Embed Size (px)

DESCRIPTION

Audit & Assurance in an interactive world. Assurance bij de “XBRL- jaarrekening ” 2009/2010 van Deloitte. Rob Vervoort. Although XBRL adoption is growing, no assurance obligations exist today. The expectations about assurance. Sc. : Traditional FS converted to XBRL format. GAAP. - PowerPoint PPT Presentation

Citation preview

Audit & Assurance in an interactive worldAssurance bij de “XBRL-jaarrekening” 2009/2010 van Deloitte

Rob Vervoort

© 2010 Deloitte Touche Tohmatsu2

Although XBRL adoption is growing, no assurance obligations exist today

The expectations about assurance

© 2010 Deloitte Touche Tohmatsu4

Information- systems Users

Manual input

FinancialStatements

Users

XBRLpreparingprocess

NL

IFRS

XBRLInstance-documentPreparing

process

Local-Dutch

Other-US

IFRS

GAAP

Sc. : Traditional FS converted to XBRL format

XBRLTaxonomies

NL-FRIS

XBRL-Presentation

viewer

OtherUs XBRL-Financial

Statements

© 2010 Deloitte Touche Tohmatsu5

Some risks in relation to the XBRL translation process

• The use of the correct taxonomy

• Correct and complete translation (mapping or tagging) of original data in an instance document

• There is no standard representation of an instance document (although the presentation view provides significant guidance)

• A fact value is not necessarily viewed in combination with closely related fact values

Quality assurance related to these risks should be considered seriously

© 2010 Deloitte Touche Tohmatsu

State of “Assurance” Discussion

• No world wide view or ‘solution’ for assurance

• IFAC is still developing a vision on the need for assurance

• SEC does not require assurance (yet)

• The current auditing standards are providing no guidance how to provide assurance on information in electronic format (audit approach)

• Major issue is that stakeholders have no view yet about the opportunities of electronic filing and their demands / needs on assurance (internal and third party)

• Nederland

• Praktijkhandreiking 1114 SBR-Kredietrapportages

• Concept notitie over digitaal rapporteren en assurance

•Opportunities for local solutions

6

Creating an XBRL Financial Statement

© 2010 Deloitte Touche Tohmatsu

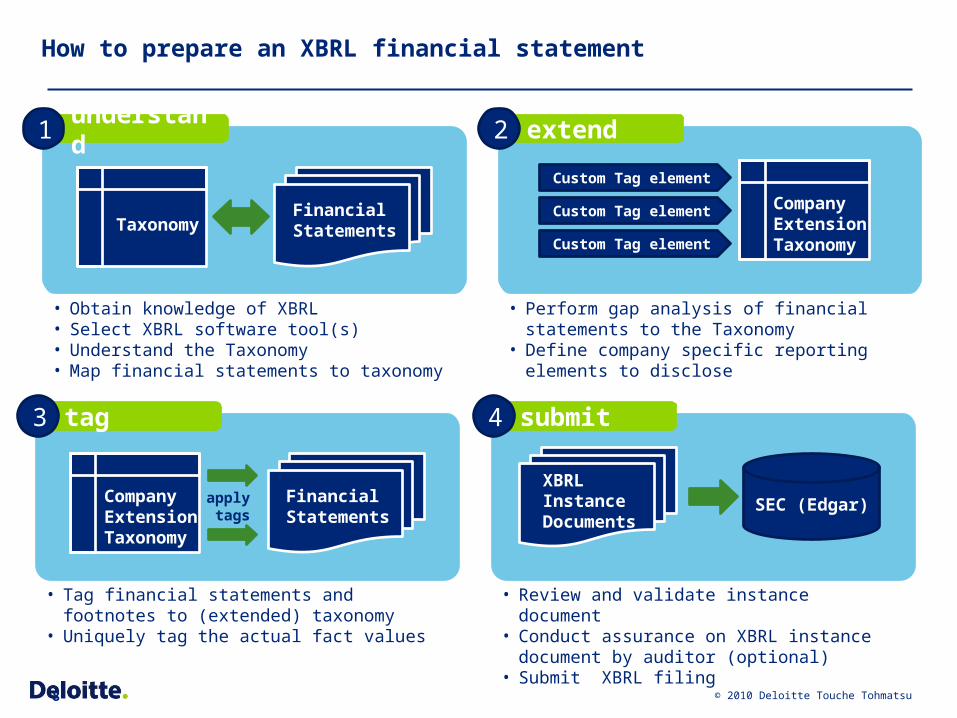

How to prepare an XBRL financial statement

8

TaxonomyFinancialStatements

CompanyExtensionTaxonomy

FinancialStatements

CompanyExtensionTaxonomy

Custom Tag element

Custom Tag element

Custom Tag element

apply tags

XBRLInstanceDocuments

SEC (Edgar)

