Embed Size (px)

DESCRIPTION

Digital Experience Report

Citation preview

AUSTRALIAN DIGITAL EXPERIENCE REPORT

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

01

C O N T E N T SExecutive Summary 02

The Digital Experience Gap 06Understanding the Gap 07Why the Gap Matters 08Business Impact of the Digital Experience 09What Matters to Consumers 11The Australian Digital Experience Index 13

The Digital Experience Gap: Industries at a Glance 15Who Leads? Who Lags? 16What’s Important to Consumers by Industry 18Industry Overview: Banking 19Industry Overview: Utilities 20Industry Overview: Telecommunications 21Industry Overview: Retail: Groceries 22Industry Overview: Retail: Consumer Goods 23Industry Overview: Insurance 24

The Rise of the Digital Influencer 26What Matters to the Digital Influencer 28Creating Delightful Digital Experiences 30

Technology Enabling the Great Digital Experience 32Know Your Customer 32Engage Your Customer 33

Case StudiesSuncorp Insurance 37Kogan.com 42

References and Further Reading 43Acknowledgements 44

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

02

E X E C U T I V E S U M M A R Y Australians are some of the most enthusiastic adopters of digital, cloud and mobile technology globally. Smartphone penetration sits at upwards of 80 per cent, while more than half of Australians (53 per cent) own a tablet, laptop and smartphone1.

The digital experience – how a brand digitally interacts with its customers during the discovery, transaction, delivery and support of a product or service – is everywhere. It has rapidly become one of the most important components of the overall customer experience.

But recent research by SAP and AMR shows that many Australian consumers have been overlooked. Some of our biggest and best‑known brands are alienating consumers due to poor digital experiences.

This isn’t just bad for consumers; it’s bad for business. Digital experiences that fail to delight consumers can negatively influence customer advocacy, lead to a loss of loyalty and ultimately affect revenue.

These are some of the major findings from SAP’s first Australian Digital Experience Report.

x 3,000

RESPONDENTS COMPLETED A 15 MINUTE ONLINE SURVEY RATING 2 TO

3 BRANDS ACROSS 6 INDUSTRIES

QUESTIONNAIRE COVERAGE

SATISFACTION WITH DIGITAL EXPERIENCE (GENERAL)

SATISFACTION WITH DIGITAL EXPERIENCE (BY INDUSTRY)

SATISFACTION WITH DIGITAL EXPERIENCE FOR INDIVIDUAL COMPANIES

NET PROMOTER SCORE

LOYALTY

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

03

This report draws on research with 3,000 Australian consumers who rated core aspects of the digital experience from two to three brands they regularly interact with. The results offer detailed insights on consumer expectations of the digital experience and the ability of brands to meet them.

Uniquely, the report assessed consumers’ direct ratings of 34 brands across six consumer-focused industries, including retail (groceries and consumer goods), telecommunications and Internet service providers, insurance, banking and utilities. From these ratings we compiled industry and brand‑level assessments of the digital experience, and the first-ever Australian Digital Experience Index, which represents ratings of nearly 7,000 digital interactions.

While this systematic assessment of the digital experience provides many organisations with a strong reference point for improvement, the killer finding is the link between the digital experience and customer loyalty and advocacy – two metrics with significant impact on revenue.

This report’s findings will be uncomfortable for many. They show:

• Australian brands aren’t delivering the digital experience consumers want. There is a significant digital experience gap in Australia – meaning there is a large discrepancy between the digital experiences that delight consumers and what Australian brands are actually delivering.

• There is a strong correlation between the size of this gap and Net Promoter Score (NPS®) and customer loyalty. Customers delighted with a digital experience are four times more likely than those who are unsatisfied to remain loyal to a brand. On average, customers delighted with the digital experience delivered a net promoter score of 63 per cent compared to a score of ‑55 per cent from those who were unsatisfied with the digital experience.

• Just one brand from the 34 ranked in the Australian Digital Experience Index attained a positive score. Those brands that performed best understood what attributes of the digital experience were most important to their customers and focused their investment and resources in those areas.

BANKING RETAIL (CONSUMER)

RETAIL (GROCERY)

INSURANCE UTILITIES TELCO

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

04

The report also highlights the important role the digitally savvy consumer plays in driving a positive digital experience score for brands. The more influential consumers are in the digital world, the better they rate a brand’s digital experience. Brands need to harness this finding by appealing to and nurturing this segment of their customer base.

SAP has taken the research a step further by interviewing the brands with the highest digital experience scores to identify the processes and culture behind best practice in Australia. Consistent across these case studies is the depth to which leading brands consider and incorporate the digital experience throughout the value chain. In other words, the digital experience is not just a channel owned by the marketing function. Rather, the digital experience is a differentiating element of the offering itself in which the entire organisation and its network invests, from inception to delivery.

Finally, the report delivers recommendations based on direct consumer input and best practice in Australia and other markets on how organisations can improve top‑line performance by delivering a superior digital experience – from awareness to advocacy. Leading brands achieve a distinct advantage by investing in simple, data-driven platforms and organisational structures that bring the front and back office together to understand and engage their customers better than any competitor.

SAP is a trusted innovator to over 3,000 Australian organisations across 25 industries and has developed and delivered solutions for more than three quarters of the ASX Top 50. With the results of this research as well as the local and global experience accumulated over the past 43 years, we are laying the facts bare. The objective is not to point out poor performance, but to help Australian organisations make decisions on how they can better serve their customers and compete in an increasingly digital and global economy.

DELIGHTED

UNSATISFIED

0

Just one brand from the 34 ranked in the Australian Digital Experience Index attained a positive score.

There is a significant digital experience gap in Australia – meaning there is a large discrepancy

between the digital experiences that

delight consumers and what Australian

brands are actually delivering.

T H E A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

05

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

06

T H E D I G I TA L E X P E R I E N C E G A PProviding a great digital experience can drive loyalty and advocacy among customers, and ultimately greater revenue. But are Australian brands getting the digital experience right?

Three thousand Australian consumers rated almost 7,000 digital interactions with 34 of the largest and best-known brands in Australia.

The core finding from these ratings was a wide digital experience gap. It suggests the vast majority of Australian brands do not deliver the digital experience consumers desire.

This gap is quantified by a digital experience score calculated by subtracting the percentage of customers unsatisfied with the digital experience from the percentage of those who are delighted.

Across the nearly 7,000 digital interactions assessed, the brands achieved an average digital experience score of ‑25 per cent.

