Embed Size (px)

Citation preview

2019 | Western Australia

Australian Farmland Values

Forward

For Australia’s farmers and agri investors, farmland value matters.

For farmers, it secures most farm debt, and underpins a large proportion of farm business balance sheets. It is a critical asset that enables farm production and provides equity which can be reinvested for growth.

As a specialist lender dedicated to Australian agribusiness, and a workforce covering the majority of Australia’s key agricultural production areas, Rural Bank knows farmland value is too important an issue to rely purely on informal and unqualified data.

We understand the robust and sometimes emotive discussion farmland values evoke. Farmers and agri investors want to know who bought what land, and how much they paid for it.

That’s why Rural Bank established its Farmland Values Report in 2014, tracking Australian farmland sales over the past 24 years.

What have we learned?

If you’re taking a long-term view, farmland values demonstrate agriculture’s strength and resilience.

The relevance of farmland values will often carry greater significance when looked at from a localised level. Therefore, we have segmented the data from national, to state and down to municipality level.

This year, there is deeper detail at the municipality level – because that’s what readers told us they were looking for.

Farmland values have comfortably outgrown CPI, which is good news for Australian landowners. And consistent with the long-term trend, we expect farmland values will continue to rise.

Climate risk is playing an increasingly significant role, as reliability of rainfall becomes paramount. Our analysis highlights investment is strongest with reliable rainfall.

The implications of these trends will – as always – be hotly debated. Rural Bank’s Australian Farmland Values report can help frame these important conversations.

These trends have implications for agriculture, and I encourage the sector to explore them.

As farms get bigger, transaction values larger and land more tightly held, what will the trend for increasing farmland value mean for new entrants?

How will Australia’s farmers access capital?

What are the alternative forms of capital or business structures to enable agricultural growth?

These questions have no simple answers. But they need to be explored and debated.

Rural Bank’s Farmland Values Report is one ingredient for an informed debate.

I look forward to discussing the report and its themes with Australia’s agricultural sector.

Alexandra Gartmann CEO, Rural Bank

2

Executive Summary

The median price per hectare of Australian farmland increased by 10.7 per cent in 2018, marking the fifth consecutive year of growth.

Keeping in-line with the long-term trend, we expect farmland values will continue to rise, underpinned by strong demand for agricultural assets and increasing profitability of farming operations in an environment of low interest rates and strong commodity prices.

Over time, we are seeing the number of farmland transactions decline. This may mean opportunities to expand become less frequent as fewer properties come on the market. Tightening access to suitable parcels of land, and increased competition for fewer parcels will play a role in driving increased values.

Across Australia the number of transactions declined 9.5 per cent year-on-year to 8,250 and saw a total of 8.7 million hectares of land transacted with a combined value of $8.99 billion.

Farmland values showed themselves again to be resilient against a backdrop of adverse seasonal conditions, following the trend that was observed from 2001 through to 2010.

Despite challenging seasonal conditions, the long-term outlook continues to point to growth for Australian agricultural productivity and profitability, and we expect this will continue to support the value of Australian farmland.

The relevance of farmland values will often carry greater significance when looked at from a localised level, which is why in 2019 Rural Bank has researched trends down to 29 regions across the country.

The Rural Bank Australian Farmland Values report draws on over 255,000 transactions, accounting for 297.5 million hectares of land with a combined value of $150.4 billion over 24 years.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$5,000

$3,500

$3,000

$4,500

$4,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

$2,500

$2,000

$1,000

$1,500

$500

0

Australia – historic performance

2018 year-on-year median price growth

2018 year-on-year transaction

volume growth

NSW 9.6% -18.0%

QLD 15.7% 0.1%

SA 17.0% -12.6%

TAS -5.0% -11.7%

VIC 14.1% -8.0%

WA 3.8% 9.1%

NT 135.5% 88.0%

3

Understanding farming’s most valuable asset is important to everyone in agribusiness, especially Australia’s farmers.

The Australian Farmland Values report tells the story of national and regional farmland performance over the past 24 years.

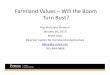

Wes

tern

Aus

tral

ia

South West-8.4%

Central8.5%

Northern34.0%

South Coast5.7%

Eastern-12.3%

Median price per hectare

$2,0052018 median price growth

3.8%Hectares of land traded

521,687Average annual growth

over 20 years

4.3%Map shows median price movement in 2018.

