Embed Size (px)

DESCRIPTION

Association for Financial Professionals of Arizona - 2013. Factors Impacting Payment Market Development. Macro/Socioeconomic Factors Demographics – Higher proportion of young people in the regional/national population could lead to faster adoption of new payment methods - PowerPoint PPT Presentation

Citation preview

AF

PA

1

A s s o c i a t i o n f o r F i n a n c i a l P r o f e s s i o n a l s o f A r i z o n a - 2 0 1 3

Steven E. BernsteinExecutive DirectorJ.P. Morgan Chase

AF

PA

2

Factors Impacting Payment Market Development

Macro/Socioeconomic Factors

Demographics – Higher proportion of young people in the regional/national population could lead to faster adoption of new payment methods

Unbanked Population – High proportion of consumers with no formal banking relationship will also lead to rapid uptake of new payment methods

GDP Growth – Rapidly growing economies generate a greater number of new market entrants and faster adoption of new types of payment methods

Average Real-Income Growth – Markets with relatively high real-income growth foster increases in average payments values and favorable returns on investments in payments innovation.

Export-Import Balance – Cross-border trade growth leads to greater opportunities for high-margin payments products (but also heightens competition)

Source: Boston Consulting Group: Winning After the Storm, 2011

AF

PA

3

Factors Impacting Payment Market Development

Macro/Socioeconomic Factors

Regulatory Outlook – Rigorous government regulation can have a dramatic impact on payments economics, sometimes necessitating strategic transformations.

Infrastructure – Active government involvement in building payments infrastructure can have large implications on the pace of market evolution and potential profit pools.

Industry Factors

Mix of Payments Instruments – Greater use of cash and checks can generate high potential to capture new payments flows, resulting in new market entrants and the likelihood of more innovation

Efficiency Level – In inefficient markets with a low degree of operational excellence, new market entrants are more likely to excel.

Source: Boston Consulting Group: Winning After the Storm, 2011

AF

PA

4

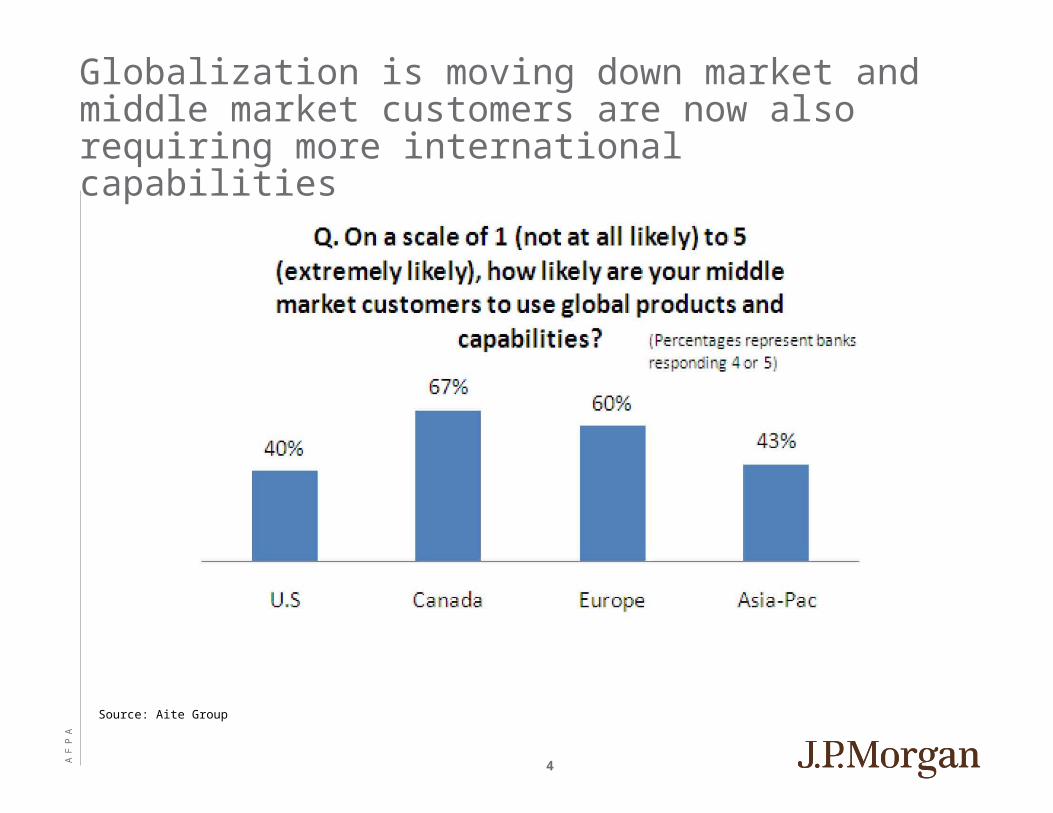

Globalization is moving down market and middle market customers are now also requiring more international capabilities

Source: Aite Group

AF

PA

5

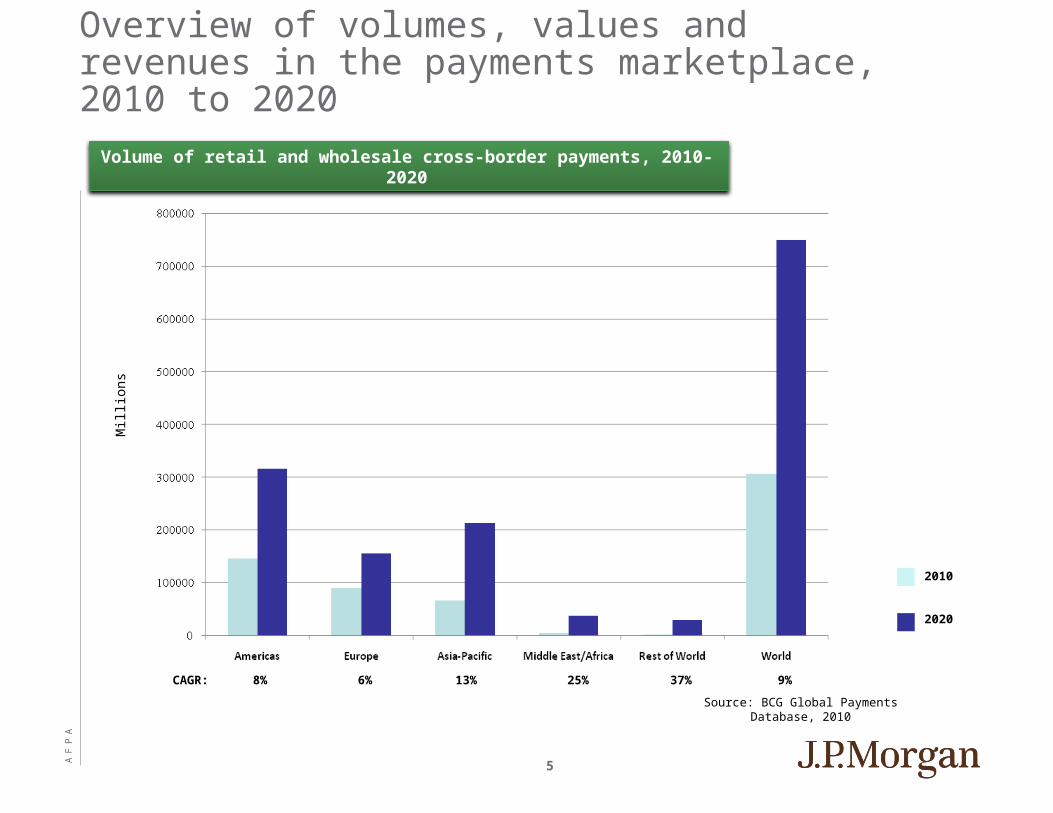

Source: BCG Global Payments Database, 2010

Volume of retail and wholesale cross-border payments, 2010-2020

6% 13%8%CAGR:

Mil

lion

s

2010

2020

25% 37% 9%

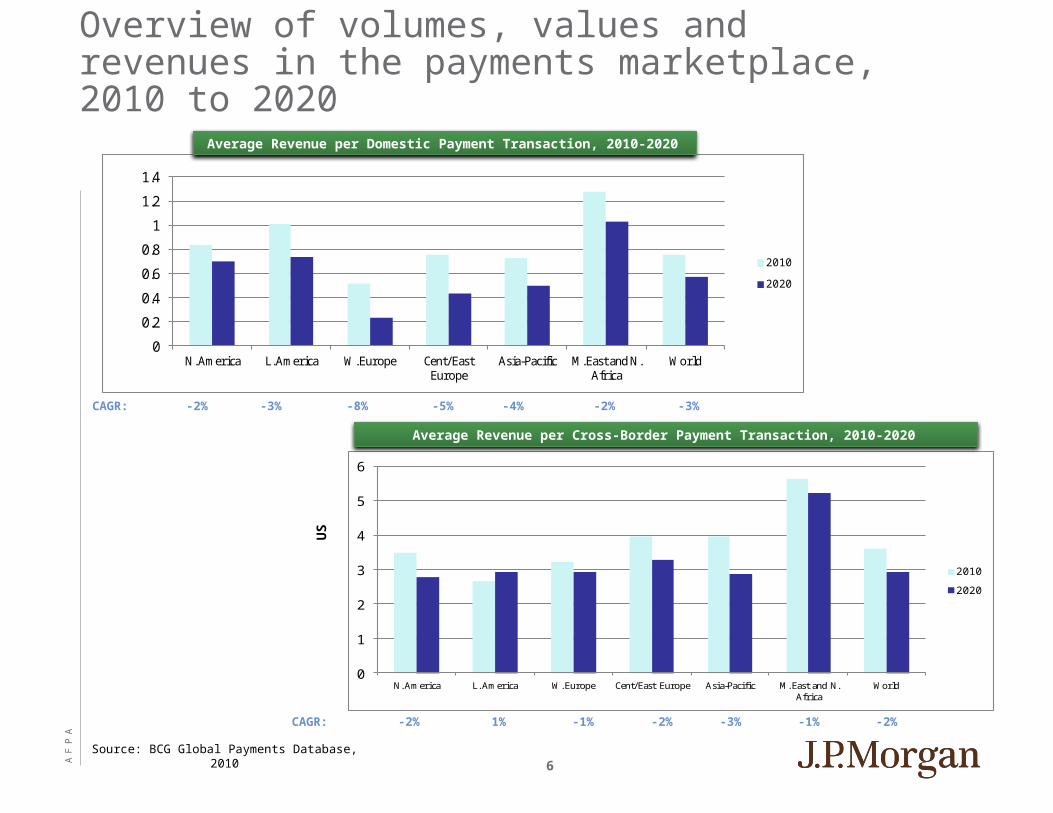

Overview of volumes, values and revenues in the payments marketplace, 2010 to 2020

AF

PA

6

0

0.2

0.4

0.6

0.8

1

1.2

1.4

N. America L. America W. Europe Cent/East Europe

Asia-Pacific M. East and N. Africa

World

2010

2020

0

1

2

3

4

5

6

N. America L. America W. Europe Cent/East Europe Asia-Pacific M. East and N. Africa

World

2010

2020

Average Revenue per Domestic Payment Transaction, 2010-2020

Source: BCG Global Payments Database, 2010

-2% -3% -8% -5%CAGR:

Average Revenue per Cross-Border Payment Transaction, 2010-2020

-2% 1% -1% -2%CAGR:

US

-4% -2% -3%

-3% -1% -2%

Overview of volumes, values and revenues in the payments marketplace, 2010 to 2020

AF

PA

7

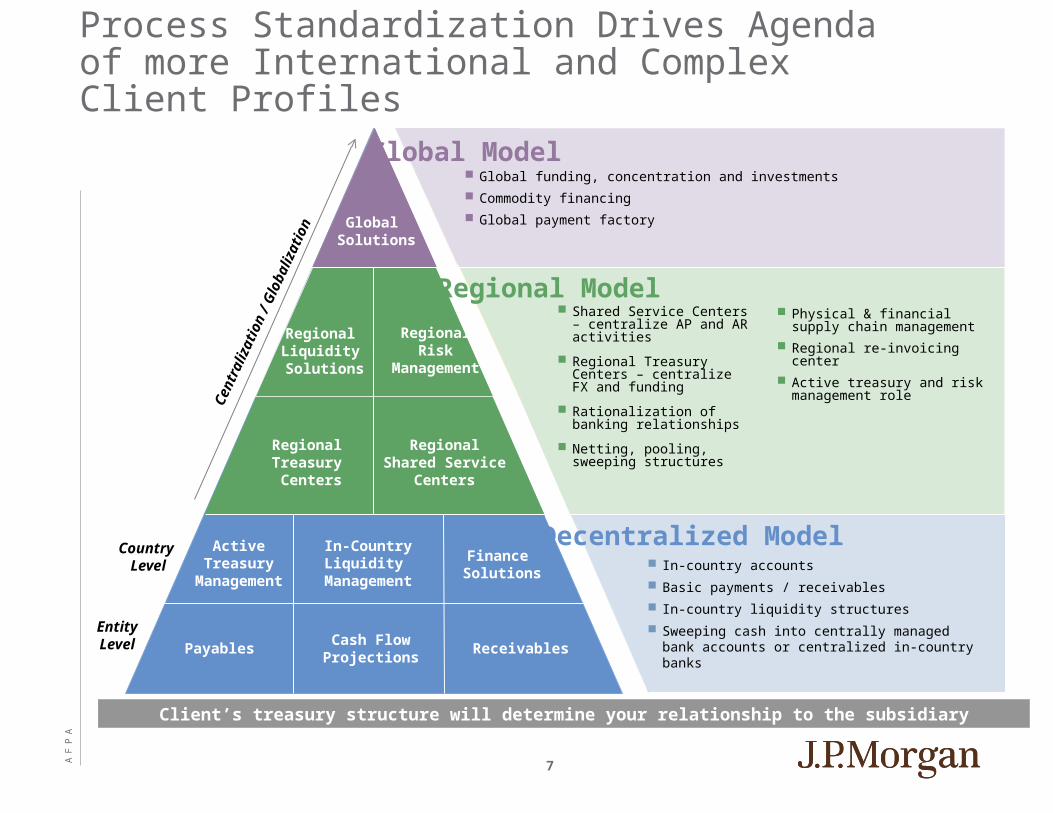

Process Standardization Drives Agenda of more International and Complex Client Profiles

ActiveTreasury

Management

Regional Treasury Centers

Regional Liquidity Solutions

Global Solutions

RegionalRisk

Management

RegionalShared Service

Centers

In-CountryLiquidity

Management

Finance Solutions

Payables Cash FlowProjections

Receivables

Country Level

EntityLevel

Cen

tral

izat

ion

/ Glo

baliz

atio

n

Global funding, concentration and investments

Commodity financing

Global payment factory

Shared Service Centers – centralize AP and AR activities

Regional Treasury Centers – centralize FX and funding

Rationalization of banking relationships

Netting, pooling, sweeping structures

In-country accounts

Basic payments / receivables

In-country liquidity structures

Sweeping cash into centrally managed bank accounts or centralized in-country banks

Global Model

Regional Model

Decentralized Model

Client’s treasury structure will determine your relationship to the subsidiary

Physical & financial supply chain management

Regional re-invoicing center

Active treasury and risk management role

AF

PA

8

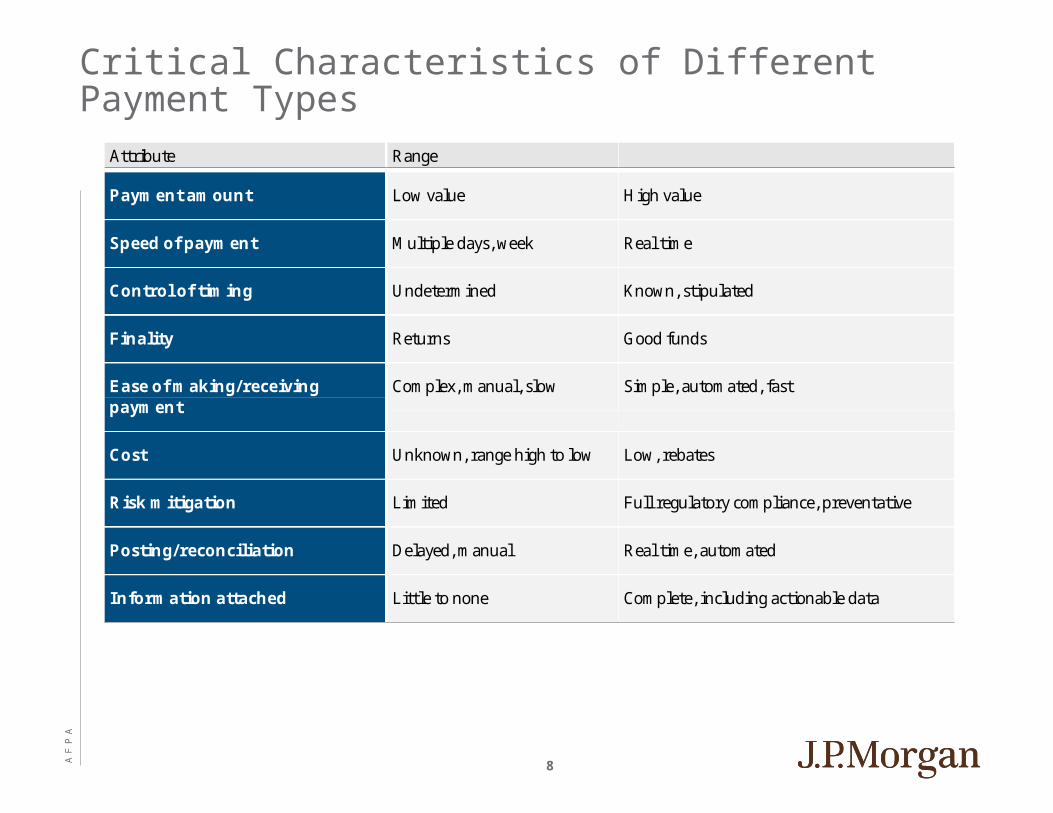

Attribute Range

Payment amount Low value High value

Speed of payment Multiple days, week Real time

Control of timing Undetermined Known, stipulated

Finality Returns Good funds

Ease of making/receiving payment

Complex, manual, slow Simple, automated, fast

Cost Unknown, range high to low Low, rebates

Risk mitigation Limited Full regulatory compliance, preventative

Posting/reconciliation Delayed, manual Real time, automated

Information attached Little to none Complete, including actionable data

Critical Characteristics of Different Payment Types

AF

PA

9

Key Concepts and Definitions

Large value payments

A somewhat generic term generally used to describe electronic, RTGS payments. What are described as wire transfers generally fall into this category. Historically, these payments types were used primarily for large payments because they were expensive. But, there is no official amount threshold that delimits them. Most international payments fall into this broad category.

Small value payments

Typically smaller electronic payments processed in batches. These payments are generally not time sensitive, and are processed on a store and forward basis. They also typically are not final and irrevocable. These payments are usually less expensive to process as their smaller amounts make it harder to justify expensive processing. US ACH payments are an example of this type of payment. Small value processing is historically limited to domestic payments, though this is gradually changing.

AF

PA

10

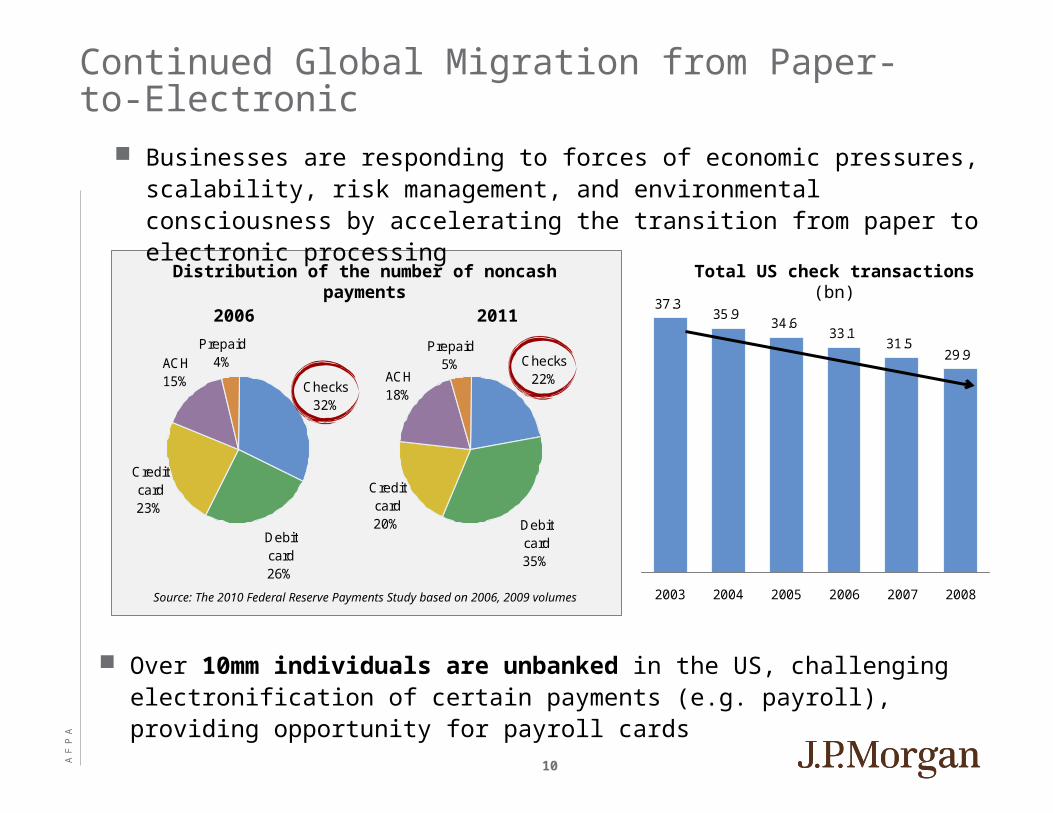

Debit card 35%

Checks 22%

Prepaid 5%

Credit card 20%

ACH 18%

37.335.9

34.633.1

31.529.9

2003 2004 2005 2006 2007 2008

Businesses are responding to forces of economic pressures, scalability, risk management, and environmental consciousness by accelerating the transition from paper to electronic processing

Source: The 2010 Federal Reserve Payments Study based on 2006, 2009 volumes

Debit card 26%

Checks 32%

Prepaid 4%

Credit card 23%

ACH 15%

Distribution of the number of noncash payments

2006 2011

Total US check transactions (bn)

Over 10mm individuals are unbanked in the US, challenging electronification of certain payments (e.g. payroll), providing opportunity for payroll cards

Continued Global Migration from Paper-to-Electronic

AF

PA

11

Let’s Dig Deeper….What is International ACH?