• Just 22 per cent of consumers were delighted with the digital experience brands offer

• 47 per cent were unsatisfied with their digital experience

• 31 per cent were ambivalent

THE DX SCORE 22%DELIGHTED

31%

AMBIVALENT

47%UNSATISFIED -25%

ACROSS A VARIETY OF INDUSTRIES MORE AUSTRALIANS ARE

UNSATISFIED THAN DELIGHTED WITH THEIR DIGITAL EXPERIENCE

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

07

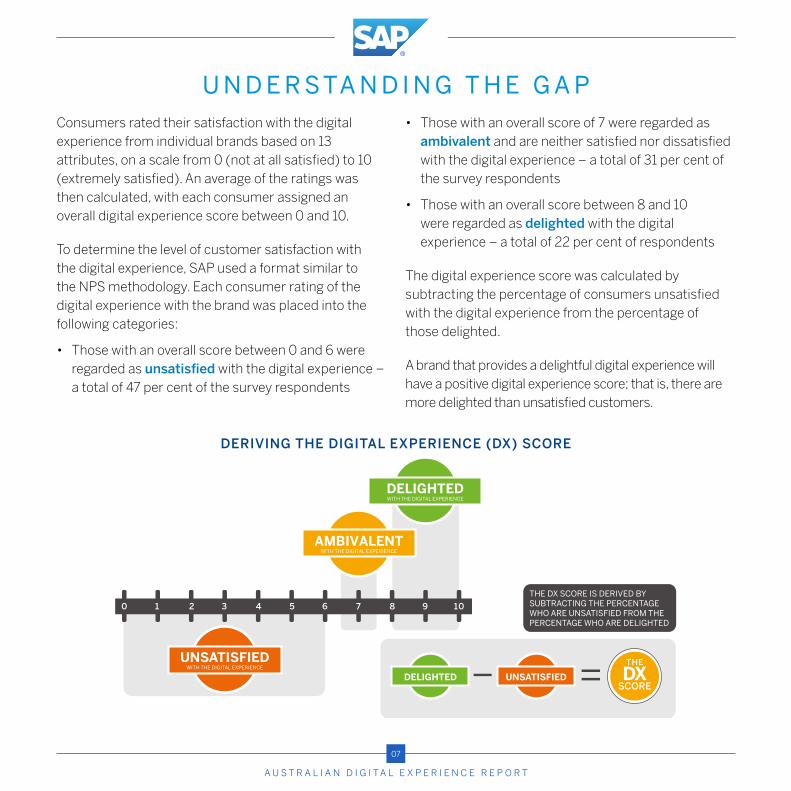

U N D E R S TA N D I N G T H E G A P Consumers rated their satisfaction with the digital experience from individual brands based on 13 attributes, on a scale from 0 (not at all satisfied) to 10 (extremely satisfied). An average of the ratings was then calculated, with each consumer assigned an overall digital experience score between 0 and 10.

To determine the level of customer satisfaction with the digital experience, SAP used a format similar to the NPS methodology. Each consumer rating of the digital experience with the brand was placed into the following categories:

• Those with an overall score between 0 and 6 were regarded as unsatisfied with the digital experience – a total of 47 per cent of the survey respondents

• Those with an overall score of 7 were regarded as ambivalent and are neither satisfied nor dissatisfied with the digital experience – a total of 31 per cent of the survey respondents

• Those with an overall score between 8 and 10 were regarded as delighted with the digital experience – a total of 22 per cent of respondents

The digital experience score was calculated by subtracting the percentage of consumers unsatisfied with the digital experience from the percentage of those delighted.

A brand that provides a delightful digital experience will have a positive digital experience score; that is, there are more delighted than unsatisfied customers.

DERIVING THE DIGITAL EXPERIENCE (DX) SCORE

THE DX SCORE IS DERIVED BY SUBTRACTING THE PERCENTAGE WHO ARE UNSATISFIED FROM THE PERCENTAGE WHO ARE DELIGHTED

THEDX

SCOREUNSATISFIED

WITH THE DIGITAL EXPERIENCEUNSATISFIED

WITH THE DIGITAL EXPERIENCEAMBIVALENT

WITH THE DIGITAL EXPERIENCEDELIGHTED

DELIGHTED

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

08

W H Y T H E G A P M AT T E R SThe research shows a strong link between digital experience and loyalty. If consumers are delighted with their digital experience, they are over four times more likely to remain a customer. A strong digital experience is also linked to stronger customer advocacy, measured in this research through NPS.

Loyalty and NPS can ultimately impact a brand’s top line. For example, according to Bain & Company, NPS leaders tend to grow at more than twice the rate of their competitors2.

As an example, a recent survey found that Australian consumers will spend 12 per cent more with brands that provide an excellent customer service. With digital now a key component of the overall customer experience, this goes to show that revenues of a brand can be impacted by how simple and engaging the digital interaction on offer is3.

On the other hand, a poor digital experience can do a lot more harm than just a lost sale or lost customer. Everyone loves to share a bad experience, so one such episode can lead to multiple losses across multiple customers within a short timeframe. SAP’s study shows this is happening in some of Australia’s biggest organisations today.

Of those identified as

unsatisfied with their digital experience (0-6):

At the same time, the net promotor score

(NPS) from this segment is a staggering

Just 17% would remain

loyal to the brand

-55%

Of those identified as delighted with their

digital experience (8-10):

Similarly, customers delighted with their digital experience

delivered an NPS of

73%would remain

loyal

63%

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

09

B U S I N E S S I M PA C T O F T H E D I G I TA L E X P E R I E N C E

Our research shows 47 per cent of Australian consumers are unsatisfied with their digital experience. But, importantly, how many within this segment plan to switch to a competitor in the future? Additionally, how many would recommend that brand to a friend based upon the digital experience?

To understand the impact of the digital experience, SAP asked consumers about their:

• Loyalty: How likely they would remain a customer of the brand in the future

• Advocacy: How likely they would recommend a brand to a friend or colleague, as with the NPS methodology

The findings are once again startling – and deeply concerning for brands failing consumers with their digital experience.

THE EFFECT ON BUSINESS OUTCOMES - LOYALTY

WITH THE DIGITAL EXPERIENCEDELIGHTED 73%

WITH THE DIGITAL EXPERIENCEAMBIVALENT

WITH THE DIGITAL EXPERIENCEUNSATISFIED

LOYALTY

34%LOYALTY

17%LOYALTY

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

10

Of those identified as unsatisfied with their digital experience (0-6):

• Just 17 per cent would remain loyal to the brand

• At the same time, the NPS from this segment is a staggering ‑55 per cent

If a brand can provide a strong digital experience, the picture is completely different. Of those who rated themselves as delighted with the digital experience (8-10):

• Almost three quarters (73 per cent) would remain loyal

• Similarly, those delighted with the digital experience delivered an average NPS score of 63 per cent – a complete about turn

It’s clear great digital experiences matter. They foster greater loyalty and advocacy from a brand’s customers, and can ultimately impact revenue.

