Embed Size (px)

Citation preview

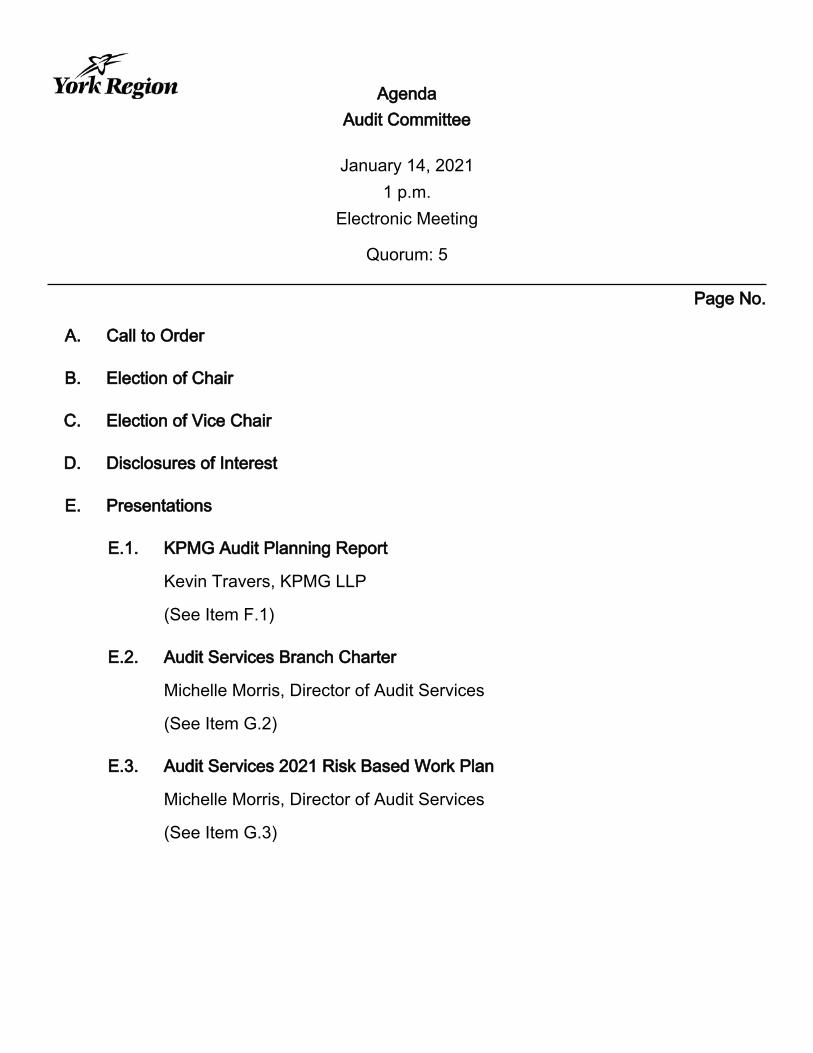

Agenda

Audit Committee

January 14, 20211 p.m.

Electronic Meeting

Quorum: 5

Page No.

A. Call to Order

B. Election of Chair

C. Election of Vice Chair

D. Disclosures of Interest

E. Presentations

E.1. KPMG Audit Planning Report

Kevin Travers, KPMG LLP

(See Item F.1)

E.2. Audit Services Branch Charter

Michelle Morris, Director of Audit Services

(See Item G.2)

E.3. Audit Services 2021 Risk Based Work Plan

Michelle Morris, Director of Audit Services

(See Item G.3)

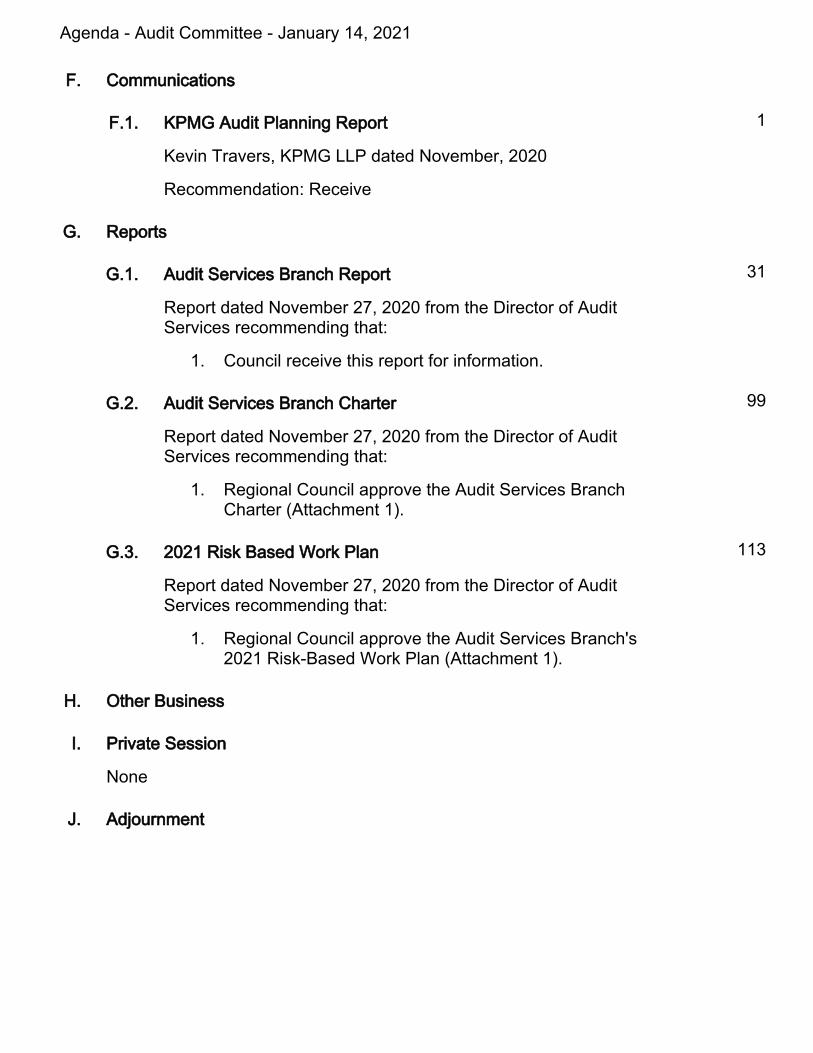

F. Communications

F.1. KPMG Audit Planning Report 1

Kevin Travers, KPMG LLP dated November, 2020

Recommendation: Receive

G. Reports

G.1. Audit Services Branch Report 31

Report dated November 27, 2020 from the Director of AuditServices recommending that:

Council receive this report for information.1.

G.2. Audit Services Branch Charter 99

Report dated November 27, 2020 from the Director of AuditServices recommending that:

Regional Council approve the Audit Services BranchCharter (Attachment 1).

1.

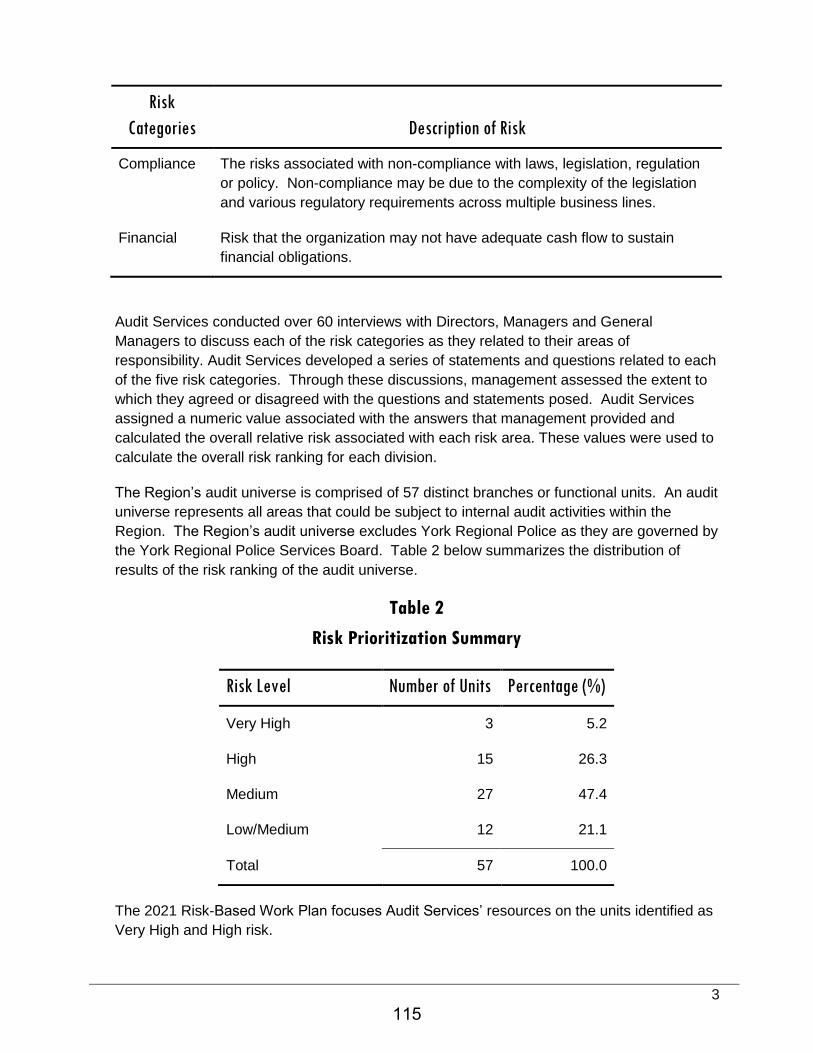

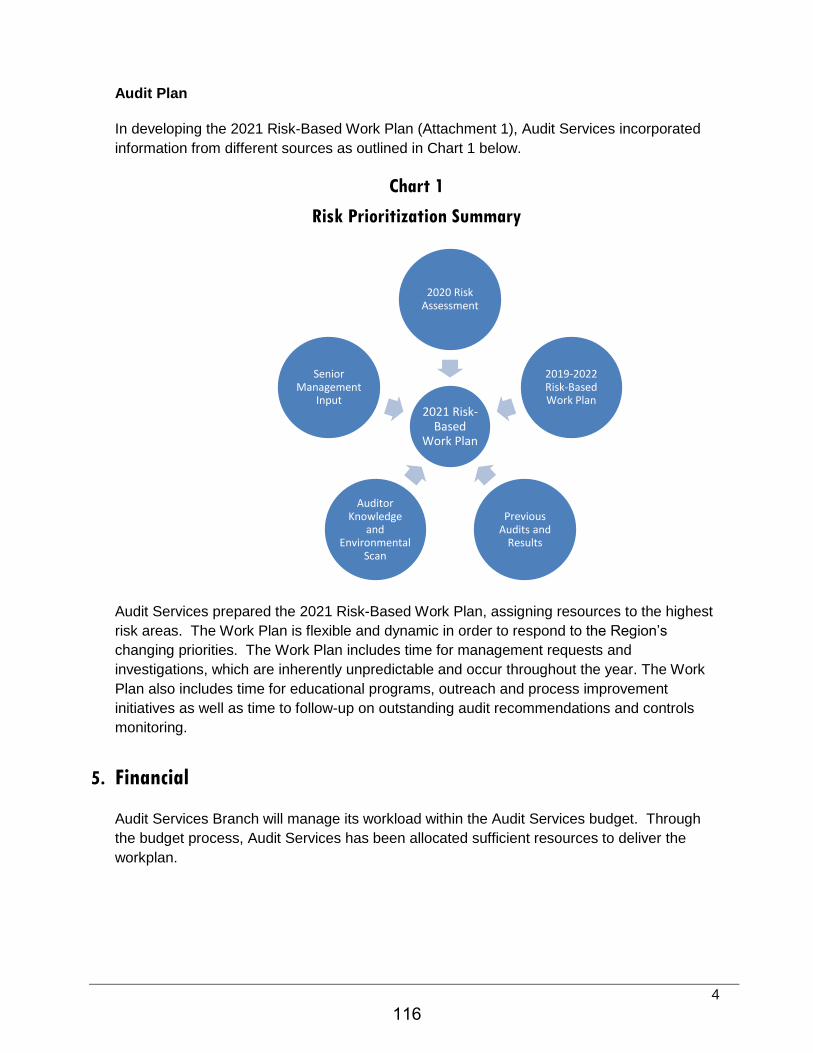

G.3. 2021 Risk Based Work Plan 113

Report dated November 27, 2020 from the Director of AuditServices recommending that:

Regional Council approve the Audit Services Branch's2021 Risk-Based Work Plan (Attachment 1).

1.

H. Other Business

I. Private Session

None

J. Adjournment

Agenda - Audit Committee - January 14, 2021

The Regional Municipality of York

Audit Planning Report for the year ending December 31, 2020

Licensed Public Accountants

November 2020

kpmg.ca/audi t

1

Audit Planning Report

Table of contents

EXECUTIVE SUMMARY 1

COVID-19: EMBEDDING RESILIENCE & READINESS 2

GROUP AUDIT SCOPE 4

AUDIT RISKS 5

MATERIALITY 11

AUDIT QUALITY AND TRANSPARENCY 13

CURRENT DEVELOPMENTS – ACCOUNTING 15

NEW AUDIT STANDARDS 19

APPENDICES 20

APPENDIX 1: REQUIRED COMMUNICATIONS 21

APPENDIX 2: USE OF TECHNOLOGY IN THE AUDIT 22

APPENDIX 3: KPMG’S AUDIT APPROACH AND METHODOLOGY 23

APPENDIX 4: LEAN IN AUDIT™ 24

APPENDIX 5: AUDIT AND ASSURANCE INSIGHTS 25

2

Audit Planning Report

KPMG contacts The contacts at KPMG in connection with this report are:

Kevin Travers

Lead Audit Engagement Partner

Tel: 416-228-7004 [email protected]

Nicole Hately

Audit Senior Manager

Tel: 416-549-7908 [email protected]

3

Audit Planning Report P a g e | 1

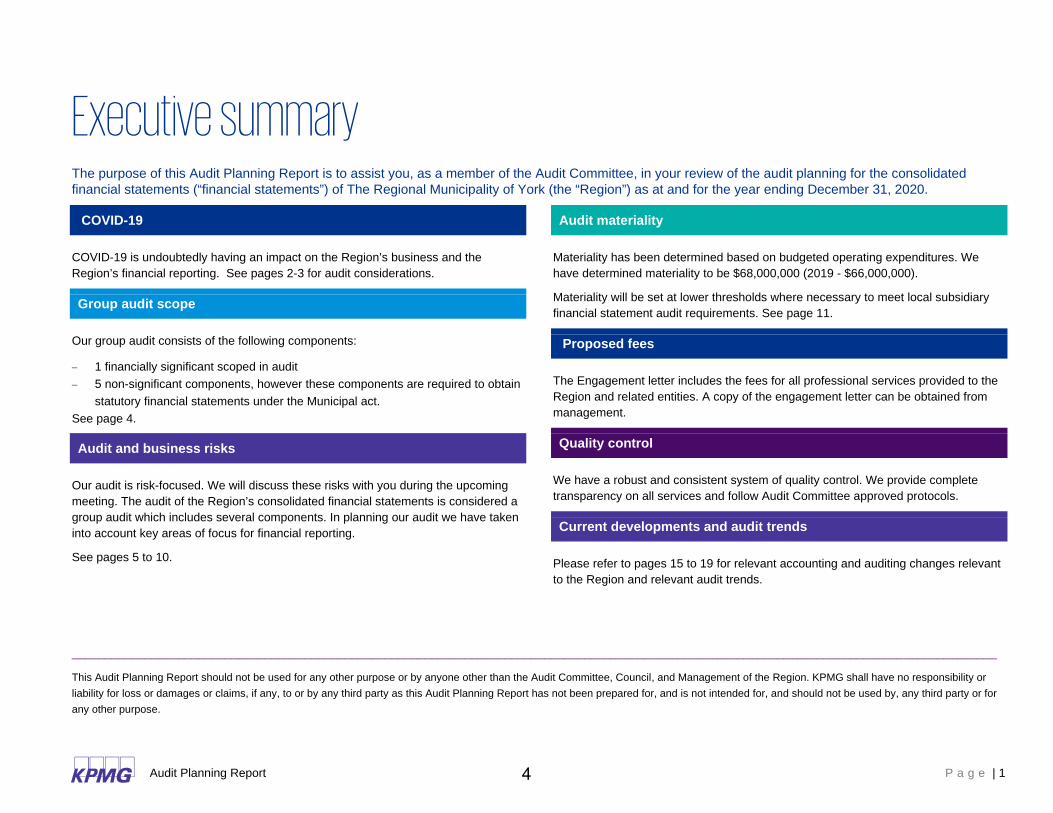

Executive summary The purpose of this Audit Planning Report is to assist you, as a member of the Audit Committee, in your review of the audit planning for the consolidated financial statements (“financial statements”) of The Regional Municipality of York (the “Region”) as at and for the year ending December 31, 2020.

