Embed Size (px)

Citation preview

A N N UA L R E P O RTF O R T H E Y E A R E N D E D 3 0 J U N E 2 0 0 6

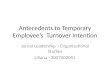

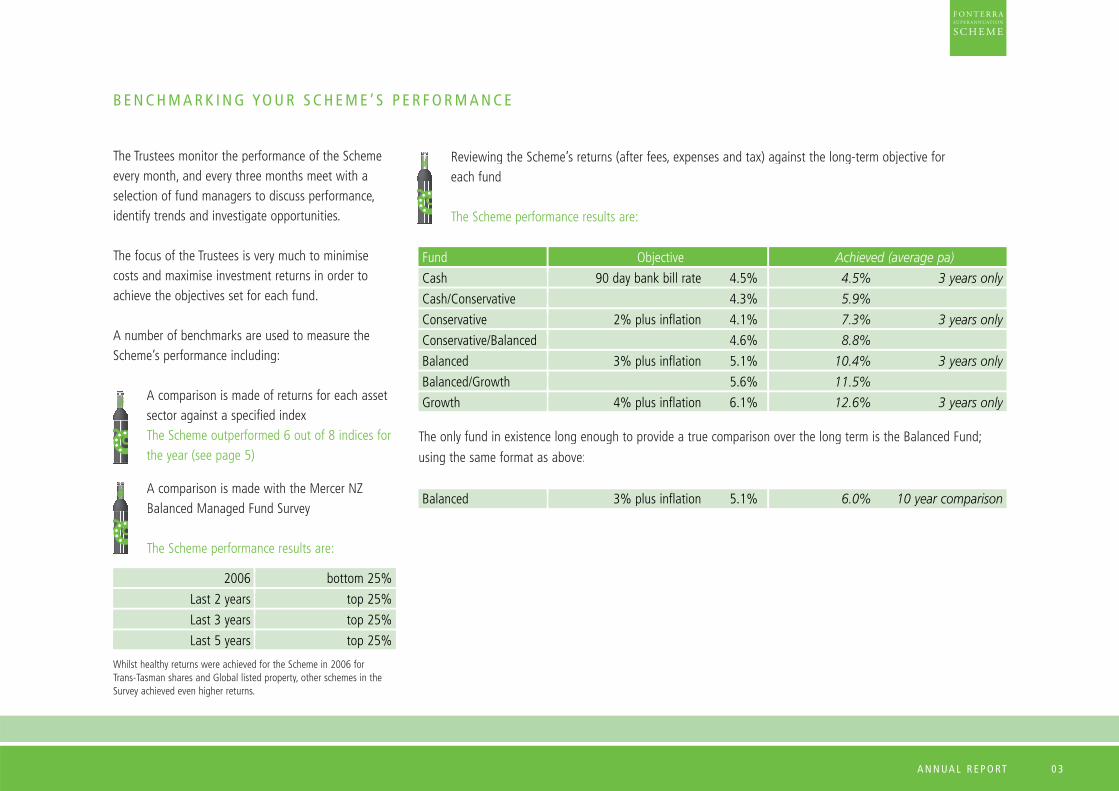

When compared with the Mercer NZ Balanced Managed Fund Survey for investment returns (before fees, expenses and tax), the Scheme ranked in the top 25% for the last three years and last five years.

A V I N TA G E Y E A R W I T H E X C E L L E N T R E T U R N S TO M E M B E R S

0%

3%

Inte

rest

cre

dite

d to

mem

ber a

ccou

nts

VINTAGEYEAR

6%

9%

-3%

-6%

VINTAGEYEAR

VINTAGEYEAR

12%

VINTAGE YEAR

Christine Allen takes careof the day to day runningof the Scheme. Please ringChristine or the MemberHelpline if there is anyaspect of the Scheme orthis report you do not understand.

Freephone: 0800 355 900Telephone: (04) 915 0416Facsimile: (04) 914 0434P O Box 2897, Wellington

INFORMATION ABOUT YOUR SCHEME

Chris Perkins (left) and Hannah Palmer (right) of Mercer Human Resource Consulting preparethe newsletters, Annual Report and other communications to members.

I ' M H E R E TO H E L P M E M B E R S E R V I C E S

Ring the Member Helpline 0800 355 900 to discuss any queries you may have about the Scheme, your Personal Benefit Statement or to discuss investment switch options

Access the Internet www.superfacts.co.nz to access an estimate of your current personal benefits, to project your retirement benefit, to update your address record and read about superannuation developments

Project your Retirement Benefit www.superfacts.co.nz has a calculator module. Simply click on the ‘your super value’ button, select the ‘Estimate your future benefits’ calculator and follow the instructions

A N N UA L R E P O RT

The Fonterra Superannuation Scheme Members’ Information Booklet and accompanying Investment Statement asdesigned by the Mercer team won the ASFONZ Gold Award in September 2005 (in the Other Communications category).

