Embed Size (px)

Citation preview

G l o b a l d e a l confidence i s h i g hI s local anx iety

A u s t r a l a s i aCapital Confidence BarometerNovem ber 2 0 16 | ey . com / au / ccb | 15th ed ition

2

D espite recen t d evelopm en ts arou n d th e w orld , d eals are still tak in g cen tre stage as com pan ies look to M & A to find rofitab e growt against a backdro of geo o itica u n certain ty , slow econ om ic con d ition s an d d igital d isru ption . T h e 15th Global Capital Confidence Barometer finds

ustra asian cor orate e ecuti es confidence around doing dea s fa ing be ind t eir g oba counter arts but wit o ati it t e new norm t e out ook for is im ro ing

n contrast to t e attitudes of g oba e ecuti es and des ite gen erally positive local econ om ic con d ition s, th e B arom eter found oca dea ans at in t e run u to t e e ection ese Au stralasian resu lts h in ged on con cern s abou t global volatility an d geo o itica instabi it and uncertaint of oca e uit a uations

es ite t e an iet seen o er t e ast few mont s re e ection t e arometer found oca dea i e ines fu of arge numbers of sma er smarter dea s and e ecuti e e ectations for oca m ark ets actu ally im provin g.

it t e e ection resu t now in standing sti is not a strategic o tion w en e er t ing is c anging for e ecuti es except th e e ectations of t eir in estors and stake o ders around ig er grow th an d retu rn s.

I n th e m ed iu m to lon g term , th ere is every reason to believe th at M & A w ill rem ain robu st an d su stain able. W e m ay see som e immediate indecision among dea makers as t e im act of t e resu t is understood ertain an s ort term e uit o ati it cou d cause a u back in acti it for a few weeks simi ar to w at w e saw post B rex it. H ow ever, con cern s over political in stability are not derai ing g oba sentiment in fact t e are increasing bein g seen as a m ean s to com bat it.

oca e ecuti es need to come to terms wit t e fact t at is an essentia e ement in de i ering rofitab e growt f

ustra asian e ecuti es and oards do not successfu im ement an ac uisiti e growt strateg as art of t eir ca ita agenda g oba com etitors wi grow at t eir e ense t s a eriod of global ch an ge an d con solid ation an d u n preced en ted d isru ption — local com pan ies m u st eith er grow or becom e irrelevan t.

Apr Oct Apr Oct Apr Oct Apr Oct Apr Oct Apr Oct Apr Oct

2 0 10 2 0 11 2 0 12 2 0 13 2 0 14 2 0 15 2 0 16

Capital Confidence Barometer a era e 4 0 %

pectation to p r e an ac i ition in t e ne t mont

Au s an d NZ G lobal

61%

46%

36% 35%

57%

41%

38% 40% 31%

25%

29% 35%

30%40%

56% 59%50%

57%

31%

20%24%

34%

32%

66%

44% 53% 41%

41%

3Capital Confidence Barometer |

Key findings

Technology and digitalisation

Industry regulation

Primary Secondary

Changes in customer behaviour

96%expect the local M&A market to improve or stay the same in the next 12 months

65%have ≥5 deals in the pipeline

#1 driver of outside sector acquisitions

Key disruptors

89%cancelled or failed to complete an acquisition

41%expect to actively pursue M&A in the next 12 months (compared with 57% globally)

54%expect growth to come from M&A, JVs and alliances

EY’s Capital Confidence Barometer is a regular survey of 1,700+ senior executives from large companies around the world conducted by the Economist Intelligence Unit (EIU). The respondent community is comprised of an independent EIU panel of senior executives and select EY clients and contacts. This report from our 15th Barometer, carried out in August and September 2016, provides a snapshot of our local findings from 136 executives in Australia and New Zealand, in the context of global results.

