Embed Size (px)

Citation preview

March 2017

Agenda

Context, strategies & priorities

Revitalizing direct selling

Digitalization

Retail

Fragrances

2016 Results

Latam

Aesop

Sustainability and Governance

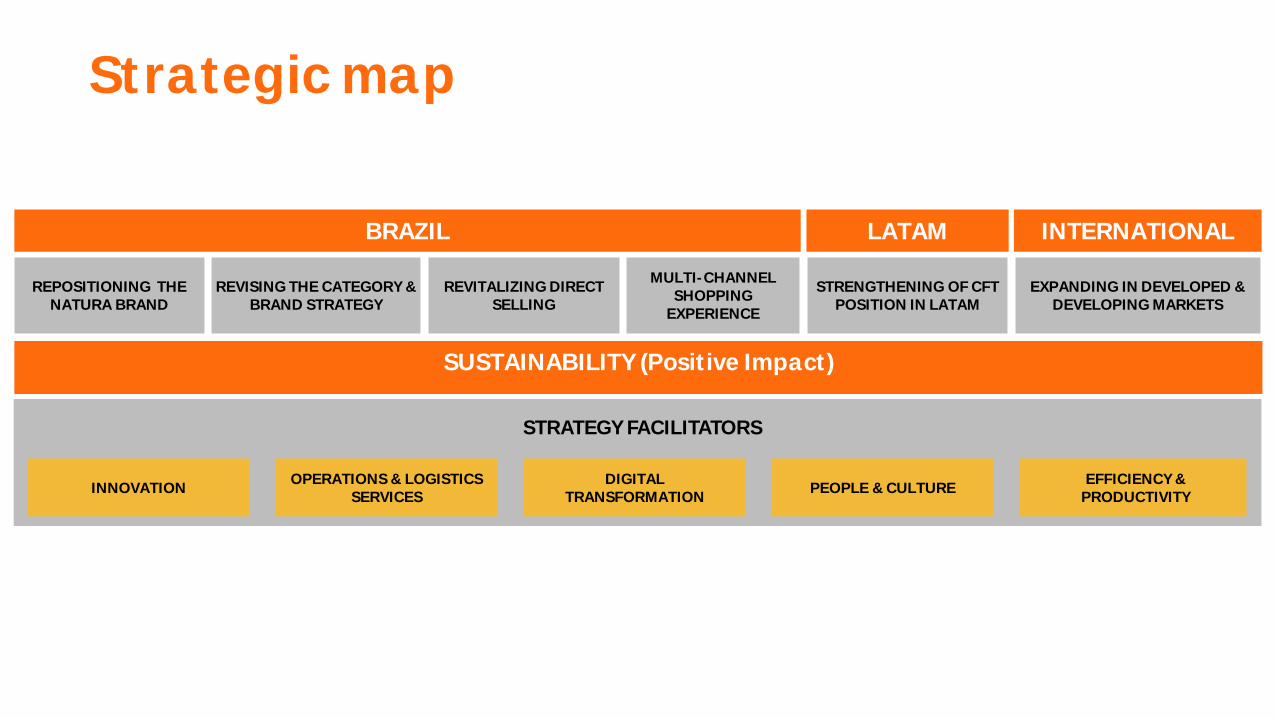

Context, strategies & priorities

BRAZIL LATAM INTERNATIONAL

REPOSITIONING THE NATURA BRAND

REVITALIZING DIRECT SELLING

REVISING THE CATEGORY & BRAND STRATEGY

MULTI-CHANNEL SHOPPING

EXPERIENCE

EXPANDING IN DEVELOPED & DEVELOPING MARKETS

STRENGTHENING OF CFT POSITION IN LATAM

SUSTAINABILITY (Positive Impact)

