Embed Size (px)

Citation preview

ARE YOU PLANNING FOR Your FUTURE?

ARE YOU PLANNING FOR Your FUTURE?

Presented byPresented byKevin D. BrewerKevin D. Brewer CFP CFP

Kevin Brewer FinancialKevin Brewer Financial

Investia Financial Services Inc.Investia Financial Services Inc.

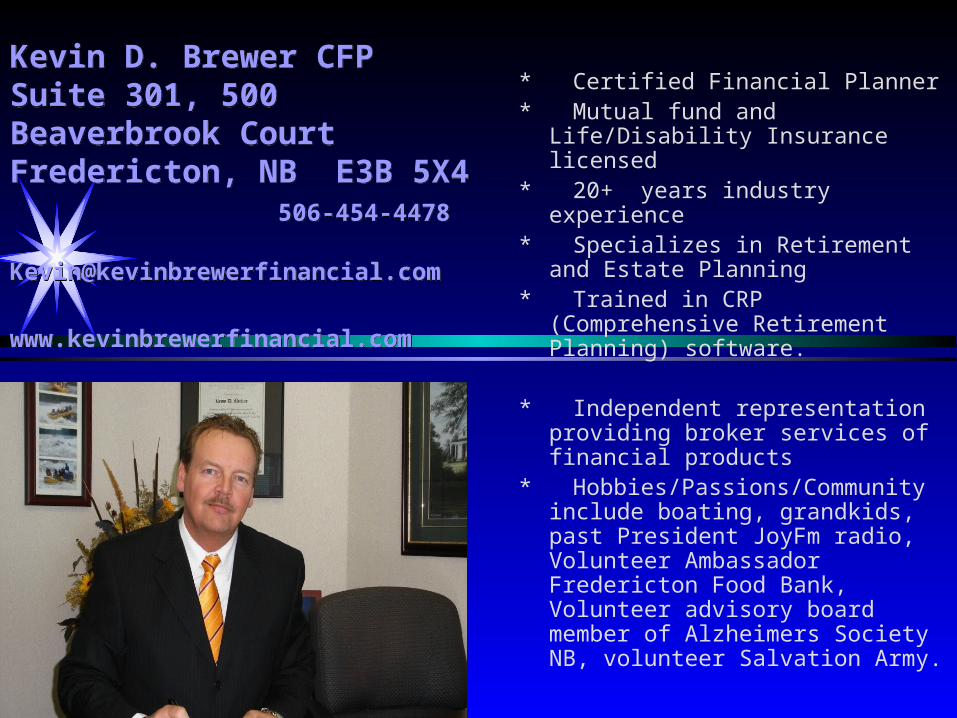

Kevin D. Brewer CFPSuite 301, 500 Beaverbrook CourtFredericton, NB E3B 5X4 506-454-4478 [email protected]

www.kevinbrewerfinancial.com

Kevin D. Brewer CFPSuite 301, 500 Beaverbrook CourtFredericton, NB E3B 5X4 506-454-4478 [email protected]

www.kevinbrewerfinancial.com

* Certified Financial Planner* Mutual fund and Life/Disability

Insurance licensed* 20+ years industry experience* Specializes in Retirement and Estate

Planning* Trained in CRP (Comprehensive

Retirement Planning) software.

* Independent representation providing broker services of financial products

* Hobbies/Passions/Community include boating, grandkids, past President JoyFm radio, Volunteer Ambassador Fredericton Food Bank, Volunteer advisory board member of Alzheimers Society NB, volunteer Salvation Army.

Today’s purpose…

Raise awareness of sound financial practices

No Sales guarantee

Free service to groups and organizations

I will not talk about specific products (except for one)

Today’s agenda… but not in this order

Tax bracketsRetirement AllowanceTaking CPPNew CPP rulesPension integrationOAS claw backPension vs. LiraPension at deathEstate Planning ideasStock MarketsInvestmentsYour questions

What Are Your Goals?What Are Your Goals?

•Retire early•Retire comfortably•Pay less income tax•Preserve my Estate

A Solid FoundationA Solid Foundation

Rules of Cash ManagementRules of Cash Management

* Spend Less Than You Earn* Read TWB - David Chilton* The dreaded B word* Pool anyone?* Pay Yourself First

Rules of Debt ManagementRules of Debt Management

* Spend Less Than You Earn* Do not borrow to pay debt

(except in some cases …)* One at a time* Is there good debt?* Never be late.

It’s Patrick!

Why Insure? Provides protection against loss …

Why Insure? Provides protection against loss …

* Loss of life (life insurance for dependents and/or CRA) Term, UL, Whole Life

* Loss of income (disability insurance)* Loss of independence (Long Term Care and Critical Illness)* Leave Inheritance to family/charity* Last expenses

• Why does insurance planning come before investment planning?