4

Oct Apr Oct Apr Oct Apr Oct Apr Oct Apr Oct

2 0 11 2 0 12 2 0 13 2 0 14 2 0 15 2 0 16

M acroecon om ic en viron m en t

A u s t r a l i a a n d N e w Z e a l a n d

ocal econom lo al econom

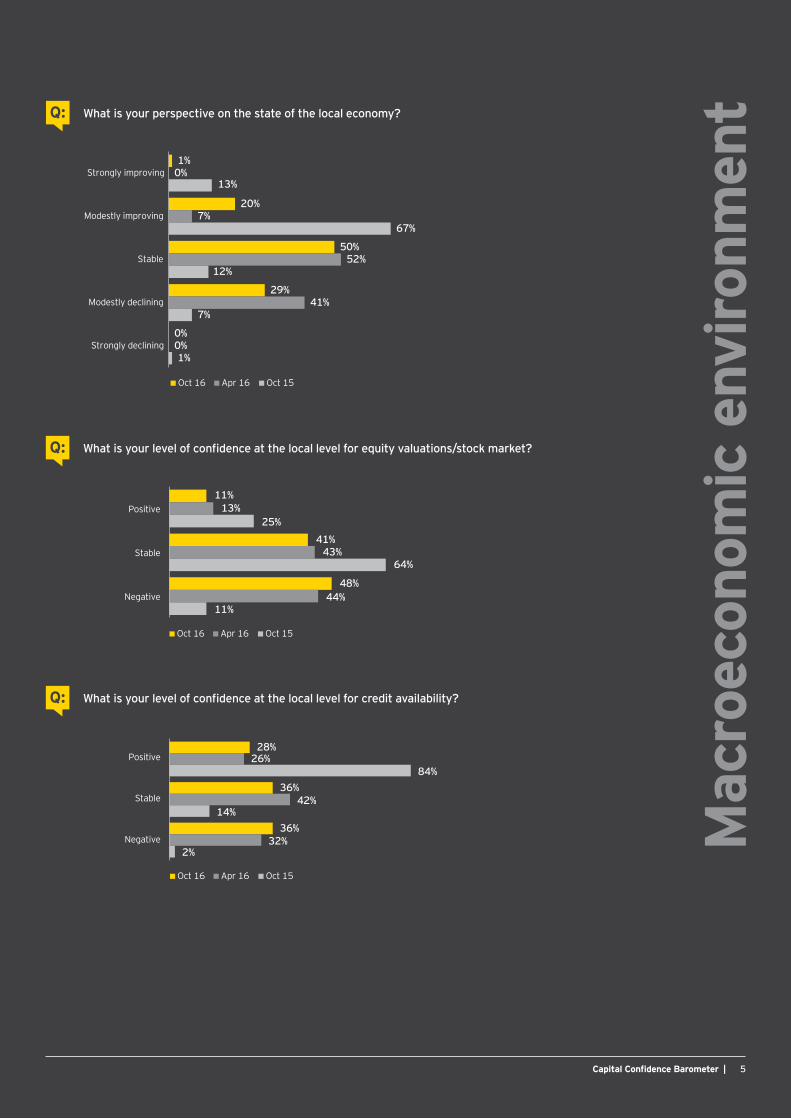

en before t e e ection ustra asian e ecuti es were u n settled by m ark et volatility an d slow in g grow th , particu larly in ig t of re it t e s owdown in ina and uncertaint surrounding

markets and its e ection outcome e ent one er cent of local respon d en ts saw th e global m ark ets as stable or m od estly im ro ing down from a ear ago

T ellin gly , local respon d en ts n ow view volatility in global capital markets and t e s owdown in g oba trade ows as t e rimar risks to t eir future growt strategies

Au stralasian ex ecu tives are m argin ally m ore positive abou t th e local econ om y th an th ey w ere six m on th s ago. T h e sligh t rebou n d in com m od ity prices, an d persisten t stren gth in con stru ction an d oth er sectors in a low in terest rate en viron m en t is d rivin g e ectations of a stabi ising oca econom

ore t an two t irds be ie e t e oca econom wi eith er rem ain stable or m od estly im prove.

at said are negati e about t e out ook of e uit valu ation s an d m ore th an a th ird ( 3 6% ) are con cern ed abou t cred it availability . T h is latter issu e m ay be d u e to B asel 3 capital re uirements and concern around credit ua it in t e cor orate sector w ic a e seen t e banks re weig ting t eir ortfo ios awa from cor orate oans to retai ome oans in t e ast 12 m on th s.

