Embed Size (px)

Citation preview

Are Capital Controls Countercyclical?

by

A.Fernandez A.Rebucci M.Uribe

June 16, 2015

1

Capital Controls: From Villain To Hero

• Early 1990s: large capital inflows to emerging countries. Capi-

tal controls were viewed, with few exceptions, as distortions that

hindered the efficient allocation of capital across countries and

thus impeded economic growth. To a large extent, policymakers

allowed capital to flow unfettered.

• Many of the booms of the early 1990s ended in sudden stops

and financial and/or exchange-rate crises (Southeast Asia and

Russia in the late 1990s, South America in the early 2000s, and

peripheral Europe in the late 2000s). Since then policymakers

view capital controls with more benign eyes.

• The strongest indication of this change of sentiment is that

the IMF now sees capital controls as an appropriate tool for

macroeconomic stabilization (IMF, 2011).

2

Prudential Capital Controls

Capital controls are imposed during booms and relaxed during

contractions.

3

Prudential Capital Controls: Theories

• Collateralized borrowing with value of collateral depending on

a price that individuals take as given: Lorenzoni, 2008; Korinek

2010; Jeanne and Korinek, 2011; Bianchi, 2011; Bianchi and

Mendoza, 2010 and 2013; Fernandez-Arias and Lombardo, 1998;

Benigno, Chen, Otrok, and Rebucci, 2012a,b; and Uribe, 2006,

2007.

• Nominal rigidity (e.g., downward nominal wage rigidity) and

suboptimal monetary policy (e.g. currency pegs): Schmitt-

Grohe and Uribe, 2012a,b; and Farhi and Werning, 2012; Ot-

tonello, 2013.

• The frictions highlighted by both of these theories generate

externalities that cause overborrowing and overspending during

booms and the reverse during contractions. Prudential capital

control policy allows agents to internalize these externalities.

4

This Paper addresses the question

Do countries in practice apply capital controls prudentially

as suggested by the new theories?

5

Preview of Main Findings

• Capital controls are remarkably stable; small standard deviation

of cyclical component.

• Unconditionally, capital controls are virtually acyclical: The

correlation between capital controls and output is about zero.

• Contrary to what a prudential stance would suggest, controls

on inflows are positively correlated with controls on outflows.

• Capital controls are virtually unchanged during economic booms

or busts.

6

Selected Related Literature

• Much of the related empirical literature has focused on deter-

mining whether capital controls are effective at stabilizing the

economy (see, among many others, Ostry et al., 2010; Klein,

2012; and Forbes, Fratzscher, and Straub, 2013). By contrast,

the present paper aims at establishing whether policymakers sys-

tematically use capital controls in a prudential or countercyclical

fashion.

• The present paper is most closely related to Aizenman and

Pasricha (2013) who argue that emerging countries that liber-

alized capital outflow controls during the 2000s did so primarily

because of concerns about net capital inflows. This paper find no

evidence of this link. Possible reason for discrepancy: Aizenman

and Pasricha’s measure of capital controls include a significant

number of financial restrictions involving residents of the same

country (e.g., foreign-currency transactions), which are not re-

garded as capital controls in the present paper.

7

Data on Capital Controls

• Starting Point: Schindler’s annual index of capital controls cov-ering the period 1995 to 2005 and 91 countries (22 developed,45 emerging, and 24 low-income).

• This paper: Extends Schindler’s data set to include the period2006-2011.

• Source: IMF’s Annual Report on Exchange Arrangements andExchange Restrictions (AREAER).

• Type of Index: De jure. Takes on 13 equally spaced valuesfrom 0 (no restrictions) to 1 (restrictions in all asset categories).

• Disaggregation: distinguishes inflows and outflows and 6 assetcategories (equity, bonds, money market instruments, mutualfunds, financial credit, and foreign direct investment.)

• All series filtered with a linear trend.

