Embed Size (px)

Citation preview

Asw

ath Dam

odaran1

Valuation

Asw

ath Dam

odaran

http://ww

w.dam

odaran.com

Asw

ath Dam

odaran2

Some Initial T

houghts

" One hundred thousand lem

mings cannot be w

rong"

Graffiti

Asw

ath Dam

odaran3

Misconceptions about V

aluation

Myth 1: A

valuation is an objective search for “true” value•

Truth 1.1: A

ll valuations are biased. The only questions are how

much and in

which direction.

•T

ruth 1.2: The direction and m

agnitude of the bias in your valuation is directlyproportional to w

ho pays you and how m

uch you are paid.

Myth 2.: A

good valuation provides a precise estimate of value

•T

ruth 2.1: There are no precise valuations

•T

ruth 2.2: The payoff to valuation is greatest w

hen valuation is least precise.

Myth 3: . T

he more quantitative a m

odel, the better the valuation•

Truth 3.1: O

ne’s understanding of a valuation model is inversely proportional to

the number of inputs required for the m

odel.

•T

ruth 3.2: Simpler valuation m

odels do much better than com

plex ones.

Asw

ath Dam

odaran4

Approaches to V

aluation

Discounted cashflow

valuation, relates the value of an asset to the present

value of expected future cashflows on that asset.

Relative valuation

, estimates the value of an asset by looking at the pricing of

'comparable' assets relative to a com

mon variable like earnings, cashflow

s,book value or sales.

Contingent claim

valuation, uses option pricing m

odels to measure the value

of assets that share option characteristics.

Asw

ath Dam

odaran5

Discounted C

ash Flow V

aluation

What is it: In discounted cash flow

valuation, the value of an asset is thepresent value of the expected cash flow

s on the asset.

Philosophical B

asis: Every asset has an intrinsic value that can be estim

ated,based upon its characteristics in term

s of cash flows, grow

th and risk.

Information N

eeded: To use discounted cash flow

valuation, you need•

to estimate the life of the asset

•to estim

ate the cash flows during the life of the asset

•to estim

ate the discount rate to apply to these cash flows to get present value

Market Inefficiency: M

arkets are assumed to m

ake mistakes in pricing assets

across time, and are assum

ed to correct themselves over tim

e, as newinform

ation comes out about assets.

Asw

ath Dam

odaran6

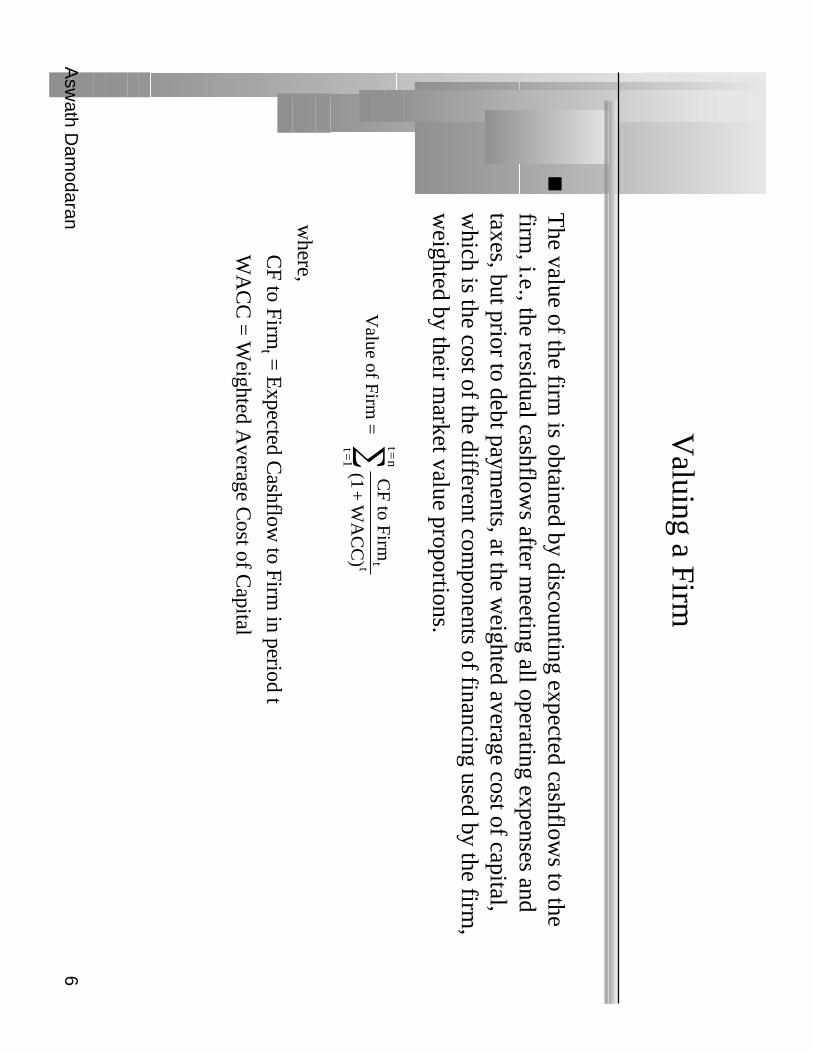

Valuing a Firm

The value of the firm

is obtained by discounting expected cashflows to the

firm, i.e., the residual cashflow

s after meeting all operating expenses and

taxes, but prior to debt payments, at the w

eighted average cost of capital,w

hich is the cost of the different components of financing used by the firm

,w

eighted by their market value proportions.

where,

CF to Firm

t = E

xpected Cashflow

to Firm in period t

WA

CC

= W

eighted Average C

ost of Capital

Value of F

irm=

C

F to F

irm

(1+

WA

CC

) ttt=

1

t=n

∑

Asw

ath Dam

odaran7

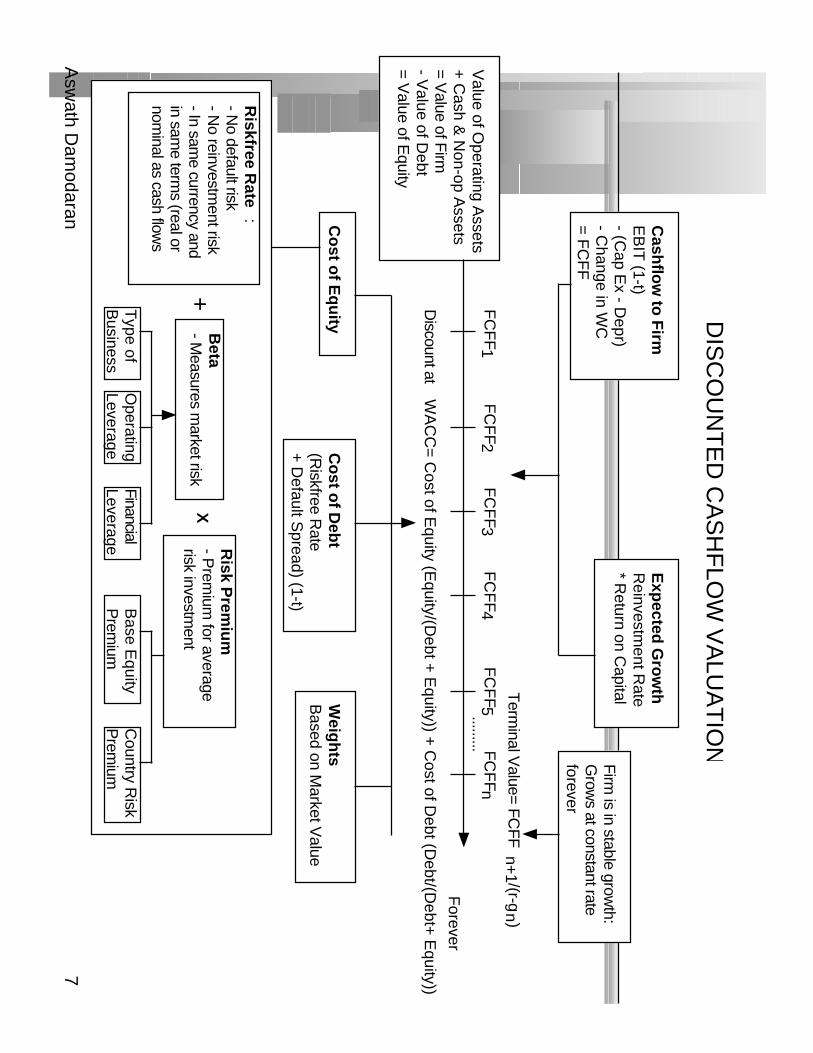

Cash

flow

to F

irmE

BIT

(1-t)- (C

ap Ex - D

epr)- C

hange in WC

= F

CF

F

Exp

ected G

row

thR

einvestment R

ate* R

eturn on Capital

FC

FF1

FC

FF2

FC

FF3

FC

FF4

FC

FF5

Forever

Firm

is in stable growth:

Grow

s at constant rateforever

Term

inal Value= F

CF

Fn+

1 /(r-gn

)

FC

FFn

.........

Co

st of E

qu

ityC

ost o

f Deb

t(R

iskfree Rate

+ D

efault Spread) (1-t)

Weig

hts

Based on M

arket Value

Discount at

WA

CC

= C

ost of Equity (E

quity/(Debt +

Equity)) +

Cost of D

ebt (Debt/(D

ebt+ E

quity))

Value of O

perating Assets

+ C

ash & N

on-op Assets

= Value of F

irm- V

alue of Debt

= Value of E

quity

Riskfree R

ate:

- No default risk

- No reinvestm

ent risk- In sam

e currency andin sam

e terms (real or

nominal as cash flow

s

+B

eta- M

easures market risk

X

Risk P

remiu

m- P

remium

for averagerisk investm

ent

Type of

Business

Operating

LeverageFinancialLeverage

Base E

quityP

remium

Country R

iskP

remium

DIS

CO

UN

TE

D C

AS

HF

LOW

VA

LUA

TIO

N

Asw

ath Dam

odaran8

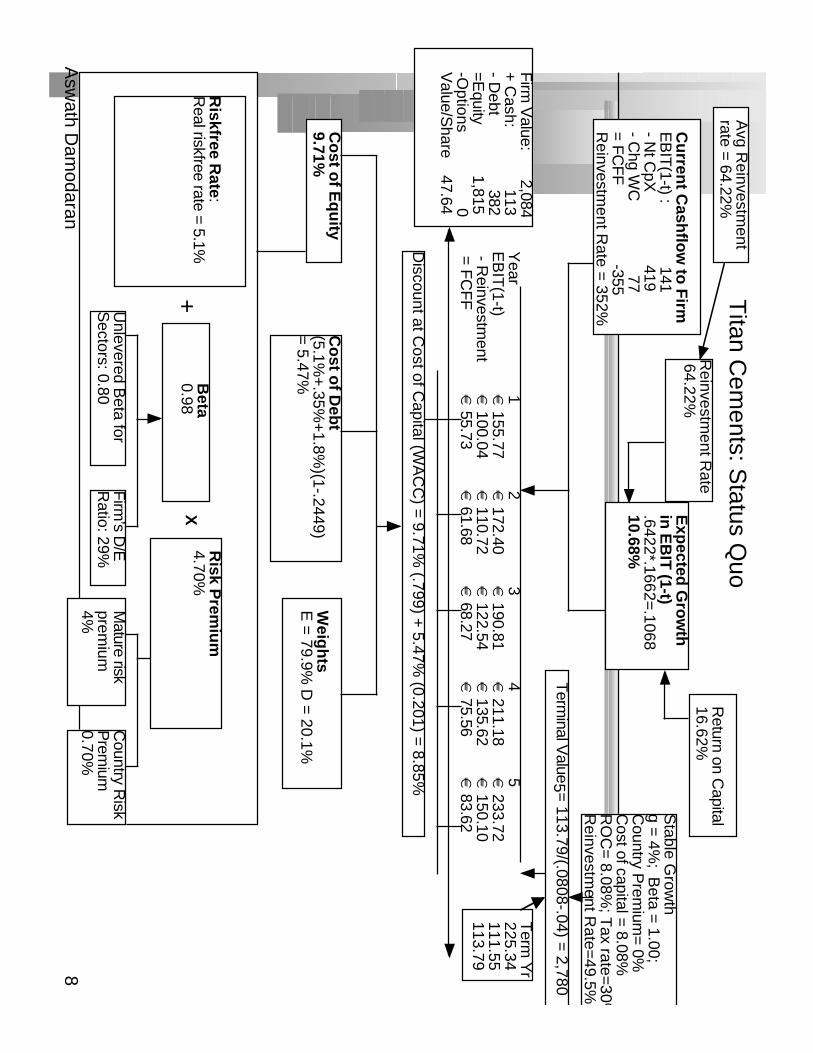

Cu

rrent C

ashflo

w to

Firm

EB

IT(1-t) : 141

- Nt C

pX 419

- Ch g W

C 77

= FC

FF

-355R

einvestment R

ate = 352%

Exp

ected G

row

th

in E

BIT

(1-t).6422*.1662=

.106810.68%

Stable G

rowth

g = 4%

; Beta =

1.00;C

ountry Prem

ium= 0%

Cost of capital = 8.08%

R

OC

= 8.08%

; Tax rate=

30 %R

einvestment R

ate=49.5%

Term

inal Value5 =

113.79/(.0808-.04) = 2,780

Co

st of E

qu

ity9.71%

Co

st of D

ebt

(5.1%+

.35%+

1.8%)(1-.2449)

= 5.47%

Weig

hts

E =

79.9% D

= 20.1%

Discount at C

ost of Capital (W

AC

C) =

9.71% (.799) +

5.47% (0.201) =

8.85%

Firm

Value: 2,084

+ C

ash: 113

- Debt 382

=Equity 1,815

-Options

0V

alue/Share 47.64

Riskfree R

ate:R

eal riskfree rate = 5.1%+

Beta

0.98X

Risk P

remiu

m4.70%

Unlevered B

eta for S

ectors: 0.80F

irm’s D

/ER

atio: 29%M

ature riskprem

ium4%

Country R

iskP

remium

0.70%

Titan C

ements: S

tatus Quo

Reinvestm

ent Rate

64.22%

Return on C

apital16.62%

Term

Yr

225.34111.55113.79

Avg R

einvestment

rate = 64.22%

Year

12

34

5E

BIT

(1-t)€

155.77€

172.40€

190.81€

211.18€

233.72 - R

einvestment

€ 100.04

€ 110.72

€ 122.54

€ 135.62

€ 150.10

= F

CF

F€

55.73€

61.68€

68.27€

75.56€

83.62

Asw

ath Dam

odaran9

FC

FF1

FC

FF2

FC

FF3

FC

FF4

FC

FF5

Forever

Term

inal Value= F

CF

Fn+

1/(r-g

n)

FC

FFn

.........

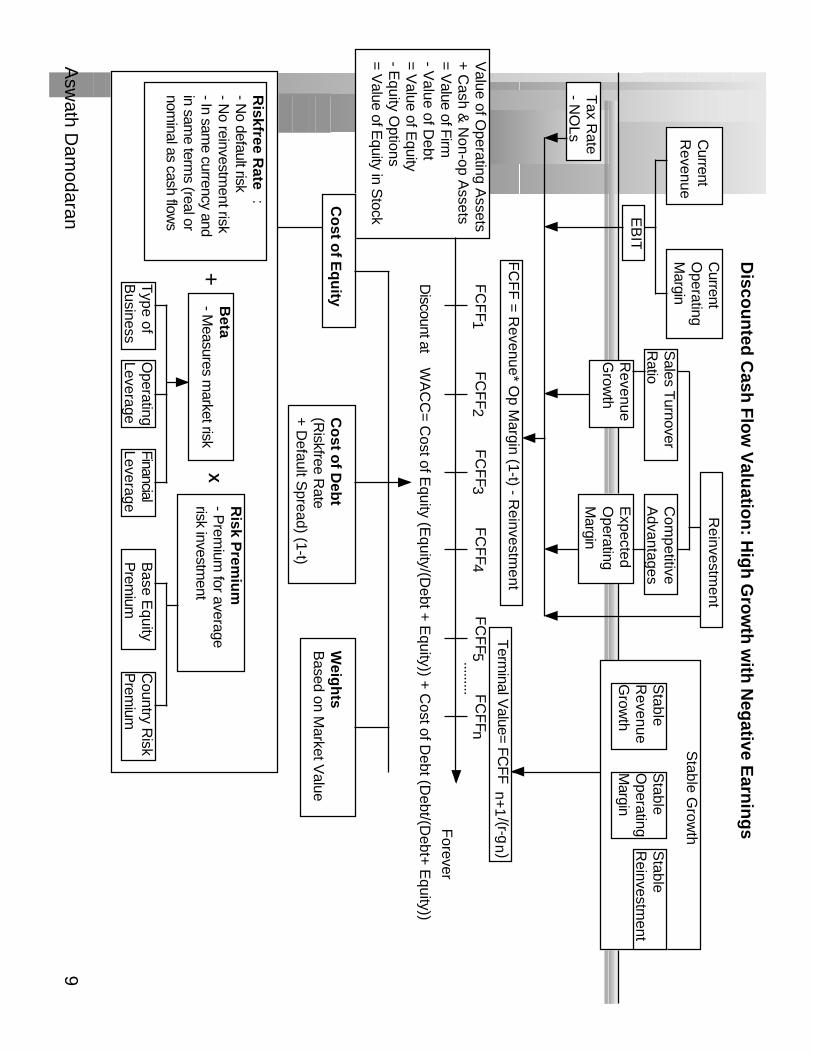

Co

st of E

qu

ityC

ost o

f Deb

t(R

iskfree Rate

+ D

efault Spread) (1-t)

Weig

hts

Based on M

arket Value

Discount at

WA

CC

= C

ost of Equity (E

quity/(Debt +

Equity)) +

Cost of D

ebt (Debt/(D

ebt+ E

quity))

Value of O

perating Assets

+ C

ash & N

on-op Assets

= Value of F

irm- V

alue of Debt

= Value of E

quity- E

quity Options

= Value of E

quity in Stock

Riskfree R

ate:

- No default risk

- No reinvestm

ent risk- In sam

e currency andin sam

e terms (real or

nominal as cash flow

s

+B

eta- M

easures market risk

X

Risk P

remiu

m- P

remium

for averagerisk investm

ent

Type of

Business

Operating

LeverageFinancialLeverage

Base E

quityP

remium

Country R

iskP

remium

Current

Revenue

Current

Operating

Margin

Reinvestm

ent

Sales T

urnoverR

atioC

ompetitive

Advantages

Revenue

Grow

thE

xpected O

perating M

argin

Stable G

rowth

Stable

Revenue

Grow

th

Stable

Operating

Margin

Stable

Reinvestm

ent

Disco

un

ted C

ash F

low

Valu

ation

: Hig

h G

row

th w

ith N

egative E

arnin

gs

EB

IT

Tax R

ate- N

OLs

FC

FF

= R

evenue* Op M

argin (1-t) - Reinvestm

ent

Asw

ath Dam

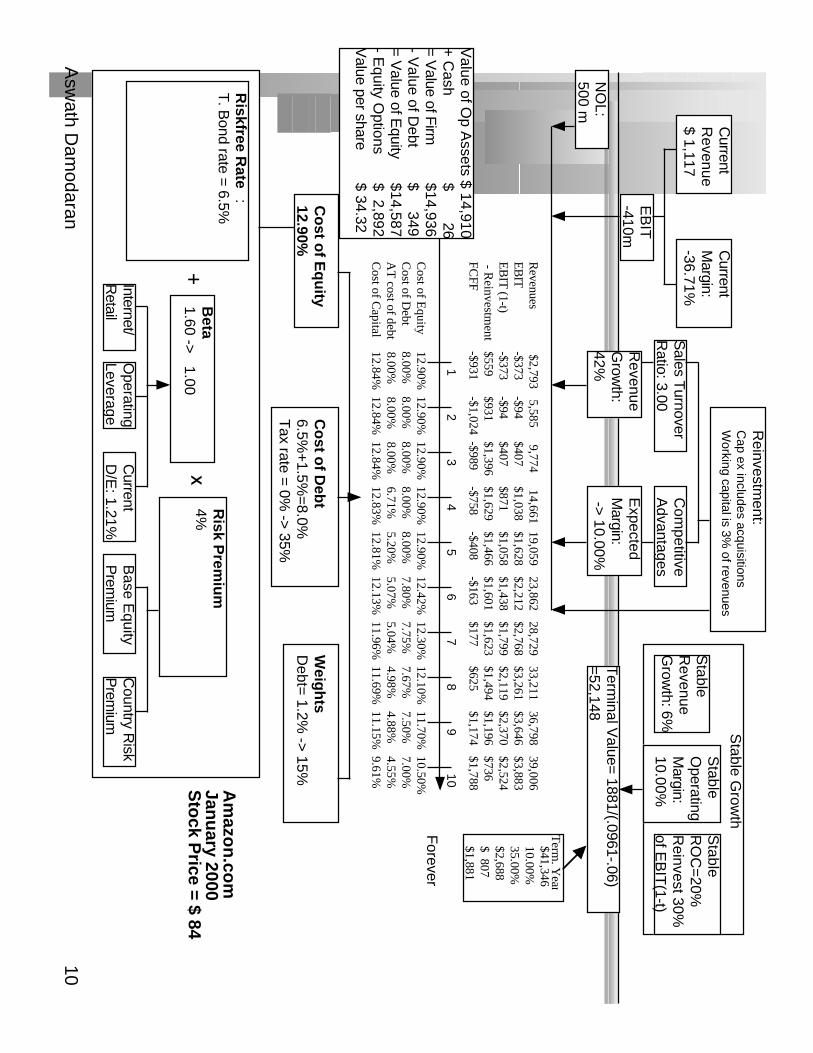

odaran10

Forever

Term

inal Value= 1881/(.0961-.06)

=52,148

Co

st of E

qu

ity12.90%

Co

st of D

ebt

6.5%+

1.5%=

8.0%T

ax rate = 0% -> 35%

Weig

hts

Debt=

1.2% ->

15%

Value of O

p Assets $ 14,910

+ C

ash $ 26

= Value of F

irm$14,936

- Value of D

ebt$ 349

= Value of E

quity$14,587

- Equity O

ptions$ 2,892

Value per share

$ 34.32

Riskfree R

ate:

T. B

ond rate = 6.5%

+B

eta1.60 ->

1.00X

Risk P

remiu

m4%

Internet/R

etailO

perating Leverage

Current

D/E

: 1.21%B

ase Equity

Prem

iumC

ountry Risk

Prem

ium

Current

Revenue

$ 1,117

Current

Margin:

-36.71%

Reinvestm

ent:C

ap ex includes acquisitionsW

orking capital is 3% of revenues

Sales T

urnoverR

atio: 3.00C

ompetitive

Advantages

Revenue

Grow

th:42%

Expected

Margin:

-> 10.00%

Stable G

rowth

Stable

Revenue

Grow

th: 6%

Stable

Operating

Margin:

10.00%

Stable

RO

C=

20%R

einvest 30%

of EB

IT(1-t)

EB

IT-410m

NO

L:500 m

$41,346 10.00%

35.00%$2,688 $ 807 $1,881

Term

. Yea r

24

31

56

89

107

Cost of E

quity12.90%

12.90%12.90%

12.90%12.90%

12.42%12.30%

12.10%11.70%

10.50%C

ost of Debt

8.00%8.00%

8.00%8.00%

8.00%7.80%

7.75%7.67%

7.50%7.00%

AT

cost of debt8.00%

8.00%8.00%

6.71%5.20%

5.07%5.04%

4.98%4.88%

4.55%C

ost of Capital

12.84%12.84%

12.84%12.83%

12.81%12.13%

11.96%11.69%

11.15%9.61%

Revenues

$2,793 5,585

9,774 14,661

19,059 23,862

28,729 33,211

36,798 39,006

E

BIT

-$373-$94

$407$1,038

$1,628$2,212

$2,768$3,261

$3,646$3,883

EB

IT (1-t)

-$373-$94

$407$871

$1,058$1,438

$1,799$2,119

$2,370$2,524

- Reinvestm

ent$559

$931$1,396

$1,629$1,466

$1,601$1,623

$1,494$1,196

$736FC

FF-$931

-$1,024-$989

-$758-$408

-$163$177

$625$1,174

$1,788Am

azon

.com

Janu

ary 2000S

tock P

rice = $ 84

Asw

ath Dam

odaran11

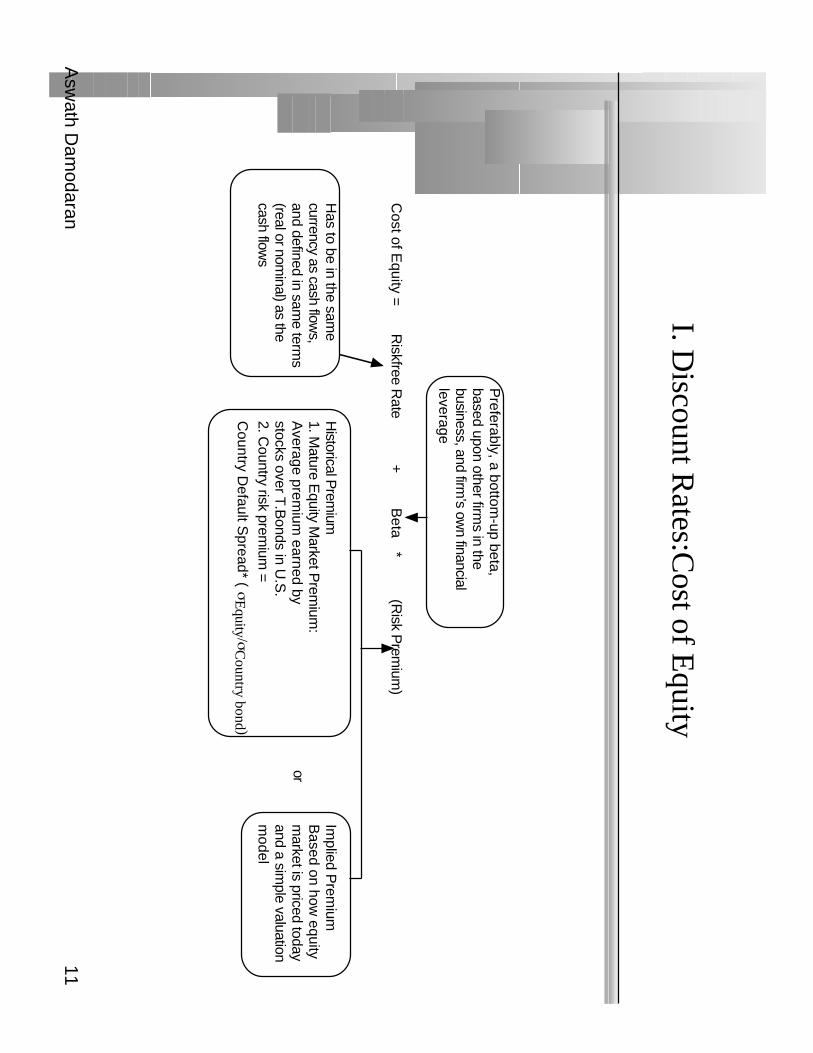

I. Discount R

ates:Cost of E

quity

Cost of E

quity =R

iskfree Rate

+B

eta*

(Risk P

remium

)

Has to be in the sam

ecurrency as cash flow

s, and defined in sam

e terms

(real or nominal) as the

cash flows

Preferably, a bottom

-up beta,based upon other firm

s in thebusiness, and firm

’s own financial

leverage

Historical P

remium

1. Mature E

quity Market P

remium

:A

verage premium

earned bystocks over T

.Bonds in U

.S.

