfixedassetsdeclinedto£4.5mintheyear(2012:£7.4m),primarilyduetolowerspendoncomputerhardware in support of the implementation of the new core software operating system.

Developmentofthenewcoresettlementsystemwhichhasbeenunderwayfor18months,reflectedintotal£16.8m further capital investment in computer hardware and software development costs to bring the new software into use. Inadditionto£17mspentin2012,totalcumulativeinvestmentintheprojectisapproximately£34m.Itisanticipatedanadditional£20mwillbespentoverthecourseofthenext18monthstobringtheimplementationtoasuccessfulcompletion.

Dividendspaidintheperiodcameto£18.1m(2012:£16.9m).

TherehasbeenacashoutflowfromthepurchaseofsharesfortheShareIncentivePlan(SIP)of£0.2mand£nilforthe DeferredProfitShareScheme(DPSP)duringtheyear,(2012:£1.9mSIPandDPSP).TheGroupinstructedthetrustees oftheDPSPtopurchase£4mofsharesaftertheendofthefinancialyear.

Investment in new technology to improve the quality of our client service, as well as lowering the cost of delivering that service, is a key initiative to achieve the strategic priority of improving operational efficiency. We will continue to develop ways of investing and successfully integrating new software solutions into our business model. This will result in future capitalinvestment,thoughatalowerlevelthanthecurrentrunrate,oncethecoresystemisfullyinplace.Freecash flow as a proportion of underlying earnings should therefore increase over time as earnings grow.

Strategic Report(continued)

25

Busin

ess re

view

Resources available to the GroupOurprimaryassets,inadditiontoouremployees,arethevalueof:

1) Clientrelationshipsacquiredviaintroductionfromnewteamsofinvestmentmanagershired;

2) Fixedtangibleassets,i.e.investmentinfixturesandfittingsinourofficesandincommunicationsandtechnologyhardwaretosupport our operations; and

3) Purchase,developmentandconfigurationofnewsoftwareapplicationstosupportouroperations.

We invest across all three categories to develop the assets of the business, securing growth and preserving and improving our operational efficiency.

As our strategy has changed in recent years from focusing solely on growth by acquiring additional client relationships to seeking also to improve operational efficiency, we have been investing more in the development of new software and less on acquiring teams of investment managers.

Pension FundTheactuariallossonthepensionfundthisyearwas£2.2m(2012:£5.1m).UnderIAS19,largeannualfluctuationscanoccur.TheGrouphasagreedtomakeadditionalpensioncontributionsof£3mperannumwiththeaimofpayingthedeficitoff,overthenextsevenyears.

Thenetpensiondeficitreducedby£0.6mduringtheyearto£9.2m(2012:£9.8m).Thisprimarilyresultedfrombetterthanexpectedinvestmentreturnsonassetsexceedingtheincreaseintheactuarialvalueofliabilities.

Capital Structure, Treasury Policy, Liquidity and Capital RequirementAt29September2013theGrouphadnetassetsof£221.6m(2012:£162.7m).Netassetsexcludingintangibleassetsandsharestobeissuedof£109.1m(2012:£61.1m)broadlyrepresenttheGroup’scapitalforregulatorypurposes.Thesenetassetswerelargelyrepresentedbynetcashandcashequivalentsof£137m(2012:£72m),including£20.3m(2012:£23.8m)ofclientsettlementmoney.TheGrouphasanagreedunsecuredoverdraftfacilityof£15m(2012:£15m).AttheperiodendtheGrouphadasurplusofnetassetsforregulatorycapitaladequacypurposesof£60.5m(2012:£11.4m),theincreaseismainlyattributable to the capital raised during the placing in May.

TheGroupaimstoholdatleast90%ofbothclients’andGroups’moneyonlyatmajorUKclearers.ClientmoneyissegregatedunderrulessetoutintheFCAClientAssetSourceBook.

Client stock is segregated and held in our nominee companies. Stock is settled via the Crest System which is owned by Euroclear,ahighlyratedbank,and,inthecaseofforeignstock,theBankofNewYorkMellon.

Market risk, foreign currency risk, liquidity risk, interest rate risk, and credit risk are small and set out in detail in note 26 to the financial statements.

26 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Post Balance Sheet EventsThere have been no material post balance sheet events.

Accounting PoliciesThere were no changes in accounting policies during the year.

Significant RelationshipsNoclientprovidesmorethan2%oftheGroup’srevenue.TheGrouphastwomainsuppliersofcomputersoftware.