Western Australia

From the field

“Broadacre farmland values in Western Australia have

been strong across most of the state particularly in

the latter part of 2018. Rises of 25 to 30 per cent in

the median price per hectare were seen in traditionally

higher rainfall areas which have enjoyed several strong

seasons. The northern Wheatbelt generally had a

very good season in 2018 and prices are expected to

grow, catching up with the rest of the state.”

James Robinson, Rural Bank, Perth.

The median price per hectare of farmland in Western Australia increased by 3.8 per cent in 2018. This follows a 6.5 per cent decline in 2017.

At a regional level, the Northern region recorded the largest growth of 34 per cent in the median price per hectare. In the Eastern region, the median price fell 12.3 per cent, mainly due to an increased proportion of transactions in the lower valued eastern districts of the region, not due to an easing market. A decline in median was also recorded in the South West where tight margins have challenged dairy and orchard industries, contributing to an 8.4 per cent fall.

The estimated number of farmland transactions increased in 2018, up by 9.1 per cent. Despite the increase, the volume of transactions remained low from a historical perspective at 18 per cent below the 20-year average.

The area of farmland traded in 2018 was approximately 522,000 hectares, an increase of 8.2 per cent from 2017. This accounted for six per cent of the total farmland area traded in Australia in 2018.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$2,500 1400

1200

1000

800

600

400

200

0

$2,000

$1,500

$1,000

$500

0

Western Australia – historic performance

6

200

50

100

0

150

$0 –1,000/ha

Num

ber o

f tra

nsac

tions

$1,000 – 2,000/ha $2,000 – 3,000/ha $3,000 – 4,000/ha $4,000 – 5,000/ha $5,000/ha+

2018

2017

Western Australia – transactions by price range

The rise in the total number of transactions of Western Australian farmland in 2018 was observed across most price ranges, with modest declines for the less than $1,000/ha and $3,000–$4,000/ha ranges. The proportion of transactions in each price range remained relatively unchanged, with only a minor shift noticeable in the profile towards the higher end of the price range.

The number of transactions below $1,000/ha declined only by 1.1 per cent in 2018 and accounted for 24 per cent of the state’s transactions, down slightly from 27 per cent in 2017. While only

a modest decline, at a state level there were contrasting trends between regions. Most notably there were 12 less transactions below $1,000/ha in the South Coast, however this was offset by an additional 14 transactions in this range in the Eastern region.

The largest growth in transaction volume was in the $4,000–$5,000/ha price range which increased by 74.2 per cent in 2018. This was predominately driven by an increase in transactions in the Central region in this price range, accounting for 74 per cent of the state’s transactions.

Growth in the median price per hectare was a consistent trend across all parcel size segments in Western Australia in 2018. The two larger parcel size segments of 500–750ha and 750ha and above recorded the strongest growth in median price in 2018, recovering from declines recorded in 2017. There were 10.8 per cent more transactions in the 750ha and above segment in 2018, as the Eastern, Central and Northern regions all recorded a rise in transaction volume.

The smallest parcel size segment recorded a seven per cent rise in median, a small recovery from its decline in 2017. This segment

has recorded strong growth over the past five years, largely driven by strength in the Central region which accounted for 40 per cent of these transactions in the state.

The median price for 250–500ha parcels recorded the lowest growth in median price in 2018, but continued to be a consistent growth segment, increasing for four consecutive years. This segment had the largest increase in transaction volume in 2018, with all regions except for the South Coast contributing to this growth.

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–250 $4,717 7.0% 1.8% 9.56 271 2.7%

250–500 $1,774 4.9% 2.7% 10.00 156 30.0%

500–750 $1,627 19.2% 3.2% 9.13 73 -6.4%

750+ $1,134 12.0% 2.2% 10.00 235 10.8%

Overall $2,005 3.8% 1.1% 9.56 735 9.1%

7

Central

The median price per hectare in Central Western Australia increased by 8.5 per cent in 2018 to $2,607/ha. This followed growth of 2.7 per cent in 2017.

Most municipalities in the region recorded double-digit median growth, with Cranbrook, Corrigin and Narrogin among the highlights.

The number of transactions also increased in 2018, up by 7.5 per cent to 257. Transaction volume in the region remains low from a historical perspective.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$3,000

$2,500

600

500

400

300

200

100

0

$2,000

$1,500

$1,000

$500

0

Central – historic performance

From the field

“Improved margins for sheep and wool producers drove strong demand for grazing

land in the Central region and is expected to push prices higher in 2019. Cropping

land also remains attractive in this high rainfall zone.”

