Embed Size (px)

DESCRIPTION

The no. 1 news magazine for Australian brokers.

Citation preview

POST APPROVED PP255003/06906$4.95

Lenders are resorting to “acts of desperation” in a bid to capture business in a low credit growth environment, and borrowers and brokers may find themselves disadvantaged by the moves.

As lenders increasingly slash rates, offer discounts and increase LVRs to draw customers, broker Daniel O’Brien of PFS Financial

banks will then no doubt attempt to seek these losses from out of my pocket or the customer’s,” he said.

It was recently reported that prudential regulator APRA issued a warning to banks over their pricing wars, cautioning lenders to maintain responsible standards and expressing concern over rising LVRs. Following the reports, CBA subsidiary Bankwest released a WA-exclusive first homeowner loan of up to 97% LVR.

Bromley said such loans skirt the boundaries of suitability. “I think we really have yet to understand if we’ve recovered from the GFC or not, and there’s a whole issue around suitability and responsible lending. I’m probably a bit old school, but I think you have to prove you can afford a deposit,” he commented.

Bankwest defended its responsible lending practices following the release of the loan, saying it had put in place credit standards such as a minimum combined income of $80,000 and a maximum purchase price of $500,000.

“It is not in our interest to lend to people who cannot afford it. We have grown our share of new lending ahead of the market whilst remaining competitive and without compromising our credit quality standards,” Bankwest head of specialist lending Ian Rakhit said.

However, for a first homebuyer couple buying a $500,000 home at

ISSUE 8.17

September 2011

Rate cut marginsFixed cutting frenzy delivers fillip for banks

Page 2

Panel face-offAggregators and lenders clash over panel updates

Page 4

Opening LMIFact sheet to make mortgage insurance transparent

Page 8

Inside this issueAnalysis 20Business size vs revenueOpinion 22Being careful of footprintsForum 23Brokers on aggregator panelsMarket talk 24Melbourne and The BlockToolkit 26Making CRMs centralCaught on camera 28AFG awards top brokersInsider 30Clients, not garbage

Bank moves to raise LVRs and lower interest rates branded unsustainable

‘Desperation’ driving bank market share bids

Services has commented that banks are showing desperation in the face of shrinking credit demand. O’Brien echoed the sentiments of LJ Hooker general manager Peter Bromley, who recently accused banks of “desperate lending tactics” amid discounting moves, and criticised the banks for wooing customers with irresponsibly high LVRs. O’Brien called the discounts “ridiculous”. “The reason I say the discounts are ridiculous is because longer term it will mean skinnier profit margins for the banks. The Page 16 cont.>>

Daniel O’Brien

2

Newswww.brokernews.com.au

Banks could have further to move on fixed rates before the current wave of cuts is over, it has been claimed.

With both major lenders and non-banks issuing a flurry of fixed rate reductions in the past weeks, National Finance Club manager of retail distribution Andrew Clouston said he believes many lenders still have room to move on fixed rates. Clouston said reductions in wholesale funding costs have been significant, and that some lenders have yet to pass on the full measure of these savings.

“Some people in the market are probably holding onto that reduction in funding costs,” Clouston said.

NFC recently reduced its three-year fixed rate by 30bps to 6.29%, a

move Clouston said represents the full impact of reductions to the lender’s funding costs. He said the move was made while still protecting profit margins.

“In reducing rates to the level we have now, we’ve managed to be able to maintain our profit margins where they were a few months ago. We’ve just seen a reduction in the cost of wholesale funding and passed on that reduction in wholesale costs in full,” he commented.

Clouston believes, however, that many lenders are building larger margins into their fixed rate reductions.

“I think there would be some lenders waiting to see where the bottom actually is. Some of them are testing the margins and building fatter margins into their funding range. We’ve just done a full pass-on of that,” he remarked.

While many lenders seem to have moved quickly to undercut each other’s fixed rate moves, Clouston believes the recent reductions merely represent changes to funding costs rather than competitive behaviour.

“Competitive behaviour will probably follow on after, but at the moment it’s predominantly a pass-on of the margin reductions,” he remarked.

This pass-on, Clouston said, has resulted in renewed customer interest. While he commented it may be too early to gauge borrower uptake of the products, he said NFC has seen a major spike in enquiries for fixed rates.

“The coming weeks will show what the result is as far as business that actually comes through, but customer enquiries have been really high,” he said.

www.brokernews.com.au

EDITOR Ben Abbott

COPY & FEATURES

NEWS EDITOR Adam Smith

PRODUCTION EDITORS Sushil Suresh, Moira Daniels

ART & PRODUCTION

DESIGN PRODUCTION MANAGER Angie Gillies

SALES & MARKETING

SALES MANAGER Simon Kerslake

ACCOUNT MANAGER Rajan Khatak

SENIOR MARKETING EXECUTIVE Kerry Corben

MARKETING EXECUTIVE Anna Keane

COMMUNICATIONS EXECUTIVE Lisa Narroway

TRAFFIC MANAGER Abby Cayanan

CORPORATE

DIRECTORS Mike Shipley, Claire Preen

CHIEF OPERATING OFFICER George Walmsley

PUBLISHING DIRECTOR Justin Kennedy

CHIEF INFORMATION OFFICER Colin Chan

HUMAN RESOURCES MANAGER Julia Bookallil

Editorial enquiriesBen Abbott tel: +61 2 8437 4716 [email protected]

Advertising salesSimon Kerslake tel: +61 2 8437 4786

Rajan Khatak tel: +61 2 8437 [email protected]

Subscriptionstel: +61 2 8437 4731 • fax: +61 2 9439 4599

Key Media www.keymedia.com.au

Key Media Pty Ltd, Regional head office, Level 10, 1 Chandos St, St Leonards, NSW 2065, Australia

tel: +61 2 8437 4700 fax: +61 2 9439 4599Offices in Singapore, Hong Kong, Toronto

www.brokernews.com.au

Copyright is reserved throughout. No part of this publication can be reproduced in whole or part without the express permission of the editor. Contributions are invited, but copies of work should be kept, as Australian

Broker magazine can accept no responsibility for loss

Australian Broker is the most-often read industry publication, according to independent research carried out by the Ehrenberg-Bass Institute for

Marketing Science at the University of South Australia in December 2008.

The research also found that brokers rate Australian Broker as the best for both news content and feature articles, followed by sister publication MPA.

Overall, on all categories, Australian Broker ranks top followed by MPA. The results were based on a sample of 405 respondents who were the

subject of telephone interviews.

Brokers are far more likely to join social networking site Twitter than they are LinkedIn, according to the MFAA.

Executive director of marketing and membership at the peak industry association, Kriti Colless, told Australian BrokerNews that broker preferences for social media start with Twitter, closely followed by Facebook, with LinkedIn struggling to find broker supporters.

“What we have found is that growing the MFAA’s likes on Facebook has been a lot more organic than trying to get brokers to actually use LinkedIn,” she said. Colless suggests this is due to the B2B nature of LinkedIn, in comparison with other more broker-friendly B2C platforms.

The MFAA suggests that it is the immediate nature and brevity of

Twitter, as well as its functionality, which is proving popular.

“Twitter is massive – absolutely massive. If you are a broker and you are not on Twitter, you are really missing out,” Colless said.

“With Twitter, you can get the information out quickly, and through that feed and through other tools you can update your other social media platforms quite easily, so it gives you efficiency.”

Colless said brokers can benefit by having regular information about the industry specifically, and more general information, delivered immediately via Twitter feeds.

Colless said the association is also running LinkedIn tutorials for people who are interested.

Melbourne-based Mortgage Fair finance consultant Emma

Lockwood said that she does use Twitter, and appreciates it particularly for its immediacy.

“Being able to interact in real time with other brokers, clients or referral partners allows me to see new initiatives as they develop,” Lockwood said. “By regularly using Twitter, I have developed my own online business identity with a range of dedicated followers. Twitter gives every business the ability to be their own PR agent.

However, Lockwood said that she uses Facebook more extensively than Twitter. “I use Facebook extensively, and LinkedIn occasionally,” Lockwood explained. “I find my core demographics use Facebook more regularly than LinkedIn, which is used mainly for developing my industry network.”

