Embed Size (px)

Citation preview

Annual Tourism Performance Report 2015

Annual Tourism Performance Report 2015

Annual Tourism Performance Report 2015

Introduction

1

Despite the economic and security challenges the region’s tourism has faced in 2015, Qatar’s tourism sector has emerged strong, marking a 3.7% growth from the previous year with 2.93 million visitors.

We had hopes to reach the 3 million visitor milestone this year, however, our statistics and analysis team revised its projections in November following a dip in arrival numbers in the fourth quarter. Nonetheless, Qatar continues to attract a growing number of visitors, and the sector’s contribution to the overall economy is on the rise.

Most significantly, the hospitality sector has continued to thrive in 2015, staying above 70% despite a 30% growth in room supply. As we introduce new standards of grading and classification to the sector this year, we look forward to a more sustainable, environmentally-friendly, and diverse hospitality sector in 2016.

QTA has stressed from the beginning, in the Qatar National Tourism Sector Strategy and in other channels, that tourism is a crucial avenue for developing a sustainable non-hydrocarbon economy in Qatar and conveying Qatari culture to the world.

This report demonstrates the importance of tourism remaining at the forefront of efforts and priorities, because of the resilience it has demonstrated throughout the past year, and because it supports the sustainability of Qatar’s economy.

This reality has come to the fore in 2015 and the job of diversifying the tourism offering and securing a place for Qatar on the map of destinations has gained even more significance. As we welcome an exciting and challenging year in 2016, QTA looks forward to working harder and collaborating closer with you, our partners and stakeholders, to achieve a sustainable and mature tourism sector in Qatar, for today, tomorrow and beyond 2030.

Annual Tourism Performance Report 2015

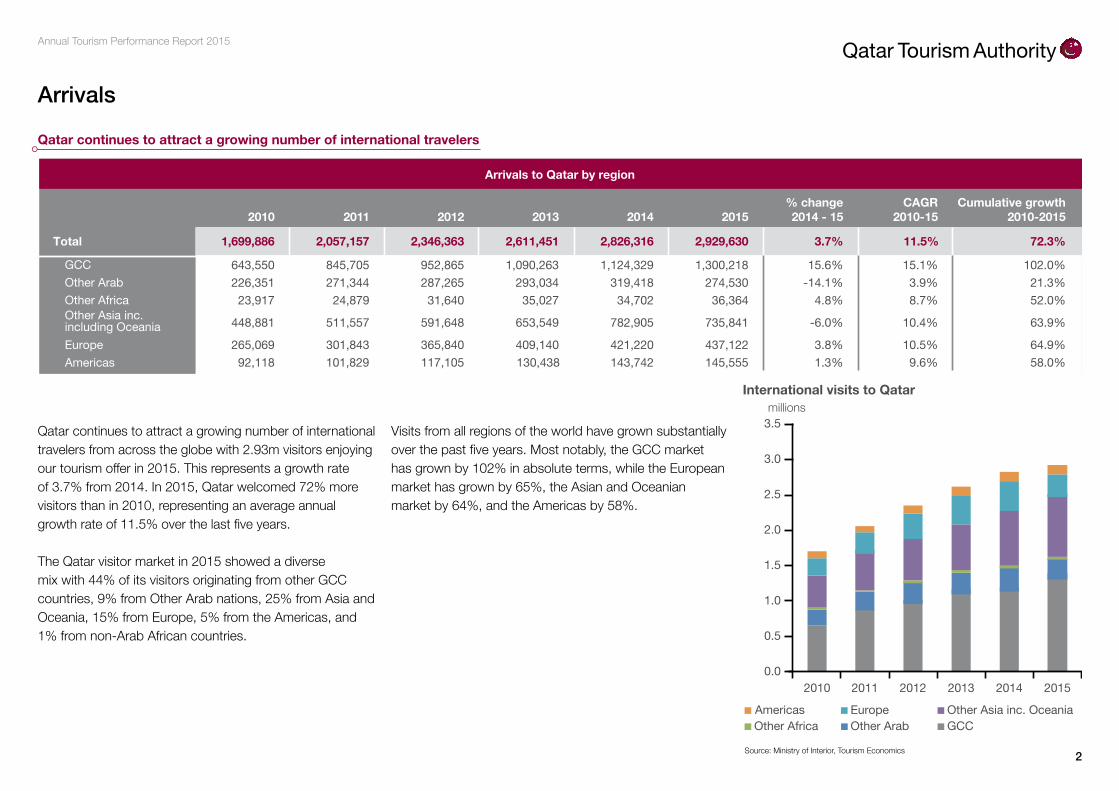

Arrivals

Qatar continues to attract a growing number of international travelers from across the globe with 2.93m visitors enjoying our tourism offer in 2015. This represents a growth rate of 3.7% from 2014. In 2015, Qatar welcomed 72% more visitors than in 2010, representing an average annual growth rate of 11.5% over the last five years.

