Embed Size (px)

Citation preview

Asia Economic Outlookand Implications for Cambodia

Presentation at the Royal School of Administration

Olaf UnteroberdoersterIMF Mission Chief for Cambodia

Phnom PenhMay 2, 2013

2

Outline and Summary

Global Setting

Financial Imbalances:New Challenges for Emerging Asia and Cambodia

Tail risks are receding, but still considerable

•Activity indicators stabilizing•Robust domestic demand•Strengthening external demand•Inflation remains low

•Improved financial conditions •Stronger capital inflows•Financial imbalances building

Asia Outlook

Common policy challenges:•Need for rebuilding space•Scope for macroprudential measures

3

Global tail risks are receding…

Global Setting

Selected Europe: Sovereign CDS Spreads (CDS Spreads in basis points, 5-year senior

debt)

Advanced Economies: Stock Market Performance

(Index; December 31, 2010 =100)

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-

12

Aug-1

2

Sep-1

2

Oct

-12

Nov-1

2

Dec-

12

Jan-1

3

Feb-1

3

Mar-

13

Apr-

13

0

100

200

300

400

500

600

700

800

900

0

200

400

600

800

1000

1200

1400

1600

1800

Italy France

Spain Ireland (RHS)

Portugal (RHS)

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-

12

Aug-1

2

Sep-1

2

Oct

-12

Nov-

12

Dec-

12

Jan-1

3

Feb-1

3

Mar-

13

Apr-

13

70

80

90

100

110

120

5

15

25

35

US: S&P 500UK: Financial Times All SharesEuro Area: STOXX Broad Price IndexVIX (actual level, RHS)

4

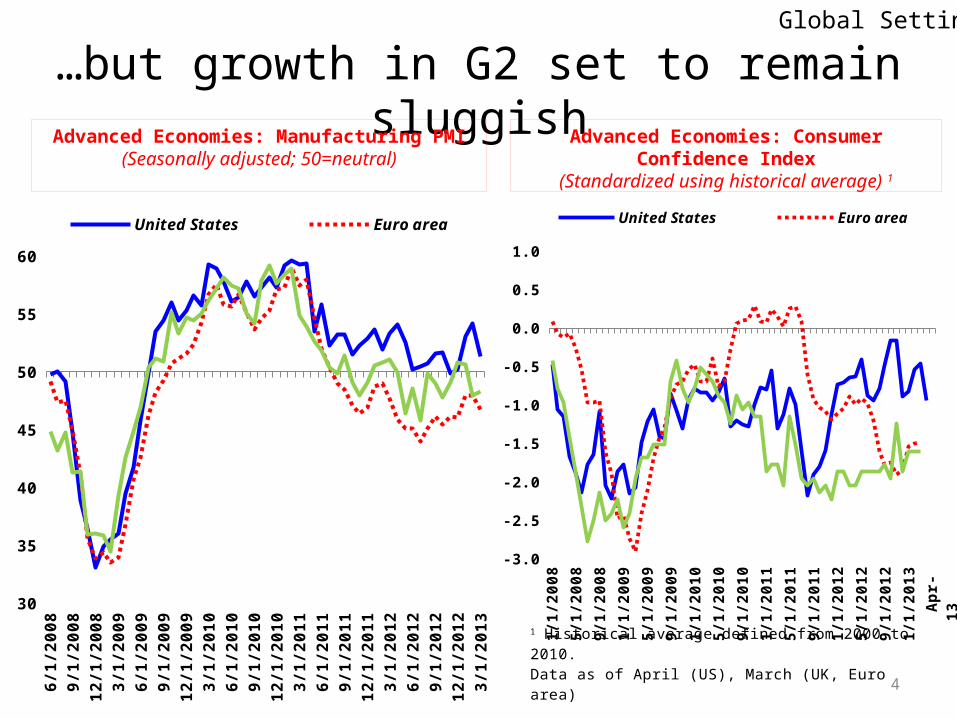

…but growth in G2 set to remain sluggish

Global Setting

Advanced Economies: Manufacturing PMI(Seasonally adjusted; 50=neutral)

