Embed Size (px)

Citation preview

ASSESSMENT OF THE UN-HABITAT

SLUM UPGRADING FACILITY

FINAL REPORT

SUBMITTED TO SWEDISH INTERNATIONAL DEVELOPMENT COOPERATION AGENCY (SIDA)

MAY 24, 2006

PREPARED BY

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 2

PM GLOBAL INFRASTRUCTURE INC

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. i

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY

FINAL REPORT

Table of Contents Table of Contents............................................................................................................................. i Acronyms .......................................................................................................................................iii Executive Summary........................................................................................................................ v 1 Introduction............................................................................................................................ 1

1.1 Study Background .....................................................................................................................1 1.2 Objectives of the Study..............................................................................................................2 1.3 Basic Approach ..........................................................................................................................3 1.4 Outline of the Report .................................................................................................................4

2 Urbanization and the Financial Challenge........................................................................... 5 2.1 The Urban Setting......................................................................................................................5 2.2 The Financial Challenge............................................................................................................5 2.3 Mobilizing Local Resources for Housing.................................................................................7 2.4 Mobilizing Local Resources for Municipal Infrastructure ....................................................9 2.5 Risk Mitigation Strategies.......................................................................................................11 2.6 The Role of Credit Enhancements..........................................................................................13 2.7 The Rationale for SUF.............................................................................................................15

3 The Need for a Slum Upgrading Facility ............................................................................ 16 3.1 Slum Upgrading Experiences..................................................................................................16 3.2 Donor Support for Slum Upgrading ......................................................................................18 3.3 The Objective of SUF...............................................................................................................24

4 The Slum Upgrading Facility .............................................................................................. 25 4.1 SUF’s Functions .......................................................................................................................25 4.2 SUF’s Clients ............................................................................................................................26 4.3 SUF Organization ....................................................................................................................27

5 The Pilot Program................................................................................................................ 30 5.1 The Contracting Out Solution ................................................................................................30 5.2 The Selected Team ...................................................................................................................30 5.3 The Pilot Operations................................................................................................................31 5.4 The Operations Manual ..........................................................................................................34 5.5 Coordination Issues and Other Issues....................................................................................34

6 SUF Budget and Work Program ......................................................................................... 36 6.1 General Considerations ...........................................................................................................36 6.2 Work Plan and Staffing Considerations ................................................................................36 6.3 Tentative 3-Year Budget .........................................................................................................38

7 Other Issues .......................................................................................................................... 39 8 Benefits and Risks ................................................................................................................ 40

8.1 Benefits of Slum Upgrading ....................................................................................................40 8.2 The Benefits of SUF .................................................................................................................40

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. ii

8.3 Main Risk Factors....................................................................................................................41 9 Conclusions and Recommendations.................................................................................... 43 ANNEX 1: Terms of Reference .................................................................................................. 45 ANNEX 2: SUF Pilot Operations............................................................................................... 48 ANNEX 3: Persons Met or Interviewed ..................................................................................... 53

Text Tables Table 1: Technical Assistance and Small Grant Facilities Part 1 ................................................ 22 Table 2: Technical Assistance and Small Grant Facilities Part 2 ................................................ 23 Table 3: Indicative Budget for SUF in 2008 (US$) ..................................................................... 38

Text Boxes Box 1: SUF Implementation Phases .............................................................................................. 2 Box 2: Are Mortgage Loans Right for the Urban Poor? ................................................................ 8 Box 3: The Community Led Infrastructure Financing Facility (CLIFF) ..................................... 13 Box 4: Common Types of Credit Enhancements......................................................................... 14 Box 5: The Kampung Improvement Program in Indonesia ......................................................... 16 Box 6: Pilot Phase Terminology .................................................................................................. 29

Text Figures Figure 1: SUF’s Development Partners ........................................................................................ 18 Figure 2: The Organizational Context of SUF............................................................................. 28

The PM Global Team

This report was prepared by Per Ljung, team leader, and Ann Elwan, urban development specialist

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. iii

Acronyms

ADB Asian Development Bank

CBO Community based organization

CGAP Consultative Group to Assist the Poorest

CLIFF Community Led Infrastructure Financing Facility

CODI Community Organizations Development Institute (Thailand)

DCA Development Credit Authority (USAID guarantee program)

DFI Development finance institution

DFID Department for International Development (UK)

EAIF Emerging Africa Infrastructure Fund

ECA Export credit agency

FIRST Financial Sector Reform and Strengthening Initiative

GDP Gross domestic product

GEF Global Environmental Facility

Habitat Foundation The United Nations Habitat and Human Settlements Foundation

HDFC Housing Development Finance Corporation (India)

HFI Housing finance institution

HI Homeless International, an NGO

IBRD International Bank for Reconstruction and Development (the World Bank)

IDA International Development Association

IDB Inter-American Development Bank

IFC International Finance Corporation

INR Indian Rupees

IULA International Union of Local Authorities

LGUGC Local Government Unit Guarantee Corporation (Philippines)

MDB Municipal Development Bank

MDG Millennium Development Goal

MFI Micro-finance institution

MM Mahila Milan (an Indian NGO)

NGO Non-governmental organization

NSDF National Slum Dwellers Federation (India)

Nurcha National Urban Reconstruction and Housing Agency (S. Africa)

O&M Operation and maintenance

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. iv

ODA Official Development Assistance

OPP Orangi Pilot Project (Pakistan)

PIDG Private Infrastructure Development Group

PIDG-TAF PIDG’s Technical Assistance Facility

PM Global PM Global Infrastructure Inc.

PMU SUF Program Management Unit

PPIAF Public-Private Infrastructure Advisory Facility

RFP Request for Proposals

SEWA Self-Employed Women’s Association (India)

Sida Swedish International Development Cooperation Agency

SPARC Society for the Promotion of Area Resources Centres (India)

SPV Special Purpose Vehicle

SUF Slum Upgrading Facility

SUF-DT SUF Design Team

SUF-PMU SUF Programme Management Unit

SUF-PT SUF Pilot Team

TA Technical assistance

TOR Terms of Reference

UCDO Urban Community Development Office (Thailand)

UMP Urban Management Programme

UNCHS United Nations Centre for Human Settlements (Habitat) Since 2002 known as UN-HABITAT

UNDP United Nations Development Program

UN-HABITAT United Nations Human Settlements Programme

USAID US Agency for International Development

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. v

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY

FINAL REPORT

Executive Summary Background

Governments in the developing world find it difficult to cope with unprecedented urban growth. The most visible signs of their failure to manage this process are the mushrooming slum areas that permeate the larger cities. About one billion people—orsome 40% of the urban population—live precariously in these settlements and, if present trends continue, the number of slum dwellers will increase to around 1,600 million by 2020. The situation is most acute in Sub-Saharan Africa and South-Central Asia, where around 70 % and 60 % of the urban population, respectively, live in slums. Given the well-established links between poverty and inadequate housing and related infrastructure, the international community has given increased importance to upgrading existing slums and slowing down the creation of new ones. Indeed, at the UN Millennium Summit in September 2000, world leaders pledged to achieve a significant improvement in the lives of at least 100 million slum dwellers by the year 2020 (MDG Target 11). They have also agreed to cut in half the number of people without safe drinking water and basic sanitation facilities by 2015 (MDG target 10). Slums are not only the result of urban poverty but also the product of failed policies, poor governance, inappropriate legal and regulatory frameworks, dysfunctional land markets, unresponsive financial systems, and—last but not least—a lack of political will. Thus, the slum problem in developing countries needs to be tackled in many different ways. First, the growth of slums needs to be slowed down and eventually stopped through legal and land market reforms (in part to provide security of tenure) and revamping zoning and regulations and building codes to make housing more affordable. Improved access to credit for housing construction and increased public sector infrastructure investments are essential elements in any strategy to prevent and upgrade slums. The financing needs for addressing the slum problem are massive and external financing from donors and private investors and lenders can play only a minor role. Thus, the bulk of the financing has to be mobilized locally. Unfortunately, the urban poor and municipalities in low and lower middle income countries have virtually no access to credit. Indeed, in most of Sub-Saharan Africa only a few percent of the urban population has access to mortgage loans for home construction or home purchases. Local governments have little resources available for investments. The fact that the urban poor

