Embed Size (px)

Citation preview

Australian Water SummitAustralian Water SummitSydney March 2006Sydney March 2006

Is privatisation of water infrastructure and services the answer?

Phillip Mills

Director of Water Services, Water UK

www.water.org.uk

Australian Water Summit 2006 2

Is privatisation of water Is privatisation of water infrastructure and services the infrastructure and services the answer?answer?

1. Understanding the UK privatisation experience

2. The appropriate role of regulation

3. Asset management and risk management

4. Key issues for large scale capital projects

5. Customers

6. Challenges in the UK

Australian Water Summit 2006 3

Understanding the UK privatisation Understanding the UK privatisation experienceexperience

• Privatisation in England and Wales – 1989• Water Authorities to Water PLCs

• Water only Companies continue

• Changes in Scotland and Northern Ireland• A different approach

Australian Water Summit 2006 4

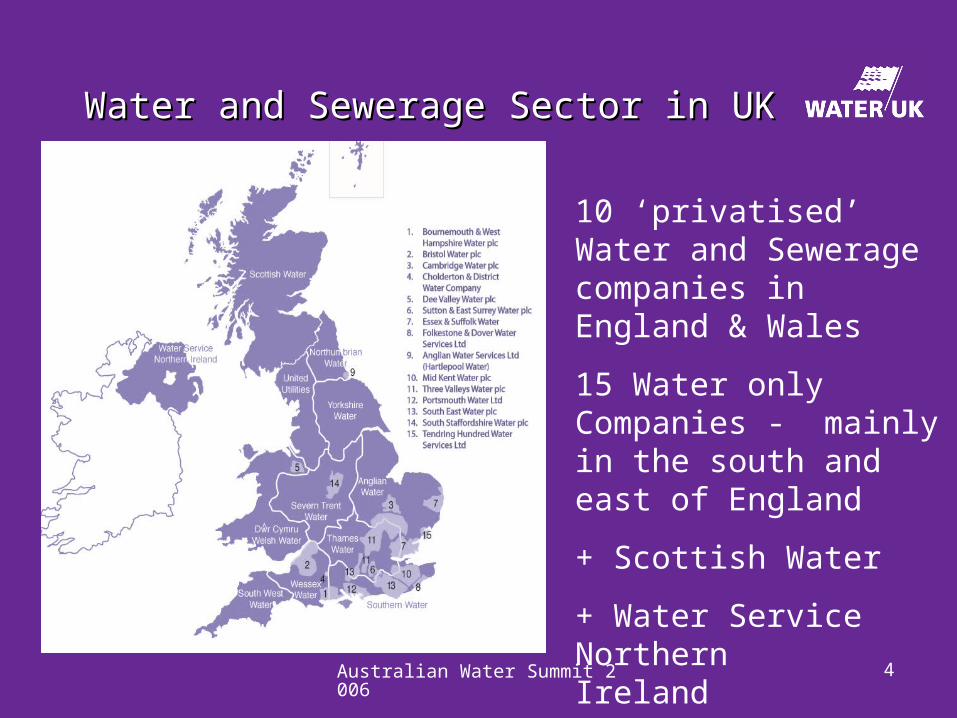

10 ‘privatised’ Water and Sewerage companies in England & Wales

15 Water only Companies - mainly in the south and east of England

+ Scottish Water

+ Water Service Northern Ireland

Water and Sewerage Sector in UKWater and Sewerage Sector in UK

Australian Water Summit 2006 5

Understanding the UK privatisation Understanding the UK privatisation experienceexperience

• Privatisation in England and Wales – 1989• Water Authorities to Water PLCs

• Water only Companies continue

• Changes in Scotland and Northern Ireland• A different approach

• Vertically integrated companies

• Early issues

• Developing businesses

• Ownership changes

Australian Water Summit 2006 6

Understanding the UK privatisation Understanding the UK privatisation experience - benefitsexperience - benefits

• Companies have control (within regulatory framework)• Companies can manage own relationships

• Stakeholders• Investors• Supply Chain

• Significant investment • Improved service – to customers and environment

Privatisation has delivered in Water - but accept its not the only way

Australian Water Summit 2006 7

The appropriate role of regulationThe appropriate role of regulation

Key regulators -

Water companiesWater companies

guardians of drinking water qualityDRINKING WATER INSPECTORATE

Australian Water Summit 2006 8

The appropriate role of The appropriate role of (economic) regulation(economic) regulation

