Embed Size (px)

Citation preview

Journal of Businesr Finance tY Accounting, 23 (l), January 1996,0306-686X

AUDIT FEES AND AUDITOR CHANGE; AN INVESTIGATION OF THE PERSISTENCE OF FEE

REDUCTION BY TYPE OF CHANGE

ALAN GREGORY AND PAUL COLLIER*

INTRODUCTION

Recent concern expressed within the accountancy profession about the issue of fee cutting has culminated in the Chartered Accountants’ Joint Ethics Committee (CAJEC) producing substantially strengthened guidance on fees.’ This practice of ‘low-balling’ was defined by DeAngelo (1981) as the setting of the initial audit fee below the sum of audit start-up costs plus normal profits. If ‘low-balling’ was shown to exist, there may be implications for auditor independence. Simon and Francis ( 1988) note the US Commission on Auditors’ Responsibilities concern about this issue, based upon the initial audit price reduction effectively representing an ‘investment’ in the client’s continued financial success. They then point out that a necessary (though not sufficient) condition for this to apply is for substantial price cutting to exist. They proceed to show that substantial fee reductions do indeed exist in the US market, a finding consistent with the prediction of the DeAngelo (1981) ‘low-balling’ model.

A question which arises here is whether or not such fee reductions raise social concerns because of a possible compromising of auditor independence. In DeAngelo’s model, low-balling is a consequence of the ability to earn future economic quasi-rents, with the auditor having an incentive to retain the client in order to realise these future rents. The initial investment would be regarded as an irrelevant sunk cost in keeping with economic tradition. By contrast, Simon and Francis ( 1988) argue that ‘recent work on the psychology of sunk costs provides evidence that sunk costs do significantly affect subsequent decision making, contrary to predictions from economic theory’ and that this may lead to an auditor independence problem during the period of investment

* The authors are respectively, from the Department of Accounting and Finance, University of Glasgow, and the Department of Economics, University of Exeter. They wish to record their thanks to Karen Cassar for her assistance with the data collection on this research project, together withJane Black, Bernard Pearson and the anonymous referee for their helpful comments; any errors or omissions remain the responsibility of the authors. They also wish to thank the Institute of Chartered Accountants in England and Wales for their financial support in respect of this data collection. (Paper received July 1994, revised and accepted October 1994)

Address for correspondence: Alan Gregory, Department of Accounting and Finance, University of Glasgow, 65-71 Southpark Avenue, Glasgow G12 8LE, UK

8 Blackwell Publishers Ltd. 1996, 108 Cowley Road, Oxford OX4 IJF, UK and 238 Main Street, Cambridge, M.4 02142, USA. 13

14 GREGORYAND COLLIER

recovery. This problem is in addition to the normal problems of auditor independence. A critical aspect of this type of low-balling behaviour is the initial reduction of the audit fee followed by later price recovery. NO theoretical predictions exist for the period of this recovery, but the Francis and Simon evidence shows that by years four to five of an audit engagement fees are a statistically insignificant 6% or so below normal.‘

It would also raise social concerns if price reduction was at the expense of audit quality. For example, a cut in audit fees may be achieved by reducing the number of hours spent on checking procedures. Whilst a temporary cut in fees would be consistent with low-balling, ‘short-cutting’ may be associated with a permanent reduction in audit fees. Alternatively, assuming such price reductions were found to exist, audit quality may be unaffected if either the price cuts reflected some genuine efficiency improvement through improved productivity from the factors of audit production, if there were economies of scale or scope in the audits carried out, or if increasing competitive pressures simply reduced economic rents accruing to these factors.

It may, of course, be the case that firms change auditors for reasons unconnected with fee reduction. For example, companies may wish to change to a ‘Big Six’ firm if they believe that such an alteration in the auditor would add credibility to the company’s reported profits in the financial markets. In cases where the objective is simply credibility enhancement, the company may not seek a reduction in the audit fee at the time of the change. In fact, they may even be prepared to pay a higher fee, an example of bonding expenditure in agency theory terms. At the same time, the amount of this bonding expenditure may be mitigated by the competitive market for audits amongst ‘Big Six’ firms.

In addition, there may be other reasons why auditors are changed. Examples of these reasons might include: disagreements over the scope of the audit; concerns over the quality of the audit; personality clashes between the directors and audit partners; and a policy to rotate auditors. Finally, there is the added possibility that an involuntary change occurs by virtue of the audit firm being taken over.

AUDIT FEES AND AUDRORCHANGE

One problem with analysing the long term consequences of auditor change is that there is little firm (as opposed to anecdotal) evidence of the relationship between auditor change and the audit fee in the UK. The only evidence which exists is the US study of Simon and Francis (1988). Recently, Pong and Whittington (1994) have analysed the impact of initial (first year) auditor change, and suggests that there was ‘a persistent tendency, robust across models, for newly appointed auditors to charge less, on average, than

8 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITORCHANGE 15

incumbent auditors’. However, the paper did not investigate whether or not there was evidence of subsequent price recovery. As explained in the next section, price recovery is a necessary condition for there to be evidence of ‘low- balling’.

Whilst the competitive market amongst ‘Big Six’ firms may be similar between the US and the UK, given the international operations of these auditors, key differences may exist between the US and the UK markets for audits. Examples may be the differing degree of regulation imposed by auditing standards and guidelines or the litigious climate in the US. However, it is difficult to be specific on precise areas of difference for as Needles (1989) observed there is ‘a need for research in the field of international auditing that focuses on theory-building and empirical testing’. Furthermore, anecdotal evidence suggests that the audit market has become more competitive in recent years, and therefore ‘low-balling’ may have become more pronounced in later years (Pong and Whittington’s sample period covered the years 198 1-8).

