Embed Size (px)

Citation preview

ARC Resources Ltd.2017 Investor Day

November 13, 2017

Agenda

8:00 – 8:05 am Welcome

Bevin Wirzba, Senior Vice President, Business Development and Capital Markets

8:05 – 8:25 am Built to Last

Terry Anderson, Senior Vice President and Chief Operating Officer

Van Dafoe, Senior Vice President and Chief Financial Officer

Lisa Olsen, Vice President, Human Resources

Myron Stadnyk, President and Chief Executive Officer

8:25 – 9:05 am Portfolio Strategy and Pace of Development

Lara Conrad, Vice President, Engineering and Planning

David Kehrig, Manager, Facilities

Sean Stuart, Manager, Completions

9:05 – 9:20 am Break

9:20 – 10:00 am How We Achieve Long-term Profitability

Ryan Berrett, Vice President, Marketing

Kris Bibby, Vice President, Finance

Sean Calder, Vice President, Production

10:00 – 10:40 am ARC’s Approach to Long-term Sustainable Development

Terry Anderson, Senior Vice President and Chief Operating Officer

Chris Baldwin, Vice President, Geosciences

Armin Jahangiri, Vice President, Operations

10:40 – 10:45 am Summary

Myron Stadnyk, President and Chief Executive Officer

10:45 – 11:00 am Questions

Our Plan

2017

Reduced the

dividend

Sold Saskatchewan

assets

Eliminated DRIP

and SDP plans

118,000 boe per day

2018

Sustain Montney

businesses

Progress Sunrise

Phase II

Advance Attachie

piloting activities

130,000 to 134,000

boe per day

2019

Maintain consistent

investment levels

Bring on Sunrise

Phase II

Progress Dawson

Phase IV to add

~17,500 boe per day

ARC’s Plan Is Fully Funded and Will Result in 10 Per Cent Production CAGR over a Three-year Period

2016

Brought on Dawson

Phase III

Rebuilt liquids

production from

divestments

Achieved success

in Lower Montney

and Attachie

120,000 to 124,000

boe per day

BUILT TO LAST

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

High-quality,

Long-life

Assets

Top Talent

and Strong

Leadership

Culture

HSE and

Operational

Excellence

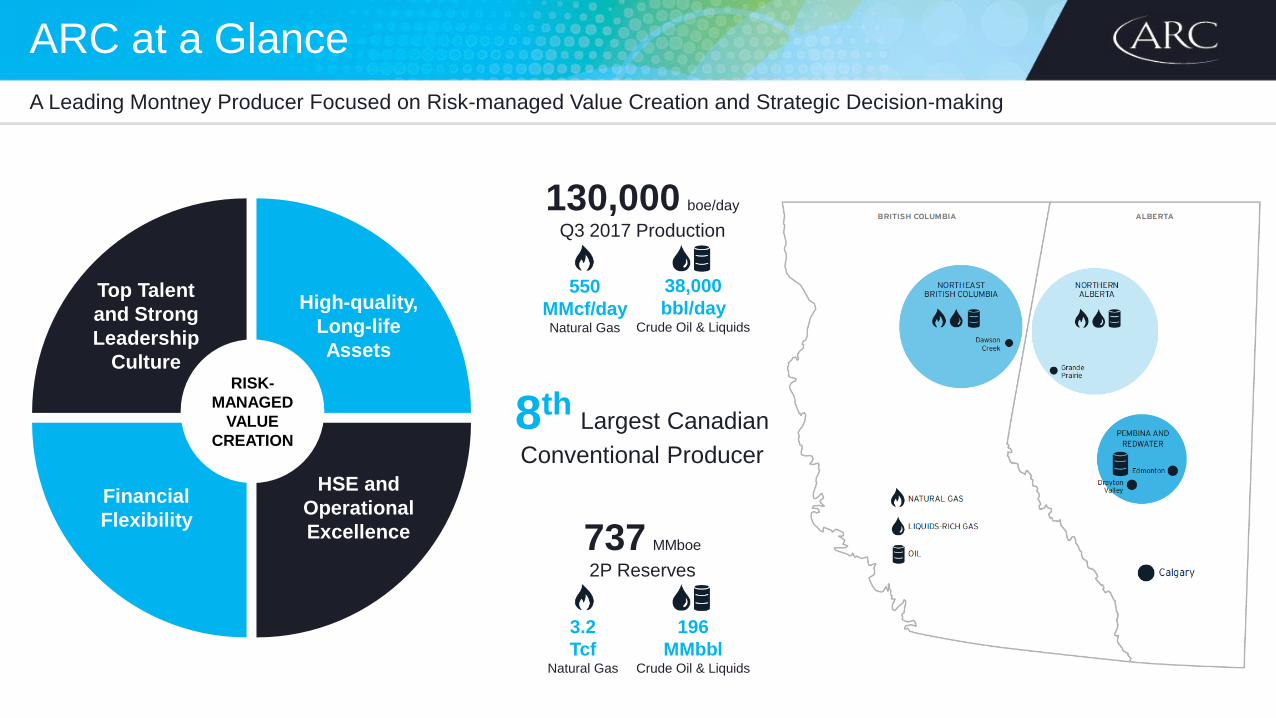

ARC at a Glance

A Leading Montney Producer Focused on Risk-managed Value Creation and Strategic Decision-making

8thLargest Canadian

Conventional Producer

130,000 boe/day

Q3 2017 Production

550

MMcf/dayNatural Gas

38,000

bbl/day Crude Oil & Liquids

737 MMboe

2P Reserves

3.2

TcfNatural Gas

196

MMbbl Crude Oil & Liquids

Long-term Value Creation

Strategic Decisions Have Created a Resilient Business and Positioned ARC for Future Success

(400%)

300%

1000%

1700%

2400%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

ARX Total Return Performance vs. Indices (1)

ARX SPTSX Comp SPTSX E&P

>$6 Billionof Distributions /

Dividends & 13%

Annualized Total Return

Stayed within

Target of 1.0 to 1.5xNet Debt to

Funds from Operations

10%Return on Average

Capital Employed

TransitionedAsset Base to

World-class Montney

ARX: 13%

SPTSX E&P: 9%

SPTSX Comp: 8%

(1) Returns to November 10, 2017.

2,400%

1,700%

1,000%

300%

(400%)

To

tal R

etu

rn

Renais

sance E

nerg

y

Ta

lism

an E

nerg

y

Su

ncor

Inc.

Alb

ert

a E

nerg

y (

EnC

ana &

Cen

ovus)

Canadia

n O

ccid

en

tal

Canadia

n N

atu

ral R

esourc

es

An

ders

on E

xplo

ration

Cre

sta

r E

nerg

y

Po

co P

etr

ole

um

s

Norc

an E

nerg

y

Wascana E

nerg

y

Ranger

Oil

Gulf C

anada R

eso

urc

es

Pa

nC

anadia

n P

etr

ole

um

(E

nC

ana)

Rig

el E

nerg

y

Ta

rragon

Oil

& G

as

Ela

n E

nerg

y

Nort

hsta

r E

nerg

y

Mo

rris

on P

etr

ole

um

s

Ab

acan R

esourc

es

Pe

nn W

est P

etr

ole

um

(O

bsid

ian E

nerg

y)

Pin

na

cle

Resourc

es

Sceptr

e R

esourc

es

Chie

ftain

Inte

rnatio

nal

Tri L

ink R

esourc

es

Chauvco R

esourc

es

Rio

Alto E

xplo

ration

Num

ac E

nerg

y

Cabre

Explo

ratio

n

Sta

mp

eder

Explo

ratio

n

Blu

e R

ange R

esourc

e

Gulfstr

ea

m R

esourc

es

CS

Resourc

es

Uls

ter

Petr

ole

um

s

En

cal E

nerg

y

AR

C R

esourc

es L

td.

Jord

an P

etr

ole

um

Nort

hro

ck R

esourc

es

Be

au C

an

ada E

xplo

ratio

n

Ba

rrin

gto

n P

etr

ole

um

Mo

rgan H

ydro

carb

ons

Ocelo

t E

nerg

y

Dors

et E

xplo

ration

Inte

nstity

Resourc

es

Su

mm

it R

esourc

es

Arc

her

Reso

urc

es

Pe

trom

et R

esourc

es

TSX Oil & Gas Producers (1)

July 1996

Survivor Bias

• Only six of the companies from the TSX Oil & Gas Producers group in July 1996 still exist today

ARC Has Transformed Its Business to Be Competitive in Today’s Energy Sector

Still in Business

No Longer in Business

(1) Quoted market value of Oil & Gas Producers group on the Toronto Stock Exchange in July 1996.

