Embed Size (px)

Citation preview

Azman Mohd Noor International Islamic University Malaysia, Seminar on Insurance and Risk in Asia PacificKyoto International Community House24 September 2010

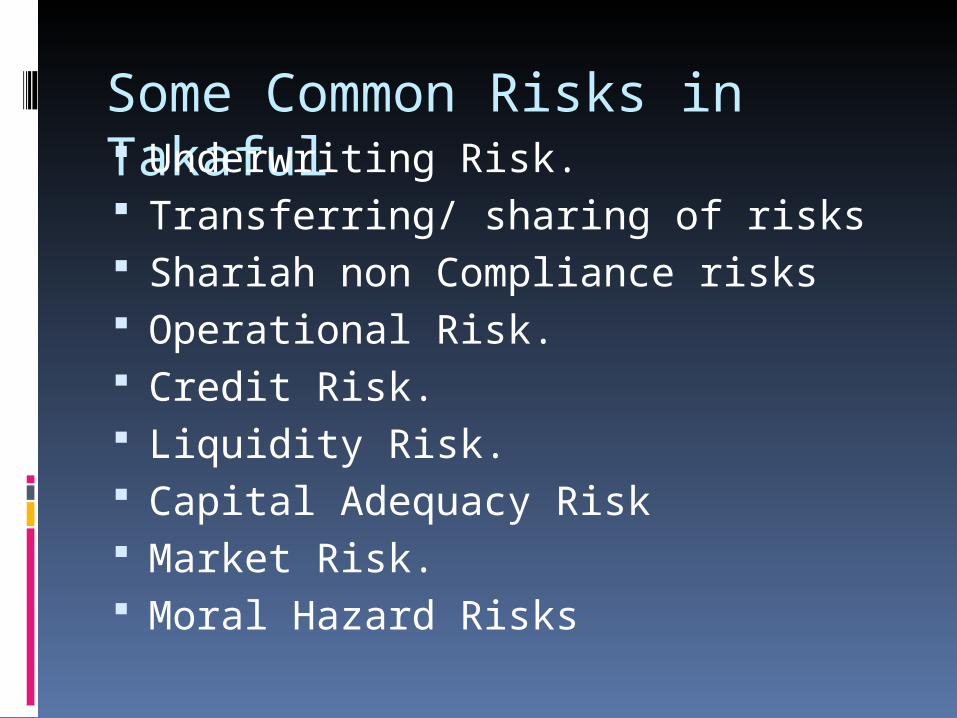

Some Common Risks in Takaful Underwriting Risk. Transferring/ sharing of risks Shariah non Compliance risks Operational Risk. Credit Risk. Liquidity Risk. Capital Adequacy Risk Market Risk. Moral Hazard Risks

