Embed Size (px)

Citation preview

ANNUAL REPORT ON THE UAE

INSURANCE SECTOR

2015

P a g e | 2

Foreword

I am pleased to present the Annual Report on the Insurance Sector in the United Arab Emirates

for 2015. The report identifies important aspects related to the insurance market in the UAE,

serves its purpose in shedding light on the key achievements of this important sector, and

illustrates the developments that were accomplished during the year 2015. The Report also

serves as a significant reference for researchers and those interested in the insurance affairs in

the UAE and abroad.

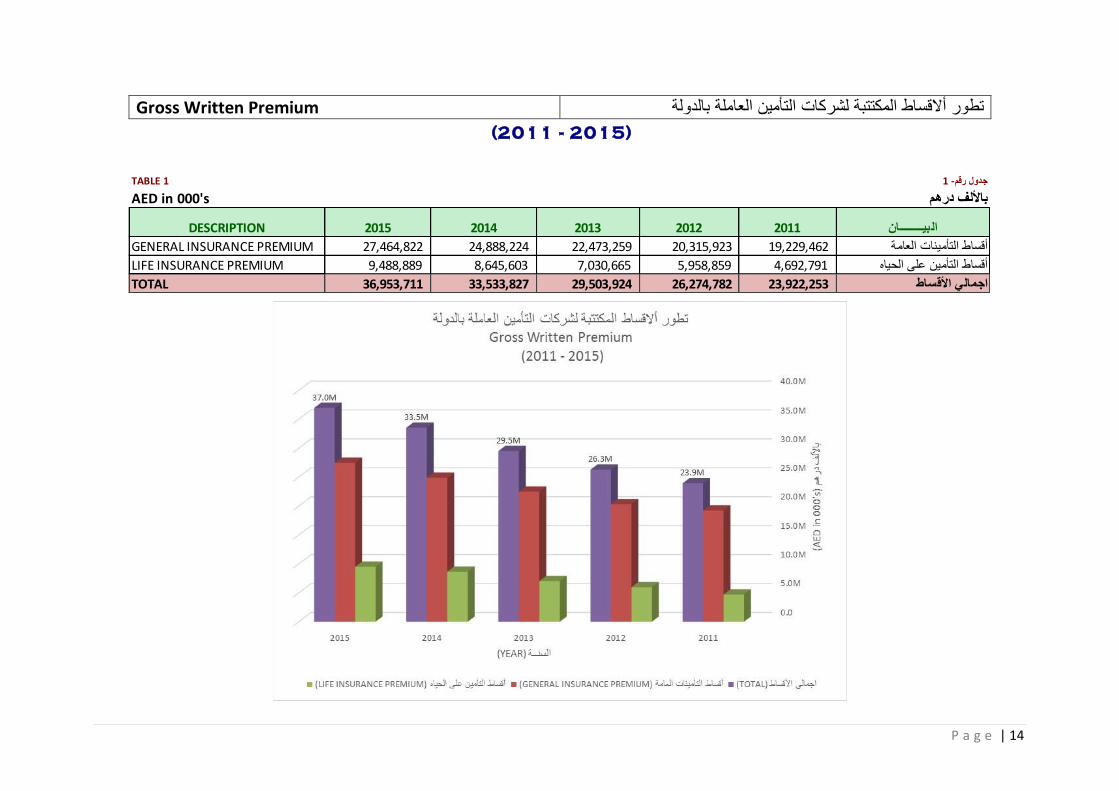

Gross written premiums for all insurance classes amounted to AED 37.0 billion, accounting

for an increase of 10.2% as compared to 2014. The importance of this sector and its vital role

to the national economy is demonstrated by the volume of money invested therein, which

amounted to AED 45.7 billion in 2015, of which 60.5% is invested in stocks and bonds,

followed by 20.7% in deposits. Shareholders’ total equity in the national insurance companies

amounted to AED 17.5 billion.

The insurance industry in the UAE has great growth opportunities. The UAE insurance market

is expected to see large growth in the upcoming years so that it can effectively contribute to

the economic development. It is worth mentioning that the UAE and Gulf Cooperation

Council states have huge potential that will help the insurance sector play a significant and

leading role in the Arab region.

In 2015, the Insurance Authority (“IA”) worked on completing the issuance of legislations that

regulate the sector. As part of the IA’s efforts and endeavours to boost the legislative base for

the regulation of the UAE insurance sector its goals are to promote the performance of local

insurance market and the entities operating therein based on solid legal, technical, and financial

foundations and to enhance the competitiveness of the sector at the regional and international

levels as per the best practices prevailing worldwide.

In this regard, I would like to thank all members of the Board of Directors, the Director General,

and the staff of the IA as well as the personnel working in the insurance companies and related

professions in the UAE for their efforts and cooperation towards achieving the objectives and

strategies of the IA.

I pray to Allah Almighty to grant us success to serve the UAE, our dear country, under the

leadership of H.H. Sheikh Khalifa bin Zayed Al Nahyan, President of the UAE, H.H. Sheikh

Mohammed bin Rashid Al Maktoum, Vice-President of the UAE, and their Highness brothers,

members of the Federal Supreme Council.

Eng. Sultan bin Saeed Al-Mansouri

Minister of Economy

Chairman of Insurance Authority Board of Directors

P a g e | 3

Report on the

Activity of the Insurance Sector in the UAE

For 2015

Introduction

The Insurance Authority (“IA”) is pleased to present the Annual Report on the activity of the

insurance sector in the UAE for 2015. The report provides the financial and technical indicators

which reflect the development accomplished by the insurance market in the State.

The importance of this sector and its vital role in the national economy are emphasized by the

amount of money invested therein, which amounted to AED 45.7 billion as of the end of 2015.

Further, the gross written premiums in the insurance sector in the State amounted to AED 37.0

billion.

The aim of this report is to recognize the various aspects of the insurance sector in the UAE

and to achieve the intended objective thereof which is to shed light on the key achievements of

the insurance sector in the State.

I. General Framework of the Insurance Sector in the UAE:

1. Legal Framework Regulating the Insurance Sector:

The UAE insurance sector is governed by Federal Law No. (6) of 2007 concerning

Establishment of the Insurance Authority & Organization of its Operations, which

came into effect on 28/08/2007. In addition, the legal framework is also governed

by the Board of Directors Resolution No. (2) of 2009 issuing the Executive

Regulation of the Federal Law No. (6) of 2007, as well as all the regulations,

instructions, and decisions issued in application of the provisions of the law.

2. Organizational Structure of the UAE Insurance Market:

2.1 Insurance Authority:

The Federal Law No. (2) of 2007 concerning Establishment of the Insurance

Authority & Organization of its Operations entrusts the IA to enforce its provisions

and to undertake its role in supervising and controlling the insurance companies and

insurance-related professions. The aims are to ensure a suitable environment for the

development of the insurance sector; to enhance the role of the insurance industry

to secure lives, properties, and liabilities against risks in order to protect the national

economy; to collect, develop, and invest the national savings to sustain the

economic development of the State; to encourage fair and effective competition; to

provide the best insurance services with technically sound premiums and adequate

coverages; and to Emiratize jobs in the insurance markets.

P a g e | 4

2.2 Emirates Insurance Association (“EIA”)

The EIA was registered as per the Ministerial Decree No. (62) of 1988 issued on

27/09/1988. Its members include all the insurance companies operating in the State

in addition to many of the insurance-related professionals.

3. General Framework of the Insurance Companies and Insurance-related

Professions:

The number of entities registered in the records at the IA as of the end of 2015 is

stated below:

Insurance Companies: (61) insurance companies, including (34) national

insurance companies and (27) foreign insurance companies. The total number

of companies underwriting all insurance classes (insurance of persons & fund

accumulation operations, and property & liability insurance) includes (11)

national companies and (2) foreign companies. The number of companies

underwriting only property and liability insurance includes (20) national

companies and (18) foreign companies. The number of insurance companies

underwriting only insurance of persons and fund accumulation operations

includes (2) national companies and (7) foreign companies. There is (1) national

company underwriting export credit insurance. It is worth noting that (11)

national companies operate pursuant to the provisions of Takaful Insurance

Regulations.

Insurance Agents: (19)

Insurance Brokers: (143) insurance brokerage companies in the State

including (139) national brokerage companies and (4) foreign companies.

Insurance Consultants: (16)

Loss adjusters and damage estimators: (40) companies operating in loss

adjustment and damage estimation

Actuaries: (35) actuarial experts registered in the State.

Health insurance TPA companies: (23) companies operating in the State.

P a g e | 5

II. Economic climate and its implication for the insurance business in the State:

The UAE economy is distinguished with a stable investment, economic, and political

environment that can continue economic growth despite the instability seen in the world

economy during various periods, including periods when oil prices are dropping. This

stability is due to adopting economic policies that promote economic diversity in which

the UAE has succeeded in increasing the contribution of non-oil sectors to the national

economy and in providing the State with financial reserves which enable continuous

funding needed for all its projects. In addition, the adopted open-door economy policy

is bringing in foreign investments. The UAE ranked in the 13th position worldwide and

the 1st position in the Middle East with respect to foreign investments from 2013 to

2015.

The advancement of the economic, construction, and social activities in the State has a

positive impact on the insurance sector. The gross premiums written in the property and

liability insurance classes rose from AED 24.9 billion in 2014 to AED 27.5 billion in

2015, an increase rate of 10.4%.

III. The insurance market business volume in the State and insurance indicators for

2015:

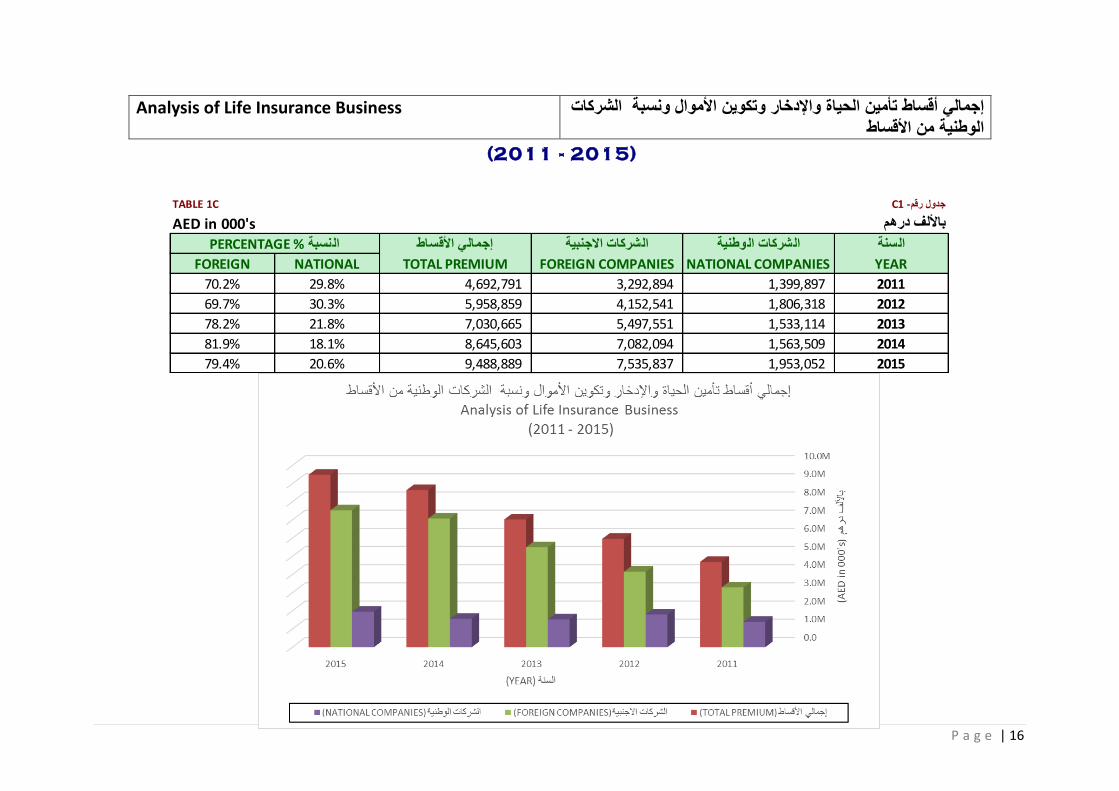

1. Gross written premiums for the insurance of persons and fund accumulation

operations classes amounted to AED 9.5 billion. The share of national companies

amounted to 20.6% while that of foreign company branches amounted to 79.4%.

2. Gross written premiums for the property and liability insurance classes amounted

to AED 27.5 billion. The share of the national companies amounted to 74.1% while

that of foreign company branches amounted to 25.9%. The percentage share by

class of property and liability insurance to the total written premiums is as follows:

Medical insurance: 47.8%

Accidents and Liability: 34.3%

Fire: 8.4%

Land, Sea, and Air Transportation: 6.0%

Other risks: 3.5%

3. The overall premium retention ratio for the property and liability insurance classes

by the national insurance companies amounted to 52.4%. The retention ratio for

each class is a follows:

Medical insurance: 59.1%

Accidents and Liability: 62.4%

P a g e | 6

Fire: 15.8%

Land, Sea, and Air Transportation: 20.9%

Other risks: 40.2%

4. Gross earned premiums for the property and liability insurance classes amounted to

AED 26.4 billion.

5. Gross incurred losses for the property and liability insurance classes before

deducing the reinsurers’ share amounted to AED 20.7 billion.

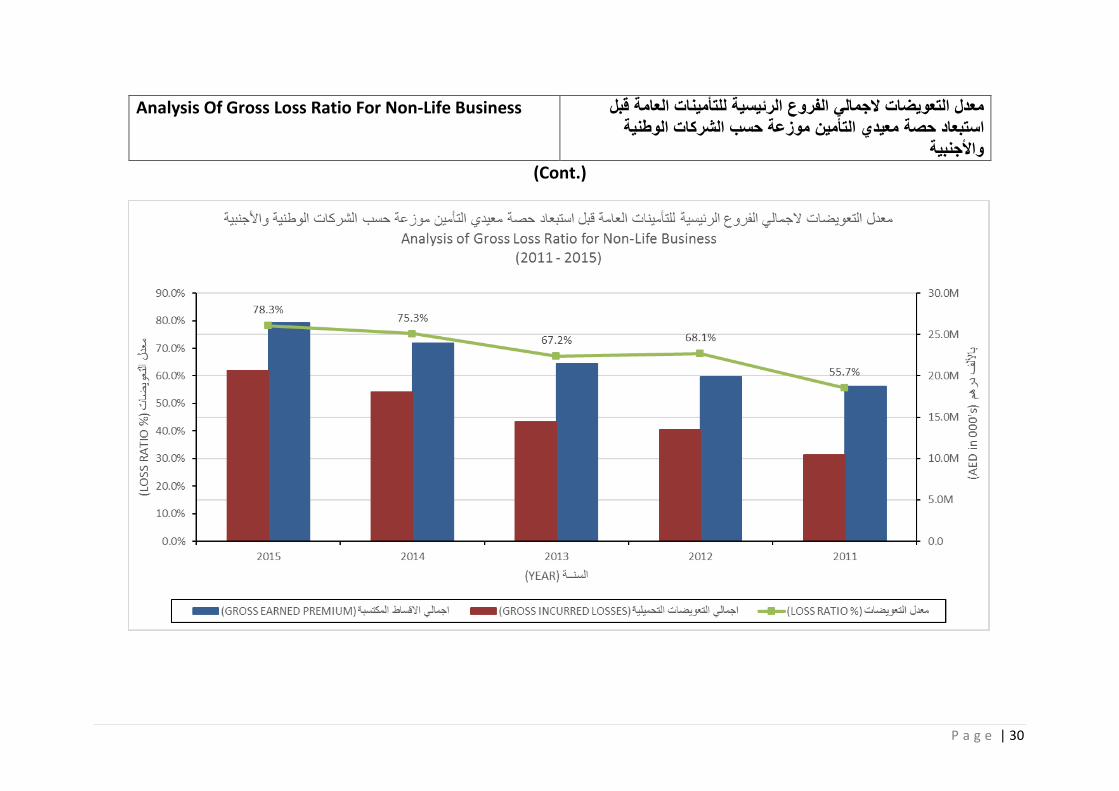

6. The gross loss ratio for the property and liability insurance classes before deducing

the reinsurers’ share amounted to 78.3% in 2015 versus 75.3% in 2014. The 2015

loss ratio for each class is as follows:

Medical insurance: 91.9%

Accidents and Liability: 73.1%

Fire: 90.2%

Land, Sea, and Air Transportation: 42.5%

Other risks: 6.9%

7. Gross technical provisions for the insurance of persons and fund accumulation

operations amounted to AED 17.0 billion. Further, the technical provisions for

property and liability insurance amounted to AED 18.7 billion.

8. The total shareholders’ equity of national insurance companies amounted to AED

17.5 billion as at 31 December 2015.

9. The total funds invested in the sector amounted to AED 45.7 billion. 60.5% of

which is invested in financial securities followed by 20.7% in bank deposits.

P a g e | 7

IV. Emiratization in the Insurance Sector:

Emiratization in the insurance sector is a strategic objective of the IA and one of its

priorities. To achieve this objective, the collective efforts and cooperation among all

parties is required. The IA continues taking more practical actions to increase the

Emiratization rate in the insurance sector and improve the skills and experiences of

UAE nationals working in the sector.

A detailed plan to execute the Cabinet Resolution issued in 2015 concerning

adopting the Emitratization strategy in the banking and insurance sector was

finalized. The plan included workshops and the issuing of manuals for adopting the

strategy which is based on a points system in the insurance sector.

Number of UAE Nationals working in the Insurance Companies

Total number of employees in the technical departments in the insurance companies

operating in the State by the end of 2015 amounted to 2,900 employees, including

340 UAE nationals constituting 11.7% of the total number of employees in these

departments as shown in the table below:

Item 2015

Total number of employees in the technical departments in

the insurance companies of various nationalities 2,900

Number of UAE nationals working in the technical

departments in the insurance companies 340

Percentage 11.7%

Training and Qualification

Education and training in the insurance sector are a significant element in the IA

strategy and the programs are in line with the vision of prudent Leadership in the

State. Further, the IA has a comprehensive and long-term vision of Emiratization in

the insurance sector which not only seeks to increase the number of UAE

employees, but also to develop technical qualifications at all levels and to enable

the UAE nationals to assume leading positions in top and med-level management

in the insurance companies in order to develop an even a more mature and vital

sector.

In cooperation with various government entities, the IA supports education in the

insurance sector. An integrated education plan was developed and which seeks to

provide human competencies of the UAE nationals who are academically and

practically qualified and to adopt the initiatives aiming at promoting functionality

of the insurance sector.

P a g e | 8

Insurance Authority Achievements for 2015

In 2015, the IA accomplished excellent achievements and results that contributed to the

increasing growth of the insurance business in the State and boosted the competitiveness of the

UAE insurance market. This leading role on a regional level was accomplished under the

prudent guidance of H.H. Sheikh Khalifa bin Zayed Al Nahyan, President of the UAE and H.H.

Sheikh Mohammed bin Rashid Al Maktoum, Vice-President and Prime Minister of the UAE

and Ruler of Dubai.

The strategy of the IA aims at building an insurance business sector to a high level of

professionalism and competiveness and at making the UAE insurance market a role model in

the Middle East and North Africa. The aim is to continue boosting the insurance premiums,

which are the largest and of the best performance in the region, which leads to the growth of

the insurance sector and increasing of its contribution to the national economy.

Law Development

To complement the legislative framework of the sector, and with the objective of rising the

legislative environment in line with the international principles on regulation, supervision,

and control, in 2015 the IA completed a package of legislation that regulate the insurance

operations in the UAE insurance sector. Chief among these legislations are:

o The IA Board of Directors Resolution No. (7) of 2015 amending some provisions of

the IA Board of Directors Resolution No. (9) of 2011 concerning instructions of health

insurance TPA companies licensing and regulation and control of operations thereof.

o The IA Board of Directors Resolution No. (13) of 2015 concerning the instructions of

actions to counter money-laundering and terrorism funding in the insurance activities.

o Administrative decision No. (79) of 2015 concerning the manual of countering money-

laundering and terrorism funding crimes in the insurance activities.

o Cabinet Resolution No. (28) of 2015 concerning extending the additional grace period

granted to the insurance companies in accordance with the provisions of Article (25) of

the Federal Law No. (6) of 2007 concerning the Establishment of the Insurance

Authority & Organization of its Operations.

o The IA Board of Directors Resolution No. (25) of 2015 amending some provisions of

the Ministerial Decree No. (54) of 1987 concerning unifying the motor insurance

policies.

o Further, a number of insurance principles were established to solve many of the

difficulties facing the sector from time to time. The principles contribute to unifying

the concepts and simplifying the procedures related to the policyholders and

beneficiaries by presenting clarifications and advice that help promote the insurance

awareness in the State.