WT

I C

rud

e O

il (

US

$/b

bl)

Banded Commodity Price Environment

ARC’s Response Has Been to Focus on the Montney, Reduce Costs, Improve Efficiencies, and Maintain a Strong Balance Sheet

(1) Forecasted pricing based on November 10, 2017 forward price curve.

NY

ME

X H

en

ry H

ub

Na

tura

l G

as

(U

S$

/MM

Btu

)

Crude Oil and Natural Gas Pricing (1)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018F 2019F 2020F 2021F

WTI Crude Oil (LHS) NYMEX Henry Hub Natural Gas (RHS)

Building Sustainable Businesses in the Montney

Businesses Sustain Production and Generate Free Cash Flow at Low Reinvestment Rates

0

30,000

60,000

90,000

120,000

150,000

2009 Non-coreDispositions

2010 2011 2012 2013 2015 2015 2017 2019

Sunrise

Phase II

Dawson

Phase III

Tower

Battery

ExpansionSunrise

Phase IParkland/Tower

Phase II

Ante Creek

Phase IDawson

Phase IIDawson

Phase I

Montney Production

Cardium & Non-core Production

Montney Businesses

Ryan BerrettVice President

Marketing

Kris BibbyVice President

Finance

Sean CalderVice President

Production

Lara ConradVice President

Engineering & Planning

Terry AndersonSenior Vice President &

Chief Operating Officer

Chris BaldwinVice President

Geosciences

Wayne LentzVice President

Business Analysis

Lisa OlsenVice President

Human Resources

Myron StadnykPresident & CEO

Van DafoeSenior Vice President &

Chief Financial Officer

Armin JahangiriVice President

Operations

Our Team

Our Team Has the Proven Ability to Execute and Is Committed to Building an Enduring Company

Bevin WirzbaSenior Vice President

Business Development &

Capital Markets

Consistent and Sustainable Strategy

Delivering on Our Strategy of Risk-managed Value Creation

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

High-quality,

Long-life

Assets

Top Talent

and Strong

Leadership

Culture

HSE and

Operational

Excellence

Top Talent and Strong Leadership Culture

High-performance Culture Creates an Environment Where Employees Are Committed to Achieving Superior Business Results

STRATEGIC DECISION-MAKING:

• Building a functional organization with

multi-disciplinary teams

• Focusing on long-term talent development

and succession

• Aligning compensation programs with the

interests of shareholders

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

High-quality,

Long-life

Assets

HSE and

Operational

Excellence

Top Talent

and Strong

Leadership

Culture

High-quality, Long-life Assets

Portfolio Strategy and Pace of Development Support Ongoing Value Creation

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

Top Talent

and Strong

Leadership

Culture

HSE and

Operational

Excellence

STRATEGIC DECISION-MAKING:

• Completing Montney transformation

• Creating full-cycle businesses

• Allocating strategic capital to liquids-rich

Attachie and Lower Montney

• Implementing full-stack development

of Montney assets

High-quality,

Long-life

Assets

HSE and Operational Excellence

Leveraging Expertise to Develop ARC’s High-quality Assets and Continuing to Drive Efficiencies

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

Top Talent

and Strong

Leadership

Culture

High-quality,

Long-life

Assets

STRATEGIC DECISION-MAKING:

• Focusing on safety performance

• Investing in owned-and-operated infrastructure

• Creating and retaining capital and

operating efficiencies

• Advancing ESG considerations across

the business

• Managing pace of development as part

of managing risk

HSE and

Operational

Excellence

Financial Flexibility

Managing a Profitable Business within Banded Commodity Price Environment

RISK-

MANAGED

VALUE

CREATION

Top Talent

and Strong

Leadership

Culture

High-quality,

Long-life

Assets

HSE and

Operational

Excellence

STRATEGIC DECISION-MAKING:

• Preserving access to capital

• Maintaining discipline around debt levels

• Executing an integrated physical and financial

risk management diversification strategy

• Continually assessing long-term profitability

of business plans

Financial

Flexibility

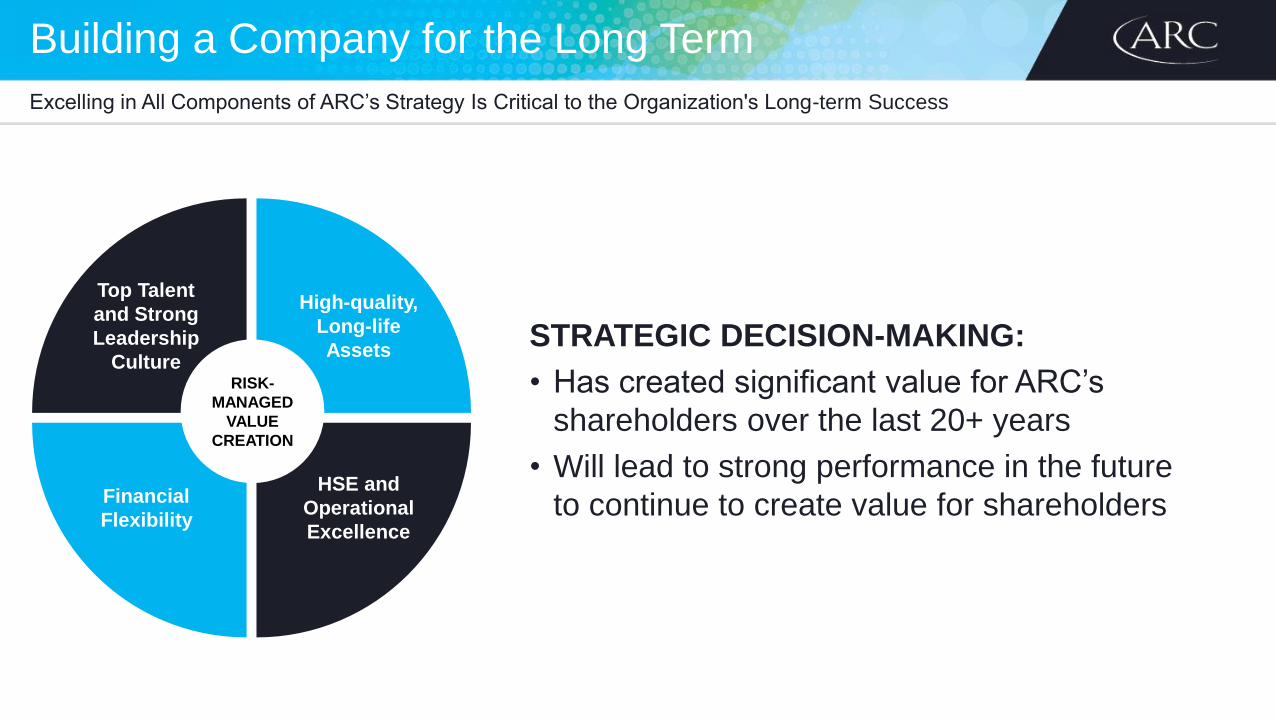

Building a Company for the Long Term

Excelling in All Components of ARC’s Strategy Is Critical to the Organization's Long-term Success

STRATEGIC DECISION-MAKING:

• Has created significant value for ARC’s

shareholders over the last 20+ years

• Will lead to strong performance in the future

to continue to create value for shareholders

RISK-

MANAGED

VALUE

CREATION

Financial

Flexibility

High-quality,

Long-life

Assets

Top Talent

and Strong

Leadership

Culture

HSE and

Operational

Excellence

PORTFOLIO STRATEGY

& PACE OF

DEVELOPMENT

Proven Development Model

Inventory at All Stages Allows for Self-funding and Full-cycle Returns across Portfolio

Dawson Phase I & II

Sunrise Phase I

Attachie East

Parkland/Tower Phase I & II

Net Cash Flow +

Blueberry

Sundown

Attachie West (Pilot)

Redwater

Pembina

Growth for Future Phase

• Exploration

• Appraisal / Piloting

• Geographic and Commodity

Diversity

Development Phase

• Develop to Commercialize

• Exploit

Free Cash Flow Phase

• Optimization

• Maintenance

Growth & Development Capital

$275 million

Sustaining Capital

$390 million

Ante Creek (Central)

Dawson Phase III

Pouce Coupe

Dawson Phase IV

Ante Creek (South)

2018 Budget

$690 million (1)

Sunrise Phase II

Parkland/Tower Phase III

Septimus

(1) Includes $25 million of non-core and corporate capital.