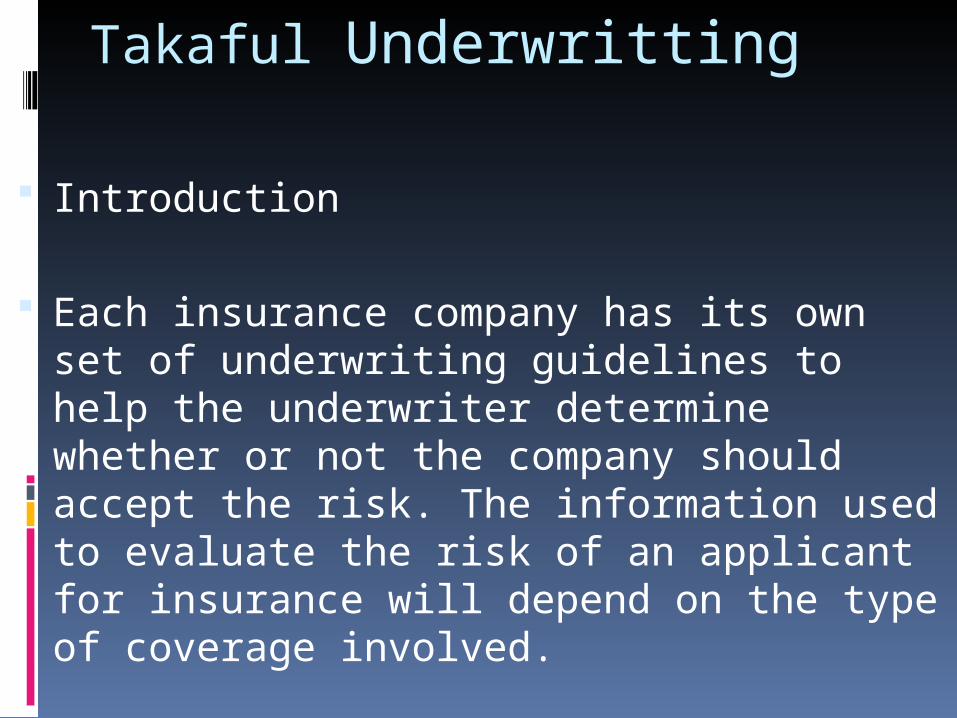

Takaful Underwritting

Introduction

Each insurance company has its own set of underwriting guidelines to help the underwriter determine whether or not the company should accept the risk. The information used to evaluate the risk of an applicant for insurance will depend on the type of coverage involved.

intro

Insurance underwriters evaluate the risk and exposures of potential clients. They decide how much coverage the client should receive, how much they should pay for it, or whether even to accept the risk and insure them. Underwriting involves measuring risk exposure and determining the premium that needs to be charged to insure that risk.

Takaful Underwriting: Key Points for Consideration Concept and Objectives. Contractual relations between the

takaful operator and the policyholders and the participants among themselves.

Shariah Governance Adopting conventional Insurance

principles and actuarial skills in underwriting as long as they are not against Shariah.

Adopting conventional Insurance principles and actuarial skills in underwriting as long as they are not against Shariah -Conventional insurance principles includes

insurable interest, subrogation, proximate lost, indemnity, utmost good faith and contribution.

-Conventional insurance principles in determining risks such as being definable, probable of happening, accidental, non-catastropic, a large number of homogenous, measurable and lawful.

Other actuarial skills and applications.

Shariah Requirement in ccepting Risks (Underwitting)

The requirements are very essential to: Ensure acceptance, validity and enforceability from

Islamic Law (Shariah) point of view. Ensure that any risk to be accepted comply with the

Shariah principles Fulfill the goal and objectives of takaful operator to

be Shariah compliant business entity. Meet the religious requirements of Muslims in line

with their belief and faith

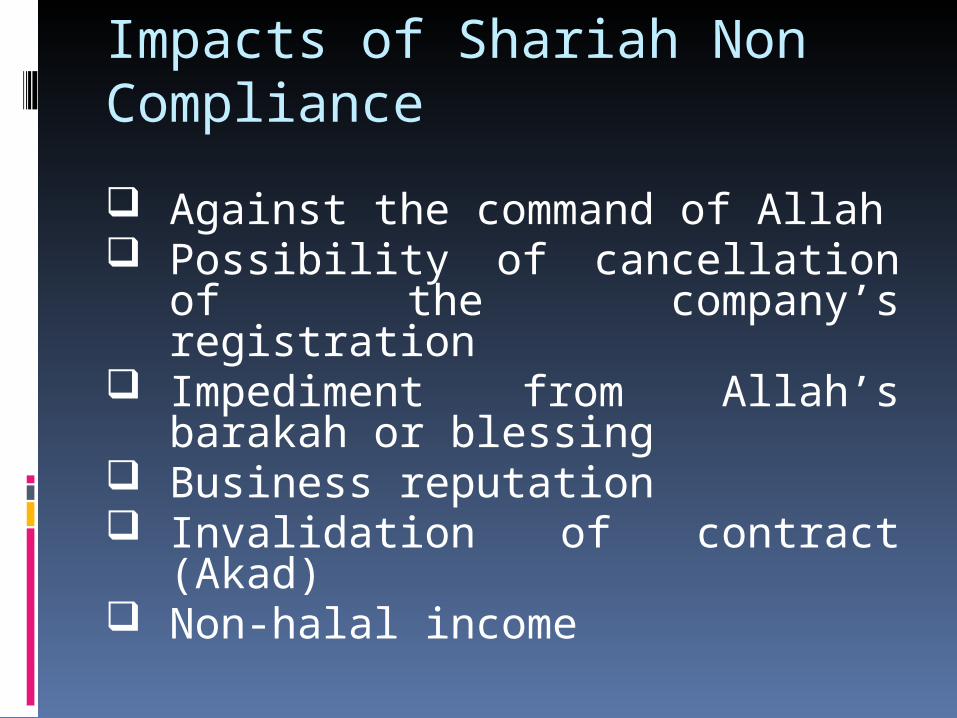

Impacts of Shariah Non Compliance

Against the command of Allah Possibility of cancellation of the company’s

registration Impediment from Allah’s barakah or blessing Business reputation Invalidation of contract (Akad) Non-halal income