P a g e | 9

Regulatory Control

The IA undertakes a supervisory and regulatory control role over the insurance companies

and related professionals to ensure the regulation of and oversight over the insurance sector.

In this role the IA verifies compliance with the relevant legislation and ensures soundness

of the financial positions of the companies and insurance professions. In this context, the

IA carried out field inspections in 2015 for 120 insurance companies and related

professionals.

For the purpose of establishing the regulatory financial and technical rules of the insurance

companies, the IA issued the financial instructions for the insurance and Takaful insurance

companies early in 2015. These instructions were considered a quantum leap in the

regulation of the UAE insurance market for their comprehensiveness by addressing all the

financial and technical aspects of the assets and investments of the insurance companies

and methodology of measuring solvency as per the best international practices.

In a related aspect, the IA launched the third version (Version 1.1) of the financial eForms

which represents a control tool through which a comprehensive financial information

database on the insurance sector in the State will be created and financial and technical

indicators will be provided based on a risk-based methodology.

The financial eForms include a comprehensive analysis of all the financial and technical

aspects related to insurance which include an analysis of the financial data, investments,

insurance premiums, commissions, expenses, technical provisions, reinsurance,

receivables, and transactions with related parties, among others.

Further, the supervisory eForms establish a methodology for unifying and comparing the

financial and technical indicators adopted for all the insurance companies in line with the

purposes of issuing the financial instructions. Namely, they provide an early warning

system to follow up on the financial status of the insurance companies which improves the

ability to handle financial deficiencies at early stages, will contribute to strengthening

control and monitoring over the insurance companies, and will enhance the ability of the

insurance companies to absorb any financial crises they may encounter. This in turn

contributes to stabilizing and boosting competitiveness of the insurance market in the State.

The number of complaints received by the IA from policyholders and beneficiaries of the

insurance and related professions were 3,900 of which 3,783 complaints were solved, or a

percentage of 97%.

P a g e | 10

Insurance Awareness

In line with realizing the IA vision and strategic objectives in relation to developing the

insurance awareness and boosting and improving the competitiveness of the UAE market,

as well as ensuring insurance protection of the policyholders and beneficiaries, in 2015 the

IA implemented an aggressive awareness campaign for the public which included

launching diverse and appropriate awareness programs using multimedia, media, and

booths of specialized exhibitions in all Emirates countrywide.

The IA concentrated on visual and printed media by producing three awareness raising

videos targeting the public entitled: “Know Your Insurance Policy”, “Choose Excellent

Insurance Service”, and “Avoid Dealing with Entities not licensed by the IA”. These videos

were promoted through a wide campaign in TV and cinemas nationwide. Appropriate

artistic brochures were printed including awareness messages and the services presented

by the IA for the policyholders, customers, partners, and the public.

The IA executed multiple awareness campaigns nationwide in addition to the campaigns

that introduce and promote its activities and services. These services included broadcasting

awareness videos and the distribution of thousands of awareness brochures to policyholders

and the public.

The IA organized periodic awareness campaigns at the national level through the

participation at specialized exhibitions, such as the technology fair “GITEX 2015” and

Smart Government Fair in Dubai, in addition to two awareness fairs in Abu Dhabi and

Sharjah.

The IA also participated in the GCC Traffic Week 2015 in Abu Dhabi and the Gulf 15 Expo

in Sharjah. The events included familiarizing the policyholders and the public with their

insurance rights and financial and technical obligations. Many awareness and educational

seminars were organized for the public in general; some of them were about the motor and

medical insurance as well as dealing with insurance companies.

For conferences, in March 2015 the IA organized the Global Islamic Insurance Conference

under the patronage of H.H. Sheikh Mansour bin Zayed Al Nahyan, Deputy Prime Minister

and Minister of Presidential Affairs. Four hundred persons participated in the conference

from the UAE and aboard representing the regulatory and supervisory authorities,

companies. experts, specialists, universities, and specialized institutes on the Arab and

Islamic region in addition to the organizations and councils specialized in the Islamic

financial services worldwide.

At the conclusion of the conference the participants issued many recommendations, most

importantly, the importance of enhancing the Sharia legal and technical regulations to

develop the rules of Islamic insurance and support the Takaful industry. In addition, the

importance of cooperation between the supervisory authorities and the financial and Sharia

councils to overcome the challenges facing the Islamic insurance companies was

P a g e | 11

recommended in order to increase their contributions in the insurance sector and the gross

domestic product of the economies of the nations. Another key recommendation was to

form a supreme committee for Fatwa and Sharia control in the countries practicing Takaful

insurance in order to unify the general Sharia controls and criteria of Takaful insurance

operations.

Foreign Relations

The foreign relations network of the IA notably expanded in 2015 as a result of signing

numerous memorandums of mutual cooperation, organizing conferences and meetings to

introduce and develop the UAE insurance market, and taking part in formal meetings of

regulatory authorities and organizations overseeing the insurance sector at the Arab,

Islamic and international levels. In addition, the IA participated in conferences and forums

associated with insurance and financial affairs in different parts of the world.

At the local level, in 2015 the IA signed memoranda of understanding and agreements with

five local entities, namely the Ministry of Labour, Emirates Identity Authority, Emirates

Transport, Abu Dhabi Statistics Centre, and Dubai Trade.

The IA also signed a memorandum of understanding with Abu Dhabi Securities Exchange

aimed at enhancing cooperation in the area of supervising the insurance business and the

exchange of relevant supervisory and regulatory information and consequently achieving

common goals in line with the UAE economic and development directions.

On the Arab level, under a specific initiative of the IA, a brainstorming meeting was

organized for the members of the Arab Forum of Insurance Regulatory Commissions

(AFIRC) and the General Arab Insurance Federation in Cairo. The goals of the meeting

were to examine the reality of the Arab insurance industry as well as the prerequisites of

advancement of the insurance industry, enhancing its role in the Arab economy, and

increasing its contribution in the Arab gross domestic product.

The Secretariat General of the Gulf Cooperation Council (Commercial Cooperation

Committee) approved the initiative presented by the UAE to coordinate the insurance

legislation in the GCC states. It was decided to form a Working Group on insurance in the

GCC states entitled GCC Top-level Insurance Officials Working Group. The GCC Top-

level Insurance Officials Committee was also formed at the Secretariat General in Riyadh,

Kingdom of Saudi Arabia. The recommendations of the committee were submitted to the

Commercial Cooperation Committee meeting which in turn endorsed the

recommendations. The Working Group will also present its recommendations to the

Commercial Cooperation Committee and the Committee of Governors of Central Banks at

the GCC states.

As part of the AFIRC meeting, the IA proposal to establish a permanent office for AFIRC

in the UAE, under the title Arab Federation of Insurance Supervision and Control, was

approved.

P a g e | 12

The UAE, represented by H.E. Ebrahim Obaid Al Zaabi, Director General of the IA, was

elected as Vice-Chairman of the AFIRC (Arab Forum of Insurance Regulatory

Commissions).

Smart Services

The latest IA app, available through smart phones, is a leap into the future in the delivery

of services and the use of multiple channels of communication with customers including

policyholders, the public, companies and related professions. In addition to simplifying

procedures, the app was designed in line with the prudent leadership and guidance in regard

to business environment development, government performance development, and meeting

customers and public needs.

In this regard, IA was 100% successful in smart-transforming its 11 priority services

according to the official Telecommunications Regulatory Authority report. The IA also

managed to transform 38 out of 47 general services, that previously required manual paper

work, into smart services through portable smart phones and tablets. This will transfer the

IA itself into a smart agency with modern competitive services to build a superior modern

UAE community. Smart services offered by IA include:

Receiving insurance-related complaints and inquiries.

Registration renewal for national and foreign insurance companies, and registering and

renewing the registration of their branches.

Registration renewal for corporate insurance agents, brokers, surveyors and loss

adjustors, actuaries, insurance consultants, and health insurance TPA companies, and

registering and renewing the registration of their branches.

Requesting amendment to the data of insurance companies, health insurance TPA

companies, and corporate and individual insurance related professions in the Register.

E-Payment of service charges.

P a g e | 13

Institutional Development

In 2015, the IA accomplished many achievements in the area of institutional development

and government excellence as it obtained ISO 9001:2008 certification for all the

organizational divisions of the IA.

Additionally, the IA held a brainstorming session for the managers of the insurance

companies on innovative provision of insurance services. Both an innovation strategy and

innovation action plan were developed. Further, the suggestions program / ideas bank was

launched. The IA performed many internal and external initiatives aiming at self-

development and unleashing the spirit of innovation through many brainstorming sessions

and innovation initiatives.

In line with the UAE Vision 2021 and the government excellence system, the IA held

workshops and brainstorming sessions about the concepts, mechanisms, and methods of

“Forecasting the Future” for members of the Joint Council for Planning and Excellence.

P a g e | 14

Gross Written Premium بالدولة العاملة التأمين لشركات المكتتبة أالقساط تطور

TABLE 1جدول رقم- 1

AED in 000'sباأللف درهم

بيــــــــان 20112012201320142015DESCRIPTIONال

GENERAL INSURANCE PREMIUM 27,464,822 24,888,224 22,473,259 20,315,923 19,229,462أقساط التأمينات العامة

LIFE INSURANCE PREMIUM 9,488,889 8,645,603 7,030,665 5,958,859 4,692,791أقساط التأمين على الحياه

TOTAL 36,953,711 33,533,827 29,503,924 26,274,782 23,922,253اجمالي األقساط

(2011 - 2015)

P a g e | 15

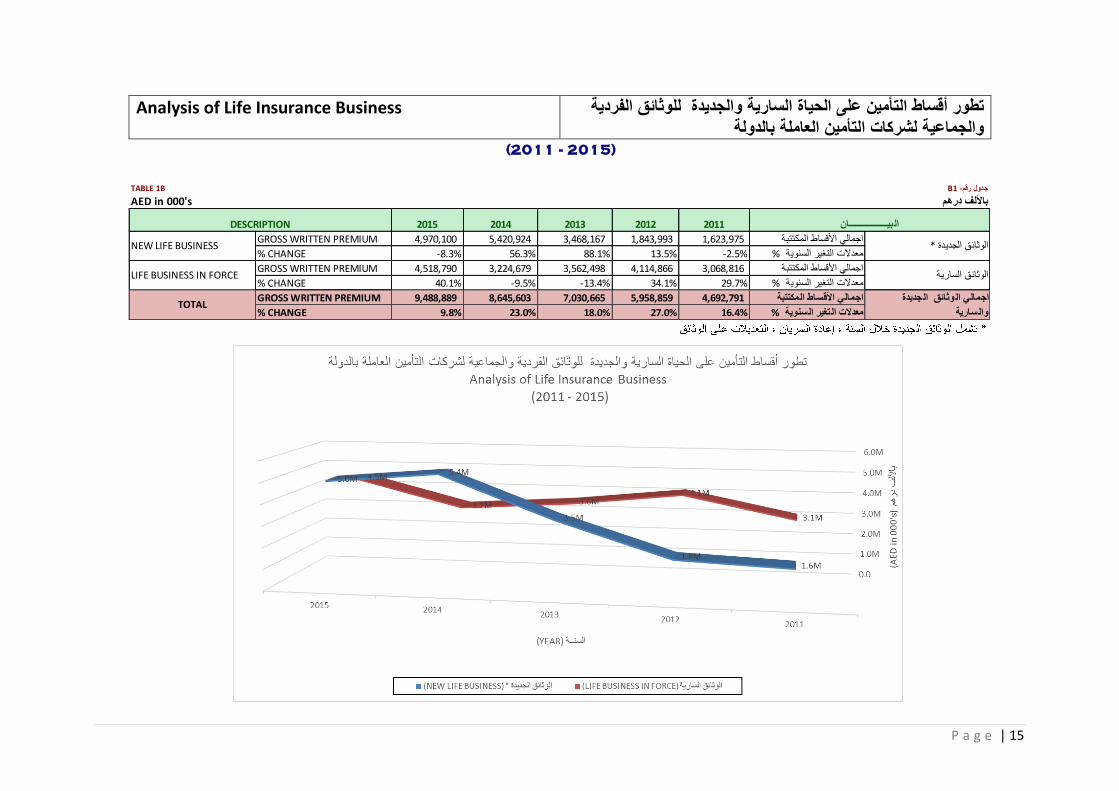

Analysis of Life Insurance Business الفردية للوثائق والجديدة السارية الحياة على التأمين أقساط تطور بالدولة العاملة التأمين لشركات والجماعية

B1 -جدول رقمTABLE 1B

AED in 000'sباأللف درهم

20112012201320142015

GROSS WRITTEN PREMIUM 4,970,100 5,420,924 3,468,167 1,843,993 1,623,975اجمالي األقساط المكتتبة

CHANGE %%8.3-%56.3%88.1%13.5%2.5-معدالت التغير السنوية %

GROSS WRITTEN PREMIUM 4,518,790 3,224,679 3,562,498 4,114,866 3,068,816اجمالي األقساط المكتتبة

CHANGE %%40.1%9.5-%13.4-%34.1%29.7معدالت التغير السنوية %

GROSS WRITTEN PREMIUM 9,488,889 8,645,603 7,030,665 5,958,859 4,692,791اجمالي األقساط المكتتبة

تغير السنوية % CHANGE %%9.8%23.0%18.0%27.0%16.4معدالت ال

(2011 - 2015)

NEW LIFE BUSINESS

LIFE BUSINESS IN FORCE

TOTAL

DESCRIPTION بيـــــــــــــــــان ال

وثائق الجديدة اجمالي ال

والسارية

الوثائق الجديدة *

الوثائق السارية

P a g e | 16

Analysis of Life Insurance Business الشركات ونسبة األموال وتكوين واإلدخار الحياة تأمين أقساط إجمالي األقساط من الوطنية

C1 -جدول رقمTABLE 1C

AED in 000'sباأللف درهم

النسبة % PERCENTAGEإجمالي األقساطالشركات االجنبيةالشركات الوطنيةالسنة

YEARNATIONAL COMPANIESFOREIGN COMPANIESTOTAL PREMIUMNATIONALFOREIGN

20111,399,897 3,292,894 4,692,791 29.8%70.2%

20121,806,318 4,152,541 5,958,859 30.3%69.7%

20131,533,114 5,497,551 7,030,665 21.8%78.2%

20141,563,509 7,082,094 8,645,603 18.1%81.9%

20151,953,052 7,535,837 9,488,889 20.6%79.4%

(2011 - 2015)

P a g e | 17

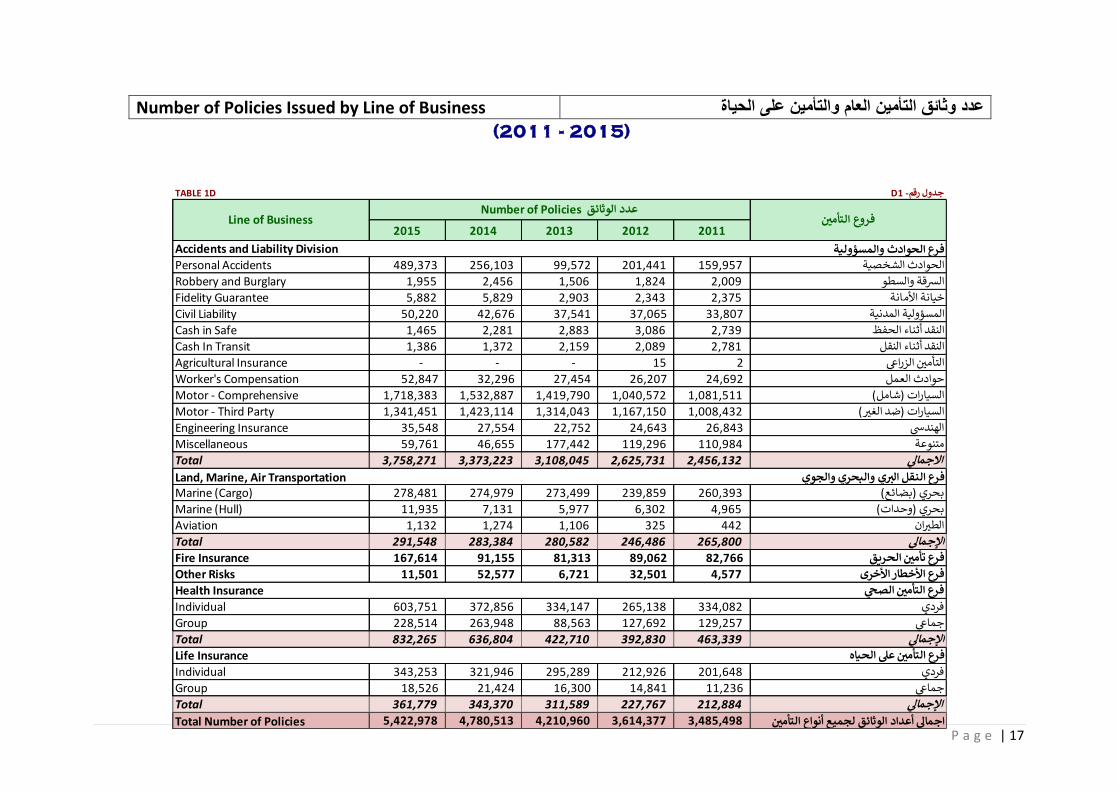

Number of Policies Issued by Line of Business ةالحيا على والتأمين العام التأمين وثائق عدد

D1 -جدول رقمTABLE 1D

20112012201320142015

Accidents and Liability Divisionفرع الحوادث والمسؤولية

Personal Accidents 489,373 256,103 99,572 201,441 159,957الحوادث الشخصية

Robbery and Burglary 1,955 2,456 1,506 1,824 2,009الرسقة والسطو

Fidelity Guarantee 5,882 5,829 2,903 2,343 2,375خيانة األمانة

Civil Liability 50,220 42,676 37,541 37,065 33,807المسؤولية المدنية

Cash in Safe 1,465 2,281 2,883 3,086 2,739النقد أثناء الحفظ

Cash In Transit 1,386 1,372 2,159 2,089 2,781النقد أثناء النقل

ن الزراعي Agricultural Insurance - - - 15 2التأمي

Worker's Compensation 52,847 32,296 27,454 26,207 24,692حوادث العمل

Motor - Comprehensive 1,718,383 1,532,887 1,419,790 1,040,572 1,081,511السيارات )شامل(

) Motor - Third Party 1,341,451 1,423,114 1,314,043 1,167,150 1,008,432السيارات )ضد الغي

Engineering Insurance 35,548 27,554 22,752 24,643 26,843الهندسي

Miscellaneous 59,761 46,655 177,442 119,296 110,984متنوعة

Total 3,758,271 3,373,223 3,108,045 2,625,731 2,456,132االجمالي

ي والبحري والجوي Land, Marine, Air Transportationفرع النقل البرMarine (Cargo) 278,481 274,979 273,499 239,859 260,393بحري )بضائع(

Marine (Hull) 11,935 7,131 5,977 6,302 4,965بحري )وحدات(

ان Aviation 1,132 1,274 1,106 325 442الطي

Total 291,548 283,384 280,582 246,486 265,800اإلجمالي

ن الحريق Fire Insurance 167,614 91,155 81,313 89,062 82,766فرع تأمي

Other Risks 11,501 52,577 6,721 32,501 4,577فرع األخطار األخرى

ن الصحي Health Insuranceفرع التأمي

Individual 603,751 372,856 334,147 265,138 334,082فردي

Group 228,514 263,948 88,563 127,692 129,257جماعي

Total 832,265 636,804 422,710 392,830 463,339اإلجمالي

ن عىل الحياه Life Insuranceفرع التأمي

Individual 343,253 321,946 295,289 212,926 201,648فردي

Group 18,526 21,424 16,300 14,841 11,236جماعي

Total 361,779 343,370 311,589 227,767 212,884اإلجمالي ن Total Number of Policies 5,422,978 4,780,513 4,210,960 3,614,377 3,485,498اجمالي أعداد الوثائق لجميع أنواع التأمي

(2011 - 2015)

Line of Business ن فروع التأمي Number of Policies عدد الوثائق

P a g e | 18

Number of Policies Issued by Line of Business ةالحيا على والتأمين العام التأمين وثائق عدد

(Cont.)