THE EFFECT ON BUSINESS OUTCOMES - NPS

WITH THE DIGITAL EXPERIENCEDELIGHTED

WITH THE DIGITAL EXPERIENCEAMBIVALENT

WITH THE DIGITAL EXPERIENCEUNSATISFIED

3%NPS

-55%NPS

63%NPS

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

11

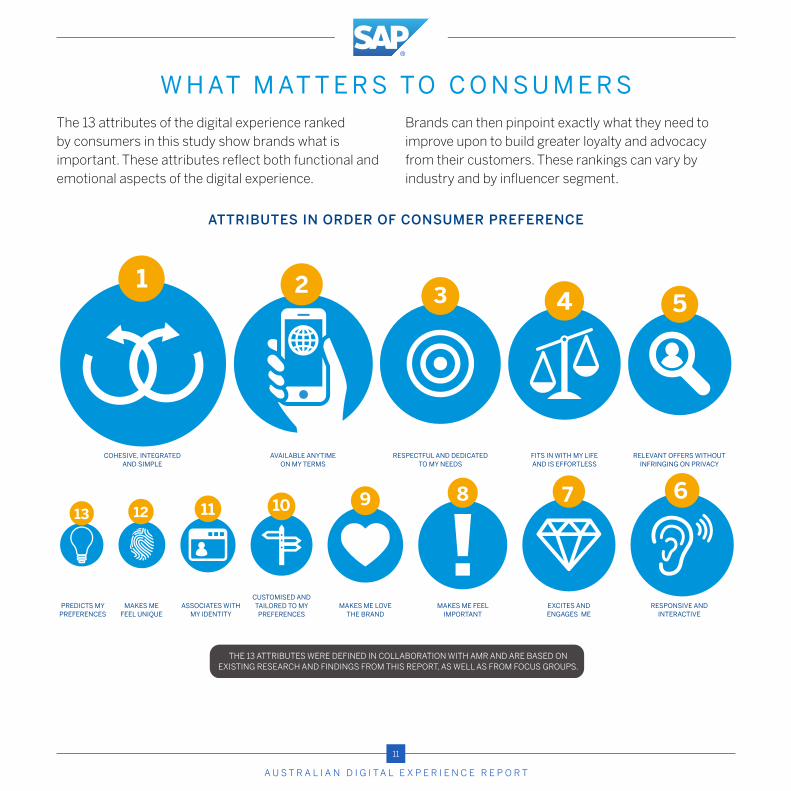

W H AT M AT T E R S T O C O N S U M E R SThe 13 attributes of the digital experience ranked by consumers in this study show brands what is important. These attributes reflect both functional and emotional aspects of the digital experience.

Brands can then pinpoint exactly what they need to improve upon to build greater loyalty and advocacy from their customers. These rankings can vary by industry and by influencer segment.

ATTRIBUTES IN ORDER OF CONSUMER PREFERENCE

COHESIVE, INTEGRATED AND SIMPLE

AVAILABLE ANYTIME ON MY TERMS

RESPECTFUL AND DEDICATED TO MY NEEDS

FITS IN WITH MY LIFE AND IS EFFORTLESS

RELEVANT OFFERS WITHOUT INFRINGING ON PRIVACY

RESPONSIVE AND INTERACTIVE

EXCITES AND ENGAGES ME

MAKES ME FEEL IMPORTANT

MAKES ME LOVE THE BRAND

CUSTOMISED AND TAILORED TO MY PREFERENCES

ASSOCIATES WITH MY IDENTITY

MAKES ME FEEL UNIQUE

PREDICTS MY PREFERENCES

1 3 4 5

678910111213

2

THE 13 ATTRIBUTES WERE DEFINED IN COLLABORATION WITH AMR AND ARE BASED ON EXISTING RESEARCH AND FINDINGS FROM THIS REPORT, AS WELL AS FROM FOCUS GROUPS.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

12

THE 13 ATTRIBUTES FIT INTO THREE GENERAL PREFERENCE AREAS

SIMPLIFY MY LIFE

Service that’s simple just works, and consumers expect this from the brands they interact with. A digital experience should be cohesive, integrated and easy. It has to fit in with the consumer’s life effortlessly, available anytime, anywhere.

BE WHO I AM

Consumers want experiences that are dedicated to them as individuals, experiences that appeal to or even predict their preferences, but without infringing on their privacy. Brands need to appeal to a customer’s individual identity, making them feel important and unique.

ENGAGE ME

An engaging digital experience is one that listens to consumers and allows them to interact with and control the experience when needed. It should be interactive and responsive, triggering an emotional response from the customer.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

13

T H E A U S T R A L I A N D I G I TA L E X P E R I E N C E I N D E XSAP’s Australian Digital Experience Report takes its analysis deeper by presenting all brand‑level digital experience scores as an index. This index anonymises the brands; however provides the additional context of how brands’ performances are distributed by industry.

To qualify for the index, brands had to be rated by at least 60 respondents.

Across the entire index, just one brand, an insurance company, managed a positive digital experience score. In second place was a grocery retailer with a digital experience score of -6 per cent, while in third was a consumer goods retailer with ‑7 per cent. Utilities made up the three lowest scores in the index.

SAP intends to expand on this index each year and help provide a living picture of the development of the digital experience in Australia.

THE DIGITAL EXPERIENCE INDEX

-40%

-30%

-20%

-10%

0.0%

10%

20%

-7

-12

-15

-19-21

-25

-34

-16

-11

-20

-23

-28

-31

-6

-12

-16

-9-11

-21

-25-27

-33

-30

-38-40 -40

13

-12

-15

-20 -21-23 -24

-34

BANKING RETAIL (CONSUMER)

RETAIL (GROCERY)

INSURANCE UTILITIES TELCO

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

14

T H E A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

14

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

15

T H E D I G I TA L E X P E R I E N C E G A P : I N D U S T R I E S AT A G L A N C E

A digital experience gap was evident across all industries that make up the Australian Digital Experience Report, with the negative digital experience scores varying across each.

A correlation between the digital experience score and the level of digital disruption in each industry is evident. Industries that achieved the higher digital experience scores are those further along a journey of digital disruption.

Those with the lower scores are yet to be hit by mass disruption. Dominated by a few major brands, the

products and services these industry players provide are more functional and transactional in nature.