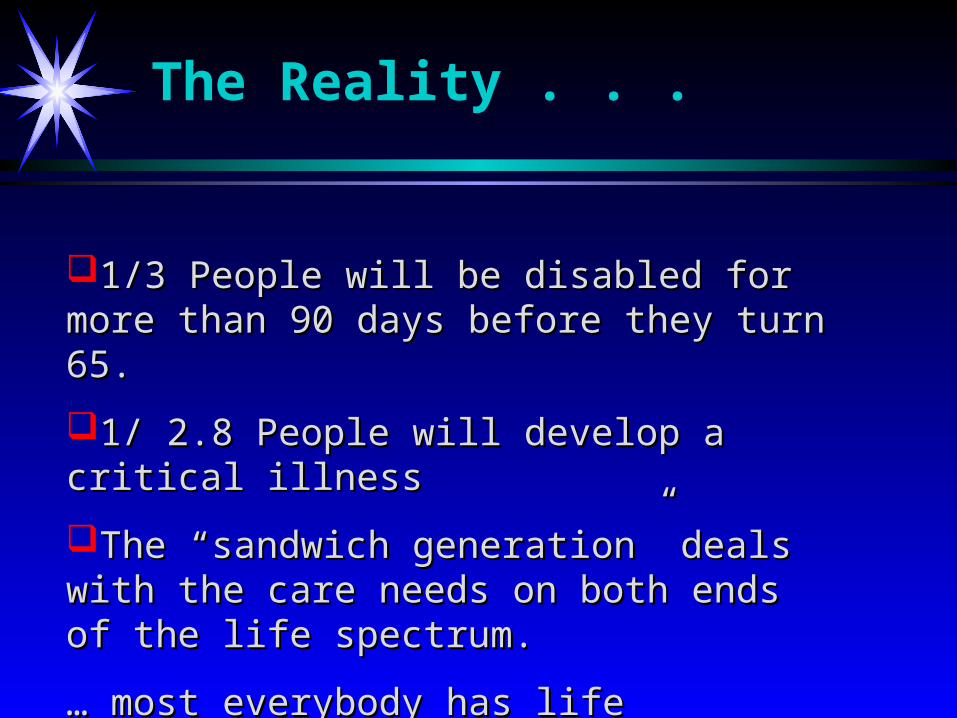

The Reality . . .

1/3 People will be disabled for more than 90 1/3 People will be disabled for more than 90 days before they turn 65.days before they turn 65.

1/ 2.8 People will develop a critical illness1/ 2.8 People will develop a critical illness

The “sandwich generation” deals with the care The “sandwich generation” deals with the care needs on both ends of the life spectrum.needs on both ends of the life spectrum.

… … most everybody has life insurance but few are most everybody has life insurance but few are prepared for the sickness or disability.prepared for the sickness or disability.

Running with the Bear!

Running with the Bear!

Market VolatilityMarket Volatility

Today’s marketToday’s market

Past experience with market fluctuationsPast experience with market fluctuations

Good or bad time to buy??Good or bad time to buy??

What to buy??What to buy??

Best time I’ve seen or worse??Best time I’ve seen or worse??

What about the headlines??What about the headlines??

July 9th, 1979

DOW JONES = 852.99

DOW JONES 10yrs later = 2,487.86

$1,000 invested in the Dow Jones on the day this issue hit the stands would have been worth $2,917 ten years later.

(almost tripling in 10 years)

July 9th, 1979

December 3rd, 1984

DOW JONES = 1,182.42

DOW JONES 10yrs later = 3,745.62

$1,000 invested in the Dow Jones on the day this issue hit the stands would have been worth $3,168 ten years later.

(more than tripling in 10 years)

December 3rd, 1984

November 2nd, 1987

DOW JONES = 2,014.09

DOW JONES 10yrs later = 7,442.08

$1,000 invested in the Dow Jones on the day this issue hit the stands would have been worth $3,695 ten years later.

