Embed Size (px)

Citation preview

1 | P a g e

AUTOMOBILE INDUSTRY REPORT

December 11th, 2013

SECTORAL REPORTS

B. Anil Kumar

Equity Analyst

Equity Research Desk

Highlights

The India auto industry closed 2012-13 with a sales dip of 6.7%, the

first drop in 12 years. The outlook for 2013-14 isn't much brighter,

with expects a growth of 3-5%.

During April-November 2013, overall automobile exports grew by

5.52 percent. Passenger Vehicles, Three Wheelers and Two Wheelers

registered growth at 9.64 percent 16.98 percent and 3.41 percent

respectively, while Commercial Vehicles declined by 12.31 percent

during April-November 2013 compared to the same period last year.

The cumulative foreign direct investment (FDI) inflow into the Indian

automobile industry during April 2000 to July 2013 was recorded at

US$ 8,932 million, amounting to 4.5 per cent of the total FDI inflows.

Hero MotoCorp will plan to enter into 50 countries with 20

manufacturing facilities across the globe and 100 million cumulative

two-wheelers sold by 2020.

Nissan Motor India has entered into an agreement with Ennore Port

Ltd (EPL), to export at least 60,000 cars a year through the port for the

next 10 years.

HMIL has invested US$ 2 billion in two state-of-the-art passenger car

manufacturing facilities in India. Moreso, India contributes 25 per cent

of the firm’s global sales.

The Government of India plans to introduce fuel-efficiency ratings for

automobiles to encourage sale of cars that consume less petrol or

diesel.

Global suppliers are setting up R&D centers in India to increase local

content in vehicles and at the same time leverage it as a global hub for

design and technology.

Japanese auto-maker Isuzu Motors is setting up its first car plant in

South India at an investment of Rs 3,000 crore and is expected to

become operational by 2016.

The automotive sector’s contribution to the gross domestic product

(GDP) is expected to double reaching a turnover worth US$ 145 billion

in 2016, according to the Automotive Mission Plan (AMP) 2006-2016.

2 | P a g e

CONTENTS

1. Industry Overview 03

2. Performance of Automobile Industry in India 2013 03

3. Automobile Industry in India 07

4. Production in the Indian Automobile Industry 09

5. Trends in the Indian Automobile Industry 10

6. Growth drivers for Automobile Sector 11

7. Automobile Industry Companies in India 12

MARUTI SUZUKI INDIA LTD

TATA MOTORS LTD

MAHINDRA & MAHINDRA LTD

HERO MOTOCORP LTD

BAJAJ AUTO LTD

EICHER MOTORS LTD

TVS MOTOR COMPANY LTD

ATUL AUTO LTD

8. Advantages in India 54

9. Key Developments & Investments 55

10. Increasing investments by global car manufacturers 56

11. Government initiatives 56

12. Industry Challenges Industry 57

13. Key Opportunities 58

14. Conclusion 59

3 | P a g e

1. Industry Overview

With the increasing growth in demand on back of rising income, expanding middle class and young population

base, in addition to a large pool of skilled manpower and growing technology, will propel India to be among the

world's top five auto-producers by 2015. India is also one of the key markets for hybrid and electric medium-

heavy-duty trucks and buses.

Indian automobile industry contributes significantly to the overall GDP of the nation and also provides significant

business and employment opportunities. It is an engine of growth for the Indian economy. It is one of the key

industries whose well being is very important in our vision of improving the living standard of our population.

According to the Society for Indian Automobile Manufacturers (SIAM), the automobile industry has already

invested Rs. 70,000 crores in the past four years in building new factories, adding fresh capacity and bringing out

new products. It is driven by a sustained increase in vehicle population and an increasing preference towards

higher-end vehicles with rising consumer aspirations (Volvo registered 155% increased growth of its luxury

segment in 2012).

In Export business, during April-November 2013, overall automobile exports grew by 5.52 percent. Passenger

Vehicles, Three Wheelers and Two Wheelers registered growth at 9.64 percent 16.98 percent and 3.41 percent

respectively, while Commercial Vehicles declined by 12.31 percent during April-November 2013 compared to

the same period last year.

2. Performance of Automobile Industry in India 2013

Two-wheelers

Improved income prospects to drive two-wheeler sales in 2013-14

After a robust 2010-11, growth in total domestic two-wheeler sales slowed to 14.1 per cent in 2011-12. In

2012-13, growth in domestic two-wheeler sales slowed further to 2.9 per cent, as slow in incomes, especially

in rural areas, high fuel prices impacted consumer sentiment. Exports declined by 1 per cent y-o-y over a 27

per cent growth in 2011-12, mainly due to the drop in export incentives post the withdrawal of the DEPB

scheme, unfavorable policy actions in key Asian markets and higher competition in African markets.

In 2013-14, growth is expected to recover modestly to 6-8 per cent on expectations of normal monsoons

aiding healthy rural incomes, recovery urban incomes and lower fuel prices. However the growth will remain

in single digits. Over the long term, the under penetrated rural market will hold the key to the industry’s

growth.

4 | P a g e

Exports growth to remain robust with new launches by players

Two-wheeler exports grew by 27 per cent in 2011-12, as volumes remained buoyant despite the

discontinuation of the DEPB scheme during the year.

In 2012-13, however, two-wheeler exports fell by 1 per cent owing to the following reasons:

The withdrawal of the DEPB scheme and subsequent reductions in incentives under the Duty Drawback

scheme forced to players to hike prices across markets. Since most of these are price-sensitive segments

(economy motorcycles account for over 50 per cent of total exports), the price hikes directly impacted

demand.

Unfavorable policy actions in some major markets like Sri Lanka, wherein 100 per cent import duties

were imposed on two-wheelers.

Higher competition in African markets where Honda Motorcycles (Japan) and a number of Chinese

manufactures entered the market with aggressively priced products.

In 2013-14, growth is expected to recover to 11-13 per cent because of fewer policy-related disruptions and

new launches.

Commercial vehicles

CV Sales Volumes decline in 201-13, to revive in 2013-14 on higher GDP expectations

Key macroeconomic indicators such as IIP, rail freight loading, mining, road awarding and execution, and

growth in port traffic remained weak during 2012-13, thereby impacting CV sales. CV sales declined by 2 per

cent (y-o-y) in 2012-13, after growing by 28.5 per cent and 18 per cent respectively in 2010-11 and 2011-12.

Sales of medium and heavy commercial vehicles (MHCV’s), which are directly linked to the level of economic

activity, declined by 25.9 per cent in 2012-13 following deceleration in GDP growth to 5.0 per cent. Lower

Industrial and agricultural output, weak transporter sentiments – weighed down by increase in fuel prices,

high interest rates, inflation and higher vehicle prices – continued to impact MHCV sales. Other factors that

had a bearing on sales growth were availability of finance, and subdued freight rtes. In contrast, LCV sales

proved to be relatively resilient to the slowdown in GDP growth, and grew at 15.9 per cent.

5 | P a g e

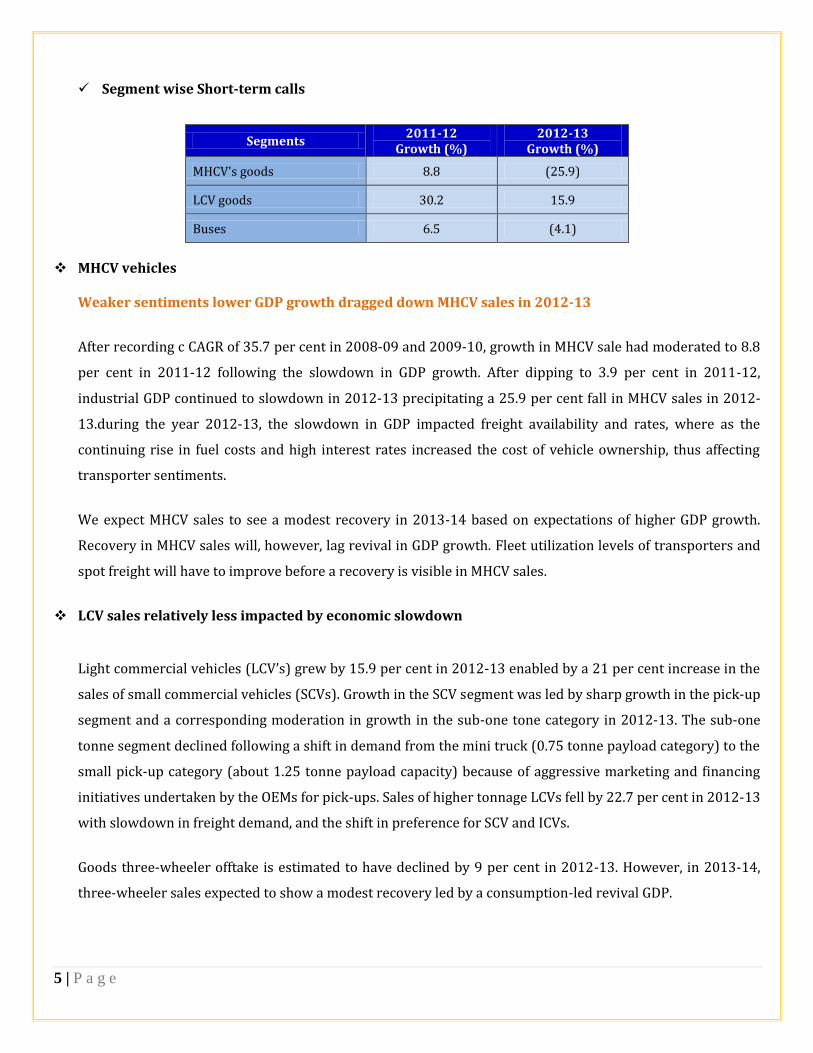

Segment wise Short-term calls

Segments 2011-12

Growth (%) 2012-13

Growth (%)

MHCV's goods 8.8 (25.9)

LCV goods 30.2 15.9

Buses 6.5 (4.1)

MHCV vehicles

Weaker sentiments lower GDP growth dragged down MHCV sales in 2012-13

After recording c CAGR of 35.7 per cent in 2008-09 and 2009-10, growth in MHCV sale had moderated to 8.8

per cent in 2011-12 following the slowdown in GDP growth. After dipping to 3.9 per cent in 2011-12,

industrial GDP continued to slowdown in 2012-13 precipitating a 25.9 per cent fall in MHCV sales in 2012-

13.during the year 2012-13, the slowdown in GDP impacted freight availability and rates, where as the

continuing rise in fuel costs and high interest rates increased the cost of vehicle ownership, thus affecting

transporter sentiments.

We expect MHCV sales to see a modest recovery in 2013-14 based on expectations of higher GDP growth.

Recovery in MHCV sales will, however, lag revival in GDP growth. Fleet utilization levels of transporters and

spot freight will have to improve before a recovery is visible in MHCV sales.

LCV sales relatively less impacted by economic slowdown

Light commercial vehicles (LCV’s) grew by 15.9 per cent in 2012-13 enabled by a 21 per cent increase in the

sales of small commercial vehicles (SCVs). Growth in the SCV segment was led by sharp growth in the pick-up

segment and a corresponding moderation in growth in the sub-one tone category in 2012-13. The sub-one

tonne segment declined following a shift in demand from the mini truck (0.75 tonne payload category) to the

small pick-up category (about 1.25 tonne payload capacity) because of aggressive marketing and financing

initiatives undertaken by the OEMs for pick-ups. Sales of higher tonnage LCVs fell by 22.7 per cent in 2012-13

with slowdown in freight demand, and the shift in preference for SCV and ICVs.

Goods three-wheeler offtake is estimated to have declined by 9 per cent in 2012-13. However, in 2013-14,

three-wheeler sales expected to show a modest recovery led by a consumption-led revival GDP.

6 | P a g e

Small trucks continue to spur LCV sales

Small commercial vehicles (SCVs), comprising mini trucks and pick-ups, will remain the fastest growing

category in the light commercial vehicles (LCVs) segment. Led by player initiatives, pick-ups will continue to

outrun sub-one tonne sales in the near term. Sales of LCVs is expected to grow by 10-12 per cent in 2013-14.

While mini-trucks have almost entirely replaced the use of large three-wheelers, sales of micro-trucks will

drive sales growth.

Passenger vehicles

Bus sales growth fell in 2012-13

Bus sales declined by 4 percent in 2012-13, owing to slowdown in demand from State Transport

Undertakings (STUs) and cautious approach undertaken by private operators towards new investments.

Demand form private operators, particularly contract operators plying buses for school and corporate

segments, has been affected by the slowdown in the service sector (especially the IT/ITeS sector) and in

ability of these operators to pass on the continues increase in fuel cost. A revival in sales is, however, likely in

2013-14, with expected improvement in demand from contrast operators, following a recovery in the

services sector, as well as from STUs.

PV sales grew at sub-5 per cent levels for second consecutive year

Domestic sales of cars and utility vehicles (UVs) grew by merely 2 per cent in 2012-13 despite a low base in

2011-12. Domestic car sales, which had increased by 3 per cent in 2011-12, declined by 7 percent in 2012-13.

Growth was impacted due to weak macroeconomic growth, uncertainly over income growth, increasing

petrol prices, high interest rates and lower disposable income caused by high inflation. Additionally, a

lockout at market leader Maruti Suzuki India’s Ltd (MSIL) Manesar production facility, and the consequent

disruption in production, impacted growth marginally.

On the other hand, domestic utility vehicles (UVs) including vans, grew by 32 per cent during 2012-13

because of new model launches during the year and also due to increased preference for diesel vehicles.

Domestic car and UV sales to recover slowly in 2013-14

We expect passenger vehicle sales to grow by 5-7 per cent in 2013-14 over a 2 per cent growth in 2012-13.

Macroeconomic recovery and decline in petrol prices would aid a revival in small car sales. We expect utility

vehicle sales to continue to grow, led by new model launches. However, growth will be capped at 9-11 per

7 | P a g e

cent on account of diesel price hikes. Long term growth prospects will remain healthy until 2017-78, as

passenger vehicle penetration is currently at low levels.

Exports stage a recovery in 2012-13

Exports of cars & utility vehicles (UVs) grew by 9 per cent in 2012-13 after a marginal decline of 0.4 per cent

in 2011-12.weak global demand, especially in Europe, one of the largest export markets, had impacted

demand in 2011-12. In 2012-13, sluggish demand in Europe and increase in import and excise duty rates in

Sri Lanka, which accounts for nearly 5 per cent of the total exports like MSIL, restricted growth to single

digits.

3. Automobile Industry in India

The Indian automotive industry is currently going through one of its most challenging phases so far. Vehicle sales

are set to register a negative growth in 2013 – first time in more than a decade – compared with the previous

year. Official data shows that vehicle sales in India declined at a high single digit rate year on year in the first nine

months of 2013 compared to 2012. This downward spiral has prompted automakers and suppliers to cut

production to avoid excess inventory build-up. Besides, there's little respite on the cost front. Though there has

recently been some softening in raw materials prices, other costs such as wages, cost of power and finance

expenses, continue to erode suppliers' operating margins. Car sales in India are expected to fall in the current

financial year, marking a second straight year of decline, as high interest rates and a slowing economy force

consumers to delay purchases.

The weakness in the automotive market has taken its toll on the investment drive of many suppliers. While

international suppliers have continued their investments in India, citing the country's long-term growth

prospects, local suppliers have almost put their expansion plans on hold until there is a sustained recovery in

vehicles sales. The Indian automotive industry at the moment is facing multiple challenges such as slowing

economic growth, high inflation and high interest rates – compared with many of its peers. IHS however is

sanguine about the country's growth trend in the medium to long term and forecasts recovery in vehicle sales in

2014, and high single-digit growth in vehicle sales for the rest of this decade. IHS expects vehicle sales in India to

grow at an average rate of 12.2% annually between 2014 and 2020; sales are expected to reach 7.1 million units

by 2020 compared with 3.6 million in 2012.

Key Statistics

The Indian automobile industry produced a total 1.69 million vehicles including passenger vehicles, commercial

vehicles, three wheelers and two wheelers in August 2013 as against 1.56 million in August 2012, registering a

growth of 8.18 percent over the same month last year.