COVID-19

COVID-19 is undoubtedly having an impact on the Region’s business and the Region’s financial reporting. See pages 2-3 for audit considerations.

Group audit scope

Our group audit consists of the following components:

− 1 financially significant scoped in audit − 5 non-significant components, however these components are required to obtain

statutory financial statements under the Municipal act. See page 4.

Audit and business risks

Our audit is risk-focused. We will discuss these risks with you during the upcoming meeting. The audit of the Region’s consolidated financial statements is considered a group audit which includes several components. In planning our audit we have taken into account key areas of focus for financial reporting.

See pages 5 to 10.

Audit materiality

Materiality has been determined based on budgeted operating expenditures. We have determined materiality to be $68,000,000 (2019 - $66,000,000).

Materiality will be set at lower thresholds where necessary to meet local subsidiary financial statement audit requirements. See page 11.

Proposed fees

The Engagement letter includes the fees for all professional services provided to the Region and related entities. A copy of the engagement letter can be obtained from management.

Quality control

We have a robust and consistent system of quality control. We provide complete transparency on all services and follow Audit Committee approved protocols.

Current developments and audit trends

Please refer to pages 15 to 19 for relevant accounting and auditing changes relevant to the Region and relevant audit trends.

___________________________________________________________________________________________________________________________________________

This Audit Planning Report should not be used for any other purpose or by anyone other than the Audit Committee, Council, and Management of the Region. KPMG shall have no responsibility or liability for loss or damages or claims, if any, to or by any third party as this Audit Planning Report has not been prepared for, and is not intended for, and should not be used by, any third party or for any other purpose.

4

P a g e | 2

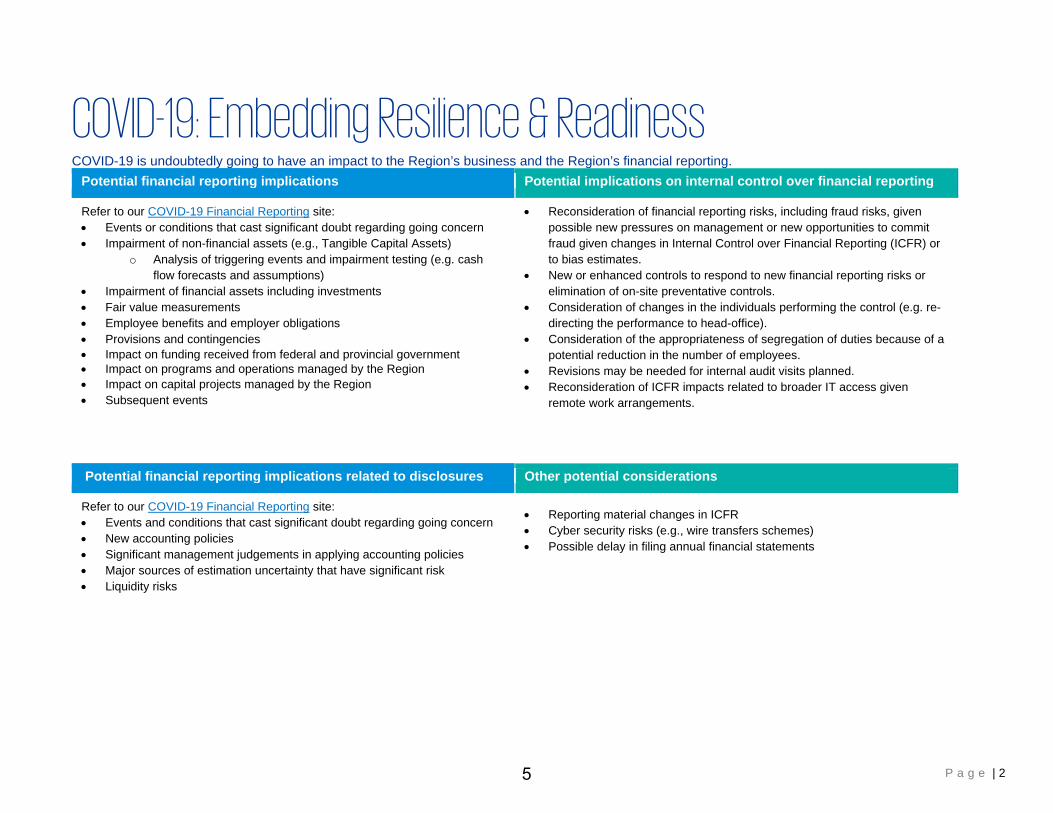

COVID-19: Embedding Resilience & Readiness COVID-19 is undoubtedly going to have an impact to the Region’s business and the Region’s financial reporting.

Potential financial reporting implications Potential implications on internal control over financial reporting

Refer to our COVID-19 Financial Reporting site: • Events or conditions that cast significant doubt regarding going concern • Impairment of non-financial assets (e.g., Tangible Capital Assets)

o Analysis of triggering events and impairment testing (e.g. cash flow forecasts and assumptions)

• Impairment of financial assets including investments • Fair value measurements • Employee benefits and employer obligations • Provisions and contingencies • Impact on funding received from federal and provincial government • Impact on programs and operations managed by the Region • Impact on capital projects managed by the Region • Subsequent events

• Reconsideration of financial reporting risks, including fraud risks, given possible new pressures on management or new opportunities to commit fraud given changes in Internal Control over Financial Reporting (ICFR) or to bias estimates.

• New or enhanced controls to respond to new financial reporting risks or elimination of on-site preventative controls.

• Consideration of changes in the individuals performing the control (e.g. re-directing the performance to head-office).

• Consideration of the appropriateness of segregation of duties because of a potential reduction in the number of employees.

• Revisions may be needed for internal audit visits planned. • Reconsideration of ICFR impacts related to broader IT access given

remote work arrangements.

Potential financial reporting implications related to disclosures Other potential considerations

Refer to our COVID-19 Financial Reporting site: • Events and conditions that cast significant doubt regarding going concern • New accounting policies • Significant management judgements in applying accounting policies • Major sources of estimation uncertainty that have significant risk • Liquidity risks

• Reporting material changes in ICFR • Cyber security risks (e.g., wire transfers schemes) • Possible delay in filing annual financial statements

5

P a g e | 3

COVID-19: Embedding Resilience & Readiness (Continued) Similarly, COVID-19 is a major consideration in the development of our audit plan for your 2020 financial statements

Potential audit implications

Planning and risk assessment:

• Understanding the expected impact on the relevant metrics for determining materiality (including the benchmark) and the implication of that in identifying the risks of material misstatement, responding to such risks and evaluating uncorrected misstatements.

• Understanding the potential financial reporting impacts, the changes in Region’s environment, and changes in the Region’s system of internal control, and their impact on our: o identified and assessed risks of material misstatement. o audit strategy, including the involvement of others (e.g., our internal

specialists or use of internal audit’s work or internal audit in a direct assistance capacity) and the nature, timing and extent of tests of controls and substantive procedures.

Executing:

• Remote auditing: o Increased use of other collaboration tools (Teams, Skype etc.) and the

need for written management acknowledgement for their use o Potential increased use of electronic evidence (and understanding the

Region’s processes to provide such evidence to us) • Timing of procedures may need to change:

o Tests of controls may need to be deferred (to allow the Region to put new or revised controls in operation and to be able to re-perform such controls).

6

P a g e | 4

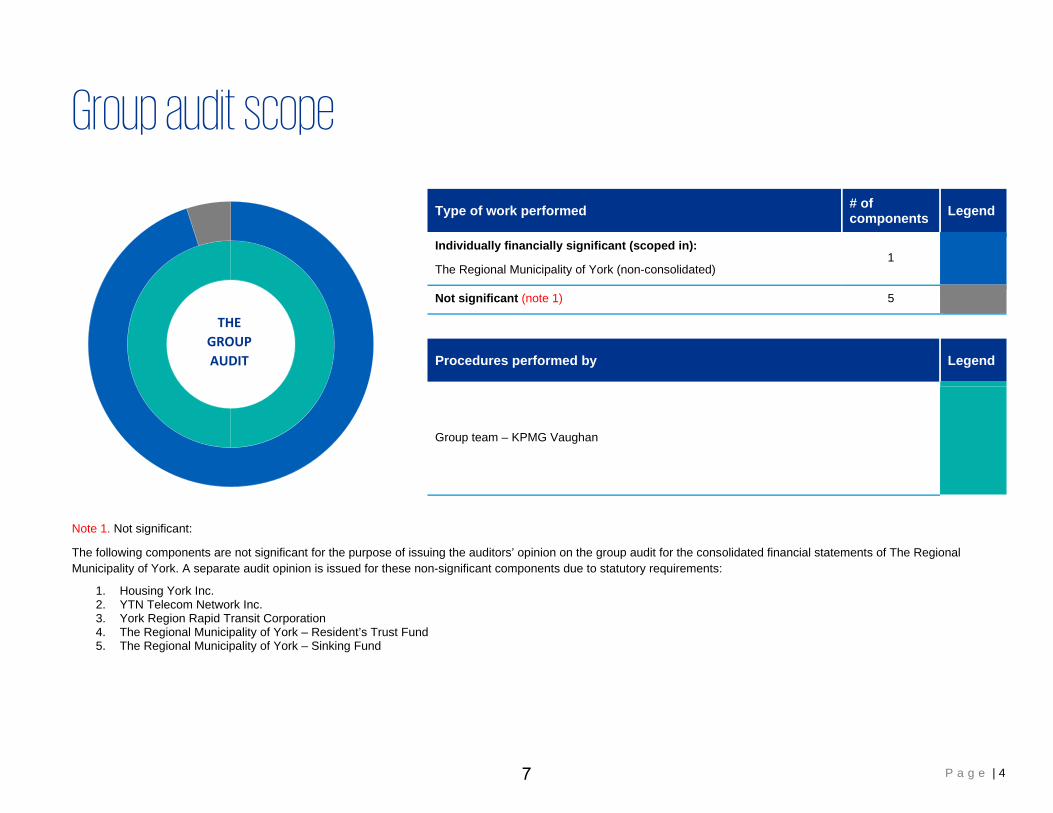

Group audit scope

Type of work performed # of components Legend

Individually financially significant (scoped in):

The Regional Municipality of York (non-consolidated) 1

Not significant (note 1) 5

Procedures performed by Legend

Group team – KPMG Vaughan

Note 1. Not significant:

The following components are not significant for the purpose of issuing the auditors’ opinion on the group audit for the consolidated financial statements of The Regional Municipality of York. A separate audit opinion is issued for these non-significant components due to statutory requirements:

1. Housing York Inc. 2. YTN Telecom Network Inc. 3. York Region Rapid Transit Corporation 4. The Regional Municipality of York – Resident’s Trust Fund 5. The Regional Municipality of York – Sinking Fund

THEGROUPAUDIT

7

P a g e | 5

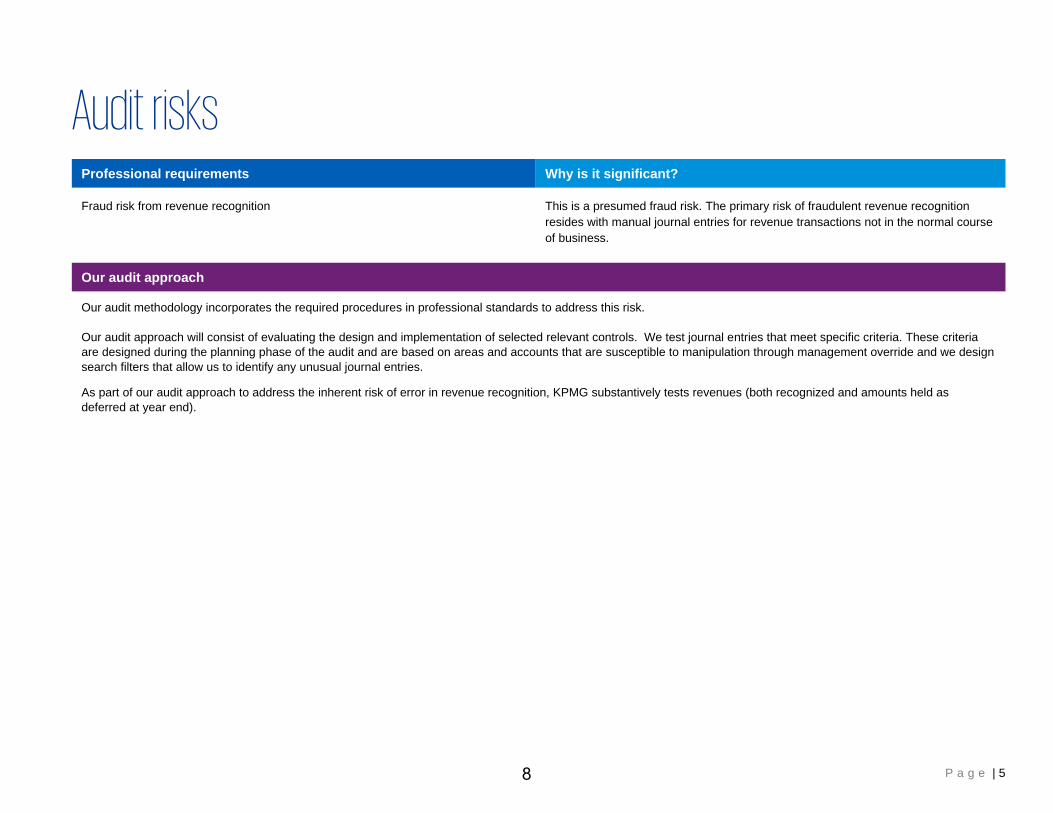

Audit risks Professional requirements Why is it significant?

Fraud risk from revenue recognition This is a presumed fraud risk. The primary risk of fraudulent revenue recognition resides with manual journal entries for revenue transactions not in the normal course of business.

Our audit approach

Our audit methodology incorporates the required procedures in professional standards to address this risk.

Our audit approach will consist of evaluating the design and implementation of selected relevant controls. We test journal entries that meet specific criteria. These criteria are designed during the planning phase of the audit and are based on areas and accounts that are susceptible to manipulation through management override and we design search filters that allow us to identify any unusual journal entries.

As part of our audit approach to address the inherent risk of error in revenue recognition, KPMG substantively tests revenues (both recognized and amounts held as deferred at year end).

8

P a g e | 6

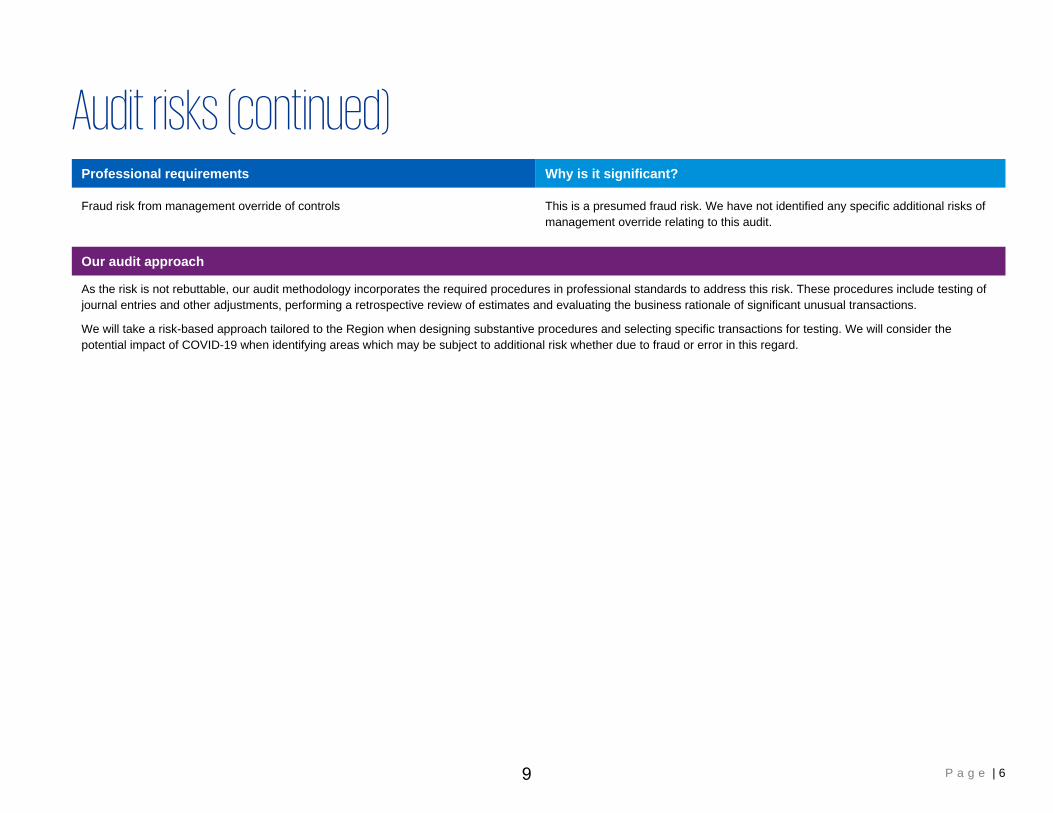

Audit risks (continued) Professional requirements Why is it significant?

