Embed Size (px)

Citation preview

ANNUAL REPORT2016

SN POWER

10

20

15

8

Financial Statements

Message from the CEO

Our Presence & Operations

Board of Directors’ Report

About SN Power

3

THIS IS SN POWER

About SN Power .................................3Key Figures ..........................................4Key Events ...........................................5Message from the CEO ....................8Presence and Operations ............. 10Corporate Governance ...................12Prorata Income Statement .......... 14Board of Directors’ Report ........... 15

FINANCIAL STATEMENTS

SN POWER GROUPAccounts 2016 ................................. 21Notes 2016 ....................................... 25

SN POWER ASAccounts 2016 .................................48Notes 2016 ....................................... 52

Auditor’s Report .............................. 59

SN POWER ANNUAL REPORT 2016 3

SN POWER

YEAR 2016

ABOUT

THIS IS SN POWER

About the Company

SN Power (SN Power AS) was re-established in June 2014, after a restructuring of the company founded in 2002 (Statkraft Norfund Power Invest AS). The ownership is split 50/50 between the two founding partners Statkraft and Norfund.SN Power is operating on commercial terms with the objective of investing in renewable energy production in developing markets globally. The overall business concept is to acquire, develop, construct, own and operate sustainable hydropower projects.

SN Power has diversified its portfolio across different regions and are currently operating hydropower plants in the Philippines, Laos, Zambia and Panama. In addition to the operating markets the company is looking at new greenfield in the regions where it operates.

The operational part of the business in Africa and Central America is currently operated through the subsidiary Agua Imara AS where Bergenshalvøens Kommunale Kraftselskap (BKK) is a significant co-owner.

Our Owners With Statkraft as one of its owners, SN Power has a strong industrial foundation, built on more than 120

years of experience in developing, owning and operating hydropower in Norway. Statkraft is a European leader within renewable energy, with approximately 66 TWh in annual power production. Through Statkraft, SN Power has access to significant experience and expertise.

Norfund is the Norwegian Investment Fund for Developing Countries, which invests risk capital in profitable private enterprises in Africa, Asia and Central America. Through Norfund, SN Power has access to significant experience and expertise in investing in developing markets.

Where we are heading SN Power, as a business, has clear core competencies, the network, the knowledge and the financial capacity to actively seek out exciting opportunities in high potential, yet often challenging, markets, alongside a proven ability to optimize return from existing assets.

Key to SN Power’s strategy is the company’s overall strategy to be a long-term industrial investor, capitalizing on Norwegian and international hydropower competence and expertise.

It is a part of SN Power’s mission to contribute to a sustainable development through its investment. All projects we enter into shall have a minimal adverse effect on society and the environment, and yield positive impact and benefits for both local communities and society through the increased generation of renewable energy. Read more on www.snpower.com

VISIONPowering development through renewable energy.

MISSIONTo become a leading hydropower company in emerging

markets, contributing to economic growth and sustainable development.

COMPETENCE: using knowledge and experience to achieve ambitious goals and be recognized as a leader.

RESPONSIBILITY:creating value while showing respect for employees, customers, the environment and society.

INNOVATION:thinking creatively, identifying opportunities and developing effective solutions.

CORE VALUES

ABOUT SN POWER

SN POWER ANNUAL REPORT 2016 4

KEY FIGURES

YEAR 2016

SN POWER

KEY FIGURES

THIS IS SN POWER

1) Consolidated numbers, excluding income from associated companies/joint ventures. 2) Long-term and short term liabilities to financial institutions / Total equity 3) Equity / Assets

UNIT 2016 2015GROSS POWER PORTFOLIOSN Power share of installed capacity MW 450 450 Gross production, actual GWh 3,826 3,934 Net production (SN Power share) GWh 1,213 1,157

FINANCIALSGross operating revenue MUSD 33 28 Income from associated companies / JVs MUSD 48 57 EBITDA 1) MUSD 3 -5 Net Earnings after tax MUSD -37 34 Cash Flow from operational activities MUSD 93 46 Cash and cash equivalents MUSD 220 148 Equity MUSD 954 1,015 Equity investments from SN Power MUSD 1 6 Repaid capital on investments to SN Power MUSD - 57 New equity MUSD - - Interest bearing debt\equity ratio 2) % 15% 24%Equity ratio 3) % 80% 80%

HUMAN CAPITALEmployees Number 136 136 Sickness absence % 1.9 % 1.5 %Total recordable injury rate - Operations 1.6 2.4 Total recordable injury rate - Projects 3.3 6.1

ENVIRONMENT Environmental fines MUSD - -

SN POWER ANNUAL REPORT 2016 5

KEY EVENTS

YEAR 2016

SN POWER

KEY EVENTS 2016

THIS IS SN POWER

JANUARY

PHASE II OF MIDDLE YEYWA FEASIBILITY STUDY

In 2014 SN Power signed an MOU with the Government of Myanmar for the development of a project east of Mandalay and is now working on the feasibility study to be completed during the third quarter of 2017. During this period SN Power will agree with the Government on the basic commercial terms, and do an Environmental and Social Impact Assessment.

SN Aboitiz Power started the construction of the Maris Canal Project in the Philippines which is located approximately 5.5 km downstream from the Magat dam, with the Maris reservoir situated between the two dams.

The Maris Canal Project will have an installed capacity of 8.5 MW and produce 45 GWh of energy per year.

The project includes the refurbishment of 12 irrigation control gates located on the intake to the Maris South Canal and is projected to be completed by February 2018.

CONSTRUCTION START OF MARIS CANAL

SN POWER ANNUAL REPORT 2016 6

KEY EVENTS 2016

THIS IS SN POWER

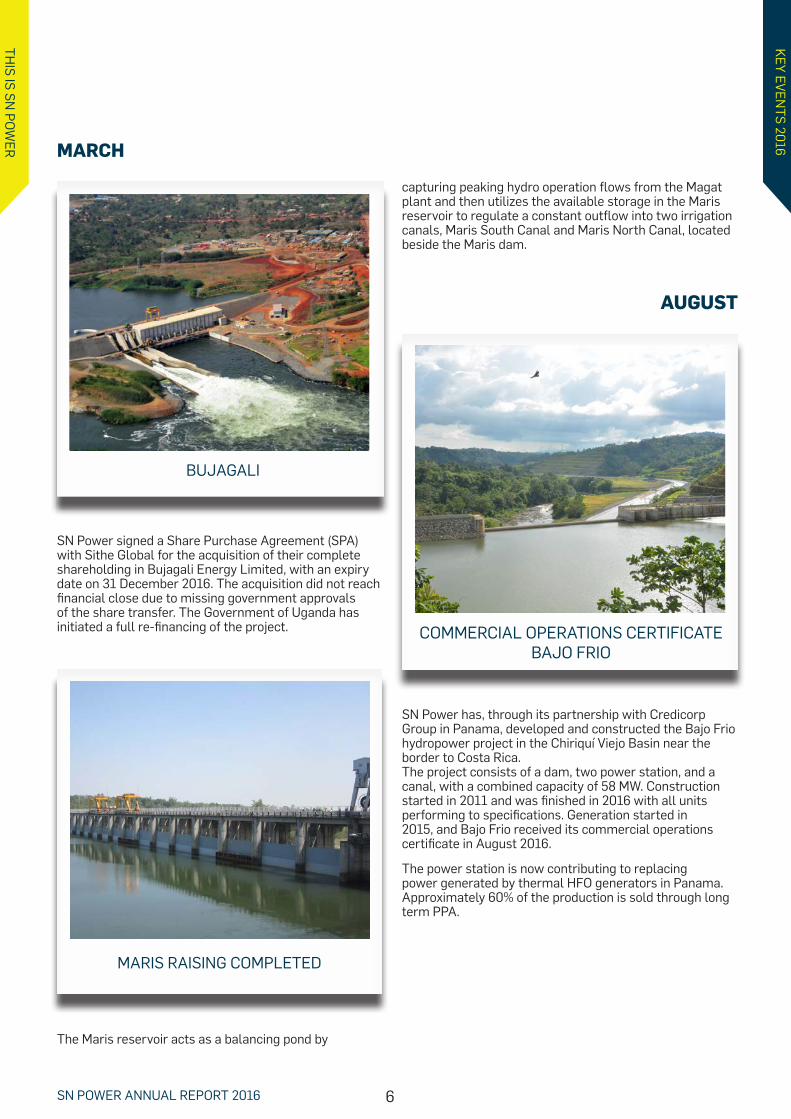

SN Power has, through its partnership with Credicorp Group in Panama, developed and constructed the Bajo Frio hydropower project in the Chiriquí Viejo Basin near the border to Costa Rica. The project consists of a dam, two power station, and a canal, with a combined capacity of 58 MW. Construction started in 2011 and was finished in 2016 with all units performing to specifications. Generation started in 2015, and Bajo Frio received its commercial operations certificate in August 2016.

