Embed Size (px)

Citation preview

Australian National Waste Report 2016

PREPARED FOR

Department of the Environment and Energy

PREPARED IN ASSOCIATION WITH

Disclaimer

This report has been prepared for Department of the Environment and Energy in accordance with the terms and conditions of appointment dated 30 May 2016, and is based on the assumptions and exclusions set out in our scope of work. While all professional care has been undertaken in preparing this report, Blue Environment Pty Ltd cannot accept any responsibility for any use of or reliance on the contents of this report by any third party.

The mention of any company, product or process in this report does not constitute or imply endorsement by Blue Environment Pty Ltd.

© Department of the Environment and Energy and Blue Environment Pty Ltd

Blue Environment prints on 100% recycled content paper

Blue Environment Pty Ltd ABN 78 118 663 997 Suite 208, 838 Collins St, Docklands Vic 3008 Email: [email protected] Web: www.blueenvironment.com.au Phone: +61 3 9081 0440 / +61 3 5426 3536

Report title Australian National Waste Report 2016

Client Department of the Environment and Energy

Status Final

Author(s) Dr Joe Pickin and Paul Randell

Reviewer(s) Christine Wardle, Karen Cosson and Jenny Trinh

Project number P726

Report date 20 June 2017

Contract date 30 May 2016

Information current to Varies by data source

Copyright Department of the Environment and Energy & Blue Environment Pty Ltd

Australian National Waste Report 2016 Final

Page i

Contents

At a glance ................................................................................................................................... vi

1. Introduction .......................................................................................................................... 1

1.1 Scope ....................................................................................................................................... 1 1.2 Data collation methods ........................................................................................................... 1 1.3 Data in this report may differ from state and territory data .................................................. 2 1.4 Data quality ............................................................................................................................. 3 1.5 Report structure ...................................................................................................................... 3 1.6 Data layout .............................................................................................................................. 4

2. Context ................................................................................................................................. 5

2.1 Population growth ................................................................................................................... 5 2.2 Economic growth ..................................................................................................................... 5 2.3 Access to recycling markets..................................................................................................... 6 2.4 Carbon policy ........................................................................................................................... 6 2.5 Waste policies .......................................................................................................................... 6

3. The national picture .............................................................................................................. 9

3.1 Overall waste quantities analysis ............................................................................................ 9 3.2 Waste stream analysis ........................................................................................................... 15 3.3 Waste materials analysis ....................................................................................................... 19

4. International comparisons ................................................................................................... 26

4.1 Waste generation and fate .................................................................................................... 26 4.2 Municipal waste generation and fate ................................................................................... 27

5. Industry perspectives .......................................................................................................... 28

6. Current and emerging challenges ......................................................................................... 32