Regardless, the findings of the Australian Digital Experience Report illustrate that the digital experience should be pushed to its full potential to maximise loyalty and advocacy. Digital disruption has already occurred across many industries – it would be naïve to suggest it won’t happen to all sooner than later.

The research provided much more rich data on how each industry performs, which will be the subject of subsequent vertical-specific reports.

WHERE AUSTRALIANS INTERACT DIGITALLY

0

20

40

60

80

100

BANKING

84%

TELCO

66%

RETAIL (CONSUMER)

62%

UTILITIES

50%

INSURANCE

47%

RETAIL (GROCERY)

32%

Banking is the industry most Australians interact with digitally followed by telecommunications, consumer retail and government.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

16

W H O L E A D S ? W H O L A G S ?Top performing industries included:

• Retail groceries (-10 per cent)

• Banking (-18 per cent)

The common thread among these industries is the huge amount of change in recent years driving the need for digital experiences that go far beyond just OK to delightful.

The arrival of overseas brands as well as niche providers in the retail groceries sector has increased the competition faced by the big local providers. Customers demand more control over the experience, and retailers are competing based on their ability to deliver that control via the digital experience – just as they compete on factors such as price or supply‑chain optimisation.

Disruption has also occurred in the retail banking sector. Consumers now look beyond the big four banks for their banking services. Transactional relationships no longer suffice, and consumers choose banks based upon a multitude of factors, not just the ability to access money.

Insurance is another sector grappling with increased competition – a prime example of an industry now challenged by non‑traditional competitors. Brands are bundling everyday services from across industries to make life easier for the consumer. When grocery shopping online, a consumer may be only one tap away from also switching insurance providers.

DIGITAL EXPERIENCE SCORE BY INDUSTRY

BANKING

INSURANCE

RETAIL (GROCERY)

RETAIL (CONSUMER)

TELCO

UTILITIES

-18%

-10%

-19%

-20%

-26%

-33%

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

17

Industries with lower digital experience scores included:

• Telecommunications and ISPs (-26 per cent)

• Utilities (-33 per cent)

Competition in these sectors is limited. While these industries do, on the whole, provide functional digital services – after all, many consumers may simply wish to pay a bill and be done with the matter – there remains plenty of room for innovation.

Utilities is a prime example. As smart devices and the Internet of Things become more pervasive in Australian households, consumers will have a greater level of visibility and control over how they consume energy and resources. Utilities will need to provide digital experiences that enable this visibility and control based on real-time data, and will compete with one another increasingly solely on this basis. The days of quarterly statements are numbered.

-26%

TELCO

-33%

UTILITIES

-10%

RETAIL (GROCERY)

-18%

BANKING

LEADING

LAGGING

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

18

W H AT ’ S I M P O R TA N T T O C O N S U M E R S B Y I N D U S T R Y

The two most important attributes of the digital experience were consistent across industries: cohesive integrated and simple and available anytime on my

terms. Only the telecommunications industry differed in its top two, with respectful and dedicated to my needs of slightly higher importance than in other industries.

THE TOP DIGITAL-EXPERIENCE ATTRIBUTES BY INDUSTRY

FITS IN WITH THE REST OF

MY LIFE AND IS EFFORTLESS

COHESIVE, INTEGRATED AND SIMPLE

RESPECTFUL AND DEDICATED

TO MY NEEDS

BANKING INSURANCE RETAIL (CONSUMER)

RETAIL (GROCERY)

UTILITIES TELCO

AVAILABLE ANYTIME

ON MY TERMS

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

19

B A N K I N G

Compared to most, the banking sector performed well. It is also the most digitally engaged – 84 per cent of respondents in the study have interacted digitally with their bank.

Importantly, on average banks scored positively on the three attributes of the digital experience most important to their customers, but underperformed especially in digital experiences tailored to the individual.

Customer engagements need to be consistent across all digital channels. The same rich experience a customer achieves on an ATM should also register on a mobile bank app or an online banking portal. Regardless of the channel or device chosen, the user must still receive focused service and product recommendations.

Australian banks can continue to improve their score by investing in these areas.

ATTRIBUTES BANKS SCORED WELL ON ARE:WHEN IT COMES TO AREAS OF THE DIGITAL EXPERIENCE BANKS COULD IMPROVE ON:

Respectful and dedicated to my needs

Responsive and interactive

Relevant offers without infringing on privacy

Available anytime on my terms

Cohesive, integrated and simple

Fits in with my life and is effortless

BAN

KIN

G

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

20

U T I L I T I E S

Conversely, the utilities industry struggled to score positively. More importantly, it scored low in the areas most relevant to its consumers. Also, it ranked low in terms of digital engagement: only 50 per cent of consumers indicated they had interacted digitally with their utility company.

The industry in Australia is ripe for disruption. Even marginal innovation to the top digital experience attributes could quickly put a first-mover utility ahead of its competition.

ONLY 50 PER CENT OF CONSUMERS INDICATED THEY HAD INTERACTED DIGITALLY WITH THEIR UTILITY COMPANY.

UTILITIES INDUSTRY STRUGGLED TO SCORE POSITIVELY

Available anytime

on my terms

Cohesive, integrated and simple

Responsive and interactive

Respectful and dedicated

to my needs

Fits in with my life and is e�ortless

Relevant o�ers without

infringing on privacy

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

21

T E L E C O M M U N I C AT I O N S

The telecommunications industry fared better than utilities, scoring positively for being available anytime on my terms. It also scored well for digital engagement – with 66 per cent of respondents interacting with a telco digitally.

However, the results indicated that the industry is still of the one‑to‑many mindset for its digital engagement as opposed to offering a tailored experience. In Australia, the telecommunications industry stands to make fast gains by investing in tools that allow it to better understand and deliver better control to its consumers.

Respectful and dedicated to my needs

Fits in with my life and is effortless

Responsive and interactive Relevant offers without infringing on privacy

TELCOExcites and engages me

Available anytime on my terms

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

22

R E TA I L : G R O C E R I E S

The grocery sector achieved the best overall digital experience score. However, it had the lowest level of engagement, with only 32 per cent of respondents doing their shopping online. This suggests that Australia’s online grocery shoppers are still a small yet engaged group of digitally savvy consumers. Telling as well, the retail groceries industry scored positively in the three attributes its consumers hold most dear.

Nonetheless, there are numerous attributes where the industry scored negatively, and where the relatively few players in this industry in Australia could quickly invest to gain market share.