The power station is now contributing to replacing power generated by thermal HFO generators in Panama. Approximately 60% of the production is sold through long term PPA.

AUGUST

MARIS RAISING COMPLETED

COMMERCIAL OPERATIONS CERTIFICATE BAJO FRIO

SN Power signed a Share Purchase Agreement (SPA) with Sithe Global for the acquisition of their complete shareholding in Bujagali Energy Limited, with an expiry date on 31 December 2016. The acquisition did not reach financial close due to missing government approvals of the share transfer. The Government of Uganda has initiated a full re-financing of the project.

MARCH

BUJAGALI

capturing peaking hydro operation flows from the Magat plant and then utilizes the available storage in the Maris reservoir to regulate a constant outflow into two irrigation canals, Maris South Canal and Maris North Canal, located beside the Maris dam.

The Maris reservoir acts as a balancing pond by

SN POWER ANNUAL REPORT 2016 7

KEY EVENTS 2016

THIS IS SN POWER

DECEMBER

THPC

SN Power signed a Head of Terms agreement with Industrial Promotion Services (IPS) and started a due diligence process to potentially enter the 147 MW Ruzizi III hydropower project located on the river bordering the Democratic Republic of the Congo (Congo) and Rwanda as IPS’ technical partner, and replace Sithe Global. As a result of a total evaluation of the project the Board of SNP decided not to pursue this opportunity. Norfund decided on this basis to continue the development of the project on a 100% basis, based on a full management service agreement with SN Power.

The expected start of construction is in 2019 and the estimated commercial operation date in 2024.

RUZIZI III

Fifty-two of the fifty-six villages (96%) included in THPC’s Social and Economic development (SED) program reached the consumption targets, set under the program. The reminder of the villages are expected to graduate THPC’s program by the end of 2017.

OCTOBER

SAFE OPERATIONS PROJECT LHPC

SN Power’s 51% owned subsidiary Lunsemfwa Hydro Power Company (LHPC) started the Safe Operations project, which will secure and stabilize energy supply from its two aging power stations, Lunsemfwa and Mulungushi, for the years to come. The project will be completed by the end of the first quarter of 2017.

SN POWER ANNUAL REPORT 2016 8

TORGER LIEN

PRESIDENT & CEO

THIS IS SN POWER

MESSAGE FROM

MESSAGE FROM

THE CEO

For SN Power, 2016 was a year with good operational results, high activity on business and project development, improved HSE benchmarking figures and important restructuring activities in the organization.

Overall the year was relatively dry in all our four operating countries, but in the last part of the year precipitation picked up and we experienced good inflows and increasing reservoir levels well into 2017.

Spot prices in Panama and Philippines have remained relatively low, mainly due to increased overall generation capacity and low coal and gas prices. Our two construction projects, Maris Canal in the Philippines, and the Safety Upgrade project in Zambia, are developing according to plan.

Focus on growth on a sound commercial basis.The new management structure implemented during 2015, has resulted in a handful of promising project opportunities in Africa and South East Asia. These have been further developed during 2016. The development strategy has been adjusted to increase the commercial efforts in the early stages of the projects, delaying costly technical and environmental studies until solutions to the main commercial challenges have been found. The main hurdle and challenge for hydropower projects in developing markets is the power off-take solution. Power Purchase Agreements (PPAs), governmental guaranties, and license arrangements are prerequisites for viability of projects. With the high number of projects failing in the

development phase due to unacceptable commercial conditions, additional financing of early stage activity combined with reduced development costs are required to stay competitive. This work has started and we already see concrete results.

Making hydropower competitive in a fast-developing renewable energy marketNew renewable generation such as solar PV and wind, gain competitive ground year by year. Cost of generation is now in many markets at grid parity, and the steady yearly cost reduction per kilowatt installed capacity seems to continue. From an environmental perspective, this is very welcome, but for SN Power, concentrating on hydropower, it becomes more and more difficult to compete on a pure energy basis, as hydropower is delivering a different product. It is still the dominant renewable flexible

SN POWER ANNUAL REPORT 2016 9

MESSAGE FROM

THE CEO

THIS IS SN POWER

SN Power is well positioned to continue to be a major player within the renewable power sector

in developing countries for years to come

“Torger Lien, CEO

generation source, and it has by far the best ability to deliver grid services required in modern grid structures. Even with a six to eight hours storage capacity, a run of river hydro plant delivers a totally different product than solar and wind which are 100% intermittent. By fully utilizing the features of hydro generation and making the most out of its comparative advantages, we are convinced that hydropower will continue to have a strong position in the renewable energy sector.

Fossil fuels still dominant in many markets.Even if new renewables are growing with an impressive rate, power generation based on fossil fuels will still be dominant in many of our markets and will therefore be central in price formation in these markets in the coming years. In Panama, existing fuel oil and new gas power plants based on LNG will be the price setters. As a result of lower future fuel price outlook, we have been forced to revise our market outlook for electricity prices, reducing expected future earnings. This is a fundamentally different situation from the one we expected four to five years ago. For new projects under development, robustness against lower energy cost, and certainty through firm PPA’s, will be given increased weight going forward.

Adapting to new market conditionsHydro power projects take more time to develop than most other power generating alternatives. On the other hand, they have a lifetime far exceeding these alternatives. To be competitive as a hydropower

Torger LienPresident & CEO

developer in today’s market the cost of development must be on par with short-time-to-market solar and wind projects. In SN Power, we have adapted the organization to the new situation and Agua Imara has been restructured to become a pure asset management company. Business- and project development is concentrated in SN Power. Local offices have been reduced or scaled down. Local knowledge through local employees is prioritized over expatriates from the head office in Oslo. Local partnerships and consortium structures reducing cost during development and construction are under implementation.

With these measures, I am convinced that hydropower remains a strong competitive alternative, and that it offers products that will be in demand also in the future electricity markets. SN Power is well positioned to continue to be a major player in developing flexible renewable generation projects in developing countries in Africa and South East Asia.

SN POWER ANNUAL REPORT 2016 10

PRESENCE &

OPERATIONSYEAR 2016

SN POWER

THIS IS SN POWER

PRESENCE AND OPERATIONS

PHILIPPINES SN Power entered the Filipino market in 2006. The Joint Venture between SN Power and the Aboitiz Group owns three hydro power plants in the country, Ambuklao, Binga and Magat as well as the Maris Canal 8.5 MW project which is under construction and will be commissioned this year. The joint venture has a pipeline of other possible projects in the Philippines.

Ambuklao Ambuklao was commissioned by the National Power Corporation in 1956 and is one of the oldest hydropower plants in the Philippines. In 2008, SN Aboitiz Power (SNAP) bought the plant and it has since then gone through a major rehabilitation. The plant was recommissioned in 2011 with a new installed capacity of 105 MW from previously 75 MW.

Location: Benguet Province, Luzon Installed capacity: 105 MW Average output: 332 GWh

SN Power Ownership: 50% Other Owners: Aboitiz Power 50% Commercial operation: 1956 Power Purchase: The electricity generated is sold in the spot market or through bilateral contracts at Wholesale Electricity Spot Market (WESM) or in the reserve market as ancillary services.

Binga The Binga hydropower plant is also currently in operation and has gone through a major rehabilitation including replacement of most electrical and mechanical components. The project has been uprated from 100 MW to 140 MW

Location: Benguet Province, Luzon Installed capacity: 140 MW Average output: 430 GWh SN Power Ownership: 50% Other Owners: Aboitiz Power 50% Commercial operation: 1960 Power Purchase: The electricity generated is sold in the spot market or through bilateral contracts at WESM or in the reserve market as ancillary services.

Magat Magat is a multipurpose dam. As it is the source for almost 85,000 hectares of rice fields downstream, the main purpose of the dam is irrigation.

Location: Ifugao and Isabel Provinces, Luzon Installed capacity: 380 MW Average output: 929 GWh SN Power Ownership: 50% Other Owners: Aboitiz Power 50% Commercial operation: 1983 Power Purchase: The electricity generated is sold in the spot market or through bilateral contracts at Wholesale Electricity Spot Market (WESM) or in the reserve market as ancillary services.

Ambuklao spillway, Philippines

LAOSTheun Hinboun In September 2014 SNP acquired 20% of the shares in the Theun Hinboun Power Company (THPC) in Laos from Statkraft, who had been a partner in the project since the beginning in 1993. The project was developed in two stages, the second of which was commissioned in late 2012. THPC’s other shareholders are EdL Generation PLC from Laos with 60% and GMS Power Public Company Limited from Thailand with 20%. THPC was the first privately developed and financed hydropower project in Laos and has won several international awards for its development.

