Embed Size (px)

Citation preview

Asda Pension Plan

Annual statement regarding governance by the Chair of the

Trustee

This Statement has been prepared to confirm the Plan’s compliance with the governance

requirements1 for the year to 5 April 2019. It provides the information required in relation to the

following:

The Default Arrangement, Processing of core financial transactions, Member borne charges and transaction costs, Value for Members, and Trustee knowledge and understanding.

Default arrangement

The Trustee of the Asda Pension Plan is the legal owner of the Plan’s assets and is responsible for governance and decision-making with regards to these assets. The Trustee is required to design default arrangements in members' interests and keep them under review. The Trustee will need to take account of the level of costs and the risk profile that are appropriate for the Scheme's DC membership in light of the overall objective of the default arrangement.

The investment principles governing the default investment strategy are:

to maximise the value of members’ retirement benefits;

to reduce investment risk towards members’ retirement in order to reduce the likelihood of significant falls in outcomes close to retirement;

to avoid over-complexity in order to keep administration costs reasonable and facilitate member understanding.

To ensure the Plan’s investment strategies are in line and comply with regulations regarding responsible investment. The Trustee will take into account the risk-adjusted returns, long-term investment risk and return profile of Plan members whilst ensuring that the underlying objectives of the Plan’s investment funds are not compromised.

The main objective of the default arrangement is to provide good member outcomes at retirement while subject to a level of investment risk appropriate to the majority of members who do not make active investment choices.

The default arrangement is continuously monitored with quarterly performance information being reviewed at each Trustee meeting. The most recent formal review was undertaken during the year ending 5 April 2018, in September 2017. The Trustee is expected to review the default investment strategy at least every three years, or without delay after any significant change in investment policy or membership demographics. The next review is therefore due in the 2020/2021 Plan year and no later than September 2020, unless any significant relevant changes happen in the interim.

The review was undertaken by Hymans Robertson LLP in line with this expectation. The review looked at the current design framework, analysis of asset class return assumptions, assessment of

1 As required by Regulation 23 of the Occupational Pension Schemes (Scheme Administration) Regulations

1996 (SI 1996 No. 1715) as amended by the Occupational Pension Schemes (Charges and Governance) Regulations 2015 (SI 2015 No. 879)

the available funds and comparison of the at-retirement solution with other market provider solutions. This showed that;

The design framework for the current default remains in place and we believe it continues to be appropriate in meeting the long-term investment objectives of the Plan

Equities are still expected to be the highest-returning asset class and the most appropriate for meeting the Plan’s objectives

The current strategies used for hourly paid and salaried colleagues, who have been automatically enrolled, and for salaried colleagues in step up remain appropriate

One change was introduced from the last strategy review – an introduction of an allocation to a multi-factor equity fund within the Asda Equity Blend.

The Trustee is satisfied that the default options remain appropriate for the majority of the Plan’s members. However, further reviews will be undertaken on a regular basis.

Further details of the Trustee’s investment principles are given in the Statement of Investment Principles which is appended to this statement.

Processing financial transactions

The Trustee has appointed Legal & General to administer the Plan on their behalf. A portion of the Plan’s assets is held with Prudential, who also perform an administration function on these assets.

The Trustee monitors the core financial transactions including:

Investment of contributions;

Switches of assets between investment options;

Inward transfers of funds; and

Payments of benefits (including outward transfers of funds).

The Trustee receives regular reports from the administrators on the processing of financial transactions against agreed service levels. The Auditor also independently tests sample transactions for accuracy and timeliness.

The Trustee is satisfied that there is a suitable process in place for monitoring core financial transactions and that during the period covered by this Statement, the core financial transactions were processed promptly and efficiently.

The Trustee understands that the provider monitors its performance against agreed service levels for the following areas:

New Joiner are processed within 2 working days;

Review contribution files, complete validation and notify payroll of any errors within 1 working day

Provision of retirement pack and quotation of benefits within 5 working days;

Payment of transfer value to new provider within 5 working days;

Provision of leaver option pack within 5 working days;

Processing individuals transferring in to the Plan within 5 working days;

Response to members enquiries within 1 working day;

Provision of statements upon request within 5 working days; and

Processing of investment switches on the same day if received before 4pm, if not the next working day

Legal & General aims to ensure that 95% of all these processes are completed within these service levels.

For the With Profits Fund, The Trustee understands that the provider monitors its performance against agreed service levels for the following areas:

Response to member queries within 5 working days

Provision of retirement packs and quotations within 5 working days

Payment of Lump sums within 5 working days

Processing contribution files within 5 working days

Payment of transfers out to new providers within 5 working days

Handling of death claims within 5 working days

Prudential aims to ensure that 95% of all these processes are completed within these service levels.

The Trustee is satisfied that the service standards are competitive because:

Over the year covered by this Statement, Legal & General has maintained an average service level of 99.95%

Over the year covered by this Statement, Prudential has maintained an average service level of 93%. Although this falls short of the 95% target, the Trustee is satisfied that this was due to higher than expected volumes of claims transactions and that following implementation of an improvement plan, the SLA performance had recovered by the end of Q1 2019.

The Trustee receives quarterly reports from the providers which are presented at each Trustee meeting and provide details on adherence to service level agreement (SLA) and level of errors and complaints

L&G have straight through processing capabilities which minimises manual intervention

Members can make administrative changes online or by phone

The Asda Pensions Team have regular operational governance calls/meetings with L&G to ensure continued high level performance

The Trustee monitored core financial transactions and administration service levels during the year by:

Checking that contributions deducted from members’ earnings have been paid promptly to the Plan by the Employer;

Receiving quarterly reports from both providers on the processing of financial transactions and other administration processes against the agreed service levels;

Considering the reasons for and resolution of any breaches of service standards;

Reviewing the competitiveness of the service standards against other administrators/providers;

Receiving reports from the Plan’s Auditor, who independently tests sample transactions for accuracy and timeliness; and considering member feedback including any complaints.

