Embed Size (px)

Citation preview

Australia’s International Business Survey 2017

2

3

AIB

S 2017

Table of contents

Research team and partners ................................................................................................................. 4

Glossary of terms ..................................................................................................................................... 5

Executive summary ................................................................................................................................. 6

1 Introduction ..................................................................................................................................... 10

2 1) The diversity of Australia’s international business activity ........................................... 14

2.1 Internationalbusinessactivities......................................................................................................16

2.2 Internationalrevenuefrominternationalactivity.................................................................... 24

2.3 Internationaltradeambitions......................................................................................................... 32

3 2) Australia’s international business activity in focus .......................................................... 34

3.1 Accesstofinance................................................................................................................................ 37

3.2Australia’sfreetradeagreement(FTA)activity...................................................................... 39

3.3Barrierstocommencinginternationaltrade............................................................................. 57

3.4Trade-relatedfactorsInfluencingInternationalrevenue..................................................... 60

4 3) Innovation in Australia’s international business activity, and future outlook ........... 62

4.1 Innovationbusinessactivityandexportsales..........................................................................64

4.2Internationaloperations–futureoutlook..................................................................................66

Appendix A – AIBS methodology ...................................................................................................... 69

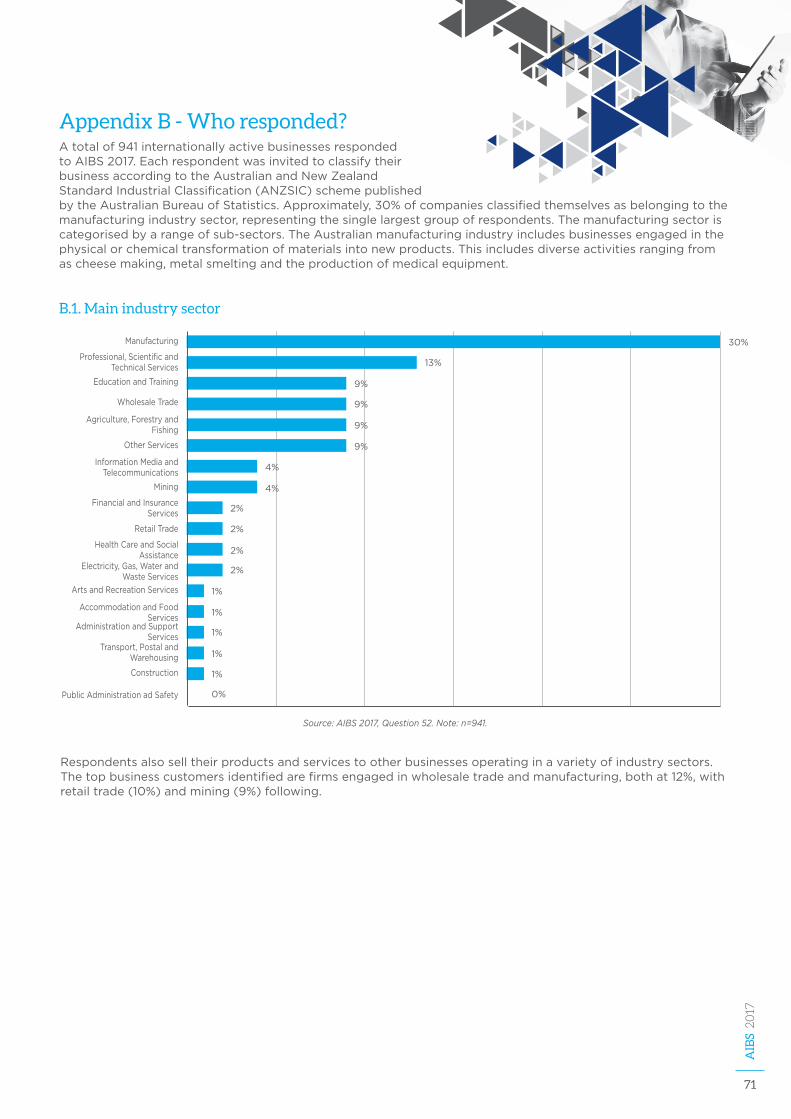

Appendix B - Who responded? .......................................................................................................... 71

Reference list .......................................................................................................................................... 77

4

Research team and partners

Research investigators

AssociateProfessorRenuAgarwal

AssociateProfessorChrisBajada

ProfessorRoyGreen

DrHussainRammal

DrMoiraScerri

Research associates

MsKatrinaSkellern

Research assistants

MsSamanthaLuff

MrStephenSoco

DrMikhailShashnov

Contributing authors

LisaMcAuley

GeirKristiansen

Citation

Agarwal,R.,Bajada,C.,Green,R.,Rammal,H.,Scerri,M.(2017).Australia’sInternationalBusinessSurvey2017,UniversityofTechnologySydney.

For further information about this research study, please contact Associate Professor Renu Agarwal at email address: [email protected].

5

AIB

S 2017

Glossary of terms

AANZFTA ASEAN-Australia-NewZealandFreeTradeArea

Austrade AustralianTradeandInvestmentCommission

ABS AustralianBureauofStatistics

AMR AdvancedMarketingResearch

ANZSIC AustralianandNewZealandStandardIndustrialClassification

CBSI CentreforBusinessandSocialInnovation

CoO CertificateofOrigin

DFAT DepartmentofForeignAffairsandTrade

ECA ExportCouncilofAustralia

Efic ExportFinanceandInsuranceCorporation

FTA FreeTradeAgreement

GVCs GlobalValueChains

IP IntellectualProperty

LNG LiquefiedNaturalGas

MRA MutualRecognitionAgreement

RoO RulesofOrigin

SMEs SmalltoMediumEnterprises

UTS UniversityofTechnologySydney

6

Executive summary

Australianbusinessescontributesignificantlytoeconomicgrowththroughcommercialactivityininternationalmarkets.Theseareasofactivityinclude:foreigndirectinvestment,tradeingoodsandservices,andotherinternationalactivities–suchasmanufacturingproductsoverseasthroughlicensing,undertakingR&Doverseasandemploymentoftemporarystaff.

Since2014,Australia’sInternationalBusinessSurvey(AIBS)hasaidedintheunderstandingofAustralia’sinternationalbusinessactivity,aswellinevaluatingtheimpactofinternationaleconomictrendsonAustralianbusinesses.

Thisyear,theExportCouncilofAustralia(ECA)commissionedtheCentreforBusinessandSocialInnovation(CBSI)attheUniversityofTechnologySydney(UTS)toconducttheresearchstudyandproducetheAIBS2017Report.

Atotalof1068AustralianbusinessesweresurveyedforAIBS2017,ofwhich941wereengagedininternationalbusinessactivity.Theremaining127respondentswerenotcurrentlyinvolvedininternationalbusinessactivity,andinsteadrespondedbyhighlightingareasthatcouldassisttheminengaginginsuchactivities.

ThisreportanalysesAIBS2017responsesinthecontextofthefollowingareas:

1) ThediversityofAustralia’sinternationalbusinessactivity

2) Australia’sinternationalbusinessactivityinfocus

3) InnovationinAustralia’sinternationalbusinessactivity,andfutureoutlook

7

AIB

S 2017

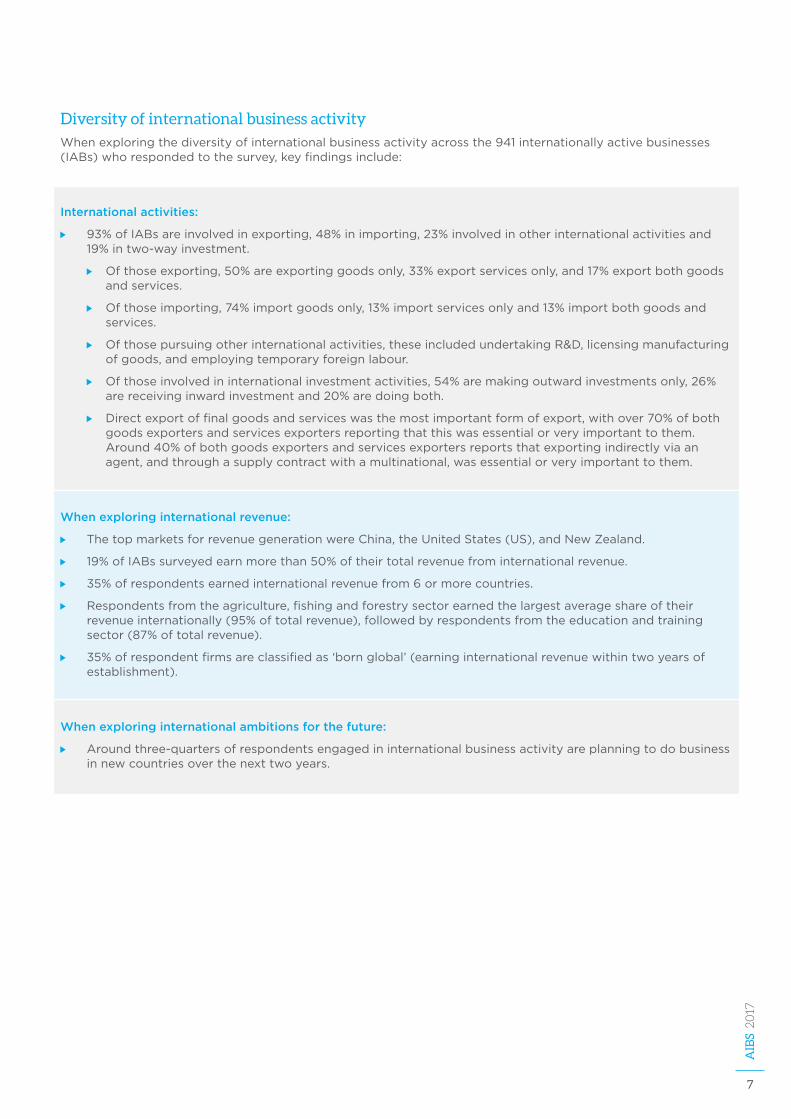

Diversity of international business activity

Whenexploringthediversityofinternationalbusinessactivityacrossthe941internationallyactivebusinesses(IABs)whorespondedtothesurvey,keyfindingsinclude:

International activities:

93%ofIABsareinvolvedinexporting,48%inimporting,23%involvedinotherinternationalactivitiesand19%intwo-wayinvestment.

Ofthoseexporting,50%areexportinggoodsonly,33%exportservicesonly,and17%exportbothgoodsandservices.

Ofthoseimporting,74%importgoodsonly,13%importservicesonlyand13%importbothgoodsandservices.

Ofthosepursuingotherinternationalactivities,theseincludedundertakingR&D,licensingmanufacturingofgoods,andemployingtemporaryforeignlabour.

Ofthoseinvolvedininternationalinvestmentactivities,54%aremakingoutwardinvestmentsonly,26%arereceivinginwardinvestmentand20%aredoingboth.

Directexportoffinalgoodsandserviceswasthemostimportantformofexport,withover70%ofbothgoodsexportersandservicesexportersreportingthatthiswasessentialorveryimportanttothem.Around40%ofbothgoodsexportersandservicesexportersreportsthatexportingindirectlyviaanagent,andthroughasupplycontractwithamultinational,wasessentialorveryimportanttothem.

When exploring international revenue:

ThetopmarketsforrevenuegenerationwereChina,theUnitedStates(US),andNewZealand.

19%ofIABssurveyedearnmorethan50%oftheirtotalrevenuefrominternationalrevenue.

35%ofrespondentsearnedinternationalrevenuefrom6ormorecountries.

Respondentsfromtheagriculture,fishingandforestrysectorearnedthelargestaverageshareoftheirrevenueinternationally(95%oftotalrevenue),followedbyrespondentsfromtheeducationandtrainingsector(87%oftotalrevenue).

35%ofrespondentfirmsareclassifiedas‘bornglobal’(earninginternationalrevenuewithintwoyearsofestablishment).

When exploring international ambitions for the future:

Aroundthree-quartersofrespondentsengagedininternationalbusinessactivityareplanningtodobusinessinnewcountriesoverthenexttwoyears.

8

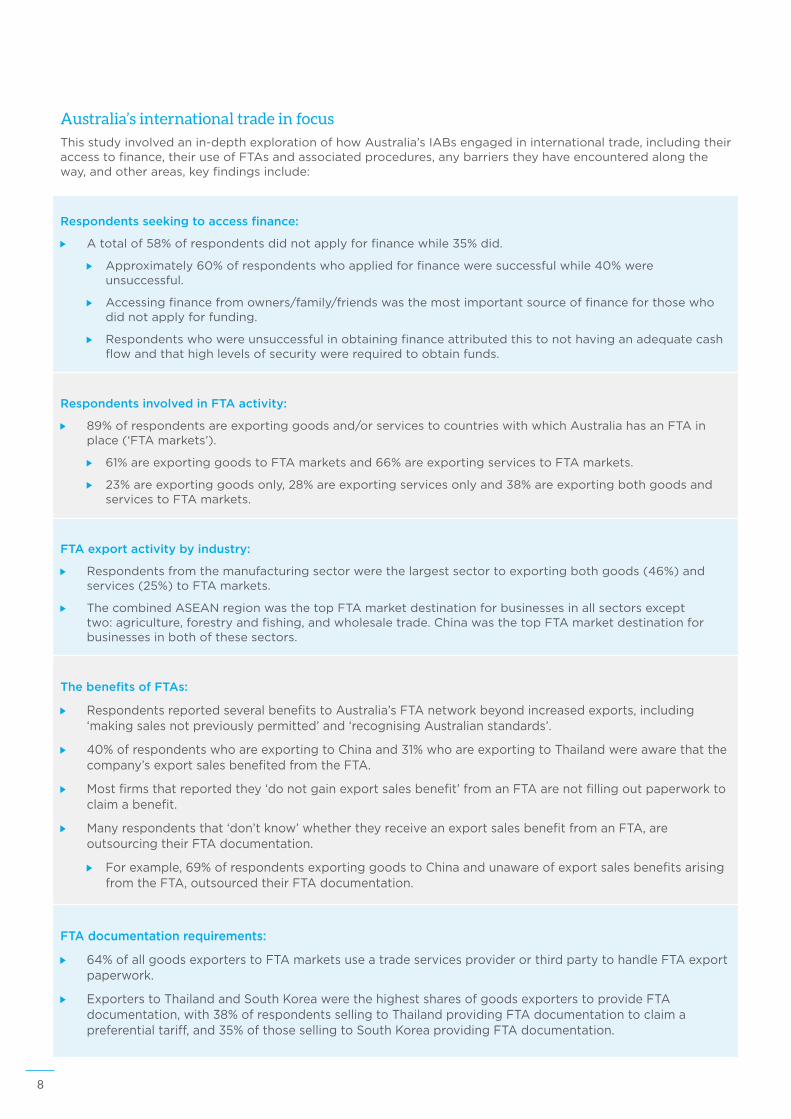

Australia’s international trade in focus

Thisstudyinvolvedanin-depthexplorationofhowAustralia’sIABsengagedininternationaltrade,includingtheiraccesstofinance,theiruseofFTAsandassociatedprocedures,anybarrierstheyhaveencounteredalongtheway,andotherareas,keyfindingsinclude:

Respondents seeking to access finance:

Atotalof58%ofrespondentsdidnotapplyforfinancewhile35%did.

Approximately60%ofrespondentswhoappliedforfinanceweresuccessfulwhile40%wereunsuccessful.

Accessingfinancefromowners/family/friendswasthemostimportantsourceoffinanceforthosewhodidnotapplyforfunding.

Respondentswhowereunsuccessfulinobtainingfinanceattributedthistonothavinganadequatecashflowandthathighlevelsofsecuritywererequiredtoobtainfunds.

Respondents involved in FTA activity:

89%ofrespondentsareexportinggoodsand/orservicestocountrieswithwhichAustraliahasanFTAinplace(‘FTAmarkets’).

61%areexportinggoodstoFTAmarketsand66%areexportingservicestoFTAmarkets.

23%areexportinggoodsonly,28%areexportingservicesonlyand38%areexportingbothgoodsandservicestoFTAmarkets.

FTA export activity by industry:

Respondentsfromthemanufacturingsectorwerethelargestsectortoexportingbothgoods(46%)andservices(25%)toFTAmarkets.

ThecombinedASEANregionwasthetopFTAmarketdestinationforbusinessesinallsectorsexcepttwo:agriculture,forestryandfishing,andwholesaletrade.ChinawasthetopFTAmarketdestinationforbusinessesinbothofthesesectors.

The benefits of FTAs:

RespondentsreportedseveralbenefitstoAustralia’sFTAnetworkbeyondincreasedexports,including‘makingsalesnotpreviouslypermitted’and‘recognisingAustralianstandards’.

40%ofrespondentswhoareexportingtoChinaand31%whoareexportingtoThailandwereawarethatthecompany’sexportsalesbenefitedfromtheFTA.

Mostfirmsthatreportedthey‘donotgainexportsalesbenefit’fromanFTAarenotfillingoutpaperworktoclaimabenefit.

Manyrespondentsthat‘don’tknow’whethertheyreceiveanexportsalesbenefitfromanFTA,areoutsourcingtheirFTAdocumentation.

Forexample,69%ofrespondentsexportinggoodstoChinaandunawareofexportsalesbenefitsarisingfromtheFTA,outsourcedtheirFTAdocumentation.

FTA documentation requirements:

64%ofallgoodsexporterstoFTAmarketsuseatradeservicesproviderorthirdpartytohandleFTAexportpaperwork.

ExporterstoThailandandSouthKoreawerethehighestsharesofgoodsexporterstoprovideFTAdocumentation,with38%ofrespondentssellingtoThailandprovidingFTAdocumentationtoclaimapreferentialtariff,and35%ofthosesellingtoSouthKoreaprovidingFTAdocumentation.

9

AIB

S 2017

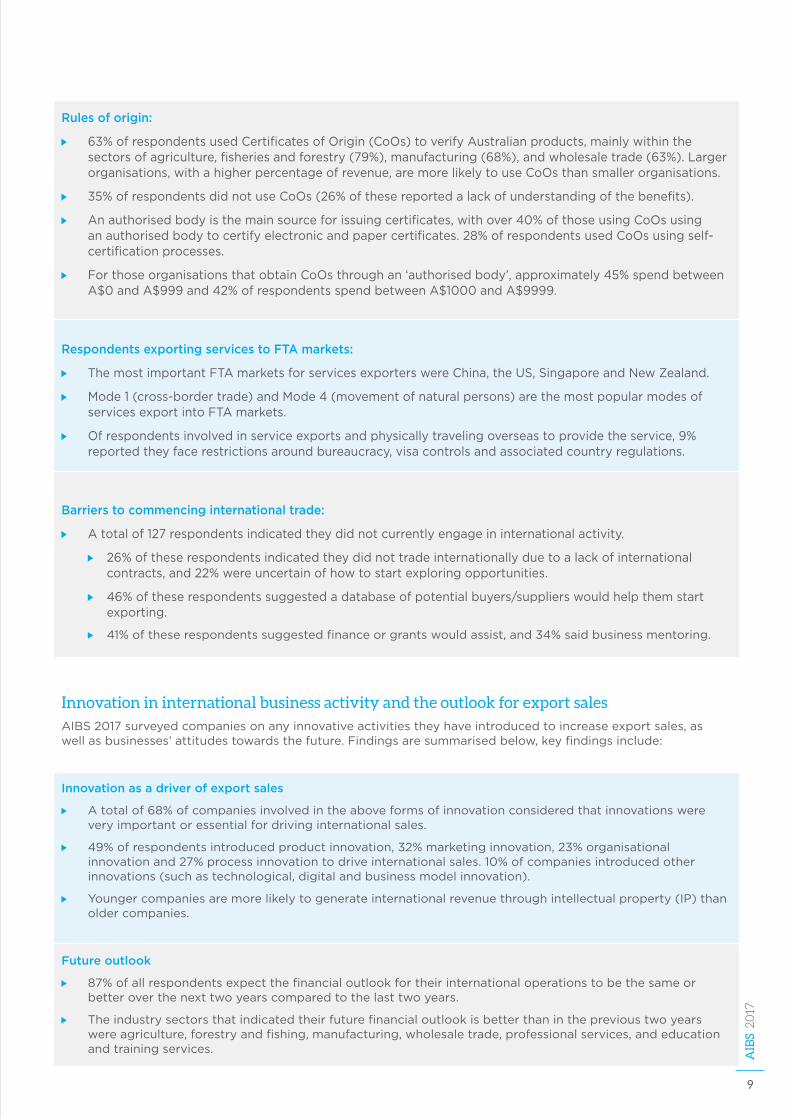

Rules of origin:

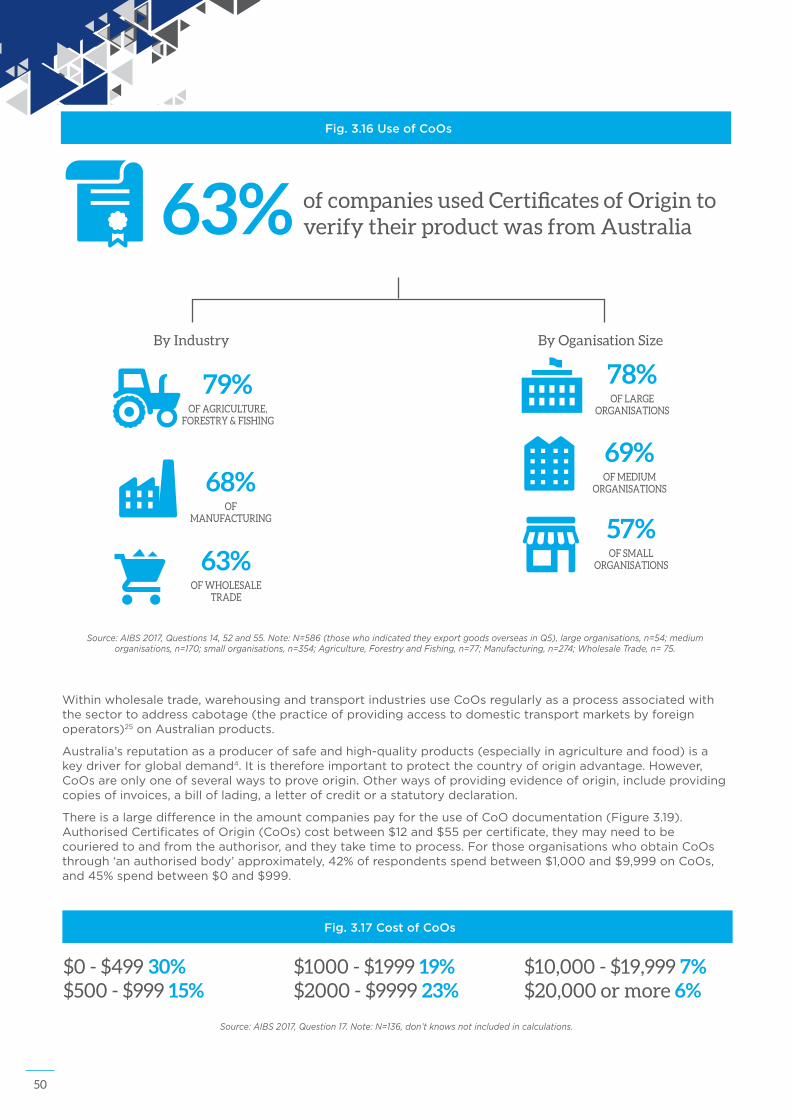

63%ofrespondentsusedCertificatesofOrigin(CoOs)toverifyAustralianproducts,mainlywithinthesectorsofagriculture,fisheriesandforestry(79%),manufacturing(68%),andwholesaletrade(63%).Largerorganisations,withahigherpercentageofrevenue,aremorelikelytouseCoOsthansmallerorganisations.