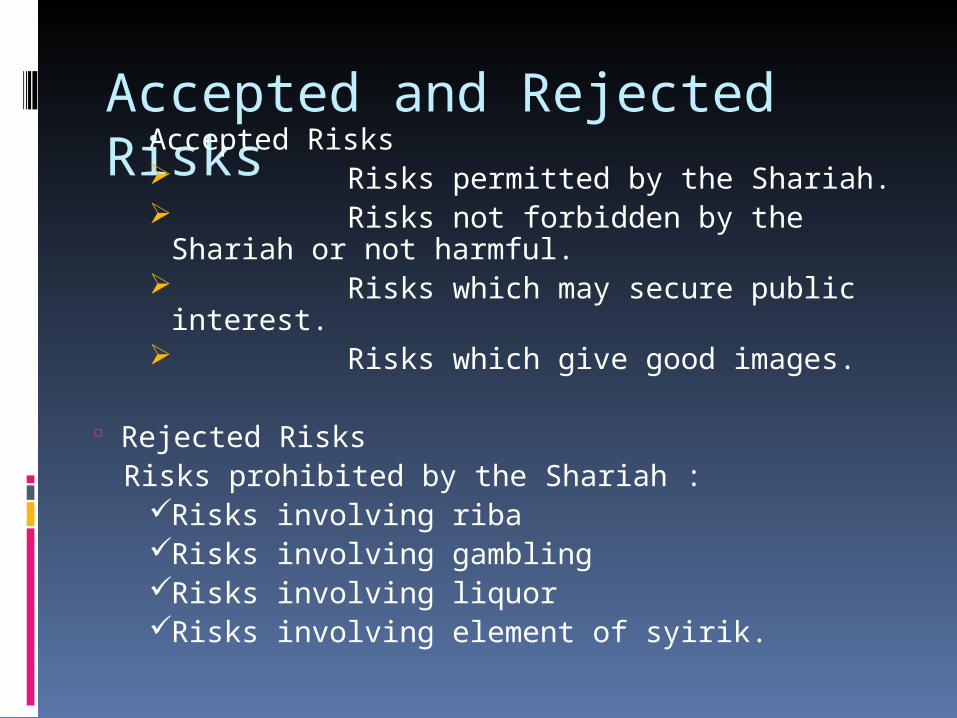

Accepted and Rejected RisksAccepted Risks

Risks permitted by the Shariah. Risks not forbidden by the Shariah or not

harmful. Risks which may secure public interest. Risks which give good images.

Rejected RisksRisks prohibited by the Shariah :

Risks involving riba Risks involving gambling Risks involving liquor Risks involving element of syirik.