Charges and transaction costs

Default arrangements The Trustee is required to determine the costs and charges borne by Scheme members on their DC funds, and to show these in the Statement.

Where information about charges and costs paid by members is not available, the Trustee has to make this clear, together with an explanation of what steps are being taken to obtain the missing information.

These charges comprise:

explicit charges (the Total Expense Ratio (TER)), which provides a clear picture of the total annual costs of running the fund. It includes the annual management charge (AMC) and any other expenses such as trading, legal and auditor fees. The TER gives the total of the explicit charges described above each year expressed as a percentage of the fund value;

implicit transaction costs, such as the costs borne within the fund for activities such as buying and selling of securities within the fund's portfolio.

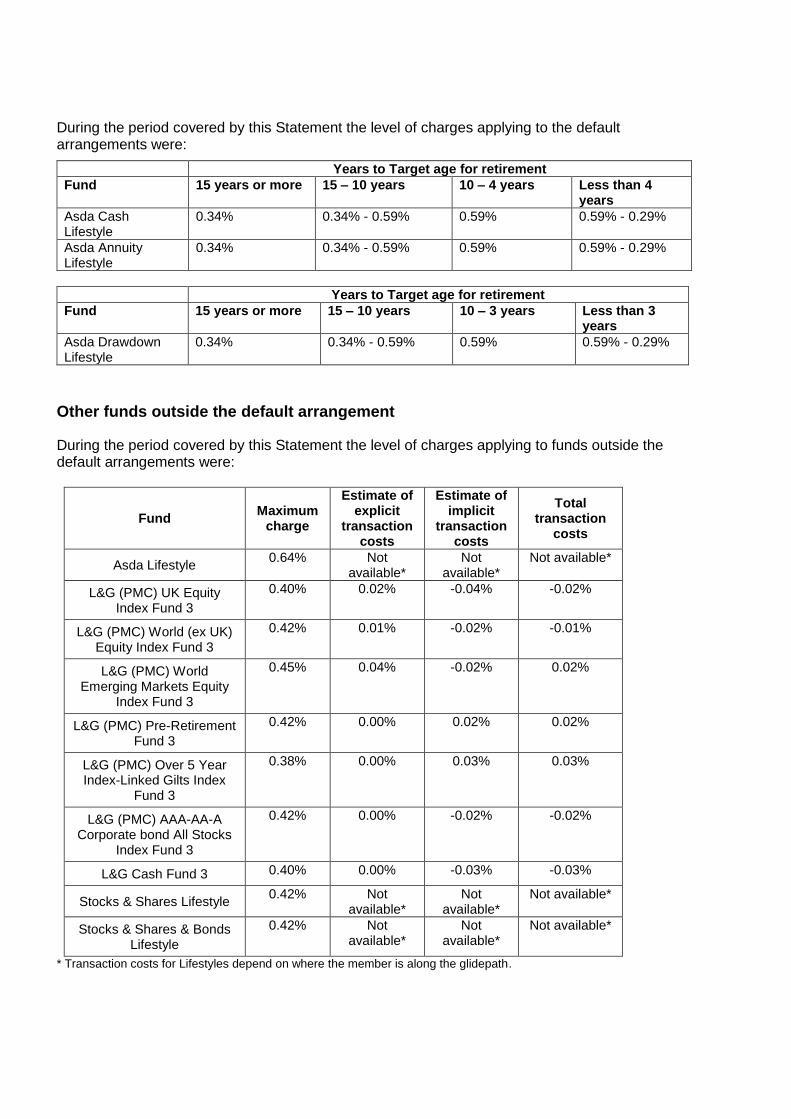

During the period covered by this Statement the level of charges applying to the default arrangements were:

Years to Target age for retirement

Fund 15 years or more 15 – 10 years 10 – 4 years Less than 4 years

Asda Cash Lifestyle

0.34% 0.34% - 0.59% 0.59% 0.59% - 0.29%

Asda Annuity Lifestyle

0.34% 0.34% - 0.59% 0.59% 0.59% - 0.29%

Years to Target age for retirement

Fund 15 years or more 15 – 10 years 10 – 3 years Less than 3 years

Asda Drawdown Lifestyle

0.34% 0.34% - 0.59% 0.59% 0.59% - 0.29%

Other funds outside the default arrangement

During the period covered by this Statement the level of charges applying to funds outside the default arrangements were:

Fund Maximum

charge

Estimate of explicit

transaction costs

Estimate of implicit

transaction costs

Total transaction

costs

Asda Lifestyle 0.64% Not

available* Not

available* Not available*

L&G (PMC) UK Equity Index Fund 3

0.40% 0.02% -0.04% -0.02%

L&G (PMC) World (ex UK) Equity Index Fund 3

0.42% 0.01% -0.02% -0.01%

L&G (PMC) World Emerging Markets Equity

Index Fund 3

0.45% 0.04% -0.02% 0.02%

L&G (PMC) Pre-Retirement Fund 3

0.42% 0.00% 0.02% 0.02%

L&G (PMC) Over 5 Year Index-Linked Gilts Index

Fund 3

0.38% 0.00% 0.03% 0.03%

L&G (PMC) AAA-AA-A Corporate bond All Stocks

Index Fund 3

0.42% 0.00% -0.02% -0.02%

L&G Cash Fund 3 0.40% 0.00% -0.03% -0.03%

Stocks & Shares Lifestyle 0.42% Not

available* Not

available* Not available*

Stocks & Shares & Bonds Lifestyle

0.42% Not available*

Not available*

Not available*

* Transaction costs for Lifestyles depend on where the member is along the glidepath.

Member Transaction charges

The estimated transaction costs are for the year to 31 March 2019

The estimated explicit transaction costs include what gets paid directly from the fund to its service providers such as broker fees and taxes.

The estimated implicit costs include costs that are not known until after they have already occurred. They can be negative as they may include some profit, which can arise due to a difference between the actual price paid and the quoted price expected at the time a transaction was placed.