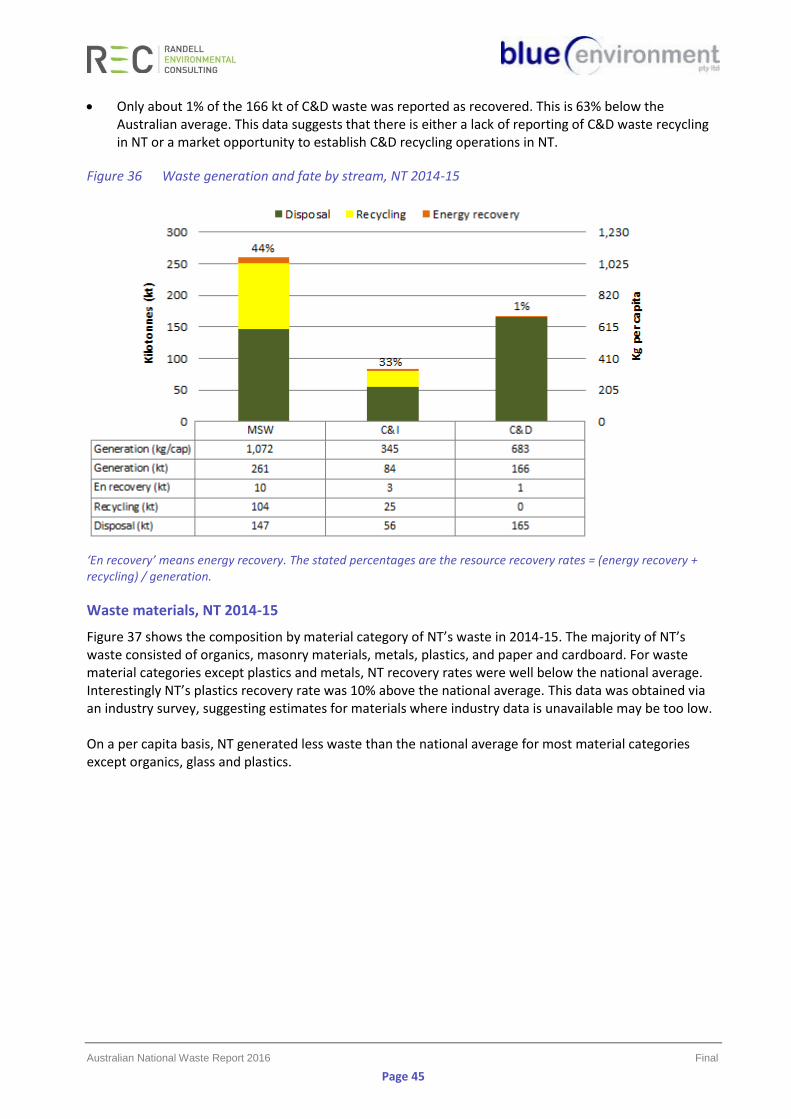

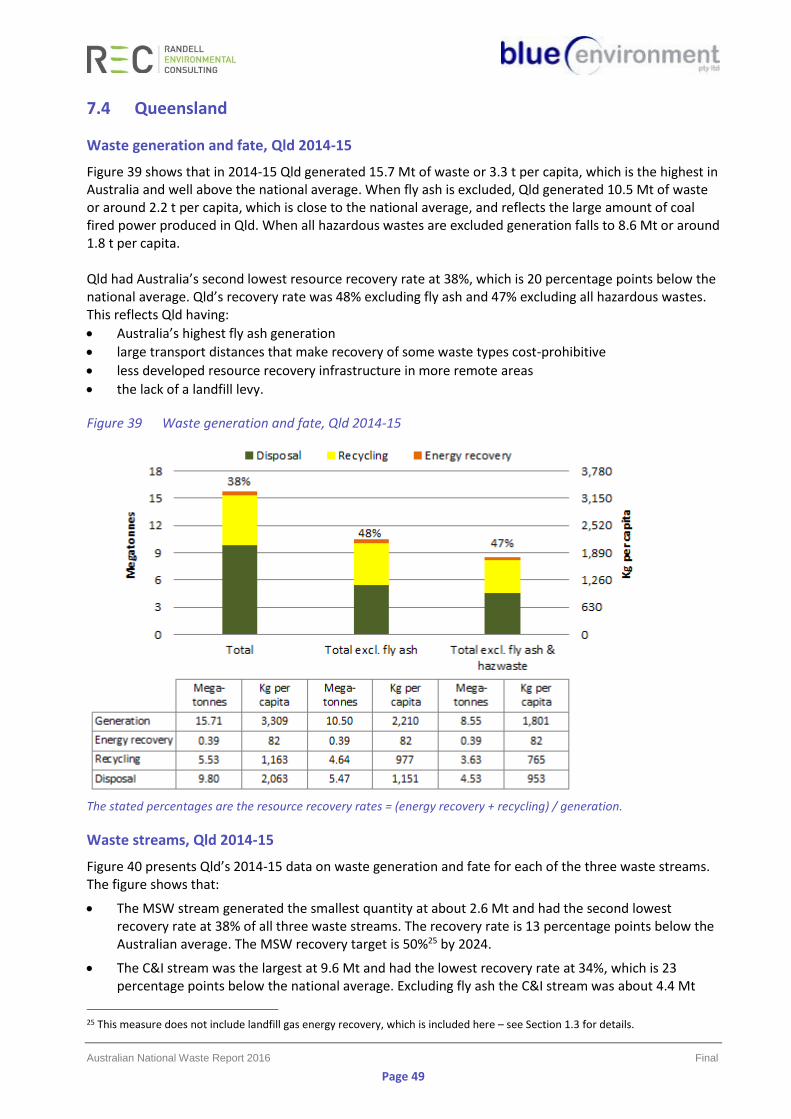

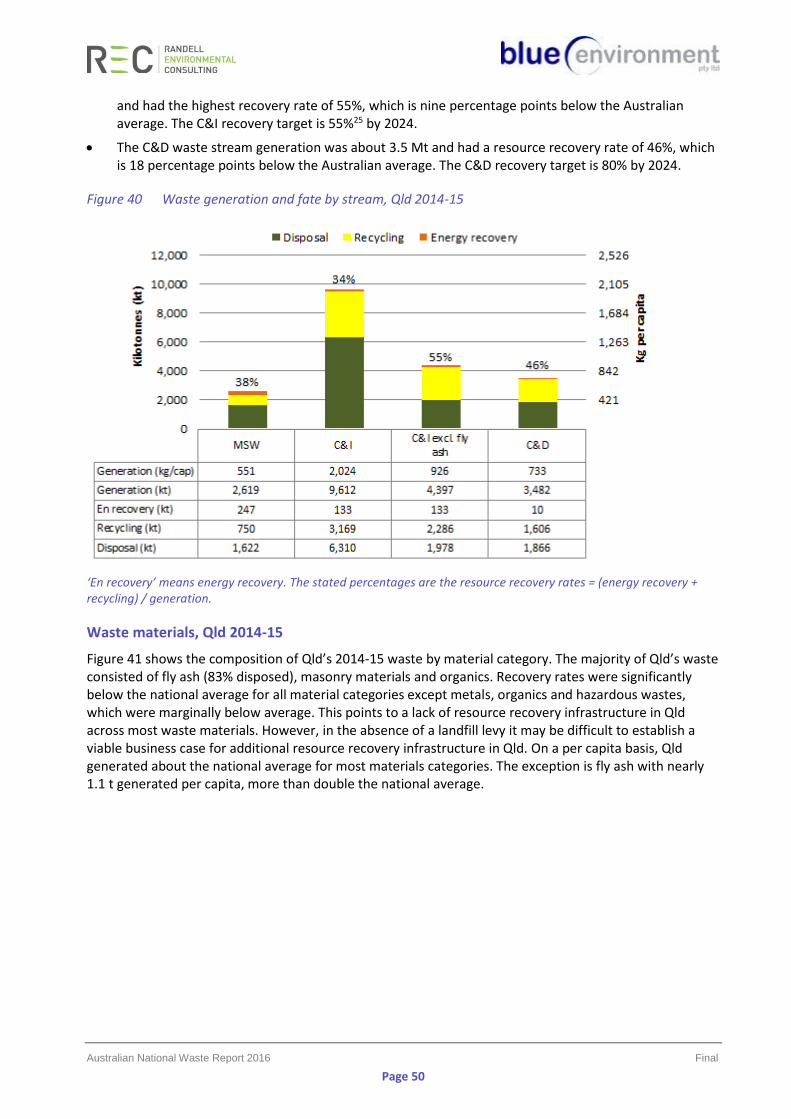

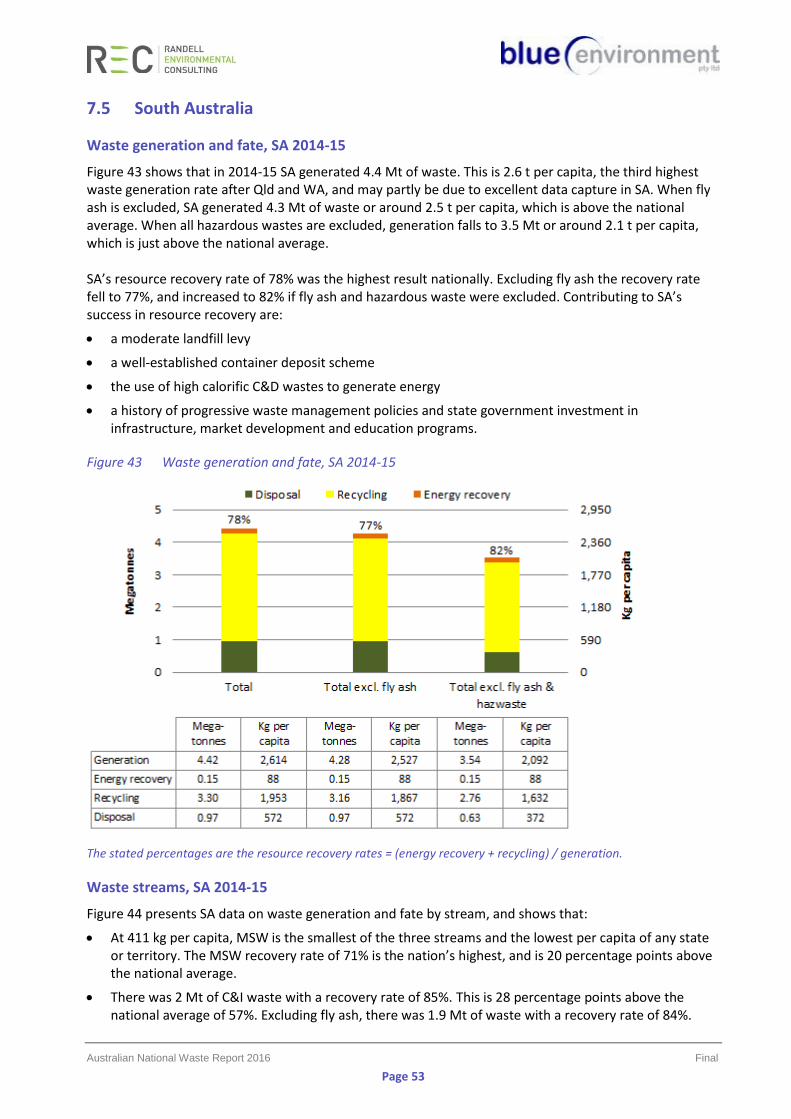

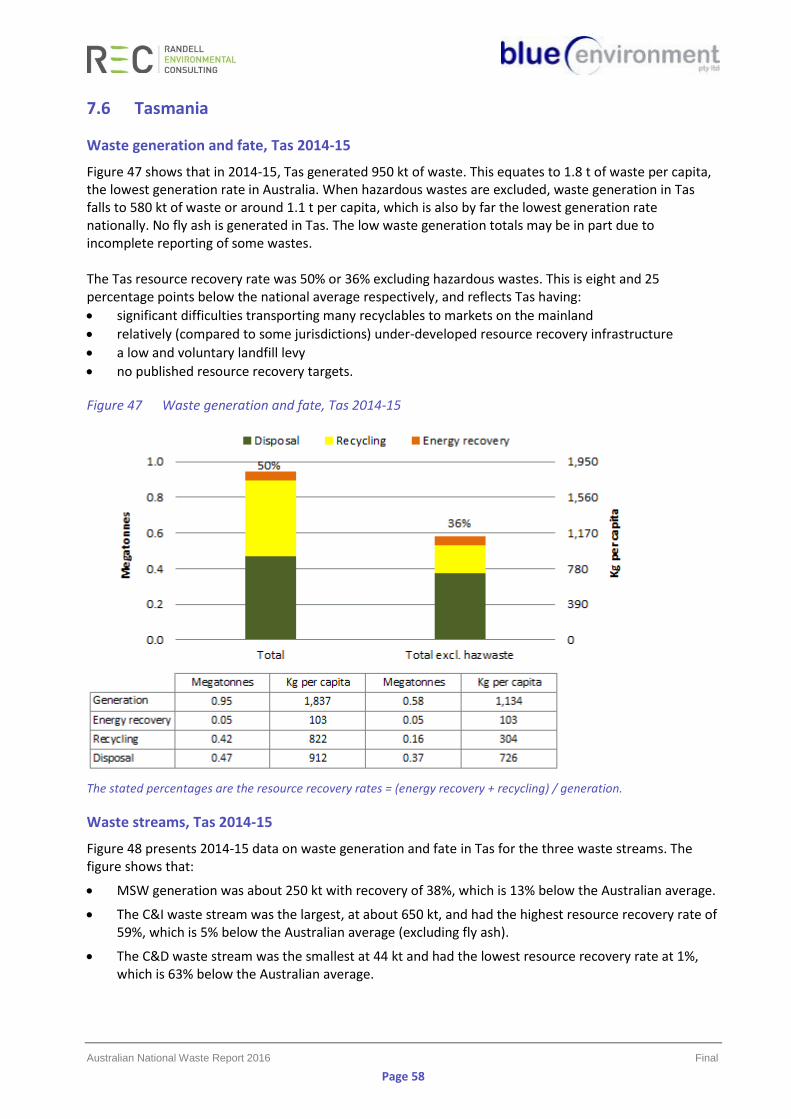

7. Waste generation and fate by state and territory ................................................................. 35

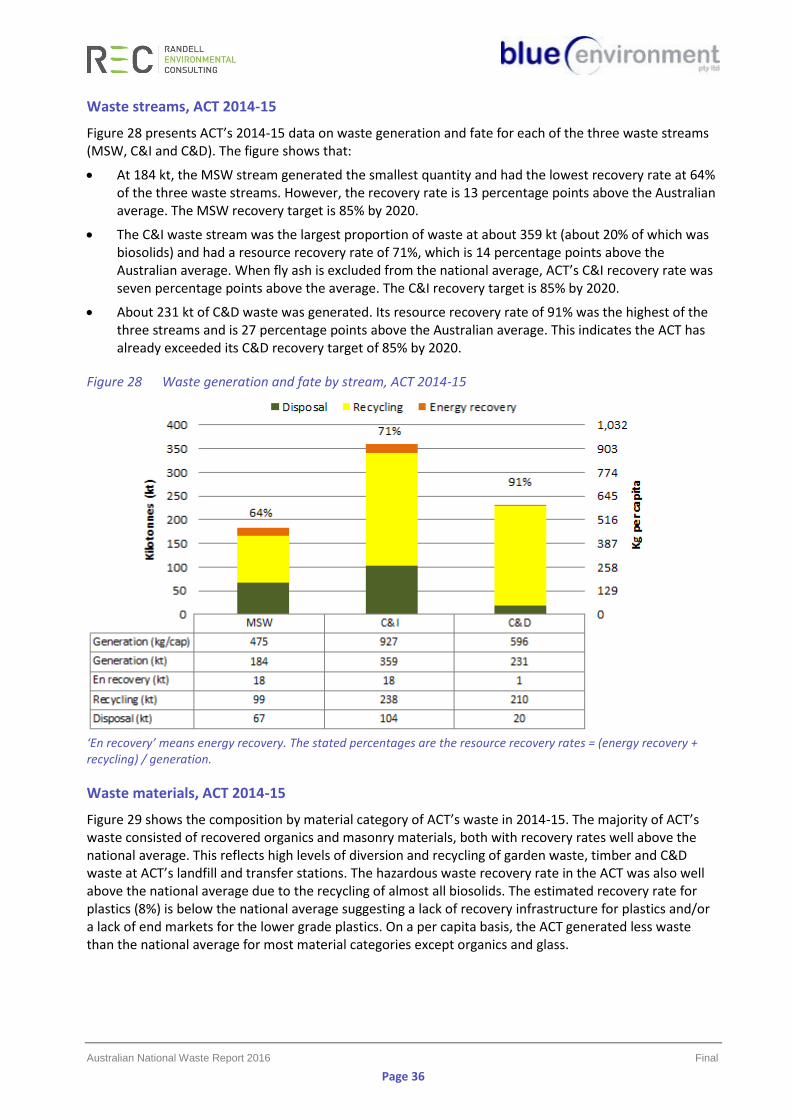

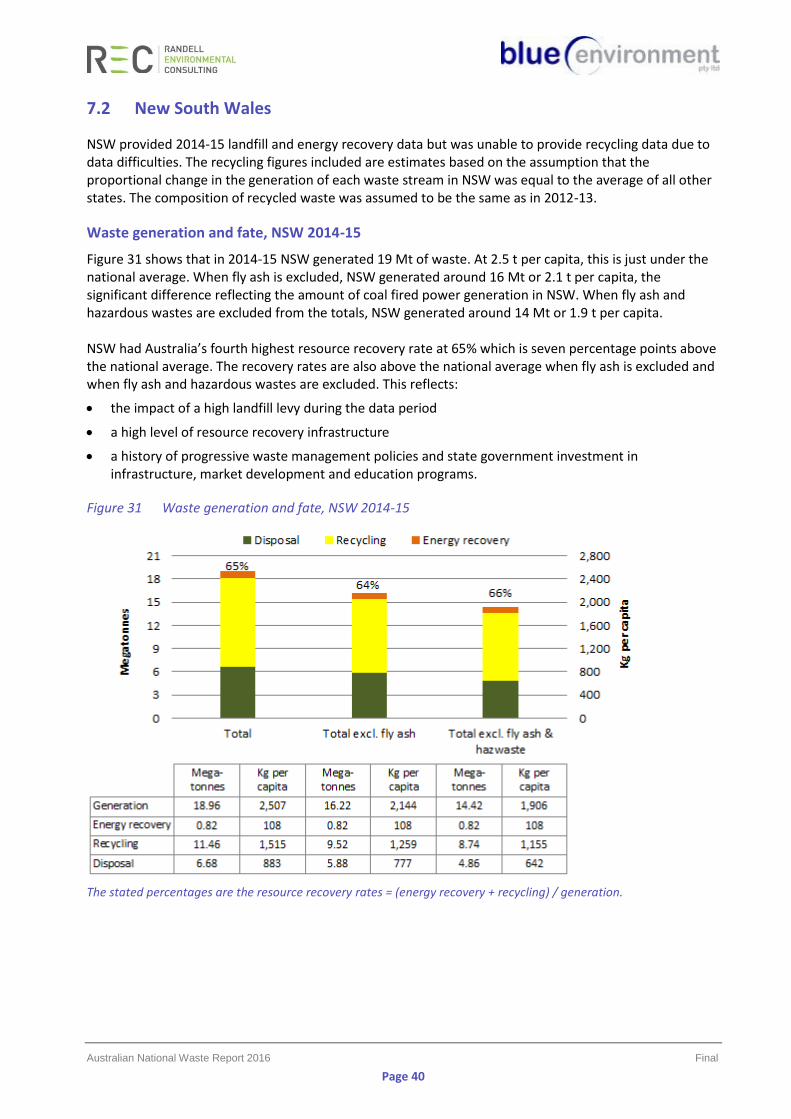

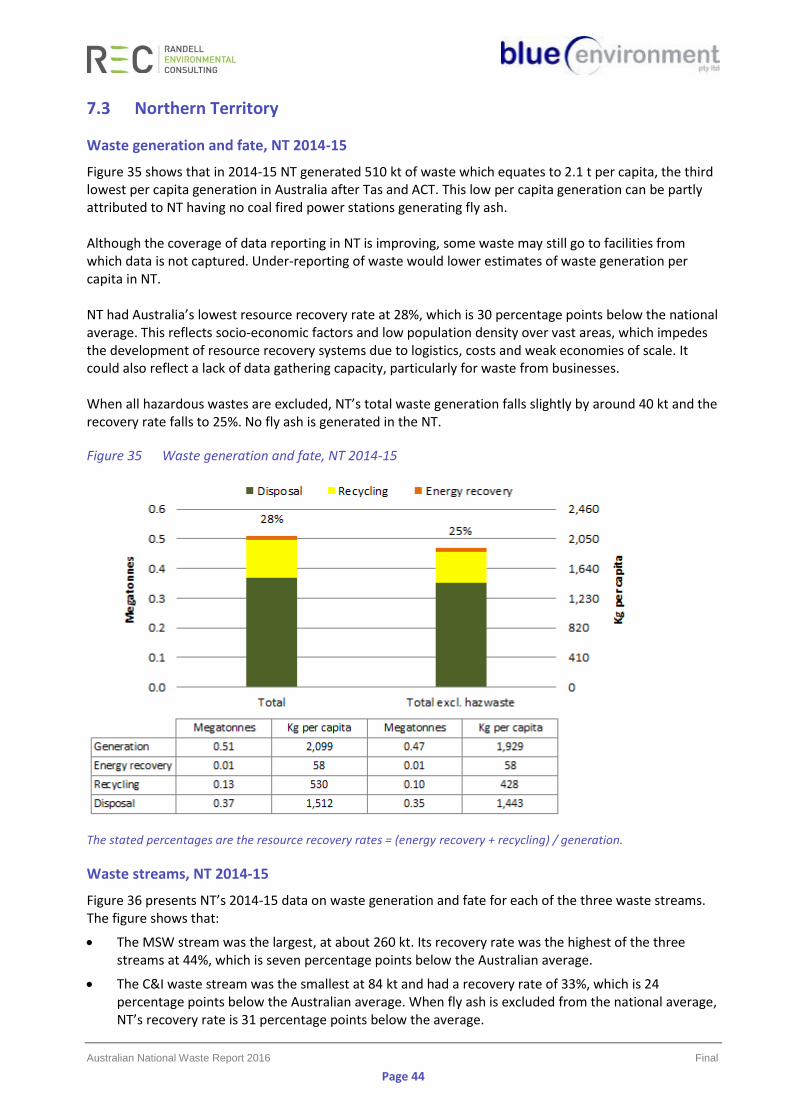

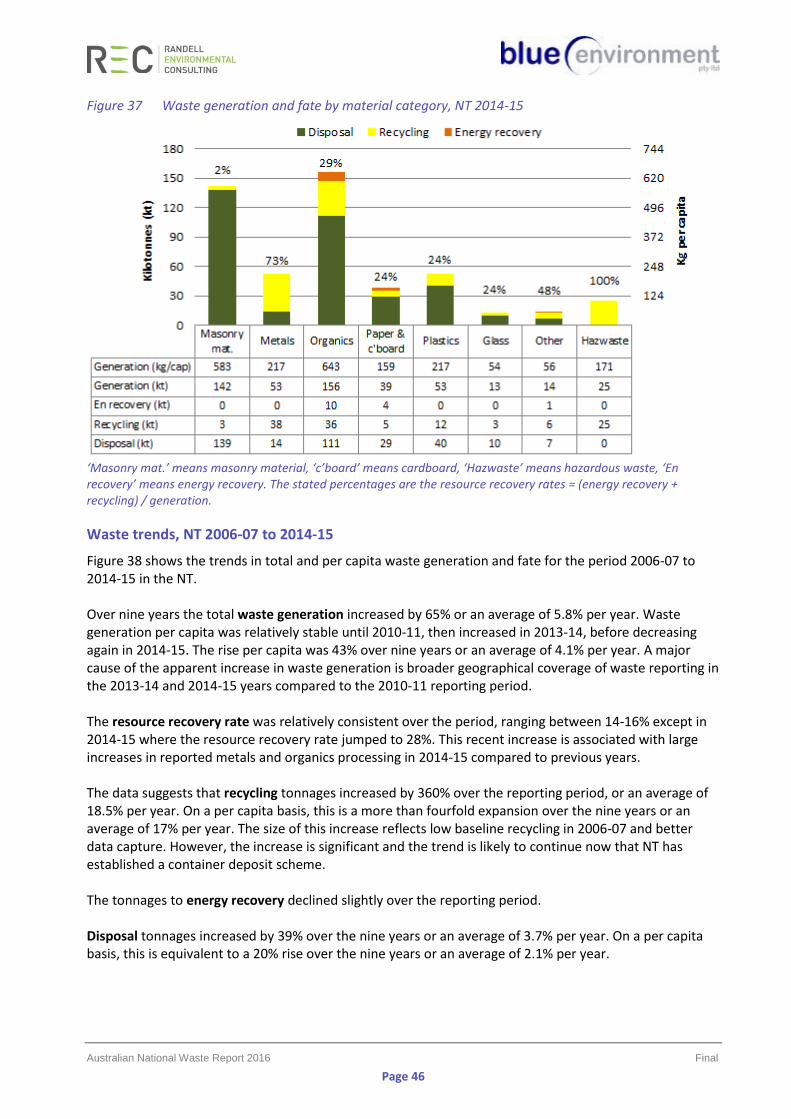

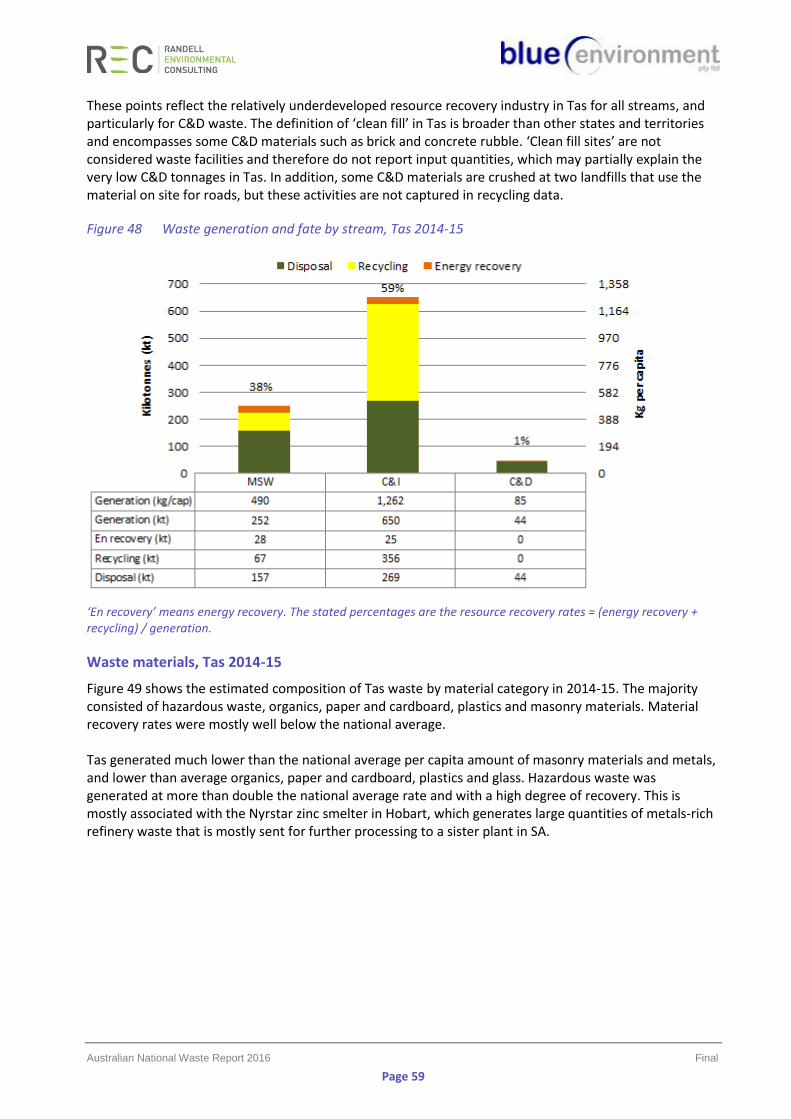

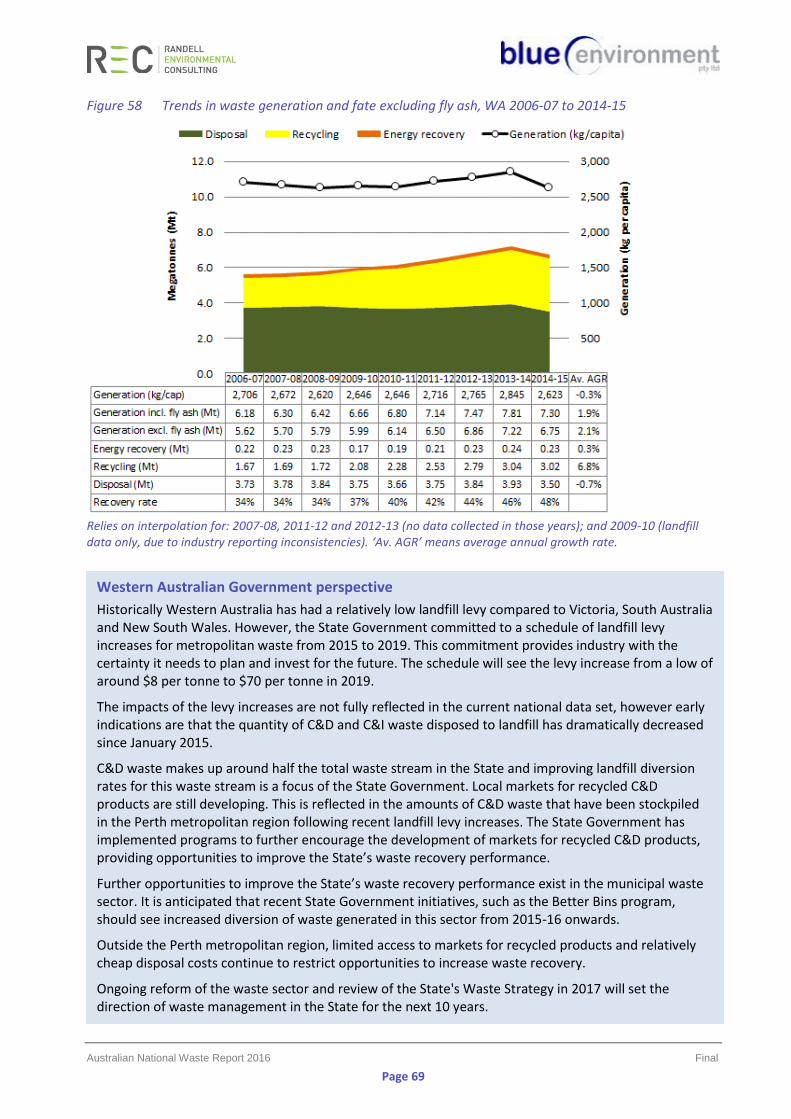

7.1 Australian Capital Territory ................................................................................................... 35 7.2 New South Wales .................................................................................................................. 40 7.3 Northern Territory ................................................................................................................. 44 7.4 Queensland ............................................................................................................................ 49 7.5 South Australia ...................................................................................................................... 53 7.6 Tasmania................................................................................................................................ 58 7.7 Victoria .................................................................................................................................. 62 7.8 Western Australia .................................................................................................................. 66

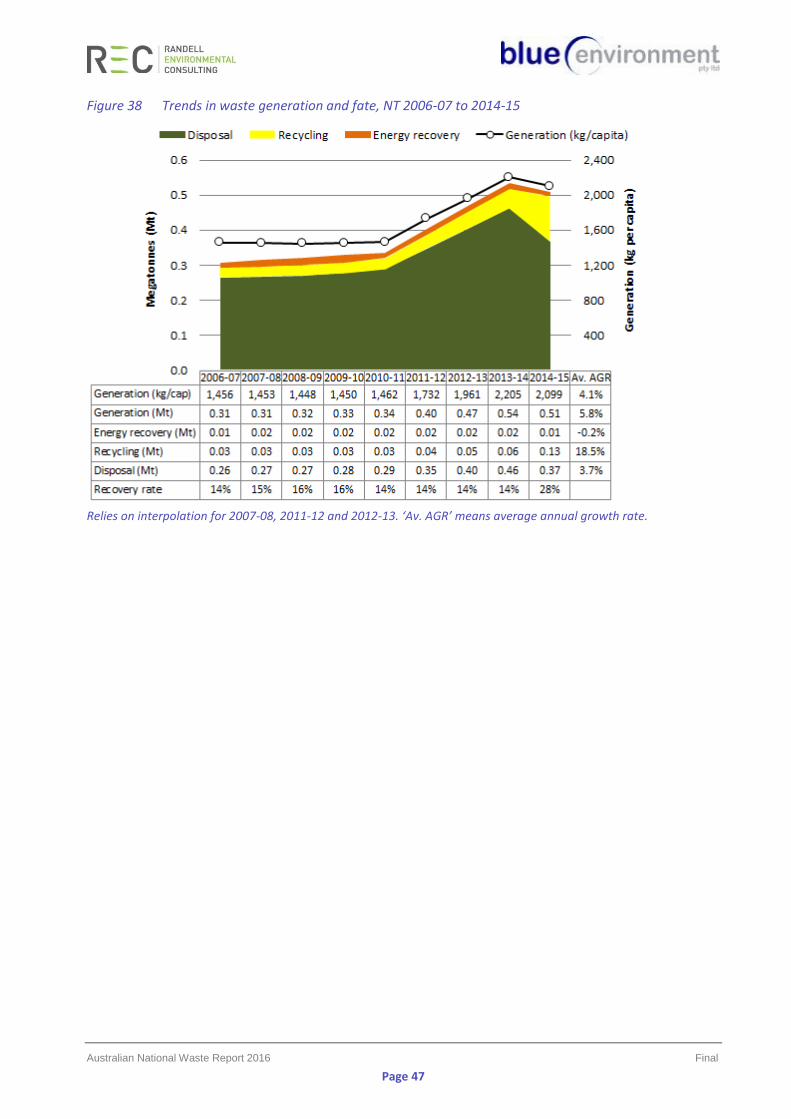

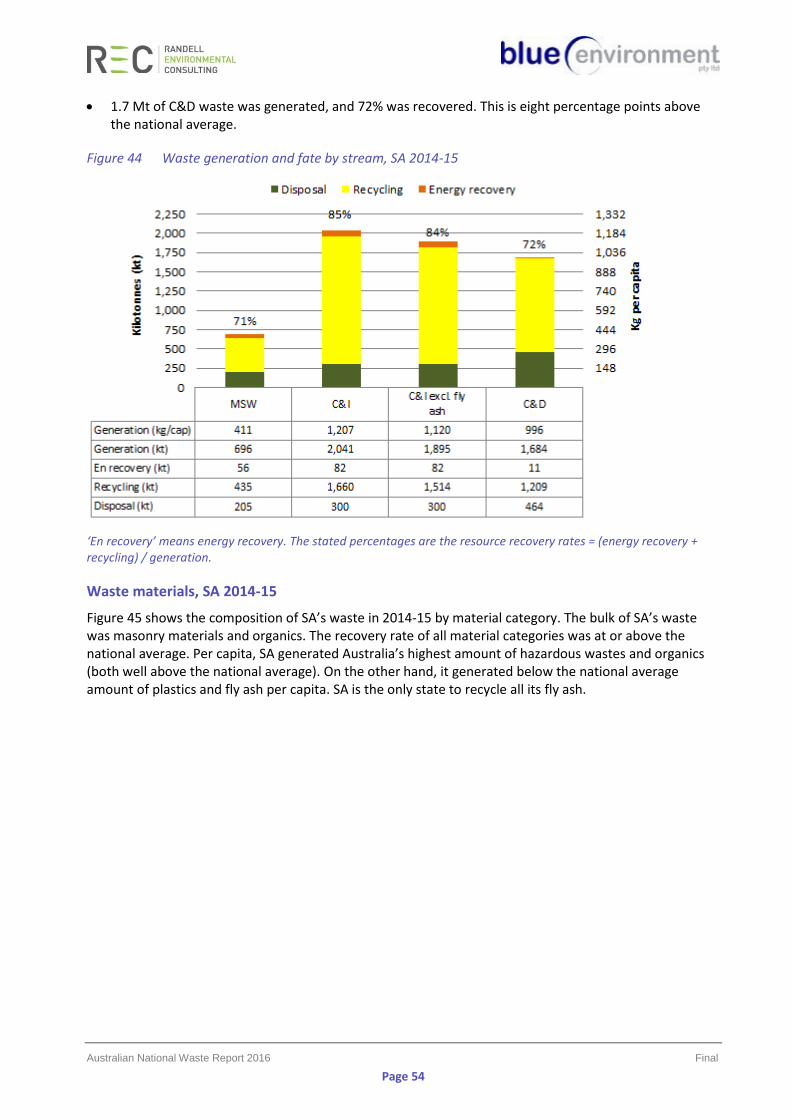

8. Data sources and assumptions ............................................................................................. 70

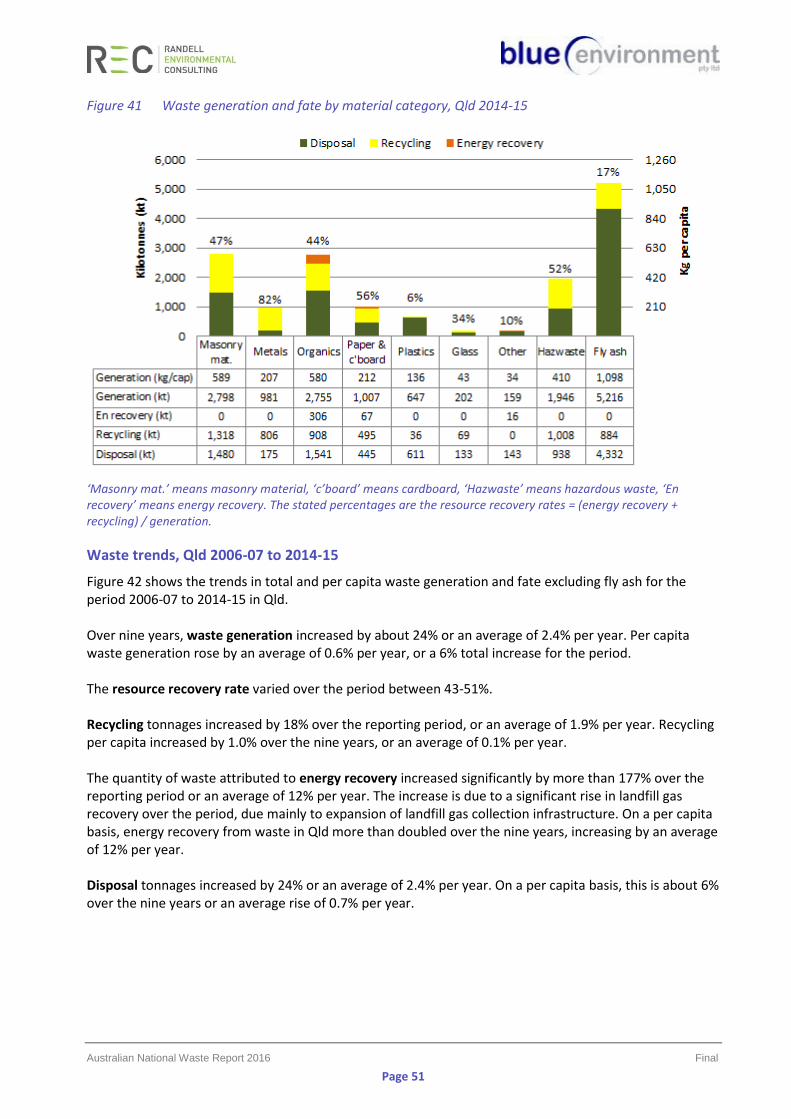

8.1 Data sources .......................................................................................................................... 70 8.2 Assumptions .......................................................................................................................... 71

Bibliography ................................................................................................................................ 72

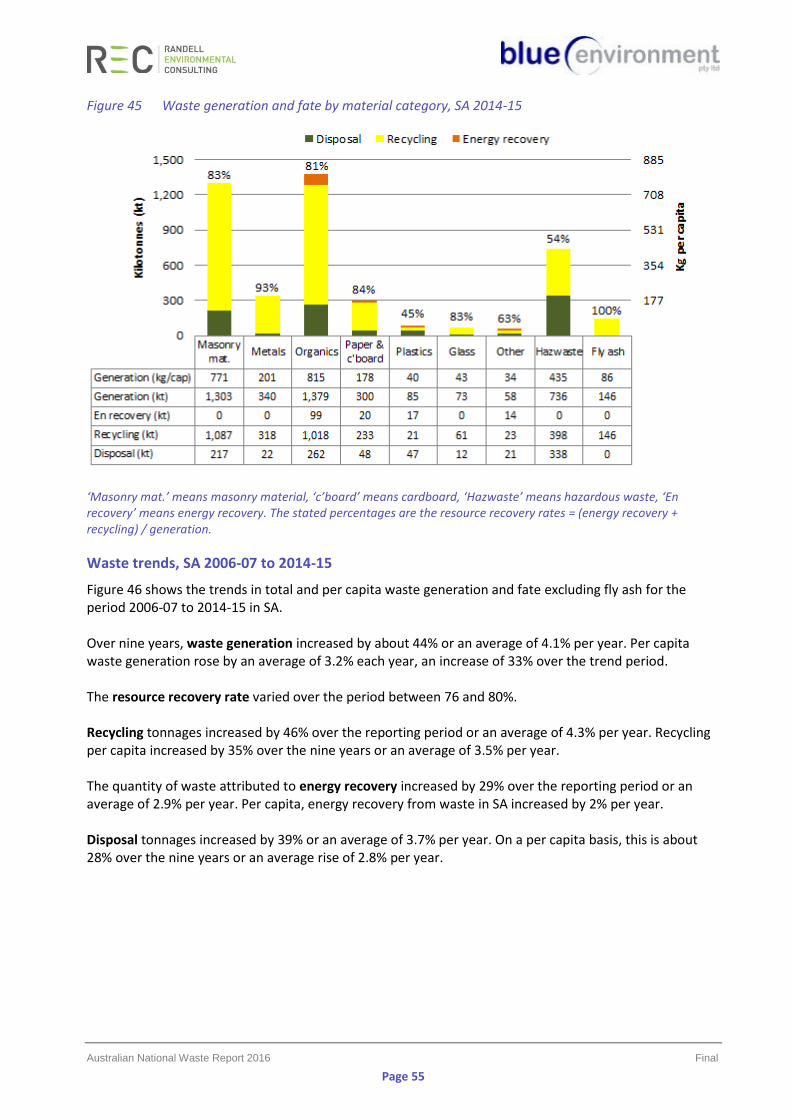

Australian National Waste Report 2016 Final

Page ii

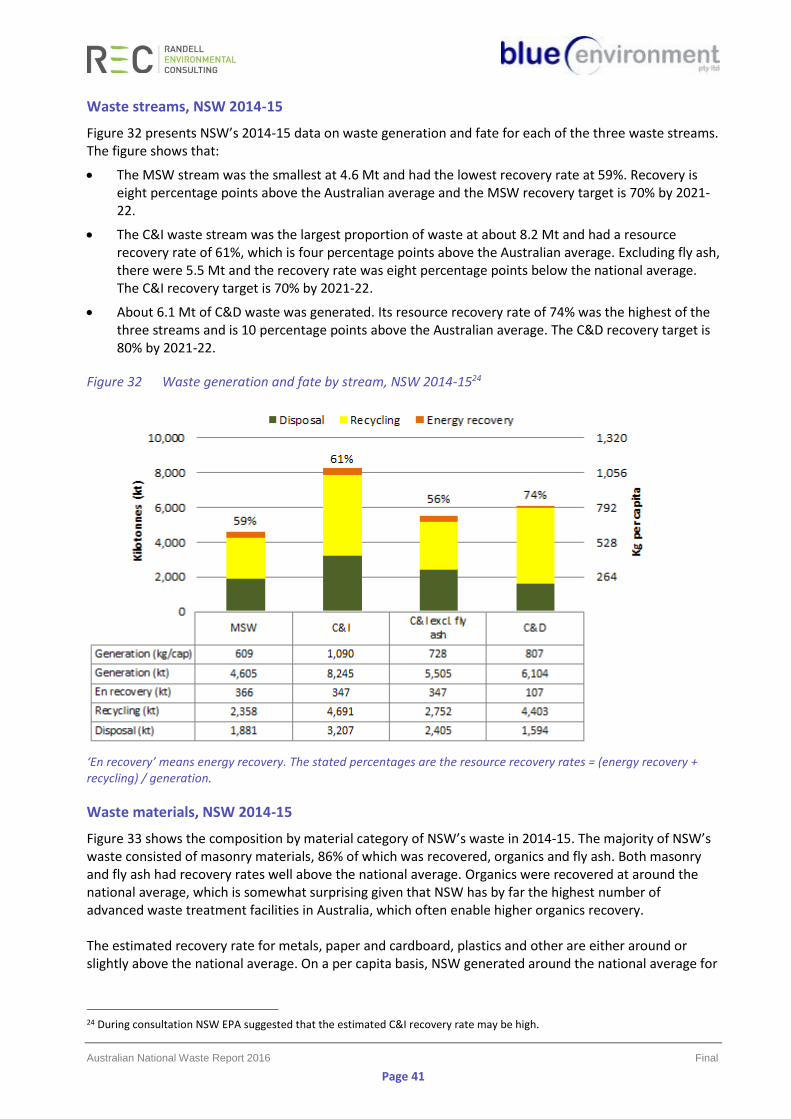

Figures Figure 1 Data inputs and outputs in the national waste data set reporting tool ........................................ 2 Figure 2 Australian population by state and territory, 2006-07 to 2014-15 ............................................... 5 Figure 3 Australian economic activity by state and territory (GSP), 2006-07 to 2014-15 ........................... 6 Figure 4 Waste generation and fate, Australia 2014-15 .............................................................................. 9 Figure 5 Waste generation and fate by state and territory, 2014-15 (megatonnes) ................................ 10 Figure 6 Waste generation and fate per capita by state and territory, 2014-15 (kilograms per capita) .. 10 Figure 7 Trends in waste generation and fate, Australia 2006-07 to 2014-15 .......................................... 12 Figure 8 Trends in waste generation and fate excluding fly ash, Australia 2006-07 to 2014-15 .............. 12 Figure 9 Trends in waste generation per capita by state and territory, 2006-07 to 2014-15 ................... 13 Figure 10 Waste generation and fate by stream, Australia 2014-15 ........................................................... 15 Figure 11 Waste generation and fate per capita by waste stream and state and territory, 2014-15 ......... 16 Figure 12 Trends in municipal waste generation and fate, Australia 2006-07 to 2014-15 ......................... 17 Figure 13 Trends in commercial and industrial waste generation and fate excluding fly ash, Australia

2006-07 to 2014-15 ..................................................................................................................... 18 Figure 14 Trends in construction and demolition waste generation and fate, Australia 2006-07 to

2014-15 ........................................................................................................................................ 18 Figure 15 Waste generation and fate by material category, Australia 2014-15 ......................................... 19 Figure 16 Trends in masonry material waste generation and fate, Australia 2006-07 to 2014-15............. 20 Figure 17 Trends in metal waste generation and fate, 2006-07 to 2014-15 ............................................... 20 Figure 18 Non-hazardous and hazardous organic waste generation and fate, Australia 2014-15 ............. 21 Figure 19 Food waste generation and fate by source sector, Australia 2014-15 ........................................ 22 Figure 20 Trends in organic waste generation and fate excluding hazardous organic wastes, Australia

2006-07 to 2014-15 ..................................................................................................................... 22 Figure 21 Trends in paper and cardboard waste generation and fate, Australia 2006-07 to 2014-15 ....... 23 Figure 22 Trends in plastic waste generation and fate, Australia 2006-07 to 2014-15 ............................... 24 Figure 23 Trends in glass waste generation and fate, Australia 2006-07 to 2014-15 ................................. 24 Figure 24 Trends in fly ash waste generation and fate, Australia 2006-07 to 2014-15 ............................... 25 Figure 25 Comparison of waste generation and fate per capita, Australia and selected OECD