This magazine is printed on paper produced from 100% sustainable forestry, grown and managed specifically for the paper pulp industry

Brokers prefer Twitter to LinkedIn

Banks building ‘fatter margins’ from fixed rate cuts

Andrew Clouston

For all the latest mortgage industry news, visit www.brokernews.com.au

4

Newswww.brokernews.com.au

Australian Mortgage Brokers CEO Paul Gollan has defended the market’s aggregators against accusations they are too slow to appoint new panel lenders.

Last edition, Australian Broker published an anonymous letter from a small non-conforming lender, which claimed that aggregators were too slow in updating their panels with good businesses, to the detriment of both brokers and their clients (‘Have aggregators forgotten their roots?’ Australian Broker edition 8.16, page 22)

However, Gollan has hit back by saying one of the main

responsibilities of an aggregator or broker firm is to complete adequate due diligence on potential panel lenders to ensure its members’ ongoing commission entitlements are not compromised.

Gollan said that this conservative approach to new panel appointments proved itself during the global financial crisis, when some mortgage managers without robust business models disappeared, leaving brokers out of pocket.

“Our members would be very pleased that other than the HLP Mortgage debacle – where we lost five trails in total – our members have continued to earn

trail on business settled through all approved panel lenders,” Gollan said.

Gollan said licensing – and the restriction of credit reps to panel lenders – made life difficult for “back door” BDMs and lenders who thrived pre-GFC era by “piggybacking off the hard work done by others”. He explained that pre-GFC, brokers were tempted via commission offers to submit deals to off-panel mortgage managers, which cut out the aggregator, reducing their return on investment in mentoring and training.

Gollan said that in a licensed environment, risks for aggregators

had also increased. “One hundred per cent of our members are authorised credit representatives under our licence and we do not charge for that,” Gollan said. “The additional risk, however, means we have to be very selective about which lenders we have on our panel and we complete an authorised product review every three months.”

Gollan added that it was also important for aggregators not to “clutter” brokers’ heads with too many competing panel members. “It’s not just about having every possible option available,” he said.

Aggregators accused of ‘restraint of trade’

Gollan defends aggregator lender panels

Aggregators who restrict credit representatives to dealing with only their panel lenders could be guilty of ‘restraint of trade’, one lender has claimed.

Premium Capital head of sales Andrew Rae said the case for aggregators restricting credit reps to panels is understandable, when it comes to risk mitigation and providing blanket professional indemnity cover for their member brokers.

However, he said that this restrictive approach is “unsubstantiated” as yet, and that ASIC could be quite happy for these brokers to become credit representatives of both their aggregator and a mortgage manager, in effect having more than one credit representation.

“At end of day their approach could potentially be perceived as restraint of trade,” Rae said.

A number of agreements already exist at some aggregators that allow select brokers to deal with off-panel lenders, usually due to long-standing broker relationships with those lenders.

Rae has also implored all brokers who have credit representative status to consider obtaining their own Australian Credit Licence, so they can “control their own destiny”.

“I’ve been speaking to a lot of brokers over the past couple of weeks, and in a lot of cases they didn’t get an ACL because they were told by their aggregator it was all going to be too hard,” he said.

Rae said that aggregators were understandably trying to protect their income streams, as well as their brokers’ income streams, by limiting lending to panel lenders. However, he said a “fair dinkum” aggregator would

open up a panel to provide more choice to their members.

Rae said brokers should do their own research, and also ask what value they are getting from their aggregators. “Brokers have got to start asking what they are getting out of their aggregators, as opposed to them being one large post office box,” he said.

Rae has also refuted claims from Australian Mortgage Brokers’ CEO Paul Gollan, which

suggested that smaller lenders locked out of lending to aggregator credit reps would begin to ‘push the envelope’ of NCCP as they were ‘starved’ of new business.

“As mortgage managers, we are bound by our funder’s credit policy, and in a lot of cases, we need to work with the mortgage insurers as well,” he said. “We are nearly working with two different credit policies on most occasions. It’s not happening at all.”

Flashback: Off-panel deals fraught with dangerCredit reps authorised by their aggregators to do off-panel deals could face extreme legal danger, according to Darren Loades of Insurance Advisernet. Speaking with Australian BrokerNews earlier this year, Loades said that if a credit rep writes business under another licensee’s banner, his group would not indemnify the other licensee. “Our position is clear that if you are a credit rep, and you’re placing loans via more than one licensee, you should have your own PI cover,” he said at the time. Were a deal to go badly and litigation to take place, Loades said both the lender and credit rep would find themselves as defendants.

For all the latest mortgage industry news, visit www.brokernews.com.au

Read the latest issue of Australian Broker online www.brokernews.com.au

6

Newswww.brokernews.com.au

‘Volatility’ delays CUA’s broker return

CBA ‘rock solid’ amid global turmoil

First homebuyers most savvy

Economic volatility has delayed CUA’s re-entry to the broker market, the mutual has indicated.

In December, CUA general manager of strategy and marketing Andrew Hadley told Australian Broker the credit union was eyeing a return to the third-party channel, given the right market conditions. Hadley has now said recent economic instability has proven a setback in the company’s plans.

“If you had asked me a month ago, I would have said we were absolutely making progress, but we really do need this period of volatility to settle itself out and see where the dust settles,” Hadley said.

CUA had set about strategising its return to the broker channel, Hadley said, but difficult conditions mean such strategies will have to be re-evaluated. Hadley stated, however, that the mutual remains committed to seeing third-party origination become a reality.

“Conditions had improved and we were doing some fairly advanced modelling. The market volatility doesn’t help, but we’re still absolutely committed when we know we can make the model work

to return to the broker channel,” he remarked.

Hadley conceded that CUA has lost out by not being open to brokers, and indicated that mortgage growth was more challenging without utilising the channel.

“With 40% of the market dominated by brokers, the fact that we’re not in it means we’re playing in a much smaller pond. We’re pleased that we’ve been able to grow 50% above the market, but it’s been a fairly significant challenge,” he said.

While market conditions have remained volatile, Hadley said, this volatility has led to a better funding position. In light of this, CUA has joined the rush of lenders making cuts to fixed rate products. The lender recently lowered its three-year fixed rate to 6.39%.

“There’s absolutely been some significant changes in wholesale prices as a result of the market volatility. The market is not pricing in a number of rate decreases, and it provides us the opportunity to secure funds at a relatively cheap rate,” Hadley said.

First homebuyers – though typically more leveraged than other market segments – show the best arrears performance, Westpac has indicated.

In its third quarter results, Westpac CEO Gail Kelly indicated that among the range of borrower demographics in its portfolio, the bank’s first homeowner customers had the best performance and lowest level of delinquencies.

The bank’s general manager of mortgage broker distribution Huw Bough said this could be due to first homebuyers becoming savvier about the terms and details of home loans.

“We know that first homebuyers have more access to financial education, seminars, internet online tools, and social media specifically targeted at them. This could mean they are most likely to understand the details of their home loan under the current economic environment where there is a focus on paying down debt and saving more,” Bough commented.

The bank posted a $1.55bn cash profit for the third quarter. The result is down 2% from the bank’s second quarter result, but up 11% on the same quarter last year. Westpac has claimed subdued

demand for credit saw it grow its mortgage portfolio in line with weakened system growth. The group’s flagship brand grew 1.2 times system, while it claimed subsidiary St.George saw “improved momentum”.

While growth was subdued, Bough said the bank currently saw more than 40% of its home loan portfolio growth through the broker channel, and would continue to drive this channel through building relationships between brokers and local branch staff.

“We are doing this by introducing brokers to our bank managers and their teams locally to build strengthened partnerships that will benefit the customer,” he said.

Kelly indicated slow credit growth is likely to continue for some time, with credit demand unlikely to recover to pre-GFC levels. She said consumer wariness had seen increased deleveraging by both households and businesses, and that market volatility and weak demand for credit were expected to continue for the near future.

Andrew Hadley

Huw Bough

The Commonwealth Bank is in a strong position to weather any further shocks to the global financial system, according to CBA executive general manager of third party and mobile banking Kathy Cummings.

Following the bank’s announcement of a $6.8bn profit for the year to 30 June, Cummings said that the bank was in a “rock solid” position to meet any further problems with the global economy, which she described as “extremely volatile” at present.