The Qatar visitor market in 2015 showed a diverse mix with 44% of its visitors originating from other GCC countries, 9% from Other Arab nations, 25% from Asia and Oceania, 15% from Europe, 5% from the Americas, and 1% from non-Arab African countries.

Visits from all regions of the world have grown substantially over the past five years. Most notably, the GCC market has grown by 102% in absolute terms, while the European market has grown by 65%, the Asian and Oceanian market by 64%, and the Americas by 58%.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2010 2011 2012 2013 2014 2015

Americas Europe Other Asia inc. Oceania Other Africa Other Arab GCC

Source: Ministry of Interior, Tourism Economics

International visits to Qatarmillions

Qatar continues to attract a growing number of international travelers

2010 2011 2012 2013 2014 2015% change2014 - 15

CAGR2010-15

Cumulative growth2010-2015

Total 1,699,886 2,057,157 2,346,363 2,611,451 2,929,630 3.7% 11.5% 72.3%

GCC 643,550 845,705 952,865 1,090,263 1,300,218 15.6% 15.1% 102.0%Other Arab 226,351 271,344 287,265 293,034 274,530 -14.1% 3.9% 21.3%Other Africa

Other Asia inc.including Oceania

Europe

Americas 92,118 101,829 117,105 130,438 145,555 1.3% 9.6% 58.0%

Arrivals to Qatar by region

2,826,316

1,124,329319,418

23,917 24,879 31,640 35,027 36,364 4.8% 8.7% 52.0%34,702

448,881 511,557 591,648 653,549 735,841 -6.0% 10.4% 63.9%782,905

265,069 301,843 365,840 409,140 437,122 3.8% 10.5% 64.9%421,220143,742

2

Annual Tourism Performance Report 2015

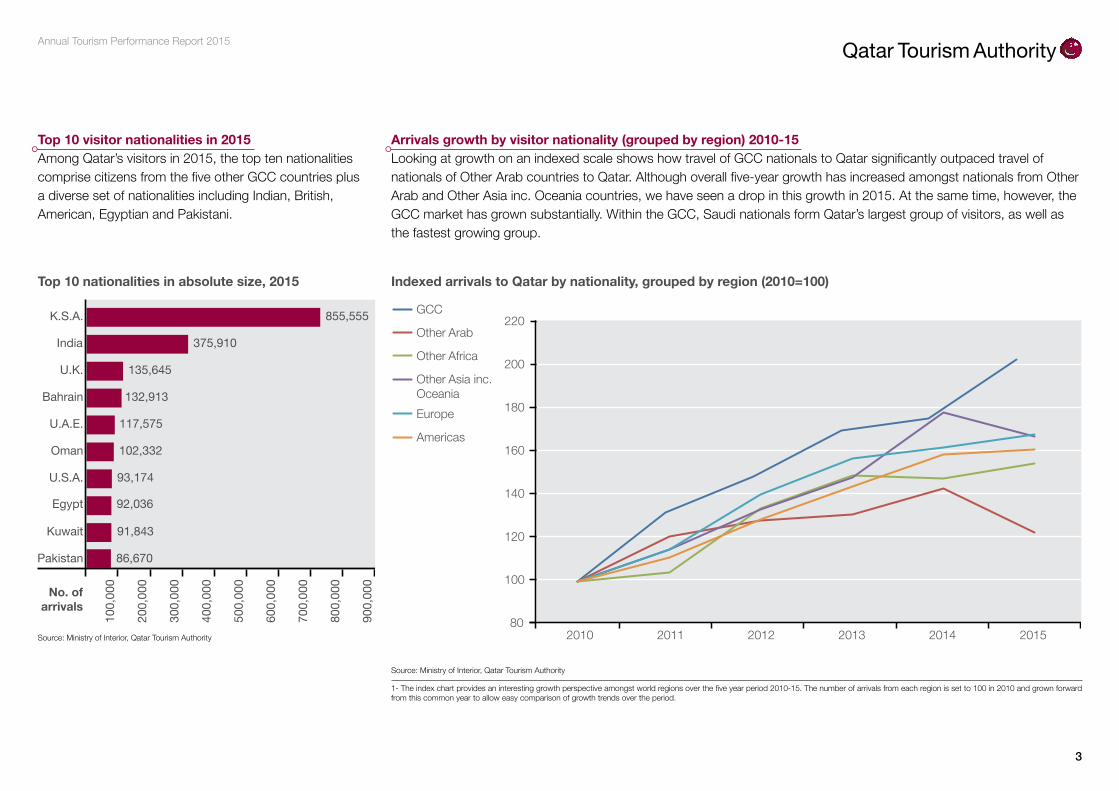

