Embed Size (px)

Citation preview

27/03/2012

Coping with Demand

Yomi Benson

ARE THE LOGISTICS IN PLACE

2

27/03/2012

3

27/03/2012

Sahara Group’s activities span across the energy value chain. Its assets

and operating competencies are vested in 15 operating companies.

Sahara Group Overview

Established in 1996,

15 operating companies – spanning the entire energy value chain, 450 employees,

Offices in Nigeria (Abuja, Lagos & Port Harcourt), Cote D’Ivoire, Ghana, Benin, United Kingdom, Singapore, Dubai, Angola and Switzerland,

Annual turnover is in excess of US$13 Billion,

Our vision: “The provider of choice wherever energy is consumed”

4

27/03/2012

The Sahara Group’s interests demonstrate our capabilities across the

entire energy value chain.

Bulk Storage Property Exploration & Production

Logistics Shipping Power Production

5

27/03/2012

Global Market Overview

• Africa is a global player in both Crude Oil and Refined Product trade flow

• Of the 90 Mbbls/day worldwide consumption of Crude, Africa produces

10Mbbls/day, whilst only consuming 3Mbbls/day

• Global trade flows are affected by

• Economics

• Supply/Demand

• Logistics

• Without key logistics and Infrastructure, there is inherent effect on product

supply and demand profiles

6

27/03/2012

Oil Trade

• Oils is more traded internationally than anything else worldwide.

• Market balances between over or under-supplied

• Adequate Infrastructure is required to accommodate the required flow.

• Current key trade flows – Shipping flows. Of the 1850 MRs and Handies

globally, 20% flow to the WAF/African region for product supply

• Transportation and storage play a critical additional role here. This is the

physical link between the product source and product requirement

7

27/03/2012

Africa Oversight

• Africa represents 4% of total global petroleum Product consumption

• Total demand for petroleum products in Africa is 75 Million MT, with over

a third of demand in West Africa, predominantly Nigeria.

• Africa only exports approx 4% of global world product extorts, with 40%

being exported to Europe only.

• Major development and urbanisation spurred by population growth will

increase demand requirements of product in Africa – Country Demography

• With current refining capacity and utilisation, numerous infrastructure

limitations exist – road transportation and trucking is the the most

common mode of product transportation.