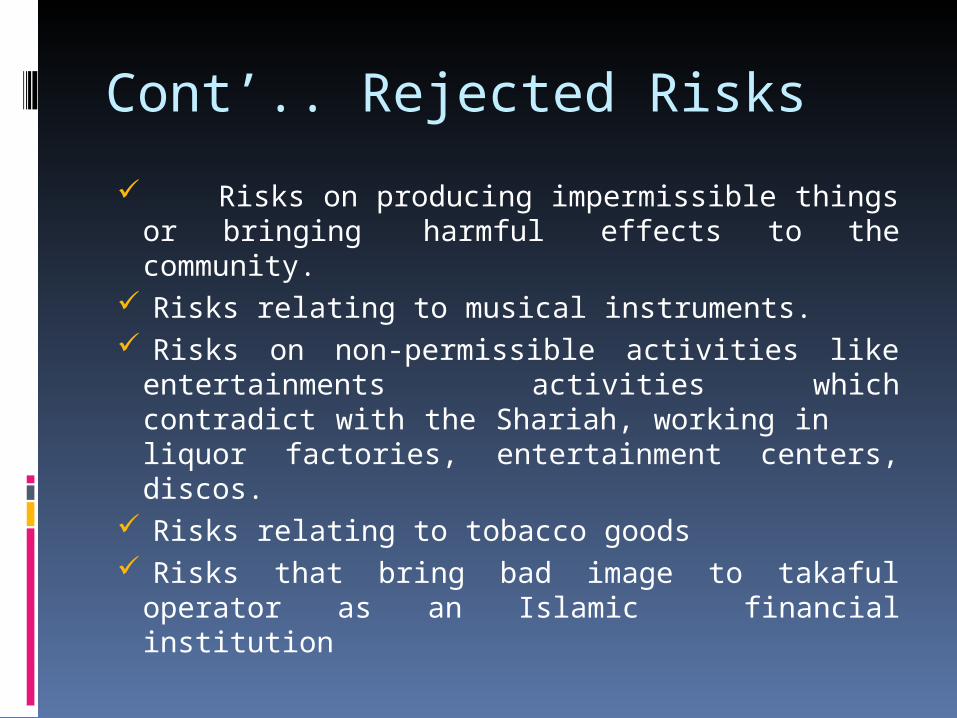

Cont’.. Rejected Risks

Risks on producing impermissible things or bringing harmful effects to the community.

Risks relating to musical instruments.Risks on non-permissible activities like entertainments

activities which contradict with the Shariah, working in liquor factories, entertainment centers, discos.

Risks relating to tobacco goodsRisks that bring bad image to takaful operator as an

Islamic financial institution

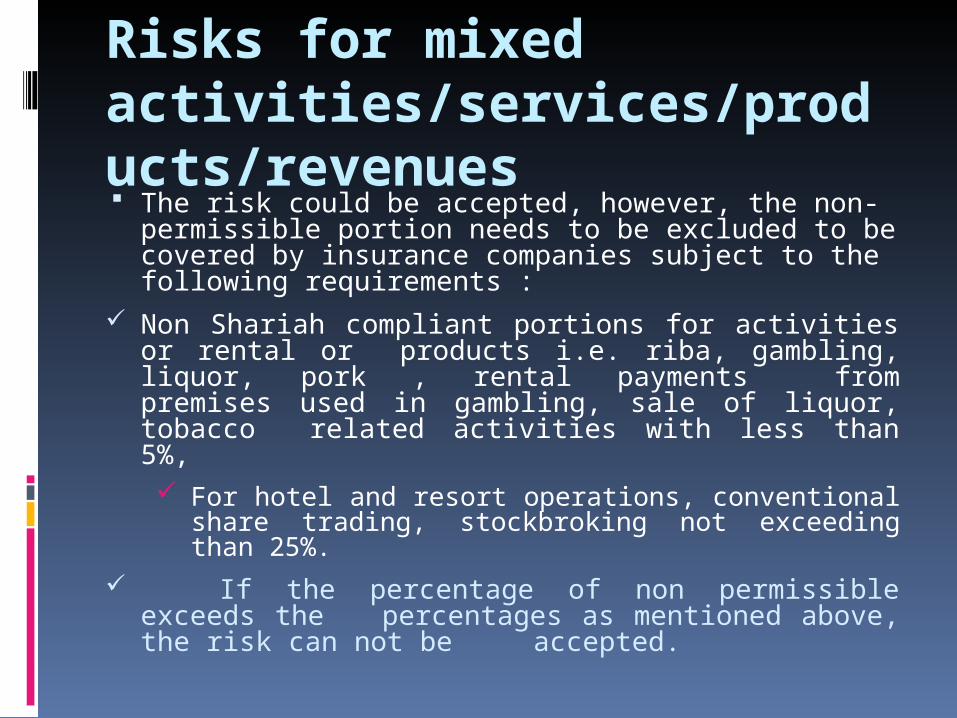

Risks for mixed activities/services/products/revenues

The risk could be accepted, however, the non-permissible portion needs to be excluded to be covered by insurance companies subject to the following requirements :

Non Shariah compliant portions for activities or rental or products i.e. riba, gambling, liquor, pork , rental

payments from premises used in gambling, sale of liquor, tobacco related activities with less than 5%,

For hotel and resort operations, conventional share trading, stockbroking not exceeding than 25%.

If the percentage of non permissible exceeds the percentages as mentioned above, the risk can not be accepted.