Certainly, the question of the extent to which fee cutting or predatory pricing is practised in the UK has proved a subject of sufficient concern for CAJEC to issue on 2nd December 1993, new guidance on fees.3 The strengthened ethical guidance followed a discussion paper on predatory pricing in June 1992,4 and a draft ethical guidance issued in March 1993.5 In none of these papers was there any specific evidence that ‘low-balling’ was a problem in the UK context. However, there was reference to similar concerns expressed by other countries with references to US and Australian pronouncements. There was also reference to the view expressed in the Cadbury report (Cadbury Committee, 1992, pp. 26-37) that competition between audit firms on price may be at the expense of meeting the needs of shareholders. Further, Brinn and Peel (1993) have found evidence of ‘low- balling’ in the unquoted company sector.

One problem with the simple model presented in DeAngelo (1981) is that although it explains ‘low-balling’ as the rational behaviour in the initial bid for an audit, it predicts that clients will not change auditors. The basic model shows that the incumbent auditor prevents switching by setting a long-run fee which is lower than the long-run costs faced by a new auditor (including start- up and switching costs). One way of allowing a change of auditor is to make competitors’ fees stochastic (DeAngelo, 1981, p. 121). The alternative is to allow for the influence of auditor quality. Thornton and Moore (1993) assume that high quality auditors are associated with a higher multiple of reported earnings. Assuming that high quality auditors charge higher fees (and have higher costs) than low quality auditors and that client company managers wish to maximise the value of the firm,6 switching from low to high quality auditors would be worthwhile if the gain in market value was greater than the present value of the increased auditing costs.

8 Blackwell Publishers Ltd 1996

16 GREGORYAND COLLIER

RESEARCH DESIGN AND SAMPLE SELECTION

T o provide further evidence on the relationship between auditor change and the audit fee in the UK, we wish to investigate whether there is any evidence of a reduction in audit fee following a change in the auditors. We further wish to see if there is any evidence of price recovery taking place in later years, which would be compatible with the idea of ‘low-balling’. Formally, the hypotheses compatible with ‘low-balling’ that we test can be stated as:

HI : There will be a negative relationship between a change ofauditor and the audit fee in the short term.

For the purpose of testing this hypothesis, we define the short term as being up to three years from the financial year end date of the change in auditor.

H2: Any negative relationship between auditor change and the audit fee will not continue to exist in the longer term.

For the purpose of testing this hypothesis, we define the longer term as being four to five years.

‘Low-balling’ is a phenomenon associated with a voluntary change of auditor. By contrast, fee reductions attributable to economies of scale or scope should be associated with both voluntary and involuntary changes of auditor, the latter being associated with the take-over of an existing auditor or the existing auditor merging with another firm. We therefore wish to examine the proposition that only voluntary changes of auditor lead to fee reduction. An involuntary change would not be expected to lead to a fee reduction for auditees since such a change is not associated with competitive audit fee underpricing. We can thus state our third hypothesis as:

H3: A change of auditor resulting from a take-over ofan auditing firm will not be associated with any decrease in audit fee.

This hypothesised relationship is an important one since it can be viewed as providing a control group for economies of scale or scope. If auditors could achieve these through expansion of the number of clients, then given a competitive market for audit services we should expect to see a reduction in audit fees following a take-over. Furthermore, this reduction would be permanent and would also be indistinguishable from the effect observed on a voluntary change of auditor. It is worth noting a t this point that Pong and Whittington (1 994) do not distinguish between voluntary and involuntary changes, and it may be that this is a partial explanation of why they observe lower fee reductions when the switch is made to a ‘Big Eight’ (now Big Six) auditor.

As is usual in the literature on audit fee modelling, our approach to testing these three hypotheses is to run a cross-sectional regression ofaudit fees on a set ofexplanatory variables including those ofprimary interest, dummy variables

8 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITORCHANGE 17

representing the timing ofa change of auditor. T o test our hypotheses, we need a model of the audit fee generating process. From previous theoretical and empirical work (Simunic, 1980; Francis and Simon, 1987; Simon and Francis, 1988; Palmrose, 1989; Haskins and Williams, 1988; Gist, 1992; Thornton and Moore, 1993; Chan, Ezzamel and Gwilliam, 1993; and Pong and Whittington, 1994), we develop two cross-sectional regression models of UK audit fees, to investigate the association between auditor change and ‘low- balling’ based on a sample oflisted UK companies. As Pong and Whittington (1994) note, such models implicitly estimate the supply curve for audit services, with the assumptions that the demand curve shifts across auditees and that the supply curve is a common cost function applying across all audits.

The first of these empirical models is of the logarithmic form found in most US studies and in the UK model of Chan, Ezzamel and Gwilliam. The second uses untransformed data and inter-active variables, as Pong and Whittington (1994). The sample was constructed by selecting all those firms, excluding the financial group and investment trusts, which were members of the Financial Times All Share Index (FTASI) in December 1991 ,’ for which a continuous record of the name of the auditor was available for the years ended in 1987 to 1991 inclusive and for which accounting records (on the Stock Exchange Micro-Fiche Service) were available for the financial year ended 1991. The requirement for five years auditor data to be available is imposed by the variable requirements of the model, which investigates the impact of a change in auditor over the past 5 years; our sources for this information were the Stock Exchange OfJicial Yearbooks, 1987-91. The accounting records (microfiche copies of the annual report and accounts) were used to identify the relevant financial and non-financial numbers used in the models described below. Our sample comprises a total of 399 firms and summary data on these is presented in Tables 1 and 2.’ These data constraints raise issues of survival bias and FTASI membership bias, and therefore we must acknowledge that the sample being used is not representative of the entire UK market for audit services.

An issue in the literature is the selection of appropriate proxies for auditee size, complexity and risk. Typically, size has been measured by total assets, with a natural logarithm transformation being employed in most cases. Attempts have also been made to employ multiple measures of size, including sales and number of employees in addition to assets, with the multicollinearity problem being avoided through the use of factor analysis (Brinn and Peel, 1992). More recently, Pong and Whittington (1994) have used multiple measures and suggested that multicollinearity is not a problem.