P a g e | 19

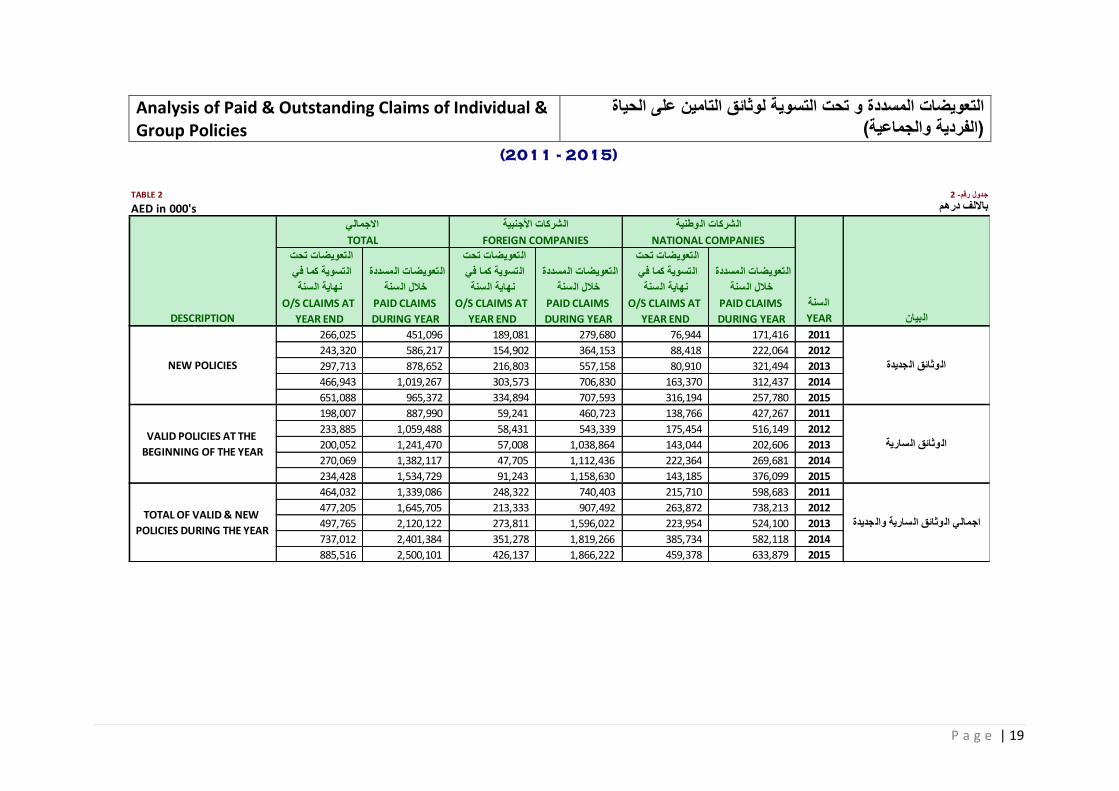

Analysis of Paid & Outstanding Claims of Individual & Group Policies

الحياة على التامين لوثائق التسوية تحت و المسددة التعويضات (والجماعية الفردية)

TABLE 2جدول رقم- 2

AED in 000'sباأللف درهم وطنية الشركات ال

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

السنة

بيان YEARDESCRIPTIONال

2011171,416 76,944 279,680 189,081 451,096 266,025

2012222,064 88,418 364,153 154,902 586,217 243,320

2013321,494 80,910 557,158 216,803 878,652 297,713

2014312,437 163,370 706,830 303,573 1,019,267 466,943

2015257,780 316,194 707,593 334,894 965,372 651,088

2011427,267 138,766 460,723 59,241 887,990 198,007

2012516,149 175,454 543,339 58,431 1,059,488 233,885

2013202,606 143,044 1,038,864 57,008 1,241,470 200,052

2014269,681 222,364 1,112,436 47,705 1,382,117 270,069

2015376,099 143,185 1,158,630 91,243 1,534,729 234,428

2011598,683 215,710 740,403 248,322 1,339,086 464,032

2012738,213 263,872 907,492 213,333 1,645,705 477,205

2013524,100 223,954 1,596,022 273,811 2,120,122 497,765

2014582,118 385,734 1,819,266 351,278 2,401,384 737,012

2015633,879 459,378 1,866,222 426,137 2,500,101 885,516

PAID CLAIMS

DURING YEAR

O/S CLAIMS AT

YEAR END

O/S CLAIMS AT

YEAR END

O/S CLAIMS AT

YEAR END

NEW POLICIES

PAID CLAIMS

DURING YEAR

PAID CLAIMS

DURING YEAR

(2011 - 2015)

FOREIGN COMPANIES NATIONAL COMPANIESTOTAL

االجمالي الشركات األجنبية

وثائق الجديدة ال

VALID POLICIES AT THE

BEGINNING OF THE YEAR

TOTAL OF VALID & NEW

POLICIES DURING THE YEARجديدة وثائق السارية وال اجمالي ال

وثائق السارية ال

P a g e | 20

Analysis of Paid & Outstanding Claims of Individual & Group Policies

الحياة على التامين لوثائق التسوية تحت و المسددة التعويضات (والجماعية الفردية)

(Cont.)

P a g e | 21

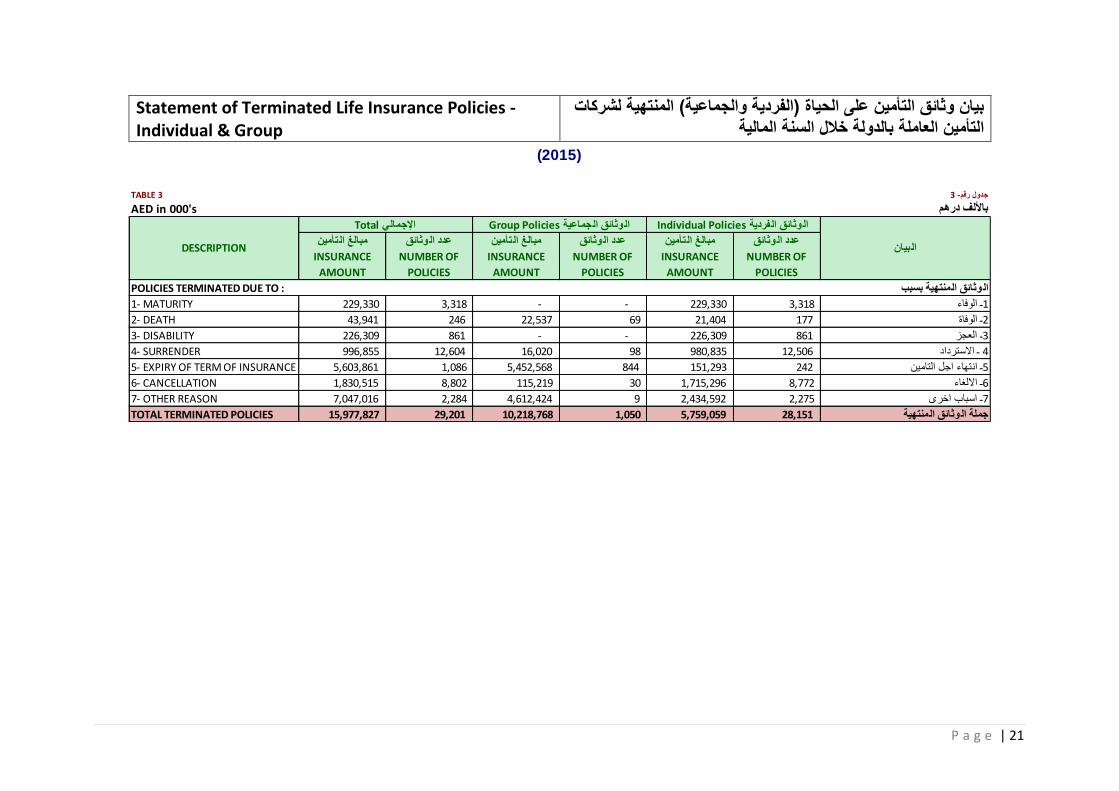

Statement of Terminated Life Insurance Policies - Individual & Group

لشركات المنتهية( والجماعية الفردية) الحياة على التأمين وثائق بيان المالية السنة خالل بالدولة العاملة التأمين

TABLE 3جدول رقم- 3

AED in 000'sباأللف درهم Individual Policies فردية وثائق ال وثائق الجماعية Group Policiesال اإلجمالي Totalال

وثائق تأمينعدد ال وثائقمبالغ ال تأمينعدد ال وثائقمبالغ ال تأمينعدد ال مبالغ ال

NUMBER OFINSURANCENUMBER OFINSURANCENUMBER OFINSURANCE

POLICIESAMOUNTPOLICIESAMOUNTPOLICIESAMOUNT

وثائق المنتهية بسبب : POLICIES TERMINATED DUE TOال

MATURITY -1 229,330 3,318 - - 229,330 13,318ـ الوفاء

DEATH -2 43,941 246 22,537 69 21,404 2177ـ الوفاة

DISABILITY -3 226,309 861 - - 226,309 3861ـ العجز

SURRENDER -4 996,855 12,604 16,020 98 980,835 412,506 ـ االسترداد

EXPIRY OF TERM OF INSURANCE -5 5,603,861 1,086 5,452,568 844 151,293 5242ـ انتهاء اجل التامين

CANCELLATION -6 1,830,515 8,802 115,219 30 1,715,296 68,772ـ االلغاء

OTHER REASON -7 7,047,016 2,284 4,612,424 9 2,434,592 72,275ـ اسباب اخرى

وثائق المنتهية TOTAL TERMINATED POLICIES 15,977,827 29,201 10,218,768 1,050 5,759,059 28,151جملة ال

(2015)

بيان DESCRIPTIONال

P a g e | 22

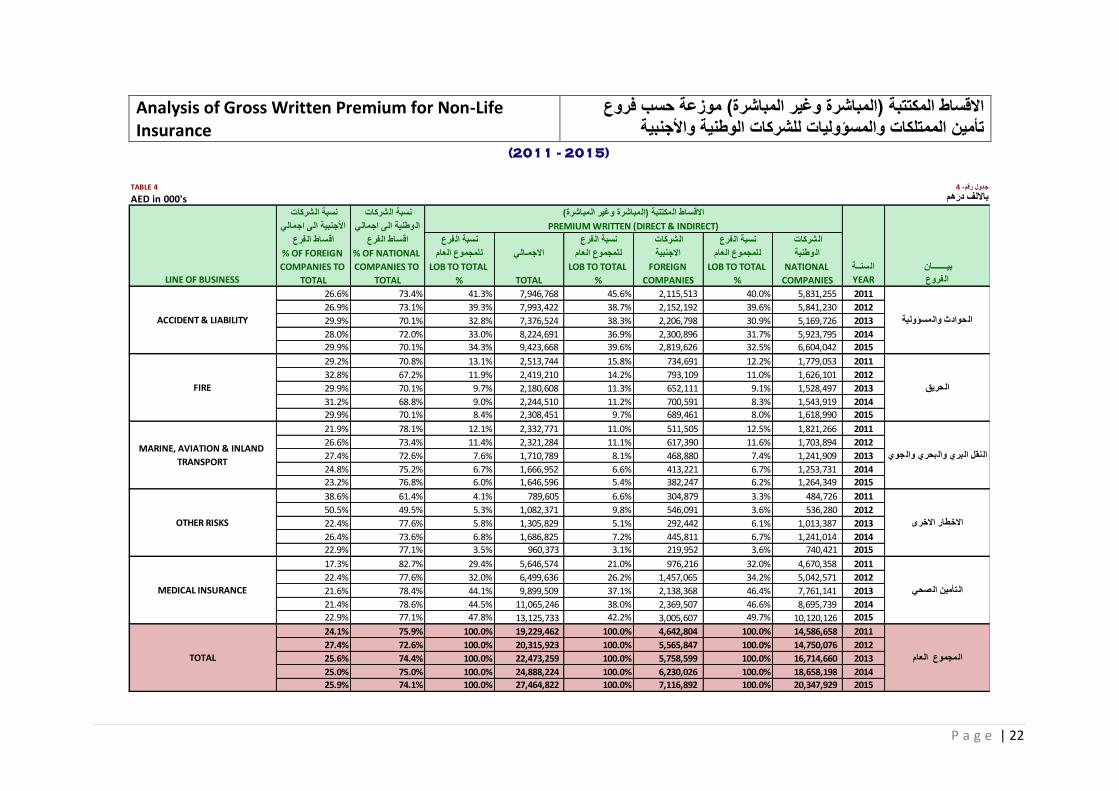

Analysis of Gross Written Premium for Non-Life Insurance

فروع حسب موزعة( المباشرة وغير المباشرة) المكتتبة االقساط واألجنبية الوطنية للشركات والمسؤوليات الممتلكات تأمين

TABLE 4جدول رقم- 4

AED in 000'sباأللف درهم نسبة الشركات نسبة الشركات االقساط المكتتبة )المباشرة وغير المباشرة(

PREMIUM WRITTEN (DIRECT & INDIRECT)وطنية الى اجمالي األجنبية الى اجماليال

فرعالشركات فرعالشركات نسبة ال فرع نسبة ال فرعنسبة ال فرعاقساط ال اقساط ال

وطنية للمجموع العاماالجمـاليللمجموع العاماالجنبيةللمجموع العامال

السنــةبيـــــــان

فروع YEARLINE OF BUSINESSال

20115,831,255 40.0%2,115,513 45.6%7,946,768 41.3%73.4%26.6%

20125,841,230 39.6%2,152,192 38.7%7,993,422 39.3%73.1%26.9%

20135,169,726 30.9%2,206,798 38.3%7,376,524 32.8%70.1%29.9%

20145,923,795 31.7%2,300,896 36.9%8,224,691 33.0%72.0%28.0%

20156,604,042 32.5%2,819,626 39.6%9,423,668 34.3%70.1%29.9%

20111,779,053 12.2%734,691 15.8%2,513,744 13.1%70.8%29.2%

20121,626,101 11.0%793,109 14.2%2,419,210 11.9%67.2%32.8%

20131,528,497 9.1%652,111 11.3%2,180,608 9.7%70.1%29.9%

20141,543,919 8.3%700,591 11.2%2,244,510 9.0%68.8%31.2%

20151,618,990 8.0%689,461 9.7%2,308,451 8.4%70.1%29.9%

20111,821,266 12.5%511,505 11.0%2,332,771 12.1%78.1%21.9%

20121,703,894 11.6%617,390 11.1%2,321,284 11.4%73.4%26.6%

20131,241,909 7.4%468,880 8.1%1,710,789 7.6%72.6%27.4%

20141,253,731 6.7%413,221 6.6%1,666,952 6.7%75.2%24.8%

20151,264,349 6.2%382,247 5.4%1,646,596 6.0%76.8%23.2%

2011484,726 3.3%304,879 6.6%789,605 4.1%61.4%38.6%

2012536,280 3.6%546,091 9.8%1,082,371 5.3%49.5%50.5%

20131,013,387 6.1%292,442 5.1%1,305,829 5.8%77.6%22.4%

20141,241,014 6.7%445,811 7.2%1,686,825 6.8%73.6%26.4%

2015740,421 3.6%219,952 3.1%960,373 3.5%77.1%22.9%

20114,670,358 32.0%976,216 21.0%5,646,574 29.4%82.7%17.3%

20125,042,571 34.2%1,457,065 26.2%6,499,636 32.0%77.6%22.4%

20137,761,141 46.4%2,138,368 37.1%9,899,509 44.1%78.4%21.6%

20148,695,739 46.6%2,369,507 38.0%11,065,246 44.5%78.6%21.4%

201510,120,126 49.7%3,005,607 42.2%13,125,733 47.8%77.1%22.9%

201114,586,658 100.0%4,642,804 100.0%19,229,462 100.0%75.9%24.1%

201214,750,076 100.0%5,565,847 100.0%20,315,923 100.0%72.6%27.4%

201316,714,660 100.0%5,758,599 100.0%22,473,259 100.0%74.4%25.6%

201418,658,198 100.0%6,230,026 100.0%24,888,224 100.0%75.0%25.0%

201520,347,929 100.0%7,116,892 100.0%27,464,822 100.0%74.1%25.9%

الحوادث والمسؤولية

الحريق

جوي بحري وال نقل البري وال ال

TOTAL

MEDICAL INSURANCE

ACCIDENT & LIABILITY

FIRE

MARINE, AVIATION & INLAND

TRANSPORT

OTHER RISKS

(2011 - 2015)

NATIONAL

COMPANIES

LOB TO TOTAL

%

FOREIGN

COMPANIES

LOB TO TOTAL

%TOTAL

LOB TO TOTAL

%

% OF NATIONAL

COMPANIES TO

TOTAL

% OF FOREIGN

COMPANIES TO

TOTAL

المجموع العام

تأمين الصحي ال

االخطار االخرى

P a g e | 23

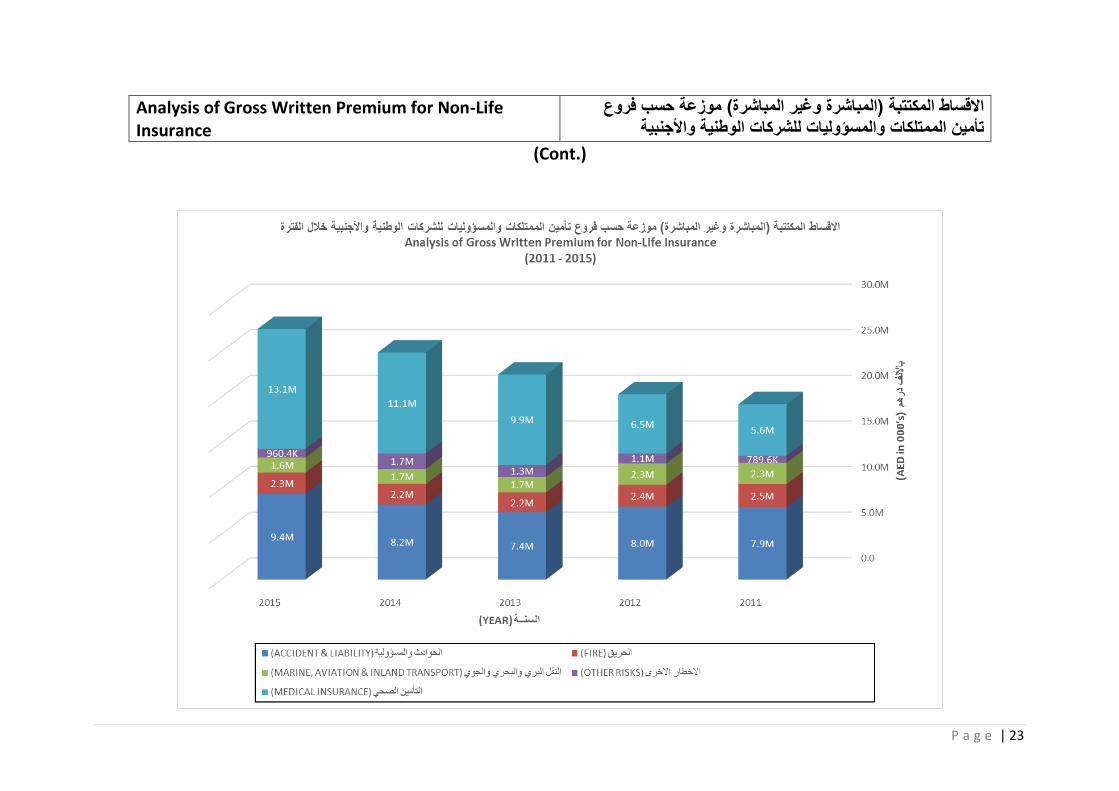

Analysis of Gross Written Premium for Non-Life Insurance

فروع حسب موزعة( المباشرة وغير المباشرة) المكتتبة االقساط واألجنبية الوطنية للشركات والمسؤوليات الممتلكات تأمين

(Cont.)

