Embed Size (px)

Citation preview

Appendix 4: Economic Policy Review December 2016

ContentsIntroduction...........................................................................................................................................3

1 SwindonandWiltshireStrategicEconomicPlan(DRAFT2015-2026).............................................4

2 SwindonandWiltshireLEPStrategicEconomicPlan(2012-2026)..................................................8

3 WiltshireCoreStrategy(2015)......................................................................................................12

4 WiltshireWorkspace&EmploymentLandReview(2011-2026)..................................................14

5 ReviewofEmploymentProjectionsandLandRequirementsinSouthWiltshire(2011)..............17

6 SwindonBoroughLocalPlan2006-2026.......................................................................................19

7 SwindonCoreStrategy:EconomicTesting(2012)........................................................................21

8 AnEconomicStrategyforSwindon(2012-26)..............................................................................23

9 SwindonEmploymentLandReview(2007)...................................................................................25

10 SwindonWorkspaceStrategyandDeliveryPlan.........................................................................26

Conclusion...........................................................................................................................................29

3

Introduction

This document formsAppendix 4 to the SwindonandWiltshire Functional EconomicMarketAreaAssessment. It summarises the keypoints of the relevantpolicydocuments for the SwindonandWiltshireLEPareasince2007.Thereportsincludedare:

• SwindonandWiltshireStrategicEconomicPlan2015-2026• SwindonandWiltshireLEPStrategicEconomicPlan2012-2026• WiltshireCoreStrategy2006-2026• WiltshireWorkspace&EmploymentLandReview2011-2026• SwindonBoroughLocalPlan2006-2026• SwindonCoreStrategy:EconomicTesting• EconomicStrategyforSwindon2012-2026• SwindonWorkplaceStrategyandDeliveryPlan• SwindonEmploymentLandReview2007

Thesereportswereassessedfortheirfindingsonthefollowingissues:

• Scaleandambitionofgrowth• Keysectorsidentified• Employmentlandrequirements• SWOTfactors• Functionaleconomicgeography• Infrastructurechanges

Theviewspresentedinthissummaryarepresentedasfoundineachreport.AnynotesprovidedbyHJAforthereader’sbenefitareprovidedinbrackets.

4

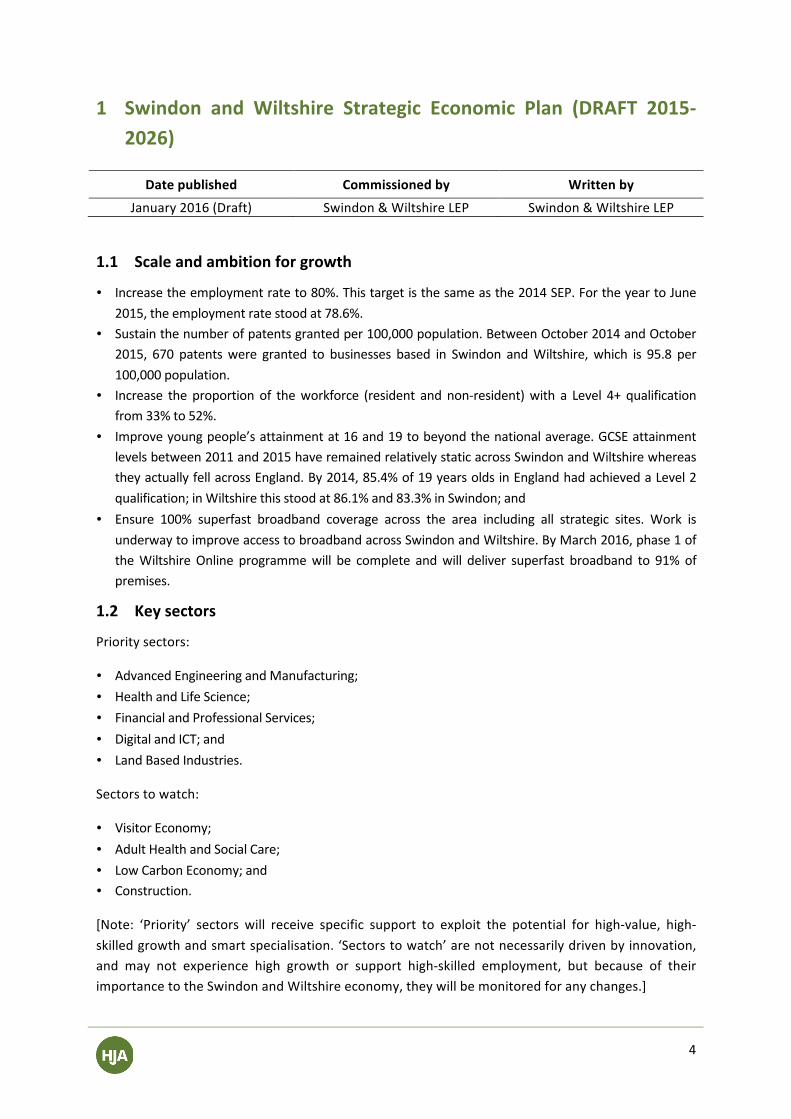

1 Swindon and Wiltshire Strategic Economic Plan (DRAFT 2015-2026)

Datepublished Commissionedby Writtenby

January2016(Draft) Swindon&WiltshireLEP Swindon&WiltshireLEP

1.1 Scaleandambitionforgrowth

• Increasetheemploymentrateto80%.Thistargetisthesameasthe2014SEP.FortheyeartoJune2015,theemploymentratestoodat78.6%.

• Sustainthenumberofpatentsgrantedper100,000population.BetweenOctober2014andOctober2015, 670 patentswere granted to businesses based in Swindon andWiltshire,which is 95.8 per100,000population.

• Increase the proportion of theworkforce (resident and non-resident)with a Level 4+ qualificationfrom33%to52%.

• Improveyoungpeople’sattainmentat16and19tobeyondthenationalaverage.GCSEattainmentlevelsbetween2011and2015haveremainedrelativelystaticacrossSwindonandWiltshirewhereastheyactuallyfellacrossEngland.By2014,85.4%of19yearsoldsinEnglandhadachievedaLevel2qualification;inWiltshirethisstoodat86.1%and83.3%inSwindon;and�

• Ensure 100% superfast broadband coverage across the area including all strategic sites. Work isunderwaytoimproveaccesstobroadbandacrossSwindonandWiltshire.ByMarch2016,phase1oftheWiltshireOnline programmewill be complete andwill deliver superfast broadband to 91% ofpremises.

1.2 Keysectors

Prioritysectors:

• AdvancedEngineeringandManufacturing;� • HealthandLifeScience;� • FinancialandProfessionalServices;� • DigitalandICT;and� • LandBasedIndustries.

Sectorstowatch:

• VisitorEconomy;� • AdultHealthandSocialCare;� • LowCarbonEconomy;and• Construction.

[Note: ‘Priority’ sectors will receive specific support to exploit the potential for high-value, high-skilledgrowthandsmartspecialisation.‘Sectorstowatch’arenotnecessarilydrivenbyinnovation,and may not experience high growth or support high-skilled employment, but because of theirimportancetotheSwindonandWiltshireeconomy,theywillbemonitoredforanychanges.]

5

1.3 SWOTfactors

Strengths

• Centralsouthern locationwithgeographicproximitytomajoreconomiccentres(includingLondon),keyairports,andcoastalports;�

• Knowledge based economy with clusters in Life Sciences, AdvancedManufacturing, Financial andProfessionalServices,DigitalandICT,andLandBasedIndustries;�

• Ruraleconomywithattractivelandscape,heritage,andvisitorattractions;� • Militarypresence;� • Strongsmallandmediumsizedenterprise(SME)growthwithhighlevelsof �innovationandbusiness

survival;� • Vibranteconomywithaskilledworkforceandlowunemployment;� • Rapidlygrowingpopulation[Note:populationgrowthwasrapidbetween2001and2011censusdata,

butsince2010populationgrowthhasreturnedtothenationalaverage];• Goodbusinesssurvivalrates.

Weaknesses

• Declining competitiveness. SWLEP sawGVA growth of just 50% from 2001-2013 compared to thenationalaverageof+61.6%GVA.

• Youthunemployment.InOctober2015,16-24madeup25.4%oftheclaimantcount.• Below national average attainment at 16 and 19, and low HE participation. National average for

studentswithAleveloralevel3qualificationmovingintoHEis58%-figureforWiltshireis54%andSwindonis35%.ThelackofHEprovisionintheareacausesadrainonthesectionofthepopulationwhodochoosetostudyfurther,andoftenthosewhodoleavedon’treturntothearea.