Cont’ Risks of mixed activities

The public perception or image of the company is good, and,

Core activities of the risk owner are important and considered maslahah (benefit) to the Muslim ummah and the country and the non-permissible elements are very small and involving

matters such as umum balwa common plight and difficult to avoid), `uruf (custom) and the rights of the non-Muslim community which are recognised by Islam.

Non Shariah Compliant Businesses According to Malaysian Securities Commission Guidelines First CriterionThe primary activity of the company is

based on riba as practised by conventional financial institutions, including commercial banks, merchant banks, finance companies, etc.

Second CriterionA company whose primary activity is

gambling, such as companies running, casinos, gaming and others.

Third CriterionThe primary activity of a company is the production and sale of goods and services that are prohibited in Islam, including:(a) Processing, producing and marketing

alcoholic drinks;

(b) Supplying non-halal meat like pork, etc.; and(c) Providing immoral services like prostitution, pubs, discos, etc.Fourth CriterionThe primary activity of the company is gharar (uncertainty) such as conventional insurance trading.

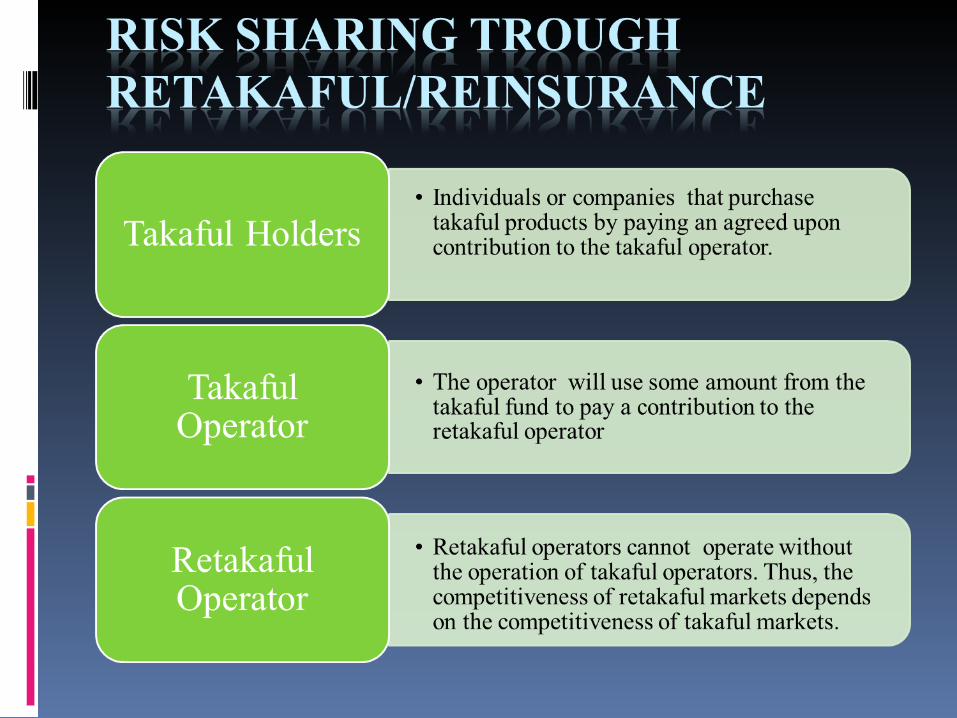

The Importance of Retakaful in Takaful Business

Generally, to assist takaful operatorsby: Protecting the solvency of the takaful

operator and its participants. Providing underwriting flexibility and

the capacity to accept risk. Stabilizing claims cost and therefore

giving greater stability to takaful contribution pricing

Allowing takaful operator to effectively utilize the assets of the retakaful provider to give coverage to its clients