The arguments concerning model specification and proxy choice are well covered in Chan et al. (1993) and Pong and Whittington (1994), so are not dealt with here.

Our preferred logarithmic model, which implies a multiplicative relationship between the untransformed independent variables, is sales based

0 Blackwell Publishers Ltd 1996

18 GREGORY AND COLLIER

and has the form:

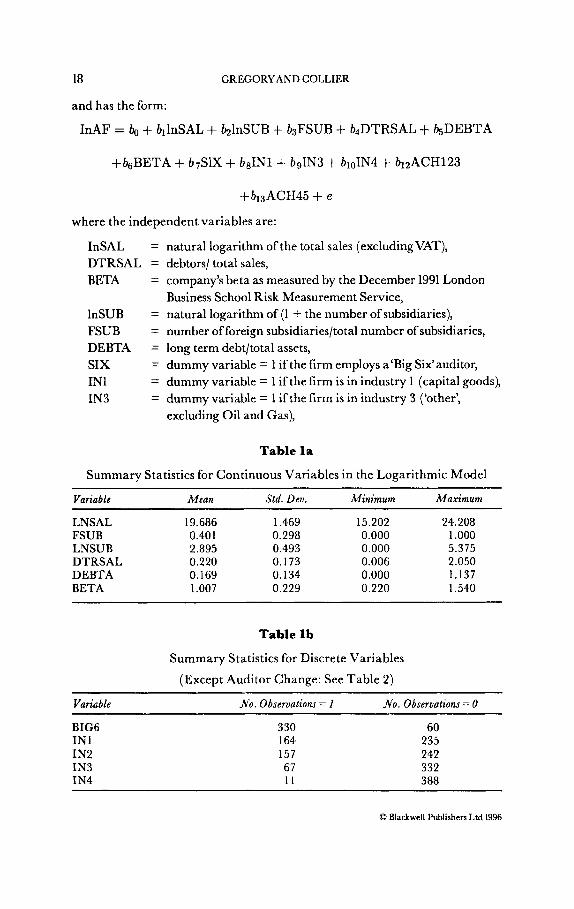

InAF = + bllnSAL + blnSUB + b3FSUB + b4DTRSAL + BsDEBTA

+b6BETA + b7SK + bsINl+ bgIN3 + b10IN4 + blzACH123

+ bl3ACH45 + e

where the independent variables are:

InSAL DTRSAL BETA

lnSUB FSUB DEBTA SIX IN1 IN 3

= natural logarithm of the total sales (excluding VAT), = debtors/ total sales, = company’s beta as measured by the December 1991 London

= natural logarithm of (1 + the number of subsidiaries), = number of foreign subsidiaries/total number of subsidiaries, = long term debtltotal assets, = dummy variable = 1 if the firm employs a‘Big Six’auditor, = dummy variable = 1 if the firm is in industry 1 (capital goods), = dummy variable = 1 if the firm is in industry 3 (‘other’,

Business School Risk Measurement Service,

excluding Oil and Gas),

Table l a

Summary Statistics for Continuous Variables in the Logarithmic Model

Variable Mean Std. Deu. Minimum Maximum

LNSAL 19.686 1.469 15.202 24.208 FSUB 0.401 0.298 0.000 1 .ooo LNSUB 2.895 0.493 0.000 5.375 DTRSAL 0.220 0.173 0.006 2.050 DEBTA 0.169 0.134 0.000 1.137 BETA 1.007 0.229 0.220 1.540

Table lb

Summary Statistics for Discrete Variables

(Except Auditor Change: See Table 2)

Variable No. observations = I No. Observations = 0

BIG6 IN1 IN2 IN3 IN4

330 164 157 67 11

60 235 242 332 388

0 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITOR CHANGE 19

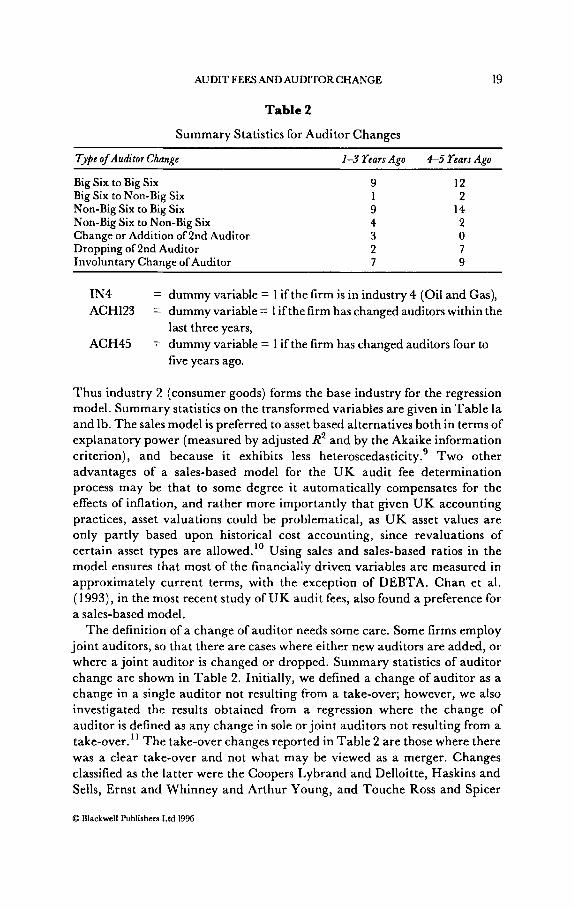

Table 2

Summary Statistics for Auditor Changes

Tyke of Auditor Change 1-3 Years Ago 6 5 Years Ago

Big Six to Big Six 9 12 Big Six to Non-Big Six 1 2 Non-Big Six to Big Six 9 14 Non-Big Six to Non-Big Six 4 2 Change or Addition of 2nd Auditor 3 0 Dropping of 2nd Auditor 2 7 Involuntary Change ofAuditor 7 9

IN4 ACH123

ACH45

= dummy variable = 1 if the firm is in industry 4 (Oil and Gas), = dummy variable = 1 ifthe firm has changed auditors within the

= dummy variable = 1 if the firm has changed auditors four to last three years,

five years ago.