The explicit and implicit charge figures shown are rounded. The total charges are the sum of the two and any discrepancies are due to roundings.

Information on transaction costs for some funds is not available.

It is possible for a transaction cost to be negative due to price movements in assets between the time a transaction order is placed and executed.

The Trustee has reviewed transaction costs where available and, with the help of their investment advisers, can confirm that they believe the costs outlined above provide reasonable value for members (having considered the funds and the underlying asset classes within the funds). With Profits The Plan includes investments in the Prudential Assurance Company Limited With Profits Fund under a “Cash Accumulation” contract. The charges and transaction costs for With Profits Funds are deducted from the overall fund before bonus rates are set for all policyholders. As a result, it is not possible to determine the exact charges and costs borne by members. The average transaction charge over the last 5 years has been 0.05%. It should be noted that the implicit charges for the With Profits Fund cover the cost of guarantees and reserving as well as investment management and administration.

The next review of the fund will take place in 2019/20.

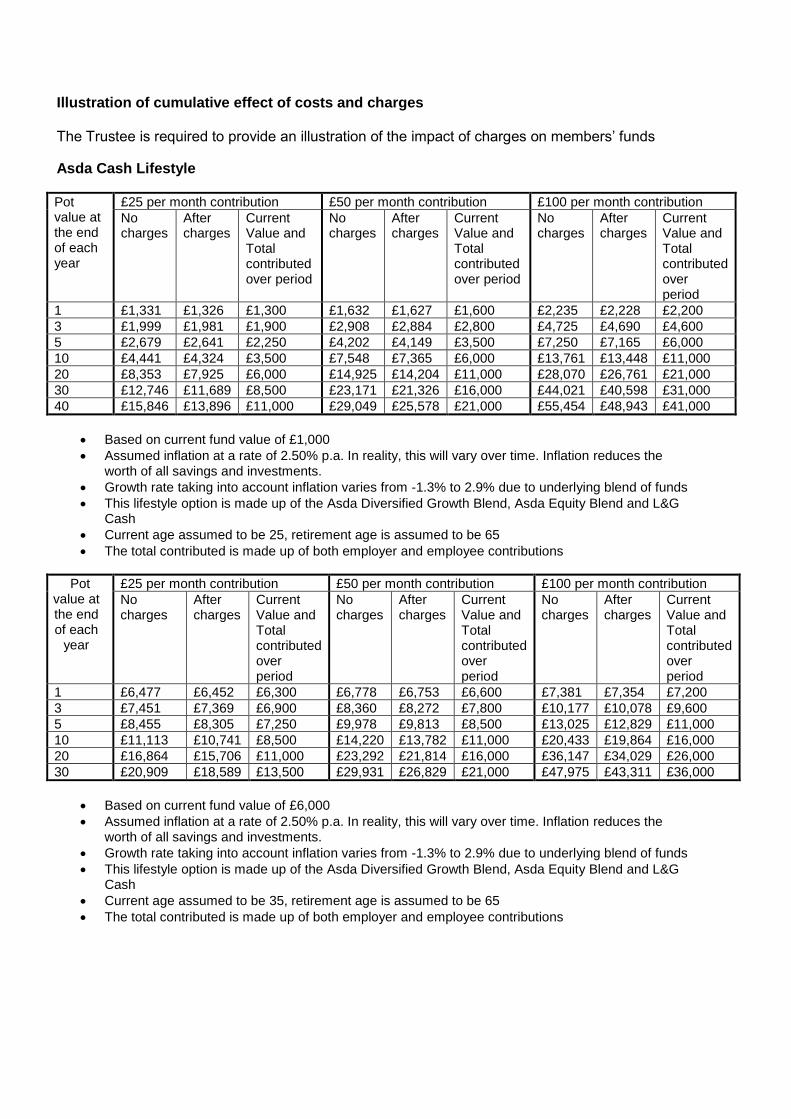

Illustration of cumulative effect of costs and charges The Trustee is required to provide an illustration of the impact of charges on members’ funds

Asda Cash Lifestyle

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £1,331 £1,326 £1,300 £1,632 £1,627 £1,600 £2,235 £2,228 £2,200

3 £1,999 £1,981 £1,900 £2,908 £2,884 £2,800 £4,725 £4,690 £4,600

5 £2,679 £2,641 £2,250 £4,202 £4,149 £3,500 £7,250 £7,165 £6,000

10 £4,441 £4,324 £3,500 £7,548 £7,365 £6,000 £13,761 £13,448 £11,000

20 £8,353 £7,925 £6,000 £14,925 £14,204 £11,000 £28,070 £26,761 £21,000

30 £12,746 £11,689 £8,500 £23,171 £21,326 £16,000 £44,021 £40,598 £31,000

40 £15,846 £13,896 £11,000 £29,049 £25,578 £21,000 £55,454 £48,943 £41,000

Based on current fund value of £1,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 25, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

Pot value at the end of each

year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £6,477 £6,452 £6,300 £6,778 £6,753 £6,600 £7,381 £7,354 £7,200

3 £7,451 £7,369 £6,900 £8,360 £8,272 £7,800 £10,177 £10,078 £9,600

5 £8,455 £8,305 £7,250 £9,978 £9,813 £8,500 £13,025 £12,829 £11,000

10 £11,113 £10,741 £8,500 £14,220 £13,782 £11,000 £20,433 £19,864 £16,000

20 £16,864 £15,706 £11,000 £23,292 £21,814 £16,000 £36,147 £34,029 £26,000

30 £20,909 £18,589 £13,500 £29,931 £26,829 £21,000 £47,975 £43,311 £36,000

Based on current fund value of £6,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 35, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

