Embed Size (px)

Citation preview

AAPP CCAA

False Premises EncourageFalse Premises EncourageMisdirected Farm PoliciesMisdirected Farm Policies

Daryll E. Ray and Harwood SchafferUniversity of Tennessee Institute of Agriculture

Agricultural Policy Analysis Center

Organization for Competitive Markets15th Annual Food and Agriculture Conference

Kansas City, MissouriAugust 9, 2013

AAPP CCAA

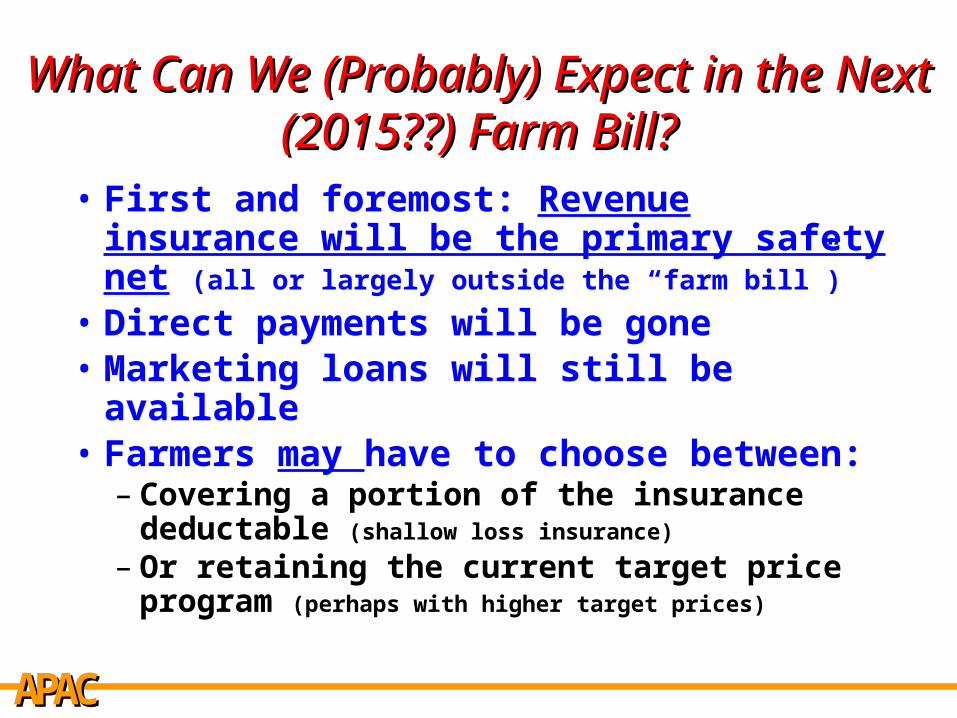

What Can We (Probably) Expect in What Can We (Probably) Expect in the Next (2015??) Farm Bill?the Next (2015??) Farm Bill?• First and foremost: Revenue

insurance will be the primary safety net (all or largely outside the “farm bill”)

• Direct payments will be gone• Marketing loans will still be available• Farmers may have to choose between:

– Covering a portion of the insurance deductable (shallow loss insurance)

– Or retaining the current target price program (perhaps with higher target prices)

AAPP CCAA

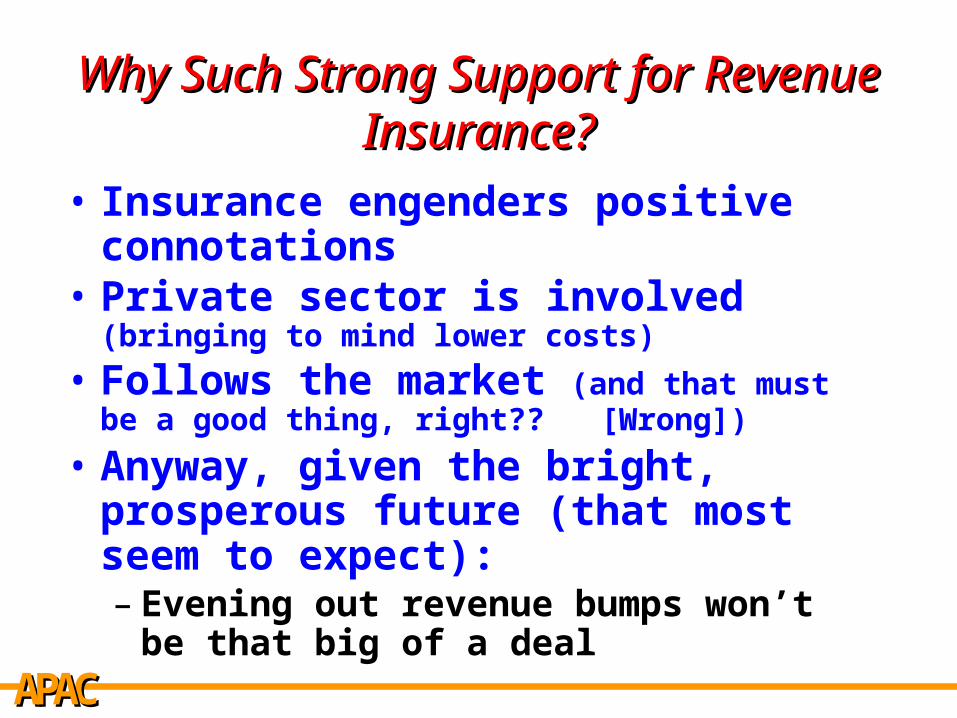

Why Such Strong Support for Why Such Strong Support for Revenue Insurance?Revenue Insurance?

