Embed Size (px)

Citation preview

“Shaping Shire’s Future”

Dr Wilson TottenGroup R&D Director

1st October 2003

A Strategic Review

THE “SAFE HARBOR” STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Statements included herein that are not historical facts, are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialise, Shire’s results could be materially affected. The risks and uncertainties include, but are not limited to, risks associated with the inherent uncertainty of pharmaceutical research, product development manufacturing and commercialisation, the impact of competitive products, including, but not limited to, the impact on Shire’s Attention Deficit Hyperactivity Disorder (ADHD) franchise, patents, including but not limited to, legal challenges relating to Shire’s ADHD franchise, government regulation and approval, including but not limited to the expected product approval date of lanthanum carbonate (FOSRENOL®) and METHYPATCH®, and other risks and uncertainties detailed from time to time in our filings, including the Annual Report filed on Form 10-K by Shire with the Securities and Exchange Commission.

Trade mark Information:The following are trade marks of Shire or companies within the Shire Group, which are the subject of trade mark registrations in certain territories.ADDERALL XR® (mixed amphetamine salts), ADDERALL® (mixed amphetamine salts), AGRYLIN® (anagrelide hydrochloride), AMATINE® (midodrine hydrochloride), CALCICHEW® (calcium carbonate), CARBATROL® (carbamazepine), COLAZIDE® (balsalazide), DEXTROSTAT® (dextroamphetamine salt), EMUTROL™, ENSOTROL®, FARESTON™ (toremifene)FLUVIRAL® S/F (split-virion influenza vaccine), FOSRENOL® (lanthanum carbonate), METHYPATCH® (methylphenidate), MICROTROL®, MICROTROL DR™, MICROTROL PR™, MICROTROL XR™, OPTISCREEN®, PROAMATINE® (midodrine hydrochloride), PROSCREEN™, RAPITROL™, SOLARAZE® (diclofenac sodium 3%), SOLUTROL™, TROXATYL® (troxacitabine), XAGRID® (anagrelide hydrochloride).The following are trade marks of third parties: 3TC (lamivudine) (trade mark of GlaxoSmithKline (GSK)), ADEPT (4% icodextrin solution) (trade mark of ML Laboratories plc), AZT (trade mark of GSK), BIO-HEP B (trade mark of Berna Biotech AG), COMBIVIR (trade mark of GSK), EPIVIR (trade mark of GSK), HEPAVAX GENE (trade mark of Berna Biotech AG), NEISVAC-C (trade mark of Baxter International Inc.), PENTASA (trade mark of Baxter International Inc.), REMINYL (galantamine hydrobromide) (trade mark of Johnson & Johnson), TRIZIVIR (trade mark of GSK), ZEFFIX (lamivudine) (trade mark of GSK), Concerta (trade mark of Johnson & Johnson), Metadate CD (trade mark of Celltech), Ritalin LA (trade mark of Novartis), Strattera (trade mark of Eli Lilly), Focalin (trade mark of Novartis), ASACOL (trade mark of Procter & Gamble).