2. Country risk prem

ium =

Country D

efault Spread* (

σE

quity /σC

ountry bond )

Implied P

remium

Based on how

equitym

arket is priced todayand a sim

ple valuationm

odel

or

Asw

ath Dam

odaran12

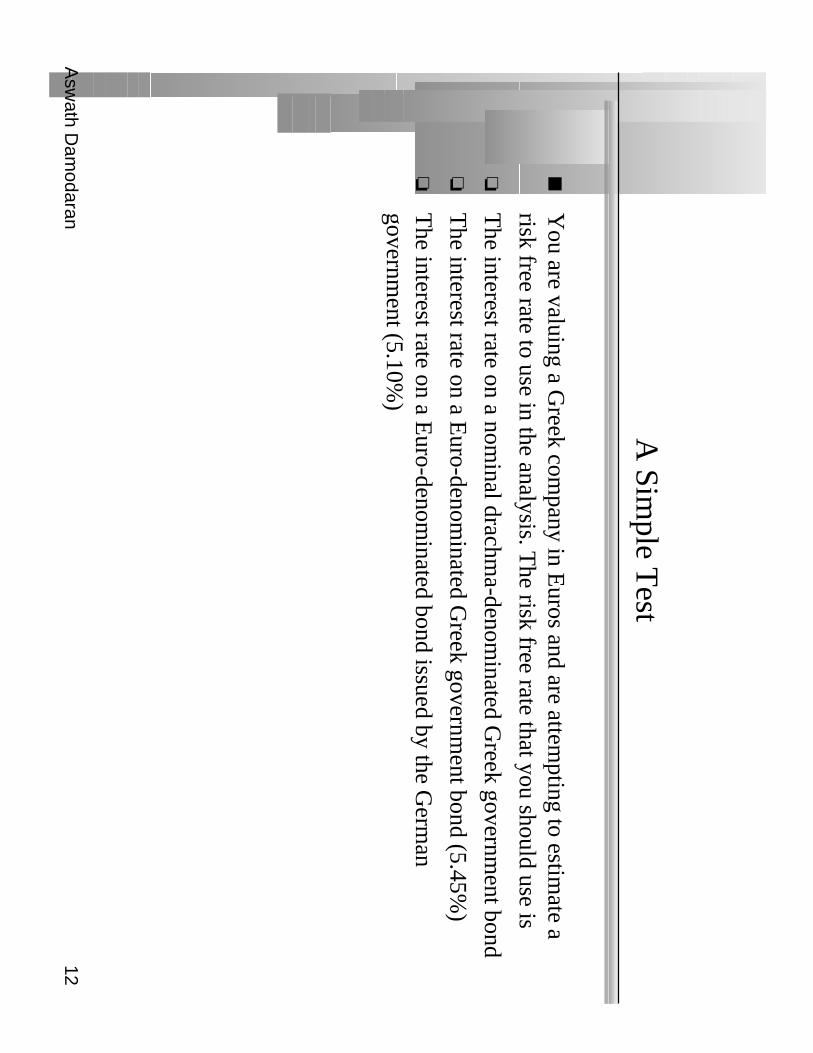

A Sim

ple Test

You are valuing a G

reek company in E

uros and are attempting to estim

ate arisk free rate to use in the analysis. T

he risk free rate that you should use is

The interest rate on a nom

inal drachma-denom

inated Greek governm

ent bond

The interest rate on a E

uro-denominated G

reek government bond (5.45%

)

The interest rate on a E

uro-denominated bond issued by the G

erman

government (5.10%

)

Asw

ath Dam

odaran13

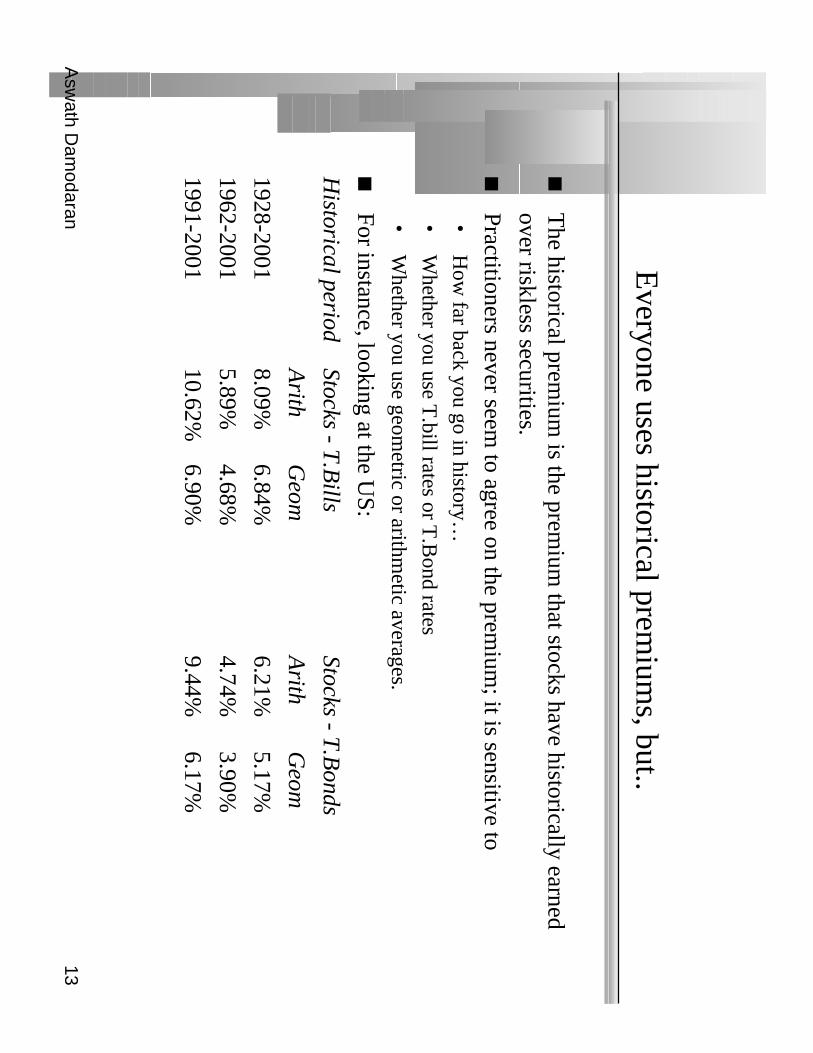

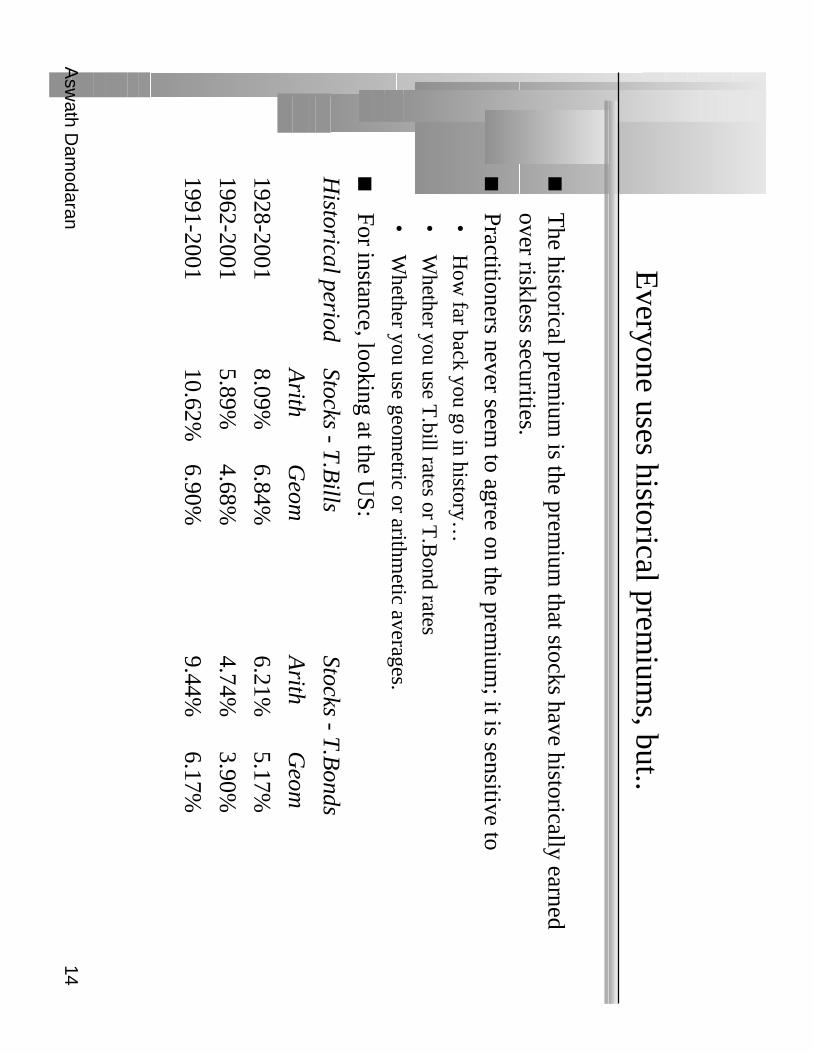

Everyone uses historical prem

iums, but..

The historical prem

ium is the prem

ium that stocks have historically earned

over riskless securities.

Practitioners never seem to agree on the prem

ium; it is sensitive to

•H

ow far back you go in history…

•W

hether you use T.bill rates or T

.Bond rates

•W

hether you use geometric or arithm

etic averages.

For instance, looking at the US:

Historical period

Stocks - T.B

illsStocks - T

.Bonds

Arith

Geom

Arith

Geom

1928-20018.09%

6.84%6.21%

5.17%

1962-20015.89%

4.68%4.74%

3.90%

1991-200110.62%

6.90%9.44%

6.17%

Asw

ath Dam

odaran14

Everyone uses historical prem

iums, but..

The historical prem

ium is the prem

ium that stocks have historically earned

over riskless securities.

Practitioners never seem to agree on the prem

ium; it is sensitive to

•H

ow far back you go in history…

•W

hether you use T.bill rates or T

.Bond rates

•W

hether you use geometric or arithm

etic averages.

For instance, looking at the US:

Historical period

Stocks - T.B

illsStocks - T

.Bonds

Arith

Geom

Arith

Geom

1928-20018.09%

6.84%6.21%

5.17%

1962-20015.89%

4.68%4.74%

3.90%

1991-200110.62%

6.90%9.44%

6.17%

Asw

ath Dam

odaran15

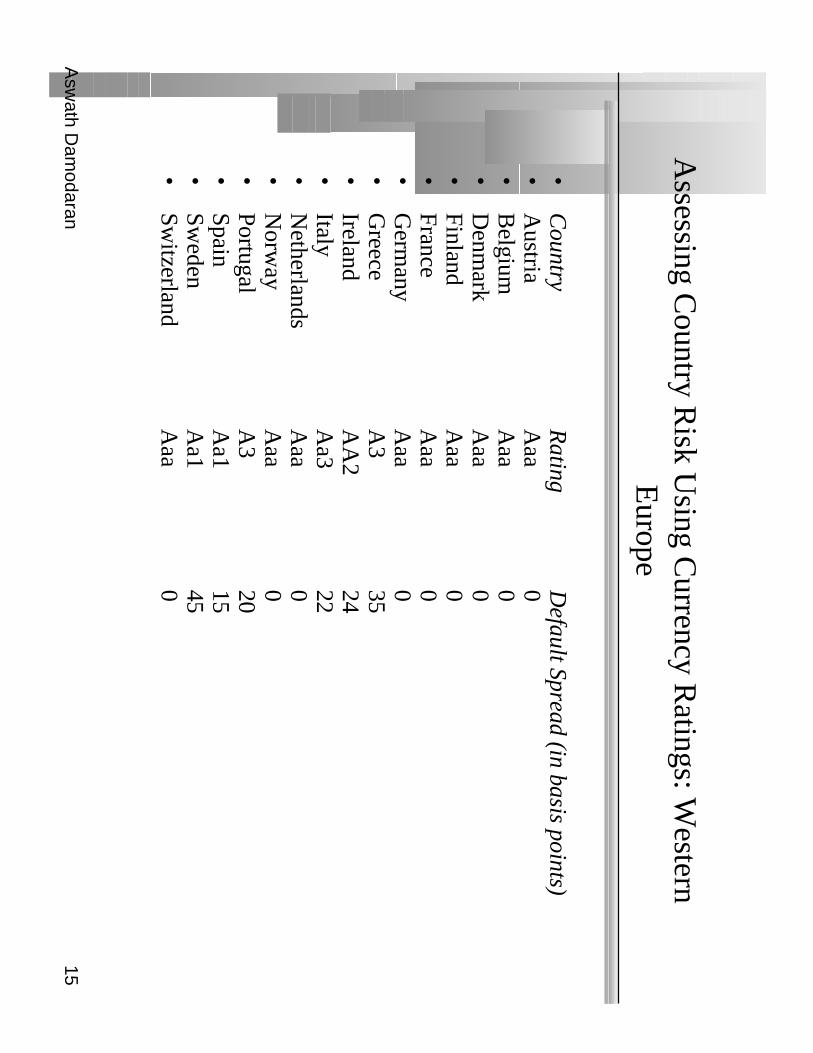

Assessing C

ountry Risk U

sing Currency R

atings: Western

Europe

•C

ountryR

atingD

efault Spread (in basis points)•

Austria

Aaa

0•

Belgium

Aaa

0•

Denm

arkA

aa0

•Finland

Aaa

0•

FranceA

aa0

•G

ermany

Aaa

0•

Greece

A3

35•

IrelandA

A2

24•

ItalyA

a322

•N

etherlandsA

aa0

•N

orway

Aaa

0•

PortugalA

320

•Spain

Aa1

15•

Sweden

Aa1

45•

Switzerland

Aaa

0

Asw

ath Dam

odaran16

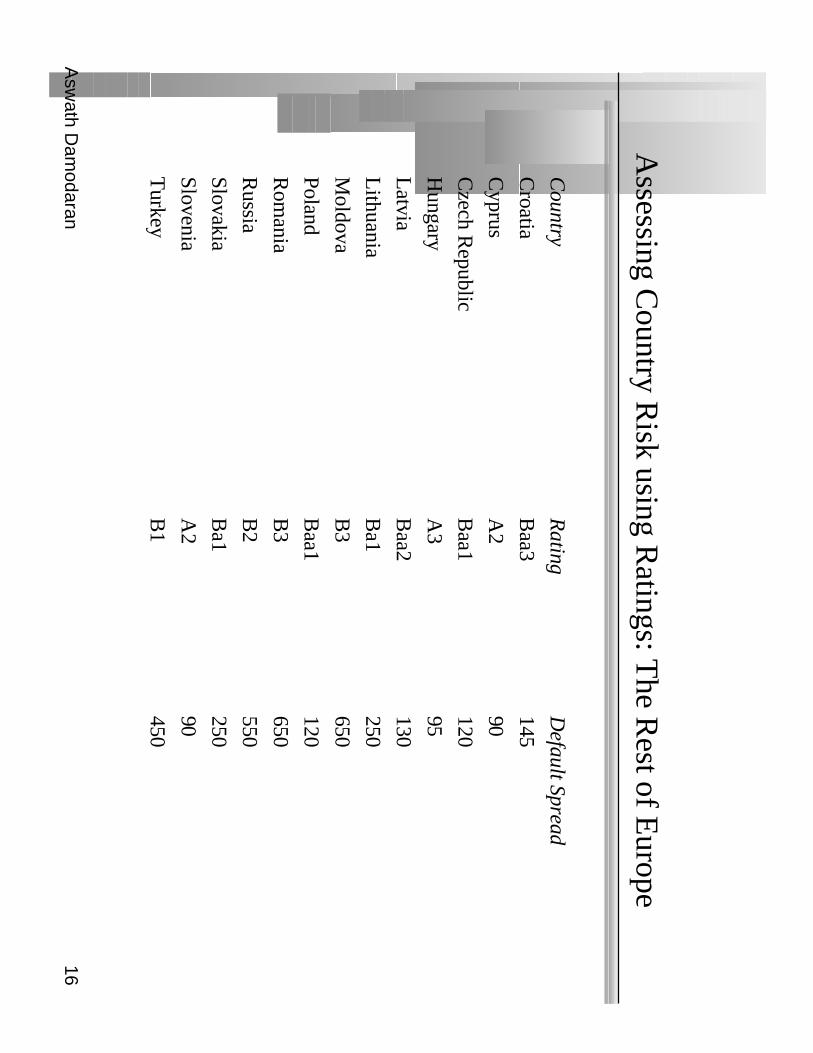

Assessing C

ountry Risk using R

atings: The R

est of Europe

Country

Rating

Default Spread

Croatia

Baa3

145

Cyprus

A2

90

Czech R

epublicB

aa1120

Hungary

A3

95

Latvia

Baa2

130

Lithuania

Ba1

250

Moldova

B3

650

PolandB

aa1120

Rom

aniaB

3650

Russia

B2

550

SlovakiaB

a1250

SloveniaA

290

Turkey

B1

450

Asw

ath Dam

odaran17

Using C

ountry Ratings to E

stimate E

quity Spreads

Country ratings m

easure default risk. While default risk prem

iums and equity

risk premium

s are highly correlated, one would expect equity spreads to be

higher than debt spreads.•

One w

ay to adjust the country spread upwards is to use inform

ation from the U

Sm

arket. In the US, the equity risk prem

ium has been roughly tw

ice the defaultspread on junk bonds.

•A

nother is to multiply the bond spread by the relative volatility of stock and bond

prices in that market. For exam

ple,–

Standard Deviation in G

reek ASE

(Equity) =

32%

–Standard D

eviation in Greek E

uro Bond =

16%

–A

djusted Equity Spread =

0.35% (32/16) =

0.70 %

Asw

ath Dam

odaran18

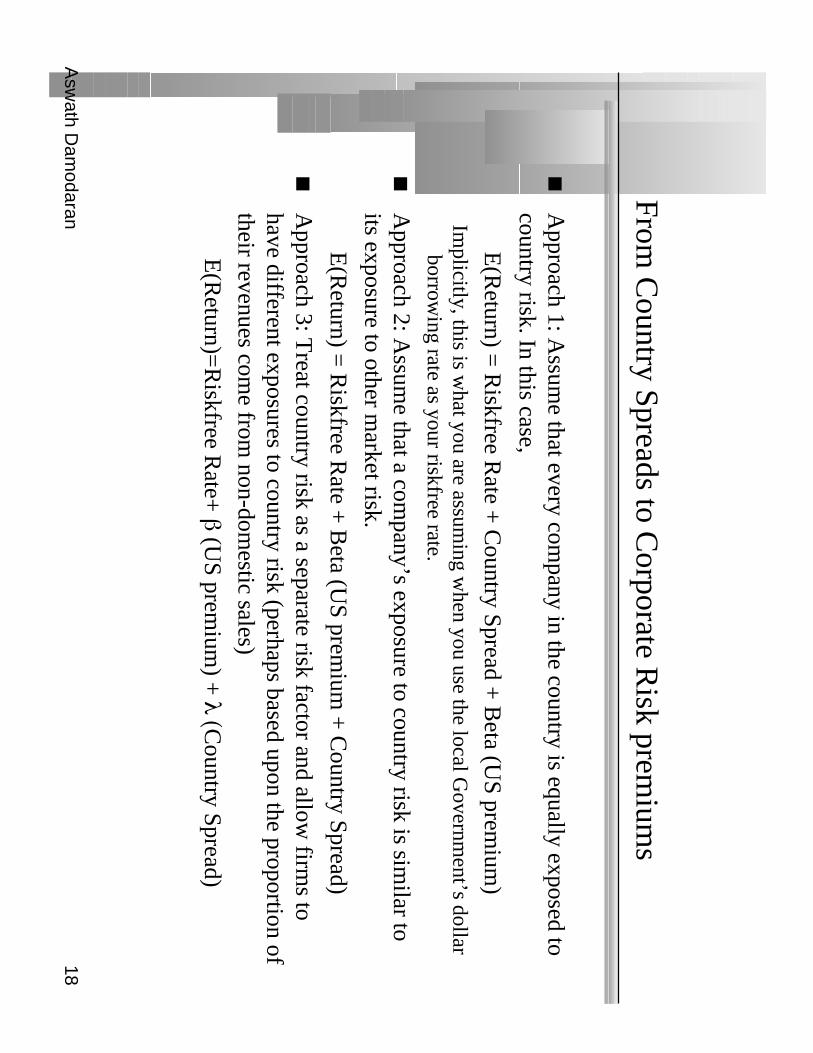

From C

ountry Spreads to Corporate R

isk premium

s

Approach 1: A

ssume that every com

pany in the country is equally exposed tocountry risk. In this case,

E(R

eturn) = R

iskfree Rate +

Country Spread +

Beta (U

S premium

)Im

plicitly, this is what you are assum

ing when you use the local G

overnment’s dollar

borrowing rate as your riskfree rate.

Approach 2: A

ssume that a com

pany’s exposure to country risk is similar to

its exposure to other market risk.

E(R

eturn) = R

iskfree Rate +

Beta (U

S premium

+ C

ountry Spread)

Approach 3: T

reat country risk as a separate risk factor and allow firm

s tohave different exposures to country risk (perhaps based upon the proportion oftheir revenues com

e from non-dom

estic sales)

E(R

eturn)=R

iskfree Rate+

β (US prem

ium) +

λ (Country Spread)

Asw

ath Dam

odaran19

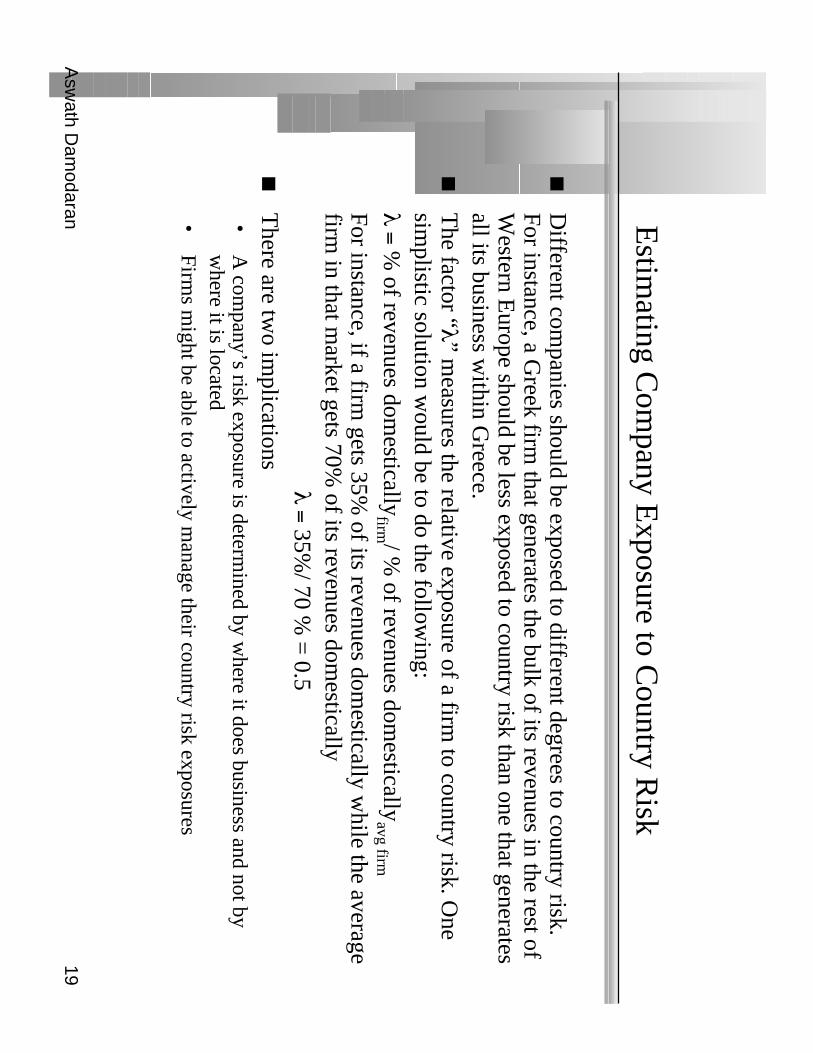

Estim

ating Com

pany Exposure to C

ountry Risk

Different com

panies should be exposed to different degrees to country risk.For instance, a G

reek firm that generates the bulk of its revenues in the rest of

Western E

urope should be less exposed to country risk than one that generatesall its business w

ithin Greece.

The factor “λ” m

easures the relative exposure of a firm to country risk. O

nesim

plistic solution would be to do the follow

ing:λ = %

of revenues domestically

firm / % of revenues dom

esticallyavg firm

For instance, if a firm gets 35%

of its revenues domestically w

hile the averagefirm

in that market gets 70%

of its revenues domestically

λ = 35%/ 70 %

= 0.5

There are tw

o implications

•A

company’s risk exposure is determ

ined by where it does business and not by

where it is located

•Firm

s might be able to actively m

anage their country risk exposures

Asw

ath Dam

odaran20

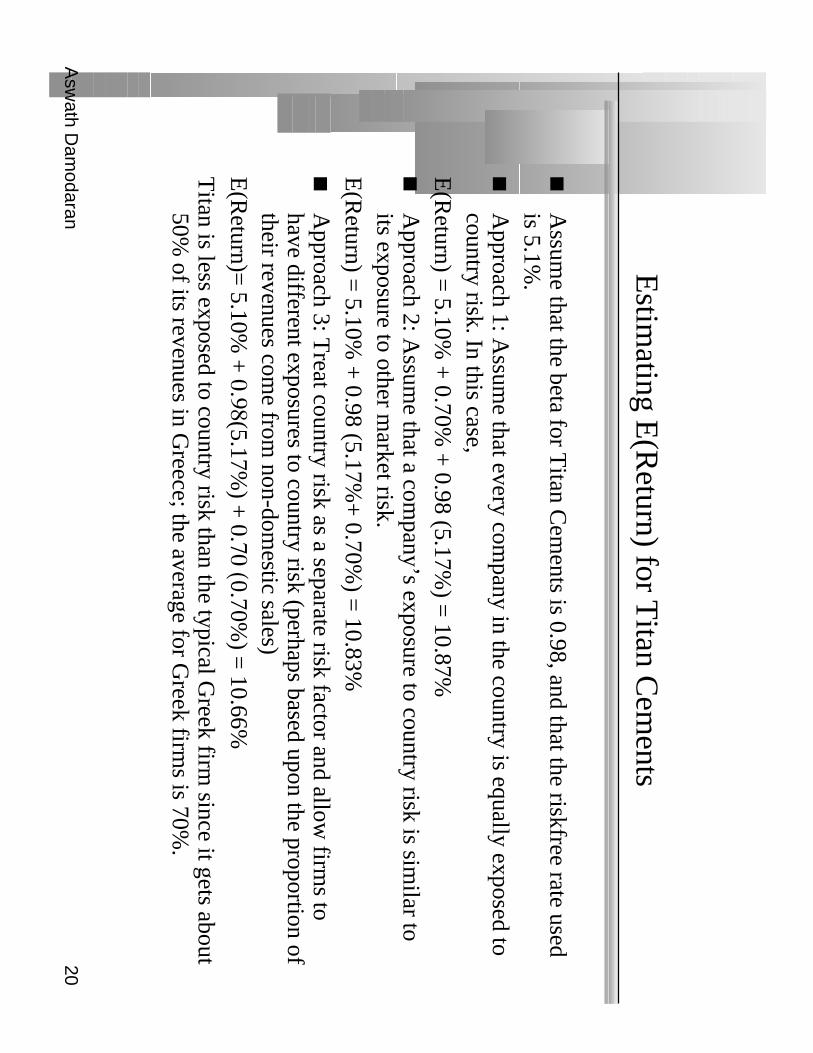

Estim

ating E(R

eturn) for Titan C

ements

Assum

e that the beta for Titan C

ements is 0.98, and that the riskfree rate used

is 5.1%.

