Embed Size (px)

Citation preview

AnnuitiesAnnuities

©Dr. B. C. Paul 2001 revisions 2008©Dr. B. C. Paul 2001 revisions 2008

Note – The subject covered in these slides is considered to be “common Note – The subject covered in these slides is considered to be “common knowledge” to those familiar with the subject and books or articles covering the knowledge” to those familiar with the subject and books or articles covering the concepts are widespread. Information of repayment terms for student loans were concepts are widespread. Information of repayment terms for student loans were based on such sources as Bankrate.com and Staffordloan.com or the Department based on such sources as Bankrate.com and Staffordloan.com or the Department of Education web site.of Education web site.

Back to the Story of Back to the Story of Lanna LoanerLanna Loaner

Lanna Loaner has just graduated from Lanna Loaner has just graduated from College with a debt of $102,325College with a debt of $102,325

Of course student loan programs don’t Of course student loan programs don’t expect Lanna to pay off her loan on expect Lanna to pay off her loan on graduation day.graduation day. They’ll have her pay it off over the next say 10 They’ll have her pay it off over the next say 10

years in monthly installmentsyears in monthly installments Lets also say she consolidates at 5.5% with Lets also say she consolidates at 5.5% with

monthly compounding.monthly compounding.

Step #1 in Problem Step #1 in Problem SolvingSolving

Let pick the perspective for the story Let pick the perspective for the story problem. (We have the bank that has problem. (We have the bank that has money loaned out and is going to collect money loaned out and is going to collect payments - or we have Lanna).payments - or we have Lanna).

This time I’m going to pick the banks This time I’m going to pick the banks perspective (I could make it work either perspective (I could make it work either way)way)

Drawing Pretty PicturesDrawing Pretty Pictures

0 1 2 3 4

5 6 7 8 9 15

This time I’m going to sweep all the money into a potat year #5. (Partially because I’ve already done half theproblem and I’m lazy).

What I already KnowWhat I already Know

0 1 2 3 4

5 6 7 8 9 15

If I sweep all that money the bank loaned forwardto year 5, it is equal to the bank having $102,325 dollarsout on loans.

New PictureNew Picture

55y 1m ---------------------------------------------------------------- 15y

-$102,325

I have to get my banker paid back over a period of 120 equalpayments with 5.5% interest compounding monthly.

Magic Number Come Out Magic Number Come Out and Playand Play

I need magic number that will sweep these I need magic number that will sweep these future payments of unknown size, back into future payments of unknown size, back into my money pot.my money pot.

Two ObservationsTwo Observations I have 120 numbers to be swept back - if I I have 120 numbers to be swept back - if I

have to do 120 P/F magic numbers I’m going have to do 120 P/F magic numbers I’m going to puketo puke

I don’t know how big these 120 numbers are.I don’t know how big these 120 numbers are.

Equal Payments Have a Equal Payments Have a Special NameSpecial Name

AnnuityAnnuity An annuity is a series of equal paymentsAn annuity is a series of equal payments Common occurrences of this type of cash Common occurrences of this type of cash

flowflow Mortgage PaymentsMortgage Payments Payments out of Retirement FundsPayments out of Retirement Funds Engineers projecting the same earnings Engineers projecting the same earnings

from their project year after year.from their project year after year.

Enter a New Super HeroEnter a New Super Hero

A/PA/P A/P stands for an AnnuityA/P stands for an Annuity

who's Present Valuewho's Present Value

A/P * Present Value =A/P * Present Value = An Annuity with the sameAn Annuity with the same total valuetotal value

What do I knowWhat do I know I know I have a banker who is out $102,325.I know I have a banker who is out $102,325. How much money do I have to sweep back How much money do I have to sweep back

into his pot before he is going to be happy?into his pot before he is going to be happy? Because I’m not paying him off on Because I’m not paying him off on

graduation day - I’ll have to sweep the graduation day - I’ll have to sweep the money back with interestmoney back with interest

I have a present valueI have a present value $102,325 * A/P = size of those annuity payments$102,325 * A/P = size of those annuity payments