Cummings said the bank was currently “very well funded”, with 61% of its funding sourced from deposits with its local branch networks. The bank is also purchasing additional wholesale funding three to six months in advance, to avoid short-term variances and shocks to wholesale pricing caused by any developments in Europe and the United States.

Commenting on the bank’s mortgage lending book,

Cummings said the bank was seeing the most competitive environment in 30 years, and the concern was that its loan book would churn out amid tough price competition from other banking institutions, some of whom she said were currently pursuing unprofitable strategies.

However, Cummings said the bank was committed to maintaining a system growth rate, and as a result was focused on taking a strong partnership approach to mortgage broking distribution, to ensure brokers supported the bank despite home loan price differences.

Cummings said the bank continued to source approximately 40% of its home loans from mortgage brokers.

While acknowledging the record $6.8bn profit result represented “a lot of money”, she said CBA was a “major engine” of the economy, and its return on assets was low compared with some other companies and industries.

At the bank’s results announcement, CBA warned of growing funding pressures due to economic “headwinds”. Outgoing CEO Ralph Norris said the 2011 financial year had been challenging for the group and many of its customers. He identified fragile consumer and

corporate confidence, political uncertainty, a strong currency and natural disasters.

Cummings said that the current minority Australian Government was a key contributor to poor consumer sentiment, including policies such as the proposed carbon tax.

Kathy Cummings

For all the latest mortgage industry news, visit www.brokernews.com.au

For all the latest mortgage industry news, visit www.brokernews.com.au

8

Newswww.brokernews.com.au

Swan champions bank ‘tick and flick’

LMI education to become mandatory

The Federal Government has released a plan that will give consumers the ability to switch banking institutions “with the stroke of a pen”, according to Treasurer Wayne Swan.

Following an inquiry into the viability of full account portability, the Treasurer announced a package in August that opted for an approach that will instead focus on removing the burden of having to change the details of automatic debit and credit transactions.

“Customers will sign just one form that authorises their new institution to do all the heavy lifting for them,” the Treasurer said at the policy announcement. “The new institution will arrange the transfer of all automatic transactions linked to the customer’s account and inform

associated creditors and debtors about the new details,” he said.

The statement came with the release of a report authored by Reserve Bank governor Bernie Fraser, which investigated options available for increasing account transferability. As a result of the report’s recommendations, the government stopped short of adopting full account number portability, which Swan said “would not deliver enough benefits to justify the huge costs it would impose on business and consumers”.

However, Swan said the initiative would give consumers the power to easily switch to another bank, building society or credit union to seek out better value and service. The plan is to be finalised after industry consultation by 1 July 2012.

The Australian Bankers’ Association reacted by claiming there are already high levels of switching, though it committed to working with the government.

ABA chief executive Steven Munchenberg said the Fraser inquiry found 8–10% of customers already switch transaction accounts, which was comparable with other countries.

Likewise, when it came to home loan customers, the ABA said data on mortgage refinancing suggests customers have little difficulty in switching their home loan provider.

“ABS housing finance statistics have consistently shown that around 30% of new housing loan applications are applications for refinancing,” Munchenberg said.

“While there’s already a lot of switching going on and

independent polling shows three out of four customers are satisfied with their current bank, the industry will work to bring in a simpler, easier system for customers,” he added.

Mortgage insurer Genworth said a new mandatory one- page mortgage fact sheet for homebuyers, which will contain key details on lenders mortgage insurance, will enable them to better compare “apples with apples”.

Announced by Federal Treasurer Wayne Swan as part of the Federal Government’s banking competition reform package, the new LMI fact sheet will allow consumers to compare quotes side-by-side, including the difference in premiums and rebate schedules.

Treasury has advised against the introduction of a scheme to allow the transfer of LMI between lenders, citing the expense, the extreme complexity of administration, and the conclusion it would benefit only 1% of all borrowers.

Genworth said in a statement following the government’s announcement that the mandatory fact sheet should be similar to the Key Fact Sheet for home loans, and could be handed out by lenders just prior to borrowers signing their home loan contract.

The insurer said it would benefit borrowers to be aware of the reason for lenders requiring LMI, how LMI reduces the interest rate that borrowers with a smaller deposit have to pay, the frequent capitalisation of LMI into the loan, and the availability and structure of refunds. This would include understanding that some lenders choose to provide a discounted mortgage insurance cost to borrowers at the outset of the loan in lieu of refunds, the company said.

“Genworth believes it is important that homebuyers know

how lenders mortgage insurance works and the benefits it offers, plus their potential rights in relation to existing refund schedules if they switch home loans,” Genworth CEO Ellie Comerford said.

According to Genworth, recently conducted consumer research shows that overall, most consumers consider LMI important due to the help it gives Australians getting onto the property ladder sooner. Genworth said homebuyers also like the fact that LMI was introduced as a government policy and was run as a government-owned business for many years.

“Consumers also valued that LMI is a community priced product, as opposed to a risk

based priced one (which could negatively impact those in less affluent areas),” Comerford explained. “Community pricing means that borrowers who take out loans (in the same loan to value category) pay the same for lenders mortgage insurance whether they live in – for example – western Sydney, Brisbane or regional Australia,” she said.

Wayne Swan

For all the latest mortgage industry news, visit www.brokernews.com.au

For all the latest mortgage industry news, visit www.brokernews.com.au

For all the latest mortgage industry news, visit www.brokernews.com.au

For all the latest mortgage industry news, visit www.brokernews.com.au

10

Newswww.brokernews.com.au

Brokers should look to outsource as operating costs become more difficult, Vow Financial has said.

As NCCP compliance brings greater operating costs to bear on mortgage brokers, Vow Financial CEO Tim Brown has said brokers must look to cut their overheads.

“Look to outsource as many non-revenue activities as possible,” Brown said. “This way they become variable rather than fixed, which helps when volumes are mixed.”

Aggregators and lenders are also facing increasing costs in the compliance environment. Brown said aggregators should look to reduce overheads while trying to maintain service levels to brokers. The main costs faced by aggregators relate to compliance and software.

“They are inter-related as the first is driving the cost of the other. Add to this the natural increases the rest of the market is suffering such as wages, travel and cost of living etc,” he said.

These costs, Brown predicted, will lead to further consolidation of aggregators. “As margins contract and expenses increase, so will the need for scale and efficiency, so no doubt there will be further consolidation and rationalisation.”

Lenders and aggregators must be proactive in finding cost efficiencies in order to maintain their proposition to the market in an environment of low credit growth, Brown said.

“From an aggregator’s perspective having software that

enables compliance, commissions processing and reporting would reduce costs to the business. From a lender’s perspective, giving aggregators information on brokers who have poor conversion assists with improving loan numbers which again improves productivity and revenue for all concerned,” he said.

As aggregators increasingly consolidate to achieve scale, brokers should also look to consolidate costs with other businesses, according to Brown. “I believe from a broker’s perspective sharing the cost of an office and sales support can reduce their overheads while improving productivity. Brokers don’t get paid from being good at administration.”

Business credit has seen an upswing, and one lender has claimed it represents an opportunity for brokers.

Veda Advantage’s latest Business Credit Demand Index shows business appetite for credit has shown strong gains over the quarter. Credit enquiries for the June quarter were up 17.4% over the previous quarter, and 3.6% year-on-year.

Bankwest head of business broker sales Aaron Milburn has said there has been a corresponding rise in brokers wanting to enter the commercial lending market.

“We are seeing increased demand from brokers both with a commercial background and brokers new to commercial dealings. I think to say there is a substantial shift from residential to commercial may be premature; however, that said, the enquiry level we are seeing is definitely on the rise, as are the requests for education in the commercial field from brokers looking to diversify,” Milburn commented.

As the residential market sees increasingly waning demand, Milburn said commercial finance could present a revenue opportunity for brokers. Milburn commented

that aggregators are now helping brokers unfamiliar with commercial lending transition into the sector.

“Those brokers who are looking to start to transact within the commercial space are well positioned to get clear advice and education as to how to start writing commercial deals. Aggregators are focusing more on having bespoke commercial managers to assist in the transition and banks such as Bankwest are offering free tailored training sessions to encourage diversification,” he said.

Milburn said the best point of entry for brokers was to examine their existing client base for self-employed clients that hold smaller SME businesses with one to four employees.