Approach 1: A

ssume that every com

pany in the country is equally exposed tocountry risk. In this case,

E(R

eturn) = 5.10%

+ 0.70%

+ 0.98 (5.17%

) = 10.87%

Approach 2: A

ssume that a com

pany’s exposure to country risk is similar to

its exposure to other market risk.

E(R

eturn) = 5.10%

+ 0.98 (5.17%

+ 0.70%

) = 10.83%

Approach 3: T

reat country risk as a separate risk factor and allow firm

s tohave different exposures to country risk (perhaps based upon the proportion oftheir revenues com

e from non-dom

estic sales)E

(Return)=

5.10% +

0.98(5.17%) +

0.70 (0.70%) =

10.66%T

itan is less exposed to country risk than the typical Greek firm

since it gets about50%

of its revenues in Greece; the average for G

reek firms is 70%

.

Asw

ath Dam

odaran21

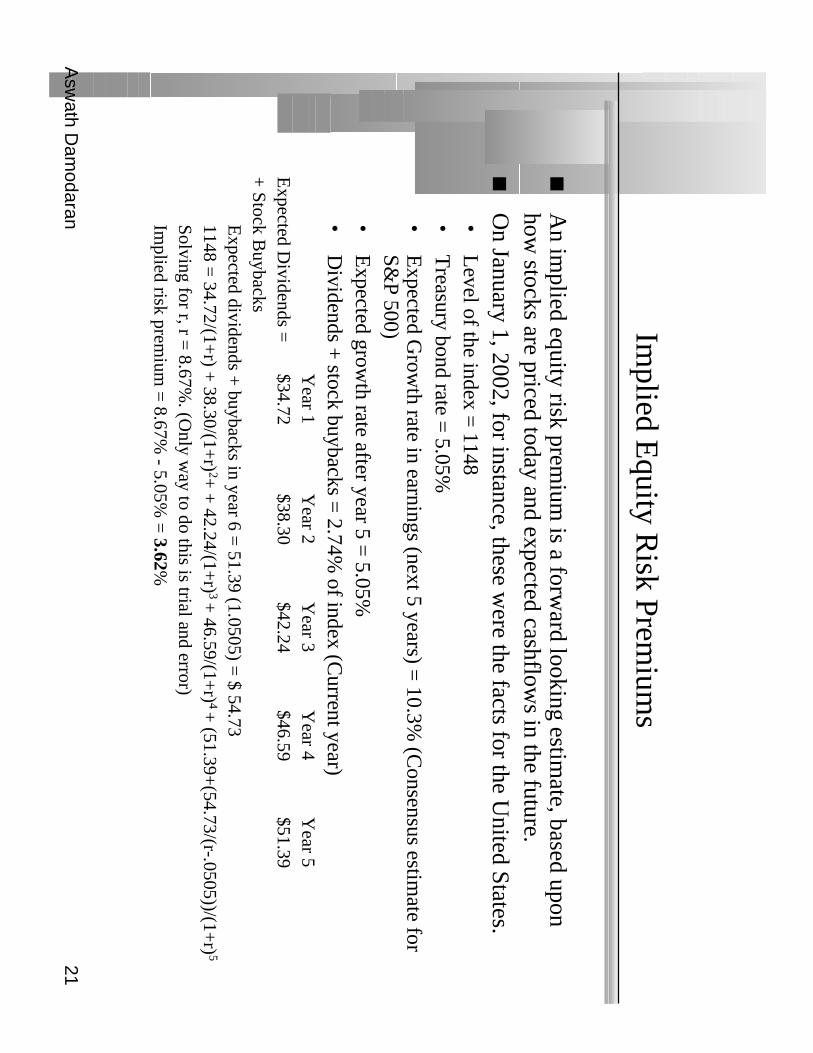

Implied E

quity Risk Prem

iums

An im

plied equity risk premium

is a forward looking estim

ate, based uponhow

stocks are priced today and expected cashflows in the future.

On January 1, 2002, for instance, these w

ere the facts for the United States.

•L

evel of the index = 1148

•T

reasury bond rate = 5.05%

•E

xpected Grow

th rate in earnings (next 5 years) = 10.3%

(Consensus estim

ate forS&

P 500)•

Expected grow

th rate after year 5 = 5.05%

•D

ividends + stock buybacks =

2.74% of index (C

urrent year)Y

ear 1Y

ear 2Y

ear 3Y

ear 4Y

ear 5E

xpected Dividends =

$34.72$38.30

$42.24$46.59

$51.39+

Stock Buybacks

Expected dividends +

buybacks in year 6 = 51.39 (1.0505) =

$ 54.731148 =

34.72/(1+r) +

38.30/(1+r) 2+

+ 42.24/(1+

r) 3 + 46.59/(1+

r) 4 + (51.39+

(54.73/(r-.0505))/(1+r) 5

Solving for r, r = 8.67%

. (Only w

ay to do this is trial and error)Im

plied risk premium

= 8.67%

- 5.05% =

3.62%

Asw

ath Dam

odaran22

U.S. E

quity Risk Prem

iums - 1960 - 2002

Imp

lied P

remiu

m fo

r US

Eq

uity M

arket

0.0

0%

1.0

0%

2.0

0%

3.0

0%

4.0

0%

5.0

0%

6.0

0%

7.0

0%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Year

Implied Premium

Asw

ath Dam

odaran23

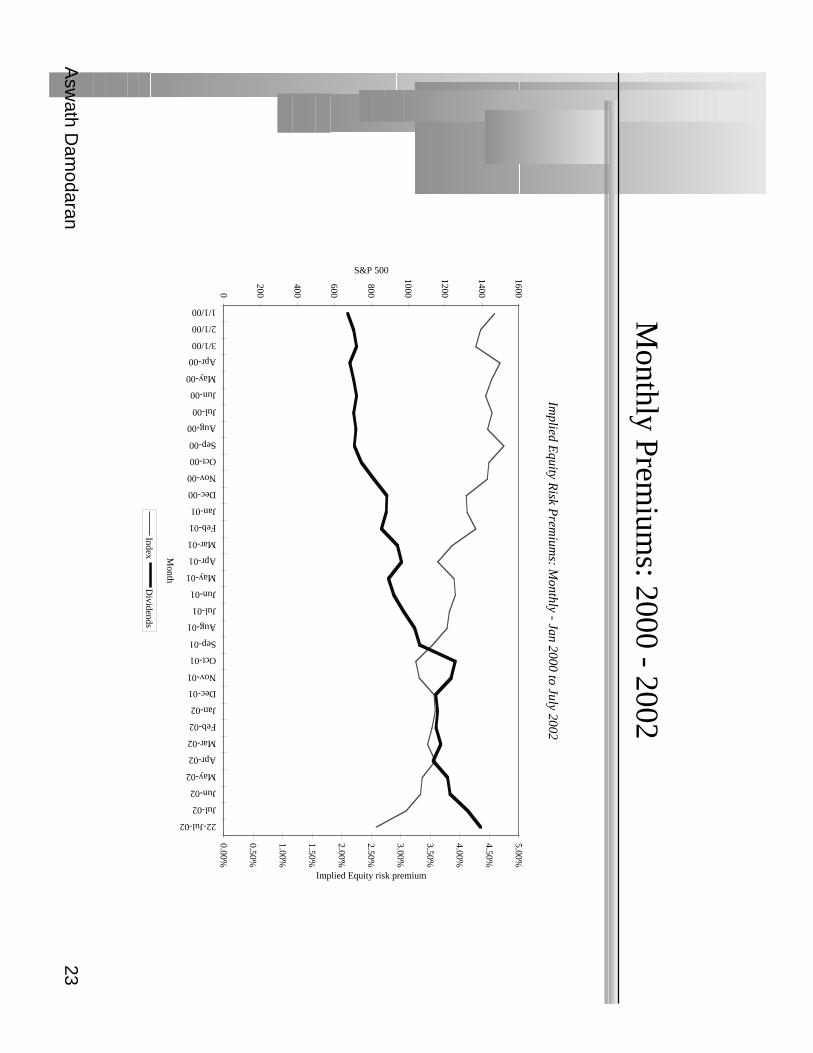

Monthly Prem

iums: 2000 - 2002

Implied E

quity Risk P

remium

s: Monthly - Jan 2000 to July 2002

0

200

400

600

800

1000

1200

1400

1600

1/1/00

2/1/00

3/1/00

Apr-00

May-00

Jun-00

Jul-00

Aug-00

Sep-00

Oct-00

Nov-00

Dec-00

Jan-01

Feb-01

Mar-01

Apr-01

May-01

Jun-01

Jul-01

Aug-01

Sep-01

Oct-01

Nov-01

Dec-01

Jan-02

Feb-02

Mar-02

Apr-02

May-02

Jun-02

Jul-02

22-Jul-02

Month

S&P 500

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

Implied Equity risk premium

IndexD

ividends

Asw

ath Dam

odaran24

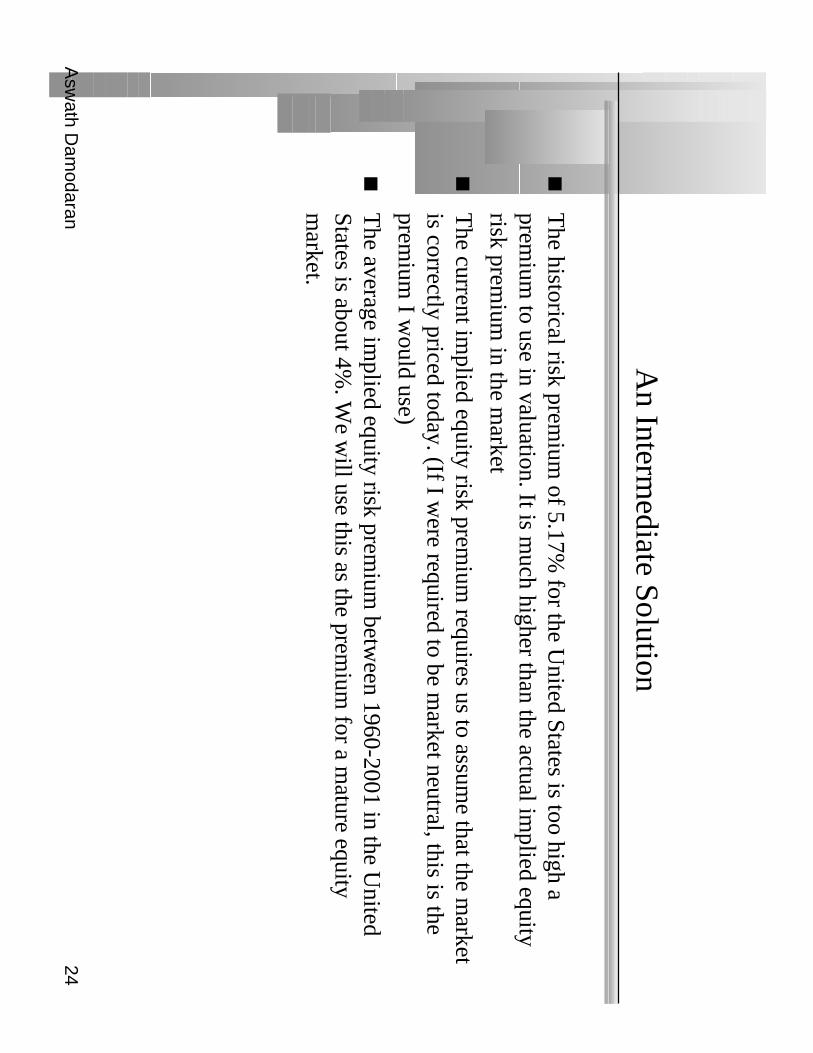

An Interm

ediate Solution

The historical risk prem

ium of 5.17%

for the United States is too high a

premium

to use in valuation. It is much higher than the actual im

plied equityrisk prem

ium in the m

arket

The current im

plied equity risk premium

requires us to assume that the m

arketis correctly priced today. (If I w

ere required to be market neutral, this is the

premium

I would use)

The average im

plied equity risk premium

between 1960-2001 in the U

nitedStates is about 4%

. We w

ill use this as the premium

for a mature equity

market.

Asw

ath Dam

odaran25

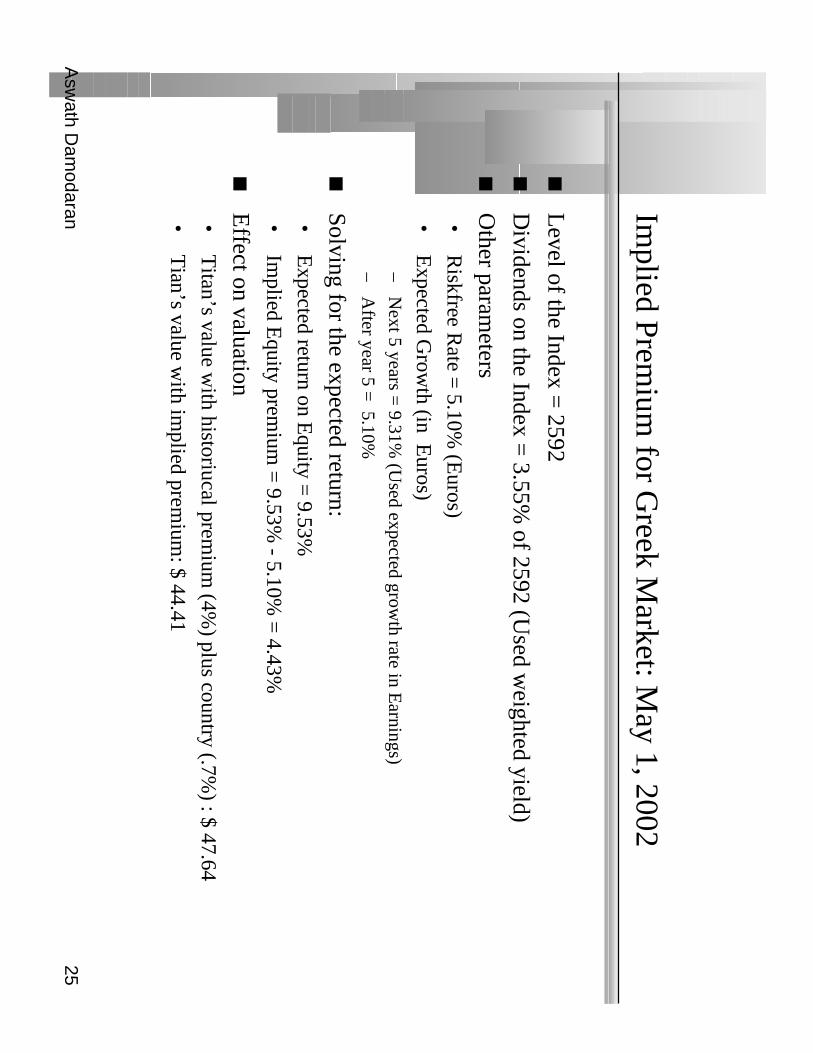

Implied Prem

ium for G

reek Market: M

ay 1, 2002

Level of the Index =

2592

Dividends on the Index =

3.55% of 2592 (U

sed weighted yield)

Other param

eters•

Riskfree R

ate = 5.10%

(Euros)

•E

xpected Grow

th (in Euros)

–N

ext 5 years = 9.31%

(Used expected grow

th rate in Earnings)

–A

fter year 5 = 5.10%

Solving for the expected return:•

Expected return on E

quity = 9.53%

•Im

plied Equity prem

ium =

9.53% - 5.10%

= 4.43%

Effect on valuation•

Titan’s value w

ith historiucal premium

(4%) plus country (.7%

) : $ 47.64

•T

ian’s value with im

plied premium

: $ 44.41

Asw

ath Dam

odaran26

Estim

ating Beta

The standard procedure for estim

ating betas is to regress stock returns (Rj )

against market returns (R

m ) -

Rj =

a + b R

m

•w

here a is the intercept and b is the slope of the regression.

The slope of the regression corresponds to the beta of the stock, and m

easuresthe riskiness of the stock.

This beta has three problem

s:•

It has high standard error

•It reflects the firm

’s business mix over the period of the regression, not the current

mix

•It reflects the firm

’s average financial leverage over the period rather than thecurrent leverage.

Asw

ath Dam

odaran27

Beta E

stimation: A

mazon

Asw

ath Dam

odaran28

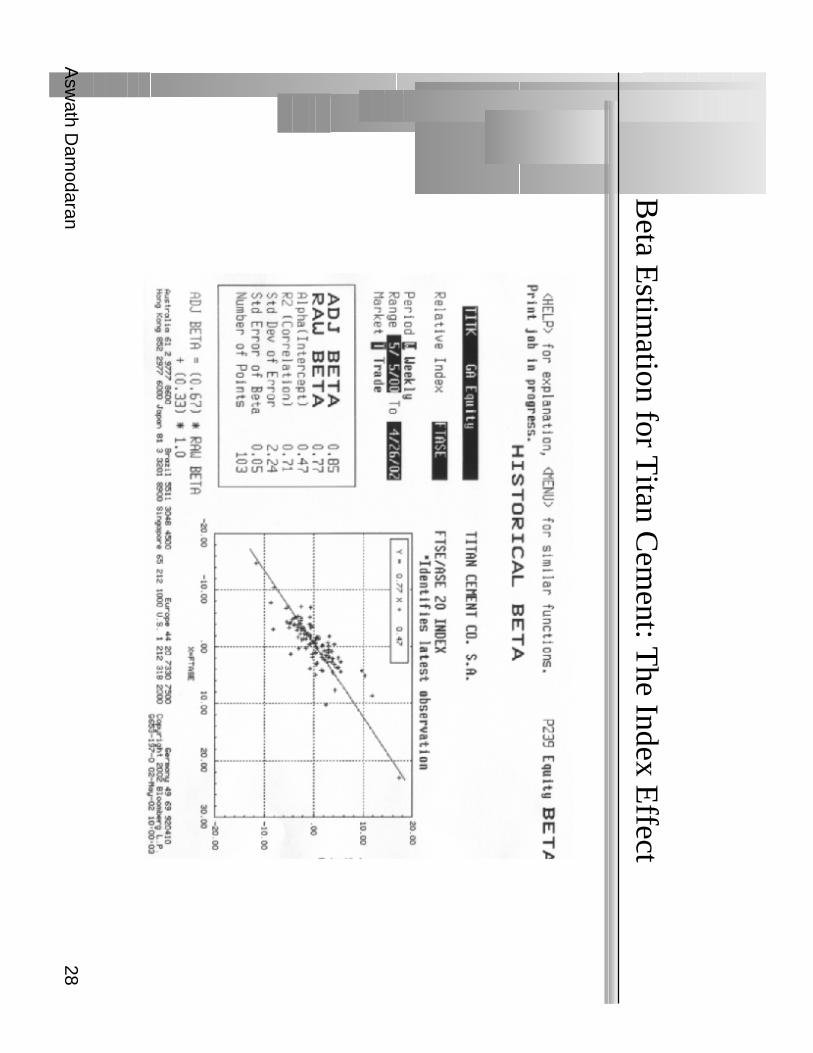

Beta E

stimation for T

itan Cem

ent: The Index E

ffect

Asw

ath Dam

odaran29

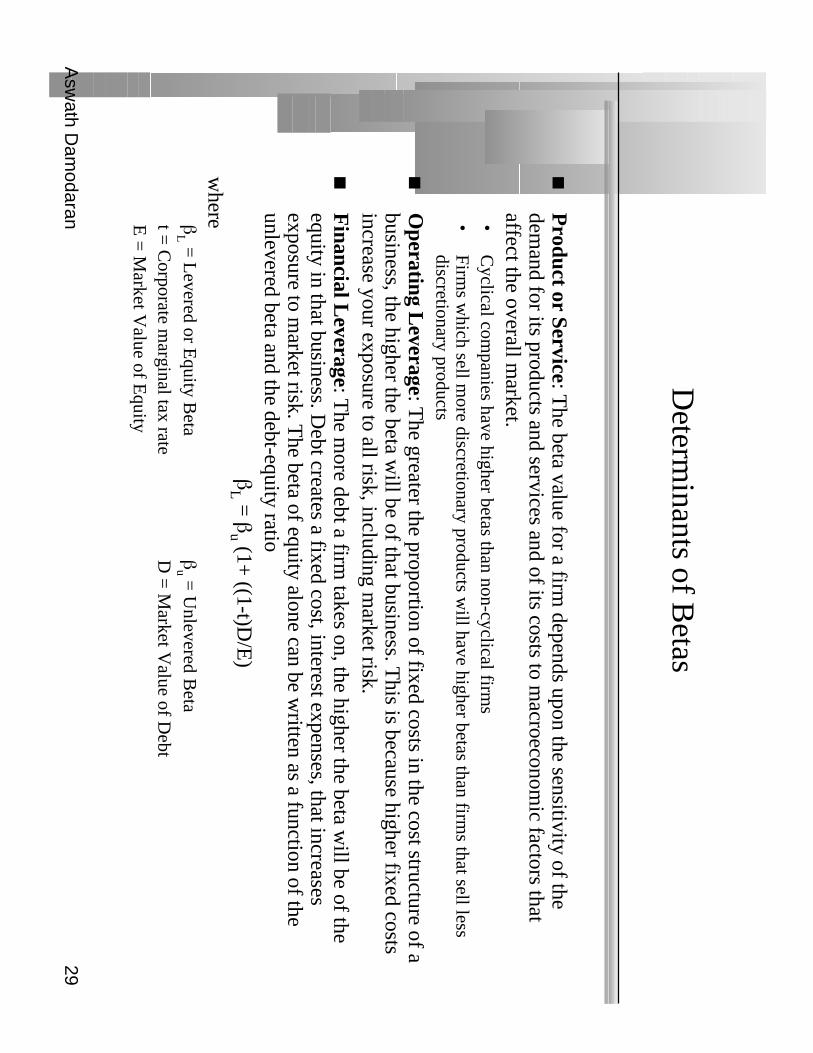

Determ

inants of Betas

Product or Service: T

he beta value for a firm depends upon the sensitivity of the

demand for its products and services and of its costs to m

acroeconomic factors that

affect the overall market.

•C

yclical companies have higher betas than non-cyclical firm

s•

Firms w

hich sell more discretionary products w

ill have higher betas than firms that sell less

discretionary products

Operating L

everage: The greater the proportion of fixed costs in the cost structure of a

business, the higher the beta will be of that business. T

his is because higher fixed costsincrease your exposure to all risk, including m

arket risk.F

inancial Leverage: T

he more debt a firm

takes on, the higher the beta will be of the

equity in that business. Debt creates a fixed cost, interest expenses, that increases

exposure to market risk. T

he beta of equity alone can be written as a function of the

unlevered beta and the debt-equity ratioβ

L = βu (1+

((1-t)D/E

)w

hereβL =

Levered or E

quity Beta

βu =

Unlevered B

etat =

Corporate m

arginal tax rateD

= M

arket Value of D

ebtE

= M

arket Value of E

quity

Asw

ath Dam

odaran30

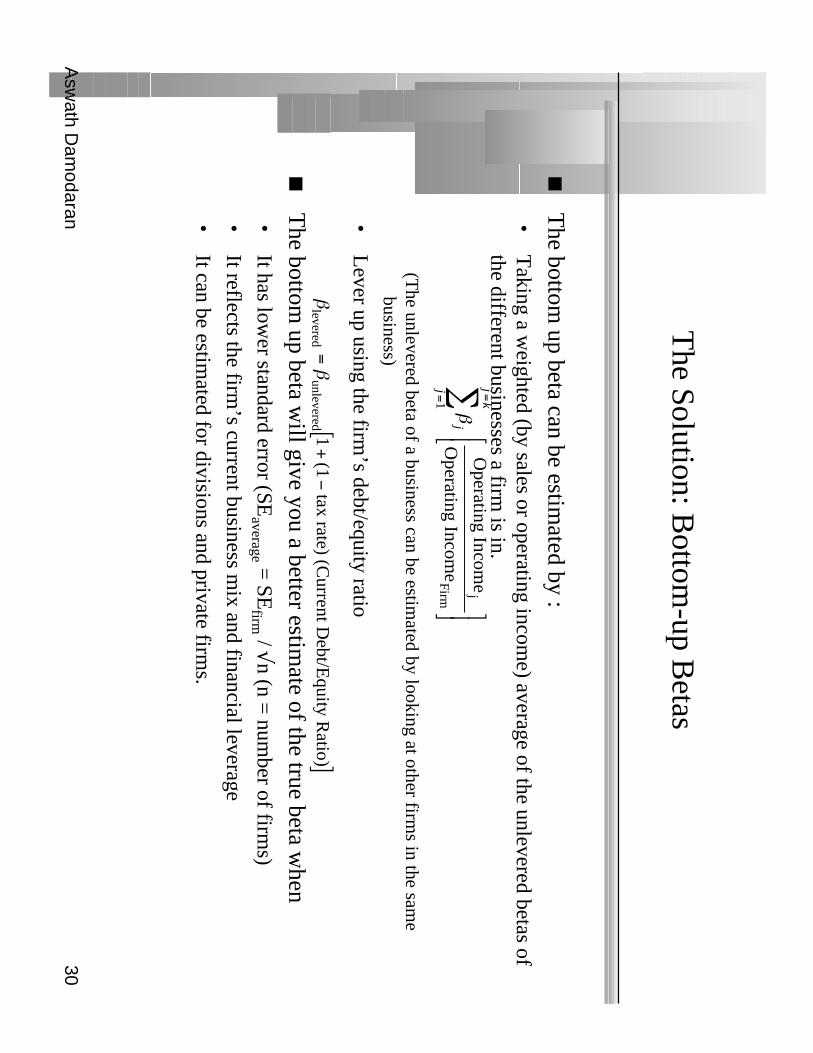

The Solution: B

ottom-up B

etas

The bottom

up beta can be estimated by :

•T

aking a weighted (by sales or operating incom

e) average of the unlevered betas ofthe different businesses a firm

is in.

(The unlevered beta of a business can be estim

ated by looking at other firms in the sam

ebusiness)

•L

ever up using the firm’s debt/equity ratio

The bottom

up beta will give you a better estim

ate of the true beta when

•It has low

er standard error (SEaverage = SE

firm / √n (n = num

ber of firms)

•It reflects the firm

’s current business mix and financial leverage

•It can be estim

ated for divisions and private firms.