OK, Now I Have OK, Now I Have Everything but the Stupid Everything but the Stupid Formula for A/PFormula for A/P

A/P A/P i, ni, n = {( i * [ 1 + i ] = {( i * [ 1 + i ] nn)/( [ 1 + i ])/( [ 1 + i ]nn - 1) } - 1) }

This sounds like a formula to put in a spread This sounds like a formula to put in a spread sheet or to save in a calculator so that sheet or to save in a calculator so that nimble fingers can’t punch it in wrongnimble fingers can’t punch it in wrong

I didn’t do a derivation of the formulaI didn’t do a derivation of the formula Thing I remember most about that derivation Thing I remember most about that derivation

was that I never wanted to see it againwas that I never wanted to see it again Look at the Formula and Say “I Believe”!Look at the Formula and Say “I Believe”!

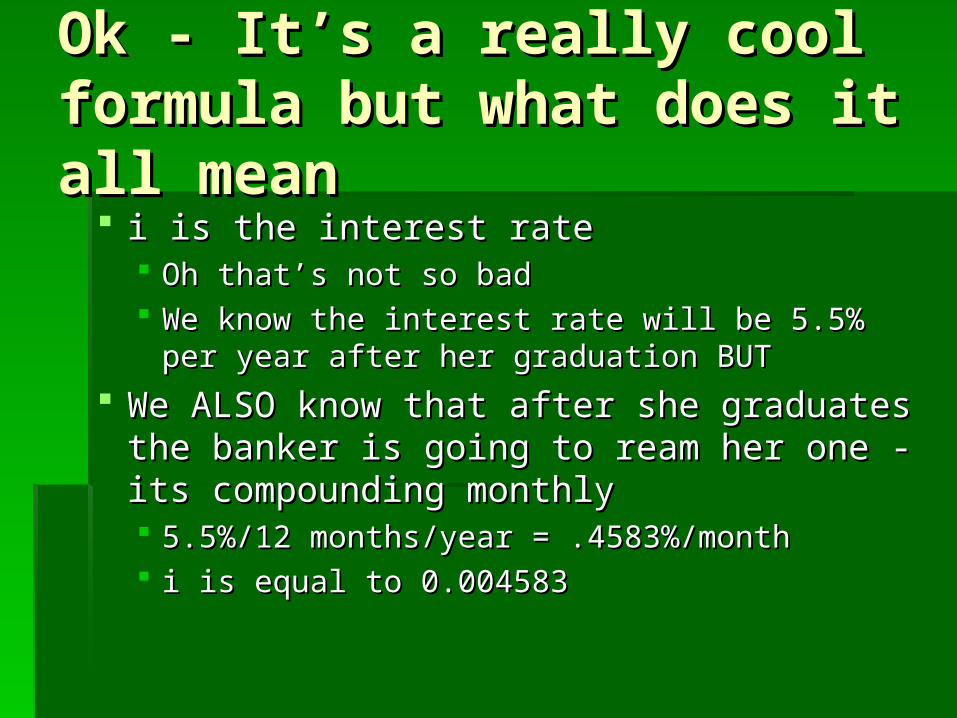

Ok - It’s a really cool Ok - It’s a really cool formula but what does it formula but what does it all meanall mean

i is the interest ratei is the interest rate Oh that’s not so badOh that’s not so bad We know the interest rate will be 5.5% per year We know the interest rate will be 5.5% per year

after her graduation BUTafter her graduation BUT

We ALSO know that after she graduates the We ALSO know that after she graduates the banker is going to ream her one - its banker is going to ream her one - its compounding monthlycompounding monthly 5.5%/12 months/year = .4583%/month5.5%/12 months/year = .4583%/month i is equal to 0.004583i is equal to 0.004583

More Coolness with the More Coolness with the FormulaFormula

n is the number of payments andn is the number of payments and the number of compounding periodsthe number of compounding periods

In this case Lanna will makeIn this case Lanna will make monthly payments for 10 years ormonthly payments for 10 years or 120 payments120 payments

n = 120n = 120 Plug and CrankPlug and Crank

A/P A/P i, ni, n = {( 0.004583 * [ 1 + 0.004583 ] = {( 0.004583 * [ 1 + 0.004583 ] 120120)/( [ 1 + )/( [ 1 +