8 | P a g e

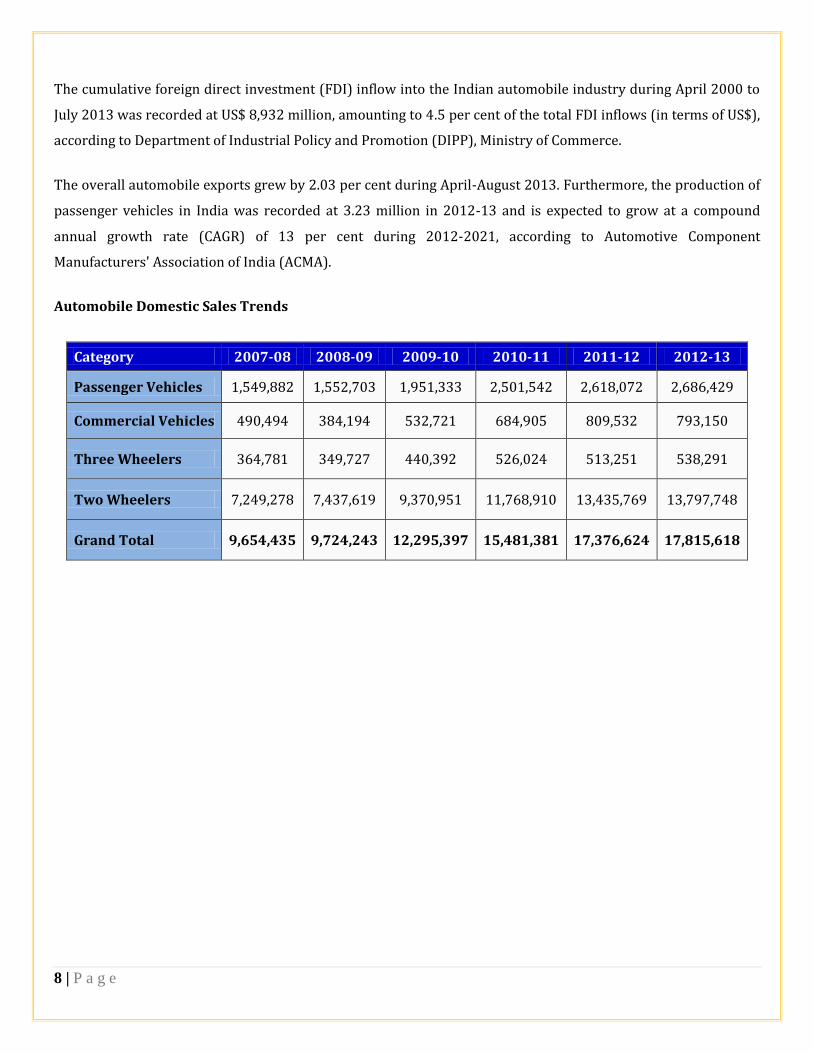

The cumulative foreign direct investment (FDI) inflow into the Indian automobile industry during April 2000 to

July 2013 was recorded at US$ 8,932 million, amounting to 4.5 per cent of the total FDI inflows (in terms of US$),

according to Department of Industrial Policy and Promotion (DIPP), Ministry of Commerce.

The overall automobile exports grew by 2.03 per cent during April-August 2013. Furthermore, the production of

passenger vehicles in India was recorded at 3.23 million in 2012-13 and is expected to grow at a compound

annual growth rate (CAGR) of 13 per cent during 2012-2021, according to Automotive Component

Manufacturers' Association of India (ACMA).

Automobile Domestic Sales Trends

Category 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Passenger Vehicles 1,549,882 1,552,703 1,951,333 2,501,542 2,618,072 2,686,429

Commercial Vehicles 490,494 384,194 532,721 684,905 809,532 793,150

Three Wheelers 364,781 349,727 440,392 526,024 513,251 538,291

Two Wheelers 7,249,278 7,437,619 9,370,951 11,768,910 13,435,769 13,797,748

Grand Total 9,654,435 9,724,243 12,295,397 15,481,381 17,376,624 17,815,618

9 | P a g e

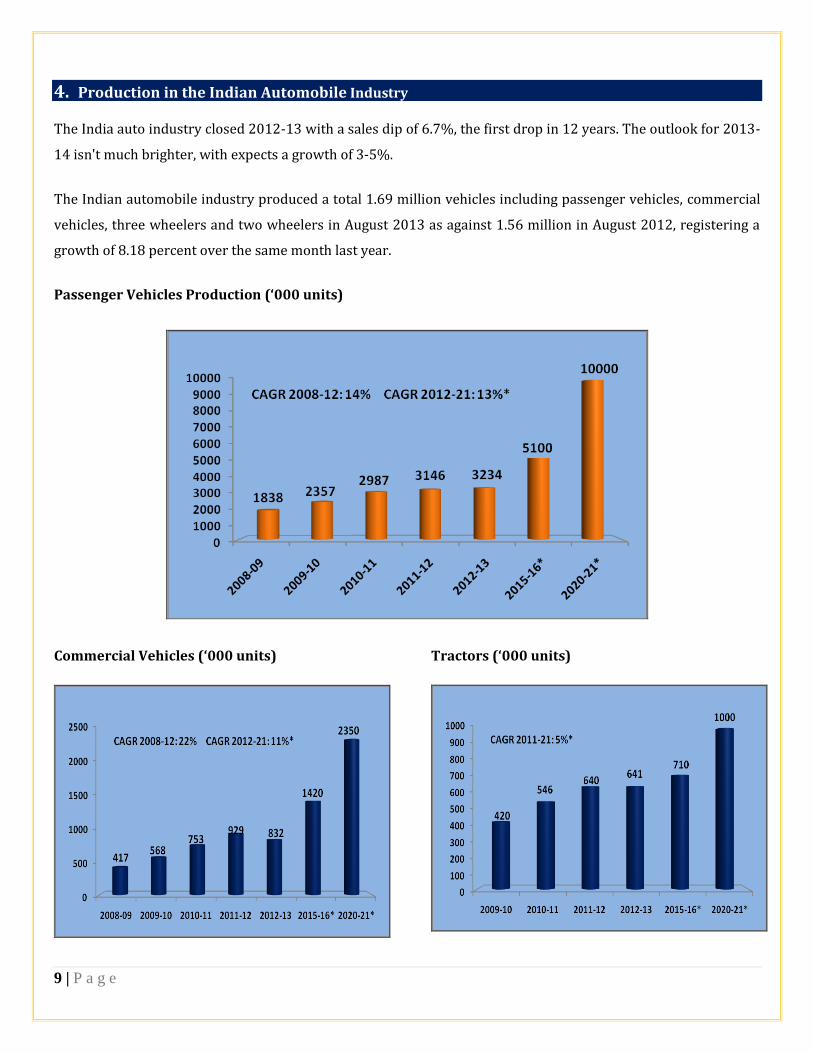

4. Production in the Indian Automobile Industry

The India auto industry closed 2012-13 with a sales dip of 6.7%, the first drop in 12 years. The outlook for 2013-

14 isn't much brighter, with expects a growth of 3-5%.

The Indian automobile industry produced a total 1.69 million vehicles including passenger vehicles, commercial

vehicles, three wheelers and two wheelers in August 2013 as against 1.56 million in August 2012, registering a

growth of 8.18 percent over the same month last year.

Passenger Vehicles Production (‘000 units)

Commercial Vehicles (‘000 units)

Tractors (‘000 units)

10 | P a g e

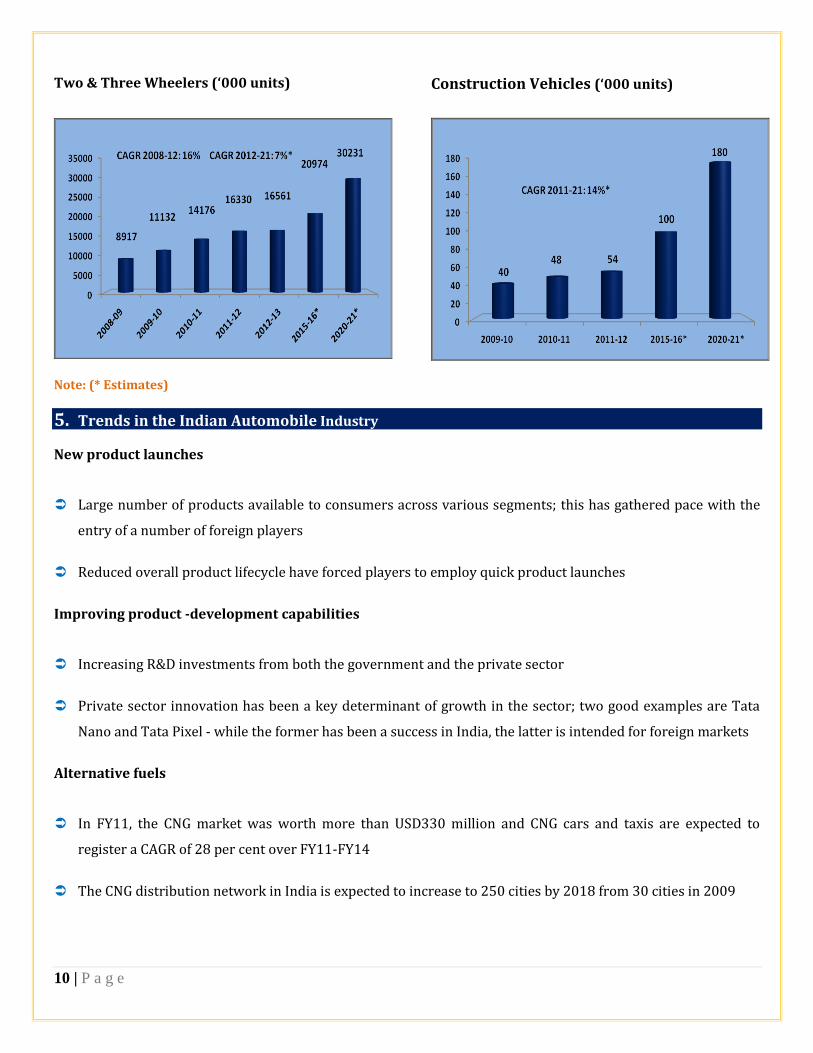

Two & Three Wheelers (‘000 units)

Construction Vehicles (‘000 units)

Note: (* Estimates)

5. Trends in the Indian Automobile Industry

New product launches

Large number of products available to consumers across various segments; this has gathered pace with the

entry of a number of foreign players

Reduced overall product lifecycle have forced players to employ quick product launches

Improving product -development capabilities

Increasing R&D investments from both the government and the private sector

Private sector innovation has been a key determinant of growth in the sector; two good examples are Tata

Nano and Tata Pixel - while the former has been a success in India, the latter is intended for foreign markets

Alternative fuels

In FY11, the CNG market was worth more than USD330 million and CNG cars and taxis are expected to

register a CAGR of 28 per cent over FY11-FY14

The CNG distribution network in India is expected to increase to 250 cities by 2018 from 30 cities in 2009

11 | P a g e

Upcoming trends

India is emerging as a strong automotive R&D hub with foreign players like Hyundai, Suzuki, and General

Motors setting up base in India. This move is further enhanced by Government’s support towards setting up

centres for development and innovation. Tata Nano’s successful entry in the Indian market has steamed up

the opportunities of growth available in alternative segments like electric cars, vehicles run on natural gas,

etc.

6. Growth drivers for Automobile Sector

Factors that will drive growth in the sector

Rising incomes among Indian population will lead to increased affordability, increasing domestic demand for

vehicles, especially in the small car segment.

Fuel economy and demand for greater fuel efficiency is a major factor that affects consumer purchase

decision that will bring leading companies across two-wheeler and four-wheeler segment to focus on

delivering performance-oriented products.

Product innovation and market segmentation will channelize growth. Vehicles based on alternative fuels will

be an area of interest for both consumers and auto makers.

Focus on establishing India as auto-manufacturing hub is reigning in policy support in form of Government’s

technology modernization fund.

Industry will seek to augment sales by tapping into rural markets, youth, women and luxury segments.

12 | P a g e

7. Automobile Industry Companies in India

MARUTI SUZUKI INDIA LTD

Maruti Suzuki India Limited (MSIL, formerly known as Maruti Udyog Limited) is a subsidiary of Suzuki Motor

Corporation, Japan. Maruti Suzuki has been the leader of the Indian car market for over two and a half decades.

The company has two manufacturing facilities located at Gurgaon and Manesar, south of New Delhi, India. Both

the facilities have a combined capability to produce over a 1.5 million (1,500,000) vehicles annually. The

company plans to expand its manufacturing capacity to 1.75 million by 2013. Maruti Suzuki is India’s largest

passenger vehicle company with a market share close to 40% which offers 14 models with over 200 variants

across the Industry segments like: Passenger cars, Utility vehicles and Vans.

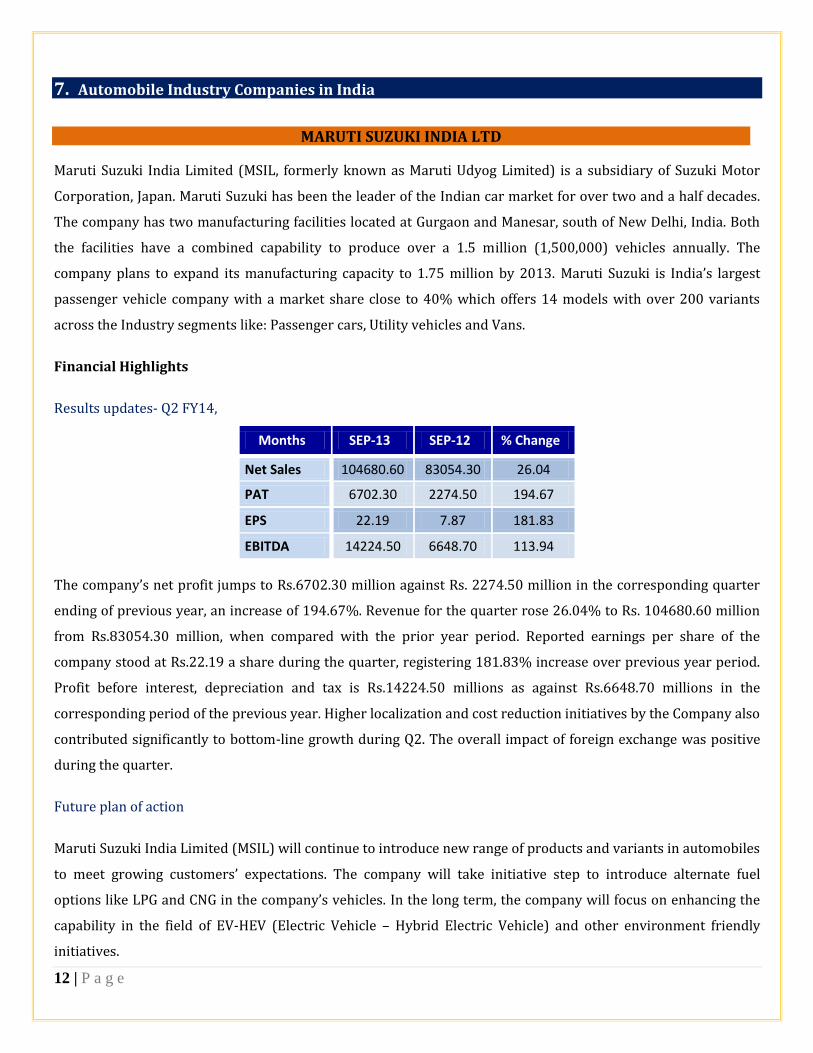

Financial Highlights

Results updates- Q2 FY14,

Months SEP-13 SEP-12 % Change

Net Sales 104680.60 83054.30 26.04

PAT 6702.30 2274.50 194.67

EPS 22.19 7.87 181.83

EBITDA 14224.50 6648.70 113.94

The company’s net profit jumps to Rs.6702.30 million against Rs. 2274.50 million in the corresponding quarter

ending of previous year, an increase of 194.67%. Revenue for the quarter rose 26.04% to Rs. 104680.60 million

from Rs.83054.30 million, when compared with the prior year period. Reported earnings per share of the

company stood at Rs.22.19 a share during the quarter, registering 181.83% increase over previous year period.

Profit before interest, depreciation and tax is Rs.14224.50 millions as against Rs.6648.70 millions in the

corresponding period of the previous year. Higher localization and cost reduction initiatives by the Company also

contributed significantly to bottom-line growth during Q2. The overall impact of foreign exchange was positive

during the quarter.

Future plan of action

Maruti Suzuki India Limited (MSIL) will continue to introduce new range of products and variants in automobiles

to meet growing customers’ expectations. The company will take initiative step to introduce alternate fuel

options like LPG and CNG in the company’s vehicles. In the long term, the company will focus on enhancing the

capability in the field of EV-HEV (Electric Vehicle – Hybrid Electric Vehicle) and other environment friendly

initiatives.