βj

j jk

= =

∑

1

O

perating Income

Operating Incom

ej

Firm

ββ

leveredunlevered

1(1

tax rate) (Current D

ebt/Equity R

atio)=

+−

[]

Asw

ath Dam

odaran31

Titan’s B

ottom-up B

eta

Business

Unlevered

D/E

Ratio

Levered beta

Proportion of V

alue

Cem

ent.82

25.21%0.98

100%

Levered B

eta= U

nlevered Beta ( 1 +

(1- tax rate) (D/E

Ratio)

= 0.82 ( 1 +

(1-.2449) (.2521)) = 0.98

A H

ypothetical scenario: Assum

e that Titan had been in tw

o businesses- cement and

technology. You could estm

ate a beta for the combined firm

as follows

Com

parable firms

Business

Revenues

Value/Sales U

nlevered betaV

alueW

eightW

eight*Beta

Cem

ent623

3.00.82

186979%

.79*.82

Technology

1005.0

1.20 500

21%.21*1.20

Firm=

.90

Asw

ath Dam

odaran32

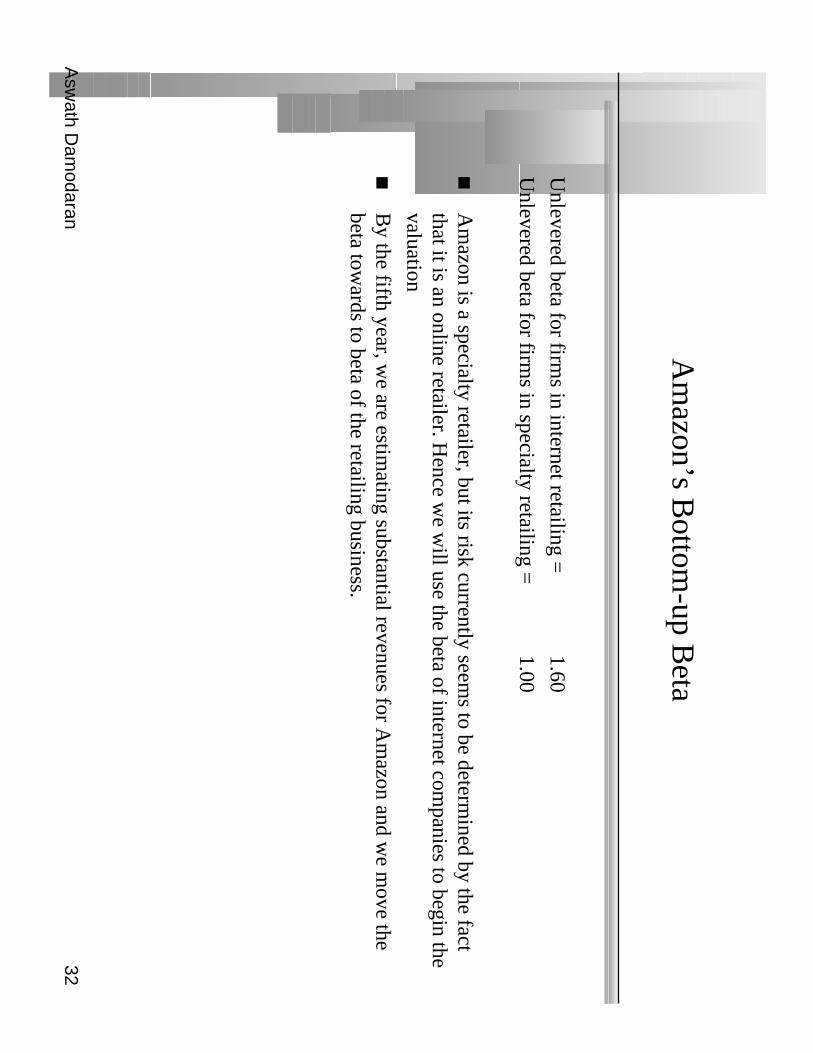

Am

azon’s Bottom

-up Beta

Unlevered beta for firm

s in internet retailing =1.60

Unlevered beta for firm

s in specialty retailing =

1.00

Am

azon is a specialty retailer, but its risk currently seems to be determ

ined by the factthat it is an online retailer. H

ence we w

ill use the beta of internet companies to begin the

valuation

By the fifth year, w

e are estimating substantial revenues for A

mazon and w

e move the

beta towards to beta of the retailing business.

Asw

ath Dam

odaran33

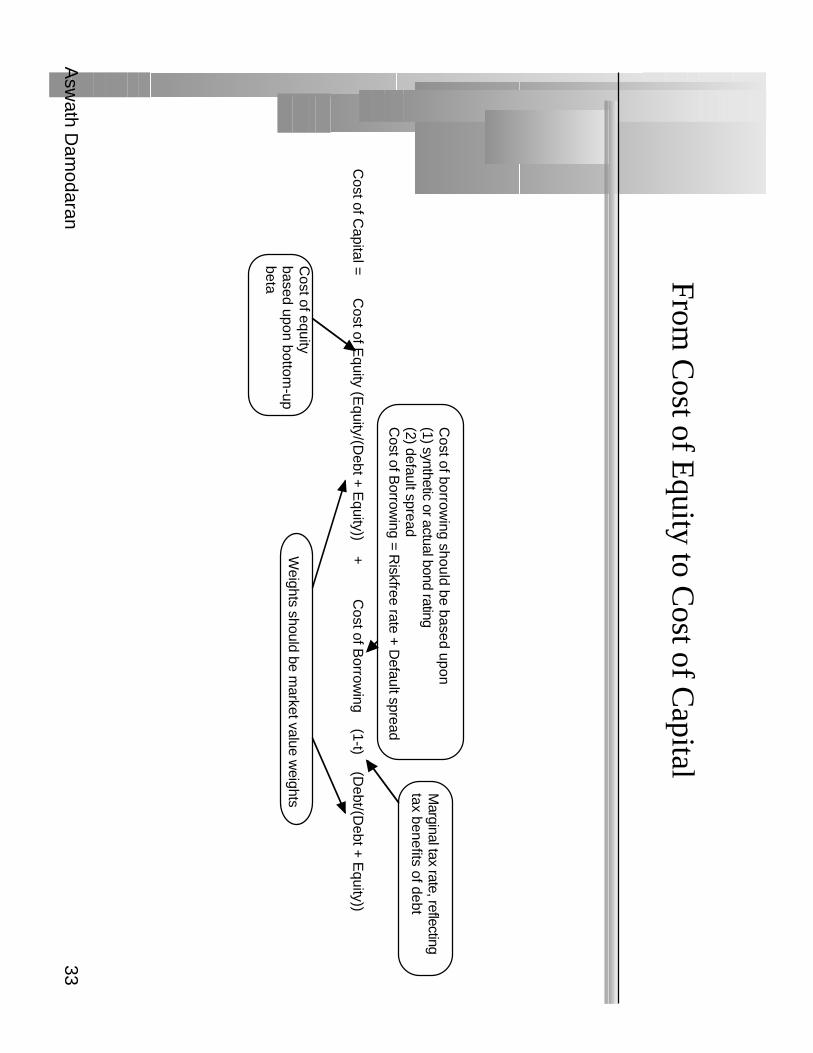

From C

ost of Equity to C

ost of Capital

Cost of C

apital =C

ost of Equity (E

quity/(Debt +

Equity))

+C

ost of Borrow

ing (1-t)

(Debt/(D

ebt + E

quity))

Cost of borrow

ing should be based upon(1) synthetic or actual bond rating(2) default spreadC

ost of Borrow

ing = Riskfree rate + D

efault spread

Marginal tax rate, reflecting

tax benefits of debt

Weights should be m

arket value weights

Cost of equity

based upon bottom-up

beta

Asw

ath Dam

odaran34

Estim

ating Synthetic Ratings

The rating for a firm

can be estimated using the financial characteristics of the

firm. In its sim

plest form, the rating can be estim

ated from the interest

coverage ratioInterest Coverage R

atio = E

BIT

/ Interest Expenses

For Titan’s interest coverage ratio, w

e used the interest expenses and EB

ITfrom

2000.

Interest Coverage R

atio = 186.40/ 26 =

7.17

Am

azon.com has negative operating incom

e; this yields a negative interestcoverage ratio, w

hich should suggest a low rating. W

e computed an average

interest coverage ratio of 2.82 over the next 5 years.

Asw

ath Dam

odaran35

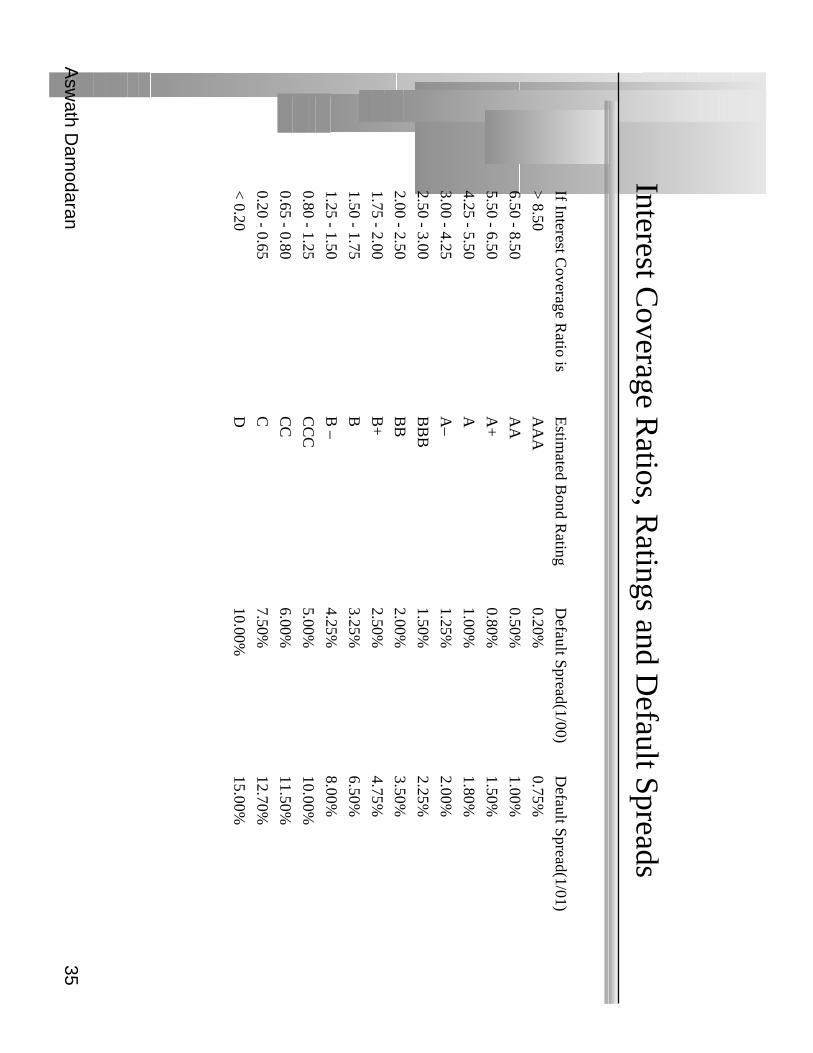

Interest Coverage R

atios, Ratings and D

efault Spreads

If Interest Coverage R

atio isE

stimated B

ond Rating

Default Spread(1/00)

Default Spread(1/01)

> 8.50

AA

A0.20%

0.75%

6.50 - 8.50A

A0.50%

1.00%

5.50 - 6.50A

+0.80%

1.50%

4.25 - 5.50A

1.00%1.80%

3.00 - 4.25A

–1.25%

2.00%

2.50 - 3.00B

BB

1.50%2.25%

2.00 - 2.50B

B2.00%

3.50%

1.75 - 2.00B

+2.50%

4.75%

1.50 - 1.75B

3.25%6.50%

1.25 - 1.50B

–4.25%

8.00%

0.80 - 1.25C

CC

5.00%10.00%

0.65 - 0.80C

C6.00%

11.50%

0.20 - 0.65C

7.50%12.70%

< 0.20

D10.00%

15.00%

Asw

ath Dam

odaran36

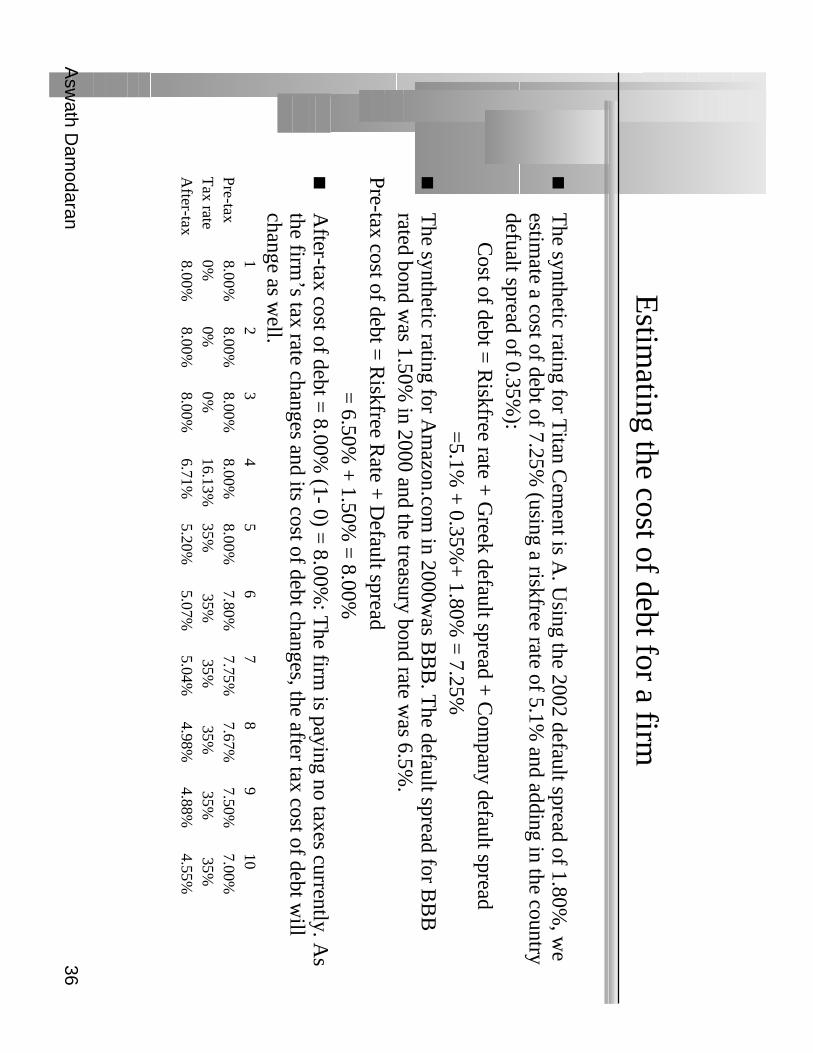

Estim

ating the cost of debt for a firm

The synthetic rating for T

itan Cem

ent is A. U

sing the 2002 default spread of 1.80%, w

eestim

ate a cost of debt of 7.25% (using a riskfree rate of 5.1%

and adding in the countrydefualt spread of 0.35%

): C

ost of debt = R

iskfree rate + G

reek default spread + C

ompany default spread

=5.1%

+ 0.35%

+ 1.80%

= 7.25%

The synthetic rating for A

mazon.com

in 2000was B

BB

. The default spread for B

BB

rated bond was 1.50%

in 2000 and the treasury bond rate was 6.5%

.Pre-tax cost of debt =

Riskfree R

ate + D

efault spread=

6.50% +

1.50% =

8.00%A

fter-tax cost of debt = 8.00%

(1- 0) = 8.00%

: The firm

is paying no taxes currently. As

the firm’s tax rate changes and its cost of debt changes, the after tax cost of debt w

illchange as w

ell.1

23

45

67

89

10P

re-tax8.00%

8.00%8.00%

8.00%8.00%

7.80%7.75%

7.67%7.50%

7.00%

Tax rate

0%0%

0%16.13%

35% 35%

35%

35% 35%

35%A

fter-tax8.00%

8.00%8.00%

6.71%5.20%

5.07%5.04%

4.98%4.88%

4.55%

Asw

ath Dam

odaran37

Weights for the C

ost of Capital C

omputation

The w

eights used to compute the cost of capital should be the m

arket valuew

eights for debt and equity.

There is an elem

ent of circularity that is introduced into every valuation bydoing this, since the values that w

e attach to the firm and equity at the end of

the analysis are different from the values w

e gave them at the beginning.

As a general rule, the debt that you should subtract from

firm value to arrive at

the value of equity should be the same debt that you used to com

pute the costof capital.

Asw

ath Dam

odaran38

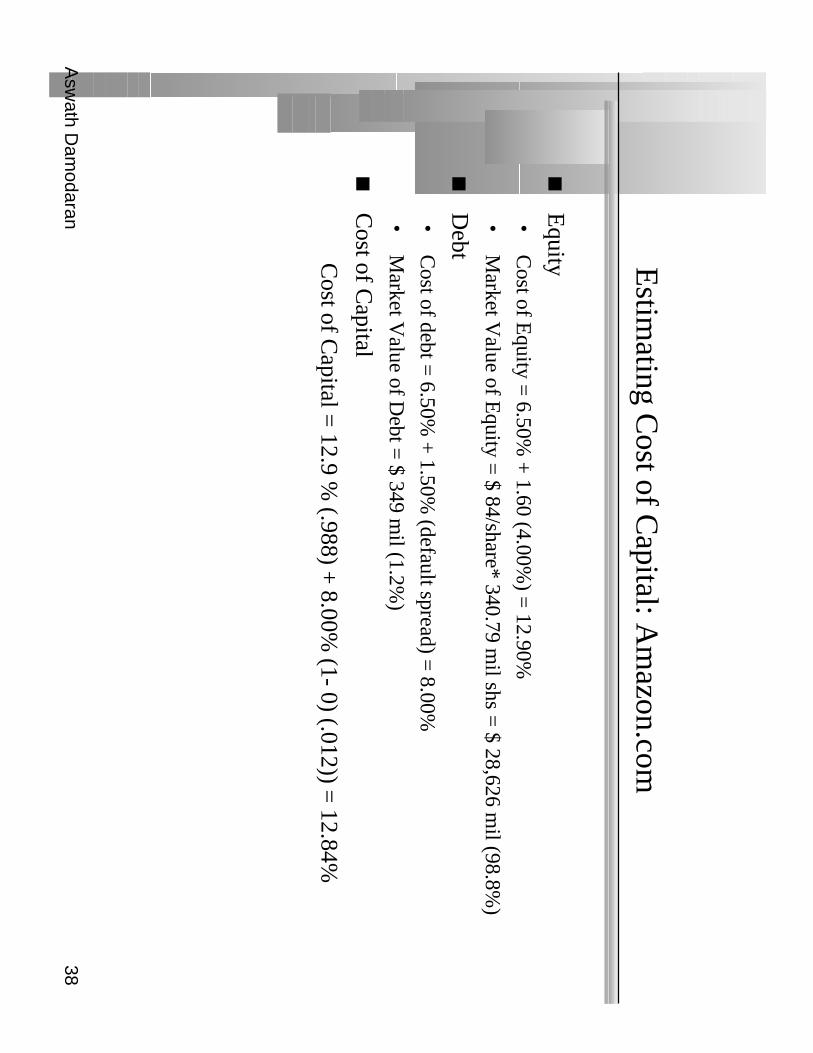

Estim

ating Cost of C

apital: Am

azon.com

Equity•

Cost of E

quity = 6.50%

+ 1.60 (4.00%

) = 12.90%

•M

arket Value of E

quity = $ 84/share* 340.79 m

il shs = $ 28,626 m

il (98.8%)

Debt

•C

ost of debt = 6.50%

+ 1.50%

(default spread) = 8.00%

•M

arket Value of D

ebt = $ 349 m

il (1.2%)

Cost of C

apital

Cost of C

apital = 12.9 %

(.988) + 8.00%

(1- 0) (.012)) = 12.84%

Asw

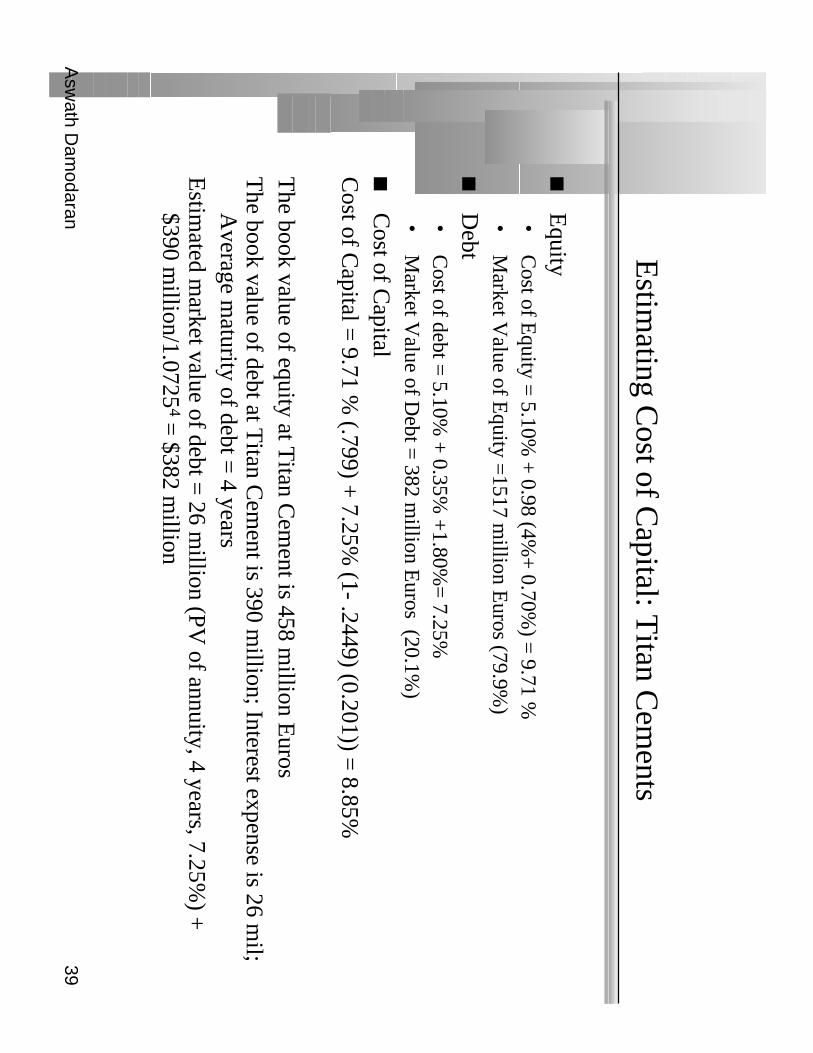

ath Dam

odaran39

Estim

ating Cost of C

apital: Titan C

ements

Equity•

Cost of E

quity = 5.10%

+ 0.98 (4%

+ 0.70%

) = 9.71 %

•M

arket Value of E

quity =1517 m

illion Euros (79.9%

)

Debt

•C

ost of debt = 5.10%

+ 0.35%

+1.80%

= 7.25%

•M

arket Value of D

ebt = 382 m

illion Euros (20.1%

)

Cost of C

apitalC

ost of Capital =

9.71 % (.799) +

7.25% (1- .2449) (0.201)) =

8.85%

The book value of equity at T

itan Cem

ent is 458 million E

urosT

he book value of debt at Titan C

ement is 390 m

illion; Interest expense is 26 mil;

Average m

aturity of debt = 4 years

Estim

ated market value of debt =

26 million (PV

of annuity, 4 years, 7.25%) +

$390 million/1.0725

4 = $382 m

illion

Asw

ath Dam

odaran40

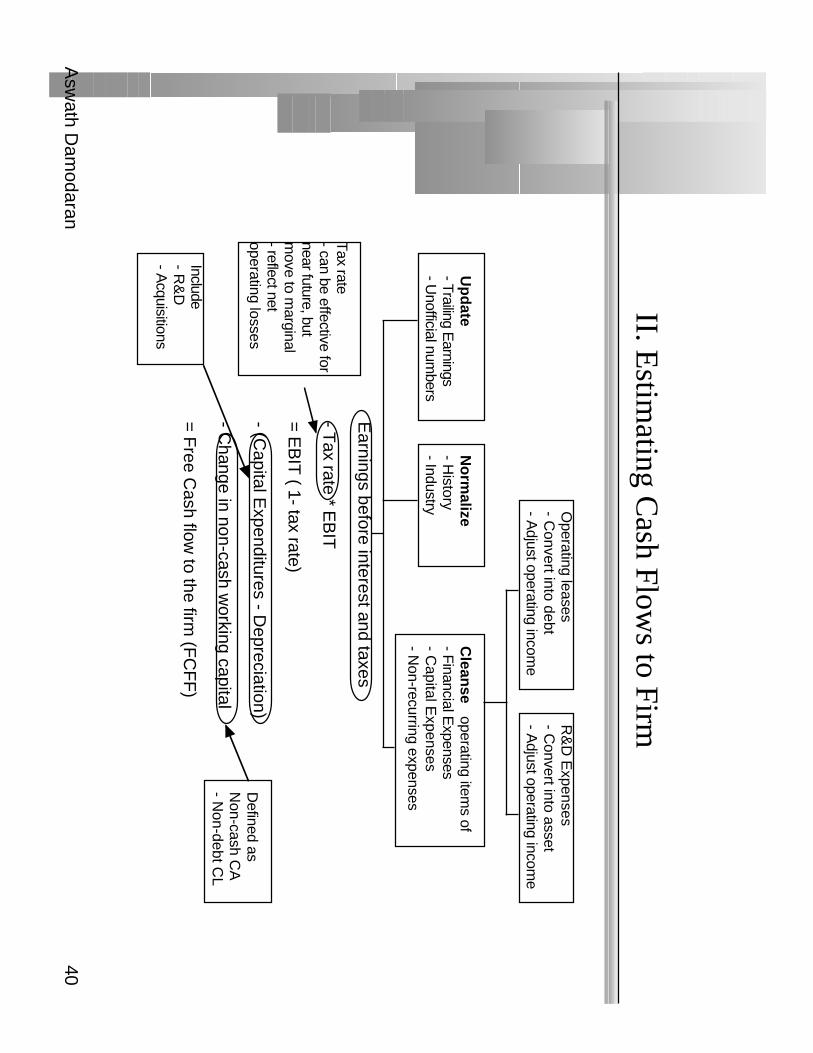

II. Estim

ating Cash Flow

s to Firm

Earnings before interest and taxes

- Tax rate * E

BIT

= EB

IT ( 1- tax rate)

- (Capital E

xpenditures - Depreciation)

- Change in non-cash w

orking capital

= F

ree Cash flow

to the firm (F

CF

F)

Up

date

- Trailing Earnings

- Unofficial num

bers

No

rmalize

- History

- Industry

Clean

se operating item

s of- F

inancial Expenses

- Capital E

xpenses- N

on-recurring expenses

Operating leases

- Convert into debt

- Adjust operating incom

e

R&

D E

xpenses- C

onvert into asset- A

djust operating income

Tax rate

- can be effective for near future, but m

ove to marginal

- reflect net operating losses

Include- R

&D

- Acquisitions

Defined as

Non-cash C

A- N

on-debt CL

Asw

ath Dam

odaran41

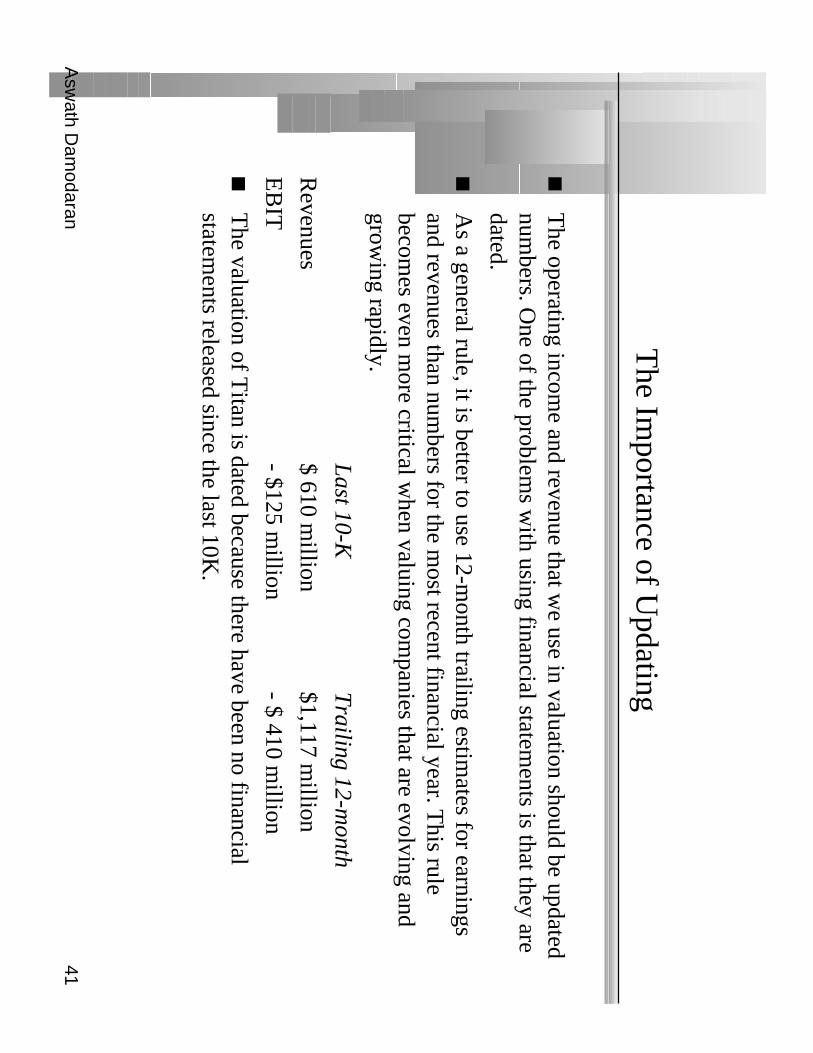

The Im

portance of Updating

The operating incom

e and revenue that we use in valuation should be updated

numbers. O

ne of the problems w

ith using financial statements is that they are

dated.