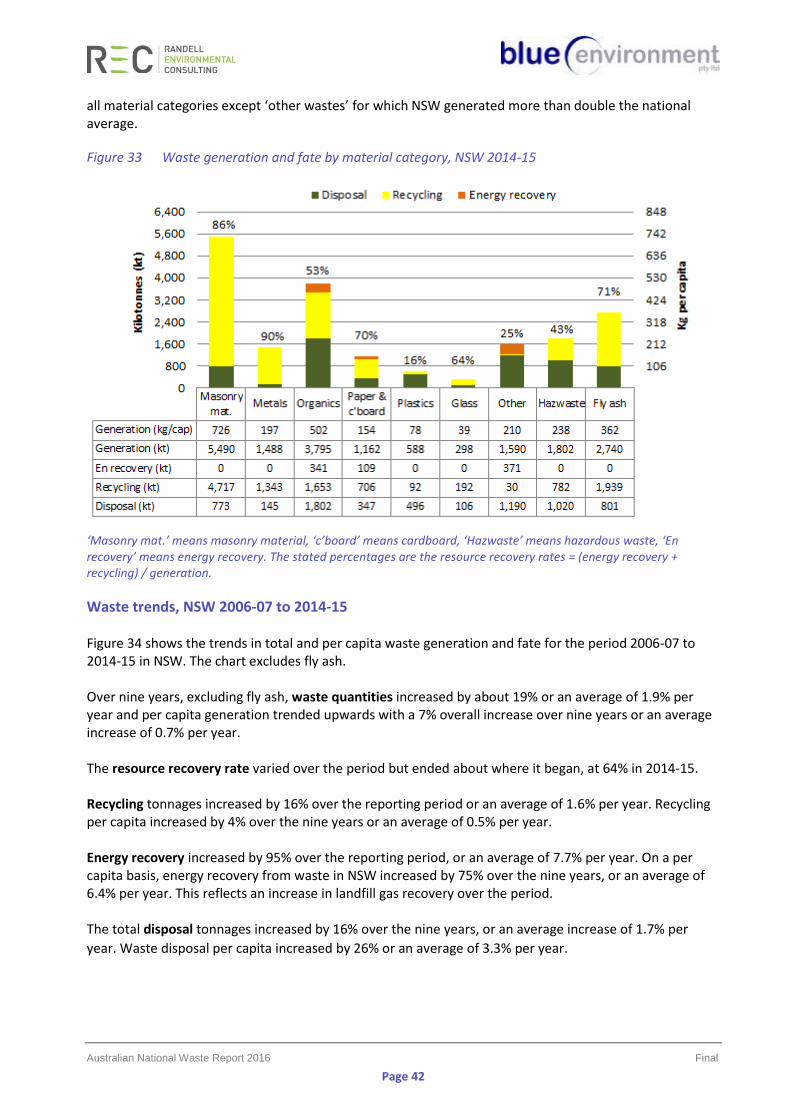

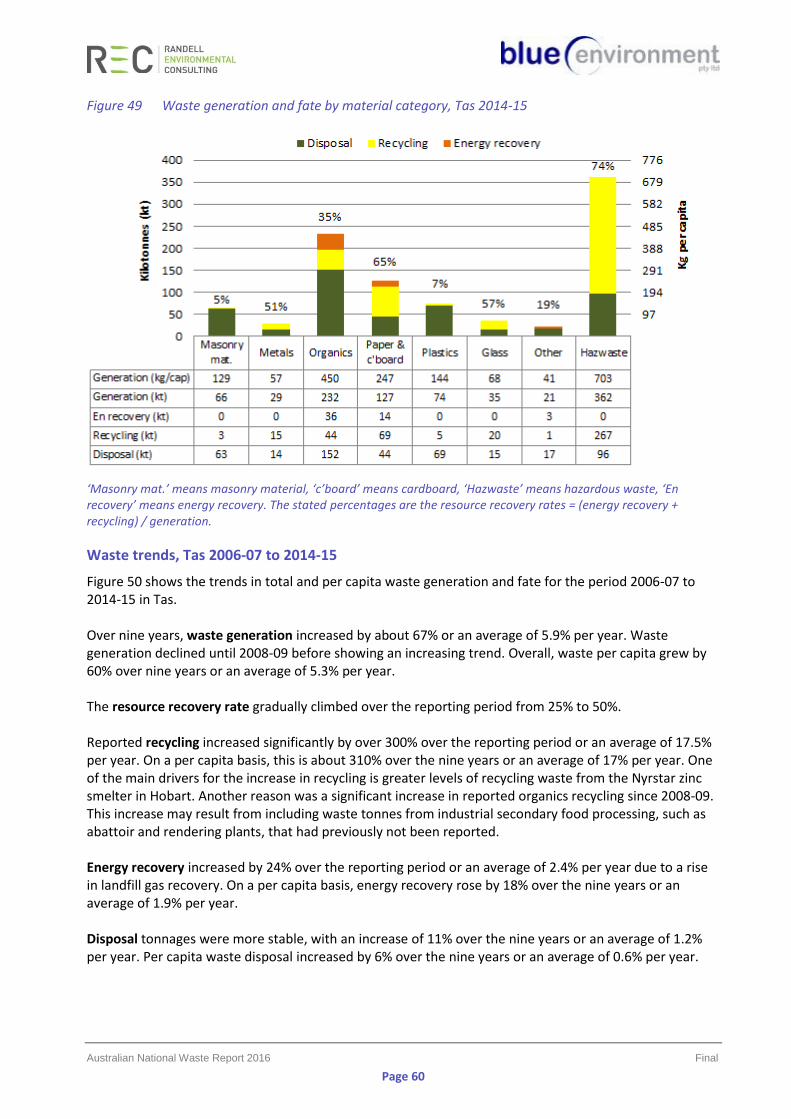

countries ...................................................................................................................................... 26 Figure 26 Comparison of MSW generation, disposal, recycling, recovery and composting per capita in

selected OECD countries .............................................................................................................. 27 Figure 27 Waste generation and fate, ACT 2014-15 .................................................................................... 35 Figure 28 Waste generation and fate by stream, ACT 2014-15 ................................................................... 36 Figure 29 Waste generation and fate by material category, ACT 2014-15 ................................................. 37 Figure 30 Trends in waste generation and fate, ACT 2006-07 to 2014-15 .................................................. 38 Figure 31 Waste generation and fate, NSW 2014-15 .................................................................................. 40 Figure 32 Waste generation and fate by stream, NSW 2014-15 ................................................................. 41 Figure 33 Waste generation and fate by material category, NSW 2014-15 ................................................ 42 Figure 34 Trends in waste generation and fate excluding fly ash, NSW 2006-07 to 2014-15 ..................... 43 Figure 35 Waste generation and fate, NT 2014-15 ..................................................................................... 44 Figure 36 Waste generation and fate by stream, NT 2014-15 .................................................................... 45 Figure 37 Waste generation and fate by material category, NT 2014-15 ................................................... 46 Figure 38 Trends in waste generation and fate, NT 2006-07 to 2014-15 .................................................... 47 Figure 39 Waste generation and fate, Qld 2014-15 .................................................................................... 49 Figure 40 Waste generation and fate by stream, Qld 2014-15 ................................................................... 50 Figure 41 Waste generation and fate by material category, Qld 2014-15 .................................................. 51 Figure 42 Trends in waste generation and fate excluding fly ash, Qld 2006-07 to 2014-15 ....................... 52 Figure 43 Waste generation and fate, SA 2014-15 ...................................................................................... 53 Figure 44 Waste generation and fate by stream, SA 2014-15 ..................................................................... 54 Figure 45 Waste generation and fate by material category, SA 2014-15 .................................................... 55

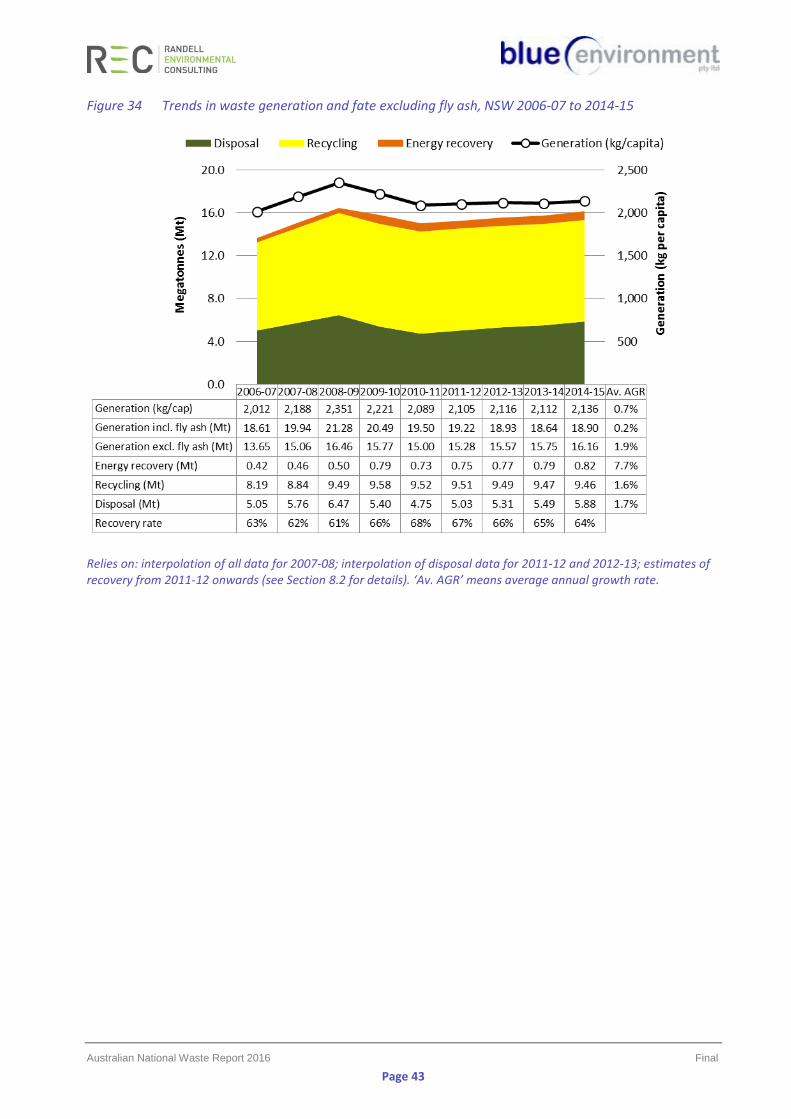

Australian National Waste Report 2016 Final

Page iii

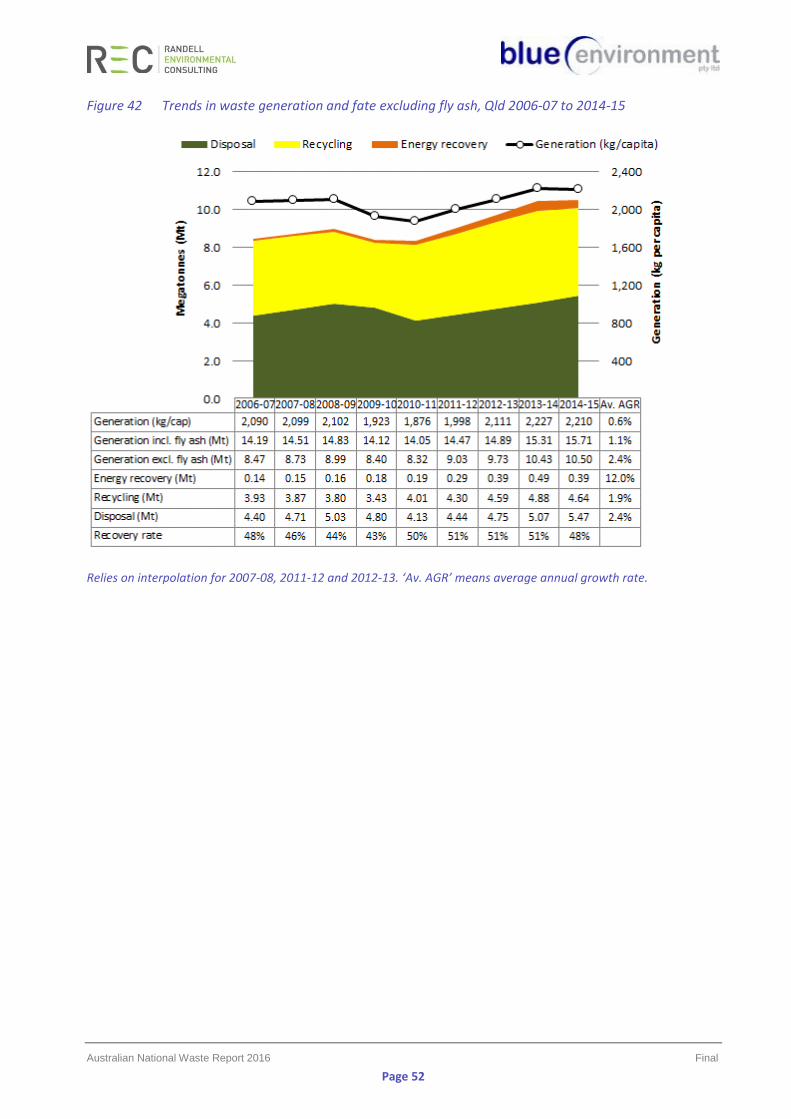

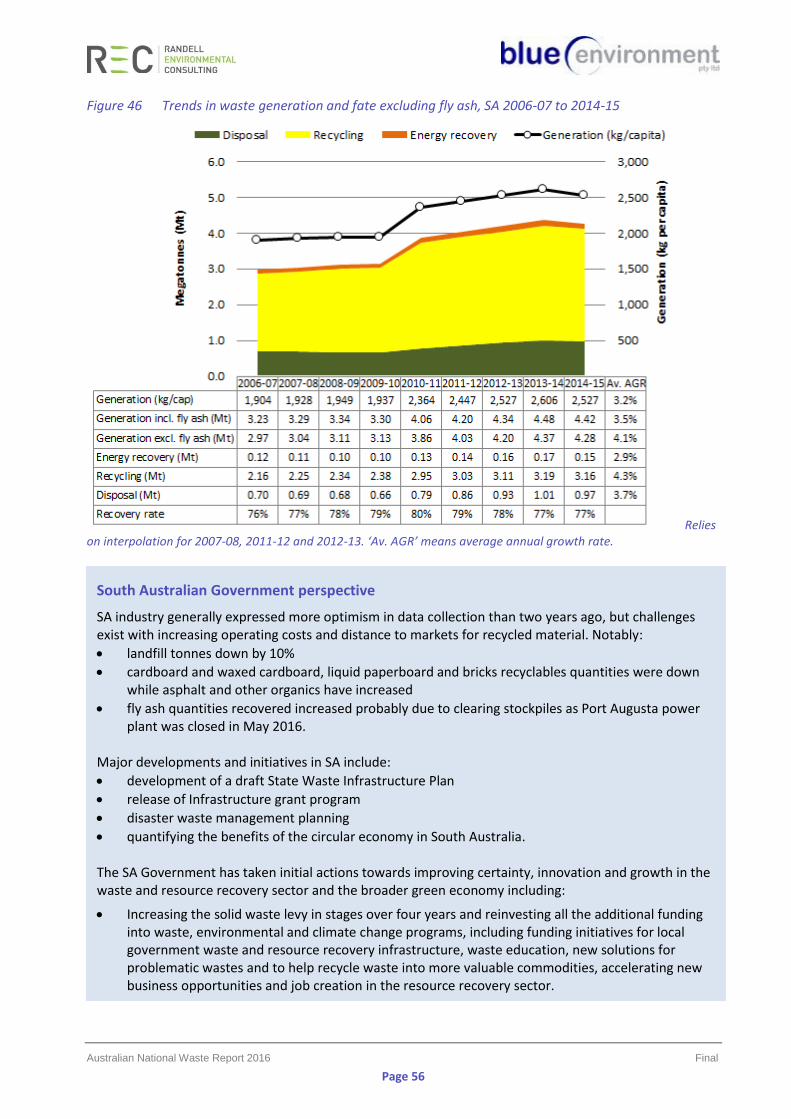

Figure 46 Trends in waste generation and fate excluding fly ash, SA 2006-07 to 2014-15......................... 56 Figure 47 Waste generation and fate, Tas 2014-15 ..................................................................................... 58 Figure 48 Waste generation and fate by stream, Tas 2014-15.................................................................... 59 Figure 49 Waste generation and fate by material category, Tas 2014-15 .................................................. 60 Figure 50 Trends in waste generation and fate, Tas 2006-07 to 2014-15 ................................................... 61 Figure 51 Waste generation and fate, Vic 2014-15 ..................................................................................... 62 Figure 52 Waste generation and fate by stream, Vic 2014-15 .................................................................... 63 Figure 53 Waste generation and fate by material category, Vic 2014-15 ................................................... 64 Figure 54 Trends in waste generation and fate excluding fly ash, Vic 2006-07 to 2014-15 ........................ 65 Figure 55 Waste generation and fate, WA 2014-15 .................................................................................... 66 Figure 56 Waste generation and fate by stream, WA 2014-15 ................................................................... 67 Figure 57 Waste generation and fate by material category, WA 2014-15 .................................................. 68 Figure 58 Trends in waste generation and fate excluding fly ash, WA 2006-07 to 2014-15 ....................... 69

Tables Table 1 Waste categories and types analysed in this report ...................................................................... 4 Table 2 Summary of state and territory waste policy settings ................................................................... 7 Table 3 Apparent 9-year percentage change in waste fate per capita by state and territory,

excluding fly ash, 2006-07 to 2014-15 ......................................................................................... 14 Table 4 Descriptions of the waste sources included in the data compared in Figure 25 ......................... 26 Table 5 Australia’s ranking in various aspects of MSW generation and management against the 28

countries listed in Figure 26 ......................................................................................................... 27 Table 6 Data from sources other than the states and territories ............................................................ 70

Australian National Waste Report 2016 Final

Page iv

Abbreviations and glossary

ABS Australian Bureau of Statistics

ACOR Australian Council of Recycling

ACT Australian Capital Territory

ALOA Australian Landfill Owners Association

AORA Australian Organics Recycling Association

AGR annual growth rate

biosolids solid, semi-solid or slurry material produced by the treatment of urban sewage

capita person

C&D construction and demolition

C&I commercial and industrial

commercial and industrial waste

Waste that is produced by institutions and businesses; includes waste from schools, restaurants, offices, retail and wholesale businesses, and industries including manufacturing.

construction and demolition waste

Waste produced by demolition and building activities, including road and rail construction and maintenance and excavation of land associated with construction activities.

disposal The deposit of solid waste in a landfill or incinerator, net of recovery of energy.

DoEE Department of the Environment and Energy

EPA Environment(al) Protection Agency / Authority (names vary with jurisdiction)

e-waste electrical or electronic waste

energy recovery The process of recovering energy that is embodied in solid waste (the amount of solid waste recovered is net of any residuals disposed).

EPR extended producer responsibility

fate What happens to a waste i.e. recycling, energy recovery or disposal.

fly ash Ash produced by burning coal or other materials that is driven out of the boiler with the flue gases and captured by pollution control equipment.

gross state product

The total market value of goods and services produced in a state or territory within a given period after deducting the cost of goods and services used up in the process of production but before deducting allowances for the consumption of fixed capital.

GSP gross state product

hazardous waste (or ‘hazwaste’)

Waste that, by its characteristics, poses a threat or risk to public health, safety or to the environment. In this report, this comprises wastes that cannot be imported to or exported from Australia without a permit under the Hazardous Waste (Regulation of Exports and Imports) Act 1989, or wastes that a jurisdiction regulates as requiring particularly high levels of control.

HDPE high-density polyethylene

kg kilograms

kt kilotonnes (thousands of tonnes)

LDPE low-density polyethylene

MSW municipal solid waste

municipal solid waste

Waste produced primarily by households and council facilities.

Mt megatonnes (millions of tonnes)

NGER National Greenhouse and Energy Reporting

NSW New South Wales

NT Northern Territory

OECD Organisation for Economic Cooperation and Development

per capita per person

PET polyethylene terephthalate

PP polypropylene

product stewardship

A policy approach recognising that manufacturers, importers, governments and consumers have a shared responsibility for the environmental impacts of a product throughout its full life cycle. Product stewardship schemes establish a means for relevant parties in the product chain to share responsibility for the products they produce, handle, purchase, use and discard.

PS polystyrene

PVC polyvinyl chloride

Australian National Waste Report 2016 Final

Page v

Qld Queensland

recycling Activities in which solid wastes are collected, sorted, processed (including through composting), and converted into raw materials to be used in the production of new products (the amount of solid waste recycled is net of any residuals disposed).

resource recovery For data collation purposes, this is the sum of materials sent to recycling and energy recovery net of contaminants and residual wastes sent to disposal.

resource recovery rate

The proportion calculated by dividing resource recovery by waste generation (also referred to as the ‘recovery rate’).

SA South Australia

solid waste Waste that can have an angle of repose of greater than 5 degrees above horizontal, or does not become free-flowing at or below 60 degrees Celsius or when it is transported, or is generally capable of being picked up by a spade or shovel.

t tonne(s)

Tas Tasmania

Vic Victoria

WA Western Australia

waste Materials or products that are unwanted or have been discarded, rejected or abandoned. This includes materials or products that are recycled, converted to energy, or disposed.

waste generation For data collation purposes, this is the sum of resource recovery and disposal.

WMAA Waste Management Association of Australia

Acknowledgements

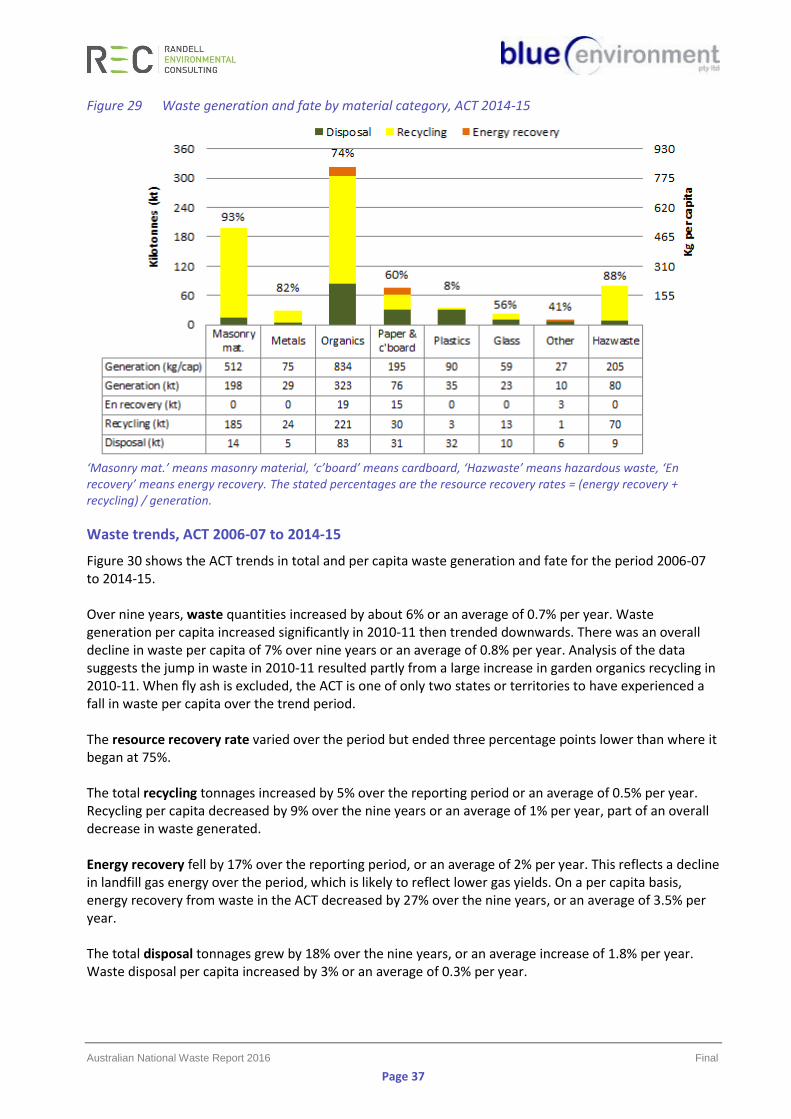

We thank the states and territories for sharing their data, perspectives and commentary for this report. We are grateful to the waste industry associations for their contributions to Section 5, namely the Australian Council of Recycling, the Australian Landfill Owners Association, the Australian Organics Recycling Association, and the Waste Management Association of Australia.

