Embed Size (px)

Citation preview

ASSESSING RISK AND VALUE CREATION OF PUBLIC AND PRIVATE TIMBERLAND

INVESTMENTS

by

ANTHONY J. CASCIO

(Under the Direction of Michael L. Clutter)

ABSTRACT

This dissertation assesses elements of the financial risk and return of timberland investments

within the United States by applying modern portfolio theory, the capital asset pricing model and the

efficient markets hypothesis. The first study applies modern portfolio theory to assist in the optimal

construction of portfolios of sub-regional timberland assets within the US South. First, we develop a

unique set of synthetic timberland returns for 22 sub-US South regions, for a 19 year time horizon.

Portfolio optimization is performed with these 22 return series, and an efficient frontier identified with

portfolios having risk levels ranging from 3.9% to 13.8%, and expected return levels of 10.4% to 13.4%.

The optimal tangency portfolio is identified having expected return and risk levels of 11.2% and 4.2%,

respectively. Monte Carlo simulation is utilized to estimate the value at risk (VAR) of a hypothetical ten

year, regionally-diversified timberland investment. The second study estimates the systematic risks and

risk-adjusted required returns of timberland investments in different geographic regions within United

States using the Capital Asset Pricing Model (CAPM). We estimate low, positive betas for timberland in

the Pacific Northwest, Northeast and South. These estimates are not significantly different than zero, but

are however higher than many past estimates from earlier time periods. Required return rates of 5.7%-

6.6% are estimated for the three regions, respectively. From 1995 to 2002, nine mergers and acquisitions

of publicly-held, vertically-integrated forest products companies occurred in the United States. Investors

not able to directly own timberland may choose to own shares of these firms as a method of indirect

timberland investment. The third study employs event study methodology, based on the concept of

market efficiency, to test the null hypothesis of no shareholder value creation from these mergers and

acquisitions. We find that $4.7B of market value was created upon the announcement of these nine

combinations. We find that target firms enjoyed a statistically significant, nearly 15% average return

attributable to the merger announcements. The returns to acquiring firms averaged a statistically

insignificant 0.34%. The aggregate return was a statistically significant 7.66%.

INDEX WORDS: Timberland investments, portfolio theory, mergers, financial risk

ASSESSING RISK AND VALUE CREATION OF PUBLIC AND PRIVATE TIMBERLAND

INVESTMENTS

by

ANTHONY J. CASCIO

B.S., James Madison University, 1986

M.S., North Carolina State University, 1998

A Dissertation Submitted to the Graduate Faculty of The University of Georgia in Partial Fulfillment of

the Requirements for the Degree

DOCTOR OF PHILOSOPHY

ATHENS, GEORGIA

2006

© 2006

Anthony J. Cascio

All Rights Reserved

ASSESSING RISK AND VALUE CREATION OF PUBLIC AND PRIVATE TIMBERLAND

INVESTMENTS

by

ANTHONY J. CASCIO

Major Professor: Michael L. Clutter

Committee: Peter S. Bettinger David H. Newman John T. Scruggs

Electronic Version Approved: Maureen Grasso Dean of the Graduate School The University of Georgia August 2006

iv

ACKNOWLEDGEMENTS

A dissertation has one name on it – the student’s. This person is responsible for 100% of the

content therein. This is as it should be. However, total responsibility in no way implies completely

independent work. We all receive help along the way, in varying degrees and from many sources, even as

the vast majority of the effort is our own. Help is received by the committee of professors who convey

guidance and nurture progress. Other professors lend help, both formally in the classroom through

structured teaching, and informally in the hallways, hashing out ideas over a cup of coffee. Data does not

grow on trees, and fall neatly into our laps. People from outside of the ivory tower are priceless conduits

to the data we want, and to the data we actually need but didn’t know about. It is amazing how much

people want to help, so long as they are treated courteously and with respect. Fellow graduate students

provide an incredible amount of support. We are the university catalog suggesting what courses should be

taken; the unofficial tutors to get us through those classes; the artist’s apprentice helping us to create and

shape ideas; the physician’s assistant to help us fix our broken models. Most of all, our fellow students

provide the invaluable encouragement and support that creates such a strong sense of teamwork, lending

another oar in the lifeboat on the graduate student’s journey to his new destination. Again, this is as it

should be.

For this help, I wish to recognize and thank my committee: Mike Clutter, my advisor and mentor

– you provided guidance and ideas, you opened doors and created a stage upon which I could perform;

David Newman, you are a wise old sage of this academic world – your advice in matters both academic,

professional and personal is greatly appreciated; Pete Bettinger, you’ve traveled a similar path as mine,

making your guidance all the more valuable; John Scruggs, you gave perhaps the best lectures I attended

at this university, and yes, you challenged and stimulated me to ‘be curious’.

v

Tom Harris, you’ve been around a long time, and I bet you would be willing to echo Roger

Lowenstein’s assertion that “No investment…can be judged on the basis of half a cycle alone“1. Thanks

for the interesting and worthwhile balance of your perspective. Ray Sheffield and Tony Johnson of the

United States Forest Service, you guys and your staff bent over backwards to accommodate my data

requirements; without your help my research and results would be much shallower. Wade Camp of the

Southern Forest Products Association likewise provided valuable data assistance. Sara Baldwin of Timber

Mart-South – you have a lot of good data and information, and the willingness to assist others in its use.

Carol Hyldahl, your support during my first year was very important in my transition back to being a

student again.

David Jones, you preceded me by one semester and your fresh wake in the water gave me a

helpful path to follow. Brooks Mendell, if someone can’t feel confident after talking to you, then they’re

really in trouble. Tim Sydor, I don’t know if I’ve met a student more willing to help another student along

their journey. Your attitude is matched only by your intellect. You are going to make a great professor.

Julie, my wife. I mention you last, because frankly that is the position you have occupied for the

past three years. You have sacrificed many of your dreams to support this part of our plan. Yes, our plan.

For that is what you made it. You have walked this journey hand in hand with me, every step of the way.

No matter how much I have been grumpy, or self-centered, or just generally not available to enjoy life the

way I should have - the way you deserved, you’ve been there providing the kind of love and support that

is quite more than I deserve. Thank you, and I love you.

1 From When Genius Failed, p. 233.

vi

TABLE OF CONTENTS

Page

ACKNOWLEDGEMENTS......................................................................................................................... iv

CHAPTER

1 INTRODUCTION..................................................................................................................... 1

2 ASSESSING RISK AND RETURN WITHIN A PORTFOLIO OF US SOUTH

TIMBERLAND INVESTMENTS ..................................................................................... 40

3 RISK AND RETURN ASSESSMENTS OF EQUITY TIMBERLAND INVESTMENTS IN

THE UNITED STATES..................................................................................................... 79

4 RECENT MERGERS AND ACQUISITIONS OF VERTICALLY-INTEGRATED,

AMERICAN FOREST PRODUCTS COMPANIES: HAS SHAREHOLDER VALUE

BEEN CREATED? .......................................................................................................... 112

5 CONCLUSION ..................................................................................................................... 143

REFERENCES ......................................................................................................................................... 148

1

CHAPTER 1

INTRODUCTION

As a proportion of the world of equity investments, direct investments in timberland within the

United States are quite small. However, they are growing. Such investments can be made in

timberland directly by purchasing either the land itself, or shares of companies whose exclusive

business is owning and managing timberland. Timberland can be invested in indirectly by

purchasing shares of publicly-owned corporations that own both timberland and other assets.

Timberland investments can be made by both individuals, and by institutions representing the

fiduciary interests of individuals, firms and municipalities.

Timberland investments are growing not because of an increase in the amount of

investment-grade timberland in the United States. Rather, the ownership of this land has seen a

large and steady change in recent years from publicly-owned, vertically-integrated forest products

companies, to financial institutions that own timberland via closed-end funds, which are often

commingled. These institutions usually own timberland via intermediary firms that purchase,

manage and dispose of the timberland for them. Therefore, what we are actually seeing is a

decrease in the amount of indirect investments in timberland, and an increase in direct timberland

investment, coupled with an increase in investment by institutions. All of these investors require

information about the financial performance of timberland investments so that informed decisions

can be made.

