Embed Size (px)

Citation preview

Independent Pricing and Regulatory Tribunal

Annual taxi licence release for Sydney 2013/14

Transport — Final ReportFebruary 2013

Annual taxi licence release for Sydney 2013/14

Transport — Final Report February 2013

ii IPART Annual taxi licence release for Sydney 2013/14

© Independent Pricing and Regulatory Tribunal of New South Wales 2013 This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism and review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgement of the source is included.

ISBN 978-1-922127-65.5

The Tribunal members for this review are: Dr Peter J Boxall AO, Chairman Mr James Cox PSM, Chief Executive Officer and Full Time Member Mr Simon Draper, Part Time Member

Inquiries regarding this document should be directed to a staff member: Jennifer Vincent (02) 9290 8418 Ineke Ogilvy (02) 9290 8473

Independent Pricing and Regulatory Tribunal of New South Wales PO Box Q290, QVB Post Office NSW 1230 Level 8, 1 Market Street, Sydney NSW 2000 T (02) 9290 8400 F (02) 9290 2061 www.ipart.nsw.gov.au

Contents

iii IPART Annual taxi licence release for Sydney 2013/14

Contents

1 Introduction 1 1.1 Purpose of this review 2 1.2 Our approach to recommending the number of new licences 3 1.3 Estimated outcomes of the recommended number of licences 4 1.4 Final recommendations in this report 6 1.5 How the review was conducted 7 1.6 Differences between draft and final report 7 1.7 Structure of this report 8

2 Overview of the Sydney taxi industry 9 2.1 Taxi industry structure 9 2.2 Types of licence in the Sydney taxi market 13 2.3 Number of licences by type in Sydney taxi market 15

3 Context for the review: objectives and factors 17 3.1 Circumstances that led to the 2009 amendments 17 3.2 Factors in the 2009 amendments and other objectives we must consider 18 3.3 Approach used to determine number of new annual licences to be

released to date 22 3.4 Success of this approach in meeting the amendment’s objectives to date 23

4 The demand for taxi services 28 4.1 How changes in demand relate to the change in licence numbers 29 4.2 Estimating changes in demand due to external factors 29 4.3 Estimating latent demand 34 4.4 Measuring the overall change in demand based on taxi trip data 39

5 The number and mix of licences to be released 42 5.1 Balancing a more affordable means of entry into the taxi market with

avoiding unreasonable impacts on existing licence-holders 44 5.2 Determining the mix of unrestricted and Peak Availability Licences

(PALs) 48 5.3 Estimated effects of releasing 160 unrestricted licences and 200 PALs in

2013/14 54 5.4 Could the outcomes be different from our estimates? 65

Contents

iv IPART Annual taxi licence release for Sydney 2013/14

6 Making an allowance for replacement licences and Wheelchair Accessible Taxi licences 69 6.1 Additional licences that need to be released 69 6.2 What should be done to help operators relinquish a more expensive

licence in favour of a cheaper one 71

7 Process for setting a price and restrictions on who may hold licences 74 7.1 Tender process 74 7.2 The need for a reserve price 76 7.3 Reserving some licences for drivers and/or restricting the number that

can be granted to the same applicant 77

Appendices 81 A Terms of Reference 83 B List of submissions 85 C Taxi industry model 88

Glossary 91

1 Introduction

Annual taxi licence release for Sydney 2013/14 IPART 1

1 Introduction

By 31 March each year, Transport for NSW must determine how many new annual taxi licences it will release in Sydney from 1 July that year.1 To assist Transport for NSW to make its next determination, the NSW Government has asked the Independent Pricing and Regulatory Tribunal of NSW (IPART) to review and make recommendations on the required number of new licences for the year commencing 1 July 2013.

Our recommendation is that 225 unrestricted annual licences, 230 Peak Availability Licences (PALs) and 1 Fringe Area (Richmond/Windsor) Licence should be released, comprising:

160 new unrestricted licences and 200 new PALs to allow for growth and peak demand

an additional 70 unrestricted licences and 30 PALs to replace licences we expect to be handed back or not renewed (including new licences effectively swapped for existing licences to get a better price)

an adjustment to subtract 5 licences to take into account the expected issue of additional Wheelchair Accessible Taxi licences, outside the annual licence tender process

1 Fringe Area (Richmond/Windsor) Licence to replace one that was not renewed in September 2012.

We are recommending a slightly different balance of unrestricted licences and PALs compared to our draft report.

1 Excluding licences for Wheelchair Accessible Taxis, which are available on demand. See Section

32C of the Passenger Transport Act 1990.

1 Introduction

2 IPART Annual taxi licence release for Sydney 2013/14

1.1 Purpose of this review

Prior to 2009, the number of taxi licences in Sydney did not keep pace with the growth in Sydney’s population, household and business income, economic activity or tourism numbers. This meant that there were not enough taxis on the road to meet passenger demand. As a result, taxi licences became a scarce commodity and were very expensive to buy and lease. This increased the costs of operating a taxi business as well as fares for taxi services. In 2008/09 taxi licences were around $365,0002 to buy outright, or around $26,000 (not including GST)3 to lease for a year, making up around 20% of the costs of providing taxi services and fares paid by passengers.

To address these problems, the Passenger Transport Act 1990 (the Act) was amended in 2009. The amendments included the introduction of Transport for NSW’s determinations of the number of new Sydney annual taxi licences to be released each year. Between the end of 2009 and the end of 2012, the Sydney taxi fleet has increased in size by around 8%.4 However, lease costs for licences leased through networks continued to increase in real terms (that is, by more than the rate of inflation) to the end of 2011, followed by a slight drop during 2012.5 It is not significantly more affordable to enter the taxi market than it was at the time of the reforms in 2009.

IPART has been asked to review and recommend the number of new taxi licences that should be released in 2013/14. We must consider the objectives of the 2009 amendments, which were to:

ensure the supply of taxis responds closely to growth in passenger demand balance the need for more affordable entry into the taxi market with the need

to avoid unreasonable impacts on existing licence holders

reduce barriers to entry and encourage competition place downward pressure on fares over time, and simplify existing taxi licence structures.

2 Average licence transfer value for 2008/09 (in 2008/09 dollars) based on information from

Transport for NSW. 3 In 2008/09 dollars. IPART calculation, based on the CIE survey data 2011 deflated by NSW

Taxi Council information about lease prices from a sample of taxi networks provided for IPART fare reviews between 2008 and 2012.

4 Information provided by Transport for NSW for 1 January 2010 compared to 1 January 2013. 5 Information about lease prices from a sample of taxi networks received from the NSW Taxi

Council on a commercial-in-confidence basis.

1 Introduction

Annual taxi licence release for Sydney 2013/14 IPART 3

We must also consider the factors in section 32C(3) of the Act, which are:

the likely passenger demand for taxi-cab services, including latent demand the performance of existing taxi-cab services the demand for new taxi-cab licences

the viability and sustainability of the taxi-cab industry, and any other matters considered relevant, having regard to the objective of

ensuring improved taxi-cab services.

(The full terms of reference for our review are provided at Appendix A.)

1.2 Our approach to recommending the number of new licences

We firstly considered the external sources of demand for taxi services, such as population, tourism, household and business income and business activity. The range of indicators suggests that demand from these external factors is likely to grow by 2.5% per year on average. We recommend for this review and the next 4 annual reviews of taxi licences that the minimum increase in the number of licences is 2.5%, reflecting a longer term estimate of growth in demand for taxi services resulting from external factors. For simplicity and certainty we consider that the 2.5% should be applied to the current number of taxi licences of 5,647,6 so that a minimum of 140 new unrestricted licences is released each year.

However, if the growth in licence numbers simply keeps pace with the growth in demand caused by external factors, lease costs are likely to be maintained in real terms.7 This would mean that many of the objectives of the amendments would not be met – it will not become more affordable to provide taxi services, so no downward pressure would be placed on fares, and there would be no improvements in the waiting times for customers.

On the other hand, if the growth in licence numbers greatly exceeds the growth in demand from external factors, the income for existing licence owners from the lease payments they receive would fall substantially. Our terms of reference require us to balance the 2 objectives of providing more affordable entry to the market for operators and avoiding unreasonable impacts on licence holders.

Determining how many additional licences to release over and above the base level of demand cannot be accomplished by a simple formula. The taxi industry consists of complex interactions between supply of taxis, demand for taxi services, waiting time and fares. Different classes of licence (such as PALs) also have a different impact on the way the market works.

6 As at 1 January 2013. 7 Assuming fares and all other costs of operating taxi services increase in line with inflation.

1 Introduction

4 IPART Annual taxi licence release for Sydney 2013/14

1.3 Estimated outcomes of the recommended number of licences

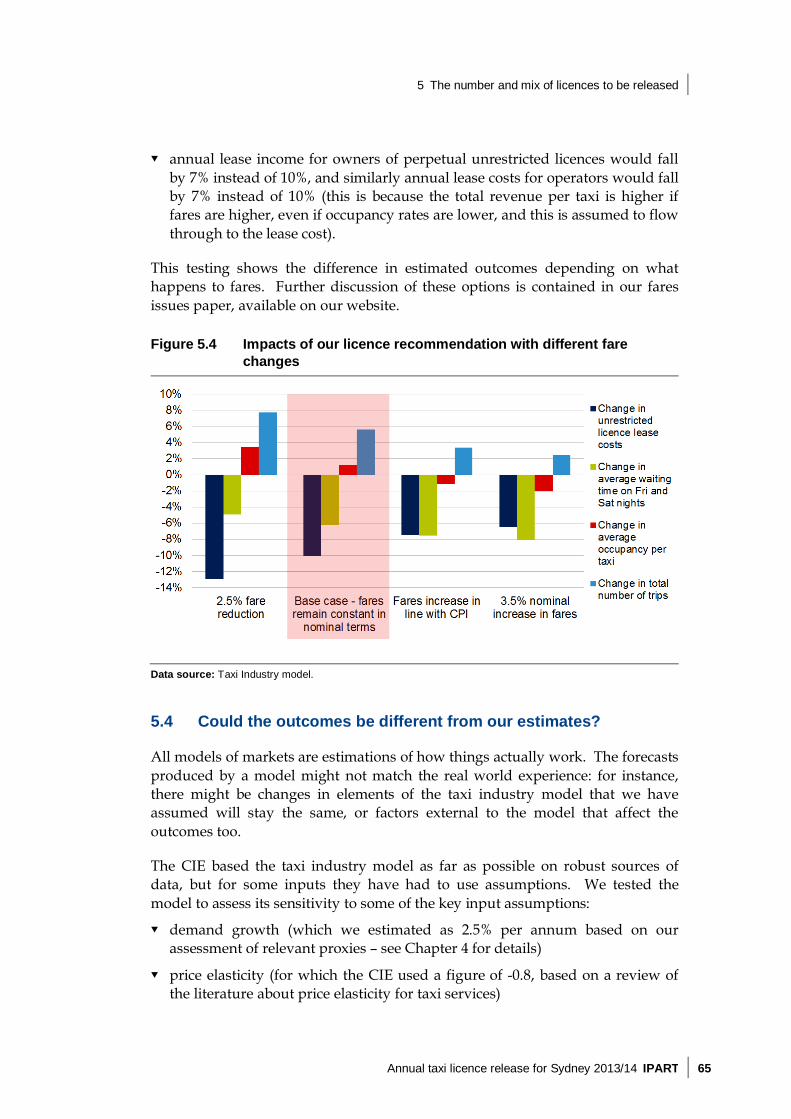

We used a model of the taxi industry developed by the Centre for International Economics (the CIE) to help us to understand the likely outcomes of adding different numbers and types of licence to the Sydney taxi market.8 The model estimates the outcomes in terms of changes to passenger demand for taxis, percentage of time a taxi spends occupied, waiting time for passengers and likely licence lease costs.