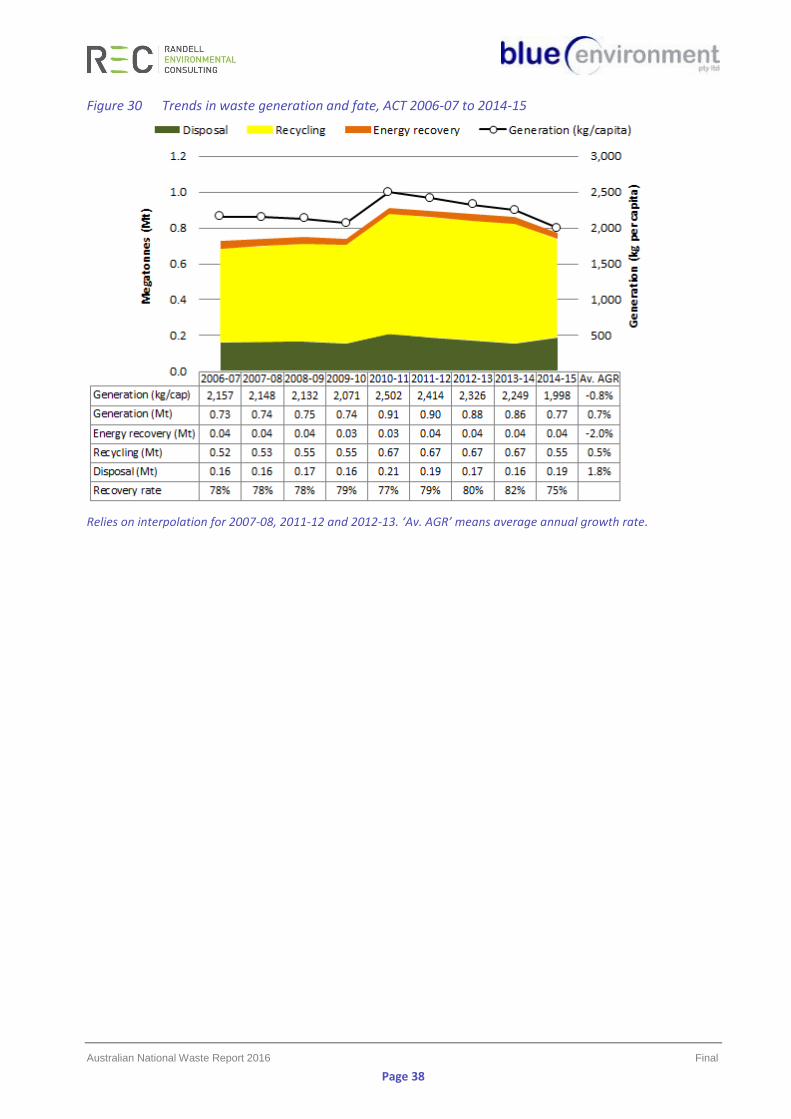

Page vi

At a glance

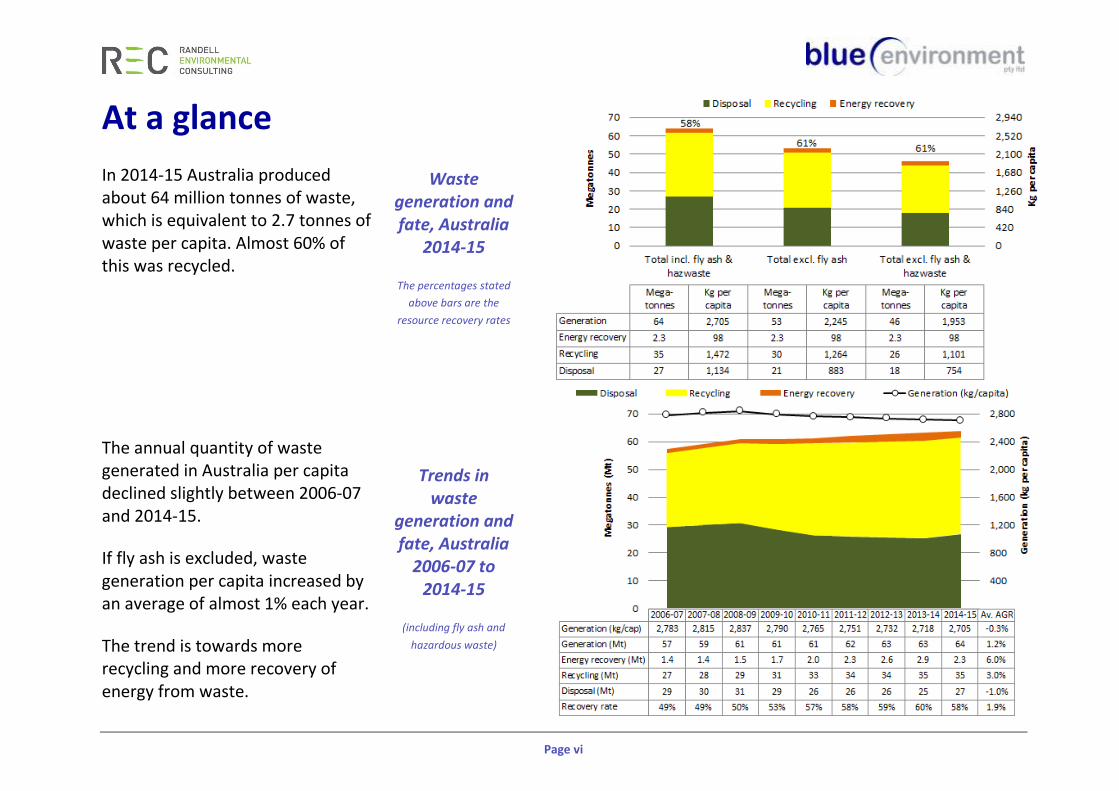

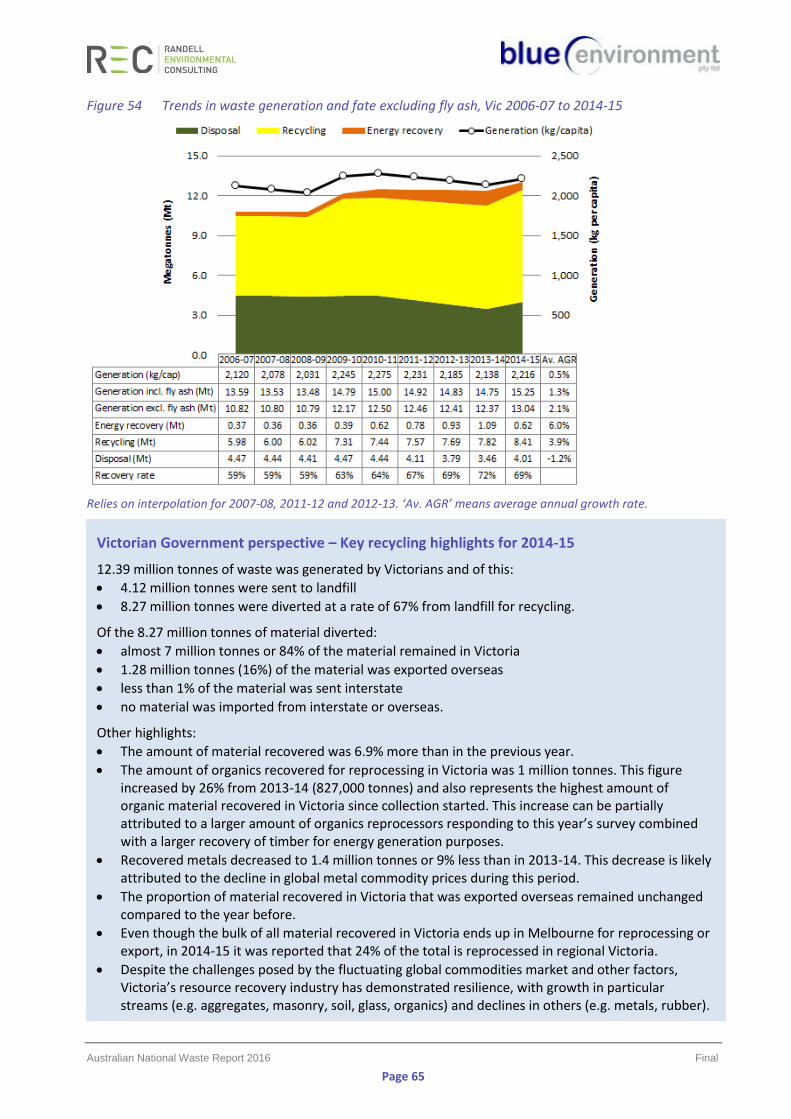

In 2014-15 Australia produced about 64 million tonnes of waste, which is equivalent to 2.7 tonnes of waste per capita. Almost 60% of this was recycled. The annual quantity of waste generated in Australia per capita declined slightly between 2006-07 and 2014-15.

If fly ash is excluded, waste generation per capita increased by an average of almost 1% each year.

The trend is towards more recycling and more recovery of energy from waste.

Waste generation and fate, Australia

2014-15

The percentages stated

above bars are the

resource recovery rates

Trends in waste

generation and fate, Australia

2006-07 to 2014-15

(including fly ash and

hazardous waste)

Page vii

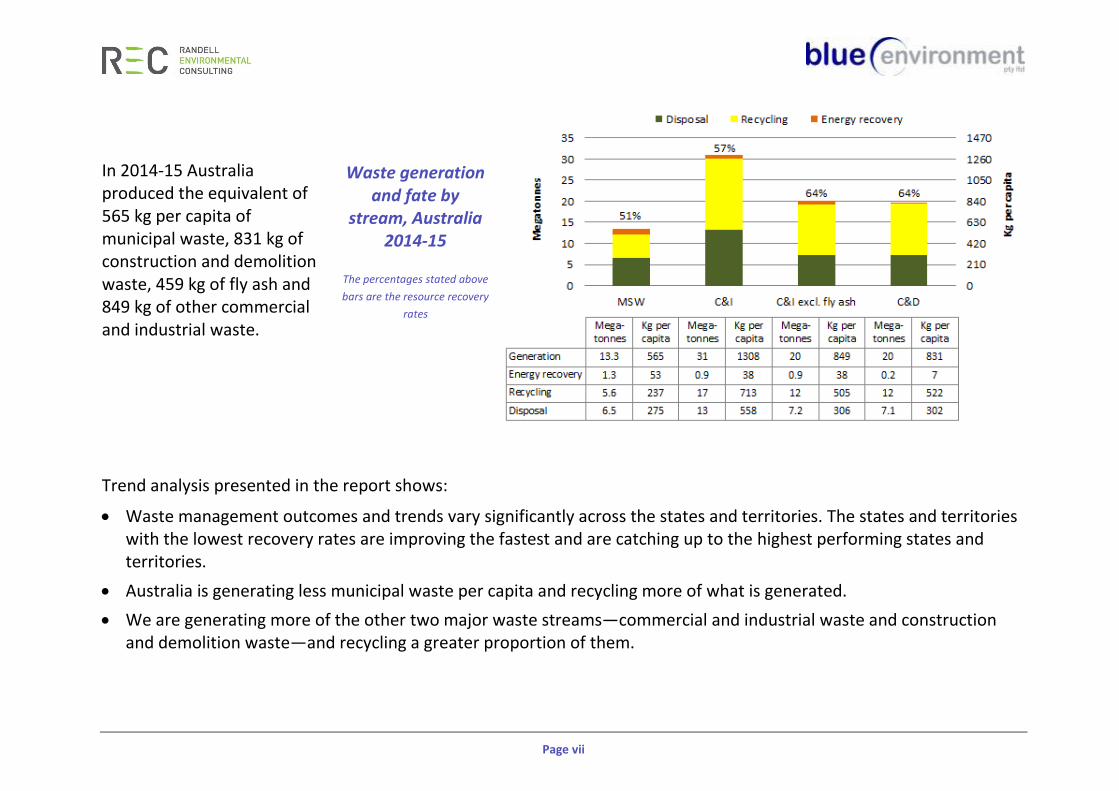

In 2014-15 Australia produced the equivalent of 565 kg per capita of municipal waste, 831 kg of construction and demolition waste, 459 kg of fly ash and 849 kg of other commercial and industrial waste.

Trend analysis presented in the report shows:

• Waste management outcomes and trends vary significantly across the states and territories. The states and territories with the lowest recovery rates are improving the fastest and are catching up to the highest performing states and territories.

• Australia is generating less municipal waste per capita and recycling more of what is generated.

• We are generating more of the other two major waste streams—commercial and industrial waste and construction and demolition waste—and recycling a greater proportion of them.

Waste generation and fate by

stream, Australia 2014-15

The percentages stated above

bars are the resource recovery

rates

Page viii

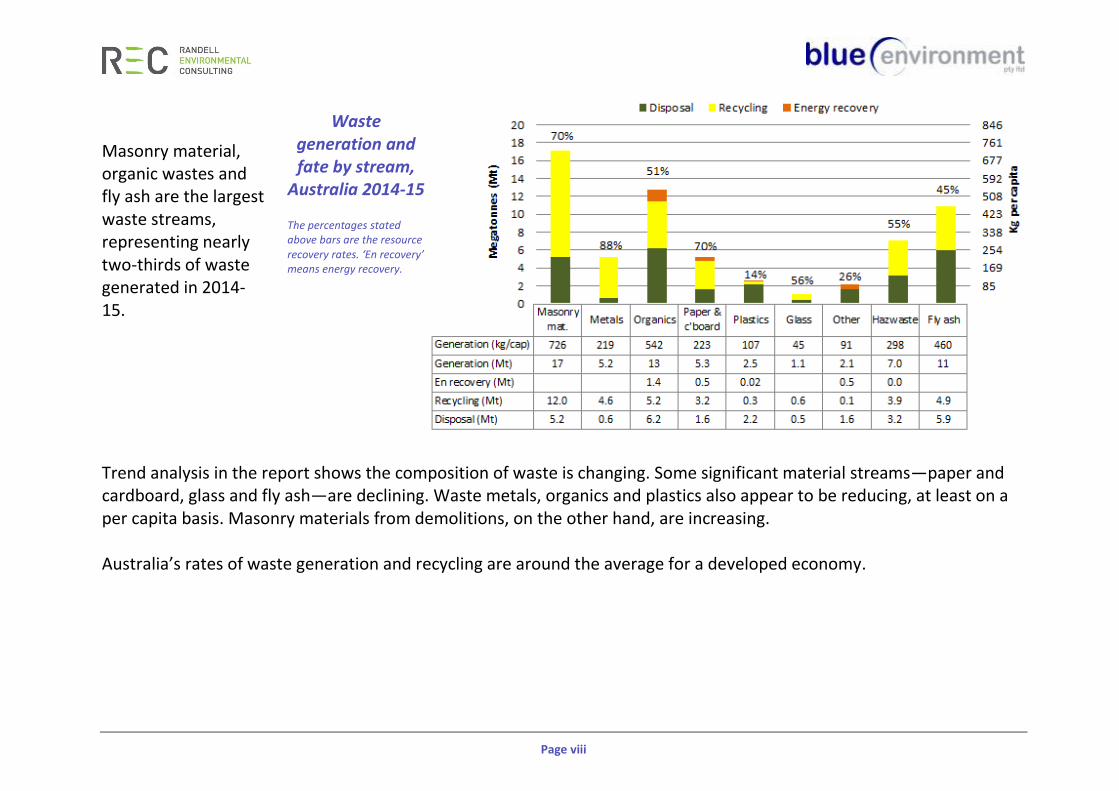

Masonry material, organic wastes and fly ash are the largest waste streams, representing nearly two-thirds of waste generated in 2014-15.

Trend analysis in the report shows the composition of waste is changing. Some significant material streams—paper and cardboard, glass and fly ash—are declining. Waste metals, organics and plastics also appear to be reducing, at least on a per capita basis. Masonry materials from demolitions, on the other hand, are increasing. Australia’s rates of waste generation and recycling are around the average for a developed economy.

Waste generation and fate by stream,

Australia 2014-15

The percentages stated above bars are the resource recovery rates. ‘En recovery’ means energy recovery.

Australian National Waste Report 2016 Final

Page 1

1. Introduction

This report was prepared on commission to the Australian Government Department of the Environment and Energy (DoEE). It provides a detailed picture of the status of solid waste generation, source streams, materials and fates in Australia during the financial year 2014-15. It also examines trends since 2006-07, and considers their causes. The report builds on the 2013 National Waste Report, which focused on data from 2010-11, and other earlier reports titled Waste and Recycling in Australia. The data in those reports has been updated for inclusion in the trends shown here, based on the current compilation method. Most of the data included in this report was obtained from state and territory governments, which collect it for their own monitoring and reporting. This data is supplemented, and sometimes replaced, by national industry data or other national estimates1. Quantity data is presented in kilograms (kg), tonnes (t), thousands of tonnes (kilotonnes or kt) or millions of tonnes (megatonnes or Mt). This report covers all Australian states and territories: Australian Capital Territory (ACT); New South Wales (NSW); Northern Territory (NT); Queensland (Qld); South Australia (SA); Tasmania (Tas); Victoria (Vic); and Western Australia (WA).

1.1 Scope

The report covers waste generated in Australia, including solid non-hazardous materials and all hazardous wastes including liquids (an accompanying report, Hazardous Waste in Australia 20172, considers hazardous waste in detail). The report excludes waste from primary production activities (agriculture, mining and forestry), waste that is reused (such as in ‘tip shops’), pre-consumer waste that is recycled as part of a production process, and clean fill/soil (whether or not it is sent to landfill). Waste sources are considered in three streams: municipal solid waste (MSW) from households and council operations; commercial and industrial (C&I) waste; and construction and demolition (C&D) waste. Waste fates are categorised into three types: disposal, which overwhelmingly means landfill; recycling; and energy recovery, which refers to processes such as conversion of organic waste into methane that is subsequently combusted to generate electricity. The term ‘resource recovery’ is used to represent the sum of recycling and energy recovery. ‘Waste generation’ is used to represent the sum of disposal and resource recovery.

1.2 Data collation methods

To obtain a national picture on waste, a common set of assumptions and categories must be applied to the collected data. This requires some manipulation of state and territory data, including recategorisation, applying assumed compositional splits and adjusting for cross-border transport. To facilitate these manipulations, in consultation with the states and territories, Randell Environmental Consulting and Blue Environment designed a national waste data set reporting tool as part of a previous

1 See Section 8 for more detail.

2 BE & AWE (2017)

Australian National Waste Report 2016 Final

Page 2

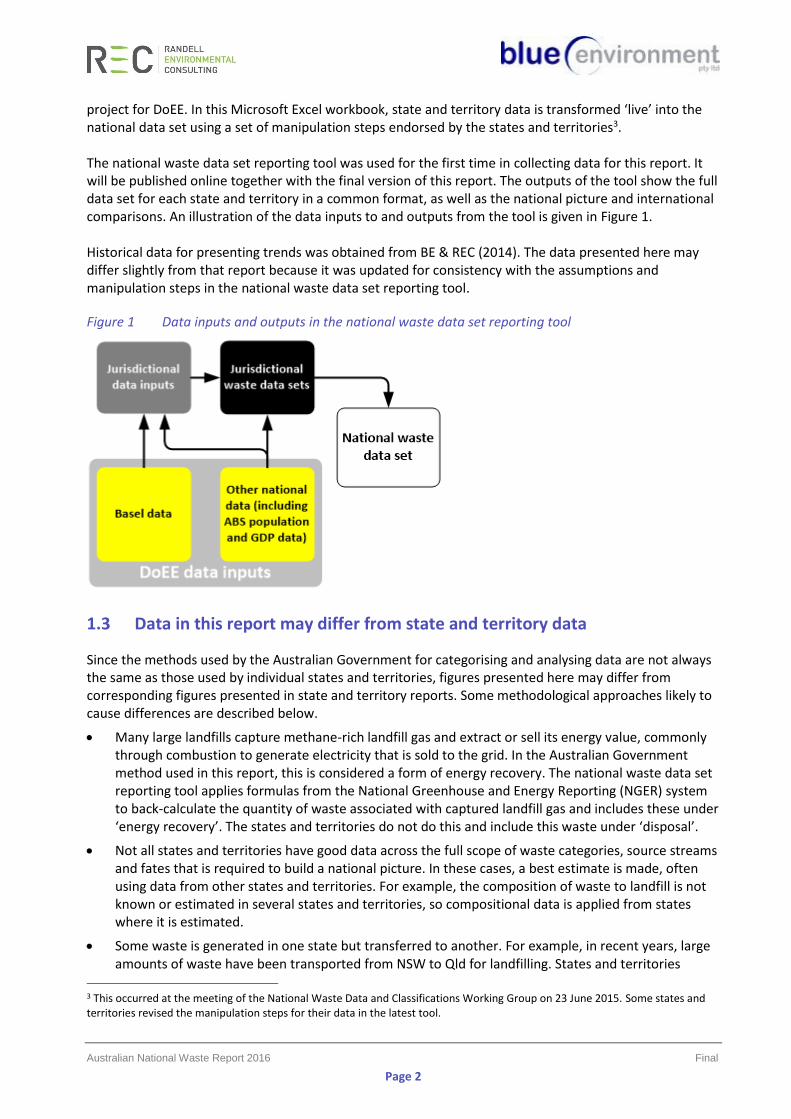

project for DoEE. In this Microsoft Excel workbook, state and territory data is transformed ‘live’ into the national data set using a set of manipulation steps endorsed by the states and territories3. The national waste data set reporting tool was used for the first time in collecting data for this report. It will be published online together with the final version of this report. The outputs of the tool show the full data set for each state and territory in a common format, as well as the national picture and international comparisons. An illustration of the data inputs to and outputs from the tool is given in Figure 1. Historical data for presenting trends was obtained from BE & REC (2014). The data presented here may differ slightly from that report because it was updated for consistency with the assumptions and manipulation steps in the national waste data set reporting tool.

Figure 1 Data inputs and outputs in the national waste data set reporting tool

1.3 Data in this report may differ from state and territory data

Since the methods used by the Australian Government for categorising and analysing data are not always the same as those used by individual states and territories, figures presented here may differ from corresponding figures presented in state and territory reports. Some methodological approaches likely to cause differences are described below.

• Many large landfills capture methane-rich landfill gas and extract or sell its energy value, commonly through combustion to generate electricity that is sold to the grid. In the Australian Government method used in this report, this is considered a form of energy recovery. The national waste data set reporting tool applies formulas from the National Greenhouse and Energy Reporting (NGER) system to back-calculate the quantity of waste associated with captured landfill gas and includes these under ‘energy recovery’. The states and territories do not do this and include this waste under ‘disposal’.

• Not all states and territories have good data across the full scope of waste categories, source streams and fates that is required to build a national picture. In these cases, a best estimate is made, often using data from other states and territories. For example, the composition of waste to landfill is not known or estimated in several states and territories, so compositional data is applied from states where it is estimated.

• Some waste is generated in one state but transferred to another. For example, in recent years, large amounts of waste have been transported from NSW to Qld for landfilling. States and territories

3 This occurred at the meeting of the National Waste Data and Classifications Working Group on 23 June 2015. Some states and territories revised the manipulation steps for their data in the latest tool.

Australian National Waste Report 2016 Final

Page 3

typically report only waste that is recovered or disposed within their boundaries but in this report, where data is available, transfers are reassigned to the jurisdiction where the waste was generated.

• This report covers wastes that are sometimes excluded from state and territory reports, such as biosolids from sewage treatment plants, fly ash from power stations and other types of hazardous waste (including hazardous liquid wastes).

• This report uses national instead of state and territory data for some wastes, including plastics and biosolids.

1.4 Data quality

Because waste data is often difficult and expensive to collect, the requirements, scope and mechanisms for collecting and reporting waste data vary across jurisdictions, industries and fates. The level of uncertainty in some of the presented data is likely to be high. For example, and as highlighted above, the composition of waste to landfill is estimated on the basis of periodic audits at a few landfills. In recognition of these limitations, data is generally presented to only two or three significant figures. There are data quality differences between states and territories:

• Data on waste to landfill: States with controlled fees or landfill levies (ACT, NSW, SA, Vic and WA) tend to have the most comprehensive data on waste to landfill, although Qld’s data is also good. WA’s is restricted to the Perth area.

• Data on recycling: ACT, NSW, Qld, SA, Vic and WA survey their recycling sectors and generate the most thorough data. NSW was unable to provide accurate 2014-15 recycling data for this report due to quality difficulties with the survey so the 2013-14 and 2014-15 data has been estimated (see Section 8.2 for details).

• Hazardous waste: NSW, Qld, SA, Vic and WA run hazardous waste tracking systems and generate the most comprehensive data on hazardous wastes. However, analysis of the Qld data found significant data quality problems (see BE & AWE 2017 for details).

The quality and quantity of the data on waste quantities, source streams and materials is continually improving. We are confident that the national data presented in this report is the most accurate to date.

1.5 Report structure

Section 2 provides further context for the report and discusses influences on waste generation and fate, namely population and economic growth, access to recycling markets, carbon policy, and state and territory waste policies. Section 3 aggregates state and territory data to present the national picture on waste. Section 4 compares the status of waste in Australia with various other countries and considers both waste generation and fate. Section 5 presents the perspectives of the four national industry associations on the status, challenges, opportunities and future of the industry. Section 6 presents the authors’ views on challenges and emerging issues. Section 7 presents the status of waste in each state and territory in alphabetical order, using the data layout described below. Commentary on the data from the state or territory is included where provided.

Australian National Waste Report 2016 Final

Page 4

A final section describes data sources and assumptions in more detail.

Technical terms and abbreviations used throughout are explained in the glossary on pages iv and v.

1.6 Data layout

State and territory data is presented in Section 7 in the following order:

1. Overall waste generation and fate (recycling, energy recovery or disposal) is presented on a total and per capita (or per person) basis.

2. This same data is presented by source stream (MSW, C&I, C&D).

3. Waste generation and fate is shown for eight or nine broad material categories as shown in Table 1.

4. A final subsection presents trends over the period 2006-07 to 2014-15 in waste disposal, recycling, energy recovery, generation and generation per capita.

National data is presented with more detail including trends by stream and material. Fly ash—a waste from coal-fired power plants—is emphasised in the report because it is generated in large volumes, it is mostly managed separately from the main waste management system, and it is generated in only five of the states and territories (NSW, Qld, SA, Vic and WA). Many charts and data sets in this report show quantities with and without fly ash so its significance can be understood and aggregated data on other wastes can be seen separately. Fly ash is excluded from the trend charts in Section 7 so that state and territory trends are readily comparable, whether or not they produce it.

Hazardous waste—both liquid and solid—is included in all the charts and data sets except where stated. The charts showing total quantities generated nationally and by state and territory show quantities with and without hazardous waste so its significance can be understood and aggregated data on other wastes can be seen separately.

Table 1 Waste categories and types analysed in this report

4 For the purposes of this report biosolids are all assumed to be contaminated and included with hazardous waste. For further detail, see Hazardous Waste in Australia 2017 (BE & AWE 2017).

Waste categories Waste types included in this category

Masonry materials Asphalt, bricks, concrete, rubble (including non-hazardous foundry sands), plasterboard and cement sheeting.

Metals Steel, aluminium, other non-ferrous metals.

Organics

Food, garden organics, timber, other organics, non-contaminated biosolids. Excludes:

• paper, cardboard, leather, textiles and rubber (included in separate categories)

• except where specified, hazardous organic wastes (these are included in the ‘hazardous’ category).

Paper and cardboard Liquid paperboard, newsprint and magazines, office paper.

Plastics PET (1), HDPE (2), PVC (3), LDPE (4), PP (5), PS (6), Other (7).

Glass

Other Leather and textiles, rubber excluding tyres, other unclassified wastes.

Hazardous

Acids; alkalis; inorganic chemicals; reactive chemicals; paints, resins, inks and organic sludges; organic solvents, pesticides, oils, putrescible/organic waste; organic chemicals; contaminated soils; asbestos; other soil/sludges (including contaminated biosolids)4; clinical and pharmaceutical; tyres; other miscellaneous.

Fly ash

Australian National Waste Report 2016 Final

Page 5

2. Context

This section discusses five factors that influence Australia’s waste generation and management:

• population growth

• economic growth

• access to recycling markets

• carbon policy

• the main waste policy initiatives established in each state and territory.