ACH (Automated Clearing House) is a US system/process for lower value, non-urgent payments and collections

International ACH—an international payment and collection process that leverages in-country clearing systems

Provides a cost effective method for corporate clients to make high volume payments such as Payroll Accounts Payable Dividends Expense Reimbursement

Payments and/or Collections are made to Vendors Businesses Consumers Employees

AF

PA

12

Why International ACH?

Customers looking for cost effective reliable payment channels

Improved experience for the beneficiary No lifting fees on originated transactions

Increased awareness in the market Customers are asking for International ACH

Provides dual revenue source Fee income Foreign exchange revenue

Leverages domestic ACH system Intelligent use of communication, delivery channels and billing

processes and expertise

AF

PA

13

Customer Benefits and Value Proposition

Reduced funds movement costs

More predictable cash flow

Integrated disbursements

Electronic return reporting

Fast confirmation

Settlement on a specified value date

Full value of item received by beneficiary

Reduced need to maintain multiple bank relationships globally

AF

PA

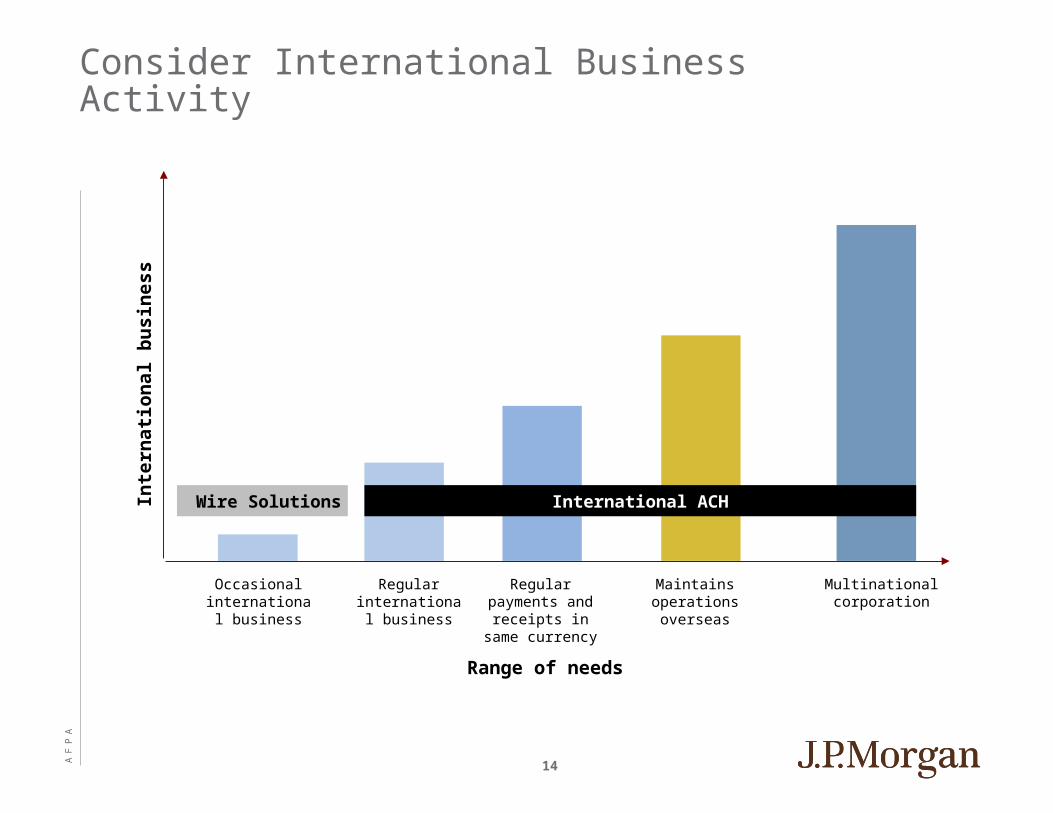

14

Inte

rnat

ion

al b

usi

nes

s

Occasional international

business

Regular international

business

Regular payments and receipts in same currency

Maintains operations overseas

Multinational corporation

International ACHWire Solutions

Range of needs

Consider International Business Activity

AF

PA

15

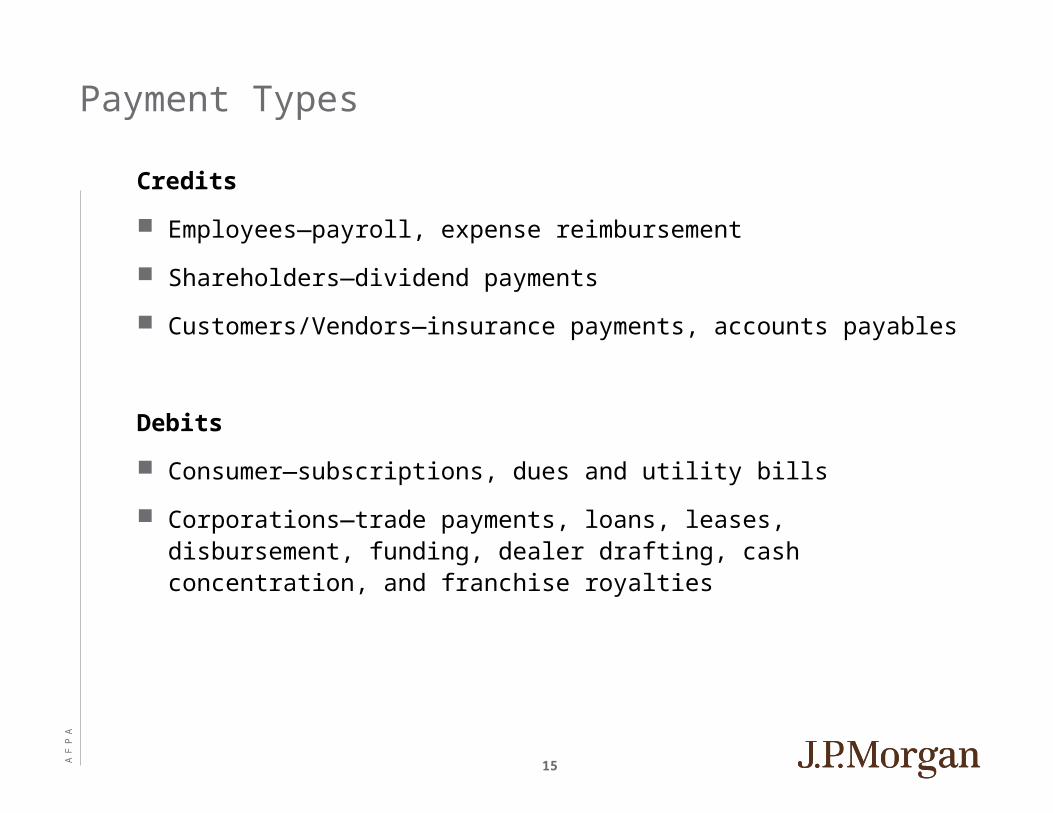

Payment Types

Credits

Employees—payroll, expense reimbursement

Shareholders—dividend payments

Customers/Vendors—insurance payments, accounts payables

Debits

Consumer—subscriptions, dues and utility bills

Corporations—trade payments, loans, leases, disbursement, funding, dealer drafting, cash concentration, and franchise royalties

AF

PA

16

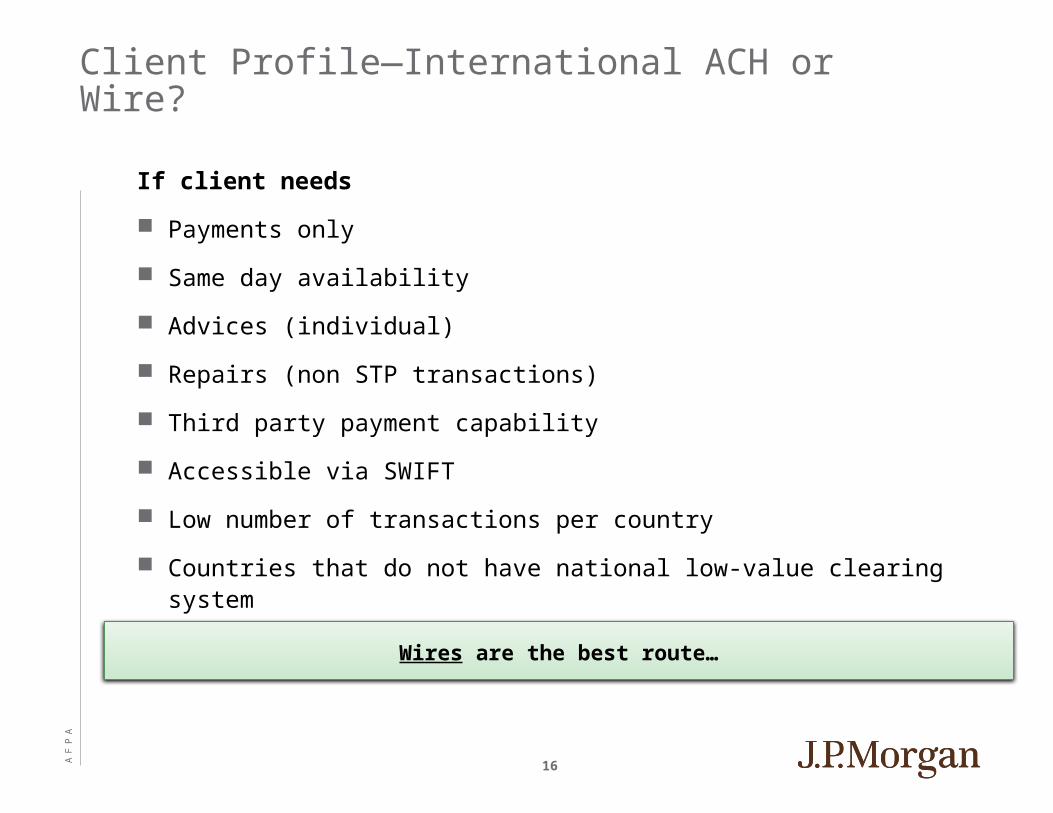

Client Profile—International ACH or Wire?

If client needs

Payments only

Same day availability

Advices (individual)

Repairs (non STP transactions)

Third party payment capability

Accessible via SWIFT

Low number of transactions per country

Countries that do not have national low-value clearing system

Wires are the best route…

AF

PA

17

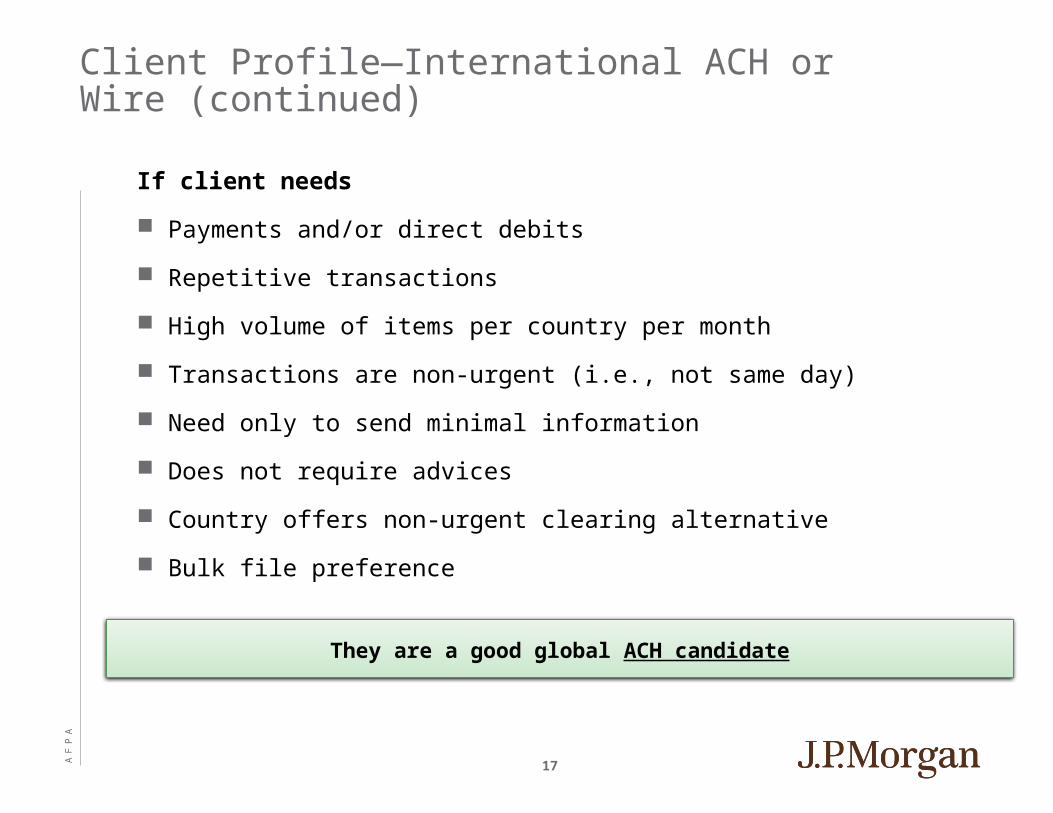

Client Profile—International ACH or Wire (continued)

If client needs

Payments and/or direct debits

Repetitive transactions

High volume of items per country per month

Transactions are non-urgent (i.e., not same day)

Need only to send minimal information

Does not require advices

Country offers non-urgent clearing alternative

Bulk file preference

They are a good global ACH candidate

AF

PA

18

Typical Customer Industries for International ACH

Travel services/hospitality

Oil/drilling/energy

Engineering services

Legal services

Manufacturing

Insurance

Securities dealer

Educational services

Computer software

Churches

AF

PA

19

International ACH Parties

Originator

Company originating the ACH item

Originating Gateway Operator (OGO)

Originating financial institution

Re-formats file to local country specifications

Creates settlement by country to originator

Receiving Gateway Operator (RGO)

Receives file from OGO

Distributes file into local country payment system

Beneficiary

Recipient of payment in foreign country

AF

PA

20

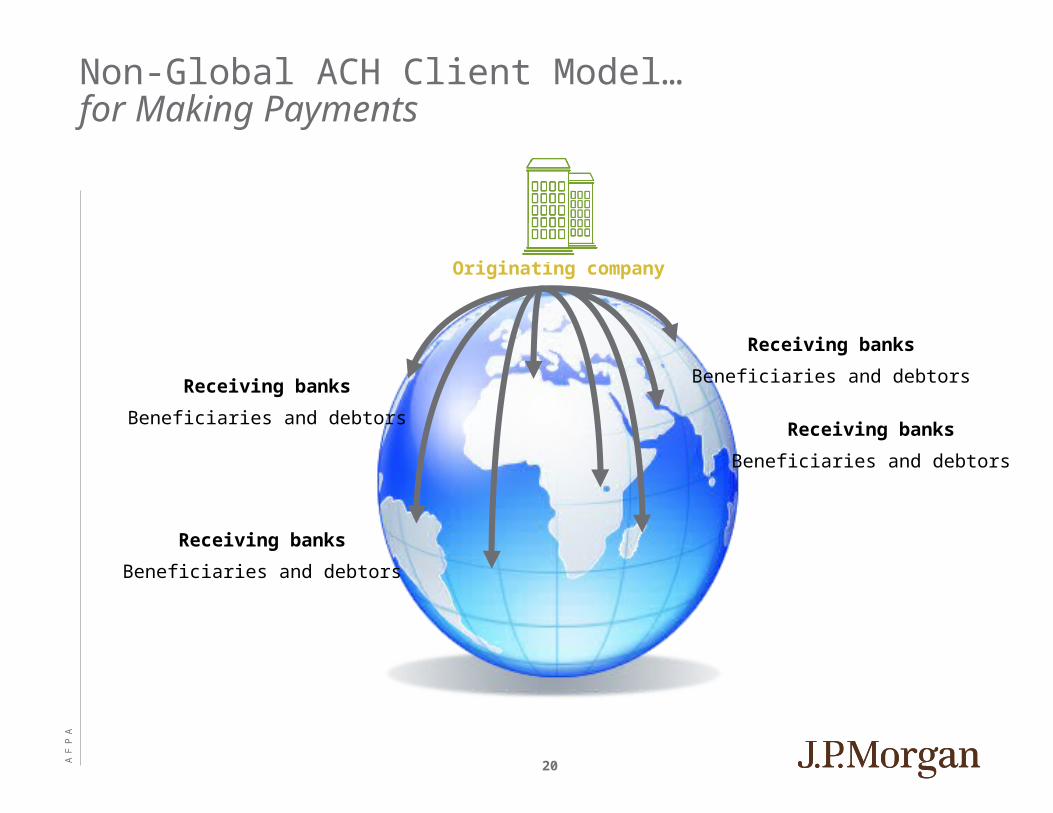

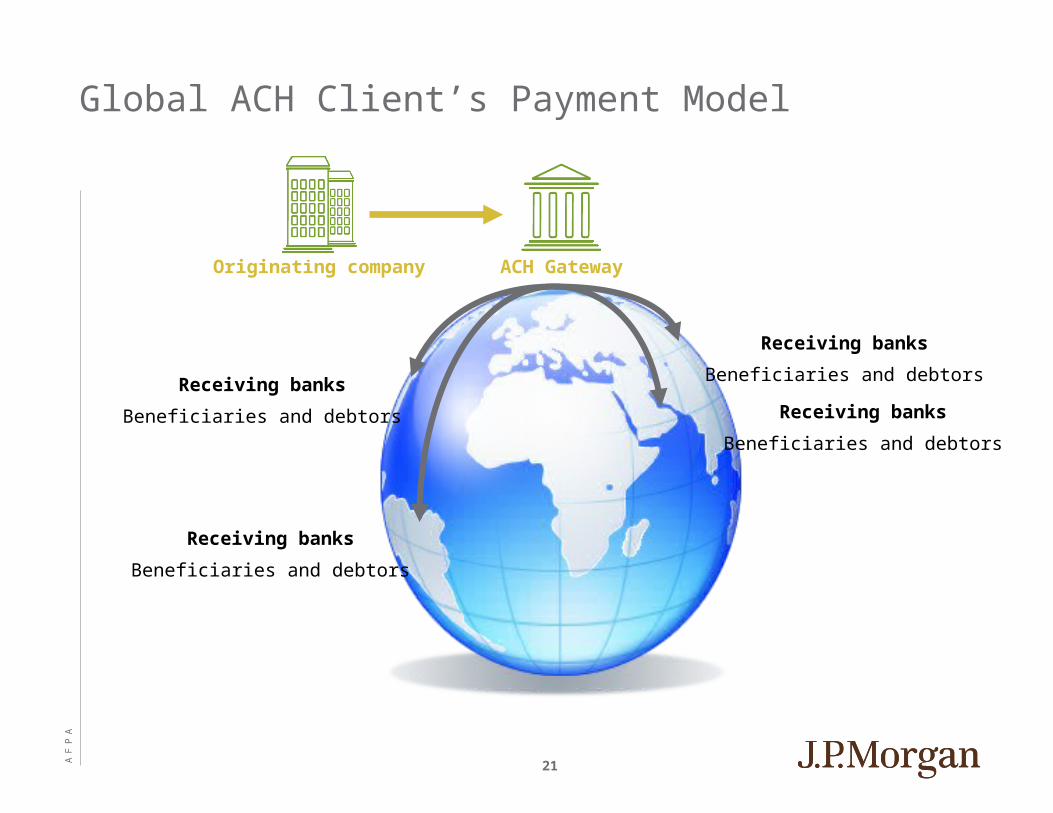

Originating company

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Non-Global ACH Client Model… for Making Payments