As a general rule, it is better to use 12-m

onth trailing estimates for earnings

and revenues than numbers for the m

ost recent financial year. This rule

becomes even m

ore critical when valuing com

panies that are evolving andgrow

ing rapidly.

L

ast 10-KT

railing 12-month

Revenues

$ 610 million

$1,117 million

EB

IT- $125 m

illion- $ 410 m

illion

The valuation of T

itan is dated because there have been no financialstatem

ents released since the last 10K.

Asw

ath Dam

odaran42

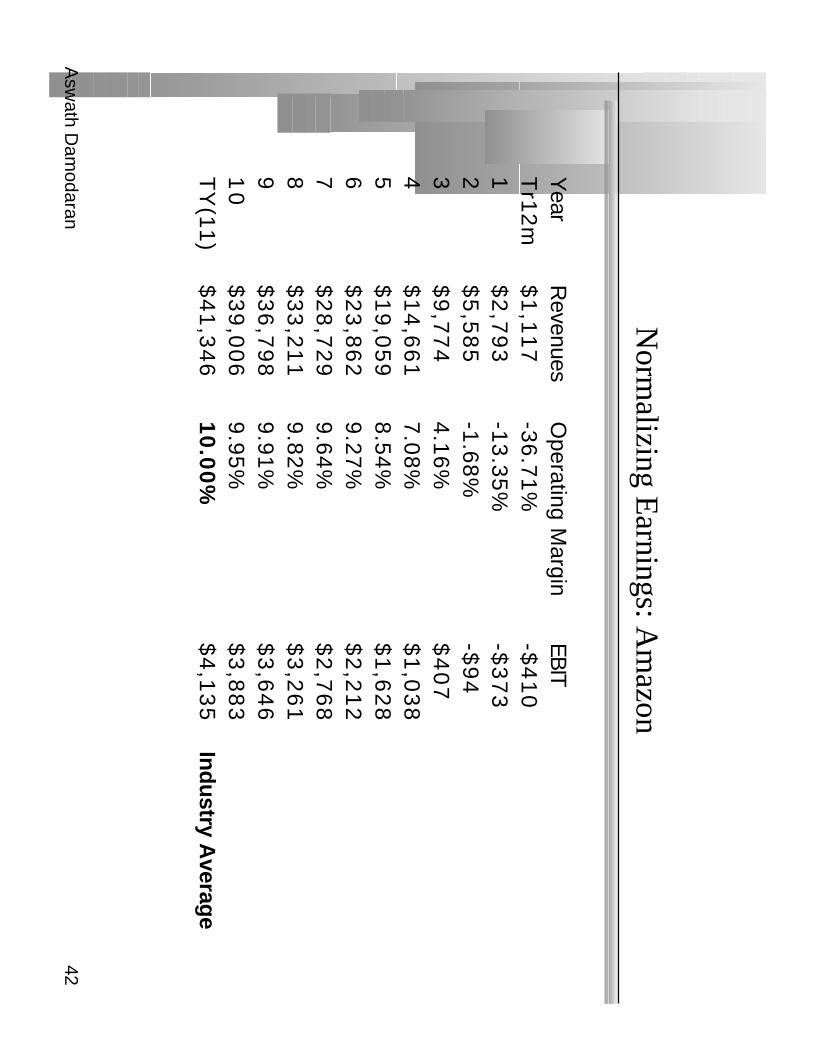

Norm

alizing Earnings: A

mazon

Year

Revenues

Operating M

arginE

BIT

Tr1

2m

$1

,11

7-3

6.7

1%

-$4

10

1$

2,7

93

-13

.35

%-$

37

32

$5

,58

5-1

.68

%-$

94

3$

9,7

74

4.1

6%

$4

07

4$

14

,66

17

.08

%$

1,0

38

5$

19

,05

98

.54

%$

1,6

28

6$

23

,86

29

.27

%$

2,2

12

7$

28

,72

99

.64

%$

2,7

68

8$

33

,21

19

.82

%$

3,2

61

9$

36

,79

89

.91

%$

3,6

46

10

$3

9,0

06

9.9

5%

$3

,88

3T

Y(1

1)

$4

1,3

46

10

.00

%$

4,1

35

Ind

ustry A

verage

Asw

ath Dam

odaran43

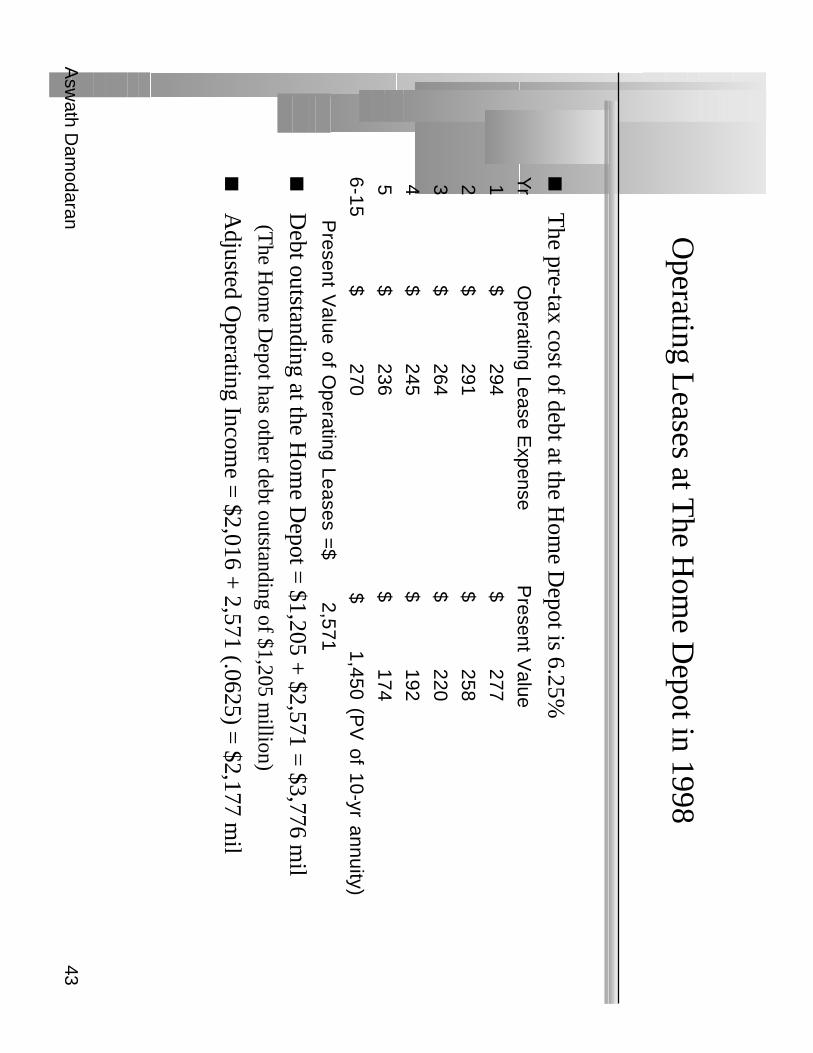

Operating L

eases at The H

ome D

epot in 1998

The pre-tax cost of debt at the H

ome D

epot is 6.25%Y

rO

perating Lease Expense

Present V

alue 1

$ 294 $ 277

2$ 291

$ 258 3

$ 264 $ 220

4$ 245

$ 192 5

$ 236 $ 174

6-1

5

$ 270 $ 1,450 (P

V of 10-yr annuity)

Present V

alue of Operating Leases =

$ 2,571

Debt outstanding at the H

ome D

epot = $1,205 +

$2,571 = $3,776 m

il(T

he Hom

e Depot has other debt outstanding of $1,205 m

illion)

Adjusted O

perating Income =

$2,016 + 2,571 (.0625) =

$2,177 mil

Asw

ath Dam

odaran44

Capitalizing R

&D

Expenses: Shire Pharm

aceuticals

To capitalize R

&D

,•

Specify an amortizable life for R

&D

(2 - 10 years)•

Collect past R

&D

expenses for as long as the amortizable life

•Sum

up the unamortized R

&D

over the period. (Thus, if the am

ortizable life is 5 years, the research asset canbe obtained by adding up 1/5th of the R

&D

expense from five years ago, 2/5th of the R

&D

expense from four

years ago...:

R &

D w

as assumed to have a 5-year life.

Year

R&

DU

namortized R

&D

Am

ortizationC

urrent£48.12

1.00£48.12

£0.00-1

£37.420.80

£29.94£7.48

-2£28.99

0.60£17.39

£5.80-3

£17.880.40

£7.15£3.58

-4£8.18

0.20£1.64

£1.64-5

£4.560.00

£0.00£0.91

£104.24£19.41

Value of research asset =

£104.24A

mortization of research asset in 2000 =

£19.41A

djustment to O

perating Income =

Add back R

&D

and subtract Am

ortization of R&

DA

djusted Operating Incom

e = £41.03 +

£48.12 - £19.41 = £

69

.74

Asw

ath Dam

odaran45

The E

ffect of Net O

perating Losses: A

mazon.com

’s Tax

Rate

Year

12

34

5

EB

IT-$373

-$94$407

$1,038$1,628

Taxes

$0$0

$0$167

$570

EB

IT(1-t)

-$373-$94

$407$871

$1,058

Tax rate

0%0%

0%16.13%

35%

NO

L$500

$873$967

$560$0

After year 5, the tax rate becom

es 35%.

Asw

ath Dam

odaran46

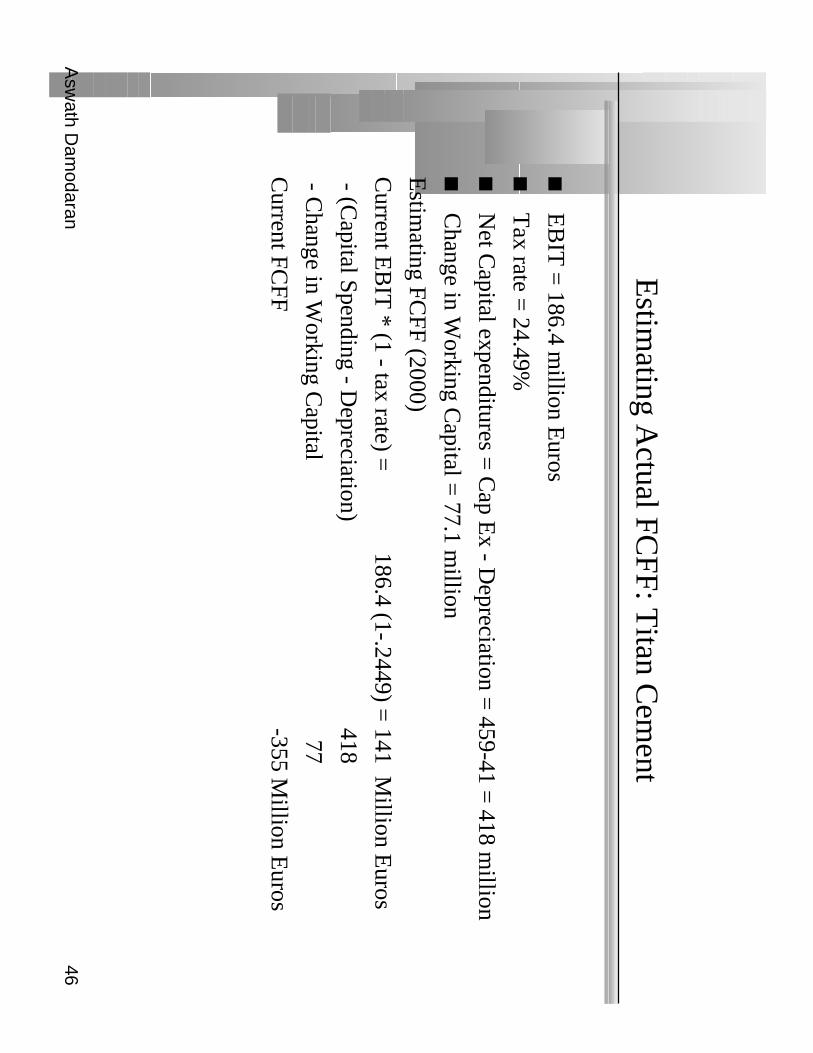

Estim

ating Actual FC

FF: Titan C

ement

EB

IT =

186.4 million E

uros

Tax rate =

24.49%

Net C

apital expenditures = C

ap Ex - D

epreciation = 459-41 =

418 million

Change in W

orking Capital =

77.1 million

Estim

ating FCFF (2000)

Current E

BIT

* (1 - tax rate) =186.4 (1-.2449) =

141 Million E

uros

- (Capital Spending - D

epreciation)418

- Change in W

orking Capital

77

Current FC

FF-355 M

illion Euros

Asw

ath Dam

odaran47

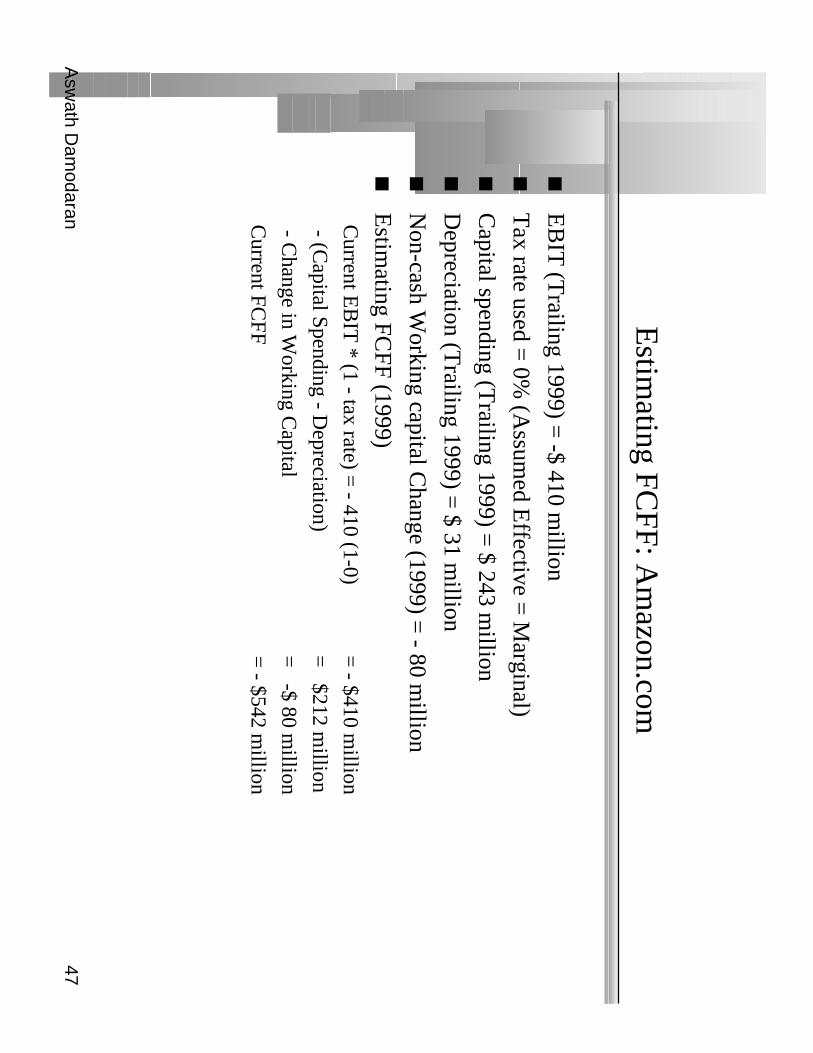

Estim

ating FCFF: A

mazon.com

EB

IT (T

railing 1999) = -$ 410 m

illion

Tax rate used =

0% (A

ssumed E

ffective = M

arginal)

Capital spending (T

railing 1999) = $ 243 m

illion

Depreciation (T

railing 1999) = $ 31 m

illion

Non-cash W

orking capital Change (1999) =

- 80 million

Estim

ating FCFF (1999)

Current E

BIT

* (1 - tax rate) = - 410 (1-0)

= - $410 m

illion

- (Capital Spending - D

epreciation)

= $212 m

illion

- Change in W

orking Capital

= -$ 80 m

illion

Current FC

FF=

- $542 million

Asw

ath Dam

odaran48

IV. E

xpected Grow

th in EB

IT and Fundam

entals

Reinvestm

ent Rate and R

eturn on Capital

gE

BIT

= (N

et Capital E

xpenditures + C

hange in WC

)/EB

IT(1-t) * R

OC

= R

einvestment R

ate * RO

C

Proposition: No firm

can expect its operating income to grow

over time

without reinvesting som

e of the operating income in net capital expenditures

and/or working capital.

Proposition: The net capital expenditure needs of a firm

, for a given growth

rate, should be inversely proportional to the quality of its investments.

Asw

ath Dam

odaran49

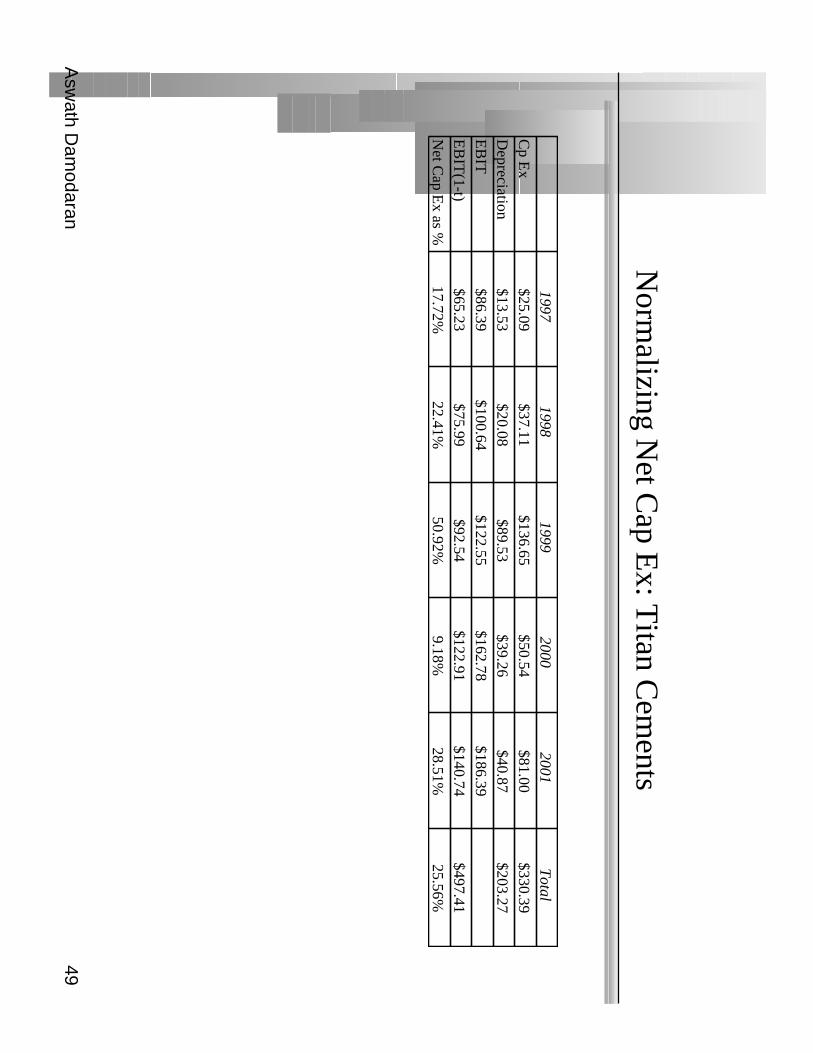

Norm

alizing Net C

ap Ex: T

itan Cem

ents

19971998

19992000

2001T

otalC

p Ex

$25.09$37.11

$136.65$50.54

$81.00$330.39

Depreciation

$13.53$20.08

$89.53$39.26

$40.87$203.27

EB

IT$86.39

$100.64$122.55

$162.78$186.39

EB

IT(1-t)

$65.23$75.99

$92.54$122.91

$140.74$497.41

Net C

a p Ex as %

o17.72%

22.41%50.92%

9.18%28.51%

25.56%

Asw

ath Dam

odaran50

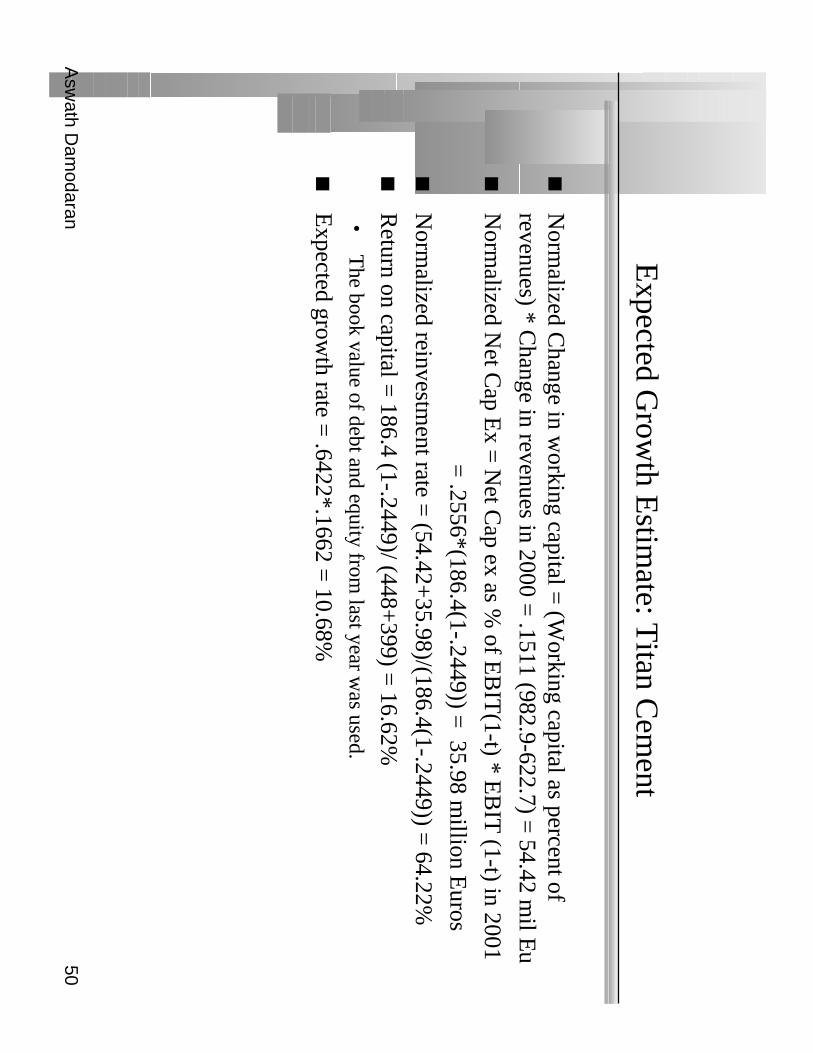

Expected G

rowth E

stimate: T

itan Cem

ent

Norm

alized Change in w

orking capital = (W

orking capital as percent ofrevenues) * C

hange in revenues in 2000 = .1511 (982.9-622.7) =

54.42 mil E

u

Norm

alized Net C

ap Ex =

Net C

ap ex as % of E

BIT

(1-t) * EB

IT (1-t) in 2001

= .2556*(186.4(1-.2449)) =

35.98 million E

uros

Norm

alized reinvestment rate =

(54.42+35.98)/(186.4(1-.2449)) =

64.22%

Return on capital =

186.4 (1-.2449)/ (448+399) =

16.62%•

The book value of debt and equity from

last year was used.

Expected grow

th rate = .6422*.1662 =

10.68%

Asw

ath Dam

odaran51

Revenue G

rowth and O

perating Margins

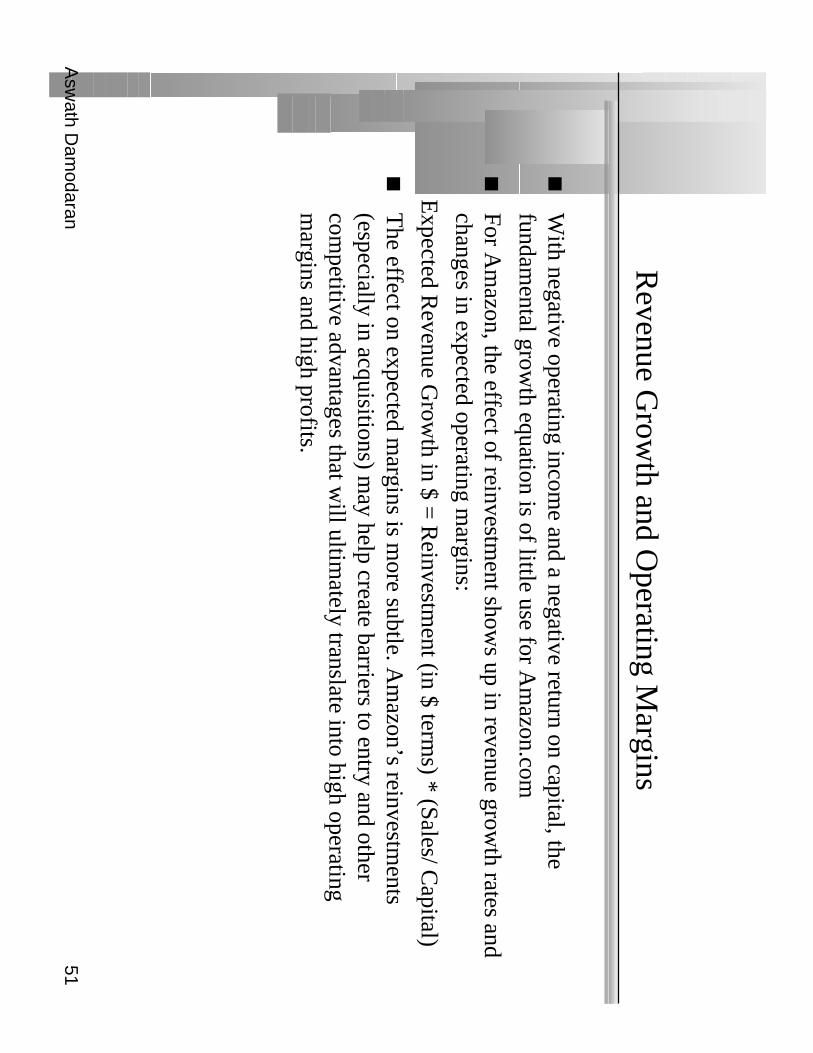

With negative operating incom

e and a negative return on capital, thefundam

ental growth equation is of little use for A

mazon.com

For Am

azon, the effect of reinvestment show

s up in revenue growth rates and

changes in expected operating margins:

Expected R

evenue Grow

th in $ = R

einvestment (in $ term

s) * (Sales/ Capital)

The effect on expected m

argins is more subtle. A

mazon’s reinvestm

ents(especially in acquisitions) m

ay help create barriers to entry and othercom

petitive advantages that will ultim

ately translate into high operatingm

argins and high profits.