INNOVATIONOPERATIONS & LOGISTICS

SERVICESDIGITAL

TRANSFORMATIONPEOPLE & CULTURE

EFFICIENCY & PRODUCTIVITY

STRATEGY FACILITATORS

Strategic map

2017 Priorities

Brazil

Fragrances & gifts

Relaunching direct selling

Accelerating digitalization

New Channels

Maintaining Latam momentum

Culture & Organization Program

Revitalizing direct selling

Improve qualification of new recruits

Project Goals

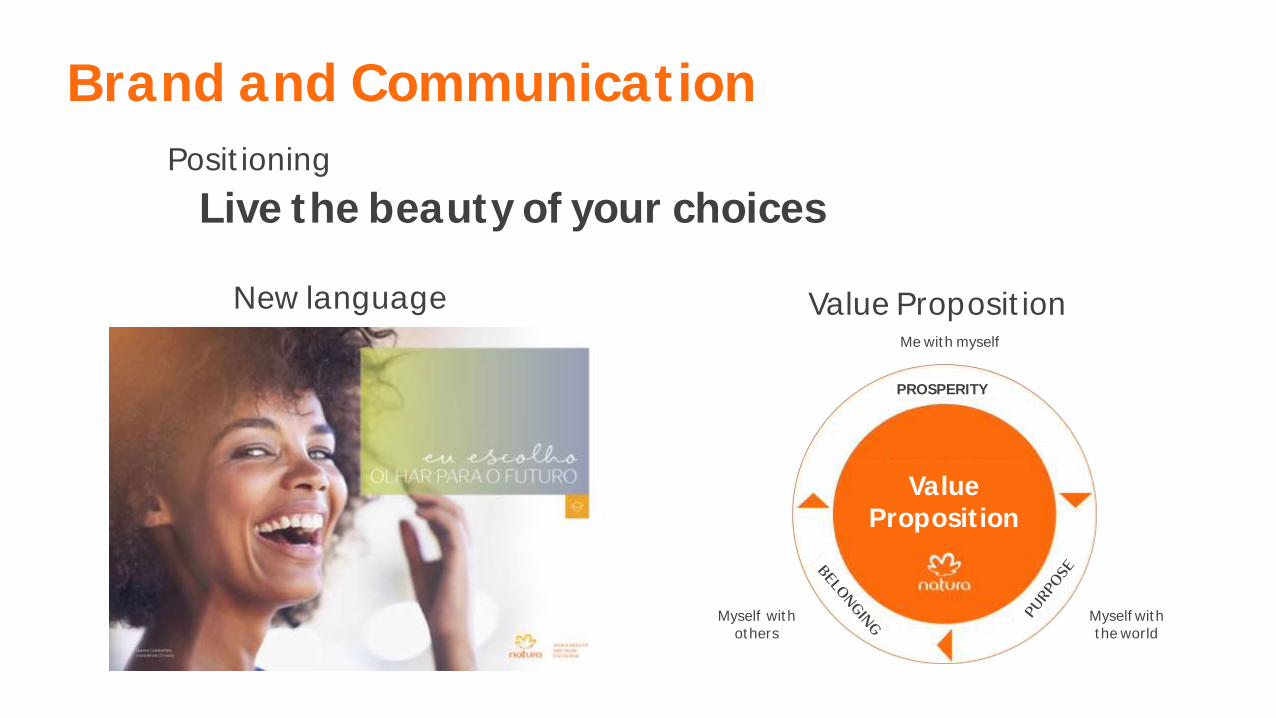

Live the beauty of your choicesPositioning

New language Value Proposition

Brand and Communication

Me with myself

Myself with the world

Myself with others

PROSPERITY

Value Proposition

Natura Beauty Specialists

Channel segmentation

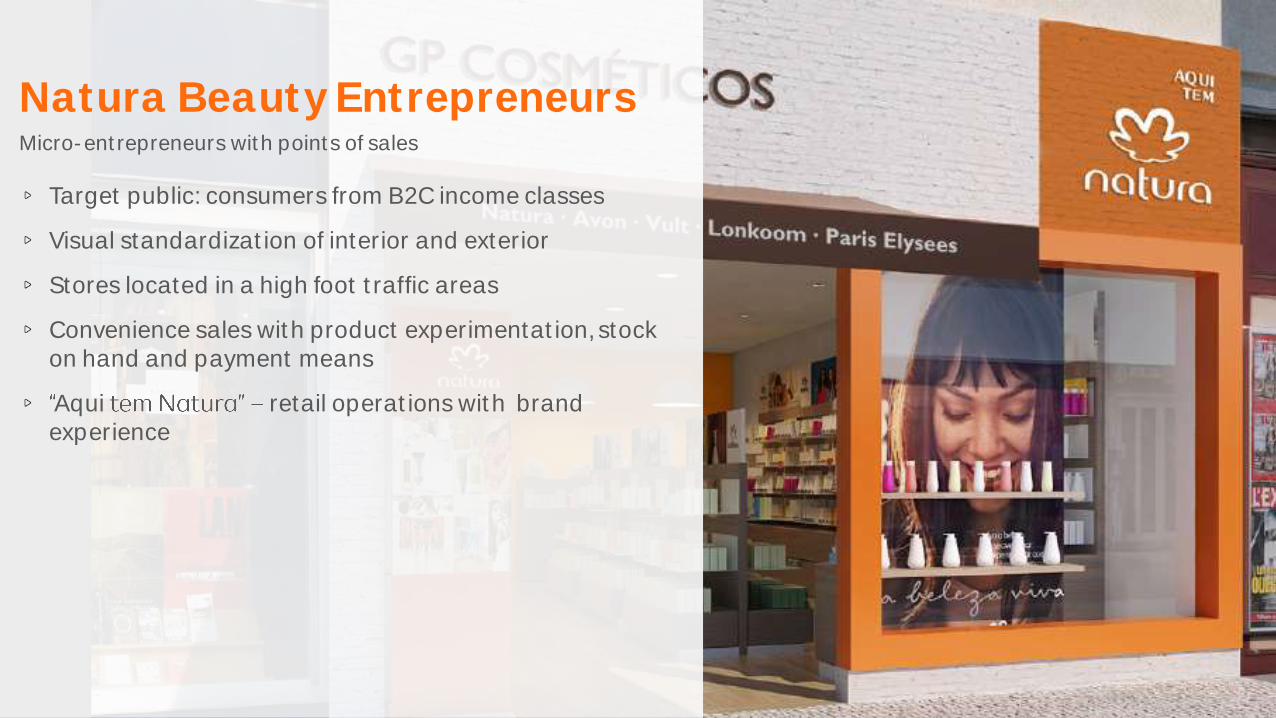

Natura Beauty Entrepreneurs

Natura Beauty Consultants

Natura Beauty Entrepreneurs Micro-entrepreneurs with points of sales

Target public: consumers from B2C income classes

Visual standardization of interior and exterior

Stores located in a high foot traffic areas

Convenience sales with product experimentation, stock on hand and payment means

Aqui retail operations with brand experience

Before After

Natura Beauty Entrepreneurs

Natura Beauty SpecialistsProfessionals connected to the universe of beauty, with higher education levels and ideal profile for selling "core beauty"

Consulting as a career: self-fulfillment and pleasure

Focus on face care and makeup

Unique experience: assistance and experimentation

Exclusive opportunities :

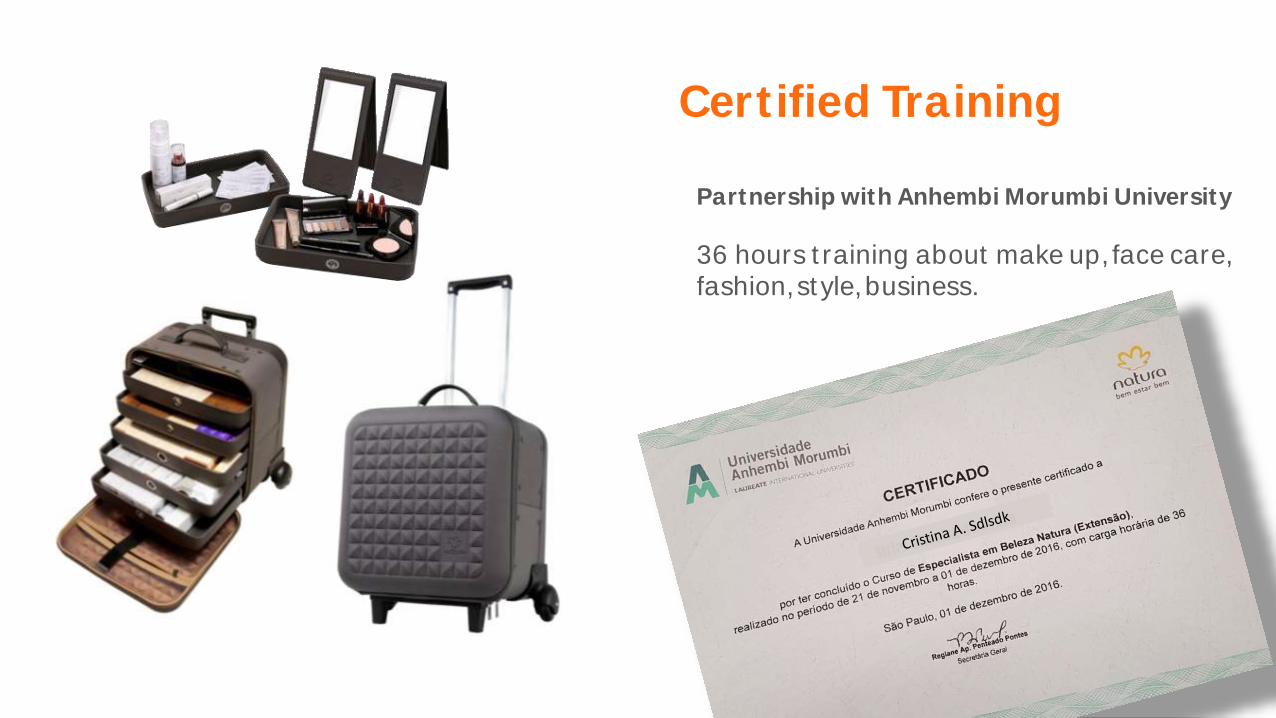

Training in partnership with Anhembi MorumbiUniversity

Independent career development

Demonstration kit and samples

Specific recruitment and selection

Digital tool for service level improvement

36 hours training about make up, face care, fashion, style, business.

Partnership with Anhembi Morumbi University

Certified Training

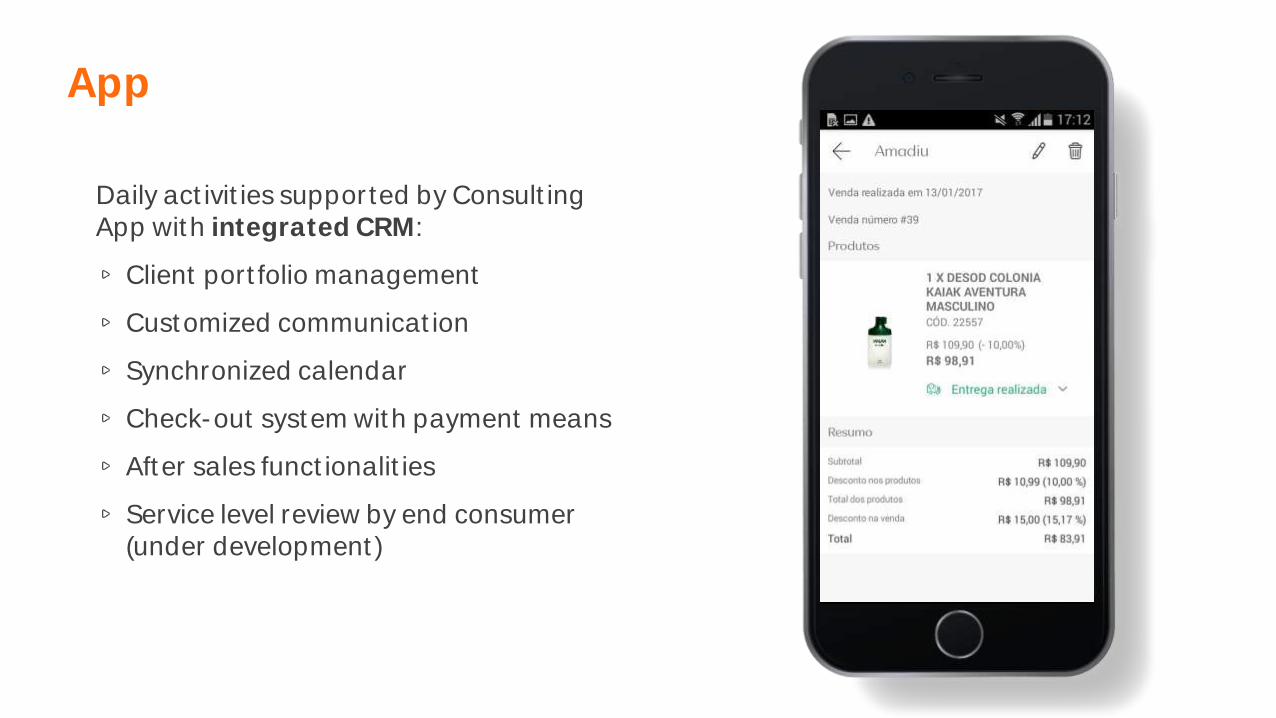

Daily activities supported by Consulting App with integrated CRM:

Client portfolio management

Customized communication

Synchronized calendar

Check-out system with payment means

After sales functionalities

Service level review by end consumer (under development)

App

Natura Beauty ConsultantsLarge or midsized consultants that dedicate a significant amount of time to direct selling

Reclaim the value of Natura Consulting

Increase average income

Accelerate opportunity for career growth

Improve quality recruiting and initial training

Strength of the relationship

Digitalization

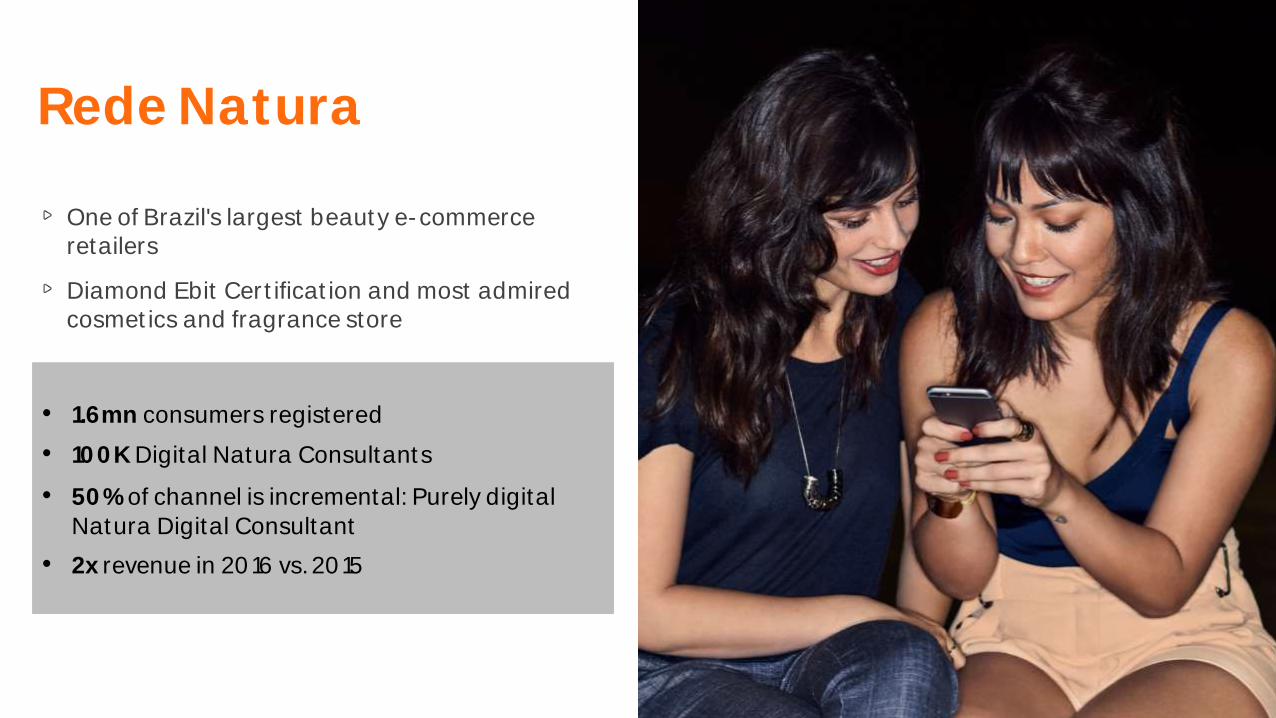

Rede Natura

One of Brazil's largest beauty e-commerce retailers

Diamond Ebit Certification and most admired cosmetics and fragrance store

• 1.6mn consumers registered

• 100K Digital Natura Consultants

• 50% of channel is incremental: Purely digital Natura Digital Consultant

• 2x revenue in 2016 vs. 2015

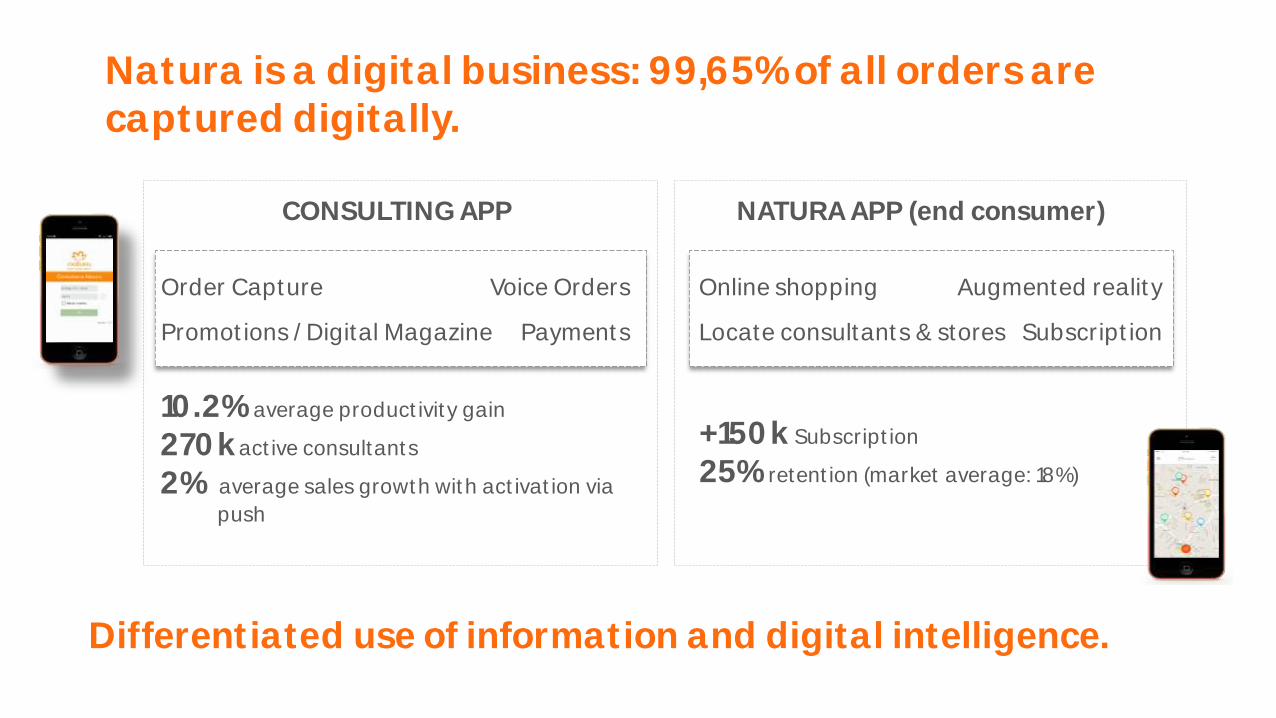

Natura is a digital business: 99,65% of all orders are captured digitally.

CONSULTING APP

10.2% average productivity gain

270k active consultants

2% average sales growth with activation via

push

Order Capture

Promotions / Digital Magazine

Voice Orders

Payments

NATURA APP (end consumer)

+150k Subscription

25% retention (market average: 18%)

Online shopping

Locate consultants & stores

Augmented reality

Subscription

Differentiated use of information and digital intelligence.