Top 10 visitor nationalities in 2015Among Qatar’s visitors in 2015, the top ten nationalities comprise citizens from the five other GCC countries plus a diverse set of nationalities including Indian, British, American, Egyptian and Pakistani.

Arrivals growth by visitor nationality (grouped by region) 2010-15 Looking at growth on an indexed scale shows how travel of GCC nationals to Qatar significantly outpaced travel of nationals of Other Arab countries to Qatar. Although overall five-year growth has increased amongst nationals from Other Arab and Other Asia inc. Oceania countries, we have seen a drop in this growth in 2015. At the same time, however, the GCC market has grown substantially. Within the GCC, Saudi nationals form Qatar’s largest group of visitors, as well as the fastest growing group.

Top 10 nationalities in absolute size, 2015

Source: Ministry of Interior, Qatar Tourism Authority

Pakistan

Kuwait

U.S.A.

Egypt

Oman

U.A.E.

Bahrain

U.K.

India

K.S.A.

86,670

91,843

93,174

92,036

102,332

117,575

132,913

135,645

375,910

855,555

No. ofarrivals

100

,000

200

,000

300

,000

400

,000

500

,000

600

,000

700

,000

800

,000

900

,000

Indexed arrivals to Qatar by nationality, grouped by region (2010=100)

Source: Ministry of Interior, Qatar Tourism Authority

1- The index chart provides an interesting growth perspective amongst world regions over the five year period 2010-15. The number of arrivals from each region is set to 100 in 2010 and grown forward from this common year to allow easy comparison of growth trends over the period.