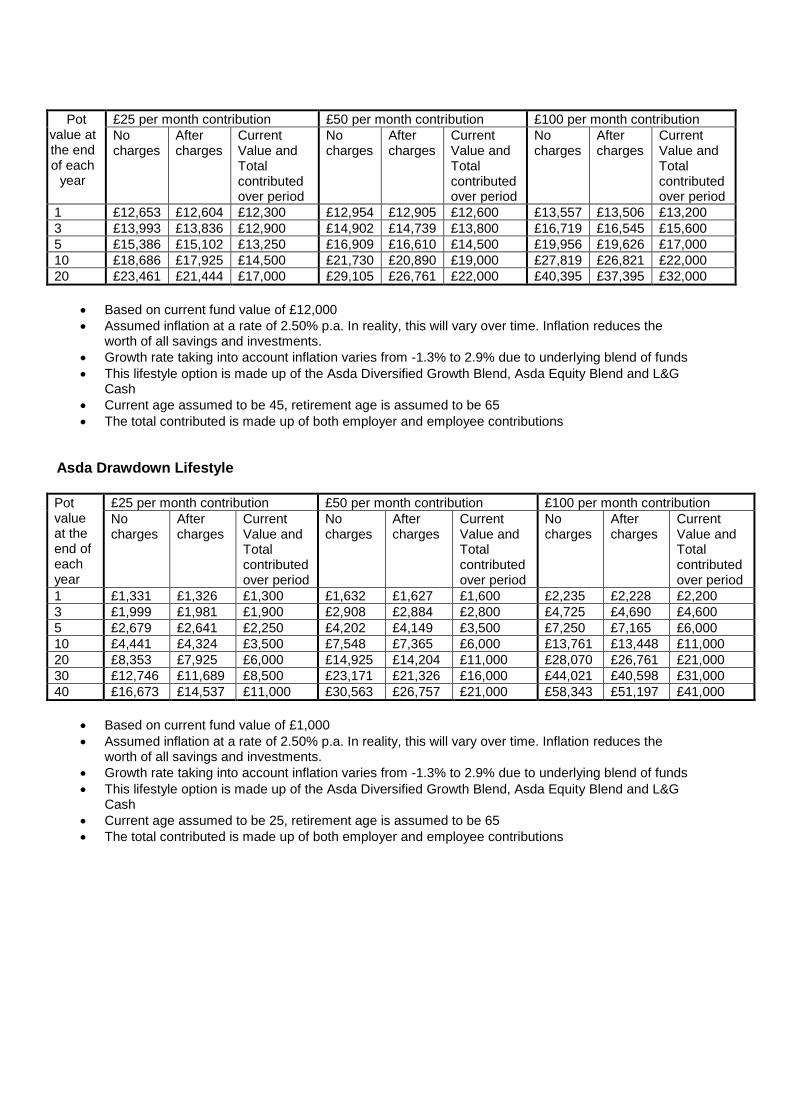

Pot value at the end of each

year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £12,653 £12,604 £12,300 £12,954 £12,905 £12,600 £13,557 £13,506 £13,200

3 £13,993 £13,836 £12,900 £14,902 £14,739 £13,800 £16,719 £16,545 £15,600

5 £15,386 £15,102 £13,250 £16,909 £16,610 £14,500 £19,956 £19,626 £17,000

10 £18,686 £17,925 £14,500 £21,730 £20,890 £19,000 £27,819 £26,821 £22,000

20 £23,461 £21,444 £17,000 £29,105 £26,761 £22,000 £40,395 £37,395 £32,000

Based on current fund value of £12,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 45, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

Asda Drawdown Lifestyle

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £1,331 £1,326 £1,300 £1,632 £1,627 £1,600 £2,235 £2,228 £2,200

3 £1,999 £1,981 £1,900 £2,908 £2,884 £2,800 £4,725 £4,690 £4,600

5 £2,679 £2,641 £2,250 £4,202 £4,149 £3,500 £7,250 £7,165 £6,000

10 £4,441 £4,324 £3,500 £7,548 £7,365 £6,000 £13,761 £13,448 £11,000

20 £8,353 £7,925 £6,000 £14,925 £14,204 £11,000 £28,070 £26,761 £21,000

30 £12,746 £11,689 £8,500 £23,171 £21,326 £16,000 £44,021 £40,598 £31,000

40 £16,673 £14,537 £11,000 £30,563 £26,757 £21,000 £58,343 £51,197 £41,000

Based on current fund value of £1,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 25, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