• Lowratesofbusinessformation.• Transport infrastructure, especially north-south connectivity, is not adequate to support expansion

plans.

Opportunities

• Becomeahubforinnovation.• ExploitpotentialtoattractfurtherinwardinvestmentandsupportthedevelopmentofSMEsinhigh

valuesectorstobalancegrowthintheSouthEast;� • ExtendreputationasahubforspecialistsectorsinLifeSciences,AdvancedManufacturing;Financial

andProfessionalServices;DigitalandICT,andLandBasedIndustries.� • Rapidpopulationgrowth[Iwouldquestionthisclaim];and� • Strong jobs growth forecasted - according to econometric forecasts in the 2013 Local Economic

Assessment (summarised elsewhere), 30,000 additional jobs are forecast between 2010 and 2020across Swindon and Wiltshire, twice the rate of growth predicted nationally owing to goodrepresentationinsectorspredictedtoperformwell,suchasProfessionalServices.

6

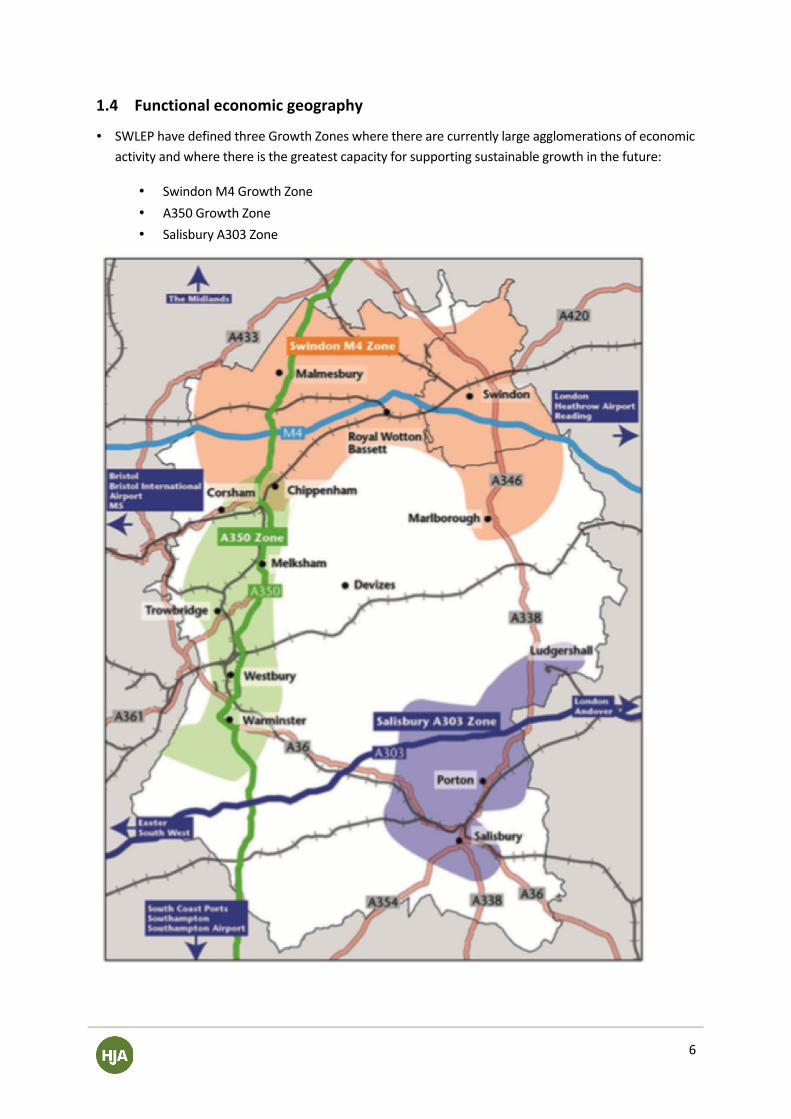

1.4 Functionaleconomicgeography

• SWLEPhavedefinedthreeGrowthZoneswheretherearecurrentlylargeagglomerationsofeconomicactivityandwherethereisthegreatestcapacityforsupportingsustainablegrowthinthefuture:

• SwindonM4GrowthZone • A350GrowthZone • SalisburyA303Zone

7

• ChippenhamisincludedinboththeSwindon-M4GrowthZoneandtheA350GrowthZoneasapivotallocationinthedevelopmentofboththeM4andA350economiccorridors.

• ItsinclusionintheSwindonM4GrowthZoneisimportantasitoffersthepotentialtoextendgrowthintotheareathathasdevelopedoutofLondonthroughtoReadingandSwindon;aswellasthepotentialtodrawininvestmentfromthewestoutofBristolandBaththroughthedevelopmentpotentialatJunction17.

• ItisanimportantlinkintheA350Corridorwithconditionsthatpromotebusinessdevelopmentandcreatingclustersoflike-mindedbusinesses,whichextendsfromMalmesburytothenorthandWarministertothesouth.

8

2 SwindonandWiltshireLEPStrategicEconomicPlan(2012-2026)

Datepublished Commissionedby Writtenby

March2014 Swindon&WiltshireLEP Swindon&WiltshireLEP

2.1 Scaleandambitionforgrowth

• Deliveryof40,600jobs.• Estimatedadditional£3billionGVA.• Raisetheemploymentratetoitspre-recessionlevel(from74.7%to80%);• Sustaintheproportionofbusinessesapplyingforpatentsattwicethenationalaverage;• Increasetheproportionoftheworkforce(residentandnon-resident)withadegreelevelqualification

from33.6%todayto52%,equivalentto83,000morepeoplewithaLevel4andabovequalification;• Improve young people’s attainment at 16 and 19 including in English andMaths to beyond the

nationalaverage;and• Ensure100%superfastbroadbandcoverageacrosstheareaincludingallstrategicsites.

2.2 Keysectors

• Advancedengineeringandmanufacturing;� • Militaryanddefence;� • HealthandLifeSciences;� • Informationeconomy–includingdigitalindustriesandinformationtechnology;� • Professionalandbusinessservices:� • Tourism;and • Land-Basedindustriesincludingfood.�

2.3 Infrastructurechangesandemploymentlandrequirements

SEPinvestmentprogrammetodeliver318haofemploymentland:

• SwindonTownCentreBusExchange:5ha• SwindonTownCentreRailwayCrossing:13ha• Wichelstowe:13ha• EasternVillages:40ha• CorshamA4access:10ha• CorshamDigitalCommunity:50ha• CorshamRailStation:6ha• Corsham:3.5ha• ChippenhamLangleyPark:3ha

• ChippenhamTransportPackage:16ha• A350Chippenhambypassimprovements:14ha• MelkshamGrowthStrategy:10ha• A350WestAshtonimprovements:14.7ha• TrowbridgeTransportPackage:12ha• MilitaryTowns:47.5ha• PortonSciencePark:8ha• SalisburyTransportPackage:24ha• SalisburyChurchfields:7ha