80

100

120

140

160

180

200

220

2010 2011 2012 2013 2014 2015

GCC

Other Arab

Other Africa

Other Asia inc.Oceania Europe

Americas

3

Annual Tourism Performance Report 2015

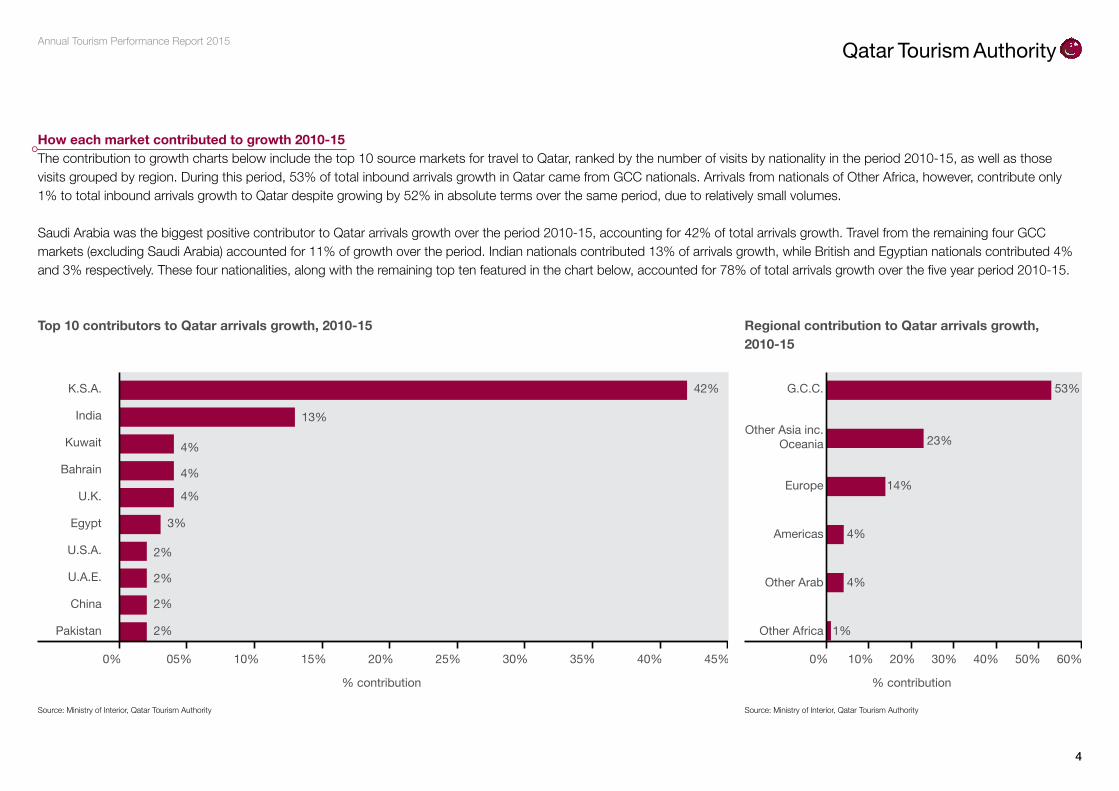

How each market contributed to growth 2010-15 The contribution to growth charts below include the top 10 source markets for travel to Qatar, ranked by the number of visits by nationality in the period 2010-15, as well as those visits grouped by region. During this period, 53% of total inbound arrivals growth in Qatar came from GCC nationals. Arrivals from nationals of Other Africa, however, contribute only 1% to total inbound arrivals growth to Qatar despite growing by 52% in absolute terms over the same period, due to relatively small volumes.

Saudi Arabia was the biggest positive contributor to Qatar arrivals growth over the period 2010-15, accounting for 42% of total arrivals growth. Travel from the remaining four GCC markets (excluding Saudi Arabia) accounted for 11% of growth over the period. Indian nationals contributed 13% of arrivals growth, while British and Egyptian nationals contributed 4% and 3% respectively. These four nationalities, along with the remaining top ten featured in the chart below, accounted for 78% of total arrivals growth over the five year period 2010-15.

Regional contribution to Qatar arrivals growth,2010-15

Source: Ministry of Interior, Qatar Tourism AuthoritySource: Ministry of Interior, Qatar Tourism Authority

G.C.C.

Other Asia inc.Oceania

Europe

Americas

Other Arab

Other Africa

53%

1%

4%

4%

14%

23%

0% 10% 20% 30% 40% 50% 60%

% contribution

42%

2%

2%

2%

2%

3%

4%

4%

4%

13%

0% 05% 10% 15% 20% 25% 30% 35% 40% 45%

% contribution

Pakistan

China

U.A.E.

U.S.A.

Egypt

U.K.

Bahrain

Kuwait

India

K.S.A.