Brazil Retail

Natura Shopping Anália Franco, SP

Natura Stores

AB1 consumers

5 stores in São Paulo in 2016

Scale up in 2017

Makeup and face care

More premium portfolio mix: Ekos, Chronos & Una

Natura Shopping Anália Franco, SP

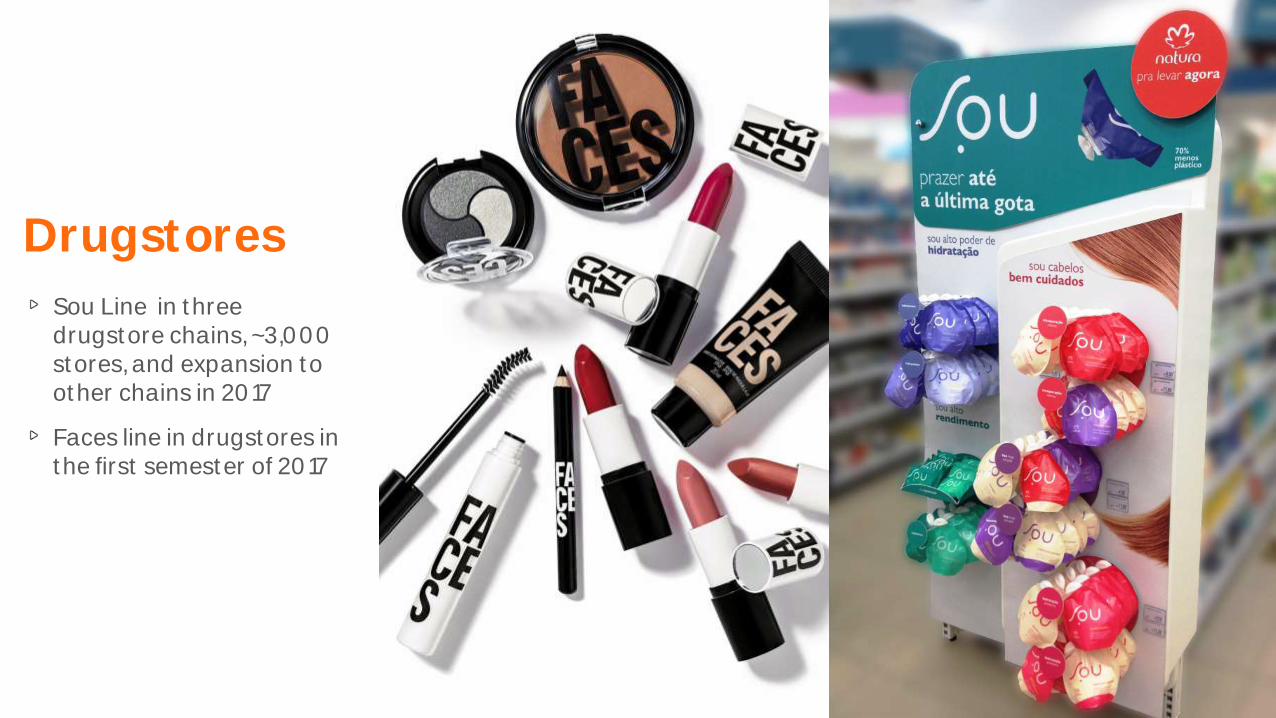

Drugstores

Sou Line in three drugstore chains, ~3,000 stores, and expansion to other chains in 2017

Faces line in drugstores in the first semester of 2017

Fragrances

Fragrances

Natura is world's tenth largest player and is:

» Leader in fragrances for men in Brazil

» Second in fragrances for women in Brazil

Largest CFT category in Brazil

Source: Euromonitor/ Kantar

Natura Day 2016 [Confidencial]

Sustainable Innovations

Natura FragrancesOur differentials

Quality Our BrandsArt of Perfumery

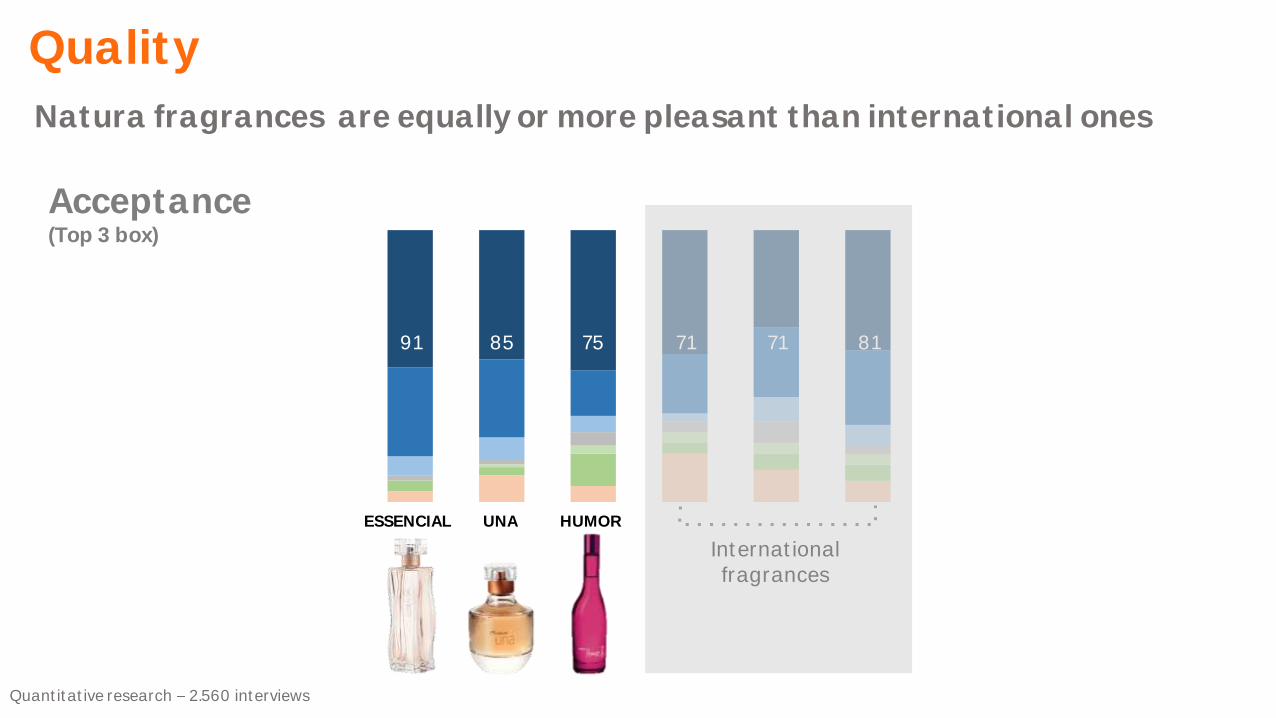

91 85 75 71 71 81

ESSENCIAL UNA HUMOR

Natura fragrances are equally or more pleasant than international ones

Quality

Acceptance(Top 3 box)

Quantitative research 2.560 interviews

International fragrances

67 66 73 75 71 65 64 63 71

5. Muito mais forte

4. Um pouco mais forte

3. Ideal, como eu gosto

2. Um pouco mais fraca

1. Muito mais fraca

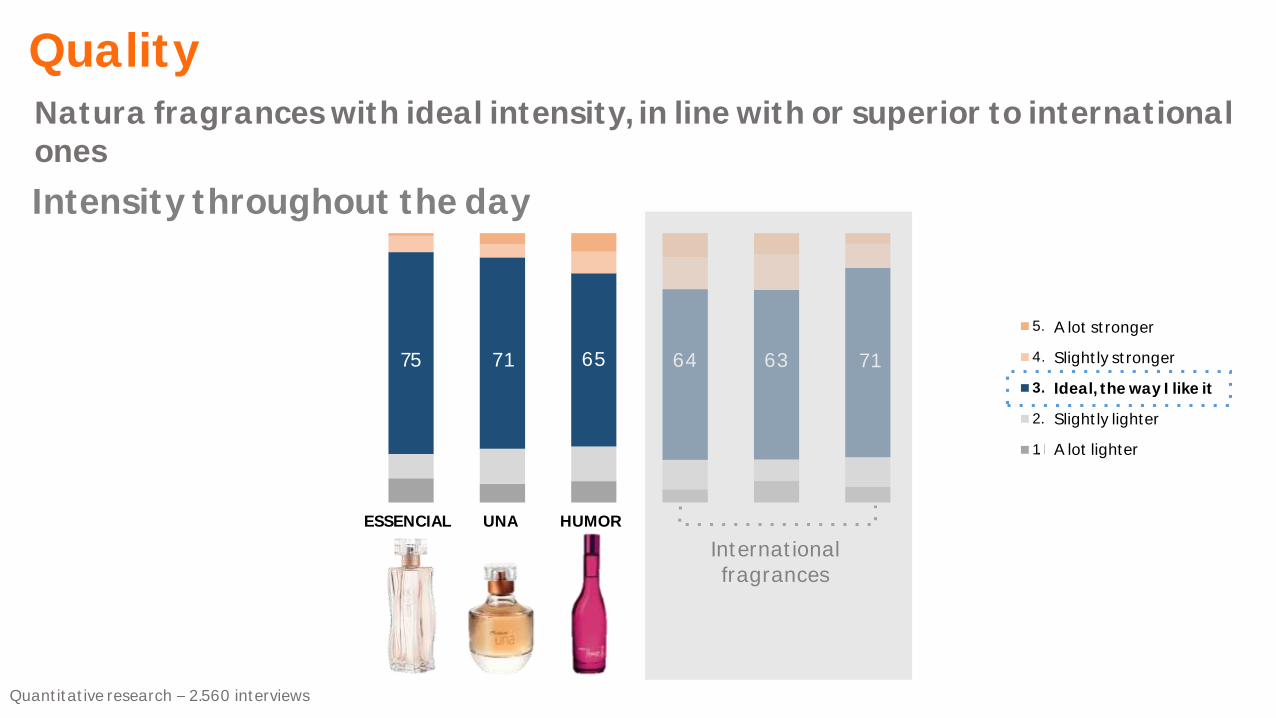

Quality

Intensity throughout the day

Natura fragrances with ideal intensity, in line with or superior to international ones