58%

84%74%

90%

90%95% 99% 100%

94%

72%

86%83%92%

82%89%

80%

96% 96% 98%92%

71%

59%

What is your perspective on the state of the local economy?Q:

What is your level of confidence at the local level for equity valuations/stock market?Q:

What is your level of confidence at the local level for credit availability?Q:

Mac

roec

onom

ic e

nviro

nmen

t

1%

20%

50%

29%

0%

0%

7%

52%

41%

0%

13%

67%

12%

7%

1%

Strongly improving

Modestly improving

Stable

Modestly declining

Strongly declining

Oct 16 Apr 16 Oct 15

Oct 16 Apr 16 Oct 15

Positive

Stable

Negative

28%

36%

36%

26%

42%

32%

84%

14%

2%

Oct 16 Apr 16 Oct 15

11%

41%

48%

13%

43%

44%

25%

64%

11%

Positive

Stable

Negative

Capital Confidence Barometer | 5

6

C orporate strategy

re local oard ndere timatin t e importance o di ital di r ptionigita tec no og is at t e to of t e agenda for g oba boards

but oca res ondents on ut it fourt on t eir ist be ow s are o der acti ism and identif ing o ortunities for growt t ma be t at t e oca agenda as mo ed on from a strategic board e e discussion to e ecution in t e form of ertain access to new tec no ogies was a ke dri er of in t eir own sector for oca com anies nd a most two t irds of oca ex ecu tives believe th at ad van ces in tech n ology an d d igitisation wi be one of t e to two disru tors to t eir core business o er th e n ex t 12 m on th s.

owe er t e findings a so suggest t at oca com anies ma be underestimating t e erfect storm of acce erating inno ation

sector con vergen ce an d ch an gin g cu stom er beh aviou r th at is d isru ptin g bu sin ess m od els arou n d th e globe. T h e rapid rise of new wa s of doing business redominant t roug digita c anne s and wit inno ati e wa s of using abour is ch an gin g operatin g m od els. G lobal com pan ies are respon d in g by reim agin in g th eir valu e proposition an d reorgan isin g th em selves to better com pete in a d igital w orld .

I n th is d isru ptive, rapid ly ch an gin g en viron m en t, in organ ic grow th can offer a uicker route to inno ation t an organic growt

M & A w ill be n eed ed to n avigate th e com plex ity an d d igital disru tion we see in t e market w ic is turbo c arging c anging con su m er beh aviors an d d rivin g sector con vergen ce.

o ld corporate do more to elp ape t e re lator en ironment went eig t ercent of oca res ondents be ie e t at industr

regu lation w ill be th e prim ary d isru ptor to th eir core bu sin ess over th e n ex t 12 m on th s.

e findings reinforce t e im ortance of regu ators and industr con tin u in g to w ork togeth er. G reater collaboration w ill create m ore robu st evid en ce bases an d en able better con versation s betw een regu lators an d in d u stry .

is wi e su ort t e de e o ment of fit for ur ose regu ation t at best manages t e ositi e and negati e effects of disru ti e forces and a ortions t e regu ator burden more e uitab

Q :

28%

20%

15%

14%

13%

10%

I n d u stry regu lation

Prod u ct in n ovation

Sector con vergen ce/ in creasecom petition f rom com pan ies in

oth er sectors

I n creasin g globalisation

C h an gin g cu stom er beh avioran d ex pectation s

Ad van ces in tech n ologyan d d igitalisation

14%

8%

13%

5%

7%

53%

Prim ary d isru ptor Secon d ary d isru ptor

Q :

