Embed Size (px)

Citation preview

9/11/2015

1

FHA Office of Single Family Housing

1

ATLANTAHOMEOWNERSHIP

CENTER2015 Appraisal Training

N. Dan Rogers III, AHOC Director

Glenn Dumont, AHOC Deputy Director

Valerie D Williams, Processing and Underwriting Division Director

FHA Office of Single Family Housing

2

On Behalf of The AHOC and Training Team,We Welcome you Today.

PLEASE BE CONSIDERATE OFOTHERS

1. Please silence your cell phones and pagers.

2. If you must answer your phone, please step out.

3. If you must text, please respect your instructorand neighbors.

FHA Office of Single Family Housing

3

Presenter

Frank J. Coleman, Senior Review AppraiserTechnical Branch I

Processing and Underwriting DivisionAtlanta Homeownership Center

Federal Housing Administration (FHA)

Atlanta Home Ownership Center (AHOC)40 Marietta Street

Five Points Plaza 7th FloorAtlanta, GA. 30303

9/11/2015

2

FHA Office of Single Family Housing

4

Archived Webinars

The official archived webinars are available at:http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/eve

nts/sfh_hb_webinars

FHA Office of Single Family Housing

5

The Presentation

• Based on The Single Family Housing PolicyHandbook 4000.1.

• Summary of salient features, changes andclarification and is not intended to replace theguidance of the Department SF HandbookArchived Webinars.

FHA Office of Single Family Housing

6

Handbook 4000.1

• Issued: August 26, 2015

• Effective: September 14, 2015

• Available at:http://portal.hud.gov/hudportal/documents/huddoc?id=40001HSGH.pdf

9/11/2015

3

FHA Office of Single Family Housing

7

AppraisalsModule 3A

FHA Office of Single Family Housing

8

FHA Office of Single Family Housing

9

Introduction

• The Appraiser and Property Requirements for Title II Forwardand Reverse Mortgages section of the Handbook 4000.1contains the Property Acceptability Criteria for FHA mortgageinsurance which include Minimum Property Requirements(MPR) and Minimum Property Standards (MPS), and includeby reference, associated rules and regulations.

9/11/2015

4

FHA Office of Single Family Housing

10

Objective

We will review some of the policies which we have providedclarity for effectively conducting an appraisal.

Appraisers are expected to exercise both sound judgmentand due diligence in the appraisal of properties to be insuredby FHA.

FHA Office of Single Family Housing

11

Components of Appraisal Guidance

• Property Requirements

– FHA requires underwriting of property condition as well asvaluation.

• Appraiser Requirements to Observe, Analyze, Report

– Appraisers’ requirements spelled out in one place, clearly.

FHA Office of Single Family Housing

12

Components of Appraisal Guidance (cont.)

• Report and Data Format Requirements

– A separate section dealing with forms, data andformats required, and “how to” instructions posted toHUD.gov.

• FHA Appraiser Roster

– Doing Business with FHA section of the Handbook.

• FHA Appraiser Quality Control and Oversight

– Legal and disciplinary issues.

9/11/2015

5

FHA Office of Single Family Housing

13

Enhancements to Note

• Zoning and Legal Non-Conforming Use

– Now requires appraiser to comment if improvementscan be rebuilt.

• Stationary Storage Tanks

– No distinction for above- or below-ground.

• Accessory Dwelling Units

– Emphasizes Highest and Best Use to determineproperty type of classification.

FHA Office of Single Family Housing

14

FHA Office of Single Family Housing

Enhancements to Note (cont.)

Attic and Crawl Space Inspection Requirements

– Clarifies that FHA requires an inspection―more than just “head and shoulders” if possible.

General Acceptance Criteria, Property Eligibility,

Nonresidential Use of Property

– Making sure that mixed use properties comply with zoning.

14

FHA Office of Single Family Housing

15

FHA Office of Single Family Housing

Enhancements to Note (cont.) Cost and Income Approach for Value

– Clarifies that ALL appropriate approaches must be utilized•when applicable.

Photograph Requirements

– Interior photos are required, as are photos of the attic andcrawl space.

– Spells out all requirements in one place.

Sales history of Comps

– 3 years+ instead of 1 year.– Due diligence by the appraiser for analyzing prior sales of

comparable properties.15

9/11/2015

6

FHA Office of Single Family Housing

16

FHA Office of Single Family Housing

Enhancements to Note (cont.)

Measurement and Reporting of Contributory Value of energyefficiency components or alternate systems (solar, etc.):

– Valuation of Solar Components is not limited to pairedsales only.

– Appraiser must follow proper appraisal practice including:

Contribution (Principle of Contribution);

Contributory Value;

Direct Sales Comparison Approach;

Cost Approach;

Income Approach; and

Reconciliation of the Approaches.

16

FHA Office of Single Family Housing

17

FHA Office of Single Family Housing

Enhancements to Note (cont.)

High Voltage Transmission Lines

– The Appraiser must notify the Mortgagee of the deficiencyof MPR or MPS if:

The Overhead Electric Power Transmission Lines or theLocal Distribution Lines pass directly over any dwelling,Structure or related property improvement, includingpools, spas, or water features; or

The dwelling or related property improvements arelocated within an Easement or if they appear to belocated within an unsafe distance of any power line ortower.

17

FHA Office of Single Family Housing

18

FHA Office of Single Family Housing

Enhancements to Note (cont.)

Mineral and Oil Reservations

– If currently under lease, the appraiser must analyze andinclude a summary of the effect on the property.

– Appraiser to comment on:

Impairment;

Property damage; or

Environmental concerns.

18

9/11/2015

7

FHA Office of Single Family Housing

19

FHA Office of Single Family Housing

Enhancements to Note (cont.)

A separate legal description for the surplus land is notrequired.

– Highest and Best Use (HABU) test of additional parcels orlarger than typical sites determines whether excess orsurplus applies (reminder-all FOUR tests of HABU).

Leasehold Valuation

– Reminder that appraiser to analyze terms of ground leaseand Mortgagee must ensure that appraiser has a copy.

19

FHA Office of Single Family Housing

20

FHA Office of Single Family Housing

Enhancements to Note (cont.)

Methamphetamine Contaminated Properties

– Contaminated properties have potentially significantenvironmental risks due to use and/or storage ofdangerous chemicals on the property.

– If the Mortgagee notifies the Appraiser or the Appraiserhas evidence that a Property is contaminated by thepresence of methamphetamine (meth), either by itsmanufacture or by consumption, the Appraiser mustrender the appraisal subject to the Property being certifiedsafe for habitation.

– The Appraiser must analyze and report any long-termstigma caused by the Property’s contamination by methand the impact on value or marketability.

20

FHA Office of Single Family Housing

21

FHA Office of Single Family Housing

Enhancements to Note (cont.)

Valuation Approaches

– Reminder to follow Uniform Standards of ProfessionalAppraisal Practice (USPAP) – apply all APPROPRIATE

methods.

Roofs Covered with Snow

– Reminder to report what can be seen inside the property.

Manufactured Home Additions

– Appraiser to require inspection by State Agency if anyAdditions or Structural changes are observed.

21

9/11/2015

8

FHA Office of Single Family Housing

22

FHA Office of Single Family Housing

High Efficiency Components

New Building Components

– Contributory value of building components that enhanceefficiency or energy savings must be analyzed and

reported.

– FHA requires that the appraiser utilize all appropriatemethods of valuation and does not restrict this to only a

matched pairs analysis.

22

FHA Office of Single Family Housing

23

FHA Office of Single Family Housing

Requirements for Reporting: SF HousingAppraisal Report and Data Delivery Guide

Posted to the HUD website.

Describes line by line reporting requirements for the fiveappraisal report forms utilized by FHA.

Includes Fannie Mae/Freddie Mac Uniform Appraisal Dataset(UAD) formats and requirements where applicable.

Appraisal software companies will use this document toensure that their products will comply with FHArequirements.

23

FHA Office of Single Family Housing

24

FHA Office of Single Family Housing

Underwriting the Property

Module 3B

Single Family Housing Policy Handbook 4000.1

Title II Insured Housing Program Forward Mortgages Origination

through Post-Closing/Endorsement

24

9/11/2015

9

FHA Office of Single Family Housing

25

FHA Office of Single Family Housing

Objective

Review Underwriting the Property section of Handbook4000.1.

During our review, we will:

– Clarify some of our current FHA polices;

– Discuss some of our policy revisions upon the effectivedate of the Handbook; and

– Continue to familiarize ourselves with the structure of theHandbook.

25

FHA Office of Single Family Housing

26

FHA Office of Single Family Housing

Introduction

The Mortgagee must underwrite the completed appraisalreport to determine if the property provides sufficientcollateral for the FHA insured mortgage.

The appraisal and the property must comply with therequirements in Appraiser and Property Requirements forTitle II Forward and Reverse Mortgages section of the

Handbook 4000.1.

The appraisal must be reported in accordance withAcceptable Appraisal Reporting Forms and Protocols.

•4001.1 II 3 Qtr. 2 FY 15 26

FHA Office of Single Family Housing

27

FHA Office of Single Family Housing

Mortgagee Responsibility for AppraisalIntegrity

The Mortgagee is responsible for identifying any problems orpotential problems with the integrity, accuracy, andthoroughness of an appraisal submitted to FHA for mortgageinsurance purposes.

•4001.1 II 1 A Qtr. 2 FY 15 27

9/11/2015

10

FHA Office of Single Family Housing

28

Communications with Third Parties: Appraisal

Just a Reminder:

• Mortgagees may not discuss the contents of the appraisal

with anyone other than the borrower.

• Yes, this includes Real Estate Agents.

28

FHA Office of Single Family Housing

29

FHA Office of Single Family Housing

Property Acceptability Criteria

The Mortgagee must evaluate the appraisal and anysupporting documentation to determine if the propertycomplies with HUD’s Property Acceptability Criteria.

Existing and New Construction properties must comply withApplication of Minimum Property Requirements (MPR) andMinimum Property Standards (MPS) by Construction Status.

•4001.1 II 3 a Qtr. 2 FY 15 29

FHA Office of Single Family Housing

30

FHA Office of Single Family Housing

Defective Conditions

The Mortgagee must evaluate the appraisal in accordancewith the Appraiser and Property Requirements of the4000.1, Section 3. Acceptable Appraisal Reporting Tools and

Protocols, Defective Conditions to determine if the propertyis eligible for an FHA-insured mortgage.

If defective conditions exist and correction is not feasible, theMortgagee must reject the property.

•4001.1 II 3 a Qtr. 2 FY 15 30

9/11/2015

11

FHA Office of Single Family Housing

31

FHA Office of Single Family Housing

Defective Conditions (cont.)

Defective construction evidence of continuing settlement,excessive dampness, leakage, decay, termites, environmentalhazards, or other conditions affecting the health and safety ofoccupants, collateral security or structural soundness of thedwelling.

The Mortgagee must render the property ineligible until thedefects or conditions have been remedied and the probabilityof further damage eliminated.

•4001.1 II C Qtr. 2 FY 15 31

FHA Office of Single Family Housing

32

Case Study• The contract of sale identifies the subject property may be

contaminated by methamphetamine.

• Does the contamination automatically establish a DefectiveCondition? Yes - Health and Safety.

• Is the property ineligible? Yes until the property (site anddwelling) is certified safe for habitation.

The appraiser must address any long-term stigma caused bythe property’s contamination by meth and the impact onvalue and/or marketability.

FHA Office of Single Family Housing

33

FHA Office of Single Family Housing

Defective Conditions: Inspection Requirements Examples of conditions that require an inspection by qualified individuals or

Entities include, but are not limited to:

– Standing water against the foundation and/or excessively dampbasements;– Hazardous materials on the site or within the improvements;– Faulty or defective mechanical systems (electrical, plumbing or heating);– Evidence of possible structural failure (e.g., settlement or bulgingfoundation

wall, unsupported floor joists, cracked masonry walls or foundation);– Evidence of possible pest infestation; or– Leaking or worn-out roofs.– Chipped, Peeling, Loose Lead-Based Paint (on homes built 1978 or prior)

The reason for or indication of a particular problem must be given whenrequiring an inspection of any mechanical system, structural system, etc.

•4001.1 II C Qtr. 2 FY 15 33

9/11/2015

12

FHA Office of Single Family Housing

34

•FHA Office of Single Family Housing

Minimum Property Requirements andMinimum Property Standards

The Mortgagee must evaluate the appraisal and property

eligibility in accordance with:

– Minimum Property Requirements for Existing and NewConstruction properties; and

– Minimum Property Standards for New Constructionproperties.

If the appraiser cannot determine that a property meets

HUD’s MPR or MPS, the Mortgagee may obtain an inspection

from a Qualified Entity to make the determination.

•4001.1 II 3 a Qtr. 2 FY 15 34

FHA Office of Single Family Housing

35

FHA Office of Single Family Housing

Minimum Repair Requirements

The appraisal report or inspection from a Qualified Entityindicates that repairs are required to make the property meetHUD’s MPR or MPS, the Mortgagee must comply with RepairRequirements.

•4001.1 II 3 a Qtr. 2 FY 15 35

FHA Office of Single Family Housing

36

FHA Office of Single Family Housing

Minimum Repair Requirements (cont.)

The underwriter will determine which repairs for existingproperties must be made for the property to be eligible forFHA-insured financing.

•4001.1 II 3 a Qtr. 2 FY 15 36

9/11/2015

13

FHA Office of Single Family Housing

37

FHA Office of Single Family Housing

Minimum Repair Requirements (cont.)

Required repairs are limited to those repairs necessary tomaintain safety, security and soundness.

Required repairs are those necessary to preserve thecontinued marketability of the property and protect thehealth and safety of the occupants.

If an element is functioning well but has not reached the endof its useful life, the appraiser should not recommendreplacement because of age.

•4001.1 II C Qtr. 2 FY 15 37

FHA Office of Single Family Housing

38

Required Documentation for Underwriting theProperty

• If additional inspections, repairs or certifications are noted bythe appraisal or are required to demonstrate compliance withProperty Acceptability Criteria, the Mortgagee must obtainevidence of completion of such inspections, repairs orcertifications.

4001.1 II 3 c Qtr. 2 FY 15

FHA Office of Single Family Housing

39

FHA Office of Single Family Housing

Appraisal Review

The appraisal process is the Mortgagee’s tool for determiningif a property meets the minimum requirements and eligibilitystandards for a Federal Housing Administration (FHA)-insuredmortgage.

Mortgagees bear primary responsibility for determiningeligibility; however, the appraiser is the onsite representativefor the Mortgagee and provides preliminary verification thatthe Property Acceptability Criteria have been met.

•4001.1 II C Qtr. 2 FY 15 38

9/11/2015

14

FHA Office of Single Family Housing

40

FHA Office of Single Family Housing

Quality of Appraisal

The Mortgagee must evaluate the appraisal and ensure itcomplies with the requirements in the Appraiser andProperty Requirements of the 4000.1, Section 3. AcceptableAppraisal Reporting Tools and Protocols, Valuation andReporting Protocols and any additional appraisalrequirements that are specific to the subject property.

•4001.1 II 3 b Qtr. 2 FY 15 39

FHA Office of Single Family Housing

41

Initial Appraisal Validity 30-Day Extension

The 120-day Validity period of an appraisal may be extended for30 days at the option of the Mortgagee if:

1. The Mortgagee Loan Approval or HUD-issued Firm

Commitment is issued prior to the expiration of the original

appraisal; or

2. The Borrower signed a valid sales contract prior to the

expiration date of the appraisal.

41

FHA Office of Single Family Housing

42

Appraisal Update• Appraisal update must be performed before the initial

appraisal has expired.

• An appraisal cannot be updated if an appraisal extension has

been issued.

• The valid period for an updated appraisal is 240 days after the

Effective Date of the initial appraisal report.

42

9/11/2015

15

FHA Office of Single Family Housing

43

Restrictions on Property FlippingFor case numbers assigned on or after January 1, 2015:

• If a property is resold within 90 days or fewer following the

date of acquisition by the seller, the property is not eligible for

an FHA-insured mortgage.

43

FHA Office of Single Family Housing

44

Restrictions on Property Flipping• Seller’s Date of Acquisition:

– FHA defines the seller’s date of acquisition as the date of

settlement on the seller’s purchase of that property.

• Resale Date:

– FHA defines the resale date as the date of execution of the

sales contract by all parties intending to finance the

property with an FHA-insured mortgage.

44

FHA Office of Single Family Housing

45

9/11/2015

16

FHA Office of Single Family Housing

46

FHA Office of Single Family Housing

47

Transferring Existing Appraisals• The Mortgagee, at the borrower’s request, must transfer the

appraisal to the second Mortgagee within 5 business days.

• The original Mortgagee may not charge the borrower a fee forthe transfer of any documents.

• A fee may be negotiated between the original Mortgagee andthe new Mortgagee. However, a fee for the transfer ofdocuments for Streamline Refinance transactions is notpermitted.

47

FHA Office of Single Family Housing

48

Transferring Existing Appraisal-New Borrower

• When an existing appraisal is being used for a different

borrower, the Mortgagee must:

– Enter the new borrower’s information in FHAC;

– Collect the appraisal fee from the new borrower and

refund the fee to the original borrower; and

– Have the appraiser review the purchase contract and

revise the appraisal report for value adjustments

accordingly.

48

9/11/2015

17

FHA Office of Single Family Housing

49

Second Appraisal Warning Screen

FHA Office of Single Family Housing

50

Material Deficiencies

• Material deficiencies on appraisals are those deficiencies thathave a direct impact on value and marketability.

• Material deficiencies are evident on the effective date of theappraisal.

FHA Office of Single Family Housing

51

Material Deficiencies (cont.)Material deficiencies include, but are not limited to:

• Failure to report readily observable defects that impact thehealth and safety of the occupants and/or structuralsoundness of the house;

• Reliance upon outdated or dissimilar comparable saleswhen more recent and/or comparable sales were availableas of the effective date of the appraisal; and

• Fraudulent statements or conclusions when the appraiserhad reason to know or should have known that suchstatements or conclusions compromise the integrity,accuracy and/or thoroughness of the appraisal submittedto the client.

9/11/2015

18

FHA Office of Single Family Housing

52

Opinion of Market Value

• The Mortgagee must ensure the Market Value of the propertyis sufficient to adequately secure the FHA-insured mortgage.

4001.1 II 3 b Qtr. 2 FY 15

FHA Office of Single Family Housing

53

Reconsideration of Value

• The underwriter may request a reconsideration of value whenthe appraiser did not consider information that was relevanton the effective date of the appraisal.

• The underwriter must provide the appraiser with all relevantdata that is necessary for a reconsideration of value.

FHA Office of Single Family Housing

54

Material Deficiencies

• May order secondappraisal but, not forvalue

• Typically, appraiserperformance negligence

Reconsideration of Value

• Second appraisalprohibited

• Typically, newcomparables becomeavailable after theeffective date.

Material Deficiencies vs. Reconsideration of Value

9/11/2015

19

FHA Office of Single Family Housing

55

• The Direct EndorsementUnderwriter/HUD ReviewerAnalysis of Appraisal Reportshould not be used tomodify value or forcomments.

(HUD-54114)

The Direct Endorsement Underwriter/HUDReviewer Analysis of Appraisal Report

FHA Office of Single Family Housing

56

Form HUD-92800.5B, Conditional CommitmentDirect Endorsement Statement of Appraised Value

• The underwriter must complete form HUD-92800.5B asdirected in the form instructions.

• Form HUD 92800.5B serves as the Mortgagee's conditionalcommitment/direct endorsement statement of value of FHAmortgage insurance on the property. The form provides asection for a statement of the property's appraised value andother required FHA disclosures to the homebuyer, includingspecific conditions that must be met before HUD can endorsea firm commitment for mortgage insurance. HUD uses theinformation only to determine the eligibility of a property formortgage insurance.

FHA Office of Single Family Housing

57

Conditional Commitment (Form HUD-92800.5b)Direct Endorsement Statement of Appraised ValueThe Conditional Commitment (Form HUD-92800.5b) Direct Endorsement Statement ofAppraised Value are not required in connection with:

– HUD REO sales;

– FHA’s 203(k) mortgage program;

– Sales in which the seller is:

o Fannie Mae;

o Freddie Mac;

o VA;

o USDA Rural Housing Services;

Sales in which the Borrower will not be an owner-occupant (for example, sales tononprofit agencies).

o Other Federal, State, and Local Government Agencies;o A Mortgagee disposing of REO assets; oro A Seller at a foreclosure sale; or

9/11/2015

20

FHA Office of Single Family Housing

58

Appraisal Review: Chain of Title

Mortgagee must review the appraisal to determine if the subjectproperty was sold within 12 months prior to the case numberassignment date.

4001.1 II A 3 b Qtr. 2 FY 15

4001.1 II 3 b Qtr. 2 FY 15

FHA Office of Single Family Housing

59

Acceptable Appraisal FormsProperty/Assignment Type AcceptableReporting Form

Fannie Mae Form 1004 MC/Freddie Mac Form 71, Market Conditions Addendum to the Appraisal Report, must be completed for every

appraisal.

Single Family, Detached, Attachedor Semi-Detached

Residential Property

Fannie Mae Form 1004/Freddie Mac Form 70, Uniform Residential Appraisal

Report (URAR); MISMO 2.6 GSE format

Single Unit Condominium Fannie Mae Form 1073/Freddie Mac Form 465, Individual Condominium Unit

Appraisal Report; MISMO 2.6 GSE format

Manufactured(HUD Code) Housing Fannie Mae Form 1004C/Freddie Mac Form 70B, Manufactured Home

Appraisal Report; MISMO 2.6 Errata 1 format

Small Residential Income Properties (Two to Four Units) Fannie Mae Form 1025/Freddie Mac Form 72, Small Residential Income

Property Appraisal Report; MISMO 2.6 Errata 1 format

Update of Appraisal

(All PropertyTypes)

Summary Appraisal Update Report Section of Fannie Mae Form

1004D/Freddie Mac Form 442, Appraisal Update and/or Completion Report;

MISMO 2.6 Errata 1 format

Complianceor Final Inspectionfor New Constructionor

ManufacturedHousing

Form HUD-92051, Compliance Inspection Report, in Portable Document

Format (PDF)

Complianceor Final Inspectionfor Existing Property Certification of Completion Section of Fannie Mae Form 1004D/Freddie Mac

Form 442, Appraisal Update and/or Completion Report; MISMO 2.6 Errata 1

format

FHA Office of Single Family Housing

60

Photograph RequirementsFHA Minimum Photograph Requirements

Photograph Exhibit Minimum Photograph Requirement

Subject Property Exterior Front and rear at opposite angles to show all sides of the dwelling

Improvements with Contributory Value not captured in the front or rear photograph

Street scene photograph to include a portion of the subject site

For New Construction, include photographs that depict the subject’s grade and drainage

For Proposed Construction, a photograph that shows the grade of the vacant lot

Subject Property Interior Kitchen, main living area, bathroom, bedrooms

Any other room representing overall condition

Basement, attic, and/or crawl space

Recent updates, such as restoration, remodeling and renovation

For two- to four-unit properties, also include photographs of common areas, hallways,

etc.

Comparable Sales, Listings, Pending Sales,

Rentals, etc.

Front view of each comparable utilized

Photographs taken at an angle to depict both the front and the side when possible

Multiple Listing Service (MLS) photographs are acceptable to exhibit comparable

condition at the time of sale. However, appraisers must include their own photographs as

well to document compliance.

Subject Property Deficiencies Photographs of the deficiency or condition requiring inspection or repair

Condominium Projects Additional photographs of the common areas and shared amenities of the Condominium

Project

4001.1 II C Qtr. 2 FY 15

9/11/2015

21

FHA Office of Single Family Housing

61

Site Section

FHA Office of Single Family Housing

62

Flood Zone: Determination & Responsibilities

• A property is not eligible for FHA insurance if:

– A residential building and related improvements tothe property are located within SFHA Zone A, a SpecialFlood Zone Area ,or Zone V, a Coastal Area, andinsurance under the National Flood InsuranceProgram (NFIP) is not available in the community; or

– The improvements are, or are proposed to be, locatedwithin a Coastal Barrier Resource System (CBRS).

FHA Office of Single Family Housing

63

Observing the Site

• FHA requires the appraiser to disclose any hazards thatendanger:

– Physical improvements;

– Affect livability;

– Marketability; and

– Health and safety of occupants.

4001.1 II C Qtr. 2 FY 15

9/11/2015

22

FHA Office of Single Family Housing

64

Individual Water Supply and Sewage Systems

• The Mortgagee is required to ensure the well and septic meetHUD and state and local jurisdiction requirements.

• The underwriter, not the appraiser, is required to determinefeasibility of connecting improvements to public water and/orseptic system.

• The appraiser and/or Mortgagee must require inspections ofreadily observable deficiencies of well or septic systems.

4001.1 II C Qtr. 2 FY 15

FHA Office of Single Family Housing

65

Improvements Section

• Number of Units

• Stories

• Property Type

• Design

• Year Built

• Effective Age

FHA Office of Single Family Housing

66

Accessory Units• An Accessory Dwelling Unit

(ADU) refers to a habitableliving unit added to, createdwithin, or detached from aprimary one-unit singlefamily dwelling, whichtogether constitute a singleinterest in real estate.

• It is a separate additionalliving unit, including:

– Kitchen;

– Sleeping; and

– Bathroom facilities.

4001.1 II C Qtr. 2 FY 15

9/11/2015

23

FHA Office of Single Family Housing

67

Interior: Materials Condition

• Appraiser is to statewhat they saw anddescribe whennecessary.

• What is readilyobservable?

• What upgrades didhe/she see?

4001.1 II C Qtr. 2 FY 15

FHA Office of Single Family Housing

68

The Attic

• The appraiser is required to observe the interiors of all attic spaces.

• The appraiser is not required to disturb insulation, move personal items,furniture, equipment or debris that obstructs access or visibility. If unable toview the improvements safely in their entirety, the appraiser must contactthe Mortgagee and reschedule a time when a complete visual observationcan be performed, or complete the appraisal subject to inspection by aqualified third party. Photograph required.

FHA Office of Single Family Housing

69

Mechanical Systems

All utilities must be on at the time of appraisal.

9/11/2015

24

FHA Office of Single Family Housing

70

Improvements Section

FHA Office of Single Family Housing

71

Property Condition Requirements

• Determine the overall quality and condition of property.

• Identify items that require immediate repair and areDefective Conditions (health & safety, structural soundness).

• Identify items where maintenance has been deferred, whichmay not require immediate repair.

FHA Office of Single Family Housing

72

Reconciliation

• The three approaches to value are reconciled with a briefdescription of the validity of each approach with respect tothe subject property appraisal:− Comparison;− Cost; and − Income.

9/11/2015

25

FHA Office of Single Family Housing

73

Identifying the Appraisal Report

Clarity

As Is No repairs, alterations or required inspections;Establish the “as is” value for 203(k); orAppraiser is recommending the property for rejection

Subject To Completion perPlans & Specs

Subject is less than 90% complete

Subject To Repairs orAlterations

The subject property is 90% or more complete

Subject To RequiredInspection (s)

The subject property is subject to inspection by aqualified individual or entity when the observationreveals evidence of a potential safety, soundness, orsecurity issue beyond the appraiser’s ability to assess.(termite, electrician, structural, etc.)

FHA Office of Single Family Housing

74

Addressing Unique Properties

• Must be:

− Legal zoning;

− Structurally sound;

− Marketable; and

− Highest & Best Use.

If zoning is Legal Non-Conforming-evidence property can be rebuilt.

Mixed Use Properties requires aminimum of 51% of the entire buildingsquare footage is for Residential use.

FHA Office of Single Family Housing

75

Required Exhibits

Maps

• Local street map showing location subject & each comparable sale.

• Show proposed roadways and street names.

Location Map

9/11/2015

26

FHA Office of Single Family Housing

76

Required Exhibits (cont.)

Exterior Sketch

FHA Office of Single Family Housing

77

No Contributory Value?

• Zero value is often placed on accessory structures that:

− Were added without permits; or

− Exhibit costly defects.

• Appraisers are not to assign “zero” value just to avoidaddressing FHA requirements!

• Zero value may mean removal of the structure.

FHA Office of Single Family Housing

78

Underwriting HUD Real Estate OwnedProperties

9/11/2015

27

FHA Office of Single Family Housing

79

HUD-owned Properties

• Permissible transactions (203b):

– Insurable; or

– As is with no repairs, alterations or inspections required.

FHA Office of Single Family Housing

80

HUD-owned Properties (cont.)

• 203(b) Insurable with Escrow.

• Subject property will meet MPR if repairs estimated to cost nomore than $5,000 are completed.

FHA Office of Single Family Housing

81

HUD-owned Properties (cont.)

Uninsurable:

• For FHA financing, must go 203(k).

• Subject property will meet MPR if repairs estimated to costmore than $5,000 are completed.

9/11/2015

28

FHA Office of Single Family Housing

82

Manufactured Homes

82

FHA Office of Single Family Housing

83

Modular? Manufactured? Site Built?

83

You can no longer tellsitting at the curb.

FHA Office of Single Family Housing

84

Manufactured Home Appraisal

84

9/11/2015

29

FHA Office of Single Family Housing

85

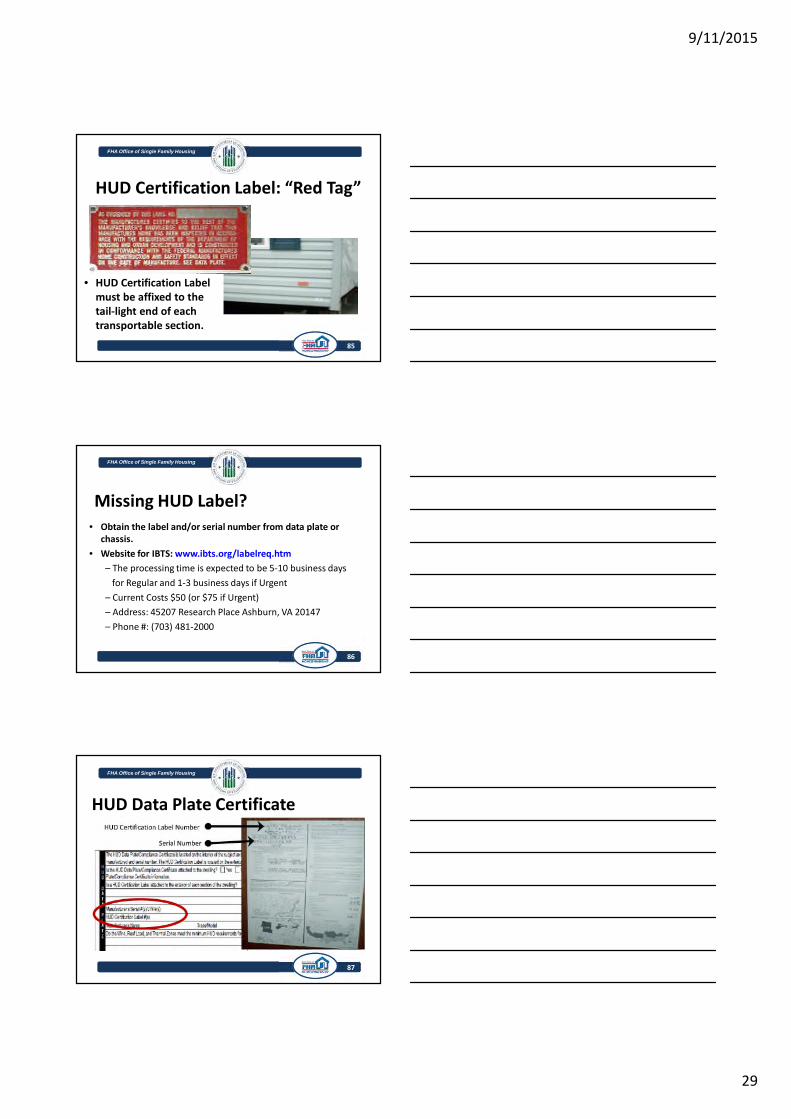

HUD Certification Label: “Red Tag”

85

• HUD Certification Labelmust be affixed to thetail-light end of eachtransportable section.

FHA Office of Single Family Housing

86

• Obtain the label and/or serial number from data plate orchassis.

• Website for IBTS: www.ibts.org/labelreq.htm

– The processing time is expected to be 5-10 business days

for Regular and 1-3 business days if Urgent

– Current Costs $50 (or $75 if Urgent)

– Address: 45207 Research Place Ashburn, VA 20147

– Phone #: (703) 481-2000

86

Missing HUD Label?

FHA Office of Single Family Housing

8787

HUD Data Plate Certificate

9/11/2015

30

FHA Office of Single Family Housing

88

Foundations

88

FHA Office of Single Family Housing

89

Additions to Manufactured Housing

• If the appraiser observes additions or structuralchanges to the original house, the appraiser mustcondition the appraisal upon inspection by the state orlocal jurisdiction administrative agency that inspectsManufactured Housing for compliance, or a licensedstructural engineer may report on the structuralintegrity of the manufactured dwelling and theaddition if the state does not employ inspectors.

• Note: Required for HUD REO.

89

FHA Office of Single Family Housing

90

Selection of Comparable Sales

90

• At least two of thecomparable salesmust be closedmanufacturedhomes.

9/11/2015

31

FHA Office of Single Family Housing

91

Skirting

• Is vinyl skirting attached to frameworkacceptable for a manufactured home?

• HUD requires manufactured homes to haveskirting that is permanent or attached to apermanent foundation.

91

FHA Office of Single Family Housing

92

FHA Condominium Project Approval

Site Condominium or Single Family Home?

FHA Office of Single Family Housing

93

FHA Condominium Project Approvals (cont.)

Condominium or Attached Single Family Residence?

9/11/2015

32

FHA Office of Single Family Housing

94

FHA Condominium Project Approvals (cont.)

Condominium or Manufactured Home?

FHA Office of Single Family Housing

95

FHA Condominium Project Approvals (cont.)

Condominium?

FHA Office of Single Family Housing

96

Condominiums

• Any mortgage covering a one-family unit in a project coupledwith an undivided interest in the common areas andfacilities which serve the project.

• May include dwelling units in detached, semi-detached, rowgarden-type, low or high rise structures.

• Remaining Economic Life is to be entered.

9/11/2015

33

FHA Office of Single Family Housing

97

FHA Condo Case Numbers

• Case numbers cannot be assigned to condominium unitsunless and until the condominium project is approved.

• To be eligible for FHA insurance, the project must be on thelist of FHA-approved condominiums.

FHA Office of Single Family Housing

98

Condominium Project Policy-Status• As stated in the Origination/Underwriting Section:

– A Condominium Project must be FHA approved before amortgage on an individual condominium unit can be insured.

• Currently, FHA’s Condominium Project Approval requirements arein the formal rulemaking phase. This process must be completedbefore the guidance is published.

• Our existing Condominium Project Approval requirements, locatedin Mortgagee Letter 2012-18, and the Condominium ProjectApproval and Processing Guide attached to Mortgagee Letter 2011-22 continue to be applicable.

FHA Office of Single Family Housing

99

Condominiums: FHA Connection

9/11/2015

34

FHA Office of Single Family Housing

100

Individual Condominium Unit Appraisal Report:Fannie Mae Form 1073

FHA Office of Single Family Housing

101

Site Condos

• Site Condominiums refer to a project of single family, totallydetached dwellings encumbered by a declaration ofcondominium covenants or a condominium form ofownership.

• They have no shared garages or any other attached buildings.Project approval is required for Site Condominiums that donot meet this definition.

• The appraiser must report the appraisal on Fannie Mae Form1073/Freddie Mac Form 465, Individual Condominium UnitAppraisal Report.

FHA Office of Single Family Housing

102

FHA Office of Single Family Housing

Module 8B

Programs and Products - Continued

Single Family Housing Policy Handbook 4000.1Title II Insured Housing Program Forward Mortgages

Origination through Post-Closing/Endorsement

102

9/11/2015

35

FHA Office of Single Family Housing

103

FHA Office of Single Family Housing

Energy Efficient Mortgage (EEM)

103

FHA Office of Single Family Housing

104

FHA Office of Single Family Housing

Energy Efficient Mortgage (EEM) Program

• Allows the Mortgagee to offer financing for cost-effective,energy efficient improvements to an existing property at thetime of purchase or refinancing, or for upgrades above theestablished residential building code for new construction.

104

FHA Office of Single Family Housing

105

FHA Office of Single Family Housing

EEM: Eligible Programs and Transactions Types

The EEM program can be used in conjunction with any

mortgage insurance under Title II, including:

– 203(b);

Purchase; or

No cash-out refinance.

– 203(h) Mortgage Insurance for Disaster Victims;

– 203(k) (Standard and Limited [former Streamline]); and

– Weatherization Policy (Existing Construction only).

105

9/11/2015

36

FHA Office of Single Family Housing

106

FHA Office of Single Family Housing

EEM: Energy Package

The energy package is the set of improvements agreed to by

the Borrower based on recommendations and analysis

performed by the qualified home energy rater.

The improvements can include:

– Materials, labor, inspections, and the home energyassessment by a qualified energy rater;

– If the Borrower desires, labor may include the cost of anEEM Facilitator (general contractor); and

– Borrower labor (Sweat Equity) is not permitted to beincluded in the loan amount.

106

FHA Office of Single Family Housing

107

FHA Office of Single Family Housing

EEM: EEM Facilitator (General Contractor)

Who is a EEM Facilitator?

– They are project managers.

What is an EEM Facilitator’s responsibility? They:

– Arrange the inspections, obtain the required documents forMortgagee, and on behalf of the Mortgagee; and

– Ensure that the improvements comply withrecommendations Home Energy Report.

107

FHA Office of Single Family Housing

108

FHA Office of Single Family Housing

EEM: Cost-Effective Test

Cost-Effective refers to the costs of the energy efficiencyimprovements including maintenance and repair, and isone where the cost of the improvements is less than thevalue of the energy saved over the estimated useful life ofthose improvements.

108

9/11/2015

37

FHA Office of Single Family Housing

109

FHA Office of Single Family Housing

EEM: Cost Effective Test for New Construction

For new construction any upgrades greater than existing codemay not bare out any additional savings.

A property classified as a energy efficient home must meetthe requirements of the 2000 IECC standards.

More information on this energy code can be obtained fromthe Department of Energy or the International Code Council.

109

FHA Office of Single Family Housing

110

FHA Office of Single Family Housing

EEM: Cost Effective Test for New Construction

(cont.)

The financed portion of an energy package includes only

those cost-effective energy improvements over and above

the greater of the following:

– The requirements of the 2006 International EnergyConservation Code (IECC);

– A successor energy code standard that has been adoptedby HUD for its Minimum Property Standards (MPS),

pursuant to 42 U.S.C. § 12709; or

– The applicable IECC year used by the state or localbuilding code for New Construction.

110

FHA Office of Single Family Housing

111

FHA Office of Single Family Housing

EEM: Home Energy Report/Assessment

The Borrower must obtain a home energy assessment.

The purpose of the energy assessment under the EEM

program is to identify opportunities for improving the

energy efficiency of the home and their cost-effectiveness.

The assessment must be conducted by a qualified energy

rater, assessor, or auditor using whole-home assessment

standards, protocols, and procedure.

111

9/11/2015

38

FHA Office of Single Family Housing

112

FHA Office of Single Family Housing

EEM: Qualifications of Energy Raters/Assessors

Qualified home energy rater/assessors must be trained and

certified as one of the following and meet local and state

jurisdictional requirements:

– Building Performance Institute Building AnalystProfessional;

– Building Performance Institute Home Energy ProfessionalEnergy Auditor; or

– Residential Energy Services Network Home Energy Rater.

112

FHA Office of Single Family Housing

113

FHA Office of Single Family Housing

EEM: Required Documentation

The Mortgagee must obtain a copy of the home energyreport:

– Must not be more than 120 days old.

The Mortgagee must submit two forms HUD 92900-LT:

– FHA Loan Underwriting; and

– Transmittal Summary.

113

FHA Office of Single Family Housing

114

FHA Office of Single Family Housing

EEM: Maximum Financeable Energy Package

The maximum amount of the energy package that can beadded to the Base Loan Amount is the lesser of:

– The dollar amount of a cost-effective energy package asdetermined by the home energy audit; or

– The lesser of 5 percent of: The Adjusted Value;

115 percent of the median area price of a Single Familydwelling; or

150 percent of the national conforming mortgage limit.

114

9/11/2015

39

FHA Office of Single Family Housing

115

FHA Office of Single Family Housing

EEM: Maximum Mortgage Amount for ExistingConstruction

The maximum final Base Loan Amount is determined byadding:

− The maximum financeable energy package amount tothe initial maximum Base Loan Amount.

115

FHA Office of Single Family Housing

116

FHA Office of Single Family Housing

EEM: Maximum Mortgage Amount For

New Construction

Determine Adjusted Value to calculate the Base Loan

Amount:

– The cost of the financeable energy package includedin the purchase contract must be subtracted from

the sales price when computing the Adjusted Value.

116

FHA Office of Single Family Housing

117

FHA Office of Single Family Housing

EEM: Maximum Mortgage Amount for

New Construction (cont.)

The steps for calculating the maximum mortgage amount fornew construction are:

– Determine the Adjusted value;

– Determine maximum financeable energy package usingthe EEM calculator in FHAC; and

– Determine the maximum FHA mortgage.

117

9/11/2015

40

FHA Office of Single Family Housing

118

FHA Office of Single Family Housing

EEM: Appraisals

For Existing and New Construction, the appraisal does notneed to reflect the value of the energy package that will beadded to the property.

If the appraisal does include the value of the energy package,the value must be subtracted from the Property Value whencomputing the Adjusted Value.

On the 203(k) program, the after-improved value is to be usedfor the EEM process.

118

FHA Office of Single Family Housing

119

FHA Office of Single Family Housing

Completion Requirements for Energy EfficientMortgages (EEMs)

With the exception of 203(k), the energy package is to beinstalled within 90 Days of the mortgage closing.

If the work is not completed within 90 Days, the Mortgageemust apply the EEM funds to a prepayment of the mortgageprincipal.

119

FHA Office of Single Family Housing

120

FHA Office of Single Family Housing

Completion Inspection

The Mortgagee, the rater, or an FHA fee inspector may inspectthe installation of the improvements.

An FHA fee inspector must be currently approved andcurrently on the roster.

The Borrower may be charged an inspection fee

120

9/11/2015

41

FHA Office of Single Family Housing

121

FHA Office of Single Family Housing

Weatherization

121

FHA Office of Single Family Housing

122

FHA Office of Single Family Housing

Weatherization

The weatherization product permits the Borrower to financethe cost of eligible energy-related weatherizationimprovements, in conjunction with a purchase or refinance.

122

FHA Office of Single Family Housing

123

FHA Office of Single Family Housing

Eligible Programs and Transaction Types

Weatherization improvements may be financed in conjunction

with the following:

– Section 203(b); purchase or no cash out refinance;

– Section 203(h) Mortgage Insurance for Disaster Victims;and

– Energy Efficient Mortgages (EEMs).

For financing of weatherization under the 203(k)Rehabilitation Mortgage Insurance Program, refer to 203(k)Rehabilitation Mortgage Insurance Program.

123

9/11/2015

42

FHA Office of Single Family Housing

124

FHA Office of Single Family Housing

Eligible Property Types

Weatherization improvements may be used on the followingproperty types:

– Existing properties (one- to four-units);

– Condominiums (one unit); and

– Manufactured Housing (single unit).

124

FHA Office of Single Family Housing

125

FHA Office of Single Family Housing

Eligible Weatherization Items

Eligible energy-related weatherization items include:

– Air sealing (including weather-stripping doors, caulkingwindow and plumbing penetrations);

– Insulation (attic, floors, walls, basement);

– Duct sealing and insulation;

– Smart thermostats and equipment controls; and

– Windows and doors.

125

FHA Office of Single Family Housing

126

FHA Office of Single Family Housing

Weatherization Combined with an EEM

For existing Properties, energy-related weatherization itemsmay be combined with the EEM.

126

9/11/2015

43

FHA Office of Single Family Housing

127

FHA Office of Single Family Housing

Escrows

The Mortgagee must establish an escrow account for theremaining costs of the energy improvements if theinstallation of weatherization items is not complete by thetime of closing.

Any funds remaining in the escrow account at the end of theimprovement period must be applied to pay down themortgage principal.

Escrows may not include costs for labor or work performed

by the Borrower (Sweat Equity).127

FHA Office of Single Family Housing

128

FHA Office of Single Family Housing

Mortgagees Assurance of Completion

When funds to complete weatherization improvements areescrowed:

– The Mortgagee must execute form HUD-92300,Mortgagee’s Assurance of Completion, to indicate that theescrow for weatherization improvements has beenestablished.

128

FHA Office of Single Family Housing

129

FHA Office of Single Family Housing

Time of Completion for Weatherization Items

Installation of weatherization improvements must becompleted within:

– 30 Days of the mortgage Disbursement; or– 90 Days of the mortgage Disbursement if the improvements

are part of an energy package for an EEM.

The Mortgagee must apply the remaining weatherizationescrow funds to a prepayment of the mortgage principal if thework is not completed within the required time frames.

129

9/11/2015

44

FHA Office of Single Family Housing

130

FHA Office of Single Family Housing

Inspection

The Mortgagee or their agent must inspect theweatherization items or obtain evidence from a localauthority that the system was installed in accordance withlocal requirements.

130

FHA Office of Single Family Housing

131

FHA Office of Single Family Housing

Case Binder: Specialized Program Documents

Specialized Product Eligibility Documents are to be located onthe Left Side of the case binder.

Refer to HUD Handbook 4000.1 for order of stacking.

131

FHA Office of Single Family Housing

132

FHA Office of Single Family Housing

New Construction

132

9/11/2015

45

FHA Office of Single Family Housing

133

FHA Office of Single Family Housing

New Construction

New Construction refers to properties that are Proposed,Under Construction, or were completed within one year.

Each type of New Construction has separate/distinctguidance.

Each is covered in this section.

133

FHA Office of Single Family Housing

134

FHA Office of Single Family Housing

Proposed Construction

Proposed Construction refers to a property where noconcrete or permanent material has been placed.

Digging of footing and placement of rebar is notconsidered permanent.

134

FHA Office of Single Family Housing

135

FHA Office of Single Family Housing

Under Construction

Under Construction refers to the period from:

– The first placement of permanent material to 100percent completion; and

– With no Certificate of Occupancy (CO) or equivalent.

135

9/11/2015

46

FHA Office of Single Family Housing

136

FHA Office of Single Family Housing

Existing for Less than One Year

Existing for Less than One Year refers to a property that:

– Is 100 percent complete; and

– Has been completed less than one year from the date ofthe issuance of the CO or equivalent.

The property must have never been occupied.

136

FHA Office of Single Family Housing

137

FHA Office of Single Family Housing

Inspections or Warranties for MaximumFinancing Site Built Housing or CondominiumsProposed Construction

A 10-year warranty and final inspection issued by the localauthority with jurisdiction over the property or an FHARoster Inspector.

137

FHA Office of Single Family Housing

138

FHA Office of Single Family Housing

Inspections or Warranties for Maximum

Financing Site Built Housing or Condominiums

Under Construction

The Mortgagee must obtain:

– Copies of the building permit and CO (or equivalent); or

– A 10-year warranty and final inspection issued by thelocal authority with jurisdiction over the property or an

FHA Roster Inspector.

138

9/11/2015

47

FHA Office of Single Family Housing

139

FHA Office of Single Family Housing

Inspections or Warranties for MaximumFinancing Site Built Housing or Condominiums

Existing for Less than One Year (100% Complete)

The Mortgagee must obtain:

– Copies of the building permit and CO (or equivalent); or

– A 10-year warranty and final inspection issued by the localauthority with jurisdiction over the property or an FHA

Roster Inspector; or

– An appraisal evidencing property is 100 percent complete.

139

FHA Office of Single Family Housing

140

FHA Office of Single Family Housing

Additional Required Documentation forMaximum Financing

All New Construction Typesand All Property Types

140

FHA Office of Single Family Housing

141

FHA Office of Single Family Housing

Additional Required Documentation

The Mortgagee must obtain and include the following

documents in the case binder:

– Form HUD-92541, Builder’s Certification of Plans,Specifications, and Site; and

– Form HUD-92544, Warranty of Completion ofConstruction.

141

9/11/2015

48

FHA Office of Single Family Housing

142

FHA Office of Single Family Housing

Additional Required Documentation (cont.)

Evidence that the property was pre-approved or the 10-yearwarranty plan:

– Evidence of pre-approval is the Early Start Letter or copy ofbuilding permit issued by local authority prior to start ofconstruction; and

– For a 10-year warranty plan, evidence of acceptance orenrollment in the plan is required.

The application alone is not acceptable.

142

FHA Office of Single Family Housing

143

FHA Office of Single Family Housing

Required Inspectionsfor Maximum Financing

All New Construction Typesand All Property Types

143

FHA Office of Single Family Housing

144

FHA Office of Single Family Housing

Required Inspections

The Mortgagee must obtain and include the followingdocuments in the case binder.

144

9/11/2015

49

FHA Office of Single Family Housing

145

FHA Office of Single Family Housing

New Construction: Required Inspections

Wood Infestation Report, unless the Property is located in anarea of no-to-slight infestation as indicated on HUD’s“Termite Treatment Exception Areas” list.

Form HUD-NPMA-99-A, Subterranean Termite ProtectionBuilder’s Guarantee.

If the building is constructed with steel, masonry, or concretebuilding components with only minor interior wood trim androof sheathing, no treatment is needed.

The Mortgagee must ensure that the builder notes on theform that the construction is masonry, steel, or concrete.

145

FHA Office of Single Family Housing

146

•FHA Office of Single Family Housing

New Construction: Required Inspections (cont.)

Form HUD-NPMA-99-B, New Construction SubterraneanTermite Service Record, is required when the proposedProperty is treated with a soil chemical termiticide.

The Mortgagee must reject the use of post construction soiltreatment when the termiticide is applied only around theperimeter of the foundation.

Local Health Authority well water analysis and/or septicreport, where required by the local jurisdictional authority.

146

FHA Office of Single Family Housing

147

FHA Office of Single Family Housing

New Construction: Financing LTV Limit

Properties that are Under Construction or Existing for Less

than One Year are limited to a 90 percent LTV unless they:

– Meet the Pre-Approval requirements; or

– Are covered with a HUD-accepted insured 10-yearprotection plan; and

– Meet the Required Documentation for MaximumFinancing.

147

9/11/2015

50

FHA Office of Single Family Housing

148

FHA Office of Single Family Housing

New Construction: Financing LTV Limit

For a Mortgage with an LTV of 90 percent or less, theMortgagee must obtain:

– Form HUD-92541, Builder’s Certification of Plans,Specifications, and Site;

– Final inspection or appraisal, if the Property is 100 percentcomplete; and

– Wood Infestation Report, unless the Property is located inan area of no to slight infestation as indicated on HUD’s

“Termite Treatment Exception Areas” list.

148

FHA Office of Single Family Housing

149

FHA Office of Single Family Housing

New Construction Financing 90% or Less (cont.)

Form HUD-NPMA-99-A, Subterranean Termite ProtectionBuilder’s Guarantee, is required for all New Construction.

If the building is constructed with steel, masonry, orconcrete building components with only minor interiorwood trim and roof sheathing, no treatment is needed.

The Mortgagee must ensure that the builder notes on theform that the construction is masonry, steel, or concrete.

149

FHA Office of Single Family Housing

150

FHA Office of Single Family Housing

New Construction Financing 90% or Less (cont.)

Form HUD-NPMA-99-B, New Construction SubterraneanTermite Service Record, is required when the proposedProperty is treated with a soil chemical termiticide.

The Mortgagee must reject the use of post constructionsoil treatment when the termiticide is applied onlyaround the perimeter of the foundation.

Local Health Authority well water analysis and/or septicreport, where required by the local jurisdictionalauthority.

150

9/11/2015

51

FHA Office of Single Family Housing

151

•FHA Office of Single Family Housing

Documents to be Provided to Appraiser atAssignment

The Mortgagee must provide the appraiser with a fully-

executed Form HUD-92541.

– Signed and dated no more than 30 Days prior to the datethe appraisal was ordered.

151

FHA Office of Single Family Housing

152

•FHA Office of Single Family Housing

Documents to be Provided to Appraiser atAssignment (cont.)

Stage of Completion

Properties 90 Percent

Completed or less

Documents Needed to Be Provided

Floor plans, plot plan, and any other

exhibits necessary to allow them to

determine the size and level of the

finished house.

Properties Greater than

90 Percent but Less than

100 Percent Completed

A list of components to be installed or

completed after the date of

inspection.

152

FHA Office of Single Family Housing

153

•FHA Office of Single Family Housing

New Construction: Mortgagee Review ofAppraisal

New Construction, like existing construction, must meetHUD’s:

– Minimum Property Requirements (MPR); and

– Minimum Property Standards (MPS).

HUD Form 92541 requirements.

HUD Handbook 4000.1; Property and Appraisal•Requirements Section.

153

9/11/2015

52

FHA Office of Single Family Housing

154

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations

Environmental

– The Mortgagee must require corrective work to mitigateany condition that arises during construction that mayaffect the:

Health and safety of the occupants;

Property’s ability to serve as collateral; and

Structural soundness of the improvements.

154

FHA Office of Single Family Housing

155

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Operating Oil or Gas Wells

– If a proposed or newly constructed dwelling is locatedwithin 75 feet of an operating oil or gas well theMortgagee must:

Reject the property unless mitigation measures arecompleted.

155

FHA Office of Single Family Housing

156

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Slush Pits

– If a property is Proposed Construction near an active orabandoned Slush Pit:

The appraiser must require a survey to locate the pit;and

The Mortgagee is to assess any impact on the subjectproperty.

156

9/11/2015

53

FHA Office of Single Family Housing

157

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Special Airport Hazards

– If a proposed or newly constructed property is locatedwithin Runway Clear Zones (also known as RunwayProtection Zones) at civil airports or within Clear Zones atmilitary airfields the Mortgagee must reject the propertyor insurance.

157

FHA Office of Single Family Housing

158

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations

Flood Hazard Areas

– The Mortgagee must reject the property if any portionof the property improvements is located within a SpecialFlood Hazard Area (SFHA) (the dwelling and relatedstructures/equipment essential to the value of theproperty and subject to flood damage) unless:

158

FHA Office of Single Family Housing

159

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Flood Hazard Areas (cont.)

– The Mortgagee must include the LOMA, LOMR, or floodelevation certificate with the case when it is submitted

for endorsement.

– The Mortgagee must ensure that insurance under theNFIP is obtained when a flood elevation certificate

documents that the property remains located within an

SFHA.

– A manufactured home in a flood zone is not permittedeven with insurance.

159

9/11/2015

54

FHA Office of Single Family Housing

160

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Individual Water Supply Systems (Wells)

– The Mortgagee must ensure that new wells are:

Drilled;

No less than 20 feet deep; and

Cased.

160

FHA Office of Single Family Housing

161

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Individual Water Supply Systems (Wells) (cont.)

– Casing should be steel or other casing material that isdurable, leak-proof, and acceptable to either the local

health authority or the trade or profession licensed todrill and repair wells in the local jurisdiction.

– A well located within the foundation walls of newconstruction is not acceptable except in arctic or sub-

arctic regions.

161

FHA Office of Single Family Housing

162

FHA Office of Single Family Housing

Mortgagee Review of Site Considerations (cont.)

Shared Well

– A shared well is permitted only if the Mortgagee obtainsevidence that:

It is not feasible to serve the housing by an acceptable

public or community water system; and

The housing is located in an area other than in an areawhere local officials have certified that installation ofpublic or adequate community water and sewersystems are economically feasible.

162

9/11/2015

55

FHA Office of Single Family Housing

163

FHA Office of Single Family Housing

Sales Comparison Approach:Comparable Selection

For properties in new subdivisions, the selectedcomparable sales must include:

– At least one sale outside the subdivision or project; and

– At least one sale from within the subdivision or project.

163

FHA Office of Single Family Housing

164

FHA Office of Single Family Housing

Completion of Construction

Regardless of the inspection process used, the Mortgageemust certify on Form HUD-92900-A, HUD/VA Addendum toUniform Residential Loan Application, that the property is100 percent complete and meets HUD’s MPR and MPS.

164

FHA Office of Single Family Housing

165

203(k) and ConsultantRequirements

Module 9

9/11/2015

56

FHA Office of Single Family Housing

166

Introduction

• The Section 203(k) program is the agency’sprimary program for the rehabilitation andrepair of Single Family properties.

FHA Office of Single Family Housing

167

How is the 203(k) Program Different?

FHA Office of Single Family Housing

168

• How the Program Can Be Used

• Benefits of the 203(k)

• Basic Eligibility

9/11/2015

57

FHA Office of Single Family Housing

169

203(k) Programs for Two DifferentRenovation Project Needs

• There are two types of 203(k) rehabilitationmortgages as described below:

– Standard 203(k); and– Limited 203(k).

• The guidance per the Program and Product section isapplicable to both the Standard 203(k) and Limited203(k) mortgages, unless noted otherwise.

FHA Office of Single Family Housing

170

203(k) Programs: The Limited 203(k)

• The Limited 203(k) (formally known as the Streamlined (k),may only be used for minor remodeling and non-structuralrepairs.

• The Limited 203(k) does not require the use of a 203(k)Consultant, but a Consultant may be used.

• The total rehabilitation cost must not exceed $35,000.There is no minimum rehabilitation cost.

FHA Office of Single Family Housing

171

Property Eligibility

• The property must be an existing propertythat has been completed for at least one yearprior to the case number assignment date.

9/11/2015

58

FHA Office of Single Family Housing

172

Acceptable Property Types• One- to four-unit Single Family Structures

• Condominiums– Individual Condominium Unit

– Site Condominium Unit

• Manufactured Housing

• Mixed Use

• HUD Real Estate Owned (REO)

FHA Office of Single Family Housing

173

Mixed Use 203(k) Specific Policies:

Mixed Use property with one- to four-residentialdwelling units, is acceptable provided:

• Fifty-one percent of gross building area is forresidential use; and

• Any commercial use will not affect the health andsafety of the occupants of the residential property.

FHA Office of Single Family Housing

174

Gross Building Area: Clarified• Fifty-one percent of gross building area is for

residential use.

• Gross Building Area (GBA) is the entire floor space ofthe building, as opposed to Gross Living Area. Thisincludes unfinished and finished non-living areas, suchas unfinished mechanical areas, laundry areas,entryways, stairs, unfinished storage, etc.

• This also includes any commercial space within thebuilding.

9/11/2015

59

FHA Office of Single Family Housing

175

Acceptable Property Types: HUD RealEstate Owned (REO)

• The property is identified as eligible for 203(k)financing as evidenced in the sales contract oraddendum.

• HUD REOs that are listed as uninsurable can only be anFHA loan as a 203(k).

• Good Neighbor Next Door and $100 Down Programscan be used with 203(k).

• Investor purchases of HUD REO properties are noteligible for 203(k) financing.

FHA Office of Single Family Housing

176

Sample HUD REO Sales Contract

FHA Office of Single Family Housing

177

Standard 203(k)• A Standard 203(k) has the following general requirements:

– A minimum of $5,000 in eligible improvements are required toqualify for the product.

– Fees and costs related to the renovation can be rolled into the loanamount.

– Standard FHA credit and cash investment requirements apply.

– Standard FHA property guidelines apply, unless otherwise stated in203(k) policies.

– A 203(k) HUD-approved Consultant is required.

9/11/2015

60

FHA Office of Single Family Housing

178

The Origination Process of a Standard 203(K)• Borrower selects a property;

• Borrower selects a FHA approved lender;

• Mortgagee takes loan application;

• Mortgagee selects 203(K) Consultant;

• Consultant visits property with Borrower;

• Consultant prepares “Work Write-up”;

• Borrower hires Contractor;

• Work write-up and bids are provided to the Mortgagee;

• Mortgagee processes, underwrites, closes, and funds the transaction;

• FHA insures the loan; and

• Improvement process to the property begins.

FHA Office of Single Family Housing

179

Repair/Improvements Begin• Contractor completes first phase of the project.

• Borrower contacts the 203(k) Consultant who inspects work completedat this point by the contractor for a draw request to be completed forrelease of funds.

• The Consultant and Borrower sign the draw request.

• Draw Request is submitted to the Mortgagee.

• Mortgagee disburses a check made payable to Borrower and Contractor.

• This process continues until the work is completed.

FHA Office of Single Family Housing

180

Project Completion• Final draw is requested.

• Borrower provides release letter indicating work iscompleted.

• Consultant verifies completion.

• Remaining Rehabilitation Escrow Account funds are released.

• Note: The project should be completed within 6 months

9/11/2015

61

FHA Office of Single Family Housing

181

Eligible ImprovementsTypes of eligible improvements include, but are notlimited to:• –Reconstructing a Structure that has been, or will

be demolished, provided the complete existingfoundation system is not affected and will still beused;

• –Repairing, reconstructing, or elevating anexisting foundation where the Structure will notbe demolished;

FHA Office of Single Family Housing

182

Eligible Improvements (cont.)• Installing or repairing wells and/or septic systems;

Note: Lot size requirements removed.

• Repairing or removing an in-ground swimming pool;

Note: $1,500 limitation removed.

• Constructing a windstorm shelter.

Note: $5,000 limitation removed.

FHA Office of Single Family Housing

183

Improvement Standards

• All improvements to existing Structures must comply withHUD’s MPR.

• All new construction must comply with HUD’s MPS.• For a newly constructed addition to the existing Structure,

the energy improvements must meet or exceed local codesand the requirements of the 2006 International EnergyConservation Code (IECC) or a successor energy codestandard that has been adopted by HUD for its MPS.

9/11/2015

62

FHA Office of Single Family Housing

184

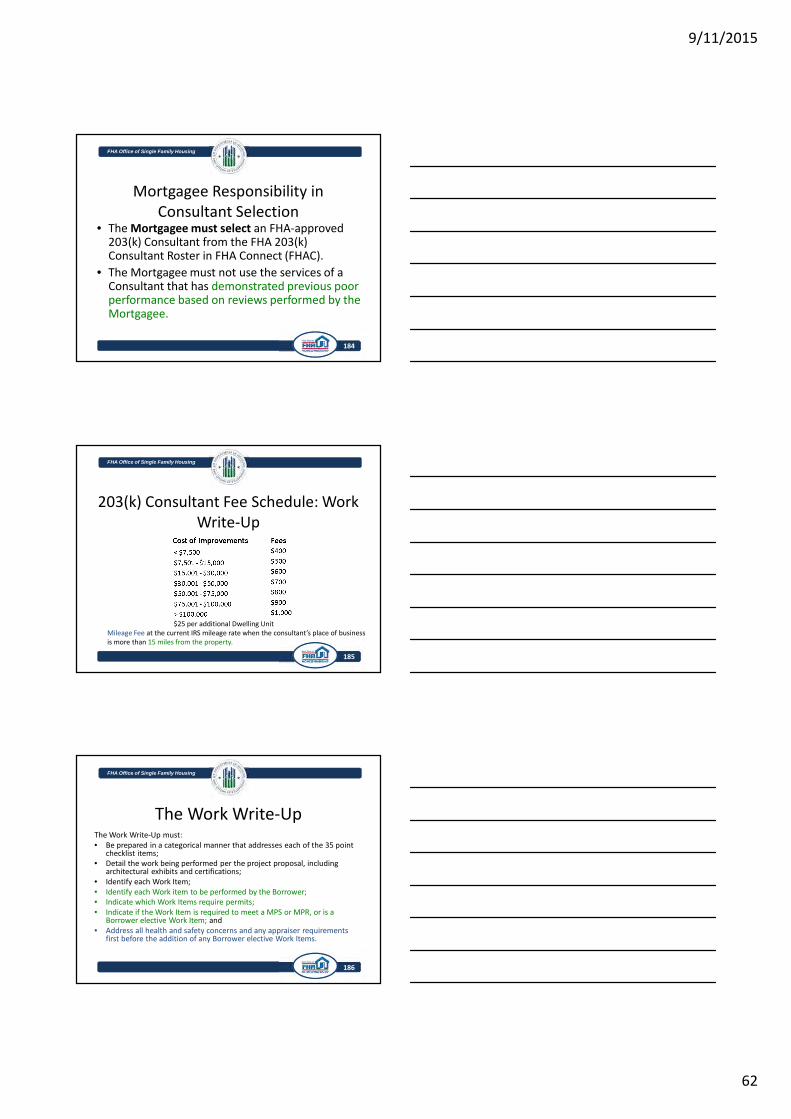

Mortgagee Responsibility inConsultant Selection

• The Mortgagee must select an FHA-approved203(k) Consultant from the FHA 203(k)Consultant Roster in FHA Connect (FHAC).

• The Mortgagee must not use the services of aConsultant that has demonstrated previous poorperformance based on reviews performed by theMortgagee.

FHA Office of Single Family Housing

185

203(k) Consultant Fee Schedule: WorkWrite-Up

$25 per additional Dwelling UnitMileage Fee at the current IRS mileage rate when the consultant’s place of businessis more than 15 miles from the property.

FHA Office of Single Family Housing

186

The Work Write-UpThe Work Write-Up must:• Be prepared in a categorical manner that addresses each of the 35 point

checklist items;• Detail the work being performed per the project proposal, including

architectural exhibits and certifications;• Identify each Work Item;• Identify each Work item to be performed by the Borrower;• Indicate which Work Items require permits;• Indicate if the Work Item is required to meet a MPS or MPR, or is a

Borrower elective Work Item; and• Address all health and safety concerns and any appraiser requirements

first before the addition of any Borrower elective Work Items.

9/11/2015

63

FHA Office of Single Family Housing

187

Borrowers Doing Own Work (Self-Help)

• The Mortgagee must:– Ensure all permits are obtained prior to

commencement of work;

• The Borrower must not be reimbursed for laborcosts.

FHA Office of Single Family Housing

188

Borrowers Doing Own Work (Self-Help)Cost Estimates

• The Mortgagee must:

– Include the costs for labor and materials for eachWork Item to be completed by the Borrowerunder a Rehabilitation (Self-Help) LoanAgreement.

FHA Office of Single Family Housing

189

Standard 203(k) Financeable Repairand Improvement Costs and Fees

• The following repair and improvement costs and fees may befinanced:

–Costs of construction, repairs, and rehabilitation;–Architectural/engineering professional fees;–The 203(k) Consultant fee (limited to the 203(k) Consultant

Fee Schedule - 9. Section 203(k) Consultant);–Inspection fees performed during the construction period,

provided the fees are reasonable and customary for the area;–Title update fees; and–Permits.

9/11/2015

64

FHA Office of Single Family Housing

190

Review of Contractor Qualifications

• Prior to closing, the Mortgagee must ensure thata qualified general or specialized contractor hasbeen hired and by contract has:

– Agreed to complete the work described inthe Work Write-Up for the amount of theCost Estimate; and

– Within the allotted time frame

FHA Office of Single Family Housing

191

Appraisal Reports• An appraisal by an FHA-approved roster appraiser is

always required to establish the after-improved valueof the property.

• Except in cases of Property Flipping and refinancetransactions, the Mortgagee is not required to obtainan as-is appraisal and may use alternate methods perthe 203(k) policies to establish the Adjusted As-IsValue.

• If an as-is appraisal is obtained, the Mortgagee mustuse it in establishing the Adjusted As-Is Value.

FHA Office of Single Family Housing

192

203(k) Resource Documents

• 203(k) Resource Documents :

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/203k/sample_documents

9/11/2015

65

FHA Office of Single Family Housing

193

Conditional Commitment (Form HUD-92800.5b)Direct Endorsement Statement of Appraised

Value

FHA Office of Single Family Housing

194

Repairs Noted by the Appraiser

• When an appraisal report identifies the need forhealth and safety repairs that were not includedin the Consultant’s Work Write-Up, Borrower’swork plan, or contractor’s proposal, theMortgagee must ensure the repairs are includedin the Consultant’s Final Work Write-Up or theBorrower’s final work plan.

FHA Office of Single Family Housing

195

Limited 203(k)• The Limited 203(k), as stated earlier, may only be

used for minor remodeling and non-structuralrepairs.

• The Limited 203(k) does not require the use of a203(k) Consultant. However, the Borrower canelect to hire a Consultant but the fee cannot befinanced.

• The total rehabilitation cost must not exceed$35,000

9/11/2015

66

FHA Office of Single Family Housing

196

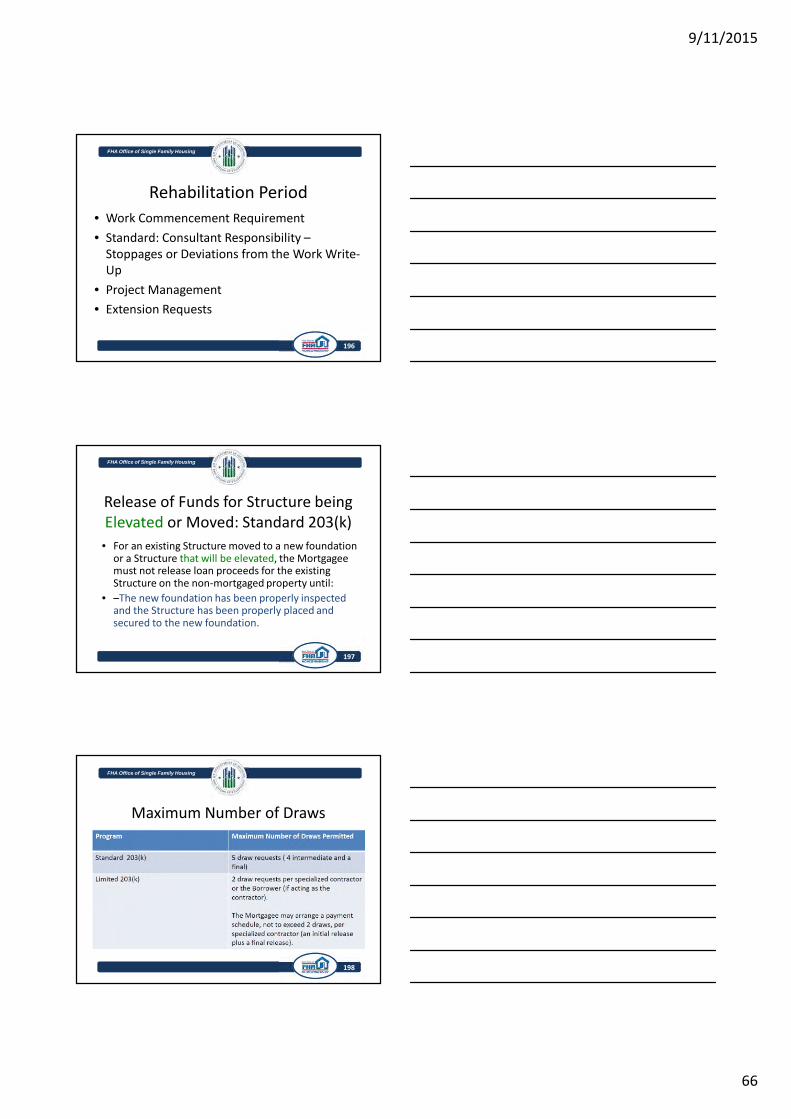

Rehabilitation Period

• Work Commencement Requirement

• Standard: Consultant Responsibility –Stoppages or Deviations from the Work Write-Up

• Project Management

• Extension Requests

FHA Office of Single Family Housing

197

Release of Funds for Structure beingElevated or Moved: Standard 203(k)

• For an existing Structure moved to a new foundationor a Structure that will be elevated, the Mortgageemust not release loan proceeds for the existingStructure on the non-mortgaged property until:

• –The new foundation has been properly inspectedand the Structure has been properly placed andsecured to the new foundation.

FHA Office of Single Family Housing

198

Maximum Number of Draws

9/11/2015

67

FHA Office of Single Family Housing

199

Discoveries During Rehabilitation

• Health and Safety Items

• Change Order Request: Standard 203(k)

• Change Order Request: Limited 203(k)

• Contingency Reserve Funds WhenRehabilitation is Not Complete