(more than tripling in 10 years)

November 2nd, 1987

Wall St Journal, Sept 20/21, 2008

THE WEEK THAT CHANGED THE WEEK THAT CHANGED AMERICAN CAPITALISMAMERICAN CAPITALISM

THE WEEK THAT CHANGED THE WEEK THAT CHANGED AMERICAN CAPITALISMAMERICAN CAPITALISM

January 1, 2009 to March 2009 Trough

-15.5

-19.0

-20.4

-24.3

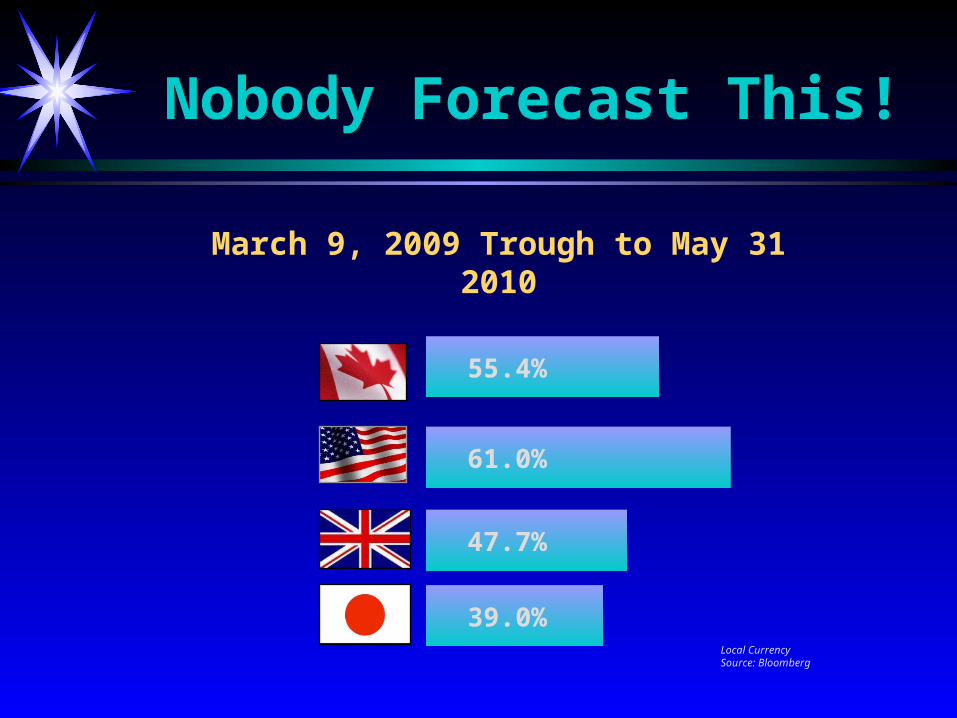

A Rough Start to 2009 Nobody Forecast This! A Rough Start to 2009 Nobody Forecast This!

Local CurrencySource: Bloomberg

March 9, 2009 Trough to May 31 2010

61.0%

39.0%

47.7%

55.4%

Nobody Forecast This! Nobody Forecast This!

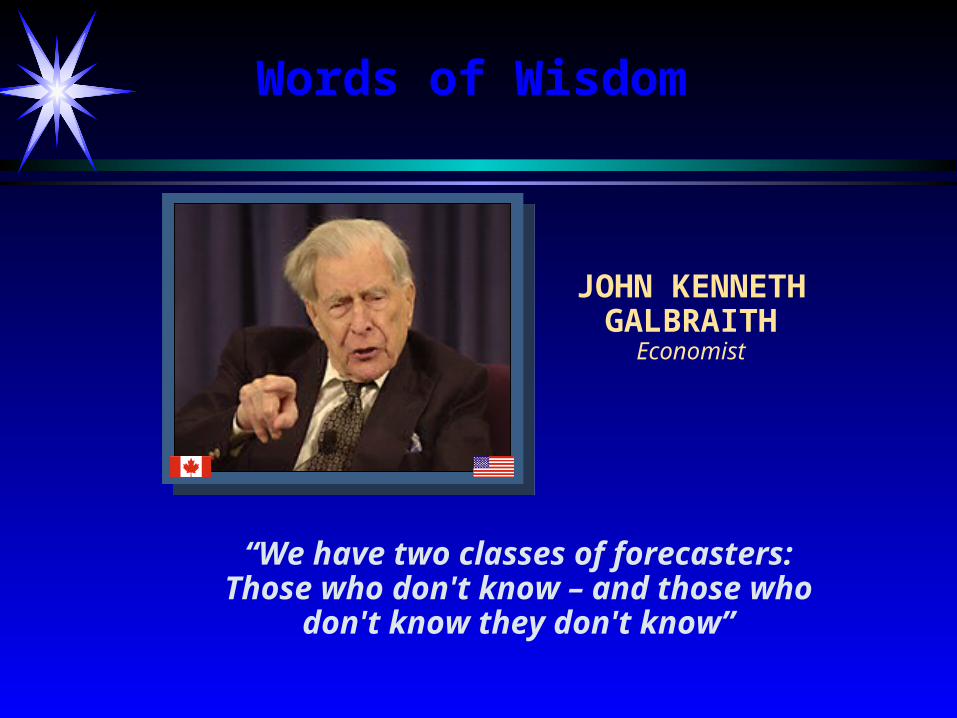

“We have two classes of forecasters:Those who don't know – and those who don't

know they don't know”

JOHN KENNETH GALBRAITH

Economist

Words of Wisdom

Three Places to Invest Three Places to Invest

Interest Interest / Dividends

Capital Gains

Low Variability

Medium Variability

High Variability

.25 – 2.5 % 2.5 -5 % 5 – ? %

Pros and ConsPros and Cons

Capital gains and Dividends received preferred tax Capital gains and Dividends received preferred tax treatment (only on non-reg investments).treatment (only on non-reg investments).

