Embed Size (px)

Citation preview

April 23, 2008

Conference Call and Webinar

“The Power of a Properly Designed Retirement Plan”Jim Allfrey, Director of 401(k) Administration, and

Del Hargis, Director of Client Development atAmerican Pension Services

Mathew N. Sorensen, Attorney at Law

Hosted By: Mark J. Kohler, CPA, Attorney at Law

www.kkolawyers.comTelephone 435.586.9366 / Facsimile 435.586.9491

©Kyler Kohler & Ostermiller, LLP 2008

Disclaimer- Although the information contained in this Presentation may be extremely useful and helpful, please understand that the presentation of this information does not constitute an attorney-client relationship. Moreover, the information contained in this Presentation is for general guidance only. It is strongly recommended that each individual or entity obtain their own legal advice, particularly applied to their own set of circumstances, facts and specific situation. Kyler Kohler & Ostermiller, LLP is not responsible or liable for any advice that is taken and applied in a situation without direct consultation and representation specific to that individual’s or company’s needs.

Instructor Notes

© Kyler Kohler & Ostermiller, LLP 2008

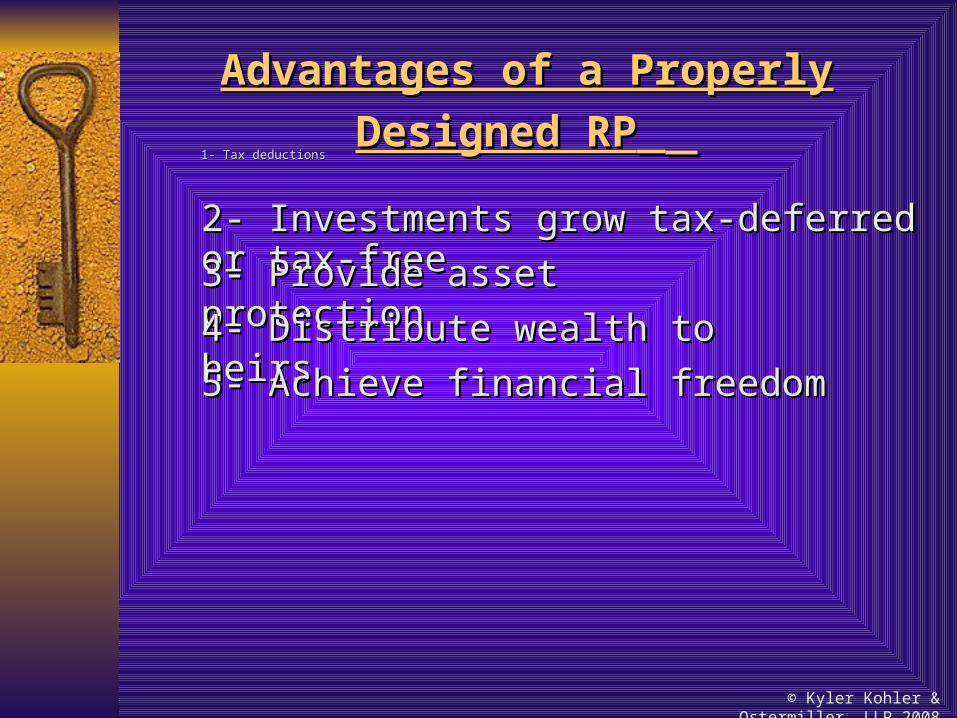

Advantages of a Properly Designed RPAdvantages of a Properly Designed RP 1- Tax deductions1- Tax deductions

2- Investments grow tax-deferred or tax-free 2- Investments grow tax-deferred or tax-free

3- Provide asset protection 3- Provide asset protection

4- Distribute wealth to heirs 4- Distribute wealth to heirs

5- Achieve financial freedom5- Achieve financial freedom

© Kyler Kohler & Ostermiller, LLP 2008

Top 10 RP MistakesTop 10 RP Mistakes 10- Not having a RP10- Not having a RP

9- Not starting early 9- Not starting early

8- Not fully contributing to your RP8- Not fully contributing to your RP

© Kyler Kohler & Ostermiller, LLP 2008

Top 10 RP MistakesTop 10 RP Mistakes 10- Not having a RP10- Not having a RP

9- Not starting early 9- Not starting early

8- Not fully contributing to your RP8- Not fully contributing to your RP

7- Not listing beneficiaries individually 7- Not listing beneficiaries individually