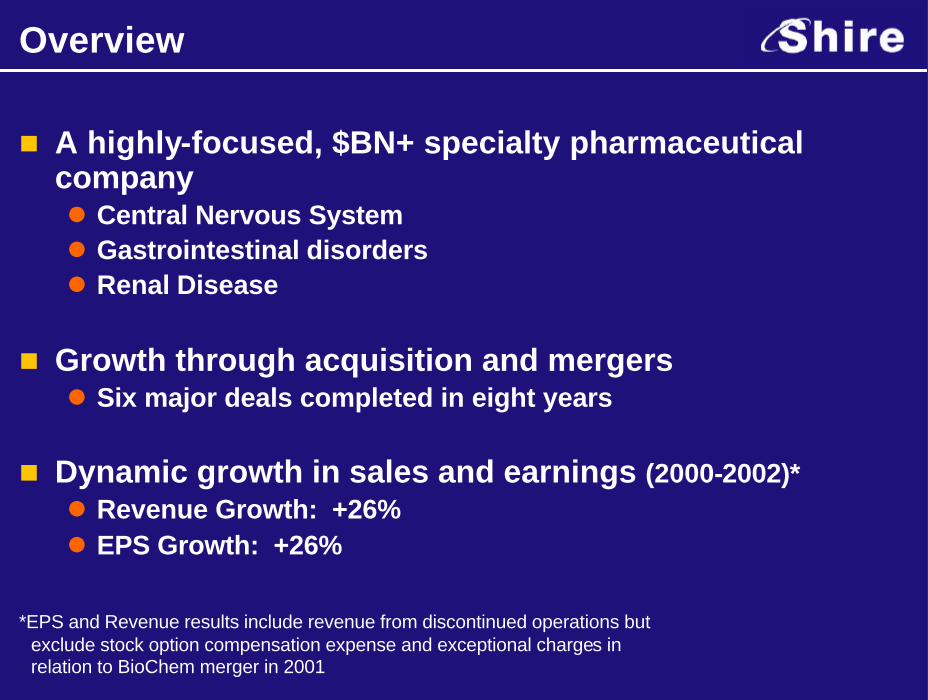

Overview

n A highly-focused, $BN+ specialty pharmaceutical companyl Central Nervous Systeml Gastrointestinal disordersl Renal Disease

n Growth through acquisition and mergersl Six major deals completed in eight years

n Dynamic growth in sales and earnings (2000-2002)*l Revenue Growth: +26%l EPS Growth: +26%

*EPS and Revenue results include revenue from discontinued operations but exclude stock option compensation expense and exceptional charges in relation to BioChem merger in 2001