P a g e | 24

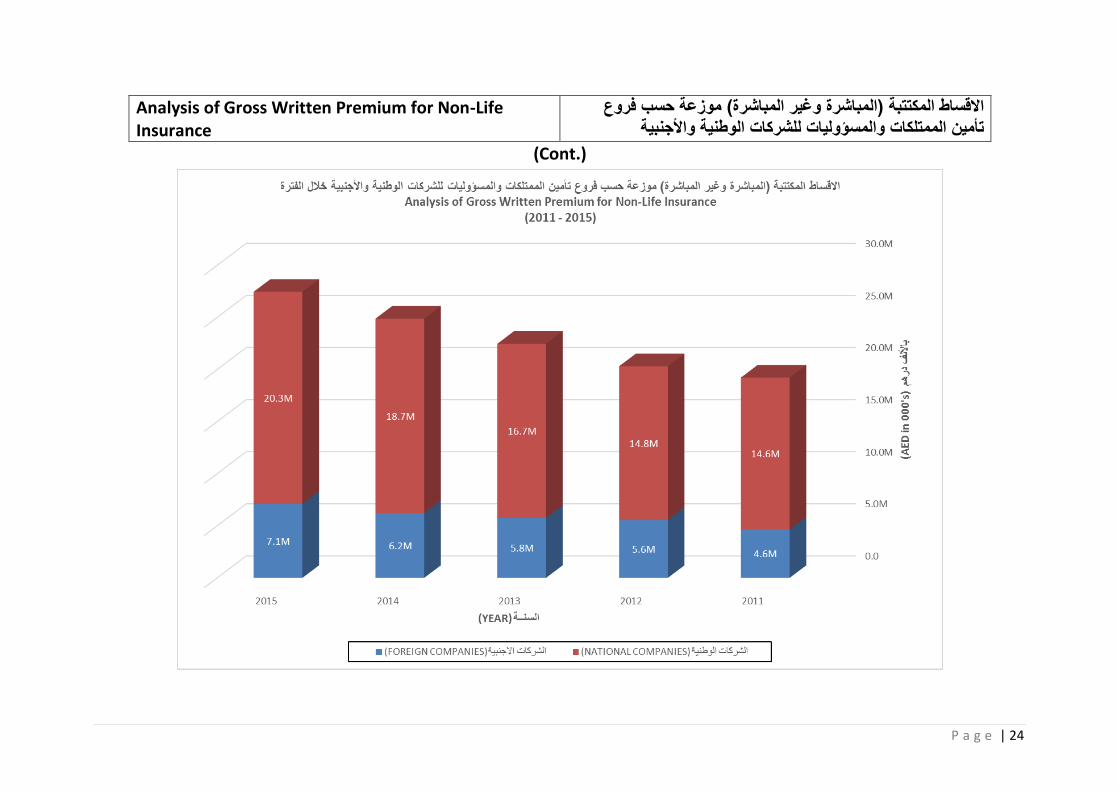

Analysis of Gross Written Premium for Non-Life Insurance

فروع حسب موزعة( المباشرة وغير المباشرة) المكتتبة االقساط واألجنبية الوطنية للشركات والمسؤوليات الممتلكات تأمين

(Cont.)

P a g e | 25

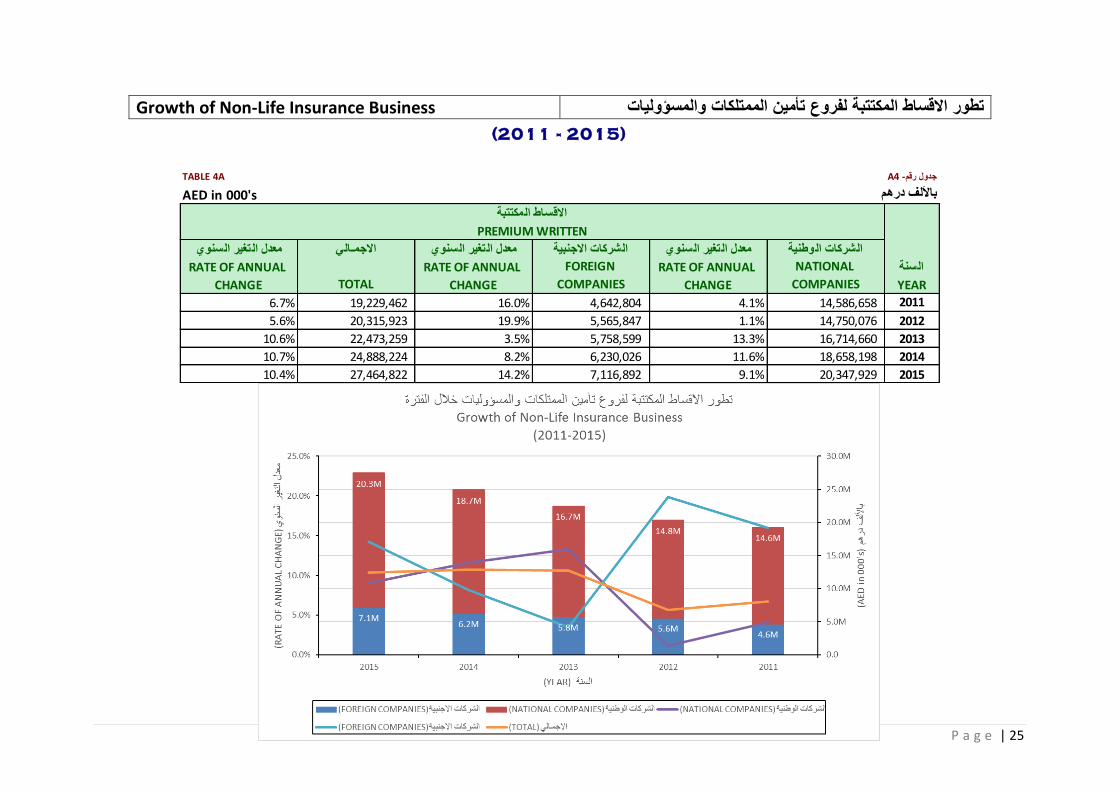

Growth of Non-Life Insurance Business والمسؤوليات الممتلكات تأمين لفروع المكتتبة االقساط تطور

A4 -جدول رقمTABLE 4A

AED in 000'sباأللف درهم االقساط المكتتبة

PREMIUM WRITTEN

تغير السنويالشركات الوطنية تغير السنويالشركات االجنبيةمعدل ال تغير السنوياالجمـاليمعدل ال معدل ال

السنة

YEAR

201114,586,658 4.1%4,642,804 16.0%19,229,462 6.7%

201214,750,076 1.1%5,565,847 19.9%20,315,923 5.6%

201316,714,660 13.3%5,758,599 3.5%22,473,259 10.6%

201418,658,198 11.6%6,230,026 8.2%24,888,224 10.7%

201520,347,929 9.1%7,116,892 14.2%27,464,822 10.4%

NATIONAL

COMPANIES

RATE OF ANNUAL

CHANGE

RATE OF ANNUAL

CHANGE

(2011 - 2015)

FOREIGN

COMPANIESTOTAL

RATE OF ANNUAL

CHANGE

P a g e | 26

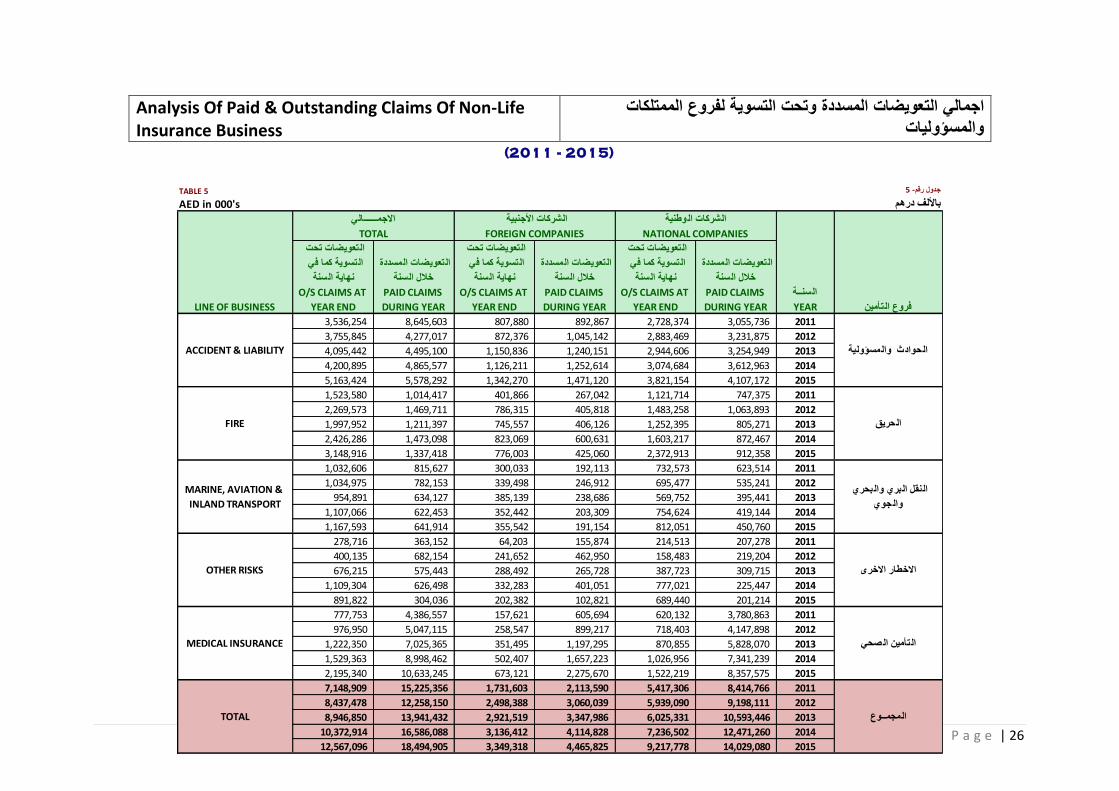

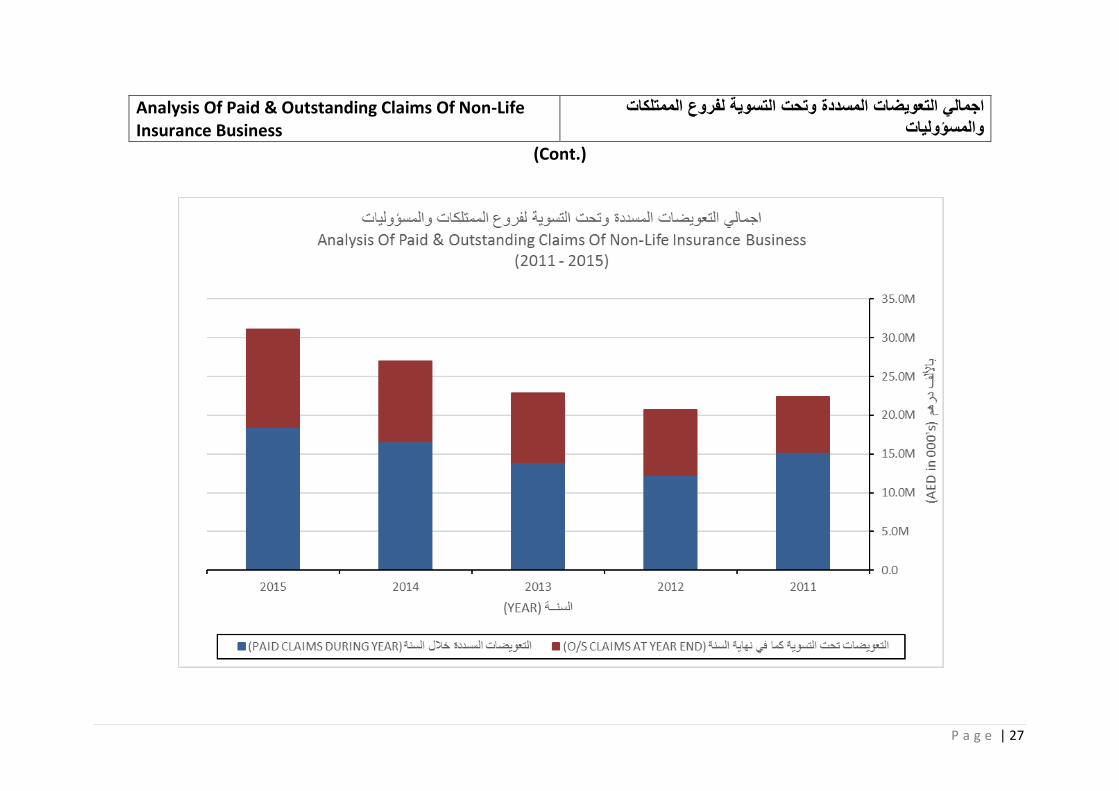

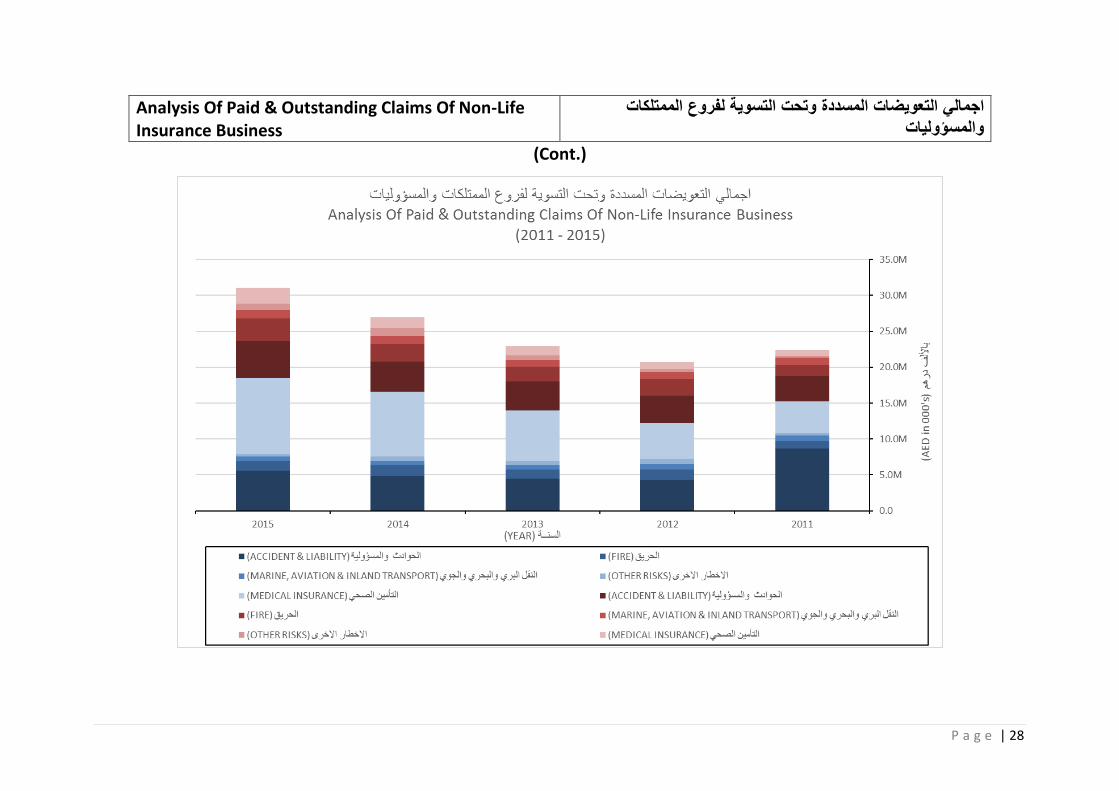

Analysis Of Paid & Outstanding Claims Of Non-Life Insurance Business

الممتلكات لفروع التسوية وتحت المسددة التعويضات اجمالي والمسؤوليات

TABLE 5جدول رقم- 5

AED in 000'sباأللف درهم

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

تعويضات المسددة ال

خالل السنة

تعويضات تحت ال

التسوية كما في

نهاية السنة

السنــة

تأمين YEARLINE OF BUSINESSفروع ال

20113,055,736 2,728,374 892,867 807,880 8,645,603 3,536,254

20123,231,875 2,883,469 1,045,142 872,376 4,277,017 3,755,845

20133,254,949 2,944,606 1,240,151 1,150,836 4,495,100 4,095,442

20143,612,963 3,074,684 1,252,614 1,126,211 4,865,577 4,200,895

20154,107,172 3,821,154 1,471,120 1,342,270 5,578,292 5,163,424

2011747,375 1,121,714 267,042 401,866 1,014,417 1,523,580

20121,063,893 1,483,258 405,818 786,315 1,469,711 2,269,573

2013805,271 1,252,395 406,126 745,557 1,211,397 1,997,952

2014872,467 1,603,217 600,631 823,069 1,473,098 2,426,286

2015912,358 2,372,913 425,060 776,003 1,337,418 3,148,916

2011623,514 732,573 192,113 300,033 815,627 1,032,606

2012535,241 695,477 246,912 339,498 782,153 1,034,975

2013395,441 569,752 238,686 385,139 634,127 954,891

2014419,144 754,624 203,309 352,442 622,453 1,107,066

2015450,760 812,051 191,154 355,542 641,914 1,167,593

2011207,278 214,513 155,874 64,203 363,152 278,716

2012219,204 158,483 462,950 241,652 682,154 400,135

2013309,715 387,723 265,728 288,492 575,443 676,215

2014225,447 777,021 401,051 332,283 626,498 1,109,304

2015201,214 689,440 102,821 202,382 304,036 891,822

20113,780,863 620,132 605,694 157,621 4,386,557 777,753

20124,147,898 718,403 899,217 258,547 5,047,115 976,950

20135,828,070 870,855 1,197,295 351,495 7,025,365 1,222,350

20147,341,239 1,026,956 1,657,223 502,407 8,998,462 1,529,363

20158,357,575 1,522,219 2,275,670 673,121 10,633,245 2,195,340

20118,414,766 5,417,306 2,113,590 1,731,603 15,225,356 7,148,909

20129,198,111 5,939,090 3,060,039 2,498,388 12,258,150 8,437,478

201310,593,446 6,025,331 3,347,986 2,921,519 13,941,432 8,946,850

201412,471,260 7,236,502 4,114,828 3,136,412 16,586,088 10,372,914

201514,029,080 9,217,778 4,465,825 3,349,318 18,494,905 12,567,096

PAID CLAIMS

DURING YEAR

PAID CLAIMS

DURING YEAR

PAID CLAIMS

DURING YEAR

TOTAL المجمــوع

تأمين الصحي ال

االخطار االخرى

الحريق

OTHER RISKS

MEDICAL INSURANCE

الحوادث والمسؤولية

بحري نقل البري وال ال

جوي وال

ACCIDENT & LIABILITY

FIRE

MARINE, AVIATION &

INLAND TRANSPORT

O/S CLAIMS AT

YEAR END

(2011 - 2015)

وطنية الشركات ال

NATIONAL COMPANIESTOTAL

االجمــــــالي الشركات األجنبية

FOREIGN COMPANIES

O/S CLAIMS AT

YEAR END

O/S CLAIMS AT

YEAR END

P a g e | 27

Analysis Of Paid & Outstanding Claims Of Non-Life Insurance Business

الممتلكات لفروع التسوية وتحت المسددة التعويضات اجمالي والمسؤوليات

(Cont.)

P a g e | 28

Analysis Of Paid & Outstanding Claims Of Non-Life Insurance Business

الممتلكات لفروع التسوية وتحت المسددة التعويضات اجمالي والمسؤوليات

(Cont.)