Garry Harvey, Rural Bank, Perth.

WA

2018 median price growth

8.5%

Hectares of land traded

116,793

Average annual growth over 20 years

4.4%

Median price per hectare

$2,607

8

Growth in the number of transactions occurred exclusively for properties priced above $4,000/ha. Small declines of less than 10 per cent were recorded for all other price ranges.

The region saw 25 more transactions in the $4,000–$5,000/ha price range, of which 16 were in the Great Southern sub-region and seven in the Central West mixed farming area. The greater proportion of transactions in this higher price range, while all others remained relatively stable, helped shift the profile of transactions slightly more towards the upper price ranges.

The median price per hectare increased for all parcel size segments in 2018. The largest growth was recorded for the mid-sized segments which both recovered from declines in 2017. Small parcel sizes of 50–250ha accounted for 43 per cent of the region’s transactions in 2018, the most consistent median price growth segment for four consecutive years. The median price for transactions larger than 750ha increased for the third consecutive year in 2018. Median price growth occurred alongside a 19.4 per cent rise in transaction volume for this segment.

80

20

40

0

60

$0 –1,000/ha

Num

ber o

f tra

nsac

tions

$1,000 – 2,000/ha $2,000 – 3,000/ha $3,000 – 4,000/ha $4,000 – 5,000/ha $5,000/ha+

2018

2017

Central – transactions by price range

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–250 $3,171 5.1% 0.5% 10.00 110 -1.8%

250–500 $2,384 33.1% 3.3% 10.00 72 26.3%

500–750 $2,077 25.6% 2.2% 8.69 32 -5.9%

750+ $2,101 10.9% 4.8% 10.00 43 19.4%

Overall $2,607 8.5% 1.4% 10.00 257 7.5%

9

EasternWA

The median price per hectare in Eastern Western Australia declined by 12.3 per cent in 2018 to $705/ha.

Kulin recorded the strongest growth in median price within the region. Many municipalities, particularly in lower valued parts of the region such as Yilgarn, experienced large declines in median price per hectare.

The number of transactions increased in 2018, up by 18.4 per cent to 122.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$900

$800

180

160

140

120

80

40

20

60

100

0

$700

$600

$500

$400

$300

$200

$100

0

Eastern – historic performance

From the field

“Values for good farming land in the Lake Grace area showed strong gains in 2018.

Increasing corporate activity in the area combined with fewer properties coming

onto the market were the main factors driving higher prices.”

Ron Dewson, Elders, Lake Grace.

2018 median price growth

-12.3%

Hectares of land traded

141,681

Average annual growth over 20 years

3.8%

Median price per hectare

$705

10

Much of the growth in the region’s transaction volume in 2018 occurred in the lower price ranges of the market, with the number of transactions less than $750/ha accounting for 52 per cent of the region’s transactions, up from 47 per cent in 2017. Yilgarn had the largest increase in transactions less than $750/ha and accounted for 27 per cent of the region’s transactions in this segment, up from eight per cent in 2017. The largest rise in transaction volume occurred for the $1,000–$1,250/ha price range, which doubled in 2018 due to rising volumes in Kondinin and Lake Grace. The highest price range recorded the largest decline in transaction volume in 2018, falling 36 per cent with fewer transactions in this segment in Lake Grace, Koorda and Merredin.

Growth in the median price per hectare only occurred in the 50–500ha segment. There were more transactions in this segment in 2018 with Kondinin and Kulin showing the largest growth in the number of transactions. These were two of the four municipalities in the region to record growth in the median price per hectare.

The larger parcel size segments reflected the median price trend of the region, declining from 2017 levels but showing an increase compared to 2016. Transaction volume increased for all parcel size segments except for 500–1,000ha which fell by 31.4 per cent.

35

5

15

0

25

10

20

30

$0 – 250/ha

Num

ber o

f tra

nsac

tions

$250 – 500/ha $500 – 750/ha $750 –1,000/ha $1,000 –1,250/ha $1,250/ha+

Eastern – transactions by price range

2018

2017

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–500 $865 27.6% -0.3% 7.39 44 46.7%

500–1,000 $682 -20.1% -0.3% 7.39 24 -31.4%

1,000–1,500 $642 -26.0% -2.0% 7.39 24 71.4%

1,500+ $474 -42.8% -1.7% 5.21 30 25.0%

Overall $705 -12.3% -0.6% 7.39 122 18.4%

11

NorthernWA

Northern Western Australia recorded a 34 per cent increase in the median price per hectare of farmland in 2018, rising to $1,194/ha. This was the largest growth of all Western Australian regions and followed a 35 per cent decline over the last two years.