13 | P a g e

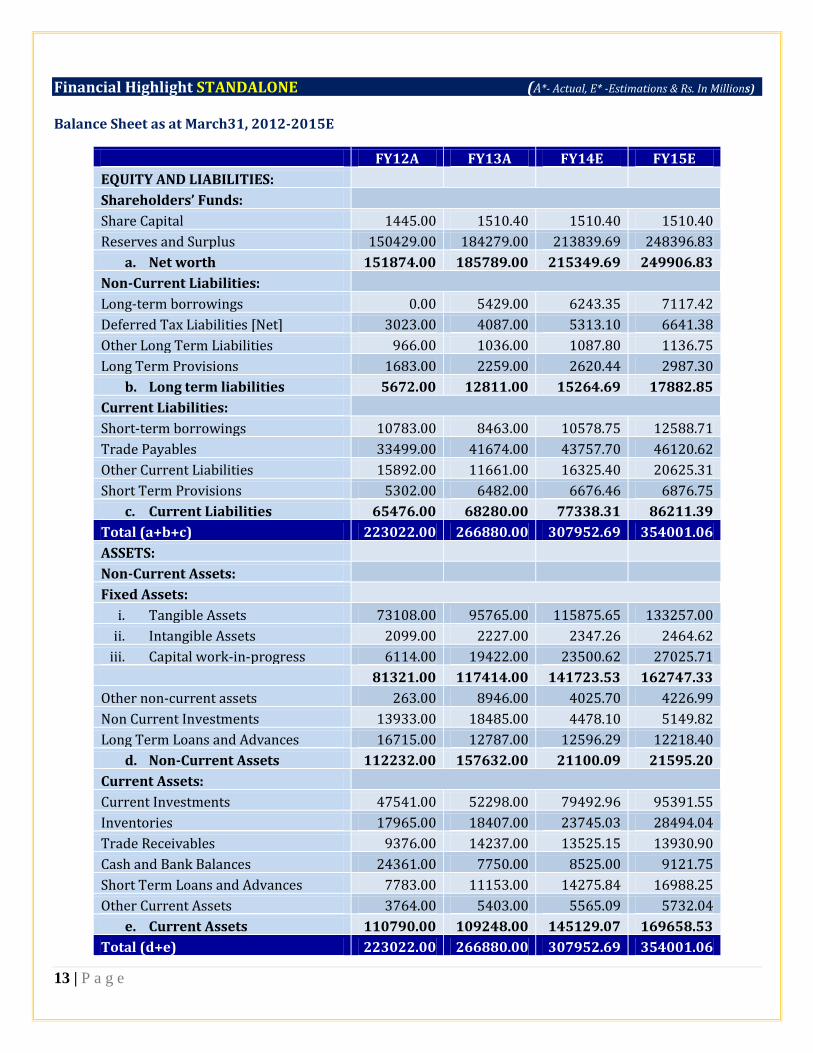

Financial Highlight STANDALONE (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March31, 2012-2015E

FY12A FY13A FY14E FY15E

EQUITY AND LIABILITIES: Shareholders’ Funds: Share Capital 1445.00 1510.40 1510.40 1510.40

Reserves and Surplus 150429.00 184279.00 213839.69 248396.83

a. Net worth 151874.00 185789.00 215349.69 249906.83

Non-Current Liabilities: Long-term borrowings 0.00 5429.00 6243.35 7117.42

Deferred Tax Liabilities [Net] 3023.00 4087.00 5313.10 6641.38

Other Long Term Liabilities 966.00 1036.00 1087.80 1136.75

Long Term Provisions 1683.00 2259.00 2620.44 2987.30

b. Long term liabilities 5672.00 12811.00 15264.69 17882.85

Current Liabilities: Short-term borrowings 10783.00 8463.00 10578.75 12588.71

Trade Payables 33499.00 41674.00 43757.70 46120.62

Other Current Liabilities 15892.00 11661.00 16325.40 20625.31

Short Term Provisions 5302.00 6482.00 6676.46 6876.75

c. Current Liabilities 65476.00 68280.00 77338.31 86211.39

Total (a+b+c) 223022.00 266880.00 307952.69 354001.06

ASSETS: Non-Current Assets: Fixed Assets: i. Tangible Assets 73108.00 95765.00 115875.65 133257.00

ii. Intangible Assets 2099.00 2227.00 2347.26 2464.62

iii. Capital work-in-progress 6114.00 19422.00 23500.62 27025.71

81321.00 117414.00 141723.53 162747.33

Other non-current assets 263.00 8946.00 4025.70 4226.99

Non Current Investments 13933.00 18485.00 4478.10 5149.82

Long Term Loans and Advances 16715.00 12787.00 12596.29 12218.40

d. Non-Current Assets 112232.00 157632.00 21100.09 21595.20

Current Assets: Current Investments 47541.00 52298.00 79492.96 95391.55

Inventories 17965.00 18407.00 23745.03 28494.04

Trade Receivables 9376.00 14237.00 13525.15 13930.90

Cash and Bank Balances 24361.00 7750.00 8525.00 9121.75

Short Term Loans and Advances 7783.00 11153.00 14275.84 16988.25

Other Current Assets 3764.00 5403.00 5565.09 5732.04

e. Current Assets 110790.00 109248.00 145129.07 169658.53

Total (d+e) 223022.00 266880.00 307952.69 354001.06

14 | P a g e

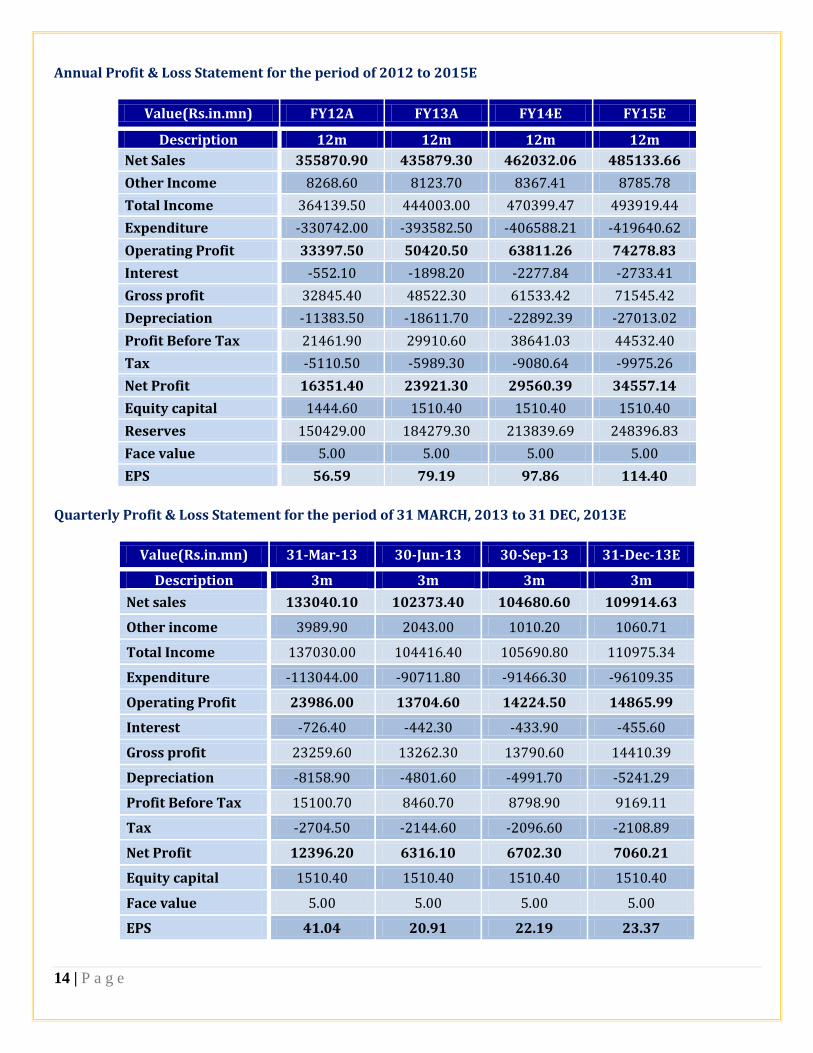

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 355870.90 435879.30 462032.06 485133.66

Other Income 8268.60 8123.70 8367.41 8785.78

Total Income 364139.50 444003.00 470399.47 493919.44

Expenditure -330742.00 -393582.50 -406588.21 -419640.62

Operating Profit 33397.50 50420.50 63811.26 74278.83

Interest -552.10 -1898.20 -2277.84 -2733.41

Gross profit 32845.40 48522.30 61533.42 71545.42

Depreciation -11383.50 -18611.70 -22892.39 -27013.02

Profit Before Tax 21461.90 29910.60 38641.03 44532.40

Tax -5110.50 -5989.30 -9080.64 -9975.26

Net Profit 16351.40 23921.30 29560.39 34557.14

Equity capital 1444.60 1510.40 1510.40 1510.40

Reserves 150429.00 184279.30 213839.69 248396.83

Face value 5.00 5.00 5.00 5.00

EPS 56.59 79.19 97.86 114.40

Quarterly Profit & Loss Statement for the period of 31 MARCH, 2013 to 31 DEC, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 133040.10 102373.40 104680.60 109914.63

Other income 3989.90 2043.00 1010.20 1060.71

Total Income 137030.00 104416.40 105690.80 110975.34

Expenditure -113044.00 -90711.80 -91466.30 -96109.35

Operating Profit 23986.00 13704.60 14224.50 14865.99

Interest -726.40 -442.30 -433.90 -455.60

Gross profit 23259.60 13262.30 13790.60 14410.39

Depreciation -8158.90 -4801.60 -4991.70 -5241.29

Profit Before Tax 15100.70 8460.70 8798.90 9169.11

Tax -2704.50 -2144.60 -2096.60 -2108.89

Net Profit 12396.20 6316.10 6702.30 7060.21

Equity capital 1510.40 1510.40 1510.40 1510.40

Face value 5.00 5.00 5.00 5.00

EPS 41.04 20.91 22.19 23.37

15 | P a g e

Ratio Analysis

Particulars FY12A FY13A FY14E FY15E

EPS (Rs.) 56.59 79.19 97.86 114.40

EBITDA Margin (%) 9.38% 11.57% 13.81% 15.31%

PBT Margin (%) 6.03% 6.86% 8.36% 9.18%

PAT Margin (%) 4.59% 5.49% 6.40% 7.12%

P/E Ratio (x) 28.25 20.19 16.34 13.98

ROE (%) 10.77% 12.88% 13.73% 13.83%

ROCE (%) 27.53% 34.57% 37.34% 37.57%

EV/EBITDA (x) 13.83 9.58 7.57 6.50

Book Value (Rs.) 525.66 615.03 712.89 827.29

P/BV 3.04 2.60 2.24 1.93

Outlook and Conclusion

At the current market price of Rs.1599.00, the stock P/E ratio is at 16.34 x FY14E and 13.98 x FY15E

respectively.

Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.97.86 and

Rs.114.40 respectively.

Net Sales and Operating Profit of the company are expected to grow at a CAGR of 11% and 28% over 2012 to

2015E respectively.

On the basis of EV/EBITDA, the stock trades at 7.57 x for FY14E and 6.50 x for FY15E.

Price to Book Value of the stock is expected to be at 2.24 x and 1.93 x respectively for FY14E and FY15E.

16 | P a g e

TATA MOTORS LTD

Tata Motors Limited is India's largest automobile company, with consolidated revenues of INR 1,88,818 crores

(USD 34.7 billion) in 2012-13. Through subsidiaries and associate companies, Tata Motors has operations in the

UK, South Korea, Thailand, Spain, South Africa and Indonesia.

It is the leader in commercial vehicles in each segment, and among the top in passenger vehicles with winning

products in the compact, midsize car and utility vehicle segments. It is also the world's fifth largest truck

manufacturer and fourth largest bus manufacturer.

The Tata Motors Group's over 60,000 employees are guided by the mission "to be passionate in anticipating and

providing the best vehicles and experiences that excite their customers globally."

Financial Highlights

India's largest automobile company, Tata Motors reported consolidated revenues (net of excise) of Rs.

568822.80 million for the quarter ended September 30, 2013, a growth of 31.06% over Rs. 434028.80 million for

the corresponding quarter of the previous year, despite weak operating environment in the India business which

was more than offset by increase in wholesale volumes and richer product and market mix at Jaguar Land Rover

(JLR). The Consolidated Profit before tax for the quarter was Rs.47523.90 million, a growth of 53.87% over

Rs.30886.00 million for the corresponding quarter of the previous year. The Consolidated Profit after tax (post

minority interest and profit/loss in respect of associate companies) for the quarter was Rs. 35418.60 million, a

growth of 70.71% over Rs. 20747.30 million for the corresponding quarter of the previous year.

During the quarter, Jaguar Land Rover has reported revenues of GBP 4,612 million, represented a growth of

40.3% over GBP 3,288 million in the corresponding quarter last year. During Q2 FY14, Operating margins stood

at 17.8%. Operating profit (EBITDA) of GBP 823 million in the quarter, represented a growth of 69.3% over GBP

486 million in the corresponding quarter last year. Continued strong revenue growth and operating performance

were supported by increase in wholesale volume, richer product mix, launch of new Range Rover Sport, new

Range Rover and Jaguar F-TYPE. PAT for the quarter grew by 66.2% to GBP 507 million against GBP 305 million

in the corresponding quarter last year. During the quarter, Tata Daewoo Commercial Vehicles Co. Ltd. registered

net revenues of KRW 202 billion and Net profit of KRW 4.4 billion as compared to KRW 205 billion and KRW 0.5

billion, respectively, in Q2 FY13.

The standalone revenues (net of excise) for the quarter ended September 30, 2013 stood at Rs. 88680 million, as

compared to Rs. 124810 million in Q2 FY13. For the quarter Q2 FY14, the operating margin stood at 2.0%.

17 | P a g e

Continued slowdown in economic activity, low level of transport freight and infrastructure activity, frequent

diesel price increases and tight financing environment, have impacted the industry during the quarter.

Tata Motors has entered into an Australian market with a sale of Tata Xenon through distributor Fusion

Automotive and it is an important milestone in the continued expansion of Tata Motors global footprint. The

Company plans to launch the new Tata Aria, the Tata Prima KL3TXF 6X4 Truck Tractor and Tata Ultra 812 Truck

in South Africa in 2014. JLR performance to remain strong led by product actions and continued growth in

emerging markets, particularly China.

Results updates- Q2 FY14,

Months Sep-13 Sep-12 % Change

Net Sales 568822.80 434028.80 31.06

PAT 35418.60 20747.30 70.71

EPS 11.00 6.50 69.18

EBITDA 88672.20 55404.40 60.05

Latest Updates

Standalone sales (including exports) of commercial and passenger vehicles for the quarter ended September

30, 2013, stood at 1,50,930 units, a decline of 32.5% as compared to the corresponding quarter last year.

During the quarter September 30, 2013, Jaguar Land Rover wholesale and retail volumes grew by 31.6% and

21.1% over the corresponding period last year to stood at 101,931 units and 102,644 units, respectively.

Tata Motors Group global sales in September 2013, including Jaguar Land Rover, were 87,316 nos.

Cumulative sales for the fiscal were 503,887 nos.

Tata Motors’ total sales (including exports) of Tata commercial and passenger vehicles in October 2013 were

1,638 vehicles. The company’s domestic sales of Tata commercial and passenger vehicles for October 2013

were 46,926 nos. Cumulative sales (including exports) for the company for the fiscal were 356,380 nos.

Tata Motors has released the new Tata Xenon for sale in Australia through distributor Fusion Automotive.

Entry into the Australian market marks an important milestone in the continued expansion of Tata Motors

global footprint.

18 | P a g e

Tata Motors has launched of the new Tata Nano CNG emax. The Tata Nano CNG emax is powered by a fuel

efficient, state-of-the-art engine, with CNG and Petrol bi-fuel system options.

PT Tata Motors Distribusi Indonesia (TMDI), wholly owned subsidiary of Tata Motors Ltd forayed into the

Indonesian automotive industry with the launch of three new exciting Tata passenger vehicles - the Tata Aria,

the Tata Vista and the Tata Safari Storme.

Tata Motors has launched the Tata Xenon Pick-up with best-in-class looks, operating economics and fuel

efficiency in the Nepal market.

Tata Motors has entered into partnership with DRB-HICOM, Malaysia's biggest conglomerate, for the import,

distribution and assembly of Tata Motors Commercial Vehicles in Malaysia.