A N N UA L R E P O RT 0 1

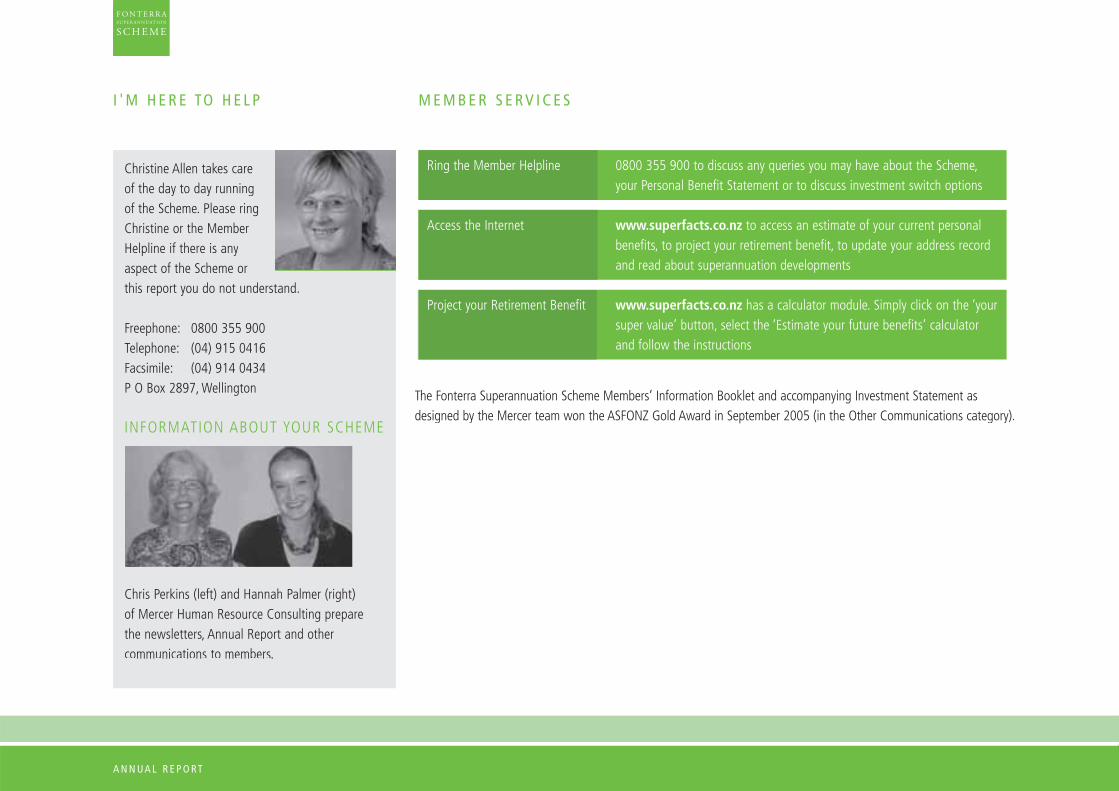

Vintage years do not happen that often but they do occur, as illustrated on the front cover. Bumper returns have now been produced in the last three years to offset the poor returns in the years 2001 to 2003.

Exceptional returns were provided by Trans-Tasman shares 18%, international shares (40% hedged) 27%,Trans-Tasman property 28% and Global listed property 29%. Fixed interest and cash returns were 4% - 8% and were affected by rising interest rates which reduced the value of the underlying securities held. The returns quoted are before tax and fees. The pleasing aspect was that the sharemarket gains were widespread, with Japanand Emerging Markets outperforming Europe and the USA. Stimulus to the market was provided by consumerdemand driving corporate profits, global growth and merger/acquisition activity. Markets reacted negatively inthe last quarter as Central Banks contemplated further interest rate hikes in response to fears of rising inflation.

The return from international shares was also assisted by the decline in the New Zealand dollar, which fell 12%against the US dollar over the year. A further benefit was the Trustees lowering the level of foreign exchangecover on international shares from 50% to 40%.

The vintage year is reflected in the interest rates credited to member accounts as shown in the table below:

Year ended 30 June 2006 2005 2004 2003 2002

4.89% 5.41% 3.12% 3.12% 5.41% 4.89% Cash fund

6.42% 6.60% 4.61% 4.61% 6.60% 6.42% Cash/Conservative

7.94% 7.79% 6.10% 6.10% 7.79% 7.94% Conservative fund

9.91% 8.41% 8.19% 8.19% 8.41% 9.91% Conservative/Balanced

11.88% 9.03% 10.27% 2.14% -3.80%2.14% 10.27% 9.03% 11.88% Balanced fund

13.36% 9.32% 11.78% 11.78% 9.32% 13.36% Balanced/Growth

14.83% 9.60% 13.28%9.60% 14.83% Growth fund

As advised to members in the December newsletter, the Trustees have further diversified the Scheme by including analternative asset sector in the Balanced and Growth Funds. The initial investment into the alternative asset sectoris a fund of hedge funds with $4 million invested at 30 June 2006. With its absolute return focus, the Trusteesare attempting to reduce the amount of fluctuations in returns which can be expected from investing in shares. An explanation of hedge funds is provided later in this report.

C H A I R M A N ’ S R E P O RT

A year of vintage returns

Shares and property performed exceptionally well

Lower forward exchange cover and a declining NZ dollar boosts returns

Balanced and Growth funds show the highest returnsfor the year but they are more volatile in performance than the Conservative and Cash funds