The model is a long-term equilibrium model. That is, it shows what the estimated outcomes are when the market has fully adjusted to the changes brought about by additional licences. It does not map out the transition path, or the time it takes to achieve the outcomes, but it is clear about the direction of the path. In short, our recommended increase in the number of licences will ensure that the supply of taxis responds closely to the growth in passenger demand, reduce barriers to entry into the taxi market, and improve services to customers through reduced waiting times.

We consider that releasing 225 unrestricted annual licences and 230 PALs is the combination that best meets the requirement to consider demand and latent demand and provides an appropriate balance between: positive outcomes for passengers (reduced waiting times and more taxi trips),

driver income (taxi occupancy and driver hourly earnings), operator costs (lower annual licence costs)

impacts on existing licence-holders (lower income from leasing out licences).

We also consider that the mix of licences we are recommending will help to mitigate transition effects.

1.3.1 A mix of PALs and unrestricted licences improves benefits for passengers and drivers

Releasing a mix of PALs and unrestricted licences produces larger passenger benefits for a given impact on licence owners: peak waiting times are reduced significantly compared with the release of only unrestricted licences.

PALs also provide a more affordable opportunity for drivers to invest in their own taxi business: without low cost PALs it is not viable for drivers to drive their own cab without also hiring other drivers (and it is likely to be that way for some time).

The number of licences we have recommended will also increase demand for driver labour, which should have a positive effect on driver incomes.

8 See Appendix C for information on the Taxi Industry Model. The model is also available on our

website, www.ipart.nsw.gov.au.

1 Introduction

Annual taxi licence release for Sydney 2013/14 IPART 5

1.3.2 The impact on licence owners is not unreasonable

We expect our recommendations to reduce income from perpetual licence leases by around 10%, all other things being equal.9 Some reduction is necessary in order to achieve the objective of more affordable entry into the taxi market. We consider that an initial reduction in licence lease costs of 10% provides an appropriate balance between improved affordability for operators and reduced income for licence owners. Smaller impacts do not provide much in the way of benefits to customers; the reduction in waiting times under our recommendations is twice what it would be under an estimated 5% reduction in lease income.

This is in the context of a reduction of licence lease costs of 25% over the next 5 years. In the event that we are given a referral to recommend licence numbers for 2014, we would re-evaluate the context, taking account of the experience of the first year.

1.3.3 What will be the transition effects on the industry?

The transition process largely depends on the timing of the adjustment of lease costs. The NSW Taxi Council has submitted that lease costs will be slow to adjust and drivers and operators will go out of business before lease costs adjust. However, it is quite feasible that lease costs will adjust more quickly than envisaged by the NSW Taxi Council, and we consider that the Taxi Council could assist the industry to make a quicker transition.

Issuing more licences as PALs should also help to accelerate the transition to lower cost licences, by offering an alternative, more affordable business model to operators immediately. It will bring forward greater benefits for passengers (in the form of shorter waiting times at peak periods) without additional impacts on existing licence owners.

There will be the opportunity to review progress when the determination of annual taxi licences for 2014/15 commences. However, given that new licences for the current determination will only commence from the second half of 2013, only a preliminary assessment of any changes to the industry will be possible.

Nevertheless, it is important to emphasise that transition effects are by definition temporary and that the change is in the long term interests of the industry as a whole.

9 That is, fares stay at their current levels, while all other costs of operating taxi services increase

at the same rate as the cost of living.

1 Introduction

6 IPART Annual taxi licence release for Sydney 2013/14

1.4 Final recommendations in this report

Transport for NSW should release 225 unrestricted annual licences, 230 Peak Availability Licences (PALs) and 1 Fringe Area licence for tender in 2013/14, comprising:

160 new unrestricted annual licences and 200 new peak availability licences (PALs) 43

65 unrestricted licences and 30 PALs to replace licences we expect to be handed back or not renewed. This includes an adjustment to account for the expected issue of additional Wheelchair Accessible Taxi licences outside the annual tender process. 70

1 Fringe Area (Richmond/Windsor) Licence 70

Transport for NSW should retain the current tender process:

Transport for NSW should continue to use the existing tender process, that is, a sealed electronic tender, with pay-as-bid prices for successful tenderers. 75

Transport for NSW should continue to release licences in accordance with the same timetable followed in previous years. 76

Transport for NSW should publish the provisional results of tenders for annual licences (for example, by publishing the median and mean successful bids) within 2 weeks after tenders have closed. 76

No reserve price should be set for licences tendered. 77

No restrictions should be placed on who may bid for licences or on the number of licences that any one person may hold. 79

Other recommendations:

Transport for NSW should investigate the cost and feasibility of mandating a regulator data set. 40

Roads and Maritime Services should require authorised Sydney taxi networks to provide reports on utilisation of all affiliated taxis for a sample of 4 weeks per year commencing in June 2013. 41

Transport for NSW should ensure that its administration processes and tender documentation support annual licence churn as a positive mechanism operators can use to reduce their annual licence costs. 73

Transport for NSW should remove any unnecessary administrative costs of churn, such as the requirement for a blue slip and deregistration/registration of the same vehicle with a new licence. 73

1 Introduction

Annual taxi licence release for Sydney 2013/14 IPART 7

1.5 How the review was conducted

We released an issues paper in October 2012, which set out the key issues we had identified as part of the review, and sought comment from interested parties.

Submissions were due by 9 November 2012. We received 42 submissions. Prior to the due date for submissions we held a public roundtable on 24 October to provide stakeholders with a further opportunity for input.

We released our draft report on 10 December 2012, with submissions due by 21 January 2013. We received 66 submissions.

Appendix B contains a list of all submissions received.

All the publications associated with the review, including reports, submissions and a transcript of the public roundtable, are available on our website, www.ipart.nsw.gov.au. A copy of the taxi industry model developed for the review is also available on our website.

1.6 Differences between draft and final report

In our draft report, we recommended slightly more PALs be released (280 compared to 230) and slightly fewer unrestricted licences (205 compared to 225).

We have also added 2 recommendations following consideration of submissions and discussion with Transport for NSW: That Transport for NSW remove any unnecessary administrative costs of

churn, such as the requirement for a blue slip and deregistration/registration of the same vehicle with a new licence.

That Transport for NSW publish the provisional results of tenders for annual licences (for example, by publishing the median or mean successful bids) within 2 weeks after tenders have closed.

1 Introduction

8 IPART Annual taxi licence release for Sydney 2013/14

1.7 Structure of this report

This report sets out our decisions and recommendations. It is structured as follows: Chapter 2 provides an overview of the taxi industry in Sydney

Chapter 3 provides the context for the review, including the objectives and factors in our terms of reference

Chapter 4 explains how we have forecast the change in demand for taxi services

Chapter 5 explains our recommendation on the number and mix of new licences to be released for 2013/14 and presents the likely impacts on the various segments of the taxi industry

Chapter 6 considers what adjustment needs to be made to allow for some licences that will be handed back to Transport for NSW (or not renewed) and to allow for the Wheelchair Accessible Taxi licences that may also be issued by Transport for NSW

Chapter 7 explains our decisions on whether new licences should be released by auction or sealed tender, and how the price of those licences should be set, as well as whether some licences should be reserved for drivers and whether restrictions should be placed on how many can be issued to one applicant.

2 Overview of the Sydney taxi industry

Annual taxi licence release for Sydney 2013/14 IPART 9

2 Overview of the Sydney taxi industry

Sydney’s taxi industry involves many participants, as well as a range of different taxi licence types. To help stakeholders understand the context for this review, the sections below provide an overview of the industry’s structure, and the licence types and numbers available.

2.1 Taxi industry structure

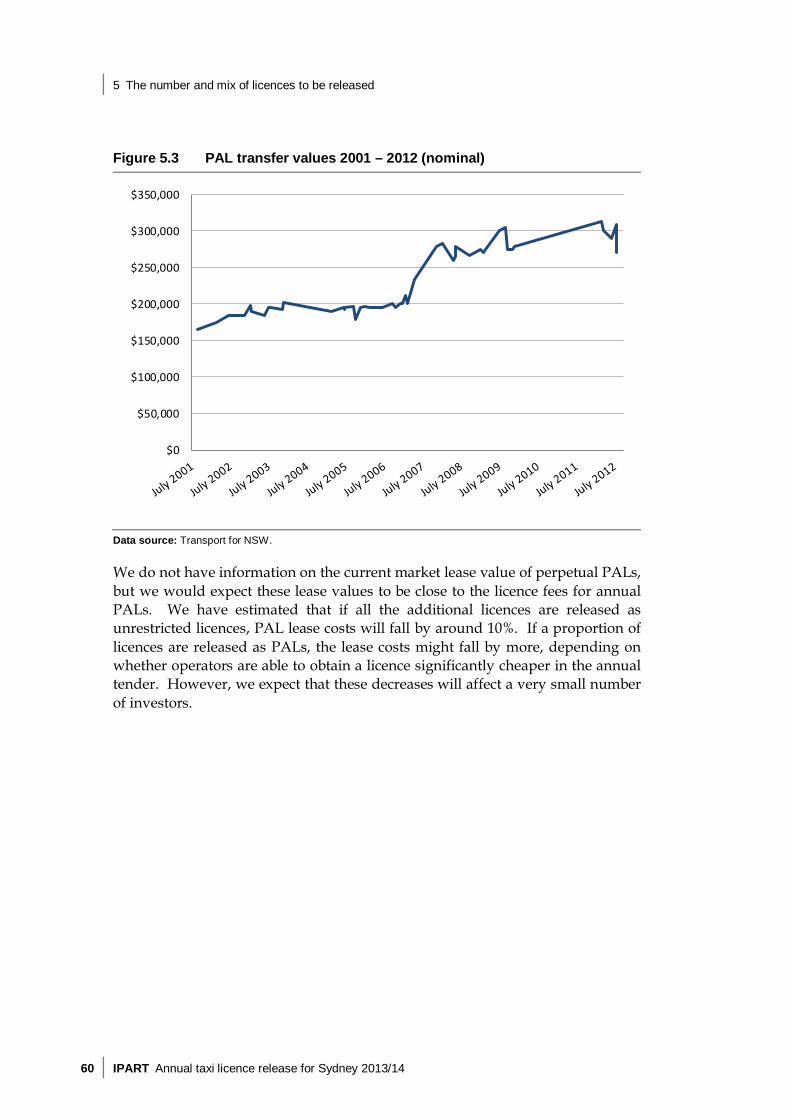

The taxi industry involves a range of participants with different roles and responsibilities – including regulators, networks, operators, drivers and licence owners. Some of these participants play several roles within the ‘supply chain’ for taxi services. For example, many operators are also drivers, networks may own licences, and some licence-owners also operate and drive a taxi.