16

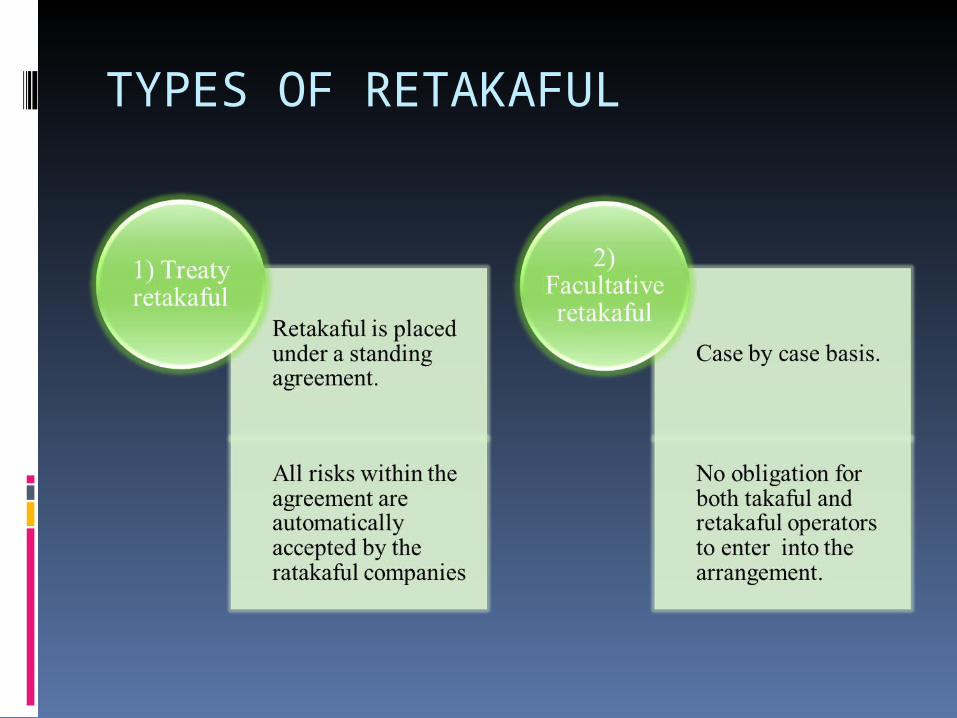

TYPES OF RETAKAFUL

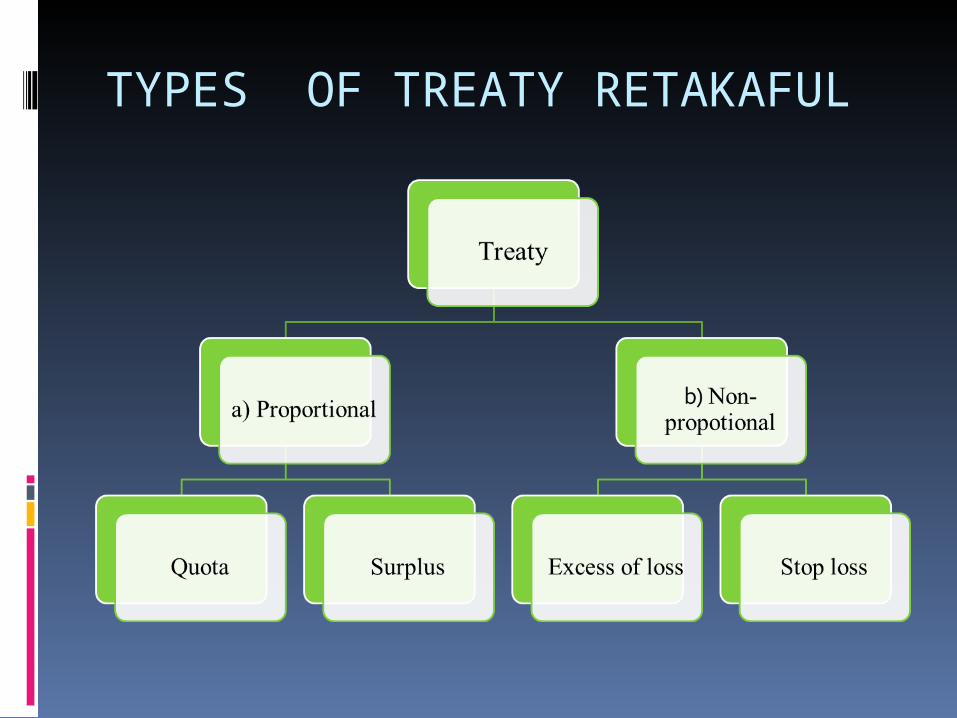

TYPES OF TREATY RETAKAFUL

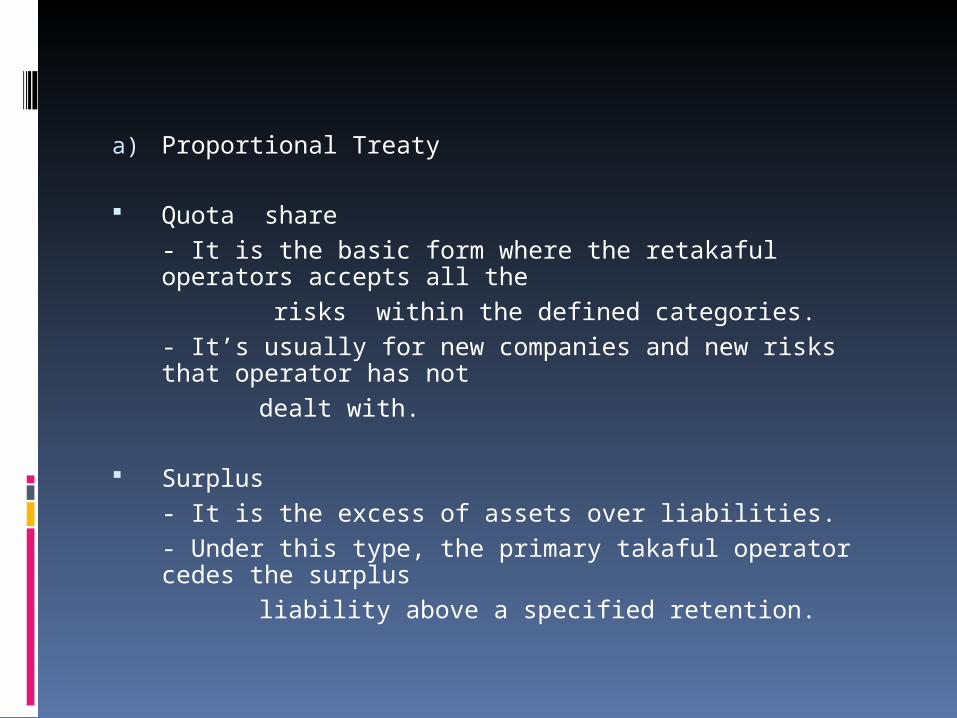

a) Proportional Treaty

Quota share

- It is the basic form where the retakaful operators accepts all the

risks within the defined categories.

- It’s usually for new companies and new risks that operator has not