35%ofrespondentsdidnotuseCoOs(26%ofthesereportedalackofunderstandingofthebenefits).

Anauthorisedbodyisthemainsourceforissuingcertificates,withover40%ofthoseusingCoOsusinganauthorisedbodytocertifyelectronicandpapercertificates.28%ofrespondentsusedCoOsusingself-certificationprocesses.

ForthoseorganisationsthatobtainCoOsthroughan‘authorisedbody’,approximately45%spendbetweenA$0andA$999and42%ofrespondentsspendbetweenA$1000andA$9999.

Respondents exporting services to FTA markets:

ThemostimportantFTAmarketsforservicesexporterswereChina,theUS,SingaporeandNewZealand.

Mode1(cross-bordertrade)andMode4(movementofnaturalpersons)arethemostpopularmodesofservicesexportintoFTAmarkets.

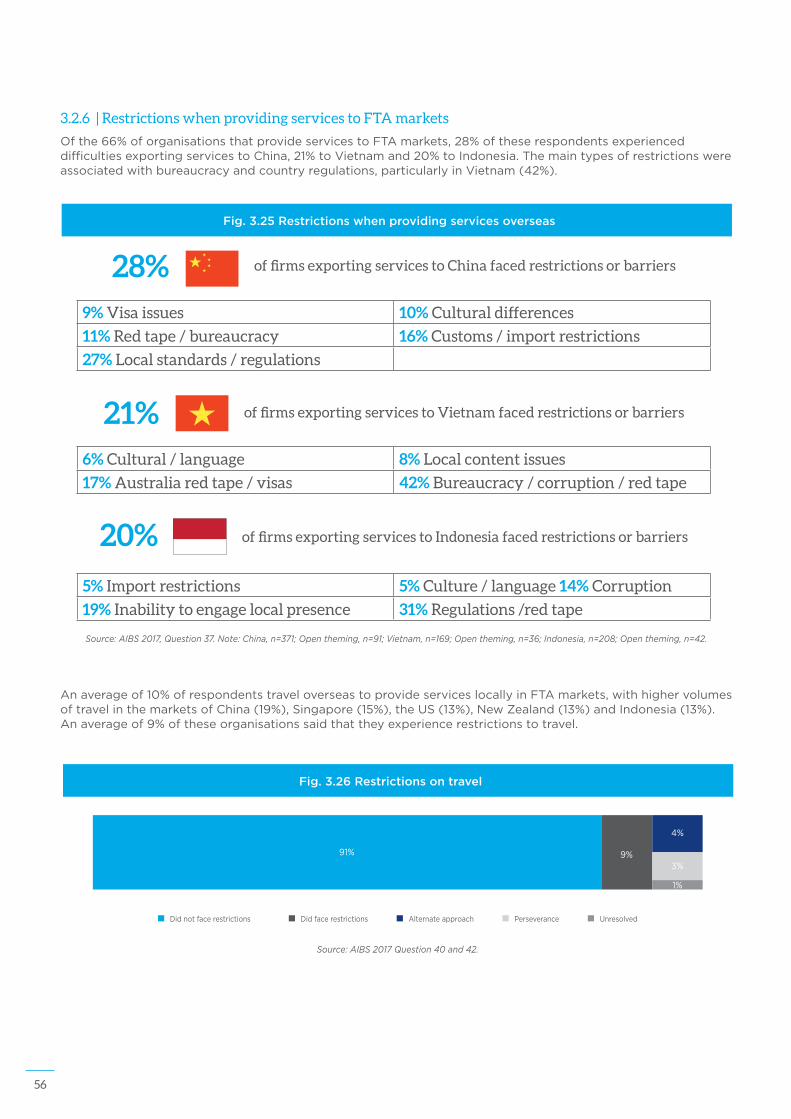

Ofrespondentsinvolvedinserviceexportsandphysicallytravelingoverseastoprovidetheservice,9%reportedtheyfacerestrictionsaroundbureaucracy,visacontrolsandassociatedcountryregulations.

Barriers to commencing international trade:

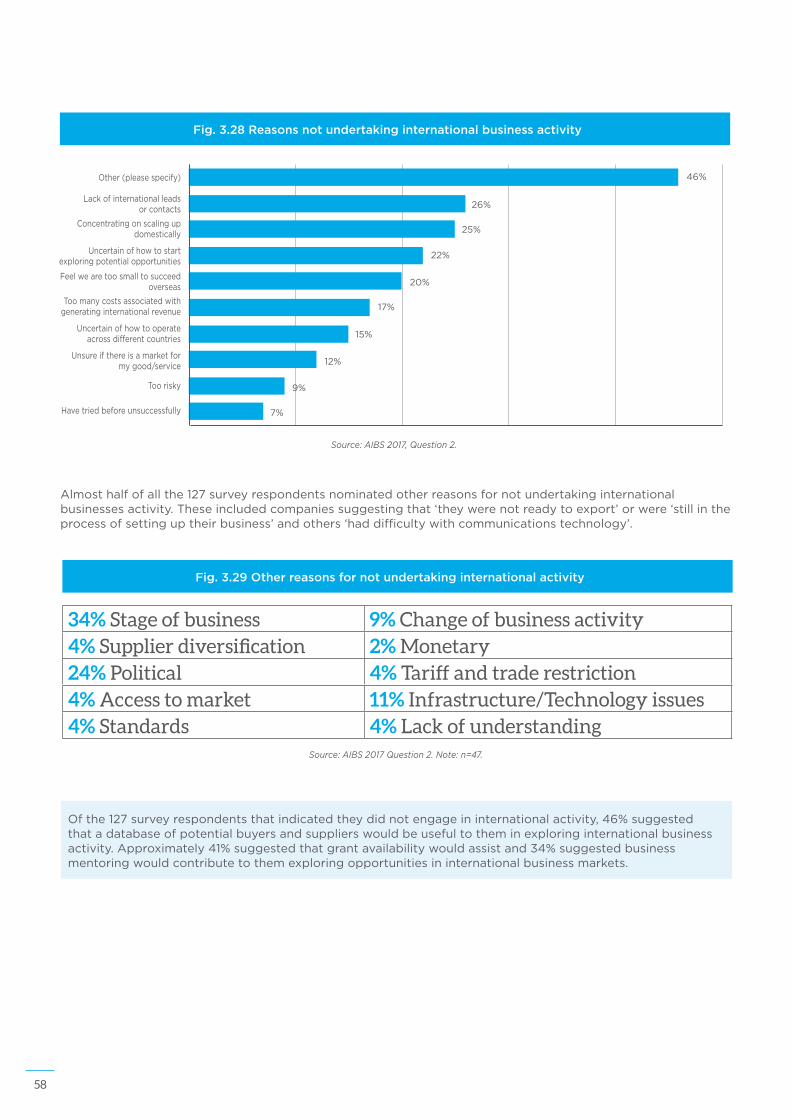

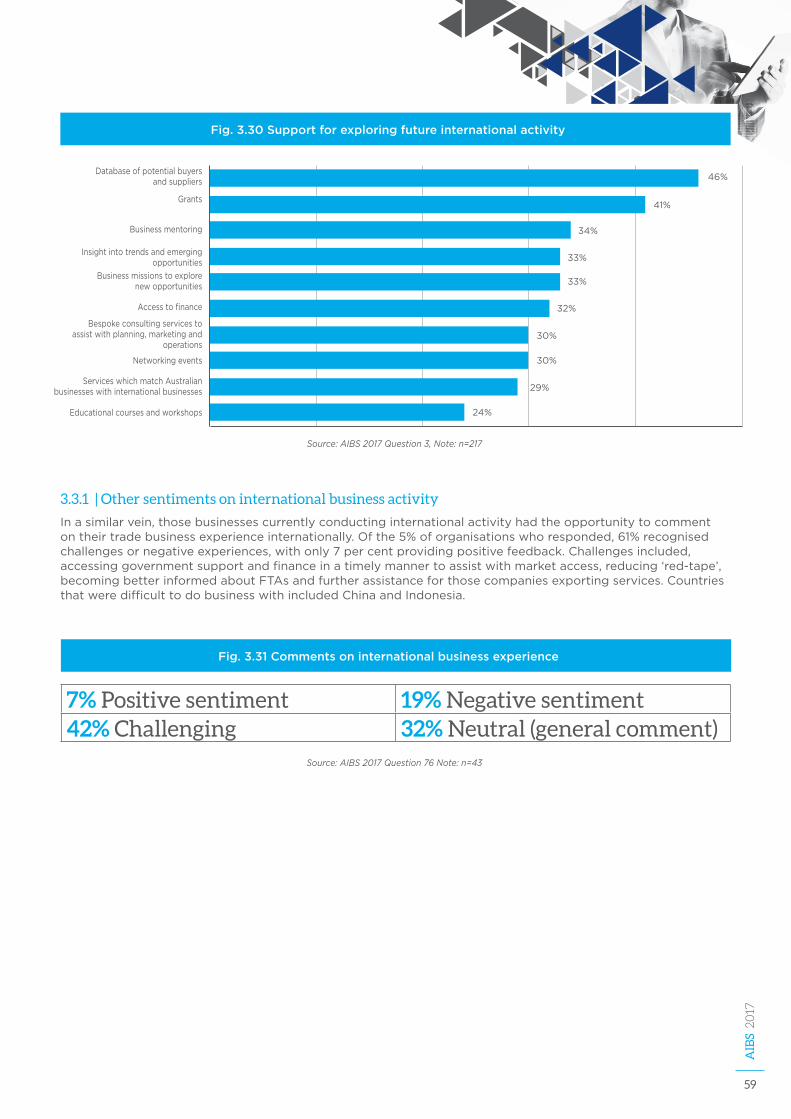

Atotalof127respondentsindicatedtheydidnotcurrentlyengageininternationalactivity.

26%oftheserespondentsindicatedtheydidnottradeinternationallyduetoalackofinternationalcontracts,and22%wereuncertainofhowtostartexploringopportunities.

46%oftheserespondentssuggestedadatabaseofpotentialbuyers/supplierswouldhelpthemstartexporting.

41%oftheserespondentssuggestedfinanceorgrantswouldassist,and34%saidbusinessmentoring.

Innovation in international business activity and the outlook for export sales

AIBS2017surveyedcompaniesonanyinnovativeactivitiestheyhaveintroducedtoincreaseexportsales,aswellasbusinesses’attitudestowardsthefuture.Findingsaresummarisedbelow,keyfindingsinclude:

Innovation as a driver of export sales

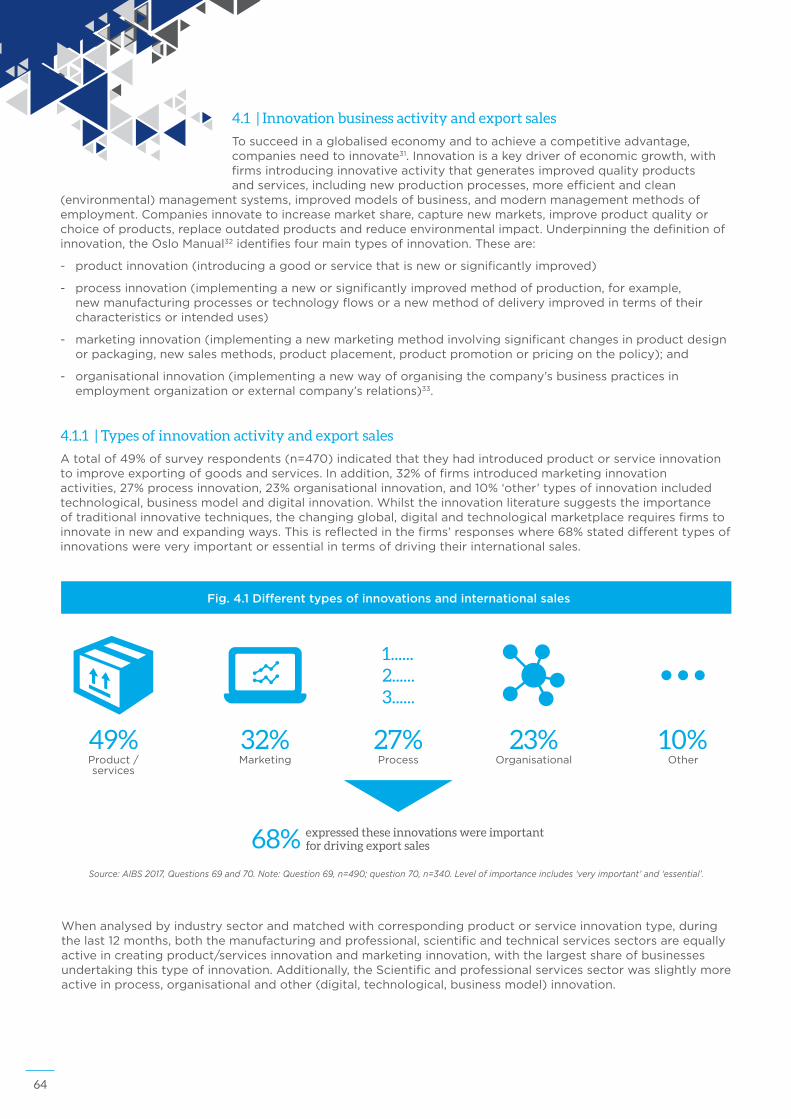

Atotalof68%ofcompaniesinvolvedintheaboveformsofinnovationconsideredthatinnovationswereveryimportantoressentialfordrivinginternationalsales.

49%ofrespondentsintroducedproductinnovation,32%marketinginnovation,23%organisationalinnovationand27%processinnovationtodriveinternationalsales.10%ofcompaniesintroducedotherinnovations(suchastechnological,digitalandbusinessmodelinnovation).

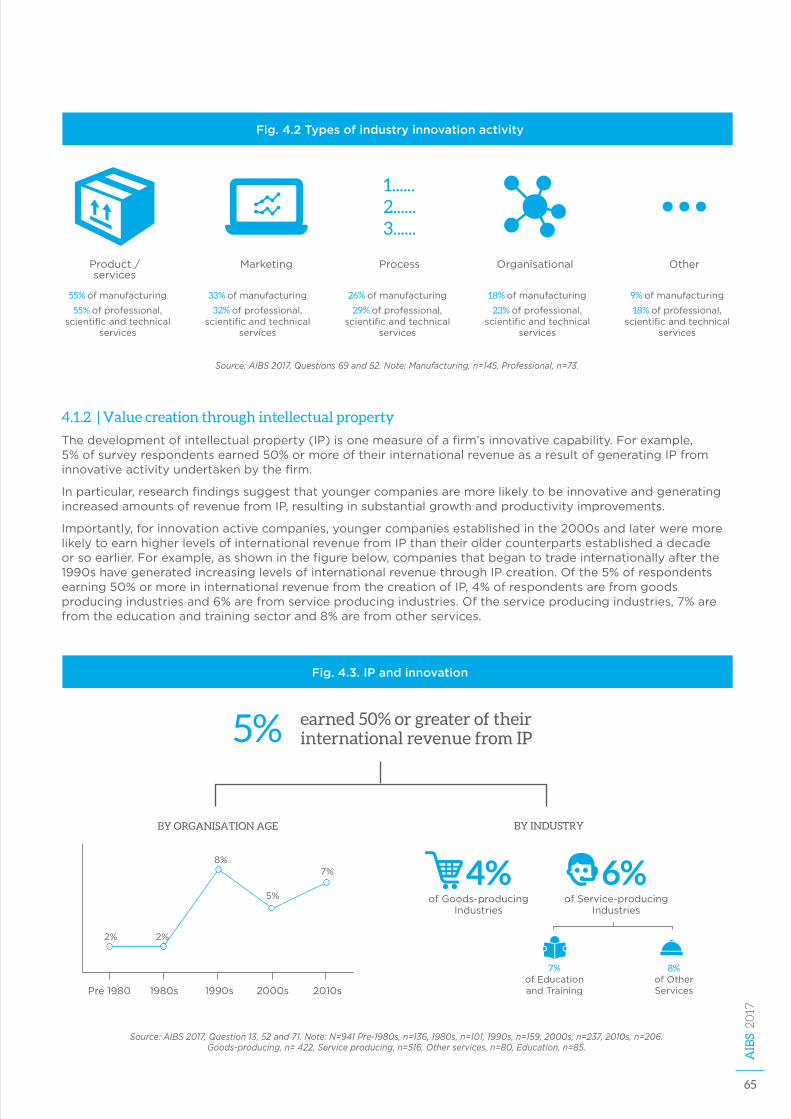

Youngercompaniesaremorelikelytogenerateinternationalrevenuethroughintellectualproperty(IP)thanoldercompanies.

Future outlook

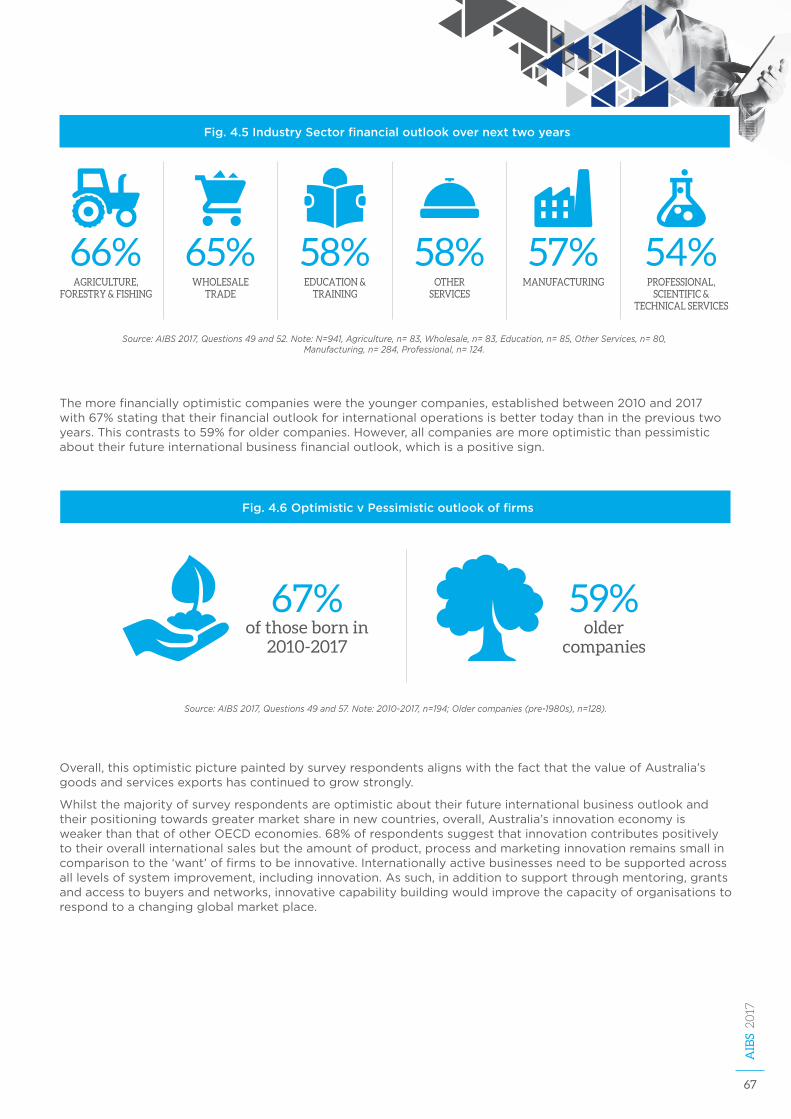

87%ofallrespondentsexpectthefinancialoutlookfortheirinternationaloperationstobethesameorbetteroverthenexttwoyearscomparedtothelasttwoyears.

Theindustrysectorsthatindicatedtheirfuturefinancialoutlookisbetterthanintheprevioustwoyearswereagriculture,forestryandfishing,manufacturing,wholesaletrade,professionalservices,andeducationandtrainingservices.

10

1 | IntroductionInternationalbusinessisessentialtosustainingAustralia’songoingeconomicprosperity.Technological,political,socialandculturalchange,togetherwithinternationaltrade,havemadeiteasierfororganisations,largeandsmall,toincreasetheirmarketshareforproductsandservices.Acomprehensiveunderstandingofthecriticalchallenges,andsuccessfactors,thatcontributetoAustralianbusinesssuccessinglobalmarketsisessentialtodeliverbetterstrategiesandsupportforAustralianbusiness.

ThisreportaimstobetterunderstandtheinternationalbusinessactivityofAustralianfirms,throughtheresultsofanextensivesurveyofbusinessestradingwithandinoverseasmarkets.