Markowitz (1952) pioneered the concept that investors should not be concerned with the

risk of individual securities, but rather should pay attention to the overall risk of their portfolio. In

other words, the additional risk contributed by a security to a portfolio is what matters.

Markowitz’s modern portfolio theory is centered on the recognition that securities’ returns

2

through time are correlated to some degree. By effectively combining assets that are not perfectly

correlated a portfolio can be constructed that has less risk than the weighted sum of the individual

assets’ risk. This logic has been utilized by previous researchers to identify the role that

timberland can play in a diversified portfolio of investments (Mills and Hoover 1982, Zinkhan

and Mitchell 1990, Caulfield 1998, and others).

Within this framework of analysis, previous work has compared the risk and return of

timberland in portfolios with traditional major investment categories such as large and small

capitalization stocks, and corporate and US Government bonds. These analyses have focused on

timberland investments at the US national and three major regional levels – the South, Pacific

Northwest and Northeast. Researchers have found that timberland, as an asset class, warrants a

position within the diversified portfolios of investors. While enough data exists to perform asset

class allocations of timberland and other assets using a portfolio optimization framework, the next

step is more difficult. Continuing the asset allocation analysis at a more refined, detailed level, or

performing security selection of specific timberland properties within a portfolio optimization

framework has been prohibitive due to the lack of sufficient return data. The second chapter of

this dissertation applies Markowitz’s portfolio optimization framework to address portfolio

opportunities of timberland investments within a US region, the South, once the investor has

decided to include southern timberland within a diversified portfolio.

The Capital Asset Pricing Model (CAPM) was developed as an outgrowth to Markowitz’

portfolio research by Sharpe (1964), Lintner (1965) and Mossin (1966). The CAPM asserts that

the return required of an asset is proportional to the systematic, or market risk of that asset. It

stipulates that the required return is equivalent to the risk free rate and a premium representing the

asset’s market risk.

The relationship between return and systematic risk has been used extensively to address

such questions as: 1) what is the risk of timberland investments compared to that of the broader

financial market; 2) given that level of risk, what return should investors require of timberland; 3)

3

does the market sensitivity risk of timberland vary by major geographic region in the United

States? The majority of this prior research predates the existence of an asset-based timberland

return series. The third chapter of this dissertation adds to this body of research by utilizing 19

years of returns (1987-2005) for the timberland index maintained and reported by the National

Council of Real Estate Investment Fiduciaries (NCREIF) to address these questions. In addition,

the systematic risk and required return of timberland in different regions within the US South is

assessed.

While institutions and high net worth individuals can readily invest directly in timberland

by utilizing the services of timberland investment management organizations (TIMOs), the

majority of individual investors wishing to invest in timberland cannot usually meet the minimum

capital requirements of the investment vehicles offered by these organizations. Most individuals

therefore invest in timberland by purchasing ownership shares of public corporations owning

timberland. Very few such firms have owned timberland as their exclusive asset, or line of

business. Historically, most firms owning timberland have been vertically-integrated forest

products companies. These firms traditionally owned timberland as a controlled source of timber

inventory for their conversion lines of business, such as lumber, paper and panel products mills.

In recent years significant consolidation has taken place within the United States forest

products industry. During the time period 1995-2002, nine mergers and acquisitions of publicly-

held, vertically-integrated forest products companies occurred. Collectively, these firms owned

approximately 33 million acres of timberland. For both institutional and individual investors who

chose to invest in timberland by owning shares of these firms, a reasonable question to ask is

whether this form of corporate project has created value.

We employ event study methodology in Chapter 4 to address this question. A key tenet of

this technique is the assumption of market efficiency. The efficient market hypothesis stipulates

that current security prices reflect all available information about those securities. By analyzing

the price movement of the stock of a firm immediately after news of a merger is announced, the

4

value of that merger, as assessed by the market, can be measured. The CAPM also plays a key

role in this analysis by projecting what the return of a stock should be during the post-merger

announcement period, against which the actual return is differenced to yield a measure of value

creation or destruction.

Modern portfolio theory, the capital asset pricing model and market efficiency are three

fundamental pillars of modern finance. Each has been extensively employed to assist both

researchers and practitioners in their understanding of the risks and return potential of financial

assets. Each concept has been applied to help better understand the investment characteristics of

timber and timberland. These concepts are employed in this dissertation to expand the knowledge

base of timberland investments both into new areas, and familiar ones with a degree of

refinement, depth and modernity. The remainder of this chapter explores the literature to review

the theory behind these aforementioned techniques, and their past application to timberland

investments.

Literature Review

Modern Portfolio Theory

A fundamental assumption of investment analysis is that investors are risk averse. Hence,

all else being equal, investors prefer greater returns, while taking a minimal amount of risk. While

investors have known for centuries that diversification, or spreading one’s funds (value) among

several investments carries less risk than investing in a sole asset, Harry Markowitz (1952)

formalized the relationship of diversification and the combination of assets. He showed that,

while the expected return of a portfolio of assets is simply the expected return of each asset

multiplied by the asset’s weight in the portfolio:

[ ] [ ]P i ii

E R x E R=∑ ,

5

the risk of the portfolio is much more than a simple function of each asset’s own risk and

portfolio weighting. Rather, the most important aspect concerning an individual asset and

portfolio risk is the correlation of that asset’s returns through time with the other assets in the

portfolio. Rubenstein (2002) states:

‘Probably the most important aspect of Markowitz’s work was to show that it is

not a security’s own risk that is important to an investor, but rather the

contribution the security makes to the variance of his entire portfolio – and that

this was primarily a question of its covariance with all other securities in his

portfolio’.

In a portfolio of n assets, where xi represents the proportion of funds allocated to asset i,

and σi is the standard deviation of asset i, Markowitz (1952) stated the risk of the portfolio as the

variance of a weighted sum:

2

1 1,

n n

P i j ij i ji j

x xσ ρ σ σ= =

=∑∑

where iσ and jσ are the standard deviations of assets i and j, ijρ is the correlation between

assets i and j, and ij i jρ σ σ is the covariance between the two assets. Standard deviation, the

conventional measure of portfolio risk, is the square root of this equation. Two important facts

about portfolio risk bear discussion. It is intuitive from the above equation that the lower the

measure of correlation of two assets in a portfolio, the lower will be the portfolio variation. Two

stocks whose historical movements are perfectly linearly correlated will have a correlation

coefficient of 1, resulting in a contribution to portfolio variance equivalent to the weighted

6

average of their individual standard deviations. So, anything less than perfect correlation between

two stocks will contribute to a lower portfolio variance, and hence less financial risk.

There is a limit, or floor to portfolio variance reduction possible through diversification.

The risk that is removed from diversification is termed firm-specific, or idiosyncratic risk. This

risk is due to specific actions, events, and news pertaining to the individual firm. The risk that

remains is termed market risk, or systematic risk. This is the risk due to economy-wide events and

news, and that affects most all firms. Systematic risk cannot be removed from the portfolio with

diversification.

The impact of covariance between assets in the calculation of portfolio standard deviation

prevents an investor from determining the optimal portfolio of assets by examining their

individual expected returns and risks. Instead, the combined risk of the group of assets,

determined primarily by their co-movement, or covariance, must be examined holistically.

Markowitz utilized these portfolio expected return and risk equations to calculate the

optimal combination of return and risk levels by varying portfolio asset weights. For each

possible level of portfolio expected return, the weights of each asset in the portfolio can be altered

to yield a minimum portfolio standard deviation. Such a portfolio is said to be minimum variance.