Quantitative research 2.560 interviews

International fragrances

ESSENCIAL UNA HUMOR

A lot stronger

Slightly stronger

Ideal, the way I like it

Slightly lighter

A lot lighter

Revised marketing strategy

Regional initiatives

Sales force incentives

Portfolio improvement

New style of communication

2017

2016 RESULTS

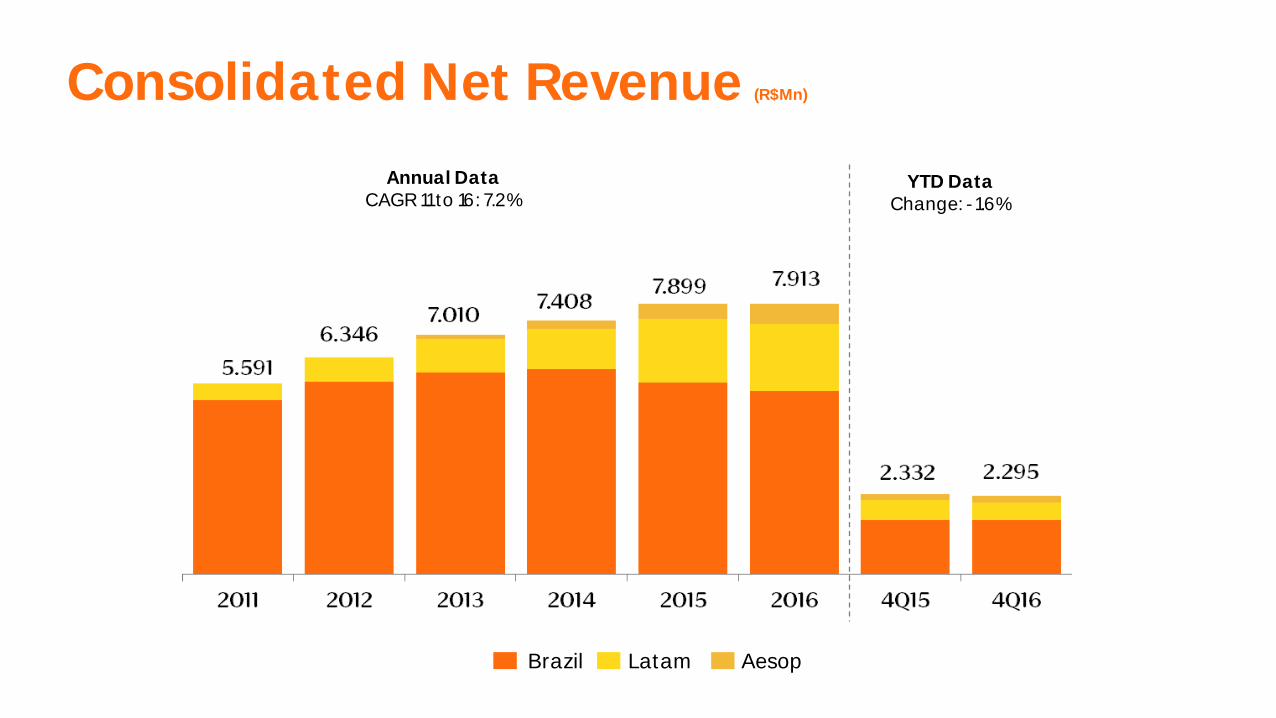

Consolidated Net Revenue (R$Mn)

Annual DataCAGR 11 to 16: 7.2%

YTD DataChange: -1.6%

LatamBrazil Aesop

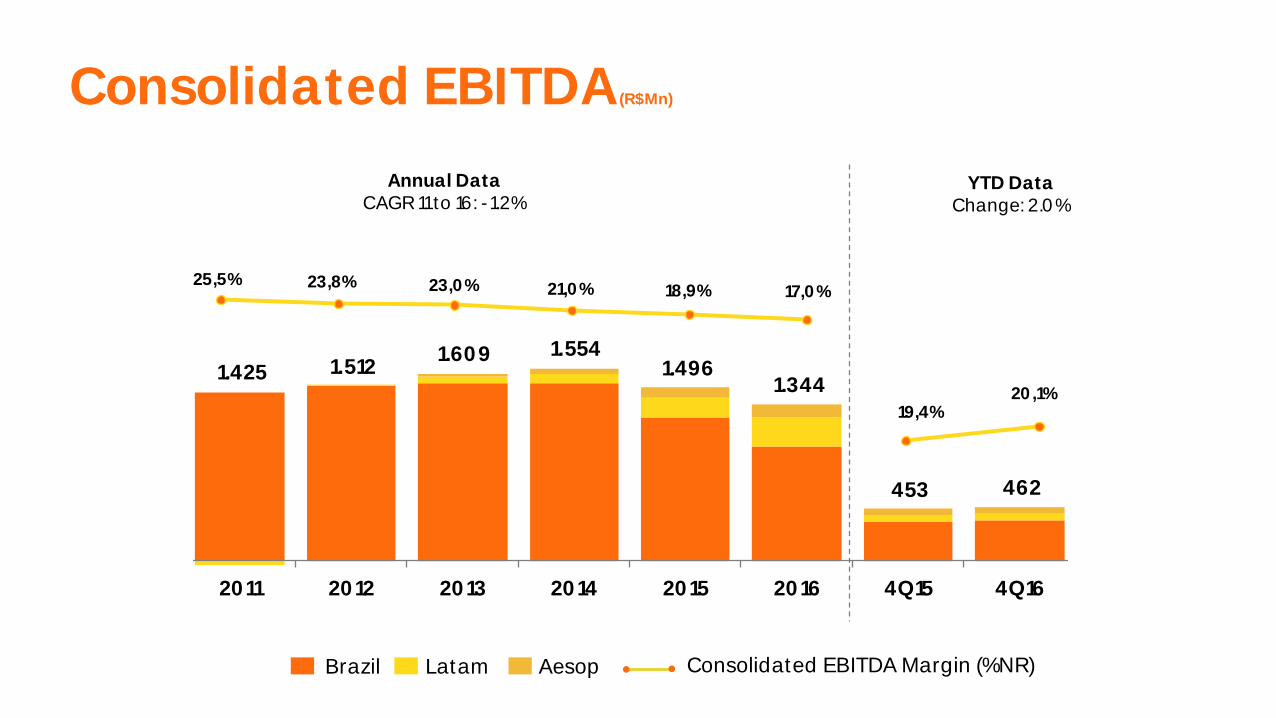

Consolidated EBITDA (R$Mn)