30%

19%

16%

15%

10%

10%

9%

7%

6%

18%

4%

56%

Sh areh old er activism , in clu d in gretu rn in g cash to sh areh old ers

I d en tif y in g opportu n ities f or grow thin clu d in g M & A, J V s an d allian ces

Portf olio an aly sis, in clu d in g strategicd ivestm en t ( spin - of f / I PO)

I m pact of d igital tech n ology on y ou rbu sin ess m od el, e. g. , n ew sales

ch an n els/ m ark ets, I oT , C y bersecu rityI m pact of in creased econ om ic an d

political in stability

Sector con vergen ce/ in creasedcom petition f rom com pan ies

in oth er sectors

M ost important S econd most important

34%

19%

16%

12%

11%

8%

20%

10%

9%

9%

10%

42%

I m pact of d igital tech n ology ony ou r bu sin ess m od el, e. g. , n ewsales ch an n els/ m ark ets, I oT , …

G lobalA ustralia and New Z ealand

Sh areh old er activism , in clu d in gretu rn in g cash to sh areh old ers

I d en tif y in g opportu n ities f or grow th , in clu d in g M & A, J V s an d allian ces

I m pact of in creased econ om ican d political in stability

Portf olio an aly sis, in clu d in gstrategic d ivestm en t ( spin - of f / I PO)

Sector con vergen ce/ in creased com petition f rom com pan ies in oth er sectors