Figure 2.1 below provides an overview of the taxi industry structure in NSW. The following sections outline the key participants’ roles and responsibilities.

2.1.1 Regulators

While taxi-cabs are a privately (rather than publicly) owned mode of transport, taxi services are usually regulated by government to ensure they meet acceptable safety and quality standards. In NSW, the main regulator is Transport for NSW.

Transport for NSW’s role includes issuing taxi driver authorities, taxi operator accreditations and taxi licences. It also authorises taxi networks, and enforces taxi service standards for networks, vehicles, operators and drivers. In addition, Transport for NSW is responsible for setting taxi fares.

IPART reviews and recommends changes in taxi fares each year. However, Transport for NSW makes the final fare decisions. For the first time, we have also been asked to review and recommend the number of new taxi licences to be released. Again, Transport for NSW will make the final decision.

2 Overview of the Sydney taxi industry

10 IPART Annual taxi licence release for Sydney 2013/14

Figure 2.1 Overview of the taxi industry in NSW

Source: The CIE, Reweighting of the taxi cost index – final report, April 2012, p 14.

2.1.2 Taxi networks

All taxis must be affiliated with a taxi network.10 Taxi networks provide a radio booking service to the taxi operators who are affiliated with them, as well as security monitoring services for taxi drivers and passengers. In some cases, they also provide additional services to operators and drivers, such as training, leasing or sub-leasing taxi licences, insurance broking, and repairs and maintenance. In addition, they monitor and enforce service standards for operators, drivers and vehicles. Networks must be authorised by Transport for NSW.

There are currently 12 networks operating in Sydney, some of which are linked to each other through their business structures.11

10 Passenger Transport Act 1990, S 30(1). 11 Information provided by Transport for NSW.

PROVIDERS OF TAXI SERVICES

Licence plate holders

Operators Drivers

Passengers

Phone and internet bookings

Annual network fees

Licence plate lease payments

Pay-ins or revenue sharing

Booking dispatch

Fares

Taxi services

Transport for NSW

Sets network

standards

Monitors/ enforces standards

May issue new licences

Payment for new licences

Networks

Sets and enforces

regulations

2 Overview of the Sydney taxi industry

Annual taxi licence release for Sydney 2013/14 IPART 11

2.1.3 Taxi operators

Taxi operators are responsible for the day-to-day management of one or more taxi cabs. Operators may be individuals or corporations, and must be accredited by Transport for NSW. They must also be affiliated with an authorised network, and are required to fit out their vehicle with that network’s livery and install the network’s communications equipment. They must insure and maintain their vehicle(s).

In addition, operators must hold a taxi licence for each vehicle they operate. Licensing entry to an industry is a common method of ensuring that participants are qualified to be in the industry, and that they maintain standards of safety and quality. However, the taxi industry is one of the few industries where the number of operators is restricted by the number of licences issued.

The cost to an operator of holding a taxi licence varies, depending on whether:

the operator owns or leases the licence the type of licence it is the source of the licence (secondary market or Transport for NSW), and

the market conditions at the time of obtaining the licence (and any change to market conditions subsequently, for leased licences).

Currently, some 60% of operators lease their taxi licences, while the other 40% either own them or hold the new annual licences issued by Transport for NSW since 2010.12 As at 1 January 2013, there were 2,609 active accredited operators in Sydney, many of whom operate just one taxi.13

Many operators are individuals who also drive their own taxis. In Sydney, most operators also arrange for other drivers to drive their taxis by charging the driver a fixed fee to take out (“bail”) the taxi.14 The maximum fee that the operator can charge the driver is set per shift by the Industrial Relations Commission, and currently ranges from $266.55 for a Friday or Saturday night shift, down to $175 for all day shifts.15

12 The CIE, Reweighting of the taxi cost index – final report, April 2012, p 44. 13 Information provided by Transport for NSW. 14 This arrangement is determined by the Industrial Relations Commission through the Taxi

Industry (Contract Drivers) Contract Determination 1984. The fixed fee arrangement is known as “Method 2.” Alternatively, operator and driver can agree to divide the taxi fares collected on the shift – usually 50/50 (“Method 1”). While a shared-fare arrangement is common in other states in Australia, it is rarely used in Sydney.

15 See www.industrialrelations.nsw.gov.au/biz_res/oirwww/pdfs/Awards/Award_0103.pdf.

2 Overview of the Sydney taxi industry

12 IPART Annual taxi licence release for Sydney 2013/14

2.1.4 Taxi drivers

A taxi driver must be licensed to drive in NSW and authorised by Transport for NSW. Drivers must wear the approved uniform of the network to which their vehicle is affiliated, and be logged in to that network while available for hire. Drivers are responsible for paying for fuel and car washing under bailment Method 2 (fixed pay-in).

As at 1 March 2012, there were 18,791 authorised drivers in Sydney, although not all were active.16

2.1.5 Licence owners

Although a taxi operator must hold a licence (either by owning or leasing it) in order to conduct a taxi business, there is no requirement for a taxi licence owner in NSW to play any part in providing taxi services – and many do not. This means that taxi licences are comparable to other financial assets. The expected profits of owning a licence are determined by how profitable it is to either operate a taxi now and into the future, or how profitable it is to lease the licence to another party.

There are currently 5,647 licences in the Sydney taxi market (as at 1 January 2013).17 Most of these licences are owned by individuals, and more than half are owned by individuals with only 1 licence each. The taxi networks own 446 licences between them.18 The taxi networks also manage licences for individual owners by organising to lease or sub-lease them to operators.

Transport for NSW advises that about 75% of taxi licences are operated by someone other than the licence owner.19 This includes licences owned by taxi networks and operated by affiliated operators. The NSW Taxi Council pointed out in its submission on the draft report that this also includes operators who ‘are registered under a different name to the entity registered as their licence owner (eg, their own superannuation fund, family trust or company) despite the fact that the operator is the beneficial owner of the licence’.20 Nevertheless, we remain of the view that a large proportion of owners hold a licence simply as an investment, whether or not they were previously involved in the taxi industry (such as retired taxi operators).

16 Information provided by Transport for NSW for the 2012 taxi fare review. 17 Information provided by Transport for NSW. Transport for NSW has advised that 55 of the

licences are ‘on hold’ – that is, the licence is in force, but a taxi is not currently being operated using the licence.

18 Information provided by Transport for NSW. 19 Transport for NSW information return for 2012 review of fares, ‘Leased taxis as at 1 March

2012’. 20 NSW Taxi Council submission, 21 January 2013, p 29.

2 Overview of the Sydney taxi industry

Annual taxi licence release for Sydney 2013/14 IPART 13

2.2 Types of licence in the Sydney taxi market

A range of different types of taxi licence are currently valid in NSW. These include perpetual licences, ordinary licences, short-term licences and annual licences. In addition, some licences are unrestricted, while others have restrictions on when, where and how the taxi can be operated.

2.2.1 Perpetual licences

Prior to 1990, perpetual taxi licences were issued to drivers from time to time by ballot. At first, the transfer (ie, sale) of these licences was permitted only to another driver and under certain conditions (eg, only after 10 years or in case of ill-health or death). However, the restrictions on their transfer were gradually removed, and in the 1980s perpetual licences became fully tradeable.

New perpetual licences have not been issued in Sydney since 1990. However, existing licences can still be obtained on the secondary market. In 1989, the average transfer value for an unrestricted perpetual licence was $164,000.21

2.2.2 Ordinary licences

From 1990, ordinary licences with 50-year terms were issued by the transport department on request at the prevailing price for perpetual licences. These licences came with the right to renew them at the end of their term, so they are effectively perpetual. However, the market assessed ordinary licences as less valuable than perpetual licences (possibly because of the prospect of a renewal fee being charged). As a result, prospective licence owners preferred to purchase perpetual licences in the secondary market.

New ordinary licences have not been issued in Sydney since 2009.22 However, existing licences can still be transferred on the secondary market. Existing licences now transfer at prices similar to perpetual licences. During 2012 the average transfer price for ordinary and perpetual licences was $410,000.23

21 Information provided by Transport for NSW. 22 But they continue to be available from Transport for NSW on application for areas outside

Sydney. 23 Information provided by Transport for NSW.

2 Overview of the Sydney taxi industry

14 IPART Annual taxi licence release for Sydney 2013/14

2.2.3 Short-term licences

From the late 1990s, some short-term licences with a term of up to 6 years were issued. Their owners can lease them to another person, but cannot transfer them, and they expire at the end of their term. New short-term licences have not been issued in Sydney since 2009, and as they expire they are being replaced by new annual licences.24 No short-term licences will expire during 2013/14.

2.2.4 Annual licences

In December 2009, taxi licensing legislation was amended to introduce an annual review and determination of the number of new licences (other than Wheelchair Accessible Taxi (WAT) licences) to be released in the Sydney Metropolitan Transport District by tender or auction each year. The licences are annual, and are automatically renewable for a term of up to 10 years. The owners of these licences can lease but not transfer them.

Transport for NSW can issue the licences to increase the number of licences in the market as well as to replace short-term licences as they expire. Transport for NSW must formally determine by 31 March each year how many new annual licences to release from 1 July that year. This year IPART is reviewing and recommending to Transport for NSW how many new licences should be released from 1 July 2013.

2.2.5 Unrestricted and restricted licences

While some taxi licences are issued without restrictions, others have restrictions on them. The most common types of restricted licences are: Peak Availability Licences (PALs) (have restricted hours of operation).