Advanced Economies: Consumer Confidence Index

(Standardized using historical average) 1

Jun-0

8S

ep-0

8D

ec-

08

Mar-

09

Jun-0

9S

ep-0

9D

ec-

09

Mar-

10

Jun-1

0S

ep-1

0D

ec-

10

Mar-

11

Jun-1

1S

ep-1

1D

ec-

11

Mar-

12

Jun-1

2S

ep-1

2D

ec-

12

Mar-

13

30

35

40

45

50

55

60

United States Euro area

Jan-0

8

May-0

8

Sep-0

8

Jan-0

9

May-0

9

Sep-0

9

Jan-1

0

May-1

0

Sep-1

0

Jan-1

1

May-1

1

Sep-1

1

Jan-1

2

May-1

2

Sep-1

2

Jan-1

3

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

United States Euro areaUnited Kingdom

1 Historical average defined from 2000 to 2010.Data as of April (US), March (UK, Euro area)

Apr-

13

5

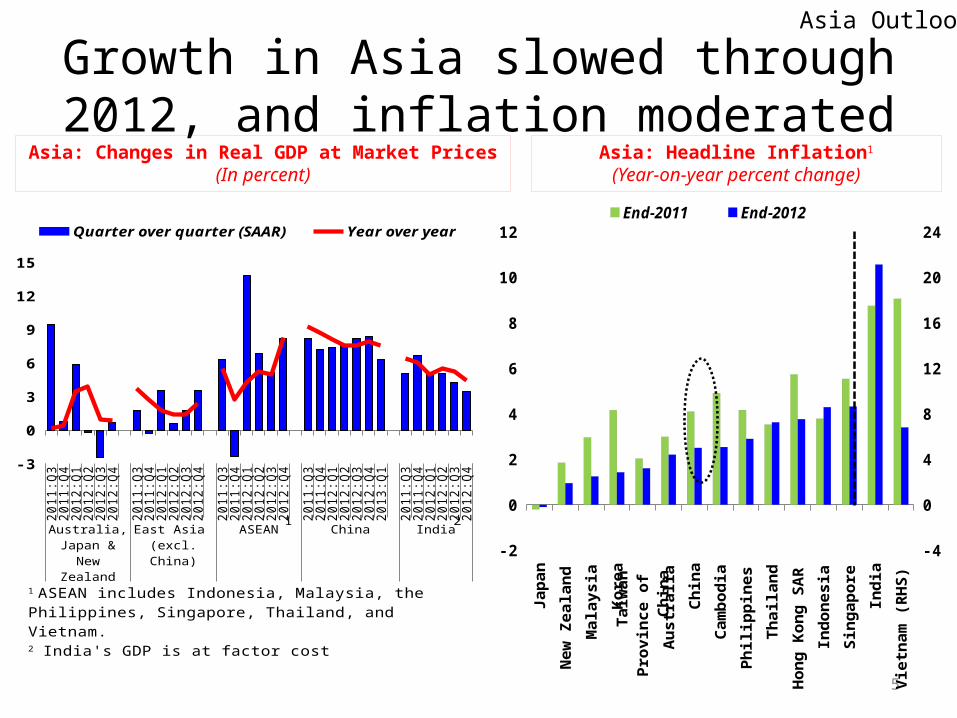

Growth in Asia slowed through 2012, and inflation moderated

Asia Outlook

Asia: Changes in Real GDP at Market Prices(In percent)

Asia: Headline Inflation1

(Year-on-year percent change)

Japan

New

Zeala

nd

Mala

ysia

Kore

a

Austr

alia

Chin

a

Cam

bodia

Philip

pin

es

Thailand

Hong K

ong S

AR

Indonesia

Sin

gapore

India

Vie

tnam

(R

HS

)

-2

0

2

4

6

8

10

12

-4

0

4

8

12

16

20

24End-2011 End-2012

Taiw

an P

rov

-in

ce o

f C

hin

a

2011:Q

32011:Q

42012:Q

12012:Q

22012:Q

32012:Q

4

2011:Q

32011:Q

42012:Q

12012:Q

22012:Q

32012:Q

4

2011:Q

32011:Q

42012:Q

12012:Q

22012:Q

32012:Q

4

2011:Q

32011:Q

42012:Q

12012:Q

22012:Q

32012:Q

42013:Q

1

2011:Q

32011:Q

42012:Q

12012:Q

22012:Q

32012:Q

4

Australia, Japan &

New Zea-land

East Asia (excl. China)