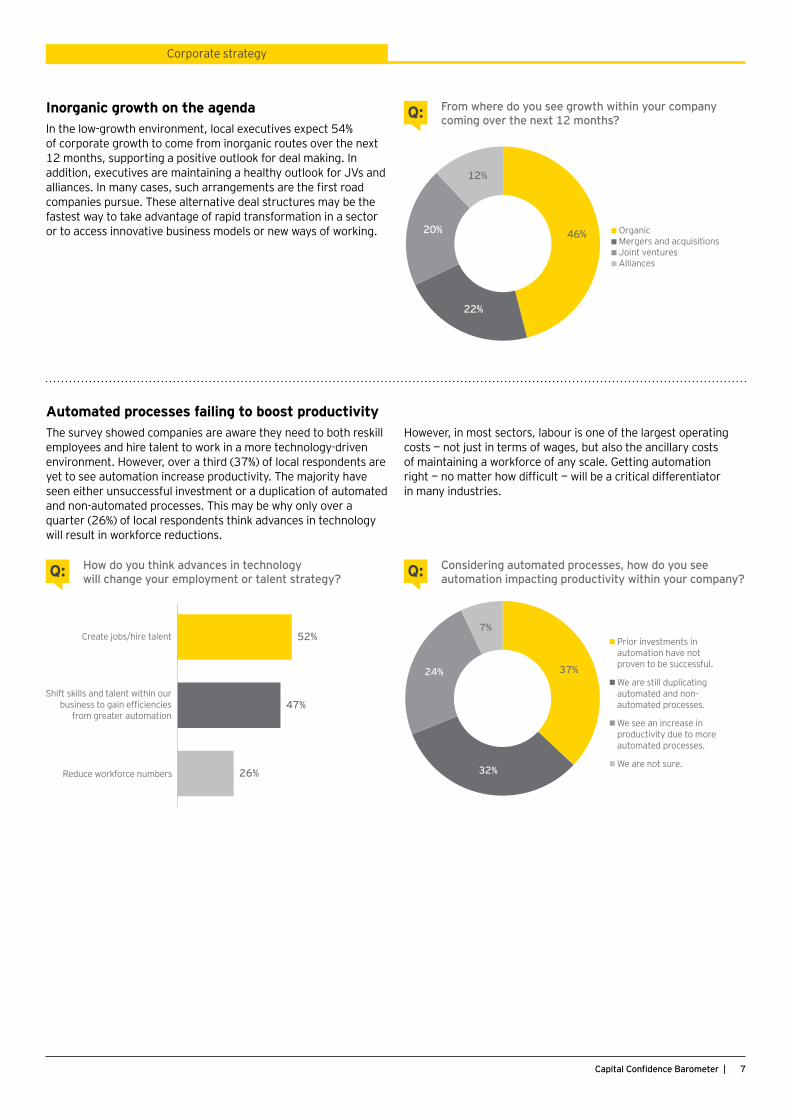

I n o r g a n i c g r o w t h o n t h e a g e n d an t e ow growt en ironment oca e ecuti es e ect of cor orate growt to come from inorganic routes o er t e ne t

mont s su orting a ositi e out ook for dea making n addition e ecuti es are maintaining a ea t out ook for s and a iances n man cases suc arrangements are t e first road com pan ies pu rsu e. T h ese altern ative d eal stru ctu res m ay be th e fastest wa to take ad antage of ra id transformation in a sector or to access inno ati e business mode s or new wa s of working

7

tomated proce e ailin to oo t prod cti itT h e su rvey sh ow ed com pan ies are aw are th ey n eed to both resk ill em o ees and ire ta ent to work in a more tec no og dri en en ironment owe er o er a t ird of oca res ondents are y et to see au tom ation in crease prod u ctivity . T h e m aj ority h ave seen eit er unsuccessfu in estment or a du ication of automated and non automated rocesses is ma be w on o er a

uarter of oca res ondents t ink ad ances in tec no og wi resu t in workforce reductions

owe er in most sectors abour is one of t e argest o erating costs not ust in terms of wages but a so t e anci ar costs of maintaining a workforce of an sca e etting automation rig t no matter ow difficu t wi be a critica differentiator in m an y in d u stries.

C orporate strategy

Q :

Q : Q :

46%

22%

20%

12%

Organ icM ergers an d acq u isition sJ oin t ven tu resAllian ces

37%

32%

24%

7%Prior in vestm en ts inau tom ation h ave n ot proven to be su ccessf u l.

W e are still d u plicatin gau tom ated an d n on -au tom ated processes.

W e see an in crease inprod u ctivity d u e to m oreau tom ated processes.

W e are n ot su re.

52%

47%

26%

C reate j obs/ h ire talen t

Sh if t sk ills an d talen t w ith in ou rbusiness to gain efficiencies

f rom greater au tom ation

Reduce workforce numbers

Q :

Oct 16 Apr 16 Oct 15

49%

47%

4%

16%

60%

24%

47%

47%

6%

I m prove

Stay th e sam e

D eclin e

Oct 16 Apr 16 Oct 15

65%

29%

2%

0%

4%

32%

27%

22%

15%

4%

35%

23%

25%

14%

3%

≥5

4

3

2

1

Oct 16 Apr 16 Oct 15

0%

9%

77%

14%

0%

38%

31%

31%

1%

1%

6%

92%

G reater th an U S$ 5b

U S$ 1. 1b – U S$ 5b

U S$ 2 51m – U S$ 1b

U S$ 0 – U S$ 2 50 m

8

Q :Q :

M & A ou tlook

W ith sh areh old ers con tin u in g to d em an d h igh top lin e an d earn in gs grow th , an d on ly low organ ic grow th rates available to m ost com pan ies, it’ s h ard to im agin e h ow ex ecu tives w ill d eliver acce tab e rofitab e growt wit out regaining t eir a etite for dea making er a s t is is w of res ondents be ie e oca M & A m ark ets w ill stay th e sam e or im prove over th e n ex t y ear.

ore t maller deal in t e pipelinearger dea i e ines a so su ort a future u tick in acti it ecuti es re ort a big increase in t e number of otentia targets

t e are re iewing wit sa ing t e a e fi e or more dea s in t eir ac uisition i e ines and e ecting t e i e ine to in crease in th e n ex t 12 m on th s.