Attachie West Phase I

Dawson Phase V

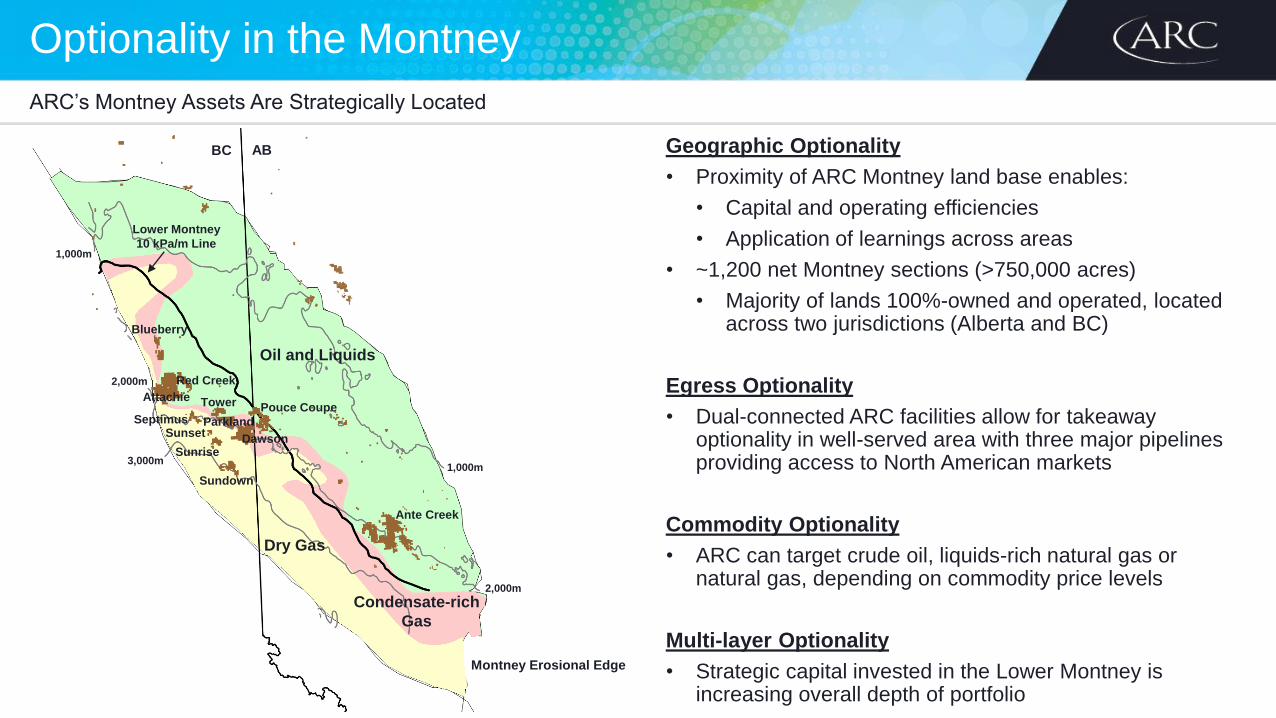

Optionality in the Montney

ARC’s Montney Assets Are Strategically Located

Geographic Optionality

• Proximity of ARC Montney land base enables:

• Capital and operating efficiencies

• Application of learnings across areas

• ~1,200 net Montney sections (>750,000 acres)

• Majority of lands 100%-owned and operated, located across two jurisdictions (Alberta and BC)

Egress Optionality

• Dual-connected ARC facilities allow for takeaway optionality in well-served area with three major pipelines providing access to North American markets

Commodity Optionality

• ARC can target crude oil, liquids-rich natural gas ornatural gas, depending on commodity price levels

Multi-layer Optionality

• Strategic capital invested in the Lower Montney is increasing overall depth of portfolio

Oil and Liquids

Dry Gas

ABBC

Blueberry

Red Creek

Attachie

Septimus

Tower

ParklandSunset

Sunrise

Sundown

Dawson

Pouce Coupe

Ante Creek

1,000m

2,000m

3,000m1,000m

Montney Erosional Edge

2,000m

Lower Montney

10 kPa/m Line

Condensate-rich

Gas

Demonstrating Optionalityat Ante Creek:A Case Study

Step Changes in Execution at Ante Creek

2017 Operational Results Are Allowing Ante Creek to Now Compete with Our Other Montney Assets

2014 20182016

2015 2017

New well design applied:

• Transverse orientation

• Monobore

• Slickwater fracturing

• 2016 drilling program deferred;

optimization activities become

key focus

• Modernized Royalty Framework

• Technical learnings from NE BC

integrated into exploitation strategy

• 2017 drilling program set

• Drilling program to

sustain production

• FEED studies for next

phase of development

• Regulatory application

Oil prices begin

to deteriorate

• NDP government elected

• Royalty review initiated

• 2016 drilling program set

0

1,000

2,000

3,000

4,000

5,000

0 2 4 6 8 10 12

Days

Drilling Times

Capital Efficiency Improvements at Ante Creek

Improvements in Drilling Times and Costs Are Sustainable across ARC’s Asset Base

0

150

300

450

600

750

0

150

300

450

600

750

2014 Pacesetter 2015 Pacesetter Q3 2016 Q1 2017 Q2 2017

Drilling Costs

Cost per Meter

Meters Drilled per Day

2014

2017

35%Reduction in

Overall Drill Times

(1) Change is relative to 2015 Pacesetter well.

60%Increase in

Meters Drilled

25%Reduction in Costs (1)

De

pth

(m

)

Co

st

pe

r M

ete

r ($

/m)

Me

ters

Dri

lle

d p

er

Da

y (

m/d

ay)

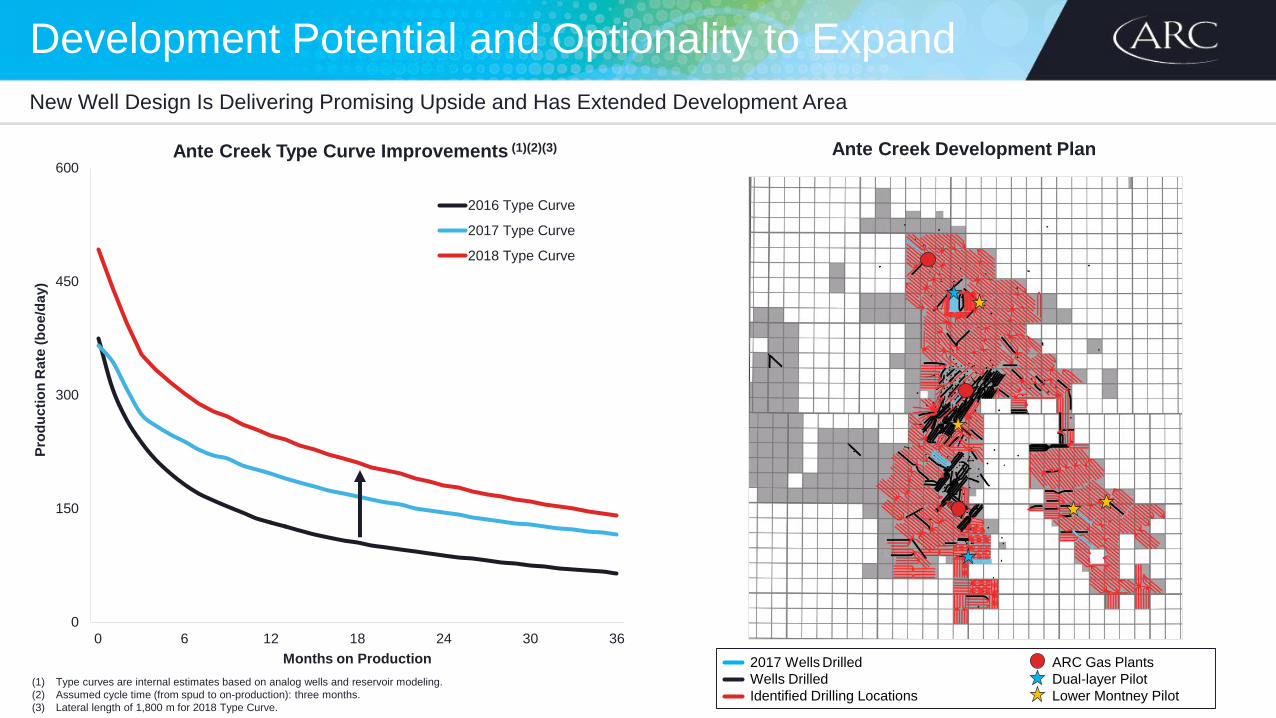

Development Potential and Optionality to Expand

New Well Design Is Delivering Promising Upside and Has Extended Development Area

Ante Creek Development Plan

0

100

200

300

400

0 6 12 18 24 30 36

Pro

du

cti

on

Ra

te

(bo

e/d

ay)

Months on Production

2017 Type Curve

2016 Type Curve

0

150

300

450

600

0 6 12 18 24 30 36

Pro

du

cti

on

Ra

te (

bo

e/d

ay)

Months on Production

2016 Type Curve

2017 Type Curve

2018 Type Curve

Ante Creek Type Curve Improvements (1)(2)(3)

(1) Type curves are internal estimates based on analog wells and reservoir modeling.