2.1 Population growth

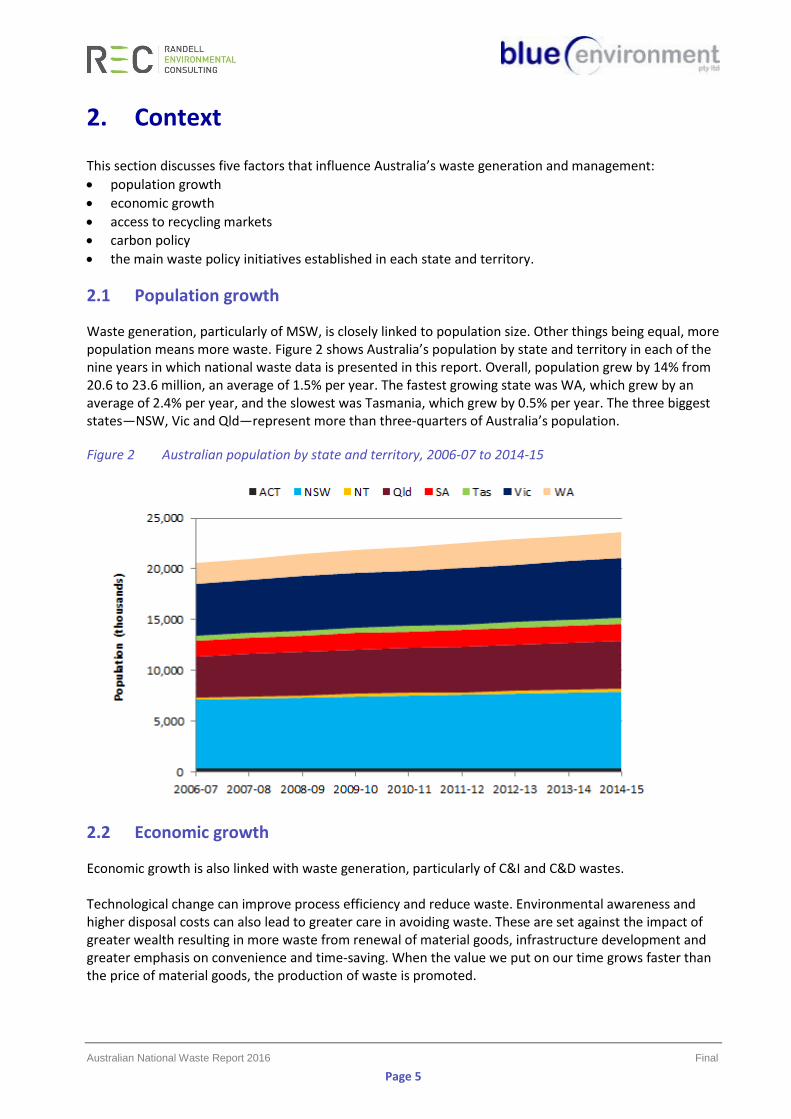

Waste generation, particularly of MSW, is closely linked to population size. Other things being equal, more population means more waste. Figure 2 shows Australia’s population by state and territory in each of the nine years in which national waste data is presented in this report. Overall, population grew by 14% from 20.6 to 23.6 million, an average of 1.5% per year. The fastest growing state was WA, which grew by an average of 2.4% per year, and the slowest was Tasmania, which grew by 0.5% per year. The three biggest states—NSW, Vic and Qld—represent more than three-quarters of Australia’s population.

Figure 2 Australian population by state and territory, 2006-07 to 2014-15

2.2 Economic growth

Economic growth is also linked with waste generation, particularly of C&I and C&D wastes. Technological change can improve process efficiency and reduce waste. Environmental awareness and higher disposal costs can also lead to greater care in avoiding waste. These are set against the impact of greater wealth resulting in more waste from renewal of material goods, infrastructure development and greater emphasis on convenience and time-saving. When the value we put on our time grows faster than the price of material goods, the production of waste is promoted.

Australian National Waste Report 2016 Final

Page 6

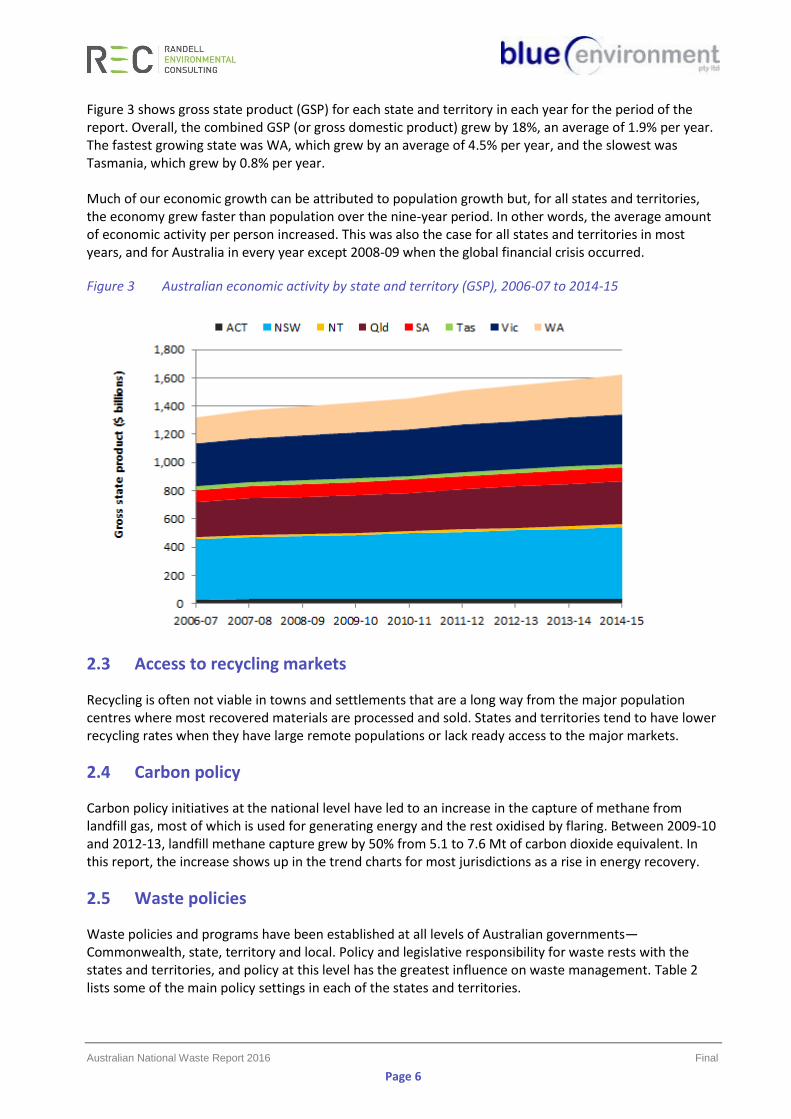

Figure 3 shows gross state product (GSP) for each state and territory in each year for the period of the report. Overall, the combined GSP (or gross domestic product) grew by 18%, an average of 1.9% per year. The fastest growing state was WA, which grew by an average of 4.5% per year, and the slowest was Tasmania, which grew by 0.8% per year. Much of our economic growth can be attributed to population growth but, for all states and territories, the economy grew faster than population over the nine-year period. In other words, the average amount of economic activity per person increased. This was also the case for all states and territories in most years, and for Australia in every year except 2008-09 when the global financial crisis occurred.

Figure 3 Australian economic activity by state and territory (GSP), 2006-07 to 2014-15

2.3 Access to recycling markets

Recycling is often not viable in towns and settlements that are a long way from the major population centres where most recovered materials are processed and sold. States and territories tend to have lower recycling rates when they have large remote populations or lack ready access to the major markets.

2.4 Carbon policy

Carbon policy initiatives at the national level have led to an increase in the capture of methane from landfill gas, most of which is used for generating energy and the rest oxidised by flaring. Between 2009-10 and 2012-13, landfill methane capture grew by 50% from 5.1 to 7.6 Mt of carbon dioxide equivalent. In this report, the increase shows up in the trend charts for most jurisdictions as a rise in energy recovery.

2.5 Waste policies

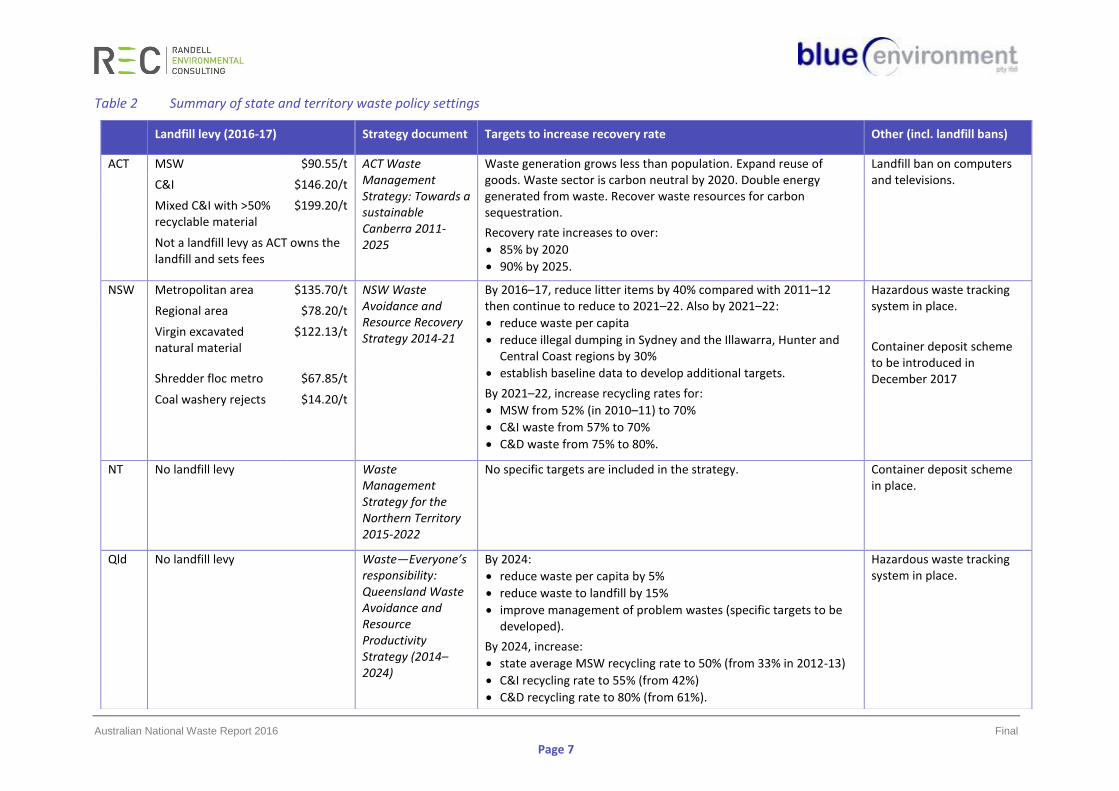

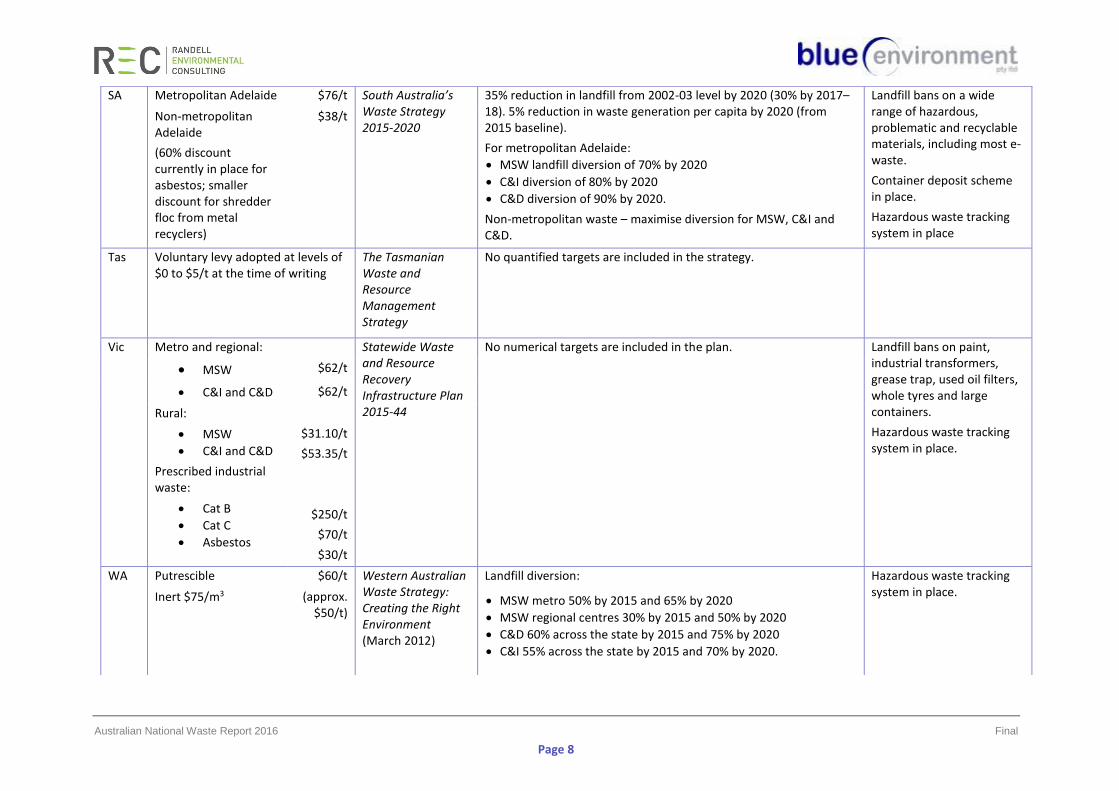

Waste policies and programs have been established at all levels of Australian governments—Commonwealth, state, territory and local. Policy and legislative responsibility for waste rests with the states and territories, and policy at this level has the greatest influence on waste management. Table 2 lists some of the main policy settings in each of the states and territories.

Australian National Waste Report 2016 Final

Page 7

Table 2 Summary of state and territory waste policy settings

Landfill levy (2016-17) Strategy document Targets to increase recovery rate Other (incl. landfill bans)

ACT MSW $90.55/t ACT Waste Management Strategy: Towards a sustainable Canberra 2011-2025

Waste generation grows less than population. Expand reuse of goods. Waste sector is carbon neutral by 2020. Double energy generated from waste. Recover waste resources for carbon sequestration.

Recovery rate increases to over:

• 85% by 2020

• 90% by 2025.

Landfill ban on computers and televisions.

C&I $146.20/t

Mixed C&I with >50% recyclable material

$199.20/t

Not a landfill levy as ACT owns the landfill and sets fees

NSW Metropolitan area $135.70/t NSW Waste Avoidance and Resource Recovery Strategy 2014-21

By 2016–17, reduce litter items by 40% compared with 2011–12 then continue to reduce to 2021–22. Also by 2021–22:

• reduce waste per capita

• reduce illegal dumping in Sydney and the Illawarra, Hunter and Central Coast regions by 30%

• establish baseline data to develop additional targets.

By 2021–22, increase recycling rates for:

• MSW from 52% (in 2010–11) to 70%

• C&I waste from 57% to 70%

• C&D waste from 75% to 80%.

Hazardous waste tracking system in place.

Container deposit scheme to be introduced in December 2017

Regional area $78.20/t

Virgin excavated natural material

$122.13/t

Shredder floc metro $67.85/t

Coal washery rejects $14.20/t

NT No landfill levy Waste Management Strategy for the Northern Territory 2015-2022

No specific targets are included in the strategy. Container deposit scheme in place.

Qld No landfill levy Waste—Everyone’s responsibility: Queensland Waste Avoidance and Resource Productivity Strategy (2014–2024)

By 2024:

• reduce waste per capita by 5%

• reduce waste to landfill by 15%

• improve management of problem wastes (specific targets to be developed).

By 2024, increase:

• state average MSW recycling rate to 50% (from 33% in 2012-13)

• C&I recycling rate to 55% (from 42%)

• C&D recycling rate to 80% (from 61%).

Hazardous waste tracking system in place.

Australian National Waste Report 2016 Final

Page 8

SA Metropolitan Adelaide $76/t South Australia’s Waste Strategy 2015-2020

35% reduction in landfill from 2002-03 level by 2020 (30% by 2017–18). 5% reduction in waste generation per capita by 2020 (from 2015 baseline).

For metropolitan Adelaide:

• MSW landfill diversion of 70% by 2020

• C&I diversion of 80% by 2020

• C&D diversion of 90% by 2020.

Non-metropolitan waste – maximise diversion for MSW, C&I and C&D.

Landfill bans on a wide range of hazardous, problematic and recyclable materials, including most e-waste.

Container deposit scheme in place.

Hazardous waste tracking system in place

Non-metropolitan Adelaide

(60% discount currently in place for asbestos; smaller discount for shredder floc from metal recyclers)

$38/t

Tas Voluntary levy adopted at levels of $0 to $5/t at the time of writing

The Tasmanian Waste and Resource Management Strategy

No quantified targets are included in the strategy.

Vic Metro and regional: Statewide Waste and Resource Recovery Infrastructure Plan 2015-44

No numerical targets are included in the plan. Landfill bans on paint, industrial transformers, grease trap, used oil filters, whole tyres and large containers.

Hazardous waste tracking system in place.

• MSW $62/t

• C&I and C&D $62/t

Rural:

• MSW

• C&I and C&D

Prescribed industrial waste:

• Cat B

• Cat C

• Asbestos

$31.10/t

$53.35/t

$250/t

$70/t

$30/t

WA Putrescible $60/t Western Australian Waste Strategy: Creating the Right Environment (March 2012)

Landfill diversion:

• MSW metro 50% by 2015 and 65% by 2020

• MSW regional centres 30% by 2015 and 50% by 2020

• C&D 60% across the state by 2015 and 75% by 2020

• C&I 55% across the state by 2015 and 70% by 2020.

Hazardous waste tracking system in place. Inert $75/m3 (approx.

$50/t)

Australian National Waste Report 2016 Final

Page 9

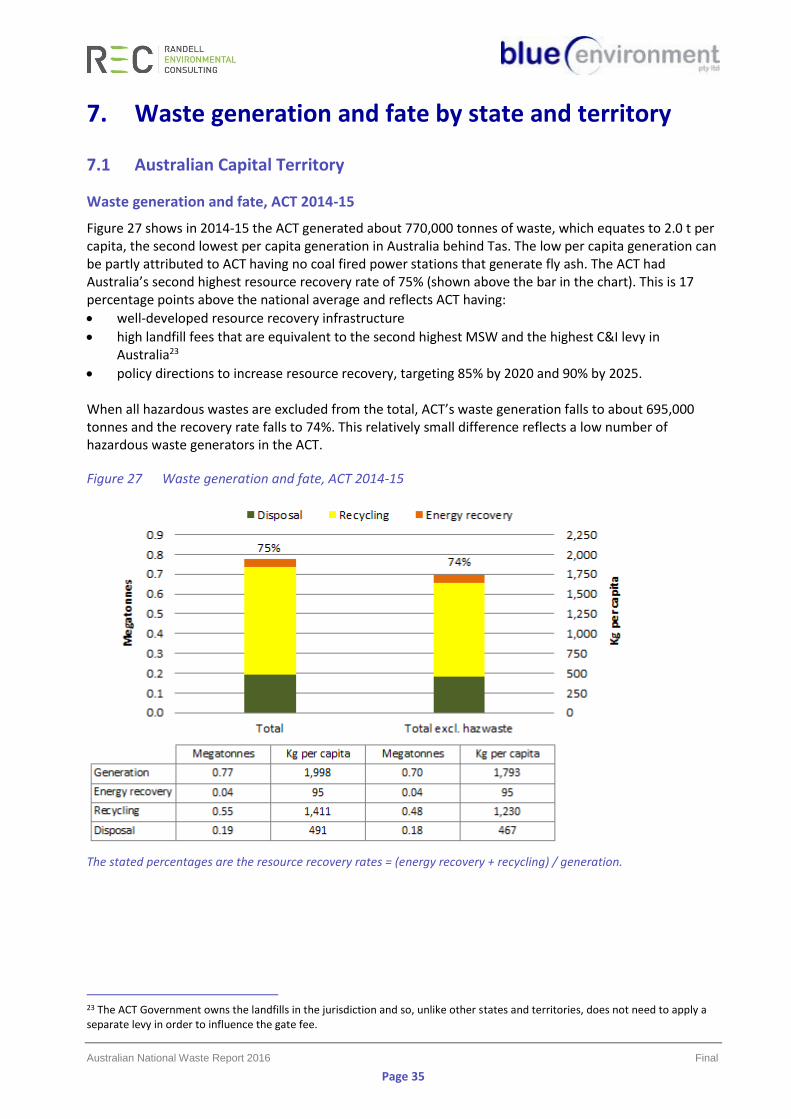

3. The national picture

3.1 Overall waste quantities analysis

Overall waste generation and fate, Australia 2014-15

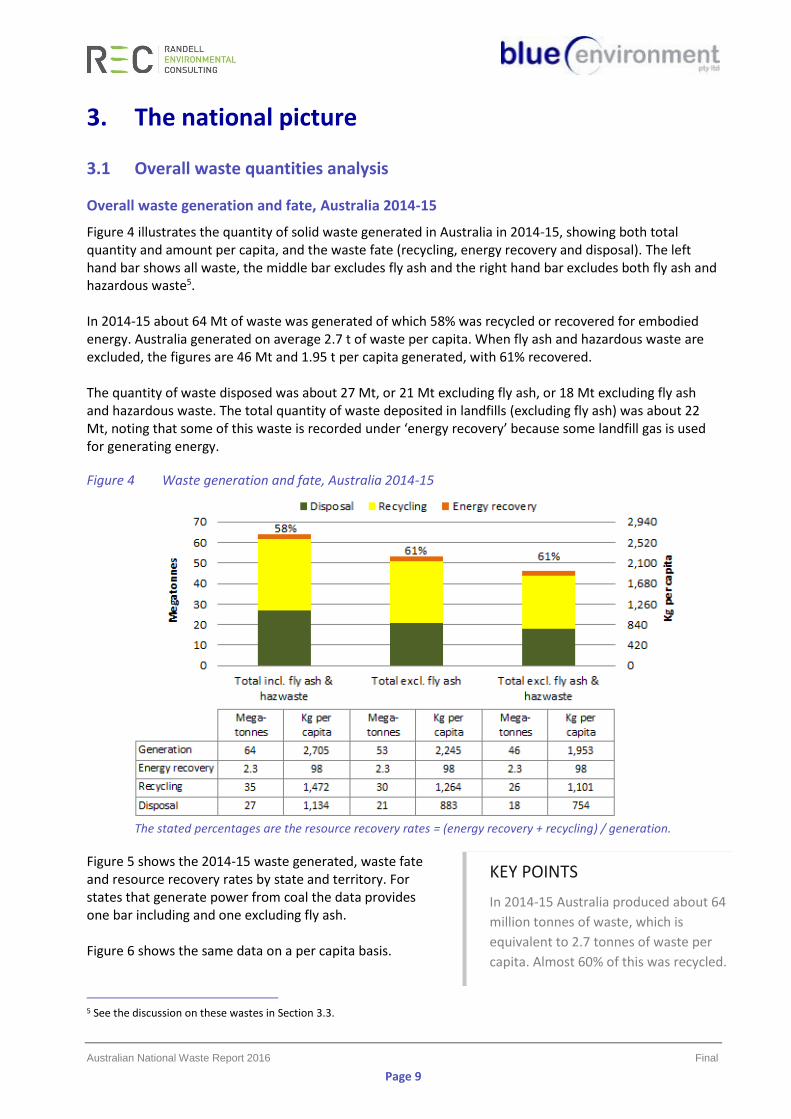

Figure 4 illustrates the quantity of solid waste generated in Australia in 2014-15, showing both total quantity and amount per capita, and the waste fate (recycling, energy recovery and disposal). The left hand bar shows all waste, the middle bar excludes fly ash and the right hand bar excludes both fly ash and hazardous waste5. In 2014-15 about 64 Mt of waste was generated of which 58% was recycled or recovered for embodied energy. Australia generated on average 2.7 t of waste per capita. When fly ash and hazardous waste are excluded, the figures are 46 Mt and 1.95 t per capita generated, with 61% recovered. The quantity of waste disposed was about 27 Mt, or 21 Mt excluding fly ash, or 18 Mt excluding fly ash and hazardous waste. The total quantity of waste deposited in landfills (excluding fly ash) was about 22 Mt, noting that some of this waste is recorded under ‘energy recovery’ because some landfill gas is used for generating energy.

Figure 4 Waste generation and fate, Australia 2014-15

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

Figure 5 shows the 2014-15 waste generated, waste fate and resource recovery rates by state and territory. For states that generate power from coal the data provides one bar including and one excluding fly ash. Figure 6 shows the same data on a per capita basis.

5 See the discussion on these wastes in Section 3.3.

KEY POINTS

In 2014-15 Australia produced about 64

million tonnes of waste, which is

equivalent to 2.7 tonnes of waste per

capita. Almost 60% of this was recycled.

Australian National Waste Report 2016 Final

Page 10

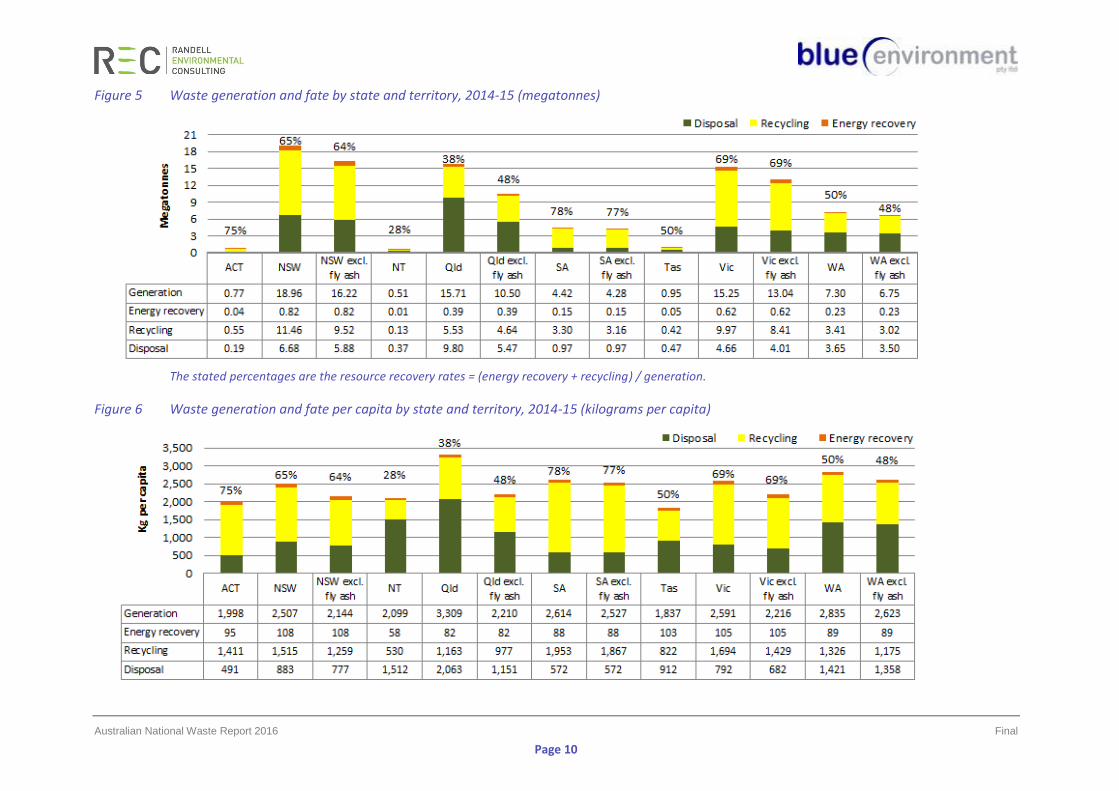

Figure 5 Waste generation and fate by state and territory, 2014-15 (megatonnes)

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

Figure 6 Waste generation and fate per capita by state and territory, 2014-15 (kilograms per capita)

Australian National Waste Report 2016 Final

Page 11

Figure 5 and Figure 6 show:

• Overall waste quantities correlate with population and GSP in each state and territory with NSW, Vic and Qld dominating, followed by WA and SA, and then Tas, ACT and NT.