• Insurance engenders positive connotations

• Private sector is involved (bringing to mind lower costs)

• Follows the market (and that must be a good thing, right?? [Wrong])

• Anyway, given the bright, prosperous future (that most seem to expect):– Evening out revenue bumps won’t be

that big of a deal

AAPP CCAA

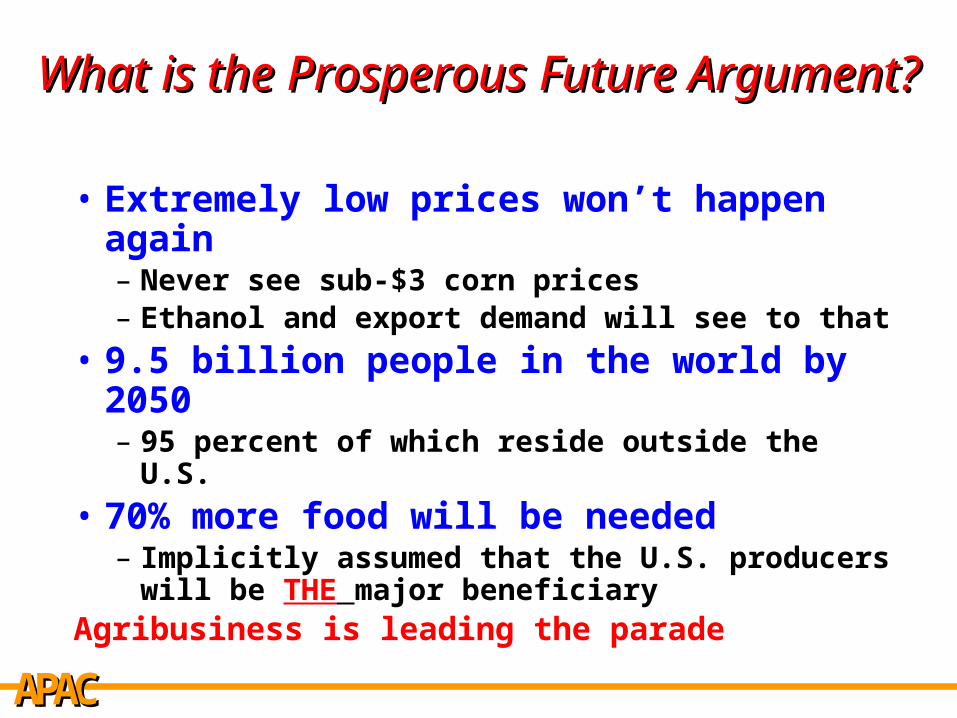

What is the Prosperous Future What is the Prosperous Future Argument?Argument?

• Extremely low prices won’t happen again– Never see sub-$3 corn prices– Ethanol and export demand will see to that

• 9.5 billion people in the world by 2050– 95 percent of which reside outside the U.S.

• 70% more food will be needed– Implicitly assumed that the U.S. producers

will be THE major beneficiaryAgribusiness is leading the parade

AAPP CCAA

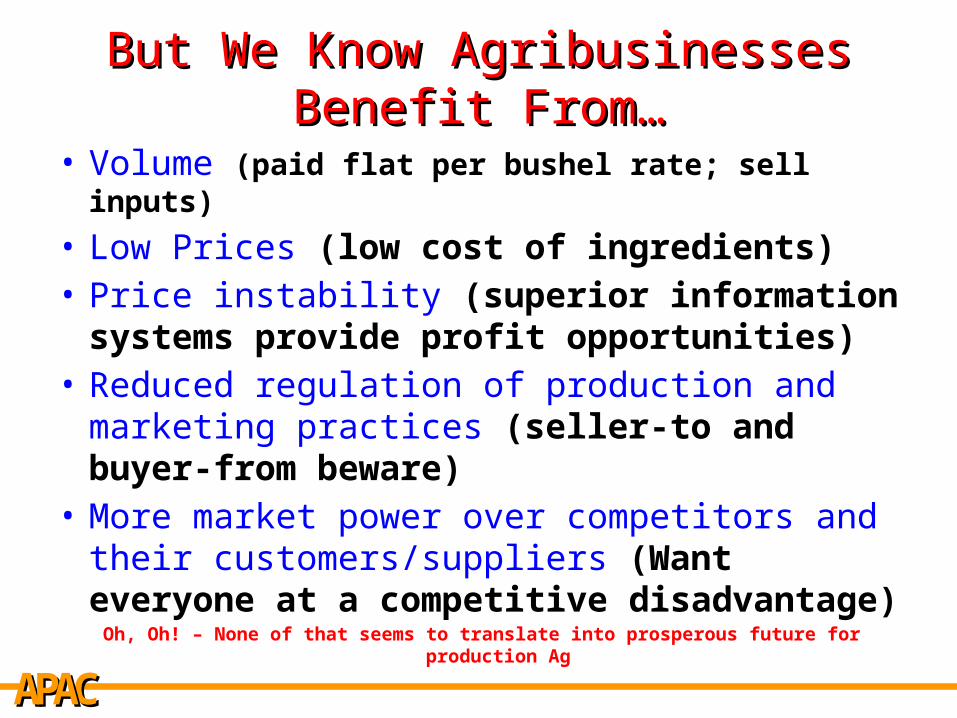

But We Know Agribusinesses But We Know Agribusinesses Benefit From…Benefit From…

• Volume (paid flat per bushel rate; sell inputs)

• Low Prices (low cost of ingredients)• Price instability (superior information

systems provide profit opportunities)• Reduced regulation of production and marketing practices (seller-to and buyer-from beware)

• More market power over competitors and their customers/suppliers (Want everyone at a competitive disadvantage)

Oh, Oh! – None of that seems to translate into prosperous future for production Ag