19 | P a g e

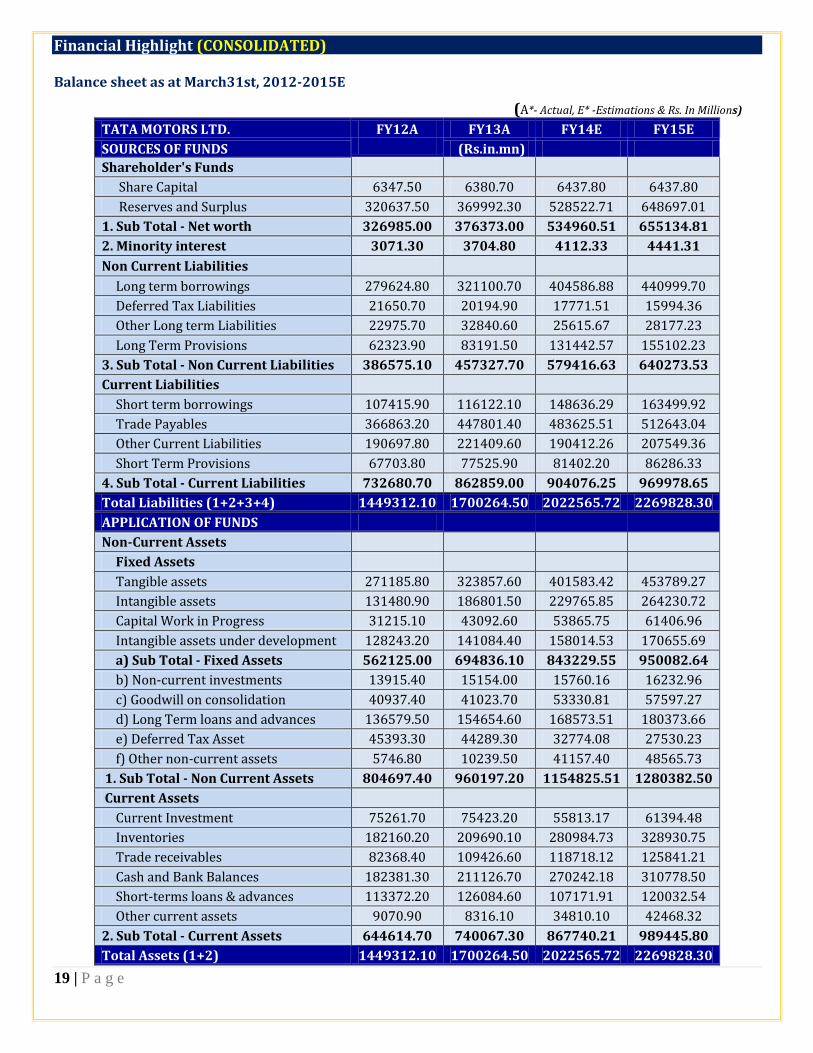

Financial Highlight (CONSOLIDATED)

Balance sheet as at March31st, 2012-2015E

(A*- Actual, E* -Estimations & Rs. In Millions)

TATA MOTORS LTD. FY12A FY13A FY14E FY15E

SOURCES OF FUNDS (Rs.in.mn)

Shareholder's Funds

Share Capital 6347.50 6380.70 6437.80 6437.80

Reserves and Surplus 320637.50 369992.30 528522.71 648697.01

1. Sub Total - Net worth 326985.00 376373.00 534960.51 655134.81

2. Minority interest 3071.30 3704.80 4112.33 4441.31

Non Current Liabilities

Long term borrowings 279624.80 321100.70 404586.88 440999.70

Deferred Tax Liabilities 21650.70 20194.90 17771.51 15994.36

Other Long term Liabilities 22975.70 32840.60 25615.67 28177.23

Long Term Provisions 62323.90 83191.50 131442.57 155102.23

3. Sub Total - Non Current Liabilities 386575.10 457327.70 579416.63 640273.53

Current Liabilities

Short term borrowings 107415.90 116122.10 148636.29 163499.92

Trade Payables 366863.20 447801.40 483625.51 512643.04

Other Current Liabilities 190697.80 221409.60 190412.26 207549.36

Short Term Provisions 67703.80 77525.90 81402.20 86286.33

4. Sub Total - Current Liabilities 732680.70 862859.00 904076.25 969978.65

Total Liabilities (1+2+3+4) 1449312.10 1700264.50 2022565.72 2269828.30

APPLICATION OF FUNDS

Non-Current Assets

Fixed Assets

Tangible assets 271185.80 323857.60 401583.42 453789.27

Intangible assets 131480.90 186801.50 229765.85 264230.72

Capital Work in Progress 31215.10 43092.60 53865.75 61406.96

Intangible assets under development 128243.20 141084.40 158014.53 170655.69

a) Sub Total - Fixed Assets 562125.00 694836.10 843229.55 950082.64

b) Non-current investments 13915.40 15154.00 15760.16 16232.96

c) Goodwill on consolidation 40937.40 41023.70 53330.81 57597.27

d) Long Term loans and advances 136579.50 154654.60 168573.51 180373.66

e) Deferred Tax Asset 45393.30 44289.30 32774.08 27530.23

f) Other non-current assets 5746.80 10239.50 41157.40 48565.73

1. Sub Total - Non Current Assets 804697.40 960197.20 1154825.51 1280382.50

Current Assets

Current Investment 75261.70 75423.20 55813.17 61394.48

Inventories 182160.20 209690.10 280984.73 328930.75

Trade receivables 82368.40 109426.60 118718.12 125841.21

Cash and Bank Balances 182381.30 211126.70 270242.18 310778.50

Short-terms loans & advances 113372.20 126084.60 107171.91 120032.54

Other current assets 9070.90 8316.10 34810.10 42468.32

2. Sub Total - Current Assets 644614.70 740067.30 867740.21 989445.80

Total Assets (1+2) 1449312.10 1700264.50 2022565.72 2269828.30

20 | P a g e

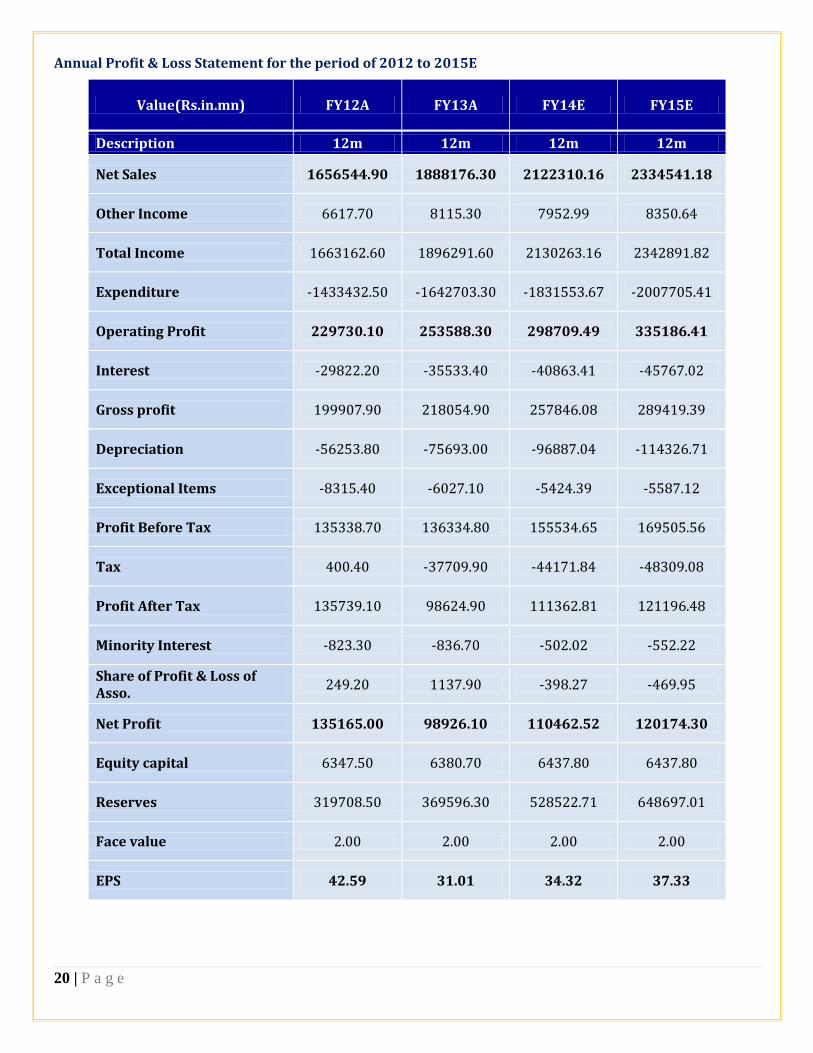

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 1656544.90 1888176.30 2122310.16 2334541.18

Other Income 6617.70 8115.30 7952.99 8350.64

Total Income 1663162.60 1896291.60 2130263.16 2342891.82

Expenditure -1433432.50 -1642703.30 -1831553.67 -2007705.41

Operating Profit 229730.10 253588.30 298709.49 335186.41

Interest -29822.20 -35533.40 -40863.41 -45767.02

Gross profit 199907.90 218054.90 257846.08 289419.39

Depreciation -56253.80 -75693.00 -96887.04 -114326.71

Exceptional Items -8315.40 -6027.10 -5424.39 -5587.12

Profit Before Tax 135338.70 136334.80 155534.65 169505.56

Tax 400.40 -37709.90 -44171.84 -48309.08

Profit After Tax 135739.10 98624.90 111362.81 121196.48

Minority Interest -823.30 -836.70 -502.02 -552.22

Share of Profit & Loss of Asso.

249.20 1137.90 -398.27 -469.95

Net Profit 135165.00 98926.10 110462.52 120174.30

Equity capital 6347.50 6380.70 6437.80 6437.80

Reserves 319708.50 369596.30 528522.71 648697.01

Face value 2.00 2.00 2.00 2.00

EPS 42.59 31.01 34.32 37.33

21 | P a g e

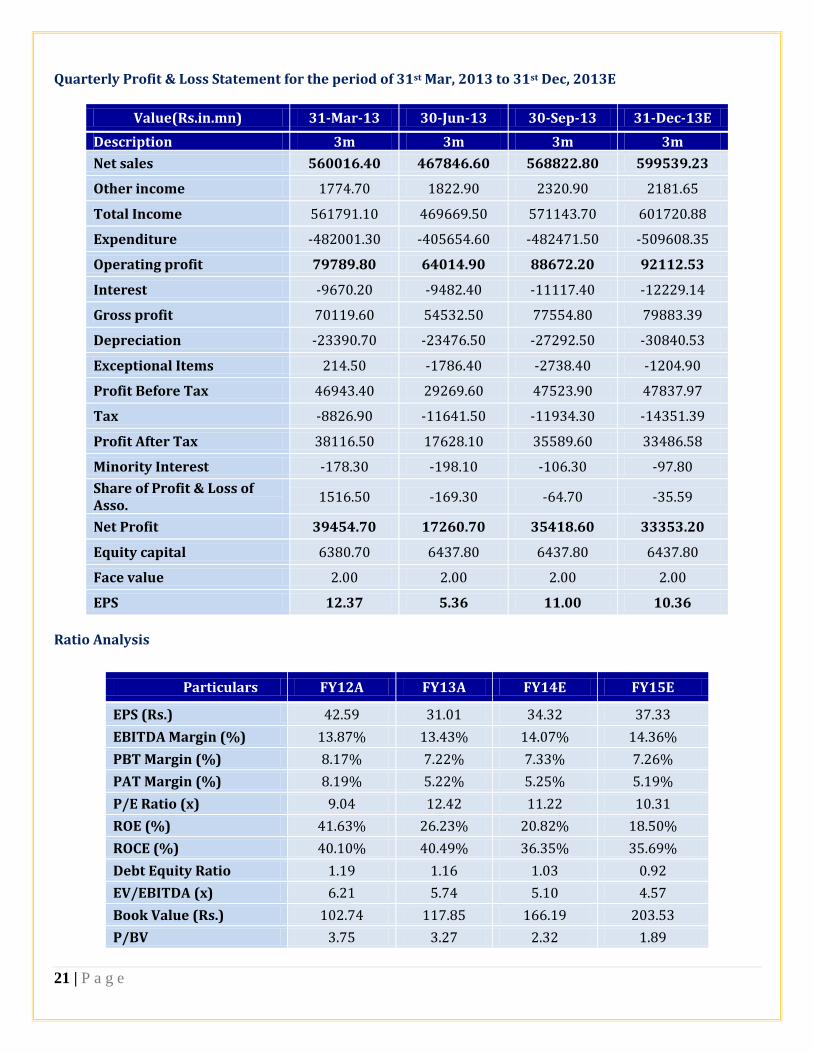

Quarterly Profit & Loss Statement for the period of 31st Mar, 2013 to 31st Dec, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 560016.40 467846.60 568822.80 599539.23

Other income 1774.70 1822.90 2320.90 2181.65

Total Income 561791.10 469669.50 571143.70 601720.88

Expenditure -482001.30 -405654.60 -482471.50 -509608.35

Operating profit 79789.80 64014.90 88672.20 92112.53

Interest -9670.20 -9482.40 -11117.40 -12229.14

Gross profit 70119.60 54532.50 77554.80 79883.39

Depreciation -23390.70 -23476.50 -27292.50 -30840.53

Exceptional Items 214.50 -1786.40 -2738.40 -1204.90

Profit Before Tax 46943.40 29269.60 47523.90 47837.97

Tax -8826.90 -11641.50 -11934.30 -14351.39

Profit After Tax 38116.50 17628.10 35589.60 33486.58

Minority Interest -178.30 -198.10 -106.30 -97.80

Share of Profit & Loss of Asso.

1516.50 -169.30 -64.70 -35.59

Net Profit 39454.70 17260.70 35418.60 33353.20

Equity capital 6380.70 6437.80 6437.80 6437.80

Face value 2.00 2.00 2.00 2.00

EPS 12.37 5.36 11.00 10.36

Ratio Analysis

Particulars FY12A FY13A FY14E FY15E

EPS (Rs.) 42.59 31.01 34.32 37.33

EBITDA Margin (%) 13.87% 13.43% 14.07% 14.36%

PBT Margin (%) 8.17% 7.22% 7.33% 7.26%

PAT Margin (%) 8.19% 5.22% 5.25% 5.19%

P/E Ratio (x) 9.04 12.42 11.22 10.31

ROE (%) 41.63% 26.23% 20.82% 18.50%

ROCE (%) 40.10% 40.49% 36.35% 35.69%

Debt Equity Ratio 1.19 1.16 1.03 0.92

EV/EBITDA (x) 6.21 5.74 5.10 4.57

Book Value (Rs.) 102.74 117.85 166.19 203.53

P/BV 3.75 3.27 2.32 1.89

22 | P a g e

Outlook and Conclusion

At the current market price of Rs.385.00, the stock P/E ratio is at 11.22 x FY14E and 10.31 x FY15E

respectively.

Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.34.32 and

Rs.37.33 respectively.

Net Sales and Operating Profit of the company are expected to grow at a CAGR of 12% and 13% over 2012 to

2015E respectively.

On the basis of EV/EBITDA, the stock trades at 5.10 x for FY14E and 4.57 x for FY15E.

Price to Book Value of the stock is expected to be at 2.32 x and 1.89 x respectively for FY14E and FY15E.

23 | P a g e

MAHINDRA & MAHINDRA LTD

A USD 16.2 billion multinational group based in Mumbai, India, Mahindra employs more than 155,000 people in

over 100 countries. M&M was set up in 1945 to make general purpose utility vehicles for the Indian market and

soon it started manufacturing agricultural tractors and light commercial vehicles (LCVs). Later the company

expanded its operations to secure a significant presence in many more significant sectors. M&M also has

controlling stake in REVA Electric Car Company and acquired South Korea's SsangYong Motor Company in 2011.

Financial Highlights

The Gross Revenues and Other Income of Mahindra & Mahindra Ltd for the quarter ended 30th September 2013

is Rs. 98906.10 million as against Rs. 108913.5 million in the corresponding period last year. The profit after tax

for the quarter is Rs. 9895.00 million as against Rs. 9018.00 million in Q2 FY13 – a growth of 9.7%. Mahindra

Vehicle Manufacturers Ltd (MVML) is a 100% subsidiary of the company with a view to sourcing contemporary

products for expanding the market offerings of the company.

The Gross Revenues and Other Income of Mahindra & Mahindra Ltd and MVML (Entity) for the quarter ended

30th September 2013 is Rs. 98876.00 million as against Rs. 107867.00 million during the corresponding period

last year. The profit before tax of Entity for the current quarter is Rs. 13036.00 million as against Rs.13272.00

million in Q2 previous year. After providing for tax, the profit is Rs. 10276.00 million against Rs. 9781.00 million

in Q2 last year - a growth of 5.1%. The operating margin of the Entity for the current quarter is 14.5% as

compared to 13.8% in Q2 last year. The deceleration in the Gross Revenues in the quarter is due to the

challenging times the Indian auto industry, with volumes shrinking by 4% during Q2 FY14. Despite this, the

entity could deliver a growth in the profits in the quarter due to a strong sales performance by its Farm

Equipment Sector and a tight control on material costs and all expenses.

In the Passenger Utility Vehicle segment, the Entity sold 47388 vehicles in the current quarter with a market

share of 39.6%. In the Cars segment, the Entity sold 2879 Verito and Verito Vibe Cars. The Entity also exported

8059 Vehicles in Q2 FY14. The domestic tractor industry continued to show robust growth with sales of 141171

tractors in Q2 FY14 against 116524 tractors sold in Q2 FY13 - a growth of 21.2%. In this period, the Company’s

domestic sales at 57549 tractors grew by 22.3% over the 47065 tractors sold in Q2 last year. Company’s market

share was 40.5% as against 40.2% in Q2 last year.

