Embed Size (px)

Citation preview

Unit 2: Managing Financial Resources and Decisions 21

Assignment 1

Pearson BTEC Level 5 HND in Business (QCF)

Unit and code: 2 Managing Financial Resources and Decisions (K/601/0548)

Level: 4

Activity title: Sources of finance

Assignment reference: MFRD1 (Assignment 1 of 2)

Issue date: / / Date due: / / Date submitted: / /

Lecturer name(s): _____________________________________

Student name: _____________________________________

Outcome Summative feedback Lecturer’s

decision

1.1

1.2

LO1 Understand the sources of finance available to a business 1.1 Identify the sources of finance available to a business 1.2 Assess the implications of the different sources 1.3 Evaluate appropriate sources of finance for a business project

1.3

2.1

2.2

2.3

LO2 Understand the implications of finance as a resource within a business 2.1 Analyse the costs of different sources of finance 2.2 Explain the importance of financial planning 2.3 Assess the information needs of different decision makers 2.4 Explain the impact of finance on the financial statements

2.4

Unit 2: Managing Financial Resources and Decisions 22

M1 Identify and apply strategies to find appropriate solutions

M1

M2 Select/design and apply appropriate methods/techniques

M2

M3 Present and communicate appropriate findings

M3

D1 Use critical reflection to evaluate own work and justify valid conclusions

D1

D2 Take responsibility for managing and organising activities

D2

D3 Demonstrate convergent/lateral/ creative thinking

D3

Statement of authenticity

I confirm that this is my own work

Student’s signature

Unit 2: Managing Financial Resources and Decisions 23

Formative feedback

Action plan

Student comment Lecturer signature Date

Student signature Date

Summative feedback

Action plan

Student comment Lecturer signature Date

Student signature Date

Unit 2: Managing Financial Resources and Decisions 24

Scenario Anna Lian is a software and computer developer who has a strong ethical interest in charitable giving. She realises that charitable giving too often relies on outmoded ways of collecting money either in the street or by door-to-door collections. The amount being collected is declining both because fewer people are donating money and because many are giving less. The age profile of givers is increasing and young people seem uninterested in charitable giving. By 2013 only 3% of all donations come from people under the age of 30.

To change this Anna has developed a system called Mayday, which uses contactless payment technology of the type used in metro systems and supermarkets. Using her earnings from the royalties generated by some apps she sells through the iStore and her savings, Anna has been able to develop the software and a prototype terminal in the shape of bear that growls ‘Thank you’ and gives a high five using a prosthetic arm. She hopes eventually that these terminals would be placed in public places throughout the country.

A number of charities have expressed enthusiasm for her product and its associated software but they feel it is beyond their remit to fund further development of the idea. Because of its focus on charitable giving a number of possible business partners have been lukewarm about the idea as there is no immediate commercial benefit.

Anna is more optimistic as she feels that there are many areas where contactless payment systems can be used, for example making a donation to a specific cause or institution such as spontaneous giving to a museum or theatre restoration fund. At present the recipient (museum or theatre) does not know who gave the money so cannot thank them. Her software would allow spontaneous givers to be tracked and followed up so increasing the number of givers and the frequency and the amount they donate. She wants to consider the possibility of keeping control of her idea and developing it into a business.

She thinks she would like to employ other software developers to write and improve the software. She has possible orders from one charity, Vision, which helps fund research into conditions that cause blindness. Anna likes the idea of developing a small manufacturing business using disadvantaged young people to assemble the bear terminals from bought in components. At present she operates as a sole trader with help and support from contractors and friends. She would like to incorporate as a business and trade as Bear Necessities.

Although she has heard of schemes such as Nesta and the National Funding Scheme she does not know how to go about establishing a business. She has decided to ask for advice and her local authority has a unit that offers help on growing a business.

Unit 2: Managing Financial Resources and Decisions 25

Required Task 1

You work for a business advice and development unit in a local authority and have been asked to provide guidance about developing Anna Lian’s business. The service provides tailor-made reports and you are to produce one for Anna in which you:

Explain the importance of financial planning for businesses such as Anna’s both at start-up and once they become established

Identify the sources of finance available to start and grow a business such as Anna’s which may after a period be significantly large and have gone from being a sole trader to a company

Assess the implications and analyse the costs of the different sources of finance that a business such as Anna’s might need for its software and manufacturing activities

Evaluate appropriate sources of finance for her project to acquire premises on a light industrial estate to assemble the bear terminals, to buy components and equipment, and to pay running costs such as wages, administration and utilities

(1.1, 1.2, 1.3, 2.1, 2.2)

Task 2

You have decided to offer some further advice to support Anna, explaining that various stakeholders will want information about the business. Extend the report with guidance for Anna in which you:

Assess the information needs of different decision makers who are likely to be involved in a business such as Anna’s, explaining the impact of finance on the financial statements that Anna’s business will need to produce for the different decision makers

(2.3, 2.4)

Tasks 1 and 2 will generate evidence for M1, M2, M3, D1, D2 and D3.

Unit 2: Managing Financial Resources and Decisions 26

Grading Pass Work has met the requirements of all the assessment

criteria identified in the assignment.

Merit The report considers a complex business problem and in considering the issues faced by a new/growing business concludes by making effective judgements about the alternatives available to the owner of the business

An effective approach to studying is demonstrated by ensuring the deadline to submit the tasks has been met

(M1)

The report demonstrates the use and application of relevant accounting and finance concepts to a new/growing business and uses a range of valid sources of information

(M2)

All components of the report are logically structured and the results of the investigation into sources of business finance and the information needs of the business are presented in an appropriate format for the owner of the business

(M3)

Distinction A critical view of the business problem being considered has been carried out and justified conclusions have been drawn as a result of applying financial ideas and techniques to the analysis of the business and the owner’s needs

(D1)

The research for the report has been self managed and conducted autonomously in ways that ensure its completion within the agreed timeframe

(D2)

The research for the report has involved considering a novel situation and thinking about how the needs of the business can best be met through the application of innovative ideas

(D3)

Unit 2: Managing Financial Resources and Decisions 27

Centre guidance notes for this assignment Use recognised business formats for presenting the work.