Going ConcernTheGrouphassubstantialoperationalgearingarisingfromitsfixedcostbase;thisismitigatedbyvariablestaffcostswhichifincomefallswouldreducevariablecosts.Cashbalancesrangedbetween£28mand£124movertheyear.

TheGroup’sbusinessactivities,performanceandposition,togetherwiththefactorslikelytoaffectitsfuturedevelopment,aresetoutintheStrategicReportwhichalsodescribesthefinancialpositionoftheGroupincludingitsliquiditypositionandborrowing facilities.

TheGroup’sobjectives,policiesandprocessesformanagingitscapital,itsfinancialriskmanagementobjectives,detailsofitsfinancialinstrumentsanditsexposuretocreditriskandliquidityriskaredescribedinnote26tothefinancialstatements.

TheDirectorsbelievethattheGroupiswellplacedtomanageitsbusinessriskssuccessfully.TheGroup’sforecastsandprojections,takingaccountofpossibleadversechangesintradingperformance,showthattheGrouphasadequateresourcestocontinueinoperationalexistencefortheforeseeablefuture.Accordingly,theDirectorscontinuetoadoptthegoingconcernbasis for the preparation of the financial statements.

Strategic Report(continued)

27

Busin

ess re

view

F. Principal Risks and Uncertainties

RisksTheGroup’sprincipalrisksanduncertaintiestogetherwiththekeymitigantsandcontrolsaresetoutonpages28and29.

DetailsoftheriskframeworkandgovernancearesetoutintheRiskCommitteereport(pages44–45).

TheoriginsandnatureoftheGroup’sprincipalriskschangeovertimeandaretheresultof,amongotherfactors,themarketenvironmentandtheGroup’sstrategy.

AsdiscussedabovewhenexplainingtheGroup’scurrentstrategy,managementtakescarefulconsiderationoftheriskimplications of different strategic initiatives. The strategic refocus instigated by the new management team has in part been drivenbytheappreciationthattheGroup’sriskprofilewasincreasingovertimeasaresultofexternalfactorssuchasincreasedregulatoryscrutinyandcompetitivepressuresaswellasfromtheGroup’sformerstrategyofinorganicgrowth.

The current strategy is aimed at managing and where possible reducing the operational, business and strategic risks over time.Forexample,initiativesalreadyunderway,suchasthestandardisationofthebusinessmodelandwithdrawalfromcertainactivities and services, should result in reduced risks.

Equally, the increased focus on organic growth will limit the addition of further risk relating to acquisitions. Risks resulting from the past strategy, however, may remain.

Inthelongterm,successfulimplementationofthestrategyandrealisationofstrategicprioritieswillreducetheGroup’sstrategicrisk by making it more competitive and better able to continue to prosper in a challenging market environment.

In the short term, however, strategic risks may well increase due to the challenges of delivering the business transformation itself.Inparticular,theinabilitytoimplementchangeduetoculturalinertia,vestedinterestsorpoorprojectmanagementisanemergent risk as the refocused strategy is implemented.

28 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Risk Type Risk Description Key Mitigants & Control

Business & Strategic Risks

Strategy & Business Model

Acquisitions & Disposals

Weak due diligence on target companies or poorexecutionoftransactions and associated commercial terms

• Alignmentwithvendorsthroughearnoutarrangements

• Robustboardgovernanceandchallengefromindependentnonexecutives

• 3rdpartylegal,accountingandcommercialdue diligence commissioned

Profitability&Resilience

Failuretomanagevolumes,margins, earnings volatility, diversification, resilience to market dislocation and cost control or impact of industry levies and long term contractual commitments

• Initiativestoenhancemarginandreducefixedoperatingcostbase

• Initiativestoensureconsistentpricingofservices

• Variablestaffincentivepaylinkedtoprofitability

•Managematerialonerousleaseexposuresthrough subletting/assignment

Products,Clients & Reputation

ProductDifferentiation& Disintermediation

Failuretoinnovate,respondto new entrants to the market, offer distinct services at a competitive pricing level, and meet or respond to client needs

• Longtermloyalclientrelationshipsandfocuson personalised service

• Strategicinitiativestokeepinnovatingclientservice

• Initiativestoinnovateandofferwealth/investment management services to as broad as possible client types e.g. development of Direct to Client, managed services, intermediary propositions

• Diversifiedclientbase

Concentration

Over-relianceonkeyclientsor limited product range, or the failure to attract new business

Capacity & Constraints to Growth

Change Management

Inability to implement change due to cultural inertia, vested interests,orpoorprojectmanagement