(2) Assumed cycle time (from spud to on-production): three months.

(3) Lateral length of 1,800 m for 2018 Type Curve.

2017 Wells Drilled ARC Gas Plants

Wells Drilled Dual-layer Pilot

Identified Drilling Locations Lower Montney Pilot

0

20000000

40000000

60000000

80000000

100000000

120000000

140000000

160000000

180000000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

Fa

cilit

y I

nve

stm

en

t ($

)

Months

Creating Optionality through Facility Design

Upfront Investment and Templated Approach to Facility Design Creates Flexibility within ARC’s Long-term Plans

Build Asset Confidence

Initiate Low

Investment Up Front

Infrastructure

Optionality Strategy

Facility Investment Profile

• Identify Plant Location

• Process Design

• Noise & Emission Modelling

• FEED Engineering

• Regulatory Applications

• Long-lead Items (e.g., Turbines)

• Water Infrastructure

Managing the Pace of Development at Attachie:A Case Study

A Paced Approach to Development at Attachie

ARC’s Disciplined Approach Has Allowed for Learnings to be Applied from Other Fields and for Efficiencies to Be Captured

2010 20182016

2017

Tower completion

design applied

to five wells

(25 m IFS & 1.9 T/m)

• Piloted production

through third-party facility

• Second well drilled

(liquids-rich)

88 net sections

acquired through

land sales

First well

drilled

(wet gas)

2011 2014

2015 2019 2020

21 net sections

acquired through

land sales

• First multi-

well pad on

production

• Lower Montney

test

Refined completion

design applied

to two wells

(18 m IFS & 1.9 T/m)

Targeted in-

service date for

TCPL North

Montney Mainline

307 net sections

97 net sections

acquired through

land transactions

0

25

50

75

100

125

0 100 200 300 400 500 600

Cu

mu

lati

ve

Oil &

Co

nd

en

sate

Pro

du

cti

on

(M

bb

l)

Days on Production

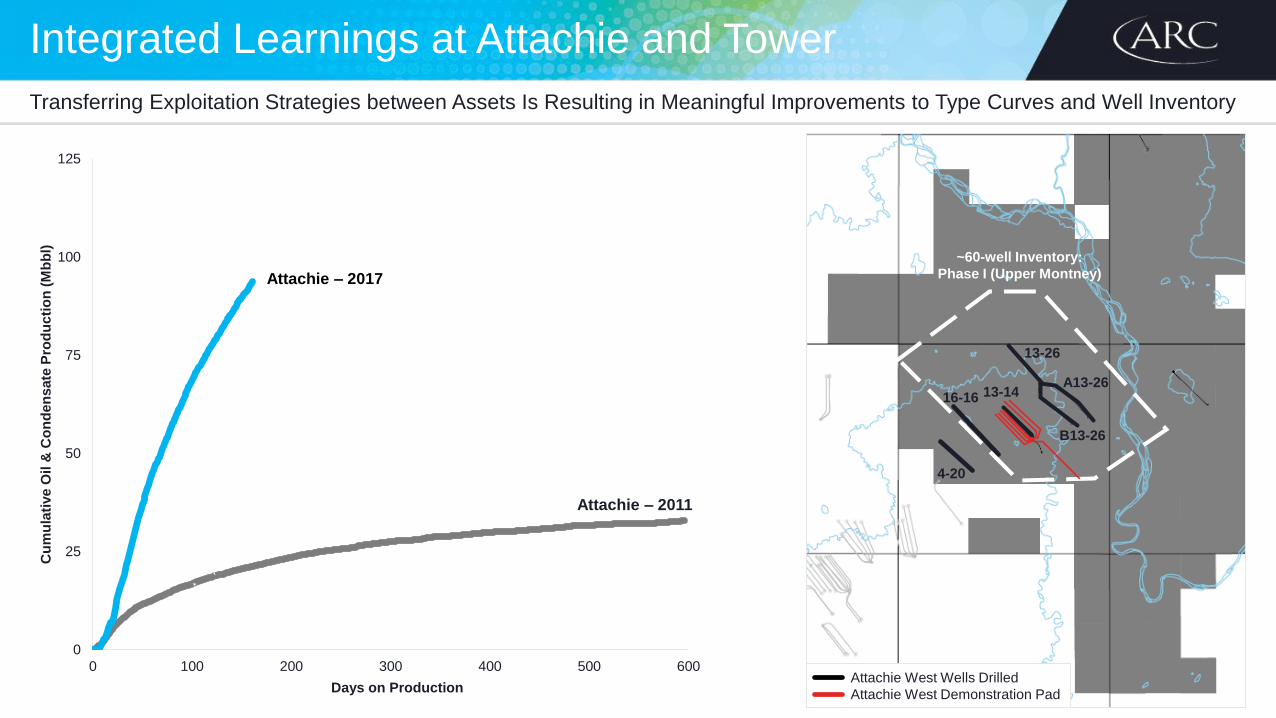

Integrated Learnings at Attachie and Tower

Transferring Exploitation Strategies between Assets Is Resulting in Meaningful Improvements to Type Curves and Well Inventory

Attachie – 2011

Attachie – 2017

13-14

13-26

B13-26

~60-well Inventory:

Phase I (Upper Montney)

16-16

4-20

A13-26

Attachie West Wells Drilled

Attachie West Demonstration Pad

Progressing Attachie Towards Commercialization

De-risking and Piloting Attachie for Optimal Infrastructure Design

Manage Pace of

Development

Takeaway Secured on

TCPL North Montney

Mainline for Phase I

Further Delineation of

Upper and Lower Montney

for Phase II+ Sanctioning TCPL North Montney Mainline

(Targeted In-service Date: H1 2019)

ARC 4-20

Demonstration

Battery

(Phases I & II)

Progress

Farrell Creek

(180 MMcf/day)

Canbriam/

Pembina

Liquids

HOW WE ACHIEVE

LONG-TERM

PROFITABILITY

Why Invest in Sunrise?

High Well Deliverability and Competitive Cost Structure Create Significant Value and Superior Full-cycle Economics

Low Cost Structure

Significant Resource

Competes Continentally

Strong Economics

Full-stack Development at Sunrise

Significant Natural Gas Resource Base with Excellent Capital and Operating Efficiencies

Sunrise Full-stack Development (1)

Up

pe

r M

on

tney

Lo

we

r M

on

tne

y

Existing Horizontal Wells, Development

Existing Horizontal Wells, Pilots

Potential Horizontal Wells(1) Spacing and completions approach varies by project area.ARC Montney Lands with 2P

Reserves Booked as of YE 2016

Sunrise Phase II Expansion

ARC’s Next Growth Driver Is a High-rate-of-return Project

Sunrise Phase I60 MMcf/day sales capacity

Sunrise Phase II180 MMcf/day sales capacity

(1) After-tax rate of return run at US$50/bbl WTI and Cdn$2.50/GJ AECO flat pricing.

(2) Economics have been normalized to a 10-year project life.

0

60

120

180

240

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Na

tura

l G

as

Pro

du

cti

on

(M

Mc

f/d

ay)

Sunrise Production Profile

Third-party Processing Facility ARC Sunrise 13-36

>25%Full-cycle

Economics (1)(2)

85%Half-cycle

Economics (1)

80%Reduction in

Processing Costs for

Repatriated Volumes

>99%Facility Run-time

Moving Our Sunrise Gas to Market

Competitive Cost Structure and Long-term Approach to Takeaway Is Resulting in Favourable Netbacks

Operated Sunrise Costs $0.85

Transportation $1.05

ARC Cost to Chicago $1.90

Operated Sunrise Costs $0.85

Transportation $1.30

ARC Cost to Henry Hub $2.15Henry Hub

Chicago

Market Access

Market

Diversification

Price

Optimization

Operated Sunrise Cost Structure

(Cdn$/Mcfe)

AECOF&D Costs $0.45

Operating Expenses &

Royalties $0.40

Operated Sunrise Costs $0.85

Natural Gas Pricing Exposure

ARC Continues to Physically and Financially Diversify to Downstream Markets to Manage Risk and to Achieve Optimal Pricing

Hedged

38%

Pac-NW US

4%

Dawn

8%

AECO

11%

2018 Physical and Financial

Diversification Activities

2017 YTD Physical and Financial

Diversification Activities (Cdn$/Mcfe)

Average Price before

Diversification Activities (1) $2.37

Diversification Activities (1) $0.30

Realized Gains on Risk

Management Contracts $0.72

Overall Corporate Price $3.39

Midwest

30%

(1) ARC’s average realized natural gas price is a combination of average price before diversification activities and diversification activities.