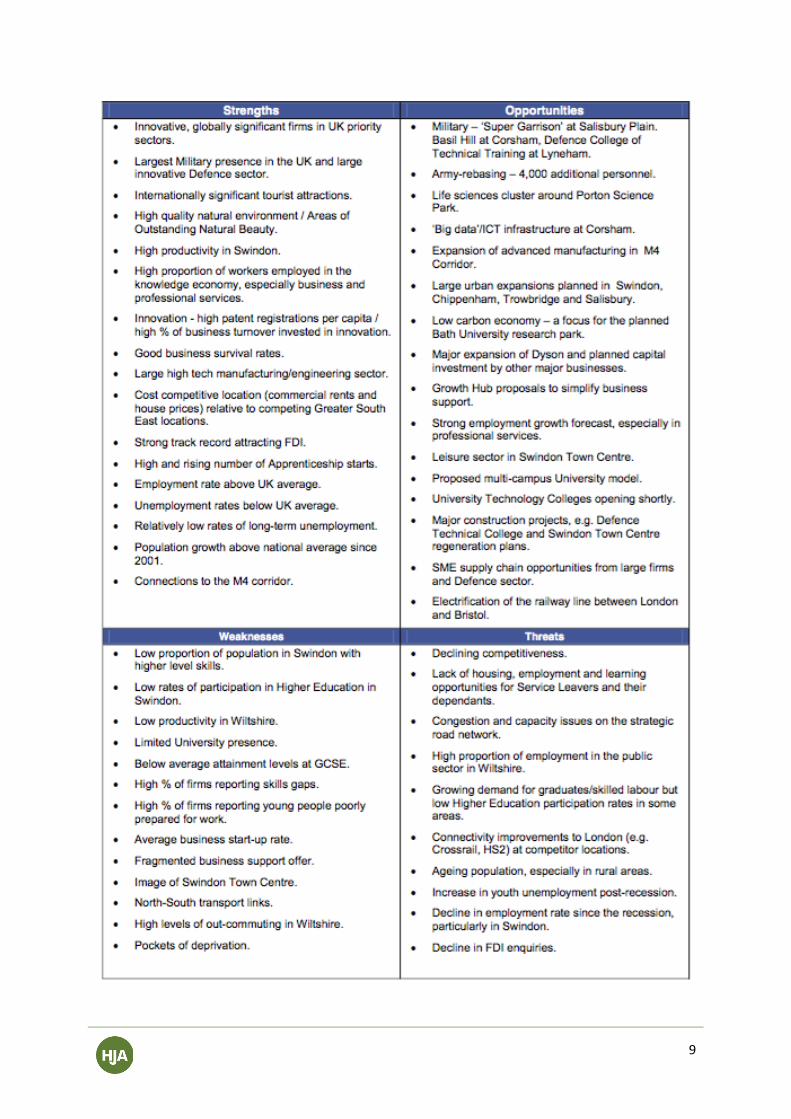

2.4 SWOTfactors

ThefollowingfigureshowstheSWOTanalysisincludedinthereport:

9

10

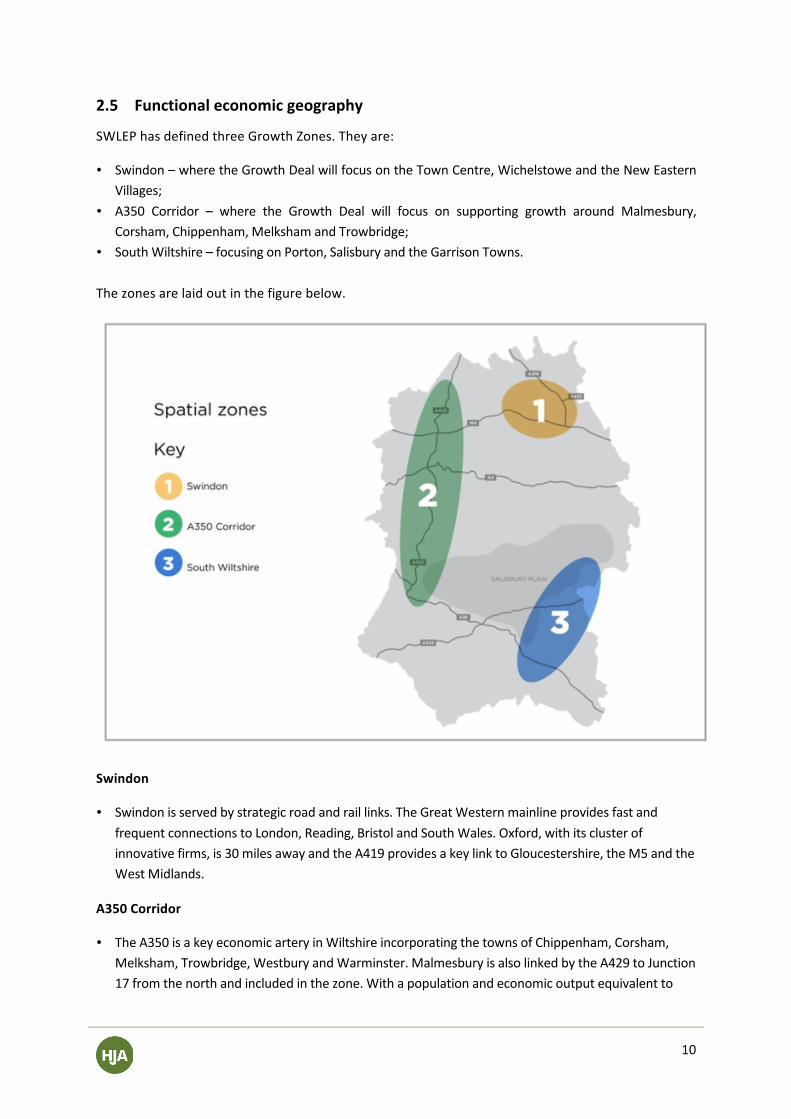

2.5 Functionaleconomicgeography

SWLEPhasdefinedthreeGrowthZones.Theyare:

• Swindon–wheretheGrowthDealwillfocusontheTownCentre,WichelstoweandtheNewEasternVillages;

• A350 Corridor – where the Growth Deal will focus on supporting growth around Malmesbury,Corsham,Chippenham,MelkshamandTrowbridge;

• SouthWiltshire–focusingonPorton,SalisburyandtheGarrisonTowns.

Thezonesarelaidoutinthefigurebelow.

Swindon

• Swindonisservedbystrategicroadandraillinks.TheGreatWesternmainlineprovidesfastandfrequentconnectionstoLondon,Reading,BristolandSouthWales.Oxford,withitsclusterofinnovativefirms,is30milesawayandtheA419providesakeylinktoGloucestershire,theM5andtheWestMidlands.�

A350Corridor

• TheA350isakeyeconomicarteryinWiltshireincorporatingthetownsofChippenham,Corsham,Melksham,Trowbridge,WestburyandWarminster.MalmesburyisalsolinkedbytheA429toJunction17fromthenorthandincludedinthezone.Withapopulationandeconomicoutputequivalentto

11

Swindon(£3.4bninGVA),theareaishometomanyofWiltshire’smostimportantbusinesses,with60%ofthe‘Wiltshire100’inthecorridorincludingSiemens,HermanMiller,andKnorrBremse.�

• Inthelastyear,jobswerecreatedinthezoneataratethreetimesfasterthantherestofWiltshire.InadditionthereissignificantMODpresenceatCorshamandWarminster,andaround2,500Militarypersonnelstationedinthearea,17%ofthetotal.�

SouthWiltshire• TheSouthWiltshirezoneishometo113,750people,witharound51,500employeesemployedby

justover4,900businesses.ItgeneratesatotalGVAofaround£2.1bn,equivalentto15%oftheLEP’sGVA.�

• ThemainsourcesofemploymentinthezoneareHealth,Professional,ScientificandTechnical,Military,and,AccommodationandFood,whichgivesitquiteadifferentprofilefromtheotherLEPgrowthzones.ThezonehasparticularstrengthsintheHealthandLifeSciences,whereitaccountsformorethan1in2jobsinthesectoracrosstheLEP,andtheMilitarysector,whereArmyRebasingintheSalisburyPlainareawillpositivelyimpactoncommunitiesandthelocaleconomy.�

12

3 WiltshireCoreStrategy(2015)

Datepublished Commissionedby Writtenby

January2015 WiltshireCouncil WiltshireCouncil

3.1 Scaleandambitionforgrowth

Thestrategymakesprovisionforthegrowthofaround27,500jobsandatleast42,000newhomesfrom2006to2026.

3.2 Keysectors

• Advancedengineeringandmanufacturing;• Businessservices;• Bioscience;• Environmentaltechnologies;• Foodanddrink;• ICTandcreativeindustries;• Agricultureandland-basedindustries;and• Tourism.

3.3 Employmentlandrequirements

The 178ha of new strategic employment landwill be provided by a combination of the followingtypesofsites:

• Newstrategicemploymentallocations;• Provisionofemploymentlandaspartofmixeduseurbanextensions;and• RetainedLocal/DistrictPlanallocationsforemploymentland.