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. vi

and the middle class as well as municipalities are regarded as not creditworthy does not mean that they can not or will not repay loans. Rather it is because lenders (commercial banks or capital market institutions) can not assess and mitigate the risks associated with lending to the urban poor or to municipalities. To make the urban poor and municipalities “bankable” requires the development of new financial instruments and a high degree of “financial engineering.” Over the last half-dozen years, a number of donor initiatives have been established to help mitigate the risk associated with lending to people and organizations—especially municipalities—that earlier had no access to credit. Under its Development Credit Authority (DCA), USAID has provided guarantees for loans to micro finance institutions and municipalities. The Private Infrastructure Development Group (PIDG—comprising a number of European donors) has established GuarantCo that provides guarantees in support of local currency borrowings by private infrastructure developers and municipalities. Sida and some other bilateral donors have guarantee programs that can be used to support housing and urban development projects. IFC, in cooperation with the World Bank, has set up a Municipal Fund that can provide guarantees for local government borrowings. The Community Led Infrastructure Financing Facility (CLIFF) and organizations like ACCION have also demonstrated the viability of using guarantees to help mobilize financing for low-income housing and slum upgrading. Making slum upgrading schemes “bankable” (i.e. able to attract commercial financing) requires creative use of targeted subsidies, the formation of “special purpose vehicles” (i.e. organizations that undertake parts of a project in a financially viable manner and are creditworthy), “financial engineering” to attract financing from various sources, development of new financial instruments, and reshaping of project plans to minimize risks. The approach will have to vary from country to country and from project to project. However, no organization (donor supported or commercial) exist that can provide advice to slum dwellers and municipalities on how to go about doing this. The Slum Upgrading Facility (SUF)

This realization led UN-HABITAT in 2003 to commission a study (financed by DFID and Sida) concerning the feasibility of establishing of a Slum Upgrading Facility (SUF) that could play a catalytic role in mobilizing local financing for slum upgrading, low-income housing, and related infrastructure for the urban poor. After consultations with potential donors and the Cities Alliance, a SUF Design Team (SUF-DT) was established in September 2004. The SUF-DT undertook scoping missions to ten countries, verified that there was a need for an institution like SUF and identified a number of pilot operations in four countries (Indonesia, Ghana, Sri Lanka and Tanzania). A comprehensive Operations Manual was developed and a team of consultants were recruited. The consultant team is lead by Emerging Markets Group, a major international firm specializing in financial markets development but with broad expertise also in areas like municipal finance and micro finance. The team also includes veteran consultants with

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. vii

extensive experience in slum upgrading, housing finance as well as private-public partnerships and infrastructure project finance. Indeed, in both slum upgrading and housing finance, the senior staff is “top-notch.” Overall, the team is very strong. SUF is now ready to go into the Pilot Phase (expected to last 2-1/2 to 3 years—see chart below). UN-HABITAT has obtained US$10 million from DFID but is seeking more money from the donor community. The purpose of this report, which was commissioned by Sida, is to review the progress so far, examine the proposed operations of SUF during the Pilot Phase, assess the financial resources needed, make an overall evaluation of the benefits and risks associated with SUF during the Pilot Phase, and make appropriate recommendations regarding Sida’s eventual financing and the future operations of the Facility. This report is based on: (i) a review of the original feasibility study and all relevant documents that were prepared during the design phase, including (but not limited to) the Operations Manual, scoping papers, trip reports, country strategy papers, progress reports, budget proposals and the proposal by the winning consortium for the SUF-PT; (ii) visits to two of the four identified pilot countries (Sri Lanka and Tanzania); (iii) interviews with UN-HABITAT staff at the headquarters in Nairobi as well as interviews with other people familiar with SUF; and (iv) a mapping of related donor initiatives. Chart: SUF Implementation Phases

Feasibility StudyConsultation & Mobilization of Financing 1Design PhaseConsultation & Mobilization of Financing 2Pilot PhaseConsultation & Mobilization of Financing 3Full-Scale "Global" Implementation

2007 2008 2009 20102003 2004 2005 2006

The main functions of SUF, in the words of UN-HABITAT, are:

¾ “Advisory Services. In the first place SUF is a technical advisory service designed to assist SUF partners (slum dweller groups, NGOs, professional bodies, municipalities, commercial banks, and capital market institutions) in the financing aspects of their slum upgrading, low income housing, and associated infrastructure projects. An advisory hub will be created in each of the SUF Sub-regions (West and East Africa; South and South-East Asia), and this service will extend to neighboring countries

¾ Referral Functions. SUF will adopt a referral function, connecting identified needs with local, regional and international institutional support by others, bringing to local projects the expertise and partnership networks of multilateral programs and international NGOs. Institutional support of this kind can augment the financial packaging assistance of SUF, promoting policy and legislative

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. viii

reform, strengthening the capacity of municipalities, and improving other aspects of slum upgrading.

¾ Financial Packaging. Taking slum upgrading and low income housing projects to scale requires access to multiple forms of investment, and the use of several kinds of corresponding financial instruments and products. A major focus of SUF will be to structure and package financing for such projects such that they become “bankable” – so that they will provide domestic providers of private capital (the largest available source of finance in the world) with the necessary risk/return profile and confidence to lend money into, and to invest in, longer term investments that target infrastructure and superstructure projects for the urban poor.

¾ Development of Financial Products. SUF seeks to assist in the design and application of new financial instruments and products that will enable investors to work with and provide loans to various upgrading initiatives. The types of instruments and products developed with the assistance of SUF will reflect the different forms of available domestic capital (loans, municipal bonds, etc.) and term debt financing from the local currency capital market. In some cases this will also involve international guarantees.”

Implicit, but not explicit in SUF’s functions, is the provision of catalytic financing in the form of seed money, bridge or working capital financing, and funding of pilot operations to help promote innovations as well as jump-starting upgrading schemes. Also implicit in the SUF documents is the provision of credit enhancements of different forms, most likely in the form of guarantees. SUF is part of the recently created Human Settlements Financing Division1 (also referred to as Sub-Programme Four). Besides the SUF, the Division will have a Programme Development Branch (PDB) that is expected to carry out normative functions including the consolidation and analysis of financial tools and instruments, fund raising, and partnerships with international financial institutions. The branch will also be responsible for the development of longer-term programs that can fulfill the mandate of the Habitat Foundation -- to mobilize resources for shelter and related urban infrastructure. PDB will make tools and practices available to SUF, and draw upon, consolidate and disseminate lessons learned from SUF field operations. PDB will be staffed by professionals with expertise in project and investment finance, micro finance, grant-making, and inter-institutional relations. It is our understanding that the PDB is still to be established. SUF will be headed by a Programme Manager who oversees two units: the Programme Management Unit (PMU) and the SUF Pilot Team (SUF-PT). The SUF-PT is made up by the team of consultants led by the Emerging Markets Group (EMG) and will be responsible for the pilot operations in Indonesia, Ghana, Sri Lanka and Tanzania.