• Ports and terminals restrictions limits maximisation of

Economies of Scale

8

27/03/2012

Gasoline Trade Flows

9

27/03/2012

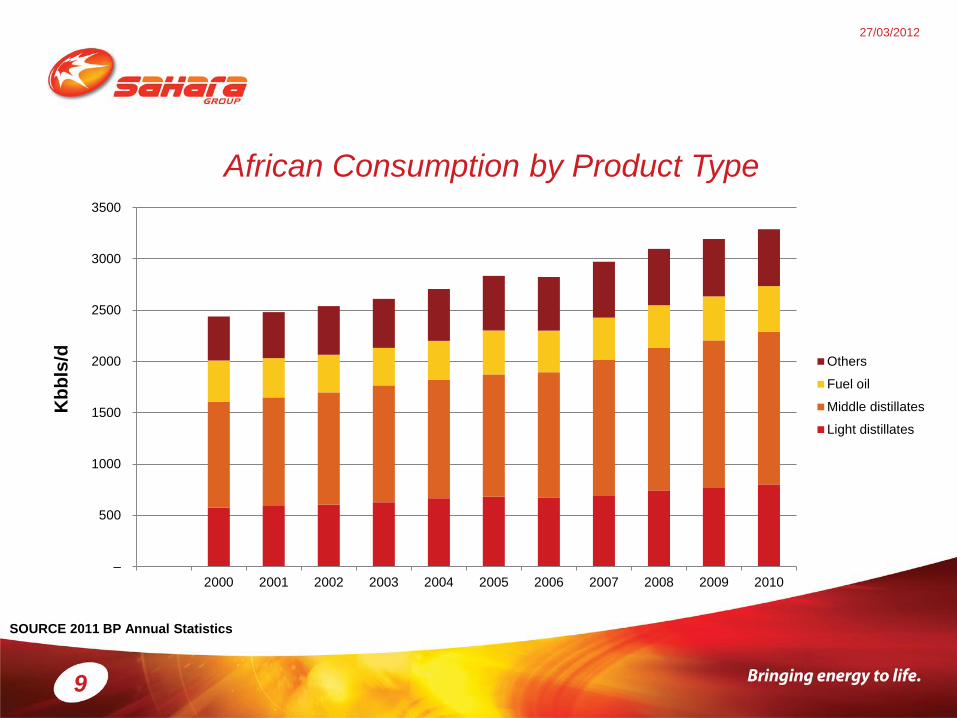

African Consumption by Product Type

–

500

1000

1500

2000

2500

3000

3500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Others

Fuel oil

Middle distillates

Light distillates

Kb

bls

/d

SOURCE 2011 BP Annual Statistics

10

27/03/2012

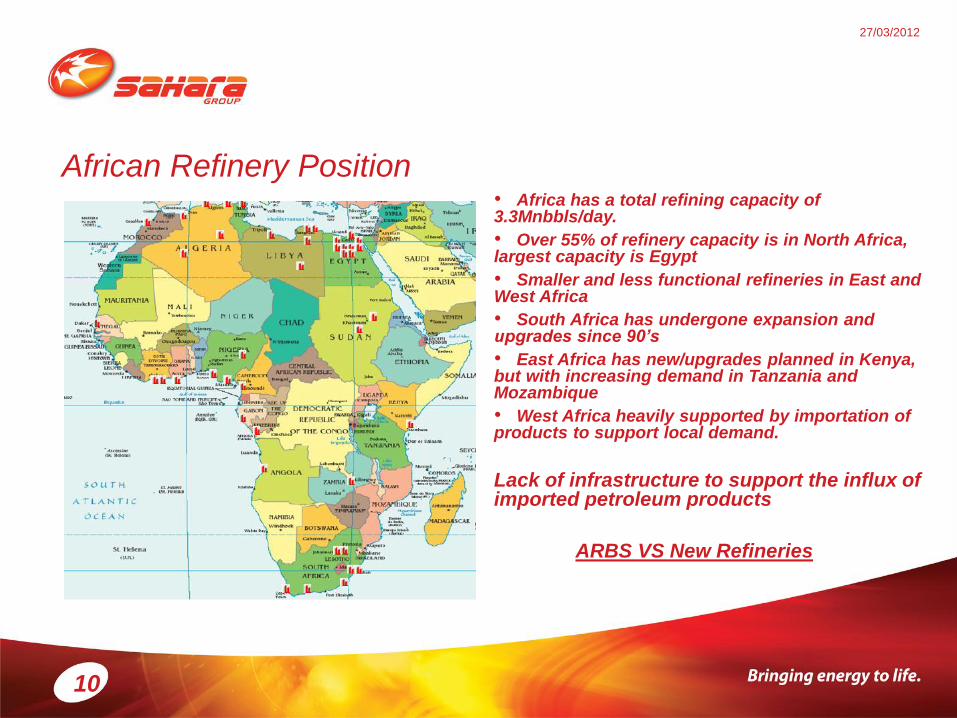

African Refinery Position • Africa has a total refining capacity of 3.3Mnbbls/day.

• Over 55% of refinery capacity is in North Africa, largest capacity is Egypt

• Smaller and less functional refineries in East and West Africa

• South Africa has undergone expansion and upgrades since 90’s

• East Africa has new/upgrades planned in Kenya, but with increasing demand in Tanzania and Mozambique

• West Africa heavily supported by importation of products to support local demand.

Lack of infrastructure to support the influx of imported petroleum products

ARBS VS New Refineries

11

27/03/2012

African Ports

• Key choke ports in Africa – Beira, Cotonu, Dar el Salam, Durban, Lagos,

Mombasa, Tema.

• All suffer Infrastructure Challenges

• Require requisite infrastructure to ensure universal access and efficient

and reliable supply of energy services

• Maritime traffic has been growing rapidly across all cargo types

• Several ports suffer from low capacity (terminal Storage), maintenance

and dredging capabilities – resulting in Congestion

• High terminal port and operational costs

• Charges per ton offloaded in SSA are approx 40% above world rates

12

27/03/2012

New Infrastructure Projects

• North Africa

- Emirates National Oil

Company has inaugurated a

new US$180mn facility

- Storage for up to 500k

cu/month

- Access to road tankers and

Vessels

- Strategically positioned at

crossing 2 major maritime

routes

• East Africa

- Biggest African Project

- Kenya, Ethiopia, South Sudan

launch $25bn joint project - port,

refinery and railway at Lamu

- 32 port berths in the region by

new rail and pipeline to South

Sudanese refinery

• West Africa

• Lekki Free Trade Zone

development

• 15 hectares of land

• 750kbbls/d refinery

• Capacity to handle up to

160’000DWT vessel for

finished grades

13

27/03/2012

Vessel Tracking by Barry Rogliano Salles

14

27/03/2012

27/03/2012

Sahara Trading Offices

Geneva:

7, Quai du Mont-Blanc

1201 Geneva

Switzerland

Tel +41 22 786 6131

Fax +41 22 786 6132

Singapore:

3 Temasek Avenue

20-06A Centennial Tower

Singapore 039190

Tel +65 6836 5377

Fax +65 6836 6257

Isle of Man:

12-14 Finch Road

Douglas

Isle of Man IM99 I TT

Tel +44 (0) 1624 646 723

Fax +44 (0) 1624 620 588