Strong median price growth was recorded in many municipalities in the region, with Dalwallinu and Greater Geraldton being the standouts. Moora and Three Springs recorded the largest decline in median price in 2018.

The number of transactions in the region also increased in 2018, up by 34.1 per cent.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$1,600

$1,400

200

180

160

140

120

80

40

20

60

100

0

$1,200

$1,000

$800

$600

$400

$200

0

Northern – historic performance

From the field

“Prices in the Northern region firmed in 2018 with good demand in the prime

localities of Chapman Valley and Northampton. Some areas in the Northern region

have seen a tightening of listed properties.”

Kevin Bright, Rural Bank, Perth.

2018 median price growth

34%

Hectares of land traded

133,222

Average annual growth over 20 years

4.8%

Median price per hectare

$1,194

12

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–500 $1,750 0.7% 3.6% 7.82 33 73.7%

500–1,000 $1,543 93.6% 4.5% 10.00 29 123.1%

1,000–1,500 $931 16.0% -2.1% 6.08 24 9.1%

1,500+ $904 56.5% 0.7% 8.69 28 -9.7%

Overall $1,194 34.0% 1.3% 8.69 114 34.1%

All price ranges recorded an increased number of transactions in 2018 except for the lowest price range, which had 15 per cent fewer transactions. The number of transactions increased significantly for the $1,000–$1,500/ha range, up by 85 per cent, and the $1,500–$2,000/ha range, up by 91 per cent.

The result was a shift in the profile of transactions towards the upper price ranges in the region, raising the region’s median price per hectare.

Smaller parcels of less than 1,000ha accounted for a larger proportion of transactions in the Northern region in 2018, rising from 38 to 54 per cent. There were 30 more transactions of properties less than 1,000ha, and all municipalities in the region except Dalwallinu contributed to this growth. Transactions greater than 1,000ha declined by one.

Growth in the median price per hectare occurred for all parcel size segments. The 500–1,000ha segment recorded the largest growth, followed by 1,500ha and above.

30

5

15

0

25

10

20

$0 – 500/ha

Num

ber o

f tra

nsac

tions

$500 –1,000/ha $1,000 –1,500/ha $1,500 – 2,000/ha $2,000 – 2,500/ha $2,500/ha+

Northern – transactions by price range

2018

2017

13

South CoastWA

The median price per hectare in the South Coast region increased by 5.7 per cent in 2018 to $3,236/ha. This was the fourth consecutive year of growth and followed a 2.6 per cent increase in 2017.

Esperance had the largest rise in median price in the region, up by 88.8 per cent. Ravensthorpe was the only municipality to record a decline in median price in 2018.

The number of transactions in the region continued to trend lower in 2018, declining by 3.8 per cent.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$3,500

$3,000

300

250

200

150

100

50

0

$2,500

$2,000

$1,500

$1,000

$500

0

South Coast – historic performance

From the field

“Prices have been on the rise thanks to a lack of supply, and some high valued

auctions helped to drive the market higher. Demand has been sound for large

acreages, while there has been less interest in lifestyle blocks. Higher values are

expected to bring some more properties on to the market.”

Brian Western, Rural Bank, Albany.

2018 median price growth

5.7%

Hectares of land traded

122,994

Average annual growth over 20 years

5.8%

Median price per hectare

$3,236

14

The South Coast recorded fewer transactions in the lower price ranges and more transactions in the upper price ranges in 2018, shifting the profile of the region’s transactions higher.

The number of transactions in the two lower price ranges both fell by 13 per cent in 2018. Transactions below $1,000/ha are becoming less frequent in Esperance as values rise.

Manjimup, Denmark and Albany all contributed to the 50 per cent rise in transactions above $10,000/ha.

The rise in number of transactions valued $10,000/ha and above corresponds to a rise in the number of small parcel size transactions, shown by a 9.7 per cent increase in the number of transactions in the 50–250ha segment. Growth in transaction volume in this segment occurred in Albany, Denmark, Manjimup and Ravensthorpe. This parcel size segment also recorded the largest rise in median price.