Additionalemploymentlandisearmarkedforthefollowinglocations:

• Churchfields&EngineSheds–5ha• FormerImerysQuarry,Salisbury–4ha• FugglestoneRed,Salisbury–8ha• HortonRoad,Devizes–8.4ha• NursteadRoad,Devizes–1.5ha• KingstonFarmandMoultonEstate,Bradford-

on-Avon–3ha• Longhedge(OldSarum),Salisbury–8ha• MillLane,Hawkeridge–14.7ha• NorthAcreIndustrialEstate–3.8ha• AshtonPark,Trowbridge–15ha• WestAshtonRoad,Trowbridge–10ha• UKLF,Wilton–3ha• WestofWarminster–6ha

• BoscombeDown–7ha• PortonDown–10ha• LandEastofBeversbrook–3.2ha• LandnorthofTetburyHill,Malmesbury–1ha• LandatGardenCentre,Malmesbury–4ha• HamptonBusinessPark–6ha• E12landatMere–3ha• LandatMalboroughRoad,Pewsey–1.66ha• LandtotheWestofTemplarsWay,Royal

WoottonBassett–3.7ha• Brickworks,Purton–1ha• LandnorthofTidworthRoad,Tidworth–12ha• HindonLane,Tisbury–1.4ha• WestWarminsterUrbanExtension–6ha

13

3.4 Functionaleconomicgeography

• ThecityofSalisburyservesalargesurroundingruralarea.DuetoStonehengeitisapopulartouristdestination.

• Trowbridgeplaysaroleasanemployment,administrationandservicecentreforthewestWiltshirearea,andhasgoodtransportlinkstomanynearbysettlements,includingBathandBristol.

• ChippenhamisafocusforemploymentgrowthduetoitsproximityandgoodaccesstotheM4andraillinks.IthasdirecttransportlinkswithSwindon,Bath,BristolandLondon.

• Wiltshire has relationshipswith the surrounding large urban centres of Bath, Bristol, Swindon andSouthampton, and lies within 115 miles of London. The larger centres provide a wider range ofemployment,leisure,andculturalopportunitiesthancanbefoundacrossWiltshire,andresultinout-commutingofWiltshire’sresidentsforworkandleisureactivities.

• EvidencealsoidentifiesthatinsomeinstancesworkersarecommutingintoWiltshire,whilstresidingin larger centres such as Bristol and Southampton and this could be due to cheaper housing andenhancedleisurefacilitiesprovidingagreaterdraw.

• TheairandseaportsrelatedtothesesettlementsarealsowidelyusedbyWiltshireresidents.• Wiltshirehasnetout-commutingflowstoseveralemploymentcentresbeyondthecountyboundary.• Evidencesuggeststhatpaydifferentialsareamajordrivermeaningthathigherearnerscommuteout

ofthecountytowork.• Out-commuting may have some beneficial effect on the local economy through income earned

outside the area being spent inWiltshire, but this is far outweighed by the negative impacts onsustainability.

3.5 Infrastructurechanges

• TheA350nationalprimaryrouteatYarnbrook/WestAshtonwillbeimproved.

Chippenham

• BathRoadCarPark/BridgeCentreSite - to formaretailextensiontothetowncentretoprovideasupermarketandcomparisonunits.

• Langley Park - to deliver a mixed-use site solution for a key redevelopment opportunity area tosupporttheretentionofsignificantbusinessusesonpartofthesite.

Melksham

• The proposedMelksham link project would provide a canal link to the south west of MelkshambetweentheKennetandAvonCanalandtheRiverAvon,andtothenortheastofMelkshambetweentheRiverAvonandthehistoricalignmentoftheWiltsandBerksCanal.

Salisbury

• The area around theMaltings, Central Car Park and Library is allocated for a retail-ledmixed-usedevelopment.Itwillconsistofconvenienceandcomparisonshopping,leisureuses,housing,offices,libraryandculturalquarter.Retail,residentialandleisureareaswillbelinkedbyopen,pedestrianisedstreetsandpublicspaces.

14

4 WiltshireWorkspace&EmploymentLandReview(2011-2026)

Datepublished Commissionedby Writtenby

December2011 WiltshireCouncil RogerTym&Partners

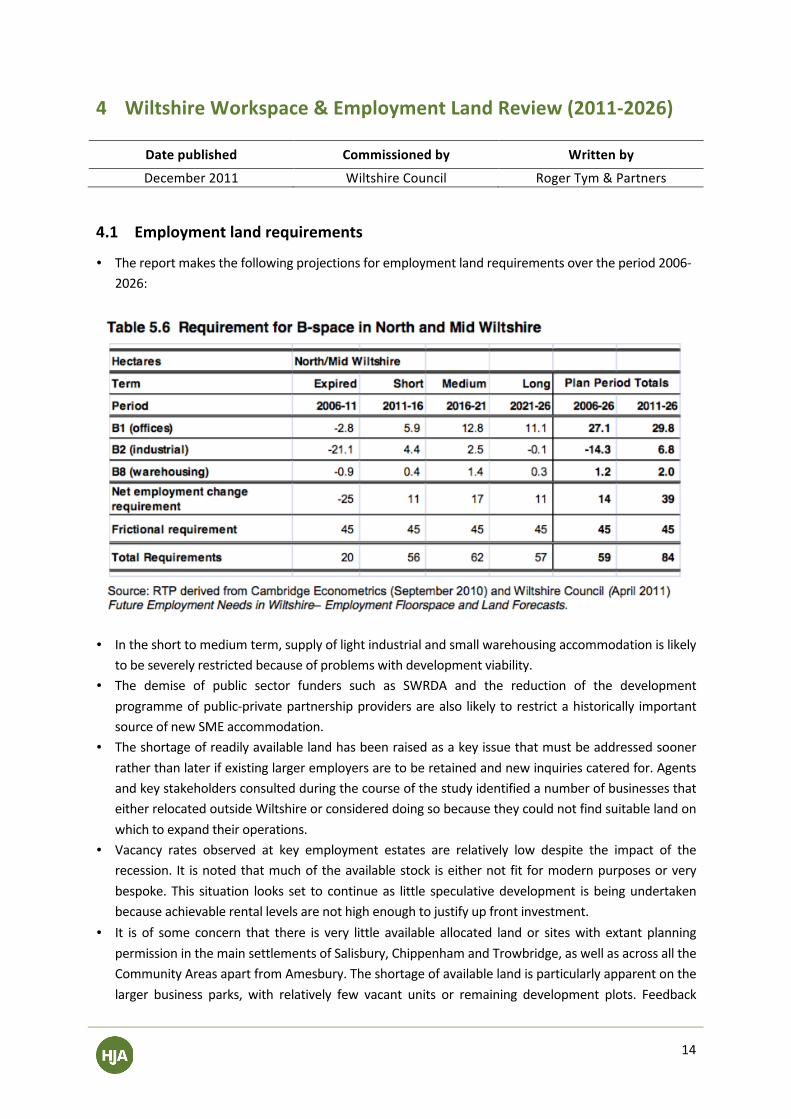

4.1 Employmentlandrequirements

• Thereportmakesthefollowingprojectionsforemploymentlandrequirementsovertheperiod2006-2026:

• Intheshorttomediumterm,supplyoflightindustrialandsmallwarehousingaccommodationislikelytobeseverelyrestrictedbecauseofproblemswithdevelopmentviability.

• The demise of public sector funders such as SWRDA and the reduction of the developmentprogrammeofpublic-privatepartnershipprovidersarealso likelytorestrictahistorically importantsourceofnewSMEaccommodation.

• Theshortageofreadilyavailablelandhasbeenraisedasakeyissuethatmustbeaddressedsoonerratherthanlaterifexistinglargeremployersaretoberetainedandnewinquiriescateredfor.AgentsandkeystakeholdersconsultedduringthecourseofthestudyidentifiedanumberofbusinessesthateitherrelocatedoutsideWiltshireorconsidereddoingsobecausetheycouldnotfindsuitablelandonwhichtoexpandtheiroperations.

• Vacancy rates observed at key employment estates are relatively low despite the impact of therecession. It isnotedthatmuchoftheavailablestock iseithernotfit formodernpurposesorverybespoke.This situation looks set tocontinueas little speculativedevelopment isbeingundertakenbecauseachievablerentallevelsarenothighenoughtojustifyupfrontinvestment.�

• It is of some concern that there is very little available allocated landor siteswithextant planningpermissioninthemainsettlementsofSalisbury,ChippenhamandTrowbridge,aswellasacrossalltheCommunityAreasapartfromAmesbury.Theshortageofavailablelandisparticularlyapparentonthelarger business parks, with relatively few vacant units or remaining development plots. Feedback

15

indicatedthatthislackofavailabilityresultedinWiltshiremissingoutonanumberoflargerinwardinvestmentinquiries.�

• ProportionallyhighersharesofemploymentallocationsshouldbegiventotheprimarysettlementsinChippenhamandTrowbridge.Theseurbansettlementshavemorescopeformeetingobjectivessuchasthealignmentofresidentswithachoiceofjobs,linkingbusinesseswithinfrastructuretosupportbusiness growth and economic development through generous land allocations, and attractingunforeseeninwardinvestments.�

• Trowbridgehasanurgentrequirementforaconsiderablequantumofavailablelandintheshortterm.ThislookslikelytocontinueasboththeAshtonParkUrbanExtensionandWestAshtonRoadsitesareunlikely to become available until expensive new road links are established. There is howeverpotential fornewallocations atWestbury to cater for land requirements for thearea in the shortterm.�

• Basedonthesiteassessmentsandknowndemand,itisrecommendedthatalloftheexistingsitesshouldeitherberetainedasemploymentsitesorredevelopedwhollyfornewBspaceorformixeduseincludingB-space.