B u t d eals in th e pipelin e are gettin g sm aller — an d sm arter. T h e ig t to sma er transactions fo ows t e wor dwide trend in

w ic as been s ifting towards mid ca si ed dea s it a degree of conser atism in boards com anies are de risking t eir ac uisiti e growt strategies b ooking for strategic bo t ons of c ose a igned businesses to fi s ecific ortfo io or ca abi it ga s rat er t an undertake riskier transformations

i en t e a ai abi it of ca ita and t e sma er si e of target ac uisitions res ondents e ect dea com etions to acce erate in th e n ex t 12 m on th s. T h ose com pan ies th at regu larly u n d ertak e bo t on ac uisitions wi bui d t eir cor orate ca abi it and ca acit to s ot e ecute and de i er a ue from integration

c uisition targets ike to de i er growt more readi and at low er risk , in clu d e: d irect com petitors, su ppliers, d istribu tors, peers in geograph ies w h ere th e com pan y d oes n ot cu rren tly operate an d im m ed iately ad j acen t in d u stries.

Q :

1%

12%

87%

18%

55%

27%

23%

47%

30%

D ecrease

No ch an ge

I n crease

Oct 16 Apr 16 Oct 15

22%

22%

19%

16%

16%

5%

10%

6%

13%

22%

11%

38%

I n vestor or board scru tin y

C om petition f rom oth er bu y ers

G ap betw een bu y er an d sellerex pectation s too w id e

I ssu es u n covered d u rin g d u e d iligen ce

C on cern s abou t regu latoryor an titru st review s

E con om ic an d political in stability

M ost im portan tSecon d m ost im portan t

60%

30%

10%

55%

29%

16%

78%

17%

5%

Positive

Stable

Negative

21%

50%

29%

25%

51%

24%

85%

8%

7%

Positive

Stable

Negative

Number of acquisition opportunities

Likelihood of closing acquisitions

Oct 16 Apr 16 Oct 15

9

M & A ou tlook

Q : Q :