8

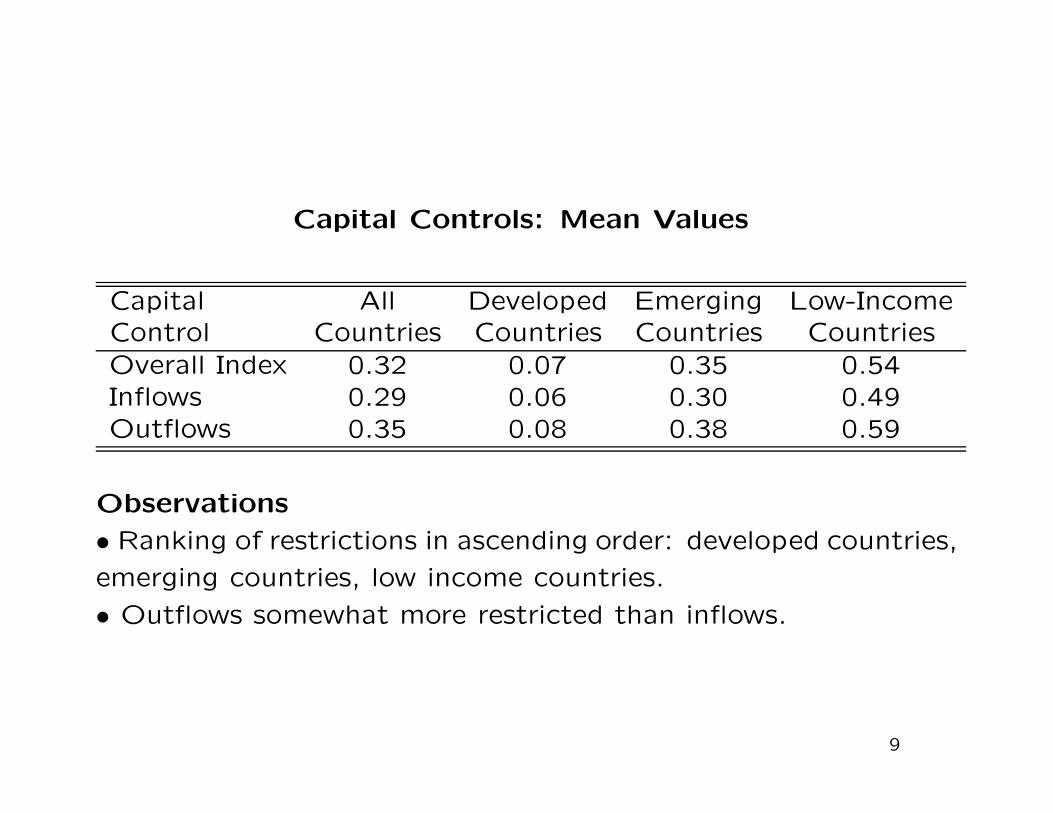

Capital Controls: Mean Values

Capital All Developed Emerging Low-IncomeControl Countries Countries Countries Countries

Overall Index 0.32 0.07 0.35 0.54Inflows 0.29 0.06 0.30 0.49Outflows 0.35 0.08 0.38 0.59

Observations

• Ranking of restrictions in ascending order: developed countries,

emerging countries, low income countries.

• Outflows somewhat more restricted than inflows.