Minimum 5 year period required for equity Minimum 5 year period required for equity investments (7-10 would be better)investments (7-10 would be better)

Real risk tolerance not known until something bad Real risk tolerance not known until something bad happenshappens

Financial planner’s rule of risk = 100 - ageFinancial planner’s rule of risk = 100 - age

Traditional Wisdom Says:

Time not Timing determines Success.

Traditional Wisdom Says:

Time not Timing determines Success.

Asset Allocation with systematic rebalancing is the key to strong and steady performance with reduced risk.

“ BUY LOW – SELL HIGH – REPEAT”

Kevin Brewer

……What is the single largest What is the single largest expense we, as Canadians expense we, as Canadians will face in our lifetimes?will face in our lifetimes?

TAX!

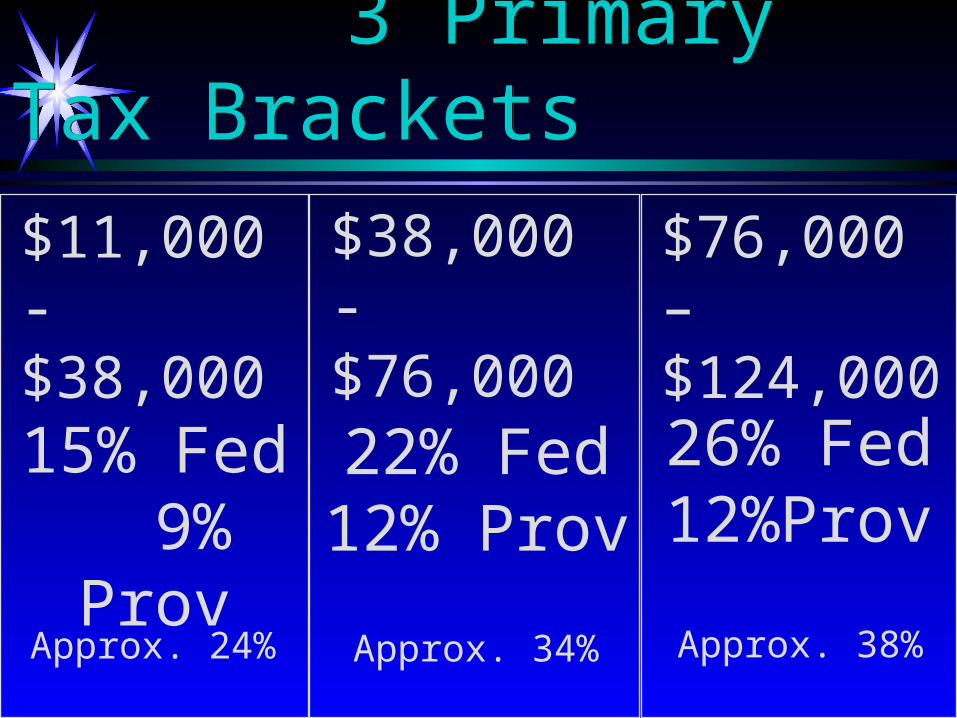

3 Primary Tax Brackets 3 Primary Tax Brackets

15% Fed 9% Prov

22% Fed12% Prov

26% Fed12%Prov

$11,000 - $38,000

$38,000 - $76,000

$76,000 – $124,000

Approx. 24% Approx. 34% Approx. 38%

Tax deductible non-registered investment strategies (use existing cash to purchase…)

Buy RRSP/RRIF InsuranceBorrow to top up allowable RRSP limit (use good debt to pay bad).

Borrow X2

Earn Dividends or Capital Gains (not Interest). This applies to non-registered accounts only.

Income splitting

Can you pay less tax?Can you pay less tax?

Save for your goals tax-free!Save for your goals tax-free!