• When fly ash is included, Qld generated the most waste per capita at about 3.3 t. When fly ash is excluded, WA and SA were the highest waste generators, producing over 2.5 t. Tas was the lowest with 1.8 t.

• SA was the clear leader in resource recovery with a rate of almost 80%. The ACT followed at 75%, then Vic at 69% and NSW at 65%. WA, Tas and Qld (excluding fly ash) recovered about 50% and NT had the lowest recovery rate at an estimated 28%.

• NSW, Vic and Tas had the highest per capita levels of energy recovery due to large landfills collecting methane for electricity generation. With several dedicated energy from waste facilities planned for WA and NSW, energy recovery from waste in those states may increase significantly in future years.

• Recycling per capita was highest in SA followed, in order, by Vic, NSW, ACT, WA, Qld, Tas and NT.

• Disposal per capita excluding fly ash was lowest in the ACT, followed, in order, by SA, Vic, NSW, Tas, Qld, WA and NT.

Trends in overall waste generation and fate, Australia 2006-07 to 2014-15

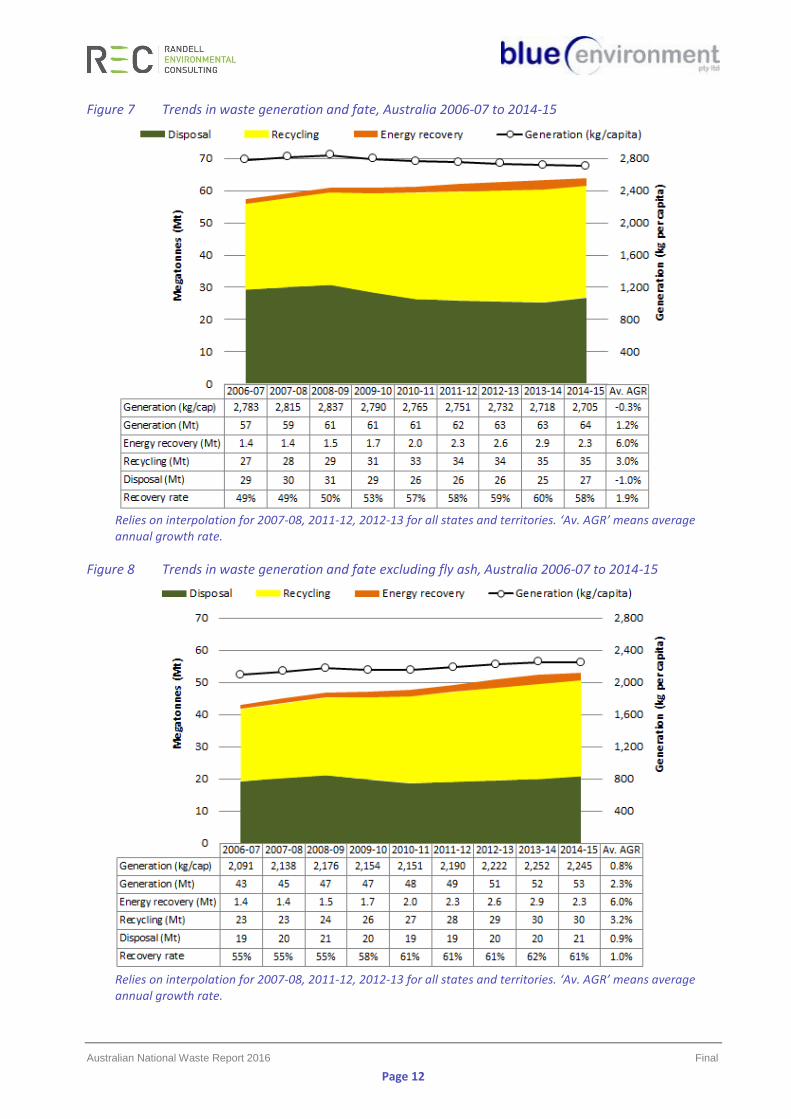

This section looks at the overall trends in waste generation and fate for Australia for the period 2006-07 to 2014-15, the period for which a reasonably consistent data set and compilation method is available. Figure 7 shows waste generation and fate in total and per capita over the period; Figure 8 is similar but excludes fly ash. Highlights include:

• Australia continued to produce more waste as the population grew. - Waste generation increased from about 57 to 64 Mt over the period, a growth rate of 11% over

nine years, or an average of 1.2% per year. Population increased by an average of 1.5% per year, so waste generation grew about 20% more slowly than population. Waste generation per capita declined by 3% over the period, or an average of 0.3% per year, when you include fly ash.

- Excluding fly ash, waste generation increased from about 43 to 53 Mt over the period, a growth rate of 23% over nine years. This is an average growth rate of 2.3% per year, about 50% greater than population growth. Waste generation per capita increased by 7% over the period, or an average of 0.8% per year.

- The decline of coal fired power reduced fly ash to such an extent that waste per capita slightly decreased. But excluding fly ash, waste per capita increased.

• The quantity of material recycled in Australia increased significantly. - Recycling increased by 30% over the period

from 27 to 35 Mt or 1.4% per capita per year. - Excluding fly ash, recycling increased by 32%

from 23 to 30 Mt or 1.6% per capita per year.

• Energy recovery increased markedly from about 1.4 to 2.3 Mt over the period, or an average of 6% per year. Energy recovery per capita increased by an average of 4.4% per year. However, there appears to have been a significant decline in gas recovery in the last year of the period.

KEY POINTS

• The annual quantity of waste

generated in Australia per capita

declined slightly between 2006-07

and 2015-15.

• If you exclude fly ash, waste

generation in Australia per capita

increased by almost 1% each year.

• The trend is towards more recycling

and more recovery of energy from

waste.

Australian National Waste Report 2016 Final

Page 12

Figure 7 Trends in waste generation and fate, Australia 2006-07 to 2014-15

Relies on interpolation for 2007-08, 2011-12, 2012-13 for all states and territories. ‘Av. AGR’ means average annual growth rate.

Figure 8 Trends in waste generation and fate excluding fly ash, Australia 2006-07 to 2014-15

Relies on interpolation for 2007-08, 2011-12, 2012-13 for all states and territories. ‘Av. AGR’ means average annual growth rate.

Australian National Waste Report 2016 Final

Page 13

• Australia’s disposal tonnages were fairly stable. - Disposal fell by 8% from about 29 to 27 Mt over the period. This is a decline per capita of about

2.5% per year. - Excluding fly ash, disposal increased by 9% from about 19 to 21 Mt. This is an average decline

per capita of about 0.6% per year.

• The resource recovery rate in Australia increased from 49% to 58% over the period. Excluding fly ash, it grew from 55% to 61%.

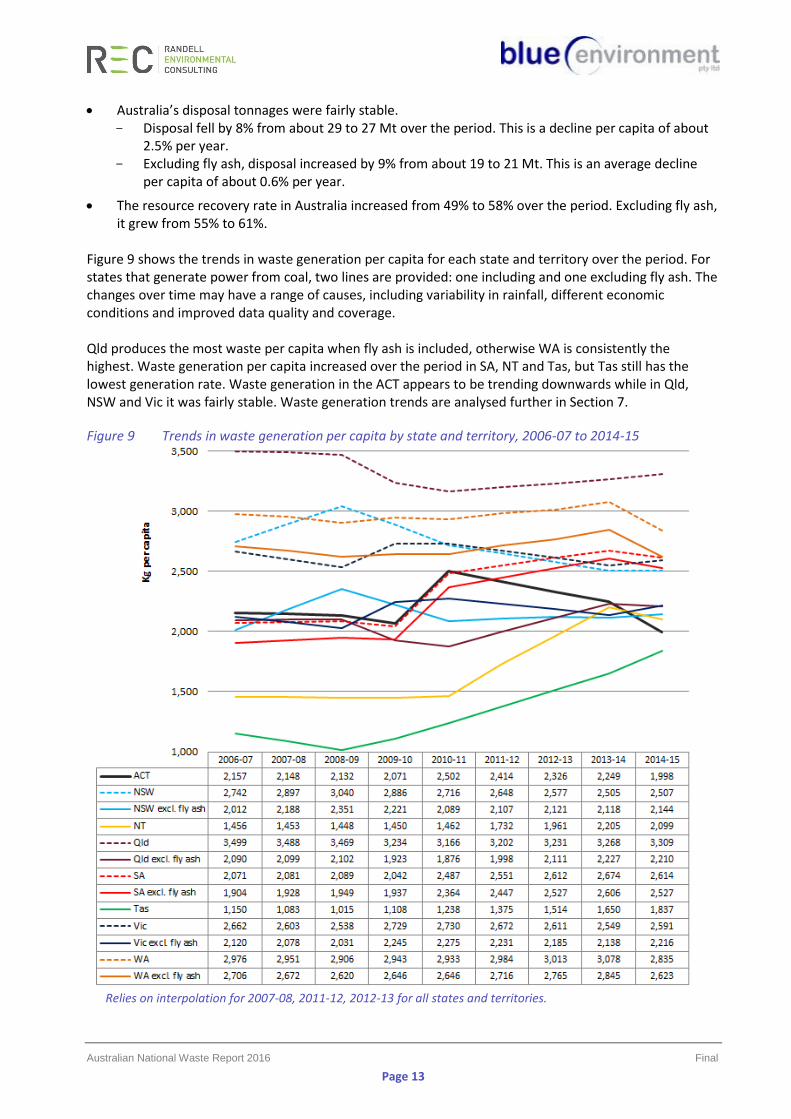

Figure 9 shows the trends in waste generation per capita for each state and territory over the period. For states that generate power from coal, two lines are provided: one including and one excluding fly ash. The changes over time may have a range of causes, including variability in rainfall, different economic conditions and improved data quality and coverage. Qld produces the most waste per capita when fly ash is included, otherwise WA is consistently the highest. Waste generation per capita increased over the period in SA, NT and Tas, but Tas still has the lowest generation rate. Waste generation in the ACT appears to be trending downwards while in Qld, NSW and Vic it was fairly stable. Waste generation trends are analysed further in Section 7.

Figure 9 Trends in waste generation per capita by state and territory, 2006-07 to 2014-15

Relies on interpolation for 2007-08, 2011-12, 2012-13 for all states and territories.

Australian National Waste Report 2016 Final

Page 14

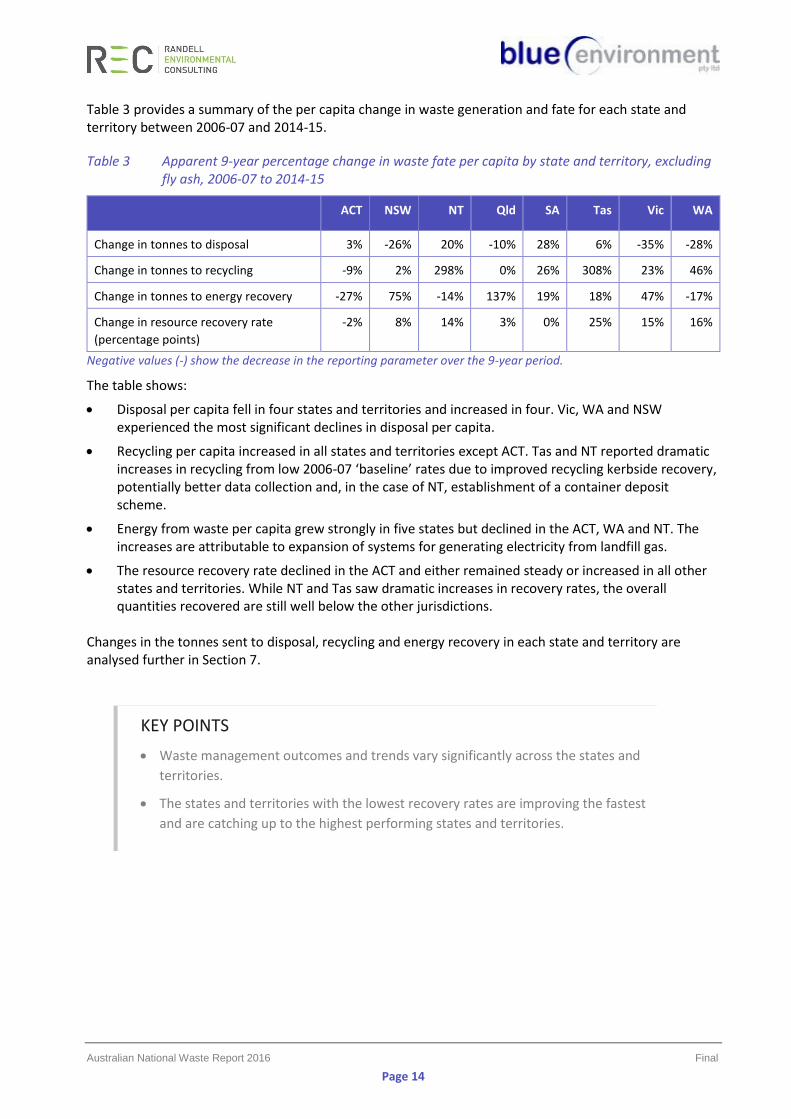

Table 3 provides a summary of the per capita change in waste generation and fate for each state and territory between 2006-07 and 2014-15.

Table 3 Apparent 9-year percentage change in waste fate per capita by state and territory, excluding fly ash, 2006-07 to 2014-15

Negative values (-) show the decrease in the reporting parameter over the 9-year period.

The table shows:

• Disposal per capita fell in four states and territories and increased in four. Vic, WA and NSW experienced the most significant declines in disposal per capita.

• Recycling per capita increased in all states and territories except ACT. Tas and NT reported dramatic increases in recycling from low 2006-07 ‘baseline’ rates due to improved recycling kerbside recovery, potentially better data collection and, in the case of NT, establishment of a container deposit scheme.

• Energy from waste per capita grew strongly in five states but declined in the ACT, WA and NT. The increases are attributable to expansion of systems for generating electricity from landfill gas.

• The resource recovery rate declined in the ACT and either remained steady or increased in all other states and territories. While NT and Tas saw dramatic increases in recovery rates, the overall quantities recovered are still well below the other jurisdictions.

Changes in the tonnes sent to disposal, recycling and energy recovery in each state and territory are analysed further in Section 7.

ACT NSW NT Qld SA Tas Vic WA

Change in tonnes to disposal 3% -26% 20% -10% 28% 6% -35% -28%

Change in tonnes to recycling -9% 2% 298% 0% 26% 308% 23% 46%

Change in tonnes to energy recovery -27% 75% -14% 137% 19% 18% 47% -17%

Change in resource recovery rate

(percentage points)

-2% 8% 14% 3% 0% 25% 15% 16%

KEY POINTS

• Waste management outcomes and trends vary significantly across the states and

territories.

• The states and territories with the lowest recovery rates are improving the fastest

and are catching up to the highest performing states and territories.

Australian National Waste Report 2016 Final

Page 15

3.2 Waste stream analysis

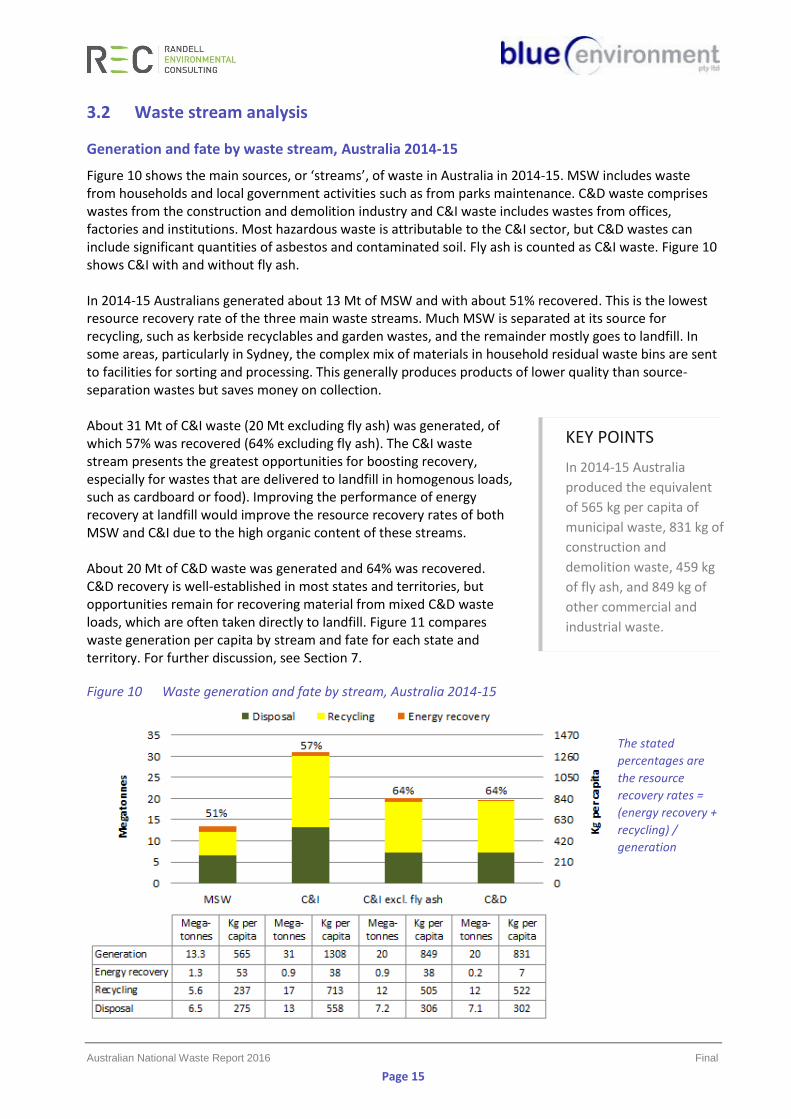

Generation and fate by waste stream, Australia 2014-15

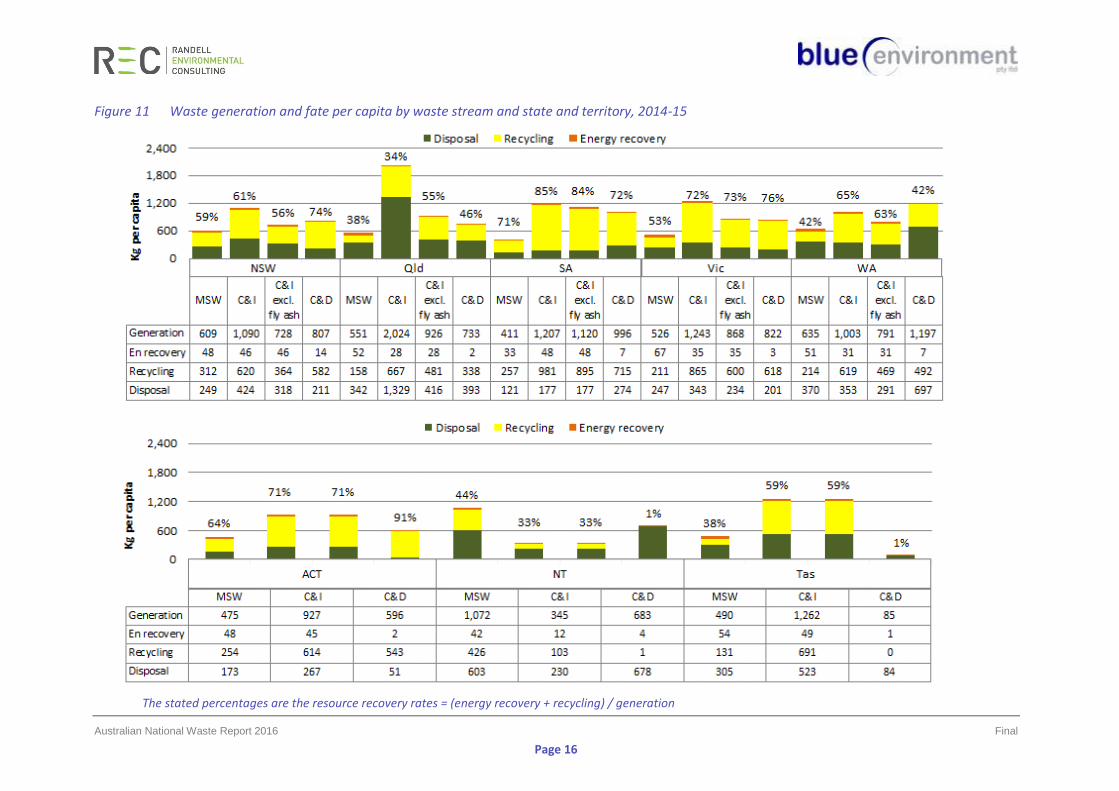

Figure 10 shows the main sources, or ‘streams’, of waste in Australia in 2014-15. MSW includes waste from households and local government activities such as from parks maintenance. C&D waste comprises wastes from the construction and demolition industry and C&I waste includes wastes from offices, factories and institutions. Most hazardous waste is attributable to the C&I sector, but C&D wastes can include significant quantities of asbestos and contaminated soil. Fly ash is counted as C&I waste. Figure 10 shows C&I with and without fly ash. In 2014-15 Australians generated about 13 Mt of MSW and with about 51% recovered. This is the lowest resource recovery rate of the three main waste streams. Much MSW is separated at its source for recycling, such as kerbside recyclables and garden wastes, and the remainder mostly goes to landfill. In some areas, particularly in Sydney, the complex mix of materials in household residual waste bins are sent to facilities for sorting and processing. This generally produces products of lower quality than source-separation wastes but saves money on collection. About 31 Mt of C&I waste (20 Mt excluding fly ash) was generated, of which 57% was recovered (64% excluding fly ash). The C&I waste stream presents the greatest opportunities for boosting recovery, especially for wastes that are delivered to landfill in homogenous loads, such as cardboard or food). Improving the performance of energy recovery at landfill would improve the resource recovery rates of both MSW and C&I due to the high organic content of these streams. About 20 Mt of C&D waste was generated and 64% was recovered. C&D recovery is well-established in most states and territories, but opportunities remain for recovering material from mixed C&D waste loads, which are often taken directly to landfill. Figure 11 compares waste generation per capita by stream and fate for each state and territory. For further discussion, see Section 7.

Figure 10 Waste generation and fate by stream, Australia 2014-15

The stated

percentages are

the resource

recovery rates =

(energy recovery +

recycling) /

generation

KEY POINTS

In 2014-15 Australia

produced the equivalent

of 565 kg per capita of

municipal waste, 831 kg of

construction and

demolition waste, 459 kg

of fly ash, and 849 kg of

other commercial and

industrial waste.

Australian National Waste Report 2016 Final

Page 16

Figure 11 Waste generation and fate per capita by waste stream and state and territory, 2014-15

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation

Australian National Waste Report 2016 Final

Page 17

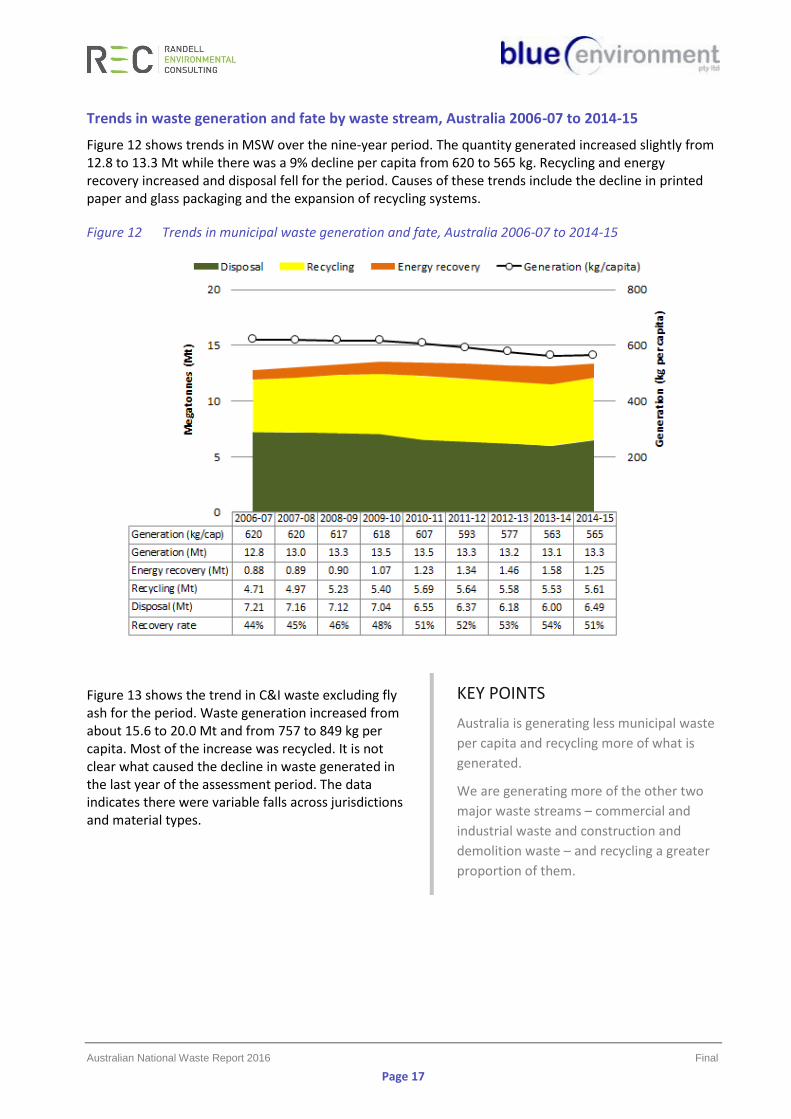

Trends in waste generation and fate by waste stream, Australia 2006-07 to 2014-15

Figure 12 shows trends in MSW over the nine-year period. The quantity generated increased slightly from 12.8 to 13.3 Mt while there was a 9% decline per capita from 620 to 565 kg. Recycling and energy recovery increased and disposal fell for the period. Causes of these trends include the decline in printed paper and glass packaging and the expansion of recycling systems.

