Embed Size (px)

Citation preview

1

Approach Towards

GST Governance

GST Governance – A Glance

Central Levies

• Central Excise Duty

• Countervailing Duty

• Special Additional Duty

• Cess

• Service Tax

State Levies

• VAT & CST

• Entry Tax

• Entertainment tax

• Luxury Tax

• State Cesses and Surcharges

GST

• Central GST *

• State GST *

• Integrated GST *

* Destination based Consumption Tax

Input Tax Credit

• Highly Critical

• Determines the Output Tax

• Audit Perspective

• Reco - Working, GL, Portal

Output Tax• Reverser Credit

• Reco - Working, GL, Portal

• Stringent Timelines

2

GST Governance – Critical Elements

GST Governance

Type of Sale

GSTR-2A : RECON

GSTR2

Goods & Services Received

Tax Invoice

Supplier Compliance

Documents Required

Sales

Sales Return

Stock Transfer

Post Sale Discount

GSTR-1 : Outward

Order of Utilization

IGST -> IGST/CGST/SGST

CGST -> CGST / IGST

SGST -> SGST / IGST

Type of Invoice

Supplementary Invoice

Job Work / FOC / Interstate Sale

SGST -> SGST / IGST

Invoice Content Check

Paid Tax

Filed Returns

GST Portal Update

Tax Invoice(Local / Interstate)

Debit Note(Price Estimation)

ISD Invoices(Dist. Of Comm. Cost)

Bill of Entry(Import)

RCM (Goods & Services UnReg.)

GSTR-3 : Balance Payable

GSTR-3B : Payment

3

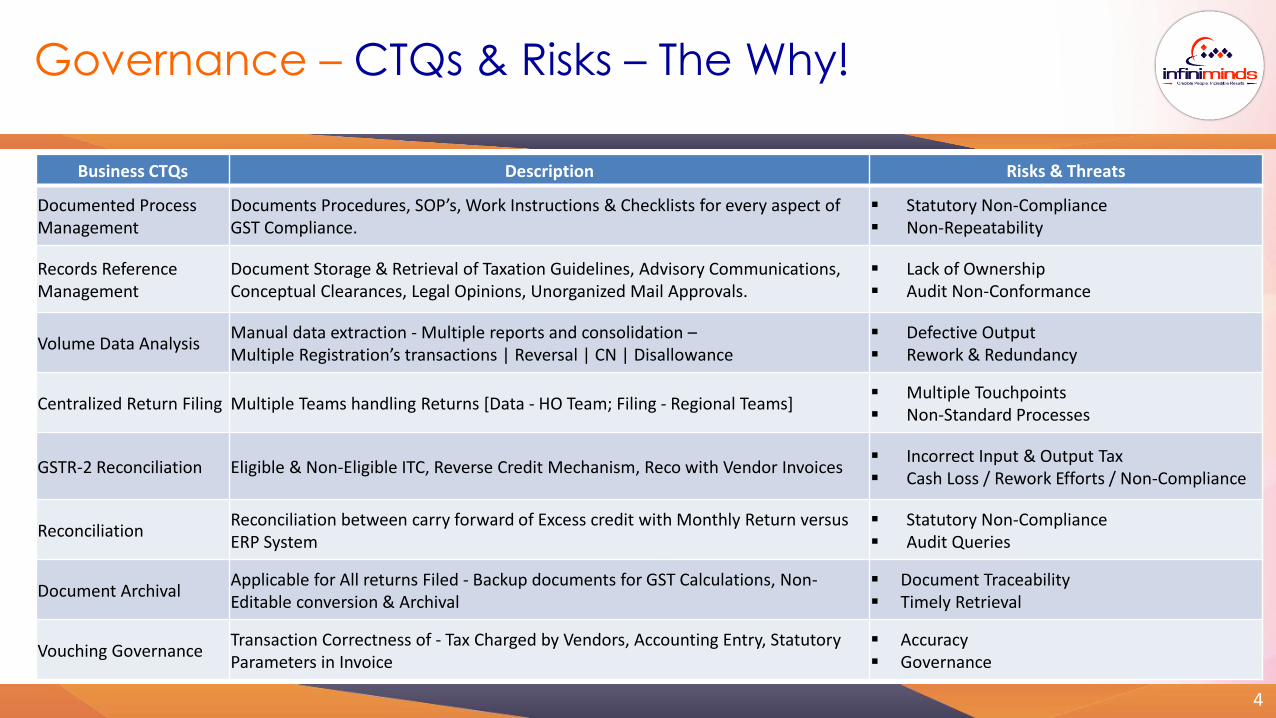

Governance – CTQs & Risks – The Why!

Business CTQs Description Risks & Threats

Documented Process Management

Documents Procedures, SOP’s, Work Instructions & Checklists for every aspect of GST Compliance.

▪ Statutory Non-Compliance ▪ Non-Repeatability

Records Reference Management

Document Storage & Retrieval of Taxation Guidelines, Advisory Communications, Conceptual Clearances, Legal Opinions, Unorganized Mail Approvals.