AAPP CCAA

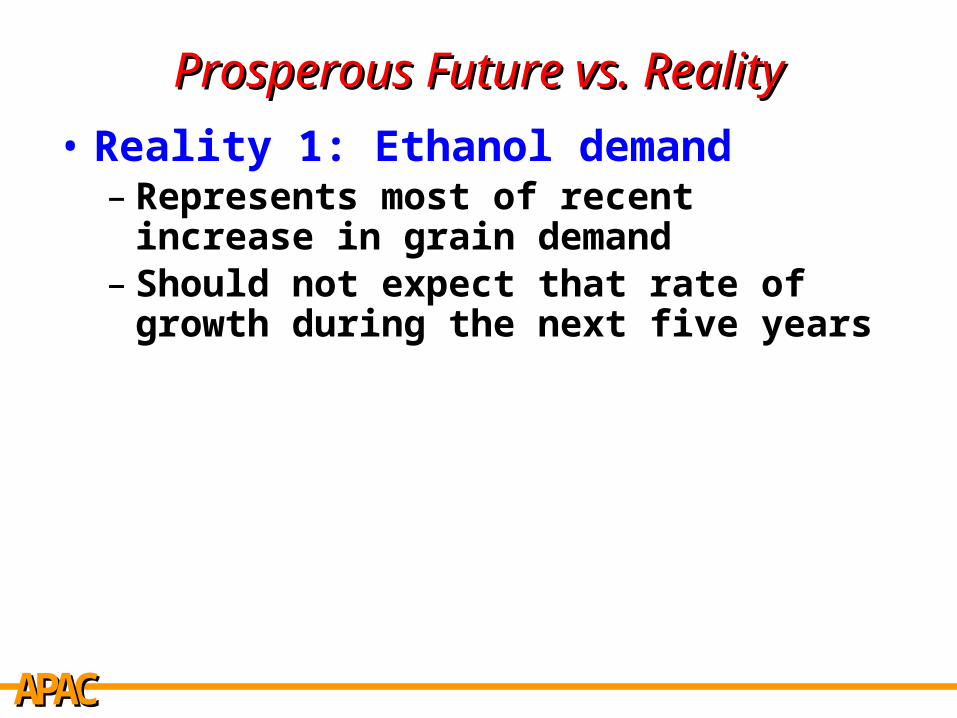

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 1: Ethanol demand– Represents most of recent increase in

grain demand– Should not expect that rate of growth

during the next five years

AAPP CCAA

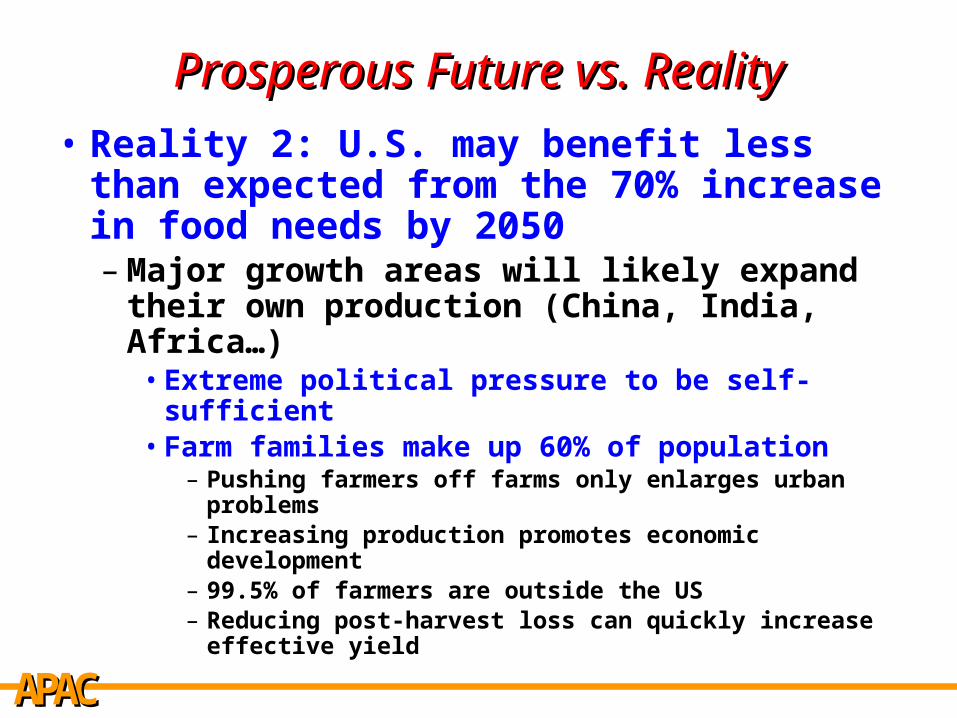

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 2: U.S. may benefit less than expected from the 70% increase in food needs by 2050– Major growth areas will likely expand their

own production (China, India, Africa…)• Extreme political pressure to be self-sufficient• Farm families make up 60% of population

– Pushing farmers off farms only enlarges urban problems

– Increasing production promotes economic development

– 99.5% of farmers are outside the US– Reducing post-harvest loss can quickly increase