Since2014,Australia’sInternationalBusinessSurvey(AIBS)1hashighlightedkeyinsightsandissuesforAustralia’sinternationalbusinesscommunity,atthesametimepresentingoveralleconomictrends.In2017,theExportCouncilofAustralia(ECA)hascommissionedtheCentreforBusinessandSocialInnovation(CBSI)attheUniversityofTechnologySydney(UTS)toproducethe2017Australia’sInternationalBusinessSurvey(AIBSReport).

11

AIB

S 2017

Background

In2014-15,theAustralianBureauofStatistics(ABS)reportedtheproportionofAustralianbusinessessellinggoodsorservicesinoverseasmarketswas7.1%,afigurethathasremainedfairlystableoverthelastthreeAIBSsurveyperiods,althoughtheabsolutenumberofexportershasincreasedoverthesameperiod.Nevertheless,theshareofAustralianfirmsundertakinginternationalactivityhasdeclinedoverthepast10years2.

Buildingoninternationalbusinessliterature,theUTSBusinessSchoolhasbeencommissionedbyECAwiththesupportofpartners,AustradeandEfic,toexpandthereachofthisfourthAIBSsurveytogenerateadeeperinsightandcomprehensiveunderstandingofthecriticalchallengesandsuccessfactorscontributingtoAustralianbusinesssuccessininternationalmarkets.ThisAIBS2017reportaddressesthecriticalresearchquestion:

What are the international business activities of Australian businesses operating globally?

Importance of international business research

Despitethegrowingpaceandbreadthofresearch,thereisaneedforfurtherinvestigationthatconsidersinternationalfirmsascompletesystems4.Muchinternationalbusinessresearchtodateeitherinvolvesthestudyofanissuewithlittleornoregardtodifferencesbetweencountries(orcultures),oritfocusesoncomparisonsbetweencountriesand/orculturesacrossdifferentnations.Astheworld’seconomieshavebecomemoreintegratedandinternationalbusinessmoreglobalised,sohavethetrendsininternationalbusinessresearch.Examplesincludetheriseofresearchintocomplexglobalmanagementinformationsystems,andinternationalcollaborationnetworksandalliances4.A1990surveyofinternationalmanagementresearchneedsidentifiedresearchoninternationalcoalitionsaspossiblythesinglemostimportantandchallengingareaforinternationalbusinessresearchers2.Another,recentdriverofresearchactivityisinternationalentrepreneurshipandtheinternationalisationofsmallbusinesses2.

Traditionallyfirmshavefocusedongrowingtheirdomesticmarketsbeforeexploringinternationalopportunities.However,evidence5suggeststhatsomesmall,youngfirms,withverylimitedresources,begintoexpandoverseasnotlongaftertheirestablishment.Thesesmallandmediumenterprises(SMEs),includingstart-ups,haveanincreasingpresenceininternationalbusiness.

Inthisglobalenvironment,theseentrepreneursandsmallbusinessesarebecominglessreliantondomestictradeandinsteadlooktotheinternationalmarket.Suchfirmsareknownas‘born-global’firms3.Despitetheemergenceoftheseborn-globalfirms,themorecommonroutetointernationalisationfortraditionalSMEstendstobeagradualone–startingwithsporadicinternationalsalesintheearlystagestomoresystematicanddeepengagementinforeignmarkets.Incontrast,the‘bornglobal’SMEs,areofteninternationallyorientedfromtheircreationandtypicallyaresobyexploitingthebenefitsofbelongingtointernationalnetworkstoopenopportunitiestocustomersandpotentialforeignpartners.Similarly,someSMEfirmsareabletointegrateintoglobalvaluechains(GVCs)bysellingeitherdirectlyorindirectlythroughlargefirmssituatedintheirhomecountries6.Ontheotherhand,theissuesofclimatechangeandthetransitiontolowercarboneconomiescontinuetochallengetraditionalbusinessmodels,raisingconcernsfortheenvironmentandprovidinganewunifyingthemeinfluencinginternationaltrade7.

Fig. 1.1. International activity in goods and services 2006-20153

9.1%2006-07

7.1%2014-15

-2%

12

Thereare,forexample,jointventuresbetweenAustralianandinternationalfirmsinresearchanddevelopmentintorenewableenergy,biotechnologies(especiallypharmaceuticals),precisionelectronics(computerchips),smartmanufacturingandvariousagri-businesses,openingthedoortopotentiallyveryprofitablecommercialopportunitiesforAustralianbusinesses.

Despitethenarrowfocusofmostinternationalbusinessresearch,therealchallengefacedbybusinessesoperatinginternationallynowisintegrationofinternationalactivities8.Astheproducts,productionprocessesandmarketsofmodernglobalmanagementbecomeincreasinglydiversified,integrationoftheseactivitiesgrowsinimportance.JohnDunning8notesthesignificanceofthisforinternationalbusinessresearchers:‘Duetobothexogenousandendogenousfactors,thepracticeofinternationalbusinessisinvolvinganincreasingratiooftransactiontototalcosts.Butinordertostudyandexplainthisphenomenon,internationalbusinessscholarsneednotonlytodrawupondifferentdisciplinesbuttodosoinacoordinatedway’.Newmodesofresearchstudyareneededthatconsiderholisticandsystem-basedapproaches,includingtheinterdisciplinaryaspectsoftheinternationalfirms.Dynamicvaluechains,forexample,arekeytotheintegrationandalignmentoftheneedsofcustomers,consumers,end-users,suppliersandthirdpartiesthroughcollaborationforcreatinganddelivering9.Adynamicapproachaimstodevelopnewbusinessmodelsandnetworks9basedonwhatinternationalcustomerswant.Thisisachangeinmindsetfromfunctionalspecialisationtowardsembeddingtheprinciplesandpracticesofthesupplychain,andvalue-networkthinking,withinthephilosophyofthefirm.

About this survey

ThisreportanalysestheinternationalbusinessresponsesofAIBS2017facilitatedbyAMRbetweenAprilandJune2017.Asaresult,thisreportprovidesinsightsgatheredfrom941Australianinternationally-activebusinessesdrawnfrom19industrysectorsandoperatingacrossmorethan90internationalmarkets.Thesesurveyrespondentswereinvolvedacrossarangeofinternationaltradingsettingsincludingtheexportandimportofgoodsandservices,makingoutwardinvestments,receivinginwardinvestments,earningrevenuefromintellectualpropertyandundertakinginternationalresearchanddevelopmentactivities.Keyfeaturesandhighlightsinclude:

a) anexaminationoftheimportanceofinternationalmarketsandthediversityandtypesofinternationalbusinessactivity,

b) thekeyimpactsofAustralia’sFTAsonexportearningsandpotentialforgrowthininternationalmarkets,

c) thechangingnatureofinternationalbusinessactivityanditsimplicationsforthefutureofAustralianbusinesses,

d) thebarrierstoandopportunitiesforinternationalbusinessactivities,

e) thecontributionthatinnovationmakestointernationalbusinessactivityandtrade,and

f) theexistingchannelsofsupportandassistanceprovidedtointernationalbusinesseswhenoperatingininternationalmarkets.

AIBS2017alsocaptured127responsesfrombusinessesthatarenotcurrentlyengagedininternationalactivities,mainlyduetoalackofinternationalbusinessawarenessandacurrentconcentrationondomesticoperations.Inthiscontext,AIBS2017providesanin-depthunderstandingofthesuccessfactorsandchallengesexperiencedbyAustralianfirmswhenengagingacrossmultipleinternationalsettings.

AIBS2017isacriticalcontributiontoprovidinginsightsintothe941internationallyactivebusinesseswhorespondedtothesurveyandthe127respondentswhoarenotengagedininternationalbusinessactivity.Whilsttheaboverecommendationsandsuggestionsaimtosteereffortstowardsassistinginternationalbusinessesgrow,furtherresearchcouldbeundertakenonsomeofthecriticaltradeinfluencingfactorsthatunderpinsuccessforinternationalbusinesses.

13

AIB

S 2017

Fig. 1.2 AIBS report structure

Diversityofinternationalbusinessactivity

SECTION 2

Australia’sinternationaltradeinfocus

SECTION 3

Supportinginternationalactivityinachangingglobalmarketplace

SECTION 4

SECTION 2 examinestheactivitiesininternationalmarketsandexploresthediversityandtypesofinternationalbusinessactivityreportedbysurveyrespondents.

SECTION 3 determinestheessentialfinancingrequirementsforundertakinginternationalbusinessactivity,keyimpactsofAustralia’sFTAsandthebarriersandopportunitiesaffectinginternationalbusinessopportunities.

SECTION 4 examinestheexistingchannelsofsupportandassistanceprovidedforinternationalbusiness,theeffectsofinnovationongrowingaglobalbusiness,andexpectationsbyAustralianbusinessesoffutureinternationalbusinessactivity.

Importance of facilitating international business activity

ThisreportaimstoprovideanoverviewofcurrentinternationalbusinessactivitydrawingfromtheresultsoftheAIBS2017.WhilecurrentAustralianBureauofStatistics(ABS)tradedataprovidesdatacollectiononthevalueandvolumeofinternationalbusinessactivities,thisreportdrawsontheindividualexperiencesandpracticesofbusinessesnotmeasuredinnationaltradedata.ThisuniquecontributingfeatureprovidesspecificinsightsintotheinternationalbusinessactivitiesofAustralianbusinesses.

ThesurveydataprovidesaninsightfulperspectiveintoAustralianbusinesses’internationaltradingbehaviours,frictionslimitingtheirlikelihoodofengagingininternationalbusiness,aswellasanappreciationofthedifferenceinexperiencesacrossindustriesandsizeoforganisations.

14

The diversity of Australia’s international business activity2

What the survey says

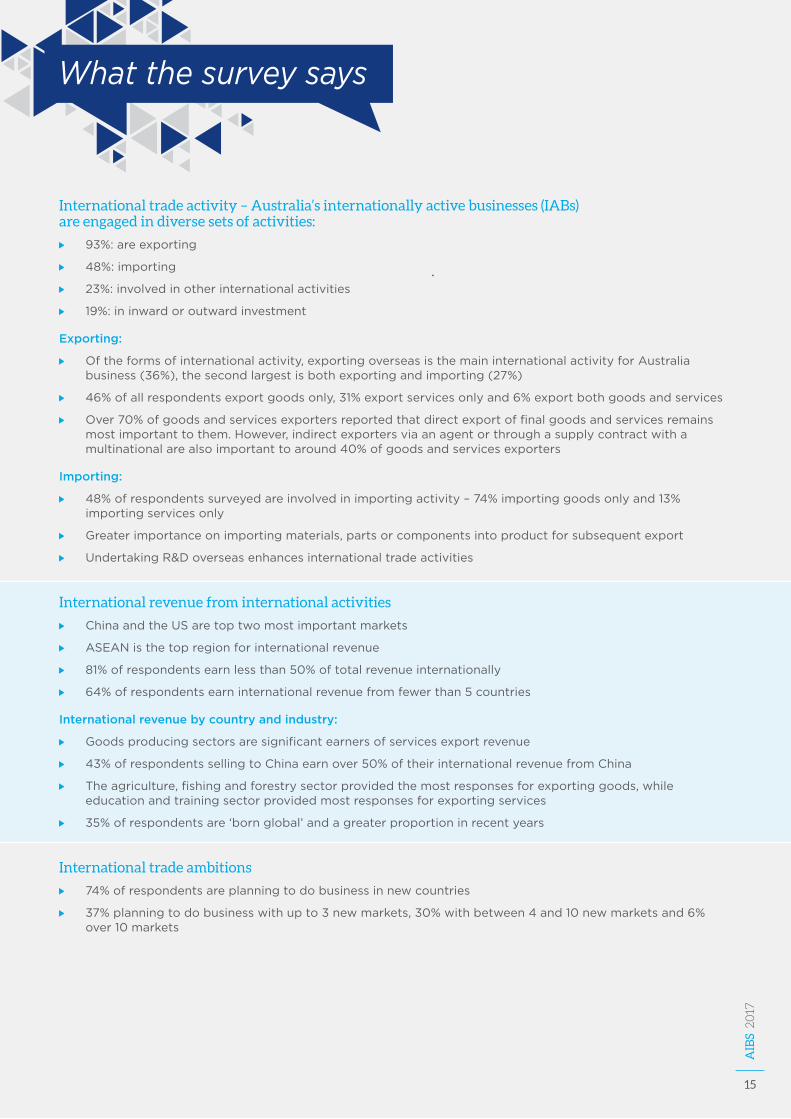

International trade activity – Australia’s internationally active businesses (IABs) are engaged in diverse sets of activities:

93%:areexporting

48%:importing

23%:involvedinotherinternationalactivities

19%:ininwardoroutwardinvestment

Exporting:

Oftheformsofinternationalactivity,exportingoverseasisthemaininternationalactivityforAustraliabusiness(36%),thesecondlargestisbothexportingandimporting(27%)

46%ofallrespondentsexportgoodsonly,31%exportservicesonlyand6%exportbothgoodsandservices

Over70%ofgoodsandservicesexportersreportedthatdirectexportoffinalgoodsandservicesremainsmostimportanttothem.However,indirectexportersviaanagentorthroughasupplycontractwithamultinationalarealsoimportanttoaround40%ofgoodsandservicesexporters

Importing:

48%ofrespondentssurveyedareinvolvedinimportingactivity–74%importinggoodsonlyand13%importingservicesonly

Greaterimportanceonimportingmaterials,partsorcomponentsintoproductforsubsequentexport

UndertakingR&Doverseasenhancesinternationaltradeactivities

International revenue from international activities

ChinaandtheUSaretoptwomostimportantmarkets

ASEANisthetopregionforinternationalrevenue

81%ofrespondentsearnlessthan50%oftotalrevenueinternationally

64%ofrespondentsearninternationalrevenuefromfewerthan5countries

International revenue by country and industry:

Goodsproducingsectorsaresignificantearnersofservicesexportrevenue

43%ofrespondentssellingtoChinaearnover50%oftheirinternationalrevenuefromChina

Theagriculture,fishingandforestrysectorprovidedthemostresponsesforexportinggoods,whileeducationandtrainingsectorprovidedmostresponsesforexportingservices

35%ofrespondentsare‘bornglobal’andagreaterproportioninrecentyears

International trade ambitions

74%ofrespondentsareplanningtodobusinessinnewcountries

37%planningtodobusinesswithupto3newmarkets,30%withbetween4and10newmarketsand6%over10markets

15

AIB

S 2017

16

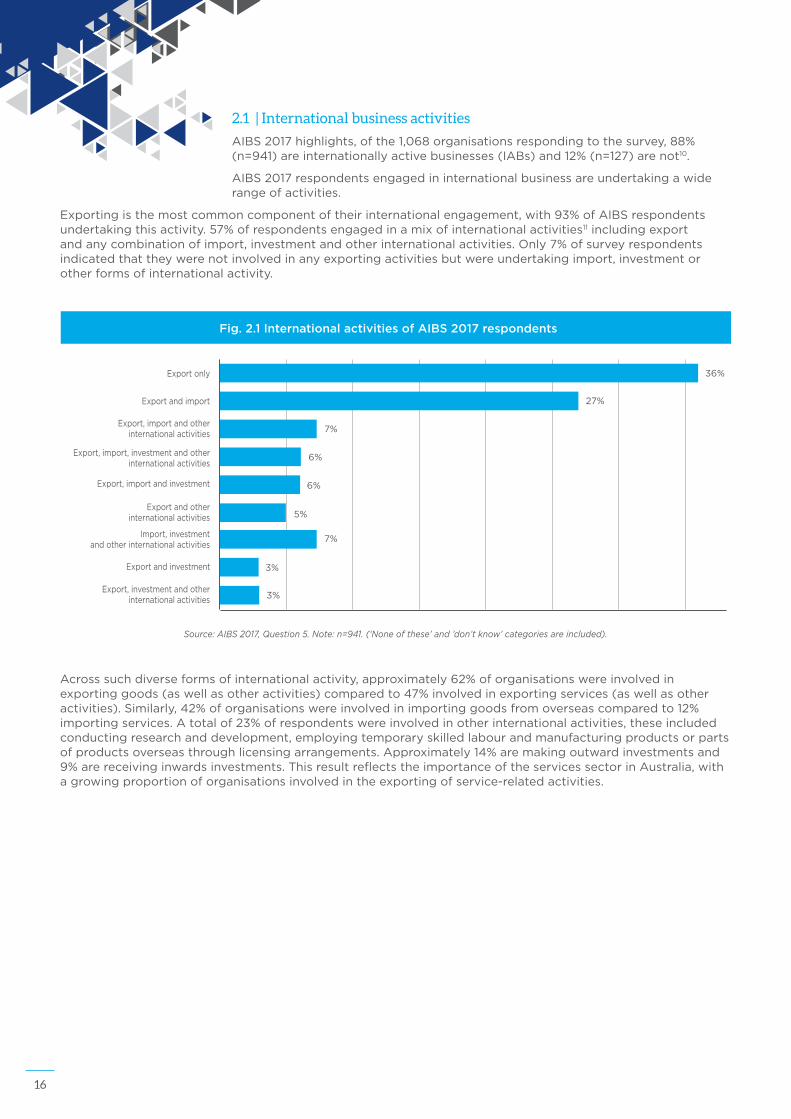

2.1 | International business activities

AIBS2017highlights,ofthe1,068organisationsrespondingtothesurvey,88%(n=941)areinternationallyactivebusinesses(IABs)and12%(n=127)arenot10.

AIBS2017respondentsengagedininternationalbusinessareundertakingawiderangeofactivities.

Exportingisthemostcommoncomponentoftheirinternationalengagement,with93%ofAIBSrespondentsundertakingthisactivity.57%ofrespondentsengagedinamixofinternationalactivities11includingexportandanycombinationofimport,investmentandotherinternationalactivities.Only7%ofsurveyrespondentsindicatedthattheywerenotinvolvedinanyexportingactivitiesbutwereundertakingimport,investmentorotherformsofinternationalactivity.

Acrosssuchdiverseformsofinternationalactivity,approximately62%oforganisationswereinvolvedinexportinggoods(aswellasotheractivities)comparedto47%involvedinexportingservices(aswellasotheractivities).Similarly,42%oforganisationswereinvolvedinimportinggoodsfromoverseascomparedto12%importingservices.Atotalof23%ofrespondentswereinvolvedinotherinternationalactivities,theseincludedconductingresearchanddevelopment,employingtemporaryskilledlabourandmanufacturingproductsorpartsofproductsoverseasthroughlicensingarrangements.Approximately14%aremakingoutwardinvestmentsand9%arereceivinginwardsinvestments.ThisresultreflectstheimportanceoftheservicessectorinAustralia,withagrowingproportionoforganisationsinvolvedintheexportingofservice-relatedactivities.

Fig. 2.1 International activities of AIBS 2017 respondents

Exportonly

Exportandimport

Export,importandotherinternationalactivities

Export,import,investmentandotherinternationalactivities

Export,importandinvestment

Exportandotherinternationalactivities

Import,investmentandotherinternationalactivities

Exportandinvestment

Export,investmentandotherinternationalactivities

27%

7%

6%

6%

5%

7%

3%

3%

36%

Source: AIBS 2017, Question 5. Note: n=941. (‘None of these’ and ’don’t know’ categories are included).

17

AIB

S 2017

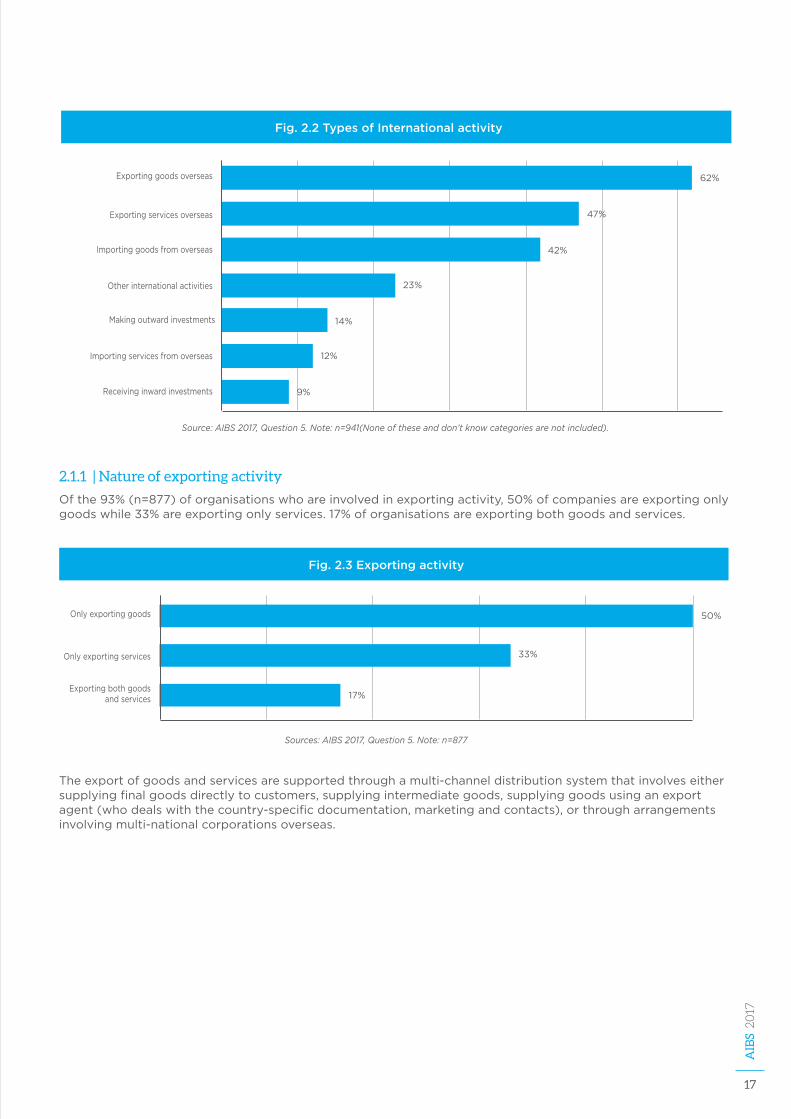

Fig. 2.2 Types of International activity

Exportinggoodsoverseas

Exportingservicesoverseas

Importinggoodsfromoverseas

Otherinternationalactivities

Makingoutwardinvestments

Importingservicesfromoverseas

Receivinginwardinvestments

62%

47%

42%

23%

14%

12%

9%

Source: AIBS 2017, Question 5. Note: n=941(None of these and don’t know categories are not included).