P a g e | 29

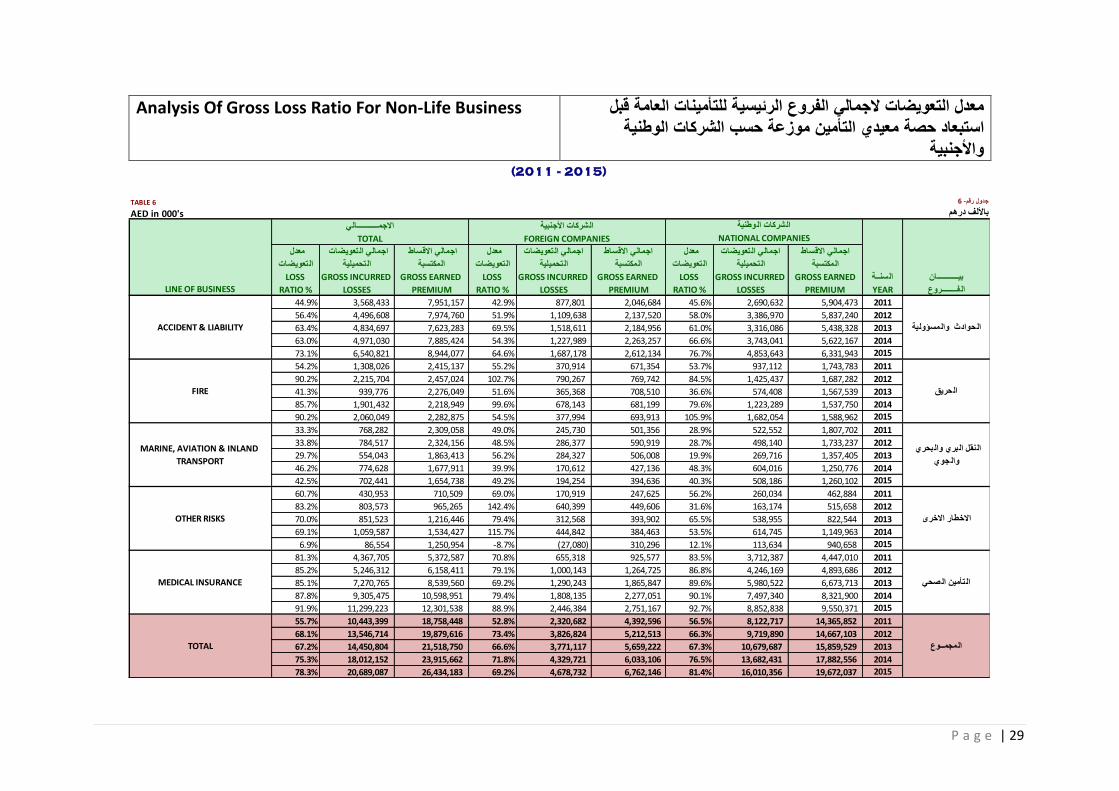

Analysis Of Gross Loss Ratio For Non-Life Business قبل العامة للتأمينات الرئيسية الفروع الجمالي التعويضات معدل الوطنية الشركات حسب موزعة التأمين معيدي حصة استبعاد

واألجنبية

TABLE 6جدول رقم- 6

AED in 000'sباأللف درهم

تعويضاتاجمالي االقساط تعويضاتاجمالي االقساطاجمالي ال اجمالي ال

تحميليةالمكتسبة تحميليةالمكتسبةال ال

السنــةبيـــــــــــان

فــــــــروع YEARLINE OF BUSINESSال

20115,904,473 2,690,632 45.6%2,046,684 877,801 42.9%7,951,157 3,568,433 44.9%

20125,837,240 3,386,970 58.0%2,137,520 1,109,638 51.9%7,974,760 4,496,608 56.4%

20135,438,328 3,316,086 61.0%2,184,956 1,518,611 69.5%7,623,283 4,834,697 63.4%

20145,622,167 3,743,041 66.6%2,263,257 1,227,989 54.3%7,885,424 4,971,030 63.0%

20156,331,943 4,853,643 76.7%2,612,134 1,687,178 64.6%8,944,077 6,540,821 73.1%

20111,743,783 937,112 53.7%671,354 370,914 55.2%2,415,137 1,308,026 54.2%

20121,687,282 1,425,437 84.5%769,742 790,267 102.7%2,457,024 2,215,704 90.2%

20131,567,539 574,408 36.6%708,510 365,368 51.6%2,276,049 939,776 41.3%

20141,537,750 1,223,289 79.6%681,199 678,143 99.6%2,218,949 1,901,432 85.7%

20151,588,962 1,682,054 105.9%693,913 377,994 54.5%2,282,875 2,060,049 90.2%

20111,807,702 522,552 28.9%501,356 245,730 49.0%2,309,058 768,282 33.3%

20121,733,237 498,140 28.7%590,919 286,377 48.5%2,324,156 784,517 33.8%

20131,357,405 269,716 19.9%506,008 284,327 56.2%1,863,413 554,043 29.7%

20141,250,776 604,016 48.3%427,136 170,612 39.9%1,677,911 774,628 46.2%

20151,260,102 508,186 40.3%394,636 194,254 49.2%1,654,738 702,441 42.5%

2011462,884 260,034 56.2%247,625 170,919 69.0%710,509 430,953 60.7%

2012515,658 163,174 31.6%449,606 640,399 142.4%965,265 803,573 83.2%

2013822,544 538,955 65.5%393,902 312,568 79.4%1,216,446 851,523 70.0%

20141,149,963 614,745 53.5%384,463 444,842 115.7%1,534,427 1,059,587 69.1%

2015940,658 113,634 12.1%310,296 (27,080) -8.7%1,250,954 86,554 6.9%

20114,447,010 3,712,387 83.5%925,577 655,318 70.8%5,372,587 4,367,705 81.3%

20124,893,686 4,246,169 86.8%1,264,725 1,000,143 79.1%6,158,411 5,246,312 85.2%

20136,673,713 5,980,522 89.6%1,865,847 1,290,243 69.2%8,539,560 7,270,765 85.1%

20148,321,900 7,497,340 90.1%2,277,051 1,808,135 79.4%10,598,951 9,305,475 87.8%

20159,550,371 8,852,838 92.7%2,751,167 2,446,384 88.9%12,301,538 11,299,223 91.9%

201114,365,852 8,122,717 56.5%4,392,596 2,320,682 52.8%18,758,448 10,443,399 55.7%

201214,667,103 9,719,890 66.3%5,212,513 3,826,824 73.4%19,879,616 13,546,714 68.1%

201315,859,529 10,679,687 67.3%5,659,222 3,771,117 66.6%21,518,750 14,450,804 67.2%

201417,882,556 13,682,431 76.5%6,033,106 4,329,721 71.8%23,915,662 18,012,152 75.3%

201519,672,037 16,010,356 81.4%6,762,146 4,678,732 69.2%26,434,183 20,689,087 78.3%

بحري نقل البري وال ال

جوي وال

TOTAL

(2011 - 2015)

الحوادث والمسؤولية

الحريق

االخطار االخرى

تأمين الصحي ال

المجمــوع

GROSS INCURRED

LOSSES

GROSS EARNED

PREMIUM

LOSS

RATIO %

ACCIDENT & LIABILITY

LOSS

RATIO %

FIRE

MARINE, AVIATION & INLAND

TRANSPORT

OTHER RISKS

MEDICAL INSURANCE

NATIONAL COMPANIES

GROSS EARNED

PREMIUM

GROSS INCURRED

LOSSES

LOSS

RATIO %

GROSS EARNED

PREMIUM

GROSS INCURRED

LOSSES

معدل

تعويضات ال

معدل

تعويضات ال

معدل

تعويضات ال

تعويضات اجمالي ال

تحميلية ال

اجمالي االقساط

المكتسبة

وطنية الشركات ال

FOREIGN COMPANIES

االجمـــــــــــاليالشركات األجنبية

TOTAL

P a g e | 30

Analysis Of Gross Loss Ratio For Non-Life Business قبل العامة للتأمينات الرئيسية الفروع الجمالي التعويضات معدل الوطنية الشركات حسب موزعة التأمين معيدي حصة استبعاد

واألجنبية(Cont.)

P a g e | 31

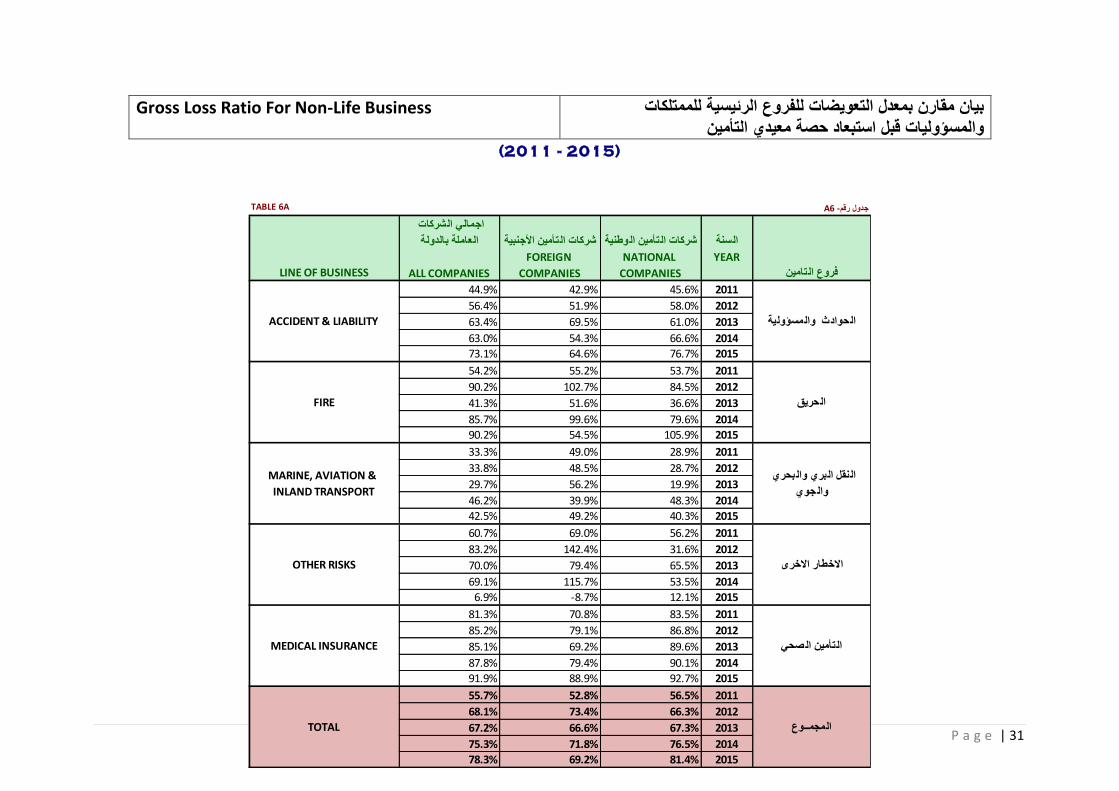

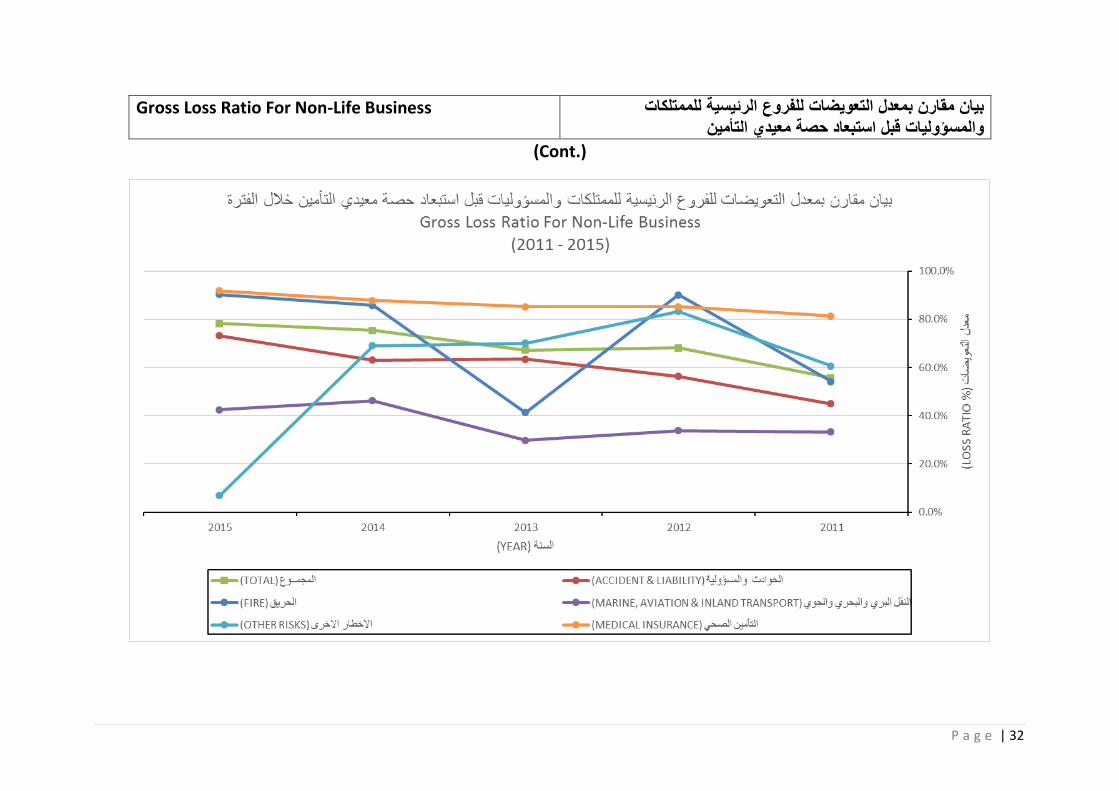

Gross Loss Ratio For Non-Life Business للممتلكات الرئيسية للفروع التعويضات بمعدل مقارن بيان التأمين معيدي حصة استبعاد قبل والمسؤوليات

A6 -جدول رقمTABLE 6A

وطنيةالسنة تأمين ال تأمين األجنبيةشركات ال شركات ال

اجمالي الشركات

العاملة بالدولة

YEAR

تامين LINE OF BUSINESSفروع ال

201145.6%42.9%44.9%

201258.0%51.9%56.4%

201361.0%69.5%63.4%

201466.6%54.3%63.0%

201576.7%64.6%73.1%

201153.7%55.2%54.2%

201284.5%102.7%90.2%

201336.6%51.6%41.3%

201479.6%99.6%85.7%

2015105.9%54.5%90.2%

201128.9%49.0%33.3%

201228.7%48.5%33.8%

201319.9%56.2%29.7%

201448.3%39.9%46.2%

201540.3%49.2%42.5%

201156.2%69.0%60.7%

201231.6%142.4%83.2%

201365.5%79.4%70.0%

201453.5%115.7%69.1%

201512.1%-8.7%6.9%

201183.5%70.8%81.3%

201286.8%79.1%85.2%

201389.6%69.2%85.1%

201490.1%79.4%87.8%

201592.7%88.9%91.9%

201156.5%52.8%55.7%

201266.3%73.4%68.1%

201367.3%66.6%67.2%

201476.5%71.8%75.3%

201581.4%69.2%78.3%

MARINE, AVIATION &

INLAND TRANSPORT

OTHER RISKS

MEDICAL INSURANCE

TOTAL المجمــوع

بحري نقل البري وال ال

جوي وال

االخطار االخرى

تأمين الصحي ال

(2011 - 2015)

الحوادث والمسؤولية

الحريق

ALL COMPANIES

FOREIGN

COMPANIES

NATIONAL

COMPANIES

ACCIDENT & LIABILITY

FIRE

P a g e | 32

Gross Loss Ratio For Non-Life Business للممتلكات الرئيسية للفروع التعويضات بمعدل مقارن بيان التأمين معيدي حصة استبعاد قبل والمسؤوليات

(Cont.)

P a g e | 33

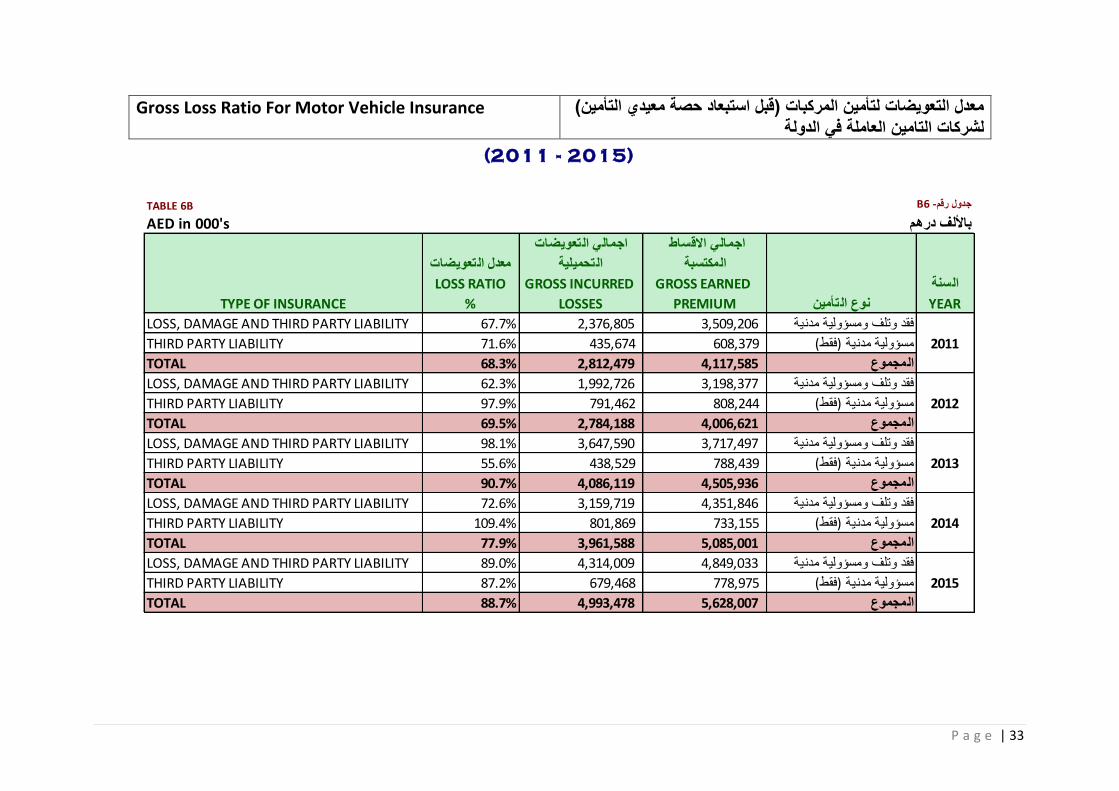

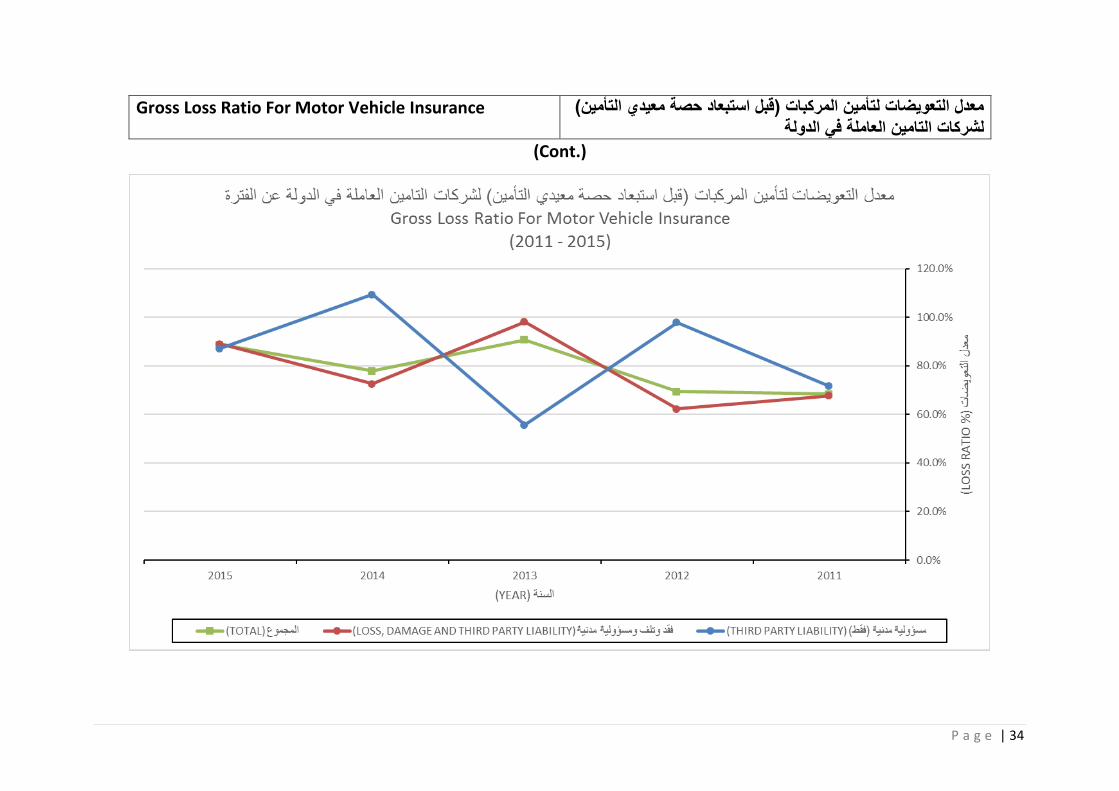

Gross Loss Ratio For Motor Vehicle Insurance ( التأمين معيدي حصة استبعاد قبل) المركبات لتأمين التعويضات معدل الدولة في العاملة التامين لشركات

B6 -جدول رقمTABLE 6B

AED in 000'sباأللف درهم تعويضات اجمالي ال

تحميلية ال

LOSS RATIOالسنة

YEARتأمين TYPE OF INSURANCE%نوع ال

LOSS, DAMAGE AND THIRD PARTY LIABILITY%67.7 2,376,805 3,509,206فقد وتلف ومسؤولية مدنية

THIRD PARTY LIABILITY%71.6 435,674 608,379مسؤولية مدنية )فقط(2011

TOTAL%68.3 2,812,479 4,117,585المجموع

LOSS, DAMAGE AND THIRD PARTY LIABILITY%62.3 1,992,726 3,198,377فقد وتلف ومسؤولية مدنية

THIRD PARTY LIABILITY%97.9 791,462 808,244مسؤولية مدنية )فقط(2012

TOTAL%69.5 2,784,188 4,006,621المجموع

LOSS, DAMAGE AND THIRD PARTY LIABILITY%98.1 3,647,590 3,717,497فقد وتلف ومسؤولية مدنية

THIRD PARTY LIABILITY%55.6 438,529 788,439مسؤولية مدنية )فقط(2013

TOTAL%90.7 4,086,119 4,505,936المجموع

LOSS, DAMAGE AND THIRD PARTY LIABILITY%72.6 3,159,719 4,351,846فقد وتلف ومسؤولية مدنية

THIRD PARTY LIABILITY%109.4 801,869 733,155مسؤولية مدنية )فقط(2014

TOTAL%77.9 3,961,588 5,085,001المجموع

LOSS, DAMAGE AND THIRD PARTY LIABILITY%89.0 4,314,009 4,849,033فقد وتلف ومسؤولية مدنية

THIRD PARTY LIABILITY%87.2 679,468 778,975مسؤولية مدنية )فقط(2015

TOTAL%88.7 4,993,478 5,628,007المجموع

(2011 - 2015)

GROSS EARNED

PREMIUM

GROSS INCURRED

LOSSES

اجمالي االقساط

تعويضاتالمكتسبة معدل ال

P a g e | 34

Gross Loss Ratio For Motor Vehicle Insurance ( التأمين معيدي حصة استبعاد قبل) المركبات لتأمين التعويضات معدل الدولة في العاملة التامين لشركات

(Cont.)