Fund of hedge funds introduced to Balanced andGrowth funds

A N N UA L R E P O RT0 2 A N N UA L R E P O RT0 2

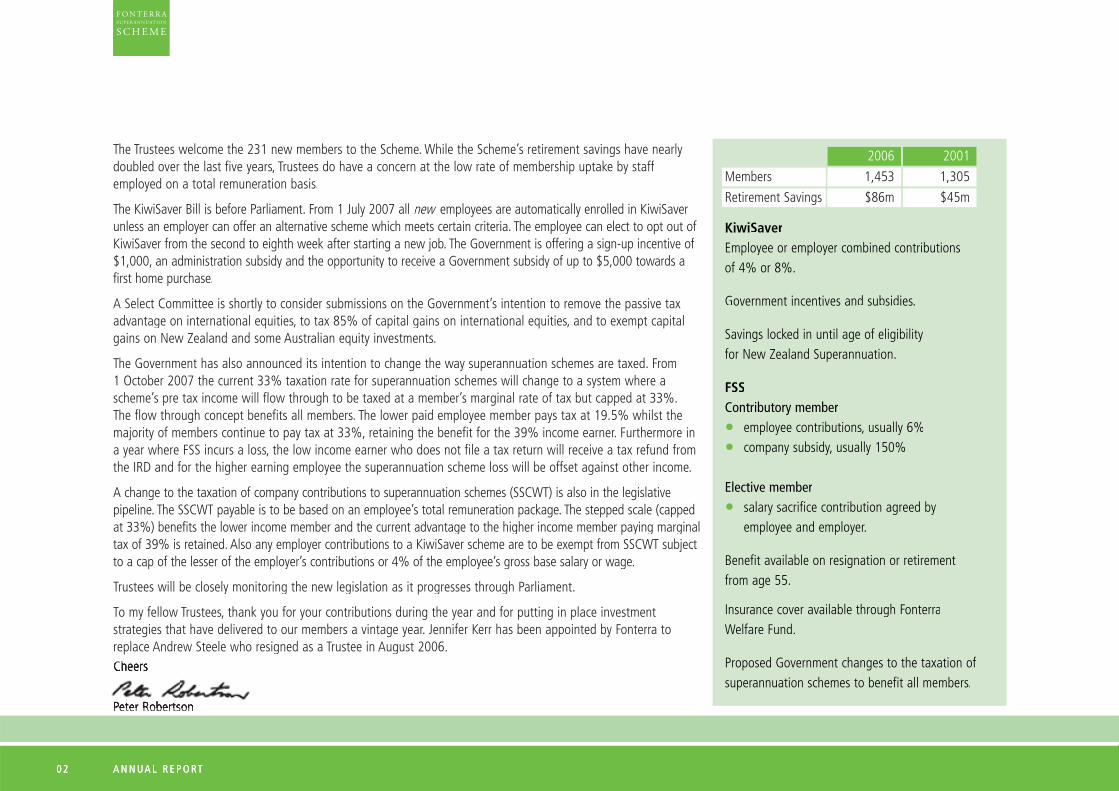

The Trustees welcome the 231 new members to the Scheme. While the Scheme’s retirement savings have nearlydoubled over the last five years, Trustees do have a concern at the low rate of membership uptake by staff employed on a total remuneration basis.

The KiwiSaver Bill is before Parliament. From 1 July 2007 all new employees are automatically enrolled in KiwiSaver wunless an employer can offer an alternative scheme which meets certain criteria. The employee can elect to opt out of KiwiSaver from the second to eighth week after starting a new job. The Government is offering a sign-up incentive of $1,000, an administration subsidy and the opportunity to receive a Government subsidy of up to $5,000 towards afirst home purchase.

A Select Committee is shortly to consider submissions on the Government’s intention to remove the passive taxadvantage on international equities, to tax 85% of capital gains on international equities, and to exempt capitalgains on New Zealand and some Australian equity investments.

The Government has also announced its intention to change the way superannuation schemes are taxed. From 1 October 2007 the current 33% taxation rate for superannuation schemes will change to a system where ascheme’s pre tax income will flow through to be taxed at a member’s marginal rate of tax but capped at 33%.The flow through concept benefits all members. The lower paid employee member pays tax at 19.5% whilst themajority of members continue to pay tax at 33%, retaining the benefit for the 39% income earner. Furthermore ina year where FSS incurs a loss, the low income earner who does not file a tax return will receive a tax refund from the IRD and for the higher earning employee the superannuation scheme loss will be offset against other income.

A change to the taxation of company contributions to superannuation schemes (SSCWT) is also in the legislative pipeline. The SSCWT payable is to be based on an employee’s total remuneration package. The stepped scale (capped at 33%) benefits the lower income member and the current advantage to the higher income member paying marginal tax of 39% is retained. Also any employer contributions to a KiwiSaver scheme are to be exempt from SSCWT subject to a cap of the lesser of the employer’s contributions or 4% of the employee’s gross base salary or wage.

Trustees will be closely monitoring the new legislation as it progresses through Parliament.

To my fellow Trustees, thank you for your contributions during the year and for putting in place investmentstrategies that have delivered to our members a vintage year. Jennifer Kerr has been appointed by Fonterra toreplace Andrew Steele who resigned as a Trustee in August 2006.Ch

Peter Robertson

2006 2001

1,453 1,3051,453 Members

$86m $45m$86m Retirement Savings

KiwiSaverEmployee or employer combined contributionsof 4% or 8%.

Government incentives and subsidies.

Savings locked in until age of eligibility for New Zealand Superannuation.

FSSContributory member

• employee contributions, usually 6%

• company subsidy, usually 150%

Elective member

• salary sacrifice contribution agreed by employee and employer.

Benefit available on resignation or retirementfrom age 55.

Insurance cover available through FonterraWelfare Fund.

Proposed Government changes to the taxation of superannuation schemes to benefit all members.

A N N UA L R E P O RT 0 3

The Trustees monitor the performance of the Schemeevery month, and every three months meet with aselection of fund managers to discuss performance, identify trends and investigate opportunities.

The focus of the Trustees is very much to minimise costs and maximise investment returns in order toachieve the objectives set for each fund.

A number of benchmarks are used to measure theScheme’s performance including:

A comparison is made of returns for each assetsector against a specified indexThe Scheme outperformed 6 out of 8 indices for the year (see page 5)

A comparison is made with the Mercer NZBalanced Managed Fund Survey

The Scheme performance results are:

bottom 25%2006

top 25%Last 2 years

top 25%Last 3 years

top 25%Last 5 years

B E N C H M A R K I N G YO U R S C H E M E ’ S P E R F O R M A N C E

Reviewing the Scheme’s returns (after fees, expenses and tax) against the long-term objective foreach fund

The Scheme performance results are:

Fund Objective Achieved (average pa)

90 day bank bill rate 4.5%Cash 4.5% 3 years only

4.3%Cash/Conservative 5.9%

2% plus inflation 4.1%Conservative 7.3% 3 years only

4.6%Conservative/Balanced 8.8%

3% plus inflation 5.1%Balanced 10.4% 3 years only

5.6%Balanced/Growth 11.5%

4% plus inflation 6.1%Growth 12.6% 3 years only

The only fund in existence long enough to provide a true comparison over the long term is the Balanced Fund;

using the same format as above:

3% plus inflation 5.1%Balanced 6.0% 10 year comparison

Whilst healthy returns were achieved for the Scheme in 2006 for Trans-Tasman shares and Global listed property, other schemes in the Survey achieved even higher returns.