2.1.1 | Nature of exporting activity

Ofthe93%(n=877)oforganisationswhoareinvolvedinexportingactivity,50%ofcompaniesareexportingonlygoodswhile33%areexportingonlyservices.17%oforganisationsareexportingbothgoodsandservices.

Theexportofgoodsandservicesaresupportedthroughamulti-channeldistributionsystemthatinvolveseithersupplyingfinalgoodsdirectlytocustomers,supplyingintermediategoods,supplyinggoodsusinganexportagent(whodealswiththecountry-specificdocumentation,marketingandcontacts),orthrougharrangementsinvolvingmulti-nationalcorporationsoverseas.

Fig. 2.3 Exporting activity

Onlyexportinggoods 50%

Onlyexportingservices 33%

Exportingbothgoodsandservices 17%

Sources: AIBS 2017, Question 5. Note: n=877

18

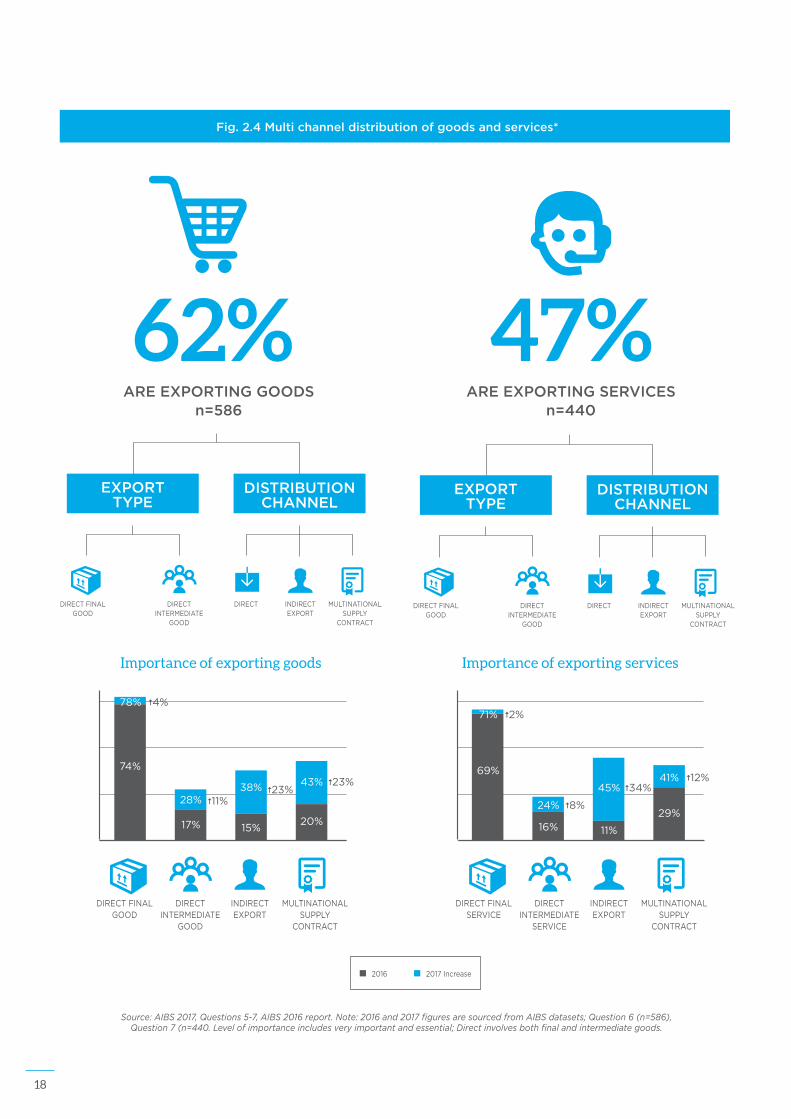

Source: AIBS 2017, Questions 5-7, AIBS 2016 report. Note: 2016 and 2017 figures are sourced from AIBS datasets; Question 6 (n=586), Question 7 (n=440. Level of importance includes very important and essential; Direct involves both final and intermediate goods.

Fig. 2.4 Multi channel distribution of goods and services*

2016 2017Increase

62%ARE EXPORTING GOODS

n=586

DIRECTFINALGOOD

DIRECTINTERMEDIATE

GOOD

DIRECT INDIRECTEXPORT

MULTINATIONALSUPPLY

CONTRACT

EXPORT TYPE

DISTRIBUTION CHANNEL

47%ARE EXPORTING SERVICES

n=440

EXPORT TYPE

DISTRIBUTION CHANNEL

DIRECTFINALGOOD

DIRECTINTERMEDIATE

GOOD

DIRECT INDIRECTEXPORT

MULTINATIONALSUPPLY

CONTRACT

DIRECTFINALSERVICE

DIRECTINTERMEDIATE

SERVICE

INDIRECTEXPORT

MULTINATIONALSUPPLY

CONTRACT

69%

71%

16%

24%

11%

45%

29%

41%

2%

8%

34%12%

Importance of exporting services

DIRECTFINALGOOD

DIRECTINTERMEDIATE

GOOD

INDIRECTEXPORT

MULTINATIONALSUPPLY

CONTRACT

74%

17%

28%

15%

38%

20%

4%

11%23%

43% 23%

Importance of exporting goods

78%

19

AIB

S 2017

Services,andgoods,canbedistributedaseitherafinalorintermediategoodorservice.However,finalgoodsandservicesreachthecustomerthroughavarietyofdifferentdistributionchannels.

Forthe93%ofsurveyrespondentswhoareexporting,exportingoffinalgoodswasthemostcommonmodeofexporting,with78%ofsurveyrespondentsindicatingthatfinalgoodsexportsdirectlytocustomerswasimportantincontributingtotheirinternationalrevenue,upfrom74%in201612.

Dealingdirectlywithcustomerstoexportfinalgoodsisagrowingtrendespeciallysincecustomersarebecomingincreasinglyaccustomedtosourcinggoodsdirectlyfromoverseas.Thishasenabledopportunitiesfor‘smart’andinnovativefirmstoprovideservicesinsupportofthesepurchases.Inaddition,opportunitiestobuildbrandsanddeepencustomerrelationshipsthroughimprovedbusinessintelligenceanddataanalyticshasbecomepossiblethroughthedirectdealingwithcustomersmodeofdistribution.Improvedunderstandingof,andsharingofinformationabout,thewaysAustralianfirmsareengagingdirectlywithitscustomers,iscriticaltoenablingmorefirmstoexpandtheirexportmarkets.

Similarly,importingfinalservicesisthemostcommonformforexportingservices,where71%ofsurveyrespondentsindicatedthatfinalservicesexportsdirectlytocustomerswasveryimportantincontributingtotheirinternationalrevenue.Thisfigureisupfrom69%in2016.(Note: whilst a comparison with AIBS 2016 highlights an increase in the proportion of respondents’ importance, the organisational sample types differ from those of the 2017 survey).

Usingexportagentsasadistributionchannelrankedthirdfordistributinggoodsimportance(38%)andsecondfordistributingservicesimportance(45%)incontributingtointernationalearnings.Anagentisgenerallypaidbytheexporterbasedonacommissionofsalesvaluegenerated13.Academicliterature14,suggestsorganisationsemployagentstoovercometheir“smallness”,languageissuesandsocialproblemsthatmaybeexperiencedwhendealinginforeigncountries.

Exportinggoodsusingsupplycontractsinvolvingoverseasmultinationalcompanieswasconsideredtobeveryimportantandessentialby43%ofrespondents(41%forservices).ThisisanincreasefromAIBS2016of23%forgoodsand12%forservices.Withmorecompaniesengagingwithmulti-nationalcorporationsanddrawingupontheservicesofagents,theseindirectdistributionchannelsareexpectedtoplayanincreasinglysignificantroleinsupportinginternationalbusiness.Organisationsdivestingresponsibilitiestothirdpartieswillbenefitthroughimprovedawarenessandknowledgeregardingmarketaccess,FTAarrangementsandotherrelevantconsiderationsinvolvedininternationaltransactions.Theincreasinginvolvementofmulti-nationalcorporationsalsosignalspotentialopportunitiesfornetworking,collaborationandaccessintonewmarkets.

20

Fig. 2.5 Distribution channels – manufacturing sector

Fig. 2.5 Importance of manufacturing distribution channels

Finalgood 79%

Intermediategood 30%

Incountryagent 37%

Multi-national 45%

Multi-channel distribution on goods and services – Focus on manufacturing sector

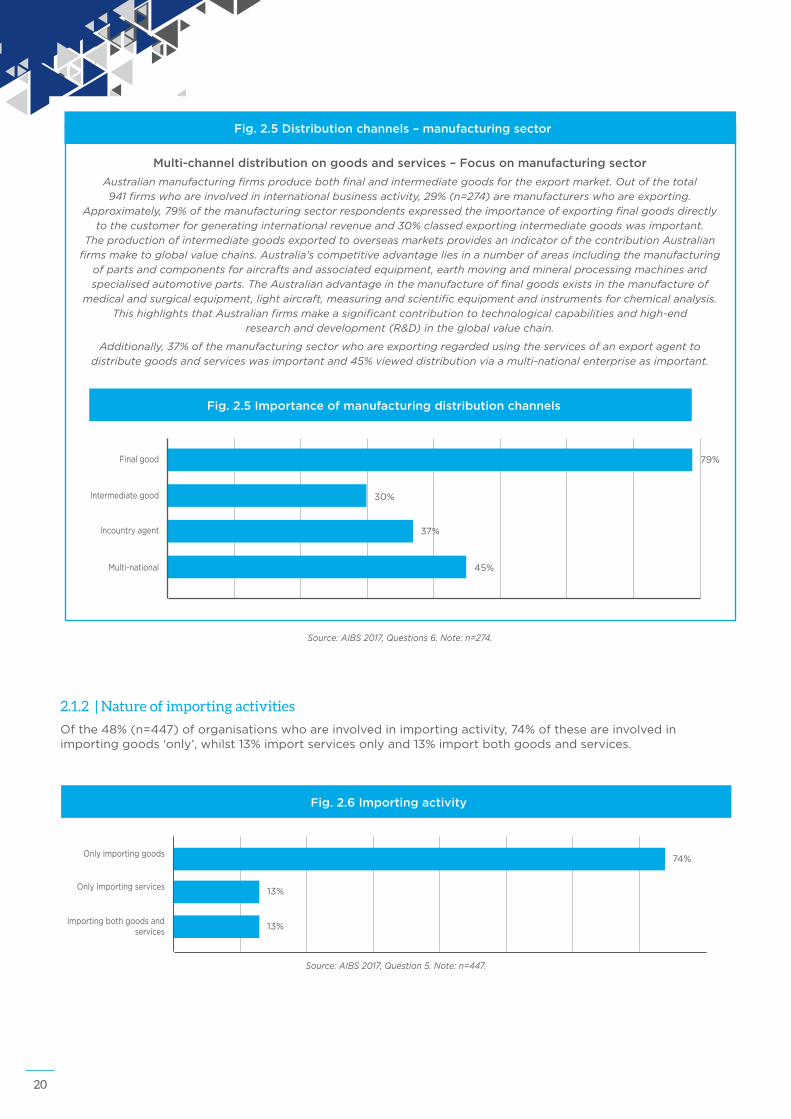

Australian manufacturing firms produce both final and intermediate goods for the export market. Out of the total 941 firms who are involved in international business activity, 29% (n=274) are manufacturers who are exporting.

Approximately, 79% of the manufacturing sector respondents expressed the importance of exporting final goods directly to the customer for generating international revenue and 30% classed exporting intermediate goods was important.

The production of intermediate goods exported to overseas markets provides an indicator of the contribution Australian firms make to global value chains. Australia’s competitive advantage lies in a number of areas including the manufacturing

of parts and components for aircrafts and associated equipment, earth moving and mineral processing machines and specialised automotive parts. The Australian advantage in the manufacture of final goods exists in the manufacture of

medical and surgical equipment, light aircraft, measuring and scientific equipment and instruments for chemical analysis. This highlights that Australian firms make a significant contribution to technological capabilities and high-end

research and development (R&D) in the global value chain.

Additionally, 37% of the manufacturing sector who are exporting regarded using the services of an export agent to distribute goods and services was important and 45% viewed distribution via a multi-national enterprise as important.

Source: AIBS 2017, Questions 6. Note: n=274.

2.1.2 | Nature of importing activities

Ofthe48%(n=447)oforganisationswhoareinvolvedinimportingactivity,74%oftheseareinvolvedinimportinggoods‘only’,whilst13%importservicesonlyand13%importbothgoodsandservices.

Fig. 2.6 Importing activity

Onlyimportinggoods74%

Onlyimportingservices 13%

Importingbothgoodsandservices

13%

Source: AIBS 2017, Question 5. Note: n=447.

21

AIB

S 2017

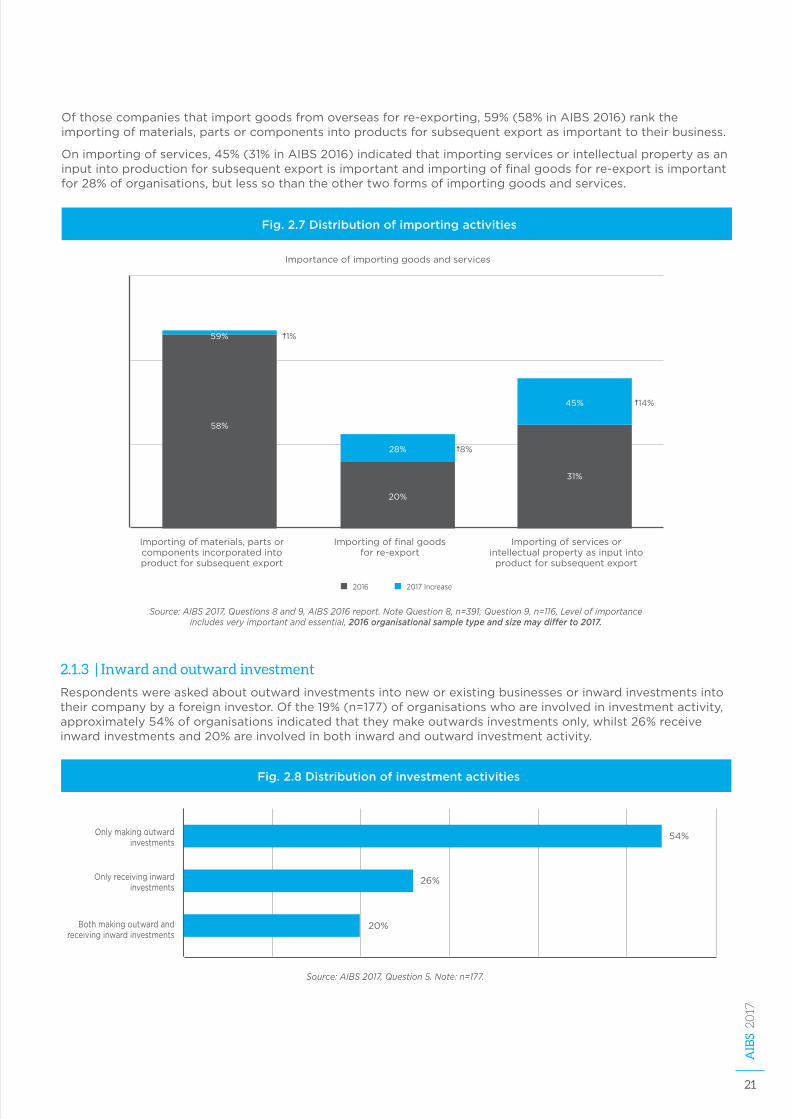

Ofthosecompaniesthatimportgoodsfromoverseasforre-exporting,59%(58%inAIBS2016)ranktheimportingofmaterials,partsorcomponentsintoproductsforsubsequentexportasimportanttotheirbusiness.

Onimportingofservices,45%(31%inAIBS2016)indicatedthatimportingservicesorintellectualpropertyasaninputintoproductionforsubsequentexportisimportantandimportingoffinalgoodsforre-exportisimportantfor28%oforganisations,butlesssothantheothertwoformsofimportinggoodsandservices.

2.1.3 | Inward and outward investment

Respondentswereaskedaboutoutwardinvestmentsintoneworexistingbusinessesorinwardinvestmentsintotheircompanybyaforeigninvestor.Ofthe19%(n=177)oforganisationswhoareinvolvedininvestmentactivity,approximately54%oforganisationsindicatedthattheymakeoutwardsinvestmentsonly,whilst26%receiveinwardinvestmentsand20%areinvolvedinbothinwardandoutwardinvestmentactivity.

Fig. 2.8 Distribution of investment activities

Onlymakingoutwardinvestments

Onlyreceivinginwardinvestments

Bothmakingoutwardandreceivinginwardinvestments

54%

26%

20%

Source: AIBS 2017, Question 5. Note: n=177.

Source: AIBS 2017, Questions 8 and 9, AIBS 2016 report. Note Question 8, n=391; Question 9, n=116, Level of importance includes very important and essential, 2016 organisational sample type and size may differ to 2017.

Fig. 2.7 Distribution of importing activities

58%

1%

20%

28% 8%

31%

45% 14%

Importingofmaterials,partsorcomponentsincorporatedintoproductforsubsequentexport

Importingoffinalgoodsforre-export

Importingofservicesorintellectualpropertyasinputinto

productforsubsequentexport

Importanceofimportinggoodsandservices

2016 2017Increase

59%

22

Fig. 2.9 Importance of investment activity in generating international revenue

21%

34%

26%

58%

52%

72%

13%

32%

20%

Investinginanexistingoverseasbusinessi.e.viaa

merger/acquisition

Receivingcapitalfromanoverseasinvestor

Investinginanewoverseasoperationeg.salesbranch,subsidiary,manufacturing

facility

2016 2017Increase

Importanceofinternationalinvestment

Source: AIBS 2017, Questions 10-12. Note: Question 10, n=131; Question 11, n=81. Level of importance includes very important and essential; 2016 data from AIBS 2016 report.2016 organisational sample type and size may differ to 2017.

Ofthoseorganisationsthatareexporting,14%aremakingoutwardsinvestments.Thesefindingssuggestthatorganisationspursuingmarketgrowthstrategiesoverseasdependonsecuringinvestmentsabroadasaleveragepointtolifttheirsales.

Ofthe131respondentsreceivinginwardinvestmentsintotheirbusinessbyaforeigninvestor,58%consideredreceivingcapitalfromanoverseasinvestorasimportantforgeneratinginternationalrevenuecomparedto26%in2016.

Approximately,72%ofrespondentsinvestinginnewoverseasoperationsincludingsalesbranches,manufacturingfacilitiesetc.,ratedthisoutwardinvestmentasimportantforgeneratinginternationalrevenuecomparedto52%for2016.Investinginanexistingoverseasbusinessviaamergeroracquisitionwasalsoratedasimportanttotheirbusinessby34%ofrespondents.

23

AIB

S 2017

2.1.4 | Other international activity

Atotalof23%ofsurveyrespondentsindicatedtheywereinvolvedinotherinternationalactivities.Byfarthelargestoftheseactivitieswasresearchanddevelopmentactivitiesoverseasratedasimportantby58%ofrespondents.SincethelastAIBSsurveyin2016,investmentandR&Dhasbecomemoreimportantforsupportinginternationalbusinessactivities.

Fig. 2.10 Importance of other international activity

Manufacturingofproductsorpartsofproductsoverseasthroughlicensing

Undertakingresearchanddevelopmentactivitiesoverseas

Employingtemporaryskilledlabourfromoverseas

(e.g.457visa)

14%

20% 35%

58%

17%

21%6%

23%

4%

2016 2017Increase

Importanceofotherinternationalactivities

Source: AIBS 2017, Question 12. Note: Question 12, n=217. Level of importance includes very important and essential. 2016 organisational sample type and size may differ to 2017.