1 The organization chart for the Human Settlements Financing Division, see Figure 2 in Section 4.3.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. ix

The PMU manages the day-to-day activities of SUF. The PMU will be staffed with a Regional Advisor for Asia (serving also as Deputy Program Manager), a Regional Advisor for Africa, and a Communications, Monitoring and Evaluation Officer. Further, the PMU is to include Country Project Consultants (national experts in project finance) in Tanzania, Ghana, Sri Lanka and Indonesia. The PMU will monitor the activities of the consultants (SUF-PT) and pursue—on its own—projects in Bangladesh, Cambodia, Kenya, Senegal, Uganda and Zambia. The PMU will also work with SUF-PT in developing generic SUF assistance, monitoring, and response methodologies for the implementation of the Pilot Projects in the pilot countries, and in the other SUF countries on a regional basis. The SUF Operations Manual defines SUF’s clients in the following terms:

“The key clients of SUF are municipal authorities, CBOs, NGOs, together with their relevant departments of central government, as well as the local, private sector, including retail banks, property developers, housing finance institutions, service providers, micro-finance institutions, and utility companies.”

Assessment

A review of related donor facilities indicates that there are important technical and financial assistance needs related to slum upgrading, low-income housing, and related infrastructure that are not adequately met at present. Most importantly, there is no organization that provides direct “hands-on” advice to slum dwellers, municipalities and other government agencies in how to structure slum upgrading and low-income housing projects and related infrastructure facilities to mitigate risks and make it possible to mobilize commercial financing for such projects. SUF is designed to fill this void. During the Design Phase, SUF has made progress in creating an in-house capacity to deal with financing of slum upgrading. SUF also prepared a comprehensive Operations Manual. We believe that the manual is very well written and thought through. It reflects an in-depth understanding of the issues involved in the mobilization of financing for slum upgrading, low-income housing and related infrastructure. The manual provides a solid foundation for SUF’s operations during the Pilot Phase. As noted earlier, the consultants hired to staff the SUF-PT are of high caliber and should be able to come up with innovative financing solutions. Thus, the basic requirements for a successful implementation of the SUF Pilot Phase have been met. We have estimated that an indicative budget for the next three years would be in the range of US$22-25 million (with the potential to productively absorb up to around US$30 million). This estimate is based two premises: the capacity of UN-HABITAT to do meaningful normative work in the Human Settlements Financing area needs to be gradually built up; and the number of potential projects and financial products pursued during the Pilot Phase needs to be increased beyond the limited priority projects identified in the four pilot countries. The target should be to bring at least four operations to the stage where commercial financing has been committed.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. x

However, it is important to realize that SUF represents a long-term investment for the donors. In the short run (i.e. over the next couple of years) the benefits in helping to improve slums will be modest. However, as SUF reach more countries and projects, as innovative tools are disseminated the impact will multiply and the benefits can become very large. The development of new financial instruments and packaging of projects to attract long-term financing will also provide new investment opportunities for pension funds, insurance companies, etc. and contribute to financial deepening. Recommendations

UN-HABITAT has proposed that the SUF-PT (i.e. the consultants from EMG) focus on eight priority schemes in four countries:

¾ 1st Priority Physical Projects: o Ghana: Pilot Slum Upgrading Projects in Shama Ahanta East Metropolitan

Area (SAEMA); o Indonesia: Cooperative Housing Project in Yogyakarta; o Sri Lanka: Pilot Slum Upgrading Projects in Moratuwa; and o Tanzania: Housing Project with TAWLAT Cooperatives.

¾ 1st Priority Financial Products: o Ghana: Low Income Home Improvement Finance Product; o Indonesia: Scaling up of Co-BILD Initiative; o Sri Lanka: Low Income Housing Finance Product; and o Tanzania: Additional Housing Loan Guarantee Facility.

It has also proposed that the SUF-PMU (rather than the SUF-PT) undertake work in six other countries (Bangladesh, Cambodia, Kenya, Senegal, Uganda and Zambia) using its own staff and its own consultants (i.e. not from EMG). We believe that that there is a high risk that a large percentage of these projects might not be completed within the Pilot Phase. We also consider it important that the SUF-PT works with a broader set of projects and products, reflecting a greater variety of client groups, participatory approaches and country situations. In addition, we see coordination problems with the suggested “split” of countries handled by the SUF-PT and the PMU. For these and other reasons, we recommend that the mandate for the EMG consultants should be expanded to cover field activities in all the ten countries proposed by UN-HABITAT. The PMU should not undertake field activities on its own but participate in the field work undertaken by EMG. We and other observes have long felt that UN-HABITAT has lacked adequate expertise in urban and housing finance. The establishment of the Human Settlements Financing Division and SUF represents a first step in addressing this problem. The EMG team will ensure that the field activities are competently handled. In addition, UN-HABITAT needs to build-up its own in-house capacity to deal with financing issues. This requires significant increases in staffing compared to the present situation.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. xi

We regard the basic staffing of PMU, as described earlier, to be inadequate for its tasks of monitoring progress, digesting the lessons learnt as well as handling SUF’s advisory and referral functions. The Programme Development Branch (PDB) is not yet staffed. The PDB is expected to carry out the normative work and develop new tools, etc. We believe that in the near term, it makes more sense to have the PMU responsible for these activities (to ensure a rapid learning from the field). The PMU should be properly staffed to do so. We believe that SUF should not act as a financial institution or a donor. There is a significant moral hazard involved: “catalytic financing” could become a substitute for poor project preparation and financial packaging. Still, during the pilot phase, the amounts involved are likely to be small and it might be too time consuming to mobilize this type of financing from donors or other donor facilities. Thus, any such funding should be limited and granted only in exceptional circumstances and be approved in a transparent manner. We believe that the procedures adopted by the Cities Alliance for “medium” and “large” grant requests can serve as a suitable model for review and approval of proposals for pilot operations and bridge financing. Similarly, we believe that SUF in the longer term should not provide guarantees and other forms of credit enhancements. During the Pilot Phase, however, the amount of credit enhancement for any given project is likely to be modest. The transaction cost (and time involved) would not justify participation by GuarantCo or other guarantee facilities. Thus, we recommend that SUF should be able to provide guarantees and other forms of credit enhancements during the Pilot Phase. Appraisal and approval procedures for credit enhancements must be very stringent and meet sound commercial standards (which imply, inter alia, that the risk of a guarantee being called has to be appropriately low). We regard this as an “expedient exception” to the general principle that SUF should not be a financial institution. We recommend that the amount of catalytic financing and credit enhancements be limited to no more than 30% of the SUF budget (with credit enhancements accounting for the major share of this amount). Any proposals for credit enhancements should be subject to an external, professional review. The choice of financing channel (through Cities Alliance, which is the case at present, through the Habitat Foundation or directly to a specific project) is essentially a policy or operational decision for Sida. However, if Sida and other donors decide to “by-pass” Cities Alliance, the governance structure for SUF should be strengthened. We believe that the risks associated with the SUF Pilot Phase are moderate and can be mitigated. We recommend that Sida supports the next phase of SUF.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 1