Top 10 contributors to Qatar arrivals growth, 2010-15

4

Annual Tourism Performance Report 2015

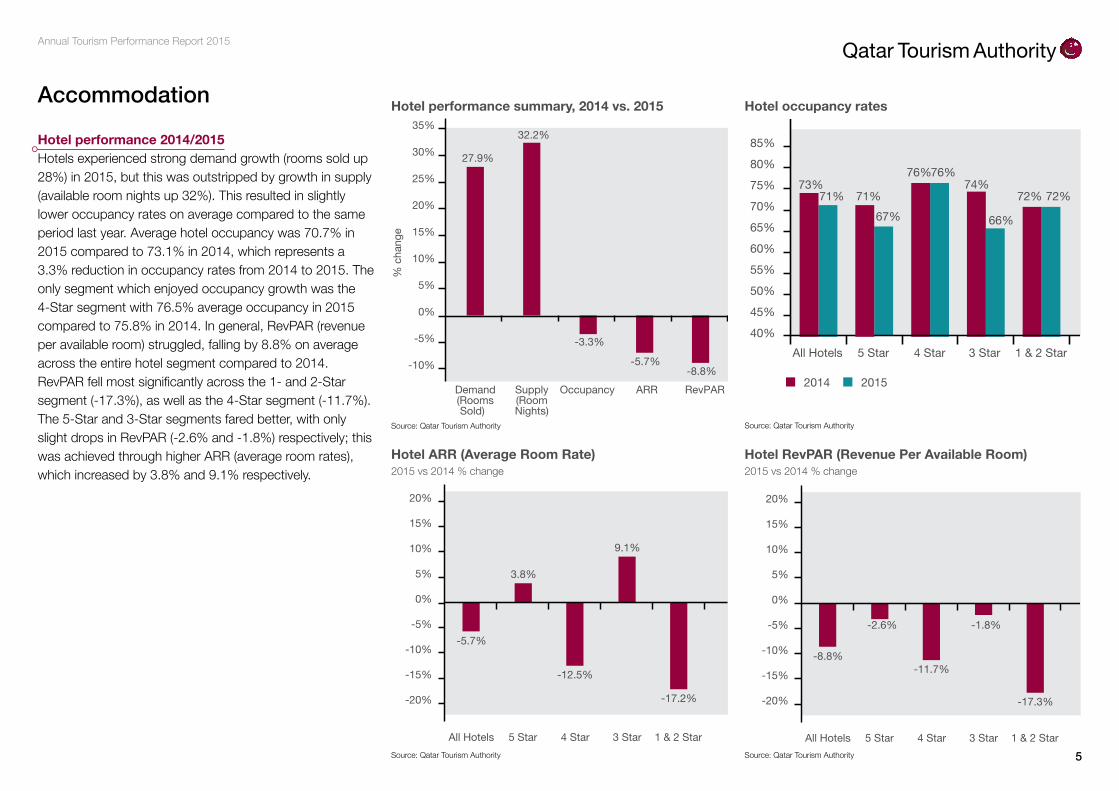

Hotel performance 2014/2015 Hotels experienced strong demand growth (rooms sold up 28%) in 2015, but this was outstripped by growth in supply (available room nights up 32%). This resulted in slightly lower occupancy rates on average compared to the same period last year. Average hotel occupancy was 70.7% in 2015 compared to 73.1% in 2014, which represents a 3.3% reduction in occupancy rates from 2014 to 2015. The only segment which enjoyed occupancy growth was the 4-Star segment with 76.5% average occupancy in 2015 compared to 75.8% in 2014. In general, RevPAR (revenue per available room) struggled, falling by 8.8% on average across the entire hotel segment compared to 2014. RevPAR fell most significantly across the 1- and 2-Star segment (-17.3%), as well as the 4-Star segment (-11.7%). The 5-Star and 3-Star segments fared better, with only slight drops in RevPAR (-2.6% and -1.8%) respectively; this was achieved through higher ARR (average room rates), which increased by 3.8% and 9.1% respectively.

-5.7%

3.8%

-12.5%

9.1%

-17.2%-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

All Hotels 5 Star 4 Star 3 Star 1 & 2 Star

Demand(RoomsSold)

Supply(RoomNights)

RevPAR

73% 76% 76%

74% 72% 71% 71%

67% 66%

72%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

All Hotels 5 Star 4 Star 3 Star 1 & 2 Star

2014 2015

-8.8%

-2.6%

-11.7%

-1.8%

-17.3%-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

All Hotels 5 Star 4 Star 3 Star 1 & 2 Star

Hotel ARR (Average Room Rate)2015 vs 2014 % change

Hotel occupancy rates

Hotel RevPAR (Revenue Per Available Room)2015 vs 2014 % change

Occupancy ARR RevPAR

0%

5%

10%

15%

% c

hang

e

-10%

-5%

20%

25%

30%

35%

Demand(RoomsSold)

Supply(RoomNights)