dealt with.

Surplus

- It is the excess of assets over liabilities.

- Under this type, the primary takaful operator cedes the surplus

liability above a specified retention.

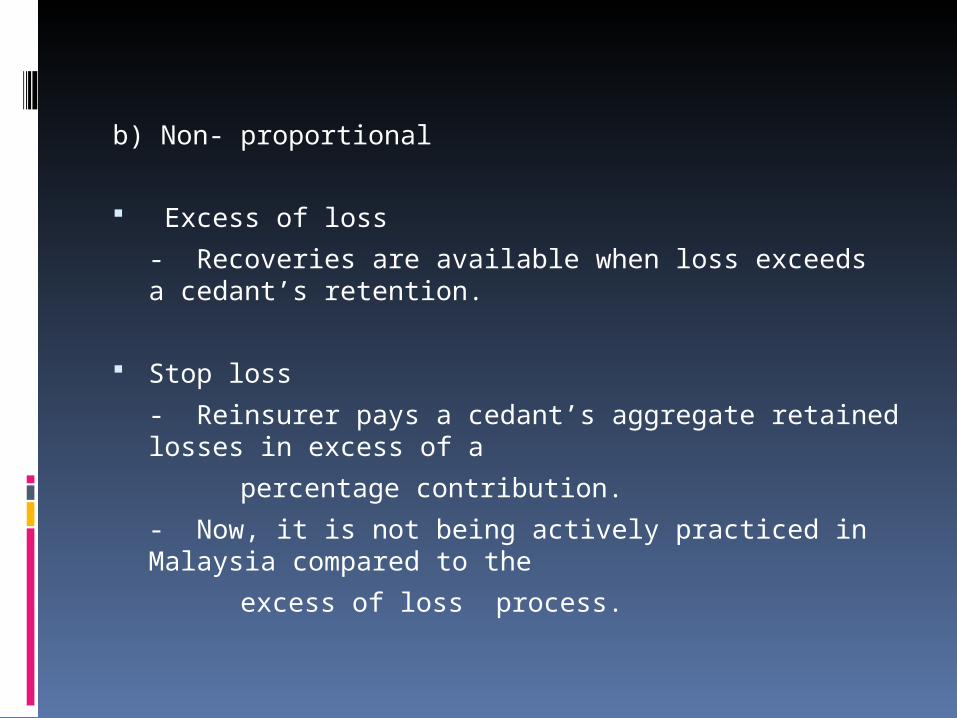

b) Non- proportional

Excess of loss

- Recoveries are available when loss exceeds a cedant’s retention.