A N N UA L R E P O RT0 4 A N N UA L R E P O RT0 4

at 30 June 2006

at 1 July 2006

$17m $48m $14m $7m

$17m $48m $14m $7m

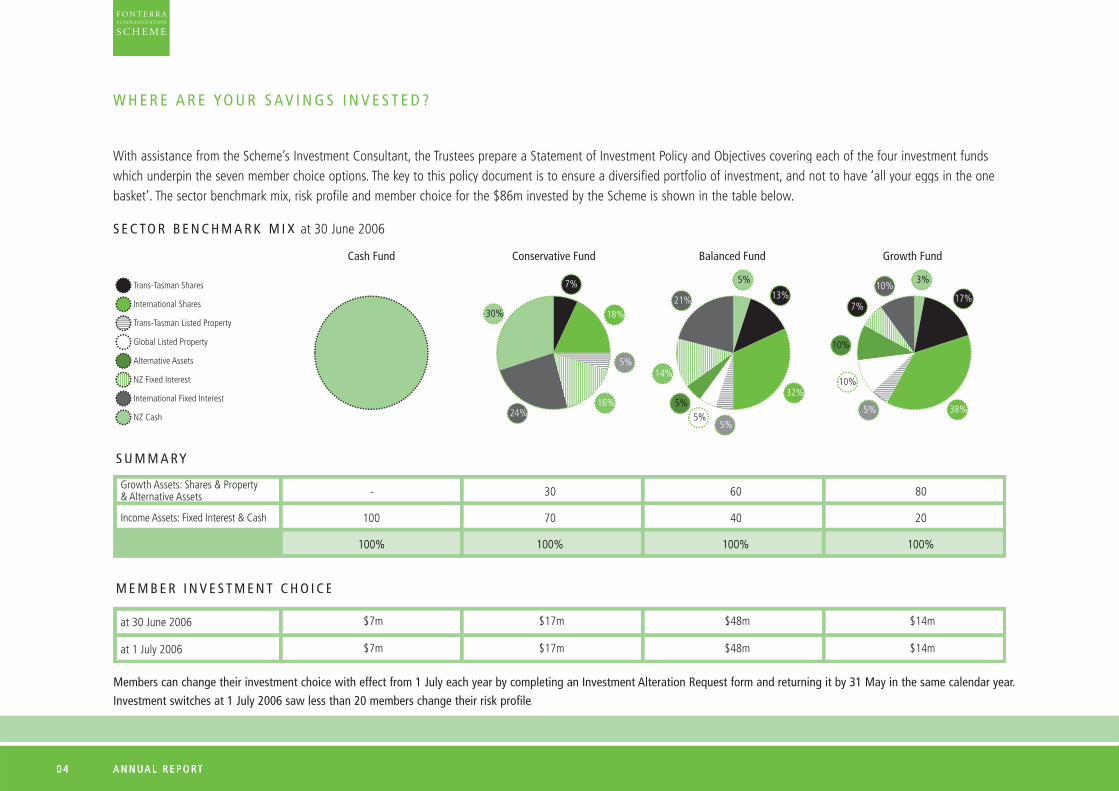

With assistance from the Scheme’s Investment Consultant, the Trustees prepare a Statement of Investment Policy and Objectives covering each of the four investment fundswhich underpin the seven member choice options. The key to this policy document is to ensure a diversified portfolio of investment, and not to have ‘all your eggs in the onebasket’. The sector benchmark mix, risk profile and member choice for the $86m invested by the Scheme is shown in the table below.

S E C TO R B E N C H M A R K M I X at 30 June 2006

S U M M A RY

M E M B E R I N V E S T M E N T C H O I C E

W H E R E A R E YO U R S AV I N G S I N V E S T E D ?

Members can change their investment choice with effect from 1 July each year by completing an Investment Alteration Request form and returning it by 31 May in the same calendar year.Investment switches at 1 July 2006 saw less than 20 members change their risk profile.

A N N UA L R E P O RT 0 5A N N UA L R E P O RT 0 5

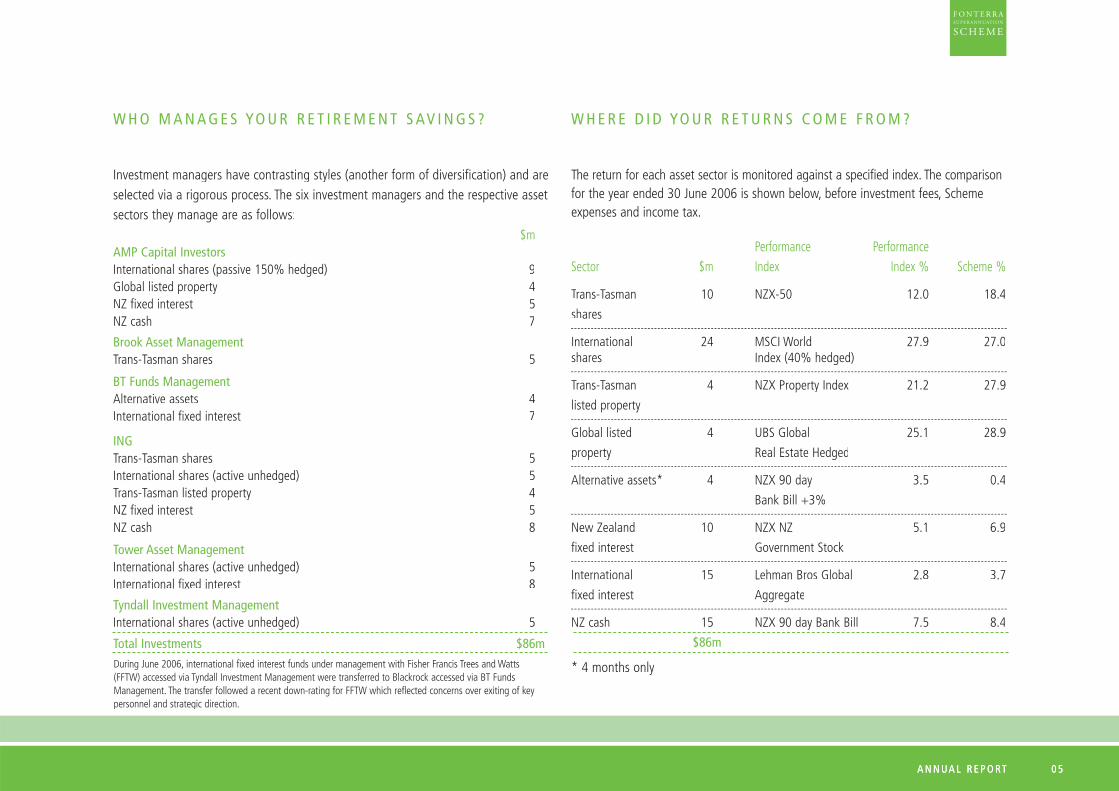

W H O M A N A G E S YO U R R E T I R E M E N T S AV I N G S ?