• Obtain knowledge of XBRL• Select XBRL software tool(s)• Understand the Taxonomy• Map financial statements to taxonomy

• Perform gap analysis of financial statements to the Taxonomy

• Define company specific reporting elements to disclose

• Tag financial statements and footnotes to (extended) taxonomy

• Uniquely tag the actual fact values

• Review and validate instance document• Conduct assurance on XBRL instance document

by auditor (optional)• Submit XBRL filing

understand1 extend2

tag3 submit4

© 2010 Deloitte Touche Tohmatsu9

© 2010 Deloitte Touche Tohmatsu10

Nederlandse Taxonomie 2010 / Commercieel Jaarrapport / Geconsolideerd / Groot

Instance document = audit object

© 2010 Deloitte Touche Tohmatsu11

<kvk-rj: IntangibleAssetsNet contextRef="I -2010-E" unitRef="u-EUR" decimals="-3">16084000</kvk-rj: IntangibleAssetsNet>

<kvk-rj: IntangibleAssetsNet contextRef="I -2009-E" unitRef="u-EUR" decimals="-3">19050000</kvk-rj: IntangibleAssetsNet>

© 2010 Deloitte Touche Tohmatsu12

© 2010 Deloitte Touche Tohmatsu13

The quest for assurance

© 2010 Deloitte Touche Tohmatsu15

Assurance bij de “XBRL-jaarrekening” van Deloitte

Doelstellingen assurance:

• Belangrijke stap zetten in assurance discussie rondom XBRL

• Niet alleen conclusie ten aanzien van juistheid van de data (zogenaamde “ontleend aan”-verklaring)

• Ook conclusie ten aanzien van de overeenstemming van het XBRL document met de uitgangspunten en criteria van de Nederlandse Taxonomie

© 2010 Deloitte Touche Tohmatsu16

Possible assurance model

1. Assurance procedures:

• Traditional procedures on the true and fair view of the financial statements according tot ISAs (audit of historical of F/S)

2. Additonal assurance procedures on:

• Use of the correct taxonomie;

• Correctness and completeness of the tagging/mapping

• Technical validity of the XBRL instance document

• Completeness and correctness of the XBRL instance document

• XBRL-Presentation viewer

• Completeness of data

• Compliance with criteria of the taxonomy

• Unique identification via a ‘hash-number’

3. Auditors report based on ISA 800 or Assurance report based on ISA 3000

© 2010 Deloitte Touche Tohmatsu17

Assurance bij de “XBRL-jaarrekening” van Deloitte

© 2010 Deloitte Touche Tohmatsu18

Assurance bij de “XBRL-jaarrekening” van Deloitte

© 2010 Deloitte Touche Tohmatsu

New XBRL reporting process will need new assurance model

19

Information- systems

Financialinstitutions

Chamber ofCommerce

Government

Oversight-bodies

Analyst

XBRL Taxonomies

Shareholders

Manual input

NL GAAP

US GAAP

IFRS

tReportingsoftware

Financial statements/

Other reports

XBRL

Instance-document

© 2010 Deloitte Touche Tohmatsu20

Possible assurance model which fits needs of users 1. Assurance procedures:

• Procedures to test the internal controls regarding the financial reporting processes

2. Additional assurance procedures on controls regarding the translation process of data to an XBRL instance document:

• Use of the correct taxonomy;

• Correctness and completeness of the tagging process

• Correctness of the technical aspects of the XBRL instance document

• Completeness of data

• Compliance with taxonomy criteria

3. Assurance report on controls (like Third party service organizations or SAS-70 reports)

© 2010 Deloitte Touche Tohmatsu

Moving from content assurance to process assurance

21

Information- systems

XBRL Taxonomies

Manual input

NL GAAP

US GAAP

IFRS

tReportingsoftware

XBRL

Instance-document

A specific ISA 30xx for an Assurance Engagements to provide a conclusion on the XBRL preparing process

Users

© 2010 Deloitte Touche Tohmatsu22

Conclusions

Short term: Content assurance

Long term: Content assurance will be replaced by process assurance in combination with content assurance for specific users.

Essential: The stakeholders must clearly understand their information needs, the possibilities of electronic reporting and last but not least clarify their assurance needs.