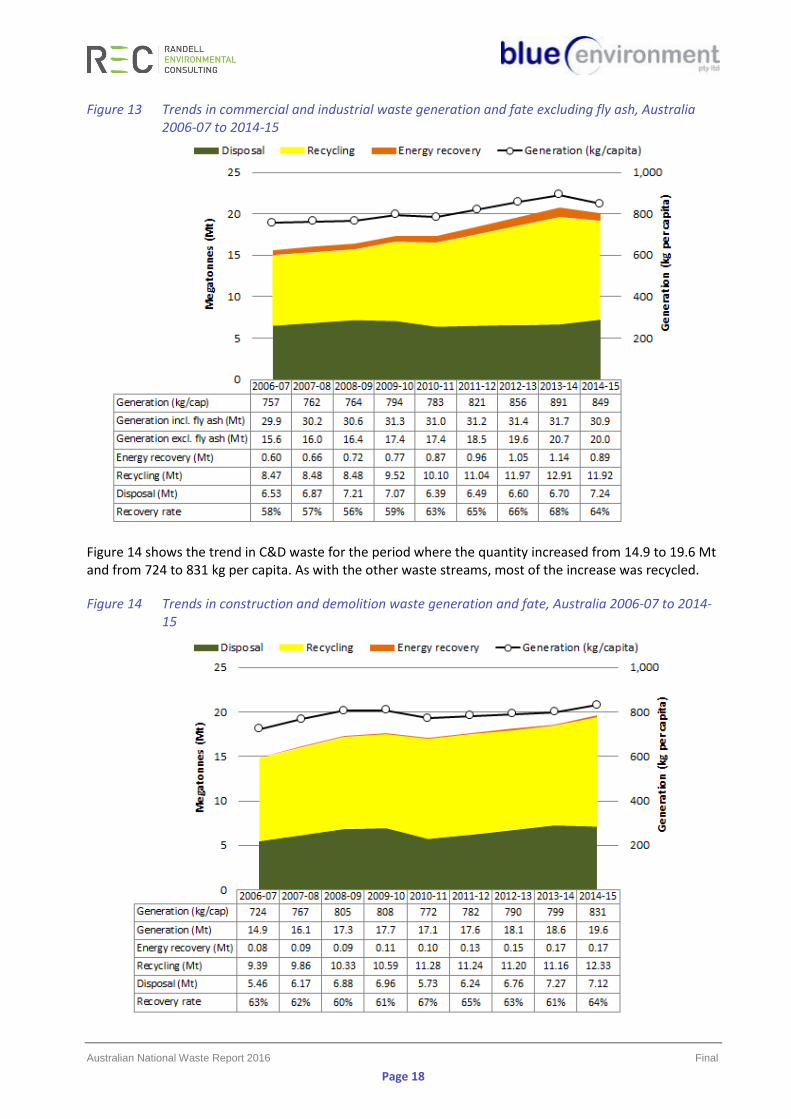

Figure 12 Trends in municipal waste generation and fate, Australia 2006-07 to 2014-15

Figure 13 shows the trend in C&I waste excluding fly ash for the period. Waste generation increased from about 15.6 to 20.0 Mt and from 757 to 849 kg per capita. Most of the increase was recycled. It is not clear what caused the decline in waste generated in the last year of the assessment period. The data indicates there were variable falls across jurisdictions and material types.

KEY POINTS

Australia is generating less municipal waste

per capita and recycling more of what is

generated.

We are generating more of the other two

major waste streams – commercial and

industrial waste and construction and

demolition waste – and recycling a greater

proportion of them.

Australian National Waste Report 2016 Final

Page 18

Figure 13 Trends in commercial and industrial waste generation and fate excluding fly ash, Australia 2006-07 to 2014-15

Figure 14 shows the trend in C&D waste for the period where the quantity increased from 14.9 to 19.6 Mt and from 724 to 831 kg per capita. As with the other waste streams, most of the increase was recycled.

Figure 14 Trends in construction and demolition waste generation and fate, Australia 2006-07 to 2014-15

Australian National Waste Report 2016 Final

Page 19

3.3 Waste materials analysis

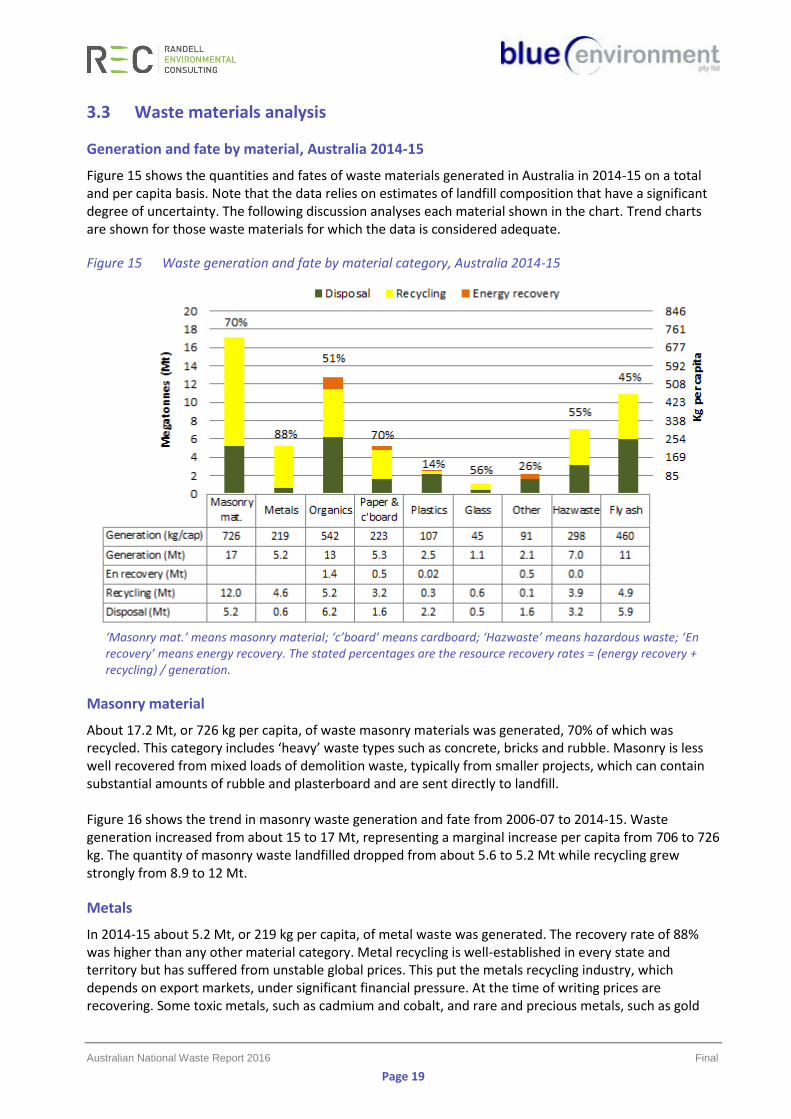

Generation and fate by material, Australia 2014-15

Figure 15 shows the quantities and fates of waste materials generated in Australia in 2014-15 on a total and per capita basis. Note that the data relies on estimates of landfill composition that have a significant degree of uncertainty. The following discussion analyses each material shown in the chart. Trend charts are shown for those waste materials for which the data is considered adequate.

Figure 15 Waste generation and fate by material category, Australia 2014-15

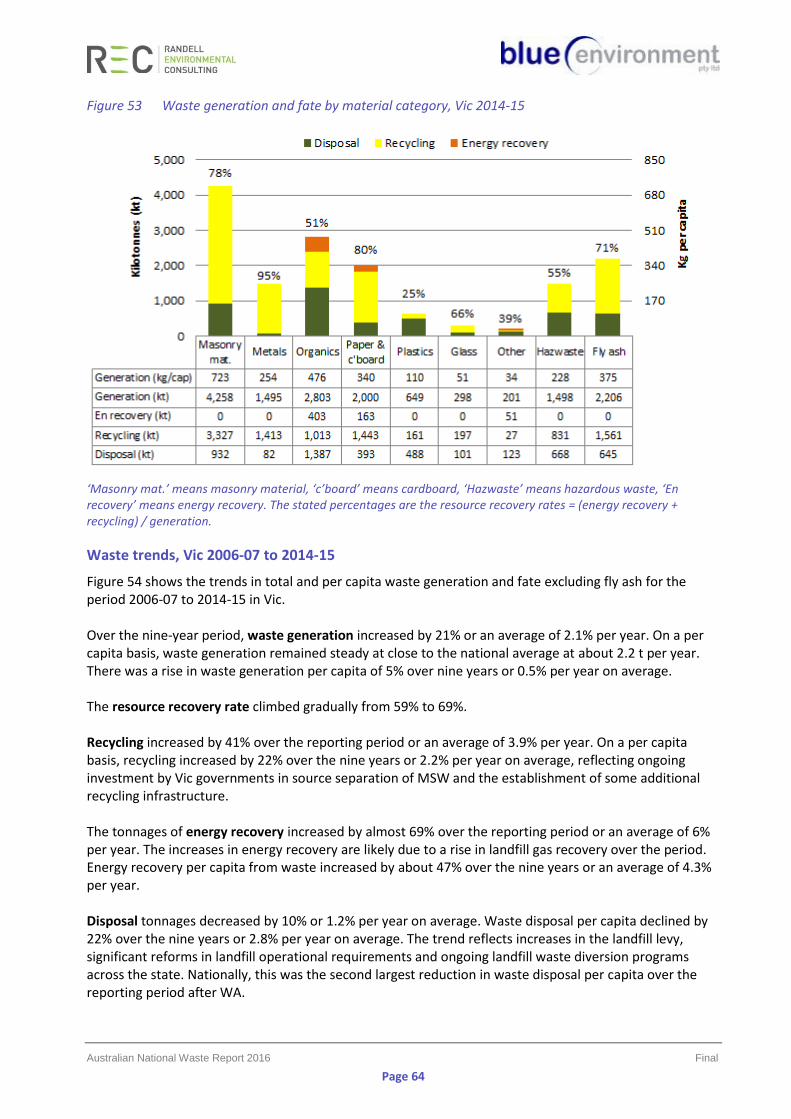

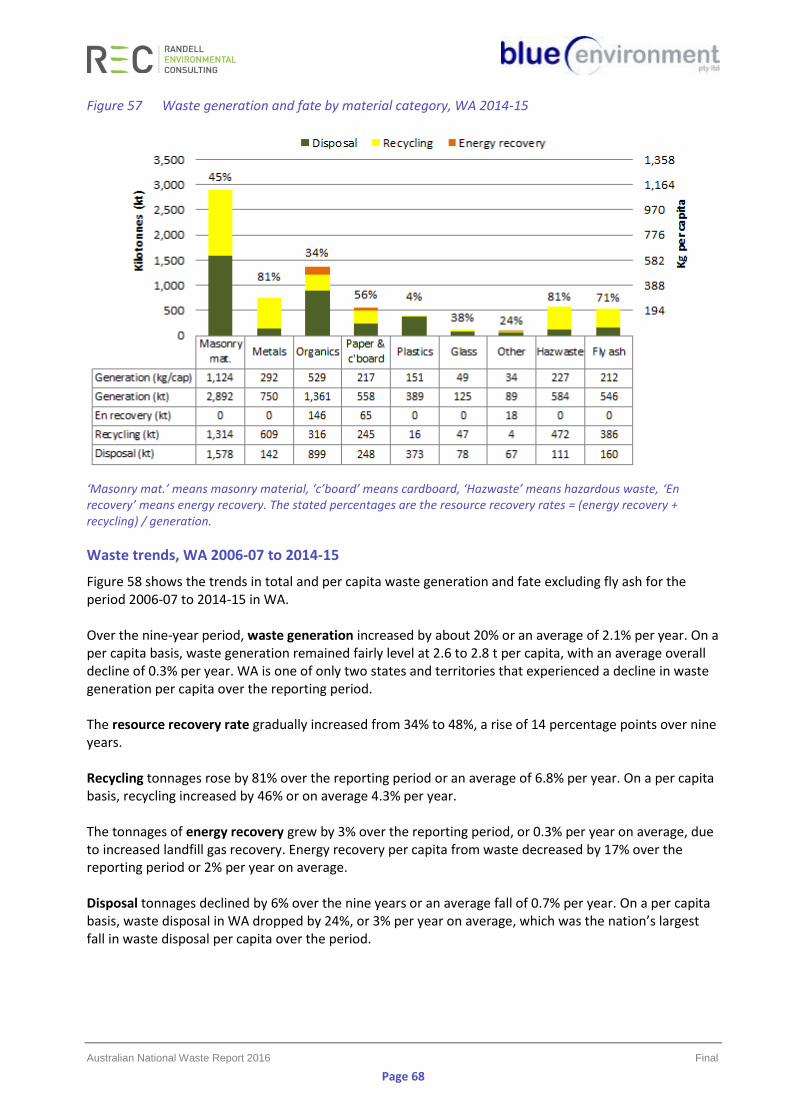

‘Masonry mat.’ means masonry material; ‘c’board’ means cardboard; ‘Hazwaste’ means hazardous waste; ‘En recovery’ means energy recovery. The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

Masonry material

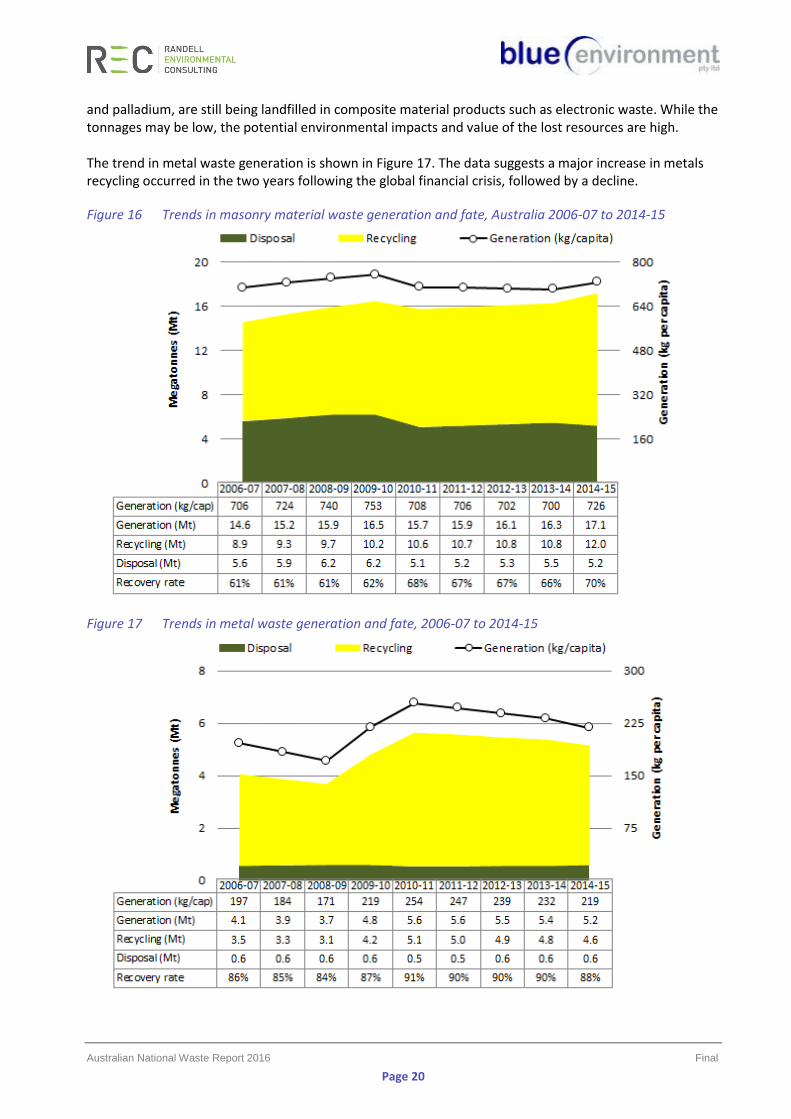

About 17.2 Mt, or 726 kg per capita, of waste masonry materials was generated, 70% of which was recycled. This category includes ‘heavy’ waste types such as concrete, bricks and rubble. Masonry is less well recovered from mixed loads of demolition waste, typically from smaller projects, which can contain substantial amounts of rubble and plasterboard and are sent directly to landfill. Figure 16 shows the trend in masonry waste generation and fate from 2006-07 to 2014-15. Waste generation increased from about 15 to 17 Mt, representing a marginal increase per capita from 706 to 726 kg. The quantity of masonry waste landfilled dropped from about 5.6 to 5.2 Mt while recycling grew strongly from 8.9 to 12 Mt.

Metals

In 2014-15 about 5.2 Mt, or 219 kg per capita, of metal waste was generated. The recovery rate of 88% was higher than any other material category. Metal recycling is well-established in every state and territory but has suffered from unstable global prices. This put the metals recycling industry, which depends on export markets, under significant financial pressure. At the time of writing prices are recovering. Some toxic metals, such as cadmium and cobalt, and rare and precious metals, such as gold

Australian National Waste Report 2016 Final

Page 20

and palladium, are still being landfilled in composite material products such as electronic waste. While the tonnages may be low, the potential environmental impacts and value of the lost resources are high. The trend in metal waste generation is shown in Figure 17. The data suggests a major increase in metals recycling occurred in the two years following the global financial crisis, followed by a decline.

Figure 16 Trends in masonry material waste generation and fate, Australia 2006-07 to 2014-15

Figure 17 Trends in metal waste generation and fate, 2006-07 to 2014-15

Australian National Waste Report 2016 Final

Page 21

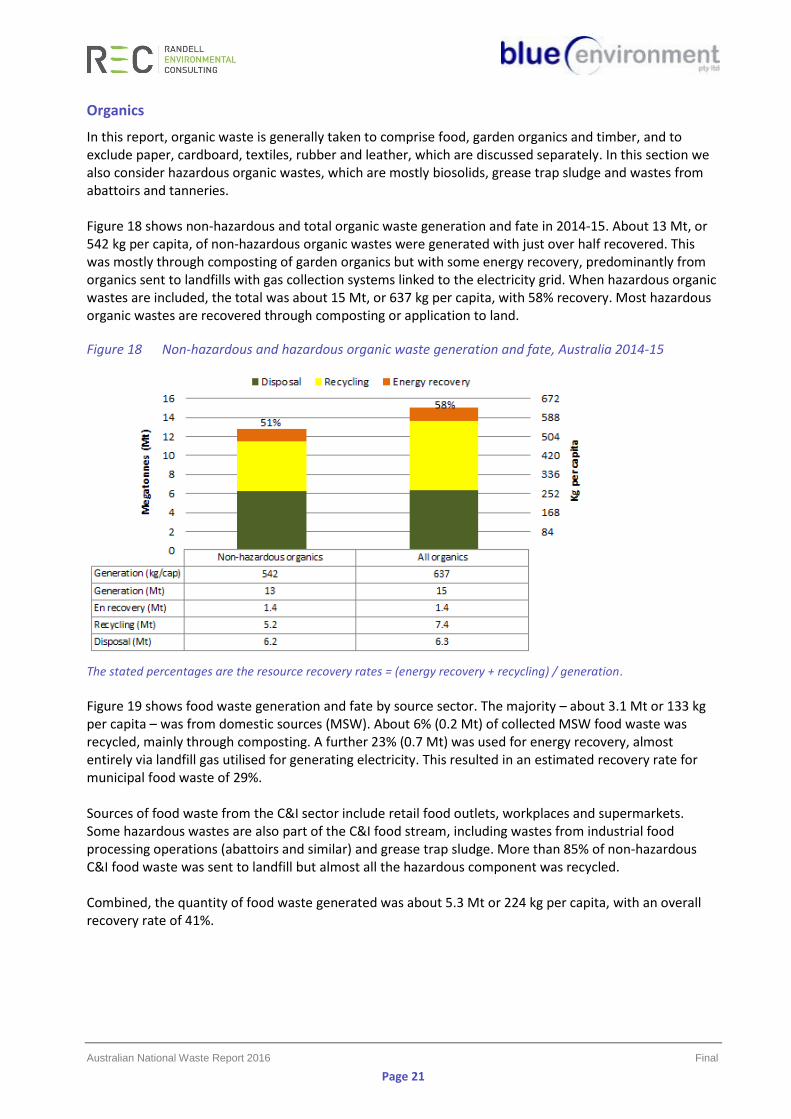

Organics

In this report, organic waste is generally taken to comprise food, garden organics and timber, and to exclude paper, cardboard, textiles, rubber and leather, which are discussed separately. In this section we also consider hazardous organic wastes, which are mostly biosolids, grease trap sludge and wastes from abattoirs and tanneries. Figure 18 shows non-hazardous and total organic waste generation and fate in 2014-15. About 13 Mt, or 542 kg per capita, of non-hazardous organic wastes were generated with just over half recovered. This was mostly through composting of garden organics but with some energy recovery, predominantly from organics sent to landfills with gas collection systems linked to the electricity grid. When hazardous organic wastes are included, the total was about 15 Mt, or 637 kg per capita, with 58% recovery. Most hazardous organic wastes are recovered through composting or application to land.

Figure 18 Non-hazardous and hazardous organic waste generation and fate, Australia 2014-15

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

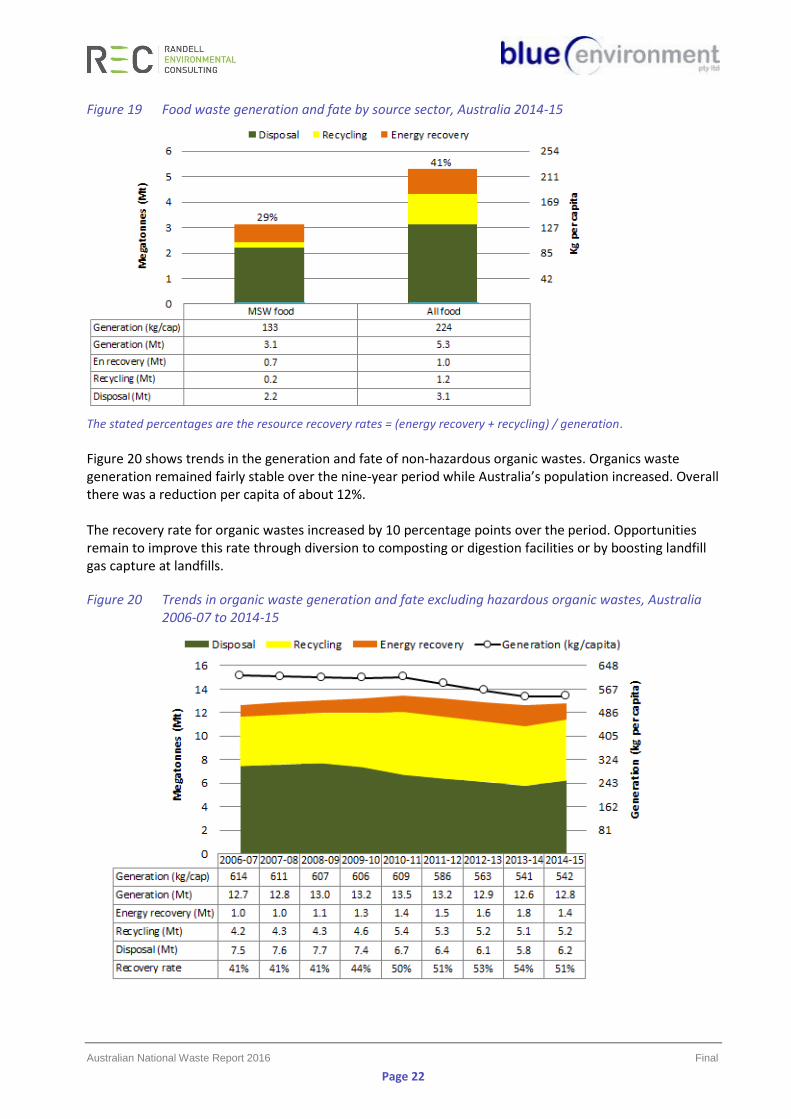

Figure 19 shows food waste generation and fate by source sector. The majority – about 3.1 Mt or 133 kg per capita – was from domestic sources (MSW). About 6% (0.2 Mt) of collected MSW food waste was recycled, mainly through composting. A further 23% (0.7 Mt) was used for energy recovery, almost entirely via landfill gas utilised for generating electricity. This resulted in an estimated recovery rate for municipal food waste of 29%. Sources of food waste from the C&I sector include retail food outlets, workplaces and supermarkets. Some hazardous wastes are also part of the C&I food stream, including wastes from industrial food processing operations (abattoirs and similar) and grease trap sludge. More than 85% of non-hazardous C&I food waste was sent to landfill but almost all the hazardous component was recycled. Combined, the quantity of food waste generated was about 5.3 Mt or 224 kg per capita, with an overall recovery rate of 41%.