AF

PA

21

Global ACH Client’s Payment Model

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Receiving banks

Beneficiaries and debtors

Originating company ACH Gateway

AF

PA

22

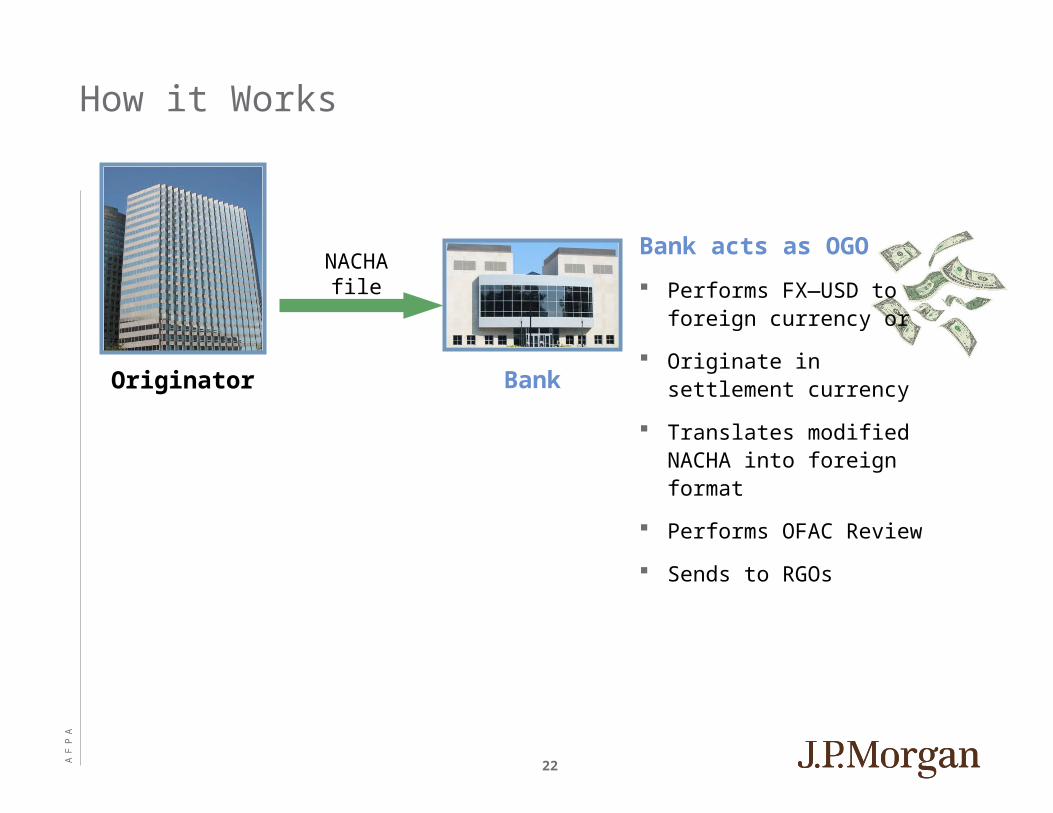

NACHA file

BankOriginator

Bank acts as OGO

Performs FX—USD to foreign currency or

Originate in settlement currency

Translates modified NACHA into foreign format

Performs OFAC Review

Sends to RGOs

How it Works

AF

PA

23

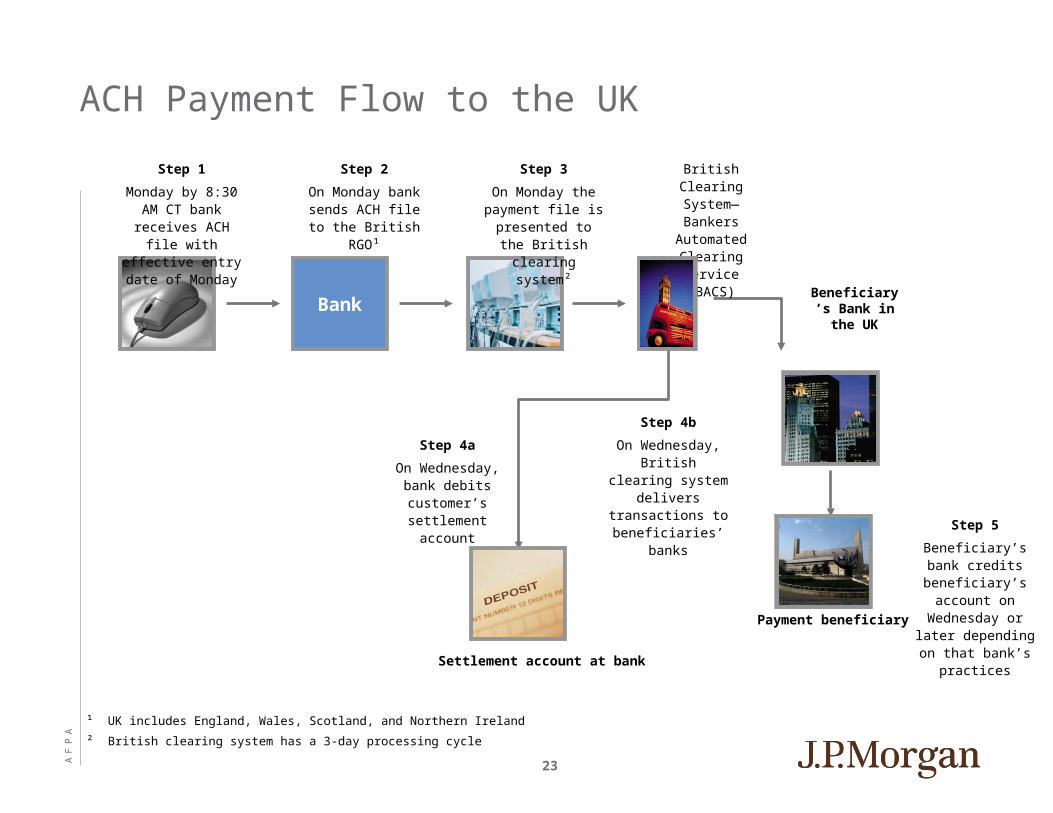

¹ UK includes England, Wales, Scotland, and Northern Ireland

² British clearing system has a 3-day processing cycle

Step 1

Monday by 8:30 AM CT bank receives

ACH file with effective entry date

of Monday

Step 2

On Monday bank sends ACH file to the

British RGO¹

Bank

Step 3

On Monday the payment file is

presented to the British clearing

system²

British Clearing System—Bankers

Automated Clearing

Service (BACS)

Settlement account at bank

Step 4a

On Wednesday, bank debits customer’s

settlement account

Beneficiary’s Bank in the

UK

Step 4b

On Wednesday, British clearing system delivers transactions to

beneficiaries’ banks

Payment beneficiary

Step 5

Beneficiary’s bank credits beneficiary’s

account on Wednesday or later depending on that bank’s practices

ACH Payment Flow to the UK

AF

PA

24

Differences Between US ACH and International ACH

There is no such thing as true Global or International ACH!

No international standard

No standards or common rules

No centralized system

No “international version” of US prenotification process

Longer settlement time/varies by country

Different formats for account numbers and routing numbers

Different holiday schedules

In most countries, reversals are not allowed

In most countries, must pay in local currency

Differing debit rules in country

Some countries have no low value system or it is an immature system

Local language requirements for clearing systems

AF

PA

25

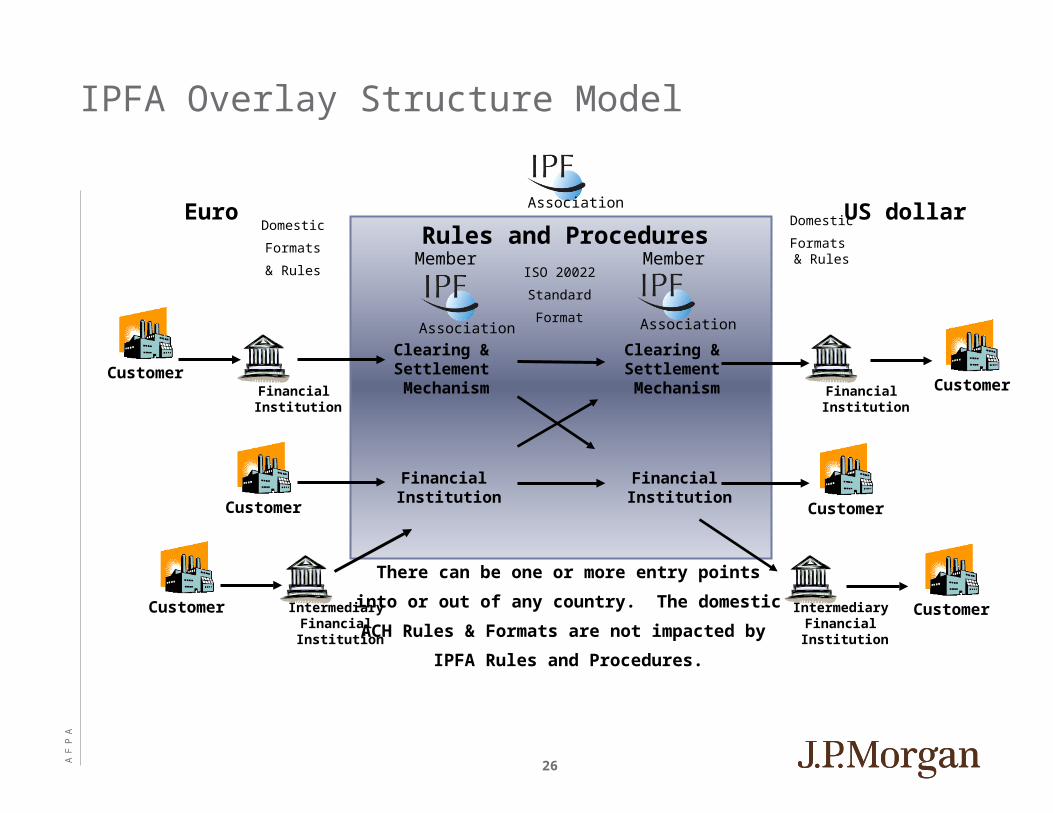

IPFA Concept

Defining rules, standards and operating framework

Simplifying non-urgent cross-border credit transfers

Leveraging existing payment networks and international standards e.g. ISO 20022

Enabling interoperability between domestic and regional non-urgent payments systems and banks

Why?

Globalization is continuing to drive a broader base of clients who demand cost-effective, less complex payment services with a wider reach

The International Payments Framework approach is to enable locally originated non-urgent credit transfers to reach markets around the world

Leverage existing “railways”, enhancing existing “rules” and deploying existing international “standards”

Increased regulatory requirements requires institutions to collaborate with counter-parts in order to ensure compliance

AF

PA

26

Rules and Procedures

Financial Institution

Domestic

Formats

& Rules

Domestic

Formats & Rules

There can be one or more entry points

into or out of any country. The domestic

ACH Rules & Formats are not impacted by

IPFA Rules and Procedures.

Euro US dollar

ISO 20022

Standard

Format

Member Member

Intermediary Financial Institution

Clearing & Settlement Mechanism

Financial Institution

Customer

Customer

Customer

Clearing & Settlement Mechanism

Financial Institution

Financial Institution

Customer

Customer

Intermediary Financial Institution

Customer

Association

Association Association

IPFA Overlay Structure Model

AF

PA

27

IPFA Governance

International Payments Framework Association (IPFA) was established as a U.S. not-for-profit association in February 2010

Two membership categories

Primary Member – financial institution or a clearing & settlement mechanism

Affiliate Member – an association that represents one or more FIs (but is not a FI) a standard-setting body, an industry vendor or a user of payment services.

Has a nine member Board of Directors

Is run by a Chief Executive Officer

Cooperates with Observers from international and national organizations / regulatory bodies

AF

PA

28

North America:

Snapshot:

Paper checks are still heavily used (representing almost half of the non-cash value in the region) and credit cards are leveling off. Payments are growing but slower than rest of the world.

Trends:

Debit card use continues to grow rapidly

Demand for more detailed remittance data included with payment

Consumers are moving from the credit-based economy of the past decade to a savings based economy

Europe:

Snapshot:

Credit transfer and debit card are most frequently used non-cash payment types. Credit cards have not been embraced in this region, except in the UK. Innovation is not as extensive as in developing regions due to high level of electronic payment adoption and low unbanked population.

Trends:

Significant margin pressure across region (e.g. SEPA-driven consolidation and regulations are shrinking transaction fees) pushing need to manage costs

Less mature markets (e.g. Eastern Europe) will experience double-digit growth in payments value

Payment Behavior and Trends differ Greatly by Region

Source: BCG, KPMG, and McKinsey reports, and EPS analysis

AF

PA

29

Source: BCG, KPMG, and McKinsey reports, and EPS analysis

Latin America:

Snapshot:

Still heavily cash based, and fear of inflation remains a strong driver of payment choice. Credit transfers are most frequently used non-cash instrument. Significant unbanked population.

Trends:

Credit cards are growing rapidly, as the banked population has increased significantly, banks are aggressively pushing electronic payment enablers (such as POS network), and banks and retailers have successfully partnered

Asia Pacific:

Snapshot:

Large divergence on trends and initiatives based on high and low income countries. Region offers attractive structural opportunities for innovation in payments. Domestic payments growing quickly. Cards represent about half of non-cash transactions. Large unbanked population.

Trends:

China: government encouraging migration to e-payments, and Alipay has become the dominant e-wallet (more registered users than PayPal globally)

Hong Kong: smart cards (e.g. Octopus) are replacing cash for micro payments

Japan and South Korea: increasing use of mobile payments Australia and New Zealand: likely to follow the lead of the North American or European models

Payment Behavior and Trends differ Greatly by Region

AF

PA

30

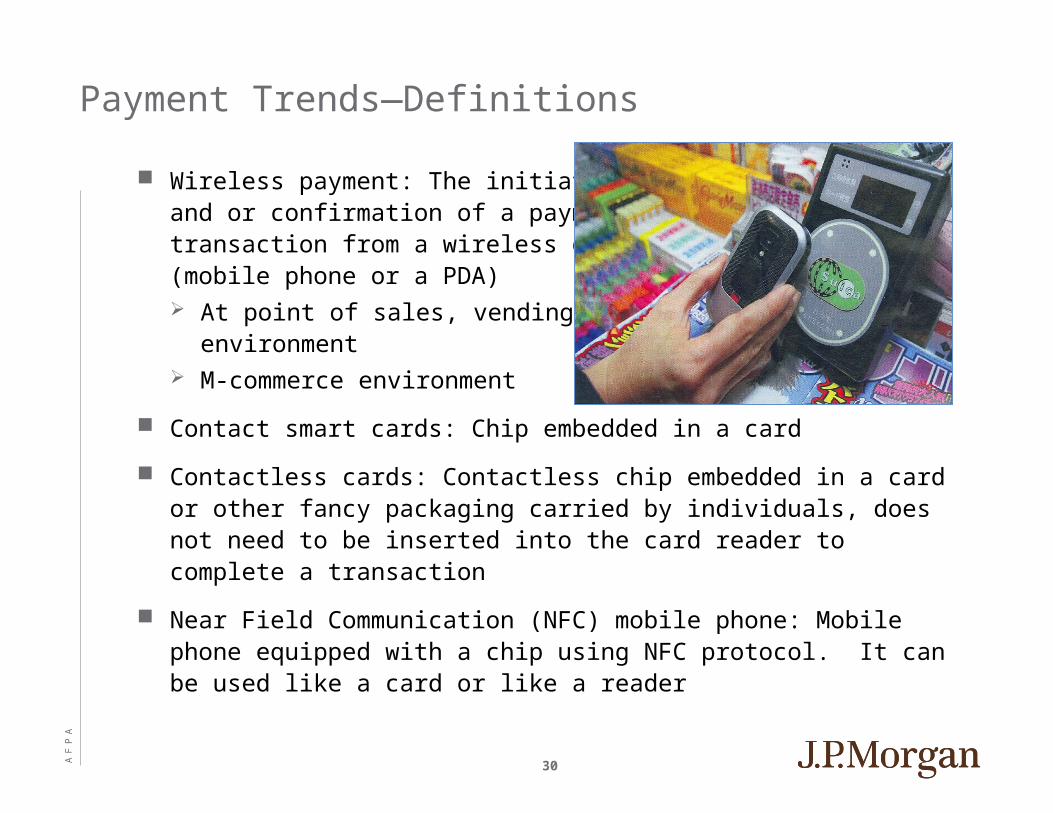

Payment Trends—Definitions

Wireless payment: The initiation and or confirmation of a payment transaction from a wireless device (mobile phone or a PDA) At point of sales, vending

environment M-commerce environment

Contact smart cards: Chip embedded in a card

Contactless cards: Contactless chip embedded in a card or other fancy packaging carried by individuals, does not need to be inserted into the card reader to complete a transaction

Near Field Communication (NFC) mobile phone: Mobile phone equipped with a chip using NFC protocol. It can be used like a card or like a reader

AF

PA

31

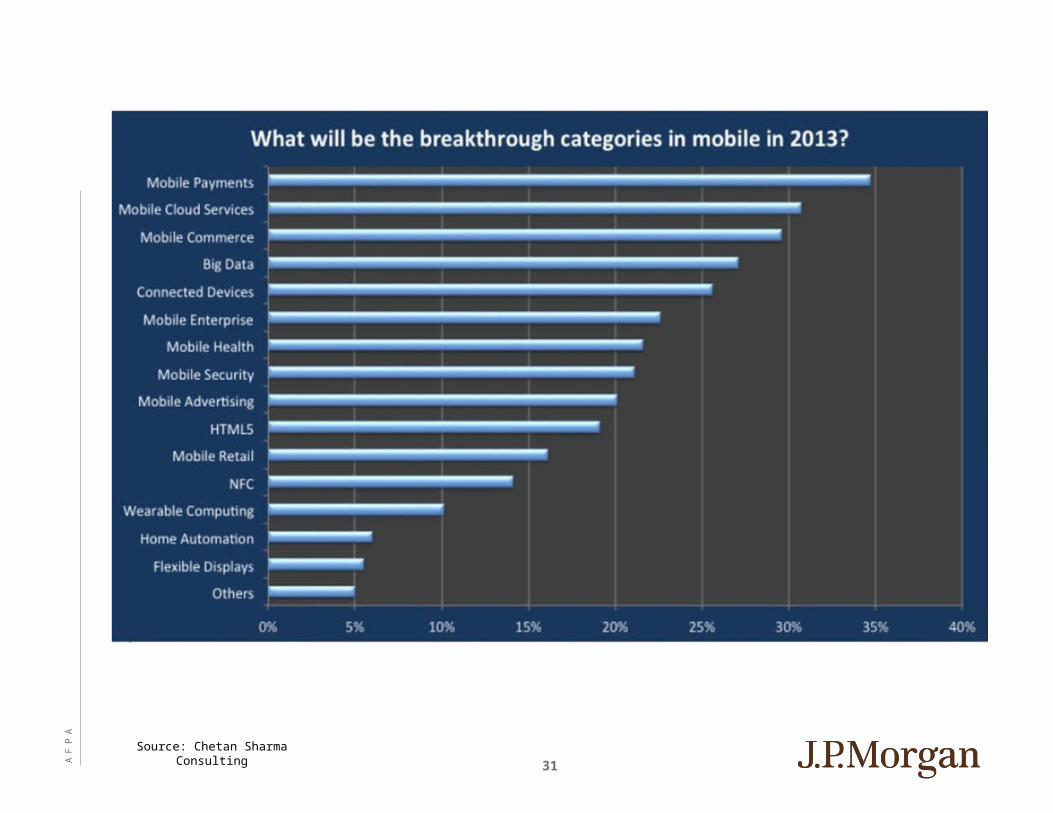

Source: Chetan Sharma Consulting

AF

PA

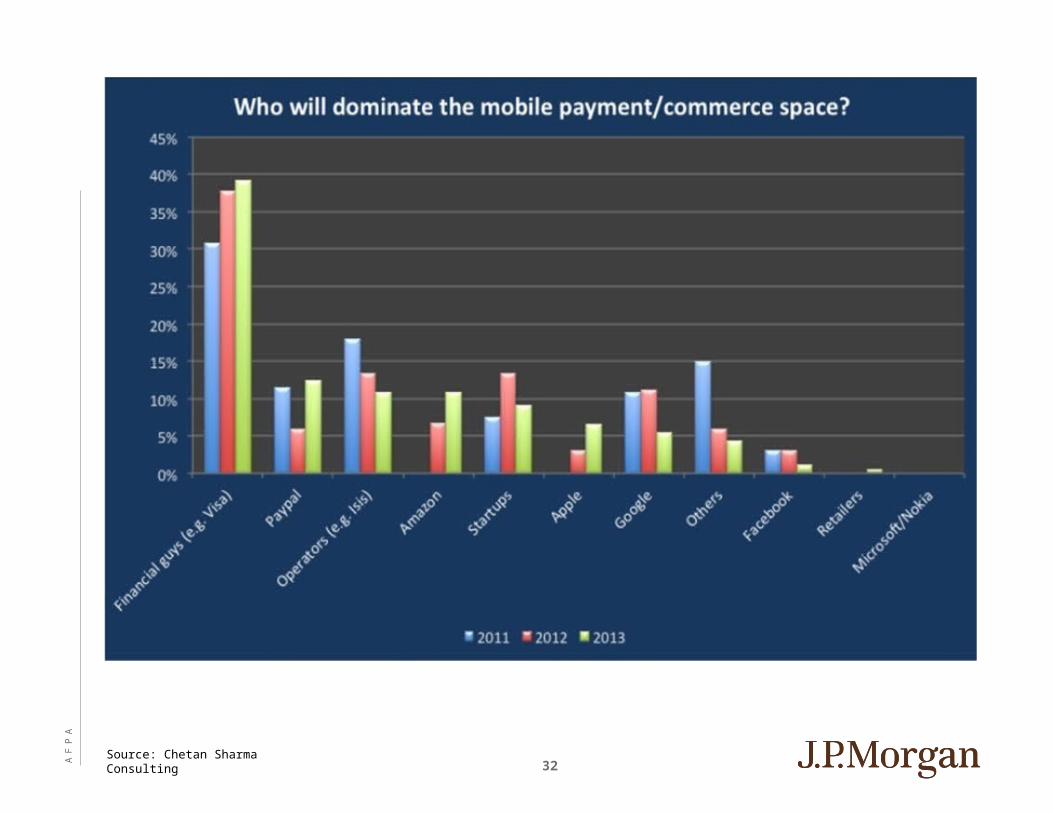

32Source: Chetan Sharma Consulting

AF

PA

33

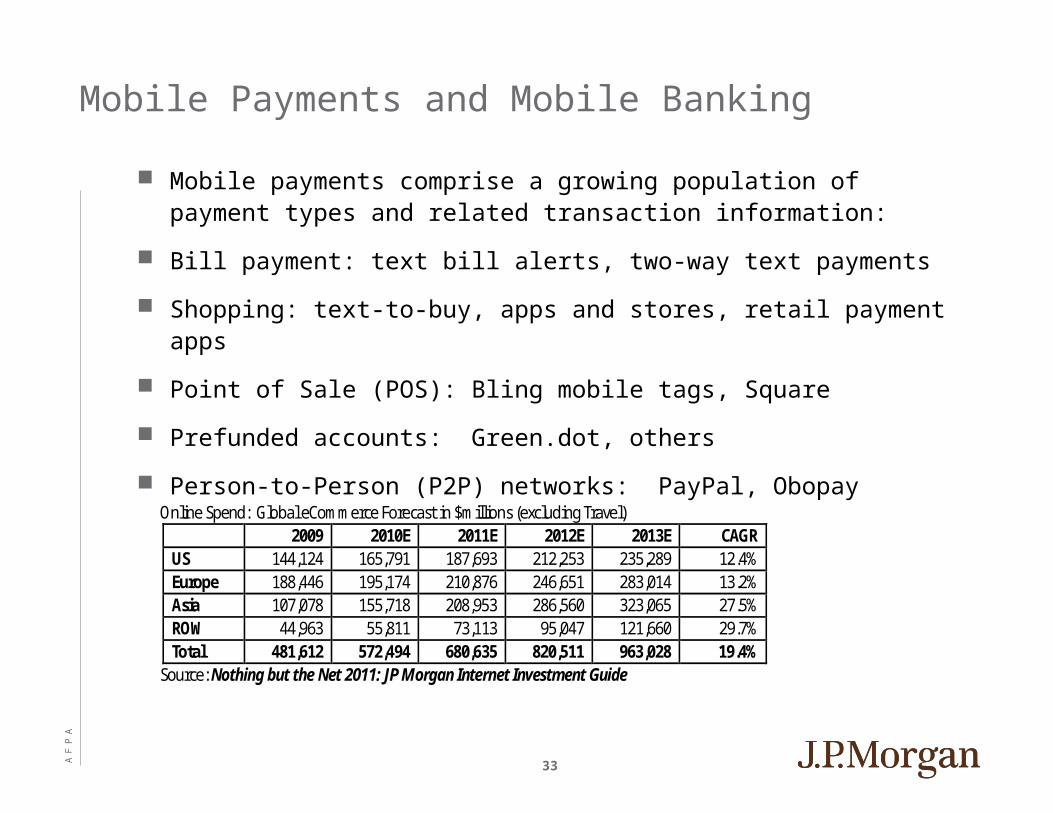

Online Spend: Global eCommerce Forecast in $millions (excluding Travel) 2009 2010E 2011E 2012E 2013E CAGR