24

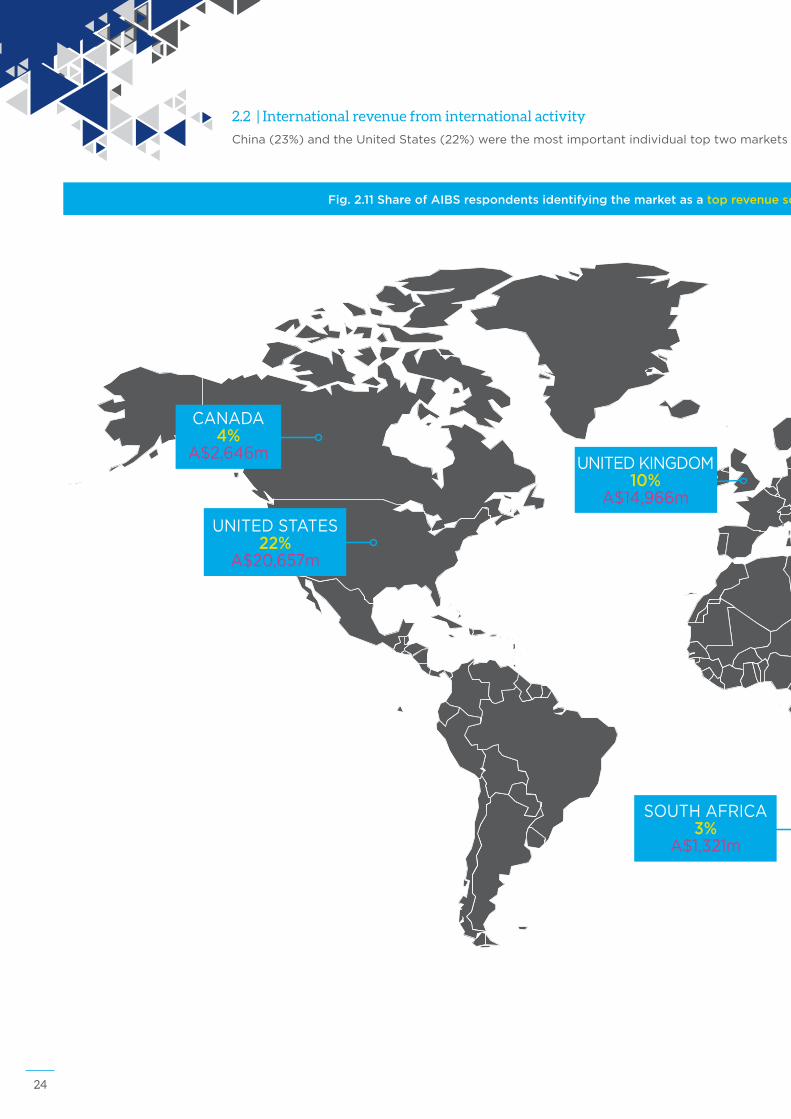

2.2 | International revenue from international activity

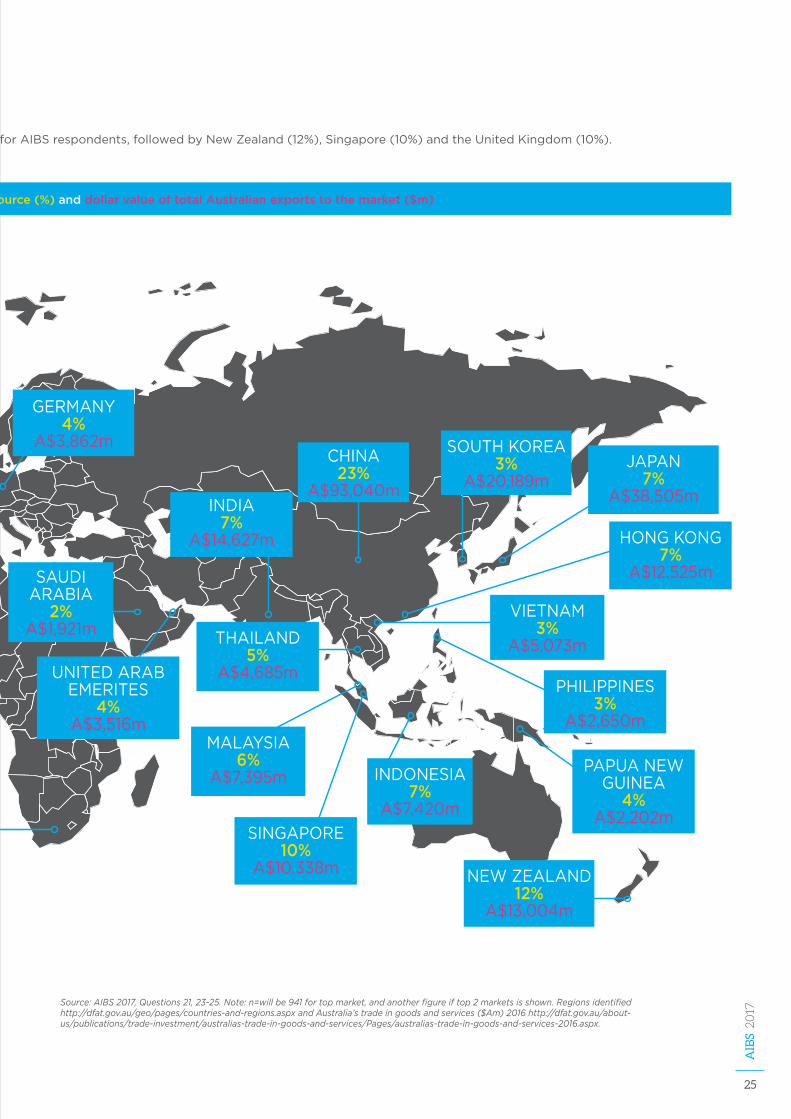

China(23%)andtheUnitedStates(22%)werethemostimportantindividualtoptwomarketsforAIBSrespondents,followedbyNewZealand(12%),Singapore(10%)andtheUnitedKingdom(10%).

Fig. 2.11 Share of AIBS respondents identifying the market as a top revenue source (%) and dollar value of total Australian exports to the market ($m)

CANADA4%

A$2,646m

UNITEDSTATES22%

A$20,657m

UNITEDKINGDOM10%

A$14,966m

SOUTHAFRICA3%

A$1,321m

25

AIB

S 2017

2.2 | International revenue from international activity

China(23%)andtheUnitedStates(22%)werethemostimportantindividualtoptwomarketsforAIBSrespondents,followedbyNewZealand(12%),Singapore(10%)andtheUnitedKingdom(10%).

Source: AIBS 2017, Questions 21, 23-25. Note: n=will be 941 for top market, and another figure if top 2 markets is shown. Regions identified http://dfat.gov.au/geo/pages/countries-and-regions.aspx and Australia’s trade in goods and services ($Am) 2016 http://dfat.gov.au/about-us/publications/trade-investment/australias-trade-in-goods-and-services/Pages/australias-trade-in-goods-and-services-2016.aspx.

Fig. 2.11 Share of AIBS respondents identifying the market as a top revenue source (%) and dollar value of total Australian exports to the market ($m)

GERMANY4%

A$3,862m

SAUDIARABIA

2% A$1,921m

UNITEDARABEMERITES

4% A$3,516m

INDIA7%

A$14,627m

CHINA23%

A$93,040m

SOUTHKOREA3%

A$20,189mJAPAN

7% A$38,505m

HONGKONG7%

A$12,525m

PHILIPPINES3%

A$2,650m

INDONESIA7%

A$7,420m

THAILAND5%

A$4,685m

PAPUANEWGUINEA

4% A$2,202m

NEWZEALAND12%

A$13,004m

VIETNAM3%

A$5,073m

SINGAPORE10%

A$10,338m

MALAYSIA6%

A$7,395m

26

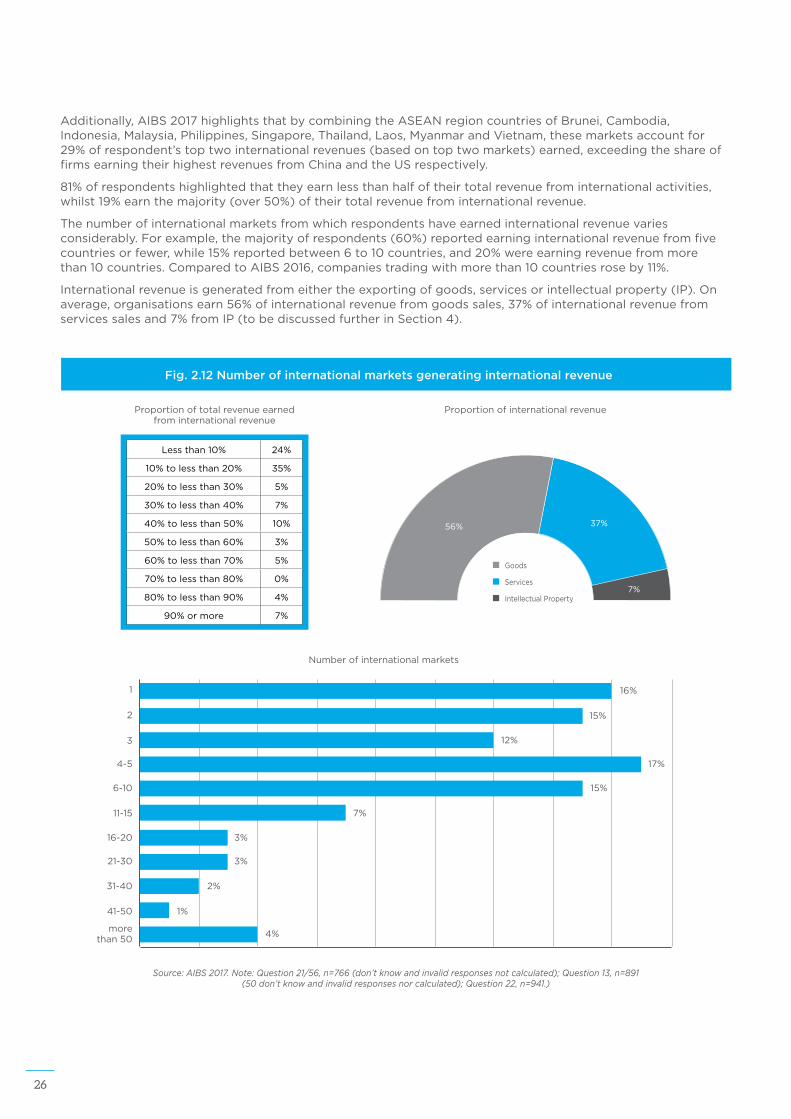

Additionally,AIBS2017highlightsthatbycombiningtheASEANregioncountriesofBrunei,Cambodia,Indonesia,Malaysia,Philippines,Singapore,Thailand,Laos,MyanmarandVietnam,thesemarketsaccountfor29%ofrespondent’stoptwointernationalrevenues(basedontoptwomarkets)earned,exceedingtheshareoffirmsearningtheirhighestrevenuesfromChinaandtheUSrespectively.

81%ofrespondentshighlightedthattheyearnlessthanhalfoftheirtotalrevenuefrominternationalactivities,whilst19%earnthemajority(over50%)oftheirtotalrevenuefrominternationalrevenue.

Thenumberofinternationalmarketsfromwhichrespondentshaveearnedinternationalrevenuevariesconsiderably.Forexample,themajorityofrespondents(60%)reportedearninginternationalrevenuefromfivecountriesorfewer,while15%reportedbetween6to10countries,and20%wereearningrevenuefrommorethan10countries.ComparedtoAIBS2016,companiestradingwithmorethan10countriesroseby11%.

Internationalrevenueisgeneratedfromeithertheexportingofgoods,servicesorintellectualproperty(IP).Onaverage,organisationsearn56%ofinternationalrevenuefromgoodssales,37%ofinternationalrevenuefromservicessalesand7%fromIP(tobediscussedfurtherinSection4).

Fig. 2.12 Number of international markets generating international revenue

1

2

3

4-5

6-10

11-15

16-20

21-30

morethan50

31-40

41-50

16%

15%

12%

17%

15%

7%

3%

3%

4%

2%

1%

Numberofinternationalmarkets

Lessthan10% 24%

10%tolessthan20% 35%

20%tolessthan30% 5%

30%tolessthan40% 7%

40%tolessthan50% 10%

50%tolessthan60% 3%

60%tolessthan70% 5%

70%tolessthan80% 0%

80%tolessthan90% 4%

90%ormore 7%

Proportionoftotalrevenueearnedfrominternationalrevenue

7%

37%56%

Goods

Services

IntellectualProperty

Proportionofinternationalrevenue

Source: AIBS 2017. Note: Question 21/56, n=766 (don’t know and invalid responses not calculated); Question 13, n=891 (50 don’t know and invalid responses nor calculated); Question 22, n=941.)

27

AIB

S 2017

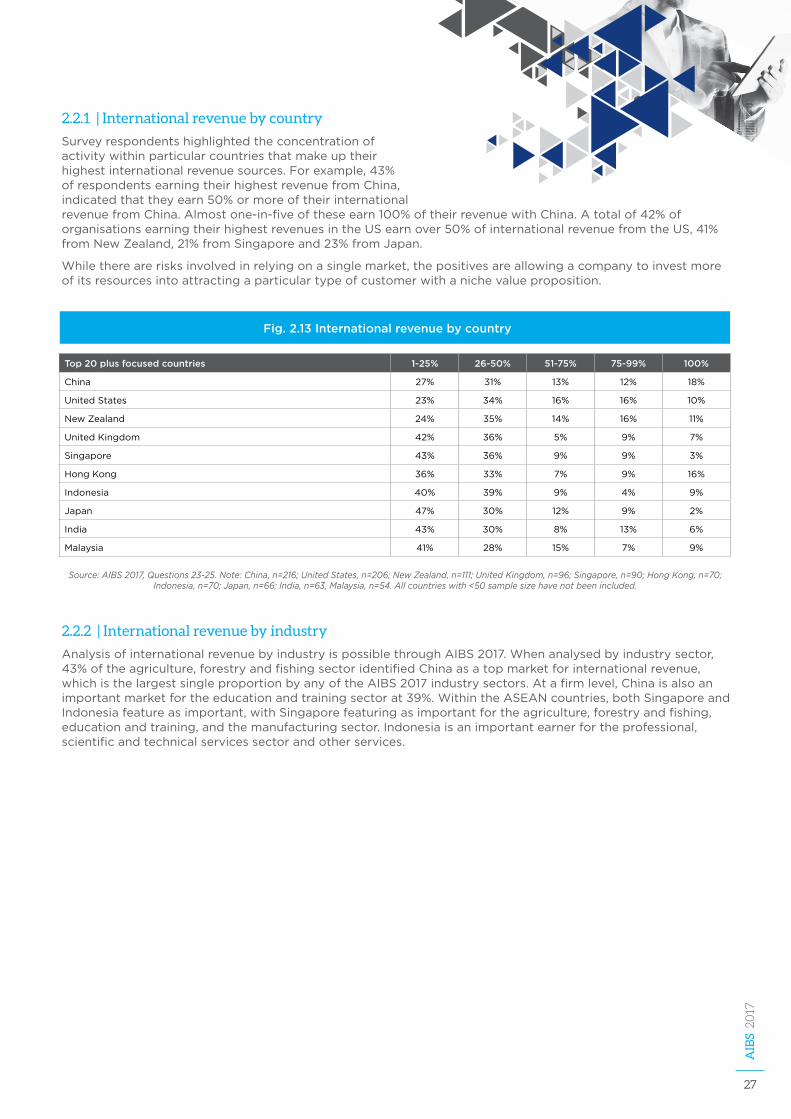

2.2.1 | International revenue by country

Surveyrespondentshighlightedtheconcentrationofactivitywithinparticularcountriesthatmakeuptheirhighestinternationalrevenuesources.Forexample,43%ofrespondentsearningtheirhighestrevenuefromChina,indicatedthattheyearn50%ormoreoftheirinternationalrevenuefromChina.Almostone-in-fiveoftheseearn100%oftheirrevenuewithChina.Atotalof42%oforganisationsearningtheirhighestrevenuesintheUSearnover50%ofinternationalrevenuefromtheUS,41%fromNewZealand,21%fromSingaporeand23%fromJapan.

Whiletherearerisksinvolvedinrelyingonasinglemarket,thepositivesareallowingacompanytoinvestmoreofitsresourcesintoattractingaparticulartypeofcustomerwithanichevalueproposition.

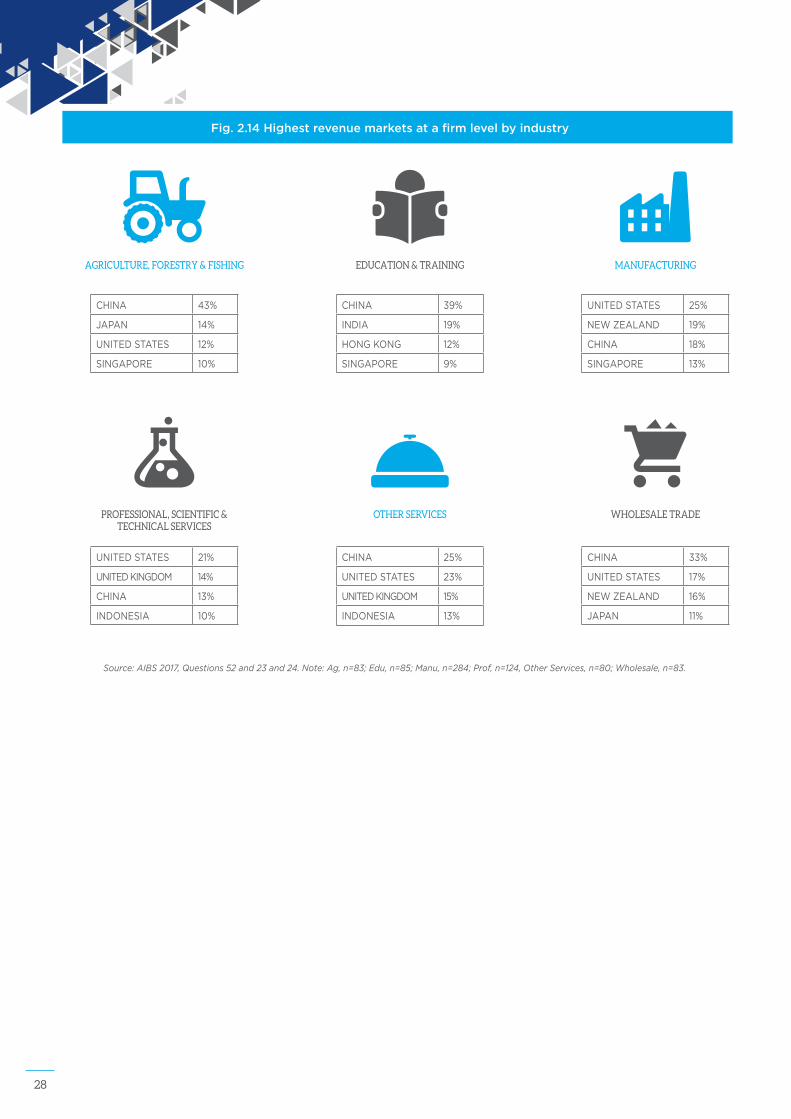

2.2.2 | International revenue by industry

AnalysisofinternationalrevenuebyindustryispossiblethroughAIBS2017.Whenanalysedbyindustrysector,43%oftheagriculture,forestryandfishingsectoridentifiedChinaasatopmarketforinternationalrevenue,whichisthelargestsingleproportionbyanyoftheAIBS2017industrysectors.Atafirmlevel,Chinaisalsoanimportantmarketfortheeducationandtrainingsectorat39%.WithintheASEANcountries,bothSingaporeandIndonesiafeatureasimportant,withSingaporefeaturingasimportantfortheagriculture,forestryandfishing,educationandtraining,andthemanufacturingsector.Indonesiaisanimportantearnerfortheprofessional,scientificandtechnicalservicessectorandotherservices.

Fig. 2.13 International revenue by country

Top 20 plus focused countries 1-25% 26-50% 51-75% 75-99% 100%

China 27% 31% 13% 12% 18%

UnitedStates 23% 34% 16% 16% 10%

NewZealand 24% 35% 14% 16% 11%

UnitedKingdom 42% 36% 5% 9% 7%

Singapore 43% 36% 9% 9% 3%

HongKong 36% 33% 7% 9% 16%

Indonesia 40% 39% 9% 4% 9%

Japan 47% 30% 12% 9% 2%

India 43% 30% 8% 13% 6%

Malaysia 41% 28% 15% 7% 9%

Source: AIBS 2017, Questions 23-25. Note: China, n=216; United States, n=206; New Zealand, n=111; United Kingdom, n=96; Singapore, n=90; Hong Kong, n=70; Indonesia, n=70; Japan, n=66; India, n=63, Malaysia, n=54. All countries with <50 sample size have not been included.

28

Fig. 2.14 Highest revenue markets at a firm level by industry

CHINA 43%

JAPAN 14%

UNITEDSTATES 12%

SINGAPORE 10%

AGRICULTURE, FORESTRY & FISHING

CHINA 39%

INDIA 19%

HONGKONG 12%

SINGAPORE 9%

EDUCATION & TRAINING

UNITEDSTATES 25%

NEWZEALAND 19%

CHINA 18%

SINGAPORE 13%

MANUFACTURING

UNITEDSTATES 21%

UNITEDKINGDOM 14%

CHINA 13%

INDONESIA 10%

PROFESSIONAL, SCIENTIFIC & TECHNICAL SERVICES

CHINA 25%

UNITEDSTATES 23%

UNITEDKINGDOM 15%

INDONESIA 13%

OTHER SERVICES

CHINA 33%

UNITEDSTATES 17%

NEWZEALAND 16%

JAPAN 11%

WHOLESALE TRADE

Source: AIBS 2017, Questions 52 and 23 and 24. Note: Ag, n=83; Edu, n=85; Manu, n=284; Prof, n=124, Other Services, n=80; Wholesale, n=83.

29

AIB

S 2017

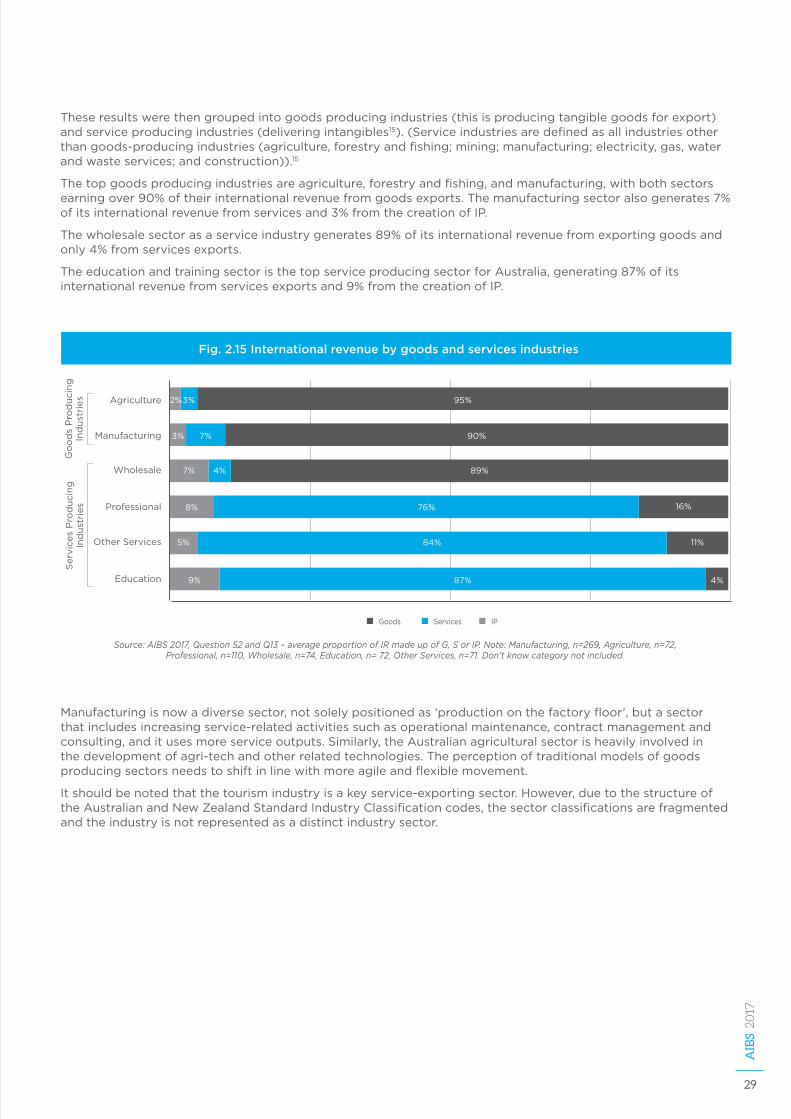

Theseresultswerethengroupedintogoodsproducingindustries(thisisproducingtangiblegoodsforexport)andserviceproducingindustries(deliveringintangibles15).(Serviceindustriesaredefinedasallindustriesotherthangoods-producingindustries(agriculture,forestryandfishing;mining;manufacturing;electricity,gas,waterandwasteservices;andconstruction)).15

Thetopgoodsproducingindustriesareagriculture,forestryandfishing,andmanufacturing,withbothsectorsearningover90%oftheirinternationalrevenuefromgoodsexports.Themanufacturingsectoralsogenerates7%ofitsinternationalrevenuefromservicesand3%fromthecreationofIP.

