Embed Size (px)

Citation preview

156 | P a g e

ASSESSING THE ECONOMIC OPTION

OFACQUIRINGMACHINERIES

Mr. M.Dhivakar Karthick1, Mr. B.Dhilip Kumar

2, Mr. S.Satheeshkumar

3

1,2,3Assistant Professor, Civil Engineering Department,

Kongunadu College of Engineering and Technology, Thottiyam, Tamil Nadu, (India)

ABSTRACT

In modern era, Consumer is using or choosing construction equipment based upon their maximum possible

uses, initial cost, maintenance cost, depreciation cost, idle cost and salvage value which are the factors

responsible for the profit margin. According to this study, identifying the cost factors that influence the

equipment utilization in various mode of acquisition. With those identifications the cost analysis is carried out

with respect to depreciation rate and discounted cash flow of the equipment. For which the questionnaire survey

is conducted on engineers and contractors practicing the equipment management system in their construction

projects. Accordingly the response from the respondents are analyzed by Relative Importance Index method and

the objectives are established with respect real time requirements on equipment utilization. Net Present Value is

used as a cost analysis technique to determine the best mode of acquisition. Hence equipment acquisition model

is framed using Microsoft Excel Application specifying right mode of acquiring the equipment for profit

maximization of the construction firm.

Keywords: Equipment; Rent; Buy; Lease; Custom Hire; Net Present Value; Ms Excel.

I. NEED FOR MECHANIZATION

The need for Mechanization arises due to the following reasons, Magnitude & Complexity of the Project,

Projects involving large quantities of material handling, Complexity of Projects using high grade materials,

High quality standards, Importance of keeping the Time Schedules, Optimum use of Material, Manpower and

Finance, shortage of skilled and efficient Manpower.

A. Scope of the Project

1. This research will optimize the investment on equipment’s of a construction firm.

2. Thereby it increases the profit margin of the construction firm.

3. It creates value & support to the construction firm.

B. Objective of the Project

1. To carry out the study review on prevailing mixer, material handling equipment, screening equipment,

vibrator, handling & compacting equipment.

2. To study the factors affecting like initial and maintenance cost, depreciation cost, idle cost and overheads

involved in usage at various types of construction work.

3. To disparate and equate the performance of the equipment’s under the influence of study focusing cost

aspects

157 | P a g e

II. LITERATURE REVIEW

The major cost consequences in construction operations are mostly due to the machineries and equipment

expenses of the project. The typical method of obtaining the machineries for the construction operation may be

achieved by personal financing or through loans at permissible interest rates or leasing the equipment [1]. Thus

the contractors or engineers preferring the option of acquiring due to increased equipment cost, maintenance

cost, obsolescence of owned equipment and limited sources of outside capital. These options includes leasing,

renting, purchasing equipment, and obtaining machinery service from custom operators.

2.1 Equipment Acquistion

The major issues faced by the contractor and engineer in running their companies to a successful turnover

depends on the mode of acquisition of equipment for their construction projects [2]. This consideration mostly

lies on the contractors and engineers undertaking CLASS II, III, IV, V works in case of government projects and

some significant private contracts. They doesn’t know the right time to acquire the equipment as owned and to

replace the equipment. Because the timely owning and replacement of equipment will definitely increases the

profit margin of the construction firm. There are various factors to be considered before going for the

acquisition of equipment. The factors are both financial and non-financial factors that influence the equipment

acquisition methods [2].

2.2 Equipment Cost

Equipment cost may in the range of 10% to 40% of overall construction cost [9]. The equipment cost is

considered as a major problem before and after acquiring it. The costs included in the equipment are tangible

and intangible [3]. By which the tangible cost of the equipment can easily be recorded and estimated using cost

accounting methods. Where the equipment cost management lies between the capital cost and operating

inferiority.

The substantial portion of the equipment production includes its ownership and operating cost. Hence the

equipment cost make up a significant part of fixed and variable cost of construction operation [4]. The fixed cost

generally include depreciation, interest, shelter and taxes, insurance. And operating cost includes fuel,

lubrication, labor, repairs.