US 144,124 165,791 187,693 212,253 235,289 12.4% Europe 188,446 195,174 210,876 246,651 283,014 13.2% Asia 107,078 155,718 208,953 286,560 323,065 27.5% ROW 44,963 55,811 73,113 95,047 121,660 29.7% Total 481,612 572,494 680,635 820,511 963,028 19.4%

Source: Nothing but the Net 2011: JP Morgan Internet Investment Guide

Mobile Payments and Mobile Banking

Mobile payments comprise a growing population of payment types and related transaction information:

Bill payment: text bill alerts, two-way text payments

Shopping: text-to-buy, apps and stores, retail payment apps

Point of Sale (POS): Bling mobile tags, Square

Prefunded accounts: Green.dot, others

Person-to-Person (P2P) networks: PayPal, Obopay

AF

PA

34

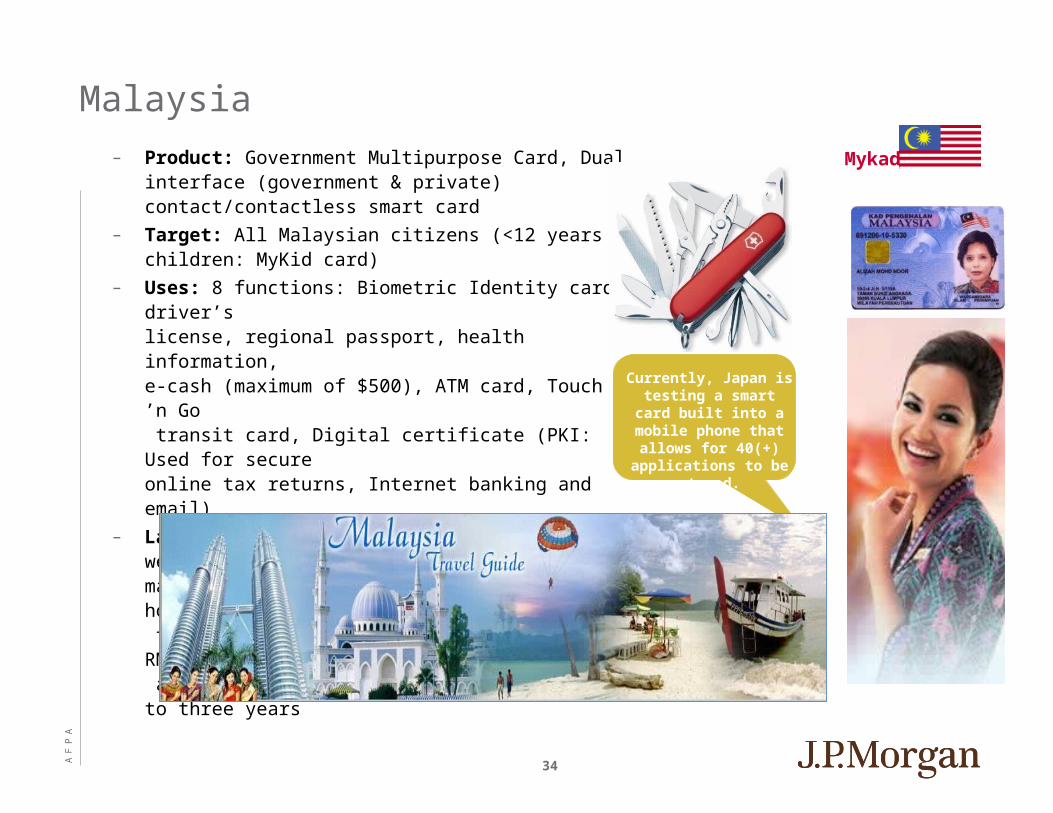

– Product: Government Multipurpose Card, Dual interface (government & private) contact/contactless smart card

– Target: All Malaysian citizens (<12 years children: MyKid card)

– Uses: 8 functions: Biometric Identity card, driver’s license, regional passport, health information,e-cash (maximum of $500), ATM card, Touch ’n Go transit card, Digital certificate (PKI: Used for secure online tax returns, Internet banking and email)

– Launched in 2001. By 2005, all citizens were mandated to carry the card outside the home. Failure to do so may incur a fine of between RM3,000 ($622) and RM20,000 ($6,218) or jail term of up to three years

Currently, Japan is testing a smart card built into a mobile phone that allows

for 40(+) applications to be

stored.

Myka

d

Malaysia

AF

PA

35

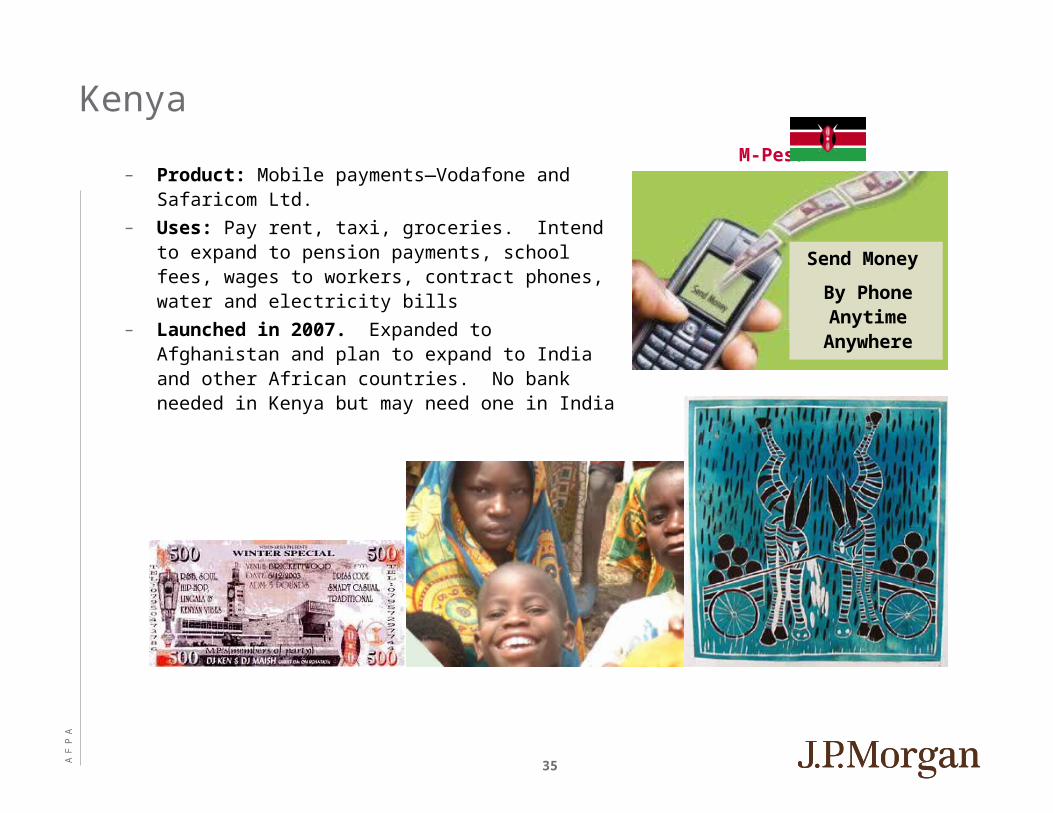

– Product: Mobile payments—Vodafone and Safaricom Ltd.

– Uses: Pay rent, taxi, groceries. Intend to expand to pension payments, school fees, wages to workers, contract phones, water and electricity bills

– Launched in 2007. Expanded to Afghanistan and plan to expand to India and other African countries. No bank needed in Kenya but may need one in India

Send Money

By Phone Anytime

Anywhere

M-Pesa

Kenya

AF

PA

36

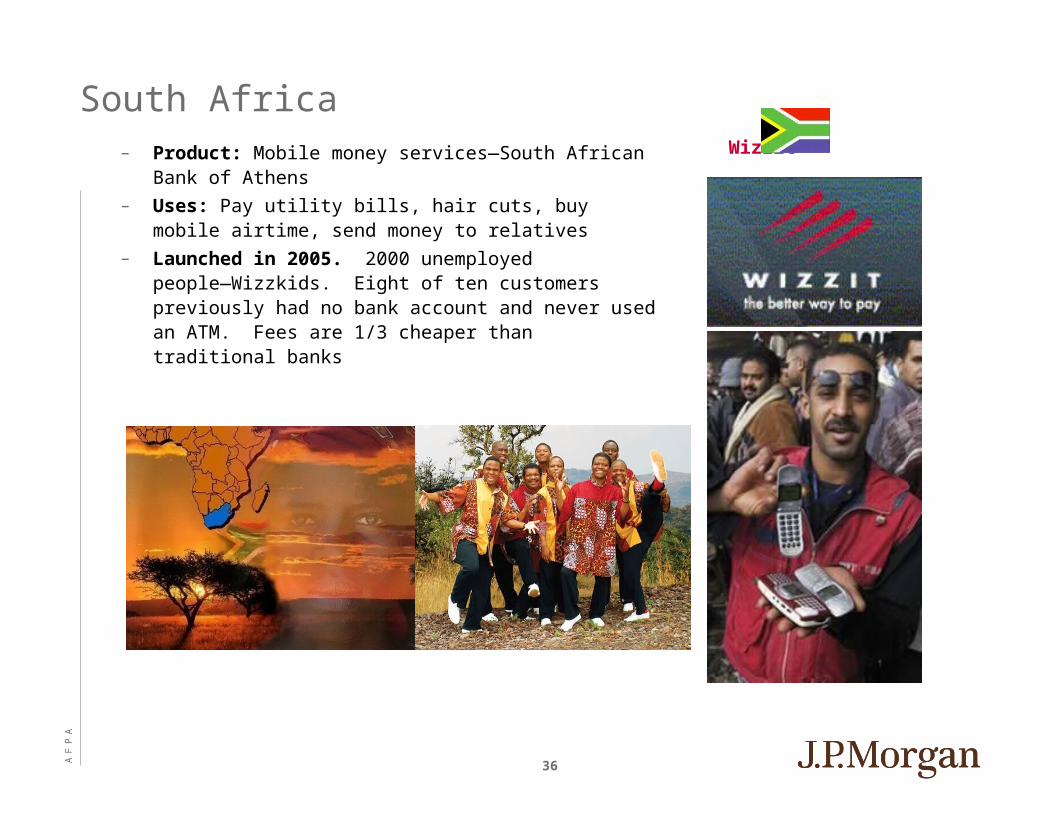

– Product: Mobile money services—South African Bank of Athens

– Uses: Pay utility bills, hair cuts, buy mobile airtime, send money to relatives

– Launched in 2005. 2000 unemployedpeople—Wizzkids. Eight of ten customers previously had no bank account and never used an ATM. Fees are 1/3 cheaper than traditional banks

Wizzit

South Africa

AF

PA

37

mobileAxept

– Product: Mobile payments - Directly charges an existing credit card or a bank account, either by customers calling or sending a SMS to a specified number

– Uses: Purchase goods and services online or at physical locations, and donate money (e.g. several Norwegian churches are collecting donations from people via mobileAxept payments instead of small notes or coins)

– Launched in 2003. Piloting customers from different countries, and currently has operations in Norway, Denmark, Sweden, and USA

mobileAxept

Norway

AF

PA

38

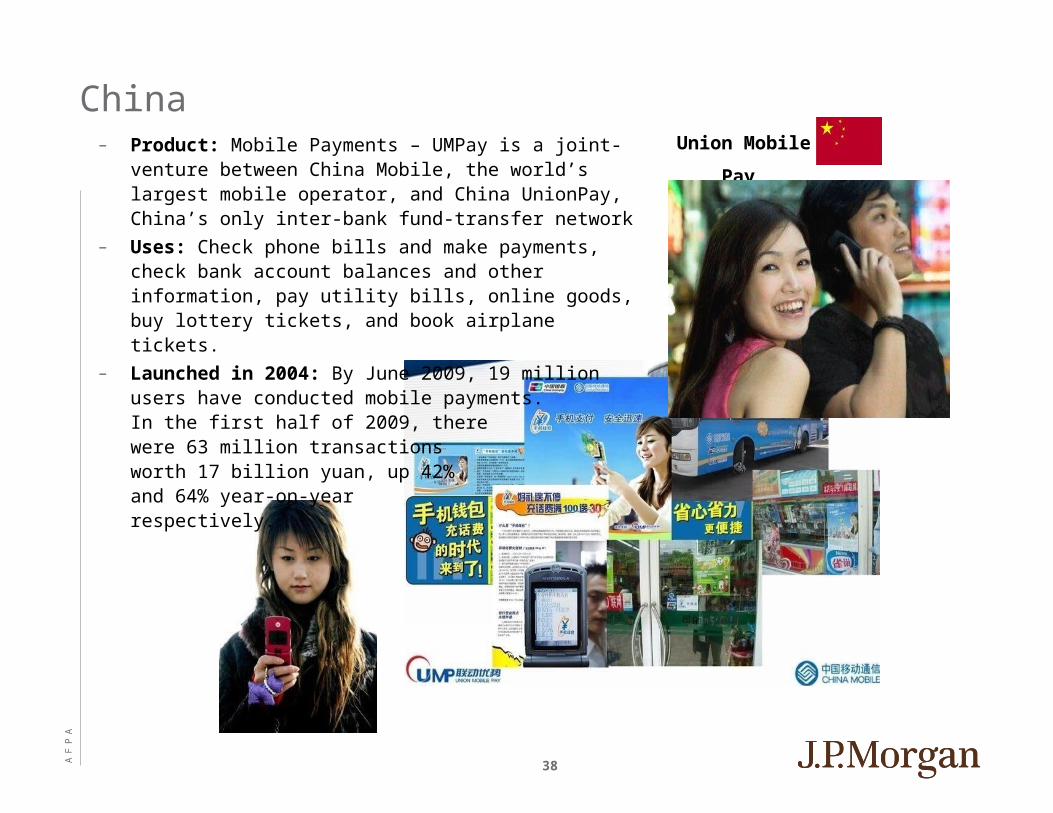

– Product: Mobile Payments – UMPay is a joint-venture between China Mobile, the world’s largest mobile operator, and China UnionPay, China’s only inter-bank fund-transfer network

– Uses: Check phone bills and make payments, check bank account balances and other information, pay utility bills, online goods, buy lottery tickets, and book airplane tickets.

– Launched in 2004: By June 2009, 19 million users have conducted mobile payments. In the first half of 2009, there were 63 million transactions worth 17 billion yuan, up 42% and 64% year-on-year respectively.

Union Mobile

Pay

China

AF

PA

39

Euro Overview – Key Changes

Payment Services Directive (PSD) legislation affecting delivery time and charge practices

The PSD affects payments where the first and last bank in the chain are EU residents

Harmonisation of the high-value, national clearing systems by the implementation of TARGET2

Introduction of a single EU payment scheme for credit & debit transfers as part of the single euro payment area (SEPA)

Increased competition among banks resulted in a greater focus on costs to remain competitive

Escalation in the volume and cost of processing third-party bank charges for commercial payments driven by regulatory change

Wide-scale use of the SWIFT bank identifier code (BIC) and international bank account number (IBAN) on payments within the European area

EC Regulation 1781/2006 required ordering financial institutions make sure all wire transfers carry specified information about the payer, through the payment chain

AF

PA

40

International Banking Account Number (IBAN)

Description

An international standard that identifies bank accounts across national borders and merges existing country specific account number formats into a global standardized framework

Required for European payments

Mandatory to ensure straight through processing

Objective

The IBAN number reduces routing errors that result in payments delays and extra costs incurred

Allows for payment information validation at the point of data entry using:

Country code

Appropriate number of characters (by country)

Specified format

AF

PA

41

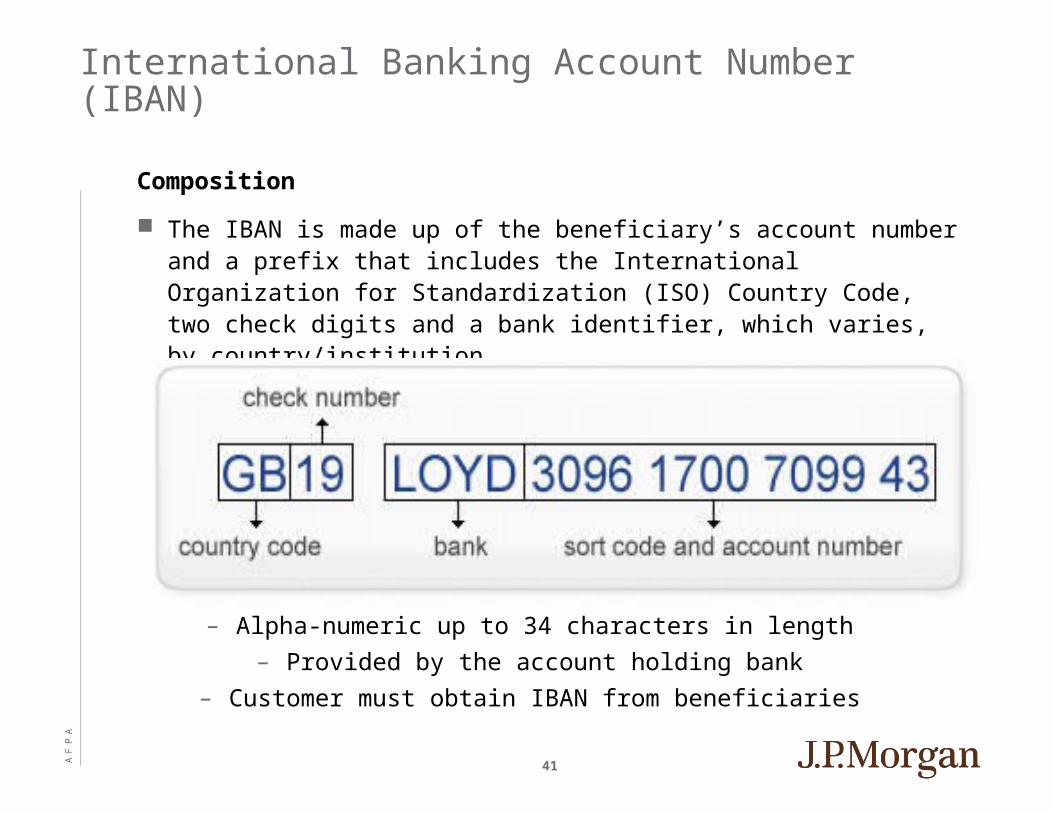

– Customer must obtain IBAN from beneficiaries

International Banking Account Number (IBAN)

Composition

The IBAN is made up of the beneficiary’s account number and a prefix that includes the International Organization for Standardization (ISO) Country Code, two check digits and a bank identifier, which varies, by country/institution.

– Provided by the account holding bank

– Alpha-numeric up to 34 characters in length

AF

PA

42

Single Euro Payments Area (SEPA)

“SEPA harmonizes the way we make and process retail payments in euro”

SEPA enables customers to make cashless euro payments to anyone located anywhere in Europe, using a single payment account and a single set of payment instruments.

SEPA Credit Transfer (SCT)

A payment initiated by the payer. The payer sends a payment instruction to his/her bank. The bank moves the funds to the receiver’s bank. This can happen via several intermediaries.

SEPA Direct Debit (SDD)

A transfer initiated by the receiver via his/her bank. Direct debits are often used for recurring payments, such as utility bills. They require a pre-authorization (“mandate”) from the payer. Direct debits are also used for one-off payments. In this case, the payer authorizes an individual payment.

SEPA Card Clearing (SCC)

Debit cards - allow the cardholder to charge purchases directly and individually to an account.

Credit cards - allow purchases within a certain credit limit. The balance is settled in full by the end of a specified period. Alternatively, it is partly settled. The remaining balance is taken as extended credit on which the cardholder must pay interest.