• Effortstocommunicatetoemployeesthestrategicbenefits:improvedclientservice,higherjobsatisfactionandcareerprogression, better efficiency and growth opportunities and consequent reward potential

• Strongprojectgovernancewiththirdpartyspecialisthelp,directexecutiveoversightand board scrutiny

• Promotionofchangeadvocacynetworks intheGroup

Infrastructure

Failuretoinvestintechnologyand legacy systems, facilities or other support infrastructure

• Investinginnewsystemstechnologyandreplacing legacy systems

Management, Staff & Internal Culture

Development & Succession

Over-relianceonkeyemployees, a lack of career progression, inadequate training, and poor role handover

• Teamapproachtomanagingclientrelationships is a key aspect of the strategic initiatives to improve efficiency

• Activesuccessionplanningforkeymanagement roles underway

• Incentivepoliciestocreatesignificantequitytie-ins

Strategic Report(continued)

29

Busin

ess re

view

Risk Type Risk Description Key Mitigants & Control

Financial Risks

PensionObligation Risk

Pensiondeficit

Increased funding requirements to meet financial obligations under a defined benefit scheme

• Schemeclosedtonewmembers

• RecoveryplanagreedwithTrustees

Operational Risks

Processes,Technology &ExternalServices

Trading ErrorsDealing errors, fat fingers, lateormis-bookedtradesand missed fund deal dates

• DedicatedemployeesundertakeallGroupdealing

• Closemanagementsupervisionofdealers

• Errorwarningsintegratedintodealingsystems

•Monitoringofhighvaluetradespreandposttrade

•Multiplevalidationsonequitytradingplatform

• Comprehensiveinsurancecoverforerrorsandlosses

•Monitoringoflossesandunderlyingcauses

ServiceProviders

Over-relianceorcriticaldependency due to lack of alternatives, or internal skills /capacity

• Internalcompetenciesbeingdevelopede.g.projectmanagement,changeandtransformationskills

• Keyvendorssubjecttoactivemanagementandgovernance framework, SLAs etc

•Monitoringofkeyriskindicators

Business Continuity

FailureofBusinessContinuityPlan(BCP)arrangementsdue to either an inadequacy or failure to test regularly

• DedicatedbusinesscontinuityfunctionwithintheGroup

• Largebranchnetworkwithappropriatecontinuity plans in place to ensure service can be maintained

• UseofexternalfacilitiestoenhancetheresilienceoftheGrouptoabusinesscontinuityevent

• BCPsubjecttoperiodictesting

• Rapidresponsetosignificantsystemsfailuresorinterruptions

Investment Suitability & Mandate Breaches

Investment Advice & Suitability

Insufficient or inadequate information on clients’ needs or capacity for loss, unsuitable advice, portfolio holdings inconsistent with clients’ attitude to risk, or failure to adhere to investment mandate.

• TreatingCustomersFairlyembeddedwithintheethosoftheGroup

• Implementationofnewinvestmentprocesssupported by new technologies

• RobustTraining&Competencyprogramme

• DedicatedBusinessStandardsTeamtoreviewbusiness quality

•MonitoringundertakenbyRisk&RegulationDepartment

•Managementinformation

• Effectivecomplainthandlingprocessandinsurance cover to mitigate losses

30 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Strategic Report(continued)

Risk Type Risk Description Key Mitigants & Control

Operational Risks (continued)

Regulatory Compliance &FinancialCrime

RegulatoryFailure

Breaches of regulatory obligations, including client money/asset rules, and AML/KYC, conflicts of interest, breach of data protection obligations and failure to respond to regulatory change.

• ProactiveandeffectiveRegulation&Riskand Internal Audit functions

• Supervisoryprocessinplaceforstaffholding a controlled function

• Annualdeclarationstobemadebyallstaffreviewed by Regulation & Risk

• ClientAssetOversightCommitteeestablished to strengthen governance over client money and custody arrangements

• ClientAssetreviewsundertakenbyRegulation & Risk and Internal Audit

• Risk-basedAMLmethodologyusedforassessing all clients

• Systemsandcontrolstoensureemployeesaccess rights to data are appropriate

• PersonalAccountDealingandGiftspoliciesin effect and overseen centrally

• Regulation&RiskDepartmentadviseonimpact of regulatory change to prompt timely business responses

Fraud

Misappropriation of client or firm's assets, deliberate mis-reportingormisroutingof payments.