Thus industry 2 (consumer goods) forms the base industry for the regression model. Summary statistics on the transformed variables are given in Table la and lb. The sales model is preferred to asset based alternatives both in terms of explanatory power (measured by adjusted R2 and by the Akaike information criterion), and because it exhibits less hetero~cedasticity.~ Two other advantages of a sales-based model for the UK audit fee determination process may be that to some degree it automatically compensates for the effects of inflation, and rather more importantly that given UK accounting practices, asset valuations could be problematical, as UK asset values are only partly based upon historical cost accounting, since revaluations of certain asset types are allowed.'' Using sales and sales-based ratios in the model ensures that most of the financially driven variables are measured in approximately current terms, with the exception of DEBTA. Chan et al. (1993), in the most recent study of IJK audit fees, also found a preference for a sales-based model.

The definition of a change of auditor needs some care. Some firms employ joint auditors, so that there are cases where either new auditors are added, or where a joint auditor is changed or dropped. Summary statistics of auditor change are shown in Table 2. Initially, we defined a change of auditor as a change in a single auditor not resulting from a take-over; however, we also investigated the results obtained from a regression where the change of auditor is defined as any change in sole or joint auditors not resulting from a take-over." The take-over changes reported in Table 2 are those where there was a clear take-over and not what may be viewed as a merger. Changes classified as the latter were the Coopers Lybrand and Delloitte, Haskins and Sells, Ernst and Whinney and Arthur Young, and Touche Ross and Spicer

0 Blackwell Publishers Ltd 1996

20 GREGORYAND COLLIER

and Oppenheim mergers; none of these changes were counted as an ‘auditor change’ for the purpose of our study.

Given the relatively small percentage of firms that change auditors in any one year, we decided to pool the change data into the two categories used in the regression model described; changes that occurred within the past three years, and changes which occurred within the past four to five years. If ‘low- balling’ occurs, ACHl23 should have a significant negative co-efficient; if there is subsequent price recovery, the term ACH45 should not be significantly different from zero.

An alternative to the logarithmic model is the untransformed variable specification of Pong and Whittington ( 1994). The reason for their use of this type of model is that a logarithmic model assumes a multiplicative relationship between the untransformed model variables, whereas the ‘raw’ model assumes an additive relationship. The latter has useful properties if it is suspected that there may be complex relationships between the independent variables, as Pong and Whittington find in the case of the ‘Big Eight’ premium.

Our prior beliefis that ‘low-balling’ is likely to manifest itselfin the form of a simple percentage fee reduction, which explains our initial preference for a logarithmic transformation of the data. In addition, such a transformation eliminates a great deal of the heteroscedasticity associated with the non-log model. Nonetheless, to investigate the inter-relationships between auditor change and other fee determinant variables, we estimated several models of the form used in Pong and Whittington. We included all those inter- dependent (or ‘slope-shifting’) variables in the Pong and Whittington models, together with additional inter-dependent variables capturing the inter-action between auditor change and size, complexity, risk and profitability. In our data set, clear indications of multi-collinearity were found, including high F-statistics but low t-ratios, together with counter intuitive signs on many co-efficients.

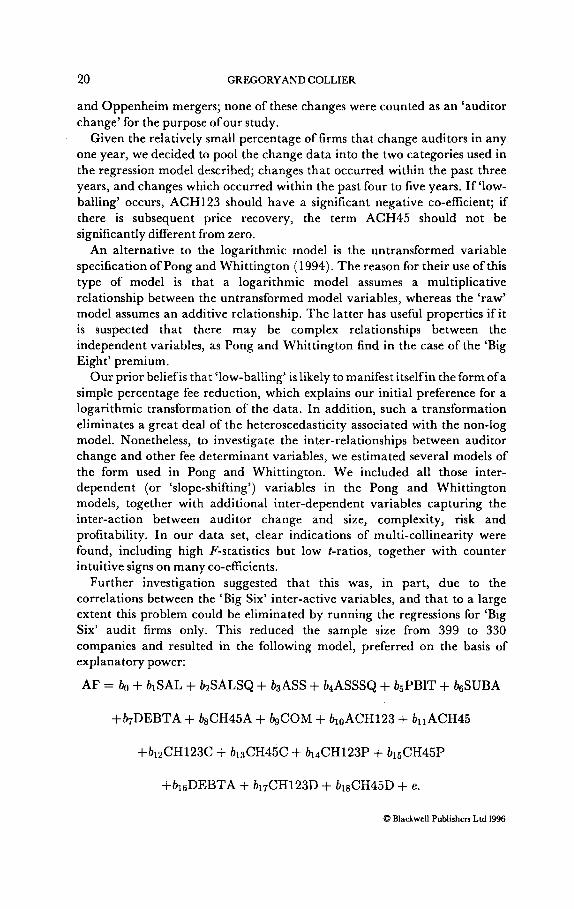

Further investigation suggested that this was, in part, due to the correlations between the ‘Big Six’ inter-active variables, and that to a large extent this problem could be eliminated by running the regressions for ‘Big Six’ audit firms only. This reduced the sample size from 399 to 330 companies and resulted in the following model, preferred on the basis of explanatory power:

AF = bo + blSAL + bzSALSQ + b3ASS + b4ASSSQ + b5PBlT + hSUBA

+b7DEBTA + bsCH45A + bgCOM + bloACH123 + bllACH45

+blzCH123C + b13CH45C + b14CH123P + b15CH45P

0 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITORCHANGE 21

Where, in addition to those defined above, the variables are:

AF SAL SALSQ ASS ASSSQ PBIT SUBA CH123A CH45A COM CH123C CH45C CH123P CH45P CH123D CH45D

= auditfee = Sales

= Total assets = ASS2 = Profit before interest and tax = COMxASS = ACH123xASS = ACH45xASS = Total number of subsidiaries = ACH123xCOM = ACH45xCOM = ACH123 x PBIT = ACH45xPBIT = ACH123 x DEBTA = ACH45 x DEBTA

= S A L ~

The general logic of using inter-active variables in audit fee modelling is discussed in Pong and Whittington. Our choice of inter-active variables in the above model is driven by our a priori reasoning that at least size and complexity will influence audit fee reduction, and a wish to investigate whether profitability or risk (as measured by DEBTA) are associated with greater or lesser fee reductions.