Fringe Area Licences (must be operated predominantly in nominated geographical areas on the outskirts of Sydney).

Wheelchair Accessible Taxi (WAT) licences (must be operated to give preference to transporting wheelchair users).

PALs can only be operated between 12 noon and 5 am, and are typically driven for a single shift per day. This means that many of these taxis are on the road at 3 pm and 3 am changeover times, which helps address the shortage of taxis on the road at these times.

24 But they continue to be available from Transport for NSW on application for areas outside

Sydney.

2 Overview of the Sydney taxi industry

Annual taxi licence release for Sydney 2013/14 IPART 15

Taxis with a Fringe Area Licence are authorised for hire only within the area of operation. They can only accept hires that originate outside their area of operation where the hiring has been pre-booked and the person is being taken to a place within the area of operation.

For the Sydney Metropolitan Transport District, new and replacement PALs and Fringe Area Licences are now issued through the annual release process, and are part of IPART’s review. Annual WAT licences will continue to be available from Transport for NSW on application for $1,000 a year (and therefore do not form part of our review).

2.3 Number of licences by type in Sydney taxi market

Currently there are 5,647 taxi licences in the Sydney market as at 1 January 2013 compared to 5,231 as at 1 January 2010. The taxi fleet has increased by 8%, comprised of:

net 310 additional unrestricted licences since January 2010, increasing the taxi fleet by 5.9%

net 21 additional PALs, increasing the taxi fleet by 0.4%

net 90 additional WAT licences, increasing the taxi fleet by 1.7%.

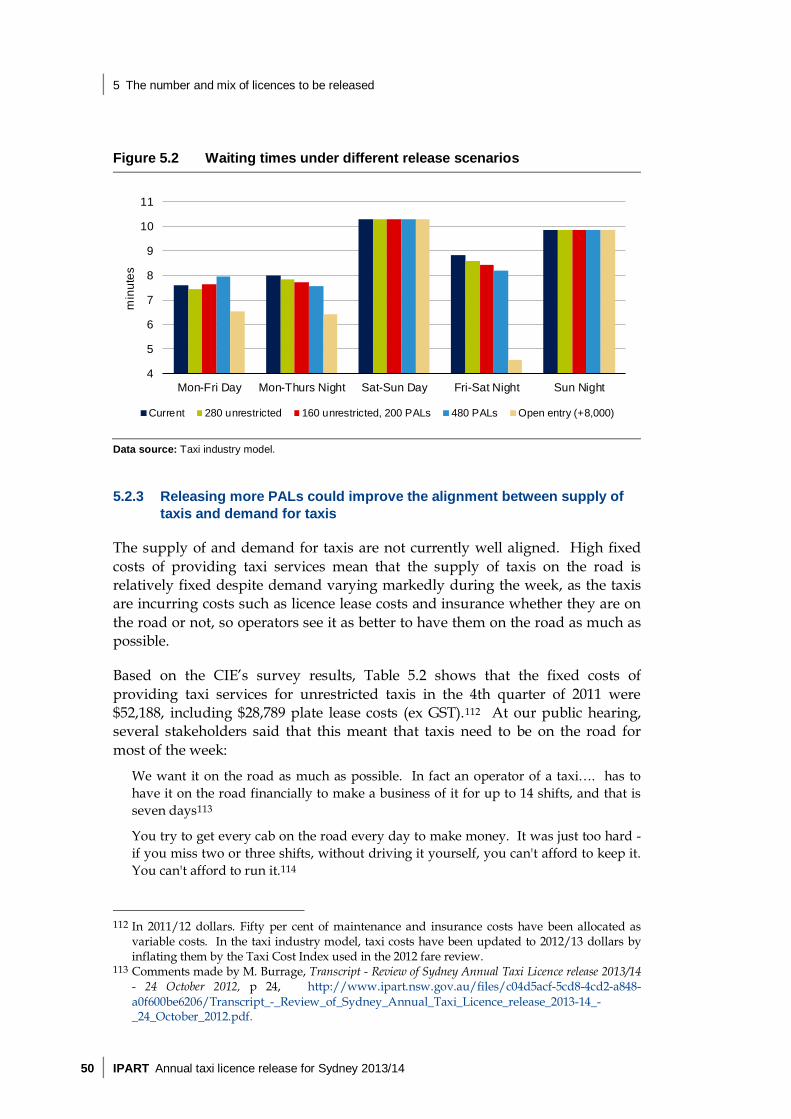

Figure 2.2 shows the change in licence numbers and composition in Sydney since November 2008.

Figure 2.2 Change in licence numbers and composition, Sydney taxi market

Data source: Transport for NSW.

2 Overview of the Sydney taxi industry

16 IPART Annual taxi licence release for Sydney 2013/14

As shown above, most licences in operation are unrestricted. PALs currently make up around 5% of all licences in the Sydney market. Fringe Area Licences make up a smaller part of the total fleet, with 14 Fringe Area Licences currently being operated.25

25 A Fringe Area Licence was handed back in September 2012 and we propose that a replacement

should be tendered in 2013/14; 2 WAT licences were reclassified as Fringe WATs in December 2012. (Information provided by Transport for NSW).

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 17

3 Context for the review: objectives and factors

As previous chapters indicated, the current approach to releasing new taxi licences in Sydney has been in use since December 2009, when the Passenger Transport Act 1990 (the Act) was amended.26 The amendments establish that each year, Transport for NSW must review and determine the number of new licences (other than Wheelchair Accessible Taxi (WAT) licences) to be released in the Sydney Metropolitan Transport District by tender or auction each year.

To help stakeholders understand this approach, and what it – and our review – is intended to achieve, the sections below discuss: the circumstances that led to the 2009 amendments to the Act

the factors that we must consider in recommending the number of new licences to be released in 2013

the approach used to determine this number in 2010, 2011 and 2012

the success of this approach in meeting the amendment’s objectives to date.

3.1 Circumstances that led to the 2009 amendments

From around 1980 to 2009, growth in the number of taxi licences in Sydney did not keep pace with the growth in the city’s population, household and business income, or economic and tourism activity. The restriction on the supply of taxis meant that licences became a scarce commodity, which pushed up the costs of buying or leasing a licence.

In general, this situation benefited the owners of these licences, as it increased the return they could earn on their investment. However, it imposed additional costs on other participants in the taxi industry, and ultimately on passengers. For example, by 2008/9 operators were required to pay around $26,000 per year (not including GST) in lease costs just to enter the market27 (or invest $365,000 if they chose to purchase a licence).28 Then they had to collect enough revenue through

26 Amendments were made by the Passenger Transport Amendment (Taxi Licensing) Act 2009,

No 118. 27 In 2008/09 dollars. IPART calculation, based on the CIE survey data 2011 deflated by NSW

Taxi Council information about lease prices from a sample of taxi networks provided for IPART fare reviews between 2008 and 2012.

28 Information from Transport for NSW for 2008/09 transfer values (in 2008/09 dollars).

3 Context for the review: objectives and factors

18 IPART Annual taxi licence release for Sydney 2013/14

fares or pay-ins from drivers to cover that cost, so pay-ins were higher than they would otherwise have been. In addition, fares had to be set high enough to provide sufficient revenue for drivers to afford the pay-ins. Passengers paid the cost of these higher fares. With the cost of a licence lease amounting to around 20% of the cost of keeping a taxi on the road for a year,29 potentially $4 of every $20 fare went to pay for the licence lease. Passengers also paid the cost of the imbalance between the supply and demand for taxis – for example, by experiencing longer waiting times for taxis, or not being able to get a taxi when they wanted one.

3.2 Factors in the 2009 amendments and other objectives we must consider

The intention of the 2009 amendments was to reduce the effects of past restrictions on the supply of taxi licences described above. This is clearly reflected in our terms of reference, which list the objectives of the amendments and the factors in the legislation that we must consider in making our recommendation.

3.2.1 Objectives of the amendments

The terms of reference for this review list the objectives of the 2009 amendments as:

ensuring the supply of taxis responds closely to growth in passenger demand balancing the need for more affordable entry into the taxi market with the

need to avoid unreasonable impacts on existing licence holders

reducing barriers to entry and encouraging competition placing downward pressure on fares over time simplifying existing taxi licence structures.

Ensuring the supply of taxis responds closely to the growth in passenger demand

This objective suggests that the number of new licences released should ensure that the supply of taxis increases as the demand for taxi services grows.

This suggests the approach used to determine this number must include estimating how demand for taxi services changes over time. Passenger demand for taxi services is driven by factors that include population, household and business income, economic activity, and tourism numbers. Growth in these is likely to increase the size of the potential market of taxi users, and increase the frequency with which people use taxi services.

29 The CIE, Reweighting of the taxi cost index – final report, April 2012, p 9.

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 19

In addition, the factors that must be considered in determining the number of new licences to be released specify that the consideration of passenger demand must include not only likely (or actual) demand, but also latent demand (see section 3.2.2 below).

Balancing the need for a more affordable means of entry into the taxi market with the need to avoid unreasonable impacts on existing licence holders

The findings of the CIE’s 2011 survey of drivers and operators conducted for IPART’s taxi fare review indicate that the average cost of leasing a taxi licence for a standard urban taxi in Sydney was $28,789 (excluding GST) per year at the time of the survey (4th quarter of 2011), or around 20% of the total cost of keeping a taxi on the road for a year.30 The other costs include driver labour, fuel, insurance, car lease costs, maintenance, operator labour and network fees.

To update the CIE’s estimated lease cost from 2011 to the current year, we have compared the average annual licence fee for all licences on foot as at 31 December 2012 with the annual average licence fee for all licences on foot as at 31 December 2011.31 We consider that this is likely to be a reliable indicator of the general movement in market lease rates. The change from 2011 to 2012 was -2.2%, which gives an estimated average lease cost as at the end of 2012 of $28,155.

As licence leases derive their value from their scarcity, increasing the supply of licences should reduce lease costs. However, if the growth in licence numbers simply keeps pace with the growth in demand from external factors, lease costs are likely to be maintained in real terms.32 In order to achieve the objective of a more affordable means of entry into the taxi market, more licences need to be released than the number that is required to meet the annual increase in passenger demand.

On the other hand, if the additional licence numbers greatly exceed the growth in demand, lease costs will fall substantially, which means a bigger impact on the incomes of existing owners of perpetual licences. Our terms of reference require us to balance the two objectives of providing more affordable leases for operators and avoiding unreasonable impacts on licence holders.