ASEAN China India

-3

0

3

6

9

12

15

Quarter over quarter (SAAR) Year over year

1 ASEAN includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam.2 India's GDP is at factor cost

1 2

6

Near-term outlook: gradual growth pickupAsia Outlook

Indicator Model for Asia: Projected vs. Actual Real GDP Growth

(In percent; q/q SAAR)

Real GDP Growth in 2013(WEO forecast; In percent)

0.000 to 3.0003.000 to 5.0005.000 to 8.0008.000 to 40.000No data

1 3 5 7 9

11

13

15

17

19

21

23

25

27

29

31

33

-6

-3

0

3

6

9

12

15

confidencerval

WEO forecast

Actual growth rate (PPP weighted)

Model forecast

2013:

Q2

7

…underpinned by robust domestic demandAsia Outlook

Asia: Contributions to Projected Growth(In percentage points; year over year)

2012 2013 2012 2013 2012 2013 2012 2013 2012 2013Australia, Japan & New Zealand

China East Asia(excl. China)

India ASEAN

-2

0

2

4

6

8

10

12

Net exports Public domestic demand Private domestic demand Growth

1 ASEAN includes Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam

1

8

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

201010

12

14

16

18

20

22

24

26

28

Capital goodsConsumption goodsIntermediate goods

ASEAN Intraregional Exports by Category

(In percent of total exports in each category)

Internal demand dynamics are becoming more favorable

15 25 35 45 55 65 750.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

0.884498506326379

0.62703801838355

0.775451110556515

0.442055725100394

0.707132910596549

1.01479075045515

0.89686428023659

Dem

and f

rom

Japan a

nd C

hin

a r

ela

tive

to d

em

and f

rom

U.S

. and E

U

Total export value added in percent of GDP

Greater openness and reliance on China

and Japan

Selected Asia: External Dependence(Value-added basis; average 2005-10)

9

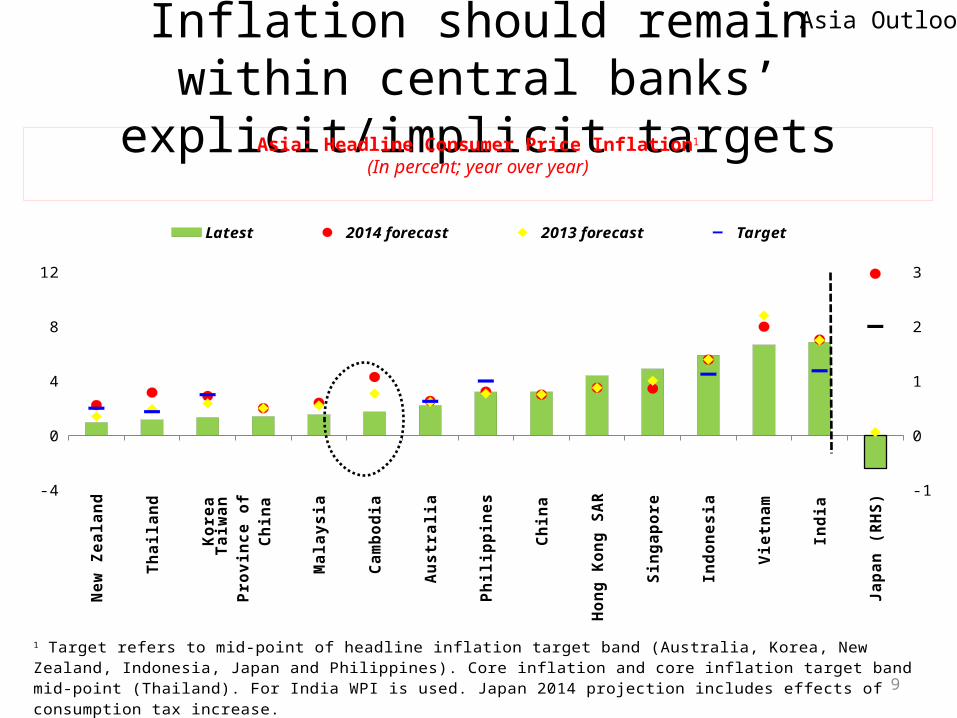

Inflation should remain within central banks’ explicit/implicit targets

Asia Outlook

Asia: Headline Consumer Price Inflation1

(In percent; year over year)