effective yield

AAPP CCAA

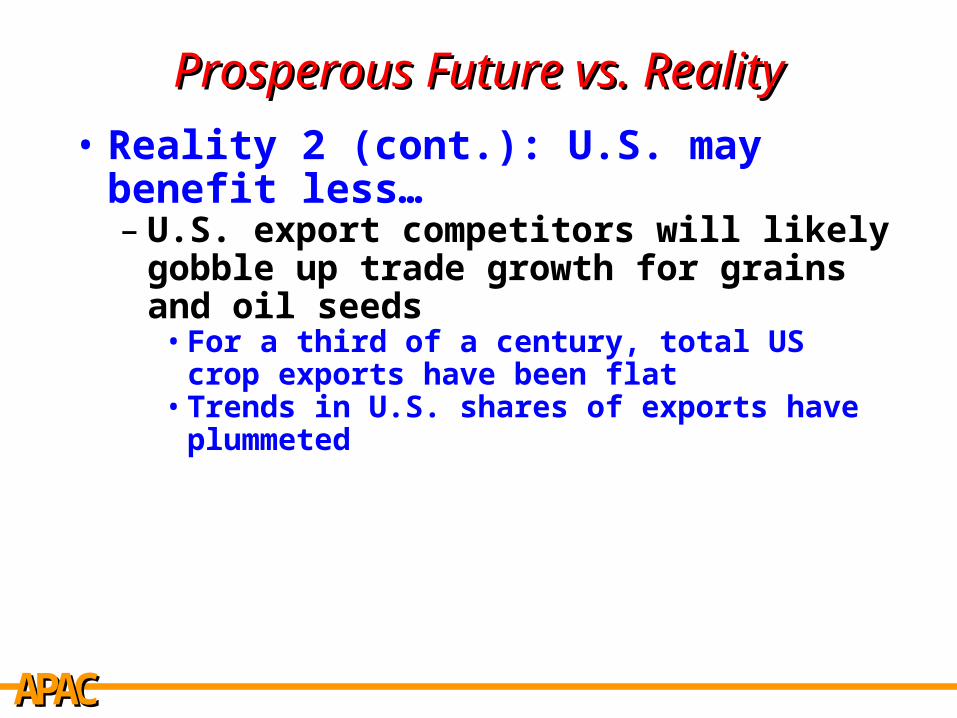

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 2 (cont.): U.S. may benefit less… – U.S. export competitors will likely gobble

up trade growth for grains and oil seeds• For a third of a century, total US crop exports

have been flat• Trends in U.S. shares of exports have

plummeted• Export competitors have more head room

than the U.S. to increase agricultural production

– Open land available in S. America and other countries

– Yields can be increased by closing technology gaps

AAPP CCAA

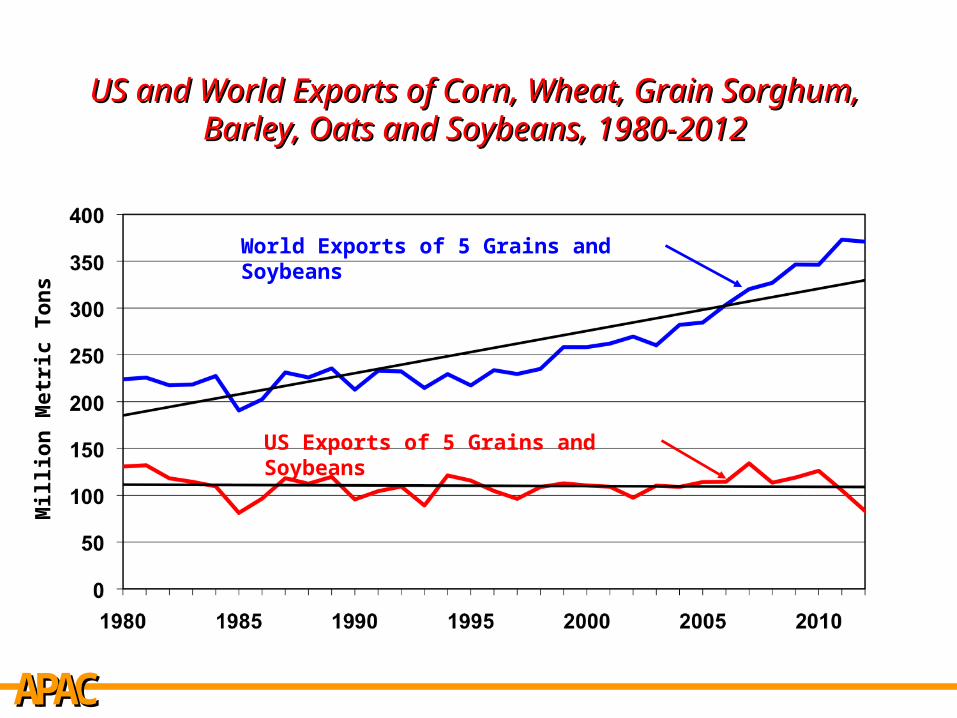

US and World Exports of Corn, Wheat, Grain US and World Exports of Corn, Wheat, Grain Sorghum, Barley, Oats and Soybeans, 1980-Sorghum, Barley, Oats and Soybeans, 1980-

20122012

Mill

ion

Met

ric

To

ns

World Exports of 5 Grains and Soybeans

US Exports of 5 Grains and Soybeans

AAPP CCAA

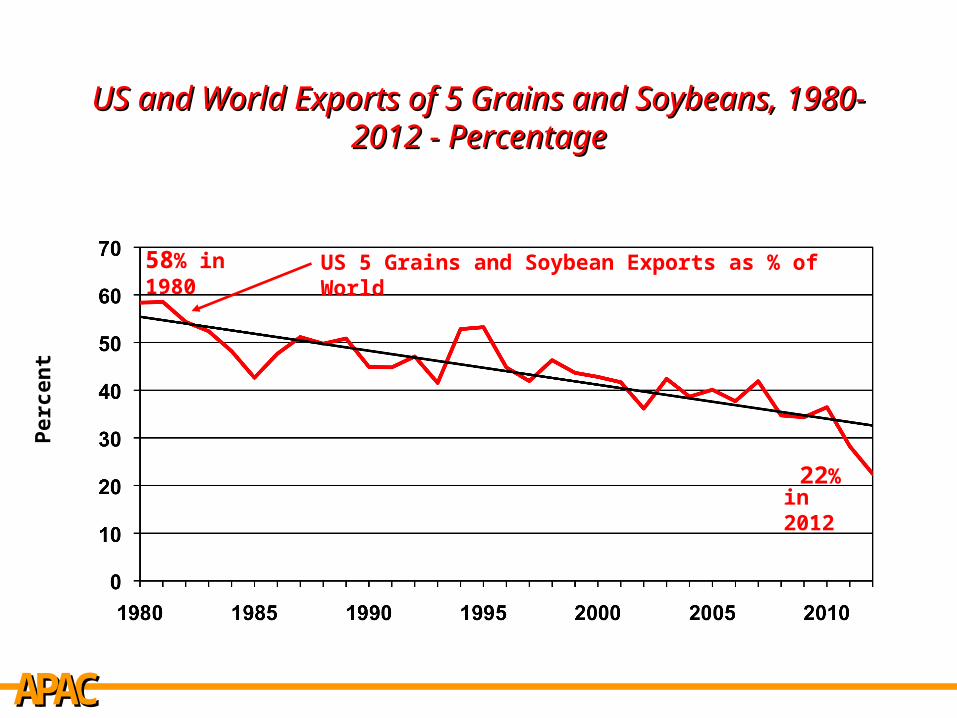

US and World Exports of 5 Grains and US and World Exports of 5 Grains and Soybeans, 1980-2012 - PercentageSoybeans, 1980-2012 - Percentage