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY

FINAL REPORT

Introduction

Study Background On January 1, 2002, the UN Centre for Human Settlements was transformed into the United Nations Human Settlements Programme, known as UN-HABITAT. In order to meet its expanded mandate, UN-HABITAT decided to create a new Sub-Programme 4 titled Human Settlements Financing. A 2003 study2 financed by DFID and Sida recommended the creation of a Slum Upgrading Facility (SUF) that would play a catalytic role in mobilizing local financing for slum upgrading, low-income housing, and related infrastructure for the urban poor. SUF would bring together and leverage four strategic client groups: municipalities and government agencies; NGOs and CBOs; local banks and other financial institutions like housing microfinance organizations; and existing or planned donor programs and facilities. The study also recommended that SUF would operate under the umbrella of the Cities Alliance but be managed by UN-HABITAT as an independent program. After a series of consultations with potential donors (especially DFID and Sida) and the Cities Alliance, SUF was established in December 2004. During the consultations it had been decided that the main operational part of SUF would be contracted out rather than being run “in-house” as proposed by the consultant study. In order to better define the tasks to be carried out by the consultants and to initiate the work while the consultancy services were being procured, a “SUF Design Phase” was introduced. During this phase, a core team was established at UN-HABITAT and several short term consultants were hired with interim financing from DFID and Sida. The SUF Design Team (SUF-DT) was established in September 2004. It has undertaken some 20 scoping and follow-up missions and identified four countries (Ghana, Indonesia, Sri Lanka and Tanzania) for implementation of pilot operations. Although the design phase was expected to last only 10-12 months, it will de facto end only in May 2006 when the consulting team will be mobilized and the pilot phase will start (see Box 1). UN-HABITAT has received a commitment of US$10 million from DFID for the pilot phase and has approached Sida and other donors for financial support to reach a funding level of US$30 million for the three year pilot phase. However, Sida has declared that its support for the pilot phase will depend on a comprehensive evaluation of the pre-

2 PM Global Infrastructure Inc. Meeting the Challenge: Proposal for the Creation of a Global Slum Upgrading Facility. Final Report submitted to UN-HABITAT on December 31, 2003.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 2

implementation/design phase. Sida has employed PM Global Infrastructure Inc. (PM Global) to undertake this evaluation.

Box 1: SUF Implementation Phases

Objectives of the Study The main objectives of the Evaluation of the Pre-Implementation Phase of the Slum Upgrading Facility, as set out in the Terms-of-Reference3 are:

¾ To provide a general overview of the short-term and long-term purpose and organization of the Slum Upgrading Facility;

¾ To evaluate the effectiveness of the Slum Upgrading Facility;

¾ To evaluate the effectiveness and capacity of the Slum Upgrading Facility in relation to other methodologies and alternative implementing organizations;

3 The Terms-of-Reference are provided in Annex 1.

A Feasibility Study was undertaken by PM Global Infrastructure Inc. in 2003. This study demonstrated the need for SUF and outlined the basic operations of the facility. After consultations with DFID, Sida and the Cities Alliance, SUF was established in late 2004. The Design Phase that followed was aimed at validating the conclusions of the feasibility study and refining SUF’s staffing, policies and procedures. The design phase also involved defining in detail the terms-of-reference for and recruitment of consultants that would be responsible for the bulk of the field activities during the next phase. The Pilot Phase is expected to last 2-1/2 to 3 years. During this phase, the consultants and UN-HABITAT are expected to work with clients in four countries (Ghana, Indonesia, Sri Lanka and Tanzania) and to successfully help mobilize financing for at least two slum upgrading schemes (with at least two more projects being close to “financial closure”). Operations will also be initiated in 5-6 other countries. Full-Scale “Global” Implementation would follow after successful completion of the pilot phase. This phasing of the work is captured in the chart below.

Feasibility StudyConsultation & Mobilization of Financing 1Design PhaseConsultation & Mobilization of Financing 2Pilot PhaseConsultation & Mobilization of Financing 3Full-Scale "Global" Implementation

2007 2008 2009 20102003 2004 2005 2006

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 3

¾ To evaluate the goals of the Slum Upgrading Facility and to what extent it fills identified financial gaps in housing provision systems in developing countries; and

¾ To evaluate the goals of the Slum Upgrading Facility and to what extent it fills identified financial gaps in housing provision systems in developing countries in relation to other methodologies and alternative implementing organizations.

Basic Approach In order to approach the work in a cost-effective manner, PM Global divided the work into several elements:

¾ Review of relevant documents. The SUF Programme Management Unit shared with the PM Global team all relevant documents (in total around 100) that had been prepared during the design phase, including (but not limited to) scoping papers, trip reports, country strategy papers, progress reports, budget proposals and the proposal by the winning consortium for the SUF-PT. In assessing the overall objectives and approaches of SUF, we have primarily relied on the Operations Manual and the SUF Design Phase--Draft Final Report (dated March 31, 2006) as providing the most comprehensive and up-to-date description of SUF and the progress to date.

¾ Field visits for “ground proofing.” Since virtually all the documents were produced by UN-HABITAT and the SUF-DT, there was a need to examine whether these documents reflected actual progress on the ground and to assess the likelihood that the identified pilot operations will go ahead, as well as to examine the merit of each pilot program. This was undertaken by visiting two of the four identified pilot countries: Sri Lanka and Tanzania. These visits were arranged with the help of the Habitat Programme Managers in the two countries. In the field, we met with most of the relevant stakeholders in the proposed pilot operations.

¾ Interviews with UN-HABITAT Staff. Useful perspectives on the progress so far and the prospects were obtained through interviews and discussions with UN-HABITAT staff at the headquarters in Nairobi.

¾ Interviews with other people familiar with SUF. We also had brief discussions with people who had served as consultants to the SUF-DT and been part of the SUF Consultative Board.

¾ Mapping of related donor initiatives. We have examined the operations of related donor initiatives to examine the relevant niche for SUF.

¾ Report preparation. The findings of all the above elements of our assessment have been incorporated in the present report.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 4

Outline of the Report Chapter 2 provides the rationale for the creation of SUF. It discusses the challenges associated with financing rapid urbanization and addressing the problem of mushrooming slum settlements. The chapter also reviews the approaches that have been taken and could be taken to mobilize local financing for slum upgrading, low-income housing, and associated infrastructure. Chapter 3, after an introductory review of global slum upgrading experiences, examines the role of SUF in relation to other donor supported programs. It reviews in some detail the technical assistance facilities that deal with urbanization and/or financing issues. This review concludes that SUF provides a type of service that is not provided by any other facility. Chapter 4 assesses the key features of SUF, namely its functions, clients and organization. It raises certain concerns regarding SUF’s present focus, and makes recommendations regarding its future orientation and staffing. Chapter 5 looks at the Pilot Program. It first makes an assessment of the selected consultants. This is followed by a review of the proposed pilot operations. Finally, the chapter raises some coordination issues. Chapter 6 builds on the observations in the preceding chapters. It examines the work program and budget for SUF from a strategic perspective (rather than commenting on individual line items in UN-HABITAT’s budget proposal). Chapter 7 raises a couple of issues concerning the process of channeling money to SUF and related governance arrangements. Chapter 8 discusses the benefits of SUF and outlines the major risk factors. Chapter 9 provides our overall conclusions and summarizes our recommendations.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 5

Urbanization and the Financial Challenge

The Urban Setting Governments in the developing world find it difficult to cope with unprecedented urban growth. The most visible signs of their failure to manage this process are the mushrooming slum areas that permeate the larger cities. About one billion people—orsome 40% of the urban population—live precariously in these settlements and, if present trends continue, the number of slum dwellers will increase to around 1,600 million by 2020. The situation is most acute in Sub-Saharan Africa and South-Central Asia, where around 70 % and 60 % of the urban population, respectively, live in slums. Urban slums are not only eyesores; they also pose multiple threats to the health and safety of their inhabitants. The lack of the most basic infrastructure makes the provision of social services, such as health care, ineffectual. Similarly, the lack of infrastructure increases the cost of necessities, such as drinking water or fuel for cooking, to the urban poor and reduces their productivity and economic opportunities. Given the well-established links between poverty and inadequate housing and related infrastructure, the international community has given increased importance to upgrading existing slums and slowing down the creation of new ones. Indeed, at the UN Millennium Summit in September 2000, world leaders pledged to achieve a significant improvement in the lives of at least 100 million slum dwellers by the year 2020 (MDG Target 11). They have also agreed to cut in half the number of people without safe drinking water and basic sanitation facilities by 2015 (MDG target 10).