AF

PA

43

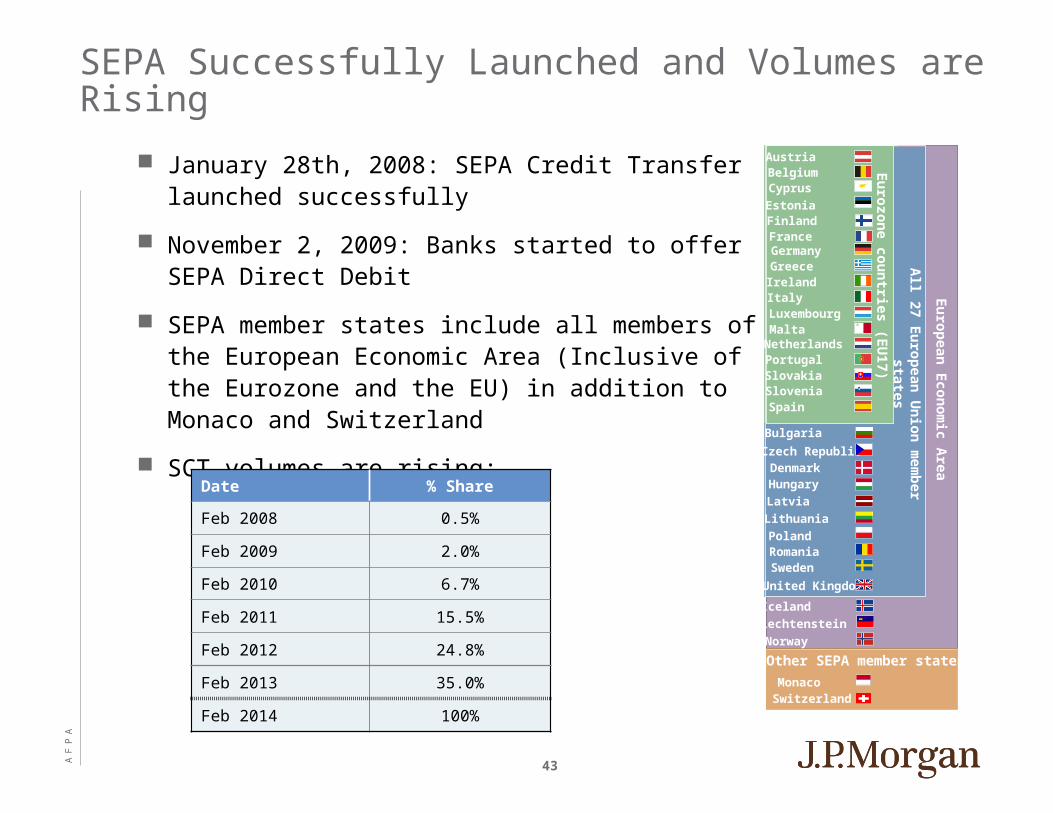

SEPA Successfully Launched and Volumes are Rising

January 28th, 2008: SEPA Credit Transfer launched successfully

November 2, 2009: Banks started to offer SEPA Direct Debit

SEPA member states include all members of the European Economic Area (Inclusive of the Eurozone and the EU) in addition to Monaco and Switzerland

SCT volumes are rising:

Date % Share

Feb 2008 0.5%

Feb 2009 2.0%

Feb 2010 6.7%

Feb 2011 15.5%

Feb 2012 24.8%

Feb 2013 35.0%

Feb 2014 100%

FinlandFranceGermanyGreece

Italy

NetherlandsPortugal

Ireland

Cyprus

LuxembourgMalta

SloveniaSpain

31

SEPA

cou

ntrie

s in

clu

din

g a

ll 27

Eu

rop

ean

Un

ion

mem

ber s

tate

s

Eu

rozon

e c

ou

ntrie

s (E

U1

6)

Denmark

Czech Republic

Hungary

Latvia

Lithuania

Slovakia

Bulgaria

Poland

Liechtenstein *Norway *

Iceland *

Estonia

Austria

FranceGermanyGreece

Italy

NetherlandsPortugal

Ireland

Cyprus

LuxembourgMalta

SloveniaSpain

Eu

rop

ean

Econ

om

ic A

rea

Eu

rozon

e c

ou

ntrie

s (E

U1

7)

DenmarkCzech Republic

HungaryLatvia

Lithuania

Slovakia

Bulgaria

Poland

Estonia

Switzerland *

Switzerland Monaco

BelgiumAustria

Finland

All 2

7 E

uro

pean

Un

ion

mem

ber

sta

tes

Other SEPA member states

Bulgaria

Czech RepublicDenmarkHungaryLatviaLithuania

SwedenRomaniaPoland

United Kingdom

Norway

Iceland Liechtenstein

AF

PA

44

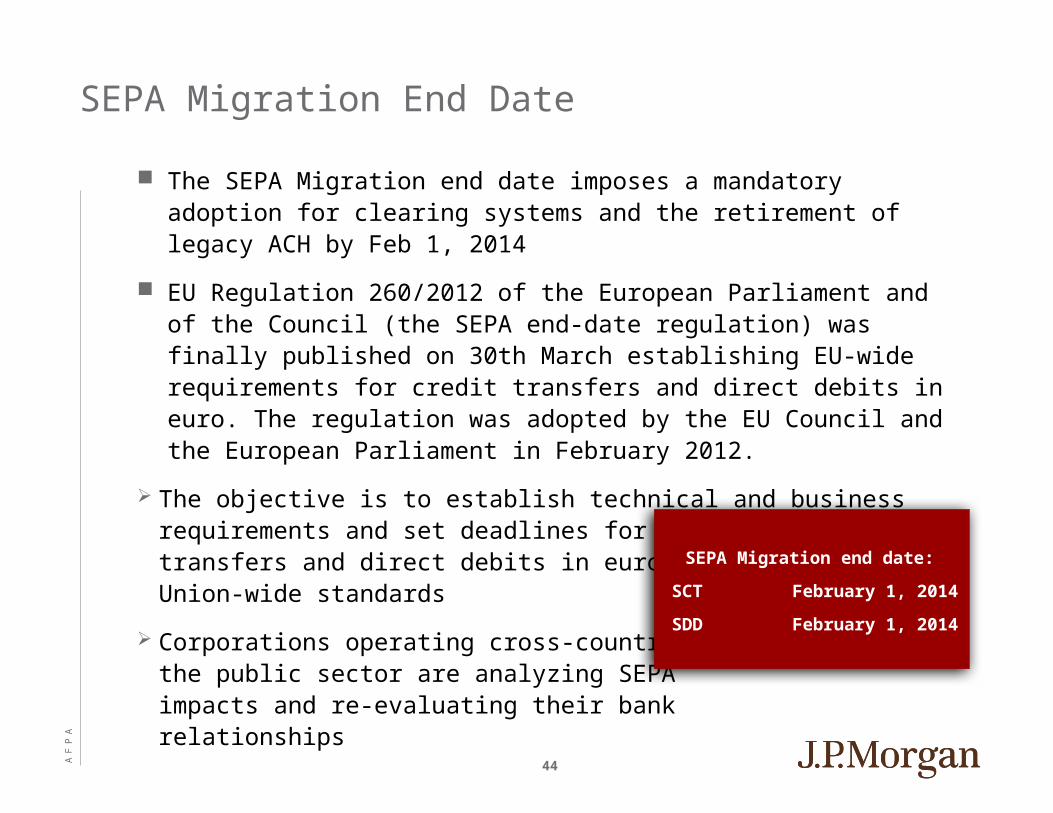

SEPA Migration End Date

The SEPA Migration end date imposes a mandatory adoption for clearing systems and the retirement of legacy ACH by Feb 1, 2014

EU Regulation 260/2012 of the European Parliament and of the Council (the SEPA end-date regulation) was finally published on 30th March establishing EU-wide requirements for credit transfers and direct debits in euro. The regulation was adopted by the EU Council and the European Parliament in February 2012.

The objective is to establish technical and business requirements and set deadlines for migrating credit transfers and direct debits in euro from national to Union-wide standards

Corporations operating cross-country and the public sector are analyzing SEPA impacts and re-evaluating their bank relationships

SEPA Migration end date:

SCT February 1, 2014

SDD February 1, 2014

AF

PA

45

SEPA Migration End Date

The day after publication of EU Regulation 260/2012, the following entered into force:

Reachability for euro Credit Transfers and Direct Debits (the latter only where national Direct Debits are available to consumers)

Payment accessibility across EU Member States, implying accounts can be held in any European Member State

Removal for €50,000 limit on equal charging practices aligning cross border with domestic charges for payments of the same value and in the same currency

Impact on banks:

National timeframes for winding down niche services

Complying with interoperability requirements

Flexibility with national variances

The removal of the obligation for customers to provide BIC with the IBAN.

AF

PA

46

Are all banks now reachable for SEPA DD&CT?

Within the Eurozone

All consumer / retail and commercial banks in the Eurozone are reachable

SCT was launched in January 2008 and currently has more than 4,400 European banks registered with the EPC for this service

EC Regulation 924 that came into force on 1st November 2009 mandated the SDD reachability of all Eurozone banks – currently 2,600 European banks have registered with the European Payment Council (EPC) for the SDD Core service and 2,400 banks for SDD Business to Business service

Outside the Eurozone

Limited reach for banks outside the Eurozone and some private / special institutions

Dependent on countries: UK and Switzerland are leading here, some eastern European non-euro countries already have BIC & IBAN as mandatory. If banks offer Euro accounts then they are SEPA ready

Generally SCT reach into non-Eurozone countries is good. For instance, in excess of 100 banks are reachable in Switzerland

SDD reachability is considerably lower at this point in these countries. Most have less than 10% of their banks as reachable for the Core DD service and participation is lower still for the Business to Business DD service

AF

PA

47

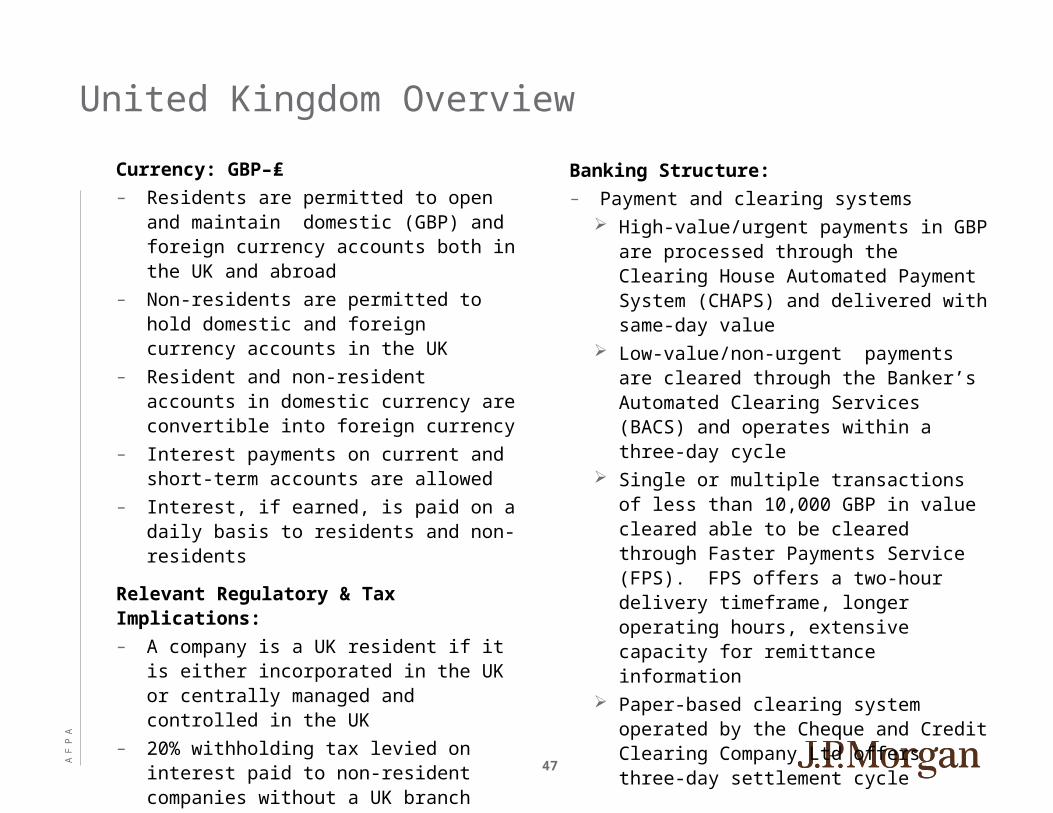

Currency: GBP–₤

– Residents are permitted to open and maintain domestic (GBP) and foreign currency accounts both in the UK and abroad

– Non-residents are permitted to hold domestic and foreign currency accounts in the UK

– Resident and non-resident accounts in domestic currency are convertible into foreign currency

– Interest payments on current and short-term accounts are allowed

– Interest, if earned, is paid on a daily basis to residents and non-residents

Relevant Regulatory & Tax Implications:

– A company is a UK resident if it is either incorporated in the UK or centrally managed and controlled in the UK

– 20% withholding tax levied on interest paid to non-resident companies without a UK branch

Banking Structure:

– Payment and clearing systems High-value/urgent payments in GBP are

processed through the Clearing House Automated Payment System (CHAPS) and delivered with same-day value

Low-value/non-urgent payments are cleared through the Banker’s Automated Clearing Services (BACS) and operates within a three-day cycle

Single or multiple transactions of less than 10,000 GBP in value cleared able to be cleared through Faster Payments Service (FPS). FPS offers a two-hour delivery timeframe, longer operating hours, extensive capacity for remittance information

Paper-based clearing system operated by the Cheque and Credit Clearing Company Ltd offers three-day settlement cycle

United Kingdom Overview

AF

PA

48

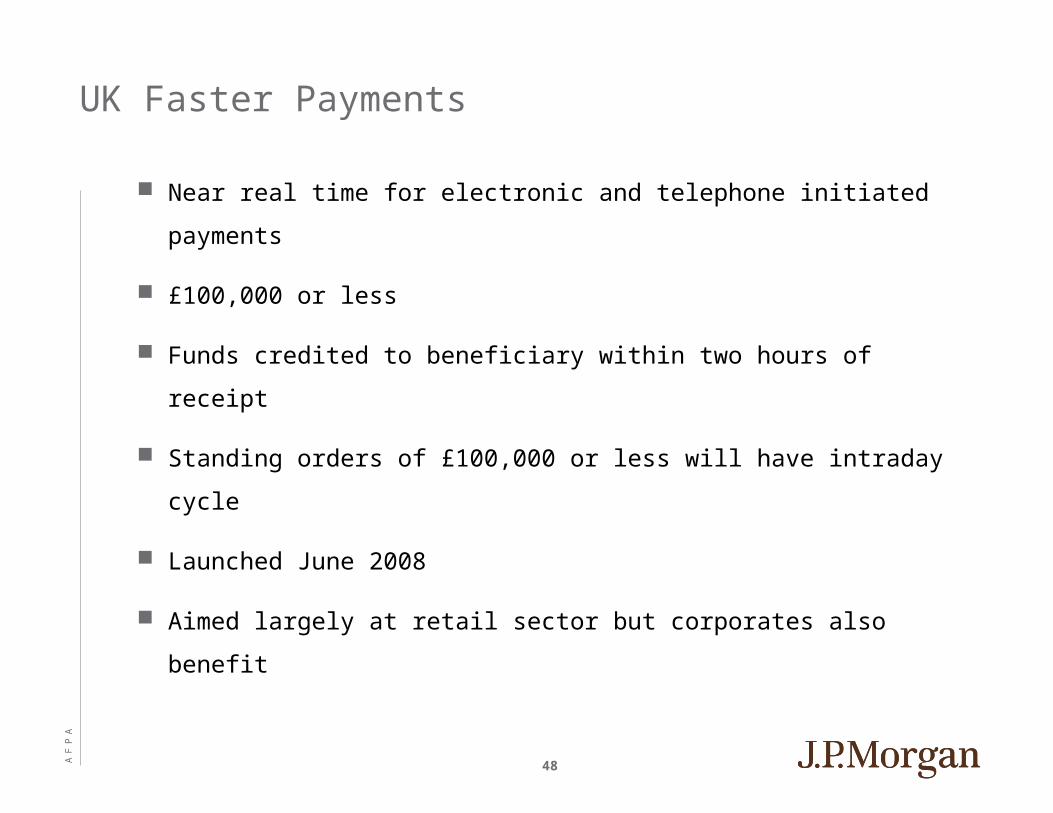

UK Faster Payments

Near real time for electronic and telephone initiated payments

£100,000 or less

Funds credited to beneficiary within two hours of receipt

Standing orders of £100,000 or less will have intraday cycle

Launched June 2008

Aimed largely at retail sector but corporates also benefit

AF

PA

49

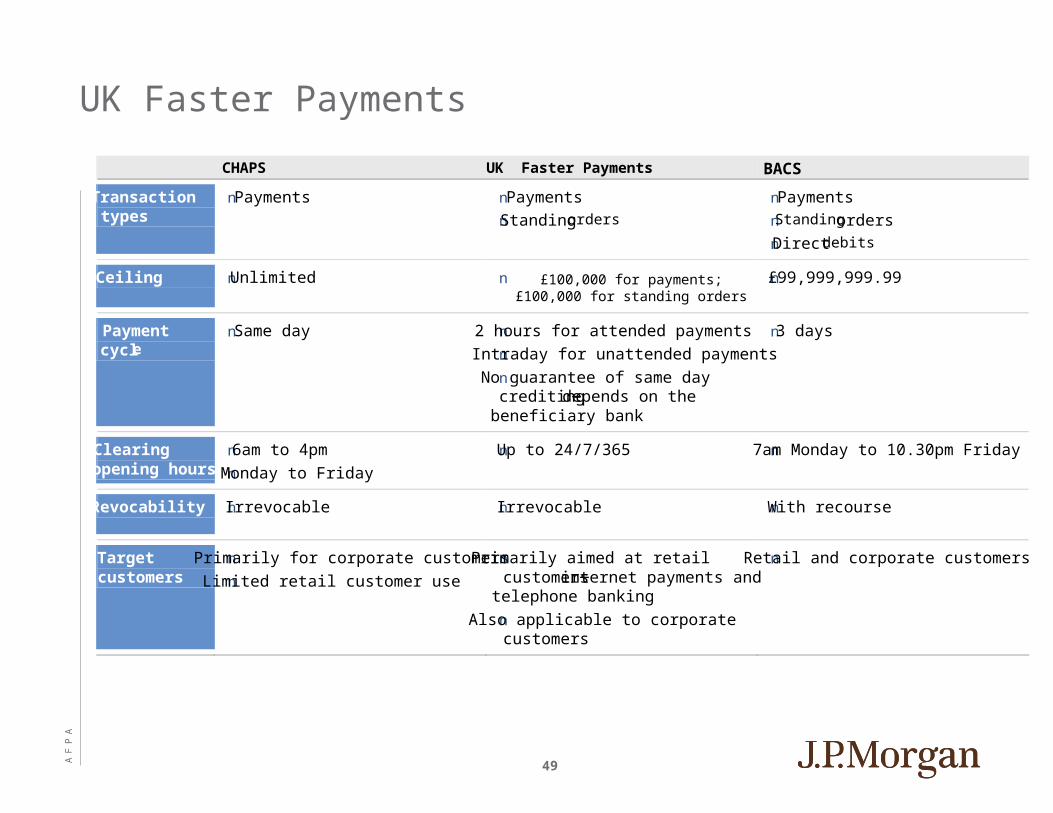

CHAPS UK Faster Payments BACS

Transaction types

n Payments n Payments

n Standing orders

n Payments

n Standing orders

n Direct debits

Ceiling n Unlimited n £100,000 for payments; £100,000 for standing orders

n £99,999,999.99

Payment cycle

n Same day n 2 hours for attended payments

n Intraday for unattended payments

n No guarantee of same day crediting—depends on the beneficiary bank

n 3 days

Clearing opening hours

n 6am to 4pm

n Monday to Friday n Up to 24/7/365 n 7am Monday to 10.30pm Friday

Revocability n Irrevocable n Irrevocable n With recourse

Target customers

n Primarily for corporate customers

n Limited retail customer use n Primarily aimed at retail

customers—internet payments and telephone banking

n Also applicable to corporate customers

n Retail and corporate customers

UK Faster Payments

AF

PA

50

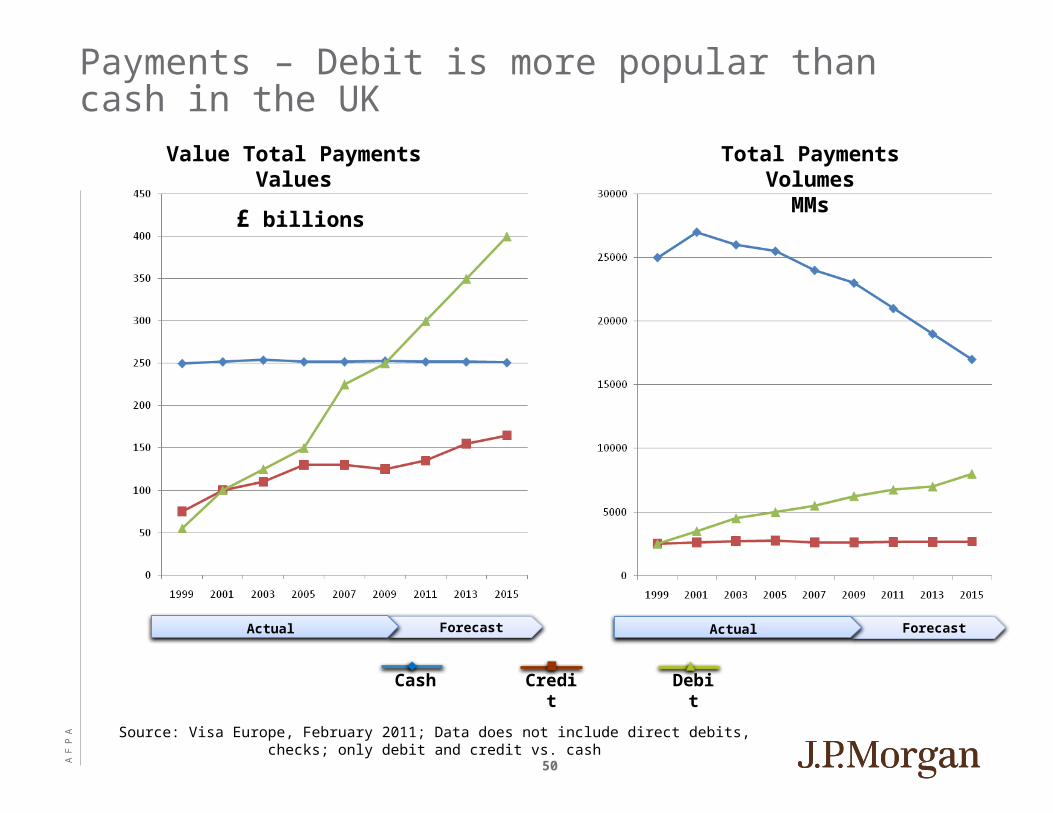

Source: Visa Europe, February 2011; Data does not include direct debits, checks; only debit and credit vs. cash