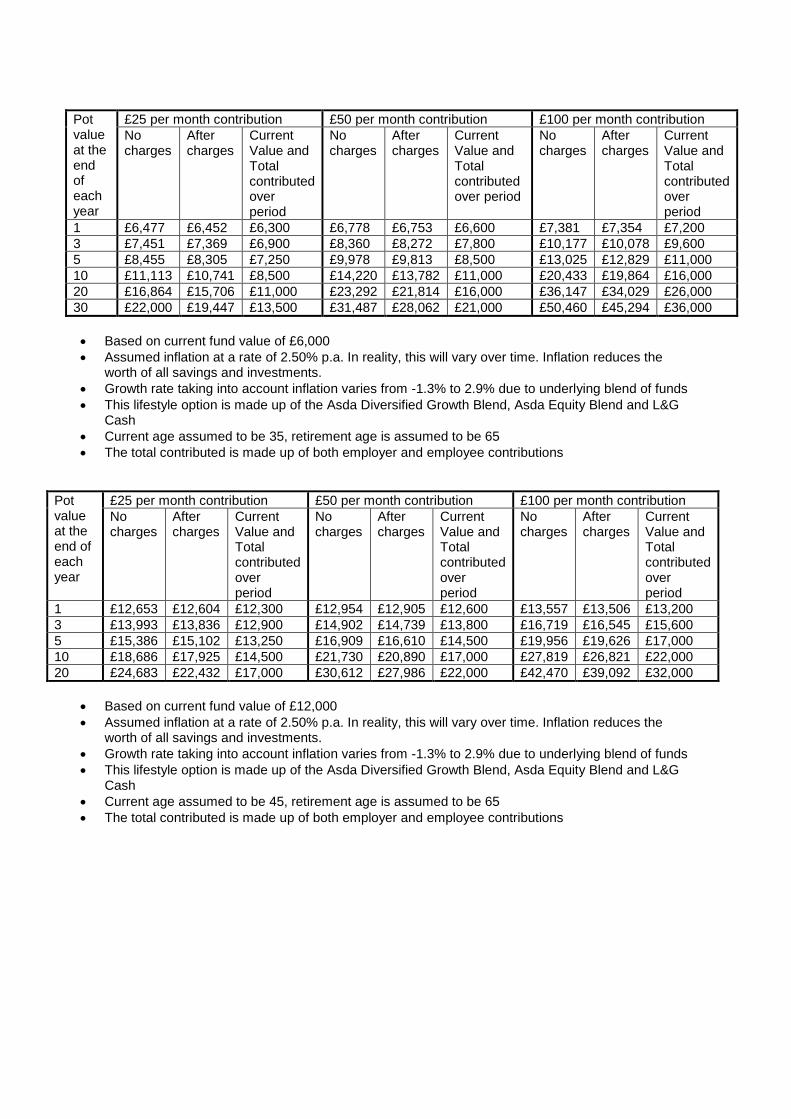

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £6,477 £6,452 £6,300 £6,778 £6,753 £6,600 £7,381 £7,354 £7,200

3 £7,451 £7,369 £6,900 £8,360 £8,272 £7,800 £10,177 £10,078 £9,600

5 £8,455 £8,305 £7,250 £9,978 £9,813 £8,500 £13,025 £12,829 £11,000

10 £11,113 £10,741 £8,500 £14,220 £13,782 £11,000 £20,433 £19,864 £16,000

20 £16,864 £15,706 £11,000 £23,292 £21,814 £16,000 £36,147 £34,029 £26,000

30 £22,000 £19,447 £13,500 £31,487 £28,062 £21,000 £50,460 £45,294 £36,000

Based on current fund value of £6,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 35, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £12,653 £12,604 £12,300 £12,954 £12,905 £12,600 £13,557 £13,506 £13,200

3 £13,993 £13,836 £12,900 £14,902 £14,739 £13,800 £16,719 £16,545 £15,600

5 £15,386 £15,102 £13,250 £16,909 £16,610 £14,500 £19,956 £19,626 £17,000

10 £18,686 £17,925 £14,500 £21,730 £20,890 £17,000 £27,819 £26,821 £22,000

20 £24,683 £22,432 £17,000 £30,612 £27,986 £22,000 £42,470 £39,092 £32,000

Based on current fund value of £12,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 45, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

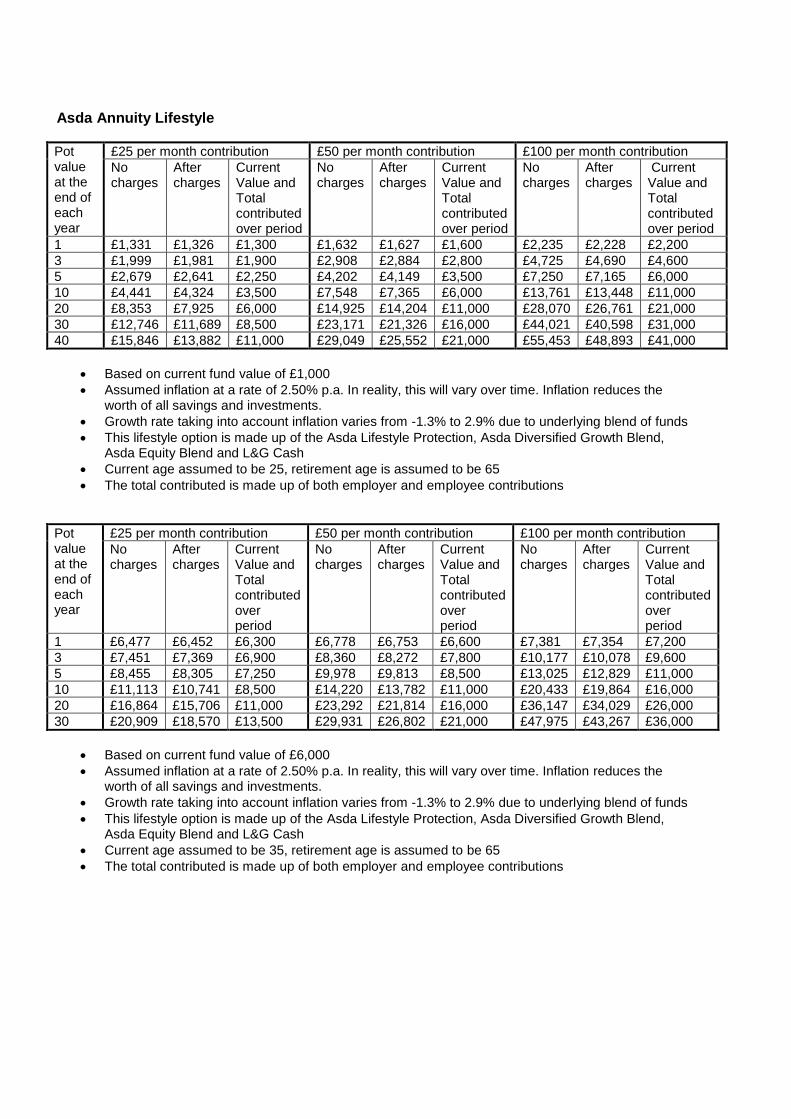

Asda Annuity Lifestyle

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £1,331 £1,326 £1,300 £1,632 £1,627 £1,600 £2,235 £2,228 £2,200

3 £1,999 £1,981 £1,900 £2,908 £2,884 £2,800 £4,725 £4,690 £4,600

5 £2,679 £2,641 £2,250 £4,202 £4,149 £3,500 £7,250 £7,165 £6,000

10 £4,441 £4,324 £3,500 £7,548 £7,365 £6,000 £13,761 £13,448 £11,000

20 £8,353 £7,925 £6,000 £14,925 £14,204 £11,000 £28,070 £26,761 £21,000

30 £12,746 £11,689 £8,500 £23,171 £21,326 £16,000 £44,021 £40,598 £31,000

40 £15,846 £13,882 £11,000 £29,049 £25,552 £21,000 £55,453 £48,893 £41,000

Based on current fund value of £1,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Lifestyle Protection, Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 25, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £6,477 £6,452 £6,300 £6,778 £6,753 £6,600 £7,381 £7,354 £7,200