While urban poverty is certainly one factor contributing to the growth of slums, they are also the product of failed policies, bad governance, inappropriate legal and regulatory frameworks, dysfunctional land markets, unresponsive financial systems, and—last but not least—a lack of political will. Addressing this multi-faceted problem requires not only the concerted effort of governments, enterprises and civil society in the developing world, but also financial and technical assistance from the international community.

The Financial Challenge Housing and related infrastructure investments in developing countries tend to be in the range of 3-8% of GDP, depending largely on the per capita income level of the country concerned. In aggregate, these investments are around US$300 billion,4 including around US$ 100 billion for urban infrastructure (excluding health and education facilities in urban areas) and around US$ 200 billion for housing. These investments fall well short of the needs and often do not reach the poor.

4 Dillinger (1994) estimates that annual government expenditures on urban services in developing countries were in the range of US$100 to US$200 billion (or 2.5-5% of GDP). This estimate included water supply, sewerage, intra-city roads, subsidies to mass transit, primary education and health. (UMP, 1994)

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 6

The total investment for 670 million slum dwellers would, according to the Millennium Project , be close to US$ 300 billion (annually US$18.5 billion) during the period 2005-2020 and would include security of tenure, housing improvement, physical infrastructure (water, sanitation, drainage, roads, electricity), primary schools and health clinics.5 The Millennium Project’s Task Force on slums assumed that 30% of this funding would be in the form of small loans to slum dwellers to help them build and improve their houses and that the families would directly contribute 10% from their own savings. Governments and donors were assumed to finance another 30% each. These assumptions imply that micro-housing finance institutions and donors each would contribute around US$5.5 billion annually for improvements in slum areas. The World Panel on Financing Water Infrastructure (2003) estimates that, in order to meet the MDG targets related to water supply and sanitation, annual investments need to double from the present level of US$30-35 billion. Most of these investments would be made in urban areas. This estimate includes water and sanitation in slum areas and, consequently, there is some double counting. Multilateral and bilateral assistance for housing and urban infrastructure appears to be less than US$5 billion annually, of which less than US$1 billion is earmarked for slum upgrading.6

While private investments in infrastructure facilities increased rapidly during the 1990s and amounted to more than US$890 billion over the 1984-2004 period, only about 5% of this total has been devoted to urban water supply and sanitation.7 After a peak in the late 1990s, it appears that the amount of investments in private water and sanitation projects have stabilized in the range of US$1.5 billion to US$2 billion annually. However, most of the private sector investments have gone to projects in middle income countries. Investments in private water and sewerage projects located in low income countries amounted to only US$17 million over the 2001-2004 period. Thus, it is clear that international financing, be it from private or public sources, only plays a miniscule role in meeting the financing needs.

The scarcity of foreign funds for urban infrastructure, housing, and slum upgrading is not the main reason why such investments should be financed domestically to the extent possible. Such investments generate no revenues in foreign currency and expose the borrowers to significant foreign exchange risks. Nearly all expenditures are in local

5A home in the city, Achieving the Millennium Development Goals, Task force 8, Millennium Project,

2005, Earthscan, London. 6 Multilateral financing is around US$3 billion per year, of which around 14% is dedicated to slum upgrading. 7 Source: the World Bank’s Private Participation in Infrastructure (PPI) database at ppi.worldbank.org. It should be noted that the investment amounts in this database give a somewhat exaggerated picture of the amount of private investments. First, the investment figures are commitments (that may or may not materialize). Second, the figures comprises investments from all sources (including governments and donors) and not only investments made, or to be made, by the private equity investors and lenders.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 7

currency; payments from beneficiaries of the projects are in local currency as well; and the government, investors, lenders and project beneficiaries are generally not able to assume the foreign exchange risk.8 Indeed, the use of foreign currency loans, channeled through domestic banks, for real estate investments was a major factor contributing to the Asian financial crisis in 1997. With foreign currency loans, the lender faces the risk that the recipient country will not have adequate foreign exchange reserves to service the debt or make other payments in foreign currencies. This “country risk” is included in the interest rate that the lender would charge or in the fee that a guarantee institution would impose. Thus, the cost to the borrower/beneficiaries of local funding would be lower, as it would only include the cost associated with the commercial risks of the program/project and not that associated with the sovereign and currency exchange risks. In short, financing for urban development, slum upgrading and housing should, as far as possible, be mobilized locally through taxes, user fees and loans from banks and capital markets. Indeed, housing and infrastructure projects can offer pension funds and insurance companies suitable instruments for long-term investments. Thus, such long-term financial instruments would contribute to financial sector deepening and development of capital markets.

Mobilizing Local Resources for Housing In industrialized countries, formal housing finance institutions, (i.e. commercial banks providing mortgage finance, specialized housing banks, building societies/savings and loans schemes, cooperatives, etc.) constitute a large and important part of the financial sector and the overall economy. In the US, Norway and Sweden, the value of all outstanding mortgage loans is around 50% of GDP. In developing countries, and especially in low income countries, these institutions play only limited roles in meeting the housing needs of the urban poor (as well as the broad middle class).9 In Uganda, for example, only about 200 mortgage loans are issued every year while the number of new dwellings (however modest they may be) in urban areas probably approaches 50,000. In Kenya, less than 5% of new dwellings in urban areas are constructed with mortgage financing; indeed, there is a common saying in Nairobi that “only bankers can get mortgages.” In Zambia the total stock of mortgages is less than US$2 million and in Tanzania less than US$3 million.

8 Since most developing country currencies tend to depreciate against those of the industrialized countries, the loan amount would continuously (but unpredictably) increase in the domestic currency, making financial planning and management difficult. 9 Because of the embryonic nature of housing finance markets in low and lower-middle income countries and the lack of credit information, property titles, informal sector incomes etc., innovations in mortgage lending that have swept the industrialized and upper-middle income countries have largely bypassed most of the developing world.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 8

Of low-income countries, India has the best developed housing finance industry. More than 80 private housing finance institutions have been established during the last decade, some of whom rely on refinancing from the National Housing Bank, an apex bank. They are also responding to incentives that form part of India’s system of directed lending. Still, only about 22% of new dwellings in urban areas are financed with mortgages. However, some mortgage lenders have started to address the needs of low income borrowers. The Housing Development Finance Company (HDFC), the leading private sector mortgage lender in India, relies on NGOs and self-help groups to channel loans to low income families. HDFC had experienced a recovery rate of nearly 100% on such loans. Birla Home Finance has a new scheme that targets urban poor households with monthly incomes less than INR 6,000 (about US$135). In recent years, a new—and often more appropriate10—option has become available to some of the urban poor: small loans for home improvements from micro-finance institutions (MFIs) such as Grameen Bank in Bangladesh, the Self-Employed Women’s Association (SEWA) Bank in India, the National Cooperative Housing Union (NACHU) in Kenya, or Mibanco in Peru. Most of these organizations are general micro-finance institutions while a few, such as NACHU, were originally set up to provide housing loans. Micro housing finance represents an evolution of the model for lending to micro-enterprises. Traditionally, these institutions have provided small, short term loans to low-income families only for “productive” purposes. House improvement loans respond to strong client demand, and reflect the realization that, in the words of SEWA Bank, “especially for poor women, their homes are not only their place of shelter, but also their workplace, storehouse, security and usually their biggest asset.”