RESULTS

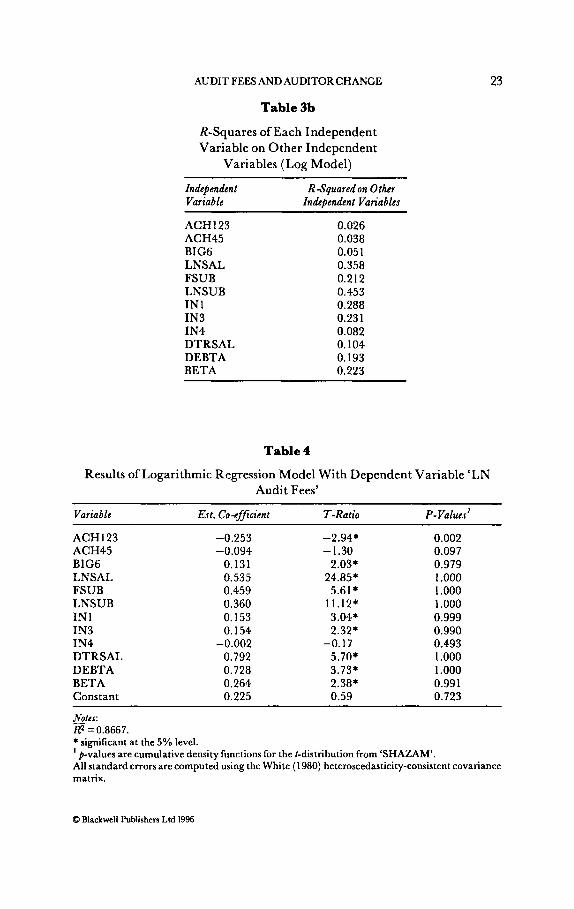

Results of the logarithmic model are reported in Table 4; the chi-squared test did not suggest any particular problem with non-normality of the residuals (although the Jarque-Bera test was significant at the 5% level), and the Ramsey (1969) test did not show any evidence of heteroscedasticity; however, the Breusch-Pagan test proved significant at the 5% level. Checking the data revealed no obvious source of heteroscedasticity12 and so the White (1 980) Heteroscedastic-Consistent Covariance matrix estimation was used to correct the estimates of co-efficient variance V ( @ . These corrected estimates are then used to form the t-ratios reported in Table 4. A further test for model specification error is the Ramsey (1969) reset test,13 which proved insignificant at the 5% level.

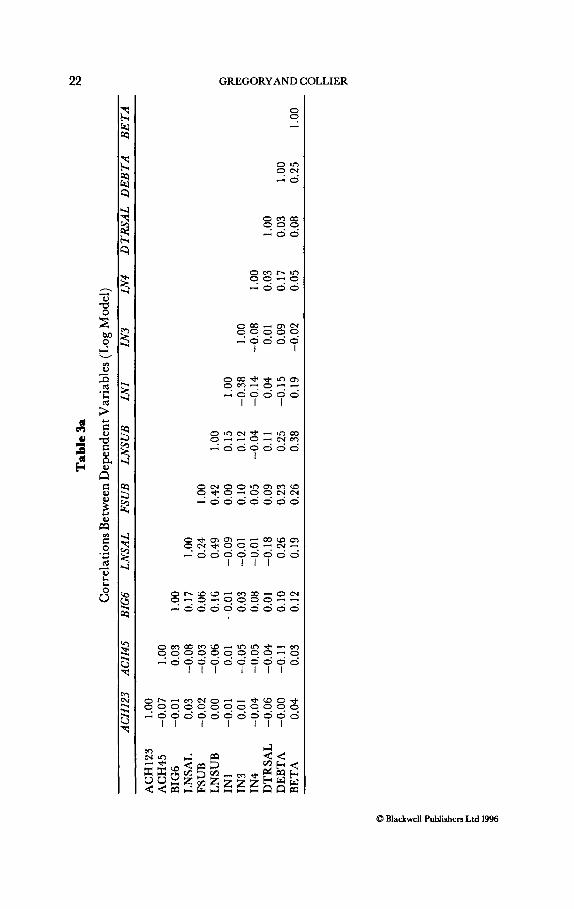

As a further check on model validity,'* we report statistics showing the correlations between independent variables (Table 3a) and the R-squared of each independent variable on other independent variables (Table 3b). These statistics suggest that there is no particular multi-collinearity problem.