Fraud risk from management override of controls This is a presumed fraud risk. We have not identified any specific additional risks of management override relating to this audit.

Our audit approach

As the risk is not rebuttable, our audit methodology incorporates the required procedures in professional standards to address this risk. These procedures include testing of journal entries and other adjustments, performing a retrospective review of estimates and evaluating the business rationale of significant unusual transactions.

We will take a risk-based approach tailored to the Region when designing substantive procedures and selecting specific transactions for testing. We will consider the potential impact of COVID-19 when identifying areas which may be subject to additional risk whether due to fraud or error in this regard.

9

P a g e | 7

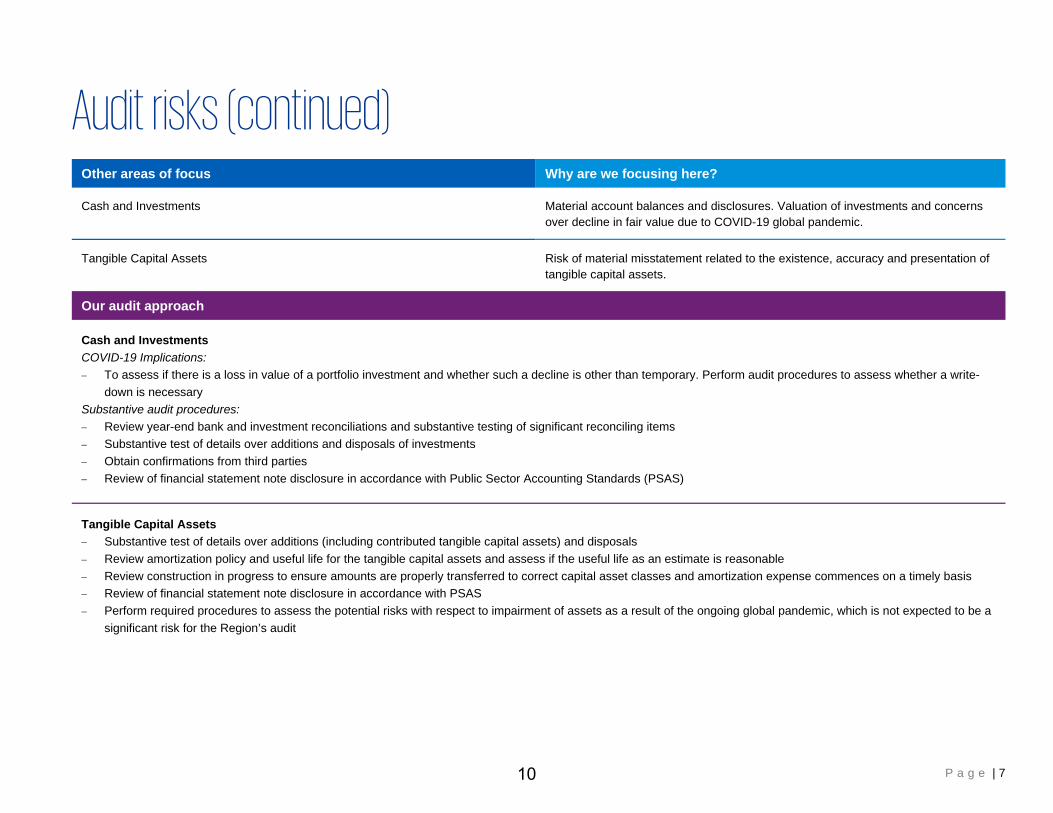

Audit risks (continued) Other areas of focus Why are we focusing here?

Cash and Investments Material account balances and disclosures. Valuation of investments and concerns over decline in fair value due to COVID-19 global pandemic.

Tangible Capital Assets Risk of material misstatement related to the existence, accuracy and presentation of tangible capital assets.

Our audit approach

Cash and Investments COVID-19 Implications: − To assess if there is a loss in value of a portfolio investment and whether such a decline is other than temporary. Perform audit procedures to assess whether a write-

down is necessary Substantive audit procedures: − Review year-end bank and investment reconciliations and substantive testing of significant reconciling items − Substantive test of details over additions and disposals of investments − Obtain confirmations from third parties − Review of financial statement note disclosure in accordance with Public Sector Accounting Standards (PSAS)

Tangible Capital Assets − Substantive test of details over additions (including contributed tangible capital assets) and disposals − Review amortization policy and useful life for the tangible capital assets and assess if the useful life as an estimate is reasonable − Review construction in progress to ensure amounts are properly transferred to correct capital asset classes and amortization expense commences on a timely basis − Review of financial statement note disclosure in accordance with PSAS − Perform required procedures to assess the potential risks with respect to impairment of assets as a result of the ongoing global pandemic, which is not expected to be a

significant risk for the Region’s audit

10

P a g e | 8

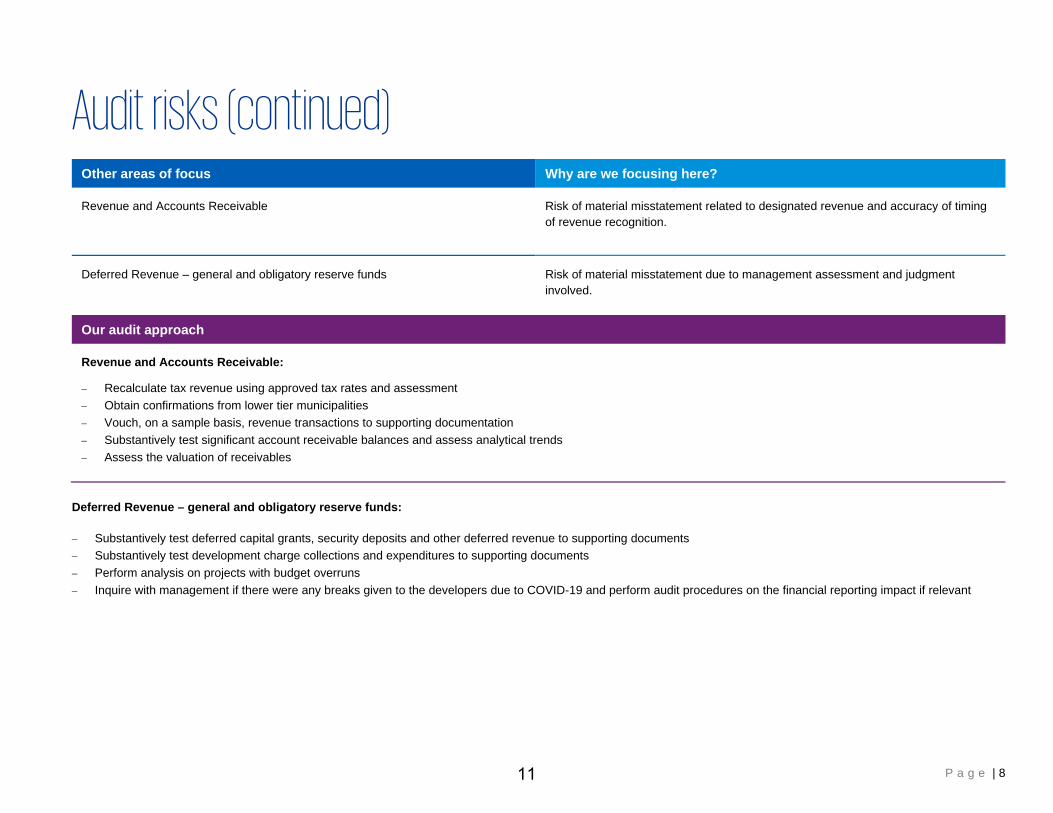

Audit risks (continued) Other areas of focus Why are we focusing here?

Revenue and Accounts Receivable

Risk of material misstatement related to designated revenue and accuracy of timing of revenue recognition.

Deferred Revenue – general and obligatory reserve funds Risk of material misstatement due to management assessment and judgment involved.

Our audit approach

Revenue and Accounts Receivable:

− Recalculate tax revenue using approved tax rates and assessment − Obtain confirmations from lower tier municipalities − Vouch, on a sample basis, revenue transactions to supporting documentation − Substantively test significant account receivable balances and assess analytical trends − Assess the valuation of receivables

Deferred Revenue – general and obligatory reserve funds: − Substantively test deferred capital grants, security deposits and other deferred revenue to supporting documents − Substantively test development charge collections and expenditures to supporting documents − Perform analysis on projects with budget overruns − Inquire with management if there were any breaks given to the developers due to COVID-19 and perform audit procedures on the financial reporting impact if relevant

11

P a g e | 9

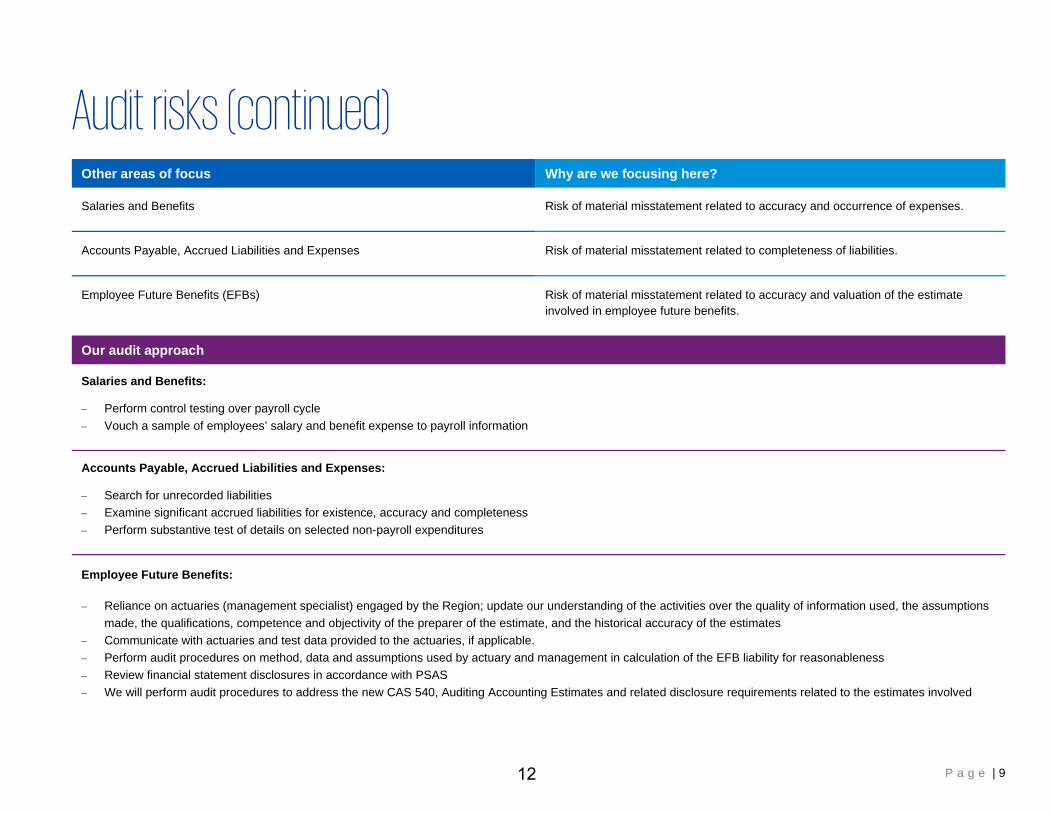

Audit risks (continued) Other areas of focus Why are we focusing here?

Salaries and Benefits Risk of material misstatement related to accuracy and occurrence of expenses.

Accounts Payable, Accrued Liabilities and Expenses Risk of material misstatement related to completeness of liabilities.

Employee Future Benefits (EFBs) Risk of material misstatement related to accuracy and valuation of the estimate involved in employee future benefits.

Our audit approach

Salaries and Benefits:

− Perform control testing over payroll cycle − Vouch a sample of employees’ salary and benefit expense to payroll information

Accounts Payable, Accrued Liabilities and Expenses:

− Search for unrecorded liabilities − Examine significant accrued liabilities for existence, accuracy and completeness − Perform substantive test of details on selected non-payroll expenditures

Employee Future Benefits: − Reliance on actuaries (management specialist) engaged by the Region; update our understanding of the activities over the quality of information used, the assumptions

made, the qualifications, competence and objectivity of the preparer of the estimate, and the historical accuracy of the estimates − Communicate with actuaries and test data provided to the actuaries, if applicable. − Perform audit procedures on method, data and assumptions used by actuary and management in calculation of the EFB liability for reasonableness − Review financial statement disclosures in accordance with PSAS − We will perform audit procedures to address the new CAS 540, Auditing Accounting Estimates and related disclosure requirements related to the estimates involved

12

P a g e | 10

Audit risks (continued) Other areas of focus Why are we focusing here?

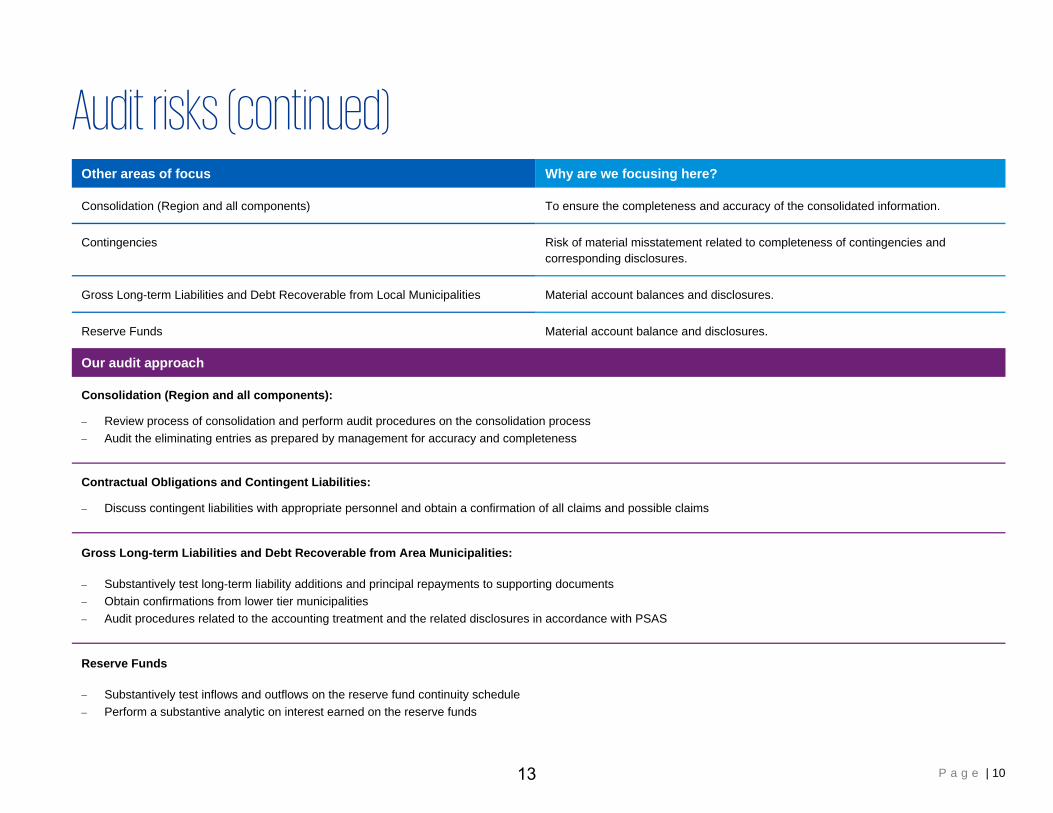

Consolidation (Region and all components) To ensure the completeness and accuracy of the consolidated information.

Contingencies Risk of material misstatement related to completeness of contingencies and corresponding disclosures.

Gross Long-term Liabilities and Debt Recoverable from Local Municipalities Material account balances and disclosures.

Reserve Funds Material account balance and disclosures.