P a g e | 35

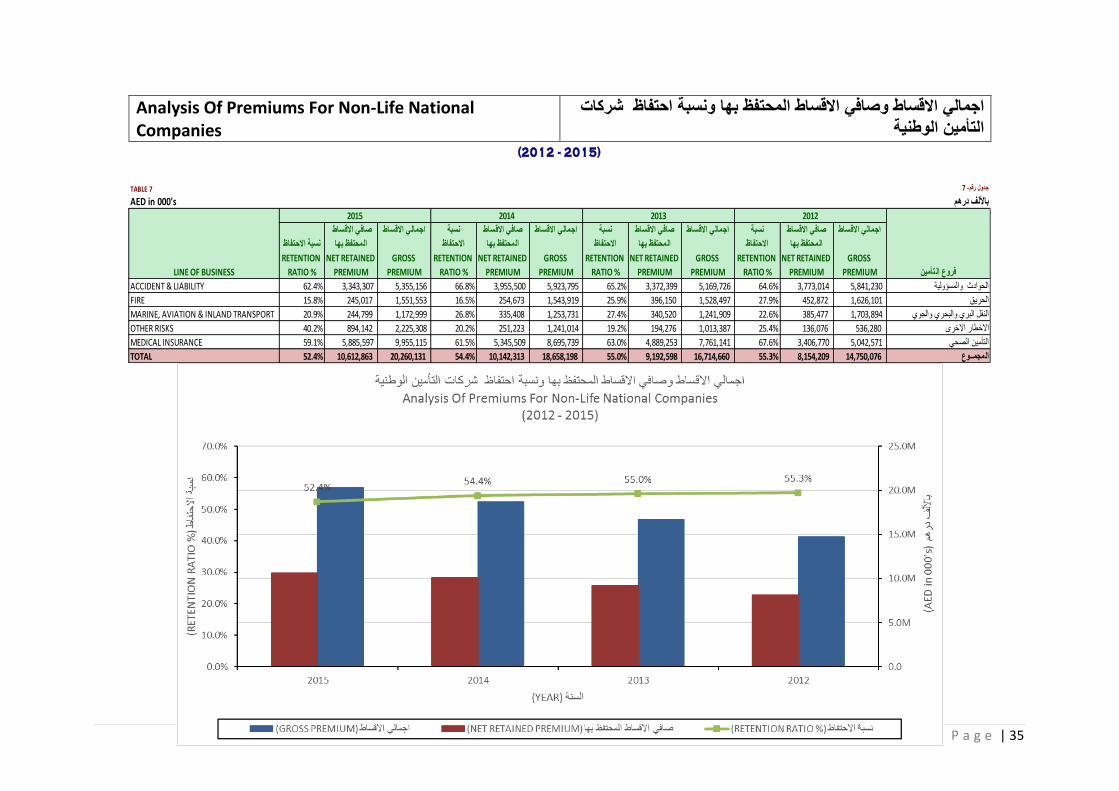

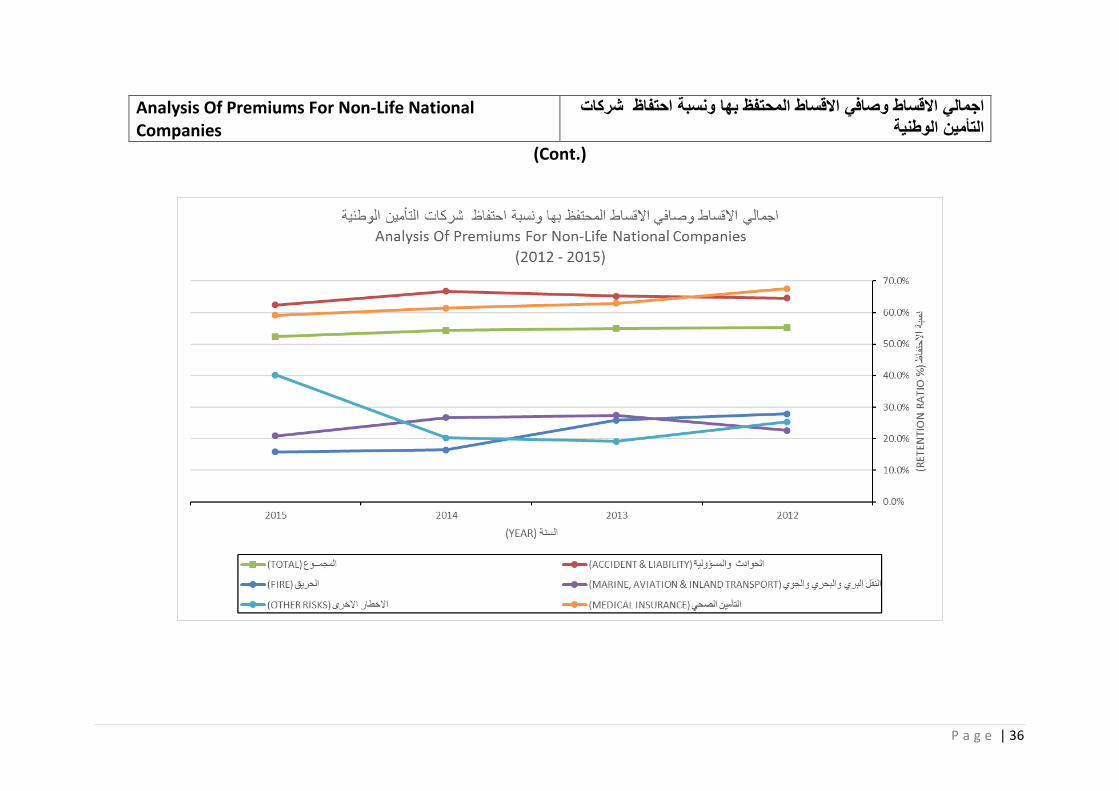

Analysis Of Premiums For Non-Life National Companies

شركات احتفاظ ونسبة بها المحتفظ االقساط وصافي االقساط اجمالي الوطنية التأمين

TABLE 7جدول رقم- 7

AED in 000'sباأللف درهم

اجمالي االقساطنسبةصافي االقساطاجمالي االقساطنسبةصافي االقساطاجمالي االقساطنسبةصافي االقساطاجمالي االقساط

االحتفاظالمحتفظ بهااالحتفاظالمحتفظ بهااالحتفاظالمحتفظ بها

تأمين LINE OF BUSINESSفروع ال

ACCIDENT & LIABILITY%62.4 3,343,307 5,355,156%66.8 3,955,500 5,923,795%65.2 3,372,399 5,169,726%64.6 3,773,014 5,841,230الحوادث والمسؤولية

FIRE%15.8 245,017 1,551,553%16.5 254,673 1,543,919%25.9 396,150 1,528,497%27.9 452,872 1,626,101الحريق

MARINE, AVIATION & INLAND TRANSPORT%20.9 244,799 1,172,999%26.8 335,408 1,253,731%27.4 340,520 1,241,909%22.6 385,477 1,703,894النقل البري والبحري والجوي

OTHER RISKS%40.2 894,142 2,225,308%20.2 251,223 1,241,014%19.2 194,276 1,013,387%25.4 136,076 536,280االخطار االخرى

MEDICAL INSURANCE%59.1 5,885,597 9,955,115%61.5 5,345,509 8,695,739%63.0 4,889,253 7,761,141%67.6 3,406,770 5,042,571التأمين الصحي

TOTAL%52.4 10,612,863 20,260,131%54.4 10,142,313 18,658,198%55.0 9,192,598 16,714,660%55.3 8,154,209 14,750,076المجمــوع

(2012 - 2015)

GROSS

PREMIUM

NET RETAINED

PREMIUM

RETENTION

RATIO %

GROSS

PREMIUM

NET RETAINED

PREMIUM

2015 20132014 2012

GROSS

PREMIUM

NET RETAINED

PREMIUM

RETENTION

RATIO %

نسبة االحتفاظ

GROSS

PREMIUM

NET RETAINED

PREMIUM

RETENTION

RATIO %

RETENTION

RATIO %

صافي االقساط

المحتفظ بها

P a g e | 36

Analysis Of Premiums For Non-Life National Companies

شركات احتفاظ ونسبة بها المحتفظ االقساط وصافي االقساط اجمالي الوطنية التأمين

(Cont.)

P a g e | 37

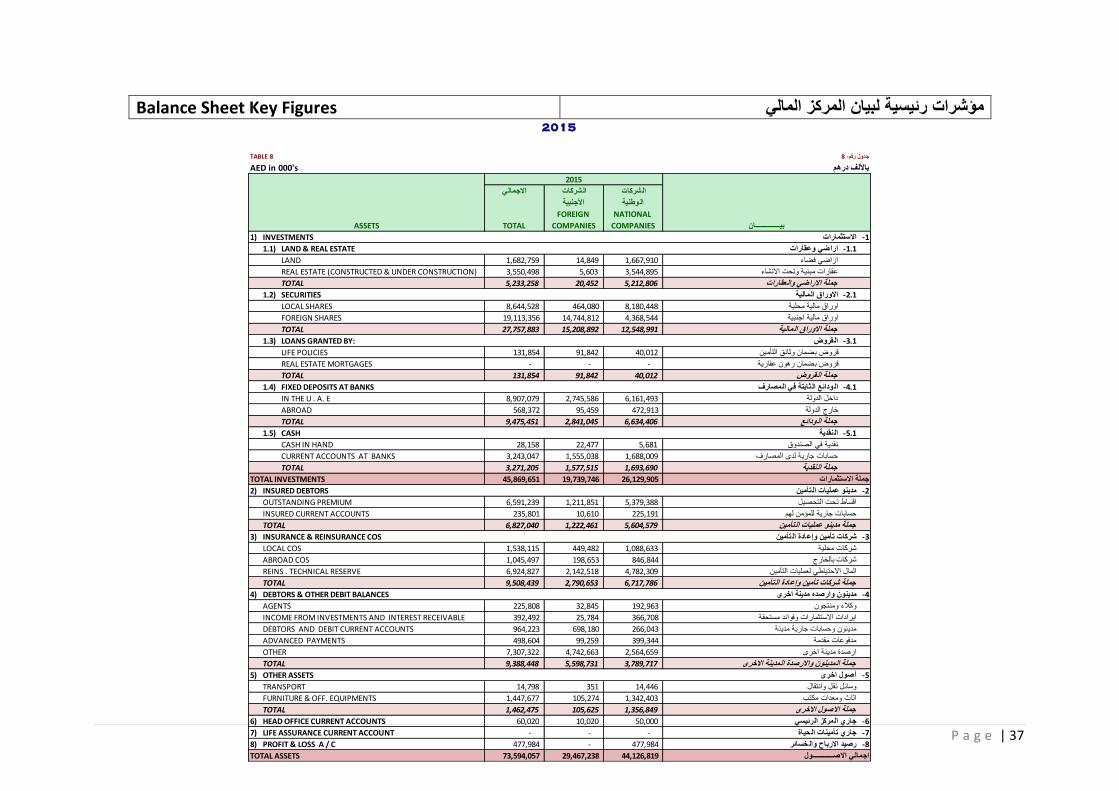

Balance Sheet Key Figures المالي المركز لبيان رئيسية مؤشرات

TABLE 8جدول رقم- 8

AED in 000'sباأللف درهم

االجماليالشركات الشركات

وطنية األجنبيةال

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTAL

(INVESTMENTS 1االستثمارات1-

(LAND & REAL ESTATE1.1اراضي وعقارات1.1-

LAND 1,682,759 14,849 1,667,910اراضي فضاء

REAL ESTATE (CONSTRUCTED & UNDER CONSTRUCTION) 3,550,498 5,603 3,544,895عقارات مبنية وتحت االنشاء

TOTAL 5,233,258 20,452 5,212,806جملة االراضي والعقارات

(SECURITIES 1.2االوراق المالية2.1-

LOCAL SHARES 8,644,528 464,080 8,180,448اوراق مالية محلية

FOREIGN SHARES 19,113,356 14,744,812 4,368,544اوراق مالية اجنبية

TOTAL 27,757,883 15,208,892 12,548,991جملة االوراق المالية

(LOANS GRANTED BY:1.3القروض3.1-

LIFE POLICIES 131,854 91,842 40,012قروض بضمان وثائق التأمين

REAL ESTATE MORTGAGES - - -قروض بضمان رهون عقارية

TOTAL 131,854 91,842 40,012جملة القروض

ثابتة في المصارف4.1- ودائع ال (FIXED DEPOSITS AT BANKS 1.4ال

IN THE U . A. E 8,907,079 2,745,586 6,161,493داخل الدولة

ABROAD 568,372 95,459 472,913خارج الدولة

ودائع TOTAL 9,475,451 2,841,045 6,634,406جملة ال

نقدية5.1- (CASH1.5ال

CASH IN HAND 28,158 22,477 5,681نقدية في الصندوق

CURRENT ACCOUNTS AT BANKS 3,243,047 1,555,038 1,688,009حسابات جارية لدى المصارف

نقدية TOTAL 3,271,205 1,577,515 1,693,690جملة ال

TOTAL INVESTMENTS 45,869,651 19,739,746 26,129,905جملة االستثمارات

تأمين2- (INSURED DEBTORS2مدينو عمليات ال

OUTSTANDING PREMIUM 6,591,239 1,211,851 5,379,388اقساط تحت التحصيل

INSURED CURRENT ACCOUNTS 235,801 10,610 225,191حسابات جارية للمؤمن لهم

تأمين TOTAL 6,827,040 1,222,461 5,604,579جملة مدينو عمليات ال

تأمين3- (INSURANCE & REINSURANCE COS 3شركات تأمين وإعادة ال

LOCAL COS 1,538,115 449,482 1,088,633شركات محلية

ABROAD COS 1,045,497 198,653 846,844شركات بالخارج

REINS . TECHNICAL RESERVE 6,924,827 2,142,518 4,782,309المال االحتياطي لعمليات التأمين

تأمين TOTAL 9,508,439 2,790,653 6,717,786جملة شركات تأمين وإعادة ال

(DEBTORS & OTHER DEBIT BALANCES4مدينون وارصده مدينة اخرى4-

AGENTS 225,808 32,845 192,963وكالء ومنتجون

INCOME FROM INVESTMENTS AND INTEREST RECEIVABLE 392,492 25,784 366,708ايرادات االستثمارات وفوائد مستحقة

DEBTORS AND DEBIT CURRENT ACCOUNTS 964,223 698,180 266,043مدينون وحسابات جارية مدينة

ADVANCED PAYMENTS 498,604 99,259 399,344مدفوعات مقدمة

OTHER 7,307,322 4,742,663 2,564,659ارصدة مدينة اخرى

TOTAL 9,388,448 5,598,731 3,789,717جملة المدينون واالرصدة المدينة االخرى

(OTHER ASSETS5أصول اخرى5-

TRANSPORT 14,798 351 14,446وسائل نقل وانتقال

FURNITURE & OFF. EQUIPMENTS 1,447,677 105,274 1,342,403اثاث ومعدات مكتب

TOTAL 1,462,475 105,625 1,356,849جملة االصول االخرى

(HEAD OFFICE CURRENT ACCOUNTS6 60,020 10,020 50,000جاري المركز الرئيسي6-

حياة7- (LIFE ASSURANCE CURRENT ACCOUNT 7 - - -جاري تأمينات ال

خسائر8- (PROFIT & LOSS A / C 8 477,984 - 477,984رصيد االرباح وال

TOTAL ASSETS 73,594,057 29,467,238 44,126,819اجمالي االصــــــــــــول

ASSETS بيــــــــــــــان

2015

2015

P a g e | 38

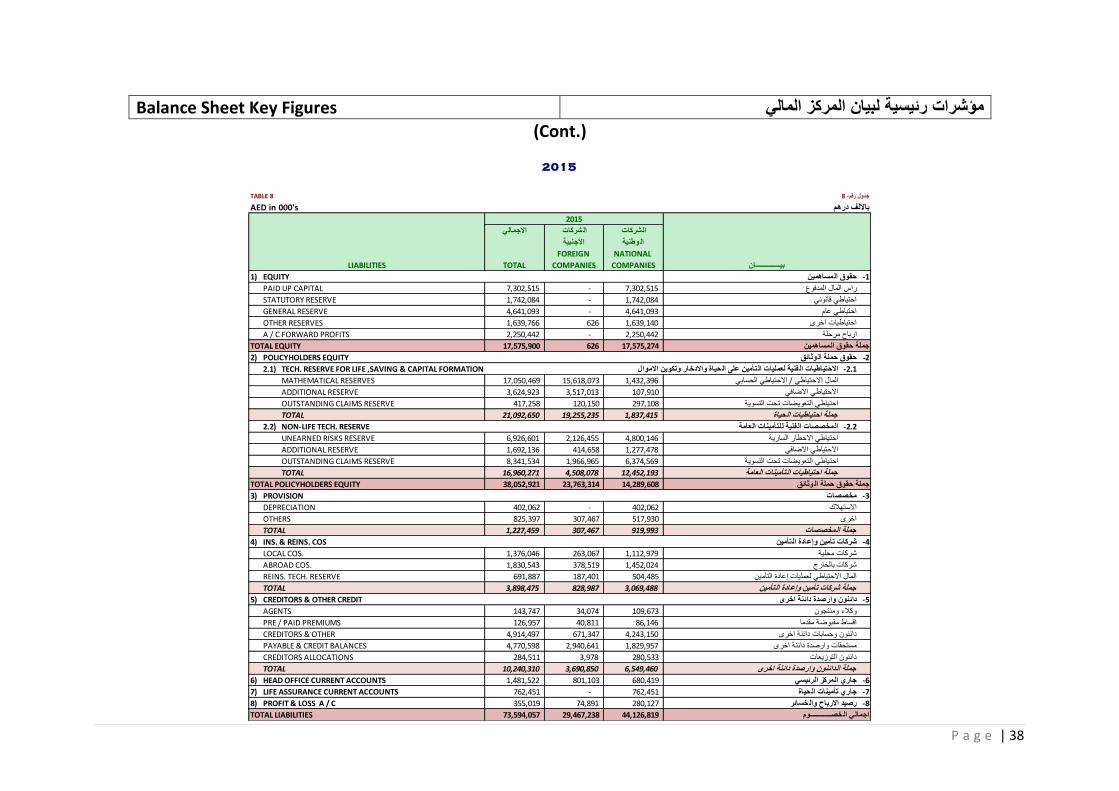

Balance Sheet Key Figures المالي المركز لبيان رئيسية مؤشرات

(Cont.)