Asw

ath Dam

odaran52

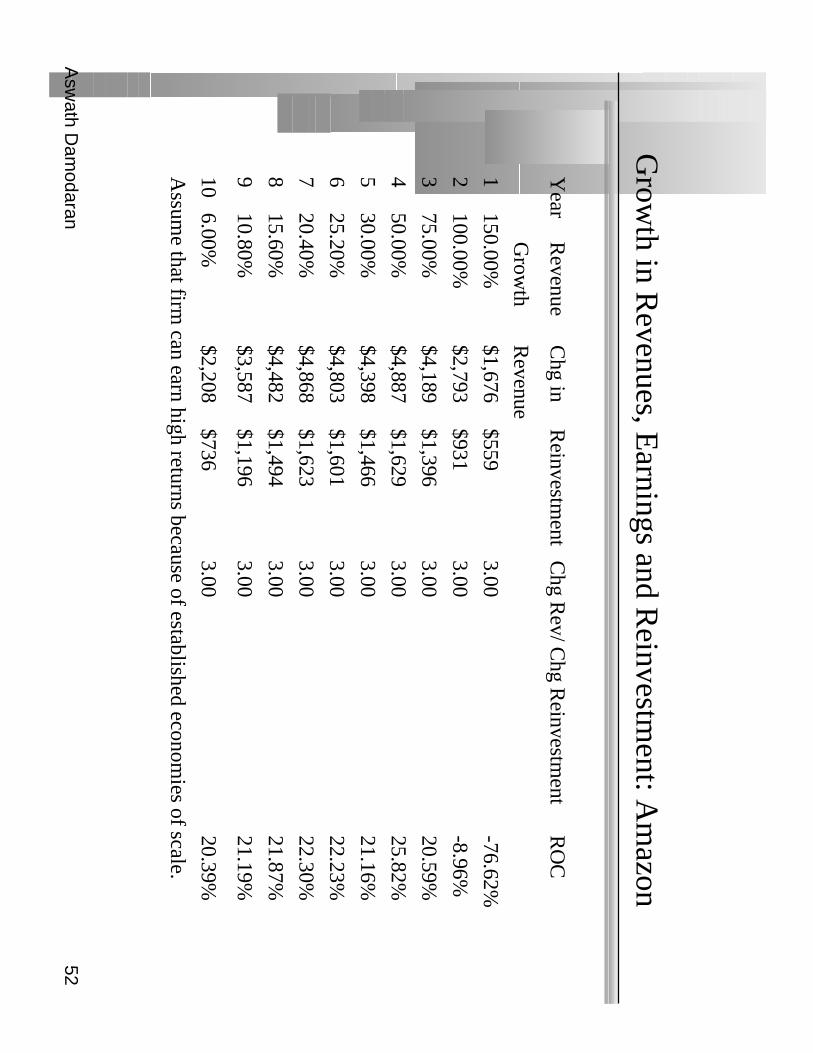

Grow

th in Revenues, E

arnings and Reinvestm

ent: Am

azon

Year

Revenue

Chg in

Reinvestm

entC

hg Rev/ C

hg Reinvestm

entR

OC

Grow

thR

evenue

1150.00%

$1,676$559

3.00-76.62%

2100.00%

$2,793$931

3.00-8.96%

375.00%

$4,189$1,396

3.0020.59%

450.00%

$4,887$1,629

3.0025.82%

530.00%

$4,398$1,466

3.0021.16%

625.20%

$4,803$1,601

3.0022.23%

720.40%

$4,868$1,623

3.0022.30%

815.60%

$4,482$1,494

3.0021.87%

910.80%

$3,587$1,196

3.0021.19%

106.00%

$2,208$736

3.0020.39%

Assum

e that firm can earn high returns because of established econom

ies of scale.

Asw

ath Dam

odaran53

V. G

rowth Patterns

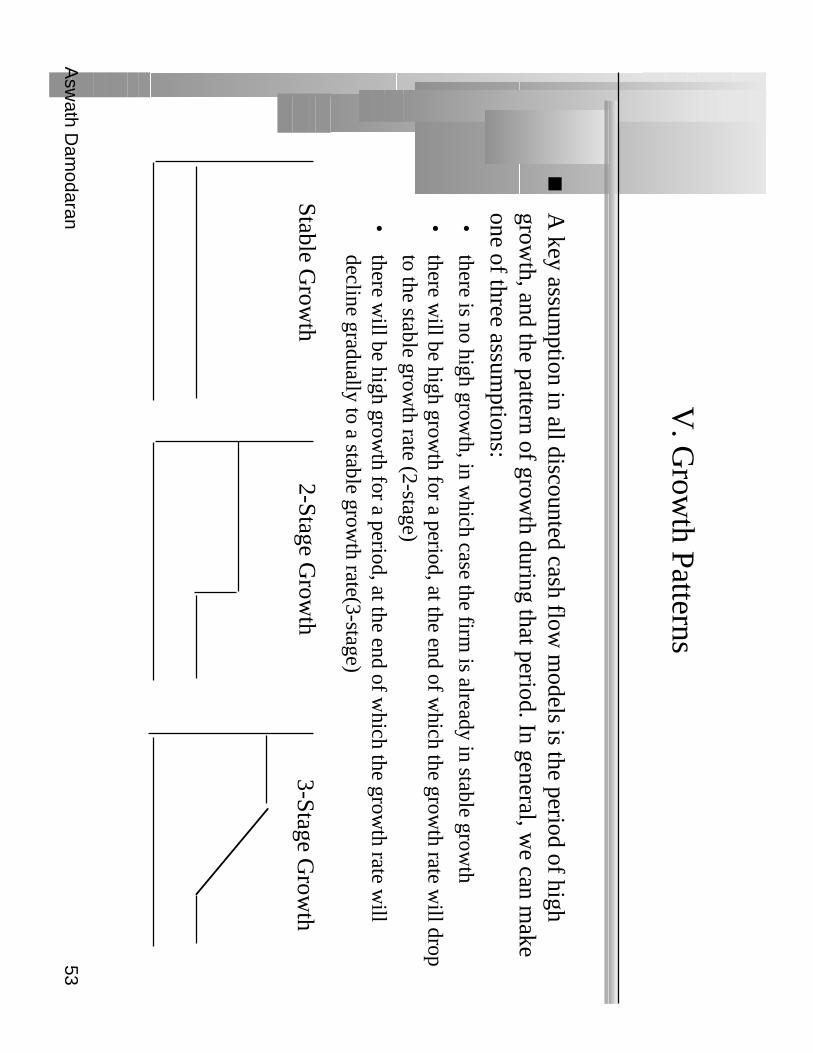

A key assum

ption in all discounted cash flow m

odels is the period of highgrow

th, and the pattern of growth during that period. In general, w

e can make

one of three assumptions:

•there is no high grow

th, in which case the firm

is already in stable growth

•there w

ill be high growth for a period, at the end of w

hich the growth rate w

ill dropto the stable grow

th rate (2-stage)

•there w

ill be high growth for a period, at the end of w

hich the growth rate w

illdecline gradually to a stable grow

th rate(3-stage)

Stable Grow

th2-Stage G

rowth

3-Stage Grow

th

Asw

ath Dam

odaran54

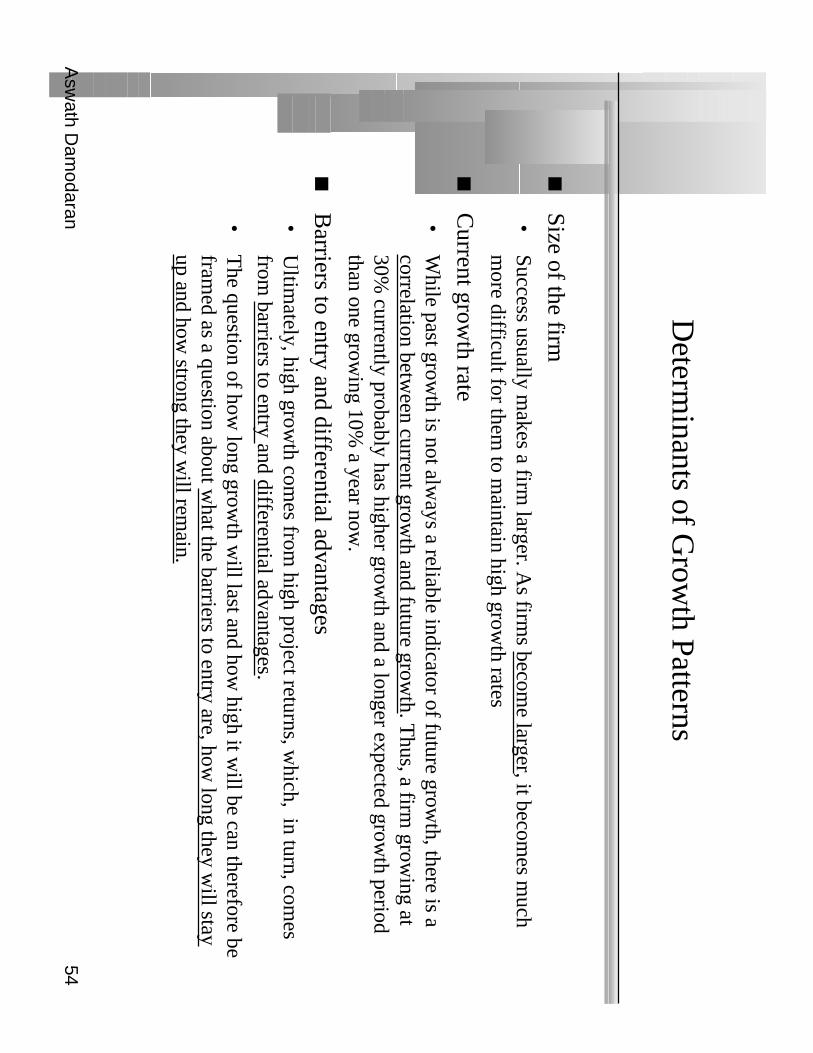

Determ

inants of Grow

th Patterns

Size of the firm•

Success usually makes a firm

larger. As firm

s become larger, it becom

es much

more difficult for them

to maintain high grow

th rates

Current grow

th rate•

While past grow

th is not always a reliable indicator of future grow

th, there is acorrelation betw

een current growth and future grow

th. Thus, a firm

growing at

30% currently probably has higher grow

th and a longer expected growth period

than one growing 10%

a year now.

Barriers to entry and differential advantages•

Ultim

ately, high growth com

es from high project returns, w

hich, in turn, comes

from barriers to entry and differential advantages.

•T

he question of how long grow

th will last and how

high it will be can therefore be

framed as a question about w

hat the barriers to entry are, how long they w

ill stayup and how

strong they will rem

ain.

Asw

ath Dam

odaran55

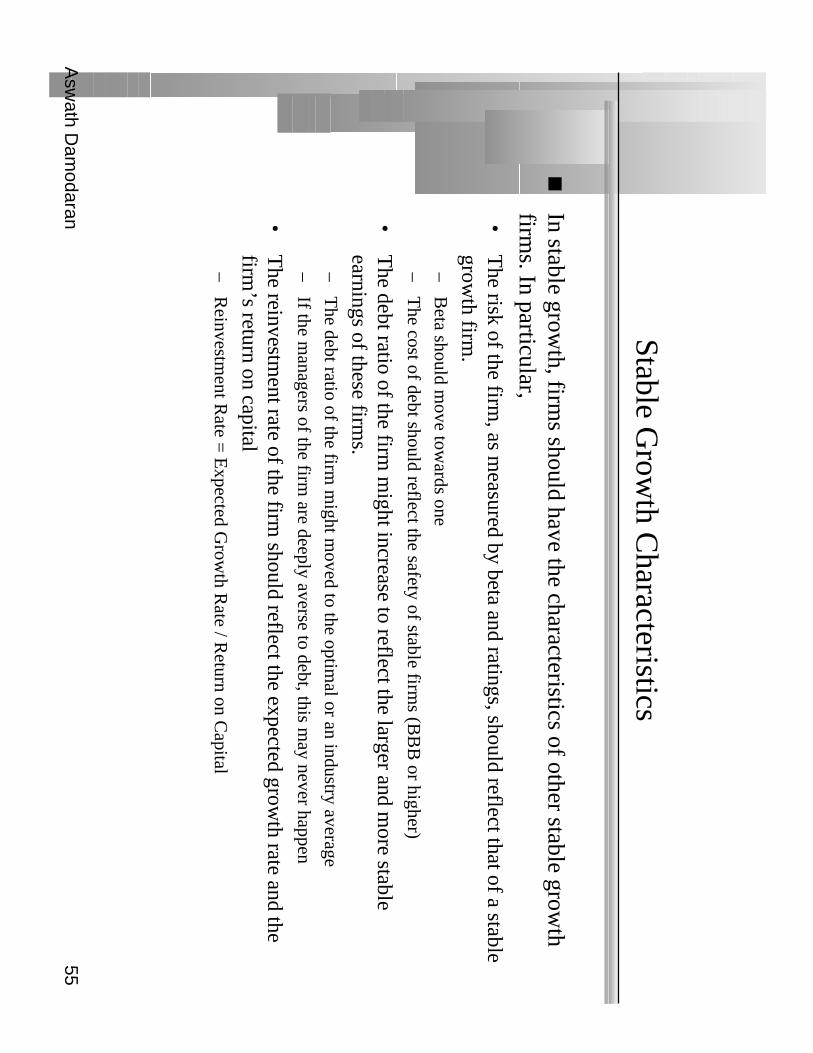

Stable Grow

th Characteristics

In stable growth, firm

s should have the characteristics of other stable growth

firms. In particular,

•T

he risk of the firm, as m

easured by beta and ratings, should reflect that of a stablegrow

th firm.

–B

eta should move tow

ards one

–T

he cost of debt should reflect the safety of stable firms (B

BB

or higher)

•T

he debt ratio of the firm m

ight increase to reflect the larger and more stable

earnings of these firms.

–T

he debt ratio of the firm m

ight moved to the optim

al or an industry average

–If the m

anagers of the firm are deeply averse to debt, this m

ay never happen

•T

he reinvestment rate of the firm

should reflect the expected growth rate and the

firm’s return on capital

–R

einvestment R

ate = E

xpected Grow

th Rate / R

eturn on Capital

Asw

ath Dam

odaran56

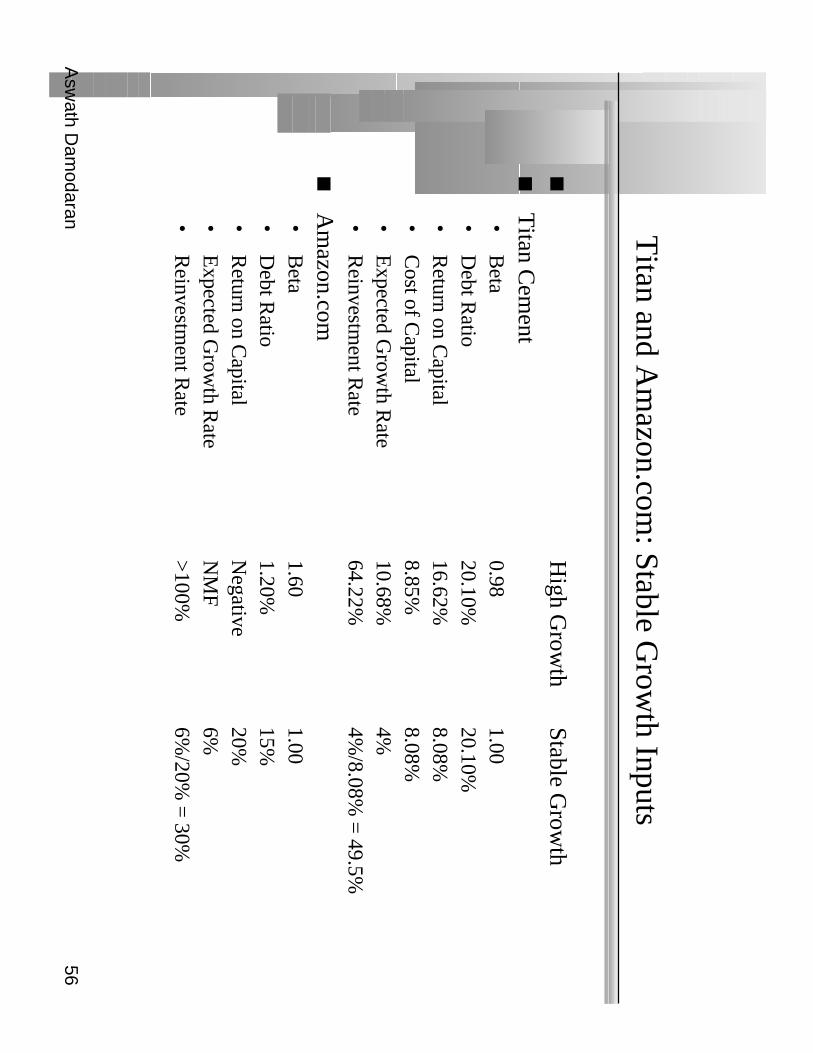

Titan and A

mazon.com

: Stable Grow

th Inputs

H

igh Grow

thStable G

rowth

Titan C

ement

•B

eta0.98

1.00•

Debt R

atio20.10%

20.10%•

Return on C

apital16.62%

8.08%•

Cost of C

apital8.85%

8.08%•

Expected G

rowth R

ate 10.68%

4%•

Reinvestm

ent Rate

64.22%4%

/8.08% =

49.5%

Am

azon.com•

Beta

1.601.00

•D

ebt Ratio

1.20%15%

•R

eturn on Capital

Negative

20%•

Expected G

rowth R

ateN

MF

6%•

Reinvestm

ent Rate

>100%

6%/20%

= 30%

Asw

ath Dam

odaran57

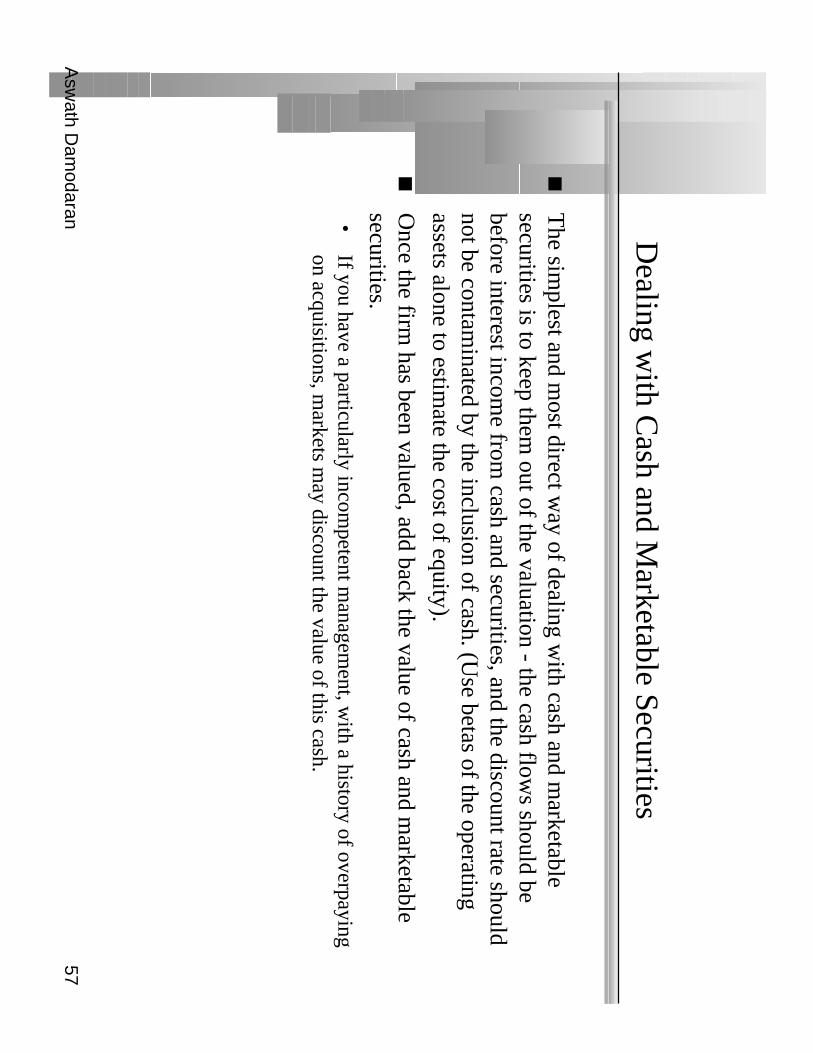

Dealing w

ith Cash and M

arketable Securities

The sim

plest and most direct w

ay of dealing with cash and m

arketablesecurities is to keep them

out of the valuation - the cash flows should be

before interest income from

cash and securities, and the discount rate shouldnot be contam

inated by the inclusion of cash. (Use betas of the operating

assets alone to estimate the cost of equity).

Once the firm

has been valued, add back the value of cash and marketable

securities.•

If you have a particularly incompetent m

anagement, w

ith a history of overpayingon acquisitions, m

arkets may discount the value of this cash.

Asw

ath Dam

odaran58

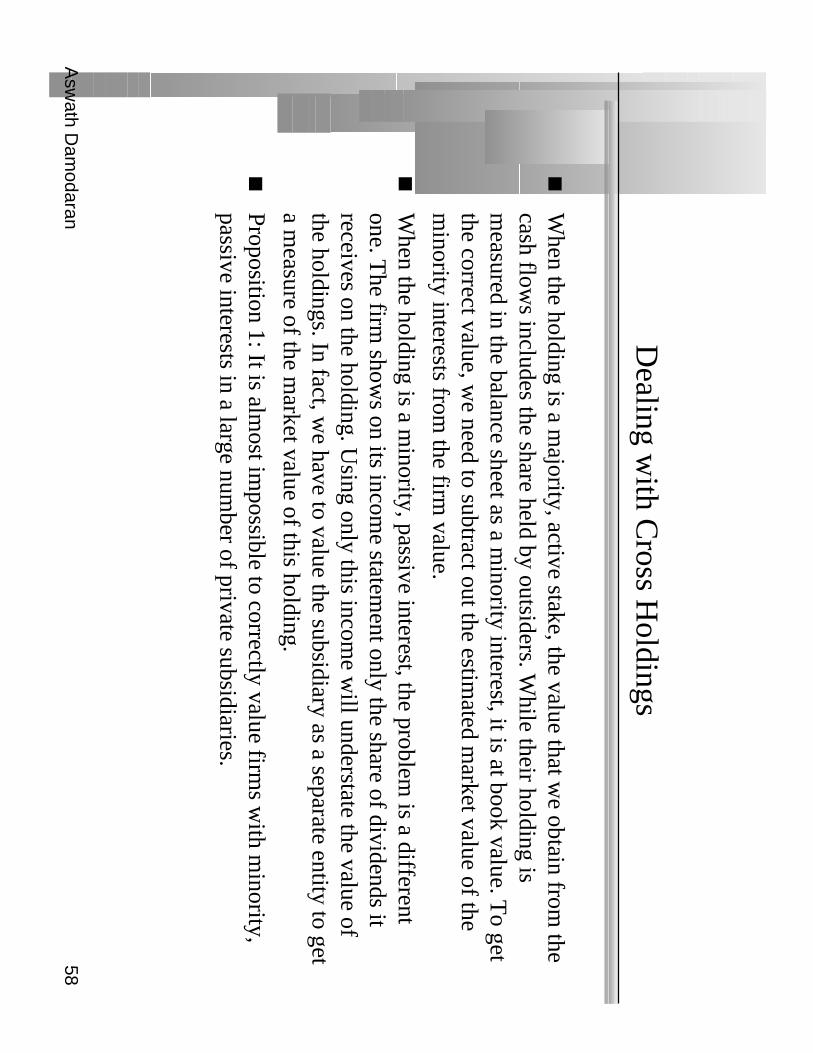

Dealing w

ith Cross H

oldings

When the holding is a m

ajority, active stake, the value that we obtain from

thecash flow

s includes the share held by outsiders. While their holding is

measured in the balance sheet as a m

inority interest, it is at book value. To get

the correct value, we need to subtract out the estim

ated market value of the

minority interests from

the firm value.

When the holding is a m

inority, passive interest, the problem is a different

one. The firm

shows on its incom

e statement only the share of dividends it

receives on the holding. Using only this incom

e will understate the value of

the holdings. In fact, we have to value the subsidiary as a separate entity to get

a measure of the m

arket value of this holding.

Proposition 1: It is almost im

possible to correctly value firms w

ith minority,

passive interests in a large number of private subsidiaries.