24 | P a g e

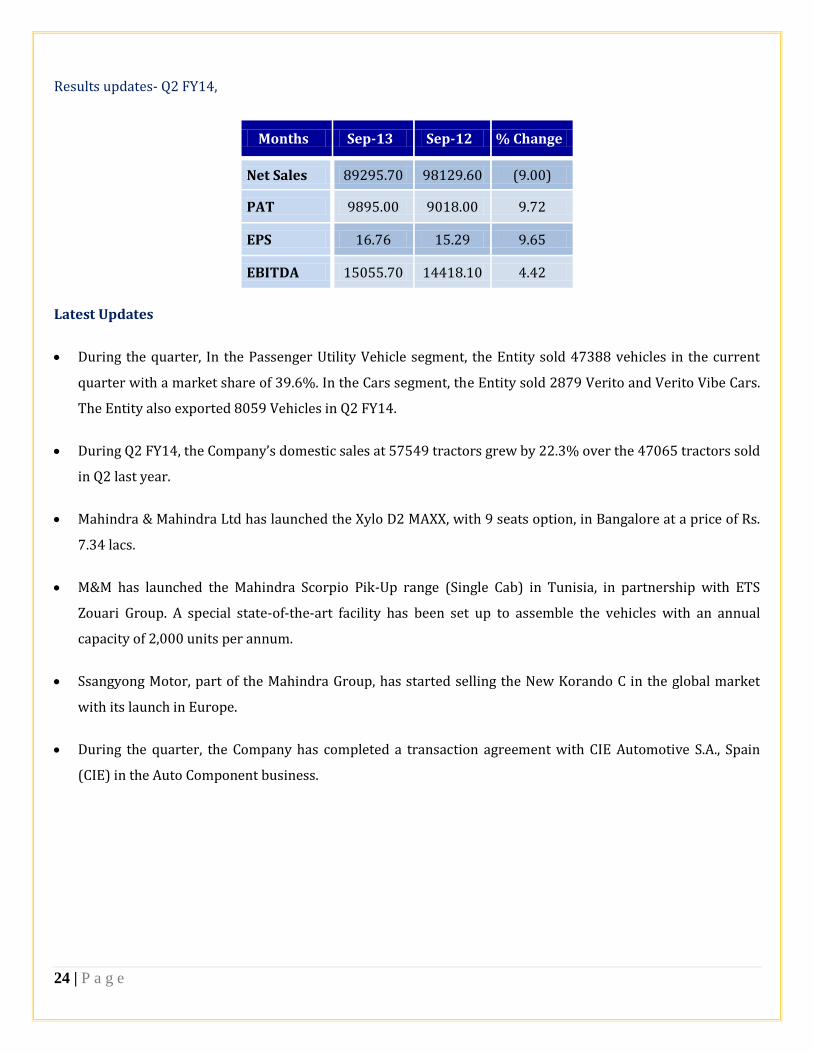

Results updates- Q2 FY14,

Months Sep-13 Sep-12 % Change

Net Sales 89295.70 98129.60 (9.00)

PAT 9895.00 9018.00 9.72

EPS 16.76 15.29 9.65

EBITDA 15055.70 14418.10 4.42

Latest Updates

During the quarter, In the Passenger Utility Vehicle segment, the Entity sold 47388 vehicles in the current

quarter with a market share of 39.6%. In the Cars segment, the Entity sold 2879 Verito and Verito Vibe Cars.

The Entity also exported 8059 Vehicles in Q2 FY14.

During Q2 FY14, the Company’s domestic sales at 57549 tractors grew by 22.3% over the 47065 tractors sold

in Q2 last year.

Mahindra & Mahindra Ltd has launched the Xylo D2 MAXX, with 9 seats option, in Bangalore at a price of Rs.

7.34 lacs.

M&M has launched the Mahindra Scorpio Pik-Up range (Single Cab) in Tunisia, in partnership with ETS

Zouari Group. A special state-of-the-art facility has been set up to assemble the vehicles with an annual

capacity of 2,000 units per annum.

Ssangyong Motor, part of the Mahindra Group, has started selling the New Korando C in the global market

with its launch in Europe.

During the quarter, the Company has completed a transaction agreement with CIE Automotive S.A., Spain

(CIE) in the Auto Component business.

25 | P a g e

FINANCIAL HIGHLIGHT (STANDALONE) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March31st, 2012 -2015E

M&M LTD. FY12A FY13A FY14E FY15E

SOURCES OF FUNDS (Rs.in.mn)

Shareholder's Funds

Share Capital 2945.20 2951.60 2951.60 2951.60

Reserves and Surplus 118101.70 143637.60 175105.62 211877.81

1. Sub Total - Net worth 121046.90 146589.20 178057.22 214829.41

Non Current Liabilities

Long Term Borrowing 31738.30 31724.40 38069.28 35785.12

Deferred Tax Liability (Net) 5271.30 6148.50 7685.63 6455.93

Other Long term Liabilities 2747.70 4154.00 6231.00 7352.58

Long Term Provisions 3634.90 4415.90 5078.29 5586.11

2. Sub Total - Non Current Liabilities 43392.20 46442.80 57064.19 55179.74

Current Liabilities

Short Term Borrowing 3.90 546.30 1043.43 1210.38

Trade Payables 47363.50 55797.10 56913.04 58620.43

Other Current Liabilities 12267.00 10521.70 17676.46 20327.92

Short Term Provisions 13626.10 14638.80 8344.12 9095.09

3. Sub Total - Current Liabilities 73260.50 81503.90 83977.05 89253.83

Total Liabilities (1+2+3) 237699.60 274535.90 319098.46 359262.97

APPLICATION OF FUNDS

Non-Current Assets

Fixed Assets

Tangible assets 40526.10 47510.60 55112.30 61725.77

Intangible assets 2407.40 2068.00 2295.48 2456.16

Capital Work in Progress 5699.30 4955.40 5153.62 5411.30

Intangible assets under development 2248.00 3679.40 4599.25 5289.14

a) Sub Total - Fixed Assets 50880.80 58213.40 62561.39 69593.23

b) Non- Current Investments 92604.50 105715.00 116910.54 126263.38

c) Long Term loans and advances 14766.80 20874.70 25049.64 29057.58

d) Other non-current assets 364.50 298.50 785.50 903.33

1. Sub Total - Non Current Assets 158616.60 185101.60 205307.07 225817.52

Current Assets

Current Investment 10369.00 12619.60 20443.75 24532.50

Inventories 23583.9 24197.70 29279.22 33085.52

Trade receivables 19285.30 22083.50 29591.89 34918.43

Cash and Bank Balances 11884.30 17814.10 15141.99 18170.38

Short-terms loans & advances 9309.90 7634.00 12977.80 15555.50

Other current assets 4650.60 5085.40 6356.75 7183.13

2. Sub Total - Current Assets 79083.00 89434.30 113791.39 133445.45

Total Assets (1+2) 237699.60 274535.90 319098.46 359262.97

26 | P a g e

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 318535.20 404411.60 436764.53 480440.98

Other Income 4657.90 5491.70 7413.80 7858.62

Total Income 323193.10 409903.30 444178.32 488299.60

Expenditure -279745.30 -356412.40 -384352.78 -422788.06

Operating Profit 43447.80 53490.90 59825.54 65511.54

Interest -1627.50 -1911.90 -2217.80 -2506.12

Gross profit 41820.30 51579.00 57607.73 63005.42

Depreciation -5761.40 -7108.10 -8174.32 -9155.23

Profit Before Tax 36058.90 44470.90 49433.42 53850.19

Tax -7270.00 -10942.70 -11369.69 -12385.54

Net Profit 28788.90 33528.20 38063.73 41464.65

Equity capital 2945.20 2951.60 2951.60 2951.60

Reserves 118656.60 143529.20 175105.62 211877.81

Face value 5.00 5.00 5.00 5.00

EPS 48.87 56.80 64.48 70.24

Quarterly Profit & Loss Statement for the period of 31st Mar, 2013 to 31st Dec, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 104865.30 100225.20 89295.70 98225.27

Other income 921.90 1642.30 3606.30 1622.84

Total Income 105787.20 101867.50 92902.00 99848.11

Expenditure -91262.30 -87350.80 -77846.30 -85455.98

Operating profit 14524.90 14516.70 15055.70 14392.12

Interest -511.10 -493.30 -622.60 -653.73

Gross profit 14013.80 14023.40 14433.10 13738.39

Depreciation -1986.00 -1806.30 -1970.10 -2029.20

Profit Before Tax 12027.80 12217.10 12463.00 11709.19

Tax -3135.90 -2838.00 -2568.00 -2576.02

Net Profit 8891.90 9379.10 9895.00 9133.17

Equity capital 2951.60 2951.60 2951.60 2951.60

Face value 5.00 5.00 5.00 5.00

EPS 15.06 15.89 16.76 15.47

27 | P a g e

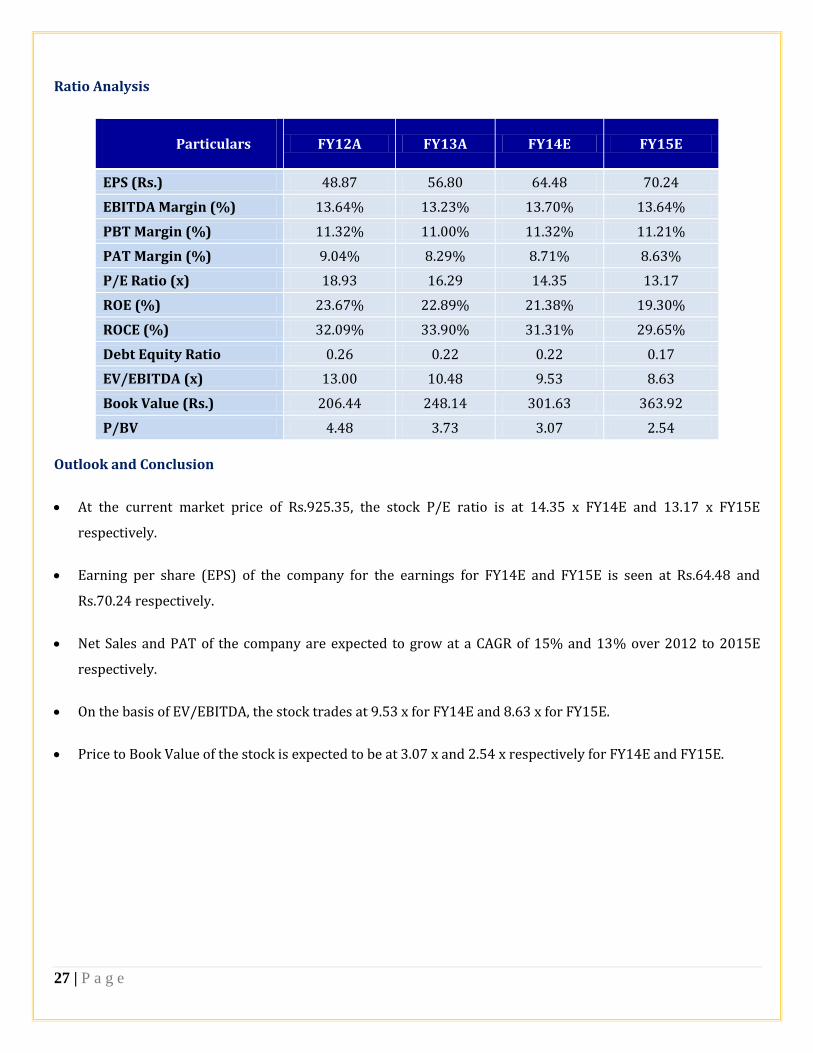

Ratio Analysis

Particulars FY12A FY13A FY14E FY15E

EPS (Rs.) 48.87 56.80 64.48 70.24

EBITDA Margin (%) 13.64% 13.23% 13.70% 13.64%

PBT Margin (%) 11.32% 11.00% 11.32% 11.21%

PAT Margin (%) 9.04% 8.29% 8.71% 8.63%

P/E Ratio (x) 18.93 16.29 14.35 13.17

ROE (%) 23.67% 22.89% 21.38% 19.30%

ROCE (%) 32.09% 33.90% 31.31% 29.65%

Debt Equity Ratio 0.26 0.22 0.22 0.17

EV/EBITDA (x) 13.00 10.48 9.53 8.63

Book Value (Rs.) 206.44 248.14 301.63 363.92

P/BV 4.48 3.73 3.07 2.54

Outlook and Conclusion

At the current market price of Rs.925.35, the stock P/E ratio is at 14.35 x FY14E and 13.17 x FY15E

respectively.

Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.64.48 and

Rs.70.24 respectively.

Net Sales and PAT of the company are expected to grow at a CAGR of 15% and 13% over 2012 to 2015E

respectively.

On the basis of EV/EBITDA, the stock trades at 9.53 x for FY14E and 8.63 x for FY15E.

Price to Book Value of the stock is expected to be at 3.07 x and 2.54 x respectively for FY14E and FY15E.

28 | P a g e

HERO MOTOCORP LTD

Hero MotoCorp Ltd. (Formerly Hero Honda Motors Ltd.) is the world's largest manufacturer of two - wheelers,

based in India. HMCL offer one of the widest ranges of two wheelers with over 19 different products across the

100 cc, 125 cc, 150 cc, 225 cc and scooter categories. Hero MotoCorp Limited manufactures and sells motorized

two-wheelers and spare parts, as well as provides related services in India. The company provides motorcycles

and scooters.

Financial Highlights

With sales of 14,16,276 two-wheelers in Q2 FY’14, the company registered a total turnover of Rs. 57262.10 mn

and net profit after tax (PAT) of Rs 4814.10 mn. HMCL had reported a total turnover of Rs. Rs. 51874.60 mn and

PAT of Rs 4405.80 mn in the corresponding quarter in the previous fiscal. EBIDTA margin for the second quarter

of this financial year stood at 14.5 per cent. The cumulative sales for first half of the year (April-Sept’13) stands at

29,75,558 two-wheelers. The company registered a total turnover of Rs 118857.30 mn and net profit after tax of

Rs 10299.90 mn in this period. EBIDTA margin for the H1 FY14 stood at 14.7 per cent. HMCL recently

commenced construction of its Rs 450 Crore “Hero Centre of Global Innovation and Research & Design (R&D)” at

Kukas, Jaipur in Rajasthan.

In July 2013, Hero MotoCorp began its quest in Africa with the launch of brand Hero in Kenya, Burkina Faso and

Ivory Coast. HMCL has also set-up its first international assembly unit at Nairobi in Kenya. The company followed

it with the launch of operations in Peru in Latin America. As of today, Hero two-wheelers sell in 11 markets

across the globe. The Company has reached the historic milestone of 50 million unit’s production. Over the past

two years, it has been working hard to build a foundation to realize their aspirations of a New Hero. This New

Hero will plans to enter into 50 countries with 20 manufacturing facilities across the globe and 100 million

cumulative two-wheelers sold by 2020. In the short term, HMCL will plans to launch Brand Hero in 10 more

international markets by the end of this year. And by next year, it will plan to have six assembly facilities spread

across three continents.

Results updates- Q2 FY14,

Months Sep-13 Sep-12 % Change

Net Sales 57262.10 51874.60 10.39

PAT 4814.10 4405.80 9.27

EPS 24.11 22.06 9.27

EBITDA 9481.60 8185.30 15.84

29 | P a g e

A NEW vision for a NEW Hero

With HMCL fast augmenting its presence globally and further strengthening its leadership in the domestic

market, the company unveiled a global vision for brand ‘Hero’- to be achieved by year 2020:

Surpass 100 million units in cumulative production

Annual bike and scooter sales of 12 million

More than 20 manufacturing and assembly plants across the globe

Sales in more than 50 countries

Turnover of Rs 60,000 crore

Latest Updates

HMCL recently commenced construction of its Rs 450 Crore “Hero Centre of Global Innovation and Research

& Design (R&D)” at Kukas, Jaipur in Rajasthan.

HMCL has launched brand ‘Hero’ and its range of two-wheelers in Peru, marking the iconic brand’s foray into

the Latin American market. And also entered into a partnership with MOTOCORP S.A.C– a part of the reputed

EFE Group of Peru - to bring its two-wheelers to this market.

The Company has reached the historic milestone of 50 million unit’s production. Over the past two years, it

has been working hard to build a foundation to realize their aspirations of a New Hero. This New Hero will

plans to enter into 50 countries with 20 manufacturing facilities across the globe and 100 million cumulative

two-wheelers sold by 2020.

In the short term, HMCL will plans to launch Brand Hero in 10 more international markets by the end of this

year. And by next year, it will plan to have six assembly facilities spread across three continents.

HMCL has recently showcased next-gen features to be introduced in its new product line-up, namely, i3S

Technology (Idle Stop & Start System) for two-wheelers which will soon make its debut in the all-new

Splendor iSmart; Integrated Braking System (IBS) that is being introduced in the all-new Pleasure and

Electronic Immobilizer which will debut on the new 150cc Xtreme. Hero has filed for patents for these

technological innovations.

Hero MotoCorp Ltd is setting up two new plants at Neemrana, Rajasthan and Gujarat and it has integrated a

R&D Centre at Kukas, Jaipur with an investment of Rs. 2500 crore.

HMCL launched the country's first-ever warranty of 5 years on all its two-wheelers (5 years or 70,000 km on

motorcycles, whichever is earlier and 5 years or 50,000 km on scooters, whichever is earlier).

30 | P a g e

Investments

Hero MotoCorp’s newly-incorporated wholly-owned American subsidiary - HMCL (NA).