Box 2: Are Mortgage Loans Right for the Urban Poor?

A few micro-lending institutions have reached significant scale in their housing finance operations such as Mibanco with a housing portfolio of US$15 million, Grameen Bank and Bolivia’s Banco Sol with US$20 million. What is striking, however, is the relatively small scale of the operations of many of the leading actors: SEWA Bank has a housing finance portfolio of about US$900,000; the Homeless People’s Federation of the Philippines (HPFP) has assets of about US$700,000; and NACHU “recycles” about US$600,000 in funds once received from USAID and the Ford Foundation. These figures pale in comparison with the assets of the formal housing finance system. While

10 See Box 2

Traditional mortgage instruments tend to be inflexible and not suited for situations where people build their houses in stages. There is also a growing awareness that traditional mortgage loans might not be attractive to the urban poor, even if they might be able to obtain such loans. Most slum dwellers not only have low incomes, but they also suffer from a high degree of income insecurity. Thus, they can ill afford fixed monthly mortgage payments and face the risk of losing the house in case of temporary loss of income

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 9

exact aggregate figures are hard to come by, it appears that, in aggregate, micro-finance institutions in most countries have an outstanding housing loan volume of only a few percent of the assets of the formal mortgage lending institutions. Thus, in most developing countries, not only the poor but also the broad middle class have no access to finance for house construction and improvements. What is required is a two-pronged approach—both from-the-top-down and from-the-bottom-up:

¾ Making the formal housing finance institutions “move down” and reach people with lower incomes. This will require: adoptions of new corporate lending policies and procedures; strategic and operational partnerships with NGOs and/or micro-finance institutions; creation of secondary mortgage markets; etc.

¾ Scaling up the operations of micro housing finance organizations. Inter alia, this involves providing them with resources to expand the client base as well as getting access to longer term sources of financing.

Mobilizing Local Resources for Municipal Infrastructure The provision of basic services and local infrastructure is usually seen as the domain of municipal governments that are closer to the inhabitants and, thus, better understand their needs. In reality, local governments have typically failed to keep pace with rapid population growth and to meet the needs of the urban poor. In Sub-Saharan Africa (with the exception of South Africa), municipalities are marginal actors, generally accounting for less than one-twentieth of all public expenditures. Municipalities in Asia have some greater capabilities and resources, especially in the middle-income countries. The financial problems of many municipalities have worsened over the last decade. Many countries have sought to decentralize service delivery to local governments but this has often not been associated with a commensurate increase in their revenue sources. In most low-income countries, municipal investment budgets are extremely limited. The Lusaka City Council, for example, has an annual investment budget of around US$1.50 per inhabitant. The corresponding figure for Douala is around US$2.00.11 Thus, central government ministries and agencies tend to finance and build all major infrastructure facilities, leaving local governments with responsibility for only marginal activities, such as solid waste collection and disposal, bus terminals and slaughterhouses. In Senegal, for example, most urban projects are built by Agetip, the central public works organization, and financed through grants from FECL, the government’s municipal development fund. In Sri Lanka, the Urban Development Authority is responsible for slum upgrading and general environmental improvements (as well as urban planning); NWSDB, for water supply and sewerage; Department of Roads and Highways, for major roads. The Colombo Municipal Council is only responsible for solid waste collection and minor investments in roads and public spaces. The situation in Tanzania is basically the same—central government agencies implement all major infrastructure projects. However, at least in Sub-Saharan Africa, the amount of public sector investments appear to have

11 This can be compared with US$400 per resident in Stockholm.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 10

dropped drastically from over 4% of GDP in the early 1980s to less than 2% of GDP around 2000 (Estache et al. 2005). Municipal budgets are typically approved by the central government. In Tanzania, until recent reforms (supported in part by Sida), the central government approved all municipal budgets and determined the amount of transfers based on “scaled-down” expenditure programs, taking into account what the municipalities can raise on their own. (Thus, improved revenue performance was partly “rewarded” through reduced transfers.) By implication, the central government would need to approve any long-term borrowing by municipalities and its approval is often perceived as a guarantee that sufficient funding would be available for debt service. Central governments control all major revenue sources. What municipalities are left with are a few rather inelastic revenue sources, often best described as “nuisance” taxes. In Senegal, for example, municipalities levy more than 300 different fees and business taxes. Often, the central government also limits the local governments’ freedom to set tax rates, thereby further reducing their ability to mobilize resources. In spite of the importance of transfers to local governments, most countries do not have a rational, transparent system for allocating funds to municipalities. Transfers tend to be determined based on political considerations and vary from year to year, which make it virtually impossible to plan large-scale infrastructure investments that may require several years of capital outlays. However, a few countries, such as Bolivia where municipalities receive 20% of all central government revenues, have established automatic systems for such transfers. Statutory restrictions on municipalities’ ability to borrow frequently preclude this option. The reasons for such restrictions vary from a desire to control or limit public sector debt and prevent moral hazard problems (in that the central government might have an explicit or implicit obligation to “bail out” municipalities that cannot service their debt). For example, municipalities in Sri Lanka have the legal right to borrow and to issue general obligations bonds. However, the Municipal Ordinance does not allow municipalities to pledge assets or revenue streams as security, which in practice has prevented them from accessing financing from banks and bond markets. Even where municipalities do carry out and finance their own projects, commercial lenders are extremely cautious about dealing with them. Municipalities’ basic lack of creditworthiness is due, in part, to the generally inadequate fiscal and regulatory frameworks (including lack of clarity in service responsibilities among the various government levels, and inadequate capacity for revenue generation at the local level, as discussed above). Strengthening municipalities’ ability to effectively deliver services to their inhabitants requires actions on many different levels. In most developing countries, the fiscal system needs to be reformed, increasing local governments’ taxing authority. Transfers to municipalities should be made automatic, predictable, and transparent. The amount

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 11

should be linked to some easily established criteria such as population, number of school children, etc. Municipalities should generally be given greater fiscal autonomy and be free to determine their expenditures without central government approval (subject, of course, to proper audits). Given the difficulties that municipalities face in accessing funds on the commercial market—whether through bonds or through bank loans—more than 50 countries have established special credit intermediaries, commonly referred to as municipal development banks, to lend funds to local governments. Although some of these institutions have been around for almost three decades, they have largely remained vehicles for channeling funds from international institutions and central governments. Generally, their financial performance has been poor—except for those institutions that have collateralized the loans, generally through the right to intercept transfers from the central government to the borrowing municipality. Thus, if they operate on sound commercial principles, municipal development banks can help local governments gain access to domestic capital markets. Careful attention to the need for collateral has opened up a municipal bond market in India. In 1998, Ahmedabad was the first city to place a bond without guarantee from the state government. The bond issue was rated AA by CRISIL, the Indian rating agency. Ahmedabad managed to achieve an investment grade rating by channeling its octroi12 revenues through an escrow account. The bond holders have first claim on the money in the escrow account. A similar approach is being adopted for a planned bond issue by the municipality of Douala in Cameroon. In the Philippines, the bankers’ association took initiative for the creation of the Local Government Units Guarantee Corporation (LGUGC) that guarantees municipal bond issues. The LGUGC charges an upfront fee of 2.5% to 3.5%. In case of a default, LGUGC assumes the debt service obligation. However, LGUGC has the right to intercept the transfers from the central government to the municipality. Since its creation in 1998, LGUGC has provided guarantees for about 20 municipal bond issues. The above examples show that with creative approaches, municipalities can gain access to debt financing for infrastructure development.