Our audit approach

Consolidation (Region and all components):

− Review process of consolidation and perform audit procedures on the consolidation process − Audit the eliminating entries as prepared by management for accuracy and completeness

Contractual Obligations and Contingent Liabilities:

− Discuss contingent liabilities with appropriate personnel and obtain a confirmation of all claims and possible claims

Gross Long-term Liabilities and Debt Recoverable from Area Municipalities: − Substantively test long-term liability additions and principal repayments to supporting documents − Obtain confirmations from lower tier municipalities − Audit procedures related to the accounting treatment and the related disclosures in accordance with PSAS

Reserve Funds − Substantively test inflows and outflows on the reserve fund continuity schedule − Perform a substantive analytic on interest earned on the reserve funds

13

P a g e | 11

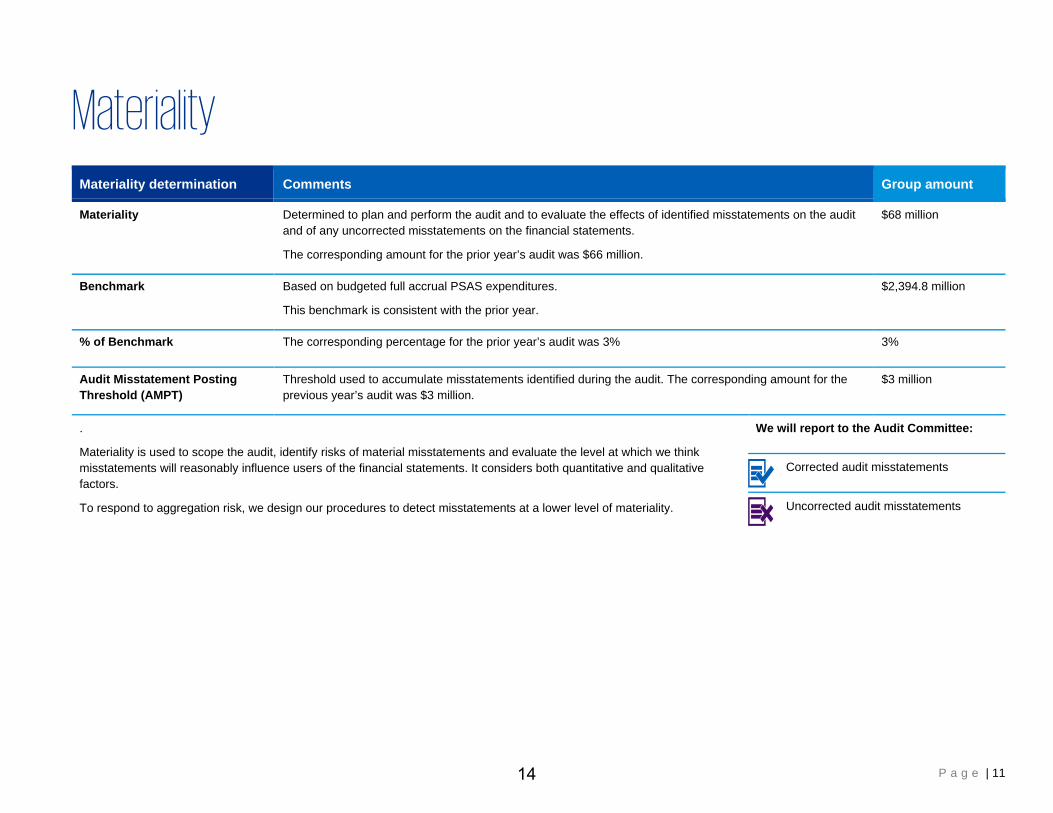

Materiality

Materiality determination Comments Group amount

Materiality Determined to plan and perform the audit and to evaluate the effects of identified misstatements on the audit and of any uncorrected misstatements on the financial statements.

The corresponding amount for the prior year’s audit was $66 million.

$68 million

Benchmark Based on budgeted full accrual PSAS expenditures.

This benchmark is consistent with the prior year.

$2,394.8 million

% of Benchmark The corresponding percentage for the prior year’s audit was 3% 3%

Audit Misstatement Posting Threshold (AMPT)

Threshold used to accumulate misstatements identified during the audit. The corresponding amount for the previous year’s audit was $3 million.

$3 million

.

Materiality is used to scope the audit, identify risks of material misstatements and evaluate the level at which we think misstatements will reasonably influence users of the financial statements. It considers both quantitative and qualitative factors.

To respond to aggregation risk, we design our procedures to detect misstatements at a lower level of materiality.

We will report to the Audit Committee:

Corrected audit misstatements

Uncorrected audit misstatements

14

P a g e | 12

Audit Quality Matters

15

Audit Planning Report P a g e | 13

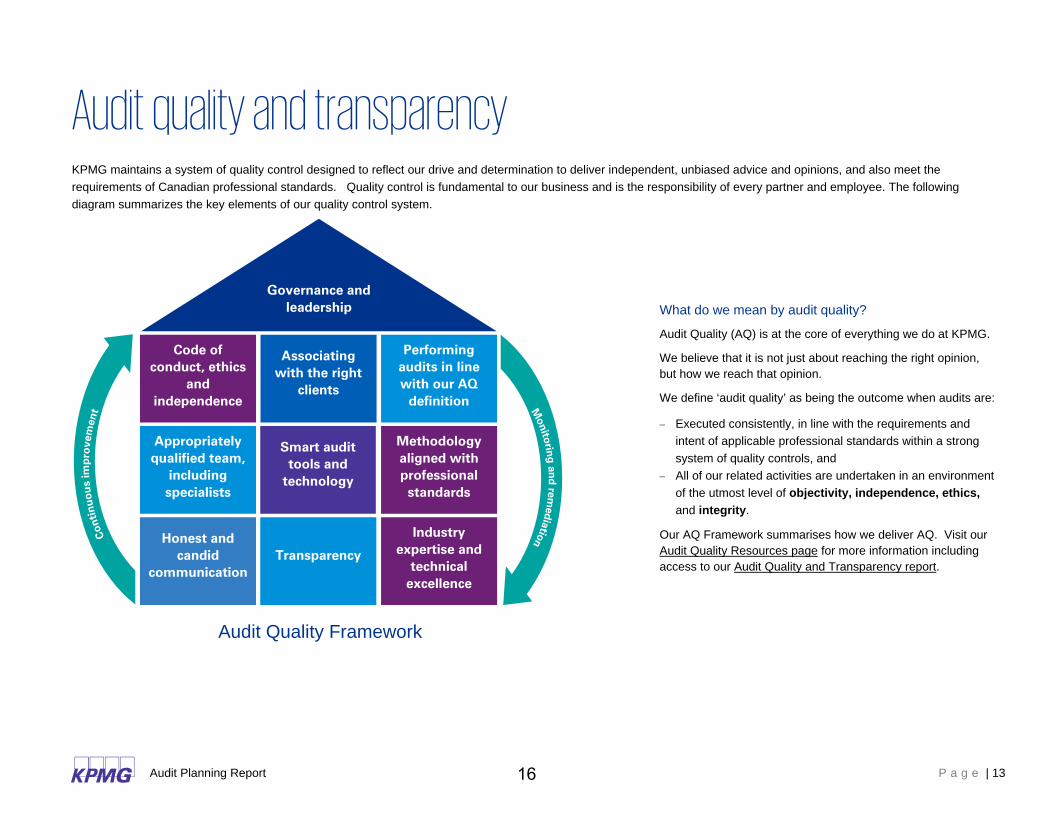

Audit quality and transparency KPMG maintains a system of quality control designed to reflect our drive and determination to deliver independent, unbiased advice and opinions, and also meet the requirements of Canadian professional standards. Quality control is fundamental to our business and is the responsibility of every partner and employee. The following diagram summarizes the key elements of our quality control system.

What do we mean by audit quality?

Audit Quality (AQ) is at the core of everything we do at KPMG.

We believe that it is not just about reaching the right opinion, but how we reach that opinion.

We define ‘audit quality’ as being the outcome when audits are:

− Executed consistently, in line with the requirements and intent of applicable professional standards within a strong system of quality controls, and

− All of our related activities are undertaken in an environment of the utmost level of objectivity, independence, ethics, and integrity.

Our AQ Framework summarises how we deliver AQ. Visit our Audit Quality Resources page for more information including access to our Audit Quality and Transparency report.

Audit Quality Framework

Governance and leadership

Code of conduct, ethics

and independence

Associating with the right

clients

Performing audits in line with our AQ

definition

Appropriately qualified team,

including specialists

Smart audit tools and

technology

Methodology aligned with professional

standards

Honest and candid

communication Transparency

Industry expertise and

technical excellence

16

Audit Planning Report P a g e | 14

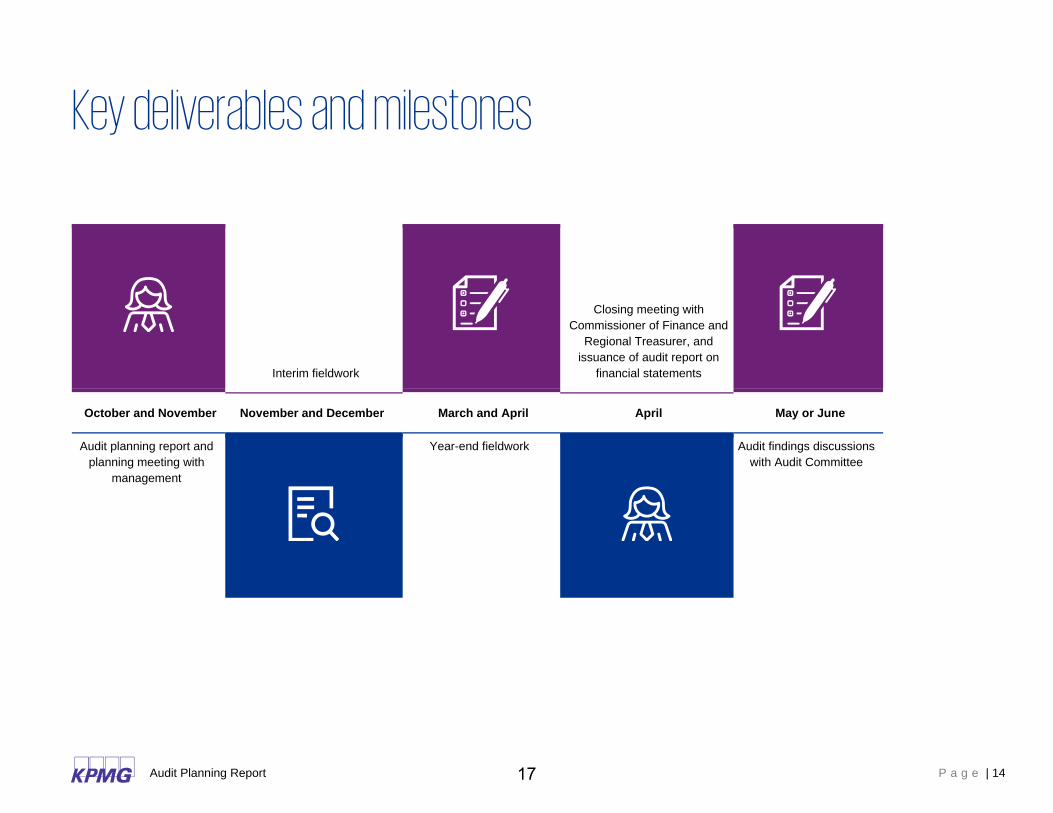

Key deliverables and milestones

Interim fieldwork

Closing meeting with

Commissioner of Finance and Regional Treasurer, and

issuance of audit report on financial statements

October and November November and December March and April April May or June

Audit planning report and planning meeting with

management

Year-end fieldwork

Audit findings discussions with Audit Committee

17

Audit Planning Report P a g e | 15

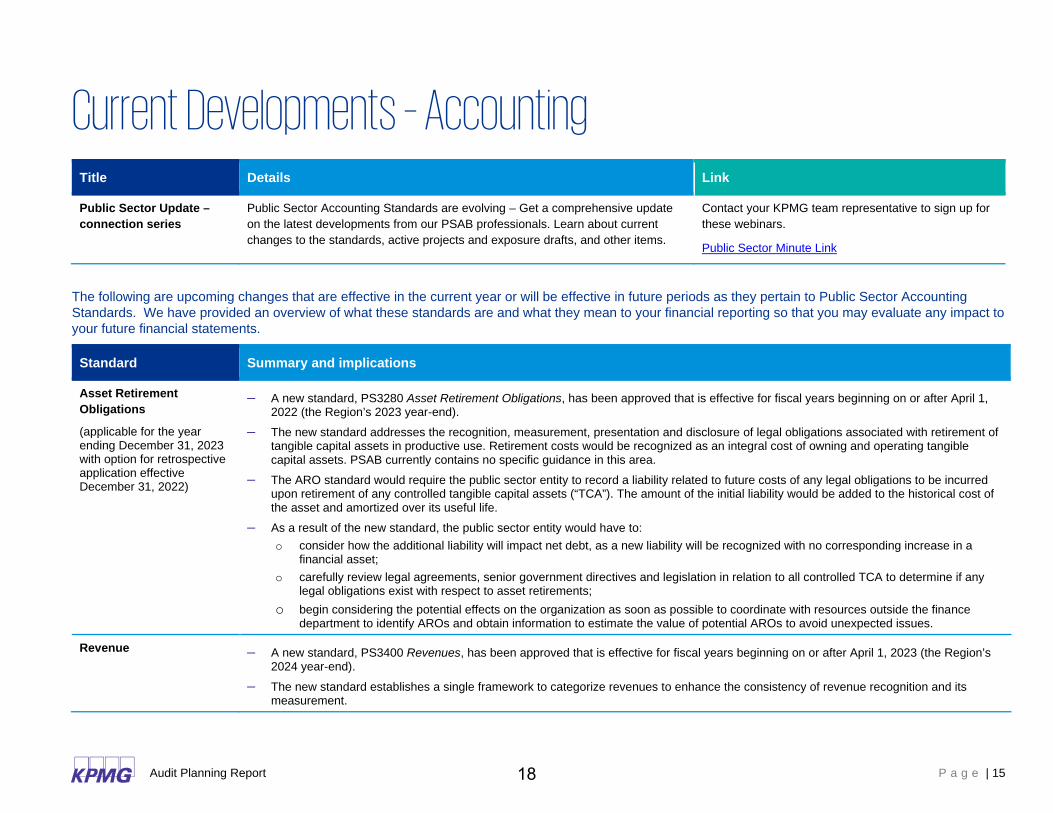

Current Developments – Accounting Title Details Link

Public Sector Update – connection series

Public Sector Accounting Standards are evolving – Get a comprehensive update on the latest developments from our PSAB professionals. Learn about current changes to the standards, active projects and exposure drafts, and other items.

Contact your KPMG team representative to sign up for these webinars.

Public Sector Minute Link

The following are upcoming changes that are effective in the current year or will be effective in future periods as they pertain to Public Sector Accounting Standards. We have provided an overview of what these standards are and what they mean to your financial reporting so that you may evaluate any impact to your future financial statements.

Standard Summary and implications

Asset Retirement Obligations

(applicable for the year ending December 31, 2023 with option for retrospective application effective December 31, 2022)

– A new standard, PS3280 Asset Retirement Obligations, has been approved that is effective for fiscal years beginning on or after April 1, 2022 (the Region’s 2023 year-end).

– The new standard addresses the recognition, measurement, presentation and disclosure of legal obligations associated with retirement of tangible capital assets in productive use. Retirement costs would be recognized as an integral cost of owning and operating tangible capital assets. PSAB currently contains no specific guidance in this area.

– The ARO standard would require the public sector entity to record a liability related to future costs of any legal obligations to be incurred upon retirement of any controlled tangible capital assets (“TCA”). The amount of the initial liability would be added to the historical cost of the asset and amortized over its useful life.

– As a result of the new standard, the public sector entity would have to: o consider how the additional liability will impact net debt, as a new liability will be recognized with no corresponding increase in a

financial asset; o carefully review legal agreements, senior government directives and legislation in relation to all controlled TCA to determine if any

legal obligations exist with respect to asset retirements; o begin considering the potential effects on the organization as soon as possible to coordinate with resources outside the finance

department to identify AROs and obtain information to estimate the value of potential AROs to avoid unexpected issues.

Revenue – A new standard, PS3400 Revenues, has been approved that is effective for fiscal years beginning on or after April 1, 2023 (the Region’s 2024 year-end).

– The new standard establishes a single framework to categorize revenues to enhance the consistency of revenue recognition and its measurement.