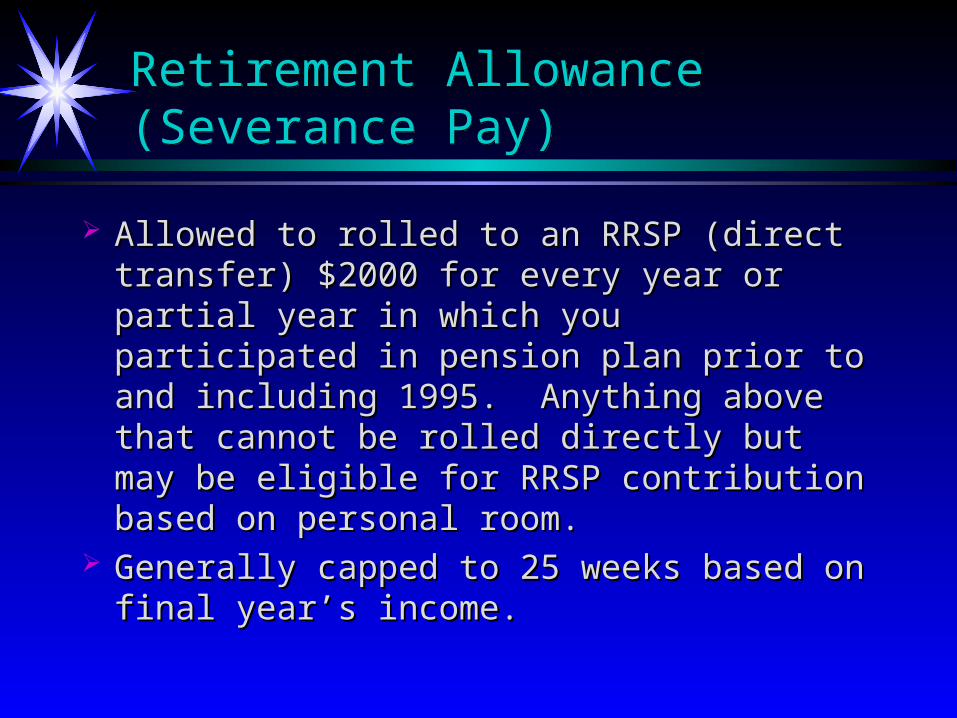

Retirement Allowance (Severance Pay)Retirement Allowance (Severance Pay)

Allowed to rolled to an RRSP (direct transfer) Allowed to rolled to an RRSP (direct transfer) $2000 for every year or partial year in which you $2000 for every year or partial year in which you participated in pension plan prior to and including participated in pension plan prior to and including 1995. Anything above that cannot be rolled 1995. Anything above that cannot be rolled directly but may be eligible for RRSP contribution directly but may be eligible for RRSP contribution based on personal room.based on personal room.

Generally capped to 25 weeks based on final Generally capped to 25 weeks based on final year’s income.year’s income.

Retirement Allowance (New Options)Retirement Allowance (New Options)

Effective March 31, 2013, management and nonEffective March 31, 2013, management and non

union employees in parts 1,11, and 111 will nounion employees in parts 1,11, and 111 will no

longer accumulate retirement allowance credits.longer accumulate retirement allowance credits.

OPTIONSOPTIONS

1.1. Obtain a payout in lieu of ret. allowance based on Obtain a payout in lieu of ret. allowance based on credits accum’td and salary to Mar 31, 2013.credits accum’td and salary to Mar 31, 2013.

2.2. Defer your retirement allowance until retirement Defer your retirement allowance until retirement based on current credits and salary at time of based on current credits and salary at time of retirement.retirement.

Retirement Allowance (New Options)Retirement Allowance (New Options)

Question of the day: Question of the day:

Do I take the money now or defer it a few yearsDo I take the money now or defer it a few years

until I retire?until I retire?

Retirement Allowance (New Options)Retirement Allowance (New Options)

Example:Example:

Joe, age 45, 15 accumulated pension years creditJoe, age 45, 15 accumulated pension years credit

Salary $52,000 ($1000 week)Salary $52,000 ($1000 week)

Pay in lieu of retirement allowance = $15,000Pay in lieu of retirement allowance = $15,000

Assumption: intent is to work another 15 yearsAssumption: intent is to work another 15 years

until retirement.until retirement.

Retirement Allowance (New Options)Retirement Allowance (New Options)

Based on the previous assumption, the investmentBased on the previous assumption, the investment

simply has to outpace the rate of salary increasessimply has to outpace the rate of salary increases

each year (or the average). Ie: if the salary for thiseach year (or the average). Ie: if the salary for this

job description only increases by CPI of 2 or 3%job description only increases by CPI of 2 or 3%

each year, the investment portfolio only has toeach year, the investment portfolio only has to

make 2 or 3% to match the eventual outcome.make 2 or 3% to match the eventual outcome.