(60)

0

60

120

180

240

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7F

201

8F

201

9F

202

0F

$ m

illio

ns

Financial Risk Management

Realized Gains (Losses)

Station 2

9%

-35,000

-30,000

-25,000-20,000-15,000-10,000

-5,000

05,00010,00015,00020,000

25,00030,000

35,000

($200,000,000)

($150,000,000)

($100,000,000)

($50,000,000)

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

2017F

2018F

2019F

2020F

2021F

2022F

2023F

2024F

2025F

2026F

2027F

-35,000

-30,000

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

($200,000,000)

($150,000,000)

($100,000,000)

($50,000,000)

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

0

2,000

4,000

6,000

8,000

0 10 20 30 40 50 60

Delivering Full-cycle and Corporate Returns

Efficiently Converting Resources into Corporate Earnings for Shareholders

Single-well

Economics

(Half-cycle)

Proportional Facility

and Appropriate

Timing Included:

Project Economics

(Full-cycle)

Corporate Costs

ROACE of 10% since

Inception

Aft

er-

tax R

ate

of

Retu

rn

Pro

du

cti

on

Rate

(M

cf/

da

y)

Months on Production

Field NetbackCapital Expenditures, excluding Facility Expenditures

Facility Expenditures Production

Net Cash Flow

Sunrise Type Curves & Single-well Economics (Half-cycle)

Full-cycle and Corporate Returns

~$225 million of capital

investment for facility start-up

~$400 million of capital

investment to sustain facility

Projected Sunrise Phase II Cash Flows

2017 Type Curve (Previous Well Design: 2,000 m)

2018 Type Curve (New Well Design: 2,440 m)

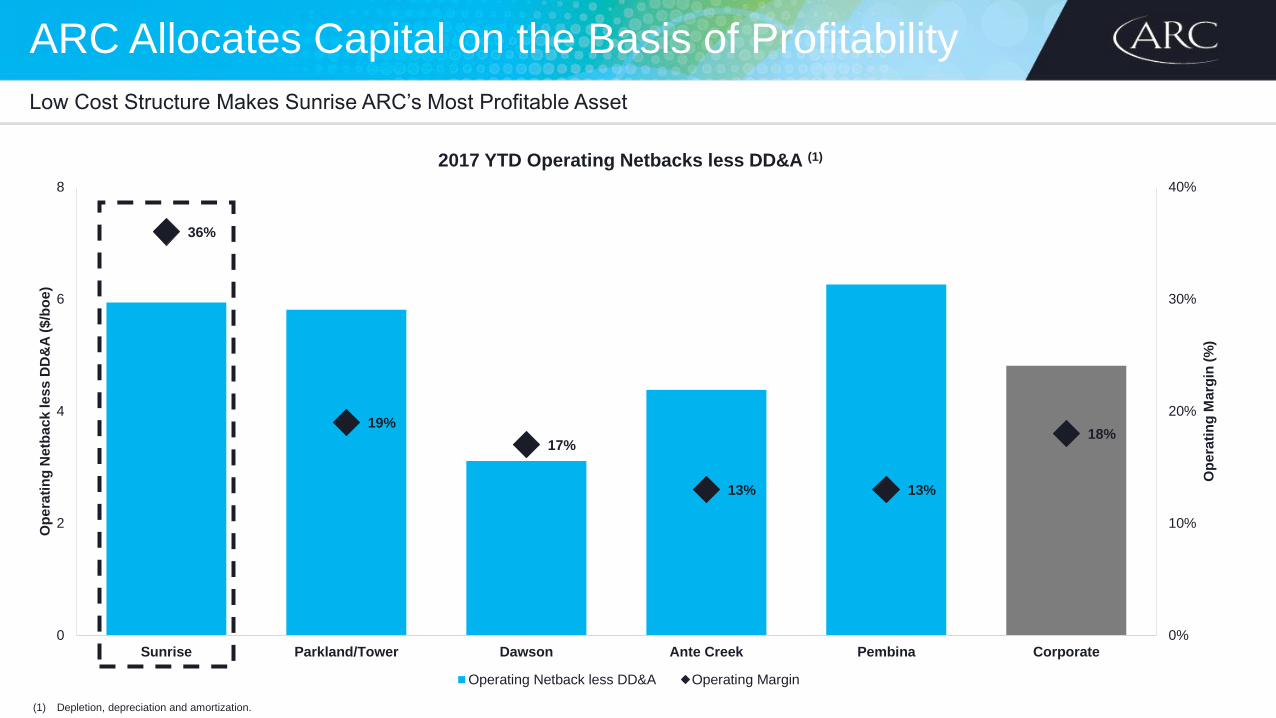

ARC Allocates Capital on the Basis of Profitability

Low Cost Structure Makes Sunrise ARC’s Most Profitable Asset

36%

19%

17%

13% 13%

18%

0%

10%

20%

30%

40%

0

2

4

6

8

Sunrise Parkland/Tower Dawson Ante Creek Pembina Corporate

Op

era

tin

g M

arg

in (

%)

Op

era

tin

g N

etb

ac

k le

ss

DD

&A

($

/bo

e)

2017 YTD Operating Netbacks less DD&A (1)

Operating Netback less DD&A Operating Margin

(1) Depletion, depreciation and amortization.

How We Choose to Fund Our Business

• ARC is currently funding its business through the use of cash and long-term debt

ARC’s Funding Choices Have the Lowest Cost of Capital

Cash

Debt

Equity

Asset Sale PDP

Midstream Joint Venture(Includes Operating Expense Dilution)

Upstream Joint Venture(Includes Asset Dilution)

Q4 2016 sale of

Saskatchewan assets

Incre

asin

g C

ost

of

Cap

ital

Dividends

Sustaining Capital

Growth Capital

Funds from Operations

2016 DispositionProceeds

Dividends

Sustaining Capital

Growth Capital

Funds from Operations

DRIP/SDP

Equity Proceeds

Net A&D Proceeds

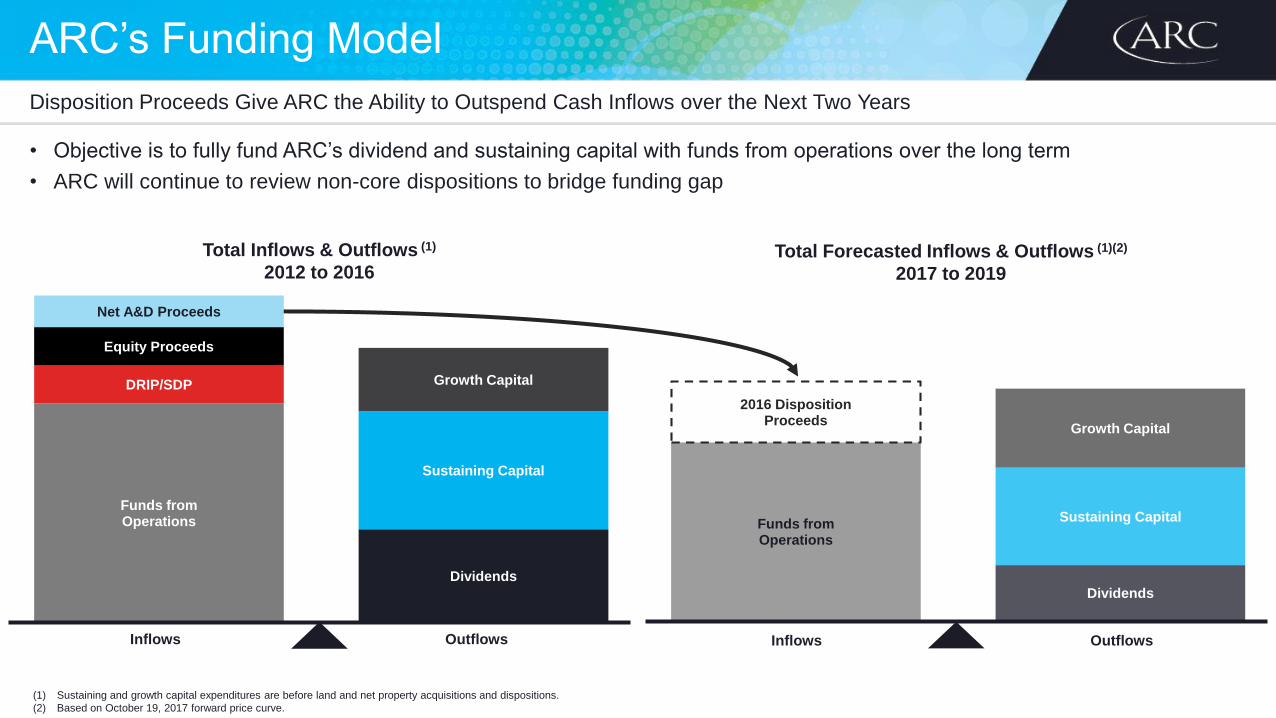

ARC’s Funding Model

• Objective is to fully fund ARC’s dividend and sustaining capital with funds from operations over the long term