Plotting each of these minimum risk levels for a change in expected return yields a curve we term

the efficient frontier. Conversely, the efficient frontier can be calculated by iteratively specifying

a required portfolio standard deviation and then varying the asset weights until a maximum

portfolio expected return is determined. A portfolio constructed in this manner is said to be mean-

variance efficient. This process of developing the efficient frontier is often referred to as

Markowitz portfolio optimization. Computationally, this process is a constrained optimization

problem, where, in the case of maximizing return for a given risk 2Pσ , it can be described

mathematically as:

7

max [ ],PxE R

subject to the constraints:

1

2

1 1

1,n

iin n

i j ij Pi j

x

x x σ σ

=

= =

=

=

∑

∑∑

for an n-asset portfolio, with each asset having portfolio weight xi. Constraining the sum of the

asset weights to 1 enforces the rule of not allowing any short sales for any particular asset, and

that the portfolio must be fully invested. Markowitz portfolio optimization is referred to as a one-

period model. The portfolio return and risk based on any combination of asset allocations can

only be expected to hold for one period, where the length of this period matches the frequency of

the time series of data used in the model. However, analysts and investors do not always limit

their horizon of return and risk expectations to one period. This approach to optimal portfolio

construction is widely used among institutional investment managers today (Rubenstein, 2002).

By utilizing the risk-free rate, the optimal portfolio can be identified. This portfolio is the

one that results in the steepest slope of the line drawn from the risk-free rate on the y-axis to the

tangency point on the efficient frontier. The slope of this line is termed the reward-to-variability

ratio. We can use this ratio, also termed the Sharpe ratio, to solve for the optimal portfolio

allocations by stating it as the objective function:

( [ ] )max .P f

xP

E R Rσ−

8

To assess different investments within a portfolio optimization context, historical return

series for each asset are needed. Using these series, the three data elements for conducting

portfolio optimization can be estimated: asset expected return and risk matrices of correlations

and covariances can be computed. Historical return data for timberland investments are

unfortunately sparse. Before discussing historical timberland return data, and the portfolio

research that has been conducted with it, we first discuss a significant outgrowth of modern

portfolio theory, the Capital Asset Pricing Model, which also requires timberland return data.

Capital Asset Pricing Model

The CAPM builds upon the foundation laid by Markowitz (1952), who proved that the

risk of an individual investment should not be important to investors, but rather the investment’s

contribution to the investor’s overall portfolio risk. The risk of a financial asset is referred to as

the variability of its returns over time, and is commonly denoted by the standard deviation of

periodic returns. Risk can be stratified into two components. Idiosyncratic or firm-specific risk is

that component of total risk that is specific to the asset, resulting from actions, events and news

pertaining to the asset but not to other assets or firms. Firm-specific risk can be removed from the

portfolio through diversification. The risk that remains is termed market risk, or systematic risk.

This is risk due to economy-wide events and news, and that affects all firms. Systematic risk

cannot be removed from the portfolio with diversification.

The contribution of the CAPM is its ability to relate the impact of systematic risk upon

the returns of an investment. It does so with the following form:

( ) [ ( ) ],i f i m fE R R E R Rβ= + −

9

where E(Ri)is the expected or required return on asset i, Rf is the risk free rate of return and

E(Rm)is the expected return on the total market portfolio of assets. The quantity E(Rm)- Rf is

referred to as the market risk premium, or the additional expected return of the market portfolio

over the risk-free rate. βi is a measure of the sensitivity of the expected returns of asset i to

variance in the total market portfolio. It is a measure of the asset’s systematic risk, that portion of

the asset’s total risk that cannot be diversified away. An asset having a beta greater than one is

more risky than the market, and commands a higher required return, while an asset with a beta

less than one is less risky than the market, and requires a lower return.

CAPM theory states that the market return should reflect the return on all traded and non-

traded risky assets, to include human capital. A major criticism of the CAPM is that such a return

is of course, unobservable. For empirical work, a proxy is chosen that reflects a broad market

portfolio of assets. Historical returns for the S&P 500 composite index, or other similar broad

market index are commonly used.

The CAPM was designed as a one-period model. As such, the choice of a proxy for the

risk-free rate does not receive much attention. US Treasury securities with a short maturity are

usually chosen, the 30 and 90-day Treasury bills being common. These assets are more reflective

of a truly risk-free asset than long term US Treasury bonds. Treasury bonds make periodic

coupon payments which have some degree of reinvestment risk. However, Bruner (2003) and

Damodaran (2006a) emphasize that the choice of the risk-free rate should match the return period

for the asset data employed. In other words, if the choice is to invest in a closed-end timberland

fund having a ten year horizon, the most appropriate risk-free alternative would be the 10-year

US Treasury bond.

Bruner (2003) surveyed a collection of corporations, financial advisors, and academic

and trade corporate finance textbooks. The survey questions addressed practices used when

estimating the cost of capital. When asked the question of which risk-free rate to use when using

the CAPM to estimate a required return, the overwhelming response by both corporations and

10

advisors is to use a long term Treasury bond yield. 70% of practitioners utilize a maturity of 10

years or longer, while only 4% stated the use of Treasury-bill yields. Bruner concludes with the

recommendation of matching the maturity of the risk-free investment to the character of the

investment being analyzed, and recommends the yield on the 10-year or longer maturity US

Treasury bond for most capital project evaluations.

Estimates of the market risk premium can vary widely, and according to Perold (2004)

can be the most difficult component of the model to estimate. Practitioners have a choice of using

either an historical estimate of the premium earned by equities over riskless investments, or

somehow looking forward to estimate this differential. The obvious assumption in using historical

premiums is that future expectations can be reasonably characterized by past experiences. The

technique usually involves differencing the average realized return on a risk-free government

security from the average realized return on a broad market index. However, Damodaran (2006b)

describes three questions the analyst must answer that can significantly influence the result.

First, the number of years of historical returns can have influence. Using a longer time

period yields averages that are much more robust, yet at the cost of including potentially stale or

misleading data. Damodaran (2006b) documents that the large standard errors resulting in using

time periods of less than 50 years can be larger than the estimated risk premium itself. Second,

the choice of short term treasury bills as the risk-free asset will result in a market risk premium

approximately 1.5% larger than if long term treasury bonds are used. This choice is easily

decided for us, as consistency is required with our aforementioned choice of the risk free rate that

matches the investment.

Third, the choice of using arithmetic versus geometric averaging of market and riskless

returns will make a difference. The arithmetic average is the simple mean return. The geometric

average is the compound return, more reflective of an investor’s buy-and-hold experience (Bruner

2003). The more variable a return series is, the lower its geometric average will be compared to

its arithmetic average. While US Treasury bonds and bills will not be greatly influenced by this

11

choice, stock indices will, due to their increased volatility. The arithmetic average annual return

of large capitalization stocks from 1926-2005 is 11.6%, while the geometric average is 9.6%2. A

requirement of using the arithmetic average of returns is that they be independent over time.

However Fama and French (1988), among others, have documented significant negative

autocorrelation of returns over time, making the geometric average the more accurate choice.

When analyzing timberland investments, the proper choice is therefore to use a broad-market

return index coupled with long-term US Treasury bonds as the risk-free investment, with annual

returns for each series averaged geometrically.

While the CAPM is designed to be a forward looking model, it is often used to estimate

an asset’s beta by evaluating historical returns. This is because we cannot know or observe the

expected returns required in the model. Following Jensen (1969), the excess returns version of the

single-index model regresses historical returns for the asset less the risk-free rate (the asset’s risk

premium) against the market risk premium:

( ) ( ) ,i f i i m f iR R R R eα β− = + − +

where Ri, Rf and Rm are time series of historical returns for the asset, the risk-free rate and the

market proxy, respectively, and ei is an error term. αi, or the Jensen’s alpha parameter, is an

estimate of the risk-adjusted excess return generated by the asset. If significantly positive, the

asset has generated a return in excess of that warranted by its market risk sensitivity. When

choosing a risk-free investment, a zero-coupon US Treasury security having the same maturity as

the frequency of return data should be used.