-- $52,000 @ 2% increase over 15 years = final $52,000 @ 2% increase over 15 years = final salary of $69,985 and ret allowance of $20,188.salary of $69,985 and ret allowance of $20,188.

-- $15,000 @ 2% increase over 15 Yrs = $20,188$15,000 @ 2% increase over 15 Yrs = $20,188

Retirement Allowance (New Options)Retirement Allowance (New Options)

So if you think that investment performance

will outpace your salary increase then the choice based on that alone would be to take

the money today. However …What if the expectation is that you will move up

the ladder to a more senior position in Govt over the years and thus retire with a salary much larger than your present one? What would that increase in salary have to be to

offset an investment return of 4%, 5%, or 6%?

Retirement Allowance (New Options)Retirement Allowance (New Options)

$15,000@ 4% return over 15 Yrs = $27,014$15,000@ 4% return over 15 Yrs = $27,014

$93,648 = $1800.93/wk X 15 wk = $27,014$93,648 = $1800.93/wk X 15 wk = $27,014

$15,000 @ 5% return over 15 Yrs = $31,184$15,000 @ 5% return over 15 Yrs = $31,184

$108,104 = $2078.92/wk X 15 wk = $31,184$108,104 = $2078.92/wk X 15 wk = $31,184

$15000@ 6% return over 15 Yrs = $35,948$15000@ 6% return over 15 Yrs = $35,948

$124,620 = $2396.54/wk X 15wk = $35,948$124,620 = $2396.54/wk X 15wk = $35,948

Salary must double to be equiv. to 5% return!Salary must double to be equiv. to 5% return!

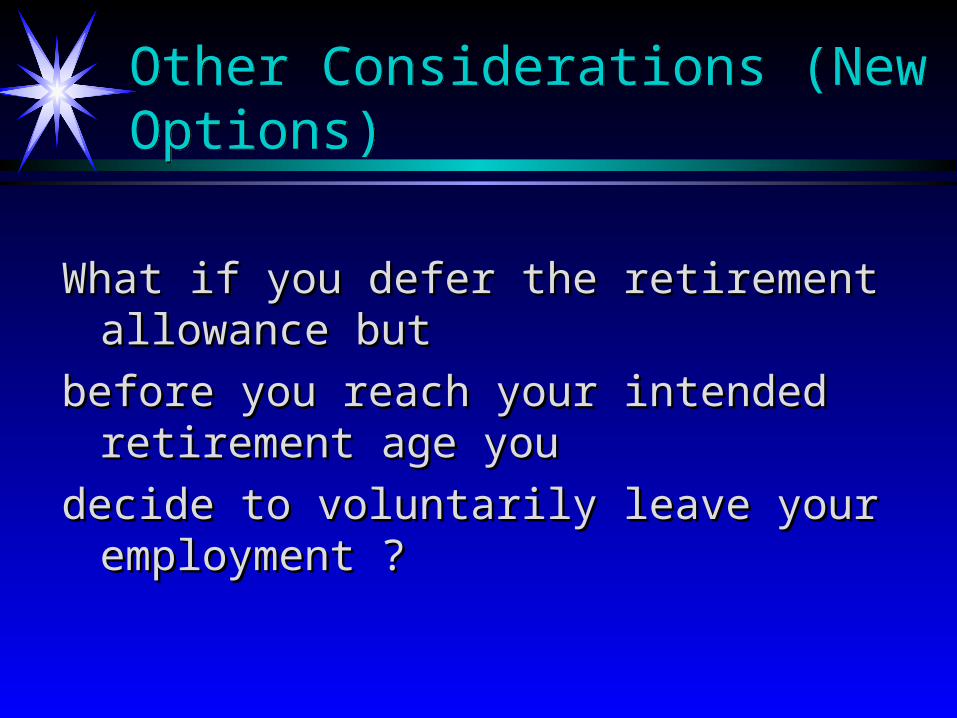

Other Considerations (New Options)Other Considerations (New Options)

What if you defer the retirement allowance butWhat if you defer the retirement allowance but

before you reach your intended retirement age youbefore you reach your intended retirement age you

decide to voluntarily leave your employment ?decide to voluntarily leave your employment ?

Other Considerations (New Options)Other Considerations (New Options)

What if you defer the retirement allowance butWhat if you defer the retirement allowance but

before you reach your intended retirement age youbefore you reach your intended retirement age you

decide to voluntarily leave your employment ?decide to voluntarily leave your employment ?

Under the old rules you would not qualify for theUnder the old rules you would not qualify for the

retirement allowance. Based on availableretirement allowance. Based on available

information there is no guarantee you wouldinformation there is no guarantee you would

receive it in this scenario either.receive it in this scenario either.