Hero MotoCorp is investing US$25 million for a total stake of 49.2% in the share capital of Erik Buell Racing

(EBR). The first tranche of US$15 million has already been invested by HMCL. The second tranche of US$10

million is proposed to be invested within the next nine months. The equity partnership with EBR is reflective

of its long-term vision of transforming Hero MotoCorp to a truly global two-wheeler major with footprints

spread across continents, offering a wide range of technologically-advanced two-wheelers.

Hero MotoCorp recently launched its own retail finance arm, Hero FinCorp, with a phase-wise expansion

plan. Having been launched in Delhi, the retail financing services will shortly be extended to the National

Capital Region and then to the rest of the northern market in the next phase. The initial plan is to make Hero

FinCorp services available at about 200 dealerships in various parts of the country by March 2014, and

extend it to as many as 450 dealerships by March 2015.

Expansion

Setting up a fourth plant at Neemrana in Rajasthan with an annual installed capacity of 750,000 units.

Setting up a fifth plant at Halol in Gujarat, with an annual installed capacity of 1.2 million in the initial phase,

which will grow to 1.8 million in the next phase.

Setting up a new state-of-the-art integrated R&D centre at Kukas, Rajasthan.

Consistent expansion across all three existing plants.

Setting up a Global Parts Centre (GPC) at Neemrana, Rajasthan.

31 | P a g e

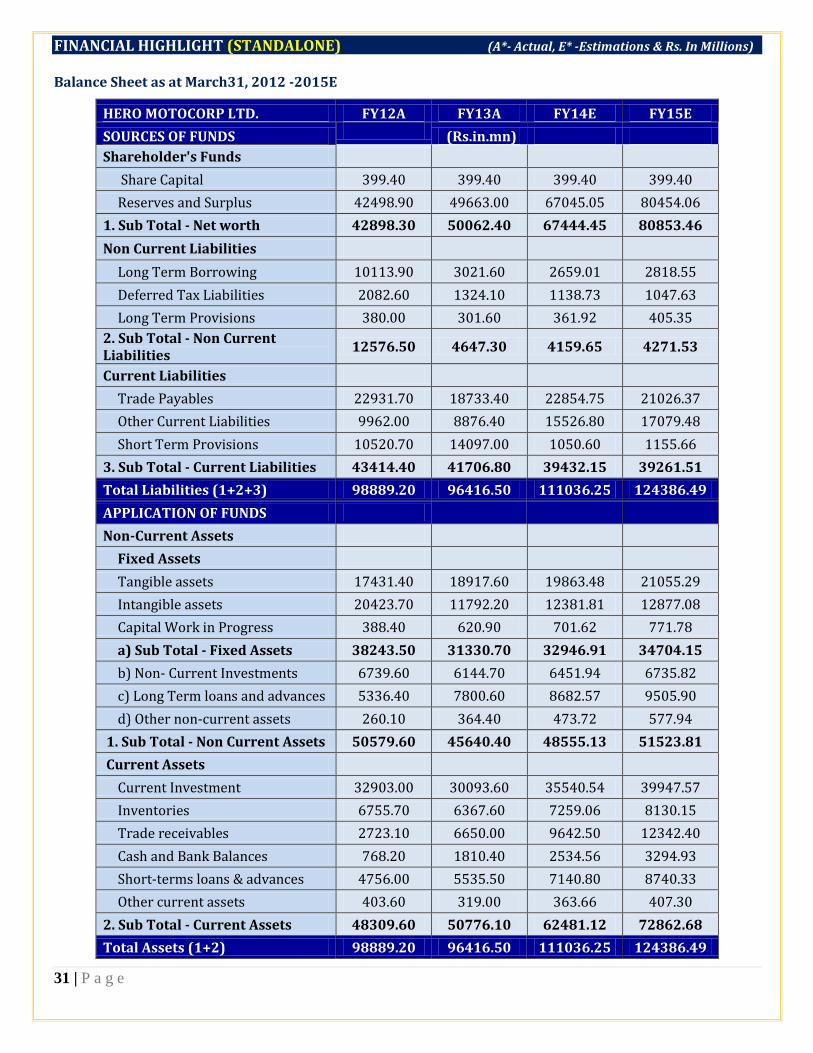

FINANCIAL HIGHLIGHT (STANDALONE) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March31, 2012 -2015E

HERO MOTOCORP LTD. FY12A FY13A FY14E FY15E

SOURCES OF FUNDS (Rs.in.mn)

Shareholder's Funds

Share Capital 399.40 399.40 399.40 399.40

Reserves and Surplus 42498.90 49663.00 67045.05 80454.06

1. Sub Total - Net worth 42898.30 50062.40 67444.45 80853.46

Non Current Liabilities

Long Term Borrowing 10113.90 3021.60 2659.01 2818.55

Deferred Tax Liabilities 2082.60 1324.10 1138.73 1047.63

Long Term Provisions 380.00 301.60 361.92 405.35

2. Sub Total - Non Current Liabilities

12576.50 4647.30 4159.65 4271.53

Current Liabilities

Trade Payables 22931.70 18733.40 22854.75 21026.37

Other Current Liabilities 9962.00 8876.40 15526.80 17079.48

Short Term Provisions 10520.70 14097.00 1050.60 1155.66

3. Sub Total - Current Liabilities 43414.40 41706.80 39432.15 39261.51

Total Liabilities (1+2+3) 98889.20 96416.50 111036.25 124386.49

APPLICATION OF FUNDS

Non-Current Assets

Fixed Assets

Tangible assets 17431.40 18917.60 19863.48 21055.29

Intangible assets 20423.70 11792.20 12381.81 12877.08

Capital Work in Progress 388.40 620.90 701.62 771.78

a) Sub Total - Fixed Assets 38243.50 31330.70 32946.91 34704.15

b) Non- Current Investments 6739.60 6144.70 6451.94 6735.82

c) Long Term loans and advances 5336.40 7800.60 8682.57 9505.90

d) Other non-current assets 260.10 364.40 473.72 577.94

1. Sub Total - Non Current Assets 50579.60 45640.40 48555.13 51523.81

Current Assets

Current Investment 32903.00 30093.60 35540.54 39947.57

Inventories 6755.70 6367.60 7259.06 8130.15

Trade receivables 2723.10 6650.00 9642.50 12342.40

Cash and Bank Balances 768.20 1810.40 2534.56 3294.93

Short-terms loans & advances 4756.00 5535.50 7140.80 8740.33

Other current assets 403.60 319.00 363.66 407.30

2. Sub Total - Current Assets 48309.60 50776.10 62481.12 72862.68

Total Assets (1+2) 98889.20 96416.50 111036.25 124386.49

32 | P a g e

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 235790.30 237681.10 254318.78 272121.09

Other Income 3645.70 3983.80 4461.86 4729.57

Total Income 239436.00 241664.90 258780.63 276850.66

Expenditure -199602.50 -204836.30 -217696.87 -232663.53

Operating Profit 39833.50 36828.60 41083.76 44187.13

Interest -213.00 -119.10 -126.25 -133.82

Gross profit 39620.50 36709.50 40957.51 44053.30

Depreciation -10973.40 -11417.50 -11760.03 -12348.03

Profit Before Tax 28647.10 25292.00 29197.49 31705.28

Tax -4865.80 -4110.40 -6773.82 -7292.21

Net Profit 23781.30 21181.60 22423.67 24413.06

Equity capital 399.40 399.40 399.40 399.40

Reserves 42498.90 49663.00 67045.05 80454.06

Face value 2.00 2.00 2.00 2.00

EPS 119.09 106.07 112.29 122.25

Quarterly Profit & Loss Statement for the period of 31st Mar, 2013 to 31st Dec, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 61457.50 61595.20 57262.10 63560.93

Other income 1045.10 1122.60 1154.60 1108.42

Total Income 62502.60 62717.80 58416.70 64669.35

Expenditure -52959.70 -52443.00 -48935.10 -54814.95

Operating profit 9542.90 10274.80 9481.60 9854.40

Interest -30.70 -29.50 -29.60 -28.42

Gross profit 9512.20 10245.30 9452.00 9825.98

Depreciation -2655.30 -2743.80 -2869.10 -2983.86

Profit Before Tax 6856.90 7501.50 6582.90 6842.12

Tax -1114.60 -2015.70 -1768.80 -1594.21

Net Profit 5742.30 5485.80 4814.10 5247.91

Equity capital 399.40 399.40 399.40 399.40

Face value 2.00 2.00 2.00 2.00

EPS 28.75 27.47 24.11 26.28

33 | P a g e

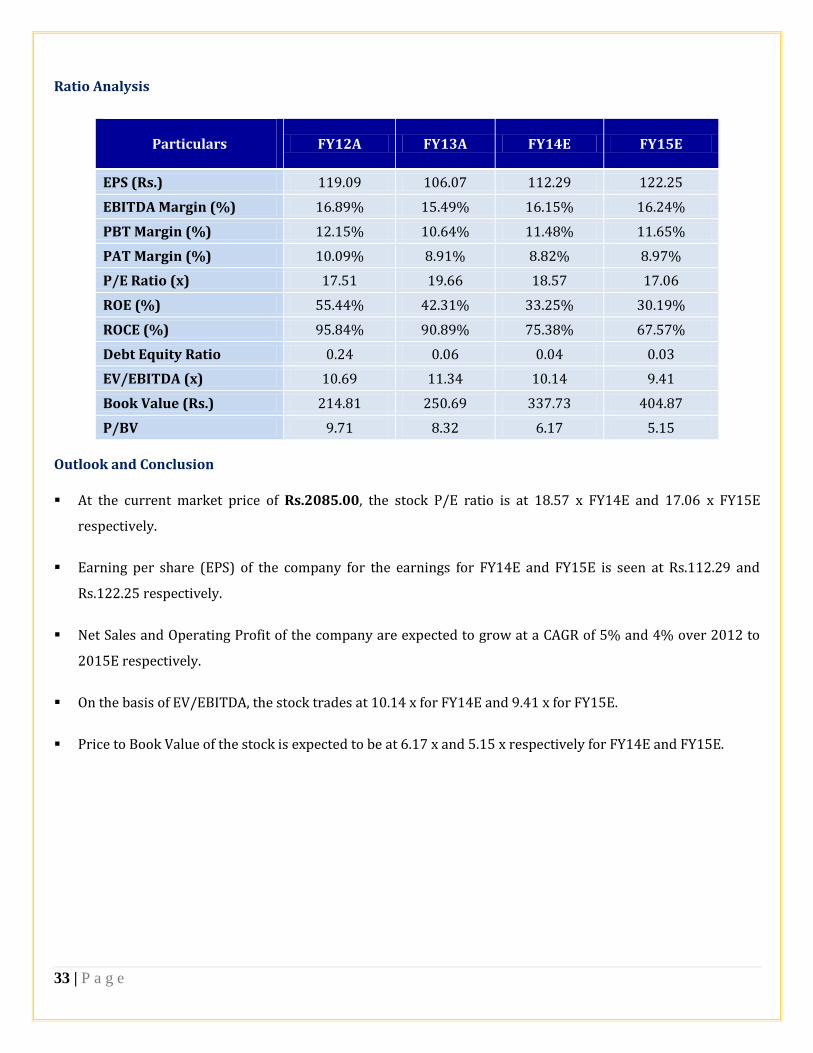

Ratio Analysis

Particulars FY12A FY13A FY14E FY15E

EPS (Rs.) 119.09 106.07 112.29 122.25

EBITDA Margin (%) 16.89% 15.49% 16.15% 16.24%

PBT Margin (%) 12.15% 10.64% 11.48% 11.65%

PAT Margin (%) 10.09% 8.91% 8.82% 8.97%

P/E Ratio (x) 17.51 19.66 18.57 17.06

ROE (%) 55.44% 42.31% 33.25% 30.19%

ROCE (%) 95.84% 90.89% 75.38% 67.57%

Debt Equity Ratio 0.24 0.06 0.04 0.03

EV/EBITDA (x) 10.69 11.34 10.14 9.41

Book Value (Rs.) 214.81 250.69 337.73 404.87

P/BV 9.71 8.32 6.17 5.15

Outlook and Conclusion

At the current market price of Rs.2085.00, the stock P/E ratio is at 18.57 x FY14E and 17.06 x FY15E

respectively.

Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.112.29 and

Rs.122.25 respectively.

Net Sales and Operating Profit of the company are expected to grow at a CAGR of 5% and 4% over 2012 to

2015E respectively.

On the basis of EV/EBITDA, the stock trades at 10.14 x for FY14E and 9.41 x for FY15E.

Price to Book Value of the stock is expected to be at 6.17 x and 5.15 x respectively for FY14E and FY15E.

34 | P a g e

BAJAJ AUTO LTD

Bajaj Auto was founded in 1926. Bajaj Auto is world’s fourth largest two- and three-wheeler manufacturer. Bajaj

Auto is into manufacturing motorcycles, scooters and three wheelers. In India, Bajaj Auto has a distribution

network of 791 dealers and over 1,600 authorized services centers. It has total 3750 rural outlets in rural areas.

In FY2013, Bajaj Auto sold over 3.76 million motorcycles in India and abroad. The manufacturing units are

located in the Industrial estates of Waluj (Aurangabad) and Chakan (Pune) in Maharashtra and Pantnagar in

Uttarakhand.

Financial Highlights

Bajaj Auto posted net profit of Rs 8371.60 mn is the highest ever quarterly profit. The company recorded an all

time high operating EBITDA of Rs 12561.20 mn in Q2 FY14. During the quarter, EBITDA margin edged up to

23.1% from 21.3% in Q1 FY14 and 18.7% in Q2 FY13. After payment of dividend and cash thereon amounting to

Rs. 15180 mn during Q2 September 2013, as on 30 September 2013, surplus cash and cash equivalents stood at

Rs. 65160 mn. As on 30th June 2013, surplus cash and cash equivalents stood at Rs 63910 mn.

The company’s outperformance in margins can be attributed to factors including transforming itself into an

Indian multi national company with international business contributing 40% of total revenue. Over the last five

years, strategic initiatives taken to enter into difficult markets, like Africa, is yielding rich dividends. The benefits

are now further enhanced with rupee depreciation. The company has focused on high margin products with 75%

of Bajaj Auto's revenue generated by business verticles which operate on EBITDA margins in excess of 20%. The

company also operates on an essentially variable cost structure with fixed cost, including depreciation, interest

and even employee cost was under 8%. This protects the company from any slowdown in demand as being

witnessed in the domestic market over last few quarters.

Results updates- Q2 FY14,

Months Sep-13 Sep-12 % Change

Net Sales 51748.90 49724.00 4.07

PAT 8371.60 7406.70 13.03

EPS 28.93 25.60 13.03

EBITDA 12561.20 10819.30 16.10

35 | P a g e

Latets Updates

The Company’s current installed capacity is 5.4 million units per annum. The Company plans to increase the

installed capacity to 6.06 million units per annum by March 2014.

The 4 Wheeler project is going on as per plan and is being implemented at Waluj. Commercial production of

the four-wheeler RE 60 is slated for second half of 2013-14.