Use appropriate software in producing the work.

Use 11 point Arial or Trebuchet script.

Use common formats for the reports, the calculation of financial data and the presentation of financial data and ensure they are clearly and logically structured. The report should be around 2,000 to 2,500 words long, excluding any appendices and supporting information.

The report and any financial presentations within it should use common formats and be logically structured. It must be referenced using a standard referencing system.

Complete the title page and sign the statement of authenticity.

Detach the title page and fix it to the front of your assignment before submitting your work.

Use a butterfly or treasury tag to keep the pages of your work together.

Work must be checked by a plagiarism checker and the institution’s plagiarism policy will apply to all student assignment work. A copy of the plagiarism checker report must be attached to the assignment that is handed in, otherwise it will be rejected for marking.

Submit the work to {insert name} in the faculty office by {insert date and time}. Late work and non-submission of work will be dealt with in line with the institution’s assessment policy.

Unit 2: Managing Financial Resources and Decisions 28

Topic 6: Analysis of costs The purpose of these activities is to provide an understanding of how unit costs are calculated.

Activity 6.1

Provide learners with copies of the handout on page 29 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Use the information on the feedback slide as a basis for discussing how to distinguish between different types of cost and the importance of this in analysing the performance of a business and making decisions about how a business works, including setting prices for products and services.

Activity 6.2

Provide learners with copies of the handout on page 30 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Use the information on the feedback slide as a basis for discussing how to distinguish between different types of stock valuation, showing the advantages/disadvantages of each and their financial effects.

Activity 6.3

Provide learners with copies of the handout on page 31 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Use the information on the feedback slide as a basis for discussing how to apportion costs in a business and the financial effect on the business.

Unit 2: Managing Financial Resources and Decisions 29

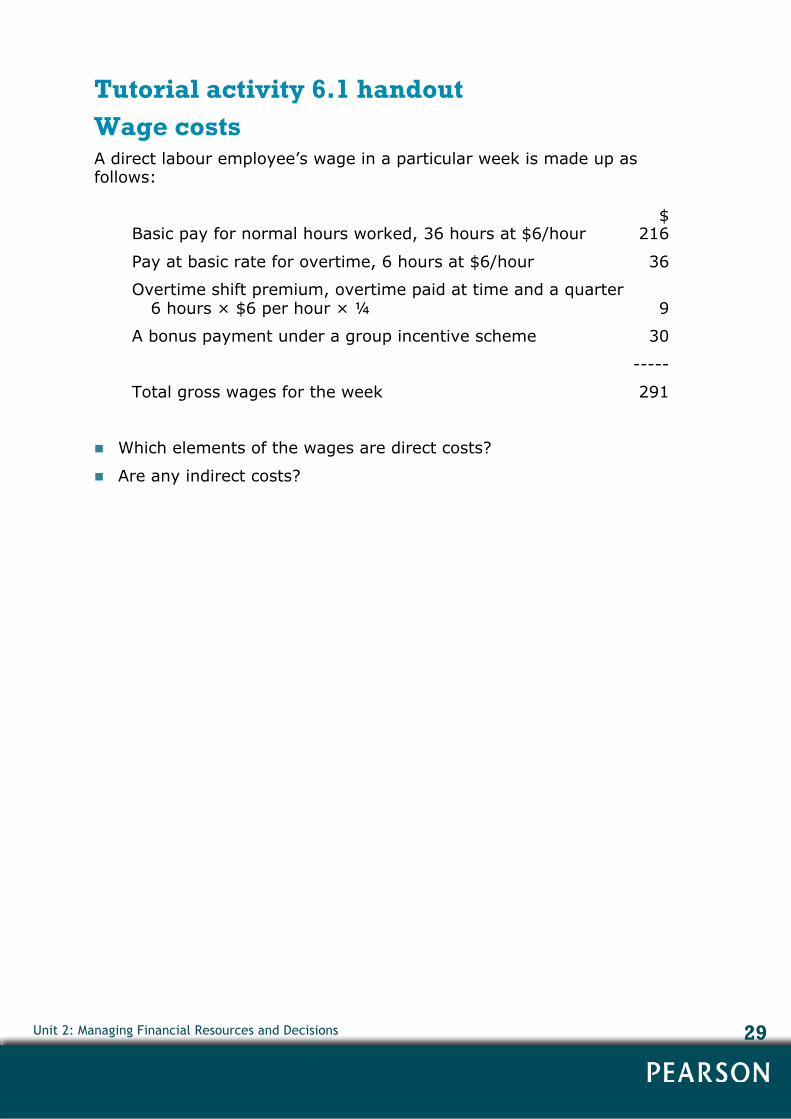

Tutorial activity 6.1 handout Wage costs A direct labour employee’s wage in a particular week is made up as follows:

$ Basic pay for normal hours worked, 36 hours at $6/hour 216

Pay at basic rate for overtime, 6 hours at $6/hour 36

Overtime shift premium, overtime paid at time and a quarter 6 hours × $6 per hour × ¼ 9

A bonus payment under a group incentive scheme 30

-----

Total gross wages for the week 291

Which elements of the wages are direct costs?

Are any indirect costs?