Other Considerations (New Options)Other Considerations (New Options)

Is it better to put this investment in my spouse’sIs it better to put this investment in my spouse’s

name (Spousal RRSP) for tax purposes?name (Spousal RRSP) for tax purposes?

Other Considerations (New Options)Other Considerations (New Options)

Is it better to put this investment in my spouse’sIs it better to put this investment in my spouse’s

name (Spousal RRSP) for tax purposes?name (Spousal RRSP) for tax purposes?

Much of the advantage in doing a spousal RRSPMuch of the advantage in doing a spousal RRSP

has been negated with the introduction of the newhas been negated with the introduction of the new

Pension Income Splitting rule. However, it mayPension Income Splitting rule. However, it may

still be worth consideration.still be worth consideration.

Summary (New Options)Summary (New Options)

This decision is made more difficult because itThis decision is made more difficult because it

must be made based on these unknown variablesmust be made based on these unknown variables

and assumptions: and assumptions:

What will be the performance of my investment What will be the performance of my investment versus versus

What will be my final salary at retirement (if I What will be my final salary at retirement (if I make it to retirement age).make it to retirement age).

Summary (New Options)Summary (New Options)

Bottom line:Bottom line:

A Bird In The Hand …A Bird In The Hand …

Procedures/Paperwork (New Options)Procedures/Paperwork (New Options)

For allowances less that $10,000:For allowances less that $10,000:

1)1) CRA Letter of Intent Regarding a Deductible CRA Letter of Intent Regarding a Deductible Contribution to an RRSPContribution to an RRSP

2)2) Province of NB Financial Institution FormProvince of NB Financial Institution Form

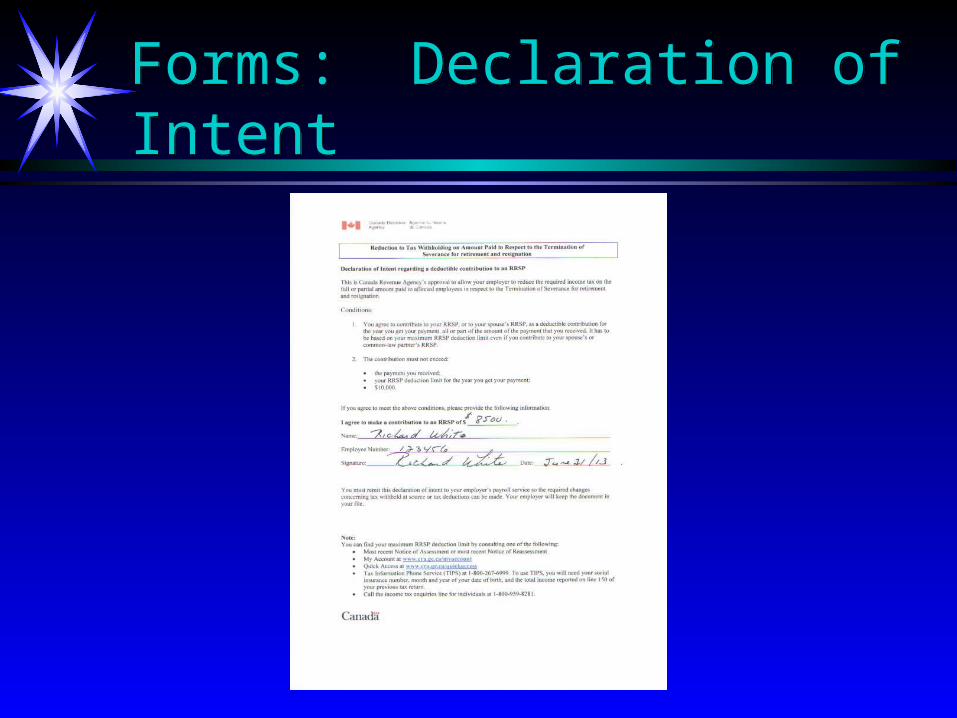

Forms: Declaration of IntentForms: Declaration of Intent

Form: Financial Institution Information FormForm: Financial Institution Information Form

Procedures/Paperwork (New Options)Procedures/Paperwork (New Options)

For allowances greater than $10,000:For allowances greater than $10,000:

1)1) Apply to CRA using CRA form T1213 for Apply to CRA using CRA form T1213 for permission for Province to do a direct transfer permission for Province to do a direct transfer to your financial institution of choice. Allow 4-to your financial institution of choice. Allow 4-6 weeks for their response. Then provide their 6 weeks for their response. Then provide their response along with the form below to Provinceresponse along with the form below to Province

2)2) Province of NB Financial Institution FormProvince of NB Financial Institution Form

Form: CRA T1213Form: CRA T1213

Procedures/Paperwork (New Options)Procedures/Paperwork (New Options)

In the first case (less than $10,000) you areIn the first case (less than $10,000) you are

indicating to the Province that you have the roomindicating to the Province that you have the room

to transfer to an RRSP. In the second case (moreto transfer to an RRSP. In the second case (more

than $10,000) proof is required from CRA. IF thisthan $10,000) proof is required from CRA. IF this

is the case, you must submit your request to CRAis the case, you must submit your request to CRA

in plenty of time to get a response before Sept 30.in plenty of time to get a response before Sept 30.