Per

cen

t

US 5 Grains and Soybean Exports as % of World58% in 1980

22% in 2012

AAPP CCAA

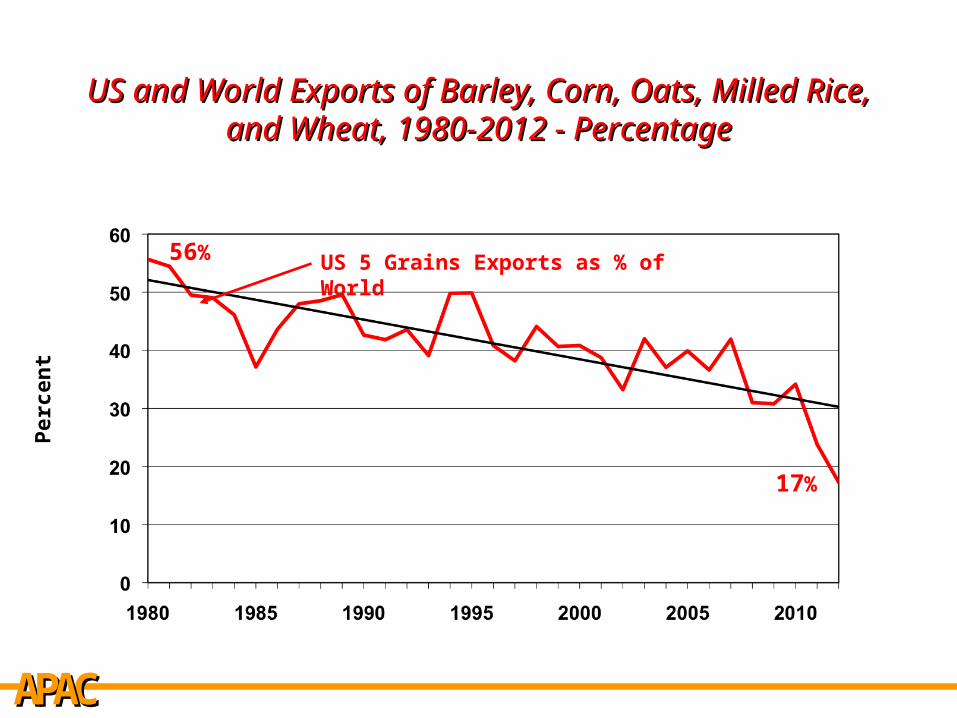

US and World Exports of Barley, Corn, US and World Exports of Barley, Corn, Oats, Milled Rice, and Wheat, 1980-2012 - Oats, Milled Rice, and Wheat, 1980-2012 -