Asw

ath Dam

odaran59

Am

azon: Estim

ating the Value of E

quity Options

Details of options outstanding

•A

verage strike price of options outstanding =$ 13.375

•A

verage maturity of options outstanding =

8.4 years

•Standard deviation in ln(stock price) =

50.00%

•A

nnualized dividend yield on stock =0.00%

•T

reasury bond rate =6.50%

•N

umber of options outstanding =

38 million

•N

umber of shares outstanding =

340.79 million

Value of options outstanding (using dilution-adjusted B

lack-Scholes model)

•V

alue of equity options = $ 2,892 m

illion

Asw

ath Dam

odaran60

Forever

Term

inal Value= 1881/(.0961-.06)

=52,148

Co

st of E

qu

ity12.90%

Co

st of D

ebt

6.5%+

1.5%=

8.0%T

ax rate = 0% -> 35%

Weig

hts

Debt=

1.2% ->

15%

Value of O

p Assets $ 14,910

+ C

ash $ 26

= Value of F

irm$14,936

- Value of D

ebt$ 349

= Value of E

quity$14,587

- Equity O

ptions$ 2,892

Value per share

$ 34.32

Riskfree R

ate:

T. B

ond rate = 6.5%

+B

eta1.60 ->

1.00X

Risk P

remiu

m4%

Internet/R

etailO

perating Leverage

Current

D/E

: 1.21%B

ase Equity

Prem

iumC

ountry Risk

Prem

ium

Current

Revenue

$ 1,117

Current

Margin:

-36.71%

Reinvestm

ent:C

ap ex includes acquisitionsW

orking capital is 3% of revenues

Sales T

urnoverR

atio: 3.00C

ompetitive

Advantages

Revenue

Grow

th:42%

Expected

Margin:

-> 10.00%

Stable G

rowth

Stable

Revenue

Grow

th: 6%

Stable

Operating

Margin:

10.00%

Stable

RO

C=

20%R

einvest 30%

of EB

IT(1-t)

EB

IT-410m

NO

L:500 m

$41,346 10.00%

35.00%$2,688 $ 807 $1,881

Term

. Year

24

31

56

89

107

Cost of E

quity12.90%

12.90%12.90%

12.90%12.90%

12.42%12.30%

12.10%11.70%

10.50%C

ost of Debt

8.00%8.00%

8.00%8.00%

8.00%7.80%

7.75%7.67%

7.50%7.00%

AT

cost of debt8.00%

8.00%8.00%

6.71%5.20%

5.07%5.04%

4.98%4.88%

4.55%C

ost of Capital

12.84%12.84%

12.84%12.83%

12.81%12.13%

11.96%11.69%

11.15%9.61%

Revenues

$2,793 5,585

9,774 14,661

19,059 23,862

28,729 33,211

36,798 39,006

E

BIT

-$373-$94

$407$1,038

$1,628$2,212

$2,768$3,261

$3,646$3,883

EB

IT (1-t)

-$373-$94

$407$871

$1,058$1,438

$1,799$2,119

$2,370$2,524

- Reinvestm

ent$559

$931$1,396

$1,629$1,466

$1,601$1,623

$1,494$1,196

$736FC

FF-$931

-$1,024-$989

-$758-$408

-$163$177

$625$1,174

$1,788Am

azon

.com

Janu

ary 2000S

tock P

rice = $ 84

Asw

ath Dam

odaran61

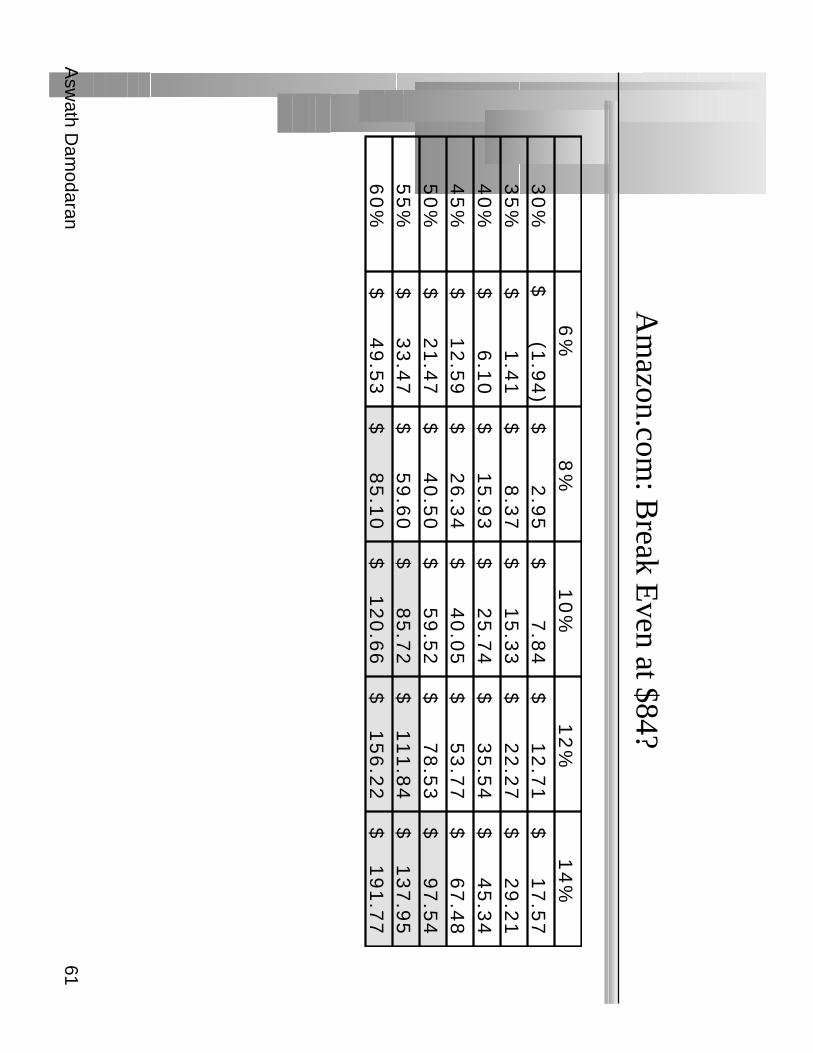

Am

azon.com: B

reak Even at $84?

6%

8%

10

%1

2%

14

%3

0%

(1.9

4)

$ 2

.95

$ 7

.84

$ 1

2.7

1$

17

.57

$ 3

5%

1.4

1$

8.3

7$

15

.33

$ 2

2.2

7$

29

.21

$ 4

0%

6.1

0$

15

.93

$ 2

5.7

4$

35

.54

$ 4

5.3

4$

45

%1

2.5

9$

26

.34

$ 4

0.0

5$

53

.77

$ 6

7.4

8$

50

%2

1.4

7$

40

.50

$ 5

9.5

2$

78

.53

$ 9

7.5

4$

55

%3

3.4

7$

59

.60

$ 8

5.7

2$

11

1.8

4$

13

7.9

5$

60

%4

9.5

3$

85

.10

$ 1

20

.66

$ 1

56

.22

$ 1

91

.77

$

Asw

ath Dam

odaran62

Forever

Term

inal Value= 1064/(.0876-.05)

=$ 28,310

Co

st of E

qu

ity13.81%

Co

st of D

ebt

5.1%+

4.75%=

9.85%T

ax rate = 0% -> 35%

Weig

hts

Debt=

27.38% ->

15%

Value of O

p Assets $ 7,967

+ C

ash & N

on-op $ 1,263

= Value of F

irm$ 9,230

- Value of D

ebt$ 1,890

= Value of E

quity$ 7,340

- Equity O

ptions$ 748

Value per share

$ 18.74

Riskfree R

ate:

T. B

ond rate = 5.1%

+B

eta2.18->

1.10X

Risk P

remiu

m4%

Internet/R

etailO

perating Leverage

Current

D/E

: 37.5%B

ase Equity

Prem

iumC

ountry Risk

Prem

ium

Current

Revenue

$ 2,465

Current

Margin:

-34.60%

Reinvestm

ent:C

ap ex includes acquisitionsW

orking capital is 3% of revenues

Sales T

urnoverR

atio: 3.02C

ompetitive

Advantages

Revenue

Grow

th:25.41%

Expected

Margin:

-> 9.32%

Stable G

rowth

Stable

Revenue

Grow

th: 5%

Stable

Operating

Margin:

9.32%

Stable

RO

C=

16.94%R

einvest 29.5%

of EB

IT(1-t)

EB

IT-853m

NO

L:1,289 m

$24,912$2,322$1,509$ 445$1,064

Term

. Year

24

31

56

89

107

Debt R

atio27.27%

27.27%27.27%

27.27%27.27%

24.81%24.20%

23.18%21.13%

15.00%B

eta2.18

2.182.18

2.182.18

1.96 1.75

1.53 1.32

1.10 C

ost of Equity

13.81%13.81%

13.81%13.81%

13.81%12.95%

12.09%11.22%

10.36%9.50%

AT

cost of debt10.00%

10.00%10.00%

10.00%9.06%

6.11%6.01%

5.85%5.53%

4.55%C

ost of Capital

12.77%12.77%

12.77%12.77%

12.52%11.25%

10.62%9.98%

9.34%8.76%

Am

azon

.com

Janu

ary 2001S

tock p

rice = $14

Revenues

$4,314$6,471

$9,059$11,777

$14,132$16,534

$18,849$20,922

$22,596$23,726

$24,912E

BIT

-$703

-$364$54

$499$898

$1,255$1,566

$1,827$2,028

$2,164$2,322

EB

IT(1-t)

-$703-$364

$54$499

$898$1,133

$1,018$1,187

$1,318$1,406

$1,509 - R

einvestment

$612$714

$857$900

$780$796

$766$687

$554$374

$445FC

FF-$1,315

-$1,078-$803

-$401$118

$337$252

$501$764

$1,032$1,064

Asw

ath Dam

odaran63

Cu

rrent C

ashflo

w to

Firm

EB

IT(1-t) : 141

- Nt C

pX 419

- Ch g W

C 77

= FC

FF

-355R

einvestment R

ate = 352%

Exp

ected G

row

th

in E

BIT

(1-t).6422*.1662=

.106810.68

%

Stable G

rowth

g = 4%

; Beta =

1.00;C

ountr y Prem

ium= 0%

Cost of capital = 8.08%

R

OC

= 8.08%

; Tax rate=

30%R

einvestment R

ate=49.5%

Term

inal Value5 =

113.79/(.0808-.04) = 2,780

Co

st of E

qu

ity9.71%

Co

st of D

ebt

(5.1%+

.35%+

1.8%)(1-.2449)

= 5.47%

Weig

hts

E =

79.9% D

= 20.1%

Discount at C

ost of Capital (W

AC

C) =

9.71% (.799) +

5.47% (0.201) =

8.85%

Firm

Value: 2,08 4

+ C

ash: 113

- Debt 382

=Equit y 1,815

-Options

0V

alue/Share 47.64

Riskfree R

ate:

Real riskfree rate = 5.1%

+B

eta 0.98

X

Risk P

remiu

m4.70%

Unlevered B

eta for S

ectors: 0.80F

irm’s D

/ER

atio: 29%M

ature riskprem

ium4%

Country R

iskP

remium

0.70%

Titan C

ements: S

tatus Quo

Reinvestm

ent Rate

64.22%

Return on C

apital16.62%

Term

Yr

225.34111.55113.79

Avg R

einvestment

rate = 64.22%

Year

12

34

5E

BIT

(1-t)€

155.77€

172.40€

190.81€

211.18€

233.72 - R

einvestment

€ 100.04

€ 110.72

€ 122.54

€ 135.62

€ 150.10

= F

CF

F€

55.73€

61.68€

68.27€

75.56€

83.62

Asw

ath Dam

odaran64

Value E

nhancement: B

ack to Basics

Asw

ath Dam

odaran

http://ww

w.stern.nyu.edu/~adam

odar

Asw

ath Dam

odaran65

Price Enhancem

ent versus Value E

nhancement

Asw

ath Dam

odaran66

The Paths to V

alue Creation

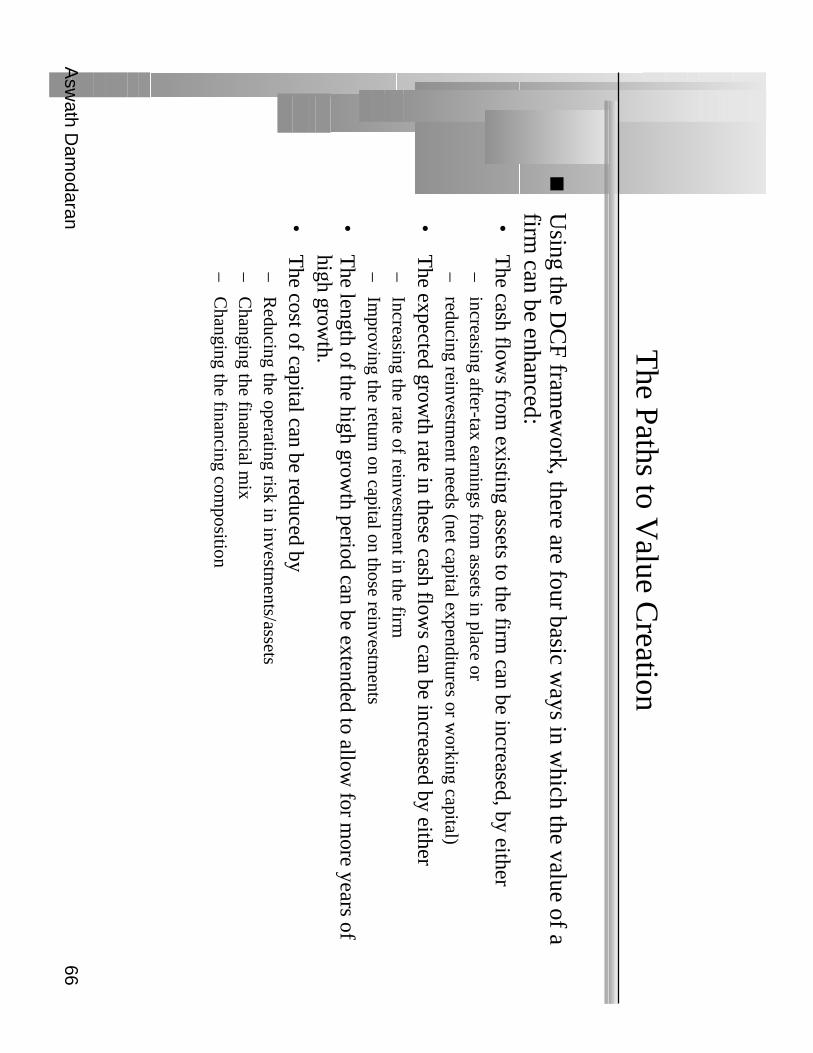

Using the D

CF fram

ework, there are four basic w

ays in which the value of a

firm can be enhanced:

•T

he cash flows from

existing assets to the firm can be increased, by either

–increasing after-tax earnings from

assets in place or–

reducing reinvestment needs (net capital expenditures or w

orking capital)

•T

he expected growth rate in these cash flow

s can be increased by either–

Increasing the rate of reinvestment in the firm

–Im

proving the return on capital on those reinvestments

•T

he length of the high growth period can be extended to allow

for more years of

high growth.

•T

he cost of capital can be reduced by–

Reducing the operating risk in investm

ents/assets–

Changing the financial m

ix–

Changing the financing com

position

Asw

ath Dam

odaran67

A B

asic Proposition

For an action to affect the value of the firm, it has to

•A

ffect current cash flows (or)

•A

ffect future growth (or)

•A

ffect the length of the high growth period (or)

•A

ffect the discount rate (cost of capital)

Proposition 1: A

ctions that do not affect current cash flows, future

growth, the length of the high grow

th period or the discount rate cannotaffect value.

Asw

ath Dam

odaran68

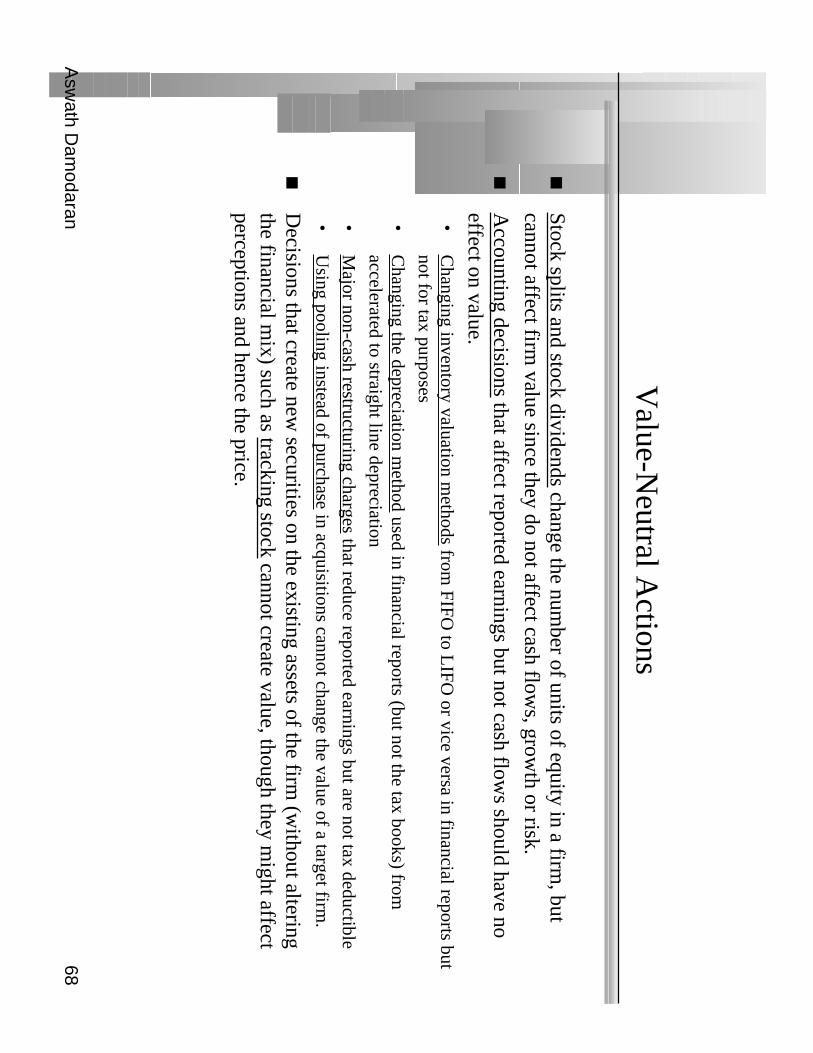

Value-N

eutral Actions

Stock splits and stock dividends change the number of units of equity in a firm

, butcannot affect firm

value since they do not affect cash flows, grow

th or risk.

Accounting decisions that affect reported earnings but not cash flow

s should have noeffect on value.

•C

hanging inventory valuation methods from

FIFO to L

IFO or vice versa in financial reports but

not for tax purposes

•C

hanging the depreciation method used in financial reports (but not the tax books) from

accelerated to straight line depreciation

•M

ajor non-cash restructuring charges that reduce reported earnings but are not tax deductible

•U

sing pooling instead of purchase in acquisitions cannot change the value of a target firm.

Decisions that create new

securities on the existing assets of the firm (w

ithout alteringthe financial m

ix) such as tracking stock cannot create value, though they might affect

perceptions and hence the price.

Asw

ath Dam

odaran69

I. Ways of Increasing C

ash Flows from

Assets in Place

Revenues

* Operating M

argin

= E

BIT

- Tax R

ate * EB

IT

= E

BIT

(1-t)

+ Depreciation

- Capital E

xpenditures- C

hg in Working C

apital=

FC

FF

Divest assets that

have negative EB

IT

More efficient

operations and cost cuttting: H

igher Margins

Reduce tax rate

- moving incom

e to lower tax locales

- transfer pricing- risk m

anagement

Live off past over- investm

ent

Better inventory

managem

ent and tighter credit policies

Asw

ath Dam

odaran70

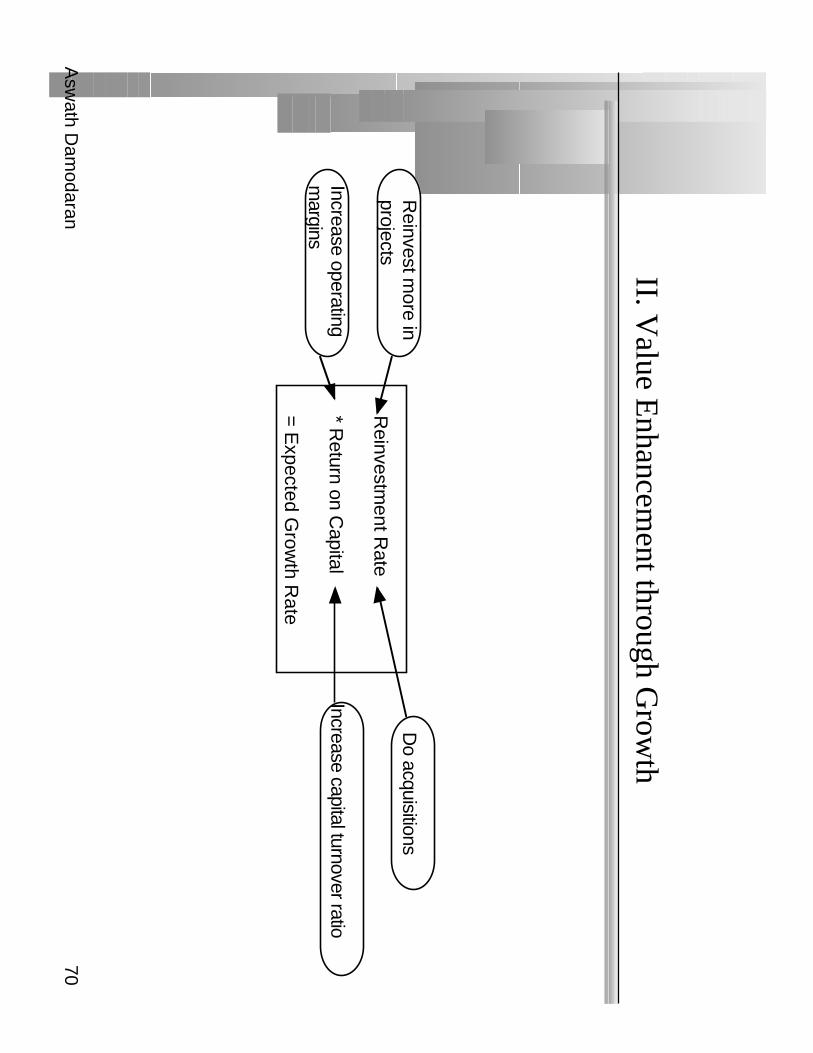

II. Value E

nhancement through G

rowth

Reinvestm

ent Rate

* Return on C

apital

= E

xpected Grow

th Rate

Reinvest m

ore inprojects

Do acquisitions

Increase operatingm

arginsIncrease capital turnover ratio

Asw

ath Dam

odaran71

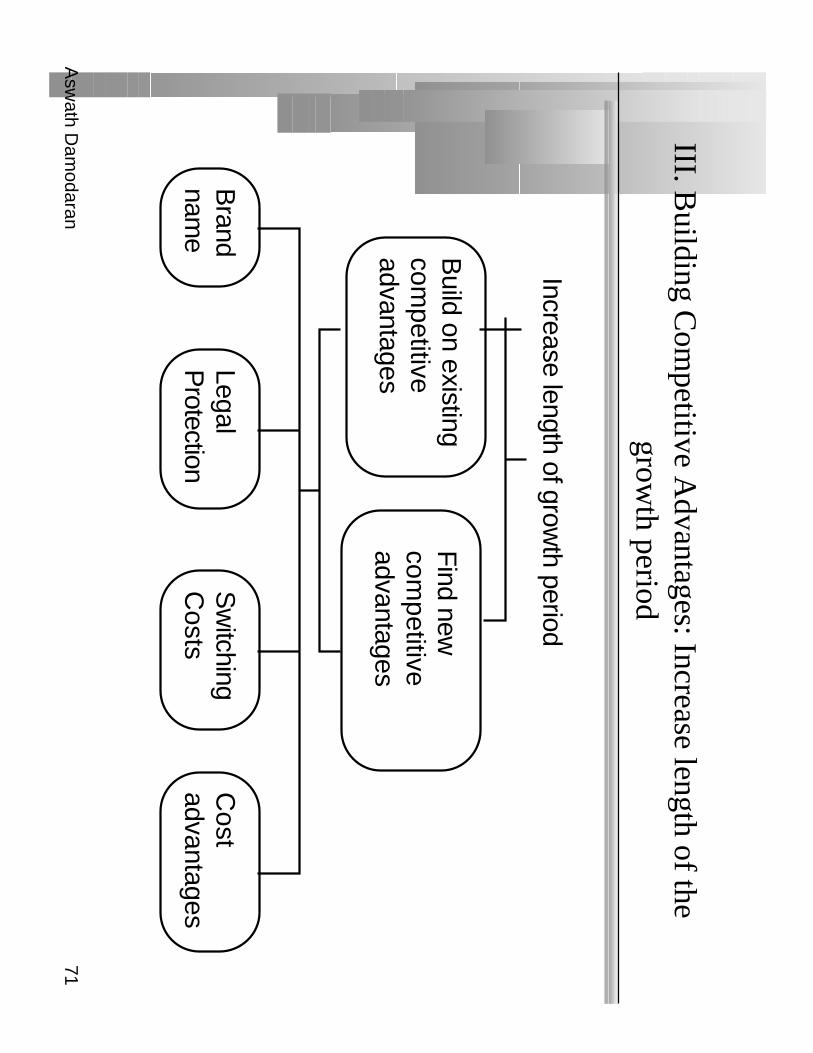

III. Building C

ompetitive A

dvantages: Increase length of thegrow

th period

Increase length of growth period

Build on existing

competitive

advantages

Find new

com

petitive advantages

Brand

name

Legal P

rotectionS

witching

Costs

Cost

advantages

Asw

ath Dam

odaran72

3.1: The B

rand Nam

e Advantage

Some firm

s are able to sustain above-normal returns and grow

th because theyhave w

ell-recognized brand names that allow

them to charge higher prices

than their competitors and/or sell m

ore than their competitors.

Firms that are able to im

prove their brand name value over tim

e can increaseboth their grow

th rate and the period over which they can expect to grow

atrates above the stable grow

th rate, thus increasing value.

Asw

ath Dam

odaran73

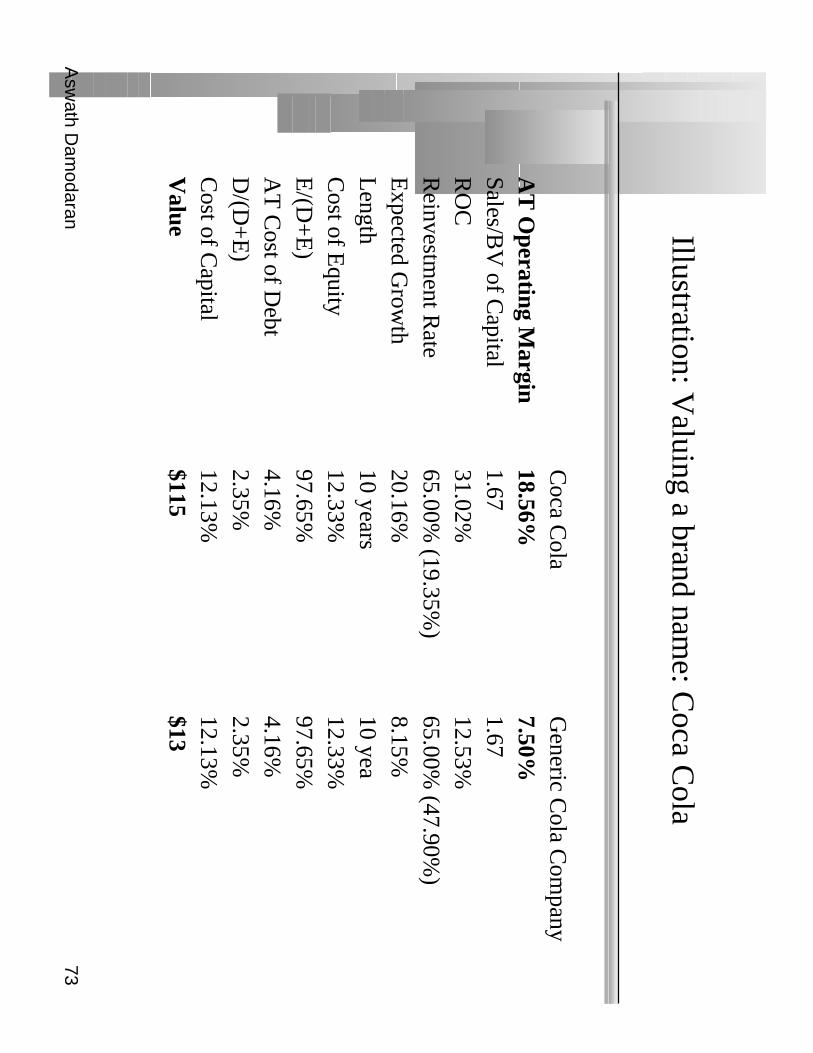

Illustration: Valuing a brand nam

e: Coca C

ola

Coca C

olaG

eneric Cola C

ompany

AT

Operating M

argin18.56%

7.50%Sales/B

V of C

apital1.67

1.67R

OC

31.02%12.53%

Reinvestm

ent Rate

65.00% (19.35%

)65.00%

(47.90%)

Expected G

rowth

20.16%8.15%

Length

10 years10 yea

Cost of E

quity12.33%

12.33%E

/(D+

E)

97.65%97.65%

AT

Cost of D

ebt4.16%

4.16%D

/(D+

E)

2.35%2.35%

Cost of C

apital12.13%

12.13%V

alue$115

$13

Asw

ath Dam

odaran74

3.2: Patents and Legal Protection

The m

ost complete protection that a firm

can have from com

petitive pressureis to ow

n a patent, copyright or some other kind of legal protection allow

ing itto be the sole producer for an extended period.