0 Blackwell Publishers Ltd 1996

h3 Table 3a N

Correlations Between Dependent Variables (Log Model) ACH123 ACH45 BIG6 LNSAL FSUB LNSUB IN1 IN3 IN4 DTRSAL DEBTA BETA

ACH 123 ACH45 BIG6 LNSAL FSUB LNSUB IN1 IN3 IN4 DTRSAL DEBTA BETA

1 .oo -0.07 1 .oo -0.01 0.03 1 .oo

-0.02 -0.03 0.06 0.24 1 .oo

-0.01 0.01 -0.01 -0.09 0.00 0.15 1 .oo -0.04 -0.05 0.08 -0.01 0.05 -0.04 -0.14 -0.08 1 .oo -0.06 -0.04 0.01 -0.18 0.09 0.11 0.04 0.01 0.03 1 .oo -0.00 -0.11 0.10 0.26 0.23 0.25 -0.15 0.09 0.17 0.03 1 .oo

0.03 -0.08 0.17 1 .oo

0.00 -0.06 0.16 0.49 0.42 1 .oo

0.01 -0.05 0.03 -0.01 0.10 0.12 -0.38 1 .oo

0.04 0.03 0.12 0.19 0.26 0.38 0.19 -0.02 0.05 0.08 0.25 1 .oo

AUDIT FEES AND AUDITORCHANGE

Table 3b

R-Squares of Each Independent Variable on Other Independent

Variables (Log Model)

23

Independent RSquared on Other Variable Indebendent Variables

ACH123 ACH45 BIG6 LNSAL FSUB LNSUB IN1 IN3 IN4 DTRSAL DEBTA BETA

0.026 0.038 0.05 1 0.358 0.212 0.453 0.288 0.231 0.082 0.104 0.193 0.223

Table 4

Results of Logarithmic Regression Model With Dependent Variable ‘LN Audit Fees’

Variable Est. Co-tfficient T-Ratio P-Values’

ACHl23 -0.253 -2.94* 0.002 ACH45 -0.094 -1.30 0.097 BIG6 0.131 2.03* 0.979 LNSAL 0.535 24.85* 1 .ooo FSUB 0.459 5.61* 1.000 LNSUB 0.360 11.12* 1 .ooo IN1 0.153 3.04* 0.999 IN3 0.154 2.32* 0.990 IN4 -0.002 -0.17 0.493 DTRSAL 0.792 5.70* 1 .ooo DEBTA 0.728 3.73* 1 .ooo BETA 0.264 2.38* 0.991 Constant 0.225 0.59 0.723

ah: Rz = 0.8667. * significant at the 5% level. ’ p-values are cumulative density functions for the f-distribution from ‘SHAZAM’. All standard errors are computed using the White (1980) heteroscedasticity-consistent covariance matrix.

0 Blackwell Publishen Ltd 1996

24 GREGORYAND COLLIER

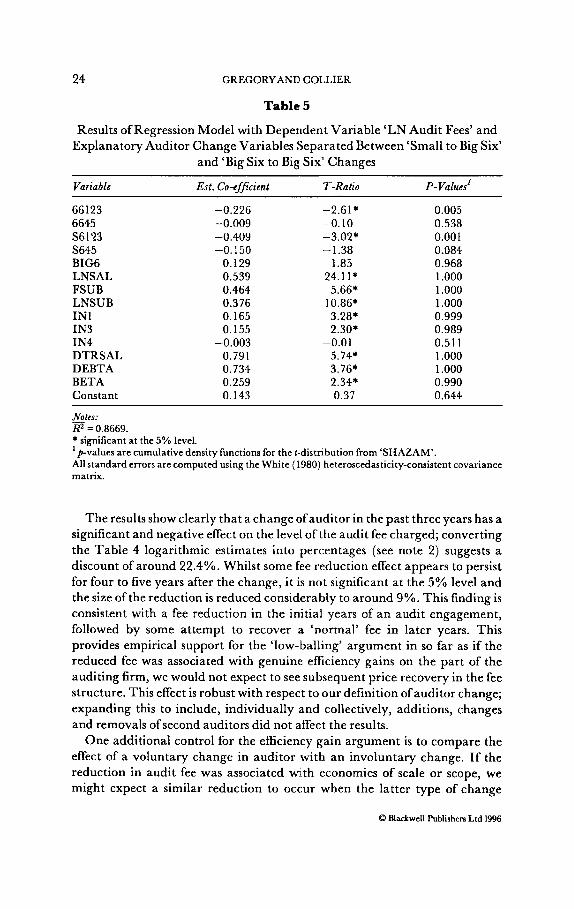

Table 5

Results of Regression Model with Dependent Variable ‘LN Audit Fees’ and Explanatory Auditor Change Variables Separated Between ‘Small to Big Six’

and ‘Big Six to Big Six’ Changes

Variable Est. Co -efficient I-Ratio P-Values’

66123 6645 S6123 S645 BIG6 LNSAL FSUB LNSUB IN1 IN3 IN4 DTRSAL DEBTA BETA Constant

-0.226 -0.009 -0.409 -0.150

0.129 0.539 0.464 0.376 0.165 0.155

0.791 0.734 0.259 0.143

-0.003

-2.61 * -0.10 -3.02* -1.38

1.85 24.11*

5.66* 10.86; 3.28* 2.30*

5.74* 3.76* 2.34* 0.37

-0.01

0.005 0.538 0.001 0.084 0.968 1 .ooo 1 .ooo 1 .ooo 0.999 0.989 0.511 1 .ooo 1 .ooo 0.990 0.644

&Notes: Ra = 0.8669. * significant at the 5% level. ’ p-values are cumulative density functions for the t-distribution from ‘SHAZAM’. All standard errors are computed using the White (1980) heteroscedasticity-consistent covariance matrix.

The results show clearly that a change ofauditor in the past three years has a significant and negative effect on the level ofthe audit fee charged; converting the Table 4 logarithmic estimates into percentages (see note 2) suggests a discount of around 22.4%. Whilst some fee reduction effect appears to persist for four to five years after the change, it is not significant at the 5% level and the size of the reduction is reduced considerably to around 9%. This finding is consistent with a fee reduction in the initial years of an audit engagement, followed by some attempt to recover a ‘normal’ fee in later years. This provides empirical support for the ‘low-balling’ argument in so far as if the reduced fee was associated with genuine efficiency gains on the part of the auditing firm, we would not expect to see subsequent price recovery in the fee structure. This effect is robust with respect to our definition ofauditor change; expanding this to include, individually and collectively, additions, changes and removals of second auditors did not affect the results.