Consolidated EBITDA Margin (%NR)LatamBrazil Aesop

1.425 1.512 1.609 1.554

1.496 1.344

453 462

2011 2012 2013 2014 2015 2016 4Q15 4Q16

25,5% 23,8% 23,0% 21,0% 18,9% 17,0%

19,4%20,1%

Annual DataCAGR 11 to 16: -1.2%

YTD DataChange: 2.0%

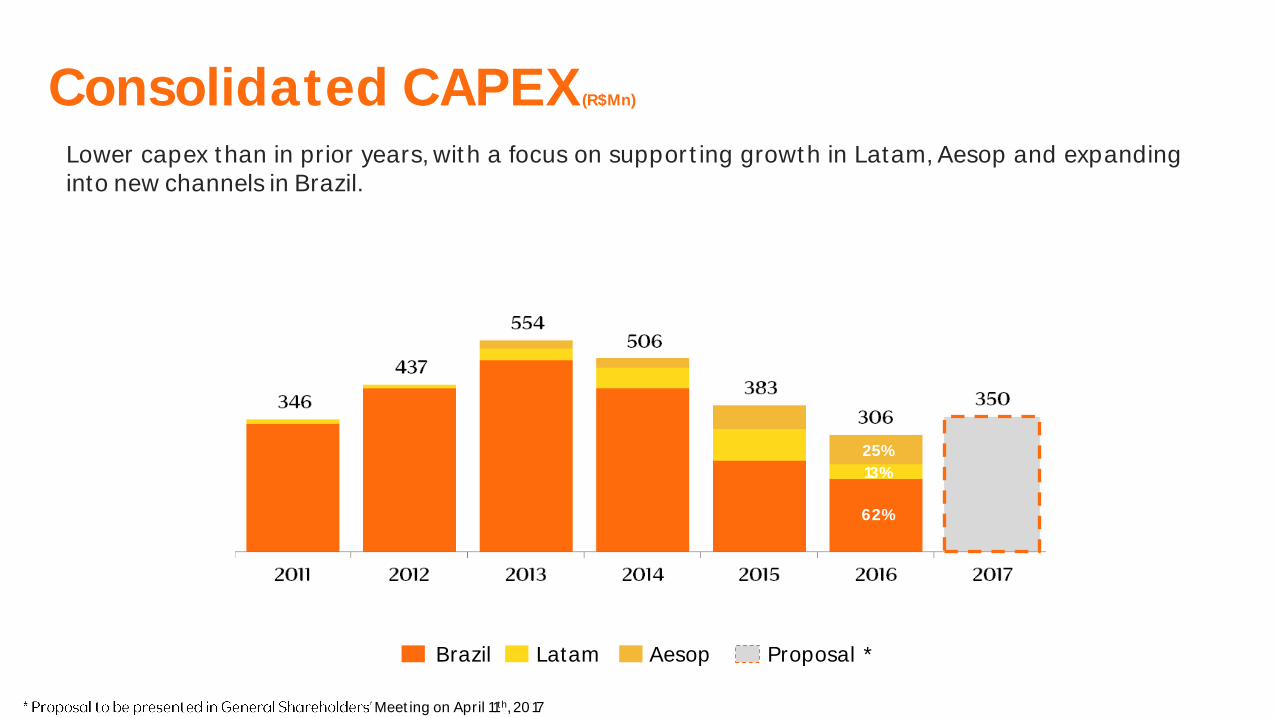

Consolidated CAPEX (R$Mn)

Lower capex than in prior years, with a focus on supporting growth in Latam, Aesop and expandinginto new channels in Brazil.

LatamBrazil Aesop

25%

62%

13%

Proposal *

Meeting on April 11th, 2017

Sustainability

Crer para Ver product Line

Funding of R$38.2mn in 2016 (+27%)

Natura Consultant Education Program

12,000 beneficiaries between July and December 2016

We are advancing towards 2020 goals:

Indicator 2016 2020

Relative carbon emissions

3.17 Kg CO2/

Kg prod billed

2.15 Kg CO2/

Kg prod billed

% post consumption recycled materials

4.3 % 10.0 %

Cumulative business volume in the Pan-

Amazon regionR$ 972.6 mn R$ 1 bn

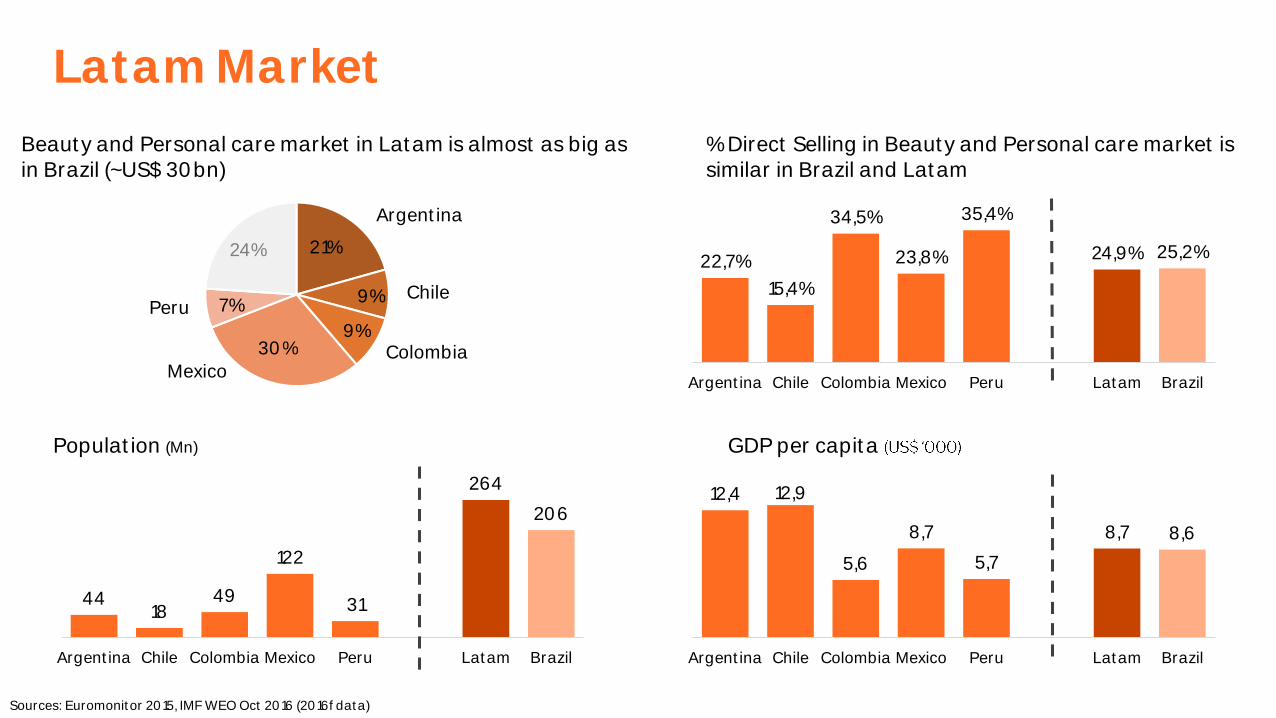

Latam

4418

49

122

31

264

206

Argentina Chile Colombia Mexico Peru Latam Brazil

Latam Market

21%

9%

9%30%

7%

24%22,7%

15,4%

34,5%

23,8%

35,4%

24,9% 25,2%

Argentina Chile Colombia Mexico Peru Latam Brazil

Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)

Beauty and Personal care market in Latam is almost as big as in Brazil (~US$ 30bn)

% Direct Selling in Beauty and Personal care market is similar in Brazil and Latam

Population (Mn) GDP per capita

Argentina

ChilePeru

MexicoColombia

12,4 12,9

5,6

8,7

5,7

8,7 8,6

Argentina Chile Colombia Mexico Peru Latam Brazil

487

164

Latam Brazil

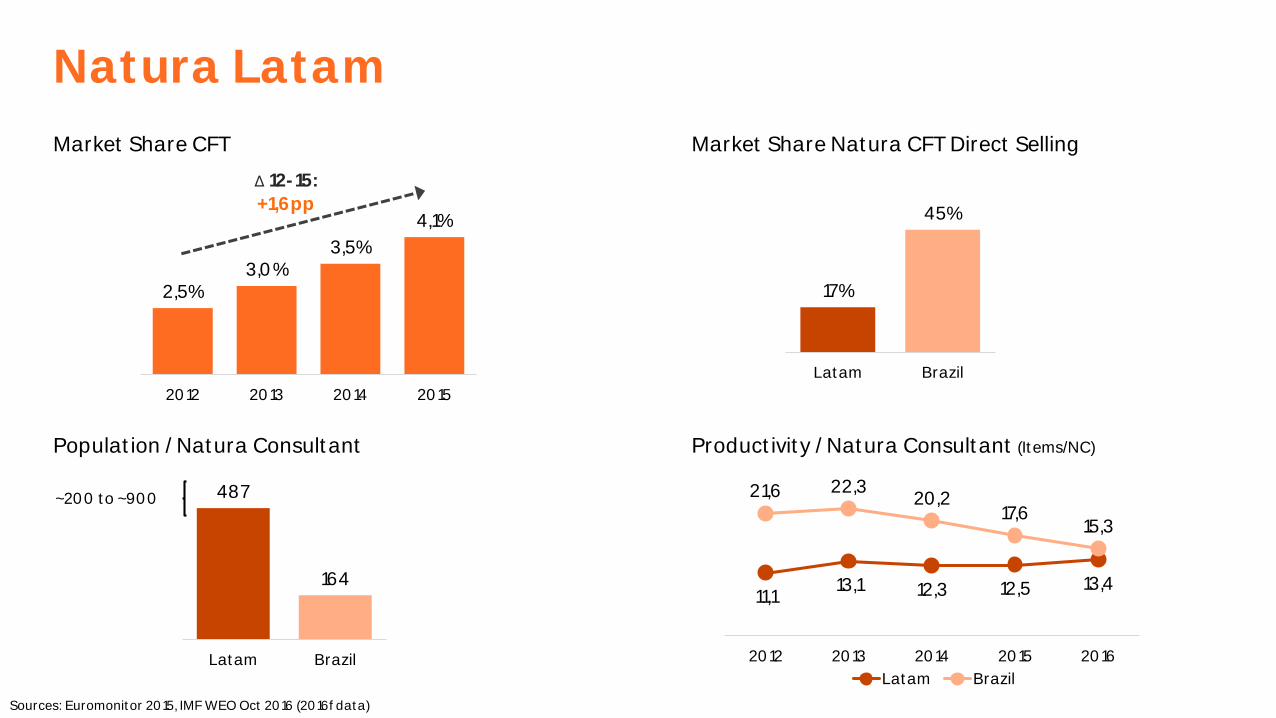

Natura Latam

Market Share CFT Market Share Natura CFT Direct Selling

Population / Natura Consultant Productivity / Natura Consultant (Items/NC)