Risk Mitigation Strategies While successful examples have been given above, the fact remains that slum upgrading involves the two categories of actors that are least creditworthy: the urban poor and municipalities. Banks and bond buyers generally lack the ability to assess and mitigate risks associated with this type of lending. The nature of the risks varies from country to country and from case to case. Thus, various approaches are needed to mitigate the risk for the lenders.

12 Octroi is a tax levied on goods brought into the city.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 12

Risks are allocated and mitigated not only through the loan documents but through the whole design and implementation of a project. For example, some risk can be mitigated by designing the project in such a way that part of the land can be sold to middle income families who make a significant down payment up front; and risks can be minimized by using a fixed-price turnkey contract. Some factors cut across all aspects of a project. Land ownership and tenure security is perhaps the most important. If an upgrading project is associated with enhanced tenure security, experience has shown that slum dwellers are willing to pay more for the infrastructure services and are more interested in using their savings for house improvements. This in turn will enhance the financial viability of the project. Although micro housing finance lenders typically do not require a mortgage, they often want to see some evidence that the borrower has the right to stay on the site and be satisfied that the risk of eviction is minimal. Thus, enhanced tenure security will also make the slum dwellers more creditworthy. Similarly, a commercial bank or investor is more interested in supporting a project if there is no risk that ownership disputes will halt implementation. Zoning regulations and building codes similarly impact all aspects of an upgrading project. They will, for example, influence the ability to sell some lots or houses on fully commercial terms and to utilize the proceeds for cross-subsidies to the existing residents. (The sale of residential and commercial space and transferable development permits is a key element in the financial viability of the CLIFF residential projects in Mumbai—see Box 3.) In other cases, they might impose too costly standards and spoil the financial viability of the scheme. Ambiguous or changing codes and regulations can also introduce new risk elements that keep lenders away. Once the basic steps have been taken to reduce the overall risks, the next is to identify the various revenue streams of a project and assess how dependable they are. Lenders (or types of lenders) are likely to vary in their assessment of the risks associated with different project components and revenue streams. For example, a commercial bank might be willing to take the risks associated with sale of developed land but not those associated with financing house construction for low income residents—a risk that might be taken willingly by micro housing finance institutions. One key problem might occur when a municipality or government agency, which is not creditworthy, seeks to implement a project that in itself is highly justified and profitable. In such a case, the lender would like to make sure that the revenues from the project are “ring-fenced” and not used for meeting non-related spending needs. This is typically achieved by creating a separate development company or a “special purpose vehicle” (SPV). An SPV in its simplest form is not much more than a special banking account through which project expenditures and revenues as well as loan disbursements and repayments are channeled.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 13

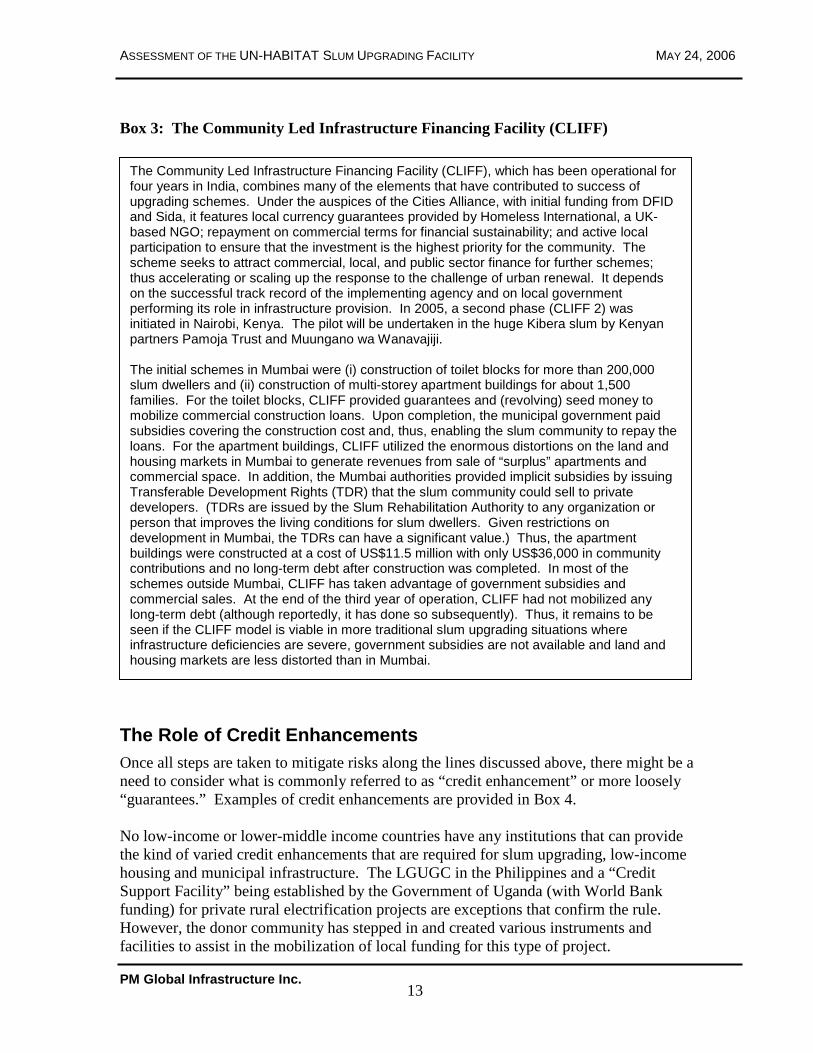

Box 3: The Community Led Infrastructure Financing Facility (CLIFF)

The Role of Credit Enhancements Once all steps are taken to mitigate risks along the lines discussed above, there might be a need to consider what is commonly referred to as “credit enhancement” or more loosely “guarantees.” Examples of credit enhancements are provided in Box 4. No low-income or lower-middle income countries have any institutions that can provide the kind of varied credit enhancements that are required for slum upgrading, low-income housing and municipal infrastructure. The LGUGC in the Philippines and a “Credit Support Facility” being established by the Government of Uganda (with World Bank funding) for private rural electrification projects are exceptions that confirm the rule. However, the donor community has stepped in and created various instruments and facilities to assist in the mobilization of local funding for this type of project.