• Centralisedindependentinvoiceprocessingand payment

• AuthorisationprocessinplaceforkeydepartmentsthatdealwithclientsorGroupassets

• SegregationofdutiesacrosstheGroup

• Paymentauthorisationcontrols

•Monitoringofpaymentsandtransfers

• Comprehensiveinsurancecover

31

Busin

ess re

view

G. Future DevelopmentsThe risks of not adapting our business model to a changing environment are significant and would erode shareholder value. Therefore we have developed an ambitious strategy to evolve the business and become the leading provider of Discretionary Wealth Management and the firm of choice for our clients, employees and shareholders.

We will continue to invest in our people, processes and technology to improve the client offering and if we achieve these goals, we will deliver significant value for shareholders, clients and employees.

H. Corporate ResponsibilityTheCorporateResponsibilityreportonpages36to38includesinformationonenvironmentalmatters,employees(includinggenderratios)andcommunityissues.

ApprovedbytheBoardofDirectorson3December2013andsigneditsbehalfby:

David Nicol Andrew WestenbergerChiefExecutive FinanceDirector

Simon Edward Callum Miller (n)(r) Chairman

SimonMillerwasappointedChairmaninMarch2013.HejoinedtheBoardin2005andbecame DeputyChairmanandSeniorIndependentDirectorin2012.HereadlawatCambridgeandwas calledtothebar.HesubsequentlyworkedforLazardBrothersandCountyNatwest.Since1994 hehasbeenChairmanofDunedinLLP.HeisalsoChairmanofArtemisAlphaTrust,Blackrock NorthAmericanIncomeTrustandJPMorganGlobalConvertibleIncomeFund.

David Richardson Nicol, CA, Chartered FCSI (n) Chief Executive

DavidNicolisacharteredaccountant.HewasaDirectorofMorganStanleyInternationalPLCfrom2004to2010.HeworkedforMorganStanleyfor26yearsinanumberofOperationsandFinancerolesandwasappointedEMEACAOin2004.DavidwasaNon-ExecutiveDirectorofEuroclearplcfrom1998to2010.Hetrainedandqualifiedin1980asaCharteredAccountantwithErnst&YoungandspenttwoyearsworkingforKPMGinHongKongbeforejoiningMorganStanleyinLondonin1984.DavidNicolisontheBoardoftheChartered Institute of Securities and Investments, the Council of the Institute of Chartered Accountants of ScotlandandisamemberoftheAppointmentCommitteeoftheHermesPropertyUnitTrust.DavidjoinedtheBoardasaNon-ExecutiveDirectorinMarch2012andwassubsequentlyappointedasChiefExecutiveinMarch 2013.

Andrew Westenberger, FCA Finance Director

AndrewWestenbergerjoinedtheBoardinJanuary2013.HewasGroupFinanceDirectorofEvolutionGroupPLCfrom2009untilAugust2011andaDirectorofitsprincipalsubsidiaryWilliamsdeBroeLimited.AndrewqualifiedasacharteredaccountantwithCoopers&Lybrand,andfrom2000to2008heldvariousseniorfinancerolesinLondonandNewYorkwithBarclaysCapital.

Stephen Ford, FCSI, CAIA Head of Investment Management

StephenFordjoinedBrewinDolphininMarch2000andhasheldanumberofseniormanagement roles.HewasappointedasaDirectoroftheoperatingcompany,BrewinDolphinLimitedin2009andofBrewinDolphinHoldingsPLCinMarch2013.Stephenpreviouslyledthefinancialservicesdivisionataregional Building Society and holds the Chartered Wealth Manager and Chartered Alternative Investment Analyst designation.

The Board of the Company has been restructured with the appointment of three new ExecutiveDirectors,DavidNicol–ChiefExecutive,AndrewWestenberger–FinanceDirector andStephenFord–HeadofInvestmentManagementwhohavejoinedfellow ExecutiveDirector,MichaelWilliams.

Directors and their biographies

32 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Michael John Ross Williams, FCSI Executive Director

MichaelWilliamsjoinedBrewinDolphin&Co.in1968andbecameapartnerin1978.Hehas consistentlybeeninvolvedinportfoliomanagement.HejoinedtheBrewinDolphinHoldingsBoard onincorporationin1987.

Francis Edward (Jock) Worsley, OBE, FCA (a)*(n)(r)rk) Senior Independent Director

JockWorsleyisacharteredaccountant.HewasappointedtotheBoardinSeptember2003.HewasafounderoftheFinancialTrainingCompanyanditsExecutiveChairmanfrom1972until1993.HehasbeenPresidentoftheInstituteofCharteredAccountantsofEnglandandWales,DeputyChairmanofLautro,amember of the Building Societies Commission and Independent Complaints Commissioner for SIB and theFSA.HewasChairmanoftheCancerResearchCampaignfrom1998untilitsmergerin2002withtheImperialCancerResearchFund.