PERFORMED POSITIVELY FOR BEING:

BUT REQUIRED ATTENTION FOR THESE ATTRIBUTES:

Cohesive, integratedand simple

Fits in with my life and is effortless

Available anytime on my terms

Relevant offers without

infringing on privacy

Responsive and

interactive

Customised and tailored to my preferences

Makes me love the brand

Makes me feel important

Excites and engages me

Associates with my identity

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

23

R E TA I L : C O N S U M E R G O O D S

Similar to its groceries counterpart, the consumer-goods retail industry scored positively for the three digital-experience attributes most important to its customers. Unlike groceries, it is one of the most digitally engaged, with 62 per cent of respondents confirming an interaction.

Connected consumers are redefining the shopping experience. A vast majority of shoppers start purchases on a PC or mobile device and want to be digitally engaged in their shopping experiences4. Expectations have never been higher for retailers to deliver consistent shopping experiences through online channels, mobile technology and social networks.

CONSUMER GOODS RETAIL INDUSTRY SCORED POSITIVELY FOR:

BUT REQUIRED ADDITIONAL FOCUS FOR:

Respectful and dedicated

to my needs

Responsive and interactive

Cohesive, integrated and simple

Fits in with my life and is eortless

Relevant o�ers without infringing on privacy

Excites and engages me

Available anytime on my terms

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

24

I N S U R A N C E

The insurance sector in Australia scored positively for two of the digital-experience attributes most important to its consumers. It is also one of the better performing sectors. Its digital engagement, however, is one of the lowest, at 47 per cent.

To succeed, insurers must provide customer care and not just financial services. This approach also helps ensure that a company doesn’t lose hard‑won customers to a more responsive competitor. The ability to understand customer needs and quickly respond with the right products delivered through the right channels earns customer loyalty.

Available anytime on my terms

Cohesive, integrated and simple

Respectful and dedicated to my needs

Fits in with my life and is effortless

Responsive and interactive Predicts my preferences

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

25

T H E A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

25

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

26

T H E R I S E O F T H E D I G I TA L I N F L U E N C E RPrioritising and improving the 13 attributes of the digital experience are critical for a brand to increase its number of delighted customers. However, the research uncovered another extremely important factor that can help a company boost loyalty and advocacy: the digital influencer.

A digital influencer is someone who demonstrates the ability to change opinions and behaviours, and drive measurable outcomes online. Effectively harnessing and expanding this segment of the customer base is essential for a brand to improve satisfaction with its digital experience.

To provide insight into the digital influence of Australian consumers, respondents rated their level of digital

engagement. Based on their responses they were categorised into four groups:

Influencers: Those who frequently posted content, received a high volume of responses and had a large following of people who read their posts and comments

Contributors: Those who contributed content on digital media and received responses from others

Observers: Those who frequently viewed content posted by others on digital media but seldom actively participated

Passives: Those who had little engagement with digital media

PERCENTAGE OF RESPONDENTS BY INFLUENCER SEGMENT

OBSERVERS

CONTRIBUTORS

PASSIVES

INFLUENCERS

9% 16% 37% 38%

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

27

The study shows that as people become increasingly influential in the digital arena, the higher they rate their digital experience.

Influencers delivered a significant positive digital experience score of 33 per cent across all industries, meaning that there were far more delighted consumers in this category than unsatisfied.

Those identified as contributors delivered a digital experience score of -3 per cent, observers fared far worse with a score of -33 per cent, and finally passives scored ‑41 per cent.

The message for brands seeking to improve loyalty and advocacy is to harness the power of the digital influencer, while also helping to educate the other consumer groups and bring them along the digital journey from passive through to influencer.

AS PEOPLE BECOME INCREASINGLY INFLUENTIAL IN THE DIGITAL ARENA,

THE HIGHER THEY RATE THEIR DIGITAL EXPERIENCE

DX SCOREBY INFLUENCER SEGMENT

INFLUENCERS

33%

CONTRIBUTORS

-3%

OBSERVERS

-33%

PASSIVES

-41%

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

28

W H AT M AT T E R S T O T H E D I G I TA L I N F L U E N C E RContributors, observers and passives all rank available anytime on my terms and cohesive, integrated and simple as their top two digital experience attributes. Influencers, however, rank fits in with my life and is effortless and respectful and dedicated to my needs as their top attributes. Rather than being more functionally led, digital influencers preferred attributes reflecting a tailored, emotive experience.

Additionally, two emotional attributes creep into the influencers’ top five which are not seen in the other groups; namely relevant offers without infringing on privacy and excites and engages me. This again points to the fact that influencers seek out the emotional attributes of the digital experience.

WHAT MATTERS TO INFLUENCERS

OBSERVERS

CONTRIBUTORS

PASSIVES

INFLUENCERS

FITS IN WITH THE REST OF

MY LIFE AND IS EFFORTLESS

RESPONSIVE AND INTERACTIVE

COHESIVE, INTEGRATED AND SIMPLE

RESPECTFUL AND DEDICATED

TO MY NEEDS

AVAILABLE ANYTIME

ON MY TERMS

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

29

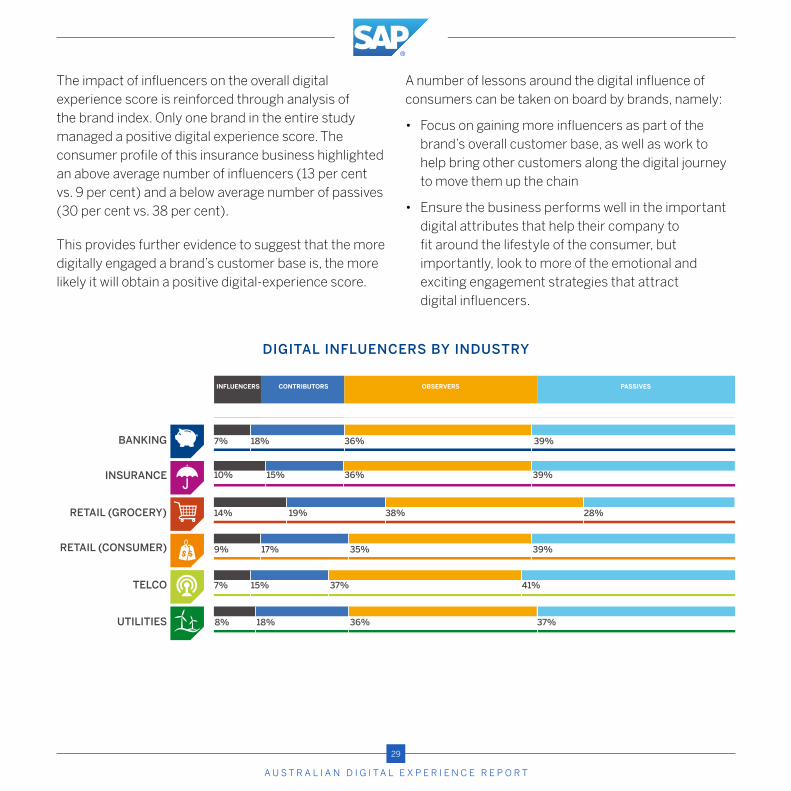

The impact of influencers on the overall digital experience score is reinforced through analysis of the brand index. Only one brand in the entire study managed a positive digital experience score. The consumer profile of this insurance business highlighted an above average number of influencers (13 per cent vs. 9 per cent) and a below average number of passives (30 per cent vs. 38 per cent).