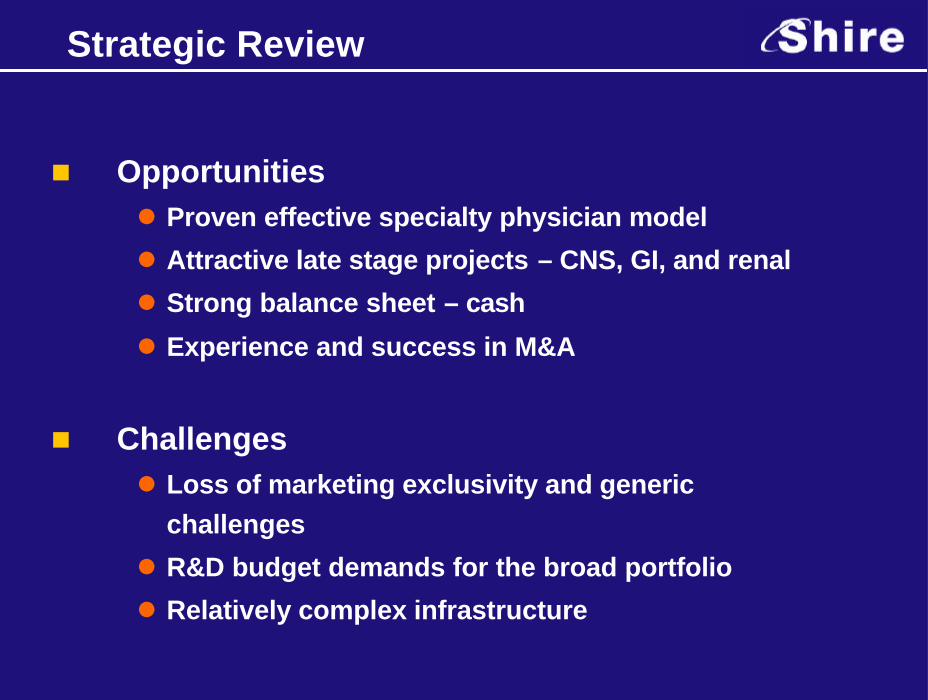

Strategic Review

n Opportunitiesl Proven effective specialty physician model

l Attractive late stage projects – CNS, GI, and renal

l Strong balance sheet – cash

l Experience and success in M&A

n Challengesl Loss of marketing exclusivity and generic

challenges

l R&D budget demands for the broad portfolio

l Relatively complex infrastructure

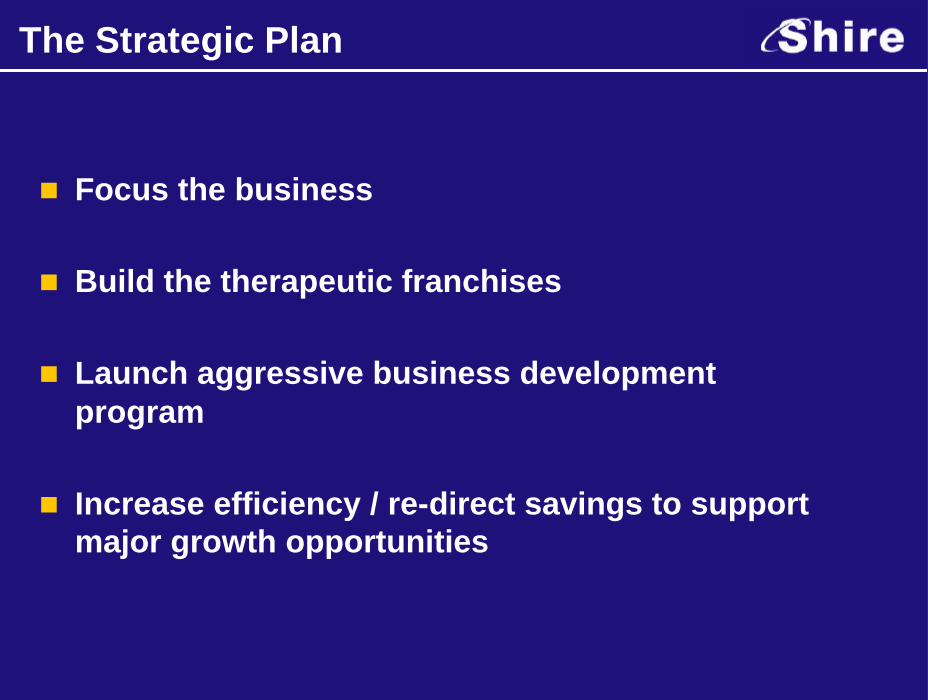

The Strategic Plan

n Focus the business

n Build the therapeutic franchises

n Launch aggressive business development program

n Increase efficiency / re-direct savings to support major growth opportunities

Focus R&D

n Close early stage research (lead optimization)l $15 million annual savings

Actions - July 31, 2003

n Spin off vaccine business (H1 2004)l Includes four Phase I projects and revenue stream (Fluviral)l Maximize shareholder value

n Exit oncology l Out-license Troxatyl®

n Seek partner for anti-infective l Seek partner for SPD754 - HIV

n Rationalize technology effortsl Maintain focus on advanced drug delivery platforms

R&D Portfolio FocusP/C and Phase I Phase II / III / Reg In Market R&D Support

Troxatyl AMLTroxatyl Pancreatic

Xagrid Agrylin

SPD473SPD483SPD465

SPD503Methypatch

Carbatrol Bipolar

ReminylAdderall XR

Carbatrol

SPD476SPD480

Pentasa 500mg

PentasaColazide

Fosrenol ProAmatineAdept

SPD756 (HIV) SPD754 (HIV) 3TC

SPD707 (Flu T-) Fluviral SPD701 (Flu)

SPD703 (S.pneu)SPD704 (N.menin)SPD705 (P.aeru)

Haematology

CNS

GI

Other

Anti-viral

SPD451

Continue R&D

Out-license / Exit

Legend:

Haematology

CNS

GI

Other

Anti-viral

Oncology

Vaccines

RegistrationPhase 3Phase 2

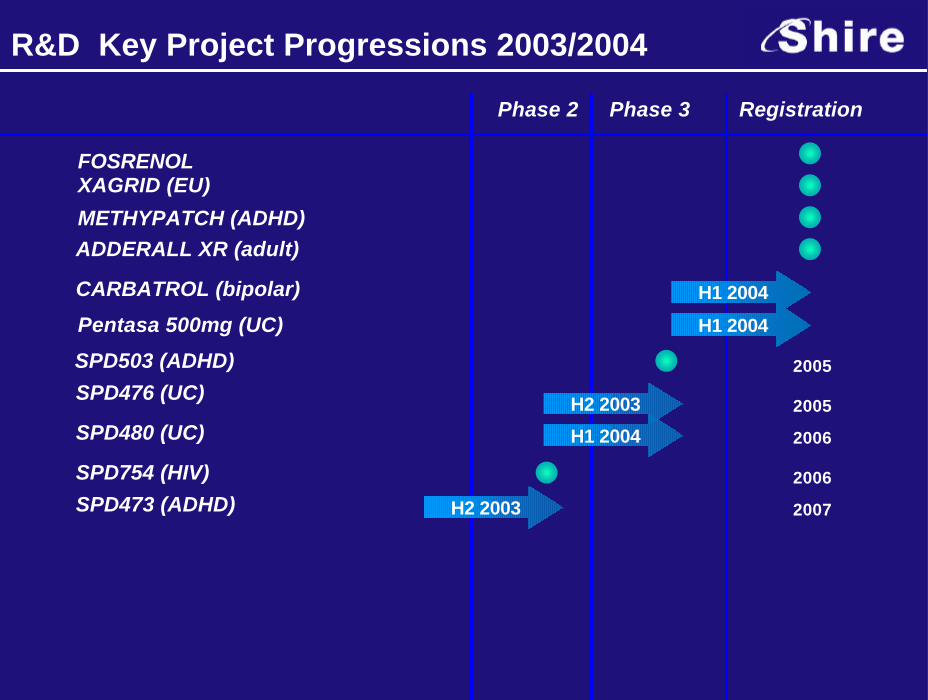

R&D Key Project Progressions 2003/2004

XAGRID (EU)FOSRENOL

SPD503 (ADHD) 2005

METHYPATCH (ADHD)ADDERALL XR (adult)