2.3 Equipment Mainteinance

Profitability of construction projects depends on the effective equipment maintenance, because the equipment is

one of the key factor for improving contractor’s capability in performing their work more effectively and

efficiently [5]. The economic production of construction machineries depends on keeping the equipment in good

condition. Construction firm faces finance loses due to improper maintenance, equipment failure and

breakdown.

2.4 Decesion Options

Decision to acquire the equipment makes the value and profit to the construction firm. There are other options

and conditions reviewed during decision making. The general thumb rule is that percentage contribution of

equipment less than 60% should go for renting [6]. This consideration favors purchasing the equipment with

158 | P a g e

cost significant cost consequences. The decision making also goes with consideration of taxes, incentives,

capital investment, interest rates, depreciation and resale value also influence the decision making process.

Consumer going for equipment acquisition need to know the elements involved in the life cycle of equipment

and its estimated time period to be used with its frequency in that period [7]. Other sensible factors during

decision making are reliable service for long time, down payment, tax benefits, and depreciation dispose of [8].

The condition in lease contract is that leases are structured to last at least a year. Canceling the lease contract

prior to the contract period may end up with penalty.

There are some immeasurable factors like flexibility, ease of use, repetitions, which are responsible for the

decision making on equipment acquisition. The measurable factors includes tax advantages, depreciation,

maintenance cost and repair cost [9].

2.5 Evaluation of Decision Options

Cost benefit analysis is used to determine the appropriate contracting method. Cost benefit analysis includes two

various methods such as Present Value Method & Net Present Value Method [7]. The method of estimating

machinery cost over multiple time periods is in order to compare the options of leasing, renting, purchasing,

custom hire [1]. The net present value analysis is used to evaluate the decision option in equipment acquisition.

The DIRTI formula which is used to calculate the annual depreciation, interest, repairs, taxes and insurance [1].

The discounted after tax rate can also be analyzed by NPV method. The analysis is made worthwhile under the

consideration of equipment productive hours and its useful life [9].

This research focuses on construction contractor and engineer practicing equipment management in Erode

district, especially in Mettur canal division, Bhavani, Gobi, Erode, to identify the factors considered in

equipment acquisition and evaluate the various decision modes of equipment acquisition on cost benefit analysis

method.

III. RESEARCH METHODOLOGY

A detailed literature review was carried out to collect the information about the objectives of this study by

considering construction practitioners in various locations. Through the literature review helped to establish the

research topic in detail and general.The construction equipments considered for this research includes seven

categories or eleven no. of machineries includes concreting equipments, concrete handling equipment, screening

equipment, compaction equipment, handling equipment, bar bending equipment, earth compactor.

The resources from various literature of this study are international and national conference papers. Documents,

internet, journal articles, magazines, books, etc. These are collectively named as secondary data sources, used to

identify the financial factors affecting on construction equipment acquiring method [2].

3.1 Establishing Objectives

The design of questionnaire meant for surveying with contractors and engineers are literally achieved through

various literatures. The primary data that are obtained from the sources of contractors and engineers with open

ended questions. This survey is used for identification of factors affecting on construction equipments

acquisition methods.