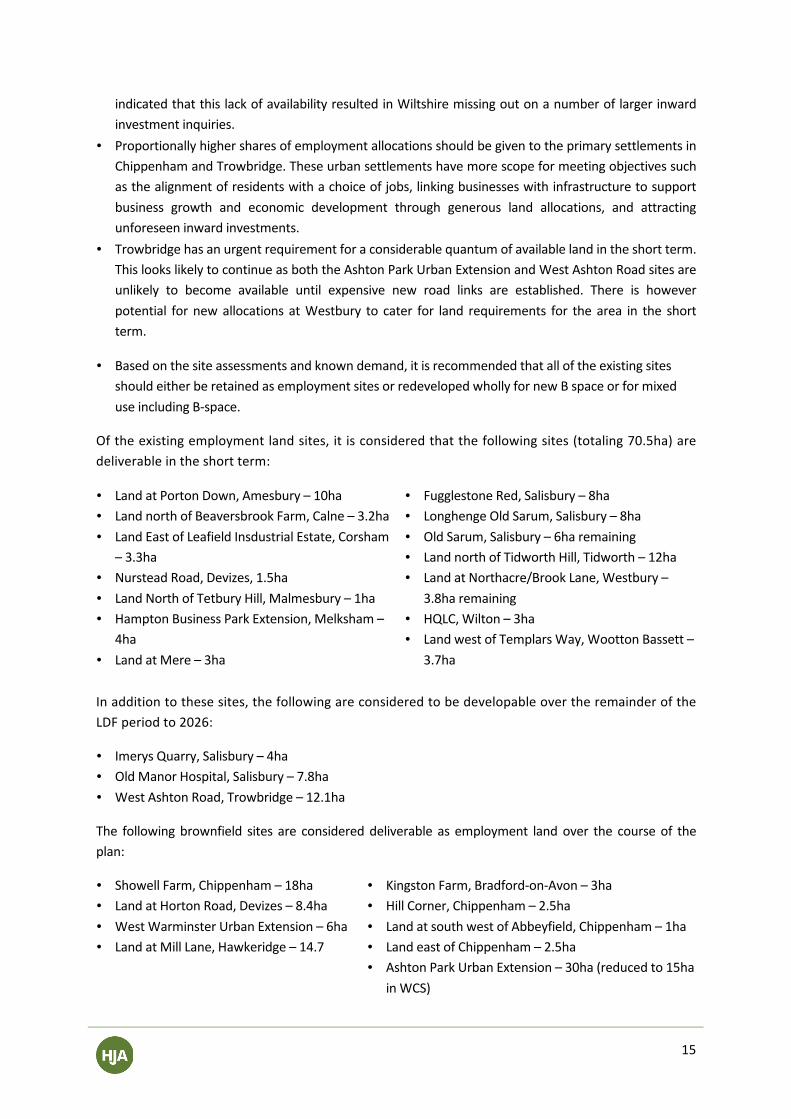

Oftheexistingemploymentlandsites,itisconsideredthatthefollowingsites(totaling70.5ha)aredeliverableintheshortterm: �

• LandatPortonDown,Amesbury–10ha• LandnorthofBeaversbrookFarm,Calne–3.2ha• LandEastofLeafieldInsdustrialEstate,Corsham

–3.3ha• NursteadRoad,Devizes,1.5ha• LandNorthofTetburyHill,Malmesbury–1ha• HamptonBusinessParkExtension,Melksham–

4ha• LandatMere–3ha

• FugglestoneRed,Salisbury–8ha• LonghengeOldSarum,Salisbury–8ha• OldSarum,Salisbury–6haremaining• LandnorthofTidworthHill,Tidworth–12ha• LandatNorthacre/BrookLane,Westbury–

3.8haremaining• HQLC,Wilton–3ha• LandwestofTemplarsWay,WoottonBassett–

3.7ha Inadditiontothesesites,thefollowingareconsideredtobedevelopableovertheremainderoftheLDFperiodto2026:

• ImerysQuarry,Salisbury–4ha• OldManorHospital,Salisbury–7.8ha• WestAshtonRoad,Trowbridge–12.1ha

The followingbrownfield sites are considereddeliverable as employment landover the courseof theplan:

• ShowellFarm,Chippenham–18ha• LandatHortonRoad,Devizes–8.4ha• WestWarminsterUrbanExtension–6ha• LandatMillLane,Hawkeridge–14.7

• KingstonFarm,Bradford-on-Avon–3ha• HillCorner,Chippenham–2.5ha• LandatsouthwestofAbbeyfield,Chippenham–1ha• LandeastofChippenham–2.5ha• AshtonParkUrbanExtension–30ha(reducedto15ha

inWCS)

16

Twonon-allocated sites are identified as havingpotential for employmentuse, particularly for B8occupiers:

• LandoffJunction17• LandoffA350

Thesitesareflatandfewconstraintswereidentifiedinthecourseofcompilingthisreport.

• Analysisofrequirementsagainstplannedsupply(above)revealsthatthereisenoughlandtomeettherequiredquantumofspaceidentifiedinTable5.6.Thebestsitesforcommercialattractivenessanddeliverabilityshouldbeprioritized,andtheamountoflandbeingplannedforshouldbereducedtoavoidreducingviabilitylevelsfurther.�

• Acommonmisunderstandingisthatbecauseoftherecession(withunemploymentincreasing),plannersshouldbeallocatingmoredevelopmentlandtobuildmoreeconomicfloorspace.Howeverinreality,theexactoppositeistrue.Thisisbecausethefloorspacevacatedintherecessionisstillavailableforoccupation,andthereforethephysicalspacecapacitytoemploypeoplehasnotbeentakenaway.Therecessionhasundermineddeveloperconfidenceandthevacantspacedepressedvalues.Addingfurthersupplybyallocatingtoomuchnewlandmayonlydepressvaluesfurtherandunderminemarketconfidence.�

17

5 Review of Employment Projections and Land Requirements inSouthWiltshire(2011)

Datepublished Commissionedby Writtenby

January2011 WiltshireCouncil WiltshireCouncil

5.1 Employmentlandrequirements

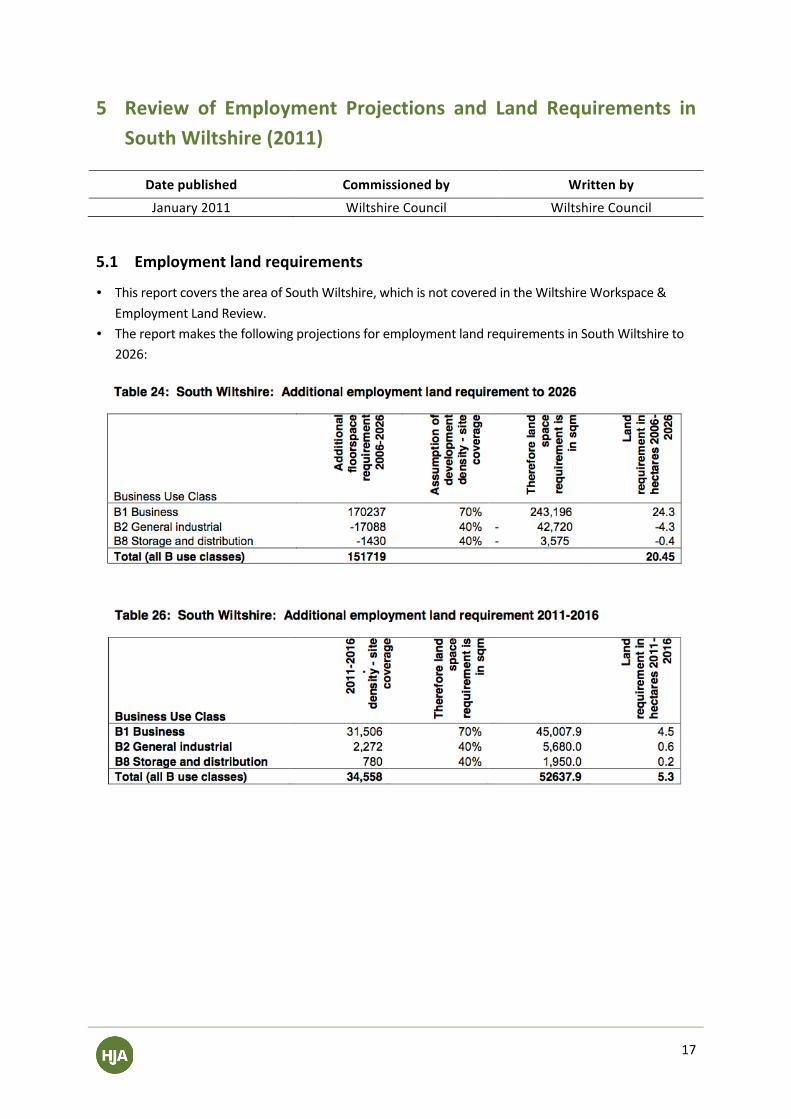

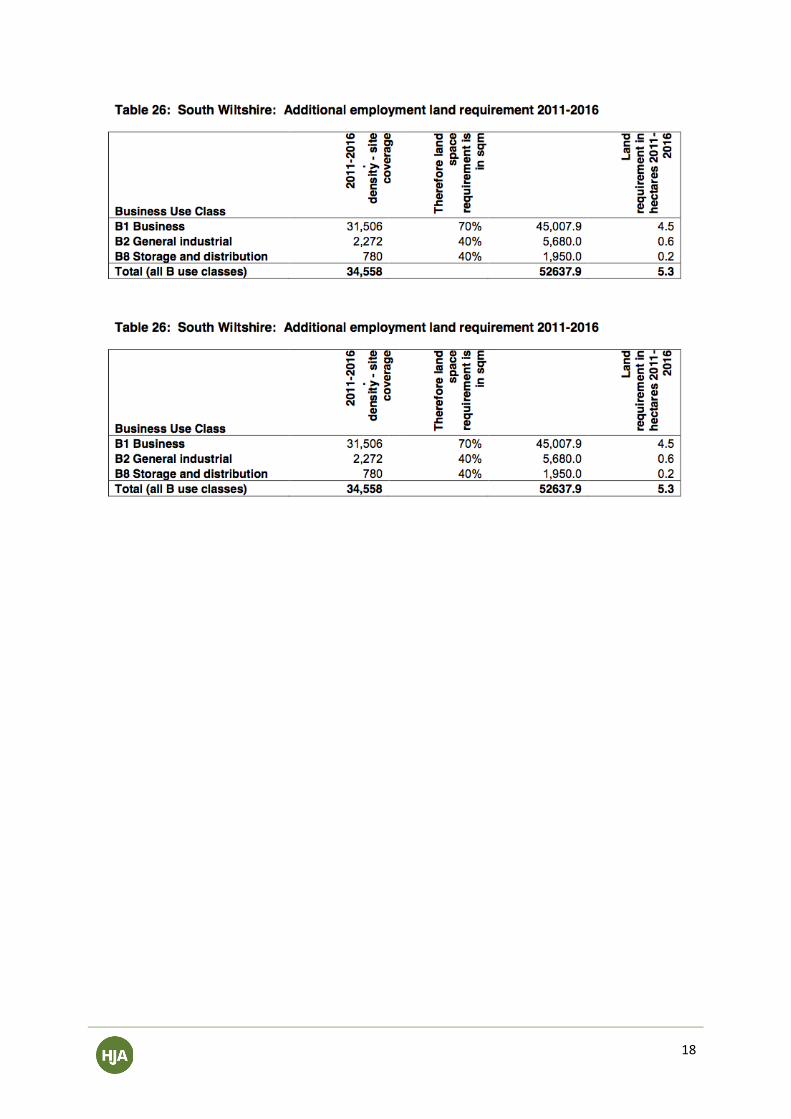

• ThisreportcoverstheareaofSouthWiltshire,whichisnotcoveredintheWiltshireWorkspace&EmploymentLandReview.

• ThereportmakesthefollowingprojectionsforemploymentlandrequirementsinSouthWiltshireto2026:

18

19

6 SwindonBoroughLocalPlan2006-2026

Datepublished Commissionedby Writtenby

March2015 SwindonBoroughCouncil SwindonBoroughCouncil

6.1 Scaleandambitionforgrowth

Thehighgrowthscenarioof+19,600jobsfor2011-2026hasbeenadoptedasthetarget.

6.2 Keysectors

• SpecialistmanufacturingineastSwindon• FinancialandbusinessservicesintheCentralArea• DistributionandlogisticsontheA419corridor• Environment• Tourismandleisure• ICT• Education• Health• Retail• Creativeindustries• Lowcarbondevelopmentandmanufacturing

6.3 Employmentlandrequirements

Sustainable economic and housing growth will be delivered in Swindon Borough during the planperiodthroughtheprovisionof119.5hectaresofemploymentland(B-useclass)through:

• 77.5hectaresofadditionalemploymentland;and • 42hectareswithextantpermissionandexistingallocationscarriedforward.

Theareasthroughwhichadditionalemploymentlandwillbeprovidedare:

• Wichelstowe–12.5ha• Commonhead–15ha• TadpoleFarm–5ha• NewEasternVillages–approx.40ha• Highworth–5ha

Theareasthatalreadyhaveextantpermissionandexistingallocationsare:

• Delta300–0.3ha• EdisonRoad,Dorcan–2.42ha• PennyLane,Drake’sWay–1.12ha• Europa/Brittania–1.65ha• AdjacenttoAbbeyStadium–4ha• Hillmead–7.9ha

• Keypoint–K3–2.9ha• Rivermead–1.3ha• SouthMarstonPark–2.75ha• G-Park–15.25ha• WindmillHill–2.38ha

20

6.4 Infrastructurechanges

Targeted investment in the following priority transport corridors, to promote travel choices, willsupporttripstoSwindonTownCentre:

• CovinghamDrive/DorcanWay; • CrickladeRoad; • GreatWesternWay; • MarlboroughRoad/QueensDrive; • MeadWay; • OxfordRoad/DrakesWay;and • ThamesdownDrive/OakhurstWayCorridor.�

21

7 SwindonCoreStrategy:EconomicTesting(2012)

Datepublished Commissionedby Writtenby

September2012 SwindonBoroughCouncil RegenerisConsultingLtd

Thiswaswrittenonthebasisofa2011draftoftheSwindonCoreStrategy(whichwaslaterrenamedasSwindonBoroughLocalPlan–seesection6),andservestoprovidecommentontheveracityofthefindingsinthedraftreport.

7.1 Scaleandambitionforgrowth

The report provides a base case forecast. This closely follows the forecasts of CambridgeEconometrics-growthof10,400jobs(8.5%)representing700netnewjobspa.

The higher growth scenario is for growth of around 19,600 jobs (16%) between 2011 and 2026,representing1,300netnewjobspa.This issomewhathigherthanthegrowthrate(c.900pa)thatSwindonachievedbetween1995and2008,although thedatashowssomesignificant fluctuationsduringthe2000s.Inthisrespect,itwouldbeastretchingandambitioustargettoadopt.

[Note:theSwindonBoroughLocalPlanadoptedthehighergrowthfigures]

7.2 Employmentlandrequirements

The total quantity of employment land allocated in the draft Core Strategy exceeded therequirement implied by the scale of employment growth assumed to drive the housing needrequirement,suggestingthatthereismorethanadequateemploymentlandallocated.However,theamount of employment land needed is highly sensitive to the demands from large scalewarehousing.The2007ELRassumedtheneedfor17.5haoflandforevery1,000distributionjobs.