Theun Hinboun, Laos

SN POWER ANNUAL REPORT 2016 11

THIS IS SN POWER

PRESENCE AND OPERATIONS

Location: Bolikhamxay and Khammouane provinces of Southeast Laos Installed capacity: 500 MW Average output: 3,292 GWh SN Power Ownership: 20% Other Owners: EdL Generation in Laos 60% and GMS Power in Thailand 20% Commercial operation: 210 MW in 1998 and 290 MW in 2012 Power Purchase: Long term contracts to Laos and Thailand

ZAMBIA In 2011, Agua Imara acquired a 51% shareholding in Lunsemfwa Hydropower Company Ltd (LHPC). LHPC currently owns two hydropower plants, Mulungushi and Lunsemfwa with a combined generation capacity of 56 MW.

Mulungushi The Mulungushi power station comprises a regulation reservoir, a canal and penstocks to a surface powerhouse. The power station has been developed in stages with the first unit installed in 1925.

Location: Near Kabwe in the Central Province Installed capacity: 32 MW Average output: 238 GWh Agua Imara ownership: 51% Other owners: Wanda Gorge Investments (WGI) Commercial operation: 1925

Lunsemfwa The Lunsemfwa power station comprises a reservoir, a canal and penstocks to a surface powerhouse. The power station was constructed in 1945 with two 6 MW units. The power plant was operated as a run-of-river scheme until 1958 when the Mita Hills dam was built. A third 6 MW unit was installed in 1961. With a fourth unit installed in 2012, Lunsemfwa hydropower project today has the capacity of 24 MW.

Location: Near Kabwe in the Central Province Installed capacity: 24 MW Average output: 190 GWh Agua Imara ownership: 51% Other owners: Wanda Gorge Investments (WGI) Commercial operation: 1945

Muchinga LHPC fully owns the Muchinga Power Company which has a license to develop a new hydropower plant with a potential capacity of 150 – 250 MW. A new Muchinga hydropower plant will harness the hydropower potential of the Lunsemfwa and Mkushi rivers and would be located downstream of the existing Lunsemfwa plant.

Myitnge River, Myanmar

PANAMA SN Power has been present in Panama since 2010, and have an office in Panama City through its Subsidiary Agua Imara. Agua Imara owns 50.1% of Fountain Intertrade Corporation. The remaining share is owned by our local partner in Panama, the Credicorp Group. SN Power has two projects in the country – Bajo Frio and Burica. Bajo Frio started production in 2015, while Burica is still in the early construction planning phase.

Bajo Frio Bajo Frio is a run-of river hydropower scheme with two powerhouses and a dam. It’s located in the lower part of the Chiriquí Viejo River in the Chiriquí province in western Panama. Location: Chiriquí province in western Panama Installed capacity: 58 MW Agua Imara ownership: 50.1% Other owners: Credicorp Group 49.9% Generation started: 2015 Commercial operations Certificate: 2016

Burica Burica is located directly downstream of the Bajo Frio project in the Chiriquí Viejo Basin.

Location: Chiriquí province in western Panama Installed capacity: 63 MW Owner: Burica Hydropower SA Agua Imara Ownership: 50.1% Other owners: Credicorp Group 49.9%

Bajo Frio, Panama

Muchinga, Zambia

MYANMAR SN Power has been monitoring developments in Myanmar for several years, more extensively since 2011 as major reforms swept through the country. In 2014 SN Power signed a Memorandum of Understanding (MoU) with the Government of Myanmar. SN Power completed a pre-feasibility study and is now working on a feasibility study on a hydro power project located east of Mandalay.

SN POWER ANNUAL REPORT 2016 12

CORPORATE GOVERNANCE

YEAR 2016

SN POWER

THIS IS SN POWER

CORPORATE GOVERNANCE

SN Power complies with international corporate governance practices, and its principles are based on the Norwegian Code of Practice for Corporate Governance (NUES). Non-compliances are attributable to the fact that SN Power is not a publicly listed company as it is owned by Statkraft and Norfund, and restrictions contained in the Articles of Association. A statement concerning follow-up of the items in the Norwegian Code of Practice for Corporate Governance is given below.1. Corporate governance statement The basis for the board of SN Power’s corporate governance work is the Norwegian Code of Practice for Corporate Governance.

The code has been applied to the extent permitted by the company’s organisation and ownership. Non-compliances are attributable to the fact that SN Power is not a publicly listed company, that it is owned by Statkraft and Norfund, as well as restrictions contained in the Articles of Association. The non-compliances relate to non-discrimination of shareholders, tradability of shares, the annual general meeting, nomination committee, the corporate assembly, and take over.

SN Power’s policy for corporate governance establishes the relationship between the company’s owners, board of directors, and management.

2. Business SN Power’s Articles of Association state that: “The company’s objectives are, alone, in cooperation with or through ownership in other companies, to develop, construct, acquire, own and manage renewable energy plants in South East Asia, Sub-Sahara Africa and Central America, with focus on hydro power projects and other naturally related activities, including financial and physical power trading”.

SN Power AS is registered in Norway and its

management structure is based on Norwegian company law and the Limited Companies Act. In addition, the company’s Articles of Association, vision, values, code of conduct, corporate governance policies and ethical guidelines are guiding for the company’s business.

A summary of the vision, values, and code of conduct can be viewed at www.snpower.com

3. Share capital and dividend SN Power AS’ share capital is NOK 5,176,315,600 divided on 51,763,156 shares, with a nominal value of NOK 100 each. The legal share capital in NOK corresponds to booked share capital of USD 852,643,426 due to the fact that SN Power AS’ functional currency is USD.

It is the joint intention and purpose of the shareholders that SN Power shall be a going concern and shall be independently viable in all possible aspects. The shareholders shall exert their individual best efforts to make the company viable and profitable.

The company’s long term goal is to have an annual pay-out ratio of at least 40% of net profit.

See note 3 and 22 for more information about the management of the capital structure and note 19 for shares and shareholder information.

4. Equal treatment of shareholders and transactions with related parties 50% of the shares in SN Power AS are owned by the state-owned enterprise Statkraft AS and the remaining 50% by the Norwegian investment fund for developing countries, Norfund. The Shareholder Agreement defines the treatment of shareholders and transactions with related parties.

See note 24 and 8 for further information about related parties.

5. Freely negotiable N/A, shares are not traded in the open market.

6. General meeting The shareholders exercise supreme authority over SN Power AS through the annual general meeting. In accordance with the Articles of Association the annual general meeting shall be held annually before the end of June.

The company’s annual accounts and the auditor’s statement must be presented at the general meeting, and the following items must be discussed and resolved:

1. Approval of profit and loss accounts and balance sheet, including distribution of annual profit or coverage of loss.

2. Approval of group profit and loss accounts and group balance sheet.

3. Other matters that according to law or the articles

SN POWER ANNUAL REPORT 2016 13

THIS IS SN POWER

CORPORATE GOVERNANCE

of association fall within the scope of the general meeting.

7. Nomination committee N/A. There is no nomination committee.

8. The corporate assembly and board of directors, composition and independence Pursuant to the Norwegian Public Limited Liability Companies Act, SN Power AS does not have a corporate assembly as it has fewer than 200 employees.

SN Power’s board of directors shall have 2 - 8 members. The chairperson of the board and one board member or the general manager are jointly authorised to sign for the company. The company has per December 2016 6 directors. 3 directors, including the chairperson, are nominated by Statkraft and 3 are nominated by Norfund.

The board members are evaluated on the basis of their expertise and independence. The board shall furthermore be independent of the company’s executive employees. The current challenges facing the company are taken into consideration in establishing the composition of the board.

9. The work of the board of directors The board has established rules of procedure for the board of SN Power AS that lay down guidelines for the board’s work and decision-making procedures. The board’s tasks are described in general by Norwegian company law and the company’s Articles of Association. The rules of procedure also define the tasks and obligations of the chairperson and CEO in relation to the board.

Due to its size and that SN Power AS is not publicly listed, it does not have an audit committee nor a compensation committee. The board will undertake an annual evaluation of its own performance. The purpose of the evaluation is to improve board effectiveness. The chairperson will act on the results of the performance evaluation by recognizing the strengths and addressing the weaknesses of the board. The annual general meeting determines the remuneration of the board members.

See Report from the Board of Directors for more information about the work of the board of directors.

10. Risk management and internal control SN Power’s investments are made in emerging markets in South East Asia, Sub-Sahara Africa and Central America, and are to a great extent exposed to a high level of risk in terms of their future return. SN Power is continuously working to improve its methods for risk management to measure, mitigate, and manage this risk exposure.

Comprehensive risk analysis techniques covering financial, economic, social, environmental, and political factors have been established in the company’s project management system. The methods identify risk at an early phase in the valuation process and implement appropriate mitigation plans which are monitored through the projects.

As part of the Group’s internal control system, Statkraft’s corporate audit function assists the SN Power board and management in making an independent and impartial evaluation of the Group’s key risk management and control procedures. Statkraft Corporate Audit shall also contribute to on-going quality improvement in internal management and control systems. The annual corporate audit report and auditing plan for the coming year shall be submitted to the board.