The Community Led Infrastructure Financing Facility (CLIFF), which has been operational for four years in India, combines many of the elements that have contributed to success of upgrading schemes. Under the auspices of the Cities Alliance, with initial funding from DFID and Sida, it features local currency guarantees provided by Homeless International, a UK-based NGO; repayment on commercial terms for financial sustainability; and active local participation to ensure that the investment is the highest priority for the community. The scheme seeks to attract commercial, local, and public sector finance for further schemes; thus accelerating or scaling up the response to the challenge of urban renewal. It depends on the successful track record of the implementing agency and on local government performing its role in infrastructure provision. In 2005, a second phase (CLIFF 2) was initiated in Nairobi, Kenya. The pilot will be undertaken in the huge Kibera slum by Kenyan partners Pamoja Trust and Muungano wa Wanavajiji. The initial schemes in Mumbai were (i) construction of toilet blocks for more than 200,000 slum dwellers and (ii) construction of multi-storey apartment buildings for about 1,500 families. For the toilet blocks, CLIFF provided guarantees and (revolving) seed money to mobilize commercial construction loans. Upon completion, the municipal government paid subsidies covering the construction cost and, thus, enabling the slum community to repay the loans. For the apartment buildings, CLIFF utilized the enormous distortions on the land and housing markets in Mumbai to generate revenues from sale of “surplus” apartments and commercial space. In addition, the Mumbai authorities provided implicit subsidies by issuing Transferable Development Rights (TDR) that the slum community could sell to private developers. (TDRs are issued by the Slum Rehabilitation Authority to any organization or person that improves the living conditions for slum dwellers. Given restrictions on development in Mumbai, the TDRs can have a significant value.) Thus, the apartment buildings were constructed at a cost of US$11.5 million with only US$36,000 in community contributions and no long-term debt after construction was completed. In most of the schemes outside Mumbai, CLIFF has taken advantage of government subsidies and commercial sales. At the end of the third year of operation, CLIFF had not mobilized any long-term debt (although reportedly, it has done so subsequently). Thus, it remains to be seen if the CLIFF model is viable in more traditional slum upgrading situations where infrastructure deficiencies are severe, government subsidies are not available and land and housing markets are less distorted than in Mumbai.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 14

Box 4: Common Types of Credit Enhancements

Some of the institutions that are currently are in the business of structuring and providing credit enhancements in one form or another include:

¾ GuarantCo. Set up by DFID, Sida and selected other donor organizations, GuarantCo provides credit enhancements on private and municipal (including publicly owned utilities if they meet certain criteria) infrastructure related projects. These generally take the form of guarantees.

¾ USAID’s Development Credit Authority (DCA) Facility. The DCA has been used to provide guarantees (covering up to 50% of the principal) for a broad range of activities relevant to SUF’s mandate. The DCA was used to give credibility to the Local Government Unit Guarantee Corporation in the Philippines (by backing-up LGUGC’s guarantees). The DCA has been used to support municipal bond issues and “pooled funding” for water projects in the Indian States of Tamil Nadu and Karnataka. The DCA has also been used to support borrowing by micro-finance institutions, including housing.

¾ Sida and some other bilateral donors have guarantee programs that can be used to support housing and urban development projects.

¾ IFC (with staffing support from the World Bank) has created a “Municipal Fund” that can provide guarantees in support of borrowings by municipalities and municipal utilities. So far, these guarantees have supported projects that are located in countries that are considerably wealthier than SUF’s target countries.

Partial credit guarantees covering up to 100% of outstanding principal and accrued interest in case of borrower default. For bank loans, the percentage would be lower, requiring the lender to take some of the credit risk. In the case of bonds, the capital markets and/or other prudential authorities might require a full guarantee. The partial credit guarantees can be structured in many ways; for example with higher coverage for later maturities or be made to cover “first loss”, which limits the exposure of the lender.

Rolling guarantees that would temporarily “top-up” the borrower’s cash flow if the debt-service ratio fell below a certain level.

Financial options (put options benefiting senior lenders) if lenders have difficulties in managing maturity structure of their assets and liabilities. In case of a liquidity squeeze, the lender would have a right to “put” the loan to the guarantee agency.

A roll-over or refinance guarantee is also designed to address the problems associated with the lender’s asset-liability mismatch. However, it is structured in a different way: the borrower gets a short-term loan with the explicit understanding from the lender that the loan will be rolled-over as long as the borrower meets its obligations. The guarantee agency would provide an assurance that it would provide a loan if the original bank was not able to roll-over its loan.

Hedging via forward financial contracts provided by the guarantee agency could help mitigate interest rate or foreign exchange risks (since such markets do not exist in virtually all low income countries).

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 15

¾ The World Bank has recently established a local currency guarantee facility that could potentially be used for this type of projects.

The Community Led Infrastructure Financing Facility (CLIFF ) has also demonstrated the viability of using guarantees to help mobilize financing for low-income housing (see Box 3 above)

The Rationale for SUF The discussion in the preceding sections demonstrates both that mobilizing funding for urban development is a major challenge. It is also clear that innovative solutions have been found, but unfortunately, they are few and far between. There is a great need for cross-fertilization and systematic efforts to adapt these solutions so that they fit other country and project settings. Indeed, because conditions vary so much from case-to-case, mobilizing financing from commercial banks and capital markets for urban development project in general and for slum upgrading in particular, requires extensive “financial engineering” to mitigate risks and making projects “bankable.”13 At present, precious little expertise in this area exist. SUF is designed to fill this void.

13 “Bankable” implies that banks and other lenders regard the person, firm or project as an acceptable credit risk and are willing to lend. In simple terms, “bankable” means the same thing as “creditworthy.”

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 16

The Need for a Slum Upgrading Facility

Slum Upgrading Experiences Approaches to slum upgrading, low-income housing, and related infrastructure in developing countries are still evolving.14 They vary from case to case, depending on a large number of political, institutional, social and economic factors. Some government-supported upgrading schemes have managed to reach a scale that has had a city or country-wide impact on the living conditions of the urban poor. Tunisia, for example, managed to reduce the percentage of slum dwellings from 24% of the housing stock in 1975 to less than 3% by the mid-1990s. The Kampung Improvement Program in Indonesia has benefited almost 30 million people (Box 5).

Box 5: The Kampung Improvement Program in Indonesia

A new breed of ‘bottom-up’ initiatives in community-based approaches and micro-finance for housing has mushroomed. One of the earliest community driven schemes was the Orangi Pilot Project (OPP) in Karachi, Pakistan. The OPP as well as numerous other community based projects have demonstrated that slum dwellers are willing to contribute both their own labor as well as cash for such schemes. Furthermore, the schemes help to empower the residents and encourage them to actively lobby the government and thereby influence public sector priorities and investment programs. The work of the Society for the Promotion of Area Resource Centres (SPARC) and Mahila Milan in India are other examples of grassroots involvement in slum upgrading. Their work is now partly supported through CLIFF (see Box 3 above). Similar approaches have been used by housing micro-finance organizations like SEWA Bank in India and Nachu in Kenya that have used savings and home improvement loans as vehicles for organizing and empowering slum dwellers to be followed by active

14 For a comprehensive overview of the factors contributing to the growth of slums and slum upgrading approaches, see the Global Report on Human Settlements 2003: The Challenge of Slums prepared by UN-HABITAT (2003).

In 1969, the Government of Indonesia initiated the Kampung improvement Program (KIP). Since its inception the concept has spread to 800 cities to benefit almost 30 million people. It is considered to be one of the best urban poverty relief programs in the world. Initially, it was engineering oriented, but realizing the need to tailor upgrading to the varying conditions, the KIP soon started to use community based organizations (CBOs) as project initiators to encourage an active, innovative, and self-sustained community in which upgrading could take place. In the 1990s, the KIP was gradually decentralized and, in the process, it lost much of its momentum since local governments lacked the technical and financial capacity to properly implement the schemes. However, Indonesia is presently undergoing a much more drastic decentralization process and with significant increases in local government resources and with systematic efforts to build local capacity.

ASSESSMENT OF THE UN-HABITAT SLUM UPGRADING FACILITY MAY 24, 2006

PM Global Infrastructure Inc. 17

engagement with the local authorities. Thus, these grassroots initiatives can become powerful agents of change. In short, many of these ‘bottom-up initiatives’, with their strong rooting in individual and community resources, hold promise for ‘scaling up’ to reach more of the urban poor. Not only do these approaches offer ways to improve shelter conditions while longer term institutional reforms are taking place, they also offer opportunities to actively promote change.