If an asset’s beta is known, or has been estimated, then its required return can be

estimated. This required return can be used as a benchmark for measuring potential investments

2 Data from the Center for Research in Security Prices, University of Chicago, as published in Bodie, et al (2005).

12

or projects. If evaluating a potential timberland acquisition, the first step would be to estimate the

future cash flows for the property, to include timber sales, lease revenues, tax payments, etc. The

estimated cost of capital would then be used to discount these figures to arrive at a present value.

For an existing property, the required return can be used to evaluate periodic silviculture

investments in that asset, such as fertilization or subsoil plowing, based on their expected impacts

on growth and subsequent cash flow.

The CAPM is widely used as a model to explain the sensitivity of an asset’s returns to its

undiversifiable risk. It is used extensively by practitioners to quantify this risk, and to develop an

asset’s required return given this risk. However, like any model, the CAPM has its flaws, and

certainly like any other model, is a simplification of reality and cannot therefore be considered

absolutely correct. Over time researchers have slowly constructed evidence against the ability of

the CAPM to accurately portray the relationship between an asset’s market risk and required

return.

Early tests of the CAPM (Fama and MacBeth 1973, Gibbons 1982, among others) have

confirmed the positive relationship between beta and asset return. This relationship has also been

found to be mostly linear, as the CAPM predicts. Researchers have, however found the beta-

return relationship to be ‘flatter’ than that predicted by the CAPM (Fama and MacBeth 1973,

Black et al 1972, Fama and French 2004, among others). For example, low-beta assets often have

a positive Jensen’s alpha, or y-intercept rather than a predicted value of zero, while high beta

stocks have been shown on average to have negative Jensen’s alpha values.

Fama and French (2004) document a divergence of opinion among researchers for the

imperfect empirical record of the CAPM. Some believe financial markets are not as efficient as

once believed, a requirement of the CAPM. Market efficiency stipulates that current security

prices reflect all available information regarding the security, resulting in the inability to predict

the direction or magnitude of the security’s future price movements. Some believe that investors

overreact to past stock price performance, which researchers have potentially identified by adding

13

factors to asset pricing models that may capture this behavior (DeBondt and Thaler 1987, and

others).

Others believe that more risk factors are required to explain asset prices, in addition to

market risk. The three factor model of Fama and French (1993) is an example. Still others (Roll

1977) believe that the CAPM has never been, nor can be, accurately tested due to the impossible

selection of a proxy for the entire market portfolio of assets. While Fama and French (2004)

discourage use of the CAPM for empirical work, 80% of corporations and financial advisers

surveyed by Bruner (2003) nevertheless use the CAPM to estimate the cost of equity capital.

100% of text and trade books included in the survey also recommend primarily using the CAPM

for this purpose.

To conduct portfolio optimization and CAPM risk and required return analyses for

timberland, historical time series of timberland returns are required. Unfortunately, a robust data

series, one based solely upon market transactions, does not exist. Timberland is not traded on an

organized exchange like common stocks, bonds or commodities. Compared to equity

investments, timberland is an extremely thinly traded sector, meaning that very few market

transactions occur during a time period from which a return series can be developed. Only in

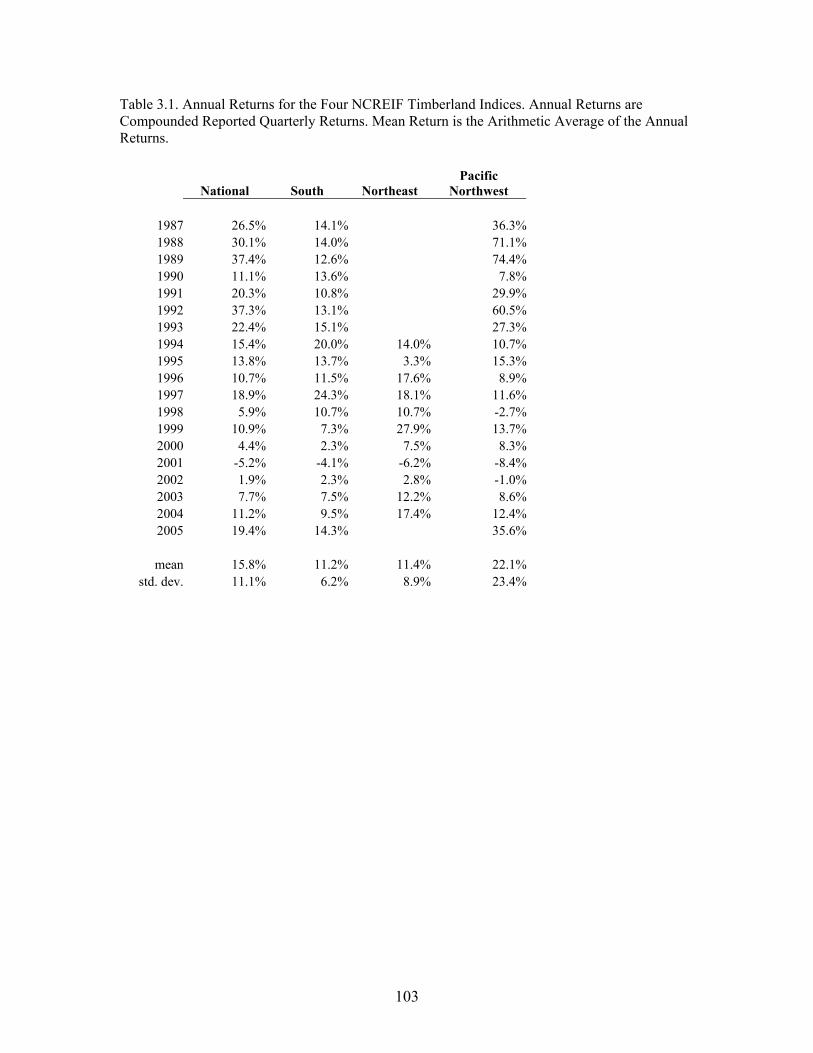

1994 did the National Council of Real Estate Investment Fiduciaries (NCRIEF) begin publishing

their Timberland Index, with returns dating back to 1987. Before this series developed sufficient

length, researchers chose between two alternative approaches. Recognizing that timber price

appreciation is a key factor in the timberland return generation process, some researchers simply

used time series of prices of commercial timber species in their analyses. Others developed

synthetic timberland return series based upon the factors that drive timberland returns, for which

available data could be gathered.

14

Timberland Return Drivers

Timberland investment returns are generated through two components: income and

capital appreciation. Income is received primarily from the periodic sale of timber, which in turn

is used in the manufacture of lumber; panel products such as plywood, oriented-strand board

(OSB) and fiberboard; paper; packaging; and several types of specialty chemicals. An attractive

characteristic of selling timber is that it can be withheld from the market during times of low

prices at no cost. There is no ‘storage fee’ direct cost, and in fact the timber continues to grow

and often appreciate until more favorable market conditions return. There is however the

opportunity cost of foregoing harvest until a later time. Annual income is also often received from

the leasing of recreation rights on the land, primarily for hunting.

Capital appreciation is realized from the continuous biological growth of the trees. In

addition, larger trees are generally more valuable per unit than are smaller trees, due to the fact

that telephone poles, plywood veneer and the larger sizes of lumber, some of the highest valued

products made from trees, can only be manufactured from larger trees. Therefore as a tree crosses

a certain threshold from one size class to another, its value per unit increases. For southern yellow

pine species, there are three predominant size classes: pulpwood, from which is made paper and

OSB; chip-n-saw, from which small dimension lumber is made; and sawtimber, used in the

manufacture of wider dimension lumber, poles and plywood.

The price paid for timber varies by tree size, region and season. Finished good prices also

have an impact on timber prices. However, Binkley (2000) documented how the price of southern

pine sawtimber has increased at a compound annual real rate of 2.6% from 1910 to 2000. Timber

price increases are exhibited not only in the income component of timberland returns, but also in

the capital appreciation component, because a key element of the capital appreciation of

timberland is the increase in the value of the land itself (Caulfield 1994). This increase is

attributable to two factors: first, the increase in the value of the land for producing timber due to

price increases (Washburn 1992), and the conversion of a portion of a timberland portfolio to a

15

higher-valued use than the production of timber, such as residential or commercial development,

during the investment period.