Risk management and internal control has been further discussed in the Report from the Board of Directors and note 3.

11. Board remuneration The board’s remuneration is not related to the company’s results.

See note 8 for information about the board remuneration.

12. Remuneration to executive employees The salary and other remuneration of the CEO are decided by a convened meeting of the board. The remuneration of other executive management is decided by the CEO, based on a structure agreed by the board to enhance value creation by the company through shared goals.

The board reviews the CEO’s performance in meeting on an annual basis based on agreed goals and objectives.

See note 8 for information about the remuneration to executive employees.

13. Information and communication SN Power emphasises open and honest communications with all its stakeholders and places the greatest focus on the stakeholders who are directly affected by SN Power’s business. The information the company provides to its owners, lenders and the financial markets in general shall permit an evaluation of the company’s underlying values and risk exposure. To ensure predictability, the owners and the financial markets shall be treated equally, and information shall be communicated in a timely manner. SN Power’s financial reports shall be transparent, and provide the reader with a broad, relevant and reliable overview of its strategies, targets and results, as well as its consolidated financial performance.

14. Take-over of the company N/A. Shares not traded.

15. Auditor The annual general meeting appoints the auditor based on the board’s proposal and approves the auditor’s fees. The auditor serves until a new auditor is appointed. The external auditing contract is normally put out to tender at regular intervals.

The board has meetings with the external auditor to review the annual financial statements and otherwise as required. The board evaluates the external auditor’s independence and has established guidelines for the use of the external auditor for consultancy purposes. In accordance with the requirement to maintain the auditor’s independence, SN Power will only make limited use of the external auditor for tasks other than statutory financial audits.

SN POWER ANNUAL REPORT 2016 14

PRORATA INCOME

STATEMENT01/01/2016-31/12/2016

SN POWER

THIS IS SN POWER

PPORATA INCOME STATEM

ENT

In order to have a better and more complete picture of SN Power’s financial status, prorated numbers adjusted for changes in fair value are used for internal reporting.

SN Power’s business model is to a large extent built on development of joint projects with local partners and in such projects the power to govern financial and operational matters will be shared between the shareholders. In the financial statements these investments are treated in accordance with the equity method, and presented as a single line item in the income statement and in the balance sheet. For internal reporting purposes, in order to have a better and more complete picture of the financial result, prorated numbers are used.

Figures in USD million Consolidated Non-controlling interests

Associated companies and

joint venturesAdjustments Prorata

2016 2016 2016 2016 2016Income statementOPERATING REVENUES AND EXPENSESSales revenues 33 -22 161 173 Energy purchase and other costs related to power sales -4 3 -22 -24 Salary and personnel costs -13 4 -4 -13 Depreciation, amortization and impairment -74 41 -17 -50 Other operating costs -13 4 -13 -22 Income from investments in associated companies and joint ventures 48 0 -0 -59 -11

Earnings before financial items and tax -22 29 104 -59 52

FINANCIAL INCOME AND EXPENSES

Financial income 6 -0 4 10 Financial expenses -17 9 -38 -47 Gain (loss) on derivatives - - 1 1 Net financial items -11 8 -33 - -36

Profit before tax -34 38 71 -59 16

This year's tax expense -3 -6 -12 -21

NET PROFIT FOR THE YEAR -37 32 59 -59 -5

Attributable to:Equity holders of the parent -5 Non-controlling interests -32 NET PROFIT FOR THE YEAR -37

SN POWER ANNUAL REPORT 2016 15

BOARD OF DIRECTORS’

REPORTYEAR 2016

SN POWER

Asbjørn Grundt

Kjersti Rønningen

Simen Bræin Hilde Merete Nafstad

Øystein Øyehaug

Kjell Roland

THIS IS SN POWER

BOARD OF DIRECTORS’ REPORT

1. Introduction SN Power AS (SNP) is owned by Norfund (50%) and Statkraft (50%). SNP’s business strategy is to develop, build, acquire, own and operate sustainable hydropower projects in developing countries on commercial terms. The company’s mission is to become a leading hydropower company in developing countries, contributing to economic growth and sustainable development.

Statkraft Norfund Power Invest AS (SNPI), SN Power for short, was established in 2002. In 2013 Norfund and Statkraft decided to restructure the company. SNP was incorporated and in 2014 SNPI’s portfolio in Africa, South East Asia and Central America was transferred to SNP. SNPI’s remaining portfolio in South Asia and South America was integrated with Statkraft International Hydro’s assets in South East Europe. The transfer of assets and people from SNPI to SNP took place in June 2014.

The rationale for investing in developing countries is the attractiveness of these markets due to expected long-term economic growth, increased need for environmentally friendly energy, and the potential for hydropower development. 2. Important Events in 2016

• The Bajo Frio project in Panama started commercial operations.

• The Burica pre-construction works in Panama were almost completed, and put on hold.

• Started site activities on the safe operations project in Zambia (refurbishment and upgrading of existing units/equipment).

• Feasibility study for the Middle Yeywa project in Myanmar started, covering the commercial and basic technical aspects.

• Maris Raising project in the Philippines completed.

• Start of the construction of the Maris Canal project in the Philippines.

• Closing of SN Power’s office in Singapore.

• Signed MoU with Industrial Promotion Services (”IPS”) and started a due diligence process to potentially enter the 147 MW Ruzizi III hydropower project located on the river bordering the Democratic Republic of the Congo (”Congo”) and Rwanda, as IPS’

SN POWER ANNUAL REPORT 2016 16

BOARD OF DIRECTORS’ REPORT

THIS IS SN POWER technical partner. The Project is continuing with

Norfund as owner

• Signed Share Purchase Agreement with Sithe Global for the acquisition of their complete shareholding in Bujagali Energy Limited in Uganda. However, the transaction did not close by the Agreement’s expiry date of 31 December.

3. The Financial Statements SN Power Group 2016 is the second full year of operation for SN Power Group and SN Power AS. The sales amounted to USD 33.0 million (28.4). As for 2015 the 2016 sales figures were characterized by dryer than normal conditions in Laos in the first half year due to el Niño, and due to drought in Zambia.

Operating expenses were USD -103.6 million (-39.5) including impairment for the year of USD -64.3 million (0). Income from investments in joint ventures was USD 48.1 million (56.8). Net financial items amounted to USD -11.3 million in 2016 (-7.0). The net result was USD -37.1 million in 2016 (33.8).

The SN Power Group’s cash and cash equivalents were at USD 219.6 million as of 31 December 2016 compared to 148.0 as of 31 December 2015. Net cash flow from operational activities was USD 92.8 million (46.1), while net cash flow to investment activities was USD 13.8 million (-15.4) and cash flow to financing activities was USD 7.8 million compared to -17.9 in 2015. Total assets amounted to USD 1,187.4 million at the end of the year 2016 (1,269.7). The equity as a percentage of total debt and equity was 80% as of 31 December 2016 which is no change from 2015.

SN Power AS The parent company, SN Power AS, had an operating loss of USD -8.8 million (-6.9). Net financial items amounted to USD -31.0 million (59.2), and net profit was USD -39.8 million in 2016 (52.3). Net profit includes a write-down of 53.4 MUSD of the shares in Agua Imara AS as a consequence of the impairment of the Bajo Frio project. The impairment was caused by a delayed completion, cost overrun and declining spot prices.

The company’s operational expenses for 2016 were USD -9.2 million (-7.8). The increase mainly comes from project related activities.

SN Power AS’ cash and cash equivalents were USD 119.4 million as per 31 December 2016 (106.0). Net cash flow from operational activities was USD 13.4 million (52.7), while investment in SN Power AS was USD 0.1 million (-35.9). There was no new paid in equity in 2016 (0). The Company has no interest bearing debt.

Total Assets at the end of 2016 were USD 872.8 million

(913.7). The equity as a percentage of total debt and equity was 99.6% as of 31 December 2016 (99.5%).

Allocation of this year’s net loss and continued operations SN Power AS’ Board of Directors has suggested that no dividend is distributed for 2016 and that this year’s net profit is allocated as follows:

The Board confirms that the company is in a situation of going concern.

It is the Board’s opinion that the annual accounts give a true and fair view of SN Power Group’s financial results in 2016 and the Group’s financial situation as of 31 December 2016. According to the Norwegian Accounting Act, the Board confirms that the Annual Accounts have been prepared based on the Group as a going concern.

International Financial Reporting Standards (IFRS) The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards as adopted by the European Union. SN Power Group’s presentation currency is USD. 4. Health and Safety

The health and safety of SNP’s employees and the employees of contractors and consultants is a key priority for SNP. Our goal is to meet international Health, Safety and Environmental (HSE) standards in all of our activities.

The Total Recordable Injury (TRI)-rate for Operation in 2016 was 1.6 (2.4), which is below the target. (TRI ≤ 3). This is a decrease from previous years.