Unit 2: Managing Financial Resources and Decisions 30

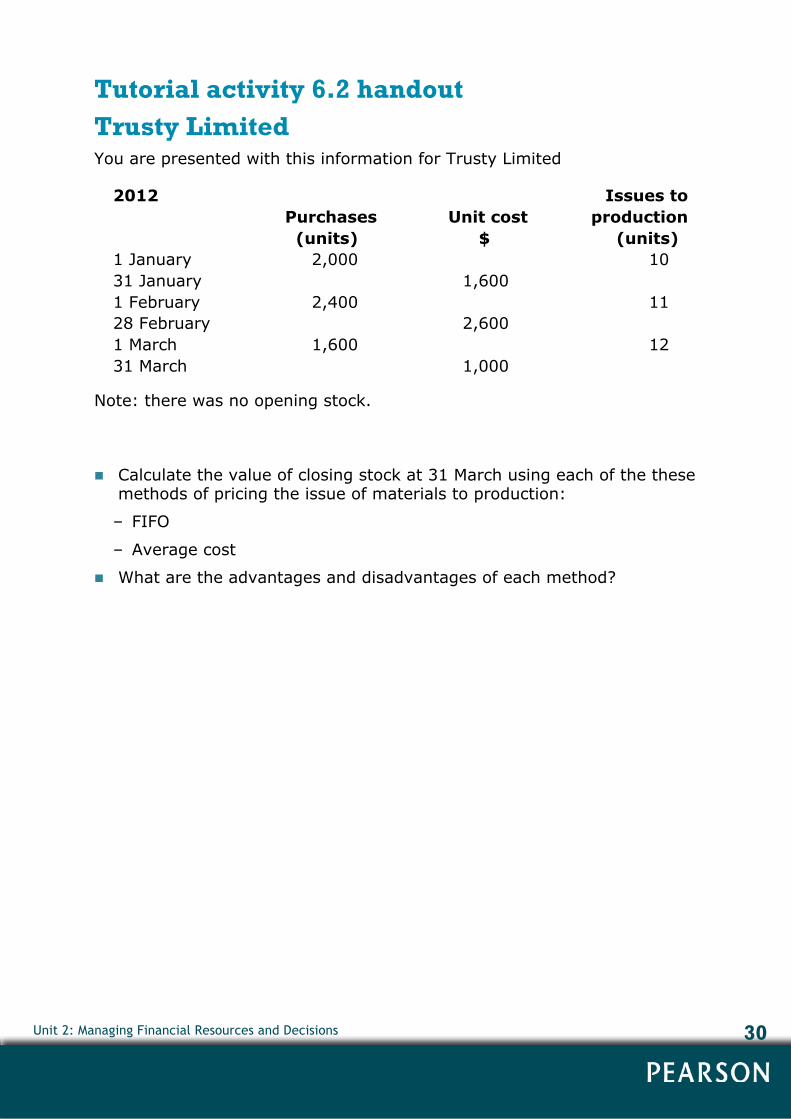

Tutorial activity 6.2 handout Trusty Limited You are presented with this information for Trusty Limited

2012 Issues to Purchases Unit cost production (units) $ (units) 1 January 2,000 10 31 January 1,600 1 February 2,400 11 28 February 2,600 1 March 1,600 12 31 March 1,000

Note: there was no opening stock.

Calculate the value of closing stock at 31 March using each of the these methods of pricing the issue of materials to production:

– FIFO

– Average cost

What are the advantages and disadvantages of each method?

Unit 2: Managing Financial Resources and Decisions 31

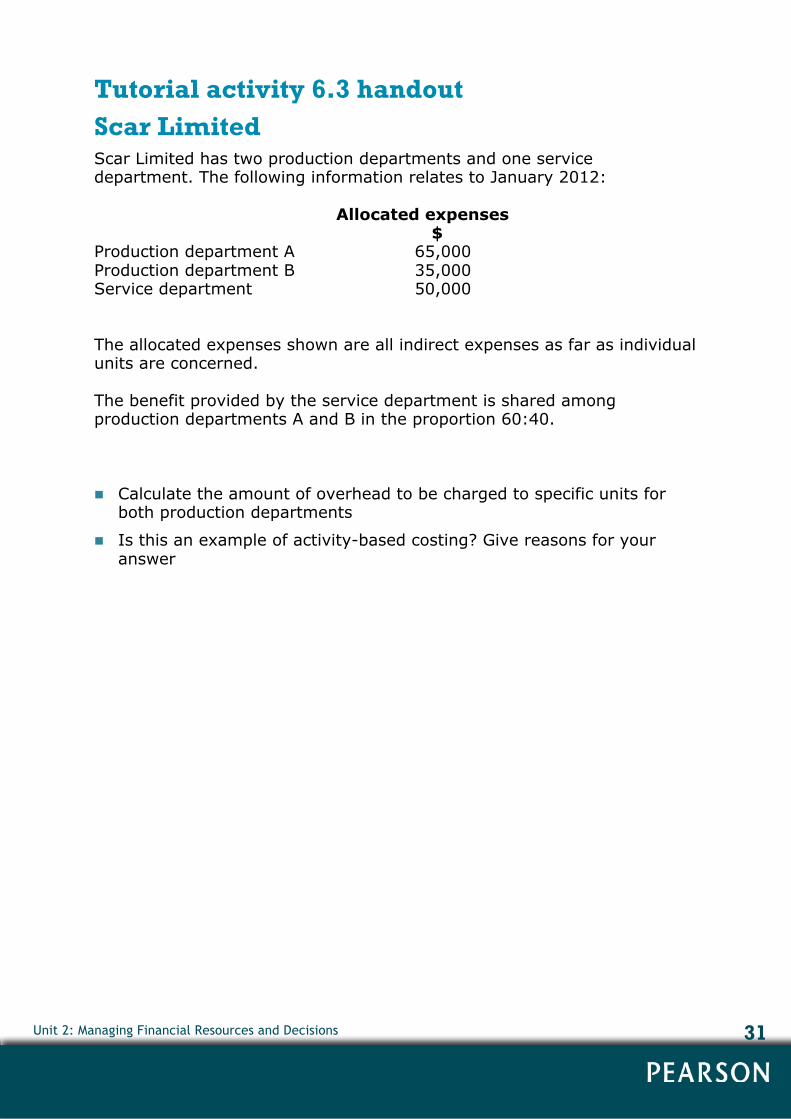

Tutorial activity 6.3 handout Scar Limited Scar Limited has two production departments and one service department. The following information relates to January 2012:

Allocated expenses $ Production department A 65,000 Production department B 35,000 Service department 50,000

The allocated expenses shown are all indirect expenses as far as individual units are concerned.