159 | P a g e

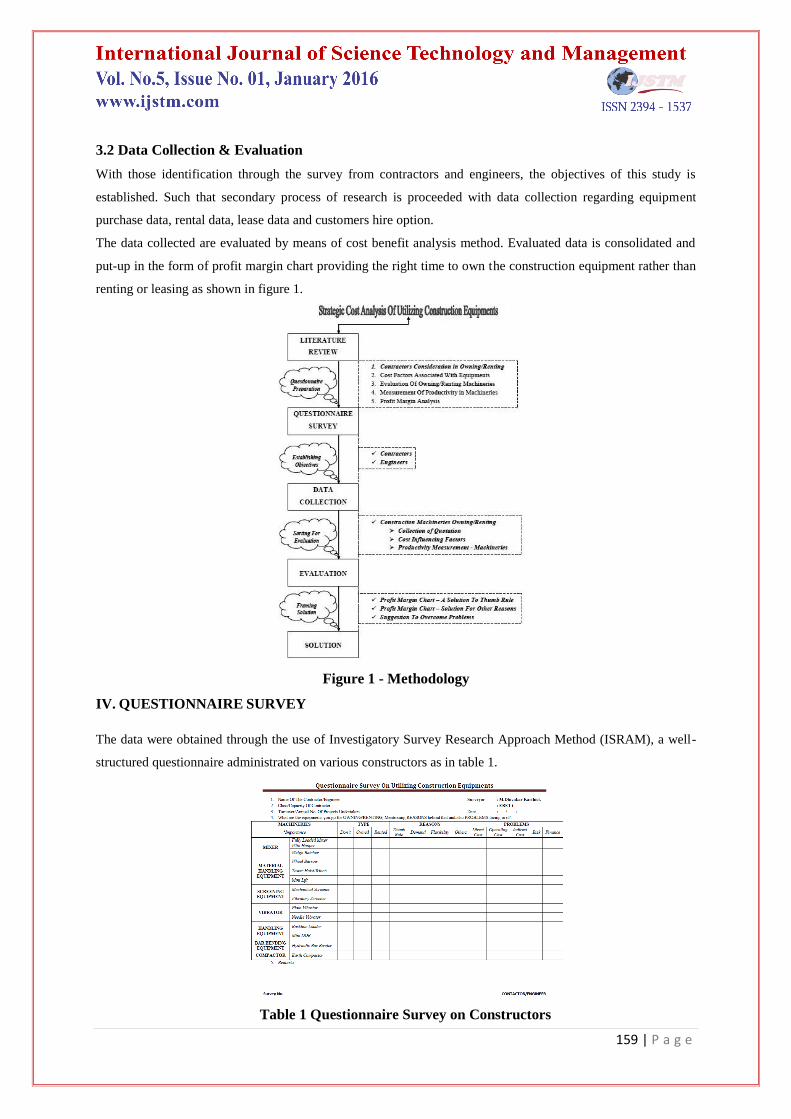

3.2 Data Collection & Evaluation

With those identification through the survey from contractors and engineers, the objectives of this study is

established. Such that secondary process of research is proceeded with data collection regarding equipment

purchase data, rental data, lease data and customers hire option.

The data collected are evaluated by means of cost benefit analysis method. Evaluated data is consolidated and

put-up in the form of profit margin chart providing the right time to own the construction equipment rather than

renting or leasing as shown in figure 1.

Figure 1 - Methodology

IV. QUESTIONNAIRE SURVEY

The data were obtained through the use of Investigatory Survey Research Approach Method (ISRAM), a well-

structured questionnaire administrated on various constructors as in table 1.

Table 1 Questionnaire Survey on Constructors

160 | P a g e

4.1 Contractors

The survey is triggered with contractors practicing equipment management system in public projects.

Contractors so identified are from sources of tamilnadu public works department in mettur lower canal division

followed up by the sub division’s ammapettai, bhavani, komarapalayam. The group so surveyed focused on

CLASS I – V contractors, where priority is given to lower class contractors. This is because of logical reason

that the premium class contractor’s holds maximum assets and so equipment management may not be major

problem in acquisition. The survey is conducted through in-person interview with them respectively.

4.2 Engineers

The equipment management system other than public works covers private contracts such as residential building

construction, commercial construction and other civil works. Here engineers are involved in large proportions.

Hence the survey made effective with in-person interview with engineers performing private contracts. Survey

with engineers are achieved through civil engineers association situated in gobi, and erode.