9

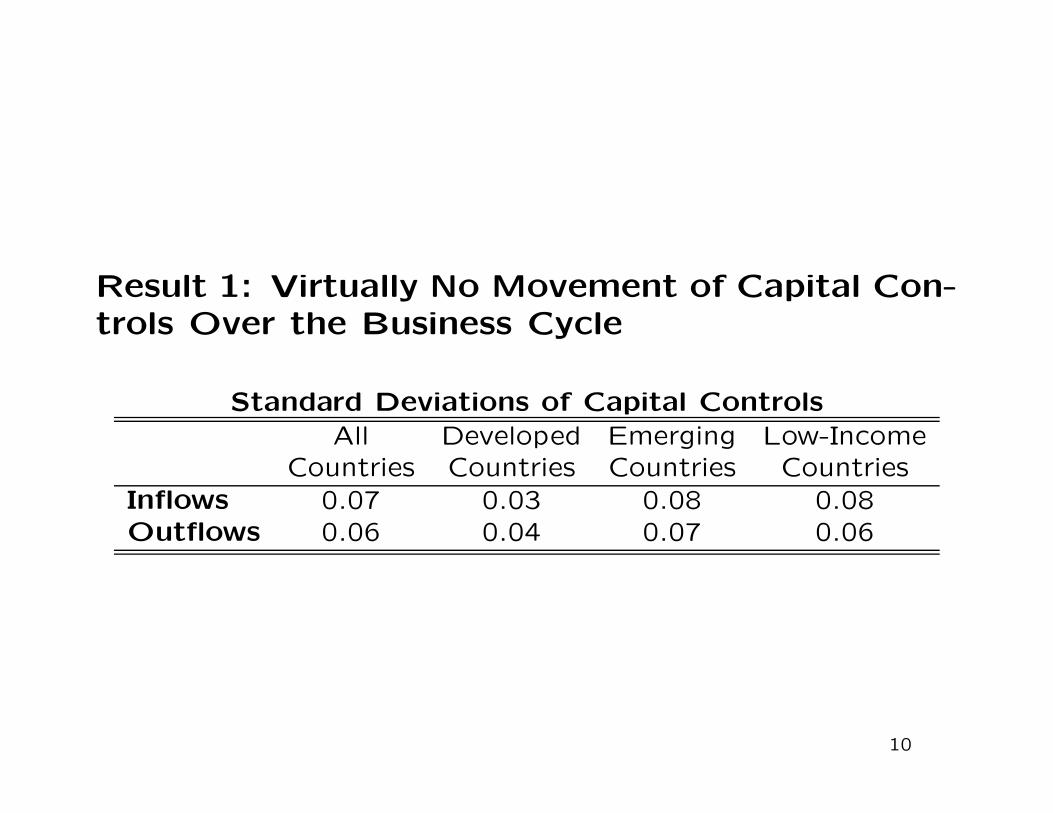

Result 1: Virtually No Movement of Capital Con-trols Over the Business Cycle

Standard Deviations of Capital Controls

All Developed Emerging Low-IncomeCountries Countries Countries Countries

Inflows 0.07 0.03 0.08 0.08Outflows 0.06 0.04 0.07 0.06

10

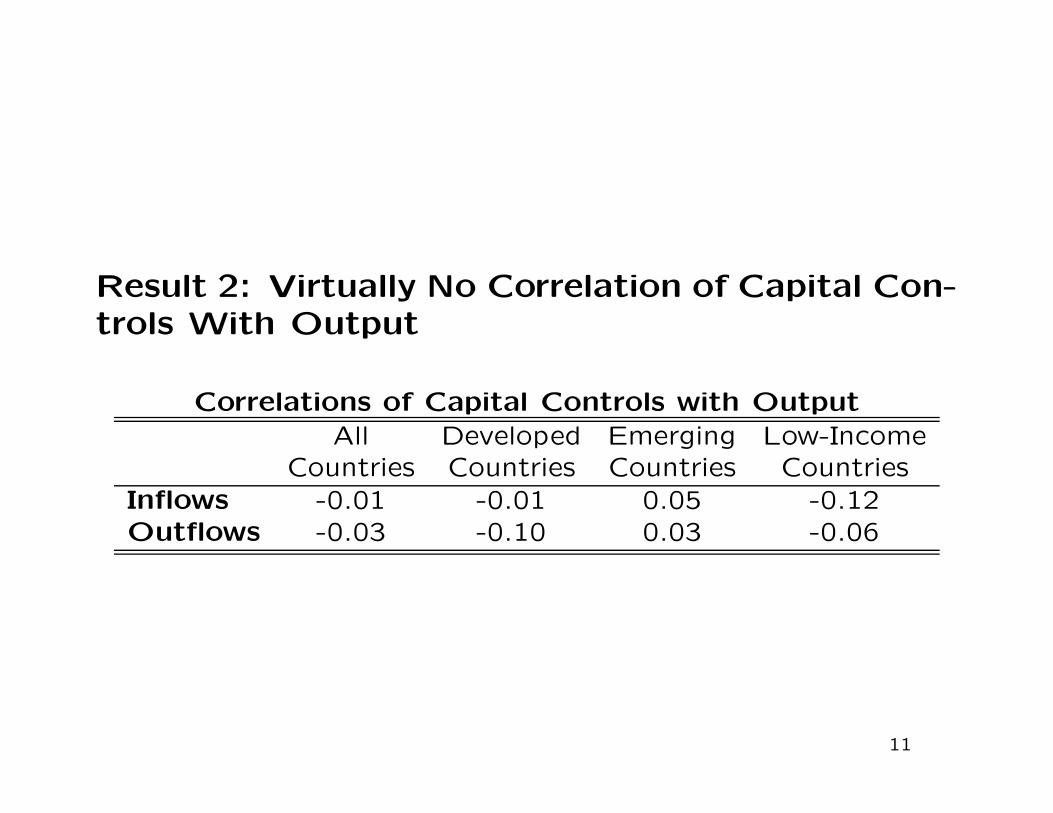

Result 2: Virtually No Correlation of Capital Con-trols With Output

Correlations of Capital Controls with Output

All Developed Emerging Low-IncomeCountries Countries Countries Countries

Inflows -0.01 -0.01 0.05 -0.12Outflows -0.03 -0.10 0.03 -0.06

11

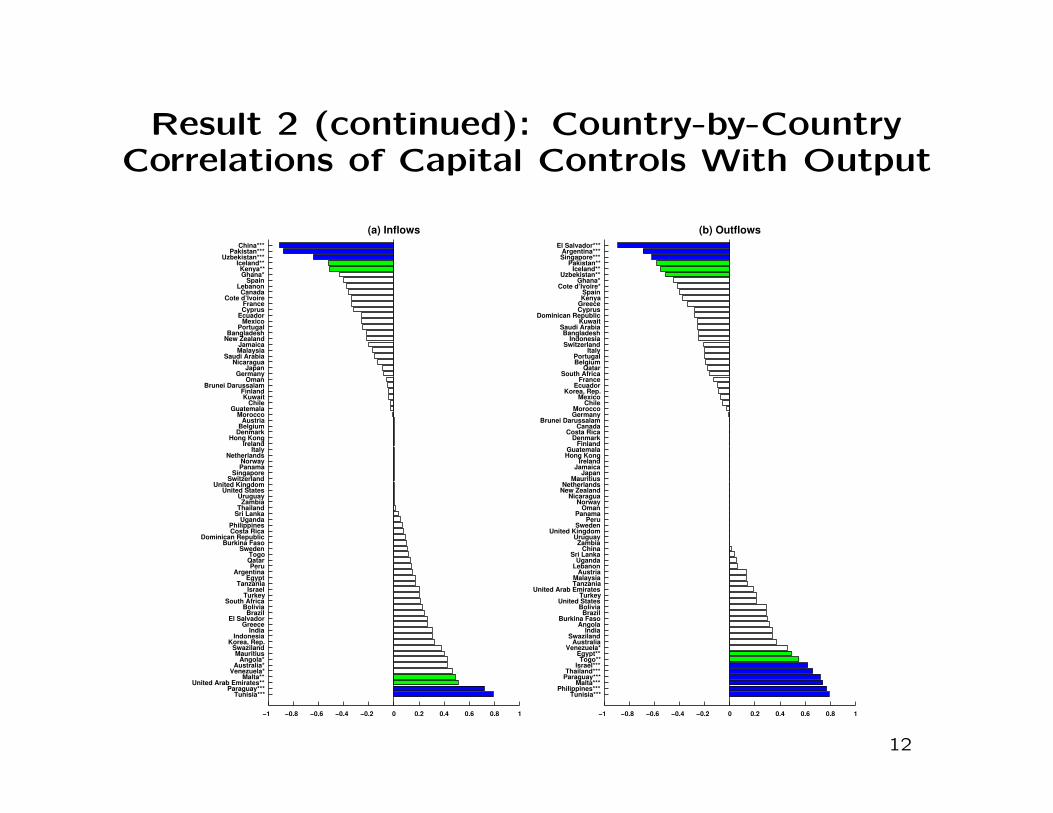

Result 2 (continued): Country-by-CountryCorrelations of Capital Controls With Output