0.004583 ]0.004583 ] 120 120 - 1) } = 0.01085 - 1) } = 0.01085

Turning on our SweeperTurning on our Sweeper

55y 1m ---------------------------------------------------------------- 15y

-$102,325

$102,325 * 0.01085 = $1108.68 per month

Try That With Class Try That With Class AssistantAssistant

Out comes A/PApply it $102,325 * 0.01085 = $1108.68

Magic # Calculator

Enter Annual Interest Rate in %Do not use the % key during data entry

Annual Int Rate 5.512 Enter the number of compounding periods/year

in % in decimalPeriod Int Rate 0.458333333 0.004583

Enter # Compouning Periods to Move Cash (value of n) 2The value should be an interger

F/P 1.009187674 (used to move one cash flow element n compounging period into the future)

P/F 0.990895971 (used to move one cash flow element n compounging periods back)

Enter # of payments (or repeating earnings) in the annuity 120The value should be an interger

P/A 92.14358207 (used to convert an annuity to a single sum of money one compounding period before first payment)

A/P 0.010852628 (used to convert a single sum of money into a series of n payments starting one compounding period in the future)

5.5% compounded 12 times a year

10years*12 months =120 payments

$1108.68! – one way to $1108.68! – one way to reduce is to spread out over reduce is to spread out over more timemore time

Magic # Calculator

Enter Annual Interest Rate in %Do not use the % key during data entry

Annual Int Rate 5.512 Enter the number of compounding periods/year

in % in decimalPeriod Int Rate 0.458333333 0.004583

Enter # Compouning Periods to Move Cash (value of n) 20The value should be an interger

F/P 1.095769917 (used to move one cash flow element n compounging period into the future)

P/F 0.912600341 (used to move one cash flow element n compounging periods back)

Enter # of payments (or repeating earnings) in the annuity 240The value should be an interger

P/A 145.3726488 (used to convert an annuity to a single sum of money one compounding period before first payment)

A/P 0.006878873 (used to convert a single sum of money into a series of n payments starting one compounding period in the future)

Could Make thePayments over20 years

102,325 *0.00688 = $704/month

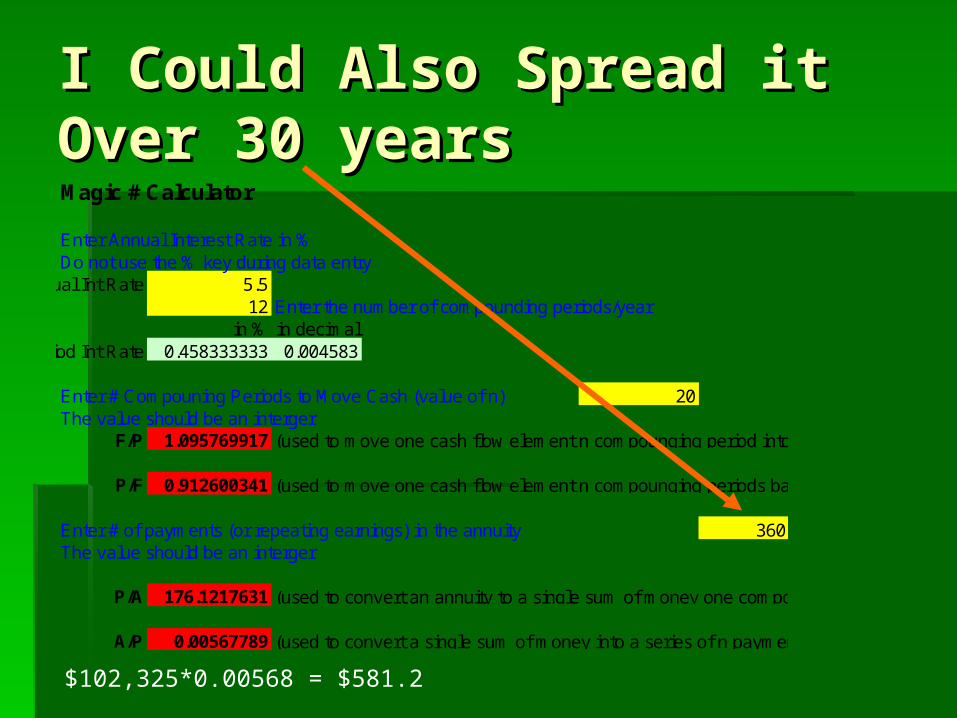

I Could Also Spread it I Could Also Spread it Over 30 yearsOver 30 yearsMagic # Calculator