Thewholesalesectorasaserviceindustrygenerates89%ofitsinternationalrevenuefromexportinggoodsandonly4%fromservicesexports.

TheeducationandtrainingsectoristhetopserviceproducingsectorforAustralia,generating87%ofitsinternationalrevenuefromservicesexportsand9%fromthecreationofIP.

Manufacturingisnowadiversesector,notsolelypositionedas‘productiononthefactoryfloor’,butasectorthatincludesincreasingservice-relatedactivitiessuchasoperationalmaintenance,contractmanagementandconsulting,anditusesmoreserviceoutputs.Similarly,theAustralianagriculturalsectorisheavilyinvolvedinthedevelopmentofagri-techandotherrelatedtechnologies.Theperceptionoftraditionalmodelsofgoodsproducingsectorsneedstoshiftinlinewithmoreagileandflexiblemovement.

Itshouldbenotedthatthetourismindustryisakeyservice-exportingsector.However,duetothestructureoftheAustralianandNewZealandStandardIndustryClassificationcodes,thesectorclassificationsarefragmentedandtheindustryisnotrepresentedasadistinctindustrysector.

Fig. 2.15 International revenue by goods and services industries

95%3%2%

90%7%3%

89%4%7%

87%9%

84%5%

76%8% 16%

11%

4%

Goods Services IP

Agriculture

Manufacturing

Wholesale

Professional

OtherServices

Education

Go

od

sP

rod

ucin

g

Ind

ust

ries

Serv

ices

Pro

du

cin

g

Ind

ust

ries

Source: AIBS 2017, Question 52 and Q13 – average proportion of IR made up of G, S or IP. Note: Manufacturing, n=269, Agriculture, n=72, Professional, n=110, Wholesale, n=74, Education, n= 72, Other Services, n=71. Don’t know category not included.

30

2.2.3 | Born global companies

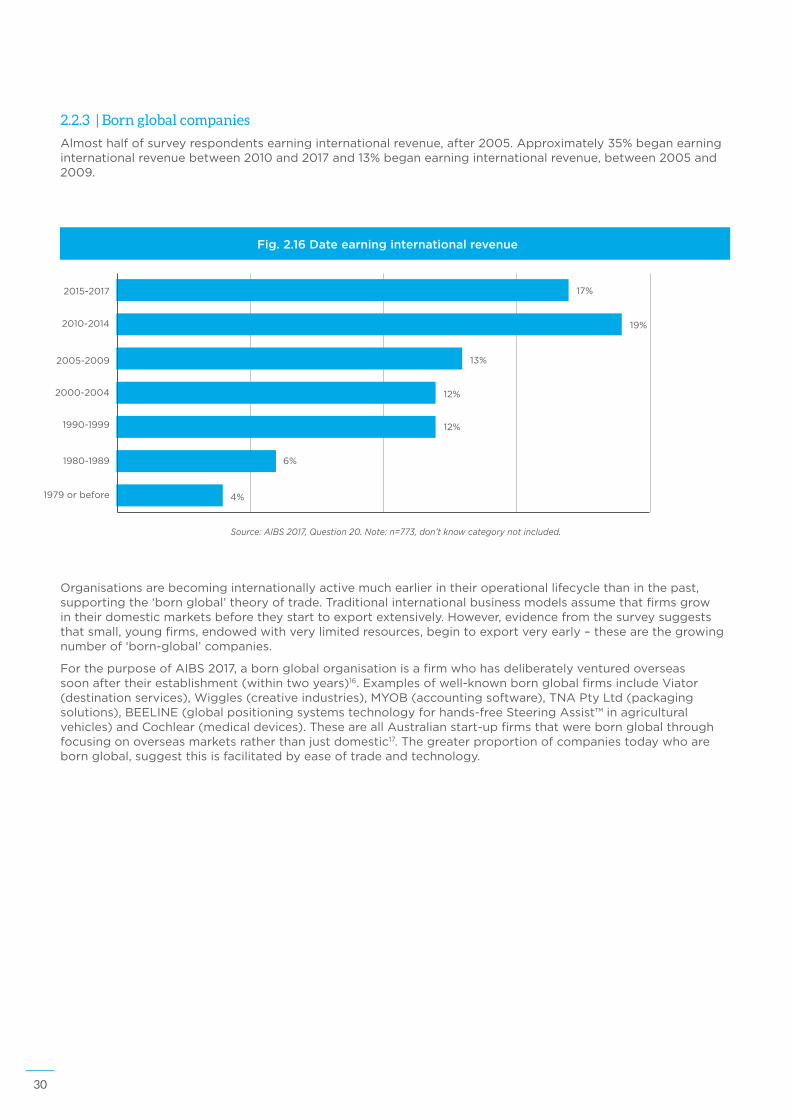

Almosthalfofsurveyrespondentsearninginternationalrevenue,after2005.Approximately35%beganearninginternationalrevenuebetween2010and2017and13%beganearninginternationalrevenue,between2005and2009.

Fig. 2.16 Date earning international revenue

2015-2017

2010-2014

2005-2009

2000-2004

1990-1999

1980-1989

1979orbefore

17%

19%

13%

12%

12%

6%

4%

Source: AIBS 2017, Question 20. Note: n=773, don’t know category not included.

Organisationsarebecominginternationallyactivemuchearlierintheiroperationallifecyclethaninthepast,supportingthe‘bornglobal’theoryoftrade.Traditionalinternationalbusinessmodelsassumethatfirmsgrowintheirdomesticmarketsbeforetheystarttoexportextensively.However,evidencefromthesurveysuggeststhatsmall,youngfirms,endowedwithverylimitedresources,begintoexportveryearly–thesearethegrowingnumberof‘born-global’companies.

ForthepurposeofAIBS2017,abornglobalorganisationisafirmwhohasdeliberatelyventuredoverseassoonaftertheirestablishment(withintwoyears)16.Examplesofwell-knownbornglobalfirmsincludeViator(destinationservices),Wiggles(creativeindustries),MYOB(accountingsoftware),TNAPtyLtd(packagingsolutions),BEELINE(globalpositioningsystemstechnologyforhands-freeSteeringAssist™inagriculturalvehicles)andCochlear(medicaldevices).TheseareallAustralianstart-upfirmsthatwerebornglobalthroughfocusingonoverseasmarketsratherthanjustdomestic17.Thegreaterproportionofcompaniestodaywhoarebornglobal,suggestthisisfacilitatedbyeaseoftradeandtechnology.

31

AIB

S 2017

Fig. 2.17 Born global organisations

16%MANUFACTURING

14%WHOLESALE TRADE

12%AGRICULTURE, FORESTRY AND FISHING

10%OTHER SERVICES

14%PROFESSIONAL,

SCIENTIFIC AND TECHNICAL SERVICES

TOP INDUSTRIES

OF THE SAMPLE ARE BORN GLOBAL COMPANIES

6% EARN ALL TOTAL REVENUE FROM INTERNATIONAL, while 58% are earning 10% OR LESS of their revenue off international revenue.

BORN GLOBAL COMPANIES STARTING OPERATION IN 2010-2017

54% are earning less than $1 million in total revenue

56%MICRO

26%SMALL

15%MEDIUM

3%LARGE

ORGANISATION SIZE

Pre1980

0%

20%

40%

60%

1980s 1990s 2000s 2010sBO

RN

GLO

BA

L B

Y D

EC

AD

E

Source: AIBS 2017, Questions 20, 21, 22, 52, 55 and 56. Note: n=941 for overall, 2010-2017 (n=145); classed as born global if they began trading internationally within two years of beginning their operation.

4%8%

15%

31%

44%

59%1 or 2

21%3 to 5

9%6 to 10

10%MORE THAN 10

NUMBER OF MARKETS

32

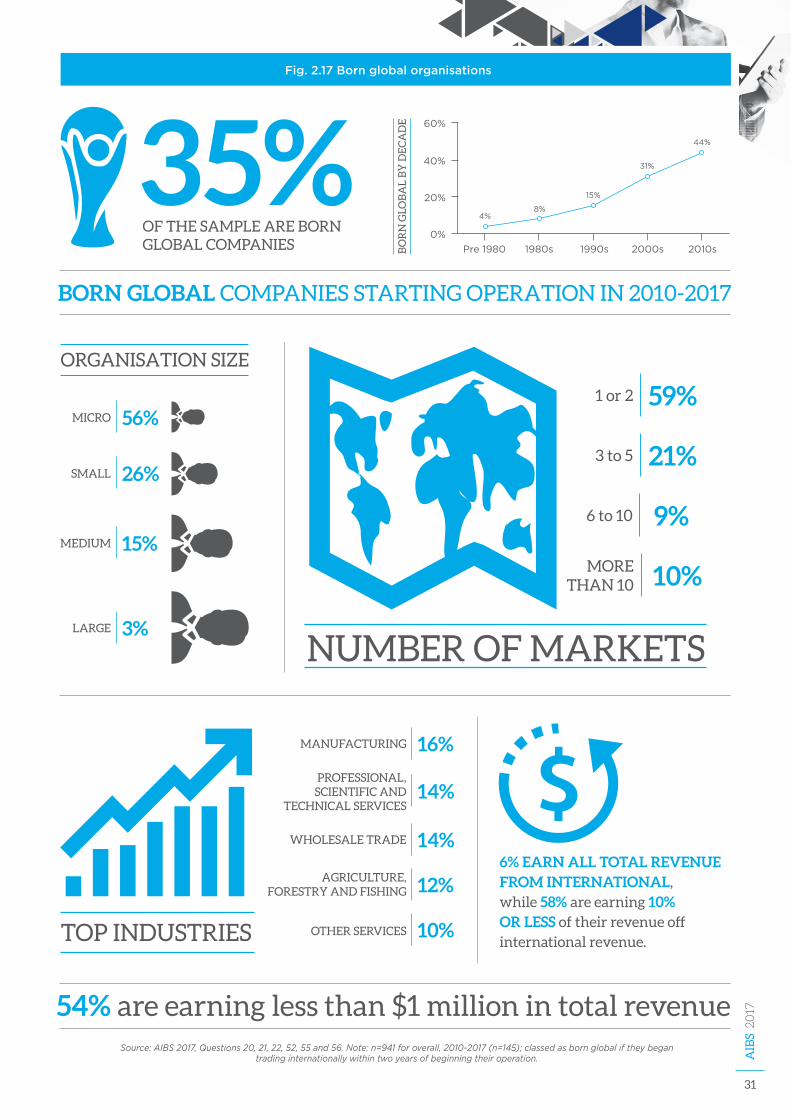

Bornglobalsurveyrespondentstotal35%ofthesample(n=941).Whenthisfigureisdistributedacrossseveraldecades,findingsindicatethatthehighestproportionofbornglobalcompaniesoperatedinthe2010s,thatistosaythattheyearntinternationalrevenuewithinthefirsttwoyearsofoperation.Bornglobalrespondentsarefoundacrossthevariousindustrysectorsbutweremore

prominentinmanufacturing,professionalservicesandwholesaletradesectors.Mostbornglobalorganisationsaremicro-sizedorganisationsemployingbetween0and4peopleandthat58%oftheseearnlessthanA$1millionintotalrevenue.

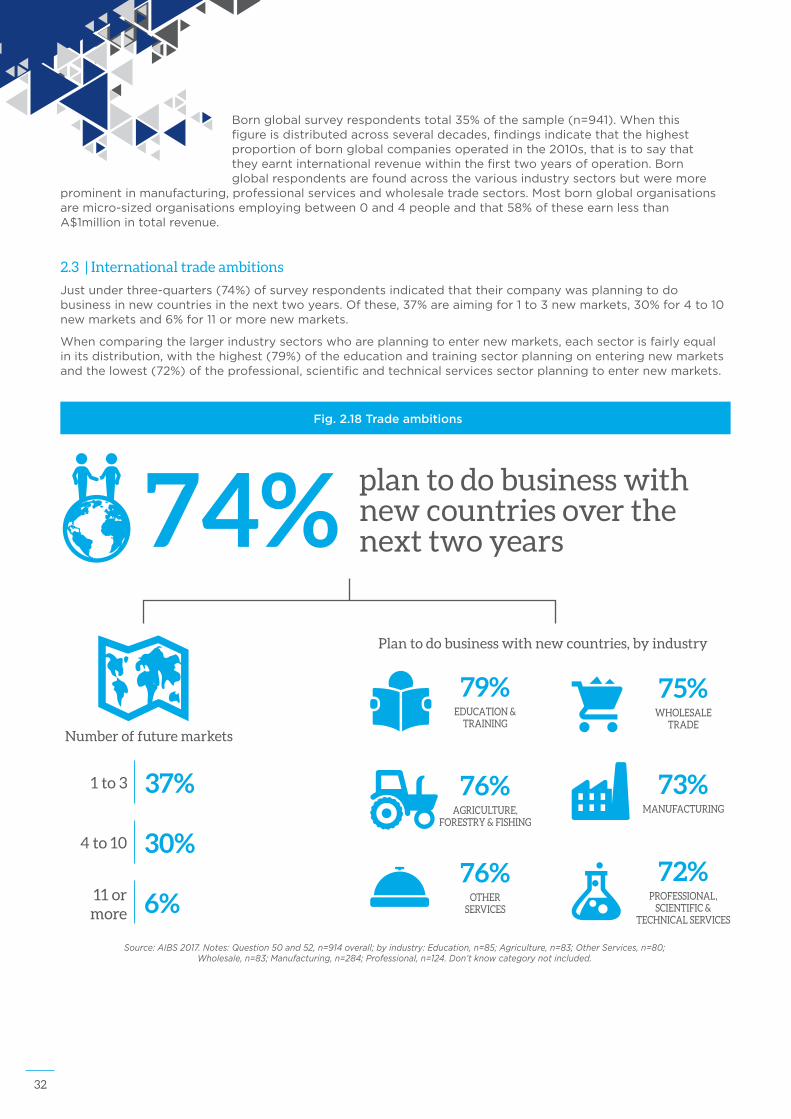

2.3 | International trade ambitions

Justunderthree-quarters(74%)ofsurveyrespondentsindicatedthattheircompanywasplanningtodobusinessinnewcountriesinthenexttwoyears.Ofthese,37%areaimingfor1to3newmarkets,30%for4to10newmarketsand6%for11ormorenewmarkets.

Whencomparingthelargerindustrysectorswhoareplanningtoenternewmarkets,eachsectorisfairlyequalinitsdistribution,withthehighest(79%)oftheeducationandtrainingsectorplanningonenteringnewmarketsandthelowest(72%)oftheprofessional,scientificandtechnicalservicessectorplanningtoenternewmarkets.

Source: AIBS 2017. Notes: Question 50 and 52, n=914 overall; by industry: Education, n=85; Agriculture, n=83; Other Services, n=80; Wholesale, n=83; Manufacturing, n=284; Professional, n=124. Don’t know category not included.

Fig. 2.18 Trade ambitions

74% plan to do business with new countries over the next two years

Plan to do business with new countries, by industry

AGRICULTURE, FORESTRY & FISHING

76%MANUFACTURING

73%

EDUCATION & TRAINING

79%WHOLESALE

TRADE

75%

OTHER SERVICES

76%PROFESSIONAL,

SCIENTIFIC & TECHNICAL SERVICES

72%

Number of future markets

37%1 to 3

30%4 to 10

6%11 or more

33

AIB

S 2017

Australia’sinternationallyactivebusinessesarenotonlyengagedinexportsandimportsofgoodsandservices,butarealsoactiveinoutwardinvestmentandreceivinginvestments.UndertakingresearchanddevelopmentoverseasisacommonactivityforAustralianbusinessesandwithsupport,theseinvestmentscanbetransformedintonichecommercialactivity,contributingtothegrowthofinternationalbusinesspartnershipsandcollaboration.However,whilstthissectionanalysesexistinginternationalbusinessactivity,futuremarketsanddoingbusinessinnewandmultiplecountriesarealsointhesightsofAustralianbusinesses,contributingtowardsthefuturegrowthofAustralia’sinternationaleconomy.

34

Australia’s international business activity in focus3

What the survey says

Access to additional finance

58%didnotapplyforanyfinance,35%did

Overall27%oflargefirmssecuredadditionalfinance(32%applied)and18%ofsmallsecuredfinance(35%applied)

60%ofthoseapplyingforadditionalfinanceweresuccessful,40%unsuccessful

Fundingsourcesfromowners/family/friends,overseasinvestorandretainedearningsimportant

Reasonsthatcompaniescitedunsuccessfulaccesstoadditionalfinancewereduetoinadequatecashflowandhighsecurityrequirements

Australia’s FTA activity

89%areexportinggoodsand/orservicestoFTAmarkets

38%areexportingbothgoodsandservicestoFTAmarkets

23%areexportingonlygoodstoFTAmarkets

28%areexportingonlyservicestoFTAmarkets

FTA export activity by industry

LargestshareofexportersofgoodsandservicestoFTAmarketsinmanufacturingsector,followedbyprofessional,scientificandtechnicalservices

ASEANisatopFTAmarketforallsectors

FTA ‘goods’ export activity

ASEANregionismostcommongoodsexportmarket,40%,followedbyNewZealand,USandChina

ChinawasthebiggestFTAmarketforagriculture,forestryandfishing(goods),andwholesaletrade,NewZealandformanufacturedgoods,theUSforprofessionalservicesandMalaysiaforeducationandtrainingservices

Benefits of FTAs

40%respondentsexportingtoChinaand31%toThailandsaidFTAsbenefitedtheirexportsales

13%gainedadditionalFTAbenefitsincluding‘recognisedAustralianstandards’and‘allowedorganisationtomakesalesnotpreviouslypermitted’

FTA documentation requirements

64%ofallgoodsexporterstoFTAmarketsuseatradeservicesproviderorthirdpartytohandleFTAexportpaperwork

ExporterstoThailandandSouthKoreareportedthehighestsharesofgoodsexportersprovidingFTAdocumentationwith38%ofrespondentssellingtoThailandprovidingFTAdocumentationtoclaimapreferentialtariff,and35%ofthosesellingtoSouthKorea

Negotiating rules of origin

63%ofrespondentsusedCertificatesofOrigin(CoOs)toverifyAustralianproducts,mainlywithinthesectorsofagriculture,fisheriesandforestry(79%)manufacturing(68%)andwholesaletrade(63%).LargerorganisationsaremorelikelytouseCoOsthansmallerorganisations

35%ofrespondentsdidnotuseCoOsand26%ofthesehighlightedthiswasduetoalackofunderstandingofthebenefits

Anauthorisedbodyisthemainsourceforissuingcertificates,withover40%ofthoseusingCoOsusinganauthorisedbodytocertifyelectronicandpapercertificates.28%ofrespondentsusingCoOsuseself-certificationprocesses

ForthoseorganisationsthatobtainCoOsthroughan‘authorisedbody’,approximately45%betweenA$0andA$999and42%ofrespondentsspendbetweenA$1000andA$9999

35

AIB

S 2017

36

FTA ‘Services’ activity

MostpopularFTAserviceexportmarketsaretheASEANregion,China,US,SingaporeandNewZealand

Mode1,servicingoverseasmarketsviacallcentresetc.andMode4bytravellingoverseasaremostsignificant

9%ofthosethattraveloverseasfacedrestrictions

Barriers to commencing international trade

Ofthosecompaniesthatdonotengageininternationalactivity,26%reportthisisduetoalackofinternationalleadsand22%areuncertainhowtobegin

46%suggestedadatabaseofpotentialbuyers/supplierswouldhelpstart,41%suggestedgrants,34%mentoring

Key trade factors influencing international revenue

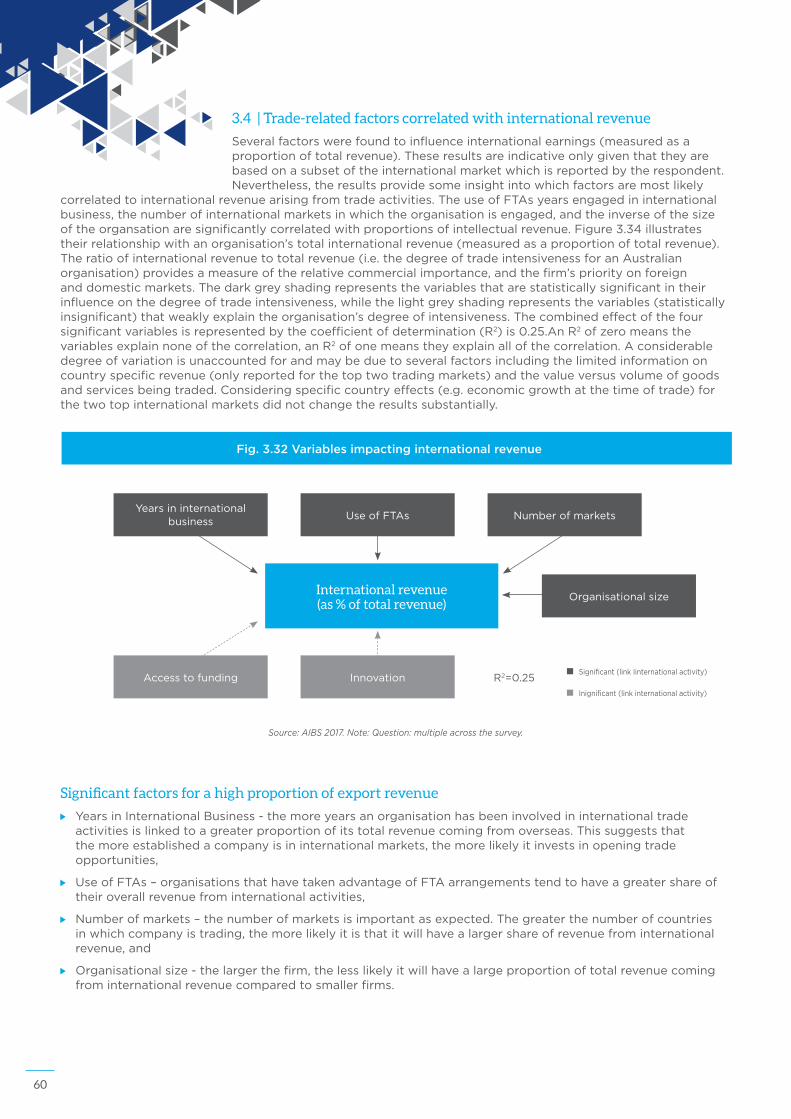

Significantfactorscorrelatingtohigherexportintensityinclude:moreyearsengagedininternationaltrade,smallerorganisations,inlargermarkets,andtheusingofFTAs.