−1 −0.8 −0.6 −0.4 −0.2 0 0.2 0.4 0.6 0.8 1

China***Pakistan***

Uzbekistan***Iceland**Kenya**Ghana*

SpainLebanon

CanadaCote d’Ivoire

FranceCyprus

EcuadorMexico

PortugalBangladesh

New ZealandJamaicaMalaysia

Saudi ArabiaNicaragua

JapanGermany

OmanBrunei Darussalam

FinlandKuwait

ChileGuatemala

MoroccoAustria

BelgiumDenmark

Hong KongIreland

ItalyNetherlands

NorwayPanama

SingaporeSwitzerland

United KingdomUnited States

UruguayZambia

ThailandSri Lanka

UgandaPhilippinesCosta Rica

Dominican RepublicBurkina Faso

SwedenTogoQatarPeru

ArgentinaEgypt

TanzaniaIsrael

TurkeySouth Africa

BoliviaBrazil

El SalvadorGreece

IndiaIndonesia

Korea, Rep.SwazilandMauritius

Angola*Australia*

Venezuela*Malta**

United Arab Emirates**Paraguay***

Tunisia***

(a) Inflows

−1 −0.8 −0.6 −0.4 −0.2 0 0.2 0.4 0.6 0.8 1

El Salvador***Argentina***Singapore***

Pakistan**Iceland**

Uzbekistan**Ghana*

Cote d’Ivoire*SpainKenya

GreeceCyprus

Dominican RepublicKuwait

Saudi ArabiaBangladesh

IndonesiaSwitzerland

ItalyPortugalBelgium

QatarSouth Africa

FranceEcuador

Korea, Rep.Mexico

ChileMoroccoGermany

Brunei DarussalamCanada

Costa RicaDenmark

FinlandGuatemalaHong Kong

IrelandJamaica

JapanMauritius

NetherlandsNew Zealand

NicaraguaNorway

OmanPanama

PeruSweden

United KingdomUruguayZambia

ChinaSri Lanka

UgandaLebanon

AustriaMalaysiaTanzania

United Arab EmiratesTurkey

United StatesBoliviaBrazil

Burkina FasoAngola

IndiaSwaziland

AustraliaVenezuela*

Egypt**Togo**

Israel***Thailand***

Paraguay***Malta***

Philippines***Tunisia***

(b) Outflows

12

Result 3: Positive Correlation Between Controlson Inflows and Controls on Outflows

Correlations Between Capital Controls on Inflows

and Capital Controls on Output

All Developed Emerging Low-IncomeCountries Countries Countries Countries

0.28 0.21 0.32 0.31

13

Result 3 (continued): Correlation BetweenControls on Inflows and Controls on Outflows

−1 −0.8 −0.6 −0.4 −0.2 0 0.2 0.4 0.6 0.8 1

South Africa**El Salvador**

United Arab Emirates**Indonesia

BoliviaAngola

Korea, Rep.Malaysia

PhilippinesAustria

BelgiumBrunei Darussalam

CanadaCosta Rica

DenmarkFinland

GuatemalaHong Kong

IrelandItaly

JapanMauritius

NetherlandsNew Zealand

NicaraguaNorway

OmanPanama

PeruSingapore

SwedenSwitzerland

United KingdomUnited States

UruguayZambia

Dominican RepublicPortugal

TogoThailand

EgyptBurkina Faso

ChinaGreece

LebanonArgentinaMorocco

Bangladesh*Australia**Pakistan**Kuwait***France***

Ecuador***Qatar***

Mexico***Brazil***

Cote d’Ivoire***Israel***Chile***

Venezuela***India***

Jamaica***Saudi Arabia***

Kenya***Turkey***

Malta***Germany***

Swaziland***Cyprus***Ghana***

Uzbekistan***Tanzania***

Iceland***Paraguay***

Spain***Sri Lanka***

Tunisia***Uganda***

14

The Behavior of Capital Controls AroundBooms and Busts

Definition of a Boom (Bust): At least 3 consecutive years of

output above (below) trend.

Features of Idenfified Booms (Busts):

• Average magnitude of peaks (troughs), 8% above (below)

trend.

• Average duration of booms (busts), 7 years.

15

Boom-Bust Episodes and Capital Controls

−2 −1 0 1 2−0.31

0

0.34

Years

Boom

0

5

10

−2 −1 0 1 2−0.34

0

0.38

Years

Bust

−8

−7

−6

−5

−4

−3

−2

−2 −1 0 1 2−0.34

0

0.33

Years

Boom

0

5

10

−2 −1 0 1 2−0.36

0

0.42

Years

Bust

−8

−7

−6

−5

−4

−3

−2

−2 −1 0 1 2−0.37

0

0.39

Years

Boom

0

5

10

−2 −1 0 1 2−0.4

0

0.44

Years

Bust

−8

−7

−6

−5

−4

−3

−2

Average Index (lhs) Average Output Gap (rhs) Two Standard Deviation for the Index (lhs)

(a) Overall Index

(b) Inflows

(c) Outflows

16

Boom-Bust Episodes and Capital Controls: FourDecompositions

• By level of development.