4.3 Consoildation

The overall survey with contractors and engineers are consolidated for evaluation of research objectives as

below as in table 2,

Table 2 Consolidated Survey Results

Machineries Acquisition Reasons Problems

Factors Evaluation D O R T D F O D O R F

Fully Loaded Mixer 0 23 17 28 0 12 0 0 27 0 13

Weigh Batcher 34 3 3 7 0 0 33 0 10 10 20

Wheel Barrow 4 20 16 26 1 9 4 0 23 0 17

Tower Hoist/Winch 7 13 20 25 2 7 6 0 18 7 13

Mini Lift 11 12 17 21 1 5 13 5 12 6 15

Mechanical Screener 15 10 15 21 1 4 14 0 14 0 26

Vibratory Screener 38 2 0 2 1 1 36 0 0 16 24

Plate Vibrator 40 0 0 0 0 1 39 12 8 11 9

Needle Vibrator 2 20 18 26 3 9 2 0 18 4 13

Backhoe Loader 8 9 23 21 3 10 6 16 13 3 4

Mini DOR 9 13 18 25 1 7 7 11 16 5 2

Hydraulic Bar Bender 40 0 0 0 0 0 40 21 7 9 3

Earth Compactor 22 8 10 14 2 3 21 0 18 7 13

V. CONSOLIDATED SURVEY RESULTS

The data collection is done for acquisition evaluation. Data are consolidated based on its mode of acquisition

reasons for acquisition, problems in acquisition.

161 | P a g e

5.1 Survey Response on Mode of Acquisition

52 Survey Response on Reason for Acquisition

5.3 Survey Response on Problems in Acquisition

162 | P a g e

VI. EVALUATION

6.1 Extracted Objectives Based on Questionnaire Survey

6.2 Purchase Model

The present value of purchase data is calculated with various factors such as depreciation of equipment,

marginal tax rate, self-employment rate, down payment, loan period, loan interest rate, after tax discount rate as

per the input given by the owner for assessment. Further calculations are proceeded with the following data’s for

NPV analysis,

(1). Tax Depreciation equals tax deduction and allowable depreciation based on MACRS schedule

(2). Fixed and Variable Cost is total of annual insurance, housing, repairs, labour and fuel, oil from given input

(3). Book Value is equal to the purchase price less accumulated tax depreciation

(4). Salvage Value is market value of machine when sold

(5). Balancing Charge equals the depreciation recapture [(Salvage Value - Book Value) * (Tax Rate - Self

Employment Rate)] in period machine sold

(6). Tax Reduction reflects the tax benefit due to eligible deductions [Tax Reduction = (Interest + Tax

Depreciation + FV Cost) * Marginal Tax Rate - (Balancing Charge)]

(7). After Tax Cash Flows equals [After Tax Cashflow = (Loan Payment + Fixed & Variable Cost) - (Salvage

Value) - (Tax Reduction)]

(8). Present Value Factor is based on discount rate and is calculated as [1/(1+(after tax discount rate/100))^Year]

(9). PV after Tax Cash Flow reflects discounted cash flow value [PV after Tax Cashflow = After Tax Cashflow

* Present Value Factor]

6.3 Lease Model

The present value of lease data is calculated with various factors such as first lease payment due immediately

(no deposit), lease term, lease payment, marginal tax rate, after tax discount rate as per the input given by the

owner for assessment. Further calculations are proceeded with the following data’s for NPV analysis,

163 | P a g e

(1). Fixed And Variable Cost is total of annual insurance, housing, repairs, labour and fuel, oil from given input

(2). Tax Reduction equals lease payment plus v.c times the marginal tax rate [Tax Reduction = (Lease Payment

+ Variable Cost) * Marginal Tax Rate]

(3). After Tax Cash Flows equals lease payment plus v.c minus tax reduction [After Tax Cashflow = (Lease

Payment + Variable Cost) - Tax Reduction]

(4). Present Value Factor is based on discount rate and is calculated as [1/ (1+ (after tax discount rate/100))

^Year]

(5). PV after Tax Cash Flow reflects discounted cash flow value [PV after Tax Cashflow = After Tax Cashflow

* Present Value Factor]