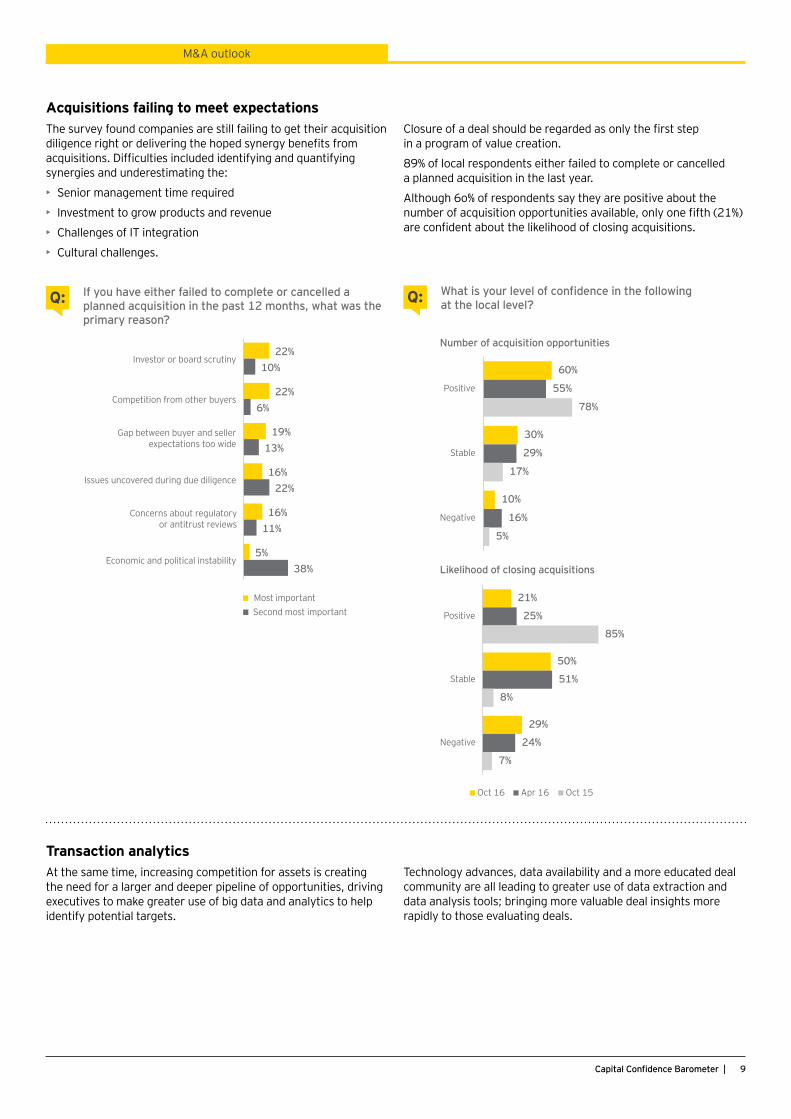

c i ition ailin to meet e pectatione sur e found com anies are sti fai ing to get t eir ac uisition

di igence rig t or de i ering t e o ed s nerg benefits from ac uisitions ifficu ties inc uded identif ing and uantif ing sy n ergies an d u n d erestim atin g th e:

• enior management time re uired

• I n vestm en t to grow prod u cts an d reven u e

• a enges of integration

• C u ltu ral ch allen ges.

osure of a dea s ou d be regarded as on t e first ste in a rogram of a ue creation

of oca res ondents eit er fai ed to com ete or cance ed a anned ac uisition in t e ast ear

t oug o of res ondents sa t e are ositi e about t e number of ac uisition o ortunities a ai ab e on one fift are confident about t e ike i ood of c osing ac uisitions

ran action anal tict t e same time increasing com etition for assets is creating

t e need for a arger and dee er i e ine of o ortunities dri ing e ecuti es to make greater use of big data and ana tics to e identif otentia targets

T ech n ology ad van ces, d ata availability an d a m ore ed u cated d eal communit are a eading to greater use of data e traction and d ata an aly sis tools; brin gin g m ore valu able d eal in sigh ts m ore rapid ly to th ose evalu atin g d eals.

10

Bre it concern no lon er a top in e tment de tination co ld t e ollo it

efore t e e ection g oba and oca res ondents were ursuing ac uisitions wit in t e ke de e o ed and argest emerging economies but t e ost re it was a notab e e ce tion nstead t e referred destinations of t e of oca res ondents ursuing outbound in estment were t e ina and erman

ereas si mont s ago t e was t e fourt most o u ar destination and erman didn t make t e to fi e ist oba and oca e ecuti es a e a ower degree of confidence to in est h eavily in to d evelopin g cou n tries, as th e risk s in h eren t in th ose cou n tries h ave proven to be real.

W ith a T ru m p presid en cy , it w ill be in terestin g to see w h eth er e ecuti e a etite for in estment wanes at east unti t e n ew ad m in istration ’ s policy d irection becom es clear.

M & A ou tlook

Q :

T op d estin ation s are based on a w eigh ted scorin g of res ondents to t ree in estment destinations in order of im ortance

1 3

25

4

As in previou s B arom eters, th e k ey d eveloped an d largest em ergin g econ om ies d om in ate ex ecu tives’ in vestm en t plan s.

Global contactsSteve KrouskosEY Global Vice Chair Transaction Advisory Services EY Global Limited [email protected] +44 20 7980 0346 Follow me on Twitter: @SteveKrouskos

Julie HoodEY Deputy Global Vice Chair Transaction Advisory Services EY Global Limited [email protected] +44 20 7980 0327 Follow me on Twitter: @JulieHood

11Capital Confidence Barometer |

For a conversation about your capital strategy, please contact us:

David LaroccaTransaction Advisory Services Leader+61 2 9248 [email protected]