• By Exchange-Rate Regime.

• By level of external indebtedness.

• By asset category.

17

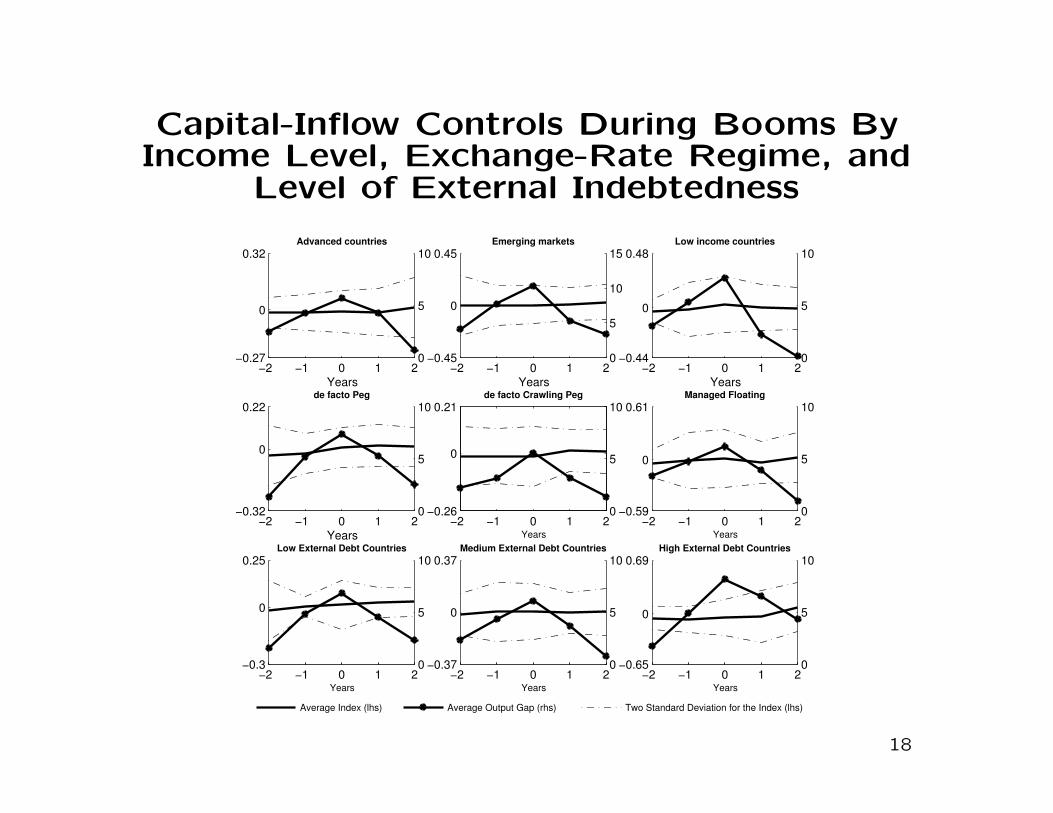

Capital-Inflow Controls During Booms ByIncome Level, Exchange-Rate Regime, and

Level of External Indebtedness

−2 −1 0 1 2−0.27

0

0.32

Years

Advanced countries

0

5

10

−2 −1 0 1 2−0.45

0

0.45

Years

Emerging markets

0

5

10

15

−2 −1 0 1 2−0.44

0

0.48

Years

Low income countries

0

5

10

−2 −1 0 1 2−0.32

0

0.22

Years

de facto Peg

0

5

10

−2 −1 0 1 2−0.26

0

0.21

Years

de facto Crawling Peg

0

5

10

−2 −1 0 1 2−0.59

0

0.61

Years

Managed Floating

0

5

10

−2 −1 0 1 2−0.3

0

0.25

Years

Low External Debt Countries

0

5

10

−2 −1 0 1 2−0.37

0

0.37

Years

Medium External Debt Countries

0

5

10

−2 −1 0 1 2−0.65

0

0.69

Years

High External Debt Countries

0

5

10

Average Index (lhs) Average Output Gap (rhs) Two Standard Deviation for the Index (lhs)

18

Acyclicality of Granular Measures ofCapital-Inflow Controls

−2 −1 0 1 2−0.49

0

0.49

Years

eq

0

5

10

−2 −1 0 1 2−0.46

0

0.43

Years

bo

0

5

10

−2 −1 0 1 2−0.54

0

0.56

Years

di

0

5

10

−2 −1 0 1 2−0.63

0

0.66

Years

eq−plbn

0

5

10

−2 −1 0 1 2−0.6

0

0.63

Years

bo−plbn

0

5

10

−2 −1 0 1 2−0.56

0

0.63

Years

dii

0

5

10

−2 −1 0 1 2−0.56

0

0.54

Years

eq−siar

0

5

10

−2 −1 0 1 2−0.66

0

0.6

Years

bo−siar

0

5

10

−2 −1 0 1 2−0.48

0

0.49

Years

ldi

0

5

10

Average Inflow Index (lhs) Average Output Gap(rhs) Two Standard Deviation for the Index(lhs)

19

Capital Controls, the Real Exchange Rate,and the Current Account

• Based on a meta analysis of more than 30 empirical studies,

Magud, Reinhart, and Rogoff (2011), find that two important

reasons why policymakers impose capital controls are:

– To reduce real exchange-rate pressure.

– To reduce the volume of capital flows.