Reducing barriers to entry and encouraging competition

We consider the main barrier to entry is the cost of taxi licences, discussed above. However, other structural issues might also affect entry into the taxi industry and competition within it. These include the number of licences one person can hold; how a person obtains a licence (holding it themselves, or leasing it from an owner 30 The CIE, Reweighting the Taxi Cost Index Final Report, March 2012, p 9. 31 Information provided by Transport for NSW. 32 That is, assuming fares and all other costs of providing taxi services increase in line with

inflation, lease costs would also increase in line with inflation.

3 Context for the review: objectives and factors

20 IPART Annual taxi licence release for Sydney 2013/14

or through a third party); and whether licence owners are involved in the industry as drivers, operators, licence owners or as 2 or 3 of these roles.

Placing downward pressure on fares over time

As Chapter 2 noted, we review and recommend taxi fares to Transport for NSW each year. In recent years, we have based our recommended fare increases on the annual change in the cost of providing taxi services as measured by a Taxi Cost Index. As part of our 2012 review of taxi fares we decided to set the licence lease cost inflator to zero. As part of our next 2013 fare review we will reconsider this, as increasing the supply of taxi licences and thus reducing lease costs should put downward pressure on fares.

Simplifying existing taxi licence structures

Existing short-term licences are gradually being replaced as they expire by new annual licences. While no new ordinary or perpetual licences will be issued in Sydney, existing ones will not be replaced or revoked, so there is a limit to the extent to which the release of new licences can simplify existing taxi licence structures.

3.2.2 Factors to be considered in determining the number of new taxi licences per year

Section 32C(3) of the Act indicates that in determining the number of new annual licences to be released in any year, the following factors must be considered: the likely passenger demand for taxi-cab services, including latent demand

the performance of existing taxi-cab services the demand for new taxi-cab licences the viability and sustainability of the taxi-cab industry

and any other matters considered relevant, having regard to the objective of ensuring improved taxi-cab services.

Likely passenger demand and latent demand for taxi-cab services

As noted above, demand for taxis is driven by a range of factors, including population, household and business income, economic activity, and tourism numbers. We could also directly observe demand for taxis by looking at the number of taxi trips taken in a year.

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 21

But as most people see taxis as a discretionary service, there is likely to also be latent demand for taxi travel – that is, demand that we cannot directly observe. This includes the demand by people who would have liked to travel by taxi but didn’t. For example, they might have thought taxi travel was too expensive or the waiting time would be too long or the taxi might not turn up, and so made alternative arrangements, such as driving their own car, catching public transport, or booking a hire car instead. Alternatively, they might have decided not to travel at all.

We commissioned Taverner Research to conduct a survey of 2000 Sydney residents to help us understand the behaviour of taxi users to inform our estimates of responsiveness to price and the time taken to catch a taxi.33 The results of the survey were published at the same time as our taxi licence review draft report.

The performance of existing taxi-cab services

Performance of existing taxi services could be considered an indicator of the balance between supply and demand. For example, increases in the numbers of trips, length of waiting time, or number of bookings where there is ‘no car available’ to complete the job could indicate that demand has grown (or supply is too low). Deterioration in the quality and safety of services, or in customers’ satisfaction with taxi services, could indicate operators are trying to lower costs to match lower fare revenue because demand has fallen (or supply is too high).

Some performance measures of taxis in Sydney are available through the network standards and KPIs set by Transport for NSW and reported against by the taxi networks. However, these only apply to booked trips, which constitute a minority of all trips. The Taverner Research survey confirmed that only around a quarter of trips are booked through a taxi company.34 To date there has been no regular survey of customer satisfaction in NSW. IPART uses information on customer complaints and compliments from the Customer Feedback Management System operated by Transport for NSW as an indicator of service standards in our fare reviews, but we have recommended adoption of regular customer surveys as a better measure.

The Taverner Research survey sought to get a better understanding of the performance of taxi services from customers’ perspective. In general, 65% of people who had taken a taxi in the past 6 months were satisfied with the overall performance of the service. Customers were more dissatisfied with fares than with other aspects of taxi services. 36% of passengers said that they were dissatisfied with fares, whereas only 10% to 16% were dissatisfied with other aspects (such as waiting time, knowledge of Sydney and route taken). The highest rated aspects of the journey were the directness of the route (59% were

33 Taverner Research, Survey of Taxi Use in Sydney, November 2012. 34 Data from Taverner Research, Survey of Taxi Use in Sydney, November 2012, analysed by IPART.

3 Context for the review: objectives and factors

22 IPART Annual taxi licence release for Sydney 2013/14

very satisfied or satisfied) with driver courtesy and helpfulness somewhat lower (48%) but still well above the fare charged (26%).35

Most people felt that the quality of taxi services has not changed since last year. The main exception was for fares. Over half of taxi users surveyed (55%) said that the cost of fares is worse than it was last year, while only 6% considered this had improved. The next worse trend was in journey times with 16% saying this was worse against 8% saying it was better. Driver behaviour and the time taken to make a booking both attracted slightly more ratings of ‘better’ than of ‘worse’.36

The demand for new taxi-cab licences

The demand for new taxi licences is driven by factors such as the income a potential taxi operator expects to earn, the existence of other employment opportunities (including driving but not operating a taxi) and their expected incomes, and the availability and price of taxi licences and leases on the secondary market.

The viability and sustainability of the taxi-cab industry

Our approach for deciding on the number of licences to be released needs to consider the impacts on drivers and operators, as well as those on existing licence owners (discussed above) so that the industry continues to be viable in both the short and the longer term.

Any other matters considered relevant, having regard to the objective of ensuring improved taxi-cab services

Other matters can be considered in determining the number of licences to be released, provided they relate to improving taxi services for the community. We note that previous reviews have not considered additional matters. We have not identified any other matters for consideration.

3.3 Approach used to determine number of new annual licences to be released to date

In January 2010, immediately after the 2009 amendments came into effect, Transport for NSW released 100 new annual licences as an interim measure. Later that year, and in March 2011 and 2012, it made annual determinations of new annual licences to be released each year, in line with the amendments.

35 Taverner Research, Survey of Taxi Use in Sydney, November 2012, pp 46-47. 36 Taverner Research, Survey of Taxi Use in Sydney, November 2012, pp 59-60.

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 23

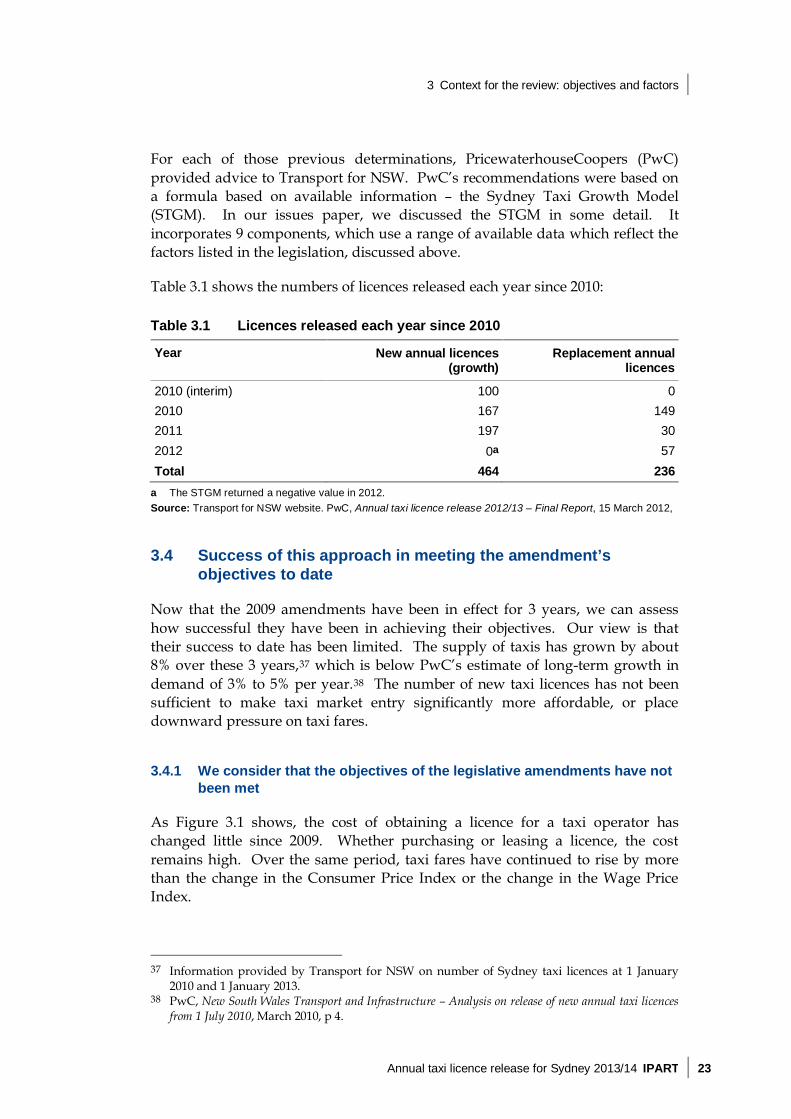

For each of those previous determinations, PricewaterhouseCoopers (PwC) provided advice to Transport for NSW. PwC’s recommendations were based on a formula based on available information – the Sydney Taxi Growth Model (STGM). In our issues paper, we discussed the STGM in some detail. It incorporates 9 components, which use a range of available data which reflect the factors listed in the legislation, discussed above.

Table 3.1 shows the numbers of licences released each year since 2010:

Table 3.1 Licences released each year since 2010

Year New annual licences (growth)

Replacement annual licences

2010 (interim) 100 0 2010 167 149 2011 197 30 2012 0a 57 Total 464 236

a The STGM returned a negative value in 2012. Source: Transport for NSW website. PwC, Annual taxi licence release 2012/13 – Final Report, 15 March 2012,

3.4 Success of this approach in meeting the amendment’s objectives to date

Now that the 2009 amendments have been in effect for 3 years, we can assess how successful they have been in achieving their objectives. Our view is that their success to date has been limited. The supply of taxis has grown by about 8% over these 3 years,37 which is below PwC’s estimate of long-term growth in demand of 3% to 5% per year.38 The number of new taxi licences has not been sufficient to make taxi market entry significantly more affordable, or place downward pressure on taxi fares.