• ARC will continue to review non-core dispositions to bridge funding gap

Disposition Proceeds Give ARC the Ability to Outspend Cash Inflows over the Next Two Years

Inflows Outflows

(1) Sustaining and growth capital expenditures are before land and net property acquisitions and dispositions.

(2) Based on October 19, 2017 forward price curve.

Total Inflows & Outflows (1)

2012 to 2016

Inflows Outflows

Total Forecasted Inflows & Outflows (1)(2)

2017 to 2019

Positioned for Continued Long-term Profitability

Low Sustaining Capital Requirements, Efficient Investment of Growth Capital and Low-cost Funding Decisions Lead to Profitability

(10%)

0%

10%

20%

30%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F

Return on Average Capital Employed (1)

(1) 2017F ROACE based on October 19, 2017 forward price curve.

ROACE of 10% since Inception ROACE

Trailing Three-year ROACE

ARC’S APPROACH

TO LONG-TERM

SUSTAINABLE

DEVELOPMENT

Unlocking the Lower Montney

Benefits of Multi-layer Development

Significant Future Delineation Opportunities

Attachie Septimus Sunrise Tower Parkland Dawson Pouce Coupe

Montney

A

Montney

B

Montney

C

Montney

D

Montney

E

Existing Horizontal Wells, Development Existing Horizontal Wells, Pilots Potential Horizontal Wells

Up

pe

r M

on

tney

Lo

we

r M

on

tne

y

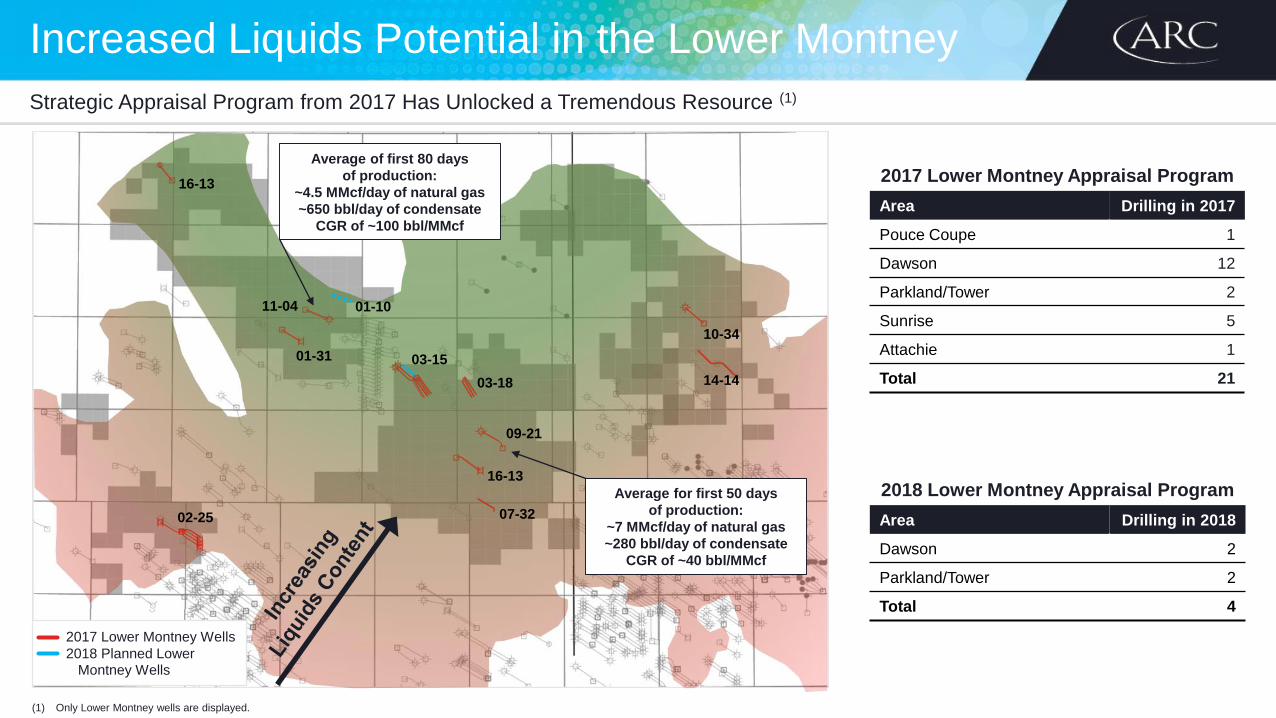

Increased Liquids Potential in the Lower Montney

Strategic Appraisal Program from 2017 Has Unlocked a Tremendous Resource (1)

(1) Only Lower Montney wells are displayed.

2017 Lower Montney Appraisal Program

Area Drilling in 2017

Pouce Coupe 1

Dawson 12

Parkland/Tower 2

Sunrise 5

Attachie 1

Total 21

2018 Lower Montney Appraisal Program

Area Drilling in 2018

Dawson 2

Parkland/Tower 2

Total 4

10-34

14-14

07-32

16-13

09-21

03-18

03-15

11-04

01-31

02-25

2017 Lower Montney Wells

2018 Planned Lower Montney Wells

01-10

16-13

Average of first 80 days

of production:

~4.5 MMcf/day of natural gas

~650 bbl/day of condensate

CGR of ~100 bbl/MMcf

Average for first 50 days

of production:

~7 MMcf/day of natural gas

~280 bbl/day of condensate

CGR of ~40 bbl/MMcf

Montney Exploitation Approach Improves Efficiencies

ARC Has Advanced Its Understanding of the Full-stack Development Potential for All Project Areas in Order to Execute Efficiently

Dawson Full-stack Development (1)

(1) Spacing and completions approach varies by project area.

ARC’s ESG Considerations for Infrastructure Development

Protection

and

Conservation

Water Strategy Limits Impact and Creates Efficiencies

Integrated Approach with Collaboration Between Technical Experts and Participation in Industry Discussions and Partnerships

ARC’s Guiding Principles of Water Stewardship

Transport,

Store and

Dispose

Responsibly

Measure,

Monitor and

Set Targets

Strategy in Action:

$80 million investment planned for water-related infrastructure over the next three years

Reduce fresh water usage by 80% in Dawson, Parkland and Tower

Reduce northeast BC frac water costs by 70 to 80% by 2019

Lead and Support

Research,

Collaboration and

Technology

Sustainable

and Economic

Water Supply

Evaluate

Opportunities

for Reduction

Carbon and Emissions Management Strategy

Committed to Minimizing Emissions that Pose Potential Risks While Recognizing the Importance of Economic Viability

ARC’s Guiding Principles of Carbon and Emissions Management

Measure,

Monitor and

Set Targets

Participate in

Carbon

Incentives

Participate in

Emissions

Dialogue

Reduced corporate emissions intensity by 30% since 2010

Strategy in Action:

~15% reduction in emissions intensity by 2019 through planned electrification of facilities

Planned solar pump conversion project will reduce methane emissions by 1,100 tonnes of CO2e per year

Dawson Phase III waste heat recovery project will reduce our corporate CO2 emissions by 2% per year

Lead and Support

Research,

Collaboration and

Technology

Proven Expertise in NE BC Facility Development

Best-in-class Capital Efficiency

$550 million>500 MMcf/day natural gas

>17 Mbbl/day liquids-handling

✓ Increased Reliability (ARC-owned and Operated)

✓ Low-cost Operator

✓Continuous Improvement

✓Design for Future Flexibility

Investment in Strategic Infrastructure Has Resulted in Best-in-class Efficiencies

Dawson Phase I

(2010)

Dawson Phase II

(2011)

Parkland/Tower

Phase II

(2013)

Sunrise Phase II

(2019 Est.)