20

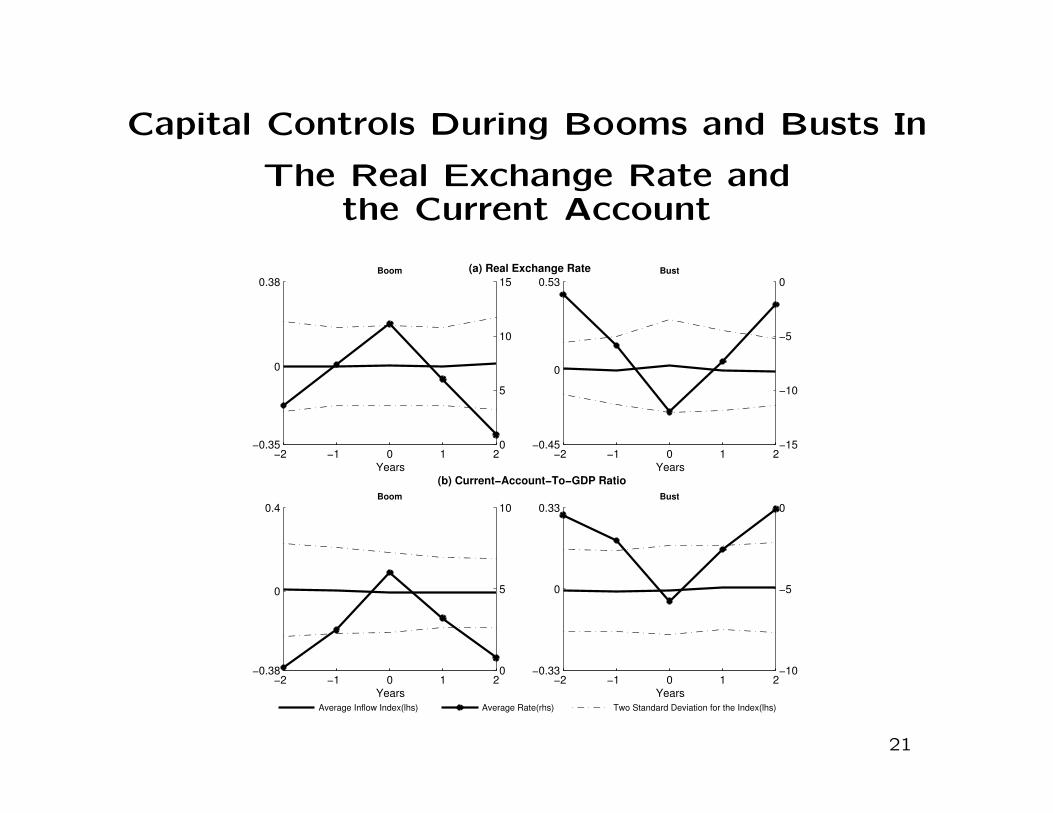

Capital Controls During Booms and Busts In

The Real Exchange Rate andthe Current Account

−2 −1 0 1 2−0.35

0

0.38

Years

Boom

0

5

10

15

−2 −1 0 1 2−0.45

0

0.53

Years

Bust

−15

−10

−5

0

−2 −1 0 1 2−0.38

0

0.4

Years

Boom

0

5

10

−2 −1 0 1 2−0.33

0

0.33

Years

Bust

−10

−5

0

Average Inflow Index(lhs) Average Rate(rhs) Two Standard Deviation for the Index(lhs)

(a) Real Exchange Rate

(b) Current−Account−To−GDP Ratio

21

Capital Controls Around the Great Contraction

• Endogeneity Problem: Some recessions may not be identi-

fied precisely because capital controls were successful at making

them not happen.

• The global recession of 2007-2009 is a useful natural experi-

ment. It originated in the United States and then spread globally.

For most countries, it was an exogenous negative shock.

• Question: Do we observe any systematic movement in cap-

ital controls across countries before, during, or after the great

contraction?