6- Making poor investment choices6- Making poor investment choices

5- Taking un-advised loans5- Taking un-advised loans

4- Not rolling over RP properly4- Not rolling over RP properly

3- Not understanding the hidden fees 3- Not understanding the hidden fees

© Kyler Kohler & Ostermiller, LLP 2008

Hidden Costs in Mutual FundsHidden Costs in Mutual Funds

1.1. Investments in an Annuity?Investments in an Annuity?

2. All Mutual Funds have expenses!2. All Mutual Funds have expenses!

3. Other expenses may include… 3. Other expenses may include…

• Annuity charge (1.25% of funds)Annuity charge (1.25% of funds)

• Annual operating expenses Annual operating expenses • 12(b)1 fees (up to 2%)12(b)1 fees (up to 2%)

• Front end loads Front end loads • Contingent deferred sales charges Contingent deferred sales charges • Redemption fees.Redemption fees.

© Kyler Kohler & Ostermiller, LLP 2008

IRA’s vs. 401(k)’sIRA’s vs. 401(k)’s• Maximum Contribution Maximum Contribution of $5,000 Annuallyof $5,000 Annually

• $1,000 Catch-up amount $1,000 Catch-up amount over age 50over age 50

• Contributions subject to Contributions subject to AGI limits & filing statusAGI limits & filing status

• Tax deductible (Pre-Tax)Tax deductible (Pre-Tax)

• Roth Account (Post-tax) Roth Account (Post-tax)

• Conversion to Roth IRA Conversion to Roth IRA limited by AGI until 2010limited by AGI until 2010

• Maximum Contribution up to Maximum Contribution up to $46,000 Annually$46,000 Annually

• $5,000 Catch-up amount $5,000 Catch-up amount over age 50over age 50

• No limits on AGI for your No limits on AGI for your contributions to the Plancontributions to the Plan

• Personal contributions of Personal contributions of 100% up to $15,500100% up to $15,500

• Tax Deductible (Pre-Tax)Tax Deductible (Pre-Tax)

• Roth Account (Post-Tax)Roth Account (Post-Tax)

© Kyler Kohler & Ostermiller, LLP 2008

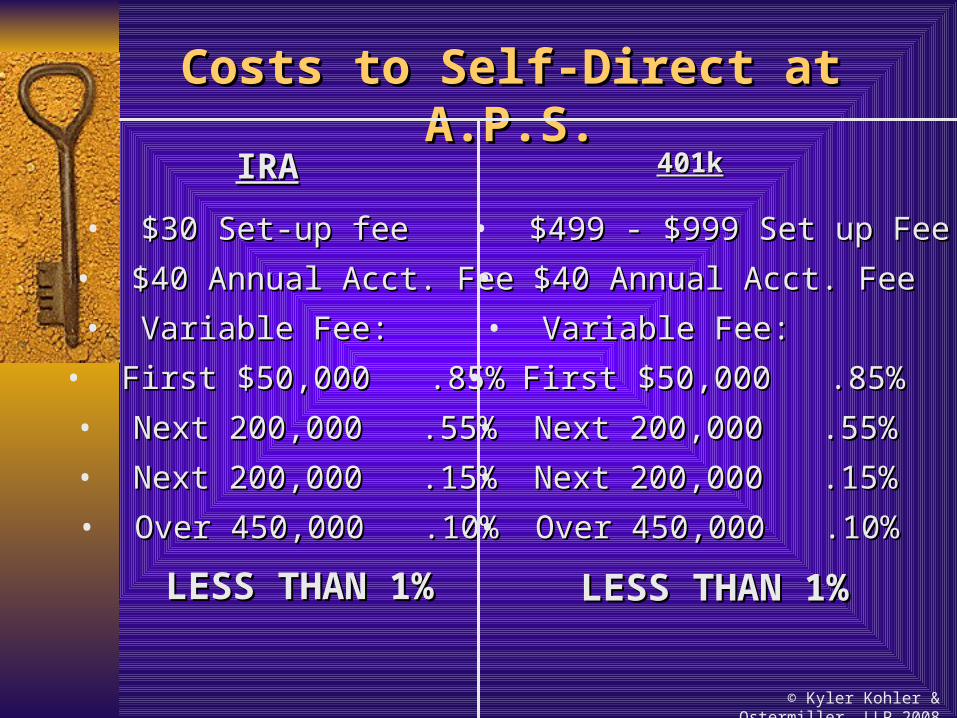

IRAIRA

• $30 Set-up fee$30 Set-up fee

• $40 Annual Acct. Fee$40 Annual Acct. Fee

• Variable Fee:Variable Fee:

• First $50,000 .85%First $50,000 .85%

• Next 200,000 .55%Next 200,000 .55%

• Next 200,000 .15%Next 200,000 .15%

• Over 450,000 .10%Over 450,000 .10%

LESS THAN 1%LESS THAN 1%

401k401k

• $499 - $999 Set up Fee$499 - $999 Set up Fee

• $40 Annual Acct. Fee$40 Annual Acct. Fee

• Variable Fee:Variable Fee:

• First $50,000 .85%First $50,000 .85%

• Next 200,000 .55%Next 200,000 .55%

• Next 200,000 .15%Next 200,000 .15%

• Over 450,000 .10%Over 450,000 .10%

LESS THAN 1%LESS THAN 1%

Costs to Self-Direct at A.P.S.Costs to Self-Direct at A.P.S.

© Kyler Kohler & Ostermiller, LLP 2008

APS Contact InfoAPS Contact Info

American Pension Services, Inc.American Pension Services, Inc.4168 West 12600 South4168 West 12600 South

Riverton, UT 84065Riverton, UT 84065(801) 571-0667(801) 571-0667

www.aps-utah.comwww.aps-utah.com

© Kyler Kohler & Ostermiller, LLP 2008

Do’s and Don’ts of Structuring Your Self

Directed Retirement Plan (“SDRP”) Investments

© Kyler Kohler & Ostermiller, LLP 2008

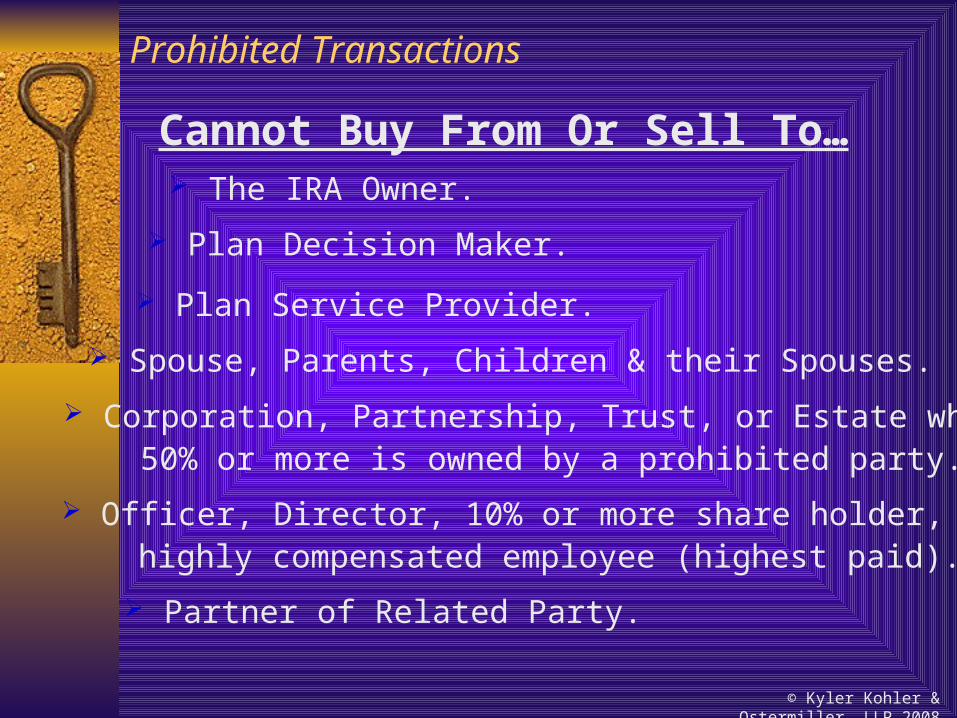

Prohibited Transactions

Cannot Buy From Or Sell To… The IRA Owner.

Plan Decision Maker.

Plan Service Provider.

Spouse, Parents, Children & their Spouses.

Corporation, Partnership, Trust, or Estate where 50% or more is owned by a prohibited party.

Officer, Director, 10% or more share holder, or highly compensated employee (highest paid).

Partner of Related Party.

© Kyler Kohler & Ostermiller, LLP 2008

Wiggle Room

The IRS allows your The IRS allows your IRAIRA to sell to and buy from to sell to and buy from brothers, sisters, aunts, uncles, cousins, nieces, brothers, sisters, aunts, uncles, cousins, nieces, nephews, and step Relatives.nephews, and step Relatives.