Enter Annual Interest Rate in %Do not use the % key during data entry

Annual Int Rate 5.512 Enter the number of compounding periods/year

in % in decimalPeriod Int Rate 0.458333333 0.004583

Enter # Compouning Periods to Move Cash (value of n) 20The value should be an interger

F/P 1.095769917 (used to move one cash flow element n compounging period into the future)

P/F 0.912600341 (used to move one cash flow element n compounging periods back)

Enter # of payments (or repeating earnings) in the annuity 360The value should be an interger

P/A 176.1217631 (used to convert an annuity to a single sum of money one compounding period before first payment)

A/P 0.00567789 (used to convert a single sum of money into a series of n payments starting one compounding period in the future)

$102,325*0.00568 = $581.2

A Nasty Fact of LifeA Nasty Fact of Life Lanna borrowed $22,137+4*15,137 = $82,685Lanna borrowed $22,137+4*15,137 = $82,685 Over 10 year Lanna Pays BackOver 10 year Lanna Pays Back

$1,108.69*120 = $133,048$1,108.69*120 = $133,048 $133,048 - $82,685 = $50,357 interest$133,048 - $82,685 = $50,357 interest

Over 20 years Lanna would PayOver 20 years Lanna would Pay $704*240 = $168,959$704*240 = $168,959

$168,959 - $82,685 = $86,273$168,959 - $82,685 = $86,273 Over 30 years Lanna would PayOver 30 years Lanna would Pay

$581.2*360 = $209,234$581.2*360 = $209,234 $209,234 - $82,685 = $126,548$209,234 - $82,685 = $126,548

I Wonder Why Everyone Wants to Tell You I Wonder Why Everyone Wants to Tell You How Easy it is to borrow money, but no one How Easy it is to borrow money, but no one wants to tell you what it will be like to pay it wants to tell you what it will be like to pay it back?back?

Example DisclaimersExample Disclaimers Interest rate I used was for a Stafford Student loanInterest rate I used was for a Stafford Student loan

But there are borrowing limits on Stafford loans – you could But there are borrowing limits on Stafford loans – you could not borrow $82,000not borrow $82,000

The loan accumulated interest while Lanna was in school – The loan accumulated interest while Lanna was in school – Stafford loans don’t (Plus loans to parents do – and have a Stafford loans don’t (Plus loans to parents do – and have a higher interest rate)higher interest rate)

There were no up front fees for the loans (Stafford and Plus There were no up front fees for the loans (Stafford and Plus loans can have fees)loans can have fees)

Student loans are distributed at the start of each semester – Student loans are distributed at the start of each semester – not the start of each year so the example borrowed some not the start of each year so the example borrowed some money sooner than would be allowed.money sooner than would be allowed.

Most Private Student loans have variable interest rates Most Private Student loans have variable interest rates that can explode upwardsthat can explode upwards

Over-all the example is a little optimisticOver-all the example is a little optimistic I’m adding a spreadsheet under Resources that can I’m adding a spreadsheet under Resources that can

help estimate Student loan optionshelp estimate Student loan options

Limitations and PointLimitations and Point

My calculation did not consider that the value of My calculation did not consider that the value of that money will change over timethat money will change over time

It Does Work in the My Money EquationIt Does Work in the My Money Equation

Income = Necessities + Good Stuff + Taxes + Insurance + Savings +

Investments + Interest - Debts

Income is some number

If interest is a big number then some of the other stuff such as Good StuffInsurance, Savings, or Investments will have to be smaller

(Interest plunders your future quality of life)

Can You Ever Win with Can You Ever Win with Debt?Debt?