The benefit provided by the service department is shared among production departments A and B in the proportion 60:40.

Calculate the amount of overhead to be charged to specific units for both production departments

Is this an example of activity-based costing? Give reasons for your answer

Unit 2: Managing Financial Resources and Decisions 32

Topic 7: Budgets The purpose of these activities is to provide an understanding of how to prepare and interpret budgets.

Activity 7.1

Provide learners with copies of the handout on page 33 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart of whiteboard.

Use the information on the feedback slide as a basis for discussing the importance of budgeting for all business activities, not just production. Highlight the interlocking nature of budgets, showing in this case how the production requirement drives the labour requirement.

Activity 7.2

Provide learners with copies of the handout on page 34 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart of whiteboard.

Use the information on the feedback slide as a basis for discussing the importance of budgetary analysis as a way of understanding why actual activity diverges from planned activity. By understanding the reasons for the variances they can be brought under control and corrective action can be taken.

Activity 7.3

Ask learners to consider budgeting in a college and in a hospital, using the prompts on the activity slide. Ask two or three of the learners to put their answers on a flipchart of whiteboard.

Use the information on the feedback slide as a basis for discussing budgetary principles and how decision making can be shaped by budgetary activity.

Unit 2: Managing Financial Resources and Decisions 33

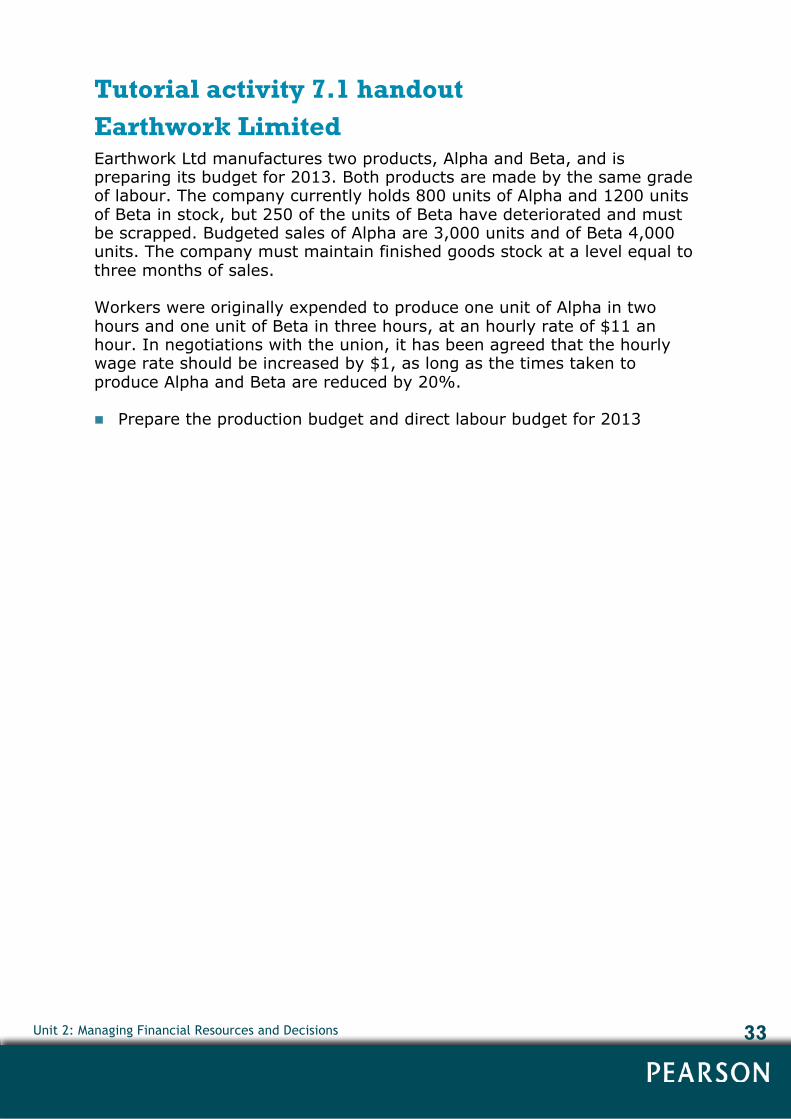

Tutorial activity 7.1 handout Earthwork Limited Earthwork Ltd manufactures two products, Alpha and Beta, and is preparing its budget for 2013. Both products are made by the same grade of labour. The company currently holds 800 units of Alpha and 1200 units of Beta in stock, but 250 of the units of Beta have deteriorated and must be scrapped. Budgeted sales of Alpha are 3,000 units and of Beta 4,000 units. The company must maintain finished goods stock at a level equal to three months of sales.

Workers were originally expended to produce one unit of Alpha in two hours and one unit of Beta in three hours, at an hourly rate of $11 an hour. In negotiations with the union, it has been agreed that the hourly wage rate should be increased by $1, as long as the times taken to produce Alpha and Beta are reduced by 20%.