3 £7,451 £7,369 £6,900 £8,360 £8,272 £7,800 £10,177 £10,078 £9,600

5 £8,455 £8,305 £7,250 £9,978 £9,813 £8,500 £13,025 £12,829 £11,000

10 £11,113 £10,741 £8,500 £14,220 £13,782 £11,000 £20,433 £19,864 £16,000

20 £16,864 £15,706 £11,000 £23,292 £21,814 £16,000 £36,147 £34,029 £26,000

30 £20,909 £18,570 £13,500 £29,931 £26,802 £21,000 £47,975 £43,267 £36,000

Based on current fund value of £6,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Lifestyle Protection, Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 35, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

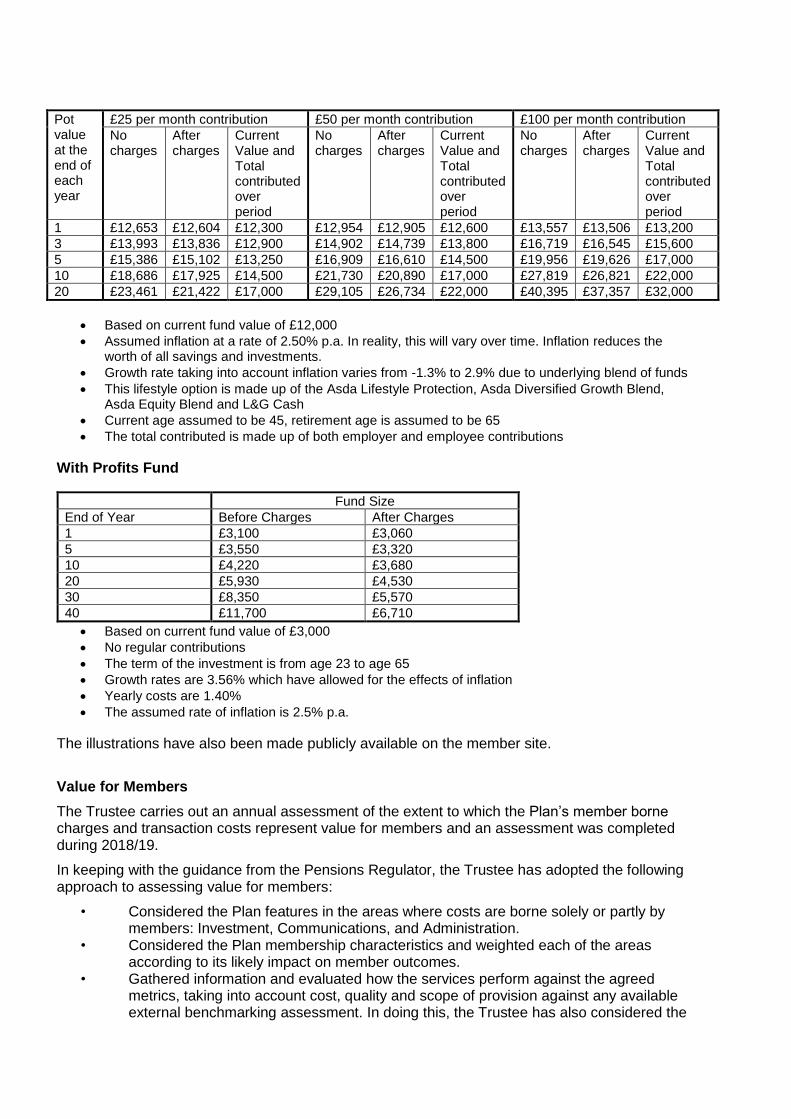

Pot value at the end of each year

£25 per month contribution £50 per month contribution £100 per month contribution

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

No charges

After charges

Current Value and Total contributed over period

1 £12,653 £12,604 £12,300 £12,954 £12,905 £12,600 £13,557 £13,506 £13,200

3 £13,993 £13,836 £12,900 £14,902 £14,739 £13,800 £16,719 £16,545 £15,600

5 £15,386 £15,102 £13,250 £16,909 £16,610 £14,500 £19,956 £19,626 £17,000

10 £18,686 £17,925 £14,500 £21,730 £20,890 £17,000 £27,819 £26,821 £22,000

20 £23,461 £21,422 £17,000 £29,105 £26,734 £22,000 £40,395 £37,357 £32,000

Based on current fund value of £12,000

Assumed inflation at a rate of 2.50% p.a. In reality, this will vary over time. Inflation reduces the worth of all savings and investments.

Growth rate taking into account inflation varies from -1.3% to 2.9% due to underlying blend of funds

This lifestyle option is made up of the Asda Lifestyle Protection, Asda Diversified Growth Blend, Asda Equity Blend and L&G Cash

Current age assumed to be 45, retirement age is assumed to be 65

The total contributed is made up of both employer and employee contributions

With Profits Fund

Fund Size

End of Year Before Charges After Charges

1 £3,100 £3,060

5 £3,550 £3,320

10 £4,220 £3,680

20 £5,930 £4,530

30 £8,350 £5,570

40 £11,700 £6,710

Based on current fund value of £3,000

No regular contributions

The term of the investment is from age 23 to age 65

Growth rates are 3.56% which have allowed for the effects of inflation

Yearly costs are 1.40%

The assumed rate of inflation is 2.5% p.a.

The illustrations have also been made publicly available on the member site.

Value for Members

The Trustee carries out an annual assessment of the extent to which the Plan’s member borne charges and transaction costs represent value for members and an assessment was completed during 2018/19.