2,5%3,0%

3,5%

4,1%

2012 2013 2014 2015

∆ 12-15:

+1,6pp

Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)

17%

45%

Latam Brazil

~200 to ~900

11,113,1 12,3 12,5 13,4

21,6 22,320,2

17,615,3

2012 2013 2014 2015 2016

Latam Brazil

1

53 65

170

248

53 58

9,1%11,1%

0,1%

5,4% 5,6%

9,1%

12,5%

-0,1

-0,05

0

0,05

0,1

2012 2013 2014 2015 2016 4Q15 4Q16

-

50

100

150

200

250

300

350

EBITDA Latam

EBITDA (R$ Mn) EBITDA Margin

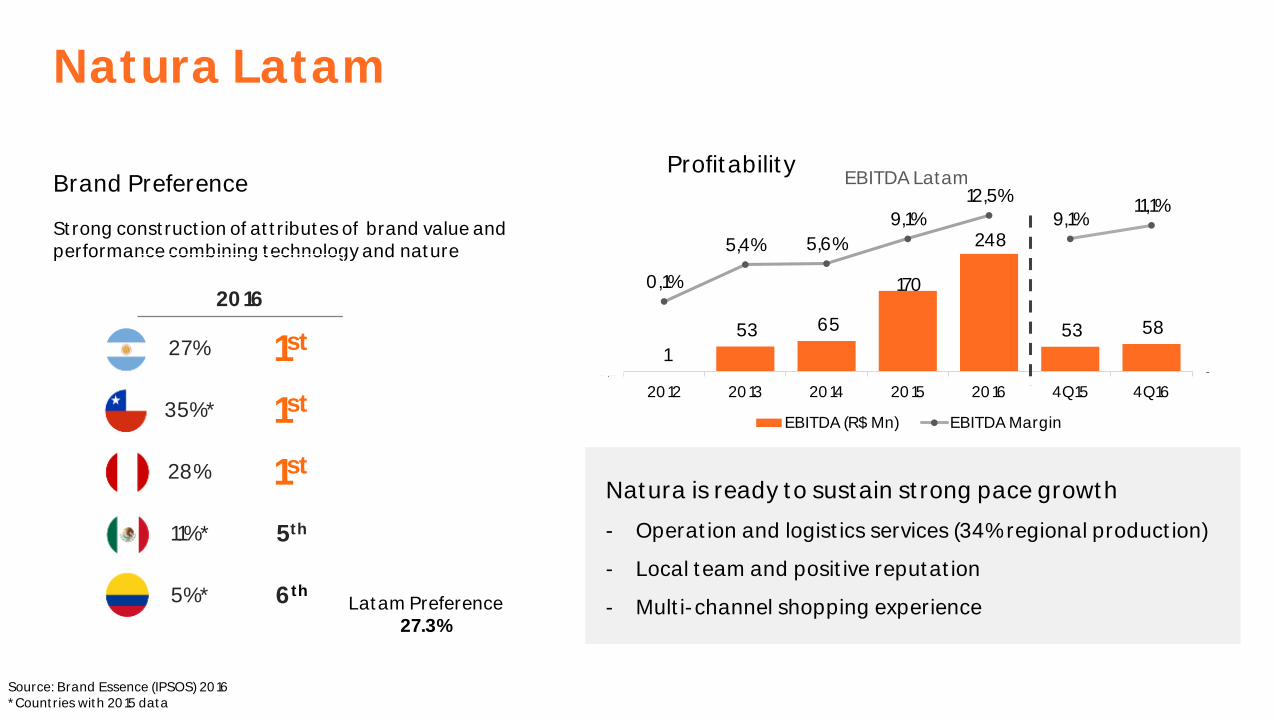

Natura Latam

Brand PreferenceProfitability

Latam Preference27.3%

Strong construction of attributes of brand value and performance combining technology and nature

Natura is ready to sustain strong pace growth

- Operation and logistics services (34% regional production)

- Local team and positive reputation

- Multi-channel shopping experience

Source: Brand Essence (IPSOS) 2016* Countries with 2015 data

2016

27% 1st

35%* 1st

28% 1st

11%* 5th

5%* 6th

-

2,0

4,0

6,0

8,0

10,0

12,0

14,0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Unilever

P&G

L'Oréal

Colgate

Avon

Natura

Belcorp

BeiersdorfJafra

J&J

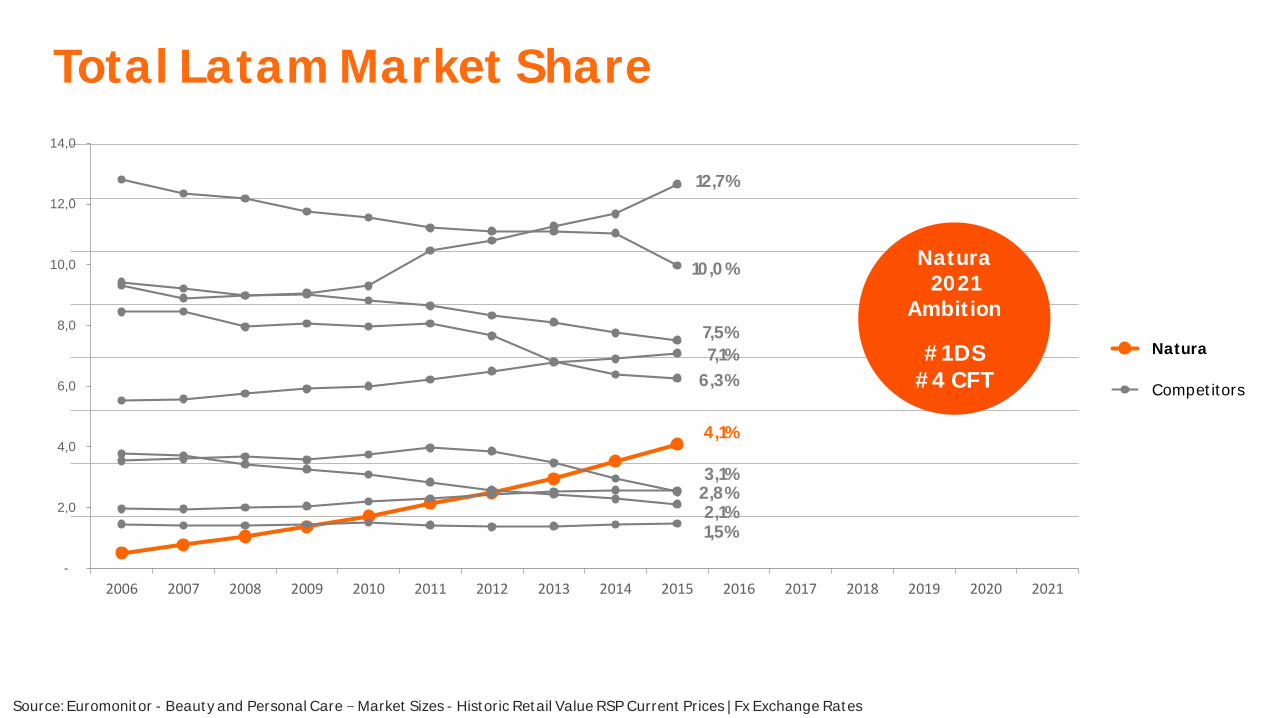

Natura 2021

Ambition

#1 DS#4 CFT

1,5%

10,0%

12,7%

7,5%

4,1%

3,1%

6,3%

2,1%2,8%

Source: Euromonitor - Beauty and Personal Care Market Sizes - Historic Retail Value RSP Current Prices | Fx Exchange Rates