27.9%

32.2%

-3.3%

-5.7%-8.8%

Hotel performance summary, 2014 vs. 2015

Source: Qatar Tourism Authority

Source: Qatar Tourism Authority Source: Qatar Tourism Authority

Source: Qatar Tourism Authority

Accommodation

5

Annual Tourism Performance Report 2015

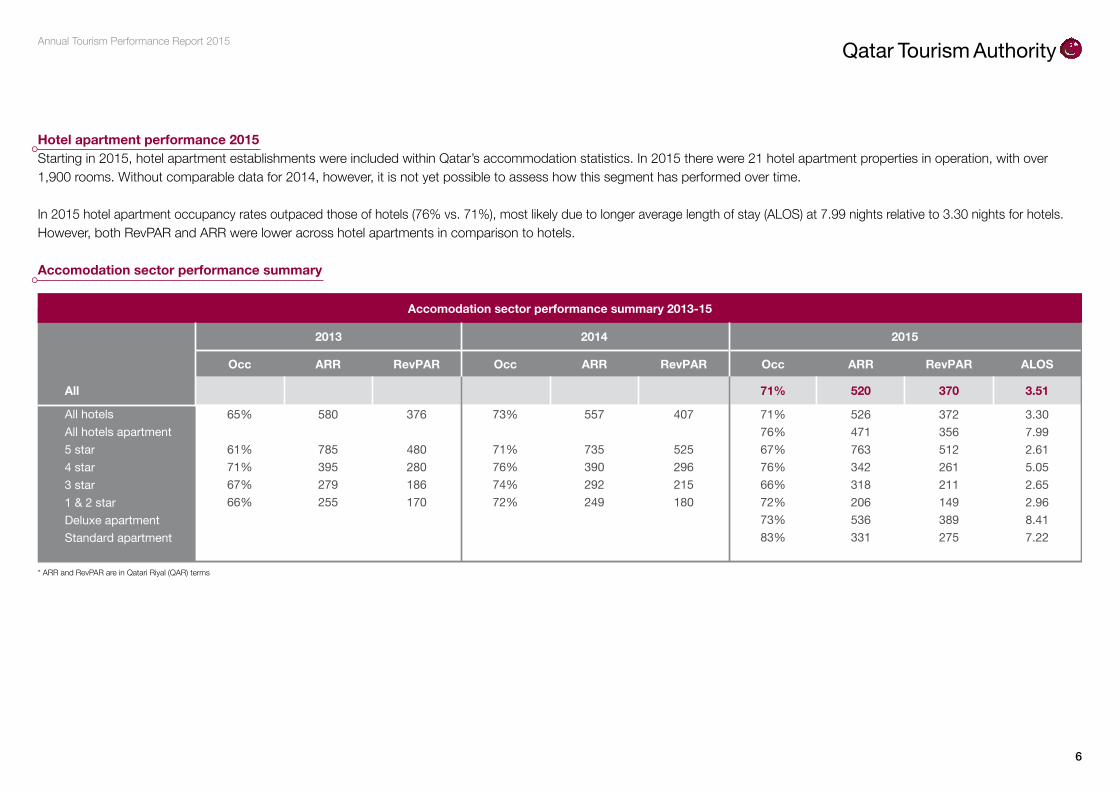

Hotel apartment performance 2015Starting in 2015, hotel apartment establishments were included within Qatar’s accommodation statistics. In 2015 there were 21 hotel apartment properties in operation, with over 1,900 rooms. Without comparable data for 2014, however, it is not yet possible to assess how this segment has performed over time.

In 2015 hotel apartment occupancy rates outpaced those of hotels (76% vs. 71%), most likely due to longer average length of stay (ALOS) at 7.99 nights relative to 3.30 nights for hotels. However, both RevPAR and ARR were lower across hotel apartments in comparison to hotels.

Accomodation sector performance summary

Occ ARR RevPAR Occ ARR RevPAR

2013 2014

Occ ARR RevPAR ALOS

All 71% 520 370

All hotels 65%

61%71%67%66%

580

785395279255

376

480280186170

All hotels apartment5 star4 star3 star1 & 2 starDeluxe apartmentStandard apartment