While Veda said the demand for business credit was strengthening significantly, the company’s head of commercial risk, Moses Samaha, said it had yet to reach pre-GFC levels. However, he commented that the upswing could signal a renewed trend, giving momentum to demand. “Assuming we can move beyond the current market volatility, we should see growth in credit demand gather pace in the second half,” he said.

Outsource to reduce overheads: Brown

Business demand a broker opportunity

Stop using our logo: ASICASIC has warned licensees to stop using the regulator’s name and logo in their advertising.

The watchdog has issued a caution to the industry after a licensee was found displaying the ASIC name and logo on its website to advertise the company’s ACL. ASIC said the action breached intellectual property laws, and could have the potential to mislead consumers.

The regulator further called on consumers to report individuals or companies “suspected of misusing ASIC’s name or logo”.

“ASIC is concerned that use of the ASIC name and logo in conjunction with these identification requirements could

cause consumers to believe the business or company is in some way endorsed or approved by ASIC,” commissioner Peter Boxall said.

An ASIC spokesperson told Australian Broker the company in question displayed the ASIC name and logo on its home page “alongside a number of other organisations’ logos”. She said it was the only case of misuse the regulator had found to date.

Though the incident may have been isolated, Boxall warned that licensees had to follow protocol for advertising their ACL. He commented that it was important to make consumers aware of industry licensing standards.

“This is an important part of

informing consumers that they are dealing with a licensed and regulated entity,” he said.

Boxall reminded licensees that ACL numbers would have to be included in a number of documents, and in all advertising, with the onset of NCCP regulations.

“ASIC reminds licensees that the correct way to inform the public that they hold a credit licence is to display the Australian credit licence number. Credit licensees must include their credit licence number in certain prescribed documents, including advertisements, from 1 April 2012. Licensees should have started the process of updating documentation

which identifies them as holders of an Australian credit licence to avoid breaching the National Credit Act,” he said.

Tim Brown

Peter Boxall

Business credit demand: the key statsCredit cards Up 53.8% on July 2010, and up 21.7% on March 2011

Business loans Up 9% on July 2010, and up 27.6% on March 2011

Asset finance Up 6% on July 2010, and 10.3% on March 2011

Trade credit Remained flat at 0.1% year-on-year, but was up 15.7% on March 2011

Source: Veda Advantage

For all the latest mortgage industry news, visit www.brokernews.com.au

11www.brokernews.com.au

For all the latest mortgage industry news, visit www.brokernews.com.au

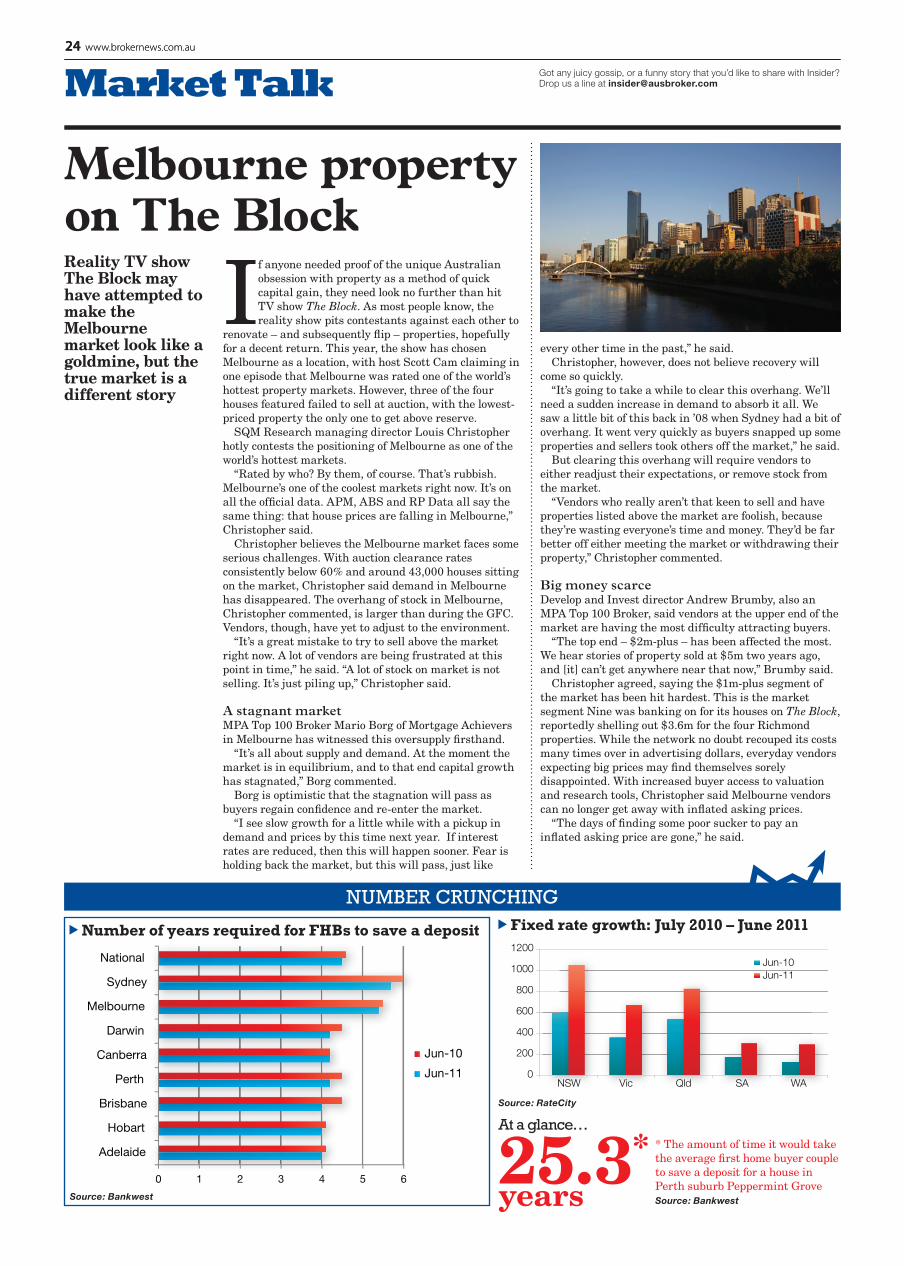

Falling house prices have led to only marginal improvements in affordability, it has been claimed.

Comparison site RateCity has claimed a falling housing market combined with rising incomes means housing is now more affordable than five years ago. However, RP Data has stated that housing has some way to go to combat affordability concerns.

“As property values ease and the cost of goods and services continue to increase, property becomes relatively more affordable. Therefore, it’s unlikely that a couple of quarters of falling values will result in a substantial improvement in affordability; however, if property values continue to grow at a rate below the growth in inflation (as we anticipate) affordability will continue to improve,” RP Data researcher Cameron Kusher said.

Kusher said inflation-adjusted data shows property values have fallen 2.4% in real terms for the quarter. The data has also indicated capital city property values have declined

5.8% from their peak during the March 2010 quarter.

Despite these recent declines, Kusher said property growth has outpaced inflation for much of the last 15 years, resulting in property becoming more expensive in relative terms. If growth remains subdued, though, Kusher said the property market could make headway on affordability.

“Given the expectation of limited value growth as a result of consumer conservatism and limited availability of finance, by inflation-adjusted terms and real terms homes are likely to continue to become relatively more affordable. This is great news for potential homeowners as it will make home ownership a more realistic prospect over time,” he remarked.

In further contrast to RateCity’s claim is new data that has shown the time needed for a first-time buyer couple to save a deposit has significantly increased in the last five years. The Bankwest First Time Buyer Deposit Report has shown the time needed to save a

deposit increased from 3.8 years in 2006 to 4.1 years in 2011.

Bankwest senior analyst Tim Crawford said first homebuyer participation has fallen 35% since last year, and has hit a seven-year low.

“The fact that first-time buyers are taking longer to save a deposit, especially in capital cities, directly contributes to this drop in new buyers entering the property market,” Crawford said.