One additional control for the efficiency gain argument is to compare the effect of a voluntary change in auditor with an involuntary change. If the reduction in audit fee was associated with economies of scale or scope, we might expect a similar reduction to occur when the latter type of change

8 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITOR CHANGE 25

occurred. To test for this, we re-ran our regression model with the inclusion of two further dummy variables, ICH123 (set to 1 if an involuntary change occurred in the last three years) and ICH45 (set to 1 if an involuntary change occurred four to five years ago). Whilst the size and significance of the ACH 123 and ACH45 variables remain virtually identical to those reported in Table 4, the ICH123 variable has a co-efficient of 0.0913 ( t = 0.5101) while that of ICH45 is -0.1007 ( t = 0.551 1) . This strongly suggests that there is no fee reduction associated with such changes, providing further evidence in support of a ‘low-balling’ model of behaviour. This needs to be qualified to some extent because of the low number of observations for the involuntary change variables (seven and nine cases respectively).

A further area of inquiry was to investigate whether the type of change made any difference to the fee reduction experienced. Table 2 clearly shows a trend amongst our sample companies to change to a ‘Big Six’ firm. In total, of 53 voluntary changes in sole auditors only three were from ‘Big Six’ to ‘non- Big Six’ firms, whilst only six were between ‘non-Big Six’ firms. There were 2 1 changes between ‘Big Six’ firms, and 23 changes from ‘non-Big Six’ to ‘Big Six’ firms. Given the numbers involved, only the latter two changes are investigated. A separate regression is run with separate dummy variables included for changes between ‘Big Six’ firms (66123 and 6645)) and changes from ‘non-Big Six’ to ‘Big Six’ firms (S6123 and S645). These results are reported in Table 5; in this regression the sample size is reduced to 390. Both types of change in years 1, 2 and 3 are highly significant, with the largest co- efficient being associated with changes from ‘non-Big Six’ to ‘Big Six’ firms. Note that the increased cost of a ‘Big Six’ audit is separately controlled for (this is around the order of 13.7%), and that the size of the reduction is around 33.6%, as opposed to 20.2% for a change between ‘Big Six’ firms. This implies that large auditors have to forego the ‘Big Six’ premium, in addition to offering initial fee discounts, as an incentive to persuade the auditees of smaller firms to switch auditors.

Whilst the evidence of price recovery is particularly strong in the case of changes between ‘Big Six’ firms, i t is more ambiguous in the case of a change from ‘non-Big Six’ to ‘Big Six’ firms. The fee reduction drops to a statistically insignificant 13.9%, similar to the ‘Big Six’ (‘quality’) premium. This might be taken as providing weak evidence compatible with ‘low-balling’ behaviour by the large accounting firms, with recovery to ‘normal’ fee levels but no immediate recovery of the auditor quality premium. However, this conclusion must be tempered by the reduced sample size involved in splitting the auditor change variable over two types.

We then adopt the Pong and Whittington (1994) methodology in an attempt to shed further light on the nature of the audit fee reduction process. The full results are not reported here because of space constraints, but using the untransformed variable model described above, we obtain results which are compatible with those of Pong and Whittington.’’ However, there is

0 Blackwell Publishers Ltd 1996

26 GREGORYAND COLLIER

some concern about multi-collinearity in our model, and in the case of all the alternatives we estimated, the Ramsey (1969) reset test proved significant a t the 5% level. This suggests that for our data set, using untransformed variables may not be the most appropriate form of model specification. Although these problems mean that our results from this model need to be treated with some caution, they may still provide useful insights into the factors that influence fee reduction associated with a change in auditor. Confirming the general fee reduction found in the logarithmic transformation. size and complexity are associated with lower initial audit fees, with both CH!23A and CH123C having significant negative co- efficients. This reduction is partly off-set by a significant profitability driven increase, so that more profitable firms experience a lower fee reduction than less profitable ones. Although there is some evidence that risk (high gearing) is associated with lower fee reductions, it is not a statistically significant effect.I6 Nor is there any evidence to suggest that the fixed cost reduction, as captured by ACH 123, is significant. Evidence of subsequent fee recovery is found in the lack of significance of any of the ACH45 based inter-active variables, or the fixed cost element. The hypothesis that audit fees paid by firms 4 to 5 years after any change of auditor are no different from those paid by firms which do not change auditor cannot therefore be rejected, confirming the result of the logarithmic model.

Because of the relatively small numbers of changes in the ‘66’ and ‘S6’ categories discussed above and the large number of inter-active variables required, we did not attempt to present a Pong and Whittington-type formulation of the logarithmic model which forms the basis of the results presented in Table 5 .

CONCLUSIONS

The evidence is compatible with ‘low-balling’ behaviour, of a type predicted by the DeAngelo (1981) model, in at least a part of the UK market for audits, with subsequent price recovery (at least to some extent) in later years. The initial fee reduction is both large (around 22.4%) and significant; the scale of this change is similar to that found by Simon and Francis in the US. Furthermore, by investigating the effect of involuntary auditor changes, we provide additional evidence that it really is ‘low-balling’ which is being observed, rather than economies of scale or scope. However, we need to be cautious in infering that our conclusions apply to the entire UK market for audits, because of the sample selection issues discussed above.

I t would also appear that companies changing from ‘non-Big Six’ to ‘Big Six’ firms may experience an even greater reduction in fees; this reduction seems to at least compensate for the ‘Big Six’ premium. There is also evidence that substantial and significant fee reductions (around the order of20.2%) are

8 Blackwell Publishers Ltd 1996

AUDIT FEES AND AUDITORCHANGE 27

available to firms switching between ‘Big Six’ firms. For both types of auditor change there is, consistent with a ‘low-balling’ model, evidence of price recovery.