ForecastActual

Value Total Payments Values

£ billions

Total Payments VolumesMMs

Cash Credit Debit

ForecastActual

Payments – Debit is more popular than cash in the UK

AF

PA

51

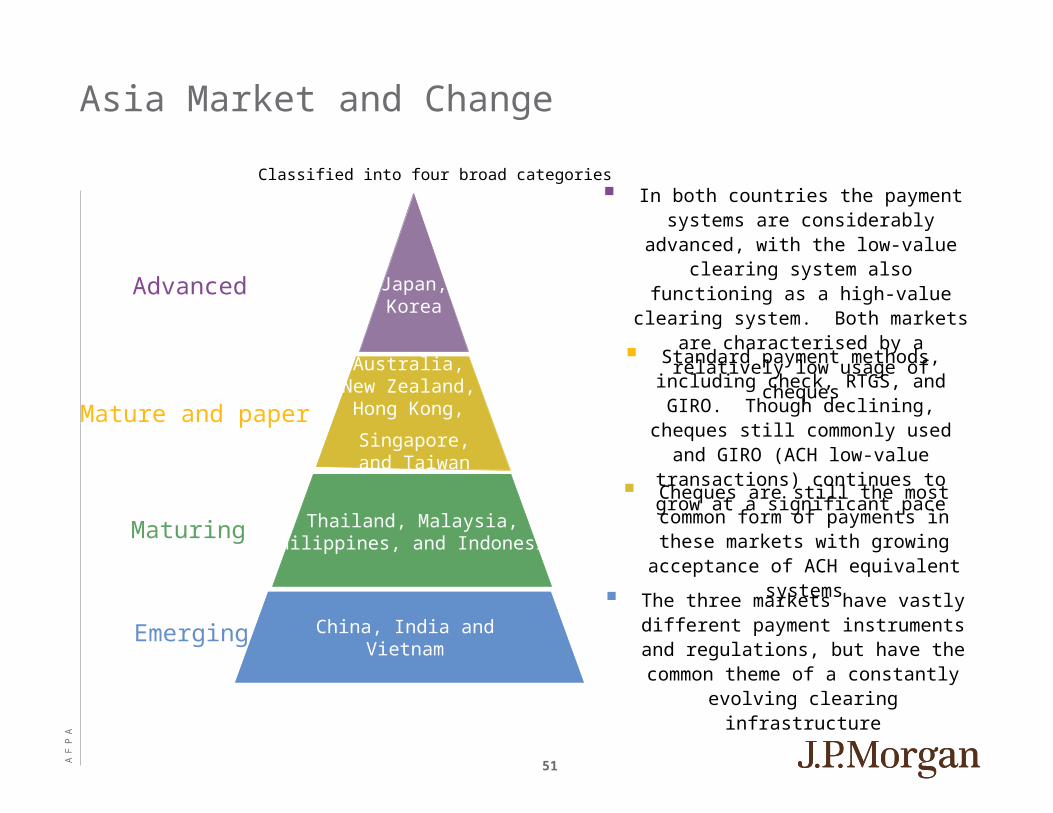

Asia Market and Change

Classified into four broad categoriesClassified into four broad categories

China, India andVietnam

Thailand, Malaysia,Philippines, and Indonesia

Japan,Korea

Maturing

In both countries the payment systems are considerably advanced, with the low-value clearing system also functioning as

a high-value clearing system. Both markets are characterised by a relatively

low usage of cheques

Standard payment methods, including check, RTGS, and GIRO. Though

declining, cheques still commonly used and GIRO (ACH low-value transactions) continues to grow at a significant pace

Cheques are still the most common form of payments in these markets with

growing acceptance of ACH equivalent systems

Emerging

The three markets have vastly different payment instruments and regulations,

but have the common theme of a constantly evolving clearing

infrastructure

China, India andVietnam

Thailand, Malaysia,Philippines, and Indonesia

Australia, New Zealand, Hong Kong,

Singapore,and Taiwan

Japan,Korea

Advanced

Mature and paper

AF

PA

52

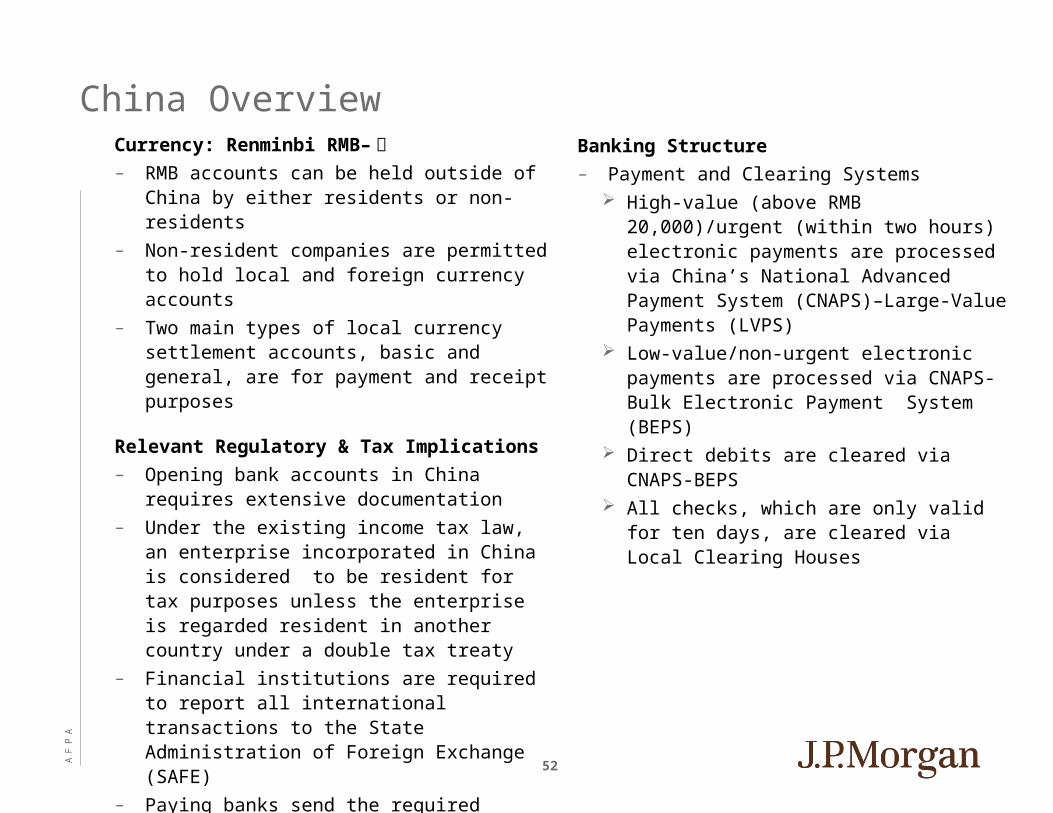

Currency: Renminbi RMB– 元– RMB accounts can be held outside of China by

either residents or non-residents

– Non-resident companies are permitted to hold local and foreign currency accounts

– Two main types of local currency settlement accounts, basic and general, are for payment and receipt purposes

Relevant Regulatory & Tax Implications

– Opening bank accounts in China requires extensive documentation

– Under the existing income tax law, an enterprise incorporated in China is considered to be resident for tax purposes unless the enterprise is regarded resident in another country under a double tax treaty

– Financial institutions are required to report all international transactions to the State Administration of Foreign Exchange (SAFE)

– Paying banks send the required information for international payments, though a company, whether the remitter or the beneficiary, must also send supporting data to SAFE

Banking Structure

– Payment and Clearing Systems High-value (above RMB 20,000)/urgent

(within two hours) electronic payments are processed via China’s National Advanced Payment System (CNAPS)–Large-Value Payments (LVPS)

Low-value/non-urgent electronic payments are processed via CNAPS- Bulk Electronic Payment System (BEPS)

Direct debits are cleared via CNAPS-BEPS All checks, which are only valid for ten days,

are cleared via Local Clearing Houses

China Overview

AF

PA

53

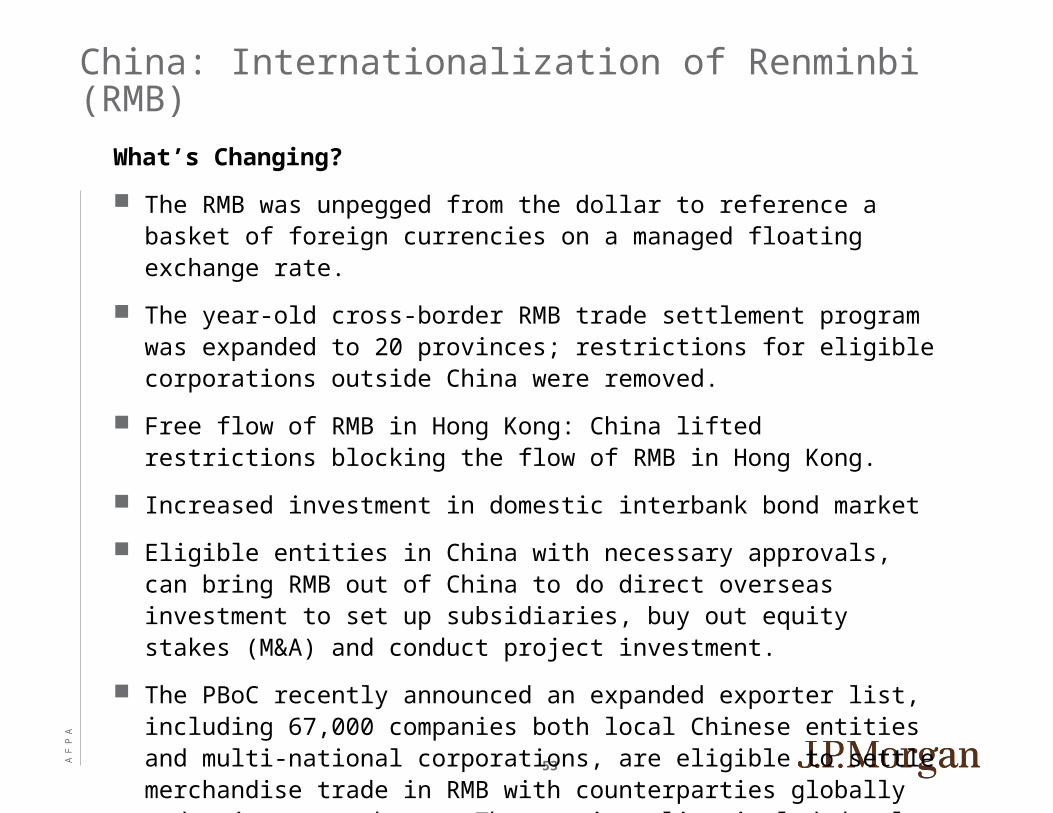

China: Internationalization of Renminbi (RMB)

What’s Changing?

The RMB was unpegged from the dollar to reference a basket of foreign currencies on a managed floating exchange rate.

The year-old cross-border RMB trade settlement program was expanded to 20 provinces; restrictions for eligible corporations outside China were removed.

Free flow of RMB in Hong Kong: China lifted restrictions blocking the flow of RMB in Hong Kong.

Increased investment in domestic interbank bond market

Eligible entities in China with necessary approvals, can bring RMB out of China to do direct overseas investment to set up subsidiaries, buy out equity stakes (M&A) and conduct project investment.

The PBoC recently announced an expanded exporter list, including 67,000 companies both local Chinese entities and multi-national corporations, are eligible to settle merchandise trade in RMB with counterparties globally and enjoy tax rebates. The previous list included only 400 eligible companies.

AF

PA

54

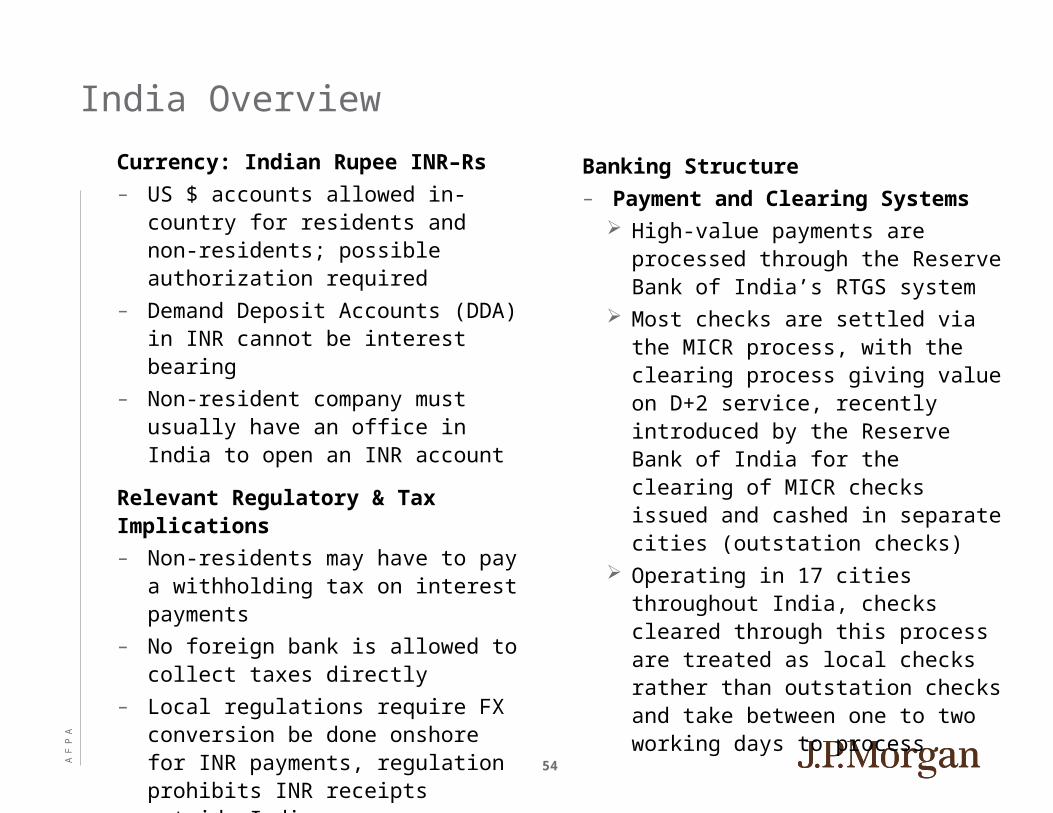

Currency: Indian Rupee INR–₨

– US $ accounts allowed in-country for residents and non-residents; possible authorization required

– Demand Deposit Accounts (DDA) in INR cannot be interest bearing

– Non-resident company must usually have an office in India to open an INR account

Relevant Regulatory & Tax Implications

– Non-residents may have to pay a withholding tax on interest payments

– No foreign bank is allowed to collect taxes directly

– Local regulations require FX conversion be done onshore for INR payments, regulation prohibits INR receipts outside India

Banking Structure

– Payment and Clearing Systems High-value payments are processed

through the Reserve Bank of India’s RTGS system

Most checks are settled via the MICR process, with the clearing process giving value on D+2 service, recently introduced by the Reserve Bank of India for the clearing of MICR checks issued and cashed in separate cities (outstation checks)

Operating in 17 cities throughout India, checks cleared through this process are treated as local checks rather than outstation checks and take between one to two working days to process

India Overview

AF

PA

55

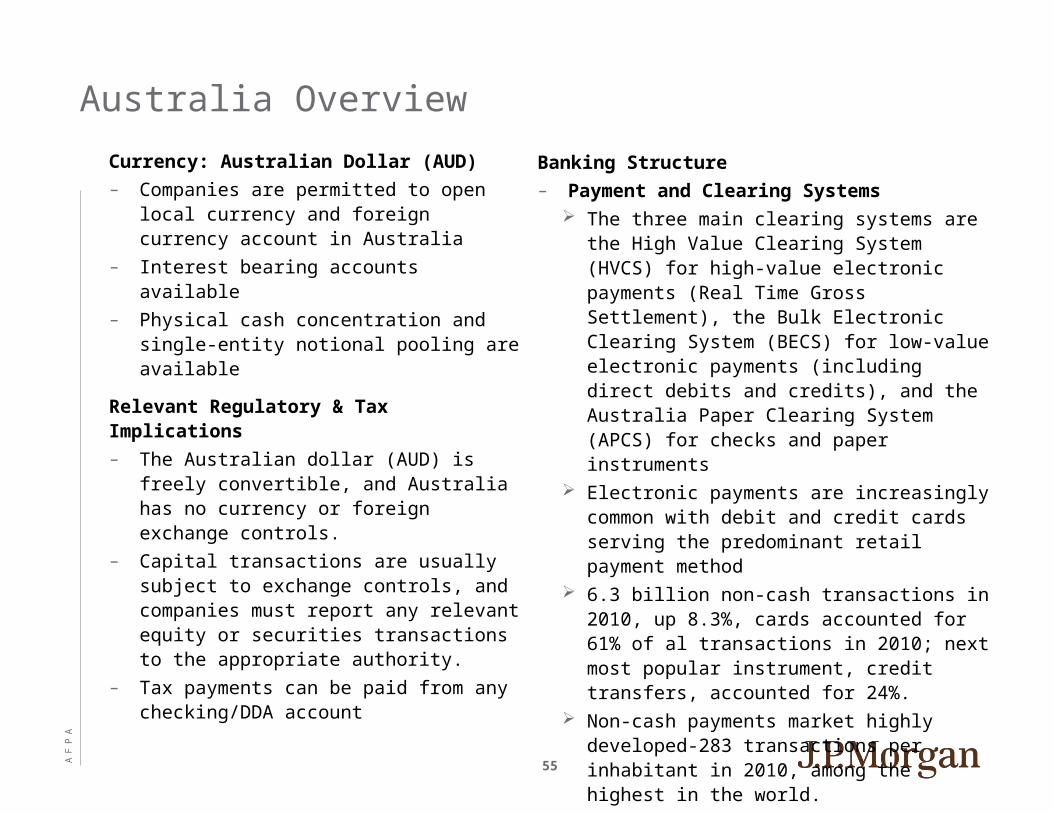

Currency: Australian Dollar (AUD)

– Companies are permitted to open local currency and foreign currency account in Australia

– Interest bearing accounts available

– Physical cash concentration and single-entity notional pooling are available

Relevant Regulatory & Tax Implications

– The Australian dollar (AUD) is freely convertible, and Australia has no currency or foreign exchange controls.

– Capital transactions are usually subject to exchange controls, and companies must report any relevant equity or securities transactions to the appropriate authority.

– Tax payments can be paid from any checking/DDA account

Banking Structure

– Payment and Clearing Systems The three main clearing systems are the High

Value Clearing System (HVCS) for high-value electronic payments (Real Time Gross Settlement), the Bulk Electronic Clearing System (BECS) for low-value electronic payments (including direct debits and credits), and the Australia Paper Clearing System (APCS) for checks and paper instruments

Electronic payments are increasingly common with debit and credit cards serving the predominant retail payment method

6.3 billion non-cash transactions in 2010, up 8.3%, cards accounted for 61% of al transactions in 2010; next most popular instrument, credit transfers, accounted for 24%.

Non-cash payments market highly developed-283 transactions per inhabitant in 2010, among the highest in the world.