New

Zeala

nd

Thailand

Kore

a

Mala

ysia

Cam

bodia

Austr

alia

Philip

pin

es

Chin

a

Hong K

ong S

AR

Sin

gapore

Indonesia

Vie

tnam

India

Japan (

RH

S)

-4

0

4

8

12

-1

0

1

2

3

Latest 2014 forecast 2013 forecast Target

1 Target refers to mid-point of headline inflation target band (Australia, Korea, New Zealand, Indonesia, Japan and Philippines). Core inflation and core inflation target band mid-point (Thailand). For India WPI is used. Japan 2014 projection includes effects of consumption tax increase.

Taiw

an P

rov-

ince

of

Chin

a

10

Global risks have become more balanced, but considerable downside risks remain.

Risks

Asia: Real GDP Growth (Central forecast and selected confidence intervals; in percent)

2009 2010 2011 2012 2013 20140

1

2

3

4

5

6

7

8

9

Series550 percent confidence interval 70 percent confidence interval90 percent confidence interval (2012)

Central forecast

11

Financial stability risks amid renewed capital inflows and robust credit growth?

Risks

Emerging Asia: Equity and Bond Funds—Weekly Net Flows during 2010‒13 1

(In billions of U.S. dollars)

Asia: Change in Credit to GDP, 20121

(In percentage points)

2010:Q

1

2010:Q

2

2010:Q

3

2010:Q

4

2011:Q

1

2011:Q

2

2011:Q

3

2011:Q

4

2012:Q

1

2012:Q

2

2012:Q

3

2012:Q

4

2013:Q

1

-20000

-15000

-10000

-5000

0

5000

10000

15000

20000

25000

30000

Bond funds Equity fundsPeak in 2006-2007

1 Includes exchange traded fund flows and mutual fund flows for Emerging Asia, Singapore, Hong Kong SAR, Tai-wan Province of China, and Korea.