The TRI-rate for Projects in 2016 was 3.3 (6.1) and below the target (TRI ≤ 5). This result could partly be contributed to low construction activity, but both Maris Canal Project in the Philippines and the Safe Operation Project in Zambia has performed well in 2016. In Zambia we had, however, an accident with permanent disability. One of our employees lost sight on one eye.

SNP experienced no fatalities in 2016.

The focus in 2016 has been on building competence within own organization, particularly focusing on the country offices. As part of this, SNP plans to adopt as much as possible from Statkraft’s Step Change program in 2017. 5. Projects and Operations 2016 The Philippines SNP and its partner Aboitiz Power, own on a 50/50-basis three hydropower plants in the Philippines with a total capacity of 625 MW. The financial performance in 2016 was affected by lower deliveries of ancillary services in Magat as well as lower spot prices. This has however to some extent been compensated by a good portfolio of longer fixed price contracts. The annual demand growth in the Luzon grid is estimated at 9.5%. Generation capacity, mainly coal, natural gas and some renewables, mainly solar, have increased and spot prices were 18% lower than

SN POWER ANNUAL REPORT 2016 17

BOARD OF DIRECTORS’ REPORT

THIS IS SN POWER 2015.

All three plants Magat, Ambuklao and Binga provided ancillary services to the grid.

SN Aboitiz Power Magat refinanced and topped up its debt in USD and PHP with a PHP 19 billion fixed rate corporate note facility. Bank of the Philippine Islands is lead arranger and China Banking Corporation is the joint lead arranger.

The Maris Raising project was completed in March 2016. Construction has started on the 8.5 MW Maris Canal project and Commercial Operation Date is targeted early 2018.

The Alimit hydropower generation project is in its feasibility stage.

Laos SNP owns 20% of the shares in Theun Hinboun Power Company (THPC) in Laos. THPC has a capacity of 500 MW and the power is sold on long-term contracts to Thailand and Laos. THPC’s other shareholders are EDL Generation Plc from Laos with 60% and GMS Power International Pte. Ltd. from Singapore with 20%. The production and sales during 2016 were lower than in 2015 and significantly lower than that of 2014 because of a lack of water partly caused by the El Niño effect. This lack of water ended with the arrival of the rainy season in June 2016 when production went back to normal again.

Myanmar SNP has a Memorandum of Understanding with the Government of Myanmar for the development of a large scale Middle Yeywa hydropower project on the Myitnge river. During 2016 SNP has been working on a Feasibility study and an Environmental and Social Impact Assessment for the project, and the studies will be ready in 2017.

Zambia SNP’s subsidiary Agua Imara owns a 51% share in Lunsemfwa Hydro Power Company (LHPC) in Zambia. LHPC owns and operates two hydropower plants with a combined capacity of 56 MW. LHPC is the only private power generating company connected to the Southern African Power Pool (SAPP). The operations of LHPC were severely affected by drought for the third consecutive year in 2016. This has depleted both reservoirs, which will impact the production also in 2017. During the second half of the year, site activities on the safe operations project started. The project aims at refurbishing the existing units and equipment. The Lunsemfwa plant is completed and the Mulungushi plant is scheduled to be completed during the first quarter of 2017.

LHPC also owns Muchinga Power Company (MPC) in Zambia. MPC has a license to develop a hydropower plant with a potential capacity of 180-300 MW, downstream of the existing LHPC power plants. USD 6.9 million has been written down in 2016 related to MPC, due to suspension of the current scope of the project.

Panama SNP has through Agua Imara one subsidiary and one joint venture in Panama, Fountain Intertrade Corporation (FIC) and Hidro Burica SA (Burica). Agua Imara holds a 50.1% ownership share in both companies.

FIC has developed and constructed the 58 MW Bajo Frio run of river hydropower project, in the Chiriquí Viejo Basin near the border to Costa Rica. Bajo Frio started to generate energy in June 2015 and the regulator issued the Commercial Operations Certificate in August 2016. The first half of 2016 was affected by the El Niño phenomenon, which implied a lower than average hydrology and therefore lower production than in a normal year. Approximately 60% of the production is currently sold through a long term PPA which runs to the end of 2027.

USD 57.4 million was written down in 2016 related to Bajo Frio, due to higher cost and later start-up than expected as well as a revised future market outlook.

Burica is developing the 63 MW run of river hydropower plant immediately downstream of Bajo Frio. Due to the synergies with the Bajo Frio project, the construction of the Burica intake was completed in 2015. An international tender process for construction companies and equipment providers was put on hold early in 2016 due to uncertainty related to the approval of the 63 MW license. The approval was given in June 2016 and Burica is preparing for the new Power Purchase Agreement auction expected to take place in the third quarter of 2017.

Mozambique SNP’s and Agua Imara’s office in Mozambique has been closed down in 2016, due to lack of progress on development of new projects. However, SNP and Agua Imara will continue to monitor the potential for projects in the country.

Uganda On 3 March 2016 SNP signed a Share Purchase Agreement (SPA) with Sithe Global for the acquisition of their complete shareholding in Bujagali Energy Limited, with an expiry date on 31 December 2016.

The SPA was not extended at the end of the year due to missing government approvals of the share transfer. The Uganda Government initiated a full re-financing of the project.

Rwanda/Burundi/DRC SNP signed a Memorandum of Understanding with Industrial Promotion Services (IPS) and started a due diligence process to potentially enter the 147 MW Ruzizi III hydropower project located on the river bordering the Democratic Republic of the Congo (Congo) and Rwanda as IPS’ technical partner, and replace Sithe Global.

The Ruzizi III project represents an opportunity to enter a fairly matured project with a well-structured commercial framework. The expected start of construction is in 2019 and the estimated commercial operation date in 2024. The host countries and the region in general represents a risk profile that is fairly high. As a result of a total evaluation of the project the Board of SNP decided not to pursue this

SN POWER ANNUAL REPORT 2016 18

BOARD OF DIRECTORS’ REPORT

THIS IS SN POWER opportunity. Norfund decided on this basis to continue

the development of the project on a 100% basis, based on a full management service agreement with SN Power.

Indonesia SNP is exploring opportunities for hydro power projects in Indonesia. A pre-feasibility study is being conducted for one project in the Lariang river in Sulawesi in partnership with Aboitiz Power and The Indonesian Industrial group Astra. 6. Employees and OrganizationMid-2016 SNP, due to strategic reasons, decided to downsize its non-operational office in Singapore with effect as of 1 January 2017.

SNP’s consolidated companies had 136 employees at the end of 2016 (136). Of these, 12 (16) worked at the company’s headquarters in Oslo together with 8 (7) employees in Agua Imara AS in addition to 6 (6) in the Philippines, 8 during the year and 0 at year end (8) in Singapore, 4 (4) in the Netherlands, 62 (55) in Zambia, 6 (0) in Bangkok and 30 (40) in Panama. Including joint ventures, the total number of employees at the end of 2016 was 660 (675). Of the additional employees in joint ventures, 201 (188) worked in the Philippines (SN Aboitiz Power (SNAP)/Manila Oslo Renewable Energy (MORE)), 2 (10) in Panama (Hidro Burica SA) and 321 (341) in Laos (Theun-Hinboun Power Company Ltd).

The Management team of the group continues to be divided into two units; one focusing on development and the other on operational matters. In this way, the SN Power Group has developed to be a leaner matrix based organization, working across different cultures.

In 2016, sick leave in SNP was 654 days, equivalent to 1.87% of the total number of working days. SN Power AS and Agua Imara AS had 38 (74) sick leave days, equivalent to 0.73% (1.40%) of the total number of working days.

At the end of the year, two of the six (33.3%) Board members in SN Power AS were females, with one female (10%) present in the top management. 25.38% of SN Power AS’s workforce is female.

To ensure that SNP does not discriminate on grounds of gender, religion, ethnic background, physical challenges or otherwise, appropriate procedures are in place concerning selection to jobs, promotions to higher positions, transfers and redundancies. Procedures entail transparent recruitment processes whereby job opportunities normally are advertised internally as a minimum, but in general also made available to the public through advertisements. Employment decisions are made in cooperation between at least two managers and the HR function to ensure compliance with statutory regulations and SNP’s internal guidelines.

7. Society and the Environment

SNP is committed to comply with international environmental and social standards set by the International Finance Corporation (IFC) and the UN Global Compact. The standards are integrated into the Company’s Group CSR and Environmental Policy and Procedures and into the Company’s project management tool.

SNP is keeping its strong focus on anti-corruption. The Company’s policy on reporting of concerns is focusing on a transparent, open line to report possible irregularities, and at the same time, protecting the integrity of the whistle-blower (reporter). In addition, SNP’s recording system ensures confidential reporting of any issue related to integrity and corruption. The same policy and system have been introduced to SNP’s joint ventures and subsidiaries. IFC has adopted SNP’s methodology for dealing with stakeholders in a systematic manner, and SNP and IFC mutually exchange knowledge and methodologies within this field.