Jeremy Barker Consumer and Industrial Products +61 2 9276 9821

Richard Bowman Real Estate +61 3 9288 8085

Stuart Bright Valuations & Business Modelling +61 2 8295 6483

Nick Cardno Energy +61 2 9248 4817

Tim Coyne Financial Services +61 3 9288 8056

Andrew Ettridge Middle Market +61 2 9248 4588

Darrin Grimsey Government and Public Sector +61 3 9655 2519

Grant Hodges New Zealand +64 9 300 8027

Ishwar Madhyastha Technology, Media & Entertainment and Telecommunications +61 2 9248 5865

Peter Magill Mergers and Acquisitions +61 8 9217 1330

John Matthews Infrastructure Advisory +61 3 9288 8830

Paul Murphy Markets Leader and Mining & Metals +61 3 9288 8708

Gary Nicholson Transaction Support +61 3 9288 8704

Adam Nikitins Corporate Restructuring +61 3 8650 7528

Daryn Saretzki Operational Transactions Services +61 2 8295 6638

Marcus Willison Real Estate Advisory Services +61 3 8650 7270

Julie Wolstenholme Australian Diversified Business +61 2 8295 6876

Reid Zulpo Transaction Tax +61 7 3243 3772

Contacts

E Y | Assu ran ce | T ax | T ran saction s | Ad visory

A b o u t E YE Y is a global lead er in assu ran ce, tax , tran saction an d ad visory ser ices e insig ts and ua it ser ices we de i er e bui d trust and confidence in t e ca ita markets and in economies th e w orld over. W e d evelop ou tstan d in g lead ers w h o team to de i er on our romises to a of our stake o ders n so doing we a a critica ro e in bui ding a better working wor d for our

eo e for our c ients and for our communities

refers to t e g oba organi ation and ma refer to one or more of t e member firms of rnst oung oba imited eac of w ic is a se arate ega entit rnst oung oba

imited a com an imited b guarantee does not ro ide ser ices to c ients or more information about

our organi ation ease isit e com

o t ran action d i or er iceow ou manage our ca ita agenda toda wi define

y ou r com petitive position tom orrow . W e w ork w ith clien ts to create social an d econ om ic valu e by h elpin g th em m ak e better more informed decisions about strategica managing ca ita and transactions in fast c anging markets et er ou re reser ing o timi ing raising or in esting ca ita s ransaction d isor er ices combine a set of ski s insig t

and e erience to de i er focused ad ice e can e ou dri e com petitive ad van tage an d in creased retu rn s th rou gh im proved decisions across a as ects of our ca ita agenda

© 2 0 16 E rn st & Y ou n g, Au stralia. All R igh ts R eserved .

o E D Non e

is materia as been re ared for genera informationa ur oses on and is not intended to be re ied u on as accounting ta or ot er rofessiona ad ice ease refer to our ad isors for s ecific ad ice

Abou t th is su rveyT h e Global Capital Confidence Barometer gau ges cor orate confidence in t e economic out ook and identifies boardroom trends and ractices in th e w ay com pan ies m an age th eir C apital

gendas s framework for strategica m an agin g capital.

e arometer is a regu ar sur e of senior e ecuti es from large com pan ies arou n d th e w orld , con d u cted by th e E con om ist nte igence nit ur ane com rises se ected g oba c ients and contacts and regu ar contributors

n ugust and e tember we sur e ed a ane of more t an 1, 7 0 0 ex ecu tives in 4 5 cou n tries. Nearly 50 % w ere C E Os, C F Os and ot er e e e ecuti es e ecuti es were sur e ed from t e

Res ondents re resented sectors inc uding financia ser ices consumer roducts and retai tec no og ife scien ces, au tom otive an d tran sportation , oil an d gas, pow er an d uti ities mining and meta s di ersified industria roducts and con stru ction an d real estate.

ur e ed com anies annua g oba re enues were as fo ows ess t an m m m

b b b b and greater t an b

oba com an owners i was as fo ows ub ic isted ri ate owned fami owned

and go ernment state owned