CARBATROL (bipolar) H1 2004

Pentasa 500mg (UC) H1 2004

SPD476 (UC) H2 2003 2005

SPD480 (UC) 2006H1 2004

SPD473 (ADHD) H2 2003 2007

SPD754 (HIV) 2006

Antivirals 16%

Others 13%

Adderall XR® 31%

Adderall® 11%

ProAmatine® 5%Pentasa®

8%

Carbatrol® 4%

Agrylin® 12%

Total Revenue: $1.037 BillionTotal Revenue: $1.037 Billion

2002 Product Sales & Royalties2002 Product Sales & Royalties

Building the franchise: Adderall XR

n Near-term

l Successful conversion and defense of Adderall XR®

l Highly effective marketing and sales program aimed at high-prescribing specialists

l Exclusivity

n Hatch-Waxman to October 2004n Potential Pediatric extension: April 2005 n Drug product patent to 2018n Additional patent issued August 12 2003

Building the franchise: ADHD

Prevalence Diagnosed TreatedPrevalence Diagnosed Treated

US Pediatric Patients*

Million

US Adult Patients*

8.2

4.8

.37

1.5

.36

1.4

*National Institute for Mental Health, 1999

US ADHD

33%$ GrowthJuly 2002-July 2003

16%Growth in TRxJuly 2002-July 2003

$1.7 Billion$ MarketJune 2002-June 2003

*source IMS data

Building the franchise: ADHD

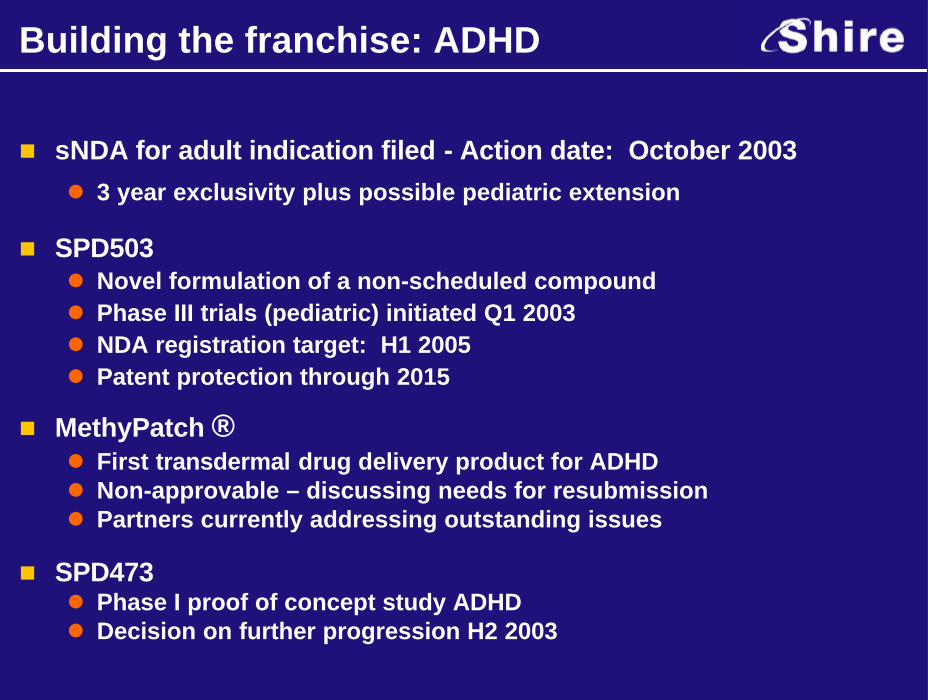

n sNDA for adult indication filed - Action date: October 2003

l 3 year exclusivity plus possible pediatric extension

n SPD503l Novel formulation of a non-scheduled compoundl Phase III trials (pediatric) initiated Q1 2003l NDA registration target: H1 2005l Patent protection through 2015

n MethyPatch ®l First transdermal drug delivery product for ADHD l Non-approvable – discussing needs for resubmissionl Partners currently addressing outstanding issues

n SPD473l Phase I proof of concept study ADHDl Decision on further progression H2 2003

Building the franchise: Carbatrol®

Prevalence Diagnosed TreatedPrevalence Diagnosed Treated

Epilepsy*

Million

2.3 2.3

1.6

Bipolar Mood Disorder*

1.5

.75 .65

*Epilepsy Foundation of America

Bipolar Mood Disorder

Billion

June 2002-2003 2007 L.E.