This provides further evidence to suggest that the more digitally engaged a brand’s customer base is, the more likely it will obtain a positive digital-experience score.

A number of lessons around the digital influence of consumers can be taken on board by brands, namely:

• Focus on gaining more influencers as part of the brand’s overall customer base, as well as work to help bring other customers along the digital journey to move them up the chain

• Ensure the business performs well in the important digital attributes that help their company to fit around the lifestyle of the consumer, but importantly, look to more of the emotional and exciting engagement strategies that attract digital influencers.

DIGITAL INFLUENCERS BY INDUSTRY

BANKING

INSURANCE

RETAIL (GROCERY)

RETAIL (CONSUMER)

TELCO

UTILITIES

INFLUENCERS

9% 16% 37% 38%

CONTRIBUTORS OBSERVERS PASSIVES

7% 18% 36% 39%

36% 39%15%10%

38% 28%19%14%

35% 39%17%9%

37% 41%15%7%

36% 37%18%8%

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

30

C R E AT I N G D E L I G H T F U L D I G I TA L E X P E R I E N C E SThis report has illustrated the business impact of digital experiences both great and poor. However, the findings also point to where organisations can begin to assess, improve and optimise the digital experience they deliver for their customers. In this assessment, representatives from across an organisation’s functions (Marketing, Service, IT, Finance and even HR) – and

preferably those organisation’s customers – need to be involved. As Forrester has claimed and as our interviews with leading Australian brands support, the digital experience is not just a channel owned by the Marketing function5. Rather, the digital experience is a differentiating element of the offering itself in which the entire organisation invests, from inception to delivery.

DISCOVER DEVELOP DISRUPTIn discussions with several brands assessed in this report, even top performers didn’t have a complete view of their customers’ preferences when it comes to the digital experience. The first step to developing competitive advantage through the digital experience is for a brand to understand what its specific gap is or at least what the gap is for its industry. Then, by breaking down the digital experience into its attributes and how these attributes rank among their customers, a brand can identify where it should most effectively invest to bridge the gap.

Examine how the digital experience gap influences your customers’ NPS and loyalty scores and prioritise how you improve your digital experience accordingly. Not all attributes of the digital experience are cherished equally, so focus on which ones strike a chord with your customer base. Also, help your customers develop as digital influencers. As the research findings suggest, the more digitally influential a customer, the more likely they are to be delighted by the digital experience.

Especially in industries grappling with significant disruption, choosing the right attributes to invest in may not be obvious. Often a brand and its consumers won’t know what they don’t know until a disruptor comes by and shows them. To fend off disruptors or – better yet – to become disruptors themselves, brands can also invest in those digital-experience attributes that appeal most to digital influencers.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

31

T H E A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

31

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

32

T E C H N O L O G Y E N A B L I N G T H E G R E AT D I G I TA L E X P E R I E N C E

Moving from a transactional digital experience to one that engages and delights takes more than a new app or fresh digital presence. It also takes more then simply putting a physical process “online.” As noted in the previous section, experts from across the organisation need to contribute to design and deliver a delightful digital experience.

Instrumental as well is a thorough understanding of the value technology holds as the foundation for the digital experience, helping organisations know their customers better and thereby engage with them better.

KNOW YOUR CUSTOMERAs digital services first expanded in the market, many consumers didn’t mind the less personal nature of the experience. It worked, and that was it. Now, as consumers have become more digitally active, they once gain desire the level of personalisation many had received when the experience was exclusively over the counter.

As the research shows, Australian consumers are increasingly demanding digital experiences that not only work but also trigger an emotional affinity to the brand. This level of engagement requires a deep level of personalisation, which in turn requires data – lots of data – to have the clearest possible view of a customer and his or her preferences.

Today, organisations can leverage structured data (as in spreadsheets) and unstructured data (as in audio or video content). They can make use of obvious sources such as point-of-sale data, and they can use less traditional sources such as third‑party and social media data, as well as signal data from sensors or machine‑to‑machine data from networked automation systems.

How the organisation manages the data is as important as the data itself. Organisations must break down their data silos: The architecture of the systems and tools that collect, store and display data must be integrated across sales, service, financials, supply-chain and other systems to ensure that every role within the organisation can make decisions based on the single view of the customer.

Knowing your customer also means building the right teams and honing the right skills internally to engage with the data and deliver business insights. Data scientists, line of business analysts and IT architects who understand the business and who can design systems that integrate data sources from across functions are instrumental in developing an effective digital strategy.

However, it’s not enough for the view of the customer to be complete; it also has to be in real time. In retail, for example, there is tremendous value in making an offer to a customer at the opportune moment. Montreal’s public transport agency Société de Transport de Montréal (STM) has developed an app

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

33

that runs on real‑time data to personalise the commute of thousands of residents. STM and its network of entertainment providers, food and beverage outlets and retailers, offer special discounts and one-off promotions to commuters as they move in and out of the transport system. Bookstores are able to offer commuters moving toward its store the opportunity to download a sample chapter of a book that is on sale, the Montreal Opera House offers special prices on unsold seats for the coming afternoon’s performance. Supermarkets offer their specials on bus routes for commuters who are likely to be thinking about what to cook for dinner. All of this is accomplished in real‑time and without infringing on commuters’ privacy6.

In Australia, Fire and Rescue New South Wales has recognised the significance of real-time and implemented SAP’s in‑memory database platform SAP HANA so internal users can understand instantaneously the location of assets and the skill level of their employees and volunteers so as to best deploy resources in times of emergency7. Organisations must lay the real‑time foundation for these types of differentiating capabilities not at the application level, not even at the business intelligence level, rather at the data platform level.

KNOW YOUR CUSTOMER• Capture data from traditional and

non-traditional sources

• Break down data silos

• Harness the power of real-time data

ENGAGE YOUR CUSTOMERThe focus of this research has been on the digital experiences brands deliver to their customers in Australia. However, although the digital experience is rapidly dominating the overall customer journey, it is of course not the only way consumers interact with brands. Important to the overall customer experience is an integration of all channels to the consumer, digitally online and physically in store, to deliver a consistent experience and meaningful customer engagement.