IRS Ruling 2004-8: In a IRS Ruling 2004-8: In a Roth IRARoth IRA, brother and , brother and sister are considered a Prohibited Party, so you sister are considered a Prohibited Party, so you cannot sell to or buy from them in your cannot sell to or buy from them in your Roth IRARoth IRA..

© Kyler Kohler & Ostermiller, LLP 2008

Real Estate is the “Key”

Rules are specific to real estate

Must be Real Estate Operating Company if the Retirement Plan and IRA Owner own more than 25% of the LLC/LP. See 29 CFR Section 2510.3-101.

Cannot have 100% control of LLC/LP.

If not Real Estate or you want to take a salary for managing the company, you, your SDRPs and Prohibited Parties Cannot own 50% or more of the company.

© Kyler Kohler & Ostermiller, LLP 2008

The Right Structure for You

Option 1

Tax QualifiedPlan$$

Self DirectedRetirement

Plan$$

Raw Land

$$ LOANSecured byReal Estate

- No Debt- No LLC/LP- No Partners- Direct Investment in name of IRA

For Illustration Purposes OnlyMay not be reproduced without theExpress written permission of KKO Lawyers©

Createor Transfer

© Kyler Kohler & Ostermiller, LLP 2008

Option 2

Rental Property(Income Producing)

Non-RecourseLoan

MortgageCompany

- Non-Recourse Debt- No Personal Guaranty- No Sweat Equity- No LLC/LP- No Partners- Direct Investment in name of IRA

The Right Structure for You

Tax QualifiedPlan$$

Self DirectedRetirement

Plan$$

For Illustration Purposes OnlyMay not be reproduced without theExpress written permission of KKO Lawyers©

Createor Transfer

© Kyler Kohler & Ostermiller, LLP 2008

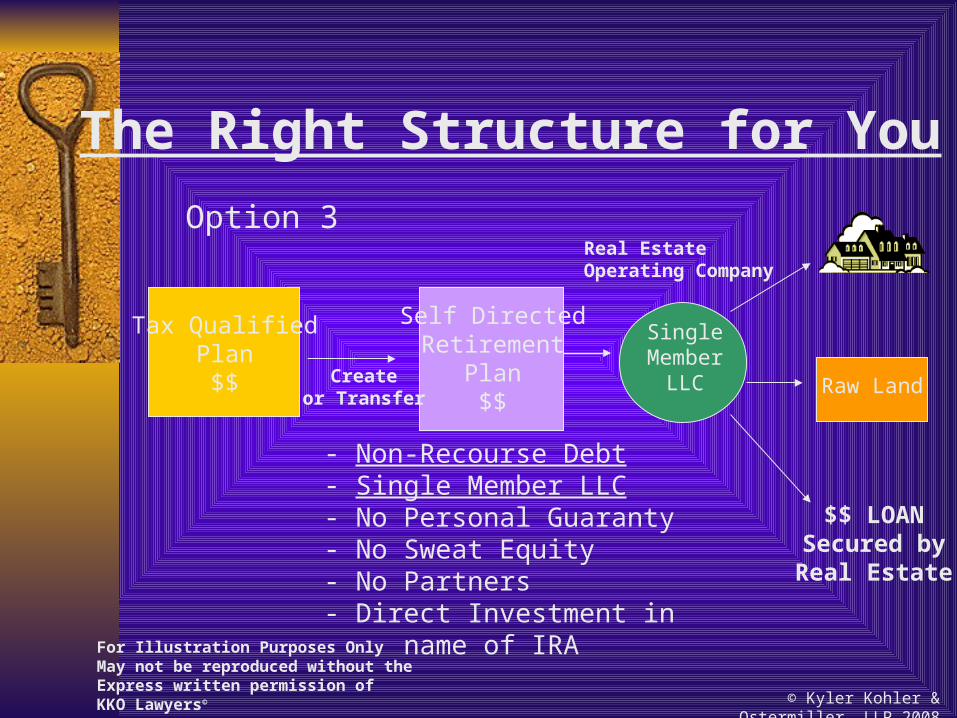

Option 3

- Non-Recourse Debt- Single Member LLC- No Personal Guaranty- No Sweat Equity- No Partners- Direct Investment in name of IRA

SingleMember

LLC

The Right Structure for You

Raw Land

$$ LOANSecured byReal Estate

Tax QualifiedPlan$$

Self DirectedRetirement

Plan$$

For Illustration Purposes OnlyMay not be reproduced without theExpress written permission of KKO Lawyers©