Prepare the production budget and direct labour budget for 2013

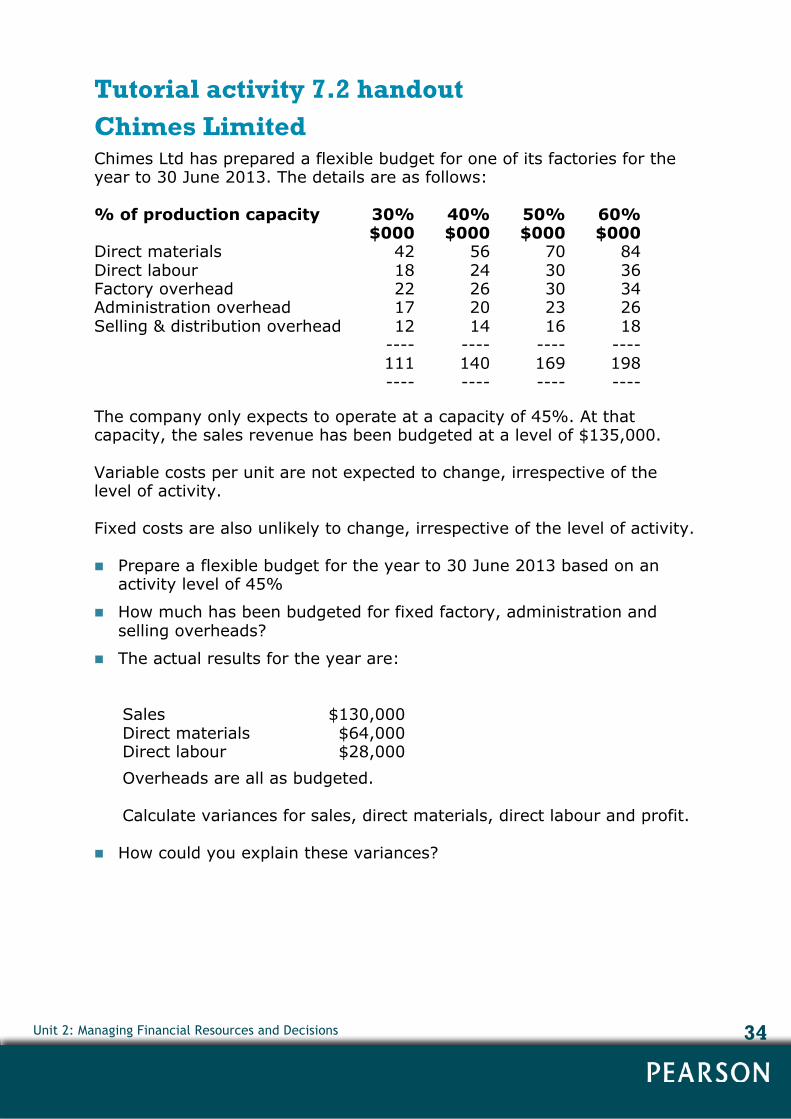

Unit 2: Managing Financial Resources and Decisions 34

Tutorial activity 7.2 handout Chimes Limited Chimes Ltd has prepared a flexible budget for one of its factories for the year to 30 June 2013. The details are as follows:

% of production capacity 30% 40% 50% 60% $000 $000 $000 $000 Direct materials 42 56 70 84 Direct labour 18 24 30 36 Factory overhead 22 26 30 34 Administration overhead 17 20 23 26 Selling & distribution overhead 12 14 16 18 ---- ---- ---- ---- 111 140 169 198 ---- ---- ---- ----

The company only expects to operate at a capacity of 45%. At that capacity, the sales revenue has been budgeted at a level of $135,000.

Variable costs per unit are not expected to change, irrespective of the level of activity.

Fixed costs are also unlikely to change, irrespective of the level of activity.

Prepare a flexible budget for the year to 30 June 2013 based on an activity level of 45%

How much has been budgeted for fixed factory, administration and selling overheads?

The actual results for the year are:

Sales $130,000 Direct materials $64,000 Direct labour $28,000

Overheads are all as budgeted.

Calculate variances for sales, direct materials, direct labour and profit.

How could you explain these variances?

Unit 2: Managing Financial Resources and Decisions 35

Topic 8: Pricing and production decisions The purpose of these activities is to explain the concepts of marginal cost, contribution and breakeven analysis, and to review how to use them when decision making.

Activity 8.1

Divide learners into pairs and ask them to consider the opportunity cost of studying at college. You can ask them to draw on their own experience as well.

Ask each pair to make a summary of points on a flipchart. Get each pair to explain one or two points by making a brief presentation to the rest of the class.

Widen the discussion to consider how decision making uses the values attached to different activities even if the activity has no obvious monetary value. This is as true of businesses as it is of individuals.

Activity 8.2

Provide learners with copies of the handout on page 36 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Use the information on the feedback slide as a basis for discussing the importance of understanding costs and revenues in order to establish breakeven points and the consequences for businesses of knowing at what point they break even.

Activity 8.3

Divide the learners into small groups for this activity. Ask each group to make a presentation explaining why the company should (or should not) accept the order.

Discuss the importance of engaging in activity which in the short term may be unprofitable but may have longer-term benefits, such as ensuring cash flow, retaining the labour force and ultimately securing the company’s future when there is an upturn in activity.