If income rises more rapidly than debt + If income rises more rapidly than debt + interestinterest

Example – CollegeExample – College With debt and interest paid off over 30 years With debt and interest paid off over 30 years

Lanna spends $209,234Lanna spends $209,234 Using early 2000s data (its even more now)Using early 2000s data (its even more now)

HS lifetime earnings average $1.2 millionHS lifetime earnings average $1.2 million College Grad $2.1 millionCollege Grad $2.1 million $900,000 > $209,234$900,000 > $209,234

If We Consider That Lanna If We Consider That Lanna Was Wise and Chose Was Wise and Chose Engineering the Outlook is Engineering the Outlook is Even BetterEven Better

Median Annual Earnings

0100002000030000400005000060000700008000090000

100000

High S

choo

l

College

Mas

ters

Doctora

te

Civil E

ng EE

Petro

leum

$/ye

ar

Series1

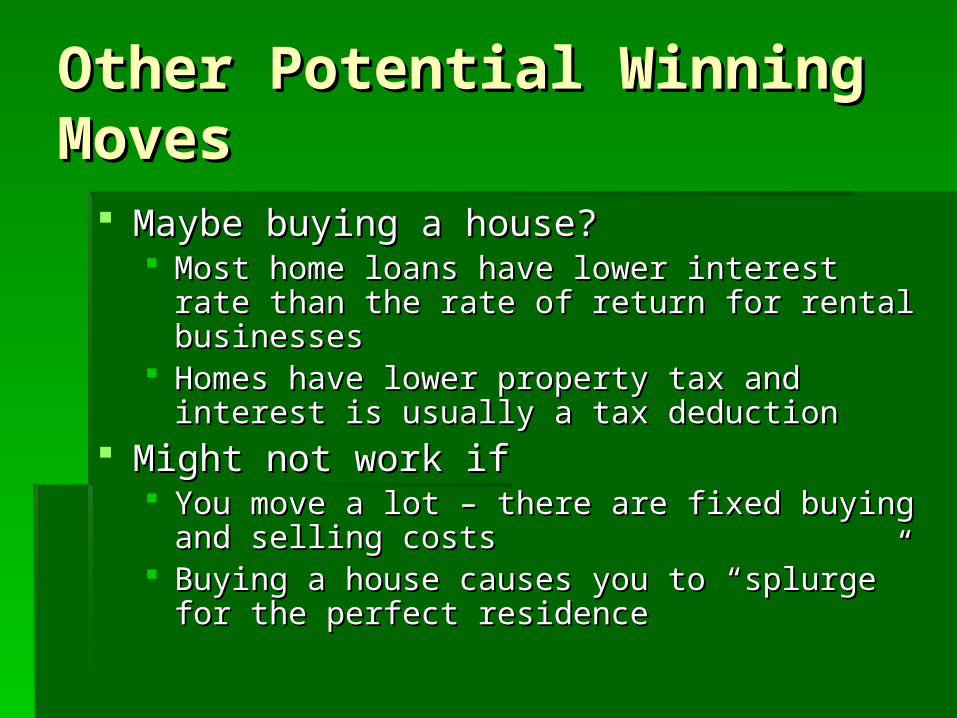

Other Potential Winning Other Potential Winning MovesMoves

Maybe buying a house?Maybe buying a house? Most home loans have lower interest rate than the Most home loans have lower interest rate than the

rate of return for rental businessesrate of return for rental businesses Homes have lower property tax and interest is Homes have lower property tax and interest is

usually a tax deductionusually a tax deduction Might not work ifMight not work if

You move a lot – there are fixed buying and selling You move a lot – there are fixed buying and selling costscosts

Buying a house causes you to “splurge” for the Buying a house causes you to “splurge” for the perfect residenceperfect residence

Good Loosing MovesGood Loosing Moves

Taking vacations and buying Taking vacations and buying consumables using debtconsumables using debt The goods are gone – the debt remainsThe goods are gone – the debt remains

Consumer DurablesConsumer Durables Debt makes them cost more and they Debt makes them cost more and they

usually don’t add to income or reduce usually don’t add to income or reduce expensesexpenses