Createor Transfer

Real EstateOperating Company

© Kyler Kohler & Ostermiller, LLP 2008

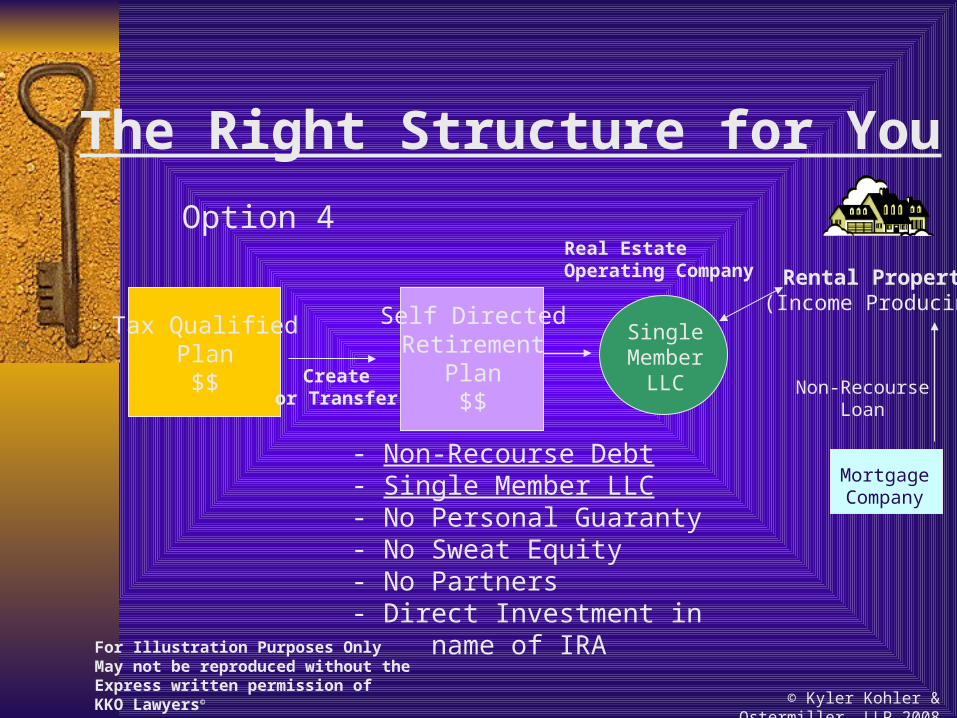

Option 4

Rental Property(Income Producing)

Non-RecourseLoan

MortgageCompany

- Non-Recourse Debt- Single Member LLC- No Personal Guaranty- No Sweat Equity- No Partners- Direct Investment in name of IRA

SingleMember

LLC

The Right Structure for You

Tax QualifiedPlan$$

Self DirectedRetirement

Plan$$

For Illustration Purposes OnlyMay not be reproduced without theExpress written permission of KKO Lawyers©

Createor Transfer

Real EstateOperating Company

© Kyler Kohler & Ostermiller, LLP 2008

Option 5

50%

Limited Liability Co.

orLimited Php.

IRAOwner

40-45%

MortgageCompany

Guarantor

Rental Properties

3rd PartyOwner

5-10%- Recourse Debt - YES- Partners -YES- LLC/LP- Yes

The Right Structure for You

Tax QualifiedPlan$$

Self DirectedRetirement

Plan$$

For Illustration Purposes OnlyMay not be reproduced without theExpress written permission of KKO Lawyers©

Createor Transfer

Real EstateOperating Company

© Kyler Kohler & Ostermiller, LLP 2008

Self Directed IRA Issues

Prohibited Transactions Transactions with Prohibited parties Use of Property Compensation of IRA ownerUnrelated Business Taxable Income (“UBTI”)

1. Rents, interest, dividends and capital gains exempt.

2. Watch out for development activities and non-real estate activities.

Unrelated Debt Financed Income (“UDFI”)1. Tax is paid on the portion of gains attributable to

the debt on the property. Administration Duties Annual report/valuation to Custodian Bookkeeping and tax return

© Kyler Kohler & Ostermiller, LLP 2008

For more information, please contact us at:

KYLER KOHLER & OSTERMILLER, LLPTel: 435.586.9366 Fax: 435.586.9491

www.kkolawyers.com

THANK YOU!!THANK YOU!!

© Kyler Kohler & Ostermiller, LLP 2008