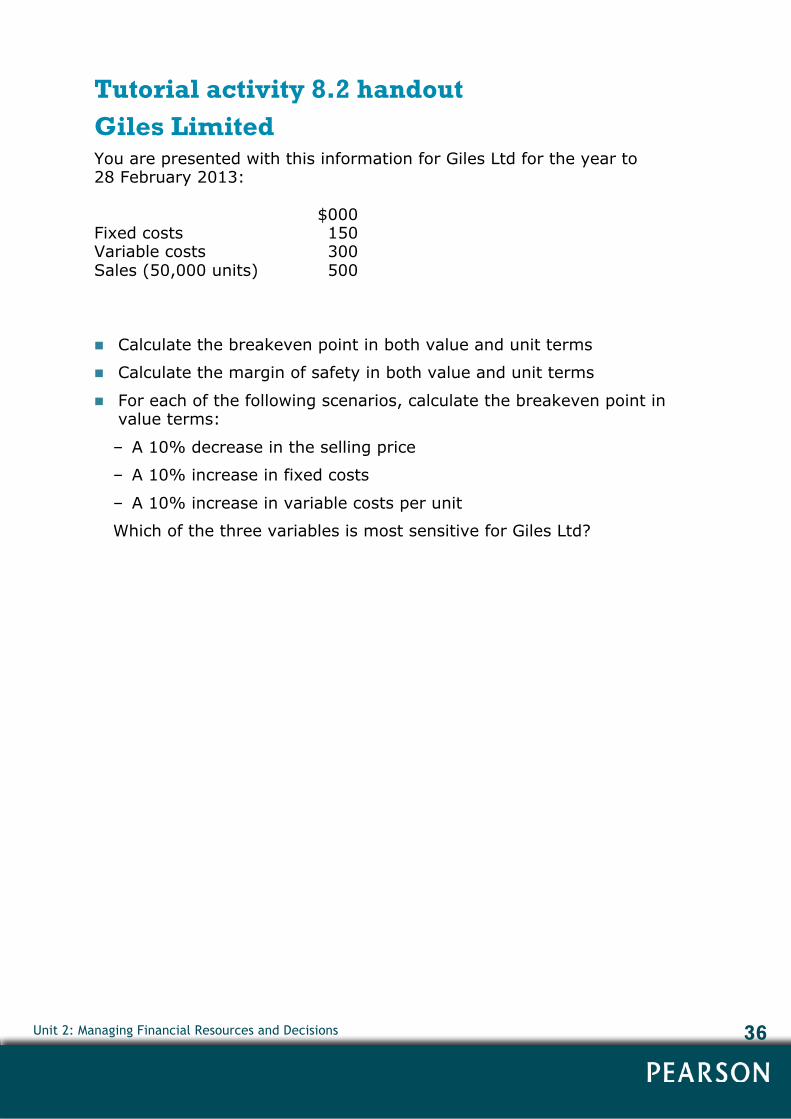

Unit 2: Managing Financial Resources and Decisions 36

Tutorial activity 8.2 handout Giles Limited You are presented with this information for Giles Ltd for the year to 28 February 2013:

$000 Fixed costs 150 Variable costs 300 Sales (50,000 units) 500

Calculate the breakeven point in both value and unit terms

Calculate the margin of safety in both value and unit terms

For each of the following scenarios, calculate the breakeven point in value terms:

– A 10% decrease in the selling price

– A 10% increase in fixed costs

– A 10% increase in variable costs per unit

Which of the three variables is most sensitive for Giles Ltd?

Unit 2: Managing Financial Resources and Decisions 37

Topic 9: Investment and project appraisal The purpose of these activities is to apply payback period, accounting rate of return, net present value and internal rate of return in evaluating the viability of an investment project.

Activity 9.1

Provide learners with copies of the handout on page 38 and ask them to complete the exercise. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Activity 9.2

This follows on from Activity 9.1 using the handout on page 38. Ask two or three of the learners to put their answers on a flipchart or whiteboard.

Activity 9.3

This completes the set of exercises based on the handout on page 38. Again, ask two or three of the learners to put their answers on a flipchart or whiteboard.

Use the information from the three activities as a basis for a discussion on how best a business should consider whether or not to invest in a project. Some techniques offer a short-term view of investment but other techniques are better suited to projects that have a longer life. All decision making that looks into the future carries with it a degree of risk and uncertainty.