37

AIB

S 2017

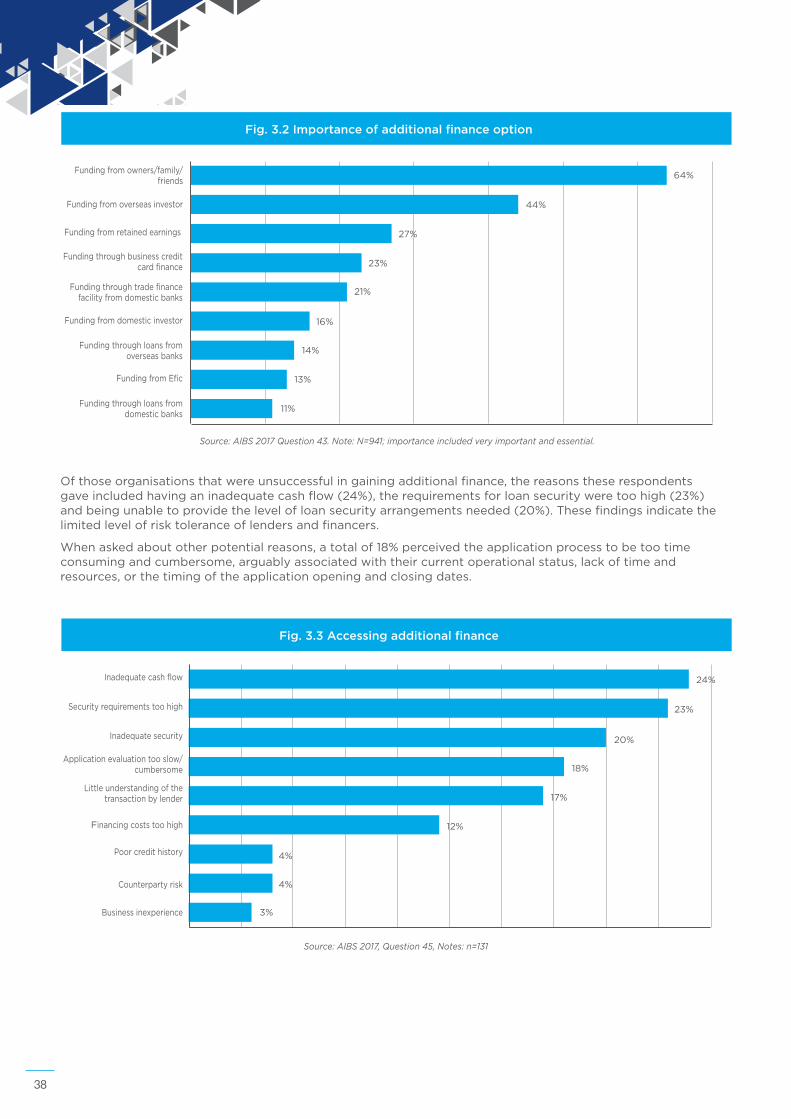

Theimportanceofadditionalfinanceoptionsforfinancingexportoperationstoserviceoverseasmarketswascanvassedacrossthesurveyparticipantsample.Atotalof64%ofrespondentspreferencedthatthemainsourceoffinanceisthroughowners/family/friendsratherthangrantsorfinancialinstitutions.Approximately44%ofrespondentsconsideredfundingfromanoverseasinvestorasimportant,while27%ofrespondentsconsideredfinancingactivitiesusingretainingearningsasimportant.21%and11%ofrespondentsfoundtradefinanceandloans(respectively)fromdomesticbanksimportant,loansfromanoverseasbankwasimportantfor14%andfundingfromEficwasimportantfor13%.

Introduction

Internationaltradeisakeydriverofjobsgrowth,productivity,innovationandlong-termeconomicgrowth.Hence,developinganunderstandingofthedriversoftradeiscriticalindevelopingAustralia’slong-termdomesticeconomicpolicysettings.Section3seekstoidentifysomeofthesedriversthroughcloseranalysisofAIBS2017responsesregarding:

Accesstofinance,

Australia’sfreetradeagreement(FTA)activityandprocesses,

Barriersexperiencedbyfirmswhoarenotcurrentlyundertakinginternationalbusinessactivity,and

Tradefactorsinfluencinginternationalrevenue.

3.1 | Access to finance

Surveyrespondentsreportedaccessingarangeofdifferentfundingsourcestofinancetheirexportoperations.Accesstoadditionalfinanceplaysacriticalroleinthesupportofinternationaltrade.Whilstatotalof58%ofrespondentsdidnotapplyforanyfinancetosupportinternationalbusinessactivity,35%ofcompaniesdidseekadditionalfinance.Approximately60%oftheseindicatedtheyweresuccessfulinobtainingfinancewhiletheremaining40%indicatedtheywereunsuccessful.Ofthelargebusinessesthatappliedforadditionalfinance,84%ofthemweresuccessful.Thepropositionwas51%forsmallbusinesses.SmallerorganisationsareseekingoverseasfinancebecausetheyfinditdifficulttoaccessfundingfromwithinAustraliaaslendersherearegenerallyriskaversetolendingtosmallorganisationsandseethesefirmshavingpoorcash-flowsystems.AccesstofundingforglobalexpansionofAustralianSMEssupportsgrowthofbothdomesticandinternationalmarketshare,provideseconomiesofscale,developsskillsandcapabilitiesforimprovementinbusinessmanagement,andprovidesincreasedresilience10.

Source: AIBS 2017, Questions 44 Note: n=941, by organisation employee size, small (0 – 19), n=566, medium (20-199), n=250, large (200 or more), n=113; 7% who selected ‘don’t know’ not included in figure

Fig. 3.1 Accessing additional finance

58% Did not apply for additional finance 35% Applied for additional

finance

were not successful

40%were successful

60%

Successful Unsuccessful Didnotseekadditionalfinance

18%

17%62%

26%

12%54%

27%

5%45%

SMALL MEDIUM LARGE

By organisational size

38

Ofthoseorganisationsthatwereunsuccessfulingainingadditionalfinance,thereasonstheserespondentsgaveincludedhavinganinadequatecashflow(24%),therequirementsforloansecurityweretoohigh(23%)andbeingunabletoprovidethelevelofloansecurityarrangementsneeded(20%).Thesefindingsindicatethelimitedlevelofrisktoleranceoflendersandfinancers.

Whenaskedaboutotherpotentialreasons,atotalof18%perceivedtheapplicationprocesstobetootimeconsumingandcumbersome,arguablyassociatedwiththeircurrentoperationalstatus,lackoftimeandresources,orthetimingoftheapplicationopeningandclosingdates.

Fig. 3.2 Importance of additional finance option

Fundingfromowners/family/friends

Fundingfromoverseasinvestor

Fundingfromretainedearnings

Fundingthroughbusinesscreditcardfinance

Fundingfromdomesticinvestor

Fundingthroughloansfromoverseasbanks

FundingfromEfic

Fundingthroughloansfromdomesticbanks

Fundingthroughtradefinancefacilityfromdomesticbanks

64%

44%

27%

23%

16%

14%

13%

11%

21%

Source: AIBS 2017 Question 43. Note: N=941; importance included very important and essential.

Fig. 3.3 Accessing additional finance

Inadequatecashflow

Inadequatesecurity

Securityrequirementstoohigh

Applicationevaluationtooslow/cumbersome

Littleunderstandingofthetransactionbylender

Financingcoststoohigh

Poorcredithistory

Counterpartyrisk

Businessinexperience

24%

20%

23%

18%

17%

12%

4%

4%

3%

Source: AIBS 2017, Question 45, Notes: n=131

39

AIB

S 2017

Forthoserespondentsthatdidnotseekadditionalfinance,68%highlightedthattheydidnotneedit,8%expressedconcernsthattheydidnotseekfinancebasedonpastexperiencesand4%suggestedalackofbusinessexperiencepreventedthemfromseekingadditionalfinance.

Finance made easy

Ofthoseorganisationsthatappliedforadditionalfinance,whethersuccessfulornot,theeaseofsourcingfinancewasexplored.Approximately27%ofthosethatappliedhighlightedthattheprocesswasthesameforinternationalanddomesticbusinessopportunities,27%saiditwaseasiertosourcefinancefordomesticbusinessopportunities,whereas,19%saiditwasmucheasiertosourcefinanceforinternationalbusinessopportunities.

Fig. 3.4 Reasons for not accessing additional finance

68% Did not need additional debt to fund international business opportunities

8% Did not expect to be able to secure additional funding based on past experiences

4% Balance sheet could not accommodate additional debt; Business inexperience

Source: AIBS 2017, Question 46, Notes: n=543 , ‘other’ and ‘none of these’ categories not included in figure

Overall,itiseasiertosourcefinancefordomesticbusinessopportunitiesthanitistosourcefinanceforinternationalactivityandwhilstsurveyrespondentsrepresentingsmallerorganisationshighlightdifficultiesinsourcingfinance,thedifferenceisnotsignificantlydifferentwhencomparedtoalargeorganisation.

3.2 | Australia’s free trade agreement (FTA) activity

AnFTAisaninternationaltreatywhichaimstoremovebarriersandfacilitatestrongertradeandcommercialties,contributingtoincreasedeconomicintegrationbetweenparticipatingcountries18.FTAscancoverentireregions(RegionalFreeTradeAgreementsorRTAs),withmultiplemembersorbebilateralbetweentwoeconomies18.

ThereisanexpandingglobalnetworkofFTAs,withAustralia’scurrentFTApolicyaimedatmaximisingtheeconomicbenefitsflowingtoAustraliafromthenegotiationoftradeagreements18.AustraliacurrentlyhasninebilateralFTAs,namelythosewithThailand,Singapore,theUS,Japan,China,Chile,SouthKorea,MalaysiaandNewZealand.

The10countriesoftheASEANregionincludeIndonesia,thePhilippines,Cambodia,Vietnam,Malaysia,Thailand,Laos,Brunei,SingaporeandMyanmar,andareincludedintheASEAN-Australia-NewZealandFTA.AllFTAmarketscombinedaccountfor67%ofAustralia’stotaltwo-wayinternationaltrade18.

19% Easier to source finance for international business opportunities

27% About the same for international and domestic business opportunities

27% Easier to source for domestic business opportunities

Fig. 3.5 Ease of sourcing additional Finance

Source: AIBS 2017, Question 47. Note: Answered by those who applied, successful or not – international versus domestic opportunities N=329.

40

AustraliaisengagedinseveralFTA,RTAandmultilateralnegotiations,whichinclude:

Australia-EuropeanUnionFreeTradeAgreement,

Australia-GulfCooperationCouncil(GCC)FTA,

Australia-HongKongFreeTradeAgreement,

Australia-IndiaComprehensiveEconomicCooperationAgreement,

ComprehensiveandProgressiveAgreementsonTrans-PacificPartnership

EnvironmentalGoodsNegotiations,

Indonesia-AustraliaComprehensiveEconomicPartnershipAgreement,

PacificAllianceFreeTradeAgreement,

RegionalComprehensiveEconomicPartnership,and

TradeinServicesAgreement,

TherearemanybenefitsoftheFTAarrangementsforAustralia17.AnFTAcan:

Fosterfreertradeflowsandcreatestrongertieswithglobaltradingpartners,

Eliminatetariffsandaddressbehind-the-borderbarriersthatimpedetheflowofgoodsandservicesbetweenparties,

Encourageinvestment,enhancecooperation,addressintellectualproperty,e-commerceandgovernmentprocurementissues,

IncreaseAustralia’sproductivityandcontributetohigherGDPgrowthbyallowingdomesticbusinessesaccesstocheaperinputs,

Introducenewtechnologiesandfostercompetitionandinnovation,

Promoteregionaleconomicintegrationandbuildsharedapproachestotradeandinvestment,includingadoptingcommonRulesofOrigin(RoO)andbroaderacceptanceofproductstandards,

EnhancethecompetitivenessofAustralianexportsintheinternationalpartnermarketandaddtotheattractivenessofAustraliaasaninvestmentdestination,and

Deliverenhancedtradingopportunitiesthatcontributetothesustainableeconomicgrowthofless-developedeconomies.

However,despiteongoingfacilitationandimplementationofdirectandregionalFTApolicy,barriersforinternationalbusinessesinexpandinginternationalbusinessactivitiescontinuetoexist,forexporters18.Suchcomplexitiesinclude:

Culturalandsocialbarriers,and

Politicalandregulatorybarrierssuchastariffsandstandards.

ShiftingeconomiccircumstancesalsoinfluenceAustralia’srelativeinternationalcompetitivenessandaffectstheabilitytoattractforeigndirectinvestment(FDI)intoAustralia–therebyshapingthegeneraloperatingenvironmentforAustralianbusinessesandinstitutionsconductinginternationalbusinessactivities.Theseissueswillbeexploredlaterinthisreport.

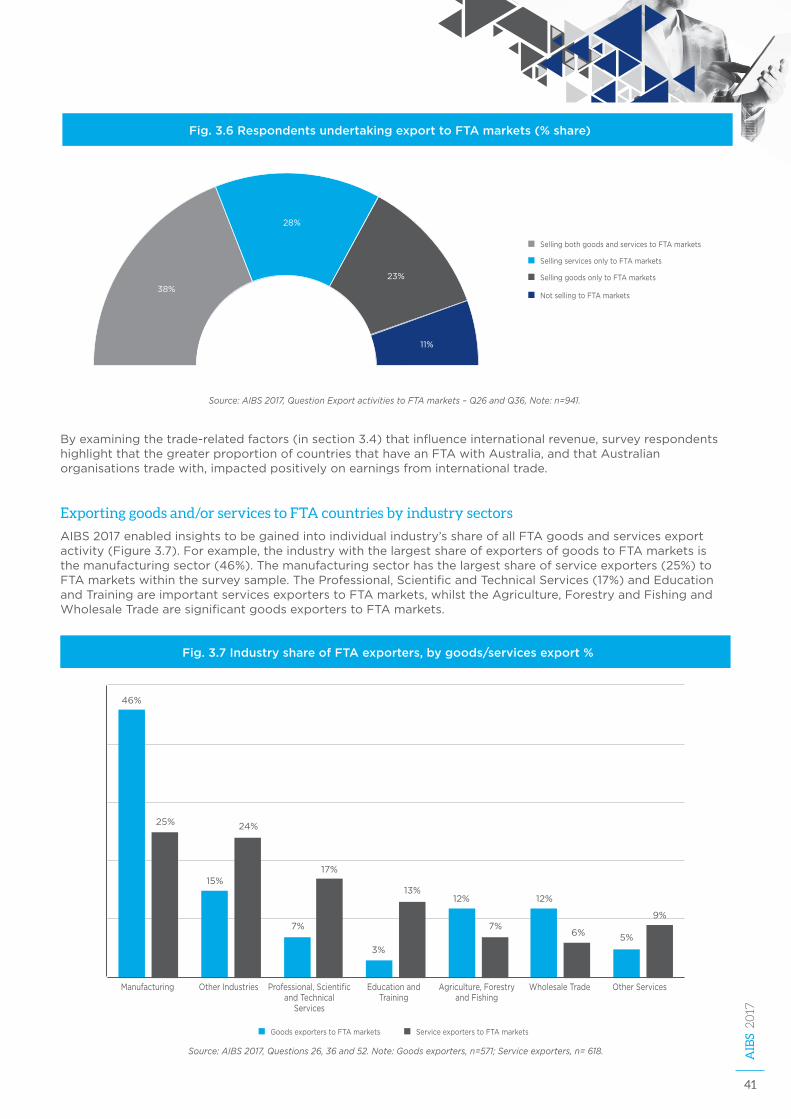

3.2.1 | Overall goods and services to FTA markets

AustraliahasactivelypursuedFTAsforgoodsandservicesexportsandthesehaveresultedinfavourablemarketaccessforAustralianbusinessesinvolvedintradingintermediateand/orfinalgoodsandservices.WhiletheFTAshavefocussedprimarilyonagriculturalandmerchandisegoods,thedatabaseoftheGeneralAgreementonTradeinServices(GATS)identifiesAustralia’sagreementswithChile,Japan,SingaporeandUnitedStatesasincludingsignificantcommitmentsfortheservicessector.

Approximately89%ofAIBSrespondents(n=941)areexportinggoodsand/orservicestoFTAmarkets.Fromwithinthesurveysample(n=941),61%ofrespondentsareexportinggoodstoFTAmarkets(eithergoodsonly,oracombinationofgoodsandservices)and66%areexportingservices(eitherservicesonly,oracombinationofservicesandgoods).

41

AIB

S 2017

Fig. 3.6 Respondents undertaking export to FTA markets (% share)

38%

28%

23%

11%

SellingbothgoodsandservicestoFTAmarkets

SellingservicesonlytoFTAmarkets

NotsellingtoFTAmarkets

SellinggoodsonlytoFTAmarkets

Source: AIBS 2017, Question Export activities to FTA markets – Q26 and Q36, Note: n=941.

Byexaminingthetrade-relatedfactors(insection3.4)thatinfluenceinternationalrevenue,surveyrespondentshighlightthatthegreaterproportionofcountriesthathaveanFTAwithAustralia,andthatAustralianorganisationstradewith,impactedpositivelyonearningsfrominternationaltrade.

Exporting goods and/or services to FTA countries by industry sectors

AIBS2017enabledinsightstobegainedintoindividualindustry’sshareofallFTAgoodsandservicesexportactivity(Figure3.7).Forexample,theindustrywiththelargestshareofexportersofgoodstoFTAmarketsisthemanufacturingsector(46%).Themanufacturingsectorhasthelargestshareofserviceexporters(25%)toFTAmarketswithinthesurveysample.TheProfessional,ScientificandTechnicalServices(17%)andEducationandTrainingareimportantservicesexporterstoFTAmarkets,whilsttheAgriculture,ForestryandFishingandWholesaleTradearesignificantgoodsexporterstoFTAmarkets.

Fig. 3.7 Industry share of FTA exporters, by goods/services export %

Manufacturing OtherIndustries Professional,ScientificandTechnical

Services

EducationandTraining

Agriculture,ForestryandFishing

WholesaleTrade OtherServices

46%

15%

7%

3%

12% 12%

5%

25% 24%

17%

13%

7%6%

9%

GoodsexporterstoFTAmarkets ServiceexporterstoFTAmarkets

Source: AIBS 2017, Questions 26, 36 and 52. Note: Goods exporters, n=571; Service exporters, n= 618.