Timberland Return Data

The only timberland return index currently in existence3 that is based on actual

timberland transactions and appraisals is the National Council of Real Estate Investment

Fiduciaries Timberland Property Index (NCREIF 1994). NCREIF publishes historical return data

for timberland investments managed by its members, at two geographic levels: the United States,

and three regions within the US: the Pacific Northwest, the Northeast and the South. The

NCREIF Timberland Property Index segregates a total return into income and capital appreciation

elements, and is based on actual data reported by its members managing timberland investments.

Hancock Timber Resource Group (2003a) describes how NCREIF began compiling and

publishing a quarterly index of timberland property returns in 1994, with data retroactive to 1987

for the Southern and Pacific Northwest regions in the United States, and to 1994 for the

Northeast. This index tracks changes in value of timberland properties that are a) held in a

fiduciary environment, as opposed to the myriad other ownership objectives shared by many

other timberland owners; and b) “marked to market” at least annually. If the property does not

experience a change in ownership during a year via a sale, then it is appraised at year end to yield

a new value. As a timberland investment organization joins NCREIF, they submit historic returns

for their properties to augment the index.

The Timberland index is built and maintained similarly to NCREIF’s other commercial

real estate indices. The index has four basic components: the market value of all properties in the

index; the EBITDDA return for the properties; the capital return; and the total return. The

EBITDDA return, or earnings before interest expenses, taxes, depreciation, depletion and

3 The Timberland Performance Index (TPI) (Caulfield,1994) is similar to the NCREIF index, however is no longer in existence.

16

amortization, is based primarily on the sale of harvested timber during the quarter. However,

many timberland property owners lease recreation use rights to clubs or individuals, the income

from which is also included in the EBITDDA portion of the total return. It must be noted that the

EBITDDA figure is gross of applied management fees charged by the property manager, and

therefore overstates the true net income received by the investor (Healey 2003). The EBITDDA

income component of the return is analogous to the dividend component of a stock return.

The capital appreciation component is basically the ratio of the difference in period-to-

period property market value, minus capital expenditures in the current period, to the market

value of the previous period. Timberland appreciation is measured by periodic appraisals.

Appraisals are conducted both externally by consultants and internally by the managing

organization. Major, externally-conducted appraisals often occur on a three year cycle, although

more frequent timing is becoming common (Clutter 2006). Annual external updates (in the other

years) are performed by some management organizations, while others use internal updates of

various types. All organizations perform quarterly updates that are based on harvested timber

removals, merchantable timber growth, and timber price changes. These quarterly updates rarely

include land appreciation, nor account for changes in the value of premerchantable timber

(Clutter 2006). The majority of external appraisals are conducted in the fourth quarter of the year.

Since appraisals are not evenly distributed throughout the year, reported quarterly property

returns are less meaningful. For analysis purposes, it is recommended that annual returns be used

(Hancock Timber Resource Group 2003a).

Investing in timberland by institutions is relatively new. It can be tracked to the passage

of the Employee Retirement Income Security Act (ERISA) in 1974 that required institutional

investors to diversify their portfolios away from traditional common stocks and fixed income

securities to broader classes (Zinkhan 2003, Healey 2003). Investments in timberland by

institutions grew by a factor of ten during the 1990’s to some $17 billion by 2005 (Cambridge

Associates 2002; Dana 2006). This is reflected in the time span of the NCREIF Timberland

17

Property Index. Although the NCREIF series is regarded as the best data available describing the

performance of institutional investments in timberland, the need to analyze the financial

performance of timberland predates the existence of this index. Before this time, most analysts

constructed synthetic return indices with several management assumptions for use in timberland

investment analyses.

Timberland returns value to the owner through a combination of periodic income and

capital appreciation, as previously discussed. The return formula common to financial security

appreciation is applicable for measuring timberland returns:

1

1,t tt

t

NI CVRCV −

+= −

where:

Rt = total return per acre of the asset during period t;

CVt = capital value per acre of the asset during period t;

NIt = net income received per acre of the asset during period t.

Many assumptions about forest management practices must be made when developing a

synthetic timberland return series. One that is common among most authors is that the

hypothetical forest being modeled is fully-regulated. This implies that the volume of timber

harvested each period is equal to the volume grown. The standing volume of timber in the forest

is therefore static over time, and there are equal amounts of area in each age class. This allows

any capital appreciation of the forest to be reflective of timber or land price appreciation,

inflation, or some other factor, but not from any implied change in the inventory of the asset.

Revenue realized from the sale of harvested timber represents the periodic income component.

18

Researchers’ use of both synthetic and reported timberland return data to examine the role of

timberland within a diversified portfolio is discussed next.

Previous Assessments of the Role of Timberland in Diversified Portfolios

Mills and Hoover (1982) and Mills (1988) used this basic formula to synthesize time

series of returns from hypothetical uneven aged, multi-species hardwood forests in west central

Indiana. Annual rates of return from 1959-1978 were estimated. No direct empirical data for the

return formula components existed at that time, requiring the authors to incorporate several

assumptions reflecting forest management practices and productivity, disaster occurrence

probabilities, lumber market conditions and land appreciation, with which they could estimate the

income and capital value components. The authors likewise developed synthetic annual return

series representing agriculture investments, both crop and livestock. They then analyzed these

investments in a portfolio optimization context along with traditional financial assets. Their

results suggested that portfolios of forestland assets alone might yield low, risky returns relative

to portfolios of typical financial assets. However, they found that by combining forestland

investments with more traditional financial investments in their portfolio, investors could expect

moderate returns with decreased risk, as opposed to portfolios with financial assets alone.

Conroy and Miles (1989) developed a monthly return series from 1976-1986 representing

a hypothetical commercial Southern pine forest. Assumptions were made for silvicultural costs,

management prescriptions, and harvest volumes. Timber product prices reported in Timber Mart-

South were used, along with representative farmland values for the land appreciation component.

The authors altered the rotation age to determine the impact on average monthly return and

standard deviation. They then formed optimal portfolios with timberland and the traditional

financial asset categories of large and small capitalization stocks, and US treasury bonds and

bills. Conroy and Miles (1989) found that timberland occupied a significant position in the

optimal portfolio depending on the required portfolio return.

19

Zinkhan and Mitchell (1990) utilized a synthetic return series for Southern pine from

1977-1987, developed by a timberland investment firm, to analyze portfolio allocation. The

return series utilized published south-wide pine stumpage prices, timber harvests from a typical

southern pine management regime, and proprietary land appreciation rates. They found that

including timberland in a portfolio of representative financial assets reduced the risk of efficient

portfolios by an average 43%, and timberland was allocated asset weights of as much as 30% of

the portfolio value.

Geographic diversification of timberland investments has long been known to reduce

overall risk from damage by natural disasters, such as insect, fire and storm damage. Hancock

Timber Resource Group (2005) discussed how damage to some of their timberland holdings in

Mississippi, Louisiana and Alabama suffered as much as a 12% loss in market value due to

damage caused by the Hurricanes Katrina and Rita in 2005. Yet when viewing their total

Southern timberland portfolio, the loss in market value from these two storms was less than one

percent. Likewise, losses dropped even further when viewing their total North American

timberland portfolio.

Hancock Timber Resource Group (2003b) used synthetic timberland return data in

tandem with NCREIF return data to evaluate regional and global diversification potential within a

portfolio optimization context. Their model, the John Hancock Timberland Index (JHTI) uses

only one time series data component: the quarterly stumpage price of the appropriate timber

species group for the region modeled. For the US South, the stumpage price is a composite price

equal to the equally-weighted average price of pine pulpwood and sawtimber. The return income

component is simply the quarterly stumpage price multiplied by a subjective factor that represents

the regional ratio of periodic income to the capital value of the representative forest. The capital

value component is a weighted average of the previous eight quarters stumpage prices, with

progressively less weight given to each preceding quarter’s price. Each year’s four quarterly

returns were then averaged to yield an annual return. Hancock Timber Resource Group estimated

20

return series from 1960-1986 to provide a longer history of timberland returns than possible using

the NCREIF series alone, which begins in 1987. By combining these two return series, Hancock

Timber Resource Group (2003b) was able to analyze portfolio opportunities utilizing returns

spanning 1960-2002. They found the different US regional and international return series were

not highly correlated, allowing significant reduction in portfolio risk by combining regional assets

into a global timberland portfolio.