Little headway for affordability

Source: RP Data

CPI-adjusted capital home value changeCapital city Peak quarter Change to home

values, June 2011

Sydney Sept 2003 -7.9%

Melbourne Sept 2010 -6.2%

Brisbane March 2008 -12.3%

Adelaide June 2010 -6.8%

Perth Sept 2007 -11.3%

Hobart March 2010 -6.3%

Darwin March 2010 -7.2%

Canberra June 2010 -3.9%

Combined capitals March 2010 -5.8%

Cameron Kusher

12

Newswww.brokernews.com.au

Connective posts three months above $1bn

ING Direct has offered ATM fee rebates to its home loan customers as lenders increasingly make moves to attract new mortgage business.

The second tier bank has advised it will refund ATM fees to home loan customers who use their ING Direct transaction account at any ATM in Australia. The rebate will apply to the bank’s Orange Everyday transaction accounts, which will not charge for withdrawals or balance checks.

ING Direct executive director of delivery Lisa Claes said she expected the offer to provide further incentive to potential home loan customers.

“We know Australians loathe paying ATM fees to conduct a simple, everyday transaction so

we’re providing further value to our home loan customers by rebating these completely,” she commented.

Claes said the changes to the bank’s transaction account were not merely a promotional move, but would instead be permanent for home loan customers.

“This is not a promotion, but an enhancement to our transaction account. We’re hoping this feature will be very popular amongst our home loan customers and as a result we aim to embed this into our product suite long term,” she commented.

Amid a wave of recent fixed rate cuts and dramatic discounts to draw new home loan business, Claes indicated that lenders will have to be creative in their

offering to potential borrowers. “As competition heats up in the

market, lenders are looking at other ways to add value to their offers in order to attract new or refinancing borrowers. We believe this will be a real drawcard when customers are looking for a point of difference between lenders and have customers further consider ING Direct for more of their everyday banking,” she said.

The second tier bank also announced in August that it would waive fees on its SmartPack and fixed rate home loans for borrowers with LVRs up to 80%. The offers apply to any new loans unconditionally approved from 15 August until further notice.

ING Direct’s head of broker sales Mark Woolnough said the

offer reflected the current aggressive competition within the home loan market.

“We’re conscious that it’s a very competitive environment at the moment and these offers prove that we’re very keen to maintain our position as a true alternative to the major banks,” Woolnough commented.

ING Direct waives ATM, setup fees

Connective has reached three consecutive months of more than $1bn in settlements.

The company surpassed the $1bn mark in May, June and July, and principal Mark Haron said the milestone is one the aggregator had been edging in on for some time.

“Our average monthly settlements had been sitting just shy of the $1bn mark and we’ve previously come very close to reaching the milestone. To actually surpass the target, and to do so across three consecutive months, is very satisfying,” he remarked.

Connective previously reached $966m in December, and more

than $800m in June 2010. Haron previously told Australian Broker he believed the company was well-positioned to surpass $1bn in settlements during 2011, adding after December’s result that brokers had been distracted by licensing concerns. He said the result was pleasing in the midst of a difficult market.

“This achievement is testament to the dedication of our member brokers and is a reminder of the opportunities which still remain despite challenging market conditions,” Haron said.

While Connective initially set a goal of reaching the $1bn mark by March, Haron indicated he was

buoyed by the consistency of the results in May, June and July.

“Aggregators often experience spikes in lending volumes due to the seasonal nature of home lending. We’ve now achieved three record months of settlements and set a benchmark that we’re confident we’ll be able to consistently reach moving forward,” he commented.

In spite of recent slowdowns in credit demand, Haron expressed optimism that brokers could continue to see good returns, and added that revenue diversification had become increasingly important.

“Expanding one’s offering and diversifying revenue has become

increasingly important for brokers in the current market. We believe there are still many opportunities in traditional residential mortgages for the proactive broker but it makes a lot of sense for brokers to add complementary products to their suite. Connective has been very focused on assisting brokers to diversify their offering and our member brokers have responded especially well, particularly with insurance products,” he said.

Mark Haron

Lisa Claes

13www.brokernews.com.au

Smartline’s new WA state manager has stated that brokers must assist clients in wealth creation by filling the role of debt and risk advisers.

The company has announced the appointment of David Devenish. Devenish previously worked as the director of Profound Property and an associate director of Macquarie Bank.

Devenish commented that the operating environment in the mortgage broking industry has seen significant change, and that brokers now fill the role of debt advisers.

“Consumers are now more conservative and less inclined to make quick, emotive purchase decisions – and they’re looking for trusted advisers to help them do that,” Devenish said.

Devenish said brokers must fill the role of helping clients create wealth by aiding in the management of debt and risk.

“For many people debt is the thing that keeps them awake at night. Our role is to advise our clients on the most appropriate strategies and solutions to reduce risk, assist in wealth creation and, consequently, allow them to rest easy,” he commented.

Smartline said Devenish would be mandated with raising the company’s

profile in the WA marketplace, and boost support to franchisees. Devenish said he would look to further develop support structures available to the state’s 31 existing franchisees, as well as ramp up recruitment of new franchisees. He commented that the WA market presented unique challenges to brokers, with many potential borrowers working in the resources sector.

“Many people are managing fly-in- fly-out roles, they tend to purchase and share rental accommodation and have a lifestyle that demands solutions tailored to those specific needs,” Devenish remarked.

Devenish encouraged brokers to embrace changes in the industry that have come about through the onset of licensing and regulation. He predicted further industry change was “around the corner”.

“In the last few years, we’ve seen the industry change dramatically with much tighter lending, more regulation and consolidation, so professional development is critical,” he commented.

Consumers have jumped on board the Choice mortgage switching campaign, but its feasibility is still being questioned.

The Choice-led One Big Switch campaign has drawn 40,000 consumers, who have registered their interest in the campaign’s drive to obtain group discounts from mortgage lenders. The scheme has drawn controversy, with both Choice and One Big Switch set to collect commissions, but Intouch CEO Paul Ryan believes the campaign is unrealistic.

Ryan called One Big Switch “optimistic and romantic”, but said it was unlikely to yield results. The idea of securing a lender discount based on collective bargaining is not feasible, Ryan remarked.

“The notion of trying to help a collective group of thousands of people achieve a better home loan deal is great but the challenge is in the execution. When you are talking home loans there are so many variables. Every loan is different and deserves individual attention as per the responsible lending guidelines outlined by ASIC,” he said.

The campaign has also drawn regulatory scrutiny, with ASIC reportedly examining whether Choice’s involvement necessitates the group holding an ACL. The regulator is also reportedly examining whether One Big Switch is following responsible lending guidelines under the NCCP. Ryan said it is doubtful

the campaign’s structure can abide by these guidelines.

“For example, if Mr and Mrs Smith at Campbelltown have registered their interest, then who will be the qualified person to help them with their home loan application and assessment under the collective bargaining? Will they qualify for what’s available, will the loan suit them, who approves their loan and at what cost?”Ryan asked.

And should the campaign fail, Ryan believes it is borrowers who will be hurt most.

“I’ve been in the industry for 20 years now and just get incredibly frustrated when I hear about another quick fix idea. Inevitably it’s the consumer who loses out and is left disenchanted,” he said.

Smartline appointment sees wealth creation role for brokers

Choice campaign will leave consumers ‘disenchanted’

David Devenish

Paul Ryan

For all the latest mortgage industry news, visit www.brokernews.com.au

14

Newswww.brokernews.com.au

Australia booming compared to US: RP DataNot for profit property developer

group Urban Taskforce has blasted the Council of Australian Governments (COAG), saying it has failed to take any action on housing affordability.

Urban Taskforce CEO Aaron Gadiel said that COAG has failed to act on a Productivity Commission report into zoning and development assessments. A COAG communication on the report claimed states and territories were “continuing to improve significantly” in planning and development. Gadiel called this assertion “nonsense”.

“There is no sign that state governments have taken any note of the Productivity Commission’s report, and clearly the Commonwealth hasn’t insisted that they should,” Gadiel said.

The Productivity Report, Gadiel said, identified practices pertaining to property zoning and development which could “dramatically improve the efficiency and responsiveness of state planning systems”.

“They advocated broad and simplified development rules, more rational and transparent rules for infrastructure levies and

eliminating impacts on the viability of existing businesses as a town planning consideration,” he commented.