Natura

Competitors

7,1%

Total Latam Market Share

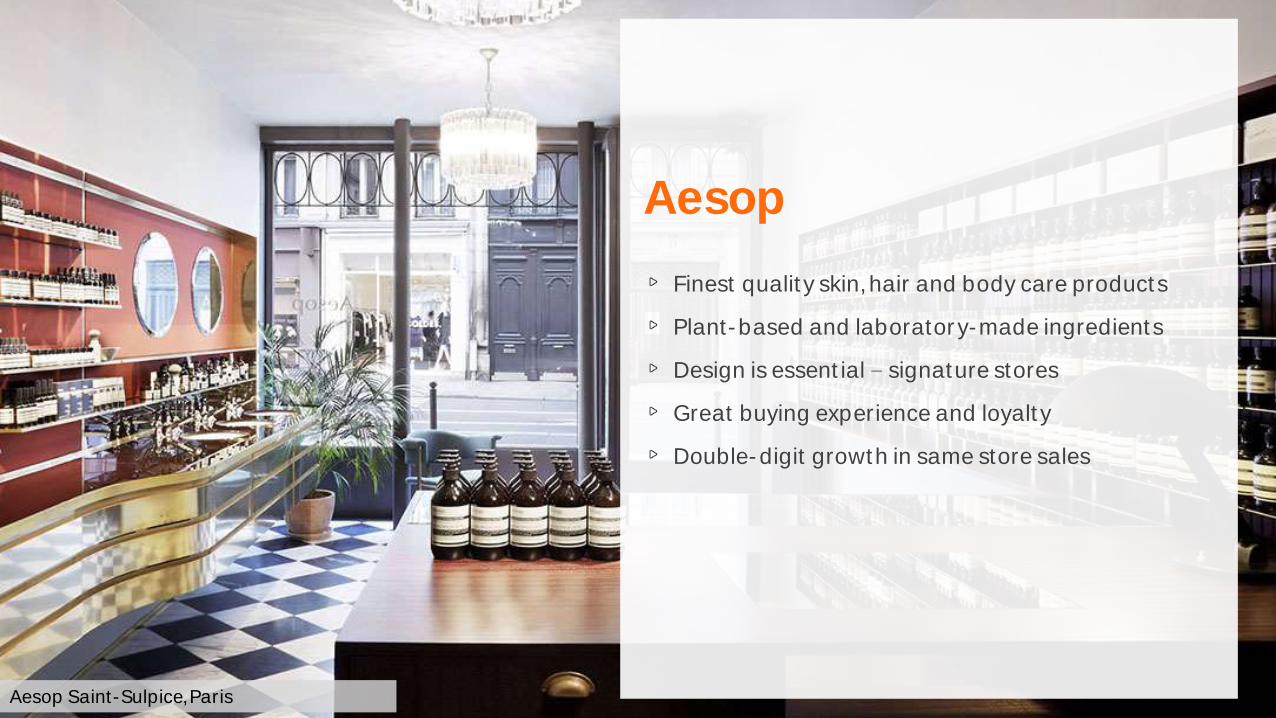

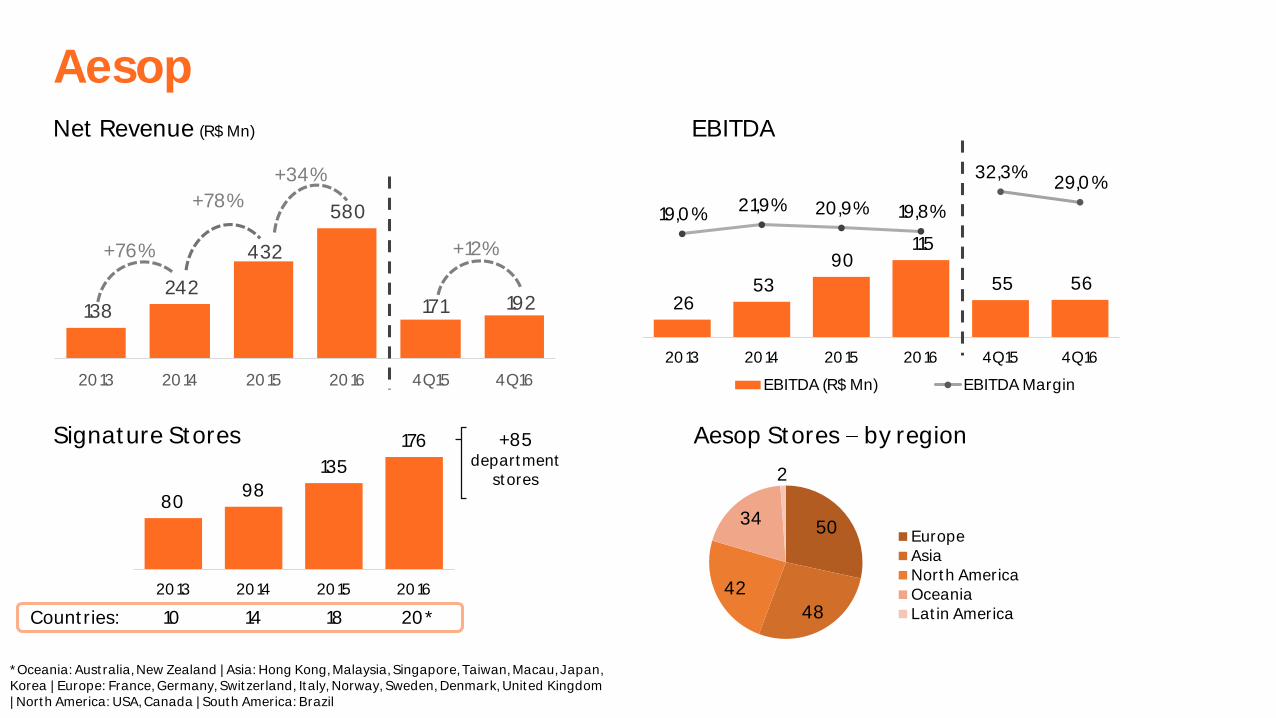

Aesop

Aesop Saint-Sulpice, Paris

Aesop

Finest quality skin, hair and body care products

Plant-based and laboratory-made ingredients

Design is essential signature stores

Great buying experience and loyalty

Double-digit growth in same store sales

Aesop Saint-Sulpice, Paris

138 242

432

580

171 192

2013 2014 2015 2016 4Q15 4Q16

+76%

+78%

+12%

+34%

26 53

90 115

55 56

32,3%29,0%

19,0% 21,9% 20,9% 19,8%

-0,2

-0,1

0

0,1

0,2

0,3

-30

20

70

120

170

220

2013 2014 2015 2016 4Q15 4Q16

EBITDA (R$ Mn) EBITDA Margin

AesopNet Revenue (R$ Mn)

8098

135

176

2013 2014 2015 2016

Signature Stores

14 18 20*Countries:

* Oceania: Australia, New Zealand | Asia: Hong Kong, Malaysia, Singapore, Taiwan, Macau, Japan,Korea | Europe: France, Germany, Switzerland, Italy, Norway, Sweden, Denmark, United Kingdom| North America: USA, Canada | South America: Brazil

10

EBITDA

+85 department

stores

Aesop Stores by region

50

48

42

34

2

EuropeAsiaNorth AmericaOceaniaLatin America

Sustainability andGovernance

Sustainability

Sustainable Innovations in fragrances: 100% organic alcohol; 20% recycled glass; 100% recycled PET for refills

New Technologies and Traditional Communities Project

Launch of Natura Amazonia Challenge: Businesses for the Standing Forest

Carbon Neutral Program

EP&L Project in implementation (Environmental Accounting):

Innovation in business performance analysis by effective TBL evaluation

Recognition in 2016

Época Empresas Verdes case Ekos Ucuuba

Exame Sustainability Guide

Corporate Sustainability Index (ISE)

20 most sustainable companies corporations in the world (Corporate Knights)

Robust and Consolidated Governance Model

One of the first companies listed on Novo Mercado segment

Board of Directors, created in 1998, currently has 9 members, 5 of which are independent

Luiz Seabra, Guilherme Leal, Pedro Passos, Carla Schmitzberger, Giovanni Giovanneli, Marcos Lisboa, PlínioMusetti, Roberto de Oliveira Marques and Silvia Lagnado

Support committees

Corporate Governance

Audit, Risk Management & Finance

Strategic

People & Organizational Development

Largest publicly traded B-Corporation

Component of major stock indexes

Corporate Governance

Key takeaways

Brazil recovery

Direct Selling transformation

Multi-channel experience focused on end consumer

Ready to offer distinct service level

Cost control and focus on cash generation

Three businesses at different development stages

Thank you.