Thereportdevelopedemploymentlandfiguresonbasecaseandhighergrowthscenariosasfollows:

• Basecase–16-23hadependingupontheapproachtoB8allocationsandassumptionsaboutB1officedevelopments.Witha20%safetymarginaddedtotherequirement,therangewouldbe19-27ha.�

• Highergrowth–41-55hadependingupon theapproach toB8andB1officedevelopment.A20%safetymarginwouldincreasetherangeto50-66ha.�

7.3 Functionaleconomicgeography

• The analysis of Swindon’s population and labour force suggests that the size and growth of theborough’sresidentworkforceshouldnotmeanthatemployersfacefuturelabourshortagesinoverallterms.However,evidencethat theboroughhasa lowerthanaverageproportionof residentswithhigherqualificationsandskillsdoespresentachallengethatneedstobeaddressed.Thecontinuedgrowthofthebusinessservicessector,theexpansionoftheICTindustryandthegeneralshifttowardshigherskillsrequirementsacrosstheeconomypointstopotentialshortagesinthiscomponentoftheresidentlabourforce.�

• Todate,traveltoworkdatasuggeststhatSwindon’semployershavebeenabletodrawonawiderlabourmarkettomeetthisrequirement,withtheareaaroundtheboroughprovidinganattractive

22

locationforhigherskilledandhigherpaidpeopletolive.Theimplicationisthattherewillneedtobechange–eitherSwindonattractsmore �residentswhoseskillsfittheseoccupations,oritmanagestoupskillexistingresidents,or ithastoacceptcontinuedpull fromitswidertraveltoworkarea(withconsequenttrafficimplications).

• However, it cannot be assumed that this patternwill continue to fullymeet employers’ needs infuture.TheimplicationisthatSwindon’seconomicstrategywillneedtoidentifyasapriorityasetofactionswhich leadto improvements inthequalification levelsof its residentsandencouragemorehighly qualified people to choose to live in the borough. Such issues could be addressed throughpriorities on theprovisionof higher education facilities in the townaswell as theplanningof thefuturehousingmixandlivingenvironmentthattheboroughseekstoachieve.�

23

8 AnEconomicStrategyforSwindon(2012-26)

Datepublished Commissionedby Writtenby

January2013 SwindonBoroughCouncil SwindonBoroughCouncil

8.1 Scaleandambitionforgrowth

Base Case scenario – Swindon achieves a level of employment growth that is consistent withnational and regional forecasts, andwhich reflectsexpectationsabouta recoveryof theeconomythatislikelytobeslowtoarrive,andmodestinscale.Thissuggestsemploymentgrowthofaround10,500netnewjobsto2026,returningtoalevelslightlyinexcessof2001levels.

Higher Growth scenario – the pace and extent of Swindon’s recovery outstrips that of otherlocationsandtheUKasawhole. In thisscenario,nearly20,000netnew jobswouldbecreated inSwindonby2026,withanincreaseof12,000jobsover2001levels.

ItisalsosensibletoconsideraMidRange scenario,whichwouldrepresentnetemploymentgrowthofaround14,000jobs.

8.2 Keysectors

• Business,Professional,andFinancialServices• TourismandLeisure(HotelsandCatering)• LogisticsandDistribution• ICT• ManufacturingandAdvancedEngineering• RetailandPrivateServices• HealthandEducationServices

8.3 SWOTfactors

Strengths

• Maintainingstrongproductivityperformance(GVApercapita);• LocationofSwindon-M4corridor,A417/M5,proximitytoLondon;• Diversityofbusinessbaseandsectorsrepresentedineconomy;• Highproportionofprivatesectoremployment; • Low proportion of public sector employment means more resilience to public sector austerity

measures;• Strongmanufacturingbase;• Presence of HQ functions in a broad range of sectors including ICT, financial services, insurance,

businessservices,andmanufacturing;• Relatively cost competitive, offering lower than average house prices and mid range commercial

propertyprices;and• Proximity of scientific research assets (eg. OxfordUniversity, PortonDown) and presence in town

(ResearchCouncils,TSB).

24

Weaknesses

• GVAgrowthhasslowedoverlastdecaderelativetocompetitorlocations;• Higherthanaverageproportionofresidentswithlowqualificationlevels;• Highlevelofyouthunemployment;• Towncentreinneedofsignificantregeneration; • Limited range of good quality cultural and leisure assets drawing visitors to town and providing

facilitiesforresidents;• Risingout-commutingmayreflectlackofsuitableemploymentintown;• LackofawarenessornegativeimageofSwindonexternally; • AbsenceofasignificantHEIpresence;• Weakcommercialofficemarket,particularlyintowncentre;• Unreliablejourneytimesandpriceofrailservices;• SlowandinfrequentraillinktoHeathrow;and• Distance fromneighbouringcitiesand townsmeansSwindon is isolated [Note:not sureabout this

onegiventheyalsouselocationasastrength].

Opportunities

• Expandingpopulation,withforecastsforagrowingworkingagepopulation;• Deliveryofmajorregenerationprojects–RegentCircus,Oasis,UnionSquare;• Potentialtodrawadditionalvisitorsandgenerateadditionalvisitorspend;• UKinitiativestodevelopindigenoussupplychainforautomotiveindustry;• Rising labour costs in China, India etc. has potential to make Swindon a more competitive

manufacturinglocation;• HighlevelofpatentactivityinSwindonpointstopotentialtogeneratemorecommercialinnovation,

buildingonbaseinautomotive,ICT,electronics,pharmaceuticals;• Investmentingreenenergyinfrastructure,lowcarbontransportandlocalenergygeneration;and• [Great?](sic)WesternaccesstoHeathrowandelectrification.

Threats

• Major employers in globally competitive sectors makes Swindon vulnerable to recession impactsincludingclosures;

• Double dip recession andweakness of recovery is broader threat to Swindon’s business base andabilitytocreateandsustainjobs;

• ProgressofcompetitorlocationsonM4corridorandhomecounties,capturinglimitedpoolofmajorcommercialinvestment;

• Failuretodevelopmoreknowledgeintensivebusinessactivity;• Failuretodelivermajorregenerationprojects;• Lackofsuitablesitesandpremisestounderpinexpansionofeconomyincludingoffices,logisticsand

distribution;and• Lack of public sector resources available to support infrastructure development, business support,

regeneration.

25

9 SwindonEmploymentLandReview(2007)

Datepublished Commissionedby Writtenby

June2007 SwindonBoroughCouncil NathanielLichfieldandPartners

9.1 Employmentlandrequirements

ThereportprovidesaheadlinefigureforgrossemploymentlandrequirementsforSwindonBorough2006-2016and2006-2026:

2006-16 Lowergrowthscenario(ha) Highergrowthscenario(ha)

Industrialspace 62 90Office/non-industrialspace 18 20TotalBspace 80 110

2006-26 Lowergrowthscenario(ha) Highergrowthscenario(ha)

Industrialspace 135 160Office/non-industrialspace 35 40TotalBspace 170 200

It is important to factor in that these estimates were based on pre-recession scenarios of highgrowth(+3.2%GVA)andlowgrowth(+2.8%GVA).GVAgrowthdidnotgetnearthoselevelsduringtheyearsafterthefinancialcrisis.

Withthatinmind,itcanbeextrapolatedfromthetwotablesabovewhattherecommendationsforgrossemploymentlandrequirementsforSwindonBorough2016-26are:

2016-2026 Lowergrowthscenario(ha) Highergrowthscenario(ha)

Industrialspace 73 70Office/non-industrialspace 17 20TotalBspace 90 90

Themostobvioussitesforconsiderationasemploymentlandare:

• EnlargingthecurrentA420/A419allocationsitetotheeastandsouth,orpossiblyaspartofalarger,mixeduseEasternDevelopmentArea,shouldthatdirectionofgrowthbeconfirmedintheapprovedRegionalSpatialStrategyfortheSouthWest(RSS);�

• AnewgreenfieldallocationeastoftheA419tothenorthoftheGroundwellIndustrialEstate;� • Ifpossible,amodestamountofadditionalofficespaceinthetowncentre;� • LandonthenorthsideoftheSwindonurbanarea,closetotheA419;� • PossiblyasmallextensionoftheBlackworthIndustrialEstateinHighworth;and� • If itwereconsideredstrategicallyacceptabletodevelopsouthoftheM4motorway, locationsnear

Junction16couldbeconsideredifadequateroadaccesscouldbeachieved.

26

10 SwindonWorkspaceStrategyandDeliveryPlan

Datepublished Commissionedby Writtenby

May2009 SwindonBoroughCouncilandSWRDA GVAGrimleyLtd

This reportwascommissioned inorder toassess thepotential forSwindontodeviatesignificantlyfrom the recommendations and requirements that the2007Employment LandReview (section8,above)putforward.Thiswas in largepartduetothechange ineconomiccircumstancesthattookholdnotlongafterthereportwaspublished.

10.1 Scaleandambitionforgrowth

• ThereportdoesnotmakeanestimateofGVAgrowth,butitusestheCambridgeEconometricsfigureof3.2%GVAgrowthperannum.