A policy on security was implemented in 2016.

During 2016, there were no records of serious violations of SNP’s environmental standards for emission or other serious environmental risks, and no serious ethical or integrity cases were reported.

The Company’s operations do not result in pollution or spillage harmful to the external environment. 8. Market and Regulatory UpdateGlobal fuel prices have come down significantly the last year implying that the costs of conventional thermal generation are declining in most power markets. In combination with the global investment boom in wind and solar power this will inevitably reduce power prices also in SNP’s markets, including the Philippines and Panama. Against this backdrop of uncertain global fuel prices and spot prices in most emerging markets, SNP will primarily focus on investments backed by long-term power purchase agreements rather than merchant plants, with the exception of a few markets where spot prices alone may still justify plants with full spot exposure (i.e. notably the Philippines and Panama).

In the Philippines, the spot prices have come down significantly the last couple of years, and SN Aboitiz Power have reduced their spot exposure by developing a contract portfolio with favorable prices.

In Panama, a large contract for a liquefied natural gas fired combined cycle gas power plant has been awarded to American energy company AES, which will alter the power balance from 2019.

On the regulatory side, the guidelines from 2013 preventing hydropower plants with reservoirs to set the spot price are to be changed, which will be favorable to Bajo Frio, and bring the regulatory system in line with the other cost-based pools in Latin America.

SN POWER ANNUAL REPORT 2016 19

BOARD OF DIRECTORS’ REPORT

THIS IS SN POWER

Oslo, 1 March 2017

9. Risk Management

SNP’s growth targets and the nature of its business make it important to monitor and understand the risk picture continuously at all levels. A global framework for risk management is implemented in all business areas and constantly improved. Important risk exposures for SNP are related to hydrology, market, political and regulatory environment, construction, health and safety, finance markets, and corruption. The company has in 2016 focused on monitoring and controlling risks and uncertainties by further developing procedures and tools to ensure quality in project development, investment decisions, project execution, and operations.

In some countries in which SNP operates, exposure to political and regulatory risk is considered to be high. All markets are particularly closely monitored in this regard and mitigation measures such as political risk insurance is evaluated and acquired if necessary.

The company manages the financial risks associated with foreign currencies, interest rates and liquidity primarily by using currency forward contracts and interest rate swap agreements.

Through the maximization of dividends, repayment of previously contributed capital, share issues and refinancing operations of the operative project companies, the capital structure is optimized to maximize the Group’s value and reinvestment capability.

The Group relies on project financing in which lenders are not entitled to recourse against the parent or sister companies. In some cases, capped parent company guarantees will still have to be issued in order to cover risks that cannot be allocated to lenders, typically construction related risks.

SNP has established a uniform and comprehensive set of HSE standards, which are monitored by its regional organizations and representatives in the Boards, the SNP management team, and through HSE audits. Serious injuries are subject to independent accident investigations. 10. Priorities for SN Power in 2017SNP has operating assets in the Philippines, Laos, Zambia and Panama. As the plant in Panama enters its first full year of regular operations and the plants in Zambia restart after the safe operations refurbishments, excellent operational performance will be a main priority. After dry years in many places we expect normal hydrology in 2017.

SNP’s work with the project pipeline in 2016 has focused on narrowing the scope to focus on a few projects where the likelihood that the projects will reach completion is deemed to be high. For 2017, the main priority will be to bring these preferred projects forward and limit the search for new projects to countries where we are already present or to where the particular hydropower project will have a competitive advantage compared to other power sources.

SN POWER ANNUAL REPORT 2016 20

FINANCIAL STATEMENT

FINANCIAL STATEMENTS

YEAR 2016

SN POWERFINANCIAL STATEMENTS

SN POWER ANNUAL REPORT 2016 21

FINANCIAL STATEMENTS

SN POWER GROUP

Income statement and consolidated statement of comprehensive income

SN POWER GROUP

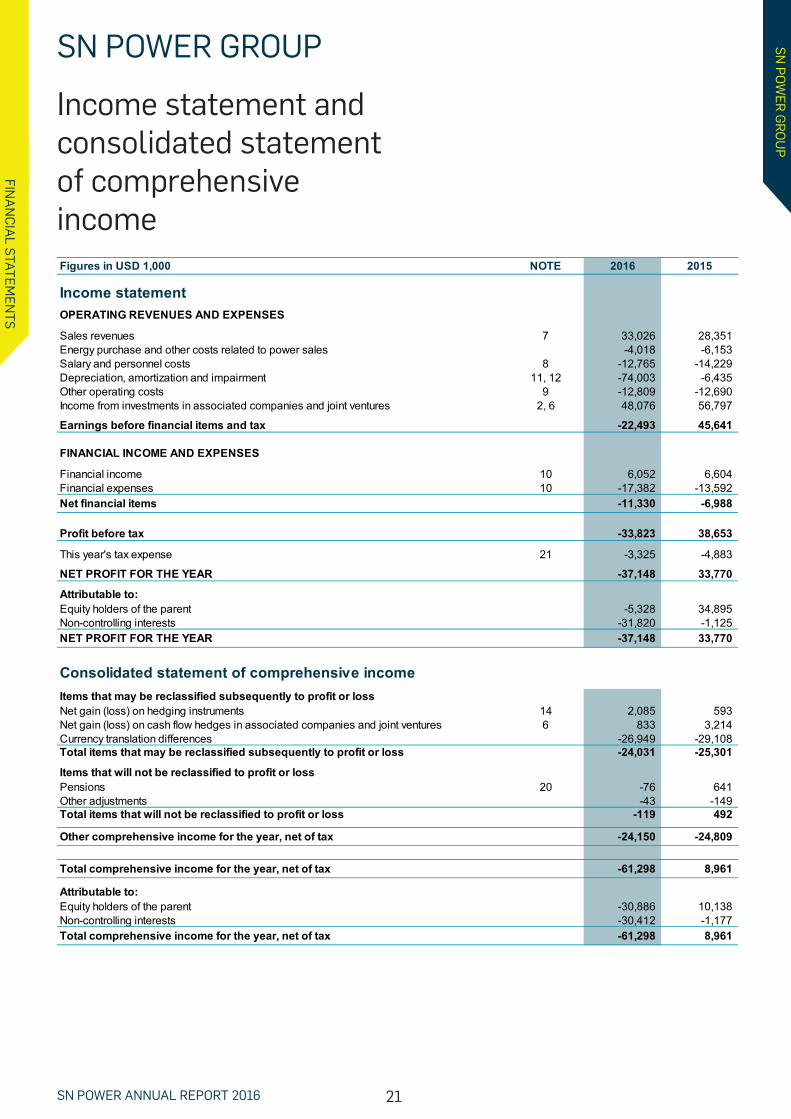

Figures in USD 1,000 NOTE 2016 2015

Income statementOPERATING REVENUES AND EXPENSES

Sales revenues 7 33,026 28,351 Energy purchase and other costs related to power sales -4,018 -6,153 Salary and personnel costs 8 -12,765 -14,229 Depreciation, amortization and impairment 11, 12 -74,003 -6,435 Other operating costs 9 -12,809 -12,690 Income from investments in associated companies and joint ventures 2, 6 48,076 56,797

Earnings before financial items and tax -22,493 45,641

FINANCIAL INCOME AND EXPENSES

Financial income 10 6,052 6,604 Financial expenses 10 -17,382 -13,592 Net financial items -11,330 -6,988

Profit before tax -33,823 38,653

This year's tax expense 21 -3,325 -4,883

NET PROFIT FOR THE YEAR -37,148 33,770

Attributable to:Equity holders of the parent -5,328 34,895 Non-controlling interests -31,820 -1,125 NET PROFIT FOR THE YEAR -37,148 33,770

Consolidated statement of comprehensive incomeItems that may be reclassified subsequently to profit or lossNet gain (loss) on hedging instruments 14 2,085 593 Net gain (loss) on cash flow hedges in associated companies and joint ventures 6 833 3,214 Currency translation differences -26,949 -29,108 Total items that may be reclassified subsequently to profit or loss -24,031 -25,301

Items that will not be reclassified to profit or lossPensions 20 -76 641 Other adjustments -43 -149 Total items that will not be reclassified to profit or loss -119 492

Other comprehensive income for the year, net of tax -24,150 -24,809

Total comprehensive income for the year, net of tax -61,298 8,961

Attributable to:Equity holders of the parent -30,886 10,138 Non-controlling interests -30,412 -1,177 Total comprehensive income for the year, net of tax -61,298 8,961

SN POWER ANNUAL REPORT 2016 22

FINANCIAL STATEMENTS

SN POWER GROUP

Balance Sheet at December 31

SN POWER GROUP

Figures in USD 1,000 NOTE 2016 2015

ASSETS Deferred tax asset 21 - - Intangible assets 2, 11, 12 5,105 13,522 Property, plant and equipment 2, 11, 12 365,370 420,774 Investment in associated companies and joint ventures 2, 6 577,597 670,730 Financial assets 16 8,207 5,842 Total non-current assets 956,279 1,110,868 Spare parts 87 - Receivables 17 11,422 10,877 Bank deposits, cash and cash equivalents 18 219,563 147,971 Total current assets 231,072 158,848