Customers are seizing control of the marketplace. They are more digitally connected, socially networked and better informed than ever before. They have become savvy consumers in their personal lives and sophisticated buyers at work. When they finally decide to interact with a business, they expect to be able to do their research, make a purchase and get assistance on any channel they choose. They expect that each new interaction will be personalised and occur within the context of the last one. Their tolerance for fragmented experiences is lower than ever, and they are very much in control of their own journey.

Ultimately, successful integration of these channels leads to omnichannel commerce—the seamless integration of systems that allows shoppers to browse, buy and take possession of goods more flexibly and conveniently, leading to more sales. For example, research from IDC shows that omnichannel shoppers spend 3.5 times more than single-channel shoppers 8.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

34

The greater proportion of interaction that is digital relative to other channels, the less suited a traditional CRM solution, where a brand enters opportunities and leads. Rather best suited is an omnichannel platform that goes beyond CRM to help a brand serve its customers on their terms by integrating not only salesforce automation, but customer and employee collaboration, quote-to-cash processes, commerce, support, fulfilment and marketing.

A digitally native business such as Uber is an extreme case, but one that clearly illustrates the need for brands to go beyond just CRM to engage their customers. A location-aware mobile app finds the user when you launch the app, immediately makes you an offer based on your preferred vehicle, fulfils the order based on credit card data on file, learns your preferences as you use the service and integrates behavioural feedback into every feature to optimise the experience. Without a fleet of sales and marketing professionals, this is simply impossible without the right technology.

Take Lorna Jane for example. To succeed in Australia and overseas, the women’s sports apparel retailer invested in an e‑commerce platform that aligns channels and delivers a consistent and integrated customer experience across its mobile, Web and call centre instances as well as across its bricks and mortar stores. Online conversion via mobile devices has since grown by 200 per cent9.

The customer is in full control. To compete and win in today’s digital world, brands have to create an environment where true, digital engagement with customers is possible. And to meet customer expectations and fend off rivals, brands must be able to respond to them in real-time, whenever, wherever and on whatever device they choose to use.

ENGAGE YOUR CUSTOMER• Align digital experience to other channels

(omnichannel)

• Personalise the experience

• Go beyond CRM

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

35

DATA-DRIVEN CUSTOMER ENGAGEMENTEN

GAG

E YO

UR C

USTO

MER

STR

UCTU

RED

DATA

UNSTRUCTURED DATA

ENGAG

E YOUR CUSTO

MER

KNOW

YO

UR

CUST

OM

ERKN

OW YO

UR CUSTO

MER

PERFECT D

IGIT

AL E

XPERIENCE POWERED BY TECH

NOLOGY

B U S I N E S S I N T E L L I G E N C E P L AT F O R M

R E A L -T I M E D ATA P L AT F O R M

PROCUREMENTFINANCE HUMAN RESOURCES

MARKETINGSALES

O M N I C H A N N E L E N G A G E M E N T

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

36

T H E A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

36

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

37

C A S E S T U DY: S U N C O R P I N S U R A N C ESuncorp Insurance has the distinction of being the only brand in the research to attain a positive digital experience score. Insights into the organisation’s digital practices help explain why.

Over the past five years, Suncorp has experienced a significant increase in digital interactions with its insurance customers. According to Head of PI eCommerce & Specialist Brands, Ivan Owide, the digital experience is now their customers’ preferred window to the organisation. Increasingly, customers want much more from the digital experience than functionality. “Yes, they want it to be convenient and timely, but

they now want the experience to be tailored and meaningful,” Owide says.

The ability of the team at Suncorp Insurance to accommodate these more nuanced digital demands of its customers is evident in the company’s exceptional scores across the majority of digital-experience attributes. In fact, Suncorp Insurance scored positively in 11 of the 13 attributes. “Our digital philosophy is underpinned by the notion that the customer should think more highly of the brand after the experience than before,” Owide says.

SUNCORP DX SCORE

THE DX SCORE

31%

AMBIVALENT

13%28%

UNSATISFIED

41%DELIGHTED

WHO IS DELIGHTED WITH THE DIGITAL EXPERIENCE PROVIDED BY SUNCORP

INSURANCE AND WHO IS NOT?

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

38

Suncorp Insurance tallied by far the highest percentage of delighted customers, at 41 per cent. Across all segments Suncorp Insurance enjoys higher‑than‑average loyalty and NPS.

The high scores also demonstrate Suncorp’s ability to excel not only in the functional attributes, but also in the more emotional – specifically: responsive and interactive, respectful and dedicated to my needs, fits in with my life and is effortless and customised and tailored to my preferences. These attributes are valued especially among digital influencers, an important driver behind Suncorp Insurance’s high digital‑experience score.

As the research shows, digital influencers tend to deliver a higher digital-experience score, and for Suncorp Insurance this segment makes up an above‑average percentage of the brand’s customer base (13 per cent vs. average of 9 per cent). Similarly, the organisation had a lower than average percentage of passives (30 per cent vs. average of 38 per cent).

The digital experience has significantly shaped Suncorp Insurance’s business over the past five years. It hasn’t necessarily reduced the number of calls the organisation receives, rather – more importantly – it’s changed the type of conversations customers are having with the brand during these calls.

AFFECTING SUNCORP’S BUSINESS OUTCOMES - LOYALTY

73%LOYALTY

45%LOYALTY

28%LOYALTY

WITH THE DIGITAL EXPERIENCEDELIGHTED

WITH THE DIGITAL EXPERIENCEAMBIVALENT

WITH THE DIGITAL EXPERIENCEUNSATISFIED

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

39

“Our digital experience allows our consultants to focus on immediately helping our customers rather than spending the first 10 minutes of the conversation gathering information,” Owide says. The omnichannel experience here is key: “There is no ‘online customer.’ We look to integrate our online experiences with our offline conversations to build a similar experience across channels.”

Suncorp prides itself on recognising the evolving demands of its customers early and investing ahead of them. “Digital isn’t any one person’s job, it’s a highly collaborative process across the business,” Owide says.

Suncorp relies on an in-house team of digital experts to work with the departments, process owners and customers, iteratively testing and challenging the experience so that it best complements the customer journey.

“It’s not about replicating the offline online. It’s about enhancing a process and making it more valuable in a digital context,” Owide says. “Customer experience is the battle ground in our industry, and digital is such a massive enabler for a delightful experience. Digital is an enabler for organisations to exceed customers’ expectations like never before,” he concludes.