36 | P a g e

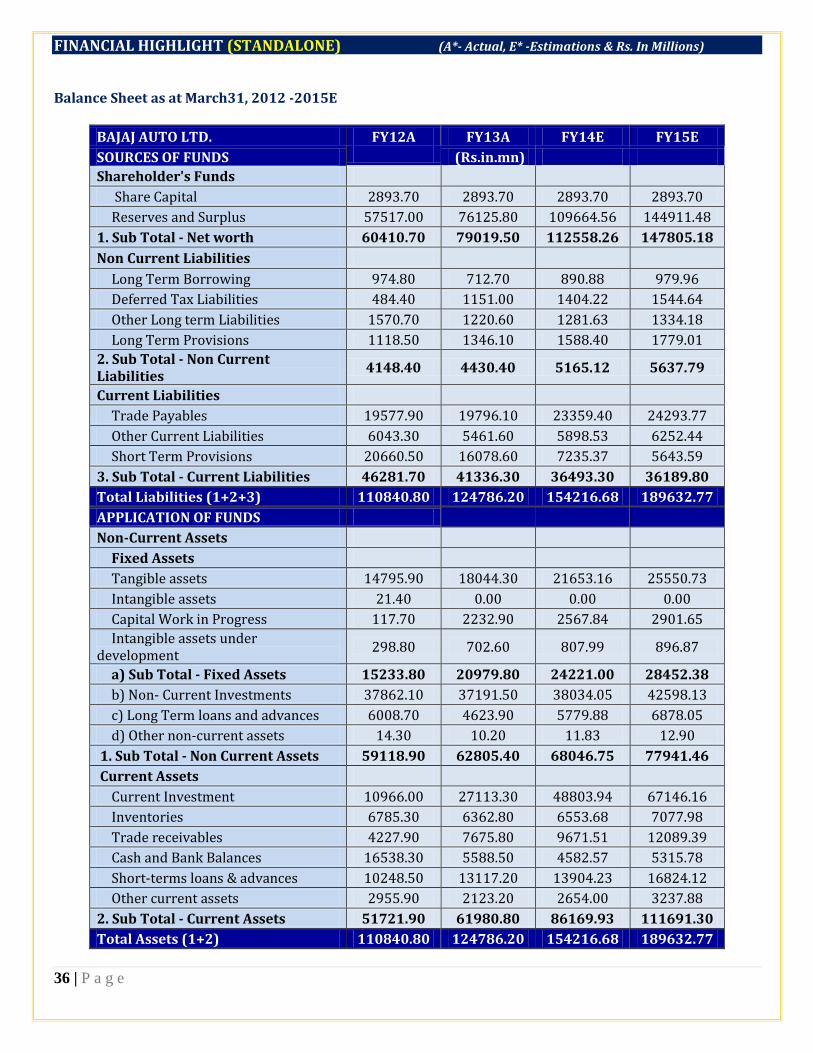

FINANCIAL HIGHLIGHT (STANDALONE) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as at March31, 2012 -2015E

BAJAJ AUTO LTD. FY12A FY13A FY14E FY15E

SOURCES OF FUNDS (Rs.in.mn)

Shareholder's Funds

Share Capital 2893.70 2893.70 2893.70 2893.70

Reserves and Surplus 57517.00 76125.80 109664.56 144911.48

1. Sub Total - Net worth 60410.70 79019.50 112558.26 147805.18

Non Current Liabilities

Long Term Borrowing 974.80 712.70 890.88 979.96

Deferred Tax Liabilities 484.40 1151.00 1404.22 1544.64

Other Long term Liabilities 1570.70 1220.60 1281.63 1334.18

Long Term Provisions 1118.50 1346.10 1588.40 1779.01

2. Sub Total - Non Current Liabilities

4148.40 4430.40 5165.12 5637.79

Current Liabilities

Trade Payables 19577.90 19796.10 23359.40 24293.77

Other Current Liabilities 6043.30 5461.60 5898.53 6252.44

Short Term Provisions 20660.50 16078.60 7235.37 5643.59

3. Sub Total - Current Liabilities 46281.70 41336.30 36493.30 36189.80

Total Liabilities (1+2+3) 110840.80 124786.20 154216.68 189632.77

APPLICATION OF FUNDS

Non-Current Assets

Fixed Assets

Tangible assets 14795.90 18044.30 21653.16 25550.73

Intangible assets 21.40 0.00 0.00 0.00

Capital Work in Progress 117.70 2232.90 2567.84 2901.65

Intangible assets under development

298.80 702.60 807.99 896.87

a) Sub Total - Fixed Assets 15233.80 20979.80 24221.00 28452.38

b) Non- Current Investments 37862.10 37191.50 38034.05 42598.13

c) Long Term loans and advances 6008.70 4623.90 5779.88 6878.05

d) Other non-current assets 14.30 10.20 11.83 12.90

1. Sub Total - Non Current Assets 59118.90 62805.40 68046.75 77941.46

Current Assets

Current Investment 10966.00 27113.30 48803.94 67146.16

Inventories 6785.30 6362.80 6553.68 7077.98

Trade receivables 4227.90 7675.80 9671.51 12089.39

Cash and Bank Balances 16538.30 5588.50 4582.57 5315.78

Short-terms loans & advances 10248.50 13117.20 13904.23 16824.12

Other current assets 2955.90 2123.20 2654.00 3237.88

2. Sub Total - Current Assets 51721.90 61980.80 86169.93 111691.30

Total Assets (1+2) 110840.80 124786.20 154216.68 189632.77

37 | P a g e

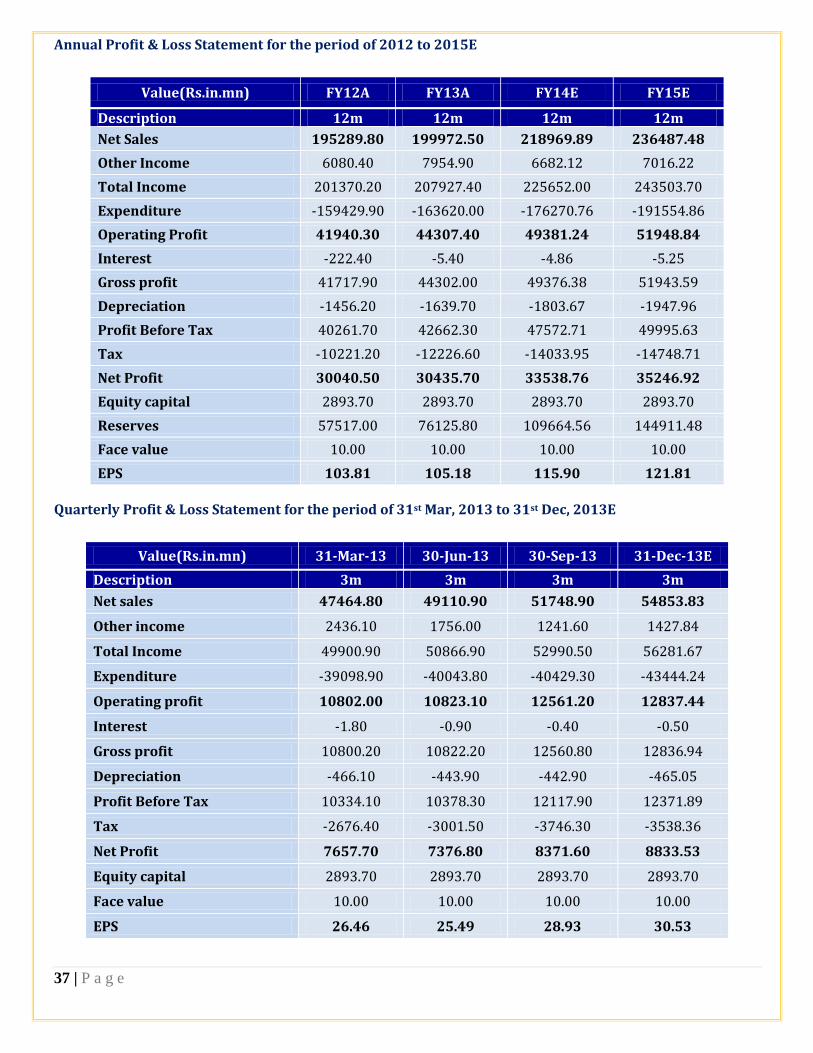

Annual Profit & Loss Statement for the period of 2012 to 2015E

Value(Rs.in.mn) FY12A FY13A FY14E FY15E

Description 12m 12m 12m 12m

Net Sales 195289.80 199972.50 218969.89 236487.48

Other Income 6080.40 7954.90 6682.12 7016.22

Total Income 201370.20 207927.40 225652.00 243503.70

Expenditure -159429.90 -163620.00 -176270.76 -191554.86

Operating Profit 41940.30 44307.40 49381.24 51948.84

Interest -222.40 -5.40 -4.86 -5.25

Gross profit 41717.90 44302.00 49376.38 51943.59

Depreciation -1456.20 -1639.70 -1803.67 -1947.96

Profit Before Tax 40261.70 42662.30 47572.71 49995.63

Tax -10221.20 -12226.60 -14033.95 -14748.71

Net Profit 30040.50 30435.70 33538.76 35246.92

Equity capital 2893.70 2893.70 2893.70 2893.70

Reserves 57517.00 76125.80 109664.56 144911.48

Face value 10.00 10.00 10.00 10.00

EPS 103.81 105.18 115.90 121.81

Quarterly Profit & Loss Statement for the period of 31st Mar, 2013 to 31st Dec, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 47464.80 49110.90 51748.90 54853.83

Other income 2436.10 1756.00 1241.60 1427.84

Total Income 49900.90 50866.90 52990.50 56281.67

Expenditure -39098.90 -40043.80 -40429.30 -43444.24

Operating profit 10802.00 10823.10 12561.20 12837.44

Interest -1.80 -0.90 -0.40 -0.50

Gross profit 10800.20 10822.20 12560.80 12836.94

Depreciation -466.10 -443.90 -442.90 -465.05

Profit Before Tax 10334.10 10378.30 12117.90 12371.89

Tax -2676.40 -3001.50 -3746.30 -3538.36

Net Profit 7657.70 7376.80 8371.60 8833.53

Equity capital 2893.70 2893.70 2893.70 2893.70

Face value 10.00 10.00 10.00 10.00

EPS 26.46 25.49 28.93 30.53

38 | P a g e

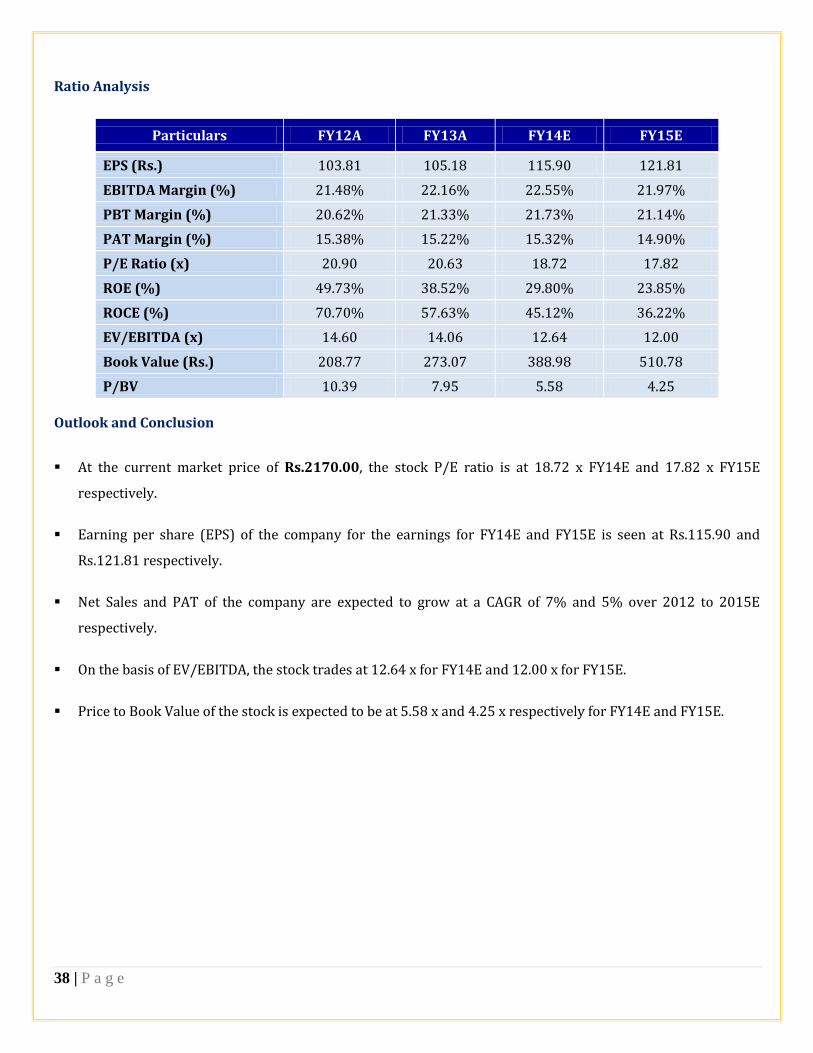

Ratio Analysis

Particulars FY12A FY13A FY14E FY15E

EPS (Rs.) 103.81 105.18 115.90 121.81

EBITDA Margin (%) 21.48% 22.16% 22.55% 21.97%

PBT Margin (%) 20.62% 21.33% 21.73% 21.14%

PAT Margin (%) 15.38% 15.22% 15.32% 14.90%

P/E Ratio (x) 20.90 20.63 18.72 17.82

ROE (%) 49.73% 38.52% 29.80% 23.85%

ROCE (%) 70.70% 57.63% 45.12% 36.22%

EV/EBITDA (x) 14.60 14.06 12.64 12.00

Book Value (Rs.) 208.77 273.07 388.98 510.78

P/BV 10.39 7.95 5.58 4.25

Outlook and Conclusion

At the current market price of Rs.2170.00, the stock P/E ratio is at 18.72 x FY14E and 17.82 x FY15E

respectively.

Earning per share (EPS) of the company for the earnings for FY14E and FY15E is seen at Rs.115.90 and

Rs.121.81 respectively.

Net Sales and PAT of the company are expected to grow at a CAGR of 7% and 5% over 2012 to 2015E

respectively.

On the basis of EV/EBITDA, the stock trades at 12.64 x for FY14E and 12.00 x for FY15E.

Price to Book Value of the stock is expected to be at 5.58 x and 4.25 x respectively for FY14E and FY15E.

39 | P a g e

EICHER MOTORS LTD

Eicher Motors Limited (EML) is the flagship company of the Eicher Group, which was a catalyst in the green

revolution in India with the production of India’s first agricultural tractor in 1959. EML is now a leading player in

the Indian automotive space. Its 50-50 joint venture with the Volvo group, VE Commercial Vehicles Limited,

designs, manufactures and markets reliable, fuel-efficient trucks and buses; and is leading the path in driving

modernization in commercial transportation in India and other developing markets. Eicher Motors also owns the

iconic Royal Enfield motorcycle business, which leads the premium motorcycle segment in India. The oldest

motorcycle company in continuous production world-wide, Royal Enfield has witnessed a huge surge in demand

in the recent past, and is charting its course to be the leading player in the mid-size motorcycle segment globally.

EML’s 50:50 strategic joint venture with US based Polaris Industries Inc., Eicher Polaris Private Ltd. is in start-up

phase, and is currently designing and developing, and will soon manufacture and sell a full new range of personal

vehicles. In 2012, Eicher Motors recorded its highest ever sales of INR 7,000 crores (USD 1.3 billion).

Royal Enfield has also substantially expanded and upgraded its network across the country. In 2012 it added 63

new dealerships taking the total dealership network to 249.

Financial Highlights

In Q3 2013, Eicher Motors Limited reported its best ever standalone results- relating entirely to Royal Enfield

motorcycle operations, with a quarterly total income from operations at Rs. 4589.70 million, an increase of

66.23% over Rs. 2761.10 million in Q3 2012. The quarterly operating profit (EBIT) recorded an increase of

116.9% at Rs. 805 million in Q3 2013 over Rs. 371 million in Q3, 2012. Royal Enfield has maintained its

phenomenal growth trajectory even in Q3 2013 registering the best ever quarter results. Royal Enfield has

registered year-on-year unit sales growth of 60.6% with record sales of 48,242 units as compared to 30,046 units

in Q3 2012. It is continuing to extract operating leverage from the business, thus improving the EBIT margin to

17.5% in Q3 2013 as compared to 13.4% in Q3 2012.

The Company continued to improve their overall market share in commercial vehicles through 50:50 joint

venture with the Volvo Group – VE Commercial Vehicles (VECV). For the nine month period ending September

30, 2013, the industry declined by 33.6%, but the Company Heavy Duty market share increased to 4.5% from

3.7% in the corresponding period last year. The products in the bus segment continue to do well. For the third

quarter ending September 30, 2013, the Company has reported a consolidated total income from operations at

Rs. 17361 million. Earnings before interest and tax (EBIT) are increased by 95.8% in Q3 2013.

VECV’s Eicher Trucks and Buses division is preparing to launch its full new range of trucks and buses. These are

absolutely world-class products that will completely renew ETB’s product portfolio. Royal Enfield has created

40 | P a g e

and been leading the premium category of motorcycles in India for all these years with evocative products such

as the Classic and the Thunderbird. In September 2013, Royal Enfield had its first successful global launch with

the all new Continental GT- a motorcycle that perfects the essential elements of the most influential idea in

motorcycling history – café racing.