PercentagePercentage

Per

cen

t

US 5 Grains Exports as % of World56%

17%

AAPP CCAA

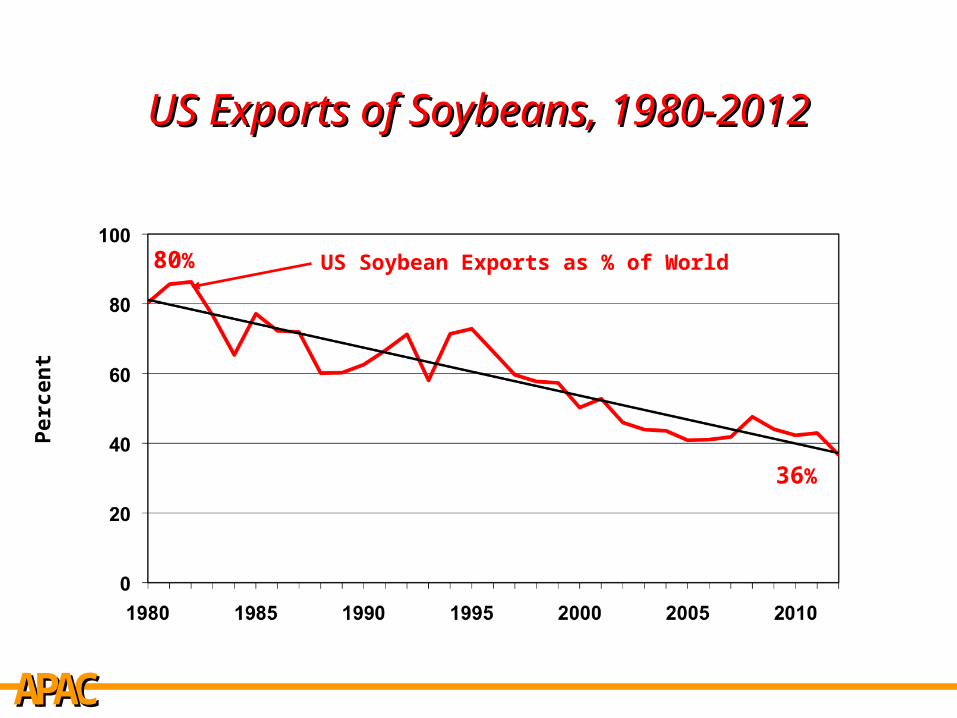

US Exports of Soybeans, 1980-2012US Exports of Soybeans, 1980-2012

Per

cen

t

US Soybean Exports as % of World80%

36%

AAPP CCAA

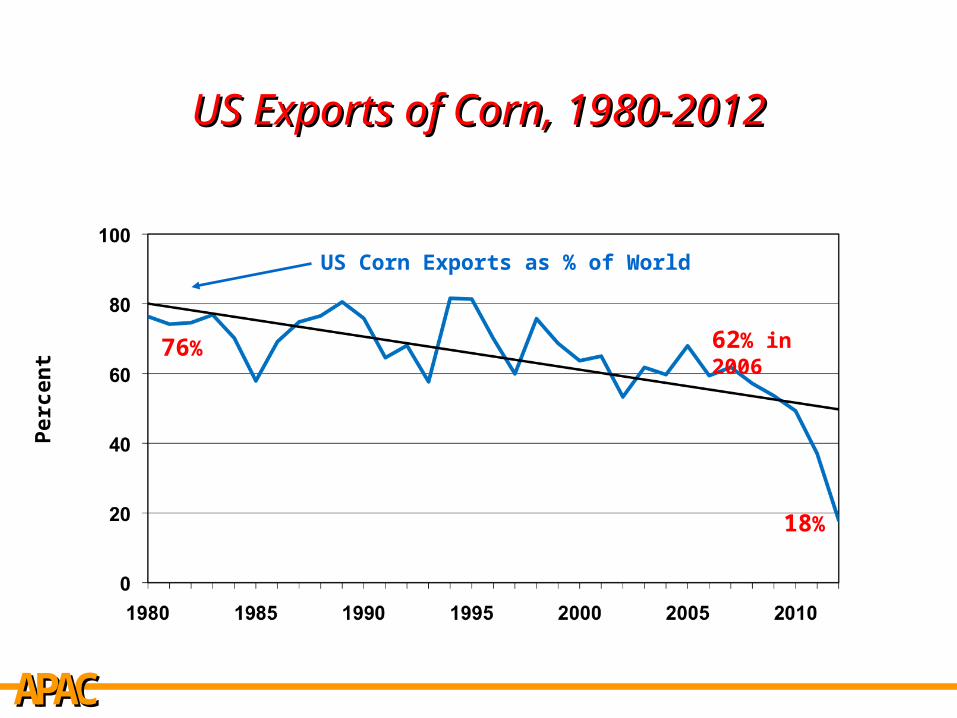

US Exports of Corn, 1980-2012US Exports of Corn, 1980-2012

Per

cen

t

US Corn Exports as % of World

76%

18%

62% in 2006

AAPP CCAA

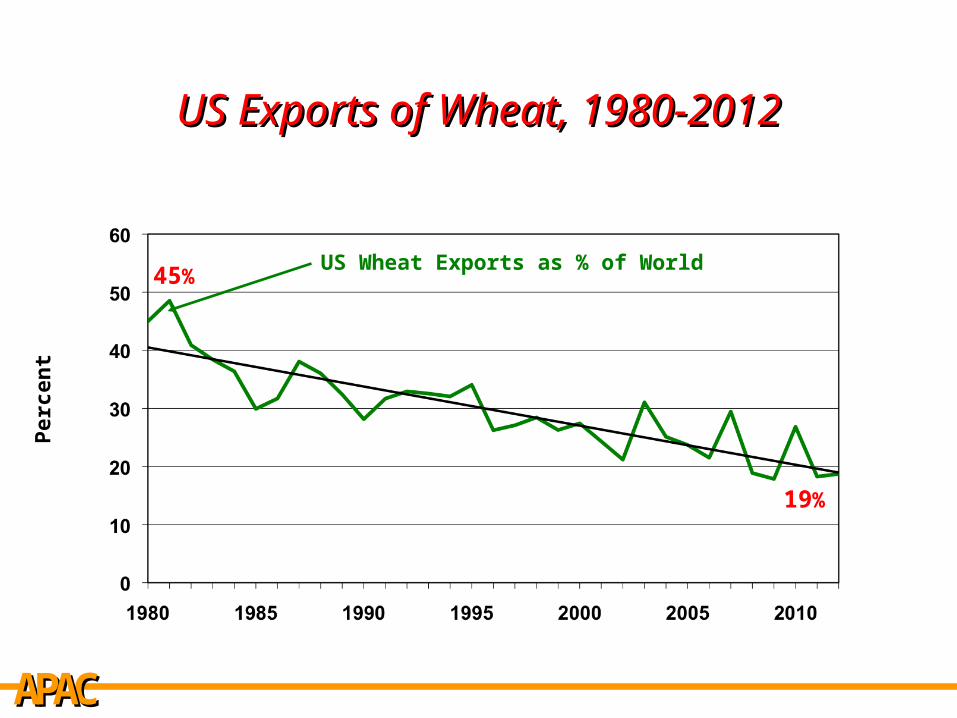

US Exports of Wheat, 1980-2012US Exports of Wheat, 1980-2012

Per

cen

t

US Wheat Exports as % of World45%

19%

AAPP CCAA

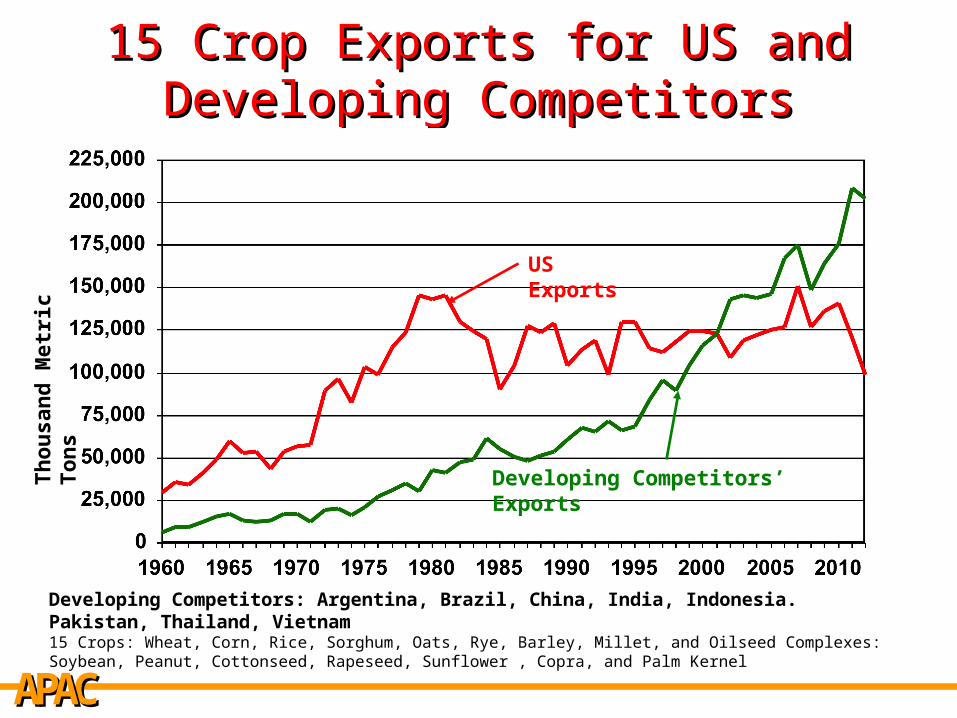

15 Crop Exports for US and 15 Crop Exports for US and Developing CompetitorsDeveloping Competitors

Developing Competitors: Argentina, Brazil, China, India, Indonesia. Pakistan, Thailand, Vietnam15 Crops: Wheat, Corn, Rice, Sorghum, Oats, Rye, Barley, Millet, and Oilseed Complexes: Soybean, Peanut, Cottonseed, Rapeseed, Sunflower , Copra, and Palm Kernel

Th

ou

san

d M

etri

c T

on

s US Exports

Developing Competitors’ Exports

AAPP CCAA

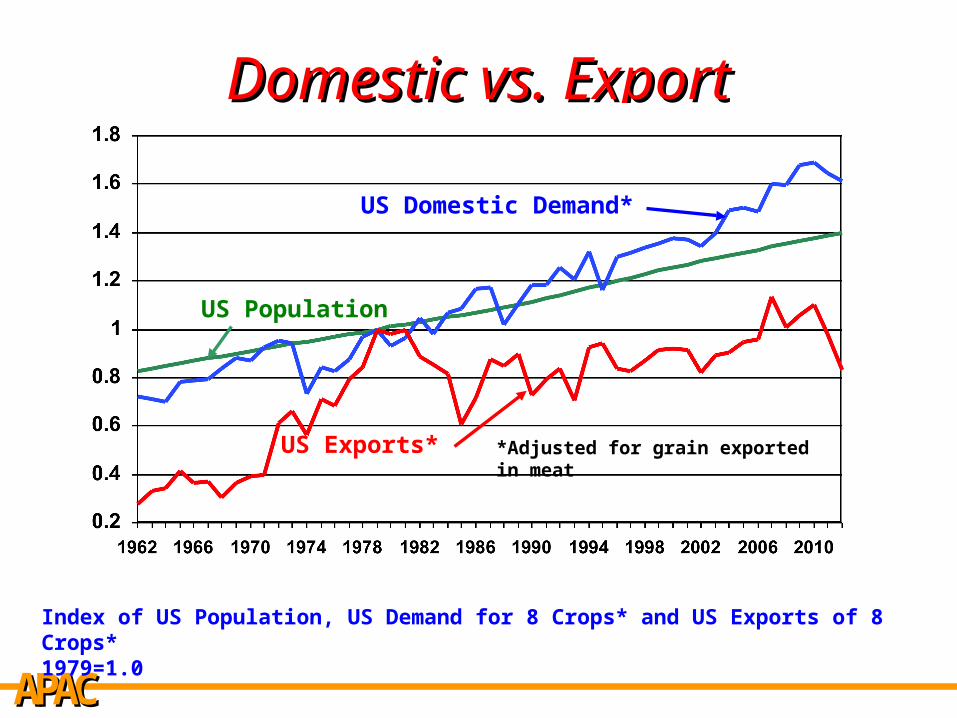

Domestic vs. ExportDomestic vs. Export

Index of US Population, US Demand for 8 Crops* and US Exports of 8 Crops*1979=1.0

US Population

US Exports*

US Domestic Demand*

*Adjusted for grain exported in meat

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 2 (cont.): U.S. may benefit little… – U.S. export competitors will likely gobble

up trade growth for grains and oil seeds• For a third of a century, total US crop exports

have been flat• Trends in U.S. shares of exports have

plummeted• Export competitors have more head room

than the U.S. to increase agricultural production

– Open land available in S. America and other countries

– Yields can be increased by closing technology gaps

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 3: There are no price floors– Yes, the price standard for corn increased

from $1 per bushel to $2 following the 1970s• Commodity Credit Corp supported crop prices and

did so at a higher level reflecting inflation

– Nothing now to stop a catastrophic drop in prices

• The CCC non-recourse loans cannot do it• Loan deficiency and other payments cannot do it• Revenue insurance cannot do it (stay tuned…)• Future growth in ethanol and export demand would be

helpful but doubtfully a floor

– Corollary: Land prices could easily be the new “house of cards”

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 4 : Possible conclusion from all this…– Should not rule out worldwide excess

capacity and multiple years of very low prices

• This happened after the price surge in the 1970s– Other countries responded to the high prices and fear of food

insecurity by increasing production over time– U.S. export demand collapsed– The resulting U.S. excess agricultural capacity in the early 1980s

turned out to be over 30 million acres– And became known as the Conservation Reserve Program

• What about this time?– Our export competitors are expanding production for export– Our import customers are ramping up domestic production– U.S and world output likely to outpace demand growth– Like the three price run-ups over the 100 years: prices drop