Accomodation sector performance summary 2013-15

3.51

2015

73%

71%76%74%72%

557

735390292249

407

525296215180

71%76%67%76%66%72%73%83%

526471763342318206536331

372356512261211149389275

3.307.992.615.052.652.968.417.22

* ARR and RevPAR are in Qatari Riyal (QAR) terms

6

Annual Tourism Performance Report 2015

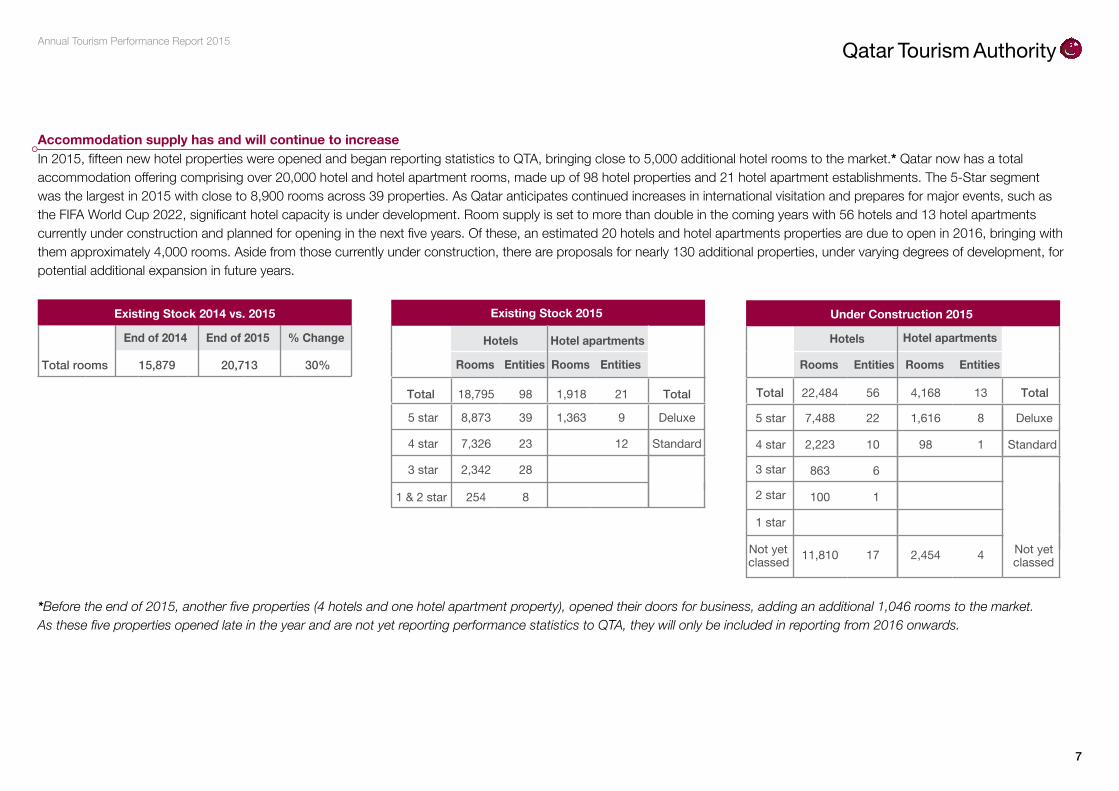

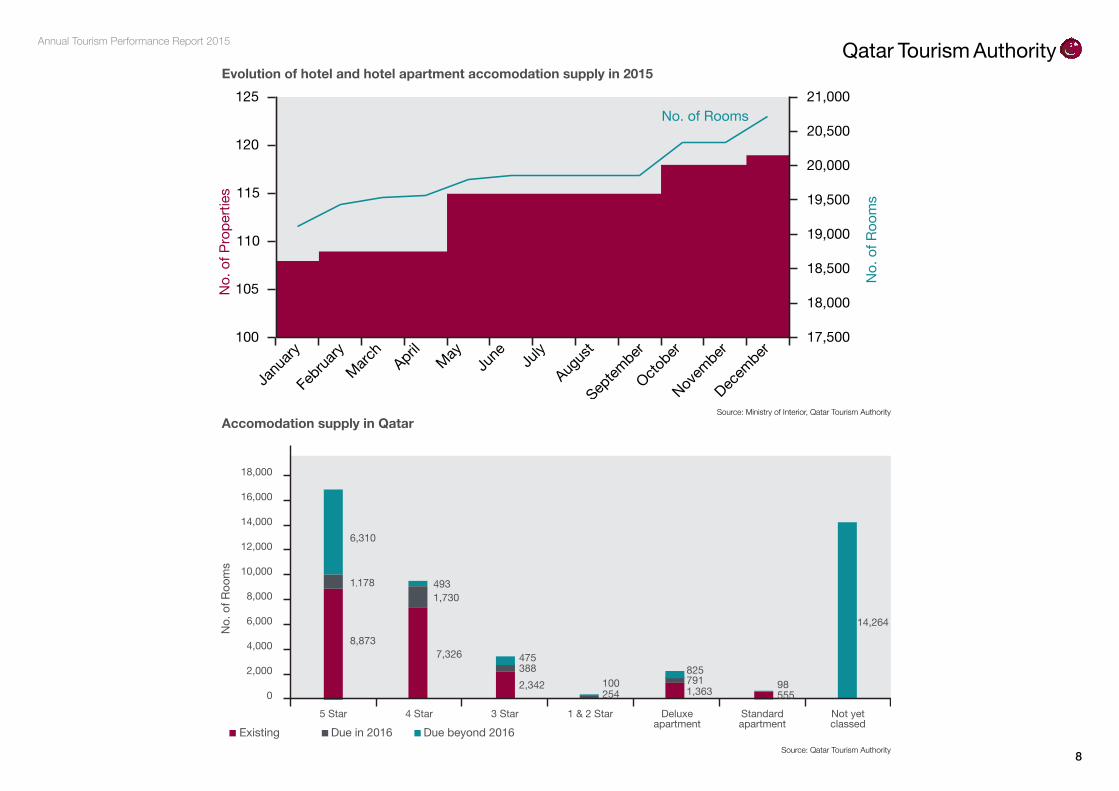

Accommodation supply has and will continue to increaseIn 2015, fifteen new hotel properties were opened and began reporting statistics to QTA, bringing close to 5,000 additional hotel rooms to the market.* Qatar now has a total accommodation offering comprising over 20,000 hotel and hotel apartment rooms, made up of 98 hotel properties and 21 hotel apartment establishments. The 5-Star segment was the largest in 2015 with close to 8,900 rooms across 39 properties. As Qatar anticipates continued increases in international visitation and prepares for major events, such as the FIFA World Cup 2022, significant hotel capacity is under development. Room supply is set to more than double in the coming years with 56 hotels and 13 hotel apartments currently under construction and planned for opening in the next five years. Of these, an estimated 20 hotels and hotel apartments properties are due to open in 2016, bringing with them approximately 4,000 rooms. Aside from those currently under construction, there are proposals for nearly 130 additional properties, under varying degrees of development, for potential additional expansion in future years.