Australian National Waste Report 2016 Final

Page 22

Figure 19 Food waste generation and fate by source sector, Australia 2014-15

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

Figure 20 shows trends in the generation and fate of non-hazardous organic wastes. Organics waste generation remained fairly stable over the nine-year period while Australia’s population increased. Overall there was a reduction per capita of about 12%. The recovery rate for organic wastes increased by 10 percentage points over the period. Opportunities remain to improve this rate through diversion to composting or digestion facilities or by boosting landfill gas capture at landfills.

Figure 20 Trends in organic waste generation and fate excluding hazardous organic wastes, Australia 2006-07 to 2014-15

Australian National Waste Report 2016 Final

Page 23

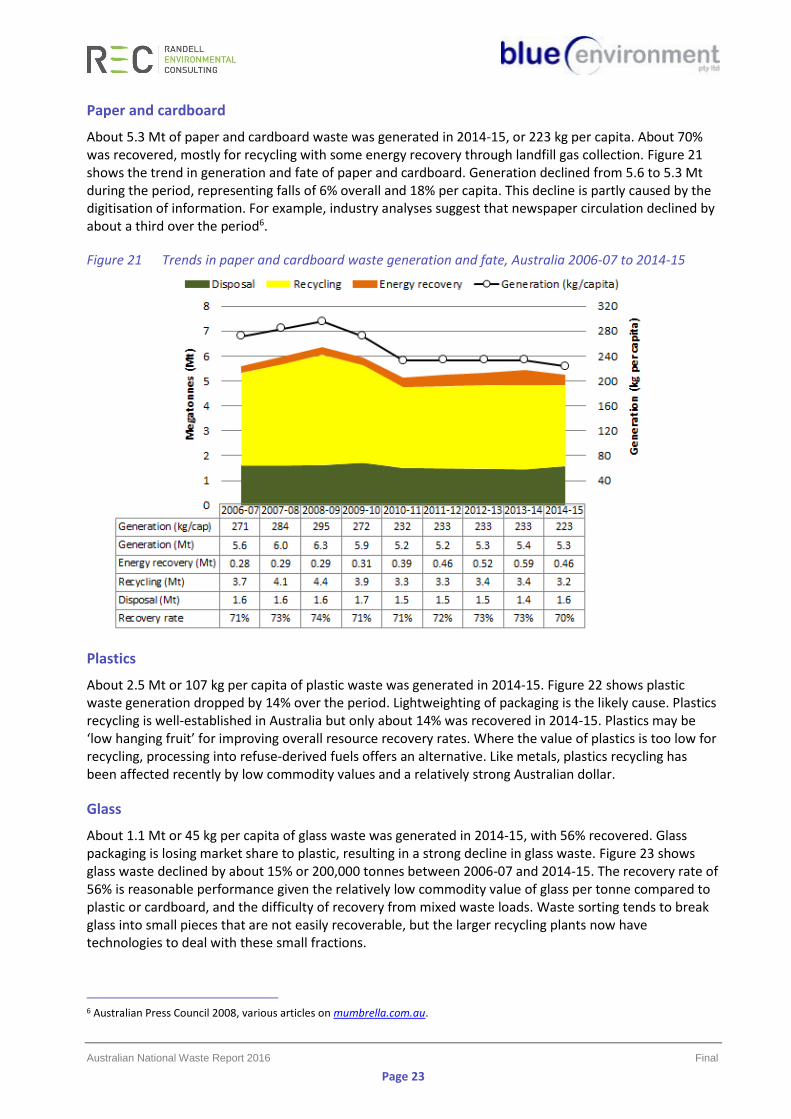

Paper and cardboard

About 5.3 Mt of paper and cardboard waste was generated in 2014-15, or 223 kg per capita. About 70% was recovered, mostly for recycling with some energy recovery through landfill gas collection. Figure 21 shows the trend in generation and fate of paper and cardboard. Generation declined from 5.6 to 5.3 Mt during the period, representing falls of 6% overall and 18% per capita. This decline is partly caused by the digitisation of information. For example, industry analyses suggest that newspaper circulation declined by about a third over the period6.

Figure 21 Trends in paper and cardboard waste generation and fate, Australia 2006-07 to 2014-15

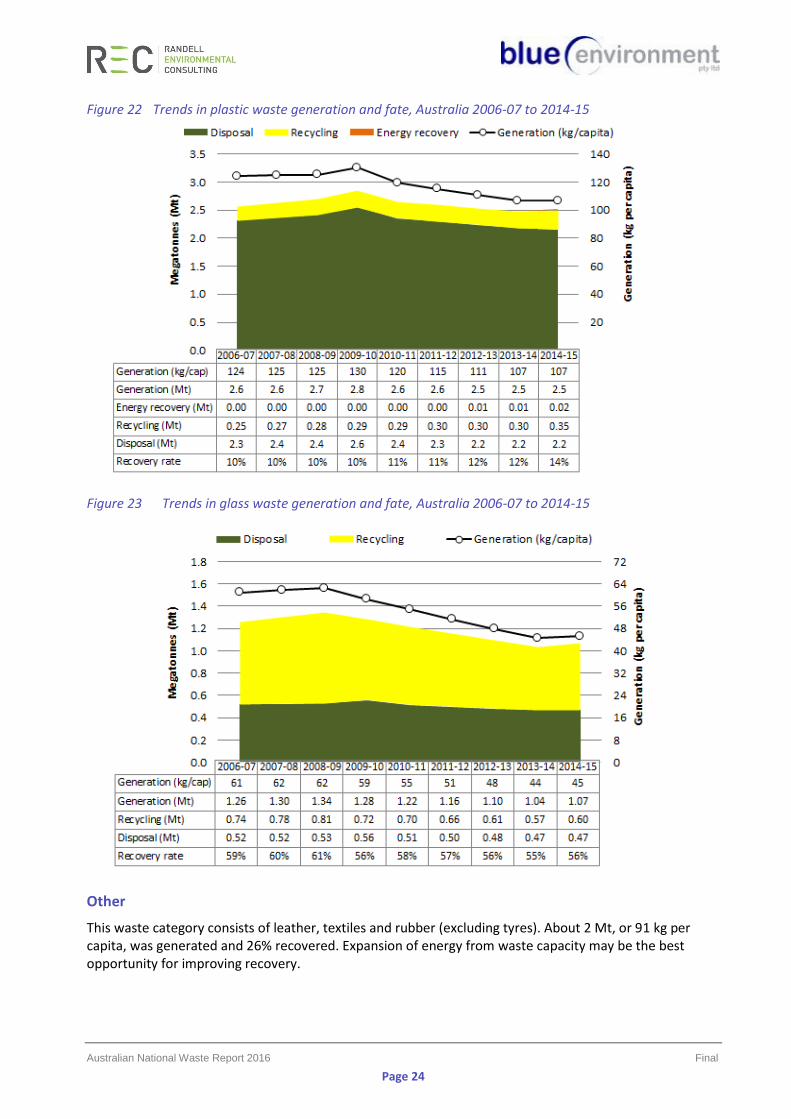

Plastics

About 2.5 Mt or 107 kg per capita of plastic waste was generated in 2014-15. Figure 22 shows plastic waste generation dropped by 14% over the period. Lightweighting of packaging is the likely cause. Plastics recycling is well-established in Australia but only about 14% was recovered in 2014-15. Plastics may be ‘low hanging fruit’ for improving overall resource recovery rates. Where the value of plastics is too low for recycling, processing into refuse-derived fuels offers an alternative. Like metals, plastics recycling has been affected recently by low commodity values and a relatively strong Australian dollar.

Glass

About 1.1 Mt or 45 kg per capita of glass waste was generated in 2014-15, with 56% recovered. Glass packaging is losing market share to plastic, resulting in a strong decline in glass waste. Figure 23 shows glass waste declined by about 15% or 200,000 tonnes between 2006-07 and 2014-15. The recovery rate of 56% is reasonable performance given the relatively low commodity value of glass per tonne compared to plastic or cardboard, and the difficulty of recovery from mixed waste loads. Waste sorting tends to break glass into small pieces that are not easily recoverable, but the larger recycling plants now have technologies to deal with these small fractions.

6 Australian Press Council 2008, various articles on mumbrella.com.au.

Australian National Waste Report 2016 Final

Page 24

Figure 22 Trends in plastic waste generation and fate, Australia 2006-07 to 2014-15

Figure 23 Trends in glass waste generation and fate, Australia 2006-07 to 2014-15

Other

This waste category consists of leather, textiles and rubber (excluding tyres). About 2 Mt, or 91 kg per capita, was generated and 26% recovered. Expansion of energy from waste capacity may be the best opportunity for improving recovery.

Australian National Waste Report 2016 Final

Page 25

Hazardous waste

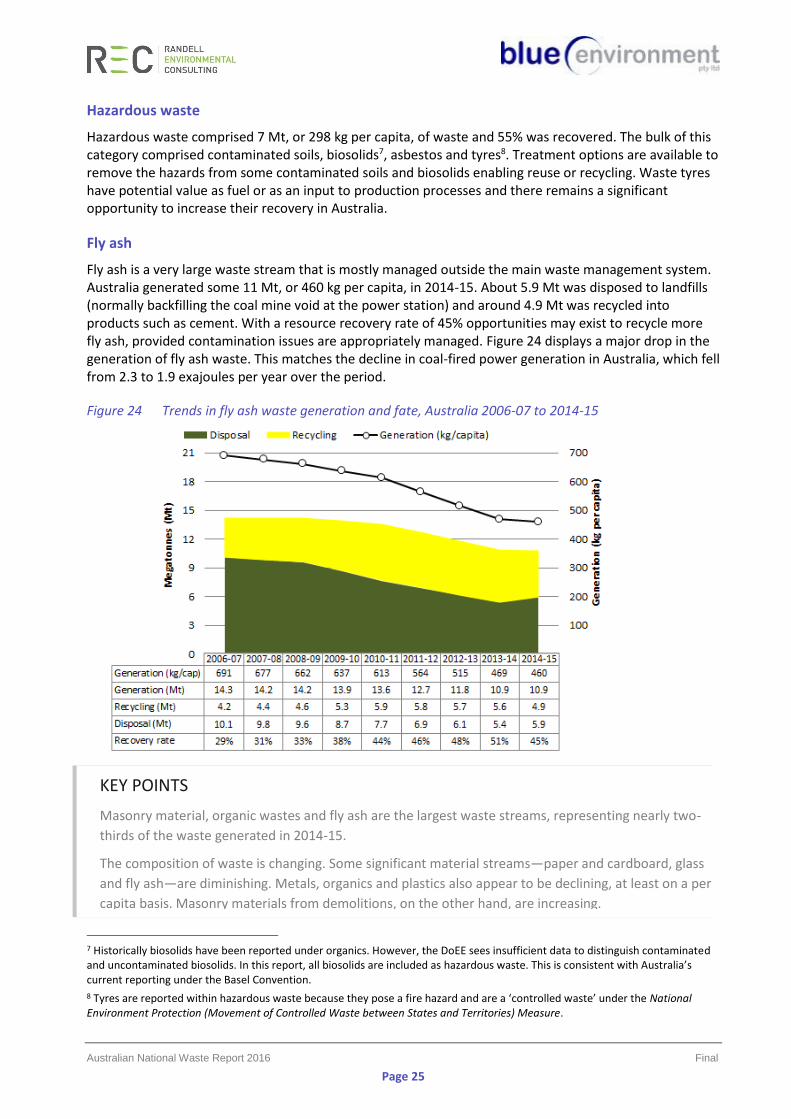

Hazardous waste comprised 7 Mt, or 298 kg per capita, of waste and 55% was recovered. The bulk of this category comprised contaminated soils, biosolids7, asbestos and tyres8. Treatment options are available to remove the hazards from some contaminated soils and biosolids enabling reuse or recycling. Waste tyres have potential value as fuel or as an input to production processes and there remains a significant opportunity to increase their recovery in Australia.

Fly ash

Fly ash is a very large waste stream that is mostly managed outside the main waste management system. Australia generated some 11 Mt, or 460 kg per capita, in 2014-15. About 5.9 Mt was disposed to landfills (normally backfilling the coal mine void at the power station) and around 4.9 Mt was recycled into products such as cement. With a resource recovery rate of 45% opportunities may exist to recycle more fly ash, provided contamination issues are appropriately managed. Figure 24 displays a major drop in the generation of fly ash waste. This matches the decline in coal-fired power generation in Australia, which fell from 2.3 to 1.9 exajoules per year over the period.

Figure 24 Trends in fly ash waste generation and fate, Australia 2006-07 to 2014-15

7 Historically biosolids have been reported under organics. However, the DoEE sees insufficient data to distinguish contaminated and uncontaminated biosolids. In this report, all biosolids are included as hazardous waste. This is consistent with Australia’s current reporting under the Basel Convention.

8 Tyres are reported within hazardous waste because they pose a fire hazard and are a ‘controlled waste’ under the National Environment Protection (Movement of Controlled Waste between States and Territories) Measure.

KEY POINTS

Masonry material, organic wastes and fly ash are the largest waste streams, representing nearly two-

thirds of the waste generated in 2014-15.

The composition of waste is changing. Some significant material streams—paper and cardboard, glass

and fly ash—are diminishing. Metals, organics and plastics also appear to be declining, at least on a per

capita basis. Masonry materials from demolitions, on the other hand, are increasing.

Australian National Waste Report 2016 Final

Page 26

4. International comparisons

4.1 Waste generation and fate

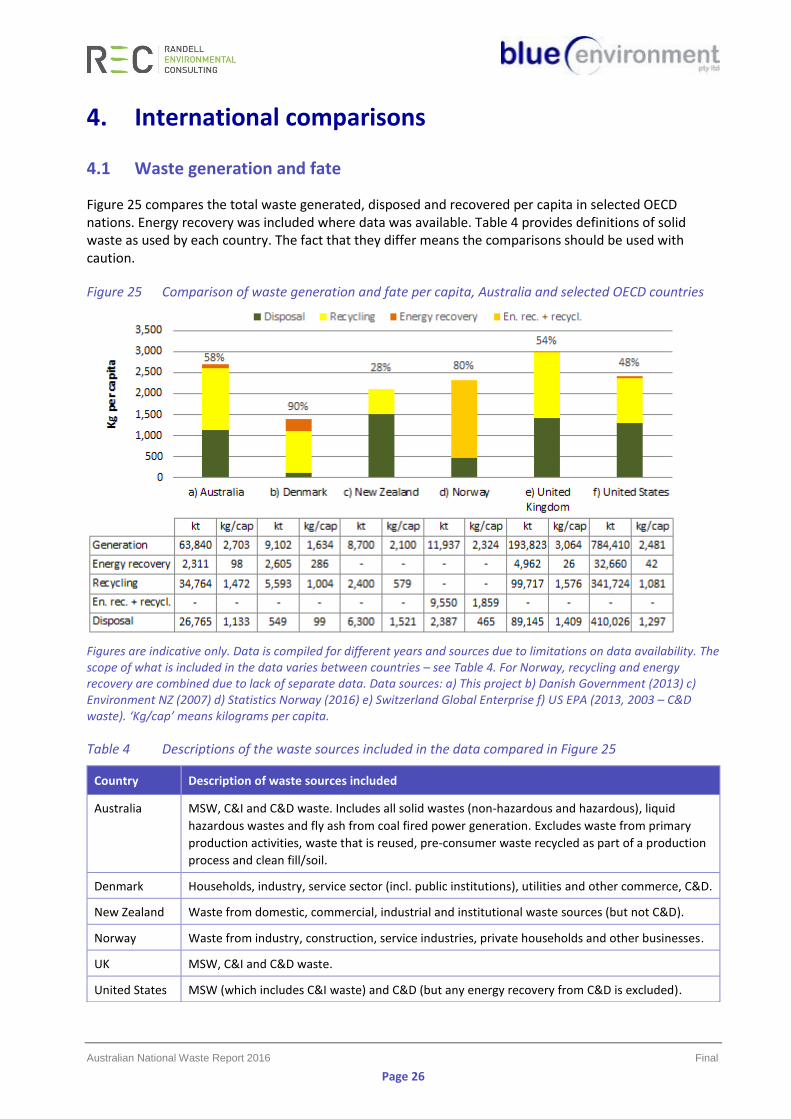

Figure 25 compares the total waste generated, disposed and recovered per capita in selected OECD nations. Energy recovery was included where data was available. Table 4 provides definitions of solid waste as used by each country. The fact that they differ means the comparisons should be used with caution.

Figure 25 Comparison of waste generation and fate per capita, Australia and selected OECD countries

Figures are indicative only. Data is compiled for different years and sources due to limitations on data availability. The scope of what is included in the data varies between countries – see Table 4. For Norway, recycling and energy recovery are combined due to lack of separate data. Data sources: a) This project b) Danish Government (2013) c) Environment NZ (2007) d) Statistics Norway (2016) e) Switzerland Global Enterprise f) US EPA (2013, 2003 – C&D waste). ‘Kg/cap’ means kilograms per capita.

Table 4 Descriptions of the waste sources included in the data compared in Figure 25

Country Description of waste sources included

Australia MSW, C&I and C&D waste. Includes all solid wastes (non-hazardous and hazardous), liquid

hazardous wastes and fly ash from coal fired power generation. Excludes waste from primary

production activities, waste that is reused, pre-consumer waste recycled as part of a production

process and clean fill/soil.

Denmark Households, industry, service sector (incl. public institutions), utilities and other commerce, C&D.

New Zealand Waste from domestic, commercial, industrial and institutional waste sources (but not C&D).

Norway Waste from industry, construction, service industries, private households and other businesses.

UK MSW, C&I and C&D waste.

United States MSW (which includes C&I waste) and C&D (but any energy recovery from C&D is excluded).

Australian National Waste Report 2016 Final

Page 27

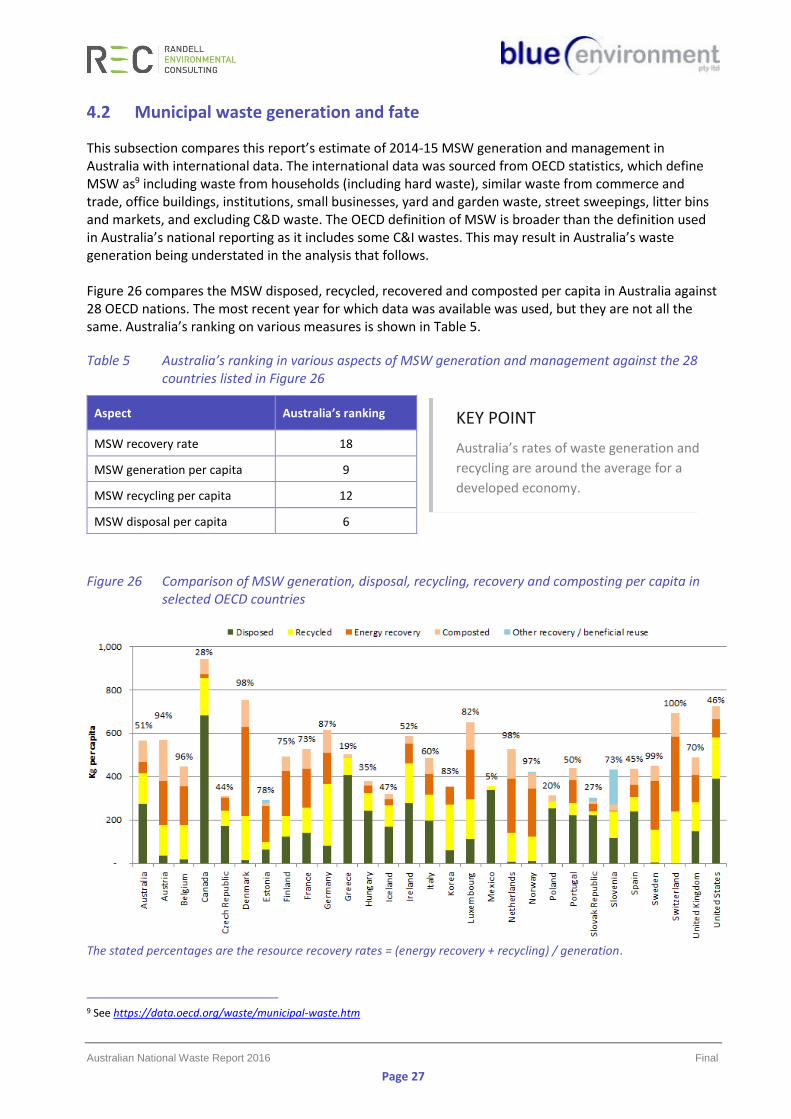

4.2 Municipal waste generation and fate

This subsection compares this report’s estimate of 2014-15 MSW generation and management in Australia with international data. The international data was sourced from OECD statistics, which define MSW as9 including waste from households (including hard waste), similar waste from commerce and trade, office buildings, institutions, small businesses, yard and garden waste, street sweepings, litter bins and markets, and excluding C&D waste. The OECD definition of MSW is broader than the definition used in Australia’s national reporting as it includes some C&I wastes. This may result in Australia’s waste generation being understated in the analysis that follows. Figure 26 compares the MSW disposed, recycled, recovered and composted per capita in Australia against 28 OECD nations. The most recent year for which data was available was used, but they are not all the same. Australia’s ranking on various measures is shown in Table 5.

Table 5 Australia’s ranking in various aspects of MSW generation and management against the 28 countries listed in Figure 26

Figure 26 Comparison of MSW generation, disposal, recycling, recovery and composting per capita in selected OECD countries

The stated percentages are the resource recovery rates = (energy recovery + recycling) / generation.

9 See https://data.oecd.org/waste/municipal-waste.htm

Aspect Australia’s ranking

MSW recovery rate 18

MSW generation per capita 9

MSW recycling per capita 12

MSW disposal per capita 6

KEY POINT

Australia’s rates of waste generation and

recycling are around the average for a

developed economy.

Australian National Waste Report 2016 Final

Page 28

5. Industry perspectives

Four peak associations representing the solid waste sector or elements of it were invited to provide their perspective in this National Waste Report. The associations were the Australian Council of Recycling (ACOR), Australian Landfill Owners Association (ALOA), Australian Organics Recycling Association (AORA) and the Waste Management Association of Australia (WMAA). Each of these organisations was asked to provide their perspective on the status of waste management, the challenges and opportunities facing the industry and where the industry should aim to be in 10 years.

Status of waste management Australia is one of the richest countries in the world yet we are losing the recycling race, ranked 17th among OECD nations. Australia’s waste generation has increased significantly by 23% between 2006-07 and 2014-

15. Australians are also generating more waste at 2.2 tonnes of waste per person per year. Waste is Australia’s most rapidly increasing environmental and economic metric, according to the ABS (2016). Challenges The recycling and resource recovery industry is being undermined by bad landfill levy design at the state level, with the technologically and commercially unavoidable residues from recycling subject to the landfill levy and, at the time of writing, one mainland state without a landfill levy. Levy alignment led by the Commonwealth would stop perverse outcomes such as interstate waste trafficking. In addition, waste levy revenue should be confined to waste management and resource recovery initiatives and illegal dumping, not propping up state budgets. While extended producer responsibility (EPR) is typically mandatory in many other OECD countries for problematic wastes, Australia is still behind with the only non-voluntary scheme being a co-regulatory National TV and Computer Recycling Scheme with a mere 50% target at the time of writing. Government procurement policies typically focus on lowest cost, with purchasing of recycled materials not mandated. Opportunities Given our advanced technology and economic development, there are great opportunities for the sector. Standardisation across states and territories, enhanced product stewardship and EPR schemes as well as better waste education to the public, are some examples of the opportunities facing the sector. Within 10 years, Australia should have a mandatory national product stewardship scheme for tyres, batteries and fluorescent lights and no e-waste should go to landfill. By 2026 Ten years from now, Australia should be aiming for world leading recycling rates and a vibrant and innovative reprocessing sector, delivering not only an essential service to the community, but also: reducing greenhouse gas emissions; reducing the amount of waste sent to landfills; conserving natural resources such as timber, water, and minerals; preventing pollution by reducing the need to collect new raw materials; saving energy; sustaining the environment for future generations; and creating new and innovative high technology jobs in the recycling and re-manufacturing industries. This report is a valuable resource that will assist us on an evidence-based path to a more viable, profitable and sustainable industry delivering benefits to the entire community.

Plastics baled for recycling

Australian National Waste Report 2016 Final

Page 29

Status of waste management In general terms, Australia’s waste management industry meets international best practice and provides a sustainable balance between meeting resource recovery expectations and keeping costs at affordable levels. The industry is committed to improving employee safety, enhancing environmental protection and minimising climate change impacts.

Challenges The waste industry currently recycles around half of the waste generated in Australia. The remainder – residuals from recycling and mixed putrescible wastes – is landfilled. Each of these activities has its challenges:

• Recycling – The recycling industry comprises three segments construction materials; organics; and discarded packaging. Notwithstanding recent advances in processing technology across the three segments, growth continues to be hindered by the availability of secure markets for the various products produced.

• Landfill – Major landfill practices have improved significantly over the past twenty years and now are at world's best practice. This is evidenced by most sites embracing composite liners, leachate extraction and disposal capability, landfill gas combustion and responsible long term rehabilitation and after use. Unfortunately, many smaller regional landfills are not at this standard and more needs to be done to close the poorer quality sites and provide local waste transfer facilities.

Other challenges facing landfills include the permitting of replacement facilities and managing the receipt of recoverable materials such as e-waste and tyres. Opportunities As concern over climate change continues to influence environmental policy, the waste industry is well positioned to contribute to emission reduction by diverting organics from landfills for processing. This initiative has commenced in some city markets but has considerable scope for expansion. Diverting organics from landfill has a double benefit – reduced landfill gas emissions and sequestered soil carbon contributing to improved farm production. Other opportunities are also now becoming available from the use of mechanised waste sorting technology that allows acceptance of organic wastes with higher levels of contamination without compromising product quality. By 2026 The waste industry has seen much change over the past 20 years and this trend will continue for the next 10. Many of these changes will be driven as new harmonisation programs lift the service levels in regional levels. Further, it is expected that energy from waste will begin to be introduced over the next decade.

Woodlawn landfill is licensed to accept over a million tonnes of waste per year from Sydney and surrounds.

Picture kindly supplied by Veolia Environmental Services

Australian National Waste Report 2016 Final

Page 30