10.2 Keysectors• SpecialistManufacturing� • DistributionAndLogistics� • Financial&BusinessServices� • ‘OtherBusinessServices’(ICTandCreativeIndustries)� • Biotechnology/‘Green’/EnergyIndustries� • Tourism&Leisure�

10.3 Employmentlandrequirements

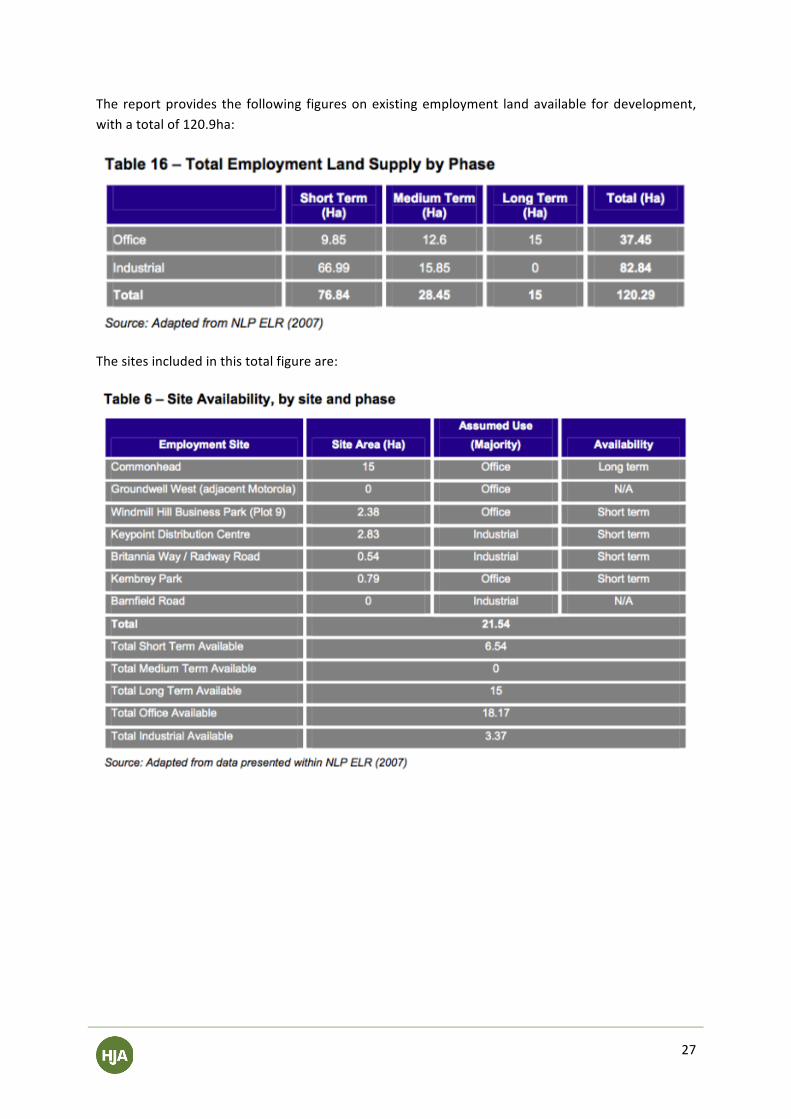

Thereportprovidesthefollowingbaselineforecastsforfutureemploymentlandrequirements,withaheadlinefigureof144.5hafrom2006-2026:

27

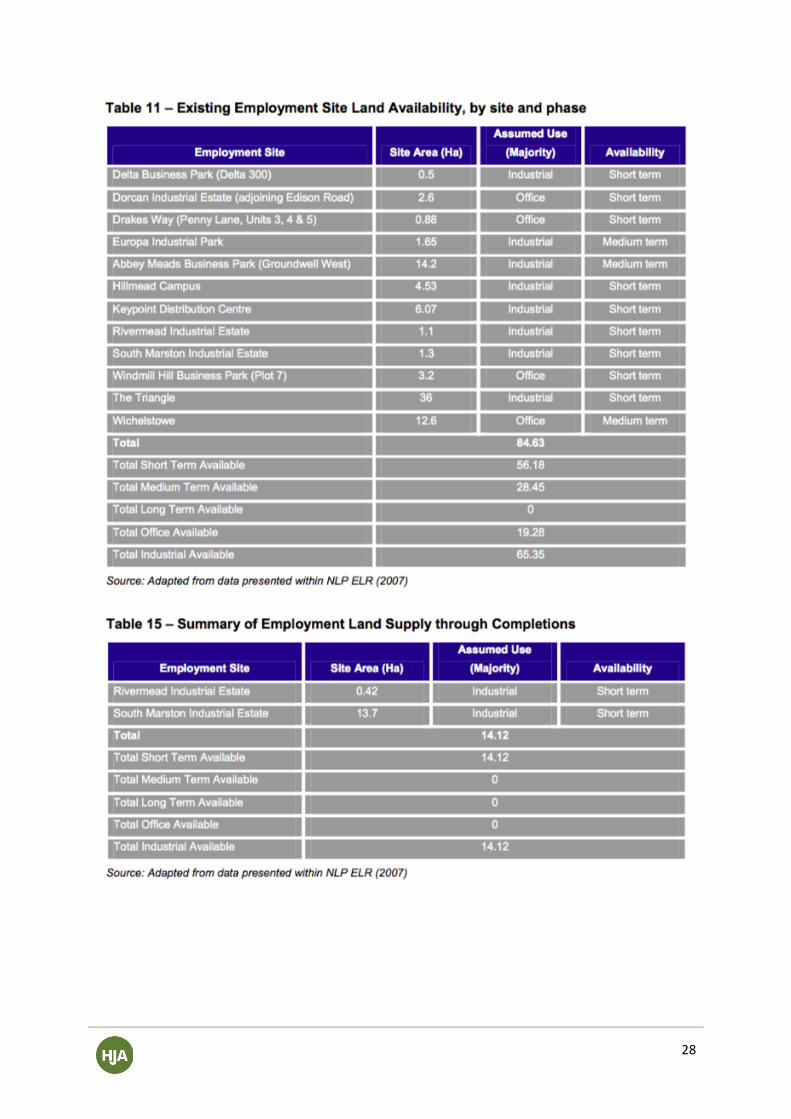

The reportprovides the following figuresonexistingemployment landavailable fordevelopment,withatotalof120.9ha:

Thesitesincludedinthistotalfigureare:

28

29

Conclusion

Thispolicyreviewcoversabreadthofgeographiesandtimeperiods.SomeofthereviewedreportsfocusonSwindon,othersonWiltshire,andothersonboth.Simultaneously,somereportsconsideratime period from 2006 -2026, with others based on figures for 2010-2020. Given the lack ofconsistency, the findings below are very generalised and aim to give an informal picture ofwhatexistingpoliciesrecommendonthemainissuesathand,whichare:

• Thescaleandambitionofgrowth–abroadrangeoffiguresemergeacrossdifferenttimeperiodsandgeographies.

• Keysectors–thesectorsthatareconsideredvitaltotheSwindonand/orWiltshireeconomyandappearinthreeormoreofthereportsare:AdvancedEngineeringandManufacturing(6);FinancialandProfessionalServices(6);DigitalandICT(6);TourismandLeisure(6);Health,LifeSciencesandPharmaceuticals(4);LandBasedIndustries(3);HealthandSocialCare(3);EnvironmentalTechnologies(3);CreativeIndustries(3);DistributionandLogistics(3).

• Employmentlandrequirements–theestimatesforWiltshirerangefrom104ha(takenbycombiningthefiguresinReviewofEmploymentProjectionsandLandRequirementsinSouthWiltshireandWiltshireWorkspace&EmploymentLandReview)to178ha.TheestimatesforSwindonrangefromaveryconservative16hatoapre-recessionforecastof200ha.ThereisnoofficialfigureforthewholeofSwindonandWiltshire,butusingthesefigures,theestimatecouldbeanythingfrom120hato378ha.

• SWOTfactors–seeAppendix3foracompletelistofthestrengths,weaknesses,opportunitiesandthreatstotheSwindonandWiltshireeconomy.

• Functionaleconomicgeography–thereportsthatcoverthewholeofSwindonandWiltshiresuggestthattheeconomyprimarilyfunctionsinthreemainzones,whichare:Swindon/M4corridorGrowthZone, A350corridorGrowthZone,andSalisburyA303corridorZone.

• Infrastructurechanges–thereisinsufficientinformationinthereportstodrawanyconclusionsonthisissue.