22

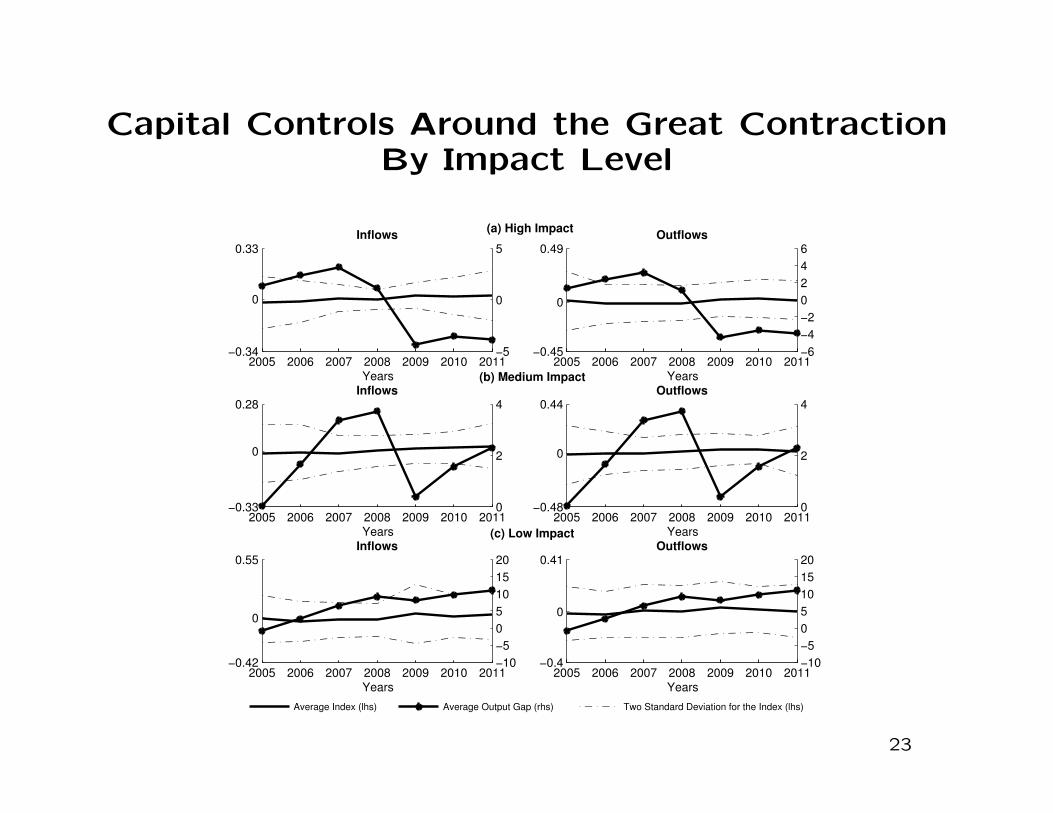

Capital Controls Around the Great ContractionBy Impact Level

2005 2006 2007 2008 2009 2010 2011−0.34

0

0.33

Years

Inflows

−5

0

5

2005 2006 2007 2008 2009 2010 2011−0.45

0

0.49

Years

Outflows

−6

−4

−2

0

2

4

6

2005 2006 2007 2008 2009 2010 2011−0.33

0

0.28

Years

Inflows

0

2

4

2005 2006 2007 2008 2009 2010 2011−0.48

0

0.44

Years

Outflows

0

2

4

2005 2006 2007 2008 2009 2010 2011−0.42

0

0.55

Years

Inflows

−10

−5

0

5

10

15

20

2005 2006 2007 2008 2009 2010 2011−0.4

0

0.41

Years

Outflows

−10

−5

0

5

10

15

20

Average Index (lhs) Average Output Gap (rhs) Two Standard Deviation for the Index (lhs)

(a) High Impact

(b) Medium Impact

(c) Low Impact

23

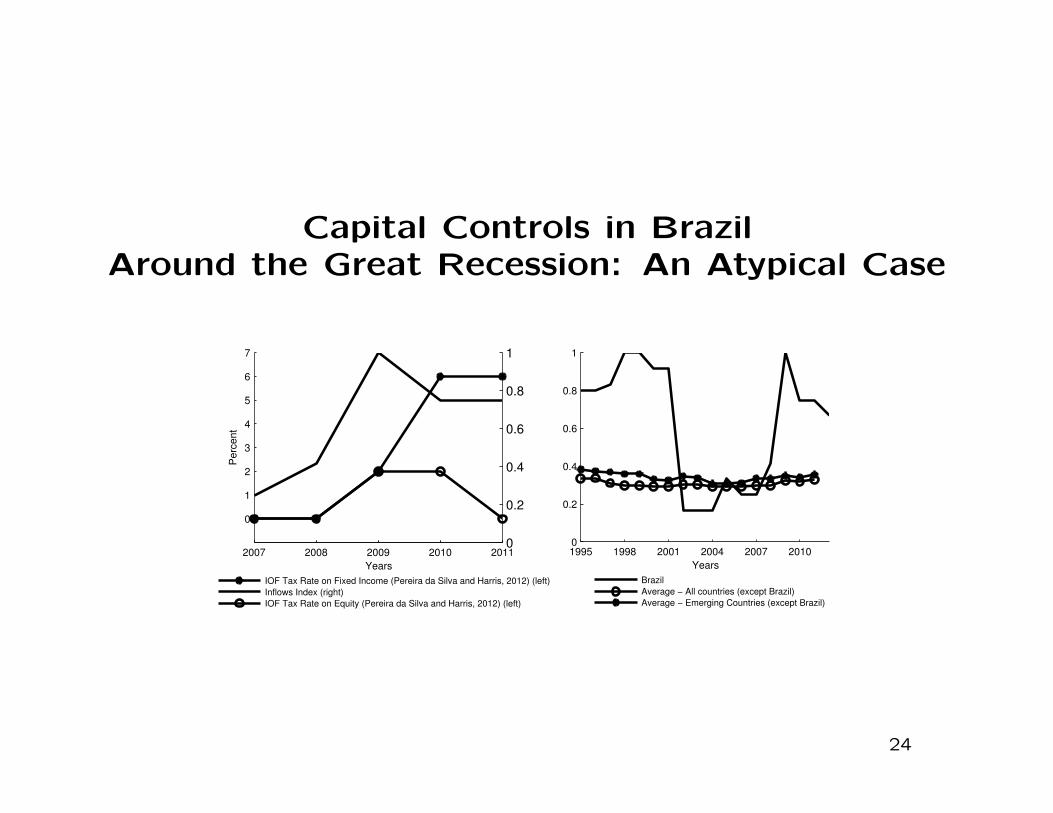

Capital Controls in BrazilAround the Great Recession: An Atypical Case

1995 1998 2001 2004 2007 20100

0.2

0.4

0.6

0.8

1

Years

Brazil

Average − All countries (except Brazil)

Average − Emerging Countries (except Brazil)

2007 2008 2009 2010 2011

0

1

2

3

4

5

6

7

Years

Perc

ent

0

0.2

0.4

0.6

0.8

1

IOF Tax Rate on Fixed Income (Pereira da Silva and Harris, 2012) (left)

Inflows Index (right)

IOF Tax Rate on Equity (Pereira da Silva and Harris, 2012) (left)

24

Observations

(1) The updated Schindler index for Brazil captures well recently

observed movements in the Brazilian IOF capital control tax,

which takes intensity into account since it measures the actual

tax rate.