6.4 Rent Model

The present value of rent data is calculated with various factors such as first rent payment due immediately after

use, rent term, rent payment, rent inflation rate, marginal tax rate, after tax discount rate as per the input given

by the owner for assessment. Further calculations are proceeded with the following data’s for NPV analysis,

(1). Fixed And Variable Cost is total of annual insurance, housing, repairs, labour and fuel, oil from given input

(2). Tax Reduction equals Rent payment plus v.c times the marginal tax rate [Tax Reduction = (Rent Payment +

Variable Cost) * Marginal Tax Rate]

(3). After Tax Cash Flows equals Rent payment plus v.c minus tax reduction [After Tax Cashflow = (Rent

Payment + Variable Cost) - Tax Reduction]

(4). Present Value Factor is based on discount rate and is calculated as [1/ (1+ (after tax discount rate/100))

^Year]

(5). PV after Tax Cash Flow reflects discounted cash flow value [PV after Tax Cashflow = After Tax Cashflow

* Present Value Factor]

6.5 Custome Hire Model

The present value of custom hire data is calculated with various factors such as first rent payment due

immediately, custom hire term, custom hire payment, custom hire inflation rate, marginal tax rate, after tax

discount rate as per the input given by the owner for assessment. Further calculations are proceeded with the

following data’s for NPV analysis,

(1). Tax Reduction equals custom rate payment times the marginal tax rate [Tax Reduction = Custom Hire

Payment * Marginal Tax Rate]

(2).After Tax Cash Flows equals custom rate payment minus tax reduction [After Tax Cashflow = Custom Hire

Payment - Tax Reduction]

(3).Present Value Factor is based on discount rate and is calculated as [1/ (1+ (after tax discount rate/100))

^Year]

(4).PV After Tax Cash Flow reflects discounted cash flow value [PV after Tax Cashflow = After Tax Cashflow

* Present Value Factor]