3.4.1 We consider that the objectives of the legislative amendments have not been met

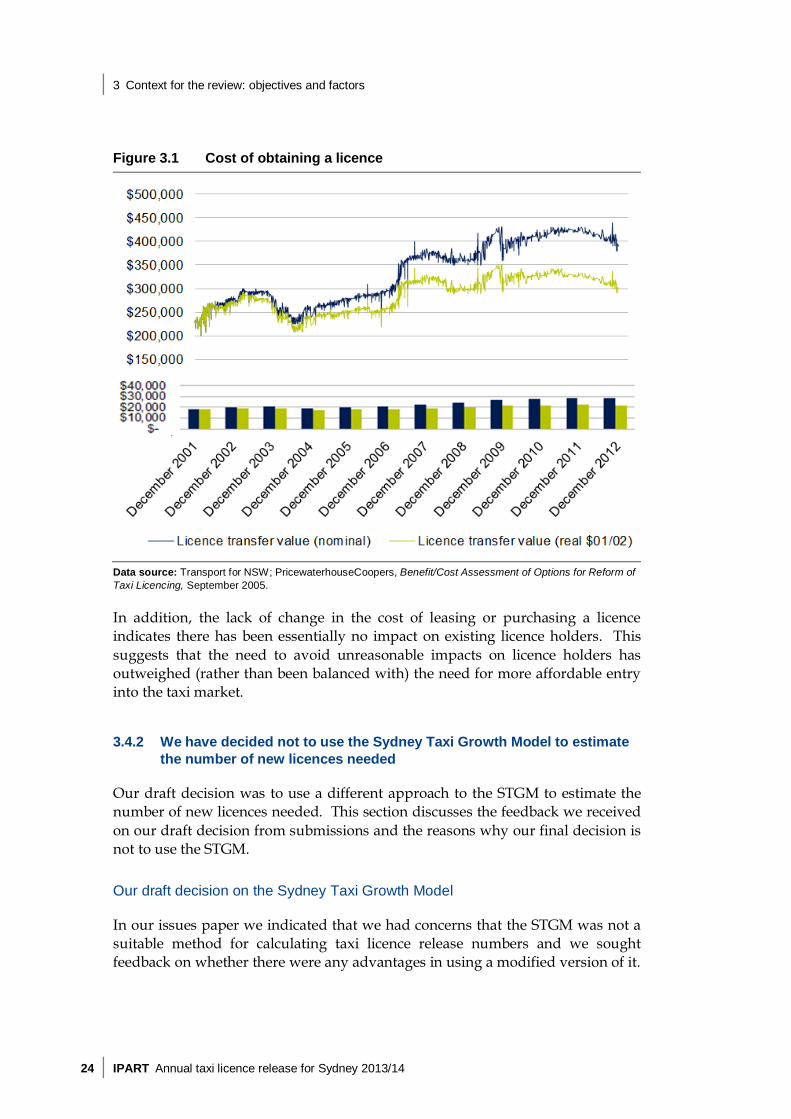

As Figure 3.1 shows, the cost of obtaining a licence for a taxi operator has changed little since 2009. Whether purchasing or leasing a licence, the cost remains high. Over the same period, taxi fares have continued to rise by more than the change in the Consumer Price Index or the change in the Wage Price Index.

37 Information provided by Transport for NSW on number of Sydney taxi licences at 1 January

2010 and 1 January 2013. 38 PwC, New South Wales Transport and Infrastructure – Analysis on release of new annual taxi licences

from 1 July 2010, March 2010, p 4.

3 Context for the review: objectives and factors

24 IPART Annual taxi licence release for Sydney 2013/14

Figure 3.1 Cost of obtaining a licence

Data source: Transport for NSW; PricewaterhouseCoopers, Benefit/Cost Assessment of Options for Reform of Taxi Licencing, September 2005.

In addition, the lack of change in the cost of leasing or purchasing a licence indicates there has been essentially no impact on existing licence holders. This suggests that the need to avoid unreasonable impacts on licence holders has outweighed (rather than been balanced with) the need for more affordable entry into the taxi market.

3.4.2 We have decided not to use the Sydney Taxi Growth Model to estimate the number of new licences needed

Our draft decision was to use a different approach to the STGM to estimate the number of new licences needed. This section discusses the feedback we received on our draft decision from submissions and the reasons why our final decision is not to use the STGM.

Our draft decision on the Sydney Taxi Growth Model

In our issues paper we indicated that we had concerns that the STGM was not a suitable method for calculating taxi licence release numbers and we sought feedback on whether there were any advantages in using a modified version of it.

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 25

In its submission on the issues paper, the NSW Taxi Council argued that most of the components in the model are required to comply with the requirements of the Act, and proposed modifications to overcome some of the concerns about data.39 However, as we noted in our draft report, the requirements of the Act do not have to be incorporated into a single formula, and in fact including components that are not specifically demand-related in a formula has helped to preserve the existing balance between supply and demand for taxis in Sydney, by acting as an in-built brake on the number of growth licences released. For example, when taxi service levels begin to improve, or the transfer values of existing licences start to decline, the STGM recommends fewer new taxi licences be released.

One submission argued that the STGM should be run in parallel with a new model as a validation exercise.40 However, this would only be worthwhile if we thought that the STGM was a valid method.

In our draft report, we decided that ‘given our own concerns about the STGM, and the lack of support or compelling arguments for maintaining it in a modified form, our draft decision is that a new approach is warranted.’41

Submissions on the draft report supporting the STGM

The NSW Taxi Council submitted that we should use the STGM for this review, with improvements as suggested by the NSW Taxi Council’s submission to the issues paper.42 St George Cabs reiterated that the STGM should be used in parallel to validate IPART’s recommendations.43

The NSW Taxi Council’s submission states that the STGM is simpler, more transparent, more understandable and predictable than IPART’s proposed approach, takes account of real-world performance and ensures the supply of taxis responds closely to growth in passenger demand. The submission also states that ‘the only justification that IPART has provided for rejecting the STGM is that it has not produced rapid enough change.’44

39 NSW Taxi Council submission, 9 November 2012, p 12. 40 St George Cabs submission, 9 November 2012, p 3. 41 IPART, Annual taxi licence release for Sydney 2013/14 – Draft Report, December 2012, p 21. 42 NSW Taxi Council submission, 21 January 2013, p 37. 43 St George Cabs submission, 21 January 2013. 44 NSW Taxi Council submission, 21 January 2013, p 35.

3 Context for the review: objectives and factors

26 IPART Annual taxi licence release for Sydney 2013/14

Our response to submissions supporting the STGM

While we did not reproduce the arguments in our draft report, our issues paper did discuss our concerns with the STGM approach.45 In summary, the STGM is not, despite its name, a model of the demand for taxi services, but an index constructed from available data, some of which are related to demand and some of which are not. The factors in the STGM which are directly related to demand are not included based on their quantitative relationship to demand, but in an arbitrary fashion. Some of these problems were acknowledged by PWC when they developed the STGM, and the STGM was proposed as a ‘next best’ solution that used objective inputs, was simple and transparent and enabled a ‘balanced consideration of factors’.46

While the STGM is certainly simple and transparent, during the time it was in use PwC and others expressed concerns about the data inputs,47 and it proved not particularly stable or predictable, returning a negative number in the third year it was used.48

The NSW Taxi Council acknowledged these data and stability shortcomings of the STGM in its submission on our issues paper, proposing improvements.49 Some of the NSW Taxi Council’s suggested changes (such as using longer term averages for proxy measures of demand) are consistent with the approach we have taken to estimating demand from external factors. (Chapter 4 discusses our approach to estimating demand from external factors in more detail).

However, we consider that the NSW Taxi Council’s proposed improvements do not address a fundamental problem with the STGM: that the inclusion of factors intended to capture measures of changes to ‘industry viability’ and ‘performance of existing services’ preserve the existing relationship between supply and demand for taxis. The NSW Taxi Council argues that we are required by our terms of reference to develop a formula that includes all the factors in the terms of reference (which in turn come from the Passenger Transport Act).50 We agree that we must meet our terms of reference; however, we do not agree that considering factors requires them to be included in a formula.

45 IPART, Annual taxi licence release for Sydney 2013/14 - Issues Paper, October 2012. 46 PwC, New South Wales Transport and Infrastructure – Analysis on release of new annual taxi licences

from 1 July 2010, March 2010, pp 12-19. 47 PwC, Annual taxi licence release 2012/13: Final Report, March 2012, p18 (network bookings not

representative of overall passenger demand), p 20 (errors in reporting of network bookings data).

48 Ibid, p 5. 49 NSW Taxi Council submission, 9 November 2012, p 11. 50 NSW Taxi Council submission, 21 January 2013, p 35.

3 Context for the review: objectives and factors

Annual taxi licence release for Sydney 2013/14 IPART 27

Submissions on the draft report proposing a different approach and our response

Several submissions supported releasing an unlimited number of licences at a fixed price below the current market price, but only to operator/drivers.51 The submission from a former Victorian Taxi Inquiry commissioner noted that this approach had also been recommended by the Victorian Taxi Inquiry. His submission continued ‘although IPART may be constrained by its terms of reference, it is suggested that consideration again be given to the possible adoption of a price-based rationing system in NSW.’52

Our response to submissions proposing alternative approaches

As we noted in our issues paper, the legislation that governs the annual licence determination process does not permit this approach. A decision was made by Government when the amendments were made to the legislation in 2009 that release of licences should be determined by quantity rather than by price. Therefore our terms of reference ask us to recommend a fixed number of new licences, rather than recommend a price for an unlimited number of licences.

51 E Mollenhauer submission, 21 January 2013, p 2; NSW Taxi Drivers’ Association (NSWTDA)

submission, 21 January 2013, p 3; Australian Taxi Drivers’ Association (ATDA) submission, 23 January 2013.

52 D Cousins submission, 15 January 2013, pp 2-3.

4 The demand for taxi services

28 IPART Annual taxi licence release for Sydney 2013/14

4 The demand for taxi services

Under Section 32C(3) of the Passenger Transport Act 1990, regard must be had to the likely passenger demand for taxi-cab services, including latent demand, and the performance of existing taxi-cab services.

We firstly considered the external factors that are likely to increase the demand for taxi services, such as growth in population, household and business income, economic activity and tourism. Growth in these factors is likely to increase the size of the potential market of taxi users, and increase the frequency with which people use taxi services.

By examining trends in NSW state final demand, population growth and airport passenger numbers, we consider that demand for taxi services is likely to grow by around 2.5% per year over the longer term. In our view, at least an additional 140 new unrestricted licences should be issued each year to keep pace with this growth. We recommend that this be set as the minimum number of licences that will be issued each year over the next 5 years. These are the same as the decisions we made in our draft report.

We also considered the demand that would be generated by changes to the number of taxis on the road, and the price of taxi services. In particular: if there were more taxis on the road, additional trips would be taken because

passengers would not have to wait as long to catch a taxi if fares were to fall, additional trips will be taken because it costs less to use

taxi services.

This is known as latent demand, because some people are not currently making these trips, but would make them if waiting time or prices were reduced. As part of our assessment of latent demand we looked at the performance of existing taxi services by surveying Sydney residents to measure the current time taken to catch a taxi. Chapter 5 provides more information on the impact of latent demand on our recommendations.