Vie

tnam

Kore

a

Japan

Austr

alia

India

New

Zeala

nd

Indonesia

Philip

pin

es

Hong K

ong S

AR

Mala

ysia

Chin

a

Thailand

Cam

bodia

Sin

gapore

Euro

are

a

Lati

n A

meri

ca

Unit

ed S

tate

s

-30

-20

-10

0

10

20

30

Change from 2011 Deviation from trend

1 Latest available in 2012. Trend calculated using HP filter over the period 2001‒11.

Taiw

an

Pro

v-

ince

of

Ch

ina

12

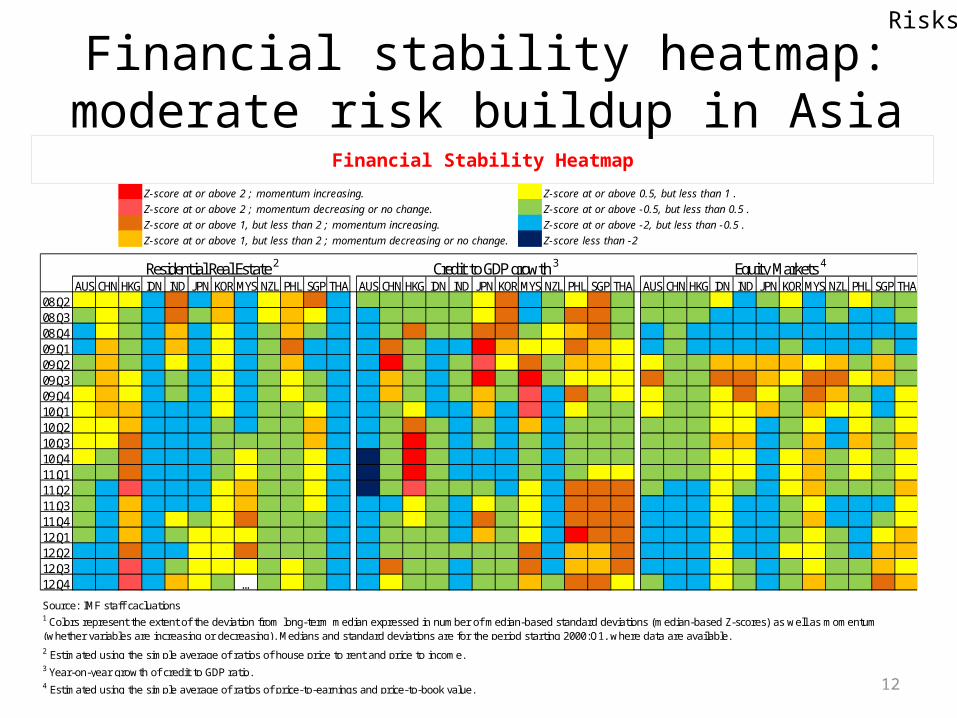

Financial stability heatmap:moderate risk buildup in Asia

Risks

Financial Stability Heatmap

Z-score at or above 2 ; momentum increasing. Z-score at or above 0.5, but less than 1 .

Z-score at or above 2 ; momentum decreasing or no change. Z-score at or above -0.5, but less than 0.5 .

Z-score at or above 1, but less than 2 ; momentum increasing. Z-score at or above -2, but less than -0.5 .

Z-score at or above 1, but less than 2 ; momentum decreasing or no change. Z-score less than -2

AUS CHNHKG IDN IND JPN KORMYS NZL PHL SGP THA AUS CHNHKG IDN IND JPN KORMYS NZL PHL SGP THA AUS CHNHKG IDN IND JPN KORMYS NZL PHL SGP THA08:Q2 1 1 1 -1 3 -1 2 -1 1 2 3 -1 0 0 0 0 0 1 3 -1 0 1 3 0 0 0 0 1 -1 0 1 -1 0 1 0 008:Q3 0 1 0 -1 3 0 2 -1 1 2 1 -1 -1 0 0 0 0 1 3 -1 0 3 3 0 0 0 0 -1 -1 -1 0 -1 0 -1 -1 008:Q4 -1 1 0 -1 2 -1 1 -1 0 2 0 -1 -1 0 3 0 0 3 3 0 1 2 3 0 -1 0 -1 -1 -1 -1 -1 -1 -1 -1 -1 -109:Q1 -1 2 0 -1 2 -1 1 -1 0 3 -1 -1 -1 3 0 -1 -1 5 2 1 1 3 2 1 -1 0 -1 -1 -1 -1 0 -1 -1 -1 0 -109:Q2 0 2 0 -1 1 -1 1 -1 0 2 -1 -1 -1 5 0 -1 0 4 1 3 0 2 2 1 1 0 0 2 2 2 2 1 2 0 2 009:Q3 0 2 1 -1 0 -1 1 -1 0 1 0 -1 -1 2 0 -1 0 5 0 5 0 1 1 1 3 0 0 3 3 2 1 3 3 1 2 009:Q4 1 2 1 -1 0 -1 1 -1 0 1 0 -1 -1 2 0 -1 0 2 0 4 -1 3 0 1 1 0 0 1 3 1 0 3 2 0 -1 110:Q1 1 2 2 -1 -1 -1 1 -1 0 0 1 -1 -1 0 1 -1 -1 2 -1 4 -1 1 0 0 1 0 0 1 1 2 0 2 1 1 -1 110:Q2 1 1 2 -1 -1 -1 0 -1 0 0 2 -1 -1 0 3 0 -1 0 -1 2 -1 0 0 0 0 0 0 1 1 -1 0 1 -1 1 0 110:Q3 1 1 3 -1 -1 -1 0 0 0 0 2 -1 -1 0 5 0 -1 0 -1 0 -1 0 0 0 0 0 0 2 2 -1 0 2 -1 2 0 210:Q4 1 0 3 -1 -1 -1 0 1 0 0 1 -1 -2 0 5 0 -1 -1 -1 0 -1 0 0 0 0 0 0 1 1 -1 1 2 0 1 0 111:Q1 0 0 3 -1 -1 -1 0 1 0 0 1 -1 -2 0 5 0 -1 -1 -1 0 -1 0 1 1 0 0 0 1 1 -1 1 2 0 1 0 111:Q2 0 -1 4 -1 -1 -1 1 2 0 0 1 -1 -2 0 4 0 0 0 -1 1 -1 3 3 3 0 -1 -1 1 0 -1 1 2 0 0 0 211:Q3 0 -1 2 -1 -1 -1 1 2 0 0 1 -1 -1 -1 1 0 -1 1 0 1 -1 3 3 3 -1 -1 -1 1 -1 -1 0 1 -1 -1 -1 111:Q4 0 -1 2 -1 1 0 1 3 0 0 0 -1 -1 0 1 0 -1 3 0 1 -1 3 3 3 -1 -1 -1 1 -1 -1 0 2 -1 -1 0 112:Q1 0 -1 2 -1 0 1 1 1 0 0 0 -1 -1 0 0 0 -1 2 0 1 -1 5 3 3 -1 -1 -1 1 -1 -1 0 1 0 -1 1 212:Q2 -1 -1 3 -1 -1 1 1 3 0 0 0 -1 -1 0 0 0 0 0 0 3 -1 2 2 3 -1 -1 -1 1 -1 -1 1 1 0 -1 2 212:Q3 -1 -1 4 -1 0 1 1 1 0 1 0 -1 -1 3 0 0 -1 0 0 3 -1 2 2 3 -1 -1 -1 1 0 -1 0 1 0 0 2 112:Q4 -1 -1 4 -1 2 1 0 … 0 1 0 -1 -1 1 0 0 -1 0 0 2 0 3 3 1 0 -1 -1 1 0 -1 0 2 0 0 3 2