Caulfield (1998) used the Timberland Performance Index (TPI) to evaluate the

timberland asset class from 1981-1996 within a portfolio optimization context. The TPI is similar

to the NCREIF index in that it is an actual asset-based index. However, it is no longer in

existence. Like Hancock Timber Resource Group (2003b), Caulfield found that adding

timberland to a diversified portfolio increased expected returns for given levels of risk.

The role of risk reduction for a timberland investment portfolio via species diversification

has been explored within a portfolio optimization context by Thompson (1987, 1992). He

developed synthetic return series for pine, ash, oak and gum species in Louisiana, and for white

pine, red pine, aspen and red oak species in Minnesota. Similar to Mills and Hoover (1982),

Thompson developed explicit hypothetical forest management regimes to arrive at estimates of

annual income and capital appreciation components for the return equation. He included costs and

revenues reflecting land rent, site preparation, planting, administration, taxes and timber revenue.

In comparing portfolios of Southern and Midwestern timberland investments, Thompson (1987)

found that Southern timberland portfolios offered superior returns for any given risk level. He

similarly found that portfolios of assets from both regions dominated the Southern timberland

portfolio. Finally, he found that portfolios combining timberland and a broad market investment

(S&P 500 Composite Index) dominated timberland-only portfolios.

21

Value at Risk

A typical institutional investment in timberland is made via a closed-end, co-mingled

fund having a horizon of ten to fifteen years. Additions to the timberland portfolio are sometimes

made during the fund lifetime. Segments of the portfolio are also sometimes disposed of before

the fund expires. This is usually done for portions of properties that experience a significant

increase in value for uses other than growing timber, such as development. Fund managers

commonly perform an analysis of all properties on an annual basis to determine whether they

should be retained in the portfolio or sold. However, the bulk of the timberland properties in the

fund remain fixed during the fund’s lifetime. Therefore, although Markowitz portfolio

optimization gives a one-period solution, that approach generally suffices for institutional

timberland investments. It is nevertheless interesting to examine this type of investment

performance over its lifetime. An element of such a long-term timberland investment that has not

been previously explored is its value at risk (VAR). The final section of Chapter 2 develops and

compares VAR estimates of three intra-South timberland investment portfolios. Methods for

modeling a portfolio over multiple periods are next discussed, followed by a discussion of VAR

estimation.

Thomson (1991) analyzed the expected performance of timberland within a portfolio of

financial assets from both a short and long term perspective, using the same synthetic timberland

return series from Thomson (1987). In addition to employing Markowitz portfolio optimization to

arrive at portfolio asset weights, Thomson (1991) also used a power utility function, an approach

which attempts to maximize long-term portfolio wealth by maximizing the logarithm of portfolio

returns, subject to a specified proxy for risk tolerance. Similar to previous analyses, his results

showed that diversification among financial and timber assets generated the highest risk-adjusted

expected returns, and that diversification among timber species also reduced risk. Thomson found

that the two portfolio construction approaches of Markowitz single period optimization and the

power utility function generated similar results for both one- and multi-period solutions.

22

Thomson’s (1991) technique for conducting long-term portfolio analyses utilizing

Markowitz optimization begins by solving for a one period solution. Then, stochastic techniques

are used to estimate the portfolio value at the end of the investment horizon. The fundamental

premise is to assume that the expected return for each portfolio asset in any year of the

investment horizon is equally likely to be one of the returns within the asset’s time series of

historical returns used to develop the portfolio allocations. An index, or period of the historical

returns is randomly chosen, and each asset’s return corresponding to that index is multiplied

against that asset’s weight in the portfolio, which remains constant across the investment horizon.

These weighted returns are summed to yield one portfolio return. Choosing each asset’s return

from the same point in time ensures that the correct asset correlations are maintained. This

process is repeated for each year in the horizon. Portfolio returns are compounded to yield a total

return. This process is repeated 1,000 times. The 1,000 total returns, t1000, are then converted to

compound rates of return, or geometric mean returns, by raising each t to one over the length of

the horizon. The 1,000 geometric mean returns are then averaged to yield a mean expected

compound rate of return and an estimated standard deviation.

In the mid 1990’s a metric for characterizing the financial risk of an investment was

developed in the wake of several significant disasters involving derivatives investments (Jorion

1996, Culp, et al 2003). Value at risk is a method of measuring the financial risk of a portfolio

over some specified period of time. VAR estimates the maximum reasonable loss that could be

expected. ‘Reasonable’ is usually defined as the portfolio value at the 5% probability level of a

distribution of possible returns. The portfolio value at this level could be positive or negative. A

key characteristic of VAR is that its unit of measure is in dollars, not percent, which may more

acutely and accurately convey the message of the possible loss (Jorion 1996).

Manfredo and Leuthod (1999) describe the two classes of procedures for estimating

VAR: parametric and full-valuation methods. Parametric methods are based on the assumption of

a normal distribution of expected returns for the investment. With this assumption, only the mean

23

and variance of the outcome distribution, which fully characterize it, need to be known. The 5%

VAR will equal the expected portfolio value less 1.645 standard deviations of the expected return.

If the expected outcome distribution is not normal, then a full-valuation procedure must

be used to estimate the VAR. To estimate the VAR of an investment the distribution of expected

returns for the given portfolio of assets and allocations must be estimated. Simulation methods

are generally used to generate the full distribution of expected returns, often using randomly

chosen past values of portfolio asset returns as future values. Once a full distribution of returns is

estimated, the return at the 5% level is used as the VAR estimate, or worst-case scenario. To date,

VAR estimates for institutional timberland investments have not been addressed in the literature.

Previous Assessments of the Financial Risk of Timberland Investments

What is the sensitivity of timberland returns to market risk? What return is required of

timberland? Has timberland performed well with respect to its market risk? The use of the CAPM

by other researchers to answer these questions is now discussed. As with the portfolio

optimization studies, timberland CAPM studies began in the 1980’s, examining timberland

performance from the early 1950’s through the middle 1990’s. A wide range of CAPM betas have

been found by previous researchers, many of them negative. A negative beta would imply that the

inclusion of certain types of timberland in a diversified portfolio can actually reduce the overall

portfolio risk, and that timberland should have a required rate of return less than the risk-free rate.

Redmond and Cubbage (1988) constructed species-based synthetic timberland return

series for multiple commercial timber species in the United States. Return series based on

particular timber products were developed as well, such as southern pine sawtimber and

pulpwood. The formula was based on a sum of annual stumpage price change and a measure of

average annual timber growth. Redmond and Cubbage used these return series to estimate CAPM

betas for the respective species and products. The S&P 500 composite index was used for the

market proxy, along with an unspecified risk free rate. 18 of the 22 product series’ beta estimates

24

were negative, and only two were significant at the α = 0.05 level. Estimated betas ranged from -

0.93 to 0.20.

Zinkhan (1988) utilized a synthetic annual return series for Southern pine from 1956-

1986, developed by a timberland investment firm, to estimate a timberland beta and cost of

capital. The return series utilized published south-wide pine stumpage prices, timber harvests

from a typical southern pine management regime, and proprietary land appreciation rates. The

S&P500 composite index was used for the market proxy, and 90-day Treasury bills for the risk-

free rate. Zinkhan estimated a beta of -0.21. Statistical significance was not stated, and must be

considered questionable.