Observations About A/PObservations About A/P

A/P is sometimes called a capital A/P is sometimes called a capital recovery factorrecovery factor

In many problems you will have an initial In many problems you will have an initial capital outlay.capital outlay. If you multiply this initial outlay by the A/P If you multiply this initial outlay by the A/P

factor it tells you how big the payments will factor it tells you how big the payments will have to be starting with the next have to be starting with the next compounding period to pay back the capitalcompounding period to pay back the capital

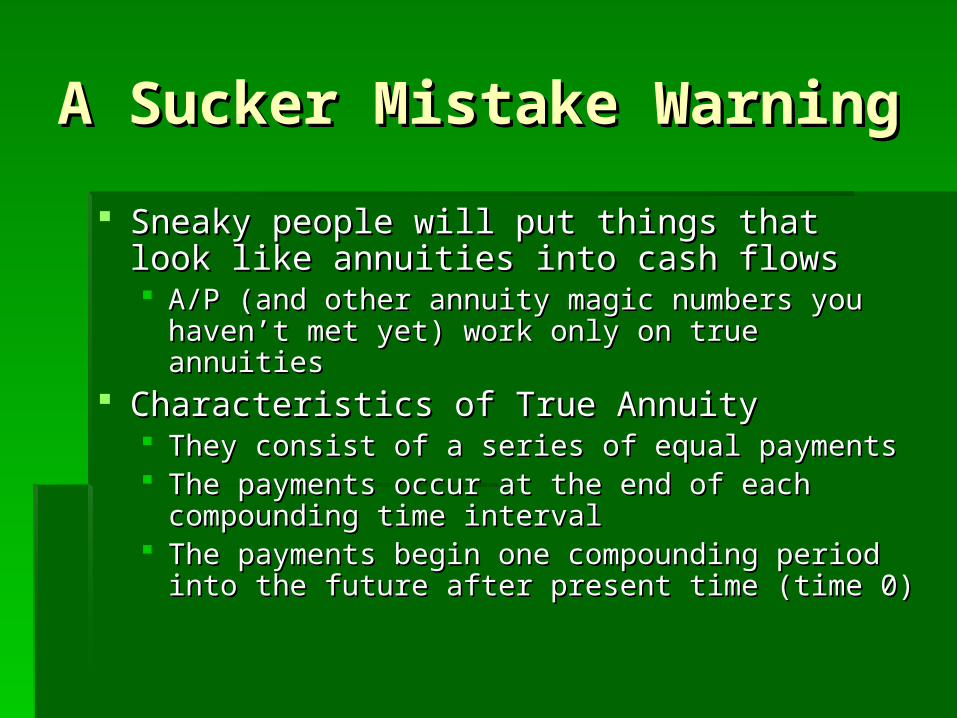

A Sucker Mistake A Sucker Mistake WarningWarning

Sneaky people will put things that look like Sneaky people will put things that look like annuities into cash flowsannuities into cash flows A/P (and other annuity magic numbers you haven’t A/P (and other annuity magic numbers you haven’t

met yet) work only on true annuitiesmet yet) work only on true annuities Characteristics of True AnnuityCharacteristics of True Annuity

They consist of a series of equal paymentsThey consist of a series of equal payments The payments occur at the end of each The payments occur at the end of each

compounding time intervalcompounding time interval The payments begin one compounding period into The payments begin one compounding period into

the future after present time (time 0)the future after present time (time 0)

Now Its Your TurnNow Its Your Turn

Do Assignment #4Do Assignment #4

You will be helping Harry Homebuyer figure out his house You will be helping Harry Homebuyer figure out his house payments (another form of annuity). payments (another form of annuity).

![THE ETHICS APPLICABLITY, DEFINITIONS, INTERPRETATIONS, … · 2021. 7. 3. · Revised March 2013, revisions effective May 31, 2013.] .07 Covered member. A covered member is a. an](https://img.pdfslide.net/doc/110x75/6145e98e8f9ff812541fede7/the-ethics-applicablity-definitions-interpretations-2021-7-3-revised-march.jpg)