Transaction reporting requirements to the central bank both in/out of Australia and if deposits are greater than AUD10,000

Australia Overview

AF

PA

56

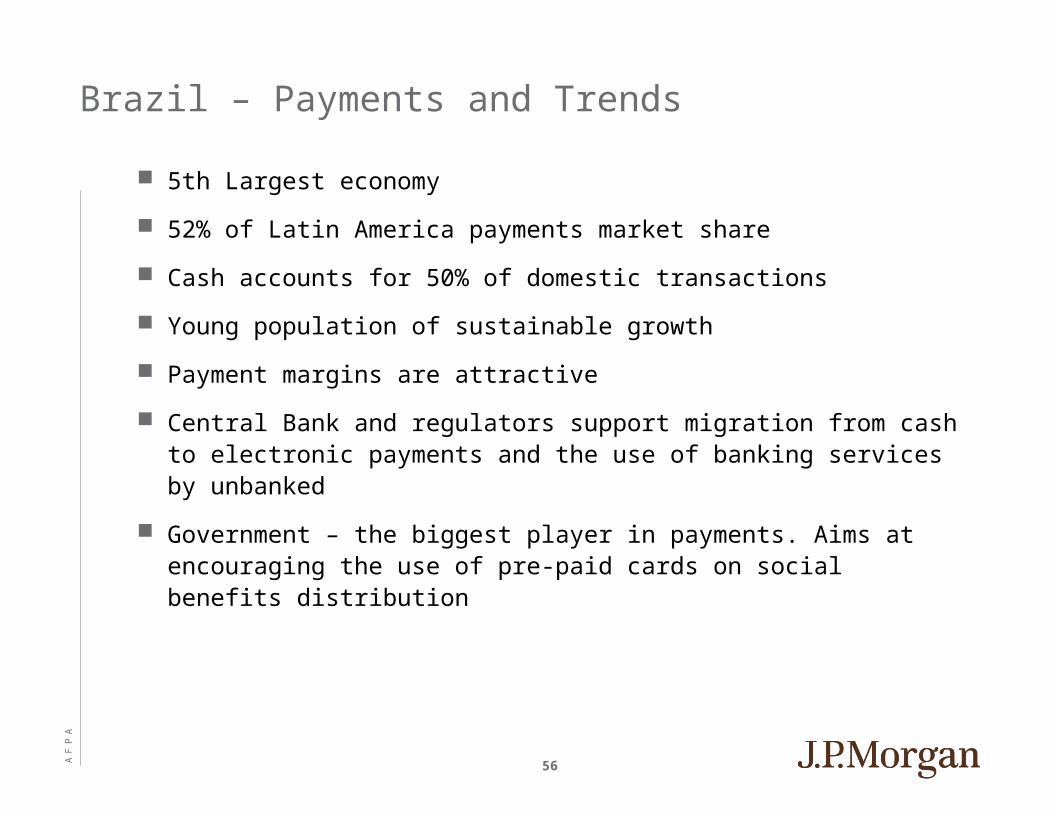

Brazil – Payments and Trends

5th Largest economy

52% of Latin America payments market share

Cash accounts for 50% of domestic transactions

Young population of sustainable growth

Payment margins are attractive

Central Bank and regulators support migration from cash to electronic payments and the use of banking services by unbanked

Government – the biggest player in payments. Aims at encouraging the use of pre-paid cards on social benefits distribution

AF

PA

57

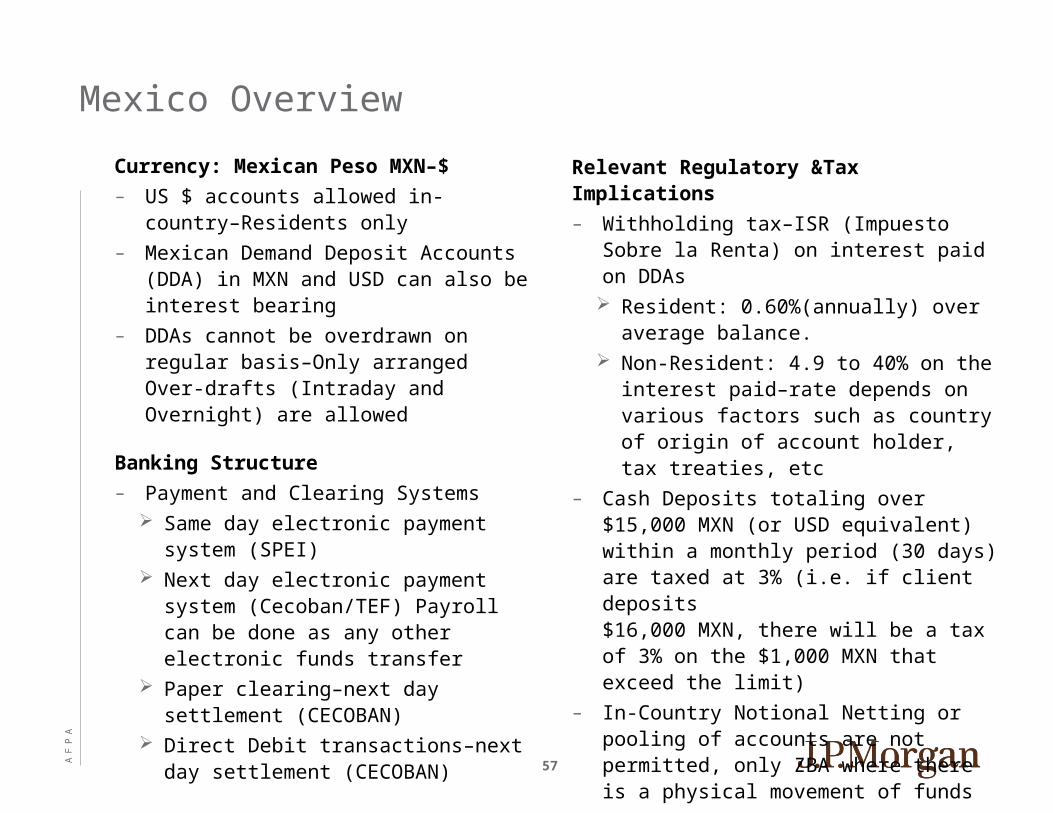

Currency: Mexican Peso MXN–$

– US $ accounts allowed in-country–Residents only

– Mexican Demand Deposit Accounts (DDA) in MXN and USD can also be interest bearing

– DDAs cannot be overdrawn on regular basis–Only arranged Over-drafts (Intraday and Overnight) are allowed

Banking Structure

– Payment and Clearing Systems Same day electronic payment system

(SPEI) Next day electronic payment system

(Cecoban/TEF) Payroll can be done as any other electronic funds transfer

Paper clearing–next day settlement (CECOBAN)

Direct Debit transactions–next day settlement (CECOBAN)

Relevant Regulatory &Tax Implications

– Withholding tax–ISR (Impuesto Sobre la Renta) on interest paid on DDAs Resident: 0.60%(annually) over average

balance. Non-Resident: 4.9 to 40% on the interest

paid–rate depends on various factors such as country of origin of account holder, tax treaties, etc

– Cash Deposits totaling over $15,000 MXN (or USD equivalent) within a monthly period (30 days) are taxed at 3% (i.e. if client deposits $16,000 MXN, there will be a tax of 3% on the $1,000 MXN that exceed the limit)

– In-Country Notional Netting or pooling of accounts are not permitted, only ZBA where there is a physical movement of funds

– No withholding tax on cross border transactions

Mexico Overview

AF

PA

58

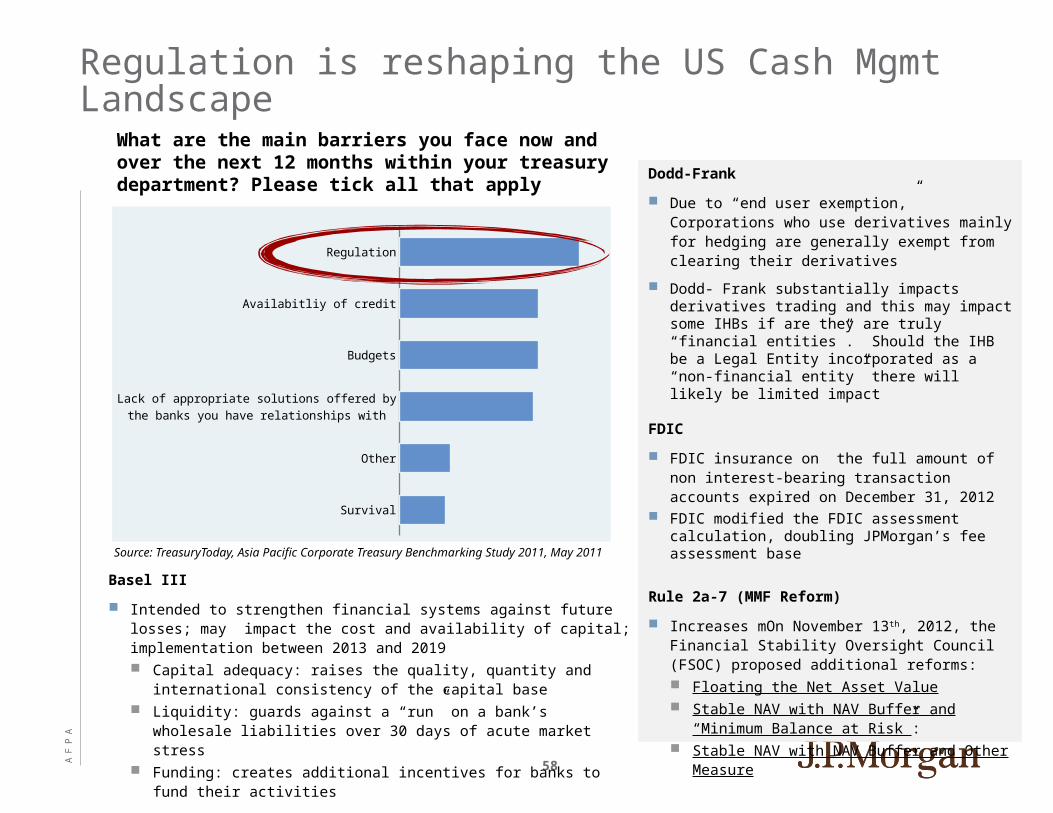

Regulation

Availabitliy of credit

Budgets

Lack of appropriate solutions offered by the banks you have relationships with

Other

Survival

Regulation is reshaping the US Cash Mgmt Landscape

Dodd-Frank

Due to “end user exemption,” Corporations who use derivatives mainly for hedging are generally exempt from clearing their derivatives

Dodd- Frank substantially impacts derivatives trading and this may impact some IHBs if are they are truly “financial entities”. Should the IHB be a Legal Entity incorporated as a “non-financial entity” there will likely be limited impact

FDIC

FDIC insurance on the full amount of non interest-bearing transaction accounts expired on December 31, 2012

FDIC modified the FDIC assessment calculation, doubling JPMorgan’s fee assessment base

Rule 2a-7 (MMF Reform)

Increases mOn November 13th, 2012, the Financial Stability Oversight Council (FSOC) proposed additional reforms: Floating the Net Asset Value Stable NAV with NAV Buffer and “Minimum

Balance at Risk”: Stable NAV with NAV Buffer and Other Measure

Source: TreasuryToday, Asia Pacific Corporate Treasury Benchmarking Study 2011, May 2011

W h a t a r e th e m a in b a r r ie r s y o u fa c e n o w a n d o v e r th e

n e x t 1 2 m o n th s w i th in y o u r t r e a s u r y d e p a r tm e n t? P le a s e

t ic k a l l th a t a p p ly

What are the main barriers you face now and over the next 12 months within your treasury department? Please tick all that apply

Basel III

Intended to strengthen financial systems against future losses; may impact the cost and availability of capital; implementation between 2013 and 2019 Capital adequacy: raises the quality, quantity and international

consistency of the capital base Liquidity: guards against a “run” on a bank’s wholesale liabilities over 30

days of acute market stress Funding: creates additional incentives for banks to fund their activities

AF

PA

59

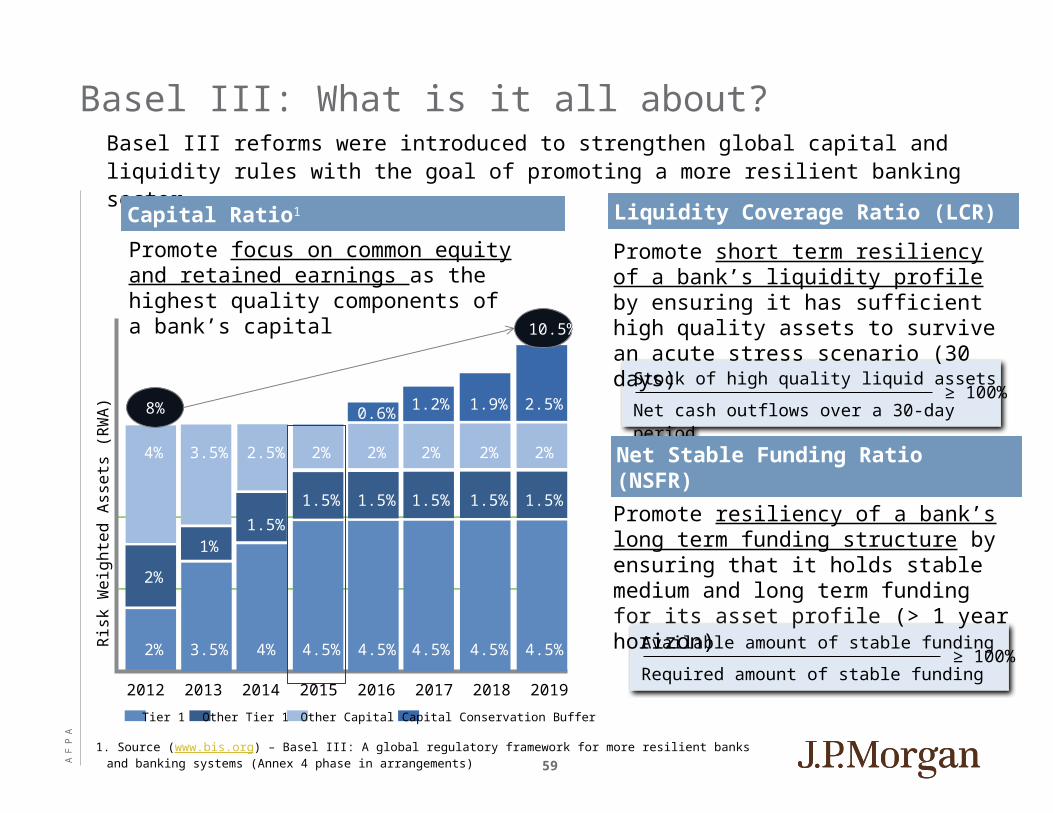

Basel III reforms were introduced to strengthen global capital and liquidity rules with the goal of promoting a more resilient banking sector.

2012 2013 2014 2015 2016 2017 2018 2019

Ris

k W

eig

hte

d A

sse

ts (

RW

A)

2% 3.5% 4% 4.5% 4.5% 4.5% 4.5% 4.5%

2%

1%1.5%

1.5% 1.5% 1.5% 1.5% 1.5%

4% 3.5% 2.5% 2% 2% 2% 2% 2%

0.6%1.2% 1.9% 2.5%

Tier 1 Other Tier 1 Other Capital Capital Conservation Buffer

8%

10.5%

Stock of high quality liquid assets

Net cash outflows over a 30-day period≥ 100%

Available amount of stable funding

Required amount of stable funding≥ 100%

Capital Ratio1Capital Ratio1 Liquidity Coverage Ratio (LCR)Liquidity Coverage Ratio (LCR)

Net Stable Funding Ratio (NSFR)Net Stable Funding Ratio (NSFR)

Promote short term resiliency of a bank’s liquidity profile by ensuring it has sufficient high quality assets to survive an acute stress scenario (30 days)

Promote resiliency of a bank’s long term funding structure by ensuring that it holds stable medium and long term funding for its asset profile (> 1 year horizon)

Promote focus on common equity and retained earnings as the highest quality components of a bank’s capital

1. Source (www.bis.org) – Basel III: A global regulatory framework for more resilient banks and banking systems (Annex 4 phase in arrangements)

Basel III: What is it all about?

AF

PA

60

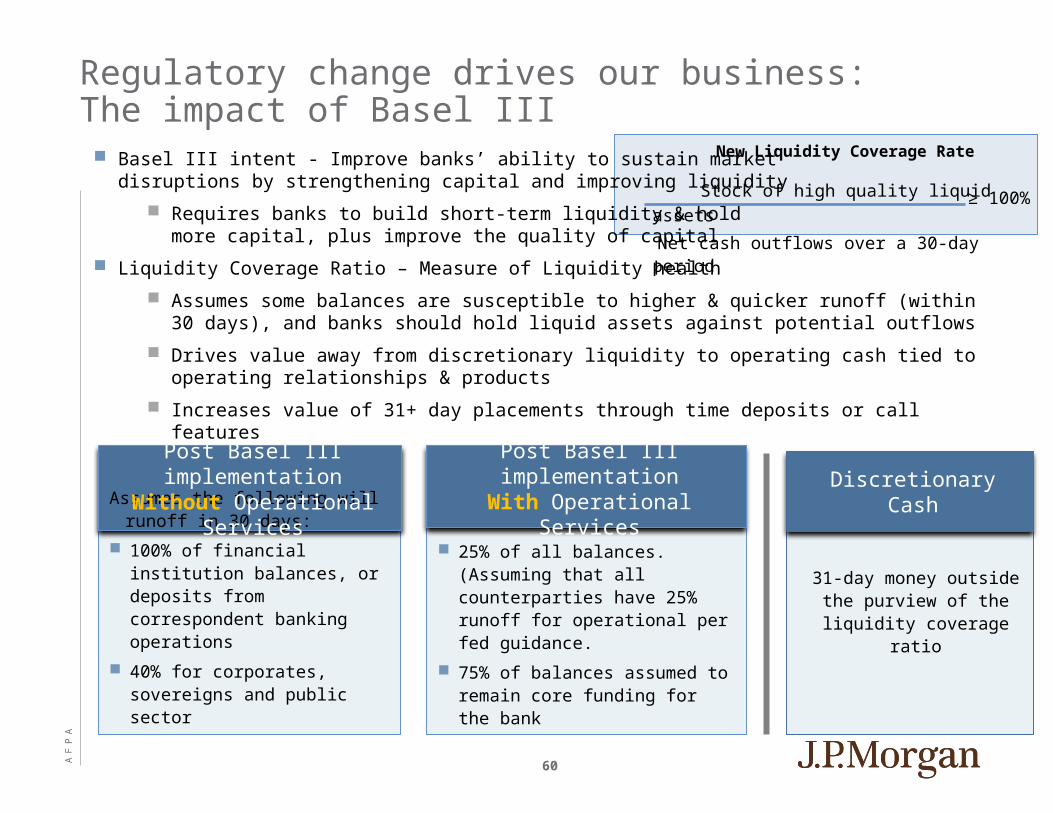

New Liquidity Coverage Rate

Stock of high quality liquid assets

Net cash outflows over a 30-day period

Regulatory change drives our business: The impact of Basel III

Basel III intent - Improve banks’ ability to sustain market disruptions by strengthening capital and improving liquidity

Requires banks to build short-term liquidity & hold more capital, plus improve the quality of capital

Liquidity Coverage Ratio – Measure of Liquidity health

Assumes some balances are susceptible to higher & quicker runoff (within 30 days), and banks should hold liquid assets against potential outflows

Drives value away from discretionary liquidity to operating cash tied to operating relationships & products

Increases value of 31+ day placements through time deposits or call features

31-day money outside the purview of the liquidity

coverage ratio

Discretionary Cash

Assumes the following will runoff in 30 days:

100% of financial institution balances, or deposits from correspondent banking operations

40% for corporates, sovereigns and public sector

Assumes the following will runoff in 30 days:

25% of all balances.(Assuming that all counterparties have 25% runoff for operational per fed guidance.

75% of balances assumed to remain core funding for the bank

Post Basel III implementationWith Operational Services

Post Basel III implementationWithout Operational Services

≥ 100%

AF

PA

61

Corporate Needs Implications to Corporates

Credit / Liquidity (incl. Trade /

Working Capital Loans)

Commercial Paper

Intraday Lines

Both committed and uncommitted credit lines will get expensive (and banks will be more judicious in extending credit)

Structured trade (high risk weights) will costs more

Commercial paper market is expected to shrink and cost likely will increase3 where CP issuance is issued with maturities

under 30 days Bank facilities that back CP programs

are counted as contingent liabilities

Intraday lines may become costly for banks to both fund and to absorb risk, putting financial pressure on low margin, high volume payment services based on Basel III committee guidance5

10% draw on committed credit lines1

100% draw on committed liquidity facilities1 for non – financial institutions, sovereigns, and central banks

100 % conversion on trade finance (exception – one year maturity floor for issued and confirmed LC 2 under certain conditions)

A 100% minimum liquidity1 (cash or certain liquid assets) against net outflows less than 30 days

Regulation advocates an approach that places an emphasis to have adequate systems in place to measure and manage intraday liquidity risks4,5

Basel III Guidance

1. 2. 5. Source (www.bis.org) – Basel III: International framework for liquidity risk measurement, standards and monitoring (II.1.97. page 21)

3. Source (www.bis.org) – J.P. Morgan North America Fixed Income Strategy (27 September 2010) – Short Term Market Outlook and Strategy

4. Source – Financial Stability Paper No. 11 – June 2011 (Intraday Liquidity: risk and regulation); Bank of England

Credit implications of Basel III to corporations

AF

PA

62

Dodd Frank Section 1073

Two completely different public policies are covered

Congress seems to express support for an interest in expansion of international remittances

Federal Reserve Board required to report to Congress every two years on growth of international remittances and on factors that limit growth

Congress establishes new consumer protections and requires the Consumer Financial Protection Bureau (CFPB) to implement those protections by rule making

AF

PA

63

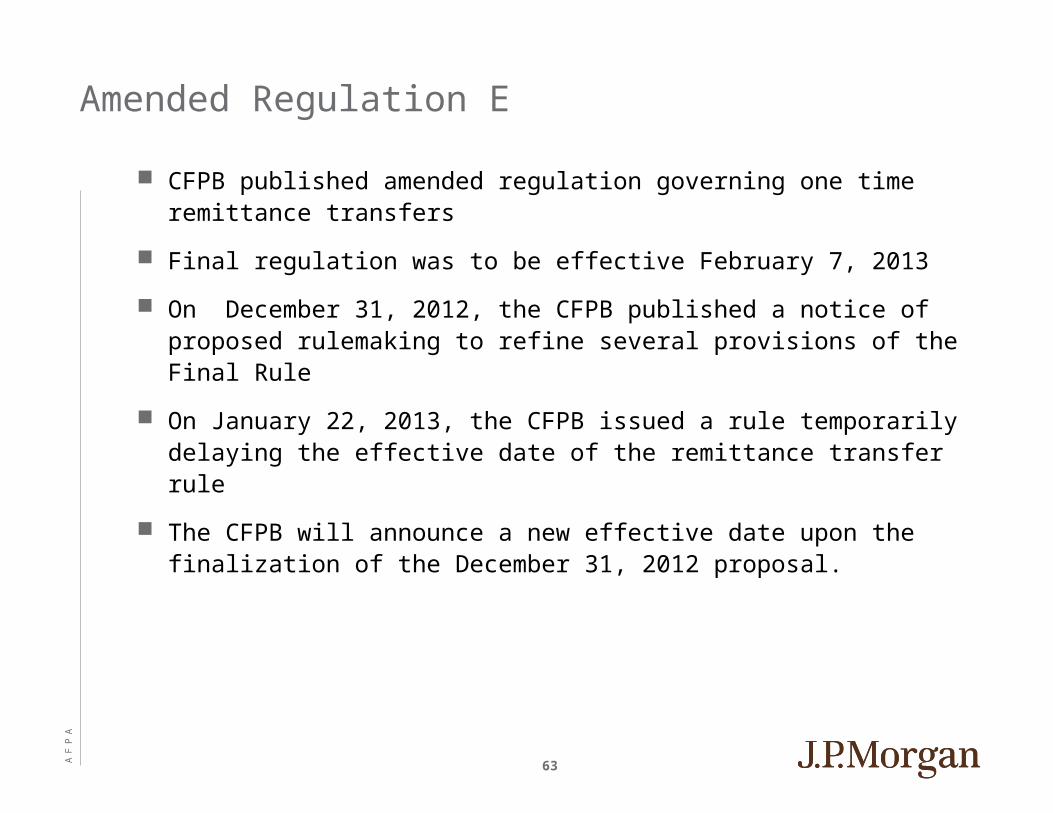

Amended Regulation E

CFPB published amended regulation governing one time remittance transfers

Final regulation was to be effective February 7, 2013

On December 31, 2012, the CFPB published a notice of proposed rulemaking to refine several provisions of the Final Rule

On January 22, 2013, the CFPB issued a rule temporarily delaying the effective date of the remittance transfer rule

The CFPB will announce a new effective date upon the finalization of the December 31, 2012 proposal.