The 750ha and above segment accounted for 32 per cent of the region’s transactions and experienced strong growth in the median price.

80

20

0

60

40

$0 – 2,000/ha

Num

ber o

f tra

nsac

tions

$2,000 – 4,000/ha $4,000 – 6,000/ha $6,000 – 8,000/ha $8,000 – 10,000/ha $10,000/ha+

South Coast – transactions by price range

2018

2017

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–250 $8,157 22.1% 2.0% 10.00 79 9.7%

250–500 $2,005 -12.7% 2.5% 6.95 25 -21.9%

500–750 $1,449 -12.7% 1.3% 5.65 17 -19.0%

750+ $1,509 17.7% 4.1% 9.56 57 -5.0%

Overall $3,236 5.7% 6.0% 10.00 178 -3.8%

15

South WestWA

The median price per hectare in South West Western Australia declined by 8.4 per cent in 2018, down to $8,772/ha. This was a continuation of the downward trend since the median peaked at $14,799/ha in 2008.

The largest growth in median price in the region occurred in Capel, while Waroona saw the largest decline.

The number of transactions increased by 3.2 per cent in 2018, continuing a six-year period of relatively stable transaction volume.

Number of transactions (RHS)Median price $/ha (LHS)

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

$16,000

$14,000

160

140

120

100

80

60

40

20

0

$12,000

$10,000

$8,000

$6,000

$4,000

$2,000

0

South West – historic performance

From the field

“The South West has lagged behind other regions with low margins for dairy farms

and orchards weighing on the market. Sentiment is good among beef producers,

but few properties are changing hands.”

Garry Harvey, Rural Bank, Perth.

2018 median price growth

-8.4%

Hectares of land traded

6,997

Average annual growth over 20 years

2.9%

Median price per hectare

$8,772

16

There was a large rise in the number of lower priced transactions in the South West in 2018, with Collie contributing significantly to the rise in transactions less than $6,000/ha. Fewer transactions between $6,000–$12,000/ha in the Busselton and Donnybrook-Balingup municipalities resulted in a 41 per cent decline in transactions in this range for the region.

The combined effect of an increase in lower priced transactions and fewer mid priced transactions shifted the profile of the region towards the lower end of the price spectrum, pushing the median lower.

The median price per hectare increased in the smallest parcel size segment and the 120–160ha segment but declined for all others. The 80–120ha segment has been on a downwards trajectory with three consecutive years of declining median prices, while the 120–160ha segment recorded its first rise in median price since 2014.

While the region’s transaction volume remained relatively stable, there were some significant shifts in the number of transactions for different parcel size ranges. A 64.3 per cent decline in the number of transactions in the 80–120ha parcel size segment partially offset increases in all other segments.

25

10

0

5

20

15

$0 – 3,000/ha

Num

ber o

f tra

nsac

tions

$3,000 – 6,000/ha $6,000 – 9,000/ha $9,000 –12,000/ha $12,000 –15,000/ha $15,000/ha+

South West – transactions by price range

2018

2017

Performance by land size

Parcel size (ha)