$1.9

$2.4

$ Market*

* Decision Resources Report on Bipolar Mood Disorder: February 2003

Building the franchise: Carbatrol®

n Phase III trials in bipolar patients well advanced

n Benefits:l Excellent mood stabilizerl Unique formulation with smooth response

n sNDA registration target: H1 2004

n Eligible for 3 year exclusivity under Hatch-Waxman

n Drug product patent valid until 2011

n Paragraph IV letter received in July 2003

Meeting the Challenge: GIInflammatory Bowel Disease*

500,000

600,000

Ulcerative Colitis Crohn’s Disease

Prevalence Treated

500,000500,000

*Crohn’s and Colitis Foundation of America, 2001

Inflammatory Bowel Disease

13%$ GrowthJuly 2002-July 2003

$658 Million$ MarketJune 2002-June 2003

Building the franchise: GI

n Pentasa® (ulcerative colitis) – Near-term

l Phase II development under way: 500 mg / double-strength

l Greater convenience and compliancel sNDA filing H1 2004

n SPD476: Ulcerative colitis – mesalamine

l High strength to improve compliance in long-term therapy

l NDA filing 2005l Patent protection through 2020

Establishing a franchise: Fosrenol®

n Approvable letter received from FDA

n Discussions ongoing with FDA and EU

n No new issues raised by regulatorsl Generating data requested (submission H2 2003)

n Continued confidence in safety

n No CNS toxicity seen in animal and clinical studiesl Not found to cross blood brain barrier

n Patent protection through 2016

n Global opportunity

sevelamersevelamer

PhosloPhoslo

Establishing a franchise: Fosrenol®

455,000410,000

End Stage Renal DiseaseUS Market Profile

Diagnosed Treated

US Renal Data System, 2002

$223 Million(June 2002-2003)

OtherOther

Enhanced Business Development

n Primary Screens

l Products targeted at the specialist physicianl Prefer those aligned with / complementary to current therapeutic

targets but will consider attractive new areal Patent protectedl Provide revenue growth

n Both “incremental” and “transformational”

n Opportunities most prevalent in US

n Strong cash position plus debt capacity provide flexibility

Enhanced Business Development

n Commitment to R&D / late-stage focus

n Skilled registration/regulatory group

n Expert commercialization

n Reputation/access to high-Rx specialist MDs

n Sales force productivity

n “Big enough, but not too big”

Shire: A Partner of Choice

Increase efficiency

n Restructure for growth

l Ongoing review of operating sites

l Ongoing review of organizational structure

l Providing greater efficiency in global operations

l Improve communications and team work

Financial Performance – Q2 2003

+10%38 centsADS

+10%$65.5 millionNet Income

+25%$94.2 millionOperating Income

+21%$299 millionRevenue

Growth overGrowth overQ2 2002Q2 2002

Balance Sheet - $ Millions

1,185Gross Cash*

807Net Cash

1,713Net Assets

As of 6/30/03

*Cash, cash equivalents and marketable securities

Financial Outlook – 2003 Guidance

Mid to high teensRevenue Growth

High single to low double digit*EPS Growth (per ADS)

30% rangeOperating Margin

*Excludes closure of Lead Optimization Business: Impact approx. $.03

Shaping Shire’s Future

n Clear Strategy

l Focus R&D on late-stage development / key franchisesl Protect and grow major franchisesl Supplement growth through licensing/M&A

n Clear Strengths

l Proven, highly successful business modell Franchise life cycle opportunitiesl Strong pipeline – CNS, GI, Renall Management commitment to sharpen focus/reduce costs

“Shaping Shire’s Future”

Dr Wilson TottenGroup R&D Director

1st October 2003

A Strategic Review

![[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF …investors.shire.com/~/media/Files/S/Shire-IR/...[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE](https://img.pdfslide.net/doc/110x75/5f536ae70417e549e05359bf/x-annual-report-pursuant-to-section-13-or-15d-of-mediafilessshire-ir.jpg)

![[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR …investors.shire.com/~/media/Files/S/Shire-IR/annual-interim...united states . securities and exchange commission . washington, d.c. 20549](https://img.pdfslide.net/doc/110x75/5ab138327f8b9ac3348c160c/x-annual-report-pursuant-to-section-13-or-mediafilessshire-irannual-interimunited.jpg)