Dawson Phase III

(2017)

Sunrise Phase I

(2015)

ARC’s Approach toLong-term Planning

Building Our Integrated Long-term Plan

Collaborative Approach Facilitates Learnings, Leverages Technical Expertise and Creates Both Ownership and Optionality

Economic Screening

Scenario Analysis

Financials and Lookbacks

Test and Optimize

Data Collection and Review

Integrating

Learnings

at All Stages

of Development

Determine Well

Designs

Evaluate

Results

Optimize

Exploitation

Strategy

Further Our

Understanding

of the Asset

Establish

Project

Sequencing

Rigour and

Expertise

Dialogue and

Ownership

Highest Quality Inputs

2018 Budget and Guidance

2018 Guidance

Focused on Profitability and Long-term Value Creation

$690 million

Invest to drill

64 gross

Allowing

ARC to:

While managing operating costs

at $6.50 – $6.90/boe

Maintain Balance Sheet Strength

Facilitate an Orderly Pace of Development

Create Shareholder Value

Keeping gas plants in

our core Montney areas

at capacity

Ensuring the safe and responsible

execution of the capital program

operated wells

37,500 – 40,500 bbl/day

of Liquids Production

555 – 565 MMcf/day

of Gas Production

To produce

130,000 – 134,000boe/day

2018 Budget – Our Most Capitally Efficient Year

Capital Budget of $690 Million Focuses on Overall Capital Efficiency and Profitability

ABBC

Blueberry

Red CreekAttachie

Septimus

Tower

ParklandSunset

Sunrise

Sundown

Dawson

Pouce Coupe

Ante Creek

Attachie

$45MM • 2 wells

Advance towards

commercialization with

multi-well pad and long-term

infrastructure evaluation

Ante Creek

$75MM • 8 wells

Focus on results from new

wells and advance technical

learnings through

optimization activities

Pembina

$30MM

Manage production declines

and maximize free cash

flow generation from light

oil production

Parkland/Tower

$175MM • 13 wells

Sustain production at

current facility capacity

and interconnect Parkland

and Dawson assets

Sunrise

$190MM • 23 wells

Phase II facility construction

and pipeline infrastructure

and drill wells to fill facility

(on-stream mid-year 2019)

Pembina

Redwater

Dawson

$150MM • 17 wells

Manage overall pace

of development and

continue to develop

Lower Montney

$390MM - Sustaining Capital

$275MM - Growth and Development Capital

$25MM - Non-core and Corporate Capital

SUMMARY

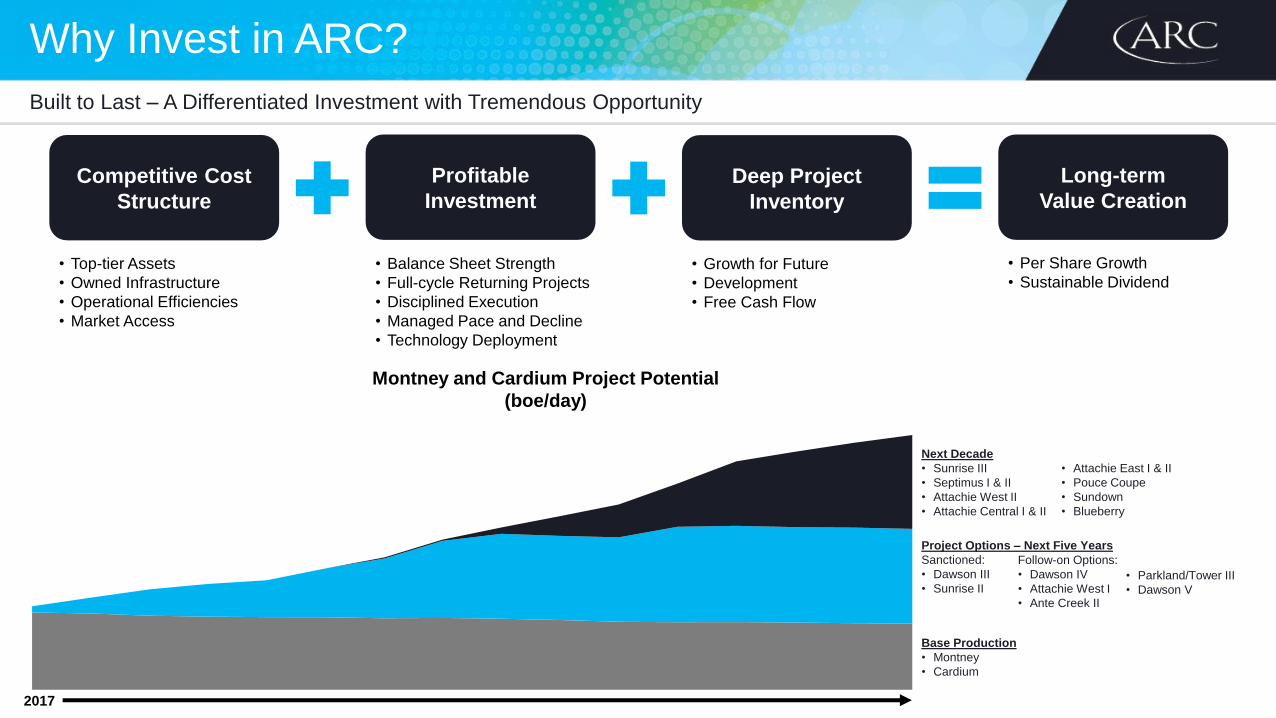

Why Invest in ARC?

Built to Last – A Differentiated Investment with Tremendous Opportunity

• Top-tier Assets

• Owned Infrastructure

• Operational Efficiencies

• Market Access

• Balance Sheet Strength

• Full-cycle Returning Projects

• Disciplined Execution

• Managed Pace and Decline

• Technology Deployment

• Growth for Future

• Development

• Free Cash Flow

• Per Share Growth

• Sustainable Dividend

Montney and Cardium Project Potential

(boe/day)

2017

Competitive Cost

Structure

Profitable

Investment

Deep Project

Inventory

Long-term

Value Creation

Base Production

• Montney

• Cardium

Project Options – Next Five Years

Sanctioned:

• Dawson III

• Sunrise II

Next Decade

• Sunrise III

• Septimus I & II

• Attachie West II

• Attachie Central I & II

• Attachie East I & II

• Pouce Coupe

• Sundown

• Blueberry

Follow-on Options:

• Dawson IV

• Attachie West I

• Ante Creek II

• Parkland/Tower III

• Dawson V

Our Plan

2017

Reduced the

dividend

Sold Saskatchewan

assets

Eliminated DRIP

and SDP plans

118,000 boe per day

2018

Sustain Montney

businesses

Progress Sunrise

Phase II

Advance Attachie

piloting activities

130,000 to 134,000

boe per day

2019

Maintain consistent

investment levels

Bring on Sunrise

Phase II

Progress Dawson

Phase IV to add

~17,500 boe per day

ARC’s Plan Is Fully Funded and Will Result in 10 Per Cent Production CAGR over a Three-year Period

2016

Brought on Dawson

Phase III

Rebuilt liquids

production from

divestments

Achieved success

in Lower Montney

and Attachie

120,000 to 124,000

boe per day

APPENDIX

This presentation contains forward-looking information as to ARC’s internal projections, expectations or beliefs relating to future eventsor future performance and includes information as to our future well inventory in our core areas, our exploration and development drillingand other exploitation plans for 2017, 2018 and beyond, and related production expectations, costs and cash flow, expenses, our plansfor constructing and expanding facilities, the volume of ARC's oil and gas reserves and the volume of ARC's oil and gas resources in thenortheast British Columbia Montney (“NE BC Montney”), the recognition of additional reserves and the capital required to do so, the lifeof ARC's reserves, the volume and product mix of ARC's oil and gas production, future results from operations and operating metrics.These statements represent Management’s expectations or beliefs concerning, among other things, future operating results and variouscomponents thereof or the economic performance of ARC. The projections, estimates and beliefs contained in such forward-lookingstatements are based on Management's assumptions relating to the production performance of ARC’s oil and gas assets, the cost andcompetition for services, the continuation of ARC’s historical experience with expenses and production, changes in the capitalexpenditure budgets, future commodity prices, continuing access to capital and the continuation of the current regulatory and tax regimein Canada and necessarily involve known and unknown risks and uncertainties, such as changes in oil and gas prices, infrastructureconstraints in relation to the development of the Montney in British Columbia, risks associated with the degree of certainty in resourceassessments and including the business risks discussed in ARC’s annual and quarterly MD&A and other continuous disclosuredocuments, and related to Management’s assumptions, which may cause actual performance and financial results in future periods todiffer materially from any projections of future performance or results expressed or implied by such forward-looking statements.Accordingly, readers are cautioned that events or circumstances could cause actual results to differ materially from those predicted.Other than the 2017 and 2018 Guidance, which is discussed quarterly, ARC does not undertake to update any forward-lookinginformation in this document whether as to new information, future events or otherwise except as required by securities lawsand regulations.