Gadiel claimed Australia was currently experiencing a housing shortfall of 200,000 homes, and forecast that this would grow to 308,000 by 2014. He slammed COAG’s claim that “work [is] already under way [on] ... housing supply and affordability reform”, saying that COAG has accomplished “almost nothing” it previously promised.

“The requirement to start producing solid reform proposals by mid-June 2010 was intended to spur on officials to get on with this urgent work,” Gadiel said.

The report, commissioned by COAG in April, asked the Productivity Commission’s Housing Supply and Affordability Reform Working Party to investigate potential reform to zoning and planning processes, the development of consistent principles for development charges, the role of local governments in planning approval processes and extending land audit work to examine underutilised land.

The Australian housing market is a “boomtown” compared to the United States, RP Data has claimed.

The company’s Property Pulse publication has pointed to continued declines in US home values, where nearly one-quarter of loans are in negative equity. The company has claimed its data indicates relatively few Australian homes are in negative equity.

Arrears in Australia are also extremely low compared to the US, RP Data contended. The percentage of US homes delinquent by 90 days or more is more than 8%, while comparable arrears for Australian homes are below 1%.

However, both Australia and the US are experiencing lagging demand, with transaction volumes in the US 33% below five-year averages and Australian transaction volumes 16% below five-year averages.

RP Data research director Tim Lawless said the US housing market may see a boost from the recent Federal Reserve announcement that rates will remain on hold for at least the next two years. Lawless commented that the Australian market has no such guarantee of stability.

“The certainty around US interest rates is in direct contrast to the Australian mortgage market where the direction of interest rates over the short to medium term still seems to be up in the air,” Lawless remarked.

Australian mortgage holders are also more sensitive to interest rate movements, Lawless said.

“The vast majority of Australian mortgages are on a variable rate. This means that any change in the interest rate environment has an immediate impact on most mortgage holders and consumer behaviours,” he commented.

Though there are significant differences between the two markets, Lawless said the Australian housing market would be well served to learn from the US market. Lawless warned that the relative health of Australian housing compared to the US should not make the market “complacent”.

Property developers take COAG to task

Australia is struggling in a low growth, high inflation environment, the Reserve Bank has claimed.

RBA deputy governor Ric Battellino has commented that the Reserve’s board has had to balance higher-than-anticipated inflation with slowed economic growth. Battellino said upward revisions of mining investment mean that inflation for 2011 is likely to trend higher than was forecast last year, while growth estimates have had to be revised downward amid global economic uncertainty and this year’s natural disasters.

“As the year has progressed, the resources boom has strengthened, but the divergence between the mining and non-mining sectors of the economy has increased and the mix of growth and inflation has turned out to be less favourable than expected a year ago – ie there has been less growth but more inflation,” he told a gathering in Sydney.

Battellino indicated that inflation forecasts have risen, with longer term outlooks predicting inflation above the RBA’s target range. However, he commented that growth had been hampered both by production

slowdowns due to natural disasters and falling consumer sentiment. Battellino said global economic growth had slowed noticeably by the RBA’s July board meeting. In addition to global forecasts trending downward, Battellino said the July meeting revealed domestic growth would be lower than expected, and that employment growth was expected to slow.

“In Australia, households remained cautious and the housing market was soft. Also, it now appeared that the slow recovery in coal production would mean that earlier GDP forecasts

for 2011 would not be met,” Battellino said.

This dwindling growth had stayed the RBA’s hand in 2011, Battellino said. However, he said the Bank still remained concerned about inflation, and indicated that devising monetary policy taking into account waning growth and growing inflation would prove a challenge.

“With the recent volatility in financial markets adding to the uncertainty about the economic outlook, it does not look like the challenge will become any easier over the months ahead,” he commented.

Low growth, high inflation challenges RBA

Missing in action: Affordability reports yet to be releasedIn April last year, COAG asked the Housing Supply and Affordability Reform Working Party to prepare a report on:• The potential to reform land aggregation, zoning and planning processes• Nationally consistent principles for housing development

infrastructure charges• The merits of measures to ensure greater consistency across

jurisdictions, including local governments’ planning approval processes, in the application of building regulations

• Extending the land audit work to examine underutilised land and to examine private holdings of large parcels of land

Moody’s not so sunny on Aussie housingMoody’s senior credit officer Ilya Serov said in July the agency expects arrears and defaults to rise in Australia over the coming decade.

“Default and delinquency rates in the mortgage market are likely to be both variable and, in our view, on average higher over the coming decade than in the past,” Serov commented.

Moody’s said the sustainability of Australian house prices was in question, and stated that massive increases in value over the past decade were “only partially explained by fundamentals”.

“We consider the possibility of major regional house price drops to be a material risk for the Australian market,” Serov said.

For all the latest mortgage industry news, visit www.brokernews.com.au

15www.brokernews.com.au

Bank ranks have little impact on behaviour

Brokers missing e-lodgement benefits

Top brokers have claimed that customer satisfaction rankings do not necessarily reflect actual client behaviour when it comes to banks.

Outgoing CBA chief executive Ralph Norris and 11 other CBA executives reportedly lost out on more than $15m in pay due to the company’s slide in the Roy Morgan customer satisfaction rankings. However, The Selector Group’s Brett Abikhair believes the rankings reflect little more than a philosophical stance on the part of consumers.

Abikhair said he has noticed no hesitance on the part of consumers to use the bank, even amid negative publicity following CBA’s out-of-cycle rate rise. For consumers, Abikhair said, price is more important than public perception.

“Most people have zero loyalty to the bank they happen to be with at

the time,” he said. “Zero loyalty means they always chase the better deal, or at the very least go with the lender who can do what the client is wanting.”

Abikhair indicated that the lack of customer loyalty has been driven by lenders who increasingly outsource customer service.

“The banks are the very reason this has occurred, as they have made a loan purely a commodity. This is the very reason mortgage brokers actually exist, as the banks have passed the relationship aspect of their banking to brokers,” he said.

MPA Top 100 Broker Justin Doobov of Intelligent Finance agrees, and said price and product drive customer behaviour, while customer service is largely the role of the broker.

“When Intelligent Finance arranges brokers a loan for a

client we act as the conduit between the client and the lender. So long as we as a broker are providing fantastic service to our client, this is all our client cares about, as they generally have more contact with us than the lender,” he commented.

Doobov, however, defended service levels for CBA, saying the fact that so much of Norris’ pay

packet was tied to satisfaction results showed a commitment to customer service.

“I am sure that this poor survey result is mainly due to the out-of-cycle rate rise by CBA. We survey our clients regularly and the clients whose loans we have put with CBA are generally the most satisfied with their lender,” he said.

Mortgage brokers are rendering a large part of their CRM functionality “defunct” by not using their system as an e-lodgement gateway, according to Stargate.

Speaking with Australian Broker, Stargate CEO Brett Spencer said many brokers are choosing to use free online bank e-lodgement systems, rather than the electronic gateway provided by CRM systems such as Stargate’s Symmetry CRM.

During the last 12 months, Spencer said that 164,000 loans went through the Symmetry system, but there were only

30,000 e-lodgements that went through the platform.

“That means that the CRM system for many is becoming defunct,” Spencer said. “You are not getting all the back-channel messaging, you are not getting the status updates, and it is not going into their CRM system – they are getting that information on their mobile phone.

“So they can’t then utilise the marketing and reporting – all the things that appear in CRM systems – to manage their customer loans. That is the biggest issue we see – there are alternatives out there, and they

would rather take the free approach to doing that,” he said.

Spencer said the cost of e-lodgement – which is facilitated by the likes of NextGen.Net and Pisces – can vary depending on whether brokers pay a fee per transaction, or choose to pay a monthly user fee. However, he said a single transaction may cost brokers $10.

“If you’re a big broker and you are lodging over 20 transactions a month, you are spending over $200 on your e-lodgement, and some of them just won’t spend that,” he said.

While acknowledging the cost, Spencer said brokers miss out on

the functionality, which would enable them to monitor through regular reports the entire loan process – eliminating problems such as ‘forgetting’ or tardy lender responses – allowing them to stay on top of their customers.

Spencer said the cost and time efficiencies that could be achieved are in the vicinity of two to three hours per loan file, when taking into account 30 minutes to enter two sets of data, and manually updating back-channel messaging that is not automatically coming into the system.