In keeping with the guidance from the Pensions Regulator, the Trustee has adopted the following approach to assessing value for members:

• Considered the Plan features in the areas where costs are borne solely or partly by members: Investment, Communications, and Administration.

• Considered the Plan membership characteristics and weighted each of the areas according to its likely impact on member outcomes.

• Gathered information and evaluated how the services perform against the agreed metrics, taking into account cost, quality and scope of provision against any available external benchmarking assessment. In doing this, the Trustee has also considered the

views of their advisers on other options available in the market given the Plan’s characteristics.

• Agreed an action plan with clear timescales where the Trustee believes areas could be further improved.

With help from their advisers the Trustee has assessed how well the Plan delivers value for members in each area including using appropriate metrics to compare the Plan against other pension schemes and other options available in the market. The Value for Members assessment carried out for the Plan is a cost-benefit analysis. It is an application of both quantitative and qualitative criteria, where the costs of membership are generally quantitative and the benefits of membership are mostly qualitative.

Value Definition Provides excellent value (3)

The Trustee considers the Plan offers excellent value for members; providing services of a high quality/cost range compared with other options or similar schemes in the market.

Provides value (2) The Trustee considers the Plan offers value for members, providing similar services at similar quality/cost compared with other options or similar schemes in the market.

Provides poor value (1)

The Trustee considers the Plan offers poor value for members providing services of a low quality/cost range compared with other options or similar schemes in the market.

Category Weighting Overall rating Key rationale

Investment 70% 2019

Provides

excellent

value (3)

2018

3

• The average charges for the default funds are

broadly in line with a 2016 Landscape and Charges

DWP survey.

• The default arrangement is closely monitored with

quarterly performance information being reviewed

at each Trustee meeting.

• With the assistance of the investment adviser, the

Trustee negotiated competitive (as assessed by the

investment adviser) fund charges in 2017/18. There

will be an exercise to perform a market review of

charges once these current terms expire in 2021.

This process is likely to kick off in 2020 as part of the

platform provider review.

• The Trustee considers that the default funds and

range of self-select funds are suitable given

membership characteristics.

• Performance for most funds has been within

expectations of respective benchmarks (net of

fees). The Trustee regularly monitors charges and

receives quarterly detailed investment reports.

• Transaction cost data has also been compared

relative to other pension schemes but also mainly

also against expectations of typical asset class

trading costs. The Trustee, with the help of their

investment adviser, believes that transaction costs

incurred for the default arrangement and self-select

funds are within this range of expectations. It is too

early to be able to make comparisons across

pension scheme data as these have only been fully

disclosed under the current legislated methodology

for the past couple of years.

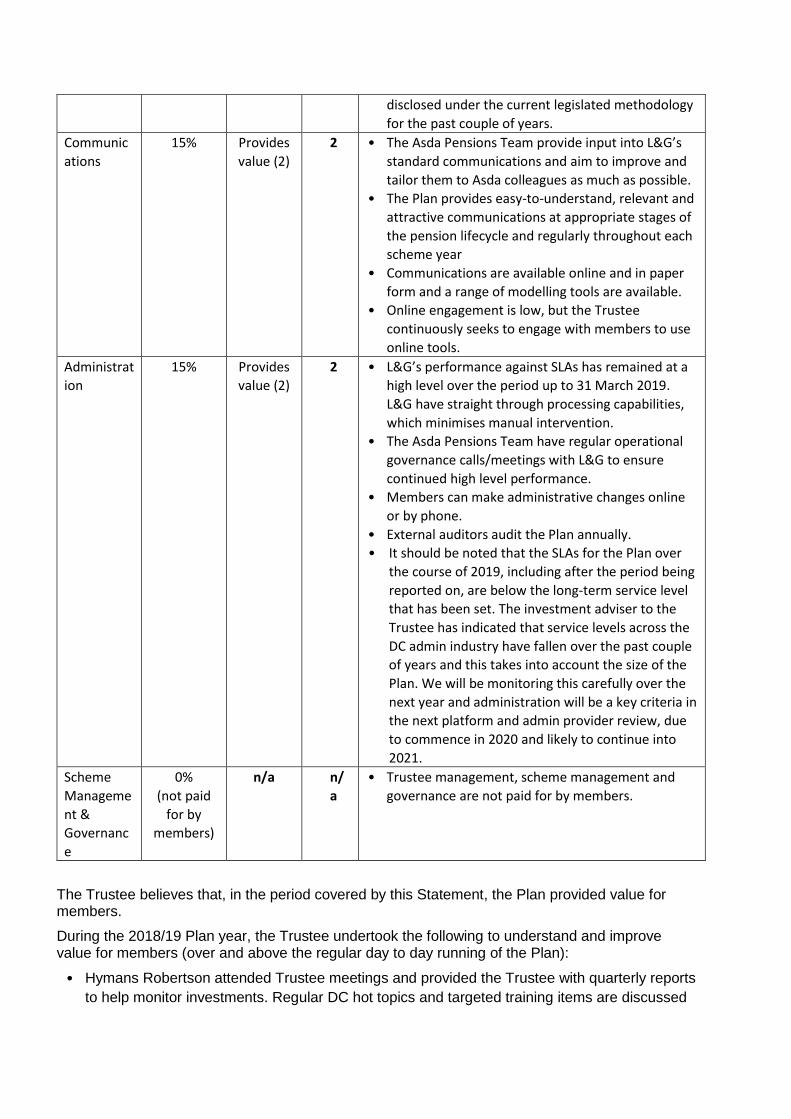

Communic

ations

15% Provides

value (2)

2 • The Asda Pensions Team provide input into L&G’s

standard communications and aim to improve and

tailor them to Asda colleagues as much as possible.

• The Plan provides easy-to-understand, relevant and

attractive communications at appropriate stages of

the pension lifecycle and regularly throughout each

scheme year

• Communications are available online and in paper

form and a range of modelling tools are available.

• Online engagement is low, but the Trustee

continuously seeks to engage with members to use

online tools.