Median $/ha No. of transactions

2018 % change 10yr CAGR Decile 2018 % change

50–80 $11,551 15.6% -1.9% 6.52 38 2.7%

80–120 $5,871 -21.3% -4.8% 3.04 5 -64.3%

120–160 $5,903 74.5% -7.9% 5.65 10 100.0%

160+ $5,139 -41.7% -7.0% 3.91 11 83.3%

Overall $8,772 -8.4% -3.5% 4.34 64 3.2%

17

WA

Farmland sales by municipality

MunicipalityMedian $/ha Number of transactions

2018 2018 % change 10yr CAGR Decile 2018 2018

% changeCentral

Beverley $3,280 7.2% -1.0% 6.95 9 -10.0%

Boyup Brook $4,111 34.5% 1.0% 9.13 20 42.9%

Brookton $3,625 50.8% -0.7% 8.69 6 -45.5%

Broomehill-Tambellup $3,915 18.9% 5.2% 10.00 11 120.0%

Bruce Rock $1,374 10.6% 3.9% 9.56 8 100.0%

Corrigin $1,740 61.6% 5.6% 10.00 13 160.0%

Cranbrook $2,545 44.1% -1.2% 9.13 17 6.3%

Cuballing $4,049 63.8% 3.6% 10.00 5 0.0%

Cunderdin -49.1% -9.6% 2.17 3 -25.0%

Dowerin $1,181 -29.8% -5.2% 4.34 4 -66.7%

Dumbleyung $1,612 29.9% 2.3% 9.13 12 33.3%

Goomalling $1,889 -20.7% -2.3% 5.65 5 -16.7%

Katanning $2,611 -21.1% 5.5% 8.69 5 -28.6%

Kellerberrin $1,023 -5.7% -1.8% 5.21 6 20.0%

Kojonup $2,950 -5.0% -1.9% 7.82 18 12.5%

Narrogin $3,778 38.8% -0.3% 9.13 9 -18.2%

Northam $5,098 -1.5% -2.5% 8.26 11 10.0%

Pingelly $4,024 34.4% 2.7% 9.56 4 -33.3%

Quairading $2,773 38.5% 7.6% 10.00 13 62.5%

Tammin $1,219 -55.6% -1.6% 5.65 5 400.0%

Toodyay 188.6% 0.7% 10.00 3 -25.0%

Trayning $732 15.9% -3.0% 6.52 6 50.0%

Victoria Plains $4,075 93.8% -0.4% 9.56 8 166.7%

Wagin $2,856 24.4% 6.0% 9.56 11 120.0%

Wandering $3,570 -29.3% 3.0% 9.13 4 -20.0%

West Arthur $2,352 13.0% -1.1% 6.95 10 -44.4%

Wickepin $2,091 30.0% -0.4% 9.13 6 50.0%

Williams $3,125 95.7% -1.6% 7.39 4 -42.9%

Wongan-Ballidu $1,057 -9.0% -2.6% 5.65 5 -37.5%

Woodanilling $3,594 115.0% 9.2% 9.13 5 25.0%

Wyalkatchem $1,213 59.7% -1.7% 8.26 5 400.0%

York $4,897 16.8% -1.5% 9.13 6 -45.5%

SUB-TOTAL $2,607 8.5% 0.2% 10.00 257 7.5%

Eastern

Kondinin $938 8.1% 1.1% 9.56 20 100.0%

Koorda $488 -17.4% -2.1% 6.08 7 -46.2%

Kulin $1,118 39.5% 0.3% 10.00 8 -11.1%

Lake Grace $952 -4.6% 1.3% 8.26 20 25.0%

Merredin $947 4.4% 0.8% 9.13 9 -50.0%

Mount Marshall $585 8.0% 4.1% 9.56 13 44.4%

Mukinbudin $508 -6.5% 0.5% 8.69 5 0.0%

Narembeen $725 -19.3% -2.2% 6.95 16 220.0%

Nungarin $309 -31.4% -6.1% 3.04 5 -16.7%

Westonia -86.2% -10.3% 1.30 1 -75.0%

Yilgarn $389 -38.9% -2.5% 4.78 18 125.0%

SUB-TOTAL $705 -12.3% -0.3% 7.39 122 18.4%

18

MunicipalityMedian $/ha Number of transactions

2018 2018 % change 10yr CAGR Decile 2018 2018

% changeNorthern

Carnamah 153.1% 7.8% 10.00 2 -66.7%

Chapman Valley $1,548 72.6% 0.6% 6.08 4 0.0%

Coorow $1,030 0.5% -5.0% 8.26 12 140.0%

Dalwallinu $1,188 78.4% 7.9% 10.00 13 18.2%

Dandaragan $1,198 -19.2% -1.8% 6.08 11 22.2%

Greater Geraldton $722 52.8% -4.0% 3.47 11 -8.3%

Irwin $1,644 124.7% 18.5% 9.56 5 -16.7%

Mingenew $1,750 -5.8% 2.6% 9.13 5 25.0%

Moora $1,767 -46.0% 0.9% 6.95 8 60.0%

Morawa $497 30.8% 6.5% 6.95 9 350.0%

Northampton $1,050 1.7% -0.5% 6.08 16 23.1%

Perenjori $811 2.2% 3.7% 9.13 6 50.0%

Three Springs $1,499 -34.3% -1.9% 7.39 12 200.0%

SUB-TOTAL $1,194 34.0% 1.6% 8.69 114 34.1%

South Coast

Albany $5,991 8.4% 5.2% 7.39 27 17.4%

Bridgetown-Greenbushes $5,926 23.1% -2.0% 7.82 7 -41.7%

Denmark $9,870 14.5% -0.9% 8.26 15 25.0%

Esperance $2,453 88.8% 4.5% 10.00 19 -48.6%

Gnowangerup $2,141 0.7% 4.4% 9.56 9 -18.2%

Jerramungup $1,442 4.9% 2.7% 9.13 15 50.0%

Kent $1,270 4.1% 0.6% 8.69 23 91.7%

Manjimup $10,290 30.7% -0.1% 8.69 14 7.7%

Nannup 14.0% -4.6% 6.95 3 -50.0%

Plantagenet $4,626 11.6% 2.5% 9.13 29 -19.4%

Ravensthorpe $1,107 -19.2% -2.1% 6.52 17 30.8%

SUB-TOTAL $3,236 5.7% 6.5% 10.00 178 -3.8%

South West

Boddington $4,534 -47.6% -2.0% 6.95 4 100.0%

Busselton $13,628 33.3% 2.0% 9.56 5 -64.3%

Capel $13,414 94.6% -2.9% 9.13 6 20.0%

Collie $3,497 -12.8% -11.6% 3.47 9 350.0%

Dardanup $16,425 24.9% -2.3% 7.82 5 -28.6%

Donnybrook-Balingup $7,101 -3.9% -4.4% 6.08 10 -28.6%

Harvey $8,825 -7.1% -6.5% 5.21 12 9.1%

Murray $11,209 18.8% -4.8% 5.21 8 100.0%

Waroona $8,734 -50.0% -3.3% 6.08 5 66.7%