Investment managers have contrasting styles (another form of diversification) and areselected via a rigorous process. The six investment managers and the respective assetsectors they manage are as follows:

$mAMP Capital InvestorsInternational shares (passive 150% hedged) 9Global listed property 4NZ fixed interest 5NZ cash 7

Brook Asset ManagementTrans-Tasman shares 5

BT Funds ManagementAlternative assets 4International fixed interest 7

INGTrans-Tasman shares 5International shares (active unhedged) 5Trans-Tasman listed property 4NZ fixed interest 5NZ cash 8

Tower Asset ManagementInternational shares (active unhedged) 5International fixed interest 8

Tyndall Investment ManagementInternational shares (active unhedged) 5

Total Investments $86m

W H E R E D I D YO U R R E T U R N S C O M E F R O M ?

The return for each asset sector is monitored against a specified index. The comparison for the year ended 30 June 2006 is shown below, before investment fees, Schemeexpenses and income tax.

Performance PerformanceSector $m Index Index % Scheme %

Trans-Tasman 10 NZX-50 12.0 18.4

shares

International 24 MSCI World 27.9 27.0shares Index (40% hedged)

Trans-Tasman 4 NZX Property Index 21.2 27.9

listed property

Global listed 4 UBS Global 25.1 28.9

property Real Estate Hedged

Alternative assets* 4 NZX 90 day 3.5 0.4

Bank Bill +3%

New Zealand 10 NZX NZ 5.1 6.9

fixed interest Government Stock

International 15 Lehman Bros Global 2.8 3.7

fixed interest Aggregate

NZ cash 15 NZX 90 day Bank Bill 7.5 8.4

$86m

* 4 months onlyDuring June 2006, international fixed interest funds under management with Fisher Francis Trees and Watts (FFTW) accessed via Tyndall Investment Management were transferred to Blackrock accessed via BT FundsManagement. The transfer followed a recent down-rating for FFTW which reflected concerns over exiting of keypersonnel and strategic direction.

A N N UA L R E P O RT0 6

1,446At 1 July 2005

171New members

60Transfers in

(22)Transfers out

(146)Resignations

(5)Retirements

(48)Redundancies

0 Deaths

1,456 At 30 June 2006

Members

A N N UA L R E P O RT0 6

Membership of the Scheme comprises contributing members and elective members. The uptake of membership by contributing members where a separate company subsidy is applicable is very high; whereas for elective memberswho are paid on a totally remunerated basis the uptake of membership is very low.

Trustees recognise that employees on total remuneration packages are provided with greater options such aswhere to invest for their retirement, or to repay a home mortgage at a faster rate, or to improve their currentstandard of living.

The concern of Trustees is whether totally remunerated staff are setting aside monies for their retirement,or if invested in another superannuation scheme, the performance of that scheme relative to the FonterraSuperannuation Scheme. Non-members of the Scheme are to be surveyed once this annual report is publishedto encourage membership.

M E M B E R S H I P

M E M B E R S H I P H I S TO RY

Membership is not growing. The increase in numbers in2003 relates to the transfer in of 417 new membersfrom the Dairy Industry Superannuation Scheme andNZ Dairy Group schemes.

0

500

1,000

1,500

2,000

2002 2003 2004 2005 2006

All transfers relate to the New Zealand Dairy Foods Limited Superannuation Plan as part of the sale andpurchase agreement between Fonterra and Goodman Fielder.

A N N UA L R E P O RT 0 7A N N UA L R E P O RT 0 7

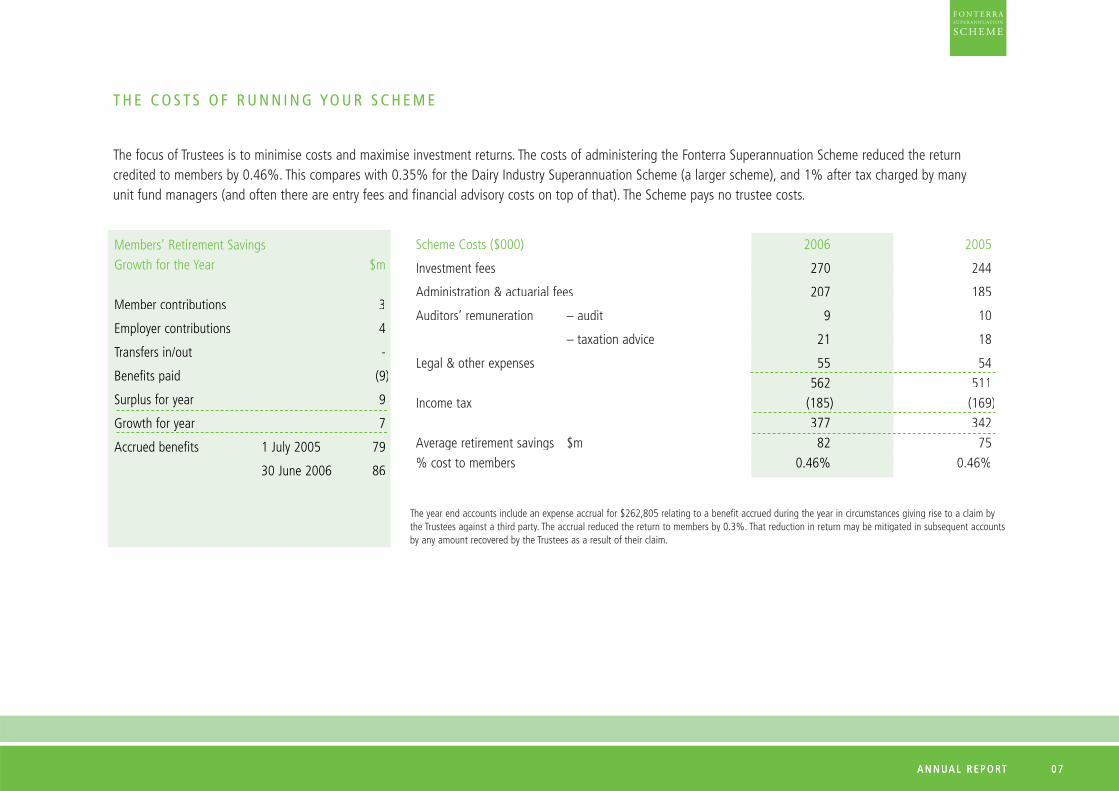

T H E C O S T S O F R U N N I N G YO U R S C H E M E

Scheme Costs ($000) 2006 2005

Investment fees 270 244270

Administration & actuarial fees 207 185207

Auditors’ remuneration – audit 9 109

– taxation advice 21 1821

Legal & other expenses 55 5455 562 511562 Income tax (185) (169)(185) 377 342377 Average retirement savings $m 82 7582 % cost to members 0.46% 0.46%0.46%