Source: IMF staff cacluations

2 Estimated using the simple average of ratios of house price to rent and price to income.3 Year-on-year growth of credit to GDP ratio. 4 Estimated using the simple average of ratios of price-to-earnings and price-to-book value.

Residential Real Estate 2 Credit to GDP growth 3 Equity Markets 4

1 Colors represent the extent of the deviation from long-term median expressed in number of median-based standard deviations (median-based Z-scores) as well as momentum (whether variables are increasing or decreasing). Medians and standard deviations are for the period starting 2000:Q1, where data are available.

13

Corporate balance sheets generally sound

Risks

Selected Asia: Nonfinancial Sector Corporate Debt-to-Equity Ratio1

(In percentage points; cap-weighted mean; 2011)

KO

REA

PH

ILIP

PIN

ES

JAP

AN

IND

ON

ES

IA

AU

STR

ALIA

NEW

ZEA

LA

ND

MA

LA

YS

IA

IND

IA

VIE

TN

AM

CH

INA

TH

AIL

AN

D

HO

NG

KO

NG

SA

R

SIN

GA

PO

RE

EU

RO

ZO

NE

LA

TA

M

AS

IAN

AV

ER

AG

E

UN

ITED

STA

TES

-100

-80

-60

-40

-20

0

20

40

60

80

100Difference from 2009 Difference from Median (2002-2007)

1 Vietnam's data start in 2006.

TA

IWA

N

PR

OV

-IN

CE O

F C

HIN

A

14

Banks’ buffers increasing, although below international comparators in some cases

Risks

Selected Asia: Commercial Banks' Loss-Absorbing Buffers1

(In percent of risk-weighted assets; asset-weighted mean)

India

Austr

alia

Japan

New

Zeala

nd

Kore

a

Thailand

Chin

a

Mala

ysia

Hong K

ong S

AR

Philip

pin

es

Indonesia

Sin

gapore

-2

0

2

4

6

8

Tier-1 capital in excess of 8.5 % Loan loss reserves less nonperforming loansEffective buffer Latin AmericaUnited States Euro AreaAsia

1 Loss absorbing buffers are calculated as Tier-1 capital in excess of 8.5 percent plus loan loss reserves less impaired loans as percent of total risk-weighted assets.

Taiw

an P

rov-

ince

of

Chin

a

15

Cambodia: Rapid credit growth increasingly fuelled by foreign funds

Risks

Monetary Developments, 2008-12(Contribution to broad money growth, in percent)

Feb-0

8

Apr-

08

Jun-0

8

Aug-0

8

Oct

-08

Dec-

08

Feb-0

9

Apr-

09

Jun-0

9

Aug-0

9

Oct

-09

Dec-

09

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct

-10

Dec-

10

Feb-1

1

Apr-

11

Jun-1

1

Aug-1

1

Oct

-11

Dec-

11

Feb-1

2

Apr-

12

Jun-1

2

Aug-1

2

Oct

-12

Dec-

12

Feb-1

3

-20

0

20

40

60

80

100

120

-20

0

20

40

60

80

100

120 Net domestic assets Net foreign assets

Broad money growth 1/ Private sector credit 1/

1/ Year-on-year percent change.