(2) Brazilian capital controls around the global recession are

atypical, in the sense that they move much more markedly than

observed in the rest of the world.

25

Alternative Indices of Capital Controls and Coun-tries with Active Capital Control Policy

– The Quinn index.

– The Chinn-Ito index

• (3) Episodic Capital Controls

26

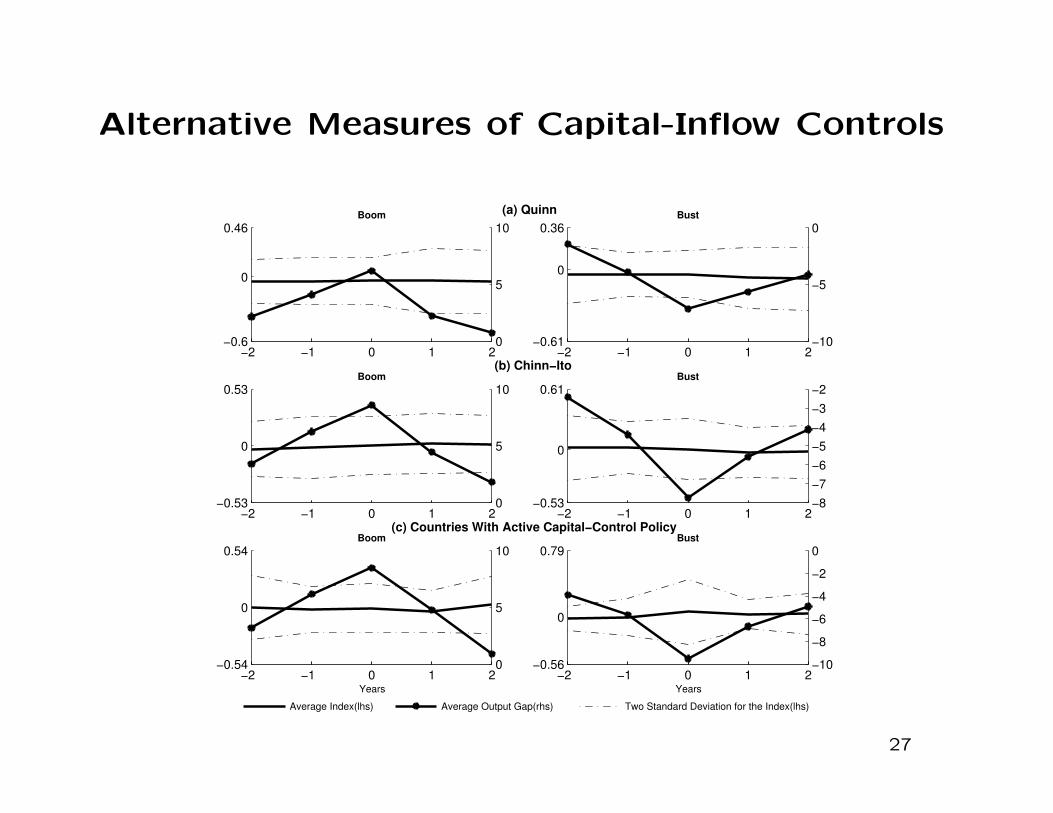

Alternative Measures of Capital-Inflow Controls

−2 −1 0 1 2−0.6

0

0.46Boom

0

5

10

−2 −1 0 1 2−0.61

0

0.36Bust

−10

−5

0

−2 −1 0 1 2−0.53

0

0.53Boom

0

5

10

−2 −1 0 1 2−0.53

0

0.61Bust

−8

−7

−6

−5

−4

−3

−2

−2 −1 0 1 2−0.54

0

0.54

Years

Boom

0

5

10

−2 −1 0 1 2−0.56

0

0.79

Years

Bust

−10

−8

−6

−4

−2

0

Average Index(lhs) Average Output Gap(rhs) Two Standard Deviation for the Index(lhs)

(a) Quinn

(b) Chinn−Ito

(c) Countries With Active Capital−Control Policy

27

Conclusion

• New theories of capital controls suggest that they should be

applied in a prudential or countercyclical fashion.

• The present empirical investigation finds that on average pol-

icymakers have not applied capital controls in ways consistent

with the new theories.

• In particular, on average capital controls are remarkably acycli-

cal.

• Two Interpretations:

(1) We are in the presence of a case of theory running ahead of

policymaking. Under this view, observed movements in capital

controls (or lack thereof) are suboptimal. As time goes by and

theories percolate policy circles, we should observe changes in

the cyclical behavior of capital controls.

(2) Policymakers know more than theorists. Under this view,

actual capital control policy may be optimal, and more feedback

from policy to theory is needed.

28