Embed Size (px)

Citation preview

ATHLETIC BLACK BOOK NIKE, UNDER ARMOUR, ADIDAS, FOOT LOCKER, HIBBETT, DICK’S, FINISH LINE

DEC 18, 2014

BRIAN MCGOUGH ALEC RICHARDS

HEDGEYE 2

DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye Risk Management is not a broker dealer and does not provide investment advice for individuals. This research does not constitute an offer to sell, or a solicitation of an offer to buy any security. This research is presented without regard to individual investment preferences or risk parameters; it is general information and does not constitute specific investment advice. This presentation is based on information from sources believed to be reliable. Hedgeye Risk Management is not responsible for errors, inaccuracies or omissions of information. The opinions and conclusions contained in this report are those of Hedgeye Risk Management, and are intended solely for the use of Hedgeye Risk Management’s clients and subscribers. In reaching these opinions and conclusions, Hedgeye Risk Management and its employees have relied upon research conducted by Hedgeye Risk Management’s employees, which is based upon sources considered credible and reliable within the industry. Hedgeye Risk Management is not responsible for the validity or authenticity of the information upon which it has relied. TERMS OF USE This report is intended solely for the use of its recipient. Re-distribution or republication of this report and its contents are prohibited. For more detail please refer to the appropriate sections of the Hedgeye Services Agreement and the Terms of Use at www.hedgeye.com

LEGAL

HEDGEYE 3

1

2

3

KEY CONCLUSIONS

ECONOMIC CYCLE TRUMPS THE SNEAKER CYCLE There is no doubt that a sneaker cycle exists – or rather – used to exist. But now that the industry is maturing in the US, the economic cycle trumps all.

INNOVATION COMES IN ALL SHAPES AND SIZES Product innovation is critical in this space, but we think that Nike will soon start to innovate in other areas that will turn this industry upside down.

BRICK & MORTAR RETAIL MIGHT NEVER GROW AGAIN By our math, we need to 6% footwear growth in a given year for B&M stores to grow.

HEDGEYE 4

4

5

6

KEY CONCLUSIONS

SURVEY SAYS… Our consumer survey show how disadvantaged the traditional retailers are, and how ill equipped they are to handle this change. Nike is done placating those that won’t evolve. Evolution costs money.

CONTENT WINS Perhaps a cliché, but in this instance, it really matters. Brands can capture almost 20 points in higher gross margins by changing up the online experience and offering a better alternative to the 40-year-old model. Nike is the clear winner, and should drive its online sales from 6% of total today to 18% in five years. That’s an extra $7bn in sales at a 70% gross margin.

BUT IT’S STILL A ZERO SUM GAME Best ideas on the short side include FL, HIBB, and DKS. We think that all of these names will show a meaningful falloff in margins, asset utilization and earnings over the next 2-3 years.

HEDGEYE 5

YOU ARE NO LONGER UNINFORMED

DATA SOURCE: NIKE DOCUMENTS

ATHLETIC FOOTWEAR & APPAREL SIZE AND SCOPE

HEDGEYE 7

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

APPAREL IS BIGGER AND MORE STABLE

SPORTS APPAREL ’13 MARKET SHARE Sports Apparel is about 2.5x the size of the footwear industry and remains massively fragmented. The average person buys 10.5 units/yr at $17.50 ASP.

GROWTH IN APPAREL VS FOOTWEAR Apparel has proven to be more resilient than footwear in aggregate dollars – though margins associated with those sales are considerably more volatile.

SOURCE: HEDGEYE & EUROMONITOR

76.5%

Other

Nike

Under Armour

adidas

The North Face

Columbia

Lululemon Athletica Reebok

Puma

$57.9B

-2% -2%

3%

7%

7% 4% 5%

-8% -5%

5%

6%

8%

2% 4%

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8%

10% Sports Apparel Sports Footwear

HEDGEYE 8

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

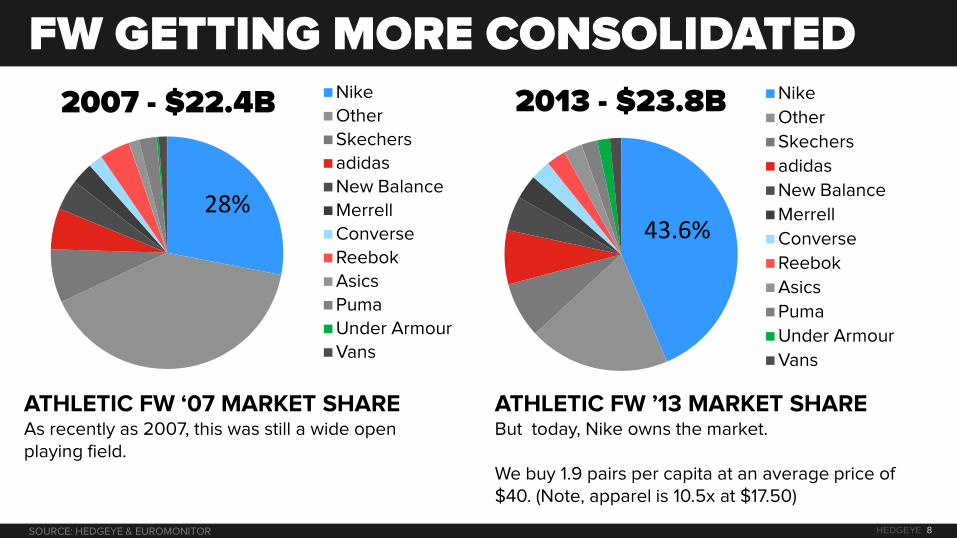

FW GETTING MORE CONSOLIDATED

28%

2007 - $22.4B Nike

Other

Skechers

adidas

New Balance

Merrell

Converse

Reebok

Asics

Puma

Under Armour

Vans

ATHLETIC FW ‘07 MARKET SHARE As recently as 2007, this was still a wide open playing field.

ATHLETIC FW ’13 MARKET SHARE But today, Nike owns the market. We buy 1.9 pairs per capita at an average price of $40. (Note, apparel is 10.5x at $17.50)

SOURCE: HEDGEYE & EUROMONITOR

43.6%

2013 - $23.8B Nike

Other

Skechers

adidas

New Balance

Merrell

Converse

Reebok

Asics

Puma

Under Armour

Vans

HEDGEYE 9

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

ADIBOK WAS NIKE’S BIGGEST WIN

US FOOTWEAR SALES 2006 VS 2013 In the years following the AdiBok merger, the industry did not grow meaningfully.

ADIDAS HANDED SHARE TO NIKE Without stepping up its marketing spend, or any other capital cost, Nike took almost 1,000bp share from AdiBok – then another 500bp from others.

SOURCE: HEDGEYE, NSGA, & EUROMONITOR

-10%

-5%

0%

5%

10%

$0

$5

$10

$15

$20

$25

$30 Dollars (Bil) Growth - Right

30%

17%

44%

10%

0%

10%

20%

30%

40%

50% 2006 2013

Adi

Rbk

HEDGEYE 10

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

COMBINED ATHLETIC MARKET

INDUSTRY GROWTH All in, the industry is coming off of five very respectable years – much like we’re seeing from the rest of retail.

MARKET SHARE 2013 With all its hype and success, UA has to win in footwear to overtake Adidas, never mind threaten Nike.

SOURCE: HEDGEYE, NSGA & EUROMONITOR

19.1%

4.1% 2.9%

Nike adidas Under Armour The North Face Skechers Champion Timberland Columbia New Balance Reebok Puma Lululemon Athletica Merrell Asics Converse Others

$81.7B

-3.9% -2.7%

3.9%

6.5% 6.8%

3.5% 4.8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

HEDGEYE 11

DISTRIBUTION IN A NUTSHELL

ATHLETIC DISTRIBUTION, USING NIKE AS A PROXY

This map shows the channel distribution of Nike’s US business. It’s a fair proxy for the traditional brands.

NIKE USA

Nike Stores

16%

Nike.com

6%

$12.8B

FL & FINL

23% 6%

17%

Specialty Retailers

17% Dept. Stores

Sporting Goods Stores

14% 2%

6%

15%

Pro Shops

9%

SOURCE: COMPANY REPORTS, BLOOMBERG, & HEDGEYE ESTIMATES

THE ‘MYTH’ OF THE SNEAKER CYCLE

HEDGEYE 13

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40% DOLLARS UNITS ASP

IT USED TO BE REAL – BUT PRODUCT DRIVEN

SNEAKER CYCLE – REAL OR MYTH? -1982 Nike Air Force 1 -1984 Nike Air Jordan -1989 Reebok Pumps -1990 New Bal. m574 -1993 Jordan leaves -1995 Jordan returns -1996 ”NBA Best Sneaker Year” -1998-1999 Nike Slows -2000 Nike Shox & Nike restructures -2006 Nike Free -2010 Toning/Minimal/ lightweight shoes -2012 Lebron shoes up 50% 2013: Flyknit

DATA SOURCE: HEDGEYE, SGMA AND NPD

HEDGEYE 14

NOW ONLY ONE CYCLE MATTERS The industry is at a point where the cycle that matters most is the economic one.

DATA SOURCE: HEDGEYE, SGMA AND NPD

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0% ATHLETIC FOOTWEAR 10-YEAR GROWTH DOLLARS UNITS ASP

©2013 HEDGEYE RISK MANAGEMENT

THE TAIL WAGS THE DOG RETAIL IS THE DOG

HEDGEYE 16

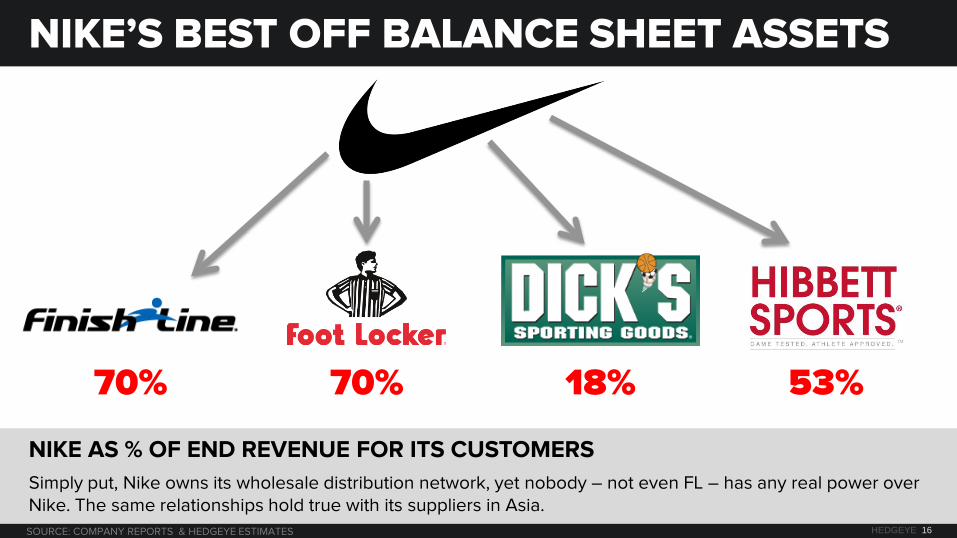

NIKE’S BEST OFF BALANCE SHEET ASSETS

NIKE AS % OF END REVENUE FOR ITS CUSTOMERS

Simply put, Nike owns its wholesale distribution network, yet nobody – not even FL – has any real power over Nike. The same relationships hold true with its suppliers in Asia.

70% 70% 18% 53%

SOURCE: COMPANY REPORTS & HEDGEYE ESTIMATES

HEDGEYE 17

FL 68% FINL 70%

COGS $4,505 COGS $1,123

COGS From Nike $3,063 COGS From Nike $786

Estimated Margin on Nike 33% Estimated Margin on Nike 33%

End Revenue From Nike $4,572 End Revenue From Nike $1,173

Total Rev $6,505 Total Rev $1,670

% of Total End Rev 70% % of Total End Rev 70%

HIBB 52% DKS 18%

COGS $557 COGS $4,272

COGS From Nike $291 COGS From Nike $769

Estimated Margin on Nike 36% Estimated Margin on Nike 31%

End Revenue From Nike $455 End Revenue From Nike $1,114

Total Rev $852 Total Rev $6,213

% of Total End Rev 53% % of Total End Rev 18%

DEPENDENCY MATH

HERE’S THE MATH OUTLINED ON THE PRIOR PAGE

*Blue number is Nike Inc. as % of purchases as per company 10-k

SOURCE: COMPANY REPORTS, FACTSET, & HEDGEYE ESTIMATES

HEDGEYE 18

1972

INNOVATION #1 = PRODUCT

2014

HEDGEYE 19

INNOVATION #2: MANUFACTURING

Nike ‘Considered’ 2005

Nike Free 4.0 Flyknit 2014

Everyone ‘Gets It’ that Flyknit is a scalable innovation. But what is misunderstood is how this will shape Nike’s distribution.

HEDGEYE 20

FLYKNIT CONSERVATION STATS

SOURCE: NIKE SUSTAINABILITY REPORT

QUESTION Why is it that footwear and

apparel retail is one of the few industries that is operating

today as it did 30 years ago?

HEDGEYE 22

•

MOST INDUSTRIES EVOLVE T

HE

N

NO

W

HEDGEYE 23

ON-SITE CUSTOMIZATION IN 2015

“I want you to imagine if it's possible to provide highly customized product, specific to your body, your own feet, maybe different separate left foot from right foot, manufactured locally in the market that you live, delivered within hours, if not minutes, profitably at scale.” -Erik Sprunk (October 2013)

SOURCE: COMPANY REPORTS

HEDGEYE 24

• Kiosks at Nike retail. Manufacturing in the back room.

• This takes 3-4 weeks wait time for NikeID down to 3-4 days. On-site it’s 3-4 hours.

• Likely to be opened up to select retailers – at no cost to Nike.

• The changes the retailers will need to make in order to get this technology are a bigger deal.

NIKEID = IMMEDIATE GRATIFICATION

HOW THIS IMPACTS DISTRIBUTION

HEDGEYE 26

NIKE STORE COUNT

NIKE’S STORE GROWTH

91 101 99 96 100 104

117 132

150

170 171 178 184

204 209 213

0

50

100

150

200

250 Nike Factory Stores Nike Stores

NIKETOWN Employee Only Stores

Punchline, Nike has very few retail stores outside of factory outlets. That will change. Currently 1 Nike Women’s Store.

SOURCE: COMPANY REPORTS & HEDGEYE

HEDGEYE 27

ARE WE OVERSTORED?

SOURCE: COMPANY WEBSITES, GOOGLE, & HEDGEYE

HEDGEYE 28

NIKE, UNDER ARMOUR, ADIDAS

UA, NKE, ADI FULL PRICE ADI

NKE UA

SOURCE: COMPANY WEBSITES, GOOGLE, & HEDGEYE

HEDGEYE 29

B&M MIGHT NEVER BE UP AGAIN

Online will account for more than 100% of the growth in this industry – for the first time. ATHLETIC FOOTWEAR SALES BY CHANNEL (WHOLESALE EQUIVALENT)

SOURCE: NSGA & COMPANY REPORTS

HEDGEYE 30

‘NON-ONLINE’ MIGHT NEVER GROW AGAIN UNLESS WE SEE 6%+ GROWTH IN THE INDUSTRY

-15%

-10%

-5%

0%

5%

10%

15%

-$800

-$600

-$400

-$200

$0

$200

$400

$600

$800

2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Online + Factory Industry (less factory & online) Industry YY % Growth

HEDGEYE 31

$11,000

$12,000

$13,000

$14,000

$15,000

$16,000

$17,000

$18,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

B&M Factory Online

INDUSTRY SALES GROWTH WATERFALL FW WILL GROW, BUT WILL SHOW UP ON DIFFERENT P&LS

HEDGEYE 32

WHOLESALE CAN’T COMPETE

NIKE ONLINE MARGIN MATH An online sale carries a margin nearly 20 points higher than the base wholesale business. Not to mention a higher price point and better attachment rate online.

SOURCE: COMPANY REPORTS & HEDGEYE

Wholesale Margin Math On-Line Margin Math Price at Retail 100.0 Online Direct Price 100.0

Apparel Attachment Rate 25%

'At Once' Cost 50.0 Net Revenue 125.0

- Futures Discount 5.0

Retailer's Cost 45.0 Online Servicing Cost 6.3

Incr Mktg/Cust Acquisition 5.0

Cost of Goods 27.5

Nike Revenue 45.0 Nike Revenue 125.0

Cost of Goods 22.0 Total Costs 38.75

Nike Margin 23.0 Nike Margin 86.25

GM % 51.1% GM % 69.0%

HEDGEYE 33

DOT.COM GOING FROM 6% TO 18% OF SALES

ONLINE IS FUELING NIKE GROWTH Dot.com already accounts for about 20% of Nike’s global growth – weighted heavily towards the US. That should accelerate to 50% over the next 5-years.

1,860

2,678

3,797

5,077

6,537

8,199

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0%

10%

20%

30%

40%

50%

60%

2015 2016 2017 2018 2019 2020

Nike Online Sales Percent of Growth

SOURCE: INTERNET RETAILER , COMPANY REPORTS, & HEDGEYE

HEDGEYE 34

8 YEAR E-COMMERCE CAGR

DOT.COM GROWTH SCORECARD Biggest Surprises 1. How small

Nike is. 2. UA’s growth 3. Spread

between DKS and TSA

4. HIBB X Axis = e-comm CAGR ’05-’13 Logo size represents size of online business.

SOURCE: INTERNET RETAILER & HEDGEYE

HEDGEYE 35

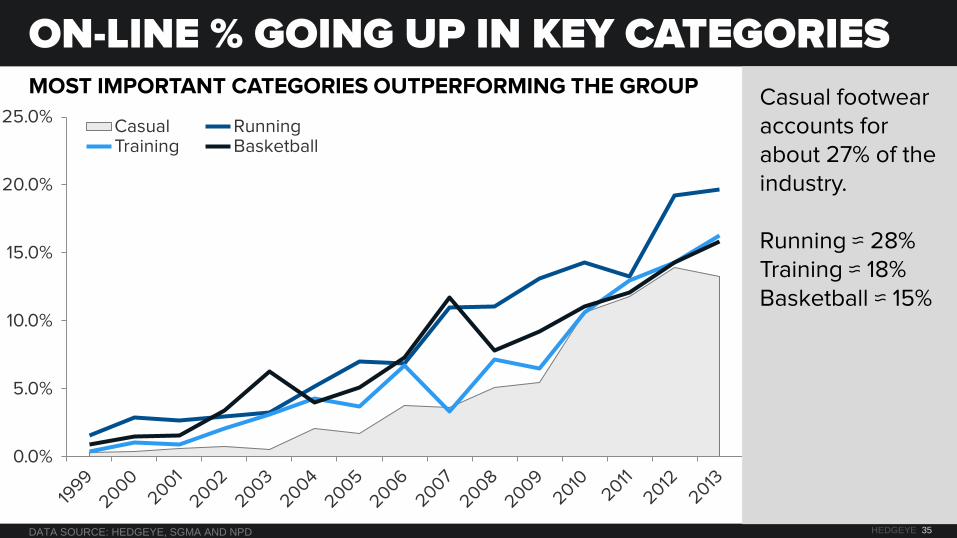

MOST IMPORTANT CATEGORIES OUTPERFORMING THE GROUP

ON-LINE % GOING UP IN KEY CATEGORIES

Casual footwear accounts for about 27% of the industry. Running ≈ 28% Training ≈ 18% Basketball ≈ 15%

DATA SOURCE: HEDGEYE, SGMA AND NPD

0.0%

5.0%

10.0%

15.0%

20.0%

25.0% Casual Running Training Basketball

HEDGEYE 36

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900 Amazon (Apparel & Foot) - Right Axis Zappos (Apparel & Foot) - Right Axis Foot Locker Nike Dick's Sporting Goods The Finish Line Under Armour adidas The Sports Authority Hibbett

US ONLINE SALES ($MM)

E-COMMERCE LANDSCAPE How can FL not be worried about this chart? Nike is accelerating… +70% last Q. Amazon and Zappos doing significant sales in the category.

SOURCE: INTERNET RETAILER, EUROMONITOR, COMPANY REPORTS, & HEDGEYE

ONLINE DEEP DIVE (SURVEY)

HEDGEYE 38

COMPARED TO A YEAR AGO ARE YOU TAKING MORE OR LESS OF PHYSICAL STORE PURCHASES ONLINE IN THE FOLLOWING CATEGORIES?

ONLINE CATEGORY SHIFT All three athletic categories are higher than industry mean as it relates to shift online.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

15% 13%

20%

13%

16%

20% 19% 17%

20%

5%

8%

12% 13%

23%

18%

22%

17% 17%

31%

0%

5%

10%

15%

20%

25%

30%

35%

HEDGEYE 39

PURCHASE SPREAD: 18-44 AGE GROUP LESS 45+

AGE DISPERSION BY CATEGORY A positive reading suggests that the key 18-44 demographic is shifting more on line.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

0 bps

500 bps

1000 bps

1500 bps

2000 bps

2500 bps

HEDGEYE 40

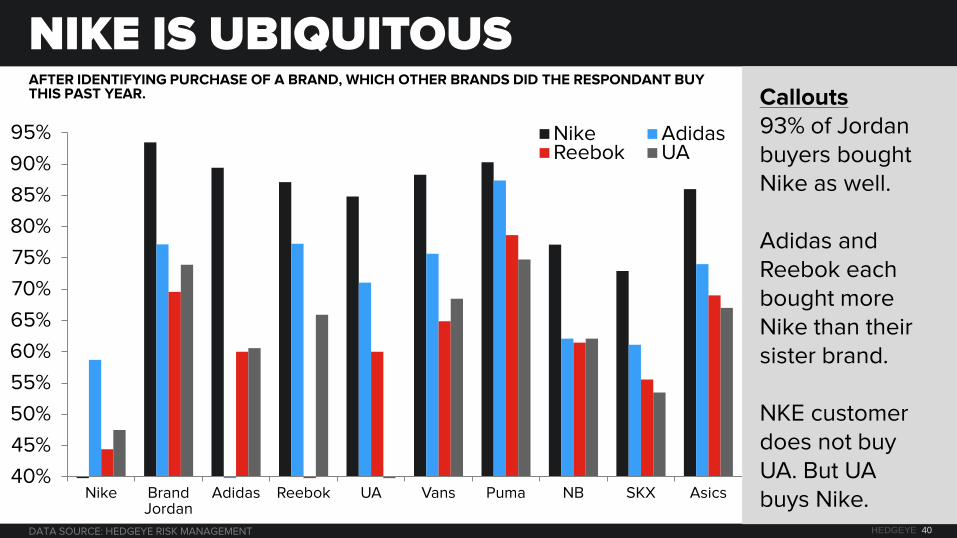

AFTER IDENTIFYING PURCHASE OF A BRAND, WHICH OTHER BRANDS DID THE RESPONDANT BUY THIS PAST YEAR.

NIKE IS UBIQUITOUS Callouts 93% of Jordan buyers bought Nike as well. Adidas and Reebok each bought more Nike than their sister brand. NKE customer does not buy UA. But UA buys Nike.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

Nike Brand Jordan

Adidas Reebok UA Vans Puma NB SKX Asics

Nike Adidas Reebok UA

HEDGEYE 41

EXCLUSIVE BUYERS VS # BRANDS PURCHASED

BRAND LOYALTY NKE has the most exclusive buyer group (14% Nike-only), but followed close by…Skechers? AdiBok’s loyalty is dead. UA = opportunity Bubble size = US athletic apparel & footwear market share.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, EUROMONITOR

Nike

Jordan

Adi

Reebok UA

Vans

Puma

NB

SKX

Asics

0%

2%

4%

6%

8%

10%

12%

14%

16%

4.0x 5.0x 6.0x 7.0x 8.0x Average # of brands purchased

% o

f e

xclu

sive

bu

yers

HEDGEYE 42

WHEN SHOPPING THE FOLLOWING CATEGORIES WOULD YOU PREFER TO SHOP IN A PHYSICAL STORE OR ONLINE?

PURCHASE METHOD INTENT BY CATEGORY This is a spread between the percent of people that would like to shop in a physical store net of those who would rather shop the category on-line. Positive = Physical Store Preference Negative = Online

DATA SOURCE: HEDGEYE RISK MANAGEMENT

23% 22%

11%

24%

7%

-7%

-17%

19%

0%

65%

56%

13% 11%

-51% -42%

-6%

-17% -10%

-22%

-60%

-40%

-20%

0%

20%

40%

60%

80%

HEDGEYE 43

PREFERENCES VS ACTUAL

WHAT THEY SAY VS WHAT THEY DO

How to Interpret: For Sporting Goods, 57.8% of our 1,000 person sample prefers to buy Sporting Goods online. But 28.7% of their SG purchases actually were online. Only 13.1% of SG retailers actually ARE ‘on the line’.

57.8%

40.2%

49.8%

28.7%

22.6%

29.7%

13.1% 16.1%

11.6%

0%

10%

20%

30%

40%

50%

60%

70%

Sporting Goods Athletic Footwear Athletic Apparel

Online Prefererence % of Purchases Online Actual Online %

SOURCE: EUROMONITOR, NGSA, HEDGEYE RISK MANAGEMENT

HEDGEYE 44

WHICH METHOD OF SHOPPING WOULD YOU PREFER TO USE WHEN PURCHASING ATHLETIC FOOTWEAR?

ATHLETIC FOOTWEAR BY AGE When dissecting the Footwear category’s net 19% score in favor of a store vs online, it is grossly skewed toward the 55+ demographic. The more relevant 18-44 demo is more a push.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

5% 1%

5%

22%

43%

61%

0%

10%

20%

30%

40%

50%

60%

70%

18-24 25-34 35-44 45-54 55-64 65+

Average

HEDGEYE 45

WHEN SHOPPING FOR NIKE PRODUCT, WHICH PHYSICAL STORE ARE YOU MOST LIKELY TO VISIT FIRST?

RETAILER PREFERENCE (IN-STORE) Nike scored lower than we suspected (30%), though the footprint of its own store base is nothing remotely close to FL.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

37%

23%

6%

14%

5%

14%

9%

25%

7%

19% 21%

15%

19%

40%

4%

0% 0% 0% 0%

9%

5%

24%

18%

8% 6%

30%

0% 5%

10% 15%

20% 25% 30% 35% 40% 45%

HEDGEYE 46

WHEN SHOPPING FOR NIKE PRODUCT, WHICH ONLINE STORE ARE YOU MOST LIKELY TO VISIT FIRST?

RETAILER PREFERENCE (ONLINE)

As people shift away from Brick & Mortar, they certainly don’t go to the B&M retailer’s web site. This is where content wins.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

26%

13%

0%

12%

0%

13%

4%

16%

2%

13% 16%

13%

0%

23%

4%

0%

4%

10%

5%

37%

11%

21%

2% 5%

15% 12%

0% 0% 0%

46%

0% 5%

10% 15%

20% 25% 30% 35% 40% 45% 50%

HEDGEYE 47

WHAT PHYSICAL RETAILER AND ONLINE RETAILER WOULD YOU VISIT FIRST WHEN BUYING NIKE PRODUCT?

PREFERENCE IN BUYING NIKE PRODUCT Every traditional retailer of Nike product loses relevance once online purchasing enters the equation.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

0% 5%

10% 15%

20% 25% 30% 35% 40% 45% 50% In-Store

Online

HEDGEYE 48

NIKE.COM = GREATER BRAND ACCESS

E-COMMERCE IS GREAT EQUALIZER

% of shoppers who would visit either a Nike store or nike.com first when shopping for Nike footwear & apparel In-store reach limited by unit count, but website offers greater & cost effective access to consumer at much higher margin.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

32%

46%

20%

25%

30%

35%

40%

45%

50%

Existing Customers

In-Store Online

HEDGEYE 49

AMZN & ZAPPOS EXPOSURE

THE ‘SHORT HIBB’ CHART This measures the percent of customers that also shop AMZN and Zappos, vs the size of the company’s dot.com business.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, INTERNET500

FL

FINL

M

JCP

KSS

SHLD

JWN

DKS

HIBB

35%

40%

45%

50%

55%

60%

65%

70%

75%

10% 20% 30% 40% 50% Zappos Exposure

Am

azo

n e

xpo

sure

HEDGEYE 50

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

WHY GO SHOP ONLINE?

MULTI-BRAND RETAILER WEBSITE Over half of the people list price as the first reason. Then discounts. Not very defendable factors long-term.

NIKE.COM Over half of the people go to nike.com because of the selection. Followed by product research. Both are extremely Brand-enhancing long-term.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

10% 13%

17% 20%

25% 25% 30% 30% 32%

34%

57%

0%

10%

20%

30%

40%

50%

60%

9% 11% 12% 12% 13%

15% 16% 20%

23% 24% 25%

31%

52%

0%

10%

20%

30%

40%

50%

60%

HEDGEYE 51

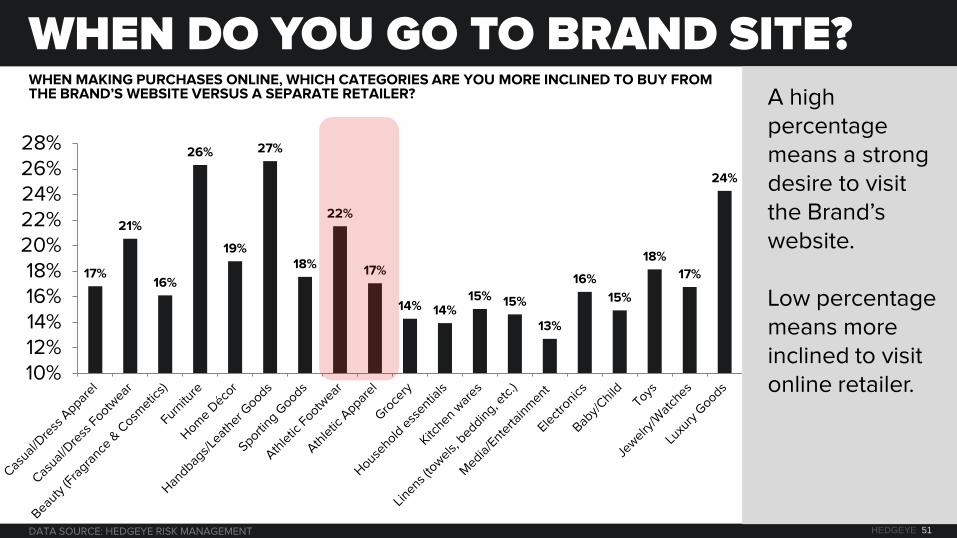

WHEN MAKING PURCHASES ONLINE, WHICH CATEGORIES ARE YOU MORE INCLINED TO BUY FROM THE BRAND’S WEBSITE VERSUS A SEPARATE RETAILER?

WHEN DO YOU GO TO BRAND SITE? A high percentage means a strong desire to visit the Brand’s website. Low percentage means more inclined to visit online retailer.

DATA SOURCE: HEDGEYE RISK MANAGEMENT

17%

21%

16%

26%

19%

27%

18%

22%

17%

14% 14% 15% 15%

13%

16%

15%

18%

17%

24%

10% 12% 14% 16% 18%

20% 22% 24% 26% 28%

RECENT ONLINE TRENDS

HEDGEYE 53

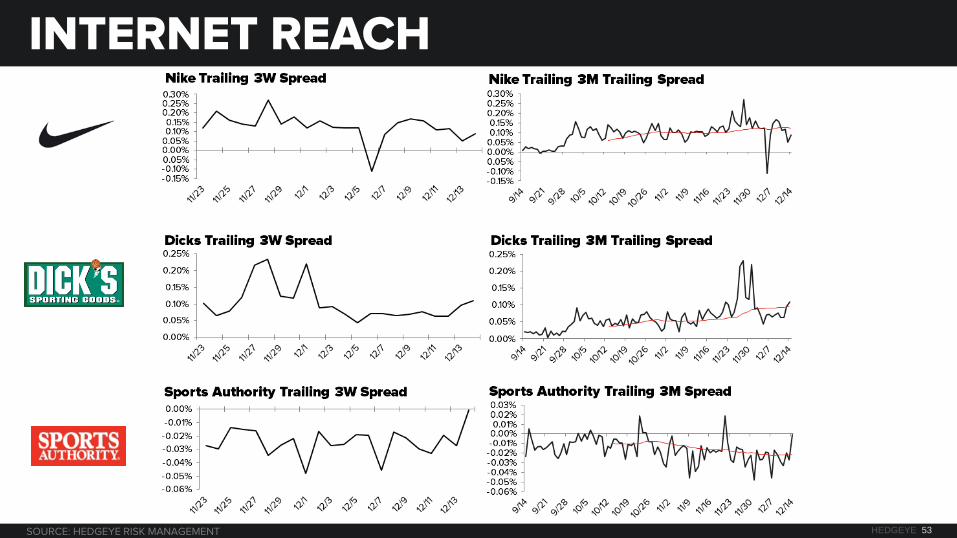

INTERNET REACH

SOURCE: HEDGEYE RISK MANAGEMENT

HEDGEYE 54

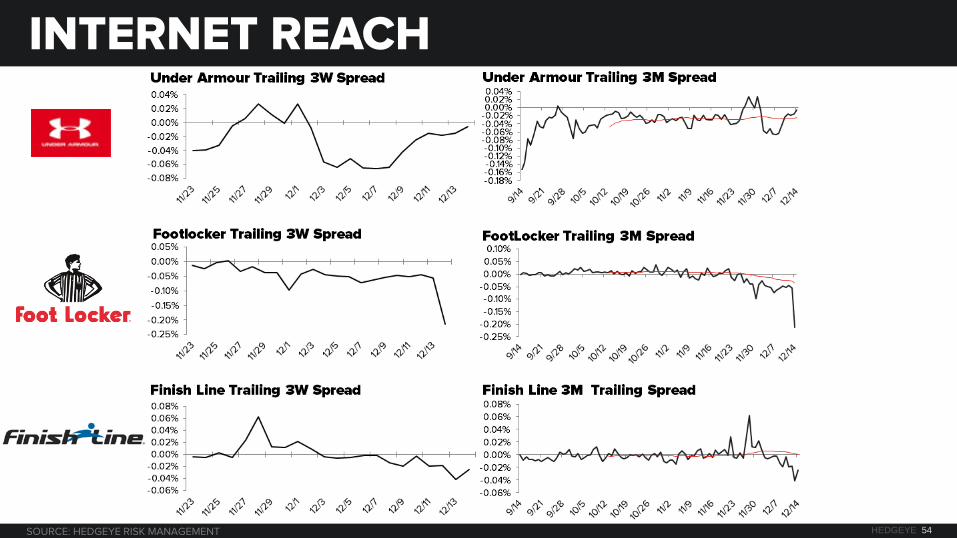

INTERNET REACH

SOURCE: HEDGEYE RISK MANAGEMENT

HEDGEYE 55

INTERNET REACH

SOURCE: HEDGEYE RISK MANAGEMENT

ATHLETE ENDORSEMENT TRENDS

HEDGEYE 57

NIKE IN SPORTS

1978: Nike signs John McEnroe.

1982: Nike signs first English Football player and team.

1984: Nike signs Michael Jordan .

1990: Football / Baseball player Bo Jackson promotes Nike’s Cross Trainers.

1999: Derek Jeter joins Jordan Brand.

1996: Nike supplies 4 NFL teams with jerseys.

1994/1996: Nike chosen to equip American, Nigerian, Dutch and Brazilian National teams.

2000: Nike loses NFL jerseys to Reebok.

2003: Lebron James signed out of High School.

2012: Nike regains NFL jersey sponsorship.

2009: Nike Debuts new Pro Combat football and basketball jersey designs.

2014: Nike extends US Olympic sponsorship through 2020.

1996: Nike signs Tiger Woods

2006: Signs Indian Cricket team.

2004: Nike loses last of NBA jersey contracts.

1997: Nike joins several others in NBA jersey rights.

1970: Steve Prefontaine, runner at the U of Oregon & U.S. Olympic Team, becomes the first Nike sponsored athlete.

HEDGEYE 58

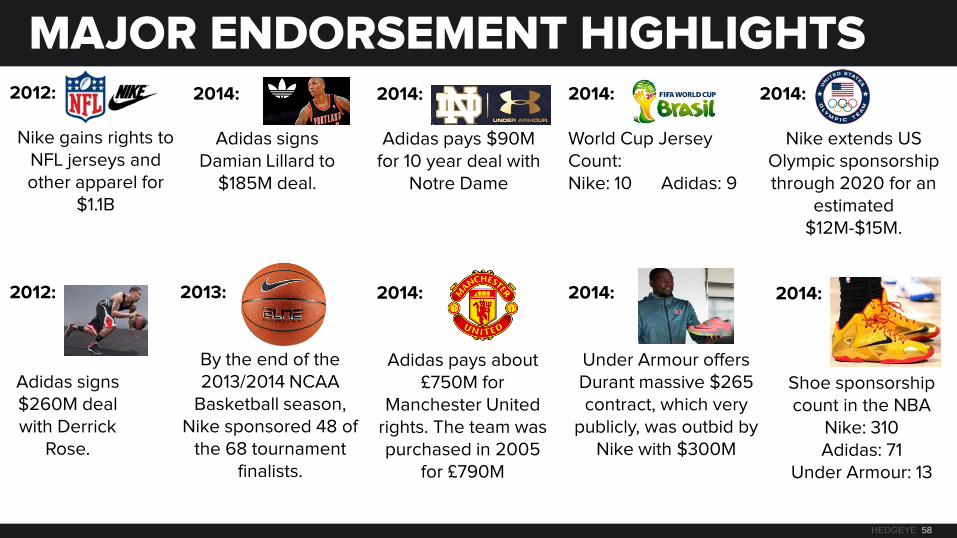

2014:

Adidas signs Damian Lillard to

$185M deal.

2014:

Under Armour offers Durant massive $265 contract, which very

publicly, was outbid by Nike with $300M

2012:

Adidas signs $260M deal with Derrick

Rose.

2014:

Adidas pays $90M for 10 year deal with

Notre Dame

2014:

Shoe sponsorship count in the NBA

Nike: 310 Adidas: 71

Under Armour: 13

2014:

Adidas pays about £750M for

Manchester United rights. The team was purchased in 2005

for £790M

MAJOR ENDORSEMENT HIGHLIGHTS 2012:

Nike gains rights to

NFL jerseys and other apparel for

$1.1B

2014:

Nike extends US Olympic sponsorship through 2020 for an

estimated $12M-$15M.

2014: World Cup Jersey Count: Nike: 10 Adidas: 9

2013:

By the end of the 2013/2014 NCAA

Basketball season, Nike sponsored 48 of

the 68 tournament finalists.

HEDGEYE 59

NKE DWARFS UA, BUT THE GAP IS CLOSING

ENDORSEMENT MINIMUMS

No two ways about it – UA is starting to play with the big boys and spend even bigger dollars.

$1 $44 $54 $76 $78 $168 $170 $158 $273

$1,642

$2,794

$3,828

$4,202

$3,790

$4,444

$3,828 $3,603

$4,704

0%

1%

2%

3%

4%

5%

6%

7%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

UnderArmour Nike UA as % of NKE (right)

HEDGEYE 60

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

BIGGER BETS

ENDORSEMENT % BY DURATION This table looks at the payment percent contractually obligated by year.

LT ENDORSEMENT OBLIGATIONS Both companies are signing longer-dated deals. Defer costs – but the assets better work out.

SOURCE: HEDGEYE ESTIMATES AND COMPANY DOCUMENTS

0%

5%

10%

15%

20%

25%

30%

35% NKE UA

©2013 HEDGEYE RISK

MANAGEMENT

DATA SOURCE: CENSUS.GOV

2007 2008 2009 2010 2011 2012 2013 1 Year

NKE 18% 17% 18% 18% 22% 25% 21%

UA 27% 34% 38% 26% 31% 37% 30%

2-3 Yrs

NKE 29% 30% 32% 35% 39% 38% 31%

UA 52% 52% 43% 43% 53% 52% 35%

4-5 Yrs

NKE 23% 22% 24% 24% 22% 21% 19%

UA 20% 13% 14% 29% 15% 9% 17%

5+ Yrs

NKE 29% 31% 26% 23% 16% 16% 29%

UA 0% 1% 5% 2% 1% 2% 19%

HEDGEYE 61

SPONSORSHIPS AS A % OF DEMAND CREATION

UA AND NKE ARE SPOT ON HERE Surprisingly, UA is already right in line with Nike as it relates to endorsements and a % of Demand Creation.

SOURCE: HEDGEYE ESTIMATES AND COMPANY FILINGS

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010 2011 2012 2013 2014

UA NKE

©2014 HEDGEYE RISK MANAGEMENT

COMPANY CAPSULES

HEDGEYE 63

NIKE, INC (NKE) 1. Our Expectations for Tonight’s Print: Nickel beat ($0.75). Double digit C$ Futures.

2. A lot of good news in it today, but what people are missing is the duration over which the product engine will crank.

3. About to change the shoe manufacturing paradigm.

4. Online should go from $1.4 to $8 bn over 5-6 years -- at a 70% GM%.

5. Adidas, it's top competitor globally, is due for a massive restructuring, which helps Nike.

6. Will step up repo/dividend again to prevent ROIC/ROE dispersion.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

$3.83

$4.48

$5.10

$6.16

$7.29

$3.61 $4.16

$4.82

$5.43

$6.23

$3.00 $3.50 $4.00 $4.50 $5.00 $5.50 $6.00 $6.50 $7.00 $7.50 $8.00

2015E 2016E 2017E 2018E 2019E

Hedgeye EPS ($) Consensus ($)

HEDGEYE 64

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

NIKE FINANCIAL TRAJECTORY

NIKE SIGMA Headed in the right direction. But inventories still heavy as of last quarter. Nonetheless this bodes well for the 2Q print.

NIKE RNOA ROADMAP This might be the most compelling chart as to why you want to own Nike long term. Winning market share, margins heading higher, and capital efficiency (online) getting better.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS

HEDGEYE 65

NIKE FINANCIAL SUMMARY

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

HEDGEYE 66

UNDER ARMOUR (UA) • UA took a page out of Nike’s

playbook, but ran the plays better.

• The fact that the company has not stumbled in over half a decade is impressive.

• We’re not against owning it. But everything has a price. We don’t think 70x earnings is a fair price for 25-30% earnings growth.

• And that’s not even accounting for the fact that it is growing in Footwear and International, where the competition is tougher, and cost to grow is higher than its core apparel business.

• Endorsements = risk

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

$0.96 $1.29

$1.63

$1.97 $2.21

$0.94 $1.20

$1.53

$1.93

$2.29

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2014E 2015E 2016E 2017E 2018E

Hedgeye EPS ($) Consensus ($)

HEDGEYE 67

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

UA FINANCIAL TRAJECTORY

UA SIGMA Inventories finally rightsized. Nothing really to call out here as it relates to the near-term P&L.

UA RNOA ROADMAP Turns are eroding, but that hasn’t stopped the stock from going parabolic over the past three years. The market is paying for growth and consistency.

SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS

HEDGEYE 68

UA FINANCIAL SUMMARY

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

HEDGEYE 69

FOOT LOCKER (FL) 1. Never has a mediocre business been more loved.

2. Hicks executed on the 'restructuring BOGO'. Two restructurings for the price of one. If a third was possible, he'd still be here.

3. The rapidly closing gap between FL’s ecommerce and nike.com is alarming.

4. Peak sales productivity x peak GM% x trough SG&A% x entering the tail end of a cycle x NKE going rogue on distribution = trouble for FL.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

$3.47 $3.62 $3.46

$2.75 $3.19

$3.49 $3.87

$4.25

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

2014E 2015E 2016E 2017E 2018E

Hedgeye EPS ($) Consensus ($)

HEDGEYE 70

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

FL FINANCIAL TRAJECTORY

FL SIGMA Has been solid – but latest move is negative. Note, FL has been in the upper right for 6 years, after being in the lower left for 10.

FL RNOA Both margins and turns eroding. Not what we want to see for a name at a peak multiple that is universally loved.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS

HEDGEYE 71

FL FINANCIAL SUMMARY

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

Footlocker Inc. (FL) $55.78

FY14 ends Jan 2015 4QE 2014E 2015E 2016E 2017E 2018E EPS % P/E Price EV/EBITDA

Hedgeye EPS ($) 0.91 3.47 3.62 3.46 2.75 3.19 2014E 21.7% 16.0 x 56 8.1 x

Consensus ($) 0.92 3.49 3.87 4.25 2015E 4.2% 14.0 x 51 6.8 x

Variance % -1.0% -0.6% -6.6% -18.7% 2016E -4.4% 14.0 x 48 6.6 x

2017E -20.5% 13.0 x 36 5.6 x

Sales ($MM) 7,133 7,402 7,482 7,315 7,404 2018E 16.1% 13.0 x 41 6.1 x

EBIT Margin 11.2% 11.0% 10.1% 8.0% 9.1%

EBITDA ($MM) 943 980 941 779 860

FCF Per Share ($) 2.71 2.90 2.97 3.10 3.17

Book Value Per Share ($) 17.89 18.84 18.93 17.51 19.44

Net Debt to Total Capital

P/E 16.1 x 15.4 x 16.1 x 20.3 x 17.5 x

EV/EBITDA 8.1 x 7.6 x 7.7 x 9.2 x 8.3 x

Price/Book 3.1 x 3.0 x 2.9 x 3.2 x 2.9 xCash Yield 4.9% 5.2% 5.3% 5.5% 5.7%

Targeted Valuation RangeFinancial and Valuation Summary

Investment Thesis Snapshot1. Never has a mediocre business been more loved.

2. Hicks executed on the 'restructuring BOGO'. Two restructurings for the price of one. If a third was possible, he'd still be here.

3. Peak sales productivity x peak GM% x trough SG&A% x entering the tail end of a cycle x NKE going rogue on distribution = trouble for FL.

HEDGEYE 72

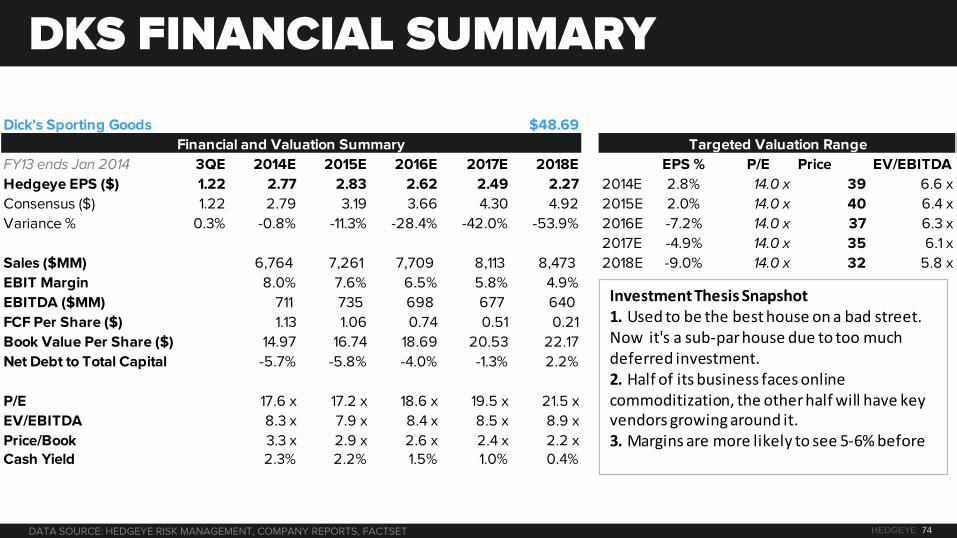

DICK’S SPORTING GOODS (DKS) 1. Used to be the best house on a bad street. Now it's a sub-par house due to too much deferred investment.

2. Half of its business faces online commoditization, the other half will have key vendors growing around it.

3. DKS needs 9-10% sales growth to leverage occupancy. In the absence of meaningful comp, it suggests DKS should add more stores, when it should really stop.

4. Margins are more likely to see 5-6% before they revisit peak of 9%.

$2.77 $2.83 $2.62 $2.49 $2.27 $2.79

$3.19 $3.66

$4.30 $4.92

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

2014E 2015E 2016E 2017E 2018E

Hedgeye EPS ($) Consensus ($)

SOURCE: HEDGEYE RISK MANAGEMENT, FACTSET, COMPANY REPORTS

HEDGEYE 73

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

DKS FINANCIAL TRAJECTORY

DKS SIGMA DKS showed signs of life (i.e. rightsizing inventories) and then it didn’t.

DKS RNOA This is even worse than KSS.

DATA SOURCE: HEDGEYE RISK MANGEMENT, COMPANY REPORTS

HEDGEYE 74

DKS FINANCIAL SUMMARY

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

Dick's Sporting Goods $48.69

FY13 ends Jan 2014 3QE 2014E 2015E 2016E 2017E 2018E EPS % P/E Price EV/EBITDA

Hedgeye EPS ($) 1.22 2.77 2.83 2.62 2.49 2.27 2014E 2.8% 14.0 x 39 6.6 x

Consensus ($) 1.22 2.79 3.19 3.66 4.30 4.92 2015E 2.0% 14.0 x 40 6.4 x

Variance % 0.3% -0.8% -11.3% -28.4% -42.0% -53.9% 2016E -7.2% 14.0 x 37 6.3 x

2017E -4.9% 14.0 x 35 6.1 x

Sales ($MM) 6,764 7,261 7,709 8,113 8,473 2018E -9.0% 14.0 x 32 5.8 x

EBIT Margin 8.0% 7.6% 6.5% 5.8% 4.9%

EBITDA ($MM) 711 735 698 677 640

FCF Per Share ($) 1.13 1.06 0.74 0.51 0.21

Book Value Per Share ($) 14.97 16.74 18.69 20.53 22.17

Net Debt to Total Capital -5.7% -5.8% -4.0% -1.3% 2.2%

P/E 17.6 x 17.2 x 18.6 x 19.5 x 21.5 x

EV/EBITDA 8.3 x 7.9 x 8.4 x 8.5 x 8.9 x

Price/Book 3.3 x 2.9 x 2.6 x 2.4 x 2.2 xCash Yield 2.3% 2.2% 1.5% 1.0% 0.4%

Financial and Valuation Summary Targeted Valuation Range

Investment Thesis Snapshot1. Used to be the best house on a bad street. Now it's a sub-par house due to too much deferred investment.2. Half of its business faces online commoditization, the other half will have key vendors growing around it.3. Margins are more likely to see 5-6% before

HEDGEYE 75

HIBBETT SPORTS (HIBB)

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

2.80 2.88 2.79

2.37

2.75 2.76 3.03

3.46

4.11

4.80

$2.00

$3.00

$4.00

$5.00

2015E 2016E 2017E 2018E 2019E

Hedgeye EPS ($) Consensus ($)

DATA SOURCE: CENSUS GOV

1. To say that HIBB is terminal would probably be inaccurate. But the debate is worth having.

2. The reason for its success “build a store next to a WMT and use it as a traffic driver” is dying. WMT growing online. Can’t park next to WMT in cyberspace.

3. Store footprint is saturated. Growing into areas occupied by Dick’s and Academy (one of the best, but private, SG retailers).

4. NKE is growing aggressively online, but HIBB might be the only B&M retailer that does not have an internet presence. It has to build one ($) or face significant top line pressure.

5. With all these pressures, the street has earnings doubling over 5 years. We think they’re flat at best.

HEDGEYE 76

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

HIBB FINANCIAL TRAJECTORY

HIBB SIGMA Good inventory correction. But margins down 5 quarters in a row. Why not 6, 7, 8?

HIBB RNOA This is pretty much the inverse of how Nike looks on this chart.

SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS

HEDGEYE 77

HIBB FINANCIAL SUMMARY

HEDGEYE 78

AUG 2011

– Q: Do you see a day where it will be important for Hibbett to develop an e-commerce strategy?

– A: It’s in our five-year strategic plan. We’ve had some things that we’re working on that we feel are more important at this time. But as we grow, we definitely see it as part of our mix.

MAY 2012

– Q: You announced a partnership with a third-party for e-commerce. Can you talk a little bit about the thought process behind that decision and maybe how it’s done so far?

– A: Yeah, it’s just really an affiliate program. It’s a click-through and we’re getting a small royalty off of it. And in a future date, we’ll have an e-commerce strategy.

MAR 2013

– Q: Timeline for potentially discussing an e-commerce strategy?

– A: Yeah, H2 this year we’re coming up with a strategy, and as we put that together, we’ll let you know. But really we got enough on our plate between a new home office and new distribution center right now.

MAR 2014

– Q: And then as you look out the next couple years, what would be sort of a rough timeline in terms of ramp up in e-commerce capabilities?

– A: Yeah. We just finished – we’ve had some consultants in here and it will be a multi-year project and as we put more together, we will share more information with you, but we will be heading in that direction.

HIBBETT E-COMMERCE COMMENTARY

SOURCE: COMPANY REPORTS

HEDGEYE 79

CONFUSING ONLINE STORE

It looks like an online store. You can even check out the new releases! But you cant Check Out…

SOURCE: HIBBETT.COM

HEDGEYE 80

CAN’T BUY ANYTHING

When every item says not available for sale online, why do you have what appears to be an online store ?

SOURCE: HIBBETT.COM

HEDGEYE 81

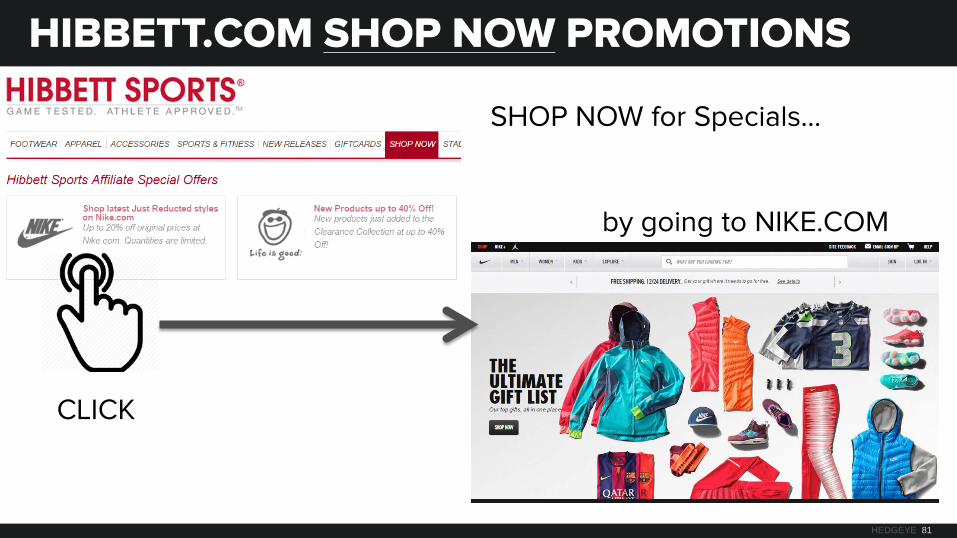

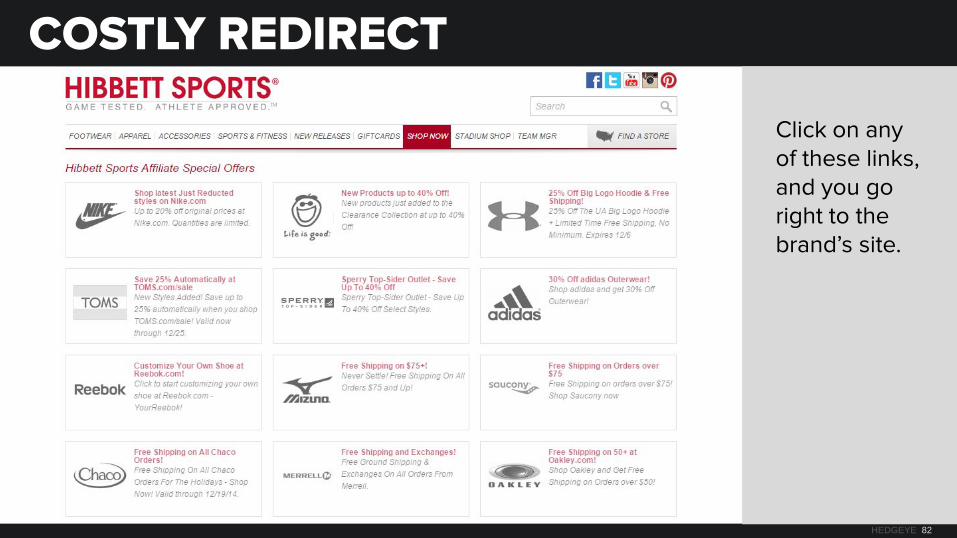

HIBBETT.COM SHOP NOW PROMOTIONS

SHOP NOW for Specials…

by going to NIKE.COM

CLICK

HEDGEYE 82

COSTLY REDIRECT

Click on any of these links, and you go right to the brand’s site.

HEDGEYE 83

ADIDAS, INC. (ADS-DE) • We want to like this one. Despite zero relevance

in the US, it is Nike’s top competitor globally, and has good assets in adidas, Reebok and TMaG.

• But over the years it has become superbly adept at being a mediocre company.

• Management is ineffective, and corporate governance is nowhere to be found.

• If this was a US company, activists would be circling. But much tougher to change up ADS.

• Unfortunately, the company German-engineered a series of acquisitions, and took away their ability to be nimble in their local markets.

• That needs to be undone. But it will be painful. Either way, it’s not this management team who should be leading the charge.

DATA SOURCE: HEDGEYE RISK MANAGEMENT, COMPANY REPORTS, FACTSET

$30

$50

$70

$90

$110 Stock Price

CHART APPENDIX

HEDGEYE 85

BASKETBALL SHOES DEMOGRAPHICS

0% 20% 40% 60% 80% 100%

Under 14 14 - 17 18 - 24 25 - 34 35 - 44 45 - 64 65 & OLDER

22.2%

0% 20% 40% 60% 80% 100%

UNDER $15,000 $15,000 - $24,999 $25,000 - $34,999 $35,000 - $49,999

$50,000 - $74,999 $75,000 - $99,999* $100,000 $149,999 $150,000 & OVER

0% 20% 40% 60% 80% 100%

NEW ENGLAND MID ATLANTIC E. NO. CENTRAL W. NO. CENTRAL SO ATLANTIC E. SO. CENTRAL W. SO. CENTRAL MOUNTAIN PACIFIC

88% 81%

11% 18%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100% MALE FEMALE Sex

Age

Income

Region

SOURCE: NSGA

HEDGEYE 86

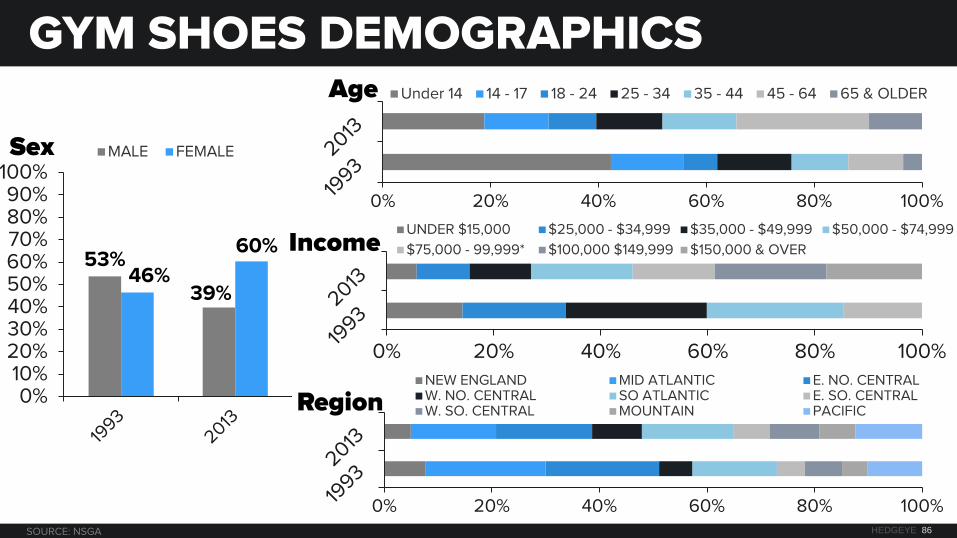

GYM SHOES DEMOGRAPHICS

0% 20% 40% 60% 80% 100%

Under 14 14 - 17 18 - 24 25 - 34 35 - 44 45 - 64 65 & OLDER

0% 20% 40% 60% 80% 100%

UNDER $15,000 $25,000 - $34,999 $35,000 - $49,999 $50,000 - $74,999

$75,000 - 99,999* $100,000 $149,999 $150,000 & OVER

0% 20% 40% 60% 80% 100%

NEW ENGLAND MID ATLANTIC E. NO. CENTRAL W. NO. CENTRAL SO ATLANTIC E. SO. CENTRAL W. SO. CENTRAL MOUNTAIN PACIFIC

53%

39% 46%

60%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100% MALE FEMALE Sex

Age

Income

Region

SOURCE: NSGA

HEDGEYE 87

RUNNING SHOES DEMOGRAPHICS

0% 20% 40% 60% 80% 100%

Under 14 14 - 17 18 - 24 25 - 34 35 - 44 45 - 64 65 & OLDER

0% 20% 40% 60% 80% 100%

UNDER $15,000 $15,000 - $24,999 $25,000 - $34,999 $35,000 - $49,999 $50,000 - $74,999 $75,000 - 99,999* $100,000 $149,999 $150,000 & OVER

0% 20% 40% 60% 80% 100%

NEW ENGLAND MID ATLANTIC E. NO. CENTRAL W. NO. CENTRAL SO ATLANTIC E. SO. CENTRAL W. SO. CENTRAL MOUNTAIN PACIFIC

62%

39% 38%

61%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100% MALE FEMALE Sex

Age

Income

Region

SOURCE: NSGA

HEDGEYE 88

QUESTIONS?