16

Cambodia: When is credit growth too fast?

Risks

Credit to GDP Relative to Peers(In percent)

Credit Gap(In percent)

Jul-

04

Mar-

05

Nov-0

5Ju

l-06

Mar-

07

Nov-0

7Ju

l-08

Mar-

09

Nov-0

9Ju

l-10

Mar-

11

Nov-1

1Ju

l-12

Mar-

13

Nov-1

3Ju

l-14

Mar-

15

Nov-1

5

0

10

20

30

40

50

60

70

80Credit-to-GDPWith 30 percent credit growthWith 20 percent credit growthLIC median (2009)

Jul-

04

Mar-

05

Nov-0

5Ju

l-06

Mar-

07

Nov-0

7Ju

l-08

Mar-

09

Nov-0

9Ju

l-10

Mar-

11

Nov-1

1Ju

l-12

Mar-

13

Nov-1

3Ju

l-14

Mar-

15

Nov-1

5

-5

0

5

10

15

20

25

30 Credit-to-GDP gap

Gap with 30 percent credit growth

Gap with 20 percent credit growth

17

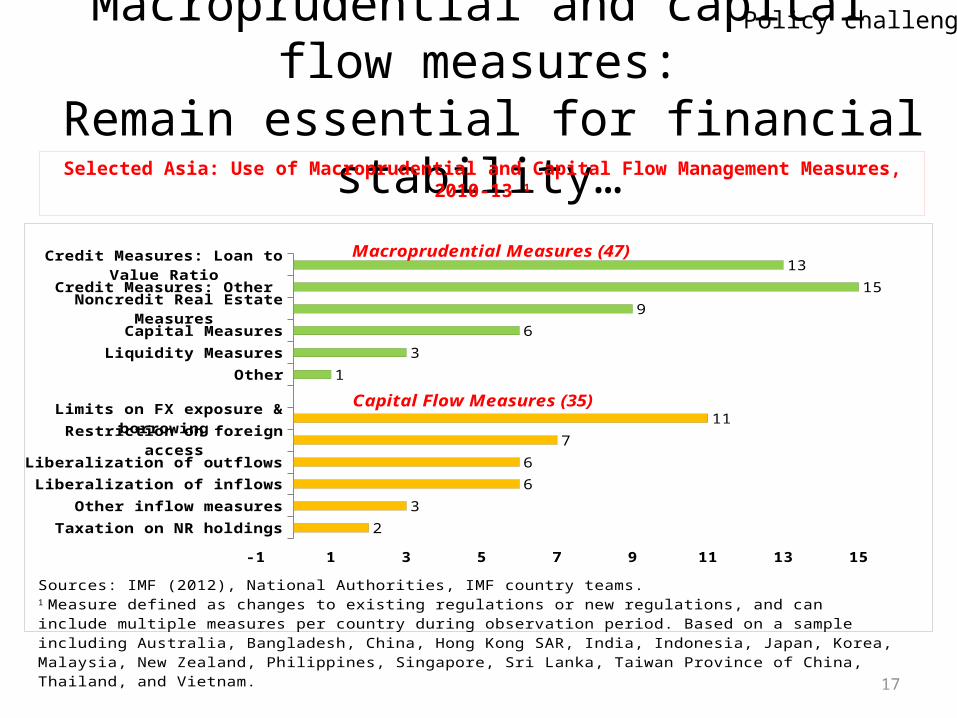

Macroprudential and capital flow measures: Remain essential for financial stability…

Policy challenges

Selected Asia: Use of Macroprudential and Capital Flow Management Measures, 2010-13 1

Taxation on NR holdings

Other inflow measures

Liberalization of inflows

Liberalization of outflows

Restriction on foreign access

Limits on FX exposure & borrowing

Other

Liquidity Measures

Capital Measures

Noncredit Real Estate Measures

Credit Measures: Other

Credit Measures: Loan to Value Ratio

-1 1 3 5 7 9 11 13 15

2

3

6

6

7

11

1

3

6

9

15

13Macroprudential Measures (47)

Capital Flow Measures (35)

Sources: IMF (2012), National Authorities, IMF country teams.1 Measure defined as changes to existing regulations or new regulations, and can include multiple measures per country during observation period. Based on a sample including Australia, Bangladesh, China, Hong Kong SAR, India, Indonesia, Japan, Korea, Malaysia, New Zealand, Philippines, Singapore, Sri Lanka, Taiwan Province of China, Thailand, and Vietnam.