▪ Lack of Ownership▪ Audit Non-Conformance

Volume Data AnalysisManual data extraction - Multiple reports and consolidation –Multiple Registration’s transactions | Reversal | CN | Disallowance

▪ Defective Output▪ Rework & Redundancy

Centralized Return Filing Multiple Teams handling Returns [Data - HO Team; Filing - Regional Teams]▪ Multiple Touchpoints▪ Non-Standard Processes

GSTR-2 Reconciliation Eligible & Non-Eligible ITC, Reverse Credit Mechanism, Reco with Vendor Invoices▪ Incorrect Input & Output Tax▪ Cash Loss / Rework Efforts / Non-Compliance

ReconciliationReconciliation between carry forward of Excess credit with Monthly Return versus ERP System

▪ Statutory Non-Compliance▪ Audit Queries

Document ArchivalApplicable for All returns Filed - Backup documents for GST Calculations, Non-Editable conversion & Archival

▪ Document Traceability▪ Timely Retrieval

Vouching GovernanceTransaction Correctness of - Tax Charged by Vendors, Accounting Entry, Statutory Parameters in Invoice

▪ Accuracy▪ Governance

4

Document Management

Reports & Dashboards

Support Services

Process Study Value Stream Mapping

Standard Operating Procedures

Checklists & Work Instructions

Record Governance Model

Metrics & Dashboards

Issue Tracker Document Archival

Structure for GST Returns Filing

Facilitate GSTR-2 |Vouching

Reconciliation Working vs GL vs

GST Portal

CSAT Governance & Compliance

AS-IS StudyTO-BE Process

Model

Governance - Broad Scope – The What!

5

ASIS Process Study – Segmented Approach & Document Preparation by ISO Certified Documentation Experts

Simplification of Volume Data Analysis – BA Tool [One Click Algorithms & Macro Based Solutions]

GST Reference Manual [SOP, Process Guidelines, Interpretations, Advisory Communications, Legal Opinions]

Coding Storage & Retrieval methodology [Record Reference | Conceptual Clearances | Mail Approvals]

RACI Matrix Approach – Responsibility & Accountability at all levels for Centralised GST Returns Filing Model

GSTR2 & ITC RECO – Competent & Hands-on expertise in Reconciliation | Dispute Management Desk

Record Archival – Calendarized Model, Checklist Driven, Structed Governance [Maker, Checker, Audits]

Customized Vouching Audits - Audit Plans, Schedules, Procedures, Guidelines, Checklists etc. – Post Audit Analytics

Our Quality Approach – The How!

6

The Framework

7

Advocacy• ROT Adherence

• Compliance on Mandates

• Applicable Advanatages

• Early Assessment of Tax Impact

• Ease of Future Reference

Baseline• Operating Model

• Sourcing

• Distribution

• SCM Process

• Contracting

• Multi-level Drilldown

Impact Assessment

• Revenue Stream

• Procurement

• Availability of Credit of GST

• Transitional Credits

Accounting & Reporting

• Tax Credit, Payments and accounting

• Change assessment in accounting entries (incl. revised chart of accounts, compliance with standards)

Compliance• Compliance with

GST Requirement

• Tax credit transitions

• Return Reporting

• Other Statutory compliance

• High Quality Analytics

Governance• Process PITSTOP

• PMO Tools

• Compliance Manager

7

Team Structure – The Who?

Team

Program Director

Program Manager

GSTR-1[Output Tax

Liability]

GSTR-2[ITC]

GSTR-3B

DMD

V-Team

R-Team

Centralized Team Structure

Competent & Skilled

Relevant Exposure

Taxation Expertise

CA Certified SME

Centralized Monitoring

Macro Driven

8

GSTR1 Process

STARTReports from Systems & identified sources

for GSTR-1

Validation of Output Tax

System Reports• Sales Report• Transfer Price (TP)• GL Dump [IGST / CGST / SGST]• Credit Notes & Debit Notes• Stock Outward Movements• Scrap Sales• Unregistered Purchases

Inputs from Other Sources• Revenue Files• Fixed Asset Reports• Inter-Unit Transfer (IUT) Movements• IUT Cost Transfer• IUT Manual Entries• Other Incomes

Compilation of GSTR 1 in specified format

[GSTN wise]

Random Sample Checking

Reconciliation with GLConsolidated of

SchedulesIssue list Sign-off

Summary of GSTR-1 Filing Input

Business Dashboards &

Reports

Data Duplications Cancellations, ReversalsAny Specific errors etc.

Archival Process – Final Files and Working files

END

9

GSTR2 Process

NO

YES

START Reports for GSTR-2Compilation of Inward supply

• ITC Ledger• RCM Report• Exempted Purchase

Vouching ProcessExpense GL

Mapping

Determination on Eligibility of ITC

Business Dashboards & Reports

Archival Process – Final Files and Working files

END

Eligible ITC?

ITC ReversalReconciliation of

ITC with 2AValidation of

Exempted Purchase

RCM ProcessReconciliation –

ITC vs. GLIssue list Sign-off

• Stock Inward Movements• Asset in• Import Purchases

10

The Next Steps & Time Line (Kickoff Goal 45 Days)C

ust

om

er

1. Letter of Indent

2. Volume Data Sharing

3. Scoping

Co

mb

ined

1. Team Structure

2. Commercial Signoff

3. Award of Contract

INFI

NIM

IND

S

1. Team Onboarding

2. Project Kick-off

WK-1 to WK-4

WK-5 to WK-8

WK-9 to WK-12

Beyond

Team Onboarding

Process Study Transition Signoff

Sustenance

11

12