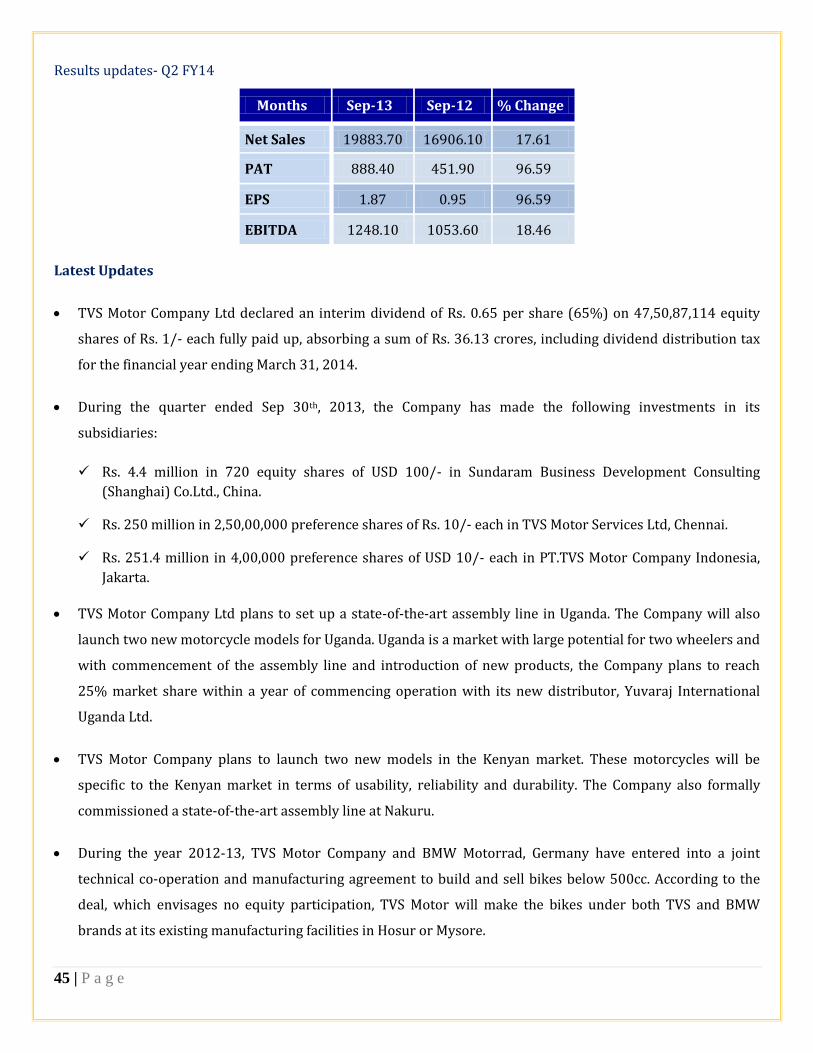

Results updates- Q3 CY13

Months Sep-13 Sep-12 % Change

Net Sales 4589.70 2761.10 66.23

PAT 617.90 329.70 87.41

EPS 22.88 12.21 87.34

EBITDA 906.20 454.60 99.34

Latest Updates

Royal Enfield has registered year-on-year unit sales growth of 60.6% with record sales of 48,242 units as

compared to 30,046 units in Q3 2012.

The Company has sold 1858 buses in Q3 2013 compared to 2326 buses over same period last year,

registered a degrew of 20.12%

Eicher Motors has recently started production at VECV’s Medium Duty Engine Plant at Pithampur, Madhya

Pradesh. The plant has been set up with an initial capacity of 25,000 units per annum in Phase I, at an

investment of Rs 375 crores. The capacity will be increased in a phased manner to 100,000 units per annum

as per the market requirements with an additional investment of around Rs 125 crores.

Starting end 2013 till 2015, VECV’s Eicher Trucks and Buses division (ETB) will be renewing its entire

product portfolio by launching its new range of trucks and buses across light, medium and heavy duty. The

Company continues to invest in all their strategic projects in VECV. By end of CY 2014, it would have invested

Rs. 2500 crores since the creation of the joint venture in mid 2008.

During the quarter ended June, 2013, VE Commercial Vehicles has set up a wholly owned subsidiary V E C V

Lanka (Private) Ltd in Sri Lanka for the purpose of expanding its commercial vehicles operations in Sri Lanka

with an investment of Rs. 54.3 million.

41 | P a g e

Financial Highlight STANDALONE

Balance sheet as at December 31st, 2011-2014E

(A*- Actual, E* -Estimations & Rs. In Millions)

EICHER MOTORS LTD. CY11A CY12A CY13E CY14E

SOURCES OF FUNDS (Rs.in.mn)

Shareholder's Funds

Share Capital 269.90 270.00 270.10 270.10

Reserves and Surplus 5130.50 6020.50 8767.26 11927.00

1. Sub Total - Net worth 5400.40 6290.50 9037.36 12197.10

Non Current Liabilities

Long Term Borrowing 5.80 0.00 0.00 0.00

Deferred Tax Liability (net) 39.20 62.60 105.20 82.06

Other Long term Liabilities 27.30 32.30 38.11 42.69

Long Term Provisions 80.90 92.60 103.71 112.01

2. Sub Total - Non Current Liabilities 153.20 187.50 247.03 236.75

Current Liabilities

Short term borrowings 136.70 200.10 322.16 373.71

Trade Payables 1058.70 1775.00 2396.25 2731.73

Other Current Liabilities 595.10 1168.10 1366.68 1503.34

Short Term Provisions 479.70 621.20 93.18 102.50

3. Sub Total - Current Liabilities 2270.20 3764.40 4178.27 4711.27

Total Liabilities (1+2+3) 7823.80 10242.40 13462.65 17145.13

APPLICATION OF FUNDS

Non-Current Assets

Fixed Assets

Tangible assets 1097.50 1338.30 1900.39 2394.49

Intangible assets 25.50 38.70 50.31 62.38

Capital Work in Progress 42.10 603.30 868.75 1042.50

a) Sub Total - Fixed Assets 1165.10 1980.30 2819.45 3499.37

b) Non-current investments 54.40 109.40 114.87 119.46

c) Long Term loans and advances 348.10 613.00 472.01 528.65

d) Other non-current assets 57.60 61.80 77.87 89.55

1. Sub Total – Non Current Assets 1625.20 2764.50 3484.20 4237.04

Current Assets

Current Investments 5125.70 6384.50 8133.86 10483.55

Inventories 452.7 754.10 942.63 1150.00

Trade receivables 41.00 62.00 150.50 204.68

Cash and Bank Balances 29.80 35.00 96.00 126.72

Short-terms loans & advances 138.70 239.40 652.40 939.46

Other current assets 410.70 2.90 3.07 3.69

2. Sub Total - Current Assets 6198.60 7477.90 9978.46 12908.09

Total Assets (1+2) 7823.80 10242.40 13462.65 17145.13

42 | P a g e

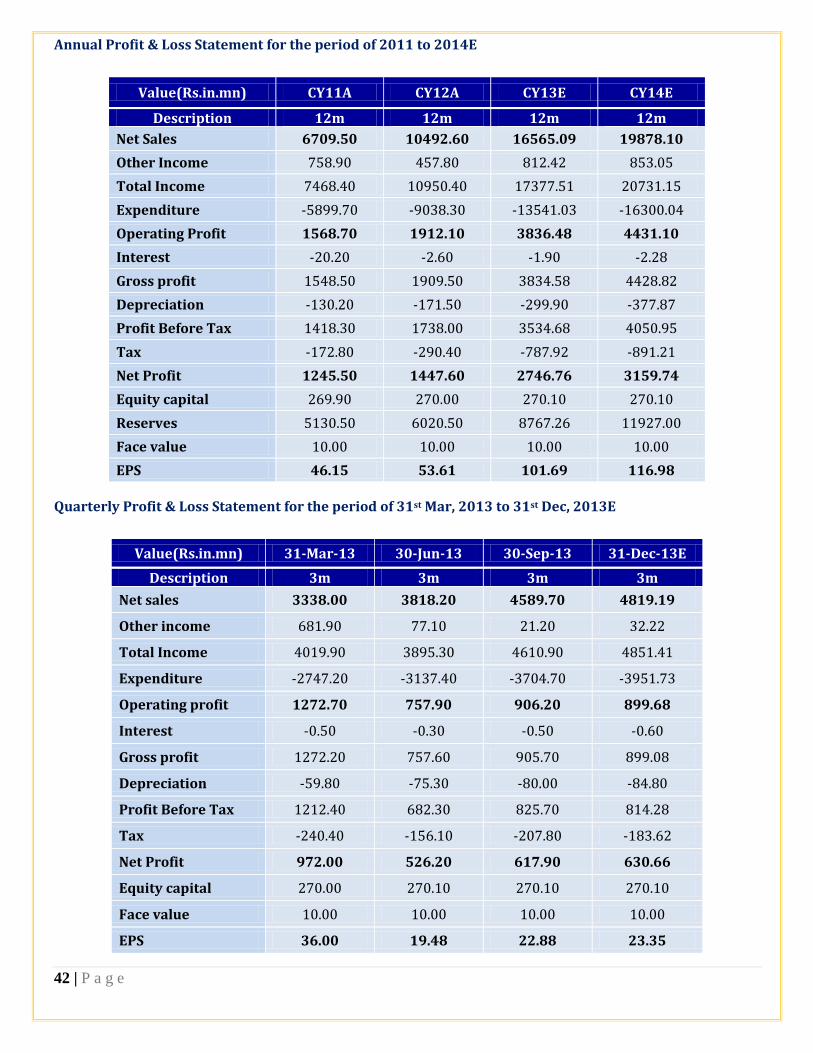

Annual Profit & Loss Statement for the period of 2011 to 2014E

Value(Rs.in.mn) CY11A CY12A CY13E CY14E

Description 12m 12m 12m 12m

Net Sales 6709.50 10492.60 16565.09 19878.10

Other Income 758.90 457.80 812.42 853.05

Total Income 7468.40 10950.40 17377.51 20731.15

Expenditure -5899.70 -9038.30 -13541.03 -16300.04

Operating Profit 1568.70 1912.10 3836.48 4431.10

Interest -20.20 -2.60 -1.90 -2.28

Gross profit 1548.50 1909.50 3834.58 4428.82

Depreciation -130.20 -171.50 -299.90 -377.87

Profit Before Tax 1418.30 1738.00 3534.68 4050.95

Tax -172.80 -290.40 -787.92 -891.21

Net Profit 1245.50 1447.60 2746.76 3159.74

Equity capital 269.90 270.00 270.10 270.10

Reserves 5130.50 6020.50 8767.26 11927.00

Face value 10.00 10.00 10.00 10.00

EPS 46.15 53.61 101.69 116.98

Quarterly Profit & Loss Statement for the period of 31st Mar, 2013 to 31st Dec, 2013E

Value(Rs.in.mn) 31-Mar-13 30-Jun-13 30-Sep-13 31-Dec-13E

Description 3m 3m 3m 3m

Net sales 3338.00 3818.20 4589.70 4819.19

Other income 681.90 77.10 21.20 32.22

Total Income 4019.90 3895.30 4610.90 4851.41

Expenditure -2747.20 -3137.40 -3704.70 -3951.73

Operating profit 1272.70 757.90 906.20 899.68

Interest -0.50 -0.30 -0.50 -0.60

Gross profit 1272.20 757.60 905.70 899.08

Depreciation -59.80 -75.30 -80.00 -84.80

Profit Before Tax 1212.40 682.30 825.70 814.28

Tax -240.40 -156.10 -207.80 -183.62

Net Profit 972.00 526.20 617.90 630.66

Equity capital 270.00 270.10 270.10 270.10

Face value 10.00 10.00 10.00 10.00

EPS 36.00 19.48 22.88 23.35

43 | P a g e

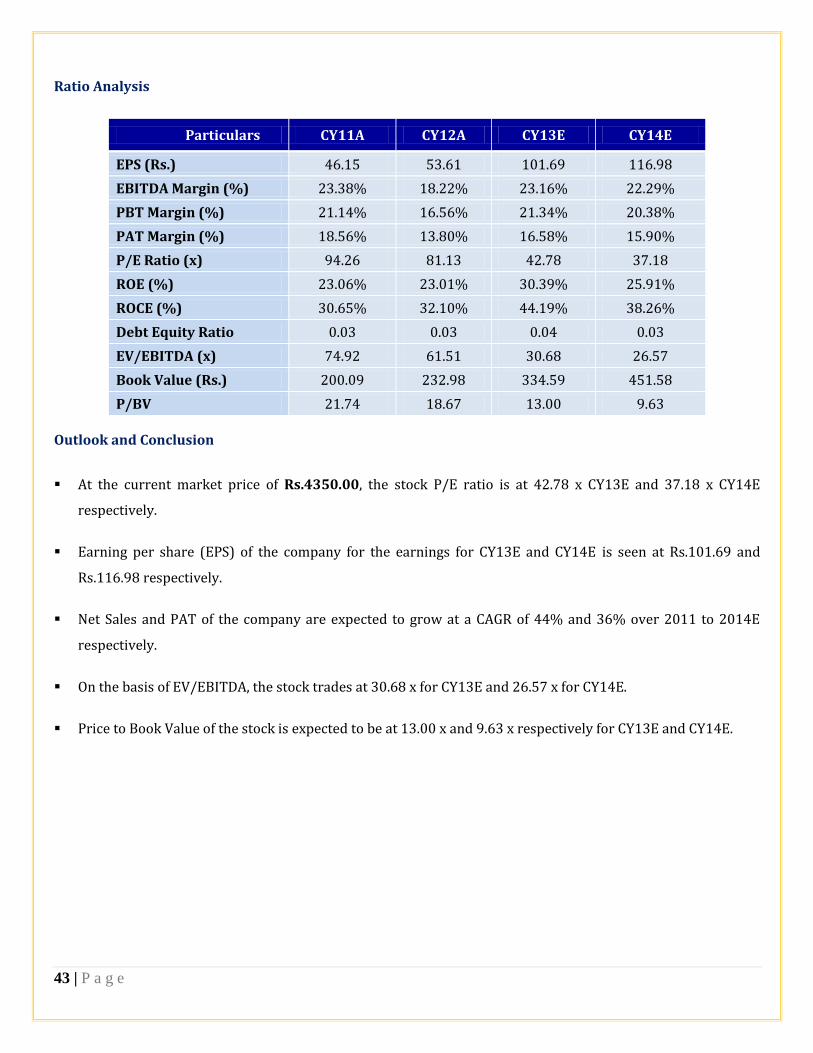

Ratio Analysis

Particulars CY11A CY12A CY13E CY14E

EPS (Rs.) 46.15 53.61 101.69 116.98

EBITDA Margin (%) 23.38% 18.22% 23.16% 22.29%

PBT Margin (%) 21.14% 16.56% 21.34% 20.38%

PAT Margin (%) 18.56% 13.80% 16.58% 15.90%

P/E Ratio (x) 94.26 81.13 42.78 37.18

ROE (%) 23.06% 23.01% 30.39% 25.91%

ROCE (%) 30.65% 32.10% 44.19% 38.26%

Debt Equity Ratio 0.03 0.03 0.04 0.03

EV/EBITDA (x) 74.92 61.51 30.68 26.57

Book Value (Rs.) 200.09 232.98 334.59 451.58

P/BV 21.74 18.67 13.00 9.63

Outlook and Conclusion

At the current market price of Rs.4350.00, the stock P/E ratio is at 42.78 x CY13E and 37.18 x CY14E

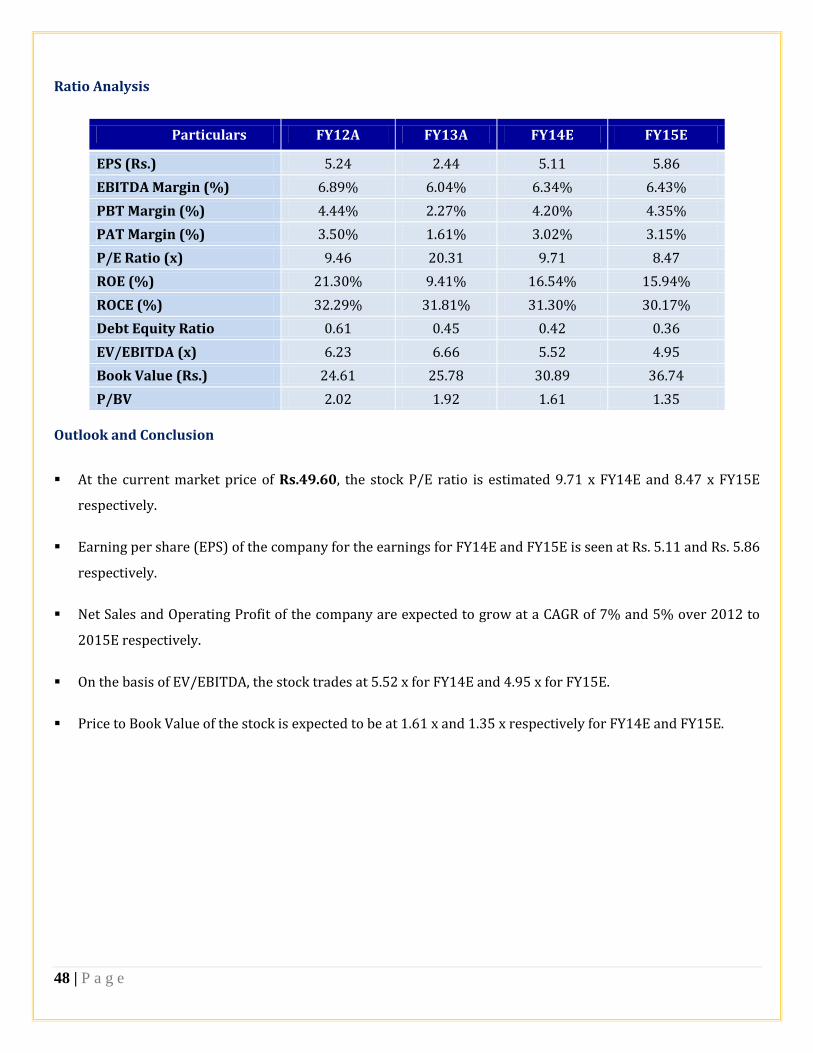

respectively.