TABLE 8جدول رقم- 8

AED in 000'sباأللف درهم

االجماليالشركات الشركات

وطنية األجنبيةال

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTAL

(EQUITY1حقوق المساهمين1-

PAID UP CAPITAL 7,302,515 - 7,302,515راس المال المدفوع

STATUTORY RESERVE 1,742,084 - 1,742,084احتياطي قانوني

GENERAL RESERVE 4,641,093 - 4,641,093احتياطي عام

OTHER RESERVES 1,639,766 626 1,639,140احتياطيات اخرى

A / C FORWARD PROFITS 2,250,442 - 2,250,442ارباح مرحلة

TOTAL EQUITY 17,575,900 626 17,575,274جملة حقوق المساهمين

وثائق2ـ (POLICYHOLDERS EQUITY 2حقوق حملة ال

حياة واالدخار وتكوين االموال2.1- تأمين على ال فنية لعمليات ال (TECH. RESERVE FOR LIFE ,SAVING & CAPITAL FORMATION2.1االحتياطيات ال

MATHEMATICAL RESERVES 17,050,469 15,618,073 1,432,396المال االحتياطي / االحتياطي الحسابي

ADDITIONAL RESERVE 3,624,923 3,517,013 107,910االحتياطي االضافي

OUTSTANDING CLAIMS RESERVE 417,258 120,150 297,108احتياطي التعويضات تحت التسوية

حياة TOTAL 21,092,650 19,255,235 1,837,415جملة احتياطيات ال

لتأمينات العامة2.2- فنية ل (NON-LIFE TECH. RESERVE2.2المخصصات ال

UNEARNED RISKS RESERVE 6,926,601 2,126,455 4,800,146احتياطي االخطار السارية

ADDITIONAL RESERVE 1,692,136 414,658 1,277,478االحتياطي االضافي

OUTSTANDING CLAIMS RESERVE 8,341,534 1,966,965 6,374,569احتياطي التعويضات تحت التسوية

تأمينات العامة TOTAL 16,960,271 4,508,078 12,452,193جملة احتياطيات ال

وثائق TOTAL POLICYHOLDERS EQUITY 38,052,921 23,763,314 14,289,608جملة حقوق حملة ال

(PROVISION3مخصصات3-

DEPRECIATION 402,062 - 402,062االستهالك

OTHERS 825,397 307,467 517,930اخرى

TOTAL 1,227,459 307,467 919,993جملة المخصصات

تأمين4- (INS. & REINS. COS4شركات تأمين وإعادة ال

.LOCAL COS 1,376,046 263,067 1,112,979شركات محلية

.ABROAD COS 1,830,543 378,519 1,452,024شركات بالخارج

REINS. TECH. RESERVE 691,887 187,401 504,485المال االحتياطي لعمليات إعادة التأمين

تأمين TOTAL 3,898,475 828,987 3,069,488جملة شركات تأمين وإعادة ال

(CREDITORS & OTHER CREDIT5دائنون وارصدة دائنة اخرى5-

AGENTS 143,747 34,074 109,673وكالء ومنتجون

PRE / PAID PREMIUMS 126,957 40,811 86,146اقساط مقبوضة مقدما

CREDITORS & OTHER 4,914,497 671,347 4,243,150دائنون وحسابات دائنة اخرى

PAYABLE & CREDIT BALANCES 4,770,598 2,940,641 1,829,957مستحقات وارصدة دائنة اخرى

CREDITORS ALLOCATIONS 284,511 3,978 280,533دائنون التوزيعات

TOTAL 10,240,310 3,690,850 6,549,460جملة الدائنون وارصدة دائنة اخرى

(HEAD OFFICE CURRENT ACCOUNTS6 1,481,522 801,103 680,419جاري المركز الرئيسي6-

حياة7- (LIFE ASSURANCE CURRENT ACCOUNTS7 762,451 - 762,451جاري تأمينات ال

خسائر8- (PROFIT & LOSS A / C 8 355,019 74,891 280,127رصيد االرباح وال

TOTAL LIABILITIES 73,594,057 29,467,238 44,126,819اجمالي الخصــــــــــــوم

2015

2015

LIABILITIES بيــــــــــــــان

P a g e | 39

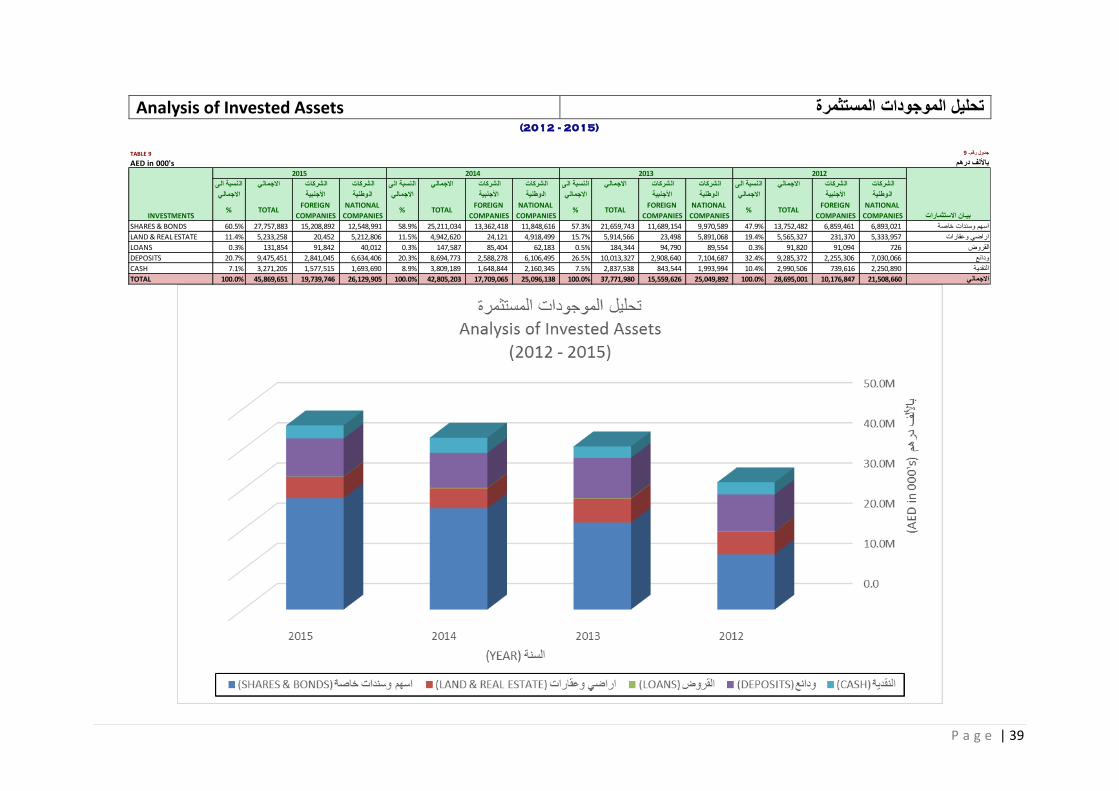

Analysis of Invested Assets المستثمرة الموجودات تحليل

TABLE 9جدول رقم- 9

AED in 000'sباأللف درهم

النسبة الىاالجماليالشركات الشركات النسبة الىاالجماليالشركات الشركات النسبة الىاالجماليالشركات الشركات النسبة الىاالجماليالشركات الشركات

وطنية وطنيةاالجمالياألجنبيةال وطنيةاالجمالياألجنبيةال وطنيةاالجمالياألجنبيةال االجمالياألجنبيةال

INVESTMENTSبيـان االستثمارات

SHARES & BONDS%60.5 27,757,883 15,208,892 12,548,991%58.9 25,211,034 13,362,418 11,848,616%57.3 21,659,743 11,689,154 9,970,589%47.9 13,752,482 6,859,461 6,893,021اسهم وسندات خاصة

LAND & REAL ESTATE%11.4 5,233,258 20,452 5,212,806%11.5 4,942,620 24,121 4,918,499%15.7 5,914,566 23,498 5,891,068%19.4 5,565,327 231,370 5,333,957اراضي وعقارات

LOANS%0.3 131,854 91,842 40,012%0.3 147,587 85,404 62,183%0.5 184,344 94,790 89,554%0.3 91,820 91,094 726القروض

DEPOSITS%20.7 9,475,451 2,841,045 6,634,406%20.3 8,694,773 2,588,278 6,106,495%26.5 10,013,327 2,908,640 7,104,687%32.4 9,285,372 2,255,306 7,030,066ودائع

CASH%7.1 3,271,205 1,577,515 1,693,690%8.9 3,809,189 1,648,844 2,160,345%7.5 2,837,538 843,544 1,993,994%10.4 2,990,506 739,616 2,250,890النقدية

TOTAL%100.0 45,869,651 19,739,746 26,129,905%100.0 42,805,203 17,709,065 25,096,138%100.0 37,771,980 15,559,626 25,049,892%100.0 28,695,001 10,176,847 21,508,660االجمالي

(2012 - 2015)

TOTAL%NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTAL

FOREIGN

COMPANIESTOTAL%

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTAL

FOREIGN

COMPANIES

NATIONAL

COMPANIES%

NATIONAL

COMPANIES

2015 20132014 2012

%

P a g e | 40

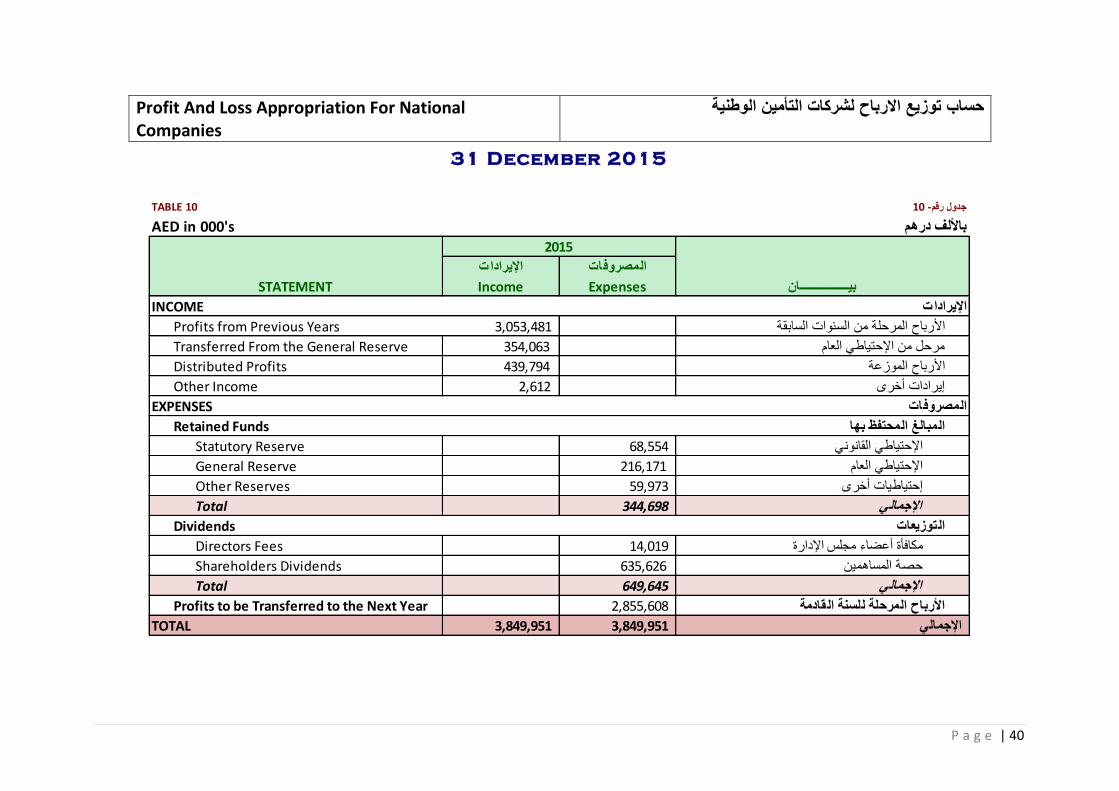

Profit And Loss Appropriation For National Companies

الوطنية التأمين لشركات االرباح توزيع حساب

TABLE 10جدول رقم- 10

AED in 000'sباأللف درهم

تالمصروفات اإليرادا

ExpensesIncomeSTATEMENTبيــــــــــــــــان

INCOMEاإليرادات

Profits from Previous Years 3,053,481األرباح المرحلة من السنوات السابقة

Transferred From the General Reserve 354,063مرحل من اإلحتياطي العام

Distributed Profits 439,794األرباح الموزعة

Other Income 2,612إيرادات أخرى

EXPENSESالمصروفات

Retained Fundsالمبالغ المحتفظ بها

Statutory Reserve 68,554اإلحتياطي القانوني

General Reserve 216,171اإلحتياطي العام

Other Reserves 59,973إحتياطيات أخرى

Total 344,698اإلجمالي

توزيعات Dividendsال

Directors Fees 14,019مكافأة أعضاء مجلس اإلدارة

Shareholders Dividends 635,626حصة المساهمين

Total 649,645اإلجمالي

قادمة Profits to be Transferred to the Next Year 2,855,608األرباح المرحلة للسنة ال

TOTAL 3,849,951 3,849,951اإلجمالي

31 December 2015

2015

P a g e | 41

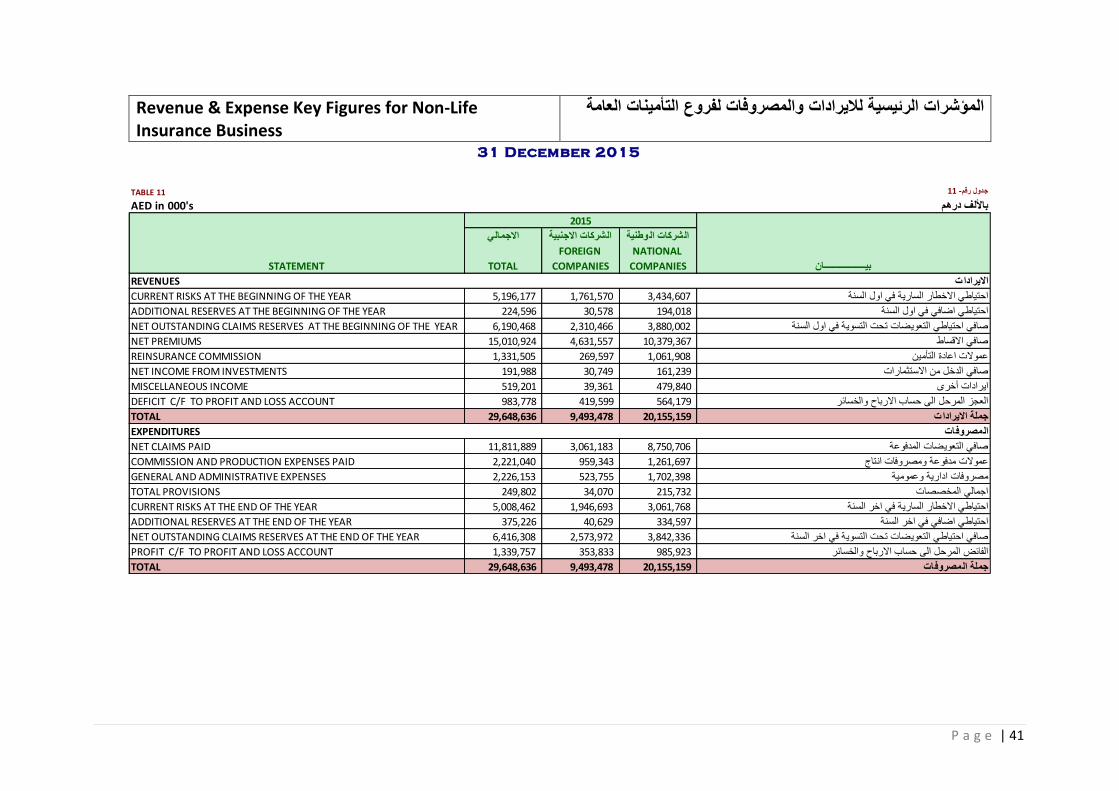

Revenue & Expense Key Figures for Non-Life Insurance Business

العامة التأمينات لفروع والمصروفات لاليرادات الرئيسية المؤشرات

TABLE 11جدول رقم- 11

AED in 000'sباأللف درهم

وطنية االجماليالشركات االجنبيةالشركات ال

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTAL

REVENUESااليرادات

CURRENT RISKS AT THE BEGINNING OF THE YEAR 5,196,177 1,761,570 3,434,607احتياطي االخطار السارية في اول السنة

ADDITIONAL RESERVES AT THE BEGINNING OF THE YEAR 224,596 30,578 194,018احتياطي اضافي في اول السنة

NET OUTSTANDING CLAIMS RESERVES AT THE BEGINNING OF THE YEAR 6,190,468 2,310,466 3,880,002صافي احتياطي التعويضات تحت التسوية في اول السنة

NET PREMIUMS 15,010,924 4,631,557 10,379,367صافي االقساط

REINSURANCE COMMISSION 1,331,505 269,597 1,061,908عموالت اعادة التأمين

NET INCOME FROM INVESTMENTS 191,988 30,749 161,239صافي الدخل من االستثمارات

MISCELLANEOUS INCOME 519,201 39,361 479,840ايرادات أخرى

DEFICIT C/F TO PROFIT AND LOSS ACCOUNT 983,778 419,599 564,179العجز المرحل الى حساب االرباح والخسائر

TOTAL 29,648,636 9,493,478 20,155,159جملة االيرادات

EXPENDITURESالمصروفات

NET CLAIMS PAID 11,811,889 3,061,183 8,750,706صافي التعويضات المدفوعة

COMMISSION AND PRODUCTION EXPENSES PAID 2,221,040 959,343 1,261,697عموالت مدفوعة ومصروفات انتاج

GENERAL AND ADMINISTRATIVE EXPENSES 2,226,153 523,755 1,702,398مصروفات ادارية وعمومية

TOTAL PROVISIONS 249,802 34,070 215,732اجمالي المخصصات

CURRENT RISKS AT THE END OF THE YEAR 5,008,462 1,946,693 3,061,768احتياطي االخطار السارية في اخر السنة

ADDITIONAL RESERVES AT THE END OF THE YEAR 375,226 40,629 334,597احتياطي اضافي في اخر السنة

NET OUTSTANDING CLAIMS RESERVES AT THE END OF THE YEAR 6,416,308 2,573,972 3,842,336صافي احتياطي التعويضات تحت التسوية في اخر السنة

PROFIT C/F TO PROFIT AND LOSS ACCOUNT 1,339,757 353,833 985,923الفائض المرحل الى حساب االرباح والخسائر

TOTAL 29,648,636 9,493,478 20,155,159جملة المصروفات

2015

STATEMENTبيــــــــــــــــــان

31 December 2015

P a g e | 42

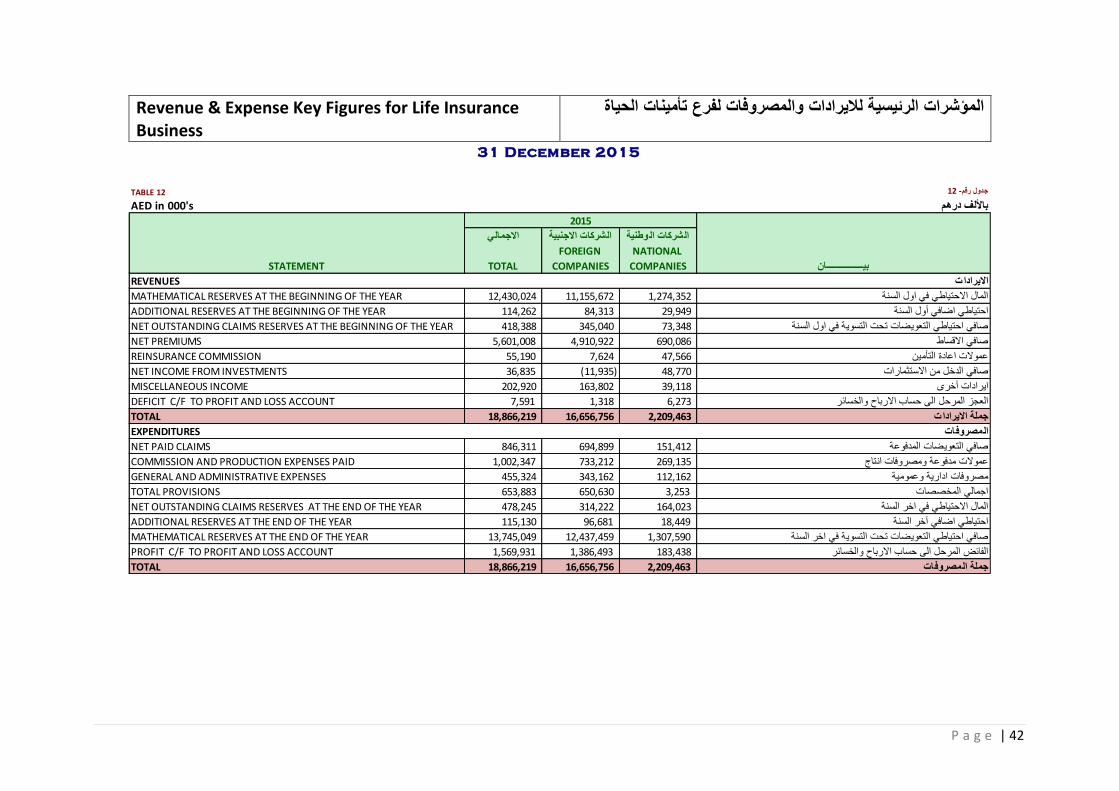

Revenue & Expense Key Figures for Life Insurance Business

الحياة تأمينات لفرع والمصروفات لاليرادات الرئيسية المؤشرات

TABLE 12جدول رقم- 12

AED in 000'sباأللف درهم

وطنية االجماليالشركات االجنبيةالشركات ال

بيــــــــــــــــان

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTALSTATEMENT

REVENUESااليرادات

MATHEMATICAL RESERVES AT THE BEGINNING OF THE YEAR 1,274,35211,155,67212,430,024المال االحتياطي في اول السنة