Washburn and Binkley (1990) studied eleven sawtimber annual stumpage price series

reported by the US Forest Service and the State of Louisiana. The S&P500 composite index was

used for the market proxy, and 30-day Treasury bills for the risk-free rate. Three different

methods were used to calculate appropriate asset periodic rates of change. For southern pine

sawtimber in Louisiana they estimated insignificant betas of between 0.17 and 0.18, while for

southern pine sawtimber on national forests they estimated insignificant betas of 0.35 to 0.37. The

beta estimates for national forest Douglas-fir sawtimber ranged from 0.95 to 0.98, and were

significant at the α =0.05 level.

Binkley et al. (1996) utilized the John Hancock Timberland Index (Hancock Timber

Resource Group 2003b) to create synthetic timberland return series from 1960-1994 for the

Pacific Northwest, Northeast and South, with which to estimate timberland systematic risk

measures and excess returns. The authors used a portfolio of large and small company common

stocks, corporate bonds and US Treasury securities of varying maturities for the market portfolio

proxy. US Treasury bills of unspecified maturity were used for the risk-free rate. The authors

found significant betas of -0.88 (α = 0.05), -0.54 (α = 0.05) and -0.21 (α = 0.10) for the Pacific

Northwest, South and Northeast, respectively. Significant alpha estimates of 10.2%, 5.9% and

2.8% were found for the same regions, (α = 0.05).

25

Sun and Zhang (2001) compared CAPM and APT estimates for eight different forestry-

related investment classes. Two of the investment vehicles modeled were the Timber

Performance Index and the NCREIF timberland index. NCREIF quarterly returns from 1987-

1997 were used as a return series. The S&P500 composite index was used for the market proxy,

and US Treasury bills of unspecified maturity were used for the risk-free rate. Sun and Zhang

(2001) estimated insignificant betas of 0.07 for the now-defunct TPI, and -0.05 for the NCREIF

Timberland Index. By using quarterly rather than annual returns for the NCREIF series, the beta

estimates must be considered suspect. This is due to the aforementioned common practice of

appraising timberland properties in the fourth calendar quarter, as well as often adding timber

growth only in the fourth quarter, resulting in an artificial change in capital value during that

time.

Mergers Within the Forest Products Industry

When two firms merge, many questions arise. Why did they merge? Do the two firms

think they will hold a competitive advantage over others in their industry as one, larger firm?

Who will control the new firm? Is it clear that the management of one former firm will dominate

the decision making of the new firm? Will assets be shed? Will lines of business be discontinued?

What about the shareholders of the two firms? Are they better off because of the merger?

Historically most individuals who have wished to invest in timberland have done so indirectly, by

owning shares of vertically-integrated forest products companies. Nine mergers of such firms

occurred from 1995-2002.

Chapter 4 addresses the question of shareholder value creation as a result of these nine

mergers. The remainder of this review discusses mergers and acquisitions of public corporations.

The fundamental question that is analyzed is how researchers have defined and measured whether

shareholders are better off when their firm merges with another. Previous research assessing the

success of mergers that occurred throughout the latter half of the twentieth century from the

26

perspective of shareholders is reviewed. No studies of mergers within the United States forest

products industry have been performed, against which to compare the results of this study.

A merger can be defined as the amicable integration of two firms into one, where

management of both firms work together to define the terms of the merger: price, timeline, asset

retention and disposition, and management positions. A firm can acquire another firm by offering

to purchase its outstanding shares directly from the firm’s shareholders, bypassing any negotiated

agreement with the firm’s managers. Such takeover structures can originate as a surprising,

unsolicited offer, or possibly as a result of failed merger negotiations between the two

management teams. This latter form of tender offer is often referred to as a hostile takeover.

Andrade, Mitchell and Stafford (2001) document a decrease in hostile takeover attempts in recent

years, from 14.3% of all merger and acquisition attempts in the 1980’s to 4% in the 1990’s.

Hostile bidders succeeded in their takeover attempts approximately half of the time in both

decades.

Corporate unifications are often collectively referred to as mergers and acquisitions

(M&A). Whether the event is a merger or an acquisition, one firm is considered to be the

acquiring firm, and the other the target. Although some mergers are advertised as a ‘merger of

equals’, rarely is this the case in reality, and there is nevertheless an acquirer and target label

applied to the two firms (Weston, Mitchell and Mulherin, (2004), Grinblatt and Titman (2002),

and others).

Mergers occur for three general reasons, either singly or in any combination thereof:

synergy, agency or hubris. Weston, et. al. (2004) discuss synergies as the desired result of

increased economies of scale of operations from the natural increase in size after a merger. These

economies of scale are often evidenced in reduced inventories, human resources, accounting, and

research and development efforts. Weston, et. al. (2004) also point out that industries needing to

reduce capacity often merge so as to spread fixed costs over a larger base. Grinblatt and Titman

(2002) relate a strategy of tax savings as a form of synergy, or financial gain that, if achieved,

27

benefits all shareholders of the combined firm. These are reasons for merging that result in value

creation. If the creation of synergies or tax savings are the reasons for merging, then it is

generally accepted that the merger will create value for the two firms, if properly executed.

Agency and hubris are reasons for mergers that tend to destroy rather than create value.

In a publicly-held corporation, the shareholders are the owners, and the managers are the agents

charged with maximizing the wealth returned to the owners. An agency problem exists when the

agents act more in their own self-interests rather than in the interests of the owners/shareholders.

Jensen (1986) and Shleifer and Vishny (1989) discuss how such behavior is sometimes evidenced

in a merger where the terms of the merger support an entrenchment of key managers in new

positions, or otherwise involve investments that make the managers more valuable to the

shareholders, without directly creating value for the shareholders.

Hubris, or excessive self-confidence, is posited by Roll (1986) as a reason for some

mergers. Under the hubris theory the acquiring firm’s managers overestimate the value of the

target firm, and offer more than it is worth. The target firm naturally accepts the offer. The gain

attributed to the owners of the target firm is simply a mirror of the destruction of value suffered

by the owners of the acquiring firm that paid too much. This is analogous to the “winner’s curse”

phenomenon in an auction, where, by definition the highest bidder is likely to have bid an amount

that is greater than the intrinsic value of the object for sale. Weston et al. (2004) discuss how the

impact of Roll’s research was to evaluate mergers by measuring the cumulative change in value

of the acquirer and target firms, so as to capture any evidence of hubris, or winner’s curse.

Similar to over-estimating the value of the target, the acquiring firm’s managers may wish to

broaden their ‘empire’ of control via a merger, with less regard to the cost of doing so.

Previous M&A research has shown merger activity tends to occur in clusters within

industries and timeframes. Mulherin and Boone (2000) analyzed merger and divestiture activity

in the 1990’s and found deregulation to have an impact on merger activity within affected

industries. Similar conclusions were reached by Mitchell and Mulherin (1996) and Andrade et al.

28

(2001). In their research of industry patterns and timing related to mergers and divestitures,

Andrade and Stafford (2004) found that M&A activity can occur within an industry both as a

means of contraction or expansion. We can therefore view mergers as a mechanism by which

firms and industries attempt to react to economic change. After exhibiting strong stock price

performance relative to the S&P 500 index from the mid 1980’s through the early 1990’s, the

firms in this sample reversed course in the middle to late 1990’s and began a period of economic

underperformance. In comparing the stock price return net of the S&P 500 index return for the

three years immediately preceding their respective merger announcements, only three of eighteen

firms outperformed the index during this timeframe, with an average underperformance of 40%.

Merger Research – Measuring Value

How is success defined for the firms that merged? Much research has been done to

evaluate whether mergers tend to create or destroy value. This discussion will focus on three

aspects of this question. First, value creation is defined. Next, the methods of measuring value

creation are discussed. Finally, the empirical research on merger performance is stratified by

acquirer and target, and by method of payment.

A primary objective of the firm in a capitalistic society is to maximize the wealth of the

existing shareholders. All projects the firm chooses to undertake should support this objective.

Bruner (2004) states a clear and concise benchmark for evaluating mergers and acquisitions. As a

result of the merger or acquisition involving two firms, shareholder value is either created,

conserved or destroyed. Value is defined here as being net of the opportunity cost of the capital

employed. In other words, is the project successful above its associated risk? Therefore, if a

merger results in the conservation of value, this means that the project earned the required rate of

return, and can be considered a financial success for investors.