4 The demand for taxi services

Annual taxi licence release for Sydney 2013/14 IPART 29

4.1 How changes in demand relate to the change in licence numbers

Our terms of reference require us to consider the need for the supply of taxis to respond closely to the growth in passenger demand. We must also consider the need to reduce barriers to entry and place downward pressure on fares.

At a minimum, the number of taxi licences needs to increase in line with the demand due to external factors to ensure that lease costs do not increase in real terms (that is, after adjusting for inflation). But additional licences will be required for lease costs to fall in order to make it more affordable to provide taxi services and to place downward pressure on fares.

Additional licences will also be needed to reduce waiting time for customers. Latent demand would convert to actual demand when these new trips are taken because passengers will not have to wait as long to catch taxis.

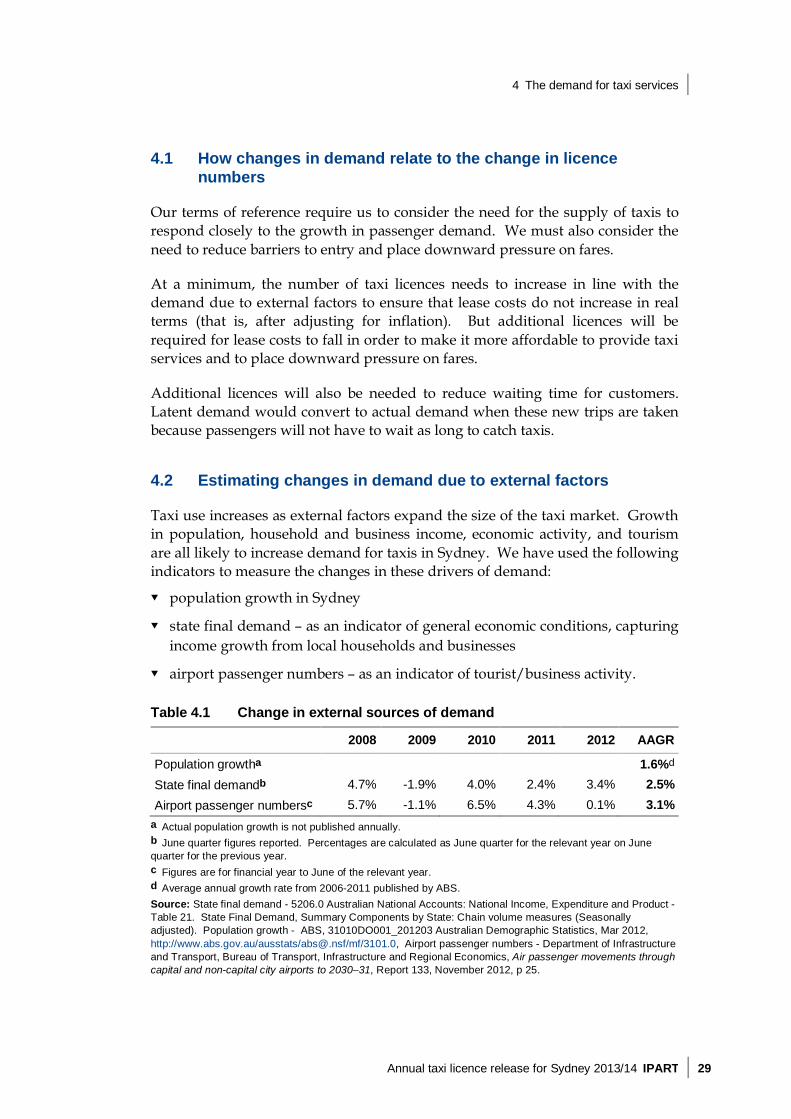

4.2 Estimating changes in demand due to external factors

Taxi use increases as external factors expand the size of the taxi market. Growth in population, household and business income, economic activity, and tourism are all likely to increase demand for taxis in Sydney. We have used the following indicators to measure the changes in these drivers of demand: population growth in Sydney

state final demand – as an indicator of general economic conditions, capturing income growth from local households and businesses

airport passenger numbers – as an indicator of tourist/business activity.

Table 4.1 Change in external sources of demand

2008 2009 2010 2011 2012 AAGR

Population growtha 1.6%d State final demandb 4.7% -1.9% 4.0% 2.4% 3.4% 2.5% Airport passenger numbersc 5.7% -1.1% 6.5% 4.3% 0.1% 3.1%

a Actual population growth is not published annually. b June quarter figures reported. Percentages are calculated as June quarter for the relevant year on June quarter for the previous year. c Figures are for financial year to June of the relevant year. d Average annual growth rate from 2006-2011 published by ABS. Source: State final demand - 5206.0 Australian National Accounts: National Income, Expenditure and Product - Table 21. State Final Demand, Summary Components by State: Chain volume measures (Seasonally adjusted). Population growth - ABS, 31010DO001_201203 Australian Demographic Statistics, Mar 2012, http://www.abs.gov.au/ausstats/[email protected]/mf/3101.0, Airport passenger numbers - Department of Infrastructure and Transport, Bureau of Transport, Infrastructure and Regional Economics, Air passenger movements through capital and non-capital city airports to 2030–31, Report 133, November 2012, p 25.

4 The demand for taxi services

30 IPART Annual taxi licence release for Sydney 2013/14

Table 4.1 shows that the recent trends indicate that demand is likely to grow by 2.5% per year on average due to external factors.

We recommend for this review and the next 4 annual reviews of taxi licences that the minimum increase in the number of licences is 2.5%, reflecting a longer term estimate of growth in demand for taxi services resulting from external factors. For simplicity and certainty we consider that the 2.5% should be applied to the current number of taxi licences as at 1 January 2013, so that a minimum of 140 new licences are released each year. We expect that increasing the number of taxi licences by this amount each year in line with the increase in demand from external sources would mean that lease costs remain unchanged in real terms.53 As mentioned previously, more licences than this will need to be released for lease costs to fall to improve affordability into the industry, and to improve waiting times for customers to convert latent demand to actual demand.

Submissions on the draft report generally did not support our view of demand. The sections below set out our reasoning, the comments made in submissions, and our response to them.

4.2.1 Indicators of external sources of demand

In submissions on the issues paper, stakeholders suggested that we should look at a range of indicators of demand for taxi services:

NSW GDP, state final demand54 employment rate, movement in wages, commercial tenancy occupancy rates55 population growth56

airport passenger numbers57 measures of economic uncertainty – rates of corporate cost cutting and

consumer spending.58

We agree that many of these factors will influence the amount of taxi use in Sydney. Regression analysis is a statistical tool that could be used to determine the strength of the relationship between these and other variables and taxi use. The outputs could then be used to estimate the change in demand from one period to another. While we consider that this would be the best way to measure

53 That is, assuming fares and all other costs of providing taxi services increase by the rate of

inflation, lease costs would also continue to rise by the rate of inflation. 54 N O’Brien submission, 9 November 2012, p 1; NSW Taxi Council submission, 9 November 2012,

p 3. 55 E Atra submission, 5 November 2012. 56 NSW Taxi Council submission, 9 November 2012, p 4; Sydney Metro Taxi Fleet submission,

November 2012; D Lipski submission, 9 November 2012, p 5; E Atra submission, 5 November 2012.

57 NSW Taxi Council submission, 9 November 2012, p 4. 58 NSWTDA submission, 9 November 2012, p 2.

4 The demand for taxi services

Annual taxi licence release for Sydney 2013/14 IPART 31

the change in demand from these factors, we do not have enough historical information of the number of trips taken in Sydney to undertake this analysis.

Therefore we have decided to focus on the same 3 indicators of external sources of demand that were used previously by PwC: state final demand, Sydney population size and Sydney airport passenger numbers. Many of the other measures suggested in submissions are closely related to these. Continuing to use these factors was generally supported in submissions on our issues paper.59

Why state final demand?

State final demand reflects the relationship between income and spending on goods and services, including taxi services. It includes government and household final consumption expenditure. State final demand has been used in previous years.60 The NSW Taxi Council supported PwC’s findings from previous reviews that state final demand was the most relevant measure of economic activity.61

Why population growth?

Population has also been used in the past to forecast the demand for taxi services. The NSW Taxi Council submitted that while it is appropriate to consider population growth, ‘there is no conclusive evidence of a strong correlation in the increased demand for taxis and population increase’.62

Why passenger numbers at Sydney Airport?

In previous reviews, the PwC considered passenger numbers at Sydney airport as an indication of the likely change in the number of taxi journeys to and from Sydney airport. The NSW Taxi Council supports using airport passenger numbers because it is a significant source of demand for taxis.63

We consider that passenger numbers at Sydney airport are an indicator not only of the trips likely to be taken at Sydney airport, but also the growth in the size of the taxi market reflecting tourism and business growth. Increases in airport passengers suggest greater tourist and business travel activity.

59 We note that PwC used network bookings to measure the change in demand. We have not

included network bookings because we do not consider them to be a good indicator of demand for taxi services.

60 PwC, Annual taxi licence release 2012/13 – Final Report, 15 March 2012. 61 NSW Taxi Council submission, 9 November 2012, p 7. 62 Ibid, p 4. 63 Ibid, p 4.