Protecting the customer, ensuring “prices are only what they need to be”, through….• Independent regulation

• Comparative competition

• Periodic Reviews (5year) and price caps [RPI ± X]

• Challenging efficiency targets and incentives

• License conditions and ringfencing

To ensure companies can finance their functions

Clear and transparent regulatory regime – minimising uncertainty and regulatory risk

Australian Water Summit 2006 9

The appropriate role of regulationThe appropriate role of regulation

Moving forward – Future Regulation

Objectives -

1. A long term strategic framework

2. More consistent and coordinated regulation

3. Regulation to deliver an appropriate risk-return balance

4. Simpler, smarter regulation

5. Enhanced accountability all round

Australian Water Summit 2006 10

Asset management and risk Asset management and risk managementmanagement

Australian Water Summit 2006 11

Asset Investment since PrivatisationAsset Investment since Privatisation

Privatisation

Actual and projected capital investment 1981 – 2010 Source: Ofwat

Capital Maintenance

Quality and other improvements

Australian Water Summit 2006 12

Asset Investment – moving forwardAsset Investment – moving forward

0

1

2

3

4

5

6

7

8

9

£ billion

Capital maintenance Supply / demandbalance

Qualityenhancements

Enhanced servicelevels

Capital Investment assumptions 2005-10

Sewerage

Water source Ofwat

Total spend

£16.8 billion

Australian Water Summit 2006 13

Asset management and risk Asset management and risk managementmanagement

Asset ManagementAsset Management

• Common Framework for Capital Maintenance

- developed with the Regulators

- forward looking risk based approach

- balance between proactive and reactive maintenance as well as opex v capex solutions.

- demonstrates economic levels of capital maintenance.

Australian Water Summit 2006 14

Asset management and risk Asset management and risk managementmanagement

Asset ManagementAsset Management• 5 year AMP programme• Ofwat challenges• Regulatory drivers - Efficiency

frontier and catch up• Building long term relationships or

Partnering• Continuous improvement

Issues?• Sustainability of Supply Chain?• Skills and available workforce?

Australian Water Summit 2006 15

Key issues for large scale capital Key issues for large scale capital projectsprojects

AMP4 Investment Programme 2005-2010

£16.8 billion (39.8bn AUD)

• Funding• Investigations• Planning delays• Changing / uncertain quality

requirements

Australian Water Summit 2006 16

Asset management and risk Asset management and risk managementmanagement

Risk Management

• At company strategic business level

• At operating level e.g. • Water Safety Plans,

• Security measures and Contingency Planning

Australian Water Summit 2006 17

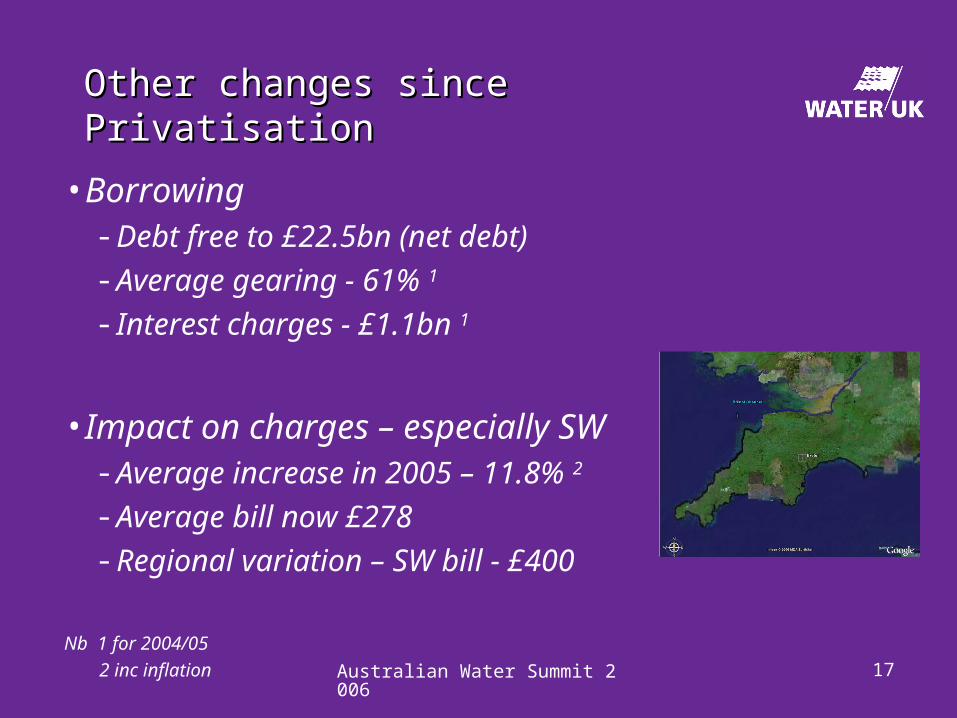

Other changes since PrivatisationOther changes since Privatisation

• Borrowing- Debt free to £22.5bn (net debt)