TOTAL ASSETS 1,187,351 1,269,716

EQUITY AND LIABILITIESPaid-in capital 19 852,643 852,643 Other equity -5,525 25,360 Non-controlling interests 106,854 137,268 Total Equity 953,972 1,015,271 Pension commitments 20 1,348 1,068 Deferred tax 21 38,816 48,251 Non-current financial instruments (derivatives) 14 4,038 6,123 Interest-bearing long term debt 22 137,012 168,812 Total long-term liabilities 181,214 224,254 Current portion long term debt 22 8,433 8,207 Tax payable 21 786 1,375 Other current liabilities 23 42,946 20,609 Total current liabilities 52,165 30,191

TOTAL EQUITY AND LIABILITIES 1,187,351 1,269,716

SN POWER ANNUAL REPORT 2016 23

FINANCIAL STATEMENTS

SN POWER GROUP

Consolidated Statement of Changes in Equity at 31 December

SN POWER GROUP

Non-controlling interests

Total equity

Figures in USD 1,000 Share capital

Retained earnings

Translation reserve

Hedging reserve

At 1 January 2015 852 643 25 401 -8 581 -1 598 117 128 984 994

Transactions with shareholdersIssue of share capital in Subsidiaries - Minority Share 11,277 11,277 Increased minority due to purchase of subsidiary 10,040 10,040 Transactions with shareholders - - - - 21,317 21,317

Other comprehensive income for the year, net of taxNet gain/losses on hedging instruments 193 400 593 Net gain/losses on cash flow hedges in associated companies 3,214 3,214 Currency translation differences -29,108 - -29,108 Pensions 579 - 62 641 Other adjustments - 365 - - -514 -149 Other comprehensive income for the year, net of tax - 944 -29,108 3,407 -52 -24,809

Recognized through Profit and LossProfit for the year - 34,895 - - -1,125 33,770 Recognized through Profit and Loss 34,895 -1,125 33,770

Total comprehensive income for the year, net of tax 35,839 -29,108 3,407 -1,177 8,959

At 31 December 2015 852,643 61,239 -37,689 1,810 137,268 1,015,271

Other comprehensive income for the year, net of taxNet gain/losses on hedging instruments 678 1,407 2,085 Net gain/losses on cash flow hedges in associated companies 833 833 Currency translation differences -26,950 1 -26,949 Pensions -76 - - -76 Other adjustments - -43 - - - -43 Other comprehensive income for the year, net of tax -119 -26,950 1,511 1,408 -24,150

Recognized through Profit and LossProfit for the year -5,328 - - -31,820 -37,148 Recognized through Profit and Loss -5,328 -31,820 -37,148

Total comprehensive income for the year, net of tax -5,447 -26,950 1,511 -30,412 -61,298

At 31 December 2016 852,643 55,792 -64,639 3,322 106,854 953,972

Other equityPaid-in capital

Attributable to equity holders of the parent

SN POWER ANNUAL REPORT 2016 24

FINANCIAL STATEMENTS

SN POWER GROUP

Cash flow statementSN POWER GROUP

Figures in USD 1,000 NOTE 2016 2015

OPERATIONAL ACTIVITIESProfit before tax -33,823 38,653 Tax paid -13,649 -8,052 Depreciation, amortization and impairment 11, 12 74,003 6,435 Loss (gain) on disposal of fixed assets 7 -101 - Difference between this year's pension expense and pension premium 356 785 Income from investments in associated companies and joint ventures 6 -48,076 -56,797 Dividends from associated companies and joint ventures 6 113,787 61,395 Effect of exchange rate changes (agio/disagio) 2,180 187 Change in spare parts -87 - Change in receivables and other current liabilities -1,813 3,479 Net cash flow from operational activities 92,776 46,085

INVESTMENT ACTIVITIESInvestment in tangible and intangible fixed assets 11, 12 -10,188 -32,731 Proceeds from sale of fixed assets 135 - Investment in associated companies and joint ventures 6 -1,405 50,769 Change in non-current financial assets -2,365 -2,652 Net cash flow to investment activities -13,823 15,386

CASH FLOW FROM FINANCING ACTIVITIESNew long-term debt 22 431 13,379 Paid installments long-term debt 22 -8,207 -6,789 New paid-in equity from non-controlling interests EQ - 11,277 Net cash flow from financing activities -7,776 17,867

Effect of exchange rate changes on cash and cash equivalents 415 -512

Net change in cash and cash equivalents 71,592 78,826 Cash and cash equivalents at 1 January 147,971 69,145 Cash and cash equivalents at 31 December 219,563 147,971

SN POWER ANNUAL REPORT 2016 25

SN POWER GROUP

Notes to the financial statments

SN POWER GROUP

NOTES TO THE FINANCIAL STATEMENTS

Note 1Summary of significant accounting principlesGeneral information SN Power AS, including subsidiaries (SN Power Group), is an international renewable energy company with projects and operations in South-East Asia, Sub-Sahara Africa and Central America. The company invests on commercial terms and is committed to social and environmental sustainability throughout the business. The company’s headquarter is in Oslo.

The consolidated financial statements of the SN Power Group for the year 2016 were authorized for issue in accordance with a resolution of the Board of Directors on 1 March 2017.

The following text describes the most important accounting principles used in the consolidated financial statements. These principles have been applied consistently to all reporting, unless otherwise stated.

Basic principles The consolidated financial statements for the Group have been prepared in accordance with the International Financial Reporting Standard (IFRS) as adopted by the EU.

The following new and revised or amended Standards and Interpretations have also been adopted in these financial statements. Their adoption has not had any significant impact on the amounts reported in these financial statements, but may affect the accounting for future transactions or arrangements.

At the time of presentation of the financial statements, the following standards and interpretations are issued by IASB, but not entered into force for the financial year 2016. Management assumes that these standards and interpretations will be applied in the Group financial statements from the financial year 2017 or later, and have not assessed the potential effect of these new standards.

Standards and Interpretations that are clearly not relevant for the Group’s financial statements have not been included in the below schedule. The impact of the standard listed below on the Group financial statements are expected to be minimal.

Standard/

InterpretationTitle Date of issue

Applicable to accounting periods commencing on or after

Amendments to IAS 1 Disclosure initiative Dec 2014 1 January 2016Amendments to IFRS 10, IFRS 12 and IAS 28

Investment entities: Applying the Consolidation Exemption

Dec 2014 1 January 2016

Amendments to IFRS 11 Accounting for Acquisitions of Interests in Joint Operations

May 2014 1 January 2016

Amendments to IAS 16 and IAS 38

Acceptable methods of depreciation and amortisation

May 2014 1 January 2016

Amendments to IAS 27 Allow the use of the Equity Method in Separate Financial Statements

August 2014 1 January 2016

Improvements to IFRSs (Various Standards and Interpretations)

Improvements to IFRSs 2012-2014 Cycle

September 2014

1 January 2016

FIGURES IN USD 1,000

SN POWER ANNUAL REPORT 2016 26

SN POWER GROUP

SN POWER GROUP

NOTES TO THE FINANCIAL STATEMENTS

Standard/

InterpretationTitle Date of issue

Applicable to accounting periods commencing on or after

Improvements to IFRSs (Various Standards and Interpretations)

Annual Improvements 2014–2016 Cycle

December 2016 1 January 2017

IFRS 9 Financial Instruments July 2014 1 January 2018IFRS 15 Revenue from Contracts with

CustomersMay 2014 1 January 2018

IAS 12 Amendments regarding the recognition of deferred tax assets for Unrealized losses

January 2016 1 January 2017

IAS 7 Disclosure initiative January 2016 1 January 2017

When entering into new investments in subsidiaries, associated companies or joint ventures, the Group will measure the cost of the business combination according to IFRS 3. Management must use judgment in defining and allocating fair values of assets, liabilities and direct costs attributable to the combination.

Contracts related to purchase and sale of energy Contracts related to purchase and sale of energy that meets the definition of financial instruments, are valued at fair value through profit and loss. The calculation of fair value on such contracts imply in most cases use of a wide range of estimates, of which the determination of future price curves in the market are the most significant.

Impairments SN Power Group has significant investments in fixed assets, associated companies and joint ventures. These assets are tested for possible impairment where indications of loss of value are present. Such indicators might be changes in market prices on energy or capital, shift in production capacity or other economic and legal circumstances. Calculating the recoverable amount requires a series of estimates concerning future cash flows, of which price curves and discount rate are the most significant.

Development costs Development costs are recognized in the balance sheet when it is probable that these will result in future economic benefits. Establishing such probability involves extensive use of judgment based on previous results and experience.