OAS and the OAS ClawbackOAS and the OAS Clawback

Amount same for everyone at age 65 = Amount same for everyone at age 65 = $546.07/mo or $6552.84/year$546.07/mo or $6552.84/year

Claw back begins at $70,954 and is depleted at an Claw back begins at $70,954 and is depleted at an income of $114,640income of $114,640

If a taxpayer in receipt of OAS benefits has net If a taxpayer in receipt of OAS benefits has net income in excess of the base amount for that year income in excess of the base amount for that year ($70,954 for 2013) he or she must repay 15% of ($70,954 for 2013) he or she must repay 15% of net income in excess of the base amount.net income in excess of the base amount.

Example: net income = 80,954 then 15% of Example: net income = 80,954 then 15% of $10,000 ($80,954-$70,954) or $1500 of OAS must $10,000 ($80,954-$70,954) or $1500 of OAS must be paid back of the $6552.84 annual payment.be paid back of the $6552.84 annual payment.

Pension Options and death of pensionerPension Options and death of pensioner

Generally offered 5 or 10 year guarantee and…Generally offered 5 or 10 year guarantee and… A reduced amount with 50% to surviving spouse or…A reduced amount with 50% to surviving spouse or… A reduced amount with 60% to surviving spouse or…A reduced amount with 60% to surviving spouse or… A reduced amount with 75% to surviving spouseA reduced amount with 75% to surviving spouse

(reduced to $0 upon death of final spouse)(reduced to $0 upon death of final spouse)

WHAT ABOUT COMMUNTED VALUES vs PENSIONS?WHAT ABOUT COMMUNTED VALUES vs PENSIONS?

* Owner controls investment choices (must have discipline)* Owner controls investment choices (must have discipline)

* Locked-in rules apply limiting maximum annual withdrawal* Locked-in rules apply limiting maximum annual withdrawal

* Locked-in rules broken at death allowing full tax sheltered transfer * Locked-in rules broken at death allowing full tax sheltered transfer to remaining spouseto remaining spouse

* Can be passed to beneficiaries upon death of final spouse but taxes * Can be passed to beneficiaries upon death of final spouse but taxes will be owingwill be owing

There is a need for estate planning in these casesThere is a need for estate planning in these cases

My Dear Children…My Dear Children…

……we love you so much

we’ve decided to leave

half our wealth to the

Canada Revenue

Agency

Estate Planning StrategiesEstate Planning Strategies Beneficiary designationsBeneficiary designations Joint ownershipJoint ownership GiftingGifting InsuranceInsurance TrustsTrusts Segregated fundsSegregated funds Annuity productsAnnuity products

About WILLs and POAs ...About WILLs and POAs ...

Prevents the courts from making decisions for you.

Allows life to carry on for those left behind the way you intended it to.

Education SavingsEducation Savings

Registered Education Savings Plans (RESPs)Registered Education Savings Plans (RESPs) Government savings programGovernment savings program 20% grant on contributions20% grant on contributions Can withdraw contributions and growth if not used, just Can withdraw contributions and growth if not used, just

have to return granthave to return grant If used, withdrawn at beneficiary’s Marginal Tax RateIf used, withdrawn at beneficiary’s Marginal Tax Rate

ConclusionConclusion

Financial planning is complexFinancial planning is complex Your true beliefs have to be taken into Your true beliefs have to be taken into

considerationconsideration Decide what you want to achieve - what’s Decide what you want to achieve - what’s

most important to you and your familymost important to you and your family Talk to those that are affected by your Talk to those that are affected by your

wisheswishes Planning is a work in progress - it requires Planning is a work in progress - it requires

ongoing review and modificationongoing review and modification

Types of Financial Plans:Types of Financial Plans:

* Fee for Service based on complexity of plan required.

* No fee but based on assumption that if good work/advice is provided then future business may occur. Fee then paid in form of commission by product manufacturer – not the client.

ONE LAST THINGONE LAST THING

In appreciation of your attendance . . .

THANK YOUQUESTIONS?