For more on CRMs, see Toolkit on page 26

Bouncing back: CBA’s satisfaction rankings since the November 2010 rate hikes

7070.5

7171.5

7272.5

7373.5

7474.5

75

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11

Source: Roy Morgan

16

Newswww.brokernews.com.au

Fixed rate cutting frenzy continues

Franchise profits after ‘demanding’ year

97% LVR, the minimum monthly mortgage repayment on a 7% variable rate would be more than $3,200, or in excess of 50% of the couple’s before-tax income. Bromley said such numbers are troubling.

“Sometimes with high LVRs, there are lower standards used around the income to qualify,” he remarked.

O’Brien has also called into question Bankwest’s assertion that the loan will combat housing affordability issues. The bank claimed its high LVR product would address housing affordability in WA, with Rakhit saying that it could stimulate first homebuyer demand.

“If first-time buyers need to save for a shorter period, this is a clear sign that affordability has improved for them. It doesn’t reduce the amount of debt that they acquire but it means that they can build equity in the property market sooner. In order for the property market to prosper there needs to be a consistent number of first-time buyers as historically this has been the catalyst for growth in the sector,” he commented.

However, O’Brien said he doubted the product would “impact the market at all”. Bromley agreed, saying he too was sceptical that a higher LVR would have any

material impact on affordability.“I don’t know if it’s going to

stimulate extra growth in housing. There are more fundamentals that need to be addressed before we see any real change in housing,” he commented.

Ultimately, Bromley said he believed the Bankwest move, along with similar moves by other banks to raise LVRs and slash rates, represented the pressure banks are under to grow market share. Though high LVRs could pose a risk to lending standards, Bromley suggested that banks may see more risk in shrinking credit demand.

“With a high LVR I would assume they’re all being mortgage insured anyway, so there’s not the sort of risk in terms of defaults. There’s more risk for banks in not getting credit growth,” he said.

The mortgage market saw a fixed rate cutting frenzy in August, as lenders increasingly bet on the probability of the RBA slashing rates.

At time of going to press, St.George Bank had issued a third round of fixed rate cuts, dropping the rates on its two-year product a further 10bps to 6.59%, and discounting its three-year fixed rate 20bps to 6.59%.

The lender also made cuts to its four and five-year rates, cutting both by 55bps. The move brought the bank’s four-year rate to 6.99%, and its five-year rate to 7.04%. St.George CEO Rob Chapman said demand for fixed rate products has been high.

St.George’s parent bank, Westpac, also made further fixed rate moves, cutting its three-year rate 20bps to 6.59%. The bank also announced discounts to variable rates on its Premier Advantage Package on loans of $500,000 or more.

Meanwhile, Citibank lowered fixed rates for a second time, moving its one-year and two-year fixed rate home loan from 6.79% to 6.34%, and its three-year fixed rate home loan from 6.79% to 6.45%.

Mortgage managers began

passing on the discounts as well, with Mortgage Ezy, Australian First Mortgage, Iden Group and Future Financial all announcing fixed rate cuts.

Mortgage Ezy announced a 30bps cut, which will give customers fixed rate options from 6.39% with no ongoing annual fees.

Mortgage Ezy said the fixed rate loan repricing also included upfront and trail commission.

Iden Group cut fixed rates on its Fair Go range of products. It is offering 6.74% on its one-year fixed rate loans, and 6.54% for two-year and three-year products.

Australian First Mortgage also reduced its two and three-year fixed rates, cutting its Flexible Option Full Doc products twice in the space of a week, bringing both two and three-year rates to 6.54%. Future Financial cut its two-year rate to 6.79% and its three-year rate to 6.89%.

Both AFM and Future Financial have opened the products to residential construction loans for owner-occupiers and investors, and both include the option of a 100% offset account. Future Financial has also touted a rollover rate of 7.19% at the end of its fixed rate period.

Profits rose for Mortgage Choice in spite of a slight slowdown in approvals, according to the listed group’s recent profit announcement for the 2010/11 financial year.

The company’s full-year results showed a 7.4% increase in net profits to $15.9m. Likewise, the group has grown its loan book to $42.4bn, up from $40bn in 2010.

Housing loan approvals, however, saw a slowdown in 2011, falling to $9.9bn from $10.1bn in 2010. The company attributed the decline in approvals to the general market slowdown in credit demand. CEO Michael Russell said the financial year was “one of the most demanding” in the history of the company, and praised the profit results.

Russell said the group saw stable productivity from its brokers, who average 58 loans each per year, and witnessed a doubling of brokers in its aggregation arm, LoanKit.

“It is satisfying to present a healthy financial performance, loan book and recruitment growth,

broker efficiency and customer satisfaction during a year of great change for the market and for Mortgage Choice, which has been steadily evolving to ensure we make the most of a new lending landscape,” Russell said. “Our sound result shows the company’s DREAM strategy – an acronym for diversification, recruitment, existing broker support, acquisitions and managing costs – is producing rewards.”

During the period, Mortgage Choice managed an overhaul of learning and development programs, the introduction of a target-driven lead conversion project, streamlining of commissions reporting and improvements to franchisee benchmarking. The group saw the addition of 19 greenfield franchises and the sale of 19 existing franchises during the period.

Commenting on the state of the market, Russell said the group executed a strategy to strengthen its presence amongst the “more experienced” borrower groups, focusing heavily on investors and

refinancers. “We understand the need to go where the business is rather than sit back and wait for conditions to return to ‘normal’, which may never happen,” he said.

“If conditions remain subdued for a number of years, our brokers

are well equipped to continue to run successful operations that concentrate on areas of growth located within both the home loan market and other realms of personal and commercial finance,” he said.

Peter Bromley

Newswww.brokernews.com.au19

INDUSTRY NEWS IN BRIEF

Keen support for non-banksFindings from MPA’s latest Brokers on Non-Banks Report suggest that brokers who regularly support non-banks are keen to increase the volume of business they do with these lenders. More than 350 brokers took part in this year’s survey, with the average non-bank supporter saying they placed 41% of their business with non-banks, but in an ideal world this figure would account for 63%. However, participants said just one-fifth of customers requested a home loan from a non-bank. Despite non-bank market share plummeting to record lows recently, 72% of those surveyed expect this trend to reverse in the coming months. Brokers taking part in the survey were also asked whether licensing and the removal of DEFs would impact their dealings with non-banks, but just 21% thought regulation would be an issue and 26% expected the exit fee ban to affect their relationship with non-banks.

Pisces snapped up by investment groupMortgage software company Pisces Group has announced it has been acquired by Santapau Limited for an undisclosed sum. Pisces, which provides a suite of mortgage software services for mortgage brokers, including CRM and electronic lodgement capabilities, was acquired by Santapau, which is backed by clients of Gleneagle Securities, a registered Australian financial services company. A statement from Pisces said the acquisition would allow the launch of a range of new financial services products in Australia. In the coming weeks, Pisces and messaging solution provider Newsnet – also acquired by Santapau – will be combined under a unified brand in the market. CEO of Pisces, Jega Rajan, said the transition would be “smooth and transparent” for customers, partners and suppliers.

ANZ focuses on fundingRetail deposit growth has driven a stronger funding position for ANZ, the bank has stated.In a market update, ANZ reported an unaudited underlying profit after tax of $4.2bn for the nine months to June, 16.1% above the previous corresponding period. The bank said it had also strengthened its funding position, with customer deposits increasingly driving its funding. “Customer funding now represents 61% of ANZ’s funding base, up from 50% in 2008,” the bank said. “This structural improvement has reduced ANZ’s reliance on both short-term and term wholesale funding.” ANZ said it saw retail deposits grow at 1.8 times, and a 10.1% increase in overall deposits year-to-date. While deposit growth outstripped lending, the bank said its commercial loan book grew by 2.4% in the third quarter, and that mortgage lending volumes were improving on the second quarter.

Divide opening up in buildingAustralia’s two-speed economy is evident in the building sector, industry advocates have claimed. Following ABS figures that showed a decline in every sector of construction except engineering, Master Builders of Australia claimed a divide is evident in the building sector. With residential building declining a seasonally-adjusted 7.6% in the June quarter, Master Builders chief economist Peter Jones said outlook for the sector is grim. “For the building and construction industry overall, a sectoral divide is opening up, with strong engineering construction fed by the mining boom contrasting with a weak building sector caught in the slow lane of a post GFC economy struggling to transition to a private sector led recovery,” he commented. Jones said the figures confirm evidence from a Master Builder’s survey, indicating falling builder sentiment in the commercial and residential sectors.