Stop loss

- Reinsurer pays a cedant’s aggregate retained losses in excess of a

percentage contribution.

- Now, it is not being actively practiced in Malaysia compared to the

excess of loss process.

Retakaful Operators in Malaysia

In Malaysia, for the time being, there are four Retakaful operators, namely, ACR Retakaful SEA Berhad, MNRB Retakaful Berhad, Munchener Ruckversicherungs-Gesellschaft (Munich Re Retakaful) and Swiss Reinsurance Company Ltd. (Swiss Re Retakaful); and one International Takaful Operator in AIA Takaful International Bhd.

Contractual Relationship Between Takaful Company and Retakaful It is again based on wakalah bi ajr

(agency with fee/hire on services) contract. But the particpants are the takaful operators on behalf of the participants

Collection of premium from takaful operators, investment of funds, maintenance and reimbursement of reserves when they are not needed, handling the risk and settlement of claims of the takaful operators

22

Model of Retakaful: Essentially about handling risk

(takaful operators) by sharing the risk with the retakaful company.

In principle, its operation is similar to that of takaful .

Therefore, all Shari’a principles applying to takaful must apply to retakaful operations

23

Retakaful or reinsurance? Sec. 23 (1), Takaful Act provides: “ An

operator shall have arrangements consistent with sound Takaful principles for r-takaful of liabilities in respect of risks undertaken or to be undertaken by the operator in the course of his carrying on takaful business. “

Shortage of retakaful capacity with paid-up capital at about USD250M. Also issue of a viable, reputable and effective retakaful with good rating

Result Re takaful capacity is constrained – perhaps fulfilling less than 14% of takaful primary gross premium. 24

cont’

“With total gross written premiums by Takaful operators of approximately US$3.9 billion in 2006, and a total reTakaful capacity of about US$400 million, it is evident that Takaful operators must avail themselves of reinsurance from conventional reinsurers”

Dr Omar Fisher, Islamic Finance News, page 28, 9th may 2008

Cont.. Retakaful or Reinsurance Based on doctrine of necessity (darurah) or

at least needs (hajah), the jurist has allowed for reinsurance, but the allocation must be made within the limits (The exercise of darurah must be made within its limits)

Abuse of doctrine of necessity by putting all the reinsurance portion (or the biggest portion) to reinsurance only without any proper investigation to the capacity and risk allocation.

Boosting and accelerating the retakaful capacity: Takaful Operators are required to cede its takaful needs within retakaful as far as possible and only to cede with reinsurance to the extent that retakaful companies cannot fulfill their needs.

Parameters for Ceding to Conventional Reinsurance

AAOIFI standards: 1. The ceding should be done initially with

retakaful operator at the maximised level. 2. The takaful operator should not hold the

reserves belong to the reinsurance operator if it is interest bearing. It is allowable to keep and invest if the arrangement is based on mudharabah and wakalah.

3. It must be on short term basis, the volume must be small compared to the total portfolio and on top of that, must be approved by their respective Sahriah Committee.

4. Takaful operator cannot take any ceding or profit commission from reinsurance company as it is not it’s agent.

Can Retakaful underwrite conventional insurance? According to AOOIFI standards it is

allowable with the following conditions: 1. The contract used must be the

Retakaful contract (where the concept, terms and conditions were approved by the Shariah Committee).

2. It is not based on treaty arrangement.

3. The subject matter/insurable interest is not against Sahriah

![[MS-AZMP]: Authorization Manager (AzMan) Policy File Format... · the Microsoft Authorization Manager (AzMan) policy. AzMan policy files are typically used in two ways: 1. Loaded](https://img.pdfslide.net/doc/110x75/5fa59701e400b433fe529e07/ms-azmp-authorization-manager-azman-policy-file-format-the-microsoft.jpg)