Note that patents only provide partial protection, since they cannot protect a

firm against a com

petitive product that meets the sam

e need but is not coveredby the patent protection.

Licenses and governm

ent-sanctioned monopolies also provide protection

against competition. T

hey may, how

ever, come w

ith restrictions on excessreturns; utilities in the U

nited States, for instance, are monopolies but are

regulated when it com

es to price increases and returns.

Asw

ath Dam

odaran75

3.3: Switching C

osts

Another potential barrier to entry is the cost associated w

ith switching from

one firm’s products to another.

The greater the sw

itching costs, the more difficult it is for com

petitors to come

in and compete aw

ay excess returns.

Firms that devise w

ays to increase the cost of switching from

their products tocom

petitors’ products, while reducing the costs of sw

itching from com

petitorproducts to their ow

n will be able to increase their expected length of grow

th.

Asw

ath Dam

odaran76

3.4: Cost A

dvantages

There are a num

ber of ways in w

hich firms can establish a cost advantage over

their competitors, and use this cost advantage as a barrier to entry:

•In businesses, w

here scale can be used to reduce costs, economies of scale can give

bigger firms advantages over sm

aller firms

•O

wning or having exclusive rights to a distribution system

can provide firms w

ith acost advantage over its com

petitors.

•O

wning or having the rights to extract a natural resource w

hich is in restrictedsupply (T

he undeveloped reserves of an oil or mining com

pany, for instance)

These cost advantages w

ill show up in valuation in one of tw

o ways:

•T

he firm m

ay charge the same price as its com

petitors, but have a much higher

operating margin.

•T

he firm m

ay charge lower prices than its com

petitors and have a much higher

capital turnover ratio.

Asw

ath Dam

odaran77

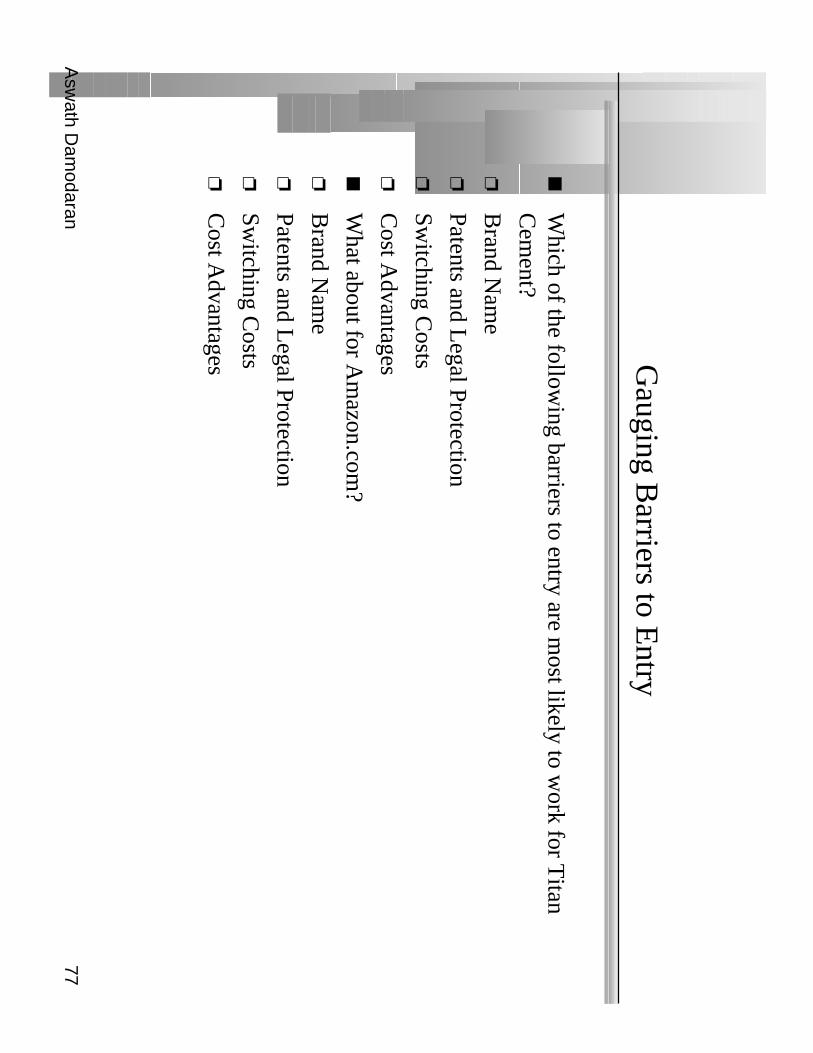

Gauging B

arriers to Entry

Which of the follow

ing barriers to entry are most likely to w

ork for Titan

Cem

ent?

Brand N

ame

Patents and Legal Protection

Switching C

osts

Cost A

dvantages

What about for A

mazon.com

?

Brand N

ame

Patents and Legal Protection

Switching C

osts

Cost A

dvantages

Asw

ath Dam

odaran78

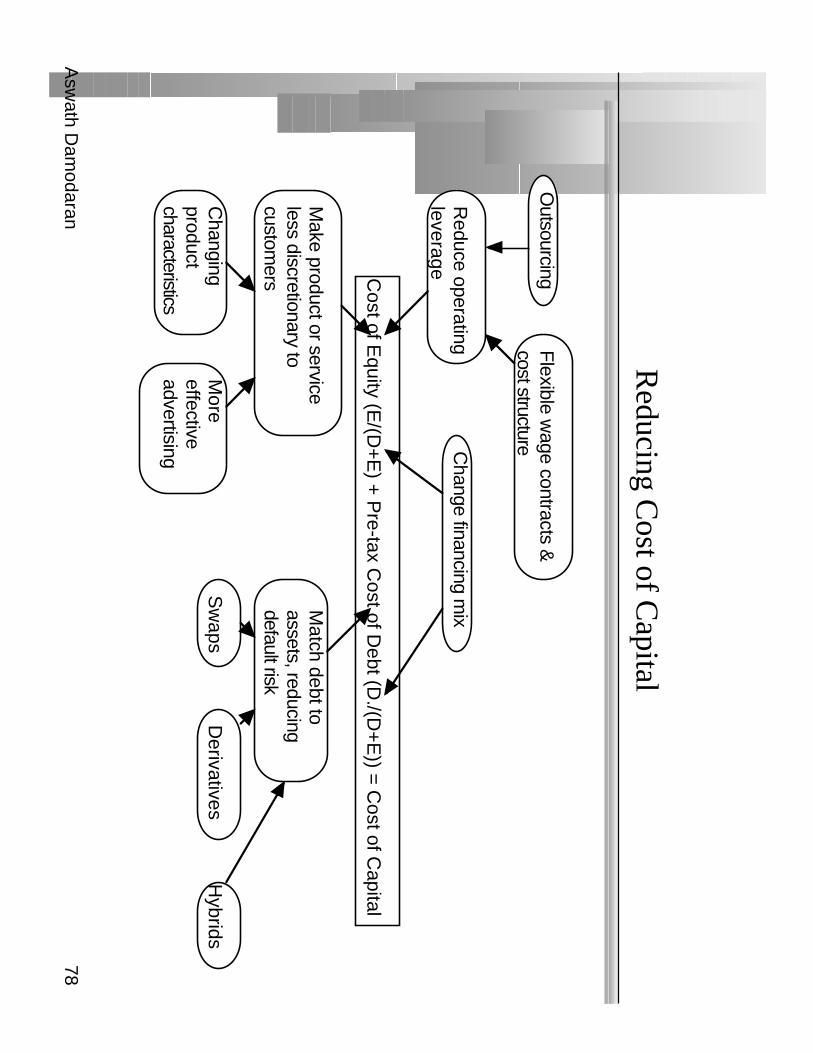

Reducing C

ost of Capital

Cost of E

quity (E/(D

+E

) + P

re-tax Cost of D

ebt (D./(D

+E

)) = C

ost of Capital

Change financing m

ix

Make product or service

less discretionary to custom

ers

Reduce operating

leverage

Match debt to

assets, reducing default risk

Changing

product characteristics

More

effective advertising

Outsourcing

Flexible w

age contracts &cost structure

Sw

apsD

erivativesH

ybrids

Asw

ath Dam

odaran79

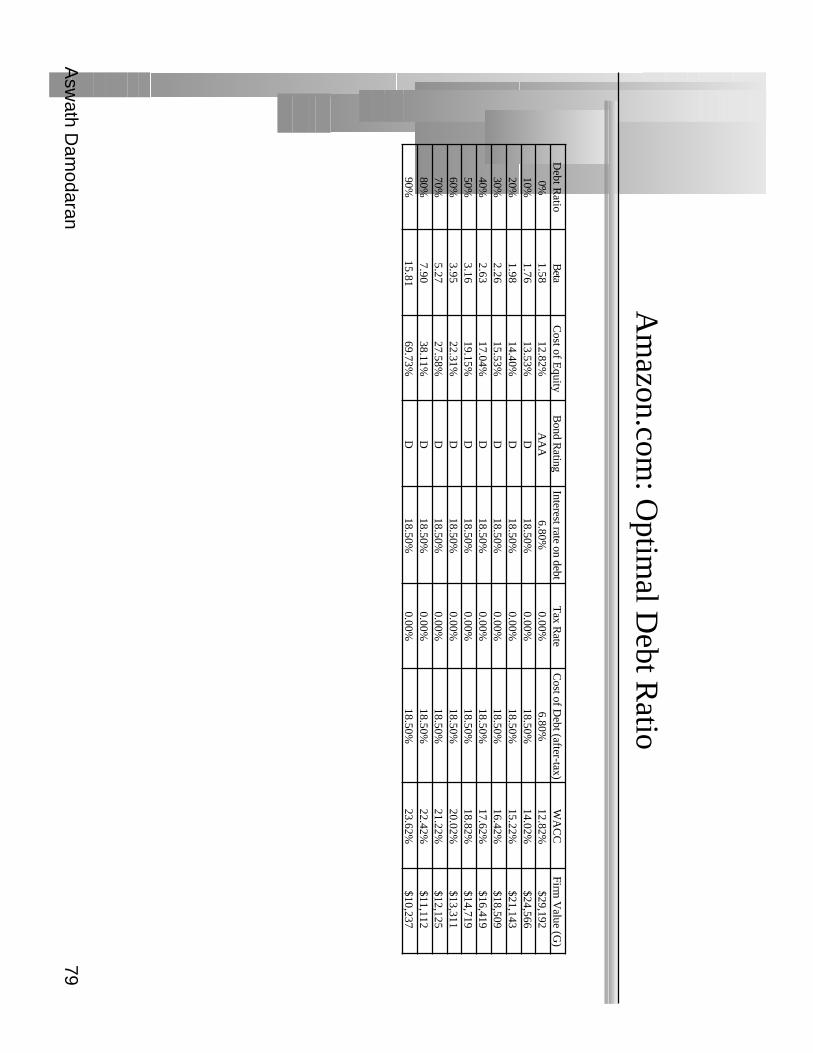

Am

azon.com: O

ptimal D

ebt Ratio

Debt R

atioB

etaC

ost of Equity

Bond R

atingInterest rate on debt

Tax R

ateC

ost of Debt (after-tax)

WA

CC

Firm V

alue (G)

0%1.58

12.82%A

AA

6.80%0.00%

6.80%12.82%

$29,19210%

1.7613.53%

D18.50%

0.00%18.50%

14.02%$24,566

20%1.98

14.40%D

18.50%0.00%

18.50%15.22%

$21,14330%

2.2615.53%

D18.50%

0.00%18.50%

16.42%$18,509

40%2.63

17.04%D

18.50%0.00%

18.50%17.62%

$16,41950%

3.1619.15%

D18.50%

0.00%18.50%

18.82%$14,719

60%3.95

22.31%D

18.50%0.00%

18.50%20.02%

$13,31170%

5.2727.58%

D18.50%

0.00%18.50%

21.22%$12,125

80%7.90

38.11%D

18.50%0.00%

18.50%22.42%

$11,11290%

15.8169.73%

D18.50%

0.00%18.50%

23.62%$10,237

Asw

ath Dam

odaran80

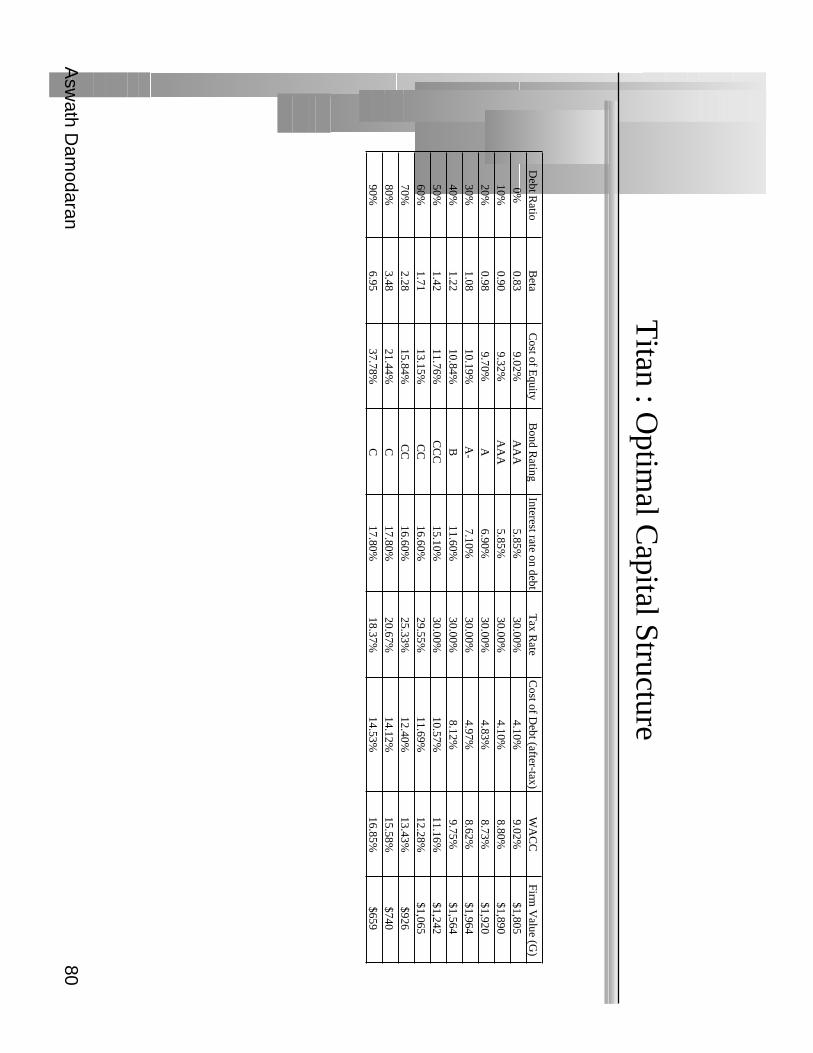

Titan : O

ptimal C

apital Structure

Debt R

atioB

etaC

ost of Equity

Bond R

atingInterest rate on debt

Tax R

ateC

ost of Debt (after-tax)

WA

CC

Firm V

alue (G)

0%0.83

9.02%A

AA

5.85%30.00%

4.10%9.02%

$1,80510%

0.909.32%

AA

A5.85%

30.00%4.10%

8.80%$1,890

20%0.98

9.70%A

6.90%30.00%

4.83%8.73%

$1,92030%

1.0810.19%

A-

7.10%30.00%

4.97%8.62%

$1,96440%

1.2210.84%

B11.60%

30.00%8.12%

9.75%$1,564

50%1.42

11.76%C

CC

15.10%30.00%

10.57%11.16%

$1,24260%

1.7113.15%

CC

16.60%29.55%

11.69%12.28%

$1,06570%

2.2815.84%

CC

16.60%25.33%

12.40%13.43%

$92680%

3.4821.44%

C17.80%

20.67%14.12%

15.58%$740

90%6.95

37.78%C

17.80%18.37%

14.53%16.85%

$659

Asw

ath Dam

odaran81

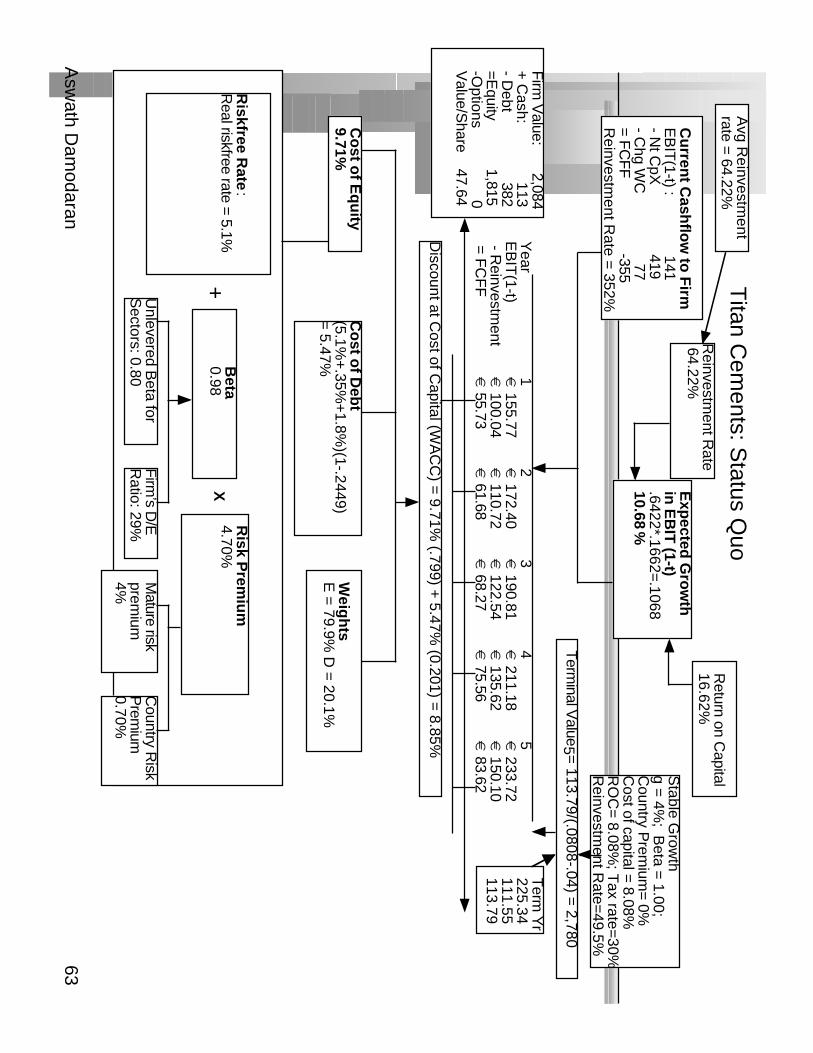

Cu

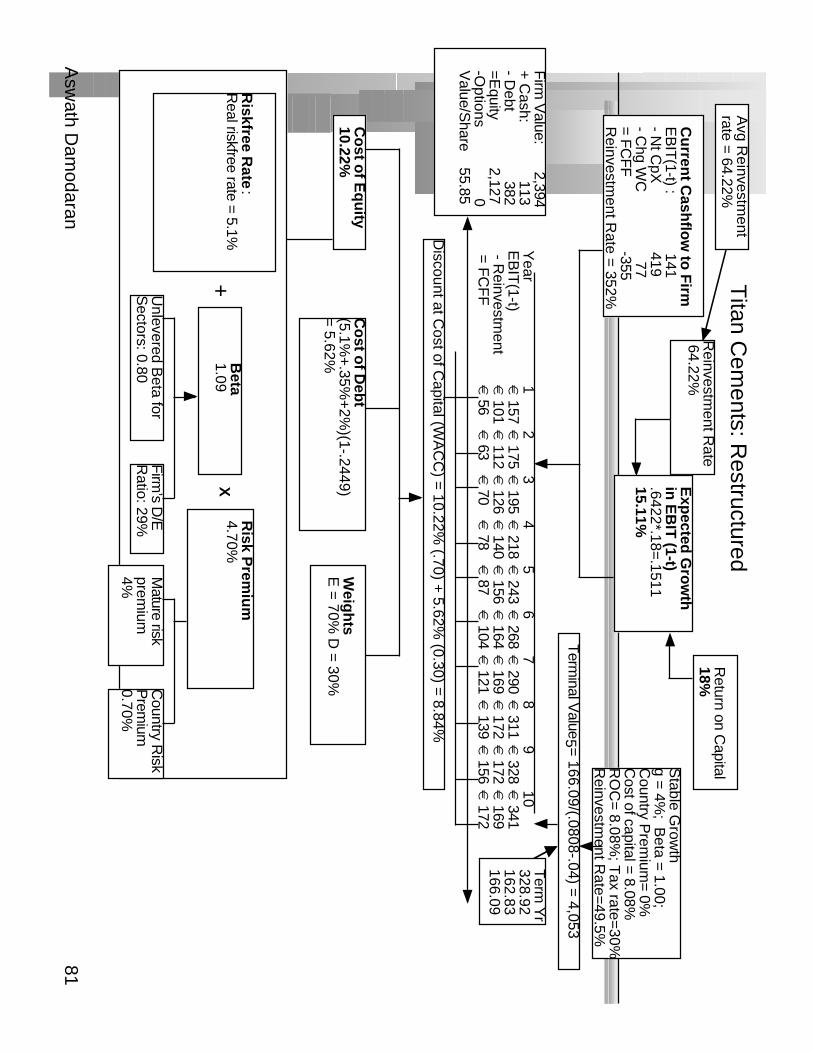

rrent C

ashflo

w to

Firm

EB

IT(1-t) : 141

- Nt C

pX 419

- Ch g W

C 77

= FC

FF

-355R

einvestment R

ate = 352%

Exp

ected G

row

th

in E

BIT

(1-t).6422*.18=

.151115.11%

Stable G

rowth

g = 4%

; Beta =

1.00;C

ountry Prem

ium= 0%

Cost of capital = 8.08%

R

OC

= 8.08%

; Tax rate=

30%R

einvestment R

ate=49.5%

Term

inal Value5 =

166.09/(.0808-.04) = 4,053

Co

st of E

qu

ity10.22%

Co

st of D

ebt

(5.1%+

.35%+

2%)(1-.2449)

= 5.62%

Weig

hts

E =

70% D

= 30%

Discount at C

ost of Capital (W

AC

C) =

10.22% (.70) +

5.62% (0.30) =

8.84%

Firm

Value: 2,394

+ C

ash: 113

- Debt 382

=Equity 2,127

-Options

0V

alue/Share 55.85

Riskfree R

ate:

Real riskfree rate = 5.1%

+B

eta 1.09

X

Risk P

remiu

m4.70%

Unlevered B

eta for S

ectors: 0.80F

irm’s D

/ER

atio: 29%M

ature riskprem

ium4%

Country R

iskP

remium

0.70%

Titan C

ements: R

estructured R

einvestment R

ate 64.22%

Return on C

apital18%

Term

Yr

328.92162.83166.09

Avg R

einvestment

rate = 64.22%

Year

12

34

56

78

910

EB

IT(1-t)

€ 157

€ 175

€ 195

€ 218

€ 243

€ 268

€ 290

€ 311

€ 328

€ 341

- Reinvestm

ent€

101€

112€

126€

140€

156€

164€

169€

172€

172€

169 =

FC

FF

€ 56

€ 63

€ 70

€ 78

€ 87

€ 104

€ 121

€ 139

€ 156

€ 172

Asw

ath Dam

odaran82

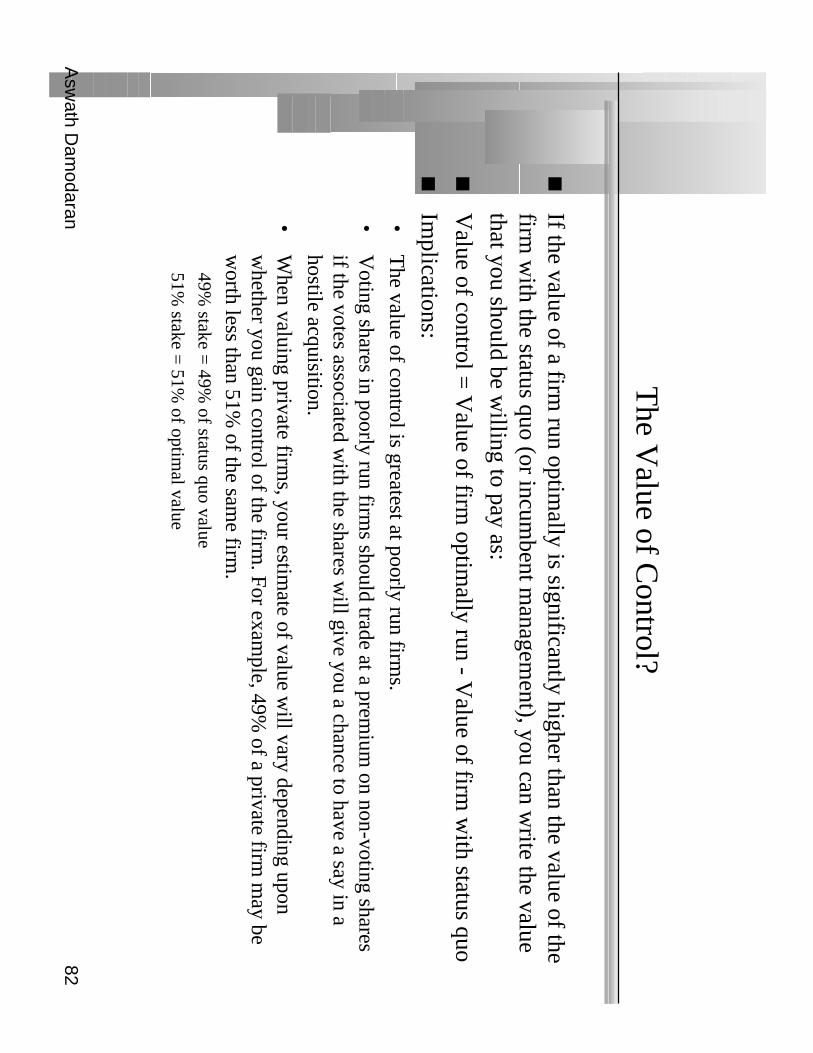

The V

alue of Control?

If the value of a firm run optim

ally is significantly higher than the value of thefirm

with the status quo (or incum

bent managem

ent), you can write the value

that you should be willing to pay as:

Value of control =

Value of firm

optimally run - V

alue of firm w

ith status quo

Implications:

•T

he value of control is greatest at poorly run firms.

•V

oting shares in poorly run firms should trade at a prem

ium on non-voting shares

if the votes associated with the shares w

ill give you a chance to have a say in ahostile acquisition.

•W

hen valuing private firms, your estim

ate of value will vary depending upon

whether you gain control of the firm

. For example, 49%

of a private firm m

ay bew

orth less than 51% of the sam

e firm.

49% stake =

49% of status quo value

51% stake =

51% of optim

al value

Asw

ath Dam

odaran83

Back to L

emm

ings...