VII. DISCUSSION

164 | P a g e

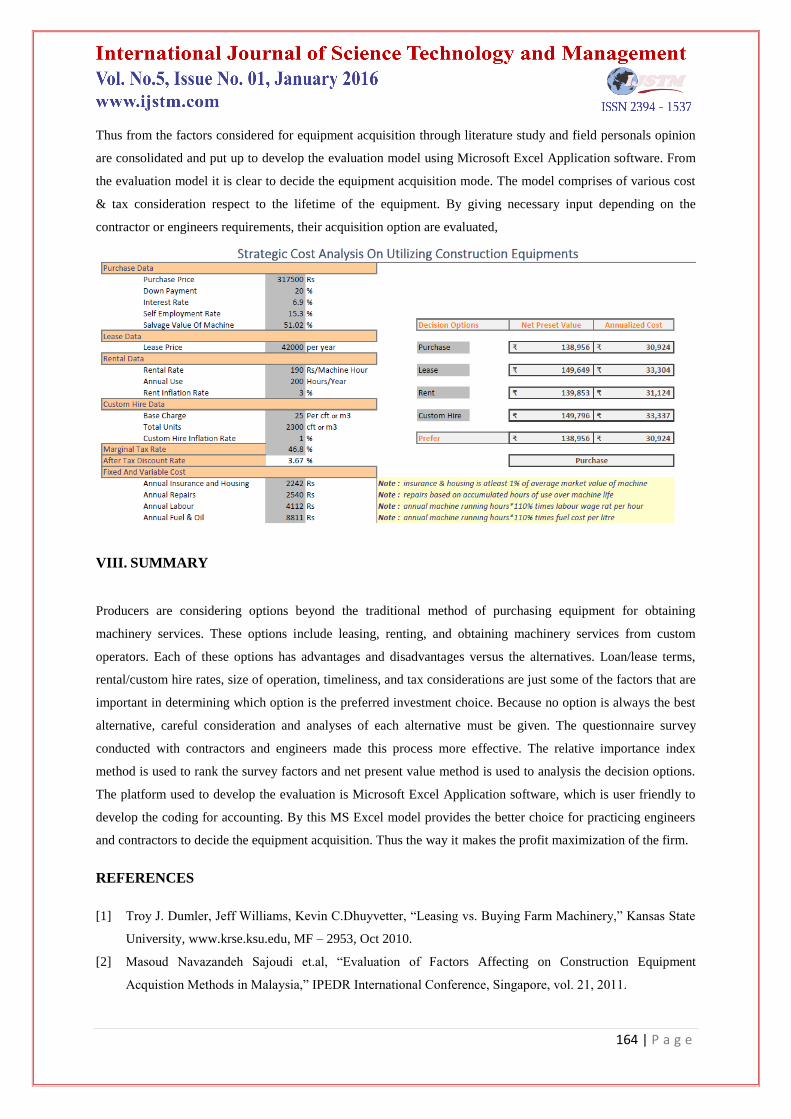

Thus from the factors considered for equipment acquisition through literature study and field personals opinion

are consolidated and put up to develop the evaluation model using Microsoft Excel Application software. From

the evaluation model it is clear to decide the equipment acquisition mode. The model comprises of various cost

& tax consideration respect to the lifetime of the equipment. By giving necessary input depending on the

contractor or engineers requirements, their acquisition option are evaluated,

VIII. SUMMARY

Producers are considering options beyond the traditional method of purchasing equipment for obtaining

machinery services. These options include leasing, renting, and obtaining machinery services from custom

operators. Each of these options has advantages and disadvantages versus the alternatives. Loan/lease terms,

rental/custom hire rates, size of operation, timeliness, and tax considerations are just some of the factors that are

important in determining which option is the preferred investment choice. Because no option is always the best

alternative, careful consideration and analyses of each alternative must be given. The questionnaire survey

conducted with contractors and engineers made this process more effective. The relative importance index

method is used to rank the survey factors and net present value method is used to analysis the decision options.

The platform used to develop the evaluation is Microsoft Excel Application software, which is user friendly to

develop the coding for accounting. By this MS Excel model provides the better choice for practicing engineers

and contractors to decide the equipment acquisition. Thus the way it makes the profit maximization of the firm.

REFERENCES

[1] Troy J. Dumler, Jeff Williams, Kevin C.Dhuyvetter, “Leasing vs. Buying Farm Machinery,” Kansas State

University, www.krse.ksu.edu, MF – 2953, Oct 2010.

[2] Masoud Navazandeh Sajoudi et.al, “Evaluation of Factors Affecting on Construction Equipment

Acquistion Methods in Malaysia,” IPEDR International Conference, Singapore, vol. 21, 2011.

165 | P a g e

[3] D. M. Naiknaware, Dr. S. S. Pimplikar, “Equipment Cost Associated With Downtime and Lack of

Availability,” IJERA, vol. 3, Issue 4, pp. 327-332, Jul-Aug 2013.

[4] Burton Pflueger, “How to Calculate Machinery Ownership and Operating Cost,”

http://agbiopubs.sdstate.edu/articles/EC920e.pdf, Feb 2005.

[5] Tsado Theophilus Yisa, “Equipment Mainteinance An Effective Aspect of Enhancing Construction Project

Profitability,” ISSN, Vol. 3, Issue 4, pp. 34-41, April 2014.

[6] John Leisner, “Deciding Whether to Buy Construction Equipment or

Rent,”http://www.constructionbussinessowner.com/topics/euipment/construction-equipment-

management/deciding-whether-buy-construction-equipment-or/page/0/1#sthash.rjPuARJ.dpuf,

Construction Bussiness Owner, Spetember 2010.

[7] Public Procurement Practice, “Lease-Purchase Decision,” Priniciple and Practice of Public Procurement

Practice.

[8] Robert Dymnet, “Renting, Leasing, Or Owning Construction Equipment,” The Aberdeen Group

Publication, #C960499 , 2011.

[9] James J Adrian, “Buy or Rent,” The Aberdeen Group Publication, #C00C057, 2009.