The focus of Trustees is to minimise costs and maximise investment returns. The costs of administering the Fonterra Superannuation Scheme reduced the return credited to members by 0.46%. This compares with 0.35% for the Dairy Industry Superannuation Scheme (a larger scheme), and 1% after tax charged by manyunit fund managers (and often there are entry fees and financial advisory costs on top of that). The Scheme pays no trustee costs.

Members’ Retirement Savings Growth for the Year $m

Member contributions 3

Employer contributions 4

Transfers in/out -

Benefits paid (9)

Surplus for year 9

Growth for year 7

Accrued benefits 1 July 2005 79

30 June 2006 86

The year end accounts include an expense accrual for $262,805 relating to a benefit accrued during the year in circumstances giving rise to a claim bythe Trustees against a third party. The accrual reduced the return to members by 0.3%. That reduction in return may be mitigated in subsequent accounts by any amount recovered by the Trustees as a result of their claim.

A N N UA L R E P O RT0 8 A N N UA L R E P O RT0 8

F U N D O F H E D G E F U N D S

Diversification is a key component in the constructionof any portfolio. Hence the Scheme’s assets comprisegrowth assets (shares and property) and income assets(fixed interest and cash). There are many components to the Scheme’s investments in shares including passive,where the fund managers track an index and active, where the fund managers’ mandates are to outperformthe index.

There are alternative forms of investing that are notindex linked. These include hedge funds which havean absolute return focus. Irrespective of whether themarket (the index) goes up or down, the hedge fundmanager targets an absolute return each year.

The Scheme has invested in Grosvenor CapitalManagement, a firm with $US15 billion undermanagement founded back in 1971. This is a fund of hedge funds which invests in over 50 separate funds, but with two main streams of investment strategiesoperating in key markets of the world:

● arbitrage, where the fund will take advantage of the price or timing differences in a security, e.g. Vodafone shares on the US and UKsharemarkets may not equate after exchangeconversion and brokerage are taken into account

• equities, where a fund will hold or short-sellshares, e.g. it may ‘borrow’ 20,000 Vodafoneshares and sell them, and replace the ‘borrowed’ shares when the anticipatedfall in Vodafone shares has occurred.

The Trustees have introduced the fund of hedgefunds to cushion some of the fluctuations normallyassociated with share investments.

A N N UA L R E P O RT 0 9A N N UA L R E P O RT 0 9

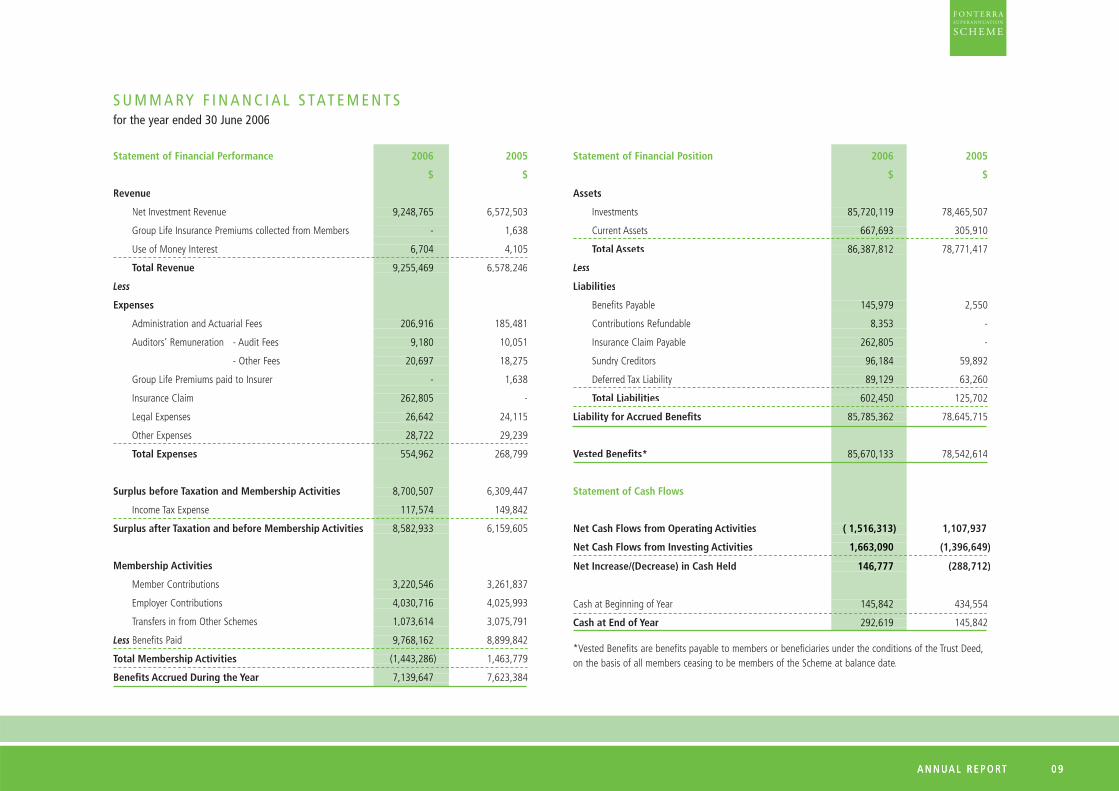

Statement of Financial Performance 2006 2005

$ $

Revenue

Net Investment Revenue 9,248,765 6,572,5039,248,765

Group Life Insurance Premiums collected from Members - 1,638-

Use of Money Interest 6,704 4,105 6,704

Total Revenue 9,255,469 6,578,2469,255,469

Less

Expenses

Administration and Actuarial Fees 206,916 185,481206,916

Auditors’ Remuneration - Audit Fees 9,180 10,0519,180

- Other Fees 20,697 18,27520,697

Group Life Premiums paid to Insurer - 1,638-

Insurance Claim 262,805 -262,805

Legal Expenses 26,642 24,11526,642

Other Expenses 28,722 29,23928,722

Total Expenses 554,962 268,799554,962

Surplus before Taxation and Membership Activities 8,700,507 6,309,4478,700,507

Income Tax Expense 117,574 149,842117,574

Surplus after Taxation and before Membership Activities 8,582,933 6,159,6058,582,933