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 5: High-price periods are the worst times to do a farm bill…– Provisions are put into the farm bill that

work during those high-price times• Decoupled payments in 1996 FB—prices were

high in 1996 when bill was passed• High interest in revenue insurance this year—

when prices are high “pure profits” could be virtually guaranteed

– But are completely inadequate/inept when prices go well below the cost of production for multiple years

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 6: Let’s get serious about insurance!– It is designed to protect against random

incidents• A relatively predictable proportion of houses in

“home insurance pools” will burn down

– It is not well-suited for incidents that affect the entire pool of insurance clients

• All houses do not burn down at once (if that is a possibility—like during wartime—those events are excluded from coverage)

– Insurance is primarily for “individual” incidents not incidents that affect everybody

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 6 (cont.): What about ag then?– Makes sense to insure against incidents that

affect production of individual farmers or subgroups of farmers

• Like yield and prevented planting problems – especially hail, wind, floods, etc.– Rates could/would differ, including by region

– Not indicated for incidents that affect all farmers (that is, incidents that are systemic)

• Like severe price drops, especially for multiple years

• Ditto price-caused drops in revenue

AAPP CCAA

Prosperous Future vs. RealityProsperous Future vs. Reality

• Reality 7: Revenue insurance tends to be an upside-down safety net– When prices are high, revenue insurance

provides protection• Depending on circumstances, could guarantee

profits well above all production costs• Courtesy of U.S. taxpayers

– When prices remain very “low,” revenue insurance does not provide a meaningful safety net

• “Guarantees” a proportion of low prices, even when prices are well below production costs

Attractively painted “revenue-insurance bandwagon” seems structurally unsound

AAPP CCAA

Modifications, then??Modifications, then??• (If) the proverbial train (bandwagon) has

left the station, what can be done?– Keep, but modify

• Protect taxpayers by limiting revenue insurance to cover no more than a portion of production costs

• Better protect farmers by requiring that revenue insurance cover at least variable production costs

• Reduce administrative costs– For example, fixed agent fee per policy (or let FSA do it!)

– Start over—let insurance do what it does best• Limit taxpayer subsidized insurance to yield shortfalls

or prevented planting (Could provide it free so no need for emergency disaster payments)

• Use other programs for price and income protection• But the first step is properly identify the source of

agriculture’s price and income problems

AAPP CCAA

My Question to US Farmers Is: What My Question to US Farmers Is: What Are You Going to Do About It?Are You Going to Do About It?

• One alternative is passively sit by, be co-opted, and let others commandeer the policy agenda– That is exactly what producers have increasingly done since

the mid-eighties!!!

– Crop producers get subsidy-tarred while real subsidy beneficiaries (integrated livestock producers and other users, sellers of inputs and marketers of output) remain above the fray

– Advocating unfettered free markets, promising export growth, or claiming a level playing field as farmers’ magic bullet, etc., ain’t workin.

AAPP CCAA

My Question to US Farmers Is: My Question to US Farmers Is: What Are You Going to Do About What Are You Going to Do About

It?It?• Must be a mindset change

– Producers and farm and commodity organizations must refuse to carry water

– Must design policies based on “the realities” not hope or wishful thinking

– Must be willing to energetically embrace other groups that genuinely share identical or complementary objectives

– Work as hard to become independent as we have “worked” to become subservient in the past

AAPP CCAA

My Question to US Farmers Is: My Question to US Farmers Is: What Are You Going to Do About What Are You Going to Do About

It?It?• Did I mention that there must be a mindset

change?

• Everything should be on the table. Take nothing for granted.– Previous programs: DNA testing (seeing what

happens when most of them are eliminated) have exonerated most of the “failed programs of the past”

– In all cases, do not contradict or ignore any of “the realities” when developing policy

AAPP CCAA

What What ISIS the Problem? the Problem? • Technology/Ac expands output faster than

population and exports expand demand• Yield variability • Market failure: lower prices do not solve

the problem in a timely fashion• Little self-correction on the demand side

– People will pay almost anything when food is short

– Low prices do not induce people to eat more• Little self-correction on the supply side

– Farmers tend to produce on all their acreage– Few alternate uses for most cropland

AAPP CCAA

Farmer-Oriented Agricultural Farmer-Oriented Agricultural PolicyPolicy

• I. Three components:– Farmer-Owned-Reserve to put a relatively-wide

band around prices– Annual general cropland set-aside, allowing

complete planting flexibility on remainder– Eliminate Direct Payments and the marketing loan

General cropland set-aside and occasional use of CCC non-recourse loan would be used to help keep within the price band of FOR.

• II. Complement set-aside in I. with additional longer-term land withdrawal in CRP or perennial energy crops, thus reducing annual set-aside acreage requirements

AAPP CCAA

In the Long Term…In the Long Term…• Solutions to chronic price and income

problems need to include:– International supply management to

manage supply on a global scale

– At the present US supply management can benefit farmers everywhere in the world

– As countries like Brazil and other developing export competitors continue to increase their capacity they will need to be a part of an effective supply management program

AAPP CCAA

SummarySummary• Conventional wisdom has seemed to be that

we are in a “new price and income era”• When we had a similar price run-up in the

1970s, worldwide production increases slammed U.S. agriculture

• This time there is no floor on crop prices• Without modification, current revenue

insurance proposals…– Provide a safety net when prices are “high”– But are not much help when prices are “low”

• So where does that leave us?– Déjà vu all over again?

• With status quo, will there be emergency payments like after the 1996 Farm Bill?

• An expanded Conservation Reserve?– Really need to rethink Ag policy

• The source of agriculture’s price and income problems• And programs that actually get to the root of Ag’s problems

AAPP CCAA

Agricultural Policy Analysis Center The University of Tennessee 310 Morgan Hall 2621 Morgan Circle Knoxville, TN 37996-4519

www.agpolicy.org

Thank YouThank You

AAPP CCAA

To receive an electronic version of our weekly ag policy column send an email to: [email protected] to be added to APAC’s Policy Pennings listserv

Weekly Policy ColumnWeekly Policy Column