*Before the end of 2015, another five properties (4 hotels and one hotel apartment property), opened their doors for business, adding an additional 1,046 rooms to the market.As these five properties opened late in the year and are not yet reporting performance statistics to QTA, they will only be included in reporting from 2016 onwards.

7

Existing Stock 2015

Hotels Hotel apartments

Rooms Entities Rooms Entities

Total 18,795 98 1,918 21 Total

5 star 8,873 39 1,363 9 Deluxe

4 star 7,326 23 12 Standard

3 star 2,342 28

1 & 2 star 254 8

Hotels Hotel apartments

Rooms Entities Rooms Entities

Total 22,484 56 4,168 13 Total

5 star

4 star

3 star

2 star

1 star

7,488 22 1,616 8 Deluxe

2,223 10 98 1 Standard

863 6

100 1

Not yet classed 11,810 17 2,454 4 Not yet

classed

Under Construction 2015

End of 2014

Total rooms 15,879 20,713 30%

End of 2015 % Change

Existing Stock 2014 vs. 2015

Annual Tourism Performance Report 2015

8,873 7,326

1,178 1,730

6,310

493

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0Not yetclassed

5 Star 4 Star 3 Star 1 & 2 Star Deluxeapartment

Standardapartment

Existing Due in 2016 Due beyond 2016

2,342 254 1,363 555

388 791

475

100 825

98

14,264

No.

of R

oom

s

No. of Rooms

17,500

18,000

18,500

19,000

19,500

20,000

20,500

21,000

100

105

110

115

120

125

No.

of R

oom

s

No.

of P

rope

rties

Accomodation supply in Qatar

Evolution of hotel and hotel apartment accomodation supply in 2015

Source: Qatar Tourism Authority

Source: Ministry of Interior, Qatar Tourism Authority

8

![LMP [arrivals] 1_2010](https://img.pdfslide.net/doc/110x75/568c4cab1a28ab4916a10c8f/lmp-arrivals-12010.jpg)

![LMP [arrivals] 2013](https://img.pdfslide.net/doc/110x75/568bd8671a28ab2034a337c9/lmp-arrivals-2013.jpg)