SUB-TOTAL $8,772 -8.4% -5.1% 4.34 64 3.2%

Price information with a small volume of transactions should be used with caution. The median price for municipalities with less than four transactions in 2018 is not reported.

19

About this researchThe Australian Farmland Values report is based on actual farm sales using data collected by the official government agency in each state and territory, which is then compiled by PriceFinder.

In this edition of the report, the Queensland East region has been separated into Queensland Central and Queensland South to better reflect differing land use in the state.

The Australian Farmland Values report is a guide to market trends of commercial farming property. To that end, where possible, transactions between family members or where one party has compulsory powers are excluded from the analysis. Further, small farms are also excluded to limit the impact of ‘lifestyle farming’ on the results.

As property settlement periods vary, some 2018 sales will not be captured in this report at the time of publication. The median price for the most recent year is preliminary and will be revised at least annually.

The values used in this report are based on the total sale price and therefore include the value of capital improvements.

The value of water entitlements attached to a land title and therefore sold with the property will be reflected in the sale price of the land. If water entitlements are sold separately from the land, this value will not be captured in the sale price.

Median prices in the report are only a guide to market activity. They are not a valuation. Median is used rather than mean as the median is not as readily distorted by unusually high or low prices. However, the median does have limitations. The mix of property sold in a given year can cause the median price to move up or down in a way that is unrelated to a move in value. For example, a higher proportion of lower-value sales can result in a lower median and vice-versa. In areas where there have been very few sales, this effect can be especially pronounced and so in these cases the median should be used with caution and may not be indicative of an actual change in farmland value.

Farmland sales volume is reported as the number of transactions. Farms can be sold as single or multiple lots, which obscures the view of the number of farms sold, particularly in cases where one farm is sold as multiple lots to multiple buyers. Accordingly, the number of ‘transactions’ should not be interpreted as the number of farms sold and should only be used as a guide to market activity.

This report is not intended for use as a farm valuation tool. A qualified professional is required to assess the value of a property.

For PriceFinder terms and conditions visit: www.pricefinder.com.au/terms-conditions/

About Rural BankRural Bank is a division of Bendigo and Adelaide Bank Limited and provides exceptional financial services, knowledge and leadership for Australian farmers to grow.

This report is intended to provide general information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Rural Bank, a Division of Bendigo and Adelaide Bank Limited, ABN 11 068 049 178 AFSL/Australian Credit Licence 237879, makes no representation as to or accepts any responsibility for the accuracy or completeness of information contained in this report. Any opinions, estimates and projections in this report do not necessarily reflect the opinions of Rural Bank and are subject to change without notice. Rural Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth therein, changes or subsequently becomes inaccurate. This report is provided for informational purposes only. The information contained in this report does not take into account your personal circumstances and should not be relied upon without consulting your legal, financial, tax or other appropriate professional.

© Copyright Rural Bank Ltd ABN 74 083 938 416 and Bendigo and Adelaide Bank Ltd ABN 11 068 049 178 (1299953 –1318070) (06/19)