Unit 2: Managing Financial Resources and Decisions 38

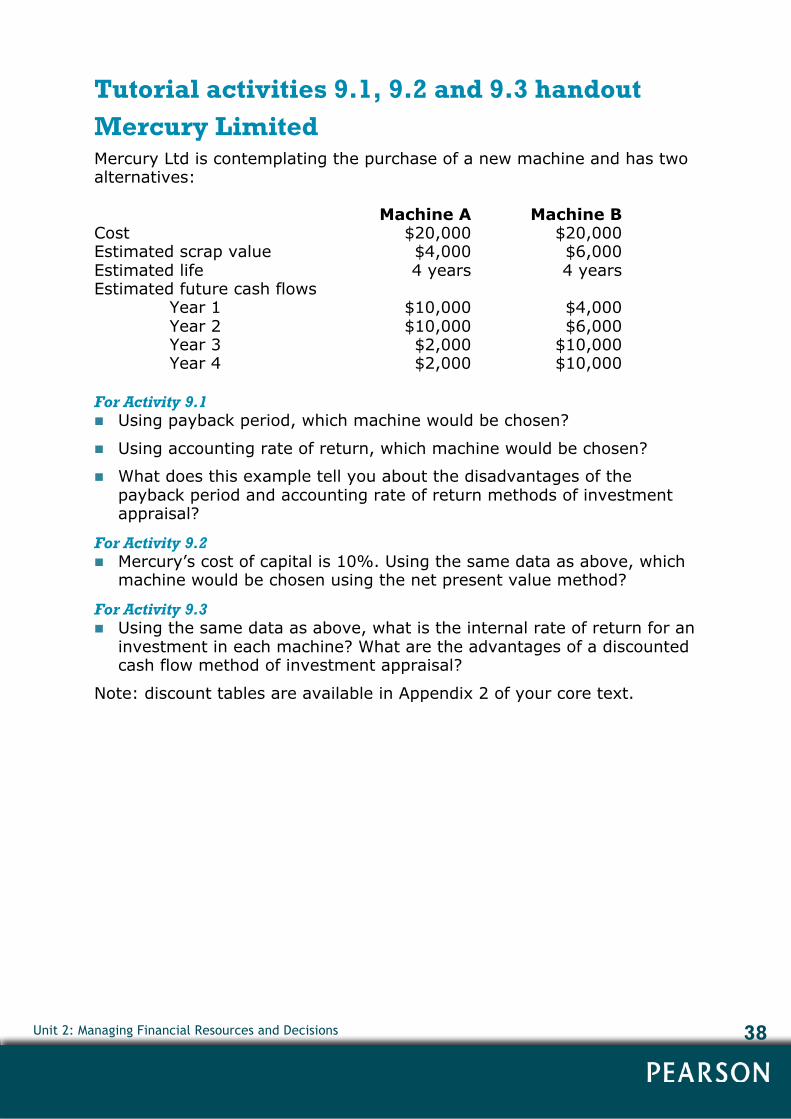

Tutorial activities 9.1, 9.2 and 9.3 handout Mercury Limited Mercury Ltd is contemplating the purchase of a new machine and has two alternatives:

Machine A Machine B Cost $20,000 $20,000 Estimated scrap value $4,000 $6,000 Estimated life 4 years 4 years Estimated future cash flows

Year 1 $10,000 $4,000 Year 2 $10,000 $6,000 Year 3 $2,000 $10,000 Year 4 $2,000 $10,000

For Activity 9.1 Using payback period, which machine would be chosen?

Using accounting rate of return, which machine would be chosen?

What does this example tell you about the disadvantages of the payback period and accounting rate of return methods of investment appraisal?

For Activity 9.2 Mercury’s cost of capital is 10%. Using the same data as above, which

machine would be chosen using the net present value method?

For Activity 9.3 Using the same data as above, what is the internal rate of return for an

investment in each machine? What are the advantages of a discounted cash flow method of investment appraisal?

Note: discount tables are available in Appendix 2 of your core text.

Unit 2: Managing Financial Resources and Decisions 39

Topic 10: Evaluating financial performance The purpose of these activities is to provide an understanding of the use of accounting ratios for profitability, liquidity, efficiency and investment.

Activity 10.1

Provide learners with copies of the handout on page 40 and ask them to complete the exercise by working in pairs. Ask each pair to summarise their results on a whiteboard or flipchart.

Get three or four pairs to comment on the results and explain their significance in a presentation to the rest of the class. Widen the discussion to consider how to measure profitability and how the ratios enable comparisons to be made between years, between businesses, across industries and across nations.

Activity 10.2

Provide learners with copies of the handout on page 41 and ask them to complete the exercise by working in pairs. Ask each pair to summarise their results on a whiteboard or flipchart.

Get three or four pairs to comment on the results and explain their significance in a presentation to the rest of the class. Widen the discussion to consider how to measure liquidity and efficiency and how the ratios enable comparisons to be made between years, between businesses, across industries and across nations in the same way as profitability ratios can.

Activity 10.3

Provide learners with copies of the handout on page 42 and ask them to complete the exercise by working in pairs. Ask each pair to summarise their results on a whiteboard or flipchart.

Get three or four pairs to comment on the results and explain their significance in a presentation to the rest of the class. Widen the discussion to consider how other aspects of business performance can be measured by different ratios and how the ratios enable comparisons to be made between years, between businesses, across industries and across nations in the same way as profitability ratios can.