Membership Activities

Member Contributions 3,220,546 3,261,8373,220,546

Employer Contributions 4,030,716 4,025,9934,030,716

Transfers in from Other Schemes 1,073,614 3,075,7911,073,614

Less Benefits Paid 9,768,162 8,899,8429,768,162

Total Membership Activities (1,443,286) 1,463,779(1,443,286)

Benefi ts Accrued During the Year 7,623,3847,139,647

Statement of Financial Position 2006 2005

$ $

Assets

Investments 85,720,119 78,465,507 85,720,119

Current Assets 667,693 305,910 667,693

Total Assets 86,387,812 78,771,417 86,387,812

Less

Liabilities

Benefits Payable 145,979 2,550 145,979

Contributions Refundable 8,353 - 8,353

Insurance Claim Payable 262,805 -262,805

Sundry Creditors 96,184 59,892 96,184

Deferred Tax Liability 89,129 63,260 89,129

Total Liabilities 602,450 125,702 602,450

Liability for Accrued Benefi ts 78,645,715 85,785,362

Vested Benefi ts* 78,542,61485,670,133

Statement of Cash Flows

Net Cash Flows from Operating Activities ( 1,516,313) 1,107,937 ( 1,516,313)

Net Cash Flows from Investing Activities 1,663,090 (1,396,649)1,663,090

Net Increase/(Decrease) in Cash Held 146,777 (288,712)146,777

Cash at Beginning of Year 145,842 434,554 145,842

Cash at End of Year 145,842292,619

S U M M A RY F I N A N C I A L S TAT E M E N T Sfor the year ended 30 June 2006

*Vested Benefits are benefits payable to members or beneficiaries under the conditions of the Trust Deed,on the basis of all members ceasing to be members of the Scheme at balance date.

A N N UA L R E P O RT

A Summary of the Scheme’s audited financialstatements for the year ended 30 June 2006 whichwere authorised for issue on 24 August 2006 is shown on page 9.

The summary financial report has been extracted from the full audited financial statements dated30 June 2006 and therefore cannot be expectedto provide as complete understanding as providedby the full financial statements of the financialperformance, position and cash flows of the entity.

A copy of the full financial statements can beobtained from the Scheme’s Secretary free of charge.

The auditor has examined the summary financialreport for consistency with the audited financialstatements and has issued an unqualified opinion.

A N N UA L R E P O RT

TO T H E M E M B E R S O F F O N T E R R A S U P E R A N N UAT I O N S C H E M EWe have audited the summary financial report of Fonterra Superannuation Scheme (“the Scheme”) for the year ended30 June 2006 as set out on page 9.

R E S P O N S I B I L I T I E S O F T H E T R U S T E E S A N D AU D I TO RThe Trustees are responsible for the preparation of a summary financial report in accordance with generally acceptedaccounting practice in New Zealand. It is our responsibility to express to you an independent opinion on the financialreport presented by the Trustees.

B A S I S O F O P I N I O NOur audit was conducted in accordance with New Zealand Auditing Standards and involved carrying out procedures toensure the summary financial report is consistent with the full financial report on which the summary financial report isbased. We also evaluated the overall adequacy of the presentation of information in the summary financial report againstthe requirements of FRS-39: Summary Financial Reports.

Our firm has also provided other services to the scheme in relation to taxation. This has not impaired our independence as auditors of the scheme. The firm has no other relationship with, or interest in, the scheme.

U N Q UA L I F I E D O P I N I O NIn our opinion:● the summary financial report has been correctly extracted from the full financial report; and● the information reported in the summary financial report complies with FRS-39: Summary Financial Reports and is consistent in all material respects with the full financial report from which it is derived and upon which we expressed an unqualified audit opinion in our report to members dated 24 August 2006.

We completed our work for the purposes of this report on 24 August 2006.