42

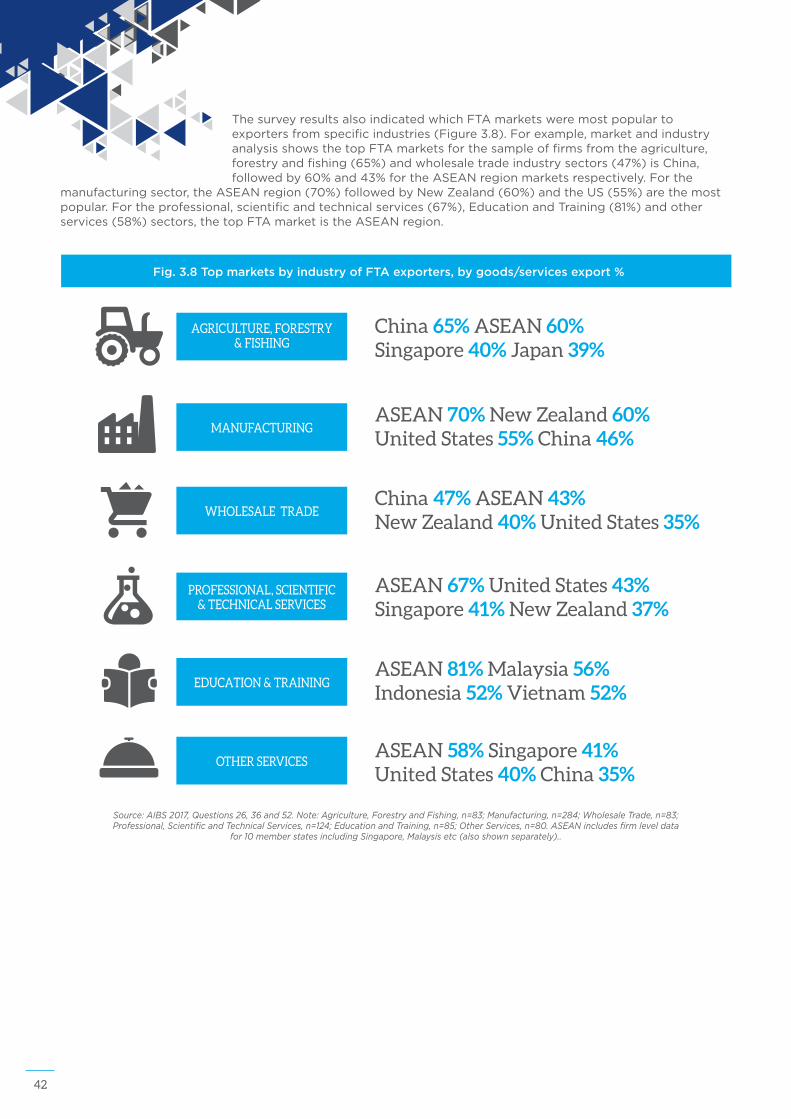

ThesurveyresultsalsoindicatedwhichFTAmarketsweremostpopulartoexportersfromspecificindustries(Figure3.8).Forexample,marketandindustryanalysisshowsthetopFTAmarketsforthesampleoffirmsfromtheagriculture,forestryandfishing(65%)andwholesaletradeindustrysectors(47%)isChina,followedby60%and43%fortheASEANregionmarketsrespectively.Forthe

manufacturingsector,theASEANregion(70%)followedbyNewZealand(60%)andtheUS(55%)arethemostpopular.Fortheprofessional,scientificandtechnicalservices(67%),EducationandTraining(81%)andotherservices(58%)sectors,thetopFTAmarketistheASEANregion.

Fig. 3.8 Top markets by industry of FTA exporters, by goods/services export %

AGRICULTURE, FORESTRY & FISHING

China 65% ASEAN 60% Singapore 40% Japan 39%

ASEAN 70% New Zealand 60% United States 55% China 46%

MANUFACTURING

ASEAN 81% Malaysia 56% Indonesia 52% Vietnam 52%

EDUCATION & TRAINING

China 47% ASEAN 43% New Zealand 40% United States 35%

WHOLESALE TRADE

ASEAN 58% Singapore 41% United States 40% China 35%

OTHER SERVICES

ASEAN 67% United States 43% Singapore 41% New Zealand 37%

PROFESSIONAL, SCIENTIFIC & TECHNICAL SERVICES

Source: AIBS 2017, Questions 26, 36 and 52. Note: Agriculture, Forestry and Fishing, n=83; Manufacturing, n=284; Wholesale Trade, n=83; Professional, Scientific and Technical Services, n=124; Education and Training, n=85; Other Services, n=80. ASEAN includes firm level data

for 10 member states including Singapore, Malaysis etc (also shown separately)..

43

AIB

S 2017

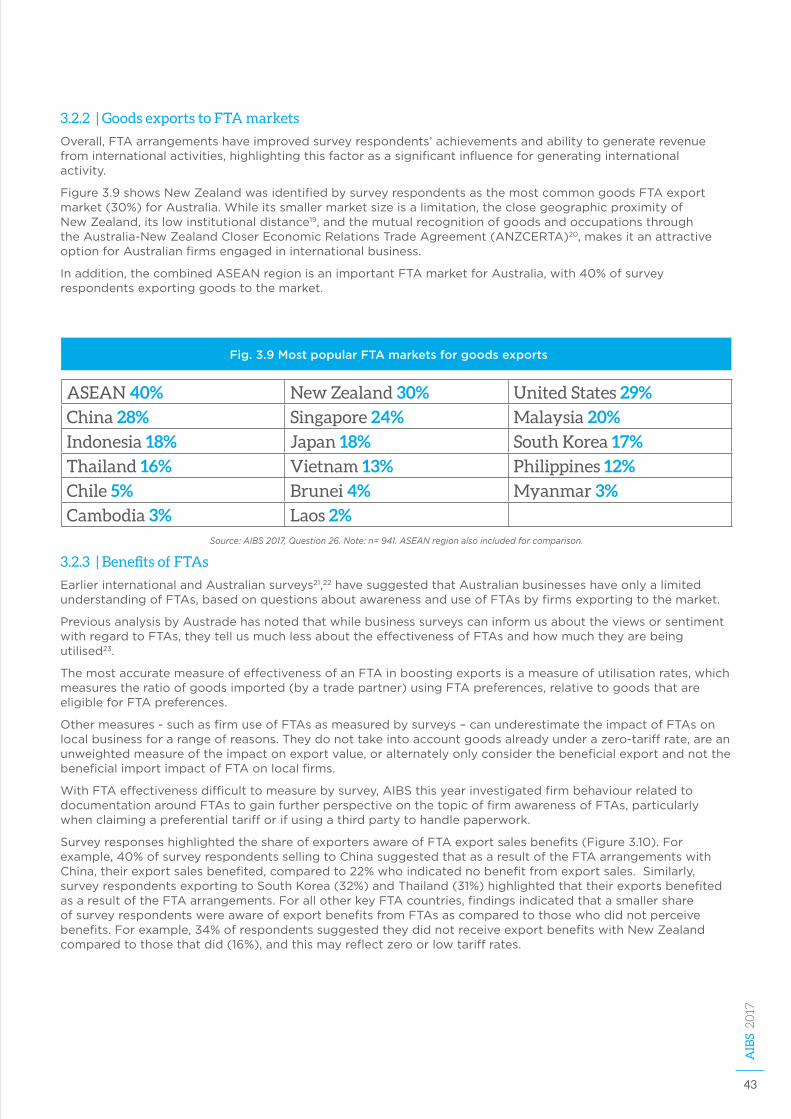

3.2.2 | Goods exports to FTA markets

Overall,FTAarrangementshaveimprovedsurveyrespondents’achievementsandabilitytogeneraterevenuefrominternationalactivities,highlightingthisfactorasasignificantinfluenceforgeneratinginternationalactivity.

Figure3.9showsNewZealandwasidentifiedbysurveyrespondentsasthemostcommongoodsFTAexportmarket(30%)forAustralia.Whileitssmallermarketsizeisalimitation,theclosegeographicproximityofNewZealand,itslowinstitutionaldistance19,andthemutualrecognitionofgoodsandoccupationsthroughtheAustralia-NewZealandCloserEconomicRelationsTradeAgreement(ANZCERTA)20,makesitanattractiveoptionforAustralianfirmsengagedininternationalbusiness.

Inaddition,thecombinedASEANregionisanimportantFTAmarketforAustralia,with40%ofsurveyrespondentsexportinggoodstothemarket.

3.2.3 | Benefits of FTAs

EarlierinternationalandAustraliansurveys21,22havesuggestedthatAustralianbusinesseshaveonlyalimitedunderstandingofFTAs,basedonquestionsaboutawarenessanduseofFTAsbyfirmsexportingtothemarket.

PreviousanalysisbyAustradehasnotedthatwhilebusinesssurveyscaninformusabouttheviewsorsentimentwithregardtoFTAs,theytellusmuchlessabouttheeffectivenessofFTAsandhowmuchtheyarebeingutilised23.

ThemostaccuratemeasureofeffectivenessofanFTAinboostingexportsisameasureofutilisationrates,whichmeasurestheratioofgoodsimported(byatradepartner)usingFTApreferences,relativetogoodsthatareeligibleforFTApreferences.

Othermeasures-suchasfirmuseofFTAsasmeasuredbysurveys–canunderestimatetheimpactofFTAsonlocalbusinessforarangeofreasons.Theydonottakeintoaccountgoodsalreadyunderazero-tariffrate,areanunweightedmeasureoftheimpactonexportvalue,oralternatelyonlyconsiderthebeneficialexportandnotthebeneficialimportimpactofFTAonlocalfirms.

WithFTAeffectivenessdifficulttomeasurebysurvey,AIBSthisyearinvestigatedfirmbehaviourrelatedtodocumentationaroundFTAstogainfurtherperspectiveonthetopicoffirmawarenessofFTAs,particularlywhenclaimingapreferentialtarifforifusingathirdpartytohandlepaperwork.

SurveyresponseshighlightedtheshareofexportersawareofFTAexportsalesbenefits(Figure3.10).Forexample,40%ofsurveyrespondentssellingtoChinasuggestedthatasaresultoftheFTAarrangementswithChina,theirexportsalesbenefited,comparedto22%whoindicatednobenefitfromexportsales.Similarly,surveyrespondentsexportingtoSouthKorea(32%)andThailand(31%)highlightedthattheirexportsbenefitedasaresultoftheFTAarrangements.ForallotherkeyFTAcountries,findingsindicatedthatasmallershareofsurveyrespondentswereawareofexportbenefitsfromFTAsascomparedtothosewhodidnotperceivebenefits.Forexample,34%ofrespondentssuggestedtheydidnotreceiveexportbenefitswithNewZealandcomparedtothosethatdid(16%),andthismayreflectzeroorlowtariffrates.

Fig. 3.9 Most popular FTA markets for goods exports

ASEAN 40% New Zealand 30% United States 29%

China 28% Singapore 24% Malaysia 20%

Indonesia 18% Japan 18% South Korea 17%

Thailand 16% Vietnam 13% Philippines 12%

Chile 5% Brunei 4% Myanmar 3%

Cambodia 3% Laos 2%Source: AIBS 2017, Question 26. Note: n= 941. ASEAN region also included for comparison.

44

Furtheranalysisthatcross-referencesthedocumentationpracticesoffirms,showthatthosefirmsthatarenotawareofexportsalesbenefits(i.e.respondentsthatansweredno,notapplicableordon’tknow),areinthemajorityofcasesnotfillingoutFTA-specificdocumentation.ForthekeyFTAmarkets,exporterstoSingaporeaccountedforthehighestrateofsurveyrespondentsthatdidnotfilloutFTAspecificdocumentation(83%),followedbyNewZealand(80%).

Fig. 3.10 Firm awareness of export sales benefits of FTA by country

Yes NotApplicableNo Don’tKnow

40% 22% 17% 22%

27%16%35%22%

32%

12%

16%

14%

31%

20% 29% 17% 33%

26% 12% 30%

32% 19% 35%

34% 20% 30%

29% 13% 47%

27% 17% 24%

China

Japan

SouthKorea

Malaysia

NewZealand

Singapore

Thailand

UnitedStates

Source: AIBS 2017, Question 31. Note: Export sales benefits of FTA, China, n=166; Indonesia, n=102; Japan, n=141; South Korea, n=132; Malaysia, n=77; New Zealand, n=128; Singapore, n=128; Thailand, n=106; United States, n=166.

45

AIB

S 2017

However,asindicatedabove,surveyquestionsbasedonfirmawarenessarenotanaccuratewayofmeasuringapplicabilityofanFTA,andinthiscase‘nobenefit’responsesmaywellindicatefirmstowhichFTAprovisionssimplydonotapply.

Inaddition,furtheranalysisofresponsesincluding‘Don’tknowiftheirgoodsexportsalesbenefitedornot’highlightthatasignificantnumberofsurveyrespondentsareoutsourcingtheirdocumentationtothirdpartiesandthereforesurveyrespondentsmaynotbeawarehowtheFTAiscontributingtotheirsales.Forexample,69%ofthoserespondentsexportinggoodstoChina,thathaverespondedthattheydon’tknowiftheirgoodsexportssalesbenefitedornot,outsourcetheirpaperworkandlogisticstoacustomsbroker,freightforwarder,consolidatororasimilartradeserviceprovider.

Fig. 3.11 Views of respondents on FTA access by market

Goodsexportsalebenefits

Nogoodsexportsalebenefits;andprovidedFTA-specificdocumentation

Nogoodsexportsalebenefits;anddidnotprovideFTA-specificdocumentation

40%

32% 8% 60%

31% 9% 59%

22% 7% 71%

20% 8% 72%

16% 4% 80%

14% 3% 83%

12% 10% 78%

5% 55%China

Japan

SouthKorea

Malaysia

NewZealand

Singapore

Thailand

UnitedStates

Source: AIBS 2017, Question 31 and 27. Note: China, n=166; South Korea, n= 132; Thailand, n= 106; Japan, n=141; United States, n=16. ‘No’ includes ‘no’, ‘not applicable’ and ‘don’t know’.

46

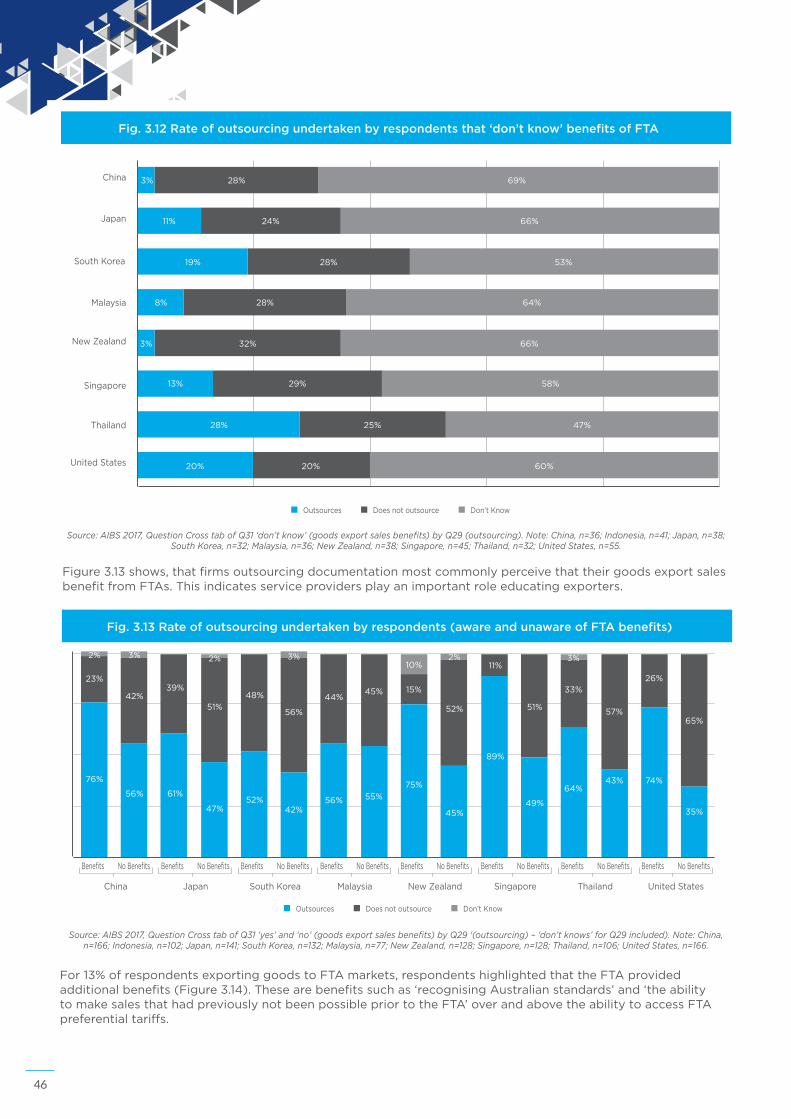

Figure3.13shows,thatfirmsoutsourcingdocumentationmostcommonlyperceivethattheirgoodsexportsalesbenefitfromFTAs.Thisindicatesserviceprovidersplayanimportantroleeducatingexporters.

Fig. 3.12 Rate of outsourcing undertaken by respondents that ‘don’t know’ benefits of FTA

China

Japan

SouthKorea

Malaysia

NewZealand

Singapore

Thailand

UnitedStates

Outsources Doesnotoutsource Don’tKnow

3% 28% 69%

11% 24% 66%

19% 28% 53%

8% 28% 64%

3% 32% 66%

13% 29% 58%

28% 25% 47%

20% 20% 60%

Source: AIBS 2017, Question Cross tab of Q31 ‘don’t know’ (goods export sales benefits) by Q29 (outsourcing). Note: China, n=36; Indonesia, n=41; Japan, n=38; South Korea, n=32; Malaysia, n=36; New Zealand, n=38; Singapore, n=45; Thailand, n=32; United States, n=55.

For13%ofrespondentsexportinggoodstoFTAmarkets,respondentshighlightedthattheFTAprovidedadditionalbenefits(Figure3.14).Thesearebenefitssuchas‘recognisingAustralianstandards’and‘theabilitytomakesalesthathadpreviouslynotbeenpossiblepriortotheFTA’overandabovetheabilitytoaccessFTApreferentialtariffs.

Fig. 3.13 Rate of outsourcing undertaken by respondents (aware and unaware of FTA benefits)

Outsources Doesnotoutsource Don’tKnow

China Japan SouthKorea Malaysia NewZealand Singapore Thailand UnitedStates

Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits Benefits NoBenefits

76%

23%

2%

56%

42%

3%

61%

39%

47%

51%

2%

52%

48%

42%

56%

3%

56%

44%

55%

45%

75%

15%

10%

45%

52%

2%

89%

11%

49%

51%

64%

33%

3%

43%

57%

74%

26%

35%

65%

Source: AIBS 2017, Question Cross tab of Q31 ‘yes’ and ‘no’ (goods export sales benefits) by Q29 ‘(outsourcing) – ‘don’t knows’ for Q29 included). Note: China, n=166; Indonesia, n=102; Japan, n=141; South Korea, n=132; Malaysia, n=77; New Zealand, n=128; Singapore, n=128; Thailand, n=106; United States, n=166.

47

AIB

S 2017

19%ofrespondentsreceivedadditionalFTAbenefitswhenexportinggoodstoChinaand16%ofrespondentswhenexportinggoodstoSouthKorea.Inthesefirms,respondentsindicatedthattheFTArecognisedAustralianstandardsandthisledtoincreasedtradeactivity.SuchincreasedtradeactivityandthehigherrateofexportersawareofadditionalbenefitssuggeststhatFTAsgaveAustralianfirmsconfidencetoenhancepartnershiparrangementswithcountriesintheAsia-Pacificregion,despitetheculturalandinstitutionaldifferences.

WhilsttheresearchteamhaveattemptedtoanalysethebenefitsofFTAsforparticipatingfirms,capturingthesebenefitsisdifficultasthereislimitedcurrentdataontheapplicabilityofFTAstofirmsexportingtothemarketandsurveysarelimitedintheirabilitytomeasurebenefits.

Fig. 3.14 FTA additional benefits

of firms perceived additional benefits from utilising FTAs from at least one FTA market13%

of firms exporting to China

19% of firms exporting to

South Korea

16%

ADDITIONAL BENEFITS

RecognisedAustralianstandardsand/oraccreditation55%

Allowedustomakesaleswewerenotpreviouslypermittedtomake46%

Allowedustostructureourbusinessinasimplerwaythanbefore39%

Providedbettervisaconditions32%

AlloweddatatobestoredinAustralia29%Source: AIBS 2017. Note: Question 34: (n=571); China, n=166; South Korea, n= 132, Question 35: (n=82), % of firms whom noted additional benefit

for at least one of the 1-3 FTA markets they are exporting goods to.

48

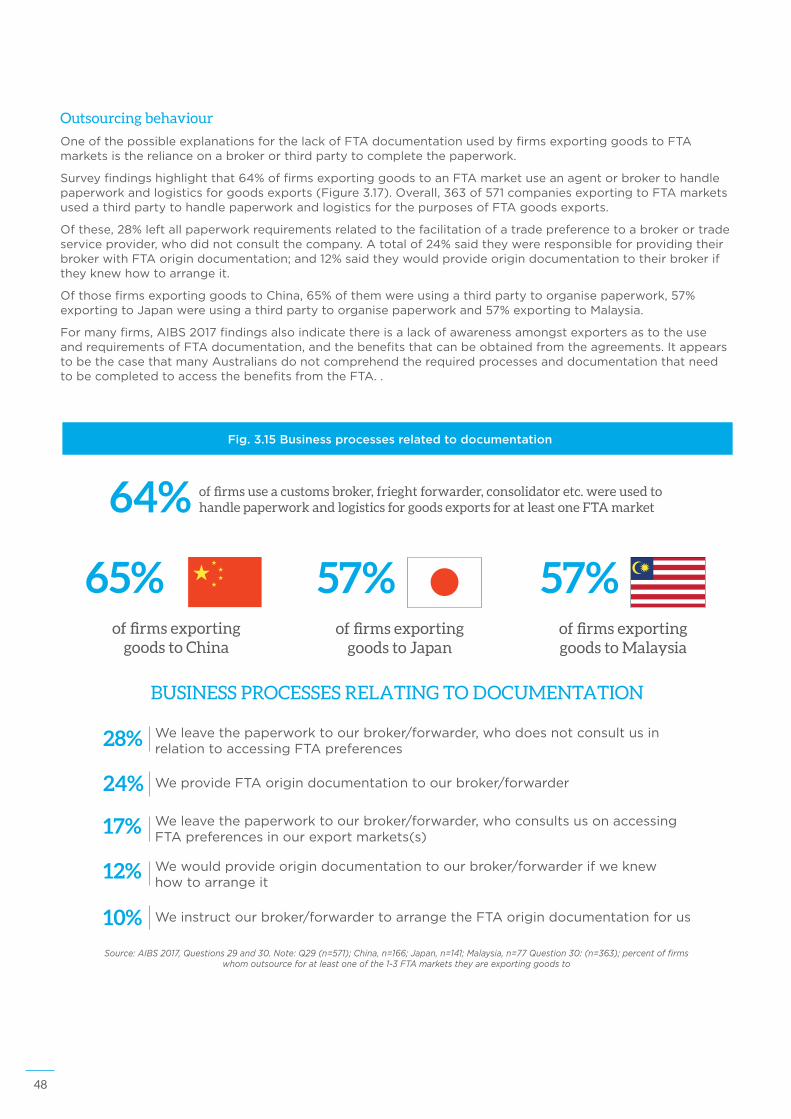

Outsourcing behaviour

OneofthepossibleexplanationsforthelackofFTAdocumentationusedbyfirmsexportinggoodstoFTAmarketsistherelianceonabrokerorthirdpartytocompletethepaperwork.