18

Audit Planning Report P a g e | 16

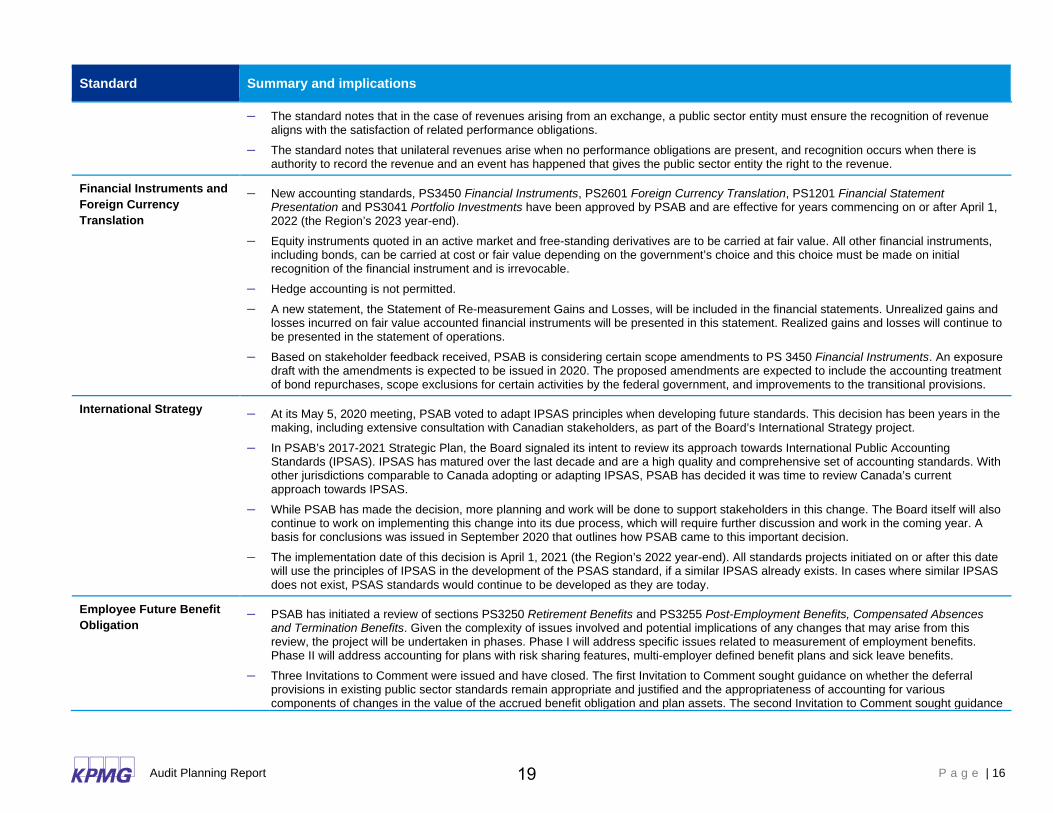

Standard Summary and implications

– The standard notes that in the case of revenues arising from an exchange, a public sector entity must ensure the recognition of revenue aligns with the satisfaction of related performance obligations.

– The standard notes that unilateral revenues arise when no performance obligations are present, and recognition occurs when there is authority to record the revenue and an event has happened that gives the public sector entity the right to the revenue.

Financial Instruments and Foreign Currency Translation

– New accounting standards, PS3450 Financial Instruments, PS2601 Foreign Currency Translation, PS1201 Financial Statement Presentation and PS3041 Portfolio Investments have been approved by PSAB and are effective for years commencing on or after April 1, 2022 (the Region’s 2023 year-end).

– Equity instruments quoted in an active market and free-standing derivatives are to be carried at fair value. All other financial instruments, including bonds, can be carried at cost or fair value depending on the government’s choice and this choice must be made on initial recognition of the financial instrument and is irrevocable.

– Hedge accounting is not permitted. – A new statement, the Statement of Re-measurement Gains and Losses, will be included in the financial statements. Unrealized gains and

losses incurred on fair value accounted financial instruments will be presented in this statement. Realized gains and losses will continue to be presented in the statement of operations.

– Based on stakeholder feedback received, PSAB is considering certain scope amendments to PS 3450 Financial Instruments. An exposure draft with the amendments is expected to be issued in 2020. The proposed amendments are expected to include the accounting treatment of bond repurchases, scope exclusions for certain activities by the federal government, and improvements to the transitional provisions.

International Strategy – At its May 5, 2020 meeting, PSAB voted to adapt IPSAS principles when developing future standards. This decision has been years in the making, including extensive consultation with Canadian stakeholders, as part of the Board’s International Strategy project.

– In PSAB’s 2017-2021 Strategic Plan, the Board signaled its intent to review its approach towards International Public Accounting Standards (IPSAS). IPSAS has matured over the last decade and are a high quality and comprehensive set of accounting standards. With other jurisdictions comparable to Canada adopting or adapting IPSAS, PSAB has decided it was time to review Canada’s current approach towards IPSAS.

– While PSAB has made the decision, more planning and work will be done to support stakeholders in this change. The Board itself will also continue to work on implementing this change into its due process, which will require further discussion and work in the coming year. A basis for conclusions was issued in September 2020 that outlines how PSAB came to this important decision.

– The implementation date of this decision is April 1, 2021 (the Region’s 2022 year-end). All standards projects initiated on or after this date will use the principles of IPSAS in the development of the PSAS standard, if a similar IPSAS already exists. In cases where similar IPSAS does not exist, PSAS standards would continue to be developed as they are today.

Employee Future Benefit Obligation

– PSAB has initiated a review of sections PS3250 Retirement Benefits and PS3255 Post-Employment Benefits, Compensated Absences and Termination Benefits. Given the complexity of issues involved and potential implications of any changes that may arise from this review, the project will be undertaken in phases. Phase I will address specific issues related to measurement of employment benefits. Phase II will address accounting for plans with risk sharing features, multi-employer defined benefit plans and sick leave benefits.

– Three Invitations to Comment were issued and have closed. The first Invitation to Comment sought guidance on whether the deferral provisions in existing public sector standards remain appropriate and justified and the appropriateness of accounting for various components of changes in the value of the accrued benefit obligation and plan assets. The second Invitation to Comment sought guidance

19

Audit Planning Report P a g e | 17

Standard Summary and implications

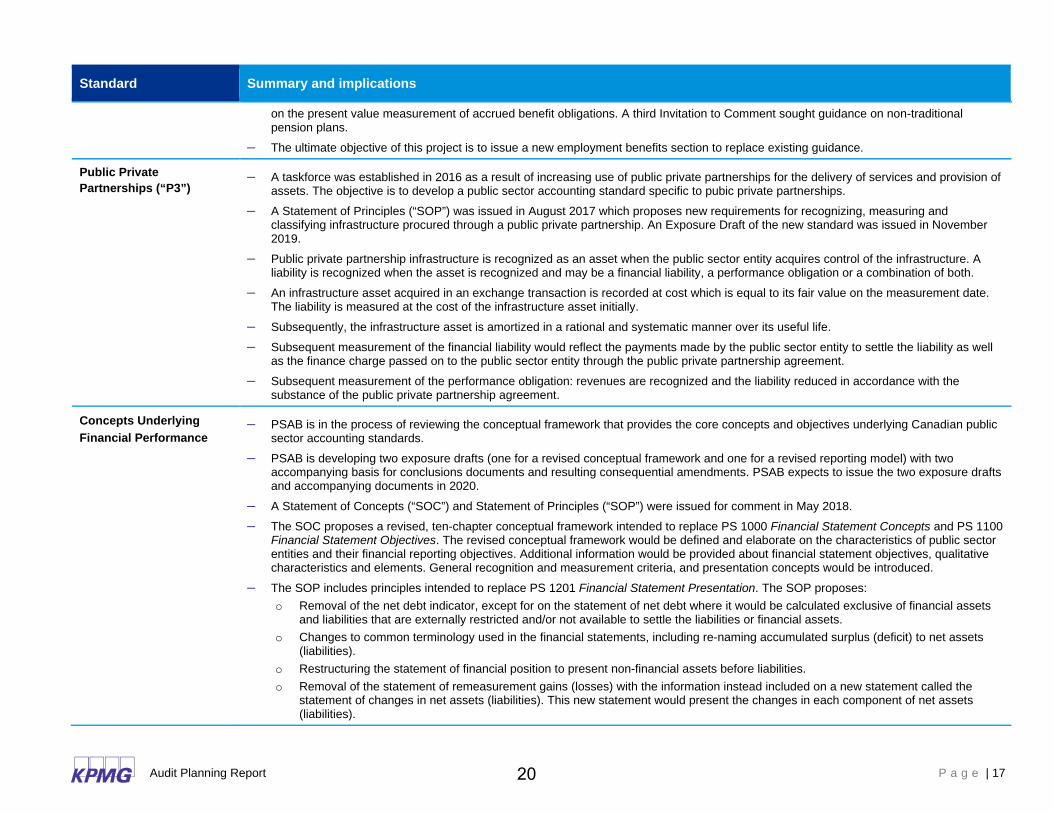

on the present value measurement of accrued benefit obligations. A third Invitation to Comment sought guidance on non-traditional pension plans.

– The ultimate objective of this project is to issue a new employment benefits section to replace existing guidance.

Public Private Partnerships (“P3”)

– A taskforce was established in 2016 as a result of increasing use of public private partnerships for the delivery of services and provision of assets. The objective is to develop a public sector accounting standard specific to pubic private partnerships.

– A Statement of Principles (“SOP”) was issued in August 2017 which proposes new requirements for recognizing, measuring and classifying infrastructure procured through a public private partnership. An Exposure Draft of the new standard was issued in November 2019.

– Public private partnership infrastructure is recognized as an asset when the public sector entity acquires control of the infrastructure. A liability is recognized when the asset is recognized and may be a financial liability, a performance obligation or a combination of both.

– An infrastructure asset acquired in an exchange transaction is recorded at cost which is equal to its fair value on the measurement date. The liability is measured at the cost of the infrastructure asset initially.

– Subsequently, the infrastructure asset is amortized in a rational and systematic manner over its useful life. – Subsequent measurement of the financial liability would reflect the payments made by the public sector entity to settle the liability as well

as the finance charge passed on to the public sector entity through the public private partnership agreement. – Subsequent measurement of the performance obligation: revenues are recognized and the liability reduced in accordance with the

substance of the public private partnership agreement.

Concepts Underlying Financial Performance

– PSAB is in the process of reviewing the conceptual framework that provides the core concepts and objectives underlying Canadian public sector accounting standards.

– PSAB is developing two exposure drafts (one for a revised conceptual framework and one for a revised reporting model) with two accompanying basis for conclusions documents and resulting consequential amendments. PSAB expects to issue the two exposure drafts and accompanying documents in 2020.

– A Statement of Concepts (“SOC”) and Statement of Principles (“SOP”) were issued for comment in May 2018. – The SOC proposes a revised, ten-chapter conceptual framework intended to replace PS 1000 Financial Statement Concepts and PS 1100

Financial Statement Objectives. The revised conceptual framework would be defined and elaborate on the characteristics of public sector entities and their financial reporting objectives. Additional information would be provided about financial statement objectives, qualitative characteristics and elements. General recognition and measurement criteria, and presentation concepts would be introduced.

– The SOP includes principles intended to replace PS 1201 Financial Statement Presentation. The SOP proposes: o Removal of the net debt indicator, except for on the statement of net debt where it would be calculated exclusive of financial assets

and liabilities that are externally restricted and/or not available to settle the liabilities or financial assets. o Changes to common terminology used in the financial statements, including re-naming accumulated surplus (deficit) to net assets

(liabilities). o Restructuring the statement of financial position to present non-financial assets before liabilities. o Removal of the statement of remeasurement gains (losses) with the information instead included on a new statement called the

statement of changes in net assets (liabilities). This new statement would present the changes in each component of net assets (liabilities).

20

Audit Planning Report P a g e | 18

Standard Summary and implications

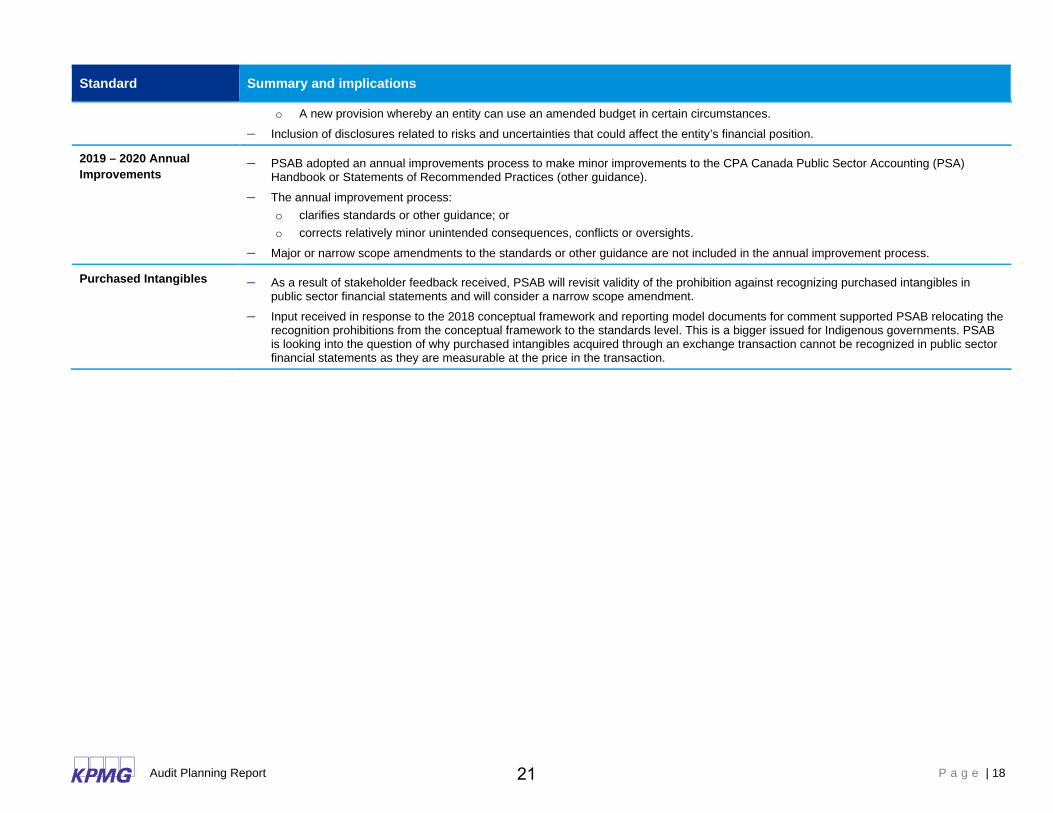

o A new provision whereby an entity can use an amended budget in certain circumstances. – Inclusion of disclosures related to risks and uncertainties that could affect the entity’s financial position.

2019 – 2020 Annual Improvements

– PSAB adopted an annual improvements process to make minor improvements to the CPA Canada Public Sector Accounting (PSA) Handbook or Statements of Recommended Practices (other guidance).

– The annual improvement process: o clarifies standards or other guidance; or o corrects relatively minor unintended consequences, conflicts or oversights.

– Major or narrow scope amendments to the standards or other guidance are not included in the annual improvement process.

Purchased Intangibles – As a result of stakeholder feedback received, PSAB will revisit validity of the prohibition against recognizing purchased intangibles in public sector financial statements and will consider a narrow scope amendment.

– Input received in response to the 2018 conceptual framework and reporting model documents for comment supported PSAB relocating the recognition prohibitions from the conceptual framework to the standards level. This is a bigger issued for Indigenous governments. PSAB is looking into the question of why purchased intangibles acquired through an exchange transaction cannot be recognized in public sector financial statements as they are measurable at the price in the transaction.

21

Audit Planning Report P a g e | 19

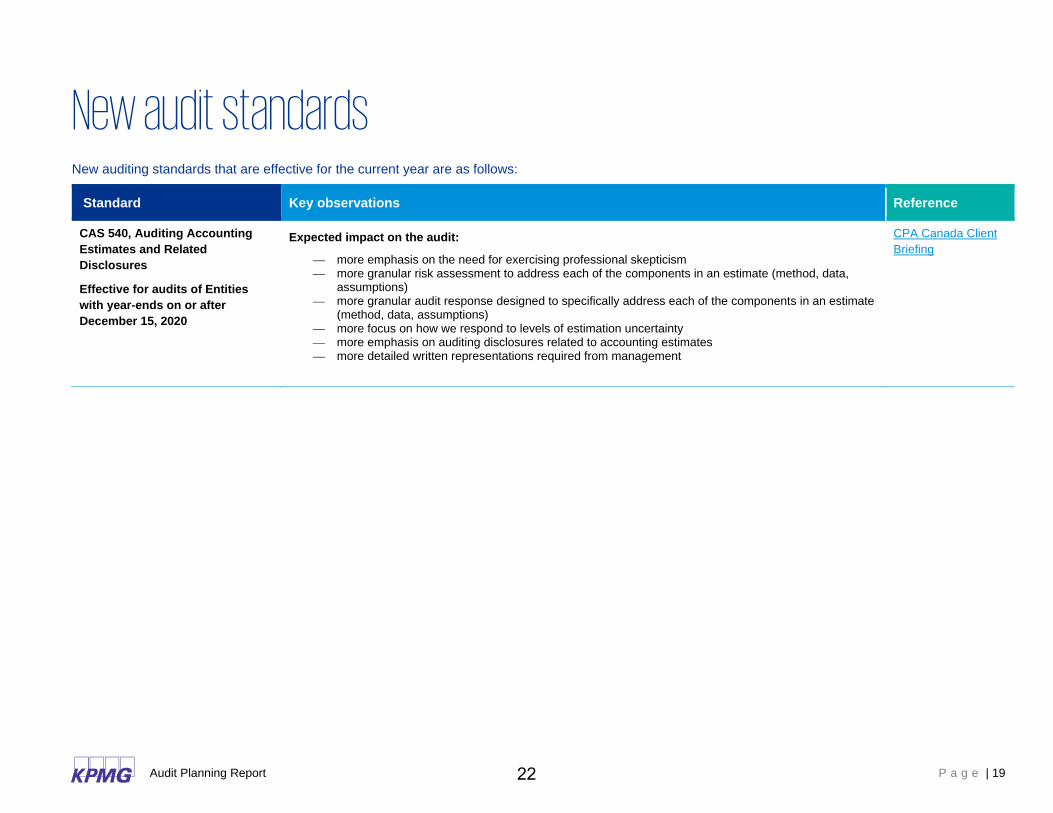

New audit standards New auditing standards that are effective for the current year are as follows:

Standard Key observations Reference

CAS 540, Auditing Accounting Estimates and Related Disclosures

Effective for audits of Entities with year-ends on or after December 15, 2020

Expected impact on the audit:

— more emphasis on the need for exercising professional skepticism — more granular risk assessment to address each of the components in an estimate (method, data,

assumptions) — more granular audit response designed to specifically address each of the components in an estimate

(method, data, assumptions) — more focus on how we respond to levels of estimation uncertainty — more emphasis on auditing disclosures related to accounting estimates — more detailed written representations required from management

CPA Canada Client Briefing

22

Appendices Content Appendix 1: Required communications

Appendix 2: Key Audit Matters

Appendix 3: Use of technology in the audit

Appendix 4: KPMG’s audit approach and methodology

Appendix 5: Lean in Audit™

Appendix 6: Audit and Assurance Insights

23

Audit Planning Report P a g e | 21

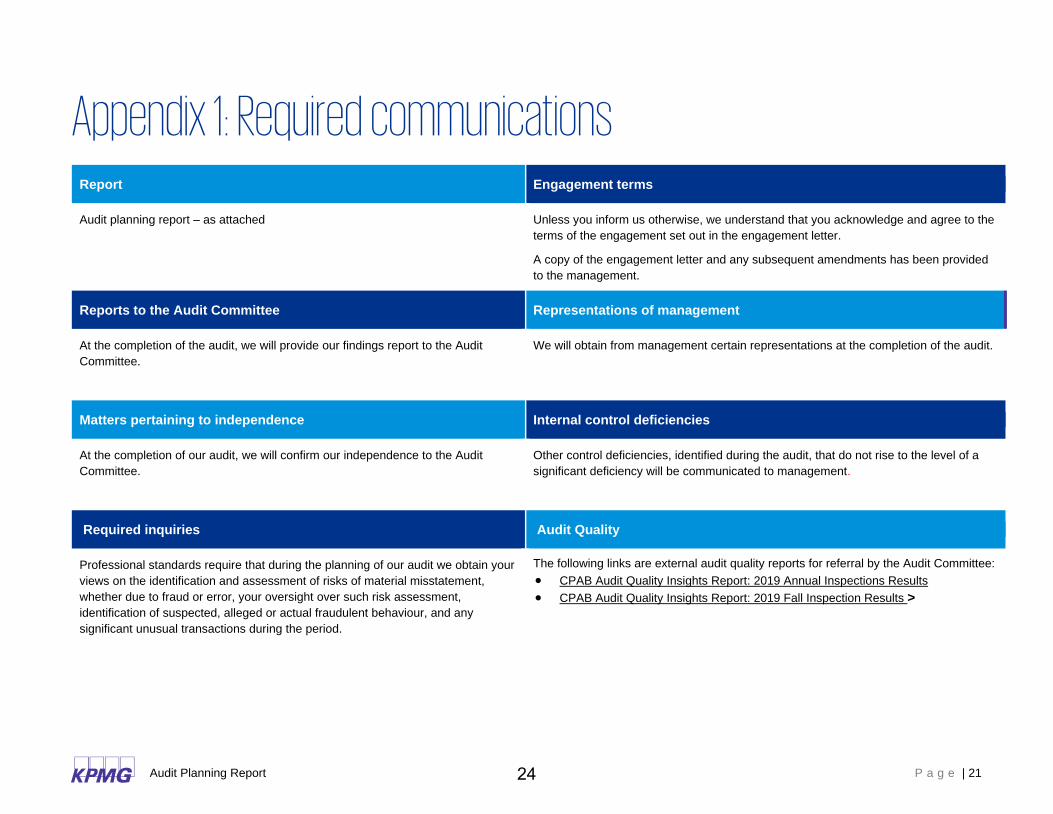

Appendix 1: Required communications Report Engagement terms

Audit planning report – as attached

Unless you inform us otherwise, we understand that you acknowledge and agree to the terms of the engagement set out in the engagement letter.

A copy of the engagement letter and any subsequent amendments has been provided to the management.

Reports to the Audit Committee Representations of management

At the completion of the audit, we will provide our findings report to the Audit Committee.

We will obtain from management certain representations at the completion of the audit.

Matters pertaining to independence Internal control deficiencies

At the completion of our audit, we will confirm our independence to the Audit Committee.

Other control deficiencies, identified during the audit, that do not rise to the level of a significant deficiency will be communicated to management.

Required inquiries Audit Quality

Professional standards require that during the planning of our audit we obtain your views on the identification and assessment of risks of material misstatement, whether due to fraud or error, your oversight over such risk assessment, identification of suspected, alleged or actual fraudulent behaviour, and any significant unusual transactions during the period.

The following links are external audit quality reports for referral by the Audit Committee: • CPAB Audit Quality Insights Report: 2019 Annual Inspections Results • CPAB Audit Quality Insights Report: 2019 Fall Inspection Results >

24

Audit Planning Report P a g e | 22

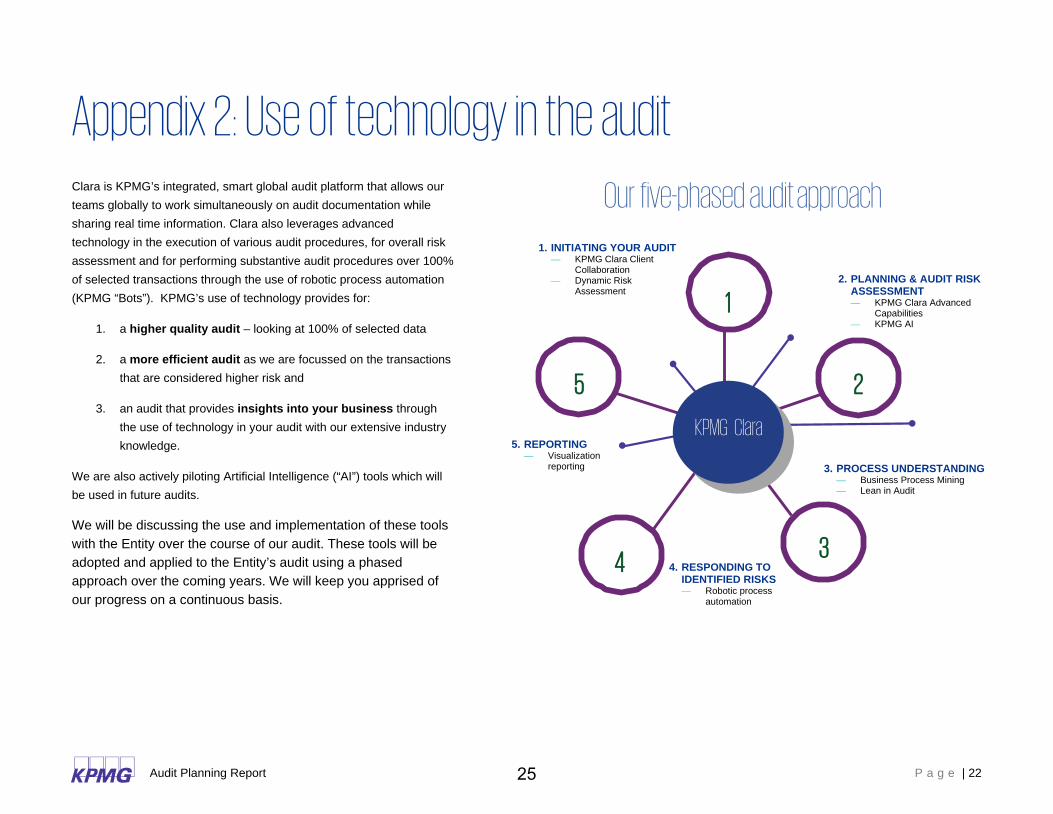

Appendix 2: Use of technology in the audit

Clara is KPMG’s integrated, smart global audit platform that allows our teams globally to work simultaneously on audit documentation while sharing real time information. Clara also leverages advanced technology in the execution of various audit procedures, for overall risk assessment and for performing substantive audit procedures over 100% of selected transactions through the use of robotic process automation (KPMG “Bots”). KPMG’s use of technology provides for:

1. a higher quality audit – looking at 100% of selected data

2. a more efficient audit as we are focussed on the transactions that are considered higher risk and

3. an audit that provides insights into your business through the use of technology in your audit with our extensive industry knowledge.

We are also actively piloting Artificial Intelligence (“AI”) tools which will be used in future audits.

We will be discussing the use and implementation of these tools with the Entity over the course of our audit. These tools will be adopted and applied to the Entity’s audit using a phased approach over the coming years. We will keep you apprised of our progress on a continuous basis.

1. INITIATING YOUR AUDIT — KPMG Clara Client

Collaboration — Dynamic Risk

Assessment

2. PLANNING & AUDIT RISK ASSESSMENT — KPMG Clara Advanced

Capabilities — KPMG AI

3. PROCESS UNDERSTANDING — Business Process Mining — Lean in Audit

4. RESPONDING TO IDENTIFIED RISKS — Robotic process

automation

5. REPORTING — Visualization

reporting

Our five-phased audit approach

KPMG Clara

1

2

3 4

5

25

Audit Planning Report P a g e | 23

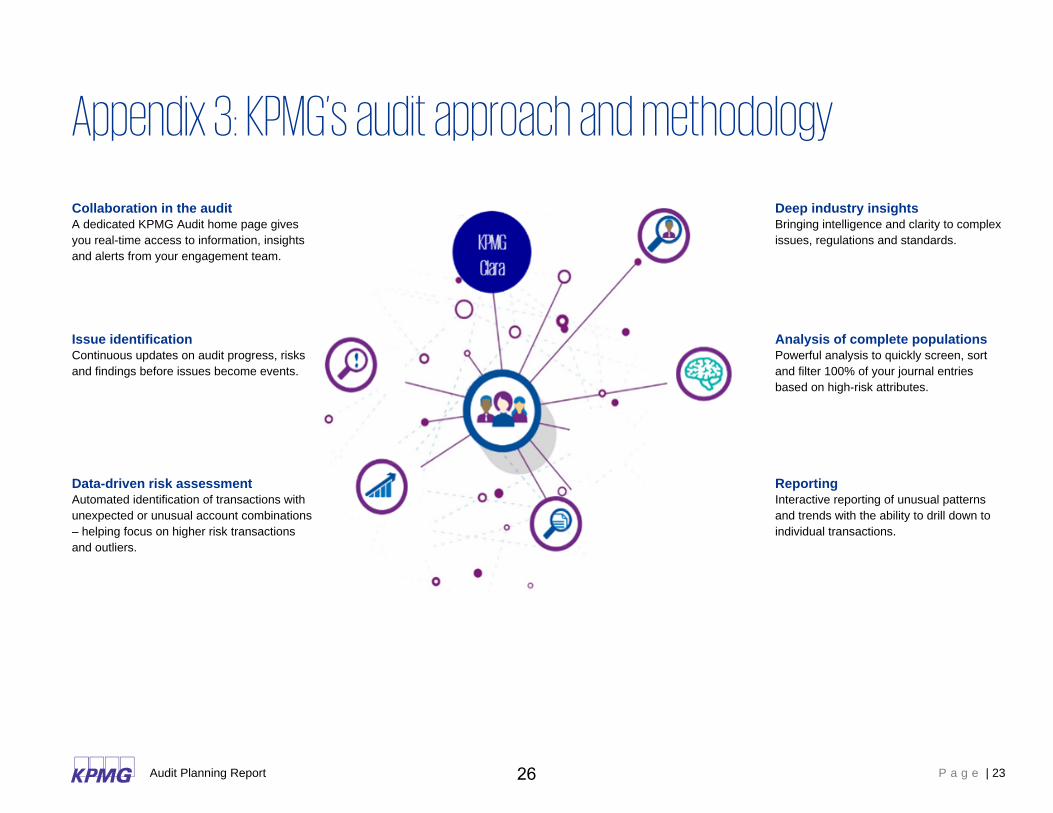

Appendix 3: KPMG’s audit approach and methodology

Collaboration in the audit A dedicated KPMG Audit home page gives you real-time access to information, insights and alerts from your engagement team.

Deep industry insights Bringing intelligence and clarity to complex issues, regulations and standards.

Issue identification Continuous updates on audit progress, risks and findings before issues become events.

Analysis of complete populations Powerful analysis to quickly screen, sort and filter 100% of your journal entries based on high-risk attributes.

Data-driven risk assessment Automated identification of transactions with unexpected or unusual account combinations – helping focus on higher risk transactions and outliers.

Reporting Interactive reporting of unusual patterns and trends with the ability to drill down to individual transactions.

26

Audit Planning Report P a g e | 24

Appendix 4: Lean in Audit™ An innovative approach leading to enhanced value and quality How it works

Our innovative audit approach, Lean in Audit, further improves audit value and productivity to help deliver real insight to you. Lean in Audit is process oriented, directly engaging organizational stakeholders and employing hands-on tools, such as walkthroughs and flowcharts of actual financial processes.

By embedding Lean techniques into our core audit delivery process, our teams are able to enhance their understanding of the business processes and control environment within your organization – allowing us to provide actionable quality and productivity improvement observations.

Any insights gathered through the course of the audit will be available to both engagement teams and management. For example, we may identify control gaps and potential process improvement areas, while management has the opportunity to apply such insights to streamline processes, inform business decisions, improve compliance, lower costs, increase productivity, strengthen customer service and satisfaction and drive overall performance.

We will be discussing the use of this of tool with management over the coming months to understand management’s assessment and appetite for the use of this tool for current and future periods.

Lean in Audit employs three key Lean techniques:

1. Lean training

Provide basic Lean training and equip our teams with a new Lean mindset to improve quality, value and productivity.

2. Interactive workshops

Perform interactive workshops to conduct walkthroughs of selected financial processes providing end-to-end transparency and understanding of process and control quality and effectiveness.

3. Insight reporting

Quick and pragmatic insight report including immediate quick win actions and prioritized opportunities to realize benefit.

27

Audit Planning Report P a g e | 25

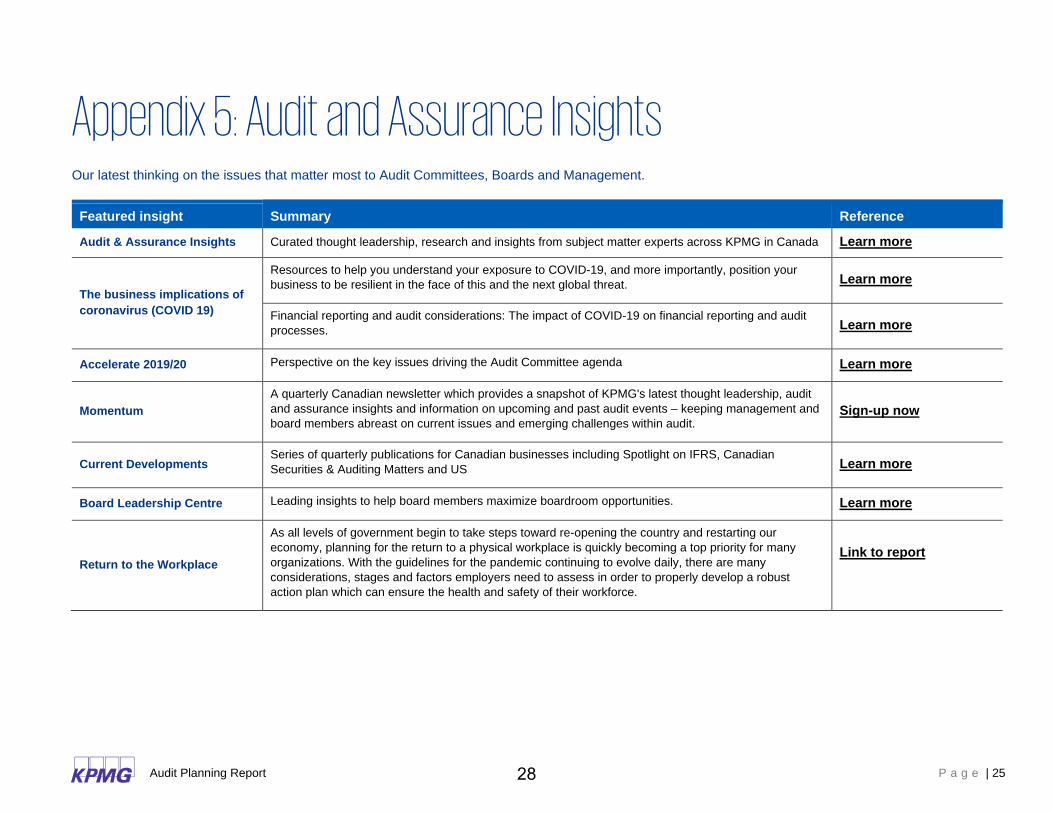

Appendix 5: Audit and Assurance Insights

Our latest thinking on the issues that matter most to Audit Committees, Boards and Management.

Featured insight Summary Reference

Audit & Assurance Insights Curated thought leadership, research and insights from subject matter experts across KPMG in Canada Learn more

The business implications of coronavirus (COVID 19)

Resources to help you understand your exposure to COVID-19, and more importantly, position your business to be resilient in the face of this and the next global threat. Learn more

Financial reporting and audit considerations: The impact of COVID-19 on financial reporting and audit processes. Learn more

Accelerate 2019/20 Perspective on the key issues driving the Audit Committee agenda Learn more

Momentum A quarterly Canadian newsletter which provides a snapshot of KPMG's latest thought leadership, audit and assurance insights and information on upcoming and past audit events – keeping management and board members abreast on current issues and emerging challenges within audit.

Sign-up now

Current Developments Series of quarterly publications for Canadian businesses including Spotlight on IFRS, Canadian Securities & Auditing Matters and US Learn more

Board Leadership Centre Leading insights to help board members maximize boardroom opportunities. Learn more

Return to the Workplace

As all levels of government begin to take steps toward re-opening the country and restarting our economy, planning for the return to a physical workplace is quickly becoming a top priority for many organizations. With the guidelines for the pandemic continuing to evolve daily, there are many considerations, stages and factors employers need to assess in order to properly develop a robust action plan which can ensure the health and safety of their workforce.

Link to report

28

kpmg.ca/audit

KPMG LLP, an Audit, Tax and Advisory firm (kpmg.ca) and a Canadian limited liability partnership established under the laws of Ontario, is the Canadian member firm of KPMG International Cooperative (“KPMG International”).

KPMG member firms around the world have 174,000 professionals, in 155 countries.

The independent member firms of the KPMG network are affiliated with KPMG International, a Swiss entity. Each KPMG firm is a legally distinct and separate entity, and describes itself as such.

© 2020 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

29

30

1

The Regional Municipality of York

Audit Committee

January 14, 2021

Report of the Director, Audit Services

Audit Services Branch Report

1. Recommendations

Council receive this report for information.

2. Summary

This report provides an update on the activities of the Audit Services Branch since the last

Audit Committee meeting held on June 10, 2020.

3. Background

The Audit Services Branch provides independent, objective assurance and consulting services

designed to add value and improve York Region’s operations. Audit Committee meets twice

yearly and receives the Audit Services Branch activities in the fulfilment of their oversight

responsibilities on the Region’s systems of internal control and the audit process.

4. Analysis

Audit Plan Execution

The Audit Services Branch Four-Year Audit Plan was approved by the Audit Committee on

January 9, 2019. As reported to Audit Committee on June 10, 2020 the Four-Year Audit

Plan has been impacted by the Regional declared emergency caused by the COVID-19

pandemic. As such, the Audit Services Branch has taken the opportunity to revise the Four-

Year Audit Plan from a four-year to a one-year basis. This change allows for flexibility in

planning to address new and emerging risks, in-year requests and is aligned with the

International Standards for the Professional Practice of Internal Auditing. The proposed

Risk-Based Work Plan for 2021 will be presented for approval under a separate report.

Audit Services continues to conduct audits where feasible, provide consulting and

investigation services upon request, follow up on outstanding audit recommendations and

maintain the quality assurance and improvement program that covers all aspects of the

internal audit activity.

31

Audit Services Branch Report 2

Management was provided the opportunity to defer providing an update on the status of

outstanding audit recommendations at this time given the organizational response to the

emergency caused by the COVID-19 pandemic.

A summary of the Audit Services Branch activities since the June 10, 2020 Audit Committee

is outlined in Attachment 1.

Audit Reports Issued

The following Audit Reports have been issued since June 10, 2020:

Corporate Services – Human Resources Workplace Health, Safety and Wellness

Audit (Attachment 2)

Finance – Information and Technology Cellular Audit (Attachment 3)

September 2020 Outstanding Audit Recommendations Follow-Up Report

(Attachment 4)

Audit Services Branch supports Vision 2051 and the 2019 to 2023 Strategic Plan

The Audit Services Branch, through its service offerings including assurance, consulting and

investigation services, assists the Region in achieving its goals and community results areas

in Vision 2051 under Open and Responsive Governance and in the 2019 to 2023 Strategic

Plan under Good Government. The internal audit activity is designed to add value and

improve an organization’s operations through a systematic and disciplined approach to

evaluate and improve the effectiveness of risk management, controls and processes.

5. Financial

Audit Services continues to manage its workload within the allocated budget.

6. Local Impact

The Audit Services Branch provides auditing services to seven of the local municipalities

through a Memorandum of Understanding on a cost recovery basis.

32

Audit Services Branch Report 3

7. Conclusion

Audit Services will continue to conduct audits where feasible, provide consulting and

investigation services upon request, follow up on outstanding audit recommendations and

maintain the quality assurance and improvement program. An update of Audit Services

activities will be brought forward to the next Audit Committee meeting scheduled for June

2021.

For more information on this report, please contact Michelle Morris, Director, Audit Services

1-877-464-9675 ext.71205. Accessible formats or communication supports are available

upon request.

Recommended by: Michelle Morris

Director, Audit Services

November 27, 2020

Attachments (4)

eDOCS #12040435

33

34

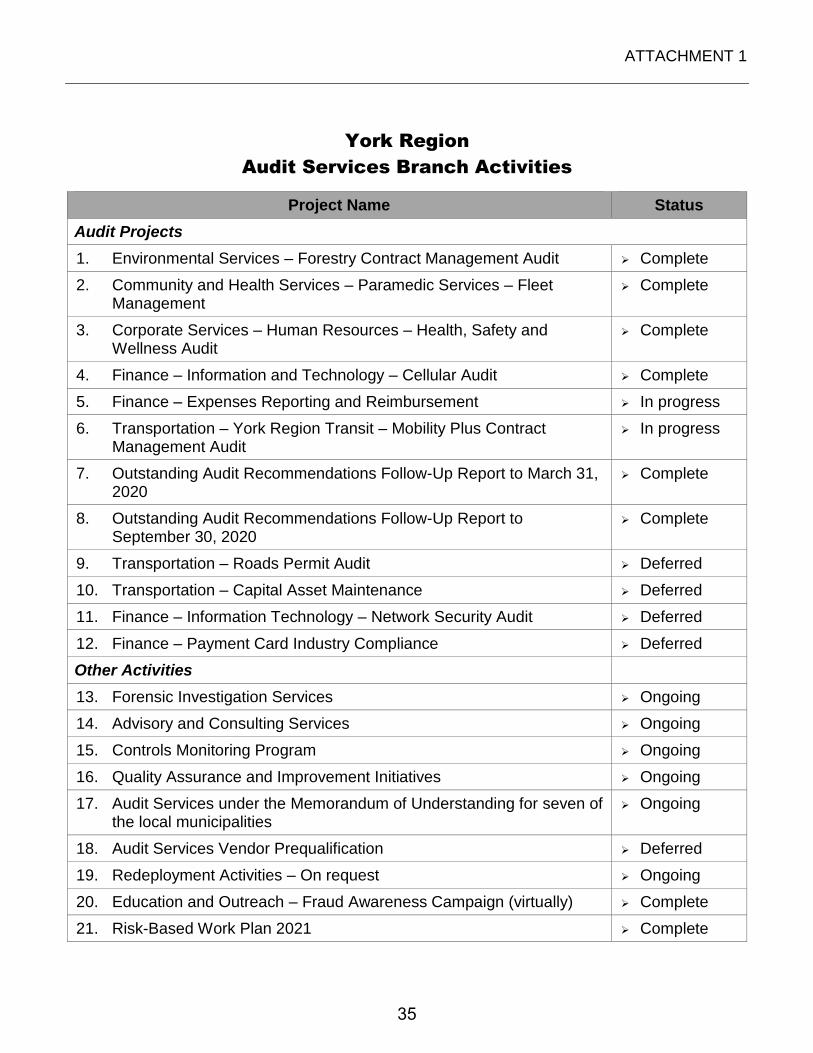

ATTACHMENT 1

York Region

Audit Services Branch Activities

Project Name Status

Audit Projects

1. Environmental Services – Forestry Contract Management Audit Complete

2. Community and Health Services – Paramedic Services – Fleet Management

Complete

3. Corporate Services – Human Resources – Health, Safety and Wellness Audit

Complete

4. Finance – Information and Technology – Cellular Audit Complete

5. Finance – Expenses Reporting and Reimbursement In progress

6. Transportation – York Region Transit – Mobility Plus Contract Management Audit

In progress

7. Outstanding Audit Recommendations Follow-Up Report to March 31, 2020

Complete

8. Outstanding Audit Recommendations Follow-Up Report to September 30, 2020

Complete

9. Transportation – Roads Permit Audit Deferred

10. Transportation – Capital Asset Maintenance Deferred

11. Finance – Information Technology – Network Security Audit Deferred

12. Finance – Payment Card Industry Compliance Deferred

Other Activities

13. Forensic Investigation Services Ongoing

14. Advisory and Consulting Services Ongoing

15. Controls Monitoring Program Ongoing

16. Quality Assurance and Improvement Initiatives Ongoing

17. Audit Services under the Memorandum of Understanding for seven of the local municipalities

Ongoing

18. Audit Services Vendor Prequalification Deferred

19. Redeployment Activities – On request Ongoing

20. Education and Outreach – Fraud Awareness Campaign (virtually) Complete

21. Risk-Based Work Plan 2021 Complete

35

36

ATTACHMENT 2

Internal Audit Report

Workplace Health, Safety and Wellness – Human Resources, Corporate Services

May 2020

37

Health, Safety & Wellness Audit Report May 2020

Internal Audit Report Page 1

TABLE OF CONTENTS

Section Page No.

1.0 MANAGEMENT SUMMARY ...................................................................................................................... 2

2.0 INTRODUCTION ........................................................................................................................................... 2

4.1 INCIDENT TRACKING ............................................................................................................................. 5 4.2 DETAILED TESTING – INSPECTIONS & COMMITTEE MEETINGS ............................................................. 5 4.3 ON-SITE OBSERVATION – INSPECTIONS ................................................................................................. 7 4.4 TRAINING .............................................................................................................................................. 8 4.5 HEALTH & SAFETY INFORMATION - INTRANET ..................................................................................... 9

38

Internal Audit Report Page 2

1.0 Management Summary

Audit Services has completed an audit of the Workplace Health, Safety and Wellness area, which

is under the Human Resources branch of the Corporate Services department. The objectives of

the review were to ensure: controls exist and are adequate to support the Occupational Health and

Safety Act R.S.O. 1990 (OHSA) requirements and manage the health and safety programs at the

Region; compliance with the OHSA requirements and internal policies and procedures; and

systems are used effectively and efficiently to support the departments objectives.

The audit scope included interviews with appropriate personnel, a review of the legislative

requirements and internal policies/systems, detailed testing of various health and safety

compliance requirements for the 2019 fiscal year, and on-site observations of monthly

inspections.

Our audit was conducted in accordance with the International Standards for the Professional

Practice of Internal Auditing.

Based on the work Audit Services performed, we concluded that overall the Workplace Health,

Safety and Wellness area is being well managed and controls are designed to support the

Region’s compliance with the OHSA requirements and internal policies. Opportunities for

control and process improvements have been noted and discussed in the body of this report.

These opportunities include enhanced tracking and management of “incidents” and “hazards”

within the Parklane software, additional training for Joint Health and Safety Committee (JHSC)

members on compliance requirements for monthly inspections, and increased awareness and

oversight on staff compliance with regulatory and mandatory training requirements.

It should also be noted that there were key areas identified during the audit where controls were

strong and working effectivity as designed. These areas include the Region’s 2019 documented

Health and Safety policy statement, adherence to the JHSC structure requirements, documented

standards exist and are being followed for reporting and tracking incidents, a robust workplace

harassment and discrimination program, and continuous improvement initiatives including the

“Safe Start” and “Mindful Approach” programs to help ensure the health and safety of all staff.

Should the reader have any questions or require a more detailed understanding of the risk

assessment and sampling decisions made during this audit, please contact the Director, Audit

Services.

Audit Services would like to thank Workplace Health, Safety and Wellness staff and management

for their co-operation and assistance provided during the audit.

2.0 Introduction

The Occupational Health and Safety Act (OHSA) is Ontario's legislation for workplace health

and safety. Other contributing legislation includes the Workplace Safety and Insurance Act

(WSIA) Part II of which deals with the prevention of occupational injury and disease.

39

Internal Audit Report Page 3

York Region’s Health, Safety and Wellness area is responsible for managing the safety, health

and well-being of every staff and has committed to creating a healthy workplace through the

integration of leadership, organizational culture and health and safety practices.

The Human Resources branch is the internal service responsible for the administration of

workplace health, safety and wellness programs at the Region. Responsibilities include helping

staff that develop an illness or are injured return to work in a safe manner, ensuring the workplace

is a safe place and providing education and training on health and safety topics. Human

Resources provide advisory services relating to health and safety to all departments within the

Region and develop the tools and direction to help ensure compliance with legislation.

The Region has thirty (30) JHSC’s in line with the size of our workforce and all locations. The

JHSC’s consists of management and worker representatives that have specific responsibilities and

together they are responsible for providing leadership in improving health and safety conditions

in the workplace by adhering to the OHSA and its regulations as well as internal policies.

The Minister of Labour governs health and safety and is responsible for enforcing the OHSA in

Ontario. Inspectors are the enforcement arm of the Ministry of Labour and their role includes the

following: inspection of workplaces, issuing orders where non-compliance is found and

investigations of accidents and work refusals.

3.0 Objectives and Scope

AUDIT OBJECTIVES The objectives of this engagement are:

To provide assurance on the adequacy and effectiveness of controls in place to support the

Occupational Health and Safety Act (OHSA) requirements and manage workplace health and

safety programs at the Region.

To evaluate compliance with relevant legislation (OHSA), regulations and internal policies

and procedures.

To ensure systems/software that support the Health and Safety program are designed to

provide adequate oversight and reporting on metrics.

AUDIT SCOPE

The audit objectives were accomplished through:

1. Interviews with appropriate personnel involved in workplace health, safety and wellness

programs.

2. A review of legislation and internal policies and procedures that support workplace health,

safety and wellness programs.

3. A review of health and safety documentation produced, collected and distributed.

4. A review of program objectives and industry best practices.

40

Internal Audit Report Page 4

5. Detailed testing and on-site observation of various health, safety and wellness programs for

compliance with legislation and internal policies and procedures, for the period November 1,

2018 to December 31, 2019.

41

Internal Audit Report Page 5

4.0 Detailed Observations

4.1 Incident Tracking

Observation

Corrective action completion date for incidents is not currently entered into the Parklane

software. The Parklane software is where all health and safety incidents are entered for tracking

and reporting. An incident is defined as “an occurrence, condition, or situation arising in the

course of work that resulted in or could have resulted in injuries, illnesses, and damage to health,

or fatalities.”

Based on discussions with the Lead, Health and Safety and a review of the Parklane system, the

completion date for corrective actions taken to resolve and/or prevent future issues is not actually

recorded in the Parklane software once all required action has been taken. The health and safety

group is involved with reviewing the incidents and they take trends to the JHSC meetings:

however, there is no clear way to report on the timeliness and completeness of addressing the

incident or to analyze long term trends. Tracking when an incident has been fully addressed may

help reduce the risk of the incident not being resolved sufficiently to prevent similar injuries from

occurring.

Recommendation

Management should update the process for incident reporting and tracking to ensure the

completion date of corrective actions is entered into the Parklane software.

Management Response

HR Health & Safety will explore methods to enter actions, responsibility, plan date and

completion date of incident corrective actions.

York Region’s Employee Incident/Injury process document will be updated to indicate new

corrective action tasks and management will be trained on new responsibilities.

Completion Date: Q3 2021

4.2 Detailed Testing – Inspections & Committee Meetings

Observation

The OHSA requires the JHSC’s to meet at least once every three months and that all workplaces

are inspected by the committee members at least once a month.

42

Internal Audit Report Page 6

Audit selected a random sample of ten (10) Regional locations and reviewed the quarterly JHSC

meeting minutes and monthly inspection reports for the period November 2018 to December

2019. The following observations were noted during the review:

Two (2) out of the ten (10) (20 percent) sample locations selected were missing evidence

of the quarterly JHSC meetings and three (3) out of the ten (10) (30 percent) sample

locations were missing evidence of the on-site monthly health and safety inspection

reports. Missing or incomplete OHSA requirements may increase the risk of non-

compliance orders and/or pose a risk to employee safety.

Digital copies of JHSC inspections and meeting minutes are not consistently maintained

in a centralized location. Based on discussions with health and safety committee

members and the Health and Safety Specialists, hard copies of the inspection reports are

posted on-site and digital copies emailed to the manager and specialist only if there are

concerns noted. Without a centralized location to house the regulatory compliance

results, there may be a risk of incomplete or missing items that may to go undetected.

Hazards identified during monthly inspections are not formally tracked and monitored for

resolution. The inspection reports are emailed to the manager of the area and the Health

and Safety Specialist; however, there is no formal follow up process for hazards

identified. Based on discussions with staff during the onsite visits, there have been

instances where issues have been reported multiple times with no resolution. Without a

formal follow up process, there may be a risk that an issue maybe unresolved.

Multiple versions of the inspection checklist template are in use and do not include a

checkoff column for the inspector to mark as complete for each area. Implementing a

standard checklist with a check mark requirement for each area may help ensure

consistency and completeness of inspections.

Recommendation

1. Management should consider centralizing the records management for monthly inspection

reports/results and committee meeting minutes to ensure completeness. Consideration should

be given to formally tracking hazards identified during the monthly inspections to allow for

an increase in oversight in addressing concerns.

2. Management should review the various inspection template checklists in use and ensure the

most current is communicated to all appropriate members. In addition, the template could be

updated to include a column for the inspector to initial each item reviewed to ensure

completeness. Once updated, the current checklist should be distributed to all locations

performing inspections.

Management Response

A database will be implemented by the HR Health & Safety team for centralizing the records

management for JHSC committee meeting minutes and monthly inspection reports/results.

The current JHSC inspection checklist available on the JHSC Portal page will be reviewed and

updated. Once updated, the current checklist will be distributed to all locations performing

inspections. The HR Health & Specialists will support customization of the inspections checklist

43

Internal Audit Report Page 7

for relevant groups where sector specific hazards apply. A column will be added on the checklist

for the inspector to verify that items noted on the previous inspection have been addressed.

Completion date: Q3 2021

4.3 On-site Observation – Inspections

Observation

Monthly health and safety inspections were not in full compliance with the OHSA requirements.

Audit Services selected a random sample of five (5) locations to attend and observe the monthly

health and safety inspection.

Please note, due to the timing of the scheduled inspections and the start of the Covid-19 public

health crisis, Audit Staff were only able to attend two (2) out of the five (5) on-site inspections.

The following concerns were observed during the on-site inspections;

The fire extinguishers and first aid kits were not inspected at both locations as required

under the OHSA.

The external inspection of the building was not completed at one of the locations as

required under the OHSA.

Non-compliance with the OHSA regulatory requirements for monthly inspections may result in

orders issued and/or pose a risk to employee safety.

Recommendation

Management should implement the following:

Education and communication with JHSC members to ensure they are aware of the

OHSA requirements and compliance areas covered within their inspections.

Increased oversight by Health and Safety Specialists to ensure committee members are

meeting the OHSA requirements for inspections.

Management Response

HR Health & Safety will create a self-learning JHSC workplace inspection training resource and

will engage the Corporate Health and Safety Advisory Committee (CHASAC) to assist in

educating JHSC members who complete workplace inspections.

The HR Health & Safety Specialists will attend two (2) JHSC inspections for each JHSC in 2021

in order to provide oversight of OHSA requirements for inspections. To become familiar with the

workplace inspection process, area management will also be invited to attend the when the H&S

Specialist is present.

Completion Date: Q4 2021

44

Internal Audit Report Page 8

4.4 Training

Observation

Training requirements are not always being met in accordance with legislation and Regional

requirements. York Region staff are required to complete specific Regional required mandatory

training and OHSA regulatory training. Exception reporting is produced annually within the

Learning Management System and is communicated to Directors.

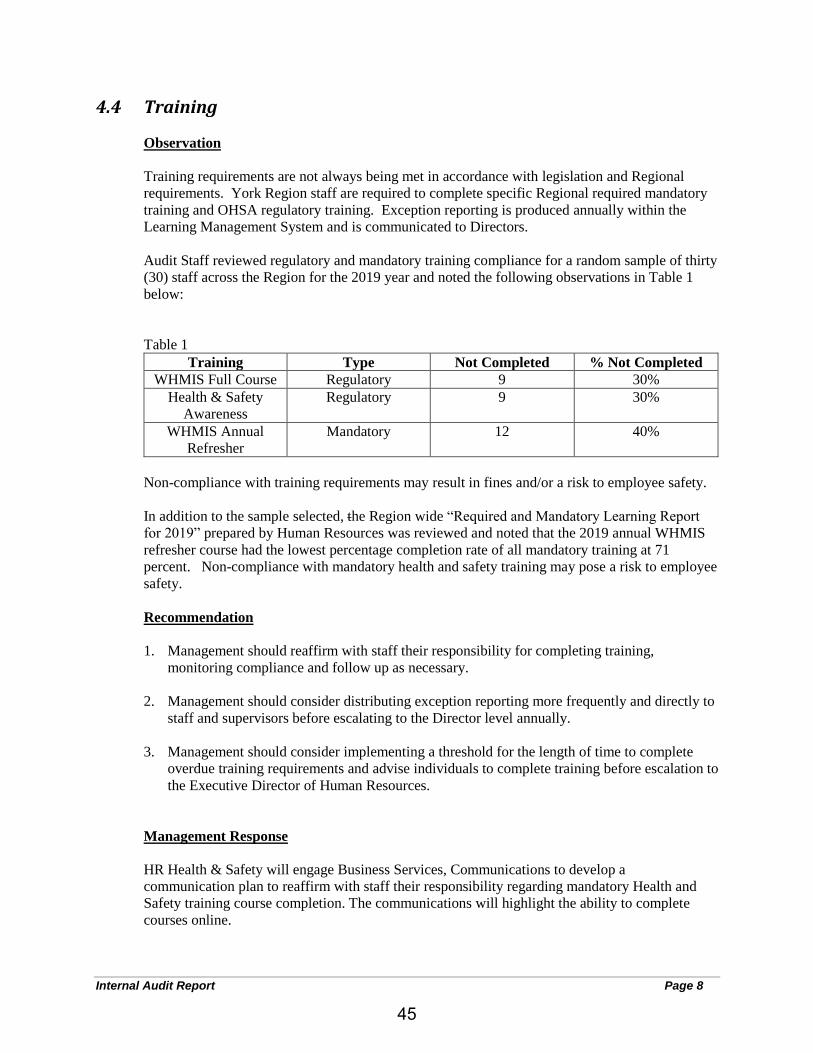

Audit Staff reviewed regulatory and mandatory training compliance for a random sample of thirty

(30) staff across the Region for the 2019 year and noted the following observations in Table 1

below:

Table 1

Training Type Not Completed % Not Completed

WHMIS Full Course Regulatory 9 30%

Health & Safety

Awareness

Regulatory 9 30%

WHMIS Annual

Refresher

Mandatory 12 40%

Non-compliance with training requirements may result in fines and/or a risk to employee safety.

In addition to the sample selected, the Region wide “Required and Mandatory Learning Report

for 2019” prepared by Human Resources was reviewed and noted that the 2019 annual WHMIS

refresher course had the lowest percentage completion rate of all mandatory training at 71

percent. Non-compliance with mandatory health and safety training may pose a risk to employee

safety.

Recommendation

1. Management should reaffirm with staff their responsibility for completing training,

monitoring compliance and follow up as necessary.

2. Management should consider distributing exception reporting more frequently and directly to

staff and supervisors before escalating to the Director level annually.

3. Management should consider implementing a threshold for the length of time to complete

overdue training requirements and advise individuals to complete training before escalation to

the Executive Director of Human Resources.

Management Response

HR Health & Safety will engage Business Services, Communications to develop a

communication plan to reaffirm with staff their responsibility regarding mandatory Health and

Safety training course completion. The communications will highlight the ability to complete

courses online.

45

Internal Audit Report Page 9

HR Health & Safety will liaise with departmental Learning and Development teams to ensure that

training exception reports are distributed to supervisors and staff at least bi-annually.

HR Health & Safety will seek Senior Management endorsement to indicate specific required

completion timelines for all regulatory health and safety courses currently outlined in the

‘required courses’ information on the Portal. Overdue thresholds will be included the training

exception reports sent to supervisors.

Completion Date: Q4 2021

4.5 Health & Safety Information - Intranet

Observation:

Audit Staff reviewed the health, safety and wellness information found on the Region’s intranet

site that is used to keep employees informed under the Human Resources area and noted the

following observations:

The “Employee Health Resources” portal page can be laid out in a more organized manner.

The format of documents appears inconsistent and the information provided in the linked

documents does not always provide clear or complete directions. Improving the organization

of information contained on the portal page may help improve employee awareness and

compliance with health and safety policies/procedures.

The policies that appear under the “Employee Health Related Policies” section are outdated.

As such, there is a risk that information contained in one or more of those policies is not

consistent with the OHSA, which was last updated in December 2017.

The extent of health and safety information and resources provided varies across the Region’s

employee portal. There is a greater level of health and safety related information found

within other areas on the Region’s intranet site compared to that found within the Human

Resources Health, Safety & Wellness page. Examples of these other areas include the Health

& Wellness tab under the Paramedic Services Resources section and the Safety tab under the

“My Life & Career” drop down menu on the home site. Decentralized information may lead

to inconsistent messaging, duplication of information, and be difficult for staff to navigate.

Recommendation:

1. Management should review the “Employee Health Resources” portal page and update to

ensure information is presented in an organized and consistent manner. Policies should

be reviewed and updated accordingly to ensure they are clear, accurate, complete and

current.

2. Management should determine the frequency with which policies should be reviewed and

updated going forward to ensure current regulations and compliance requirements are

accurately reflected in a timely manner.

46

Internal Audit Report Page 10

3. Management should review the current landscape for health and safety information

available on the portal and ensure health and safety information is presented in a clear,

consistent and coordinated manner. Consideration should be given to link the

information under the “My Life & Career” safety section to the Human Resources Health

Safety & Wellness portal page.

Management Response:

The My Life and Career and the associated tabs is where all workplace safety information is to be

housed. The Corporate Services – Human Resources – Health and Safety will be updated.

Duplicate information by other departments will be flagged and removed or redirected to the tabs

on My Life and Career page.

Management will review Health and Safety policies annually and will update information as

necessary to ensure current regulations and compliance requirements are accurately reflected.

Completion Date: Q2 2021

47

Internal Audit Report Page 11

Original signed by Original signed by

Dino Basso

Commissioner, Corporate Services

Sharon Kennedy

Executive Director, Human Resources

Original signed by

Michelle Morris

Director, Audit Services

48

ATTACHMENT 3

Internal Audit Report

Finance - Information Technology Cellular Audit Report

June 2020

49

Finance - IT Cellular Audit June 2020

Internal Audit Report Page 1

TABLE OF CONTENTS Section Page No.

1.0 MANAGEMENT SUMMARY ............................................................................................................ 2

2.0 INTRODUCTION .............................................................................................................................. 2

3.0 OBJECTIVES AND SCOPE ............................................................................................................... 3

4.0 DETAILED OBSERVATIONS AND RECOMMENDATIONS .......................................................... 4

4.1 POLICIES REQUIRE UPDATED REVIEW .................................................................................... 4 4.2 POLICIES REGARDING EMPLOYEE REIMBURSEMENT FOR PERSONAL CHARGES INCURRED ON

CELLULAR DEVICES REQUIRE CLARIFICATION ....................................................................... 5 4.3 EMPLOYEE SIGN-OFF NOT REQUIRED WHEN PROVIDED A REGION ISSUED CELLULAR DEVICE6 4.4 INFORMATION COMMUNICATED TO EMPLOYEES REQUIRES CLARIFICATION ON

EXPECTATIONS REGARDING ROAMING CHARGES ................................................................... 7 4.5 THERE IS NO FORMAL OFF-BOARDING PROCESS FOR DECOMMISSIONING CELLULAR DEVICES8 4.6 EMPLOYEES ARE NOT REQUIRED TO USE A CASE WITH THEIR REGION ISSUED CELLULAR

DEVICE ................................................................................................................................. 10

50

Finance - IT Cellular Audit June 2020

Internal Audit Report Page 2

1.0 Management Summary

Audit Services has completed an audit of Information Technology Cellular in Finance.

The audit was conducted in accordance with the Institute of Internal Auditors International

Standards for the Professional Practice of Internal Auditing.

The scope of the audit included a review of the Region’s policies that govern the process of

issuing, administrating and decommissioning cellular devices to provide secure and reliable

communication for staff. Additionally, detailed data analysis on all 2019 cellular related orders

from the Region’s main service provider, Rogers was conducted.

Testing was conducted at a sufficient level of detail to allow us to evaluate compliance with

contract terms and applicable policies / procedures.

Overall, the results of our detailed testing indicate that the cellular process operates in a manner

that helps to ensure devices are administered and used in accordance with policies and

procedures, and the billing process is in accordance with contract terms and conditions.

Opportunities for internal control improvements were noted and discussed with appropriate

management. These improvements relate to Region policy updates, the process for off-boarding

and decommissioning cellular devices, and various aspects of device administration.

It should also be noted that there were key processes identified during the audit where controls

were strong and working as designed. This includes the process for inventory management of

older devices to save the Region money on new device purchases and repair costs between the

cellular devices refresh periods, mobile device management and security initiatives, and the

process of issuing new devices to employees.

Should the reader have any questions or require a more detailed understanding of the risk

assessment and sampling decisions made during this audit, please contact the Director, Audit

Services.

Audit Services would like to thank Information Technology staff for their co-operation and

assistance provided during the audit.

2.0 Introduction

As part of our Regional Council Approved Audit Plan, the Audit Services branch performed a

Cellular Audit. The Audit Plan, approved by the Audit Committee, is developed by Audit

Services using a risk assessment methodology that helps to define the different risks associated

with the various processes at the Region. It is one tool that Audit Services uses in assessing

where best to allocate audit resources.

The IT Services branch administers the process for cellular devices used by Regional staff. This

process includes assigning devices to staff, managing billing and payments, managing device

51

Finance - IT Cellular Audit June 2020

Internal Audit Report Page 3

repairs, and off-boarding devices when no longer required. In 2019, excluding police, the Region

spent approximately $2.4 million on cellular.

Audit Services reviewed all Region policies related to cellular devices and the processes and

procedures in place to ensure administration of cellular devices in performed in compliance with

related policies.

3.0 Objectives and Scope

The main objectives of this engagement were to:

Review the internal controls regarding cellular communications at the Region to ensure

administration of devices and services is controlled.

Review Corporate and Departmental policies to ensure they are in alignment.

Ensure accurate billing based on contract terms and conditions.

The audit objectives were accomplished through:

1. A review of the Region’s policies and processes regarding the issuing and

decommissioning of cellular devices.

2. A review of contract terms for existing cellular services.

3. A review of the cellular billing process to ensure accuracy of billings.

4. A detailed analysis on all 2019 cellular billing data received from Rogers.

5. Interviews with appropriate personnel.

6. Review of other related documentation.

52

Finance - IT Cellular Audit June 2020

Internal Audit Report Page 4

4.0 Detailed Observations and Recommendations

4.1 Policies require updated review

Observation

As part of the audit, Audit reviewed all policies relating to cellular at the Region. During this

review, it was noted that the:

Responsible Use of IT policy was originally approved on November 14, 2016 and had

not been reviewed or updated since.

Privacy Policy was last updated on June 21, 2012.

Use of Social Media Policy was last updated on December 17, 2014.

Technology Acquisition Policy was last updated on November 14, 2016.

Voicemail Policy was last updated on April 30, 2014.