Bruner (2004) claims that since value creation is the objective of a merger, any other

advertised goals simply support this primary objective. For example, if the two firms undergoing

29

a merger state that the combination will create new synergies allowing the firm to be more

productive, this should directly translate into increased shareholder value. The economic return

from the project is all that need be, or should be measured. All other stated rationale should

support this concept, or are otherwise not of value to shareholders.

Bruner (2004), Weston et al. (2004) and others argue that the best measure of the

economic return for a merger or acquisition is the impact on the stock price of the two firms

involved. This is the most direct measure available. Alternatively, subsequent accounting

performance can be measured. For example, a merger may have an advertised benefit of reducing

production costs by $500 million over three years. This can be evaluated by examining

accounting reports over time to see if net income correspondingly improves. However, there is

not a direct link between the accounting performance of a firm and its stock price. Estimating

financial performance from analyzing accounting statements acts as “an indirect measure of

economic value creation” (Bruner, 2004).

Event study methodology is the preferred approach for evaluating the impact of an event,

such as a merger announcement, on a firm’s stock price, serving as an estimation of the present

value of the event to shareholders. Two temporal scales of event studies exist: short and long

term. Both approaches attempt to quantify the value of the specific event by examining stock

price movement in excess of an estimation of how the price would have moved had the event not

occurred. The two approaches are sometimes used in conjunction to evaluate an event. The

methodology of conducting a short term event study is described first.

Short Term Event Study Methodology

In a capitalistic system where investors have significant access to information about firms

and are able to make investment decisions in a relatively unrestricted manner, we expect equity

prices to be efficient. In other words, impounded in the price of an asset is all relevant information

about that asset. In theory the price is the market’s interpretation of the present value of all future

30

cash flows to the holder of a share of that security. This is the efficient market hypothesis that has

become generally accepted within academia, and to a lesser extent the professional investment

communities. Market efficiency can be stratified to three different forms: weak, semistrong and

strong. Weak-form market efficiency implies that no informational advantage can be gained

about a firm’s future stock price movement by studying its history of price movements.

Semistrong-form market efficiency implies that no advantage can be gained in the marketplace by

studying publicly-available information about a firm. Strong-form market efficiency implies that

no trading advantage can be gained by studying any information about a firm, whether of a public

or privately-held (e.g. insider information) nature. It is understood that significant, abnormal

returns can be made with the use of insider information, hence the illegality of that practice.

However markets are generally believed to be weak and semistrong-form efficient.

A key tenet of this paradigm is that the prices of assets react nearly instantaneously to

new information in the marketplace. We can therefore determine the market’s valuation of an

event involving a firm by measuring the change in that firm’s stock price at the time of the

announcement of the event. Such an event can be the announcement of actual or projected

periodic financial performance, the introduction of a new product line, or the decision to merge

with another firm. Again, upon the announcement, the market will collectively assess all available

relevant information and make trading decisions that will effect a change in the firm’s stock price.

Two important elements of market efficiency are: 1) the change in price equates to the market’s

perception of the change in the value of the firm, and 2) this change occurs before an individual

investor can take advantage of this new information. In other words, it is nearly impossible to

effect an arbitrage situation based on learning new information about a firm.

Given the general acceptance of the efficient market hypothesis, the standard technique

for quantifying the value of a merger is to conduct a short term event study around the time of the

merger announcement. Event study methodology was used to study the reaction of stock prices to

new information in the seminal work by Fama et al. (1969), and has been used extensively for

31

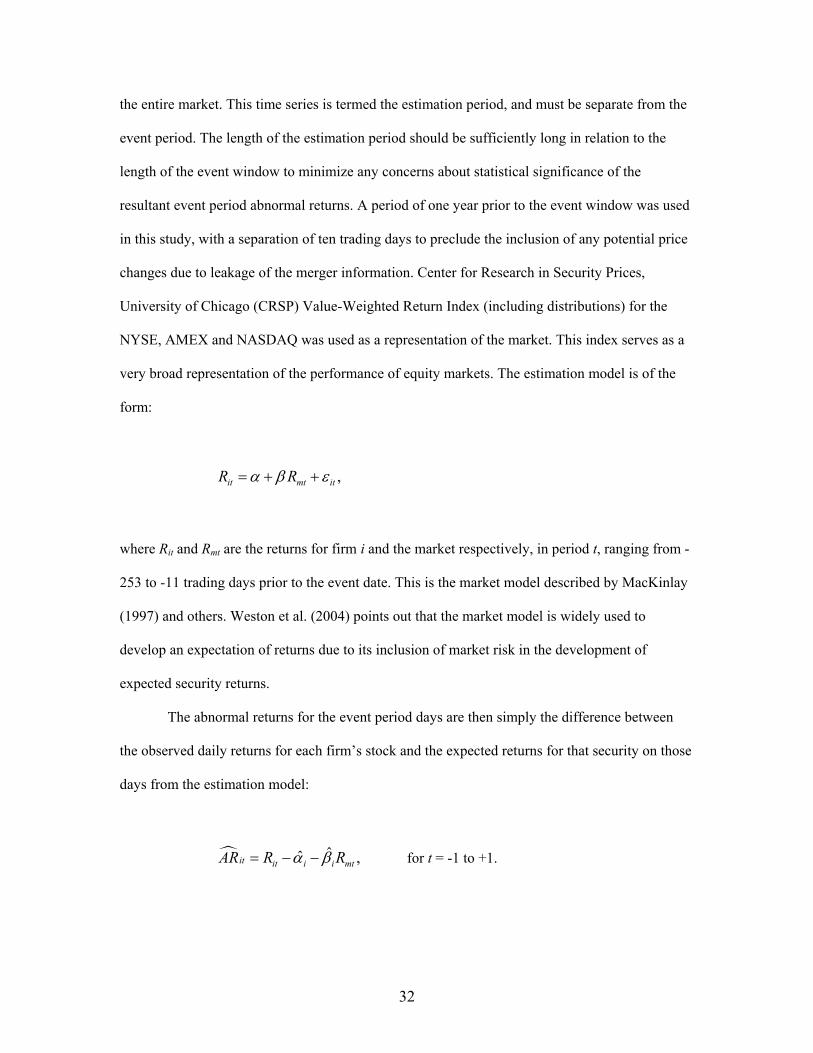

this purpose since then. It is described in detail by Henderson (1990), MacKinlay (1997),

Boehmer et al. (2002), and Weston et al. (2004), among others. A short term event study

determines an expected return for a firm during the period of the event, and then compares this to

the actual observed return. The difference is the abnormal return (AR), and can be attributed to

the market’s “collective wisdom” of the impact of the event on the firm’s value.

The first step in conducting a short term event study is to carefully determine the timing

of the event. Identifying when the event actually happened is not critical; determining when the

market was first able to react to news of the event is critical. By examining popular press releases

and Securities and Exchange Commission (SEC) filings, the date of the announcement of each

merger in our sample was identified. This day, labeled day (0), is the day we can expect to

observe the market’s reaction to the event. If the actual announcement occurred on a non-trading

day, such as a weekend, or after trading hours when financial markets were closed, the next

trading day is established as day (0). To test whether information arrived to the market before the

general announcement, we also wish to determine if an abnormal return exists prior to the day of

the event, or day (-1). Likewise, we also check to see if the market’s response to the

announcement occurred over a period longer than one day. We therefore define our event period

as three days: days -1, 0, and +1.

The actual returns during this three day period are simply the observed returns based on

the daily closing stock prices of the two firms. However we need to isolate the impact of the

event from other market-wide events that may have influenced the returns for the two firms

during the event period. We therefore develop an estimate of what we think should have been the

return for the firm during the event period.

The expected return cannot of course be known with certainty; we can only estimate what

we think the return might be, based upon some model of the market. Short term event studies

often use the single index model form of the CAPM to estimate expected returns. Firm returns