Price forecast for power A key assumption used by management in making business decisions is management’s price forecasts for power and the related market developments. In addition, these assumptions are critical input for management related to financial statement processes such as:

• Allocation of fair value in business combinations

• Valuation of contracts related to purchase and sale of energy

Functional and presentation currency The consolidated financial statements are presented in US dollars (USD), which is the functional currency of the parent company is US dollars (USD). All amounts are rounded to the nearest thousand, unless otherwise stated.

Significant accounting judgments, estimates and assumptions The preparation of the Group’s financial statements requires management to make judgments, estimates and assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the disclosure of contingent liabilities, at the reporting date. Estimates and underlying assumptions are reviewed on an ongoing basis. Changes in estimates will be recognized in the period they occur only if applicable in that period. If changes also concern future periods, the effect is distributed over both current and future periods. However, uncertainty about these assumptions and estimates could result in outcomes requiring a material adjustment to the carrying amount of the asset or liability affected in the future. The areas in the financial statements of SN Power Group that are most affected by significant accounting judgments, estimates and assumptions are:

Useful life of tangible and intangible fixed assets Depreciation is based on management estimates of the useful lives of the assets and their residual values. Estimates may change due to changes in scrap value, technological development, environmental and other conditions. Management reviews the future useful lives of each component and the residual value annually, taking into account the above mentioned factors.

Provisions and contingent liabilities IAS 37 defines when to recognize a provision in the financial statements. Management must make estimates and use judgment in determining the expected probability of an outflow of resources and a reliable estimate of the amount.

Purchase price allocation related to new investments in subsidiaries, associated companies, and joint ventures

SN POWER ANNUAL REPORT 2016 27

SN POWER GROUP

SN POWER GROUP

The process is headed and run by a team of experts across the organization. The main results are benchmarked to external references and major deviations are explained. The process aims to ensure consistency, and arrive at a balanced view of both the markets and the future power prices.

Capital management The primary objective of the Group’s capital management is to optimize the use of equity to maximize shareholder value. The Group manages its capital structure and makes adjustments to it, in light of changes in economic conditions. To maintain or adjust the capital structure, the Group may adjust debt exposure, dividend payments to shareholders, return capital to shareholders or issue new shares. The Group’s policy is to use project financing in all investments and in the long run to keep the gearing ratio in operating companies above 50 %. The gearing ratio is defined as interest bearing debt divided by Total equity and liabilities:

• Impairment testing of property, plant and equipment, intangible assets and equity accounted investments

SN Power performs an update of its price forecasts and the related expected market developments in the geographical areas where SN Power operates, annually. The update provides basis for both strategic decisions as well as the management’s expectation for future prices and revenue streams associated with the assets. The annual update is the output of a continuous process of monitoring, interpreting and analyzing global as well as local trends, market fluctuations and drivers that ultimately could affect future markets and revenues. A fundamental approach is applied to analyse the markets. Such analysis includes among others;

• Cost levels of competing technologies and fuels

• Future energy balances

• Political regulations

• Technological developments to reduce emissions of climate gases

Basis for consolidation The consolidated financial statements comprise the financial statements of the parent company SN Power AS and its controlling interests in other companies as of 31 December 2016.

Subsidiaries Subsidiaries are all entities controlled by the Group. The Group controls an entity when it is exposed, or has rights, to variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. The financial statements of subsidiaries are included in the consolidated financial statements from the date on which control commences until the date control ceases.

Business combinations The purchase method of accounting is used to account for the acquisition of subsidiaries. The consideration transferred in the acquisition is generally measured at fair value, as are the identifiable net assets acquired. The amount of the consideration which exceeds fair value of net identifiable assets is recorded as goodwill, and tested annually for impairment. Non-controlling interest Non-controlling interest is the share of profit and equity that is not held by the majority owners. Non-controlling interests are measured at their proportionate share of the acquiree’s identifiable net assets at the date of acquisition.

Investments in associated companies and joint ventures Shares in companies where the Group exercises a significant, but not controlling influence, and shares in companies with joint control are accounted for under the equity method. Significant influence normally means

that the Group owns between 20 % and 50 % of the voting capital. The Group’s share of the companies’ net result adjusted for amortization of excess value is shown on a separate line in the consolidated income statement. The investments are shown in the consolidated balance sheet as non-current assets, recognized at the value which equals the historical cost price including directly assigned transaction costs adjusted for the accumulated share of results adjusted for depreciation and amortization of excess values during the period of ownership, dividend received and possible exchange rate adjustment. Any conversion differences are recorded directly against equity. The consolidated financial statement includes the Group’s share of profit or loss from the date on which significant influence is attained and until such influence ceases. If the Group’s share of losses of an associate or a joint venture equals or exceeds the interest in the associate or joint venture, the Group discontinues recognizing its share of further losses. The interest in an associate or a joint venture is the carrying amount of the investment under the equity method together with any long-term interests that, in substance, form part of the Group’s net investment in the associate or joint venture. Such items may include long-term shareholder loans that are subordinated and unsecured.

Transactions eliminated on consolidation Intra-group balances and transactions, and any unrealized income and expenses resulting from intra-group transactions, are eliminated. Unrealized gains arising from transactions with associated companies and joint ventures are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealized losses are eliminated in the same way as unrealized gains, but only to the extent that there is no evidence of impairment.

2016 2015

Total Interest-bearing debt 175,448 177,019

Total equity and liabilities 1,187,351 1,269,716 Gearing ratio 14.8% 13.9%

NOTES TO THE FINANCIAL STATEMENTS

SN POWER ANNUAL REPORT 2016 28

SN POWER GROUP

SN POWER GROUP

Financial instruments Generally Financial instruments are initially allocated to one of the categories of financial instruments as described in IAS 39. The different categories relevant to the SN Power Group and the management that follow the instruments recognized in the respective categories are described below.

Valuation principles for different categories of financial instruments 1) Instruments at fair value through profit or loss Derivatives and financial instruments held for sale have to be measured at fair value in the balance sheet with corresponding change in fair value through profit and loss statement. For derivatives that are hedging instruments in a hedge accounting relationship, the change in value of the effective part of the hedge, following from a change in the value of the hedged risk, is not taken to profit or loss. In a fair value hedge such effects are carried against the value of the hedging object. For hedging of cash flow and hedging of net investments in foreign operations such effects are taken directly to equity. Derivatives consist of both independent derivatives and embedded derivatives that are separated from the host contract and recognized at fair value as if the derivative was an independent contract.

2) Loans and receivables Loans and receivables are initially recognized at fair value including transaction costs. In subsequent periods, loans and receivables are measured at amortized cost using the effective interest method, so that the effective interest rate becomes equal over the term of the instrument.

3) Financial liabilities Financial liabilities are initially recognized at fair value including transaction costs. In subsequent periods, financial liabilities are measured at amortized cost using the effective interest method so that the effective interest rate becomes equal over the term of the instrument.

Principles for designation of financial instruments to different categories of instruments Below is a description of the guidelines applied by the SN Power Group for designation of financial instruments to different categories of financial instruments in cases where an instrument can qualify for recognition under more than one category.

Instruments at fair value through profit or loss Derivatives must always be assessed under the category “fair value through profit or loss”. Financial contracts regarding purchase or sale of energy and CO2-quotas always have to be considered as derivative financial instruments. Physical contracts regarding purchase and sale of energy and CO2-quotas entered into as authorized by trading, or settled financially are considered as if they were financial instruments and have to be measured at fair value. Physical contracts regarding purchase and sale of energy and CO2-quotas entered into according to authorization related to own requirements or provision for own production, are normally not covered by IAS 39 as long as the contracts do not contain written options in terms of volume flexibility.

Financial instruments included in hedge accounting Identification of financial instruments designated as a hedge instrument or a hedge object in a hedge account is based on the intention of the acquisition of the financial

Foreign operations Each entity in the Group determines its own functional currency based on local operations, and items included in the financial statement of each entity are measured using that functional currency. The assets and liabilities of foreign operations, including goodwill and fair value adjustments arising on acquisition, are translated to the Group’s presentation currency (USD) at the exchange rate at the reporting date. The income and expenses of foreign operations are translated to USD at the average rate for the reporting year. Foreign exchange differences are recognized in other comprehensive income and accumulated in the translation reserve, except to the extent to the extent that the translation difference is allocated to non-controlling interest.

Revenue recognition Revenue comprises the fair value for the sale of goods and services, net of value-added tax, rebates and discounts. Intra-group sales are eliminated in the group accounts. Revenue is recorded as and when earned.

(a) Power sales Revenues from power sales and transmission are recognized as income when delivered.

(b) Rendering of services Income from rendering of services is recognized in the accounting period in which the services are rendered.

(c) Dividend income Dividend income is recognized when the right to receive payment is established, normally when approved by the General Meeting.

Borrowing costs Borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale.