Embed Size (px)

Citation preview

Are Financial Markets Signalling Recession?—August 2018

— The flattening of the US yield curve has led some to forecast a US recession (with an inverted curve seen as an accurate recession signal). While there are clear risks - including protectionism, geopolitics, emerging market concerns and the US budget deficit – our analysis indicates that a US recession is unlikely until well into next decade.

— Domestically, the conversation is different yet doubts about the sustainability of growth continue to be expressed. Overall, the trends are favourable. The labour market has strengthened, accompanied by rising business investment. Strong international trade surpluses are also being recorded – although drought is impacting farm production.

Executive Summary

— The housing and household sectors are areas of vulnerability, although consumer sentiment and spending remain sound and the RBA has observed an easing of financial risks across the economy.

— The latest inflation and wage data show subdued yet gradually improving outcomes. In the short term, the RBA is forecasting one-off factors to lower headline inflation to 1¾%, before rebounding over 2019 and 2020. Given the forward-looking nature of policy, this is likely to see the Bank begin a gradual tightening cycle by mid next year.

2Are Financial Markets Signalling Recession? — August 2018

Recent financial commentary has focussed on the ‘late-cycle’ nature of the US economic upturn (with 2018 being the 9th consecutive year of growth). Fundamental factors, such as unsustainably low unemployment and exceptionally strong profit growth, have been cited as reasons why a US recession may be approaching.

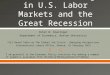

The most common signal being referenced, however, is the yield curve. An inversion of the US yield curve (when long bond yields fall below those at the shorter end of the curve) has historically been a reliable recession predictor, with the past 9 US recessions preceded by an inverted curve (there was a false signal in 1965-66). The lead time from inversion to recession has ranged from 6 to 24 months, as shown in Chart 1.

The fundamental interpretation of the yield curve signal is that an inverse curve indicates tight monetary policy (that is, high short term rates) that ultimately leads to slower growth and falling inflation. Given the predictive nature of financial markets, the bond market is credited with identifying these conditions before they materialise and, in so doing, long term bond yields are pressured downward.

Chart 1 also shows the recent ‘flattening’ of the US curve, as measured by the differential between the 10 year and 1 year bond yield. This spread, at 43bp (at the time of writing), is still positive but a simple projection of the downward trend suggests that the curve could invert in early 2019. The lags referred to above then suggest a possible recession sometime from late 2019.

Are Financial Markets Signalling Recession? —

Two questions therefore arise. The first is whether the US curve will invert within the projected time frame? The market suggests not, with ‘forward’ curves 6, 12 and 18 months out retaining a positive slope - supported by US inflation trends and the Fed’s balance sheet actions (in reducing its bond holdings). The second question is whether an inversion could be a less reliable signal this time?

CHART 1: US Yield Spread vs Recessions

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015Suncorp Macrobond

US 10y-1y Yield SpreadFalse Signal US Recession Dates-1

-2

4%

3

2

1

0

CHART 2: House Prices and Consumer Sentiment

Sep-16 Dec-17 Mar-18 Jun-18Sep-17Jun-17Mar-17Dec-16

Source: Bloomberg, Westpac, CoreLogic/RP Data

96

93

108

Consumer Sentiment Index (LHS)

4 Year High

105

102

99

136

133

148

145

142

139

Capital City House Price Index (RHS)

3Are Financial Markets Signalling Recession? — August 2018

Before addressing this second question, we’re intuitively attracted to a recent comment by BCA Research stating (in reference to this topic) that “every time is always different: there is never a previous period that perfectly matches the current environment”. Amongst the differences we see now versus history are the following.

— Real and nominal bond yields remain historically low, with global central banks having supressed long term yields through their respective quantitative easing (bond purchase) programs since the GFC.

— The US Fed Funds rate, at 2.0%, remains below the Fed’s ‘neutral rate’ estimate of 2.9%, indicating that monetary policy remains stimulatory.

— Alternative yield curve specifications that are also regarded as reliable recession signals have not flattened to the same degree as that shown in Chart 1.

Meanwhile, from a fundamental perspective, recent fiscal stimulus has bolstered US growth and leading indicators do “not suggest any considerable growth slowdown in the short-term” (source: Conference Board).

Clearly, there are risks - including protectionism, geopolitics, emerging market concerns and the escalating US budget deficit – yet there are no obvious threats likely to cause recession until well into the next decade.

“[...] there are no obvious threats likely to cause recession until well into the next decade.”

4Are Financial Markets Signalling Recession? — August 2018

Domestically, the conversation is quite different to that in the US. The yield curve remains positive and monetary policy is not being tightened. Moreover, since it’s been 26 years since Australia has experienced recession, it’s difficult to identify an accurate recession predictor. Nevertheless, that’s not to say that there aren’t unusual financial market developments, with money markets recently capturing attention, as discussed below.

— Australia’s Bank Bill Swap rate (BBSW) has increased significantly in recent months (the 90 day bill rate posting a 2 year high of 2.12% during June).

— Typically, BBSW is influenced by the RBA’s cash rate plus banking system risk and liquidity. Several explanations have been put forward for the recent lift in BBSW, without there being general agreement. What’s clear, is that the episode is unrelated to cash rate expectations (with the RBA clearly ‘on hold’). Furthermore, while there has been some slight widening of credit spreads (the risk margin paid on corporate bonds), the full extent of the BBSW move cannot be attributed to elevated credit risk.

— One impact of the lift in BBSW is the increase in bank funding costs and the resulting potential for mortgage repricing – although the RBA observes that over much of the past 12 months rates on new and outstanding variable housing loans have actually drifted lower.

— Overall, the outlook for BBSW and the degree to which it will remain elevated (and cyclical) is unclear. Encouragingly, the BBSW rate has eased in recent weeks, by 17bp, and market measures of corporate credit risk conditions have improved slightly.

Turning to the domestic implications of US developments we note that, while the US is important for global growth and financial markets, Australia’s direct exposure to the US economy has diminished over time. The US now buys less than 4% of Australian goods exports and, for some time now, the economic cycles of Australia and the US have been desynchronised.

Australian Implications and Money Market Developments —

5Are Financial Markets Signalling Recession? — August 2018

Notwithstanding the above, doubts continue to be expressed about the Australian outlook and the sustainability of domestic economic growth, with the housing market and household sector being areas of vulnerability.

Nevertheless, the latest RBA commentary retains the theme of gradual improvement. We discuss inflation and wages in the following sections yet note that the RBA forecasts unemployment to slowly fall to 5% and GDP growth to be “a little above 3 per cent” in 2018 and 2019.

Looking at the latest trends, employment growth has been strong (2.5% annually) and has been accompanied by rising business investment. Meanwhile, on the external front, Australia continues to record strong trade surpluses – although the drought continues to impact farm production.

The housing sector is an area of concern, with prices having fallen 1.6% over the year (the national house price index is shown in Chart 2). Moreover, household debt levels are high and wage growth low. To date, however, the housing slowdown is orderly (and desired by policy makers) and non-performing loans remain low. Indeed, the RBA regards financial risks as easing. Moreover, from a household perspective, improving income and labour market trends appear to be sustaining both high levels of consumer sentiment (as shown in Chart 2) and spending (with real growth of 2.9% over the past 12 months).

Domestic Growth Backdrop Remains Favourable —

6Are Financial Markets Signalling Recession? — August 2018

Australian Inflation Dynamics —By historical standards, Australian inflation remains low, given the spare capacity across the economy. That said, in-line with the improvement in growth and the labour market, annual headline and underlying CPI inflation has gradually accelerated over recent quarters, after having troughed in late 2016.

Annual ‘headline’ inflation is now running at 2.1%, with the alternative measure of ‘underlying’ inflation a little lower, at 1.9%. Noticeably, in a sign that inflation pressures are slowly broadening, the proportion of the household CPI basket that is increasing by 2% or less has drifted lower and the proportion of the CPI basket rising by 3% or more has edged higher (see Chart 3).

% expenditure items <2%pa

% expenditure items 2-3%pa

% expenditure items >3%pa

CHART 3: Australia CPI Dispersion (% expenditure items)

80%

60%

40%

20%

0%

80%

60%

40%

20%

0%

Mar-03 Mar-07 Mar-11 Mar-15 Mar-19

New Dwelliing Construction

Rents

CHART 4: CPI Housing Costs

%pa9

6

3

0

%pa9

6

3

0

Mar-02 Mar-06 Mar-10 Mar-14 Mar-18

7Are Financial Markets Signalling Recession? — August 2018

Key Inflation Drivers —In terms of the factors that have been restraining Australian inflation (in addition to technological change), there are a few factors worth highlighting. How these play out will be key to how inflation evolves.

— Housing costs, which include new dwelling construction and rents, are an important consideration for CPI. Together, these components account for just under 17% of the CPI basket. While new dwelling construction costs are currently rising at a 2.7% annual rate, growth in rents (now just 0.6% annually, as per Chart 4) is near its slowest pace since the mid-90s. Rising supply and the impact of the end of the mining boom (with rents in Perth still falling) is depressing the aggregate measure. Looking ahead, these trends look set to remain in place for a while yet.

— Elsewhere, intense competition across the retail industry has also weighed on inflation. This has been observed across the key consumer items, such as food, furniture, household appliances, clothing and footwear and audio-visual equipment. In addition to heightened competition, subdued growth in input costs and slow growth in labour costs have had an impact on retail prices.

Looking ahead, the depreciation in the Australian Dollar over the past year may generate some upward pressure on import / retail prices. However, the extent of the pass-through will depend on how much longer the margin adjustment process in the industry persists. Likewise, the evolution of wages (discussed below) will be crucial.

“[...] the extent of the pass-through will depend on how much longer the margin adjustment process in the industry persists.”

8Are Financial Markets Signalling Recession? — August 2018

Wage Growth Subdued Yet Heading in the Right Direction —Given they are the largest component of business costs, wages are a significant driver and consideration for inflation trends. Indeed, as the RBA points out, labour costs account for around 40% of final prices for services such as hairdressing, meals out, and dry-cleaning and, within this segment, inflation remains low.

That said, there are signs of improvement. Although annual wage growth remains below its long-run average of 3.3%, the latest data shows that a modest acceleration is coming through, with annual growth having bottomed out in H2 2016. The Wage Price Index (a measure of wage inflation, excluding bonuses) nudged up to 2.1% growth in Q2 2018. The underlying detail also shows that wage growth has broadened out, with 11 of the industry 16 sectors now recording annual growth of 2% or more. This is a high in since mid-2016. Elsewhere, Average Weekly Earnings (the average gross wage across the economy) rose by an improved 2.7% over the year to Q2 2018.

Looking ahead, forward-looking indicators of labour demand and economic activity point to solid employment growth being maintained. In turn, this should generate a decline excess labour capacity. When combined with the 3.5% lift in the minimum wage (from 1 July 2018), faster wage growth in recent Enterprise Bargaining Agreements and a pick-up in wage expectations (including in the RBA’s liaison data), an acceleration in wages is anticipated (this being indicated via Chart 5). However, as the RBA notes, the improvements are likely to be gradual.

CHART 5: Wage Growth & Labour Market Underutilisation

4.8

% % yoy

6.1

7.3

8.6

9.8

5.20

4.15

3.10

2.05

1.00

Mar-00 Mar-03 Mar-06 Mar-09 Mar-12 Mar-15 Mar-18

Underemployment Rate (inverse, Adv 2 Qtrs, lhs)

WPI Private Ex Bonus (rhs)

WPI Private With Bonus (rhs)

CHART 6: Admin & Utilities Inflation

20

%pa %pa

15

10

5

0

-5

20

15

10

5

-5

0

Sep-09 Sep-11 Sep-13 Sep-15 Sep-17

Child Care

Gas & Household Fuels

EducationUrban TransportHealthElectricity

9Are Financial Markets Signalling Recession? — August 2018

Inflation Pressures are Building but One-Offs will Act as a Drag in Q3 —In broad strokes, the outlook is for inflation pressures to continue to build over coming years - albeit gradually - as economic slack continues to be absorbed. However, in the near-term, there are some transitory factors that look set to act as a drag on headline inflation.

The RBA recently noted that changes in childcare subsidies, TAFE fees, NSW car registration prices as well as smaller increases in health care premiums are set to slow ‘administered’ inflation for Q3. This will compound the pull-back in electricity and gas prices, with price reductions announced by providers in some states also taking effect in Q3. Each of these developments represent a pause after a period of outsized inflation in these areas (as shown in Chart 6).

As a result, the RBA is forecasting headline CPI inflation to decelerate towards 1¾% by year-end, before rebounding over 2019 and 2020. Overall, the RBA is projecting inflation to rise to 2¼% by end-2020 and, as noted by RBA Governor Lowe, based on the forward-looking nature of policy, the Bank won’t wait for inflation to print at 2½% before beginning its modest tightening cycle. We continue to expect an initial tightening by mid-2019.

10Are Financial Markets Signalling Recession? — August 2018

Report release date 17th August 2018

For further information, please contact:

Steven Milch, Chief EconomistPhone: 02 8121 0921Email: [email protected]

Peter Dragicevich, Financial Market Strategist Phone: 02 8121 9519,Email: [email protected]

30188 20/08/18 A