- Average gearing - 61% 1

- Interest charges - £1.1bn 1

• Impact on charges – especially SW- Average increase in 2005 – 11.8% 2

- Average bill now £278

- Regional variation – SW bill - £400

Nb 1 for 2004/05

2 inc inflation

Australian Water Summit 2006 18

Customer service Customer service

Australian Water Summit 2006 19

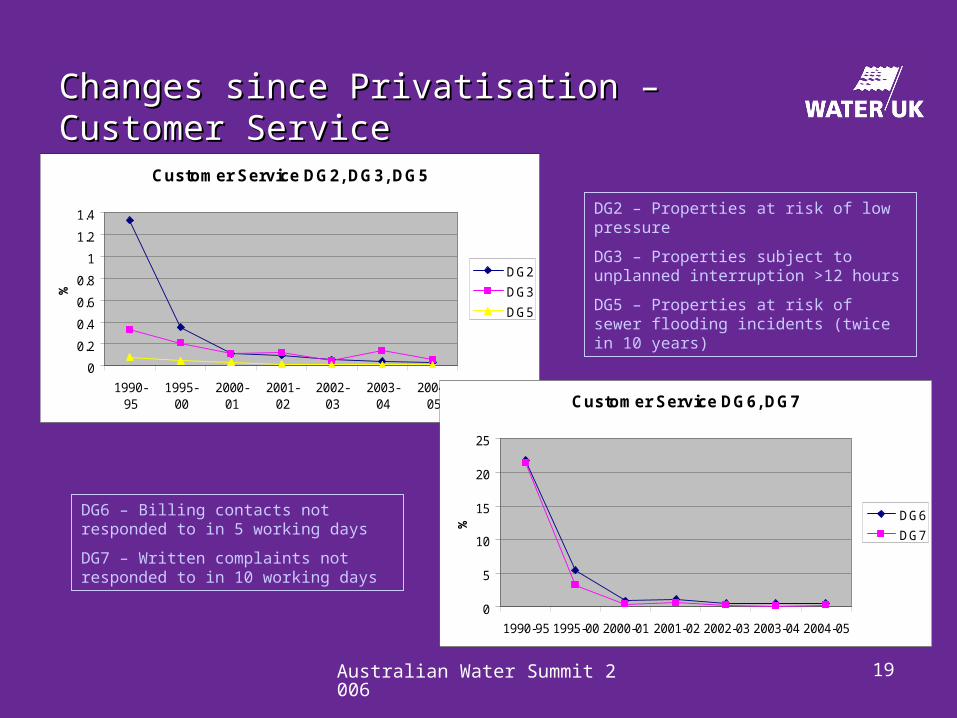

Changes since Privatisation – Customer Changes since Privatisation – Customer ServiceService

Customer Service DG2, DG3, DG5

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1990-95

1995-00

2000-01

2001-02

2002-03

2003-04

2004-05

%

DG2

DG3

DG5

Customer Service DG6, DG7

0

5

10

15

20

25

1990-95 1995-00 2000-01 2001-02 2002-03 2003-04 2004-05

%

DG6

DG7

DG2 – Properties at risk of low pressure

DG3 – Properties subject to unplanned interruption >12 hours

DG5 – Properties at risk of sewer flooding incidents (twice in 10 years)

DG6 – Billing contacts not responded to in 5 working days

DG7 – Written complaints not responded to in 10 working days

Australian Water Summit 2006 20

Challenges in the UKChallenges in the UK

• Climate Change• Demand management• Access to funding• Ongoing investment• Affordability• Competition

Australian Water Summit 2006 21

Is privatisation of water infrastructure and services the answer?

Results….Industry has delivered…

High levels of

InvestmentCustomer Service

Improvements Drinking Water Improvements Environmental

Improvements

cost effectively and efficiently