AF

PA

64

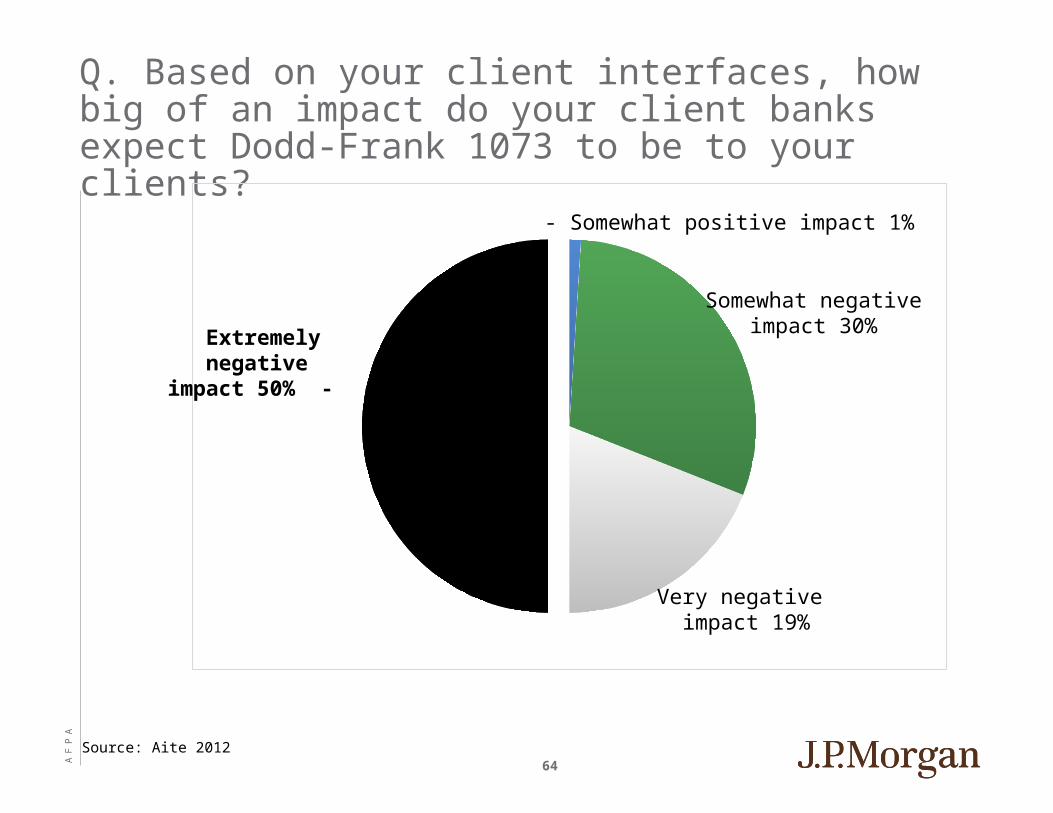

Q. Based on your client interfaces, how big of an impact do your client banks expect Dodd-Frank 1073 to be to your clients?

- Somewhat positive impact 1%

Somewhat negative impact 30%

Very negative impact 19%

Extremely negative impact 50% -

Source: Aite 2012

AF

PA

65

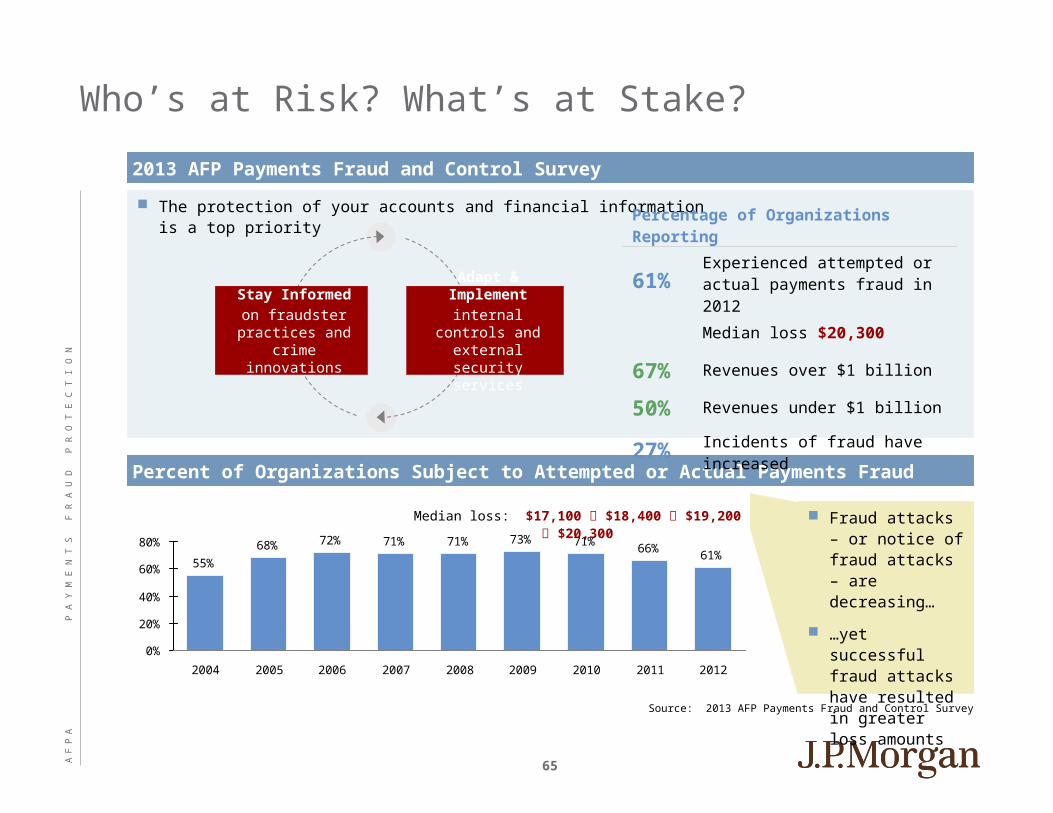

The protection of your accounts and financial information is a top priority

Who’s at Risk? What’s at Stake?

Source: 2013 AFP Payments Fraud and Control Survey

2013 AFP Payments Fraud and Control Survey2013 AFP Payments Fraud and Control Survey

Percent of Organizations Subject to Attempted or Actual Payments FraudPercent of Organizations Subject to Attempted or Actual Payments Fraud

55%

68% 72% 71% 71% 73% 71%66%

61%

0%

20%

40%

60%

80%

2004 2005 2006 2007 2008 2009 2010 2011 2012

Percentage of Organizations Reporting

61% Experienced attempted or actual payments fraud in 2012

Median loss $20,300

67% Revenues over $1 billion

50% Revenues under $1 billion

27% Incidents of fraud have increased

Fraud attacks – or notice of fraud attacks – are decreasing…

…yet successful fraud attacks have resulted in greater loss amounts

Stay Informed

on fraudster practices and crime

innovations

Adapt & Implement

internal controls and external security

services

Median loss: $17,100 $18,400 $19,200 $20,300

P A

Y M

E N

T S

F

R A

U D

P

R O

T E

C T

I O

N

AF

PA

66

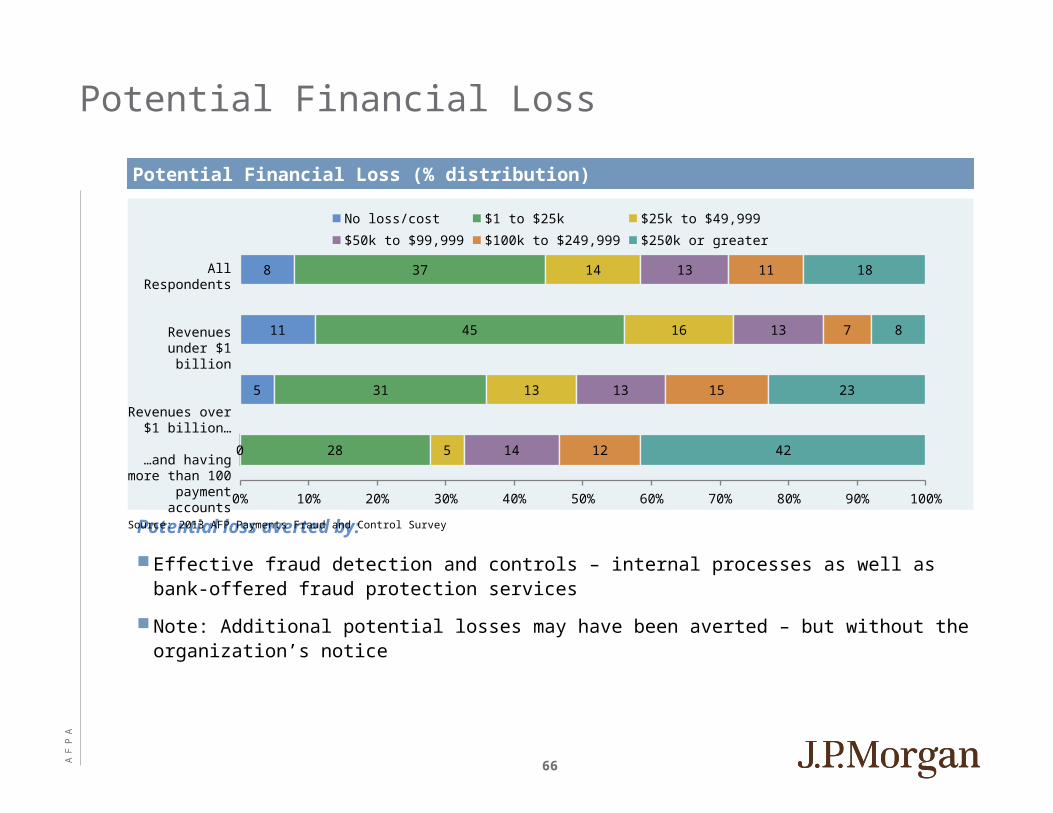

Potential Financial Loss

Potential loss averted by:

Effective fraud detection and controls – internal processes as well as bank-offered fraud protection services

Note: Additional potential losses may have been averted – but without the organization’s notice

Potential Financial Loss (% distribution)Potential Financial Loss (% distribution)

Source: 2013 AFP Payments Fraud and Control Survey

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

8

11

5

0

37

45

31

28

14

16

13

5

13

13

13

14

11

7

15

12

18

8

23

42

No loss/cost $1 to $25k $25k to $49,999 $50k to $99,999 $100k to $249,999 $250k or greater

All Respondents

Revenues under $1 billion

Revenues over $1 billion…

…and having more than 100

payment accounts

AF

PA

67

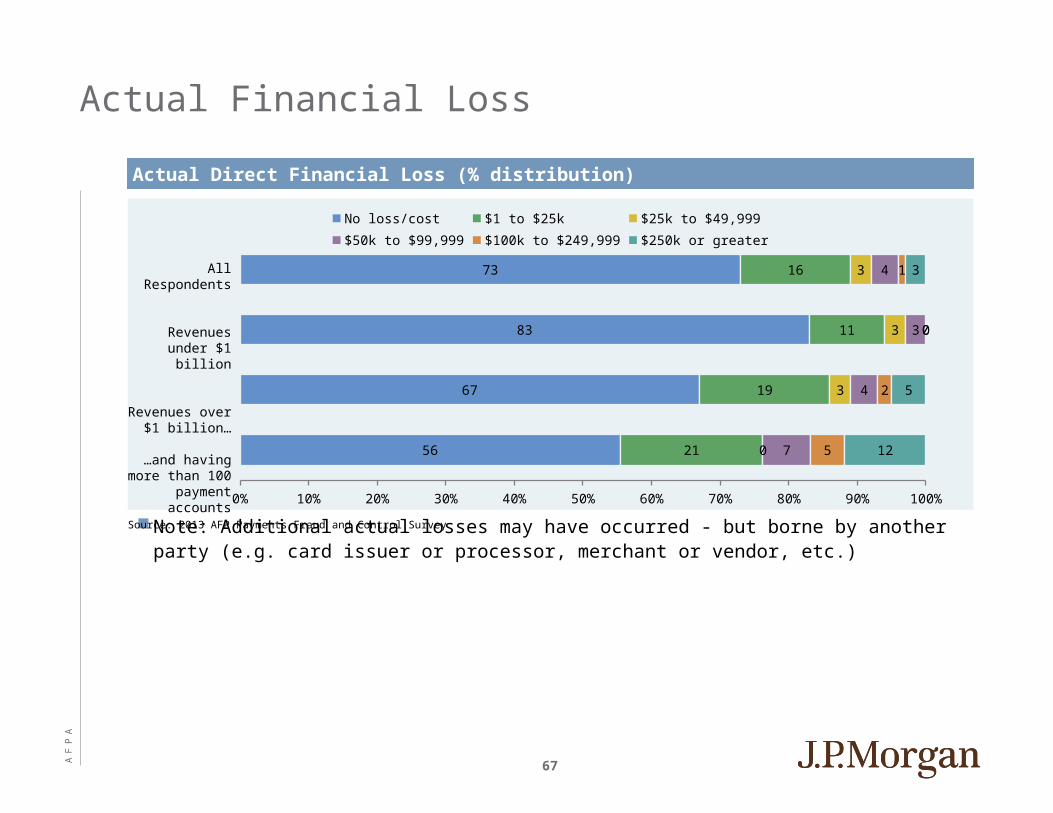

Actual Financial Loss

Note: Additional actual losses may have occurred - but borne by another party (e.g. card issuer or processor, merchant or vendor, etc.)

Actual Direct Financial Loss (% distribution)Actual Direct Financial Loss (% distribution)

Source: 2013 AFP Payments Fraud and Control Survey

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

73

83

67

56

16

11

19

21

3

3

3

0

4

3

4

7

1

0

2

5

3

0

5

12

No loss/cost $1 to $25k $25k to $49,999 $50k to $99,999 $100k to $249,999 $250k or greater

All Respondents

Revenues under $1 billion

Revenues over $1 billion…

…and having more than 100

payment accounts

AF

PA

68

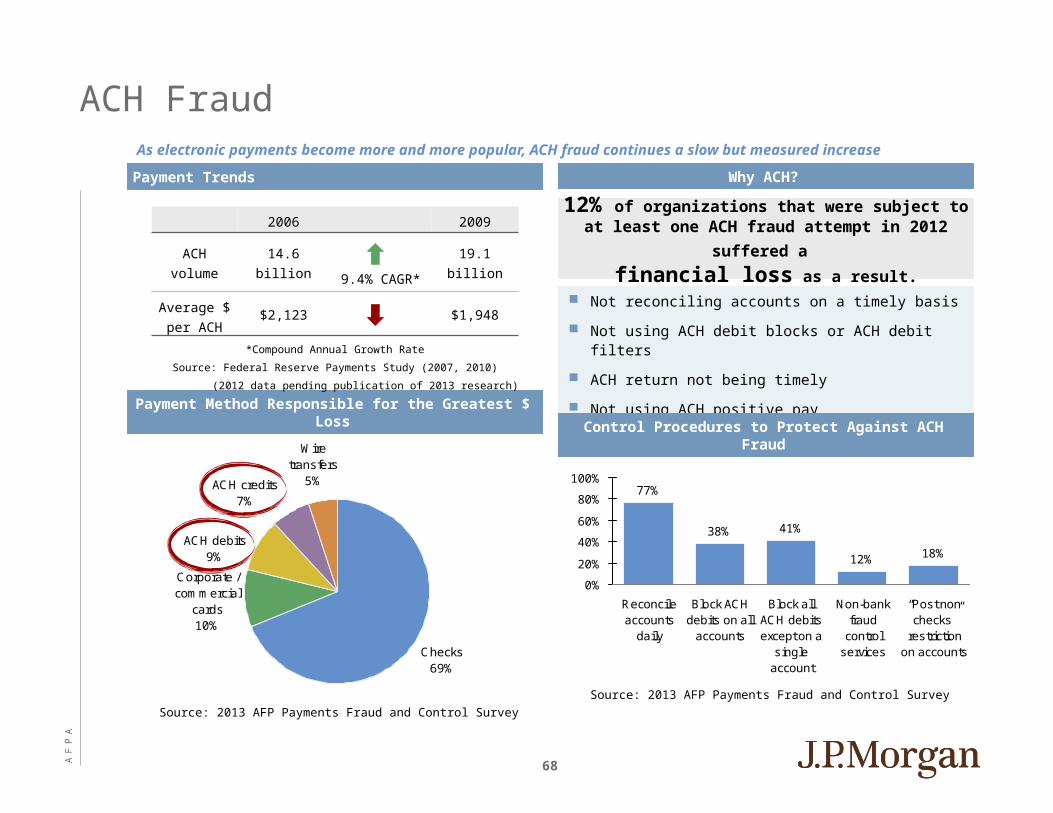

ACH FraudAs electronic payments become more and more popular, ACH fraud continues a slow but measured increase

Not reconciling accounts on a timely basis

Not using ACH debit blocks or ACH debit filters

ACH return not being timely

Not using ACH positive pay

Source: 2013 AFP Payments Fraud and Control Survey

Payment TrendsPayment Trends

Control Procedures to Protect Against ACH FraudControl Procedures to Protect Against ACH Fraud

12% of organizations that were subject to at least

one ACH fraud attempt in 2012 suffered a financial loss as a result.

77%

38% 41%

12% 18%

0%

20%

40%

60%

80%

100%

Reconcileaccounts

daily

Block ACHdebits on all

accounts

Block allACH debitsexcept on a

singleaccount

Non-bankfraud

controlservices

“Post nonchecks”

restrictionon accounts

Why ACH?Why ACH?

Payment Method Responsible for the Greatest $ LossPayment Method Responsible for the Greatest $ Loss

Source: 2013 AFP Payments Fraud and Control Survey

Checks69%

ACH debits9%

Wire transfers

5%ACH credits7%

Corporate / commercial

cards10%

2006 2009

ACH volume 14.6 billion9.4% CAGR*

19.1 billion

Average $ per ACH

$2,123 $1,948

*Compound Annual Growth Rate

Source: Federal Reserve Payments Study (2007, 2010)

(2012 data pending publication of 2013 research)

AF

PA

69

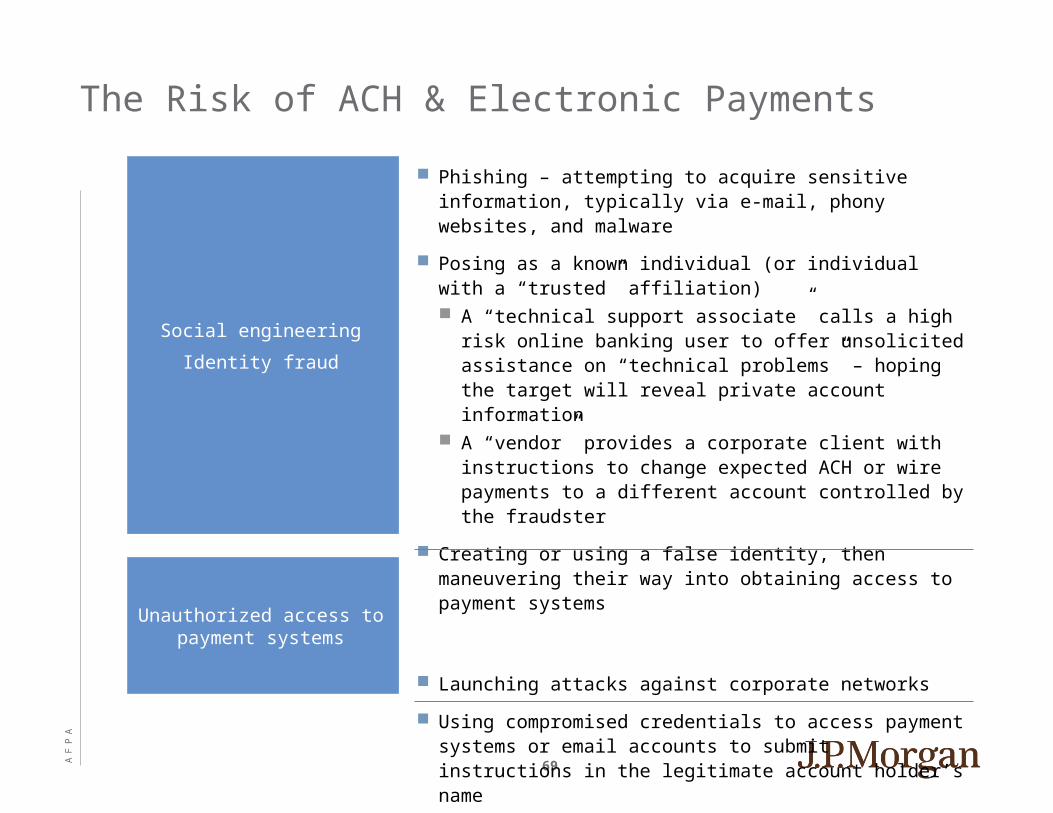

Phishing – attempting to acquire sensitive information, typically via e-mail, phony websites, and malware

Posing as a known individual (or individual with a “trusted” affiliation) A “technical support associate” calls a high risk online

banking user to offer unsolicited assistance on “technical problems” – hoping the target will reveal private account information

A “vendor” provides a corporate client with instructions to change expected ACH or wire payments to a different account controlled by the fraudster

Creating or using a false identity, then maneuvering their way into obtaining access to payment systems

Launching attacks against corporate networks

Using compromised credentials to access payment systems or email accounts to submit instructions in the legitimate account holder’s name

The Risk of ACH & Electronic Payments

Social engineering

Identity fraud

Unauthorized access to payment systems