AFFECTING SUNCORP’S BUSINESS OUTCOMES - NPS

65%NPS

10%NPS

-44%NPS

WITH THE DIGITAL EXPERIENCEDELIGHTED

WITH THE DIGITAL EXPERIENCEAMBIVALENT

WITH THE DIGITAL EXPERIENCEUNSATISFIED

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

40

WHAT’S IMPORTANT TO SUNCORP CUSTOMERS?

-20

-10

0

10

20

30

40

50RANK 1

RANK 2

RANK 3

RANK 4RANK 5

RANK 6

RANK 7

RANK 8

RANK 9 RANK 10 RANK 11

RANK 12

RANK 13

DIGI

TAL

EXPE

RIEN

CE S

CORE

(%)

50%

27%

34%

14%17%

14%

5%

16%

6% 5% 5%

-6%

-13%

INSURANCE DX RANK

Cohesive, integrated and simple

Responsive and interactive

Excites and engages me

Makes me feel unique

Relevant offers without infringing on privacy

Predicts my preferences

Customised and tailored to my preferences

Makes me feel important

Associates with my identity

Makes me love the brand

Fits in with my life and is effortless

Respectful and dedicated to my needs

Available anytime on my terms

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

41

WHAT SHOULD SUNCORP FOCUS ON?

30%

20%

10%-60% 40%-40% 20%-20% 0%

40%

25%

35%

15%

IMPROVE

IMP

OR

TAN

CE

MAINTAIN

MONITOR COMMUNICATETHE VALUETHE

DX SCORE

Cohesive, integrated and simple

Responsive and interactive

Excite and engage me

Makes me feel unique

Relevant offers without infringing on privacy

Predicts my preferences

Customised and tailored to my preferences

Make me feel important

Associates with my identity

Makes me love the brand

Fits in with my life and is effortless

Respectful and dedicated to my needs

Available anytime on my terms

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

42

C A S E S T U DY: K O G A N . C O MKogan.com is widely recognised in Australia as a disruptor to the retail industry. As a complete online, direct-to-consumer business, Kogan.com relies nearly exclusively on the digital experience when it comes to the overall customer experience.

The findings of the Australian Digital Experience Report reflect Kogan.com’s thorough understanding of what makes a strong digital experience: The organisation scored the highest among consumer-goods retailers, besting eight other large consumer‑goods retail players and delivering the third‑highest score across industries. Unique to Kogan.com is that the ambivalent segment is the largest among the top performing brands assessed, suggesting potential to further improve with relatively little investment.

Kogan.com has achieved its leadership standing through relentless focus on “simple and beautiful ways to buy tens of thousands of products at the world’s best prices,” according to David Shafer, Executive Director, Kogan.com. The team at Kogan.com continually improve the shopping experience on its Web site, but importantly the systems and processes at the backend that power their operations.

From an engagement standpoint, Kogan.com applies smart, measurable marketing to attract customers, and a leading digital experience to drive loyalty. Kogan.com carefully analyses how customers interact with their brand at every point of engagement – from its very robust searching and filtering system through to its intelligent checkout process, which remembers a customer’s key details. Kogan.com hires coders and designers who are encouraged to challenge the status quo. They develop ideas for the digital

experience based on fact, not emotion – based on what customers actually do rather than what they feel customers ought to be doing.

This digital experience is backed up by rapid delivery achieved through strong operational systems and procedures in the backend reliant on timeliness and accuracy of data. The business is highly data driven. Shafer describes Kogan.com as “a statistics business first and foremost, rather than a retailer.” He adds, “We see a big difference at the frontend based on our optimised backend.”

At 78 per cent, Kogan.com enjoys strong loyalty among customers delighted with the digital experience. This illustrates the particular importance of the digital experience for Kogan.com as the dominant point of engagement with customers. According to the Australian Digital Experience Report, Kogan.com’s leadership is defined by its superior ability to provide service anytime and on the customer’s terms, the attribute most important to customers of consumer-goods retail. Strong, too, was Kogan.com’s capability to deliver on the attributes most important to the digital influencer: fits in with my life and is effortless and respectful and dedicated to my needs.

Early 2015, Kogan.com introduced its retail grocery offering, launching it into the grocery retail sector with a very established set of competitors. From a digital experience perspective, Kogan.com is in a unique position to activate what has made it so successful in the consumer‑goods space for the grocery space and further define the delightful digital experience in Australia.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

43

R E F E R E N C E S1. Media Consumer Survey 2014: Australian Media

and Digital Preferences – 3rd Edition Deloitte, March and April 2014.

2. Measuring Your Net Promoter Score Bain & Company.

3. 2014 Global Customer Service Barometer American Express, 2014.

4. The 3 New Realities of Local Retail Google, Ipsos Media CT and Sterling Brands, October 2014.

5. The Forrester Wave™: Digital Experience Delivery Platforms, Q3 2014 Forrester Research, Inc., 2014.

6. An Instantly Rewarding Ride SAP.

7. Customer Snapshot: Saving Lives and Property with Data SAP.

8. IDC Retail Insights, John Lewis: “The Path to Omnichannel” IDC, May 2012.

9 hybris and Lorna Jane, A Growing Success Story hybris software.

F U R T H E R R E A D I N GCreating the Customer Experience SAP and Oxford Economics, 2014.

Delivering New Levels of Personalization in Consumer Engagement Forrester Consulting and SAP, November 2013.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

44

A C K N O W L E D G E M E N T SSAP Australia would like to thank customers Suncorp Insurance and Kogan.com for sharing their best practice and leadership with the digital experience in this research report, as well as addressing this topic openly and in detail for the benefit of organisations across Australia.

We also thank former SAP Australia and New Zealand President and Managing Director Andrew Barkla for his input into the conceptualisation and execution of this research.

SAP Australia extends its deep appreciation to Ray Kloss, Director of Marketing, CISCO and former Head of Marketing for SAP Australia and New Zealand for his leadership in building the framework for the research.

The development of this whitepaper benefited from the input and support provided by our partners The Factuary and Howorth Communications.

A U S T R A L I A N D I G I T A L E X P E R I E N C E R E P O R T

45

www.sap.com/australia/ausdxr

Join the conversation #ausdxr

No part of this publication may be reproduced or transmitted in any form or for any purpose without the express permission of SAP SE or an SAP affiliate company.

These materials are provided by SAP SE or an SAP affiliate company for informational purposes only without representation or warranty of any kind and SAP SE and its affiliated companies shall not be liable for errors or omissions with respect to the materials.

Copyright 2015 SAP SE or an SAP affiliate company. All rights reserved.