Australian Unity doubles broker bookFinancial services company Australian Unity has seen its broker-originated loan book grow significantly over the past year. The financial services provider announced it has seen its network of 20 mortgage brokers more than double its loan book over the past 12 months. In addition, general manager of personal financial services Steve Davis commented the company has seen a 27% increase in risk insurance revenues over the same period. “We now have a very strong business, especially when you consider that it was just a few years ago that we restructured and moved from a retail, sales driven shop approach to a modern advice driven financial services business,” he said. While primarily a financial planning business, Davis indicated the business has brokers working across every mainland state, and the ACT.

Little difference between majorsBanks are failing to differentiate on customer service, a survey has indicated. A recent Roy Morgan bank customer satisfaction survey has shown the gap between the major banks continues to narrow, with less than 2.5% separating the front-runner, ANZ, from the bottom-ranking bank, CBA. ANZ has ceded much of its lead in customer satisfaction, now only eclipsing Westpac by 10bps. ANZ posted only a 0.1% rise in satisfaction during July, increasing to 76.6%, while Westpac surged 50bps to 76.5%. NAB has also given up some of the ground it gained on Commonwealth Bank after moving ahead of CBA in March. NAB’s satisfaction ranking fell 30bps in July to 74.7%, while CBA’s rose 50bps to 74.2%. Roy Morgan said the banks were doing a poor job of differentiating their propositions.

20 www.brokernews.com.au

Analysis

Small fish in a big pond

Consolidation and scale may drive income benefits for some, but smaller independent brokerages question whether the numbers really add up

A recent research report has indicated that the scale provided by large broking franchises may lead to healthier revenue prospects for brokers.

A poll conducted by Macquarie Practice Consulting has shown that brokers in large firms earn more per broker than their solo-operator counterparts. As much of the industry argues for the benefits of scale and continued consolidation, Macquarie Practice Consulting’s Fiona Mackenzie has said brokers in larger firms may have more earning potential.

“The results are saying that with the smaller firms, which are one broker firms, they’re earning around $142,000 per broker, whereas larger firms are earning about $175,000 per broker. The main reasons we’re seeing in the results is the diversification of revenue, so they’ve got other revenue streams which are supporting the mortgage revenue,” Mackenzie said.

However, one top broker remains unconvinced. MPA Top 100 Broker Justin Doobov of Intelligent Finance has questioned the results, saying while the numbers may indicate more money overall for larger firms, not all of this is being passed on to brokers.

“When you actually read the survey it says that larger businesses have more formal referral arrangements than smaller businesses, so smaller businesses have more informal arrangements. What that actually shows me is that while larger businesses might have more income, more gross revenue per broker, I’d actually argue that the net revenue – the profit that each broker takes home – in a smaller business is probably more,” he said.

Doobov argues smaller businesses may be better positioned due to smaller overheads. He commented that large national franchises have operating costs that could end up eating into the amount of revenue their brokers actually see.

“Chances are if they’re a larger business they’ve probably got formal referral arrangements, so they’re probably paying a referral fee. Yes they may turn over more per broker, but actually the net amount that stays with the business is probably a lot less for some larger businesses,” he said.

Mortgage Choice broker Andrew Hawking agrees that bigger is not always better. He indicated that scale does not automatically equate to increased revenue, and said situations vary from franchise to franchise and broker to broker.

“I know some smaller franchises actually have a very

large income stream, whereas some large franchises have a small-to-medium income stream. It just depends where you are, what you do and how you actually have to try to generate income,” Hawking remarked.

Small business, big portfolioBigger businesses don’t necessarily equate to bigger loan books, either, according to Mackenzie.

“The smaller firms have about $51m per broker, and the larger firms around $40m, which is an interesting result,” she said.

However, Mackenzie has contended that the smaller portfolio size is reflective of income diversification rather than a difference in broker productivity.

“We’re seeing the drivers for that are that the larger firms are being more diversified, so they’re actually earning income from other products, not just mortgages,” she said.

Experience can also play a role, Mackenzie indicated.“The larger firms have more junior, less experienced

brokers coming through who are still building their book,” she remarked.

Even with the larger portfolio sizes of some small businesses, Doobov believes brokers across the board could be doing more.

“I would have expected any broker to be able to maintain $100m–$200m of portfolio, so the 50-odd million they’re talking about is actually quite low. It doesn’t matter whether you’re a big or small business,” he remarked.

Shrink to growDoobov still contends that brokers who can generate their own referrals are better off as small operators as opposed to aligning themselves with large franchise networks. While being part of a franchise may have its benefits, Doobov contends that there are greater revenue opportunities for smaller brokers.

“Being part of a large franchise will definitely assist you with a bigger stream of leads as franchises spend a large amount of money on advertising, though the conversion of leads will be nowhere as good compared to the conversion of a quality referral that you generate yourself from happy clients. From my calculations, for every $5m you settle a month as a small operator, you would have to settle between $6m-$7m per month as a franchisee broker. It is worth running the numbers before deciding to ensure you make the right decision,” he said.

22 www.brokernews.com.au

Macquarie Practice Consulting recently released a series of benchmarks on the industry’s mortgage broking businesses. Here’s what our pundits had to say about the results.VIEWPOINT

Comment

OPINION

Brokers need to be careful not to add to credit file footprints – and educating them about credit files may just be good for business, writes Joseph Trimarchi.

Since the global financial crisis, lenders have become fearful of the cost of bad credit, and as such have adopted a stringent regime in pricing the credit they extend.

Excessive enquiry on a client’s credit file - irrespective of whether it is for domestic or commercial purposes - may see your client embark upon a perilous journey, where they may be rejected outright for a loan or become subject to an interest rate significantly higher than the most competitive rate offered in the marketplace.

As finance professionals, it’s part of a mortgage broker’s job to assist their clients in maintaining credit worthiness, not only by advising clients on the best form of credit available, but also by making significant efforts to present their clients in the best possible light - as depicted by their credit file - to potential credit providers.

Finance professionals need to assess their client’s credit file at the beginning of the retainer, and not treat it as an afterthought. As

professionals, you must be in tune with how credit providers view your client’s application for finance and what impact the same has on their ability to be approved. This includes the number of footprints that appear on a credit file.

A footprint is defined as activity recorded on a credit file. Given a credit file records a large amount of information, the content of such activity could be wide and varied. Once recorded the information is a permanent fixture on the credit file and remains there for five years.

At the beginning of the retainer, it is preferable that a request be made by the broker for the client to supply a copy of a credit report obtained from Veda Advantage or Dunn & Bradstreet. By the client ordering their own report, the broker has not left a footprint on the credit file and is not alerting future potential lenders the client is shopping around for finance.

Prior to lodging any application for finance on behalf of a client, the broker must be confident the loan will be approved. In most cases, prior to lodging an application contact should be made with the prospective lender in order to establish prima facie (on the face of it or at first glance) if the application stands a good chance of being approved, whilst making it abundantly clear the request is only a preliminary attempt in order to ascertain the client’s prospects of approval and

not an application for finance. As such, this will mean that no enquiry will be noted on the client’s credit file.

Finance professionals will be served well by educating their clients about the importance of protecting their credit file’s integrity. This may be done by adopting this message as part of your monthly newsletter sent to clients, which may have the added benefit of keeping the marketing message you wish to send useful, thereby preventing your client’s from falling victim to the carnage left in the aftermath of excessive footprints. Typically, your clients should be educated about the inherent danger of browsing online websites and inadvertently lodging an application for finance.

The story you wish to tell potential lenders about your client is one of stability and a calculated borrowing capacity, not one of instability as depicted in your client’s credit file. Numerous footprints - in particular applications for finance - raise a level of suspicion as to your client’s credit worthiness and invariable lead to an application being rejected.

The above information servers only as a guide and should not be relied upon as legal advice. Joseph Trimarchi is the principal of Joseph Trimarchi & Associates solicitors.

Credit file footprints and the story they tell