Wellington

AU D I T R E P O RT

1 0

A N N UA L R E P O RTA N N UA L R E P O RT

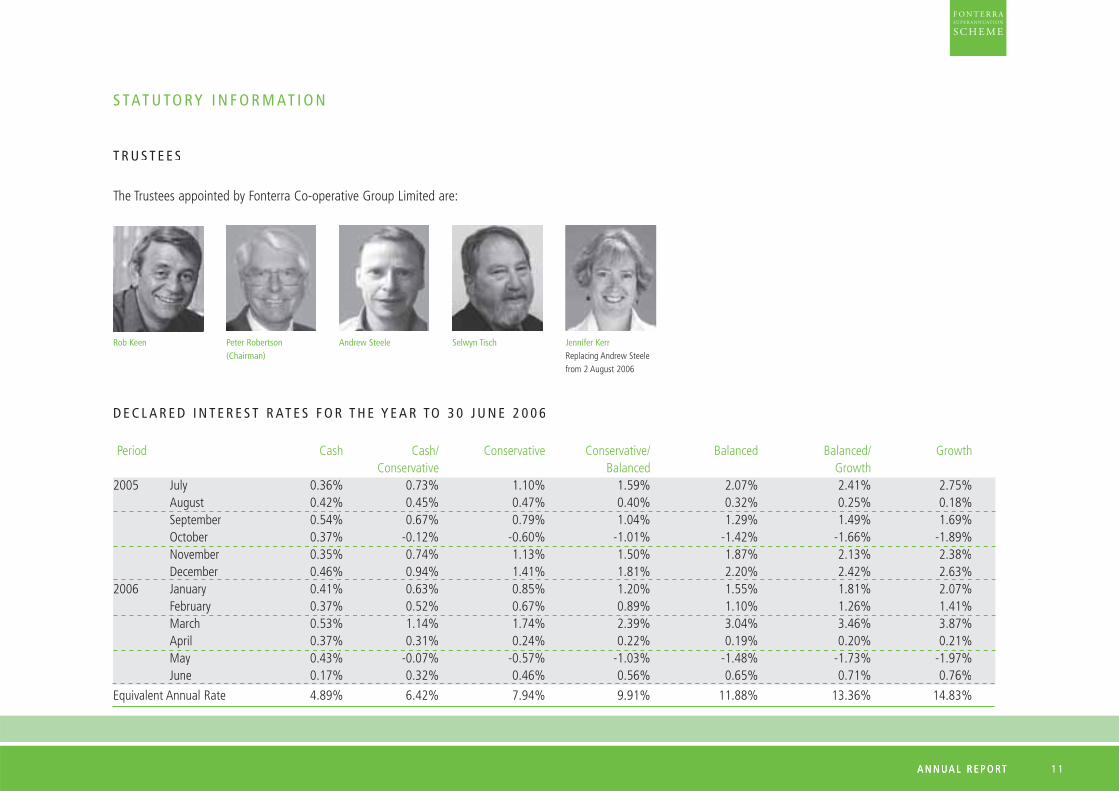

S TAT U TO RY I N F O R M AT I O N

T R U S T E E S

The Trustees appointed by Fonterra Co-operative Group Limited are:

Rob Keen Peter Robertson (Chairman)

Selwyn Tisch Jennifer KerrReplacing Andrew Steelefrom 2 August 2006

Andrew Steele

D E C L A R E D I N T E R E S T R AT E S F O R T H E Y E A R TO 3 0 J U N E 2 0 0 6

Period Cash Cash/ Conservative Conservative/ Balanced Balanced/ Growth Conservative Balanced Growth2005 July 0.36% 0.73% 1.10% 1.59% 2.07% 2.41% 2.75%

August 0.42% 0.45% 0.47% 0.40% 0.32% 0.25% 0.18%September 0.54% 0.67% 0.79% 1.04% 1.29% 1.49% 1.69% October 0.37% -0.12% -0.60% -1.01% -1.42% -1.66% -1.89% November 0.35% 0.74% 1.13% 1.50% 1.87% 2.13% 2.38%December 0.46% 0.94% 1.41% 1.81% 2.20% 2.42% 2.63%

2006 January 0.41% 0.63% 0.85% 1.20% 1.55% 1.81% 2.07% February 0.37% 0.52% 0.67% 0.89% 1.10% 1.26% 1.41% March 0.53% 1.14% 1.74% 2.39% 3.04% 3.46% 3.87% April 0.37% 0.31% 0.24% 0.22% 0.19% 0.20% 0.21%May 0.43% -0.07% -0.57% -1.03% -1.48% -1.73% -1.97%June 0.17% 0.32% 0.46% 0.56% 0.65% 0.71% 0.76%

Equivalent Annual Rate 4.89% 6.42% 7.94% 9.91% 11.88% 13.36% 14.83%

1 1

A N N UA L R E P O RT

T R U S T E E S ' S TAT E M E N T

The Trustees certify, in accordance with theSuperannuation Schemes Act 1989, that:

• all contributions required to be made to the Scheme in accordance with the terms of the Trust Deed have been made;

• all benefits required to be paid from the Scheme in accordance with the terms of the Trust Deed have been paid;

• the market value of the assets of the Scheme at 30 June 2006 equalled the total value of benefits that would have been payable had all members of the Scheme ceased to be members at that date.

P J RobertsonTrustee

Selwyn TischTrustee

A N N UA L R E P O RT

T R U S T D E E D

No changes have been made to the Trust Deed.

P R O S P E C T U S

The registration date of the Scheme’s most recent prospectus was 22 December 2005 which was amended30 June 2006.

1 2

A N N UA L R E P O RT

D I R E C TO RY

A N Y M O R E Q U E S T I O N S ?

Neil Jury is the Secretary to the Scheme. Please ring Neilif you have any questions about this report or wouldlike a copy of the Scheme’saudited financial statements.

Neil can be contacted at:

Freephone: 0800 355 900Telephone: (04) 890 7000Facsimile: (04) 914 0434P O Box 2897, Wellington

A D M I N I S T R ATO R

All correspondence should be addressed to:SecretaryFonterra Superannuation SchemeC/- Mercer Human Resource Consulting LtdP O Box 2897WellingtonFreephone: 0800 355 900Telephone: (04) 890 7000Facsimile: (04) 914 0434Administers the Scheme on behalf of the Trustees.

I N V E S T M E N T M A N A G E R S

AMP Capital Investors (NZ) LimitedBrook Asset ManagementBT Funds ManagementING Investment Services LimitedTower Asset Management LimitedTyndall Investment Management New Zealand LimitedResponsible for investing the Scheme’s assets in accordance

with the investment policy adopted by the Trustees.

I N V E S T M E N T C O N S U LTA N T

Mercer Investment ConsultingAssists the Trustees in setting investment policy and monitoring

the investment managers.

A C T UA RY

Mercer Human Resource Consulting LimitedCalculates the monthly interest rate.

AU D I TO R

KPMGAudits the Scheme’s financial statements.

I N S U R A N C E P R O V I D E R

National Mutual Life Association of New Zealand Limited(trading as AXA New Zealand Limited)Provides the cover for the insurance benefits through the

Fonterra Welfare Fund.

S O L I C I TO R S

Kensington SwanAdvises the Trustees on legal issues.

P R I VA C Y A C T

Your personal information may be held for the purposesof the Scheme and when necessary passed between youremployers, the Trustees and the Scheme’s professionaladvisers. If you wish to check or amend your personalinformation, please contact the Scheme Secretary.

L O O K I N G F O R M O R E I N F O R M AT I O N ?Internet Access: www.superfacts.co.nzMember Helpline: 0800 355 900

A N N UA L R E P O RT 1 3