Further analysis using the untransformed variable approach preferred in Pong and Whittington suggests that the fee reductions following a change of auditor may be associated with both size (assets) and complexity (number of subsidiaries), with a partially off-setting effect attributable to profitability. I t also appears that such net fee reductions are not maintained with any statistical significance in the longer term.

The cross-sectional results from both models used in this study and those in Pong and Whittington provide evidence that fee reductions can take place following a change of auditor. The contribution of this paper has been to show that, for our sample, these fee reductions do not persist in the longer term, and that the initial discount varies according to the type of auditor change (voluntary compared to involuntary) and whether or not the switch is between ‘Big Six’ firms.

NOTES

Chartered Accountants’Joint Ethics Committee (1993), Sfufement: Fces, CAJEC, London. Note that their model is estimated in logarithmic form with a reported co-efficient of 0.06. The implied fee reduction (r) could be found by:

7 = e-’ - 1

where c = reported co-efficient. Thus if this 0.06 was the exact co-efficient the implied reduction would be 5.82%. See note 1. Chartered Accountants’ Joint Ethics Committee (1992) Prcdufory Pricing: A Discussion Paper (- CAJEC, London). Chartered Accountants’ Joint Ethics Committee (1993), Fees ( includingjc undcr-cutfing): DruJt Ethicd Guiduncc (CAJEC, London). This could be because of pure altruism or because ofsome value-sharing parameter incorporated in their reward contracts Uensen and Meckling, 1976) In December 1991, this consisted of 500 companies. For the second model of audit fees, which uses untransformed variables, the sample size is reduced to 330 firms (see below). Note, however, that our general condusions reported below are robust with respect to model sDecification.

10 For example, property, aircraft fleets and shipping fleets have been valued at above historical cost in UK accounts.

11 As these results are not qualitatively different from those discussed below, they are not reported in this paper.

12 Note that the final model selected showed less evidence of heteroscedasticity than the alternatives investigated.

13 This differs from the Ramsey (1969) test for heteroscedasticity; see Maddala (1989), p. 408. 14 Given the inter-dependencies between variables that may be expected to occur in practice and

those (such as an inverse relationship between auditor quality and client risk) hypothesised by Thornton and Moore (1993).

15 The full results can be obtained from the authors upon request. 16 Alternative models incorporating beta-based risk measures also failed to identify significant risk

effects.

8 Blackwell Publishers Ltd 1996

28 GREGORYAND COLLIER

REFERENCES

Breusch, T.S. and A.R. Pagan (1979), A Simple Test For Heteroscedasticity and Random Coefficient Variation’, Economchua, Vol. 47, pp. 1287-94.

Brinn, A. and M.J. Peel (1993),‘Low-balling and the Small Firm’, Certz$ed Accountant Uanuary), pp. 37- 39.

__ ___ and R. Roberts (19921, Determinants of Audit Fees in the Unquoted Sector: Some New Evidence, Occasional Research Paper No. 11 (The Chartered Association of Certified Accountants, London).

Cadbury Committee (1992), Report of the Committee on The Financial Aspects of Corporate Goucrnance (Gee, London).

Chan, I?, M. Ezzamel and D. Gwilliam (1993), ‘Determinants of Audit Fees for Quoted UK Companies’, Journal of Business Finance B Accounting, Vol. 20, No. 6 (November), pp. 765-783.

DeAngelq L. (1981), ‘Auditor Independence, “Lowballing”, and Disclosure Regulation’, journal of Accountingand Economics,Vol3, No 3, p p 113-127.

Francis, J. and D. Simon (1987),ATest of Audit Pricing in the Small-Client Segment of the US Audit Market’, Accounting Reuiew (January), pp. 145-157.

Gist, W.E. (1992),‘ExplainingVanability in External Audit Fees’, AccountingandBusiness Research,Vol. 23 No. 89, pp. 79-84.

Haskins, M.E. and D.D. Williams (1988),‘The Association Between Client Factors and Audit Fees: A Comparison by Country and by Firm’, AccountingandBusiness Research,Vol. 18, No. 70, pp. 183-190.

Jensen, M.C. and W.H. Meckling (1976),‘Theory of the Rrm: Managerial Behaviour, Agency Costs and Ownership Structure’, journal gfFinancia1 Economics,Vol. 3.

Maddala, G.S. (1989), Introduction to Econometrics (Macmillan Publishing Co., NewYork). Needles, B.E. J n . (1989), ‘International Auditing Research Current Assessment and Future

Palmrose, Z-V (1989):The Relation of Audit ContractType to Audit Fees and Hours’, Accounting Rcuiew

Pong, C.M. and G. Whittington (1994), ‘The Determinants of Audit Fees: Some Empirical Models’,

Ramsey, J.B., (1969), Tests for Specification Errors in Classical Linear Least Squares Regression

Simon, D. and J. Francis (1988),‘The Effects of Auditor Change on Audit Fees: Tests of Price Cutting

Simunic, D.A. (1980), ‘The Pricing of Audit Services: Theory and Evidence’, journal of Accounting

Thornton, D.B. and G. Moore (1993),‘Auditor Choice and Audit Fee Determinants’, Journal OfBusincss

White, H. (1980),A Heteroskedasticity-Consistent Covariance Matrix Estimator and a DirectTest for

Direction’, Thejournal oflntcrnational Accounting, Vol. 24, pp. 1-20,

(July), pp. 488-499.

journal ofBusiness Finance B Accounting, Vol. 21, No. 8 (December), pp. 1071-1095.

Analysis’, journal of the Royal Statistlcal Socie& Series B, Vol. 31, pp. 350-71.

and Rice Recovery’, Accounting Review (April), pp. 255-269.

Research (Spring), pp. 161-190.

Finance B Accounting,Vol. 20, No. 3 (April), pp. 333-350.

Heteroskedasticity’, Economefrica, Vol. 48, pp. 817-38.

0 Blackwell Publishers Ltd 1996