4 The demand for taxi services

32 IPART Annual taxi licence release for Sydney 2013/14

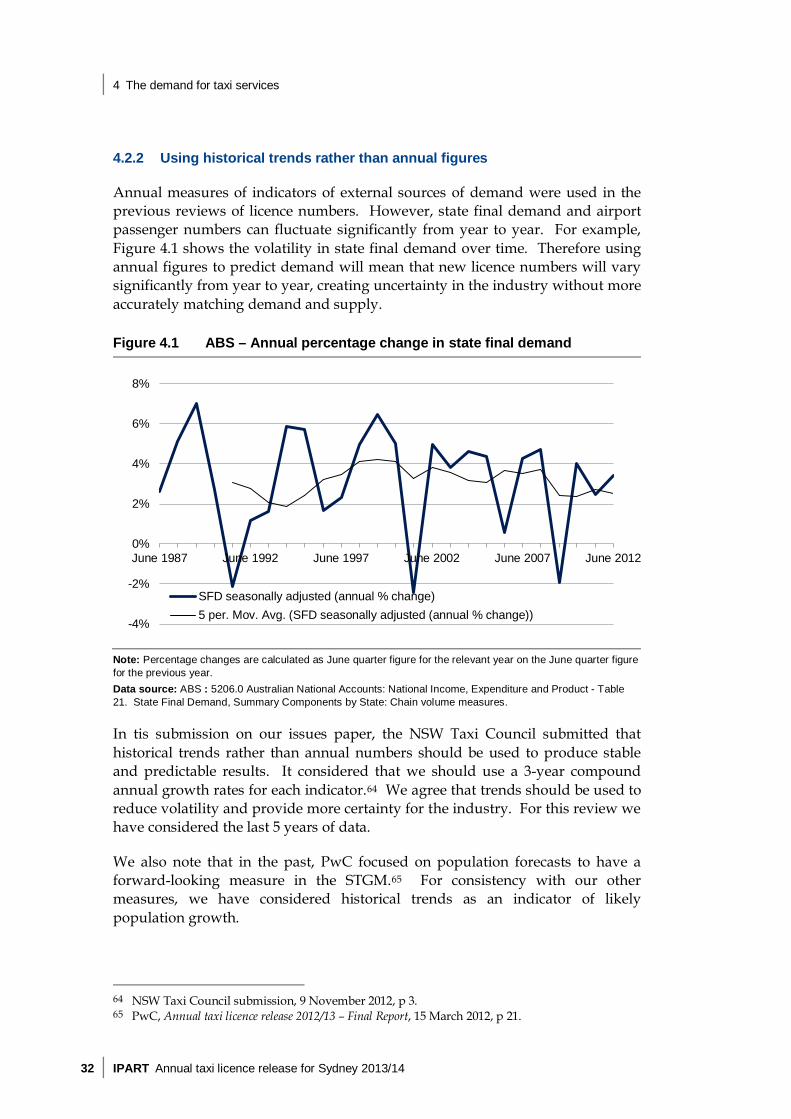

4.2.2 Using historical trends rather than annual figures

Annual measures of indicators of external sources of demand were used in the previous reviews of licence numbers. However, state final demand and airport passenger numbers can fluctuate significantly from year to year. For example, Figure 4.1 shows the volatility in state final demand over time. Therefore using annual figures to predict demand will mean that new licence numbers will vary significantly from year to year, creating uncertainty in the industry without more accurately matching demand and supply.

Figure 4.1 ABS – Annual percentage change in state final demand

Note: Percentage changes are calculated as June quarter figure for the relevant year on the June quarter figure for the previous year. Data source: ABS : 5206.0 Australian National Accounts: National Income, Expenditure and Product - Table 21. State Final Demand, Summary Components by State: Chain volume measures.

In tis submission on our issues paper, the NSW Taxi Council submitted that historical trends rather than annual numbers should be used to produce stable and predictable results. It considered that we should use a 3-year compound annual growth rates for each indicator.64 We agree that trends should be used to reduce volatility and provide more certainty for the industry. For this review we have considered the last 5 years of data.

We also note that in the past, PwC focused on population forecasts to have a forward-looking measure in the STGM.65 For consistency with our other measures, we have considered historical trends as an indicator of likely population growth.

64 NSW Taxi Council submission, 9 November 2012, p 3. 65 PwC, Annual taxi licence release 2012/13 – Final Report, 15 March 2012, p 21.

-4%

-2%

0%

2%

4%

6%

8%

June 1987 June 1992 June 1997 June 2002 June 2007 June 2012

SFD seasonally adjusted (annual % change)5 per. Mov. Avg. (SFD seasonally adjusted (annual % change))

4 The demand for taxi services

Annual taxi licence release for Sydney 2013/14 IPART 33

State final demand

Over the past 5 years annual growth in state final demand has averaged 2.5%. Over the longer term, the rolling 5-year average is in the range of 2% to 4%. The NSW Taxi Council suggested using a 3-year Compound Annual Growth Rate for state final demand, which the NSW Taxi Council calculated at 2.92%,66 but we prefer the 5-year annual average growth rate as a more stable long-term indicator.

Population growth

The most recent historical data from the ABS (2010/11) shows that population has grown on average by 1.6% per year over the past five years.67 These numbers are slightly higher than the Department of Planning forecast. Using the Department of Planning forecast, the NSW Taxi Council recommend using an increase of 1.22% in population growth based on a 3-year compound annual growth rate,68 but we have preferred the 5-year historical data for consistency with our other measures, and for more long-term stability.

Airport passenger numbers

Data from the Bureau of Infrastructure, Transport and Regional Economics (BITRE) shows an average increase of 4.6% per year since 1991/92.69 It forecasts an average 3.6% per year over the next 30 years.70 The NSW Taxi Council have noted that the most recent 3 years of data shows an average compound annual growth rate of airport passenger numbers of 2.11%.71 We have preferred the 5-year historical annual average of 3.1% for consistency with our other measures, and for more long-term stability.

66 NSW Taxi Council submission, 9 November 2012, p 7. 67 ABS, 31010DO001_201203 Australian Demographic Statistics, Mar 2012,

http://www.abs.gov.au/ausstats/[email protected]/mf/3101.0. 68 NSW Taxi Council submission, November 2012, p 8. 69 Department of Infrastructure and Transport, Bureau of Transport, Infrastructure and Regional

Economics, Air passenger movements through capital and non-capital city airports to 2030-31, Report 133, November 2012, p 25.

70 Department of Infrastructure and Transport, Bureau of Transport, Infrastructure and Regional Economics, Air passenger movements through capital and non-capital city airports to 2030-31, Report 133, November 2012, p 25.

71 NSW Taxi Council submission, November 2012, p 8.

4 The demand for taxi services

34 IPART Annual taxi licence release for Sydney 2013/14

Comments on demand from external factors from submissions

Most submissions took the view that demand is stagnant or declining, citing various reasons, including the global economic downturn, competition from hire cars, technology changing work practices, businesses restricting staff use of taxis, the strong Australian dollar reducing tourism, and the experience of cab drivers on the streets.72 Two submissions73 pointed to the declining trend in taxi bookings (an input into the STGM) as indicators of declining demand.

The NSW Taxi Council submitted that we did not explain the weighting of each indicator, nor how we obtained the figure of 2.5%. The NSW Taxi Council also opposed our longer-term recommendation that each of the next 4 reviews release at least 140 licences, describing it as a fixed growth policy that was contrary to the intention of the amendments to the Passenger Transport Act that set up an annual review process.74

Former commissioner of the Victorian Taxi Inquiry David Cousins questioned ‘the assumption that the so-called base level of demand can be adequately determined by a formula approach’, submitting that IPART had ‘strongly and effectively criticised the use of formulas to estimate demand in its draft report’.75

Response to views on demand growth from external factors raised in submissions

Our estimate of long-term annual demand growth from external factors is not based on a formula, but a judgement following examination of three relevant indicators. The measures of demand used in the STGM were quite volatile, so we preferred an approach that gave a more stable result over time. However, it is not a ‘fixed growth policy’ as there will continue to be an annual review and determination.

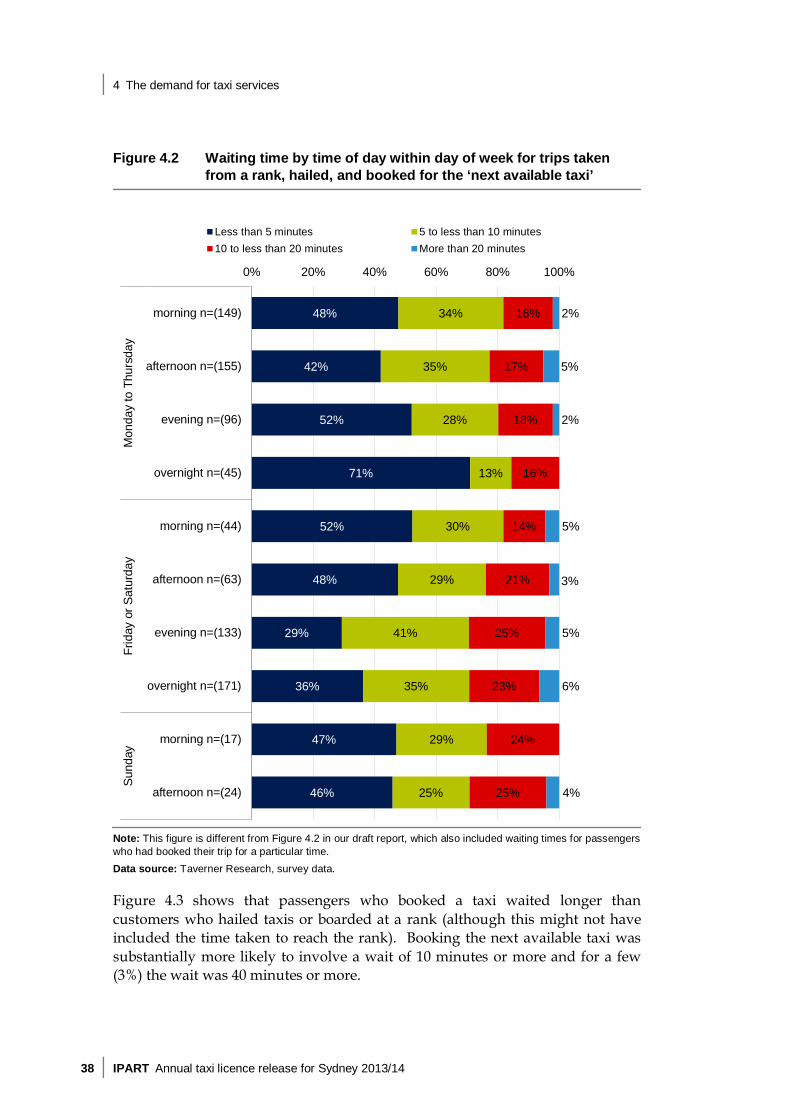

4.3 Estimating latent demand

Latent demand represents the additional taxi trips that would be taken if waiting time for taxi services fell, or if prices were reduced. New licences, in addition to the licences for growth in external sources of demand, will be required in order to reduce waiting times for customers.

72 Anonymous submission (W13/2), 3 January 2013; H Batth submission, 21 January 2013; P

Nicolopoulos submission, 21 January 2013; T Fathinia submission, 14 January 2013; D Gill submission, 10 January 2013; N O’Brien submission, 21 January 2013; M Mikhail submission, 29 December 2012; Anonymous submission (W13/48), 16 January 2013; M Gordon submission, 18 January 2013; M Burrage submission, 12 January 2013; NSWTDA submission, 21 January 2013; RSL Cabs submission, 18 January 2013; S Porcaro submission, 21 January 2013; A Yazdabadi submission, 21 January 2013; ATDA submission, 23 January 2013.

73 NSW Taxi Council submission, 21 January 2013, p 18; ATDA submission, 23 January 2013, p 5. 74 NSW Taxi Council submission, 21 January 2013, p 18. 75 D Cousins submission, 15 January 2013, p 2.

4 The demand for taxi services

Annual taxi licence release for Sydney 2013/14 IPART 35