18

Cambodia: High dollarization and foreign inflows limit effectiveness of conventional tools

Policy challenges

Effective Required Reserves(In percent)

Dollarization(In percent)

Feb-0

8

Aug-0

8

Feb-0

9

Aug-0

9

Feb-1

0

Aug-1

0

Feb-1

1

Aug-1

1

Feb-1

2

Aug-1

2

Feb-1

3

90

92

94

96

98

100

90

92

94

96

98

100

Foreign currency deposits to total deposits

Claims on private sector in foreign currency to total claims on private sector.

Feb-0

8Ju

n-0

8O

ct-0

8Feb-0

9Ju

n-0

9O

ct-0

9Feb-1

0Ju

n-1

0O

ct-1

0Feb-1

1Ju

n-1

1O

ct-1

1Feb-1

2Ju

n-1

2O

ct-1

2Feb-1

3

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40In dollars as percent of dollar deposits

In riels as percent of riel deposits

19

There is a need for rebuilding monetary and fiscal policy space

Policy challenges

Selected Asia: Policy Rates(In percent; as of December, 2012)

Selected Asia: Cyclically Adjusted Fiscal Balance

(In percent of GDP)

Ind

ia

Jap

an

Vie

tnam

Mala

ysia

Th

ailan

d

Hon

g K

on

g S

AR

Ph

ilip

pin

es

New

Zeala

nd

Ind

on

esia

Au

str

alia

Ch

ina

Kore

a

Sin

gap

ore

-10

-8

-6

-4

-2

0

2

4

6

8

2012 2013 Average: 2002-07

Taiw

an P

rov

-in

ce o

f C

hin

a

Jap

an

Sin

gap

ore

New

Zeala

nd

Th

ailan

d

Kore

a

Ch

ina

Au

str

alia

Mala

ysia

Ph

ilip

pin

es

Ind

on

esia

Vie

tnam

-4

-2

0

2

4

6

8

10

12

14

Current nominal policy rates

Real policy rates (deviation from 2002–07 av-erage, in percentage points)

Nominal policy rates end-2011

Taiw

an

Pro

v-

ince o

f C

hin

a

20

Cambodia: Fiscal Trends(In Percent of GDP)

2006 2007 2008 2009 2010 2011 2012-25

-20

-15

-10

-5

0

5

10

15

20

Capital expenditureCurrent expenditureGrantsDomestic revenueFiscal balanceDomestic financing

Selected Asia: Tax Revenue(In Percent of GDP)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

0

5

10

15

20

25

Vietnam Cambodia

Lao PDR Myanmar

Other Asian LICs 1/

Cambodia: Fiscal buffers also key for stability and medium-term growth

Policy challenges

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 3050

100

150

200

250

300

350

400

450

500

550

600

650

700

750

Median

10th/90th percentile

25th/75th percentile

Indonesia 1983

Brazil 1961

Korea 1961

Mozambique 1996

1950–2011(normalized to 100 at t = 0, the year before the start of a strong growth episode; median economy; years on x-axis)

Cambodia 1996

Note: LICs exclude countries experiencing or recovering from a serious external or internal conflict at the start of their takeoffs.

Cambodia: A longer-term growth lesson Policy challenges

22

To wrap up…• Near-term growth prospects for Asia have improved, although global recovery remains fragile and subdued

• Easy global and domestic financial conditions and prospect of continued capital inflows require vigilance in monitoring build-up of potential financial stability risks

• Macroprudential tools have a role to play along a move toward rebuilding monetary and fiscal policy space

• For Cambodia, strengthening the conventional monetary tools will also be important while fiscal buffers remain the anchor of macroeconomic stability

23

THANK YOU