Administrat

ion

15% Provides

value (2)

2 • L&G’s performance against SLAs has remained at a

high level over the period up to 31 March 2019.

L&G have straight through processing capabilities,

which minimises manual intervention.

• The Asda Pensions Team have regular operational

governance calls/meetings with L&G to ensure

continued high level performance.

• Members can make administrative changes online

or by phone.

• External auditors audit the Plan annually.

• It should be noted that the SLAs for the Plan over

the course of 2019, including after the period being

reported on, are below the long-term service level

that has been set. The investment adviser to the

Trustee has indicated that service levels across the

DC admin industry have fallen over the past couple

of years and this takes into account the size of the

Plan. We will be monitoring this carefully over the

next year and administration will be a key criteria in

the next platform and admin provider review, due

to commence in 2020 and likely to continue into

2021.

Scheme

Manageme

nt &

Governanc

e

0%

(not paid

for by

members)

n/a n/

a

• Trustee management, scheme management and

governance are not paid for by members.

The Trustee believes that, in the period covered by this Statement, the Plan provided value for members.

During the 2018/19 Plan year, the Trustee undertook the following to understand and improve value for members (over and above the regular day to day running of the Plan):

• Hymans Robertson attended Trustee meetings and provided the Trustee with quarterly reports

to help monitor investments. Regular DC hot topics and targeted training items are discussed

each quarter to allow the Trustee to assess whether ongoing value is provided to members

across all areas of the investment strategy.

• Underlying fund managers attended Trustee meetings over the course of the year to provide

updates on performance relative to risk and return objectives, an update on their forward-

looking views on markets and their strategy to deliver ongoing value for money for underlying

Plan members.

• Increased minimum contribution rates for both employer and employee, in line with legislation

in respect of members that have been automatically enrolled to the Plan.

• Carried out a review of the Common and Conditional Member Data held as part of good

governance to ensure any gaps in information are identified and rectified

• Monitored reports from Prudential and L&G with details of adherence to SLAs and level of

errors and complaints

• Reviewed the Statement of Investment Principles to ensure sufficient wording around

Environmental, Social and Governance (ESG) and other financially material considerations in

relation to the DC investment strategy. Changes were made in September 2019 (outside the

Plan year that this annual statement covers) and this was in line with legislation ahead of the

October 2019 deadline. The Trustee’s beliefs on the impact of ESG on long-term investment

returns and member outcomes and also their beliefs on non-financial considerations were

discussed and updated after training sessions and investment papers from L&G and the

Trustee’s investment advisers. This has been made available on the publicly accessible

member site

• Monitored the transaction costs paid within the funds offered to members and compared this

against the industry more widely.

• Implemented the changes to the equity allocation of the default funds as agreed in 2017/18

• There was a switch to an investment only platform with L&G which has resulted in lower fund

charges for members due to increased efficiencies

• Hymans reviewed the suitability of the current available post retirement income drawdown

products. The outcome of the review was that the existing asset allocation for the Drawdown

Lifestyle Strategy is appropriate and there were no recommended changes

• Maintained a risk register to help record and manage the risks faced in the Plan

During the 2019/20 Plan year, the Trustee intends to undertake the following work to further improve value for members and to refine the way in which the Plan is assessed for value for members:

• Begin a platform provider review.

• Review the suitability of the With Profits fund to members and whether it offers reasonable

value, the last review was carried out during the 2016/17 year

• Review the L&G Master Trust to ensure suitability for members using drawdown

• Consider further liability reduction solutions, in particular a buy-out exercise for deferred

members

The progress will be regularly monitored over the period. An update for the Plan year 2019/20 will be reported in the next Chair’s Statement.

Trustees’ knowledge and understanding

Newly appointed Trustee Directors are asked to complete the Pensions Regulator’s Trustee Toolkit within six months of becoming a Trustee Director. The Trustee has a documented plan for

ongoing training and knowledge appropriate to their duties and this is reviewed annually. This includes:

Trustee Directors are expected to have a working knowledge of the Plan’s Trust Deed and Rules;

Trustee Directors are expected to have a working knowledge of the Plan’s Statement of Investment Principles as well as the investment concepts relevant to the Scheme;

Trustee Directors are expected to have a working knowledge of all documents setting out the Trustee’s current policies;

Trustee Directors are expected to have a working knowledge of the law and legislation relating to pension schemes;

Trustee Directors are encouraged to undertake further study and qualifications which support their work as Trustee Directors;

The Trustee Directors have a documented plan in place for ongoing training appropriate to their duties;

The effectiveness of these practices and the training received are reviewed annually;

The Trustee Directors carry out regular assessments to confirm and identify any gaps in their knowledge and skills.

The Trustee Directors are satisfied that during the period covered by this Statement they have taken effective steps to maintain and develop their knowledge and understanding to properly exercise their functions as Trustee Directors of the Plan.

The Trustee has appointed recognised and suitably qualified legal advisers, investment consultants and benefit consultants to provide advice on the operation of the Plan in accordance with the Plan’s Trust Deed and Rules and in compliance with legislation. This includes the respected professional independent trustee corporation Law Debenture which sits on the Trustee board. The appointment of the Trustee’s advisers is reviewed on a periodic basis.

The Trustee also receive quarterly ‘hot topics’ from it’s adviser covering technical and legislative/regulatory changes affecting defined contribution schemes. Topics included in these updates over the past year include developments in the multi-asset fund market, an update on the impact of market falls during Q4 2018 and updates on ESG and responsible investment.

The Trustee benefits from being up-to-date on current regulatory issues (provided by our legal advisers every quarter) and the members will have confidence the Trustee is aware of any issues that could impact the Plan. The Trustee also participates in an annual quiz that tests their knowledge of investment and legal issues concerning DC pensions. The Trustee Directors are satisfied that during the period covered by this Statement they had access to suitable advice, which enabled them to properly exercise their functions as Trustee Directors of the Plan.

Signed on behalf of the Trustee by: RICHARD PHILLIPS

Chair of Asda Pension Plan Trustees Ltd