ADDITIONAL RESERVES AT THE BEGINNING OF THE YEAR 29,94984,313114,262احتياطي اضافي أول السنة

NET OUTSTANDING CLAIMS RESERVES AT THE BEGINNING OF THE YEAR 73,348345,040418,388صافي احتياطي التعويضات تحت التسوية في اول السنة

NET PREMIUMS 690,0864,910,9225,601,008صافي االقساط

REINSURANCE COMMISSION 47,5667,62455,190عموالت اعادة التأمين

NET INCOME FROM INVESTMENTS 36,835(11,935)48,770صافي الدخل من االستثمارات

MISCELLANEOUS INCOME 39,118163,802202,920ايرادات أخرى

DEFICIT C/F TO PROFIT AND LOSS ACCOUNT 6,2731,3187,591العجز المرحل الى حساب االرباح والخسائر

TOTAL 2,209,46316,656,75618,866,219جملة االيرادات

EXPENDITURESالمصروفات

NET PAID CLAIMS 846,311 694,899 151,412صافي التعويضات المدفوعة

COMMISSION AND PRODUCTION EXPENSES PAID 1,002,347 733,212 269,135عموالت مدفوعة ومصروفات انتاج

GENERAL AND ADMINISTRATIVE EXPENSES 455,324 343,162 112,162مصروفات ادارية وعمومية

TOTAL PROVISIONS 653,883 650,630 3,253اجمالي المخصصات

NET OUTSTANDING CLAIMS RESERVES AT THE END OF THE YEAR 478,245 314,222 164,023المال االحتياطي في اخر السنة

ADDITIONAL RESERVES AT THE END OF THE YEAR 115,130 96,681 18,449احتياطي اضافي آخر السنة

MATHEMATICAL RESERVES AT THE END OF THE YEAR 13,745,049 12,437,459 1,307,590صافي احتياطي التعويضات تحت التسوية في اخر السنة

PROFIT C/F TO PROFIT AND LOSS ACCOUNT 1,569,931 1,386,493 183,438الفائض المرحل الى حساب االرباح والخسائر

TOTAL 18,866,219 16,656,756 2,209,463جملة المصروفات

2015

31 December 2015

P a g e | 43

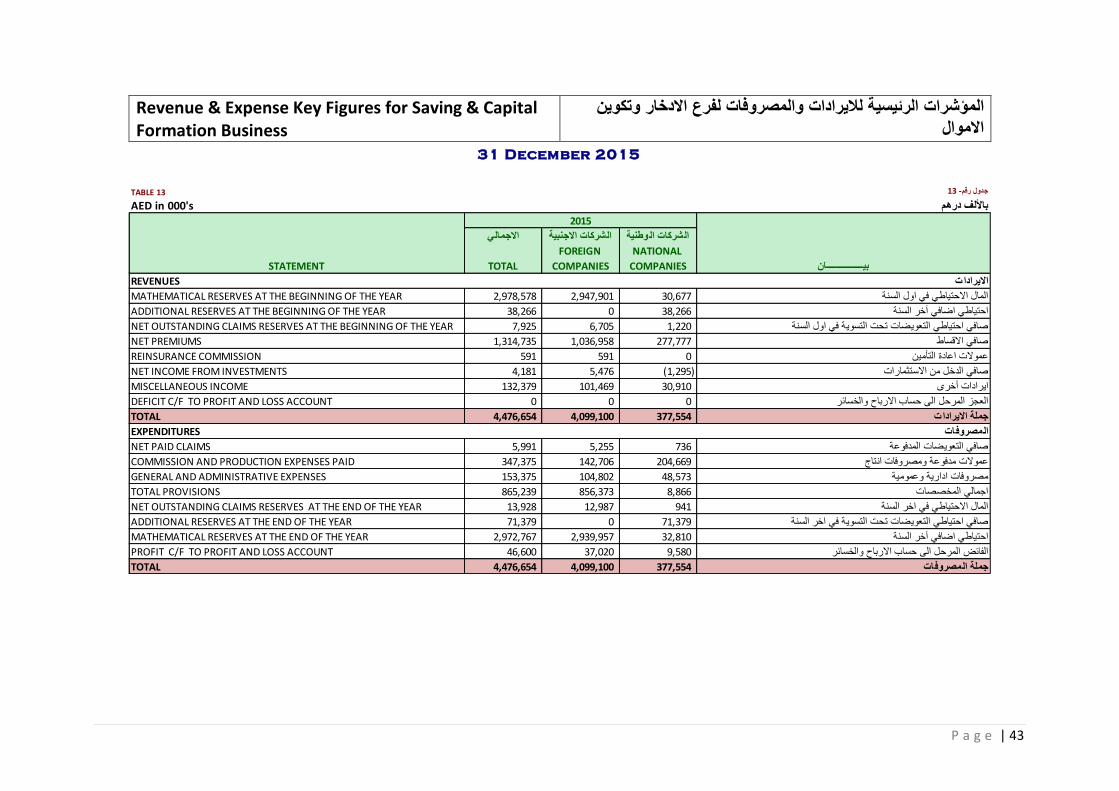

Revenue & Expense Key Figures for Saving & Capital Formation Business

وتكوين االدخار لفرع والمصروفات لاليرادات الرئيسية المؤشرات االموال

TABLE 13جدول رقم- 13

AED in 000'sباأللف درهم

وطنية االجماليالشركات االجنبيةالشركات ال

بيــــــــــــــــان

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTALSTATEMENT

REVENUESااليرادات

30,6772,947,9012,978,578MATHEMATICAL RESERVES AT THE BEGINNING OF THE YEARالمال االحتياطي في اول السنة

38,266038,266ADDITIONAL RESERVES AT THE BEGINNING OF THE YEARاحتياطي اضافي آخر السنة

1,2206,7057,925NET OUTSTANDING CLAIMS RESERVES AT THE BEGINNING OF THE YEARصافي احتياطي التعويضات تحت التسوية في اول السنة

277,7771,036,9581,314,735NET PREMIUMSصافي االقساط

0591591REINSURANCE COMMISSIONعموالت اعادة التأمين

5,4764,181NET INCOME FROM INVESTMENTS(1,295)صافي الدخل من االستثمارات

30,910101,469132,379MISCELLANEOUS INCOMEايرادات أخرى

000DEFICIT C/F TO PROFIT AND LOSS ACCOUNTالعجز المرحل الى حساب االرباح والخسائر

377,5544,099,1004,476,654TOTALجملة االيرادات

EXPENDITURESالمصروفات

7365,2555,991NET PAID CLAIMSصافي التعويضات المدفوعة

204,669142,706347,375COMMISSION AND PRODUCTION EXPENSES PAIDعموالت مدفوعة ومصروفات انتاج

48,573104,802153,375GENERAL AND ADMINISTRATIVE EXPENSESمصروفات ادارية وعمومية

8,866856,373865,239TOTAL PROVISIONSاجمالي المخصصات

94112,98713,928NET OUTSTANDING CLAIMS RESERVES AT THE END OF THE YEARالمال االحتياطي في اخر السنة

71,379071,379ADDITIONAL RESERVES AT THE END OF THE YEARصافي احتياطي التعويضات تحت التسوية في اخر السنة

32,8102,939,9572,972,767MATHEMATICAL RESERVES AT THE END OF THE YEARاحتياطي اضافي آخر السنة

9,58037,02046,600PROFIT C/F TO PROFIT AND LOSS ACCOUNTالفائض المرحل الى حساب االرباح والخسائر

377,5544,099,1004,476,654TOTALجملة المصروفات

2015

31 December 2015

P a g e | 44

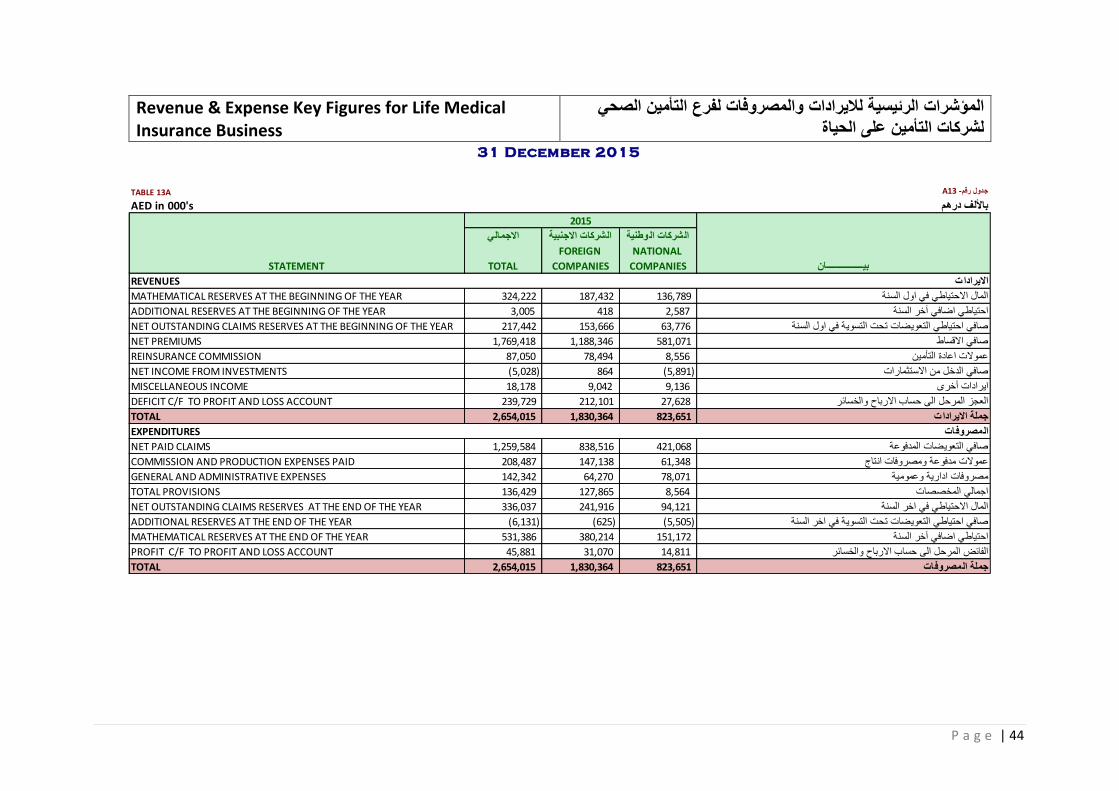

Revenue & Expense Key Figures for Life Medical Insurance Business

الصحي التأمين لفرع والمصروفات لاليرادات الرئيسية المؤشرات الحياة على التأمين لشركات

A13 -جدول رقمTABLE 13A

AED in 000'sباأللف درهم

وطنية االجماليالشركات االجنبيةالشركات ال

بيــــــــــــــــان

NATIONAL

COMPANIES

FOREIGN

COMPANIESTOTALSTATEMENT

REVENUESااليرادات

MATHEMATICAL RESERVES AT THE BEGINNING OF THE YEAR 324,222 187,432 136,789المال االحتياطي في اول السنة

ADDITIONAL RESERVES AT THE BEGINNING OF THE YEAR 3,005 418 2,587احتياطي اضافي آخر السنة

NET OUTSTANDING CLAIMS RESERVES AT THE BEGINNING OF THE YEAR 217,442 153,666 63,776صافي احتياطي التعويضات تحت التسوية في اول السنة

NET PREMIUMS 1,769,418 1,188,346 581,071صافي االقساط

REINSURANCE COMMISSION 87,050 78,494 8,556عموالت اعادة التأمين

NET INCOME FROM INVESTMENTS (5,028) 864 (5,891)صافي الدخل من االستثمارات

MISCELLANEOUS INCOME 18,178 9,042 9,136ايرادات أخرى

DEFICIT C/F TO PROFIT AND LOSS ACCOUNT 239,729 212,101 27,628العجز المرحل الى حساب االرباح والخسائر

TOTAL 2,654,015 1,830,364 823,651جملة االيرادات

EXPENDITURESالمصروفات

NET PAID CLAIMS 1,259,584 838,516 421,068صافي التعويضات المدفوعة

COMMISSION AND PRODUCTION EXPENSES PAID 208,487 147,138 61,348عموالت مدفوعة ومصروفات انتاج

GENERAL AND ADMINISTRATIVE EXPENSES 142,342 64,270 78,071مصروفات ادارية وعمومية

TOTAL PROVISIONS 136,429 127,865 8,564اجمالي المخصصات

NET OUTSTANDING CLAIMS RESERVES AT THE END OF THE YEAR 336,037 241,916 94,121المال االحتياطي في اخر السنة

ADDITIONAL RESERVES AT THE END OF THE YEAR (6,131) (625) (5,505)صافي احتياطي التعويضات تحت التسوية في اخر السنة

MATHEMATICAL RESERVES AT THE END OF THE YEAR 531,386 380,214 151,172احتياطي اضافي آخر السنة

PROFIT C/F TO PROFIT AND LOSS ACCOUNT 45,881 31,070 14,811الفائض المرحل الى حساب االرباح والخسائر

TOTAL 2,654,015 1,830,364 823,651جملة المصروفات

2015

31 December 2015

P a g e | 45

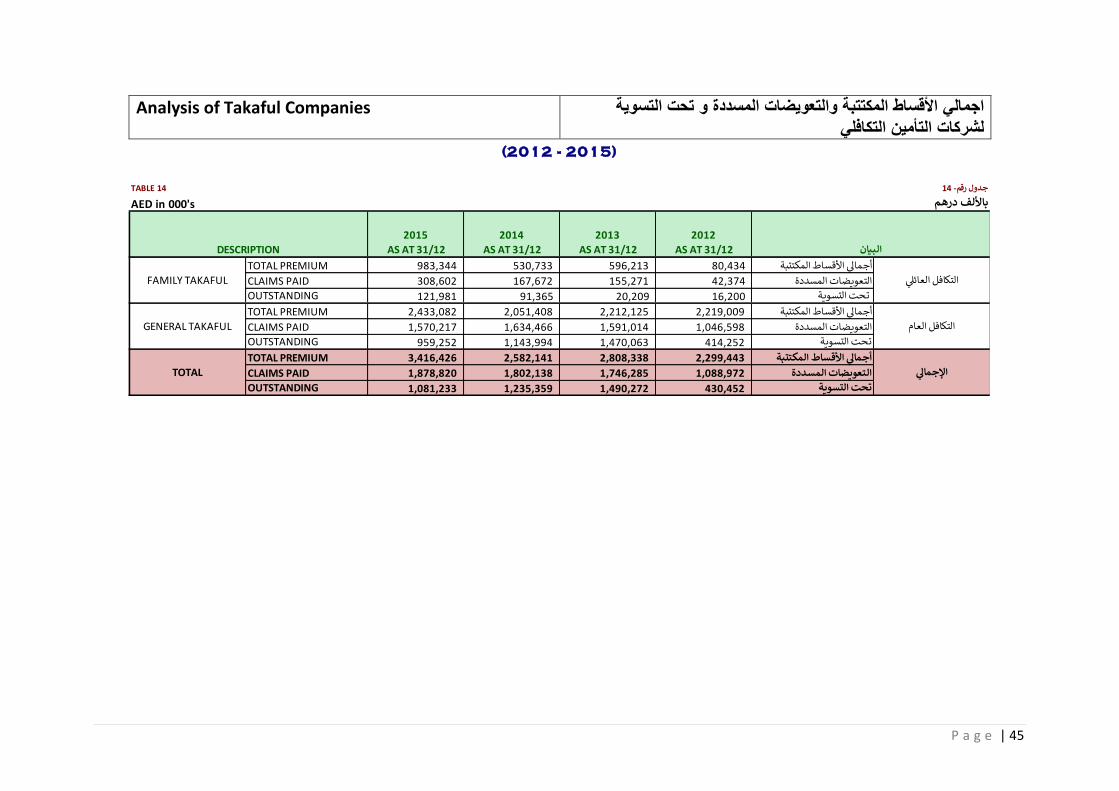

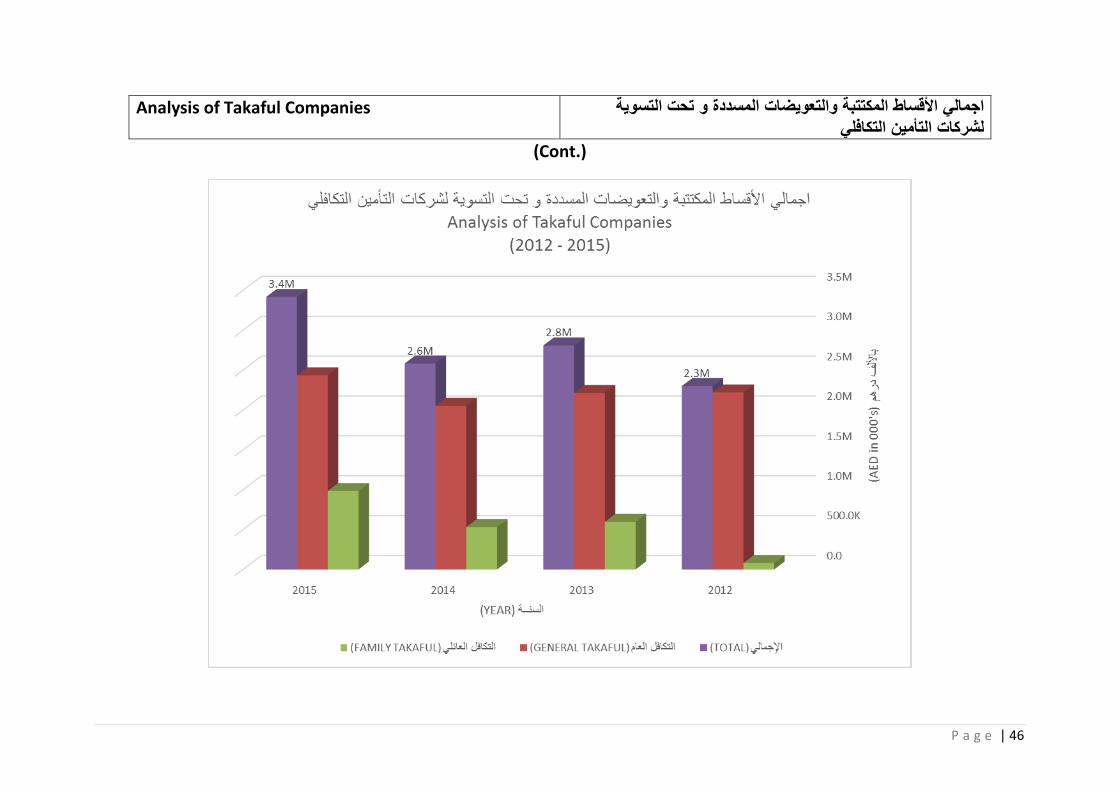

Analysis of Takaful Companies التسوية تحت و المسددة والتعويضات المكتتبة األقساط اجمالي التكافلي التأمين لشركات

TABLE 14جدول رقم- 14

AED in 000'sباأللف درهم

2012201320142015

AS AT 31/12 AS AT 31/12 AS AT 31/12 AS AT 31/12

TOTAL PREMIUM 983,344 530,733 596,213 80,434أجمالي األقساط المكتتبة

CLAIMS PAID 308,602 167,672 155,271 42,374التعويضات المسددة

OUTSTANDING 121,981 91,365 20,209 16,200 تحت التسوية

TOTAL PREMIUM 2,433,082 2,051,408 2,212,125 2,219,009أجمالي األقساط المكتتبة

CLAIMS PAID 1,570,217 1,634,466 1,591,014 1,046,598التعويضات المسددة

OUTSTANDING 959,252 1,143,994 1,470,063 414,252تحت التسوية

TOTAL PREMIUM 3,416,426 2,582,141 2,808,338 2,299,443أجمالي األقساط المكتتبة

CLAIMS PAID 1,878,820 1,802,138 1,746,285 1,088,972التعويضات المسددة

OUTSTANDING 1,081,233 1,235,359 1,490,272 430,452تحت التسويةاإلجمالي

التكافل العام

FAMILY TAKAFULالتكافل العائلي

GENERAL TAKAFUL

TOTAL

البيان

(2012 - 2015)

DESCRIPTION

P a g e | 46

Analysis of Takaful Companies التسوية تحت و المسددة والتعويضات المكتتبة األقساط اجمالي التكافلي التأمين لشركات

(Cont.)