Unit 2: Managing Financial Resources and Decisions 40

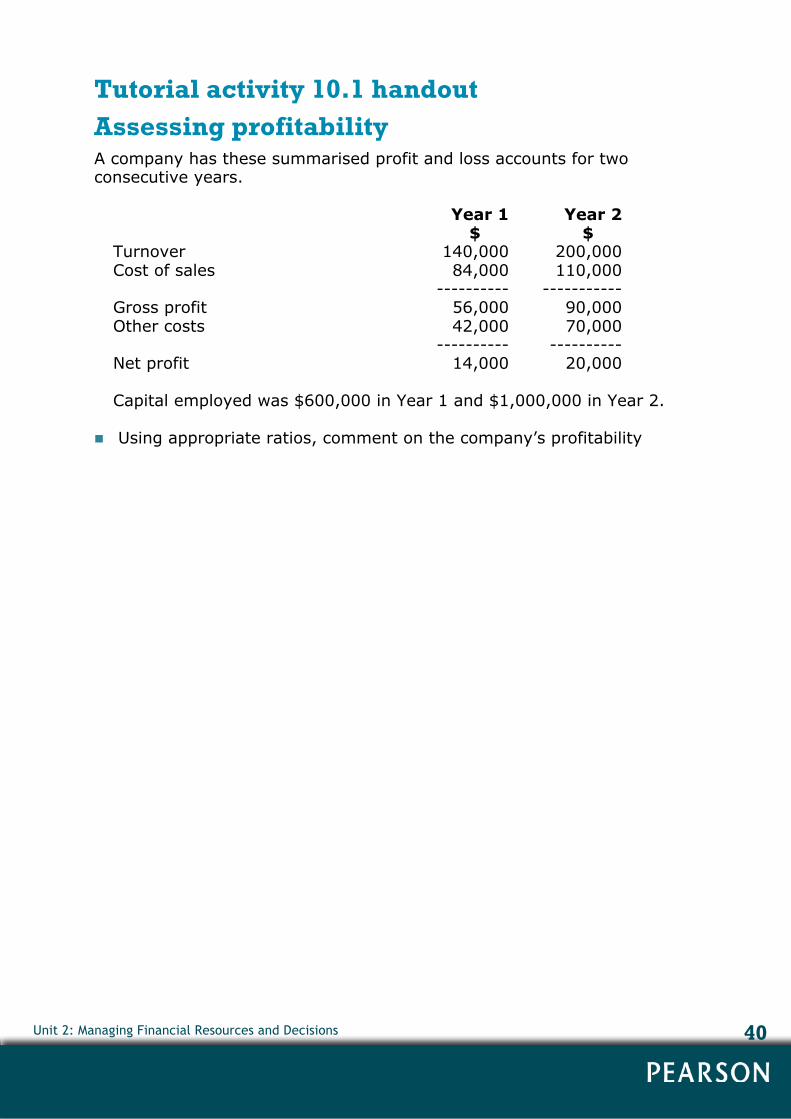

Tutorial activity 10.1 handout Assessing profitability A company has these summarised profit and loss accounts for two consecutive years.

Year 1 Year 2 $ $ Turnover 140,000 200,000 Cost of sales 84,000 110,000 ---------- ----------- Gross profit 56,000 90,000 Other costs 42,000 70,000 ---------- ---------- Net profit 14,000 20,000

Capital employed was $600,000 in Year 1 and $1,000,000 in Year 2.

Using appropriate ratios, comment on the company’s profitability

Unit 2: Managing Financial Resources and Decisions 41

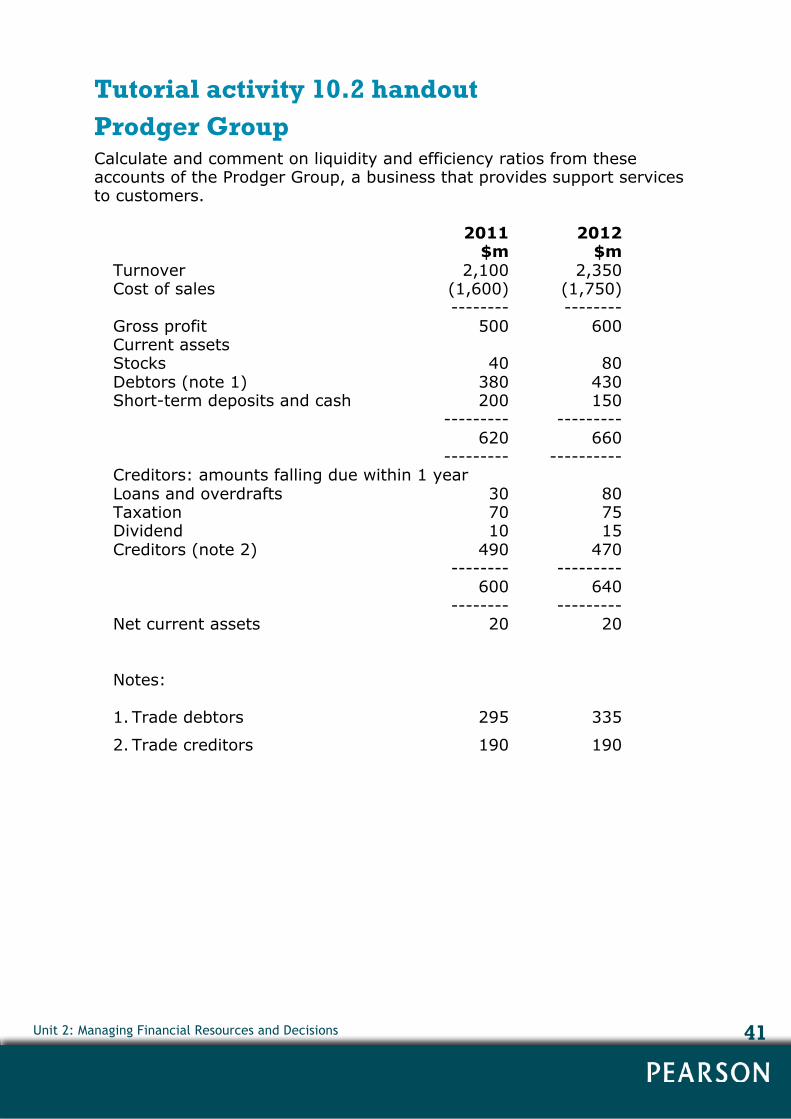

Tutorial activity 10.2 handout Prodger Group Calculate and comment on liquidity and efficiency ratios from these accounts of the Prodger Group, a business that provides support services to customers.

2011 2012 $m $m

Turnover 2,100 2,350 Cost of sales (1,600) (1,750) -------- -------- Gross profit 500 600 Current assets Stocks 40 80 Debtors (note 1) 380 430 Short-term deposits and cash 200 150 --------- --------- 620 660 --------- ---------- Creditors: amounts falling due within 1 year Loans and overdrafts 30 80 Taxation 70 75 Dividend 10 15 Creditors (note 2) 490 470 -------- --------- 600 640 -------- --------- Net current assets 20 20

Notes:

1. Trade debtors 295 335

2. Trade creditors 190 190

Unit 2: Managing Financial Resources and Decisions 42

Tutorial activity 10.3 handout Hedge plc You are presented with this information relating to Hedge plc for the year to 31 May 2012:

The company has an issued and fully paid up share capital of $500,000 ordinary shares of $1 each. There are no preference shares, but the company has a 10-year 10% debenture loan of $300,000.

The market price of the shares at 31 May 2012 was $3.50.

The net profit after taxation for the year to 31 May 2012 was $70,000.

The directors are proposing a dividend of $0.07 per share for the year to 31 May 2012.

Calculate the following accounting ratios:

Capital gearing

Dividend yield

Dividend cover

Earnings per share

Price/earnings ratio