We have adopted the standard of 6 Mcf:1 barrel when converting natural gas to barrels of oil equivalent ("boe"). Boe may be misleading,particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 barrel is based on an energy equivalency conversion method primarilyapplicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the currentprice of crude oil as compared to natural gas is significantly different than the energy equivalency of the 6:1 conversion ratio, utilizing the6:1 conversion ratio may be misleading as an indication of value.

Forward-looking Statements

Reserves and Resources Disclosure

All reserves and resources volumes for NE BC Montney and elsewhere in this presentation are, unless indicated otherwise, asat December 31, 2016 as evaluated by GLJ Petroleum Consultants Ltd. in accordance with the definitions, standards andprocedures contained in the Canadian Oil and Gas Evaluation Handbook and National Instrument 51-101 – Standards forDisclosure for Oil and Gas Activities.

TPIIP, DPIIP and UPIIP have been estimated using a one per cent porosity cut-off for shale gas and tight oil.

Reserves volumes for the NE BC Montney and elsewhere in this presentation are, unless indicated otherwise, Proved plusProbable, while the resource categories for NE BC Montney in this presentation are “Best Estimates.” “NE BC Montney”includes lands in Pouce Coupe, Alberta.

All reserves and resources volumes for NE BC Montney and elsewhere in this presentation are company gross.

Gas volumes are “sales” for reserves and resource and raw gas for DPIIP and TPIIP.

The tight oil DPIIP is a stock tank barrel.

All DPIIP and TPIIP other than cumulative production, reserves, Economic Contingent Resources and Prospective Resourceshave been categorized as unrecoverable.

The amount of natural gas and liquids ultimately recovered from ARC’s NE BC Montney resource will be primarily a function ofthe future price of both commodities.

This presentation contains metrics commonly used in the oil and natural gas industry, such as “recycle ratio,” “finding anddevelopment costs,” “finding and development recycle ratio,” “finding, development and acquisition costs,” “operatingnetbacks,” and “reserve life index.” These terms do not have a standardized meaning and may not be comparable to similarmeasures presented by other companies, and therefore should not be used to make such comparisons.

Definitions of Oil and Gas Reserves and Resources

Reserves are estimated remaining quantities of oil and natural gas and related substances anticipated to be recoverable from known accumulations, as of a given date,

based on the analysis of drilling, geological, geophysical and engineering data; the use of established technology; and specified economic conditions, which are generally

accepted as being reasonable. Reserves are classified according to the degree of certainty associated with the estimates as follows:

Proved Reserves are those reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered

will exceed the estimated proved reserves.

Probable Reserves are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities

recovered will be greater or less than the sum of the estimated proved plus probable reserves.

Possible Reserves are those additional reserves that are less certain to be recovered than probable reserves. It is unlikely that the actual remaining quantities

recovered will exceed the sum of the estimated proved plus probable plus possible reserves.

Resources encompasses all petroleum quantities that originally existed on or within the earth’s crust in naturally occurring accumulations, including Discovered and

Undiscovered (recoverable and unrecoverable) plus quantities already produced. “Total Resources” is equivalent to “Total Petroleum Initially-in-Place”. Resources are

classified in the following categories:

Total Petroleum Initially-In-Place (“TPIIP”) is that quantity of petroleum that is estimated to exist originally in naturally occurring accumulations. It includes that

quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations, prior to production, plus those estimated quantities in

accumulations yet to be discovered.

Discovered Petroleum Initially-In-Place (“DPIIP”) is that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations prior to

production. The recoverable portion of discovered petroleum initially in place includes production, reserves, and contingent resources; the remainder is unrecoverable.

Contingent Resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established

technology or technology under development but which are not currently considered to be commercially recoverable due to one or more contingencies.

Economic Contingent Resources (“ECR”) are those contingent resources which are currently economically recoverable.

Project Maturity Subclass Development Pending is defined as a contingent resource that has been assigned a high chance of development and the resolution of

final conditions for development are being actively pursued.

Forecast

Definitions of Oil and Gas Reserves and Resources

Project Maturity Subclass Development Unclarified as a contingent resources that requires further appraisal to clarify the potential for development and has been

assigned a lower chance of development until contingencies can be clearly defined.

Undiscovered Petroleum Initially-In-Place (“UPIIP”) is that quantity of petroleum that is estimated, on a given date, to be contained in accumulations yet to be

discovered. The recoverable portion of undiscovered petroleum initially in place is referred to as “prospective resources” and the remainder as “unrecoverable.”

Prospective Resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application

of future development projects.

Unrecoverable is that portion of DPIIP and UPIIP quantities which is estimated, as of a given date, not to be recoverable by future development projects. A portion of

these quantities may become recoverable in the future as commercial circumstances change or technological developments occur; the remaining portion may never be

recovered due to the physical/chemical constraints represented by subsurface interaction of fluids and reservoir rocks.

Uncertainty Ranges are described by the Canadian Oil and Gas Evaluation Handbook as low, best, and high estimates for reserves and resources as follows:

Low Estimate: This is considered to be a conservative estimate of the quantity that will actually be recovered. It is likely that the actual remaining quantities recovered

will exceed the low estimate. If probabilistic methods are used, there should be at least a 90 percent probability (P90) that the quantities actually recovered will equal or

exceed the low estimate.

Best Estimate: This is considered to be the best estimate of the quantity that will actually be recovered. It is equally likely that the actual remaining quantities

recovered will be greater or less than the best estimate. If probabilistic methods are used, there should be at least a 50 percent probability (P50) that the quantities

actually recovered will equal or exceed the best estimate.

High Estimate: This is considered to be an optimistic estimate of the quantity that will actually be recovered. It is unlikely that the actual remaining quantities recovered

will exceed the high estimate. If probabilistic methods are used, there should be at least a 10 percent probability (P10) that the quantities actually recovered will equal

or exceed the high estimate.

Non-GAAP Measures

Throughout this presentation, ARC uses the terms operating netback (“netback”) to analyze financial and operatingperformance. This non-GAAP measure presented does not have any standardized meaning prescribed by GAAP and thereforemay not be comparable with the calculation of similar measures for other entities. ARC feels that this non-GAAP measure is akey industry benchmark of performance for ARC and provide investors with information that is commonly used by other oil andgas companies.

Netback

Netback is a common non-GAAP metric used in the oil and gas industry. This measurement assists Management and investorsin evaluating operating results on a per boe basis to better analyze performance on a comparable basis. A calculation ofnetback is disclosed within ARC’s MD&A.

This presentation contains forward-looking information and statements that may be identified by words like “outlook”,“estimates” and similar expressions. These forward-looking statements are based on certain assumptions that involve a numberof risks and uncertainties and are not guarantees of future performance. Reference is made to the section titled “Forward-looking Statements” at the beginning of the presentation and also to the February 8, 2017 news release entitled, “ARCResources Ltd. Announces Fourth Quarter and Year-end 2016 Results as It Increases Capital Investment in ARC’s Multi-year,Large-scale Development Projects at Dawson, Parkland/Tower, and Sunrise” which may be found on ARC’s website atwww.arcresources.com or on SEDAR at www.sedar.com and which are hereby incorporated by reference in this presentationand which outline a number of assumptions, risks and uncertainties associated with forward-looking statements. Actual resultscould differ materially as a result of changes to ARC’s plans, the impact of changes in commodity prices, general economic,market and business conditions as well as production, development and operating performance and other risks associated withoil and gas operations.

For further information about ARC Resources Ltd. please visit our website www.arcresources.com

Or contact:Investor RelationsE-mail: [email protected] 403.503.8600Toll Free 1.888.272.4900F 403.509.6417ARC Resources Ltd.1200, 308 – 4th Avenue SWCalgary, AB T2P 0H7