Angela Ann Knight, CBE (a)(n)(r)*(rk)* Non-Executive Director

AngelaKnightwasaCouncillorandChiefWhiponSheffieldCityCouncilfrom1987to1992.SheenteredParliamentin1992asMPforErewashandwasEconomicSecretarytotheHMTreasurybetween1995and1997.ShewasChiefExecutiveofTheAssociationofPrivateClientInvestmentManagersandStockbrokersfromSeptember1997toDecember2006&ChiefExecutiveoftheBritishBankersAssociationfromApril2007toJuly2012.SheiscurrentlyChiefExecutiveofEnergyUKandanon-executivedirectorontheBoardofTullettPrebonPLCandaNon-ExecutivememberofTransportforLondon.AngelawasappointedasaNon-ExecutiveDirectorinJuly2007.

Sir Stephen Mark Jeffrey Lamport, KCVO (a)(n)*(r)rk) Non-Executive Director

SirStephenwasappointedasaNon-ExecutiveDirectorinMarch2007.HeservedintheDiplomaticServicefrom1974to1993.InMarch1993,hejoinedThePrinceofWales’sHouseholdasDeputyPrivateSecretaryandwasappointedPrivateSecretaryandTreasurertoThePrinceofWalesinOctober1996.FromOctober2002toDecember2007,hewasGroupDirectorforPublicPolicyandGovernmentAffairsforTheRoyalBankofScotland.InAugust2008hewasappointedReceiver-GeneralofWestminsterAbbey.HewasappointedKCVOin2002.HeisDeputyLieutenantforSurreyandsitsonanumberofBoards for charitable organisations.

(a) Member of the Audit Committee (n) Member of the Nomination Committee (r) Member of the Renumeration Committee (rk) Member of the Risk Committee * Denotes Committee Chairman

33

Dire

cto

rs’ Report &

G

ove

rnance

Directors’ Report

34 Brewin Dolphin Holdings PLC Annual Report and Accounts 2013

Directors’ Report

The Directors present their report and the audited accounts for the52weekperiodended29September2013.Thecomparativefiguresareforthe52weekperiodended30 September 2012.

Review of the Business and its Future Development Accompanying this Directors’ Report are the Strategic Report, CorporateGovernanceReport,CorporateResponsibilityReport, Risk Committee Report, Audit Committee Report and Directors’ Remuneration Report. These reports form part of the front half of the Annual Report.

A review of the business and its future development is set out in the Strategic Report. A description of the principal risks and uncertainties is given on page 27 of the Strategic Report.

Cautionary StatementThereviewofthebusinessanditsFutureDevelopmentin the Annual Report has been prepared solely to provide additionalinformationtoshareholderstoassesstheGroup’sstrategies and the potential for these strategies to succeed. It should not be relied on by any other party for any other purpose. The review contains forward looking statements which are made by the Directors in good faith based on information available to them up to the time of the approval of these reports and should be treated with caution due to inherent uncertainties associated with such statements. The Directors, in preparing this Strategic Report, have complied with s417 of the Companies Act 2006.

Results and DividendsTheresultsoftheGrouparesetoutindetailonpage70. The Company paid a final dividend and an interim dividend during the period, as detailed in note 14 to the financial statements.Afinaldividendof5.05penceperordinaryshareisproposedandifapproved,willbepayableon28March2014 to shareholders on the register at close of business on 28February2014.

Capital StructureDetails of the Company’s authorised and issued share capital, together with details of the movements therein are setoutinnote28tothefinancialstatements.Thisincludesthe rights and obligations attaching to shares and restrictions on the transfer of shares. The Company has one class of ordinaryshareswhichcarrynorighttofixedincome.

There are no specific restrictions on the size of a holding nor on the transfer of shares, which are both governed by the general provisions of the Articles of Association and prevailing legislation. The Directors are not aware of any agreements between holders of the Company’s shares that may result in restrictions on the transfer of securities or on voting rights. Details of employee share schemes are set out innote30.SharesheldbyComputershare(Trustees)Limitedabstainfromvoting.UndertherulesoftheGroup’sShareIncentivePlan(“BDSIP”),sharesareheldintrustforparticipantsbyEquinitiSharePlanTrusteesLimited(the“Trustee”).VotingrightsareexercisedbytheTrusteesonreceipt of the participant’s instructions; if no such instruction isreceivedbytheTrusteesthennovoteisregistered.No

person has any special rights of control over the Company’s share capital and all issued shares are either fully or nil paid.